Embed Size (px)

Citation preview

MODERN PRINCIPLES OF ECONOMICSThird Edition

Equilibrium: How Supply and Demand Determine Prices

Chapter 4

Outline

Equilibrium and the Adjustment Process A Free Market Maximizes Producer Plus

Consumer Surplus (the Gains from Trade) Does the Model Work? Evidence from the

Laboratory Shifting Demand and Supply Curves

2

Outline

Terminology: Demand Compared with Quantity Demanded and Supply Compared with Quantity Supplied

Understanding the Price of Oil

3

Definition

Equilibrium:

The price at which the quantity

demanded is equal to the quantity

supplied.

4

5

Equilibrium

equilibrium quantity

equilibrium price

Equilibrium

Equilibrium occurs at the intersection of the demand and supply curves.

Equilibrium price and quantity are the only ones that are stable in a free market.

At any other point, economic forces push prices and quantities back toward equilibrium.

6

Definition

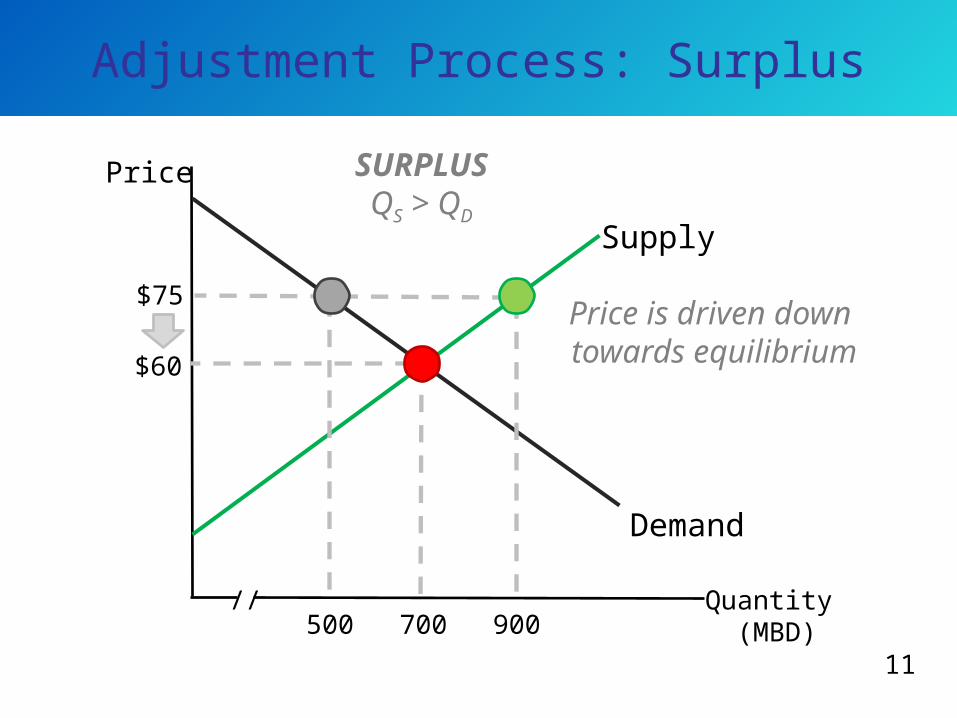

Surplus:

A situation in which quantity supplied

is greater than quantity demanded.

7

Adjustment Process: Surplus

Price

Quantity (MBD)

Supply

Demand

700

$60

//

8

Equilibrium

Adjustment Process: Surplus

Price

Quantity (MBD)700

$60

$75

500//

900

9

Supply

Demand

Price Above Equilibrium

Adjustment Process: Surplus

Price

Quantity (MBD)700

$60

$75

500//

900

10

Supply

Demand

QD = 500 QS = 900

SURPLUSQS > QD

Adjustment Process: Surplus

Price

Quantity (MBD)700

$60

$75

500//

900

11

Supply

Demand

SURPLUSQS > QD

Price is driven down towards equilibrium

12

Self-Check

When there is a surplus in a competitive market:

a. Price will increase.

b. Price will decrease.

c. Price will remain the same.

Answer: b – excess supply will causesuppliers to decrease price.

Definition

13

Shortage:

A situation in which quantity

demanded is greater than quantity

supplied.

Adjustment Process: Shortage

Price

Quantity (MBD)700

$60

$55

500//

900

14

Supply

Demand

Price Below Equilibrium

Adjustment Process: Shortage

Price

Quantity (MBD)700

$60

$55

500//

900

15

Supply

Demand

QS = 500 QD = 900

SHORTAGEQD > QS

Adjustment Process: Shortage

Price

Quantity (MBD)700

$60

$55

500//

900

16

Supply

Demand

Price is driven up towards equilibrium

SHORTAGEQD > QS

17

Self-Check

When there is a shortage in a competitive market:

a. Price will increase.

b. Price will decrease.

c. Price will remain the same.

Answer: a – excess demand will causeprice to increase.

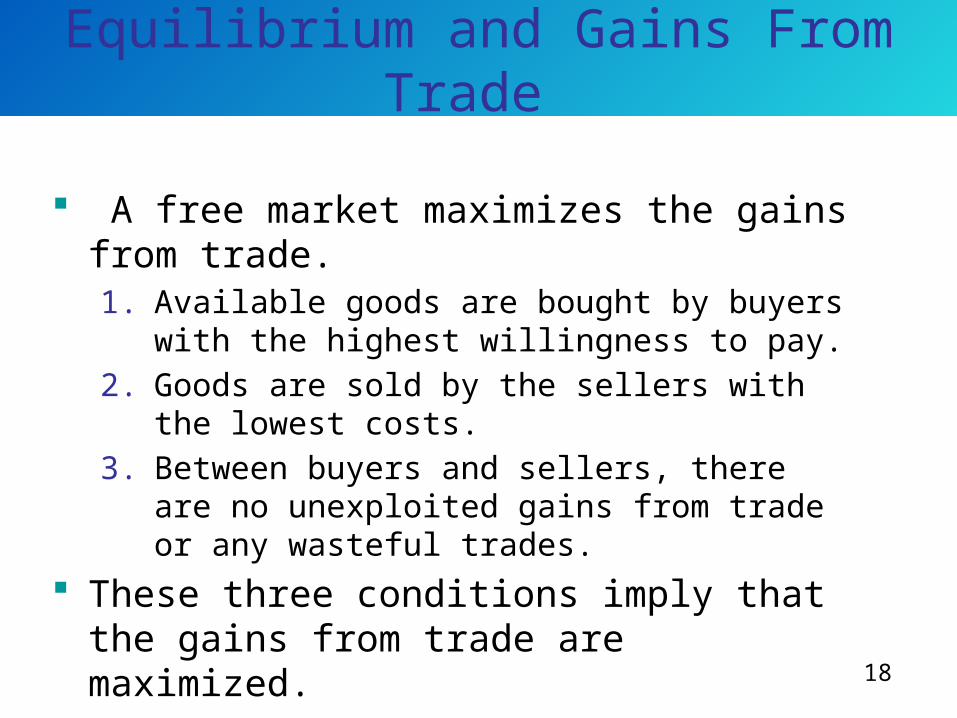

Equilibrium and Gains From Trade

A free market maximizes the gains from trade. 1. Available goods are bought by buyers with the

highest willingness to pay.

2. Goods are sold by the sellers with the lowest costs.

3. Between buyers and sellers, there are no unexploited gains from trade or any wasteful trades.

These three conditions imply that the gains from trade are maximized.

18

Buyers are willing to pay $90

Unexploited Gains From Trade

Price

Quantity (MBD)

Supply

Demand

70

$70

//

19

Suppose quantity is less than equilibrium

quantity (say 50)

50 90

$50

$90

Sellers are willing to supply for $50

Buyers are willing to pay $90

Unexploited Gains From Trade

Price

Quantity (MBD)

Supply

Demand

70

$70

//

20

50 90

$50

$90

Sellers are willing to supply for $50

Any trade between $50 and $90 will

make both parties better off

Unexploited gains from trade

Wasted Resources

Price

Quantity (MBD)

Supply

Demand

70

$70

//

21

Suppose quantity is greater than

equilibrium (say 90)

50 90

$50

$90

Sellers are willing to supply for $90

Buyers are only willing to pay $50

Wasted Resources

Price

Quantity (MBD)

Supply

Demand

70

$70

//

22

50 90

$50

$90

Sellers are willing to supply for $90

Buyers are only willing to pay $50

Sellers will not sell units they are losing

money on

Waste of resources

23

Self-Check

If the quantity traded is less than equilibrium quantity:

a. Resources will be wasted.

b. Suppliers will only supply goods at equilibrium price.

c. Some gains from trade will be lost.

Answer: c – some gains from trade will be lost.

Evidence from the Laboratory

In 1956, Vernon Smith tested the supply and demand model in a lab.

The model accurately and consistently predicted market behavior.

24

In 2002, Smith was awarded the Nobel Prize for establishing laboratory experiments as an important tool in economics.

J. SCOTT APPLEWHITE/AP PHOTO

Shifting Demand and Supply

Quantity

OriginalSupply

Demand

Price

Pa

Qa25

New Supply

Surplus

Supply increases

Creates surplus at original price

Shifting Demand and Supply

Quantity

OriginalSupply

Demand

Price

Pa

Qa26

New Supply

Competition drives price down

Surplus

Pb

Shifting Demand and Supply

Quantity

OriginalSupply

Demand

Price

Pa

Qa27

New Supply

New equilibrium at lower price, higher

quantity

PbLower price increases

quantity demanded

Qb

28

Self-Check

A decrease in supply will:

a. Increase both price and quantity.

b. Decrease price and increase quantity.

c. Increase price and decrease quantity.

Answer: c – lower supply causes a shortage, increasing price and causing consumers to buy less.

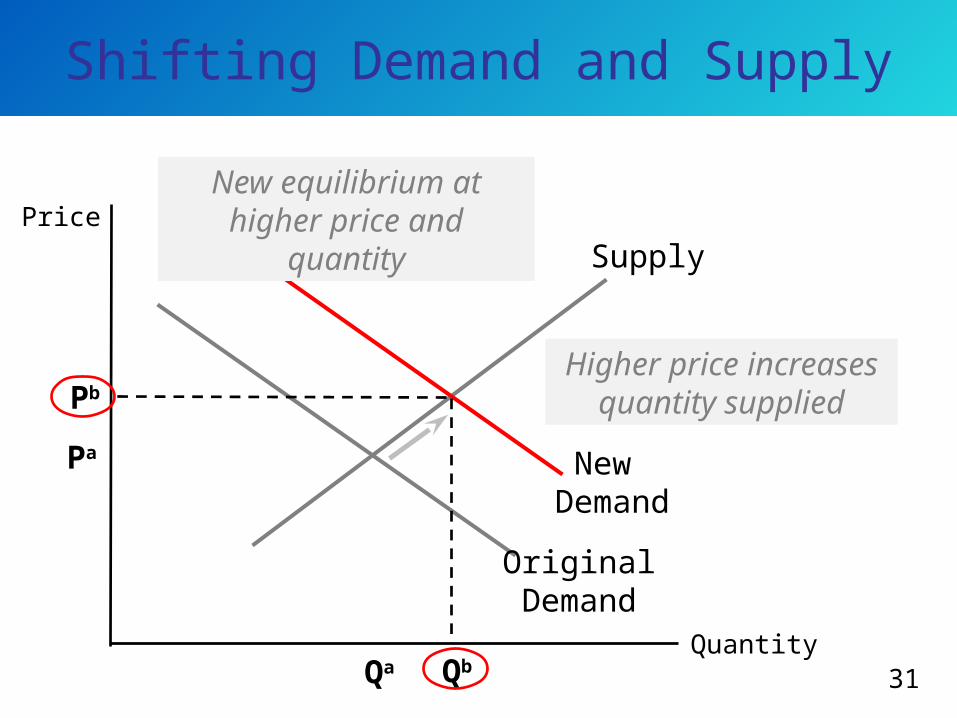

Shifting Demand and Supply

Quantity

Supply

OriginalDemand

Price

Pa

Qa29

Demand increases

Creates shortage at original price

New Demand

Shortage

Shifting Demand and Supply

Quantity

Supply

OriginalDemand

Price

Pa

Qa30

New Demand

Buyers bid prices up

Pb

Shifting Demand and Supply

Quantity

Supply

OriginalDemand

Price

Pa

Qa31

New Demand

Qb

Pb

New equilibrium at higher price and quantity

Higher price increases quantity supplied

32

Self-Check

A decrease in demand will:

a. Decrease both price and quantity.

b. Decrease price and increase quantity.

c. Increase price and decrease quantity.

Answer: a – lower demand causes a surplus, lowering prices and causing suppliers to supply less.

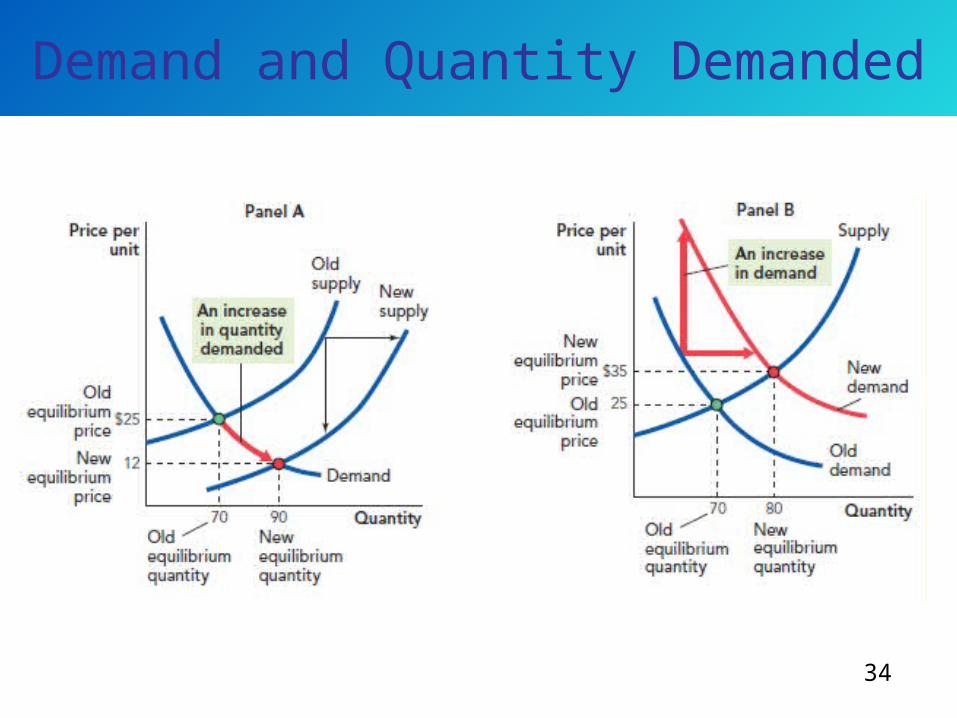

Demand and Quantity Demanded

There is a big difference between demand and quantity demanded.

A change in the quantity demanded is a movement along a fixed demand curve.

A change in demand is a shift of the entire demand curve (up and to the right).

33

Demand and Quantity Demanded

34

Supply and Quantity Supplied

A change in supply is a shift of the entire supply curve

A change in quantity supplied is a movement along a fixed supply curve.

35

Supply and Quantity Supplied

36

Understanding the Price of Oil

37The supply and demand model can explain oil prices.

38

Takeaway

We can use supply and demand to answer questions about the world.

Market competition brings about an equilibrium in which the quantity supplied is equal to the quantity demanded.

Only one price/quantity combination is a market equilibrium.

Incentives for both buyers and suppliers enforce the market equilibrium.

39

Takeaway

The sum of consumer and producer surplus (the gains from trade) is maximized at the equilibrium price and quantity.

Factors which shift supply or demand will change the equilibrium price and quantity.

A change in demand (or supply) shifts the whole curve.

A change in quantity demanded (or supplied) is a move to a different point on the existing curve.