Embed Size (px)

Citation preview

Dixons R

etail plc Annual R

eport and Accounts 2010/11

Dixons Retail plc Maylands AvenueHemel HempsteadHertfordshireHP2 7TG

Tel 0844 800 2030www.dixonsretail.com

Dixons Retail plc Annual Report and Accounts 2010/11

Bringing life to technology

Dixons Retail plcAnnual Report and Accounts 2010/11

Dixons Retail plc is a specialist electrical retailer and services company which sells consumer electronics, personal computers, domestic appliances, photographic equipment, communication products and related services.

We are one of Europe’s leading specialist electrical retailing groups. We trade through over 1,200 stores and online, spanning 28 countries and we employ 38,000 people.

www.dixonsretail.com

Designed and produced by MerchantCantos www.merchantcantos.com

Photography by Dennis Davis: Dennis Davis Photography and Dixons Retail plc Digital Studio.

Printed at St Ives Westerham Press Ltd, ISO9001, ISO14001, FSC certified and CarbonNeutral

The papers used in this report are Revive 50:50 Silk and Revive 50:50 Offset. They are produced from 50% recycled fibre from both pre- and post-consumer waste sources, together with 50% Elemental Chlorine Free fibre from well-managed forests independently certified according to the rules of the Forest Stewardship Council. The inks used are all vegetable oil based.

Dixons Retail plc 01 Annual Report and Accounts 2010/11

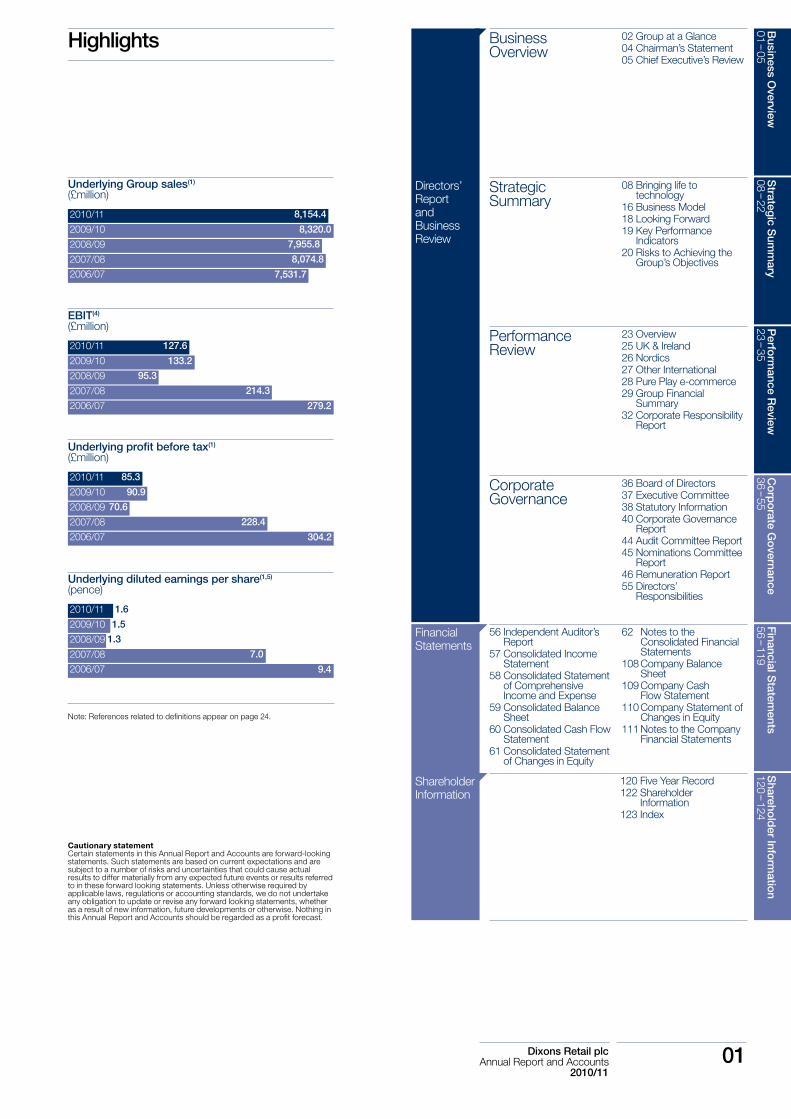

EBIT(4)

(£million)

2010/11 127.6

133.2

95.3

214.3

279.2

2009/10

2008/09

2007/08

2006/07

Underlying diluted earnings per share(1,5)

(pence)

2010/11 1.6

1.5

1.3

7.0

9.4

2009/10

2008/09

2007/08

2006/07

Underlying profit before tax(1)

(£million)

2010/11 85.3

90.9

70.6

228.4

304.2

2009/10

2008/09

2007/08

2006/07

Underlying Group sales(1)

(£million)

8,154.4

8,320.0

7,955.8

8,074.8

7,531.7

2010/11

2009/10

2008/09

2007/08

2006/07

Highlights

FinancialStatements

Shareholder Information

Directors’ Report and Business Review

CorporateGovernance

36 Board of Directors37 Executive Committee38 Statutory Information40 Corporate Governance

Report44 Audit Committee Report45 Nominations Committee

Report46 Remuneration Report55 Directors’

Responsibilities

56 Independent Auditor’s Report

57 Consolidated Income Statement

58 Consolidated Statement of Comprehensive Income and Expense

59 Consolidated Balance Sheet

60 Consolidated Cash Flow Statement

61 Consolidated Statement of Changes in Equity

62 Notes to the Consolidated Financial Statements

108 Company Balance Sheet

109 Company Cash Flow Statement

110 Company Statement of Changes in Equity

111 Notes to the Company Financial Statements

120 Five Year Record122 Shareholder

Information123 Index

Performance Review

23 Overview25 UK & Ireland26 Nordics27 Other International28 Pure Play e-commerce29 Group Financial

Summary32 Corporate Responsibility

Report

Strategic Summary

08 Bringing life to technology

16 Business Model18 Looking Forward19 Key Performance

Indicators20 Risks to Achieving the

Group’s Objectives

BusinessOverview

02 Group at a Glance04 Chairman’s Statement05 Chief Executive’s Review

Note: References related to definitions appear on page 24.

Cautionary statement Certain statements in this Annual Report and Accounts are forward-looking statements. Such statements are based on current expectations and are subject to a number of risks and uncertainties that could cause actual results to differ materially from any expected future events or results referred to in these forward looking statements. Unless otherwise required by applicable laws, regulations or accounting standards, we do not undertake any obligation to update or revise any forward looking statements, whether as a result of new information, future developments or otherwise. Nothing in this Annual Report and Accounts should be regarded as a profit forecast.

Business O

verview01 -- 05

Strategic S

umm

ary08 -- 22

Perform

ance Review

23 -- 35C

orporate G

overnance36 -- 55

Financial Statem

ents56 -- 119

Sharehold

er Information

120 -- 124

02 Dixons Retail plcAnnual Report and Accounts 2010/11

UK & IrelandFor more information please go to page 25

NordicsFor more information please go to page 26

Directors’ ReportBusiness Overview

Group at a GlanceLeading European electrical retailing and services company

Currys and PC World are the UK & Ireland’s largest specialist electrical retailing and services chains.

We operate from High Street stores, Superstores and Megastores. We are increasingly opening combined 2-in-1 Currys and PC World stores across all formats, bringing customers the benefits of both brands in one convenient location.

Dixons Travel stores are based at all major UK airports.

KNOWHOW is our new market leading services brand.

Elkjøp is the leading specialist electrical retailer across the Nordics.

Elkjøp and Lefdal stores operate in Norway, El Giganten in Sweden and Denmark and Gigantti in Finland.

www.currys.co.ukwww.pcworld.co.ukwww.dsgibusiness.comwww.knowhow.co.uk

HighlightsOur Renewal and Transformation plan is working and customers are experiencing better store environments, improved ranges and increased levels of service.

250 stores have been transformed so far, 31 of which are Megastores.

We launched KNOWHOW, our new face of service and product support which puts customers at the heart of everything we do. This features delivery and installation, set up of equipment and upgrades, help and support as well as repairs and protection.

The multi-channel offering provides customers with the convenience of online shopping alongside the accessibility of our stores, particularly through the reserve&collect facility.

Dixons Travel is expanding its brand overseas with operations now in Copenhagen, Rome, Milan and Dublin airports.

HighlightsElkjøp continues to perform strongly in all of its markets and is expanding its business significantly as we grow market share across the Nordic region. Elkjøp operates an efficient operating model with centralised warehousing in Sweden serving all four principal markets in which it operates. With the lowest store-based cost to sales ratio in the Group it provides the basis for the favoured operating model for the Group.

Elkjøp is increasing its footprint through Megastores by extending or refitting existing stores as well as refurbishing superstores to the new Group format. During the year Elkjøp delivered strong performance in Norway and delivered particularly strong improvement in Denmark, Finland and Sweden.

Underlying sales(£million)

2,268.9

Underlying sales(£million)

3,816.1Average selling area

per store(sq ft)

12,752

Average selling area per store

(sq ft)

14,818

Number of stores

285

Number of stores

642Average employees

23,091

Average employees

7,343

Selling space(‘000 sq ft)

4,223

Selling space(‘000 sq ft)

8,187

Our brandsOur brands

www.elkjop.nowww.elgiganten.sewww.elgiganten.dkwww.gigantti.fiwww.lefdal.com

Dixons Retail plc 03 Annual Report and Accounts 2010/11

Other InternationalFor more information please go to page 27

Pure play e-commerceFor more information please go to page 28

Underlying sales by division(£million)

12 34

UK & Ireland £3,816.1mNordics £2,268.9m Other International £1,226.7m Pure play e-commerce £842.7m

1

2

3

4Directors’ ReportBusiness Overview

Kotsovolos is Greece’s leading specialist electrical retailer.

In Italy, we operate Unieuro electrical stores with some as combined 2-in-1 Unieuro and PC City stores.

In the Czech Republic and Slovakia, we operate under the Electro World brand.

In Turkey, we operate the Electro World brand with a local joint venture partner.

PIXmania is one of the largest pure play electrical retailers in Europe operating in 26 countries.

Dixons.co.uk is one of the leading UK online electrical retail brands.

www.kotsovolos.grwww.unieuro.itwww.electroworld.czwww.electroworld.grwww.electroworld.com.tr

www.pixmania.comwww.dixons.co.uk

HighlightsThe turnaround in Italy remains on track and the business delivered a positive EBITDA performance in the year, the first for several years.

Trading conditions in Greece remain difficult, however, Kotsovolos continues to generate cash and as market leader is well positioned to gain further market share.

Electro World in Central Europe is already a leading brand and is well positioned for the development of the Czech and Slovakian markets in the medium term.

Electro World in Turkey remains a long term opportunity for the Group with our joint venture partner.

HighlightsOur pure play brands work together with our store based multi-channel brands to provide our customers with the shopping trip that suits their needs.

Overall the Group continues to see strong growth in the multi-channel operations.

The functionality of PIXmania’s e-merchant platform was developed further for Dixons.co.uk to provide an improved online shopping experience.

Underlying sales(£million)

1,226.7

Underlying sales(£million)

842.7Average selling area

per store(sq ft)

14,380

Average selling area per store

(sq ft)

1,412

Number of stores

308

Number of stores

17Average employees

6,191

Average employees

1,398

Selling space(‘000 sq ft)

4,429

Selling space(‘000 sq ft)

24

Our brands Our brands

Business O

verview01 -- 05

04 Dixons Retail plcAnnual Report and Accounts 2010/11

Directors’ ReportBusiness Overview

Chairman’s StatementJohn Allan

This has been a year when the economic environment has remained particularly challenging in many of the markets in which we operate. The Group has, however, remained focused on delivering a better experience for customers, which will position the business for significant progress when the economic environment improves.

I am conscious that the Group has made only limited progress in financial returns year on year, but I can assure you that the Board is alive to the need to improve returns for shareholders. The work under the Renewal and Transformation plan has continued which will make the business better for our customers, simpler for our colleagues to manage and cheaper to run. This has started to show encouraging developments with improvements in customer satisfaction measures; we have maintained gross margins over the last two years in the face of competitive and challenging markets; our operations in the Nordics continue to go from strength to strength with sales up eight per cent. over the last year; we have taken decisive action in Spain to close our operations in a market where we saw little opportunity for short to medium term profitable recovery; and we have reduced costs by £50 million in the year.

Delivering a better experience for customers will position the Group for significant progress when the economic environment recovers

In March this year we launched the KNOWHOW brand in the UK which encompasses all our after-sales services. KNOWHOW clearly puts the customer at the heart of everything we do and empowers all our colleagues to focus determinedly on our customers. Our KNOWHOW distribution and repair centre in Newark is world class. The logistics, distribution, repair and services areas are far better than many of our competitors. The efficient operation illustrates how far we have progressed in getting it right for customers first time.

During the early part of the financial year we successfully issued a £150 million bond due 2015, which enabled us to repurchase just under half of the Group’s existing 2012 Bonds as well as extend the maturity of the Group’s working capital facility to 2013. This gives the Group a much more appropriate maturity profile on its debt facilities.

We have made significant progress in transforming our stores with over 360 stores now in the Group’s new format, including 65 Megastores across the Group. With a solid base of stores now transformed and significant improvements having been made to the Group’s operational processes we can now manage our capital expenditure carefully to ensure the Group has adequate capital to repay the remaining 2012 Bonds irrespective of the trading environment.

Recognising challenging conditions in some of our markets, and the ongoing business restructuring under the Renewal and Transformation plan, we have reviewed the balance sheet and made impairment and other non-underlying charges totalling £309.4 million. The additional cash impact of these charges is estimated as £39 million, of which approximately £8 million was incurred in 2010/11.

This year, the Group selected two national charities to support, Lifelites and the e-Learning Foundation, which help to provide access to technology for disadvantaged children or those with disabilities. I am very proud of our colleagues, who have organised so many fundraising activities throughout the year for both these charities as well as a number of charities local to the communities in which our stores operate.

This year we welcomed Dharmash Mistry to the Board as a non-executive director, who has substantial retail experience in consumer-facing and internet businesses.

The year ahead remains a challenging one, particularly in the UK, Greece and Italy. Your Board is confident that the changes that have been, and are being, made to the Group will enable it to navigate the difficult environment ahead in a better shape than it has ever been. I would like to thank the management team led by John Browett, and in addition all of our colleagues across the Group, for their persistent hard work. I am convinced that we will emerge increasingly as a winner in the electricals and services market as the economy recovers.

John AllanChairman

Dixons Retail plc 05 Annual Report and Accounts 2010/11

Business O

verview01 -- 05

Directors’ ReportBusiness Overview

Chief Executive’s ReviewJohn Browett

The tough economic backdrop in many of our markets has made this a difficult year. Nonetheless, we have been able to balance improving our offer for customers whilst maintaining profitability. The shopping trip we provide to customers is more competitive and we see the impact on our business as we make our offer even better. Customers come to our stores because they are looking for great new products; however, they need a complete solution to get the best out of the latest technology. It is our job to make sure they leave our stores with the right products and services to meet all their needs. Increasingly, we are seeing the benefits of selling services effectively, particularly with the launch of KNOWHOW in the UK.

Our Customer Plan is at the heart of the business and a key element of delivering on our core purpose of bringing life to technology, so I thought I would again lay out our progress in the last year under the plan. As ever, our objective is to make the business better for customers, easier for colleagues and cheaper to operate.

They’re interested in working out what’s right for meOur unique FIVES training programme has formed the basis of ensuring all our colleagues across Europe are equipped with the right tools to understand and meet customers’ needs. This year we have continued to refine and develop FIVES training, with colleagues attending many refresher courses. Alongside this we have introduced better product learning tools under our web

based Product Learning Centre. We have also worked with suppliers in the UK to hold over 900 workshops, enabling our colleagues to immerse themselves in fully understanding the features and benefits of a wide range of products, ensuring they can explain the exciting technology we sell to our customers.We have also introduced a new colleague scheduling tool to all our shops in the UK to better ensure colleague availability meets our customer footfall patterns. This has already improved the measure of our colleague availability to our customers’ footfall in our stores by 20%.

Our objective is to be famous for great service. Our operations in the Nordics are already famed for excellent customer service and we can take many learnings from them and make further improvements as we roll out our vision to our other businesses. Through the actions so far we have made great progress with customer satisfaction metrics improving significantly since we started the Renewal and Transformation plan. In the year ahead there is much more we can do. Our new KNOWHOW services brand, launched in the UK at the beginning of 2011, embodies the behavioural attitudes that deliver a fantastic experience for our customers. Improved services and enhanced training plans will give our colleagues further tools to ensure every customer gets the right solution for their needs.

It’s an exciting place to beWe continue to develop our stores, making them exciting places to experience technology and find the right solutions for our customers’ needs. During the year we transformed over 130 stores across the Group, which included 32 Megastores. In Italy the combined 2-in-1 format of Unieuro and PC City is now open in 19 locations and is proving to be a format that is as popular with Italian customers as it is in the UK. This to me proves that a well designed store and customer offer works across many markets. In the Nordics we now have 20 Megastores and will continue to transform stores to the larger Megastore format there in the years ahead. In the UK we now operate 31 Megastores and 56 combined 2-in-1 Currys and PC World superstores. We have also introduced the 2-in-1 format to the High Street with great initial results. These new store formats are consistently delivering gross profit uplifts of between 15% and 20% and in some cases higher in the first year versus the unrefurbished estate. Encouragingly they are maintaining these uplifts into the second year.

Our objective is to make the business better for customers, easier for colleagues and cheaper to operate

Customer plan

It’s easy to shop

It’s an exciting place to be

They’re interested

in working out what’s right

for meThey deal with queries and complaints brilliantly

They make things work and keep

them working

The prices are good

I can get what I want

when I want it

06 Dixons Retail plcAnnual Report and Accounts 2010/11

Chief Executive’s Reviewcontinued

Directors’ ReportBusiness Overview

A significant validation of the changes we are making manifested itself in the fact that we were a key partner for Apple’s launch of the iPad in the UK. The fact that our stores are great places for new technology where products can be demonstrated and their features explained fully is why Apple chose to partner with us on this important product launch. In October 2010 we launched an exciting new advertising campaign around the Megastore format in the UK, featuring R2D2 and C3PO from the Star Wars films, which was hugely popular with customers. It is testament to the work we are doing that Lucas Films allowed their iconic Star Wars characters to be used to advertise ‘the greatest technology stores in our universe’. We have also started to implement in-store demonstrations which bring the features and benefits of kitchen appliances to life in our stores with the introduction of live kitchens.

Having integrated PIXmania’s market leading e-merchant platform into our UK sites we have now been able to improve the customer offer on both the pure play internet business of dixons.co.uk and our multi-channel businesses such as currys.co.uk and pcworld.co.uk.

We are also looking at ways to raise the bar in our store formats even higher and during the year we opened a trial store in Birmingham called Black. The aim is to trial new ways of merchandising and demonstrating high end technology products as well as integrating our new KNOWHOW services into the proposition. During 2011 we will learn from this trial and will be using the elements that customers like the most in all our store transformations.

It’s easy to shopOur new store layout and improved websites make it easier than ever before for our customers to choose the right product. We have made great progress this year in helping customers choose the right product for their needs through clearer signage and better information at point of sale, helping to untangle technology for our customers.

Our reserve&collect facility is proving to be a great success with our customers, giving them the ease of the internet combined with the convenience of our stores. In the last year we have seen our multi-channel internet sales, driven by reserve&collect, rise by 13% across the Group.

In the year ahead we will make further improvements to our multi-channel offering providing customers with improved information on our websites as well as access to a wider range of products online and in-store through our websites.

I can get what I want when I want itWe have launched our own label brands of Currys and PC World essentials, Logik, Advent, Goji and Sandstrøm. Having had over 70 different own brands previously, this simplified our offering and gives customers a clear good-better-best range of products from which to choose.

With our partner, Phones4U, we opened 57 shop in shops, giving our customers access to the latest smartphones and networks from one of the UK’s largest mobile phone retailers.

We must ensure that we provide excellent service to our customers every time we come into contact with them. Through our ‘At home with FIVES’ training we can ensure that a customer has everything they need when we visit their homes, reducing the need for a further call out by 52%.

Having made significant progress in managing our stock in the warehouse and in-store across the Group, this year we plan to simplify processes still further which will improve availability online and in-store while freeing up more time for our colleagues to spend with customers.

As a part of the KNOWHOW rollout to our home services team we have introduced Personal Digital Assistants (PDAs) to the team which will help improve customer feedback and time management of our colleagues.

Dixons Retail plc 07 Annual Report and Accounts 2010/11

Business O

verview01 -- 05

The prices are goodOur scale across Europe means that we are continually able to give our customers the latest products at the best prices. We monitor prices against our competitors regularly with, for example, over 300,000 products checked every week in the UK, so we know we are offering real value to our customers every day. All this is backed up by our market leading price promise to refund 110% of the difference if a customer finds the same product cheaper elsewhere.

There are further changes we plan to make in the year ahead. By simplifying our promotions processes, for example, we can give customers better deals on new products by making our own brand products even better value through cost reductions and giving customers good, better and best choices across our ranges. We are also conscious that not all of our customers are aware of the significant value we offer compared to our competitors, so we will start to improve the communication of that messaging in the year ahead.

They make things work and keep them workingThis was a significant year for our support services. We brought the majority of the service operations in house in the UK. We know we can only improve the service we offer by owning and being directly responsible for all contacts with our customers. That enabled us to launch the KNOWHOW brand bringing together the home services, distribution, contact centre and repair operations. With all these services now operating as one clear customer focused brand we have already started to see the benefits for our customers. I am immensely proud of our colleagues’ enthusiasm for the KNOWHOW brand, but more importantly their desire to really help customers as much as possible every step of the way through the lifecycle of the technology they use. Our turnaround times for repair products is faster, with 93% being returned at a pre-booked time. Our right first time delivery is one of the highest in the industry and our customer satisfaction levels are continually improving.

Under the KNOWHOW brand we will make further improvements to the services our customers receive by, for example, shortening the repair times even further; enabling customers to track their product while it is being repaired; and a ‘no lemons’ policy which means that, under our support agreements, if we fail to fix the product properly after three attempts a customer can request a replacement. We will also start to roll out the KNOWHOW services to our international businesses. This is a multi-year project which will require tailoring to each market, but our customers need our help with their products wherever they are, so this presents a major opportunity for our customers and our shareholders.

They deal with queries and complaints brilliantlyThis year we consolidated our UK call centres into one location in Sheffield as well as enabled many of our call centre colleagues to work from home, increasing the ability to match colleague availability with customer calls. By analysing the reasons why customers call us and providing them with better information to reduce the need to call us, we have reduced the number of calls we receive by 11%. Together with increased cross skilling we have increased the availability and ability of our colleagues to resolve customers’ issues. As a result we have seen increased customer satisfaction and reduced repeat calls. We have also made the processes for stores dealing with customers’ issues easier for our colleagues and better for our customers. In the year ahead we will improve our systems further so that customers and their products can be identified more easily when they call. We will continue to identify the root cause of customer calls and eliminate the need for customers to call in the first place.

As you can see, the volume of work on our Renewal and Transformation plan is still very high. Our reward is improving customer satisfaction and higher share in many of our markets. We are starting to stand out for customers and we have much more to deliver to make our customers’ shopping trip even better. These achievements would not be possible without the enthusiasm, dedication and hard work of our 38,000 colleagues across the business and I would like to thank them all for their contribution to making Dixons Retail a great business.

OutlookThe economic backdrop remains challenging, particularly in the first half as we anniversary the World Cup and iPad launch. However the Group is well prepared for this environment. We are creating a market leading differentiated customer offer, leaving us well set to emerge from the current climate ahead of the competition.

John BrowettChief Executive

08 Dixons Retail plcAnnual Report and Accounts 2010/11

“Point and shoot and the moment’s captured. Transferred over to my iPad 2 and my photos are ready to edit, print or upload to the internet to share with my mates. The guys at Currys helped me find the right camera, lens and memory card too. They explained how to use KNOWHOW online storage solutions where I can save my precious photos, music and videos. It’s amazing. It’s exactly what I need. Shoot, save and share!”

‘‘ I love to capture the moment’’

Technology at your fingertips with the iPad 2. Games, maps, apps, reading, films and photos have all been made faster and easier. Talk to your friends face to face using FaceTime and instantly upload photos and films for sharing online. Tablets are revolutonising the way we interact with our digital content.

The Nikon D5100 Digital SLR Camera delivers crystal clear images. It boasts Full HD 1080p video recording options with a 3” vari-angle LCD monitor making it easy to look back at photos and films.

Have fun taking perspective shots with the Nikon 10.5mm SLR Fisheye Lens. The 8GB Kodak High Speed Memory Card means you can take action shots in quick succession and has plenty of space for storing photos and films.

Dixons Retail plc 09 Annual Report and Accounts 2010/11

Strategic S

umm

ary08 -- 22

10 Dixons Retail plcAnnual Report and Accounts 2010/11

Dixons Retail plc 11 Annual Report and Accounts 2010/11

“You don’t need to use a controller with XBox Kinect™, just your body and voice. It’s magic! We jump, dance, drive and play and the Kinect™ senses it all. It’s even better when Mum and Dad or even Gran and Grandad join in. We can watch movies too. They look amazing on the 3DTV which the KNOWHOW man put on the wall. He even set up Mum and Dad’s Bose DVD home entertainment system and connected the Kinect™ to the internet. Our family has so much fun, I can’t wait for the weekends!”

‘‘ We just want to have fun’’

For a premium home cinema surround sound experience, connect a Bose Lifestyle® 38 DVD home entertainment system to your TV. The HD viewing quality brings your films to life. Audio can be shared in up to 14 rooms, even outdoors. It can also store up to 340 hours of digital music.

The Xbox Kinect sensor puts you into the heart of the gaming action like never before. Your body is the game controller. You don’t have to hold controllers or struggle with wires. Just jump in front of the sensor and start playing.

Put on your 3D glasses and experience breathtaking 3D films and TV programmes on the Samsung 55” HD LED 3D Smart TV with integrated Freeview. Its Smart Hub provides access to the internet with features and apps. Watch films through a connected games console or stream them through the internet.

Strategic S

umm

ary08 -- 22

12 Dixons Retail plcAnnual Report and Accounts 2010/11

“A new baby boy, a football mad son, and a tap dancing daughter equates to a mountain of washing alone. I needed a large, high performance energy-efficient washing machine. The team at Currys suggested the LG Direct Drive – the answer to my prayers!It can take a huge 11kg wash load and is packed with features such as allergen sanitisation and Scrub motion – perfect for the kids’ clothes. It’s even got a Baby care wash programme and it’s so quiet. With KNOWHOW’s WHATEVER HAPPENS Kitchen Cover, I’ve got peace of mind too.”

‘‘ That’s a load off my mind’’

Steam irons take the strain out of ironing, cutting through the pile of ironing in no time. The ceramic soleplate and variable steam settings mean you can use the GV8360 Pro Express Turbo Steam Iron as a dry iron too.

Washing larger loads is light work with the 11kg load LG Direct Drive Washing Machine. Inverter Technology means it effectively removes the dirt and bacteria that can aggravate allergies and has an A++ rating for energy efficiency.

We will deliver your appliance at a time to suit you and we’ll even recycle your old product for free. If you want us to install it, we KNOWHOW. If it needs a minor or major repair, we’ll fix it....and if we can’t, we’ll replace it. If you simply need a bit more help to get the most out of your purchase or even want an upgrade, we KNOWHOW to help you.

Dixons Retail plc 13 Annual Report and Accounts 2010/11

Strategic S

umm

ary08 -- 22

14 Dixons Retail plcAnnual Report and Accounts 2010/11

Dixons Retail plc 15 Annual Report and Accounts 2010/11

“Just bought myself a state of the art TV from Currys. Lovely stuff. Slimline LED screen, Hi Def and 3D ready to watch the footie with the lads. Trouble is, I said to the bloke who served me at Currys that I knew how to install it and set it up. Thought it would be easy. Turns out it’s pretty technical stuff and I can’t work out what goes where. I needed someone with KNOWHOW . Luckily, I called Currys and they said they will arrange for someone from the KNOWHOW team to come over and install it for me. Now all we need to worry about is keeping the beer chilled!”

‘‘ I need someone withKNOWHOW ’’

Help & SupportNeed data transferring to a new PC, help with getting rid of a virus on your laptop or help restoring missing data? We’re here to support you so you KNOWHOW to do it next time. Or, simply call us and we’ll help you 24/7 – again and again.

Deliver & InstallOur KNOWHOW team can deliver and install your new product on a day and time to suit you, seven days a week. We’ll even text you the night before to remind you we’re coming.

Set Up & UpgradeLaptops, cameras, tablets, home networks.... we KNOWHOW to set them up for you. If your PC needs more memory or you simply need us to help with a software upgrade, we can visit you at home or you can just pop into a store.

Repair & ProtectTV on the blink? Games console isn’t working quite right? We can repair your faulty PC, TV, games console and more in our state of the art repair lab and keep you up to date with its repair progress. We KNOWHOW to fix it for you.

Strategic S

umm

ary08 -- 22

16 Dixons Retail plcAnnual Report and Accounts 2010/11

Store Internet Products After-salesservice

Support

Value

Low cost operating model

Choice Service

Customer insight

Sales advice Easy to shop Playtables 2-in-1 store offering

Multi-channel Pure play reserve&collect Specialist

Great brands Wide range Exclusivity Own brand product

Delivery & installation Set up & upgrade Help & support Repair & protect

Directors’ ReportStrategic Summary

Business Model

Bringing life to technologyOur customers are at the centre of an increasingly digitised world which they can access and utilise in numerous different ways. Whether this be social media, online gaming, downloading movies, sharing pictures, cloud computing or energy efficient products, customers do not just come into our stores to buy products, but to find a solution to a need. It is our job to help find the right solution for our customers, ensuring they get the most out of the products they buy. As such we put our customers at the heart of everything we do. Our core purpose of bringing life to technology embodies our belief that in this increasingly complex world our customers need solutions and help. From this core purpose we have built our customer plan which is discussed in more detail in the Chief Executive’s Review on pages 5 to 7.

As one of Europe’s leading specialist electrical retailing and services companies we operate a business model that supports delivery of our Customer Plan.

Customer insightIn order to ensure we understand what our customers want, how they use the products they buy from us, and what they think of the service they get from us, we use extensive customer insight. This includes discussions at customer panels, interviews, home visits and other research. This is supported by mystery shopping in our own and competitors’ stores, exit surveys and customer feedback. We use this information to build our ranges, improve our stores and services as well as help us with other business decisions.

Stores and internetConvenience and ease of navigation are key in attracting customers to shop with us. Through the Renewal and Transformation plan (more detail of which can be found at www.dixonsretail.com) we are improving our stores, making them easier to shop with, for example, improved navigation, better signage, playtables to allow customers to interact with products before they buy, as well as good advice on features and benefits from our colleagues. We are also combining our PC World and Currys stores into 2-in-1 stores which give our customers greater access to our specialist computing offer combined with our market leading mixed electrical offering, and enables us to improve our sales densities and rent to space mix. We favour the combined store format and we are implementing this in our stores across the Nordics and Other International businesses.

Our FIVES sales training programme combined with our Product Learning Centres provides our colleagues with the right tools to really understand customers’ needs and to provide them with the complete solution to properly meet those needs. We will continue to improve the training of our colleagues and the ways in which we can help them be experts in the products we sell.

Many of our customers research products online before coming in to store to buy, so ease of navigation, clear descriptions of products and related information are important for our websites. We are increasingly seeing customers combining the ease of the internet with the convenience of our stores by using our reserve&collect service. In the UK, we have implemented the market leading e-merchant platform from PIXmania which enables us to continually evolve and improve our online offer to ensure customers are engaged with our internet operations.

ProductsCombining our customer insight with our market strength across Europe we can make sure we have the right range of products in our stores to suit customers’ needs. Our scale means that we can work with suppliers to showcase the latest technology and products in our stores, with areas dedicated to key suppliers’ products. This also enables us to get products exclusively in our stores, such as the iPad on launch in 2010.

Own brand products enable us to offer customers a greater range and choice of products at competitive prices. We have defined a clear good-better-best brand range of: Currys and PC World essentials; Logik; Advent; Goji; and Sandstrøm brands.

Customers are at the heart of everything we do

Dixons Retail plc 17 Annual Report and Accounts 2010/11

Directors’ ReportStrategic Summary

After-sales services and supportMany of our customers need help with their products, whether it be delivery and installation, keeping their products up and running or repairing them when things go wrong. Our business in the UK & Ireland sets the benchmark for our services infrastructure. In May 2011 we relaunched our services under the new KNOWHOW brand with four clear pillars of support for customers to choose from.

We operate the largest network of two man deliveries in the UK with around 60,000 deliveries per week enabling us to provide customers with the convenience of next day delivery in a three hour time slot or the value of a free delivery later. Our KNOWHOW team in store, in our call centre and out in the field can provide set up and upgrade services as well as online fix and back up services. Our market leading range of help and support services help ensure a customer has the backing of expertise and support that keeps their technology up and running. In the event that a customer has a problem with their product we fix it. For example our state of the art repair facility in Newark repairs 600,000 laptops and televisions each year and is able to repair and return a laptop in six days. We offer customers a choice of support agreements such as ‘Premier’ which provides them with a loan TV, for example, if theirs needs to be taken in for repair.

Business Modelcontinued

Our low cost operating model drives continuous improvement in our processes and services. This continuous improvement enables us to re-invest back into providing better value products and services to our customers.

Direct ownership of the service infrastructure from end to end means we can ensure the best service at all touch points with our customers. We believe this gives us a unique operating model for a specialist electrical retailer and a significant competitive advantage in meeting the needs of our customers.

While much of the improvement work has been focused on the UK, core elements of the business model exist in our businesses in the Nordics and Other International divisions. Further services under the KNOWHOW brand will be rolled out to these divisions over the medium term.

Low cost operating modelDixons Retail operates in a highly competitive market. In order to deliver an unbeatable customer offer we need to have a low cost to sales ratio relative to the service based business we run. This means we have to:

have sufficient scale economics in each market – usually number one or two by market share;

lean business processes – minimising wasteful activity;

design our business processes end to end to minimise cost and deliver a high quality of service; and

find new ways to continually improve what we do.

We use a technique called Lean Six Sigma to re-engineer our business processes to make them better for customers, easier for colleagues to operate and therefore cheaper to run.

Through this low cost operating model we can deliver an unbeatable offer for customers meaning that they reward us with increased market share and improved returns for our shareholders.

WEH = Whateverhappens customer support agreements

Delivery & Recycling

Built-in Cooker Installation

Cooker Installation

Washer and Dishwasher Installation

Fridge Freezer Installation

TV Set Up & Demo

TV Wallmount & Demo

Integrated Appliance Install

Home Theatre Set Up & Demo

Aerial Install & Tune

Aerial Multiroom Install and Tune

Freesat Setup & Demo

Freesat Install & Demo

Freesat + Install & Demo

Set up and Support

Store & Protect

Virus & Spyware Removal

24 7 Help and Advice

Store & Share

PC Tune Up

System Reset & Restore

Infinity

Data Transfer & Check

Data Wipe & Check

Data Rescue & Protect

Computer Set up & Personalise

Software Install & Check

Operating System Upgrade & Check

Camera Set up & Personalise

Component Install & Check

Network Set up & Secure

Memory Install & Check

Tablet Set up & Tutorial

Tablet Set up Tutorial & Internet Protection

Netbook Set up

Knowhow Appcentre

Network Fault & Fix

Aerial Fault & Fix

WEH - Computing

WEH Premier -Computing

WEH - TV

WEH Premier- TV

WEH - Kitchen

WEH Premier - Kitchen

WEH - Technology

Instant Replacement

Games Console Fault & Fix

Desktop PC Fault & Fix

Digibox Fault & Fix

Laptop Fault & Fix

TV Fault & Fix

Strategic S

umm

ary08 -- 22

18 Dixons Retail plcAnnual Report and Accounts 2010/11

Directors’ ReportStrategic Summary

Looking Forward

The Group is making significant progress under the Renewal and Transformation plan. The operational processes across the business are on a firmer foundation, the customer offer is better than it has ever been and costs are under control.

Our offer for customers must continually improve. Here we set out just some of the innovations in the business which will enable us to remain one step ahead of the competition and firmly focused on customer needs in every market in which we operate.

This year we opened an exciting new concept store called Black in Birmingham. This is a 15,000 sq ft high street store on three floors, totally new in design and positioned as the ultimate place to get up close with the most wanted gadgets around. It is a must-visit store, appealing to customers who love their brands and how their kit looks. We are using Black to conduct a variety of trials, exploring new ways of making the shopping trip and the presentation of our exciting technology and services even better for customers. A totally new store layout, department style disciplines in categories, interactive displays and new ways of merchandising are all being explored in this store. We have embedded the new KNOWHOW services brand in the store, providing areas for customers to use the services we can provide in a more interactive and relaxed environment. Our colleagues have been encouraged to explore new ways of excelling at providing high levels of services and better solutions for customers. The customer feedback has been very encouraging and we are already taking learnings from this format into the rest of the store portfolio across the Group.

Simplifying the shopping trip for our customers is key to helping them buy the right solution as well as getting the best out of the technology they buy. This is why we created the customer journey in each category. We have trialled new ways of doing this in Black and elsewhere in our portfolio. We have now developed an improved customer journey around a vision which not only simplifies the technology for customers, but also helps them choose other products and services to get the complete solution. Trials of this have proved to be very successful and set the groundwork for improved customer journeys in other categories.

Added value services are a key differentiator in our business model (as discussed on page 17) and we will continue to innovate in this area. For example, having introduced PDAs for our delivery and installation team we are looking at other ways to use this technology, such as dynamic routing of our colleagues out in the field to make sure we meet and even exceed customers’ needs, the ability to provide customers with added value services while in their homes rather than on a second call out and use of the data provided by the PDAs to improve processes.

A lot of exciting things are going on, but we won’t sit still. We will continue to innovate to deliver a better shopping trip for our customers.

Keeping ahead of the competition

Dixons Retail plc 19 Annual Report and Accounts 2010/11

Directors’ ReportStrategic Summary

Key Performance Indicators

Financial and operational

Definition PerformanceTotal underlying sales

Growth in total underlying sales. The ability to grow sales is an important measure of a brand’s appeal to customers and its competitive position.

Like for like sales

The Board measures like for like sales as sales in stores that have been open for a full financial year both at the beginning and end of the financial period and are calculated using constant exchange rates. Customer support agreement sales are excluded from all UK like for like calculations. Operations that are subject to closure have sales excluded as of the announcement date. Stores subject to a refurbishment are excluded during the period of refurbishment. All e-commerce pick-up store sales are included in like for like sales. Sales targets and growth are set relative to the market and expected economic conditions.

Market position In line with the Group’s strategy to be the leading specialist electrical retailer in Europe, this is an important measure of how well customers are being engaged by the Group’s brands in each market. Retailing operations should be, or be capable of becoming, the number one or number two specialist electrical retailer in their market, measured by market share.

No.1 market positions in:

UK & Ireland Nordics Greece Czech Republic

Underlying operating profit

Continued growth of underlying operating profit enables the Group to invest in its future and provide a return for shareholders. Targets are set relative to expected market performance.

Underlying profit before tax

Continued growth of underlying profit before tax represents a measure of Group performance to external investors and shareholders. Targets are set relative to expected market performance.

Free Cash Flow The Group defines Free Cash Flow as net cash generated from operations, less net finance costs, taxation and net capital expenditure and excluding certain discrete items such as special pension contributions. The management of cash usage, in particular working capital employed in the business, optimises resources available for the Group to invest in its future growth and to generate shareholder value.

(£million)

8,154.4

8,320.0

7,955.8

8,074.8

7,531.7

2010/11

2009/10

2008/09

2007/08

2006/07

(£million)

127.6

133.2

7,955.8

8,074.8

7,531.7

2010/11

2009/10

2008/09

2007/08

2006/07

(£million)

85.3

90.9

7,955.8

8,074.8

7,531.7

2010/11

2009/10

2008/09

2007/08

2006/07

2010/11: (2)%2009/10: +2%

2010/11: £10.0m2009/10: £(17.6)m

Shareholder

Underlying diluted earnings per share (EPS)

The level of growth in EPS provides a suitable measure of the financial health of the Group and its ability to deliver returns to shareholders each year. The Group targets growth in EPS commensurate with growth in earnings.

Total Shareholder Return (TSR)

This metric provides a relative performance measure over the longer term of the Group’s ability to deliver returns for shareholders. For 2009/10, the base which the Group used was to outperform a bespoke weighted average index of UK and European Retailers over a three year period. From 2010/11, the base has been to measure against the FTSE 250 Index (comprising FTSE 101-350 companies), excluding investment trusts, over a three year period.

See graph on page 50

2010/11: 1.6p2009/10: 1.5p

For more information on our Corporate Responsibility KPI’s see pages 32 to 35.

Strategic S

umm

ary08 -- 22

20 Dixons Retail plcAnnual Report and Accounts 2010/11

Directors’ ReportStrategic Summary

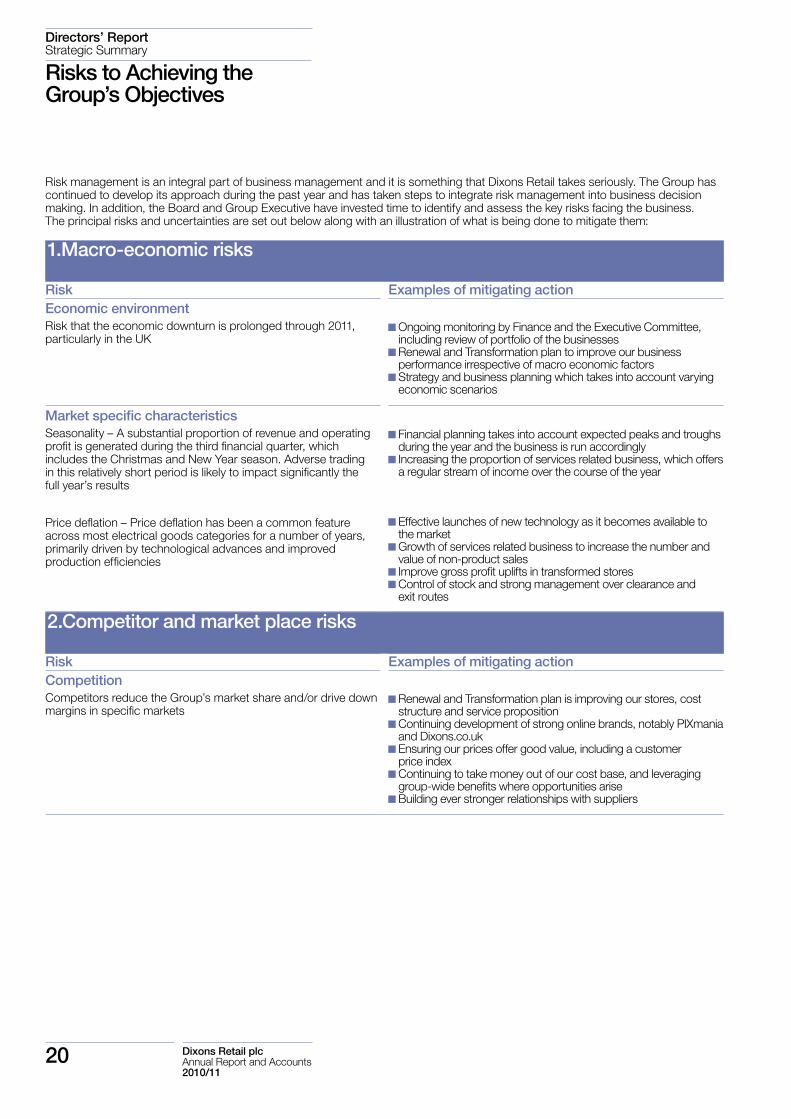

Risks to Achieving the Group’s Objectives

1.Macro-economic risks

Risk Examples of mitigating actionEconomic environmentRisk that the economic downturn is prolonged through 2011, particularly in the UK

Ongoing monitoring by Finance and the Executive Committee, including review of portfolio of the businesses Renewal and Transformation plan to improve our business performance irrespective of macro economic factors Strategy and business planning which takes into account varying economic scenarios

Market specific characteristics Seasonality – A substantial proportion of revenue and operating profit is generated during the third financial quarter, which includes the Christmas and New Year season. Adverse trading in this relatively short period is likely to impact significantly the full year’s results

Price deflation – Price deflation has been a common feature across most electrical goods categories for a number of years, primarily driven by technological advances and improved production efficiencies

Financial planning takes into account expected peaks and troughs during the year and the business is run accordingly Increasing the proportion of services related business, which offers a regular stream of income over the course of the year

Effective launches of new technology as it becomes available to the market Growth of services related business to increase the number and value of non-product sales Improve gross profit uplifts in transformed stores Control of stock and strong management over clearance and exit routes

2.Competitor and market place risks

Risk Examples of mitigating actionCompetition Competitors reduce the Group’s market share and/or drive down margins in specific markets

Renewal and Transformation plan is improving our stores, cost structure and service proposition Continuing development of strong online brands, notably PIXmania and Dixons.co.uk Ensuring our prices offer good value, including a customer price index Continuing to take money out of our cost base, and leveraging group-wide benefits where opportunities arise Building ever stronger relationships with suppliers

Risk management is an integral part of business management and it is something that Dixons Retail takes seriously. The Group has continued to develop its approach during the past year and has taken steps to integrate risk management into business decision making. In addition, the Board and Group Executive have invested time to identify and assess the key risks facing the business. The principal risks and uncertainties are set out below along with an illustration of what is being done to mitigate them:

Dixons Retail plc 21 Annual Report and Accounts 2010/11

2.Competitor and market place risks continued

Risk Examples of mitigating actionChanging technology/consumer preferencesRisk that we fail to capitalise on new technology or emerging trends to maximise revenues

Our retail brands fail to meet the expectations of customers

Strong supplier relationships (e.g. UK launch partner of Apple iPad) Delivery of Customer Plan to respond to identified changes in technology Store transformations to take into account emerging trends in store layouts Exciting product launches to make our stores the destination for the latest technology (e.g. 3D TVs)

Understanding our customers and monitoring our levels of service through mystery shopping, customer exit surveys and analysis of purchase data Continued focus on ensuring we have an excellent range acrossall price points, including own label brands Renewal and Transformation plan improving the quality and optimising the location of our stores across the Group FIVES customer service training for all colleagues and product workshops to improve product knowledge Implementation of the Customer Plan in the UK to improve the customer journey – a clear and focused plan at the heart of the business Innovations in service propositions and improved customer service levels across the Group Clearer and easier navigation of our e-commerce websites

Legislative, contractual, reputational and regulatory risksRisk that as a result of a change in legislation, a decision by a regulatory authority, or exposure in our compliance activities, the Group’s business is impacted by reputational or financial damage or a need to adapt the Group’s business and processes (e.g. competition, consumer rights, intellectual property, contractual obligations, health and safety or compromise of confidential customer data)

In-house legal teams communicate on a frequent basis and legal reports are submitted to the Board Launch of Group Ethical Conduct policy, supported by annual declaration of compliance by colleagues Monitoring changes in legislation/regulation Corporate Responsibility Committee meets regularly to discuss reputational and regulatory risks Quality checks and factory audits for own-branded product assembly Compliance Committee approves activity that may impact the terms of Group credit facilities Contact with regulatory authorities, such as in relation to the Office of Fair Trading’s (OFT) market study into extended warranties

3.Operational risks

Risk Examples of mitigating actionEmployeesRisk that we fail to attract, develop and retain the necessary talent for our business

Group-wide standardised performance management Talent reviews across the business Store structures which provide a clear career path for all employees Improved quality of training courses and development programmes with specialist focus on service, product, commercial and technical Bonus plans, which include a component relating to individual performance and business performance Reward strategy aligned to retain the best talent

Directors’ ReportStrategic Summary

Strategic S

umm

ary08 -- 22

22 Dixons Retail plcAnnual Report and Accounts 2010/11

Directors’ ReportStrategic Summary

3.Operational risks continued

Risk Examples of mitigating actionSystems failure and damage to property and consequential business interruptionRisk that a key system becomes unavailable for a period of time

The Group’s ability to distribute merchandise to its stores and to sell and distribute merchandise to its customers is reliant on its operational infrastructure, particularly the efficient functioning of its distribution centres and distribution network

Contingency plans developed that are tested regularly Evaluation, planning and implementation analysis carried out before updating or introducing new systems that have an impact on critical functions Ongoing systems implementation in key areas of the business

Disaster recovery plans are in place Insurance is purchased to mitigate against business interruption Preventative measures are constantly being updated to reduce the likelihood of an incident

Project deliveryRisk that a project delivering an element of our Renewal and Transformation plan does not deliver its anticipated benefits

The portfolio plan is clearly defined and is managed and governed through clear processes and regular meetings Post-investment analysis and performance tracking is in place including financial and customer measures Projects under the Customer Plan are aligned to our UK budget

InternetRisk we fail to build a successful internet business, both in its own right and as part of a multi-channel retailing model

Execution of online strategy Investment in site functionality and user friendliness Roll-out of our e-merchant platform across our businesses Successful marketing campaigns to raise the profile of online brands

4.Financial risks

Risk Examples of mitigating actionChanges in supplier creditRisk that credit insurance is no longer available to electrical and computing suppliers

Ongoing engagement with suppliers and credit insurers Improvements in stock management Innovations in and close scrutiny of working capital together with regular monitoring and review

Finance and treasuryRisk that the Group’s exposure to exchange rate, interest rate, liquidity and credit risks have an adverse or unexpected impact on results, funding requirements or purchasing ability

Detailed Group hedging policies reviewed through a separate Tax and Treasury Committee Balance sheet management and reviews Strong cash management Regular monitoring of receivables balances Strong pre and post investment appraisal processes Central control of treasury activity

Pensions risk and policiesRisk that the pension funding policy fails to react to or address deficits, which may arise on the Group’s pension schemes

Deficit reduction activities in place Defined benefit section of UK scheme closed to future accrual

Risks to Achieving the Group’s Objectivescontinued

Dixons Retail plc 23 Annual Report and Accounts 2010/11

Directors’ ReportPerformance Review

Business highlights Renewal and Transformation plan delivering a market leading

offer for customers.

Store transformation programme on track:

– 360 stores reformatted at the year end;

– 70 Megastores now open with average annual sales of £20 million;

– Over 80 Megastores across the Group, including 40 in the UK and 25 in the Nordics will have been reformatted by Peak 2011;

– Newly reformatted stores continue to deliver gross profit uplifts of 20% versus the unreformatted stores in the UK and 15% in the Nordics; and

– Second year trading for reformatted stores maintained.

Elkjøp performed strongly in all of its markets, gaining significant market share.

New customer services brand KNOWHOW launched in the UK encompassing all after sales and support services.

Multi-channel internet sales up 13% across the Group, reflecting the continued shift of sales to the multi-channel brands.

Closure of loss making PC City operations in Spain ahead of plan.

Cost savings on track:

– £50 million savings delivered in the financial year; and

– £50 million of additional cost savings expected in each of the next three years.

Impairment and restructuringRecognising challenging conditions in some of our markets, and the ongoing business restructuring under the Renewal and Transformation plan, we have reviewed the balance sheet and made impairment and other non underlying charges totalling £309.4 million. The additional cash impact of these charges is estimated as £39 million, of which approximately £8 million was incurred in 2010/11. The impairments primarily relate to the closure of operations in Spain (£70.6 million), the impairment of acquired goodwill in relation to Kotsovolos in Greece (£53.2 million) and PIXmania (£106.3 million).

Overview

Key highlights Margins and underlying profit before tax, at £85.3 million,

maintained in challenging market conditions.

Investment in the customer offer through the Renewal and Transformation plan is delivering.

Increasing market share across most markets and sectors, particularly in the UK and Nordics.

Step change to the customer focused business model, differentiating the offer for customers.

Further benefits to come through rolling out refurbished and Megastore formats, the transformation of the services offer through KNOWHOW, upgraded websites and a leaner operating model.

Financial highlights Total underlying Group sales(1)(2) down 2% to £8,154.4 million

(2009/10 £8,320.0 million) and down 1% on a constant currency basis.

Total Group sales, including those from businesses to be closed and closed businesses, were £8,341.8 million (2009/10 £8,532.5 million).

Group like for like sales(3) down 4% in the second half and down 2% in the full year.

Underlying Group gross margins were flat in the second half of the year and up 0.1% in the full year.

EBIT(4) of £127.6 million (2009/10 £133.2 million).

Underlying pre-tax profit(1) of £85.3 million (2009/10 £90.9 million).

Underlying diluted earnings per share(1) of 1.6 pence (2009/10(5) 1.5 pence). Basic loss per share for continuing operations of (6.6) pence (2009/10 earnings per share of 2.0 pence).

Total loss before tax, after deducting non-underlying items of £(309.4) million, was £(224.1) million (2009/10 profit before tax of £112.7 million).

Free Cash Flow(6) of £38.9 million before restructuring charges (2009/10 £28.1 million).

As at 30 April 2011 the Group had net debt of £(206.8) million (2009/10 £(220.6) million).

Rephased debt profile following issue of new 2015 Bonds and part repurchase of existing 2012 Bonds in July 2010.

Perform

ance Review

23 -- 35

24 Dixons Retail plcAnnual Report and Accounts 2010/11

Directors’ ReportPerformance Review

Underlying sales and profit analysisUnderlying sales Underlying profit/(loss)

52 weeks ended

30 April 2011 £million

52 weeks ended

1 May 2010 £million

Currency neutral (7)

% changeLike for like(3)

% change

52 weeks ended

30 April 2011 £million

52 weeks ended

1 May 2010 £million

UK & Ireland(8) 3,816.1 4,013.5 (5)% (3)% 71.3 71.1

Nordics(9) 2,268.9 2,093.7 +7% +5% 105.6 97.4

Other International(10) 1,226.7 1,291.6 (2)% (5)% (21.6) (8.3)

Pure play e-commerce(11) 842.7 921.2 (5)% (5)% 0.9 11.3

Central costs – – (15.8) (19.5)

Total Group Retail 8,154.4 8,320.0 (1)% (2)% 140.4 152.0

Property losses (12.8) (18.8)

EBIT 127.6 133.2

Underlying net finance costs (42.3) (42.3)

Group underlying profit before tax 85.3 90.9

Notes

(1) Throughout this report, references are made to underlying performance measures. Underlying results are defined as excluding trading results from the business to be closed, closed businesses, the amortisation of acquired intangibles, net restructuring and business impairment charges and other one off non-recurring items, profit on sale of investments, net fair value remeasurements of financial instruments and, where applicable, discontinued operations. These excluded items are described as ‘non-underlying’. The financial effect of these items is shown in the analyses on the face of the income statement and in note 4 to the financial statements.

(2) Business to be closed comprises PC City Spain. Closed businesses comprise the operations of PC City Sweden and Markantalo in Finland. Discontinued operations comprise operations in Poland and Hungary.

(3) Like for like sales are calculated based on stores that have been open for a full financial year both at the beginning and end of the financial period and are calculated using constant exchange rates. Customer support agreement sales are excluded from all UK like for like calculations. Operations that are subject to closure have sales excluded as of the announcement date. Stores subject to a refurbishment are excluded during the period of refurbishment. All e-commerce pick-up store sales are included in like for like sales.

(4) Underlying Earnings Before Interest and Tax (EBIT) equates to underlying operating profit and is defined as underlying earnings from retail operations, after property losses, before deduction of net finance costs and tax.

(5) The weighted average number of shares used in the calculation of earnings per share for the period prior to the rights issue, which completed on 9 June 2009, has been multiplied by an adjustment factor to reflect the bonus element of the shares issued under the terms of the rights issue (as described in note 8 to the financial statements). The adjustment factor used was 1.2138.

(6) Free Cash Flow relates to continuing operations and comprises net cash flow from operating activities before special pension contributions, less net finance costs, less income tax paid and net capital expenditure.

(7) Currency neutral change percentage reflects the year on year growth or decline in underlying sales, calculated excluding the effect of currency movements.

(8) UK & Ireland comprises Currys, CurrysDigital, Dixons Travel, PC World, operations in Ireland, DSGi Business and KNOWHOW. Like for like sales exclude DSGi Business.

(9) Nordics comprises the Elkjøp group and Dixons Travel Denmark.

(10) Other International comprises Greece (Kotsovolos), Italy (Unieuro, combined 2-in-1 Unieuro and PC City stores and Dixons Travel Italy), Czech Republic (Electro World), Slovakia

(Electro World) and Turkey (Electro World).

(11) Pure play e-commerce division comprises Dixons.co.uk and PIXmania.

(12) Unless otherwise noted, throughout this statement figures relate to continuing operations, excluding the results of the business to be closed / closed businesses. Total revenue including discontinued operations and business to be closed / closed businesses was £8,341.8 million (2009/10 £8,543.4 million).

Business performanceUnderlying Group sales (excluding discontinued operations and the business to be closed / closed businesses) were down 2% to £8,154.4 million (2009/10 £8,320.0 million) and down 2% on a like for like basis. Underlying Group sales were down 1% at constant exchange rates. Total Group sales (including the business to be closed / closed businesses) were down 2% to £8,341.8 million (2009/10 £8,532.5 million). Group gross margins were up 0.1% across the year.

Group EBIT (underlying profit before interest and tax) was £127.6 million (2009/10 £133.2 million). Group underlying profit before tax was £85.3 million (2009/10 £90.9 million). Total loss before tax, after deducting non-underlying items of £309.4 million, was £(224.1) million (2009/10 profit before tax £112.7 million).

Overview continued

Dixons Retail plc 25 Annual Report and Accounts 2010/11

Underlying sales(£million)

2010/11 3,816.1

4,013.52009/10

Underlying operating profit(£million)

2010/11 71.3

71.12009/10

Directors’ ReportPerformance Review

Dixons Travel continues to go from strength to strength with all stores now operating in the new format which allows for more customer focused ranges, with a particular focus on portable items and accessories. The demographic of its customer base in airports has meant the business has been less impacted by the consumer downturn. In addition to the UK, Dixons Travel now operates in Copenhagen, Dublin, Rome and Milan airports with further opportunities in other airports across Europe.

Internet sales continue to be driven by the shift of consumers and manufacturers to multi-channel retail outlets with significant growth in reserve&collect. At the start of the financial year, the PIXmania e-merchant platform was implemented across the UK websites significantly improving the navigation, operation and customer experience. Further work to improve the offer and extended ranges online are planned for the new financial year.

Gross margins in the UK & Ireland were up throughout the year as a result of a number of factors:

Improvements in stock control, enabling the business to exit the year with lower inventory levels than last year despite the very weak markets. This has included improved processes for exiting aged stock, limiting the need for excessive discounting;

Introduction of better promotional planning, enabling better support from suppliers, particularly as they increasingly favour multi-channel operators; and

Cost saving initiatives in the distribution and services infrastructure.

The division made good progress on the Renewal and Transformation plan through the year with 250 stores now refitted in the UK & Ireland, including 31 Megastores. The preferred format for customers and for the business is the combined 2-in-1 Currys and PC World format. All High Street and out of town Superstores will be in this format. The majority of the 70 Megastores the Group is targeting will also be in this format, with a small number of standalone Currys Megastores in larger catchments. The Group’s planned store base for the UK & Ireland is 450 stores, comprising 70 High Street stores, 310 Superstores and 70 Megastores. The portfolio will be managed to this size as existing leases expire and stores in each catchment are refitted.

The Group operates the most comprehensive end to end service offering in electrical retailing in the UK, giving the Group a unique services model versus the competition. In the spring of 2011 the new services brand of KNOWHOW was launched. This follows an intensive period of investment and significant improvement in our service offering for customers. The new brand was introduced into stores in May 2011 with roll out to all stores being completed by the autumn. The KNOWHOW brand provides customers with clear easily identifiable value for money services under four distinct categories; Deliver & Install; Set up & Upgrade; Help & Support; and Repair & Protect. Through growth and continuous process improvements the unit costs can be reduced, enabling further investment in the services offer.

UK & Ireland

Profit and margins maintained despite challenging markets.

Performing ahead of our competitors.

Launch of KNOWHOW services.

Total sales in the UK & Ireland were down 5% to £3,816.1 million (2009/10 £4,013.5 million) and like for like sales were down 3% across the year. Underlying operating profit for the full year was flat year on year at £71.3 million (2009/10 £71.1 million).

This is an encouraging performance in the context of a weak market. During the first half we benefitted from sales of TVs in the lead up to the World Cup. The ‘cash for goals’ promotion caught customers’ imagination and enabled the business to capture more than its market share of the uplift in sales of TVs. The work being done under the Renewal and Transformation plan to improve the store environment and the shopping trip for customers was recognised by Apple when they chose us as their key partner for the launch of the iPad. Trade continued to be robust in the lead up to Christmas and in the early sale period, interrupted only by very poor weather conditions in the two week period preceding Christmas. However, like for like sales in the second half were down 7% as the consumer environment weakened in the fourth quarter. Against this environment Currys and PC World traded ahead of the competition and gained market share. During the year, white goods held up well and computing has been supported by iPads and tablets, with the new iPad 2 selling very strongly. Television sales benefitted from a strong World Cup, but have been particularly weak since January.

Perform

ance Review

23 -- 35

26 Dixons Retail plcAnnual Report and Accounts 2010/11

Underlying sales(£million)

2010/11 2,268.9

2,093.72009/10

Underlying operating profit(£million)

2010/11 105.6

97.42009/10

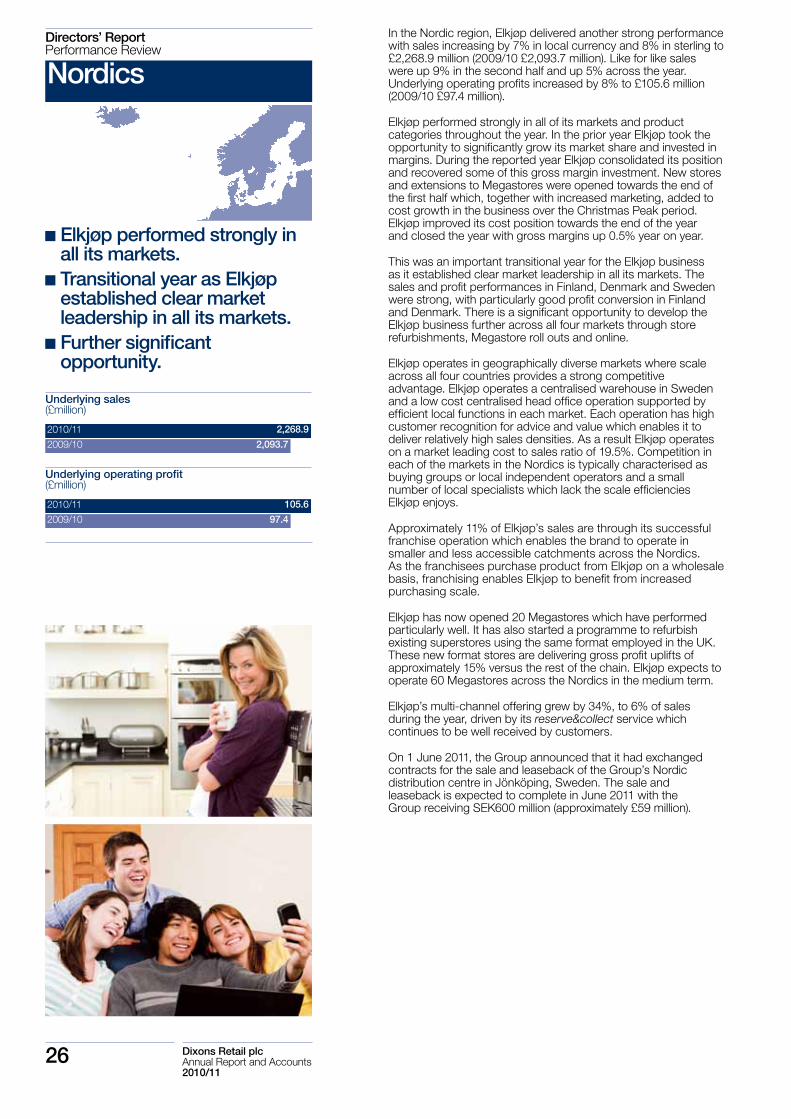

Directors’ ReportPerformance Review

In the Nordic region, Elkjøp delivered another strong performance with sales increasing by 7% in local currency and 8% in sterling to £2,268.9 million (2009/10 £2,093.7 million). Like for like sales were up 9% in the second half and up 5% across the year. Underlying operating profits increased by 8% to £105.6 million (2009/10 £97.4 million).

Elkjøp performed strongly in all of its markets and product categories throughout the year. In the prior year Elkjøp took the opportunity to significantly grow its market share and invested in margins. During the reported year Elkjøp consolidated its position and recovered some of this gross margin investment. New stores and extensions to Megastores were opened towards the end of the first half which, together with increased marketing, added to cost growth in the business over the Christmas Peak period. Elkjøp improved its cost position towards the end of the year and closed the year with gross margins up 0.5% year on year.

This was an important transitional year for the Elkjøp business as it established clear market leadership in all its markets. The sales and profit performances in Finland, Denmark and Sweden were strong, with particularly good profit conversion in Finland and Denmark. There is a significant opportunity to develop the Elkjøp business further across all four markets through store refurbishments, Megastore roll outs and online.

Elkjøp operates in geographically diverse markets where scale across all four countries provides a strong competitive advantage. Elkjøp operates a centralised warehouse in Sweden and a low cost centralised head office operation supported by efficient local functions in each market. Each operation has high customer recognition for advice and value which enables it to deliver relatively high sales densities. As a result Elkjøp operates on a market leading cost to sales ratio of 19.5%. Competition in each of the markets in the Nordics is typically characterised as buying groups or local independent operators and a small number of local specialists which lack the scale efficiencies Elkjøp enjoys.

Approximately 11% of Elkjøp’s sales are through its successful franchise operation which enables the brand to operate in smaller and less accessible catchments across the Nordics. As the franchisees purchase product from Elkjøp on a wholesale basis, franchising enables Elkjøp to benefit from increased purchasing scale.

Elkjøp has now opened 20 Megastores which have performed particularly well. It has also started a programme to refurbish existing superstores using the same format employed in the UK. These new format stores are delivering gross profit uplifts of approximately 15% versus the rest of the chain. Elkjøp expects to operate 60 Megastores across the Nordics in the medium term.

Elkjøp’s multi-channel offering grew by 34%, to 6% of sales during the year, driven by its reserve&collect service which continues to be well received by customers.

On 1 June 2011, the Group announced that it had exchanged contracts for the sale and leaseback of the Group’s Nordic distribution centre in Jönköping, Sweden. The sale and leaseback is expected to complete in June 2011 with the Group receiving SEK600 million (approximately £59 million).

Nordics

Elkjøp performed strongly in all its markets.

Transitional year as Elkjøp established clear market leadership in all its markets.

Further significant opportunity.

Dixons Retail plc 27 Annual Report and Accounts 2010/11

Underlying sales(£million)

2010/11 1,226.7

1,291.62009/10

Underlying operating loss(£million)

2010/11 (21.6)

(8.3)2009/10

Directors’ ReportPerformance Review

This division comprises operations in Italy, Greece, the Czech Republic, Slovakia and Turkey. Total sales were down 2% at constant exchange rates and by 5% in sterling to £1,226.7 million (2009/10 £1,291.6 million). Underlying operating losses were £(21.6) million (2009/10 loss of £(8.3) million). Towards the end of the financial year the Group announced that it was closing its PC City operations in Spain. The closure programme is on track, with all stores now closed and a net cash cost of closure of approximately £30 million across the 2010/11 and 2011/12 financial years. Underlying financials are reported excluding these PC City operations.

ItalyThis comprises Unieuro, combined 2-in-1 Unieuro and PC City stores and Dixons Travel Italy operating in the airports in Rome and Milan. The business has progressed well against the turnaround plan, with a positive EBITDA delivered for the first time in several years, ahead of plan. The turnaround plan has involved considerable work to improve the ranges in-store, as well as availability for customers. Significant progress has been made in improving the stock turn to improve working capital, helping cash generation. Using the same Six Sigma principles as have been employed in the UK & Ireland division, Unieuro has reduced costs. In addition the store network is being upgraded, including store reformatting, again using the work done in the UK & Ireland division, which provides a better, easier to navigate store environment for customers.

A strong first quarter driven by the World Cup was followed by a weaker sales environment as the business anniversaried the first stages of the regional digital switchover. The consumer environment remained subdued in the second half, but Unieuro continued to outperform the market as it benefitted from a further stage of the digital switchover. As the business becomes cash generative it will start to add Megastores as well as refurbish existing stores to the 2-in-1 Unieuro and PC City format that is proving to be the favoured format for customers. The business is well positioned to make further gains in the years ahead.