Embed Size (px)

DESCRIPTION

Implementation of Predictive Models – Making Models Come Alive. John Lucker – Principal – Deloitte Consulting LLP Michele Yeagley, ACAS, MAAA – Asst. Vice President - Harleysville Insurance. Casualty Actuarial Society - Predictive Modeling Special Interest Seminar September 2005. - PowerPoint PPT Presentation

Citation preview

Casualty Actuarial Society - Predictive Modeling Special Interest SeminarSeptember 2005

Implementation of Predictive Models – Making Models Come Alive

John Lucker – Principal – Deloitte Consulting LLPMichele Yeagley, ACAS, MAAA – Asst. Vice President - Harleysville Insurance

2Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

Discussion Themes

• Predictive Modeling provides the toolset to assist with a variety of critical business operations

• The market is softening and better risk assessment capabilities are needed to avoid inappropriate soft market dynamics and naïve reactions

• Predictive Models can be implemented in ways that do not require complex, expensive efforts

• The financial benefits that can be realized from predictive models are very significant – phased and rapid implementation can help fund additional future analytics and more complex implementations

• The three most important parts of any predictive modeling project are (1) implementation; (2) implementation; and (3) implementation – building a great model should be a given

Some Predictive Modeling Basics

3

4Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

Some Areas that Insurance Predictive Modeling Can Address

Risk Profitability Assessment

• Risk Attraction

• Risk Retention

• Risk Avoidance

• Non-Renewals

• Right-Pricing

Claims Management

• Claim Triage

• Duration Reduction

• Fraud Propensity

Producer Management

• Profitable Production

• Production Retention

• Recruitment

Customer Management

• Cross-Sell Success Rates

• Client View

• Geo / Market Expansion

• Book Rollover/Transfer

• Proactive Call Centers

• Audit & Billing Options

Reinsurance

• Assumed Biz Scoring

• Retro Placement/Retention

M&A

• Pre-Deal Assessment

• Post-Deal Remediation

5Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

Before Insurance Predictive Modeling – Class Underwriting

Below average

Average

Above average

135%125%

110%115%

100% 90%

80%70%

140%

63%60%

65%68%

72%

78%75%

82%

90%87%

RoofersYouthful Drivers

OverallLoss Ratioof 75%

Workers’ CompensationCommercial AutoCMP / BOPPropertyGeneral LiabilityPrivate Passenger AutoHomeowners

FloristsMiddle Aged Drivers

Numbers are Illustrative

6Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

A Predictive Modeling Approach

Building and deploying predictive models requires a specialized combination of skills covering data management, data cleansing, data mart construction, actuarial and statistical analysis, data mining and modeling, and insurance operational and business processing and technologies

External Data

External Data

Internal Data

Internal Data

Synthetic VariablesSynthetic Variables

Data Aggregation &

Data Cleansing

Data Aggregation &

Data Cleansing

Evaluate and Create Variables

Evaluate and Create Variables

Develop Predictive Model

Develop Predictive Model

Score For Each Policy

Predicted loss ratio

160%140%

120%110%100% 90%80%70%

60%

180%

Business Rules Engine

Score Driven Business Applications

7Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

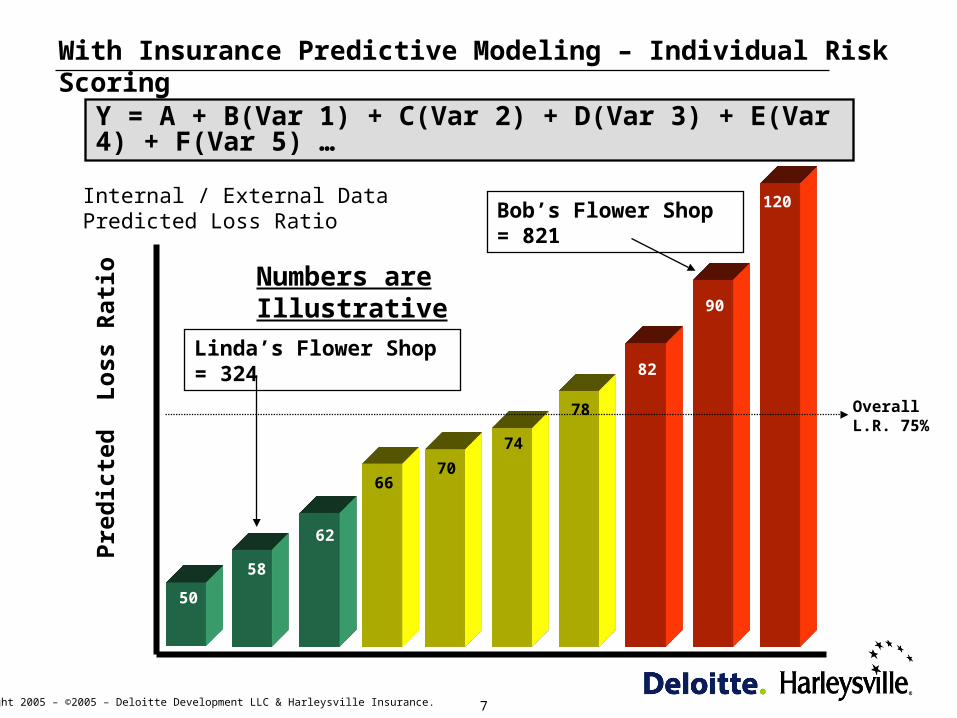

With Insurance Predictive Modeling – Individual Risk Scoring

82

66

58

62

70

74

78

90

120

OverallL.R. 75%

50

Bob’s Flower Shop = 821

Linda’s Flower Shop = 324

Pre

dict

ed L

oss

Rat

io

Internal / External DataPredicted Loss Ratio

Y = A + B(Var 1) + C(Var 2) + D(Var 3) + E(Var 4) + F(Var 5) …

Numbers are Illustrative

Laying the Groundwork for an End-To-End Implementation

8

9Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

What The Process IS NOT – What it IS

What it IS NOT

• A Black Box approach

• Stock delivery

• Replacement for underwriters

• Score used to communicate decision

• Score drives results

• A single variable magic bullet

• Actuarial and/or systems project

• Class plan underwriting

What it IS

• Scoring drivers are known / understood

• Collaborative throughout the business

• Additional underwriting toolset

• Reason codes / messages are developed

• Implementation drives results

• Relationship among variables is power

• Business initiative

• Efficient segmentation of policyholders

10

Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

Using the Lift Curve for Business Applications – Renewal Business

Highly Profitable

• Risk Attraction

• Retention Priority

• Less Loss Control

• Less Premium Audit

• More Pricing Flexibility

Highly Unprofitable

• Risk Avoidance

• Repricing Priority

• Non-Renewals

• Loss Control

• Premium Audit

Renewal BusinessUnderwriterWorkflow

Best 25%

Worst 25%

11

Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

Using the Lift Curve for Business Applications – New Business

Highly Profitable

• Risk Attraction

• Retention Priority

• Less Loss Control

• Less Premium Audit

• More Pricing Flexibility

Highly Unprofitable

• Risk Avoidance

• Repricing Priority

• Non-Renewals

• Loss Control

• Premium Audit

Best 25%

Worst 25%

New BusinessUnderwriterWorkflow

12

Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

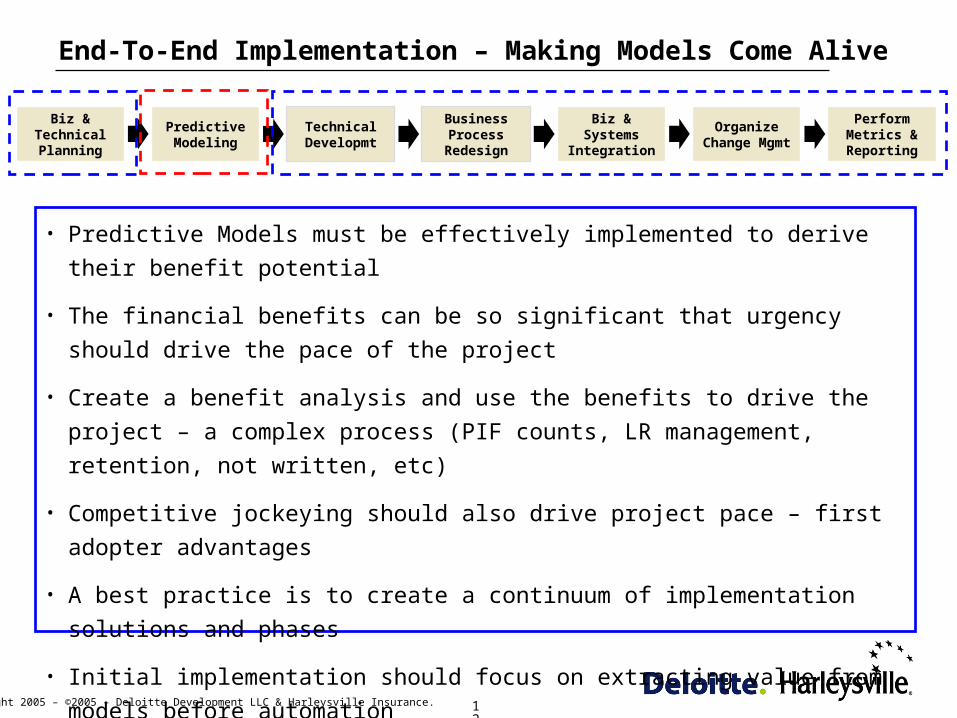

End-To-End Implementation – Making Models Come Alive

Biz & TechnicalPlanning

Predictive Modeling

Technical Developmt

Business Process

Redesign

Biz & Systems

Integration

OrganizeChange Mgmt

Perform Metrics & Reporting

• Predictive Models must be effectively implemented to derive their benefit potential

• The financial benefits can be so significant that urgency should drive the pace of the project

• Create a benefit analysis and use the benefits to drive the project – a complex process (PIF

counts, LR management, retention, not written, etc)

• Competitive jockeying should also drive project pace – first adopter advantages

• A best practice is to create a continuum of implementation solutions and phases

• Initial implementation should focus on extracting value from models before automation

• Tactical implementation can be achieved in 2-4 months

• Planning, planning, and then some more planning

13

Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

End-To-End Implementation – Making Models Come Alive

Biz & TechnicalPlanning

Predictive Modeling

Technical Developmt

Business Process

Redesign

Biz & Systems

Integration

OrganizeChange Mgmt

Perform Metrics & Reporting

• Steering Committee and Project Committee Structure

• Phased structure and focus on 80:20 Rule

• Development of End-State-Vision & Project Planning Document – some key questions are:

• How will predictive modeling guide decision making, pricing, and tier placement?

• How will predictive models impact existing business processes (e.g. by line / account)?

• How will predictive models be blended into the field and agency management process?

• What key performance measures must be achieved?

• How will underwriters/raters/other personnel’s compliance be measured?

• What level of automation is desired for various business processes?

14

Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

End-To-End Implementation – Making Models Come Alive

Biz & TechnicalPlanning

Predictive Modeling

Technical Developmt

Business Process

Redesign

Biz & Systems

Integration

OrganizeChange Mgmt

Perform Metrics & Reporting

• Extract, Transform, Load process for Internal, External, and Synthetic Data

• Management of external data vendors and external data acquisition

• Data quality and cleansing issues

• Construction of Scoring Engine(s) (real time, batch, manual, etc)

• Construction of Business Rules Engine or similar process

• Construction of operational data mart

• Design of technical architecture, data flow, messaging, data management, etc.

• Model maintenance

15

Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

End-To-End Implementation – Making Models Come Alive

Biz & TechnicalPlanning

Predictive Modeling

Technical Developmt

Business Process

Redesign

Biz & Systems

Integration

OrganizeChange Mgmt

Perform Metrics & Reporting

• Underwriting workflow (renewal business, new business, touch level)

• How model scores will be used in the U/W process (scores, reason codes, action thresholds,

risk avoidance, risk acquisition, retention management, account vs. monoline, etc)

• How will models be used as risks proceed from new to renewals (disruption issues)?

• Use of model scores for downstream processes

• Relationship of model usage to field and producer management

• Business rule creation, optimization and maintenance

16

Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

End-To-End Implementation – Making Models Come Alive

Biz & TechnicalPlanning

Predictive Modeling

Technical Developmt

Business Process

Redesign

Biz & Systems

Integration

OrganizeChange Mgmt

Perform Metrics & Reporting

• What systems modifications are required to accommodate the process?

• What will different people in different roles see throughout the process?

17

Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

End-To-End Implementation – Making Models Come Alive

Biz & TechnicalPlanning

Predictive Modeling

Technical Developmt

Business Process

Redesign

Biz & Systems

Integration

OrganizeChange Mgmt

Perform Metrics & Reporting

• Identification of all new process stakeholders (Underwriting, actuarial, systems, executive,

legal/regulatory, claims, field, agency, training, project management, etc)

• How will predictive modeling be described internally and externally to all stakeholders?

• Manage any legal/regulatory issues and concerns

• Once communicated, how to deal with questions, concerns, issues, etc. from Underwriters,

field personnel, agents, market analysts, etc.

• Development of change management, communication, and training activities and materials

• Development of necessary implementation materials for all stakeholders

• Development of feedback mechanisms using objective and subjective criteria

18

Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

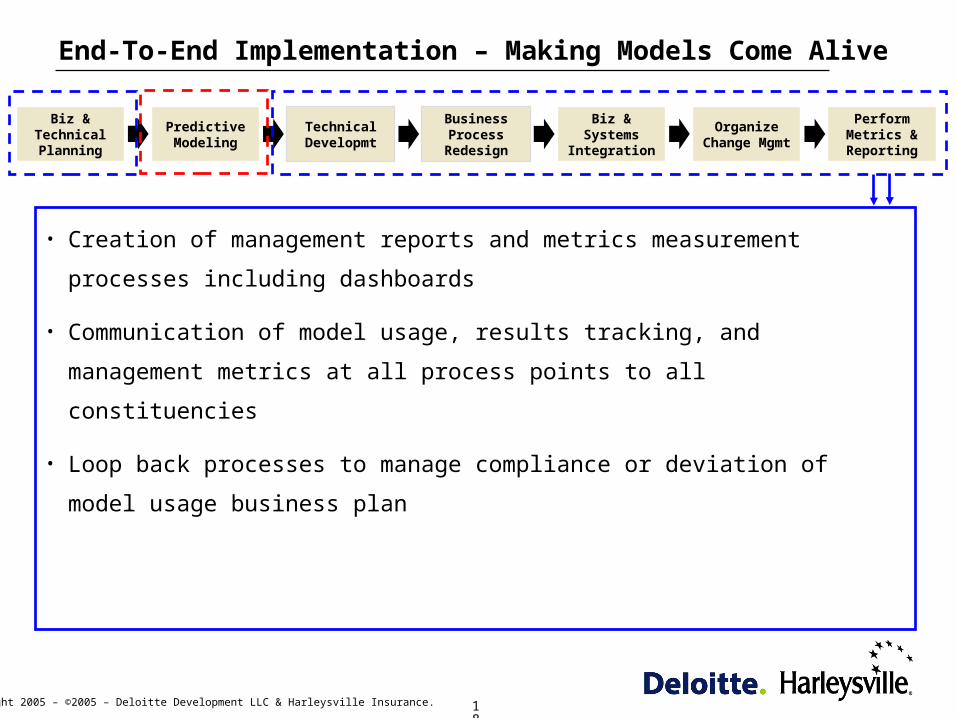

End-To-End Implementation – Making Models Come Alive

Biz & TechnicalPlanning

Predictive Modeling

Technical Developmt

Business Process

Redesign

Biz & Systems

Integration

OrganizeChange Mgmt

Perform Metrics & Reporting

• Creation of management reports and metrics measurement processes including dashboards

• Communication of model usage, results tracking, and management metrics at all process

points to all constituencies

• Loop back processes to manage compliance or deviation of model usage business plan

19

Copyright 2005 – ©2005 – Deloitte Development LLC & Harleysville Insurance.

Contact Information

John LuckerPrincipalDeloitte [email protected]

Michele YeagleyAsst. Vice PresidentHarleysville [email protected]