Embed Size (px)

Citation preview

Weekly Emerging markets 26 October 2007

Emerging Weekly

Contents

Poland 3

Hungary 4

Czech Republic 5

Slovakia 6

Romania 7

Russia 8

Turkey 9

Coordinators

Murat Toprak

+44 20 7676 7491

Gaëlle Blanchard

+33 1 42 13 44 96

Poland & Hungary

Jaroslaw Janecki

+48 22 528 41 62

Czech Rep & Slovakia

Jan Vejmelek

+420 222 008 568

Anne-Francoise Blüher

+420 222 008 524

Miroslav Frayer

+420 222 008 567

Turkey & South Africa

Murat Toprak

Russia & Romania

Gaëlle Blanchard

The markets at a glance

Despite the uncertainties surrounding the US economic outlook, EMFX continues to perform extremely well. At the beginning of the week, a spell of risk aversion hit some of the high-yielding currencies but correction has been short-lived, with investors taking advantage of the fall to re-initiate long positions. This has been particularly true for the TRY. The most impressive performance, however, has been posted by the ZAR. The South-African currency has been our favourite for several months and we made a recommendation in our half-year FX outlook publication released in July to buy the ZAR. Although, the currency has already performed well, we believe that it still retains some upward potential. Latest inflation data fuel the expectations of another rate hike, but more fundamentally, we should see a reduction in macro-economic imbalances in the coming months, which, together with the attractive carry, will be able to support the currency. Beyond the high-yielders’ space, it is worth noting that even eastern European currencies are in a catch-up process. EUR/CZK hit a new historical low and EUR/PLN fell sharply towards 3.60. In the very short terrm, the current trends should persist but for some CEE currencies the upside potential is very limited, in our view. The PLN already shows some disconnection between macro-fundamentals and its performance. The worst performer remains the HUF, which has been unable to benefit from the rebound by other currencies in the region. Its poor performance is in line with our expectations. We keep our negative view.

Next week, the main event will obviously be the Fed meeting, which is widely expected to deliver a rate cut of 25bp. The communiqué will be crucial for EM performances but we keep a constructive view. Globally speaking, EM should take a breather and a consolidation is very likely by the end of the year. The US outlook needs to become clearer. In CEE-4, market attention will be on the Hungarian central bank meeting. There is uncertainty surrounding the outcome but we believe that the NBH has enough reason to cut the key rate by 25bp to 7.25% this week and probably by another 25bp by the end of the year.

Recommendations

Poland: We recommend to receive 5y5y PLN vs EUR at +70 on any upside T/P +45, S/L +80.

Hungary: With the market anticipating high chances of a rate cut by the MPC next week, we maintain payer recommendation in the IRS 2/5/10 yr butterfly (T/P: 10 in 3 months’ time, (S/L: -10). We also recommend buying HGB 17B vs paying 10 yr IRS around -8 (T/P: 2 until year-end, S/L: -12). The recent flattening (where we had our 2/10 yr stopped out) tried to mimic Poland and concentrated only in IRS, so we expect the 10 yr paper to catch up with the derivatives' flow.

Czech Republic: We keep last week recommendation to be short EUR/CZK at 27.25 with a target at 26.90, stop at 27.45.

On 28. September we recommended: - Pay 2Y IRS rate at 3.93% with target 4.30% end of 2007, stop at 3.75%. - Buy FRA 9x12 at 3.86% with target 4.30%, stop at 3.64%.

Slovakia: On 19. September we recommended: Pay EUR 1Yx1Y forward and receive SKK 1Yx1Y forward. Current spread at 21bp, target 10bp and stop at 26bp.

Turkey: Stay short USD/TRY, target 1.1740

See FX trade recommendations on page 2

Emerging Weekly

2 26 October 2007

View & Trade summary Forex

18/10/2007 25/10/2007 Coming week Coming month

EUR/USD 1.4295 1.4305 EUR/PLN 3.6898 3.6310 EUR/CZK 27.32 27.07 EUR/SKK 33.43 33.30 EUR/HUF 250.39 251.10 EUR/TRY 1.7163 1.7138 USD/TRY 1.2004 1.1980 EUR/RUB 35.49 35.49 USD/RUB 24.81 24.81

Source: SG FX Research, SG Economic research, KB economic & strategy research, SG Poland, BRD Economic Research

Interest rates

18/10/2007 25/10/2007 Coming week Coming month

WIBOR 3M 5.15 5.17 PLN IRS 5Y 5.68 5.53 PRIBOR 3M 3.48 3.47 CZK IRS 2Y 3.94 3.90 CZK IRS 10Y 4.42 4.32 BRIBOR 3M 4.05 4.05 SKK IRS 2Y 4.56 4.46 SKK IRS 10Y 4.74 4.60

BUBOR 3M 7.41 7.39 HUF IRS 5Y 6.69 6.67 Source: SG FX Research, SG Economic research, KB economic & strategy research, SG Poland

FX Trade recommendations Cross Position Date Entry Target Stop Current P/L week * P/L total

New positions

Old positions

USD/TRY Short 21-Sep 1.2325 1.1740 1.2620 1.1980 0.20% 2.80%

USD/BRL Short 15-Oct 1.8200 1.7700 1.8500 1.7915 -0.36% 1.57%

EUR/CZK Short 18-Oct 27.25 26.90 27.45 27.07 0.92% 0.66%

Positions closed

Total P/L 5.03%

* since previous Thursday ** P/L calculated without carry

Source: SG Forex Research

Emerging Weekly

3 26 October 2007

Poland Election result raises optimism

The centre-right Civic Platform party (PO) won last Sunday’s parliamentary election, successfully defeating the former ruling conservative party, PiS. Table 1 below sets out the voting results.

Table 1. Election result

PO - Civic Platform, PiS - Law and Justice, PSL - Peasants Party, LiD – Left and Democrats, GM - German Minorities

The PO leader, Donald Tusk is the official candidate for the role of Prime Minister. Tusk has yet to be nominated by President Lech Kaczynski. The outgoing Prime Minister, Jaroslaw Kaczynski will resign on November 5 – the day the new parliament will hold its first sitting. This week Donald Tusk commenced talks with Waldemar Pawlak, the leader of the Peasants' Party (PSL) regarding a possible coalition between the two parties. The PSL wants the new government to be formed quickly, so we do not see any risk with the coalition negotiations.

We think Professor Jacek Rostowski will be one of the candidates for the job of Finance Minister. Mr. Rostowski holds degrees from London University College, The London School of Economics and The University of London. He was an advisor to the Finance Minister in 1989–1991 and was also a Professor at the School of Slavonic and East European Studies, University of London. Mr. Rostowski was chairman of the Macroeconomic Policy Committee at the Ministry of Finance in 1997-2001. Currently he is Chairman of the Economics Department of the Central European University in Budapest and is also a member of the CASE Foundation Advisory Council.

The key economic priorities of the PO will be the revision of the 2008 budget and accelerating the process of adopting the euro. The PO has stated it wants to cut the 2008 central government deficit to around PLN 20 billion from the currently programmed PLN 28 billion. Adoption of the euro is also supported by the leftist opposition party, LiD. The PO will promote 2012 as the year for adoption of the euro, it is possible that the new government will propose an actual date for this move. Indeed, fiscal tightening may even influence bringing forward the target date for Poland's adoption of the euro to January 2011 from the previously contemplated 2012-2013 timeframe. This would require Poland to enter the ERM-II (restricting the zloty to a +/- 15% fluctuation band around a central parity rate against the euro) in the middle of 2008. So, the key challenge will be the budget bill for 2008. The PO may be forced to abandon the cuts to the social contribution fee, introduced by Finance Minister Zyta Gilowska. One of the major risks for the PO-PSL coalition will be over the flat rate tax. Thus, while the PSL is willing to discuss the possibility of introducing a flat rate tax in Poland, it does not want to make any commitment to its support until all consequences of such a move have been considered. Here are some of the pre-election priorities set out by the PO:

Improving relations with EU allies Adopting the euro Quickly conclude mission in Iraq Accelerate and take advantage of economic growth Simplify taxes, introduce a flat rate tax Radically raise public sector wages Build motorway network to replace dilapidated infrastructure Reform health service with guaranteed free access Encourage emigrant Poles to return to Poland Raise the quality of education and extend Internet use Undertake a real fight against corruption

According to S&P, the election results had no immediate impact on Poland's sovereign ratings, but: "The election outcome opens the possibility of the formation of a more reform-oriented and fiscally more conservative government, which could ultimately benefit the ratings." Therefore, the zloty strengthened after the election results.

The Statistics Office revised down Poland's GDP for the first 2 quarters with Q1 GDP down to 7.2% vs 7.4% and Q2's to 6.4% vs 6.7%.

Next week the market will focus on the Central Bank’s decision but we do not expect an interest rate hike this month. MPC members will doubtless prefer to await the new government and its proposals for changes in the budget bill for next year. Thus, the next hike is expected in November, although the probability of such a move is slightly lower than it was a month ago. Firstly because two days after the November MPC meeting, Q3 GDP data will be released. According to Jan Czekaj - a moderate member of the MPC, the latter may need to await this data release: "…to really find out where the economy's going." Secondly, the unexpectedly strong zloty may influence the MPC’s strategy. The inflationary risk from the rising food prices and wages will be partially diminished by the stronger zloty. Note also that Poland's net annual inflation rate was 1.2% in September, unchanged from August. The MPC pays close attention to net inflation. 1.5% is the key level from the interest rate hike perspective.

Recommendations

We recommend to receive 5y5y PLN vs EUR at +70 on any upside T/P +45, S/L +80.

[email protected], SG Warsaw

% no. of seats PO 41.51 209 PiS 32.11 166 LiD 13.15 53 PSL 8.91 31 GM - 1

Graph 1. Stronger zloty after election results

3.60

3.65

3.70

3.75

3.80

3.85

01-0

8-07

07-0

8-07

13-0

8-07

17-0

8-07

23-0

8-07

29-0

8-07

04-0

9-07

10-0

9-07

14-0

9-07

20-0

9-07

26-0

9-07

02-1

0-07

08-1

0-07

12-1

0-07

18-1

0-07

24-1

0-07

2.50

2.60

2.70

2.80

2.90

EUR/PLN (lef t axis) USD/PLN (right axis)

Source: Reuters

Emerging Weekly

4 26 October 2007

Hungary

Focus on the interest rate decision

The NBH’s monetary policy committee will hold its next meeting on 22 October when it will decide on the interest rate level. The NBH cut rates by 25 bp at its last meeting on September 24. While a majority of analysts have changed their view and now believe the 7.50% base rate will be left on hold this month, most Hungarian foreign currency dealers expect the NBH to cut its base rate by 25 bp to 7.25% next Monday. Dealers underlined that the level of 7.25% is now already priced in. They believe that a rate cut would not undermine the forint’s strength.

The Vice President of the NBH and MPC member, Julia Kiraly, stressed that the core markets are stable. Kiraly claimed that whilst the subprime crisis is not having a direct influence on Hungary’s economy, the subprime turbulence and the credit squeeze may have an impact on some sectors of the economy in the medium term. Kiraly added that the inflation projection could well be around the Central Bank’s target in the medium time horizon, although agricultural prices need to be strictly monitored. Real interest rates are forecast at 2-3% in the coming years. The Central Bank assumes real gross wages growth to be 0% next year. Of course, wage setting is still a threat to easing the monetary policy, especially in the public sector where the discussion on pay rises continues. We maintain our view of a rate cut by 25 bp in October and we also now see more room for a further 25 bp cut in November or December this year. Given this, we change our expectations concerning the level of the key interest rate at end-2007 and set it at 7.00%.

Hungarian markets were closed on Monday and Tuesday of this week for the national holiday, marking the 61st anniversary of the start of the anti-Soviet revolution in 1956. Thousands of anti-government protesters clashed with Hungarian police on Monday near Budapest’s Opera House where Socialist Prime Minister Ferenc Gyurcsany was attending a state event. Budapest police used water cannon and tear gas to attempt to disperse several hundred far-right protesters. 19 people were injured as rioters hurled petrol bombs and overturned cars in the centre of Budapest. Hundreds were injured during a police crackdown on similar protests around this time last year.

Political tensions in Hungary have been high since last September when the state radio broadcast parts of a confidential speech by Ferenc Gyurcsany in which he had admitted to lying about the economy to win the April 2006 elections. According to the latest polls, support for Fidesz, the main centre-right opposition party, stands at around 40%, while the Socialists are at 20%, with about 75% of voters saying the country is heading in the wrong direction.

Hungary’s retail sales dropped by an annual 3.6% in August after a decline in July according to the Central Statistics Office. In the first eight months, retail sales were 2.2% lower than in the same period a year earlier. The data confirms that domestic consumption has been slowing down due to the government’s austerity measures which have reduced household’s real income. In month on month terms, retail sales were down 0.1% from July. Books and newspapers held a record 3.4% growth (m/m), which is linked to the start of the new school year. Non-food sales were unchanged m/m in August despite the 1.6% increase in textiles, clothing and footwear due to seasonality.

Hungary’s unemployment rate was 7.2% and remained unchanged in July-September, compared with June-August according to the KSH. The number of unemployed accounted for 306,900, up from 304,600 in June-August, but a fall from 318,300 last year. This year’s unemployment rate for the July-September period was down from the 7.5% rate recorded in the corresponding period in 2006.

The Hungarian government Debt Management Agency sold a total of HUF75 billion of 5-year and 10-year bonds at auction on Thursday. The average yield of the 5Y was 6.67%. AKK data showed that it sold less of the 10-year instrument than originally planned - HUF10 bln below plan and the 10Y was sold at an average yield of 6.54%.

Recommendations

With the market anticipating high chances of a rate cut by the MPC next week, we maintain payer recommendation in the IRS 2/5/10 yr butterfly (T/P: 10 in 3 months’ time, (S/L: -10). We also recommend buying HGB 17B vs paying 10 yr IRS around -8 (T/P: 2 until year-end, S/L: -12). The recent flattening (where we had our 2/10 yr stopped out) tried to mimic Poland and concentrated only in IRS, so we expect the 10 yr paper to catch up with the derivatives' flow.

[email protected], SG Warsaw

Graph 1. Possible rate cut next week

0.0

2.0

4.0

6.0

8.0

10.0

05'I III V VII IX XI 06'I III V VII IX XI 07'I III V VII IX

CPI (y/y) CB Base Rate

Source: KSH

Graph 2. Retail sales dropped by 3.6% (y/y)

-5

-3

0

3

5

8

10

13

15

05'I V IX 06'I V IX 07'I V

Retail sailes Industrial output (y/y)

Source: KSH

Emerging Weekly

5 26 October 2007

Czech Republic

Strong crown forced a pause in the CNB’s tightening cycle

Against our expectations, the CNB left its key interest rate unchanged at 3.25% this week. Two members out of seven voted for a hike. However, the new CNB inflation forecast was in line with our expectations. Governor Tuma said that the latest forecast makes no major changes to the bank’s economic outlook and is consistent with a rise in nominal interest rates. We think that the new forecast is consistent with a 25-50bp hike in Q4 (we will know more after the full forecast is released). Yet, Tuma stated that the size and timing of the interest rate increase will depend on the evolution of risks to the forecasts, which the Board actually perceives as balanced. Tuma added that a hike might happen next month or it could come at the beginning of next year. Our view is that the further development of the CZK will be important (according to CNB governor Tuma, the CZK is slightly stronger than assumed in their forecast); and also the inflation data for October, which we see accelerating significantly.

We expected a hike of 25bp, but saw a strong risk stemming from the recent strengthening of the CZK. Our last quarterly forecast was based on an average EUR/CZK for Q4 at 27.50 and thus the current level is about 1.5% lower. According to our simulations, a 1.5% stronger crown lowers our 3M PRIBOR forecast in a 1Y horizon by almost 45bp. If the Czech crown remains at such strong levels during the rest of this quarter, or at even slightly stronger levels, we will probably see the CNB postponing the hiking cycle towards the beginning of next year. But so far, we do not change our Czech crown view at 27.40 for the end of this year and at 27.00 for the end of next year. If we take into account the current CNB forecast and our inflation and mid-term CZK forecast, we think that the CNB will continue raising rates gradually towards a neutral level at 4.0-4.25% (probably in November or December 07, or Q1, Q2, Q3 08). As a result, we stick to our recommendations we gave at the end of September and await the full CNB Inflation Report, which will be released next week and which will give us deeper insight to the CNB view on interest rates.

Graph 1. External Trade disappointed recently

-25-20-15-10-5

05

101520

Jan-98 Jan-00 Jan-02 Jan-04 Jan-06

External Trade Balance in bn CZK

Source: KB Economic & Strategy Research, Ecowin

At the beginning of the week, the Czech crown continued its appreciation. The crown moved together with its regional peers and was driven by the USD depreciation. Then the crown remained in a relatively tight range, i.e. between EUR/CZK 27.15 to 27.25, but after the CNB meeting, the crown appreciated further and the EUR/CZK hit a new historical low below 27.10. We see room for further appreciation of the Czech crown in the short term. However, by the end of the year we think that it should return towards weaker levels (see also our comments above).

Foreign trade figures for September will be released next week. The figures are of greater importance this time, as the August trade figures represented a disappointment for us. A deficit on the external trade balance was recorded for the second month in a row. We expect the September trade balance to return to surplus (CZK 9.0bn, consensus not available). It would also mean an enhancement of the y/y improvement towards CZK 1.6bn after only CZK 0.5bn recorded in August. Such an outcome would fundamentally support our short term bullish view on the CZK.

Recommendations

In our last SG Forex Weekly we included the recommendation short EUR/CZK at 27.25 with a target at 26.90, stop at 27.45.

On 28. September we recommended:

- Pay 2Y IRS rate at 3.93% with target 4.30% end of 2007, stop at 3.75%.

- Buy FRA 9x12 at 3.86% with target 4.30%, stop at 3.64%.

[email protected] [email protected]

Komercni banka Prague (Société Générale group)

Emerging Weekly

6 26 October 2007

Slovakia Eurostat revises the 2006 public finance deficit to 3.7% of GDP, from 3.4%

As a result of Eurostat’s recommendation to Slovakia to incorporate state television and radio in its public finances, the 2006 deficit was revised to 3.7% of GDP, up from the original 3.4%. The finance minister, Mr. Pociatek had expected the revisions to range between 0.6% - 0.7% of GDP for 2006 and between 0.2% and 0.3% for 2007. Additionally, Eurostat ruled that the state highway company could be excluded from the calculation, which resulted in the revision being smaller than expected. According to a Finance Ministry spokesman, the change in methodology did not have any major impact on the expected fiscal data for 2007. Nevertheless, deputy finance minister Frantisek Palko said the EU may still demand the inclusion of the state highway company in Slovakia’s public finance figure, but even if this turned out to be the case, the deficit would still meet the euro zone entry condition, as the booming Slovak economy would offset the impact and keep the country on track to adopt the euro in 2009. The finance ministry revised the 2007 fiscal gap forecast down to 2.5% of GDP from 2.7%. If the highways are included, the deficit should reach a maximum of 2.7% of GDP. The comments from Eurostat as well as the finance ministry were positive given that even in a worst case scenario where the highway company’s losses are included, the end result would still be that the public finance deficit stays below the reference value of 3% of GDP. This news was reflected in a strengthening of the Slovak currency, while it had weakened sharply prior to the release of the deficit revision, i.e. it moved from EUR/SKK 33.70 to close to

33.20.

The Slovak Statistics Office revised its full-year 2006 GDP growth upwards to 8.8% y/y from the previously reported 8.3%. 2005 GDP growth was also revised upward to 6.6% y/y from the originally posted 6.0%. This revision was attributable to methodology changes required to comply with EU regulations and thanks to improved data

sources, changes in reclassification of some transactions and adjustments related to foreign trade. (The above fiscal data revision already takes into account the GDP revisions).

The NBS will hold its regular monetary policy meeting next week. In line with consensus, we expect no change in key rates and we do not foresee any impact on the market. More interesting will be the press conference afterwards and the update of the NBS forecast. The NBS indicated earlier that it may lower the impact of the exchange rate on inflation in its quarterly projection model. If the appreciation of the Slovak crown has a smaller disinflationary impact than previously thought, this would mean, firstly, that the NBS will not react as promptly as in the past to an appreciation of the Slovak crown (this seems to already have been the case for some time, see graph also) and, secondly, it improves the outlook for the long term sustainability of inflation, when the Slovak crown is replaced by the Euro.

Recommendations

On 19. September we recommended:

Pay EUR 1Yx1Y forward and receive SKK 1Yx1Y forward. Current spread at 21bp, target 10bp and stop at 26bp.

[email protected] Komercni banka Prague

(Société Générale group)

Graph 1. Fiscal gap expected to get below 3%

-4.0

-3.0

-2.0

-1.0

0.0

2004 2005 2006 2007 2008 2009 2010

Budget Deficit - MaastrichtFinMin estimateReference level

Source: KB Economic & Strategy Research, Ministry of Finance

SR

Graph 2. NBS no longer following the EUR/SKK

0.0

2.0

4.0

6.0

8.0

10.0

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

33.0

35.0

37.0

39.0

41.0

43.0

45.0

47.02W Repo, in %EUR/SKK, monthly average

Source: KB Economic & Strategy Research, EcoWin

Emerging Weekly

7 26 October 2007

Romania The challenge of growing imbalances

Economic growth slowing but still solid: Economic growth has been slowing since reaching its peak of 8.3% y/y in Q3 2006; GDP grew by 6% y/y in Q1 and 5.6% y/y in Q2 of this year. This slowdown is due to the increasingly negative contribution of net exports, while domestic demand remains very buoyant. Real export growth has indeed dropped dramatically in Q2, to 2.4% y/y from 12.9% in Q1. Meanwhile, real import growth slowed to only 20.8% y/y in Q2 after 23.8% in Q1. The continuation of a soft export growth trend would obviously be a worry, as domestic demand appears unlikely to cool significantly in the short-term. Private consumption is supported by wage growth and the development of credit, in a characteristic process of catch-up in living standards. Investment is still on the rise, up 17.2% and 19.4% y/y in Q1 and Q2, respectively. Consumption does not look like cooling down either, with the September consumer confidence index reaching a peak and employment growing at a pace close to 3% y/y. Regarding the supply side, the outlook is less clear. Business confidence remains fairly stable in the manufacturing sector, steady in the retail trade sector but slightly down in construction. The pace of manufacturing output growth has been slowing since a peak of 13% y/y in mid-2006, and is currently hovering at around 5%.

Graph 1. Contributions to GDP growth

pts of y/y grow th

-17

-12

-7

-2

3

8

13

18

23

Q1 03 Q4 03 Q3 04 Q2 05 Q1 06 Q4 06

Priv. cons Pub. consInv. inventoriesNet exports

Source: SG Economic Research, Ecowin

No rebalancing in sight: The strong growth in domestic demand has fuelled large and growing trade and current account deficits. Such trends are unavoidable in developing economies that need to import investment goods to improve production capacities and build infrastructure. This is then expected to improve productivity and boost exports, restoring the external balance over time. Romania’s industry has been restructured and exports have indeed been growing significantly in recent years, but the latest developments in exports (acutely slower growth in volume in Q2) would be a real worry if confirmed in Q3. A slowdown in exports is actually expected next year in all the new EU members, as a consequence of softer economic activity in the euro zone next year. The current account deficit, which reached

10.3% of GDP in 2006 has increased rapidly this year (from EUR3.67 bn at end-December to EUR4.44 bn at end-June) and thus should be larger than 13% of GDP for the whole year. A tighter fiscal policy would help moderate domestic demand, but the country also needs spending programmes to improve economic and social structures in the longer term. There are certainly improvements to be made in some areas of expenditure, but this is rather unlikely to occur with elections scheduled for end-2008.

Financing of imbalances could become more difficult: Up to now, the current account deficit has been easily financed by FDI inflows, but with decreasing privatisation receipts (as the process is coming to an end, at least for major deals), funding will become more difficult. Romania has also been recording large capital inflows to finance its domestic banks’ credit activity. The growth of credit to households is slowing (to 67% y/y in August from more than 80% in January) but still remains strong, and credit to businesses is not decelerating (45% y/y in August). In the context of a global financial crisis, there are risks of tighter financing conditions for countries with large imbalances. On the positive side though, the total external debt is just above 40% of GDP, which does not represent a major risk. A withdrawal of foreign financing would nevertheless have a significant effect on economic growth.

Graph 1. Trade balance

2002 2003 2004 2005 2006 2007-2.25-2.00-1.75-1.50-1.25-1.00-0.75-0.50-0.250.00

0

5

10

15

20

25

30

35 Trade balance (rhs)

Export growth

Import growth

% y/y bn euro

Source: SG Economic Research, Ecowin

A tricky situation for the central bank: The strong growth in domestic demand coupled with labour shortages has led to an acceleration in wage increases since 2006 and possiblel inflationary pressures, as GDP growth runs above potential. Until this year, inflation had been decelerating, thanks partly to the strengthening of the currency up to this summer, but the trend is starting to reverse, mainly on the back of the surge in food and oil prices (although core CPI is also moving up). The output gap would thus support a tighter monetary policy, but raising interest rates would lead to renewed strength of the leu, with all the negative implications that would have on export competitiveness and, in turn, on the current account balance. Confronted with a loose fiscal policy, rising inflation and uncertain global market conditions, the central bank could be tempted to tighten its monetary policy, as the IMF, for instance, is inviting it to do.

Emerging Weekly

8 26 October 2007

Russia Monetary policy to rely less on FX management

Liquidity conditions remain fragile: After improving sharply since the beginning of the month, conditions in the money market are tightening again ahead of the tax payment period (end of month). The overnight rate is back to 5.5-6% after reaching a 2-month low of 4.5-5% a week ago. The central bank increased its daily repo injections again, and the coming week will likely see higher overnight rates. The situation is, however, unlikely to be as tense as end-September, when the overnight rate reached 10% at one point. Indeed, since then global liquidity conditions have improved and the Russian monetary authorities have taken measures to ease the refinancing process. The CBR extended the range of collaterals it accepts at repo operations (and will extend further by accepting Eurobonds and claims on non-rated companies) and the Ministry of Finance gave up its plan to issue a further RUB100 bn in Treasury bonds (OFZ) this year due to market conditions. The Ministry of Finance also announced that it could place over 1.5 tln roubles of State treasury funds with commercial banks to improve liquidity.

Yesterday the average-weighted rate at the CBR’s 4-week deposit auction was 4.03%, down from 4.10% a week ago, confirming that some normalisation is underway. It will take time though to restore conditions in the interbank market (the 3-month rate is stuck around 7.25%, from just below 5% before the crisis), but the expected Fed rate cut should provide further support to financial markets.

Graph 1. Interbank rates

%

2

3

4

5

6

7

8

9

10

1-May 29-May 26-Jun 24-Jul 21-Aug 18-Sep 16-Oct4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0Overnight

3-month (rhs)

Source: SG Economic Research, Ecowin

The liquidity crisis may lead to a change in monetary policy management: The liquidity crisis and the tensions it generated on the money market led to a change in the central bank’s role that could have longer term consequences. Indeed, the CBR had to provide liquidity to a market that had been generally rather flooded with it, mainly through its daily repo, a tool that had not been used with such frequency for a long time. These events have actually propelled interest rates into the spotlight again, and comments by central bank officials suggest that they could become a monetary policy tool once more. Since

Russia has been flooded by oil/gas export earnings and capital inflows, there has been so much liquidity that the market was not responsive to central bank rates. This has been changing since August and the CBR is likely to take this opportunity to proceed with its project of restoring a more “traditional” monetary policy management to fight inflation, based more on interest rates and less on foreign exchange intervention. The most efficient tool so far to keep inflationary pressures under control has been the managed appreciation of the rouble. CBR officials have said this week that the bank would raise its refinancing rate (currently at 10%) by year-end, whereas it had been gradually reducing it over the past years. This rate is the ceiling for official rates and has no policy implications for the time being. The fact that the CBR intends to raise the rate is interesting nevertheless, as it means that they expect the renewed uptrend in inflation to continue.

Graph 2. Inflation fuelled by food prices

5%

10%

15%

20%

25%

30%

Mar-03 Dec-03 Sep-04 Jun-05 Mar-06 Dec-06 Sep-077%

9%

11%

13%

15%PPI

CPI (rhs)

Source: SG Economic Research, Ecowin

Controlling inflation is the priority ahead of the elections: The spike in inflation is very bad news for the government and the President. As the surge in the recent months is mainly due to food prices, the authorities have urged retailers to limit price increases. Several food producers and retailers actually signed a price freeze agreement this week, which covers essential products and will be in place up to end-January. It will be difficult to prevent year-end inflation from reaching 10%, but the central bank said it would not revalue the rouble before the end of the year as this would not be efficient in the short-term. The basket is thus likely to remain broadly stable for the coming months, which will not prevent moves on the EUR/RUB and USD/RUB.

Emerging Weekly

9 26 October 2007

Turkey

Inflation stays on a downward trend and keeps the door open for further rate cuts

The recent sessions have been quite volatile for the Turkish currency. EUR/TRY and USD/TRY moves have been large in both directions. The combination of swings in global risk appetite and fears of a military intervention in Iraq pushed EUR/TRY up to 1.78 and USD/TRY to 1.25 during the week. The TRY obviously remains vulnerable to the global environment and to geo-political variables but it is worth noting that the market tends to sell the crosses on rallies. We keep a constructive approach on the TRY as our global economic scenario relies on a stabilisation of the financial markets and a quick recovery of the US economy in the coming quarters, while the Turkish macro-economic factors are broadly moving in the right direction.

Graph 1. CPI, y/y

0

2

4

6

8

10

12

14

Jan-05 Aug-05 Mar-06 Oct-06 May-07 Dec-07

2007 target: 4% with a tolerance of +/- 2%

Source: SG FX Research, CBRT

One of the most important macro-economic factors is

clearly the downward trend in inflation. Since the spring, the annual inflation rate is on a sustained southerly path falling from a level close to 11% in March/April to 7.1% in September. Next week, the October CPI will be released and should confirm that inflation continues to converge towards the central bank’s target. The annual rate could fall slightly below 7.0% in October, keeping the door open to further rate cuts. We were among the few research teams to forecast a 50bp rate cut in October and we still believe that the CBRT will cut again by at least 50bp by the end of the year. The decline in Turkey’s core inflation with durable goods prices falling and services prices running at a much slower pace since the beginning of the year give the leeway to the central bank to cut again. Admittedly, the evolution of oil prices represents a risk for the inflation outlook as the CBRT has underlined on several occasions. Nevertheless, the strength of the TRY offers sound protection to imported inflationary pressures. Oil prices in TRY terms are growing at a much slower pace than in USD terms, less than 20% y/y vs. 40%.

Graph 2. Services prices, y/y

-5

0

5

10

15

20

25

Jan-05

May-05

Sep-05

Jan-06

May-06

Sep-06

Jan-07

May-07

Sep-07

communication

Health

Housing

Hotel & restaurant

Education

Graph 3. Oil prices, y/y change (%)

-40

-20

0

20

40

60

80

100

Jan-05

May-05

Sep-05

Jan-06

May-06

Sep-06

Jan-07

May-07

Sep-07

in USD

in TRY

Source: SG FX Research, Datastream

Despite the expected rate cuts and the uncertainties surrounding the global markets, we remain bullish TRY. For now, there is a larger potential being short USD/TRY than EUR/TRY as the USD weakness should persist for some time yet but in a medium-term perspective a short EUR/TRY position looks more attractive. Be ready to sell EUR/TRY on the next rally.

Recommendations

Stay short USD/TRY, target 1.1740

Emerging Weekly

10 26 October 2007

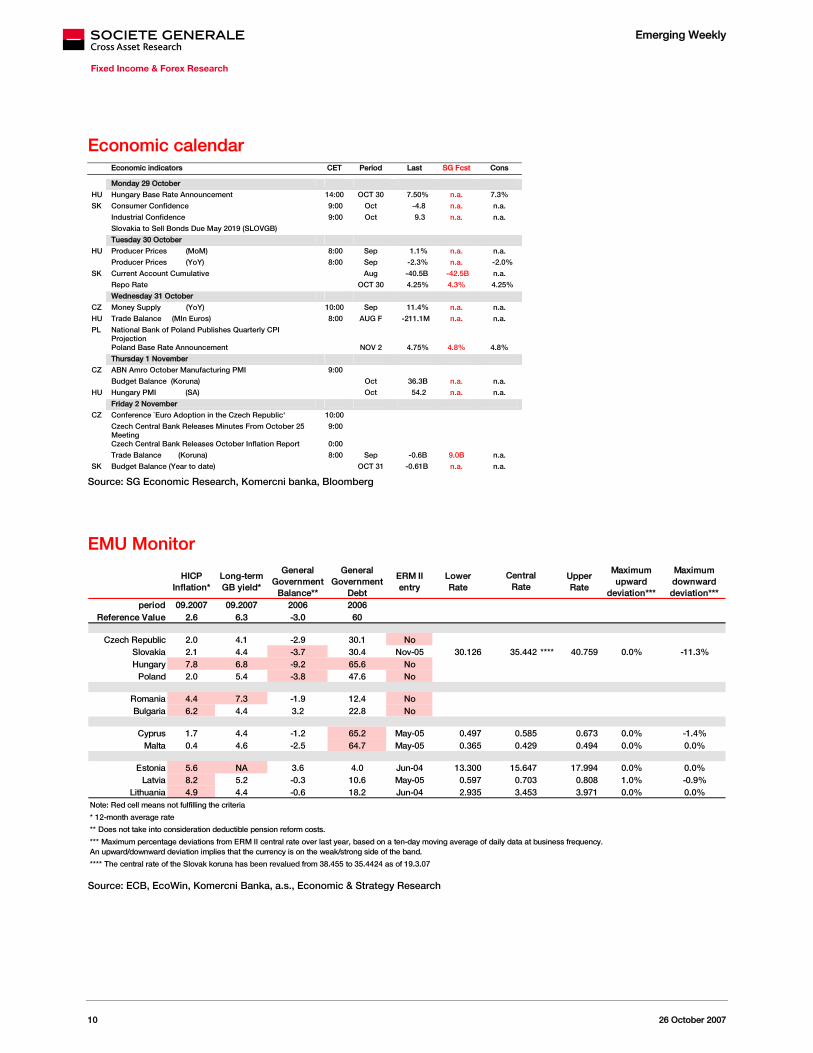

Economic calendar Economic indicators CET Period Last SG Fcst Cons

Monday 29 October

HU Hungary Base Rate Announcement 14:00 OCT 30 7.50% n.a. 7.3%

SK Consumer Confidence 9:00 Oct -4.8 n.a. n.a.

Industrial Confidence 9:00 Oct 9.3 n.a. n.a.

Slovakia to Sell Bonds Due May 2019 (SLOVGB)

Tuesday 30 October

HU Producer Prices (MoM) 8:00 Sep 1.1% n.a. n.a.

Producer Prices (YoY) 8:00 Sep -2.3% n.a. -2.0%

SK Current Account Cumulative Aug -40.5B -42.5B n.a.

Repo Rate OCT 30 4.25% 4.3% 4.25%

Wednesday 31 October

CZ Money Supply (YoY) 10:00 Sep 11.4% n.a. n.a.

HU Trade Balance (Mln Euros) 8:00 AUG F -211.1M n.a. n.a.

PL National Bank of Poland Publishes Quarterly CPI Projection

Poland Base Rate Announcement NOV 2 4.75% 4.8% 4.8%

Thursday 1 November

CZ ABN Amro October Manufacturing PMI 9:00

Budget Balance (Koruna) Oct 36.3B n.a. n.a.

HU Hungary PMI (SA) Oct 54.2 n.a. n.a.

Friday 2 November

CZ Conference `Euro Adoption in the Czech Republic' 10:00

Czech Central Bank Releases Minutes From October 25 Meeting

9:00

Czech Central Bank Releases October Inflation Report 0:00

Trade Balance (Koruna) 8:00 Sep -0.6B 9.0B n.a.

SK Budget Balance (Year to date) OCT 31 -0.61B n.a. n.a.

Source: SG Economic Research, Komercni banka, Bloomberg

EMU Monitor

HICPInflation*

Long-term GB yield*

General Government

Balance**

General Government

Debt

ERM II entry

LowerRate

UpperRate

Maximum upward

deviation***

Maximum downward deviation***

period 09.2007 09.2007 2006 2006Reference Value 2.6 6.3 -3.0 60

Czech Republic 2.0 4.1 -2.9 30.1 NoSlovakia 2.1 4.4 -3.7 30.4 Nov-05 30.126 35.442 **** 40.759 0.0% -11.3%Hungary 7.8 6.8 -9.2 65.6 No

Poland 2.0 5.4 -3.8 47.6 No

Romania 4.4 7.3 -1.9 12.4 NoBulgaria 6.2 4.4 3.2 22.8 No

Cyprus 1.7 4.4 -1.2 65.2 May-05 0.497 0.585 0.673 0.0% -1.4%Malta 0.4 4.6 -2.5 64.7 May-05 0.365 0.429 0.494 0.0% 0.0%

Estonia 5.6 NA 3.6 4.0 Jun-04 13.300 15.647 17.994 0.0% 0.0%Latvia 8.2 5.2 -0.3 10.6 May-05 0.597 0.703 0.808 1.0% -0.9%

Lithuania 4.9 4.4 -0.6 18.2 Jun-04 2.935 3.453 3.971 0.0% 0.0%

* 12-month average rate

** Does not take into consideration deductible pension reform costs.

**** The central rate of the Slovak koruna has been revalued from 38.455 to 35.4424 as of 19.3.07

CentralRate

Note: Red cell means not fulfilling the criteria

*** Maximum percentage deviations from ERM II central rate over last year, based on a ten-day moving average of daily data at business frequency. An upward/downward deviation implies that the currency is on the weak/strong side of the band.

Source: ECB, EcoWin, Komercni Banka, a.s., Economic & Strategy Research

Emerging Weekly

11 26 October 2007

Macro & Financial forecasts Macroeconomic forecasts

2005 2006 2007 2008 2005 2006 2007 2008

Poland 3.6 6.1 6.5 5.5 2.1 1.1 2.1 2.8Czech Republic 6.5 6.4 5.9 3.7 1.9 2.5 2.6 5.3Hungary 4.1 3.9 2.5 3.0 3.6 3.9 7.6 4.9Slovakia 6.1 8.3 9.1 7.7 2.7 4.5 2.3 1.9Romania 4.1 7.7 5.9 5.2 9.1 6.6 5.1 4.7Russia 6.4 6.7 7.1 6.0 12.7 9.7 8.3 7.0

Turkey 7.7 5.0 5.1 5.0 8.2 9.8 8.2 5.9

2005 2006 2007 2008 2005 2006 2007 2008Poland -1.4 -1.8 -3.5 -4.5 -4.3 -3.9 -3.4 -3.2Czech Republic -1.6 -3.1 -3.3 -3.3 -3.5 -2.9 -4.0 -3.0Hungary -6.9 -5.8 -4.9 -4.4 -7.8 -9.4 -6.6 -4.6Slovakia -8.6 -7.9 -3.3 -1.3 -2.8 -3.4 -2.7 -2.3Romania -8.7 -10.3 -11.5 -10.0 -1.4 -1.7 -2.0 -2.2Russia 11.00 11.0 7.5 4.5 7.5 7.3 4.0 2.8

Turkey -6.4 -8.2 -7.0 -6.6 -1.7 -0.7 -2.7 -2.6

GDP Inflation (year average)

Current account balance (% of GDP) Fiscal balance (% of GDP)

Interest Rates (end quarter)

Key central bank rates Dec 07 Mar 08 Jun 08 Sep 08 2007 ave 2008 ave

USA 4.50 4.50 4.75 5.00 5.06 4.78Euroland 4.00 4.25 4.25 4.50 3.80 4.35

Poland 5.00 5.00 5.25 5.25 4.25 5.20Czech Republic 3.75 4.00 4.25 4.25 2.90 4.13Hungary 7.00 6.50 6.25 6.00 7.50 6.40Slovakia 4.25 4.25 4.25 4.50 4.35 4.44Russia 10.50 10.50 10.50 10.00 10.37 10.25

Turkey 16.25 15.00 14.00 14.00 17.00 14.33South Africa 10.50 10.50 10.50 10.00 9.50 10.25Brazil 11.00 10.75 10.75 10.50 12.25 10.50

10 year bond yields (otherwise stated) Dec 07 Mar 08 Jun 08 Sep 08 2007 ave 2008 ave

USA 4.70 4.85 5.10 5.30 5.10Euroland 4.25 4.50 4.65 4.80 4.65

Poland 5.57 5.60 5.60 5.60 5.42 5.60Czech Republic 10Y IRS 4.80 5.10 5.20 5.30 4.30 5.30Hungary 6.55 6.30 6.30 6.30 7.50 6.40Slovakia 10Y IRS 4.70 4.90 5.00 5.10 4.60 5.10

Exchange Rates (end quarter) Dec 07 Mar 08 Jun 08 Sep 08 2007 ave 2008 ave

EUR/USD 1.38 1.35 1.32 1.30 1.34 1.33

EUR/PLN 3.70 3.70 3.65 3.65 3.80 3.70EUR/CZK 27.40 27.60 27.80 27.60 27.9 27.6EUR/HUF 257 260 265 265 250 260.00EUR/SKK 32.70 32.30 31.90 31.50 33.6 31.90EUR/RUB 34.70 34.00 33.60 33.50 34.80 33.70USD/RUB 25.40 25.30 25.40 25.60 25.75 25.50

EUR/TRY 1.68 1.70 1.72 1.76 1.78 1.72USD/TRY 1.20 1.25 1.30 1.35 1.34 1.30USD/ZAR 6.80 7.00 7.20 7.20 7.10 7.20USD/BRL 1.85 1.90 1.95 1.95 1.98 1.95

Source: SG FX Research, SG Economic research, KB economic & strategy research, SG Poland, BRD Economic Research

The information herein is not intended to be an offer to buy or sell, or a solicitation of an offer to buy or sell, any securities and including any expression of opinion, has been obtained from or is based upon sources believed to be reliable but is not guaranteed as to accuracy or completeness although Société Générale (“SG”) believe it to be fair and not misleading or deceptive. SG, and their affiliated companies in the SG Group, may from time to time deal in, profit from the trading of, hold or act as market-makers or act as advisers, brokers or bankers in relation to the securities, or derivatives thereof, of persons, firms or entities mentioned in this document or be represented on the board of such persons, firms or entities. Employees of SG, and their affiliated companies in the SG Group, or individuals connected to them may from time to time have a position in or be holding any of the investments or related investments mentioned in this document. SG and their affiliated companies in the SG Group are under no obligation to disclose or take account of this document when advising or dealing with or for their customers. The views of SG reflected in this document may change without notice. To the maximum extent possible at law, SG does not accept any liability whatsoever arising from the use of the material or information contained herein. Dealing in warrants and/or derivative products such as futures, options, and contracts for differences has specific risks and other significant aspects. You should not deal in these products unless you understand their nature and the extent of your exposure to risk. This research document is not intended for use by or targeted at private customers. Should a private customer obtain a copy of this report they should not base their investment decisions solely on the basis of this document but must seek independent financial advice. Notice to French Investors: This publication is issued in France by or through Société Générale ("SG") which is regulated by the AMF (Autorité des Marchés Financiers). Important Notice to UK Investors: The circumstances in which this publication has been produced are such that it is not appropriate to characterize it as impartial as referred to in the Financial Services Authority Handbook, for example because of reporting or remuneration structures or the physical location of the author of the material. However, it must be made clear that all research issued by SG will be clear, fair, and not misleading. This publication is issued in the United Kingdom by or through Société Générale ("SG") London Branch which is authorised and regulated by the Financial Services Authority ("FSA") for the conduct of its UK business. Notice to US Investors: This report is issued solely to major US institutional investors pursuant to SEC Rule 15a-6. Any US person wishing to discuss this report or effect transactions in any security discussed herein should do so with or through SG Americas Securities, LLC to conform with the requirements of US securities law. SG Americas Securities, LLC, 1221 Avenue of the Americas, New York, NY, 10020. (212) 278-6000. Some of the securities mentioned herein may not be qualified for sale under the securities laws of certain states, except for unsolicited orders. Customer purchase orders made on the basis of this report cannot be considered to be unsolicited by SG Americas Securities, LLC and therefore may not be accepted by SG Americas Securities, LLC investment executives unless the security is qualified for sale in the state. Analyst Certification: Each author of this research report hereby certifies that the views expressed in the research report accurately reflect his or her personal views about any and all of the subject securities or issuers. Notice to Japanese Investors: This report is distributed in Japan by Société Générale Securities (North Pacific) Ltd., Tokyo Branch, which is regulated by the Financial Services Agency of Japan. The products mentioned in this report may not be eligible for sale in Japan and they may not be suitable for all types of investors. Notice to Australian Investors: Société Générale Australia Branch (ABN 71 092 516 286) (SG) takes responsibility for publishing this document. SG holds an AFSL no. 236651 issued under the Corporations Act 2001 (Cth) ("Act"). The information contained in this newsletter is only directed to recipients who are aware they are wholesale clients as defined under the Act. http://www.sgcib.com. Copyright: The Société Générale Group 2007. All rights reserved.

Fixed Income, Forex & Credit Research

Global Head of Fixed Income, Forex & Credit Research Benoît Hubaud (33) 1 42 13 61 08 / (44) 20 7676 7168

Fixed Income & Forex Strategy Research Manager Denis Groven (33) 1 42 13 78 21

Head Vincent Chaigneau (44) 20 7676 7707

Credit Research

Fixed Income Adam Kurpiel (33) 1 42 13 63 42 Auto & Transportation Pierre Bergeron (33) 1 42 13 89 15

Khrishnamoorthy Sooben (44) 20 7676 7713 Stéphanie Herrault (33) 1 42 13 63 11

Ciaran O'Hagan (33) 1 42 13 58 60

Aro Razafindrakola (33) 1 42 13 64 93

Jose Sarafana (33) 1 42 13 56 59 Consumers & Services Sonia van Dorp (33) 1 42 13 64 57

Guillaume Baron (33) 1 42 13 57 07 Olivier Monnoyeur (33) 1 42 13 43 87

Caroline Duron (33) 1 58 98 30 32

Industrials Roberto Pozzi (44) 20 7676 7152

Foreign Exchange Carole Laulhere (33) 1 42 13 71 45 Ozana Breaban, CFA (44) 20 7676 7160

Murat Toprak (44) 20 7676 7491

David Deddouche (33) 1 42 13 56 22

Telecom & Media Satyajit Chatterjee (44) 20 7676 7023

Terry Nguyen, CFA (44) 20 7676 7162

Technical Analysis Hughes Naka (33) 1 42 13 51 10

Stephane Billioud (33) 1 42 13 35 55 Utilities Hervé Gay (33) 1 42 13 87 50 Fabien Manac'h (33) 1 42 13 88 35 Florence Roche (33) 1 42 13 63 99

Commodities Stéphanie Aymes (33) 1 42 13 57 03

Banks & Insurance Eleanor Yeh (44) 20 7676 7030

Quant Research

Head Julien Turc (33) 1 42 13 40 90

David Benhamou (33) 1 42 13 94 75

Benjamin Herzog (33) 1 42 13 67 49 High Yield

Marc Teyssier (33) 1 42 13 55 96 General Industries Adam Harnetty (44) 20 7676 7136

Sandrine Chapelon (33) 1 42 18 05 39 Nadia Yoshiyama, CFA (44) 20 7676 6985

Consumers & Services Sonia van Dorp (33) 1 42 13 64 57

Credit Strategy

Suki Mann (44) 20 7676 7063 ABS Jean-David Cirotteau (33) 1 42 13 72 52

Guy Stear, CFA (33) 1 42 13 40 26 Christopher Greener (44) 20 7676 7055

Juan Esteban Valencia (44) 20 7676 7059

Paris Tour Société Générale 17 cours Valmy 92987 Paris La Défense Cedex - France

London SG House – 41, Tower Hill London EC3 N 4SG United Kingdom

Hong Kong Level 38, Three Pacific Place 1 Queen's Road East Hong Kong

![[2007] Financial Contagion in Emerging Markets](https://img.dokumen.tips/doc/110x75/577d34ff1a28ab3a6b8f5564/2007-financial-contagion-in-emerging-markets.jpg)