Embed Size (px)

Citation preview

Q2 2011 / Q3 2011

new Supply

RenTAlS

occupAncy

Bangkok RETaIL MaRkETThAilAnd

www.colliers.co.th

Bangkok Retail MarkethighlighTS

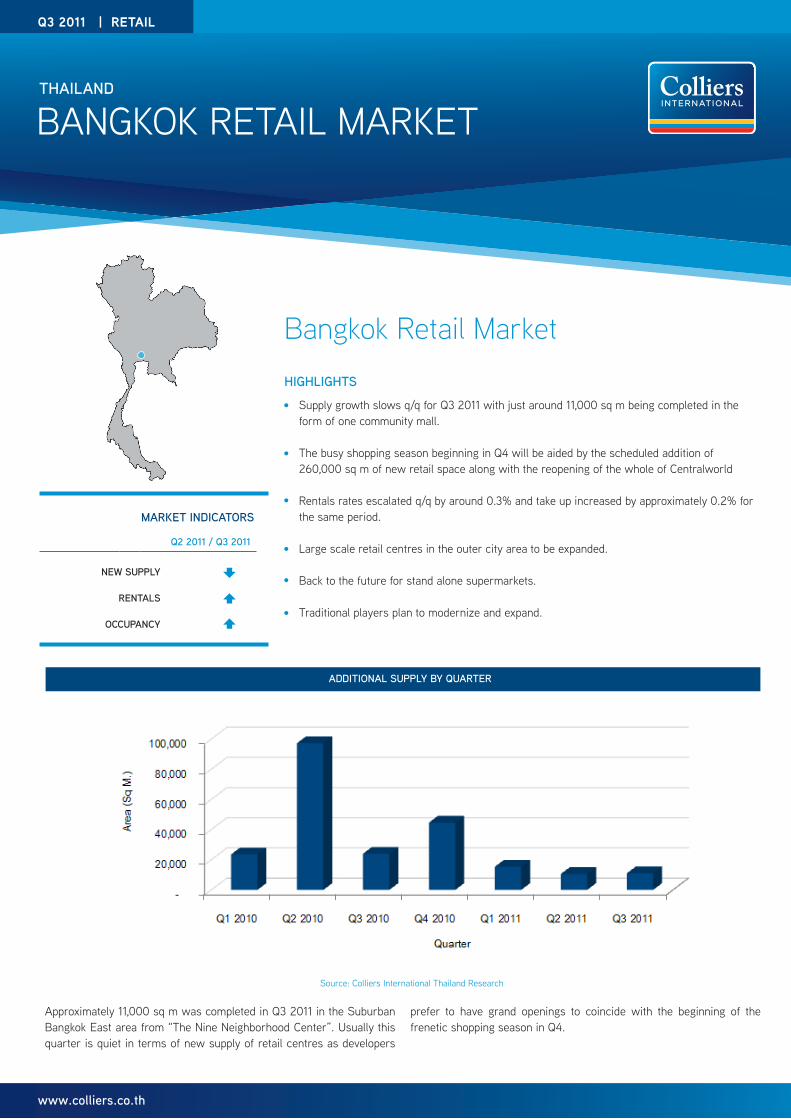

Supply growth slows q/q for Q3 2011 with just around 11,000 sq m being completed in the form of one community mall. The busy shopping season beginning in Q4 will be aided by the scheduled addition of 260,000 sq m of new retail space along with the reopening of the whole of Centralworld Rentals rates escalated q/q by around 0.3% and take up increased by approximately 0.2% for the same period. Large scale retail centres in the outer city area to be expanded. Back to the future for stand alone supermarkets. Traditional players plan to modernize and expand.

Q3 2011 | RETAIL

mARkeT indicAToRS

AddiTionAl Supply by QuARTeR

Source: Colliers International Thailand Research

approximately 11,000 sq m was completed in Q3 2011 in the Suburban Bangkok East area from “The nine neighborhood Center”. Usually this quarter is quiet in terms of new supply of retail centres as developers

prefer to have grand openings to coincide with the beginning of the frenetic shopping season in Q4.

COLLIERS INTERNATIONAL | P. 2

Community malls are an ever popular feature of the retail market. “The nine neighborhood Center” is a new community mall on Rama 9 road in Suburban Bangkok – East, developed by MBk Plc. and comprising eight buildings with a total of approximately 11,000 sq m.

Central Pattana Plc. reopened Central Plaza Ladprao on 28 august 2011, after it closed for six months for renovation with CPn spending approximately 900 million baht for redecoration of the whole plaza. The

most significant change is the modern interior and exterior design in line with recent CPn developments.

Big C has launched a new store format with “Big C Jumbo” catering to wholesalers and shopkeepers. Big C plans to change more branches of ex-Carrefour stores to this model which will be in direct competition with Makro wholesale centres.

BAngkok RETAIL MARkET REPoRT | Q3 2011

nearly 50% of total retail space in the Bangkok area is located outside the urban area; due to Suburban Bangkok being a residential area, therefore developers focus on retail projects. Many large shopping malls

and hypermarkets are located in Suburban Bangkok and an abundant supply of land plots is still available for large scale retail projects.

Source: Colliers International Thailand Research

bReAkdown of ReTAil SpAce in bAngkok by locATion, Q3 2011

cumulATive of fuTuRe Supply in bAngkok by yeAR And cATegoRy, Q3 2011

bReAkdown of hiSToRicAl TAke-up RATe of ReTAil SpAce by locATion, Q1 2010 – Q3 2011

COLLIERS INTERNATIONAL | P. 3

Source: Colliers International Thailand Research

Source: Colliers International Thailand Research

The future supply scheduled to be completed in the last quarter of 2011 amounts to more than 260,000 sq m, with approximately 215,000 sq m as shopping malls. A significant amount of space will come from Central Rama 9 and Terminal 21, with more than 124,000 sq m and both projects

are scheduled to open in Q4 2011. In addition, Centralworld is slated to reopen the remaining section that was damaged in the May 17 riots, including Zen department store. This is not included as new supply.

Take up rate for retail in Bangkok is similar to the previous quarter, although small increases were registered in all zones for Q3 2011.

fuTuRe Supply

demAnd – TAke-up

BAngkok RETAIL MARkET REPoRT | Q3 2011

COLLIERS INTERNATIONAL | P. 4

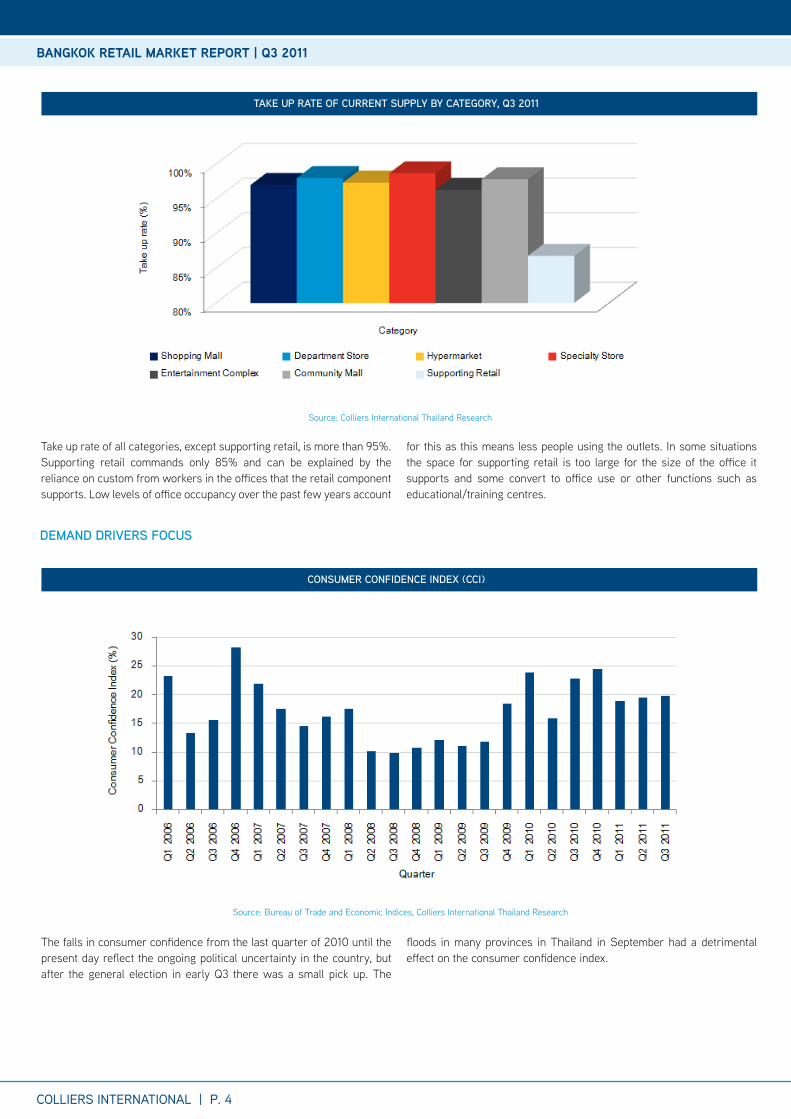

Take up rate of all categories, except supporting retail, is more than 95%. Supporting retail commands only 85% and can be explained by the reliance on custom from workers in the offices that the retail component supports. Low levels of office occupancy over the past few years account

for this as this means less people using the outlets. In some situations the space for supporting retail is too large for the size of the office it supports and some convert to office use or other functions such as educational/training centres.

The falls in consumer confidence from the last quarter of 2010 until the present day reflect the ongoing political uncertainty in the country, but after the general election in early Q3 there was a small pick up. The

floods in many provinces in Thailand in September had a detrimental effect on the consumer confidence index.

Source: Colliers International Thailand Research

Source: Bureau of Trade and Economic Indices, Colliers International Thailand Research

TAke up RATe of cuRRenT Supply by cATegoRy, Q3 2011

conSumeR confidence index (cci)

BAngkok RETAIL MARkET REPoRT | Q3 2011

demAnd dRiveRS focuS

COLLIERS INTERNATIONAL | P. 5

ReTAil SAleS index by QuARTeR

RenTAl RATe duRing The yeAR Q1 2010 – Q3 2011

Source: Bank of Thailand, Colliers International Thailand ResearchRemark: Year 2002 = 100

Source: Colliers International Thailand Research

Since the last quarter of 2010 onwards the retail sales index has been higher than the last five years due to increasing political stability and retail developers launching new marketing campaigns to boost their

centres. The floods that have been occurring in September may lead to a temporary spike in non-discretionary spending due to buyers wishing to stock up on essential items.

The rental rates in every area are similar from the previous quarter, although some new retail centre have increased their rental rate, which

has had a marginal effect on the whole market.

ReTAil SAleS

RenTAlS

BAngkok RETAIL MARkET REPoRT | Q3 2011

COLLIERS INTERNATIONAL | P. 6

Supermarkets in the past are usually located in a retail centre, however a new trend is for a supermarket chain to develop stand alone outlets due to limited sized land plots being available for development of a community mall but with demand from residential areas nearby. Many are being developed from a group of old shophouses and are often smaller in size than usual supermarkets and can often also be equated with convenience stores. In the past, before the advent of the modern retail centre, supermarkets were the only form of mass retail and were therefore stand alone, and ironically we are seeing this situation occur again.

Tesco Lotus launched their own supermarket format a long time ago, which reaches many areas throughout Thailand. Tesco Lotus Market still commands the largest share of the market followed by Tops Super and Tops Market, but this does not include Tesco Lotus Express which has less than 300 square metres per outlet with more than 850 branches in Thailand and is a direct competitor with 7 Eleven.other retail developers also wish for a share of this market. Central Food Retail Co., Ltd. have opened many Tops Super and Tops Market outside retail centres, and in addition they also have opened numerous Tops Daily outlets with a convenience store format in Bangkok and up-country. approximately half of Tops Super and Tops Market are not stand alone format, due to them being located in retail centres and the rest mostly hail back to the days before the emergence of shopping centres.

Although Foodland opened its first supermarket in Thailand more than 30 years ago, they still only have 10 branches in Bangkok and are fast losing market share. However recently they plan to expand with new branches along with an eventual listing on the SET. Max Valu, part of the Japanese aeon group, plans to expand with smaller size branches with more than ten a year being slated.

Source: Colliers International Thailand ResearchRemark : Including stand alone and inside retail centre supermarket

ShARe of numbeR of SupeRmARkeTS ThRoughouT ThAilAnd

TRendS | SupeRmARkeTS go iT Alone AgAin

BAngkok RETAIL MARkET REPoRT | Q3 2011

COLLIERS INTERNATIONAL | P. 7

The increasing land price in the urban Bangkok area along with town planning regulations makes larger retail centre development less appealing in the centre; instead more large scale retail centres are being located in the outer city and suburban areas as well as in the neighbouring provinces.

To gain market share in the centre, more retailers are reducing the size of new developments with a move from supermarket to a hybrid style convenience store. In order to accommodate for this blurring of distinctions between hypermarket, supermarket and convenience store, retailers are developing more brands to allow consumers to differentiate such as Mini Big C and Tops Deli.

Many residential developers are also looking to integrate community malls in their own projects for the convenience of residents and thus enhance the appeal of the residential property and also potentially its value

Many large scale retail centres in the outer city area plan to expand existing retail space, due to the increasing population in the catchment area. Seacon Square, Paradise Park Phase 2, Fashion Island, Central Bangna, and The Mall Bangkae all have plans in the works. The challenge for such expansions is maintaining the right balance and configuration of retail outlets throughout the existing and expanded centre as a whole.

foRecAST

BAngkok RETAIL MARkET REPoRT | Q3 2011

COLLIERS INTERNATIONAL | P. 8

Appendix

BAngkok RETAIL MARkET REPoRT | Q3 2011

COLLIERS INTERNATIONAL | P. 9

BAngkok RETAIL MARkET REPoRT | Q3 2011

ReTAil locATionS

ReTAil mARkeT cATegoRieSThe organized retail market in Thailand can be divided into seven main categories, based on size, characteristics, goods sold, and pricing:1) Shopping mall / Shopping centre2) department Store (figures for this report include stand-alone stores only; those located in shopping malls are not included)3) hypermarket 4) community mall

5) Specialty Stores6) entertainment complex (this does not include entertainment areas in shopping malls, as these represent an intrinsic part of the shopping mall mix)7) Supporting Retail

Note: For the purposes of the report, retail refers to organized retail services and excludes traditional single proprietor outlets often located in shophouses and markets consisting of predominantly small traders. Also, supermarkets have been excluded from this report.

BAngkok RETAIL MARkET REPoRT | Q3 2011

collieRS inTeRnATionAl ThAilAnd mAnAgemenT TeAm

RETaIL SERVICESasharawan Wachananont | Senior Manager oFFICE & InDUSTRIaL SERVICESnarumon Rodsiravoraphat | Senior Manager aDVISoRY SERVICES | HoSPITaLITY Jean Marc garret | Director PRoJECT SaLES & MaRkETIngMonchai orawongpaisan | Senior Manager RESIDEnTIaL SaLES & LEaSIngnapasawan Chotephard | Manager aDVISoRY SERVICESnapatr Tienchutima | associate Director

REaL ESTaTE ManagEMEnT SERVICESBandid Chayintu | associate Director

InVESTMEnT SERVICESnukarn Suwatikul | associate Director Wasan Rattanakijjanukul | Senior Manager

RESEaRCHTony Picon | associate DirectorSurachet kongcheep | Senior Manager

VaLUaTIon & aDVISoRY SERVICESnicholas Brown | associate DirectorPhachsanun Phormthananunta | associate Director Santipong kreemaha | Senior Manager Wanida Suksuwan | Manager PaTTaYa oFFICEMark Bowling | Senior Sales ManagerSupannee Starojitski | Senior Business Development Manager / Office Manager

CoLLIERS InTERnATIonAL ThAILAnd:

Bangkok Office 17/F Ploenchit Center, 2 Sukhumvit Road, klongtoey,Bangkok 10110 ThailandTel +662 656 7000fAx +662 656 7111 emAil [email protected] Pattaya Office 519/4-5, Pattaya Second Road (opposite Central Festival Pattaya Beach), nongprue, Banglamung, Chonburi 20150Tel +6638 427 771fAx +6638 427 772 emAil [email protected]

ReSeARcheR:

ThailandTony Piconassociate Director | ResearchemAil [email protected]

ReSeARcheR:

ThailandSurachet kongcheepSenior Manager | ResearchemAil [email protected]

512 offices in 61 countries on 6 continents

This report and other research materials may be found on our website at www.colliers.co.th. Questions related to information herein should be directed to the Research Department at the number indicated above. This document has been prepared by Colliers International for advertising and general information only. Colliers International makes no guarantees, representations or warranties of any kind, expressed or implied, regarding the information including, but not limited to, warranties of content, accuracy and reliability. any interested party should undertake their own inquiries as to the accuracy of the information. Colliers International excludes unequivocally all inferred or implied terms, conditions and warranties arising out of this document and excludes all liability for loss and damages arising there from. Colliers International is a worldwide affiliation of independently owned and operated companies.

www.colliers.co.th

accelerating success.

• a leader in real estate consultancy worldwide• 2nd most recognized commercial real estate brand globally • 2nd largest property manager• 979 million square feet under management• over 12,500 professionals