Embed Size (px)

Citation preview

8/6/2019 Brazil Insurance_Goldman Sachs_Nov 2010

http://slidepdf.com/reader/full/brazil-insurancegoldman-sachsnov-2010 1/12

8/6/2019 Brazil Insurance_Goldman Sachs_Nov 2010

http://slidepdf.com/reader/full/brazil-insurancegoldman-sachsnov-2010 2/12

November 23, 2010 Brazil: Insurance: Multi-Line

Goldman Sachs Global Investment Research 2

3Q2010 review: Operations and financial income improve, driving bottom line

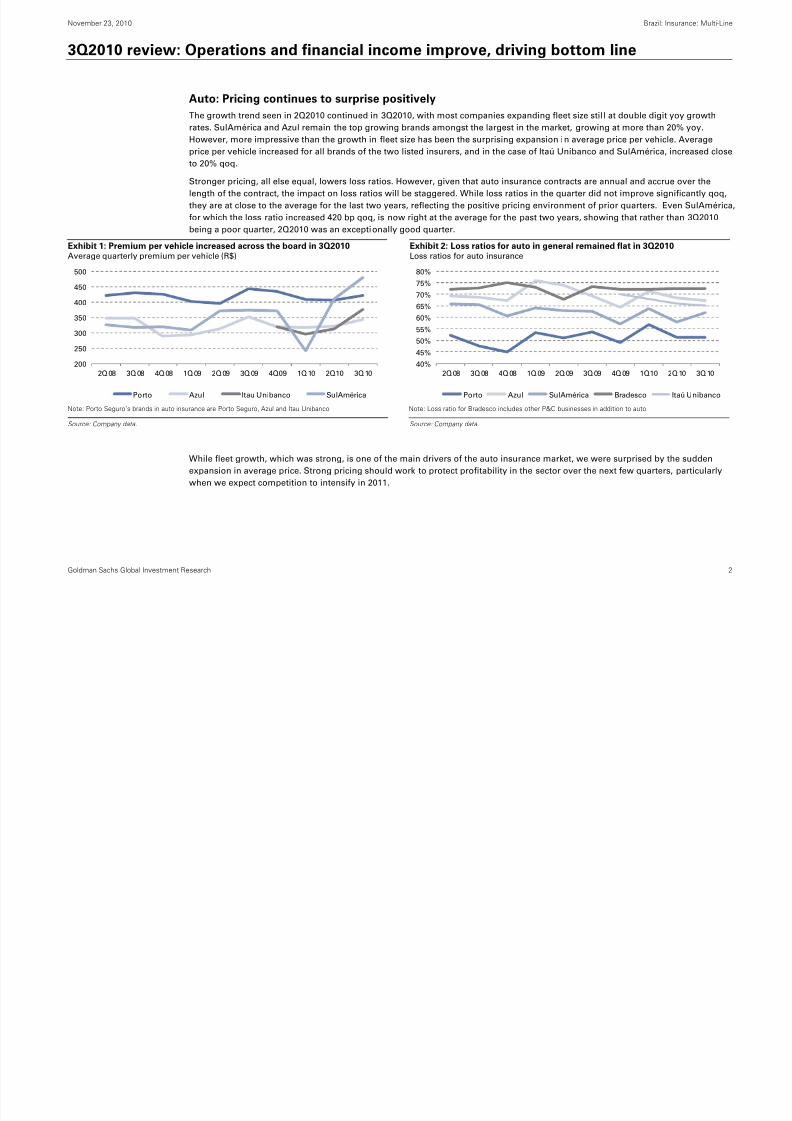

Auto: Pricing continues to surprise positivelyThe growth trend seen in 2Q2010 continued in 3Q2010, with most companies expanding fleet size still at double digit yoy growth

rates. SulAmérica and Azul remain the top growing brands amongst the largest in the market, growing at more than 20% yoy.

However, more impressive than the growth in fleet size has been the surprising expansion in average price per vehicle. Average

price per vehicle increased for all brands of the two listed insurers, and in the case of Itaú Unibanco and SulAmérica, increased close

to 20% qoq.

Stronger pricing, all else equal, lowers loss ratios. However, given that auto insurance contracts are annual and accrue over the

length of the contract, the impact on loss ratios will be staggered. While loss ratios in the quarter did not improve significantly qoq,

they are at close to the average for the last two years, reflecting the positive pricing environment of prior quarters. Even SulAmérica,for which the loss ratio increased 420 bp qoq, is now right at the average for the past two years, showing that rather than 3Q2010

being a poor quarter, 2Q2010 was an exceptionally good quarter.

Exhibit 1: Premium per vehicle increased across the board in 3Q2010Average quarterly premium per vehicle (R$)

Exhibit 2: Loss ratios for auto in general remained flat in 3Q2010Loss ratios for auto insurance

Note: Porto Seguro’s brands in auto insurance are Porto Seguro, Azul and Itau Unibanco Note: Loss ratio for Bradesco includes other P&C businesses in addition to auto.

Source: Company data. Source: Company data.

While fleet growth, which was strong, is one of the main drivers of the auto insurance market, we were surprised by the sudden

expansion in average price. Strong pricing should work to protect profitability in the sector over the next few quarters, particularly

when we expect competition to intensify in 2011.

200

250

300

350

400

450

500

2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10

Porto Azul Itau Unibanco SulAmérica

40%

45%

50%

55%

60%65%

70%

75%

80%

2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10

Porto Azul SulAmérica Bradesco Itaú Unibanco

8/6/2019 Brazil Insurance_Goldman Sachs_Nov 2010

http://slidepdf.com/reader/full/brazil-insurancegoldman-sachsnov-2010 3/12

November 23, 2010 Brazil: Insurance: Multi-Line

Goldman Sachs Global Investment Research 3

Health: Growth stronger, better loss ratio improves profitabilityYear-on-year growth in lives covered accelerated for both SulAmérica and Porto Seguro. For SulAmérica, the growth was once

again driven by SME (+5.9% qoq) and dental (+12.4% qoq), which now make up 32% of the total lives covered by the company in

group health insurance (up from 26% in 3Q2009). For Porto Seguro, the recovery of the portfolio continues after the restructuring

implemented in 2Q2009. Average premium per life also increased, though the effect was much more pronounced in individualhealth insurance (annual regulatory increase that took effect in the quarter) than in group health insurance.

The loss ratio for SulAmérica, both for group and individual health insurance, showed remarkable improvement in the quarter, and

was the lowest since 4Q2008. A part of the improvement was driven by the higher premiums, particularly on the individual health

side, but much was also a result of the company’s efforts to reduce frequency of utilization, particularly at hospitals. Loss ratios in

the remainder of the industry were flat to slightly up qoq.

Exhibit 3: Growth remained strong, almost 20% yoy across the boardYoy growth rate in number of lives covered (corporate plans)

Exhibit 4: SulAmerica’s loss ratio improved significantlyHealth loss ratio by quarter

Note: Figures for Bradesco are not pro- forma for the consolidation of Odontoprev in 1Q2010. Figures for

Amil include Amil only (not Medial), and are both for corporate and individual plans.

Note: Figures for Bradesco are not pro-forma for the consolidation of Odontoprev in 1Q2010.

Source: Company data. Source: Company data.

While growth was solid, the biggest surprise was the very strong improvement in SulAmérica’s loss ratio. We do not expect the

improvement to be fully sustainable (as costs in individual health increase throughout the year, some margin will be eroded), andthe loss ratio to track slightly closer to 80%. However, it does set the company well for the next few quarters, helping to support

profitability.

-40%

-20%

0%

20%

40%

60%

80%

100%

2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10

SulAmérica Bradesco Porto Seguro Amil

60%

65%

70%

75%

80%

85%

90%

95%

2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10

Porto SulAmérica Bradesco Amil

8/6/2019 Brazil Insurance_Goldman Sachs_Nov 2010

http://slidepdf.com/reader/full/brazil-insurancegoldman-sachsnov-2010 4/12

November 23, 2010 Brazil: Insurance: Multi-Line

Goldman Sachs Global Investment Research 4

Other categories: Good growth, but limited relevancePremiums for life insurance (both personal accident and traditional life) showed good growth at both Porto Seguro and SulAmérica.

Even though they failed to gain relevance in the product mix for either company, the fact that they are not losing share while other

lines are reporting strong growth is encouraging. One trend in the quarter, which was much more visible for the large banks that

dominate this market, was that loss ratios in life insurance increased significantly qoq, although it is not clear why that happened.

Homeowners insurance, which in our view has more short to medium term potential, also grew in line with other products for both

companies.

Exhibit 5: Personal insurance did not gain relevance for either company…Personal insurance earned premiums as a % of total earned premiums

Exhibit 6: …And neither did other P&C insuranceOther P&C insurance earned premiums as a % of total earned premiums

Source: Company data. Source: Company data.

0%

1%

2%

3%

4%

5%6%

7%

2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10

Porto Seguro SulAmérica

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10

Porto Seguro SulAmérica

8/6/2019 Brazil Insurance_Goldman Sachs_Nov 2010

http://slidepdf.com/reader/full/brazil-insurancegoldman-sachsnov-2010 5/12

November 23, 2010 Brazil: Insurance: Multi-Line

Goldman Sachs Global Investment Research 5

Operational efficiency solid, but financial income is big earnings driverOperational efficiency, as measured by the combined ratio, improved for both Porto Seguro and SulAmérica. The reasons for the

improvement were different for the two companies, however:

For Porto Seguro, the improvement in the combined ratio was driven by low growth in admin expenses, which led the admin

expense ratio to decline 90 bp qoq. This compensated for a 40 bp qoq increase in the selling expense ratio and a 20 bp qoq

increase in the loss ratio.

For SulAmérica, the improvement was driven by a 420 bp qoq decline in the loss ratio, largely a result of the lower claims in

health insurance. This offset a 10 bp qoq increase in the selling expense ratio and a 90 bp qoq increase in the admin expense

ratio.

Both companies, however, reported significantly higher financial income. This helped the extended combined ratio improve by an

average 350 bp qoq. Companies reported an average yield on invested assets of 118% of the base rate, up from 95% in 2Q2010.

Exhibit 7: Combined ratios improved for Porto Seguro and remained flat forSulAméricaCombined ratios by quarter

Exhibit 8: The extended combined ratio did not improve as significantly asfinancial results were lowerExtended combined ratios by quarter

Note: Combined ratio for Bradesco includes more profitable pension and life insurance businesses. Note: Combined ratio for Bradesco includes more profitable pension and life insurance businesses.

Source: Company data. Source: Company data.

80%

85%

90%95%

100%

105%

110%

2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10

Porto SulAmérica Bradesco

60%

65%

70%

75%80%

85%

90%

95%

100%

2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10

Porto SulAmérica Bradesco

8/6/2019 Brazil Insurance_Goldman Sachs_Nov 2010

http://slidepdf.com/reader/full/brazil-insurancegoldman-sachsnov-2010 6/12

8/6/2019 Brazil Insurance_Goldman Sachs_Nov 2010

http://slidepdf.com/reader/full/brazil-insurancegoldman-sachsnov-2010 7/12

8/6/2019 Brazil Insurance_Goldman Sachs_Nov 2010

http://slidepdf.com/reader/full/brazil-insurancegoldman-sachsnov-2010 8/12

November 23, 2010 Brazil: Insurance: Multi-Line

Goldman Sachs Global Investment Research 8

Key risksKey risks include changes in expected interest rates (insurance companies derive a significant part of their net income from

investing their reserves, and lower expected interest rates could lead to lower financial income, and vice versa), regulation (health

insurance is a highly regulated business), slower than expected economic growth (affecting real wages and, as a consequence,

demand for insurance products), competition (aggressive competitors that may target market share at the expense of margin,particularly in auto insurance), and concentration of claims (heavy rains and floods in the summer in Brazil typically lead to higher

loss ratios in auto insurance).

8/6/2019 Brazil Insurance_Goldman Sachs_Nov 2010

http://slidepdf.com/reader/full/brazil-insurancegoldman-sachsnov-2010 9/12

8/6/2019 Brazil Insurance_Goldman Sachs_Nov 2010

http://slidepdf.com/reader/full/brazil-insurancegoldman-sachsnov-2010 10/12

8/6/2019 Brazil Insurance_Goldman Sachs_Nov 2010

http://slidepdf.com/reader/full/brazil-insurancegoldman-sachsnov-2010 11/12

8/6/2019 Brazil Insurance_Goldman Sachs_Nov 2010

http://slidepdf.com/reader/full/brazil-insurancegoldman-sachsnov-2010 12/12