Embed Size (px)

Citation preview

See important disclosures, including any required research certifications, beginning on page 73

■ What's new Since September 2012 the government has introduced four key reforms (that aim to address the issues of fuel availability and the weak financials of the state utilities) in an effort to revive the power sector. While it will take time to assess the full implications, it is clear that the early beneficiaries of the reforms will be the asset owners. However, the resolution of the more complex issues faced by the independent power producers (IPP) remains a work in progress, with an uncertain timeline. ■ What's the impact As a result of the ongoing reform process, dispatches from Coal India (CIL) rose by 8% YoY for 9M FY13 (following flat growth over FY10-12), environment and forest approvals have been expedited, and a consensus has been reached between CIL and the power utilities on the signing of fuel-supply agreements (FSA) on the guaranteed levels of coal supplies to power plants. Meanwhile, the improving financial situation at the state utilities as a result of regular tariff hikes, the ability of most state regulators to

pass on fuel and power purchase costs in the form of higher tariffs, and the government’s approval of a restructuring plan, should help resolve the key hurdles faced by the power sector in terms of fuel supply and receivables. In our view, the early beneficiaries of these reforms will be NTPC and CIL. For the IPPs, each asset has a different business model, and each faces issues either with domestic coal availability or the high costs of imported coal that cannot be passed through in tariffs. Until it becomes clear that these areas will be reformed, we are less sanguine on the outlook for the IPPs, such as Adani Power and Reliance Power. The power sector has been a key driver of order flow to the capital goods companies in the past. However, given the cyclical and structural issues faced by the sector at present, we see limited orders from the power sector at this time. With orders under the 12th Five Year Plan (FYP) complete and domestic power-equipment manufacturing capacity due to increase from 10GW in FY08 to 33GW by FY14, we expect competition to remain intense over FY14-15. We forecast annual orders of only 10-12GW over the period, and so are not yet buyers of Bharat Heavy Electricals (BHEL). We expect an upturn in the capex cycle this time to be led by new drivers – such as: 1) surface transport (railways, the dedicated freight corridor [DFC], and the

development of metro lines), 2) the New Urea Investment Policy, which could drive 10m tpa/INR400bn of capex in the fertiliser segment – which are benefitting from positive government policy changes. Well-diversified players such as Larsen & Toubro (L&T) should benefit from a revival in the capex cycle. ■ What we recommend We are upgrading our rating for NTPC to Buy (1) from Outperform (2) as the current FY14E PBR of 1.4x (an eight-year low) looks attractive. CIL is our top pick given the recent share-price underperformance on the back of various concerns, which we believe are overstated. We also upgrade L&T to Buy from Outperform (2) as, following the share-price drop of 8% over the past three months, the stock is trading at a 30% discount to its average PER over the past seven years.

18 March 2013

Cutting through the noise

• Initial reforms in the power sector should benefit asset owners first; resolution of issues faced by private utilities will take time

• Power-equipment players likely to see few orders for next two years; investment cycle should be led by new drivers

• Our top picks: NTPC, Coal India, and L&T, as they should be the early beneficiaries of reforms and a revival in the capex cycle

India Power Utilities & Capital Goods Sectors

Key stock calls

Source: Daiwa forecasts.

Industrials and Utilities / India

Saurabh Mehta(91) 22 6622 1009

New Prev.Coal India (COAL IN)Rating Buy BuyTarget 423.00 423.00Upside 32.2%

NTPC (NTPC IN)Rating Buy OutperformTarget 178.00 178.00Upside 22%

Larsen & Toubro (LT IN)Rating Buy OutperformTarget 1,830.00 1,780.00Upside 21.5%

Bharat Heavy Electricals (BHEL IN)Rating Underperform UnderperformTarget 184.00 192.00Downside 7.1%

India Power Utilities & Capital Goods Sectors 18 March 2013

- 2 -

Source: Daiwa forecasts

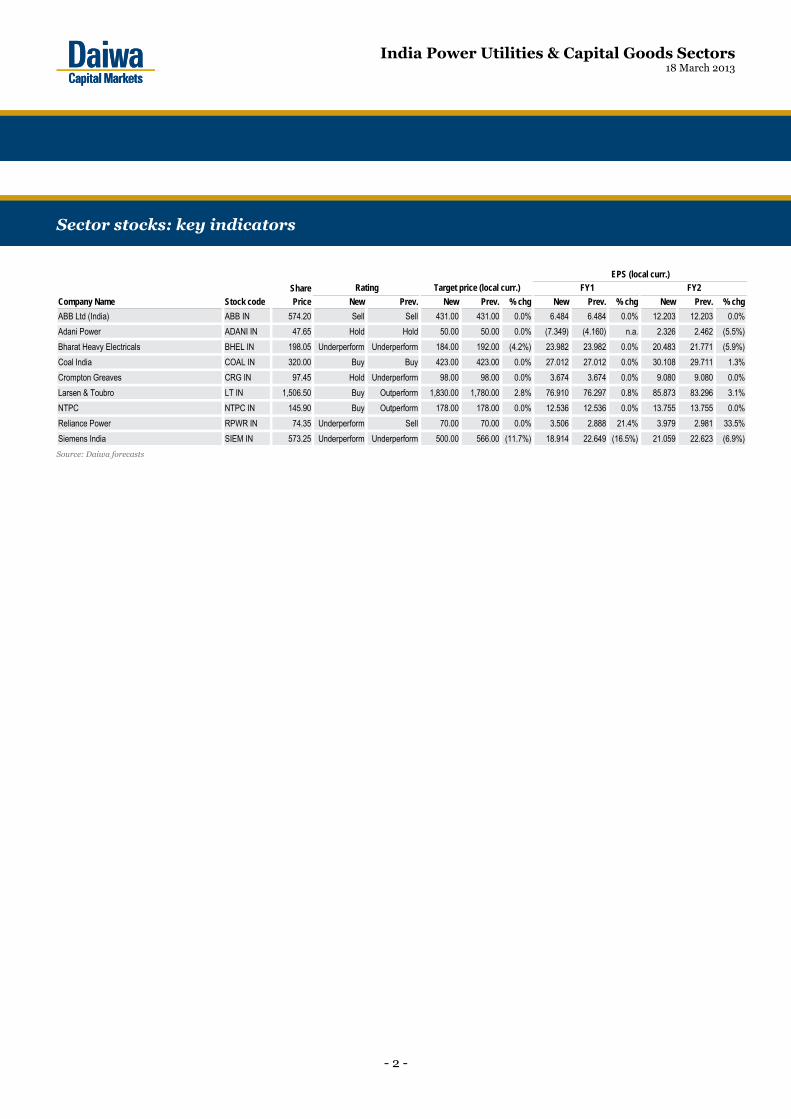

Sector stocks: key indicators

Share

Company Name Stock code Price New Prev. New Prev. % chg New Prev. % chg New Prev. % chg

ABB Ltd (India) ABB IN 574.20 Sell Sell 431.00 431.00 0.0% 6.484 6.484 0.0% 12.203 12.203 0.0%

Adani Power ADANI IN 47.65 Hold Hold 50.00 50.00 0.0% (7.349) (4.160) n.a. 2.326 2.462 (5.5%)

Bharat Heavy Electricals BHEL IN 198.05 Underperform Underperform 184.00 192.00 (4.2%) 23.982 23.982 0.0% 20.483 21.771 (5.9%)

Coal India COAL IN 320.00 Buy Buy 423.00 423.00 0.0% 27.012 27.012 0.0% 30.108 29.711 1.3%

Crompton Greaves CRG IN 97.45 Hold Underperform 98.00 98.00 0.0% 3.674 3.674 0.0% 9.080 9.080 0.0%

Larsen & Toubro LT IN 1,506.50 Buy Outperform 1,830.00 1,780.00 2.8% 76.910 76.297 0.8% 85.873 83.296 3.1%

NTPC NTPC IN 145.90 Buy Outperform 178.00 178.00 0.0% 12.536 12.536 0.0% 13.755 13.755 0.0%

Reliance Power RPWR IN 74.35 Underperform Sell 70.00 70.00 0.0% 3.506 2.888 21.4% 3.979 2.981 33.5%

Siemens India SIEM IN 573.25 Underperform Underperform 500.00 566.00 (11.7%) 18.914 22.649 (16.5%) 21.059 22.623 (6.9%)

Rating Target price (local curr.) FY1

EPS (local curr.)

FY2

India Power Utilities & Capital Goods Sectors 18 March 2013

- 3 -

Cutting through the noise ........................................................................................................... 4

Executive summary .................................................................................................................. 4

Top picks .................................................................................................................................. 6

Least preferred .......................................................................................................................... 7

Partial reforms in 2003 have put power sector in the current difficult situation .................. 9

Reforms to address the fuel shortage ..................................................................................... 10

Reforms to address the weak financials of the SEBs .............................................................. 12

Difficult measures still in progress, with limited clarity on timeline ..................................... 13

Capital goods sector is highly dependent on the power sector for orders ............................. 16

Upturn in investment cycle should be led by new drivers ..................................................... 19

Company Section

Coal India ............................................................................................................................... 29

NTPC ...................................................................................................................................... 32

Larsen & Toubro ..................................................................................................................... 37

Bharat Heavy Electricals ........................................................................................................ 42

Crompton Greaves .................................................................................................................. 47

Adani Power ............................................................................................................................ 52

Reliance Power ........................................................................................................................ 57

Siemens India .......................................................................................................................... 61

ABB Ltd (India) ...................................................................................................................... 66

Contents

India Power Utilities & Capital Goods Sectors 18 March 2013

- 4 -

Cutting through the noise

Reforms have been implemented to resolve the issues in the power sector, but many are still pending, and have uncertain timelines.

Executive summary

Asset owners should benefit first Recent reforms. Over the past six months, the government has taken unprecedented steps to tackle some of the key hurdles faced by the power sector: Fuel supply: 1) introduced initiatives to boost coal volume, which resulted in the supply of coal from CIL rising by 8% YoY for 9M FY13 (following flat growth over FY10-12), and 2) expedited environment and forest approvals, and 3) pushed CIL to sign FSAs with power producers, which should see the guaranteed supply of coal to power plants at 65% for FY13, with this increasing to 80% for FY17. Improving the financial position of the state utilities: 1) the government initiated a financial restructuring plan (FRP) for the state electricity boards (SEB), which involves the restructuring of short-term debt, along with a plan to improve the SEBs’ operational performance, 2) it is encouraging the states to implement regular tariff hikes; since April 2012, 26 states have raised tariffs, and 3) fuel power purchase cost adjustment (FPPCA) mechanisms for tariffs have been introduced by most state regulators, removing the time lag between increases in power purchase and fuel costs and passing the rises through to end users. In our opinion, early beneficiaries of these reforms will be NTPC and CIL, which remain our preferred picks. Many reforms still pending. Despite the issues addressed so far, resolution of the more complex issues faced by the IPPs, such as coal pooling, the revision of tariffs under unviable power-purchasing agreements (PPAs), and the finalisation of standard bidding documents (SBDs), are at various stages of discussion.

For the IPPs, each asset has a different business model, and each faces issues either with domestic coal availability or the high costs of imported coal that cannot be passed through in tariffs. Until it becomes clear that these areas will be reformed, we are less sanguine on the outlook for the private utilities, such as Adani Power and Reliance Power. We see a limited recovery in power-equipment orders Equipment manufacturers. The power sector has been a key driver of India’s capex cycle in the past. However, given the cyclical and structural issues faced by the sector at present, we see limited orders for it at this time. With orders under the 12th FYP complete and a likely increase in domestic power-equipment manufacturing capacity from 10GW in FY08 to 33GW by FY14, we expect competition to remain intense over FY14-15, and forecast annual orders to be only 10-12GW over the period, and so are not yet buyers of BHEL. Early signs of a capex recovery Industrial capex has been affected by the challenging domestic macroeconomic environment. However, recent policy measures taken by the government to revive the investment cycle, such as: 1) encouraging and enabling large cash-rich public-sector utilities (PSUs) to go ahead with planned investments, 2) the setting up of the Cabinet Committee on Investment (CCI) to expedite big infrastructure projects of more than INR10bn, and 3) setting an investment allowance of 15% for capex of more than INR1bn (announced in the recent budget) – together with signs of interest rates peaking (the Reserve Bank of India cut the repo rate by 25bps in January 2013) –provide the environment for a recovery in capex. Our economist, forecasts a further 75bp rate cut for this year. New drivers of capex We expect capex to be driven by new drivers, such as: 1) surface transportation (there is a several-fold increase planned in railway capex in the 12th FYP, DFC, and the planned development of metro lines), and 2) the government’s New Urea Investment Policy (10m tpa/INR400bn of capex in the fertiliser segment) Overall, we expect the capex cycle to pick up over the next 6-12 months, starting with spending by the PSUs, later followed by a revival in capex in the private sector. L&T looks best-positioned to benefit from the upturn in the capex cycles of the railways, fertiliser, and infrastructure sectors.

India Power Utilities & Capital Goods Sectors 18 March 2013

- 5 -

India industrials and utilities: valuation matrix PER (x) EV/EBITDA (x) PBR (x) ROE (%)

Company Share price (INR) Target price (INR) Rating FY14E FY15E FY14E FY15E FY14E FY15E FY14E FY15E Industrials Larsen & Toubro 1,507 1,830 Buy 17.5 15.7 11.8 10.6 2.8 2.4 17.0 16.6 BHEL 198 184 Underperform 9.7 10.4 5.2 5.4 1.5 1.4 16.2 13.8 Crompton Greaves 97 98 Hold 10.7 9.1 6.0 5.0 1.5 1.3 14.7 15.4 Siemens 573 500 Underperform 27.2 21.3 15.2 11.4 4.1 3.6 15.7 17.8 ABB India 574 431 Sell 47.1 33.3 26.2 19.4 4.3 3.8 9.5 12.2 Utilities NTPC 146 178 Buy 10.6 9.8 8.7 7.9 1.4 1.3 13.7 13.6 Adani Power 48 50 Hold 20.5 8.7 9.3 6.3 2.1 1.7 10.9 21.7 Reliance Power 74 70 Underperform 18.7 14.4 20.7 14.3 1.1 1.0 5.8 7.1 Coal India 320 423 Buy 10.6 9.6 6.5 5.4 3.6 3.0 36.8 34.3

Source: Bloomberg, Daiwa forecasts

Note: Share prices as at 15 March 2013

India industrials and utilities: share-price performance

3M average traded Absolute performance (%) Relative performance (%) Mkt. cap (USDm) volume (USDm) 1 month 3 months 6 months 1 year 1 month 3 months 6 months 1 year

Industrials Larsen & Toubro 17,185 47 4 (8) 1 11 5 (9) (4) 1 BHEL 8,976 15 (3) (12) (3) (30) (3) (13) (9) (40) Crompton Greaves 1,159 6 (1) (13) (9) (33) (0) (13) (14) (43) Siemens 3,779 2 1 (16) (15) (29) 1 (16) (20) (38) ABB India 2,256 1 (5) (18) (23) (34) (5) (18) (28) (43) BSE Capital Goods 0 (11) (3) (7) 0 (11) (8) Utilities NTPC 22,284 19 (3) (4) (13) (19) (2) (5) (18) (29) Adani Power 2,107 4 (8) (23) 10 (37) (8) (23) 5 (47) Reliance Power 3,870 12 (5) (26) (9) (44) (5) (26) (14) (54) BSE Power (3) (10) (6) (22) (3) (10) (11) (32) Coal India 37,427 14 (9) (10) (16) (6) (8) (10) (22) (16) SENSEX (0) 1 5 10 - - - -

Source: Bloomberg, Daiwa

Note: Share prices as at 15 March 2013

India industrials and utilities: PER/PBR

PER (x) PBR (x) Company Min Max Average 1-year-forward Min Max Average 1-year-forward Industrials Larsen & Toubro 11.8 54.7 24.1 16.4 2.0 12.1 4.7 2.6 BHEL 8.6 44.9 18.5 9.7 1.5 11.2 4.8 1.5 Crompton Greaves 5.1 51.0 20.8 10.7 1.5 9.5 4.3 1.5 Siemens 9.2 68.0 34.1 25.0 2.0 15.2 7.6 3.7 ABB India 18.8 258.4 72.0 43.7 3.1 16.9 7.4 4.2 Utilities NTPC 10.9 27.4 16.1 11.0 1.4 4.0 2.2 1.4 Adani Power* - - 24.3 37.2 1.9 5.0 3.6 2.3 Reliance Power* 20.0 236.8 54.8 20.0 1.1 4.7 2.1 1.1 Coal India* 10.5 16.8 13.3 10.5 3.6 6.1 4.8 3.6

Source: Bloomberg, Daiwa

Note: *Since listing, others since March 2005

India Power Utilities & Capital Goods Sectors 18 March 2013

- 6 -

Top picks

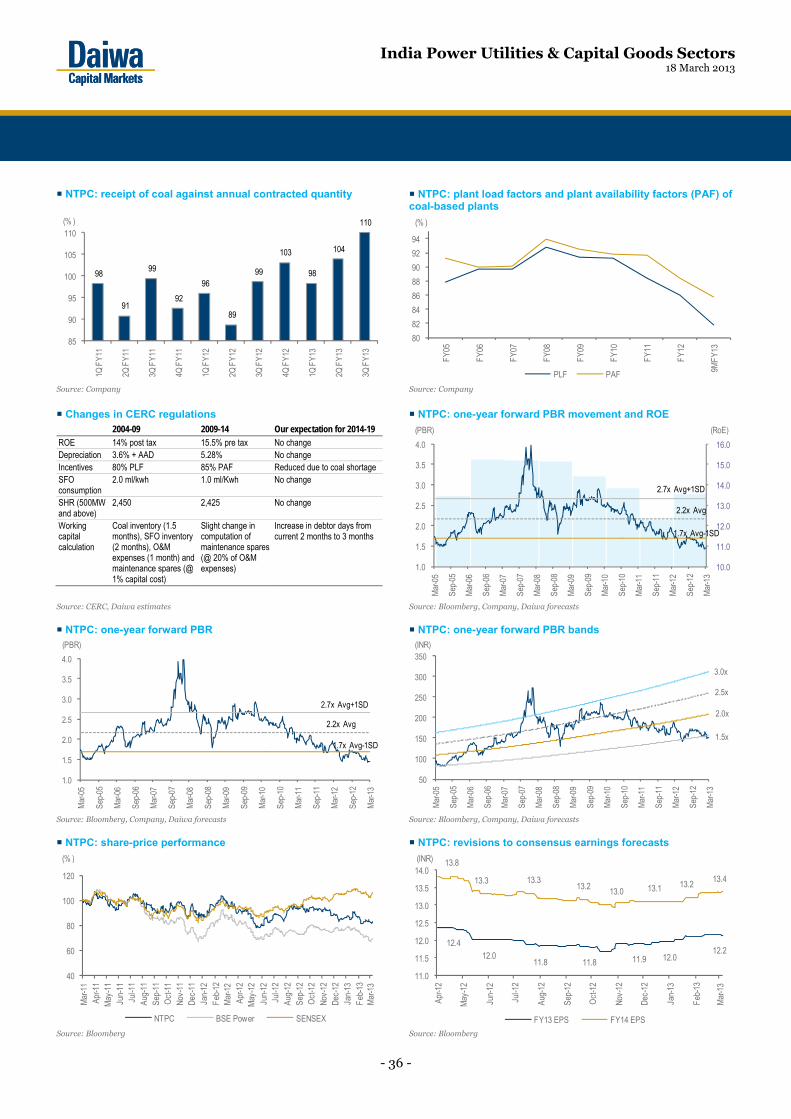

NTPC

• An early beneficiary of the reforms, NTPC saw coal availability from CIL improve by a significant 16.4% YoY for 9M FY13. In addition, the recent announcement of FRP for SEBs and regular tariff hikes by most of the SEBs over the past year should reduce the risk of delays in receivables.

• We believe NTPC will benefit from the Central Electricity Regulatory Commission’s (CERC) new tariff regulations for 2014-19, which should be finalised soon. Against the backdrop of a shortage of domestic coal availability and the weak financial positions of the SEBs, we expect the regulator to cut the levels of plant availability above which incentives are available (from 85% to 80% or lower to offset the impact of reduced coal availability).

• In addition, unlike under the 10th and 11th FYP Plans, when NTPC missed its capacity-addition targets by 2.2GW and 12.8GW, respectively, for the 12th FYP, its capacity-addition target of 14GW appears achievable, as capacity additions are front-end loaded (7GW over FY13-14).

• Trading currently at an FY14E PBR of 1.4x, an 8-year low, the stock looks attractive. On the back of the 13% fall in the share price over the past six months, we are upgrading our rating to Buy (1) from Outperform (2).

NTPC: one-year forward PBR

Source: Bloomberg, Company, Daiwa forecasts

Coal India

• CIL has also benefited from the recent reforms. The strong push by the government to boost volumes and initiatives put in place by the new chairman resulted in the company’s dispatch volume rising by 7.3% YoY for 11M FY13.

• With recent cost pressures relating to the hike in diesel costs (~INR14.4bn) and wages for contract workers (~INR2.5-3bn), coupled with the expectation of an improvement in the SEBs’ financials (recent tariff hikes and restructuring plan), we believe a price hike is in the offing over the next 3-4 months (there has been no price increase for the power sector for the past three years despite the wage settlement in January 2012).

• Despite being a direct beneficiary of the reforms and having high earnings visibility (with 80% of its sales at notified prices), CIL’s share price has underperformed the SENSEX by 22% over the past six months. We believe this is unjustified and therefore reiterate our Buy (1) rating.

CIL: one-year forward PER

Source: Bloomberg, Company, Daiwa forecasts

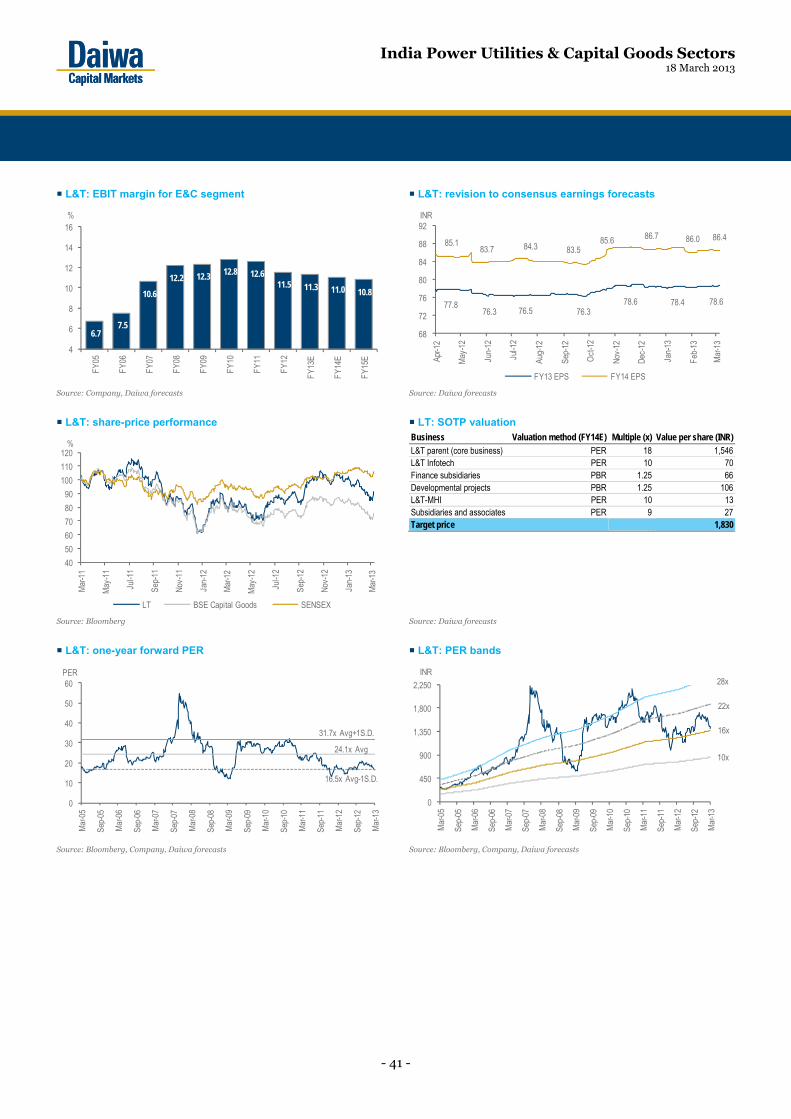

Larsen & Toubro

• In the current weak macroeconomic environment, we prefer diversified capital goods players, such as L&T, which would be a primary beneficiary of the likely revival in industrial capex.

• The company appears to us to be best-positioned to capitalise on the upturn in the capex cycle, and we forecast it to see INR893bn worth of new orders in FY14 (up 15% YoY), driven by the railways, power, and oil and gas sectors. Further orders could come from the fertiliser sector, which is benefiting from positive government policy changes. Investment in railways, for example, is set to accelerate, driven by the new DFC and metro rail line opportunities in a number of cities. Also, increased local sourcing in defence contracts could be the next demand driver.

• With the share price having fallen by 8% over the past three months, we upgrade our rating on L&T to Buy (1) from Outperform (2), and raise our SOTP-based six-month target price to INR1,830 (from INR1,780).

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Mar

-05

Sep-

05

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

2.7x Avg+1SD

1.7x Avg-1SD

2.2x Avg

(PBR)

10

11

12

13

14

15

16

17

18

Dec-

10

Mar

-11

Jun-

11

Sep-

11

Dec-

11

Mar

-12

Jun-

12

Sep-

12

Dec-

12

Mar

-13

14.8x Avg.+ 1 S.D

13.3x Avg.

11.8x Avg -1 S.D.

(PBR)

India Power Utilities & Capital Goods Sectors 18 March 2013

- 7 -

L&T: one-year forward PER

Source: Bloomberg, Company, Daiwa forecasts

Least preferred

Bharat Heavy Electricals

• With the power sector facing structural headwinds, we see a limited order pipeline for BHEL (15GW over the next 12-18 months, from state and central utilities), and expect the competition from domestic suppliers to increase, given that domestic capacity is expected to increase from 10GW in FY08 to 33GW by FY14. A revival in orders from the private sector will take time and depend on the resolution of the issues relating to fuel availability and environmental approvals, and current projects under execution turning profitable.

• In addition, BHEL’s current order backlog of INR1,137bn (down by 22% YoY for 3Q FY13), includes orders (about 12GW) placed by relatively inexperienced private players, and so could face execution delays, or cancellation, given the abovementioned headwinds.

• Further, these structural issues (such as execution delays) have started to be reflected in BHEL’s performance (3Q FY13 revenue fell by 5% YoY and the EBITDA margin dropped by 3.38pp YoY). Also, we expect the EBITDA margin to remain under pressure, due to a decline in the ASPs of recent orders, a rise in fixed costs due to the high level of installed capacity (20GW), and reduced advances due to a fall in order inflows, leading to an increase in the working-capital requirement.

• As a result we maintain our Underperform (4) rating on BHEL.

BHEL: one-year forward PER

Source: Bloomberg, Company, Daiwa forecasts

0

10

20

30

40

50

60

Mar

-05

Sep-

05

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

13

31.7x Avg+1S.D.

16.5x Avg-1S.D.

24.1x Avg

(PBR)

05

101520253035404550

Mar

-05

Sep-

05

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

25.5x Avg+1S.D.

18.5x Avg

11.5x Avg-1S.D.

(PBR)

India Power Utilities & Capital Goods Sectors 18 March 2013

- 8 -

India Power Sector: summary of reforms Reforms Steps taken/details of the scheme Impact /hurdles Companies to watch Measures already implemented

Increase supply from CIL

Strong push from the government, greater rake availability, faster environmental approvals, new Resettlement & Rehabilitation (R&R) policy.

Increases in CIL's production and dispatch volumes of 5.8% and 8.0%, respectively, for 9M FY13.

CIL, power companies with Letters of Assurance (LOA)/FSAs with CIL, NTPC a key beneficiary with 16% growth in coal supply for 9M FY13.

Expedite environmental and forest approvals

Scrapping of the no-go area concept; guidelines for environmental clearance (EC) for up to 25% one-time capacity expansion of an existing project.

Coal mines with about 600m tpa were segregated into no-go areas; one-time capacity expansion of up to 25% should aid CIL in increasing volume by 45m tpa.

CIL, all power companies, Reliance Power, Essar, JPVL

FSAs with CIL Presidential directive given to CIL to sign FSAs with 66GW of capacity between FY10 and FY17.

By the end of February, 55 power plants with a capacity of 21.7GW had signed FSAs with CIL. NTPC has still not signed an FSA with CIL.

Power companies with LOA from CIL, NTPC, Lanco, India bulls, Adani, JPVL, Reliance Power

Improve the financial health of the SEBs by way of:

a) Initiating a FRP for the SEBs

Restructuring of short-term debt, along with a plan to improve SEBs’ operational performance.

Improvement in SEBs’ balance sheets and liquidity positions - improve working-capital cycle across value chain, boost transmission & distribution (T&D) spending and revive short-term power demand Improvements in SEBs’ financials will benefit the

whole value chain – power-generation companies, T&D companies

b) Regulating tariff hikes

Since April 2012, 26 states have raised tariffs (all seven loss-making states have raised tariffs).

Regular tariff increases will reduce the gap between the cost of purchase of power and the cost of supply.

c) Introducing the FPPCA

Most states have implemented the pass-through of power and fuel costs in their tariff orders.

Removes the time lag between increase in power purchase and fuel costs, and pass through to end users, helping improve liquidity

Measures that are in the process of being implemented

Coal pooling Plugging the domestic coal shortfall with imports, and averaging prices to all consumers.

Main hurdles: 1) differences between Ministry of Coal (MOC) and Ministry of Power (MOP) on inclusion of pre-2009 FSAs, 2) resistance by SEBs.

For CIL, revenue-neutral, positive for power companies that have FSAs with CIL - Lanco, Indiabulls, Adani, JPVL, Reliance Power, negative for NTPC.

Revision of non-viable PPAs

Power companies with sales under Case I/II bids using imported coal, without a complete/partial pass-through are looking for tariff revisions, post a change in Indonesian law.

CERC is currently hearing Adani Power’s and Tata Power's cases. We believe both cases are weak; also favourable decision for any side would prompt other side to go to higher court; could lead to prolonged litigation.

Adani Power, Tata Power, Reliance Power, JSW Energy

Finalisation of SBDs Removes the risk of fuel-price rises from the project. Consensus on new norms by all stakeholders

Positive for power sector, more beneficial for companies with open capacity with no certain fuel source.

Implementing the FRP for the SEBs

50% of short-term debt has to be taken up by the state government and the other 50% has to be restructured.

Getting all seven loss-making states on board, given state governments are seeing limited support from the central government in the scheme.

Improvement in SEBs’ financials will benefit the whole value chain - power generation companies, T&D companies

Source: Daiwa

India Industrials Sector: summary of outlook for different sub-sectors Sector Ordering opportunity Key drivers Key hurdles Companies to watch Power equipment

10-12GW from central and state utilities over FY13-14

Resolution of fuel shortage (both for coal and gas) and receivables situation.

Structural: fuel and receivables,; cyclical: ordering completed for 12th FYP. L&T and Thermax

Power T&D

Driven by PGCIL and investments by SEBs to reduce aggregate technical & commercial (AT&C) losses (INR1550bn capex for the 12th FYP)

Improvement in balance sheets of SEBs with recently announced FRP. Revival in industrial capex.

Weak financials of SEBs, delays in regular electricity tariff hikes.

Transmission line segment - L&T, Kalpataru, KEC Substation equipment - CRG, Siemens, ABB, and Alstom.

Railways

I) Railways

Indian Railways to more than double its 12th FYP spend (to INR5,192bn compared with INR1,921bn under the 11th FYP).

Very high unmet demand - passenger and freight, improved cash flows following the recent passenger and freight rate hikes.

Availability of funds has been a key issue, delays in decision-making.

Railway lines - L&T and KEC. Electrification - KEC, ABB, Siemens. Rolling stock - BHEL, Titagarh, Texmaco.

II) DFC

Total project cost of Eastern and Western corridor estimated at about INR958bn, near-term award could be about INR90bn

Growing congestion on existing lines and increasing demand for freight. Delays in order decisions.

L&T, KEC could be the biggest beneficiaries initially.

III) Metro Metro rail network in tier-2 cities (about INR1,300bn over 12th FYP).

State government to reduce traffic congestion and develop infrastructure. Slower pace of work at state governments

Civil works - L&T, KEC. Electrification - KEC, ABB, Siemens. Rolling stock: Alstom, Bombardier, Siemens.

Roads 3,000ks to be awarded by NHAI by 1H FY14 (according to Union budget).

Setting up of a road regulator, easier funding and reduced interest rates.

Delays in projects due to environment and land approvals. Issues in getting financial closure.

L&T, IRB, ITNL, GMR and GVK. Competition to decline due to highly leveraged balance sheets of the players.

Airports

Development of non-metro airports (INR149bn in the 12th FYP compared with INR70bn under the 11th FYP).

Steady increase in domestic and international passenger and cargo movements. Delays in approval of investment proposals L&T, GVK, and GMR

Fertiliser About 10mtpa of capacity addition could result in about INR400bn of capex.

Approval to implement New Urea Investment Policy, high dependence on imports, current capacity running at high utilisation rate.

Weak domestic gas-supply situation, lack of regasified liquefied natural gas (RLNG) infrastructure to import liquefied natural gas (LNG ). L&T, Engineers India, and Punj Lloyd.

Oil & Gas - Upstream

Sizeable opportunity remains with ONGC over next 2-3 years).

Planned capex by ONGC as the sole driver. About INR350bn of capex for FY14 according to the Union budget

High level of competition from foreign players, delays in orders. L&T, Punj Lloyd.

Oil & Gas - Downstream

Capacity addition under 12th FYP is over 90m tpa; the majority of that will be brown-field expansion.

Diesel deregulation to decrease under-recovery amounts and encourage capacity expansion plans. Uncertain regulatory environment. EPC – L&T, Punj Lloyd, and BHEL.

Steel 35m tonnes over the 12th FYP (INR1750bn order opportunity) largely back-end loaded.

Removal of mining bans in Karnataka, Goa, and Odisha. Environment, land approvals. ABB, Siemens, L&T, Thermax and BHEL.

Source: Daiwa

India Power Utilities & Capital Goods Sectors 18 March 2013

- 9 -

Partial reforms in 2003 have put power sector in the current difficult situation

The reforms initiated by the government in the power sector during the 10th and 11th Five Year Plans (mainly the liberalisation of electricity generation through The Electricity Act, 2003) resulted in a huge investment in generation capacity from the private sector (mostly for commissioning in the periods of the 11th and 12th Five Year Plans). India: planned power generation capacity additions

Source: BHEL, Planning Commission

FYP= Five Year Plan

India Power Sector: annual power capacity additions

Source: CEA, Daiwa forecasts

Further, most of the investment from the private sector was in thermal coal-based plants. A total of about 41GW coal-based capacity was commissioned in the 11th Five Year Plan and we forecast about 78GW of addition in the 12th Five Year Plan, ie over FY12-17.

India Power Sector: annual power capacity additions by fuel

Source: CEA, Daiwa forecasts

However: 1) there was no planning with respect to providing an adequate fuel supply for the large capacity additions and 2) investments in the transmission & distribution (T&D) sector did not keep pace with the investment in the power-generation sector. Hence, over the past 2-3 years the sector has been facing challenges in these areas. Coal demand-supply scenario Based on our current capacity addition forecast of about 78GW over the 12th Five Year Plan period, about 73GW (including projects that do not have fuel sources) will come from domestic coal. Once operational, we estimate this capacity would require an additional 343m tonnes (75% plant load factor [PLF] and a gross calorific value [GCV] of 3,500kcal/kg) of coal. In addition, we forecast about 5.5GW of projects relying on imported coal to be commissioned by FY17, which we estimate in turn would require an additional 22m tonnes (adjusted for imported coal quality to a GCV of 5,000kcal/kg). On the supply side we forecast total supply to increase by 228m tonnes by FY17 for the power sector, with most of this coming from CIL (128m tonnes) and allocated captive coal blocks (67m tonnes). Hence, based on our coal-based power capacity-addition forecasts, we expect the demand for non-coking (thermal) coal to increase by a 12.3% CAGR over the FY12-17 period (compared with our CAGR forecast for supply of 9.7%), resulting in a deficit of 186m tonnes in FY17.

2 4 7 9 12 20 22

31 40 41

79 89

1 2 5 5 10 14

21 16 19 21

55

92

0102030405060708090

100

1st F

YP

2nd

FYP

3rd

FYP

4th

FYP

5th

FYP

6th

FYP

7th

FYP

8th

FYP

9th

FYP

10th

FYP

11th

FYP

12th

FYP

Target Actual

(GW)

Significant increase in target andactual capacity addition in the 11th and the 12th FYP

7.2 2.8

9.2 11.3

20.2

15.9

26.2

21.9

16.3

11.9

0

5

10

15

20

25

30

FY08 FY09 FY10 FY11 FY12 FY13E FY14E FY15E FY16E FY17E

(GW)

4.91.6

6.59.7

18.113.2

20.3 19.014.6

10.81.00.2

2.20.7

0.7

1.7

1.8 0.6

1.0

0.01.3

1.0

0.40.9

1.4

1.0

4.02.4

0.7

1.0

0

5

10

15

20

25

30

FY08 FY09 FY10 FY11 FY12 FY13E FY14E FY15E FY16E FY17E

Coal Gas Hydro & Nuclear

(GW)

India Power Utilities & Capital Goods Sectors 18 March 2013

- 10 -

India Power Sector: coal demand supply scenario FY11 FY12 FY13E FY14E FY15E FY16E FY17E

Coal demand: CIL/SCCL linkage capacity 361 383 428 466 513 564 603Capacity on captive coal 22 24 31 48 69 80 86Capacity on imported coal 11 20 30 37 40 42 43Capacity on undecided source 4 9 11 18 30 39 48Total demand (A) 397 436 500 569 653 725 779Coal production: CIL 291 312 341 364 388 413 440SCCL 32 34 36 38 40 43 45Captive 17 22 25 43 52 70 89Imported 18 20 30 37 40 42 43Total production (B) 358 388 431 481 521 568 617Gap based on domestic quality (B-A) (39) (48) (68) (88) (132) (157) (162)Adj for imported quality (GCV 5000Kcal/Kg) (22) (27) (39) (50) (75) (90) (93)Total imports (apparent +forced) 40 48 69 87 116 131 135India DD:SS deficit 10% 11% 14% 15% 20% 22% 21%

Source: CEA, MOC, Daiwa forecasts

Reforms to address the fuel shortage

Increase in supply from Coal India Over FY10-12, CIL’s production was flat and dispatch growth was 2.1%, raising concerns amongst investors of CIL’s inability to ramp up its volumes. After a strong push by the government over the past year, CIL’s production and dispatch volumes have risen by 4.3% and 7.3%, respectively, up to February FY13. What has Coal India done? CIL’s R&R policy was revised in March 2012 to facilitate the faster acquisition of land for expansion/ new projects. It provided greater flexibility to the boards of subsidiary companies to determine the rehabilitation package best suited for local needs. It also raised the lump-sum land compensation level from INR0.2m/acre to INR0.5m/acre. This should speed up land acquisition, which has been a bottleneck. 2) Rake availability: better coordination with the railways ensured a significant improvement in the rake availability for 9M FY13, which was up 10.3% YoY. 3) Area-level monitoring: CIL introduced area-level monitoring from February 2012 and has made the individual mines accountable for not achieving output targets. 4) Environmental and forest approvals: regular discussions between the MOC, CIL, and the Secretary, Ministry of Environment and Forests (MOEF) now take place to expedite the approvals process.

CIL: YoY change in the dispatches volume

Source: Company

CIL: annual production volume

Source: Company

Expediting environmental and forest approvals A number of CIL’s projects were stuck over FY10-12 due to delays in land acquisition, the introduction of the no-go area concept by the MOEF and Comprehensive Environmental Pollution Index (CEPI), and general delays in environment and forest approvals. However, following a strong push by the government over the past year, the MOEF has given some leeway by doing away with the no-go areas and relaxing the CEPI, along with making other policy changes to support faster clearances:

• The granting of environmental clearance of up to 25% for one-time capacity expansion of existing projects. As one of the measures to resolve the short-term coal supply shortage, CIL had been seeking permission to produce 25% more capacity than was currently approved for 11 of its projects that had reached their capacity limits. Finally, in December 2012, the MOEF released guidelines for granting environmental clearance for one-time expansion of existing coal mining projects by up to 25% without the need for a public hearing.

• The scrapping of the no-go areas, forest clearance accorded to Mahan, Chhatrasal

8 3 3 6

(10)(13)

(8)

11

(3)

19

13

6 2

10 6 1 8

18 18

6 8

0 1

(15)

(10)

(5)

0

5

10

15

20

Apr-1

1

May

-11

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Oct

-11

Nov-

11

Dec-

11

Jan-

12

Feb-

12

Mar

-12

Apr-1

2

May

-12

Jun-

12

Jul-1

2

Aug-

12

Sep-

12

Oct

-12

Nov-

12

Dec-

12

Jan-

13

Feb-

13

(% )

Positive impact of Gover nment's policy measur es

High base effec t

Fall in volumes

100

200

300

400

500

600

700

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

E

FY14

E

FY15

E

FY16

E

FY17

E

No gr owth(m tonnes)

India Power Utilities & Capital Goods Sectors 18 March 2013

- 11 -

and Amelia North coal mine. These coal blocks were earlier part of the no-go areas; however the MOEF scrapped the no-go system, after which the Group of Ministers (GOM) approved forest clearance for these blocks, following which even MOEF gave forest approvals.

• Setting up an additional Forest Advisory Committee (FAC). At present, there is only one FAC to process forest clearance proposals in the country. To reduce the FAC’s burden of examining all applications in a timely manner, the MOEF wants to set up another FAC to recommend in-principle approval and address environmental and development issues for projects.

• Forest approvals now to be applied to entire lease areas. The MOEF has directed mine developers to apply for forest clearance for their entire lease areas, instead of seeking clearance for a smaller section of the lease area where actual mining is proposed to take place. The companies will only have to apply once to the MOEF for complete forest clearance, instead of seeking forest clearance again and again as production ramps up.

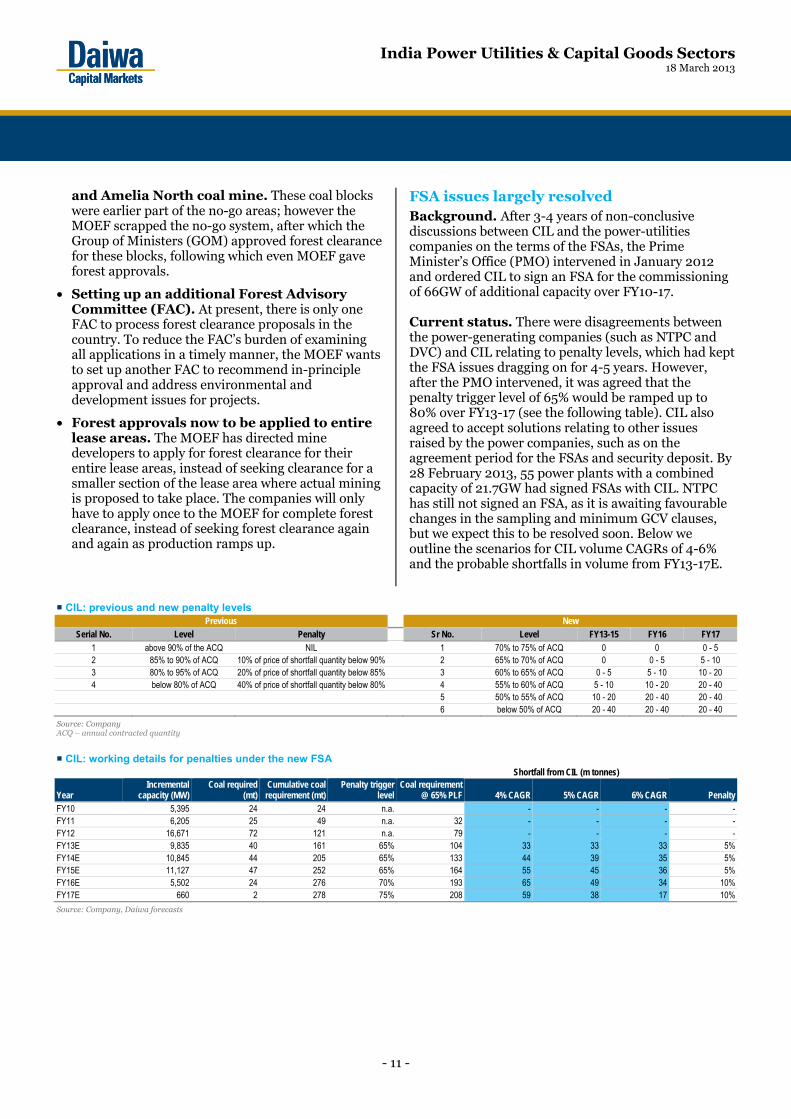

FSA issues largely resolved Background. After 3-4 years of non-conclusive discussions between CIL and the power-utilities companies on the terms of the FSAs, the Prime Minister’s Office (PMO) intervened in January 2012 and ordered CIL to sign an FSA for the commissioning of 66GW of additional capacity over FY10-17. Current status. There were disagreements between the power-generating companies (such as NTPC and DVC) and CIL relating to penalty levels, which had kept the FSA issues dragging on for 4-5 years. However, after the PMO intervened, it was agreed that the penalty trigger level of 65% would be ramped up to 80% over FY13-17 (see the following table). CIL also agreed to accept solutions relating to other issues raised by the power companies, such as on the agreement period for the FSAs and security deposit. By 28 February 2013, 55 power plants with a combined capacity of 21.7GW had signed FSAs with CIL. NTPC has still not signed an FSA, as it is awaiting favourable changes in the sampling and minimum GCV clauses, but we expect this to be resolved soon. Below we outline the scenarios for CIL volume CAGRs of 4-6% and the probable shortfalls in volume from FY13-17E.

CIL: previous and new penalty levels

Previous New Serial No. Level Penalty Sr No. Level FY13-15 FY16 FY17

1 above 90% of the ACQ NIL 1 70% to 75% of ACQ 0 0 0 - 5 2 85% to 90% of ACQ 10% of price of shortfall quantity below 90% 2 65% to 70% of ACQ 0 0 - 5 5 - 10 3 80% to 95% of ACQ 20% of price of shortfall quantity below 85% 3 60% to 65% of ACQ 0 - 5 5 - 10 10 - 20 4 below 80% of ACQ 40% of price of shortfall quantity below 80% 4 55% to 60% of ACQ 5 - 10 10 - 20 20 - 40

5 50% to 55% of ACQ 10 - 20 20 - 40 20 - 40 6 below 50% of ACQ 20 - 40 20 - 40 20 - 40

Source: Company ACQ – annual contracted quantity

CIL: working details for penalties under the new FSA

Shortfall from CIL (m tonnes)

Year Incremental

capacity (MW) Coal required

(mt) Cumulative coal requirement (mt)

Penalty trigger level

Coal requirement @ 65% PLF 4% CAGR 5% CAGR 6% CAGR Penalty

FY10 5,395 24 24 n.a. - - - -FY11 6,205 25 49 n.a. 32 - - - -FY12 16,671 72 121 n.a. 79 - - - -FY13E 9,835 40 161 65% 104 33 33 33 5%FY14E 10,845 44 205 65% 133 44 39 35 5%FY15E 11,127 47 252 65% 164 55 45 36 5%FY16E 5,502 24 276 70% 193 65 49 34 10%FY17E 660 2 278 75% 208 59 38 17 10%

Source: Company, Daiwa forecasts

India Power Utilities & Capital Goods Sectors 18 March 2013

- 12 -

Reforms to address the weak financials of the SEBs

India Cabinet approves SEB restructuring On 24 September 2012, India’s Cabinet Committee on Economic Affairs (CCEA) approved an FRP for the SEBs due to their weakening financial health, given the increase in their accumulated losses over the past few years. We believe the country’s power-distribution sector is in a similar state of flux to the power-generation sector before the Electricity Act 2003 was introduced. Even given the recent tariff hikes taken by 26 states over the past 11 months, an FRP is necessary for the SEBs with strict guidelines so that the sector does not end up in a similar situation again. Key benefits of the scheme

• SEBs’ balance sheets should improve, which would improve the long-term prospects for the power sector in terms of generation and T&D capex.

• The working-capital cycle will improve across the value chain, which has been a cause of concern among investors.

• Concerns about lenders’ non-performing assets (NPAs) will be addressed as part of the restructuring.

• Once their fundamentals have improved, the SEBs should be able to meet their short-term power demand deficits by buying at spot prices, thus reviving the merchant-power market.

Details of the scheme Some 50% of the SEBs’ short-term debt as at 31 March 2012 will be taken over by the state governments. This will first be converted into bonds issued by the SEBs to participating lenders (backed by the state governments). Some 2-5 years after that, the state governments will take over the debt from the SEBs in the form of special securities.

• The repayment of the principal amount and interest is to be undertaken by the state governments until they take over the debt from the SEBs.

• The remaining 50% is to be restructured as a short-term loan by rescheduling loans and providing a moratorium on the principal amount.

• The restructuring/rescheduling of the debt is to be accompanied by concrete and measurable action by the SEBs/states in order to improve the SEBs operating performance.

• Two committees are to be formed, one at the state and the other at the central level to monitor the turnaround plan.

• The central government is to provide incentives by way of: 1) a grant equal to the value of the additional energy saved if the SEBs cut their aggregate technical & commercial (AT&C) losses by more than that specified under the Restructured Accelerated Power Development and Reforms Programme, and 2) capital reimbursement of 25% of the principal repayment by the state governments on the debt taken over by the state governments.

• The following table shows how the state government securities will be issued to the SEBs over the FY13-17 period, as indicated by the MOP.

India Power Sector: Instalments of special securities to be issued by the state government of the 7 focus states to the SEBs

INRbn 50% of

short-term loans FY13 FY14 FY15 FY16 FY17Andhra Pradesh 32 22 9 - - -Haryana 70 25 25 20 - -Madhya Pradesh 6 1 5 - - -Punjab 58 9 10 11 13 15Rajasthan 199 26 35 40 45 52Tamil Nadu 96 9 25 29 33 -Uttar Pradesh 130 19 22 26 29 33Total 590 111 132 126 120 100

Source: Planning Commission

Constant pressure on the SEBs has resulted in tariff hikes Since April 2012, 26 states have raised tariffs (including the seven loss-making states). We do not believe these hikes will be sufficient to cover the SEBs’ losses. Nor do we believe they will help to entirely eliminate the estimated gap between revenue and cost, given the SEBs’ current cost structures. However, these tariff hikes should provide a breather for the India Power Sector overall, as well as for the lenders, with many states having raised tariffs twice over the past 1-2 years. We see this as a step in the right direction, building confidence among lenders, and encouraging them to support the SEBs’ financial turnaround.

India Power Utilities & Capital Goods Sectors 18 March 2013

- 13 -

Tariff hikes taken by the seven focus states

States Last tariff

hike Average tariff

hike (%) Previous tariff hike

Average tariff hike (%) Remarks

Andhra Pradesh Apr-12 20-25 Apr-11 n.a. Hikes in all categories except for domestic consumers using less than 50 units a month Haryana Apr-12 10-15 Jun-11 0.5 Average tariff hike of 10-15% across all consumer categories; agricultural consumers saw no increases Madhya Pradesh Apr-12 7.17 Jun-11 6.1 Average tariff hike of 7% across consumer categories, but no tariff rise for domestic consumers using less than 30 units a

month Punjab Apr-12 12.08 Apr-11 9.2 Hike across all consumer categories Rajasthan Aug-12 18 Apr-11 20.0 Tamil Nadu Apr-12 37.0 Aug-10 n.a. Hikes across all consumer categories after nine years; the August 2010 rise was only for specific consumers such as shops,

cinemas, and malls Uttar Pradesh Oct-12 17.63 Apr-10 13.0 No tariff hike for domestic and rural consumers; hike for heavy industries tariff of 30%, while for small and medium industries

18%. Commercial consumers saw a hike rise of 20%.

Source: Daiwa

Introduction of pass-through of fuel and power purchase costs Most states have implemented FPPCA, ie, the pass-through of power and fuel costs in their tariff orders. This is very positive development for SEBs given: 1) any increase in the cost of fuel is a pass-through for the generator through a fuel surcharge adjustment formula and is payable by the distribution licensees in the subsequent bills, 2) the power purchase cost being uncontrollable is passed through to consumers, but the difference in the actual cost of procurement of power and the estimated cost of the purchase of power gets adjusted by the regulator only after 2 years. The time lag of two years puts an additional burden on consumers by way of carrying cost. Extract from Delhi Electricity Regulatory Commission staff paper: mechanism and frequency of power purchases

Source: Delhi Electricity Regulatory Commission

Difficult measures still in progress, with limited clarity on timeline

Many other measures relating to the resolution of issues faced by the IPPs, like coal pooling, the revision of tariffs for unviable PPAs and the finalisation of bidding documents, are still a work in progress and there is little visibility as to when these issues might be resolved. This is particularly so as each asset of each private-sector developer has a different business model that faces issues of either domestic coal availability or higher costs of imported coal, which cannot be passed on to end users in the form of higher tariffs. Also, we believe many of these issues are difficult to resolve. Coal-pooling could resolve fuel-supply issues in the near term Background: The Ministry of Power (MOP) is working with the Central Electricity Authority (CEA) to come up with a plan to meet the near-term shortfall of domestic coal in the power sector through coal pooling. This scheme involves plugging the domestic coal shortfall with imports, and averaging prices to all consumers, thereby increasing the cost of domestic coal by 10-12%. Latest developments: On 5 February 2013, the CCEA gave ‘in-principle’ approval for the coal-pool-pricing mechanism through CIL, though the key modalities have yet to be finalised. Main hurdles: the main hurdles in the implementation of the pooling scheme would be: 1) Differences in opinion between the Ministry of Coal (MOC) and MOP on the inclusion of pre-2009 FSAs, 2) CIL wants coal pooling only on a trial basis for two years and then to review the system based on the feedback, and 3) Resistance from the SEBs.

India Power Utilities & Capital Goods Sectors 18 March 2013

- 14 -

The way forward: Our interactions with the Planning Commission, MOP and MOC indicate that coal pooling as suggested by the CEA, ie, including all pre-2009 FSAs, has not been accepted by the CCEA, mainly as the inclusion of pre-2009 FSAs would significantly affect the SEBs, which have weak financials. Going forward, MOP and MOC, in consultation with the Finance Ministry, will work on the mechanism of coal pooling, which we expect to happen after the second phase of the budget session of the Parliament (ie, after April-May). Our take: We believe coal price pooling for power customers (once it is agreed upon by all stakeholders), would remain difficult to implement both logistically and technically. 1) For CIL: we would expect it to be a revenue-neutral event for CIL. However, this could increase the intra-year volatility of CIL’s earnings when global coal prices see sharp movements, and CIL might not take simultaneous price hikes/cuts to its coal prices in the domestic market. 2) For the power producers: the primary beneficiaries of the mechanism would be the IPPs that have LOAs with CIL. IPPs that could gain from coal pooling Player Capacity (GW)Lanco 5.0Indiabulls 4.3Adani 2.6Jaiprakash Power 1.8RPWR 1.5CESC 1.5L&T 1.2GMR 1.1Tata Power 1.1KSK 0.5

Source: MOC

Finalising the standard bidding document Background. In order to resolve major issues related to the pass-through of fuel in power tariffs, the MOP published a standard bidding document (SBD) in February 2012. However, while making the changes to the document, the MOP changed the power-generation business model from a build-operate-own (BOO) to design-build-finance-operate-transfer (DBFOT), which none of the private companies, regulator or financial institutions agreed to. This is because the changes make the power-generation companies more inflexible with respect to: 1) plant design, 2) land control, 3) approvals required for each milestone achieved, and 4) the right to terminate a contract with the SEBs.

The way forward. As the IPPs have objected to many of the above-mentioned issues, the MOP has set up an advisory committee to look into the model document. Once the committee submits its recommendations to the MOP, it will submit its revised model PPA to the Cabinet for approval before the PPA is implemented. We expect the revised bidding documents to be finalised in the next 1-2 months. Our take. We believe that as the increase in fuel costs will now be passed on to end users when the bidding document becomes an agreement, IPPs’ expected returns on projects will also be much lower. Revising non-viable PPAs Background. Power companies that have previously participated in a competitive bidding process (Case I and Case II), where there was no complete or partial pass-through of any tariff hikes, have been looking for tariff hikes, following the changes in Indonesia’s coal regulations in September 2011, whereby the Indonesia Government ordered that the pricing of coal exports be benchmarked to global prices. Though the discussions between these power generators and the SEBs did not result in an amicable solution earlier, there was some confusion regarding the appropriate authority to go for arbitration. In August 2012, the Attorney General (AG) opined that the CERC could regulate and revise PPA tariffs irrespective of the contracts signed by power producers with the state distribution companies if it was with more than one state. Post the failed discussions with the SEBs, Tata Power’s plea to revise tariffs at the Mundra Ultra Mega Power Plant (UMPP) got a hearing with the CERC. The CERC had asked IPPs to initiate a consultation process with the state DISCOMs, and some IPPs (Tata Power, Adani) asked the state utilities to revise PPA tariffs upwards. The cash-strapped SEBs, which had entered into long term PPAs, have opposed such a revision. Latest updates. The CERC hearings are under way. During Tata Power’s recent post results conference call, management commented that a few hearings have been conducted by the CERC (starting in December 2012), but did not indicate any expected time frame for a verdict. Our take. We believe that as these projects were won through a competitive bidding process, both cases are on a weak footing; also, a decision on these PPAs going in the favour of any side would probably prompt the other side to go to a higher court to reverse the decision. Also, comparing Tata Power’s and Adani’s

India Power Utilities & Capital Goods Sectors 18 March 2013

- 15 -

case, Tata’s Mundra project was a Case II project which was set up on imported coal, while Adani’s Mundra project was a Case I bid, wherein the project developer is responsible for fuel. Other bidders who lost out in the competitive bids in the past for UMPPs and Case-I projects could oppose such a move and it could lead to prolonged litigation. These cases are being followed by the other IPPs, and any favourable decision to increase tariffs in the abovementioned cases would set a precedence for them to apply for tariff revisions. Finally, we believe that a solution to the above issue needs to be found if further investment in the power sector is to be encouraged. So we conclude that rather than a decision on the above case, the possible solution would be the regulator pushing both sides to come to a negotiated solution to the issue and decide what the possible tariff hike should be. What could go in favour of the project owner is that despite a tariff increase, these projects are significantly cheaper than some of the recent Case I bids (INR4-6/kWh), and with the implementation of FRP, the SEBs’ financials should improve and they would be encouraged to agree to a tariff increase. Implementing the SEB FRP

Approval of the SEB FRP in September 2012 is a positive for the power sector. However, there will be challenges getting the scheme up and running, and we have already seen an extension of the deadline to apply for restructuring from December 2012 to March 2013. Invariably, we might see a further extension given the following:

• According to the scheme, 50% of the short-term debt of the SEBs would have to be taken by the state governments, which will strain the latter’s financial position.

• With state governments seeing limited support from the central government in the scheme, many state governments have stated their reluctance to accept the scheme.

• Continued regular tariff hikes by states will require political will.

India: status of states on SEB FRP

State Agreed to FRP Loan from FIs/ Banks/

Bonds (INRbn for FY11) % of total loansAndhra Pradesh √ 299 10 Haryana √ 261 8 Madhya Pradesh x 162 5 Punjab x 169 5 Rajasthan √ 580 19 Tamil Nadu √ 251 8 Uttar Pradesh √ 325 10 Bihar √ 21 1 Jharkhand √ 8 0 Himachal Pradesh √ 37 1 Karnataka √ 182 6 States agreeing 1,965 63Total 2,297 73 All India 3,133 100

Source: PFC

Note: Highlighted text indicates the 7 major loss-making states

India Power Utilities & Capital Goods Sectors 18 March 2013

- 16 -

Capital goods sector is highly dependent on the power sector for orders

The capex cycle in India in the past has been driven by orders from the power sector. However, given the cyclical and structural issues faced by the power sector currently, we see limited orders being placed with the capital goods companies from there. Over FY08-12, the capital goods companies under our coverage saw both a drop in power sector orders as a percentage of total order inflows and a sharp decline in their order inflows from the power sector. Daiwa India Industrials: order inflow from the power sector (%)

FY08 FY09 FY10 FY11 FY12ABB 66 62 66 54 67CRG* 65 75 74 65 70Siemens 45 53 61 41 26BHEL* 84 82 76 82 64L&T 14 25 33 32 21% of power in total 52 56 54 52 35

Source: Company

Note: *for CRG/BHEL only domestic orders have been considered

Daiwa India Industrials: growth in total orders and orders from the power sector

Source: Company

Power: most ordering is already completed The Power Equipment Sector is facing cyclical and structural issues. In the 11th FYP (2007-12), there was a significant increase in capacity additions (from 21GW in the 10th FYP to 55GW in the 11th FYP); further, in the 12th FYP (2012-17) capacity additions are expected to increase to 89GW. However, ordering for India’s 12th FYP has already been completed, and at the same time, domestic power-equipment manufacturing capacity is expected to increase to 33GW by FY14 from 10GW in FY08. Also, the power sector is facing structural issues, such as coal availability and the SEBs’ still weak financials,

which will continue to pose a risk to the execution of current orders and a recovery in orders. India: targeted and actual power generation capacity additions

Source: BHEL, Planning Commission

FYP= Five Year Plan

India: China players’ market share up from 29% in the 11th Five Year Plan to 34% in the 12th Five Year Plan

Source: BHEL

India power equipment capacity by player

Source: Company, Daiwa

33

17 16 6

(28)

39

25 13

2

(52)(60)

(40)

(20)

0

20

40

60

FY08 FY09 FY10 FY11 FY12

Growth in total orders Growth in orders for power sector

(% )

2 4 7 9 12 20 22

31 40 41

79 89

1 2 5 5 10 14

21 16 19 21

55

92

0102030405060708090

100

1st F

YP

2nd

FYP

3rd

FYP

4th

FYP

5th

FYP

6th

FYP

7th

FYP

8th

FYP

9th

FYP

10th

FYP

11th

FYP

12th

FYP

Target Actual

(GW)

Significant increase in target andactual capacity addition in the 11th and the 12th FYP

49 41

29 34

22 25

0

20

40

60

80

100

11th plan 12th plan

BHEL Chinese Others

(% )

6 610 10 10

15 1520 20 20

4

4 4 42 4

23

0

5

10

15

20

25

30

35

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13E FY14E

BHEL L&T BGR Energy GB-Ansaldo Thermax -B&W

(GW)

6 610 10 10

1519

2426

33

India Power Utilities & Capital Goods Sectors 18 March 2013

- 17 -

India power equipment capacity and orders placed

Source: Company, Daiwa

Recovery in ordering still a long way off. We believe that until all the issues in the power sector are resolved, notwithstanding implementation of various reforms and further various measures under way to resolve issues in the power sector, ordering from the sector will not recover. As the current capacities under execution need to be profitable for companies to gain confidence before investing further in projects, lenders need to have clarity on approvals and fuel security of future projects before they start lending again. We do not see orders from the IPPs recovering over the next two years (FY14-15), and expect annual ordering to remain at the 10-12GW level over the period from the state and central utilities (which are slow in awarding projects). Moreover, we forecast domestic capacity to reach 33GW by FY14, and competition to remain fierce, given that players such as Thermax have no orders and the likes of JSW-Toshiba have low utilisation rates. Near-term order opportunities. The opportunities are limited to new orders from the central and state utilities. For FY13-14, we expect the following orders to be awarded:

India: ordering opportunity over FY14

Project Configuration Total (MW)

Opportunity (INRbn) Remarks

Orders under award stage RVUNL, Suratgarh and Chabra 4x660MW 2640 108 BHEL is L1, L&T is L2Orissa - IB valley 2x660MW 1320 52.8 BHEL is L1, L&T is L2NTPC, Tanda 2x660MW 1320 52.8 L&T is L1

NTPC, Unchahhar 500MW 500 20 To be awarded to BHEL

on nomination basisTotal 5780 233.6

Orders under finalisation NTPC, Khargaon 2x660MW 1320 52.8 MPGENCO, Khandawa 2x660MW 1320 52.8 TANGEDCO, Ennore 1x660MW 660 26.4 TNEB, Udangudi 2x660MW 1320 52.8 MAHAGENCO, Nashik 1x660MW 660 26.4 MAHAGENCO, Bhusawal 1x800MW 800 32 NLC 2x500MW 1000 40 AP 3x500MW 1500 60

Total 8580 343.2

Source: Companies, Daiwa

Key drivers. Resolution to the fuel shortage (both for coal and gas). Finalisation of the bidding documents, and award for UMPPs. A further improvement in the SEBs’ financials would also drive equipment ordering. Key hurdles. Delays in environment and land approvals, and securing fuel in a supply constrained environment. Key players. Diversified players with less exposure to power, as well as limited capacity to fill, namely, L&T and Thermax. Power T&D Total spend potential in the 12th FYP for transmission is pegged at INR1,800bn against INR1,400bn in the 11th FYP. This will be largely led by the central transmission utility, Power Grid Corporation of India (PGCIL) (to contribute over 55% of the total spend). India: investment in the transmission sector

Source: Planning Commission

6 3

10

15 19 20 19

7 10

12

0

5

10

15

20

25

30

35

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

E

FY14

ETotal Orders placed Total India Capacity

(GW)

185550

1000253

650

550200

250

0

500

1,000

1,500

2,000

10th plan 11th plan 12th plan

Central State Private

(INRbn)

438 1,400 1,800

India Power Utilities & Capital Goods Sectors 18 March 2013

- 18 -

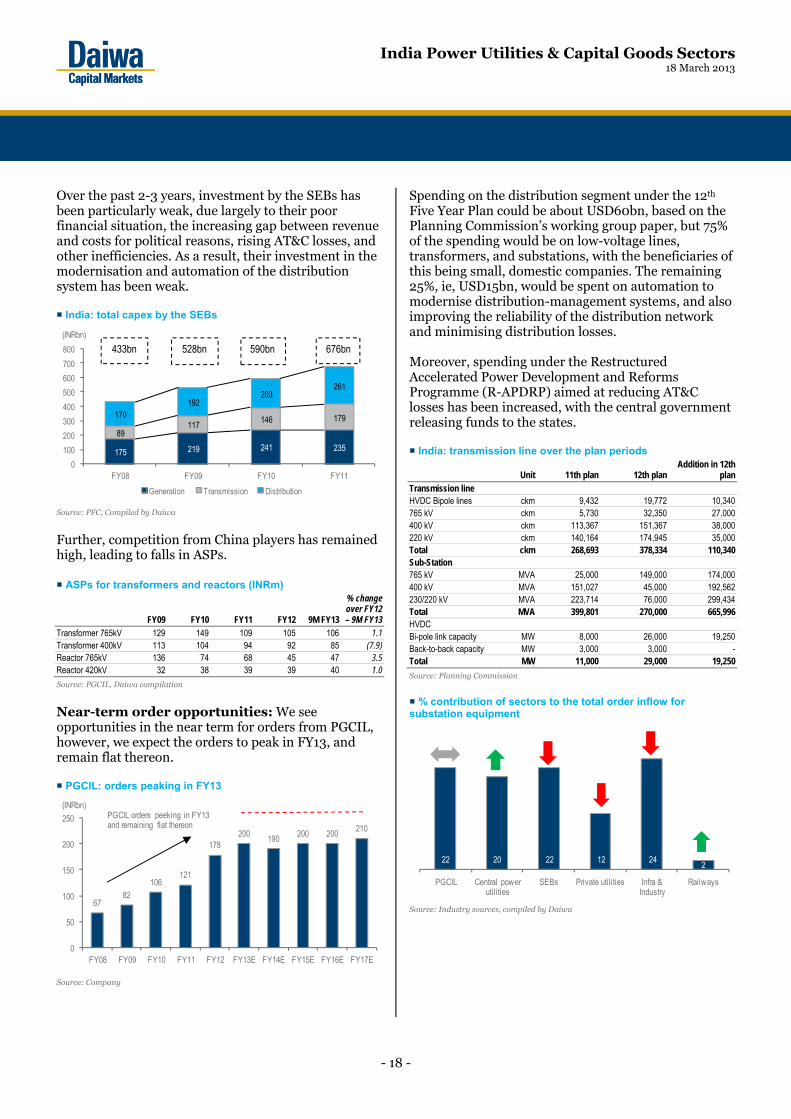

Over the past 2-3 years, investment by the SEBs has been particularly weak, due largely to their poor financial situation, the increasing gap between revenue and costs for political reasons, rising AT&C losses, and other inefficiencies. As a result, their investment in the modernisation and automation of the distribution system has been weak. India: total capex by the SEBs

Source: PFC, Compiled by Daiwa

Further, competition from China players has remained high, leading to falls in ASPs. ASPs for transformers and reactors (INRm)

FY09 FY10 FY11 FY12 9M FY13

% change over FY12 – 9M FY13

Transformer 765kV 129 149 109 105 106 1.1Transformer 400kV 113 104 94 92 85 (7.9)Reactor 765kV 136 74 68 45 47 3.5Reactor 420kV 32 38 39 39 40 1.0

Source: PGCIL, Daiwa compilation

Near-term order opportunities: We see opportunities in the near term for orders from PGCIL, however, we expect the orders to peak in FY13, and remain flat thereon. PGCIL: orders peaking in FY13

Source: Company

Spending on the distribution segment under the 12th Five Year Plan could be about USD60bn, based on the Planning Commission’s working group paper, but 75% of the spending would be on low-voltage lines, transformers, and substations, with the beneficiaries of this being small, domestic companies. The remaining 25%, ie, USD15bn, would be spent on automation to modernise distribution-management systems, and also improving the reliability of the distribution network and minimising distribution losses. Moreover, spending under the Restructured Accelerated Power Development and Reforms Programme (R-APDRP) aimed at reducing AT&C losses has been increased, with the central government releasing funds to the states. India: transmission line over the plan periods

Unit 11th plan 12th planAddition in 12th

planTransmission line HVDC Bipole lines ckm 9,432 19,772 10,340 765 kV ckm 5,730 32,350 27,000 400 kV ckm 113,367 151,367 38,000 220 kV ckm 140,164 174,945 35,000 Total ckm 268,693 378,334 110,340 Sub-Station 765 kV MVA 25,000 149,000 174,000 400 kV MVA 151,027 45,000 192,562 230/220 kV MVA 223,714 76,000 299,434 Total MVA 399,801 270,000 665,996 HVDC Bi-pole link capacity MW 8,000 26,000 19,250 Back-to-back capacity MW 3,000 3,000 -Total MW 11,000 29,000 19,250

Source: Planning Commission

% contribution of sectors to the total order inflow for substation equipment

Source: Industry sources, compiled by Daiwa

175 219 241 235

89 117

146 179 170 192

203 261

0

100

200

300

400

500

600

700

800

FY08 FY09 FY10 FY11

Generation Transmission Distribution

433bn 528bn 590bn 676bn(INRbn)

6782

106121

178200

190200 200

210

0

50

100

150

200

250

FY08 FY09 FY10 FY11 FY12 FY13E FY14E FY15E FY16E FY17E

PGCIL orders peeking in FY13 and remaining flat thereon

(INRbn)

22 20 22 12 24 2

PGCIL Central power utilities

SEBs Private utilities Infra & Industry

Railways

India Power Utilities & Capital Goods Sectors 18 March 2013

- 19 -

India T&D Sector: main sectors ordering substation equipment

Sector Share CY12 (%) Outlook for FY14

PGCIL 20~25 PGCIL orders likely to remain flat Central power utilities

20~25 Could see 10-15% YoY growth in order value with as a result of capacity-addition plans

SEBs 20~25 Slow pace of ordering due to SEBS’ weak financial health; however regular electricity tariff hikes, the introduction of FPPCA, and the SEB FRP may improve the situation in FY14-15

Private utilities 10~15 Facing structural issues, such as the availability of fuel, that could lead to a decline in the value of orders YoY

Infrastructure and industrial companies

20~25 With a revival in capex, ordering could be revived over FY14-15

Railways 2~5 Should continue to see order value growth of 15-20% YoY

Source: Industry sources, compiled by Daiwa

Key drivers: With the recent announcement of an FRP, we believe the balance sheets of the SEBs will improve, which should eventually lead to a rise in T&D capex. However, an immediate improvement seems less likely. Further, a revival in industrial capex would also boost investment in the T&D sector. Key hurdles. Regular and timely increases in electricity tariffs would require continued political will and concerted steps to reduce AT&C losses. India Power Sector: nationwide AT&C losses

Source: PFC

Key players. In the substation equipment space, CRG, Siemens, ABB, and TRIL; in the transmission line segment companies such as L&T, Kalpataru and KEC.

Upturn in investment cycle should be led by new drivers

In the long-cycle industrial-project segments of the capital goods sector, projects have been affected by the challenging domestic macroeconomic environment. The challenges have included high interest rates and constraints on the availability of funds (the credit extended to industry has moderated over the past two years, with bank loans extended to industries rising by 13.8% YoY for December 2012 compared with a CAGR of 23.1% for FY09-12). A recent report by the RBI indicated that more than 50% of central government sector projects worth more than INR1.5bn each in five sectors (roads, power, petroleum, railways and coal), had been delayed and had seen cost overruns. The main reasons for this were delays in acquiring land/receiving environmental approvals/obtaining project financing/finalising engineering designs, a lack of infrastructure support and linkages, changes in scope, and other contractual issues. Among the five sectors, the worst affected were power and roads. However, there have been recent policy measures by the government to resolve many of these issues and to revive the investment cycle. The initiatives have included: 1) encouraging and enabling large cash-rich PSUs to go ahead with planned investments, 2) the setting up of the CCI to expedite big infrastructure projects of more than INR10bn, and 3) the investment allowance of 15% for capex of more than INR1bn (announced in the recent budget), together with signs of interest rates peaking (the Reserve Bank of India cut the repo-rate by 25bps in January 2013) – provide the environment for a recovery in capex. We expect the capex cycle to improve over next 6-12 months, starting with the public sector capex cycle, which should be followed by a revival in the private sector as well over the next 12-18 months. India: projected interest rates (repo rate)

Source: Bloomberg, Daiwa forecasts

Note: CRR=cash reserve ratio

29.45

27.3726.58

26.15

20

22

24

26

28

30

FY08 FY09 FY10 FY11

(% )

0

2

4

6

8

10

Oct

-07

Jan-

08

A pr-0

8

Jul-0

8

Oct

-08

Jan-

09

Apr-0

9

Jul-0

9

Oct

-09

Jan-

10

Apr-1

0

Jul-1

0

Oct

-10

Jan-

11

Apr-1

1

Jul-1

1

Oct

-11

Jan-

12

Apr-1

2

Jul-1

2

Oct

-12

Aug-

13

Repo Rate % CRR %

Three rate cuts of 25 bps each ex pected in remainder of 2013

(% )

India Power Utilities & Capital Goods Sectors 18 March 2013

- 20 -

India: industry capacity-utilisation rate

Source: RBI

India: gross fixed-capital formation

Source: Government of India Economic survey

RBI’s estimate of amount of approved projects

Source: RBI

We believe the current upturn in the capex cycle will be led by new drivers, such as: 1) surface transportation, as a result of a several-fold increase in railway capex in the 12th Five Year Plan, the DFC, and the planned development of metro lines in a number of second-tier cities, 2) the New Urea Investment Policy, which could drive 10mtpa or INR400bn of capex in the fertiliser segment, and continued investments by ONGC.

Railways

In the 12th Five Year Plan, Indian Railways plans to more than double its expenditure, from INR1,921bn under the 11th Five Year Plan to INR5,192bn. Indian Railways: funding of expenditure in the plan period

Source: Planning Commission

To fund this expansion it will rely on the internal generation of funds and investment from the private sector. The internal requirement of funds will be met through a 12% CAGR in passenger receipts and a 9.9% increase in freight receipts (it aims for freight loading to increase by a CAGR of 7.8% to 1,405m tonnes over FY13-17) according to the working group report for the 12th Five Year Plan on the railways sector.

77

7173

72

7981 80

7677

80

83

78 77 7880

7375

646668707274767880828486

2QFY

09

3QFY

09

4QFY

09

1QFY

10

2QFY

10

3QFY

10

4QFY

10

1QFY

11

2QFY

11

3QFY

11

4QFY

11

1QFY

12

2QFY

12

3QFY

12

4QFY

12

1QFY

13

2QFY

13

(%)

05

10152025303540

FY91

FY92

FY93

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

Gross Domestic Fix ed Capital Formation (YoY)

Gross Domestic Capital Formation as a % of GDP

(% )

914

1,332

891

437

1,415

1,148

698

521

1,402

872

633

829 875

336

0

300

600

900

1,200

1,500

FY10 FY11 FY12 FY13

Q1 Q2 Q3 Q4

(INRbn)

770 1,942 667

2,250

484

1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

11th Plan 12th Plan

Budgetary support Internal generation Private sector / others

(INRbn)

1,921

5,192

India Power Utilities & Capital Goods Sectors 18 March 2013

- 21 -

Indian Railways: expenditure outlay in the 11th Five Year Plan Indian Railways: expenditure outlay in the 12th Five Year Plan

Source: Planning Commission Source: Planning Commission

Indian Railways: capacity creation in the plan period

km 10th Five Year Plan

11th Five Year Plan

12th Five Year Plan

New lines 920 2,205 4,000Gauge conversion 4,289 5,290 5,500Doubling 1,300 2,756 7,653Railway electrification 1,810 4,501 6,500Eastern and western dedicated freight corridor 3,338

Source: Planning Commission

Indian Railways: capacity creation for rolling stock units 10th Five Year Plan 11th Five Year Plan 12th Five Year Plan

Wagons 36,222 63,481 105,659Coaches 12,202 17,085 24,000Diesel locomotives 622 1,288 2,000Electric locomotives 524 1,218 2,010

Source: Planning Commission

PPP-based railway projects by category in the 12th Five Year Plan

Project Investment expected

(INRbn) Project size (INRbn)High speed corridor Mumbai-Ahmedabad 200 600Elevated Rail corridor in Mumbai 0 200Redevelopment of stations 50 100Freight terminals 50 50Port connectivity 50 50DFC 100 100Loco and coach manufacturing units 50 60Power generation 60 60Total 560 1,220

Source: Planning Commission

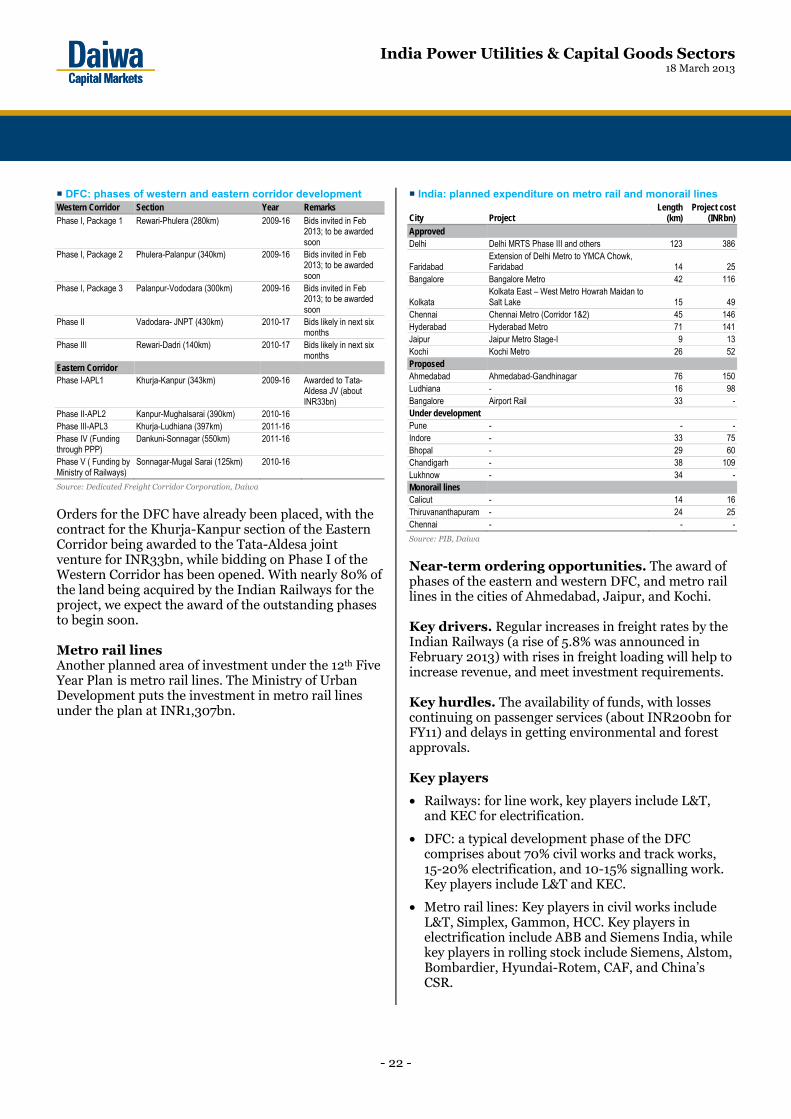

Dedicated Freight Corridor This project aims to develop rail routes for the faster and more efficient transportation of raw materials to industries and manufactured goods to ports. The project includes about 2,700km of new freight lines and about 5,000km of feeder lines (new construction and the upgrading of existing lines). The DFC on the western and the eastern routes (see the following chart) involves the construction of about 3,338km of dedicated freight lines to carry predominantly coal and steel on the Eastern Corridor and containers on the Western Corridor. The ports in

Maharashtra and Gujarat would be linked to the northern part of the country and coal from the east of the country would be moved to the power plants in the north. The total cost of the project is estimated by the Planning Commission at about INR958bn. DFC: development programme

Source: Daiwa

New Line6.4%

Gauge Conversion

7.5%

Doubling7.6%

Rolling Stock23.7%

Track Renewals9.2%

Signalling & Telecom Work

4.8%

Investment in PSU's16.3%

Others24.6%

New Line17.1%

Gauge Conversion

2.5%

Doubling4.6%

Rolling Stock22.1%

Track Renewals6.6%

Signalling & Telecom Work

2.7%

Investment in PSU's19.1%

Others25.3%

Ludhiana

Dadri

World Bank FundedPhase 1950 km KhurjaJICA Funded Jaipur APL 1

343 kmWorld Bank Funded

Bhaupur APL 2Ahmedabad 395 km

World Bank FundedVadodara

Phase 2 Allahabad584 km SuratJICA Funded

Mughalsarai122 kmGovt Funded 540 km(IR Equity) Sonnagar PPP funded

JNPT AsansolGaya

JICA- Japan International Co-operation AgencyAPL-Adaptable Program Lending Dankuni

Western CorridorEastern CorridorImportant Stations

Kanpur

Rewari

450 kmAPL 3

Palanpur

India Power Utilities & Capital Goods Sectors 18 March 2013

- 22 -

DFC: phases of western and eastern corridor development Western Corridor Section Year Remarks

Phase I, Package 1 Rewari-Phulera (280km) 2009-16 Bids invited in Feb 2013; to be awarded soon

Phase I, Package 2 Phulera-Palanpur (340km) 2009-16 Bids invited in Feb 2013; to be awarded soon

Phase I, Package 3 Palanpur-Vododara (300km) 2009-16 Bids invited in Feb 2013; to be awarded soon

Phase II Vadodara- JNPT (430km) 2010-17 Bids likely in next six months

Phase III Rewari-Dadri (140km) 2010-17 Bids likely in next six months

Eastern Corridor Phase I-APL1 Khurja-Kanpur (343km) 2009-16 Awarded to Tata-

Aldesa JV (about INR33bn)

Phase II-APL2 Kanpur-Mughalsarai (390km) 2010-16 Phase III-APL3 Khurja-Ludhiana (397km) 2011-16 Phase IV (Funding through PPP)

Dankuni-Sonnagar (550km) 2011-16

Phase V ( Funding by Ministry of Railways)

Sonnagar-Mugal Sarai (125km) 2010-16

Source: Dedicated Freight Corridor Corporation, Daiwa

Orders for the DFC have already been placed, with the contract for the Khurja-Kanpur section of the Eastern Corridor being awarded to the Tata-Aldesa joint venture for INR33bn, while bidding on Phase I of the Western Corridor has been opened. With nearly 80% of the land being acquired by the Indian Railways for the project, we expect the award of the outstanding phases to begin soon. Metro rail lines Another planned area of investment under the 12th Five Year Plan is metro rail lines. The Ministry of Urban Development puts the investment in metro rail lines under the plan at INR1,307bn.

India: planned expenditure on metro rail and monorail lines

City Project Length

(km)Project cost

(INRbn)Approved Delhi Delhi MRTS Phase III and others 123 386

Faridabad Extension of Delhi Metro to YMCA Chowk, Faridabad 14 25

Bangalore Bangalore Metro 42 116

Kolkata Kolkata East – West Metro Howrah Maidan to Salt Lake 15 49

Chennai Chennai Metro (Corridor 1&2) 45 146Hyderabad Hyderabad Metro 71 141Jaipur Jaipur Metro Stage-I 9 13Kochi Kochi Metro 26 52Proposed Ahmedabad Ahmedabad-Gandhinagar 76 150Ludhiana - 16 98Bangalore Airport Rail 33 -Under development Pune - - -Indore - 33 75Bhopal - 29 60Chandigarh - 38 109Lukhnow - 34 -Monorail lines Calicut - 14 16Thiruvananthapuram - 24 25Chennai - - -

Source: PIB, Daiwa