Embed Size (px)

Citation preview

CFS Retail Property Trust Group (CFX)Annual results for the year ended 30 June 201221 August 2012

Angus McNaughton Managing Director, Property Colonial First State Global Asset Management

2

We take a 360o approach to retail property investment, drawing on an integrated

investment and asset management platform

3

4 State of the market 16 Portfolio overview9 Financial highlights 20 Retail observations11 Acquisition 23 Development12 CFX stapling 31 Retail environment14 Capital management 34 Outlook

Debt costs are falling• Offshore debt markets are open• All in debt costs have fallen

Strong returns over the period• High yield is attracting investors in a risk-off

environment• AREITs continue to trade at a discount to NTA

but the gap is narrowing

Mixed conditions• Supported by steady wages and consumption

growth • Challenged by weak housing market, offshore

travel, low sentiment and internet sales growth

Capital markets

A-REIT sector

Retail environment

Economy

4

Solid growth continues• Supported by strong business investment

and low unemployment• Challenged by offshore conditions• Consumer spend up 5.7%

State of the marketHeadwinds and tailwinds persist

OverviewCFX has delivered solid long-term performance

5Note: Past performance is not indicative of future performance.1. Assuming the reinvestment of distributions.Source: UBS Australia 2012.

CFX cumulative total return1

Total cumulative returns since June 2002

CFX has outperformed the UBS Retail A-REIT Accumulation Index over one, three, five and 10-year periods

CFX has outperformed the UBS Retail A-REIT Accumulation Index over one, three, five and 10-year periods

Over 10-years, CFX has delivered a total securityholder return of 205%, or an average 11.8% per annum

Over 10-years, CFX has delivered a total securityholder return of 205%, or an average 11.8% per annum

-50%

0%

50%

100%

150%

200%

250%

FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

Cum

ulat

ive

retu

rns

CFX UBS Retail Property 200 Accum Index S&P/ASX Property 200 Accum Index

Michael GormanCFX Fund Manager

6

Prudent capital

management

Focused on long-term,

sustainable returns for investors

Enhance value through

intensive asset

management

7

CFX invests in quality retail assets across Australia

8

Target ResultDistribution 13.0 – 13.1 cps 13.10 cps, at the upper end of guidance

Investigate additional revenue streams Successfully stapled CFX securities to allow additional revenue streams

Recycle capital

Sold a 50% interest in The Myer Centre Brisbane

Initiated an on-market buy-back for up to $150m securities and reset interest rate swaps

Progressed planning on developments where there is strong demand

Drive portfolio performance99.7% portfolio occupancy maintained

3.0% average rental increase on specialty store re-leasing

Maintain a strong balance sheet

26.6% gearing within target 25-35% range

Diversified sources of debt and lowered weighted average cost of debt

Specialty store sales growth of 3% Specialty store sales growth of 1.7% achieved

OverviewCFX delivering on strategy

x

Decline in net profit reflects lower growth in asset valuations than in prior year

Decline in net profit reflects lower growth in asset valuations than in prior year

Financial highlightsCFX remains in a solid position

9

1. Distributable income is a key financial measure used by management to assess the performance of CFX. Distributable income equals profit excluding: net gains on revaluations of investment properties, associates and derivatives; the effect of straight-lining fixed rental increases; the movement in fair-value of unrealised performance fees; non-cash convertible notes interest expense; adjustments for convertible notes buy-back expense; and adjustments for project and other items.

2. Excluding the capital distribution of 0.2 cents per unit, or $5.7m, reinvested in CFS Retail Property Trust 2, as approved by investors on 28 May 2012. This distribution enabled the initial capitalisation of CFX2.

3. Excluding flowback.4. Adjusted for changes in ownership of properties in either of the 12-month periods, excluding development impacted centres and significant

one-off Queensland land tax refunds.

Net property income growth was 2.4% on a like-for-like basis3

Net property income growth was 2.4% on a like-for-like basis3

Key metrics FY12 FY11 Change

Net profit $409.2m $532.6m (23.2)%

Distributable income1 $371.5m $350.3m 6.1%

Distribution per security2 13.1 cents 12.7 cents 3.1%

Net property income3 $547.9m $526.4m 4.1%

Total assets4 $8.4b $8.5b (0.7)%

Net tangible asset backing (NTA) per unit $2.07 $2.05 1.0%

10

Financial highlightsNet profit reconciliation

FY12$m

FY11$m

Net profit 409.2 532.6

Adjustments:

net gain from properties and associates valuations (164.3) (201.4)

net loss/(gain) from derivatives valuations 87.9 (12.9)

straight-lining rental revenue (2.8) (4.1)

movement in fair value of unrealised performance fees 3.4 0.2

non-cash convertible notes interest expense 7.0 11.3

convertible notes buy-back expense 4.9 -

project and other items 26.2 24.6

Distributable income 371.5 350.3

transfer from undistributed reserves1 - 9.4

Distribution 371.5 359.7

Distribution per security (cents) 13.10 12.70

1. Units issued in October and November 2010 ranked equally with pre-existing units and were therefore entitled to the full distribution for the half-year ended 31 December 2010. Therefore, CFX transferred an amount from undistributed reserves to deliver a distribution of 6.3 cents per unit for the half-year ended 31 December 2010.

Initiated an on-market

buy-back for up to $150m

Paid down bank debt to reinvest in

development pipeline

Reset interest rate

swaps

11

Sold a 50% interest in The Myer Centre Brisbane

12

Delivering on strategyOptimising revenues

CFSRetail Property

Trust Group (CFX)

$8,434mTotal assets

CFX1

$8,428mTotal assets

CFX2

$6mTotal assets

• Original trust• Owns shopping centres• Distributes net rental income pre-tax

• Pursues additional income streams• Initially intended for digital advertising screens• Distributes after-tax profit

• Comprises stapled securities• Created by stapling CFX1 trust

units to CFX2 trust units

CFX stapled securities structure

CFX units stapled to enable CFX to pursue new income streams

CFX units stapled to enable CFX to pursue new income streams

Digital screens will help make CFX centres more attractive to customers and retailers

Digital screens will help make CFX centres more attractive to customers and retailers

13

Our digital strategy To drive sales through our centres

Increase the experiential nature of our centres to drive foot traffic

Convert online shoppers to real time shoppers

E-commerce initiatives such as click and collect

14

Capital managementLowering the cost of debt

1. Adjusted for the drawing of debt to repay $198.5m of August 2014 convertible notes put to CFX on 21 August 2012, the commencement of the $120m USPP (12 July 2012) and $125m five-year bank debt facility (2 September 2012), the repayment of $225m of MTNs on 2 September 2012 and interest rate swaps entered into on 26 July 2012.

2. Adjusted for the issue of $300m of July 2016 convertible notes and buy-back of $300m of August 2014 convertible notes, which settled post 30 June 2011. 3. Including line fees and margins.4. Including convertible notes and fixed-rate medium term notes. 5. Gearing equals borrowings to total assets. For this calculation, total assets exclude the fair-value of derivatives and borrowings is the amount drawn down.

Total debt profile

Capital management activities have significantly reduced CFX’s weighted average interest rate

Capital management activities have significantly reduced CFX’s weighted average interest rate

30-Jun-121 30-Jun-112

Weighted average interest rate3 5.9% 7.0%

Weighted average duration of debt 3.5 years 3.5 years

Proportion of debt hedged4 84% 92%

Undrawn debt facilities $629m $360m

Long term credit rating – S&P A A

Gearing5 26.6% 27.0%

Loan to value ratio 31% 31%

Interest cover ratio 3.2x 2.8x

Capital managementMaintaining diversity and duration

15

1. Adjusted for the drawing of debt to repay $198.5m of August 2014 convertible notes put to CFX on 21 August 2012, the commencement of the $120m USPP (12 July 2012) and $125m five-year bank debt facility (2 September 2012), the repayment of $225m of MTNs on 2 September 2012 and interest rate swaps entered into on 26 July 2012.

^ The $92.3m of August 2014 convertible notes will be redeemed at their final maturity date of 21 August 2014. The $300m of July 2016 convertible notes have an investor put option in July 2014.

Debt maturity profile $m

50 150

575

300 100 125 -

38 178

158 -

92

300

-

260

100

440

0

200

400

600

800

1,000

FY13 FY14 FY15 FY16 FY17 FY18 Beyond

42%

14%

13%

3%

28%

Bank debt Convertible notes US Private Placement Short term notes Medium term notes

CFX’s debt remains well diversified with limited near-term expiries

^

Sources of debt1

Portfolio overviewKey portfolio statistics remain steady

16

Total asset values reduced due to the sale of an interest in The Myer Centre Brisbane

Total asset values reduced due to the sale of an interest in The Myer Centre Brisbane

Occupancy costs have remained stableOccupancy costs have remained stable

1. Shopping centre portfolio excludes DFO retail outlet centres.2. Comparable centres refer to those centres that are not undergoing or have not undergone substantial redevelopment in either period of comparison.

30-Jun-12 30-Jun-11

Number of retail assets 29 29

Investment properties ($m) 8,363 8,407

Weighted average capitalisation rate (%)1 6.45 6.49

Total area (‘000s, sqm) 1,404 1,419

Number of tenants 4,194 4,192

Number of vacancies 32 36

Occupancy rate (%) 99.7 99.7

Retail sales (MAT $m) 7,557 7,497

Comparable specialty MAT/sqm ($)1 9,576 9,166

Specialty occupancy costs (%)1,2 17.1 17.1

Department stores have shown improving sales in the June half

Department stores have shown improving sales in the June half

Retail specialty stores 1.7% growthRetail specialty stores 1.7% growth

Sales performance by categoryGrowth continues, but at a slower pace

171. Comparable centres refer to those centres that are not undergoing or have not undergone substantial redevelopment in either period of comparison.2. General retail comprises giftwear, pharmacy and cosmetics, pets, discount variety, florists and toys.

Category

Comparable1 Actual

MAT30-Jun-12

$m

Annualgrowth

%

MAT30-Jun-12

$m

Annualgrowth

%

Department stores 625.7 (2.5) 659.0 (2.9)

Discount department stores 708.5 (1.9) 780.0 (2.2)

Supermarkets 1,362.5 0.8 1,568.6 0.9

Mini majors 682.4 (1.7) 758.8 0.6

Retail specialty 2,547.9 1.7 2,756.0 1.8

Other retail2 453.0 6.9 494.4 7.5

Shopping centre portfolio 6,380.0 0.6 7,016.8 0.9

DFO centres 540.0 (0.8) 540.0 (0.8)

Total portfolio 6,920.0 0.5 7,556.8 0.8

18

DFOupdate

93 leasing deals

executed in FY12

Average 30% rental uplift on

new leases

Flat MAT growth due to extensive

remixing

Comparable1 Moving Annual Turnover

Retail specialty category 30-Jun-12$m

30-Jun-11$m

Annual growth

%

Food retail 170.9 160.6 6.4

Food catering 374.1 354.9 5.4

Apparel 896.7 910.7 (1.5)

Jewellery 205.2 208.0 (1.4)

Leisure 173.3 184.6 (6.1)

General retail2 220.9 220.8 0.0

Homewares 219.6 194.7 12.8

Mobile phones 101.7 94.8 7.3

Retail services 185.5 175.6 5.6

Total retail specialty 2,547.9 2,504.7 1.7

Retail specialty sales by categoryMobile phones, services, food and cafes performing strongly

19

1. Comparable centres refer to those centres that are not undergoing or have not undergone substantial redevelopment in either period of comparison.2. General retail includes cinemas and sales reporting tenancies under 400sqm including travel agents, auto accessories, Lotto and other entertainment

and non-retail stores.

Sales productivity has grown while occupancy costs have remained stable

Sales productivity has grown while occupancy costs have remained stable

Comparable1 shopping centre portfolio

Specialty occupancy

costs

Specialty sales

per sqm

Jun 2012 17.1% $9,576

Dec 2011 17.2% $9,269

Jun 2011 17.1% $9,166

Dec 2010 17.2% $8,955

Retail observations

• Despite consumer spending growth of 5.7%, retail sector remains challenging

• Demand continues from international casual and luxury retailers in larger centres

• Mid-level apparel retailers continue to experience difficulty, particularly in smaller centres

• Discretionary categories such as food catering, and new technology e.g. mobile phones and tablet devices are keeping demand strong

CFX outcomes

• Despite challenges, healthy leasing deal rate and occupancy maintained

• Achieved a 3.0% increase on retail specialty store re-leasing (renewals and replacements) with standard 5% fixed annual increases

• Actively replacing underperforming retailers

20

Healthy deal rate and occupancy despite a challenging environment

21

Portfolio overviewEntire portfolio valued through FY12

Historical valuation trendsCFX portfolio by centre type

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

Jun-

04

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Dec

-11

Jun-

12

Cap

italis

atio

n ra

te

Regional Sub-regional Shopping centre portfolio

Entire portfolio was revalued in FY12, resulting in a $164.3m net valuation gain

Entire portfolio was revalued in FY12, resulting in a $164.3m net valuation gain

Shopping centre portfolio weighted average cap rate 6.45%

Shopping centre portfolio weighted average cap rate 6.45%

15.1%lower

emissions intensity4

Responsible property investment Makes good business sense

8.6%more energy

efficient4

29.4%more water

efficient4

2012 achievements

• 11 assets have certified NABERS ratings assessments

• Joint highest disclosure in 2011 CDP1 response in AU/NZ

• An Australian leader in 2011 GRESB2 survey

• Merited in APREA3 best practices awards

Focus in 2013

• Continue to improve the efficiency of the portfolio

• Continue to certify the portfolio for NABERS ratings

• Continue to benchmark against global best practice, including:– Global Reporting Initiative (GRI)– AA1000 standard (engagement of stakeholders)

22

1. Carbon Disclosure Project. 2. Global Real Estate Sustainability Benchmark. 3. Asia Pacific Real Estate Association. 4. Against base year FY08.

22

Tony GilchristHead of Development

23

24

Development updateTrack record

1. Including Myer Bourke Street project.2. Yield based on first year income after development completion.3. Excludes Emporium Melbourne.

Completions and targets

Redevelopment completions FY06 to FY121 CFX share

Number of projects completed 39

Total cost $1.7b

Weighted average initial yield2 7.6%

Average internal rate of return (IRR) 12.5%

Development targets

Total cost $1.7b

Target internal rate of return (IRR) >10%

Demonstrated track record of delivering on developments

Demonstrated track record of delivering on developments

$380m in additional value in excess of costs delivered in past seven years

$380m in additional value in excess of costs delivered in past seven years

Average notional development profit of 22% for CFX

Average notional development profit of 22% for CFX

Development updateKey development projects1 as at 30 June 2012

25

Dec-11 Jun -12 Dec-12 Jun -13 Dec -13 Jun-14 Dec -14 Beyond

Forest Hill Chase $25m

Bayside Shopping Centre $36m

Roxburgh Park $65m

Forest Hill Chase $20m

Brimbank Central $34m

DFO Homebush $100m

Eastlands $35m

Castle Plaza $130m

Emporium Melbourne $560m

1. CFX share.

Projects in progressProjects completed Projects planned (estimated timing)

Projects deferred

Chadstone (Stage 35) $260m

Progressing projects with

strong underlying

demand

Key development metrics

Total cost $1.12b

CFX share (50% interest) $560m

Target initial yield1 >6%

Target IRR >9%

Project commenced February 2011

Project to be complete Late 2013

Development updateEmporium Melbourne – progressing well

26

On target for 2013

completion

1. Yield based on forecast first year income after development completion.

Artist’s impression of Emporium Melbourne, Vic

New brand to Australia

will take 3,000 sqmover four

levels

Topshopto take

2,600 sqmstore over

three levels

Well progressed with luxury

and Australian designers

Emporium Melbourne Salvatore FerragamoMichael KorsScanlon & Theodoresass & bideZimmerman

2727

Development updateRoxburgh Park Shopping Centre – progressing well

28

Key development metrics

Total cost $65m

Target initial yield1 >8%

Target IRR >10%

Project commenced January 2012

Expected completion Early 2013

Project on track

1. Yield based on forecast first year income after development completion.

New large format

Coles + Aldiand 40 new

specialty stores

700 new car spaces

Refurb of existing centre

29

Development updateDFO Homebush – strong demand to expand the retail offer

Key development metrics

Total cost $100m

Target initial yield1 >7%

Target IRR >10%

Project to commence On planning approval

1. Yield based on forecast first year income after development completion.

500 new car spaces with

improved access

Centre refurb/remix,

new foodcourt,

luxury retailers

New bulky goods

retailers

ArmaniZegna

Michael Kors

30

Development updateChadstone Shopping Centre Stage 35 – planning milestone achieved

Key development metrics

Indicative cost1 $520m

CFX share (50% interest) $260m

Target initial yield2 >7%

Target IRR >10%

Project to commence On development approval

1. Retail component. 2. Yield based on forecast first year income after development completion.

Additional 30,000sqm of lettable

area allowed

Anchored by flagship

stores

Household consumption versus retail spendTemporarily out of sync

31

Australian retail turnover versus household consumptionAnnual growth rates, quarterly rests to March 2012

Consumer spend +5.7%1Consumer spend +5.7%1

Retail spend +2.8%2Retail spend +2.8%2

0%

2%

4%

6%

8%

10%

12%

0%

2%

4%

6%

8%

10%

12%

1992 1996 2000 2004 2008 2012

% C

hang

e Yo

Y

Mov

ing

annu

al tu

rnov

er, %

cha

nge

YoY

Australian retail turnover, MAT Household consumption (rhs)

Source: Australian Bureau of Statistics and CFSGAM Research.1. 12 months to 31 March 2012.2. 12 months to 30 June 2012.

• Positive economic outlook• Interest rates falling• Steady wages growth and low

unemployment• Strong consumption growth

• 8 million international travellers in FY12

• Savings rate is high but stable• Consumer sentiment is low• Growth in online sales

Headwinds

Tailwinds

32

33

Driving our existing asset base by remixing tenancies to optimise performance

Deliver capital management initiatives to maintain debt diversity and duration

Investing in the redevelopment pipeline and investigating asset recycling opportunities

Strategic focus for FY13

Supporting retailers by advancing online and social media strategies

While the retail property market still faces headwinds, we anticipate specialty retail sales growth of around 3% for FY13

Distribution guidance of 13.6 – 13.7 cents per security for the 12 months ending 30 June 20131

1. Assuming performance fees are payable for the full financial year and there is no unforeseen material deterioration to existing economic conditions.

Outlook34

Appendices

35

36. Property summary38. Reconciliation of net property income39. Gearing history and key debt covenants40. Hedge maturity profile41. Hedging profile

42. Development overview43. Flowback44. Diversification by income and expiry profile45. Weighted average capitalisation rates

Appendix 1Property summary 1

36

Ownership (%) Centre type1 Book

value ($m)MAT

growth (%)Spec MAT growth (%)

Spec MAT/sqm

Occ costs (%)

Occupancy (%) Cap rate (%) % of retail

portfolio

Chadstone Shopping Centre 50 Super-regional 1,612.3 1.1 4.4 $13,741 18.0 100.0 5.25 20.5

Chatswood Chase Sydney 100 Regional 810.0 (1.3) 2.3 $10,353 18.0 100.0 5.75 10.3

Bayside Shopping Centre 100 Regional 582.6 8.2 5.3 $ 6,701 19.4 98.6 6.50 7.4

QueensPlaza 100 CBD-regional 550.1 2.4 1.8 $17,389 14.6 100.0 5.75 7.0

Northland Shopping Centre 50 Regional 460.6 0.8 (0.4) $8,337 21.0 99.9 6.25 5.9

The Myer Centre Brisbane 50 CBD-regional 366.7 1.1 2.6 $11,576 19.4 99.7 6.50 4.7

Elizabeth Shopping Centre 100 Regional 366.6 (1.4) 0.4 $6,991 16.0 99.7 7.00 4.7

Broadmeadows Shopping Centre 100 Regional 330.6 (5.5) (3.3) $6,333 19.4 99.5 7.25 4.2

Forest Hill Chase 100 Regional 273.2 5.2 0.1 $6,359 13.1 99.8 7.25 3.5

Rockingham Shopping Centre 50 Regional 247.4 8.6 9.2 $8,577 15.0 100.0 6.50 3.2

Lake Haven Shopping Centre 100 Sub-regional 245.2 (1.2) 2.0 $8,924 13.3 99.6 7.50 3.1

Grand Plaza Shopping Centre 50 Regional 169.6 (0.5) (5.9) $8,754 16.5 99.7 6.75 2.1

Eastlands Shopping Centre 100 Sub-regional 168.1 (2.6) (4.8) $7,665 14.3 99.3 7.25 2.1

Clifford Gardens Shopping Centre 100 Sub-regional 157.5 (3.0) 0.6 $9,067 12.4 99.6 7.75 2.0

1. Regional and sub-regional centres classified as per Property Council of Australia definitions.

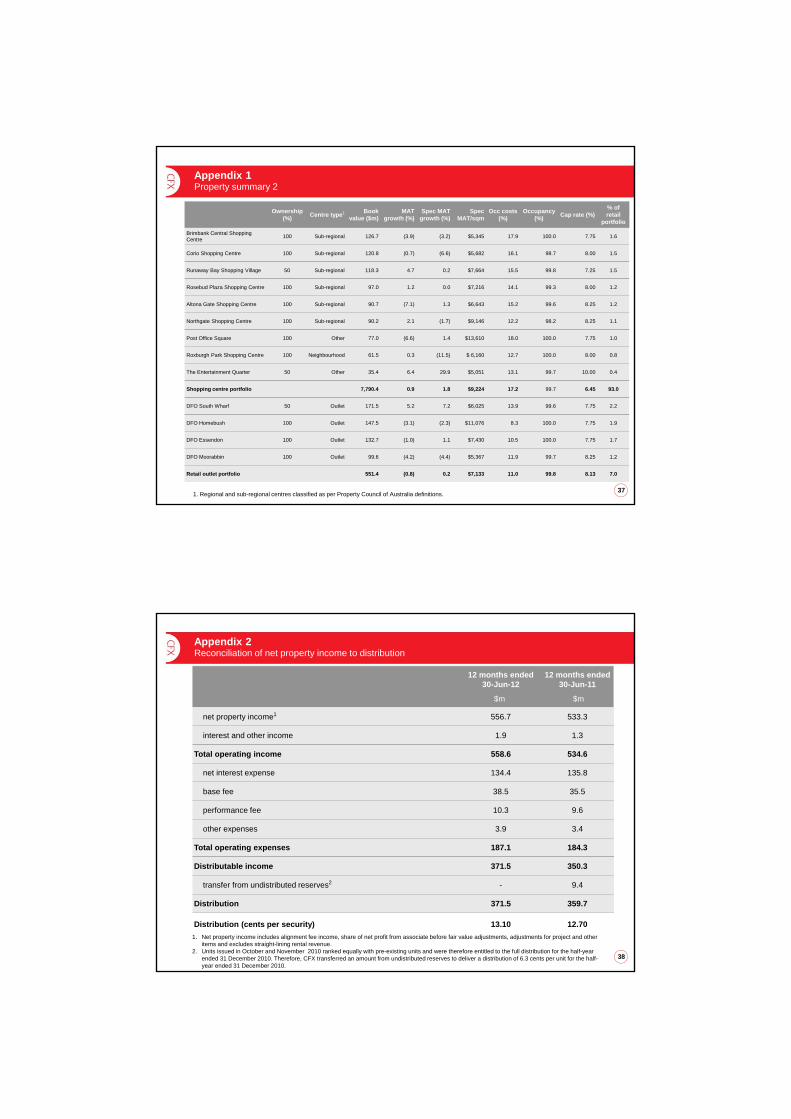

Appendix 1Property summary 2

37

Ownership (%) Centre type1 Book

value ($m)MAT

growth (%)Spec MAT

growth (%)Spec

MAT/sqmOcc costs

(%)Occupancy

(%) Cap rate (%)% of retail

portfolio

Brimbank Central Shopping Centre 100 Sub-regional 126.7 (3.9) (3.2) $5,345 17.9 100.0 7.75 1.6

Corio Shopping Centre 100 Sub-regional 120.8 (0.7) (6.6) $5,682 16.1 98.7 8.00 1.5

Runaway Bay Shopping Village 50 Sub-regional 118.3 4.7 0.2 $7,664 15.5 99.8 7.25 1.5

Rosebud Plaza Shopping Centre 100 Sub-regional 97.0 1.2 0.0 $7,216 14.1 99.3 8.00 1.2

Altona Gate Shopping Centre 100 Sub-regional 90.7 (7.1) 1.3 $6,643 15.2 99.6 8.25 1.2

Northgate Shopping Centre 100 Sub-regional 90.2 2.1 (1.7) $9,146 12.2 98.2 8.25 1.1

Post Office Square 100 Other 77.0 (6.6) 1.4 $13,610 18.0 100.0 7.75 1.0

Roxburgh Park Shopping Centre 100 Neighbourhood 61.5 0.3 (11.5) $ 6,160 12.7 100.0 8.00 0.8

The Entertainment Quarter 50 Other 35.4 6.4 29.9 $5,051 13.1 99.7 10.00 0.4

Shopping centre portfolio 7,790.4 0.9 1.8 $9,224 17.2 99.7 6.45 93.0

DFO South Wharf 50 Outlet 171.5 5.2 7.2 $6,025 13.9 99.6 7.75 2.2

DFO Homebush 100 Outlet 147.5 (3.1) (2.3) $11,076 8.3 100.0 7.75 1.9

DFO Essendon 100 Outlet 132.7 (1.0) 1.1 $7,430 10.5 100.0 7.75 1.7

DFO Moorabbin 100 Outlet 99.6 (4.2) (4.4) $5,367 11.9 99.7 8.25 1.2

Retail outlet portfolio 551.4 (0.8) 0.2 $7,133 11.0 99.8 8.13 7.0

1. Regional and sub-regional centres classified as per Property Council of Australia definitions.

Appendix 2Reconciliation of net property income to distribution

38

12 months ended30-Jun-12

$m

12 months ended30-Jun-11

$m

net property income1 556.7 533.3

interest and other income 1.9 1.3

Total operating income 558.6 534.6

net interest expense 134.4 135.8

base fee 38.5 35.5

performance fee 10.3 9.6

other expenses 3.9 3.4

Total operating expenses 187.1 184.3

Distributable income 371.5 350.3

transfer from undistributed reserves2 - 9.4

Distribution 371.5 359.7

Distribution (cents per security) 13.10 12.701. Net property income includes alignment fee income, share of net profit from associate before fair value adjustments, adjustments for project and other

items and excludes straight-lining rental revenue.2. Units issued in October and November 2010 ranked equally with pre-existing units and were therefore entitled to the full distribution for the half-year

ended 31 December 2010. Therefore, CFX transferred an amount from undistributed reserves to deliver a distribution of 6.3 cents per unit for the half-year ended 31 December 2010.

Appendix 3Gearing history and key debt covenants

39

1.Calculated as total liabilities divided by total assets.2.Calculated as earnings before interest divided by net interest expense for CFX1. For the purposes of this calculation, earnings represents net profit

excluding all fair value adjustments, straight-lining revenue, borrowing costs and net interest expense on interest rate swaps. Interest expense is the sum of borrowing costs, net interest expense on interest rate swaps, and capitalised interest; less non-cash convertible notes interest expense and adjustments for convertible notes buy-back expense.

Threshold

As at 30 June

2012

As at 30 June

2011

Loan to value ratio (LVR)1

50% or less 31% 31%

Interest cover ratio2 1.8 times or greater

3.2 times

2.8times

20.7%

26.7%28.3%28.3%

25.0%27.3%27.3%

29.5%27.0%26.6%

0%

10%

20%

30%

40%

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

Gearing history Key debt covenants

Target gearing 25-35%

Hedging profile at 30 June 20121

Appendix 4Hedge maturity profile

40

1.Adjusted for the drawing of debt to repay $198.5m of August 2014 convertible notes put to CFX on 21 August 2012, the commencement of the $120m USPP (12 July 2012) and $125m five-year bank debt facility (2 September 2012), the repayment of $225 million of MTNs on 2 September 2012 and interest rate swaps entered into on 26 July 2012.

2.Adjusted for capital management activities post the period. 3.Excluding line fees and margins.

Swap rate$m

At 30 June 20121 At 30 June 20112

Proportion of debt hedged3 84% 92%

Weighted average interest rate on hedged debt3,4 5.1% 6.1%

Weighted average durationof hedged debt 3.9 years 4.5 years

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

0

500

1,000

1,500

2,000

2,500

FY13 FY14 FY15 FY16 FY17 FY18 FY19

Face value of hedges Weighted average interest rate on hedged debt

Appendix 5Hedging profile1

41

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

Face value of hedges ($m) 1,872 1,872 1,883 1,501 765 365 266 290

Weighted average interest rate on hedged debt (%) 5.05 5.05 5.04 5.03 5.94 4.86 5.24 5.35

Average % hedged over FY 84 83 71 56 28 14 10 11

1.Adjusted for the drawing of debt to repay $198.5m of August 2014 convertible notes put to CFX on 21 August 2012, the commencement of the $120m USPP (12 July 2012) and $125m five-year bank debt facility (2 September 2012), the repayment of $225m of MTNs on 2 September 2012 and interest rate swaps entered into on 26 July 2012.

421.Yield based on first year income after development completion.2.Other projects in progress comprise Brimbank $34m, Forest Hill Chase $20m, Corio $7m and DFO South Wharf $4m (CFX share).

Appendix 6Development overview

Current projects

CFXtotal cost $m

CFXcost to

complete$m

Target yield1

%

Expected completion

date

Projects in progress

Emporium Melbourne 560 186 > 6 Late 2013

Roxburgh Park Shopping Centre 65 39 >8 Early 2013

Other projects in progress1 65 58 >7 Mid-2013

DFO Homebush 100 98 >7 TBA

Chadstone Shopping Centre 260 260 >7 TBA

Total current projects 1,050 641

Planning, concept and deferred 261 261

Total development pipeline 1,311 902

43

Appendix 7Flowback

12 months to 30 June 2012

CFSGAMProperty asset management

division CFX share

Retail assets under management $13.8b $8.4b

Development pipeline $2.4b $1.3b

Distributable income $31.2m $10.2m

Asset management division adds value to CFX portfolio and provides a share of distributable income

Asset management division adds value to CFX portfolio and provides a share of distributable income

Distribution income relating to flow-back up 29.1% on prior year due to increased development fee-related income

Distribution income relating to flow-back up 29.1% on prior year due to increased development fee-related income

44

Appendix 8Diversification by income and expiry profile

1.Including Coles, Target and Kmart and subsidiary brands.2.Including Big W, Dick Smith and subsidiary brands.

FY12

1. Wesfarmers1 7.7

2. Woolworths2 4.5

3. David Jones 3.3

4. Myer 3.2

5. Premier Investments 1.7

6. Hoyts 1.4

7. Commonwealth Bank 1.1

8. Luxottica Retail 0.9

9. Australian Pharmaceutical Industries 0.9

10. Angus & Coote 0.9

11. Speciality Fashion Group 0.9

12. Westpac 0.9

13. Country Road 0.8

14. Cotton On 0.8

15. BB Retail Capital 0.8

Top 15 29.8

22.6%

15.2%

20.9% 18.4%22.9%

0%

5%

10%

15%

20%

25%

FY13* FY14 FY15 FY16 BEYOND

Tenant (% of income)

Retail specialty store lease expiry (% gross lettable area)

4,194 retail tenants

* FY13 includes vacancies and holdovers

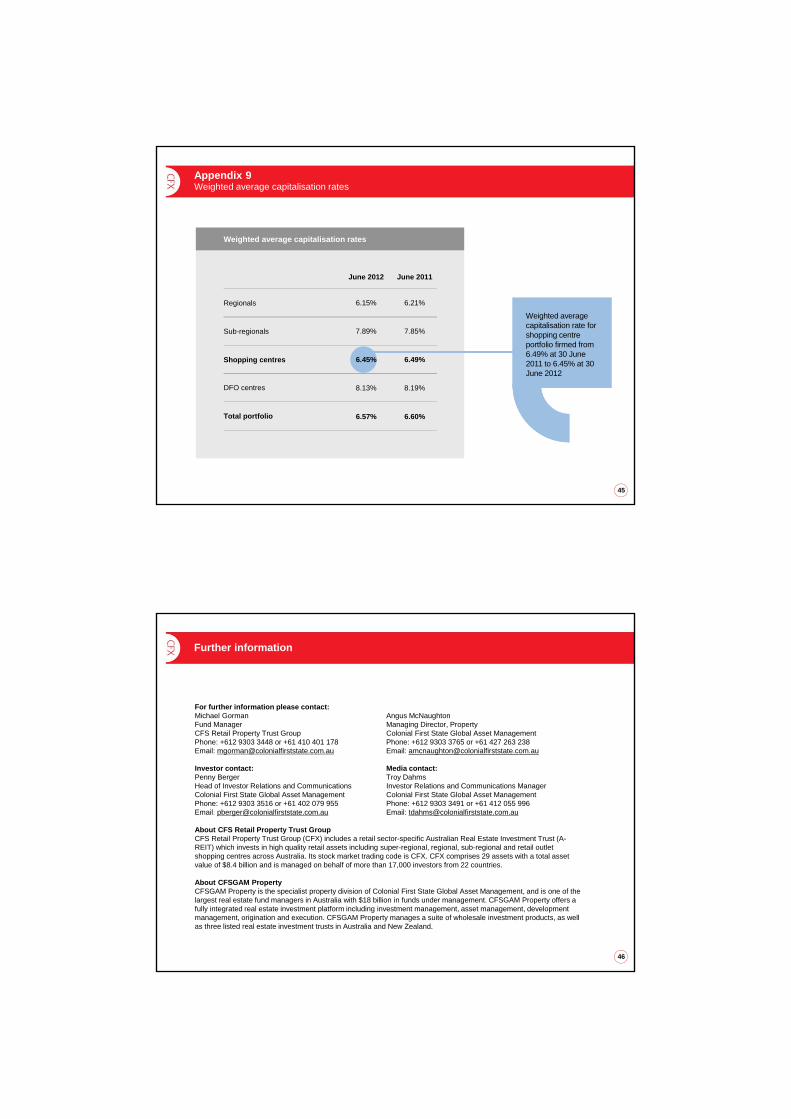

Appendix 9Weighted average capitalisation rates

45

Weighted average capitalisation rates

June 2012 June 2011

Regionals 6.15% 6.21%

Sub-regionals 7.89% 7.85%

Shopping centres 6.45% 6.49%

DFO centres 8.13% 8.19%

Total portfolio 6.57% 6.60%

Weighted average capitalisation rate for shopping centre portfolio firmed from 6.49% at 30 June 2011 to 6.45% at 30 June 2012

Weighted average capitalisation rate for shopping centre portfolio firmed from 6.49% at 30 June 2011 to 6.45% at 30 June 2012

46

Further information

For further information please contact:Michael Gorman Angus McNaughton Fund Manager Managing Director, Property CFS Retail Property Trust Group Colonial First State Global Asset ManagementPhone: +612 9303 3448 or +61 410 401 178 Phone: +612 9303 3765 or +61 427 263 238Email: [email protected] Email: [email protected]

Investor contact: Media contact: Penny Berger Troy DahmsHead of Investor Relations and Communications Investor Relations and Communications ManagerColonial First State Global Asset Management Colonial First State Global Asset ManagementPhone: +612 9303 3516 or +61 402 079 955 Phone: +612 9303 3491 or +61 412 055 996Email: [email protected] Email: [email protected]

About CFS Retail Property Trust GroupCFS Retail Property Trust Group (CFX) includes a retail sector-specific Australian Real Estate Investment Trust (A-REIT) which invests in high quality retail assets including super-regional, regional, sub-regional and retail outlet shopping centres across Australia. Its stock market trading code is CFX. CFX comprises 29 assets with a total asset value of $8.4 billion and is managed on behalf of more than 17,000 investors from 22 countries.

About CFSGAM PropertyCFSGAM Property is the specialist property division of Colonial First State Global Asset Management, and is one of the largest real estate fund managers in Australia with $18 billion in funds under management. CFSGAM Property offers a fully integrated real estate investment platform including investment management, asset management, development management, origination and execution. CFSGAM Property manages a suite of wholesale investment products, as well as three listed real estate investment trusts in Australia and New Zealand.

Neither Commonwealth Bank of Australia (the ‘Bank’) ABN 48 123 123 124 nor any of its subsidiaries guarantees or in any way stands behind the performance of the CFS Retail Property Trust 1 ARSN 090 150 280 and CFS Retail Property Trust 2 ARSN 156 647 853 (together CFS Retail Property Trust Group or ‘CFX’) or the repayment of capital by CFX. Investments in CFX are not deposits or other liabilities of the Bank or its subsidiaries, and investment-type products are subject to investment risk including possible delays in repayment and loss of income and principal invested.

The information contained in this presentation (the ‘Presentation’) is intended to provide general advice only and does not take into account your individual objectives, financial situation or needs. You should assess whether the Presentation is appropriate for you and consider talking to a financial adviser or consultant before making an investment decision.

All reasonable care has been taken in relation to the preparation and collation of the Presentation. Except for statutory liability which may not be excluded, no person, including Commonwealth Managed Investments Limited (the ‘Responsible Entity’) ABN 33 084 098 180, Colonial First State Property Retail Pty Limited ABN 19 101 384 294 or any other member of the Bank’s group of companies, accepts responsibility for any loss or damage howsoever occurring resulting from the use of or reliance on the Presentation by any person. Past performance is not indicative of future performance and no guarantee of future returns is implied or given.

Copyright and confidentialityThe copyright of this Presentation and the information contained therein is vested in the Responsible Entity, the Bank and the Bank’s group of companies. This Presentation should not be copied, reproduced or redistributed without prior consent.

Disclaimer

47