Embed Size (px)

Citation preview

1 | P a g e

PICK OF THE WEEK

Jan 22, 2018

DISHMAN CARBOGEN AMCIS LTD.

Recommendation

Buy at CMP and add on declines

Add on dips to

Rs 317-325

Sequential Targets

Rs 412 & Rs 459

Time Horizon

4-6 Quarters

Industry

Pharmaceuticals

CMP

Rs 361

FUNDAMENTAL ANALYST

Atul Karwa

HDFC Scrip Code DISCAREQNR

BSE Code 540701

NSE Code DCAL

Bloomberg DCAL IN

CMP (19-Jan-18) 360.95

Equity Capital (Rs Mn) 322.8

Face Value (Rs) 2.0

Eq. Shares O/S (Mn) 161.4

Market Cap (Rs Mn) 58255

Book Val (Rs) 302.7

Avg.52 Wk Volume 2,53,000

52 Week High 378.1

52 Week Low 275.0

Shareholding Pattern % (Dec 31, 17)

Promoters 61.4

Institutions 21.4

Non Institutions 17.2

Total 100.0

Incorporated in 1983, Dishman Pharmaceuticals was a global outsourcing partner for the pharmaceutical industry offering a portfolio of development, scale-up and manufacturing services. In Aug-2006, it acquired Carbogen Amcis, a leading service provider, offering a portfolio of drug development and commercialisation services to the pharmaceutical and biopharmaceutical industries at all stages of drug development. Post a Scheme of Arrangement, Dishman Pharma was Amalgamated with Carbogen Amcis and the merged entity was renamed as Dishman Carbogen Amcis Ltd. (DCAL) wef Jan 01, 2015. The new entity got listed on Sept 21, 2017. The company operates 23 multipurpose facilities across India, Switzerland, the Netherlands and China, and a dedicated production facility for APIs and intermediates in Bavla and Naroda. Most of its facilities have been approved/certified by health authorities.

Investment Rationale: Focus on CRAMS business

Fully integrated player gives a natural advantage

Strong R&D and product pipeline

Commercialisation of capabilities built in High Potency API

Steady growth in marketable molecules

Concerns: Regulatory compliance risk

Adverse incidents related to Niraparib

Delays in product launches

Low return ratios

Foreign exchange fluctuations

View and Valuation DCAL has a natural advantage of being an integrated player making it a preferred partner in India for global innovators. With strong visibility on commercial launches and future orders, DCAL will finally see its efforts culminating in sustainable growth starting FY18. Apart from Niraparib, there are three to four potential launches in FY18, which will not only accelerate growth, but also de-risk earnings from blockbuster products. Altogether, there are 25 candidates in Phase III, and we expect four to five products to be commercialised every year. The bulk of capex investments already made, and prudent spending over the next 2-3 years, DCAL could generate US$ 80-90mn free cash flows p.a. Higher EBITDA margins and reducing leverage would bring down interest costs and lower effective tax rate will contribute significantly to boost earnings.

At CMP of Rs 361 the stock quotes at 15.8x FY20E EPS and 8.4x FY20E EV/EBITDA. We feel investors could buy the stock at the CMP and add on dips to Rs 317-325 band (14x FY20E EPS and 7.5x FY20E EV/EBITDA) for sequential targets of Rs 412 (18x FY20E EPS and 9.5x FY20E EV/EBITDA) and Rs 459 (20x FY20E EPS and 10.5x FY20E EV/EBITDA) in 4-6 quarters.

2 | P a g e

PICK OF THE WEEK

Jan 22, 2018

DISHMAN CARBOGEN AMCIS LTD.

Consolidated Financial Summary

Particulars (Rs mn) Q2FY18 Q2FY17 YoY-% Q1FY18 QoQ-% FY17 FY18E FY19E FY20E

Operating Income 4,438 4,339 2.3 3,396 30.7 17,137 17,690 20,745 24,689

EBITDA 1,330 1,128 17.9 700 89.9 4,534 5,092 6,112 7,406

Adj. PAT 484 383 26.3 130 271.9 1,454 1,903 2,689 3,692

EPS (Rs) 3.0 2.4 0.8 9.0 11.8 16.7 22.9

P/E (x) 40.1 30.5 21.6 15.8

RoE (%) 3.0 3.9 5.3 6.9 Source: (Company, HDFC sec)

Company Overview Incorporated in 1983, Dishman Pharmaceuticals was a global outsourcing partner for the pharmaceutical industry offering a portfolio of development, scale-up and manufacturing services. In Aug-2006, it acquired Carbogen Amcis, a leading service provider, offering a portfolio of drug development and commercialisation services to the pharmaceutical and biopharmaceutical industries at all stages of drug development. Post a Scheme of Arrangement, Dishman Pharma was Amalgamated with Carbogen Amcis and the merged entity was renamed as Dishman Carbogen Amcis Ltd. (DCAL) wef Jan 01, 2015. The new entity got listed on Sept 21, 2017. The company operates 23 multipurpose facilities across India, Switzerland, the Netherlands and China, and a dedicated production facility for APIs and intermediates in Bavla and Naroda. Most of its facilities have been approved/certified by health authorities.

Revenue breakup (FY17) Segmental Revenue trend (Rs mn)

`

(Source: Company, HDFC Sec)

DCAL is a fully-integrated global CRAMS player. 72% of the total revenue flows from the CRAMS (Contract Research & Manufacturing services) segment, with the remaining coming from the ‘Marketable Molecules’ (Vitamin D analogoues,

KEY HIGHLIGHTS

The global CRAMS industry was valued at US$ 72bn in 2013, and is expected to rise to US$ 136bn in 2017.

DCAL has natural advantage of being an integrated player making it a preferred partner in India for global innovators

Overall DCAL has 400+ molecules under development, of which 15 to 16 molecules are in late-stage phase III trials

DCAL is working on nine ADCs, with one being very close to commercialisation in FY18, and the other in early Phase III.

Higher utilisation of the Hi-Po and Shanghai facilities, better EBITDA margins and financial leverage coupled with lower effective tax rate would contribute significantly to boost earnings

3 | P a g e

PICK OF THE WEEK

Jan 22, 2018

DISHMAN CARBOGEN AMCIS LTD.

generic APIs etc). Within CRAMS, DCAL is in the business of custom synthesis (CRO) and contract manufacturing (CMO) of APIs. Upon engagement, DCAL helps its customers through the entire process of development, and then the commercialisation of the drug: (1) Carbogen Amcis handles the research and clinical trials, and (2) Dishman India takes care of manufacturing of large scale commercial batches. In FY17, Dishman Pharma decided to reverse merge its 100% subsdiary, Carbogen Amcis India, with the parent entity wef Jan 01, 2015. Post the reverse merger, DCAL will receive tax benefits to the tune of ~Rs 3bn over the next 15 years, owing to the amortisation of the resultant goodwill of ~Rs 13.5bn.

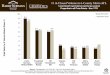

Investment Rationale Focus on CRAMS business DCAL’s focus is chiefly on its CRAMS business, which contributed ~72% of total revenue in FY17. Over the last six years, CRAMS revenues have grown at 10% CAGR, led by 16% growth in the Carbogen Amcis (CA) Switzerland subsidiary. The EBITDA margins have also improved from 22.6% in FY12 to 26.5% in FY17. At present, DCAL largely operates in four therapies that it has identified as its focus areas. These include oncology, cardiac, CNS and ophthalmology. Overall, there are 400+ molecules under development.

Breakup of CRAMS business

`

(Source: Company, HDFC Sec)

4 | P a g e

PICK OF THE WEEK

Jan 22, 2018

DISHMAN CARBOGEN AMCIS LTD.

The global CRAMS industry was valued at US$ 72bn in 2013, and was expected to rise to US$ 136bn in 2017. The CRO market for development services is expected to grow at 11-12% CAGR to US$ 44.6bn by 2018. The growing trend of outsourcing the drug development processes and proliferation of virtual biotech companies in the US are the key drivers for this uptick in the industry. The R&D spend of pharmaceutical and biotechnology companies has also not abated, increasing from US$ 108bn in 2006 to US$ 141bn in 2015. This figure is expected to increase to US$ 160bn by 2020. CRO Dev. Industry to grow to US$ 44.6bn by CY18 CRAMS industry growth pegged at 22-23% CAGR

`

(Source: Company, HDFC Sec)

India is already a preferred manufacturing destination on account of its cost advantages, skilled scientific talent pool and improving manufacturing capabilities. Hence, growth is expected to stem from both India’s gain in market share and the growth of the market itself. However, India’s share is only 8-10% of the CRAMS market at present. This indicates the vast growth opportunity available to Indian players in this segment. A CAGR of 18-20% is expected for Indian players over 2013-18. Fully integrated player gives a natural advantage The development capabilities in CA and the manufacturing capabilities in India, give DCAL a natural and significant advantage in this business. Before the acquisition of CA, DCAL was only able to focus on the development side of the process, whereas now, forward integration makes DCAL a preferred partner among innovators. Mylan, Abbott, JnJ, Novartis and Celgene are among DCAL’s main customers. The business is extremely sticky in nature, as innovators do not generally change partners during the process of development and commercialisation, as it is both cumbersome and expensive. The company believes 75% of the business is repeat.

5 | P a g e

PICK OF THE WEEK

Jan 22, 2018

DISHMAN CARBOGEN AMCIS LTD.

Present across the value chain

`

(Source: Company, HDFC Sec)

Strong R&D and product pipeline At present, DCAL has 400+ molecules under development, of which 15 to 16 molecules are in late-stage phase III, 15 to 16 in early phase III , 150 in phase II and 250 in phase I or pre-clinical. Overall, six to eight launches are likely in in FY18 and early FY19, which include Niraparib, Edaravone, an ADC, and candidates from anti-diabetes, derma and pediatric leukemia. These molecules can add ~20% to revenues and ~40-45% to earnings by FY20E. In DCAL’s CRAMs pipeline, there are fourteen molecules in phase III, of which twelve have already been filed. Eight of these filings are in oncology, two in CNS, one in CVS and one in opthalmalogy. This is indicative of the huge opportunity available to DCAL in the foreseeable future.

6 | P a g e

PICK OF THE WEEK

Jan 22, 2018

DISHMAN CARBOGEN AMCIS LTD.

Key Molecules Molecule Company Therapy Indication Status Commercial

Launch Potential peak sales (US$ mn)

Niraparib Tesaro Oncology Ovarian cancer Approved Q2FY18 1500

Sirturo J&J Anti-Infective Anti-TB Approved FY16 300

Edaravone Novartis & Treeway CNS ALS Approved Q1FY18 300

Molecule 1 - Anti-Diabetes - Approved Q3FY18 750

Molecule 2 - Derma Anti-bacterial Filed Q4FY18 500

Molecule 3 - Oncology, ADC ALL Filed Q4FY18 1000

Molecule 4 - Oncology Pediatric Leukemia Filed FY19 500

Crenolanib Arog Pharma Oncology GIST, AML, Glioma Phase III FY19 N/A (Source: Company, HDFC Sec)

Niraparib: Niraparib has now been launched in the EU after marketing approval from the EC. Post commercial launch in the US in Apr-17, niraparib is likely to deliver sales of ~US$ 120mn in CY17. Tesaro had peggged the global opportunity size of the current indication at US$1bn. However, Tesaro is determind to expand niraparib’s indications beyond the current maintenance therapy setting and into the first-line of ovarian cancer treatment. This opportunity has been pegged at US$ 4bn by the company. Niraparib API supplies could generate US$ 25-30mn on peak sales for DCAL. Edaravone: Edaravone, currently sold under the brands Radicut (Japan) and Radicava (USA), is an intravenous drug used to help with recovery following a stroke, and to treat amyotrophic lateral sclerosis (ALS). Treeway, a company based in the Netherlands, is also developing an oral version of this drug. It is our understanding that these drugs are a part of DCAL’s pipeline. Edaravone injection could translate to a ~US$ 5-6mn opportunity for DCAL. Crenolanib: Crenolanib, a next-gen tyrosine kinase inhibitor, is currently undergoing clinical trials for use in a variety of indications like Acute Myeloid Leukemia (AML), Gastro-intestinal Stromal Tumor (GIST) and Glioma. The US FDA has awarded fast track designation to crenolanib for the indication of R/R AML, while the European Union has previously granted orphan drug status to crenolanib for the treatment of AML and soft tissue sarcoma. Per the information on clinicaltrials.org (link), the phase III trial for GIST is scheduled to be completed by Aug-19, making a late FY20/early FY21 commercial launch possible. Crenolanib could translate to a double-digit US$mn product for DCAL. Commercialisation of capabilities built in High Potency API DCAL has invested in world class capabilities to address the Anti-Body Conjugates (ADC) market. Coupled with 15 years of HiPo API experience, the High Potency API business could represent a significant opportunity for step change in the company’s top and bottom line growth. DCAL has significant capabilities in two parts of the ADC. One is the warhead, the active toxin which piggybacks on the antibody and also the linker, which is the molecule that links the active toxin to the antibody. DCAL is also improving its skills in the antibody.

7 | P a g e

PICK OF THE WEEK

Jan 22, 2018

DISHMAN CARBOGEN AMCIS LTD.

DCAL is working on nine ADCs, with one being very close to commercialisation in FY18, and the other in early Phase III. Recently, it was successful in winning a project from a German pharma company for an ADC product. Advanced ADC Molecules (Commercialised To Phase III)

Molecule Company Status Indication

Adcetris (brentuximab vedotin) Seattle Genetics Marketed Hodgkin's lymphoma and anaplastic large cell lymphoma;

Kadcyla (trastuzumab emtansine) ImmunoGen Marketed HER2+ve metastatic breast cancer

Inotuzumab ozogamicin Pfizer Approved Relapsed or refractory CD22-positive acute lymphoblastic leukemia

Sacituzumab govitecan Immunomedics Phase III Triple-negative breast cancer

Mirvetuximab soravtansine Immunogen Phase III Women with platinum-resistant FR-alpha positive advanced EOC

Vadastuximab talirine (SGN-CD33A) Seattle Genetics Phase III Acute Myeloid Leukemia (Source: Company, HDFC Sec)

Steady growth in marketable molecules DCAL manufactures and supplies a range of Vitamin D and Vitamin D analogues. It also manufactures cholesterol and lanolin related products for pharmaceutical, cosmetic and related markets. It has achieved market leadership in the advanced regulated markets in the Vitamin D space. Due to the commoditisation of Vitamin D3, it has now shifted its focus to high-margin low-volume analogs and cholesterol, which fetches a significantly higher price in the global market. These are manufactured at its Netherland facility, and it is operating at only 55% of its capacity. This business makes 35%+ margins. With higher utilisation in the coming years, it will aid margin expansion. DCAL operates in a few other segments, which contributed ~14% to the FY17 revenue. Of these, the most significant is the disinfectants market, where DCAL is looking to build a presence. Through its disinfectant division, DCAL offers a range of Antiseptics and Disinfectants for application in healthcare and related industries such as disinfectants for surgical instrumentation, hand and body wash sanitisers and antiseptics, pre and post-operative surgical scrubs, antimicrobial washes. Dishman Specialty Chemicals is the global leader in the specialty chemicals segment and the leading manufacturer of Phase Transfer Catalysts. The company had a long association with the manufacture and supply of Quaternary ammonium compounds (Quats) for use as phase transfer catalysts. New launches to drive margin expansion EBITDA margins have been in an upward trend since FY16. This was mainly owing to the rationalisation of orders at Dishman India in FY15 and operating leverage in Switzerland. Further margin improvement would be driven by higher utilisation of the Hi-Po and Shanghai facilities and commercialisation of 4-5 molecules every year from the phase III pipeline.

8 | P a g e

PICK OF THE WEEK

Jan 22, 2018

DISHMAN CARBOGEN AMCIS LTD.

The management has guided for Rs 1.7-1.8bn capex in FY18, which will be spent on buying equipment for two new blocks at the Hi-Po facility and constructing a building for Carbogen Amicis’ development segment. With the bulk of capex investments already made, and prudent spending over the next 2-3 years, DCAL is expected to generate US$ 80-90mn free cash flows and fixed asset turnover is expected to scale up to ~1.2x (adjusting for idle land and goodwill). Higher EBITDA margins and reducing financial leverage would bring down interest costs and lower effective tax rate will contribute significantly to boost earnings.

Revenue: 14% CAGR Over FY17-20E EBITDA Margin: ~400bps Expansion By FY20E

(Source: Company, HDFC Sec)

Q2FY18 Results Review Dishman Carbogen (DCAL) reported strong numbers in Q2FY18. Revenue was Rs 4.4bn, up 2%/31% YoY/QoQ. EBITDA came in at Rs 1.3bn, up 20% YoY. The margin was 30%, ~400bps up YoY. PAT came in at Rs 484mn, up 26% YoY. These strong numbers were largely on account of sales deferred from Q1, commercial launch of Niraparib and the benefits of operating leverage.

Particulars (Rs mn) Q2FY18 Q2FY17 YoY (%) Q1FY18 QoQ (%)

Operating Income 4,438 4,339 2.3 3,396 30.7

Material consumed 795 900 (11.7) 474 67.5

Employee expenses 1,518 1,430 6.2 1,434 5.9

Other expenses 796 880 (9.6) 788 1.0

EBITDA 1,330 1,128 17.9 700 89.9

Depreciation 546 546 514

9 | P a g e

PICK OF THE WEEK

Jan 22, 2018

DISHMAN CARBOGEN AMCIS LTD.

EBIT 784 583 34.6 186 321.4

Other Income 90 125 66

Finance cost 134 198 114

PBT 741 510 45.4 138 437.1

Tax expenses 257 127 8

PAT 484 383 26.3 130 271.9

EPS (Rs) 3.0 2.4 0.8

EBITDA (%) 30.0% 26.0% 396 bps 20.6% 935 bps

PAT (%) 10.9% 8.8% 207 bps 3.8% 707 bps (Source: Company, HDFC sec)

Concerns Regulatory compliance risk The pharmaceutical industry is highly regulated in many countries and requires various approvals, licenses, registrations and permissions for business activities. Regulatory compliance risk, especially pertaining to the US FDA, has been a key overhang on the sector in recent years. In India, the government also controls the prices of pharmaceutical products through the drug price control order (DPCO) under price control mechanism which could erode profitability. Adverse incidents related to Niraparib Niraparib API is expected to generated US$ 25-30mn revenues for DCAL. Any adverse development for Niraparib could result in lower revenues. Delays in product launches DCAL has invested in building capabilities for high potency APIs. Delays in commercialisation of revenues from these products could result in lower growth and profitability. Low return ratios Due to the high amount of goodwill in the books and investment on idle land, return ratios for the company are very low. In FY17 RoE and RoCE stood at 3.0%/2.9% respectively. Adjusted for goodwill and idle land RoE and RoCE stood at 17.2%/12.0% Foreign exchange fluctuations The Company operates internationally and is exposed to foreign exchange risk arising from foreign currency transactions, primarily with respect to the USD, EURO, GBP, CHF and Chinese Renminbi (RMB). The Company hedges 75 to 80% of its estimated foreign currency exposure in respect of forecast sales.

10 | P a g e

PICK OF THE WEEK

Jan 22, 2018

DISHMAN CARBOGEN AMCIS LTD.

View and Valuation DCAL has a natural advantage of being an integrated player making it a preferred partner in India for global innovators. With strong visibility on commercial launches and future orders, DCAL will finally see its efforts culminating in sustainable growth starting FY18. Apart from Niraparib, there are three to four potential launches in FY18, which will not only accelerate growth, but also de-risk earnings from blockbuster products. Altogether, there are 25 candidates in Phase III, and we expect four to

five products to be commercialised every year. The bulk of capex investments already made, and prudent spending over the next 2-3 years, DCAL could generate US$ 80-90mn free cash flows p.a. Higher EBITDA margins and reducing leverage would bring down interest costs and lower effective tax rate will contribute significantly to boost earnings.

At CMP of Rs 361 the stock quotes at 15.8x FY20E EPS and 8.4x FY20E EV/EBITDA. We feel investors could buy the stock at the CMP and add on dips to Rs 317-325 band (14x FY20E EPS and 7.5x FY20E EV/EBITDA) for sequential targets of Rs 412 (18x FY20E EPS and 9.5x FY20E EV/EBITDA) and Rs 459 (20x FY20E EPS and 10.5x FY20E EV/EBITDA) in 4-6 quarters.

Peer Comparison (FY20E) (Rs Mn) CMP* Mcap Revenues % growth OPM PATM EPS BVPS P/E P/BV RoNW

Dishman Carbogen Amcis 361 58,255 24,702 18.9 31.1 15.5 22.9 343.7 15.8 1.1 6.9

Syngene International 616 123,160 18,740 18.0 34.7 24.7 23.1 126.4 26.7 4.9 18.3

Divi's Lab. 1098 291,564 49,066 11.9 37.6 28.7 53.1 284.9 20.7 3.8 19.8 * CMP as on 19-Jan-18 (Source: HDFC Sec and street estimates)p

11 | P a g e

PICK OF THE WEEK

Jan 22, 2018

DISHMAN CARBOGEN AMCIS LTD.

Consolidated Financial Statements

Income Statement Particulars (Rs mn) FY16 FY17 FY18E FY19E FY20E

Net Revenues 16,017 17,137 17,714 20,778 24,702

Growth (%) 0.8 7.0 3.4 17.3 18.9

Material Expenses 3,419 3,293 3,175 3,514 4,174

Employee Expenses 5,355 5,960 6,007 6,827 7,871

Selling and Admin. Exps 1,726 1,814 1,974 2,409 2,982

Other Operating Expenses 1,413 1,537 1,459 1,907 2,266

EBITDA 4,103 4,534 5,099 6,121 7,409

EBITDA Margin (%) 25.6 26.5 28.8 29.5 30.0

EBITDA Growth (%) 31.2 10.5 12.5 20.1 21.0

Depreciation 1,975 2,135 2,241 2,386 2,479

EBIT 2,128 2,399 2,858 3,735 4,931

Other Income (Incl. EO Items) 265 261 270 350 450

Interest 944 490 440 367 319

PBT 1,449 2,170 2,687 3,718 5,061

Tax (Incl Deferred) 421 707 779 1,023 1,367

RPAT 1,028 1,463 1,908 2,696 3,695

Minority Interest (1) (9) - - -

APAT 1,027 1,454 1,908 2,696 3,695

APAT Growth (%) -14.3 41.6 31.2 41.3 37.1

Adjusted EPS (Rs) 6.4 9.0 11.8 16.7 22.9

Balance Sheet Particulars (Rs mn) FY16 FY17 FY18E FY19E FY20E

SOURCES OF FUNDS

Share Capital - Equity 161 161 161 161 161

Reserves 48,853 47,979 49,597 52,003 55,311

Total Shareholders Funds 49,014 48,140 49,758 52,164 55,472

Long Term Debt 5,126 4,601 4,101 3,601 3,101

Short Term Debt 5,327 4,790 5,250 4,500 4,750

Total Debt 10,453 9,391 9,351 8,101 7,851

Net Deferred Taxes 818 803 150 350 450

Other Non-current Liab. & Prov. 2,474 2,263 2,299 2,549 2,799

TOTAL SOURCES OF FUNDS 62,759 60,597 61,558 63,164 66,572

APPLICATION OF FUNDS

Net Block 51,450 48,473 47,994 48,108 48,129

CWIP 1,330 1,329 1,100 950 800

Investments 53 46 46 46 46

Other Non-current Assets 1,815 2,169 2,200 2,500 2,825

Total Non-current Assets 54,648 52,017 51,340 51,604 51,800

Cash & Equivalents 1,043 1,270 2,343 2,391 4,425

Inventories 3,399 4,266 4,481 5,242 6,227

Debtors 3,153 2,856 3,000 3,509 4,169

Other Current Assets 5,349 5,335 5,373 5,856 6,408

Total Current Assets 11,901 12,457 12,854 14,607 16,804

Creditors 1,144 856 826 914 1,086

Other Current Liab. & Prov. 3,690 4,290 4,154 4,525 5,372

Total Current Liabilities 4,834 5,147 4,980 5,439 6,458

Net Current Assets 7,067 7,310 7,875 9,169 10,346

TOTAL APPLICATION OF FUNDS 62,759 60,596 61,558 63,164 66,572

12 | P a g e

PICK OF THE WEEK

Jan 22, 2018

DISHMAN CARBOGEN AMCIS LTD.

Cash Flow Particulars (Rs mn) FY16 FY17 FY18E FY19E FY20E

Reported PBT 2,334 2,170 2,687 3,718 5,061

Non-operating & EO items (74) (15) (653) 200 100

Interest net 846 229 170 17 (131)

Depreciation 1,091 2,135 2,241 2,386 2,479

Working Capital Change (835) (807) (560) (1,344) (1,253)

Tax Paid (575) (707) (779) (1,023) (1,367)

OPERATING CASH FLOW ( a ) 2,786 3,005 3,106 3,955 4,890

Capex (1,239) (2,008) (1,771) (2,350) (2,350)

Free cash flow (FCF) 1,548 997 1,335 1,605 2,540

Investments - 41 - - -

Non-operating Income (290) 1,007 270 350 450

INVESTING CASH FLOW ( b ) (1,529) (960) (1,501) (2,000) (1,900)

Debt Issuance/(Repaid) 101 (1,062) (40) (1,250) (250)

Interest Expenses (720) (490) (440) (367) (319)

FCFE 639 493 1,125 338 2,421

Dividend (323) (232) (290) (290) (386)

Others (66) - 238 - -

FINANCING CASH FLOW ( c ) (1,007) (1,784) (532) (1,906) (955)

NET CASH FLOW (a+b+c) 251 262 1,073 48 2,035

EO Items, Others - - - - -

Closing Cash & Equivalents 613 874 1,947 1,995 4,030

Key Ratios Particulars (Rs mn) FY16 FY17 FY18E FY19E FY20E

PROFITABILITY (%)

GPM 78.2 79.8 81.5 82.5 82.5

EBITDA Margin 26.2 27.7 29.7 30.5 31.1

APAT Margin 6.6 8.9 11.1 13.4 15.5

RoE 3.3 3.0 3.9 5.3 6.9

RoIC (or Core RoCE) 4.1 2.9 3.7 4.9 6.3

RoCE 3.9 2.9 3.6 4.7 6.0

EFFICIENCY

Tax Rate (%) 29.1 32.6 29.0 27.5 27.0

Fixed Asset Turnover (x) 0.3 0.3 0.3 0.3 0.3

Inventory (days) 79.1 95.3 95.3 95.3 95.3

Debtors (days) 73.4 63.8 63.8 63.8 63.8

Other Current Assets (days) 98.3 97.8 85.1 77.3 68.9

Payables (days) 26.6 19.1 17.6 16.6 16.6

Other Current Liab. & Prov. (days) 84.0 91.6 84.1 79.5 79.5

Cash Conversion Cycle (days) 140.3 146.1 142.5 140.2 131.8

Debt/EBITDA (x) 2.5 2.1 1.8 1.3 1.1

Net D/E (x) 0.2 0.2 0.1 0.1 0.1

Interest Coverage (x) 2.5 5.4 7.1 11.1 16.9

PER SHARE DATA (Rs)

EPS 6.4 9.0 11.8 16.7 22.9

Dividend 1.0 1.2 1.5 1.5 2.0

Book Value 303.7 298.3 308.3 323.2 343.7

VALUATION

P/E (x) 56.7 40.1 30.5 21.6 15.8

P/BV (x) 1.2 1.2 1.2 1.1 1.1

EV/EBITDA (x) 16.6 14.7 12.9 10.5 8.4

Dividend Yield (%) 0.3 0.3 0.4 0.4 0.6

(Acknowledgement for this report : HDFCSec Institutional research)

13 | P a g e

PICK OF THE WEEK

Jan 22, 2018

DISHMAN CARBOGEN AMCIS LTD.

Price chart since relisting:

14 | P a g e

PICK OF THE WEEK

Jan 22, 2018

DISHMAN CARBOGEN AMCIS LTD.

Fundamental Research Analyst: Atul Karwa ([email protected]) HDFC securities Limited, I Think Techno Campus, Building - B, "Alpha", Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg (East), Mumbai 400 042 Phone: (022) 3075 3400 Fax: (022) 2496 5066 Website: www.hdfcsec.com Email: [email protected].

Compliance Officer: Binkle R. Oza Email: [email protected] Phone: (022) 3045 3600 __________________________________________________________________________________________________________________________________________________________________________________________________ Disclosure: I, (Atul Karwa, MMS), authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. HSL has no material adverse disciplinary history as on the date of publication of this report. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. Research Analyst or his/her relative or HDFC Securities Ltd. does not have any financial interest in the subject company. Also Research Analyst or his relative or HDFC Securities Ltd. or its Associate does not have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Further Research Analyst or his relative or HDFC Securities Ltd. or its associate does not have any material conflict of interest. Any holding in stock – No HDFC Securities Limited (HSL) is a SEBI Registered Research Analyst having registration no. INH000002475. Disclaimer: This report has been prepared by HDFC Securities Ltd and is meant for sole use by the recipient and not for circulation. The information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. This document is for information purposes only. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete and this document is not, and should not be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments. This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be contrary to law or regulation or what would subject HSL or its affiliates to any registration or licensing requirement within such jurisdiction. If this report is inadvertently send or has reached any individual in such country, especially, USA, the same may be ignored and brought to the attention of the sender. This document may not be reproduced, distributed or published for any purposes without prior written approval of HSL. Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk. It should not be considered to be taken as an offer to sell or a solicitation to buy any security. HSL may from time to time solicit from, or perform broking, or other services for, any company mentioned in this mail and/or its attachments. HSL and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions. HSL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc. HSL and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt in the report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations described in this report.

HSL or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months. HSL or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from t date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction in the normal course of business. HSL or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither HSL nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. HSL may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the subject company or third party in connection with the Research Report.

This report is intended for non-Institutional Clients only. The views and opinions expressed in this report may at times be contrary to or not in consonance with those of Institutional Research or PCG Research teams of HDFC Securities Ltd. and/or may have different time horizons

HDFC Securities Limited, SEBI Reg. No.: NSE-INB/F/E 231109431, BSE-INB/F 011109437, AMFI Reg. No. ARN: 13549, PFRDA Reg. No. POP: 04102015, IRDA Corporate Agent License No.: HDF 2806925/HDF C000222657, SEBI Research Analyst Reg. No.: INH000002475, CIN - U67120MH2000PLC152193