Embed Size (px)

Citation preview

ON

“BAJAJ V/S HERO HONDA”

SUBMITTED TO: EXTERNAL GUIDE:

SUBMITTED BY:

Chaptet-1

INTRODUCTION

Peter Drucker called the automobile industry as "the industry of industries". During

the last few years, the production and management systems have been revolutionized

in the automobile industry (Karmokolias, 1990). One of the major changes in the

industry has been the opening up and growth of several emerging markets. In 1991,

the Government of India embarked on an ambitious structural adjustment programme

aimed at economic liberalization, based on the pillars of Delicensing, Decontrol,

Deregulation and Devaluation. Post-liberalization, the Government of India's new

automobile policy announced in June 1993 contained measures, such as delicensing,

automatic approval for foreign holding of 51% in Indian companies, abolition of

phased manufacturing programme, reduction of excise duty to 40% and import duties

of CKD to 50% and of CBU to 110%, and commitment to indigenization schedules.

The Indian automotive industry has been on a high growth path in the domestic

market, given strong demand-push factors coupled with an encouraging policy

environment. Changing lifestyles, increasing disposable income, deterioration of

public transport and accelerated urbanisation is leading to a growth in demand for

passenger vehicles and 2-wheelers. Improving rural income on account of the rise in

the agri-commodity prices and near normal monsoons together can boost the demand

for tractors. Domestic demands for cars are expected to grow at a double-digit rate for

the next three to four years. The brilliant performance of the automotive sector is

attributed to better performance of the economy and high all round growth leading to

robust GDP growth, improved infrastructure development, excise duty reduction on

passenger vehicles, improved financing of second hand vehicles, availability of

finance in rural and semi-urban areas and the emergence of India as a manufacturing

hub for the automotive industry. Investment upto Rs 30,000 crore has been planned

for the Sector, by leading Indian and global players, by 2010.

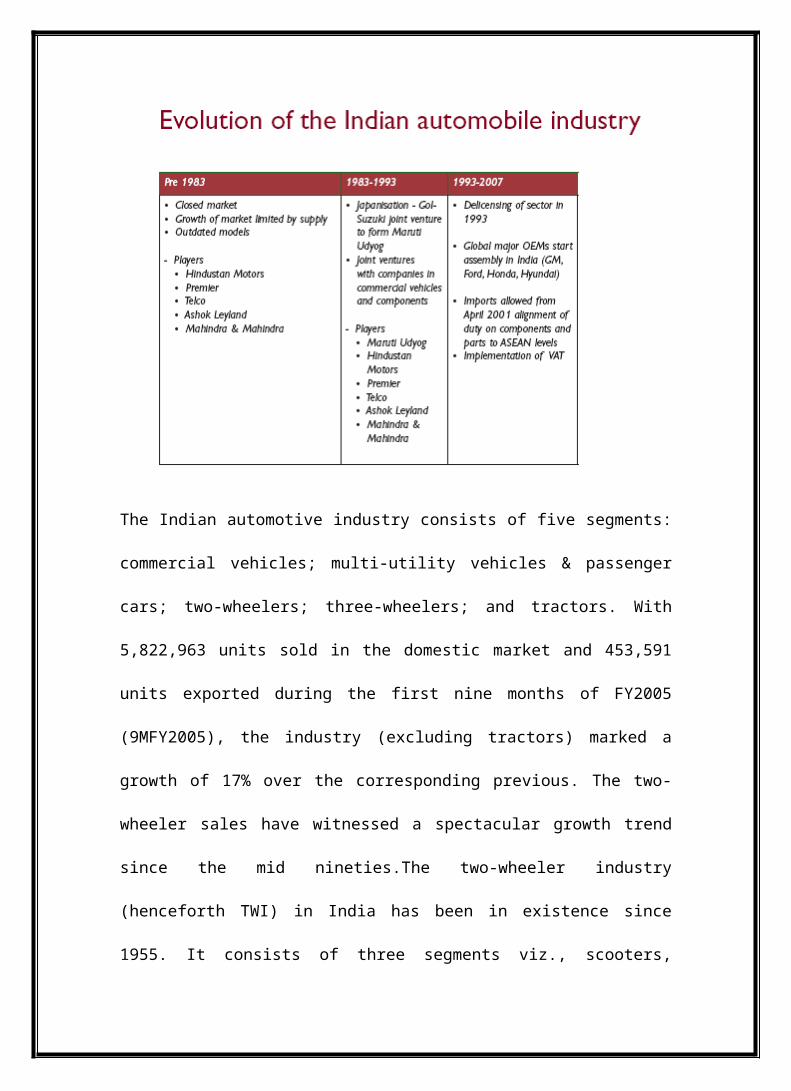

The Indian automotive industry consists of five segments: commercial vehicles;

multi-utility vehicles & passenger cars; two-wheelers; three-wheelers; and tractors.

With 5,822,963 units sold in the domestic market and 453,591 units exported during

the first nine months of FY2005 (9MFY2005), the industry (excluding tractors)

marked a growth of 17% over the corresponding previous. The two-wheeler sales

have witnessed a spectacular growth trend since the mid nineties.The two-wheeler

industry (henceforth TWI) in India has been in existence since 1955. It consists of

three segments viz., scooters, motorcycles, and mopeds. The increase in sales volume

of this industry is proof of its high growth. In 1971, sales were around 0.1 million

units per annum. But by 1998, this figure had risen to 3 million units per annum.

Similarly, capacities of production have also increased from about 0.2 million units of

annual capacity in the seventies to more than 4 million units in the late nineties. The

two-wheeler industry in India has to a great extent been shaped by the evolution of the

industrial policy of the country. Regulatory policies like FERA and MRTP caused the

growth of some segments in the industry like motorcycles to stagnate. These were

later able to grow (both in terms of overall sales volumes and number of players) once

foreign investments were allowed in 1981. The reforms in the eighties like

‘broadbanding’ caused the entry of several new firms and products which caused the

existing technologically outdated products to lose sales volume and/or exit the market.

Finally, with liberalization in the nineties, the industry witnessed a proliferation in

brands.

The technological backwardness of the Indian two-wheeler industry was one of the

reasons for the initiation of reforms in 1981. Foreign collaborations were allowed for

all two-wheelers up to an engine capacity of 100 cc. This prompted a spate of new

entries into the industry the majority of which entered the motorcycle segment,

bringing with them new technology that resulted in more efficient production

processes and products. The variety in products available also improved after

‘broadbanding’ was allowed in the industry in 1985 as a part of NEP. This, coupled

with the announcement of the MES of production for the two wheeler industry, gave

firms the flexibility to choose an optimal product and capacity mix which could better

incorporate market demand into their production strategy and thereby improve their

capacity utilization and efficiency. These reforms had two major effects on the

industry: First, licensed capacities went up to 1.1 million units per annum

overshooting the 0.675 million units per annum target set in the Sixth Plan. Second,

several existing but weaker players died out giving way to new entrants and superior

products.

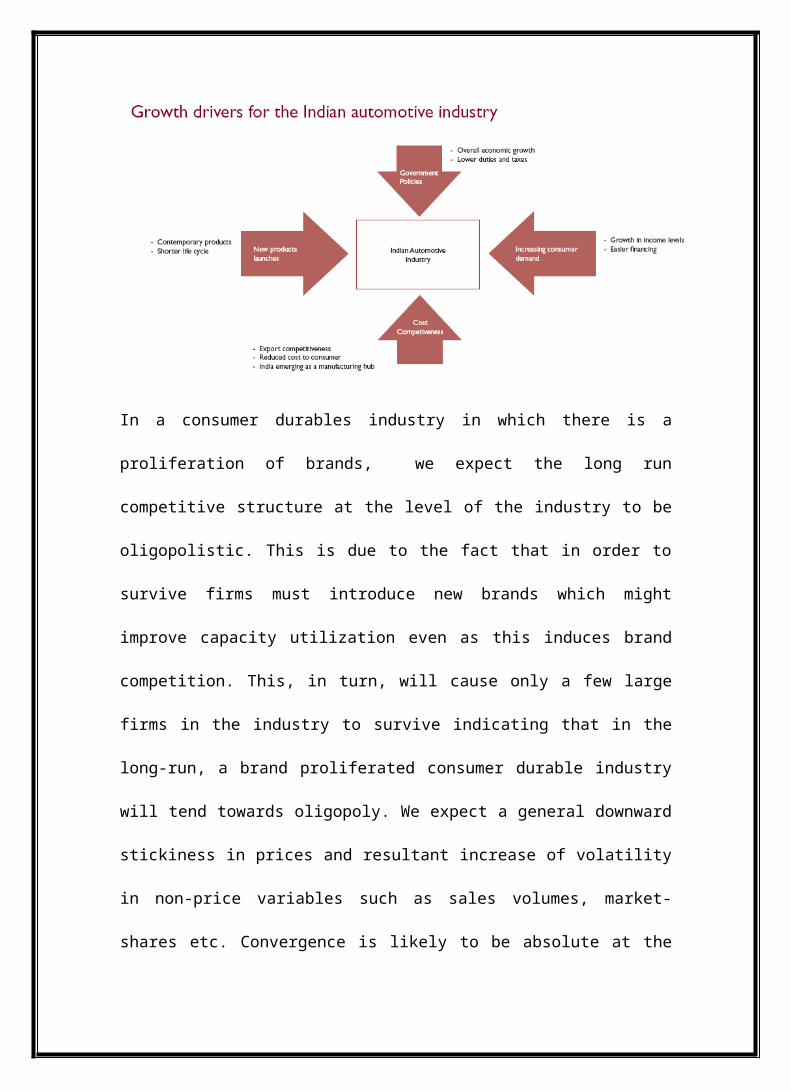

In a consumer durables industry in which there is a proliferation of brands, we expect

the long run competitive structure at the level of the industry to be oligopolistic. This

is due to the fact that in order to survive firms must introduce new brands which

might improve capacity utilization even as this induces brand competition. This, in

turn, will cause only a few large firms in the industry to survive indicating that in the

long-run, a brand proliferated consumer durable industry will tend towards oligopoly.

We expect a general downward stickiness in prices and resultant increase of volatility

in non-price variables such as sales volumes, market-shares etc. Convergence is likely

to be absolute at the level of the segment and conditional at the level of the industry.

Competitive strategies (which include product development and other strategies

aimed at innovation and technological change) are more inter-dependent at the level

of the market-segment than at the level of the industry. This is due to the fact that

within each segment the products are, to a large extent, similar. Hence we can expect

convergence to be absolute at the level of the segment and conditional at the level of

the industry.Two-wheeler sales continue to be buoyant with a 19% growth joy, driven

by its motorcycle segment that has posted a rise of 24%. Bajaj Auto’s market share in

the domestic motorcycle market has improved from 23% in FY03 to 30% in FY06.

Hero Honda, the largest motorcycle manufacturer in India, with a domestic market

share of 50% in FY06, was down from 52% in FY05, while the market share of TVS

Motors is 18%. The Indian two-wheeler industry is entering a strong secular growth

phase, driven by increasing affordability, easy availability of finance, and accelerating

exports. The next phase of earnings growth will be driven by unit volume growth,

while the four-wheeler passenger car industry is driven by low penetration, increasing

consumer aspiration levels, increasing affordability, and proliferation of new models.

Some of the features that deserve attention in respect of the Indian two wheeler

segment are as mentioned:

The total sale of two wheelers in India has touched a figure of 7.86 million units

by March, 2007, up 11.42% from the previous fiscal figures of 7.05 million.

Production during the period reached 8.63 million units.

The production of two wheelers in India is expected to reach a staggering 17.85

million units by 2011-12, more than double of the current production level.

The two-wheeler production capacity is to reach 22.31 million units in 2011-12

compared with 10.78 million in 2006-07.

India is likely to export 1.39 million two-wheelers in 2011-12 compared with

590,000 in 2006-07.

Total investment for new capacity generation in two-wheeler segment is likely to

be more than $2.2 billion (INR10, 000 crore).

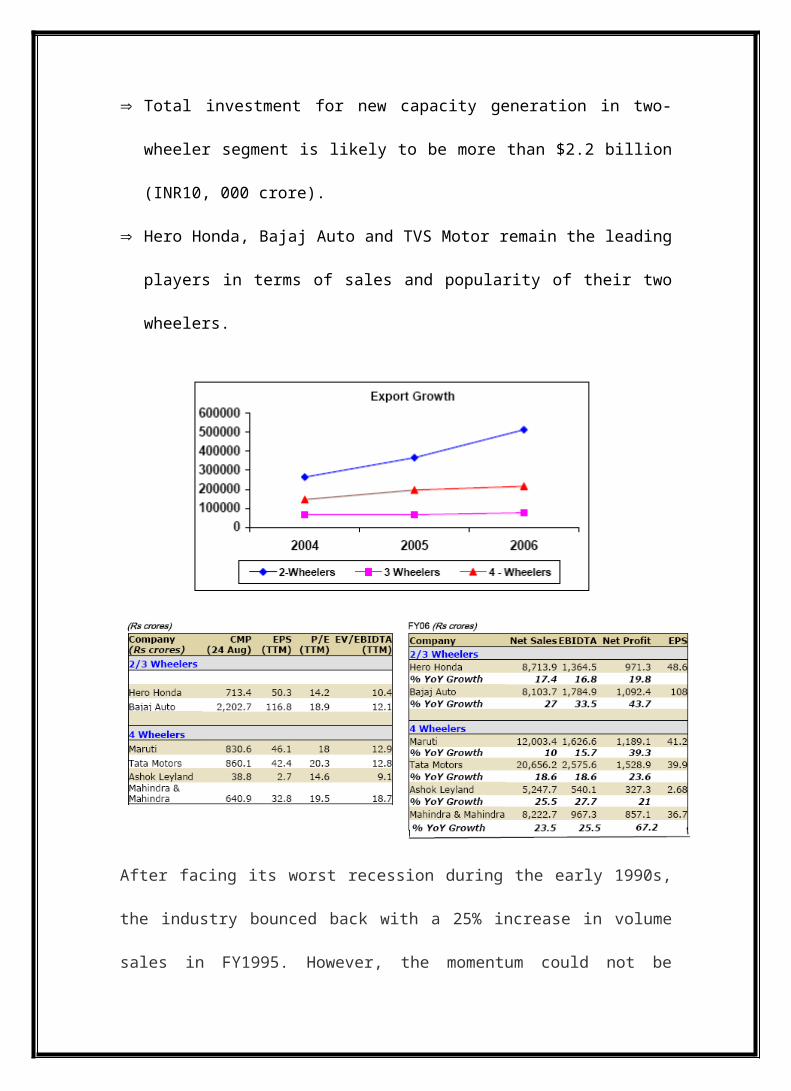

Hero Honda, Bajaj Auto and TVS Motor remain the leading players in terms of

sales and popularity of their two wheelers.

After facing its worst recession during the early 1990s, the industry bounced back

with a 25% increase in volume sales in FY1995. However, the momentum could not

be sustained and sales growth dipped to 20% in FY1996 and further down to 12% in

FY1997. The economic slowdown in FY1998 took a heavy toll of two-wheeler sales,

with the year-on-year sales (volume) growth rate declining to 3% that year. However,

sales picked up thereafter mainly on the strength of an increase in the disposable

income of middle-income salaried people (following the implementation of the Fifth

Pay Commission's recommendations), higher access to relatively inexpensive

financing, and increasing availability of fuel efficient two-wheeler models.

Nevertheless, this phenomenon proved short-lived and the two-wheeler sales declined

marginally in FY2001. This was followed by a revival in sales growth for the industry

in FY2002. Although, the overall two-wheeler sales increased in FY2002, the scooter

and moped segments faced de-growth. FY2003 also witnessed a healthy growth in

overall two-wheeler sales led by higher growth in motorcycles even as the sales of

scooters and mopeds continued to decline. Healthy growth in two-wheeler sales

during FY2004 was led by growth in motorcycles even as the scooters segment posted

healthy growth while the mopeds continued to decline. Figure 1 presents the

variations across various product sub-segments of the two-wheeler industry between

FY1995 and FY2004.

DEMAND DRIVERS

The demand for two-wheelers has been influenced by a number of factors over the

past five years. The key demand drivers for the growth of the two-wheeler industry

are as follows:

Inadequate public transportation system, especially in the semi-urban and rural

areas;

Increased availability of cheap consumer financing in the past 3-4 years;

▪ Increasing availability of fuel-efficient and low-maintenance models;

▪ Increasing urbanisation, which creates a need for personal transportation;

▪ Changes in the demographic profile;

▪ Difference between two-wheeler and passenger car prices, which makes two-

wheelers the entrylevel vehicle;

▪ Steady increase in per capita income over the past five years; and

▪ Increasing number of models with different features to satisfy diverse consumer

needs.

While the demand drivers listed here operate at the broad level, segmental demand is

influenced by segment-specific factors.

DEMAND

Segmental Classification and Characteristics

The three main product segments in the two-wheeler category are scooters,

motorcycles and mopeds. However, in response to evolving demographics and

various other factors, other sub segments emerged, viz. scooterettes, gearless scooters,

and 4-stroke scooters. While the first two emerged as a response to demographic

changes, the introduction of 4-stroke scooters has followed the imposition of stringent

pollution control norms in the early 2000. Besides, these prominent sub-segments,

product groups within these sub-segments have gained importance in the recent years.

Examples include 125cc motorcycles, 100-125 cc gearless scooters, etc.

‘Riding on Top Gear’ is what our two-wheeler update said for the first half of FY05,

wherein the industry volumes had grown over 12% on back of good monsoons. If that

was anything to be happy about, the second half of FY05 has given the industry

reasons to celebrate, with strong volume rise of nearly 16% (Apr-Feb) in motorcycles,

largely aided by faster growth in the entry level 100 cc segment. Though competition

has been on the rise in the past year, with new models and variants being launched

every alternate day, the overall market has been growing fast enough to accommodate

all of these models. The most striking feature of the year gone by was the growing

volumes in favour of the entry-level segment. Industry leaders Hero Honda and Bajaj

Auto have once again kept the other players at bay, and increased their market share

during the year. In fact, Bajaj Auto has been outperforming the industry by a good

margin for the last few months, courtesy its new launches CT100 and the Discover.

TVS Motor on the other hand has been reeling under pressure since the time its Max

100 sales started dipping at the end of FY04 while the new models are yet to taste

success in the market. Apart from the big three, the talk of the town in the past year

was the entry of Honda Motors into the Indian motorcycle segment through its

‘Unicorn’. Launched in the premium 150 cc category, the bike received spectacular

response initially with a waiting period of almost 6 weeks.

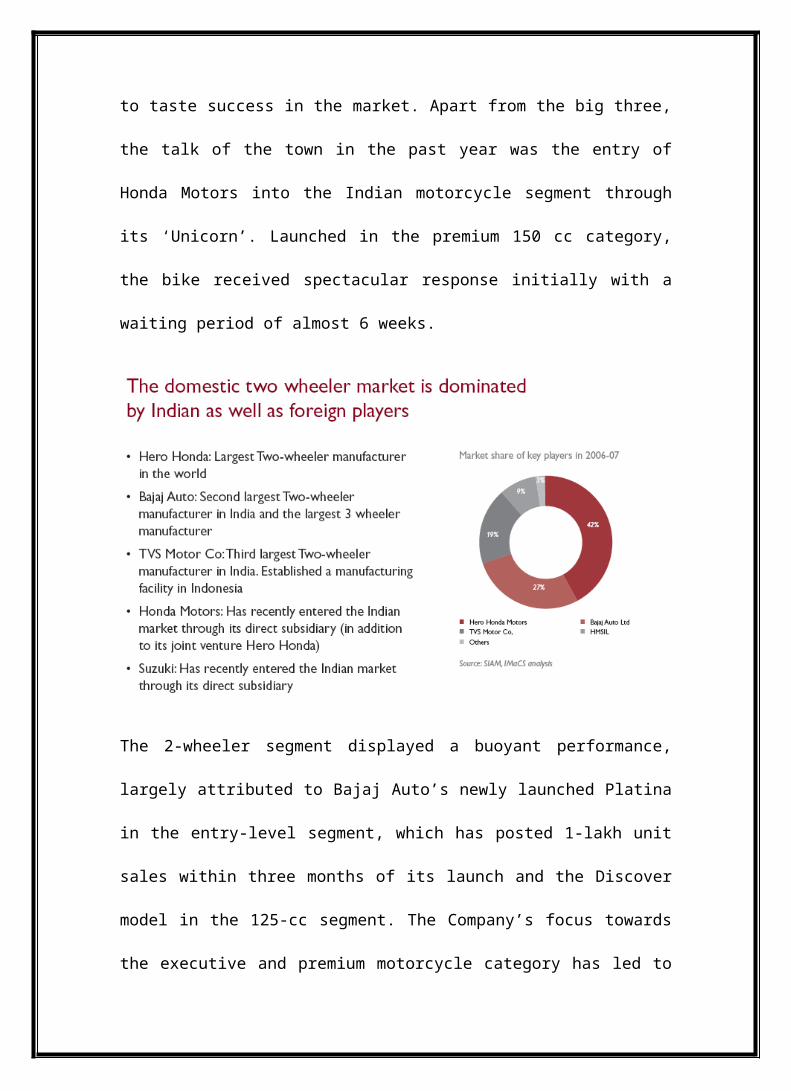

The 2-wheeler segment displayed a buoyant performance, largely attributed to Bajaj

Auto’s newly launched Platina in the entry-level segment, which has posted 1-lakh

unit sales within three months of its launch and the Discover model in the 125-cc

segment. The Company’s focus towards the executive and premium motorcycle

category has led to the expansion of the two-wheeler segment and has pushed it up the

value chain, availing better profitability. From FY06 till date, the Company has

notched up a 200-bps gain in the market share in these two segments, from 31% to

33%, respectively, eating into the market share of Hero Honda. The Company is also

likely to start manufacturing a four-wheeler low-cost goods carrier by end 2008 or

beginning 2009. Despite the strong volume growth witnessed by the industry, profits

have grown at a slower rate or even de-grown in some cases due to the cost pressures

and higher sales of economy bikes. Due to growing competition, manufacturers

resisted passing on price hikes and instead took a hit on their profits. However,

recently the companies have raised prices on most of their models by around 1-3%.

The margins for Q1FY07 for Hero Honda have been the lowest for the Company in

recent past, indicating that the margins will continue to be under pressure due to

hardened metal prices. But with hike in prices of different models, margins may show

an improvement in the current quarter as compared to last quarter’s. The Company

plans to launch seven new models in FY07, and with the launches scheduled for Q3 &

Q4, volumes are expected to grow significantly during this period. This may translate

into a richer product mix, in favour of the executive & premium segments, helping

realisations to improve. However, Hero Honda appears to be on a defensive mode,

with Bajaj Auto scoring aggressively. The first-quarter results for the automobile

sector assume great significance, given the volatility that the economy has witnessed

in the past few months. However, despite the uncertainty, the mood was upbeat

among vehicle makers and most of them posted a positive growth. With most

companies, particularly in the consumer-led 2-wheelers and passenger car space,

announcing price hikes, margins are expected to remain protected despite cost

pressures. While the Q2FY07 earnings growth should remain moderate due to the

monsoons, higher earnings are expected, Q3FY07 onwards. We advise investors to

Hold M&M, Tata Motors and Maruti, and give a BUY recommendation for Bajaj

Auto.

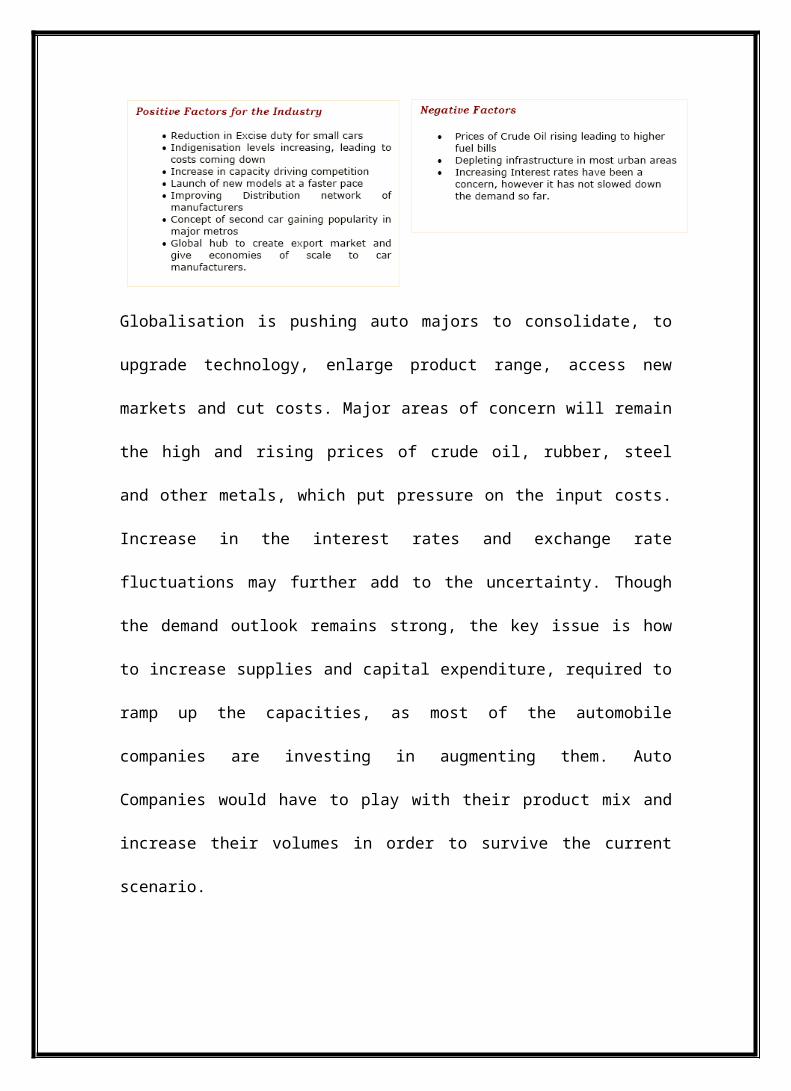

Globalisation is pushing auto majors to consolidate, to upgrade technology, enlarge

product range, access new markets and cut costs. Major areas of concern will remain

the high and rising prices of crude oil, rubber, steel and other metals, which put

pressure on the input costs. Increase in the interest rates and exchange rate

fluctuations may further add to the uncertainty. Though the demand outlook remains

strong, the key issue is how to increase supplies and capital expenditure, required to

ramp up the capacities, as most of the automobile companies are investing in

augmenting them. Auto Companies would have to play with their product mix and

increase their volumes in order to survive the current scenario.

MARKET HIGHLIGHTS

1. High Growth market

At just over 7.3 million vehicles sold in 2004-2005, the Indian automobile market is

one of the fastest growing in the world. Total unit sales grew 15.8% in 2004-05 over

the previous year.

2. 75- 125 cc motorbikes see most action

84% of the 4.9 million motorbikes sold in India in 2004-05 were in the 75-125 cc

range. This segment has the largest number of brands and variants in style and price.

Significantly, this segment has lost 3% share since 2003-04 to 125-250 cc

bikes.

3. Scooters grow 4%; 75-125 cc most popular

Scooters, geared and ungeared, are enjoying a revival of sorts, growing 4% since

2003-04 to under a million units. 63% of all scooters sold are in the 75-125 cc

segment, where all the major players have brands. Also, most of these are of

automatic gears as well.

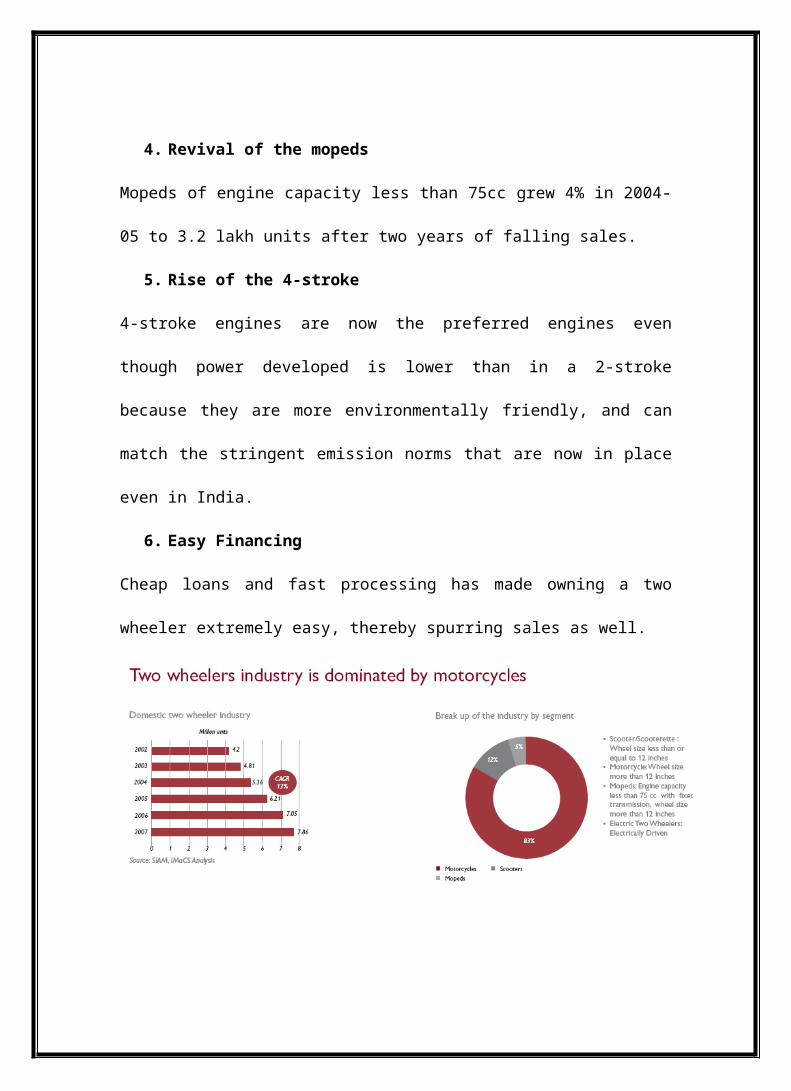

4. Revival of the mopeds

Mopeds of engine capacity less than 75cc grew 4% in 2004-05 to 3.2 lakh units after

two years of falling sales.

5. Rise of the 4-stroke

4-stroke engines are now the preferred engines even though power developed is lower

than in a 2-stroke because they are more environmentally friendly, and can match the

stringent emission norms that are now in place even in India.

6. Easy Financing

Cheap loans and fast processing has made owning a two wheeler extremely easy,

thereby spurring sales as well.

Scooters dominated the Indian two-wheeler industry till the early 1990s, when

motorcycles from Hero Honda began to appear. Within half a decade, the market

shifted decisively to motorcycles, which delivered better, styling, and power and fuel

efficiency. Today motorcycles account for three quarters of all two-wheeler sales, a

total of 49.6 lakh sold in 2004-05 against 9.2 lakh of scooters. The advent of Honda

spurred the scooter market again, with a range of ungeared and geared scooters

emerging with great style and a market positioning targeting the youth- a step

between the moped (positioned for students) and the motorcycle (upwardly mobile

young men). This strategy paid dividends to every company that adopted it; today

Honda Scooters and Motorcycles (HMSI) holds a dominant share of the scooters

market. With the rapid rise of the scooter, the moped (motorized pedal cycle) as it was

known then died a sudden death in the early 1990s. However, from 2003-04 onwards,

moped sales have again begun to creep up: chiefly because the new ranges now are a

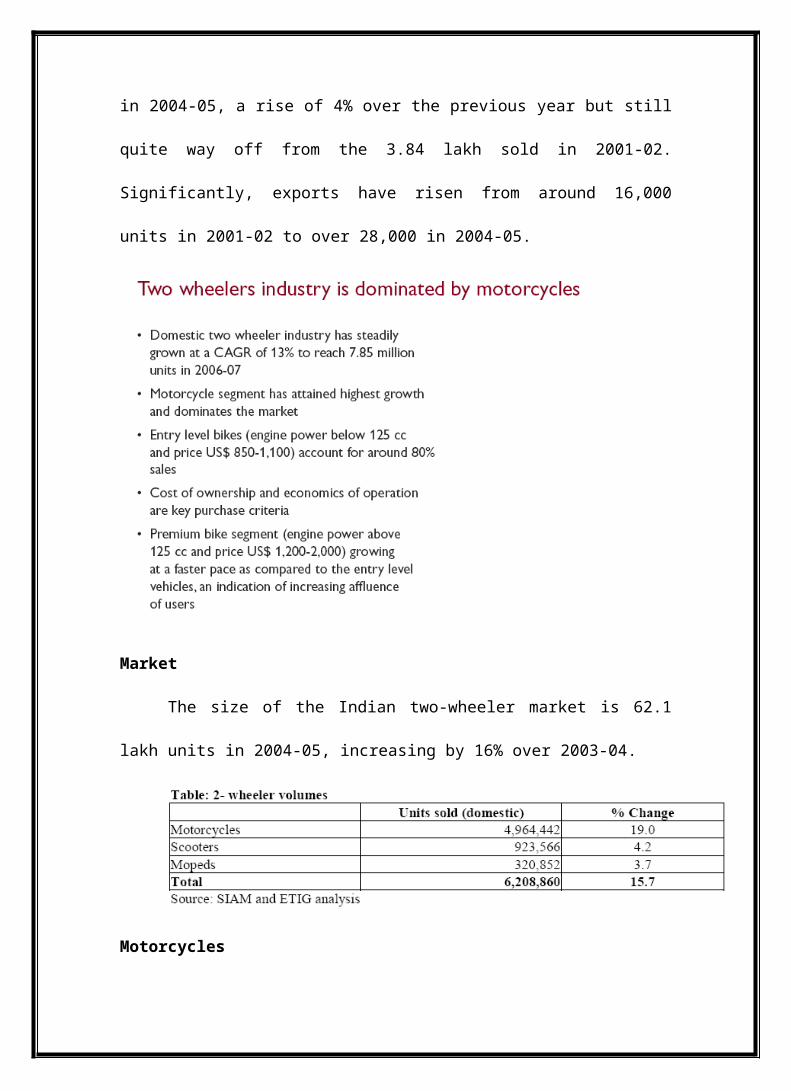

far cry in style and power from those in the late 1980s and early 1990s. 3.2 lakh

mopeds were sold in 2004-05, a rise of 4% over the previous year but still quite way

off from the 3.84 lakh sold in 2001-02. Significantly, exports have risen from around

16,000 units in 2001-02 to over 28,000 in 2004-05.

Market

The size of the Indian two-wheeler market is 62.1 lakh units in 2004-05,

increasing by 16% over 2003-04.

Motorcycles

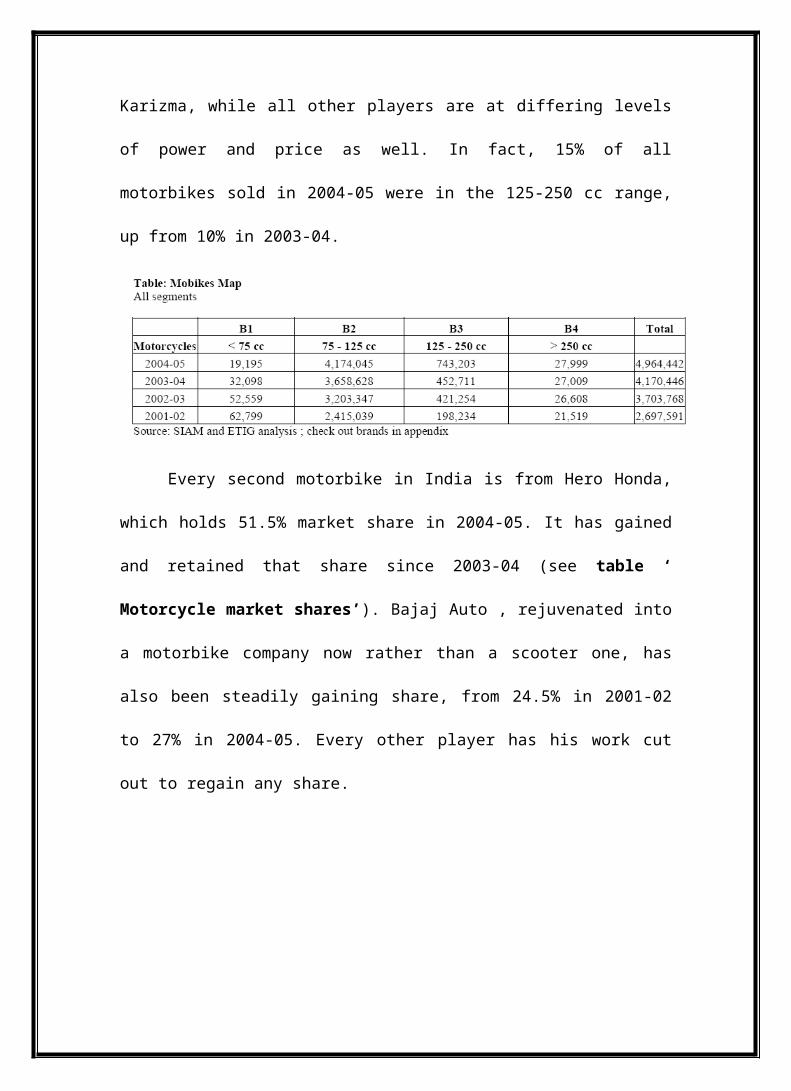

The motorcycles segment of two wheelers has seen the greatest number of

new launches as well as the most fierce competition on every plank – pricing, style,

power, fuel efficiency, pedigree and so on. The 75-125 cc segment, also called the

economy segment, remains the driver for the industry, accounting for 84% of all sales

in 2004-05 (see table ‘ Mobikes Map’). Price points in the 75-125 cc range from a

low of Rs 38,000 to as high as Rs 65-70,000. A marginal shift towards the next higher

category of power, 125-250 cc is becoming visible in

2004-05, driven by lifestyle statements, need for speed and style, greater disposable

incomes and quite simply more variety on offer in the segment. Hero Honda’s

Karizma, for example, was one of the first to be launched in this segment at over Rs

80,000 a piece, and much to the company’s surprise, sold over 2,000 units every

month in the first year of its launch. More surprisingly, its demand was coming not

just from the metros, but the semi-urban areas in North India as well. Clearly, there

was a demand for such products. Today Bajaj Auto has its hugely successful Pulsar

positioned directly against the Karizma, while all other players are at differing levels

of power and price as well. In fact, 15% of all motorbikes sold in 2004-05 were in the

125-250 cc range, up from 10% in 2003-04.

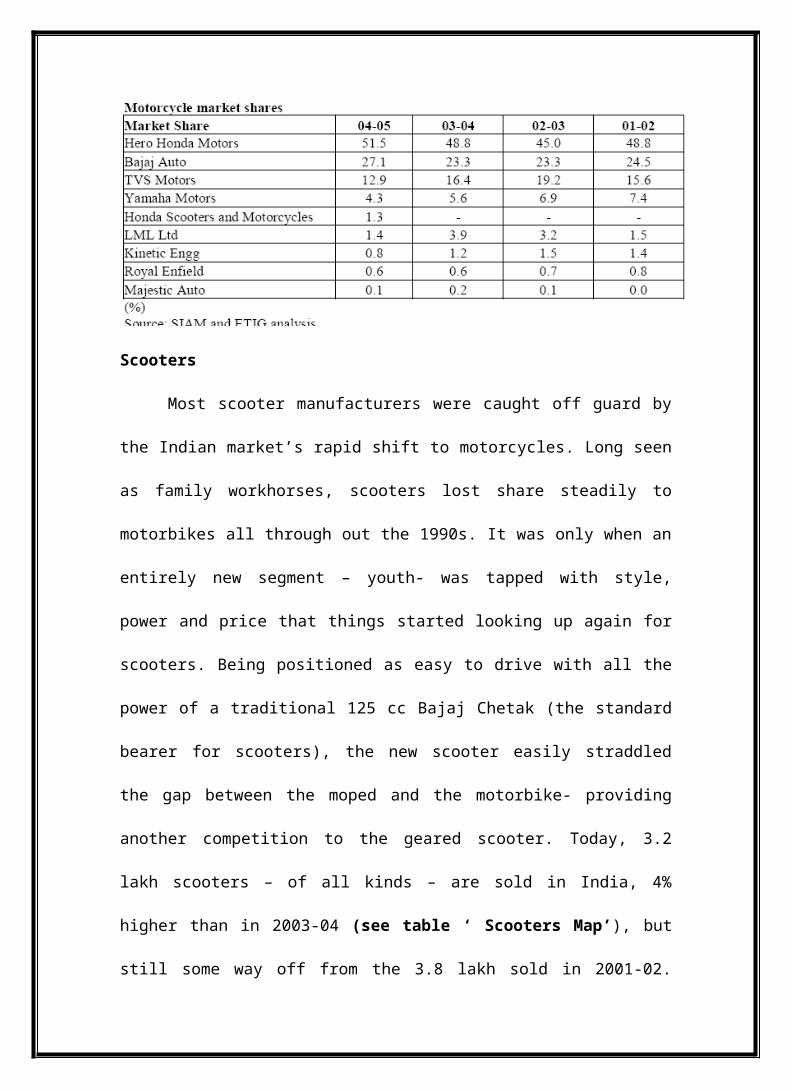

Every second motorbike in India is from Hero Honda, which holds 51.5%

market share in 2004-05. It has gained and retained that share since 2003-04 (see

table ‘ Motorcycle market shares’). Bajaj Auto , rejuvenated into a motorbike

company now rather than a scooter one, has also been steadily gaining share, from

24.5% in 2001-02 to 27% in 2004-05. Every other player has his work cut out to

regain any share.

Scooters

Most scooter manufacturers were caught off guard by the Indian market’s

rapid shift to motorcycles. Long seen as family workhorses, scooters lost share

steadily to motorbikes all through out the 1990s. It was only when an entirely new

segment – youth- was tapped with style, power and price that things started looking

up again for scooters. Being positioned as easy to drive with all the power of a

traditional 125 cc Bajaj Chetak (the standard bearer for scooters), the new scooter

easily straddled the gap between the moped and the motorbike- providing another

competition to the geared scooter. Today, 3.2 lakh scooters – of all kinds – are sold in

India, 4% higher than in 2003-04 (see table ‘ Scooters Map’), but still some way off

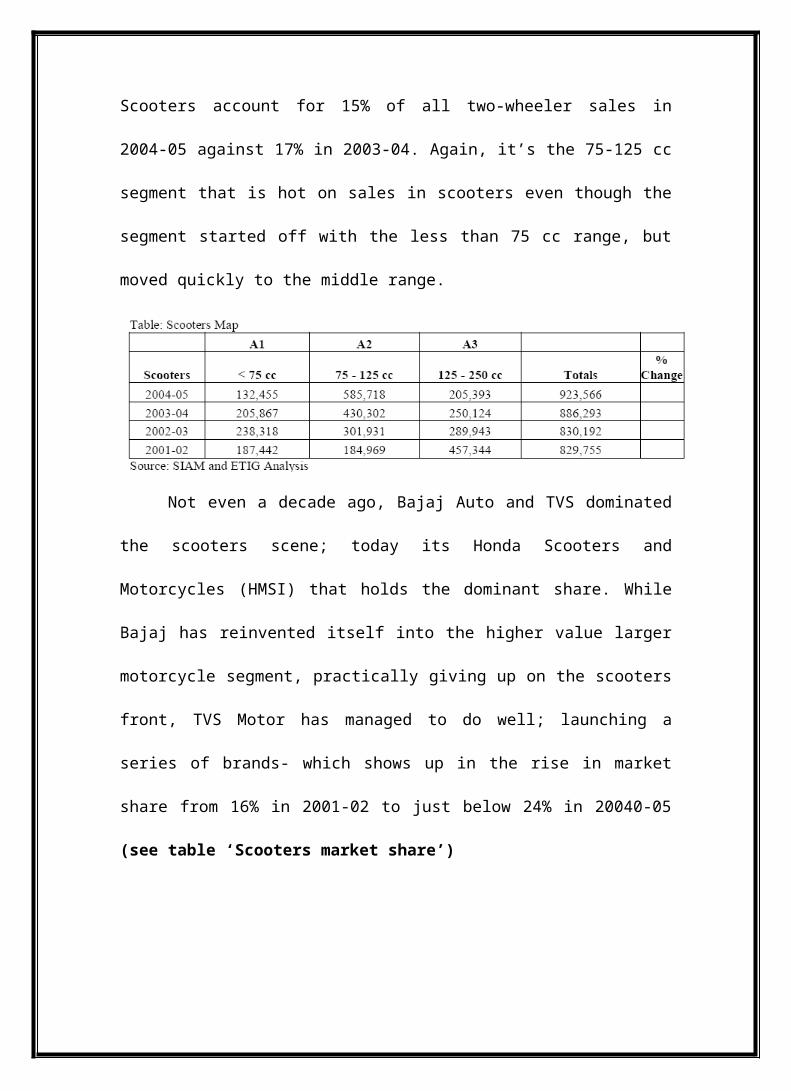

from the 3.8 lakh sold in 2001-02. Scooters account for 15% of all two-wheeler sales

in 2004-05 against 17% in 2003-04. Again, it’s the 75-125 cc segment that is hot on

sales in scooters even though the segment started off with the less than 75 cc range,

but moved quickly to the middle range.

Not even a decade ago, Bajaj Auto and TVS dominated the scooters scene;

today its Honda Scooters and Motorcycles (HMSI) that holds the dominant share.

While Bajaj has reinvented itself into the higher value larger motorcycle segment,

practically giving up on the scooters front, TVS Motor has managed to do well;

launching a series of brands- which shows up in the rise in market share from 16% in

2001-02 to just below 24% in 20040-05 (see table ‘Scooters market share’)

Mopeds

The smallest segment in two wheelers is the mopeds one, at 5% of total two

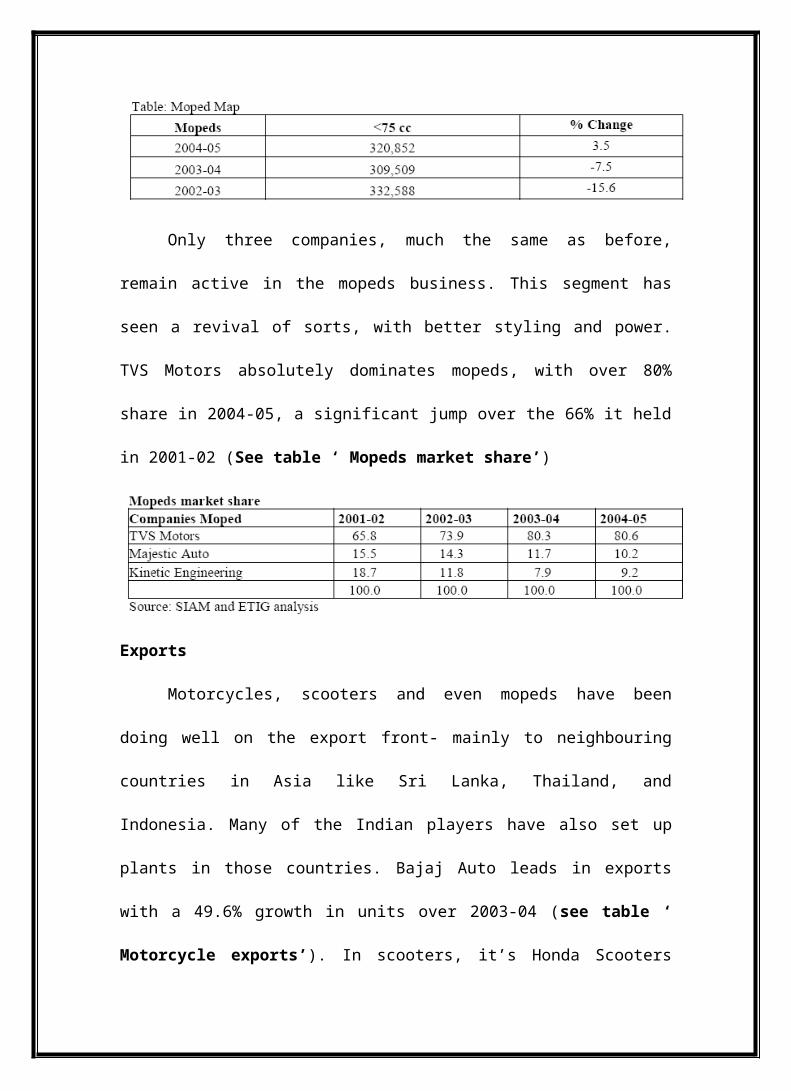

wheeler sales in 2004-05, with 3.2 lakh units sold (see table ‘ Moped Map’)

Only three companies, much the same as before, remain active in the mopeds

business. This segment has seen a revival of sorts, with better styling and power. TVS

Motors absolutely dominates mopeds, with over 80% share in 2004-05, a significant

jump over the 66% it held in 2001-02 (See table ‘ Mopeds market share’)

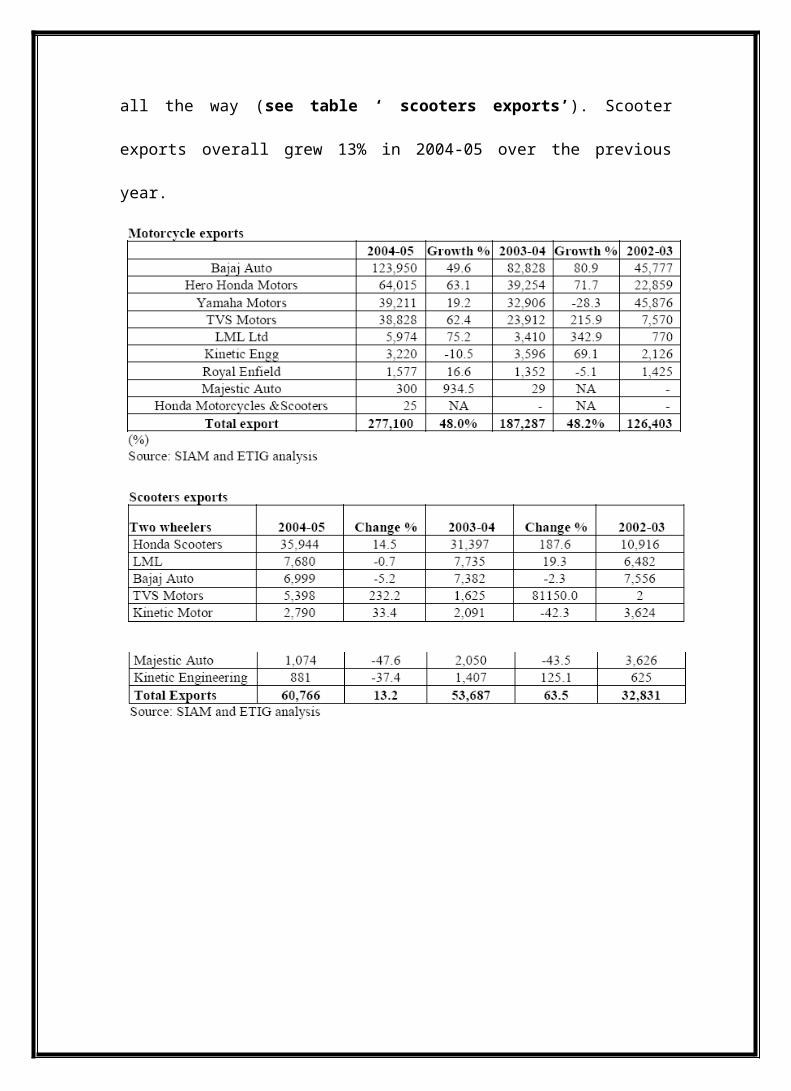

Exports

Motorcycles, scooters and even mopeds have been doing well on the export

front- mainly to neighbouring countries in Asia like Sri Lanka, Thailand, and

Indonesia. Many of the Indian players have also set up plants in those countries. Bajaj

Auto leads in exports with a 49.6% growth in units over 2003-04 (see table ‘

Motorcycle exports’). In scooters, it’s Honda Scooters all the way (see table ‘

scooters exports’). Scooter exports overall grew 13% in 2004-05 over the previous

year.

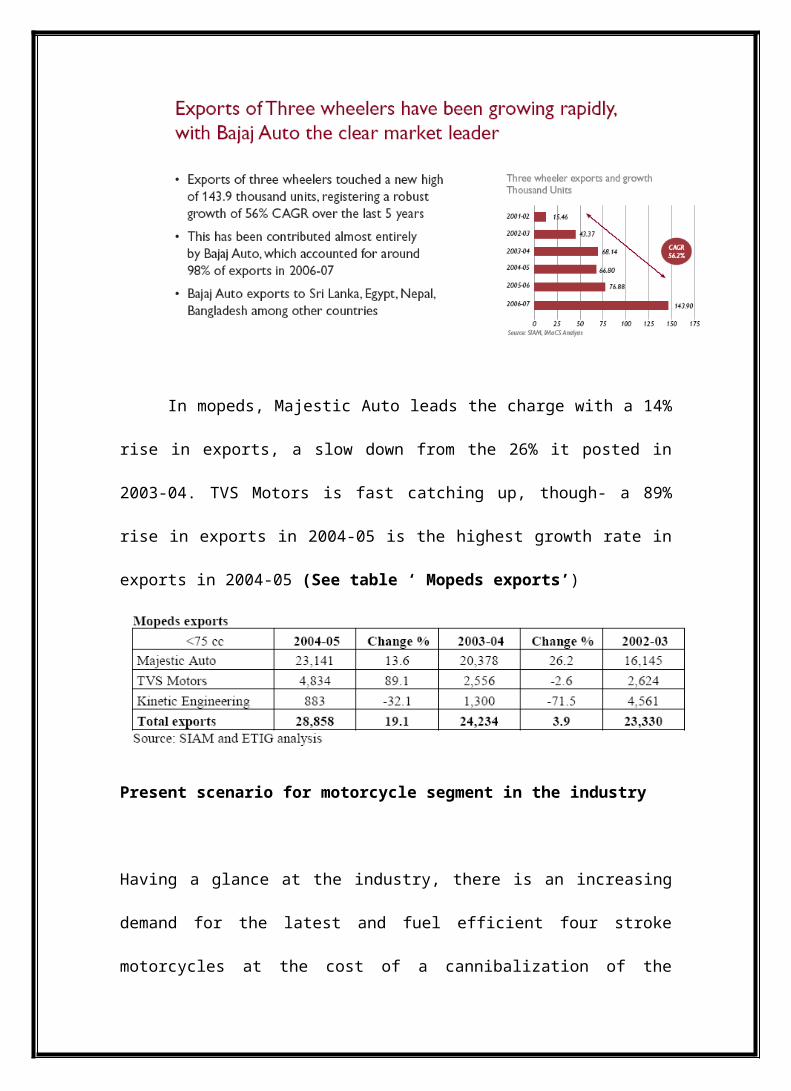

In mopeds, Majestic Auto leads the charge with a 14% rise in exports, a slow

down from the 26% it posted in 2003-04. TVS Motors is fast catching up, though- a

89% rise in exports in 2004-05 is the highest growth rate in exports in 2004-05 (See

table ‘ Mopeds exports’)

Present scenario for motorcycle segment in the industry

Having a glance at the industry, there is an increasing demand for the latest and fuel

efficient four stroke motorcycles at the cost of a cannibalization of the traditional

scooter segment. We believe the growth in motorcycle segment has remained

consistently good due to

Rise in rural demand as the per capita income of rural people have increased

More suitability on rural road conditions, comfortable long distance riding and

ease of maintenance

The stricter emission norms increase the cost of manufacturing of two stroke

vehicles which in turn brings a shift from two stroke vehicle to four stoke

motorcycles

Option of various Finance schemes available and above all

Consumer preferences for the latest, stylish and fuel-efficient motorcycles.

INDUSTRY CHALLENGES AND OPPORTUNITIES

The Indian two-wheeler industry saw an increase of 15 percent during the

year. Two-wheeler sales crossed 7.5 million units mark, which accounted for more

than 80 percent of domestic auto sales. Motorcycles shared around 82 percent of the

entire two-wheeler sales. However, industry margins came under some pressure

during the year in review because of an increase in input prices of steel, aluminum

and rubber. Operating margins were also affected on account of erratic power supplies

and high costs of back up power. Nevertheless, the upside potential for the future is

still extremely high because of the sheer potential for volume growth. According to

NCAER, there are about 225 million people - about 22 per cent of the population-who

live in households that have an annual income range of Rs. 90,000-200,000. Large

towns (population of over 500,000) have about 30 per cent of this population, while

rural India has about half of this income group. These groups are the real growth

engines for the great Indian dream, because at these levels, a number of aspirational

and discretionary purchases (which includes two-wheelers) are within reach. Against

this backdrop, your Company should be able to comfortably sustain double-digit

growth in the medium to long term, despite increasing competition.

Inputs and Technology

Technology

Hitherto, technology transfer to the Indian two-wheeler industry took place

mainly through: licensing and technical collaboration (as in the case of Bajaj Auto

and LML); and joint ventures (HHML). A third form - that is, the 100% owned

subsidiary route - found favour in the early 2000s. A case in point is HMSI, a 100%

subsidiary of Honda, Japan. Besides the below mentioned technology alliances,

Suzuki Motor Corporation has also followed the strategy of joint ventures (SMC

reportedly acquired equity stake in Integra Overseas Limited for manufacturing and

marketing Suzuki motorcycles in India).

Technological tie-ups of Select Players

Nature of Alliance Company Product

Bajaj Auto Technological tie-up Kawasaki Heavy Industries Ltd, Japan Motorcycles

Technological tie-up Tokya R&D Co Ltd, Japan Two-wheelers

Technological tie-up Kubota Corp, Japan Diesel Engines

HHML Joint Venture Honda Motor Co, Japan Motorcycles

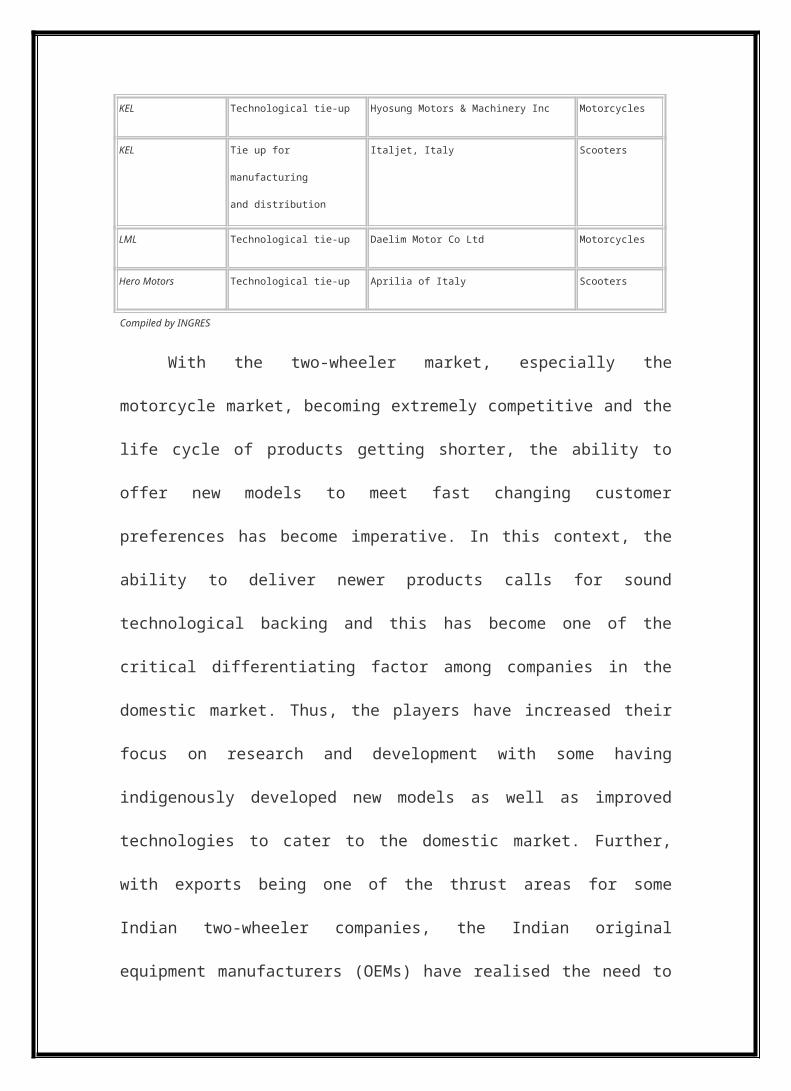

KEL Technological tie-up Hyosung Motors & Machinery Inc Motorcycles

KEL Tie up for manufacturing

and distribution

Italjet, Italy Scooters

LML Technological tie-up Daelim Motor Co Ltd Motorcycles

Hero Motors Technological tie-up Aprilia of Italy Scooters

Compiled by INGRES

With the two-wheeler market, especially the motorcycle market, becoming

extremely competitive and the life cycle of products getting shorter, the ability to

offer new models to meet fast changing customer preferences has become imperative.

In this context, the ability to deliver newer products calls for sound technological

backing and this has become one of the critical differentiating factor among

companies in the domestic market. Thus, the players have increased their focus on

research and development with some having indigenously developed new models as

well as improved technologies to cater to the domestic market. Further, with exports

being one of the thrust areas for some Indian two-wheeler companies, the Indian

original equipment manufacturers (OEMs) have realised the need to upgrade their

technical capabilities. These relate to three main areas: fuel economy, environmental

compliance, and performance. In India, because of the cost-sensitive nature of the

market, fuel efficiency had been an interest area for manufacturers. It is not only that

the OEMs are increasing their focus on in-house R&D, they also provide support to

the vendors to upgrade the technology and also assist them striking technological

alliances.

2-stroke v/s 4-stroke

The single most important change in the 2-wheeler market is that of the

movement from the 2- stroke to the 4-stroke engines driven by environmental and fuel

efficiency concerns. The 4-stroke engine, by virtue of burning fuel more completely

than the 2-stroke, emits lesser pollutants as well, as vital factor as emission norms

move from tail-pipe norms to engine norms and the margins themselves become

tighter. Because a 2-stroke engine gets a power stroke twice as often as a four-stroke

engine, it puts out about twice as much power (and makes twice as much noise) as a

four-stroke engine of the same size. Hence in times when emission and fuel wasn’t as

much a concern, powerful bikes used the 2-stroke engine. Secondly, a 2-stoke engine

is exposed to much more wear and tear in pressure and combustion than a 4-stroke,

with the result the 2-stroke engines need a good deal more high quality lubricating oil

than the 4-stroke. The net result is that 2-stroke engines can be quite expensive to run.

In the consumer market, the cruiser and economy segments sell much more than the

motor or premium range where the power/ weight ratio is key. The 4-stroke engine

adapts well to longer and continuously running times, combusting fully and with less

pollutants. Newer developments in fuel injection and timing in4-stroke engines have

improved power / weight ratio as well, so that many of the disadvantages of the lower

power in 4-stroke are gone now- much the same way as MPFI and common rail

injection in diesel have improved efficiencies for cars.

Emission standards

India is adopting increasingly stringent emission standards, which have a

direct implication on engine design and quality. 2-stroke engines are already passé,

while the four strokes are being continuously upgraded to reduce both tailpipe

emissions and engine emissions. Today India is adopting the Bharat II and III norms

for emissions, which are as stringent as those in the European markets.

Companies

Hero Honda

Hero Honda is India’s largest motorcycle company with 2004-05 sales of 26.2

lakh units, giving it a market share of 51.5% in motorcycles. Founded in 1984 in a

joint venture with Honda Motors, Japan, Hero Honda is one of the most profitable and

smoothly operating JVs for Honda Motors anywhere in the world, giving it a foothold

in one of the world’s largest and fastest growing two wheeler markets.

In 1985-86, Hero Honda sold just 43, 000 units, launching its business with

the CD-100; Five years later, in 2000-01, it sold over 10 lakh, and in another five

years, doubled that to over 25 lakh units. In 1987, it started the engines plant as well,

and produced with 100,000th bike that year. 1989 saw the launch of the Sleek, now

discontinued. It was in 1994 that Hero Honda introduced the Splendor, which would

go on to become the world’s single largest selling motorbike brand. In 1995, Hero

Honda was producing 800 bikes a day, 4 times the number of bikes it could produce a

day when it started up. By 1997, the company was producing 1200 bikes a day. In

2001, Joy and Passion were launched, and the Ambition was launched in 2002. Since

then, the company launched Karizma, at Rs 80000 one of the most expensive heavy-

cc bikes (250cc) in India, but which once again belied the general belief of India as a

low-price market.

The company was also surprised when demand for this expensive bike came

from rural and semi urban areas and it sold 2000 bikes a month for a few months. This

bike opened up a whole upper cc segment in bikes. Today Bajaj Pulsar is its biggest

competitor in the 250cc range. It was the first to herald the shift from scooters to

motorcycles with style, power and competitive pricing. For much of the early 1990s,

established players like TVS Motors and Bajaj Auto suffered reverses as the market

shifted to motorcycles. Today, the scenario is different as both these competitors have

brands that challenge Hero Honda, but market leadership still remains with Hero

Honda. It was also the first to create critical mass in the 75-125cc ranges, where most

brands compete. Hero Honda set a first with its dividend policy as well, announcing a

1000% dividend in 2003-04. With the motorcycle business doing well, Honda Motors

announced its own entry into India but not in the segments where Hero Honda

operated; also the technical JV was extended for another decade. Hero Honda sales

for March 2005 were Rs 7,421 crore, against Rs 5,832 crore in March ’04. Net profits

stood at Rs 810 crore against Rs 728 crore in March ’04.

Bajaj Auto

Founded in 1945 and reborn fifty years later. Bajaj auto is a revival story.

Long known for its scooters like the Chetak, which gave it over 90% of its sales for

most of the past few decades, today Bajaj Auto is more known for its motorcycles,

after reinventing itself in the late 1990s. Today its brands give the leader Hero Honda

a run for its money in every segment of the motorcycle business; while its scooters

have seen a revamp in style and power and are beginning to fight back against the

brands like TVS and Honda Scooters. Its come a long way since importing 2 and 3

wheelers in 1948. In 1959, it got its license to manufacture in India, and in 1971 it

introduced the 3-wheeler and one year later the Bajaj Chetak. 1976 saw the launch of

the Bajaj Super scooter and in 1977, the year the company sold 1-lakh units in the

year, it launched the rear engine rickshaw. In 1981 came the M-50 scooter, which

sells to this day specially in Pune and surrounding areas. In 1985, after 16 months of

its foundation, Bajaj Auto’s new plant at Waluj, Aurangabad started up. This plant

would produce the Kawasaki KB100 motorbike and M-80 scooters.

By 1990, the decline in the scooter market was visible, with the rapid increase

in motorbike sales. Bajaj was active in the motorbike market, but not as a core line of

business. As late as 1990, it launched the Bajaj Sunny, gearless scooter and until

1995, continued to upgrade and sell the scooters. From 1997 onwards, the pace of

new products ramped up- Spirit came in 1998, Legend, India’s first four stroke engine

scooter in the same year; and the Kawasaki Bajaj Caliber, its first serious attempt at

motorbikes also in 1998. The Caliber touched 1-lakh unit sales in less than 12months,

accelerating the shift towards the motorbike business in Bajaj Auto. In 2001, the

Eliminator (now discontinued) and the Pulsar- its first serious blockbuster- were

launched. But in 2003, the pace was frenetic. That year the Caliber 115 came in; so

did the Wind 125, and the Pulsar DTS-I. Bajaj Auto sold 1-lakh bikes in just one

month that year. 2004 was a brand change for Bajaj Auto, reflecting a new identity. In

May 2004, The Bajaj CT 100 bike was launched, in August the 4-stroke Chetak with

Wonder Gear and in September ’04, the Discover DTS-I. In June 2005, came the

latest launch, the Avenger. All the excitement, and the obvious improvement in

quality of Bajaj products, saw sales rise to match competition. From a market share of

24.5% in 2001-02 to 27% in 2004-05, Bajaj has gained at the expense of competitors

like TVS Motors, although Hero Honda also continues to grow its share. However, at

13.4 lakh motorbikes sold in 2004-05, Bajaj Auto is now a serious player in the

motorbike business.

In scooters, its work is still cut out. From a market share of 50.2% in 2001-02,

today it holds less than 14%; in the interval, Honda Scooters and Motorcycles (HMSI)

saw its share rise from 6.5% to 48.8%. TVS Motor took share from 16.3% to 23.7%.

Clearly, while it has its act right in motorbikes, a lot of work still needs to be done to

regain its pole position in the scooters market, which it once defined and dominated.

Bajaj Auto net sales for 2004-05 were Rs 5927 crore, against Rs 4916 crore in 2003-

04. Net profits were Rs 766 crore versus Rs 731 crore in 2003-04. It has also been

retiring surplus manpower: today 11,531 employees run it, against 17,213 in 1999-00.

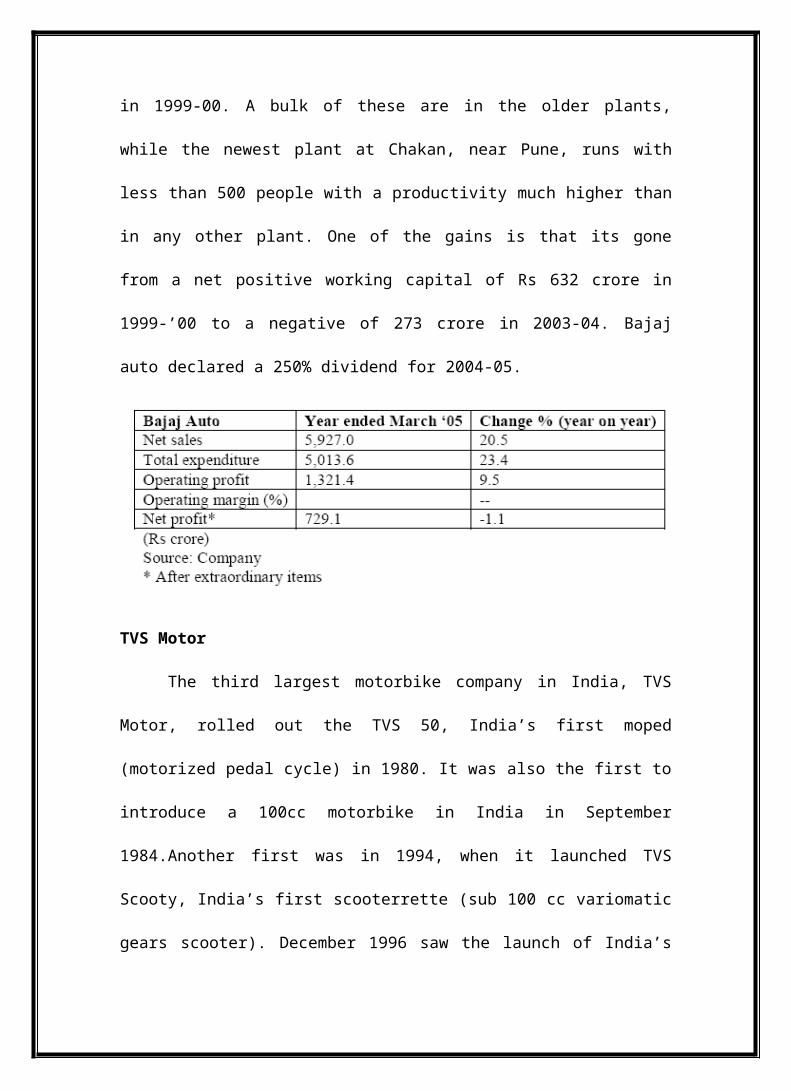

A bulk of these are in the older plants, while the newest plant at Chakan, near Pune,

runs with less than 500 people with a productivity much higher than in any other

plant. One of the gains is that its gone from a net positive working capital of Rs 632

crore in 1999-’00 to a negative of 273 crore in 2003-04. Bajaj auto declared a 250%

dividend for 2004-05.

TVS Motor

The third largest motorbike company in India, TVS Motor, rolled out the TVS

50, India’s first moped (motorized pedal cycle) in 1980. It was also the first to

introduce a 100cc motorbike in India in September 1984.Another first was in 1994,

when it launched TVS Scooty, India’s first scooterrette (sub 100 cc variomatic gears

scooter). December 1996 saw the launch of India’s first motorbike with catalytic

converters for emission control, the 110 cc TVS Shogun. The 5-speed motorbike

Shaolin came in late 1997, and 4-stroke Fiero 150cc came in 2000.In August 2001

came its real blockbuster, the TVS Victor, a 4-stroke 110cc motorbike, which the

company claimed to be India’s first indigenously developed bike. Building on the

drive towards more fuel and emission efficient bikes, TVS launched its Centra, 4-

stroke 100 cc bike in January 2004. The 100 cc TVS Star came in September 2004.

The series of launches were needed as TVS struggled to maintain its lead in

the motorbike market. In the mid 1990s, Hero Honda opened up the market in all

segments, from 75-125-250 cc categories. From selling 7.1 lakh units a year in 2002-

03, to 6.82 in 2003-04 to 6.4 lakh in 2004- 05, TVS Motor has found the going hard

against Hero Honda and a rejuvenated Bajaj Auto. Its market share rose briefly to

19.2% in 2002-03 before slipping to 12.9% in 2004-05. It has primarily lost share to

Bajaj Auto over these years. One of its concerns is that it loss has been heaviest in the

key 75-125 cc segment, where its market share has dipped from 21% in 2002-03 to

17% in 2003-04 and to 12.8% in 2004-05. At the same time, it has gained market

share in the 125-250 cc range up to 14% in 2004-05 from 8% in 2002-03. Clearly, the

company is striving to move up the value chain, into a relatively less cluttered

marketplace.

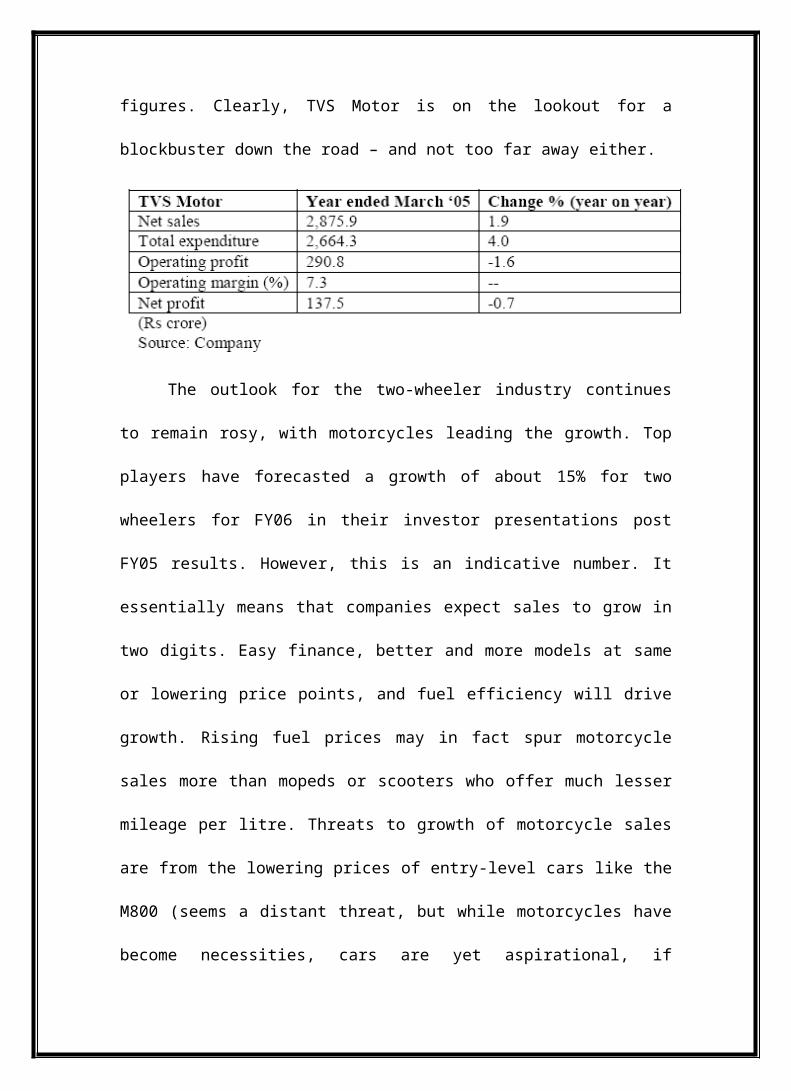

TVS Motors net sales were Rs 2875 crore for the year ended March ’05 with a

net profit of Rs 137 crore, against net sales of Rs 2820 crore and net profits of Rs 138

crore in March ’04. The concern for TVS Motor comes also from the fact that falling

unit sales aren’t been shored up by any price rises and bottom line profitability is

being hit by rising raw material prices, which cant be passed on as a result of severe

competition. Operating margins have been squeezed as well, falling from 9.2% in

April-June ’04 to 4.9% in January- March ’05.It scooters business continues to do

well, where its market share went to 23.7% (2.19 lakh units) in 2004-05 from 16.2%

(1.35 lakh) in 2001-02. However this wasn’t enough to boost overall company

figures. Clearly, TVS Motor is on the lookout for a blockbuster down the road – and

not too far away either.

The outlook for the two-wheeler industry continues to remain rosy, with

motorcycles leading the growth. Top players have forecasted a growth of about 15%

for two wheelers for FY06 in their investor presentations post FY05 results. However,

this is an indicative number. It essentially means that companies expect sales to grow

in two digits. Easy finance, better and more models at same or lowering price points,

and fuel efficiency will drive growth. Rising fuel prices may in fact spur motorcycle

sales more than mopeds or scooters who offer much lesser mileage per litre. Threats

to growth of motorcycle sales are from the lowering prices of entry-level cars like the

M800 (seems a distant threat, but while motorcycles have become necessities, cars are

yet aspirational, if aspirations come within reach, they would become necessities

shortly). Growth could be impacted by the passing on of raw material price increases

to customers, as well as better scooters that take away a swathe of fence sitters

between scooters and motorcycles.

CHANGING TECHNOLOGY AND CONSUMER

BEHAVIOUR

TheTheory.

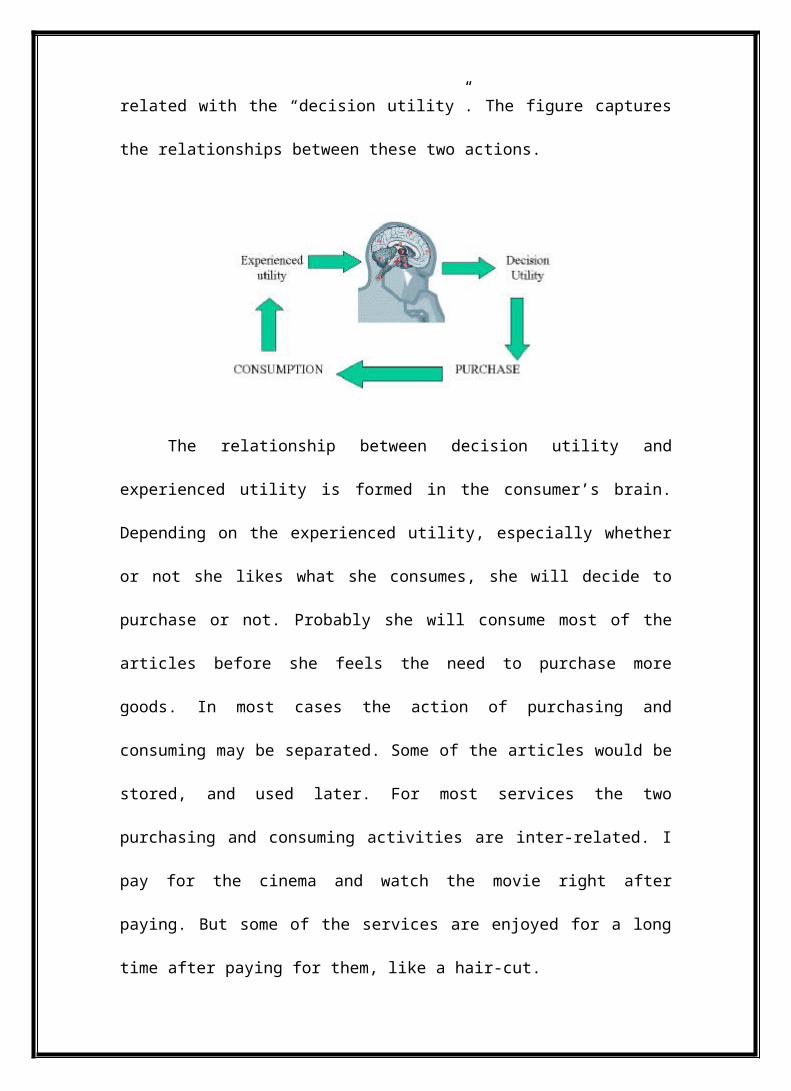

To fully understand consumer behavior we have to separate two actions by the

consumer. These two actions are interrelated. The consumer buys some goods, so she

realizes the “action of purchasing”. In this act of buying she buys several goods, at the

same time. The second action is the “action of consuming” goods. The later is related

with “experienced utility”, i.e. with the hedonistic capacity of the goods. The former

is related with the “decision utility”. The figure captures the relationships between

these two actions.

The relationship between decision utility and experienced utility is formed in

the consumer’s brain. Depending on the experienced utility, especially whether or not

she likes what she consumes, she will decide to purchase or not. Probably she will

consume most of the articles before she feels the need to purchase more goods. In

most cases the action of purchasing and consuming may be separated. Some of the

articles would be stored, and used later. For most services the two purchasing and

consuming activities are inter-related. I pay for the cinema and watch the movie right

after paying. But some of the services are enjoyed for a long time after paying for

them, like a hair-cut.

We have to think about the idea, that most of the stimuli we get over one

normal day, they do not come from the shopping. We get stimuli from our work, from

our own thoughts, from the our friends, family etc... But every now and then, we also

get stimuli from a newspaper, a new book, a new T-shirt something that we buy. But

if her arousal potential is being hold only by shopping it will mean that she needs to

keep on buying new things to feel comfortable. Novelty is a factor that is mixed in the

decision utility. Novelty makes goods important. But novelty disappears over time.

There is also the intrinsic value that a good offers to the consumer, i.e. on the capacity

to generate a positive hedonistic value. In this case the good has the potential to

become a habit. The first time somebody smokes, she does it because it is something

new for her, she wants to try. Initially there may be no addiction. But once the novelty

is gone the addictive good is still able to generate positive stimulus in the consumer.

The usual smoker does not buy cigarettes for the novelty but for the capacity that the

good in itself has to offer.

“Representation of consumer behaviour” in a model is how well the model

captures the consumer’s decision-making process in competing technologies. Models

that accurately capture consumer behaviour from empirical data are considered to be

behaviourally realistic. In addition to many financial variables about the technologies

in question, which are each technology’s capital cost and operating cost,

behaviourally realistic models can also include demographics, such as consumer

income, perceptions of risk, and the desire for new technologies. In contrast,

behaviourally weak policy models do not incorporate all of these factors in

determining technological adoption by consumers; some resort to simple decision

rules such as adopting technologies solely on the basis of financial costs.

As we approach the 21st century, the marketing function remains concerned

with serving customers and consumers effectively. While developing better marketing

processes and programs, we need to be aware that demographic shifts and emergence

of facilitating technologies in production, distribution and personal use are affecting

consumer behavior and therefore the marketing function. For example,

demographically we are witnessing the following major trends -- aging of population,

larger proportion of working women, decline of the middle class and increasing ethnic

diversity. These trends are unique that they are occurring simultaneously, have long

term impact and will effect society and the marketing function.

In the last decade, firms have been witnessing market fragmentation and

constantly evolving products and services. These changes have put pressure on the

marketing function to shift their strategies from stable markets to turbulent markets.

In fact, due largely to the evolving market place, firms have started questioning the

performance and productivity of the marketing function (Sheth and Sisodia 1993). As

firms approach the 21st century, they need to be cognizant of and anticipate changes

in customer behavior. The marketing function needs to convert anticipated customer

behavior changes into opportunities for sustained competitive advantage (c.f., Ashley

& Morrison 1997).

In the last decade there have been a rapid evolution of technologies in product

and service design and manufacturing, distribution, and personal use that have

facilitated changes in consumer behavior. For example, communication technologies

such as the internet, personal computers, and wireless communications have changed

shopping and consumption behavior. In the Indian automobile industry, consumers

(estimated at a quarter of buyers) peruse the market through various media, including

the Internet before they visit a dealer. This trend toward adopting new technologies is

expected to grow. About half of the Indian population look forward to technology

innovations.

Technology Evolution

Technological change has been extremely rapid during the past two decades,

and indications are that this rate of change will continue. The prices of most

technologies will continue to come down and the capabilities will continue to expand.

Many technologies that have already been developed will start to have

a significant impact on society (McRae 1996).

Alsop (1998) describes how technology will personalize marketing, customer

service and other areas of daily life by the year 2004. His additions include road signs

that change for each viewer, personalize electronic trading of securities, monthly

account statements from the IRS and periodicals customized for each reader. Regis

McKenna (1997) points out that current technologies produce instantaneous response

at the touch of a mouse. Consumers have changed their reference regarding sense of

time and instant satisfaction leading to an evolutionary change in judging good and

bad service. Customer expectations and satisfaction are now hyper accelerated if not

immediate for organizational response

The speed at which technologies are getting adopted has been increasing in

recent years it took 46 years for a quarter of American homes to be wired for

electricity. It took 35 years to get phones to a quarter of the population and 55 years to

get cars. Recent innovations such as the PC (16 years), cellular phones (13 years) and

the Internet (7 years) have penetrated much more rapidly (Cox and Alm 1997). The

relationship between consumer behavior and technology is a fascinating one, but has

not been examined in great detail. As Mick and Fournier (1998) point out, less than

one-fifth of one percent of studies on technology have consigned themselves with

consumer behavior. Mick and Fournier (1998) point out that technology is often

paradoxical in that it can simultaneously help and hinder customer behavior.

Facilitating Technologies and Consumer Behavior

The change in consumer behavior due to demographic trends on will be

facilitated by emerging technologies in production, distribution and personal use.

Undoubtedly, the pace of technological evolution has and will continue to have a

great impact on the lives of consumers. The new technologies are disruptive in that

they are changing consumer behavior and marketing practices at a pace not seen

earlier (Bower and Christensen 1994; Christensen 1997). Particularly, they make

incumbents vulnerable due to the impact of technology on production, distribution

and technologies for personal use.

Production Technology

Breakthroughs in production technology, such as CAD-CAM, flexible

manufacturing systems, and just-in-time production are impacting competitive

marketing in a number of ways. Other significant technologies in this area include

photorealistic visualization, groupware (e.g. conferencing systems across design

functions and across design, manufacturing and sales), virtual reality, Design-for-

Manufacturability and- Assembly databases, component performance history

databases, and 3-D physical modeling technologies such as stereolithography. These

technologies are increasing quality, reducing prices for many products, enabling a

higher level of customization and providing customers with a greater of variety.

Distribution Technology

Distribution technologies have rapidly changed in the last two decades (Ross

1996). Recent innovations in distribution technology include computer-assisted

logistics (CALS), the refinement of scanner and other product identification and

tracking technologies, electronic data interchange (EDI), point-of-sale (POS)

terminals linked to vendors, expert systems, satellite-based locational systems,

automated retail and warehouse ordering, and flow-through logistics. The benefits of

these technologies include reduced damages, reduced supplier and distributor

wholesale inventories, warehousing, transportation, administrative and manufacturing

efficiencies, reduced “forward buying”, better market coverage, fewer stock outs and

distress sales, more refined target marketing and faster response to market trends.

Technologies for Personal Use

The technologies with the fastest gains in price-performance are those

intended for personal rather than institutional use. Personal information devices have

been and will continue to ride a steep experience curve based on the unique

“economics of electronics.” One of the fundamental properties of such technologies is

their inverse economies of scale; the smaller the unit, the greater the price-

performance. This is due to the fact that smaller units can be produced in mass

quantities with very low (sometimes near zero) variable costs. Large units, on the

other hand, tend to be produced in small volumes and retain a significant proportion

of variable costs. Thus, today’s personal computers offer far more by way of “MIPS

per dollar” than do today’s mainframes or supercomputers; video games and other

lower end consumer devices tend to offer even better price-performance than that.

Consumers will rely heavily on small unit technologies, while producers will rely on a

mix of personal and institutionally-oriented technologies. As the power and

pervasiveness of the technologies at their command grow, consumers will be in the

unique and unaccustomed position of controlling a far greater share of the information

and communication flow between the buyer and seller than ever before. In other

words, customers can and will have more information about product providers in most

cases than providers will have about customers. Far from being passive “targets” of

marketing activity, customers will dictate the timing and modality of communications,

and they will determine the time and place of the resulting transaction.

The Impact on Consumer Behavior

As people start to change the way they work, communicate and spend their

leisure time, they will seek companies that will do business in the manner that they

prefer. Accustomed to always being within electronic reach of their family and

colleagues, they will seek marketers who do not demand adherence to rigidly defined

modes of commerce. Used to instantaneous response to their requirements for

information and entertainment, they will seek similar responses from marketers. With

constantly improving technology, they will seek avenues that will allow them to

acquire goods and services that require less time and effort. Future consumers will be

more demanding, more time-driven, more information intensive, and highly

individualistic. A combination of a ubiquitous broadband digital communications

network and high definition display terminals will further accelerate changes in

consumer behavior. With targeted, interactive digital media in the future, advertisers

will be able to “mass customize” their messages as well as allow for user interaction

and input. Shopping will also change. Buyers will have immediate access to a variety

of independent buying services, providing distributed expertise on demand. Because

of interactive advertising, buyers will be much more active in seeking even marketer-

provided information.

From Time and Location Bound to Time-Free and Location-Free Marketing

Commerce today, for the most part, tends to be time and location bound. That

is, transactions are constrained to occur at particular times, and/or at particular

locations (e.g., the retail store model). If the consumer is unable to transact at those

times or those locations, the transaction either does not occur at all, or occurs between

the consumer and an alternative supplier. Even if the transaction does occur, i.e., the

consumer is able to comply with the time and place requirements placed by the

supplier, it often forces undesirable tradeoffs upon the customer (e.g., higher prices at

convenience stores). For most consumers, there are alternative uses to which they

might put the same time, and the location constraint imposes an additional burden of

the time, effort and expense of making oneself physically available to transact.

Time and place constraints are slowly giving way, under the pressure of

increasingly hectic consumer lifestyles, heightened competition and myriad enabling

technologies. Behavioral barriers to the adoption of alternative modes of interacting,

be they based on engrained habits or perceived risks (Ram and Sheth 1989; Ram and

Jung 1994), have become increasingly porous and less rigid. We believe that this

forward momentum will result in a positive-feedback loop that will accelerate the rate

of consumer migration toward alternative modes of transacting. While no positive-

feedback loop can persist forever, we believe that a period of rapid, even explosive

growth lies ahead in this arena. It will subside only as a large majority of consumers

have been converted to the new model of commerce. Early examples of this

phenomena are Amazon.com and Peapod, a grocery delivery service. We are, then, in

the midst of a change from gravitational commerce (demarcated by its time and

location constraints upon customers) to an era of digital commerce, which will be

almost entirely free of those constraints. The future will see “anytime, anywhere

procurement” coupled with “anytime, anywhere consumption;” more and more

products and services will be purchased and consumed anytime, anywhere.

Consumers will demand and receive advertising and other forms of information “on

demand.”

The crucial importance of increased time and place utility is nowhere more

evident than in the banking industry. Banks face a massive dislocation in the near

future, as their vast and expensive time and location-bound distribution networks

(branches) may become obsolete. For example, Wells Fargo announced in the fall of

1995 that it planned to move 72 percent of its existing branch network into in-store

(supermarket) locations. Since in-store branches are only 20 percent to 25 percent of

the cost of conventional branches, this represents a substantial cost saving, as well as

a way to expand market coverage in terms of time as well as geography. The more

major shift, of course, is the move toward home or remote banking. This trend, still in

its early infancy, will take time and place utility to a much higher level.

With regard to supermarket retailing, the impact of increased emphasis on

time and place utility will be even greater. Already, supermarkets can offer electronic

ordering and home delivery services for relatively low start-up costs. A recent survey

indicates that over 25% of chains offer home delivery, representing more than 40% of

the population. Significant barriers to a broader adoption of home shopping are

delivery charges, which run from $7 to $10 an order. Survey research by Management

Horizons shows significant consumer resistance to any delivery charge. What is

needed is a business model that is optimized for home shopping, rather than one in

which the service is added on as an ancillary to traditional retailing. Analysis by

Management Horizons indicates substantial savings in operating a “delivery depot”

compared to a supermarket. On a typical $100 order, home delivery will cost a typical

supermarket operator an extra $10 to process, pick, check out and deliver from the

supermarket. A delivery depot can process and deliver the same order for about $10 to

$12 less in total cost than the supermarket can.

To summarize, the success of marketers in the future will be predicated upon

their ability to deliver “total customer convenience.” This includes hassle free search

(advertising-on-demand), hassle free acquisition (home delivery), hassle free

consumption (for example, products with built-in expert systems to enable maximal

value extraction) and hassle free disposal.

The future may be a balance of mass customization and mass market products

and services for two reasons. First, customers are not always looking for customized

products and they may be content in many cases with a well-designed standardized

product. Thus, the price, advertising message and/or the distribution mode may be

customized, even if the product is not. Second, new forms of aggregation of demand

will undoubtedly occur. In the past, these were driven entirely by producers. In the

future, it will become increasingly facile for the aggregation to be driven by

customers. For examples, customers who individually purchase small quantities of a

product will find it very easy to band together and pool their purchases to enjoy better

terms.

Power Shift From Marketers to Consumers

Inevitably, increased competition and greater access to more powerful

information tools will put greater power in the hands of savvy customers. As a result,

it is possible that “buyers” will increasingly be viewed as “marketers” and sellers as

“prospects” in the marketplace. Some consumers will no longer be “targets” of

marketing activity; they will be knowledgeable and demanding drivers of it.

Consumers will demand content-rich information and demonstrable product

innovations (c.f., Manu and Sriram 1996). Customer managers will be explicitly

charged with identifying, retaining and growing profitable customer relationships.

Market activity will be driven almost entirely by buyer demand as marketing

management will essentially become demand management and will entail the task of

influencing the level, timing and composition of demand in a way that will help the

organization achieve its objectives (c.f., Cahill, Thach and Warshawsky 1994).

Customer knowledge will become the cornerpiece of effective marketing, and that

knowledge will become a highly valued corporate resource (c.f., Kohli and Jaworski

1990; Ram and Jung 1990).

Consumers can already do product research online, log onto bulletin boards

and interact with other customers, provide and receive helpful hints about the product,

its use, acquisition etc. In this environment, “information invitations” may become

common; companies will have to seek permission to present their case to consumers

by inducing interest, unlike the “message clutter” of today. As

communication between marketers and customers becomes increasingly interactive,

relationship marketing will become the rule rather than the exception. Buyers and

sellers will interact in “real time.” Time and place constraints on purchase (and even

consumption of many products and services) will become obsolete. The nearly instant

gratification of customer needs will be common and lead times (e.g., for product

development, or between order placement and shipment) will have to shrink

dramatically.

The Concept of a “Personal Marketplace”

The “Personal Marketplace” (PM) is a hypothetical mechanism to make

effective use of the vast amounts of consumer and transaction data generated today.

This or a similar type of mechanism is expected to develop in the future. It is a

repository where participating marketers prepare and offer custom-tailored offerings

directly to a consumer. By selecting a particular category, the customer alerts the

market that he/she is a potential customer, and offers begin to flow in. The customer

voluntarily provides as much customizing information as needed. Participating

companies agree not to sell the data they collect outside the PM, and not to use it to

market in any other channel.

For example, the two-wheeler market today is largely comprised of

replacement buyers rather than first-time purchasers (Business Line 2002). And the

average time taken from ‘identification of need’ to ‘actual purchase’ has reduced from

months to weeks if not days. Studies examining runaway consumerism have focused

on impulse purchases, arguing that lower levels of cognition results in compulsive

often ‘mindless’ consumption. This compulsive and habitual purchase has received

much attention in terms of its negative effects manifesting as guilt, frustration,

anxiety, loss of control and even domestic dissention (O’Guinn and Faber 1989, Rook

1987). The ‘self-defining’ choice among different brands and products is assumed to

be beneficial for the individual’s identity if it is based on greater cognition and pre-

purchase information processing (Schiffman and Kanuk 2000). We argue that a

consumer who can, and does, apply a certain extent of cognition before purchase, can

yet face identity confusion rather than enhancement. The cognitive dissonance theory

(Oshikawa 1969) in the study of consumer behavior, asserts that a person has certain

cognitive elements, which are "knowledges" about oneself, one’s environment, one’s

attitudes, one’s opinions and one’s behavior. If one cognitive element follows

logically from another, they are said to be consonant to each other. They are dissonant

to each other if one does not follow logically from the other.

With increased competition, established automobile manufacturers in India are

becoming more conscious about technology and quality. These companies are

incorporating ISO 9000 certification and Total Quality Management as explicit

corporate goals. Most of the MNCs entering the Indian automobile market are

bringing in modern technology. Emission control techniques like catalytic converters

and injection technology are present in most models. The fuel efficiency of these cars

is higher than that of domestic models. Foreign models are equipped with vehicle

safety gadgets which have never been seen in Indian automobiles. In fact, some

brands in the luxury and super-luxury segments are positioning themselves on the

basis of safety and engineering excellence.

HERO HONDA- The Technological Giant

The two wheeler market in India essentially comprises of motorcycles,

scooters and mopeds. With a volume size of 84.6 lakh units in ’06-‘07 the industry

has registered a growth of 12% over ’05-’06. The industry is dominated by

motorcycles which constitute 84% of the category followed by scooters consisting of

11% and mopeds accounting for the remaining 5%. The largest player in the two

wheeler industry is Hero Honda which commands a lion’s share in the category.

With a market share of 39.4% and volume size of 33.4 lakh units in ’06-’07, the

company has registered a robust growth of 11% in volumes over ’05-’06 when it had

sold 30 lakh units. The second largest player in the industry is Bajaj Auto which

registered a growth of 18% in volumes by selling 24 lakh units in ’06-’07 compared

to 20.3 lakh units in ’05-’06. The company saw its two wheeler market share increase

marginally by 1.5% to 28.3% in the same period.

Key competition:

HMSI – HMSI launched Activa in 2001 and it was a huge success from start.

The brand enjoyed superior product and image perceptions given Honda’s

equity and global lineage. Activa was a 4 stroke, variomatic (gearless), metal

bodied offering which offered superior mileage and performance. The brand

ruled the market with a 44% market share in the gearless scooter segment.

The brand is targeted at men and family

TVS Scooty: The TVS heritage gives the brand perceptions of reliability, easy

availability of spares etc. Moreover the brand had signed up with Preity Zinta

as its endorser which further added to its popularity. The brand had entered

the market with ABS (plastic) bodied Scooty Pep (75cc) and later introduced

a more powerful Scooty Pep + (90cc). However the brand has discontinued

Scooty Pep and now focuses only on Scooty Pep +.

The brand has recently created new news by launching 99 colours for its brand

and has backed it up with a heavy media push. The brand is a clear No.2 in the

market. It had a market share of 29% before the entry of hero Honda Pleasure which

has now declined to 26.1%. While the brand is targeted at females it has tried to

maintain a unisex appeal in its advertising.

Other players: There are a number of small players in the category viz.

Eterno, Dio, Nova etc fighting for salience. It was in this scenario that Hero Honda

decided to enter the scooter market with its brand Pleasure in 2006

The Hero Honda Pleasure product truth:

ABS body

100cc

Gearless

Hero Honda Motors Ltd – is a leader in the 100 cc motorbike segment with

around 42% market share during the current fiscal 2000. During the year, the

company posted a 46.74% growth in turnover and 43.55% sales volume growth as

compared to the FY-1998-99. The company has invested in capex to bring in new

models and meet the increased market demand from internal accruals. It has posted a

sales volume growth of around 48% during the Q1 of 2000-01 as against the

corresponding period of the last year. To compare its performance with other

competitors, sales volume of July’00 for HHML (73857 units) is more than the

combined sales of Bajaj Auto (41950 units) and TVS Suzuki (28907 units). A concern

of 100% subsidiary by Honda Motors has affected HHML stock on the bourses

without really taking into account its business out performance.

At present HHML is having exclusive technology from Honda Motors. An

announcement of a 100% subsidiary company, Honda Scooters & Motors India Ltd.

(HSMIL) by Honda Motors in India has jeopardized the premium valuations enjoyed

by HHML because HHML’s excellent performance is very well backed by Honda

technology. This event adversely affected the HHML stock on the bourses and led to

a sharp fall in stock prices without giving any rating to its outstanding performance

for motorcycle segment than its peer group. As per the terms and conditions agreed

upon between Honda Motors and Munjals, this subsidiary will initially manufacture

scooters and after 2004, it will begin the manufacturing of motorbikes. So for the

medium term till 2004, HHML need not fear the competition with HSMIL. We

believe, the formation of 100% subsidiary by Honda Motors may be the emergence

out of the following reasons:

1) Honda may be not contended with the present stake of 26% in HHML

(same as Munjal family stake) due to which it is not able to dictate its

terms.

2) This can also be a negotiating tool for Honda Motors by which it may take

some steps in future i.e. post-2004 against HHML.

After 2004…the following possibilities are opening up…

1) The probability of continuation with the present scenario is medium. Honda

Motors continue with its present stake of 26% in HHML, which is same as

Munjal’s stake without disturbing the most successful world class JV because

after 2004, the growth of motorcycle segment may not be as attractive as the

present growth.

2) Honda Motors increase its stake to 52% by buying out 26% stake of Munjal

family and control the scenario in motorcycle segment. This will again place

HHML to exit with a large consideration rather than to run the show without

sound technology and a thorough research base for new products and product

upgradation. Thus, the probability of a complete takeover of HHML by Honda

Motors is also very low as that is a bit difficult task for Honda Motors and it

could also affect other JVs of Honda Motors in India.

3) Honda Motors manufacturing motorcycles in 100% subsidiary company by

exiting from the JV, which is likely to affect adversely HHML unless it gets

into a new JV or do some in-house development. But by the time Honda

Motors starts its production of motorcycles by 2004, the segment growth may

not be as attractive as today which is a negative point for Honda Motors, as

the growing requirements are going to be fulfilled by HHML upto 2004.

4) Honda Motors to increase its stake in HHML for which the probability of

Munjals agreement is very strong, which will be a win-win situation for

HHML and its investors. The following effects are likely to arise on account

of this possibility:

This would make HHML fearless on competition front in motorcycle

segment,

An assured flow of Honda Motors technology to HHML

Re-rating of HHML stock price

Honda Motors can easily control the management by dictating the

issues on its own.

The possibility of Munjal’s disagreement for the above aspect is very low.

5) It may also happen that Munjals try to increase their stake in HHML for which

the probability of Honda Motors’ agreement is very low and the vice-versa

condition may show a picture that in future HHML has to face competition

with HMSIL in motorcycle segment.

HHML has taken significant efforts to remain market leader in time to come

Due to the shift in the consumer preferences from old scooters to stylish and

the latest smart looking sleek motorcycles, the other companies like Bajaj Auto, LML,

Kinetic Motors and TVS have also begun to work hard on motorcycle segment, which

has made the competition even stronger for HHML. TVS Suzuki has launched a four-

stroke motorcycle ‘Fiero’ and Bajaj Auto is fully geared to launch ‘Eliminator’

(173.9cc), ‘Pulsar’ (150/200cc) and ‘Acer’ (100cc) in coming months of 2000. To

fight with the competitors and to dominate the market even in the future, HHML has

swiftly taken the following steps:

Expanded the production capacity of Dharuhera plant at Haryana to 3.5 lakh

vehicles from 3 lakh units to capture the upward trend of demand for

motorbikes, which it is going to fund out of its internal accruals.

‘CBZ’, a 156 cc bike with 5 gears, the only bike with a disc brake i.e. a power

bike has already become the success story of the company in the urban market.

The company has launched this hit product during year 2000 only.

HHML has also involved itself to focus on the sale of spare parts and

accessories, which has increased substantially from Rs.4.82 crore (Q1 of 99-

00) to Rs.7.69 crore (Q1 of 2000-01) which in turn has enabled the company

to maintain its net profit margins on a higher side.

It is also planning to introduce new version of Splendor by January 2001 for

which the trial production is already started in the month of Sep.’00. The

modified version of Splendor would enable the company to further capture the

market.

Hero Honda Motors Ltd., India’s largest motorcycle manufacturer reported

24.1% increase in Q2FY05 profits at Rs.1.94bn on a 39.3% increase in net sales to

Rs.17.6bn. The results have been as per our expectation on PAT levels, but higher

realisations per vehicle due to better product mix and 100bps drop in EBIDTA

margins on back of Rs.1,000 cash discount promotion offer surprised us. It has not

been all smooth sailing for Hero Honda. There have been some hiccups too. For

example, though the company claims that sales for Splendor cut across a wide

spectrum of people, Hero Honda for long did not have a bike which focused on the

entry level-segment of the market. It did launch Joy last year for the economy

segment, which did not get a very positive response. "There were two reasons for this.

First, being an entry-level product it was overpriced by about Rs 1,000. Also, that was

the time when Bajaj launched its Boxer priced at Rs 29,900, making matters worse,"

says Sobti. However, Hero Honda was quick to make amends. It phased out Joy in

less than a year, and launched Dawn as an entry-level bike. "We priced it right and we

believe that it will be the 21st century CD-100 for us. Dawn has received a great

response and has sold 10,000 pieces in the second month itself," says Sobti.

Meanwhile, the company may also phase out the CD-100 (popular during the 1985-

1995 period) at a later stage and replace it with Dawn. In 1999, Hero Honda

conducted the largest research on two-wheelers in the country covering 50,000

households, which helped the company in drawing out its strategy. "The research

helped us gauge consumer preferences and demand. It also gave us an estimate of

demand for bikes vis-à-vis scooters," says Sobti. Hero Honda has conducted a follow-

up to the research this year covering an even larger spectrum of people with an

emphasis on the rural market. Although the results of the survey are still being

compiled, it clearly shows that demand for bikes continues in the Indian market. In

fact, as per estimates, demand for bikes will continue growing in double-digit figures

in the coming years.

At one level, Hero Honda’s emergence as the largest motorcycle manufacturer

in the world’s biggest two wheeler market is the sum of two stories: the first about

how India’s middle class – used to traveling either on public transport or on scooters

—was wooed, nurtured and won in 1990s. In the 2000s, it is the continuing stories of

how college kids, and salesmen and even farmers are being enticed. In a space of 20

years, Hero Honda has not only caught up with, but has also overtaken the incumbent

in the Number 1 slot: Pune-based Bajaj Auto. At last count, Hero Honda sold 500,000

more two wheelers than Bajaj Auto in a year, according to Society for Indian

Automobile Manufacturers—the apex body for auto manufacturers in India. The

youth of India emerged as one of most important constituents for Hero Honda. They

demanded stylish and sleek products rather than those that were merely functional and

simple; and got them.

And as rural markets began to explode, motorcycles with their bigger wheels and

longer wheelbases found favour with the buyers. While the emerging trends did not