Embed Size (px)

Citation preview

Appendix C

Special Journals and Subsidiary Ledgers

Subsidiary Ledger

• Contains a large number of individual accounts with a common characteristic

• Provides detail for a Controlling Account in the General Ledger (the primary ledger)

Controlling Account

• Summarizing account in the General Ledger

• Examples:– Accounts Receivable (Customers ledger)

• Made up of individual account balances due from customer

– Accounts Payable (Creditors ledger)• Made up of individual account balances owed to

vendors

Accounts Receivable Ledger

• Maintains separate account for each customer

• Keeps track of:

– credit extended to customer

– payments received from customer

– Balance due from customer

• Total of all customer accounts in Accounts Receivable Ledger should equal balance of Accounts Receivable in the General Ledger

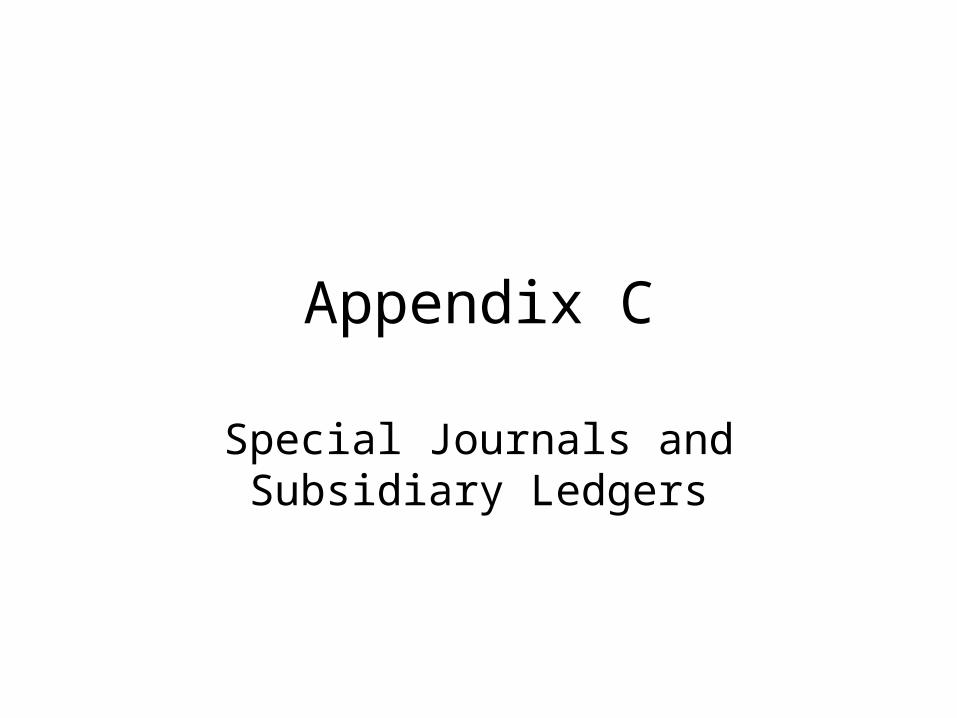

Accounts Payable Ledger

• Maintains separate account for each vendor

• Keeps track of:

– credit extended by vendor

– payments made to vendor

– Balance owed to vendor

• Total of all vendor accounts in Accounts Payable Ledger should equal balance of Accounts Payable in the General Ledger

Special Journal

• Used when a business has a large number of similar transactions

Common types of Special Journals

1) Cash Payments Journal

2) Cash Receipts Journal

3) Revenue Journal

4) Purchases Journal

Cash Payments Journal

• Used to record all cash payments

• Transactions will have a credit to Cash

• Examples of transactions:– Paying expenses– Paying amounts owed to vendors

Cash Receipts Journal

• Used to record all cash receipts

• Transactions will have a debit to Cash

• Examples of transactions– Providing services for cash– Receiving cash from customers on account

Revenue Journal

• Used to record services provided on account

• Transactions will have a debit to Accounts Receivable and a Credit to Revenue

Purchases Journal

• Used to record purchases on account

• Transactions will have a credit to Accounts payable

• Examples of transactions– Purchase of supplies on credit– Purchase of equipment on credit

General Journal

• Used to record entries that don’t fit into special journals

• Examples of transactions– Adjusting entries– Closing entries– Special transactions

Revenue Journal .

Invoice Post Accts. Rec. Dr.

Date No. Account Debited Ref Fees Earned Cr.

Customer name enter

check

mark

when

posted

to A/R

Ledger

post total of column

as a Dr. to A/R and

a Cr. to Fees Earned

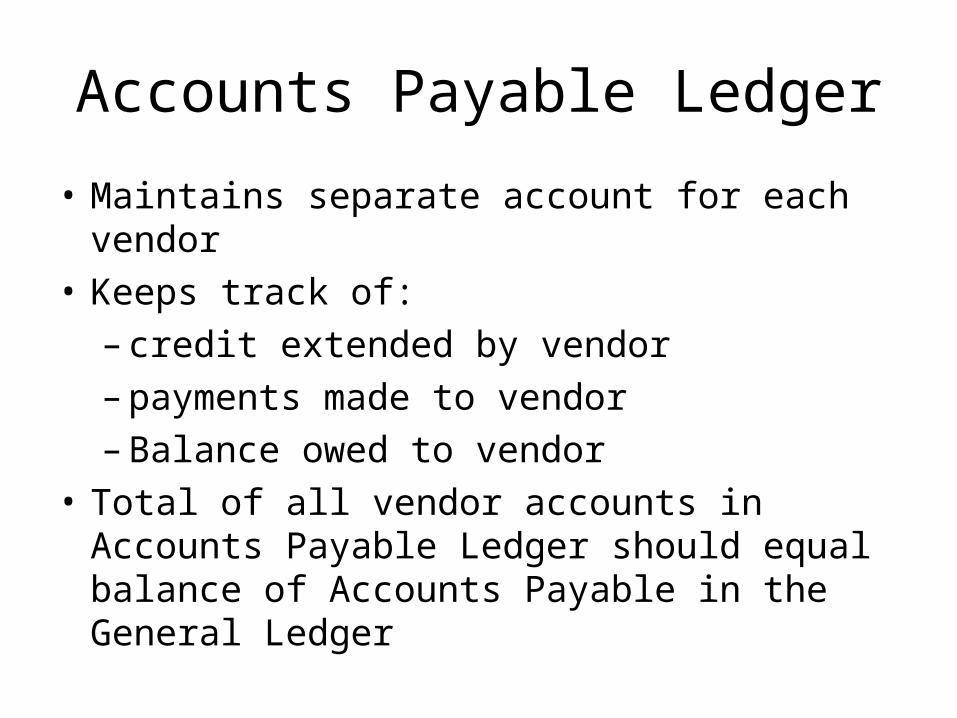

Revenue Journal Example

Nov. 1 Issued Invoice #1 to Sandoval Company for services performed, $750.

Revenue Journal Page 13

Invoice Post Accts. Rec. Dr.

Date No. Account Debited Ref Fees Earned Cr.

Nov. 1 1 Sandoval Co. 750

Accounts Receivable Subsidiary Ledger .

Customer Name: Sandoval Company

Post

Date Item Ref Dr. Cr. Balance

Nov 1 750 750

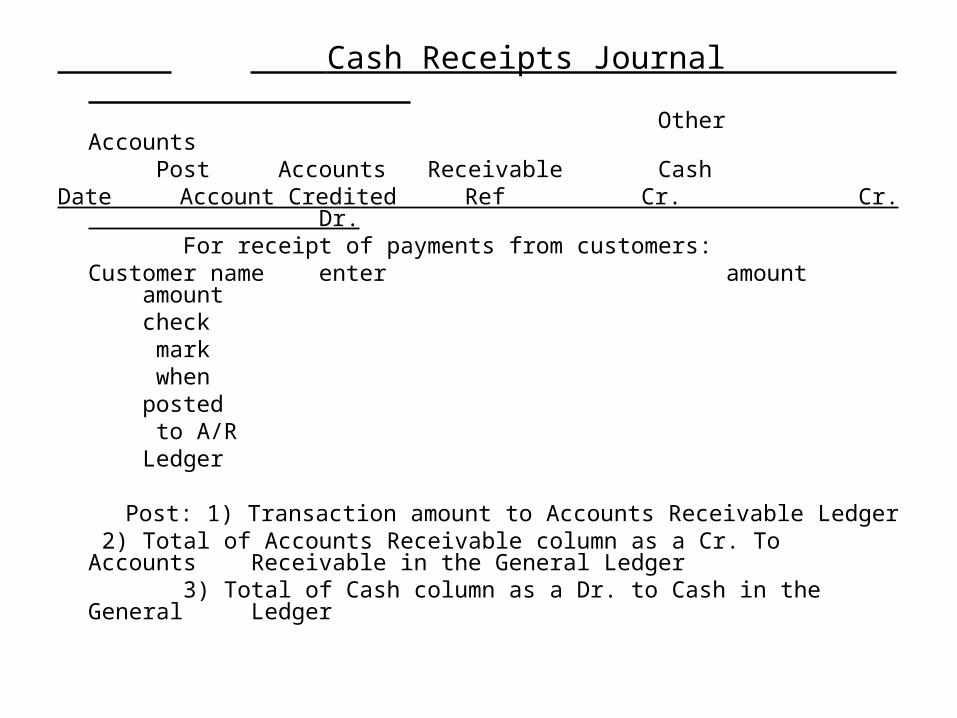

Cash Receipts Journal .

Other Accounts Post Accounts Receivable Cash

Date Account Credited Ref Cr. Cr. Dr. For receipt of payments from customers:

Customer name enter amount amount

check mark when posted to A/R Ledger

Post: 1) Transaction amount to Accounts Receivable Ledger 2) Total of Accounts Receivable column as a Cr. To

Accounts Receivable in the General Ledger 3) Total of Cash column as a Dr. to Cash in the General

Ledger

Cash Receipts Journal .

Other Accounts Post Accounts Receivable Cash

Date Account Credited Ref Cr. Cr. Dr. For receipt of cash from revenue:

Revenue revenue amount amount acct #

Post: 1) Transaction amount to revenue account in the General

Ledger 2) Total of Accounts Receivable column as a Cr. To

Accounts Receivable in the General Ledger 3) Total of Cash column as a Dr. to Cash in the General

Ledger

Cash Receipts Journal Example

Nov. 9 Received $500 from Sandoval Co. on account

Cash Receipts Journal Page 27 .

Other Accounts Post Accounts Receivable Cash

Date Account Credited Ref Cr. Cr. Dr.Nov. 8 Sandoval Co. 500 500

Accounts Receivable Subsidiary Ledger .

Customer Name: Sandoval Company

Post

Date Item Ref Dr. Cr. Balance

Nov 1 750 750

8 500

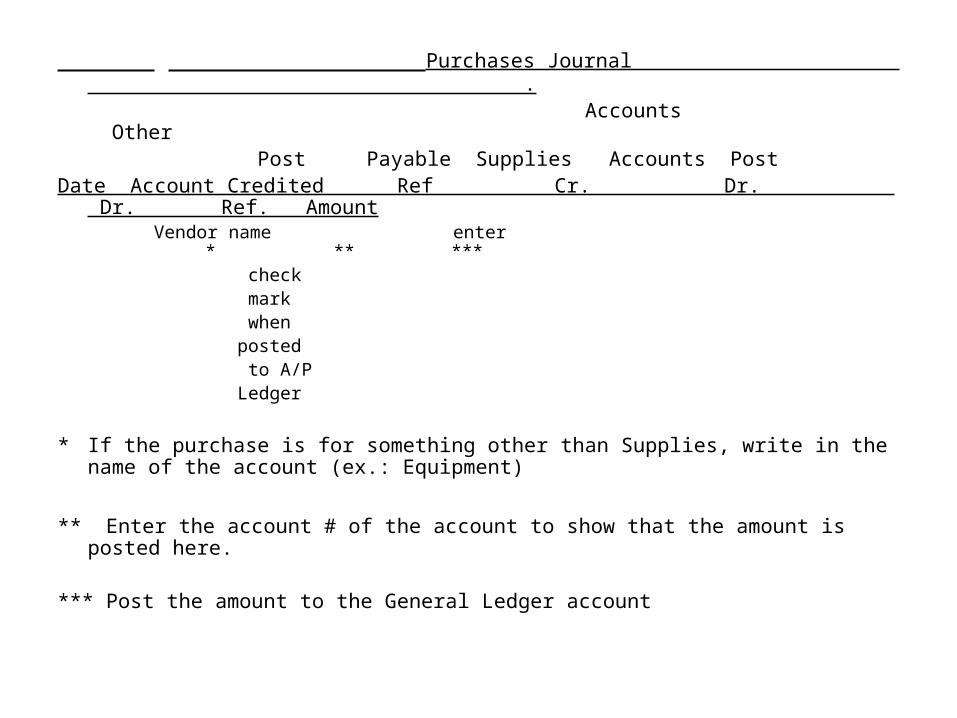

Purchases Journal .

Accounts Other Post Payable Supplies Accounts Post

Date Account Credited Ref Cr. Dr. Dr. Ref. Amount Vendor name enter * **

check mark when posted to A/P Ledger

* Every transaction will have an amount in the Accounts Payable column.

Individual transaction amounts will be posted to the Accounts Payable Ledger.The total of this column will be posted as a credit to Accounts payable in the General Ledger

** An amount is entered in this column if the purchase is for supplies, and the total of this column is posted to the Supplies account in the General Ledger.

Purchases Journal .

Accounts Other Post Payable Supplies Accounts Post

Date Account Credited Ref Cr. Dr. Dr. Ref. Amount Vendor name enter * ** ***

check mark when posted to A/P Ledger

* If the purchase is for something other than Supplies, write in the name of the

account (ex.: Equipment)

** Enter the account # of the account to show that the amount is posted here.

*** Post the amount to the General Ledger account

Accounts Payable Subsidiary Ledger .

Vendor Name:

Post

Date Item Ref Dr. Cr. Balance

Purchases journal transaction

Nov. 5 Purchased supplies on account from Walsh, Inc., $85

Purchases Journal Page 55

Accounts Other Post Payable Supplies Accounts Post

Date Account Credited Ref Cr. Dr. Dr. Ref. AmountNov. 5 Walsh, Inc 85 85

Accounts Payable Subsidiary Ledger .

Vendor Name: Walsh, Inc.

Post

Date Item Ref Dr. Cr. Balance

Nov. 5 85 85

Cash Payments Journal .

Other Accounts Post Accounts Payable

CashDate Account Debited Ref Dr. Dr. Cr. .

For payments made to vendors: Vendor name enter amount

amount check

mark when posted to A/R Ledger

Post: 1) Transaction amount to Accounts Payable Ledger 2) Total of Accounts Payable column as a Dr. to Accounts

Payable in the General Ledger 3) Total of Cash column as a Cr. to Cash in the General

Ledger

Cash Payments Journal .

Other Accounts

Post Accounts Payable Cash

Date Account Debited Ref Dr. Dr. Cr. .

For payment of cash for rent expense, utilities expense, etc.:

Name of account acct # amount amount

Post:

1) Transaction amount to account in the General Ledger

2) Total of Cash column as a Cr. to Cash in the General Ledger

Cash Payments example

Nov. 15 Paid $85 to Walsh, Inc. on account

Cash Payments Journal Page 6 .

Other Accounts Post Accounts Payable

CashDate Account Debited Ref Dr. Dr. Cr. Nov 15 Walsh, Inc. 85 85

Accounts Payable Subsidiary Ledger .

Vendor Name: Walsh, Inc.

Post

Date Item Ref Dr. Cr. Balance

Nov. 5 85 85

15 85