Embed Size (px)

Citation preview

August 13, 2016

China: Consumer Staples

Equity Research

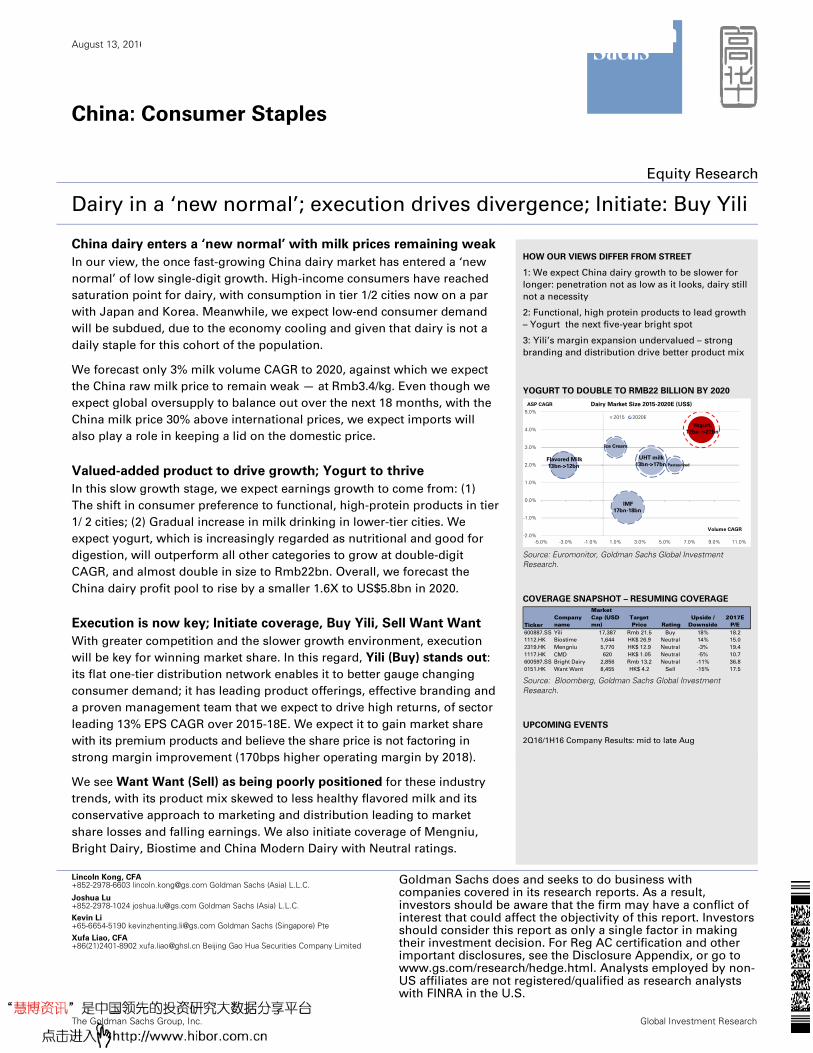

Dairy in a ‘new normal’; execution drives divergence; Initiate: Buy Yili

China dairy enters a ‘new normal’ with milk prices remaining weak

In our view, the once fast-growing China dairy market has entered a ‘new

normal’ of low single-digit growth. High-income consumers have reached

saturation point for dairy, with consumption in tier 1/2 cities now on a par

with Japan and Korea. Meanwhile, we expect low-end consumer demand

will be subdued, due to the economy cooling and given that dairy is not a

daily staple for this cohort of the population.

We forecast only 3% milk volume CAGR to 2020, against which we expect

the China raw milk price to remain weak — at Rmb3.4/kg. Even though we

expect global oversupply to balance out over the next 18 months, with the

China milk price 30% above international prices, we expect imports will

also play a role in keeping a lid on the domestic price.

Valued-added product to drive growth; Yogurt to thrive

In this slow growth stage, we expect earnings growth to come from: (1)

The shift in consumer preference to functional, high-protein products in tier

1/ 2 cities; (2) Gradual increase in milk drinking in lower-tier cities. We

expect yogurt, which is increasingly regarded as nutritional and good for

digestion, will outperform all other categories to grow at double-digit

CAGR, and almost double in size to Rmb22bn. Overall, we forecast the

China dairy profit pool to rise by a smaller 1.6X to US$5.8bn in 2020.

Execution is now key; Initiate coverage, Buy Yili, Sell Want Want

With greater competition and the slower growth environment, execution

will be key for winning market share. In this regard, Yili (Buy) stands out:

its flat one-tier distribution network enables it to better gauge changing

consumer demand; it has leading product offerings, effective branding and

a proven management team that we expect to drive high returns, of sector

leading 13% EPS CAGR over 2015-18E. We expect it to gain market share

with its premium products and believe the share price is not factoring in

strong margin improvement (170bps higher operating margin by 2018).

We see Want Want (Sell) as being poorly positioned for these industry

trends, with its product mix skewed to less healthy flavored milk and its

conservative approach to marketing and distribution leading to market

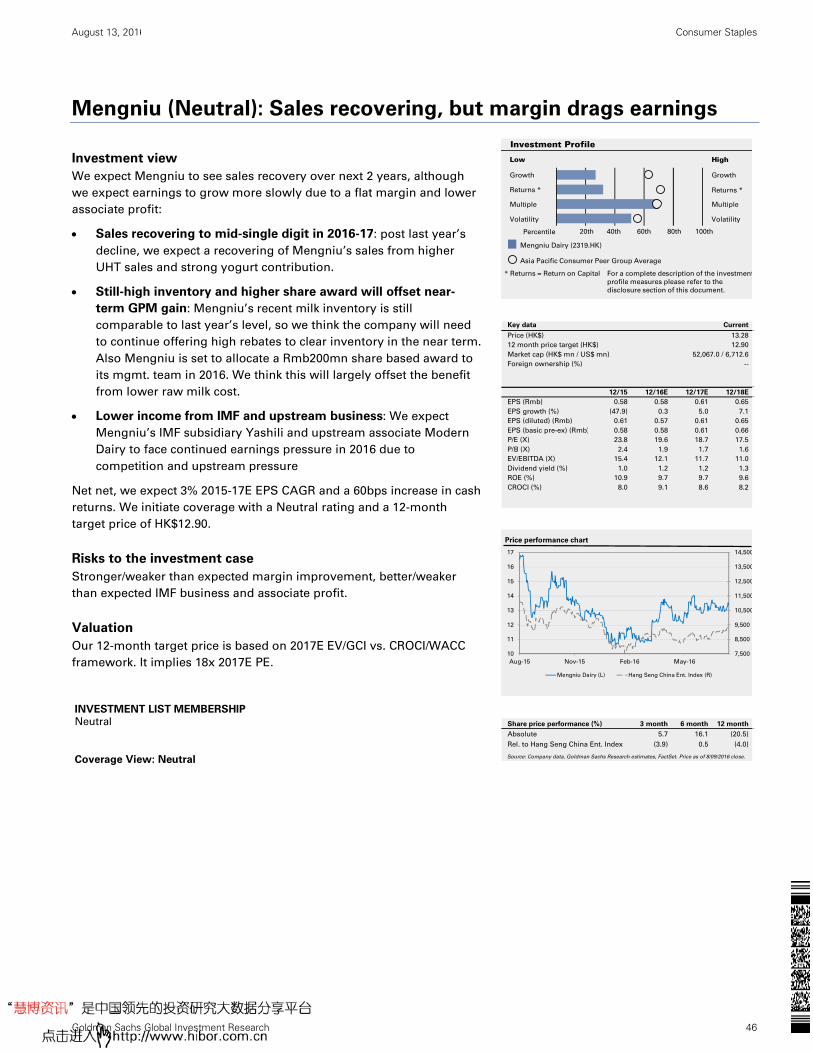

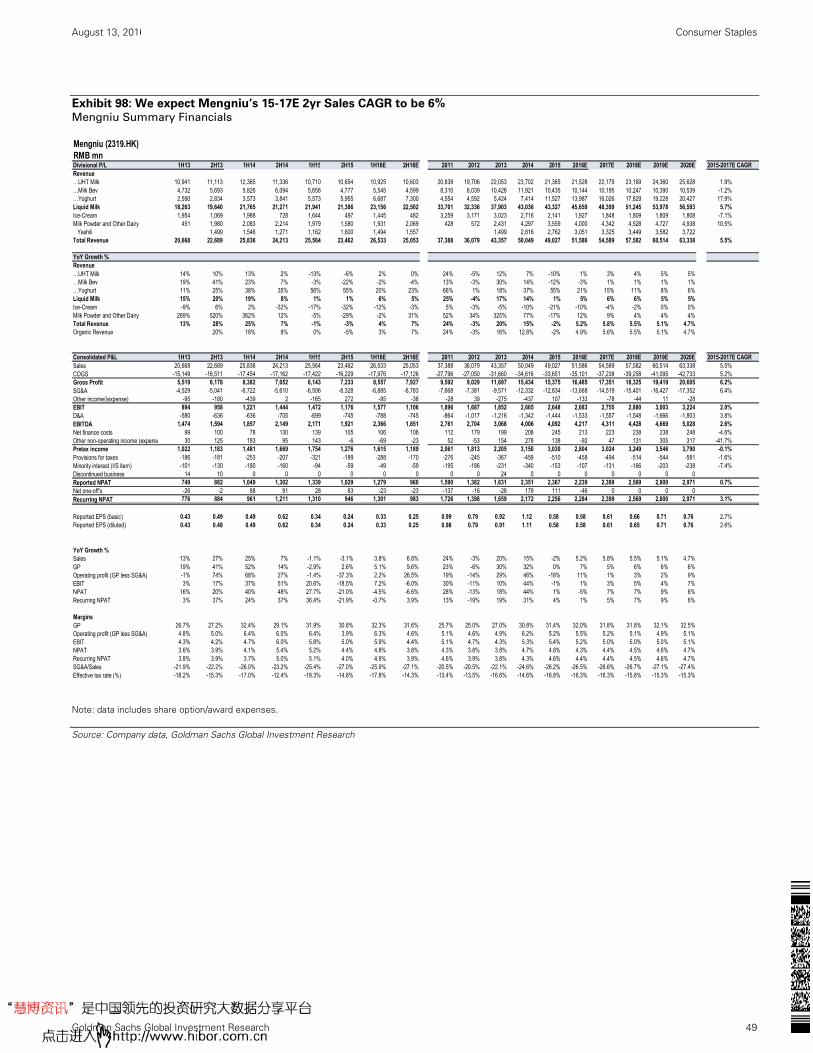

share losses and falling earnings. We also initiate coverage of Mengniu,

Bright Dairy, Biostime and China Modern Dairy with Neutral ratings.

HOW OUR VIEWS DIFFER FROM STREET

1: We expect China dairy growth to be slower for

longer: penetration not as low as it looks, dairy still

not a necessity

2: Functional, high protein products to lead growth

– Yogurt the next five-year bright spot

3: Yili’s margin expansion undervalued – strong

branding and distribution drive better product mix

YOGURT TO DOUBLE TO RMB22 BILLION BY 2020

Source: Euromonitor, Goldman Sachs Global Investment Research.

COVERAGE SNAPSHOT – RESUMING COVERAGE

Source: Bloomberg, Goldman Sachs Global Investment Research.

UPCOMING EVENTS

2Q16/1H16 Company Results: mid to late Aug

Lincoln Kong, CFA +852-2978-6603 [email protected] Goldman Sachs (Asia) L.L.C. Goldman Sachs does and seeks to do business with

companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S.

Joshua Lu +852-2978-1024 [email protected] Goldman Sachs (Asia) L.L.C. Kevin Li +65-6654-5190 [email protected] Goldman Sachs (Singapore) Pte

Xufa Liao, CFA +86(21)2401-8902 [email protected] Beijing Gao Hua Securities Company Limited

The Goldman Sachs Group, Inc. Global Investment Research

Pasteurized

UHT milk

13bn->17bnFlavored Milk

13bn->12bn

Yogurt,

12bn ->22bn

IMF

17bn-18bn

Ice Cream

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

-5.0% -3.0% -1.0% 1.0% 3.0% 5.0% 7.0% 9.0% 11.0%

Dairy Market Size 2015-2020E (US$)

2015 2020E

Volume CAGR

ASP CAGR

TickerCompany name

Market Cap (USD mn)

Target Price Rating

Upside / Downside

2017E P/E

600887.SS Yili 17,387 Rmb 21.5 Buy 18% 18.2

1112.HK Biostime 1,644 HK$ 26.9 Neutral 14% 15.0

2319.HK Mengniu 5,770 HK$ 12.9 Neutral -3% 19.4

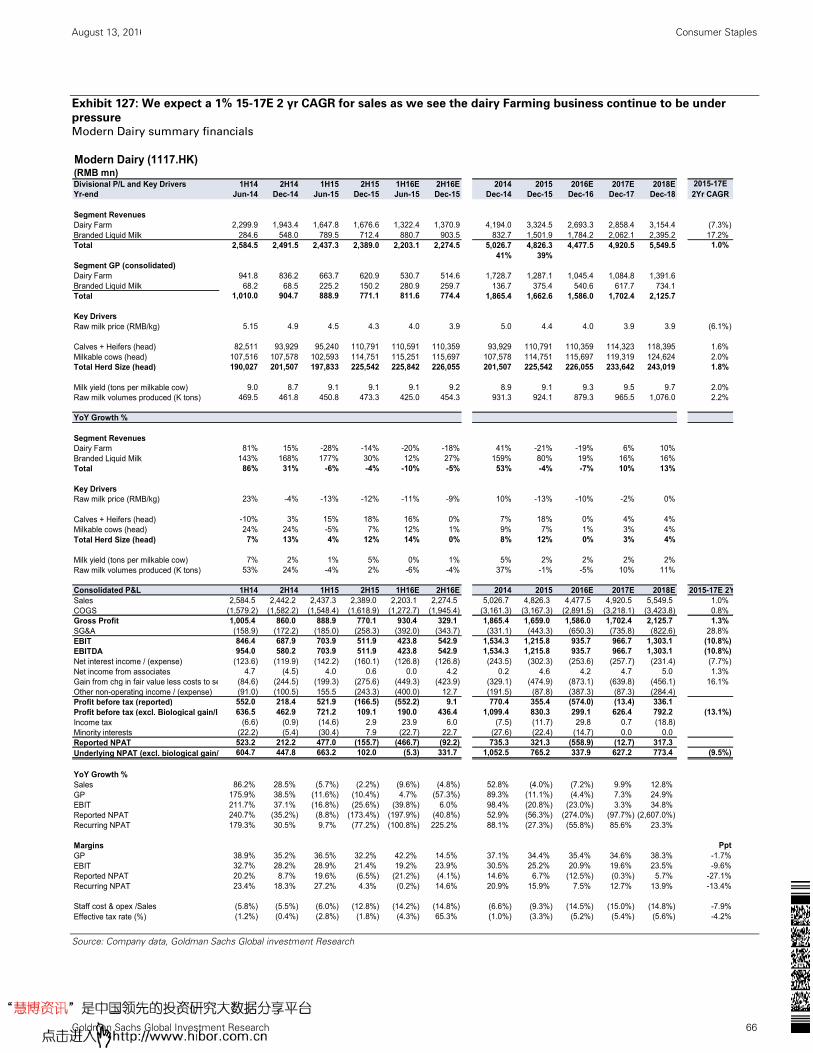

1117.HK CMD 620 HK$ 1.05 Neutral -5% 10.7

600597.SS Bright Dairy 2,856 Rmb 13.2 Neutral -11% 36.8

0151.HK Want Want 8,455 HK$ 4.2 Sell -15% 17.5

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 2

Contents

Our thesis in 6 charts 4

China dairy enters a ‘new normal’ stage; milk price to remain weak 5

Slower growth for longer 5

Global milk price recovering in 2017, but China raw milk price to remain weak 7

Next growth driver: high protein, functional; Yogurt the bright spot 11

China profit pool to increase 1.6X by 2020 to Rmb5.8bn 11

Yogurt will be the bright spot 13

Execution is now the key: Yili stands out on distribution, branding 16

Products, branding, distribution, mgmt. comparison 16

Dairy 2020: Yili to gain market share in key product categories 24

Valuation: Yili our top pick, Want Want overvalued 29

Yili (Buy): A long-term stand-out leader; fastest sales/EPS growth 33

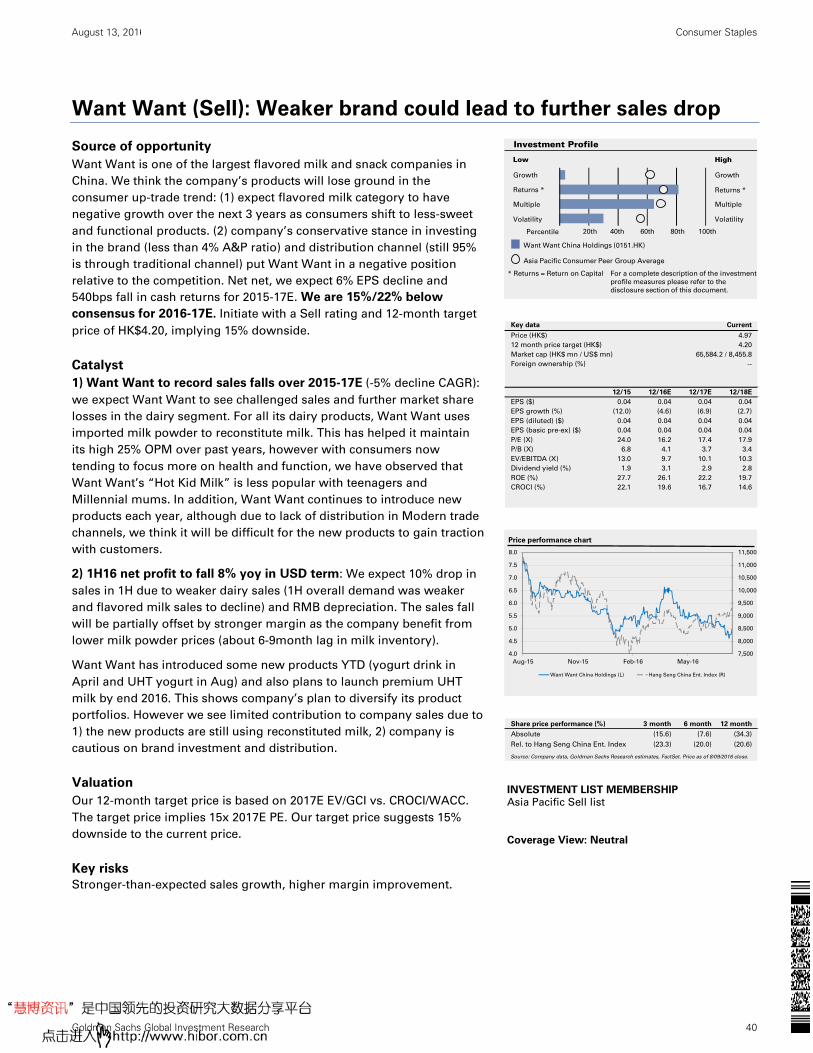

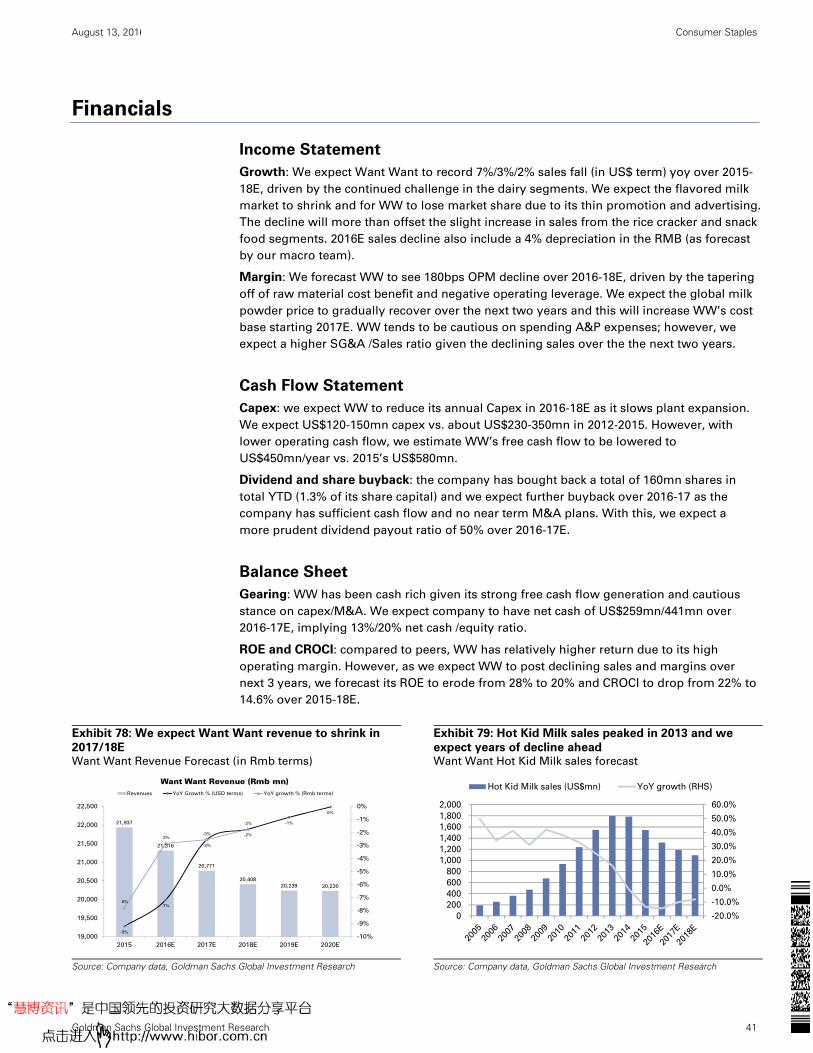

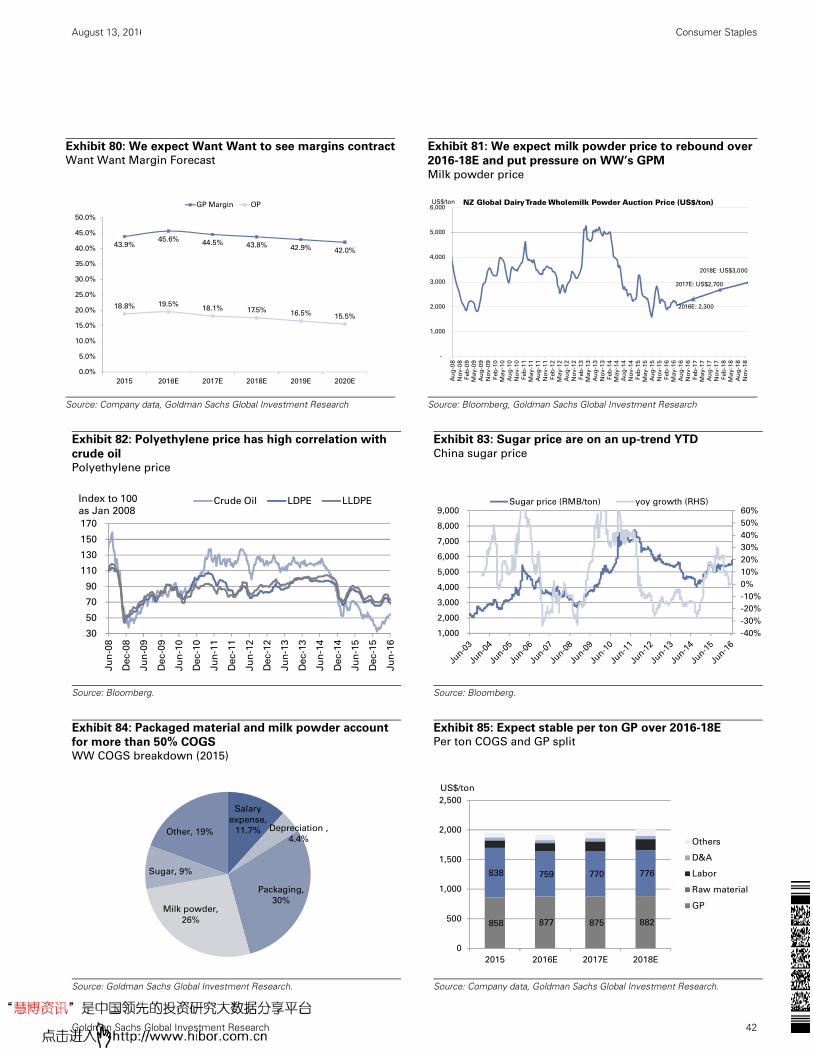

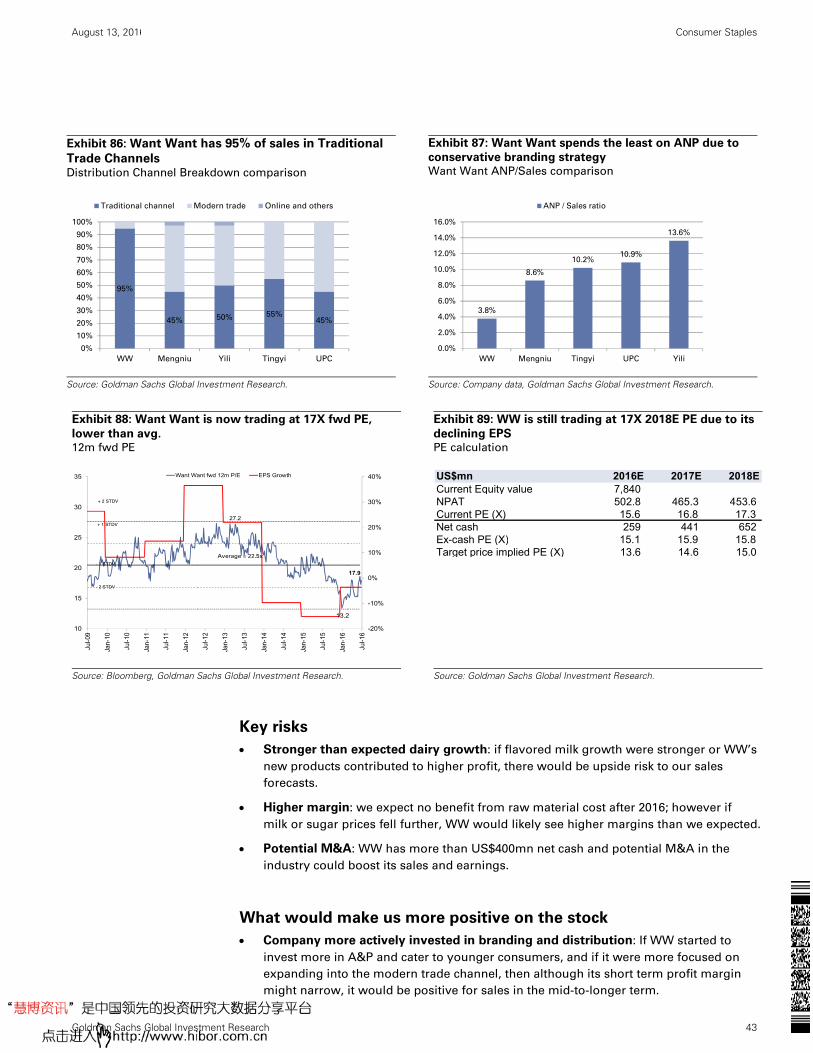

Want Want (Sell): Weaker brand could lead to further sales drop 40

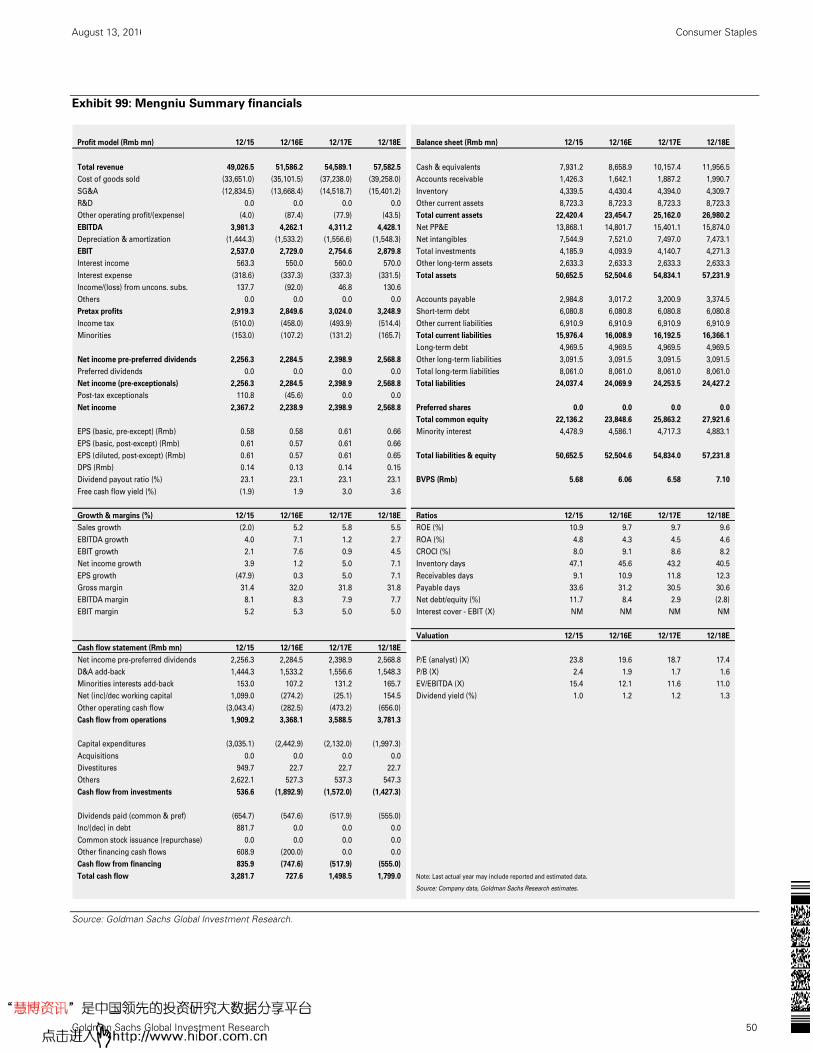

Mengniu (Neutral): Sales recovering, but margin drags earnings 46

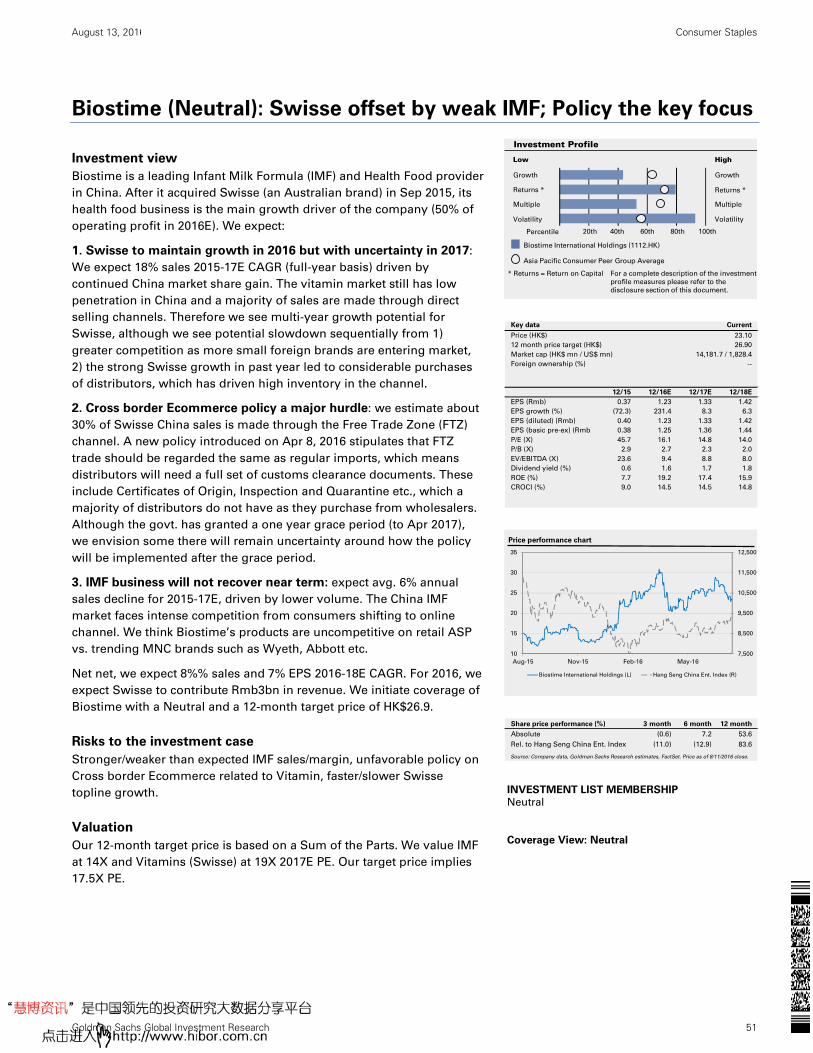

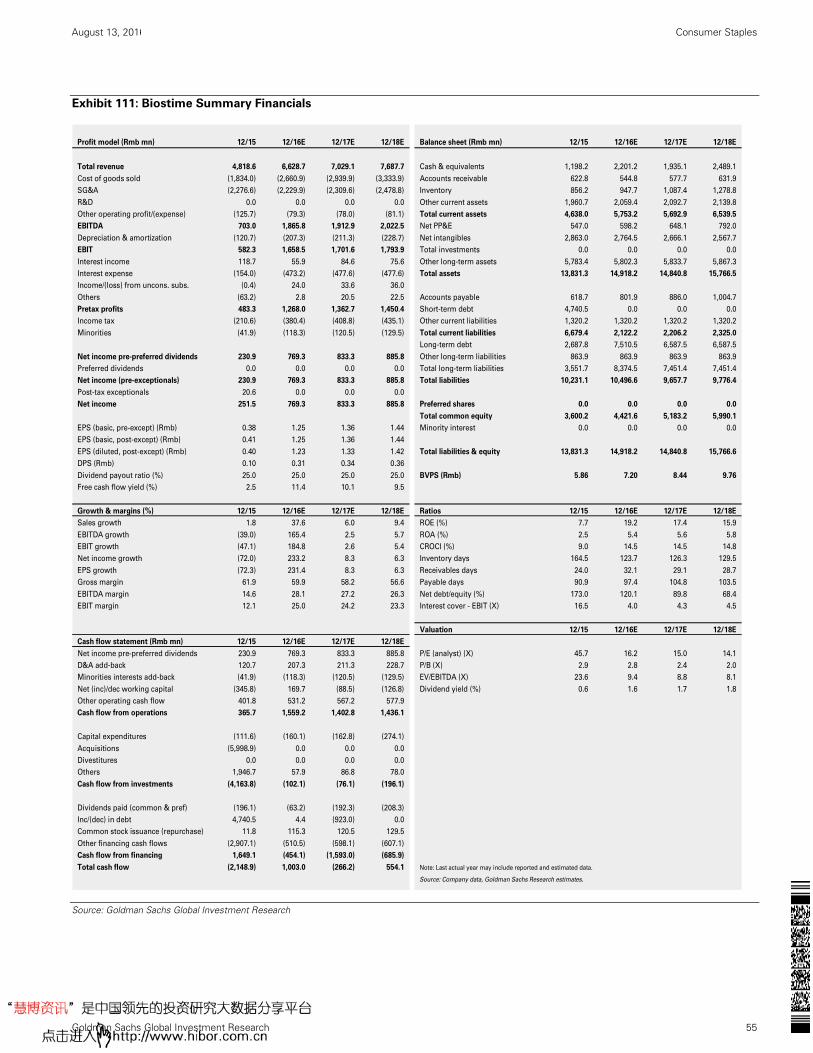

Biostime (Neutral): Swisse offset by weak IMF; Policy the key focus 51

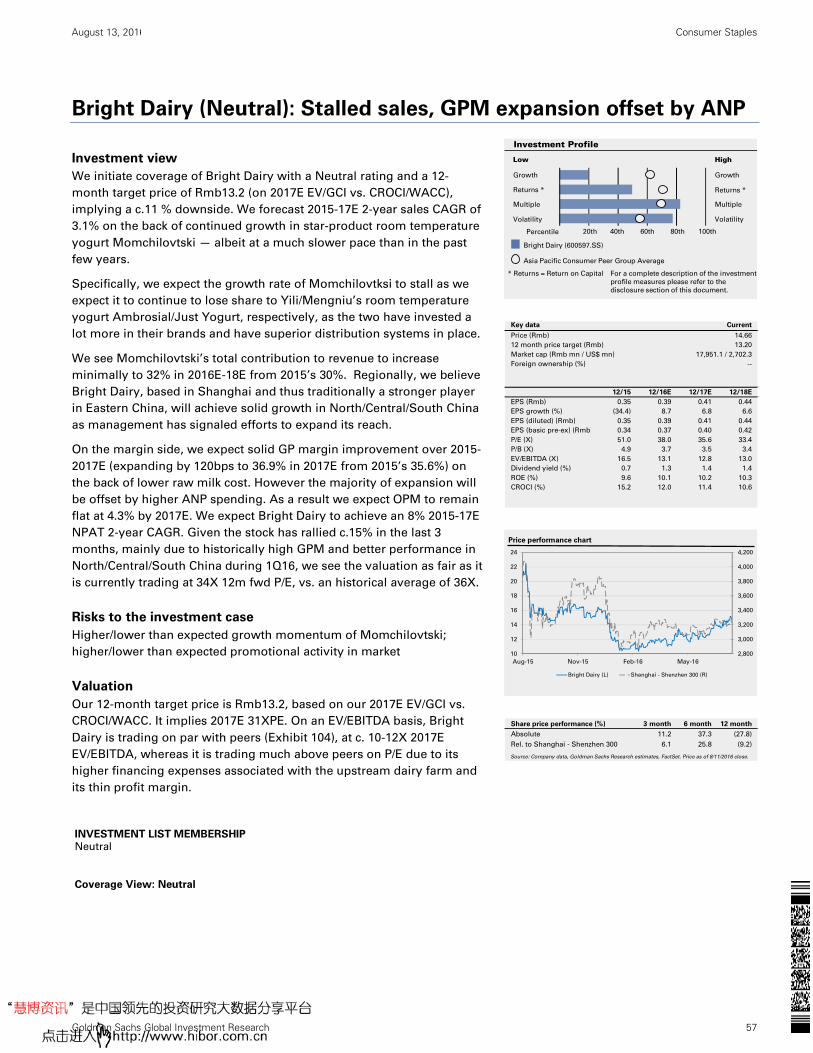

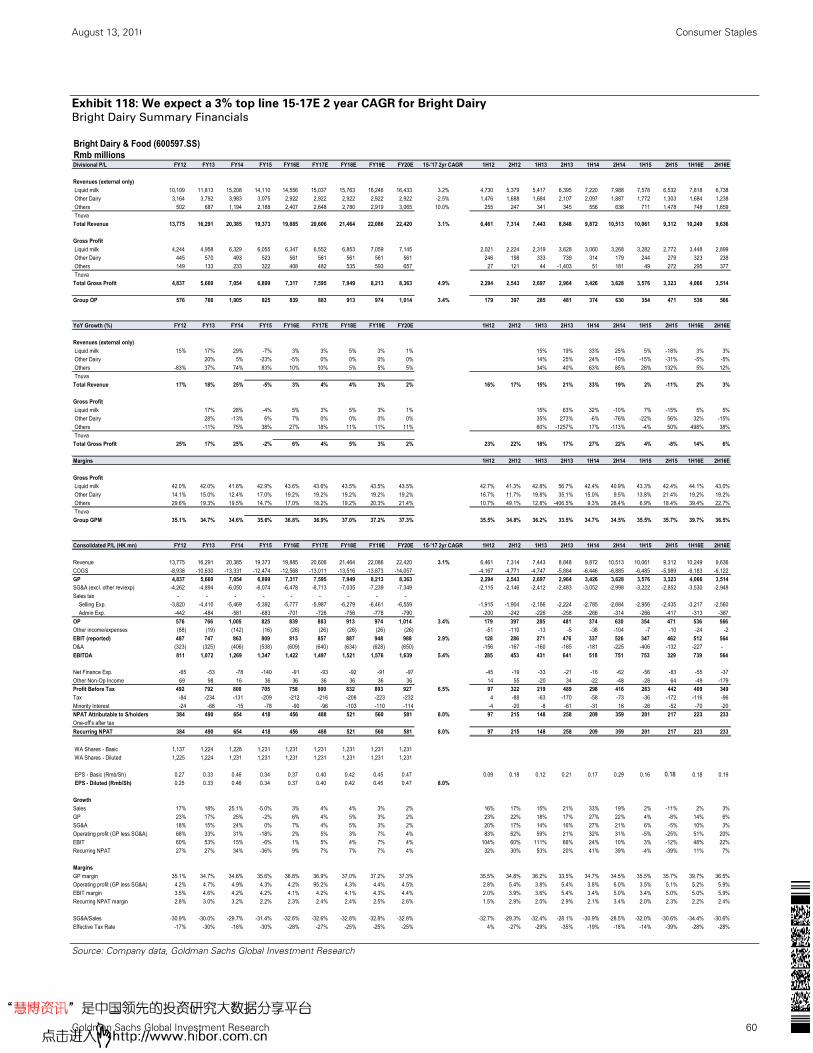

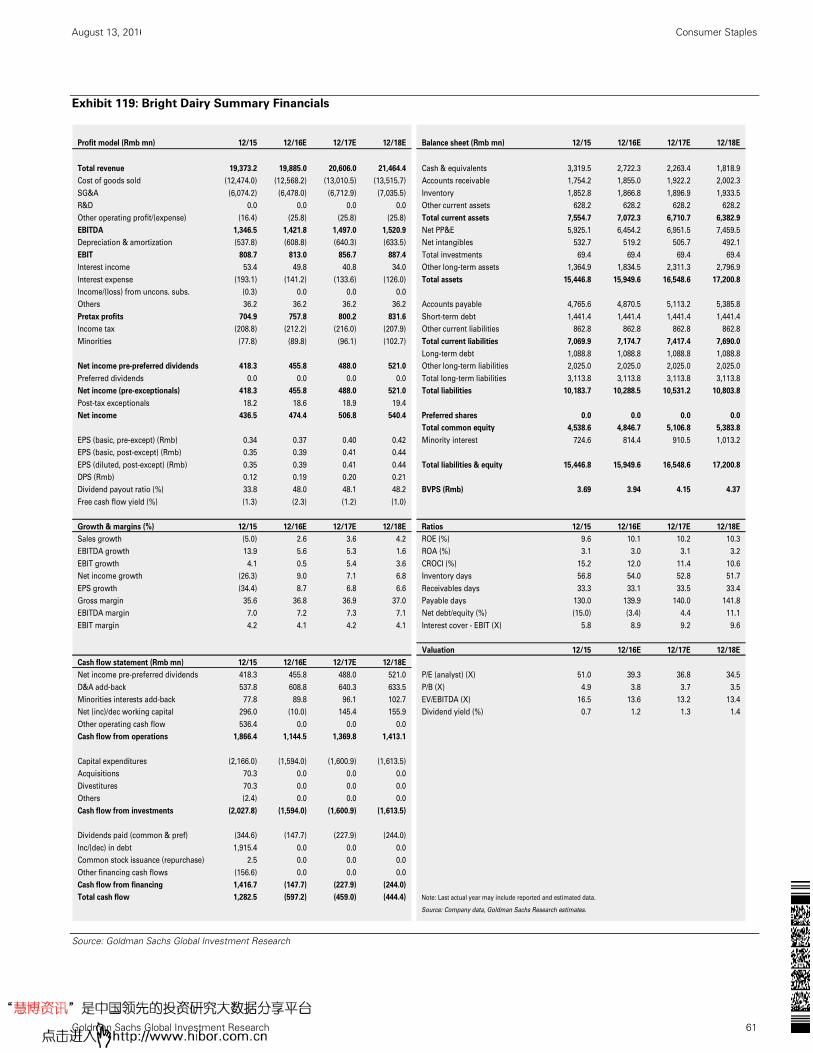

Bright Dairy (Neutral): Stalled sales, GPM expansion offset by ANP 57

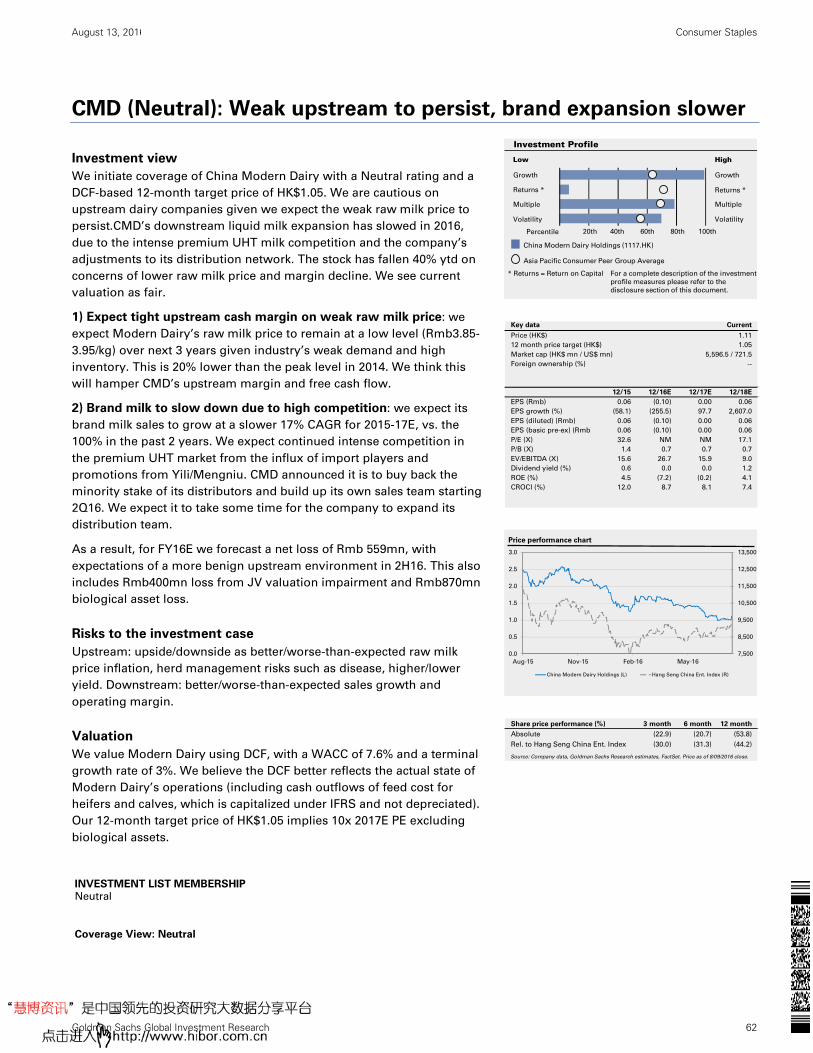

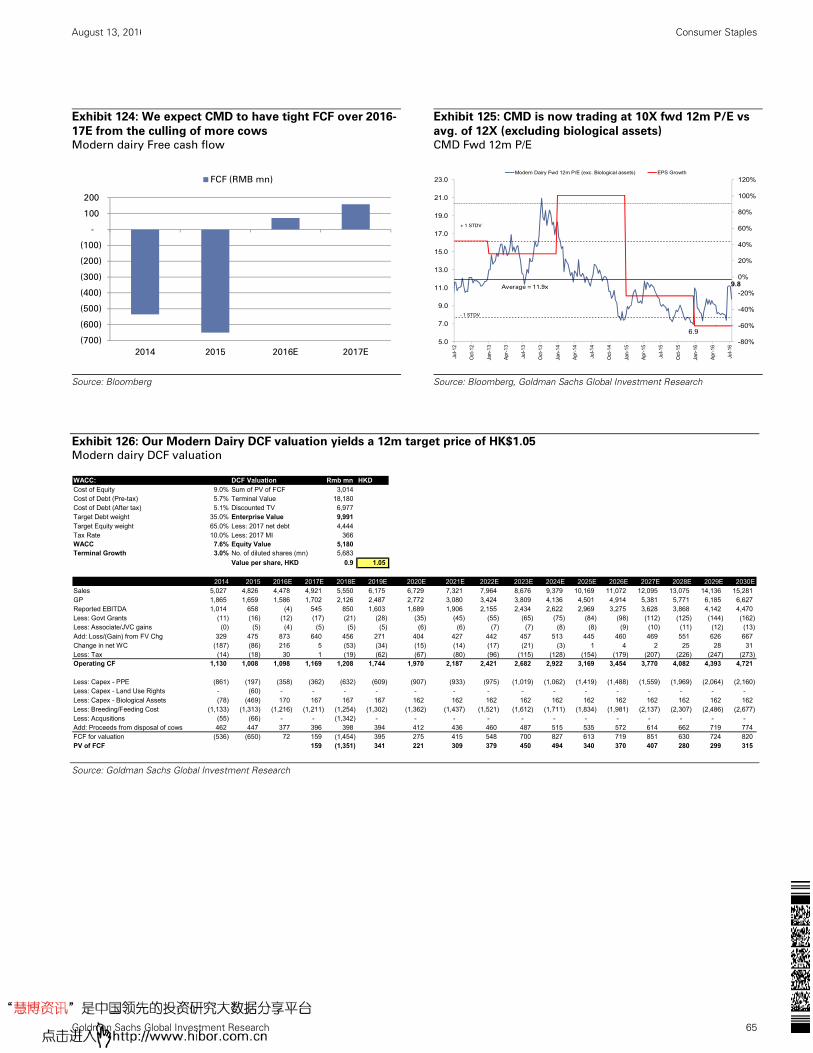

CMD (Neutral): Weak upstream to persist, brand expansion slower 62

Appendix: China dairy overview 68

Disclosure Appendix 74

Prices as of August 9, 2016 close, unless otherwise stated.

Exhibit 1: Comp Sheet (China and Global dairy)

*Conviction list, NC: Not Covered, NR: Not Rated.

Source: Bloomberg, Goldman Sachs Global Investment Research

BBG Ticker Name Mkt Cap Last GS Target List Report EPS 15-17 PE PE PEG EV/EBITDA EV/EBITDA P/B P/B Div Yield Div Yield ROE ROE

Close Rating Price Crncy Crncy 6M Chg CAGR CY16 CY17 2Yr CY16 CY17 CY15 CY16E CY16E CY17E CY16E CY17

US$m Price L.C. L.C. L.C. % % (X) (X) CAGR (X) (X) (X) (X) % % % %

China Dairy

600887 CH Yili 16,700 18.3 Buy 21.5 CNY CNY 37.0 13.5 20.5 18.1 1.5 13.4 11.6 5.6 5.0 2.9 3.3 25.5 25.9

2319 HK Mengniu 6,894 13.6 Neutral 12.9 HKD CNY 19.2 2.6 20.4 19.4 7.7 12.3 11.8 2.0 1.9 1.0 1.0 8.3 8.1

600597 CH Bright Dairy 2,770 15.0 Neutral 13.2 CNY CNY 40.1 7.8 38.8 36.3 5.0 13.3 13.0 4.1 3.8 1.2 1.3 8.7 8.7

151 HK Want Want China 8,345 5.1 Sell 4.2 HKD USD (5.2) (5.8) 16.7 17.9 (2.9) 9.7 10.2 4.5 4.1 0.4 0.4 26.0 22.2

1117 HK Modern Dairy^ 759 1.1 Neutral 1.05 HKD CNY (20.7) (14.4) 16.2 8.7 (1.1) 26.5 15.8 0.6 0.7 - - (7.1) (0.2)

Average 35,468 20.9 19.5 1.9 12.6 11.5 4.4 4.0 1.7 1.9 20.3 19.7

China IMF

1112 HK Biostime 1,918 23.6 Neutral 26.9 HKD CNY 9.0 89.5 16.7 15.4 0.2 9.4 8.8 3.4 2.8 1.3 1.4 19.2 17.4

1230 HK Yashili 1,046 1.7 NC N/A HKD CNY (4.5) 54.4 40.7 23.6 0.7 17.3 9.8 NA 1.1 1.0 0.8 3.0 4.6

002570 CH Beingmate 1,909 12.4 NC N/A CNY CNY 13.9 31.5 100.9 71.7 3.2 32.8 27.8 NA 3.4 0.2 0.1 1.5 4.5

Average 59,110 54.8 39.2 1.5 20.3 16.5 3.4 2.7 0.8 0.8 8.8 9.6

Global leaders

BN FP Danone 50,334 68.8 NR N/A EUR EUR 16.0 4.1 22.7 21.5 5.5 12.5 12.1 3.5 3.5 2.4 2.5 14.5 14.9

NESN VX Nestle 247,695 78.0 Sell 65.0 CHF CHF 7.0 4.4 23.1 21.6 5.2 15.0 14.1 NA 3.6 3.0 2.8 16.2 16.7

FSF NZ Fonterra 6,673 5.8 NC N/A NZD NZD (0.2) 15.5 10.9 10.7 0.7 7.9 7.6 NA 1.3 6.9 7.2 12.5 12.5

ALMARAI AB Almarai 11,733 55.0 Buy 72.0 SAR SAR 6.9 10.7 21.5 17.6 2.0 15.9 13.8 4.2 3.8 2.1 2.1 17.8 19.5

CHR DC CHR Hansen 8,455 427.8 Neutral 452.0 DKK EUR 8.9 13.2 37.6 34.1 2.8 25.0 21.6 33.2 25.2 0.2 0.2 78.8 57.7

MJN US Mead Johnson 16,363 88.6 Neutral 96.0 USD USD 25.3 6.0 25.2 23.0 4.2 16.8 15.6 NA NA 2.1 2.4 (114.5) (101.9)

2269 JP Meiji 14,849 9,850.0 Neutral 12,000.0 JPY JPY 6.7 6.8 20.3 20.3 3.0 11.7 10.9 3.8 3.3 1.0 1.4 15.7 14.6

Average 341,253 22.2 20.7 4.7 14.1 13.2 21.9 3.8 2.6 2.6 11.0 11.4

China F&B/FMCG

322 HK Tingyi 5,382 7.5 Neutral 6.4 HKD USD (12.5) (4.2) 24.3 18.8 (5.8) 7.8 6.8 1.8 1.8 0.2 0.3 5.6 6.9

220 HK UPC 3,470 6.2 Neutral 6.5 HKD CNY 24.6 17.5 23.7 20.3 1.4 9.1 8.0 1.9 1.9 0.7 0.9 8.2 8.9

168 HK Tsingtao 5,522 28.6 Sell 24.3 HKD CNY (0.3) (1.2) 26.0 24.9 (22.6) 12.3 11.8 2.0 1.9 1.0 1.1 7.8 7.7

600519 CH Kweichow Moutai 59,606 315.4 Buy 332.3 CNY CNY 54.7 16.1 22.2 19.0 1.4 13.2 11.1 6.2 5.4 2.3 2.6 25.1 25.4

1044 HK Hengan 10,455 66.9 NC N/A HKD HKD (0.4) 6.1 18.6 17.9 3.1 11.6 11.1 NA 4.3 3.3 2.8 23.8 22.8

288 HK WH Group 11,332 6.0 Buy* 7.4 HKD USD 39.5 9.2 12.2 10.8 1.3 6.3 5.7 2.1 1.9 0.3 0.5 14.2 14.2

Average 8,851 21.0 18.3 (0.2) 11.7 10.2 4.9 4.3 1.9 2.1 21.0 21.2 ^ Excl. biological FV chg gain / (loss)

Price

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 3

PM Summary

Slower growth for longer

China’s dairy industry was worth US$64bn in 2015, up from US$42bn in 2011. Although

total per capita consumption is still low vs. DM countries (20kg vs. 200kg in the US), we

think the market has entered a slower growth stage — and we estimate only 3%

volume CAGR over 2015-2020.

The slower growth is due to: 1) tier 1 and 2 cities already have similar penetration rates as

Japan/Korea and 2) economic slowdown is impacting low-end consumer demand (dairy is

not a staple for most low-end consumers).

Our GS proprietary global dairy Supply and Demand model (including all major milk

production and consumption countries globally) indicates a gradual recovery in the milk

price in 2017. (GSe: New Zealand Whole Milk Power price to reach US$2,700/ton by end

2017, 30% increase from now) as milk output has started to slow in both NZ and the EU.

In China, however, with the slower demand growth, our milk supply-demand model

suggests the supply gap will be filled by higher imports (given a still large price gap), and

therefore we see China raw milk prices remaining flat out to 2020 (GSe: around

Rmb3.40/kg).

Growth to come from value-added products, Yogurt to outperform

With slower volume growth, we see growth coming from the shift in consumer preferences

away from sweeter products like flavored milk towards functional, high protein products –

like probiotic yogurt.

Within all dairy subcategories, we expect yogurt will outperform the rest and almost

double in size by 2020. With further distribution expansion, we see low temp yogurt

continuing to deliver mid-teen growth whereas we expect UHT yogurt to be more of a

short-term product before gradually tapering off as distribution infrastructure improves

and consumers shift to fresher, healthier products. In all, we expect the China dairy profit

pool to grow 1.6X by 2020 to US$5.8bn over 2015, driven by growth in value-added

products and margin improvement at dairy companies (due to the change in product mix).

To capture the step change in the growth profile of the industry, we derive our 12-month

target prices from our returns-based Director’s Cut methodology (2017E EV/GCI vs.

CROCI/WACC).

Buy Yili on better execution; Sell Want Want

We think a successful downstream expansion strategy is the key for dairy players to win

market share. In this regard, Yili stands out. It has led on this front for the last three years,

and we expect it to extend this leadership out to 2020. Yilli is best positioned in the higher

growth categories and offers more targeted marketing to cater to young consumers. It also

has a more comprehensive distribution network and a prudent, proven management team.

We initiate with Buy and 12-month Rmb21.5. We expect it to deliver fastest 14% EPS CAGR

and highest cash return of 27% over 2015-17E vs. peers in an 8-15% range.

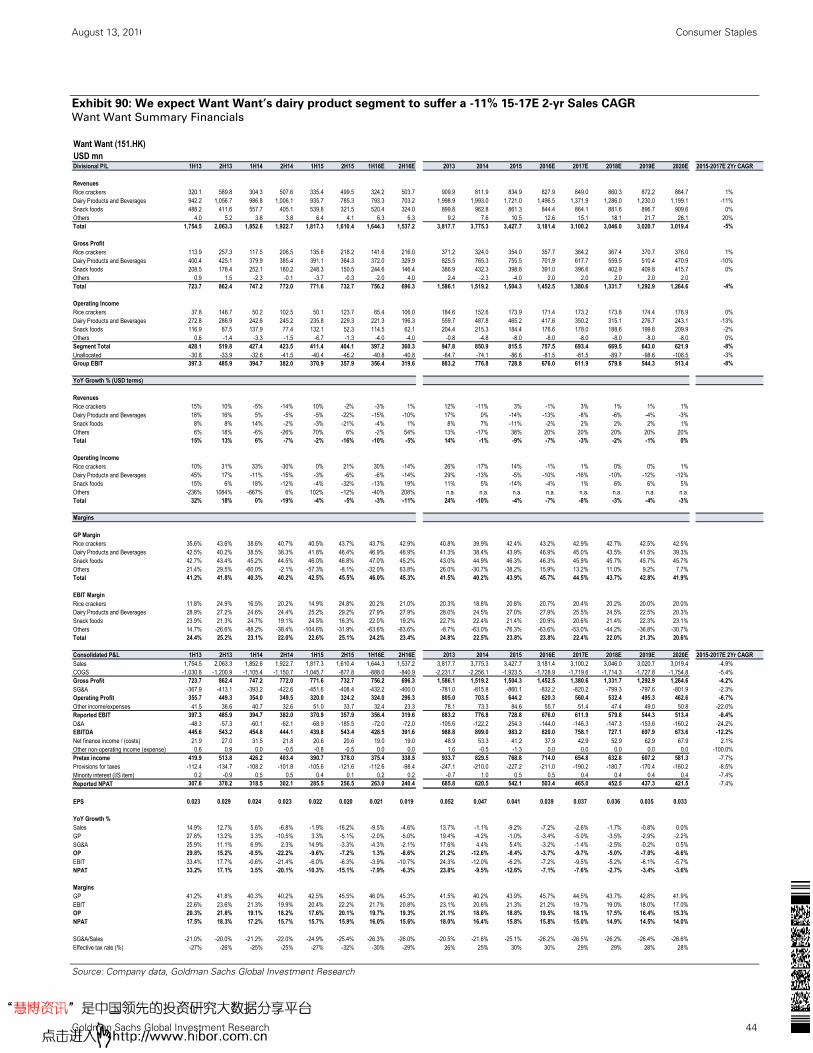

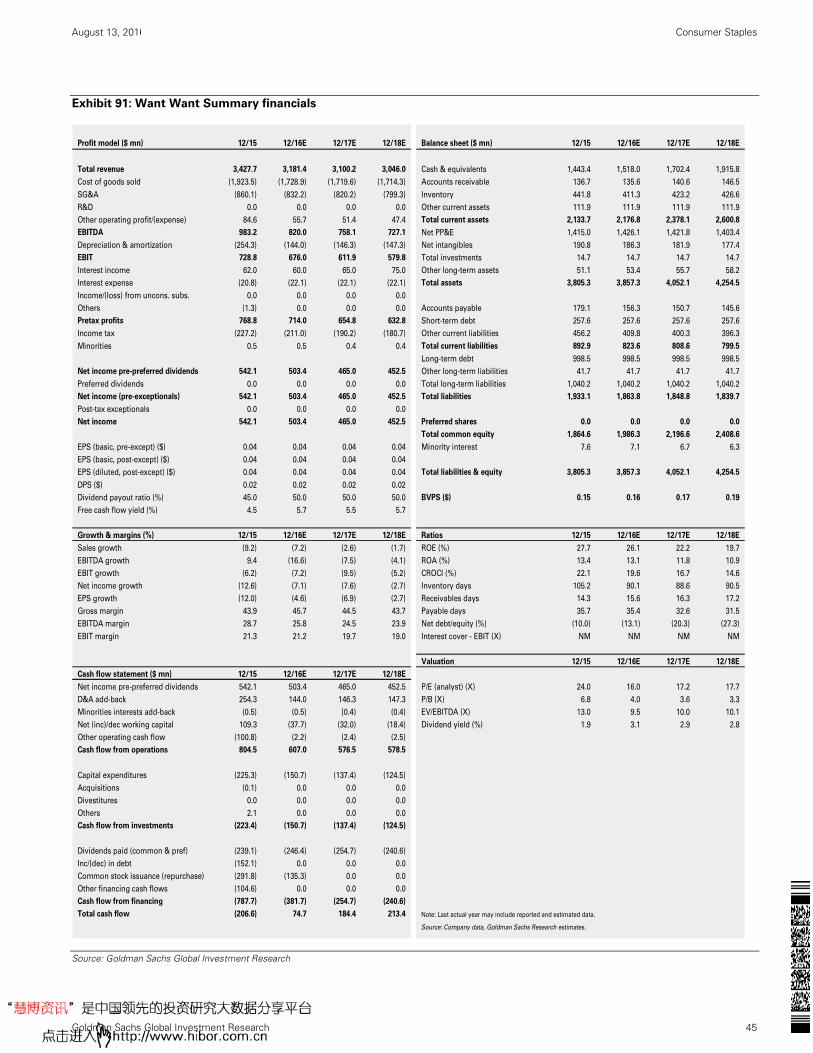

In contrast, we think Want Want stands to lose market share and register negative

growth as its product offerings of flavored milk and rice crackers are less innovative and

positioned in declining categories. We expect -4% EPS (Rmb terms) CAGR over 2015-18E.

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 4

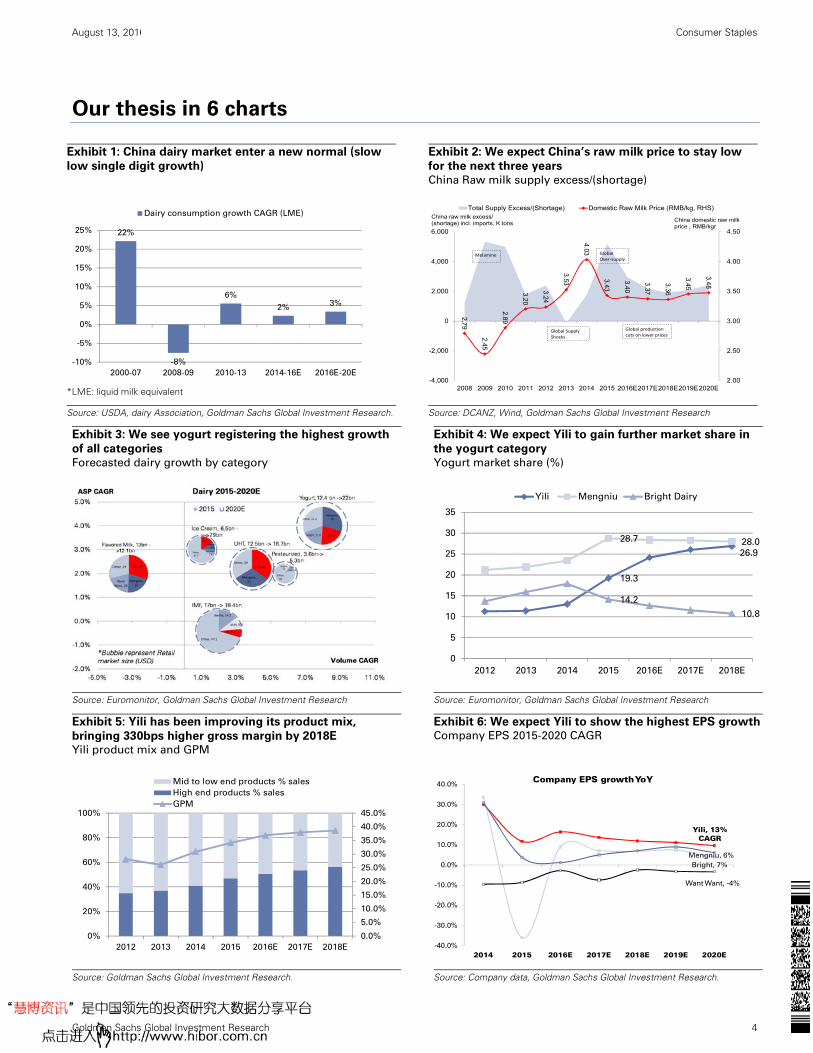

Our thesis in 6 charts

Exhibit 3: We see yogurt registering the highest growth

of all categories

Forecasted dairy growth by category

Exhibit 4: We expect Yili to gain further market share in

the yogurt category

Yogurt market share (%)

Source: Euromonitor, Goldman Sachs Global Investment Research

Source: Euromonitor, Goldman Sachs Global Investment Research

Exhibit 5: Yili has been improving its product mix,

bringing 330bps higher gross margin by 2018E Yili product mix and GPM

Exhibit 6: We expect Yili to show the highest EPS growth Company EPS 2015-2020 CAGR

Source: Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

19.3

26.9

28.7 28.0

14.2

10.8

0

5

10

15

20

25

30

35

2012 2013 2014 2015 2016E 2017E 2018E

Yili Mengniu Bright Dairy

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

0%

20%

40%

60%

80%

100%

2012 2013 2014 2015 2016E 2017E 2018E

Mid to low end products % sales

High end products % sales

GPM

Yili, 13% CAGR

Bright, 7%

Mengniu, 6%

Want Want, -4%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

2014 2015 2016E 2017E 2018E 2019E 2020E

Company EPS growth YoY

Exhibit 1: China dairy market enter a new normal (slow

low single digit growth)

Exhibit 2: We expect China’s raw milk price to stay low

for the next three years

China Raw milk supply excess/(shortage)

*LME: liquid milk equivalent

Source: USDA, dairy Association, Goldman Sachs Global Investment Research.

Source: DCANZ, Wind, Goldman Sachs Global Investment Research

22%

-8%

6%

2%3%

-10%

-5%

0%

5%

10%

15%

20%

25%

2000-07 2008-09 2010-13 2014-16E 2016E-20E

Dairy consumption growth CAGR (LME)

2.79

2.45

2.89

3.20

3.24

3.53

4.03

3.43

3.40

3.37

3.36

3.45

3.48

2.00

2.50

3.00

3.50

4.00

4.50

-4,000

-2,000

0

2,000

4,000

6,000

2008 2009 2010 2011 2012 2013 2014 2015 2016E2017E2018E2019E2020E

Total Supply Excess/(Shortage) Domestic Raw Milk Price (RMB/kg, RHS)

Melamine

China raw milk excess/ (shortage) incl. imports, K tons

China domestic raw milk price , RMB/kgr

Global Supply Shocks

Global Over‐supply

Global production cuts on lower prices

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 5

China dairy enters a ‘new normal’ stage; milk price to remain weak

We see China dairy industry growth having entered a ‘new normal’ stage and expect low

single digit volume growth over the next 3-4 years. Per capita diary penetration for high tier

cities is already comparable with levels in Japan and Korea level and in our view therefore

has reached equilibrium. On the other hand, demand in lower tier cities are more a

function of economic growth as dairy is not yet a staple among lower-income Chinese.

With the slower demand, we see the China raw milk price remaining weak even though we

expect the global S/D backdrop to gradually recover. In light of this, we are cautious on

upstream dairy farming companies.

As the industry shift from high growth to low growth, we see the earning growth driver for

dairy companies also changing. It is more difficult for companies to grow if they simply

expand their distribution network or push new products into existing channels. Going

forward we think execution will be the key to winning market share, Yili stands out with

strong results in the past years.

Slower growth for longer

China dairy: double digit volume growth before 2014, but subdued in past 2 years

The China dairy market has grown nine-fold in the past 15 years with a total addressable

market of US$64bn currently. Before 2014, dairy demand growth average 12% for more

than 10 years, with Yili and Mengniu growing their sales six-fold.

Per capita comparison not always correct, high tier city consumption already on par

with overseas peers

Compared with US/EU, China’s per capita consumption is low (roughly 20kg per person vs.

200kg in the US). Among staples categories, dairy is also one of the least penetrated at

only avg. 22% of US/EU level. However, in light of their different dietary habits, we think

US/EU’s dairy consumption is not a good comparable for China and think Japan/Korea are

better benchmarks.

Exhibit 10 shows that for liquid milk (fresh + UHT milk), China per capita is about 46% of

the Japan/Korea avg. and if we include the flavored milk, then China is already 76%. This is

higher than the relative penetration for RTD tea or instant noodles.

Exhibit 7: China dairy market enter a slow growth stage

Exhibit 8: China dairy market volume comparable with

US/W. Europe

Source: Euromonitor

Source: Euromonitor

22%

-8%

6%

2%3%

-10%

-5%

0%

5%

10%

15%

20%

25%

2000-07 2008-09 2010-13 2014-16E 2016E-20E

Dairy consumption growth CAGR (LME)

34,205

19,347

27,386

3,9641,419

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

WesternEurope

USA China Japan S. Korea

Total Dairy Market Volume ('000 Tonnes)

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 6

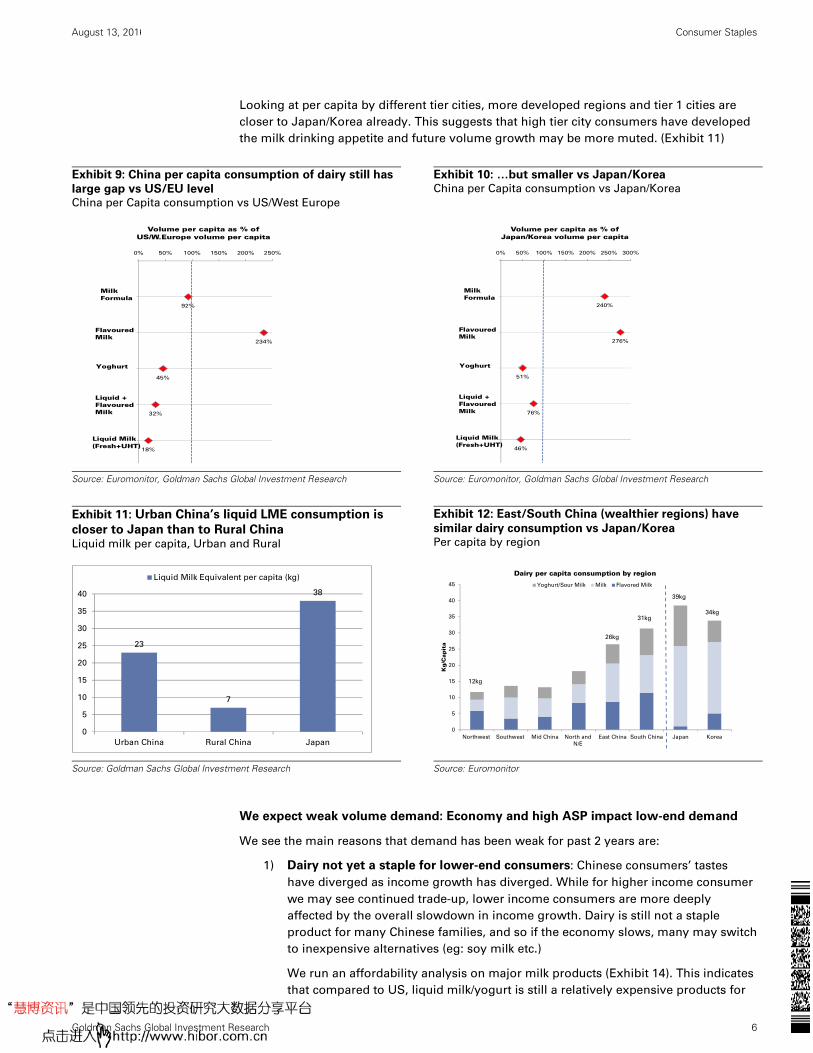

Looking at per capita by different tier cities, more developed regions and tier 1 cities are

closer to Japan/Korea already. This suggests that high tier city consumers have developed

the milk drinking appetite and future volume growth may be more muted. (Exhibit 11)

Exhibit 9: China per capita consumption of dairy still has

large gap vs US/EU level China per Capita consumption vs US/West Europe

Exhibit 10: …but smaller vs Japan/Korea China per Capita consumption vs Japan/Korea

Source: Euromonitor, Goldman Sachs Global Investment Research

Source: Euromonitor, Goldman Sachs Global Investment Research

Exhibit 11: Urban China’s liquid LME consumption is

closer to Japan than to Rural China

Liquid milk per capita, Urban and Rural

Exhibit 12: East/South China (wealthier regions) have

similar dairy consumption vs Japan/Korea Per capita by region

Source: Goldman Sachs Global Investment Research

Source: Euromonitor

We expect weak volume demand: Economy and high ASP impact low-end demand

We see the main reasons that demand has been weak for past 2 years are:

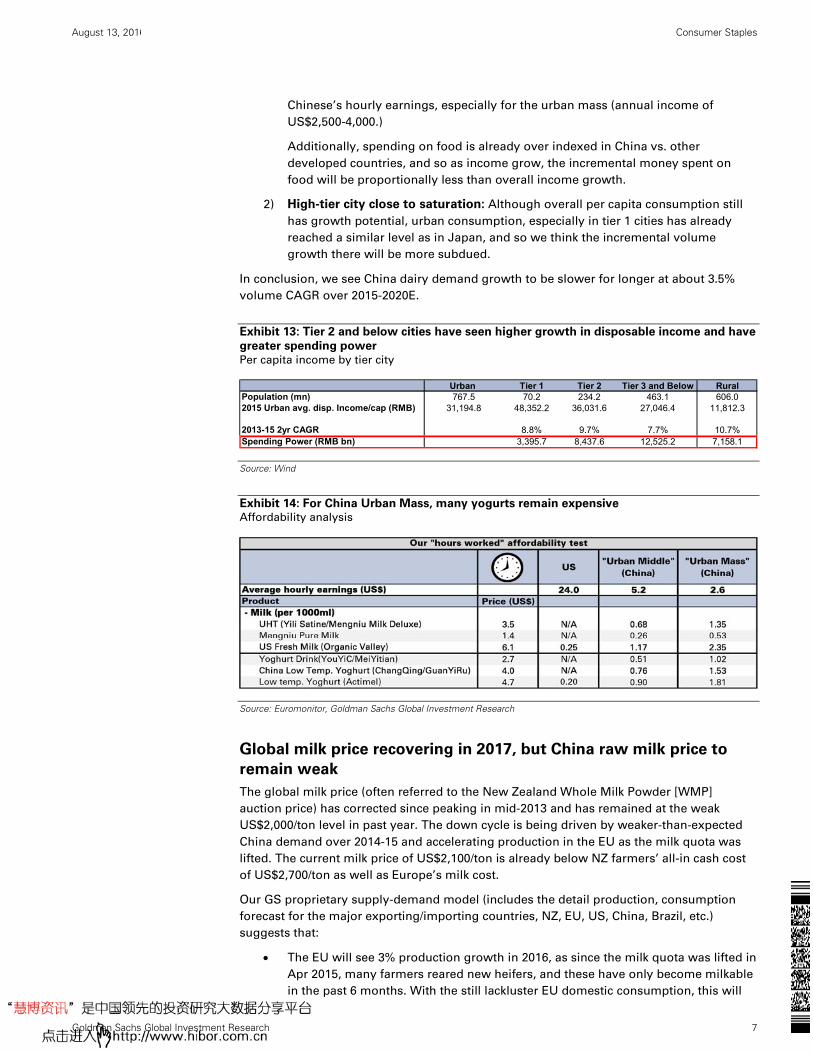

1) Dairy not yet a staple for lower-end consumers: Chinese consumers’ tastes

have diverged as income growth has diverged. While for higher income consumer

we may see continued trade-up, lower income consumers are more deeply

affected by the overall slowdown in income growth. Dairy is still not a staple

product for many Chinese families, and so if the economy slows, many may switch

to inexpensive alternatives (eg: soy milk etc.)

We run an affordability analysis on major milk products (Exhibit 14). This indicates

that compared to US, liquid milk/yogurt is still a relatively expensive products for

92%

234%

45%

32%

18%

0% 50% 100% 150% 200% 250%

0

1

2

3

4

5

Volume per capita as % of US/W.Europe volume per capita

Milk Formula

FlavouredMilk

Yoghurt

Liquid + Flavoured Milk

Liquid Milk (Fresh+UHT)

240%

276%

51%

76%

46%

0% 50% 100% 150% 200% 250% 300%

0

1

2

3

4

5

Volume per capita as % of Japan/Korea volume per capita

Milk Formula

FlavouredMilk

Yoghurt

Liquid + Flavoured Milk

Liquid Milk (Fresh+UHT)

23

7

38

0

5

10

15

20

25

30

35

40

Urban China Rural China Japan

Liquid Milk Equivalent per capita (kg)

0

5

10

15

20

25

30

35

40

45

Northwest Southwest Mid China North and

N/E

East China South China Japan Korea

Kg/C

apit

a

Dairy per capita consumption by region

Yoghurt/Sour Milk Milk Flavored Milk

26kg

31kg

39kg

34kg

12kg

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 7

Chinese’s hourly earnings, especially for the urban mass (annual income of

US$2,500-4,000.)

Additionally, spending on food is already over indexed in China vs. other

developed countries, and so as income grow, the incremental money spent on

food will be proportionally less than overall income growth.

2) High-tier city close to saturation: Although overall per capita consumption still

has growth potential, urban consumption, especially in tier 1 cities has already

reached a similar level as in Japan, and so we think the incremental volume

growth there will be more subdued.

In conclusion, we see China dairy demand growth to be slower for longer at about 3.5%

volume CAGR over 2015-2020E.

Exhibit 13: Tier 2 and below cities have seen higher growth in disposable income and have

greater spending power

Per capita income by tier city

Source: Wind

Exhibit 14: For China Urban Mass, many yogurts remain expensive Affordability analysis

Source: Euromonitor, Goldman Sachs Global Investment Research

Global milk price recovering in 2017, but China raw milk price to

remain weak

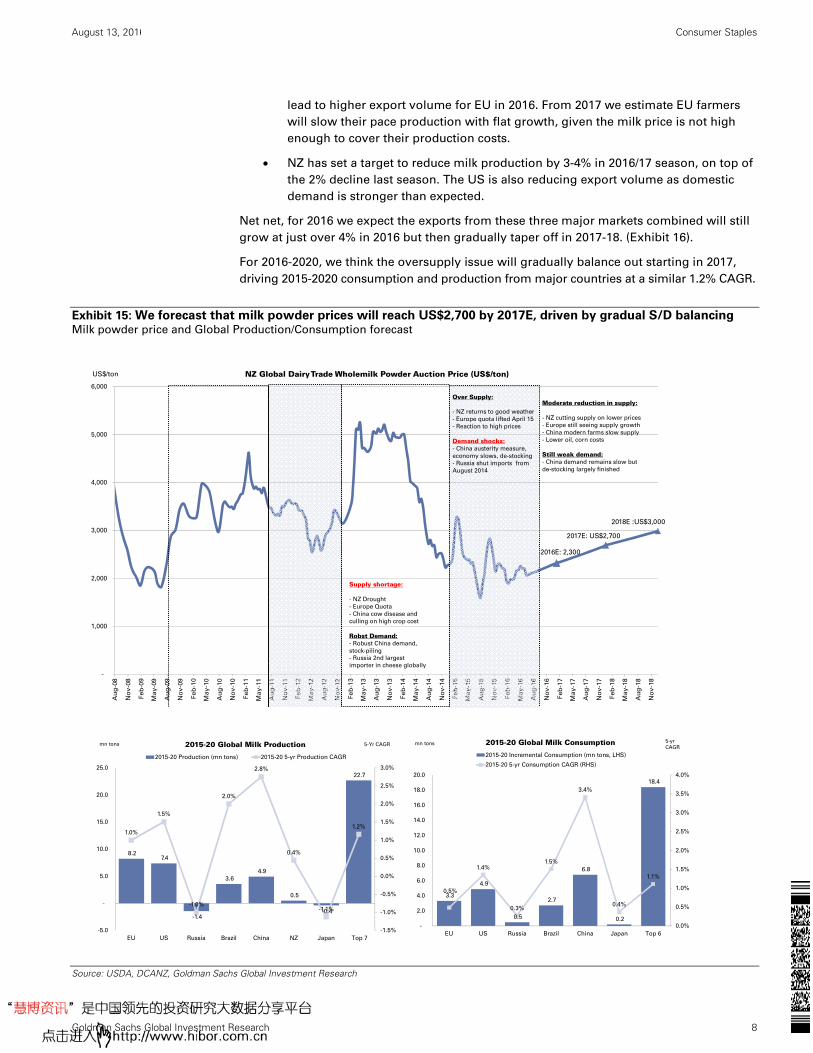

The global milk price (often referred to the New Zealand Whole Milk Powder [WMP]

auction price) has corrected since peaking in mid-2013 and has remained at the weak

US$2,000/ton level in past year. The down cycle is being driven by weaker-than-expected

China demand over 2014-15 and accelerating production in the EU as the milk quota was

lifted. The current milk price of US$2,100/ton is already below NZ farmers’ all-in cash cost

of US$2,700/ton as well as Europe’s milk cost.

Our GS proprietary supply-demand model (includes the detail production, consumption

forecast for the major exporting/importing countries, NZ, EU, US, China, Brazil, etc.)

suggests that:

The EU will see 3% production growth in 2016, as since the milk quota was lifted in

Apr 2015, many farmers reared new heifers, and these have only become milkable

in the past 6 months. With the still lackluster EU domestic consumption, this will

Urban Tier 1 Tier 2 Tier 3 and Below RuralPopulation (mn) 767.5 70.2 234.2 463.1 606.02015 Urban avg. disp. Income/cap (RMB) 31,194.8 48,352.2 36,031.6 27,046.4 11,812.3

2013-15 2yr CAGR 8.8% 9.7% 7.7% 10.7%Spending Power (RMB bn) 3,395.7 8,437.6 12,525.2 7,158.1

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 8

lead to higher export volume for EU in 2016. From 2017 we estimate EU farmers

will slow their pace production with flat growth, given the milk price is not high

enough to cover their production costs.

NZ has set a target to reduce milk production by 3-4% in 2016/17 season, on top of

the 2% decline last season. The US is also reducing export volume as domestic

demand is stronger than expected.

Net net, for 2016 we expect the exports from these three major markets combined will still

grow at just over 4% in 2016 but then gradually taper off in 2017-18. (Exhibit 16).

For 2016-2020, we think the oversupply issue will gradually balance out starting in 2017,

driving 2015-2020 consumption and production from major countries at a similar 1.2% CAGR.

Exhibit 15: We forecast that milk powder prices will reach US$2,700 by 2017E, driven by gradual S/D balancing

Milk powder price and Global Production/Consumption forecast

Source: USDA, DCANZ, Goldman Sachs Global Investment Research

2016E: 2,300

2017E: US$2,700

2018E :US$3,000

-

1,000

2,000

3,000

4,000

5,000

6,000

Au

g-0

8

No

v-0

8

Fe

b-0

9

Ma

y-0

9

Au

g-0

9

No

v-0

9

Fe

b-1

0

Ma

y-1

0

Au

g-1

0

No

v-1

0

Fe

b-1

1

Ma

y-1

1

Au

g-1

1

No

v-1

1

Fe

b-1

2

Ma

y-1

2

Au

g-1

2

No

v-1

2

Fe

b-1

3

Ma

y-1

3

Au

g-1

3

No

v-1

3

Fe

b-1

4

Ma

y-1

4

Au

g-1

4

No

v-1

4

Fe

b-1

5

Ma

y-1

5

Au

g-1

5

No

v-1

5

Fe

b-1

6

Ma

y-1

6

Au

g-1

6

No

v-1

6

Fe

b-1

7

Ma

y-1

7

Au

g-1

7

No

v-1

7

Fe

b-1

8

Ma

y-1

8

Au

g-1

8

No

v-1

8

NZ Global Dairy Trade Wholemilk Powder Auction Price (US$/ton)

Supply shortage:

- NZ Drought

- Europe Quota

- China cow disease and

culling on high crop cost

Robst Demand:- Robust China demand,

stock-piling

- Russia 2nd largest

importer in cheese globally

Over Supply:

- NZ returns to good weather

- Europe quota lifted April 15

- Reaction to high prices

Demand shocks:- China austerity measure,

economy slows, de-stocking

- Russia shut imports from

August 2014

Moderate reduction in supply:

- NZ cutting supply on lower prices

- Europe still seeing supply growth

- China modern farms slow supply

- Lower oil, corn costs

Still weak demand:- China demand remains slow but

de-stocking largely finished

US$/ton

8.2 7.4

-1.4

3.6

4.9

0.5

-0.4

22.7

1.0%

1.5%

-1.0%

2.0%

2.8%

0.4%

-1.1%

1.2%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

-5.0

-

5.0

10.0

15.0

20.0

25.0

EU US Russia Brazil China NZ Japan Top 7

2015-20 Global Milk Production

2015-20 Production (mn tons) 2015-20 5-yr Production CAGR

mn tons 5-Yr CAGR

3.3

4.9

0.5

2.7

6.8

0.2

18.4

0.5%

1.4%

0.3%

1.5%

3.4%

0.4%

1.1%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

EU US Russia Brazil China Japan Top 6

2015-20 Global Milk Consumption

2015-20 Incremental Consumption (mn tons, LHS)

2015-20 5-yr Consumption CAGR (RHS)

mn tons 5-yr

CAGR

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 9

Global milk price to recover: Although China demand has not yet picked up, with the

more radical supply side reduction, we estimate NZ WMP price will slowly recover starting

2H16 and reach US$2,700/ton by the end of 2017 (NZ farmer’s breakeven point).

Exhibit 16: We expect exports from EU/US/NZ to grow at

4% for 2016E then taper off to 0.9% in 2018E Export growth by EU/US/NZ

Exhibit 17: China’s raw milk continues to trade at a

premium against Global milk prices China raw milk price vs. Global

Source: Goldman Sachs Global Investment Research, DCANZ

Source: Bloomberg

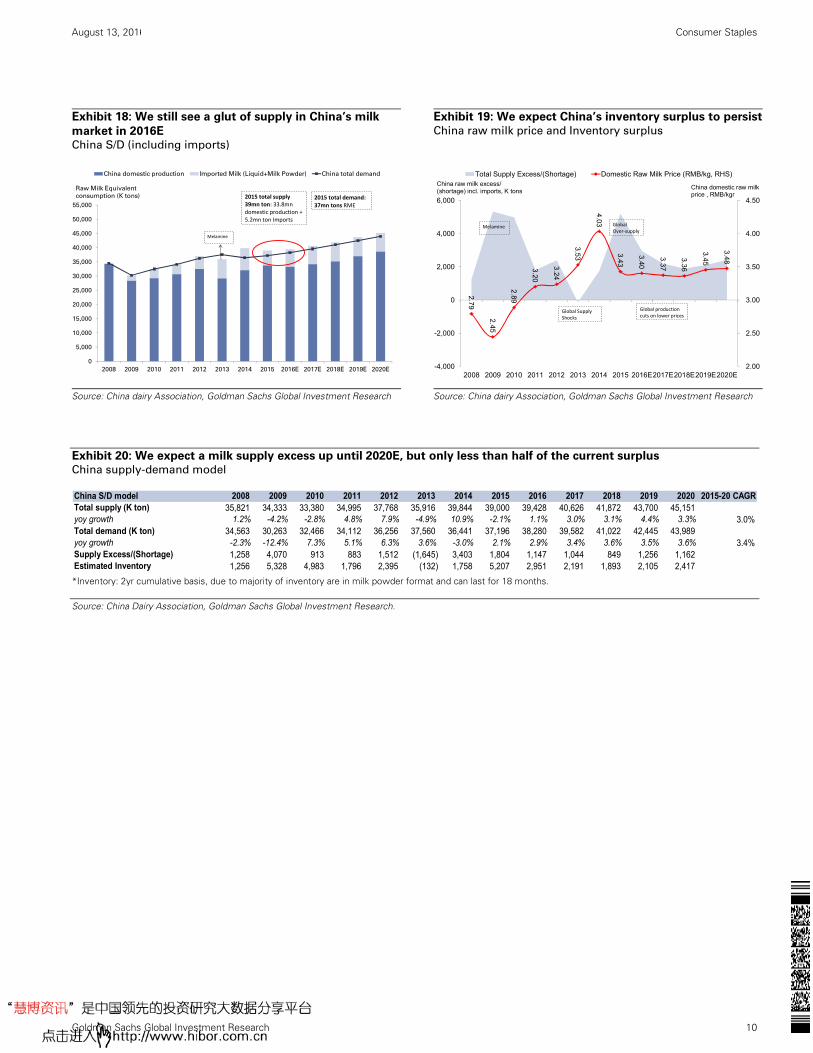

China milk prices to flat line

For China, given demand has been weaker than expected in the past 2 years, milk

oversupply has driven excess inventory and a lower milk price (down 20% from peaks). Our

China supply-demand model estimates currently there’s about 3.3mn tons of liquid milk

equivalent inventory in the market, vs. China’s annual demand of 37-38mn ton. The

excessive inventory is mostly poured into milk powder format so it can be stored for more

than 18 months.

Milk price has also been in a down cycle since 1H14 due to the industry oversupply.

Following the smaller farmers exiting market last year, in 2016 we have started to see large

scale farmers also sharply slowing down the dairy farm expansion and are having trouble

selling raw milk. (China Modern dairy poured about 11% of its milk production into milk

powder in 1H16). Therefore, we estimate in 2016 domestic supply will be reduced by 1.3%.

However, due to higher feed cost and land prices, China raw milk price has consistently

been much higher than global prices. Currently it’s still running at 55% premium to global

prices (Exhibit 17, including all transport, tariff expenses), thus we see the imports will

continue to be strong and sufficient to fill the China supply gap. (Exhibit 18) This will drive

China raw milk price to be lower for longer at around Rmb3.35-3.45/kg level, in our

view.

We are cautious about upstream dairy companies, as they will continue to have very tight

cash margin and will need to more aggressively expand into the branded milk market to

earn cash flow.

45.5 45.5

52.6

57.060.0 61.3

68.670.9

73.775.5 76.2

-0.1%

15.7%

8.3%

5.4%

2.1%

12.0%

3.3%4.0%

2.4%

0.9%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

Mn Tonnes

Dairy Export Market (3 major exporters) EU US NZ yoy growth

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

China raw milk price (Rmb/Kg)

NZ WMP equivalent price (auction only)

NZ WMP equivalent price (auction plus transport, VAT)

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 10

Exhibit 18: We still see a glut of supply in China’s milk

market in 2016E China S/D (including imports)

Exhibit 19: We expect China’s inventory surplus to persist

China raw milk price and Inventory surplus

Source: China dairy Association, Goldman Sachs Global Investment Research

Source: China dairy Association, Goldman Sachs Global Investment Research

Exhibit 20: We expect a milk supply excess up until 2020E, but only less than half of the current surplus China supply-demand model

*Inventory: 2yr cumulative basis, due to majority of inventory are in milk powder format and can last for 18 months.

Source: China Dairy Association, Goldman Sachs Global Investment Research.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

China domestic production Imported Milk (Liquid+Milk Powder) China total demand

Raw Milk Equivalent

consumption (K tons)

Melamine

2015 total supply 39mn ton: 33.8mn domestic production + 5.2mn ton Imports

2015 total demand: 37mn tons RME

2.79

2.45

2.89

3.20

3.24

3.53

4.03

3.43

3.40

3.37

3.36

3.45

3.48

2.00

2.50

3.00

3.50

4.00

4.50

-4,000

-2,000

0

2,000

4,000

6,000

2008 2009 2010 2011 2012 2013 2014 2015 2016E2017E2018E2019E2020E

Total Supply Excess/(Shortage) Domestic Raw Milk Price (RMB/kg, RHS)

Melamine

China raw milk excess/ (shortage) incl. imports, K tons

China domestic raw milk price , RMB/kgr

Global Supply Shocks

Global Over‐supply

Global production cuts on lower prices

China S/D model 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2015-20 CAGRTotal supply (K ton) 35,821 34,333 33,380 34,995 37,768 35,916 39,844 39,000 39,428 40,626 41,872 43,700 45,151 yoy growth 1.2% -4.2% -2.8% 4.8% 7.9% -4.9% 10.9% -2.1% 1.1% 3.0% 3.1% 4.4% 3.3% 3.0%Total demand (K ton) 34,563 30,263 32,466 34,112 36,256 37,560 36,441 37,196 38,280 39,582 41,022 42,445 43,989 yoy growth -2.3% -12.4% 7.3% 5.1% 6.3% 3.6% -3.0% 2.1% 2.9% 3.4% 3.6% 3.5% 3.6% 3.4%Supply Excess/(Shortage) 1,258 4,070 913 883 1,512 (1,645) 3,403 1,804 1,147 1,044 849 1,256 1,162 Estimated Inventory 1,256 5,328 4,983 1,796 2,395 (132) 1,758 5,207 2,951 2,191 1,893 2,105 2,417

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 11

Next growth driver: high protein, functional; Yogurt the bright spot

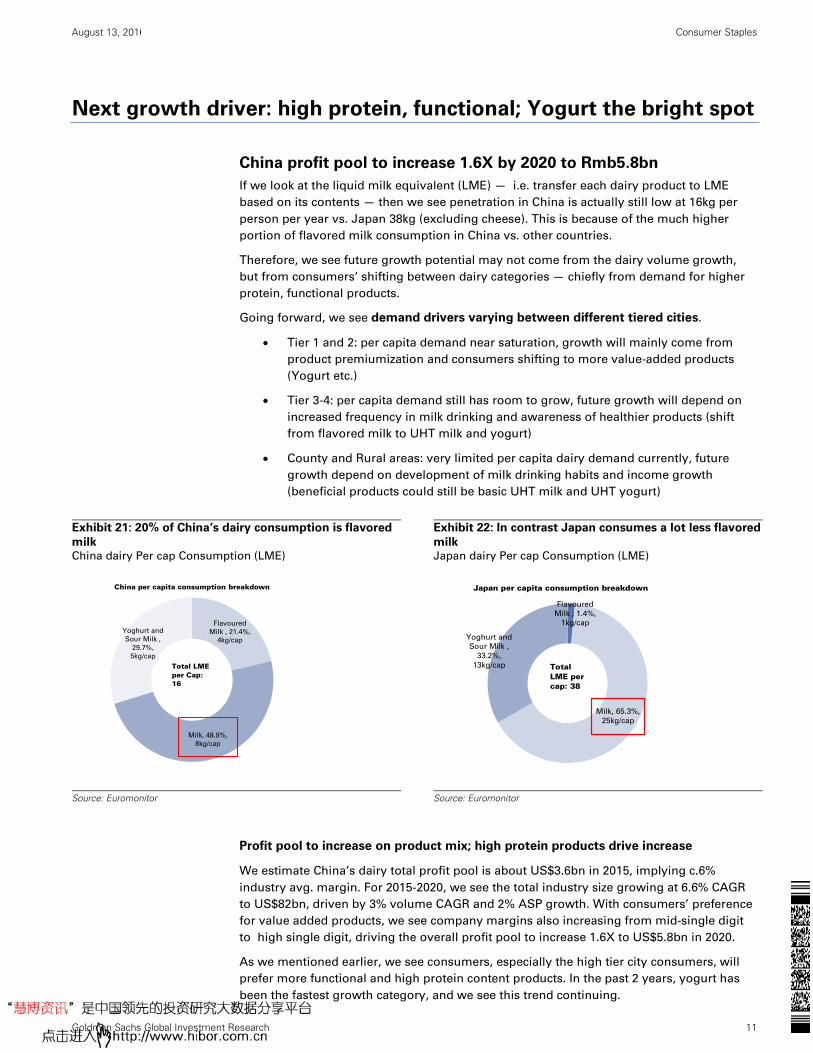

China profit pool to increase 1.6X by 2020 to Rmb5.8bn

If we look at the liquid milk equivalent (LME) — i.e. transfer each dairy product to LME

based on its contents — then we see penetration in China is actually still low at 16kg per

person per year vs. Japan 38kg (excluding cheese). This is because of the much higher

portion of flavored milk consumption in China vs. other countries.

Therefore, we see future growth potential may not come from the dairy volume growth,

but from consumers’ shifting between dairy categories — chiefly from demand for higher

protein, functional products.

Going forward, we see demand drivers varying between different tiered cities.

Tier 1 and 2: per capita demand near saturation, growth will mainly come from

product premiumization and consumers shifting to more value-added products

(Yogurt etc.)

Tier 3-4: per capita demand still has room to grow, future growth will depend on

increased frequency in milk drinking and awareness of healthier products (shift

from flavored milk to UHT milk and yogurt)

County and Rural areas: very limited per capita dairy demand currently, future

growth depend on development of milk drinking habits and income growth

(beneficial products could still be basic UHT milk and UHT yogurt)

Exhibit 21: 20% of China’s dairy consumption is flavored

milk China dairy Per cap Consumption (LME)

Exhibit 22: In contrast Japan consumes a lot less flavored

milk Japan dairy Per cap Consumption (LME)

Source: Euromonitor

Source: Euromonitor

Profit pool to increase on product mix; high protein products drive increase

We estimate China’s dairy total profit pool is about US$3.6bn in 2015, implying c.6%

industry avg. margin. For 2015-2020, we see the total industry size growing at 6.6% CAGR

to US$82bn, driven by 3% volume CAGR and 2% ASP growth. With consumers’ preference

for value added products, we see company margins also increasing from mid-single digit

to high single digit, driving the overall profit pool to increase 1.6X to US$5.8bn in 2020.

As we mentioned earlier, we see consumers, especially the high tier city consumers, will

prefer more functional and high protein content products. In the past 2 years, yogurt has

been the fastest growth category, and we see this trend continuing.

Flavoured

Milk , 21.4%,

4kg/cap

Milk, 48.9%,

8kg/cap

Yoghurt and

Sour Milk ,

29.7%,

5kg/cap

China per capita consumption breakdown

Total LMEper Cap:16

Flavoured

Milk , 1.4%,

1kg/cap

Milk, 65.3%,

25kg/cap

Yoghurt and

Sour Milk ,

33.2%,

13kg/cap

Japan per capita consumption breakdown

Total LME per cap: 38

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 12

Exhibit 23: We forecast Yogurt to be the fastest growing category with double digit volume growth, driving the China

profit pool to increase by 1.6X by 2020 Market size, volume, profit pool forecast by category

Source: Euromonitor, Goldman Sachs Global Investment Research.

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 13

By subcategory, we see the yogurt segment nearly doubling its market size to US$22bn in

2020, driven by strong volume growth. UHT milk will continue to be the dominant liquid

milk product given its convenience and consumers’ established drinking habits; hence we

see the similar volume growth as the industry average and expect roughly US$17bn in

annual sales by 2020.

On the other hand, we see flavored milk and IMF as the two categories that will shrink over

next few years. China’s flavored milk penetration is already one of highest in the world,

and with the increasing awareness of healthy and less sweet preference, we expect the size

of flavored milk to shrink by 1.3%.

For IMF, China is among the world’s largest market with annual sales of US$16bn in 2015.

This is due to per baby penetration is on par with world average and average IMF product

ASP is 50% above the EU/NZ level. For the next 5 years, we see IMF pricing remaining

under pressure with the proliferation of online and cross border channels. Absolute ASP

for IMF products, especially premium products will decline yoy, in our view; however this

will be partially offset by the product mix upgrade, driving about 1% ASP fall yoy to 2020.

The impact from the removal of the ‘one child’ policy”, initiated in 2016 will start to kick in

from the end of year, however given the trend of number of new births and increasing

promotion of breast feeding, we expect IMF volume growth to be more muted in the next 5

years at low single digits.

Yogurt will be the bright spot

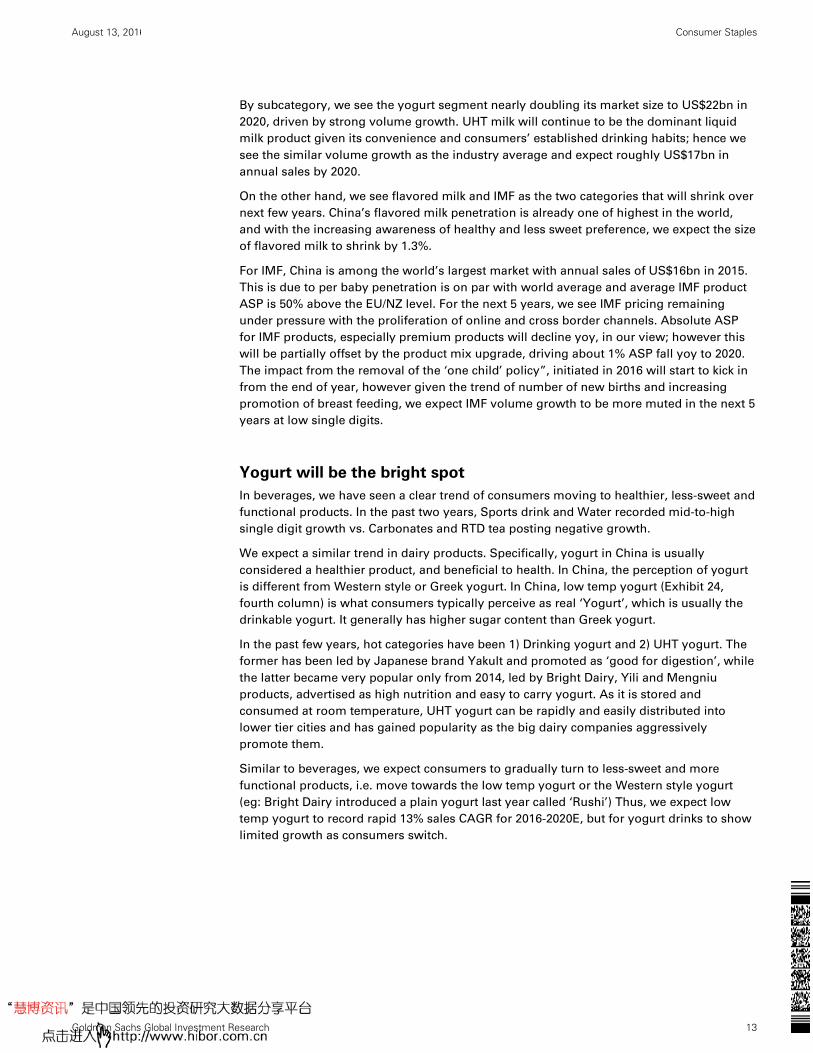

In beverages, we have seen a clear trend of consumers moving to healthier, less-sweet and

functional products. In the past two years, Sports drink and Water recorded mid-to-high

single digit growth vs. Carbonates and RTD tea posting negative growth.

We expect a similar trend in dairy products. Specifically, yogurt in China is usually

considered a healthier product, and beneficial to health. In China, the perception of yogurt

is different from Western style or Greek yogurt. In China, low temp yogurt (Exhibit 24,

fourth column) is what consumers typically perceive as real ‘Yogurt’, which is usually the

drinkable yogurt. It generally has higher sugar content than Greek yogurt.

In the past few years, hot categories have been 1) Drinking yogurt and 2) UHT yogurt. The

former has been led by Japanese brand Yakult and promoted as ‘good for digestion’, while

the latter became very popular only from 2014, led by Bright Dairy, Yili and Mengniu

products, advertised as high nutrition and easy to carry yogurt. As it is stored and

consumed at room temperature, UHT yogurt can be rapidly and easily distributed into

lower tier cities and has gained popularity as the big dairy companies aggressively

promote them.

Similar to beverages, we expect consumers to gradually turn to less-sweet and more

functional products, i.e. move towards the low temp yogurt or the Western style yogurt

(eg: Bright Dairy introduced a plain yogurt last year called ‘Rushi’) Thus, we expect low

temp yogurt to record rapid 13% sales CAGR for 2016-2020E, but for yogurt drinks to show

limited growth as consumers switch.

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 14

Exhibit 24: Consumer taste shifts towards less sweet, functional products – we see similar trends for Beverage and Milk Beverage and dairy products Comparison

Source: Company data, Goldman Sachs Global Investment Research.

UHT yogurt grew from a niche product in 2012 to an Rmb20bn market in 2015, due to the

products being easy to carry and perceived as healthy (although there’s no ‘active’

Lactobacillus in UHT yogurt). The product caters to new demand in locations that lack

sophisticated cold chain logistics and replaces some of the flavored milk and yogurt drink

demand, in our view. Bright Dairy is the leader of this category with star products

Momchilian, followed by Yili and Mengniu.

UHT yogurt is a new product category and many people are worried about the lifecycle of

the product. However, we note consumer purchase frequency of this product has only

reached 50% of that for Want Want’s “Hot kid milk”, which at its peak in 2013 was the

best-selling single SKU dairy product in China. Therefore we think UHT yogurt growth has

another 1-2 years of rapid growth ahead. That said as consumers start to realize the

difference between UHT and low temp yogurt, as well as with development of logistics in

low tier cities, we expect UHT yogurt growth to taper off and be outpaced by low temp

yogurt.

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 15

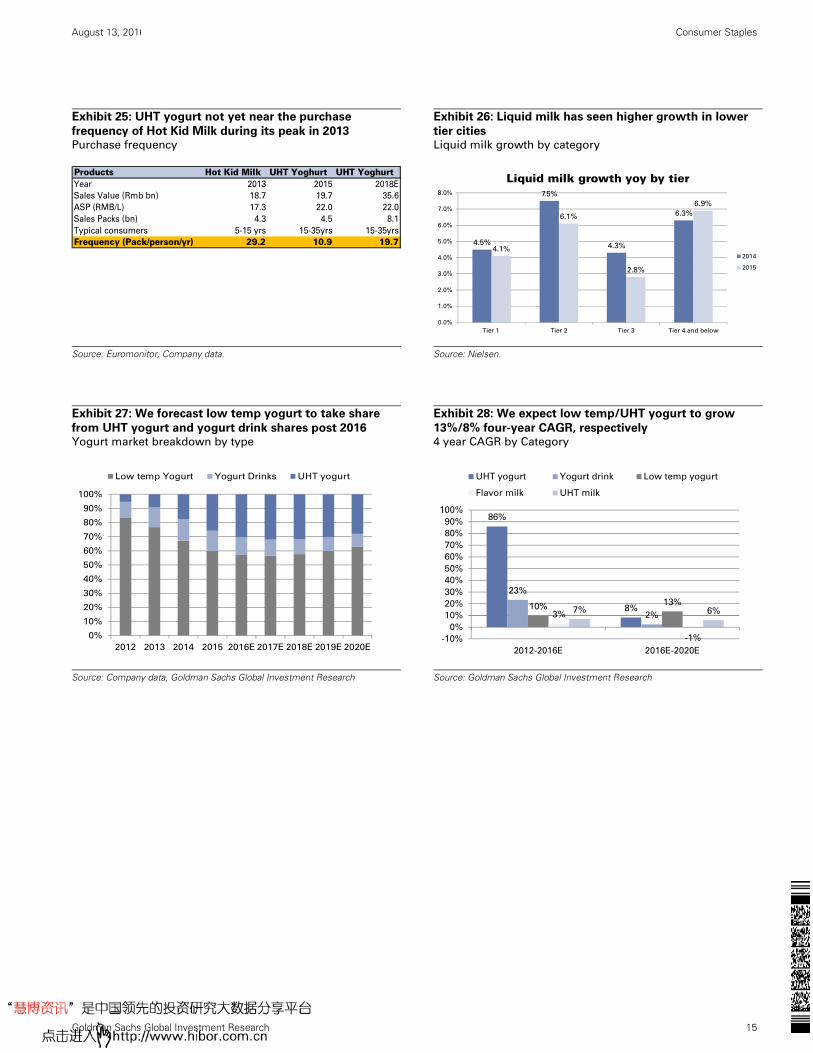

Exhibit 25: UHT yogurt not yet near the purchase

frequency of Hot Kid Milk during its peak in 2013 Purchase frequency

Exhibit 26: Liquid milk has seen higher growth in lower

tier cities Liquid milk growth by category

Source: Euromonitor, Company data.

Source: Nielsen.

Exhibit 27: We forecast low temp yogurt to take share

from UHT yogurt and yogurt drink shares post 2016 Yogurt market breakdown by type

Exhibit 28: We expect low temp/UHT yogurt to grow

13%/8% four-year CAGR, respectively 4 year CAGR by Category

Source: Company data, Goldman Sachs Global Investment Research

Source: Goldman Sachs Global Investment Research

Products Hot Kid Milk UHT Yoghurt UHT YoghurtYear 2013 2015 2018E

Sales Value (Rmb bn) 18.7 19.7 35.6

ASP (RMB/L) 17.3 22.0 22.0

Sales Packs (bn) 4.3 4.5 8.1

Typical consumers 5-15 yrs 15-35yrs 15-35yrs

Frequency (Pack/person/yr) 29.2 10.9 19.7 4.5%

7.5%

4.3%

6.3%

4.1%

6.1%

2.8%

6.9%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Tier 1 Tier 2 Tier 3 Tier 4 and below

Liquid milk growth yoy by tier

2014

2015

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

Low temp Yogurt Yogurt Drinks UHT yogurt

86%

8%

23%

2%10%

13%

3%

-1%

7% 6%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012-2016E 2016E-2020E

UHT yogurt Yogurt drink Low temp yogurt

Flavor milk UHT milk

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 16

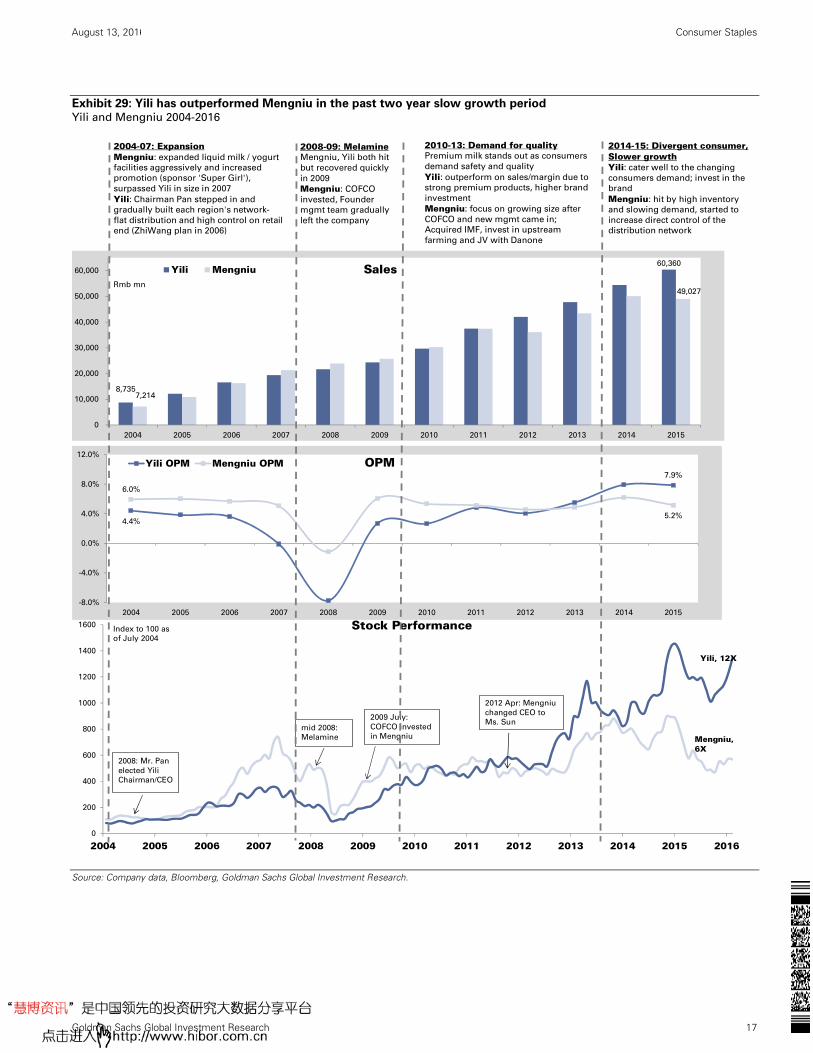

Execution is now the key: Yili stands out on distribution, branding

Since the 2008-2009 melamine incident, China consumers’ demand for quality milk has

increased substantially. Yili and Mengniu’s premium UHT milk products all gained market

share with strong growth after that event.

However, in past two years, China dairy demand has been weaker than expected and

posted subdued volume growth. But upstream dairy supply is still growing rapidly, leading

to high milk inventory in the market and increasing competition. Mengniu saw greater

challenge to its growth and its stock price corrected as much as 50% during 2014-15.

As the China dairy market has now entered a slower growth stage, individual companies’

performances have diverged more and more. The future growth and market share

dynamics depend on each company’s specific strategy on product offering, marketing and

branding and their effective execution.

We compare in detail the 4 downstream branded dairy companies and conclude that Yili as

industry leader is set to extend its leading position and gain further market share in most

categories.

Products, branding, distribution, mgmt. comparison

#1: Products: Yili and Mengniu better exposed to high-growth categories

Yili and Mengniu, as leading national players, have key products in most categories. They

both have more than 50% of their sales in the higher growth UHT milk and yogurt, with the

rest in milk beverage and milk powder. Both companies have been gaining market share in

the yogurt category.

In comparison, Want Want’s sales are more skewed to flavored milk sales, accounting for

50% with the rest rick crackers or snacks. Therefore Want Want’s dairy sales are under

significant pressure as the flavored milk market continues to shrink and the company faces

more competition from Yili/Mengniu’s children’s milk products.

Bright Dairy is a more of a regional player focusing on East China and pasteurized milk. In

the past 3 years it has successfully launched and led the UHT yogurt market with its star

product Momchilovtsi. However, as competition intensifies in the UHT yogurt market, we

see Bright’s growth coming under pressure from its dependence on a single SKU product.

(We estimate in 2016 Yili’s UHT yogurt Ambrosial will surpass the scale of Bright Dairy’s

UHT yogurt sales).

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 17

Exhibit 29: Yili has outperformed Mengniu in the past two year slow growth period Yili and Mengniu 2004-2016

Source: Company data, Bloomberg, Goldman Sachs Global Investment Research.

8,735

60,360

7,214

0

10,000

20,000

30,000

40,000

50,000

60,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Rmb mn

Sales Yili Mengniu

49,027

4.4%

7.9%

6.0%

5.2%

-8.0%

-4.0%

0.0%

4.0%

8.0%

12.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

OPMYili OPM Mengniu OPM

0

200

400

600

800

1000

1200

1400

1600

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Stock Performance

Mengniu, 6X

Yili, 12X

mid 2008:

Melamine

2009 July:

COFCO invested

in Mengniu

2012 Apr: Mengniu

changed CEO to

Ms. Sun

2008: Mr. Pan

elected Yili

Chairman/CEO

Index to 100 as

of July 2004

2004-07: ExpansionMengniu: expanded liquid milk / yogurt

facilities aggressively and increased

promotion (sponsor 'Super Girl'),

surpassed Yili in size in 2007

Yili: Chairman Pan stepped in and

gradually built each region's network-

flat distribution and high control on retail

end (ZhiWang plan in 2006)

2008-09: MelamineMengniu, Yili both hit

but recovered quickly

in 2009

Mengniu: COFCO

invested, Founder

mgmt team gradually

left the company

2010-13: Demand for qualityPremium milk stands out as consumers

demand safety and quality

Yili: outperform on sales/margin due to

strong premium products, higher brand

investment

Mengniu: focus on growing size after

COFCO and new mgmt came in;

Acquired IMF, invest in upstream

farming and JV with Danone

2014-15: Divergent consumer, Slower growthYili: cater well to the changing

consumers demand; invest in the

brand

Mengniu: hit by high inventory

and slowing demand, started to

increase direct control of the

distribution network

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 18

Exhibit 30: Yili and Mengniu has biggest exposure to Yogurt Sales by product type (2015)

Source: Company data.

#2: Branding: more effective and targeted branding crucial for young consumers

For dairy products, typical consumers are children/ students for flavored milk and

teenagers or millennials for yogurt etc. Hence we think marketing and branding aimed at

younger consumers will become more important for dairy companies. From 2013, we have

seen increasing number of dairy companies investing in the popular TV or entertainment

programs.

Yili, starting from 2014, has greatly increased its A&P expenses as they promote their star

products. Its A&P ratio reached 12% in 2015 and we expect it to continue to rise over 2016-

18E vs. Mengniu’s 8-9% and Want Want and Bright at less than 4%. Yili has invested in

television programs with higher viewership (avg. 3.0 rating vs. Mengniu’s 1.5) and has

greater presence on social media (sponsoring online video program and engaging in

WeChat events).

Also Yili spends about 60% more on advertising and roughly Rmb1bn on TV sponsorship

each year. This has translated into higher sales growth for the last two years (Exhibit 34).

Want Want on the other hand, spent less than 4% of sales on A&P, as it relies rely more on

distributors’ effort to push products. In our opinion this puts them at a disadvantage to win

market share.

36%42%

28% 20%

49%

18%27%

37%

9%

8%10%

4%

51%

26%

37%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Yili Mengniu Want Want Bright

Sales Exposure by Category

UHT Milk Milk Beverage Yogurt IMF Others Past. Milk

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 19

Exhibit 31: Yili’s higher spending on A&P has led to

higher incremental sales growth A&P comparison

Exhibit 32: Most of Yili’s selling expenses are advertising

2015 Yili vs Mengniu Selling Expenses Breakdown

Source: Company data, Goldman Sachs Global Investment Research

Source: Company data

Exhibit 33: Yili sponsored TV programs have had higher

ratings than Mengniu’s TV program sponsorship

Exhibit 34: Yili’s higher ANP spending has led to higher

sales growth vs Mengniu Yili/Mengniu A&P ratio vs Abs. sales increase

Source: tvtv.hk

Source: Company data, Goldman Sachs Global Investment Research

Yili, 13.6%

Bright, 3.6%

Mengniu, 8.9%

Want Want, 3.6%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

A&P as % of Sales

2,183

7,276

3,139

233 427806

4,085

2,310

789

2,994

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Salary Advertising Transportation Rental Others

Rmb mn

Yili Selling Expenses Breakdown

Yili Mengniu

150

610

430390

976

1275

1.6

1.3

3.53.3

2.0

0

0.5

1

1.5

2

2.5

3

3.5

4

0

200

400

600

800

1,000

1,200

1,400

2014 2015 2016

Rating pts.Rmb mnA&P expenses on TV program sponsorship

Mengniu Yili Mengniu ratings (RHS) Yili ratings (RHS)

Yili, 13.7%

Mengniu, 8.9%

-2,000

0

2,000

4,000

6,000

8,000

10,000

2%

4%

6%

8%

10%

12%

14%

16%

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

Rmb mnA&P as % of Sales vs Abs. Sales increase

Yili Abs Sales Increase Mengniu Abs. Sales Increase Yili Mengniu

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 20

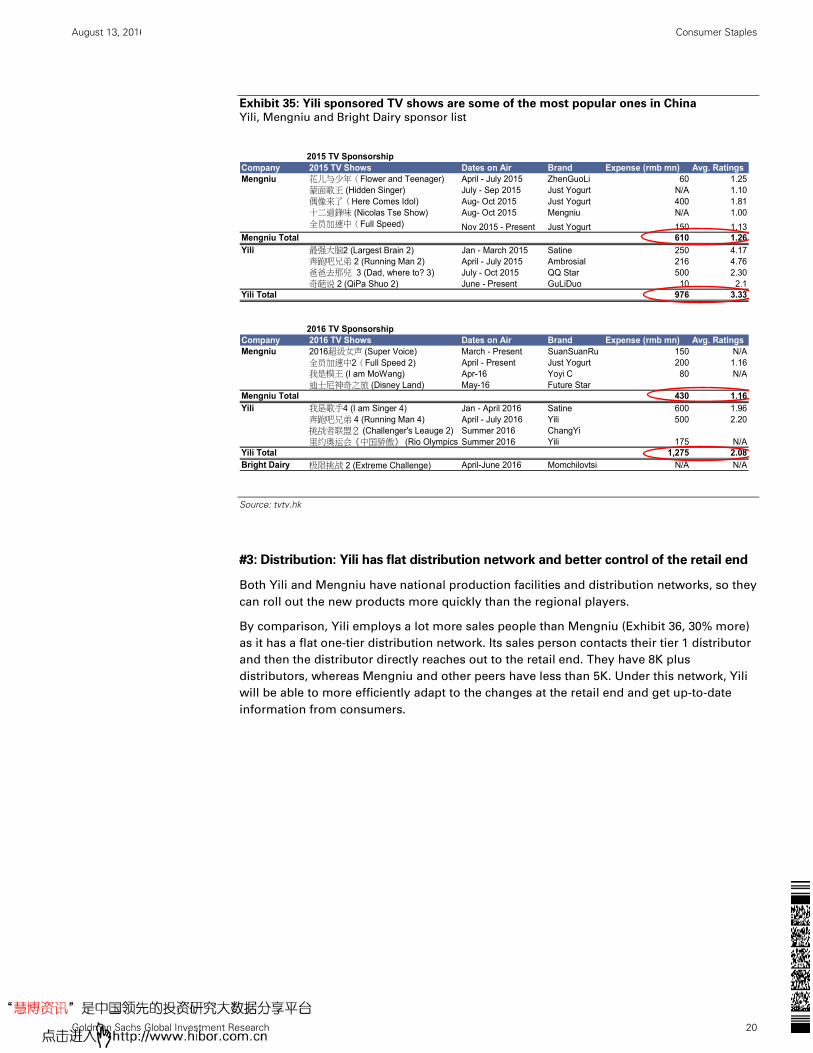

Exhibit 35: Yili sponsored TV shows are some of the most popular ones in China Yili, Mengniu and Bright Dairy sponsor list

Source: tvtv.hk

#3: Distribution: Yili has flat distribution network and better control of the retail end

Both Yili and Mengniu have national production facilities and distribution networks, so they

can roll out the new products more quickly than the regional players.

By comparison, Yili employs a lot more sales people than Mengniu (Exhibit 36, 30% more)

as it has a flat one-tier distribution network. Its sales person contacts their tier 1 distributor

and then the distributor directly reaches out to the retail end. They have 8K plus

distributors, whereas Mengniu and other peers have less than 5K. Under this network, Yili

will be able to more efficiently adapt to the changes at the retail end and get up-to-date

information from consumers.

Company 2015 TV Shows Dates on Air Brand Expense (rmb mn) Avg. RatingsMengniu 花儿与少年(Flower and Teenager) April - July 2015 ZhenGuoLi 60 1.25

蒙面歌王 (Hidden Singer) July - Sep 2015 Just Yogurt N/A 1.10偶像来了(Here Comes Idol) Aug- Oct 2015 Just Yogurt 400 1.81十二道鋒味 (Nicolas Tse Show) Aug- Oct 2015 Mengniu N/A 1.00全员加速中(Full Speed) Nov 2015 - Present Just Yogurt 150 1.13

Mengniu Total 610 1.26Yili 最强大脑2 (Largest Brain 2) Jan - March 2015 Satine 250 4.17

奔跑吧兄弟 2 (Running Man 2) April - July 2015 Ambrosial 216 4.76爸爸去那兒 3 (Dad, where to? 3) July - Oct 2015 QQ Star 500 2.30奇葩说 2 (QiPa Shuo 2) June - Present GuLiDuo 10 2.1

Yili Total 976 3.33

Company 2016 TV Shows Dates on Air Brand Expense (rmb mn) Avg. RatingsMengniu 2016超级女声 (Super Voice) March - Present SuanSuanRu 150 N/A

全员加速中2(Full Speed 2) April - Present Just Yogurt 200 1.16我是模王 (I am MoWang) Apr-16 Yoyi C 80 N/A迪士尼神奇之旅 (Disney Land) May-16 Future Star

Mengniu Total 430 1.16Yili 我是歌手4 (I am Singer 4) Jan - April 2016 Satine 600 1.96

奔跑吧兄弟 4 (Running Man 4) April - July 2016 Yili 500 2.20挑战者联盟2 (Challenger's Leauge 2) Summer 2016 ChangYi里约奥运会《中国骄傲》 (Rio Olympics)Summer 2016 Yili 175 N/A

Yili Total 1,275 2.08Bright Dairy 极限挑战 2 (Extreme Challenge) April-June 2016 Momchilovtsi N/A N/A

2015 TV Sponsorship

2016 TV Sponsorship

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 21

Exhibit 36: Yili is more directly involved in each POS, vs

Mengniu’s distributor driven model Yili vs Mengniu sales employees (2015)

Exhibit 37: Want Want still has limited exposure in

modern trade channel vs. other large staples companiesSales by channels (2015)

Source: Company data

Source: Company data, Goldman Sachs Global Investment Research.

With its wider distribution system, Yili has greater presence in lower tier cities and

traditional channels than Mengniu.

Mengniu, due to its relatively higher exposure in tier 1 and 2 cities, will face more intense

competition vs. upstream dairy players or import player on the premium UHT milk side.

This is because smaller, newer players usually have fewer resources to distribute products

into low tier city and therefore focus on premium end products. In past 12 months,

Mengniu has also started to reform its distribution network by increasing the portion of

direct selling and simplifying its layers of distributors. We think this will take time to have a

material impact on the company.

Want Want has been in China since the early 1990s and hence is well penetrated into

traditional channels. However, it is having difficulty penetrating into new channels such as

supermarkets or convenience stores in the past decade. More than 90% of its sales still

come through traditional channels as they want to protect their distributor margin.

However this makes Want Want less effective in launching new products or catering to

young consumers, in our view.

Exhibit 38: Yili has greater premium milk market share in

tier 3 and below cities Market share in different tier cities

Exhibit 39: Mengniu has a greater share in offline

channels than Yili Market share by channels

Source: Modern Dairy.

Source: Modern Dairy.

57,971

39,683

5,372

15,60411,905

1,834

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Yili Mengniu Bright Dairy

# of Employees Total employees Sales employees

95%

45% 50% 55%45%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

WW Mengniu Yili Tingyi UPC

Traditional channel Modern trade Online and others

28.8 31.7 36.2 38.2

37.4

50.147.8 47.9

0

10

20

30

40

50

60

70

80

90

100

Tier 1 Tier 2 Tier 3 Tier 4 and below

(%) Yili Mengniu

32.7 35.2 33.2 29.939.7

39.942.3

54.8 57.950.6

0

10

20

30

40

50

60

70

80

90

100

Hypermarket Supermarket Small

supermarket

Convenience

store

Brick and

Mortar

(%) Yili Mengniu

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 22

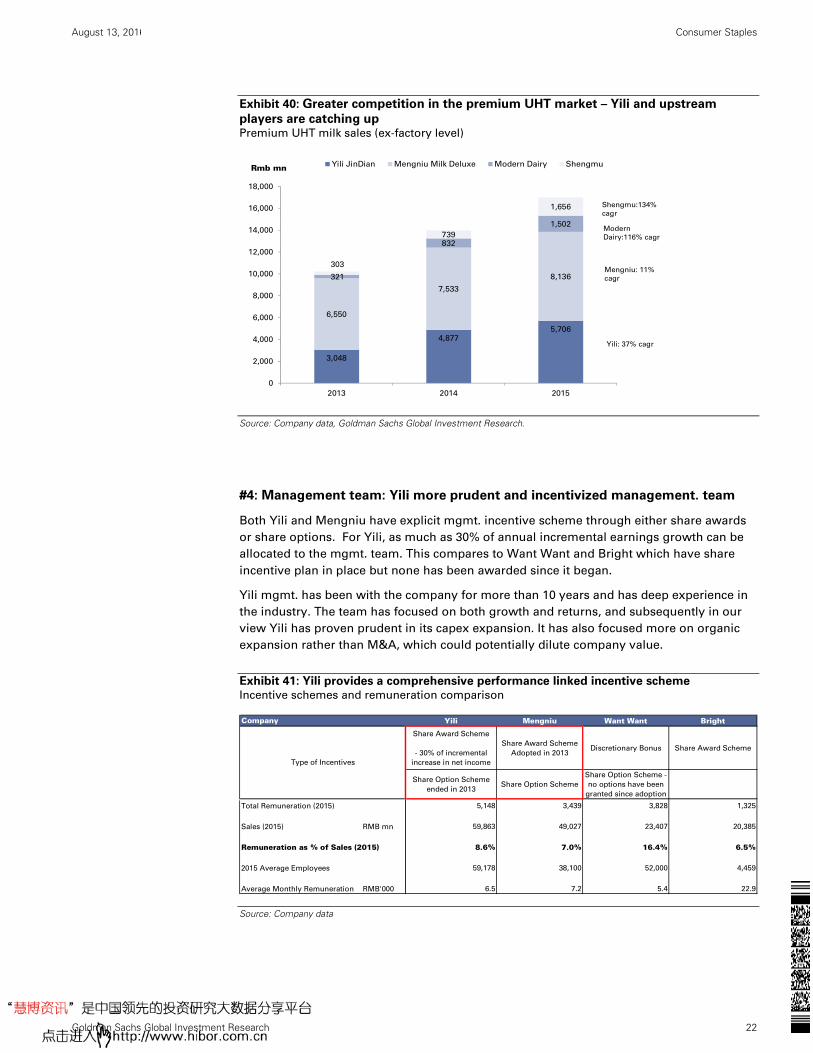

Exhibit 40: Greater competition in the premium UHT market – Yili and upstream

players are catching up

Premium UHT milk sales (ex-factory level)

Source: Company data, Goldman Sachs Global Investment Research.

#4: Management team: Yili more prudent and incentivized management. team

Both Yili and Mengniu have explicit mgmt. incentive scheme through either share awards

or share options. For Yili, as much as 30% of annual incremental earnings growth can be

allocated to the mgmt. team. This compares to Want Want and Bright which have share

incentive plan in place but none has been awarded since it began.

Yili mgmt. has been with the company for more than 10 years and has deep experience in

the industry. The team has focused on both growth and returns, and subsequently in our

view Yili has proven prudent in its capex expansion. It has also focused more on organic

expansion rather than M&A, which could potentially dilute company value.

Exhibit 41: Yili provides a comprehensive performance linked incentive scheme

Incentive schemes and remuneration comparison

Source: Company data

3,048

4,8775,706

6,550

7,533

8,136321

832

1,502

303

739

1,656

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2013 2014 2015

Rmb mn Yili JinDian Mengniu Milk Deluxe Modern Dairy Shengmu

Shengmu:134%

cagr

Modern

Dairy:116% cagr

Mengniu: 11%

cagr

Yili: 37% cagr

Company Yili Mengniu Want Want Bright

Share Award Scheme

- 30% of incremental

increase in net income

Share Award Scheme

Adopted in 2013Discretionary Bonus Share Award Scheme

Share Option Scheme

ended in 2013Share Option Scheme

Share Option Scheme -

no options have been

granted since adoption

Total Remuneration (2015) 5,148 3,439 3,828 1,325

Sales (2015) RMB mn 59,863 49,027 23,407 20,385

Remuneration as % of Sales (2015) 8.6% 7.0% 16.4% 6.5%

2015 Average Employees 59,178 38,100 52,000 4,459

Average Monthly Remuneration RMB'000 6.5 7.2 5.4 22.9

Type of Incentives

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 23

Exhibit 42: Yili has one of the highest free floats of all China dairy companies, while mgmt.

still holds nearly 8% Share ownership of each company

Source: Bloomberg

Compared with China and Global dairy companies, Yili has the highest CROCI (26%) due to

its high asset turnover. It deploys a light asset model due to years of prudence on capex

and working capital. Over 2011-2015, Yili’s CROCI grew from 15% to 26% on the back of

70% increase in Gross Cash Invested (GCI). Most of the incremental capital growth has

come from PPE investment or organic capacity expansion. We expect Yili to retain its high

CROCI of c.27% over 2016-18E.

This compares to Mengniu’s 3X higher GCI, which mainly come from higher intangibles

and working capital, as the company made a series of acquisitions in last 3 years and also

saw inventory levels go up due to milk oversupply.

Exhibit 43: Yili has highest CROCI among of peers, mainly driven by higher asset turnover

2015 CROCI breakdown comparison

Source: Company data, Goldman Sachs Global Investment Research

Dairy Companies Ownership Structure

Hohhot

Investment,

7.5%

China Security

Fund, 3.0%

China Securities

Finance, 4.3%

Gang Pan, 3.9%

Other

Executives,

4.1%

Public Investors,

77.2%

Yili

Founder

Bright Food

Group, 54.4%

Public

Investors,

43.6%

Bright Dairy

Sun Yi

Ping*(CEO),

0.4%

Public

Investors,

68.1%

COFCO Dairy

Invst. (JV of

COFCO, Arla,

Danone), 31.5%

Mengniu

Tsai Eng Meng

(Chairman),

49.8%

IWATSUKA

CONFECTIONE

RY , 5.0%JPMORGAN ,

5.0%

Public

Investors, 40.2%

Want Want

6%

8%

26%

8%

22%

15%

0.6x

1.0x

2.3x

1.2x1.1x

2.0x

17.2%

9.8%

11.2%

8.3%

28.7%

7.4%

0.6x

0.8x

0.9x

0.8x

0.7x

1.0x

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

0%

5%

10%

15%

20%

25%

30%

Danone Meiji Yili Mengniu

2015 CROCI Breakdown ComparisonCROCI Asset Turnover EBITDA Margin Cash Conversion

Want Want Bright

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 24

Exhibit 44: Yili’s increase in GCI driven by Fixed Asset

investments, leading to higher CROCI Yili CROCI/GCI breakdown

Exhibit 45: Mengniu’s acquisition in last few years

increased its intangibles, but brought down its CROCI Mengniu CROCI/GCI breakdown

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

Dairy 2020: Yili to gain market share in key product categories

For next 3 years, as the dairy market enters slow growth stage, we expect Yili will continue

to gain market share on the back of its better execution.

We expect Yili to maintain its dominant market share in UHT milk and flavored milk, and

shrink the gap vs. Mengniu in the yogurt segment. We think Yili’s UHT yogurt will take

No.1 position in the market due to its wide-spread branding and strong distribution, and

that Yili’s low temp yogurt products can catch up with Mengniu from better logistics and

further penetration. In the IMF segment, with the further influx of overseas IMF, we expect

foreign brands to continue taking share from domestic brands.

We expect Mengniu to face intense competition in the UHT milk segment; especially the

premium UHT as more upstream and import companies compete with them in the tier 1

and 2 cities.

Exhibit 46: We expect Yili to maintain market share and

Mengniu to further lose in UHT milk market

Market share – UHT milk

Exhibit 47: We expect Yili to gain market share Market share – Yogurt

Source: Goldman Sachs Global Investment Research

Source: Goldman Sachs Global Investment Research

25,805

14,168

10,740

372 0 526

CROCI, 14.9%

CROCI, 26.2%

0%

5%

10%

15%

20%

25%

30%

0

5,000

10,000

15,000

20,000

25,000

30,000

2011 Fixed Assets GrossIntangibles

NetOperating WC

Others 2015 GCI

Rm

b m

n

Yili (Historical) Gross Cash Invested & Cash Return on Cash Invested Growth

* Due to

negative Net

Operating WC

41,342

13,548

10,595

6,975

4,209

6,015 CROCI, 20.7%

CROCI, 8.0%

0%

5%

10%

15%

20%

25%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2011 GCI FixedAssets

GrossIntangibles

NetOperating

WC

Others 2015 GCI

Rm

b m

n

Mengniu (Historical) Gross Cash Invested & Cash Return on Cash Invested Growth

33.634.6 34.9

36.6 36.4 36.2 36.6

33.934.5 34.3

31.2 30.3

29.3 29.0

25.0

27.0

29.0

31.0

33.0

35.0

37.0

39.0

2012 2013 2014 2015 2016E 2017E 2018E

Yili UHT Mengniu UHT

11.3 11.413.0

19.3 24.2 26.0

26.9 21.2 21.923.4

28.7 28.4 28.3 28.0

13.7

15.917.9

14.2 12.6 11.5 10.8

0

5

10

15

20

25

30

35

2012 2013 2014 2015 2016E 2017E 2018E

Yili Mengniu Bright Dairy

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 25

Exhibit 48: We expect Yili and Mengniu to gain market

share, but Yili to gain more Market share – Flavored milk

Exhibit 49: We expect Yili to maintain its leading

domestic position Infant Milk Formula market Market share – IMF

Source: Goldman Sachs Global Investment Research

Source: Goldman Sachs Global Investment Research

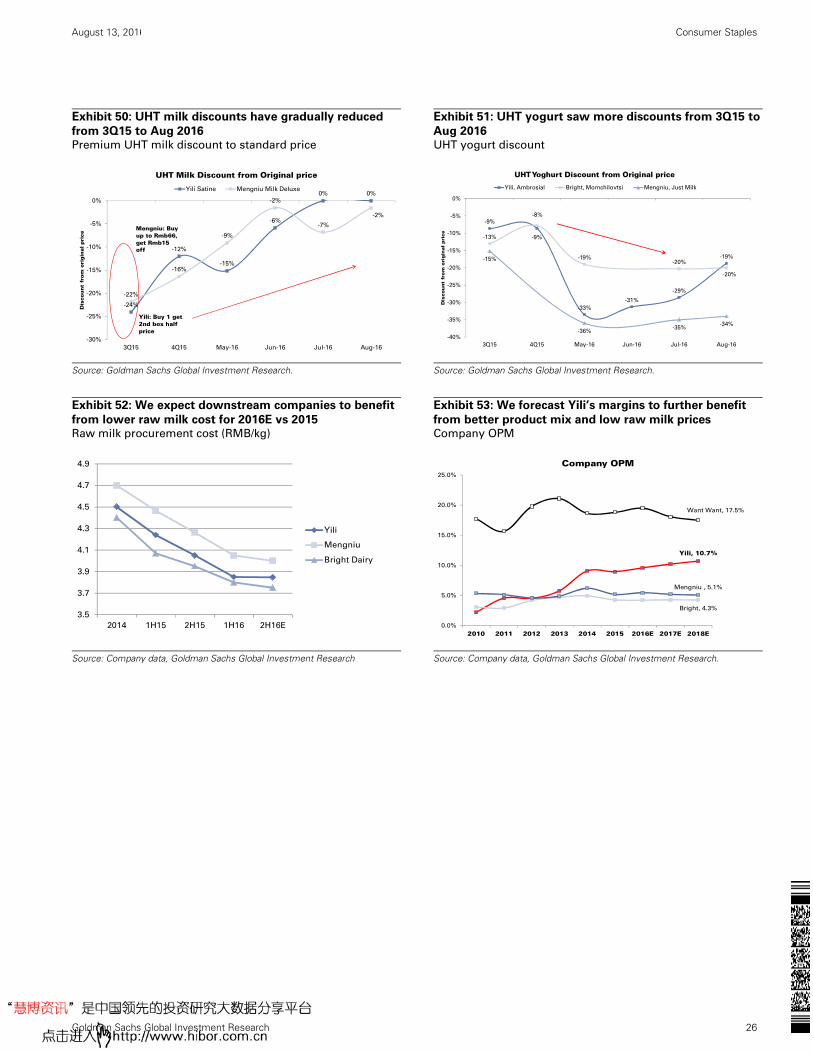

Earnings forecasts: Yili to deliver 13% EPS 3-year CAGR while Want Want will be

in negative territory

We expect Yili to deliver the fastest 7% sales 3yr CAGR 2015-2018E, driven by stronger

Yogurt and UHT premium product growth. We expect Yili to take over Bright Dairy to have

the No.1 UHT yogurt position in 2016 and narrow the gap between Mengniu for premium

UHT and yogurt products.

Margin wise, with the lower upstream raw milk price, we expect most downstream

companies to have lower raw milk procurement cost vs. 2015 (Exhibit 52). Mengniu will

benefit less vs. Yili and Bright due to its tighter connections with upstream companies

(China Modern Dairy etc.) so they need to protect their raw milk suppliers’ interest to some

extent. We expect Yili to deliver a strong 330bps GPM improvement from a better product

mix and further benefit from lower raw milk prices.

With more promotions being rolled out, there was high competitive intensity starting from

2H15 as companies aimed to clear up their excessive inventory. YTD, however, our channel

checks show that for UHT milk, especially premium milk, the discount has been reduced

(about 5% now vs. 20% in 3Q15). This suggests market inventory levels are not getting

worse in 2016. For UHT yogurt categories, there have been significant discounts, of up to

35% this year to its original price.

Net net, we expect Yili to deliver the strongest 12% CAGR 2015-2020E, vs. Mengniu’s 6%

and Want Want’s 4% decline.

25.4 26.128.1

31.6 32.3 34.0

36.1

20.321.2

22.5

20.0 20.4 20.8 21.3

10

15

20

25

30

35

40

2012 2013 2014 2015 2016E 2017E 2018E

Yili Mengniu Want Want

6.06.3

6.0 6.0

5.3 5.3 5.3

0.4

5.65.4

4.1 4.5

4.7 4.8

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2012 2013 2014 2015 2016E 2017E 2018E

Yili Mengniu

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 26

Exhibit 50: UHT milk discounts have gradually reduced

from 3Q15 to Aug 2016 Premium UHT milk discount to standard price

Exhibit 51: UHT yogurt saw more discounts from 3Q15 to

Aug 2016 UHT yogurt discount

Source: Goldman Sachs Global Investment Research.

Source: Goldman Sachs Global Investment Research.

Exhibit 52: We expect downstream companies to benefit

from lower raw milk cost for 2016E vs 2015 Raw milk procurement cost (RMB/kg)

Exhibit 53: We forecast Yili’s margins to further benefit

from better product mix and low raw milk prices Company OPM

Source: Company data, Goldman Sachs Global Investment Research

Source: Company data, Goldman Sachs Global Investment Research.

-24%

-12%

-15%

-6%

0% 0%

-22%

-16%

-9%

-2%

-7%

-2%

-30%

-25%

-20%

-15%

-10%

-5%

0%

3Q15 4Q15 May-16 Jun-16 Jul-16 Aug-16

Dis

cou

nt

fro

m o

rig

inal

pri

ce

UHT Milk Discount from Original price

Yili Satine Mengniu Milk Deluxe

Yili: Buy 1 get 2nd box half price

Mengniu: Buy up to Rmb66, get Rmb15 off

-9%

-9%

-33%

-31%

-29%

-19%

-13%

-8%

-19%-20%

-20%

-15%

-36%-35%

-34%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

3Q15 4Q15 May-16 Jun-16 Jul-16 Aug-16

Dis

cou

nt

fro

m o

rigin

al

pri

ce

UHT Yoghurt Discount from Original price

Yili, Ambrosial Bright, Momchilovtsi Mengniu, Just Milk

3.5

3.7

3.9

4.1

4.3

4.5

4.7

4.9

2014 1H15 2H15 1H16 2H16E

Yili

Mengniu

Bright DairyYili, 10.7%

Bright, 4.3%

Mengniu , 5.1%

Want Want, 17.5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

Company OPM

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 27

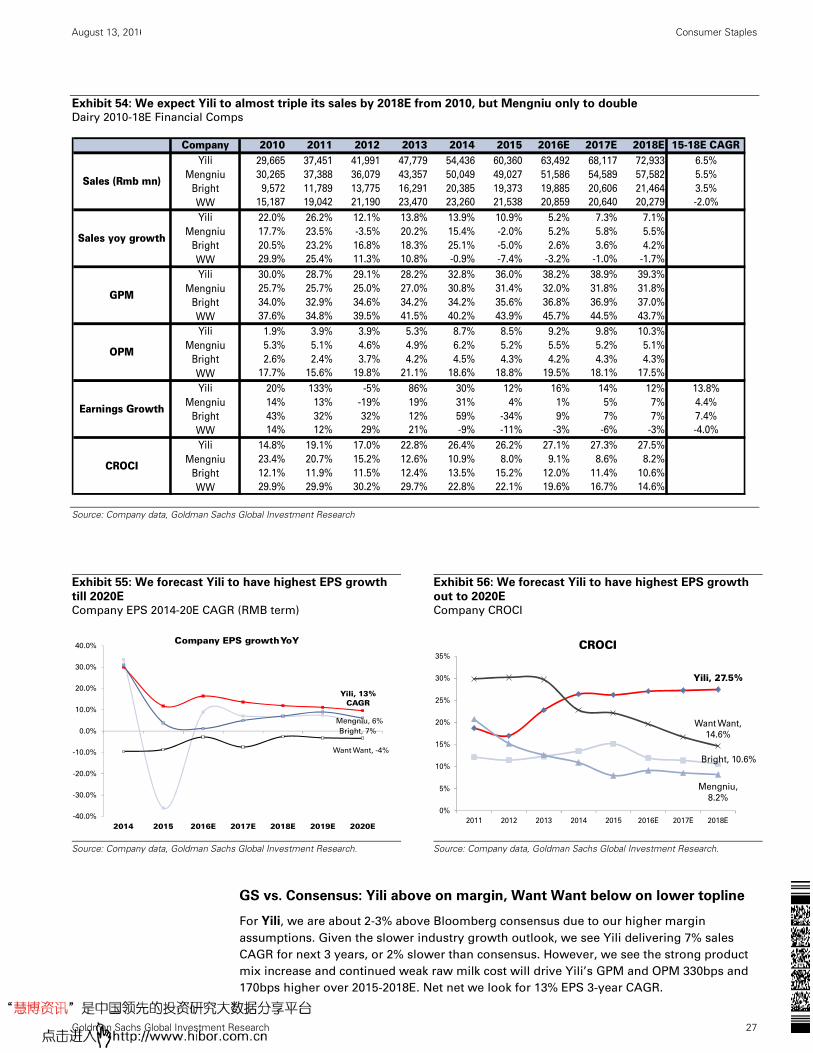

Exhibit 54: We expect Yili to almost triple its sales by 2018E from 2010, but Mengniu only to double Dairy 2010-18E Financial Comps

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 55: We forecast Yili to have highest EPS growth

till 2020E Company EPS 2014-20E CAGR (RMB term)

Exhibit 56: We forecast Yili to have highest EPS growth

out to 2020E Company CROCI

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

GS vs. Consensus: Yili above on margin, Want Want below on lower topline

For Yili, we are about 2-3% above Bloomberg consensus due to our higher margin

assumptions. Given the slower industry growth outlook, we see Yili delivering 7% sales

CAGR for next 3 years, or 2% slower than consensus. However, we see the strong product

mix increase and continued weak raw milk cost will drive Yili’s GPM and OPM 330bps and

170bps higher over 2015-2018E. Net net we look for 13% EPS 3-year CAGR.

Company 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 15-18E CAGR Yili 29,665 37,451 41,991 47,779 54,436 60,360 63,492 68,117 72,933 6.5%

Mengniu 30,265 37,388 36,079 43,357 50,049 49,027 51,586 54,589 57,582 5.5%

Bright 9,572 11,789 13,775 16,291 20,385 19,373 19,885 20,606 21,464 3.5%

WW 15,187 19,042 21,190 23,470 23,260 21,538 20,859 20,640 20,279 -2.0%

Yili 22.0% 26.2% 12.1% 13.8% 13.9% 10.9% 5.2% 7.3% 7.1%

Mengniu 17.7% 23.5% -3.5% 20.2% 15.4% -2.0% 5.2% 5.8% 5.5%

Bright 20.5% 23.2% 16.8% 18.3% 25.1% -5.0% 2.6% 3.6% 4.2%

WW 29.9% 25.4% 11.3% 10.8% -0.9% -7.4% -3.2% -1.0% -1.7%

Yili 30.0% 28.7% 29.1% 28.2% 32.8% 36.0% 38.2% 38.9% 39.3%

Mengniu 25.7% 25.7% 25.0% 27.0% 30.8% 31.4% 32.0% 31.8% 31.8%

Bright 34.0% 32.9% 34.6% 34.2% 34.2% 35.6% 36.8% 36.9% 37.0%

WW 37.6% 34.8% 39.5% 41.5% 40.2% 43.9% 45.7% 44.5% 43.7%

Yili 1.9% 3.9% 3.9% 5.3% 8.7% 8.5% 9.2% 9.8% 10.3%

Mengniu 5.3% 5.1% 4.6% 4.9% 6.2% 5.2% 5.5% 5.2% 5.1%

Bright 2.6% 2.4% 3.7% 4.2% 4.5% 4.3% 4.2% 4.3% 4.3%

WW 17.7% 15.6% 19.8% 21.1% 18.6% 18.8% 19.5% 18.1% 17.5%

Yili 20% 133% -5% 86% 30% 12% 16% 14% 12% 13.8%

Mengniu 14% 13% -19% 19% 31% 4% 1% 5% 7% 4.4%

Bright 43% 32% 32% 12% 59% -34% 9% 7% 7% 7.4%

WW 14% 12% 29% 21% -9% -11% -3% -6% -3% -4.0%

Yili 14.8% 19.1% 17.0% 22.8% 26.4% 26.2% 27.1% 27.3% 27.5%

Mengniu 23.4% 20.7% 15.2% 12.6% 10.9% 8.0% 9.1% 8.6% 8.2%

Bright 12.1% 11.9% 11.5% 12.4% 13.5% 15.2% 12.0% 11.4% 10.6%

WW 29.9% 29.9% 30.2% 29.7% 22.8% 22.1% 19.6% 16.7% 14.6%

Sales (Rmb mn)

Sales yoy growth

GPM

OPM

Earnings Growth

CROCI

Yili, 13% CAGR

Bright, 7%

Mengniu, 6%

Want Want, -4%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

2014 2015 2016E 2017E 2018E 2019E 2020E

Company EPS growth YoY

Yili, 27.5%

Bright, 10.6%

Mengniu,

8.2%

Want Want,

14.6%

0%

5%

10%

15%

20%

25%

30%

35%

2011 2012 2013 2014 2015 2016E 2017E 2018E

CROCI

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 28

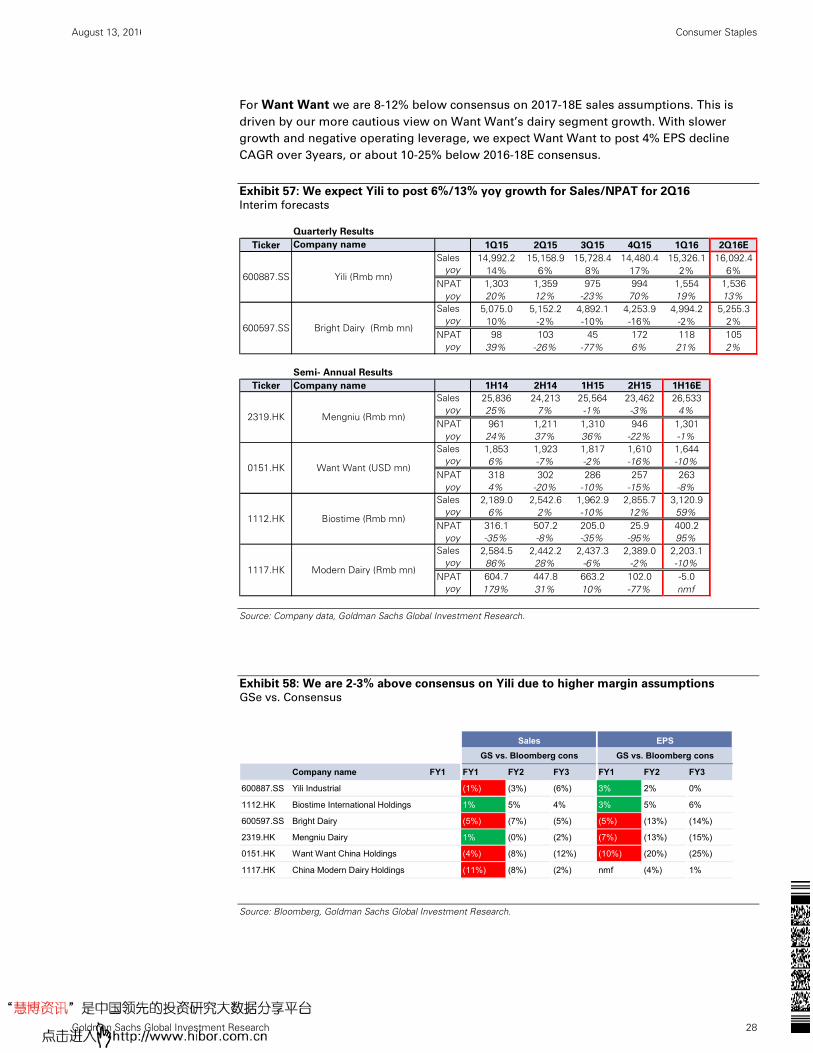

For Want Want we are 8-12% below consensus on 2017-18E sales assumptions. This is

driven by our more cautious view on Want Want’s dairy segment growth. With slower

growth and negative operating leverage, we expect Want Want to post 4% EPS decline

CAGR over 3years, or about 10-25% below 2016-18E consensus.

Exhibit 57: We expect Yili to post 6%/13% yoy growth for Sales/NPAT for 2Q16 Interim forecasts

Source: Company data, Goldman Sachs Global Investment Research.

Exhibit 58: We are 2-3% above consensus on Yili due to higher margin assumptions GSe vs. Consensus

Source: Bloomberg, Goldman Sachs Global Investment Research.

Quarterly Results

Ticker Company name 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16E

Sales 14,992.2 15,158.9 15,728.4 14,480.4 15,326.1 16,092.4 yoy 14% 6% 8% 17% 2% 6%

NPAT 1,303 1,359 975 994 1,554 1,536 yoy 20% 12% -23% 70% 19% 13%

Sales 5,075.0 5,152.2 4,892.1 4,253.9 4,994.2 5,255.3 yoy 10% -2% -10% -16% -2% 2%

NPAT 98 103 45 172 118 105 yoy 39% -26% -77% 6% 21% 2%

Ticker Company name 1H14 2H14 1H15 2H15 1H16E

Sales 25,836 24,213 25,564 23,462 26,533 yoy 25% 7% -1% -3% 4%

NPAT 961 1,211 1,310 946 1,301 yoy 24% 37% 36% -22% -1%

Sales 1,853 1,923 1,817 1,610 1,644 yoy 6% -7% -2% -16% -10%

NPAT 318 302 286 257 263 yoy 4% -20% -10% -15% -8%

Sales 2,189.0 2,542.6 1,962.9 2,855.7 3,120.9 yoy 6% 2% -10% 12% 59%

NPAT 316.1 507.2 205.0 25.9 400.2 yoy -35% -8% -35% -95% 95%

Sales 2,584.5 2,442.2 2,437.3 2,389.0 2,203.1 yoy 86% 28% -6% -2% -10%

NPAT 604.7 447.8 663.2 102.0 -5.0 yoy 179% 31% 10% -77% nmf

Mengniu (Rmb mn)2319.HK

600887.SS Yili (Rmb mn)

Semi- Annual Results

1112.HK Biostime (Rmb mn)

600597.SS Bright Dairy (Rmb mn)

0151.HK Want Want (USD mn)

1117.HK Modern Dairy (Rmb mn)

Sales EPS

GS vs. Bloomberg cons GS vs. Bloomberg cons

Company name FY1 FY1 FY2 FY3 FY1 FY2 FY3

600887.SS Yili Industrial (1%) (3%) (6%) 3% 2% 0%

1112.HK Biostime International Holdings 1% 5% 4% 3% 5% 6%

600597.SS Bright Dairy (5%) (7%) (5%) (5%) (13%) (14%)

2319.HK Mengniu Dairy 1% (0%) (2%) (7%) (13%) (15%)

0151.HK Want Want China Holdings (4%) (8%) (12%) (10%) (20%) (25%)

1117.HK China Modern Dairy Holdings (11%) (8%) (2%) nmf (4%) 1%

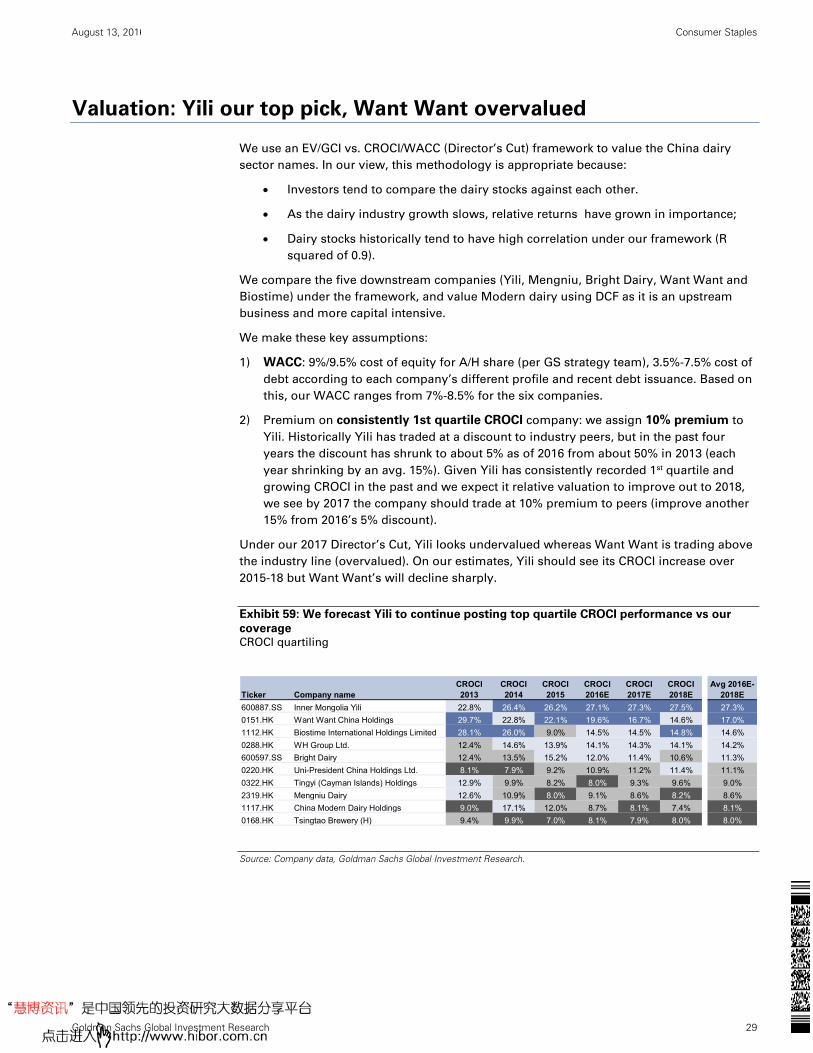

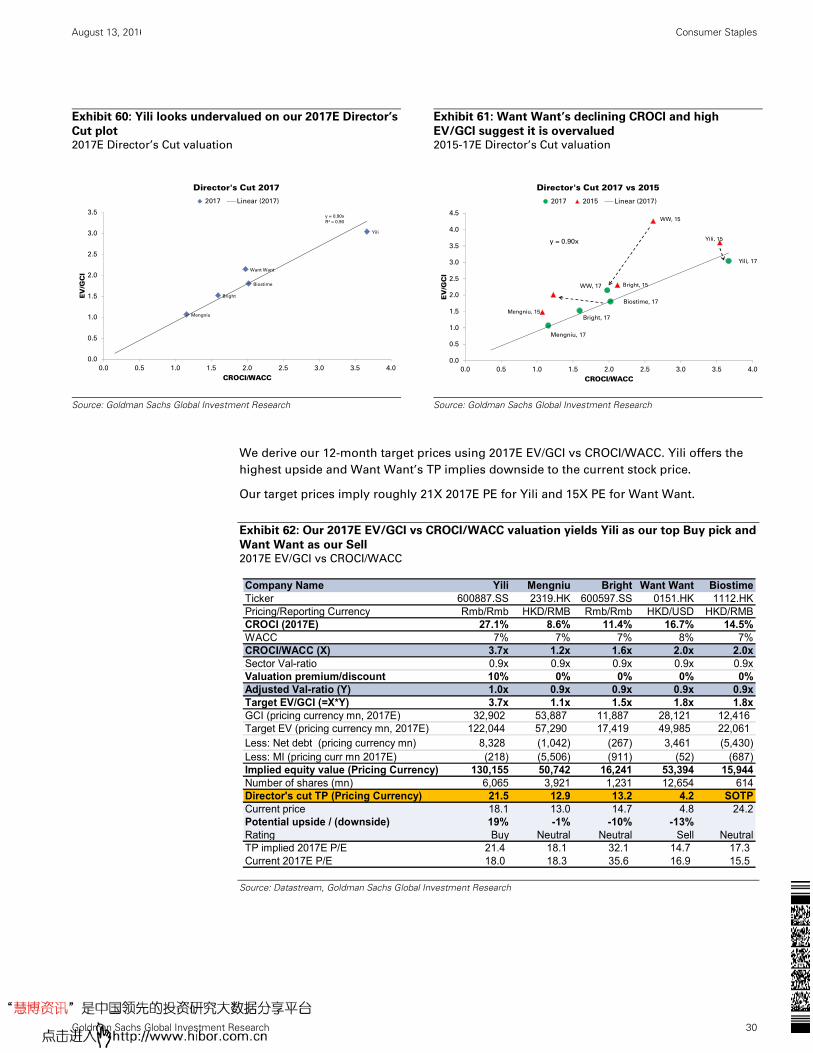

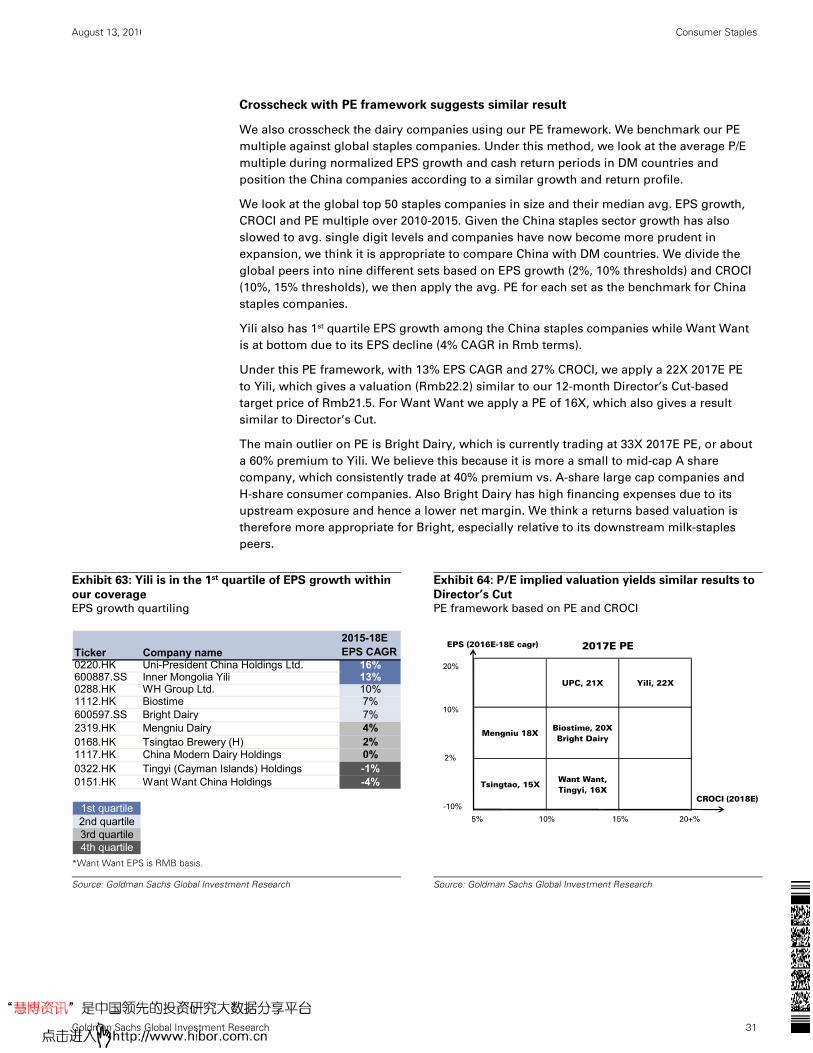

August 13, 2016 China: Consumer Staples

Goldman Sachs Global Investment Research 29