Embed Size (px)

Citation preview

Basic Services, Functional Assignments And Own Revenue Of Panchayats – Some Issues In Fiscal Decentralization for

the consideration of the Twelfth Finance Commission1.

M.A.Oommen

“ We feel that unless the panchayats are provided with adequate financial strength, it will be impossible for them to grow in stature” .

(Speech by Minister of State for Rural Development, moving the 73rd Constitution Amendment Bill in Lok Sabha on December 1, 1992)

That rural local bodies or Panchayats once an appendage of the rural development

departments have been made a ‘ third stratum’ of Indian federal polity is a great step

towards decentralized governance. Panchayat is defined in the Indian Constitution as ‘an

institution of self-government’ for the rural areas (Article 243(d) and is structured on a

three-tier basis – village, intermediate and district (Article 243 B). The hallmark of any

self-government is the degree of autonomy it enjoys in formulating and implementing

public policies in regard to those functional responsibilities assigned to it. In the three-

tier structure, the most critical level is the village or gram panchayat (GP) for a number of

reasons. It is closer to the people and is enjoined to interact with the assembly of citizen-

voters called Gram Sabha (Article 243A). The delivery of several basic services and

‘planning for economic development and social justice’ (Article 243G and 243W) can

work effectively and equitably only at the village level. More over, in almost all states

only the GPs are endowed with revenue-raising powers. The intermediate and district

tiers by and large do not enjoy substantial taxing powers (See Appendix A, A1 and A2).

Nearly a decade has passed since the decentralized development process has been

launched. The purpose of this paper is to raise some rural fiscal decentralisation issues in

the context of the twelfth finance commission (TFC). Kerala which has made significant

strides in regard to fiscal decentralisation is chosen for special mention in order to draw

possible lessons for others. The paper is organized under four heads: 1 Draft of the paper presented at the National Seminar on Panchayati Raj Finances (sponsored by the Twelfth Finance Commission) held at NIRD, Hyderabad, on January 23, 2004.

2

(i) Fiscal decentralization in India: Some conceptual and operational issues.

(ii) The reality of fiscal assignments to PRIs Vs the mandate of

decentralisation.

(iii) Own source revenue (OSR) and functional responsibilities of GPs – The

Kerala case.

(iv) Fiscal decentralisation and the TFC: Some Issues.

1.0 Fiscal decentralization in India: Some conceptual and operational issues

The theoretical framework relevant to a multi-tier federal system has evolved

from the quest to answer the basic question ‘who could do what’ to ensure the most

efficient and equitable allocation and distribution of resources consistent with the

preferences of the people. [See Oates (1972); King (1984) and Bird (2000)] .

Operationally this is the problem of fiscal decentralization which refers to the principles

and practices concerning expenditure responsibilities, revenue assignments and

rectification of vertical and horizontal imbalances with respect to the different layers of

governments. While vertical imbalance refers to the mismatches between levels of

government in responsibilities and resources, horizontal or inter jurisdictional imbalance

refers to the presence of territorial inequities. In the context of the 73rd constitutional

amendment, rectifying these imbalances has great significance for a country like India

with great regional disparities in resource endowment, level of income of the residents,

level of development, fiscal disabilities and even social deprivation.

Many of the received theories based on consumer choice may be inapplicable to

provide a neat conceptual framework for fiscal decentralization in India. The demand

driven model of consumer choice goes back to Tiebout (1956) who postulates that

individuals (households) “shop” among a large local jurisdiction in an effort to balance

marginal site costs (including all tax ‘price’ ) with the marginal evolution of public

services packages. Such costless out-migration of “consumer households” in search of

their preferred public goods package or ‘voting by feet’ as Tiebout puts it is untenable for

3

a country like India where the majority of the rural households depends on land for a

living. It is too much to expect at this stage of India’s development that rural local

governments in India can offer competitive services to their citizens. The role of local

governments best suited to India is the development concept of the citizen in a wider

community than the instrumental concept of the consumer whose choice is an expression

of self-interest. [See Mulgan (1997)] . The concept of consumer choice is also not in

sympathy with the citizen’s participatory rights guaranteed by the 73rd amendment

through such institutions as the gram sabha where all the voters in a village meet to

discuss their development problems, the reservation of seats and posts for women, and

socially backward communities and the like. Even so, ensuring some degree of

correspondence between the benefits obtained from public services in a local jurisdiction

with its revenue potential is important because it promotes autonomy and accountability.

It is argued that voter residents will hold local politicians and bureaucrats more

accountable if public services are financed by taxes they pay [See Bird (2000)] .

Two questions that immediately follow from this are (a) whether the average

Gram Panchayat (GP) jurisdiction in India enjoys a minimum population size and area

that would internalize benefits and costs of at least some of the basic services that ought

to be provided and (b) whether local governments are adequately empowered with

revenue powers, of course, supported by administrative capabilities to match expenditure

responsibilities?2 A critical population size is required for the delivery of public services

like water supply, health, education, agriculture, and the like. The average rural

population per GP in India ranges from 329 in Meghalaya to 23809 in Kerala. In

Madhya Pradesh, Himachal Pradesh, Punjab and Northeastern states the average size per

GP is below 2000 [See Indira Rajaraman (2003) Table 2.1] . Except for remote terrains,

the question of working towards a more viable population size for delivery of services

and viable Buildings a revenue base remains to be examined.

In the context of the 73rd constitutional amendments, there is a critical need to

rediscover the rural local governments because of the failure of both the national and 2 The second question is examined in section 2.0.

4

state level governments in providing a basic minimum of public services of standard

quality to their citizens irrespective of the choice of their residential location. Some

Union Finance Commissions (UFCs) have sought to improve the quality of essential

public services. But the small doze of grants recommended by them which were largely

confined to non-development, non-plan sectors had only cosmetic effects. The United

Front Government at the centre (1996-98) launched a major programme to upgrade the

quality of seven important essential services in the rural areas (these now find a place in

the XIth schedule of the constitution3) but did not proceed too far with the programme.

The tragic fact that remains is that there is considerable disparities in health care, rural

sanitations, primary education, drinking water supply, rural roads and so on [Among

others See N.J.Kurian (2000) and Deaton and Dreze (2000)] .

Article 243G enjoins that panchayats, at all the three levels should prepare plans

for ‘economic development and social justice’ . Because what this mandate means in

terms of specific responsibilities to be discharged by the panchayats has not been spelt

out in the constitution, it has to be contextually developed keeping in view the different

provisions of part IX of the Indian Constitution, besides the provisions relating to the

directive principles of state policy and fundamental rights of citizens. An examination of

XIth schedule will show that 16 subjects/functions out of the 29 listed relate to social

sectors covering education, health, women and child development, social security and

social welfare. At least 10 functions relate to the livelihood of rural people such as

agriculture, animal husbandry, fisheries, rural industries and so on, where public

intervention at the micro level will enhance production and employment opportunities.

Broadly speaking the objectives of the development plans of the Panchayati Raj

institutions (PRIs) should be to promote the national goal of ensuring and enhancing the

basic capabilities of all citizens and thereby widening their social opportunities4.

3 In July, 1996, the United Front Government convened a conference of the Chief Ministers to bring home the need to have certain basic minimum services – a carefully chosen seven, out of the 12 Minimum Needs Programme handed down from the days of the Fifth Five Year Plan. Of these drinking water, primary health and universalisation of primary education are identified by the conference as priority areas. [See Oommen (1996)] . 4 This indeed is a thesis advanced by Amartya Sen in several of his writings notably in Sen (2000).

5

Practically the public interventions required are to be addressed at the level of individual

villages and households.

The design of the transfer system be it by the Union Finance Commission (UFC)

or State Finance Commission (SFC) cannot ignore the conceptual and operational issues

raised in this section. SFC as per Article 243 I has the onerous responsibility to review

the state and local government finances, set forth the principles of vertically and

horizontal devolutions and make appropriate recommendations. UFC has to oversee

from a national perspective how the existing and emerging transfer arrangements

promote the constitutional mandate of decentralized governance within the framework of

Indian fiscal federalism.

The question of own source revenue (OSR) assumes importance here. No transfer

should promote fiscal imprudence. Indeed, it should induce revenue effort. The share of

OSR in total expenditure is the key to autonomy, participation and accountability. Only a

panchayat with revenue surplus will have greater flexibility and freedom to make

matching contributions required by a higher government and to provide the needed public

services keeping the geographical reach and better quality as it deems best for its citizens.

2.0 The constitutional mandate Vs the reality of fiscal assignments to PRIs

Decentralisation depends on the fiscal empowerment of the lower tiers and in our

context ‘ the third stratum’ of government. Fukasaku and De Mello Jr note that fiscal

decentralisation is the devolution of taxing and spending powers to lower levels of

governments [Fukasaku and De Mello (1999) P.9] . The whole transfer system is heavily

dependent on the progress made in regard to these fiscal assignments. In this section we

review the functional responsibilities and tax assignments to the PRIs with focus on the

GPs. The observations or inferences that are made in this section are based on (a) a

quick survey of the conformity acts of 16 states [See list given in Appendix A] (b) the

edited volume of Institute of Social Sciences which reviews the status of PRIs in all the

states, each state review being done by an expert with intimate knowledge of the state

6

[G.Mathew (ed) (2000)] and (c) an NIRD study of the PRIs of 18 states based on studies

and field investigations [See Choudhury and Subrahamanyam (2000)] . The major

findings from all these are spelt out below.

One, fiscal decentralisation to be really autonomous and effective, the three F’s -

functions, funds and functionaries should be transferred simultaneously. With the

singular exception of Kerala, the progress made has been halting, piecemeal and in

several cases even retrograde. Even in Kerala, the progress in regard to administrative

autonomy leaves many things to be desired.

Two, there is excessive state government control over the functional domain of

PRIs. There is very little autonomy. Andhra Pradesh, Assam, Bihar, Gujarat, Haryana,

Orissa, Punjab and Uttar Pradesh are prominent examples. Even in West Bengal widely

hailed as a good example of decentralisation, PRIs function more as agents of the state

government than as autonomous institutions. Bihar’s Panchayat Act, 1993 assigns

several functions to the PRIs, but “subject to such conditions as may be prescribed from

time to time”. Moreover the Bihar Act defines the Zilla Parishad as superior bodies over

the GPs endowed with power to suspend the executive orders of GPs. Even Gujarat with

a long tradition of PR system “has not been very successful in providing to its village

level institutions, the functional and financial autonomy which is integral to self-

governance” [P.N.Sheth (2000) in G.Mathew (ed) (2000): P.104] . While erosion of

autonomy is bad enough, the worst cases are those states where the PRIs continue to be

dominated by MPs and MLAs (e.g. Haryana).

Three, generally speaking the GPs are not adequately strengthened financially and

technically to deliver even the basic minimum services not to speak of the functional

assignments under the new dispensation. In some states several of the basic civic

services which traditionally belonged to the panchayats like street lighting, provision of

drinking water supply, sanitation and drainage, primary health care etc. have not been

entrusted to them. Instead, some of the services, if at all provided are provided by the

state departments [Subrahmanyam (2002) P.133] . In Haryana, GPs practically deal with

7

only drinking water and construction and maintenance of roads to the exclusion of all

others. [See Choudhury et al (2000): P.61] . The first state finance commission of

Karnataka identified supply of drinking water, street lighting, primary education and

primary health care as essential public services and recommended earmarked grants

based on specific norms for upgrading these services in rural areas. A few other SFCs

(e.g. Tamil Nadu, Kerala) also followed this approach. [A careful perusal of Article 243I

shows that the SFC has a role in facilitating proper fiscal assignments]

Four, because almost all the 29 subjects assigned to PRIs are state-concurrent,

there is need for role clarity to avoid duplication and over lapping. While any effort to

strengthen the reach and quality of basic services through GPs are to be welcomed, unless

there is clear role clarity as between the state on the one hand and the three-tiers on the

other in regard to functional assignments, decentralisation can only result in more

confusion, delay in implementation and add to the difficulties in evolving an efficient

transfer system. Several states have repeated the 29 subjects as functions of the three-

tiers. Some states like AP, Kerala, Gujarat and MP have broken the 29 subjects into

activities and sub-activities. Clear functional mapping is a necessary condition to ensure

efficient decentralisation.

Five, PRIs in most states have ignored the constitutional mandate to plan for

economic development and social justice. Kerala, Himachal Pradesh, Madhya Pradesh,

Bihar and West Bengal are a few states that have statutorily recognized this. But in no

state except in Kerala this important mandate has been made into a detailed bottom up

planning process [See section 3.0]. In MP, the task of planning and implementation of

schemes for economic development and social justice has been given to ‘district

governments’ created by delegating various powers and responsibilities of the state to

DPCs and calling them subordinate agencies of the government for this purpose. It is

difficult to consider this process as bottom up planning [See Articles 243 G and 243Z D] .

In Bihar, the statute gives powers to the Zilla Parishad to plan for economic development

and social justice. But this power remains only in the statute books. Bihar is one state

that has yet to take fiscal decentralisation seriously. West Bengal assigns the gram

8

sansad the responsibility to guide GP in regard to planning for economic development

and social justice. Despite an early start West Bengal too has to travel a long way

towards the goal of fiscal and administrative autonomy. In Karnataka PRI planning

continues to be “essentially a top down process” . [Satish Chandran (2000) in G.Mathew,

ed, (2000) P.144] .

It is important to note that the traditional differentiation between plan and non-

plan activities have led several SFCs to limit their recommendations to the non-plan

areas. Indeed, planning for economic development and social justice cannot be done

without reference to non-plan activities. Plan and non-plan are closely interrelated

because more plan projects and creation of assets mean more funds for operation and

maintenance, be they primary health centres, schools, minor irrigation, street taps or

streetlights5. The 29 items in the XIth Schedule cannot be developed on a dichotomous

plan versus non-plan basis because as per the constitution they are integrated expenditure

responsibilities.

Six, there are multiple channels of transferring resources some of them parallel

agencies (e.g. District Rural Development Agency) transgressing the functional domain

of PRIs. According to the Planning Commission, the share of Centrally Sponsored

Schemes (CSSs) in the plan budget of Central Ministries has currently increased to 70

percent against 30 percent in the early 1980s. Besides the CSSs, there are 26 sectoral

programmes falling under the 29 subjects of the XI Schedule which the Central

Ministries handle [See Planning Commission (2001)] . The State Governments are also

equally guilty of this. The Janmabhoomi, the Village Education Committee, Economic

Restructuring Project and the like of Andhra Pradesh all handled by the state have

virtually marginalized the PR regime of the state. The Gram Vikas Samitis of Haryana,

the Joint Forest Management Committees of Gujarat, Rajasthan’s Watershed Programme,

the Water Use Groups and Site Implementation Committees of UP and the District

5 Based on field studies, the NIRD has estimated that the annual average expenditure on maintenance of assets of PRIs in 11 states for six years from 1992-93 through 1997-98 is only 1.17percent of their total expenditure. [Choudhury and Subramanyam (2000): P.260. This is a dismal picture that needs to be corrected.

9

Government in MP are other cases to be specially mentioned in this context. Multiple

channels of resource flow and development efforts only lead to inefficient planning,

corruption and waste of resources.

Seven, turning to the tax assignments, it is clear that the pattern of pre – 73rd

Amendment regime has been repeated in a large number of states. No state seems to

have anticipated the expanding needs of decentralized governance and made appropriate

changes in the revenue assignments to local bodies. The intermediate and district

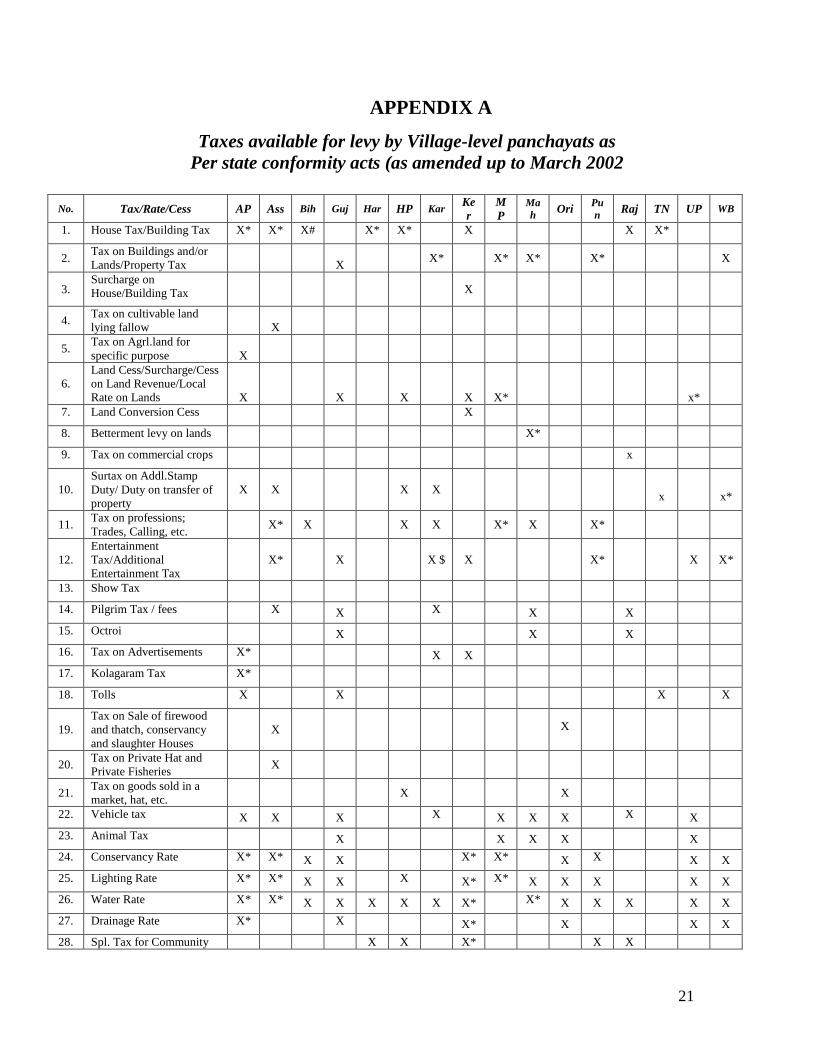

panchayats are not given substantial taxing powers [See Appendix A1 and A2] . Only GPs

are endowed with taxing powers. The number of taxes assigned to GPs range from two

in Tamil Nadu to 12 in AP and Gujarat. [See Appendix A for details] By and large, the

tax base covers property, persons and business. The taxes assigned to GPs generally are

not elastic or very productive. Even where taxes are assigned, the autonomy of the PRIs

in exercising them is considerably restricted by rules, restrictions and conditions. Of

course there are large number of fees, charges and other non-taxing items. There is also

the practice of the so-called ‘assigned taxes’ in some states (the state government

imposing a levy or surcharge on its own taxes and /or the State Government collecting

the taxes assigned to PRIs and disbursing them). In order to meet the growing demands

of decentralisation, there is need to make the taxes and non-tax revenues of the PRIs

more productive and elastic through rationalizing the tax base, rates and tax

administration along with imparting greater autonomy to the PRIs especially the GPs.

The conformity Acts in most states recognize the possibility of borrowing by local

bodies. Some experts have advocated borrowing by PRls on the basis of the experience

of municipal bonds in the United States and India and in some districts in Gujarat in

funding infrastructure development. If it is done with state guarantees, it can only add to

the fiscal worries of states most of whose finances are admittedly in doldrums. At any

rate access to capital market for PRls can be recommended only in exceptional cases.

In short to make the decentralisation process a viable and sustainable part of the

Indian federation, PRls should be made fiscally autonomous (ideally raising at least 40-

10

50 per cent of their expenditure requirements on their own). This is a function of tax

assignments, revenue efforts by PRls, the stage of development of the panchayat area,

reorganizing the transfer system keeping the best incentives to raising revenues and such

other factors. Given the shared responsibilities in a federation, every tier of government

should play its rightful role in prudent fiscal management. The discipline of 'hard budget

constraint' should inform all tiers of government to make intergovernmental finance

rational, efficient and equitable. The case for strengthening the GPs which alone enjoy

substantial revenue-raising powers and which alone has the direct link with the gram

sabha stand on unassailable ground.

3.0 OSR and the functional responsibilities of GPs – The case of Kerala.

In section 2.0 we have shown that the essence of decentralized governance is

fiscal autonomy. The autonomy of a government depends on the magnitude of OSR it

commands and the freedom it enjoys to raise and operate them. In this section we try to

examine the role of OSR in meeting the current needs and generating surplus for

development. For this we use primarily Kerala as a case study supplemented by

evidences from other states wherever possible. Kerala is chosen for two important

reasons: (1) a comprehensive study sponsored by World Bank on fiscal decentralisation

has been done recently which provides the relevant data [See Oommen (2003)] and (2)

Kerala admittedly has made remarkable progress towards decentralisation compared to

any other state in India.

Three measures of fiscal autonomy are used: (1) the number of GPs that generate

a surplus balance from current revenue and the magnitude thereof; (2) OSR of GPs and

the financing of plan expenditure. But before we examine these, a brief reference to the

salient aspects of the fiscal decentralisation that has happened in Kerala is needed to put

the discussion in proper perspective and (3) the number of GPs that cannot meet at least

selected basic services from its own revenue.

11

Kerala demonstrated considerable political will and resorted to a ‘big bang’

approach by earmarking 35-40 percent of state plan allocations and followed it up

through a state-wide decentralized plan campaign involving the State Planning Board,

local administration department, political parties, professionals and the representatives of

the local bodies from mid-August 1996. The decentralisation pursued was basically ‘a

learning by doing approach’ . More than 70 percent of the rural shares of the plan

allocations go to the GPs with the block and district panchayats getting 15 percent each.

Besides outlining a detailed methodology of bottom up planning which provides for

multiple avenues for peoples participation and scrutiny, institutional setup that ensures

certain entitlements to every panchayat and provisions for performance audit and social

audit to ensure accountability have also been made in terms of fiscal decentralisation.

OSR of GPs which was around Rs.60crores in 1993-94 increased to Rs.150 crores in

1998-99 nearly 150 percent increase in six years. The corresponding real revenue

(deflated by SDP deflator) increased by 50 percent. The per capita OSR of GPs works

out to Rs.57 in 1998-99 and taking the block average it ranges from Rs.21.4 in the

Perinthalmanna block of Malappuram district to Rs.157.2 in the Vazhakkulam block of

Ernakulam district. In 1998-99 the maximum per capita own tax revenue was Rs.328 and

non-tax revenue Rs.426. It may not be out of place to note here that in 1999-00 the per

capita OSR of the neighbouring state of Karnataka which had a longer history of rural

decentralisation is only a little over Rs.16 and that of Uttar Pradesh (UP) less than one

rupee (refers to 1997-98)6.

The per GP and per capita expenditure also have increased manifold over a span

of six years. The per GP expenditure increased from Rs.17 lakhs in 1993-94 to Rs. 78

lakhs in 1998-99 and over a crore in 1999-00. That the expenditure of local bodies as a

percentage of the combined expenditure of state and local bodies increased from 4.2

percent in 1993-94 to 12 percent in 1998-99 is something to write home about. The per

capita expenditure of GPs in Kerala in 1999-00 works out to Rs.421. In Kerala out of a

non-plan per capita expenditure of Rs.110 in 1998-99, nearly Rs 57 or over 50 percent is

6 The data for Karnataka cited in this study are based on MG Rao (2003) and the UP reference is due to an NIRD study (Choudhary and Siva Subramoniam (2000).

12

accounted for by own source revenue. This means that there is a substantial amount of

local choice. Of course when the plan expenditure is taken into account the percentage

share of OSR to total expenditure (plan and non plan) falls to 17 percent. But the

autonomy of GPs is not unduly restricted, because the GPs are free to plan their

expenditure subject to the restriction that 40 percent of the expenditure should be spent

on the productive sectors and that infrastructure expenditure must not exceed 30 percent.

To bring home the contrast with Karnataka, let me quote M.G.Rao who has done a study

on fiscal decentralisation in Karnataka recently:

“ The analysis has shown that the pattern of fiscal decentralisation has seriously

constrained flexibility and autonomy of local governments. The schematic devolution has meant that the local governments have the power to neither prioritize not design individual programmes of service delivery. Further, as the local governments do no have worthwhile revenue handles, they exercise very little fiscal autonomy. Thus, expenditure decentralisation has not helped to enhance allocative and technical efficiency in the provision of public services” [M.G.Rao (2003): P.117]

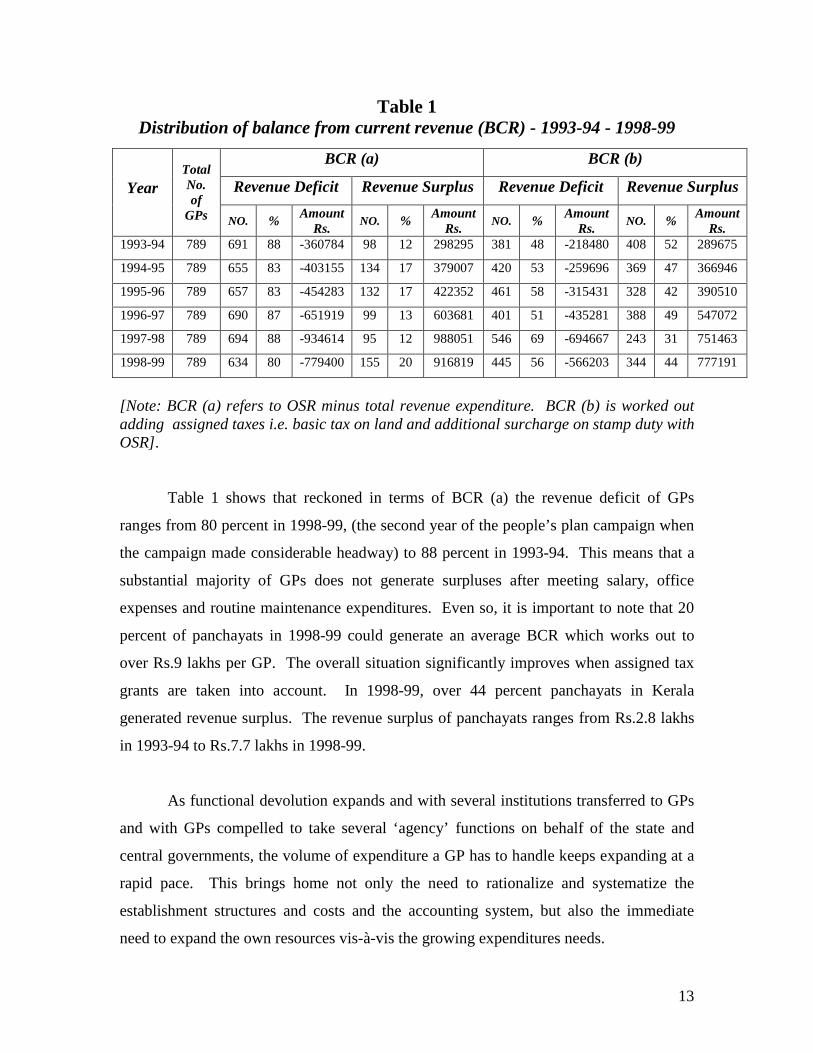

3.1 Balance from Current Revenue (BCR)

An important measure of the operational viability and financial strength of a

government is its ability to generate a surplus from the own source revenue after meeting

the current revenue expenditure. Because certain taxes statutorily assigned to gram

panchayats are collected by the state and distributed to them, we may work out an OSR

including the actuals received from these taxes also in working out the surplus. Table 1

gives the revenue deficit / surplus distribution per GP from 1993-94 through 1998-99 for

the two variants of BCR which we may call BCR (a) and BCR (b). BCR(a) refers to

OSR minus revenue expenditure and BCR(b) to OSR including the assigned taxes.

13

Table 1 Distribution of balance from current revenue (BCR) - 1993-94 - 1998-99

[Note: BCR (a) refers to OSR minus total revenue expenditure. BCR (b) is worked out adding assigned taxes i.e. basic tax on land and additional surcharge on stamp duty with OSR] .

Table 1 shows that reckoned in terms of BCR (a) the revenue deficit of GPs

ranges from 80 percent in 1998-99, (the second year of the people’s plan campaign when

the campaign made considerable headway) to 88 percent in 1993-94. This means that a

substantial majority of GPs does not generate surpluses after meeting salary, office

expenses and routine maintenance expenditures. Even so, it is important to note that 20

percent of panchayats in 1998-99 could generate an average BCR which works out to

over Rs.9 lakhs per GP. The overall situation significantly improves when assigned tax

grants are taken into account. In 1998-99, over 44 percent panchayats in Kerala

generated revenue surplus. The revenue surplus of panchayats ranges from Rs.2.8 lakhs

in 1993-94 to Rs.7.7 lakhs in 1998-99.

As functional devolution expands and with several institutions transferred to GPs

and with GPs compelled to take several ‘agency’ functions on behalf of the state and

central governments, the volume of expenditure a GP has to handle keeps expanding at a

rapid pace. This brings home not only the need to rationalize and systematize the

establishment structures and costs and the accounting system, but also the immediate

need to expand the own resources vis-à-vis the growing expenditures needs.

BCR (a) BCR (b)

Revenue Deficit Revenue Surplus Revenue Deficit Revenue Surplus Year Total No. of

GPs NO. % Amount

Rs. NO. %

Amount Rs.

NO. % Amount

Rs. NO. %

Amount Rs.

1993-94 789 691 88 -360784 98 12 298295 381 48 -218480 408 52 289675

1994-95 789 655 83 -403155 134 17 379007 420 53 -259696 369 47 366946

1995-96 789 657 83 -454283 132 17 422352 461 58 -315431 328 42 390510

1996-97 789 690 87 -651919 99 13 603681 401 51 -435281 388 49 547072

1997-98 789 694 88 -934614 95 12 988051 546 69 -694667 243 31 751463

1998-99 789 634 80 -779400 155 20 916819 445 56 -566203 344 44 777191

14

3.2 OSR and Plan Financing

Under the unfolding regime of decentralised governance, the single largest

component of the total expenditure of a GP in Kerala consists of plan expenditure

including expenditure on transferred institutions and schemes. It works out

approximately to 57-63 percent of the total expenditure. The development and material

progress of a local area has to depend heavily on this. But how the plan is financed is

crucial for autonomy and accountability. The effective linkage of local planning, basic

services and local resources can happen only when the transferred institutions and

centrally-sponsored schemes are also made an integral part of the working of a GP along

with its routine functions. Building the capacity for self-transformation to make PRIs

“ institutions of self-government” engaged in “planning for economic development and

social justice” as enjoined by Article 243 (G) of the Indian Constitution can happen only

in this fashion. For evaluating this we may use some of the data collected by the State

Planning Board using a structured format for 1998-99 for 10 districts. By 1998-99 the

bottom up planning at the GP level has been well underway with much of the guidelines

issued by the State Planning Board being firmed up by that time7. Table 2 shows the

broad scheme of financing of Annual Plan for 1998-99 based on a field study covering

645 GPs in the state. Table 2 is important because it covers the entire local plan and

includes not only the plan grants-in-aid from the State and Centrally Sponsored Schemes

but from all other sources like financial institutions, voluntary contributions, beneficiary

contributions and the own fund of the panchayats.

7 0ne can criticize this as a top down exercise. Given the present stage of development of local democratic governance in India, some initiatives from the top are inevitable to trigger the process of decentralisation. It all depends upon how the higher-level governments endeavour to foster autonomous governments at the lowest level.

15

Table 2 The Scheme of Financing of Annual Plan 1998-99 (Average for 645 GPs)

(Rs in lakhs except per capita)

I tem Grant-in-aid

Own fund

State Sponso-

red

Centrally Sponsored

Co –operati-

ves FIs

Volunt-ary

service

Benefic-iary

shares Others Total

Expenditure as Planned

37764.31 7503.89 3143.97 2361.30 1030.21 1269.04 3470.03 11945.32 1645.41 70075.85

Percentage to Total

53.89 10.71 4.49 3.37 1.47 1.81 4.95 17.05 2.35 100.00

Actual Expenditure

22897.21 1840.56 989.05 943.88 122.31 339.13 1258.78 4602.42 762.75 33756.11

Percentage to Total

67.83 5.45 2.93 2.80 0.36 1.00 3.73 13.63 2.26 100.00

Per capita (AE) 135.32 10.88 5.85 5.58 0.72 2.00 7.44 27.20 4.51 199.50

Per GP (PE) 58.55 11.63 4.87 3.66 1.60 1.97 5.38 18.52 2.55 108.64

Per GP (AE) 35.50 2.85 1.53 1.46 0.19 0.53 1.95 7.14 1.18 52.34

% of AE to PE 60.63 24.53 31.46 39.97 11.87 26.72 36.28 38.53 46.36 48.17

[FIs refers to Financial Institutions. Source: For details See Oommen (2003)]

The most striking aspect we can observe from Table 2 is the great chasm between

what is planned and what is actually spent. There is a tendency among all GPs to

exaggerate the Plan size quite often dictated by the local political pressures. We note

from Table 2 that out of over Rs.700 crore of expenditures planned only Rs.337 crore or

just 48 percent of what was planned was actually spent. This percentage ranges from 40

percent in Kollam district to 67 percent in the Alappuzha district (not reported in the

Table). Barring the negligible item of cooperatives, the exaggeration is highest in regard

to own funds. Own fund actual is as low as 24.5 percentage of what was planned.

Although 90 percent of the GPs reported that own funds would be earmarked for

financing the plan, actually 192 out of 645 GPs, or 30 percent did not make any

contribution from their own funds. While per GP planned expenditure out of own funds

was Rs.11.63 lakhs, the actual was only Rs.2.54 lakhs. As a percentage of the total actual

expenditure own funds is only 5.45 percent. With all the hiatus between the actual and

the planned, it is doubtful whether any other state panchayats could be credited with this

order of magnitude of own funds for the development of their local area.

16

3.3 Basic Services and OSR

How many GPs in Kerala cannot meet the maintenance expenditure on core

services? There are only very few panchayats in Kerala that cannot meet the

expenditures on the core services, i.e. expenditures on sanitation and drainage, drinking

water supply and street lighting. For the six years under study, the highest percentage is

only 3.4 percent and the lowest below one percent. These are the panchayats that

definitely need unconditional support from the higher-level governments. If the scopes

of basic services are enlarged, the percentage will be higher.

4.0 Some issues for the TFC

First, given the fact that one of the major objectives of fiscal transfers in Indian

federal polity is the promotion of horizontal equity and considering the failure in

achieving basic minimum services in the country as a whole, the Union Finance

Commission have a special role in the context of the 73rd Constitutional Amendment. To

deprive a citizen of adequate level of schooling, primary health care, drinking water

supply and so on because of the compulsions to choose a remote location is an injustice.

[See Oommen (2000) in D.K.Srivastava, ed, (2000): P.412] .

As we have noted in section 1.0 PRIs offer the best bet in regard to providing

basic services of reasonable quality to every part of India. But the order of magnitude

involved in achieving the goal within a reasonable time frame is huge. Based on certain

physical norms, unit cost, inflation etc, the NIRD has calculated the capital cost and

operation and maintenance (O&M) expenditure for drinking water supply, rural

sanitation, street lighting, primary education, primary health care and rural roads

considered as “core services” for five years from 2000 to 2005. Their estimate works out

to Rs.225, 731 crores. Out of this Rs.142, 128 crores or 63 percent of the total estimate is

for O & M. The annual capital outlay and O & M expenditure work out to Rs. 16721 and

Rs. 28425 crores respectively.

17

The crucial questions that arise immediately are: (a) What proportion of this can

the PRIs contribute? (b) Will the central and state governments be prepared to earmark

such a big amount by way of capital grant within a reasonable time frame? If Articles

243 G, 243 W, 243 H, 243 I, 243 Y, and 243 ZD were to be taken seriously the Twelfth

Finance Commission and the SFCs will have to set out an agenda for ensuring a

minimum of core services to every region in the country through a process of fiscal

decentralisation that will meaningfully address the problem of vertical and horizontal

imbalances.

Second, there should be some correspondence between the benefits obtained from

public services in a local jurisdiction with the revenue raised in order to promote

autonomy, accountability, ownership and a sense of participation. As we have already

noted an important precondition is to work towards a viable population size for the GP.

We have seen how most states in the country have not gone far enough in clear functional

mapping, revenue assignments and in providing financial and administrative autonomy to

the PRIs given the Terms of Reference (TOR) of the TFC to restructure public finance

and redesigning of the federal transfer system will be complete and relevant only when

the third stratum of government is also examined in an integrated fashion.

Third, that the UFC should make its recommendations regarding local

governments “on the basis of the recommendations made by the Finance Commission of

the State” [Article 280(3) (bb) and (c)] is meant to underscore the organic link in the

Indian fiscal federalism cannot be ignored. The recommendation of the Eleventh Finance

Commission (EFC) to abolish the sub-clauses (bb) and (c) because of the “heterogeneity

in approach, content and periods covered” is untenable. Clearly the EFC has failed to

appreciate adequately the letter and spirit of the Indian Constitution and the 73rd and 74th

Constitutional Amendments. Can any one expect uniformity in approach from 28

different state finance commissions (SFCs)? The historical realities and objective

conditions obtaining in the various states widely differ. The best alternative is to amend

the wording of Article 280 (3)(bb) and (c) to “after considering the recommendations of

the State Finance Commission” . Indeed the UFC has a responsibility to take initiatives

18

and offer operational guidelines to SFCs in the interest of the Indian economy and federal

finance.

Four, restructuring public finance also cannot ignore the reality that there are

multiple channels of transferring resources from the centre to the states and the local

bodies which we have documented in section 2. We reiterate the story of the ‘parallel’

flow of funds to rural areas for items falling within the 29 subjects such as anti-poverty

programme funds through the DRDA (District Rural Development Agency), literacy

promotion funds through the Saksharata Samiti and funds for fisheries, women’s

development etc. passing through various registered societies promoted by the central

government. It is strange that the Union Ministry of Rural Development which has to

monitor the progress of Panchayats in India is actively strengthening DRDAs which

ought to have been abolished by now. Apart from these, Government of India provides

extra budgetary loan facility under the RIDF (Rural Infrastructure Development Fund).

The huge special funds (Rs. 2 crore per MP) placed at the disposal of MPs (MPs Local

Area Development Fund) and MLAs to be spent on items that fall directly within the

functional domain of local bodies are other conspicuous examples of distorted transfer

arrangements prevailing at the national and sub-national level. Can the TFC ignore the

whole range of transfer arrangements in any effort at reconstructing or restructuring

public finance in the country? There is an imperative need to redraw the functions funds

matrix currently emerging in India on a more rational and constitutionally valid basis.

Imagine a rural India where a substantial proportion of the PRIs could generate a

surplus balance from current revenue. It will automatically improve the state and central

fiscal position. There is also great potential for tapping local resources. Even in Kerala

only less than 40 percent of the tax revenue potential from property tax, profession tax

and entertainment tax is collected [See Oommen (2003)] . Similarly the tremendous

potential of land revenue from states like Punjab, Haryana and Andhra Pradesh remain

untapped. The award of the service tax base in its entirety to the states and local bodies

along with strengthening the PRIs by devolving the three Fs-functions, funds and

functionaries to the local bodies, aggregate revenue of Indian federation could be

19

enhanced. On the basis of the data given in the EFC Report (Annexure VIII) the tax –

GDP ratio of PRIs in 1997-98 works out to an abysmally low 0.025. The historical trend

assuming a compound growth rate the ratio is seen to decline to 0.021 in 2006-07 the

terminal year of the Tenth Plan. It is clear that this trend has to be reversed and the PRIs

made a viable partner in the resource mobilization effort of the nation.

If the findings based on 96 village panchayats spread over 12 states conducted

by NIRD for the period 1992-93 through 1997-98 are any indication, one need not yield

to despair regarding the revenue potential and revenue raising capabilities of the PRls.

One can firmly maintain that while the taxes are not properly collected there is potential

for raising them substantially. It may be noted that the poor tax performance is due to a

variety of factors like inadequate tax assignment, less elastic nature of those taxes,

assigned low rate fixed by the State government/local government, absence of adequate

staff support for tax collection, unviable size of village panchayats and so on. It is here

that the case for promoting administratively viable GPs mentioned in section 1.0 assumes

importance.

Five, horizontal equity in a transfer system depends a great deal on the criteria

chosen for interse distribution. Need, efficiency and equity should be governing

considerations in the choice of criteria. There is nothing amiss in using different criteria

for tax-sharing as well as for grants. But the logic of using 10 percent weightage for

population for sharing of taxes and 40 percent for grants to local bodies by the EFC is

somewhat unconvincing. Population is one criterion that has been used by all the finance

commissions in the past, of course, with different weightage. This was also one criterion

demanded by the states in general. But because several other criteria such as

backwardness, tax effort, etc. (e.g per capita income distance, inverse of per capita

income, per capita tax etc.) have been deflated with population and worked out as a share

of total population, the total share effectively received turns out to be influenced

considerably by population. Alternate criteria that are not weighted by population may

also be used. For example, realizing the target of additional resource mobilization

(ARM) agreed by a state before the Planning Commission could be taken as an index of

20

tax effort. This is the best way to ensure compliance by the states most of whom have

been disregarding this target agreed before the Planning Commission with impunity.

There is also a case for building a local government component to the ARM in the future.

This is one way of ensuring shared responsibility and cooperation in a multi-tiered

federal polity.

The political economy of staying backward or proving backward to attract central

devolution has to be discouraged. States that have made real progress in terms of goals

laid down in the Constitution such as enrolment ratio of children between 6 and 14 years,

creation of public medicare facilities, progress made in effective decentralization (the

EFC made a mess of it through use of ill-informed variables in the Decentralisation Index

they used) and so on must be used as prominent criteria with appropriate weightage. The

actual devolution of funds, functions divided into relevant activities and sub-activities,

and fiscal assignments and functionaries should be the major consideration while

designing a decentralization index. The most efficient and fiscally responsible spending

consists in progressively achieving the constitutional tasks in a reasonable time frame.

Six, the Fiscal Responsibility and Budget Management Act of the centre and

similar legislations by some states are good in that they seek to provide a medium term

fiscal policy framework for the country. But what about the 2.31 lakh village panchayats

in India where accounting and budgetary process are in disarray? It is the hardware that

needs to be restructured first. The fiscal responsibility legislations can lead to fiscal

corrections in an arithmetical axing game. The concept of ‘ fiscal responsibility’ which is

not defined in the central legislation consists in channeling public resources to achieve

certain avowed social goals such as ensuring the basic minimum services in a panchayat

area, the progress in the devolution of functions, finance and administration to the local

level and so on are other constitutional tasks. The term “equitable growth” mentioned in

the TOR can take flesh and blood only in that manner.

21

APPENDIX A

Taxes available for levy by Village-level panchayats as Per state conformity acts (as amended up to March 2002

No. Tax/Rate/Cess AP Ass Bih Guj Har HP Kar Ker

MP

Mah Ori Pu

n Raj TN UP WB

1. House Tax/Building Tax X* X* X# X* X* X X X*

2. Tax on Buildings and/or Lands/Property Tax

X X* X* X* X* X

3. Surcharge on House/Building Tax X

4. Tax on cultivable land lying fallow

X

5. Tax on Agrl.land for specific purpose

X

6. Land Cess/Surcharge/Cess on Land Revenue/Local Rate on Lands

X

X

X

X

X*

x*

7. Land Conversion Cess X

8. Betterment levy on lands X*

9. Tax on commercial crops x

10. Surtax on Addl.Stamp Duty/ Duty on transfer of property

X X X X x

x*

11. Tax on professions; Trades, Calling, etc.

X* X X X X* X X*

12. Entertainment Tax/Additional Entertainment Tax

X* X X $ X X* X X*

13. Show Tax

14. Pilgrim Tax / fees X X X X X

15. Octroi X X X

16. Tax on Advertisements X* X X

17. Kolagaram Tax X*

18. Tolls X X X X

19. Tax on Sale of firewood and thatch, conservancy and slaughter Houses

X X

20. Tax on Private Hat and Private Fisheries

X

21. Tax on goods sold in a market, hat, etc.

X X

22. Vehicle tax X X X X X X X X X

23. Animal Tax X X X X X

24. Conservancy Rate X* X* X X X* X* X X X X 25. Lighting Rate X* X* X X X X* X* X X X X X 26. Water Rate X* X* X X X X X X* X* X X X X X 27. Drainage Rate X* X X* X X X 28. Spl. Tax for Community X X X* X X

22

No. Tax/Rate/Cess AP Ass Bih Guj Har HP Kar Ker

MP

Mah Ori Pu

n Raj TN UP WB

Services/Civic Purposes/Public utility works

X

29

Tax on Shops and Services

X X X

Total 12 10 5 12 4 9 7 11 8 9 8 7 7 2 8 8

* Obligatory Tax $ Other than cinematograph exhibitions # Tax on occupants of holdings. AP - Andhra Pradesh Mah - Maharastra Ass - Assam MP - Madhya Pradesh Bih - Bihar Pun - Punjab Guj - Gujarat Raj - Rajasthan Har - Hariyana TN - Tamil Nadu HP - Himachal Pradesh UP - Uttar Pradesh Kar - Karnataka Ker - Kerala Ori - Orissa WB - West Bengal

23

APPENDIX A1

Taxes available for levy by Intermediate level panchayats as Per state conformity acts (as amended up to march 2002)

No Tax/Rate/Cess AP Ass Bih Guj Har HP Kar Ker MP Mah

Ori Pun

Raj TN UP WB

1

Surcharge/Cess on Land Revenue/Land Cess/Local Rate/Local Cess Surcharge

X X

X X* X X

2 Development Tax on Agrl. Land

X

3 Addl Stamp Duty X X

4 Tax on Theatres or Public entertainments.

X*

5 Tax on Professions, trades, calling, etc.

X# X

6 Tolls on persons, vehicles, animals and ferries

X X X

7 Minor Irrigation Cess

8 Lighting Rate Tax X X X X 9 Water rate/tax/cess X X X X X X 10 Road Cess

11 Public works cess X

12 Education cess X X X

13 Surcharge on any Tax imposed by GPs

X X X X

14 Tax on Fairs X X

Total 2 3 4 3 0 0 0 0 3 2 0 4 5 1 2 3

# = Except on those not covered by Gram Panchayats. * = Obligatory Tax

24

APPENDIX A2

Taxes available for levy by District-level panchayats as Per state conformity acts (as amended up to march 2002)

Source: Conformity Acts, Oommen (1995) Appendix A and Choudhury and Subrahmanyan (2000) Vol.

No Tax/Rate/Cess AP Ass Bih Guj Har HP Kar Ker MP Ma

h Ori Pun Raj TN UP WB

1 Tax on Circumstances and Property

X

2 Spl. Tax on Lands and Buildings

X

3 Additional Stamp

Duty X X X

4

Tax on lands benefited by Irrigation works or Development Schemes

X

5 Tax on Professions, trades, calling, etc.

X X

6 Tolls on Persons, vehicles, animals and ferries

X X X X

7 Pilgrim Tax X

8 Tax on fairs, melas and other Entertainments

X

9 Water Rate X X X X X X 10 Lighting Rate X X X X 11 Conservancy Tax

12 Road Cess

13 Tax / Addl. Tax on GP Taxes

X

14 Tax on Public institutions (e.g. hospitals, schools)

X

Total 0 3 5 3 1 0 0 0 0 5 0 0 2 0 4 3

25

REFERENCE

Bird, Richard M (2000), Inter Governmental Fiscal Relations: Universal Principles, Local Applications, Andrew Young School, Georgia State University. Choudhury RC and K.Sivasubrahmanyam (2000) Functional and Financial Devolution on PRIs: A study Across selected states Vol.1, NIRD, Hyderabad. Deaton, Angus and Jean Dreze (2002) “Poverty and inequality in India: A reexamination” Economic and Political Weekly. 38 (36). Fukasaku Kiichiro and L.R.De MelLo (1999) Fiscal Decentralisation in Emerging Economics, Development center, OECD Paris. George Mathew (2000), Status of Panchayati Raj in the States and Union Territories of India, Institute of Social Sciences, New Delhi. King, David (1984), Fiscal Tiers – The Economics of Multi-level Government, George Allen and Unwin. Kurian NJ (2000) “Widening regional disparities in India” Economic and Political Weekly 12, February. Mulgan Richard (1997) “The process of accountability” , Australian Journal of Public Administration, Vol. (56)(1) March 1997. Oates Wallace E (1972), Fiscal Federalism, Harcourt Brace Javanovich lnc

Oommen.M.A (2000) “Panchayati Raj Institutions, Eleventh Finance Commission and working towards a new fiscal federalism” in D.K Sreevastava (2000) ed. ________(2003) Fiscal Decentralisation to Rural Local Bodies: A case study of Kerala, A World Bank sponsored study (to be published).

Planning Commission, (2001), Approach Paper to the Tenth Five Year Plan, Government of India, New Delhi. Pravin Sheth (2000) “Gujarat” in G.Mathew, (2000), ed. Raja Raman Indira (2003), A fiscal domain for Panchayats, Oxford University Press. Rao Govinda.M, (2003) Fiscal decentralisation to rural local bodies: A case study of Karnataka (A World Bank – Sponsored study) (To be published). Satish Chandran T.R (2000) “Karnataka” in G.Mathew, ed.

26

Sen, Amartya (2000), Development as Freedom, Oxford University Press. Siva Subrahmanyam.K (2002), “Second Generation Amends to Panchayati Raj: A suggested framework” , The Administrator, Vol. 45, December. Sree Vastava.D.K (2000) ed, Fiscal Federalism in India: Contemporary challenges. National Institute of Public Finance and` Policy, New Delhi.

![Optimal Priority Assignments in P-FRP › nsm › _docs › cosc › technical-reports › 2011 › ...Functional Reactive Programming (FRP) [28] is a declarative programming language](https://img.dokumen.tips/doc/110x75/5f0f676f7e708231d443fdde/optimal-priority-assignments-in-p-frp-a-nsm-a-docs-a-cosc-a-technical-reports.jpg)