Embed Size (px)

Citation preview

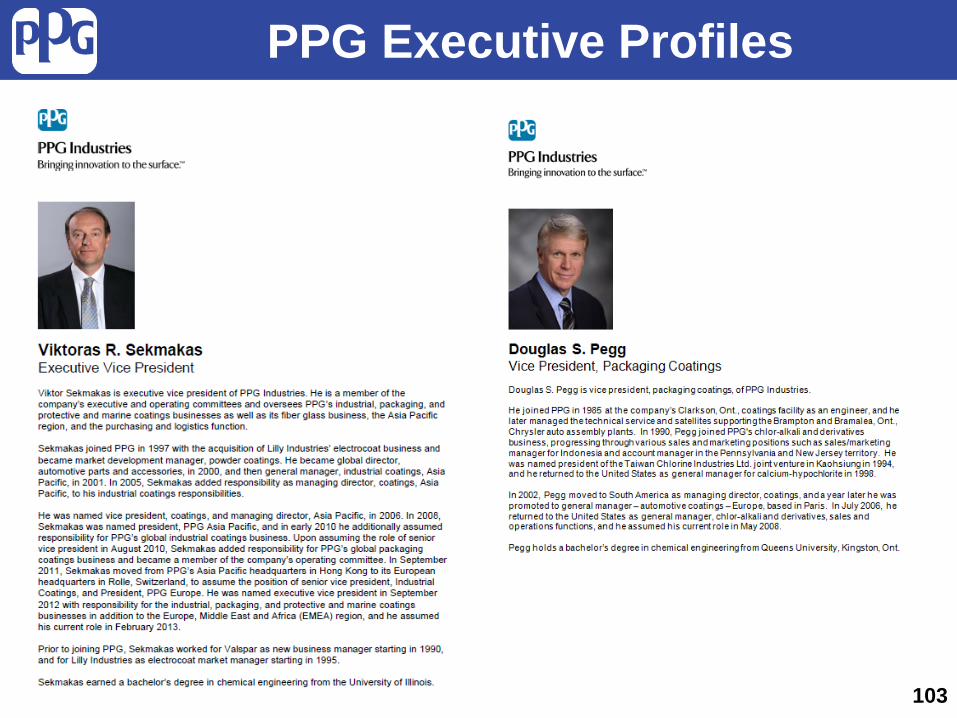

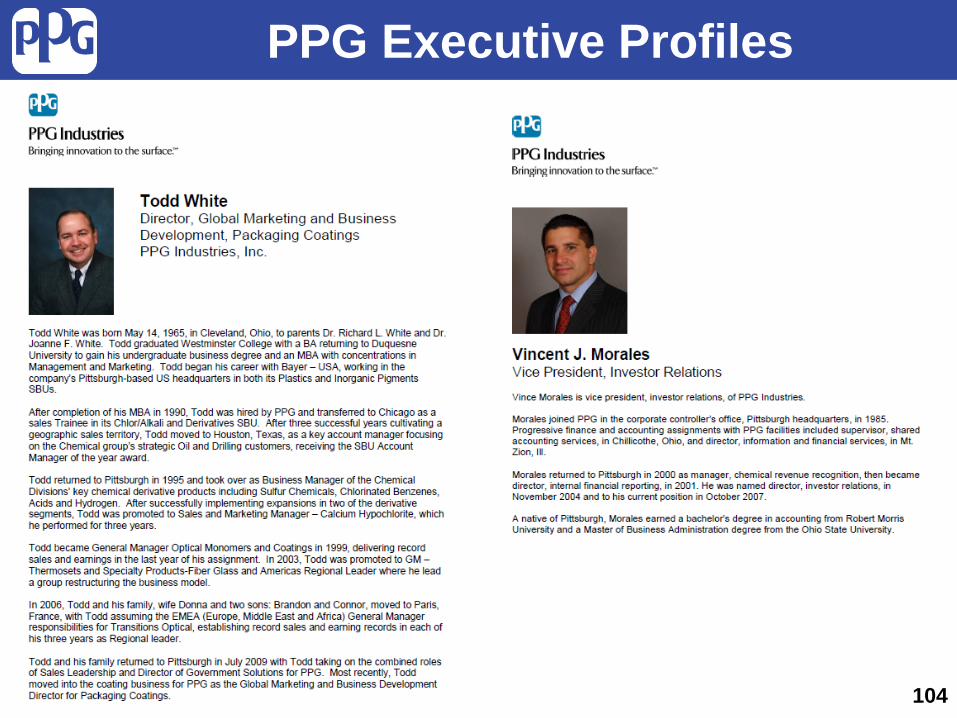

Doug Pegg Vice President, Packaging Coatings

Williamsburg, Virginia June 18, 2013

Information current as of June 18, 2013

Statements contained herein relating to matters that are not historical facts are forward-looking statements reflecting PPG’s current view with respect to future events and financial performance. These matters within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, involve risks and uncertainties that may affect PPG’s operations, as discussed in PPG’s filings with the Securities and Exchange Commission pursuant to Sections 13(a), 13(c) or 15(d) of the Exchange Act, and the rules and regulations promulgated thereunder. Accordingly, many factors could cause actual results to differ materially from the forward-looking statements contained herein. Such factors include global economic conditions, increasing price and product competition by foreign and domestic competitors, fluctuations in cost and availability of raw materials, the ability to maintain favorable supplier relationships and arrangements, the realization of anticipated cost savings from restructuring initiatives, difficulties in integrating acquired businesses and achieving expected synergies therefrom, economic and political conditions in international markets, the ability to penetrate existing, developing and emerging foreign and domestic markets, foreign exchange rates and fluctuations in such rates, fluctuations in tax rates, the impact of future legislation, the impact of environmental regulations, unexpected business disruptions, and the unpredictability of existing and possible future litigation, including litigation that could result if the asbestos settlement discussed in PPG’s filings with the Securities and Exchange Commission does not become effective. However, it is not possible to predict or identify all such factors. Consequently, while the list of factors presented here and in PPG’s Form 10-K for the year ended December 31, 2012 are considered representative, no such list should be considered to be a complete statement of all potential risks and uncertainties. Unlisted factors may present significant additional obstacles to the realization of forward-looking statements. Consequences of material differences in results compared with those anticipated in the forward-looking statements could include, among other things, business disruption, operational problems, financial loss, legal liability to third parties and similar risks, any of which could have a material adverse effect on PPG’s consolidated financial condition, results of operations or liquidity. All information in this presentation speaks only as of June 18, 2013, and any distribution of this presentation after that date is not intended and will not be construed as updating or confirming such information. PPG undertakes no obligation to update any forward-looking statement, except as otherwise required by applicable law.

Forward-Looking Statements Forward Looking Statements

2

Welcome

3

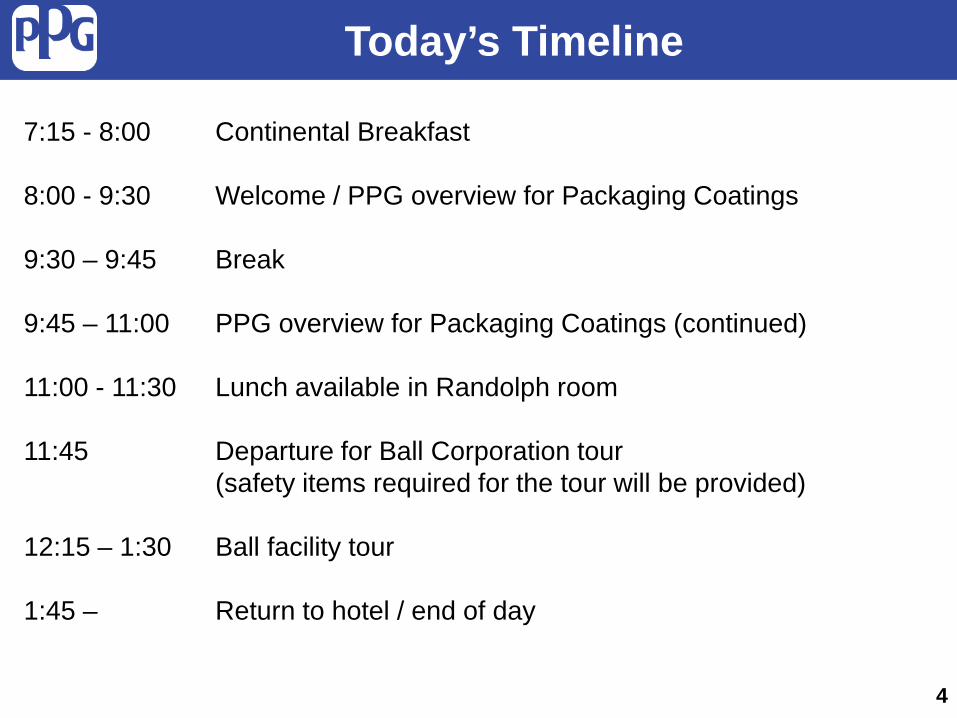

Today’s Timeline

4

7:15 - 8:00 Continental Breakfast 8:00 - 9:30 Welcome / PPG overview for Packaging Coatings 9:30 – 9:45 Break 9:45 – 11:00 PPG overview for Packaging Coatings (continued) 11:00 - 11:30 Lunch available in Randolph room 11:45 Departure for Ball Corporation tour (safety items required for the tour will be provided) 12:15 – 1:30 Ball facility tour 1:45 – Return to hotel / end of day

PPG “Deep Dive” Program

5

Meeting objective – Provide a deeper understanding of the various PPG

businesses and coatings industry sub-segments in which we operate

Typical day:

o End-use segment / industry (i.e., packaging coatings) details

o Customers

o Products / complexities

o Competitive landscape

o Geographic differences

o PPG’s participation in the segment(s)

o PPG’s growth opportunities

o Site visit to visually see PPG products “at work” for our customers

PPG “Deep Dive” Program

6

PPG Deep Dive is NOT:

o Not a PPG investor day

o Not an update on the quarter or current business trends

o Not a discussion on other PPG businesses

o Not a strategic update

Education is the focus; Strong Q&A / participation desired

Year Topic(s) Location Details

2006 Transitions Transitions HQ Tampa, FL Overview of PPG’s Transitions Optical joint venture

2007 PPG Aerospace PPG aerospace facility Huntsville, AL

Discussed PPG’s participation in the Aerospace coatings, sealants and transparency market

2008 SigmaKalon Acquisition Overview

Offsite Reviewed details (markets, customers, regional

coverage, etc.) of PPG’s largest acquisition which closed in January, 2008

2010 PPG Asia and PPG

Auto OEM Coatings

BMW facility Greenville, SC

Provided details of PPG’s Asian operations and rapid growth history/prospects. Overview of PPG’s

automotive OEM coatings business and auto OEM end-market dynamics.

2011 PPG Automotive Refinish

Penske Racing facility Charlotte, NC

Detailed review of global coatings auto collision repair market, including distribution processes and key customer requirements. Review of PPG’s new

technologies addressing market needs.

2012 PPG Industrial Coatings

Harley Davidson facility York, PA

Overview of the broad, consolidating general industrial coatings market with various product

segmentation around end-use, application methodology and substrate.

2013 PPG Packaging Coatings

Ball Container facility Williamsburg, VA

Discuss packaging coatings industry, current market and product trends and growth opportunities.

PPG “Deep Dive” Program

7

Packaging Coatings Industry Industry End-Market Mix by Dollar

Value of Sales (~$100B)

Protective & Marine

13%

Aerospace 2%

Packaging 3%

Architectural 43%

Industrial 26%

Refinish 7%

Auto OEM 6%

Source: Coatings World, Company Annual Reports, PPG estimates 8

Global Market Position Packaging Coatings

(~$3B)

PPG #2 Position

AkzoNobel #3 Position

Sherwin Williams

No meaningful presence

Axalta (formerly Dupont)

No meaningful presence

Valspar #1 Position

Global Coatings Companies – Packaging Coatings Positions

Packaging a key special purpose coating segment PPG has #2 global position

Packaging Coatings

9

Presentation Agenda

10

►Packaging Industry Overview

►Packaging Coatings Overview

►Metal Packaging Types

►PPG’s Packaging Coatings Business

►Industry Trends / Growth Opportunities

►Ball Container and Plant Tour

Packaging Coatings

Definitions and Acronyms: 2 PIECE CAN (2Pc): A metal can that has two parts; a stamped and drawn body and a

can end. Two piece cans are either Drawn and Wall Ironed (DWI or D&I) or Draw-Redraw (DRD), and are made from steel or aluminum

3 PIECE CAN (3Pc): A metal can, usually made of tinplate, whose body is welded at the side seam and has two ends.

B&B: Beer and beverage BPA: Bisphenol A, a major component of epoxy resins used in can coatings BPA-NI: BPA Non-Intent – reflects products with BPA not intentionally added COMPOUND: Also called seaming compound; a sealing material consisting of a water or

solvent emulsion of latex or synthetic rubber. Seaming compound is placed in the curl of the can end for an air tight (hermetic) seal

CSD: Carbonated soft drink DRD (D.R.D. CAN): Draw-redraw can - a can produced by forming a cup and subjecting

the cup to one or more re-drawing processes. Each re-drawing operation reduces the diameter and increases the height of the finished can

DWI (D.W.I. CAN): A drawn and wall ironed can - a two piece can made of aluminum or tinplated steel that is produced by forming a cup and then drawing and ironing the sidewall of the cup into a finished can

11

Packaging Coatings (continued)

Definitions and Acronyms: EOE (EASY OPEN END): A can end typically made of steel or aluminum that has a self-

contained fixture for opening the can and permitting removal of the contents of the container

FAEOE (FULL APERTURE EASY OPEN END): The full end of the can is opened by the use of a pull ring

FAGL: Food, Aerosol and General Line G1: PPG’s solvent-based easy open end coating used in Beer & Beverage GENERAL LINE & AEROSOLS: Cans for uses other than food and beverage LAMINATES: A thermoplastic polymer system e.g. PET, polyolefins, nylon, etc., bonded

to the coil fed metal substrate (steel or aluminum) MAT: Monobloc, aerosols and tubes RETORT: When foods are sterilized in the can using superheated steam under pressure.

Conditions are usually specified by the customer (i.e.: 90' @ 250°F) UV RIMCOAT: A coating used to coat the bottom rim on a two piece beer and beverage

can. This coating, while giving protection to the metal substrate, is intended primarily to improve the movement (mobility) of the can through the can filling line

W1: PPG’s waterborne easy open end coating for Beer & Beverage

12

Global Packaging Mix

Sources: Can Manufacturers Institute (CMI), Ernst & Young

Metal 10.9%

Rigid plastic 22.4%

Glass 10.4%

Liquid cartons

4.9%

Paper-based

containers 11.3%

Flexible packaging

39.9%

Other packaging

0.2%

Metal food can 2.3%

Metal beverage

can 7.6%

Metal aerosol

can 0.2% Metal tins

0.3%

Aluminum trays 0.1%

Collapsible metal tubes 0.1% Other

metal 0.2%

13

Today’s presentation focus is on metal packaging

All packaging types ~$400B

Global Packaging Industry

Source: CocaCola, Freedonia 14

Rigid Flexible / Plastic

Metal Glass Rigid Plastic Pouch Aseptic

Carton

Growth 2-3% 1-2% 2-4% 2-3% 4-5%

Cost vs. can 1x 2x 1.5x 0.8x 1x

Market Advantages

• Recyclability • Long shelf life • Portability • Product content

flexibility

• Recyclability • Food

protection

• Cost • Design

flexibility

• Easy to use • Brand

customization

• Resealable • Pack

perishables

Market Drawbacks

• Container not resealable

• Slower filling • Freight costs • Energy

intensity

• Shelf life • Recycling

• Shelf life • Retort

capability

• Recycling • Shelf-life

Coating Importance Key Enabler N/A N/A Decorative if any Decorative if any

Cans, 41% Plastic, 35%

Glass, 16% Paper, 6%

Box/Pouch, 2%

~240 billion units

U.S. Beverage Packaging Market

Unit Volume by Substrate

15 Source: Euromonitor, PPG estimates

Cans are the main package in a developed market like U.S. beverage

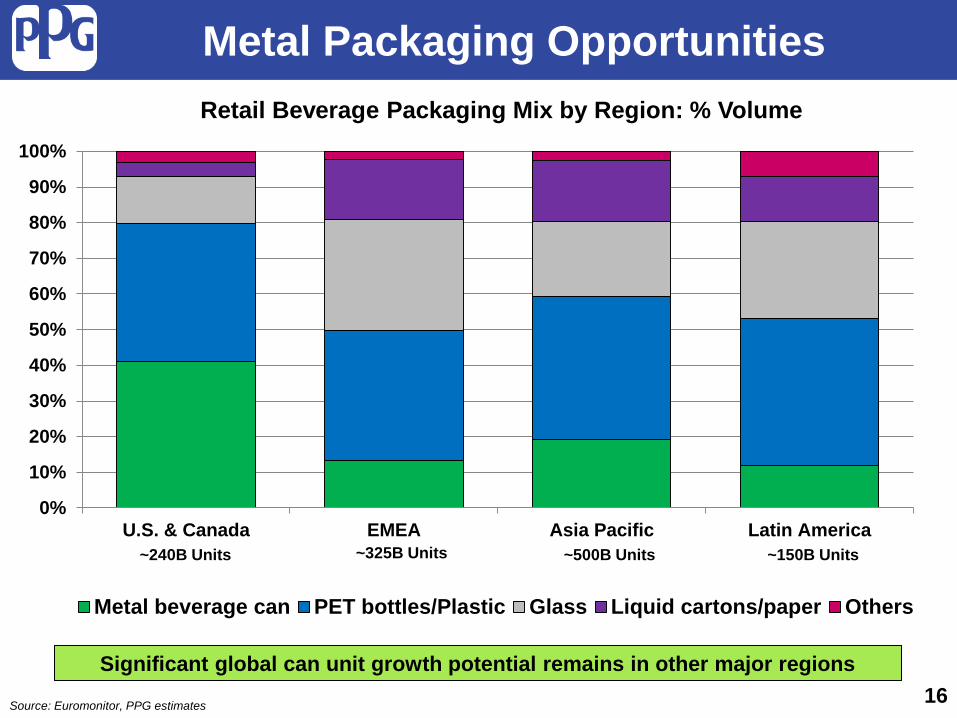

Metal Packaging Opportunities

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

U.S. & Canada EMEA Asia Pacific Latin America

Retail Beverage Packaging Mix by Region: % Volume

Metal beverage can PET bottles/Plastic Glass Liquid cartons/paper Others

~500B Units ~325B Units ~240B Units ~150B Units

Significant global can unit growth potential remains in other major regions

Source: Euromonitor, PPG estimates 16

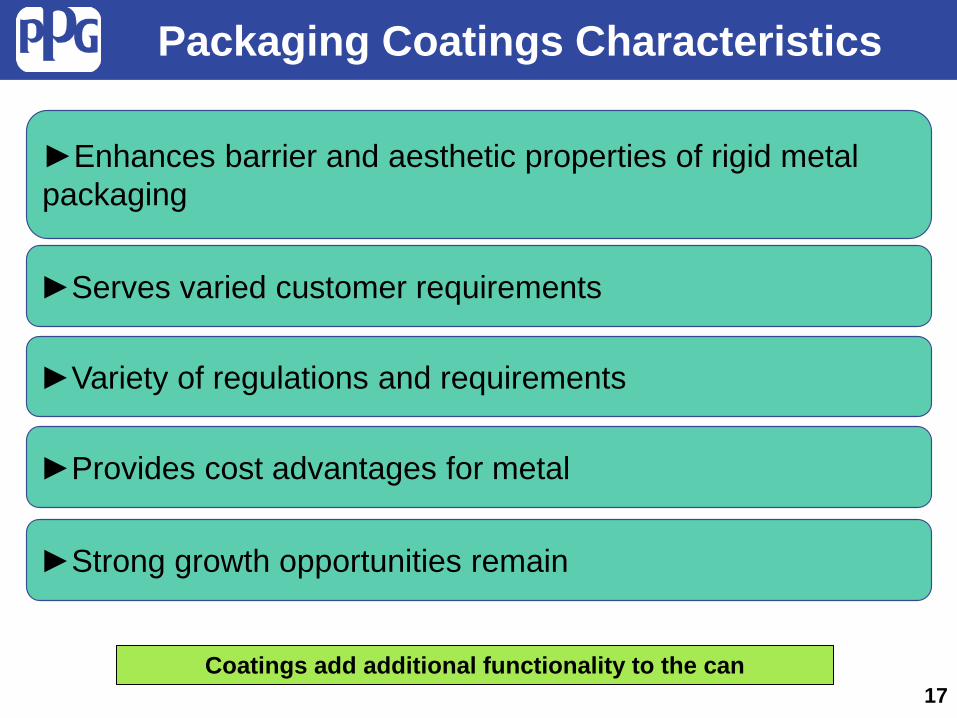

Packaging Coatings Characteristics

17

►Enhances barrier and aesthetic properties of rigid metal packaging

►Serves varied customer requirements

►Variety of regulations and requirements

►Provides cost advantages for metal

►Strong growth opportunities remain

Coatings add additional functionality to the can

Feature Description Implication Chemical Resistance Coatings must withstand a

wide variety of food types from very acidic peppers to

mild products such as beans

Coatings can keeps food safe for several years. A

failure could lead to corrosion and ultimately food

spoilage Flexibility

Coatings must be able to withstand the forming of the can or end after application

Flexible - allows for unique can designs that enable

metal reduction. Corrosion could result if the coating is

not flexible enough Application

Coatings must applied at high speed levels

Higher application speeds result in increased

productivity for the customer

Process-ability Coatings must be able to

withstand heat and pressure for cooking or retort

Retorting sterilizes the packed food ensuring food

safety

Coatings Characteristics - Metal Packaging

18

Resiliency of the Can

PET Container

1800 1900 1950 1960 1970 1980 1990 2000

Food Can

Aerosol Can

Beer Can

Tetra Pack

Al Bev Can 2pc

DWI Food Metal Tube

FAEOE Bottle Cans

• Long history of growth for metal

packaging • Sustainability, performance and

cost drive metal can growth despite availability of alternative packaging

• Innovation/design capabilities are key for customers

Packaging Can History

0

100

200

300

400

Can

s (b

illio

ns)

Global Beverage Cans Produced

Source: Canmaker Institute, EuroMonitor 19

Can Provides Unique Packaging Attributes

Sustains pasteurization & sterilization

Easily transportable around the globe

Long shelf life for consumer convenience

Nutritional value retained

Tuna Can Demonstrates Global Functionality

Thailand

Where tuna is caught

Pacific

Southern Ocean

Indian

Atlantic & Med

Where tuna is canned (Top 4 regions)

Spain, France

66%

20%

9%

5%

Where canned tuna is consumed

Philippines

Ecuador

UK 9%

25%

Japan 9%

Mexico 7%

Spain 9%

Can Remains Critical Packaging Material

Can’s functional attributes remain key factor to longevity 22

The steel food can is one of the safest types of food packaging. It is tamper resistant, provides an airtight seal, is thermally sterilized and shelf stable. – Food & Drug Administration The canning process locks in nutrients at the peak of freshness, and due to lack of oxygen during storage, canned fruits and vegetables remain stable giving them longer shelf life. – Canned Food Alliance

Source: Canned Food Alliance

Cans provide important nutrients often at a lower cost per nutrient than fresh, frozen or dried forms.

Canned foods do not necessarily need preservatives. The heating process used after the can is filled and sealed ensures the food’s quality.

Packaging Growth Continues

Metal packaging remains one of the most utilized materials in growing industry

0

200

400

600

800

1000

1200

1400

1600

2004 2009 2013

Bill

ions

of U

nits

Other

Flexible plastic

Liquid cartons

Glass

PET bottles

Metal beveragecan

CAGR

4%

5% 7%

2%

6%

3%

Source: Euromonitor 23

Metal Packaging Coatings Market Segmentation

Others Beverage

Food, Aerosol and General Line (FAGL)

Source: PPG Estimates

Market Segmentation

Beverage Bodies = interior & exterior coatings

Beverage EOE = end coatings

Food = interior, exterior & end coatings

General Line & Aerosols = interior & exterior coatings

Caps & closures = interior & exterior coatings Monobloc, Aerosols & Tubes = interior & exterior coatings

Other = inks, pretreatment, compounds 24

Packaging Coatings End-Use Markets

Estimated Market $3B 20-25% 10-15% 5-10% 25-30% 5-10% 5-10% 15-20%

Top 3 Share % 65-70% 90-95% 95-100% 45-50% 70-75% 45-50% 55-60% 25-30%

Market Growth 3% 4% 5% 2% 2% 2% 4% 2%

PPG Position Top 3 Top 3 Top 3 Top 3 Top 3 Top 3 Top 3 Top 3

# of Customers tens tens hundreds hundreds hundreds hundreds hundreds

Macro Drivers

Metal packaging serves a variety of different segments

Total Packaging

•Standard of Living

•Glass Bottle Restriction in Asia

•“Green”

•Standard of Living

•Glass Bottle Restriction in Asia

•“Green”

•Changing Consumer Tastes

• Industrial Production

•Residential Construct-ion

•Standard of Living

•Changing Consumer Tastes

•Dietary Trends

•Global GDP Growth

•Standard of Living

•Birth Rates

•Personal Care Habits

•Growing Middle Class

Caps &

Closures

Bodies

Source: IRFAB, KNG, Orr & Boss and PPG Estimates

Other

•Brand Owner Design Capability

Food

Ends

Aerosol & General Line

Food, Aerosol & General Line

Beer & Beverage Monobloc &

Tubes

25

Metal Packaging Segment Examples

Food, Aerosol, General Line (FAGL)

Beer & Beverage

Food 25-30%

Caps and Closures

5-10%

3Pc Aerosol & General Line

5-10%

Monobloc Aerosol & Tubes

5-10%

2Pc DWI

FAEOE

3Pc Food

Draw-ReDraw (DRD)

Beverage Closures

Food Closures

3Pc Aerosol

General Line / Drums

Monobloc Aerosol

Aluminum Tubes

2Pc & 3Pc Bodies 20-25%

Easy Open Ends

10-15%

Source: PPG Estimates

Other

Other 15-20%

26

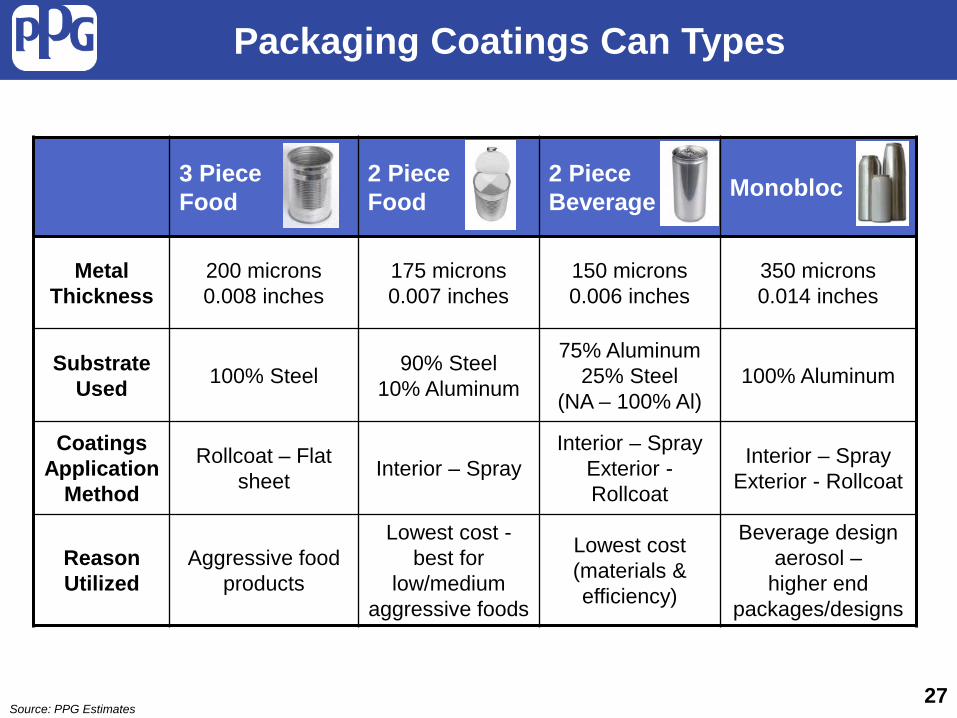

3 Piece Food

2 Piece Food

2 Piece Beverage Monobloc

Metal Thickness

200 microns 0.008 inches

175 microns 0.007 inches

150 microns 0.006 inches

350 microns 0.014 inches

Substrate Used 100% Steel 90% Steel

10% Aluminum

75% Aluminum 25% Steel

(NA – 100% Al) 100% Aluminum

Coatings Application

Method

Rollcoat – Flat sheet Interior – Spray

Interior – Spray Exterior - Rollcoat

Interior – Spray Exterior - Rollcoat

Reason Utilized

Aggressive food products

Lowest cost -best for

low/medium aggressive foods

Lowest cost (materials & efficiency)

Beverage design aerosol –

higher end packages/designs

Packaging Coatings Can Types

27 Source: PPG Estimates

Market Percent Application Method Viable For:

15-20%

Primary Purpose: For application of interior coatings of preformed cans

Advantages: Can coat non-planar surfaces

Application Challenges:

Maintain high transfer efficiency (75%), film thickness/coverage uniformity, increasing line speeds

Major Segments Used:

2Pc bev, 2Pc food, MAT

Types of Coating Application Spray Coating

28

Market Percent Application Method Viable For:

10-15%

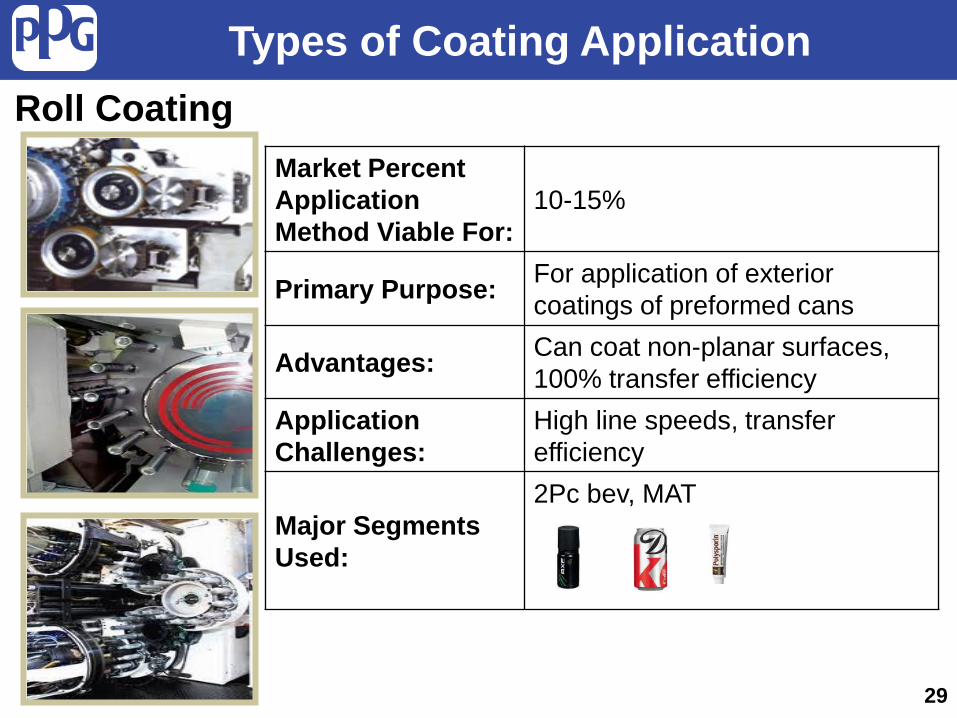

Primary Purpose: For application of exterior coatings of preformed cans

Advantages: Can coat non-planar surfaces, 100% transfer efficiency

Application Challenges:

High line speeds, transfer efficiency

Major Segments Used:

2Pc bev, MAT

Types of Coating Application Roll Coating

29

Market Percent Application Method Viable For:

60-65%

Primary Purpose: For application of interior and exterior coatings for steel/aluminum coils and sheets

Advantages: 100% transfer efficiency, low maintenance

Application Challenges:

Planar surfaces only, may require multiple layers, can formed after coating applied

Major Segments Used:

3Pc bev, 3Pc food, DRD, FAEOE, Caps and Closures, General line, 3Pc Aerosol, Bev EOE

Types of Coating Application: Coil and Sheet Coatings

30

Typical Metal Can Coatings: 3 Pc Food

3 Piece Food

Side Seam Stripe (SSS) –

Coating applied after the can is fabricated to protect the welded seam from corrosion

Ext. Clear - Protects metal from corrosion & assists in can mobility during processing

Interior Gold - Protects metal from corrosion

31

Note: Many food cans are heated after filled/sealed to sterilize contents. Coating must be

flexible due to can expansion/contraction

Typical Metal Can Coatings: 2 Pc Food DWI

2 Piece Food Drawn & Wall Ironed (DWI) Full Aperture Easy Open End (FAEOE)

Inside Spray

Washcoat

Post Repair Spray (PRS)

FAEOE Interior FAEOE Ext.

32

Typical Metal Can Coatings: 2 Pc Beverage

Over Varnish (OV) – protects the ink, allows movement in the filling can line, prevents scuffing during transportation

Inside Spray (IS) – prevents corrosion from packed product

Rim Coat - prevents corrosion of bottom of cans and allows for movement in the filling equipment

Easy Open End (EOE) Coating – prevents corrosion and assists in stamping of the end (Interior and Exterior)

2 Piece Beverage

Inks – provides decoration

33

Metal Can Coatings: General Line & Aerosol

General Line Aerosol

Interior coating: Protects metal from corrosion

Side Seam Stripe (SSS): Coating applied after the can is fabricated to protect the welded seam from corrosion

External coating: Protects metal from corrosion & assists in can mobility during processing

Inks and basecoats: Provides color and decoration

34

Typical Metal Can Coatings: Monobloc & Tubes

Monobloc Tubes

Over Varnish (OV) – protects the ink, allows movement in the filling can line, prevents scuffing during transportation

Inks and basecoats provides color and decoration

Inside Spray (IS) – prevents corrosion from packed product

Over Varnish (OV) – protects the ink, and provides various gloss effects

35

PPG Position

36

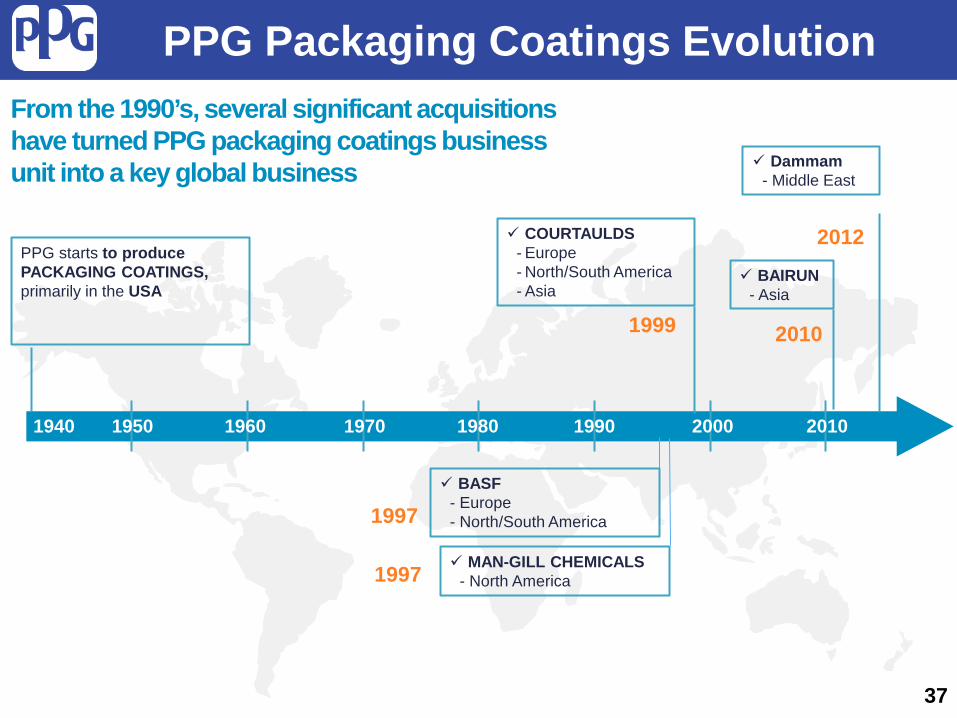

1999

1940 1950 1960 1970 1980 1990 2000 2010

From the 1990’s, several significant acquisitions have turned PPG packaging coatings business unit into a key global business

PPG starts to produce PACKAGING COATINGS, primarily in the USA

1997 MAN-GILL CHEMICALS - North America

COURTAULDS - Europe - North/South America - Asia

1999

BAIRUN - Asia

2010

PPG Packaging Coatings Evolution

Dammam - Middle East

2012

BASF - Europe - North/South America 1997

37

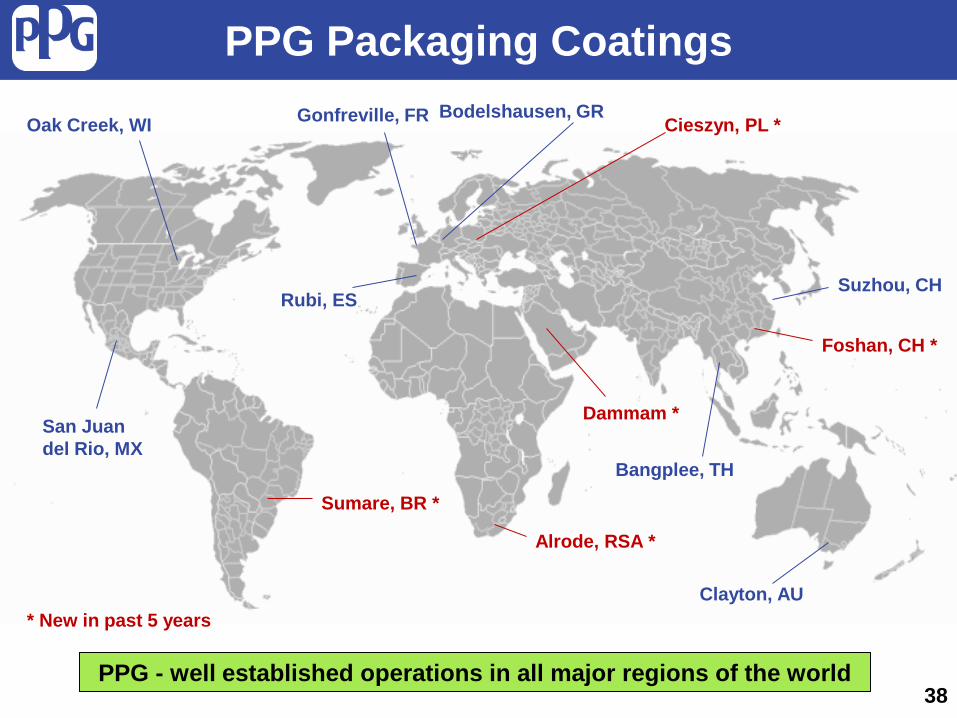

PPG Packaging Coatings

Oak Creek, WI

Sumare, BR *

Bodelshausen, GR Gonfreville, FR

Rubi, ES

Cieszyn, PL *

Alrode, RSA *

Dammam *

Suzhou, CH

Foshan, CH *

Clayton, AU

Bangplee, TH

San Juan del Rio, MX

38 PPG - well established operations in all major regions of the world

* New in past 5 years

PRODUCT RANGE

Beverage cans Food cans

Aerosols and tubes

Promotional packaging (General Line)

Complete systems ranging from pre-treatment,

coatings, compounds and

inks, for aluminium & steel cans and

ends.

Specialty packaging (General Line)

Industrial packaging

(General Line)

PPG Product Range

39

Caps & Closures

02/26/13

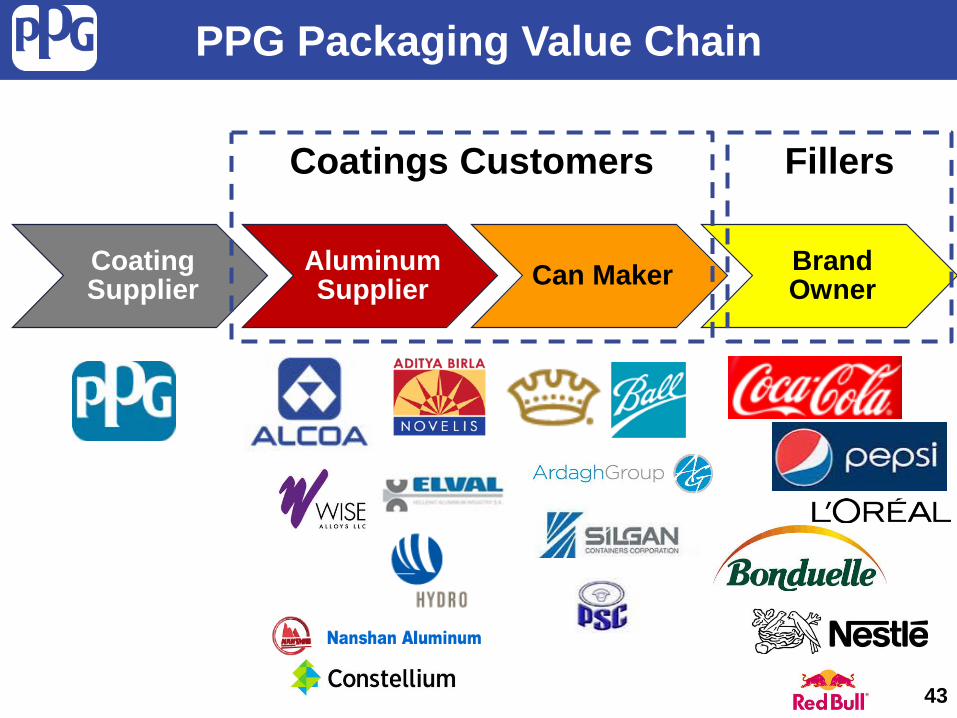

Value Chain

Coating Supplier

Aluminum Supplier Can Maker Brand

Owner

PPG Packaging Value Chain

40

02/26/13

Value Chain

Coating Supplier

Aluminum Supplier Can Maker Brand

Owner

PPG Packaging Value Chain

Coatings Customers

41

Packaging Coatings Can Makers

42 Can maker size ranges from large multi-national to local

02/26/13

Value Chain

Coating Supplier

Aluminum Supplier Can Maker Brand

Owner

PPG Packaging Value Chain

Coatings Customers Fillers

43

Packaging Coatings Fillers

44

EMEA > $1B

Customers Expected to Consolidate as Regions Mature

Others

Top 10 Customers Others

North America < $1B

Others

Asia Pacific > $0.5B

Top 10 Customers

Others

South America < $0.5B

Total Packaging Coatings Industry Customers Mix by Region

Top 10 Customers

Top 10 Customers

45 Source: PPG Estimates

Packaging Coatings Summary

46

►Highly sophisticated/technical coatings that preserve can contents and provide customers aesthetics/marketing advantages

►Array of coatings required for variety of application methods and different can types

►Global and local customers (further consolidation expected)

►High level of customer intimacy, including production yields

►Customer brand protection

►Government coatings product approval required in many cases

Food and beverage packaging coatings are highly complex

Products

Customers

Regulatory and

Legislative ►Legislative landscape driving new technologies globally

Recent Industry Trends

47

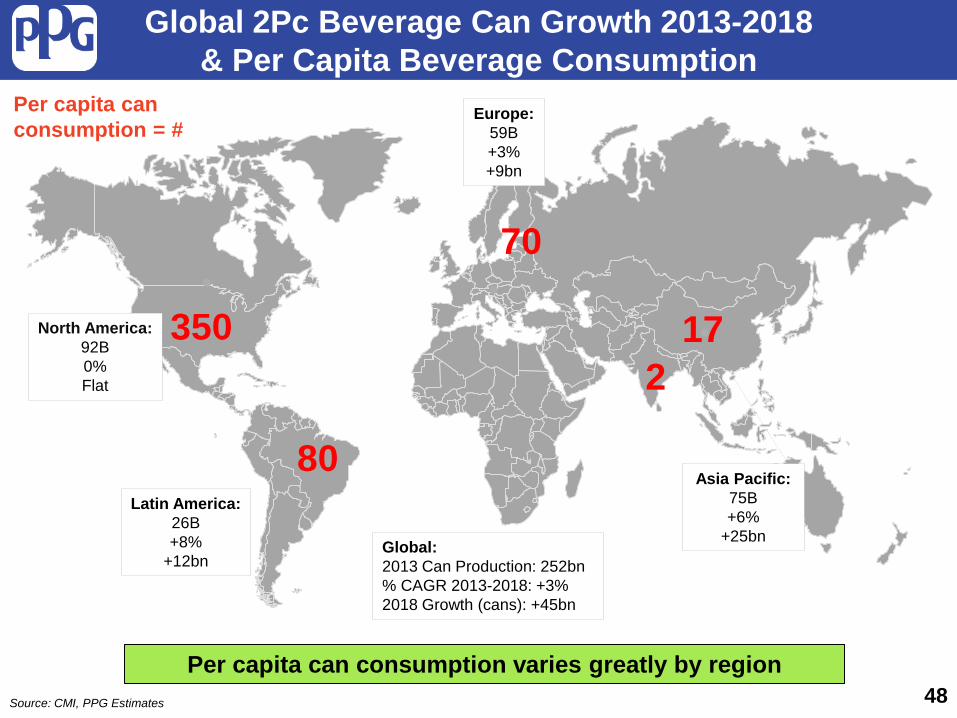

Asia Pacific: 75B +6%

+25bn

Europe: 59B +3% +9bn

Latin America: 26B +8%

+12bn

North America: 92B 0% Flat

Global 2Pc Beverage Can Growth 2013-2018 & Per Capita Beverage Consumption

Global: 2013 Can Production: 252bn % CAGR 2013-2018: +3% 2018 Growth (cans): +45bn

350 17

70

80

Per capita can consumption = #

48 Per capita can consumption varies greatly by region

Source: CMI, PPG Estimates

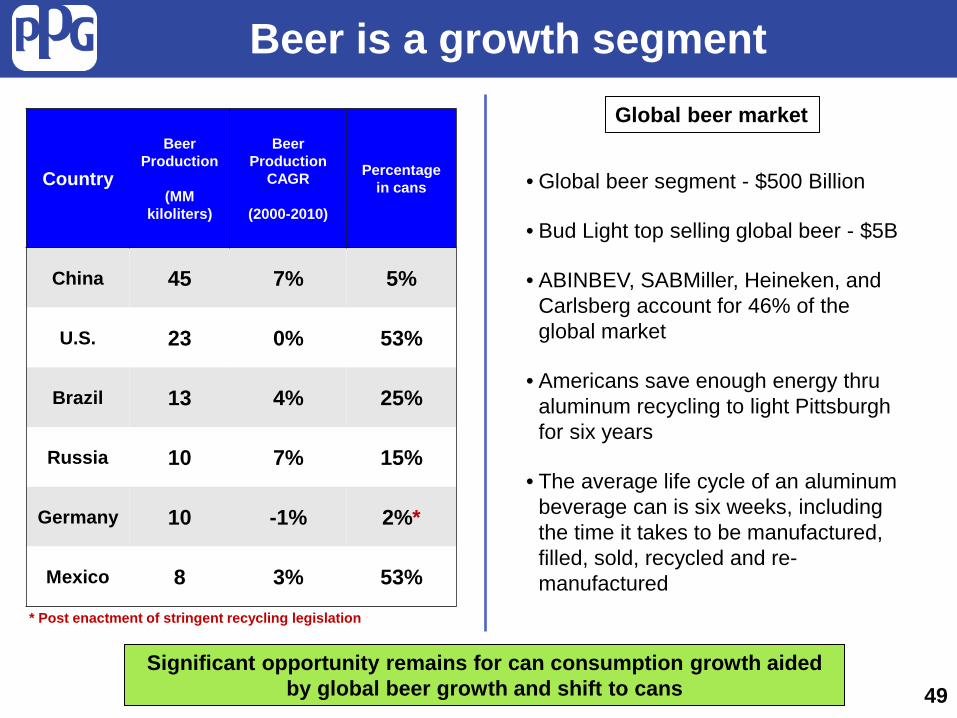

2

• Global beer segment - $500 Billion

• Bud Light top selling global beer - $5B

• ABINBEV, SABMiller, Heineken, and Carlsberg account for 46% of the global market

• Americans save enough energy thru aluminum recycling to light Pittsburgh for six years

• The average life cycle of an aluminum beverage can is six weeks, including the time it takes to be manufactured, filled, sold, recycled and re-manufactured

Country

Beer Production

(MM

kiloliters)

Beer Production

CAGR

(2000-2010)

Percentage in cans

China 45 7% 5%

U.S. 23 0% 53%

Brazil 13 4% 25%

Russia 10 7% 15%

Germany 10 -1% 2%*

Mexico 8 3% 53%

Beer is a growth segment

49 of 129 49

* Post enactment of stringent recycling legislation

Significant opportunity remains for can consumption growth aided by global beer growth and shift to cans

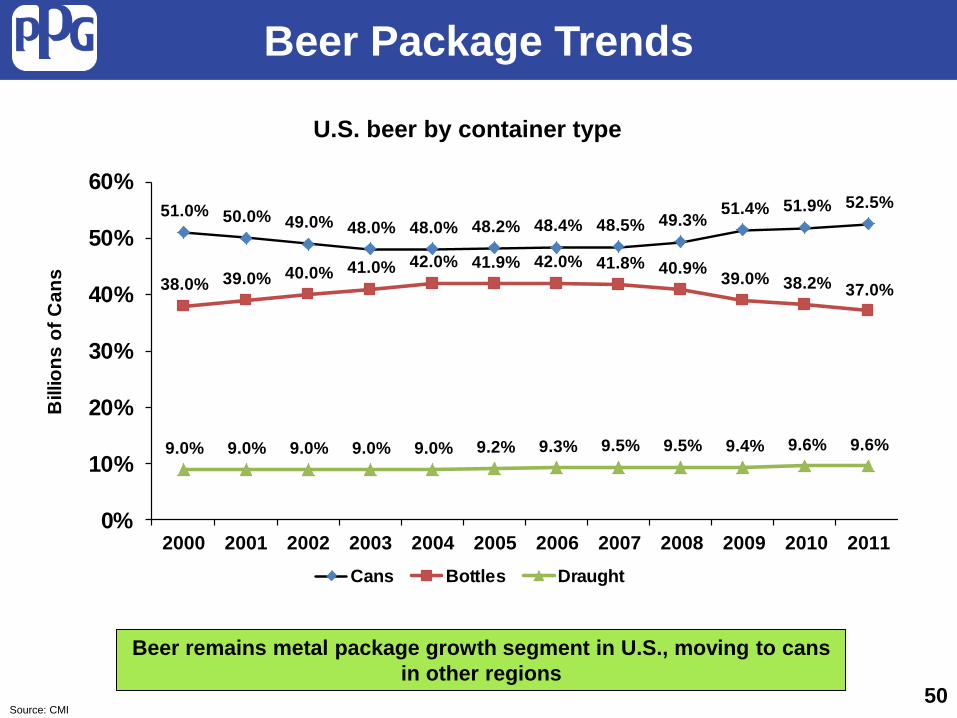

Global beer market

51.0% 50.0% 49.0% 48.0% 48.0% 48.2% 48.4% 48.5% 49.3% 51.4% 51.9% 52.5%

38.0% 39.0% 40.0% 41.0% 42.0% 41.9% 42.0% 41.8% 40.9% 39.0% 38.2% 37.0%

9.0% 9.0% 9.0% 9.0% 9.0% 9.2% 9.3% 9.5% 9.5% 9.4% 9.6% 9.6%

0%

10%

20%

30%

40%

50%

60%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Bill

ions

of C

ans

Cans Bottles Draught

Beer Package Trends

Source: CMI 50

Beer remains metal package growth segment in U.S., moving to cans in other regions

U.S. beer by container type

Packaging Innovation Concentrated around Consumption Cycle Stages

Source: CMI & Ball Corp

Green-Driven

Utility-Driven

Visual Appeal

Quality-Driven

• Creating environmentally friendly packaging

• Example: Ball’s ReAlTM metal technology

• Providing convenience and added value to consumers with features

• Example: aluminum re-sealable bottles & full aperture beverage end

• Providing features that enhance the quality of the product, perceived or actual

• Example: SmoothPour® end

• Spurring interest and intrigue with eye-catching iconic components of packaging

• Example: High-res photo quality ink printing & customizable laser-incised tabs

Post Consumption

Pre-Consumption

During Consumption

51

• Broader range of can sizes increase brand owner offering

Brand Owners Using Can to Rejuvenate Products

• 500MM bottle cans

• 3 new can manufacturing lines in U.S.

Bow-Tie Can

Slim Can

• Multiple shapes re-invigorate brands

• Can design intended to draw younger consumers to brand

• Slimmer shape targeting energy drinks and women

Bottle Can

Expanded Size

52

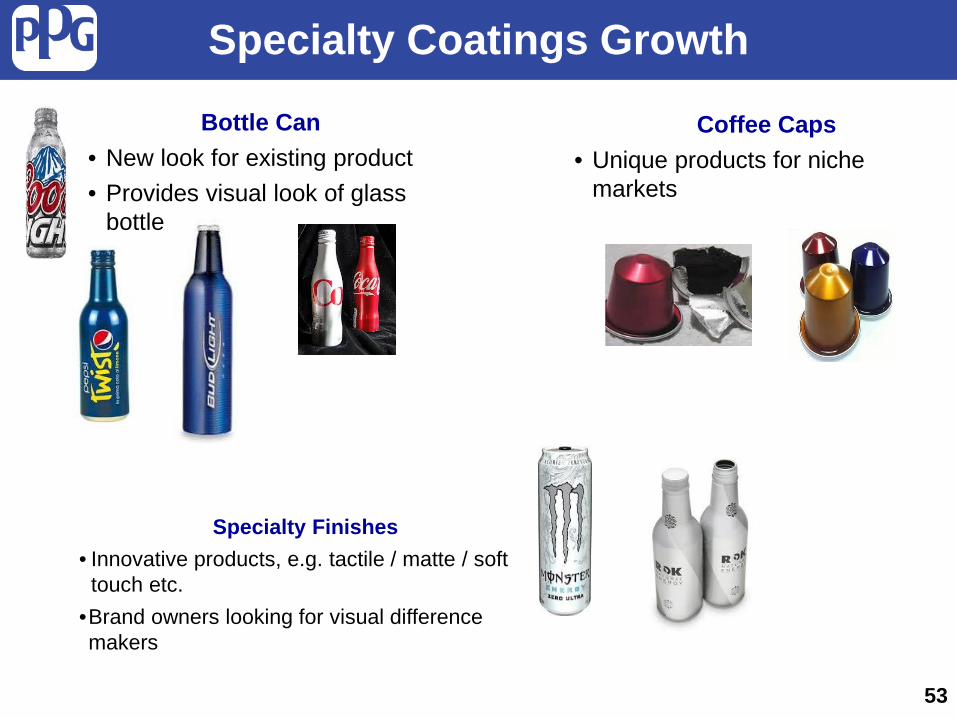

Specialty Coatings Growth

Specialty Finishes • Innovative products, e.g. tactile / matte / soft

touch etc. •Brand owners looking for visual difference makers

Bottle Can • New look for existing product • Provides visual look of glass

bottle

Coffee Caps • Unique products for niche

markets

53

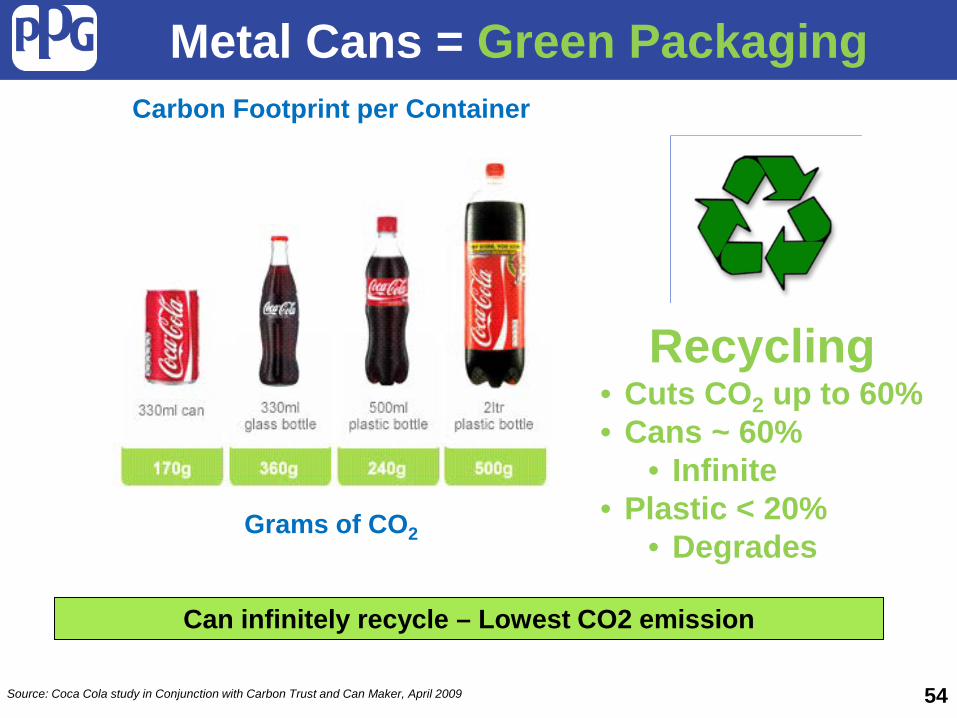

Metal Cans = Green Packaging

Can infinitely recycle – Lowest CO2 emission

Recycling • Cuts CO2 up to 60% • Cans ~ 60%

• Infinite • Plastic < 20%

• Degrades

Source: Coca Cola study in Conjunction with Carbon Trust and Can Maker, April 2009

Carbon Footprint per Container

Grams of CO2

54

U.S. Recycling Rates (%)

Aluminum Beverage Can Steel Containers

0

10

20

30

40

50

60

70

80

90

100

2003 2004 2005 2006 2007 2008 2009 2010 20110

10

20

30

40

50

60

70

80

90

100

2003 2004 2005 2006 2007 2008 2009 2010

55 Recycling rates on the rise

Source: CMI

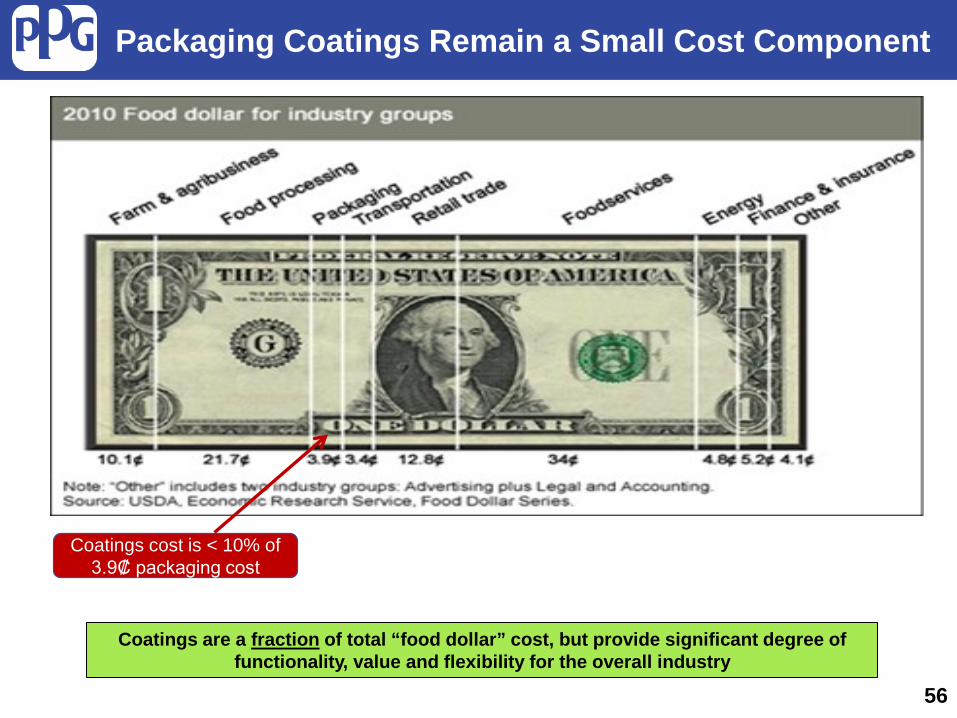

Packaging Coatings Remain a Small Cost Component

Coatings are a fraction of total “food dollar” cost, but provide significant degree of functionality, value and flexibility for the overall industry

56

Coatings cost is < 10% of 3.9₡ packaging cost

Key Industry Trends

57

• BPA-NI Development and Commercialization • Growth Opportunities in Emerging Regions

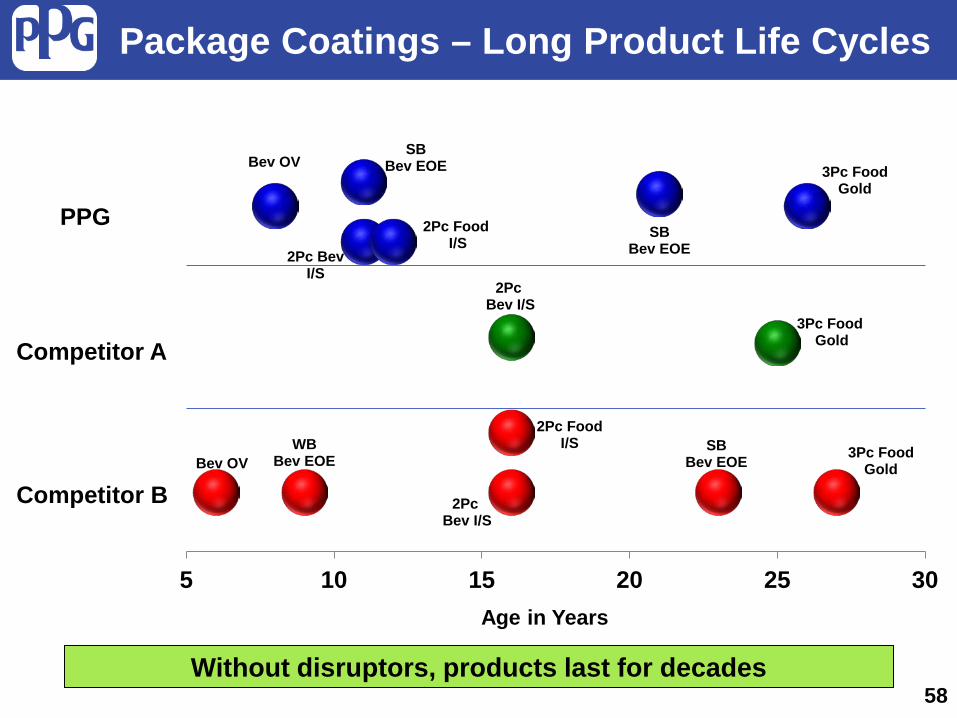

Package Coatings – Long Product Life Cycles

SB Bev EOE

WB Bev EOE

SB Bev EOE

SB Bev EOE

2Pc Bev I/S

2Pc Bev I/S

2Pc Bev I/S

3Pc Food Gold

3Pc Food Gold

3Pc Food Gold

2Pc Food I/S

2Pc Food I/S

Bev OV

Bev OV

5 10 15 20 25 30Age in Years

PPG

Competitor B

Competitor A

58 Without disruptors, products last for decades

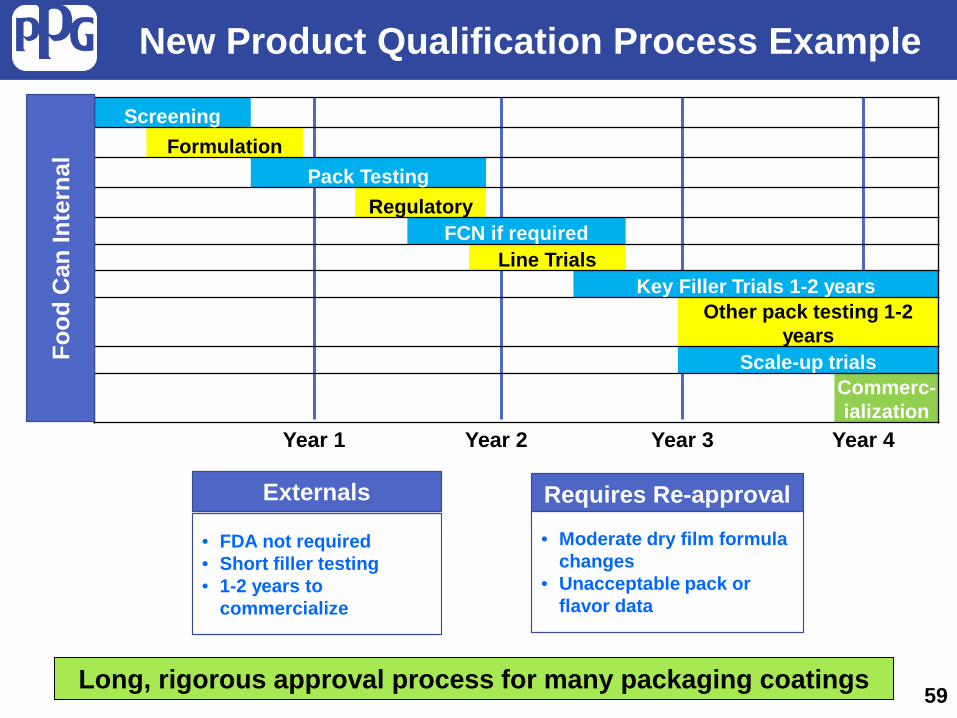

Screening Formulation

Pack Testing Regulatory

FCN if required Line Trials

Key Filler Trials 1-2 years Other pack testing 1-2

years Scale-up trials

Commerc-ialization

New Product Qualification Process Example Fo

od C

an In

tern

al

• FDA not required • Short filler testing • 1-2 years to

commercialize

Externals Requires Re-approval

• Moderate dry film formula changes

• Unacceptable pack or flavor data

Year 1 Year 2 Year 3 Year 4

59 Long, rigorous approval process for many packaging coatings

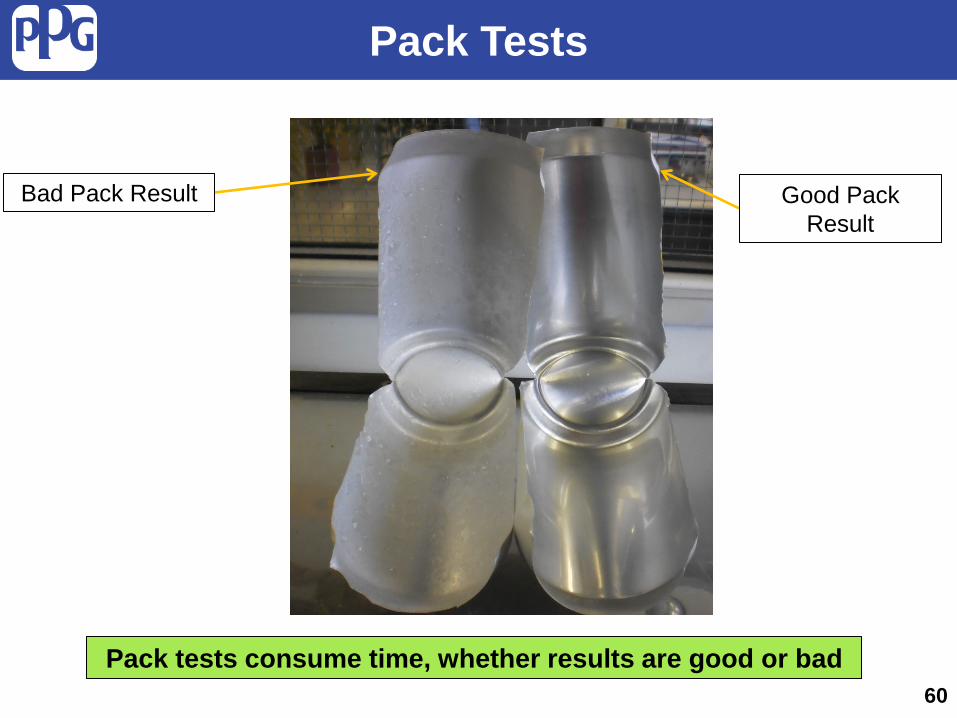

Pack Tests

Pack tests consume time, whether results are good or bad

Bad Pack Result Good Pack Result

60

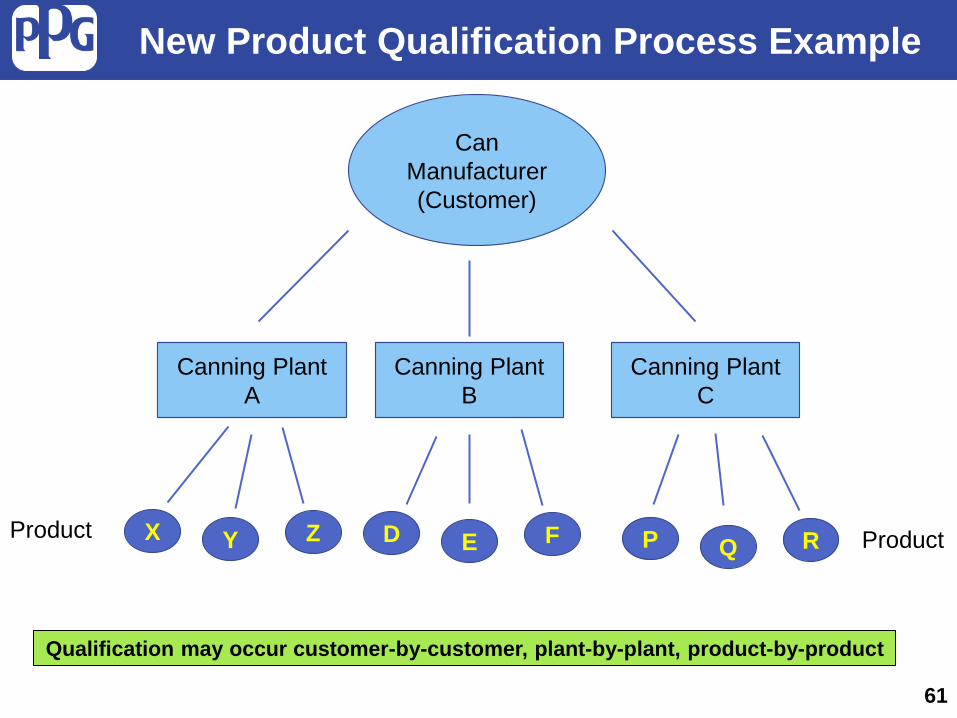

Product

61

Can Manufacturer (Customer)

Canning Plant A

Canning Plant B

Canning Plant C

Z Y X F E D R Q P Product

Qualification may occur customer-by-customer, plant-by-plant, product-by-product

New Product Qualification Process Example

Epoxy Coatings Attributes

• Excellent adhesion to various metals • Excellent corrosion resistance • Low impact on flavor • Long shelf life • Flexibility • Chemical/Pack resistance • Cost effective • Formulation and application latitude

62

New technologies need to replicate functional attributes of epoxy coatings

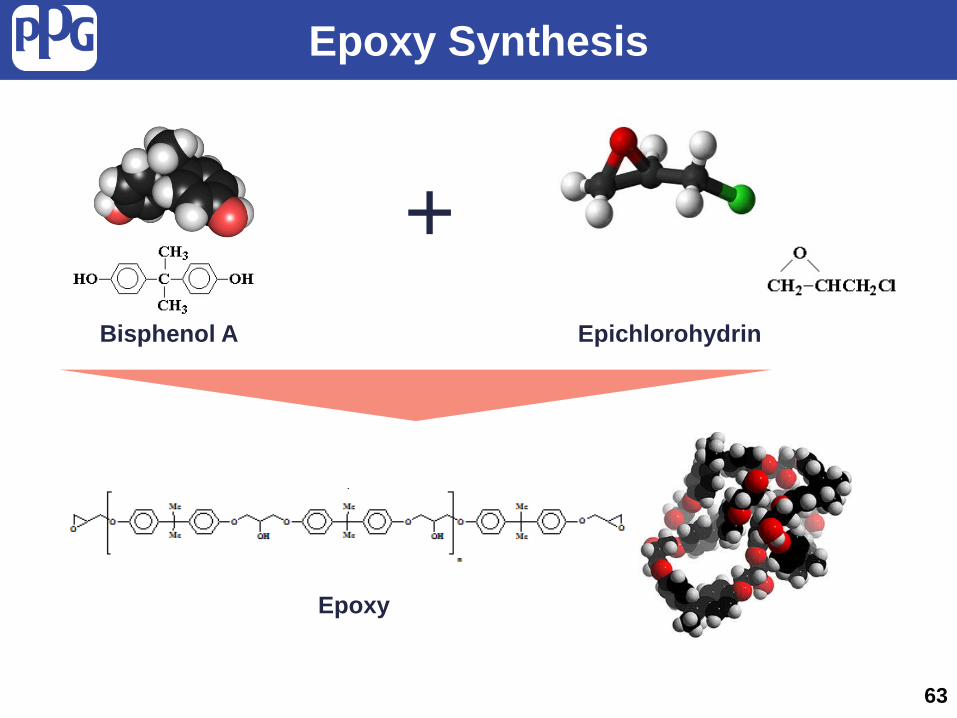

Epoxy Synthesis

+

Epoxy

Epichlorohydrin Bisphenol A

63

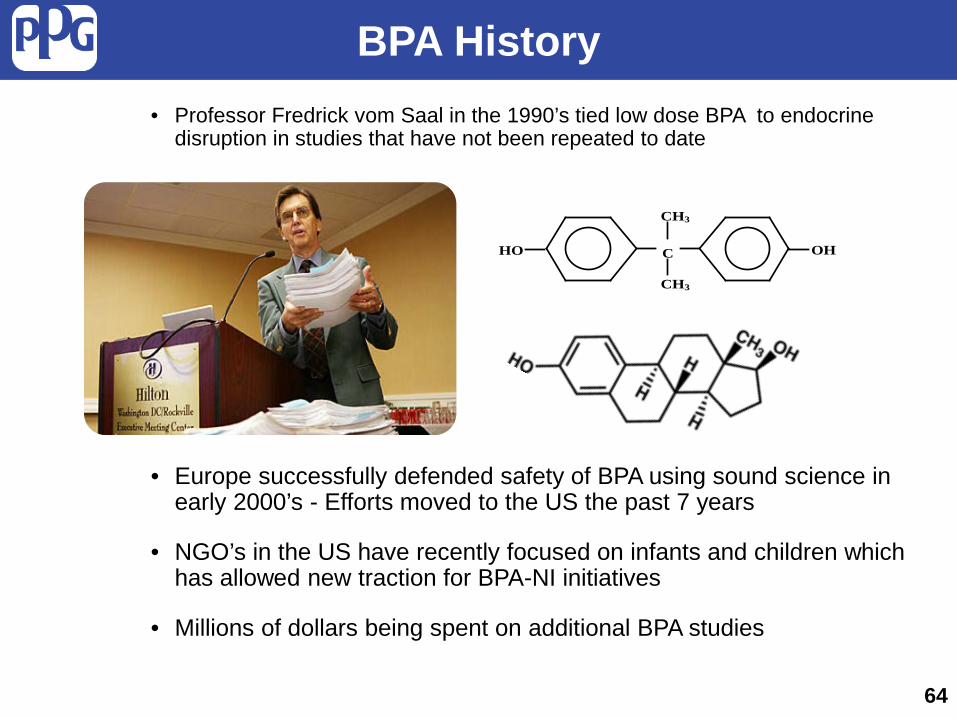

BPA History

• Professor Fredrick vom Saal in the 1990’s tied low dose BPA to endocrine disruption in studies that have not been repeated to date

• Europe successfully defended safety of BPA using sound science in early 2000’s - Efforts moved to the US the past 7 years

• NGO’s in the US have recently focused on infants and children which has allowed new traction for BPA-NI initiatives

• Millions of dollars being spent on additional BPA studies

CHO

CH3

CH3

OH

64

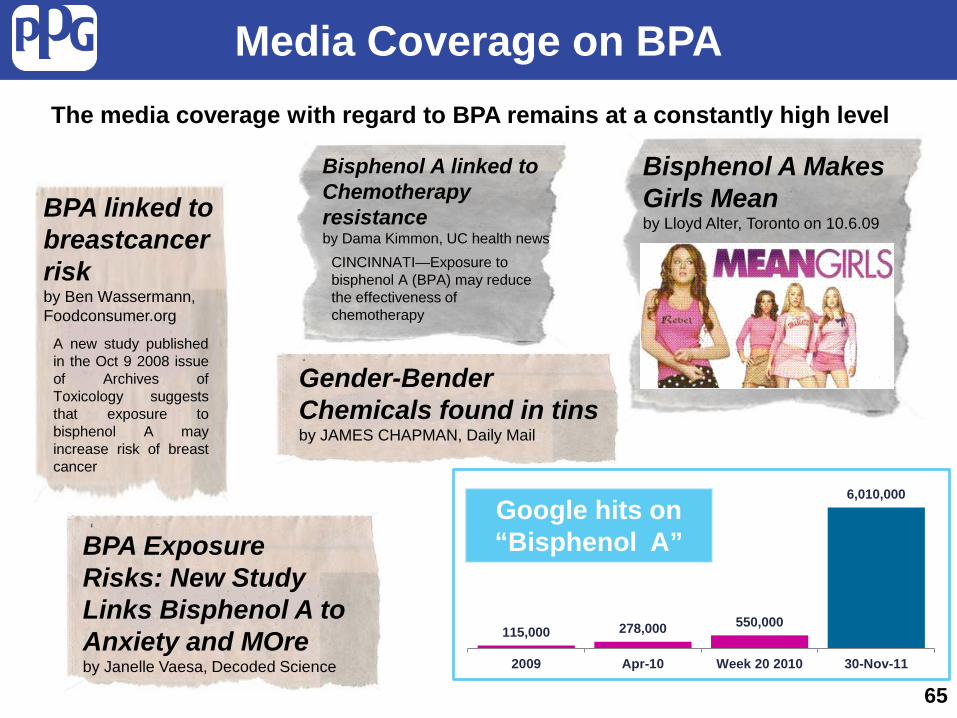

The media coverage with regard to BPA remains at a constantly high level

Media Coverage on BPA

Bisphenol A Makes Girls Mean by Lloyd Alter, Toronto on 10.6.09

BPA linked to breastcancer risk by Ben Wassermann, Foodconsumer.org

A new study published in the Oct 9 2008 issue of Archives of Toxicology suggests that exposure to bisphenol A may increase risk of breast cancer

Bisphenol A linked to Chemotherapy resistance by Dama Kimmon, UC health news

CINCINNATI—Exposure to bisphenol A (BPA) may reduce the effectiveness of chemotherapy

115,000 278,000 550,000

6,010,000

2009 Apr-10 Week 20 2010 30-Nov-11

Google hits on “Bisphenol A”

Gender-Bender Chemicals found in tins by JAMES CHAPMAN, Daily Mail

BPA Exposure Risks: New Study Links Bisphenol A to Anxiety and MOre by Janelle Vaesa, Decoded Science

65

Media Coverage on BPA (Continued)

66 October, 2010

BPA is Almost Everywhere

Electrical boards, switches, lamps, parts for kitchen tools, hair dryers, razors

Glazing, corrosion protection, concrete reinforcement, flooring

Lenses, dialysis devices, blood sample reservoirs, medical equipment, dental fillings

Mobile phone housings, CD´s, DVD´s, computer circuit boards

Front & rear light covers, interior equipment parts, covers, automotive coatings

Sports helmets, safety glasses, visors, toys, racing boats, ski/golf/tennis equipments Architecture

Medical practice

Entertainment & Communication

Automotive

Leisure and safety

Food & beverage Household equipment

food and drink cans, bottles, cutlery, food storage containers, jar sealants

House hold equipments

67

BPA Activities Around The Globe

68

1998 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Vom Saal publishes low-dose theory

Harvard Center Review

115 BPA studies globally

Canada bans BPA for baby bottles & infant formula cans

Minnesota bans BPA in baby bottles

FDA re-affirms BPA safety

Connecticut bans BPA use in infant formula cans

France proposes initial bill to ban BPA in food packaging

Sweden bans BPA in food packaging materials for children

France & Belgium ban BPA in packaging materials intended for children

France bans BPA in all food packaging

EFSA re-affirms BPA safety

Vom Saal Review Follow-up study

Nor

th A

mer

ica

Euro

pe

FDA re-affirms BPA safety

BPA Legislative Update North America EMEA

• All infant formula cans converted to BPA-NI (Connecticut law banning BPA in baby bottles, cups, and canned infant formula - October 2011)

• 30 BPA initiatives have been introduced in 13 states plus one in Puerto Rico during 2013

• Minnesota, Maine and Nevada have all recently passed BPA initiatives for 2014

• France is unmoved by EFSA report findings and proposes BPA ban for:

• January 1, 2013 – infant formula

• January 1, 2014 – all canned food products

• Belgium has proposed a law

banning BPA in food packaging material for children. Effective in January 2013

69

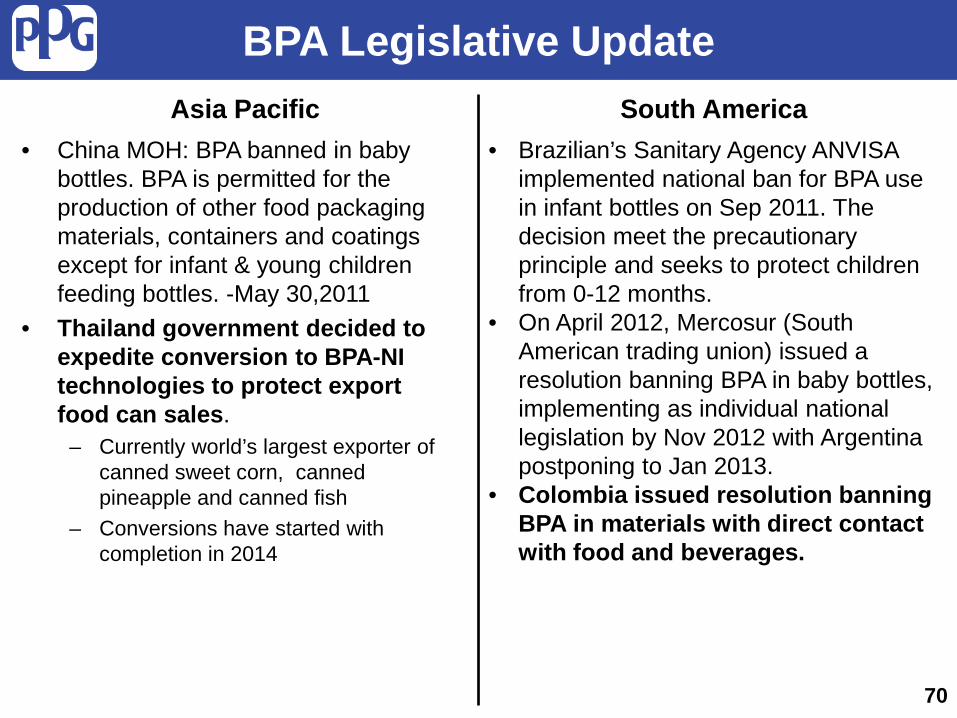

BPA Legislative Update South America Asia Pacific

• China MOH: BPA banned in baby bottles. BPA is permitted for the production of other food packaging materials, containers and coatings except for infant & young children feeding bottles. -May 30,2011

• Thailand government decided to expedite conversion to BPA-NI technologies to protect export food can sales.

– Currently world’s largest exporter of canned sweet corn, canned pineapple and canned fish

– Conversions have started with completion in 2014

• Brazilian’s Sanitary Agency ANVISA implemented national ban for BPA use in infant bottles on Sep 2011. The decision meet the precautionary principle and seeks to protect children from 0-12 months.

• On April 2012, Mercosur (South American trading union) issued a resolution banning BPA in baby bottles, implementing as individual national legislation by Nov 2012 with Argentina postponing to Jan 2013.

• Colombia issued resolution banning BPA in materials with direct contact with food and beverages.

70

Washington Post - February 23, 2010

"It doesn't matter what the FDA says. If consumers decide they don't want BPA, you don't want to be in a can that consumers don't want to buy," …said one source at a major U.S. food company who spoke on the condition of anonymity.

71

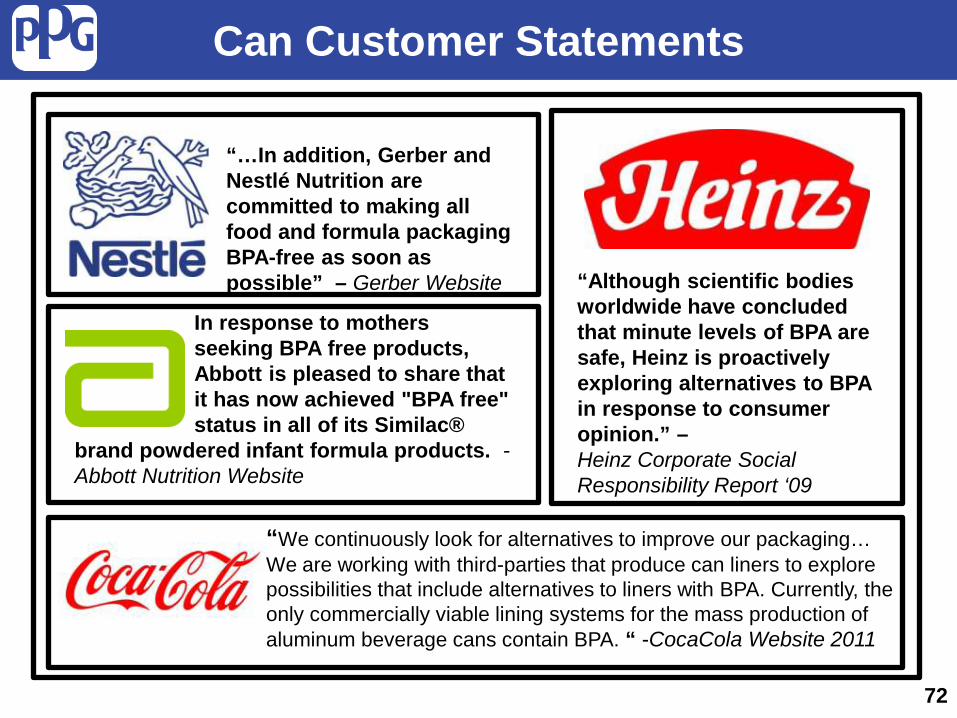

“…In addition, Gerber and Nestlé Nutrition are committed to making all food and formula packaging BPA-free as soon as possible” – Gerber Website “Although scientific bodies

worldwide have concluded that minute levels of BPA are safe, Heinz is proactively exploring alternatives to BPA in response to consumer opinion.” – Heinz Corporate Social Responsibility Report ‘09

In response to mothers seeking BPA free products, Abbott is pleased to share that it has now achieved "BPA free" status in all of its Similac®

brand powdered infant formula products. - Abbott Nutrition Website

“We continuously look for alternatives to improve our packaging… We are working with third-parties that produce can liners to explore possibilities that include alternatives to liners with BPA. Currently, the only commercially viable lining systems for the mass production of aluminum beverage cans contain BPA. “ -CocaCola Website 2011

Can Customer Statements

72

North America Customer Actions

• Infant liquid and powdered formula in cans converted 2011

• Smaller organic food companies (Amy’s Kitchen, Eden Foods) proactively converting to BPA-NI

• Campbell’s Soups announced desire (February 2012) to convert to BPA-NI - no specific timeline but conversions have started

73

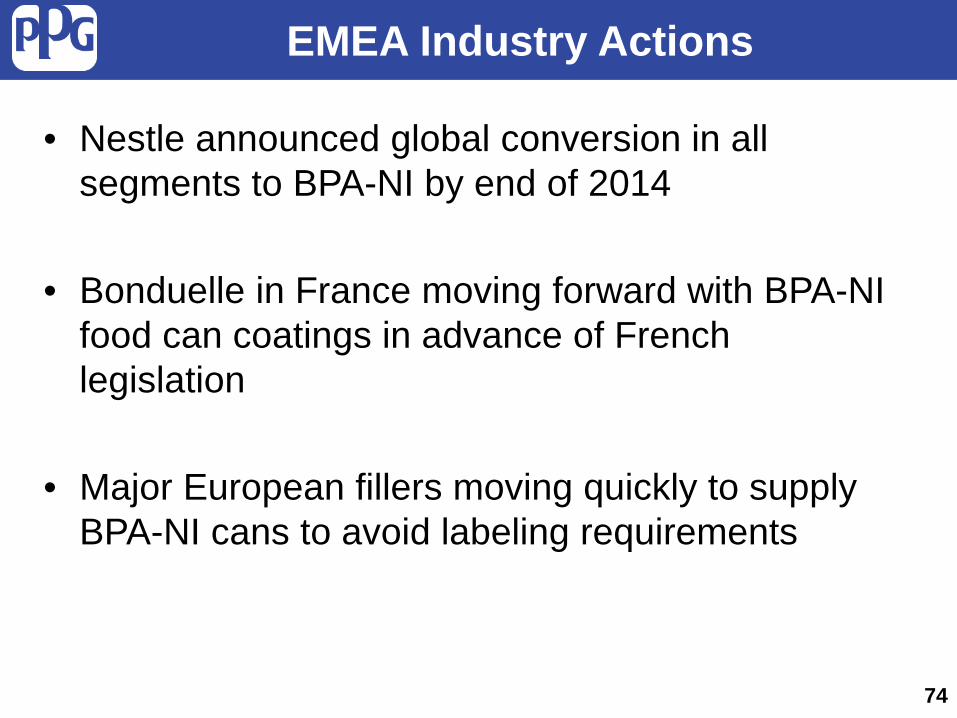

EMEA Industry Actions

• Nestle announced global conversion in all segments to BPA-NI by end of 2014

• Bonduelle in France moving forward with BPA-NI food can coatings in advance of French legislation

• Major European fillers moving quickly to supply BPA-NI cans to avoid labeling requirements

74

Regional BPA Conversion Catalysts

75

Legislative Consumer Export Likely

regional conversion

catalyst

Conversion catalyst(s) will likely differ by region

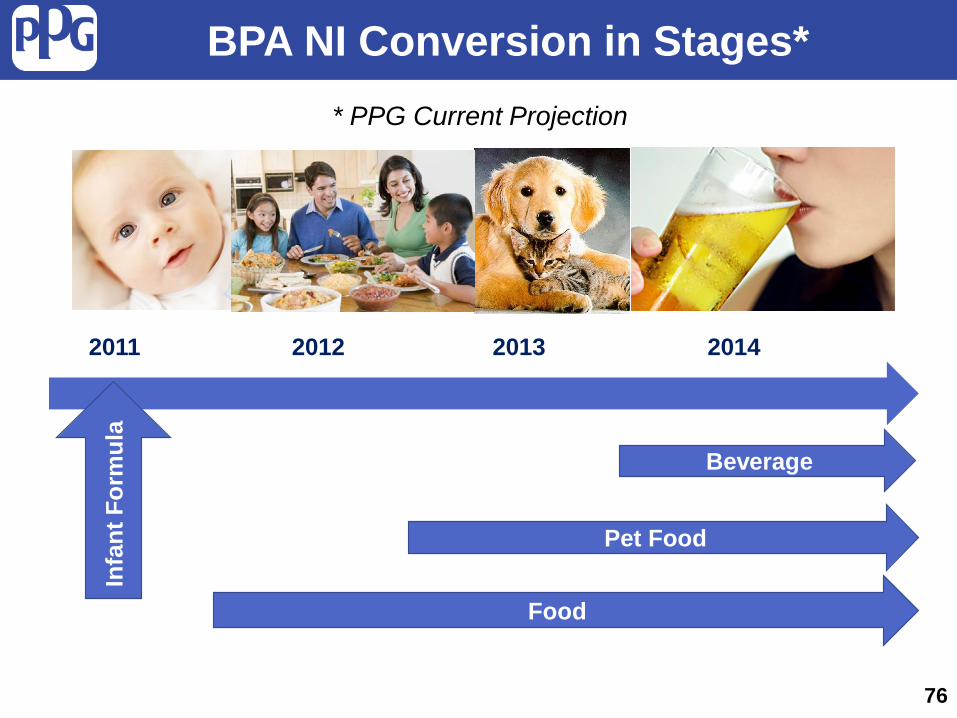

BPA NI Conversion in Stages*

2011 2012 2013 2014

Infa

nt F

orm

ula

Food

Pet Food

Beverage

* PPG Current Projection

76

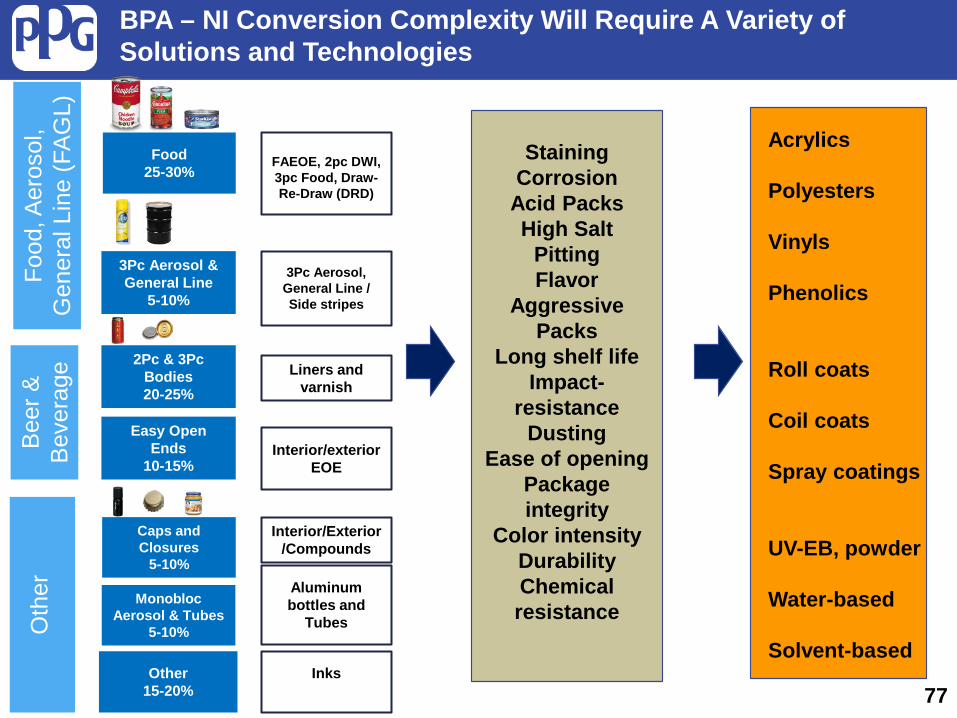

77

Food 25-30%

FAEOE, 2pc DWI, 3pc Food, Draw-Re-Draw (DRD)

3Pc Aerosol & General Line

5-10%

3Pc Aerosol, General Line / Side stripes

Food

, Aer

osol

, G

ener

al L

ine

(FA

GL)

B

eer &

B

ever

age

Oth

er

2Pc & 3Pc Bodies 20-25%

Easy Open Ends

10-15%

Caps and Closures

5-10%

Monobloc Aerosol & Tubes

5-10%

Other 15-20%

Liners and varnish

Interior/exterior EOE

Interior/Exterior/Compounds

Aluminum bottles and

Tubes

Inks

Staining Corrosion

Acid Packs High Salt

Pitting Flavor

Aggressive Packs

Long shelf life Impact-

resistance Dusting

Ease of opening Package integrity

Color intensity Durability Chemical resistance

Acrylics Polyesters Vinyls Phenolics Roll coats Coil coats Spray coatings UV-EB, powder Water-based Solvent-based

BPA – NI Conversion Complexity Will Require A Variety of Solutions and Technologies

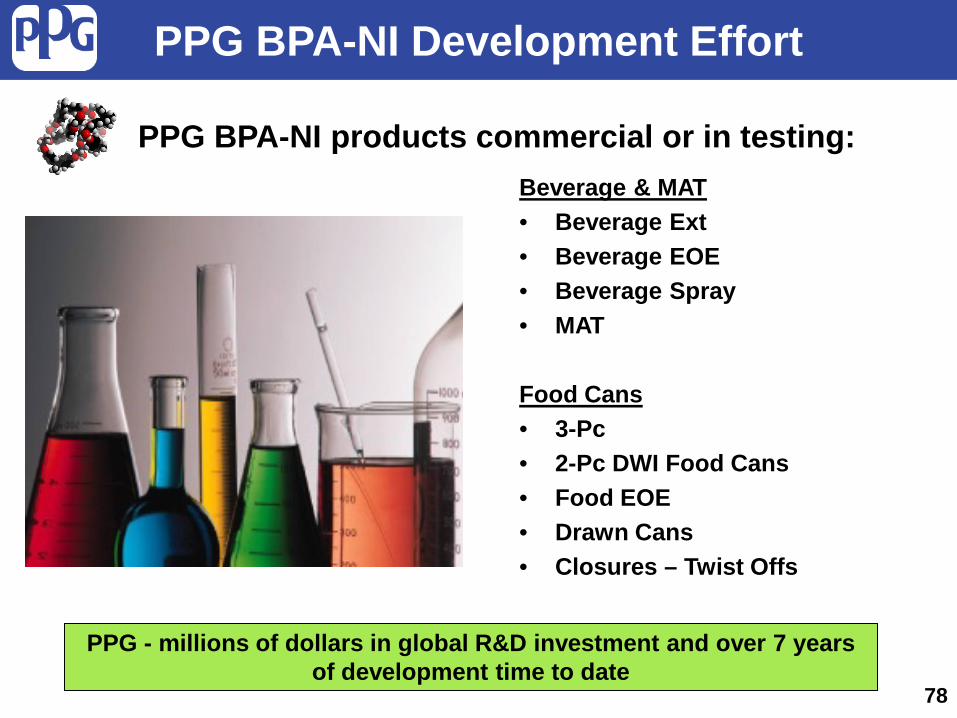

PPG BPA-NI Development Effort

PPG - millions of dollars in global R&D investment and over 7 years of development time to date

78

Beverage & MAT • Beverage Ext • Beverage EOE • Beverage Spray • MAT Food Cans • 3-Pc • 2-Pc DWI Food Cans • Food EOE • Drawn Cans • Closures – Twist Offs

PPG BPA-NI products commercial or in testing:

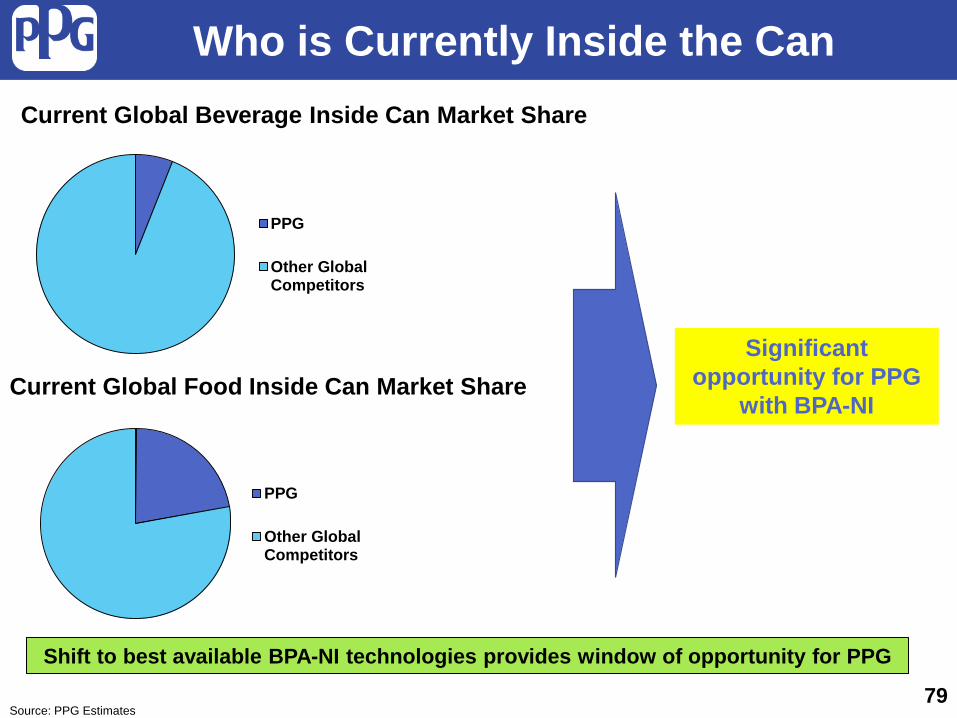

Who is Currently Inside the Can

PPG

Other GlobalCompetitors

PPG

Other GlobalCompetitors

Current Global Beverage Inside Can Market Share

Current Global Food Inside Can Market Share Significant

opportunity for PPG with BPA-NI

79

Shift to best available BPA-NI technologies provides window of opportunity for PPG

Source: PPG Estimates

Inside a Beverage Can – North America

PPG

Other GlobalCompetitors

N.A. Beverage Inside Can Market Share

80

Potential share gain opportunities for PPG in N.A. market

PPG’s history of no “inside the can” share provides market share upside as can makers

convert to best available technologies

Source: PPG Estimates

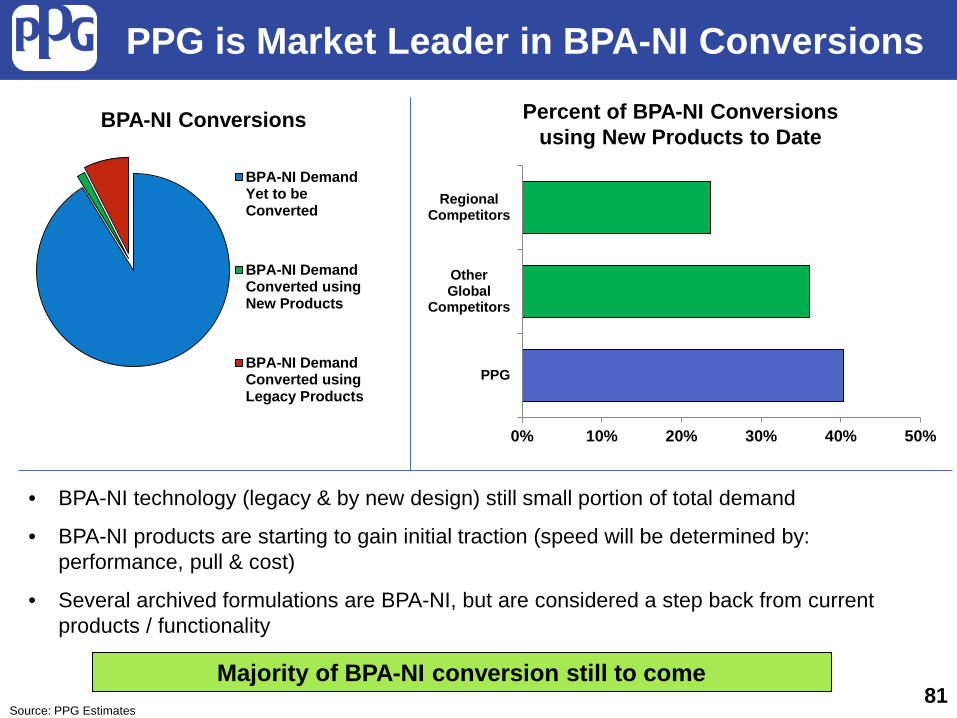

• BPA-NI technology (legacy & by new design) still small portion of total demand

• BPA-NI products are starting to gain initial traction (speed will be determined by: performance, pull & cost)

• Several archived formulations are BPA-NI, but are considered a step back from current products / functionality

BPA-NI Conversions

BPA-NI DemandYet to beConverted

BPA-NI DemandConverted usingNew Products

BPA-NI DemandConverted usingLegacy Products

0% 10% 20% 30% 40% 50%

PPG

OtherGlobal

Competitors

RegionalCompetitors

PPG is Market Leader in BPA-NI Conversions

Percent of BPA-NI Conversions using New Products to Date

81 Source: PPG Estimates

Majority of BPA-NI conversion still to come

BPA Status / Summary

• Media and NGO pressure, coupled with regional legislative action, will likely drive brand owners (fillers) to eliminate BPA from metal packaging coatings in the short-to-medium term

• New BPA-NI coating technologies are being introduced to the marketplace to replace epoxy systems

• Unique opportunity for PPG due to share position on the inside of the can

• PPG committed to developing new technologies that meet the customer’s requirements

82

Asia Pacific: 75B +6%

+25bn

Europe: 59B +3% +9bn

Latin America: 26B +8%

+12bn

North America: 92B 0% Flat

Global 2Pc Beverage Can Growth 2013-2018 & Per Capita Beverage Consumption

Global: 2013 Can Production: 252bn % CAGR 2013-2018: +3% 2018 Growth (cans): +45bn

350 17

70

80

Per capita can consumption = #

83 Emerging regions provide significant opportunity for can growth

Source: CMI, PPG Estimates

2

Packaging Production Growth

0.80

1.00

1.20

1.40

1.60

2009 2010 2011 2012 2013

Global Asia/Pacific

Metal Can Production

Source: IHS Global Insights; PPG Estimates

0.80

1.00

1.20

1.40

1.60

2009 2010 2011 2012 2013

China Metal Can ProductionChina GDP

China Metal Can Production Outpaces GDP

Asia driving recent and future growth in metal can production 84

Indexed to 2009

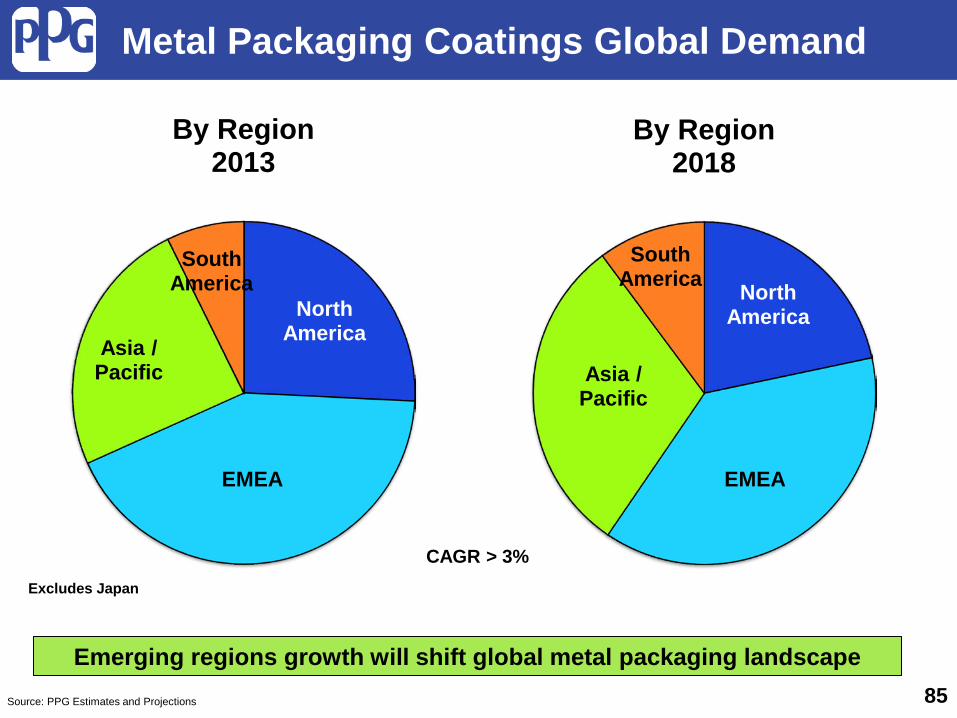

Metal Packaging Coatings Global Demand

Source: PPG Estimates and Projections

North America

EMEA

Asia / Pacific

South America

By Region 2013

Excludes Japan

North America

EMEA

Asia / Pacific

South America

By Region 2018

85

CAGR > 3%

Emerging regions growth will shift global metal packaging landscape

0

500

1000

1500

2000

Food Bev GL

Number of Global Can Lines

2012 2017

+90

= 100 Lines

740 480

275

210 115

140 155

40

+15

+75

# Lines

200

270 1,200

48

Food Lines Bev Lines GL Lines

Global Can Manufacturing Lines Increasing

Source: PPG Estimates 86

Packaging Coatings Competitive Landscape

Akzo, PPG,

Valspar

Others

Akzo, PPG,

Valspar

Others

Developed Regions Emerging Regions Top 3 = ~60% Top 3 = ~70%

Source: PPG Estimates

All values exclude Japan

87

Emerging regions less penetrated by multi-national coatings companies

Packaging Coatings Competitive Landscape

Top 5

Others

Top 5

Others

Top 5

Others

Top 5

Others

Concentration of Packaging Coatings Suppliers by Region

88

In addition to market growth, Asia remains the largest opportunity for share gains for multi-national coatings companies

Source: PPG Estimates

Korea

China

Thailand

India

Indonesia ANZ

PPG Packaging Coatings – Number 1 in Asia/Pacific

Philippines

Vietnam

Malaysia

89 PPG already well established in Asia-Pacific region

PPG share in Top 2

Source: PPG Estimates

PPG share in Top 3

PPG Supplying Global Customers in Asia

90

PPG Supplying Local Customers in China

91

太仓兴达制罐有限公司

Beer Market by Region / Can Concentration

USCA EMEA

Brazil China

China is fastest growing beer market and in early stages of can conversion aided by desire to eliminate inefficient energy usage on glass bottle production

10B liters

% in cans

92

Key: Country % share of global growth

Source: PPG Estimates

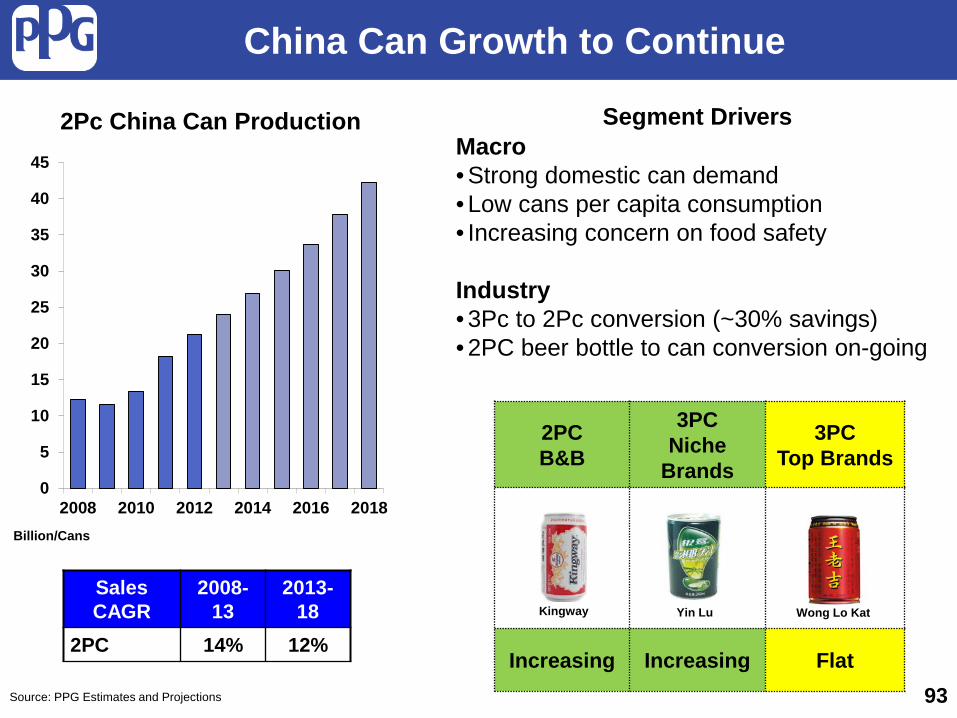

China Can Growth to Continue

2PC B&B

3PC Niche

Brands

3PC Top Brands

Increasing Increasing Flat

2Pc China Can Production

Yin Lu Wong Lo Kat Kingway Sales CAGR

2008-13

2013-18

2PC 14% 12%

Segment Drivers Macro • Strong domestic can demand • Low cans per capita consumption • Increasing concern on food safety Industry • 3Pc to 2Pc conversion (~30% savings) • 2PC beer bottle to can conversion on-going

Source: PPG Estimates and Projections 93

0

5

10

15

20

25

30

35

40

45

2008 2010 2012 2014 2016 2018Billion/Cans

China Investing in 2Pc Can Lines

16 new lines commissioned

PPG awarded coatings business on all 16 new lines

Quality products, strong customer

relationships, broad regional

presence

94

Year 2012

PPG successfully growing in China

8 new lines commissioned

PPG awarded coatings business on all 8 new lines

2013 YTD

• Population growth • Higher disposable income • New investment in metal packaging industry • Increased sophistication of distribution and

retail channels • Beer glass bottle to beer can conversion • Seafood / crop yields (e.g. tuna, sardines, sweet

corn, pineapple etc.)

Asia Expected to Remain a Growth Region

95

Trends support continued packaging growth

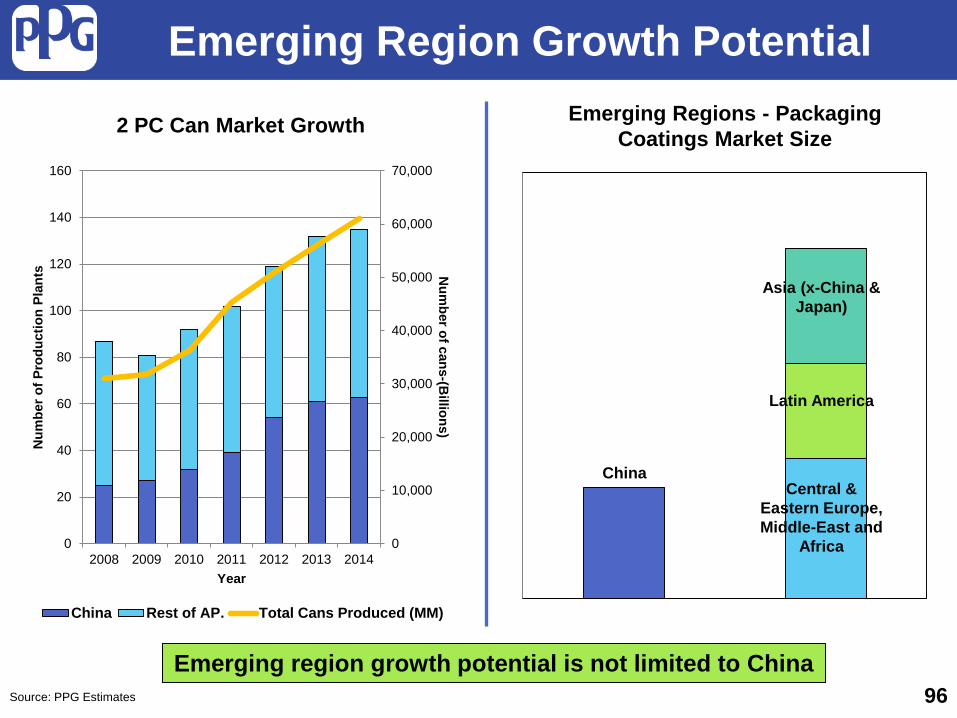

Emerging Region Growth Potential

Emerging region growth potential is not limited to China 96

Asia (x-China & Japan)

Latin America

Central & Eastern Europe, Middle-East and

Africa

China

Emerging Regions - Packaging Coatings Market Size

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

0

20

40

60

80

100

120

140

160

2008 2009 2010 2011 2012 2013 2014

Num

ber of cans-(Billions)

Num

ber o

f Pro

duct

ion

Plan

ts

Year

2 PC Can Market Growth

China Rest of AP. Total Cans Produced (MM)

Source: PPG Estimates

• Global reach • Long-term track record • Proven products with quality consistency • Diversified product portfolio • Strong customer relationship • Responsive technical service support • EHS compliance • Ethical culture

Value PPG Brings in Emerging Regions

97

PPG Presentation Summary

98

o The packaging industry, including metal cans, is a broad and growing global industry

o The metal can remains one of the most desired packaging materials due to wide functional capabilities and cost

o Packaging coatings are critical to functionality of the can o Current industry trends in packaging coatings include coatings

technology changes and emerging region growth

o PPG is a leading packaging coatings supplier serving both global and local customers in all major regions of the world

o PPG is well positioned to capitalize on these opportunities given our current market positions, global breadth and strong focus on development of new packaging coatings technologies

Ball Corporation

• Founded in 1880 by five Ball brothers • 2012 revenue of $8.7B – Fortune 300 • One of PPG’s largest packaging coatings

customers • PPG supplier to Ball for 50+ years • PPG supplies Ball globally

99

Ball Williamsburg

• Opened in 1972 • 4 line aluminum beverage can plant • Produces about 3B cans per year • Major labels are Budweiser, Bud Light, Coke,

Diet Coke, Sprite, Rockstar, Mountain Dew Kick • PPG Products

– Clear over varnish – Matte over varnish – Bottom rim coat – Pre-treatment chemicals

100

Appendix

101

PPG Executive Profiles

102

PPG Executive Profiles

103

PPG Executive Profiles

104