Embed Size (px)

Citation preview

Development of Iowa Statewide

Freight Transporta�on Network

Op�miza�on Strategy

Final Report

September 2016

© 2016 Quetica, LLC

quèt� ica

© 2016 Quetica, LLC

2 Development of Iowa Statewide Freight Transportation Network Optimization Strategy

Table of Contents

List of Figures.....................................................................................................................................................................4

List of Tables......................................................................................................................................................................6

List of Acronyms and Abbreviations..................................................................................................................................8

1. Executive Summary.......................................................................................................................................................9

1.1. Project Overview ...................................................................................................................................................9

1.2. Key Findings ........................................................................................................................................................12

1.3. Recommendations...............................................................................................................................................14

2. Introduction to Freight Transportation Network Optimization ....................................................................................17

2.1. Optimization Methodology...................................................................................................................................17

2.2. Overview of Iowa’s Freight Transportation Network..........................................................................................19

2.3 Optimization Model Architecture Overview ........................................................................................................24

3. Demand Modeling........................................................................................................................................................27

3.1. Demand Module Development Process.............................................................................................................29

3.2. Out-of-Scope Items in Demand Model ...............................................................................................................34

4. Capacity Modeling and Analysis .................................................................................................................................36

4.1. Highway Network Capacity Analysis ..................................................................................................................37

4.2. Rail Network Capacity .........................................................................................................................................40

4.3. Inland Waterway Network Capacity....................................................................................................................46

5. Quantitative and Qualitative Measurements ..............................................................................................................51

5.1. Quantitative Measurements................................................................................................................................51

5.2. Qualitative Measurements ..................................................................................................................................52

5.3. Comparing Transportation Modes using Different Measurement Criteria ........................................................53

6. Data Analysis and Key Findings .................................................................................................................................57

6.1. Baseline Model Summary ...................................................................................................................................57

6.2. Optimized Baseline Performance Summary ......................................................................................................59

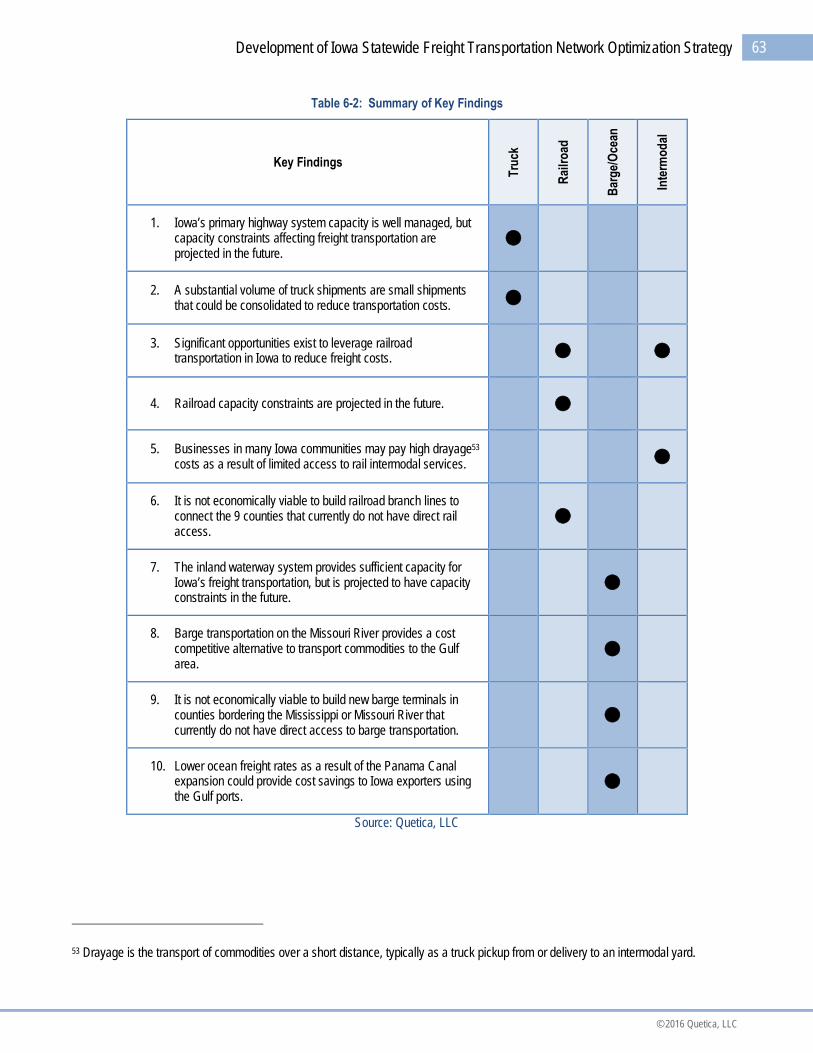

6.3. Key Findings from Baseline Analysis .................................................................................................................62

3

© 2016 Quetica, LLC

Development of Iowa Statewide Freight Transportation Network Optimization Strategy

7. Recommended Optimization Strategies .....................................................................................................................94

7.1. Explore the Opportunity to Establish and Leverage New Truck Cross-Docking Operations to Enable GreaterTruck Freight Consolidation for Iowa Businesses......................................................................................................95

7.2. Explore the Opportunity of a New Rail Intermodal Facility in Iowa to Enable Access to Lower Cost RailIntermodal Services for Iowa Businesses.................................................................................................................110

7.3. Explore the Opportunity of Additional Transload Facilities to Provide Iowa Businesses with More Access toLower Cost Rail Freight Services..............................................................................................................................129

7.4. Explore Opportunities to Leverage a Barge and Rail Multimodal Solution to Provide a Cost-Effective FreightTransportation Alternative .........................................................................................................................................143

7.5. Explore the Opportunity to Build a Logistics Park to Co-locate Cross-Docking, Intermodal, Transloading andWarehousing Facilities ..............................................................................................................................................145

7.6. Collaborate with the Railroads to Provide Iowa Businesses with More Capacity to Accommodate ForecastedGrowth in Iowa Freight Shipments............................................................................................................................148

7.7. Explore Opportunities to Improve Competitiveness of Intermodal in Iowa by Repositioning Empty Containersusing Barge and Reducing Repositioning Costs......................................................................................................149

7.8. Explore and Implement Strategies to Reduce Deadhead Truck Miles ...........................................................152

7.9. Explore Opportunities for Railroads to Provide Additional Lower Cost Rail Freight Transportation for WithinIowa High Volume Traffic Lanes ...............................................................................................................................152

8. Additional Considerations and Next Steps ..............................................................................................................153

8.1. Project Scope Considerations...........................................................................................................................153

8.2. Next Steps .........................................................................................................................................................155

Appendix A: References...............................................................................................................................................156

Appendix B: Glossary of Terms ...................................................................................................................................161

Appendix C: Iowa Freight Advisory Council Survey Questions...................................................................................165

© 2016 Quetica, LLC

4 Development of Iowa Statewide Freight Transportation Network Optimization Strategy

List of Figures

Figure 1-1: Fundamental Steps of Freight Transportation Network Optimization Analysis ..........................................................10

Figure 2-1: Fundamental Steps of Freight Transportation Network Optimization Analysis ..........................................................18

Figure 2-2: Core Components of Supply Chain Network Design ...................................................................................................18

Figure 2-3: Iowa’s Freight Transportation Network Components...................................................................................................20

Figure 2-4: Overview of Network Optimization Conceptual Architecture .......................................................................................24

Figure 3-1: Overview of Base Year Domestic Demand Module Development..............................................................................30

Figure 3-2: FAF3 Freight Volume (Percentage of Total Tonnage) Breakdown by Mode..............................................................34

Figure 4-1: Top 10 County-To-County Truck Freight Traffic Lanes (Origin-Destination Pairs) by Commodity in 2010...............39

Figure 4-2: Iowa Rail Freight Network Utilization Map Using 2013 Data .......................................................................................43

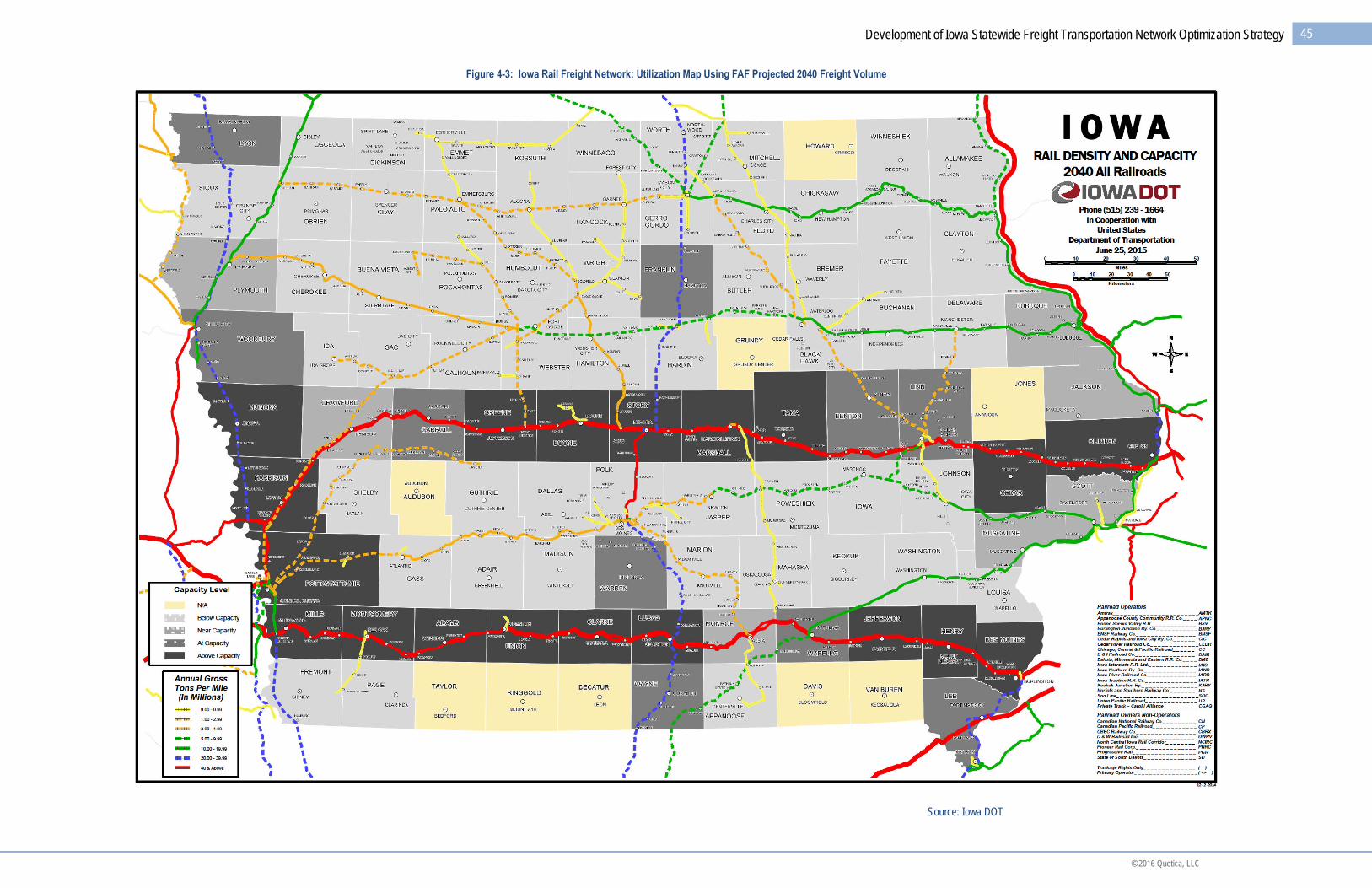

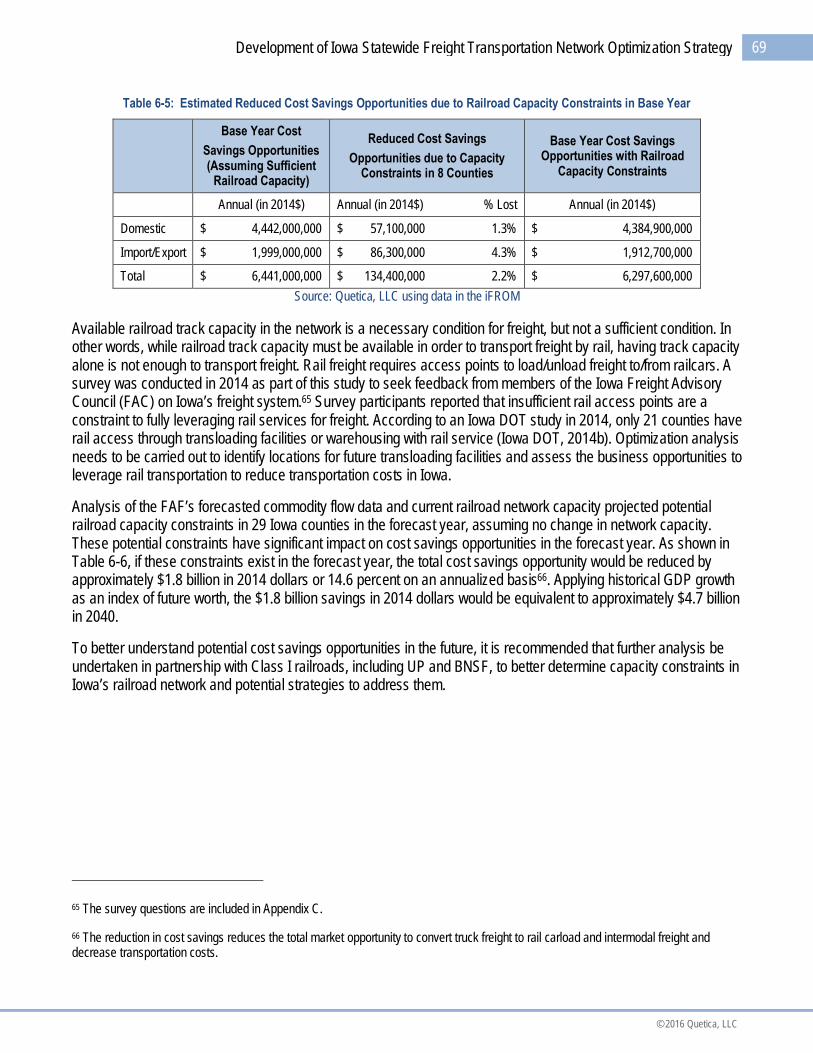

Figure 4-3: Iowa Rail Freight Network: Utilization Map Using FAF Projected 2040 Freight Volume ...........................................45

Figure 4-4: Map of Upper Mississippi and Illinois Rivers with Locks and Dams............................................................................47

Figure 5-1: U.S. Mode Share of Tonnage and Total Tonnage by Distance Band in 2007 ...........................................................56

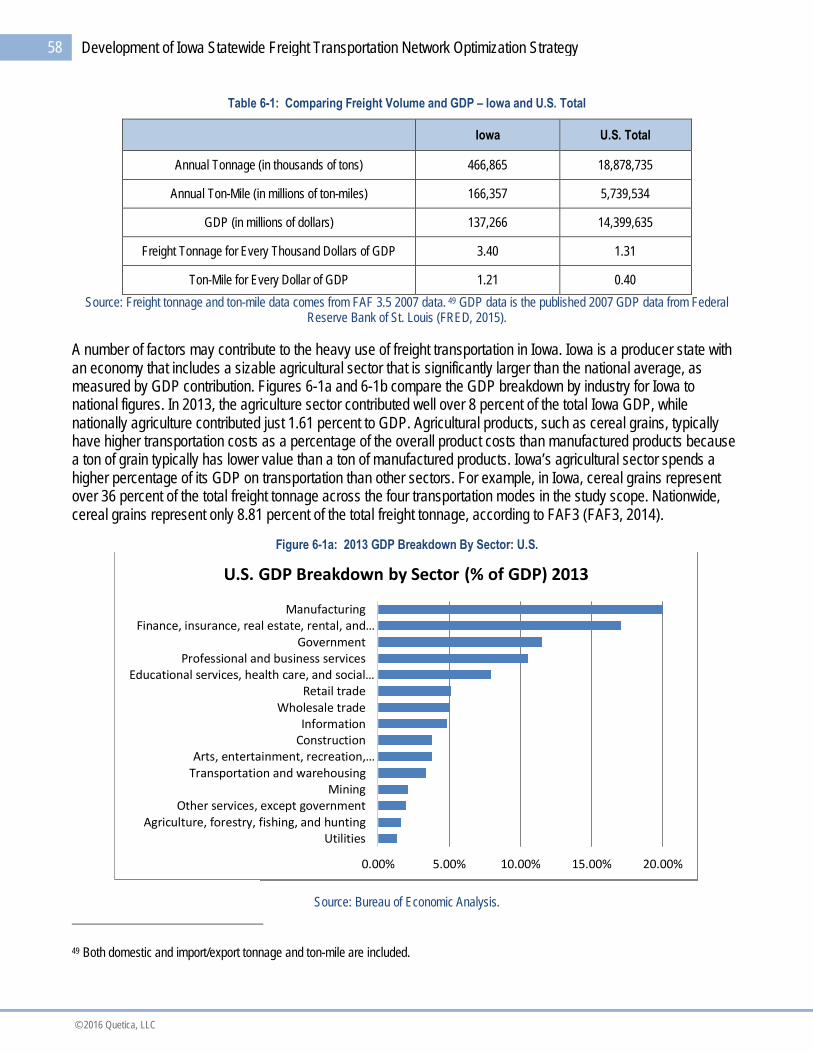

Figure 6-1a: 2013 GDP Breakdown By Sector: U.S........................................................................................................................58

Figure 6-1b: 2013 GDP Breakdown By Sector: Iowa ......................................................................................................................59

Figure 6-2: Comparing Annual Freight Volume by Mode: Baseline vs. Optimized Baseline ........................................................61

Figure 6-3: Comparing Annual Transportation Costs by Mode: Baseline vs. Optimized Baseline ..............................................62

Figure 6-4: Domestic Freight in 2012 - Percentage Breakdown of Tonnage by Mode .................................................................67

Figure 6-5: Estimated Annual Cost Savings Opportunities using Rail Carload and Rail Intermodal Transportation ..................68

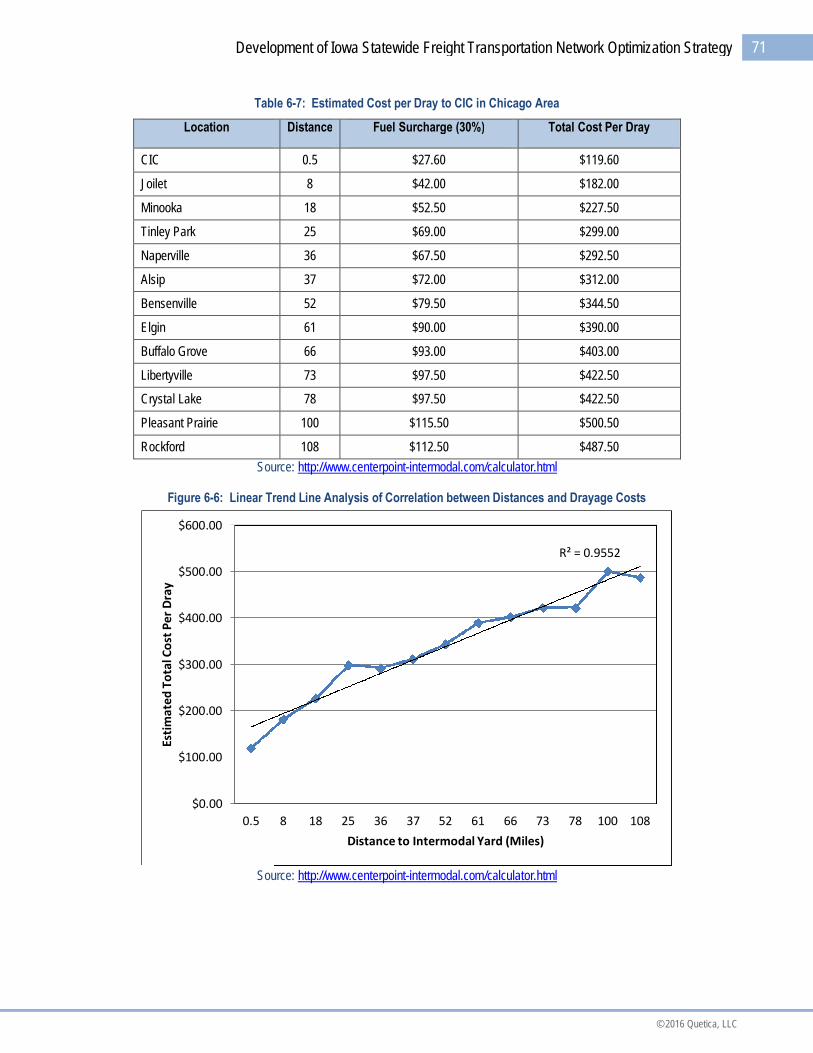

Figure 6-6: Linear Trend Line Analysis of Correlation between Distances and Drayage Costs...................................................71

Figure 6-7: Areas within 100- Mile Straight Line Radius of Existing Intermodal Yards In Iowa and Neighboring States ...........73

Figure 6-8: Annual Freight Tonnage by County That Benefits From Converting Truck to Rail ....................................................74

Figure 6-9: Ports and Navigable Waterways of the United States .................................................................................................78

Figure 6-10: Top Destination for Barge Freight Originated in Western Iowa.................................................................................79

Figure 6-11: Top Origins for Barge Freight Terminated in Western Iowa ......................................................................................80

Figure 6-12: Annual Cost Savings Opportunities with New Barge Terminals ...............................................................................82

Figure 6-13: Annual Freight Volume in Number of Barges That Would Benefit From New Barge Terminals .............................83

Figure 6-14: Average Transportation Costs to Export a 40 foot Container from Iowa to Major Foreign Markets .......................86

Figure 6-15: Cost Comparison: Trade Routes to Export Containerized Iowa Products to Major Economies in Europe ............87

Figure 6-16: Cost Comparison: Trade Routes to Export Containerized Iowa Products to Major Economies in Asia .................88

Figure 6-17: Cost Comparison: Trade Routes to Export Iowa Products to China.........................................................................89

Figure 6-18: Typical Modern Flow for Bulk Grain Export ................................................................................................................90

Figure 6-19: Iowa Areas that Could Benefit from Using Panama Canal for Grain Exports to China ............................................92

Figure 7-1: A Typical Cross-Docking Operation ..............................................................................................................................96

Figure 7-2: Comparing Total Market Opportunities (TMO) between Eastern Iowa and Central Iowa-A....................................101

5

© 2016 Quetica, LLC

Development of Iowa Statewide Freight Transportation Network Optimization Strategy

Figure 7-3: Current State Truck Shipment Network ......................................................................................................................102

Figure 7-4: Optimized State Truck Shipment Network Leveraging Cross-Dock in Eastern Iowa...............................................102

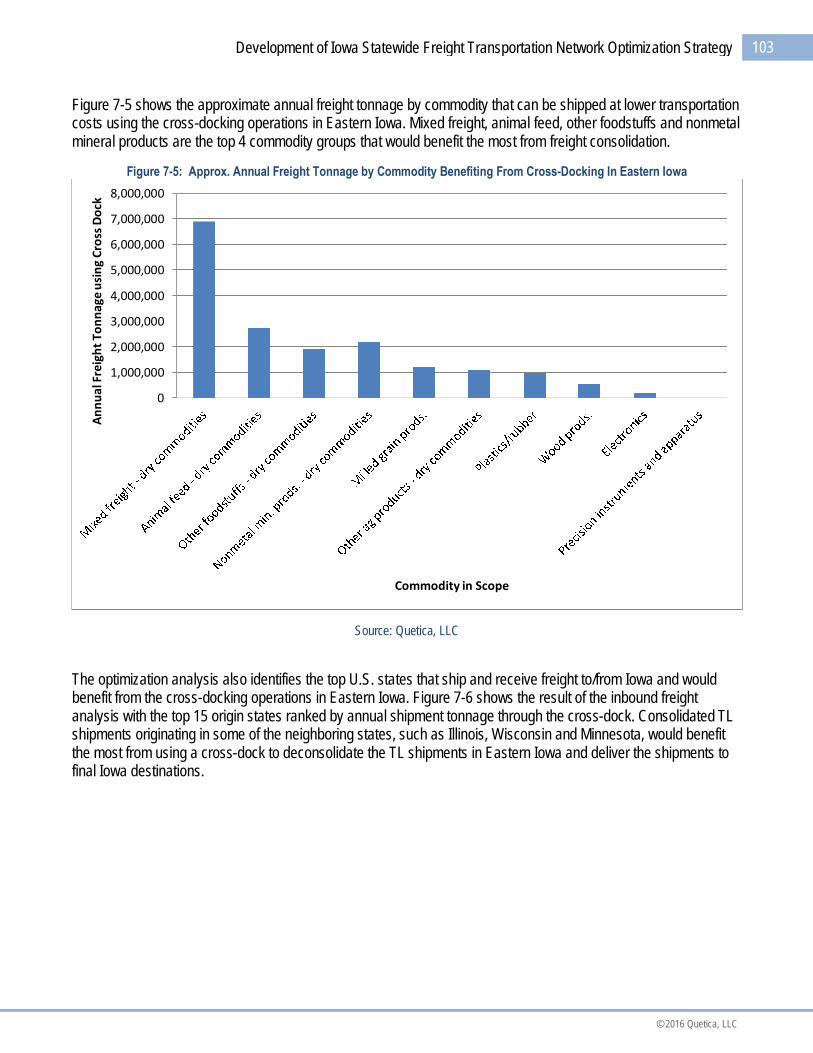

Figure 7-5: Approx. Annual Freight Tonnage by Commodity Benefiting From Cross-Docking In Eastern Iowa .......................103

Figure 7-6: Approx. Annual Freight Tonnage by Origin State Benefiting from Cross-Docking Operations in Eastern Iowa ....104

Figure 7-7: Approx. Annual Freight Tonnage by Destination State Benefiting from Cross-Docking Operations in Eastern Iowa.................................................................................................................................................................................................104

Figure 7-8: Estimated Annual EV from a Mid-Sized Cross-Dock in Eastern Iowa ......................................................................106

Figure 7-10: Aerial View of NFI’s 150-Door Cross-Dock in Breinigsville, PA ..............................................................................108

Figure 7-11: Aerial View of Reddaway’s 150-Door Cross-Dock in Fontana, CA.........................................................................108

Figure 7-12: An Intermodal Yard with Double Stacked Rail Cars.................................................................................................111

Figure 7-13: Existing Intermodal Facilities in U.S. in 2014 ...........................................................................................................111

Figure 7-14: Current Baseline Shipments That Would Benefit from an Intermodal Yard In Eastern Iowa ................................116

Figure 7-15: Optimized State Shipments Leveraging an Intermodal Yard In Eastern Iowa .......................................................116

Figure 7-16: Annual Freight Volume Measured By Container Count by Commodity in the TMO ..............................................119

Figure 7-17: Top 10 Counties with the Largest Intermodal Freight Volume (as a Percentage of Total Market Size)...............119

Figure 7-18: Aerial View of the IAIS Intermodal Facility in Council Bluffs, IA ..............................................................................125

Figure 7-19: Aerial View of the CSX Intermodal Facility in Louisville, KY....................................................................................125

Figure 7-20: Aerial View of NS Appliance Park Intermodal Facility in Louisville, KY ..................................................................126

Figure 7-21: Truck-to-Rail and Rail-to-Truck Transloading Process............................................................................................130

Figure 7-22: Estimated Total Market Opportunities in Annual Cost Savings in Three Iowa Transloading Locations ...............134

Figure 7-23: Estimated Total Market Sizes in Annual Tonnage in Three Iowa Transloading Locations....................................134

Figure 7-24: Cost Savings Opportunities by Commodity Group in Eastern Iowa Transloading Facility ....................................135

Figure 7-25: Cost Savings Opportunities by Commodity Group in Central Iowa Transloading Facility .....................................136

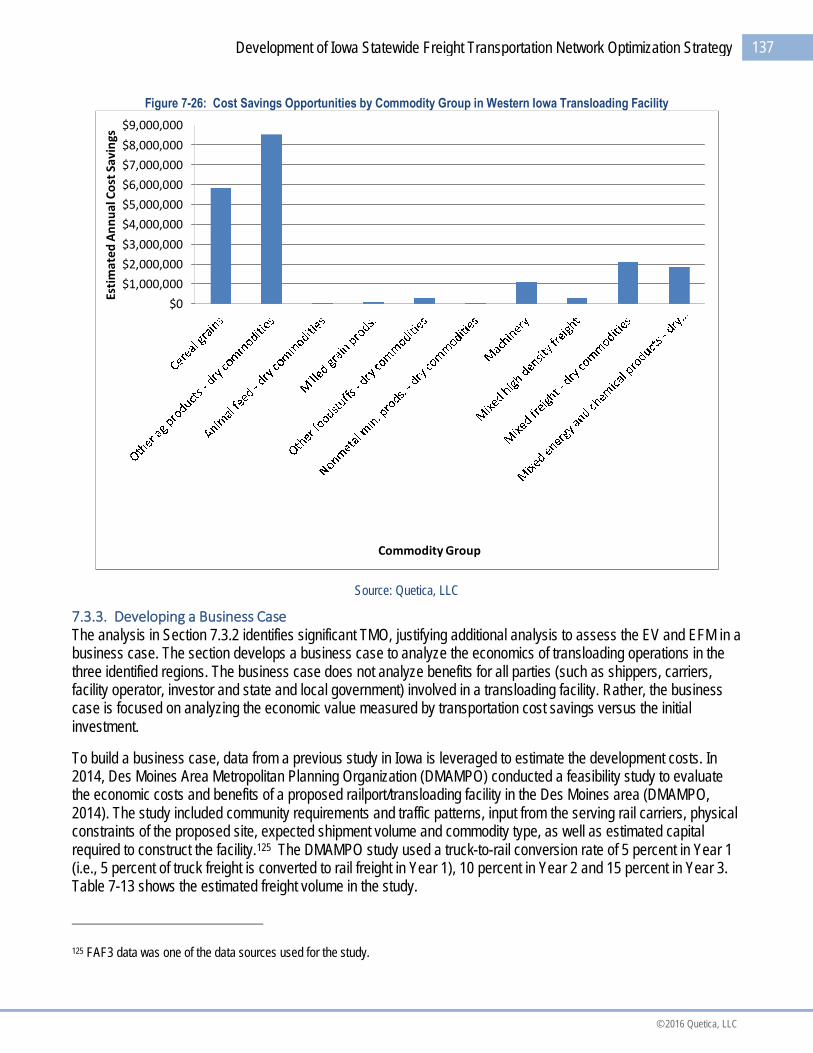

Figure 7-26: Cost Savings Opportunities by Commodity Group in Western Iowa Transloading Facility ...................................137

Figure 7-27: An Aerial View of the Trans Load Limited, Inc.’s Transloading Facility in Birmingham, AL ..................................141

Figure 7-28: An Aerial View of the Patriot Rail’s Transloading Facility in Gibsland, LA..............................................................142

Figure 7-29: Ocean Shipping Container Availability – Six-Month Snapshot of Average Weekly Throughput...........................150

© 2016 Quetica, LLC

6 Development of Iowa Statewide Freight Transportation Network Optimization Strategy

List of Tables

Table 2-1: Foreign Countries or Country Groups in the Study Scope............................................................................................21

Table 3-1: Prioritized Commodities that are Modeled Individually in the iFROM Demand Model................................................31

Table 3-2: Iowa’s Priority Commodity and Grouping Structure in the Demand Model...................................................................32

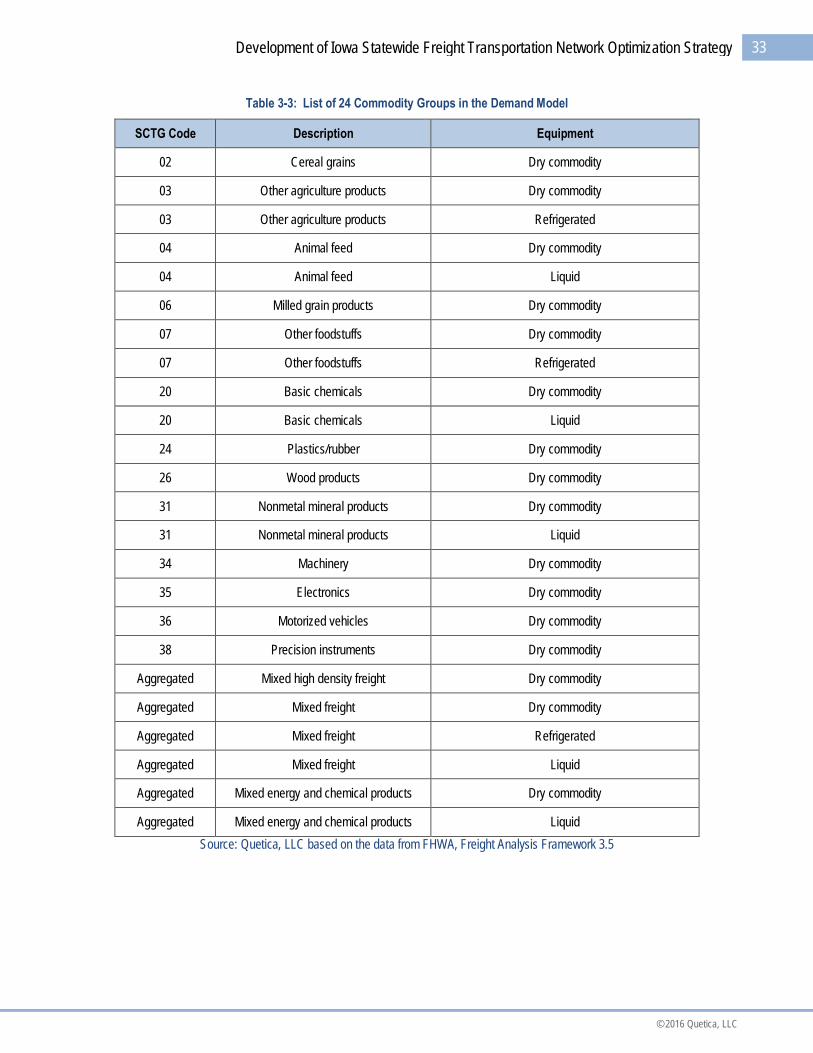

Table 3-3: List of 24 Commodity Groups in the Demand Model.....................................................................................................33

Table 4-1: Primary Highway System Utilization Level.....................................................................................................................37

Table 4-2: Summary of Financial Impact in Resilience Analysis Scenarios ..................................................................................40

Table 4-3: Rail Freight Network Utilization Level.............................................................................................................................42

Table 4-4: Growth Factors Used to Estimate Iowa Rail Freight Network Utilization in the Forecast Year ..................................44

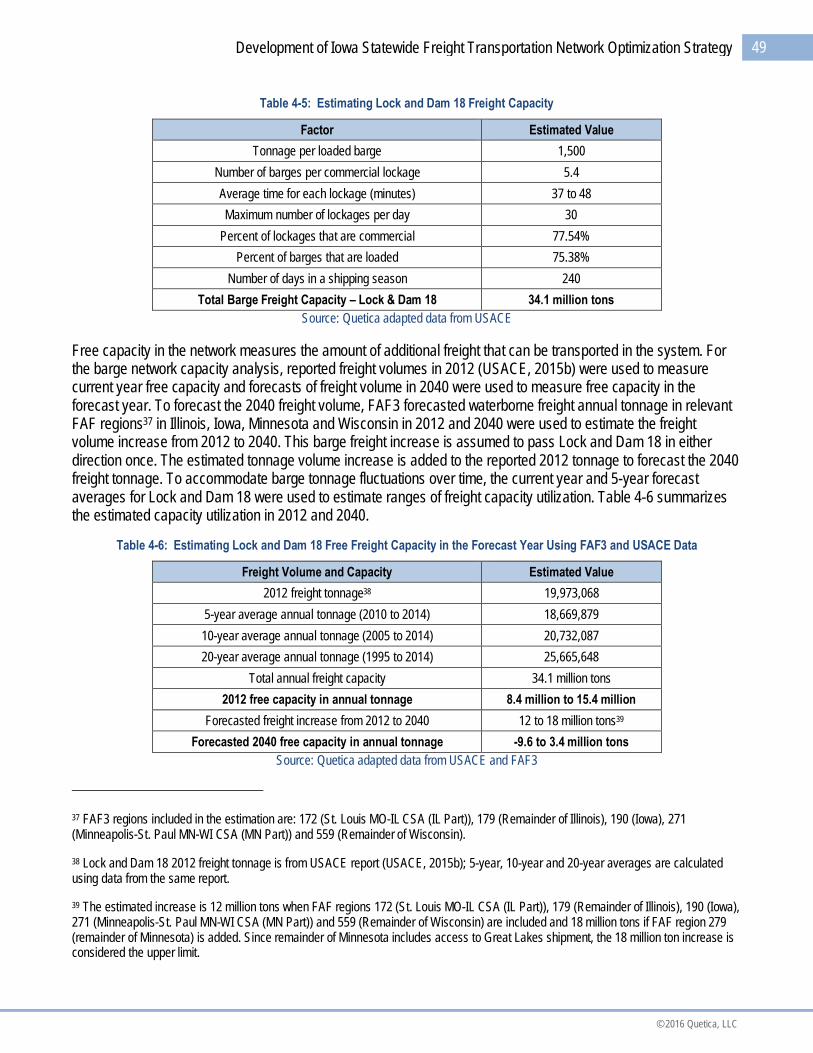

Table 4-5: Estimating Lock and Dam 18 Freight Capacity..............................................................................................................49

Table 4-6: Estimating Lock and Dam 18 Free Freight Capacity in the Forecast Year Using FAF3 and USACE Data...............49

Table 5-1: Comparing the Modes included in the Study Scope .....................................................................................................54

Table 6-1: Comparing Freight Volume and GDP – Iowa and U.S. Total .......................................................................................58

Table 6-2: Summary of Key Findings ...............................................................................................................................................63

Table 6-3: U.S. Domestic Truck Market by Mode in 2012 ..............................................................................................................65

Table 6-4: Cost per Ton-Mile Associated With Each Mode ............................................................................................................66

Table 6-5: Estimated Reduced Cost Savings Opportunities due to Railroad Capacity Constraints in Base Year ......................69

Table 6-6: Estimated Reduced Cost Savings Opportunities Due To Railroad Capacity Constraints in Forecast Year ..............70

Table 6-7: Estimated Cost per Dray to CIC in Chicago Area..........................................................................................................71

Table 6-8: High Level Financial Analysis for a Grundy County Branch Line .................................................................................76

Table 6-9: High Level Financial Analysis for a Howard County Branch Line.................................................................................77

Table 6-10: Sample Cost Per Ton Comparison between Barge and Multimodal (Rail + Barge)..................................................78

Table 6-11: Cost Comparison between Barge Transportation on the Missouri River and Rail ....................................................80

Table 6-12: Top 10 Iowa Export Counties in 2010 Based On Total Export Tonnage ...................................................................84

Table 6-13: Potential Impact of Panamax Expansion Project.........................................................................................................93

Table 7-1: Summary of Recommendations .....................................................................................................................................94

Table 7-2: Commodities Included in Analysis of Cross-Docking Operations.................................................................................98

Table 7–3: Total Market Opportunity (TMO) Before Factoring In Stop-Off Costs .......................................................................100

Table 7-4: ROM Financial Analysis for a Mid-Sized Cross-Dock in Eastern Iowa ......................................................................106

Table 7-5: Commodities Included in Optimization Strategy Analysis using Intermodal Transportation.....................................113

Table 7-6: The TMO of the Suggested Intermodal Yard in Eastern Iowa, Focusing on High Volume Traffic Lanes .................118

Table 7-7: Base Case Analysis for a New Intermodal Yard in Eastern Iowa................................................................................121

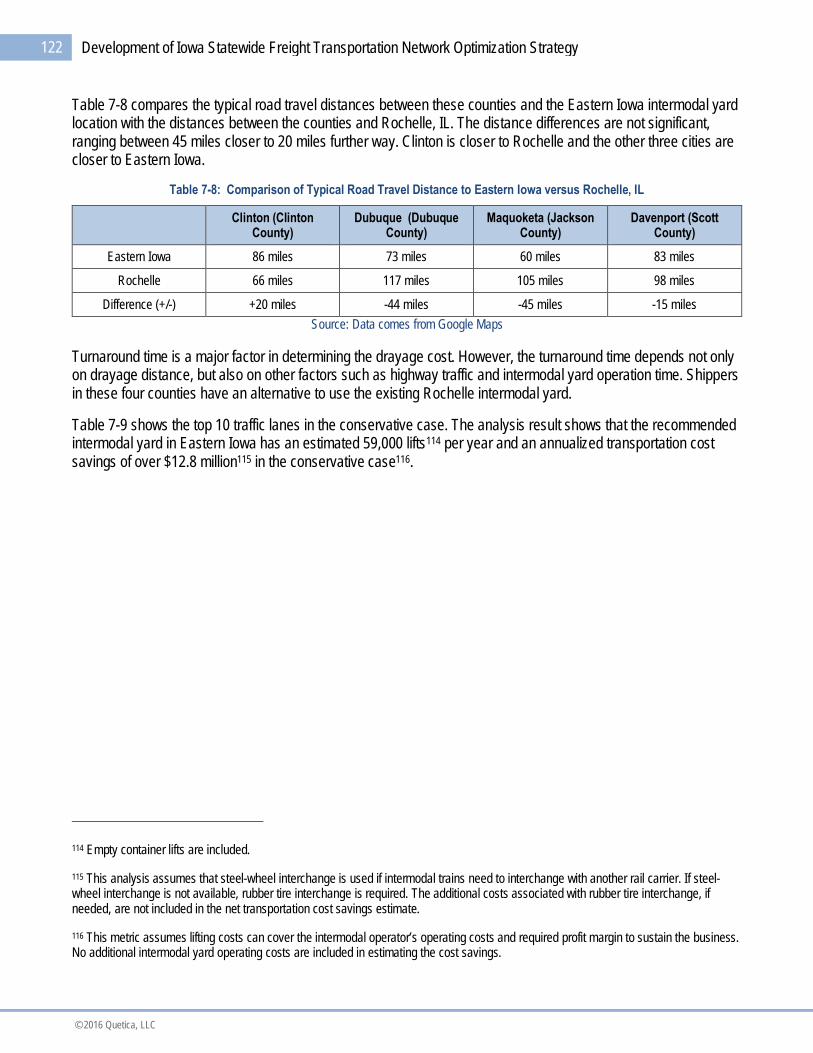

Table 7-8: Comparison of Typical Road Travel Distance to Eastern Iowa versus Rochelle, IL .................................................122

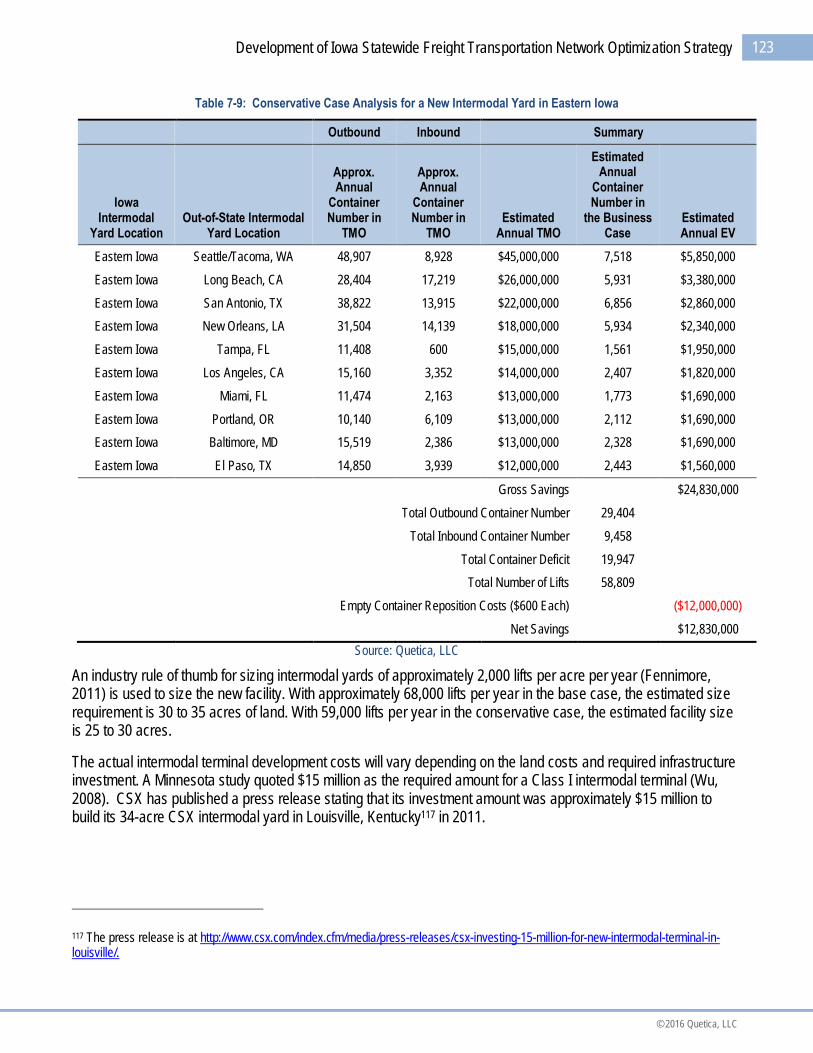

Table 7-9: Conservative Case Analysis for a New Intermodal Yard in Eastern Iowa .................................................................123

Table 7-10: Summary of the Financial Case for a New Intermodal Yard in Eastern Iowa..........................................................124

7

© 2016 Quetica, LLC

Development of Iowa Statewide Freight Transportation Network Optimization Strategy

Table 7-11: Some Small Existing Intermodal Facilities .................................................................................................................126

Table 7-12: Commodities Included In Optimization Strategy Analysis Using Transloading .......................................................132

Table 7-13: Estimated Annual Rail Carloads in DMAMPO Study ................................................................................................138

Table 7-14: Rough Order of Magnitude Initial Investment Estimates...........................................................................................138

Table 7-15: Comparing the Estimated Annual Rail Carloads between DMAMPO Study and Optimization Study ...................139

Table 7-16: Base Case vs. Conservative Case Assumptions ......................................................................................................139

Table 7-17: Base Case Financial for New Transloading Facilities ...............................................................................................140

Table 7-18: Conservative Case Financial Analysis for the New Transloading Facilities ............................................................140

Table 7-19: Cost Analysis for a Hypothetical Multimodal Solution ...............................................................................................144

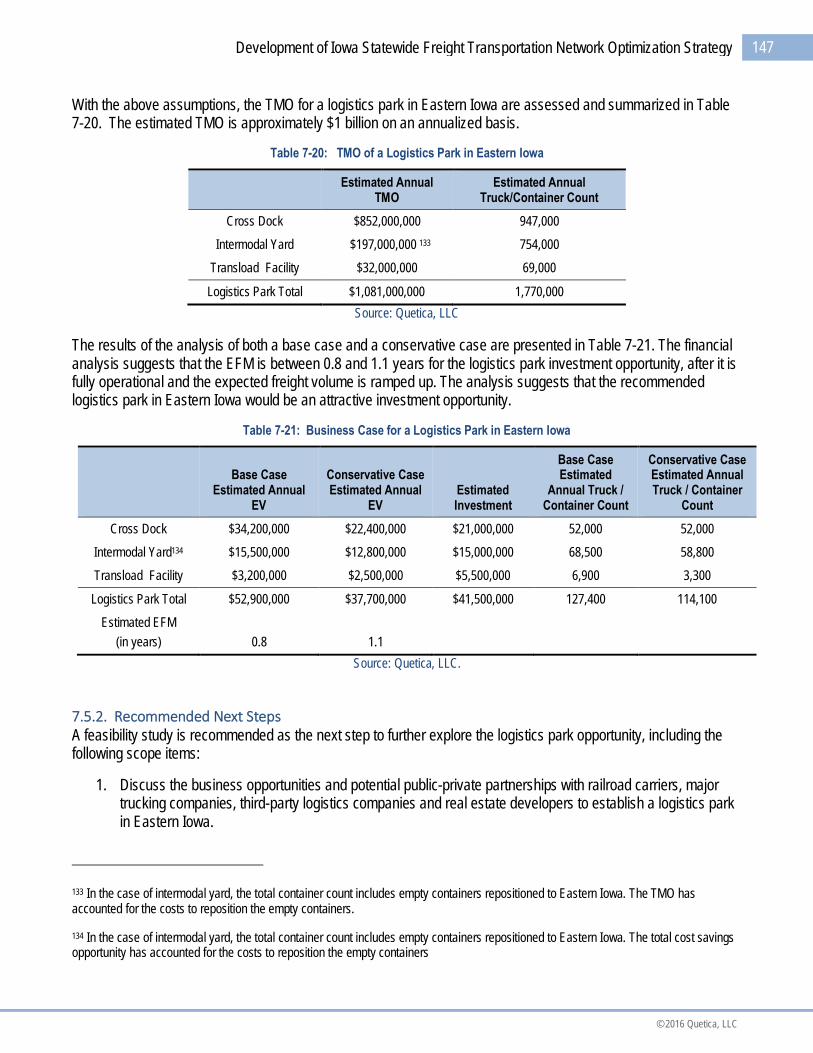

Table 7-20: TMO of a Logistics Park in Eastern Iowa..................................................................................................................147

Table 7-21: Business Case for a Logistics Park in Eastern Iowa.................................................................................................147

Table 7-22: Potential Annual Capacity in Barge Transportation to Reposition Empty Containers.............................................151

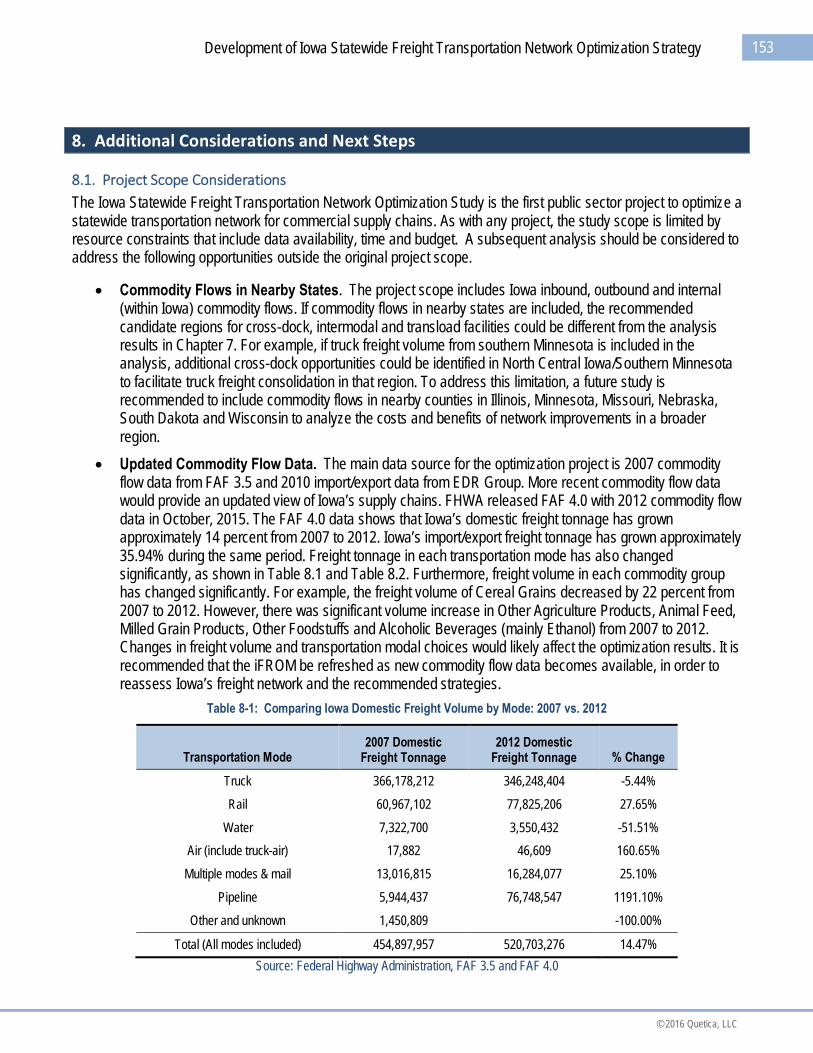

Table 8-1: Comparing Iowa Domestic Freight Volume by Mode: 2007 vs. 2012 ........................................................................153

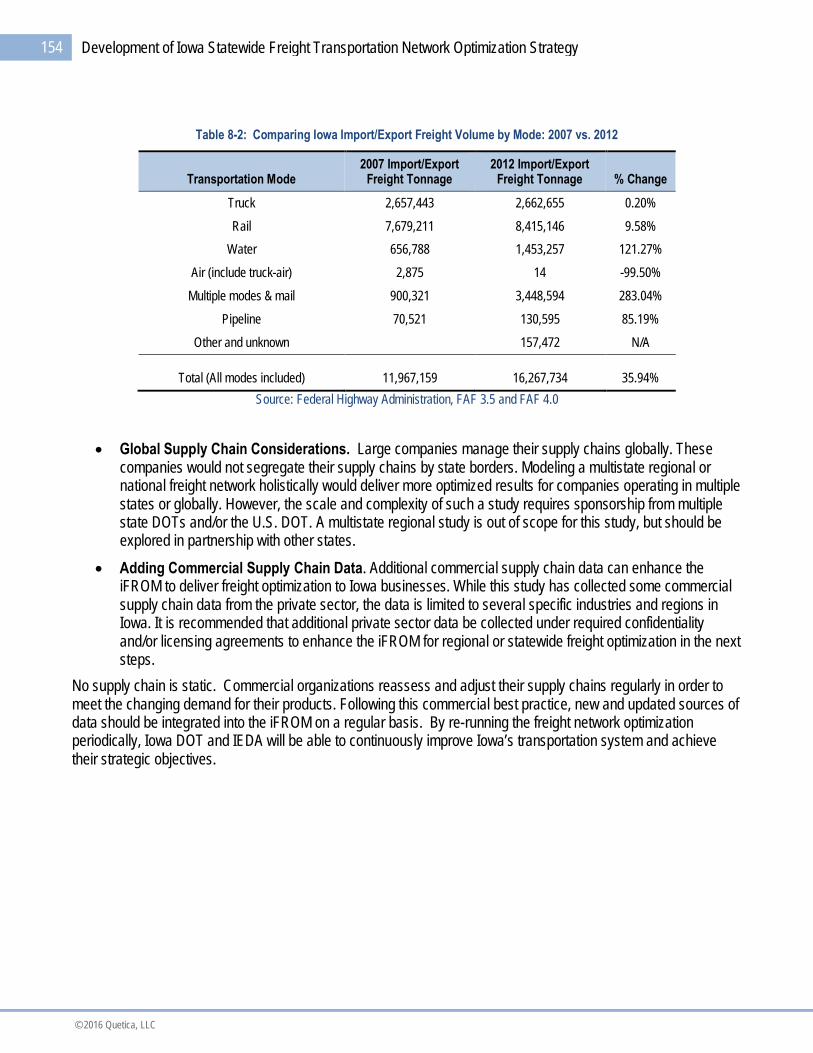

Table 8-2: Comparing Iowa Import/Export Freight Volume by Mode: 2007 vs. 2012 .................................................................154

© 2016 Quetica, LLC

8 Development of Iowa Statewide Freight Transportation Network Optimization Strategy

List of Acronyms and Abbreviations

The following is a list of acronyms and abbreviations in the report.

Acronym or Abbreviation Description

3PL Third Party Logistics

AAR Association of American Railroads

ADT Average Daily Traffic

BEA Bureau of Economic Analysis

CBP County Business Patterns

CFS Commodity Flow Survey

COFC/TOFC Container on Flat Car/Trailer on Flat Car

DOT Department of Transportation

EFM Economic Feasibility Measurement

EV Economic Value

FAF Freight Analysis Framework

FHWA Federal Highway Administration

FTL Full Truckload

GDP Gross Domestic Product

IEDA Iowa Economic Development Authority

iFROM Iowa Freight Optimization Model

iTRAM Iowa Travel Analysis Model

LTL Less Than Truckload

NAICS North American Industrial Classification System

NMFC National Motor Freight Classification

NMFTA National Motor Freight Traffic Association

SCTG Standard Classification of Transported Goods

TEU Twenty-foot Equivalent Unit

TL Truckload

TMO Total Market Opportunity

USDA United States Department of Agriculture

9

© 2016 Quetica, LLC

Development of Iowa Statewide Freight Transportation Network Optimization Strategy

1. Executive Summary

1.1. Project Overview

The primary objective of the Statewide Freight Transportation Network Optimization Study is to effectively identifyand prioritize investment opportunities that will reduce transportation costs for Iowa’s businesses and to promotebusiness growth in Iowa. The study area includes all counties in the State of Iowa. Sponsored by the IowaDepartment of Transportation (Iowa DOT) and the Iowa Economic Development Authority (IEDA), the study uses ademand-based supply chain network design and an optimization methodology to evaluate the efficiency of Iowa’sfreight transportation network, in order to make informed investment decisions. The approach, used for decades inthe private sector to optimize complex global supply chain networks for large corporations, is adopted for thisproject to optimize both public and private elements of the freight transportation network in Iowa.

A business supply chain consists of suppliers, plants, warehouses, and transportation modes used to moveproducts from point of origin to end customer. Up to 80 percent of the costs of a company’s supply chain could beimpacted by the location of the company’s facilities and its access to the multimodal networks that determine therouting of product flows between these facilities.1 In 2012, more than 490 million tons of freight moved betweenIowa and other domestic or foreign regions2, with Iowa businesses spending billions of dollars on freight transportannually.

Supply chain design and optimization is a practice used by commercial organizations to achieve a competitiveadvantage and improve profitability by reducing supply chain-related expenses. It is common in the private sectorfor companies to expect reduction in their transportation, warehousing, and other supply chain costs by 5 to 15percent by addressing supply chain constraints and optimizing their network, while improving their service andoperational agility.

A company’s supply chain, however, depends heavily on the public elements of a transportation network, such asthe highway system, interchanges, interconnectivity between different transportation modes, and inland waterwaysystems. Private companies have to design and optimize their supply chain networks around these systemconstraints, because changes to the publicly-owned transportation network are outside their direct control. Inaddition, businesses are limited to designing and optimizing their supply chains based on their own privatecompany data, without insights into other commodity movements across the region or state.

The statewide freight network optimization study builds a model using statewide commodity flow data and uses themodel to identify and assess network constraints impacting all users of Iowa’s freight network. By addressing thehigh value network constraints (the most expensive constraints in the network), Iowa DOT can effectively help Iowabusinesses to reduce their transportation costs and improve their supply chain efficiency. The statewide freightoptimization study generates recommended strategies based on the network constraints to help Iowa DOT makeinfrastructure investment decisions that deliver the greatest benefits to its freight transportation system users. It alsoprovides statewide supply chain data to key industries to help IEDA identify economic development opportunities toestablish or expand the operations of commercial businesses in Iowa.

1 Percentage is based on Quetica’s industry experience.

2 Source: Federal Highway Administration, Freight Analysis Framework version 3.5. (FAF-3.5)

© 2016 Quetica, LLC

10 Development of Iowa Statewide Freight Transportation Network Optimization Strategy

To accomplish these objectives, the Statewide Freight Transportation Network Optimization Study approachincludes four fundamental steps:

Figure 1-1: Fundamental Steps of Freight Transportation Network Optimization Analysis

Source: Quetica, LLC

The result is a set of transportation network optimization strategies and models developed to reduce the overalltransportation costs for Iowa businesses.

At the center of the study is the development of the Iowa Freight Optimization Model (iFROM), which leveragessupply chain data, supply chain network optimization algorithms and business analytics to identify transportationcost reduction opportunities for Iowa companies. The iFROM tool is designed to:

Simulate Iowa’s commodity flows using a demand module;

Simulate Iowa’s freight transportation network capacity at the county level in a capacity module; and

Evaluate optimization opportunities by applying optimization and analysis algorithms to demand andcapacity modeling and transportation cost benchmarks.

This study provides essential tools to help Iowa DOT achieve its mission to be “Smarter, Simpler, Customer Driven”and the corresponding objectives outlined in its Strategic Plan.3 By enhancing opportunities for commerce throughstrategic investment in transportation infrastructure that meets current and future needs of the transportation systemusers, the study also identifies economic development opportunities to encourage companies to establishoperations and/or expand their supply chain networks in Iowa.

3 Iowa DOT’s Strategic Plan is available at http://www.iowadot.gov/strategicplan/docs/StrategicPlanBrochure.pdf

11

© 2016 Quetica, LLC

Development of Iowa Statewide Freight Transportation Network Optimization Strategy

This study is focused on optimizing the Iowa portion of the transportation network, which may skew results towardsthe center of the state in the optimization algorithms and may understate opportunities on the edges of Iowa.Modeling a multistate region or the national freight network could deliver more balanced results for Iowa and itsadjacent states, but is beyond the scope of the current effort. It is recommended that a future study be carried out toinclude commodity flows in nearby counties in Illinois, Kansas, Minnesota, Missouri, Nebraska, South Dakota andWisconsin to analyze the costs and benefits of network improvements in a broader region.

A freight transportation network optimization is different from the traditional travel demand modeling intransportation planning. Travel demand modeling is used to “develop traffic forecasts, test alternative transportationscenarios, and evaluate transportation systems or policies” (CamSys, 2014). The results of travel demandmodeling are used to assist decision makers in making transportation planning decisions from a range ofalternatives that may include addressing congestion issues and increasing network capacity. Traditionally, a “four-step process” is used for regional transportation planning (CamSys, 2014):

1. Trip generation (how many trips will be made?);

2. Trip distribution (where will the trips go?);

3. Mode choice (what modes of transportation will the trips use?); and

4. Trip assignment (what routes will the trips take).

A freight transportation network optimization is focused on identifying opportunities to transport commodities fromorigins to destinations at lower costs for commercial users of the transportation system. The resulting optimizationstrategies typically involve leveraging more effective multimodal choices and freight consolidation methods toreduce transportation costs, truck miles, and carbon emissions. A freight network optimization study can use thetransportation network and capacity data from a travel demand model to evaluate the possible cost effectiveness ofmodal options for each origin-destination pair in commodity flows. The optimization results include quantifying thetransportation cost saving benefits to the transportation system users and projected impact to freight traffic patternssuch as an increase or reduction of truck counts, rail traffic, or barge traffic in the study area. The freight trafficpattern change data can be fed back to the travel demand model to further analyze projected changes to the overalltravel patterns after the optimization strategies are implemented. As a result, freight network optimization and traveldemand modeling can provide complementary tools to more effective transportation planning.

© 2016 Quetica, LLC

12 Development of Iowa Statewide Freight Transportation Network Optimization Strategy

1.2. Key Findings

Results of quantitative and qualitative analysis of Iowa’s multimodal transportation network, commodity flows, andfreight network cost analysis, are summarized in the following key findings:

1. Iowa’s primary highway system capacity is well managed, but capacity constraints affecting freighttransportation are projected in the future. Iowa’s 10,000 mile Primary Highway System consists ofInterstate Highways, U.S. Highways, and Iowa state highways. The primary highway network is thebackbone of the state transportation system that connects all 99 counties in Iowa. Results from the baseyear (2010) analysis show no high value network constraints for freight transportation in the base yearhighway capacity analysis. No existing capacity constraints would change truck routes and freightmovement patterns.

In the forecast year (2040), some highway segments are projected to have capacity constraints. Thesecapacity constraints could cause traffic congestion and delays, which may result in truck dispatchers andtruck drivers using alternate routes with potentially increased transportation costs.

2. A substantial volume of truck shipments are small shipments that could be consolidated to reducetransportation costs. An estimated 9.5 percent of Iowa’s domestic truck freight (inbound, outbound, andwithin Iowa) moves in small shipments weighing less than 15,000 pounds in the base year. Smallshipments typically have a higher cost per ton-mile than full truckload shipments. As a result, opportunitiesmay exist to consolidate shipments in Iowa to reduce business transportation costs.

3. Significant opportunities exist to leverage railroad transportation in Iowa to reduce freight costs.There are 18 railroads with 3,851 miles of track in Iowa that connect shippers, manufacturers, andproducers to a robust network of North American trading partners. By converting truck freight to rail freight,the estimated total annual cost savings opportunities are $670 million for inbound freight and $810 millionfor outbound freight if 100 percent of the conversion opportunities are captured.

4. Railroad capacity constraints are projected in the future. In the forecast year (2040) of the analysis,railroad capacity constraints are projected in 29 Iowa counties if no new capacity is added. These capacityconstraints limit the potential for converting some truck freight to rail freight. An estimated 14.6 percent ofthe total cost savings opportunity in truck to rail conversions could be lost in the forecast year as a result ofrailroad capacity constraints.

5. Businesses in many Iowa communities may pay high drayage4 costs as a result of limited access torail intermodal services. Shippers in a large portion of Iowa are beyond 100 miles from existingintermodal yards in Iowa and neighboring states. Iowa companies in these areas may pay high drayagecosts to access rail intermodal transportation, increasing the total transportation costs.

4 Drayage is the transport of commodities over a short distance, typically as a truck pickup from or delivery to an intermodal yard.

13

© 2016 Quetica, LLC

Development of Iowa Statewide Freight Transportation Network Optimization Strategy

6. It is not economically viable to build railroad branch lines to connect the 9 counties that currentlydo not have direct rail access. Nine out of 99 counties in Iowa do not have direct access to rail.5 Buildingrailroad branch lines to connect these counties to Iowa’s railroad network could provide transportation costsavings opportunities by converting some truck freight to rail freight. Analysis of the economic benefit, giventhe base year freight volume, estimated an Economic Feasibility Measurement (EFM)6 of approximately 16years in the best case scenario, suggesting that it is not economically viable to construct new branch lines.

7. The inland waterway system provides sufficient capacity for Iowa’s freight transportation, but isprojected to have capacity constraints in the future. Iowa has 491 miles of navigable river bordering thestate, and it is the only state in the nation bordered by two navigable rivers: Mississippi River and MissouriRiver. For some commodities, barge transportation provides significant cost savings over land-basedtransportation services and is more fuel efficient than other modes. The capacity analysis indicates thatsufficient capacity is available in the base year for barge transportation demand. However, freight capacityconstraints are projected in 2040 if the current lock and dam system on the Upper Mississippi River is notimproved to create additional capacity.

8. Barge transportation on the Missouri River provides a cost competitive alternative to transportcommodities to the Gulf area. Navigation on the Missouri River occurs from Sioux City to the mouth at St.Louis, a distance of 734 miles. Access to barge transportation on the Missouri River is available in Iowathrough barge terminals located in Council Bluffs, Sergeant Bluff, and Sioux City. Barge transportation onthe Missouri River provides approximately 5 percent in cost savings over rail carload freight costs betweenIowa and the Gulf area. More importantly, barge transportation provides additional freight capacity andtransportation modal choice to Western Iowa, improving the resiliency of Iowa’s freight transportationnetwork.

9. It is not economically viable to build new barge terminals in counties bordering the Mississippi orMissouri River that currently do not have direct access to barge transportation. Sixteen Iowacounties border either the Mississippi River or the Missouri River. However, six of these counties do nothave terminals to directly access barge transportation. 7 Quantitative network analysis indicates that there isnot enough freight volume to justify new barge terminals in these six counties. There is an opportunity forIowa companies in these six counties to leverage existing barge terminals in nearby counties to transporttheir freight.

5 The 9 Iowa counties without direct rail access are Audubon, Davis, Decatur, Grundy, Howard, Jones, Ringgold, Taylor, and Van Buren.

6 EFM is a financial metric for evaluating the economic benefits from a project. EFM is measured by the period of time required to recoupfunds expended in implementing a recommended optimization strategy, starting from the point that the freight volume reaches theexpected level in the business case. The value of EFM is equal to the estimated total implementation cost (including all design andconstruction costs) divided by the annual cost savings opportunity measured by comparing the transportation costs in build and no buildscenarios. For example, if the total implementation cost is $60 million, and the projected cost savings in the build scenario is $6 million,then the EFM is 10 years. The lower the EFM value, the stronger the business case.

7 The 6 Iowa counties bordering the rivers, but without direct barge access, are Jackson, Louisa, Monona, Harrison, Mills, and Fremont.

© 2016 Quetica, LLC

14 Development of Iowa Statewide Freight Transportation Network Optimization Strategy

10. Lower ocean freight rates as a result of the Panama Canal expansion could provide cost savings toIowa exporters using the Gulf ports. Currently, a typical Panamax cargo ship has deadweight tonnage of65,000 to 80,000 tons, due to draft limitations in the canal. After the canal expansion, the New Panamaxstandard will accommodate ships having a deadweight tonnage of up to 120,000 tons. Larger cargo shipsare typically more cost efficient for transporting commodities. It is likely that ocean carriers will pass onsome of the operational cost savings to shippers.8 If the New Panamax standard were estimated to resultin a 10 percent reduction in ocean freight rates, freight cost routing through the Panama Canal would bemore competitive than routing through the Pacific Northwest ports for an increased number of companieslocated in Iowa counties near the Mississippi River or the Missouri River. An increase of approximately 65percent in export tonnage to China and over 27 percent to the East and Southeast Asia region could benefitfrom the lower transportation costs routing through the Panama Canal than through the Pacific NorthwestPorts.

1.3. Recommendations

The key findings above present significant opportunities to enhance Iowa’s freight network. The followingrecommendations present the optimization strategies to capture the opportunities and deliver tangible benefits toIowa businesses whose supply chains rely heavily on Iowa’s freight transportation systems. The recommendedoptimization strategies include:

1. Explore the opportunity to establish and leverage new truck cross-docking operations to enablegreater truck freight Consolidation for Iowa Businesses. Cross-docking is a logistics practice ofunloading materials from an incoming semi-trailer truck or railcar and loading these materials directly intooutbound trucks, trailers, or railcars, with little or no storage in between. There are opportunities to establishnew cross-docking operations in Iowa to consolidate small truck shipments to full truckload for multipleshippers and reduce transportation costs. Quantitative analysis in truck freight consolidation estimates thatthe total market opportunity (TMO) on behalf of Iowa shippers in annual transportation cost savings isapproximately $852 million. A business case developed for a mid-sized cross dock in Eastern Iowa showsapproximately $22 million to $34 million in total annual transportation cost savings, with an EconomicFeasibility Measurement (EFM)6 of approximately one year (after the cross dock is fully operational andfreight volume has reached the expected level).

2. Explore the opportunity of a new rail intermodal facility in Iowa to enable access to lower cost railintermodal services for Iowa businesses. Rail intermodal service involves the transportation ofcontainerized freight using truck and rail, capturing the best of each mode: combining the lower cost of railline-haul, with the door-to-door flexibility of trucking. A quantitative analysis for rail intermodal marketopportunities on behalf of Iowa shippers estimates that the total market opportunity in annual transportationcost savings is approximately $197 million. A business case developed for a mid-sized intermodal facility inEastern Iowa shows approximately $12.8 million to $15.5 million in total annual transportation cost savings,with an EFM6 of approximately one year (after the intermodal facility is fully operational and freight volumehas reached the expected level).

8 The exact ocean rate saving was not available at the time when this report was authored.

15

© 2016 Quetica, LLC

Development of Iowa Statewide Freight Transportation Network Optimization Strategy

3. Explore the opportunity of additional transload facilities to provide Iowa businesses with moreaccess to lower cost railroad freight services. Transloading is the process of transferring freightbetween two modes of transportation. Truck-to-rail and rail-to-truck transloading allows shippers to takeadvantage of the trucking access capabilities for short-haul pickup/delivery and the lower cost rail for long-haul shipments. Quantitative analysis of rail carload transportation estimates that the total marketopportunity (TMO) in annual transportation cost savings is approximately $20 million to $32 million perregion, across different Iowa regions in Eastern, Central, and Western Iowa. A business case developed fora transload facility in each region shows the EFM6 is approximately 1.7 to 2.7 years9 depending on location,after a facility is fully operational and freight volume has reached the expected level.

4. Explore opportunities to leverage a barge and rail multimodal solution to provide a cost-effectivefreight transportation alternative. Barge transportation has the lowest cost structure measured by costper ton-mile among all modes of transportation, though it typically requires longer transit time. Effectivelyleveraging barge transportation for non-time sensitive, large volume shipments can produce significant costsavings opportunities for Iowa companies. However, there are several constraints for Iowa businesses tofully utilize barge transportation, including limited access to adjacent barge terminals, delays in the aginglock and dam system during peak season, and winter closures on the Upper Mississippi River. A rail andbarge multimodal solution could be a viable alternative to transport commodities during winter betweenIowa and the Gulf Coast. A cost analysis estimates that the multimodal solution has comparable cost to theall rail alternative during winter. A feasibility study is recommended to explore the economic viability of anIowa to Gulf Coast bi-direction rail/barge multimodal service option.

5. Explore the opportunity to build a logistics park to co-locate cross-docking, intermodal,transloading and warehousing facilities. A logistics park is a development concept in which warehouseand distribution centers are located in a single zone, typically with access to railroad networks and primaryhighway systems. Co-locating logistics functions in a single development provides many benefits, includingsubstantially lower transportation costs, improved transportation efficiency, more transportation options forshippers, increased transportation capacity and better facility management. Quantitative analysis hasidentified a region in Eastern Iowa as an economically viable location for a new logistics park. Theestimated annual transportation cost savings for the logistics park is approximately $37.7 million to $52.9million. The estimated EFM6 is between 0.8 and 1.1 years.

6. Collaborate with the railroads to provide Iowa businesses with more capacity to accommodateforecasted growth in Iowa freight shipments. Quantitative analysis indicates that Iowa’s railroad networkprovides significant opportunities for reducing transportation costs for Iowa shippers. Improved railroadcapacity and access points are essential for Iowa shippers to convert additional truck freight to rail in thefuture. Iowa DOT is currently in the process of developing a state rail plan. It is recommended that IowaDOT complete the development of a rail plan to identify strategic opportunities for rail transportation.

9 In business case development, two scenarios will be used to quantify the investment opportunities: a base case scenario and aconservative case scenario. The base case is the scenario with the highest likelihood. The conservative case uses a more conservative setof assumptions to evaluate economic viability. The EFM values in the section are the base case.

© 2016 Quetica, LLC

16 Development of Iowa Statewide Freight Transportation Network Optimization Strategy

7. Explore opportunities to improve competitiveness of intermodal in Iowa by repositioning emptycontainers using barge and reducing repositioning costs. There is a shortage of empty containers inIowa. Because Iowa is a production state, it ships more containerized commodities than it consumes andpotentially there is an opportunity to ship more containerized commodities in the future. Repositioningempty containers is expensive. The estimated cost to reposition an empty container from Chicago to Iowaby rail is approximately $600. Many barges go up the Mississippi River empty, load grain and othercommodities in Illinois, Iowa, Minnesota, Missouri, and Wisconsin, and transport the commodities downriver to the Gulf Coast. There are cost effective opportunities to leverage empty up river barges toreposition empty containers from cities with large container inventories, such as Memphis and NewOrleans. The concept could include a virtual container yard to track and manage containers, facilitatecontainer leasing and management of related documents, as well as container returns and exchanges.

8. Explore and implement strategies to reduce deadhead truck miles. The volume of Iowa’s outboundtruck freight is much higher than inbound volume. This flow results in many deadhead miles as trucksreturn to Iowa empty in order to haul outbound freight. It is recommended that a public-private partnershipbe established to develop a mobile and web-based freight and truck information sharing andcommunication solution for both the contractual and spot markets to help reduce deadhead miles.

9. Explore opportunities for railroads to provide additional lower cost rail freight transportation forwithin Iowa high volume traffic lanes. The driver shortage, higher insurance costs and new governmentregulations are pushing truck transportation costs higher. Railroads are making progress in the short-haulmarket, as they improve operating efficiencies and service times. It is recommended that opportunities beexplored to provide additional lower cost freight rail services for intra-Iowa high volume traffic lanes.10

The strategies recommended above can provide Iowa shippers with sustainable transportation cost reductions byaddressing current and future freight network constraints, resulting in higher profitability and more competitivetransportation options for Iowa companies. An optimized freight transportation network also encourages companiesto establish operations and/or expand their supply chain network in Iowa.

During the revision process of this final report, Iowa DOT, IEDA, and their private partners have used theoptimization recommendations and the supporting data to develop an application for the Fostering Advancements inShipping and Transportation for the Long-term Achievement of National Efficient (FASTLANE) Grant. The grantapplication proposes a logistics park in Eastern Iowa to provide cross-docking, intermodal, transloading, and otherlogistics services. The project will provide Iowa and the surrounding states with access to a high capacity, efficient,and cost-competitive facility to move goods from truck to rail and vice versa. In July 2016, Iowa DOT and its privatepartners were awarded $25.6 million in the FASTLANE grant to develop the proposed logistics park.

10 Some of these high volume traffic lanes in the base year are Polk County – Linn County – Black Hawk County, Polk County – ScottCounty, and Polk County – Woodbury County.

17

© 2016 Quetica, LLC

Development of Iowa Statewide Freight Transportation Network Optimization Strategy

2. Introduction to Freight Transportation Network Optimization

The primary objective of the Statewide Freight Transportation Network Optimization Study is to effectivelyidentify and prioritize investment opportunities that will reduce transportation costs for Iowa’s businesses and topromote business growth in Iowa. Sponsored by the Iowa Department of Transportation (DOT) and Iowa EconomicDevelopment Authority (IEDA), the project team consists of subject matter experts from Iowa DOT and IEDA, aswell as consultants in supply chain network design and optimization.

The Iowa Freight Optimization Model (iFROM) is a tool developed to:

1. Simulate Iowa’s commodity flows using a demand module;

2. Simulate Iowa’s freight transportation network capacity in a capacity module; and

3. Evaluate optimization opportunities by applying the optimization and analysis algorithms to the demand andcapacity modeling and transportation cost benchmarks.

As a result of this study, a set of transportation network optimization strategies have been developed to reduce theoverall transportation costs for Iowa businesses to support economic development within the state. The strategieshave also been used as input to the development of Iowa DOT’s freight plan.

The remainder of this chapter provides an overview of the optimization methodology used in the iFROM. The detailsof the optimization model are discussed in Chapters 3, 4, and 5. Chapter 3 discusses demand modeling, Chapter 4discusses capacity modeling and Chapter 5 discusses transportation cost benchmarks. The findings from theconstraint analysis11 are documented in Chapter 6. The design alternatives are evaluated to develop therecommended optimization strategies in Chapter 7.

2.1. Optimization Methodology

This project uses a demand-based supply chain network design and optimization methodology to evaluate theefficiency of Iowa’s freight transportation network. The same approach used for decades in the private sector tooptimize complex global supply chain networks for large corporations is adopted in this project to optimize publicly-owned or privately-owned elements of the state freight transportation network.

11 In the Theory of Constraints (TOC) (Goldratt, 1984), a constraint is anything that prevents the system from achieving its performancegoal. The TOC is based on the premise that the rate of goal achievement by a goal-oriented system is limited by at least one constraint.By following a systematic five- step process of ongoing improvement, system performance can be improved in a cost-effective way.

© 2016 Quetica, LLC

18 Development of Iowa Statewide Freight Transportation Network Optimization Strategy

The approach includes four fundamental steps described in Figure 2-1.

Figure 2-1: Fundamental Steps of Freight Transportation Network Optimization Analysis

Source: Quetica, LLC

A network optimization model is designed to objectively analyze the optimized network structure, flows and policies.The optimized network design can be mathematically determined by looking at both physical and behavioralattributes of a supply chain network (see Figure 2-2):

Figure 2-2: Core Components of Supply Chain Network Design

Source: Quetica, LLC

19

© 2016 Quetica, LLC

Development of Iowa Statewide Freight Transportation Network Optimization Strategy

The optimization process requires collecting data for the quantitative analysis, including:

Demand: Base year demand and forecast year demand

Sites: Supply (or origin) sites, consumption (or destination) sites, ports of entrance/exit for import/export

Products: Aggregated to commodity groups by source

Data was collected from both public and proprietary data sources12, as well as through interviews and surveys withindustry subject matter experts on both the infrastructure and data essential to analyze Iowa’s statewide freighttransportation network.13

The expert input on industry practices is translated into policies14 within the model to establish an optimizationcomputer model for analysis:

Sourcing: Where are the products sourced? How much product is sourced?

Transportation: What modes are used to move products from different origins to destinations? What arethe capacity and costs by mode?

2.2. Overview of Iowa’s Freight Transportation Network

A freight transportation network consists of supply sites that have commodities, demand sites that request thosecommodities and multimodal transportation systems that can transport the commodities from supply sites todemand sites. In a freight transportation network model, supply and demand sites are modeled as nodes and themultimodal transportation network is modeled as unidirectional lines connecting the nodes. Freight transportationnetwork optimization uses computer tools and algorithms to analyze possible alternatives to deliver commodities tothe demand sites, while meeting the defined optimization objectives, such as lowered costs, lowered risks and/orshortened delivery time. This study focuses on optimizing Iowa’s freight transportation network for inbound,outbound and within Iowa (Iowa internal) freight movements to achieve the primary objective which is to reducetransportation costs for Iowa businesses.

In the iFROM, a freight transportation network is modeled as a collection of interconnected nodes in the study area.A typical segment of the network is shown in Figure 2-3. Each node (identified as a circle in the diagram) representsa geographic zone and each unidirectional link between two nodes represents the freight transportation networkconnection from the origin node to the destination node. Iowa’s businesses, their commodity consumption andproduction, as well as freight transportation flows, are aggregated into one large network to represent Iowa’sstatewide freight transportation network.

12 See more detailed discussion on data sources in Chapters 3, 4 and 5.

13 External subject matter experts representing key industry stakeholders were consulted throughout the project, including Iowa’s FreightAdvisory Council (FAC), shippers, transportation service providers, as well as industry associations, regulatory authorities, educational andresearch groups.

14 Supply chain network optimization studies also include inventory policies (i.e., where to keep the right amount of inventory to meetcustomer service and revenue goals). However, since this study is focused on freight transportation network optimization, inventorypolicies are outside of the scope.

© 2016 Quetica, LLC

20 Development of Iowa Statewide Freight Transportation Network Optimization Strategy

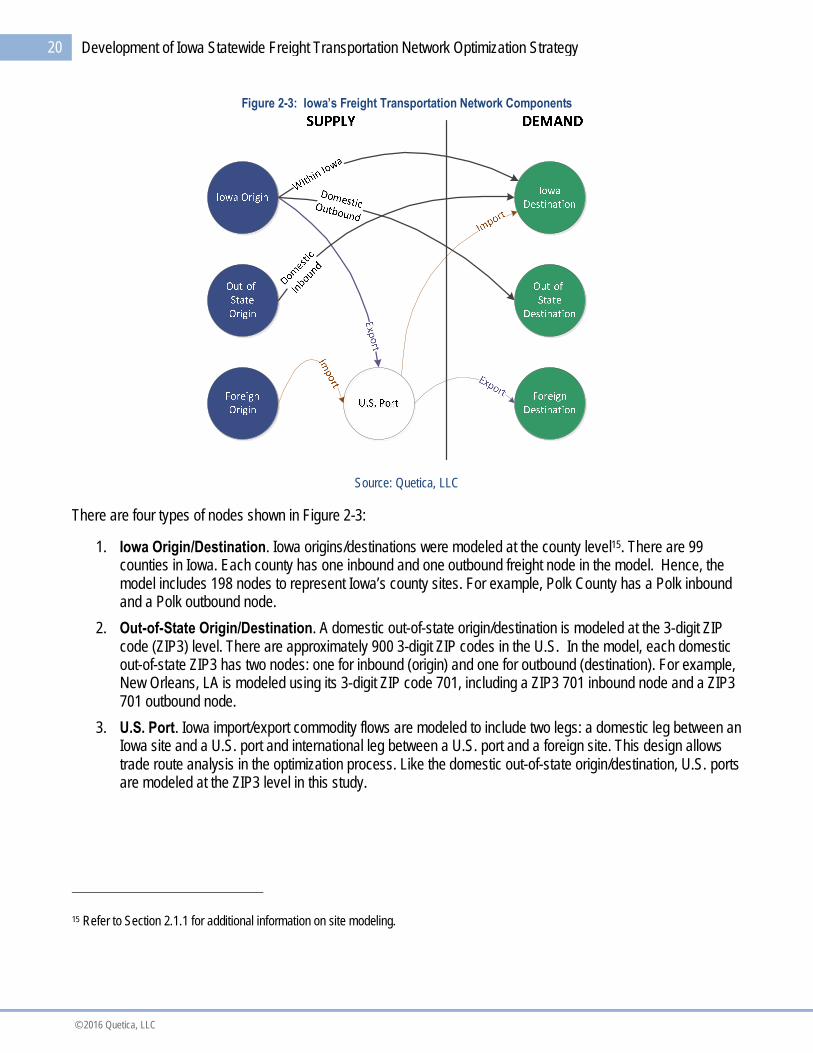

Figure 2-3: Iowa’s Freight Transportation Network Components

Source: Quetica, LLC

There are four types of nodes shown in Figure 2-3:

1. Iowa Origin/Destination. Iowa origins/destinations were modeled at the county level15. There are 99counties in Iowa. Each county has one inbound and one outbound freight node in the model. Hence, themodel includes 198 nodes to represent Iowa’s county sites. For example, Polk County has a Polk inboundand a Polk outbound node.

2. Out-of-State Origin/Destination. A domestic out-of-state origin/destination is modeled at the 3-digit ZIPcode (ZIP3) level. There are approximately 900 3-digit ZIP codes in the U.S. In the model, each domesticout-of-state ZIP3 has two nodes: one for inbound (origin) and one for outbound (destination). For example,New Orleans, LA is modeled using its 3-digit ZIP code 701, including a ZIP3 701 inbound node and a ZIP3701 outbound node.

3. U.S. Port. Iowa import/export commodity flows are modeled to include two legs: a domestic leg between anIowa site and a U.S. port and international leg between a U.S. port and a foreign site. This design allowstrade route analysis in the optimization process. Like the domestic out-of-state origin/destination, U.S. portsare modeled at the ZIP3 level in this study.

15 Refer to Section 2.1.1 for additional information on site modeling.

21

© 2016 Quetica, LLC

Development of Iowa Statewide Freight Transportation Network Optimization Strategy

4. Foreign Origin/Destination. There are 40 foreign countries or country groups in the model forimport/export analysis16. Each foreign origin/destination is modeled using the geographic location of thelargest port city in the area. A list of the foreign countries or country groups is provided in Table 2-1. Eachforeign country/country group has two nodes in the model: one for inbound and one for outbound.

Table 2-1: Foreign Countries or Country Groups in the Study Scope

Africa Asia Pacific Americas Europe

Eastern Africa

Middle Africa

Northern Africa

Remainder of SouthernAfrica

South Africa

Western Africa

Australia and New Zealand

Central Asia

China

India

Japan

Melanesia

Micronesia

Polynesia

Remainder of Eastern Asia

Remainder of Western Asia

Republic of Korea

Remainder of South-EasternAsia

Remainder of Southern Asia

Singapore

Argentina

Brazil

Canada

Caribbean

Chile

Colombia

Mexico

Remainder of CentralAmerica

Remainder of NorthernAmerica

Remainder of SouthAmerica

Eastern Europe

France

Germany

Netherlands

Remainder of NorthernEurope

Remainder of SouthernEurope

Remainder of WesternEurope

Spain

Turkey

United Kingdom of GreatBritain and Northern Ireland

Source: Economic Development Research Group (EDR Group, 2014)

The diagram in Figure 2-3 shows the 5 freight transportation scenarios modeled in the study:

1. Domestic Inbound – Freight is transported from a domestic out-of-state node to an Iowa node.

2. Domestic Outbound – Freight is transported from an Iowa node to a domestic out-of-state node.

3. Within Iowa (Iowa Internal) – Freight is transported between two Iowa nodes.

4. Import – Freight is transported from a foreign node to a U.S. port node first, then from the U.S. port node toan Iowa node.

5. Export – Freight is transported from an Iowa node to a U.S. port node first, then from the U.S. port node toa foreign node.

16 These 40 foreign countries or country groups are used in the import/export data in the model. Import/export data was acquired fromEconomic Development Research Group (EDR Group, 2014).

© 2016 Quetica, LLC

22 Development of Iowa Statewide Freight Transportation Network Optimization Strategy

Multiple modal choices may be available to transport freight between two nodes in the model. The transportationmodes in the study scope include:

Truck (both full truckload and less-than-truckload);

Rail (carload shipment);

Barge (for inland waterborne transportation);

Ocean (excluding liquid bulk); and

Multimodal (with any combination of truck, rail and barge).

These modes represent more than 98 percent of the Iowa’s freight volume in tonnage, according to the FreightAnalysis Framework Version 3.5 (FAF3) data from the Federal Highway Administration (FHWA), U.S. Departmentof Transportation (FAF3, 2014)17. Air freight, pipeline and ocean bulk tank are considered out of the study scope.

The freight network capacity modeling focuses on the Iowa portion of the network, which may skew results towardsthe center of the state in optimization algorithms and may understate opportunities on the edges of Iowa. Modelinga multistate region or the national freight network could deliver more balanced results for Iowa and its adjacentstates, but is beyond the scope of the current effort.18

The iFROM freight transportation network is modeled differently from a transportation network in a travel demandmodel. The iFROM network is focused on the amount of freight that can be transported from origin to destinationusing a specific mode in the transportation system, and the distance that the freight travels based on commerciallyused mode specific routing systems. Physical assets in a transportation network such as roads, bridges,interchanges, rail tracks and waterways are not the modeling components in the iFROM. The iFROM requiresnetwork data from the Iowa Statewide Travel Analysis Model (iTRAM, 2015) to be used to estimate freight capacityin the iFROM network, based on the physical characteristics of a transportation system.

2.2.1. Site ModelingThe primary purpose of the freight transportation network model is to enable network optimization for the definedproject objectives. Since minimizing transportation cost is the primary objective of this study, the model needs toenable effective transportation cost benchmarking. Transportation costs typically depend on a shipment’s origin,destination, transportation mode and equipment type used (e.g. dry van, refrigerated, tank). Therefore, eachcombination of origin-destination-mode-equipment in the model needs to be included in the cost benchmarkingprocess for optimization.

17 FAF Version 3.5 Year 2007 tonnage data is used in this estimate.

18 Chapter 8 discusses the suggested scope items for future study.

23

© 2016 Quetica, LLC

Development of Iowa Statewide Freight Transportation Network Optimization Strategy

The number of cost benchmarking scenarios can be estimated using the following formula:

TotalScenarioNumber = TotalOriginNodeNumber * TotalDestinationNodeNumber * TotalNumberOfModes * TotalNumberOfEquipmentTypes

Where:

TotalScenarioNumber = the total number of cost benchmarking scenarios

TotalOriginNodeNumber = the total number of origin nodes

TotalDestinationNodeNumber = the total number of destination modes

TotalNumberOfModes = the total number of transportation modes available

TotalNumberOfEquipmentTypes = the total number of transportation equipment types used

Iowa’s multimodal freight transportation network is very large, serving an area of more than 56,000 square miles,with a multitude of potential freight origin and termination zones, modal choices and equipment type combinations.To develop a model that would support relevant optimization decisions, choices were made to define Iowa’snetwork nodes that would provide a meaningful level of significance, without an overwhelming level of detail.

Iowa consists of 99 counties, with most of these counties defined by land surveys, as opposed to natural features.As a result, Iowa has a large number of “box counties” with a typical size of 576 square miles (24 mi. x 24 mi.)19. Itwas determined that building the model at a level of detail beyond county geography would increase the number ofnodes significantly, but would not meaningfully enhance the optimization results. Differences in distance and costcalculations from a higher number of nodes would be a small percentage of the total trip distance and cost. Countylevel modeling effectively balances the accuracy of the cost modeling and the model complexity in this study.

Domestic shipments using truck and rail are most commonly priced using 3-digit or 5-digit ZIP codes in thetransportation industry. There are approximately 900 3-digit ZIP Codes and 43,000 5-digit ZIP codes in the UnitedStates20. Modeling the domestic out-of-state sites at the ZIP3 level was deemed to provide sufficient accuracy fortransportation cost benchmarking in this study.

Modeling the sites at 5-digit ZIP level would have increased the number of cost benchmarking scenariossignificantly. For example:

The model examines shipments for five freight transportation modes: 1. Less-than-truckload (LTL), 2.Truckload (TL), 3. Rail (rail carload), 4. Intermodal (rail intermodal) and 5. Barge.

The model also assumes three equipment types for each mode: 1. Dry cargo trailer/container, 2.Refrigerated trailer/container (refrigerated) and 3. Liquid tank trailer or car

The model is based on 99 counties within Iowa. Each county has one inbound and one outbound node.

19 From http://factfinder.census.gov/faces/nav/jsf/pages/community_facts.xhtml

20 According to http://www.zipboundary.com/zipcode_faqs.html

© 2016 Quetica, LLC

24 Development of Iowa Statewide Freight Transportation Network Optimization Strategy

Given these parameters, using a 3-digit ZIP for out-of-state nodes (900 locations) results in a total of1,336,500 scenarios (99 x 900 x 5 x 3). Using a 5-digit ZIP for out-of-state nodes (43,000 locations) wouldhave resulted in 63,855,000 scenarios (99 x 43,000 x 5 x 3). The model using 5-digit ZIP code sites is over45 times larger than the 3-digit ZIP code model. It was determined that the additional detail resulting from5-digit ZIP code external node would add a degree of complexity that would significantly outweigh anyenhanced optimization results.

2.3 Optimization Model Architecture Overview

Figure 2-4 shows the conceptual architecture of the optimization model. The baseline model is developed torepresent the base year, freight transportation demand and network capacity and then is calibrated usingtransportation cost benchmarks to quantify baseline performance. The baseline performance is analyzed in anoptimization model to identify network constraints and design alternatives to address the constraints. The designalternatives are evaluated and used to develop a baseline optimization model to reduce transportation costs usingthe baseline transportation network. A greenfield optimization evaluates design alternatives to identifyopportunities to develop additional network elements to enhance the transportation network and address high valuenetwork constraints. Greenfield optimization is typically conducted after baseline optimization. As the final step,optimization strategies and the supporting business case are derived from the baseline and greenfield optimizationto develop the final recommendations.

Figure 2-4: Overview of Network Optimization Conceptual Architecture

Source: Quetica, LLC

25

© 2016 Quetica, LLC

Development of Iowa Statewide Freight Transportation Network Optimization Strategy

When developing Iowa’s freight transportation network model, the objectives of the model are to understand theconstraints within the network, to identify multiple network improvement opportunities and to evaluate strategies toimprove the network performance. Because the transportation network is operated and used by many independentparties, it may not be realistic to achieve the “most” optimal state of the network in an optimization. Optimizationbased on the new demand and network usage patterns would identify new improvement opportunities and furtherfine-tune the network performance.

The targeted benefits for Iowa of taking a network optimization approach, as an output of the optimization model,are:

To identify high value network constraints21 that significantly affect the freight network performance and major opportunities forimproving freight network performance;

To recommend specific and actionable optimization strategies;

To quantify investment opportunities to lower transportation costs for Iowa businesses and develop a business case for eachinvestment opportunity, using both quantitative and qualitative measurements;

To provide the building blocks to help Iowa businesses optimize their commercial supply chains to achieve sustainable costsavings; and

To develop a dynamic framework to support future analysis, as market conditions change.

A freight transportation network optimization is different from traditional travel demand modeling widely used intransportation planning. Travel demand modeling is used to “develop traffic forecasts, test alternative transportationscenarios, and evaluate transportation systems or policies” (CamSys, 2014). The results of travel demandmodeling are used to assist decision makers in making transportation planning and infrastructure investmentdecisions from a range of alternatives that may include addressing congestion issues or increasing networkcapacity. Traditionally, a “four-step process” is used for regional transportation planning (CamSys, 2014):

1. Trip generation (how many trips will be made?);

2. Trip distribution (where will the trips go?);

3. Mode choice (what modes of transportation will the trips use?); and

4. Trip assignment (what routes will the trips take).

21 High value constraints are the weakest links in a system. Addressing these constraints can deliver high cost savings, or high value to theusers of the freight transportation system.

© 2016 Quetica, LLC

26 Development of Iowa Statewide Freight Transportation Network Optimization Strategy

A freight transportation network optimization is focused on identifying opportunities to transport commodities fromorigins to destinations at lower costs for the users of the transportation system. The resulting optimization strategiestypically involve leveraging effective multimodal choices and freight consolidation methods to reduce transportationcosts, truck miles, and carbon emissions. A freight network optimization study can use the transportation networkand capacity data from a travel demand model to define the possible modal options for each origin-destination pair.These modal options are examined to select the most cost-effective mode to deliver the commodities in anoptimized network. The optimization results include quantifying the transportation cost saving benefits to thetransportation system users and projected impact to freight traffic patterns such as an increase or reduction of truckcounts, rail traffic, or barge traffic in the study area. The freight traffic pattern change data can potentially be fedback to the travel demand model to further analyze projected changes to the overall travel patterns after theoptimization strategies are implemented. As a result, freight network optimization and travel demand modeling mayprovide complementary tools to effective transportation planning.

27

© 2016 Quetica, LLC

Development of Iowa Statewide Freight Transportation Network Optimization Strategy

3. Demand Modeling

Modeling freight demand on Iowa’s multimodal networks required the assembly and normalization of Iowacommodity flow data. The data was enhanced with additional attributes, disaggregated and/or aggregated to thedesired level determined by the modeling parameters. The assembled demand data represents shipment levelinformation regarding commodity type, volume, demand nodes and supply nodes. The resulting database is acollection of shipments in the base and forecast years. Each shipment includes the following data:

Origin Site

Destination Site

Commodity/Product Group

Quantity of Commodity/Product Group22

Equipment Type Required 23

Transportation Mode(s) Available/Used

Shipment Direction (Within/Inbound/Outbound)

This study uses data from both public and proprietary sources. The primary source of the domestic commodity flowdata is FHWA’s Freight Analysis Framework (FAF), Version 3.5 data (FAF3, 2014). FAF is a compilation of datathat provides estimates of freight shipped to, from and within the United States. It provides a comprehensivenational picture of base year freight flows and forecasted trends to support policy studies. FAF3 data is builtprimarily on the 2007 Commodity Flow Survey (CFS) conducted by the U.S. Census Bureau and the Bureau ofTransportation Statistics (BTS). FAF3 data includes the following components (FAF3, 2014):

Transportation modes – Truck, Rail, Water, Air, Multiple Modes and Mail, Pipeline and Other andUnknown

Commodities – 43 commodities represented in 2-digit Standard Classification of Transported Goods(SCTG) codes (US DOT, 2007).

Domestic regions – 123 domestic regions, of which the entire state of Iowa is one region.

Foreign regions – 8 foreign regions including Canada, Mexico, Rest of Americas, Europe, Africa,Southwest & Central Asia, Eastern Asia and Southeast Asia & Oceania.

Freight tonnage22 and value -- In 2007 survey year and provisional update or forecast data in 2010, 2015,2020, 2025, 2030, 2035 and 2040.

22 All freight tonnage in both domestic and import/export models is represented in U.S. short tons, commonly referred to as a “ton”. A U.S.short ton is a unit of weight equal to 2,000 pounds (907.18474 kg).

23 Detail is covered in next part of Section 3.1.

© 2016 Quetica, LLC

28 Development of Iowa Statewide Freight Transportation Network Optimization Strategy