Embed Size (px)

Citation preview

Business Economics

Demand, Supply, andMarket Equilibrium

Thomas & Maurice, Chapter 2

Herbert Stocker

IIS, Ramkhamhaeng University& Department of Economics, University of Innsbruck

Demand and Supply

on Perfectly Competitive Markets

Demand

Quantity Demanded:

is the amount of a good that buyers arewilling and able to purchase, and

is represented by a functional relationshipbetween the price of a good or service andthe quantity demanded by consumers at agiven time, all else held constant

Demand: A Thought Experiment

Suppose, twenty people in the lecture hall receiveda voucher for a lunch in a restaurant

They would like to sell their vouchers

One starts announcing a high price and ask thepeople without vouchers, how many vouchers theyare willing to buy for this price

Lower prices are announced until everyone can sellhis/her voucher

Demand: A Thought ExperimentP QD QS

20 1 20

18 1 20

16 4 20

14 6 20

12 7 20

10 12 20

8 15 20

6 20 20

4 26 20

2 36 20

0 96 20

0

4

8

12

16

20

0 4 8 12 16 20 24 28 32 36

P

Q

D

bc

bc

bc

bc

bc

bc

bc

bc

bc

bc

S

6

Demand: A Thought Experiment

What are the determinants of demand?Apparently the price of the voucherFinancial possibilities (income, wealth)The price of alternatives (e.g., lunch at otherrestaurants)Other conditions: temperature, seasonAnd many more . . .

More systematically . . .

Determinants of Demand QD

Price (P): [P ↑⇒ QD ↓; Exception: Giffen-Goods]

Income (M): [M ↑⇒ QD ↑; Exc.: Inferior goods]

Price of Substitute Goods (PS): [PS ↑⇒ QD ↑]

Price of Complementary Goods (PC ):[PC ↑⇒ QD ↓]

Expected Price (PE )

Tastes (ℑ)

Income distribution, . . .

QD = Q (P,M ,PS ,PC ,PE ,ℑ, . . .) ,∂QD

∂P< 0

∂QD

∂M⋚ 0

∂QD

∂PS> 0

∂QD

∂PC< 0

∂QD

∂PE⋚ 0

∂QD

∂ℑ⋚ 0

Determinants of Demand

QD = Q (P,M ,PS ,PC , . . .)

∂QD

∂P< 0;

∂QD

∂M⋚ 0;

∂QD

∂PS> 0;

∂QD

∂PC< 0

Example:

QD = 1, 000− 5P + 2M + 0.3PS − 1.5PC

∂QD

∂P= −5;

∂QD

∂M= +2;

∂QD

∂PS

= +0.3;∂QD

∂PC

= −1.5

Demand Curve

Direct demand curve (”demand”) expresses quantitydemanded as a function of product price only

QD = f (P, M̄, P̄S , P̄C )

= f (P)

Note: Demand function relates the quantitiesdemanded to various prices, holding constant theeffects of income, related prices, ...→ ceteris paribus (c.p.)

Inverse Demand Curve

Price (P) is usually plotted on the vertical axis &quantity demanded (QD) is plotted on thehorizontal axis

Therefore, the equation plotted is the inversedemand function

QD = f (P) → P = f −1(QD)

Example:QD = 1000− 5P → P = 200− 0.2QD

Demand Curve: Interpretation

A point on a demand curve shows either

the maximum amount of a good that will bepurchased for a given price (direct demand), or

the maximum price consumers will pay for aspecific amount of the good (inverse demand)

In the example before:

At P = 100, QD = 1, 000− 5 · 100 = 500At QD = 500, P = 200− 0.2 · 500 = 100

Supply

Quantity supplied . . .

is the quantity supplied is the amount of agood that sellers are willing and able tosell, and

is represented by a functional relationshipbetween the price of a good or service andthe quantity supplied by sellers in a giventime, all else held constant

Determinants of Supply QS

Price (P): [P ↑⇒ QS ↑]

Input prices (PI ): [PI ↑⇒ QS ↓]

Technology (T ): [T ↑⇒ QS ↑]

Expected Price (PE )

Number of suppliers (N): [N ↑⇒ QS ↑]

Prices of goods related in production, . . .

QS = Q (P,PI ,T ,PE ,N , . . .)∂QS

∂P> 0,

∂QS

∂PI< 0,

∂QS

∂T> 0,

∂QS

∂PE⋚ 0,

∂QS

∂N> 0

Supply Curve and Inverse Supply Curve

Supply function

A supply function shows the relationship between thequantity of a good producers are willing to sell and thedeterminants of supply:

QS = QS (P,PI , . . .)

Direct supply curve (”supply”): QS = f (P)(→ holding all other determinants constant!)

Again, supply is often written as an inverse supplyfunction

QS = g(P) → P = g−1(QS)

Shifts in Curves versus

Movemens along Curves

Shifts in vs. Movements along Curves

Demand Curve:

QD = Q (P,M ,PS ,PC ,ℑ, . . .)

Change in price: Movement along the curve (priceis drawn on the vertical axis!)⇒ ”Change in Quantity Demanded”

Change of any other determinant of demand:Shifts the demand curve⇒ ”Change in Demand”

Movements along curves . . .

P

Q

∆P

Q = a0 − a1 P + a2M

∂Q∂P < 0

∆Q

Shifts in curves . . .

P

Q

Q = a0 − a1P + a2 M

∂Q∂M > 0

∂Q∂M < 0

Shifts in a curve . . .

How much a curve is shifted when income increasesfrom M1 to M2?

Q1 = a0 − a1P + a2M1

Q2 = a0 − a1P + a2M2 /−

Q1 − Q2 = a0 − a0 + a1P − a1P + a2M1 − a2M2

Q1 − Q2 = a2(M1 −M2)

⇒ ∆Q = a2∆M

[

⇒∆Q

∆M= a2

]

Shifts in a curve: Example

Example: QD = 400− 10P + 5M

01020304050607080

0 200 400 600 800

P

Q

∂Q

∂M∆M

= 5×∆M= 5× 40= 200

for M = 40

QD = 400− 10P + 5× 40

= 600− 10P

for M = 80

QD = 400− 10P + 5× 80

= 800− 10P

Endogenous and Exogenous Variables

Endogenous Variables: are determined withinthe system.

Exogenous Variables: are determined outsidethe system.

In our simple model, price and quantity areendogenous variables, all other Variables (income,price of substitutes, technology, . . . ) areexogenous variables.

Endogenous and Exogenous Variables

Endogenous variables are those drawn on the axis!

Exogeneous variables affect endogeneousvariables, but not the other way round!

Endogenous: P, Q, Exogenous: M

P

Q

M

Q P

Shifts in vs. Movements along Curves:Recap

Whenever a variable changes that is drawn on anaxis (price) we move along the demand curve!⇒ Endogenous variables

Whenever a variable changes that is not drawn onan axis the demand curve shifts!⇒ Exogenous variables

Similar holds for the supply curve: Change inquantity supplied vs. change in supply

Shifts in vs. Movements along Curves

Change in Quantity SuppliedOccurs when price changesMovement along supply curve

Change in SupplyOccurs when one of the other variables, ordeterminants of supply, changesSupply curve shifts rightward or leftward

Equilibrium Analysis

“In short, economists have powerful tools:

formal modelling,the assumption of maximizing behaviourby agents, andthe notion of equilibrium.

Using these techniques produces crisp,testable conclusions.” (Fiona Scott Morton)

Equilibrium

A situation in which, at a given price, consumerscan buy all of a good they wish and producers cansell all of the good they wish, or

the intersection of demand and supply curves

Equilibrium Price

P

Q

P∗

Q∗

QS

QD

bc

Endogenenous variables P , QD

and QS adjust until the equilib-rium values of P∗ and Q∗ arereached.

Market clearing price: As long as the price is allowedto adjust freely to the equilibrium, there will never be apermanent shortage or surplus at the market!

Why Equilibrium Analysis?

Economists hope, that an equilibrium is similar toan center of gravity, even if in the short run it’sfrequently disturbed by other forces“Economic life is continually lurching from one

out-of-equilibrium position to another.” (Joan Robinson)

“You can fool some of the people all of the time,and all of the people some of the time, but youcan not fool all of the people all of the time.”

(Abraham Lincoln)

Example

Consider the following market

QD = 1400− 10P

QS = −400 + 20P

Equilibrium requires QD = QS :

1400− 10P = −400 + 20P

Solving this equation yields

1800 = 30P

P∗ = 60

Example

At the market-clearing price P∗ = 60 we have

QD = 1, 400− 10 · 60 = 800 = Q∗

QS = −400 + 20 · 60 = 800 = Q∗

If P = 80

QD = 1, 400− 10 · 80 = 600

QS = −400 + 20 · 80 = 1, 200

Therefore

QS − QD = 1, 200− 600 = 600

⇒ Excess supply (surplus)

Controls on Prices

Controls on Prices

In a free, unregulated market system, marketforces establish equilibrium prices and exchangequantities.

While equilibrium conditions may be efficient, itmay be true that not everyone is satisfied.

Controls on prices are usually enacted whenpolicymakers believe the market price is unfair tobuyers or sellers.

Result in government-created price ceilings andprice floors.

Price Floors

P

Q

Pmin

ExcessSupply

Quantity sold

bc

Price Floor:

bindingnot binding

Examples:

Agriculture

Minimum wages. . .

A price floor that is not binding (i.e. below the equilibrium price)has no effect at all!

Example: Minimum Wage

Wage

Quantityof Labor

EquilibriumWage

MinimumWage

Unemployment

bc

Those helped

by the

minimumwage

Thosewholoosetheirjobs

Thosewho nowwant ajob but

cannotfind one

Price Ceilings

P

Q

Pmax

ExcessDemand

Quantity sold

bc

Price Ceiling:

bindingnot binding

Examples:

Rents

Energy

. . .

A price ceiling that is not binding (i.e. above the equilibriumprice) has no effect at all!

Example: Rent Controls

Rent controls are ceilings placed on the rents thatlandlords may charge their tenants

The goal of rent control policy is to help the poorby making housing more affordable

Black markets usually arise in such situations

One economist called rent control “the best wayto destroy a city, other than bombing”

Rent Controls

Short Run:P

Q

Supply

relatively

inelastic

P∗

PC

shortage

Apartments

‘lost’ due torent control

bc

Long Run:P

Q

Supply

relatively

elastic

P∗

PC

Apartments

‘lost’ due torent control

shortage

bc

Shocking the Equilibrium:

Comparative-static Analysis

Comparative-static Analysis

What is the impact of a change in income onequilibrium quantities and prices?

Comparative-static analysis is a very generalmethod for analyzing such changes

it is comparative, because it involves comparing twosituations, (before and after),it is static, because the adjustment over time is notanalyzed (as opposed to a dynamic analysis)

Comparative-static Analysis

A Comparative-static Analysis shows how theendogenous variables of a model adjust when anexogeneous variable changes

We compare two equilibrium points, before andafter the change of the exogenous variable

We could as well calculate the equilibria beforeand after the exogeneous change and comparethese two equilibria, but there are simpler ways . . .

Comparative-static Analysis

Solution involves three steps1 Set up the model regarding the demand and

supply functions⇒ Structural form

2 Solve the model in structural form for theendogenous variables⇒ Reduced form

3 Differentiate the reduced form with respect to theexogenous variables and interpret the result

Example

1. Step: Model in structural form

QS = 20 + 0.1P

QD = 80− 0.1P + 0.5M

QS = QD

2. Step: Model in reduced form

20 + 0.1P = 80− 0.1P + 0.5M

0.2P = 80− 20 + 0.5M

P∗ = 300 + 2.5M

Q∗ = 50 + 0.25M

Example

P∗ = 300 + 2.5M

Q∗ = 50 + 0.25M

3. Step: Form the (partial) derivatives of the reducedform with respect to the exogenous variables

∂P∗

∂M= 2.5

∂Q∗

∂M= 0.25

Interpretation: If income M increases by one unit(e.g., Euro) equilibrium price increases by 2.5 units(e.g., Euro) and equilibrium quantity by 0.25 units(e.g., kg).

Comparative-static Analysis

Be careful

Derivatives of a structural form eq. with respectto an exogeneous or endogeneous variable:⇒ slope of the structural equation with respect tothis variable

Derivatives of a equation of the reduced formeq. with respect to an exogeneous variable:⇒ comparative-static analysis: shows how anendogenous variable adjusts for a new equilibriumafter an exogenous variable has changed

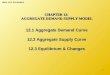

Another example

1. Step: Linear model in structural form

QS = a0 + a1P

QD = b0 − b1P + b2M

QS = QD

2. Step: Solution → reduced form

a0 + a1P = b0 − b1P + b2M

(a1 + b1)P = b0 − a0 + b2M

P∗ =b0 − a0 + b2M

a1 + b1

Another example

Solution for Q∗: we substitute P∗ in the first or secondequation

Q∗ = a0 − a1P∗ = a0 − a1

(

b0 − a0 + b2M

a1 + b1

)

Q∗ =a0b1 + a1b0 + a1b2M

a1 + b1

Another example

Solution (reduced form):

P∗ =b0 − a0 + b2M

a1 + b1

Q∗ =a0b1 + a1b0 + a1b2M

a1 + b1

3. Differentiation and interpretation

dP∗

dM=

b2a1 + b1

?

R 0;dQ∗

dM=

a1b2a1 + b1

?

R 0

Interpretation?

Comparative-static Analysis

Movement from one equilibrium to another equilibrium,caused by a change of an exogenous variable

P

Q∆Q

∆Pbc

bc

QS = a0 + a1P

QD = b0 − b1P + b2M

QS = QD

Result: (for b2 > 0)

∂Q∗

∂M=

b2a1b1 + a1

> 0

∂P∗

∂M=

b2b1 + a1

> 0

Comparative-static Analysis

Graphical Solution

Comparative-static Analysis

Graphical Solution:

3 Steps:

Decide whether the event shifts the supply ordemand curve (or both)

Decide whether the curve(s) shift(s) to the left orto the right

Examine how the shift affects equilibrium price P∗

and quantity Q∗

Comparative-static Analysis

Example:

If income increases consumer will be willing tospend more at any initial price (if it’s a normalgood), i.e., the demand curve shifts to the right

Suppliers have at the initial price no incentive tosupply more, they expand production only whenprice rises!

Therefore, a shift of the demand curve to theright causes an excess demand (shortage), thiscauses prices to rise, and suppliers adjust alongthe supply curve!

Dynamic of Adjustemnt

P

Q

bc bc

ExcessDemand

∆Q

∆P

bcAn exogeneous rise in in-come causes an excessdemand, . . .therefore price will in-crease and suppliers ad-just along the supplycurve.

Changes in Market Equilibrium

Qualitative forecast:Predicts only the direction in which an economicvariable will move

Quantitative forecast:Predicts both the direction and the magnitude of thechange in an economic variableEconometrics uses statistical tools (regressionanalysis) for making quantitative forecast

Examples

What is the effect of the following events onequilibrium quantity and price?

A strike in a firm on the goods market [⇓]

What is the effect of a decrease of average familysize on the market for 4-room apartments [⇓]

An increase in wages in a firm on the market ofthe good they produce [⇓]

Valentine’s day on the market for flowers [⇓]

A decrease in the price for Pepsi on the market forCoca-Cola [⇓]

A tax on electricity on the market for aluminium [⇓]

Skip Solutions

Example

Strike → Goods market: ⇒ decrease in supply.

P

Q∆Q

∆Pbc

bc

back

Example

Decreasing number of kids → market for largeapartments: ⇒ decrease in demand.

P

Q∆Q

∆Pbc

bc

back

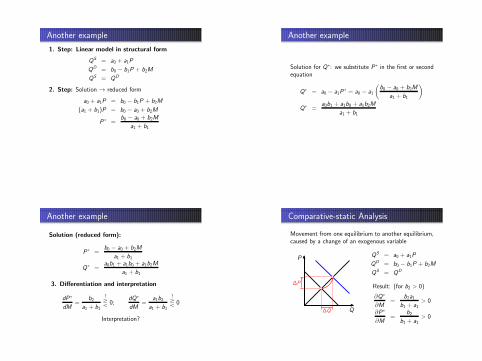

Example

Increasing wages → Goods market:⇒ decrease in supply.

P

Q∆Q

∆Pbc

bc

back

Example

Valentin’s day → Market for flowers:⇒ increase in demand.

P

Q∆Q

∆Pbc

bc

fwd., back

Example

Valentin’s day → Market for flowers:

but: Expectations of suppliers can also shift the supplycurve to the right!

P

Q∆Q

∆P bcbc

Price can increase or de-crease,but quantity will always in-crease!

back

Example

Pepsi becomes cheaper → Market Coca-Cola:⇒ decrease in demand.

P

Q∆Q

∆Pbc

bc

back

Example

Tax on electricity → Market for aluminium:⇒ decrease in supply.

P

Q∆Q

∆Pbc

bc

back

Example: Price of Coffee

Why are coffee prices very volatile?Most of the world’s coffee is produced in BrazilMany changing weather conditions affect the crop ofcoffee, thereby affecting pricePrice following bad weather conditions is usuallyshort-livedIn long run, prices come back to original levels, all elseequal

Price of Coffee (1965 - 2003, nominal prices) Price of Coffee: short-run

P

Q

S1

Q1

D

P1

S2

P2

Q2

In the short run supply is(almost) perfectly inelastic(vertical)

A freeze decreases thesupply of coffee

Price increases significantlydue to inelastic supply anddemand.

Price of Coffee: long-run

P

Q

Slr

Qlr

D

Plr

In the long run supplyis extremely elastic(almost horizontal),demand is more elasticthan in the short run

Price falls back to Plr

Quantity falls back toQlr.

Shifts in Supply and Demand

When supply and demand change simultaneously,the impact on the equilibrium price and quantityis determined by:

The relative size and direction of the change.The shape of the supply and demand models.

Example: The Price of a Education

The real price of a college education in USA rose55 percent from 1970 to 2002.

Increases in costs of modern classrooms and wagesincreased costs of production – decrease in supply.Due to a larger percentage of high school graduatesattending college, demand increased.

Example: The Price of a Education

P

Q

S1970

D1970

P∗70

Q∗70

S2002

D2002

P∗02

Q∗02

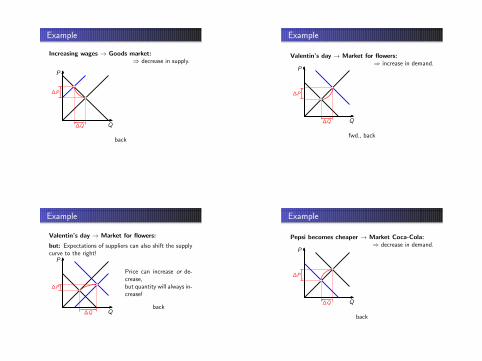

Resource Market Equilibrium

Consumption of copper has increased about ahundredfold from 1880 through 2002.

The long term real price for copper has somewhatfallen.

Increased demand as world economy grew.

Decreased production costs increased supply.

Resource Market Equilibrium

P

Q

D1900S1900

D1950S1950

D2005S2005

Long-Run Pathof Price andConsumption

Prices of Copper (1965 - 2002, real & nominal prices) Allocation function of the market

Summary:

Exogeneous changes in demand or supply causeprices to change in response to new scarcities.

This new prices affect demand and supplydecisions (prices act as ‘incentives’), behaviour ofmarket participants changes in response to pricesignals.

Therefore, competitive markets contribute to anefficient allocation of resources!(Details will follow . . . )

Value of Market Exchange:

Consumer- and Producer Surplus

Equilibrium & Welfare Economics

Market equilibrium reflects the way marketsallocate scarce resources

Whether the market allocation is desirable or notis determined by welfare positions of buyers andsellers

⇒ Welfare EconomicsBuyers and sellers receive benefits from taking part inthe market:→ Consumer surplus and producer surplusSum over consumer and producer surplus represents asociety’s total welfareEquilibrium in a market maximizes the total welfare ofbuyers and sellers

Consumer Surplus

Willingness to pay

Consumer will buy a good only if its benefit atleast covers its cost (price)

Willingness to pay: Maximum price that a buyeris willing and able to pay for a good

Reservation Price: Price at which a consumer isjust indifferent between buying and not buying →

Measures the willingness to pay.If you buy for the reservation price you are neitherbetter nor worse off, your cost equals your benefit!

Example

Willingness to Pay and Market Demand:

Willingness to payof A, B, C & D:

$A 20B 15C 10D 7

0

5

10

15

20

0 1 2 3 4

P

Q

7

bc

bc

bc

bc

bc

bc

bc

bc

bc

bc

bc

bc

Market Demand

Demand and willingness to pay

0

5

10

15

20

0 1 2 3 4

P

Q

7

bc

bc

bc

bc

Willingness to pay of A

Willingness to pay of B

WtP of C

WtP of D

Consumer Surplus

Consumer Surplus with P = 15:

0

5

10

15

20

0 1 2 3 4

P

Q

bc

bc

bc

bc

Total consumer surplus= consumer surplus of A= 1× 5 = 5A

Consumer Surplus

Consumer Surplus with P = 10:

0

5

10

15

20

0 1 2 3 4

P

Q

bc

bc

bc

bc

Total consumer Surplus= consumer surplus of A+ consumer surplus of B= 1× 10 + 1× 5 = 15

AB

Consumer Surplus

Consumer Surplus with P = 7:

0

5

10

15

20

0 1 2 3 4

P

Q

7

bc

bc

bc

bc

Total consumer Surplus= consumer surplus of A+ consumer surplus of B+ consumer surplus of C= 1× 13 + 1× 8 + 1× 3 = 24

AB

C

Consumer Surplus

Total consumer surplus and expenditures with P = 8:

0

5

10

15

20

0 1 2 3 4

P

Q

8

bc

bc

bc

bc

TotalConsumer Surplus

Total Consumer Surplus= 1× 12 + 1× 7 + 1× 2 = 21

Total Expenditures

Total Expenditures= 3× 8 = 24

Effects of a price cut

P

Q

QD

Initial consumer surplus

bc

bc

Additional consu-mer surplus toinitial consumers

bc

Consumer surplusto new consumers

(With many consumers the market demand curve is almost linear.)

Effects of a price cut

P

Q

QD

bc

Total additionalconsumer surplusof a price cut

bc

Consumer Surplus

Consumer surplus in the market is measured bythe area below the demand curve and above theequilibrium price

Consumer surplus is the amount that buyers arewilling to pay for a good minus the amount theyactually pay for it.

Consumer surplus measures the benefit thatbuyers receive from a good as the buyersthemselves perceive it

Consumer Surplus

Attention:

This concept of consumer surplus neglects tat achange in prices ceteris paribus also affects thepurchasing power!

Therefore it is only approximately valid

This concept of consumer surplus is only a limitedindicator for welfare, since it does not considerother aspects of welfare, like fairness or thedistribution of income

Producer Surplus

Producer Surplus

Producer will sell a product only when the price ofthe unit sold at least covers the cost of this unit

⇒ Marginal Cost: The cost of one additional unit(or the cost of the last produced unit respectively)

Example

Marginal Cost and Market Supply:

Marginal cost (MC)of 4 producersW, X, Y & Z:

MC ($)W 5X 12Y 17Z 22

Supply of W, X, Y & Zat different prices:

Price Seller(s) QS

P ≥ 22 W, X, Y & Z 417 ≤ P < 22 W, X & Y 312 ≤ P < 17 W & X 25 ≤ P < 12 W 1

P < 5 0

Example

Marginal Cost and Market Supply:

Marginal Cost ofW, X, Y & Z:

$W 5X 12Y 17Z 22

0

5

10

15

20

0 1 2 3 4

P

Q

bc

bc

bc

bcbc

bc

bc

bc

MC of W

MC of X

MC of Y

MC of Z

bc

bc

bc

bc

Supply Curve

Producer Surplus

At any quantity, the price given by the supplycurve shows the cost of the marginal seller, theseller who would leave the market first if the pricewere any lower

Just as consumer surplus is related to the demandcurve, producer surplus is closely related to thesupply curve

Producer Surplus: The area below the price andabove the supply curve measures the producersurplus in a market

Producer Surplus

Producer Surplus with P = 12:

0

5

10

15

20

0 1 2 3 4

P

Q

bc

bc

bc

bc

Total Producer Surplus= Producer Surplus of W= 1× (12− 5) = 7

W

12

Producer Surplus

Producer Surplus with P = 17:

0

5

10

15

20

0 1 2 3 4

P

Q

bc

bc

bc

bc

Total Producer Surplus= Producer Surplus of W+ Producer Surplus of X= 1× (17− 5) + 1× (17− 12)= 17

WX

17

Producer Surplus

Producer Surplus with P = 22:

0

5

10

15

20

0 1 2 3 4

P

Q

bc

bc

bc

bc

Total Producer Surplus= Producer Surplus of W+ Producer Surplus of X+ Producer Surplus of Y= 1× 17 + 1× 10 + 1× 5 = 32

WX

Y

22

Effects of a price increase

P

Q

QS

Initial producer surplus

bc

bc

additional pro-ducer surplusto initialproducers

producersurplus tonew producers

Effects of a price increase

P

Q

QS

Total additionalproducer surplus

bc

bc

Equilibrium & Welfare

Demand and Supply Function

0

5

10

15

20

0 1 2 3 4

P

Q

bc

bc

bc

bc

MC W: 5

MC X: 12

MC Y: 17

MC Z: 22bc

bc

bc

bc

WtP A: 20

WtP B: 15

WtP C: 10WtP D: 7

MC: Marginal Cost WtP: Willingness to Pay

Equilibrium & Welfare

Free markets allocate the supply of goods to thebuyers who value them most highly

Free markets allocate the demand for goods tothe sellers who can produce them at least cost

Free markets produce the quantity of goods thatmaximizes the sum of consumer and producersurplus

Equilibrium & Welfare

P

Q

QS

QD

bcValueto

buyersCost toproducers

Value to buyersis greater thancost to sellers!

Cost toproducers

Value tobuyers

Value to buyersis less than

cost to sellers!

Equilibrium & Welfare

Consumer-surplus

=Value toconsumers

−Amount paidby consumers

Producer-surplus

=Revenue ofproducers

−Cost toSellers

TotalSurplus

=Value to

Consumers−

Cost toSellers

Equilibrium & Welfare

P

Q

QS

QD

Consu-mer surplus

Producersurplus

bc

Market efficiency is achieved whenthe allocation of resources

maximizes totalsurplus!

P∗

Q∗

Market Efficiency

Market outcome is often not efficient

⇒ Market failure: Examples includeMarket powerExternalitiesPublic goodsAsymmetric informationPrice regulation . . .

Apart from efficiency, a social planner might alsocare about equity: Fairness of the distribution ofwell-being among the various buyers and sellers

Welfare Effects of PriceRegulations

Welfare effects of price floors

Effects of a price floor: Pmin = 7

0

2

4

6

8

10

0 2 4 6 8 10 12 14 16 18

P

Q

7Pmin = 7

bc

Consumer surplus

Producer surplus

Dead-weightloss

Welfare effects of price ceilings

Effects of a price ceiling: Pmax = 4

0

2

4

6

8

10

0 2 4 6 8 10 12 14 16 18

P

Q

bc Pmax = 4

Producer Surplus

Consumer-surplus

Dead-weightloss

Price Regulation and Deadweight Loss

Notice: The total amount of the deadweight lossdepends on ...

how distant the price floor/ceiling is away fromthe equilibrium price, and

the slopes of demand and supply curves

An Application:

International Trade

International Trade

If a country is isolated from rest of the world(under autarky) domestic price adjusts to balancedemand and supply.

The sum of consumer and producer surplusmeasures the total benefits that buyers and sellersreceive.Can international trade further improve thissituation?

International Trade

If a country has a comparative advantage, thenthe domestic price will be below the world price,and the country will be an exporter of the good.

If the country has a comparative disadvantage,then the domestic price will be higher than theworld price, and the country will be an importer ofthe good.

Two Countries before International Trade

Consumer and producer surplus under autarky:

Country 1 Country 2P

Q

P

QCountry 2 has a comparative advantage in the production of thisgood, i.e., it can produce the good cheaper!

International Trade

Consumer and producer surplus with trade:

Country 1 (Importer) Country 2 (Exporter)P

Q

PW

Imports

bc bc

QS QD

P

Q

Exports

bc bc bc bc

QSQD

International Trade

Consumer and producer surplus with trade:

Country 1 (Importer) Country 2 (Exporter)P

Q

PW

Imports

Net-gain of

consumersurplus

bc bc

QS QD

P

Q

Exports

Net-gain ofproducersurplus

bc bc bc bc

QSQD

International Trade and Welfare

Consequences for importing countries:Domestic producers of the good are worse off, anddomestic consumers of the good are better off.If welfare of producers and consumers is equallyweighted trade raises the economic well-being of thenation as a whole.

Consequences for exporting countries:Domestic producers of the good are better off, anddomestic consumers of the good are worse off.Again, trade raises the economic well-being of thenation as a whole.

Trade Policy

Tariffs

Tariffs are taxes on imported goods.

Tariffs raise the price of imported goods above theworld price by the amount of the tariff.

A tariff reduces the quantity of imports and movesthe domestic market closer to its equilibriumwithout trade.

With a tariff, total surplus in the market decreasesby an amount referred to as a deadweight loss.

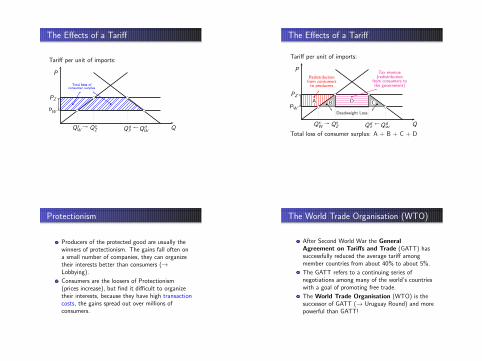

The Effects of a Tariff

Tariff per unit of imports:

P

Q

PW

QsW Qd

W

bc bc

PZ

QsZ Qd

Z

bc bc

bc bc

bc bc

Total loss ofconsumer surplus

The Effects of a Tariff

Tariff per unit of imports:

P

Q

PW

QsW Qd

W

bc bc

PZ

QsZ Qd

Z

bc bc

A

Redistributionfrom consumersto producers

D

Tax revenue(redistribution

from consumers tothe government)

B C

Deadweight Loss

bc bc

bc bc

Total loss of consumer surplus: A + B + C + D

Protectionism

Producers of the protected good are usually thewinners of protectionism. The gains fall often ona small number of companies, they can organizetheir interests better than consumers (→Lobbying).

Consumers are the loosers of Protectionism(prices increase), but find it difficult to organizetheir interests, because they have high transactioncosts, the gains spread out over millions ofconsumers.

The World Trade Organisation (WTO)

After Second World War the GeneralAgreement on Tariffs and Trade (GATT) hassuccessfully reduced the average tariff amongmember countries from about 40% to about 5%.

The GATT refers to a continuing series ofnegotiations among many of the world’s countrieswith a goal of promoting free trade.

The World Trade Organisation (WTO) is thesuccessor of GATT (→ Uruguay Round) and morepowerful than GATT!

The World Trade Organisation (WTO)

WTO Rules:

Non-discrimination: Under the ‘most favorednations clause’, any trade concession that onecountry makes one member must be granted to allsignatories.

Reciprocity: Any nation benefiting from a tariffreduction by another country must reciprocate bymaking similar tariff reductions itself.

Furthermore: General prohibition of quotas, Faircompetition, Binding tariffs.

Any questions?

Thanks!