Embed Size (px)

Citation preview

ASHK HK RBC UpdateFeifei Zhang

Rob Curtis

Jonathon Ko

Syed Haider

11 April 2017

4

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

How aware are you of the upcoming

consultation

1) Not aware

2) Somewhat aware

3) Fully aware

Question: Is my clicker working?

The Backstory

6

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Global Developments – Overview and recap

IAIS – Long term plans Global developments impact

The IAIS is an international body that promotes

effective and globally consistent supervision of the

insurance industry.

The Financial Stability Board (FSB) is an international

body that monitors and makes recommendations about

the global financial system.

HLA

ICS

BCR Basic Capital

Requirement for G-SII

Insurance Capital

Standard for IAIGs

Higher Loss

Absorbency for G-SII

All insurers Insurance groupsInternationally Active

Insurance Groups (I)

Globally Systemic

Insurance Groups

(G-SIIs)

5 Group Insurance Core Principles (ICPs)

Common Framework for

Internationally

Active Groups (ComFrame)

G-SII package

Insurance Capital

Standard (ICS)

Basic Capital

Requirement

(BCR)

Higher Loss

Absorbency

(HLA)

■ Systemic risk

and recovery

analysis

adopted by

IAIS

■ Enhanced

capital &

liquidity

planning and

management

■ Group-wide

ORSA

■ Supervisory

College

Likely

implications for

many insurers:

7

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Key IAIS Standards – (ICPs)

Important context for Hong Kong

ERM (ICP 16)

Capital Adequacy (ICP 17)

Minimum Capital Requirement (MCR)

• Prescribed Capital Requirement

(PCR)

• Internal Model Requirements:

— Statistical quality test

— Calibration test

— Use test

• Risk Governance and Control

• Risk Appetite and tolerance

• Risk Monitoring and polices

• Risk reporting and mitigation

• ORSA:

– Available capital assessment

– Economic and regulatory capital relationship

– Stress test and scenario analysis

– Continuity analysis

8

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

International Standards from the IAIS of

immediate relevance for Hong KongThere are currently 26 ICPs which can be divided into five broad categories

covering:

Supervisory Powers and

Measures

Solvency Group Supervision,

Cooperation and Crisis

Management

Conduct of Business,

Intermediaries and Fraud

Prevention

Corporate Governance and

Public Disclosure

ICP 1 Objectives, Powers and

Responsibilities of the

Supervisor

ICP 13 Reinsurance and Other

Forms of Risk Transfer

ICP 3 Information Exchange and

Confidentiality Requirements

ICP 18 Intermediaries ICP 5 Suitability of Persons

ICP 2 Supervisor ICP 14 Valuation ICP 23 Group-wide Supervision ICP 19 Conduct of Business ICP 7 Corporate Governance

ICP 4 Licensing ICP 15 Investment ICP 24 Macroprudential

Surveillance and Insurance

Supervision

ICP 21 Countering Fraud in

Insurance

ICP 8 Risk Management and

Internal Controls

ICP 6 Changes in Control and

Portfolio Transfers

ICP 16 Enterprise Risk

Management for Solvency

Purposes

ICP 25 Supervisory Cooperation

and Coordination

ICP 22 Anti-Money Laundering

and Combating the Financing of

Terrorism

ICP 20 Public Disclosure

ICP 9 Supervisory Review and

Reporting

ICP 17 Capital Adequacy ICP 26 Cross-border

Cooperation and Coordination

on Crisis Management

ICP 10 Preventive and

Corrective Measures

ICP 11 Enforcement

ICP 12 Winding-up

[1] Supervisory powers and measures

[2] Solvency

[3] Group supervision, cooperation and

crisis management

[4] Conduct of business, intermediaries

and fraud prevention

[5] Corporate governance and public

disclosure

9

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

The beginning

Hong Kong RBC development initiated

ICO ICPs 1st

Consultation

1983Oct

2011

Mid

2012

Sep

2015

2nd

Consultation

Oct

2016 -

current

Sept

2014

Dec

2014

Oct

2016

10

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

The destination

Risk Based Capital (RBC)

Pillar 1 Pillar 2 Pillar 3

Quantitative requirements

Over-arching

methodological framework

Valuation of assets and

liabilities

Capital requirement

Capital resources

Qualitative requirements

ERM

Risk governance

Risk appetite, tolerance,

limits

ORSA

Disclosure and

transparency

Public disclosures

Group-wide supervision requirements across all 3 pillars (3 tier approach)

Separate work stream

College of supervisors

Focus on relevant insurers

Pillar 1Life and GI

12

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Economic Balance Sheet (EBS)

Best estimate

of current

reserves

Eligible

assets

Margin Over

Current

Estimate

(MOCE)

Assets

Technical

provision

Other

liabilities

13

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Technical provision – Life

Economic balance

sheet approach

Margin over current

estimate

Explicit allowance of

TVOG

Product

classification

refinement for QIS

Reserves estimated

using best estimate

GPV basis

Discount rateContract boundary

definition – Alignment

to IFRS 17

Cash surrender value

and zeroisation

14

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Technical provision – GI

Reserves

projected using

best estimate

assumptions

Risk margins

required

across all

LOBs

Inclusion of both

onshore and

offshore insurance

liabilities

Discounting

applied to all LOBs

Product

classification

refinement for

QIS

15

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Economic Balance Sheet (EBS)

Best estimate

of current

reserves

Eligible

assets

Margin Over

Current

Estimate

(MOCE)

PCR

Surplus

Assets

Technical

provision

Total

available

capital

Other

liabilities

16

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

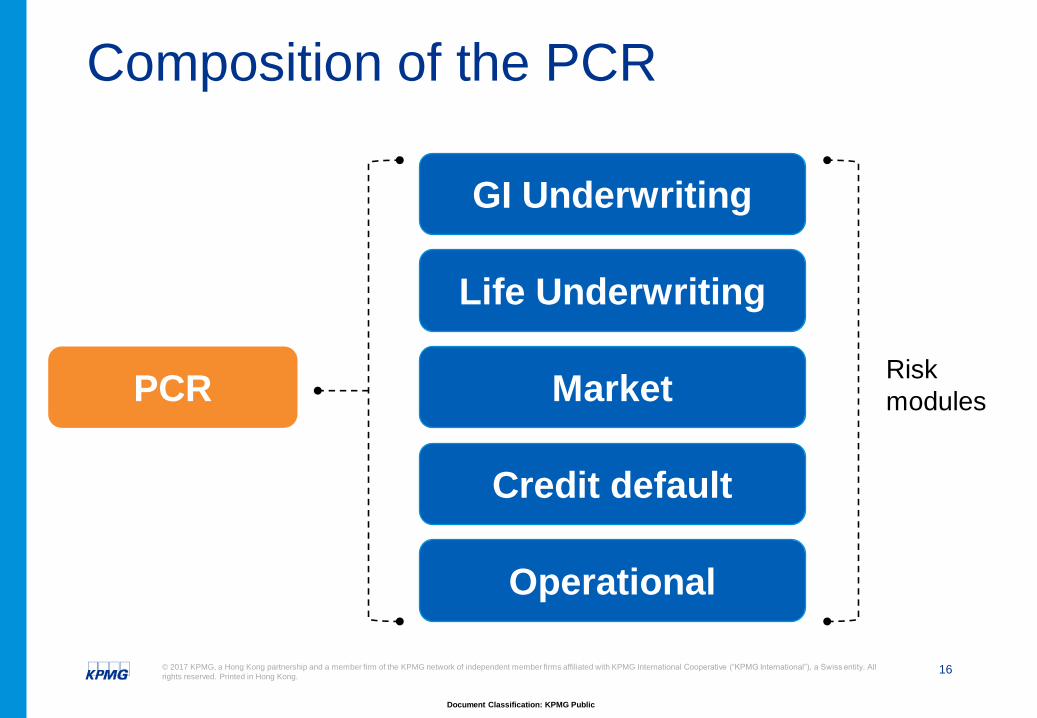

Composition of the PCR

GI Underwriting

Life Underwriting

Credit default

Market

Operational

PCR Risk

modules

17

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Catastrophes

PCR Risk modules

Premium

Reserves

DataApproach

• Valuation of

outstanding claims

and premium

liabilities under an

economic basis

• Allocation by lines of

business for QIS

• Catastrophes – TBD

• Premium and

reserves – Factor

based

• Catastrophes – TBD

GI underwriting

risk

18

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

What perils or catastrophes pose greatest

concern to the GI industry

1) Windstorm and Typhoons

2) Flood

3) Earthquake

4) Manmade losses

5) Exposure to offshore catastrophes

Question

19

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

PCR Risk modules

Mortality

Longevity

Morbidity

Expense

Lapse

DataApproach

• Liability cash flow

data

• Allocation by

product

classification for QIS

• May need to

determine the biting

stress at product

level

• Stress test

Life underwriting

risk

Mass lapse

Catastrophe

20

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

PCR Risk modules

Interest rate

Equity

Property

Credit Spread

Currency

DataApproach

• Market value

• Asset cash flow data

(fixed interest)

• Sources of data –

finance, investment

manager

• Stress test

• Factor based

• Asset look through

approach

• Allowance for

financial risk

mitigation

• Allowance for loss

absorbing capacity

Market risk

21

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

PCR Risk modules

Reinsurance

Other

counterparties

DataApproach

• Estimate

reinsurance

recoverables

• Credit rating bands

• Sources of data –

accounting,

actuarial,

reinsurance

• Factor based

Credit default

risk

22

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Operational

PCR Risk modules

DataApproach

• Volume

• Qualitative

• Losses

• Data collection for

QIS

Operational risk

23

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Of the following what do you think is the most

significant risk for life insurance companies in

HK?

1) Interest rate risk

2) Credit spread

3) Claims risks

4) Persistency

5) Credit default

Question

24

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Pillar 1 – QIS readiness checklist

Data Models Timing Resources

Training Assurance Plan for

QIS

Board /

Exec

awareness

Link to

accounting

change

25

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

What elements are you least prepared for?

1) Data or Models

2) Resources or timing

3) Training

4) Communicating awareness to Board / Senior

management

Question

Pillar 2

27

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Overview

Pillar 2 changes will feature:

A new ERM GN

A formal Own Risk and Solvency

Assessment (ORSA) requirement

28

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

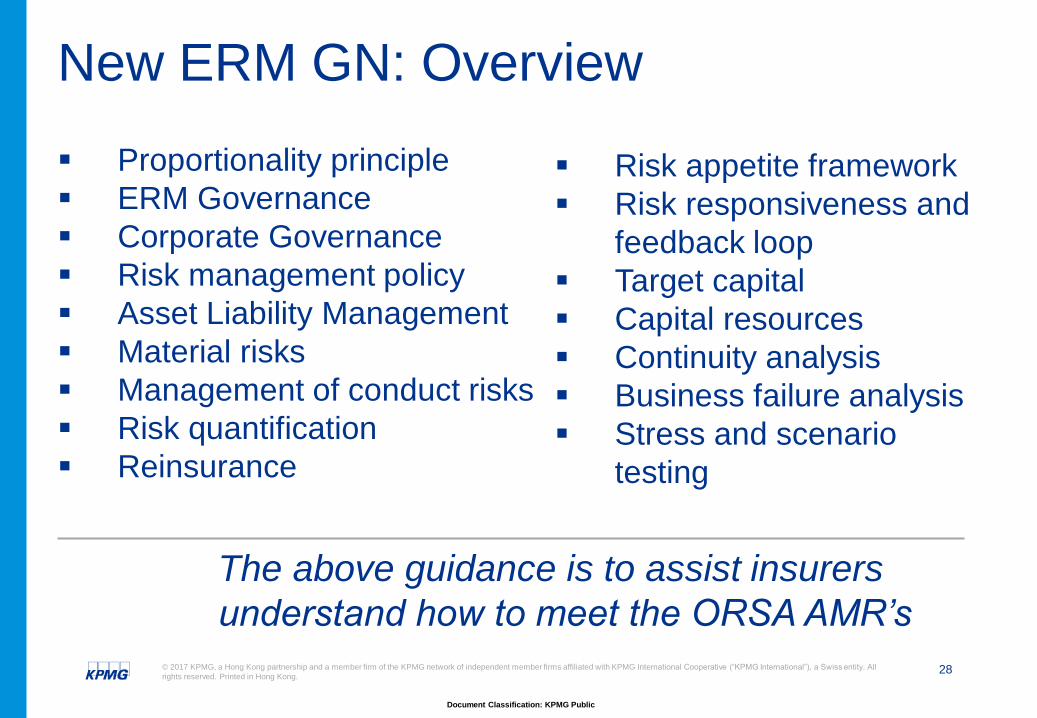

New ERM GN: Overview

Proportionality principle

ERM Governance

Corporate Governance

Risk management policy

Asset Liability Management

Material risks

Management of conduct risks

Risk quantification

Reinsurance

Risk appetite framework

Risk responsiveness and

feedback loop

Target capital

Capital resources

Continuity analysis

Business failure analysis

Stress and scenario

testing

The above guidance is to assist insurers

understand how to meet the ORSA AMR’s

29

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Have you had experience in creating or

implementing an ORSA:

1) Yes

2) Yes, but limited

3) No

Question

30

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Likely ORSA Absolute Minimum Requirements (AMRs)

6 Key AMRs:

[1] The Board of an insurer will be responsible

for approving an ORSA.

[2] The ORSA is required to consider all

material risks that are addressed within the

insurers ERM framework.

31

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Likely ORSA Absolute Minimum Requirements (AMRs)

[3] ORSA Capital Assessment:

Key elements:

Regulatory and Economic capital

Capital resources

Target capital

Risk appetite

Group-wide assessment

32

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

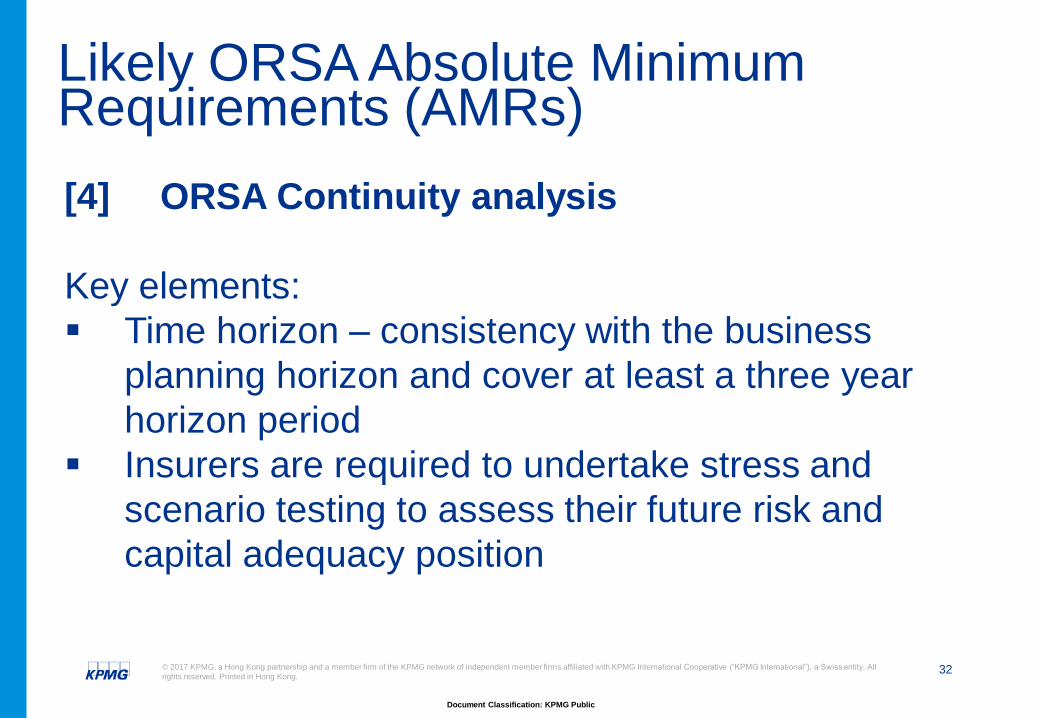

Likely ORSA Absolute Minimum Requirements (AMRs)

[4] ORSA Continuity analysis

Key elements:

Time horizon – consistency with the business

planning horizon and cover at least a three year

horizon period

Insurers are required to undertake stress and

scenario testing to assess their future risk and

capital adequacy position

33

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

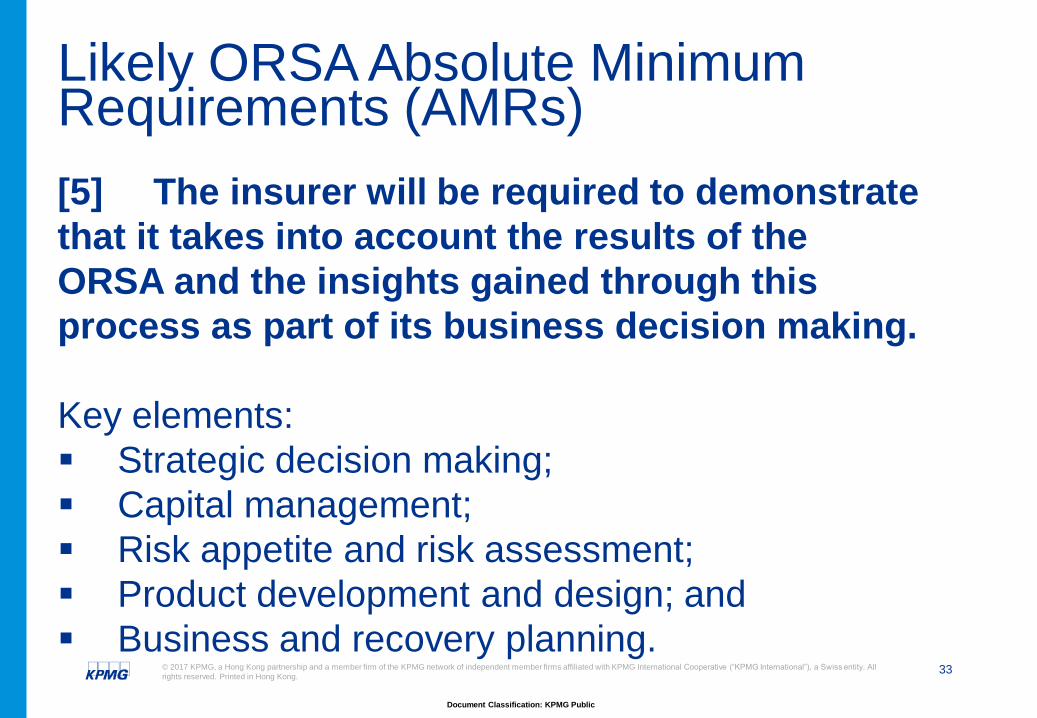

Likely ORSA Absolute Minimum Requirements (AMRs)

[5] The insurer will be required to demonstrate

that it takes into account the results of the

ORSA and the insights gained through this

process as part of its business decision making.

Key elements:

Strategic decision making;

Capital management;

Risk appetite and risk assessment;

Product development and design; and

Business and recovery planning.

34

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Likely ORSA Absolute Minimum Requirements (AMRs)

[6] The insurer is required to demonstrate that

the management of its conduct risks have been

appropriately assessed and managed, taking

into account the “fair treatment of customers”

principle.

Key elements:

The ORSA is required to consider conduct risks

which are likely to impact on the insurer’s ability

to meet its obligations to treat its customers

fairly.

35

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Do you presently have a conduct risk

framework?

1) Yes

2) No

3) Partial

4) Non insurer

Question

36

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

Likely ORSA Absolute Minimum Requirements (AMRs)

Additional Group/Subgroup ORSA AMR requirements

Include all reasonably foreseeable and relevant material

group risks considered through the ERM.

Include an assessment of group regulatory capital

requirements and sufficiency of internal capital needs.

Perform group stress and scenario testing (SST)

including recovery analysis.

Systemic risk consideration for groups including

approach to managing and mitigating systemic risks,

reducing risk posed from involvement in NTNI activities

and the systemic risks of failure.

37

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

What ORSA elements will pose concerns for

your organisation:

1) Developing the risk management framework

2) Undertaking an assessment of risk exposures

3) Undertaking prospective solvency tests

4) Performing the continuity analysis

5) Performing stress and scenario tests

6) Performing the conduct risk analysis

7) All of the above

Question

38

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All

rights reserved. Printed in Hong Kong.

The journey ahead…

Pillar

1

Pillar

2

Pillar

3

IA

IFRS

* Assume IFRS 9 deferral for all entities

QIS

Possible early

Implementation

(2022)

Expected

Full RBC

framework

IFRS 17

TBD

GN16

2017 2018 2019 2020 2021 2022 onwards

IFRS 9

disclosure

New IA

P2

Consultation

ERM GN

Consultation

in progress

RBC

guidance

Future consultations?

Future QIS?

IFRS 9

GN17

Questions ?

Document Classification: KPMG Public

© 2017 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Hong Kong.

www.kpmg.com.hk