Embed Size (px)

Citation preview

Comments on Low Carbon Fuel Standard

Re-Adoption Fuel Availability Workshop

October 2014

1

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Overview

On September 25, 2014 the California Air Resources Board (CARB) presented their findings on the

availability of low carbon intensity (CI) fuels expected to be available through 2020.

These findings are expected to have a significant impact on the following CARB analyses in process:

• Availability of low-CI fuels available in California through 2020

• Estimates of regulated parties' compliance through 2020

The following comments and questions relate to CARB's current estimate of US low-CI fuel availability

and what is expected as the re-adoption process continues

Specifically, we would like to raise the following points:

• The forecast of some of the low-CI fuels are overly optimistic (e.g. sugarcane ethanol, Brazilian cellulosic

ethanol, renewable gasoline, renewable diesel)

• CARB's forecasts appear to depend heavily on the assumption that a strong regulation ("market signal")

will drive the availability of low-CI fuels in the next five years

• There are a number of factors that should be considered going forward that were not addressed in this

workshop. These must be addressed in the following workshop currently scheduled for October 27

2

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Agenda

Sugarcane ethanol

Cellulosic ethanol

Renewable gasoline

Renewable diesel

Low-CI fuel market signal

Constraints to consider for California fuel availability

Expectations for upcoming workshop

3

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

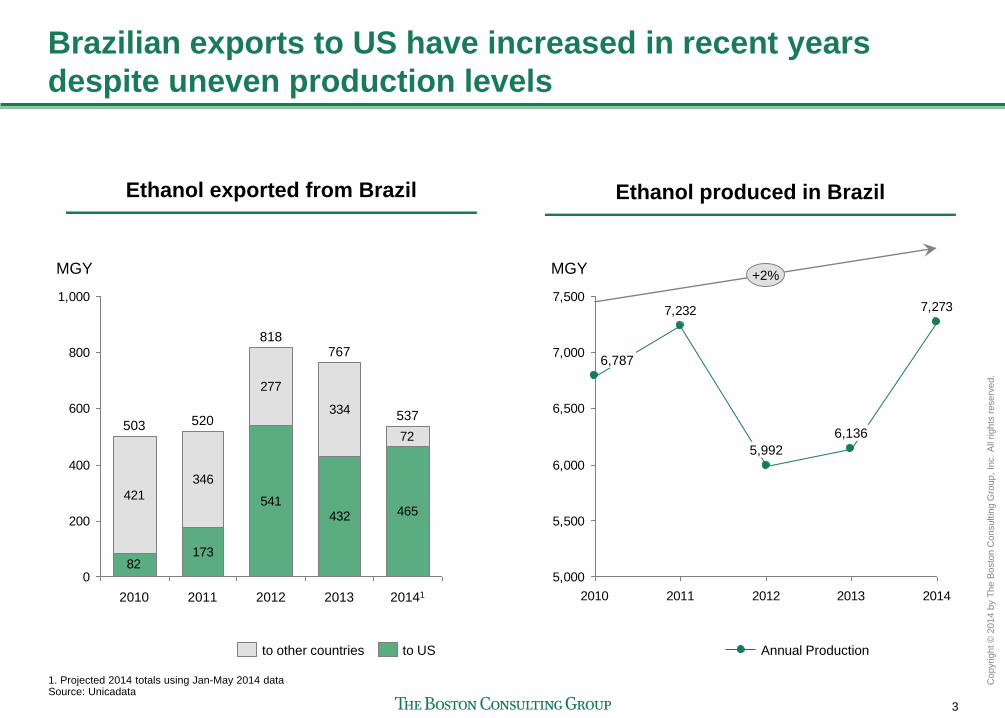

Brazilian exports to US have increased in recent years

despite uneven production levels

173

541432

421

346

277

334

82

465

72

0

200

400

600

800

1,000

MGY

2013

767

2012

818

2011

520

2010

503

20141

537

to US to other countries

Ethanol produced in Brazil Ethanol exported from Brazil

1. Projected 2014 totals using Jan-May 2014 data Source: Unicadata

7,2737,232

5,000

5,500

6,000

6,500

7,000

7,500

2010 2011 2012 2013 2014

MGY +2%

6,136

5,992

6,787

Annual Production

4

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

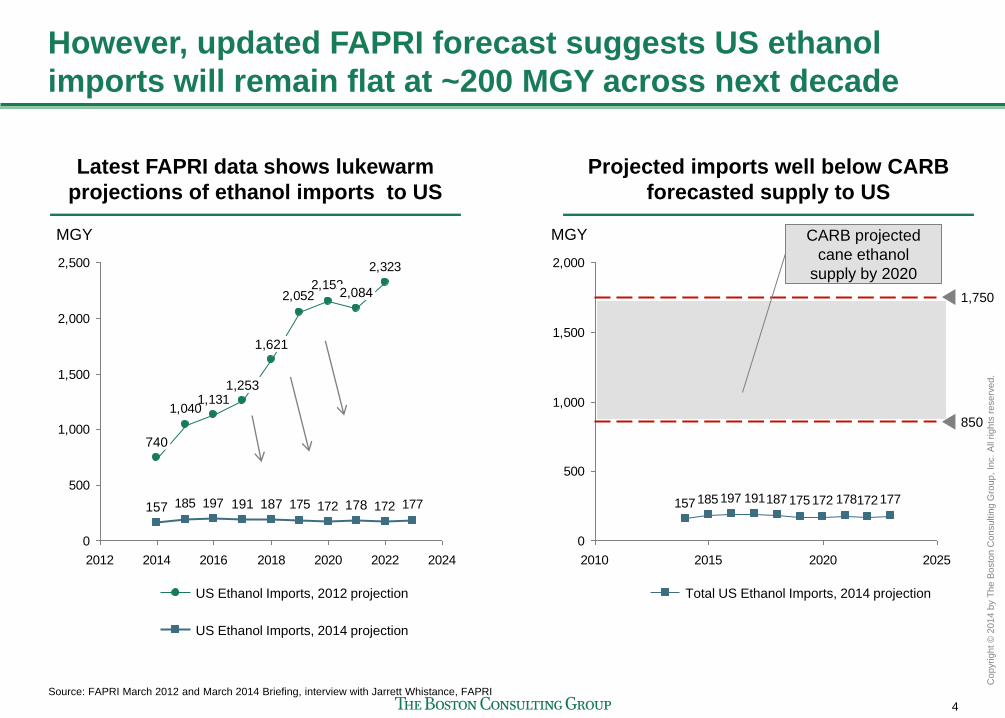

However, updated FAPRI forecast suggests US ethanol

imports will remain flat at ~200 MGY across next decade

2,323

2,1522,052

1,1311,040

177172172175197185

0

500

1,000

1,500

2,000

2,500

2012 2014 2016 2018 2020 2022 2024

1,253

157

740

178

2,084

187

1,621

191

MGY

Source: FAPRI March 2012 and March 2014 Briefing, interview with Jarrett Whistance, FAPRI

Latest FAPRI data shows lukewarm

projections of ethanol imports to US

US Ethanol Imports, 2012 projection

US Ethanol Imports, 2014 projection

177172178172175187191197185157

0

500

1,000

1,500

2,000

2010 2015 2020 2025

850

MGY

1,750

Total US Ethanol Imports, 2014 projection

Projected imports well below CARB

forecasted supply to US

CARB projected

cane ethanol

supply by 2020

5

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Long-term, several factors could affect the supply of

Brazilian sugarcane ethanol

Factors Description Effect on ethanol volume availability to CA

Weather Bad weather such as drought or

harsh winters

Reduced sugarcane crop for ethanol production

World sugar prices Greater demand driving higher

sugar prices

Reduced % of sugar cane allocated to ethanol vs.

sugar

Flex fuel adoption in Brazil

Increased level of flex-fuel

adoption

Price of hydrous < 70% of gasoline

Price of hydrous > 70% of gasoline

Brazil gasoline prices

Higher gasoline prices

Reduced domestic demand for anhydrous ethanol

if hydrous < 70% of gasoline price

No change in domestic demand for anhydrous if

hydrous > 70% of gasoline price

RIN prices in U.S. Higher RIN prices driven by

RFS2 mandates

Demand up for sugarcane ethanol in U.S.

reduces CA share

Infrastructure

constraints

State of ports Ports congested and under-

invested; not expect to change in

next four years

May not be able to export significantly high

projected ethanol volume

Domestic

logistics cost

Logistics costs from inland to

coast are high

Potentially unattractive if trying to export to U.S.

from inland Brazil

U.S. pipeline

availability

Very few dedicated ethanol

pipelines in the U.S.

Would have to ship directly to California; in

absence of it, would need trucks and rails to

transport sugarcane ethanol to California

Cyc

lic

al

Str

uc

tura

l

Key factor Source: World Ethanol Outlook to 2020, Unica, Deustsche Bank, Credit Suisse, BCG Analysis

6

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Agenda

Sugarcane ethanol

Cellulosic ethanol

Renewable gasoline

Renewable diesel

Low-CI fuel market signal

Constraints to consider for California fuel availability

Expectations for upcoming workshop

7

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Industry expectations for cellulosic fuels in the medium-

term not improving

233233233233233233233

138

176163

155

132

91

56

100

0

50

100

150

200

250

Forecasted production of

cellulosic ethanol (MGY)

2020 2019 2018 2017 2016 2015 2014 2013

-25%

AEO 2014 AEO 2013

1. Annual Energy Outlook 2. Low case Note: Converted from Quadrillion BTU to MGY using ethanol higher heating value (HHV) of 84,530 published by Oak Ridge National Laboratory Source: EIA Annual Energy Outlooks 2013 & 2014, E2

EIA has sharply dropped near-term

and moderated medium-term forecasts

163

118

12

337

267

126

0

100

200

300

400

Forecasted capacity2 (MGPY)

-52%

2015 2014 2013 2015 2014 2013

E2 has lowered forecasted short-term

capacity additions

Cell. Ethanol

2013 report 2012 report

8

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

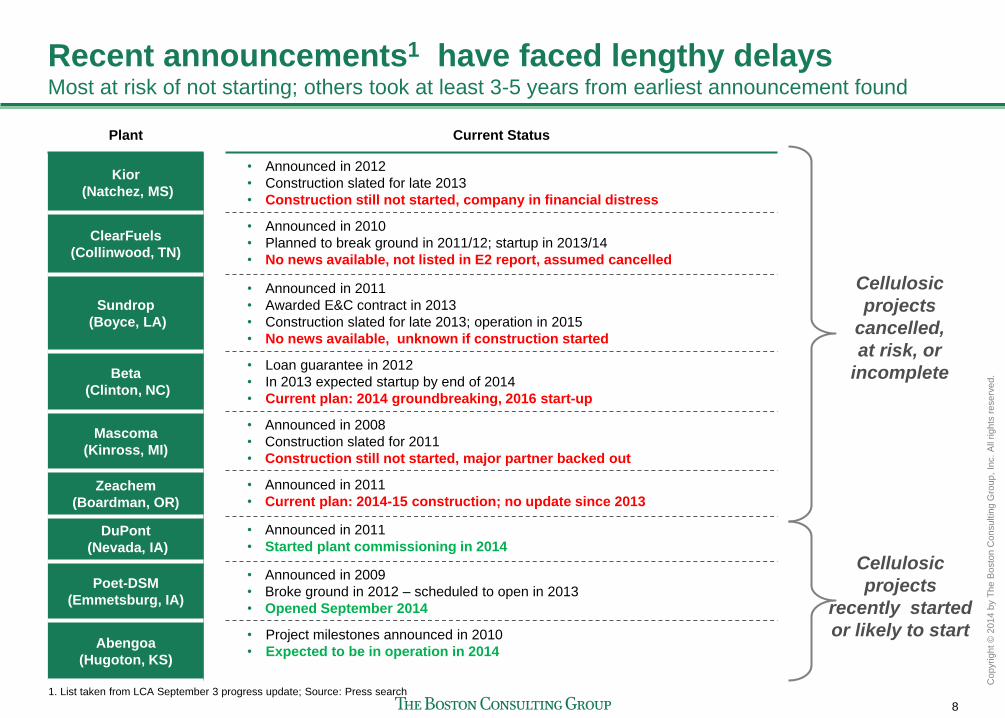

Recent announcements1 have faced lengthy delays Most at risk of not starting; others took at least 3-5 years from earliest announcement found

1. List taken from LCA September 3 progress update; Source: Press search

Plant Current Status

Kior

(Natchez, MS)

• Announced in 2012

• Construction slated for late 2013

• Construction still not started, company in financial distress

ClearFuels

(Collinwood, TN)

• Announced in 2010

• Planned to break ground in 2011/12; startup in 2013/14

• No news available, not listed in E2 report, assumed cancelled

Sundrop

(Boyce, LA)

• Announced in 2011

• Awarded E&C contract in 2013

• Construction slated for late 2013; operation in 2015

• No news available, unknown if construction started

Beta

(Clinton, NC)

• Loan guarantee in 2012

• In 2013 expected startup by end of 2014

• Current plan: 2014 groundbreaking, 2016 start-up

Mascoma

(Kinross, MI)

• Announced in 2008

• Construction slated for 2011

• Construction still not started, major partner backed out

Zeachem

(Boardman, OR)

• Announced in 2011

• Current plan: 2014-15 construction; no update since 2013

DuPont

(Nevada, IA)

• Announced in 2011

• Started plant commissioning in 2014

Poet-DSM

(Emmetsburg, IA)

• Announced in 2009

• Broke ground in 2012 – scheduled to open in 2013

• Opened September 2014

Abengoa

(Hugoton, KS)

• Project milestones announced in 2010

• Expected to be in operation in 2014

Cellulosic

projects

cancelled,

at risk, or

incomplete

Cellulosic

projects

recently started

or likely to start

9

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

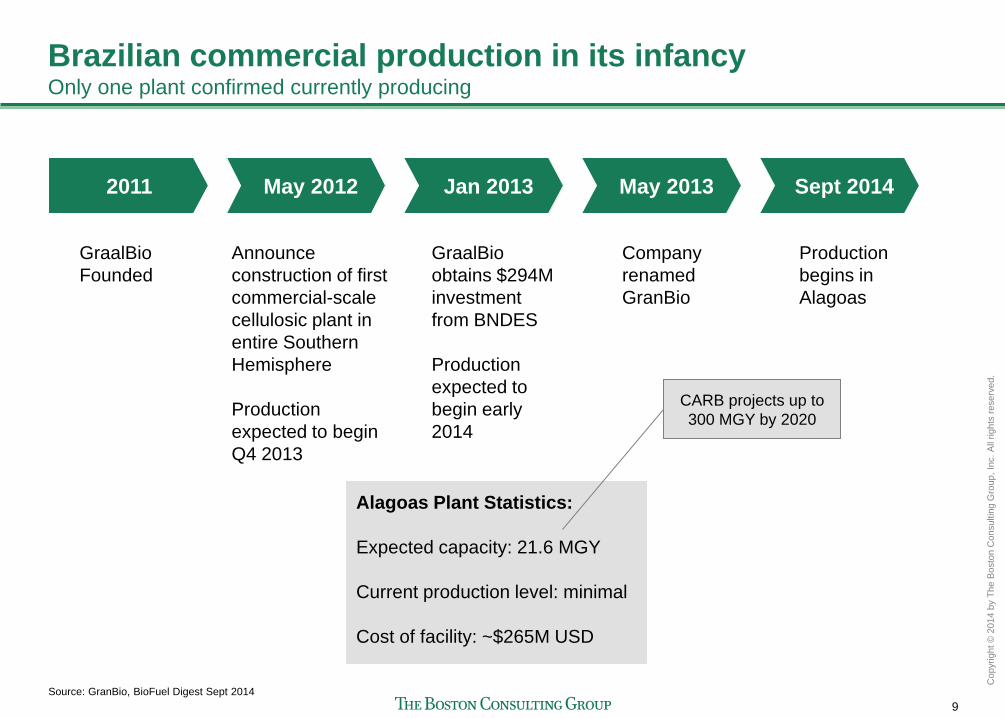

Brazilian commercial production in its infancy Only one plant confirmed currently producing

2011 May 2012 Jan 2013 Sept 2014

GraalBio

Founded

Announce

construction of first

commercial-scale

cellulosic plant in

entire Southern

Hemisphere

Production

expected to begin

Q4 2013

GraalBio

obtains $294M

investment

from BNDES

Production

expected to

begin early

2014

Production

begins in

Alagoas

May 2013

Company

renamed

GranBio

Alagoas Plant Statistics:

Expected capacity: 21.6 MGY

Current production level: minimal

Cost of facility: ~$265M USD

Source: GranBio, BioFuel Digest Sept 2014

CARB projects up to

300 MGY by 2020

10

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Agenda

Sugarcane ethanol

Cellulosic ethanol

Renewable gasoline

Renewable diesel

Low-CI fuel market signal

Constraints to consider for California fuel availability

Expectations for upcoming workshop

11

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

CARB scenarios optimistic given challenges to renewable

gasoline supply by 2020

60

10

00

50

100

150

200

Total

160

Unknown

(2018-2020)

90

Sundrop

(2017)

Cool Planet

(2016)

Current

MGY

Renewable

gasoline not

commercially

available

Status of

facility

unknown – no

update since

July 2013

No facilities

announced,

unlikely to

have operating

facilities in <5

years

CARB forecasted renewable gasoline volumes

30 100

High range projection

Low range projection

Range of 30-90 MGY

counted toward total,

despite no new facilities

announced

Source: Press search, CARB, BCG analysis

12

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Agenda

Sugarcane ethanol

Cellulosic ethanol

Renewable gasoline

Renewable diesel

Low-CI fuel market signal

Constraints to consider for California fuel availability

Expectations for upcoming workshop

13

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Renewable diesel projections unrealistic

Existing projects are not discounted

• Historically high CAPEX ($2-3MM per MGY) and ramping up of scalability have meant that

recent plants have gone 5+ years from planning to operations; others have failed

• The SG Preston facility accounts for more than 40% of "in progress" facilities. This plant

was announced in the last few months and will not be ready until 2017 at the earliest

It is unlikely that many (if any) new facilities could be built if they are not yet announced,

much less a multiple above what is currently announced as is suggested by the medium

and high cases for renewable diesel availability

Some renewable diesel facilities produce jet fuel

• While jet and diesel are similar petroleum products and some switching is possible, there

are likely specific markets or contracts for renewable jet production

As renewable diesel pathways vary significantly depending on feedstocks, does CARB

have information about the expected feedstocks of the planned facilities to determine the

CI impact?

14

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

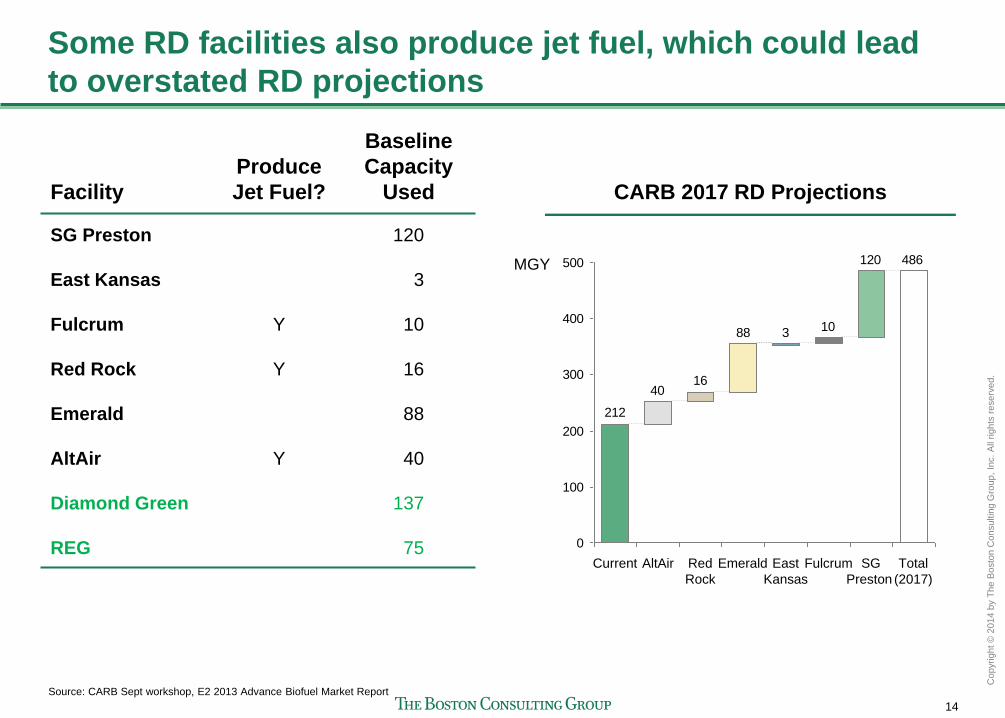

Some RD facilities also produce jet fuel, which could lead

to overstated RD projections

486120

10

1640

212

388

0

100

200

300

400

500

Fulcrum East

Kansas

Red

Rock

Emerald AltAir Current

MGY

Total

(2017)

SG

Preston

Facility

Produce

Jet Fuel?

Baseline

Capacity

Used

SG Preston

East Kansas

Fulcrum

Red Rock

Emerald

AltAir

Diamond Green

REG

Y

Y

Y

120

3

10

16

88

40

137

75

CARB 2017 RD Projections

Source: CARB Sept workshop, E2 2013 Advance Biofuel Market Report

15

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

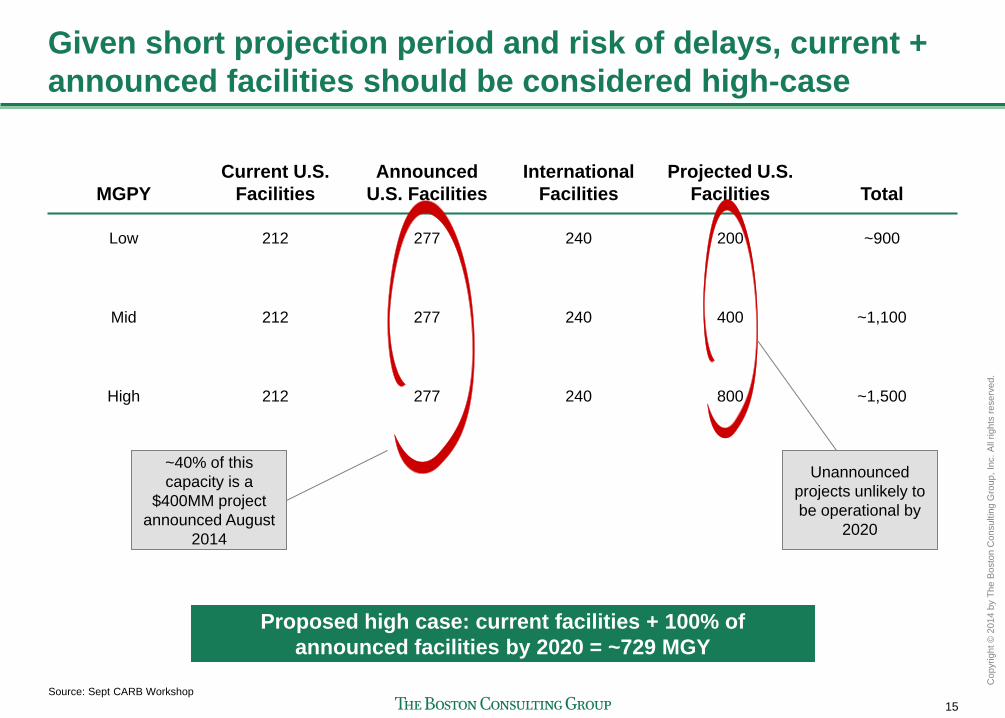

Given short projection period and risk of delays, current +

announced facilities should be considered high-case

MGPY

Current U.S.

Facilities

Announced

U.S. Facilities

International

Facilities

Projected U.S.

Facilities Total

Low

212

277

240

200

~900

Mid

212

277

240

400

~1,100

High

212

277

240

800

~1,500

Unannounced

projects unlikely to

be operational by

2020

Source: Sept CARB Workshop

~40% of this

capacity is a

$400MM project

announced August

2014

Proposed high case: current facilities + 100% of

announced facilities by 2020 = ~729 MGY

16

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Rapid increase in RD coming to California has leveled off

0

10

30

20

40

8

12Q4

7

12Q3

1

12Q2

1

12Q1

1

11Q4

1

11Q3

0

11Q2

0

11Q1

0

14Q1 13Q4

23

13Q1

Million gallons

26

30

13Q3

36

13Q2

Est. weighted CI 33.3 32.4 35.2 33.6 34.0 34.5

Source: CARB July 8, 2014 quarterly report, bCG analysis

~96 million gallons in

2013

17

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Agenda

Sugarcane ethanol

Cellulosic ethanol

Renewable gasoline

Renewable diesel

Low-CI fuel market signal

Constraints to consider for California fuel availability

Expectations for upcoming workshop

18

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

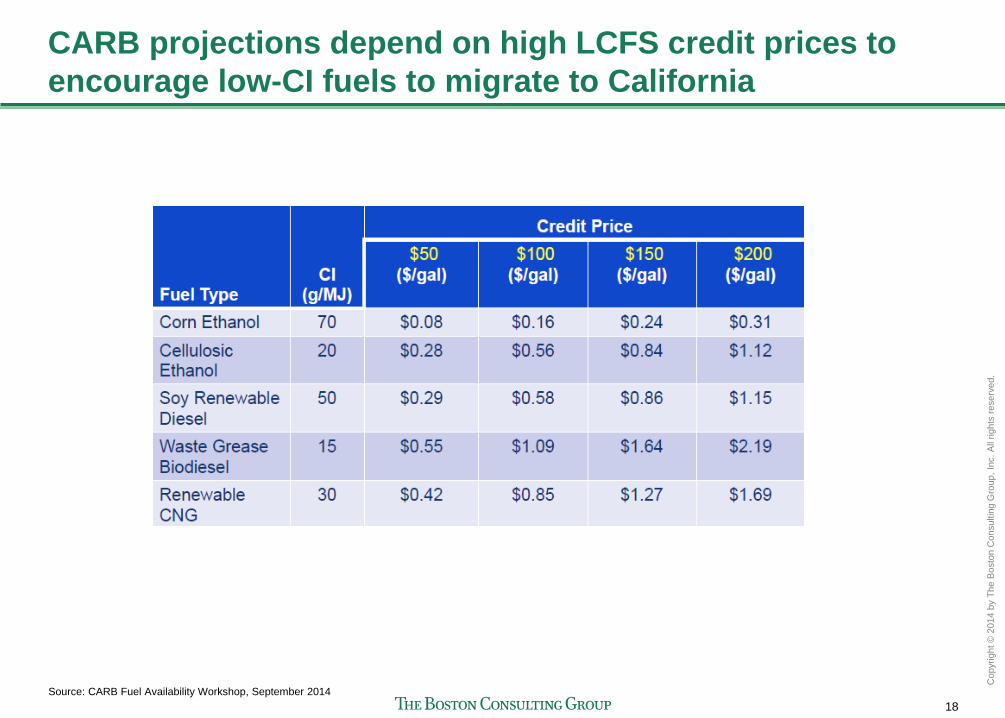

CARB projections depend on high LCFS credit prices to

encourage low-CI fuels to migrate to California

Source: CARB Fuel Availability Workshop, September 2014

19

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Any new regulation requires investment, but relying on

high credit prices to drive investment is risky

Stage Producers Product Credit Price

Early

Mid

Late

A few innovative producers

respond quickly to regulation by

investing in innovative production

techniques

High credit prices encourage

more producers to enter space

Expensive, low supply

Moderate, supply

growing

High, small supply of low-CI

fuels means few in

compliance

Lower, as larger supply of

low-CI fuels means many in

compliance

How will LCFS encourage investment differently than the RFS2?

• RFS2 consistently adjusted downward as investment has lagged expectations

As "traditional" pathways like corn ethanol improve reflect lower-CI values, the gap

required to fill with very low-CI fuels lessens, making investment even riskier.

With lower credit prices, will producers continue to invest? Will existing investments

still be making a suitable return?

20

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Agenda

Sugarcane ethanol

Cellulosic ethanol

Renewable gasoline

Renewable diesel

Low-CI fuel market signal

Constraints to consider for California fuel availability

Expectations for upcoming workshop

21

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

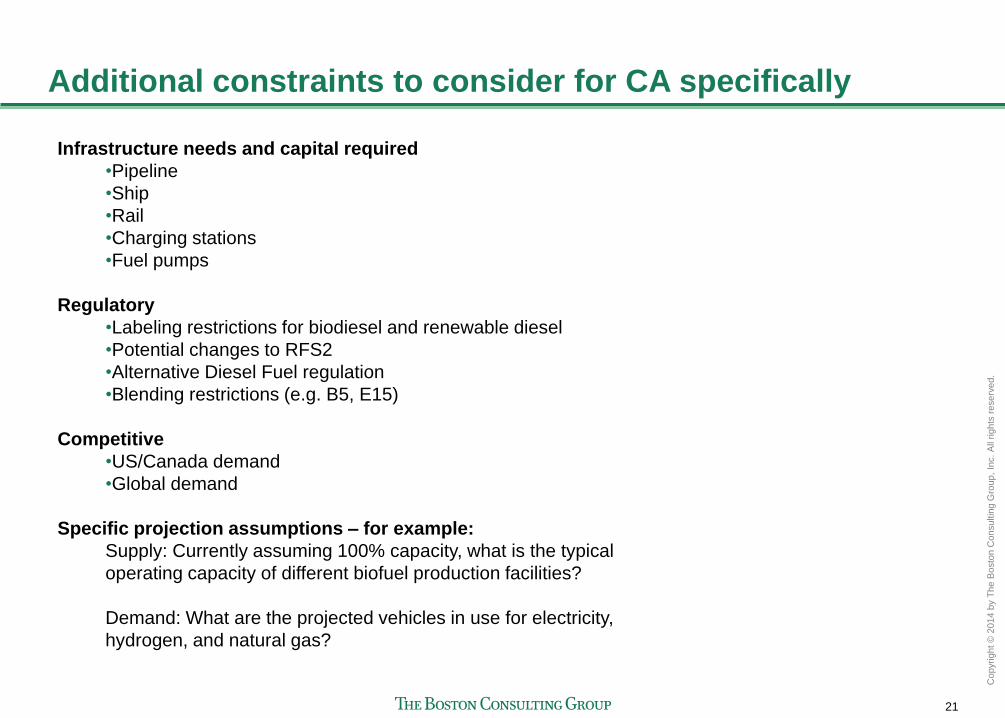

Additional constraints to consider for CA specifically

Infrastructure needs and capital required

•Pipeline

•Ship

•Rail

•Charging stations

•Fuel pumps

Regulatory

•Labeling restrictions for biodiesel and renewable diesel

•Potential changes to RFS2

•Alternative Diesel Fuel regulation

•Blending restrictions (e.g. B5, E15)

Competitive

•US/Canada demand

•Global demand

Specific projection assumptions – for example:

Supply: Currently assuming 100% capacity, what is the typical

operating capacity of different biofuel production facilities?

Demand: What are the projected vehicles in use for electricity,

hydrogen, and natural gas?

22

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Agenda

Sugarcane ethanol

Cellulosic ethanol

Renewable gasoline

Renewable diesel

Low-CI fuel market signal

Constraints to consider for California fuel availability

Expectations for upcoming workshop

23

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

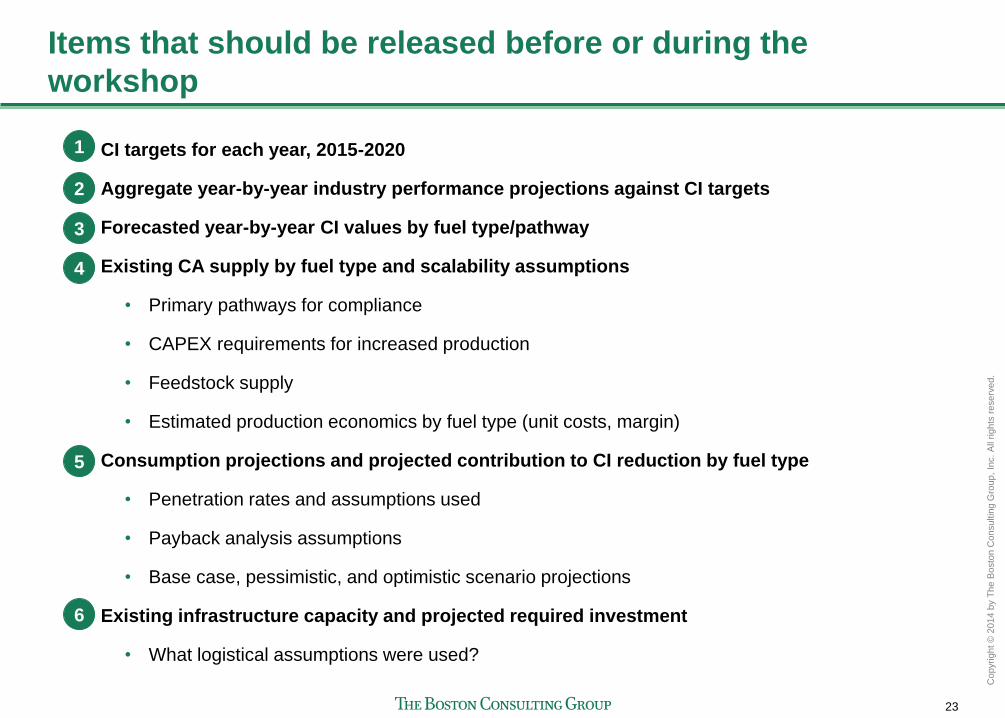

Items that should be released before or during the

workshop

CI targets for each year, 2015-2020

Aggregate year-by-year industry performance projections against CI targets

Forecasted year-by-year CI values by fuel type/pathway

Existing CA supply by fuel type and scalability assumptions

• Primary pathways for compliance

• CAPEX requirements for increased production

• Feedstock supply

• Estimated production economics by fuel type (unit costs, margin)

Consumption projections and projected contribution to CI reduction by fuel type

• Penetration rates and assumptions used

• Payback analysis assumptions

• Base case, pessimistic, and optimistic scenario projections

Existing infrastructure capacity and projected required investment

• What logistical assumptions were used?

1

2

3

4

5

6