Embed Size (px)

DESCRIPTION

BIQ issue listing 2011 Q3 Numbers

Citation preview

FLORIDA’S HURRICANESThe new agreements allowing reinsurers headquartered in Bermudato safeguard Florida’s homes, businesses and other property againstthe biggest natural peril in the United States. See page 6

‘BUSINESS-FRIENDLY’PREMIER

ALL THERESULTS &ANALYSIS

BERMUDAWINS AKEY ROLE

12

4

2BERMUDAINSURANCEQUARTERLY© 2011 Bermuda Media in association with

Q3BIQ21764F_BIQ_.qxd:ps 12/22/10 8:55 AM Page 1

“ When you want to protect your wealth for future generations, trust the people who’ve been doing just that for generations.”Joel P. Schaefer, CFA — President & CEO, Capital G Investments Limited

[email protected] Reid Streetcapitalgprivatebanking.bm

To learn more, please contact us:

Since the 1930s, the Gibbons family and Capital G have taken an innovative and personalised approach to managing wealth. And year after year, Capital G’s team of Chartered Financial Analysts builds on that experience with new ideas for meeting your unique needs. The result is a proprietary investment process, implemented through top-tier fund managers such as JP Morgan, Vanguard and Schroders. Our integrated wealth management solutions are delivered with the same high level of service we have proudly provided discerning individuals for decades. At Capital G, our legacy is protecting your legacy.

Capital G Bank Limited and its wholly owned subsidiaries are licensed to conduct Banking, Trust and Investment Business by the Bermuda Monetary Authority.

21764F_BIQ_.qxd:ps 12/15/10 2:10 PM Page 2

“In the third quarter we gen-erated an annualised operat-ing return on average com-mon equity in excess of 11percent, and grew our bookvalue per share by over sixpercent, with solid under-writing profits and strongtotal returns in our invest-ment portfolio contributing to our book valuegrowth. Our results reflect … a quiet season forland-falling US hurricanes, offset in part by$73.6 million of net negative impact from theNew Zealand earthquake.”

— Neill Currie, CEO of Renaissance Re

“ACE had a very strong thirdquarter with good earningscontributions from all of ourprincipal businesses … Basedon our strong results … andpositive outlook for thefourth quarter, we are raisingour full year 2010 operatingearnings guidance from $6.25to $6.75 per share to $7.20 to $7.40 per share.”

— Evan Greenberg, ACE Chairman and CEO

“For the first nine months of2010 we produced an annu-alised operating return onaverage common equity of11.3 percent which we viewas healthy given currentproperty and casualty insur-ance and reinsurance marketconditions, the low invest-ment yield environment and the global catastro-phe activity this year.”

— John Charman, CEO and President ofAXIS Capital

“We are extremely pleasedwith Standard & Poor’s(S&P) actions. XL has takensignificant steps to concen-trate on our core insuranceand reinsurance businesseswhile derisking our invest-ment portfolio and strength-ening our ERM. It is gratifying to have theseefforts acknowledged by S&P.”

— Mike McGavick, CEO of XL Group, afterrating agency S&P revised its outlook on the

company from “negative” to “stable”

BERMUDA INSURANCEQUARTERLY

EditorRichard Whitaker

Art DirectorPaul Shapiro

Contributing EditorChris Gibbons

Director of MarketingLissa Fisher

PublisherIan Coles

Published by Bermuda Media, Suite310, The International Centre, 26Bermudiana Road, Hamilton HM 11,Bermuda. Postal address: PO Box HM2032, Hamilton HM HX, Bermuda. Tel:292-7279 Fax: 295-3189 Email:[email protected]. Web: bermudamedia.bmPrinted in Canada.

Published four times a year in associa-tion with PricewaterhouseCoopers.

Cover image: istockphoto.com

BIQ

Bermuda insurers and reinsurersare likely to struggle through2011 against a backdrop of a

continuing soft market and fallingnet incomes, according to a reportby rating agency A M Best thatsays the market may not yet havereached the bottom of the cycle.

In the report, Favourable ResultsConceal Looming Concerns forBermuda’s Reinsurers, Best said Q3results for the 18 publicly-tradedcompanies rated by the agency,showed falling net premiums writ-ten and net earned premiums,investment income down, risingloss and expense ratios and returnon equity sharply lower.

“A M Best continues to see morechallenges than opportunities aspricing pressures persist, investmentportfolios lack sufficient yield, andloss reserve releases — which aremasking the symptoms — are like-ly drying up,” said the report.

The large volume of catastro-phes had not been enough to force

better pricing up, said Best, andnoted that even in Chile, followingthe February earthquake, priceincreases had not been enough toreflect the actual risk involved.

Best said the fundamentals wereso weak that investors were shun-ning the market and companieswere mostly trading for less thanbook value. While ACE was tradingat a ratio of 1.01 times its book value(as of December 3), XL was valuedat 0.67 times book, PartnerRe at0.76 and Everest at 0.75, accordingto Thomson Reuters data.

Best said that to survive, com-panies needed to preserve capitaland position themselves for the

next turn in the market — and saidthat made conditions ripe formergers and acquisitions.

In a separate report, NationalUnderwriter said that of the 16Bermuda companies it routinelytracked, net income drops were inthe 20–50 percent range, largelydue to the New Zealand earth-quake and other smaller events.

National Underwriter reportedthat RenaissanceRe Holdings had$73.6 million of net negativeimpact in the third quarter fromthe quake. Validus Holdingsexpects about $28.7 million inlosses, and Argo Group Inter -national about $11.3 million.

AXIS Capital Holdings, despite$85 million in net losses from thequake, made $248.1 million in netincome for the third quarter com-pared to a loss of $86.7 millionduring Q3 2009.

The magazine said the AXISresults, along with an earningsjump for XL Group, lowered thegroup results to a nine percentdrop in net income, but the overallincome drop was 24 percent forthe remaining 14 companies.

In year-to-date figures, NU saidonly Alterra, Arch Capital, AXIS,XL and Allied World had improv-ing year-to-date net income com-pared to results as of September 30last year. Only Alterra improved itscombined ratio to 86.1 from 90.5in 2009. It said year-to-date resultshad been impacted by catastropheslike the Chilean earthquake,storms in Australia, windstormXynthia in Europe, US winterstorms and the BP DeepwaterHorizon disaster.

THE QUOTES OF THE QUARTER

V o l u m e 7 , N u m b e r 1J a n u a r y 2 0 1 1

Still tough times ahead for Bermuda firmsCOMPANIES URGED TO PRESERVE CAPITAL AFTER SERIES OF CATASTROPHES IMPACTS YEAR-TO-DATE RESULTS

‘More challenges than opportunities aspricing pressures persist, investmentportfolios lack sufficient yield, and lossreserve releases — which are maskingthe symptoms — are likely drying up’

[ 1 ]

21764F_BIQ_.qxd:ps 12/15/10 2:10 PM Page 1

NEWS REVIEW

You won’t get any Bermuda rein-surance CEOs to say it publicly,but few were sorry to see the

back of Premier Dr Ewart Brownwhen he stepped down in Octoberafter four years in the job.

Dr Brown’s often confronta-tional leadership style won himfew friends in the international

business sector and controversialpolicies such as work permit termlimits further soured the relation-ship with industry executives.

Business leaders are optimisticthat the relationship with Govern -ment will be much improved underhis successor, Paula Cox.

“It’s early days but it already

seems like a lot of the tension thathad built up has gone,” said onesenior executive who asked not tobe named. “With Dr Brown wefelt we were being talked at andtolerated, rather than a partner in arelationship that is crucial to theIsland’s economy and quality of life.

“We’re optimistic that PaulaCox is someone with whom we canhave a sensible discussion on theissues. We might not always agreebut at least she has a good under-standing of the industry and weexpect our discussions to be moreconstructive.”

The new Premier was a legalcounsel with ACE Limited untilshe became Premier following herelection as leader by the Pro gressiveLabour Party. She retains her posi-tion as Finance Minister — a postformerly held by her late fatherEugene Cox — while her brotherJeremy Cox is CEO of the BermudaMonetary Authority that regulatesthe insurance industry in Bermuda.

A recent Florida newspaperreport critical of the Island’s rein-surance business, said the family’sconnections and close ties with thesector “blurred” the lines betweenregulator and regulated. Industryadvocates say those types of closerelationships are precisely whatmakes Bermuda so successfulbecause there is a greater under-standing of how the business works.

Paula Cox has already statedthat the work term limit policy —which she introduced and calls“firm but fair” — will not changeany time soon.

Indeed it may be that the poli-cy’s impact may be less than feared.Figures released by new Economy,Trade and Industry Minister KimWilson in November, showed that

Market leaders are cautiously CHRIS GIBBONS DISCOVERS WHY INDUSTRY LEADERS HAVE WELCOMEDTHE APPOINTMENT OF ‘BUSINESS-FRIENDLY’ PAULA COX

Premier and Finance MinisterPaula Cox

‘It already seemslike a lot of thetension that hadbuilt up has gone’

[ 2 ]

21764F_BIQ_.qxd:ps 12/15/10 2:11 PM Page 2

NEWS REVIEW

only 30 percent of 6,817 activework permits were subject to thesix-year term limit. Waivers hadbeen granted to 35 percent, whileanother 35 percent had beengranted extensions.

Critics say the policy portraysBermuda as hostile to foreign work-ers and makes it harder and moreexpensive to attract talented andexperienced employees to the Island.

However business leaders werepleased to see the new Premierextend the tax exemption guaran-tee for international companies,ending uncertainty caused by aperceived lack of commitment to itunder Dr Brown.

In a recent interview with TheRoyal Gazette, Evan Greenberg,CEO of ACE Limited, said it wasimportant Government recognisedthat Bermuda’s reinsurers werecompeting in a global economy.

“As a company in a marketeconomy we have to constantlyremake ourselves. I wake up everyday knowing that we have to berelevant or we disappear. Bermudaneeds to be informed and shouldbe informed by the same, in orderto remain relevant. You need to beattractive to business and thatmeans you’ve got to be competitive.

“Generally that involves anenlightened regulatory environ-ment, an infrastructure that iscost-competitive and a bureaucra-cy that is not overly burdensome.Also that it’s clear in the way it’sorganised that it wants to attractand retain business, that business isnot a source of evil. I’m not surethat message is always clearlyunderstood.”

As he pointed out, companieslike ACE, with operations aroundthe world, have plenty of optionsto improve their efficiency andcompetitiveness. Exercising thosehas already led several Bermuda-based companies to redomiciletheir holding companies in placeslike Switzerland. All claim to stillbe committed to Bermuda andretain significant operations herebut that is not guaranteed as mar-ket conditions continue to gettougher and companies cut costs

— ACE itself is to cut 17 jobs inBermuda as a result of consolidat-ing some operations to Phil -adelphia (see page 17).

In a December 3 editorial, theGazette said the Governmentshould heed Mr Greenberg’sadvice and called for a return to the“Bermuda Inc” model that helpedmake the local market such a suc-cess story over the past 25 years.

PartnerRe’s new CEO CostasMiranthis, when asked during an

interview with Bermuda InsuranceQuarterly what Bermuda could learnfrom Switzerland, where his com-pany has long had a presence, notedthat the Swiss “have always beenpro-business and pragmatic howthey deal with the business commu-nity. It has always been a very busi-ness-friendly environment.”

Bermuda’s CEOs hope that inPaula Cox they have a business-friendly Premier who can lead byexample.

optimistic about new Premier ‘We might notalways agree but at least she has a goodunderstanding of the industryand we expectour discussionsto be more constructive’

[ 3 ]

21764F_BIQ_.qxd:ps 12/15/10 2:11 PM Page 3

NEWS REVIEW

Bermuda wins key regulatory appointment

Bermuda — through theBermuda Monetary Authority(BMA) — has been appointed

Chairman of the influentialInsurance Groups and Cross-sec-toral Issues Subcommittee (IGSC)of the International Association ofIn surance Supervisors (IAIS).

The IGSC is the body that willset international regulatory stan-dards for global insurance compa-nies. Financial regulators around theworld set their national insuranceregulations based on IAIS standards.

Craig Swan, Director of Policy,Research and Risk Assessment atthe Bermuda Monetary Authority,and the leader of the team buildingBermuda’s group supervisionframework, will chair the IGSC.

The IGSC is responsible fordrafting Insurance Core Principle23, the international standards andguidance that relate specifically togroup-wide supervision. It alsoserves as liaison between the IAISand the Joint Forum, an interna-tional body focused on issues com-mon to the banking, securities andinsurance sectors, including the reg-ulation of financial conglomerates.

The Joint Forum comprisesmembers of the IAIS, the Inter -national Organisation of SecuritiesCommissioners, and the BaselCommittee of Banking Super -visors, representing the interna-

tional standard setters for theinsurance, securities and bankingindustries, respectively.

BMA CEO Jeremy Cox saidthe appointment was an opportu-nity for Bermuda to extend itscontribution to the IAIS andenhance its reputation as a respon-sible and increasingly influentialjurisdiction.

In addition to being a memberof the IAIS Executive Committee,the Authority also chairs theIAIS’s Reinsurance TransparencySubcommittee. It also has repre-sentatives on nine other IAIScommittees and/or subcommitteescovering areas such as actuarial andsolvency matters, accounting stan-dards and corporate governance.

Mr Cox said Mr Swan hadalready contributed significantly tothe development of the Groups’framework, both in Bermuda andat the IAIS level. “Given theimportance of the Groups’ initia-tive to the IAIS, I thought itappropriate for us to put forwardhis name to lead the IGSC.

“The IGSC plays a key role inshaping international standards asthey relate to insurance groups andto the regulation of financial con-glomerates. As we have seen fromthe recent financial crisis, this levelof oversight has become vital toeffective regulation globally. TheIGSC has a very full and impor-tant agenda over the next couple ofyears, and the Authority looks for-

ward to contributing and provid-ing leadership to this group in thisnew capacity.”

Commenting on the appoint-ment, Mr Swan said: “As a leadingrisk-based financial services regu-lator, the Authority has been fullyengaged with the internationalregulatory environment for sometime now. This has allowed us tonot only keep abreast of the rapidchanges in financial regulation, butalso to contribute to standards asthey are being developed. I wel-come the opportunity to act aschair of the IGSC, and to provideinput on the significant issues thatthe Committee is mandated toaddress in its work.”

The IAIS was established in1994 and Bermuda was a foundingmember. It represents insuranceregulators and supervisors of some190 jurisdictions in nearly 140countries and has also more than120 insurance professionals, insur-ers, reinsurers and trade associa-tions as observers. The IAIS issuesglobal insurance principles, stan-dards and guidance papers, pro-vides training and support onissues related to insurance supervi-sion, and organises meetings andseminars for insurance supervisors.The IAIS works closely with otherinternational institutions to pro-mote financial stability.

[ 4 ]

Allied World offers $300 million in senior notesAllied World Assurance Company Holdings Ltdhas announced that it has priced an offering of$300m aggregate principal amount of seniornotes due 2020. The senior notes will bearinterest at an annual rate of 5.50 percent peryear and were priced to yield 5.56 percent. Netproceeds from the offering will be used for gen-eral corporate purposes, including the repur-chase of their outstanding common shares.

In a separate announcement in November,Allied World reported that it had entered intoan agreement to repurchase the remainder ofits securities held by certain GS CapitalPartners and other investment funds which areaffiliates of the Goldman Sachs Group Inc and

founding shareholders of Allied World.The securities consist of 3,159,793 com-

mon shares and warrants to purchase anadditional 1,500,000 common shares. Theaggregate repurchase price for the securitieswill be $222.6 million, of which $185.4 millionwill be for the repurchase of the commonshares and $37.2 million will be for the repur-chase of the warrants.

Meanwhile, Bermuda-headquartered ValidusHoldings Ltd is to buy-back around $300 mil-lion in common shares. The buy-back for up to7,945,400 of its common shares at a price of$30 per share, was due to be by tender.

Validus also entered into separate repur-

chase agreements with funds affiliated with ormanaged by each of Aquiline Capital PartnersLLC, New Mountain Capital LLC and VestarCapital Partners to purchase 2,054,600 com-mon shares in the aggregate at the same pershare price as the tender offer, for an aggregatepurchase price of approximately $61.6 million,subject to completion of the tender offer.

As a result of these transactions, Validusexpects to repurchase an aggregate of 10 mil-lion common shares – that’s in addition to the$629 million of common shares repurchasedthrough November 3, 2010 under a previouslyauthorised share repurchase programmeannounced in February 2010.

JEREMY COX: APPOINTMENT ENHANCES ISLAND’S REPUTATION AS A RESPONSIBLE AND INFLUENTIAL JURISDICTION

Craig Swan: chair of influentialsubcommittee

Jeremy Cox: appointmentboosts Bermuda’s reputation

21764F_BIQ_.qxd:ps 12/22/10 8:47 AM Page 4

NEWS REVIEW

Solvency II head reassures business leaders

[ 5 ]

Karel Van Hulle, the manresponsible for developingSolvency II, said he was hope-

ful that Bermuda would achieveequivalency with the EuropeanUnion’s controversial new insur-ance regulations due to be imple-mented in 2013.

The proposed risk-based regu-latory framework, which willdemand that companies writingbusiness in Europe have more cap-ital and be subject to more strin-gent corporate governance andtransparency requirements, is like-ly to have a big impact on themany Bermuda reinsurers whooperate in Europe.

The Bermuda Monetary Auth -ority (BMA), which regulates theinsurance industry in Bermuda,has been working hard for someyears to ensure that Bermudameets equivalent standards.

Mr Van Hulle, Head of theInsurance and Pensions Unit in the

European Commission, was guestspeaker at the Bermuda InsuranceInstitute Christmas networkinglunch at the Fairmont HamiltonPrincess. The Royal Gazette report-ed that Mr Van Hulle had beenhappy to speak to show the EU’s“appreciation for the great efforts”made by the BMA. He said hehoped Bermuda’s equivalencyassessment would be concluded“with success.”

During his speech Mr VanHulle said the emphasis ofSolvency II was not so much capi-tal requirements but sound riskmanagement. “What is importantis that companies who are expert inhandling risks do so to the higheststandards,” he said.

And in a second address thesame day, he said it was notEurope’s intention to impose a reg-ulatory framework on the rest ofthe world. “What the world needsto do is create a fully risk-based sol-

vency standard. That’s somethingwe are doing in Europe and you inBermuda have also decided that it’sthe right thing to do.”

He said progress had beenmade in discussions with captiveinsurers. Industry leaders in Ber -muda — the world’s largest captive

domicile — have argued that cap-tives, which underwrite the risks ofparent companies, should not besubject to the same rules as insur-ers covering third party risks.

Mike McGavick, CEO of XLGroup, said the regulations wouldfavour larger insurers and forcesmaller, often more innovativecompanies out of the market. Hesuggested that had the US restruc-tured its regulations 25 years ago,Bermuda’s alternative risk marketmight never have got off theground.

“We need to make sure thatregulatory competition is still partof the world in which we do busi-ness, not one group of countriesimposing its set of rules, and with-drawing its market if those rulesare not followed,” he said.

Mr Van Hulle disagreed, sayingthat many smaller companies werevery efficient and would benefitfrom the new rules.

Karel Van Hulle: responsible fordeveloping Solvency II

21764F_BIQ_.qxd:ps 12/15/10 2:11 PM Page 5

The Florida Office of InsuranceRegulation (FOIR) has announ -ced agreements with three Ber -

muda-based reinsurers to participatein Florida’s insurance marketplaceunder modified regulatory terms.

In a statement, the FOIR saidAce Tempest Reinsurance Ltd(Ace Tempest Re), Hiscox In -surance Company (Bermuda) Lim-ited and PartnerRe would be allowedto post reduced collateral whileconducting business in the state.

Florida passed legislation in2007 allowing the FOIR to estab-lish lower collateral requirementsfor non-US reinsurers that arehighly rated and financially sound.It has now authorised six reinsur-ance companies to operate inFlorida under modified terms.Hannover Re, Hannover Insur ance(Bermuda) and XL Re Ltd wereauthorised earlier this year. USreinsurers are not required to postcollateral.

“Florida has played a key role inmodernising the US reinsurancemarket,” said Insurance Comm -issioner Kevin McCarty. “Thesecollateral agreements are intendedto encourage additional invest-ment in Florida’s property insur-ance marketplace.”

The agreements underline theimportance of Bermuda’s reinsur-ance companies to Florida in thewake of a widely publicised articlein the Sarasota Herald-Tribunethat was highly critical of theIsland’s industry. The two-partarticle in October accused them ofprofiteering from the 2004 and

2005 hurricanes that hit the state,by doubling or tripling their ratesand reducing capacity for Floridastorm coverage.

Brad Kading, President andExecutive Director of the Ass -ociation of Bermuda Insurers andReinsurers (ABIR), hit back in asubsequent comment piece carriedby the Herald-Tribune, pointingout that 60 percent of the $59 bil-lion in payments resulting fromHurricanes Katrina, Rita andWilma in 2005 were paid by for-eign insurers and reinsurers —most of them based in Bermuda.

He wrote: “With more than 60percent of the wind risk of theentire United States, Florida faceshuge challenges to insuring itshomes, businesses and other prop-erties. Insurance companies inFlorida purchase backup insurance— reinsurance — to diversify theserisks into the global private mar-kets. We are proud that much ofthis reinsurance to safeguardFlorida’s home and businessescomes from companies headquar-tered in Bermuda.”

He said no Bermuda-basedreinsurer had ever been unable topay Florida catastrophe claims.

“Bermuda reinsurance compa-nies are reliable responsive partnersfor Floridians and others in needof reinsurance around the globe.Seventeen Bermuda-based rein-surers together have 37 percent ofthe world’s property and casualtyreinsurance market, according toA M Best. In addition, there hasnever been an insolvency among

the companies that are members ofthe ABIR.”

In response to the Herald-Tribune claim that Bermuda’sindustry regulation was “famouslylight,” Mr Kading said it was“robust and sophisticated, focusingon cutting-edge practices in risk-based capital adequacy” and point-ed out that the Bermuda MonetaryAuthority, the industry’s regulatorybody, was “a well-respected quasi-government agency staffed bycareer professionals and similar tosome federal financial regulatoryagencies in the United States.”

He said the effectiveness ofBermuda’s regulatory system hadbeen recognised by the Inter -

national Monetary Fund and thatthe Florida Insurance Departmenthad a legal cooperation and legalinformation-sharing agreementwith the BMA.

“Florida hurricanes are thebiggest natural peril in the UnitedStates. Self-insuring this risk with-in Florida, particularly by depend-ing on post-event assessments fromFlorida’s small businesses and con-sumers, would be bad public policyand unsound risk management.”

He concluded: “ABIR and itsmembers will continue to con-tribute their capital, solutions, mit-igation technologies and best ideasto support a safer, stronger, moresustainable Florida.”

Florida agreementsunderline key role ofBermuda reinsurersKADING: NO BERMUDA-BASED REINSURER HAS EVER BEEN UNABLE TO PAY FLORIDA CATASTROPHE CLAIMS

NEWS REVIEW

[ 6 ]

‘Bermuda reinsurance companies are reliable responsive partners for Floridians’

A linesman in Orlando repairs lights damaged by Hurricane Charley in 2004. The storm was the second major hurricane of the season

21764F_BIQ_.qxd:ps 12/15/10 2:11 PM Page 6

reduce cost increase capability control risk

Contact: Ben Barlaba

Email: [email protected]

Phone: 441.296.9625

www.logic.bm/business

Global Connectivity and Managed Services

Logic is Bermuda’s leading provider of data connectivity and IT managed services.

What makes us different? Redundancy, reliability and more than a decade of experience. We offer:

• Presence in Bermuda, Cayman Islands, North America and Europe

• Three undersea data cables

• Seven data centers

• Next generation MPLS network

• 24/7/365 support for clients on five continents

Logic Communications Ltd. • 30 Victoria Street • Hamilton HM 12, Bermuda

CEO CIO COO

21764F_BIQ_.qxd:ps 12/15/10 2:11 PM Page 7

PROFILE

Succeeding the highly respected CEO of theworld’s fourth largest reinsurer might seemthe industry equivalent of following Sir Alex

Ferguson as manager of Manchester United.But when Costas Miranthis steps into

Patrick Thiele’s shoes when he retires in Januaryafter 10 years in the job, he is confident that hecan keep PartnerRe among the industry leaders.

After all, the 47-year-old takes over a stablefranchise in excellent shape despite the softmarket and global financial doldrums. Netincome in the third quarter was a very healthy524.9 million and at $80.18, the firm’s shareprice was up 7.4 percent for 2010 and 4.2 per-cent compared to Q3 2009. The company’sassets stood at $23.7 billion at December 31,2009 following the acquisition of PARIS RE.

“The fact that the company is successfulmakes my job easier in some respects,” acknowl-edged Mr Miranthis. “I don’t have a lot ofthings to fix or fires that I need to put out. Butthere are some risks there too. We’ve comethrough a long period where things have beensuccessful. You can become complacent and it’simportant to always guard against that.

“The world is changing and we’re in a muchtougher environment than we have been for thepast six or seven years. We need to evolve toaddress those changes. In a subtle way, it is a lit-tle more difficult to have to tell people they haveto keep changing. But if you stand still, you’velost the game.”

That philosophy also ensures that MrMiranthis is not concerned with measuring hisperformance against the past. “Sometimes, ifyou take on something that’s successful, no matterhow successful you are, it may not be perceivedas such. I’m not going to change what I do becauseI worry about what is perceived as personal success.I will do what is right for the company and howit is perceived, I can’t do a lot about. I’m not inthis job to enhance my reputation.”

Mr Miranthis, who first joined PartnerRe asan actuary in 2002 and headed PartnerReGlobal before being made President and COOin May 2010, has incrementally been assumingthe responsibility of running the company sinceJuly as the transition process has progressed. Hereturned to Bermuda full-time at the end ofSeptember. Although there will inevitably besome difference in leadership styles, he says itwill be “business as usual.”

“I think Patrick is a very straightforward per-son, has a strong sense of values and what hethinks is right and wrong and in that respectwe’re very similar. In terms of personal style wemay be a little different. I have a little less incli-nation to lead from the front. I like to orches-trate from the back,” he laughed.

“Those are personal traits and preferencesbut in terms of how you run the company andwhat values you instill, we’re very similar. Thecompany is its people and we know what westand for. We try to be straightforward and

transparent. The values we stand for — techni-cal, analytical, thoughtful — are not going tochange. We’re not an entrepreneurial companythat is looking for a quick win. We’re a steadycompany, we try to provide value to our stake-holders and we treat people with respect —that’s very important and will continue.”

Like Mr Miranthis, most of the new man-agement team have been with PartnerRe for asignificant amount of time and are well versedin those values. “Almost all of them are steppingup in their jobs and assuming more responsibil-ity,” he said.

The PartnerRe team, like the rest of theindustry, is busy figuring out how to best man-age the uncertainty in the market that lookslikely to continue for the immediate future.“Over the next couple of years, there is notgoing to be a lot of organic growth,” acknowl-edged Mr Miranthis. “It’s a tough environment.Frankly we’ve never been focused on growth. It’snever really featured in our goals as far as the topline is concerned. Growth in bottom line isanother matter.

“Over the next few years I think you need topreserve what you have got — financial andhuman capital, avoid making big mistakes, pre-serve the franchise and accept the reality whichis going to mean decent but lower returns thanin the past.

“If you try to grow too fast in that environ-ment, the likelihood is that you will make more

CHRIS GIBBONS MEETS PARTNERRE’SNEW CEO COSTAS MIRANTHIS AT THECOMPANY’S PEMBROKE OFFICES

READY FORTHE CHALLENGE

[ 8 ]

PH

OTO

: CH

RIS

GIB

BO

NS

/KA

LEID

OS

CO

PE

ME

DIA

21764F_BIQ_.qxd:ps 12/15/10 2:11 PM Page 8

[ 9 ]

mistakes and you will be increasing the risk. Sothe next few years are about guarding againstrisk rather than focusing on growth.”

Mr Miranthis is not alone in regarding theregulatory changes proposed by the EuropeanUnion under Solvency II as one of those risks.

“As a Bermudian company you want to beable to access the European insurance market.One of the big concerns with Solvency II wasthat Bermuda would not be recognised as anequivalent regulatory jurisdiction. That wouldbe a very bad day for Bermuda so Bermudaneeds to continue to work hard to make surethat it is a good regulatory environment.

“Because we have operations in differentjurisdictions, including Europe, we have a par-ticular interest on the impact of Solvency II. Wehave concerns about how long it is taking, theuncertainty, what the implications are and whenit will be implemented. It is still on track for2013 but I see a lot of people asking for anextended period of phasing in.

“For the industry in general it appears thatthe level at which capital requirements will beset are likely to be an issue. The new worldwould be a more capital-intensive world for alot of companies, and for the smaller companiesthat may be a survival issue. For us this mayultimately be an unexpected bonus in that itmay lead to an increased need for reinsurance,

but in the long term more capital for the indus-try as a whole will mean a higher cost of risktransfer. The question is who will bear that cost?It will either come in as lower profits for com-panies or higher costs to the consumer.

“Any system which is risk-based has got to bean improvement so there are some good thingshere. It’s the uncertainty we have now and thedirection of some of the discussion that con-cerns me. Often we end up discussing veryarcane and esoteric models of risk and it leavesme a little bit worried that we don’t appear tohave learned a lot from what happened in thebanking sector. It feels there is a lot of work stillto do before the industry is happy with what isbeing proposed and before we truly have a bet-ter and superior model. I think the direction isthe right one, but filling in the details will takea lot more time.”

For now, though, Mr Miranthis is focused onkeeping PartnerRe heading in the right directionand says he is looking forward to the challenge.

“I don’t plan too far ahead and it wasn’t that Ihad to become the CEO. I always want to makea change and have some kind of impact and Ithink I can contribute to the decision-makingand help people make decisions. But where youend up … part of it is circumstances, part of it isluck, but you’ve got to believe some of it is skilland that you have some value to bring.”

Age: 47Place of birth: CyprusFamily: Married, with four boys aged 4–14Education: MA in Economics fromChrist’s College, Cambridge University, UKProfessional qualifications: Fellow of the Institute of Actuaries and aMember of the American Academyof ActuariesCareer: After graduating in the UK,spent 16 years with Tillinghast TowersPerrin in London, rising to Principal.Joined PartnerRe in 2002 as ChiefActuary. Appointed Deputy CEO,PartnerRe Global in July 2007 and subsequently named CEO, PartnerReGlobal in May 2008, responsible for the executive management of theCompany’s Life operations and all non-Life reinsurance operations outsidethe US. Appointed President and ChiefOperating Officer, PartnerRe Ltd in May 2010. PartnerRe CEO effectiveJanuary 1, 2011.

Miranthis profile

21764F_BIQ_.qxd:ps 12/15/10 2:11 PM Page 9

The trend of several Bermuda-based reinsurers to redomicileto Switzerland or Ireland is

likely to continue through 2011but may not pose the long-termthreat to the Island as a majorglobal centre for the industry,according to some analysts.

Allied World is the latest majorcompany to announce that it isredomiciling its holding companyto Switzerland following earliermoves by Amlin and ACE (toSwitzerland), XL Group (toDublin) and Flagstone (to Lux -embourg). Shareholders approvedthe Allied World move onNovember 18.

For some companies, the movesare part of a strategy to establishpresence in an increasing numberof global markets, but there is nodoubt that concerns over the capi-tal requirements of Solvency II, theEuropean Union’s new regulatoryregime, is driving the trend, alongwith more competitive taxationand concerns over Bermuda Gov -ernment policies such as work per-mit time limits.

Under Solvency II, due to comeinto operation in 2013, Europeaninsurers will not be able to countreinsurance policies towards theirregulatory capital unless it is pro-vided by reinsurers operating undera comparably stringent regime.

In a letter to shareholders priorto the November 18 meeting thatapproved Allied World’s Swissmove, CEO Scott Carmilani saidthe change “will locate the compa-ny in a country that is a leadingfinancial centre with a strong repu-tation for economic and politicalstability, a shareholder-friendlygovernance environment and a cor-porate tax regime that will allow usto maintain a competitive world-wide effective corporate tax rate.”

However, Brad Kading, Exec -utive Director of the Associationof Bermuda Insurers and Re -insurers (ABIR), said the politicaland regulatory threats to localcompanies would reduce over thenext two years and that Bermuda

would maintain — and likely im -prove — its competitive edge overrival domiciles.

Speaking during a panel discus-sion about ‘The Changing Land -scape of Bermuda’ at the Standard& Poor’s/PricewaterhouseCoopers’Bermuda Reinsurance Conferenceat the Fairmont Hamilton Princessin November, Mr Kading said therisks of US social, policy and regu-latory risk in Bermuda, and theregulatory risk of Solvency II, hadincreased over the past four years.

He said: “In Bermuda over thelast three or four years all of thoserisk factors elevated over that timeand that is why we have seen someof our companies here move theirholding companies or legal enti-ties, but in 2011 and 2012 all threeof those risk buckets will be down.”

He added that Bermuda’s repu-tation as a place to do business, theBermuda Monetary Authority’sadvanced progress on achievingSolvency II equivalence and lobby-ing of the US government on taxlegislation issues by ABIR and theBermuda Government, would all

help reduce the risks.At the same conference, Neil

McConachie, CFO of LancashireHoldings, said that Bermuda “hasits problems but it’s still some-where brokers come to and there’sa good pool of talent here.”

He said the main reasons forredomiciling came down to taxationand cost and ease of operations.“Operating here is still relativelyeasy. Any time you open a newoffice you add complexity and costs.Looking at the bottom line, if it’snot going to improve things, you’rebetter off staying where you are.”

But some analysts believe theregulatory tightening in Bermudamay prove to be a double-edgedsword as it could make the Islandless attractive to future start-ups.And Bermuda’s limited space, infra-structure and talent pool may alsoaffect its future competitiveness.

“Tax might be zero in Bermudabut operating costs are high andpeople can get island fever livingthere,” Chris Waterman, an analystat ratings agency Fitch told Reutersin an October report. “A place like

Zurich also has tax advantages,great communications as it’s placedat the centre of Europe, and a high-ly skilled workforce.”

Fellow panel member WilliamPollett, Senior Vice President andTreasurer at Montpelier Re, com-mented: “Like everyone else, we’rekeeping a close eye on things. Wehave contingency plans and weknow where we will go under acertain set of circumstances but atthe moment we’re happy withBermuda.”

And he pointed out: “Otherjurisdictions have restrictions thatyou don’t have here, such as thoseon share repurchases.”

Despite the recent moves, busi-ness volumes on the Island havebeen unaffected, and all theredomiciling companies have keptsignificant operations in Bermuda.

Sebastian Kafetz, an insurancespecialist with Lloyds BankingGroup’s corporate banking divi-sion, was quoted in the sameReuters report as saying that whilecompanies were moving capital toEurope, “as a market place Ber -muda has still very much got thecluster effect, people are still grow-ing their operations there”.

In an earlier press statement onAllied World’s move, Mr Carm -ilani said the time had come “toincrease our focus on global distri-bution as well as global productcapabilities. Allied World [has]grown from a single office inBermuda to 16 offices worldwidethat service an increasingly globalcustomer base. This redomestica-tion will allow us to better manageour position in local marketsaround the world, as well as con-tinue to maintain a strong presencein the Bermuda market.”

Allied World’s new Swiss hold-ing company will remain subject toUS Securities and ExchangeCommission and New York StockExchange rules and regulations. Itwill continue to report its consoli-dated financial results in US dol-lars and under US generallyaccepted accounting principles.

[ 10 ]

NEWS REVIEW

Swiss redomiciles trend continuesALLIED WORLD IS LATEST MAJOR COMPANY TO ANNOUNCE IT IS MOVING ITS HOLDING COMPANY

Kading: Bermuda would main-tain — and likely improve — itsedge over rival domiciles

Carmilani: Allied World [will]continue to maintain a strongpresence in the Bermuda market

21764F_BIQ_.qxd:ps 12/15/10 2:11 PM Page 10

S.E. PEARMAN BUILDING

STUNNING NEW EXECUTIVE OFFICE SPACE TO RENT

Six floors of light and airy office space are now available in this dramaticglass and marble building. Floors of 5,800 sq.ft. are available as singletenancy or divided into two or three tenant options with sizes from 1,442sq.ft. to 2,761 sq.ft.

The dramatic entrance and lobby features a striking glass wall mural, thebathrooms are all finished to a high standard with elegant ceiling heightmarble and the entire color scheme of the building has been designed to

be contemporary and yet timeless, using a warm and complimentarypalette of colors. And with its location right in the heart of

Hamilton’s ‘business district’, locating your firm in thisspectacular state-of-the-art office is sure to please

your staff and impress your clients.

For a tour please contact:

MR. SANZ ‘KITTY’ PEARMAN

Tel: 535-0141 (cell) orTel: 295-5113 (office)E-mail: [email protected]

21764F_BIQ_.qxd:ps 12/15/10 2:11 PM Page 11

[ 12 ]

3

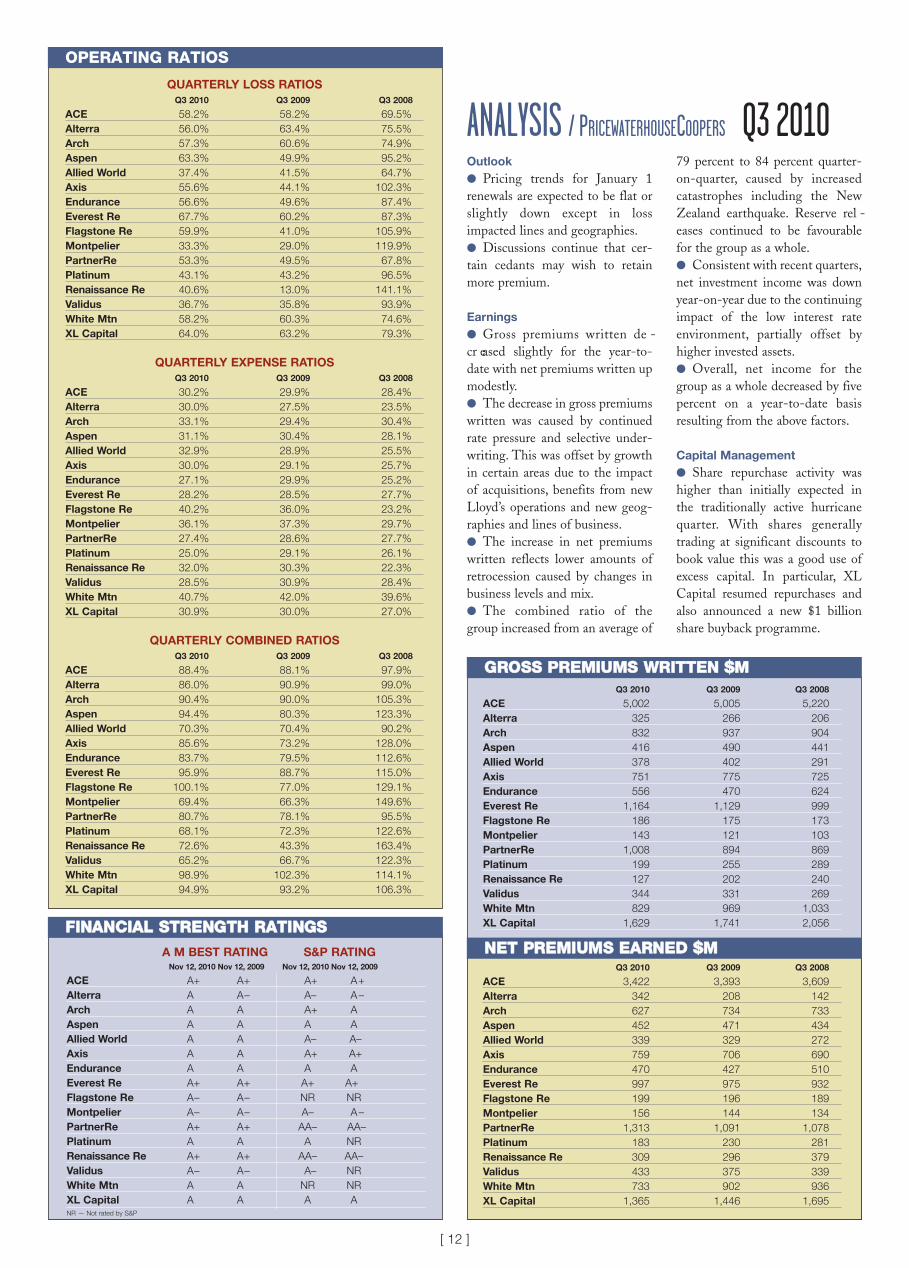

ANALYSIS / PRICEWATERHOUSECOOPERS Q3 2010

operating ratios

financial strength ratings

QuARtERLy LOss RAtiOsQ3 2010 Q3 2009 Q3 2008

ACE 58.2% 58.2% 69.5%

Alterra 56.0% 63.4% 75.5%

Arch 57.3% 60.6% 74.9%

Aspen 63.3% 49.9% 95.2%

Allied World 37.4% 41.5% 64.7%

Axis 55.6% 44.1% 102.3%

Endurance 56.6% 49.6% 87.4%

Everest Re 67.7% 60.2% 87.3%

Flagstone Re 59.9% 41.0% 105.9%

Montpelier 33.3% 29.0% 119.9%

PartnerRe 53.3% 49.5% 67.8%

Platinum 43.1% 43.2% 96.5%

Renaissance Re 40.6% 13.0% 141.1%

Validus 36.7% 35.8% 93.9%

White Mtn 58.2% 60.3% 74.6%

XL Capital 64.0% 63.2% 79.3%

QuARtERLy EXPEnsE RAtiOsQ3 2010 Q3 2009 Q3 2008

ACE 30.2% 29.9% 28.4%

Alterra 30.0% 27.5% 23.5%

Arch 33.1% 29.4% 30.4%

Aspen 31.1% 30.4% 28.1%

Allied World 32.9% 28.9% 25.5%

Axis 30.0% 29.1% 25.7%

Endurance 27.1% 29.9% 25.2%

Everest Re 28.2% 28.5% 27.7%

Flagstone Re 40.2% 36.0% 23.2%

Montpelier 36.1% 37.3% 29.7%

PartnerRe 27.4% 28.6% 27.7%

Platinum 25.0% 29.1% 26.1%

Renaissance Re 32.0% 30.3% 22.3%

Validus 28.5% 30.9% 28.4%

White Mtn 40.7% 42.0% 39.6%

XL Capital 30.9% 30.0% 27.0%

QuARtERLy COMbinEd RAtiOsQ3 2010 Q3 2009 Q3 2008

ACE 88.4% 88.1% 97.9%

Alterra 86.0% 90.9% 99.0%

Arch 90.4% 90.0% 105.3%

Aspen 94.4% 80.3% 123.3%

Allied World 70.3% 70.4% 90.2%

Axis 85.6% 73.2% 128.0%

Endurance 83.7% 79.5% 112.6%

Everest Re 95.9% 88.7% 115.0%

Flagstone Re 100.1% 77.0% 129.1%

Montpelier 69.4% 66.3% 149.6%

PartnerRe 80.7% 78.1% 95.5%

Platinum 68.1% 72.3% 122.6%

Renaissance Re 72.6% 43.3% 163.4%

Validus 65.2% 66.7% 122.3%

White Mtn 98.9% 102.3% 114.1%

XL Capital 94.9% 93.2% 106.3%

A M bEst RAting s&P RAtingnov 12, 2010 nov 12, 2009 nov 12, 2010 nov 12, 2009

ACE A+ A+ A+ A+

Alterra A A– A– A–

Arch A A A+ A

Aspen A A A A

Allied World A A A– A–

Axis A A A+ A+

Endurance A A A A

Everest Re A+ A+ A+ A+

Flagstone Re A– A– NR NR

Montpelier A– A– A– A–

PartnerRe A+ A+ AA– AA–

Platinum A A A NR

Renaissance Re A+ A+ AA– AA–

Validus A– A– A– NR

White Mtn A A NR NR

XL Capital A A A ANR — Not rated by S&P

Outlook

● Pricing trends for January 1renewals are expected to be flat orslightly down except in lossimpacted lines and geographies.● Discussions continue that cer-tain cedants may wish to retainmore premium.

Earnings

● Gross premiums written de -cr eased slightly for the year-to-date with net premiums written upmodestly.● The decrease in gross premiumswritten was caused by continuedrate pressure and selective under-writing. This was offset by growthin certain areas due to the impactof acquisitions, benefits from newLloyd’s operations and new geog-raphies and lines of business.● The increase in net premiumswritten reflects lower amounts ofretrocession caused by changes inbusiness levels and mix.● The combined ratio of thegroup increased from an average of

79 percent to 84 percent quarter-on-quarter, caused by increasedcatastrophes including the NewZealand earthquake. Reserve rel -eases continued to be favourablefor the group as a whole.● Consistent with recent quarters,net investment income was downyear-on-year due to the continuingimpact of the low interest rateenvironment, partially offset byhigher invested assets.● Overall, net income for thegroup as a whole decreased by fivepercent on a year-to-date basisresulting from the above factors.

Capital Management

● Share repurchase activity washigher than initially expected inthe traditionally active hurricanequarter. With shares generallytrading at significant discounts tobook value this was a good use ofexcess capital. In particular, XLCapital resumed repurchases andalso announced a new $1 billionshare buyback programme.

Q3 2010 Q3 2009 Q3 2008

ACE 5,002 5,005 5,220

Alterra 325 266 206

Arch 832 937 904

Aspen 416 490 441

Allied World 378 402 291

Axis 751 775 725

Endurance 556 470 624

Everest Re 1,164 1,129 999

Flagstone Re 186 175 173

Montpelier 143 121 103

PartnerRe 1,008 894 869

Platinum 199 255 289

Renaissance Re 127 202 240

Validus 344 331 269

White Mtn 829 969 1,033

XL Capital 1,629 1,741 2,056

Q3 2010 Q3 2009 Q3 2008

ACE 3,422 3,393 3,609

Alterra 342 208 142

Arch 627 734 733

Aspen 452 471 434

Allied World 339 329 272

Axis 759 706 690

Endurance 470 427 510

Everest Re 997 975 932

Flagstone Re 199 196 189

Montpelier 156 144 134

PartnerRe 1,313 1,091 1,078

Platinum 183 230 281

Renaissance Re 309 296 379

Validus 433 375 339

White Mtn 733 902 936

XL Capital 1,365 1,446 1,695

gross premiums written $m

net premiums earned $m

BIQ Q3 Dec 2010_Layout 1 12/22/10 11:50 AM Page 12

[ 13 ]

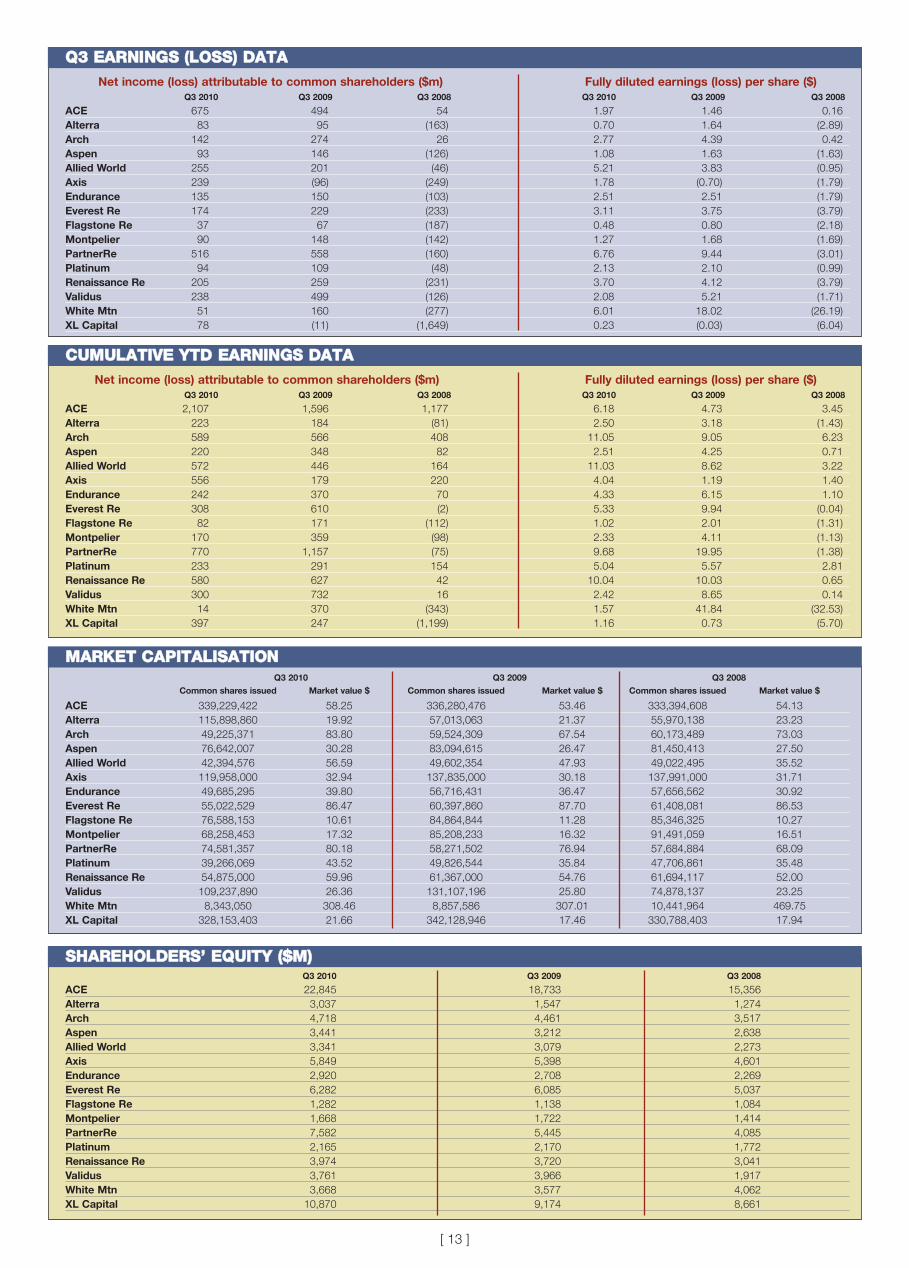

net income (loss) attributable to common shareholders ($m) Fully diluted earnings (loss) per share ($)Q3 2010 Q3 2009 Q3 2008 Q3 2010 Q3 2009 Q3 2008

ACE 675 494 54 1.97 1.46 0.16

Alterra 83 95 (163) 0.70 1.64 (2.89)

Arch 142 274 26 2.77 4.39 0.42

Aspen 93 146 (126) 1.08 1.63 (1.63)

Allied World 255 201 (46) 5.21 3.83 (0.95)

Axis 239 (96) (249) 1.78 (0.70) (1.79)

Endurance 135 150 (103) 2.51 2.51 (1.79)

Everest Re 174 229 (233) 3.11 3.75 (3.79)

Flagstone Re 37 67 (187) 0.48 0.80 (2.18)

Montpelier 90 148 (142) 1.27 1.68 (1.69)

PartnerRe 516 558 (160) 6.76 9.44 (3.01)

Platinum 94 109 (48) 2.13 2.10 (0.99)

Renaissance Re 205 259 (231) 3.70 4.12 (3.79)

Validus 238 499 (126) 2.08 5.21 (1.71)

White Mtn 51 160 (277) 6.01 18.02 (26.19)

XL Capital 78 (11) (1,649) 0.23 (0.03) (6.04)

net income (loss) attributable to common shareholders ($m) Fully diluted earnings (loss) per share ($)Q3 2010 Q3 2009 Q3 2008 Q3 2010 Q3 2009 Q3 2008

ACE 2,107 1,596 1,177 6.18 4.73 3.45

Alterra 223 184 (81) 2.50 3.18 (1.43)

Arch 589 566 408 11.05 9.05 6.23

Aspen 220 348 82 2.51 4.25 0.71

Allied World 572 446 164 11.03 8.62 3.22

Axis 556 179 220 4.04 1.19 1.40

Endurance 242 370 70 4.33 6.15 1.10

Everest Re 308 610 (2) 5.33 9.94 (0.04)

Flagstone Re 82 171 (112) 1.02 2.01 (1.31)

Montpelier 170 359 (98) 2.33 4.11 (1.13)

PartnerRe 770 1,157 (75) 9.68 19.95 (1.38)

Platinum 233 291 154 5.04 5.57 2.81

Renaissance Re 580 627 42 10.04 10.03 0.65

Validus 300 732 16 2.42 8.65 0.14

White Mtn 14 370 (343) 1.57 41.84 (32.53)

XL Capital 397 247 (1,199) 1.16 0.73 (5.70)

Q3 2010 Q3 2009 Q3 2008

ACE 22,845 18,733 15,356

Alterra 3,037 1,547 1,274

Arch 4,718 4,461 3,517

Aspen 3,441 3,212 2,638

Allied World 3,341 3,079 2,273

Axis 5,849 5,398 4,601

Endurance 2,920 2,708 2,269

Everest Re 6,282 6,085 5,037

Flagstone Re 1,282 1,138 1,084

Montpelier 1,668 1,722 1,414

PartnerRe 7,582 5,445 4,085

Platinum 2,165 2,170 1,772

Renaissance Re 3,974 3,720 3,041

Validus 3,761 3,966 1,917

White Mtn 3,668 3,577 4,062

XL Capital 10,870 9,174 8,661

market capitalisation

cumulative ytd earnings data

q3 earnings (loss) data

shareholders’ equity ($m)

Q3 2010 Q3 2009 Q3 2008

Common shares issued Market value $ Common shares issued Market value $ Common shares issued Market value $

ACE 339,229,422 58.25 336,280,476 53.46 333,394,608 54.13

Alterra 115,898,860 19.92 57,013,063 21.37 55,970,138 23.23

Arch 49,225,371 83.80 59,524,309 67.54 60,173,489 73.03

Aspen 76,642,007 30.28 83,094,615 26.47 81,450,413 27.50

Allied World 42,394,576 56.59 49,602,354 47.93 49,022,495 35.52

Axis 119,958,000 32.94 137,835,000 30.18 137,991,000 31.71

Endurance 49,685,295 39.80 56,716,431 36.47 57,656,562 30.92

Everest Re 55,022,529 86.47 60,397,860 87.70 61,408,081 86.53

Flagstone Re 76,588,153 10.61 84,864,844 11.28 85,346,325 10.27

Montpelier 68,258,453 17.32 85,208,233 16.32 91,491,059 16.51

PartnerRe 74,581,357 80.18 58,271,502 76.94 57,684,884 68.09

Platinum 39,266,069 43.52 49,826,544 35.84 47,706,861 35.48

Renaissance Re 54,875,000 59.96 61,367,000 54.76 61,694,117 52.00

Validus 109,237,890 26.36 131,107,196 25.80 74,878,137 23.25

White Mtn 8,343,050 308.46 8,857,586 307.01 10,441,964 469.75

XL Capital 328,153,403 21.66 342,128,946 17.46 330,788,403 17.94

BIQ Q3 Dec 2010_Layout 1 12/22/10 11:50 AM Page 13

NEWS REVIEW

A SOFT MARKET, LOW INTEREST RATES AND OVER CAPACITY HELP PUSH VALUATIONS DOWN DESPITE BIG RETURNS

Innovation is a primary focusThe reinsurance industry needs

to do a better job of selling itselfto investors, according to

Costas Miranthis, incoming CEOof Bermuda-based PartnerRe.

A soft market, low interest rates,and over capacity have helped pushvaluations down — with manyreinsurers valued at below bookvalue — despite impressive returns.

“Valuations are extremely frus-trating and disappointing,” MrMiranthis told the recent Standard& Poor’s/PricewaterhouseCoopers’Bermuda Reinsurance Conference.

“It’s the longest that stocks havebeen so low for so long. As anindustry we should do a better jobabout telling the investment com-munity about how good the per-formance has been. The reinsur-ance industry and insurance indus-try generally has provided returnsthat compare very favourably withalmost any other industry. Un -fortunately we don’t get the creditfor that.”

In a separate interview withBermuda Insurance Quarterly, MrMiranthis said: “I think a lot ofanalysts are too focused on insur-ance and reinsurance parochiallyand in many ways valuations in ourindustry are driven a little bit toomuch by momentum. They tend tolook ahead at what the pricingenvironment might be over thenext two years. It’s not going to begreat so they are going to markcompanies down. But the long-term track record compared toother industries is rarely looked at.

“We haven’t been good at put-ting our industry in a broader con-text compared with other capital-intensive industries. I think ourrecord stands up pretty well com-pared to other financial and capi-tal-intensive industries whetheryou look at ROE (return on equi-ty) or book value growth.

“Part of the issue is that it’s arelatively small and esoteric sectorso we don’t have the broaderappeal to the wider investmentcommunity. The people that followus are not generalists and often do

not take a broader perspective intheir valuations. From a portfoliopoint of view, a reinsurance stockis probably something everyoneshould have in their portfolio — itprovides good return, it’s not terri-bly correlated with other stocksbecause the things that drive rein-surance are not exactly the thingsthat drive other stocks.”

At the Bermuda ReinsuranceConference, industry veteran Don -ald Kramer, Chairman of ArielHoldings Ltd, was critical ofinvestors who priced reinsurancecompanies on tangible book value— a company’s total book valueless the value of any intangibleassets such as patents, intellectualproperty and goodwill.

“No other industry is valuedthat way,” he said. “None. Youwouldn’t value a bank that or alumber company or a drug compa-ny that way and certainly not

insurance broker because some ofour brokers have zero or even neg-ative book value.”

He said the collapse of interestrates had had a negative impact onlong-tail companies. “They’ve de-levered because of various solvencyrequirements, they’ve reduced theamount of assets per dollar of equi-ty and, with the yields collapsing,their investment income per dollarof equity in terms of return. If youlook at Q3 returns, this industryhas had stellar results, so you won-der about these discrepancies.”

Given the current valuations,insurance leaders say future growthis limited and that innovationwould be key.

XL Group CEO Mike Mc -Gavick said: “We are dealing witha straight third year of decliningtotal insurable premiums. This isthe first time this has happened. Itintensifies competition amongst us

and until the economy improvesthat will be a continuing trend.

“The rate of change in theworld continues to accelerate andour industry is one that likes longdatasets before we take a risk. Thatcreates a fascinating problem forthis industry to perform its role insociety if we don’t become ex -tremely focused on innovation andreinvention of these productsagainst the changing needs of ourclients. Innovation is going to be,in my view, a prime focus of com-petitive advantage creation overnext five to 10 years.”

Mr Miranthis pointed out thatinsurance premium highly corre-lated with GDP growth and islikely to be “muted or anaemic” inthe western world. “The onlyplaces that are growing — andeven their growth is slowing down— is in the emerging markets likeChina and Brazil.

“The size of the pie is not goingto change for most of us. Pene -tration is not going to changeunless we are able to meet newdemands to transfer risk. We haveto understand the change that isgoing on and come up with prod-ucts to meet that demand.”

XL CEO Mike McGavick makes a point during the recent Bermuda Reinsurance Conference flanked byJeff Consolino, Chief Financial Officer of Validus (left), and Costa Miranthis, PartnerRe’s incoming CEO

‘Analysts are too focused on insuranceand reinsurance parochially and inmany ways valuations are driven a little bit too much by momentum’

[ 14 ]

21764F_BIQ_.qxd:ps 12/15/10 2:11 PM Page 14

NEWS REVIEW

With most Bermuda reinsurers currentlyawash with excess capital as a result ofimproved loss reserves and low catastro-

phe activity in Q3 and Q4, the market is like-ly to see more share buy-back programmes inthe coming months.

Andrew Cook, EVP of Business Dev -elopment at Alterra Capital, which recentlyannounced a $200 million share repurchasescheme, said pressure to return capital was notnecessarily coming from shareholders but as aresult of deliberate management strategy inthe face of low pricing.

Speaking on a panel at the BermudaReinsurance Conference he said: “I thinkmanagement is taking pro-active action tobalance their capital base with the opportuni-ties we’re seeing in the marketplace and doingwhat they can to keep some discipline in themarketplace so we can have underwriting dis-cipline and capital management discipline.”

Bill Pollett, Senior Vice President andTreasurer of Montpelier Re Holdings, addedthat managements that had concentrated on

growing book value per share rather thanfocusing on just growing would “find it verydifficult to resist buying back their own shareswhen they are trading at a significant discountthan before.”

AXIS, Allied World, Everest Re, Hardyand Validus are among the major Bermuda-based companies to have announced multi-million dollar share repurchase programmesin recent months.

Fellow panelist Neil McConachie, ChiefFinancial Officer of Lancashire Holdings,said there was a danger of the industry fallinginto a trap by not releasing excess capital.

“It’s not completely clear why there’s somuch excess capital being held by the indus-try,” he said. “One argument you hear is ‘we’retrading below book value, it’s expensive toraise money so we need to keep a good bit ofexcess to take advantage of opportunities thatcome along.’

“But a lot of companies are trading belowbook value because the forward projections ofreturn are unexciting. If you get rid of that

excess capital, your forward returns improveand your multiple should improve. If thewhole industry was to get rid of 10 percent ofcapital, which might be in the region of $60-$70 billion, then you’re probably looking at apretty hard market, multiples improving andpeople trading above book value again. I thinkthere’s this trap that the industry as a wholehas fallen into.”

Mr Pollett said measuring excess capitaland deciding how much to hold back and howmuch to give back was a fine balancing act forall companies who are all facing greater capi-tal requirements from regulators.

“We look at required capital from manydifferent angles. We look at the regulatoryside, we look at the rating agency models andwe look at what we call client or “faith” capi-tal to be a significant player in the market.We typically look at all this following largeevents to make sure we can still play and offershareholder value. Right now it’s pretty com-pelling to deploy some of that excess intobuying back shares.”

[ 15 ]

MCGAVICK: WE STOP PRICING FOR THE UNKNOWN AND IT’S THE EASIEST GIVE-UP IN THE PRICING NEGOTIATIONS

Understand the industry’s ‘greatest flaw’Reinsurers should never stop

learning or lose their naturalappetite for risk in the current

soft market, according to leadingBermuda executives.

Answering a question on em -erging risks at the recent BermudaReinsurance Conference, ValidusHoldings President and ChiefFinancial Officer Jeff Consolinosaid: “Every time there is an event,lessons are learned. Hurricane Ikein 2008 was lost in the credit crisisbut it was a very damaging stormand what we’re learning from thatis that wind fields can extend a lotfurther from the eye than was pre-viously understood and thedestructive power of those windscan extend a lot further inland.

“All that science is going to bereflected in models and needs to befed back into pricing and riskselection and it also needs to be fedback into the insureds — even ifthey live 10 miles from the coast— in terms of the need to payattention to things like roof struc-

tures and so on.”XL Group CEO Mike Mc -

Gavick said: “Every time we gothrough one of these hyper pricingcycles what flies out the window isour appreciation of the unknown.We get very tight in our definitionof what we think is possible and weforget that every time really bad,ugly stuff happens in this industry,it happens from something wenever anticipated or knew.

“We stop pricing for theunknown and it’s the easiest give-up in the pricing negotiations.That’s the greatest flaw of theindustry. We never saw 9/11 orKRW (Hurricanes Katrina, Ritaand Wilma) coming. The data wework through is still relativelysmall and yet we price so feverish-ly with such confidence that I find

it a little bit comical. Then we areconstantly brought up short whensomething does happen that istruly unexpected and we realisethat we’ve given up pricing for thatunexpected event.”

Mr McGavick also sees the riskof governmental and regulatoryrules as “very threatening.”

He said: “If you step back andthink on a global basis, the wholeSolvency II drive — while some ofits features are very healthy for theindustry and cross-border trading— they are also an effort by one setof nations to impose a set of capi-tal regimes on the rest of theworld. I get distrustful of imposi-tions like that. It can cause deepinefficiency of how the insuranceindustry is viewed relative to othersectors because, frankly, if we’re

holding so much capital that wecannot create attractive returns,you will see that capital flow toother sectors.

“You can get into situations thatcreate peer competitive advantagesfor indigenous planners of thecountries that are imposing thestandards. All of us had better bevery focused on how these aredeveloped, particularly in the detail,or we could really wind up withsome really interesting and perhapsunfortunate market turndowns.”

Mr McGavick noted that thepace of innovation was also going tobring new opportunities and risks.

“Industries are literally going tocome in and out of existence in thespan of time that we used to want adataset before we’d consideringinsuring. You have to think how youare going to transfer your knowl-edge and experience to servicingthose kinds of industries and cur-rently untreatable needs. Our indus-try is about finding solutions forproblems that clients can’t solve.”

‘Every time really bad, ugly stuff happens … it happens from some-thing we never anticipated or knew’

Share buy-backs are a capital idea

21764F_BIQ_.qxd:ps 12/15/10 2:11 PM Page 15

While the reinsurance industryhas generally emerged fromthe global financial crisis

unscathed, it is feeling the fallout interms of increased regulatorydemands concerning enterprise riskmanagement (ERM) that are tak-ing up valuable time and resources.

Speaking at the Bermuda Re -insurance Conference, Sean Ring -sted, Chief Risk Officer and ChiefActuary of the ACE Group, saidthat while there were many goodthings in Solvency II, the Euro peanUnion’s proposed capital adequacyregime, he questioned whether someof the compliance requirements werereally necessary and suggested therewas too much emphasis on quanta-tive rather than qualitative aspectsof risk management.

“At a macro level we’re chang-ing the lifeboats as the ship cruisesalong,” he said. “Changes in acc -ounting standards, for example.They make a lot of intuitive sensebut have we really thought throughthe consequences of some of thosechanges? Are we driving downasset values at the wrong point?

“At the micro level I think we’rebeing asked to do an awful lot ofwork to satisfy the regulatorymindset. There is a real risk thatwe have a “tick box mentality” asopposed a broader perspective onwhat the issues facing the insur-

ance industry are.“If I could take some of that

money we’re spending on docu-mentation and box ticking I couldreally improve the value of thebusiness in other areas.”

He added: “Right now it’s achallenging business climate andwe don’t want to distract from thatbut these external needs are clearlyevolving. There was much goodthat was coming through inSolvency II in terms of the princi-

ples but one of the unfortunateramifications — and I think it’snatural post crisis — is that thependulum has swung a fair bit interms of how the regulators arethinking about risk managementand frameworks.”

He felt the insurance industryfared “pretty well” during the creditcrisis. “The business model workedwell. I think insurance tends to stickto its knitting, as it were.”

He added: “Our experience to

date is that much of the risk man-agement processes we developedinternally has been very much‘business as usual’. We haven’t hadto turn over the operating model orturn over how we think aboutproduct pricing or risk manage-ment because of the crisis.

“There are still challenges inhaving those discussions furtherdown in the organisation as towhat risk management means andhow we think about it.”

[ 16 ]

NEWS REVIEW

QUESTIONS RAISED OVER SOME OF THE SOLVENCY II COMPLIANCE REQUIREMENTS

Banking crisis sharpens focus on ERM

Sean Ringsted (right), Chief Risk Officer and Chief Actuary of the ACE Group, discusses a point during apanel discussion at the Bermuda Reinsurance Conference. Also pictured (left to right) are Mark Puccia,Managing Director of Standard & Poor’s, Eberhard Müller, Chief Risk Officer of Hannover Re, Germany,and Julian Cusack, Chief Risk Officer of Aspen Insurance Holdings Ltd

Hardy Underwriting Bermuda Ltd has announceda share buy-back programme in a bid to bolsterits defence against a takeover by rival specialistinsurer Beazley.

Hardy received the go ahead to buy-back 15percent of its common shares at a shareholdersmeeting in May but had not utilised the facility.On November 27, Hardy said in a statement thatif Beazley withdraws the 330p per share offerHardy rejected on November 12, it would initiatea share buy-back programme that will boostearning per share for the company’s investors.

The company also announced that it hadentered into an agreement for additional capitalfrom an unnamed third party for its underwritingbusiness, providing the Beazley bid is withdrawn.

The capital injection would support a 7.5 percentcapacity participation for the 2011 year of account.

CEO Barbara Merry said: “While Hardy hasthe capital available to support its 2011 businessplan, the group continues to see opportunities toenhance its insurance and reinsurance portfolioin 2011 and beyond. This move enhances itsability to grow the business without the need toraise additional equity capital and is designed tofacilitate mid-year increases in underwritingshould those opportunities arise.”

In a statement on November 15, Hardy saidBeazley’s second bid of 330p per share onNovember 4 “substantially” undervalued thecompany and said the proposal was an attemptto “acquire the company opportunistically, taking

advantage of both the current market environmentand recent, short-term circumstances specific toHardy.”

Beazley, which had increased its initial bidfrom 300p, said it was “disappointed” by theboard of Hardy’s “continued refusal to enter intoa dialogue with Beazley regarding its revised pro-posal or to provide access to due diligence infor-mation it requires to progress it.” It claimed theboard’s resistance was not in the interests ofHardy’s shareholders, and urged shareholders toencourage the board to adopt “a more construc-tive approach.”

The statement concluded: “In the absence ofany such encouragement, Beazley will withdrawits revised proposal.”

Hardy hoping to head off Beazley bid

21764F_BIQ_.qxd:ps 12/15/10 2:11 PM Page 16

[ 17 ]

IN BRIEF

WASHINGTON HOUSEA NEW DEVELOPMENT, IN THE

CENTRE OF HAMILTON

Recently completed and offering 62,000square feet of office space on four floorsand 24,000 square feet of retail space ontwo levels. The new building, which is partof the Washington Mall complex, spansthree city lots allowing up to 15,500 squarefeet of net rentable space on each officelevel, and the flexibility to suit a singletenant or multiple tenants.

Washington Mall is a large complex ofoffices and retail outlets on Reid Streetand Church Street. The officesaccommodate local and internationalbusinesses, while the retail outlets offera variety of products and services ofinterest to both local residents and visitors.

For more information call(+1 441) 295-4186

or e-mail: [email protected]

Under 40s tour gives valuable exposureSome of the Island’s brightest

young insurance professionalsgot the chance to broaden their

horizons during a recent tour tothe US organised by the BermudaUnder 40s Reinsurance Group.

A total of 18 employees from 14Bermuda-based companies joinedthe tour, the third — and so farlargest — biennial event organisedby the group. Participants spentthree days in New York attendingsessions on a wide range of insur-ance topics from insuring jewelleryto sophisticated catastrophe model-ling. They also travelled to Galveston,Texas, to visit the Ocean Star off-shore drilling rig and museum.

Chris Reeves, a ManagingDirector of Marsh and Presidentand Chief Operating Officer ofBowring Marsh (Bermuda) Ltd,said the tour had been “a greatopportunity” for Kara Gibbonswho works in the company’s

Property division.“At Marsh, we see career devel-

opment as a contract between thefirm and the individual, with ourrole being to provide opportunitiesto those colleagues who possessthe talent to advance their profes-sional career within our firm.”

Julia Mather, head of MillerBermuda, and social officer andtour leader for Bermuda Under40s, said: “The great thing aboutthis latest tour was that it showedthe calibre of Bermudians in theindustry, and that their employersare truly committed to seeing theserising stars advance in theircareers.”

Hiscox reduces US propertyand professional linesHiscox Ltd has reduced its under-writing of US property and largeprofessional indemnity lines due tochallenging market conditions and

is refocusing around core specialtyand wholesale lines.

In an interim managementstatement, the Bermuda-basedinsurer predicts that in the absenceof any large hurricane losses,January renewals will see pressure

on rates for US reinsurancebusiness.

Hiscox said it would expand itsoffshore energy business — energyrates are expected to rise followingthe Deepwater Horizon rig disas-ter in April.

ACE is to cut 17 of its staff in Bermuda. The company, which will have196 employees based on the Island following the cuts, says the moveis part of a global restructuring to improve efficiency. The positions willbe made redundant between May and September 2011, following thecompany’s consolidation of its financial management operations into aGlobal Finance Shared Service Centre in Philadelphia.

In a statement, ACE said: “These employees will be given priorityconsideration for appropriate open positions within the company.”

The company, which has operated in Bermuda for 25 years, said it“remains committed to Bermuda and to maintaining its insurance andreinsurance operations in the Bermuda market.”

Industry insiders say more staff cuts are likely among other majorBermuda companies as firms consolidate to cut costs or withdrawfrom unprofitable lines.

ACE to cut 17 Bermuda staff

21764F_BIQ_.qxd:ps 12/15/10 2:11 PM Page 17

[ 18 ]

The evolving landscape of riskSeasoned reinsurance executives have experi-

enced multiple cycles and periods of adversi-ty in the past — but none like the current

environment.At this year’s Monte Carlo reinsurance

Rendez-Vous, disappointing pricing fundamen-tals emerged as the chief concern for majorindustry leaders. While the major rating agen-cies reported the global reinsurance outlook as‘stable,’ macroeconomic factors such asincreased and prolonged economic growthvolatility and the potential for a longer softcycle, have put pressure on return on equity tar-gets and the reinsurance industry as whole.

Many industry CEOs have not felt the needto change their business models following thefinancial crisis. But if you examine the issuesthat are crowding in on the industry, set againsta desire to maximise future opportunity, it isclear that change is needed. The industry as awhole may be at an inflection point of a full-scale reinsurance landscape shift that could rep-resent a huge opportunity for reinsurers.

The number and complexity of the issuesthat reinsurance CEOs now face compound the

challenge of earning a return in excess of cost ofcapital. But these issues also represent opportu-nities for those companies that are able to adjusttheir business models or strategies to capitaliseon the evolving reinsurance landscape.

While it may be understandable that reinsur-ers are hunkering down, applying underwritingdiscipline and maximising the effectiveness ofexisting capital return mechanisms, they arealso, however, relying on a big loss event to turnthe underwriting cycle instead of questioningthe sustainability of their business model.

Complementary strategies, which includecapital investment and innovation during thesoft cycle, do not have to undermine thestrength of underlying businesses. There arepotential opportunities for reinsurers in at leasthalf a dozen different areas, and a lack of suit-able investment in such opportunities in themidst of this soft cycle could limit future successas the market turns. At the other end of thespectrum, a fundamental recalibration of thebusiness model with substantive investmentnow, could be the minimum required to staycompetitive in an evolving risk landscape.

Suggested action points include:Innovation: At a time of reinsurance ‘commodi-tisation’ and when the industry is facing unan-ticipated and unprecedented risk, innovation isnecessary to provide differentiation and to rap-idly capitalise on shifting demand.Distribution and risk transfer: Reinsurers’ kneejerk responses in reducing cover and pushing upprices following major dislocations has madereinsurance buyers cautious about approachingthe sector, even in times where they really oughtto be offloading risk. Reinsurers can benefitfrom providing clients with the support theyneed in times of risk adversity by creating risktransfer solutions that clients will purchase,rather than cutting back on traditional capacity.There are also opportunities to improve effi-ciency and effectiveness of risk transfer byinvesting in closer risk partnerships with clients.Solvency II: It is unclear at this point what truegrowth potential may come from Solvency IIand indeed who stands to benefit as insurancecompanies respond to demands for strongercapital, but there will be opportunities comingfrom a number of areas — an increase indemand; through innovation and product devel-opment as insurance companies seek to manage

capital positions effectively; and through merg-ers and acquisitions as small players find them-selves unable to meet new capital or compliancehurdles. Bermuda stands to benefit directly fromeach of these outcomes.Emerging markets: China and Latin Americaare obvious candidates for growth, howeverthere also less obvious, but potentially lucrativeregions that, with some positioning and invest-ment, could provide substantial returns in themedium term.Market positioning: Every jurisdiction or mar-ketplace has its strengths and limitations.Determining which approach to take withregards to underwriting lines of business is wor-thy of strategic evaluation, if not investment, inadvance of the next upturn in the cycle is crucial.Non-traditional reinsurance: Insurance-linkedsecurities deals have continued to flow this yeardespite the absence of major cat activity and theindustry loss warranties market is strong.However traditional reinsurance groups havebeen slow to react to the potential demand inthe area of non-traditional reinsurance. Makingfavourable alternative offerings available toclients could help reinsurers protect their marketshare and/or grow where ground has been lost.Mergers and acquisitions: Organic growth ofexisting businesses will be extremely difficult inthe near to medium term and in this environ-ment of deflated stock prices, mergers andacquisitions activity is likely. With several bil-lion dollar companies trading at discounts buttrading profitably, these expectations seem like-ly to be realised.

All eyes are on market dislocations that arecaused by big events. In fact, the market ischanging by increments almost irrespective ofbig events for a combination of other reasons todo with regulation, financial market uncertaintyand macro-economic drivers, changing buyerhabits, for example. Given a constantly evolvinglandscape of risk, those business models thatwill be successful will be the ones that are nim-ble to demand and opportunity and can consis-tently define and execute the full risk transferproposition to an entire spectrum of stakehold-ers: customers, investors and regulators.

In that sense, decisive and well-executedbusiness model transformation strategies may bethe only way to guarantee success when thecycle turns and markets harden.

ANALYSIS

BES LTD. is a leading provider ofRecruitment, Human Resources and

Business Solutions

� Permanent Search & Selection� Temporary & Contract Staffing� Human Resource Consulting� Immigration Processing� Secretarial & Transcribing Services

All services are tailored to meet theindividual Business needs of each client

Providing a cost effective, professionaland confidential service

Contact: Laura E. Jackson

77 Front StreetHamilton HM 12,

Bermuda

Tel: 1(441) 296-5627Fax: 1(441) 296-1749Email: [email protected]

www.bermudaemployment.com

UNFAMILIAR TIMES ARE DISPLACING FAMILIAR STRATEGIES, SAYS ARTHUR WIGHTMAN, PRICEWATERHOUSECOOPERS INSURANCE AND REINSURANCE PARTNER

21764F_BIQ_.qxd:ps 12/15/10 2:11 PM Page 18

QUOTE UNQUOTE

“The last few years have been interesting in thefinancial markets but I don’t know how muchmore interesting and exciting XL can take!”

— Mike McGavick, XL Group CEO, during a panel discussion at the Bermuda

Reinsurance Conference

“It’s much harder to find low-hanging fruit andmuch harder to distinguish yourself by pickingthe best risk. There may not be much low-hang-ing fruit but there are plenty of banana skins outthere. The way to differentiate yourself is toavoid those banana skins.” — PartnerRe’s Costas Miranthisadvocates an organic approach to

a healthy short-term strategy

“It does not matter where yourholding company is, it is whereyour people are, and Bermuda willremain the place to write rein-surance business.”— Alterra Re CEO John Berger

quoted in Bermuda:Re magazine

“Congress is still revenue-hungry, so action onan amendment incorporating Neal’s draconianreinsurance amendment is still a risk to bemanaged.”

— ABIR President and Executive DirectorBrad Kading, on the prospect of a resurrected

Neal Bill following the mid-term US elections,in Business Insurance

“I think what we would expect fromGovernment is an appreciation as to what thecurrent economic situation is doing to businesson the Island … and take those into considera-

tion when formulating its policy going forward.What would be helpful would be a seat at thetable giving constant input on what is going onso that it can achieve that goal.”

— George Hutchings, the new Chairman ofABIC (Association of Bermuda International

Companies) during an interview with TheRoyal Gazette

“Am I enjoying myself? Yes. I would be enjoyingit more with less of a challenging marketplace!”

— Ariel Re Chairman George Rivaz in aninterview with Bermuda:Re magazine