Embed Size (px)

Citation preview

Bioenergy Advancing grain-based ethanol Peter Halling, Head of Bioenergy marketing, Novozymes Claus Crone Fuglsang, Vice President R&D, Novozymes

Martin Parrish, Vice President, Alternative Fuels, Valero

This presentation and its related comments contain forward-looking statements, including statements about future events,

future financial performance, plans, strategies and expectations. Forward-looking statements are associated with words

such as, but not limited to, "believe," "anticipate," "expect," "estimate," "intend," "plan," "project," "could," "may," "might"

and other words of similar meaning.

Forward-looking statements are by their very nature associated with risks and uncertainties that may cause actual results

to differ materially from expectations, both positively and negatively. The risks and uncertainties may, among other things,

include unexpected developments in i) the ability to develop and market new products; ii) the demand for Novozymes’

products, market-driven price decreases, industry consolidation, and launches of competing products or disruptive

technologies in Novozymes’ core areas; iii) the ability to protect and enforce the company’s intellectual property rights; iv)

significant litigation or breaches of contract; v) the materialization of the company’s growth platforms, notably the

opportunity for marketing biomass conversion technologies or the development of microbial solutions for broad-acre crops;

vi) the political conditions, such as acceptance of enzymes produced by genetically modified organisms; vii) the global

economic and capital market conditions, including, but not limited to, currency exchange rates (USD/DKK and EUR/DKK in

particular, but not exclusively), interest rates and inflation; viii) significant price decreases on input and materials that

compete with Novozymes’ biological solutions. The company undertakes no obligation to update any forward-looking

statements as a result of future developments or new information.

Forward-Looking Statements

2

Session outline

• State of the U.S. ethanol market

• Innovation; key for performance

• Valero: Views from 3rd largest U.S. ethanol producer

• Innovation priorities

3

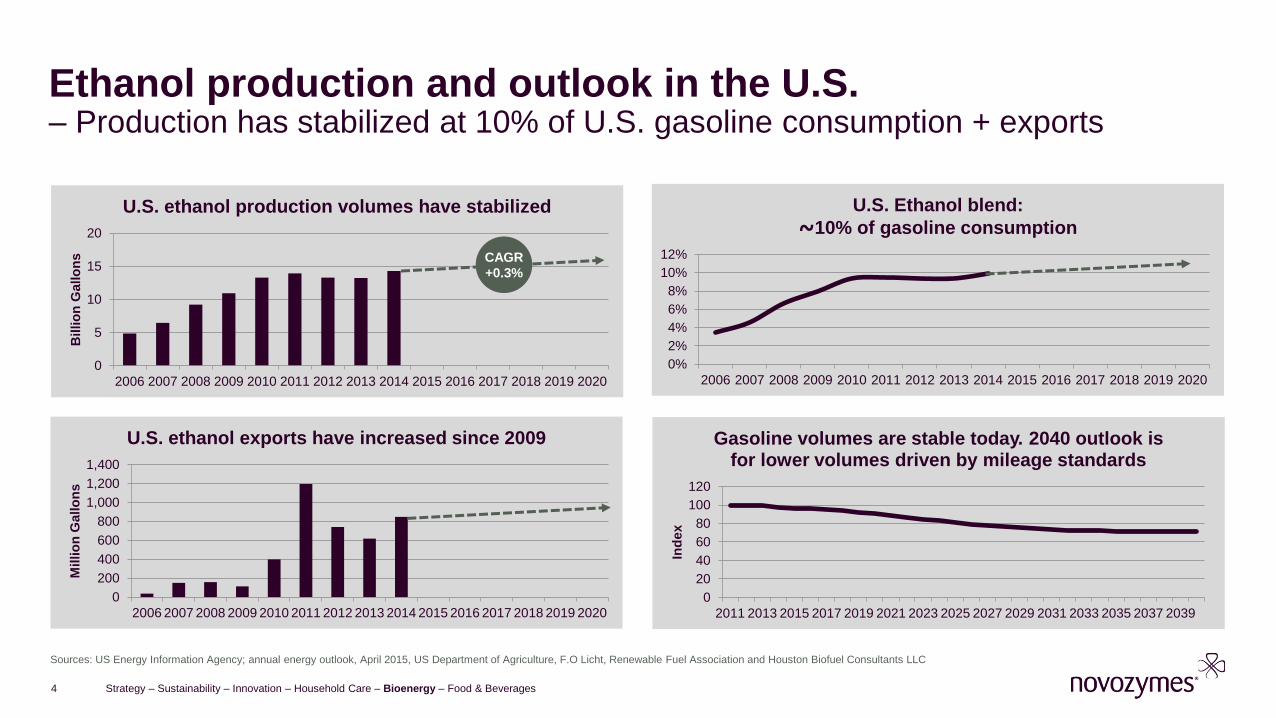

0

20

40

60

80

100

120

2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031 2033 2035 2037 2039

Ind

ex

Gasoline volumes are stable today. 2040 outlook is for lower volumes driven by mileage standards

Ethanol production and outlook in the U.S. – Production has stabilized at 10% of U.S. gasoline consumption + exports

0

5

10

15

20

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Billio

n G

allo

ns

U.S. ethanol production volumes have stabilized

0

200

400

600

800

1,000

1,200

1,400

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Millio

n G

allo

ns

U.S. ethanol exports have increased since 2009

0%

2%

4%

6%

8%

10%

12%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

U.S. Ethanol blend:

~10% of gasoline consumption

Strategy – Sustainability – Innovation – Household Care – Bioenergy – Food & Beverages

4

CAGR +0.3%

Sources: US Energy Information Agency; annual energy outlook, April 2015, US Department of Agriculture, F.O Licht, Renewable Fuel Association and Houston Biofuel Consultants LLC

Grain-based ethanol market in the U.S. – Novozymes serves a fragmented industry with overcapacity

Enzyme market players and share

Novozymes innovation drives

efficiency & growth

Industry capacity split by technology (15bn gallons/ 213 facilities)

Industry capacity split by producer

Strategy – Sustainability – Innovation – Household Care – Bioenergy – Food & Beverages

5

Dry-grind

POET

Wet milling

POET

ADM

Valero

Green Plains

Flint Hills

Cargill

Abengoa

Others2.70

gal/bu

2.85

gal/bu

3.00

gal/bu

Avantec®,

Spirizyme

Achieve®

& Olexa®

New Innovation

2012-2014 2015-2017 Eth

an

ol yie

ld

per

bu

sh

el o

f co

rn

Source: RFA ethanol and Novozymes estaimates

DuPont

+ Others

Innovation can grow the enzyme market, even in a flat production volume market

Strategy – Sustainability – Innovation – Household Care – Bioenergy – Food & Beverages

6

-20%

-10%

0%

10%

20%

30%

40%

Q1'10 Q2'10 Q3'10 Q4'10 Q1'11 Q2'11 Q3'11 Q4'11 Q1'12 Q2'12 Q3'12 Q4'12 Q1'13 Q2'13 Q3'13 Q4'13 Q1'14 Q2'14 Q3'14 Q4'14 Q1'15

U.S. quarterly ethanol volume growth rates and Novozymes organic growth (quarter over last year quarter)

NZ org. Bioenergy growth Eth.vol. growth

Avantec® launched

Spirizyme Achieve® and

Olexa® launched

Source: EIA and Novozymes

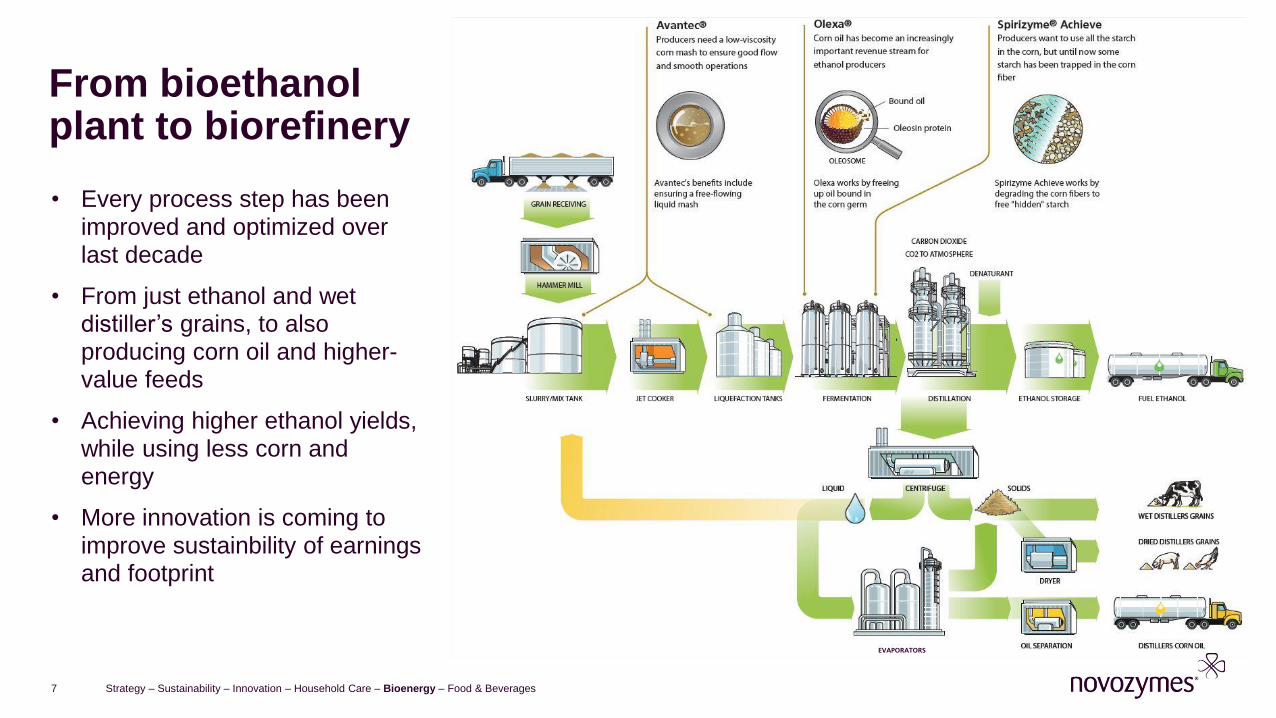

From bioethanol plant to biorefinery

• Every process step has been improved and optimized over last decade

• From just ethanol and wet distiller’s grains, to also producing corn oil and higher-value feeds

• Achieving higher ethanol yields, while using less corn and energy

• More innovation is coming to improve sustainbility of earnings and footprint

7

Strategy – Sustainability – Innovation – Household Care – Bioenergy – Food & Beverages

EVAPORATORS

Novozymes Capital Markets Days

May 2015

9

Who We Are

World’s Largest Independent Refiner

• 15 refineries, 2.9 million barrels per day (BPD) of high-complexity throughput capacity • Greater than 70% of refining capacity located in U.S. Gulf Coast and Mid-Continent • Approximately 10,000 employees

Large Logistics Infrastructure with Focus on Growth

• General partner and majority owner of Valero Energy Partners LP (NYSE: VLP), a growth-oriented, fee-based master limited partnership (MLP)

• Significant inventory of logistics assets within Valero

Wholesale Fuels Marketer

• Approximately 7,400 marketing sites in U.S., Canada, United Kingdom, and Ireland • Brands include Valero, Ultramar, Texaco, Shamrock, Diamond Shamrock, and Beacon

One of North America’s Largest Renewable Fuels Producers

• 11 corn ethanol plants, 1.3 billion gallons per year (85,000 BPD) production capacity • Operator and 50% owner of Diamond Green Diesel joint venture – 10,500 BPD renewable diesel production capacity

10

Financial Snapshot

Ticker “VLO” on New York Stock Exchange

Market Cap. $29.7 billion ($57.77/share on Mar 10, 2015)

Revenues $131 billion (Full Year 2014)

EBITDA $7.6 billion (Full year 2014)

Earnings $3.6 billion (Full year 2014)

Total Assets $46 billion (as of Dec 31, 2014)

Cash $3.7 billion (as of Dec 31, 2014)

Total Debt $5.8 billion (as of Dec 31, 2014)

Total Equity $21 billion (as of Dec 31, 2014)

Credit Rating Investment grade: S&P BBB, Moody’s Baa2, Fitch BBB

Valero ranked No. 10 on the 2014 Fortune 500 list

11

Assets Concentrated in Advantaged Locations

Refinery Capacities (MBPD) Nelson

Index Throughput Crude Oil

Corpus Christi 325 205 19.9

Houston 175 90 15.4

Meraux 135 125 9.7

Port Arthur 375 335 12.4

St. Charles 290 215 16.0

Texas City 260 225 11.1

Three Rivers 100 89 13.2

Gulf Coast 1,660 1,284 14.0

Ardmore 90 86 12.1

McKee 180 168 9.5

Memphis 195 180 7.9

Mid-Con 465 434 9.3

Pembroke 270 210 10.1

Quebec City 235 230 7.7

North Atlantic 505 440 8.9

Benicia 170 145 16.1

Wilmington 135 85 15.9

West Coast 305 230 16.0

Total or Avg. 2,935 2,388 12.4

12

Valero’s Business Segments

Refining 88%

Ethanol 2%

Corp. 10%

Assets as of 12/31/2014

Oil Refining and Marketing

• As an independent, we don’t produce or own reserves of oil

Ethanol Production

Refining 88%

Ethanol 12%

Operating Income Full Year 12/31/2014

13

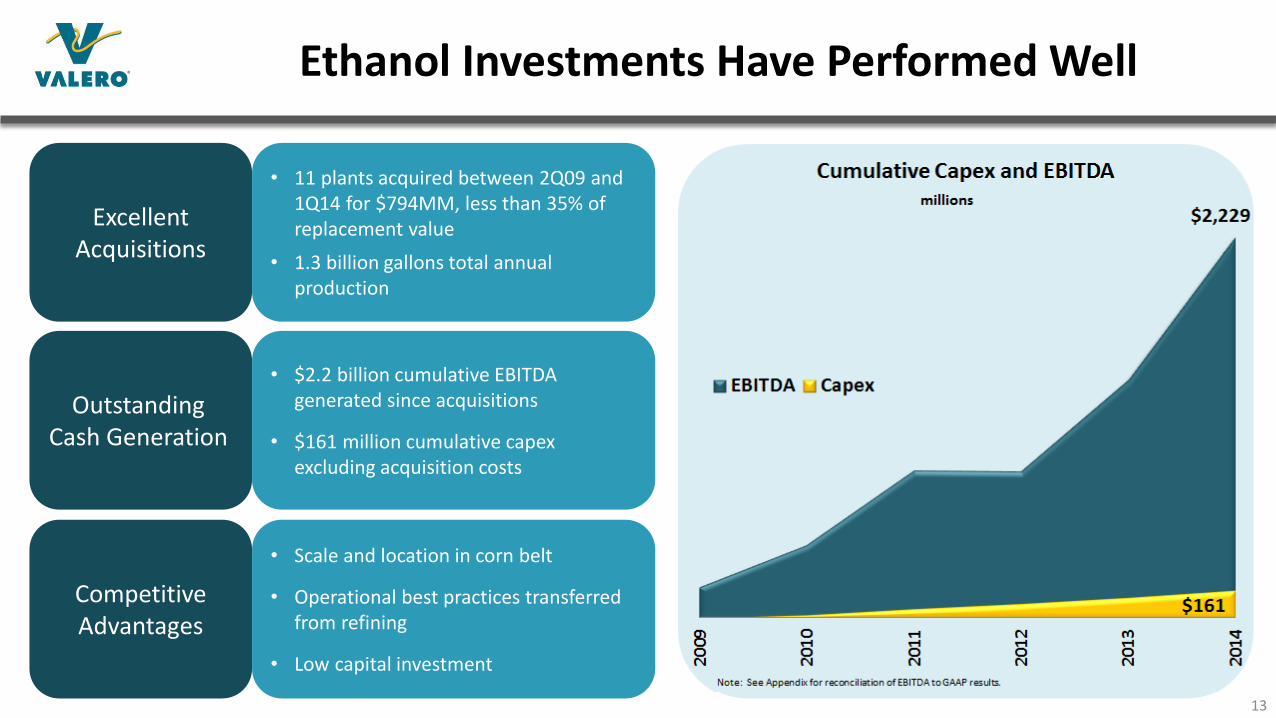

Ethanol Investments Have Performed Well

Note: See Appendix for reconciliation of EBITDA to GAAP results.

$2,229

$161

20

09

20

10

20

11

20

12

20

13

20

14

millions

Cumulative Capex and EBITDA

EBITDA CapexOutstanding

Cash Generation

Excellent Acquisitions

Competitive Advantages

• 11 plants acquired between 2Q09 and 1Q14 for $794MM, less than 35% of replacement value

• 1.3 billion gallons total annual production

• Scale and location in corn belt

• Operational best practices transferred from refining

• Low capital investment

• $2.2 billion cumulative EBITDA generated since acquisitions

• $161 million cumulative capex excluding acquisition costs

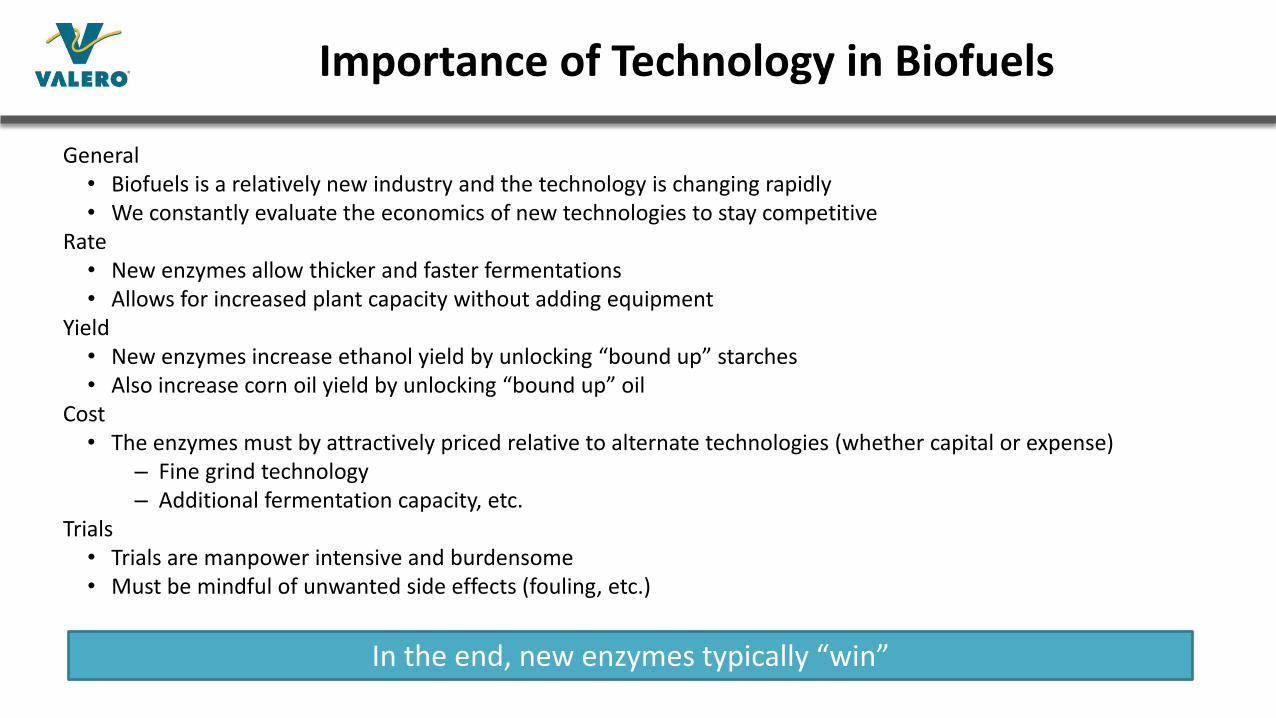

Importance of Technology in Biofuels

General • Biofuels is a relatively new industry and the technology is changing rapidly • We constantly evaluate the economics of new technologies to stay competitive

Rate • New enzymes allow thicker and faster fermentations • Allows for increased plant capacity without adding equipment

Yield • New enzymes increase ethanol yield by unlocking “bound up” starches • Also increase corn oil yield by unlocking “bound up” oil

Cost • The enzymes must by attractively priced relative to alternate technologies (whether capital or expense)

– Fine grind technology – Additional fermentation capacity, etc.

Trials • Trials are manpower intensive and burdensome • Must be mindful of unwanted side effects (fouling, etc.)

In the end, new enzymes typically “win”

Product Performance

Continuous Improvement

Technical Support

Total Cost of Ownership

Passionate about the success of

both the Customer and

Supplier

15

What is Important in a Supplier?

What’s in a corn kernel? – Refining for multiple revenue streams and lowest cost position

Strategy – Sustainability – Innovation – Household Care – Bioenergy – Food & Beverages

16

1 bushel

56 lbs

Starch 34.7 lbs

Sugars 1.0 lbs

Protein 4.8 lbs

Oil 1.8 lbs

Cellulose 1.6 lbs

Hemicellulose 3.2 lbs

Water 8.5 lbs

Germ

(high in oils)

Endosperm

(starch)

Pericarp

(gluten, high

in protein)

Bound oil Oleosin protein

Hull

(fiber)

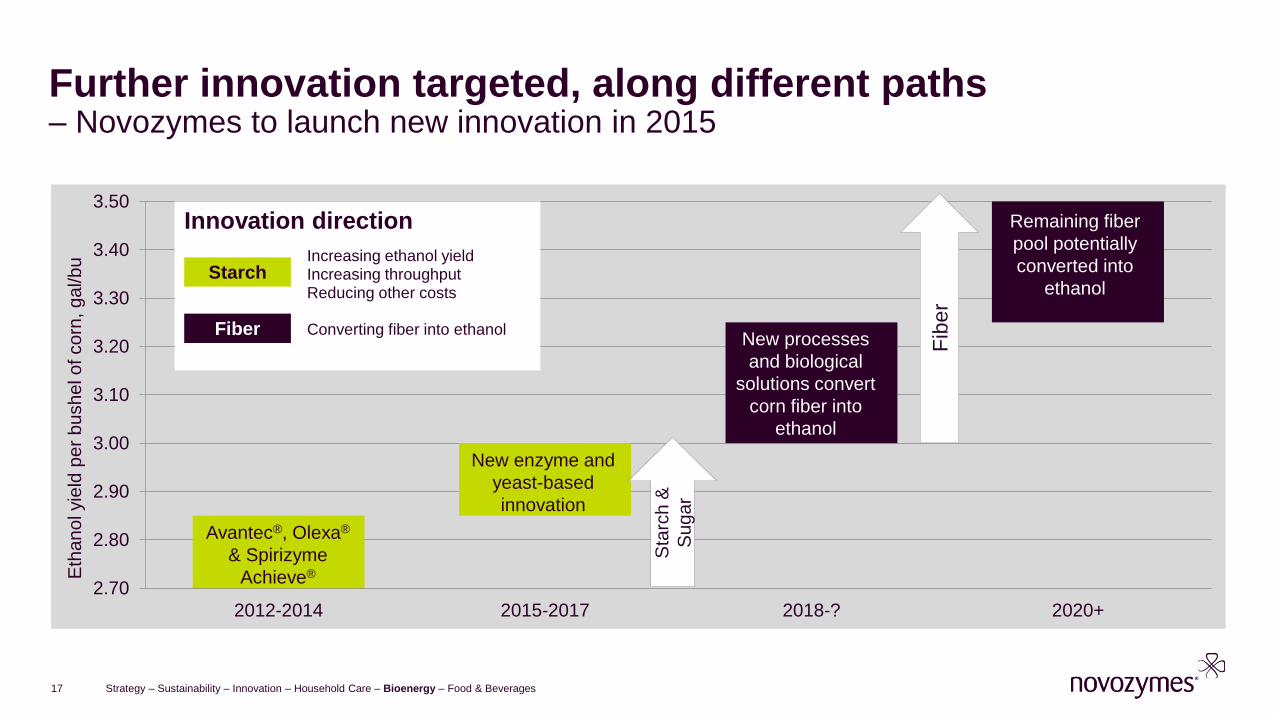

Further innovation targeted, along different paths – Novozymes to launch new innovation in 2015

2.70

2.80

2.90

3.00

3.10

3.20

3.30

3.40

3.50

2012-2014 2015-2017 2018-? 2020+

Eth

an

ol yie

ld p

er

bu

sh

el o

f co

rn, g

al/b

u

Strategy – Sustainability – Innovation – Household Care – Bioenergy – Food & Beverages

17

Sta

rch

&

Sugar

Fib

er

New processes

and biological

solutions convert

corn fiber into

ethanol

New enzyme and

yeast-based

innovation

Avantec®, Olexa®

& Spirizyme

Achieve®

Remaining fiber

pool potentially

converted into

ethanol

Innovation direction

Starch

Fiber

Increasing ethanol yield Increasing throughput Reducing other costs

Converting fiber into ethanol

Our ambition

Learn in partnership and through a strong presence at plants:

• Higher ethanol yield and throughput

• Low residual starch and ability to access beyond starch

• Co-product yield increase (corn oil)

• Co-product value increase (high-protein DDGS)

• Process low-value corn components to high value outputs (e.g. corn fiber cellulose to ethanol

• Reduction of low value by-products (e.g. glycerol, lactic acid, etc.)

Strategy – Sustainability – Innovation – Household Care – Bioenergy – Food & Beverages

Creating Unique Innovation for the

Biofuel Industry Using a Broad

Biotechnology Toolbox

18

protease cellulase

gluco-amylase

alpha-amylase

yeast phytases ?

Conclusion

• U.S. ethanol industry constantly becoming more efficient and cost-effective

• U.S. ethanol production tracks gasoline consumption and exports today. Uncertainties remain around future volume growth

• Biological solutions are a CAPEX-light means of improving plant profitability and sustainability

• Continuing innovation opportunities exist to add more value over the coming years

Strategy – Sustainability – Innovation – Household Care – Bioenergy – Food & Beverages

19