Embed Size (px)

Citation preview

-138-

- CHAPTER V

CORR~A'r TON B1ID'-n'fEEN SIZE AND. EFFICIENCY

Jh the earlier chapters the criterion to judge

the size and the existing sizes of the various units

were studied. Jh this chapter it is proposed to study

to correlation betwe~ size and efficiency, for

efficiency is the sum total of the act ion of the

various factors that have been considered as consti

-tuting the size. Size and efficiency are interrelated

that is, the size is dependent on efficiency and

efficiency on size. Normally, the efficiency of

standard size is taken to be one and the relation

-ship between the variation in size and variation

in efficiency are studied. 1n this context, the

management could be considered as possessing stan

-dard efficiency if it utilises each one of the

factors of prod:qction to the fullest extent vis~a-vis

the size operated and produces maximum net margin.

It should be reTnembered that with increasing effi

-ciency, the manageable size may also increase.

But this situation is rather the exception when the

variation in efficiency has reached unity. When

the efficiency is unity, the size is considered

as one with standarrd efficiency. The quest ion

arises Whether efficiency could be increased and

with it the size. Here, normally, after standard

J

•

-139-

-~ efficienc1an increase in efficiency is not~ ea gy.

However some units may reach an ~fficiency greater

than the standard one if the management is of

exceptionally high calibre. The exceptional

·condition arises more out of individual conditions

of managem~t,S where the management is of a very

high calibre and attempts at higher and higher

level of efficiency are made. Everi then, there is

a limit, in as much as, even in industries there is

a stage at which the law of diminish~g retums

starts operating. Therefore, it is proposed to

study the normal correlation between efficiency

and size in competitive strutture of industry.

In normal parlance, efficiency is defined

either by dividends declared on subscribed capital

.or earning,S capacity or net margin or the reserves.

In the case of joint stock companies under the

managing agency sy stern, dividend is declared, not

alwaYs with a bearing on the capacity to declare

dividends, but very oft en depending on various

other factors of interest to the managing direc

-tors or managing agents. In as much as there is

no principle ih determining the :sate of dividend

to be declared, it becomes an unreliable index

of efficiency. The net rtiargin or the eaming

capacity could normally be an index of efficiency,

. I

-140-

~~ ~ but it is defined ~for/purposes. To

cite one instance, the place of commission as a

part of profit or cost, is disputed. The mana

-ging agents as well as the income tax authorities

consider it as a part of cost while the tariff board

considers it as a part of profits. Since 11:945,

the tariff board has been allowing 10% retum on

block value which according to it should be su

-fficient both for a reasonable dividend and for

adequate renru.neration to the managing agents.*

It might appear at the out set that it should not

matter and that whichever way it. is taken, if

consistently taken should satisfy the purpose.

The correlation between size and net margin is

studied taking the net margin, both before and

after providing the commission as part of the cost,

and is studied as· an index of efficiency. The

last possible definition of efficiency mentioned above,

namely reserves are also not satisfactory as a test

of efficiencYjas they are not prdvided on any basis

of any accepted principles. The reserves include,

for instance, depreciation fund and the contribution

towards it is different on different accounts. The

income tax authority may allow a particular level

but of the profits are inadequate the management

-141-

may set aside much less than what it should be

and possibly might contribute nothing in a par

-ticular year and they tnay wait until better

profits are earned, to contribute on a much larger

scale to meet the accul'm.l.lat ed arrears of provision

for depreciation. A consequence of this is that

in a boom period ~en the profits are high, accumulated

deficit contributions to the depreciation fund may be

contributed. Thus, with the variation in the levels

of contributions which are not statutory but are

more a tnatter of convenience, the reserves, of which

depreciation _fund cent ribut ion~s a substantial part

become an mrJtmrft:iirllx'i'llfi unretiable test of effi

-ciency. Thus all the three indices of efficiency

mentioned above are 'dnreliable and so bther possible . indices have to be considered.

'T'he l"'lore scientific indices would be the

productivity per loom, productivity of labour, i.e.,

man hour production or average costs of production.

Factors like productivity and costs which have a

bearing on efficiency are more reliable, but t~ere

are limit at ions for· the reliability of the first

two factors. "rhe data available is invariably

insufficient and sometimes not very rel,a'iable and

it is a difficult proposition to get even this data.

-142-

~en here the cost of major it erns alone would be a

dependable index rather than the total cost. As has

been mentioned earlier, the cost in respect of commiss

-ion, depreciation and taxes is variable but the cost

in respect of active factors of production cannot be

managed and therefmre are dependent on efficiency.

Fence a correlation between the ~otal cost~ as well

as the cost of the major items individually, viz.;

cotton, wages, stores, fuel, repairs on the one hand

and efficiency on the other hand woyld appear to be

more conclusive as a guide. <In the paragraphs follow

-ing, the cost on the 111ajor items if is examined with

a view to take in for correlation studies such of the

major itemsas might be dependable. - ..

The first major it em is the expenditure on

cotton, the chief raw l'l1ateriatl. It a'llounts to 49.36;t

of the total expenditure • The a'Ilount spent on

cotton per loom per shift is Rs. 15.01 Naturally, it

stands to reason that the major raw material s."'lould

be purchased at as cheap a rate as possible. It

shoul:d however be verified as to whether large units . are able to secure cotton at a cheaper rate, having

the advantage of economies of large scale buying • . Of course, when there is a case of buying in bulk,

there are advantages of getting better terms. Again

~ ~' ~+-~~,f4>gc

-143-

' the /.Larger fdrms can afford to employ expert

buyers, backed up by all the resources of scienti

-fic knowledge and equipment •* But, it is

-difficult to det er'nine to what e:xt ent this

econo~ is gained by large sized firms. Here

are some of the factocrs which deserve rnent ion.

The 'disadvantage of smaller units !'!laY b.e .~

off set, when the unit is managed by agents who

"'lanage a group of mills. They definitely can

afford to buy in bulk and can also afford the

servlces of an expert. And, again, in the case of · • Ah "'led a bad Mills particularly, we have seen that

less than two dozen families control most of the

units of the centre.

Yet another point that affects the cost

of the cotton to the mills, irrespective of the

size of the unit is the intelligent as well as

lucky purchases by the managing agents. In this

case size has nothing to do with the cost.

One small point remains to be mentioned

and it is that some of the mill agents themselves

are dealing in cotton business. Hence, ·irres

-pective of the size of the -nills, they being

well conversant with the cotton tnarket, are

l

-144-

generally in a well placed position for buying

cotton. The mills they "1anage nee"' not employ tech

-nical staff and experts for the purpose. Hence,

without any consideration of the size of the mills,

the units !YJ.anaged by such 'Ilill agents are alwaYs

at an advantage.

The last point is in regard to the s!'llall .

units having strong financial reserves. And there

are quite a few in .Ahmedabad, which can be. ascer

-tained from the statement appearing at the end of

Cha'Pt er VII. These units are surely at an advantage

dn the 'llatter of purchases. These gactors clearly

indicate the size is not the only factor which

deterrnines the purchase price of cotton .but various

uncounted factors plaY their part.

The next important it em of cost is the expen

-diture on salaries and wages. This it em a'llount s to

29.28~ of the total a'ilount of expenditure. The a11ount

spent on salaries and wages per l:loom per shift is

Roo .• · 8 .91. Econol'llies of large scale do accrue in case

of labour and supervisory· cost. The advantage of division

of labour accrues to larger units only. But, in the

case of cotton textile industry this carries little

weight • The reason for it is that, for qui1re a con

-siderable period, there has not been many technical

-145-

changes which offer scope for fUrther division of

labour. 'Wen a rnoderat e sized unit can, o·fcourse

upto a certain point, enjoy the advantage of division

of labour.

Of~ourse in the case of xaknr cost on super.

-visory starr, the larger units are better placed.

Certain of the posts do not depend upon the size of

the unit. ltlat....--ever be the size of the unit, within

li"'lits, the nu'1'!ber of posts will be identical. Bor

exa~le, units which differ in size ~pto a certain li~it,

will need each one an engineer, or a spinning master

or a weaving master and such others and these posts

will not increase in number for small variations in

size. Again, larger units can afford to engage

expert and highly trainer" techn"tcal staff, which

cannot be afforded by _small~r units. But, however,

in the case o.f small units under one group of mana

-gement, this disadvantage is eliminated.

The major part of this dltem of expenditure

consists of wages to labour. Tn the case of the

Ahmedabad centre, to which this study is 'nainly confin.ed, . ' 4.M we find that sizeLvery little to do with labour cost,S.

The reasons for this are numerous. The variations

in the size of units of machinery, is one of them;

for exal'l!p~e; in the warp and the weft ring frames

-146- '

the nu.'nber of spindles varies from 292 to 440 and

352 to :J[ 492 respectively. And, the number of

workers depends upon the number of machines and

not on the number of spindles. The type of rnachi

-ner.Y used is another disturbdng factor. For

example, mills equipped with mechanical steam

enlines, high J)ressure turbines,· and elect rifi

-cation plant for power generation have varying

number of workers irrespective of the size of the

units. Yet another reason is the variations

in the designing and technique of the machines;

for e~ample, the installation of easablanka and

double zone systems, high speed winding and

warping machines and such others. A more per

-tinent factor responsible for such variations

which does not depend upon the size of the unit

is the variations in the agreements with the

labour associations, and the resultant rationali

-sation of labour in the ring spinning and the

automatic loom shed depart rnent. All these points

have been discussed at length in the third chapter.

Hence we see that the size has very little effect

on labour cost, but has a definite effect on the

supervisory costs, excepting in the case of mills

under the same management. The Tariff Board has

-147-

remarked; "Bombay has sonte advantage as compared with

An~edabarand other upcountry centres in respect of

the salaries of supervisory staff and technical s~aff,

· §gain, owing in main, to the large size of BombaY

mills."*

The ne:xt item of cost in order of importance

is the expenditure on stores and chemic'als. It amounts

to 9 .07" of the total expenditure. The amount spent on

stores and chemicals per loom per shirt is Rs. 2.76. All

~hat is . said in respe~t of cotton holds good fo·r the . purchase of stores and chemicals. And one important

point is that the consurnpt ion of and the expenses on

stores and chemicals vary in main with the variation

in different finishing processes, such as bleaching,

dyeing of yarn and cloth, printing, mercerising and

· sanforising of cloth. Naturally, fewer the processed

goods manufactured, less are the expenses incurred on

the item of store~ and chemicals irrespective of the

size of the units,

The ne:xt it em of cost is the expenditure on

fuel. It amounts to 3.68% of the total cost. The

aiJlount spent on fuel p e·r loom per shift is Rs. 1.12

An import ant point to note is that different mills

use_different types of machinery for generating

power, wh-ich we have already discussed and so the

cost of this it em varies from mill to mill, in spite

*Report of the Indian Tariff Board on Cotton te:xtile industry, 1927, Volume I, P.l22

_j

-148-

of the fact thatfhe number of spindles and looms might

remain the same.

Yet anbther it e'll of expenditure ici the sum

, total of Minor it ems totalled as 'other expenses'. These

include brokerage .for cotton purchases, yarn sales

and purchases, cloth sales, waste sales, fees to

auditors, fees to directors, interest, 'vatav', tra

-velling expenses, stationdery and postal expenses,

insurance pre'!liurns and sundries. The amount spent on

these e:xoenses id R.:;. 0.95 per loom per shirt. This

a'!lounts to 3.12% of the total expenditure. Tt should '

however be noted that the expenses in regard to fees 1

to directors, fees to auditors, travelling expenses,

stationery and po.stal charges are not likely to in-

-crease or decrease with the increase or decrease I

in the size of the unit. 'l'bereas expenses in regard

to insurance, cornrnission and brokerage on cqtton

and yarn purchases, yarn, cloth and waste sales, are

likely to increase or decrease with the increase or

decrease in the size. But so far as there is varia

-tion in the rate of commission and brokerage of the

above items, the increase or decrease in expenses

in relation to size will not be in the same proportion.

Again, the policy, as far as insurance is concerned,

is also varying. There are mills wh.ich keep some of

J

-149-

the ris.'l{s uninSU:red .- Again, the insurance premiums

depend upon the stocks of raw material, stores and

che'!licals, cotton- and cloth. The variations in

stocks depend on the fluctuation~ in the market rl pric~ either raw '11aterials or finished products.

In the case of raw materials, a rising trend in the

market prices leads to stock piling with a view to

avail of the advantages of cheaper raw material,

at a future date, when the prices would be high.

In the case of finished product, there is a tendency

to hold stocks when the ·present trend in prices

is falling and there is an expectation of a turning

over in the reasonably near future. Ih the case

of rising prices of the· finished products also if

the expectation is one of a definite upward trend,

the stocks will be storeG for the highest price to

be r~ached. All these arguments become effective

only when·the ~anaging agents are intelligent and

speculative and can stand large expenditure ~ in

advance or wait for the sales for a considerable

time. And these conditions are very variable. And I

so far as these stocks vary, there are variations

in the insurance prel'l'liums, irrespective of the

sixe of the mills.

Cost on repairs to machinery and buildings

-150-

is the next it em of expenditure • It amounts to

pc. 0.59 per loom per shift. This is 1.94% of the

total cost. There are a couple of points in r"e

-gard to this item of expenditure which need be

noted. They are th'e age of the mills, and the po

-licy of the mills in renovating the machinery and '

buildings. The average age of the 49 mills under

exa'Tlination is 34.3. years. Out of these 49 rnills,

39 belonging to groups II, III, W, V and VI have

. an average age varying between 33 and 37 years.

Out of the re1'Tlaining 6 'Tlills, those of groups I

and X have an average age of 22 and 21· years re

-spectively. ,,tlereas 2 mills of group VIII and

other 2 of group XI are respectively of the

average age of 41 and 57 years.

We can see that' nearly 80% of mills under

exalilinat ion fall in the groups which have nearly

the same average age. Hence the variation under

this it em of· expenditure is not on account of any

difference in the age of the mills. Hence it

appears that .the variat'ion 1.n cost under this

ite'll is due to the other reason. The second

factor, viz. the policy of individual units in

regard to renovation of '"'lachine:ry and buildings

-151-

is very widely varying. There are some 111ills which

spend lavishly on "'laintenance and upkeep of their

plant and machinery and there are some Mills which

follow the reverse policy. They spend less on re

-pairs but are out to buy new plant and machinery.

And this is reflected in the figures in the state

-ment of co!'!Iplete cost structure given in appendix

II. ~he range of expensesraries from~. 0.44 to

'Rc. 1.02 per loom per shift, under this j it em. The

com111ission'·paid to managing agents, which is R~.

1.11 per loom per shift or 3.65% of the total ex

-"Pend1.ture is an i"!!portant item in, the real cost.

Tt is not considered as a nart of cost for certain . L.,..~ -

sp_Pcific ~. This, does not, in any wa:y, re-

-move the importance of this item of expenditure

asttpart of real cost to the mill company. Yet

another item of expenditure is depreciation. It

a~ount s to Rs. 0.59 per loom per shift, that is,

1.94% of the total expenses. The last it em income

-tax, though strictly not a part of cost, but an

o~! go to arrive at the net retum, amounts to Rs.

0.62 per loom per shift.

So far, we have exa"'lined all the it ems of

expenditure, detailed figures for every one of

-152-

which are shown in appendix I. 1-Tow, before

scrutinising the stat 1st ics of the entire average

cost st :MJcture, we should eliminate the variable

and non-dependable items for comparing the effects

of cost on size. Such items are,

( 1) colll"l'Jission to managing agents,

( ii) provision for depreciation,

(iii) provision for incometax.

Firstly in the case of the commission to

the managing agents, it is found that it is based

on varying standards. It l!aries any where between

3~ and 5~ on the a11ount of sales or in some cases

on the al'llount of production. There are certain

units which charge it at three pies per po'l!md of

yarn. 'T'h ere are yet others which charge commi

-!lsion on a basis of percentage on profits eamed.

All these have led to variations in the it em of

expenses on commission, irrespective of the size

of the units. FUrther, the managing agents have to

forego the whole or part of their due commission

~en ~he working bas not been quite profitable~~.__

Renee it is advisable to o!'!lit this fluctuatingtitem.

The figures for the provisions of deprecia

-tion are also non-dependable for this purpose. The

varving practices in charging depreciation has

been responsible for this. Some units charg~ it

'

•

-153-

fully, all that is due. Some charge only partially

and allow it to accumulate until periods of good

profits co'lle. .Again, the amount of depre~iation

not only depends on the size of the units but it

depends on the age of the buildings and machinery •

A small 'Ylill with 'Tiostly new machinery may have to

provide for a far larg.e amount of depreciation than

a co~arst ively bi~ger mill which has old machinery.

'f-Tence, factors other than size of the unit influ

-ence the arnount of provision for depreciation

a.nd so, it is not advisable to use these figures

for the purpose of correlat jng size and cost.

Jn the case of provisions for incometax

the actual payment is rather delayed and the mills

have to maintain a fund for this purpose. ·Some

-times this fund is very large. Again, if the

mills feel that the provision is sdfficient for

the Year in review, they do not make any further

provision to that fund in that. Year, even though

the mills had eamed profits and have to pay incom9"tax

for the year. This could be seen in the statement

of COY!lJ:llete cost structure of 11ills·in appendix I.

· It is quite clear that, because of the reasons

mentioned above, we should study the figures of

expenditure on cotton, wages, stores, fuel, other

-154-

tnisc ellaneous it ems and machinery & building repairs

while studying correlation between size and costs.

As discussed before, little variations do exist even

tn the case of these items as well, but as inferences

· arw to be ·drawn on the basis of groll:p averages, the

individual rrregularity and distortions will be evened

out.

In the re'Tlaining portion of this chapter it

is pcroposed to study all the indices individually

and jointly and arrive at a correlation between size

and eff;f.ciency. In gpit e of limit at ions of the

various indices every index is studied. It will be

observed that even in the case of unreliable indices,

the general trend of the sa"ne nature is visible. The

fo~1owing is the statement of profits per loom in

the various units grouped according to their sizes.

statement overleaf

-155-

5 : 27 stat e'nent showing profits per loom in jhmedabad in 1949 *

I 1- 799

II 800- 999

ITT 1000-1199

'N 1200-13~9

v 1400-1599

VI 1600-1799

VII 1800-1999

VITI 2000-2199

IX 2200-2399

X 2400-2599

XI 2600 & over

Ol M r-t or-1 9

IH 0 •

0 z

3

4

12

9

8

6

4

2

2

2

22 .81

37 - 1.72

35 1.94

33 2.21.

33 1.55

34 2.31

41

21

57

.80-

3.10

3.30

1.64

2.96

3.09

3.39

2.73

3.38

.87

4.53

4.40

A study of profits including and excluding

commission as a part of cost, as shown in the above

stat ernent is fairly interesting. It has been dis

-cussed earlier as to what exactly is the difference

*Based on published balance sheets, year 1949

!' I

-156-

between the two. The trend of profit.s per loom in

-cluding commission as part of cost shows that the \

order of efficiency is group XI with over 2600 looms,

group X with 2400-2599 looms, group VI having 1600-

1799 looms, group IT having 1200-1399 looms and the

order of least efficiency is group I with 1-~9 looms

and group VIII with 2000-2199 looms.

An analysis of the data in the statement

above shows that there is a definite periodicity in the

trend of profits. Groups IT with 1200-1399 looms,

YI having 1600-1799 looms, X having 2400-2599 looms

indicate peak points. Group V having 1400-1599

looms and VIII having 2000-2199 looms indicate the

t~roughs; ~hat is, the low points. The graph ot

profits shows in marked relief, the steep fall in

the case of the group VIII with 2000-2199 looms

and this fall is not due to the size which is between

two cyclical points of economic size, but due to

so~me other ext !aneous factors. The cyclical points

"f. are 1200, 1600, 2000, 2400 and so on. An examina

-tion of the conditions of operation of these units

included in group VIII having 2000-2199 looms bear

out this argument. Unreliable as it is, if this

group is elimin'!tt.ed from considerations,.Atill a

periodicity is indicated. But that the trend is

-157-

a rising one is also observable. Because there is

no sa'llple beyond group XI of 2600 and over looms, it

is difficult to saY, whether the trough point beyond

group X having 2400-2599 looms is higher than the

earlier trough points. Group XI having 2600 and over

looms has only two units and group XI is not of the

same class interval, but included aY classes beyond

2600 looms. The two units, if studied individually,

show that they belong to widely varying sizes. And

taken even individually, there is no turning point

at these units and therefore, we cannot saY at what

level the next trough point would be, but we maY infer

that it might be at a level higher than the earlier

troug~ point ~dicated by group V having 1400-1599

looms. This analysis and inference thereof are not ' .

very dep.endable1 for without reference to all expen

-d:tture incurred for earning these profits, profits

can never be an index for comparative purposes. The

absolute profits do not reflect the risk involvecJ,

and the capital invested as also the utilisation of

plant and machinery for earning these profits.

Therefore, the better index of efficiency would be a

ratio of profits to either production or total

costs. The statement below gives the ratio of percen

-tage of profits to production.

statement overleaf

-158-

5 : 28 statement showing the ratio of per~entage or profits to product ion per loom in

[illmed~bad in 1949 * Group Working looms No.or Age· of % ratio of % ratio or

'!\To • per daY mills mills balance profits ba-sheet pro- · -sed on pro -fits to -duction ' production cost to

l2 roduct ion

I . 1-799 4 22 2.64 s.oo II 800-999 12 37 5.55 9.55

III 1000-1199 9 35 6.05 9.70

"N 1200-1399 8 33 6.28 9.55

v 1400-1599 6 33 4.72 8.17

VI 1600-1799 4 34 7.41 10.83

VII 1800-1999

VIII 2000-2199 2 41 2.75 3.03

IX 2200-2399

X 2400-2599 2 21 9.30 13.52

XI 2600 & over 2 57 8.94 12.09 ----------~-------------------------------------------------

'I'h e statement gives the ratio of percentage or

profit per loom to the product ion per loom. One is based

on the profits which includes ~x~~~ commission as .ipart

of costs and the other which does not. Either way, the

trend is the same. Jn both the cases, the periodicity

is. the same except that, when the commission is includ

•ed as a part of cost, the efficiency index is inter-

*Based on published balance sheets year 1949

-159-

-changed between group III and TV having 1000-1199 and

lro0-1399 looms respectively. The periodicity is almost

similar to what we found in the case of absolute profit

per loom except for the variation that in the case of

absolute profits groups ~I having 2600 and over- looms

was better than group X having 2400 to 2599 looms, vbile

when we take the ratios, group X is definitelY better.

This variation between groups X and XI conveys very

insignificant inference in as ~uch as there are hardly

two samples in each of them and again the sizes of the

two samples in group XI ame very widely different. If

the two sarnples in group iCI are taken as two indepen-

state!Ilent overleaf ,

-160-

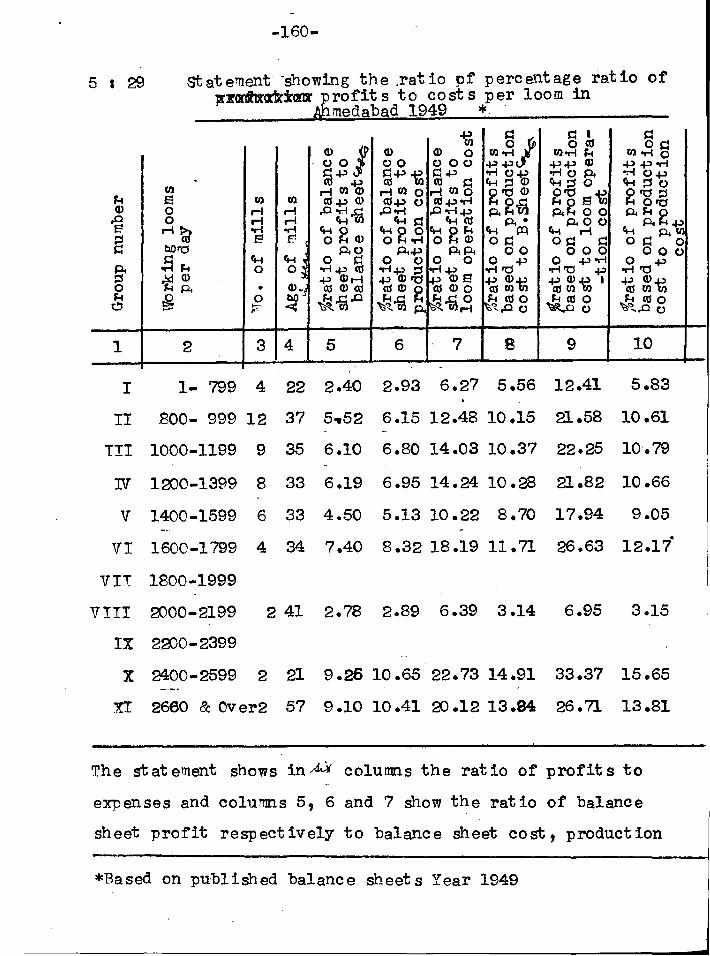

5 : 29 statement· -showing the .ratio pf percentage ratio of ]!':rcrflltd'icrtr profits to costs per loom in

Ahmedabad 1949 *

1

I

I'll r-1 r-1 ...-1 E!

ft..t 0

•

3 4 5 6 7 9

1- 799 4 22 2.40 2.93 6.27 5.56 12.41

10

5.83

rr Boo- 999 12 37 5~52 6.15 12.48 10.15 21.ss 10.61

TIT 1000-1199 9 35 6.10 6.80 14.03 10.37 22.25 10.79

"N 1200-1399 8 33 6.19 6.95 14.24 10.28 21.82 10.66

v 1400-1599 6 33 4.50 5.13 10.22 8.70 17.94 9.05

VI 1600-1799 4 34 7.40 8.32 18.19 11.71 26.63 12.1?"

VII. 1800-1999

VIII 2000-2199

IX 2200-2399

2 41 2.78 2.89 6.39 3.14 6.95 3.15

X 2400-2599 2 21 9.26 10.65 22.73 14.91 33.37 15.65

XI 2660 & Over2 57 9.10 10.41 20.12 13.94 26.71 13.81

The statement shows in 4-X columns the ratio of profits to

expenses and columns 5, 6 and 7 show the ratio of balance

sheet profit respectively to balance sheet cost, production

*Based on published balance sheets Year 1949

j .ll

'-:\· ··•.\\

•" r

l i'

-161-

cost and loom operation cost·. All the six columns

show practically the sa"le trend with the first three

ranks of efficiency. In the case of ratios of

balance sheet profits to costs, group T!l gets the

fourth rank, whiie in the case of ratios of product ion

profits to costs, group III gets the fourth rank. The

efficiency rank i_s groups X, XI and VI having ~0-2599,

2600 and over and 1200-1399 looms respectively 1n de

-cending order of efficiency. The last two, least

efficient are., no doubt, groups I and VIII having

1-799 and 2000 to 2199 looms respectively, group I being ~

least efficient if bala"t9ejprofit s are considered

and when profits based on production cost are consider

-ed, group VIII appears to be the least efficient.

This analysis also confirms the trend that has been ' ' ~

indicated in the earlier analyses.

So far, the earning capacity has been con

-sidered, and as an index of efficiency, it has been

found that it is not exclusively conclusive though

it revels a particular trend. As it has been said

earlier, more scientific index should be production

with reference either to the unit of machinery or

unit of labour. :rn either case, we could study

production in quantity or production in value.

Production in quantity has its own limitations

-162-

in the textile industry, in· that the quality and the

construction of production is not identical. Almost

every unit has a number of variable varieties of production.

Therefore, a comparison on this bas's becomes incorrect

when comparable data is meagre. The comparison cannot

be taken over the entire sample of our studY. There-

-fore it appears that it would be safer to go ·by value

of product ion~ Then every variation in quality will

have its •Wn repercussion ~n value and the quantity

being dependent on the different processes and quality,

these will be reflected in their proper posit ion.

The statement below shows the productivity. per loom

in rupees.

statement overleaf

I

----

-163-

5 :30 statement showing value of production per loom in rupees in Agmedabad 1949 *

Group Working looms 1\To .of Age of Production per No. per daY rnill s mills loom in Rs.

I 1- 799 4 22 30.69

II 800- 999 12 37 31.01

III 1000-1199 9 35 32.06

IV lroo-1399 8 33 35.21

v 1400-1599 6 33 32.82

VI 1600-1799 4 34 31.88

VII 1800-1999

VIII rooo-2199 2 41 29.11

IX 2roo-2399

X 2400-2599 2 21 33.35

XI 2600 & over 2 57 36.90

*Based on published bala'lce sheets 1949

A study of the above figures show~that

group XI having 2600 and oir'er looms has the highest

productivity, which is closely followed by group W

having lro0-1399 looms. The third place in order

of rank goes to group X having 2400-2599 looms.

Groups V and III having 1400-1599 and 1000-1199

looms respectively, follow ne:xt. The least effi

-cient groups are I and VIII having 1 to 799 and

'/ ro00-2199 looms respectively, group VIII being the

worse of the two. The production index shows a

slightly varying trend than was shown by the earli

---er indices. Fere, there are certain factors in-

-herent to the data which seem to distort the

trend to a s~all extent. The different variable

processes, particularly the finishing processes

and the different constructions of cloth invaria-

-bly affect the results. If you could get the

Yardage at the grey stage and reruce them to a

standard construct ion and evaluate the produc-

-t ion, then it would be a very good index of

efficiency. But, such data is not easily availa

-ble. It is not absolutely impossible to get the

data in as nru.ch as the primary docu11ent s are alwaYs

available with the units. From the primary documents,

-165-

the requisite data can be worked out, but they would

not be available wxcept at the authdratat ive level

of the government. Therefore, the product ion figures

actually available cannot give us a sufficient basis

for our study and there are possibilities of dis

-tortions reflected in the trend.

Labour productivity is even more elusive.

'P'ere, unless the data could be worked out on a scienti

-fic basis, no doubt, in terms of value, it can t:lever

be indicative of any results. In this case, the data

is not available and to standardise it on a

scientific basis is next tci impossible under the

existing conditions of operation of this industry.

Though theoretically, this is one of the scientific

indices, we are unable to apply this index to

test effie iency level.

Efficiency is better determined by costs.

It is therefore, that we said that cost would be

one of the most scientific of indices of efficiency

and :tt is directly correlated to size. v.hiile

studying costs, with reference to size, we should

normally take J.Ip the total costs. But,~ in the

cottr:'n textile i_ndustry, as it exists todaY, it

would not be correct to take the total costs for

-166-

reasons mentioned already. In many or the units,

the it ems of co!'Ylmission, depreciation and income ..

-tax are guided by individual decisions of the

managing agents of the units than by specific

or scientific rules• The other items of e:xpen

-diture which go to rnake up the production cost

are fairly dependable •. Therefore, it is nece

-ssary to confirm the analysis of observations

from product ion costs by an analysis of observa

-tions from loom operation costs. These two

together will give us a fairly reliable index

of efficiency, vis-a-vis the size. The state

-ment below shows the total costs and the

product ion costs.

stat etnent overleaf

-167-

5 : 31 statement showi_ng product ion costs and total costs pre in rupees per loom Ab.medabgd 1949 *

1 2

I 1- 799

• 0 z

3

4

4

22

5

~.03

§ .., I'll til .., E' E! 0 0

6

.83

II ~oo- 999 12 37 28.os 1.24

III 1000-1199 9 35 28.94 1.15

IV 1200-1399 8 33 31.80 1.18

v 1400-1599 6 33 31.01 1.18

VI 1600-1799 4 34 27.81 1.07

VII 1800-1999

VIII 2000-2199

IX 2200-2399

X 2400-2599

2 41 28.23 .07

2 21 28.81 1.43

XI 2600 & over 2 57 32 .so 1.10

7

.46

.66

.55

.73

.72

.47

.27

"< a:l

) CD E 0 0

~

8

.23

9

30.57

.61 30.56

• '71 31.30

.63 34.34

.58 32.49

.65 30 .oo

.19 28.76

.37 1.45

.73 .83 35.16

The stat,ement above shows the production costs,

commission, depreciation, incometax and the total costs

pwr loom in rupees. The production costs are built up

of costs on (1) cotton, (2) wages, (3) stores, (4)

fuel, (5) repairs and (6) other miscellanious.items

*Based on published balance sheets 1949

_ _j

-168-

of expenditure. An examination of the total costs

reveals that group VIII having 2000-2199 looms shows

the_least costs, groups VI, II and I having 1600-1'799,

800.999 and 1.799 looms respectively, following in

the second, third and fourth ranks. From what :Uas

been analysed so far, the trend appears to be high

-ly distorter". An e:xaminat ion of figures under

com.,.,_ission, depreciation and incometax reveals the

'Tlajor reasons for the distort ion. The average

expendtture on these three it ems has been very small

in the case of group VIII having g)00-2199 looms.

Therefore 1the total costs of this group becomes non

-dependable for comparison. Si>nilarly, in the

case of group I having 1-799 looms which takes the

fourth rank, figures for these three it ems are ltd

very low. In view of these observations, total

costs as such do not canst itut e a proper index. So

it is reasonable to consider the product ion costs

as an index of efficiency. An analysis of this

column showing product ion costs shows that group

VI having 1600-1799 looms has the lowest cost,

group II has the next lowest and group VIII and X

having 2000-2199, and 2400-2599 looms respectively,

follow on. The group VIII produces the cheapest

qual:i.:_ty as could be evidenced from the production

char,.et shown in the earlier statement ~:o. 5-: 30

·I

J

-169-

(i.e.~· 29.11 per loom) Therefore, if we -eliminate

group VITI, the group X having 2400-2599 looms takes the

th.i.rd rank. The trend is that group VI leads with

group II following as number two and group X as number

three. The trend is a bit surprising and appears ·'

to show that the group having 1600-1799 looms iB most

efficient while the next in efficiency is a smaller

group with 800-999 looms. The ne:A-t best is the group

with 2400-2599 looms. But, what ever it is, the

absolute cost without relation to product ion value

has its own limit at ions and therefore, such freaks

would be eXJ)lained. It is very likely that mills

producing costlier varieties of cloth will have

higher average costs per loom in spite of the units

being vetwy efficient and similarly in the converse,

it is quite likely that least efficient units manu

-facturing cheaper varieties rnay have a lower cost

per loom. Below· is given the statement showing the

production costs and the loom operation costs.

stat ernent overleaf

-170-

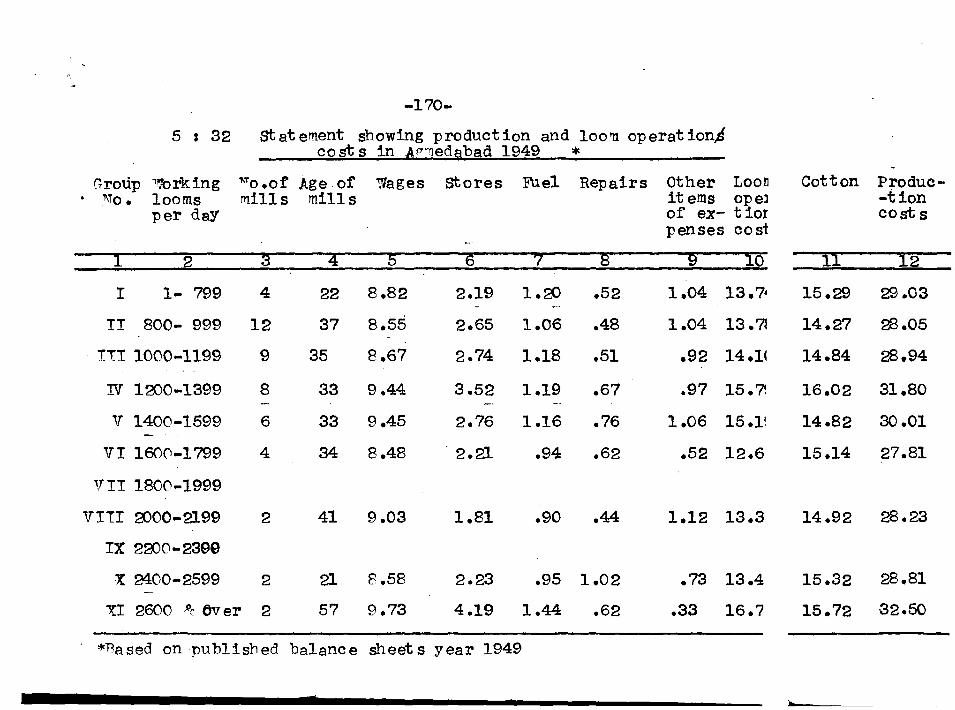

5 : 32 statement showing product ion and loo 'l1 op erat ion,S costs in A('rned~b~d 1949 *

Group ,orking "To .or .Age of ~Vages stores FUel Repairs Other Loon Cotton Pro due-. 1\To. looms mills mills items opel -tion per daY of ex- t ior costs

penses cost

! 2 ~ 4 5 ~ ? s g !o !! 12

I 1- 799 4 22 8.82 2.19 1.20 .52 1.04 13.7• 15.29 29.03

II 800- 999 12 37 8.55 2.65 1.06 .48 1.04 13.7l 14.27 28.05

· ITT 1000-1199 9 35 8.67 2.74 1.18 .51 .92 14.1~ 14.84 28.94

N 1200-1399 8 33 9.44 3.52 1.19 .67 .97 15.?. 16.02 31.80

v 1400-1599 6 33 9.45 2.76 1.16 .76 1.06 15.1! 14.82 30.01

VI 1600-1799 4 34 8.48 2.21 .94 .62 .52 12.6 15.14 27.81

VII 1800-1999

VITI roo0--2199 2 41 9.03 1.81 .90 .44 1.12 13.3 14.92 28.23

IX 2200-2399

X: 2400-2599 2 21 8.58 2.23 .95 1.02 .73 13.4 15.32 28.81

XI 2600 Pc Over 2 57 9.73 4.19 1.44 .62 .33 16.? 15.72 32.50

*Based on published balance sheets year 1949

\

-171-

An analysts of production costs shows a new

set of results, quite "different from those observed

in the earlier analYses. The first four ranks fall

to groups VI, II, VIII and X, having 1600-1799, 800-

_ggg, roo0 .. 2199 and 2400-2599 looms respectively.

Ranks itx~ second and third go to the groups II

and VIII which groups do not appear in the first

four ranks 'in the earlier analysts. The reason

is not far to seek. An exa~ination of the expen

-diture on cotton shows that these have a low

cost of cotton. !\Text stage in the examination is

to find out the quality of product ion of the units

.constituting ,thes_e groups. The indication of the

trend of per loom cost of these groups is that

they should be using the cheaper local quality

of cotton and ~hat they should be producing coar

-ser varieties. lTnit by unit analysis reveals that

the prestimpt ion is not incorrect. Therefore, the

absolute per loom production cost is not a real

index of_ efficiency by it self, for· there is no

weightage for different varieties of cotton used

or the different kinds of cloth produced. If

such weights could be obtained and the correction

ap:olied then production cost would be a correct

index. It is very difficult to g-et the real

-172-

weight age as it is one of the trade secrets. There

-fore,_ the index of product ion costs becQmes unre-

-liable. This leads to a study of loom operation

costs ·which consists of expenses on wages, stores,

fuel, repairs and other miscellaneous ite:ns. Here

again, the analysis of trend of ranks shows surpris

-ing results. The earlier trend is not reflected

in its entirety. The second and fourth places are

taken by groups VIII and I with 2000-2199 and 1-799

looms respectively. An analysis of individual cost

of these two. groups shows that their stores and fuel

costs are low. It appears that the reason for

such low cost on stores and fuel might be due t6 the

absence of the finishing processes and this is very

likelY regponsible for the low loom operation costs.

Actually, labo,,r costs in group..S VITI are fairly

high and are not very low in group I. The cost on

repairs is very negligible and will not,.therefore,

seriously affect the total costs.

The examination so far reveals that absolute

per loom cost shows a trend which is not consistent

w~t~ ~?e __ t rend observed in the earlier analy see with

reference to different criteria. This leads us to

examine the reasons for such a variation. The

-173-

reason is not far to see1(. The cost depends on the

quality produced and has therefore, reference to

quality of product ion. Hence the absolute cost,

as has earlier been eXPlained, is not co!'llparable.

rr,however, the ~cost is examined with

reference to the production .value, the result~

might be more dependable. Beww is shown the

ratio of costs and production.

stat ernent overleaf

-174-

5 : 33 stat el!lent showing ratio of costs to produc-tion in T'ercentages - A"'lmedabad 1949- *

1 2

CI-t 0

• 0 :c:

3

fJl r-1 r-1 .,; E1

CI-t 0

4 5 6

0 ~Q)

Efll~ O~r-1 Ollla1

r-1 0 > ()

CI-t ~ 0~0

0..-1 0..-l~ ..-!~()

~ f!.S F-IG>O

""""' p..~ ,,._ 0 p..

7 8

I 1- 799 4 22 94.8 97.60 44.8 99.69

II 800- 999 12 37 90.4 94.48 44.1 98.48

III 1000-1199

IV 1200-1399

v 1400-1599

VI 1600-1799 . VII 1800-1999

9

8

6

4

35 90.1 93.90 43.9 97.70

33 90·.3 93.81 44.8 97.61

33 91.8 95.47 46.2 99.31

34 89~4 92.60 40.7 96.23

VIII lCl00-2199 9- 41 96.8 97.22 45.7 98.80

IX 2200-2399

X 2400-2599

XI 2600 and over

2 21 86.7 90.80 40.5 96.17

2 57 87.9 90.90 45.5 95.09

The ratios could be worked out between total

costs and production, balance sheet cost.s and

production, production costs and production, or

loom operation costs and production. The analysis

*Based on published ba1a:rmce sheets 1949

•

-175-

of the ratio of total costs to product ion shows group

~I, with 2600 and over looms in the first rank,

group X with 2400-2599 looms in the second rank,

groups VI and TV h~ving 1600-1799 and 1000-1399

loorns respect ~vely, in the third and fourth ranks •.

The ratio of balance sheet profits to product ion

gives the ranks to 1 to 4 in the order to groups

X, U, VI and "N. The production costs gives

almost the sa"ne rank, except that :in the fourth rank,

group III gets :in instead ·or group r:t. In the

case of loom operation costs, group X again takes

the first place with groups VI and ITT in the

second and third places and group II in the fourth place.

Taking all these four ratios consolidated, it is

clear that group X takes the first place while

group XI and VI take the second and the third

places respectively •. And the fourth t'lace is taken

by group W in two cases and groups II and III

once each, but group III takes the third place once. . -

The over all picture places group X with 2400-2599

loo'7ls at the first rank, XI ~ith 2600 and over looms

and group VI with 1600-1799 looms in the second and

the third ranks and group TV with lro0-1399 looms

and group Iri with 1000-1199 looms share the fourth . rank. The weightage, however small, is for group III • .It ~~ ~ ~ ~ ~ ~<?A- .t.. .M~ ~ ~ <Ut. •.

,tk~ ~~ ~ .ft,-~l<u-v·~Ll ~~~~~ ~t\-~~4~ ~Joa-tL-!L~.

~w..¥ crv~ j

1

I

II

2

-176-

• 0 ~

3

1- '799 4. 22

800· 999 12 37

III 1000-1199 9 35

IV 1200-1399 8 33

v 1400-1599 6 33

VI 1600-1799 4 34

.VII 1800·1999

VIII rooo-2199 2 41

IX 2200ro 2899

X 2100-2599 2 21

XI 2600 & over 2 57

5 I 34 : 1 stat ement showing t production' profits

· costs -

5 6 7

2.40 ·2.93

5.52 6.15 12.48

6.10 6.80 14.03

6.19 6.95 14.24

4.50 5.13 10.22

7~40 8.32 18.19

6.39

8

s.oo 9.55

9.70

9.55

8.17

10.83

3.03

9 .ro 10 .es 22.73 _ 1s .• s2

9.1o 10.41 ao.12 12.09

9

94.8 l'l- A

90.1

90.]

90.-1

91.8

89.4

96.E

86.7

87 .s

*Based on publiShed.balance Sheets, 1949

J

-177-

percentage ratios of costs to ) product ion 1edabad 1949

I

·~~ rca o s .0 0'1""1 . ..., 'H~() 0 Q) ::s . G>'O ~i2 ~G>A ~00 . ...,

10

97.60

94.48

93.90

93.81

95.47

92.00

97.22

90.80

90.90

and profits to -. *'

Cll ...,. ..-to '-1~0 2'0""'e p.202~ "" ~-i 02 oco ~

QC)Q)fll 0 00 or~ros:::io ..., Q) 0

QS Cll ori r-1

~ "'""' "' .01.0

11

5.56

10.15

10.37

19.2.8

8.70

11.71

3.14

14.91

13.34

I

Cll 2 .f.'IP.• 'I""'G Cll '-1~0~ f!'ts..., A2 fa g

'H A~ C 0 c 0 o.

00'1""1

~'iS::~ ~02~.g ~.pI I .

12

5.83

10.61

10.79

10.66

9.05

12.17

3.15

15.65

13.81

s Cllori ..., ..., ..

..... C) fll ' "" ~ ~ 2'0S 200 A oo '-! Ar-t C . 0 c 0 0

Oof.'--rl ~ ro 02~ .p Q)~ F-4 cu Cll (1)

~CGOA .0C>Il4

.13

12.41

21..59

22·25

21.82

17.94

26.63

6.95

33.3i

26.'71

Q)

00

i""' '«<CI) .0~~

'-10 1M2'" 0 ...,

AO 0 ,a .,....,., ~~2 ~iA

14

2.64

5.55

6.05

6.28

4.72

7.41

2.75

9.30

8.94

...

t s A ori 00 'Qj~ a""' "'5.6 002 ~~3 ""'2

Oor-1 '-lA 'HOof.' 0 0 () 0 . c ::s Oof.' o ore ori

'orf.,... 2 .f.)02 ~~ ~...,

F-tt!A ~g ~I

15 16

44.8 . 99.69

44.1 98.48

43.9 97.70

44.8 97.61

46.2 99.31

40.7 . 96.23

·' 45.7 I 98.81

40.5 96.17

45.5 95.09

-178-

5 I 34 I 2

5 6

( i) X X

( ii ) XI tt •

( 111) VI VI

( iv) IV IV

( v) III III

( vi) II II

( vii) v v

(viii) VIII I

( ix) I VIII

·s 1 34 I 3

( 1)

( 1i) -( iii) . -( iv)

( v)

( .vi) 1

( vii)

(viii) 6

( ix) s

5:34:4

statement showing t different st d rds

7 8 9

X X X

XI XI XI

VI VI VI

~ 1V III III

III 1V IV

II II II

v v v

VIII I I

I VIII VIII

ment of fre

-·1

11

III

-1

5

6

-

~ ( i) ( ii) ( iii) ( iv) ( v) ( vi) ( vii) .(viii)

( ix)

G r o u

6

6

-. -

t

number of credits based on measgring efficisgcy

11 12. 13

~ X X X ~

XI n VI

VI· VI· XI

III III III

[ IV 1V IV

[ II II II

r v ,v v [. I -I .I

I VIII VIII VIII

tlCY or ranks

Nu mb e r VI VII

§ VI!I

2 '-10 -- -

--

.. -

nt or r@a

--

1

5

.6

Group X

XI 'J/I

N III II ·v I

VIII

-179- •

14 15 16

X X XI

XI VI X

VI III #I

1JI II N·

III IV. III

II I II

v XI. VIII

VIII VIII v I v I

·IX X XI f

11 1

1 9

·- - 1

- -... -

- 1

'!"'

- - -

..

.,

-180-

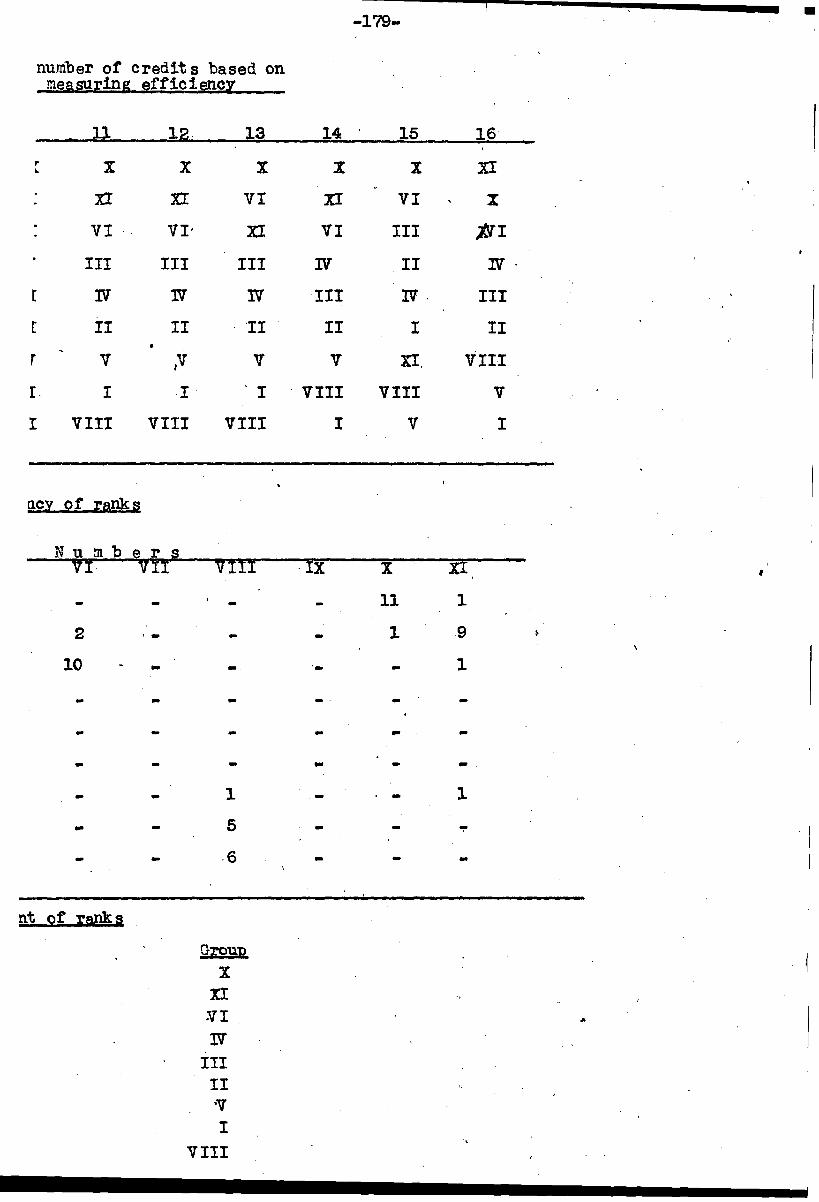

The twelve ratios have been worked out, four

relating. to costs and product ion, two relating to

profits and production, and six :r;elating to profits

and costs. Having worked out the ratios the ranks are

tabulated in the two-waY statement,S No. 5s34:2 showing

the number of times a particular rank is obtained

by each or the eleven group~. A study of the state

·~ent brings ouw prominen~ly groups X having 2400 ... 2599

looms, XI with 2600 and over looms, VI with 1600-1 '799

looms, II with 800 ... 999 looms, and V with 1400-1599

looms, each of them with well over 75% of the credits

in a particular rank. Groups X, XI and VI take the ~ .

;f'irst three ranks,igroups II and.V take the sixth and

seventh rank respectively. Groups III and IV with

1000-1199 and 1200-1399 looms t-espect ively rival

between themselves for the fourth and the fifth

ranks, while groups I and VIII with 1-799 and 2000-

.. £199 loolns respectively rival between themselves

for the eighth and the ninth ranks.

Having decided upon the first three ranks

undisput·edly between groups x, XI and VI the question

of fourth and fifth ranks have been examined in

detail because the ~race between ~ groups III and

·!Jl has been almost neck to neck. Group III gets

once rank three, five times rank four, and six times

-181-

rank fiVeJ while group rl get 1six times each ranks

fourth and f'itth. The tact that in one out or

twelve cases group III gets the third rank give

the strength or argument for t;,lac ing group III 1n

rank four. But the weighted average :ln the percen

-tage variation between the two groups clarifies

the position and shows that the ·mere attaining

or the third rank once does not give group III

the better right of being placed in rank four.

Therefore, we have placed group rl as the- fourth

in rank and group III as firth :ln rank.

Rank six and seven are distinctly occupied

by groups II and V respectively with eleven credits and

1l1r ten credits :ln those ranks. Again tor the eighth

and the ninth places there is a tie between groups

I and VIII; but a closer examination shows that

group I getting rank six once, rank eight six times

and rank nine five times is better' eligible for

rank eight than group VII which gets rank seven

once, rank eight five times and rank nine six

times. The actual ranks or the different groups

is shown in the statement of merits, 5s34:4.

The above anal~sis based on ranking vis-a-vis . ~ the twelve ratios has shown dipt inct ively that

group X with 2400-2599 looms is of the optimum

size among the samples studieq. The next higher

group, which is defined as 2600 and over looms, . ,

consists of only two units, one of them hav:1ng

2762 looms and the other 4604 looms. And because

there is a wide variation between the results of til• .

the units, on the average the group loses its

place to group x. If we had alrger number of

samples in group XI and also samples of large

sizesJin proper multiples of 400 looms, we would

have seen that the level or op-t-imum would be better

and better. The one unit whose loomage is in the

neighbourhood or 2800 shows a trend to be better

than group x, but dt cannot be accepted because

it would be an inference on the basis of a single

unit. This has led to the inference that the

best size from the observed facts is that or

group X as has been already 1ndicat ed.

The analysis further shows that the de

-gree of economy or operation places groups VI

and IV next in order, showing a periodicity of

400 with a break at the ltevel or 2000-2199 looms,

that is, group VIII. The disturbance in the

periodieity~t the level of this group is due to

the tact, as has been earlier explained, that the

-183-

average age of the group is high, and that there

are fewer fdnishing plants in the units of this

group. Further this group has only two samples

worked at diffe.rent levels of efficiency. .Had

there been sufficient samples, better indica-

.. t ions :WOuld have been observed. The analysis

shows the periodicity of economic levels start

·ing from 800 looms right upto 2400 looms at

intervals of 400 looms. The group below 800

looms is on the margin whose ratio of total

costs to product ion is 99.69 -..h.ich leaves prac

-t.ically no margin even under the controlled

economy which ensures by statutory provision

an accepted margin to every unit in operation in-

where the management is not/efficienc7t.

Therefore, this last group, that isJ group I

will tend to be unecononic under normal con

·ditions of operation of this indust,_.,.. The

marginal unit lies in the group having below

800 looms. The group just above the marginal

unit, therefore, should be taken to represent

the economic size. The analysis shows that

at intervals less than 400 looms the econom,y . ~

is distwrbing as the overhJ'ads are not fully

utilised. In the ne:xt chapter the relative

-- ------------ ----------------------

position or the different peaks above the economic

size will be studied.

'

~----------- -------~-.~-------