Embed Size (px)

Citation preview

Second Pass

Future Value of a Single Amount In situations involving the future value of a single amount, you are asked to calculate

how much money you will have in the future as a result of investing a certain amount

at the present time. If you were to receive a gift of $10,000, for instance, you might

decide to put it in a savings account and use the money as a down payment on a house

when you graduate. The future value computation will tell you how much money

would be available when you graduate.

To solve a future value problem, you need to know three items:

1. The amount to be invested .

2. The interest rate ( i ) that the amount will earn.

3. The number of periods ( n ) in which the amount will earn interest .

Since the future value concept is based on compound interest, the amount of interest

for each period is calculated by multiplying the interest rate by the principal plus any

interest not paid out in prior periods. Graphically, the calculation of the future value

of $1 for three periods and an interest rate of 4 percent may be represented as follows:

Presenttime$1

Futurevalue$1.125

Interest accumulatesover time

1 2 3

Assume that on January 1, 2014, you deposit $1,000 in a savings account at

4 percent annual interest, compounded annually. At the end of three years, the $1,000

will have increased to $1,124.90 as follows:

Year

Amount at

Start of Year 1

Interest

During the Year 5

Amount at

End of Year

2014 $1,000.0 1 $1,000.0 3 4% 5 $40 5 $1,040.0

2015 1,040.0 1 1,040.0 3 4% 5 $41.6 5 1,081.6

2016 1,081.6 1 1,081.6 3 4% 5 $43.3 5 1,124.9

We can avoid the detailed arithmetic by referring to Table 10E.1 , Future Value of

$1. For i 5 4% and n 5 3, we find the value 1.1249. We then compute the balance at

the end of year 3 as follows:

$1,000 3 1.1249 5 $1,124.90

From Table 10E.1,

Interest rate 5 4%

n 5 3

Note that the increase of $124.9 is due to the time value of money. It is inter-

est revenue to the owner of the savings account and interest expense to the savings

institution.

A P P E N D I X

10E Future Value Concepts

lib39469_app10E_10E1-10E7_olc.indd 10E-1lib39469_app10E_10E1-10E7_olc.indd 10E-1 12/3/13 8:51 AM12/3/13 8:51 AM

Second Pass

10E-2 APPENDIX 10E Future Value Concepts

FUTURE VALUE OF AN ANNUITY If you are saving money for some purpose, such as a new car or a trip to Europe, you

might decide to deposit a fixed amount of money in a savings account each month.

The future value of an annuity computation will tell you how much money will be in

your savings account at some point in the future.

The future value of an annuity includes compound interest on each payment from

the date of payment to the end of the term of the annuity. Each new payment accumu-

lates less interest than prior payments only because the number of periods remaining

to accumulate interest decreases. The future value of an annuity of $1 for three periods

at 4 percent may be represented graphically as follows:

Future valueof an annuity

$3.12

1 2 3$1 $1 $1

=

Assume that you deposit $1,000 cash in a savings account each year for three years

at 4 percent interest per year (i.e., a total principal of $3,000). You make the first

$1,000 deposit on December 31, 2014, the second deposit on December 31, 2015,

and the third and last one on December 31, 2016. The first deposit earns compound

interest for two years (for a total principal and interest of $1,081.6), the second deposit

earns interest for one year (for a total principal and interest of $1,040), and the third

deposit earns no interest because it was made on the day that the balance is computed.

Thus, the total amount in the savings account at the end of three years is $3,121.6

($1,081.6 1 $1,040 1 $1,000).

To derive the future value of this annuity, we could compute the interest on each

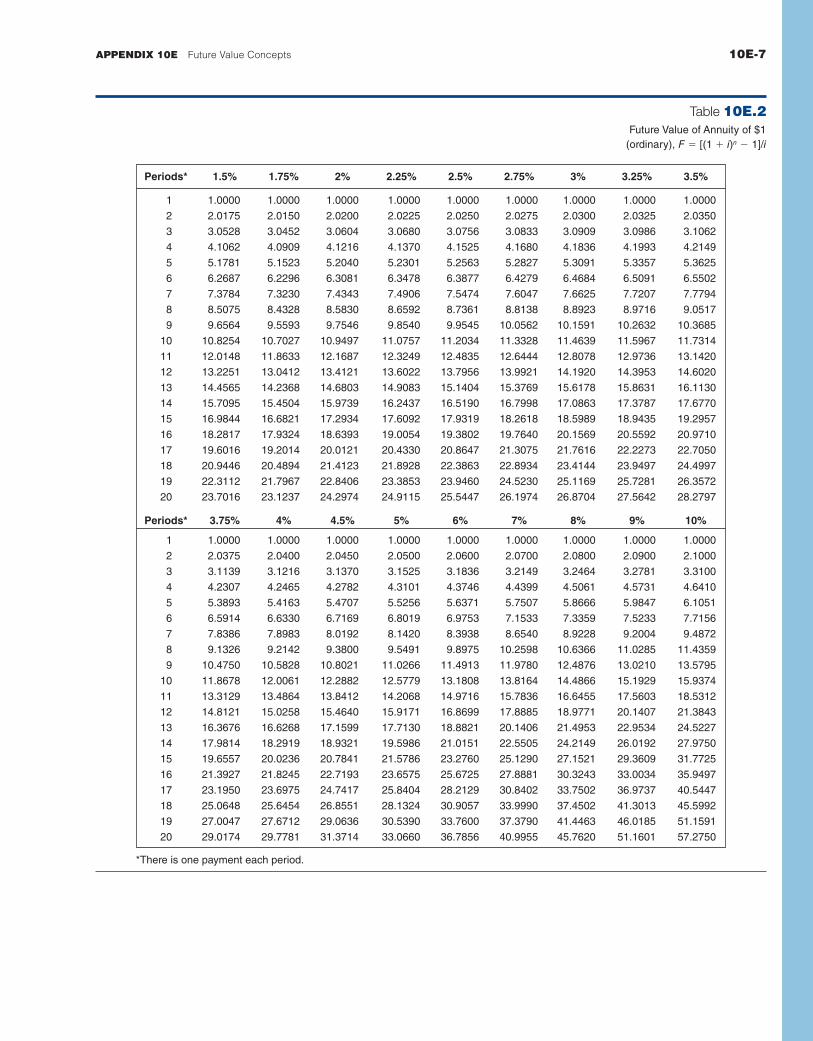

deposit. However, we can refer to Table 10E.2 , Future Value of an Annuity of $1 for

i 5 4% and n 5 3 to find the value 3.1216. The future value of your three deposits of

$1,000 each can be computed as follows:

$1,000 3 3.1216 5 $3,121.60

From Table 10E.2,

Interest rate 5 4%

n 5 3

THE POWER OF COMPOUNDING Compound interest is a remarkably powerful economic force. The ability to earn

interest on interest is the key to building economic wealth. If you start your career

on your 22nd birthday and save $1,000 per year for 10 years at an interest rate of

5 percent compounded annually until you retire at the end of your 65th year of

age, you will accumulate a total of $69,390. The money saved is $10,000 and the rest

is interest that accumulated over the 44-year period from the time you started saving

until the time you retired. If the money saved earns 6 percent instead of 5 percent

throughout the 44-year period, then the total amount increases to $101,309 on your

lib39469_app10E_10E1-10E7_olc.indd 10E-2lib39469_app10E_10E1-10E7_olc.indd 10E-2 12/3/13 8:51 AM12/3/13 8:51 AM

Second Pass

10E-3APPENDIX 10E Future Value Concepts

66th birthday, a hefty birthday present! However, if you continue to save $1,000 per year

for 44 years and earn 5 percent interest per year, then your retirement fortune jumps to

$158,700; $44,000 is money saved and the rest is compound interest. The power of com-

pounding in this specific case is illustrated in the graph below. The lesson associated with

compound interest is clear: even though it’s hard to do, you should start saving money now.

20,000

01 4 7 10 13 16 19 22 25 28 31 34 4037 43

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

Year

Dol

lar

Am

ount

Effect of Compound Interest

Money SavedFuture Value of Investment

EXERCISES

Computing Four Kinds of Present and Future Value On January 1, 2014, Wesley Company completed the following transactions (assume an annual

compound interest rate of 6 percent):

a. Deposited $12,000 in Fund A.

b. Established Fund B by agreeing to make six annual deposits of $2,000 each. Deposits are made

each December 31.

c. Established Fund C by depositing a single amount that will increase to $40,000 by the end of

year 7.

d. Decided to deposit a single sum in Fund D that will provide 10 equal annual year-end payments

of $15,000 to a retired employee (payments starting December 31, 2014).

Required (show computations and round to the nearest dollar): 1. What will be the balance of Fund A at the end of year 9?

2. What will be the balance of Fund B at the end of year 6?

3. What single amount must be deposited in Fund C on January 1, 2014?

4. What single sum must be deposited in Fund D on January 1, 2014?

Computing Growth in a Savings Account: A Single Amount On January 1, 2014, you deposited $6,000 in a savings account. The account will earn an annual

compound interest rate of 4 percent, which will be added to the fund balance at the end of each year.

Required (round to the nearest dollar): 1. What will be the balance in the savings account at the end of 10 years?

2. What is the interest for the 10 years?

3. How much interest revenue did the fund earn in 2014? 2015?

E10E–1

E10E–2

lib39469_app10E_10E1-10E7_olc.indd 10E-3lib39469_app10E_10E1-10E7_olc.indd 10E-3 12/3/13 8:51 AM12/3/13 8:51 AM

Second Pass

10E-4 APPENDIX 10E Future Value Concepts

Recording Growth in a Savings Account with Equal Periodic Payments You plan to deposit $2,000 in a savings account on each December 31. The account will earn an

annual interest rate of 9 percent, which will be added to the fund balance at year-end. The first

deposit will be made on December 31, 2014 (end of period).

Required (show computations and round to the nearest dollar): 1. Prepare the required journal entry on December 31, 2014, assuming you keep books to account

for your personal finances.

2. What will be the balance in the savings account at the end of the 10th year (i.e., after 10

deposits)?

3. What is the interest earned on the 10 deposits?

4. How much interest revenue did the fund earn in 2015? 2016?

5. Prepare all required journal entries at the end of 2015 and 2016.

Computing Growth for a Savings Fund with Periodic Deposits On January 1, 2014, you decided to plan for a trip around the world upon graduation four years

from now. Your grandmother wants to deposit sufficient funds for this trip in a savings account for

you. You estimate that the trip would cost $15,000. To be generous, your grandmother decided to

deposit $3,500 in the fund at the end of each of the next four years, starting on December 31, 2014.

The savings account will earn interest at an annual rate of 6 percent, which will be added to the

savings account at each year-end.

Required (show computations and round to the nearest dollar): 1. How much money will you have for the trip at the end of year 4 (i.e., after four deposits)?

2. What is the interest for the four years?

3. How much interest revenue did the fund earn in 2014, 2015, 2016, and 2017?

E10E–3

E10E–4

PROBLEMS

Computing Present and Future Values On January 1, 2014, Perrakis Company completed the following transactions and events (use an 8

percent annual interest rate for all transactions and assume annual compounding unless otherwise

stated):

a. Deposited $60,000 in a debt retirement fund. Interest will be computed at six-month intervals and

added to the fund at those times (i.e., semi-annual compounding). ( Hint: Think carefully about n

and i. )

b. Established a plant-addition fund of $400,000 to be available at December 31, 2015. A single

sum that will grow to $400,000 will be deposited on January 1, 2014.

c. Established a pension retirement fund of $1,000,000 to be available by December 31, 2016, by

making six equal annual deposits at year-end, starting on December 31, 2014.

d. Purchased an $180,000 machine on January 1, 2014, and paid cash, $80,000. A four-year note

payable is signed for the balance. The note will be paid in four equal year-end amounts starting

on December 31, 2014.

Required (show computations and round to the nearest dollar): 1. In transaction ( a ), what will be the balance in the fund at the end of year 4? What is the total

amount of interest revenue that will be earned during the first four years?

2. In transaction ( b ), what amount must the company deposit on January 1, 2014? What is the total

amount of interest revenue that will be earned by the end of year 5?

3. In transaction ( c ), what is the required amount of each of the six equal annual deposits? What is

the total amount of interest revenue that will be earned over the six years?

4. In transaction ( d ), what is the amount of each of the equal annual payments that will be paid on

the note? What is the total amount of interest expense that will be incurred during the four years?

Prepare journal entries to record the purchase of the machine and the payments on December 31,

2014 and 2015.

P10E–1

lib39469_app10E_10E1-10E7_olc.indd 10E-4lib39469_app10E_10E1-10E7_olc.indd 10E-4 12/3/13 8:51 AM12/3/13 8:51 AM

Second Pass

10E-5APPENDIX 10E Future Value Concepts

Computing Present and Future Values On January 1, 2014, Nader Company completed the following transactions (use an annual interest

rate of 6 percent for all transactions):

a. Deposited $300,000 in a debt retirement fund. Interest will be computed at six-month intervals

and added to the fund at those times (i.e., semi-annual compounding). ( Hint: Think carefully

about n and i. )

b. Established a plant-addition fund of $800,000 to be available at the end of year 10. A single sum

that will grow to $800,000 will be deposited on January 1, 2014.

c. Established a pension retirement fund of $600,000 to be available by the end of year 10 by

making 10 equal annual deposits at year-end, starting on December 31, 2014.

d. Purchased a $750,000 machine on January 1, 2014, and paid cash, $350,000. A four-year note

payable is signed for the balance. The note will be paid in four equal year-end amounts, starting

on December 31, 2014.

Required (show computations and round to the nearest dollar): 1. In transaction ( a ), what will be the balance in the fund at the end of year 5? What is the total

amount of interest revenue that will be earned during the first five years?

2. In transaction ( b ), what amount must the company deposit on January 1, 2014? What is the total

amount of interest revenue that will be earned by the end of year 10?

3. In transaction ( c ), what is the required amount of each of the 10 equal annual deposits? What is

the total amount of interest revenue that will be earned over the 10 years?

4. In transaction ( d ), what is the amount of each of the equal annual payments that will be paid on

the note? What is the total amount of interest expense that will be incurred during the four years?

Prepare journal entries to record the purchase of the machine and the payments on December 31,

2014 and 2015.

Computing Amounts for a Fund with Journal Entries On January 1, 2014, Jalopy Company decided to accumulate a fund to build an addition to its plant.

The company will deposit $230,000 in the fund at each year-end, starting on December 31, 2014.

The fund will earn 9 percent interest, which will be added to the fund balance at each year-end. The

fiscal year ends on December 31.

Required: 1. What will be the balance in the fund immediately after the December 31, 2016, deposit?

2. Complete the following fund accumulation schedule:

P10E–2

P10E–3

Date

Cash

Payment

Interest

Revenue

Increase

in Fund

Fund

Balance

31/12/2014

31/12/2015

31/12/2016

Total

3. Prepare adjusting journal entries on December 31 of each of the three years.

4. The plant addition was completed on January 1, 2017, for a total cost of $749,000. Prepare the

journal entry, assuming that this amount is paid in full to the contractor.

lib39469_app10E_10E1-10E7_olc.indd 10E-5lib39469_app10E_10E1-10E7_olc.indd 10E-5 12/3/13 8:51 AM12/3/13 8:51 AM

Second Pass

10E-6 APPENDIX 10E Future Value Concepts

Periods 1.5% 1.75% 2% 2.25% 2.5% 2.75% 3% 3.25% 3.5%

1 1.0150 1.0175 1.0200 1.0225 1.0250 1.0275 1.0300 1.0325 1.0350

2 1.0302 1.0353 1.0404 1.0455 1.0506 1.0558 1.0609 1.0661 1.0712

3 1.0457 1.0534 1.0612 1.0690 1.0769 1.0848 1.0927 1.1007 1.1087

4 1.0614 1.0719 1.0824 1.0931 1.1038 1.1146 1.1255 1.1365 1.1475

5 1.0773 1.0906 1.1041 1.1177 1.1314 1.1453 1.1593 1.1734 1.1877

6 1.0934 1.1097 1.1262 1.1428 1.1597 1.1768 1.1941 1.2115 1.2293

7 1.1098 1.1291 1.1487 1.1685 1.1887 1.2091 1.2299 1.2509 1.2723

8 1.1265 1.1489 1.1717 1.1948 1.2184 1.2424 1.2668 1.2916 1.3168

9 1.1434 1.1690 1.1951 1.2217 1.2489 1.2765 1.3048 1.3336 1.3629

10 1.1605 1.1894 1.2190 1.2492 1.2801 1.3117 1.3439 1.3769 1.4106

11 1.1779 1.2103 1.2434 1.2773 1.3121 1.3477 1.3842 1.4216 1.4600

12 1.1956 1.2314 1.2682 1.3060 1.3449 1.3848 1.4258 1.4678 1.5111

13 1.2136 1.2530 1.2936 1.3354 1.3785 1.4229 1.4685 1.5156 1.5640

14 1.2318 1.2749 1.3195 1.3655 1.4130 1.4620 1.5126 1.5648 1.6187

15 1.2502 1.2972 1.3459 1.3962 1.4483 1.5022 1.5580 1.6157 1.6753

16 1.2690 1.3199 1.3728 1.4276 1.4845 1.5435 1.6047 1.6682 1.7340

17 1.2880 1.3430 1.4002 1.4597 1.5216 1.5860 1.6528 1.7224 1.7947

18 1.3073 1.3665 1.4282 1.4926 1.5597 1.6296 1.7024 1.7784 1.8575

19 1.3270 1.3904 1.4568 1.5262 1.5987 1.6744 1.7535 1.8362 1.9225

20 1.3469 1.4148 1.4859 1.5605 1.6386 1.7204 1.8061 1.8958 1.9898

Periods 3.75% 4% 4.5% 5% 6% 7% 8% 9% 10%

1 1.0375 1.0400 1.0450 1.0500 1.0600 1.0700 1.0800 1.0900 1.1000

2 1.0764 1.0816 1.0920 1.1025 1.1236 1.1449 1.1664 1.1881 1.2100

3 1.1168 1.1249 1.1412 1.1576 1.1910 1.2250 1.2597 1.2950 1.3310

4 1.1587 1.1699 1.1925 1.2155 1.2625 1.3108 1.3605 1.4116 1.4641

5 1.2021 1.2167 1.2462 1.2763 1.3382 1.4026 1.4693 1.5386 1.6105

6 1.2472 1.2653 1.3023 1.3401 1.4185 1.5007 1.5869 1.6771 1.7716

7 1.2939 1.3159 1.3609 1.4071 1.5036 1.6058 1.7138 1.8280 1.9487

8 1.3425 1.3686 1.4221 1.4775 1.5938 1.7182 1.8509 1.9926 2.1436

9 1.3928 1.4233 1.4861 1.5513 1.6895 1.8385 1.9990 2.1719 2.3579

10 1.4450 1.4802 1.5530 1.6289 1.7908 1.9672 2.1589 2.3674 2.5937

11 1.4992 1.5395 1.6229 1.7103 1.8983 2.1049 2.3316 2.5804 2.8531

12 1.5555 1.6010 1.6959 1.7959 2.0122 2.2522 2.5182 2.8127 3.1384

13 1.6138 1.6651 1.7722 1.8856 2.1329 2.4098 2.7196 3.0658 3.4523

14 1.6743 1.7317 1.8519 1.9799 2.2609 2.5785 2.9372 3.3417 3.7975

15 1.7371 1.8009 1.9353 2.0789 2.3966 2.7590 3.1722 3.6425 4.1772

16 1.8022 1.8730 2.0224 2.1829 2.5404 2.9522 3.4259 3.9703 4.5950

17 1.8698 1.9479 2.1134 2.2920 2.6928 3.1588 3.7000 4.3276 5.0545

18 1.9399 2.0258 2.2085 2.4066 2.8543 3.3799 3.9960 4.7171 5.5599

19 2.0127 2.1068 2.3079 2.5270 3.0256 3.6165 4.3157 5.1417 6.1159

20 2.0882 2.1911 2.4117 2.6533 3.2071 3.8697 4.6610 5.6044 6.7275

Table 10E.1Future Value of $1, f 5 (1 1 i)n

lib39469_app10E_10E1-10E7_olc.indd 10E-6lib39469_app10E_10E1-10E7_olc.indd 10E-6 12/3/13 8:51 AM12/3/13 8:51 AM

Second Pass

10E-7APPENDIX 10E Future Value Concepts

Table 10E.2Future Value of Annuity of $1

(ordinary), F 5 [(1 1 i)n 2 1]/i

Periods* 1.5% 1.75% 2% 2.25% 2.5% 2.75% 3% 3.25% 3.5%

1 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000

2 2.0175 2.0150 2.0200 2.0225 2.0250 2.0275 2.0300 2.0325 2.0350

3 3.0528 3.0452 3.0604 3.0680 3.0756 3.0833 3.0909 3.0986 3.1062

4 4.1062 4.0909 4.1216 4.1370 4.1525 4.1680 4.1836 4.1993 4.2149

5 5.1781 5.1523 5.2040 5.2301 5.2563 5.2827 5.3091 5.3357 5.3625

6 6.2687 6.2296 6.3081 6.3478 6.3877 6.4279 6.4684 6.5091 6.5502

7 7.3784 7.3230 7.4343 7.4906 7.5474 7.6047 7.6625 7.7207 7.7794

8 8.5075 8.4328 8.5830 8.6592 8.7361 8.8138 8.8923 8.9716 9.0517

9 9.6564 9.5593 9.7546 9.8540 9.9545 10.0562 10.1591 10.2632 10.3685

10 10.8254 10.7027 10.9497 11.0757 11.2034 11.3328 11.4639 11.5967 11.7314

11 12.0148 11.8633 12.1687 12.3249 12.4835 12.6444 12.8078 12.9736 13.1420

12 13.2251 13.0412 13.4121 13.6022 13.7956 13.9921 14.1920 14.3953 14.6020

13 14.4565 14.2368 14.6803 14.9083 15.1404 15.3769 15.6178 15.8631 16.1130

14 15.7095 15.4504 15.9739 16.2437 16.5190 16.7998 17.0863 17.3787 17.6770

15 16.9844 16.6821 17.2934 17.6092 17.9319 18.2618 18.5989 18.9435 19.2957

16 18.2817 17.9324 18.6393 19.0054 19.3802 19.7640 20.1569 20.5592 20.9710

17 19.6016 19.2014 20.0121 20.4330 20.8647 21.3075 21.7616 22.2273 22.7050

18 20.9446 20.4894 21.4123 21.8928 22.3863 22.8934 23.4144 23.9497 24.4997

19 22.3112 21.7967 22.8406 23.3853 23.9460 24.5230 25.1169 25.7281 26.3572

20 23.7016 23.1237 24.2974 24.9115 25.5447 26.1974 26.8704 27.5642 28.2797

Periods* 3.75% 4% 4.5% 5% 6% 7% 8% 9% 10%

1 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000

2 2.0375 2.0400 2.0450 2.0500 2.0600 2.0700 2.0800 2.0900 2.1000

3 3.1139 3.1216 3.1370 3.1525 3.1836 3.2149 3.2464 3.2781 3.3100

4 4.2307 4.2465 4.2782 4.3101 4.3746 4.4399 4.5061 4.5731 4.6410

5 5.3893 5.4163 5.4707 5.5256 5.6371 5.7507 5.8666 5.9847 6.1051

6 6.5914 6.6330 6.7169 6.8019 6.9753 7.1533 7.3359 7.5233 7.7156

7 7.8386 7.8983 8.0192 8.1420 8.3938 8.6540 8.9228 9.2004 9.4872

8 9.1326 9.2142 9.3800 9.5491 9.8975 10.2598 10.6366 11.0285 11.4359

9 10.4750 10.5828 10.8021 11.0266 11.4913 11.9780 12.4876 13.0210 13.5795

10 11.8678 12.0061 12.2882 12.5779 13.1808 13.8164 14.4866 15.1929 15.9374

11 13.3129 13.4864 13.8412 14.2068 14.9716 15.7836 16.6455 17.5603 18.5312

12 14.8121 15.0258 15.4640 15.9171 16.8699 17.8885 18.9771 20.1407 21.3843

13 16.3676 16.6268 17.1599 17.7130 18.8821 20.1406 21.4953 22.9534 24.5227

14 17.9814 18.2919 18.9321 19.5986 21.0151 22.5505 24.2149 26.0192 27.9750

15 19.6557 20.0236 20.7841 21.5786 23.2760 25.1290 27.1521 29.3609 31.7725

16 21.3927 21.8245 22.7193 23.6575 25.6725 27.8881 30.3243 33.0034 35.9497

17 23.1950 23.6975 24.7417 25.8404 28.2129 30.8402 33.7502 36.9737 40.5447

18 25.0648 25.6454 26.8551 28.1324 30.9057 33.9990 37.4502 41.3013 45.5992

19 27.0047 27.6712 29.0636 30.5390 33.7600 37.3790 41.4463 46.0185 51.1591

20 29.0174 29.7781 31.3714 33.0660 36.7856 40.9955 45.7620 51.1601 57.2750

*There is one payment each period.

lib39469_app10E_10E1-10E7_olc.indd 10E-7lib39469_app10E_10E1-10E7_olc.indd 10E-7 12/3/13 8:51 AM12/3/13 8:51 AM