Embed Size (px)

Citation preview

Chapter 6: Revenue and Expense Recognition

Suggested TimeCase 6-1 Bella Beauty Inc.

6-2 Time-Lice Books Ltd.6-3 Ceramic Protection Company Limited6-4 Thomas Technologies Corporation

Assignment 6-1 Revenue recognition—gross or net.................. 156-2 Revenue recognition (*W)............................... 156-3 Revenue recognition—four cases.................... 206-4 Revenue recognition – critical events.............. 106-5 Revenue recognition – critical event................ 156-6 Revenue recognition........................................ 206-7 Entries for critical events (*W)........................ 356-8 Entries for critical events (*W)........................ 356-9 Removed.......................................................... 206-10 Unconditional right of return (*W).................. 406-11 Instalment sales method .................................. 356-12 Cost recovery method...................................... 156-13 Instalment and cost recovery methods............. 156-14 Warranty—two accounting methods............... 206-15 Warranty—two accounting methods............... 306-16 Multiple deliverables....................................... 106-17 Multiple deliverables....................................... 106-18 Multiple deliverables....................................... 206-19 Agricultural produce........................................ 156-20 Agricultural produce and biological assets...... 106-21 Percentage-of-completion method................... 306-22 Construction contract....................................... 256-23 Construction contract—revenue change.......... 306-24 Use data in Assignment, not text .................... 406-25 Asset exchanges—five situations.................... 30

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-1

6-26 Asset exchanges—four situations.................... 256-27 Asset exchanges—two transactions (*W)....... 206-28 Expense recognition (*W)............................... 106-29 Expense recognition......................................... 206-30 Revenue and expense recognition.................... 35

*W The solution to this exercise/problem is on the text Web site and in the Study Guide. This solution is marked WEB.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-2

Questions

1. Revenue is defined with reference to the definitions of assets and liabilities, and is therefore a derivative definition. That is, revenues are gross inflows of economic benefits (i.e., increases to assets and/or decreases to liabilities) derived from the entity’s business activities.

2. In economic terms, revenue is earned at each step in the earnings process, or as a company engages in activities that increase the utility of an item or service. For accounting purposes, revenue typically is recognized at one critical point, although it some circumstances revenue can be recognized over time or in several different discrete points.

3. To be recognized in the financial statements, an item must meet the definition of a financial statement element, be measurable, and be probable. Revenue must also be earned (the vendor has to transfer the risks and rewards of ownership) and it must be realized or realizable (cash collection must be assured).

4. Performance is acheived when the entity has substantially accomplished what it must do to be entitled to the benefits represented by the revenues. That is, the risks and rewards of ownership must have passed to the customer and the entity retains no continuing involvement. Revenue must be both realized (or realizable) and earned to be recognized.

5. There are several criteria that must be satisfied before revenue can be recognized. The last one to be satisfied is known unofficially as the critical event because it triggers the recognition of the sales transaction and the recording of revenue. All expenses are recognized at the same time. Examples of critical events include (1) delivery, (2) cash collection, and (3) fulfillment of the seller’s final obligations in connection with the sale.

6. Revenue is typically recognized on delivery because this is a point at which revenue is realized or realizable and earned. Risks and rewards of ownership usually pass in a straight-forward way on delivery, so the “earned” criteria is easily met. Realization must still be addressed, but where it is met, revenue recognition is appropriate. Customer acceptance and possession of goods is powerful evidence that the vendor has performed required tasks.

7. Revenue is recognized after delivery if significant uncertainties exist with respect to warranty or other post-sale costs, or if collection is not assured. Revenue cannot be recognized until these uncertainties are cleared up. Also, revenue cannot be recognized until estimable; this may delay revenue recognition past delivery.

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-3

©2011 McGraw-Hill Ryerson Ltd. All rights reserved Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-4

8. In order to recognize revenue when the right of return exists, the proportion of returns must be predictable. In this case, revenue is recognized and a provision for returns is used. When the returns cannot be predicted, recognition of revenue should be deferred until the return privilege expires.

If any one of these conditions is not met, no revenue is recognized. All profits are deferred, and the seller’s interest in the product is recorded at cost. The actual accounting procedures are similar to those used under the instalment sales method.

9. The instalment sales method is a method of accounting for a sale whereby gross margin is deferred when the sale is recorded (on delivery) and is subsequently recognized proportionately as cash is collected. The method is used when there is doubt about ultimate cash collection to the point where an allowance for doubtful accounts cannot be reliably estimated.

The cost recovery method (also known as the “zero profit method”) of recognizing revenue requires that all of the related costs incurred be recovered before any profit is recognized. It is used only when the ultimate realization of revenue cannot be estimated reliably that no earlier profit recognition is appropriate.

10. Ending inventory of construction in process under the percentage-of-completion method includes recognized gross profit. Therefore, the ending inventory consists of cost incurred to date plus the gross profit (or loss) recognized to date.

11. When a loss is projected on a long-term construction contract, it must be recognized in full in the period it is first projected. If income has been recognized in prior periods under the percentage-of-completion method, that income must be reversed in the period of the loss and included in the total loss recognized in the period.

12. Earnings from biological assets are recognized as the net realizable value of the assets change through growth and as the result of changes in net realizable market value. NRV is used for valuation of the assets and thus for revenue recognition through harvest or slaughter, and the harvested products are also valued at NRV. Once the harvest has been further processed into products (which are then classified as inventory), the valuation basis changes to lower of cost or NRV. The NRV of the harvest at the time it enters processing is taken as the “deemed cost” of the raw material.

13. In a barter transaction of dissimilar items, revenue is measured at the fair value of the goods or services acquired.

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-5

14. Since there is no commercial substance to the transaction, the acquired asset should be recorded at the carrying value of the asset given up, which is $12,000.

15. In this situation, the exchange has commercial substance. Therefore, the acquired asset is recorded at the fair value of the assets given up, which is the $25,000 fair value of A’s asset plus the $5,000 cash paid, for a total of $30,000.

16. The definitional approach to expense recognition refers to ‘reduction in assets or increases in liabilities’ to dictate expense recognition. Each expenditure (debit) is assessed as an asset; if it does not qualify as an asset, it is an expense. Liabilities are evaluated: if a liability exists, an expense may be created.

Matching uses revenue recognition as a trigger. Once revenues are recognized, all related expenses must also be recognized, even if they precede the revenue recognition point (they would have been deferred) or if they follow the revenue recognition point (they must be accrued).

17. Justification of bad debts policy:

Definitional approach: The asset (accounts receivable) is over-valued at its gross amount; the valuation allowance, allowance for doubtful accounts, must be recognized to accurately reflect future cash inflows.

Matching: Bad debt expense is incurred with the sale transaction and must be recognized to properly match all costs to the related revenues.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-6

Cases

Case 6-1 — Bella Beauty Inc.

Overview

BBI’s primary financial statement user is the banker who is placing reliance on the financial statements to determine whether an operating line extension will be granted.

Management is very motivated to secure this loan which may influence the selection of accounting policies. Management will want to minimize the debt to equity ratio and maximize income from continuing operations. This translates to a bias towards accounting policies which maximize the recognition of revenue and delay/minimize expense recognition.

Issues

Special Purchase Terms

The special purchase terms offered by BBI create a revenue recognition challenge. Although BBI has performed its obligations with respect to these sales by providing the product and collection is assured given upfront payment was required, there is uncertainly around the measurement criteria.

Since customers have until April 15th to return merchandise for a full refund, BBI is may be unable to predict how much revenue should be reported relating to these sales.

Financial reporting alternatives are (1) wait until the return provision expires to record revenue and related COGS or (2) record revenue and COGS and set up an estimated provision for returns. Since this is the first time BBI has offered such a promotion, historical results are not available to use a basis for an estimate of returns. Since the economy is currently in recession, it is reasonable to expect that returns will be material.

Recommendation: Wait to recognize revenue and related COGS until after the return provision expires.

Piper Inc. Sales

BBI was aggressive in recognizing the revenue related to these sales. The performance criterion was not met as of December 31, 2008. As of December 31, 2008, the customer had not accepted the product and had returned it for rework under the terms of the contract.

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-7

Recommendation: Wait to record revenue and related COGS until fiscal 2009 at which time the customer has accepted the product and the costs of rework are known.

Discontinued Operations

BBI decided to stop selling evening dresses and decided to classify the losses from these sales as discontinued operations. Since the evening dress line is not distinguishable from the rest of BBI, it does not qualify as a discontinued operation. In order to qualify as a discontinued operation, the evening dress line would have to have its own operational activities and be a separate reporting unit (i.e. have separate revenues, expenses, assets, cash flows, etc). Instead, “evening dresses” is just one product within the general revenue stream of the company.

Another issue is that of inventory valuation. Since the dresses have been selling at prices below cost, it is likely that inventory left on hand is impaired. BBI must ensure that any inventory on hand is written down to the lower of cost and net realizable value.

Contingent Gain

ASPE (as well as IFRS) specifically prohibits the reporting of contingent gains. If realization of this gain is probable, note disclosure may be appropriate.

Conclusion

Once the necessary adjustments are made to the financial statements (see below), BBI is off-side on its debt to equity covenant. BBI also reports significantly lower income from continuing operations as compared to the prior fiscal year.

This may result in the bank rejecting BBI’s application for a credit line extension. This could be very detrimental to BBI as additional financing is required in order to launch their new line which has been identified as key to their future success. These factors should be taken into account in assessing the going-concern assumption. Note disclosure may be appropriate.

BBI must approach the bank to discuss their situation as soon as possible.

Debt EquityDebt:Equity

Balance before adjustments$300,00

0$150,00

0 2.0Adjustments:

Special purchase terms +50,000 –20,000Piper Inc Sales –3,200Inventory write-down (TBD)Contingent gain –15,000

©2011 McGraw-Hill Ryerson Ltd. All rights reserved Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-8

Balance after adjustments:$350,00

0$111,80

0 3.1

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-9

Case 6-2 — Time-Lice Books Ltd.

Overview

The general objective of this case is to give students practice in applying their professional judgment to recommend an accounting policy for revenue and expense recognition. Students must identify the reporting objectives for the company, and must apply qualitative criteria in deciding what the most appropriate policy is.

Reporting objectives

1. Minimum disclosure and compliance with securities acts: The company is a public company; its shares are widely traded and are listed on the Toronto Stock Exchange. Therefore, a clean audit opinion is important. This reporting objective will cause the adoption of accounting policies that result in accounting numbers that are reliable and verifiable.

2. Cash flow prediction: The heirs of the founder own 30% of the common shares and are likely to be concerned about the dividend flow. The heirs are not actively involved in the company and retain a professional financial advisor, who may be presumed to be sophisticated. Since 30% is no doubt the largest single block of stock, the heirs probably have a substantial say in who is on the Board. Thus the needs of the heirs must be given consideration in developing accounting policies.

3. Performance evaluation: Similarly, the heirs’ analyst will be evaluating the performance of the management in order to advise the heirs on how to vote their shares.

4. Income tax deferral: The company probably will be permitted to deduct expenses when incurred and include revenues when received for income tax purposes, in view of the nature of the operations. If tax is affected by the revenue recognition policies, then the tax deferral objective is relevant, but probably be a secondary objective.

Since IFRS is somewhat flexible in the area of revenue and expense recognition, it is critical that the primary user and objective be identified at this point in time. Otherwise it will be difficult to provide a recommendation for the client.

Revenue/expense recognition alternatives

Some students may try to fit the recognition of revenue into the molds of recognition at (1) the point of production, (2) point of sale, or (3) point of cash receipt. This case does not fit into those molds, however, since all three events are occurring simultaneously (at different rates) through time. Some students may also concentrate exclusively on revenue recognition and overlook the related issues of expense recognition.

Better students will apply more basic criteria of revenue recognition, such as:

©2011 McGraw-Hill Ryerson Ltd. All rights reserved Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-10

the critical event theory,

completion of the earnings cycle, or

measurability (or relative certainty) of future cash flows for revenues and costs, and will realize that unless one simply lets the cash inflows and outflows fall where they may, costs must be deferred and/or revenues accrued in advance of receipt in order to achieve matching and satisfy the objectives of stewardship, cash flow prediction, and performance evaluation.

There are at least three conceivable alternatives to revenue and expense recognition in this case:

Recognize revenue as the books are delivered. This will require deferral of most of the revenue received from the advance sales, and also will require deferral and amortization of the initial promotional expense (the largest cost component). The stumbling block would be deferred of promotion expense, which requires measurable future benefit to be justified under IFRS, especially since the promotional materials are “internally generated” intangibles.

Recognize revenue as the cash is received, and then recognize deferred initial costs on a cost-recovery basis until all deferred costs have been recovered. Thereafter, recognize additional production costs as incurred and additional revenue as realized. Again, this approach depends on being able to justify deferral of the initial costs.

Recognize revenues as cash is received, and recognize expenses as incurred. This approach conforms to the “definitional” approach to determining revenues and expenses, which is based on changes in assets and liabilities. Under this approach most of the costs will be recognized as expense when each series is initiated while all of the revenue will be recognized later.

Advance sales — Revenue from advance sales can be reliably measured quite early in the revenue generating process, since the full amount is received at the time of subscription (after the second book is mailed). The cancellation rate is very low, and therefore the provision for cancellations would be relatively small. Most of the costs have been incurred by the time that the subscription rate is known, and recognition at the point of subscription would facilitate matching; costs would not need to be deferred. The cost of printing and binding the future books is relatively small ($5.00 on a $30.00 book) and a liability for these future costs can be established in order to match these future costs against revenue. It would appear, therefore, that the measurements would be sufficiently reliable at the time of subscription to permit revenue and expense recognition at that time for the advance sales and still satisfy the stewardship objective.

There still remains the issue of whether the revenue has been earned when only two books in the series have been produced. If the earnings process is viewed as the expenditure of effort, then the bulk of the effort (and cost) has indeed occurred, since the

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-11

major effort and expense is in the promotional stage. Thus, signing up the customers can be viewed as the critical event in the revenue generating process.

On the other hand, one could legitimately view the earnings process as not being substantively complete until the books are actually produced and delivered to the customer. Performance must be complete and TLBL has not completed its performance obligations as not all the books have been delivered. Under this approach, revenue should be recognized on a straight line basis, as the books are produced and delivered. To the extent that costs can be identified with a specific book series, they should be capitalized and offset against revenues realized. The gross profit on each series would then be recognized as each book is produced, at an amount based on the total estimated identifiable costs and total estimated revenues. Costs that cannot be identified with or reasonably allocated to specific series must be treated as period costs.

It is a short additional step to delay revenue recognition until the cash from installment purchasers is actually received. However, since the cash receipt could be spread out over a considerable period of time, it probably would be more feasible to recognize the revenue when each volume is mailed, with a provision for uncollectibles on that particular volume. TLC has been in operation for a number of years, therefore, there is past history to be able to estimate an allowance. Recognition of revenue when the amount is received is not acceptable under GAAP.

Installment sales — It would be much more difficult to estimate the revenue from the installment sales at the time of the original subscription. It is possible to estimate the net revenue, of course, after deducting a provision for uncollectibles and cancellations, but a fairly small estimation error could cause a large change in net income. Given the lack of reliability of the installment revenue measurement, recognition at the point of subscription would be difficult to rationalize. Installment earnings more naturally fit a percentage-of-completion or installment basis of reporting. Also, performance has not yet been completed.

Relationship to objectives

The foregoing discussion does consider the quality of the earnings information under the various alternatives, but it does not relate directly to the financial reporting objectives that were identified earlier. Contract compliance calls for reliable measurements, and would rather clearly rule out revenue recognition at the point of subscription for installment customers. The revenue estimate may be unexpectely off the mark, and there has been no realization of either the revenue or the production costs. For the advance sale customers, revenue should be recognized as performance is achieved. That is, revenue will be deferred and a percentage recognized as each book in the series is delivered.

For both cash flow prediction and performance evaluation, early revenue recognition for each individual series would seem to be desirable, especially for the performance evaluation objective since management makes the important decisions at the start of each series. However, early recognition depends on the predictabiliy of total revenues and

©2011 McGraw-Hill Ryerson Ltd. All rights reserved Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-12

costs, which is uncertain. Therefore, TLBL must use recognition alternatives that spread the earnings from a particular series over several accounting periods.

Spreading revenue/expense recognition over the life of the series will result in each period's reported earnings consisting largely of earnings being realized on projects started in earlier periods. This will be advantageous to the company because spreading the earnings of multiple on-going series over several years will help to stablize TLBL’s earnings and therefore the share prices.

Similarly, the overall cash flow consequences of the book series are more clearly represented if the cash flow consequences of a series is reported together, in a single period. However, revenue (and expense) recognition at the time of subscription does not lead to “high quality” earnings, because much of the revenue will not be received until a later period. The earnings may more closely approximate cash flow if a percentage-of-completion approach is used.

For tax deferral, later recognition is better than early recognition. Ideally, costs would be recognized when incurred and revenue recognized when realized. If there are many concurrent series being produced, then this approach to revenue and expense recognition may be quite appropriate. However, if series are started sporadically and the level of activity varies from period to period, then this approach would not be appropriate for financial reporting even though it would be best for income tax deferral. In that case, a percentage-of-completion or installment basis of reporting would be preferable.

In summary, it would appear that the earliest that revenue could be realized (and thereby satisfy the cash flow prediction and the performance evaluation objectives) and still have sufficient reliability to satisfy the minimum disclosure objective would be to recognize the revenue as each book is shipped. While such a method will not be very good for performance evaluation, the stewardship objective is dominant in this case due to the public reporting requirements that pertain to this company. In arriving at a decision an assumption must be made concerning which user and objective the financial statements are being tailored.

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-13

Case 6-3 — Ceramic Protection Company Limited

Overview – users and needs

Ceramic Protection Company Ltd. (CPC) is a public company. Control has recently been assumed by one shareholder, Mark Fortin, who acquired about 55% of the shares during the year. Although public companies may have a tax minimization objective, this is not relevant in the short term due to tax losses that have been incurred. Mr. Fortin’s concern is primarily cash flow. Therefore, accounting policies that reflect cash flow would meet his needs and those of the lenders, who are also interested in cash flow reporting as well as performance evaluation.

However, key personnel are entitled to bonuses based on operating income before financing charges and income tax. They would generally prefer accounting policies that maximize income to increase their bonus payments. However, since CPC will record operating losses in 20X6, no bonuses will be paid this year. These individuals should receive “fair” bonuses in the future based on their efforts or they may well become dissatisfied. Cash basis accounting may not be fair to this user group.

Representational faithfulness of the financial reporting is important for all of the users. Recommendations will be based on IFRS, except in circumstances where it may be “unfair” to the users. This is over-riding ethical concern. It should be noted that the desires of Mr. Fortin and the lenders to receive cash flow reporting are met under the IFRS requirement for a statement of cash flows.

Issues

1. Accounting for tax losses2. Inventory errors3. Potential sale of manufacturing facility4. Severance costs5. Revenue recognition

Analysis and recommendations

Accounting for tax losses

CPC will have tax losses in 20X6. These may be carried back to the three prior years to generate tax refunds if any tax was paid in those years. A receivable may be recognized with respect to the refunds, with a corresponding reduction in income tax expense. This treatment best matches the recovery of the taxes with the year in which the related loss occurred. Since the refunds should not be substantially delayed, it also approximates the cash flow.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-14

Remaining losses, if any, are available as loss carryforwards for 20 years. Under GAAP, the benefits of this can be recognized as an asset and an increase to earnings immediately if the probability of recognition is likely. Given CPC’s weak earnings record and significant losses in 20X6, the likelihood of realization is questionable. However, the reasons for the losses have been identified and corrected and significant future orders exist.

On balance, the conclusion is that the income tax asset should not be recognized. In addition to being the conservative choice under uncertain conditions, it is more consistent with cash flow. Future bonuses will not be affected since they are based on operating income before income tax. Note disclosure should be provided with respect to any unrecognized losses and their expiry dates.

Inventory errors

CPC discovered a $1,500,000 fraud in 20X6 that resulted in overstatement of inventory records in 20X4, 20X5, and 20X6. Obviously, this has to be accounted for in 20X6. Providing information for lenders about their security is paramount. The item affects 20X6, a loss year, and prior years, and thus would not change bonus entitlements of executives. Retrospective restatement as an error correction seems most appropriate, as it would result in the fairest reporting of performance for each of the years in question. Following IFRS, the following should be done:

1. Inventory balances have to be restated for 20X5 and 20X4.2. Revised cost of goods sold should be reported for 20X5 and 20X4.3. Losses due to the fraudulent activities may be shown separately in the years in which

they occurred. 4. Opening retained earnings should be restated to reflect the impact of the error

correction.5. Note disclosure should be prepared to explain the situation and its financial impact.

Potential sale of manufacturing facilities

CPC has certain manufacturing facilities for sale, although no offers have yet been received. Since CPC will still be in the ceramic ballistic armour products business after this divestiture, this disposal does not qualify as a discontinued operation. The gain or loss from sale would be reported separately on the income statement if and when the transaction occurs.

The manner in which the assets intended for sale are reported in the financial statements will depend on whether the assets fit the definition of “held for sale assets” under IFRS. If the assets qualify as held-for-sale, depreciation would cease and the assets would be reclassified (as a group) as a current asset.

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-15

In this instance, the sales status of the assets seems ambivalent; no official selling process has begun, and it appears unclear as to exactly which assets will be offered for sale. Therefore, the assets must be viewed as “idle” assets—depreciation will continue, and there will be no reclassification on the SFP. The assets should be subjected to an impairment test. The assets’ fair value less costs to sell must be assessed and compared to book value. If recoverable cost is lower than carrying value, there must be a write-down. While impairment recognition does not reflect 20X6 cash flow, it does properly reflect future cash flow and secured lenders should be appropriately treated. It is highly unlikely that recoverable cost is higher than carrying value, as the facilities are not very old and thus cost would still be largely undepreciated. Recoverable cost for used manufacturing facilities is usually low, as the market is thin (no offers to date) and the facilities are likely to be quite specialized.

Severance costs

There are two alternatives to account for the severance package:

1. Accrue the cost of all severance entitlements in the period in which the decision was made (20X6). This accrual would include the three elements of the package: one month’s salary for each year worked, a six month bonus, and the value of enhanced pension entitlements. This latter amount is not part of pension expense, as it relates specifically to the severance decision. To accrue this amount, the number of employees affected would have to be estimated. The amount should be reported as a restructuring expense in 20X6. It properly reports the cost of the decision as this decision is made, although it does not reflect cash flow. It would be reported in a loss year, and thus would not change bonus payments.

2. Expense the payments only as made. Under this alternative, the cost of the program would be reflected on the income statement as paid, in the years after employees are severed. Most of this would be paid in fiscal 20X6, as monthly pay would continue for (at most) six months. The pension entitlements would be also reflected as employees leave and withdraw from the plan.

This accounting alternative correctly portrays cash flow in 20X6. It would reduce bonus payments in 20X7 if the amounts were included in operating income, although bonuses may be calculated on income before this amount if all parties agree.

The problem with this policy is that future obligations are not completely recorded at the end of 20X6, as liabilities are not recognized and are therefore understated. Note disclosure is not a substitute for measurement. If the costs are reliably measurable, they should be accrued, which takes us back to the previous alternative of establishing a restructuring provision for unrealized costs.

The recommendation is that CPC record all restructing 20X6 costs as expenses, and establish a restructuring provision (liability) for future costs, provided that the costs are reliably measurable. In this way, future performance evaluation and bonus calculations will not be impacted and all users will have a truer picture of CPC’s financial position at

©2011 McGraw-Hill Ryerson Ltd. All rights reserved Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-16

the end of 20X6. The difficulty may be in determining the number of employees that will be affected. The agreement applies “to layoffs where necessary”; it may be that no one will be layed off. Thus, employee numbers may not be reliably estimable.

Revenue recognition

Under GAAP, revenues are generally recognized when performance is achieved and reasonable assurance regarding measurement and collectibility of the consideration exists. In the case of long-term contracts, such as CPC’s orders that take nine to fourteen months to complete, performance would be determined on the percentage of completion method. However, it can be difficult to estimate progress towards completion and remaining costs, especially since CPC has a history of cost overruns.

CPC could delay revenue recognition until delivery, which is the normal revenue recognition point for the sale of goods. There is less uncertainty with respect to performance as the risks and rewards of ownership are transferred at this point. Most costs are known with certainty and costs of any final adjustments can be accrued. This is somewhat conservative and, over the long term, will delay bonus payments.

Revenue should be recognized on delivery. Costs would be deferred as work-in-progress until the sale is recorded to ensure better matching. This alternative is the best compromise for performance evaluation and is simpler and less risky to implement than the percentage of completion method.

The Egyptian order raises issues with respect to measurement. Since attainment of the “bonus” is uncertain, it would seem prudent to record the base amount (i.e. $100,000) of revenue on delivery and the additional consideration (up to $120,000) only when the entitlement is established. It is analogous to a contingent gain and management’s confidence of its receipt may be somewhat biased.

Research and development costs

CPC will spend $200,000 to $300,000 to research and develop improved production methodologies to support the Egyptian army order. Theoretically, these amounts could be either (1) capitalized and amortized or (2) expensed as incurred.

If receipt of an increased price is reliably estimable, it may be justifyed to capitalize at least a portion of the expenditure as development cost, especially since it relates to a specific order that has benefits from a higher purchase price. Capitalization, with recognition when the benefits are realized through recognition of the higher price, would better reflect performance and thus be a better basis on which to determine bonuses.

On the other hand, if the future benefits cannot be reliably measured, expensing will be necessary. Expensing properly reflects cash flow and serves the company’s reporting objectives.

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-17

These costs should be expensed as incurred. The future benefit is uncertain and any capitalized development costs on the balance sheet would not likely be used as security by a lender. Although this will have a negative impact on bonuses in the short term, over time the impact should be neutral.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-18

Case 6-4 — Thomas Technologies Corporation

Overview

The management of Thomas Technologies seems intent on increasing reported revenue (and earnings) in 20X4 by devising contracts that support early recognition. The ethics of management’s deal-making is suspect, because they seem to be engaging in deliberate efforts to misrepresent the revenue-generating ability of the company in the short run.

Situation 1

TTC has arranged a 3-year, $6.6 million contract for engineering services that has front-loaded payments. The company has recognized revenue based on the payment scheme, with $3.0 million recognized in the first year alone.

There is no indication that TTC is performing almost half of the total contracted services in the first year, 20X4. Indeed, the company doesn’t even track the costs of services rendered under this contract, which suggests that either (1) the contract is a relatively unimportant part of TTC’s operations or (2) management is intentionally hiding the cost of services in order to justify a revenue recognition pattern that does not match the reality of services being provided to Howard. The latter reason would be quite unethical.

Instead of recognizing revenue on the basis of cash payments, TTC should recognize revenue evenly over the term of the contract. The total contract price of $6.6 million should be recognized at the rate of $2.2 million per year. The extra $0.8 million that Howard paid in 20X4 should be recorded as deferred revenue, of which $0.2 million should be recognized in 20X5 (that is, added to the $2.0 million cash received in that year) and $0.6 recognized in 20X6.

The company also should track the costs of service to determine profitability.

Situation 2

TTC has entered into a contract that has two deliverables: (1) special-purpose equipment and (2) a 4-year service contract. The equipment seems to be overpriced, and the service contract appears to be underpriced. As in Situation 1, TTC seems to be engaging in special agreements with this customer in an attempt to accelerate revenue recognition, an unethical practice. Overpricing of the equipment is apparent not only from the relatively lower price that might have been obtained from another manufacturer, but also from the fact that the manufacturing cost of $3.4 million is only about 60% of the contracted sales price—an unusually high profit margin.

Overall, the contract provides for total revenue of $11.6 million. The contract allocates $5.6 million to the equipment and $6.0 million (over four years) to the service contract. However, the equipment could be obtained elsewhere for about 20% less. Therefore, the fair value of the equipment seems to be closer to $4.5 million (that is, $5.6 million × 80%) and the fair value of the service contract is $8.0 million (i.e., $6.0 million ÷ 75%).

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-19

The auditor should require TTC to reallocate the revenue on the basis of the fair values of the two components:

Component Fair value Proportion Revenue allocationEquipment $ 4,500,000 36% $4,176,000Service contract ($1.5m × 4) ÷ .75 8,000,000 64% 7,424,000Total $12,500,000 100% $11,600,000

TTC should recognize revenue of only $4.2 million (approximately) for the equipment, with the excess $1.4 million recorded as deferred revenue to be recognized evenly over the four years of the service contract (along with Parker’s annual payments of $1.5 million).

An additional consideration is that TTC is recognizing Parker’s first $1.5 million annual payment prematurely. The contract is for the next four years, and yet the revenue was recognized in 20X4, with an accrual for cost of services not yet rendered. Parker has not paid the first year’s fee yet, and the indication is that they are not required to pay it within the next year—thus TTC’s recording of the receivable as long term.

Summary

TTC seems to be engaging in some very unethical practices in order to hype their revenue for 20X4. It would be interesting to know if the company is in financial difficulty, perhaps in near-violation of some restrictive covenents such as the times-interest-earned ratio.

It is precisely to curb such revenue manipulation that accounting standard setters have established criteria for multiple-deliverable contracts.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-20

Assignments

Assignment 6-1

a. Gross revenue, if the company actually buys the books from the publisher and bears the inventory risk.

Net revenue, if the publisher is sending the books on consignment with full return privileges and the company never acquires title to the inventory. The publisher is then bearing all of the risk.

b. Net revenue. The dealer carries no inventory. Orders are transmitted directly to the manufacturer, who bears all of the inventory risk.

c. Net revenue. Title remains with the producer until they are sold to the builder. Presumably, CanLight can return the goods to the producer if they are not sold. On the other hand, CanLight bears risk of physical loss while the goods are in its inventory. On balance, it appears that CanLight is acting as a consignee, especially since CanLight owes no money to the producer until cash has been collected from the buyer.

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-21

Assignment 6-2 (WEB)

a) Interest revenue is recognized as time passes according to amount earned.

b) Interest revenue is recognized as time passes according to amount earned.

c) Revenue would be recognized on a cost recovery basis, where payments received would be considered repayment of principal until all the principal is recovered, with any additional payments received being recognized as interest revenue.

d) Revenue recognition would be deferred until the service of transporting the passenger is completed.

e) Revenue would be recognized as soon as the transporting of the freight is completed (delivery).

f) The change in the fair value of the maturing trees can be recognized as a gain or loss each year until harvest and sale, at which point the final gain/loss will be recognized (biological assets).

g) Revenue will be recognized as the completed houses are sold and delivered to a customer. Completed houses are included in inventory at cost.

h) Revenue could and likely would be recognized on a percentage-of-completion basis, without regard to when payment is received or when the completed houses are delivered to the purchaser.

i) Either the instalment sales method or the cost recovery method would be used to recognize revenue. In this case the more usual treatment is the instalment sales method unless collectibility is in doubt.

j) Revenue would be recognized as it is earned, which in this case will be with the passage of time, i.e., straight-line over 24 months. The large initial payment will be accounted for as a deferred revenue.

k) Because it is not possible to reliably determine the costs for completion and the potential gain or loss on this project, revenue should be recognized only to the extent of costs incurred and expensed.

l) It would be permissible to recognize revenue at fair market value as the silver is produced. Subsequent increases and decreases in market value would be recognized as gains and losses. However, this is permitted under IFRS only if this practice is widely accepted in the industry. If this method is not generally accepted in the industry, revenue would be recognized only when the silver is sold.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-22

Assignment 6-3

Case A

1. Revenue recognition on delivery

2. 31 December 20x5:Cash........................................................................................ 30,000

Unearned revenue............................................................ 30,000

Some might also accrue the $70,000 account receivable and further increase unearned revenue but the transaction is partially unexecuted at year-end so this not permitted. As well, recognition would inflate both sides of the balance sheet.

3. It is tempting to record the sale on the transaction date of 31 December but delivery has not yet taken place and the risks and rewards of ownership have not yet transferred. Companies often go out of their way to make sure goods are delivered before key reporting dates for this reason.

Case B

1. Recognize revenue as time elapses (i.e., month by month)

2. 17 April 20X5:Cash........................................................................................ 30,000

Unearned revenue............................................................ 30,000

3. The critical event is the passage of time, because the “retainer” is not tied to specific services but instead represents a readiness to serve whenever called upon to do so.

Case C

1. Revenue recognition on delivery

2. 15 November 20x5Goods receivable........................................................................... 600

Sales revenue........................................................................... 600

3. A promise to pay ‘goods’ is just as valid as a promise to pay cash; the company has a claim to economic resources that can be recognized. They have delivered their own goods (risks and rewards of ownership have passed) and, as long as the goods will be delivered on schedule from the customer, revenue recognition is appropriate. The goods received are dissimilar from the goods given up, and therefore the transaction

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-23

is measured at the value of the consideration received, which is three units worth $200 each.Is this the culmination of the earnings process? If the goods were similar, they would be recorded at book value, and revenue recognition deferred until the second goods were sold.

Case D

1. Revenue recognition month by month, as revenue is earned by delivery of each month’s magazine.

2. 2 August 20x5—To recognize collection of the subscription price:

Cash........................................................................................ 720Unearned subscription revenue........................................ 720

3. The cash was collected in advance of delivery. Revenue is recognized as earned (by delivery), not when cash is collected. Only one issue was delivered in 20x5. The entry to record revenue earned in 20X5 (not required) is:

Unearned subscription revenue.............................................. 20Subscription revenue........................................................ 20

$720 × 1/36 = $20

©2011 McGraw-Hill Ryerson Ltd. All rights reserved Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-24

Assignment 6-4

a. Critical event: the end of the return period.

Carnegie is offering a generous return policy. Non-profit organizations (NPOs) can over-order and then return half of the books within 6 months. Although Carnegie may have a good historical record of average returns, there can be substantial variation, which makes it difficult to predict a sales return allowance. Gross profit recognition should be deferred until the return period ends.

Alternatively, students could argue that since 50% of the books cannot be returned, 50% of the revenue could be recognized at the time of sale, with recognition of the remaining portion of the sales delayed until expiration of the return period.

b. Critical event: production and packaging of the beans in burlap bags.

Maxwell is an intermediate processor of an agricultural commodity. The raw beans are biological assets and should be carried at fair value. On each reporting date, the carrying value should be adjusted to the fair value at that date with any gain/loss recognized in income. Once the beans have been roasted, they become an item of inventory that is reported at “deemed cost”, which is the fair value at the time of processing. Thereafter, the beans should be reported at lower of deemed cost and NRV. When the roasted beans are sold, the proceeds of the sale are recognized as revenue and the inventory carrying value (at lower of cost and NRV) is recorded as cost of sales.

c. Critical event: receipt of cash.

Heckinger will not be able to estimate the value of its shipment until the creditor-protection process has ended. At the point of shipment, Heckinger will send an invoice to the retail chain for the full price of the product, but the gross margin must be deferred until the ultimate payment is determined.

d. Critical event: production—meeting the “milestones”

Nevo delivers a service over an extended period of time, not unlike a construction project. Although Nevo has never failed to deliver the contracted software, there still is risk of delay and cost over-runs. Meeting each milestone is necessary before revenue can be recognized for that segment of the work.

Students may equate this with percentage of completion, which is not exactly the same but is an acceptable answer.

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-25

Assignment 6-5

1. The revenue should be recognized as the windows are delivered to the building site. The contractor takes title at that point, which is indicated by the fact that the contractor takes responsibility for window breakage after Luke delivers them, and the contractor also is responsible for proper installation.

Luke is still vulnerable to some risk after delivery, including (1) potential liability for design or manufacturing defects and (2) non-payment by the contractor. The risk of liability for defects is a contingent liability. The risk of non-payment can usually be estimated in advance of any financial difficulties experienced by the contractor. Even if the contractor is unable to pay, Luke still has a lien on the property and can demand payment (through the courts) from the house owner.

2. Although the contract may run for several years, the production process is not a long-term contract. Percentage of completion accounting is not appropriate!

The “bid” costs should be expensed when incurred. Luke will win some bids and lose others. Bidding is a routine part of the business—a selling cost.

Production costs should be accumulated in inventory. When the windows are delivered to the building site, the inventory cost should be moved to COS and revenue should be recognized.

Any estimates of returns or bad debts should be established when the revenue is recognized, and adjusted thereafter (if conditions have changed) until payment is received from the contractor.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-26

Assignment 6-6

Requirement 1

The most appropriate point at which to recognize revenue is likely at the time the option is exercised (early 20x6) for the following reasons:

1. The product is complete and essentially all the work is also complete, i.e., $6.5 million in costs incurred out of an eventual total of $7.3 million.

2. The remaining costs of $800,000 for testing likely could be estimated.3. Collection of the selling price is reasonably assured.4. The selling effort is complete.5. The amount of revenue is measurable.

Some students may prefer delivery, which can also be justified, although it is ratherconservative, given the above points.

Requirement 2

The research costs of $3.16 million incurred in 20x4 must be charged to expense in 20x4 because there is no reason to believe in 20x4 that a commercially saleable product has been created. Accounting standards require that research be expensed for this reason. 20x5 expenditures, which are on an established product with an obvious market, are to be deferred if revenue is deferred: these are development expenses.

Recognition of revenue and expense:a) When option is signed:

20x4 20x5 20x6 20x7Revenue $ 0 $16,000 $ 0 $ 0Expense $3,160 4,140 0 0

b) When option is exercised:20x4 20x5 20x6 20x7

Revenue $ 0 $ 0 $16,000 $ 0Expense $3,160 0 4,140 0

c) When formulas are delivered:20x4 20x5 20x6 20x7

Revenue $ 0 $ 0 $ 0 $16,000Expense $3,160 0 0 4,140

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion 6-27

Assignment 6-7 (WEB)

Requirement 1(b) Revenue Recognition on

Date (a) Delivery Cash Receipt (c) Preparation 18 July Inventory 456,000 Inventory 456,000 Inventory 456,000

Cash 456,000 Cash 456,000 Cash 456,000

24 August Inventory 60,000 Inventory 60,000 Inventory 60,000Cash 60,000 Cash 60,000 Cash

InventoryCOS

Sales

196,000516,000

60,000

712,000

10 September Accts Rec 712,000 Accts Rec 712,000 Accts Rec 712,000Sales 712,000 Inventory

Deferred gross margin

516,000

196,000

Inventory 712,000

COSInventory

516,000516,000

22 November Cash 712,000 Cash 712,000 Cash 712,000Accts Rec 712,000 Accts Rec

COSDeferred gross margin

Sales

516,000

196,000

712,000

712,000

Accts Rec 712,000

©2011 McGraw-Hill Ryerson Ltd. All rights reserved Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-28

Requirement 2

Delivery is the normal revenue recognition point, based on the presumption that the risks and rewards of ownership pass on this date and that the sales amount is realizable. Revenue recognition on cash receipt is appropriate when the account receivable is considered so doubtful that it fails the realizability test; in these circumstances, revenue cannot be recognized prior to collection. Revenue recognition on production is appropriate only for commodities with stable sales prices and markets where the sales effort and costs are trivial but is not permitted under IFRS except for biological assets and agricultural produce.

©2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edtion

6-29

Assignment 6-8 Requirement 1

Date 30 September 15 October 25 October30 August Inventory 4,300 Inventory 4,300 Inventory 4,300

Cash, etc. 4,300 Cash, etc. 4,300 Cash, etc. 4,30030 September Inventory 640 Inventory 640 Inventory 640

Cash 640 Cash 640 Cash 640Inventory 8,560COGS 4,940

Sales 13,500Bad debt exp. 155Sales returns 675

Allowance* 830

15 October Accts rec 13,500 Accts rec 13,500 Accts rec 13,500Inventory 13,500 Sales 13,500 Def’d gross margin 8,560

Inventory 4,940COGS 4,940

Inventory 4,940

Bad debt exp. 155Sales returns 675

Allowance 83025 October Allowance 675 Allowance 675 Sales returns** 675

Accts rec 675 Accts rec 675 Accts rec 675COGS 4,940Def’d gross margin 8,560

Sales 13,500Bad debt expense 155

Allowance 15530 November Cash 12,670 Cash 12,670 Cash 12,670

Allowance 155 Allowance 155 Allowance 155Accts Rec 12,825 Accts Rec 12,825 Accts Rec 12,825

* Allowance would be shown as a contra account to inventory until accounts receivable are recognized.** Or sales—this entry may be netted with the next. However, it seems more appropriate to capture the sales returns since they were problematic.

Copyright 2005 McGraw-Hill Ryerson Ltd. All rights reserved.30 Solutions Manual to accompany Intermediate Accounting, 3rd edition.

Requirement 2

At each critical event, net assets (equity) is affected by the sales and expense accounts. Prior to that point, and after that point, entries affect the distribution within net assets but not the total net amount.

Requirement 3

a. Recognition at production is appropriate for a commodity with an organized market, where sale is trivial, the producer cannot affect price, and also if all costs are known and can be accrued. This point is acceptable under IFRS, but only for biological assets and agricultural produce, and for minerals and mineral products, but then only if this valuation basis is widely used within the industry. Canadian ASPE accepts this revenue recognition point only for biological assets and agricultural produce.

b. Delivery is an appropriate critical event most of the time, as risks and rewards pass to the customer. However, sales amounts have to be realizable and all costs estimable and accrued on this date.

c. Revenue recognition after the right of return has passed is appropriate if returns cannot be predicted.

Assignment 6-9 (Removed)

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-31

Assignment 6-10 (WEB)

Requirement 1

Cash....................................................................................................... 532,000Deferred gross margin..................................................................... 244,000Inventory (48,000 × $6).................................................................. 288,000

Requirement 2

Inventory (4,500 × $6).......................................................................... 27,000Deferred gross margin*......................................................................... 20,000

Cash................................................................................................. 47,000

*(3,500 × $4) + (1,000 × $6)

©2011 McGraw-Hill Ryerson Ltd. All rights reserved6-32 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

Requirement 3

Monthof Sale

UnitsSold

SalesPrice

MonthlySales

Gross UnitsROR

Expired *

Total UnitsReturned

Net UnitsROR Expired †

ROR ExpiredSales Amount §

September 10,000 $10 $100,000 4,000 2,500 1,500 $15,000October 12,000 10 120,000 3,600 1,000 2,600 26,000November 15,000 12 180,000 3,000 1,000 2,000 24,000December 11,000 12 132,000 1,100 0 1,100 13,200Totals 48,000 $532,000 11,700 4,500 7,200 $78,200

* Gross number of units sold this month, times 10% times number of months since sale. For example, at 31 December, 20x5, four months have passed since the September sales, thus 4 × 10%, or 40% of the right of return (ROR) has expired; (40% × 10,000 units = 4,000 units).

† Equal to gross units for which ROR expired, less units returned.

§ Equal to Net units for which ROR has expired times sale price per unit for this month sales.

Realized gross margin in 20x5 = $78,200 – (7,200 units × $6) = $78,200 – $43,200 = $35,000

To record realized gross margin on expired and unused right of return unitsshipped:

Cost of Goods Sold (7,200 × $6)....................................................... 43,200Deferred gross margin........................................................................ 35,000

Sales.............................................................................................. 78,200

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-33

Requirement 4

Monthof Sale

Units Availablefor Return or

Sale**

UnitsReturned

Units Soldin 20x6 ††

Unit SalePrice

SalesAmount

September 6,000 1,000 5,000 $10 $ 50,000October 8,400 2,000 6,400 10 64,000November 12,000 2,500 9,500 12 114,000December 9,900 4,000 5,900 12 70,800

9,500 26,800 $298,800

× $6 × $6Cost of returns $57,000Costs of units sold $160,800

** Equal to total sold for this month, less those returned or recorded as sold in 20x5 (see Requirement 3).

†† Equal to Units available (column 2) less units returned.

Entry to record returns in 20x6:

Inventory (9,500 units × $6).......................................................... 57,000Deferred gross margin................................................................... 51,000

Cash........................................................................................... 108,000*

*Refund amount on returned units:(1,000 units × $10) + (2,000 units x $10) + ($2,500 units × $12) + (4,000 units × $12) = $108,000

©2011 McGraw-Hill Ryerson Ltd. All rights reserved6-34 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

Entry to record realized gross margin in 20x6 related to 20x5 sales:

Cost of goods sold...................................................................... 160,800Deferred gross margin................................................................ 138,000

Sales....................................................................................... 298,800

Reconciliation:

Total units sold in period September–December....................... 48,000Total dollar sales amount for period September–December...... $532,000Cost of units sold in period September–December.................... 288,000Total gross margin...................................................................... $ 244,000

Units: 20x5 20x6 Total

Returned................................................... 4,500 9,500 14,000Not returned (sold)................................... 7,200 26,800 34,000

Totals............................................................ 11,700 36,300 48,000

Gross Sales:Returned................................................... $ 47,000 $108,000 $155,000Not returned............................................. 78,200 298,800 377,000

Totals............................................................ $125,200 $406,800 $532,000

Cost of sales:Returned................................................... $ 27,000 $ 57,000 $ 84,000Not returned (sold)................................... 43,200 160,800 204,000

Totals............................................................ $ 70,200 $217,800 $288,000

Gross margin:Returned (not realized)............................ $ 20,000 $ 51,000 $ 71,000Not returned (sold)................................... 35,000 138,000 173,000

Totals............................................................ $ 55,000 $189,000 $244,000

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-35

Assignment 6-11

Requirement 1– Entries for 20x4 and 20x5:

Year 20x4:1 July, 20x4—instalment sale:

Cash................................................................................................. 200Instalment accounts receivable....................................................... 2,000

Inventory..................................................................................... 440Deferred gross margin................................................................ 1,760

Cost percentage: $440 ÷ $2,200 = 20%; profit 80%

Remainder of 20x4, collections:Cash................................................................................................. 300

Instalment accounts receivable................................................... 300

31 December—To recognize income regarding collections in 20x4Deferred gross margin (80%).......................................................... 400Cost of instalment sales.................................................................. 100

Sales revenue—instalment......................................................... 500

Year 20x5:To record collections and income:

Cash................................................................................................. 200Instalment accounts receivable................................................... 200

Deferred gross margin..................................................................... 160Cost of instalment sales ................................................................. 40

Sales revenue—instalment......................................................... 200

Should the repossessed inventory be recorded at market value ($700) or book value ($300)? The two alternatives follow:

1 December 20x5—To record repossession at market value:Inventory (used computers)............................................................ 700Deferred gross margin ($1,760 – $400 – $160).............................. 1,200

Instalment accounts receivable ($2,000 – $300 – $200)............ 1,500Gain on repossession.................................................................. 400

1 December 20x5—To record repossession at book value:Inventory (used computers)............................................................ 300Deferred gross margin..................................................................... 1,200

Instalment accounts receivable................................................... 1,500

©2011 McGraw-Hill Ryerson Ltd. All rights reserved6-36 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

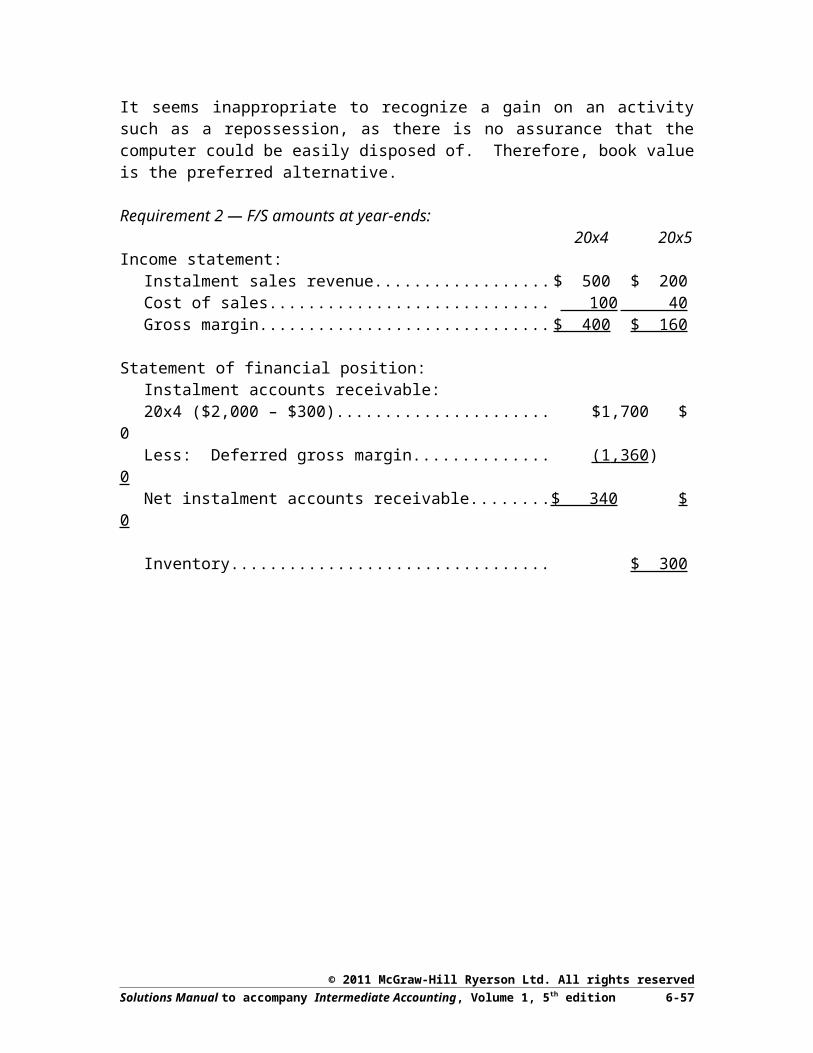

It seems inappropriate to recognize a gain on an activity such as a repossession, as there is no assurance that the computer could be easily disposed of. Therefore, book value is the preferred alternative.

Requirement 2 — F/S amounts at year-ends:20x4 20x5

Income statement:Instalment sales revenue.............................................................. $ 500 $ 200Cost of sales................................................................................. 100 40Gross margin................................................................................ $ 400 $ 160

Statement of financial position:Instalment accounts receivable:20x4 ($2,000 – $300)................................................................... $1,700 $ 0Less: Deferred gross margin....................................................... (1,360) 0Net instalment accounts receivable.............................................. $ 340 $ 0

Inventory...................................................................................... $ 300

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-37

Assignment 6-12

1 March 20x6 – Acquired inventory:

Inventory................................................................................ 10,000 Cash................................................................................... 10,000

The company may wish to segregate this speculativeinventory in financial statement presentation.

20x6 – Cash collections:

Cash........................................................................................ 4,000Inventory............................................................................ 4,000

or

Cash........................................................................................ 4,000Cost of sales........................................................................... 4,000

Sales................................................................................... 4,000Inventory............................................................................ 4,000

The latter is more accurate disclosure.

20x7 – Cash collections:

Cash........................................................................................ 5,000Inventory............................................................................ 5,000

or

Cash........................................................................................ 5,000Cost of sales........................................................................... 5,000

Sales................................................................................... 5,000Inventory............................................................................ 5,000

20x8 – Cash collections:

Cash........................................................................................ 8,000Inventory ($10,000 – $4,000 – $5,000)............................. 1,000Profit on sale...................................................................... 7,000

or

Cash........................................................................................ 8,000Cost of sales........................................................................... 1,000

Sales................................................................................... 8,000Inventory............................................................................ 1,000

©2011 McGraw-Hill Ryerson Ltd. All rights reserved6-38 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

Assignment 6-13

Requirement 1— Entries for instalment sales method:

15 March 20X0:Instalment accounts receivable 2,500

Inventory 1,900Deferred gross profit 600

[Gross profit percentage: 600 ÷ 2,500 = 24%]

Cash 1,000Instalment accounts receivable 1,000

Deferred gross profit (24% × $1,000) 240Cost of goods sold 760

Sales revenue 1,000

13 October 20X2:Cash 500

Instalment accounts receivable 500

Deferred gross profit (24% × $500) 120Cost of goods sold 380

Sales revenue 500

Requirement 2

Gross profit = $2,500 – $1,900 = $600.

Requirement 3

No gross profit would be recognized. The first $1,900 of cash received would be credited to inventory, to recover the cost. Any amounts received after the first $1,900 would be pure gross margin, with no offset to cost of goods sold.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-39

Assignment 6-14

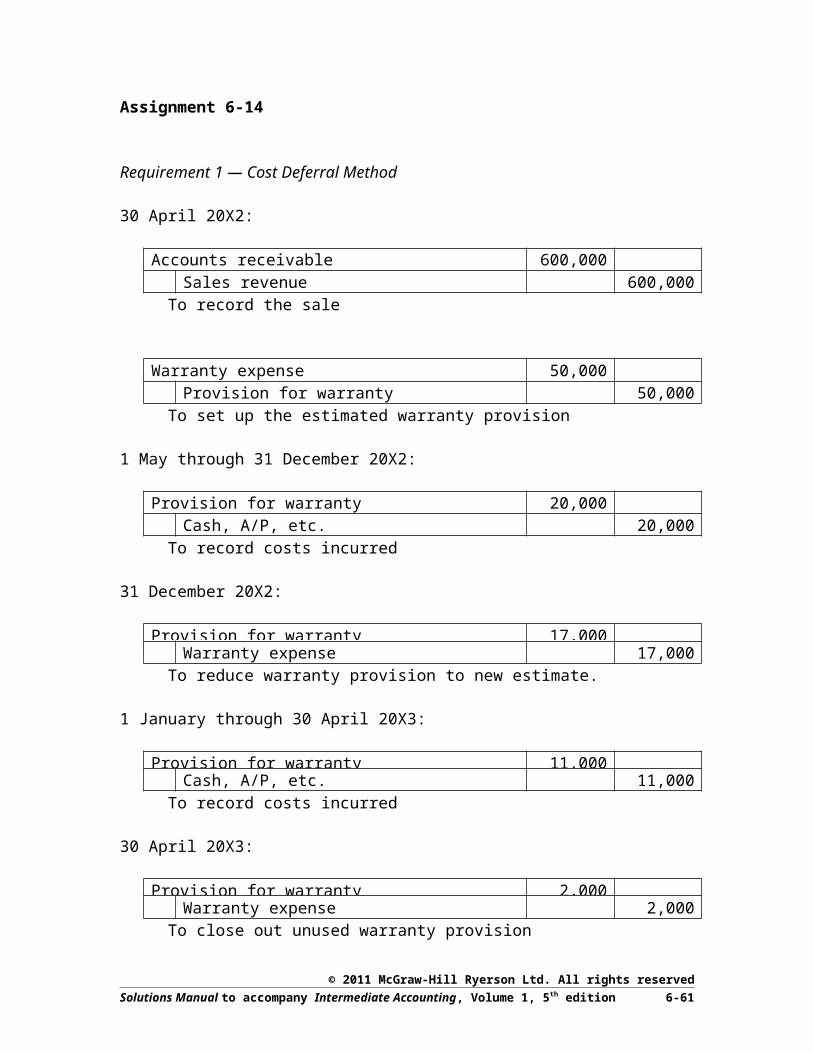

Requirement 1 — Cost Deferral Method

30 April 20X2:

Accounts receivable 600,000Sales revenue 600,000

To record the sale

Warranty expense 50,000Provision for warranty 50,000

To set up the estimated warranty provision

1 May through 31 December 20X2:

Provision for warranty 20,000Cash, A/P, etc. 20,000

To record costs incurred

31 December 20X2:

Provision for warranty 17,000Warranty expense 17,000

To reduce warranty provision to new estimate.

1 January through 30 April 20X3:

Provision for warranty 11,000Cash, A/P, etc. 11,000

To record costs incurred

30 April 20X3:

Provision for warranty 2,000Warranty expense 2,000

To close out unused warranty provision

©2011 McGraw-Hill Ryerson Ltd. All rights reserved6-40 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

Requirement 2 — Revenue Deferral Method

30 April 20X2:

Accounts receivable 600,000Sales revenue 540,000Deferred revenue 60,000

To record the sale, with deferral for warranty

1 May through 31 December 20X2:

Warranty expense 20,000Cash, A/P, etc. 20,000

To record costs incurred

Deferred revenue 40,000Sales revenue 40,000

To amortize 8/12 of deferred revenue

1 January through 30 April 20X3:

Warranty expense 11,000Cash, A/P, etc. 11,000

To record costs incurred

Deferred revenue 20,000Sales revenue 20,000

To amortize 4/12 of deferred revenue

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-41

Assignment 6-15

Requirement 1 — Cost Deferral Method

30 September 20X1:

Accounts receivable 2,000,000Sales revenue 2,000,000

To record the sale

Warranty expense 100,000Provision for warranty 100,000

To set up the estimated warranty provision

1 October through 31 December 20X1:

Provision for warranty 25,000Cash, A/P, etc. 25,000

To record costs incurred

31 December 20X1:

Warranty expense 30,000Provision for warranty 30,000

To increase warranty provision to new estimate.

1 January through 31 December 20X2:

Provision for warranty 40,000Cash, A/P, etc. 40,000

To record costs incurred

31 December 20X2:

Provision for warranty 45,000Warranty expense 45,000

To reduce warranty provision to $20,000

1 January through 30 September 20X3:

Provision for warranty 15,000Cash, A/P, etc. 15,000

To record costs incurred

30 September 20X3:

Provision for warranty 5,000Warranty expense 5,000

To close out warranty provision

Requirement 2 — Revenue Deferral Method

©2011 McGraw-Hill Ryerson Ltd. All rights reserved6-42 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

30 September 20X1:

Accounts receivable 2,000,000Sales revenue 1,880,000Deferred revenue 120,000

To record the sale, with deferral for warranty

1 October through 31 December 20X1:

Warranty expense 25,000Cash, A/P, etc. 25,000

To record costs incurred

31 December 20X1:

Deferred revenue 15,000Sales revenue 15,000

To amortize 3/24 of deferred revenue

1 January through 31 December 20X2:

Warranty expense 40,000Cash, A/P, etc. 40,000

To record costs incurred

31 December 20X2:

Deferred revenue 60,000Sales revenue 60,000

To amortize 12/24 of deferred revenue

1 January through 30 September 20X3:

Warranty expense 15,000Cash, A/P, etc. 15,000

To record costs incurred

30 September 20X3:

Deferred revenue 45,000Sales revenue 45,000

To amortize 9/24 of deferred revenue

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 6-43

Assignment 6-16

This $180,000 sale has two deliverables:

fork lift truck, sales price $140,000 3-year service contract, value $60,000

Requirement 1 — Fair Value Method:

The revenue must be divided into two components on the basis of fair values of each component:

Component Fair value Proportion Revenue allocation

Fork-lift truck $140,000 70% $126,000Service contract 60,000 30% 54,000Total $200,000 100% $180,000

Journal entry:

Accounts receivable................................................................. 180,000Revenue – equipment sales................................................ 126,000Deferred revenue – service contract.................................. 54,000

Requirement 2 — Residual Value Method:

The revenue is assigned first to the fork-lift truck, which has a known sales price of $140,000. The residual revenue is assigned to the service contract and deferred:

Journal entry:

Accounts receivable................................................................. 180,000Revenue – equipment sales................................................ 140,000Deferred revenue – service contract.................................. 40,000

©2011 McGraw-Hill Ryerson Ltd. All rights reserved6-44 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

Assignment 6-17

New subscribers are being given a new cell phone at a “special” low price for the monthly telephone service. In return, however, they will pay a higher monthly fee. In total, new subscribers pay $3,700 for product and services:

a mobile phone costing $100 36 months of service worth $100 per month, a total of $3,600

Regular subscribers pay $3,160 for the same services:

a mobile phone costing $1,000 36 months of service worth $60 per month, a total of $2,160

Revenue recognition will differ depending on which allocation method is used.

Fair Value Method

The $3,700 would be allocated proportionately to the two components:

cell phone: $3,700 × ($1,000 ÷ $3,160) = $3,700 × 31.65% = $1,171 service contract: $3,700 × ($2,160 ÷ $3,160) = $2,800 × 68.35% = $2,529

$1,171 revenue from the cell phone would be recognized immediately. Since only $100 is received up-front from a new subscriber, an asset of “unbilled revenue” of $1,071 should be recognized. The $1,071 will then be offset against the monthly $100 service payments over 36 months at $29.75 per month, thereby reducing monthly service revenue to $70.25 per month, higher than the normal charge to regular subscribers. In substance, the phone is being sold on an instalment basis, but at a price 17% higher than normal. The higher price might be due to expected defaults (and non-recovery of the phones).

Residual Value Method

In this method, the normal price of the phone, $1,000, would be recognized at the inception of the contract. The remaining $2,700 would be recognized monthly over 36 months, at $75 per month (that is, $2,700 ÷ 36).

Discussion

The company’s motivation probably is to attract new subscribers by offering the “bargain” price of $100 for an expensive phone. Nevertheless, since the bargain price is linked to a 36-month contract, the company will recover all of the value of the phone.

Either allocation method will, in this example, recognize revenue recognition that is more realistic of the value of what the company is delivering. Nevertheless, since fair values are available for both components of the deal, the market value method is preferrable.