Embed Size (px)

Citation preview

D E S I G N A N D F E A S I B I L I T YO F P E E R - T O - P E E R M O B I L E

PAY M E N T S Y S T E M S

rick van galen

master’s thesis:Rick van Galen: Design and Feasibility of Peer-to-Peer Mobile Payment SystemsUniversity of Twente - department of Computer ScienceResearch work was performed at ING Bank N.V., Amsterdam© November 2014

supervisors:Dr. Andreas Peter (UT)Dr. Maarten Everts (UT)Roderick Simons (ING)

To Dora.For all her love and words of motivation.

A B S T R A C T

Digital payment methods are becoming increasingly popular. The adventof Bitcoin and Apple Pay is an indication that digital payment systems arerelevant today and even moreso in the future. However, these payment sys-tems firmly rely on central infrastructures. Many also only bring paymentsto digital platforms, but lack the possibility for people to be paid without ad-ditional infrastructure. Lastly, privacy for payers is rarely achieved in mostcurrent commercial payment systems.

In this thesis, we investigate a novel design of digital payments especiallytargeted at smartphones and tablets to address the above shortcomings. Wename this system a peer-to-peer payment system because it transfers digitalcoins from device to device. This design choice enables two distinguishingfeatures: offline payments - the sending of payments without a third party -and receiving payments. In this thesis, we represent three protocol designsfor such mobile peer-to-peer payment systems, as well as a novel contribu-tion by introducing a method for sharing the responsibility of anonymityprotection amongst multiple partiesde.

The main result of this thesis is an assessment of the feasiblity of a peer-to-peer mobile payment system. We developed a prototype application andassessed technical choices that can be made. It was found that from theavailable local communication methods, the newly available Wi-Fi Directmedium was preferable to NFC and Bluetooth. The prototype applicationshows that the right technology is currently available to succesfully imple-ment peer-to-peer payment systems on mobile devices.

The protocol designs use a number of cryptographic constructs. An im-portant finding in our thesis is that it is possible to design an anonymous,scalable payment system using only cryptographic hashes, digital signa-tures and elliptic curve arithmetic. These basic constructs were found tostill be very demanding of these mobile devices’ computational power. Wewrote a benchmarking application and tested over 30 Android devices ontheir performance in cryptographic computations and payment protocol sce-narios. It was found that the computational performance at present leadsto some difficult tradeoffs for real-world applications. Nonetheless, we con-clude that practical applications are within the realm of possibility.

The contributions presented in this thesis are the following:

• The design of a simple peer-to-peer payment protocol

• An extension of this protocol in which a bank cannot trace paymentswithout a trusted third party

• An extension of this protocol in which multiple banks can issue coins

• A mechanism by which multiple parties can share the responsibilityof payer anonymization

• A prototype application that demonstrates a viable medium for peer-to-peer mobile communications for payments

• Benchmark results of a large number of Android devices on crypto-graphic operations used in the presented payment protocols

iii

C O N T E N T S

i background 1

1 introduction 3

2 description of digital payment systems 5

2.1 Parties and communication 5

2.2 Security properties 6

3 protocol principles 9

3.1 Online payments 10

3.2 Offline payments 11

4 cryptographic principles 15

4.1 Secure channels 15

4.2 Cryptographic assumptions 15

4.3 Public key cryptography 16

4.4 Elliptic curve arithmetic 17

4.5 Double spending prevention 19

4.6 Blind signatures 20

4.7 Fair blind signatures 21

4.8 Group signatures 24

4.9 Secret sharing 26

5 mobile security considerations 29

5.1 Offline authentication 29

5.2 Wallet protection 36

5.3 Random number generators 37

5.4 Cryptographic performance 38

5.5 NFC Security 39

6 electronic cash protocols 41

6.1 Chaum’s untraceable electronic cash 41

6.2 Gaud & Traore’s payment protocol 42

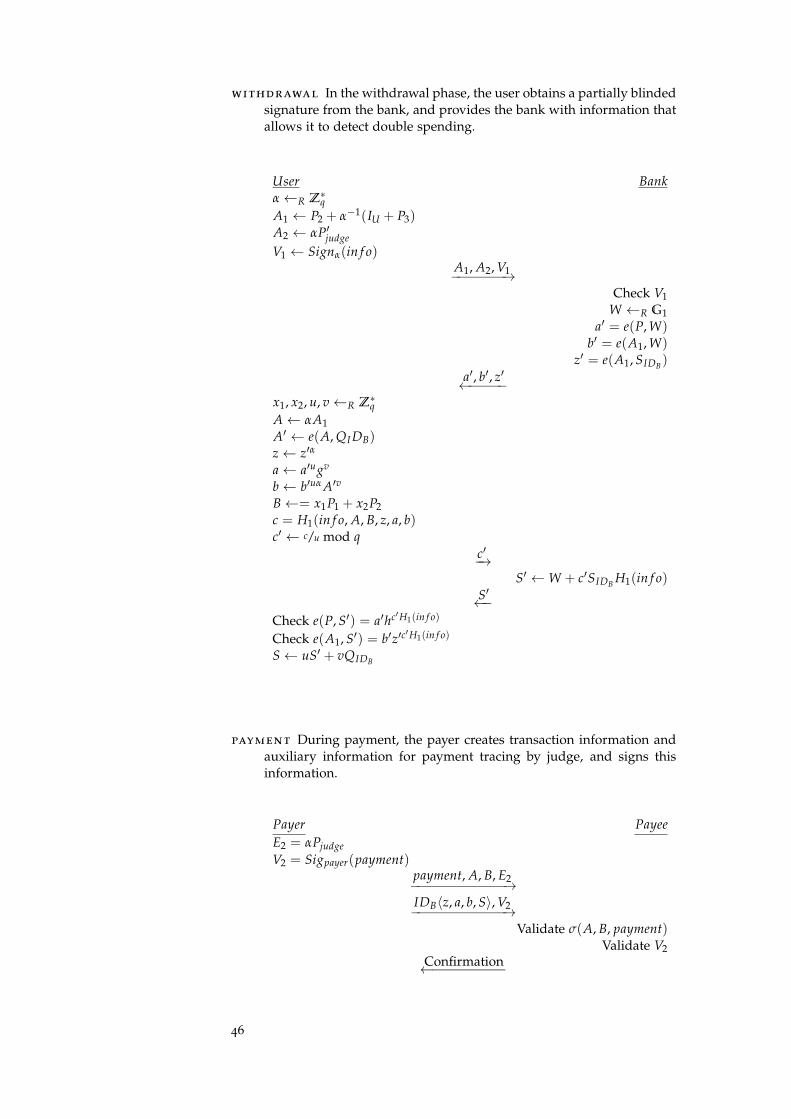

6.3 Scalable group signatures 44

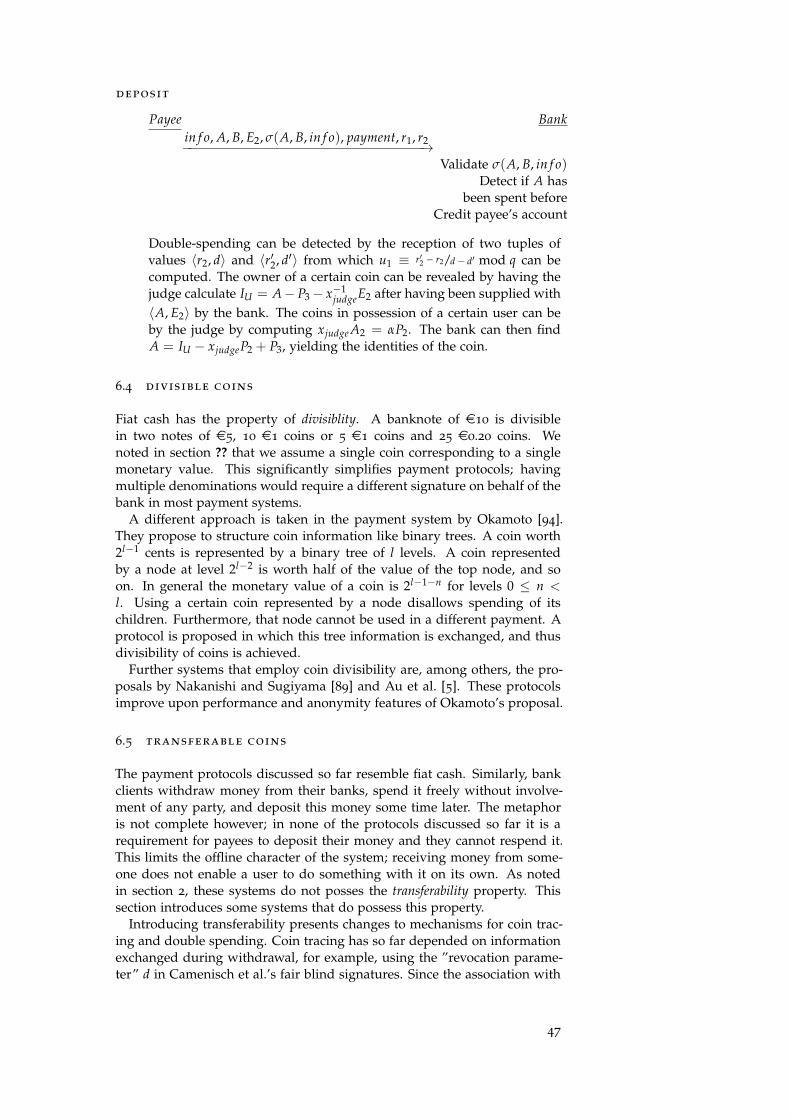

6.4 Divisible coins 47

6.5 Transferable coins 47

7 existing electronic money systems 49

7.1 EMV 49

7.2 Wireless EMV applications 51

7.3 Proton 51

7.4 Cryptocurrencies 51

ii experiment 53

8 protocol design 55

8.1 Protocol features 55

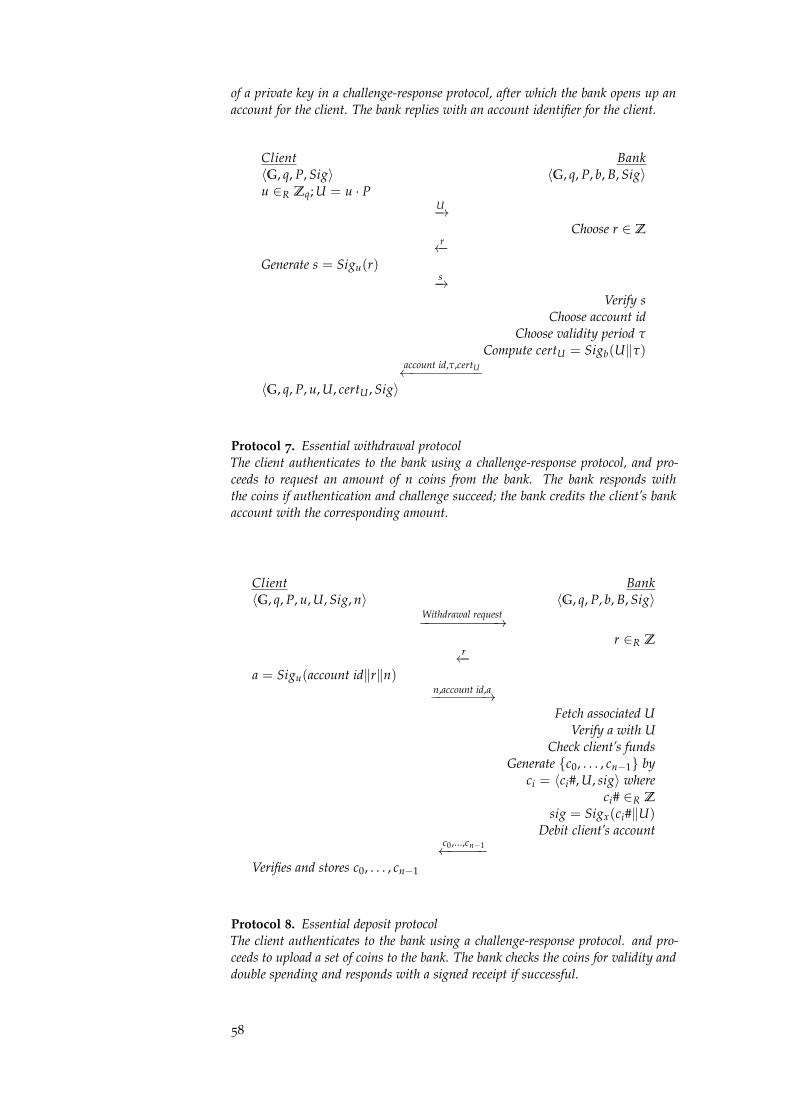

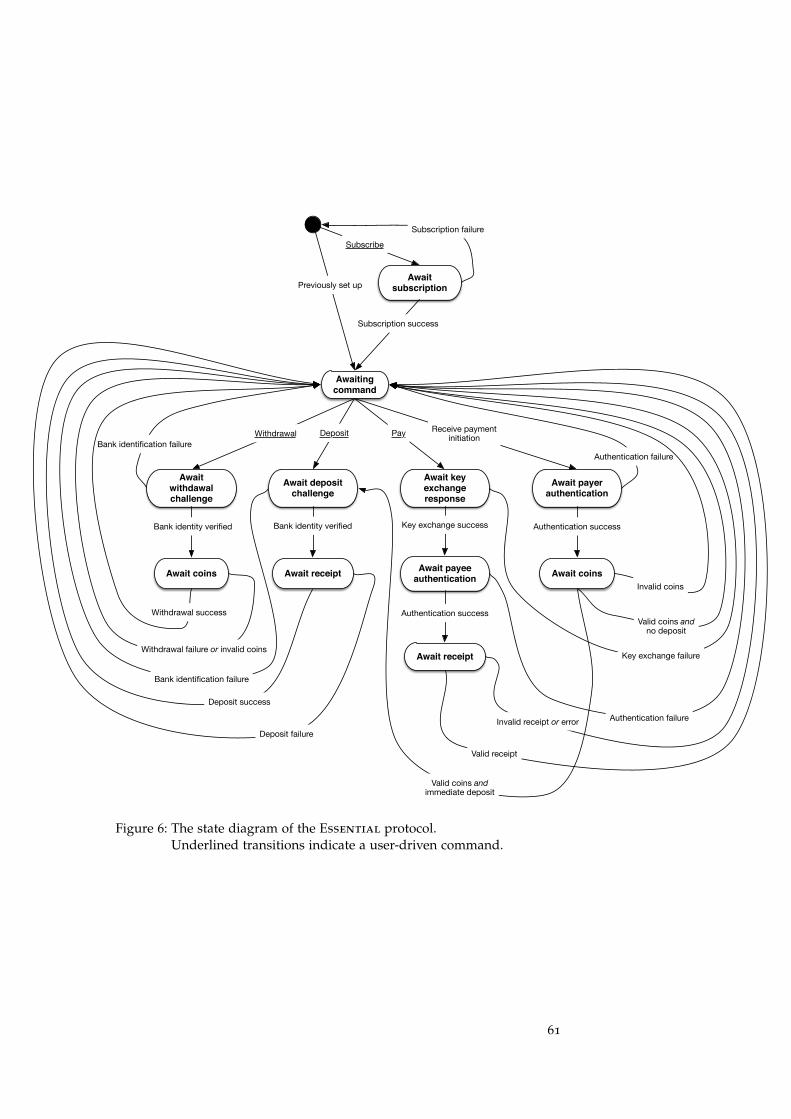

8.2 The essential protocol 57

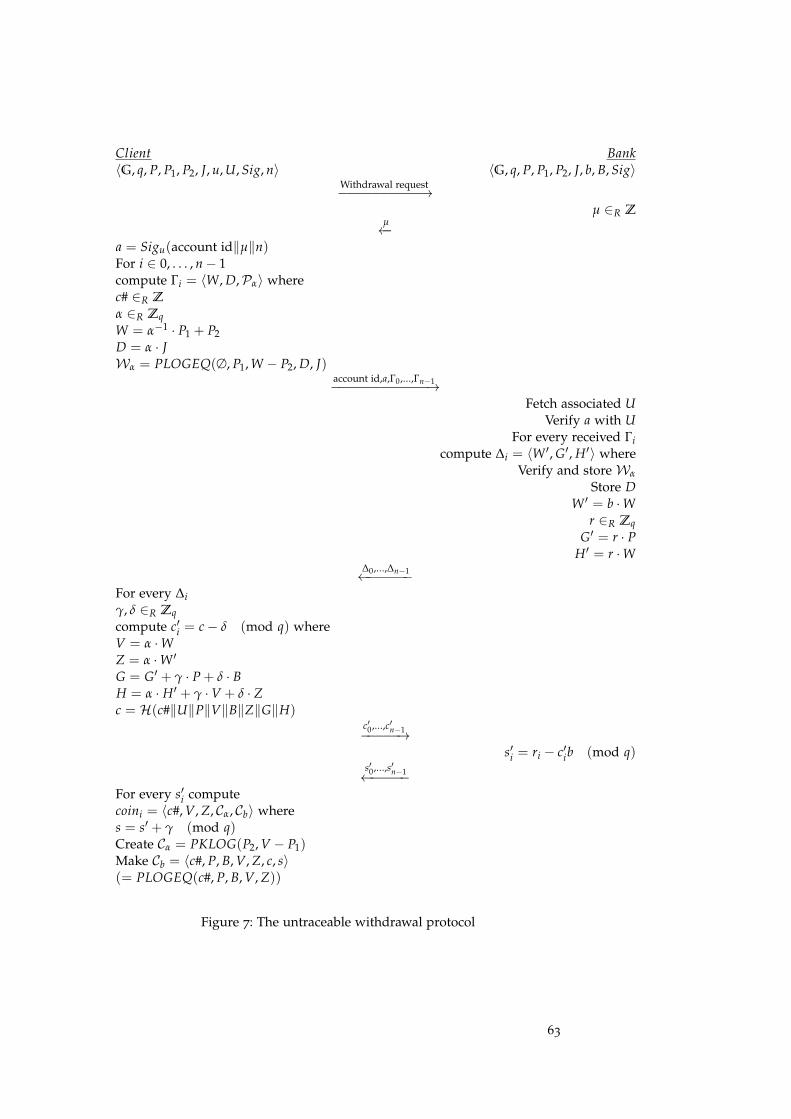

8.3 The untraceable protocol 60

8.4 The multibank protocol 64

9 prototype 71

9.1 Basic technology choices 71

9.2 Libraries 72

9.3 Mobile connectivity 73

9.4 Protocol implementation 74

v

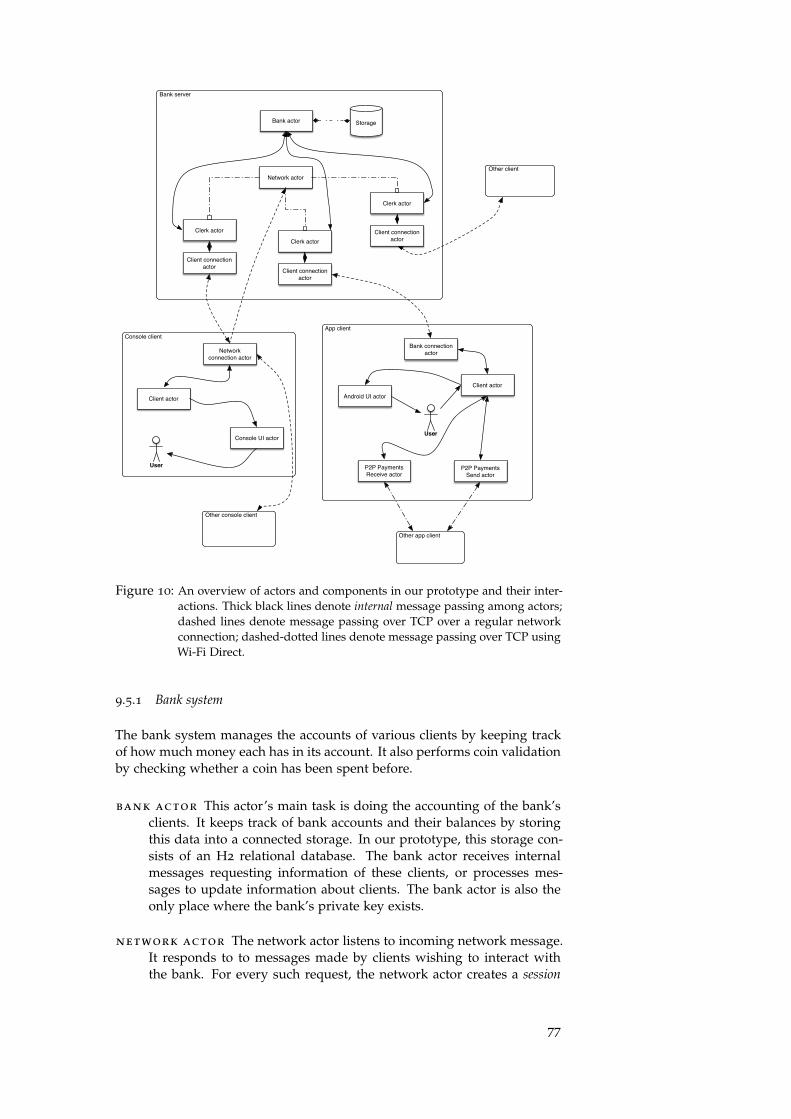

9.5 Prototype organization 76

9.6 Storage security notes 79

9.7 User interface 80

iii results 83

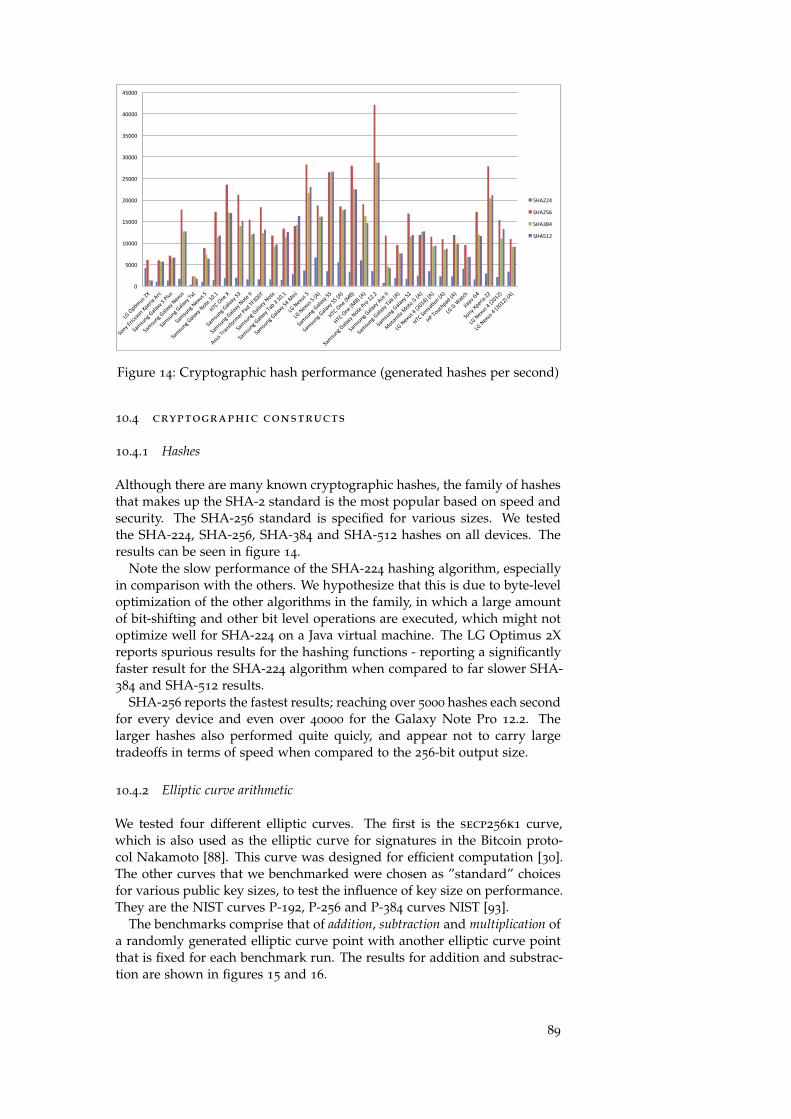

10 benchmarks 85

10.1 Description 85

10.2 Methodology 86

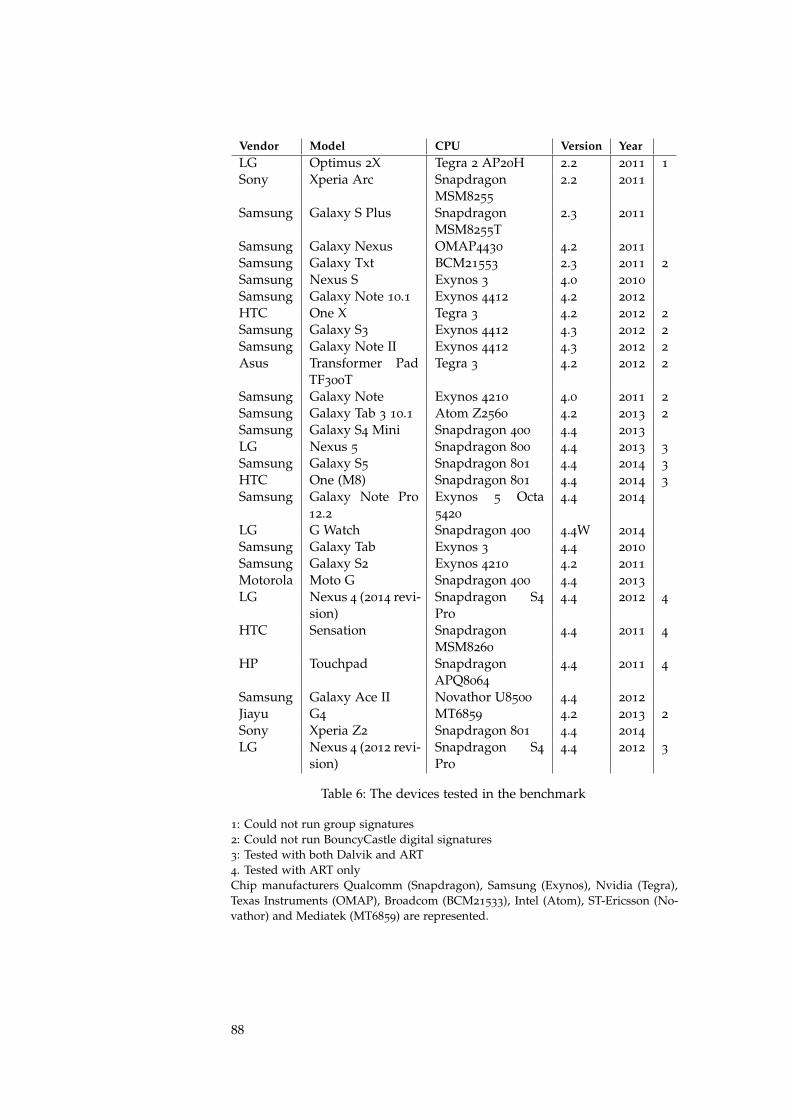

10.3 Devices 87

10.4 Cryptographic constructs 89

10.5 Proofs of knowledge 92

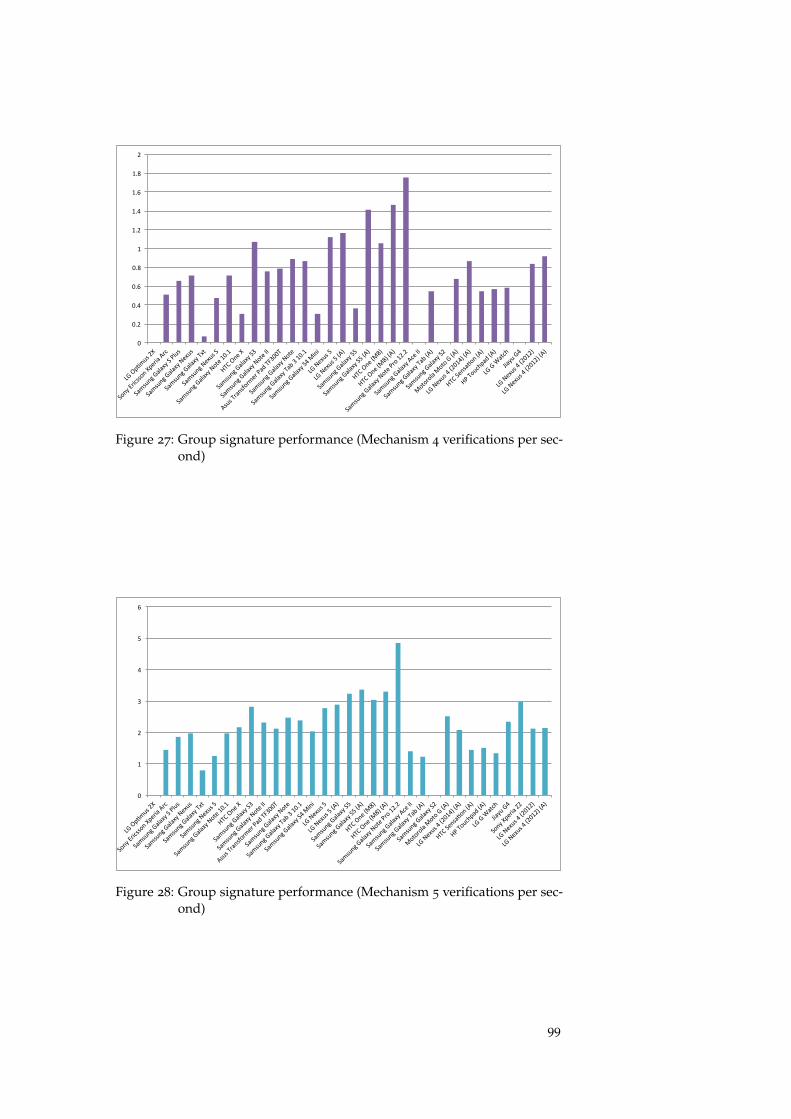

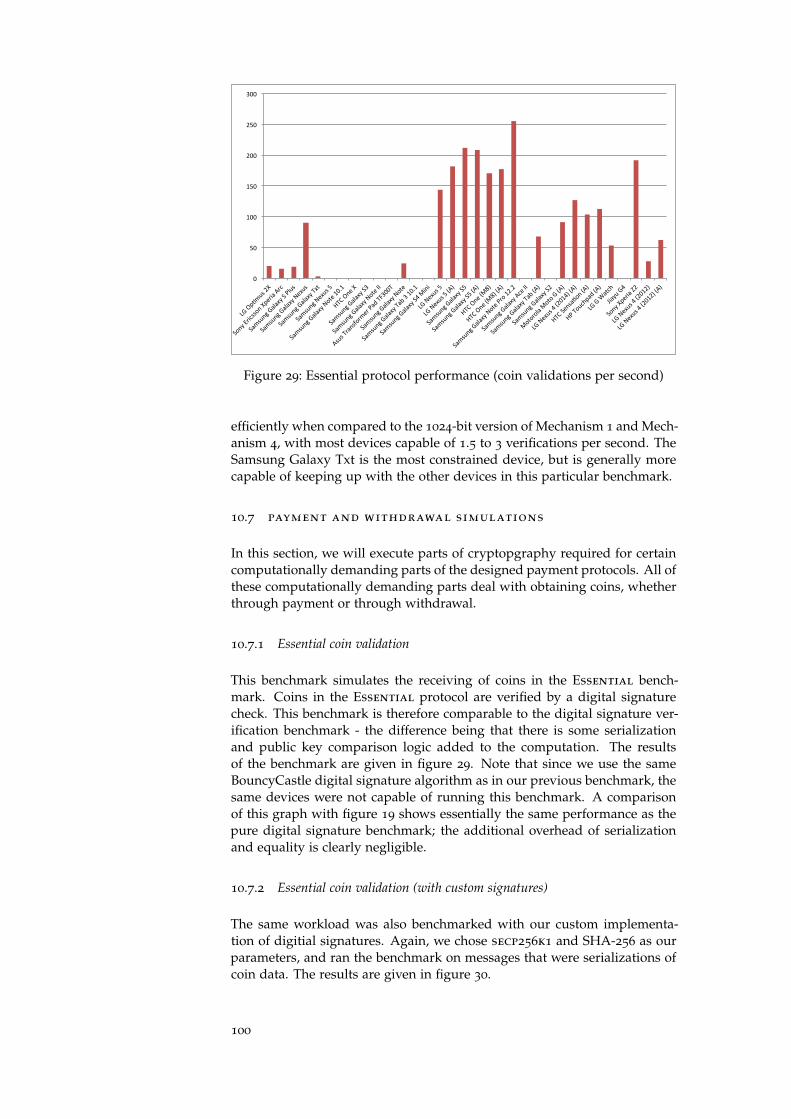

10.6 Group signatures 97

10.7 Payment and withdrawal simulations 100

11 discussion & conclusions 105

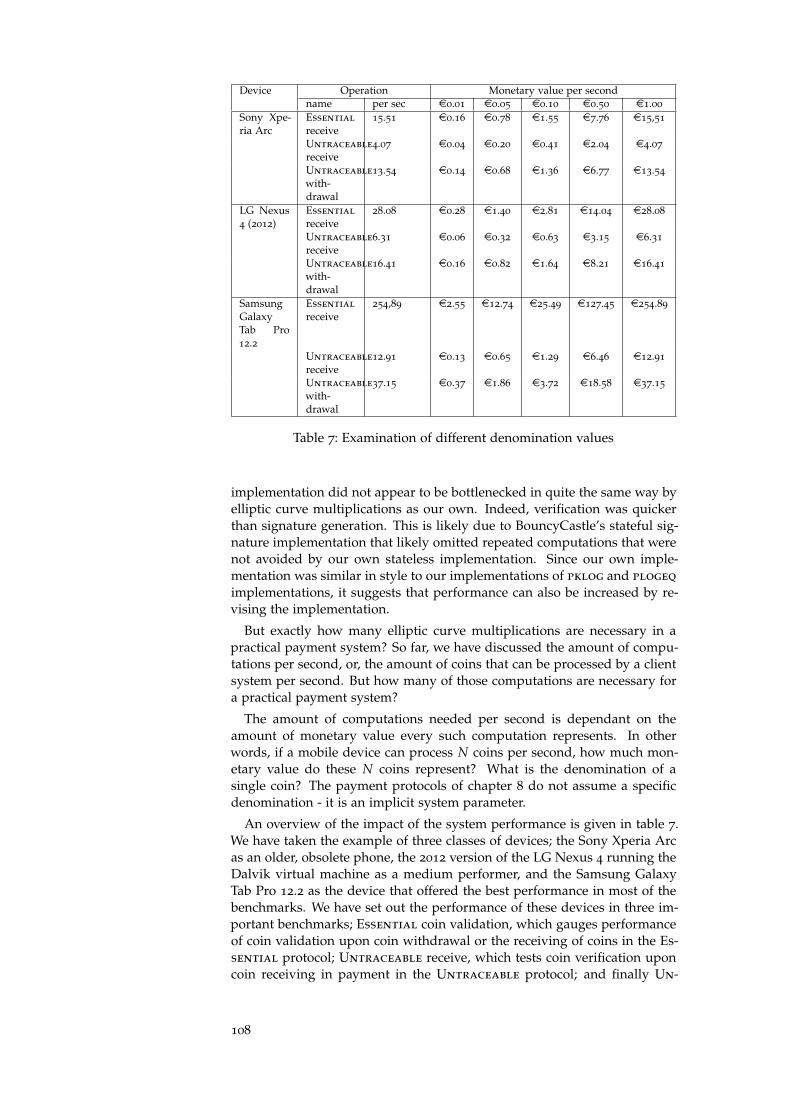

11.1 A comparison with fiat money 105

11.2 Cryptography 106

11.3 Prototype 107

11.4 Performance 107

11.5 Concluding remarks 109

12 recommendations 111

12.1 Secure element 111

12.2 Usability research 112

12.3 Implementation improvements 112

12.4 Lattice-based cryptography 112

References 115

vi

Part I

B A C K G R O U N D

1I N T R O D U C T I O N

Electronic payments systems have existed for decades. Originally employedas payment methods in telephony cards since the 1980s, many banks haveintroduced digital smart cards to serve as alternative payment methods.Adoption of electronic payment has sharply increased over the years, andthe number of cash payments has corresponingly been dropping for manyyears [58].

Smartphones have become nearly as ubiquitous as electronic payments inrecent years. Becoming ever more useful in terms of sensors, radios andprocessing power, many people always carry their smartphone with them.The mutual ubiquity of smartphones and electronic payments has led tosome initiatives for mobile payments, but none of these have succeeded.The motivation for this thesis was to create a successful mobile paymentsystem. The goal was to make describe a system that could make obsoletecash money, aiming to provide a replacement for cash on mobile devices.

Current mobile payment initiatives use the wireless capabilities of mobiledevices to communicate payment information. Phones connect to a mobilenetwork, which allows use of SMS and mobile internet services. Further-more, mobile devices can connect to other mobile devices using Bluetoothand Wi-Fi Direct. Recently, adoption of near-field communication (NFC)enabled mobile devices has surged [11]. NFC technology enables mobile de-vices to instantaneously communicate with other generic mobile devices orpurpose-made service technology. In addition, the Bluetooth 4.0 and Wi-FiDirect standards allow for a similar mode of operation for direct commu-nication between mobile devices [17, 1]. There appear to be a plethora ofmedia available for mobile payments, but few if any systems take advantageof this.

As of November 2014, popular application markets show some adoptionof these new wireless communication technologies, in accordance with somepredictions that mobile payments will be the biggest impactor in paymentbusiness in the coming years [11]. None of the initiatives presently availablein the Netherlands is a complete payment system however; they are prepaidservices that do not manage actual money. Nor are we aware of popularpayment systems in other countries. This is inconvenient from a user’sperspective; firstly a user needs to manage accounts as well as a cash sourcefor independent payment services, and secondly independent service do notreadily possess network effect for large adoption of such payment services.

Another limitation of many commercial payment systems is their unidi-rectional character. Most payment systems are developed with the focus onsendingpayments only, and receiving payments is rarely a design goal. Oftenspecial equipment and fees are necessary to receive payments, which halvesthe potential use cases for users and keeps control with the payment pro-cessor. We will use this thesis to present the design of a payment protocolwhere receiving payments is just as accessible as sending them.

3

In this thesis we will use the term mobile devices to mean consumer ori-ented portable devices that usually get marketed as ’smartphones’ or ’tablets’or similar terms. This is a loose definition that attempts to encompass thecategory of devices that many people increasingly carry along - and there-fore have readily available to use in payment transactions. We define mobilepayment technology or mobile payment systems as technology enabling digitalpayments on mobile devices [71, 100].

We will investigate a novel payment system, a so-called peer-to-peer pay-ment system, for mobile devices. The payment system consists of a descrip-tion of communication, along with a set of cryptographic computations thatfacilitate security features. The presented system in this thesis is the resultof answering the following research questions:

• What do peer-to-peer payment protocols look like on mobile devices?

– What security features do peer-to-peer payment protocols needto possess?

– Can these features be incorporated in a real-world application?

• Do there exist usable and performant communication methods forpeer-to-peer payments between mobile devices?

• Does the required cryptography for peer-to-peer payments performquickly enough on mobile devices?

This thesis is structured into three parts. The preliminary background partserves as an introduction to the concepts of digital payment systems: sec-tion 2 deals with identification of parties and responsibilities in paymentsand section 3 provides the reader with conceptual details of payment sys-tems. The next chapters explore literature that allows us to fill in details ofdigital payment protocols; generally necessary cryptographic techniques toconstruct them in section 4 and other techniques suitable for use in the mo-bile context in chapter 5. We will then see applications of these techniquesin payment systems; those from literature in chapter 6 and those currentlyon the market in chapter 7. We will then present the design and consid-erations of our protocol and experiments in system in the experiment part,in which we will present a chapter on the design of different peer-to-peerpayment protocols (chapter 8) and a chapter detailing the implementationof a demo application (chapter 9). Finally, we will conclude with a resultspart, in which we describe benchmarks and present their results in chapter11, and discuss some recommendations of further work based on this thesisin chapter 12.

4

2D E S C R I P T I O N O F D I G I TA L PAY M E N T S Y S T E M S

In this chapter, we provide the reader a conceptual description of whatdigital payment systems are. We identify the division of responsibilities ina payment protocol and also define what makes such a system secure.

2.1 parties and communication

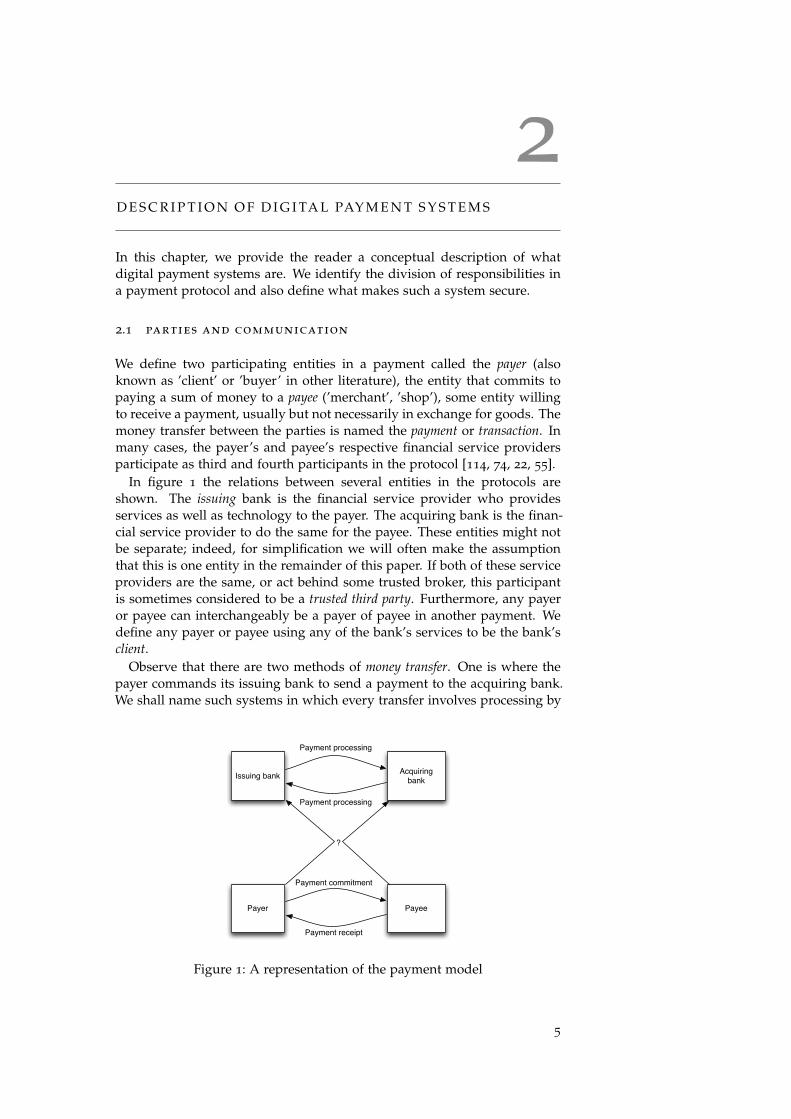

We define two participating entities in a payment called the payer (alsoknown as ’client’ or ’buyer’ in other literature), the entity that commits topaying a sum of money to a payee (’merchant’, ’shop’), some entity willingto receive a payment, usually but not necessarily in exchange for goods. Themoney transfer between the parties is named the payment or transaction. Inmany cases, the payer’s and payee’s respective financial service providersparticipate as third and fourth participants in the protocol [114, 74, 22, 55].

In figure 1 the relations between several entities in the protocols areshown. The issuing bank is the financial service provider who providesservices as well as technology to the payer. The acquiring bank is the finan-cial service provider to do the same for the payee. These entities might notbe separate; indeed, for simplification we will often make the assumptionthat this is one entity in the remainder of this paper. If both of these serviceproviders are the same, or act behind some trusted broker, this participantis sometimes considered to be a trusted third party. Furthermore, any payeror payee can interchangeably be a payer of payee in another payment. Wedefine any payer or payee using any of the bank’s services to be the bank’sclient.

Observe that there are two methods of money transfer. One is where thepayer commands its issuing bank to send a payment to the acquiring bank.We shall name such systems in which every transfer involves processing by

Payer Payee

Issuing bank Acquiring bank

Payment commitment

Payment receipt

Payment processing

Payment processing

?

Figure 1: A representation of the payment model

5

some services offered by the bank a processed payment system. Note thatprocessed payment systems by necessity are online systems since payer andpayee need to be informed of the payment traffic from their respective banks.An example of such a payment system is the debit card payment system.

Another is where the payer transfers the money directly to the payee.This is what we call a peer-to-peer payment system. During a peer-to-peerpayment, the involvement of banks is not necessary. Payers and payeeswithdraw money from their bank accounts into their own possession at adifferent time at which payments occur. An example of a peer-to-peer pay-ment system is the fiat money system.

A payment system is composed of a set of protocols that accomplish differ-ent phases in the payment process. These protocols are the following [22,36, 23, 55, 43]:

1. Setup phase – performed by the bankThe bank publishes information about its own identity and definescryptographic parameters used in the system. This phase is run onlyonce during the very start of the protocol.

2. Account setup protocol – performed by the client and the bankThe client notifies the bank that he/she desires to use the bank’s ser-vices, and the bank provides the user with the data to make use ofits services. This can be seen as the digital equivalent of opening anaccount.

3. Withdrawal protocol – performed by payer and bankThe payer withdraws money from his bank account. The bank pro-vides the payer with the corresponding amount of money, which canbe spent by the payer. The payer stores this money in his/her wallet.

4. Payment protocol – performed by two clients (one payer, one payee)The payer sends the payee an amount of money from his/her wallet:this amount gets stored by the payee. The payer can then no longervalidly spend this money.

5. Deposit protocol – performed by payee and bankThe payee sends money from his/her wallet to the bank. The bankverifies the validity of the money, and credits the payee’s account withthe corresponding monetary value.

These definitions are made in such a way that the payment system becomean analagy for the flow of fiat money.

A property a payment protocol may or may not possess is transferability.We say that a payment protocol is transferable if it is possible for a client tofirst receive money (as a payee) and immediately spend this money again (asa payer), without having to contact the bank first [6, 74]. As we will see insection 6.5, transferability in payment protocols is not easily accomplishedin digital systems. Payment protocols discussed in this paper do not possessthe transferability property unless otherwise noted.

2.2 security properties

The first security service necessary is authentication between payer and payee,and both of these parties with the trusted third party. A payer desires tomake a payment to some payee, and therefore the payee needs to authenti-cate to the payer. The payee conversely needs knowledge about the payer’s

6

authorisation and capability to fulfil payments, and therefore requires toauthenticate the payer. Payer and payee further need authentication of theadditional trusted parties in the protocol.

The second security service required is non-repudiation of a committedpayment. Once a payer commits to a payment and has transferred it to thepayee, there should be no way for the payer to later deny the creation of thiscommitment. The payee needs to ensure this to truly guarantee the validityof this payment.

Thirdly, payments should be singular. Once a payment has been commitedto by a payer, he cannot commit to a payment that includes a money unitused in a previous payment again.

The final required security service is that of integrity: once a payment istransmitted it cannot be modified in such a way that the payment details ofpayer, payee and amount transferred can be modified. Nor can additionaldetails of the payment be modified, such as time stamps or the number oftimes the payment can be repeated.

When authentication of both parties is achieved and non-repudiation andintegrity can be claimed on the payments, payments satisfy the propertythat:

1. Payments occur between the intended identities

2. Payments are final and intractable

3. Payments are singular

4. Payments cannot be modified

We define payment systems satisfying the above properties as secure pay-ment systems. In principle, the features above are defined to guarantee thatno user can illegally obtain money that was not explicitly sent to him or her.Although payment traffic can operate normally in secure payment systemsunder this definition, its properties only ensure proper operation from theperspective of the bank. Ideally however, security properties of the systemshould also provide security for the users of the system. This is becauseof the fact that, in practice, the bank’s status as trusted third party may bequestioned. Additional features can be introduced to alleviate the bank ofsome responsibilities and limit the trust users need to place in the bank’soperations. We list these additional desired features below.

The first such security feature is the confidentiality of payments when com-municated between payer and payee. Confidentiality is not always used inexisting payment systems. For example, the EMV protocol (see section 7.1)does not use cryptography to make payment communication confidential,instead relying on the physical security of contact smartcards [42] to preventeavesdropping.

Another security feature is untraceability. Untraceability decouples trans-action information from the identity of the payer. A bank can see that one ofits clients withdraws money, but cannot identify which units of money are inthe possession of their clients. This makes it impossible for involved banksto track payments executed within the system as only the payee knowsabout the identities of the payer he or she has been involved with. In ad-dition, it should be impossible for the bank to tell which money is held bywhich client. This property provides protection for payers in the system incase the bank is compromised or cannot be trusted. As an example, note thatdebit cards do not have untraceability, as issuing and acquiring bank pos-sess knowledge of the location and timing of payments made and received

7

Features of secure payment systemsAuthentication All parties can have proof that they are con-

ducting business with the payer, payee andbanks they intend.

Non-repudiation No payer can deny creating a payment after itwas received by a payee.

Singularity No payer can validly commit a payment a sec-ond time.

Integrity Once committed, a valid payment cannot bemodified into another valid payment.

Additional features of anonymous payment systemsConfidentiality Payment traffic among payer, payee and

banks cannot be eavesdropped.Untraceability The bank cannot trace the flow of money

within the system and cannot follow whichidentities possess which coins in the system.

Table 1: Overview of security features necessary for mobile payment sys-tems

using debit cards. Fiat money does possess the untraceability property, asbanks only know the timing, location and serial numbers of withdrawalsand deposits, but do not know where money has been within the system.

We define a secure payment system extended with confidentiality and un-traceability as an anonymous payment system. An overview of these featuresis given in table 1. In this thesis, we will focus on the design and impleme-nation of a payment system that is both a peer-to-peer payment system andan anonymous payment system.

8

3

P R O T O C O L P R I N C I P L E S

Before we delve into the cryptographic details of payment protocols, we willfirst introduce some principles in this chapter. This serves as a conceptualoverview, and we will fill in the required concepts. High-level descriptionsof some important building blocks for payment protocols is given below.

secure channels [28] Secure channels are prepared communication chan-nels which have the property that data passed through them cannotbe modified or eavesdropped. They are usually established by ap-plying some symmetric cipher to the communication, and are usedextensively in devices capable of network communication.

one-way functions [90] A one-way function is a function f with whichit is easy to compute f (a) = b given f and a, but it is computationallyinfeasible to compute the inverse f−1(b) = a given f and b. The irre-versibility of this function allows it to act as a trapdoor. An importantcryptographic property of the one-way function is collision resistance -that it is very hard to find distinct function inputs that result in thesame output. It is not known whether one-way functions truly exist,but many hashing algorithms are considered to be one-way in practice.

digital signatures [104] By signing a message with a private key froman assymmetric public/private key pair, integrity of the message ispreserved. Under the assumptions that the private key is kept secretby the signer and that adversaries cannot otherwise obtain the privatekey in the employed public-key cryptography scheme, digital signa-tures also provide authentication and nonrepudation. Digital signa-tures can be used to approve payment commitment, payment verifica-tion or payment acceptance by each party in a payment system.

blinding [32] Blinding is a technique used to implement untraceabilityof payments. A payer generates coins during signing, but sends thebank a transformation (called the blinded coin) of this coin to be signed.The blinded coin is signed by the bank, but the bank does not knowwhich coins it has signed, making payments untraceable. The blindingis done in such a way that the payer can afterwards unblind this coinand possess a valid signature on an unblinded coin.

double spending detection [35] Double spending detection methodsallow a bank to see when a coin has been doubly spent. This is doneby cryptographically adding information to payments that will keepsecret the identity of the payer the first time it is spent, but will revealthe identity of the payer if a single coin is used in more payments.Usually, this included information is randomized by a challenge sent tothe payer by the payee during payment. If the bank receives different

9

Construct Security propertiesSecure channels Integrity, confidentialityOne-way functions IntegrityDigital signatures Authentication, integrity, confiden-

tiality, non-repudationBlinding UntraceabilityDouble spending detection Singularity

Table 2: Relation of cryptographic constructs to security features

pieces of double spending information for the same coin for two dif-ferent challenges, the bank has legal proof that the user has spent thecoin twice.

In addition to these principles, we also need a definition of a coin. In thecontext of a digital payment protocol, a coin represents the closest analogyof the real-world concept of a coin. It is a piece of data that is indivis-able and unforgeable, and it corresponds to some monetary value. Whatdata is actually contained in the coin is based on the requirements set bythe cryptographic constructs used in the protocol. At bare minimum, thedata contained in the coin must uniquely identify each one. In addition toan identifier, a coin will usually consist of cryptographic parameters thathelp ensure its unforgeability and indivisability. In contrast to real coins,which come in many nominations corresponding to different monetary val-ues within the same currency, it is conceptually simpler to use only onesingle coin tied to one corresponding monetary value.

Using these techniques, it is possible to construct digital payment proto-cols with varying security features. A survey by the U.S. National SecurityAgency in 1996 lists the state-of-the-art in payment protocols at the time [74].Since their work provides a good conceptual explanation of payment proto-cols, this next section will summarize the concepts in this publication, withsome additions and modifications. Each protocol describes three subproto-cols: that of withdrawal in which the payer obtains money from the bank tospend. The payment part refers to the transfer of digital money from payerto payee. The deposit protocol defines the process with which the payeeredeems received payments at the bank.

3.1 online payments

The simplest version of a payment protocol with the discussed contructs isone which is fully online, and in which no attempt is being made to obscureany party’s identity. It is described as follows [74]. Please note that inthis and the subsequent sections, we assume the communication channelsbetween payer, payee and bank are secure channels.

Protocol 1. Simple online protocol

withdrawal

1. Payer sends a request for withdrawal to the bank

2. The bank prepares the coin with a digital signature

3. The bank sends the coin to the payer and withdraws the amount fromthe payer’s account

10

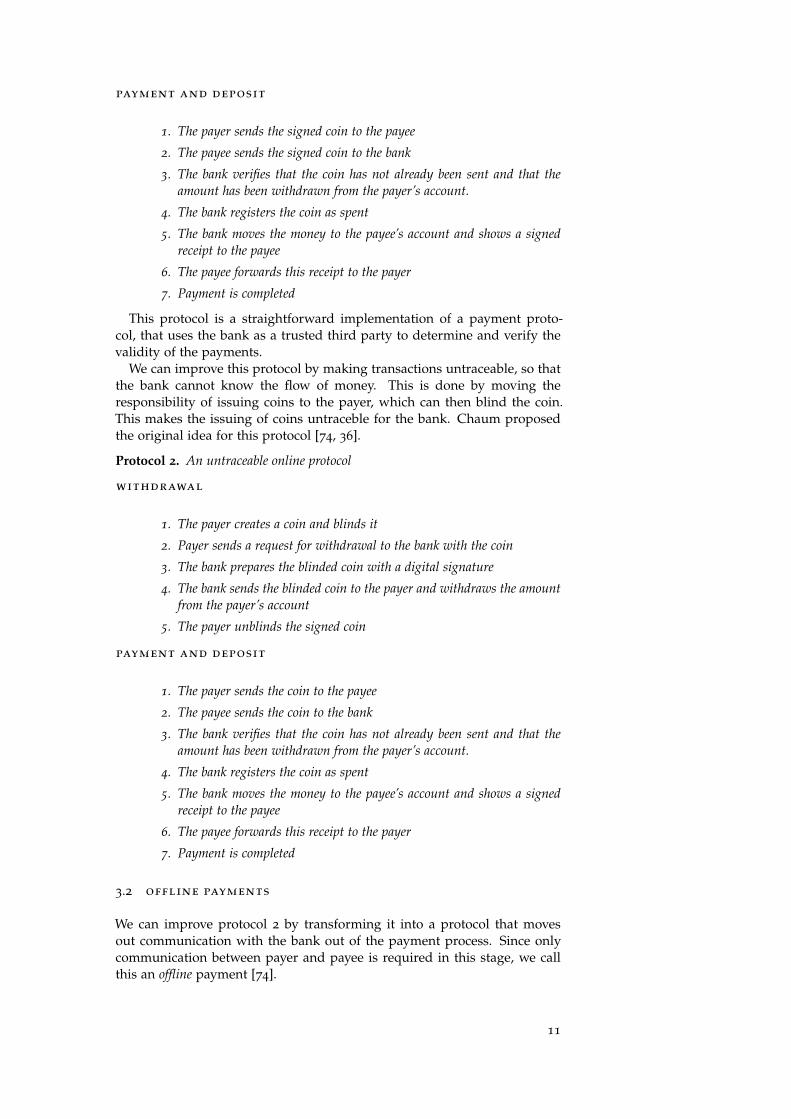

payment and deposit

1. The payer sends the signed coin to the payee

2. The payee sends the signed coin to the bank

3. The bank verifies that the coin has not already been sent and that theamount has been withdrawn from the payer’s account.

4. The bank registers the coin as spent

5. The bank moves the money to the payee’s account and shows a signedreceipt to the payee

6. The payee forwards this receipt to the payer

7. Payment is completed

This protocol is a straightforward implementation of a payment proto-col, that uses the bank as a trusted third party to determine and verify thevalidity of the payments.

We can improve this protocol by making transactions untraceable, so thatthe bank cannot know the flow of money. This is done by moving theresponsibility of issuing coins to the payer, which can then blind the coin.This makes the issuing of coins untraceble for the bank. Chaum proposedthe original idea for this protocol [74, 36].

Protocol 2. An untraceable online protocol

withdrawal

1. The payer creates a coin and blinds it

2. Payer sends a request for withdrawal to the bank with the coin

3. The bank prepares the blinded coin with a digital signature

4. The bank sends the blinded coin to the payer and withdraws the amountfrom the payer’s account

5. The payer unblinds the signed coin

payment and deposit

1. The payer sends the coin to the payee

2. The payee sends the coin to the bank

3. The bank verifies that the coin has not already been sent and that theamount has been withdrawn from the payer’s account.

4. The bank registers the coin as spent

5. The bank moves the money to the payee’s account and shows a signedreceipt to the payee

6. The payee forwards this receipt to the payer

7. Payment is completed

3.2 offline payments

We can improve protocol 2 by transforming it into a protocol that movesout communication with the bank out of the payment process. Since onlycommunication between payer and payee is required in this stage, we callthis an offline payment [74].

11

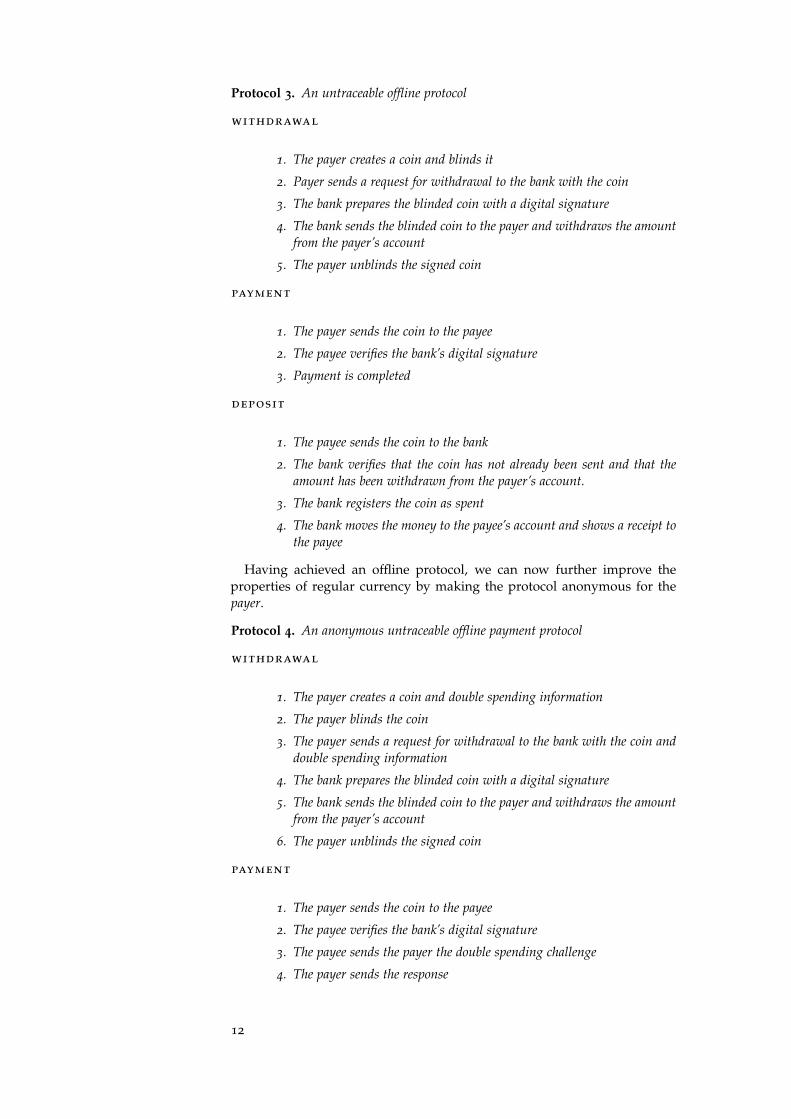

Protocol 3. An untraceable offline protocol

withdrawal

1. The payer creates a coin and blinds it

2. Payer sends a request for withdrawal to the bank with the coin

3. The bank prepares the blinded coin with a digital signature

4. The bank sends the blinded coin to the payer and withdraws the amountfrom the payer’s account

5. The payer unblinds the signed coin

payment

1. The payer sends the coin to the payee

2. The payee verifies the bank’s digital signature

3. Payment is completed

deposit

1. The payee sends the coin to the bank

2. The bank verifies that the coin has not already been sent and that theamount has been withdrawn from the payer’s account.

3. The bank registers the coin as spent

4. The bank moves the money to the payee’s account and shows a receipt tothe payee

Having achieved an offline protocol, we can now further improve theproperties of regular currency by making the protocol anonymous for thepayer.

Protocol 4. An anonymous untraceable offline payment protocol

withdrawal

1. The payer creates a coin and double spending information

2. The payer blinds the coin

3. The payer sends a request for withdrawal to the bank with the coin anddouble spending information

4. The bank prepares the blinded coin with a digital signature

5. The bank sends the blinded coin to the payer and withdraws the amountfrom the payer’s account

6. The payer unblinds the signed coin

payment

1. The payer sends the coin to the payee

2. The payee verifies the bank’s digital signature

3. The payee sends the payer the double spending challenge

4. The payer sends the response

12

5. The payee verifies the response to the payer to complete the payment

deposit

1. The payee sends the coin, challenge and response to the bank

2. The bank verifies the presence of its digital signature on the coin

3. The bank verifies that the coin has not already been spent

4. The bank enters the coin, challenge and response in a database for spentcoins

5. The bank deposits the money into the payee’s account

13

4

C RY P T O G R A P H I C P R I N C I P L E S

In the previous chapter, we have presented an outline of how cryptographicprinciples can create a secure, offline, anonymous digital payment protocol.However, we have treated the building blocks of these protocols as blackboxes. In this chapter, we will detail how these building blocks operate.Along the way, we will also cover additional cryptographic topics not previ-ously discussed, but which we will need in later chapters.

4.1 secure channels

Implementations of secure channels are widespread; the Transport Layer Se-curity (TLS) [39] and Secure Shell (SSH) [122] protocols are popular exam-ples of secure channels. Both standards are defined for different network-ing contexts, but their conceptual operation is identical. Both wrap trafficthrough a symmetric cipher (the Advanced Encryption Standard being themost popular choice) using a key exchanged by a predefined key exchangeprotocol based on public key cryptography. It is also important for theirsecurity that the channels are authenticated, for which both protocols alsodefine mechansisms.

In general, a secure channel can be established by first establishing authen-tication, negotiating a secret key. We will discuss authentication in section5.1. Once authentication and a secret key of sufficient length are established,a secure channel can me made over an insecure channel by using the com-mon key as input to symmetric cipher algorithm and message authentica-tion code mechanism. One such method preferred for packetized networktraffic is the Galois Counter Mode of the Advanced Encryption Standard(AES-GCM) [82]. This method offers both encryption and authentication.

4.2 cryptographic assumptions

The security of the following sections is dependent on a set of assumptions.These assumptions state that certain computations by are hard to perform.If a cryptographic construct is built upon one of these assumptions in sucha way that it can be shown that an adversary can break the scheme only if itcan be shown that this would break one of these assumptions, this schememay be considered secure.

cryptographic hashes are one-way functions We assume the roleof one-way functions can be fulfilled by cryptographic hashes. Crypto-graphic hashes are algorithms that accept an arbitrary amount of datato generate another, distinct, bit string. This generation has the prop-erty that, given a hash function application h(a) = b, it is easy tocompute h(a), that given b it is infeasible to compute a and infeasibleto compute a distinct a′ so that h(a′) = b [91].

15

Traditionally, the SHA family of hashes is used in integrity checkingand as one-way functions. Some concern exists however about the ca-pabilities of modern GPUs or dedicated integrated circuits to processlarge amounts of hashes to produce hash collisions. Therefore, thebcrypt [101] and scrypt [98] hashes have been proposed.

random oracle model The random oracle model is often used to provethe security of cryptographic protocols. A random oracle is a concep-tual function f that provides a completely random result f (a) for anyinput a, but will always yield the same result for any a. If a crypto-graphic protocol is shown to be secure under the random oracle model,it means that the protocol is shown to be secure if and only if everycryptographic hash function employed by the protocol is replaced bya random oracle.

The notion of ”secure under the random oracle model” is often crit-icised. This is because cryptographic hash functions are intended tobehave as random oracles, but are not known to be behaving as such.The random oracle model provides an indication of security, but is nota complete proof [29].

discrete logarithm problem We assume that certain groups exhibitthe property that it is computationally infeasible to reverse the re-peated application of the group operation on its elements. For ex-ample, given a finite multiplicative group of integers (G ⊂ Z∗, ·), itis assumed that it is computationally infeasible to find the integer agiven g ∈ G and ga ∈ G. The discrete logarithm problem is thoughtto be hard in both multiplicative groups of integers of prime order aswell as the additive group of points on certain elliptic curves, amongstothers.

computational diffie-hellman problem This assumption states thatthere exist cyclic groups G of order q for which holds that, given gen-erator g ∈ G and powers ga, gb of that generator, it is computationallyinfeasible to compute the value for gab as long as a, b ∈ Zq are notknown.

decisional diffie-hellman problem There exist cyclic groups G oforder q for which holds that, given a generator g ∈ G and three el-ements ga, gb, gc, it is computationally infeasible to decide whetherc ≡ a · b mod q for any unknown a, b, c ∈ Zq [18].

4.3 public key cryptography

An encryption scheme is said to be a public key cryptography scheme ifit seperates encryption and decryption capabilities in seperate (but related)keys named the public and private key. The public key is freely distributedto anyone, and the private key is kept secret. This division allows the holderof the private key to be the only one capable of decrypting messages thathave been encrypted using a private key, or conversely be the only one ableto encrypt messages that can be decrypted by anyone. This last propertycan be used to generate digital signatures on messages [40, 104].

The first public key cryptography schemes were based on the integer fac-torization problem (Rivest et al. [104]) or the discrete logarithm problem inmultiplicative integer groups (ElGamal [41]). Increasingly, the public key

16

-5 -4 -3 -2 -1 0 1 2 3 4 5

-3

-2

-1

1

2

3

(a) y2 = x3 − 2x

-5 -4 -3 -2 -1 0 1 2 3 4 5

-3

-2

-1

1

2

3

(b) y2 = x3 − 2x + 2

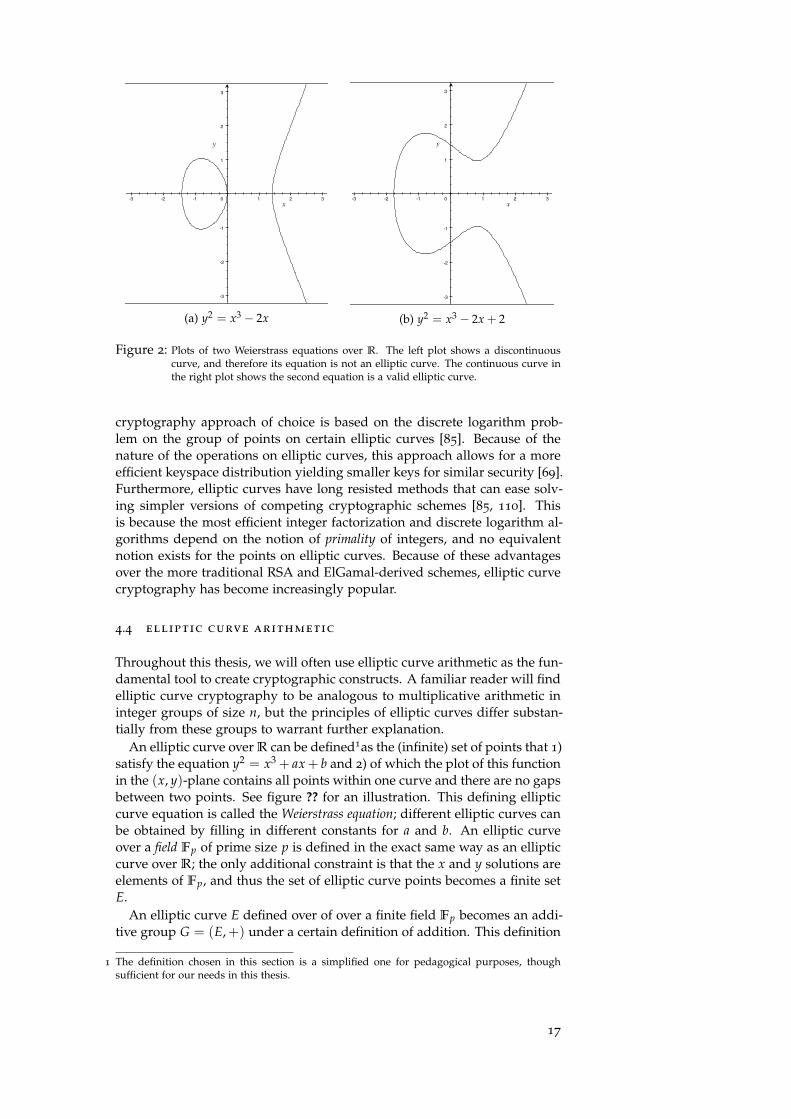

Figure 2: Plots of two Weierstrass equations over R. The left plot shows a discontinuouscurve, and therefore its equation is not an elliptic curve. The continuous curve inthe right plot shows the second equation is a valid elliptic curve.

cryptography approach of choice is based on the discrete logarithm prob-lem on the group of points on certain elliptic curves [85]. Because of thenature of the operations on elliptic curves, this approach allows for a moreefficient keyspace distribution yielding smaller keys for similar security [69].Furthermore, elliptic curves have long resisted methods that can ease solv-ing simpler versions of competing cryptographic schemes [85, 110]. Thisis because the most efficient integer factorization and discrete logarithm al-gorithms depend on the notion of primality of integers, and no equivalentnotion exists for the points on elliptic curves. Because of these advantagesover the more traditional RSA and ElGamal-derived schemes, elliptic curvecryptography has become increasingly popular.

4.4 elliptic curve arithmetic

Throughout this thesis, we will often use elliptic curve arithmetic as the fun-damental tool to create cryptographic constructs. A familiar reader will findelliptic curve cryptography to be analogous to multiplicative arithmetic ininteger groups of size n, but the principles of elliptic curves differ substan-tially from these groups to warrant further explanation.

An elliptic curve over R can be defined1as the (infinite) set of points that 1)satisfy the equation y2 = x3 + ax+ b and 2) of which the plot of this functionin the (x, y)-plane contains all points within one curve and there are no gapsbetween two points. See figure ?? for an illustration. This defining ellipticcurve equation is called the Weierstrass equation; different elliptic curves canbe obtained by filling in different constants for a and b. An elliptic curveover a field Fp of prime size p is defined in the exact same way as an ellipticcurve over R; the only additional constraint is that the x and y solutions areelements of Fp, and thus the set of elliptic curve points becomes a finite setE.

An elliptic curve E defined over of over a finite field Fp becomes an addi-tive group G = (E,+) under a certain definition of addition. This definition

1 The definition chosen in this section is a simplified one for pedagogical purposes, thoughsufficient for our needs in this thesis.

17

-4,8 -4 -3,2 -2,4 -1,6 -0,8 0 0,8 1,6 2,4 3,2 4 4,8

-3,2

-2,4

-1,6

-0,8

0,8

1,6

2,4

3,2

P

Q

R

(a) P + Q + R = 0

-4,8 -4 -3,2 -2,4 -1,6 -0,8 0 0,8 1,6 2,4 3,2 4 4,8

-3,2

-2,4

-1,6

-0,8

0,8

1,6

2,4

3,2

P

Q

R

-R

(b) P + Q = −R

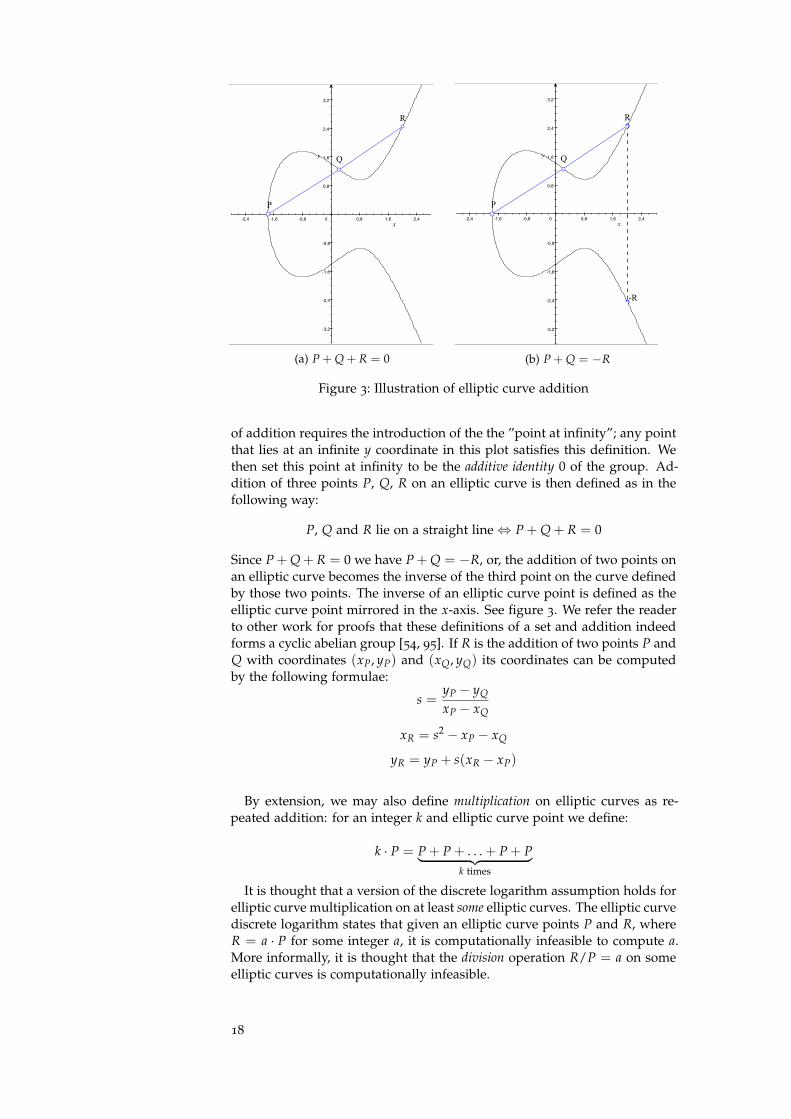

Figure 3: Illustration of elliptic curve addition

of addition requires the introduction of the the ”point at infinity”; any pointthat lies at an infinite y coordinate in this plot satisfies this definition. Wethen set this point at infinity to be the additive identity 0 of the group. Ad-dition of three points P, Q, R on an elliptic curve is then defined as in thefollowing way:

P, Q and R lie on a straight line⇔ P + Q + R = 0

Since P + Q + R = 0 we have P + Q = −R, or, the addition of two points onan elliptic curve becomes the inverse of the third point on the curve definedby those two points. The inverse of an elliptic curve point is defined as theelliptic curve point mirrored in the x-axis. See figure 3. We refer the readerto other work for proofs that these definitions of a set and addition indeedforms a cyclic abelian group [54, 95]. If R is the addition of two points P andQ with coordinates (xP, yP) and (xQ, yQ) its coordinates can be computedby the following formulae:

s =yP − yQ

xP − xQ

xR = s2 − xP − xQ

yR = yP + s(xR − xP)

By extension, we may also define multiplication on elliptic curves as re-peated addition: for an integer k and elliptic curve point we define:

k · P = P + P + . . . + P + P︸ ︷︷ ︸k times

It is thought that a version of the discrete logarithm assumption holds forelliptic curve multiplication on at least some elliptic curves. The elliptic curvediscrete logarithm states that given an elliptic curve points P and R, whereR = a · P for some integer a, it is computationally infeasible to compute a.More informally, it is thought that the division operation R/P = a on someelliptic curves is computationally infeasible.

18

The name ”discrete logarithm problem” becomes somewhat of a mis-nomer when applied to elliptic curves since the operation thought to behard is not the taking of a discrete logarithm, but the division of curvepoints. The term is derived from the analagous discrete logarithm problemin groups of integers modulo n. This is because cryptosystems based on el-liptic curve arithmetic and those based on multiplicative arithmetic modulon are both varieties of the ElGamal cryptosystem [41]. Since the ElGamalcryptosystem was first described based on the hardness of the discrete log-arithm problem in integer groups, the same term is used for the divisionproblem in elliptic curve groups.

4.5 double spending prevention

We introduced the concept of double spending prevention in section ?? asa means to include identifying information to coins that is only revealedwhen a coin is spent twice. Identifying information satisfy the propertiesthat a single transaction does not reveal information about the coin or theuser, but that a double transaction using a single coin reveals the full identiyof the user. We show two methods to accomplish this here.

Double spending prevention in other payment systems is usually depen-dent on hardware security; the devices involved in payments are simplyincapable of copying coin information, and are extremely difficult to betampered with. Indeed, Chaum [33] originally proposed equipping pay-ment devices with so-called observers; hardware devices which guaranteedcopying would be prevented or would otherwise be noticeable by other par-ties. Since observers are not generally available in mobile devices, we willnot consider such solutions in this thesis.

4.5.1 The division method

This is the method used in several electronic cash proposals [48, 120] andwas originally proposed by Ferguson [44]. We assume a payment systemthat gives users a user identity u that is representable as a unique integer foreach user. Each coin signed by the bank is associated with a bank-verifiedcoin identity i during the withdrawal phase. The trick is to have a payer gen-erated coin spending message generation depend on some independentlycheckable variable, such as a timestamp τ. This timestamp is included withother transaction information using some cryptographic hash that maps ar-bitrary strings onto the integers H : {0, 1} → Z. This requires a user tocompute the double spending information c:

c = H(other information‖i‖τ)

Which is then sent to the payee, which can verify the timestamp andother information to be correct. Then, another variable r is introduced thatcouples this cut-and-choose information to a number u representing thespender’s identity.

r = i− cu

A pair of c and r values is included with every payment. Given twoseperate payments to process, the bank obtains two sets of values {c1, r1}and {c2, r2}. Because both c1 and c2 are dependent on the cryptographichash of the timestamp the payment was made, these two sets are distinct

19

values with overhelming probability. However, both payments include thesame coin information i. Therefore, we can now compute

r1 − r2

c2 − c1=

(i− c1u)− (i− c2u)c2 − c1

=c2u− c1u

c2 − c1= u

to reveal the identity of a double spending user.

4.5.2 Cut-and-choose

A method named cut-and-choose was used in the original e-cash paper [36]for double spending detection. We present a simplified version here. A largenumber k is defined as well as a cryptographic hash function H : Z → Z

with a large output length. The integer u uniquely identifies each user ofthe system. Upon withdrawal, the payer sends the bank a signed array ofcontaining the hashes of random values a1, a2, ..., ak ∈ Z.

c = Sigskpayer (H(a1),H(a2), . . . ,H(ak))

The bank stores c. During a payment, the payee sends the payer k randomlychosen bits. For each of the k bits sent, the payer sends the following infor-mation to the payee.

c′ =

⟨{a1 z1 = 0a1 ⊕ u z1 = 1

,

{a2 z2 = 0a2 ⊕ u z2 = 1

, . . . ,

{ak zk = 0ak ⊕ u zk = 1

⟩

The payee verifies the correctness of this information, and eventually sendsit to the bank. If k is large enough, there is a large chance that the bank endsup with a pair of ai and ai ⊕ u, from which it can extract the user u. Thebank then has a signature on the hash of this value, proving that u has usedthe coin twice.

It should be noted that this method carries potentially prohibitive limita-tions with it in practice. k has to be chosen large enough to guarantee thatthe bank ends up with a pair of complementary values in this hash and krandom numbers need to be generated and stored by the bank. This createsa considerable amount of data for any coin withdrawn in the system, whichneeds to be stored on the server or by the user for every coin in his/herwallet.

4.6 blind signatures

Blind signatures are a concept that allows some authority to sign messages,without that authority obtaining any information about the message thatneeds to be signed. As described above, we use blind signatures to have thetrusted third party sign coins to be valid, without giving the authority theability to sign these messages. Blind signatures were introduced by DavidChaum in 1982 in the context of digital payments [32]. His example of blindsignatures using the RSA signature scheme is discussed here.

Suppose the bank is in possession of an RSA private key d and the payeris in possession of the corresponding public key e and the product d · e = N.Further, the payer has generated a coin transfer message C, which the payerwants to have signed by the bank. First, the payer generates the number rwhich we call the blinding factor. r must be chosen to be relatively primeto N. The payer then generates a different message C′ by computing C′ ≡

20

C · re(modN) which he/she then sends to the bank. We call C′ the blindedmessage.

The bank then signs the blinded message using the usual RSA signaturescheme, generating a blind signature s′ ≡ (C′)d(mod N) and returns this tothe payer. Now note that s′ is the result of a permutation of the originalmessage; it is a reversible operation. From the blind signature, the payee canobtain the normal signature s ≡ s′ · r−1 (mod N). Since s ≡ C (mod N) wehave a valid signature for the message C while the bank has no informationabout the actual coin that is to be spent.

Blind signatures have been extended to digital signatures based on ID-based cryptography based on the Weil pairing and elliptic curve cryptogra-phy [124].

4.7 fair blind signatures

Blind signatures were conceived by Chaum [32] in the original propositionfor digital cash. Although many works still use blind signatures in theoriginal way, practical implications of blind signatures could cause manyproblems for a real-world money system. Money, digital or not, is inherentlysubject in many illegal transactions and crime. Current cash systems can beconsidered untraceable, since no additional party is involved when cash isexchanged. Nonetheless, authorities and banks can provide some insightwhen criminal activities end up requiring the use of bank services in thecase of money withdrawal or deposit. Blind signatures effectively removethe banks’ (and authorities’) insight for this business.

This problem was first presented in a paper by von Solms and Naccache[118]. The authors show how the perfect anonymity of blind signatureswould have hypothetically prevented law enforcement to capture a criminalin the example of a Japanese kidnapping case. The perpetrator had max-imized his anonymity as much as was possible, but still had to physicallywithdraw money from the bank account he had set up to receive the ransommoney. The perpetrator’s identity was revealed by security cameras regis-tering his withdrawal from the flagged bank account at an ATM. Shouldthe victim have had access to banking services that dealed with digital cashusing blind signatures, the money in his account would be fully untraceableto anyone, and his identity would have remained secret. It is reasonable tofear that should such a fully untraceable payment system be widely avail-able, it would enable (and therefore motivate) many criminal activities thatare otherwise not undertaken because of the larger risks involved.

We therefore conclude that a further requirement for a payment system isthe ability to selectively reveal the identities of payers in the system2. Sincea protocol between both parties cannot be both anonymous and optionallytraceable, a mutually trusted third party called a judge is introduced into thepayment system [113]. The judge and bank can then run an additional pro-tocol, the link detection protocol, that ties transactions to identities. The termfor generating blind signatures using this trusted mutual party is called fairblind signatures. Different requirement sets exist for what features a protocollike this should implement [113]. Stadler et al. [113] and Davida et al. [37]distinguish two tracing types that may be provided by fair blind signatureschemes.

2 Note that we deviate from the conceptual protocols introduced in chapter 2 here.

21

• Type I: Coin tracing The judge provides the bank with information toefficiently recognize a coin once it is spent. This allows authorities torecognize the target of a transaction.

• Type II: Owner tracing The judge provides the bank with informationto efficiently find the identity of a coin owner. This allows authori-ties to recognize who withdrew a certain piece of cash from his/heraccount.

Both of these types provide different services which can address differentrequirements in a payment protocol.

Fair blind signatures build upon standard blind signatures, and encodeadditional information to allow a judge to mediate tracking of money spent.Many proposals exist for cryptographic constructs in fair blind signatures.We explain here the original proposal for fair blind signatures [23, 113];further protocols that employ fair blind signatures can be found in section6.

4.7.1 Stadler et al.’s protocol

This scheme is a derivative of Chaum’s original protocol. The followingsystem parameters are chosen: G is a multiplicative group of prime orderq for which it is hard to compute discrete logarithms; a publicly knownelement g ∈ G; y = gx, with y and x being the bank’s public and privatekeys respectively; a function Sigj which represents the judge’s signaturescheme, and a function H, a cryptographically secure hash.

A payer registers with the judge to obtain two identities in the followingway.

1. The payer sends the judge a registration request

2. The judge chooses a random A ∈ G and α ∈ Zq, and computes A′ =Aα. A and A′ represent the two payer’s identities, and the judge storesboth. The judge sends two messages 〈A, Sigj(A||0)〉, 〈α, Sigj(A||1)〉 tothe payer.

3. The payer computes A′ = Aα

The payer then has the bank sign his/her coins blindly by performing thefollowing protocol.

1. The payer sends the bank A, Sigj(A||0).

2. The bank verifies the signature and computes z = Ax and sends theresult to the payer.

3. The payer computes z′ = zα.

4. The bank chooses some r ∈ Zq and computes t1 = gr, t2 = Ar, both ofwhich are sent to the payer.

5. The payer chooses random β, γ ∈ Zq. With this, he/she computes

the following. t′1 = tβ1 gγ; t′2 = tα

2 A′γ; the hash c′ = H(m||A′||z′||t′1||t′2)where m is a coin message. The payer finally computes the blindedcoin c ≡ β/c′ (mod q) and sends it to the bank.

6. The bank computes the signature s ≡ r + cx (mod q) and returns it tothe payer.

22

7. The payer obtains the signed coin s′ ≡ βs + γ (mod q)

The resulting signature is the tuple 〈A′, Sigj(A′||1), z′, t′1, t′2, s′〉 of which thevalidity can be verified with the judge’s public key on Sigj(A′||1) , and theequivalences gs = t′1yc′ and A′s

′= t′2z′c

′. The coupling of identities for A

and A′ by the judge to the bank is sufficient for revealing the identity of thesigner of coins.

4.7.2 Passive judge protocols

A downside of Stadler et al.’s protocol is that the introduction of a judge inthe withdrawal protocol is unpractical. Schemes were found that omittedthe judge’s involvement in the withdrawal process, and made the judge apassive actor, which only needs to be contacted afterwards. Here we presenttwo ways to achieve fair blind signatures on electronic cash with a passivejudge.

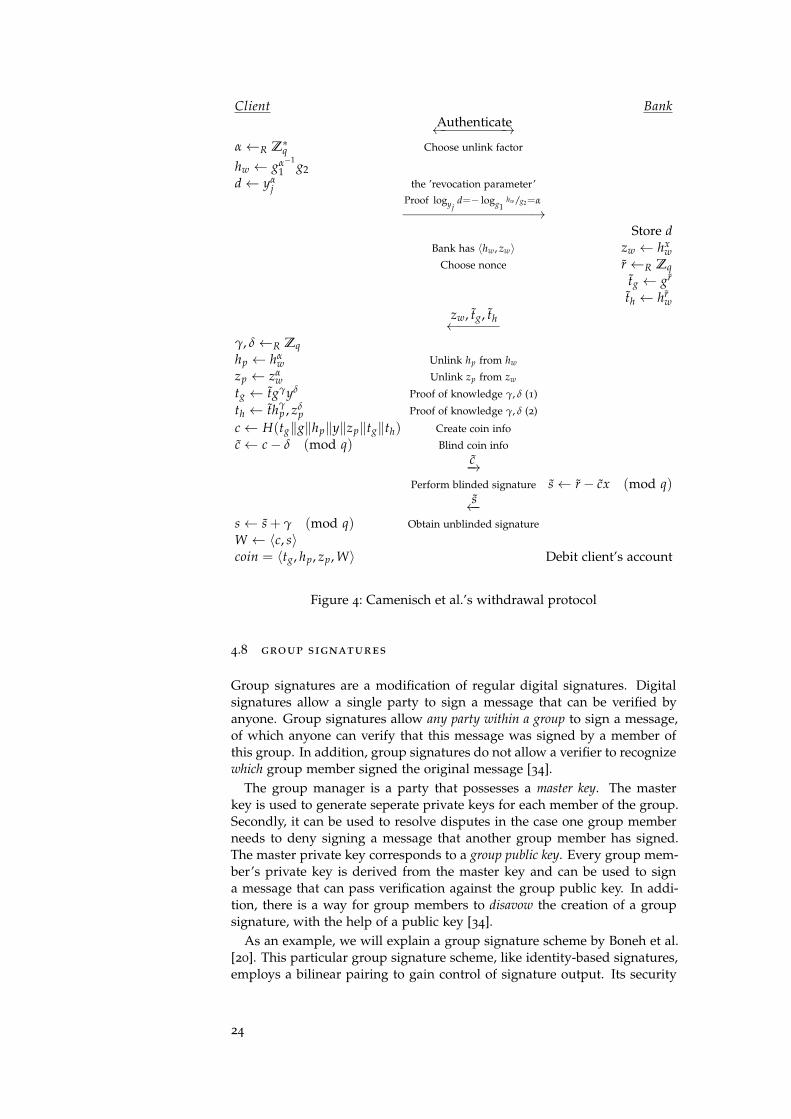

Camenish et al.’s withdrawal

The first such proposal came from Frankel et al. [45]. A passive judge sys-tem was independently introduced by Camenisch et al. [24]. The core ideaof their proposal is to have three components associated with coins: a pairof group members 〈hp, zp〉; a proof W that this pair is related by zp = hx

pwith x the bank’s signing key; a second proof V that anonymity revocationis possible. The proof W is computed blindly by the bank: it is computed ona different pair 〈hw, zw〉 and transformed by the client in the appropriate pair.The proof V is computed entirely by the client. The judge is granted the ca-pability to link the pairs 〈hp, zp〉 and 〈hw, zw〉, thus revoking coin anonymity.

Let G be a cyclic group of prime order q with three elements g, g1, g2 ∈ G.Let H be a cryptographic hash function that maps arbitrary strings onto ele-ments of G. The bank chooses a secret x ∈ Z∗q , computes the correspondingpublic key y = gx, and publishes all parameters but its secret key. The judgechooses a secret key j ∈ Z∗q and publishes public key yj = gj

2. The client andbank then run the protocol shown in figure 4 to create two unlinked pairs〈hp, zp〉 and 〈hw, zw〉.

Given a coin 〈tg, hp, zp, W〉, the judge can trace the original revocationparameter d by computing

(hp/g1)j = gα·j = d

which the bank has stored during coin generation, revealing the originalwithdrawer of the coin. The judge performs coin tracing by, given a revoca-tion parameter d, computing

g1dj−1= g1gα

2 = hp

which reveals the coin generated in the withdrawal associated with d.With each payment, the client associates a proof V that shows hp = g1gα

2 .Since each coin is associated with the value tg = gk (where k ≡ r · γ · δ · x(mod q)), the payee can request a value l ≡ k− cα (mod q) from the payer,where c is an integer based on a unique value like a timestamp or a counter.If the bank obtains two distinct pairs 〈l, c〉, 〈l′, c′〉 for the same coin he cancompute α ≡ l − l′/c′ − c (mod q) and compute the revocation parameter d =yα

j .An example of a passive judge as in Camenisch et al.’s fair blind signature

method is found in the protocol by Gaud and Traore [48].

23

Client BankAuthenticate←−−−−−−−−→

α←R Z∗q Choose unlink factor

hw ← gα−1

1 g2d← yα

j the ’revocation parameter’Proof logyj

d=− logg1hw/g2=α

−−−−−−−−−−−−−−−−→Store d

Bank has 〈hw, zw〉 zw ← hxw

Choose nonce r ←R Zqtg ← gr

th ← hrw

zw, tg, th←−−−−−γ, δ←R Zqhp ← hα

w Unlink hp from hw

zp ← zαw Unlink zp from zw

tg ← tgγyδ Proof of knowledge γ, δ (1)

th ← thγp , zδ

p Proof of knowledge γ, δ (2)

c← H(tg‖g‖hp‖y‖zp‖tg‖th) Create coin info

c← c− δ (mod q) Blind coin infoc−→

Perform blinded signature s← r− cx (mod q)s←−

s← s + γ (mod q) Obtain unblinded signature

W ← 〈c, s〉coin = 〈tg, hp, zp, W〉 Debit client’s account

Figure 4: Camenisch et al.’s withdrawal protocol

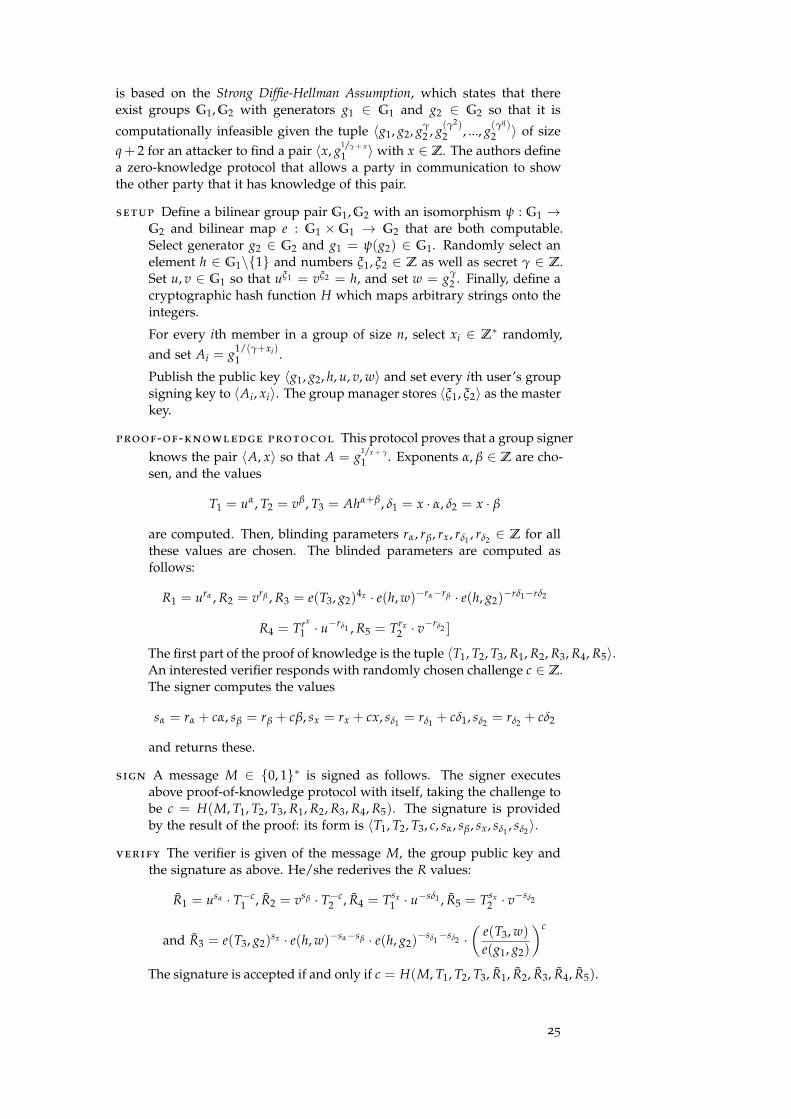

4.8 group signatures

Group signatures are a modification of regular digital signatures. Digitalsignatures allow a single party to sign a message that can be verified byanyone. Group signatures allow any party within a group to sign a message,of which anyone can verify that this message was signed by a member ofthis group. In addition, group signatures do not allow a verifier to recognizewhich group member signed the original message [34].

The group manager is a party that possesses a master key. The masterkey is used to generate seperate private keys for each member of the group.Secondly, it can be used to resolve disputes in the case one group memberneeds to deny signing a message that another group member has signed.The master private key corresponds to a group public key. Every group mem-ber’s private key is derived from the master key and can be used to signa message that can pass verification against the group public key. In addi-tion, there is a way for group members to disavow the creation of a groupsignature, with the help of a public key [34].

As an example, we will explain a group signature scheme by Boneh et al.[20]. This particular group signature scheme, like identity-based signatures,employs a bilinear pairing to gain control of signature output. Its security

24

is based on the Strong Diffie-Hellman Assumption, which states that thereexist groups G1, G2 with generators g1 ∈ G1 and g2 ∈ G2 so that it is

computationally infeasible given the tuple 〈g1, g2, gγ2 , g(γ

2)2 , ..., g(γ

q)2 〉 of size

q + 2 for an attacker to find a pair 〈x, g1/γ + x1 〉 with x ∈ Z. The authors define

a zero-knowledge protocol that allows a party in communication to showthe other party that it has knowledge of this pair.

setup Define a bilinear group pair G1, G2 with an isomorphism ψ : G1 →G2 and bilinear map e : G1 × G1 → G2 that are both computable.Select generator g2 ∈ G2 and g1 = ψ(g2) ∈ G1. Randomly select anelement h ∈ G1\{1} and numbers ξ1, ξ2 ∈ Z as well as secret γ ∈ Z.Set u, v ∈ G1 so that uξ1 = vξ2 = h, and set w = gγ

2 . Finally, define acryptographic hash function H which maps arbitrary strings onto theintegers.

For every ith member in a group of size n, select xi ∈ Z∗ randomly,and set Ai = g1/(γ+xi)

1 .

Publish the public key 〈g1, g2, h, u, v, w〉 and set every ith user’s groupsigning key to 〈Ai, xi〉. The group manager stores 〈ξ1, ξ2〉 as the masterkey.

proof-of-knowledge protocol This protocol proves that a group signerknows the pair 〈A, x〉 so that A = g1/x + γ

1 . Exponents α, β ∈ Z are cho-sen, and the values

T1 = uα, T2 = vβ, T3 = Ahα+β, δ1 = x · α, δ2 = x · β

are computed. Then, blinding parameters rα, rβ, rx, rδ1 , rδ2 ∈ Z for allthese values are chosen. The blinded parameters are computed asfollows:

R1 = urα , R2 = vrβ , R3 = e(T3, g2)4x · e(h, w)−rα−rβ · e(h, g2)

−rδ1−rδ2

R4 = Trx

1 · u−rδ1 , R5 = Trx

2 · v−rδ2 ]

The first part of the proof of knowledge is the tuple 〈T1, T2, T3, R1, R2, R3, R4, R5〉.An interested verifier responds with randomly chosen challenge c ∈ Z.The signer computes the values

sα = rα + cα, sβ = rβ + cβ, sx = rx + cx, sδ1 = rδ1 + cδ1, sδ2 = rδ2 + cδ2

and returns these.

sign A message M ∈ {0, 1}∗ is signed as follows. The signer executesabove proof-of-knowledge protocol with itself, taking the challenge tobe c = H(M, T1, T2, T3, R1, R2, R3, R4, R5). The signature is providedby the result of the proof: its form is 〈T1, T2, T3, c, sα, sβ, sx, sδ1 , sδ2〉.

verify The verifier is given of the message M, the group public key andthe signature as above. He/she rederives the R values:

R1 = usα · T−c1 , R2 = vsβ · T−c

2 , R4 = Tsx1 · u

−sδ1 , R5 = Tsx2 · v

−sδ2

and R3 = e(T3, g2)sx · e(h, w)−sα−sβ · e(h, g2)

−sδ1−sδ2 ·

(e(T3, w)

e(g1, g2)

)c

The signature is accepted if and only if c = H(M, T1, T2, T3, R1, R2, R3, R4, R5).

25

disavowal The group manager can, given the group’s public key, the mas-ter key, a message and its signature, check which group member signedthe message. This makes use of the fact that the value T3 is a linearencryption of A, T1 and T2. If the signature is valid, the managercomputes Ai = T3/Tξ1

1 · Tξ22 to reveal the original signer.

A scheme to perform blinded group signatures was proposed by Maitlandand Boyd [81].

4.9 secret sharing

The technique of secret sharing was first proposed by Shamir [108] to dis-tribute a secret among multiple parties in such a way that no informationabout the secret is obtained unless a certain number of parties work together.More formally, a secret sharing scheme describes a method to distribute in-formation of a secret s into parts s1, s2, . . . , sk, . . . , sn with the properties that:

• If a party obtains less than k parts of the secret, this party obtains noinformation about the original secret.

• If a party obtains at least k parts of the secret, then this party canefficiently compute the original secret s.

A scheme in which k secret shares are shared among n parties, wherek ≤ n, is called a (k, n)-treshold secret sharing scheme.

Shamir originally proposed a secret sharing method based on polyno-mial interpolation. He observed that given the general polynomial formf (x) = a0 + a1 · x + a2 · x2 + . . . ak · xk one can find the value for every aiby performing regression analysis on k points on that polynomial3. There-fore, one can distribute a secret s by constructing a polynomial f (x) =s + a1 · x + a2 · x2 + . . . + ak · xk with a1 . . . ak are randomly chosen integers.Next, for every ith party to which a secret share is to be distributed, com-pute the point Si = (i, f (i)) on the polynomial, and send this secret share tothe party.

If at least k parties come together to compute the secret, they can usetheir k points on the polynomial to recompute the original polynomial co-efficients. One algorithm to reconstruct a polynomial from a set of pointis the Lagrange polynomial method, which is often suggested to efficientlyrecompute the original polynomial form [13].

4.9.1 The Chinese Remainder Theorem

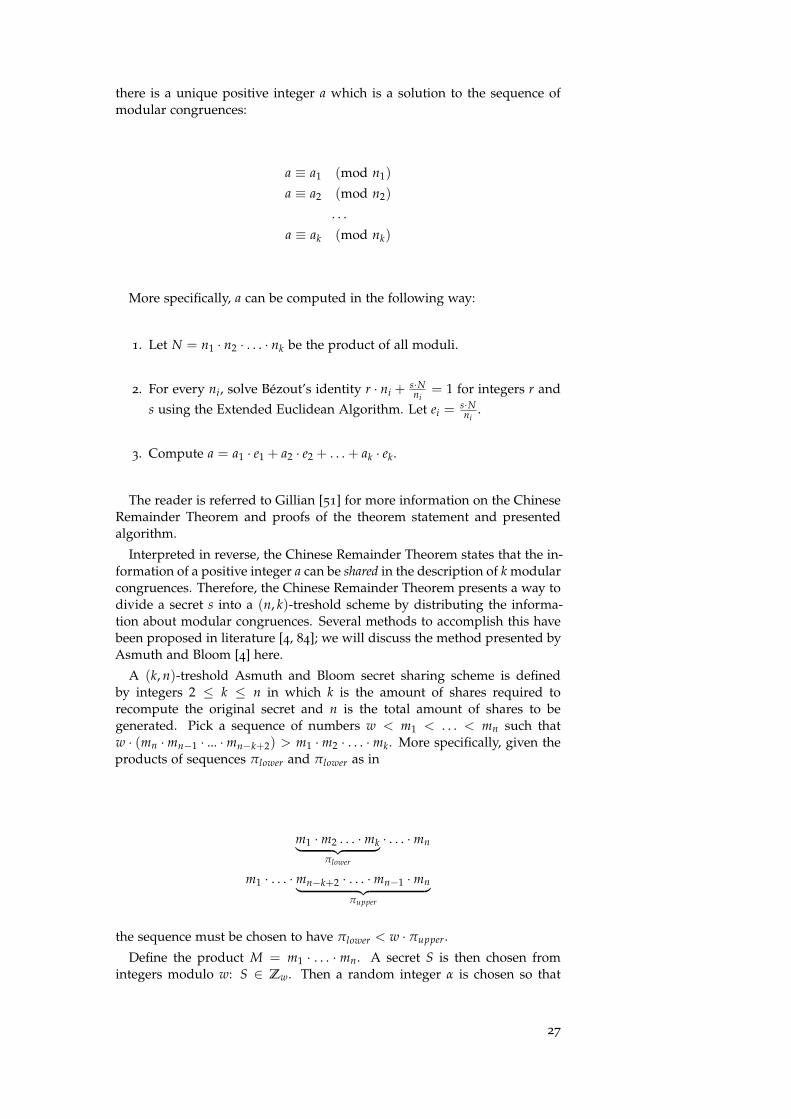

The Chinese Remainder Theorem states that given a sequence of modulin1, n2, . . . , nk which are pairwise coprime, and a sequence of integers a1, a2, . . . , ak,

3 Informally: two points are required to define a line; three points are required to define aparabola; four points are required to define a cubic curve; and so on for polynomials of higherdegree.

26

there is a unique positive integer a which is a solution to the sequence ofmodular congruences:

a ≡ a1 (mod n1)

a ≡ a2 (mod n2)

. . .

a ≡ ak (mod nk)

More specifically, a can be computed in the following way:

1. Let N = n1 · n2 · . . . · nk be the product of all moduli.

2. For every ni, solve Bezout’s identity r · ni +s·Nni

= 1 for integers r and

s using the Extended Euclidean Algorithm. Let ei =s·Nni

.

3. Compute a = a1 · e1 + a2 · e2 + . . . + ak · ek.

The reader is referred to Gillian [51] for more information on the ChineseRemainder Theorem and proofs of the theorem statement and presentedalgorithm.

Interpreted in reverse, the Chinese Remainder Theorem states that the in-formation of a positive integer a can be shared in the description of k modularcongruences. Therefore, the Chinese Remainder Theorem presents a way todivide a secret s into a (n, k)-treshold scheme by distributing the informa-tion about modular congruences. Several methods to accomplish this havebeen proposed in literature [4, 84]; we will discuss the method presented byAsmuth and Bloom [4] here.

A (k, n)-treshold Asmuth and Bloom secret sharing scheme is definedby integers 2 ≤ k ≤ n in which k is the amount of shares required torecompute the original secret and n is the total amount of shares to begenerated. Pick a sequence of numbers w < m1 < . . . < mn such thatw · (mn ·mn−1 · ... ·mn−k+2) > m1 ·m2 · . . . ·mk. More specifically, given theproducts of sequences πlower and πlower as in

m1 ·m2 . . . ·mk︸ ︷︷ ︸πlower

· . . . ·mn

m1 · . . . ·mn−k+2 · . . . ·mn−1 ·mn︸ ︷︷ ︸πupper

the sequence must be chosen to have πlower < w · πupper.

Define the product M = m1 · . . . · mn. A secret S is then chosen fromintegers modulo w: S ∈ Zw. Then a random integer α is chosen so that

27

S + α · w > M. Let x = S + α · w and compute the sequence s1, . . . , sk usingthe following system of congruences:

x ≡ s1 (mod m1)

x ≡ s2 (mod m2)

. . .

x ≡ sk (mod mk)

The secret shares are the tuples 〈s1, m1〉, . . . , 〈sk, mk〉. The value w is pub-lished and known to all parties. Using all pairs of tuples, one can use theChinese Remainder Theorem to compute x. Finally, the secret is obtainedby finding S ≡ x (mod w).

28

5

M O B I L E S E C U R I T Y C O N S I D E R AT I O N S

The previous chapters have discussed the cryptography of digital paymentprotocols. We instead focus our efforts at the circumstances a mobile plat-form presents. We address questions about connectivity, authentication,storage and other factors that are relevant for the mobile context.

5.1 offline authentication

During mobile payments, both payer and payee authenticate mutually beforeestablishing a secure channel over which to transfer money. The authentica-tion is a necessity because to assure both parties that their transaction occursbetween the intended parties, and not an intruder or an impostor.

Although subsequent improvements in infrastructure and cellular net-work technology have significantly raised availability, internet connectivityon mobile devices is subject to location (crowded or rural areas, indoors),vulnerable equipment and many other unpredictable circumstances. In ad-dition, a payment system building a reliability on an internet connection tiesa payment’s system context too strictly to devices with internet connectionsand prohibits other point-of-sale devices from functioning as a payee. Fora payment system to function reliably and scale better, authentication mustnot require an internet connection and work offline instead.

Public key cryptography is most often employed for authentication. Anexample is the Schnorr [107] identification scheme, which performs authen-tication by proving to the other party the possession of some private keycorresponding to a previously interchanged public key. The interchangeand authentication of this public key for identification is the crucial prop-erty of any authentication system. In online systems, this key is placed insome public directory, or, certificated by a set of predetermined and prede-ployed certificate authorities [70]. In an offline system, users themselves areresponsible for authentication of the public key.

This section describes two methods to accomplish this; the first is out-of-band band authentication of mutually shared secrets; the second is identity-based cryptography.

5.1.1 Out-of-band authentication methods

Out-of-band authentication is an authentication mechanism that uses availablecommunication methods outside of the channel that needs to be authenti-cated [9]. In the mobile context, users set up their secure channel in proxim-ity with one another. They can therefore reveal additional information aboutthe internal state of the cryptography by inspecting one another’s screen.When the authentication method specifically requires human interaction forapproval, this method has been named manual authentication [49].

29

For example, suppose that two users perform a key exchange using theDiffie-Hellman protocol [40]. The result is a mutually shared secret, butbased on channel communication alone, the authors cannot verify whetherthe communication was subject to man-in-the-middle attack by which anadversary has placed him/herself in the middle of the key exchange andacts as a proxy of the communication. To lift this uncertainty, mobile deviceusers can simply manually confirm whether they have agreed to the samekey. This model was proposed by Laur and Nyberg [73] and proven securein the context of the Bluetooth pairing protocol.

Bluetooth pairing requires users to enter the same PIN code on both de-vices intended to be paired [17]. Older versions of the Bluetooth pairingprotocol derived all key entropy from the entered 4-digit PIN code, andare not considered secure. This is despite the fact that formal verificationrevealed that the protocol is reasonably secure [31]. The Bluetooth specifica-tion has since then been updated to proceed with pairing using ephemeralkeys exchanged using the Diffie-Hellman protocol, which is optionally au-thenticated using a variety of methods:

• Numeric comparison: both devices display a six-digit numeric code,which has to be confirmed

• Passkey entry: the user manually enters a numberic code on both orone of the two devices to complete key exchange

• Out-of-band: another communication channel like NFC is used to con-firm the key that is exchanged over the Bluetooth channel

The usability of several of out-of-band authentication methods was in-vestigated by Kainda et al. [64] and Kumar et al. [72]. Both authors notethat security failures are a problem when it comes to authentication methodswhere the user simply needs to confirm a value. Security failures occurwhen a user erroneously rejects an agreed upon value. Kumar et al. con-clude that comparison of numeric values combines high user preferencewith a low amount of security errors, which is confirmed by Kainda et al..Both authors also looked at more exotic ways of data agreement, such asvisual comparison of images by the user (which had a larger amount of se-curity errors) as well as using microphone and camera sensors for the extrachannels (which had low user preference).

5.1.2 Secret exchange mechanisms

Having established an out-of-band method to confirm a shared secret, webriefly describe three methods that are suitable for sharing such a secret andcreating an authenticated channel.

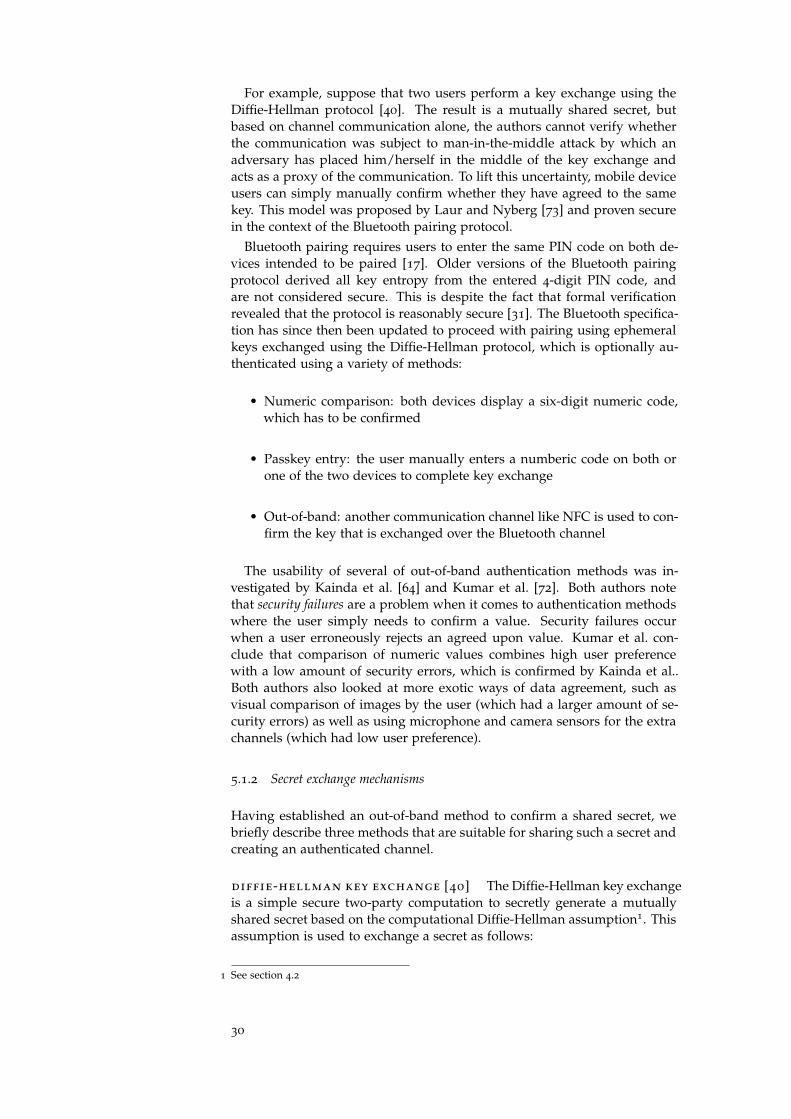

diffie-hellman key exchange [40] The Diffie-Hellman key exchangeis a simple secure two-party computation to secretly generate a mutuallyshared secret based on the computational Diffie-Hellman assumption1. Thisassumption is used to exchange a secret as follows:

1 See section 4.2

30

Alice Bobchoose prime q,G of order q, g ∈ G

a←R Zqq, G, g, A = ga−−−−−−−−−−→

b←R Zq

B = gb←−−−−−

s← Ba = (gb)a = gab s← Ab = (ga)b = gab

Where ← denotes assignment, and ←R denotes a random choice. Afterthe key is established, it can be used to symmetrically encrypt subsequentcommunication. Each encrypted subsequent message is implicitly authenti-cated with the knowledge that only both parties possess knowledge of thekey.

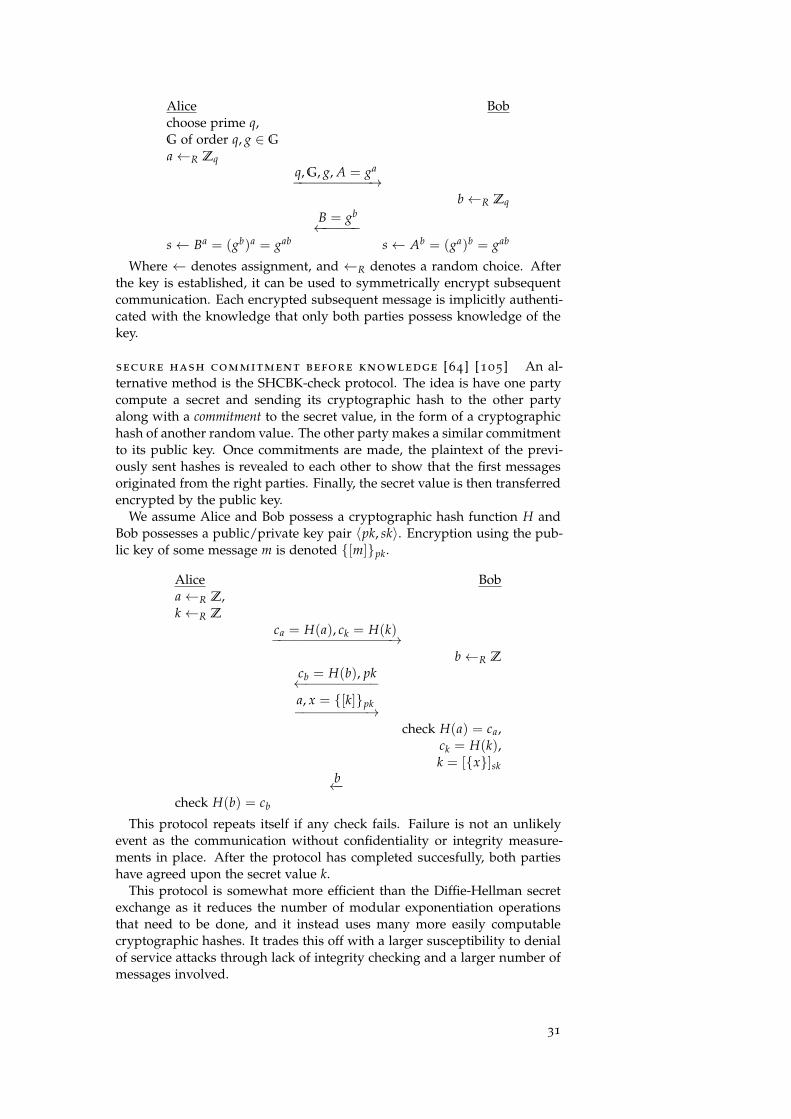

secure hash commitment before knowledge [64] [105] An al-ternative method is the SHCBK-check protocol. The idea is have one partycompute a secret and sending its cryptographic hash to the other partyalong with a commitment to the secret value, in the form of a cryptographichash of another random value. The other party makes a similar commitmentto its public key. Once commitments are made, the plaintext of the previ-ously sent hashes is revealed to each other to show that the first messagesoriginated from the right parties. Finally, the secret value is then transferredencrypted by the public key.

We assume Alice and Bob possess a cryptographic hash function H andBob possesses a public/private key pair 〈pk, sk〉. Encryption using the pub-lic key of some message m is denoted {[m]}pk.

Alice Boba←R Z,k←R Z

ca = H(a), ck = H(k)−−−−−−−−−−−−−−−→

b←R Z

cb = H(b), pk←−−−−−−−−−a, x = {[k]}pk−−−−−−−−−→

check H(a) = ca,ck = H(k),k = [{x}]sk

b←−check H(b) = cb

This protocol repeats itself if any check fails. Failure is not an unlikelyevent as the communication without confidentiality or integrity measure-ments in place. After the protocol has completed succesfully, both partieshave agreed upon the secret value k.

This protocol is somewhat more efficient than the Diffie-Hellman secretexchange as it reduces the number of modular exponentiation operationsthat need to be done, and it instead uses many more easily computablecryptographic hashes. It trades this off with a larger susceptibility to denialof service attacks through lack of integrity checking and a larger number ofmessages involved.

31

9.

The scheme works with 100% ASK only and it is not part of the ISO standard on NFC. The idea is that both devices, say Device A and Device B, send random data at the same time. In a setup phase the two devices synchronize on the exact timing of the bits and also on the amplitudes and phases of the RF signal. This is possible as devices can send and receive at the same time. After that synchronisation, A and B are able to send at exactly the same time with exactly the same amplitudes and phases.While sending random bits of 0 or 1, each device also listens to the RF field. When both devices send a zero, the sum signal is zero and an attacker, who is listening, would know that both devices sent a zero. This does not help. The same thing happens when both, A and B, send a one. The sum is the double RF signal and an attacker knows that both de-vices sent a one. It gets interesting once A sends a zero and B sends a one or vice versa. In this case both devices know what the other device has sent, because the devices know what they themselves have sent. However, an attacker only sees the sum RF signal and he cannot figure out which device sent the zero and which device sent the one. This idea is illustrated in Figure 2. The top graph shows the signals produced by A in red and by B in blue. A sends the four bits: 0, 0, 1, and 1. B sends the four bits: 0, 1, 0, and 1. The lower graph shows the sum signal as seen by an attacker. It shows that for the bit com-binations (A sends 0, B sends 1) and (A sends 1, B sends 0) the result for the attacker is absolutely the same and the attacker cannot distinguish these two cases.

Figure 2 NFC specific Key Agreement

0 1 2 3 4 5 6 7 8-2

-1

0

1

2Total Signal seen on RF field

0 1 2 3 4 5 6 7 8-3

-2

-1

0

1Send: 0/0, 0/1, 1/0 1/1 : Signal A/B

The two devices now discard all bits, where both devices sent the same value and collect all bits, where the two devices sent different values. They can either collect the bits sent by A or by B. This must be agreed on start-up, but it doesn’t matter. This way A and B can agree on an arbitrary long shared secret. A new bit is generated with a prob-ability of 50%. Thus, the generation of a 128 bit shared secret would need approximate-

Figure 5: An illustration of how interference creates an unintelligible signalfor an external observer. From Haselsteiner and Breitfuß [57]

.

radio secrets [57] Haselsteiner and Breitfuß proposed to use char-acteristics of NFC radio communication to generate a secret. Both radio-equipped parties send out a string of random bits at the same time. Thisresults in a channel collision; for an observer, the radiowaves of both signalscombine and appear to become random noise. Both parties know the orig-inal signal they sent, however, and can substract their own signal from therandom noise that was observed on the channel. Since both parties knowwhat the other party has sent, they can combine this data to a shared secretonly they know, and use this as a shared secret. See figure 5 for an illus-tration. Conceptually, this is similar to the Diffie-Hellman secret exchange.The difference is that this relies on a hardware trapdoor function instead ofmodular exponentiation.

5.1.3 Identity-based cryptography

Shamir [109] introduced the idea of identity-based (ID-based) cryptographyin 1984 to show a different approach to solve this problem. Whereas thepublic key in traditional public key cryptography the public key is an arbi-trary looking consequence of cryptographic operations on random numbers,he suggested a scheme in which the public key was chosen. The public keymay then be chosen to represent identifying information, such as a user’sname, bank account number or other properties which can convince anotherparty of authenticity. Anyone wanting to authenticate this public key canuse the information contained in it and check if this information matchesthe person claiming this public key is his or hers. Subsequently, the verifiercan be convinced that signatures that verify against this identifying stringare in fact signed by the proper private key.

One of the first practical ID-based signature schemes was introduced byBoneh and Franklin in 2001 [19]. It is based on the Weil pairing of ellipticcurves, and performs as fast as traditional signature schemes based on the

32

digital logarithm. The key difference between this scheme and traditionalschemes is that here the desired public key is an input of the key genera-tion algorithm, as opposed to the pseudorandom result of a key generationalgorithm.

The Boneh-Franklin scheme extends the regular discrete logarithm prob-lem to be able to solve this problem. Let G1 and G2 be two groups of orderp with p a large prime and a map f : G1 × G1 → G2 with the followingproperties:

bilinear For all elements P, Q ∈ G1 and all integers a, b ∈ Z it holds thatf (aP, bQ) = f (P, Q)ab.

non-degenerative f does not map all pairs in G1×G1 onto the identityof G2.

computable Computing the result of f (P, Q) can be done quickly for anyP, Q ∈ G1.

The mapping f satisfying these properties is called an admissable map. TheWeil pairing of elliptic curvers is used as the example for such an admiss-able map by Boneh and Franklin. They show that a mapping satisfyingthese properties can be used to build an identity-based cryptosystem in thefollowing way.

setup

1. Choose a large prime p, two groups G1, G2 of order p, and anadmissable bilinear map f of the two groups as described beforeand a generator P ∈ G1.