Embed Size (px)

Citation preview

© Orica Limited Group

Economic and Commodity Market Outlook

David Thurtell, Market Intelligence Lead, (AusPac & Asia), Orica January 2014

• Reliable leading indicators suggest that there will be a further pick up in the world economy in H1 2014, which

should boost the demand for resource commodities. The recovery should continue in H2 2014 and 2015.

• Recent major policy changes by Beijing should underpin economic growth and the demand for resources in

the medium/long term. However, Beijing is now responding to widespread dissent about air pollution by

moving away from burning low value coal (and low grade Iron Ore). This should benefit Australian producers,

but hurt some Indonesian, American and Vietnamese producers. Chinese coal producers are under pressure

on a number of fronts; they will likely cede more market share to overseas producers.

• The Thermal Coal price is recovering, thanks to both an improving world economy and seasonal influences

(the Northern Hemisphere winter). Supply growth will largely offset any pick-up in demand in 2014, so

margins for Thermal Coal producers will remain low/poor.

• The Coking Coal price is only US$3-4/t above the cycle lows, and margins are very low. Plentiful stocks in

China are offsetting the impact of stronger-than-expected demand by steelmakers in major consuming

nations (such as China). An improving world economy will add to the impact of supply cuts in North America

and China, but the price should remain sub US$160/t, maintaining pressure on producer margins.

• Gold has suffered from a surge of investor liquidation and heightened import restrictions by India. Further falls

could easily occur, but cost support and strong Chinese demand should kick in at the $1,000-1,100/oz mark.

• Base metals should be firm. Copper should hold at around $7,000/t, as stronger world economic growth and

a scrap shortage offset the impact of rising mine supply. Margins will therefore remain healthy in 2014. Lead

and zinc will benefit from the stronger world outlook and a looming shortage of supply, with rising margins.

Overview

2

World: Key Leading Economic Indicators

Implications

• An improving world economy will boost commodity demand and prices in the next few months,

providing some stability for customers as they work to stabilize their cost base.

• World steel demand should pick up further, helping Iron Ore and Coking Coal prices.

• Energy demand should lift in the OECD, removing some of the slack in the Thermal Coal market.

The world economy continues its recovery

• The World Purchasing Managers’ Index rose to a 2-1/2-year high in November. This suggests a (further)

significant pick-up in global industrial output growth in the coming few months.

-15

-10

-5

0

5

10

15

32

37

42

47

52

57

62

Mar-04 Mar-06 Mar-08 Mar-10 Mar-12

WORLD IND. PRODUCTION VS WORLD PMIIndex

World PMI (lhs)

World IP lagged two

months (rhs)

annual% ch.

-18

-12

-6

0

6

12

20

30

40

50

60

70

Jul-77 Jul-81 Jul-85 Jul-89 Jul-93 Jul-97 Jul-01 Jul-05 Jul-09 Jul-13

OECD IND. PRODUCTION VS US ISM NEW ORDERSIndex

US ISM New Orders

(lhs)

OECD IP,

lagged 6 months (rhs)

annual

% ch.

US: Key Economic Indicators

The U.S. Fed is now winding back its bond buying

• The U.S. Federal Reserve is moving gently towards providing less monetary stimulus without causing a large

rise in long term U.S. bond yields: the housing and auto sectors are sensitive to interest rate moves.

• Unemployment continues to decline in the U.S., falling to 7.0% in November. Jobless Claims data point to

further falls in the U.S. unemployment rate in the coming months/quarters.

1

3

5

7

9

11

13

150

240

330

420

510

600

690

Feb-70 Feb-76 Feb-82 Feb-88 Feb-94 Feb-00 Feb-06 Feb-12

Initial Jobless

Claims, lagged 8 months (rhs)

US unemployment

rate (rhs)

U.S. UNEMPLOYMENT RATEVS INITIAL JOBLESS CLAIMS ('000s) %

400

800

1200

1600

2000

2400

400

800

1200

1600

2000

2400

Sep-02 Sep-04 Sep-06 Sep-08 Sep-10 Sep-12 Sep-14

US HOUSING INDICATORS'000s, annualised

Housing

Starts

Building

Permits

Source: Bloomberg

US : Key Economic Indicators

Manufacturing improving

• The U.S. Manufacturing New Orders series hit a 4-year high in December. Suggests a rise in Chinese exports.

• The average age of consumer durable goods – long-lasting items such as furniture, appliances and computers

– is the highest since 1962. Sets the stage for a rebound in consumer spending.

• Motor vehicle sales hit a six-year high in November. Strong auto sales are a very positive sign, since

households have lacked the confidence to make big-ticket purchase decisions for many years.

Implications

U.S. data points to firm growth in 2014, providing a good locomotive for the rest of the world.

6

8

10

12

14

16

18

20

22

6

8

10

12

14

16

18

20

22

Jan-94 Jan-97 Jan-00 Jan-03 Jan-06 Jan-09 Jan-12

US VEHICLE SALES INDICATORSmn, saar

Domestic

Manufactured

Total Sales

Source: Bloomberg

mn, saar

25

35

45

55

65

75

-40

-20

0

20

40

60

Feb-93 Feb-96 Feb-99 Feb-02 Feb-05 Feb-08 Feb-11

CHINESE EXPORT GROWTHVS US ISM NEW ORDERS

Indexannual% change

Source:BloombergChinese export growth,

lagged 3 months (lhs)

US ISM New

Orders (rhs)

Asia

CrisisEurozone

Crisis

Global Financial

Crisis

China: Power Indicators

Growth in power output has accelerated

• Industrial output is highly correlated to power output. Both have seen an acceleration in recent months.

• With hydro generation now experiencing a seasonal decline, Thermal Coal-fired power generation is bearing

more of the load.

0

7

14

21

28

-10

0

10

20

30

Jul-99 Jul-01 Jul-03 Jul-05 Jul-07 Jul-09 Jul-11 Jul-13

annual% change

annual% change

CHINESE ELECTRICITY &INDUSTRIAL OUTPUT

Industrial Production

smoothed (rhs)

Electricity

Output (lhs)

0

50

100

150

200

250

300

350

400

450

500

Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Jan-12

Thermal

Other (renewable etc)

Nuclear

Hydro

CHINESE POWER OUTPUT BY TYPE('bn KWh)

GFC

Eurozone Sovereign

Debt crisis

Source: Bloomberg

LATEST OBSERVATION: OCTOBER 2013

Implications

A mix of cyclical and seasonal influences have lifted Chinese Thermal Coal demand in recent months.

China: Key Economic Indicators

0

2

4

6

8

10

12

14

0

2

4

6

8

10

12

14

Mar-94 Mar-98 Mar-02 Mar-06 Mar-10 Mar-14

CHINESE GDP GROWTH annual% change

annual% change

Source: Bloomberg

Y/Y measure

new Q/Q

measure

China: settling for 7-8% rather than 10-11%

• China is growing at ~7.5-8.0%. Leading indicators suggest that this should be maintained as 2014 begins.

• Vehicle sales in November were the 2nd highest on record, putting annual growth at 16%.

• China’s new leadership’s has resolve to provide less State support to SOEs, increase their exposure to

competition and make them pay higher dividends. Increased dividends are aimed at raising social welfare

programmes and thus encouraging private consumption.

Implications

China’s growth has rebounded from its mid-term pause, but is settling in a lower band than averaged

over much of the past decade. Beijing is reforming to try to change the sources of economic growth.

-40

0

40

80

120

160

200

240

0

250

500

750

1000

1250

1500

1750

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

CHINESE CAR SALES('000s)

Source: Bloomberg

annual %

change

level (lhs)

growth (rhs)

• Since April, there have been large falls in commodity currencies against the US$ (and hence the Yuan). The

falls relate to the prospective end of easy U.S. money and the new (lower) normal level of growth in China.

• The move in the Indonesian Rupiah over the past 8 years had already enabled Indonesia to open up a

significant gap on Australia in the seaborne Thermal Coal market. The South African Rand is now around 6%

below its GFC low, whereas the AUD is some 40% higher than its GFC low.

Currency moves of commodity-producing and consuming nations

8

Implications

Falls have restored profitability of miners in some nations, but relative competitiveness has also been

altered. Chinese miners are being crushed by the strength of the Yuan.

0

20

40

60

80

100

120

140

160

180

200

Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

AustralianDollar

Brazilian Real

South AfricanRand

Chilean Peso

Colombian Peso

IndonesianRupiah

Indian Rupee

Chinese Yuan

EXCHANGE RATE VS USDJan 2005 = 100

Canadian Dollar

Sources: Bloomberg, Orica

Russian Ruble

U.S. Fed says it's examining ending Q.E

32

-6 -6-7 -7 -8

-13 -14-15

-20 -20

-26

-6

6

-9

-2

-20

-13

-37

-17-19

-40

-61

-55

-44

-70

-60

-50

-40

-30

-20

-10

0

10

EU

RO

Ch

inese

Yuan

Co

lom

bia

n P

eso

Peru

via

n S

ol

Russia

n R

uble

Can

ad

ian D

olla

r

Yen

Ch

ilean P

eso

Austra

lian D

olla

r

Ind

ian R

up

ee

So

uth

Afric

an R

an

d

Bra

zilian

Real

Ind

onesia

n R

up

iah

since April 2013

since July 2011

EXCHANGE RATE CHANGES VS USD%

Sources: Bloomberg, Orica

40

50

60

70

80

90

100

110

120

Jan-13 Mar-13 May-13 Jul-13 Sep-13 Nov-13 Jan-14

actual price

FX-adjusted

INDONESIAN SUB-BIT COALUS$/t, FOB, Indonesia

40

50

60

70

80

90

100

110

120

Jan-13 Mar-13 May-13 Jul-13 Sep-13 Nov-13 Jan-14

actual price

FX-adjusted

AUSTRALIAN THERMAL COALUS$/t, FOB, Newcastle

Little wonder that supply is firm despite low US$ prices…

• Adjusting coal prices for the foreign currency moves of the past 7-8 months, Australian, Indonesian and South

African producers are now enjoying local currency returns that are higher than before the depreciation of

commodity currencies.

• Australian miners are maintaining production under ‘take-or-pay’ arrangements, and/or raising output to lower

unit costs.

• Indonesian producers have cut their stripping ratios.

Exchange rate-adjusted Thermal Coal prices

9

40

50

60

70

80

90

100

110

120

Jan-13 Mar-13 May-13 Jul-13 Sep-13 Nov-13 Jan-14

actual price

FX-adjusted

SOUTH AFRICAN THERMAL COALUS$/t, FOB, Richards Bay

• Of the major producers, China is the highest cost. At current prices, margins are very low in most countries.

• China became a net importer of Thermal Coal in 2009, as a result of both the changes to coal export tax

arrangements and a growing requirement for power generation, cement and fertilizer manufacture.

• Indonesia and Australia now account for 2/3 of Chinese Thermal Coal imports.

Thermal Coal producers

10

US Coal Production Update

(000's Short Tons)

2012

(act)

2013

(est)

YoY

Change

2014

(est)

2015

(est)

Appalachia Basin 291.3 276.3 -5.2% 279.8 269.8

Illinois Basin 179.0 183.3 2.4% 208.3 208.3

Western Total 539.3 527.9 -2.1% 551.9 536.9

(Wyoming - Powder River

Basin) 398.4 384.1 -3.6%

Total United States 1,009.6 987.4 -2.2% 1,040.0 1,015.0

Source: Preliminary estimates by EIA (Energy Information Administration) as of 1/7/14

US Coal producers face challenges

• US Coal market outlook shows slight

potential growth in 2014 with levels

falling back in 2015.

• Growth continues to differ by various

regions.

• Low natural gas prices and high supply

levels will continue to pressure coal

electricity generation supply into far

future.

• Export markets continue to be a

challenge, based on US regulation and

export port capacities.

Asian Thermal Coal Indicators

Chinese Thermal Coal stocks have started to rise

• Chinese Thermal Coal Imports have settled at around 15-16mt; we suspect that imports will rise in December

and January, as thermal coal power utilities consume large amounts of coal for winter heating.

• Chinese Port Stocks of Thermal Coal fell sharply in H2 2013 to 20m tonnes, but have since started to rise.

• Chinese Thermal Coal demand is likely to remain firm as winter peaks and the supply chain tightens.

• The worst of India’s growth slowdown appears to have passed. Indian coal stocks are very low, after Coal

India missed its production target by 15mt in the April-November period. Imports are almost certain to rise,

despite a very sharp fall in the Rupee in recent months.

0

500

1000

1500

2000

2500

3000

3500

Mar-10 Mar-11 Mar-12 Mar-13

CHINESE PORT STOCKSOF THERMAL COAL('000 tonnes)

Source: Bloomberg

0

3,000

6,000

9,000

12,000

15,000

18,000

21,000

Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

Others

North Korea

Vietnam

Russia

Australia

Indonesia

CHINESE THERMAL COAL IMPORTS('000 tonnes)

Source: Bloomberg

Asian Thermal Coal Influences

Japanese Thermal Coal imports have been strong since Fukushima

• Japan is struggling to cope with the loss of nuclear power from the country’s electricity grid.

• Australia Thermal Coal suppliers have been the main beneficiary of the Fukushima accident.

• Indonesian exports declined sharply in 2013, from record levels.

• South Korea recently announced a flat tax (of US$20/t, and rising to US$30/t) on Thermal Coal imports

starting next July. This will hurt Thermal Coal consumption, but also induce the burning of higher value coal.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

Indonesia Russia Australia USA Canada

JAPANESE THERMAL COAL IMPORTS('000 tonnes)

Source: Bloomberg

0

5,000

10,000

15,000

20,000

25,000

30,000

0

5,000

10,000

15,000

20,000

25,000

30,000

Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

THERMAL COAL EXPORTS('000 tonnes) ('000 tonnes)

Indonesia

Australia

Source: Bloomberg, GTIS

South Africa

United States

Vietnam

Outlook

It appears that the Northern Hemisphere winter and improving world economic activity is more than

offsetting the impact on prices of firm supply growth. From here, supply growth will slow and demand

will rise, helping prices. But the sub-US$95/t price likely for many months will keep margins tight.

Thermal Coal prices are recovering slowly

• Thermal Coal prices have risen steadily since the end of August, but at ~US$84/t, Newcastle TC is still close

to cost of production for many producers. In recent weeks, signs of an improving world economy and buying

for peak (Northern Hemisphere) winter season, have more than offset the impact on price of strong supply.

• Indonesian Sub-bit prices have finally pushed back over the US$60/t mark, as seasonal demand peaks.

Thermal Coal Prices

$0

$30

$60

$90

$120

$150

$180

$210

$0

$30

$60

$90

$120

$150

$180

$210

04-Jan-08 04-Jan-09 04-Jan-10 04-Jan-11 04-Jan-12 04-Jan-13 04-Jan-14

Average Weekly Thermal Coal Index

NewcastleThermal Coal Index (A$/t)

Newcastle Thermal Coal Index (US$/t)

Indo Sub-bit marker (US$/t)

Source: Bloomberg, McCloskey

70

80

90

100

110

120

130

140

May-13 Nov-13 May-14 Nov-14 May-15 Nov-15 May-16 Nov-16

NEWCASTLE THERMAL COAL FUTURESUS$/tonne

mid July 2013 low

9 Dec 2013

3 May 2011

Source: Bloomberg

9 January 2014

• In recent months, the differential between China’s benchmark price and Australian and Indonesian benchmarks

returned to levels last seen in 2010.

• The rise in the differential in 2011-12 explains why China’s miners lost significant market share in that period

(see next slide over).

• Australian miners are maintaining output under ‘take-or-pay’ agreements, and/or raising output to cut unit costs.

China’s competitiveness in Thermal Coal production

15

Implications

The outlook is for Australian and Indonesian coal production to continue to grow firmly, helped by the

falling currencies of their countries. China’s miners are being affected by the strength of the Yuan.

-10

10

30

50

70

90

110

130

150

0

20

40

60

80

100

120

140

160

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13

QINHUANGDAO COAL VS NEWCASTLE (spot, FOB)US$/tonne

Qinhuangdao coal price (lhs)

Newcastle coal price (lhs)

Qinhuangdao-Newcastle differential (rhs)

US$/tonne

-20

-10

0

10

20

30

40

50

60

70

80

90

100

110

120

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13

QINHUANGDAO COAL VS INDO SUB-BIT (spot)US$/tonne

Qinhuangdao coal price (lhs)

Indo Sub-Bit coal price (lhs)

Qinhuangdao-Indo Sub-Bit differential (rhs)

US$/tonne

Trends in Chinese coal production

• In trend terms, after a decade of strong growth, Chinese coal output has declined noticeably since 2011. The

noticeable fall in the Thermal Coal price over the past eighteen months explains the decline in Chinese

domestic production. Safety crack-downs in Chinese mines could have also had an impact.

• The recent decline in coal production comes despite a rise in coal-fired power, cement and fertilizer output

over that time. Coal imports have thus filled the gap.

16

Implications

China is likely to import more coal, as cheap imports steal market share from local producers.

0

50

100

150

200

250

300

350

400

0

50

100

150

200

250

300

350

400

Jan-00 Jan-03 Jan-06 Jan-09 Jan-12

CHINESE COAL-FIRED POWER OUTPUT VS COAL PRODUCTION('bn KWh) (mt/month)

Coal production -1month fwd (rhs)

Coal -firedpower output (lhs)

0

50

100

150

200

250

300

350

400

0

50

100

150

200

250

300

350

400

Jan-01 Jan-04 Jan-07 Jan-10 Jan-13

CHINESE COAL PRODUCTION VS THERMAL COAL PRICE('bn KWh) (US$/t)

Coal production (lhs)

China Thermal Coal Price (rhs)

Coking Coal Prices

Coking Coal prices have declined significantly in recent months

• The spot Coking Coal price fell during Q4 2013 and early January 2014, and at US$135/t, has now largely

reversed the gains of the August/September 2013 period. Supply has risen significantly, and anecdotes

suggest that, with comfortable stockpiles and weak demand, Chinese buyers have backed away from buying.

• Reflecting the well supplied nature of the near-term market, the front part of the Chinese futures curve dipped

sharply during November. The whole curve then shifted down noticeably during December/early January.

Outlook

• In H1 2014, North American and Chinese output cuts should combine with stronger world economic

conditions to see the seaborne market tighten modestly.

$0

$50

$100

$150

$200

$250

$300

$350

$0

$50

$100

$150

$200

$250

$300

$350

01-Dec-10 01-Jun-11 01-Dec-11 01-Jun-12 01-Dec-12 01-Jun-13 01-Dec-13

Average Weekly Aus Hard Coking Coal Price

Aus Hard Coking Coal (US$/t)

Aus Hard Coking Coal (A$/t)

Source: McCloskey140

150

160

170

180

190

200

210

220

230

240

Jul-13 Sep-13 Nov-13 Jan-14 Mar-14 May-14 Jul-14 Sep-14 Nov-14

CHINESE COKING COAL FUTURESUS$/tonne

22 March 2013

9 December 2013

9 January 2014

Source: Bloomberg

6 November 2013

Chinese Coking Coal Imports

Chinese Coking Coal imports remain strong, thanks to firm steel production

• Chinese steel production has surprised with its resilience in 2013. Weakening now, partly due to seasonal

influences.

• Chinese steel mills have sought to diversify their suppliers since the Australian floods a few years ago.

• Chinese coking coal imports remain high. Stockpiles are very comfortable, allowing steel mills to take an

opportunistic approach to buying.

0

10

20

30

40

50

60

70

80

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

CHINESE STEEL PRODUCTION mn tonnes

2009

20102011

2012

Source: National Bureau of Statistics

2013

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

Canada

Russia

USA

Australia

Others

Mongolia

CHINESE COKING COAL IMPORTS('000 tonnes)

Source: Bloomberg

Australian Coking Coal Exports

Australian Coking Coal exports hitting record levels

• Port data show that Queensland coal exports remained close to record levels in December. On a seasonally-

adjusted basis, it appears that Australian coking coal exports have been very strong since November 2012.

• Floods in late 2010/early 2011 had a major impact on production.

• ‘Take or pay’ contracts for rail and port usage have been influential.

Implications

• Price falls in recent quarters have pushed Australian miners to raise output, in order to cut unit costs .

3

6

9

12

15

18

5

8

11

14

17

20

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

AUST. COKING EXPORTS VS. QLD COAL EXPORTS

ACR QLD Coal Exports (lhs)

ABS Coking CoalExports (rhs)

mn tonnes mn tonnes

Sources:ABS, ACR

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

Others

India

Japan

South Korea

China

Taiwan

AUSTRALIAN COKING COAL EXPORTS('000 tonnes)

Source: Bloomberg

Coking Coal Exports

Seaborne supply has surged

• Australia dominates seaborne trade. Its exports have surged in recent years. The weaker AUD/USD is now

allowing Australian miners to undercut their competition.

• North American and Chinese producers are under huge pressure, thanks to their appreciating currencies.

• Mozambique?

-15

-10

-5

0

5

10

15

20

-27

-18

-9

0

9

18

27

36

Jan-92 Jan-96 Jan-00 Jan-04 Jan-08 Jan-12

WORLD STEEL PRODUCTION VS WORLD INDUSTRIAL PRODUCTION

Steel output (lhs)

World Industrial Production (rhs)

annual % ch.

annual % ch.

Sources: CPB, Bloomberg

• China is the lowest-cost producer of Coking Coal. Russia and South Africa are close behind.

• American producers are the highest cost, and are likely to be squeezed out by the impact of the falling AUD.

• Russian exports to China filled a gap left when flooding affected Australian Coking Coal production in 2011.

Coking Coal production

21

• At least 80% of the nation’s coal comes from regions where the United Nations says water supplies are

either “stressed” or in “absolute scarcity.”

• China has about 1,730 cubic metres of fresh water per person, close to the 1,700 cubic metre level the UN

deems “stressed.”

• The situation is worse in the north, where half China’s people, most of its coal and only 20% of its water,

are located.

• Shanxi – the nation’s biggest coal base, with about 28% of production – has per-capita water resources of

347 cubic metres, less than the Middle Eastern nation of Oman.

• Inner Mongolia and Shaanxi, which together contribute 40% of coal output, have less than 1,700 cubic

metres per person.

Other issues facing the Chinese coal industry 1. Water

22

• Air pollution in the major cities has become a major source of civil unrest. Environmental reform was included

in the reforms announced as a result of the recent Third Plenum meeting, which highlights the growing

importance of this area. In recent weeks, the State Council has proposed re-ignited talk of a ban on the

burning of low value coal. A draft policy is due soon.

• The Third Plenum communiqué said that the prices of electricity, fuel and other key resources would no longer

be kept artificially low. This suggests a shift away from coal-fired electricity to gas, nuclear and renewables.

• For many years, as people’s incomes and prosperity rose in line with the economy, Beijing could get away

with ignoring the environmental problems caused by lax regulations and a political system based around GDP

growth. Local officials were assessed purely on their GDP numbers. But following a series of scandals –

including the unexplained discovery of thousands of dead pigs and birds floating down one of the country’s

main rivers earlier this year, and a jump in the number of lung cancer victims – the government is now

changing its approach. Local and provincial government officials will now be held to account on environmental

and health targets, as well as targets on economic development.

• As a result of the Third Plenum, efforts to remove inefficient capacity in various industries will be intensified. In

late November 2013, Hebei Province shut down 11mt of steel capacity, with a further 50mt of capacity to be

shut. The government is moving to require the usage of higher quality ores/coal. Pollution controls are likely to

add to the cost of steelmaking over the next couple of years, reducing competitiveness.

• The environmental push may not see reduced coal consumption; growth in coal burn is crucial for economic

growth and alternatives are not of appropriate scale – indeed, increased gas output is more likely to target

refined crude products in industrial demand first. However, there is likely to be a further move to increase coal

production and consumption in Western China – with limited coal consumption growth on the Eastern

seaboard. This could be a problem for an oversupplied global thermal coal market, with the Chinese

contestable portion growing only slowly.

23

Other issues facing the Chinese coal industry 2. Air Pollution

• The Third Plenum communiqué released in mid November 2013 announced that State-Owned Enterprises

(SOEs) will be increasingly subject to market forces, and given reduced support by the Government.

• A system will be introduced to permit SOE bankruptcy so that only the “fittest survive”. The non-state sector

is encouraged to participate in SOE reform by taking equity positions.

• SOEs will be required to pay dividends of 30% of their ‘income’ by 2020, up from 10-15% at present. This

higher dividend requirement will put pressure on State-owned coal miners to cut costs and capital spending.

• China is currently feeling the impact of tighter monetary policy, and a crackdown on bank lending.

• China's State Council recently released new regulations that forbid the construction of coal mines with an

annual production capacity under 300,000 tonnes and gas outburst mines with an annual capacity less than

900,000 tonnes. Coal mines producing fewer than 90,000 tonnes annually will be phased out. The new

policies expect the Ministry of Finance (MoF) and the National Development and Reform Commission

(NDRC) to check on and remove arbitrary charges on coal miners around the country by the end of this

year. The new policies also strengthen the government's support of coal-electricity integration projects.

• In recent days, China’s National Development and Reform Commission (NDRC) and National Energy

Administration have proposed a number of reforms to China’s domestic coal industry. These reforms include

tax cuts to local coal producers, encouraging horizontal and vertical integration of coal producers, tightening

quality regulations and aiding the shutdown of loss-making coal capacity.

24

Other issues facing the Chinese coal industry 3. Lower State support and tighter finance

• The spot Iron Ore price has staged a recovery since June, as the world economy improves and the market

comes to terms with Chinese demand staying stronger than expected.

• However, the very recent (partly seasonal) slowdown in Chinese steel production and a rise in Chinese

Ports inventories of Iron Ore has hurt Iron Ore prices in the past month.

• The backwardation in futures curve has increased since the middle of the 2013, supporting the view that the

market tightened significantly in H2 2013.

Iron Ore prices have recovered...

25

$0

$50

$100

$150

$200

$250

$0

$50

$100

$150

$200

$250

04-Nov-08 04-Nov-09 04-Nov-10 04-Nov-11 04-Nov-12 04-Nov-13

Average Weekly Iron Index

Iron Ore Index (A$/t)

Iron Ore Index (US$/t)

Source: Bloomberg50

60

70

80

90

100

110

120

130

140

150

May-13 May-14 May-15 May-16

SINGAPORE IRON ORE FUTURESUS$/tonne

9 December 2013

28 Aug 2012 (cycle low)

7 Oct 2011

Source: Bloomberg

6 June 2013 (2013 low)

9 January 2014

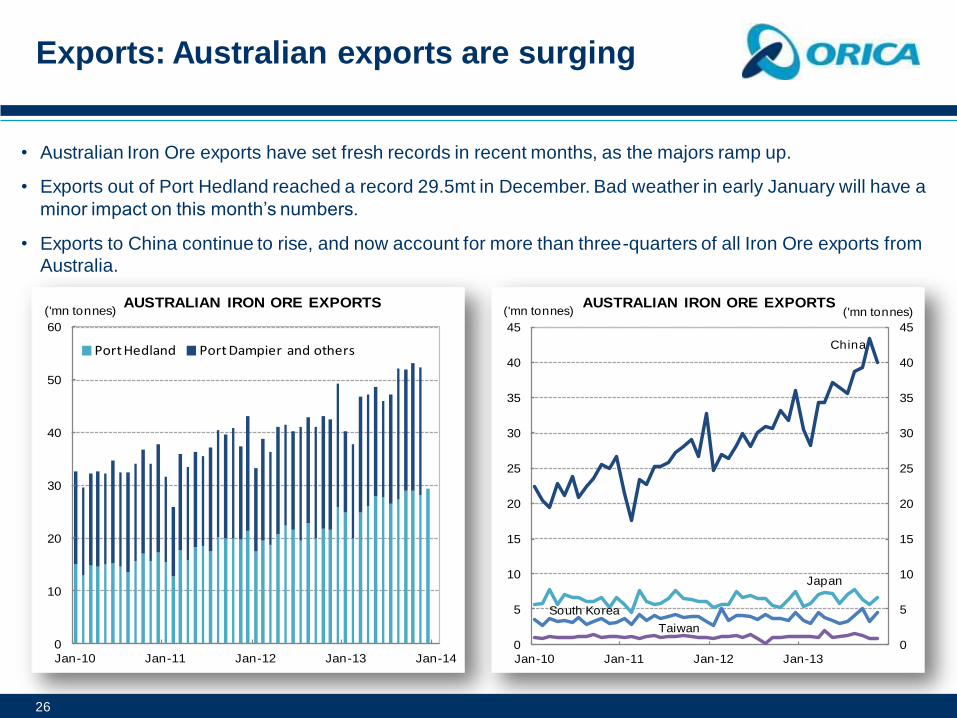

• Australian Iron Ore exports have set fresh records in recent months, as the majors ramp up.

• Exports out of Port Hedland reached a record 29.5mt in December. Bad weather in early January will have a

minor impact on this month’s numbers.

• Exports to China continue to rise, and now account for more than three-quarters of all Iron Ore exports from

Australia.

Exports: Australian exports are surging

26

0

10

20

30

40

50

60

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Port Hedland Port Dampier and others

AUSTRALIAN IRON ORE EXPORTS('mn tonnes)

0

5

10

15

20

25

30

35

40

45

0

5

10

15

20

25

30

35

40

45

Jan-10 Jan-11 Jan-12 Jan-13

AUSTRALIAN IRON ORE EXPORTS('mn tonnes) ('mn tonnes)

China

Japan

Taiwan

South Korea

• While Australian Iron Ore exports have set fresh records in recent months, exports from other countries have

been flat in trend terms.

• Indian exports remain heavily constrained. The Indian Iron Ore sector has been in crisis for the past four years

with output falling from a peak of 220mt in 2009 to 138mt in 2012. The long-running clampdown on illegal

mining has persisted this year, and Wood Mackenzie (WM) forecast output at ~125mt in 2013. WM believes

Indian output will bottom out in 2013, as production restrictions are lifted. However, exports should not reach

significant heights: in the medium-to-long term, domestic demand will (more than) absorb domestic output.

• Chinese Iron Ore output has hit record levels in recent months, as the 2013 price recovery encourages output.

Australia is winning market share

27

0

10

20

30

40

50

60

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

IRON ORE EXPORTS('mn tonnes)

Australia

Brazil

Sources: Bloomberg, Orica, GTIS

Canada

India

South Africa

0

20

40

60

80

100

120

140

0

20

40

60

80

100

120

140

Jan-01 Jan-04 Jan-07 Jan-10 Jan-13

CHINESE IRON ORE &STEEL PRODUCTIONmn tonnes

Steel Production

Chinese Iron Ore production

mn tonnes

Source Bloomberg

• With iron ore spot prices holding above USD130, all major production hubs remain profitable

• Chinese Iron Ore producers dominate the highest quartile of Wood Mackenzie’s cost curve, closely

followed by Canada.

• Note: Wood Mackenzie surveys 61 Chinese mining operations, covering approximately 25% of Chinese

marketable Iron Ore output. Average cash cost across this sample is $107/t, although this is probably

overstates the true cost, given the high proportion of large state-owned mines included in the survey.

Chinese and Canadian producers will eventually be squeezed out

28

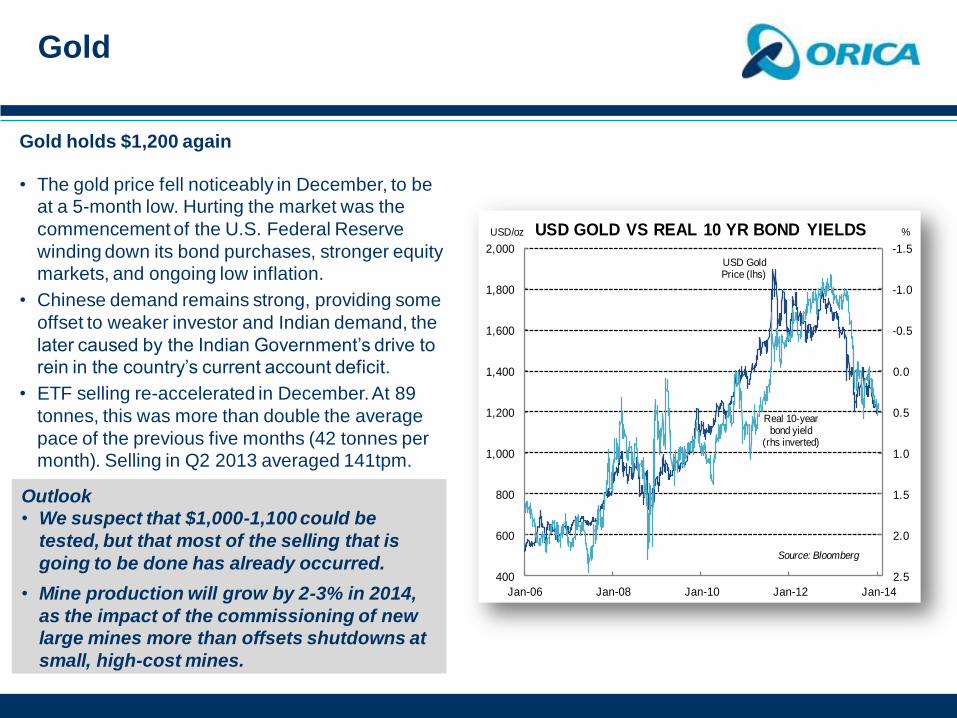

Gold holds $1,200 again

• The gold price fell noticeably in December, to be

at a 5-month low. Hurting the market was the

commencement of the U.S. Federal Reserve

winding down its bond purchases, stronger equity

markets, and ongoing low inflation.

• Chinese demand remains strong, providing some

offset to weaker investor and Indian demand, the

later caused by the Indian Government’s drive to

rein in the country’s current account deficit.

• ETF selling re-accelerated in December. At 89

tonnes, this was more than double the average

pace of the previous five months (42 tonnes per

month). Selling in Q2 2013 averaged 141tpm.

Gold

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Jan-06 Jan-08 Jan-10 Jan-12 Jan-14

USD GOLD VS REAL 10 YR BOND YIELDSUSD/oz %

Real 10-year bond yield

(rhs inverted)

USD Gold Price (lhs)

Source: Bloomberg

Outlook

• We suspect that $1,000-1,100 could be

tested, but that most of the selling that is

going to be done has already occurred.

• Mine production will grow by 2-3% in 2014,

as the impact of the commissioning of new

large mines more than offsets shutdowns at

small, high-cost mines.

• After the Global Financial Crisis (GFC), gold bar and ETF demand surged, as investors sought safe-havens.

As a result of the GFC, some managers had their mandates changed to only allow physically-backed gold

holdings. This strategy aimed to avoid the counterparty risk associated with futures contracts.

• Since the peak in November 2012, the combined holdings of Comex longs and ETFs has fallen by >1400

tonnes (40%). Bar sales have probably more than matched that. The $64 question now is ‘how much more

gold will ETF and bar investors sell?’ The risk is that Comex players go heavily ‘short’.

• So, the equivalent of over half a year’s mine supply has hit the market over the past year. This has happened

just as Indian gold consumers have had large obstacles placed in front of them by their government.

Investment demand has been important - the rally saw bar demand dwarf ETF demand

30

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2000 2002 2004 2006 2008 2010 2012

ETF's and related Products (tonnes)

Bar and coin hoarding (tonnes)

Gold Price (USD/oz)

BAR,COIN, ETF DEMAND VS GOLD PRICE

Source: World Gold Council

0

300

600

900

1200

1500

1800

2100

0

500

1000

1500

2000

2500

3000

3500

Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13

GOLD HOLDINGS - ETF & COMEXtonnes

ETF holdings (lhs)

Comex Fund Long

(rhs)

Sources: CFTC, ETF Securities

USD Gold Price

(rhs)

price

• From over 3,000 tonnes in the few years before the turn of the century, jewellery demand fell by more than 1/3

to around 2,000 tonnes per year in more recent years. The GFC wouldn’t have helped.

• Industrial demand was more resilient than jewellery demand. Typically, industrial demand comes from areas

that are less price-sensitive. That is because gold is more likely to be a small component of the overall product,

unlike gold jewellery.

• The sharp price fall so far in 2013 should stimulate jewellery and industrial demand, lending support to the price.

Gold fabrication demand has been hurt by the price gains of the past decade

31

0

450

900

1350

1800

0

180

360

540

720

1995 1998 2001 2004 2007 2010

INDUSTRIAL DEMAND VS GOLD PRICE

Industrial

demand (lhs)

Price (rhs)

$/oztonnes

550 tonnes

450 tonnes

0

300

600

900

1200

1500

1800

0

600

1200

1800

2400

3000

3600

1995 1998 2001 2004 2007 2010 2013

JEWELLERY DEMAND VS GOLD PRICE

Jewellery

demand (lhs)

Price (rhs)

$/oztonnes

2500 tonnes

2000 tonnes

3100 tonnesSource: World Gold Council

• The 1999 agreement by a group of European central

banks to restrict reserves sales to 400 tonnes per year

(and subsequent agreements capping sales at 500tpy),

gave much greater transparency to the gold market and

sparked the start of a 13-year rally in the gold price.

• Over the past decade, centrals banks collectively have

turned from being sellers of 500 tonnes per year to

being buyers of that amount: safe-haven demand

against the macroeconomic and sovereign debt

backdrop. Also, to guard against the impact of currency

de-basement that Quantitative Easing programmes

could create.

• The question from here is, will central banks follow the

pack and sell, or will they take advantage of lower

prices to increase their holdings? Central banks hold

gold for liquidity and diversification purposes, less so

because they think the price will rise. We don’t believe

central banks were participants in the recent sell-off: in

fact, some appear to have bought.

Central bank transactions

32

0

300

600

900

1200

1500

1800-750

-500

-250

0

250

500

750

1995 1998 2001 2004 2007 2010

OFFICIAL SECTOR SALESVS GOLD PRICE

Sales/Purchases

(lhs)

Price (rhs)

$/oztonnes

Source: World Gold Council

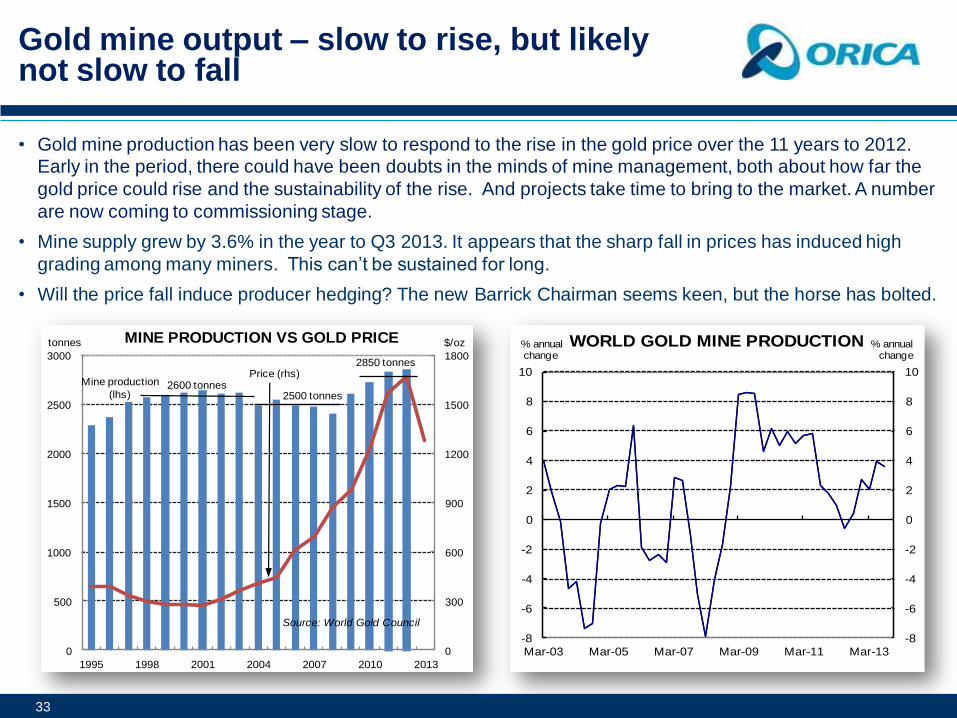

• Gold mine production has been very slow to respond to the rise in the gold price over the 11 years to 2012.

Early in the period, there could have been doubts in the minds of mine management, both about how far the

gold price could rise and the sustainability of the rise. And projects take time to bring to the market. A number

are now coming to commissioning stage.

• Mine supply grew by 3.6% in the year to Q3 2013. It appears that the sharp fall in prices has induced high

grading among many miners. This can’t be sustained for long.

• Will the price fall induce producer hedging? The new Barrick Chairman seems keen, but the horse has bolted.

Gold mine output – slow to rise, but likely not slow to fall

33

0

300

600

900

1200

1500

1800

0

500

1000

1500

2000

2500

3000

1995 1998 2001 2004 2007 2010 2013

MINE PRODUCTION VS GOLD PRICE

Mine production

(lhs)

Price (rhs)

$/oztonnes

2600 tonnes

2850 tonnes

2500 tonnes

Source: World Gold Council

-8

-6

-4

-2

0

2

4

6

8

10

-8

-6

-4

-2

0

2

4

6

8

10

Mar-03 Mar-05 Mar-07 Mar-09 Mar-11 Mar-13

WORLD GOLD MINE PRODUCTION % annualchange

% annualchange

Copper

Copper steady, and likely to remain that way...

• The copper price has been relatively stable in recent months. The market looked past a further sharp fall in

exchange stockpiles, judging it as largely a seasonal occurrence. Worries over surging mine supply have

been offset by chronic scrap shortages and strong Chinese demand.

• Activity has been strong in China’s infrastructure and construction sectors, leading to high levels of demand.

0

200000

400000

600000

800000

1000000

0

600000

1200000

1800000

2400000

3000000

Mar-00 Mar-02 Mar-04 Mar-06 Mar-08 Mar-10 Mar-12

COPPER DEMAND

China (lhs)

Germany

United States (rhs)

Developed Asia (rhs)

Source: WBMS

('000 tonnes) ('000 tonnes)

-12

-8

-4

0

4

8

12

16

-15

-10

-5

0

5

10

15

20

Jan-98 Jan-01 Jan-04 Jan-07 Jan-10 Jan-13

Industrial Production, lagged 1 quarter (rhs)

Copper demand (lhs)

COPPER DEMAND VS INDUSTRIAL PRODUCTION

annual % change

annual % change

Source: WBMS

Copper

Copper mine supply is growing firmly, after many years of problems

• Mine supply is showing strong growth at present, and after years of significant deficits, the market is likely to

show a modest surplus in 2013 and 2014.

0

300000

600000

900000

1200000

1500000

0

300000

600000

900000

1200000

1500000

Mar-95 Mar-98 Mar-01 Mar-04 Mar-07 Mar-10 Mar-13

COPPER MINE SUPPLY

Chile

NAFTA

Europe

Source: WBMS

tonnes per quarter

Oceania

Asia

Africa

tonnes per quarter

-5

0

5

10

15

Mar-96 Mar-99 Mar-02 Mar-05 Mar-08 Mar-11

COPPER MINE SUPPLYannual% ch.

Source: WBMS

Outlook

• The impact of an improvement in world economic growth is likely to be matched by rising mine supply over

the next couple of years.

• In the absence of major mine supply disruptions, the price will thus struggle to rise much above US$8,000

over that period. Chronic scrap shortages would likely see strong Chinese buying at the $6,500 mark.

Zinc and Lead

Lead and Zinc prices have recovered

• The International Lead and Zinc Study Group (ILZSG) forecasts zinc demand and supply to increase in

2014. The ILZSG projects zinc demand to increase by 5% 2014, after growth of 4.8%.

• LME lead stockpiles appear to have stabilised, after heavy falls over the past two years. ILZSG estimates

that there will have been a small 22kt surplus in the global lead market in 2013. In 2014, the market is

expected to be in deficit for the first time since 2009, with the extent of the shortage estimated at 23,000

tonnes.

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

$0

$400

$800

$1,200

$1,600

$2,000

$2,400

$2,800

$3,200

$3,600

04-Jan-08 04-Jan-10 04-Jan-12 04-Jan-14

Sto

ck

Le

ve

l (t

on

ne

s)

Pric

e

Average Weekly Lead Price & Stock Level

Lead (US$/t) Lead (A$/t) Stock Level

Source: Bloomberg50,000

250,000

450,000

650,000

850,000

1,050,000

1,250,000

1,450,000

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

04-Jan-08 04-Jan-10 04-Jan-12 04-Jan-14

Sto

ck

Le

ve

l (t

on

ne

s)

Pric

e

Average Weekly Zinc Price & Stock Level

Zinc (US$/t) Zinc (A$/t) Stock Level

Source: Bloomberg

Nickel

Nickel stocks have surged

• In December, nickel prices averaged

US$14,005/tonne for the month,

US$111/tonne higher than November’s

average.

• Nickel stocks ended the year at yet another

new high.

• Indonesia’s ban on exports of unprocessed

nickel ore is set to tighten the global nickel

market in 2014.

• Reliable leading indicators suggest that there will be a further pick up in the world economy in H1 2014, which

should boost the demand for resource commodities. The U.S. is taking over the locomotive role from China.

Hopefully, a firm Eurozone recovery will occur in 2015.

• Recent major policy changes by Beijing should underpin economic growth and the demand for resources in

the medium/long term. However, Beijing is now responding to widespread dissent about air pollution, by

moving away from burning low value coal and low grade Iron Ore. This should benefit Australian producers at

the expense of some Indonesian, American, Vietnamese and Chinese producers.

• Chinese and North American Coal and Iron Ore producers are under pressure on a number of fronts; they will

likely cede a larger share of the Chinese market to overseas producers.

• The Thermal Coal price is recovering, thanks to both an improving world economy and to seasonal influences

(the Northern Hemisphere winter). Supply growth will largely offset any pick-up in demand in 2014.

• The Coking Coal price is just US$3/t above the cycle lows. Strong supply and plentiful stocks in China are

offsetting the impact of stronger-than-expected demand by steelmakers in major consuming nations such as

China. An improving world economy will add to the impact of supply cuts in North America and China.

• Gold has suffered from a surge of investor liquidation and import restrictions by India. Further falls could

easily occur, but cost support and strong Chinese demand should kick in at the $1,000/oz mark.

• Base metals should benefit from stronger world economic growth and generally slower growth in supply.

Summary

38