Embed Size (px)

Citation preview

1

Philip Bunn and May RostomBank of England

Fourth ECB conference on household finance and consumption17 December 2015

Household debt and spending in the United Kingdom

Outline

• Motivation

• Literature/theory

• Data/methodology

• Econometric results

• Reasons for different spending responses

• Conclusion/policy implications

2

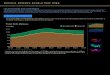

Household debt to income

3

Consumption growth

60

80

100

120

140

160

180

1987 1992 1997 2002 2007 2012

Per cent

-6

-4

-2

0

2

4

6

8

10

1987 1992 1997 2002 2007 2012

Percentage change on a year earlier

Average since 1956

Motivation

• There was a large build up of household debt in the UK before the financial crisis

• Did households who had high levels of pre-crisis debt reduce their consumption by more than others after the crisis?

• And did debt provide any support to spending before 2007?

4

Why this matters for policy

• Want to understand the reasons for weakness in household spending during the financial crisis

• More generally, it is important to understand implications of higher levels of indebtedness

• Greater risk of households suffering financial distress following shocks to income or interest rates may pose direct risks to banking system

• Larger spending cuts could have knock on effects for rest of the economy– Financial distress could increase further– Affects monetary policy decisions

5

Should debt affect household spending?

• In a simple life-cycle model, households borrow or save to smooth their consumption and debt has no causal effect on spending decisions

• But assumptions of the simple model may not hold– Households’ ability to borrow may change– Households are not certain about their lifetime incomes

• Some models do find a role for debt in affecting spending by allowing changes in income expectations or credit conditions to interact with debt (King (1994), Eggertson and Krugman (2012))

6

Literature

• Mian, Rao & Sufi (2013) – Decline in consumption was greater in regions of the US that

had higher debt prior to the crisis

• Dynan (2012) – Highly leveraged US mortgagors had larger declines in

spending between 2007-2009

• Andersen, Duus and Jensen (2014) – Negative correlation between pre-crisis LTV and change in

consumption during crisis in Denmark

7

Consumption growth

8

To help protect your privacy, PowerPoint has blocked automatic download of this picture.

Consumption relative to income

9

70

80

90

100

110

120

1992 1997 2002 2007 2012

Outright ownersRentersMortgagors: debt to income =<2Mortgagors: debt to income >2Total

Per cent

Research design

• Ideally would use household panel data to look at changes in consumption over the crisis period by debt level

• But there is no panel in the UK with good consumption and balance sheet data, only repeated cross-section

• Follow 2 different approaches:1. Create a pseudo panel (Deaton (1985)) to look at changes in

consumption for cohorts2. Look at how level of consumption varies by debt level in

cross-sectional data and how that changes over time

10

Data

11

• Living Costs and Food Survey (1992-2012)‒ Main source of UK consumption microdata‒ Repeated cross section of UK households (5300 a year)‒ Focus only on households where head is aged 21-69 ‒ Use non-housing consumption‒ Secured debt data: level of outstanding mortgage debt

• Wealth and assets survey (3 waves, 2006-12)‒ Merge in with LCFS at cohort level‒ Data on housing wealth, financial wealth and unsecured debt

Pseudo panel research design

12

• We estimate the following equation:

• Assess sensitivity to different cohort definitions:— Single birth years— Single birth years by mortgagor/non-mortgagor status— 5 birth years by mortgagor/non-mortgagor status— 10 birth years by region

• Pool 2006/07 and pre-crisis period and 2009/10 as post-crisis

• Minimum cell size of 50 (averages of 198, 110, 475 and 159)

itititititit1it eHHWYYDβC '4

'3211 βββ)/(

Pseudo panel regression results 1

13

Dependent variable: ∆ln(non-housing consumption 06/07 to 09/10)

Cohort definition

[1] [2] [3] [4] [5] [6] [7] [8]

-0.030** -0.028*** -0.026** -0.024(0.014) (0.007) (0.009) (0.014)

-0.128* -0.153*** -0.160** -0.129**(0.064) (0.038) (0.054) (0.050)

Observations 45 45 76 76 19 19 53 53

All equations also include change in income, change in housing wealth, change in financial wealth, change in number of adults,

10 birth year, region

06/07 mortgage loan-to-value ratio

change in number of children and a constant.

Single birth year Single birth year, mortgagor/non-mortgagor

5 birth year, mortgagor/non-mortgagor

06/07 mortgage debt to income ratio

All equations are estimated by OLS. Robust standard errors in parentheses, *** p<0.01, ** p<0.05, * p<0.1.

Pseudo panel regression results 2

14

Changes 2006/07 to 2009/10. Single birth year, mortgagor/non-mortgagor cohorts.

Dependent variable ∆ln(Non-housing consumption)

∆ln(Non-housing consumption)

∆ln(Durables) ∆ln(Non-durables)

[1] [2] [3] [4]

0.602*** 0.934*** 0.447***(0.117) (0.195) (0.147)

0.612***(0.120)

-0.017** -0.027*** -0.051*** -0.010(0.008) (0.007) (0.013) (0.012)

-0.020(0.122)

Observations 76 76 76 76

All equations also include change in housing wealth, change in financial wealth, change in number of adults, All equations are estimated by OLS. Robust standard errors in parentheses, *** p<0.01, ** p<0.05, * p<0.1.

change in number of children and a constant.

∆ln(Income net of mortgage interest)

∆ln(Income before mortgage interest)

Predicted 06/07 mortgage debt to income ratio

Actual 06/07 mortgage debt to income ratio

06/07 unsecured debt to income ratio

Pseudo panel regression results 3

15

Dependent variable: ∆ln(non-housing consumption)Single birth year, mortgagor/non-mortgagor cohorts

Time period 06/07 to 09/10 06/07 to 11/12 00/01 to 03/04 03/04 to 06/07

[1] [2] [3] [4]

-0.028*** -0.031*** 0.009 0.006(0.007) (0.007) (0.009) (0.008)

Observations 76 73 78 78

All equations include change in income, change in number of adults, change in number of children and a constant. All equations are estimated by OLS. Robust standard errors in parentheses, *** p<0.01, ** p<0.05, * p<0.1.

Mortgage debt to income ratio at start of period

Equations [1] and [2] also include change in housing wealth and change in financial wealth.

Cross-sectional analysis research design

ititittitititit1it eXcohortyearyearYDYDβC '5

'4

'3

'2 βββ*)/(β)/(

vector

• We estimate the following equation:

• Allow coefficient on debt to income to vary by year, relative to 2007

• Estimate from 1992-2012

• Include controls for income, birth cohort, age, household composition, education, employment status, region and house prices

Cross sectional regression results

17

Dependent variable: ln(non-housing consumption)

Mortgage debt to income ratio year interactions (reference year 2007):

2008 -0.008 (0.007)

2009 -0.024*** (0.007)

2010 -0.017** (0.007)

2011 -0.022*** (0.007)

2012 -0.029*** (0.007)

(1)

Robust t-statistics in parentheses, *** p<0.01, ** p<0.05, * p<0.1

Cross sectional regression resultsImpact of a 1 unit increase in debt to income ratio on

consumption, relative to 2007

18

-5-4-3-2-1012345

1992 1996 2000 2004 2008 2012

Significant at 5% level95% confidence intervalDebt/year interaction coefficients

Percentagedifference from

2007

Impact of debt on aggregate consumption

19

-3

-2

-1

0

1

2

1992 1996 2000 2004 2008 2012

Cross-sectional

Pseudo panel

Percentage difference from 2007

Possible explanations for why indebted households made larger spending cuts

Larger spending cuts could reflect more indebted households:

1) Being disproportionately affected by tighter credit conditions

2) Becoming more concerned about their ability to make future loan repayments:

― Lower permanent income― Increased uncertainty

3) Making larger adjustments to income expectations (perhaps because their previous expectations were too optimistic)

20

Evidence on why indebted household might have made larger cuts in spending

• Hard to prove causality from observing empirical correlations, even after controlling for other factors

• Three approaches to investigating this further:– Including proxies for the different channels in regressions– Using survey data on attitudes to spending– Developing a structural life-cycle model

21

Pseudo panel regression results 4

22

Dependent variable: ∆ln(non-housing consumption 06/07 to 09/10)

Cohort definition Single birth year, mortgagor/

non-mortgagor

5 birth year, mortgagor/

non-mortgagor

10 birth year, region

5 birth year, mortgagor/

non-mortgagor

[1] [2] [3] [4]

-0.022*** -0.014 0.004 -0.002(0.008) (0.014) (0.015) (0.027)

∆Cohort unemployment -0.280 -0.466 0.079 -0.451(0.261) (0.456) (0.478) (0.727)

∆Cohort unemployment x -0.429 -0.563 -0.961** -1.517(0.384) (0.677) (0.453) (1.457)

% Credit constrained -0.192(0.354)

Observations 76 19 53 17

All equations also include change in income, change in housing wealth, change in financial wealth, change in number of adults, change in number of children and a constant.

06/07 mortgage debt to income ratio

06/07 mortgage debt to income ratio

All equations are estimated by OLS. Robust standard errors in parentheses, *** p<0.01, ** p<0.05

Mortgage debt to income and NMG survey responses

23

0

1

2

3

Cut spending due tocredit constraints

Cut spending due todebt concerns

Worse off thanexpected since 2006

No Yes Median mortgage debt to income ratio

2010 2013

Structural life-cycle model (joint with Agnes Kovacs)

• Heterogeneous agents model where households live for T periods

• Can take out a mortgage to buy a house or withdraw equity• Maximum LTV limit on borrowing, depends on credit conditions

and house prices• Two sources of uncertainty: idiosyncratic income and house

prices• Mortgage repayments part of intertemporal budget constraint

24

Simulated permanent income shock

25

Preliminary results from structural life-cycle model

• A reduction in permanent income a key driver of the results

• Increased variance of income shocks also seems to have an effect

• Credit channels and house price falls less important

26

Conclusion

• Indebted UK households made larger cuts in spending following the financial crisis, after controlling for other factors

• Those effects have persisted, at least up until 2012

• Two different econometric approaches give broadly similar results –worth about 2% off aggregate consumption

• Empirical work does not prove a causal link

• Very provisional results from structural life-cycle model suggest that permanent income shock/increased uncertainty may have been important in explaining larger spending cuts by indebted households

27

Policy implications

• June 2014 Bank of England Financial Policy Committee recommendations:‒ Lenders should apply stress test to assess affordability if Bank

Rate rose by 3 percentage points in first 5 years of loan‒ Lenders should limit proportion of mortgages at loan to income

ratios of 4.5 or above to 15% of new mortgage lending

• FPC wanted to insure against further a significant increase in number of highly indebted households

• Evidence on indebted households making larger cuts in spending during financial crisis in UK and elsewhere was an important reason for this

28

Pseudo panel vs cross section analysis

• Pseudo panel:– Shows how consumption changed for different groups– Small number of observations– Trade off between number of cohorts and reliability of

consumption estimate for each cohort– Less variation in debt– Allows cohort level data from other sources to be merged in

• Cross section:– Can only compare difference in level of consumption for

households with similar characteristics at different points, not how it changed for an individual household

– Larger sample size– More variation in debt

29

Change in consumption relative to income(single birth year mortgagor cohorts)

30

-25

-20

-15

-10

-5

0

5

0.5 1 1.5 2 2.5 3 3.5 4

Percentage point change in non-housing consumption/income 2006/07 to 2009/10(a)

2006/07 mortgage debt to income ratio(b)

-30

-25

-20

-15

-10

-5

0

5

10

15

0.5 1 1.5 2 2.5 3 3.5 4

Percentage change in real non-housing consumption 2006/07 to 2009/10

2006/07 mortgage debt to income ratio(a)

Change in consumption (single birth year mortgagor cohorts)

31

Consumption relative to income

32

70

90

110

130

150

1992 1997 2002 2007 2012

0-11-22-33-44+

Per centMortgage debt to income ratio:

Full pseudo panel regression results

33

Dependent variable: ∆ln(non-housing consumption 06/07 to 09/10)

Cohort definition

[1] [2] [3] [4] [5] [6] [7] [8]

0.675*** 0.743*** 0.599*** 0.607*** 0.766*** 0.857*** 0.450*** 0.520***(0.122) (0.124) (0.118) (0.117) (0.123) (0.130) (0.148) (0.155)

∆Number of adults 0.267** 0.232* 0.212** 0.205** 0.115 0.081 0.342*** 0.283**(0.118) (0.121) (0.098) (0.097) (0.103) (0.100) (0.121) (0.119)

∆Number of children 0.036 0.048 0.010 0.018 0.016 0.046 0.075 0.088*(0.036) (0.037) (0.031) (0.031) (0.060) (0.057) (0.048) (0.046)

-0.030** -0.028*** -0.026** -0.024(0.014) (0.007) (0.009) (0.014)

-0.128* -0.153*** -0.160** -0.129**(0.064) (0.038) (0.054) (0.050)

∆ln(Housing wealth) 0.035 0.123 0.060 0.060 0.049 0.018 0.008 0.096(0.070) (0.096) (0.036) (0.036) (0.059) (0.061) (0.101) (0.104)

∆ln(Financial Wealth) -0.000 0.004 0.006 0.007 0.064*** 0.072*** 0.002 -0.004(0.020) (0.020) (0.023) (0.023) (0.021) (0.021) (0.032) (0.032)

Constant -0.018 -0.011 -0.027** -0.026** -0.036** -0.034** -0.026 -0.010(0.023) (0.029) (0.012) (0.012) (0.013) (0.013) (0.020) (0.020)

Observations 45 45 76 76 19 19 53 53

10 birth year, region

06/07 mortgage loan-to-value ratio

Single birth year Single birth year, mortgagor/non-mortgagor

5 birth year, mortgagor/non-mortgagor

∆ln(Income net of mortgage interest)

06/07 mortgage debt to income ratio

All equations are estimated by OLS. Robust standard errors in parentheses, *** p<0.01, ** p<0.05, * p<0.1.

Durables Non-durables

34

-8

-6

-4

-2

0

2

4

6

8

1992 1996 2000 2004 2008 2012

Significant at 5% level95% confidence intervalDebt/year interaction coefficients

Percentagedifference from 2007

-8

-6

-4

-2

0

2

4

6

8

1992 1996 2000 2004 2008 2012

Significant at 5% level95% confidence intervalDebt/year interaction coefficients

Percentagedifference from 2007

Cross sectional regression resultsImpact of a 1 unit increase in debt to income ratio on

consumption, relative to 2007

Explanations why indebted household might have made larger cuts in spending

• Highly indebted households were disproportionately affected by tighter credit conditions

– ‘Have you been put off spending because you are concerned you will not be able to get access to further credit when you need it?’

• Highly indebted households become more concerned about their ability to make future repayments

– ‘How concerned are you about your current level of debt?’, and ‘What actions are you taking to deal with your concerns?’

• Highly indebted households made larger adjustments to future income expectations

– ‘Would you say you are better or worse off financially now than you would have expected at the end of 2006, before the start of the financial crisis?’

35

Characteristics of mortgagors cutting spending due to debt concerns

36

Yes No

Median mortgage debt to income ratio

2.4 1.7

Proportion who are worse off than they expected in 2006

73% 39%

Proportion who are think that a sharp fall in income is quite likely over the next year

33% 19%

Reduced spending in response to debt concerns (2013 data)

Simulated uncertainty shock

37

House price shock

38

House price and credit shock