Embed Size (px)

Citation preview

Company Valuation 11.1

Innovation and Entrepreneurship

Company Valuation - 11

Company Valuation 11.2

Valuation – Setting

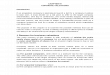

Firm with Productive

Assets

Factor Inputs

Capital

Land

Labour

Technology

Output

Consumer Market for

Products and Services

Short Term

Fixed

Intangible

GoodwillCapital Market for Stocks and

Bonds

Traded Securities

Company Valuation 11.3

Valuation – Three Major Techniques

• Asset Valuation Approach: Asset side of the Balance Sheet

• Income Valuation Approach: Profit and Loss Statement

• Market Multiple Valuation Approach: Liability side of the Balance Sheet

Company Valuation 11.4

Valuation – Asset Based Approach• Company valuation as a special case of asset

valuation• Analyze the “Asset” side of the balance sheet• Assets are where company has already spent

the money and assets will give cash flows in future

• Company’s value depends upon the size and reliability of these future cash flows

Company Valuation 11.5

Occasions for Valuation

• Equity analysis• Merger and Acquisition• Employment (when ESOPs are involved)• IPO, restructuring, divestiture• Exit of a Joint-Venture partner• Equity investment (VC Financing)• Loan decision by a banker (financial health

estimation and default probability estimation)• Management Buyout, internal share transfer

Company Valuation 11.6

Type of Companies being Valued

• Listed companies – market price (consensus of active traders, quarterly statements, guidance, forecasts)

• Companies with assets which are mostly physical – depreciation, appreciation, obsolescence

• Examples – transport operator, mechanical ancillary units

Company Valuation 11.7

Type of Companies being Valued

Knowledge-based companies have huge intangible assets

• Patents, trademarks, Copyright (Software source code)

• Processes, quality and development methodology,

• Goodwill, brand, customer base, relationships

• Team (education, experience, skills)

Company Valuation 11.8

Difficulties in Valuing Early Stage Companies• Immediate earnings are negative• No past history• No comparable companies• No market prices• Asymmetric information• Management efficacy yet to be

established

Company Valuation 11.9

Asset Valuation

• Cost of acquisition

• Depreciated value (book value)

• Appreciated value

• Replacement value (example: laptop)

• Liquidation value

Company Valuation 11.10

Assets in Combination (Synergies)

• Intellectual Property and Team

• Individual valuation difficult and problematic

• Combination valuation is meaningful

• Replacement costs are better to use as they are marked to market.

• Example: Outright sale of some working software code

Company Valuation 11.11

Major Methods of Asset Valuation

• Discounted Cash Flow (DCF)• Market multiples• Comparable companies (or assets)• Comparable deals• Ad hoc – illiquidity, intangibility

• Market as a great place – not only a place for exchange, it is a place for fair price determination

Company Valuation 11.12

Discounted Cash Flow Analysis

• Mathematics of compounding and discounting

• Time value of money: One rupee later is not worth one rupee today (inflation, uncertainties). What baskets of goods and services that rupee will buy

• Future Value (FV), Present Value (PV), Net Present Value (NPV)

Company Valuation 11.13

Net Present Value (NPV) of an Investment

• Horizon of interest: Typically 4 –5 years

• Expected future cash flows: Dividends, interests

• Residual value at the end of horizon: Market price

• Risk-free rate of return: Government bonds

• Risk premium: Investor dependent

Company Valuation 11.14

NPV for an Investment with Annual CashflowsNPV = CF1 / (1.0 + r) + CF2 / (1.0 + r) 2 + CF3 / (1.0+r) 3

+ RV / (1.0 + r) 3

r = Expected rate of returnCF i = Cash flow at the end of i th year

RV = Residual value of the asset

Where

Caveats: Expected rate of return is dependent on risky nature of the project and risk-aversion of the investor. Also “residual value” is hard to estimate.

Company Valuation 11.15

Comparable Companies and Deals

• Price/Earning Ratios: vary between 4 to 30• Price/Sales Ratios: Vary between 0.8 to 10• Return on Investment and prevalent interest

rates in the economy (when RBI Governor or FRB reduces the benchmark interest rate, stock market goes up)

Company Valuation 11.16

Market Multiples of Three IT Majors

Infosys Wipro Satyam

Sales 6986 8254 3544

PAT 1904 1628 750

Capital Employed 5421 5370 3226

Net Profit Margin 0.27 0.20 0.21

Return on Investment 0.35 0.30 0.23

EVA 1036.64 768.80 233.84

Equity (Rs Cr) 135 280 64

Share face value (Rs) 5 2 2

Outstanding shares (Cr) 27 140 32

Book Value Per Share (Rs) 200.8 38.4 100.8

Market price per share 2440.0 380.0 540.0

Earning Per Share 70.5 11.6 23.4

Price/EPS 34.6 32.7 23.0

Price/Book 12.2 9.9 5.4

Company Valuation 11.17

Range of Ratios

Ratio Conservative Aggressive

Net Profitability 0.2 0.4

Price/Earning ratio 7.5 25

Price/Sales ratio 2.5 6

VC's expected IRR 0.35 0.5

Discounting factor 1.35 1.5

Company Valuation 11.18

Example: Projected P&L of a Startup

Item Head Y1 Y2 Y3 Y4 Y5

Sales 100.0 170.0 560.0 1016.0 1726.0Net Profit 40.0 68.0 224.0 406.4 690.4Valuation1 from P/E 300.0 510.0 1680.0 3048.0 5178.0Valuation2 from P/S 250.0 425.0 1400.0 2540.0 4315.0 Valuation1 discounted to Y1 1154.8Valuation2 discounted to Y1 962.3

All figures in Rs Lakhs

Company Valuation 11.19

Buyer’s Valuation and Seller’s Valuation

• All assets are not relevant to a buyer, but the seller has spent good bit of money to acquire them

• Coca-Cola vs Parle

• Parle’s assets: bottling plants, distribution network, warehouses, brands (Thums UP)

Company Valuation 11.20

Buyer’s Strategic Intent and its Impact

• Sale of hotels by ITDC

• Buyers do the valuation Existing hoteliers

Real estate developers

Cash-rich corporates willing to diversify in the hospitality segment

Company Valuation 11.21

Qualitative Fine Tuning

• Company’s reputation

• Management capabilities

• Competitive environment prevailing in the industry

• Industry’s relationship with the economy

Company Valuation 11.22

Exercises in Valuation

• Look at financials of many types of companies and do the valuation

• Hotels, steel plants, auto manufacturers, media companies, IT companies

• See by how much the market capitalization deviates from the “fair value” that was calculated from DCF / PE multiple / PS multiple