Embed Size (px)

Citation preview

©Ofcom

Appendix 4

Nielsen Advertising Spend and Impact Data

©Ofcom 2

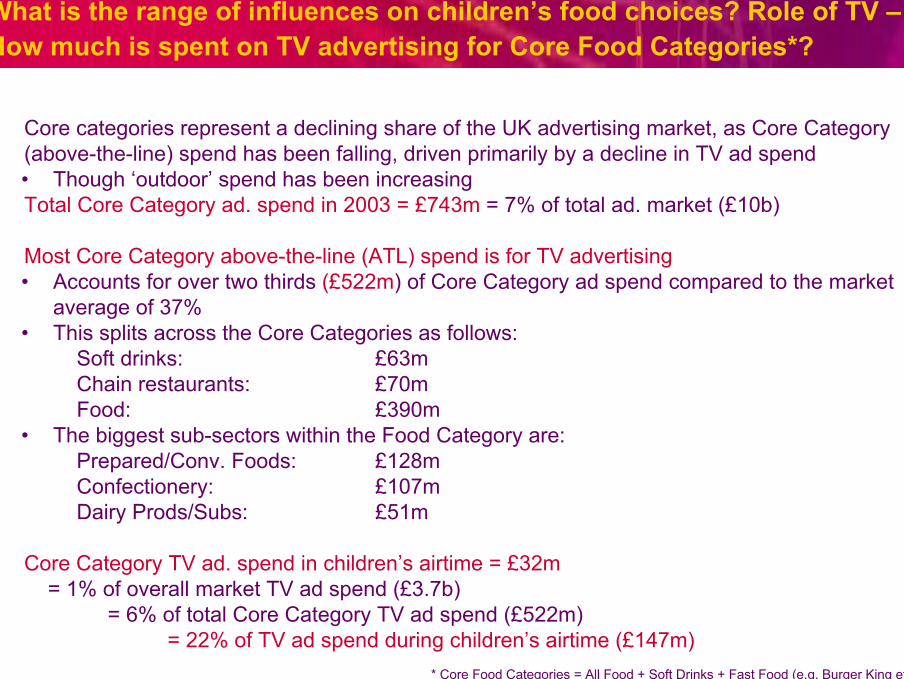

What is the range of influences on children’s food choices? Role of TV –How much is spent on TV advertising for Core Food Categories*?

• Core categories represent a declining share of the UK advertising market, as Core Category (above-the-line) spend has been falling, driven primarily by a decline in TV ad spend• Though ‘outdoor’ spend has been increasing

• Total Core Category ad. spend in 2003 = £743m = 7% of total ad. market (£10b)

• Most Core Category above-the-line (ATL) spend is for TV advertising• Accounts for over two thirds (£522m) of Core Category ad spend compared to the market

average of 37%• This splits across the Core Categories as follows:

Soft drinks: £63mChain restaurants: £70mFood: £390m

• The biggest sub-sectors within the Food Category are:Prepared/Conv. Foods: £128mConfectionery: £107mDairy Prods/Subs: £51m

• Core Category TV ad. spend in children’s airtime = £32m = 1% of overall market TV ad spend (£3.7b)

= 6% of total Core Category TV ad spend (£522m)= 22% of TV ad spend during children’s airtime (£147m)

* Core Food Categories = All Food + Soft Drinks + Fast Food (e.g. Burger King etc.)

©Ofcom 3

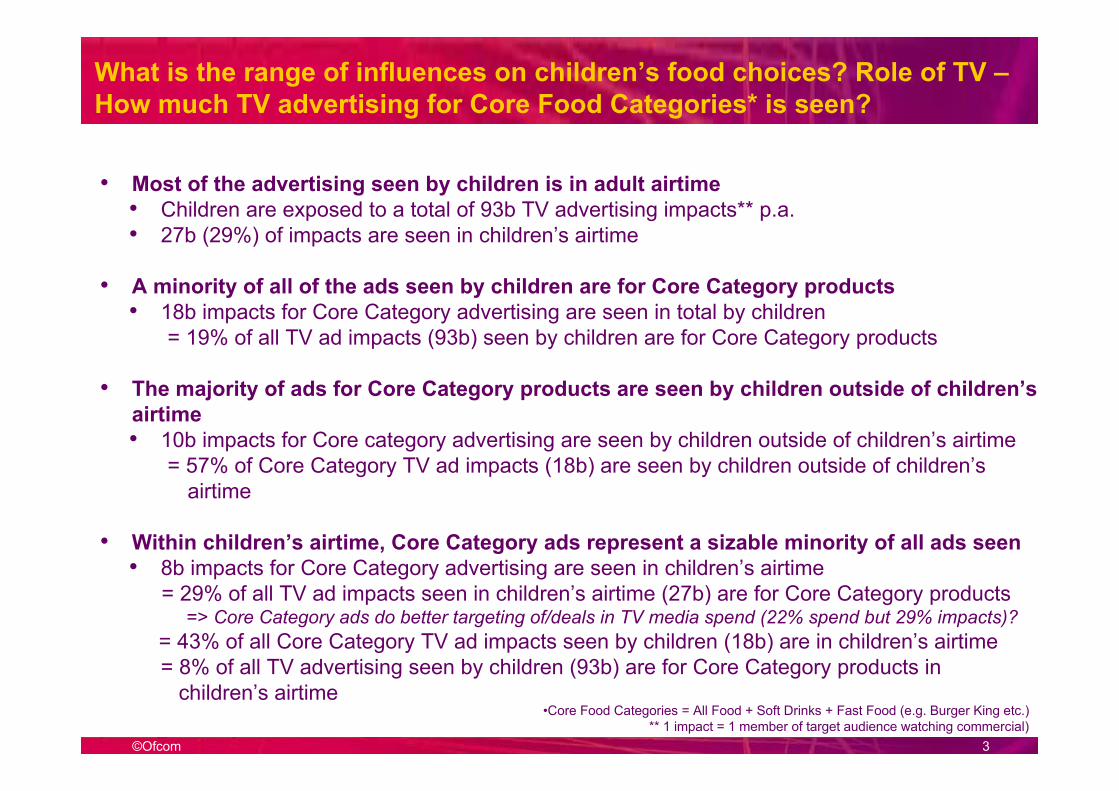

What is the range of influences on children’s food choices? Role of TV –How much TV advertising for Core Food Categories* is seen?

• Most of the advertising seen by children is in adult airtime• Children are exposed to a total of 93b TV advertising impacts** p.a. • 27b (29%) of impacts are seen in children’s airtime

• A minority of all of the ads seen by children are for Core Category products• 18b impacts for Core Category advertising are seen in total by children

= 19% of all TV ad impacts (93b) seen by children are for Core Category products

• The majority of ads for Core Category products are seen by children outside of children’s airtime• 10b impacts for Core category advertising are seen by children outside of children’s airtime

= 57% of Core Category TV ad impacts (18b) are seen by children outside of children’s airtime

• Within children’s airtime, Core Category ads represent a sizable minority of all ads seen• 8b impacts for Core Category advertising are seen in children’s airtime

= 29% of all TV ad impacts seen in children’s airtime (27b) are for Core Category products=> Core Category ads do better targeting of/deals in TV media spend (22% spend but 29% impacts)?

= 43% of all Core Category TV ad impacts seen by children (18b) are in children’s airtime = 8% of all TV advertising seen by children (93b) are for Core Category products in

children’s airtime•Core Food Categories = All Food + Soft Drinks + Fast Food (e.g. Burger King etc.)

** 1 impact = 1 member of target audience watching commercial)

©Ofcom 4

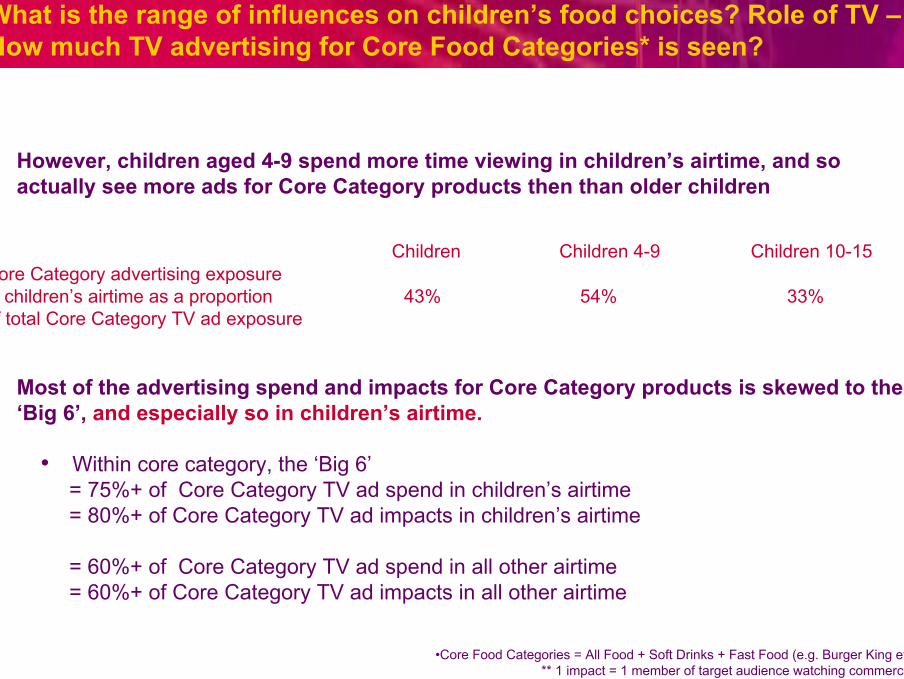

What is the range of influences on children’s food choices? Role of TV –How much TV advertising for Core Food Categories* is seen?

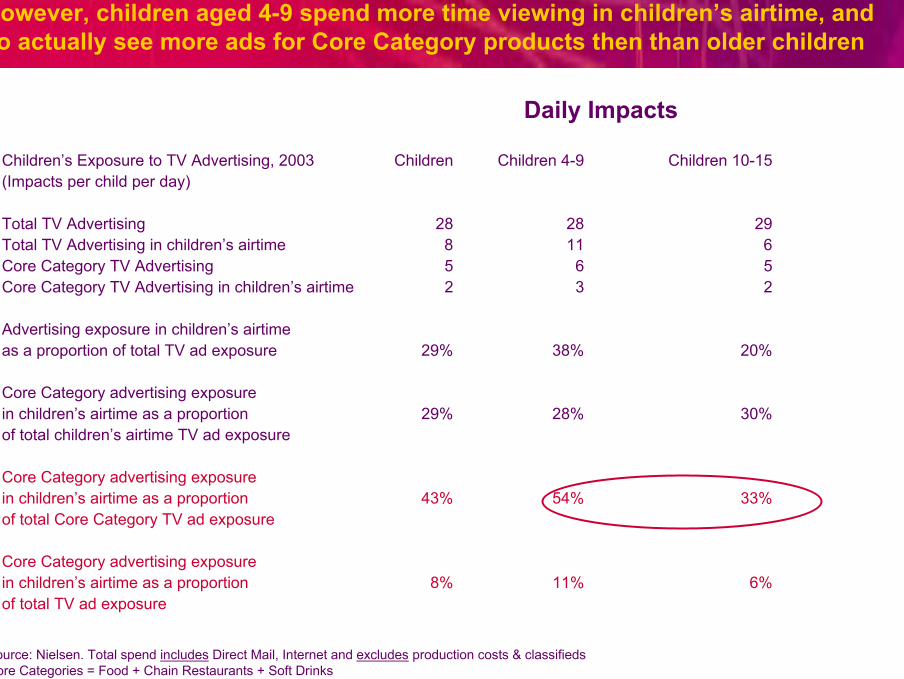

• However, children aged 4-9 spend more time viewing in children’s airtime, and so actually see more ads for Core Category products then than older children

Children Children 4-9 Children 10-15Core Category advertising exposurein children’s airtime as a proportion 43% 54% 33%of total Core Category TV ad exposure

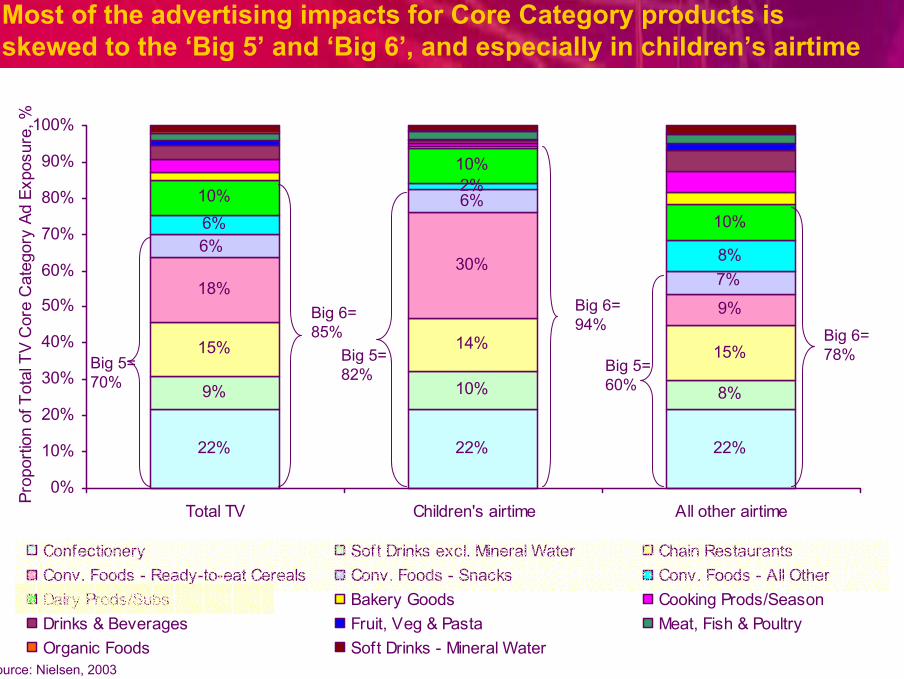

• Most of the advertising spend and impacts for Core Category products is skewed to the ‘Big 6’, and especially so in children’s airtime.

• Within core category, the ‘Big 6’ = 75%+ of Core Category TV ad spend in children’s airtime= 80%+ of Core Category TV ad impacts in children’s airtime

= 60%+ of Core Category TV ad spend in all other airtime= 60%+ of Core Category TV ad impacts in all other airtime

•Core Food Categories = All Food + Soft Drinks + Fast Food (e.g. Burger King etc.)** 1 impact = 1 member of target audience watching commercial)

©Ofcom 5

Core Categories* represent a declining share of the UK advertising market …

Source: Nielsen. Total spend excludes Direct Mail & Internet spend as continuous data is unavailable* = Food + Chain Restaurants + Soft Drinks

% of Total UK Ad Spend Represented by Core Categories

11.2%10.0% 9.6% 9.3% 8.8%

1999 2000 2001 2002 2003

% o

f Tot

al U

K Ad

Spe

nd

% of Total UK TV Ad Spend Represented by Core Categories

18.6%16.4% 15.9% 15.3% 14.1%

1999 2000 2001 2002 2003

% o

f Tot

al U

K Te

levi

sion

Ad

Spen

d

©Ofcom 6

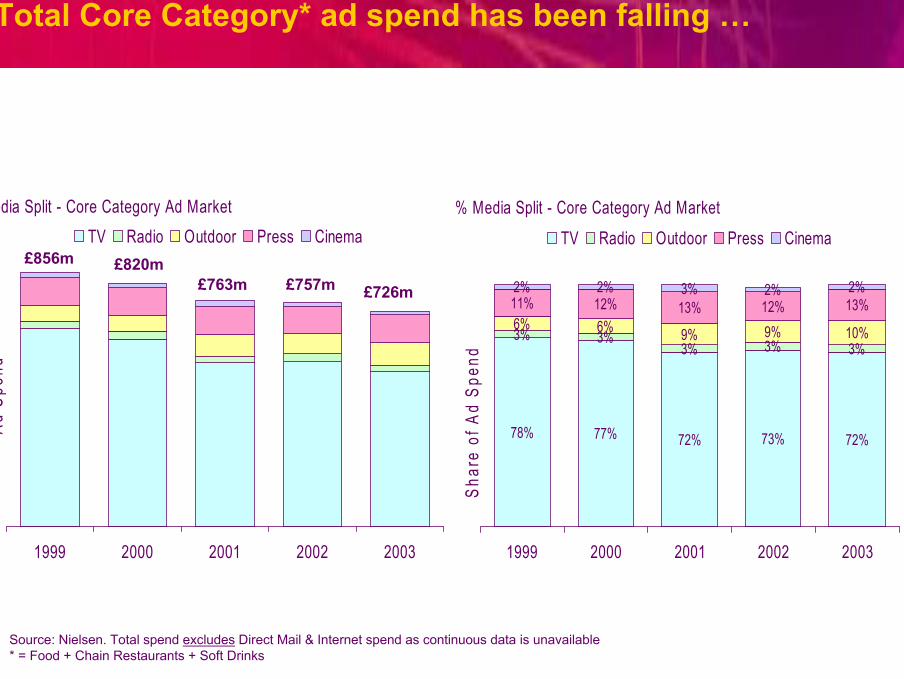

Total Core Category* ad spend has been falling …

Source: Nielsen. Total spend excludes Direct Mail & Internet spend as continuous data is unavailable* = Food + Chain Restaurants + Soft Drinks

Media Split - Core Category Ad Market

1999 2000 2001 2002 2003

Ad S

pend

TV Radio Outdoor Press Cinema£856m £820m

£763m £757m £726m

% Media Split - Core Category Ad Market

78% 77% 72% 73% 72%

3% 3%3% 3% 3%

6% 6% 9% 9% 10%

11% 12% 13% 12% 13%2% 2% 3% 2% 2%

1999 2000 2001 2002 2003

Shar

e of

Ad

Spen

d

TV Radio Outdoor Press Cinema

©Ofcom 7

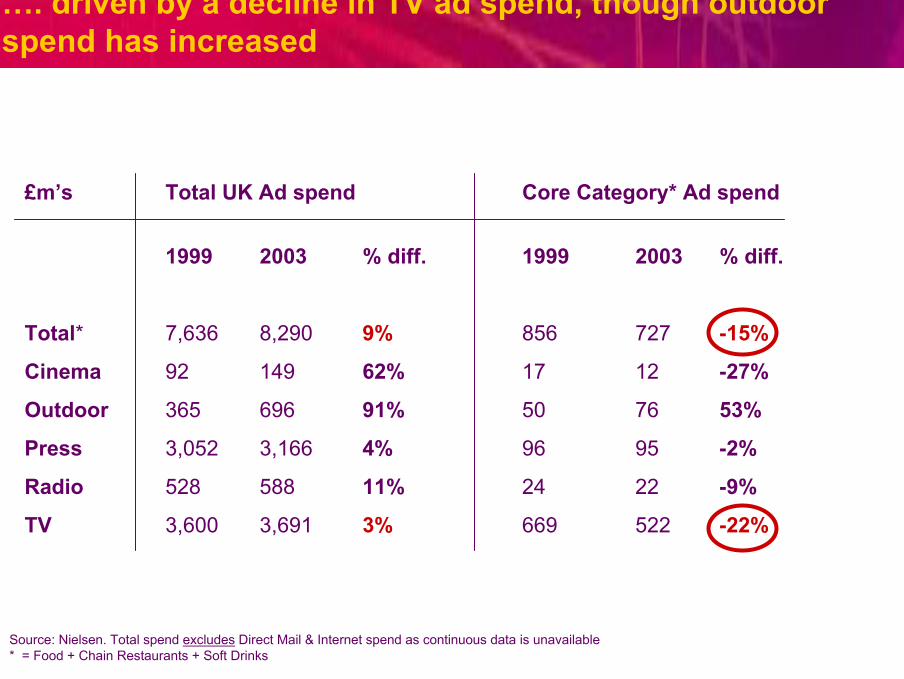

…. driven by a decline in TV ad spend, though outdoor spend has increased

£m’s Total UK Ad spend Core Category* Ad spend

1999 2003 % diff. 1999 2003 % diff.

Total* 7,636 8,290 9% 856 727 -15%

Cinema 92 149 62% 17 12 -27%

Outdoor 365 696 91% 50 76 53%

Press 3,052 3,166 4% 96 95 -2%

Radio 528 588 11% 24 22 -9%

TV 3,600 3,691 3% 669 522 -22%

Source: Nielsen. Total spend excludes Direct Mail & Internet spend as continuous data is unavailable* = Food + Chain Restaurants + Soft Drinks

©Ofcom 8

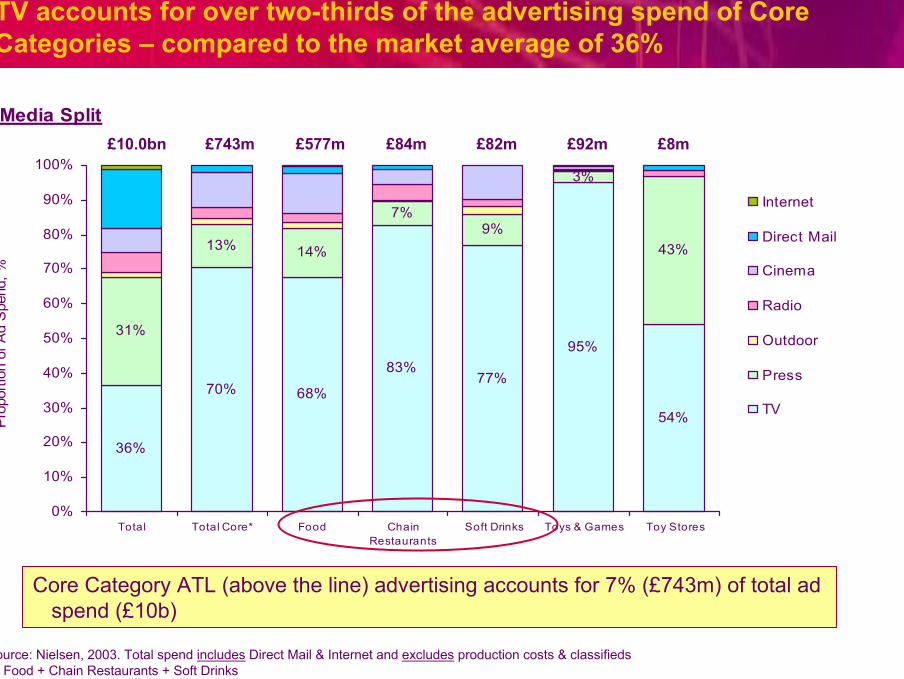

TV accounts for over two-thirds of the advertising spend of Core Categories – compared to the market average of 36%

Source: Nielsen, 2003. Total spend includes Direct Mail & Internet and excludes production costs & classifieds *= Food + Chain Restaurants + Soft Drinks

Core Category ATL (above the line) advertising accounts for 7% (£743m) of total ad spend (£10b)

Media Split

36%

70% 68%

83%77%

95%

54%

31%

13% 14%

7%9%

3%

43%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Total Total Core* Food ChainRestaurants

Soft Drinks Toys & Games Toy Stores

Pro

porti

on o

f Ad

Spe

nd, %

Internet

Direct Mail

Cinema

Radio

Outdoor

Press

TV

£10.0bn £577m £84m £82m £92m £8m£743m

©Ofcom 9Source: Nielsen, 2003. Total spend includes Direct Mail & Internet and excludes production costs & classifieds *= Food + Chain Restaurants + Soft Drinks

Core Categories* account for 14% (£522m) of the overall TV advertising market

• Spend on TV across these categories amounts to £522m – 14.1% of the total UK television advertising mkt

• This splits across Core categories as follows: - Soft Drinks £63m- Chain restaurants £70m- Food £390m

£10bn

Split in Overall Advertising Spend

93%

6%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Total Ad Spend

All Other

Soft Drinks

Chain Restaurants

Food

7.3%

£3.7bn

Split in TV Advertising Spend

86%

11%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Total TV Spend

14.1%

©Ofcom 10

The biggest sub-sectors within the Food Category are Prepared & Convenience Foods, Confectionery and Dairy Products

Split in Food Advertising Spend by Sub-sector

4%

28%

7%

13%

11%3%4%

30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Total Spend(Food)

Pro

porti

on o

f Ad

Spe

nd, %

Source: Nielsen, 2003. Total spend includes Direct Mail & Internet and excludes production costs & classifieds

The split in spend across categories is fairly consistent across the total advertising market and the TV market

£577m £390m

4%

28%

8%

13%

9%3%3%

33%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

TV Spend(Food)

Pro

porti

on o

f Ad

Spe

nd, %

Food Corporate

Food Sponsorship

Food- Internet

Organic Foods

Prepared/Conv. Foods

Meat, Fish & Poultry

Fruit, Veg & Pasta

Drinks & Beverages

Dairy Prods/Subs

Cooking Prods/Season

Confectionery

Bakery Goods

©Ofcom 11

Core Category spend during children’s airtime represents 1% of total television ad spend…

Source: Nielsen, 2003Core Categories = Food + Chain Restaurants + Soft Drinks

Non-food categories (e.g. motors, retail, finance) = 86%

Core = 14%

1%

Total TV Ad spend = £3.7bn

Core Category TV Ad spend/all airtime = £522m

Core Category TV Ad spend in

children’s airtime = £32m

©Ofcom 12

All Other media = 30%

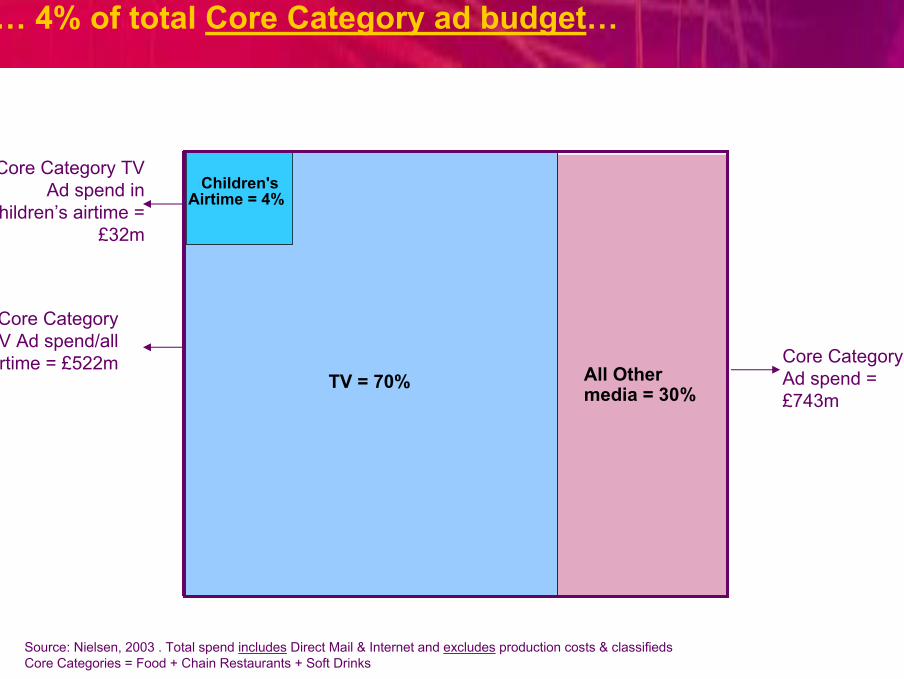

… 4% of total Core Category ad budget…

Source: Nielsen, 2003 . Total spend includes Direct Mail & Internet and excludes production costs & classifieds Core Categories = Food + Chain Restaurants + Soft Drinks

TV = 70%

Children's Airtime = 4%

Core Category Ad spend = £743m

Core Category TV Ad spend/all airtime = £522m

Core Category TV Ad spend in

children’s airtime = £32m

©Ofcom 13

Core Category TV spend = £522m

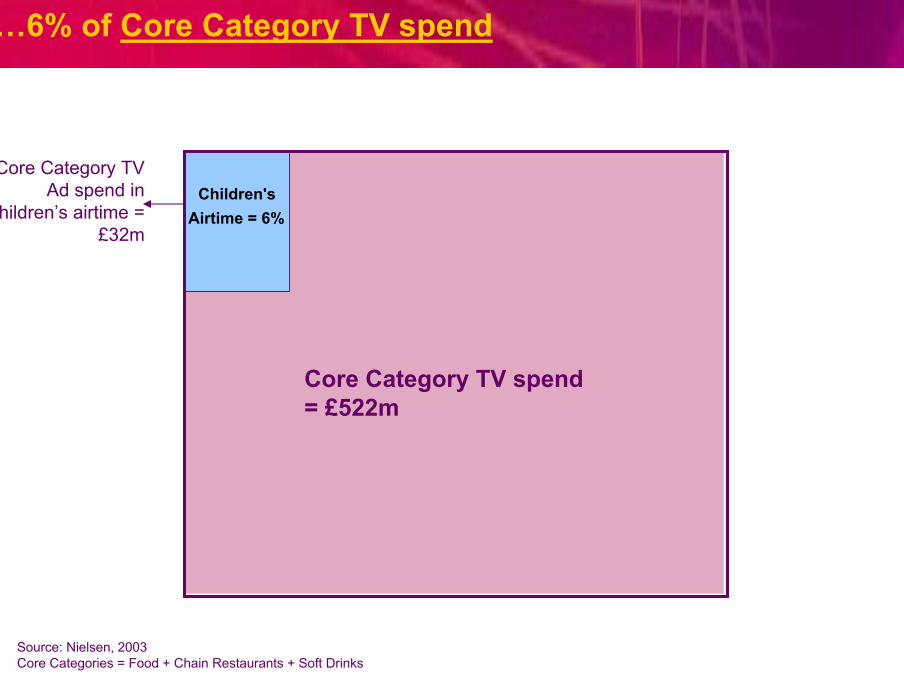

…6% of Core Category TV spend

Source: Nielsen, 2003Core Categories = Food + Chain Restaurants + Soft Drinks

Children's Airtime = 6%

Core Category TV Ad spend in

children’s airtime = £32m

©Ofcom 14

Source: Nielsen, 2003 (Child impacts)Core Categories = Food + Chain Restaurants + Soft Drinks

Children’s airtime (27bn impacts) accounts for 29% of all

advertising (93 bn impacts) seen by 4-15 year olds

©Ofcom 15

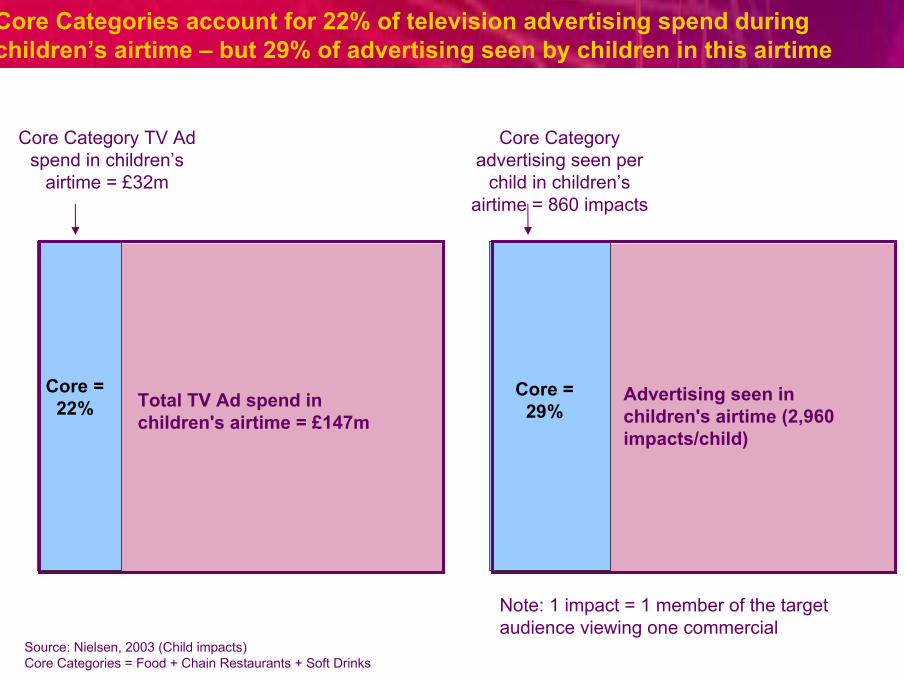

Total TV Ad spend in children's airtime = £147m

Core Categories account for 22% of television advertising spend during children’s airtime – but 29% of advertising seen by children in this airtime

Source: Nielsen, 2003 (Child impacts)Core Categories = Food + Chain Restaurants + Soft Drinks

Core = 22%

Core Category TV Ad spend in children’s

airtime = £32m

Advertising seen in children's airtime (2,960 impacts/child)

Core = 29%

Core Category advertising seen per

child in children’s airtime = 860 impacts

Note: 1 impact = 1 member of the target audience viewing one commercial

©Ofcom 16

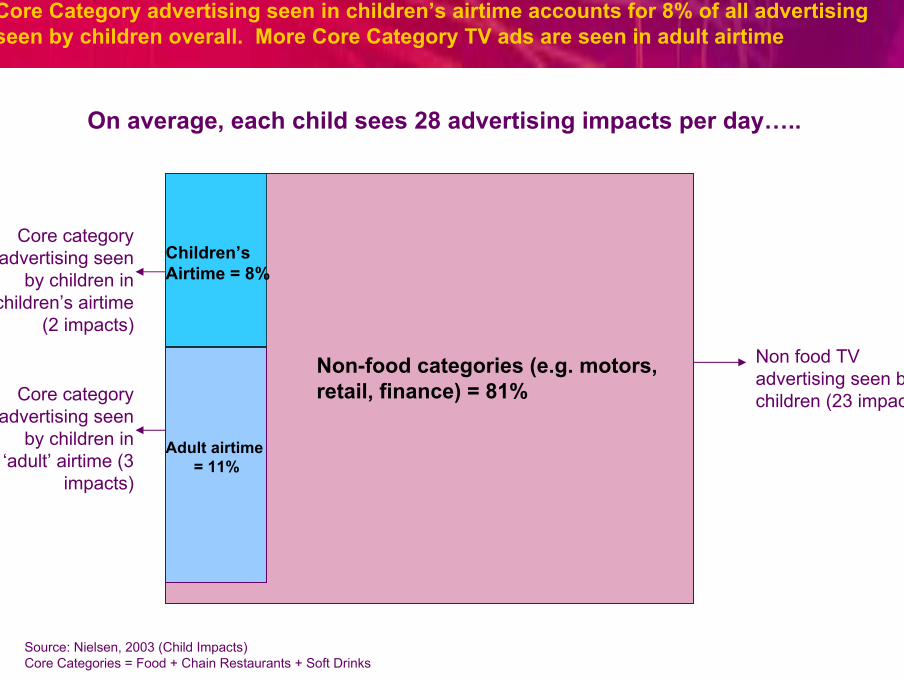

Core Category advertising seen in children’s airtime accounts for 8% of all advertising seen by children overall. More Core Category TV ads are seen in adult airtime

Source: Nielsen, 2003 (Child Impacts)Core Categories = Food + Chain Restaurants + Soft Drinks

Non-food categories (e.g. motors, retail, finance) = 81%

Adult airtime= 11%

Children’sAirtime = 8%

Non food TV advertising seen by children (23 impacts)Core category

advertising seen by children in

‘adult’ airtime (3 impacts)

Core category advertising seen

by children in children’s airtime

(2 impacts)

On average, each child sees 28 advertising impacts per day…..

©Ofcom 17

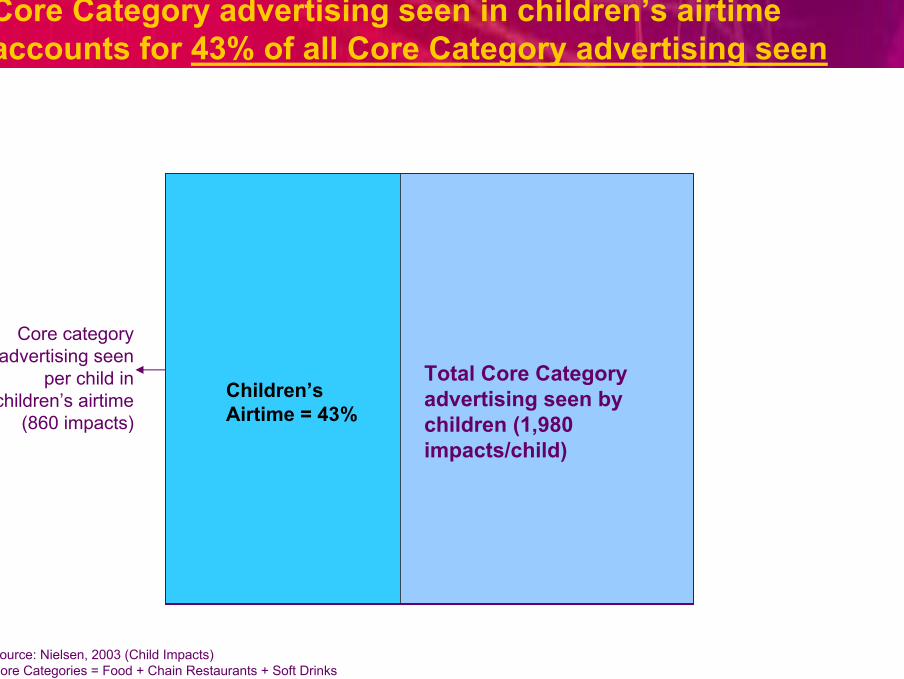

Total Core Category advertising seen by children (1,980 impacts/child)

Core Category advertising seen in children’s airtime accounts for 43% of all Core Category advertising seen

Source: Nielsen, 2003 (Child Impacts)Core Categories = Food + Chain Restaurants + Soft Drinks

Children’sAirtime = 43%

Core category advertising seen

per child in children’s airtime

(860 impacts)

©Ofcom 18

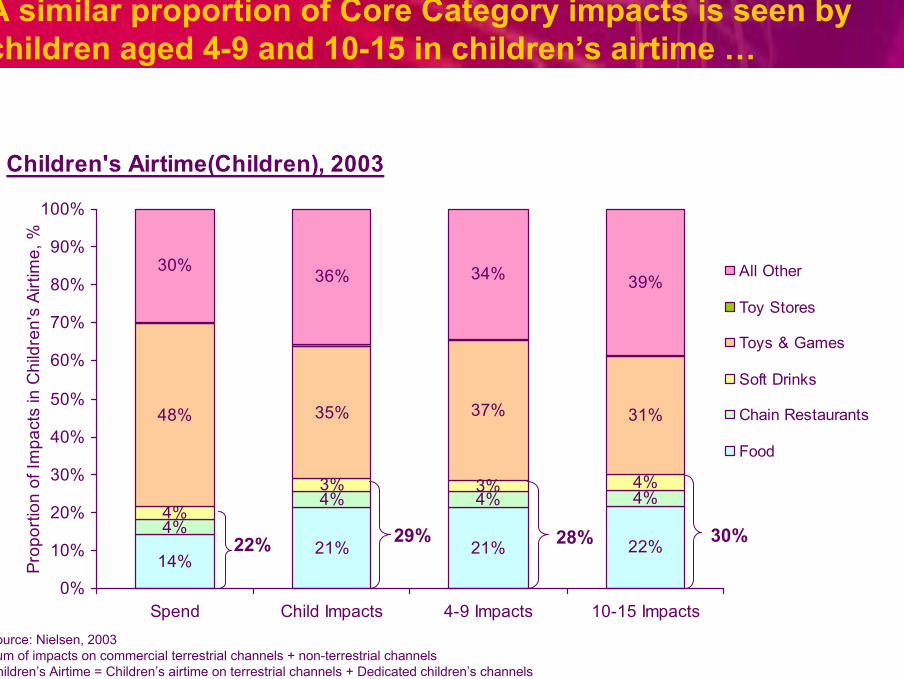

A similar proportion of Core Category impacts is seen by children aged 4-9 and 10-15 in children’s airtime …

Source: Nielsen, 2003Sum of impacts on commercial terrestrial channels + non-terrestrial channels Children’s Airtime = Children’s airtime on terrestrial channels + Dedicated children’s channels

Children's Airtime(Children), 2003

14%21% 21% 22%

4%4%

4%3%

31%

30% 36% 34% 39%

4%4%4%3%

35% 37%48%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Spend Child Impacts 4-9 Impacts 10-15 Impacts

Prop

ortio

n of

Impa

cts

in C

hild

ren'

s Ai

rtim

e, %

All Other

Toy Stores

Toys & Games

Soft Drinks

Chain Restaurants

Food

22% 29% 28% 30%

©Ofcom 19

However, children aged 4-9 spend more time viewing in children’s airtime, and so actually see more ads for Core Category products then than older children

Source: Nielsen. Total spend includes Direct Mail, Internet and excludes production costs & classifieds Core Categories = Food + Chain Restaurants + Soft Drinks

Children’s Exposure to TV Advertising, 2003 Children Children 4-9 Children 10-15(Impacts per child per day)

Total TV Advertising 28 28 29Total TV Advertising in children’s airtime 8 11 6Core Category TV Advertising 5 6 5Core Category TV Advertising in children’s airtime 2 3 2

Advertising exposure in children’s airtimeas a proportion of total TV ad exposure 29% 38% 20%

Core Category advertising exposurein children’s airtime as a proportion 29% 28% 30%of total children’s airtime TV ad exposure

Core Category advertising exposurein children’s airtime as a proportion 43% 54% 33%of total Core Category TV ad exposure

Core Category advertising exposurein children’s airtime as a proportion 8% 11% 6%of total TV ad exposure

Daily Impacts

©Ofcom 20

Most of the advertising spend for Core Category products is skewed to the ‘Big 5’ and ‘Big 6’, and especially in children’s airtime

Source: Nielsen, 2003

Big 5=59%

Big 5=77% Big 5=

58%

Big 6=95% Big 6=

77%

Big 6=78%

21% 19% 21%

10% 16% 10%

13%17%

13%

9%

19%

9%

9% 10%

10%

17%

9%

6%

6%

6%

2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Total TV Spend Children's airtime All other airtime

Prop

ortio

n of

Cor

e C

ateg

ory

Spen

d, %

Confectionery Soft Drinks excl. Mineral Water Chain RestaurantsConv. Foods - Ready-to-eat Cereals Conv. Foods - Snacks Conv. Foods - All OtherDairy Prods/Subs Bakery Goods Cooking Prods/SeasonDrinks & Beverages Fruit, Veg & Pasta Meat, Fish & PoultryOrganic Foods Soft Drinks - Mineral Water

©Ofcom 21

Most of the advertising impacts for Core Category products is skewed to the ‘Big 5’ and ‘Big 6’, and especially in children’s airtime

Source: Nielsen, 2003

22% 22% 22%

9% 10% 8%

15% 14% 15%

18%30%

9%

8%

10%

10%

10%

7%

6%

6%

2%

6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Total TV Children's airtime All other airtime

Prop

ortio

n of

Tot

al T

V C

ore

Cat

egor

y Ad

Exp

osur

e, %

Confectionery Soft Drinks excl. Mineral Water Chain RestaurantsConv. Foods - Ready-to-eat Cereals Conv. Foods - Snacks Conv. Foods - All OtherDairy Prods/Subs Bakery Goods Cooking Prods/SeasonDrinks & Beverages Fruit, Veg & Pasta Meat, Fish & PoultryOrganic Foods Soft Drinks - Mineral Water

Big 5=70%

Big 5=82% Big 5=

60%

Big 6=94%

Big 6=78%

Big 6=85%

©Ofcom 22

There is proportionally little seasonal variation in Core Category ad spend

Source: Nielsen. Total spend includes Direct Mail, Internet and excludes production costs & classifieds Core Categories = Food + Chain Restaurants + Soft Drinks

Ad spend, £ Q1 2003 Q2 2003 Q3 2003 Q4 2003 2003

Total TV Ad spend £845m £947m £863m £1,035m £3.7bnTotal Core Category Ad spend £168m £220m £182m £173m £743mTotal Core Category TV spend £125m £159m £122m £115m £522mCore Category TV spend in children’s airtime £8m £11m £8m £4m £32m

Core Category TV spend in children’s airtime as a proportion of:-Total TV spend 1% 1% 1% 0% 1%-Total Core Category Ad spend 5% 5% 5% 3% 4%-Core Category TV spend 7% 7% 7% 4% 6%

©Ofcom 23

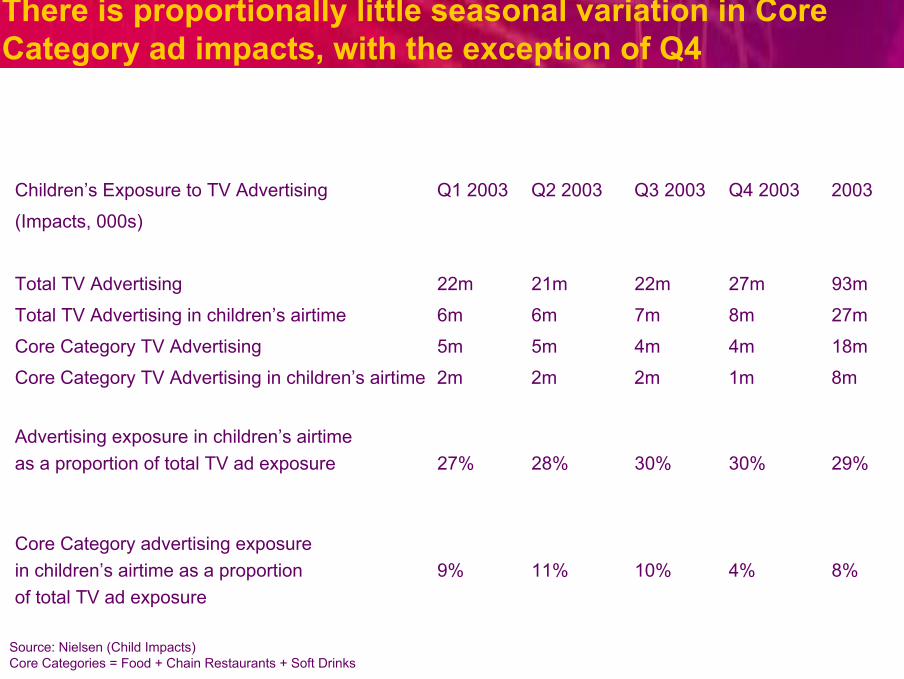

There is proportionally little seasonal variation in Core Category ad impacts, with the exception of Q4

Source: Nielsen (Child Impacts)Core Categories = Food + Chain Restaurants + Soft Drinks

Children’s Exposure to TV Advertising Q1 2003 Q2 2003 Q3 2003 Q4 2003 2003

(Impacts, 000s)

Total TV Advertising 22m 21m 22m 27m 93m

Total TV Advertising in children’s airtime 6m 6m 7m 8m 27m

Core Category TV Advertising 5m 5m 4m 4m 18m

Core Category TV Advertising in children’s airtime 2m 2m 2m 1m 8m

Advertising exposure in children’s airtimeas a proportion of total TV ad exposure 27% 28% 30% 30% 29%

Core Category advertising exposurein children’s airtime as a proportion 9% 11% 10% 4% 8%of total TV ad exposure

©Ofcom 24

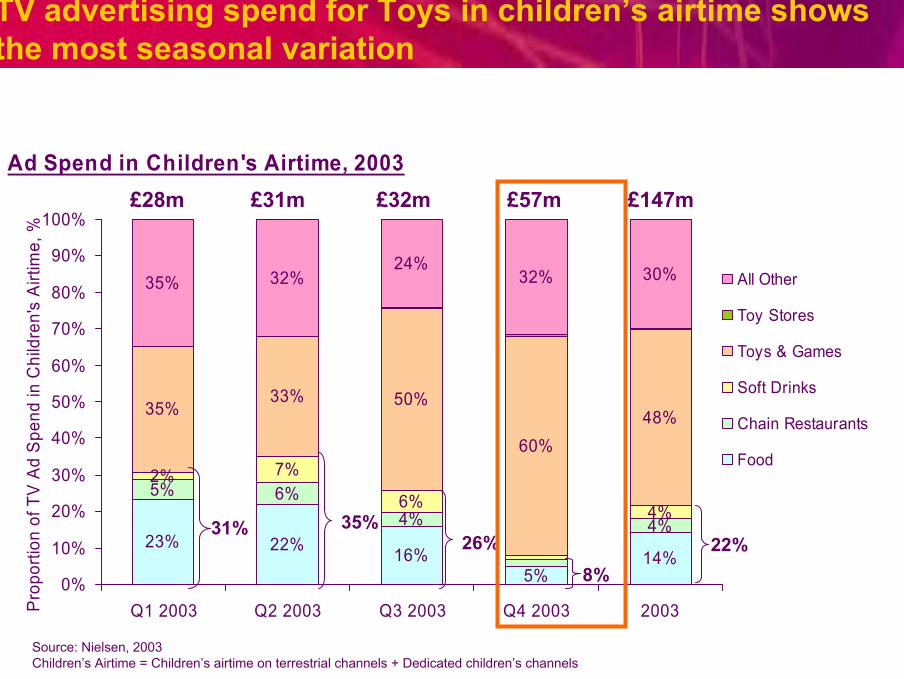

TV advertising spend for Toys in children’s airtime shows the most seasonal variation

Source: Nielsen, 2003Children’s Airtime = Children’s airtime on terrestrial channels + Dedicated children’s channels

Ad Spend in Children's Airtime, 2003

23% 22% 16%5%

14%

5%

4% 4%

2%6% 4%

60%48%

35% 32%24%

32% 30%

6%7%

33% 50%35%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1 2003 Q2 2003 Q3 2003 Q4 2003 2003Pro

porti

on o

f TV

Ad

Spe

nd in

Chi

ldre

n's

Airti

me,

%

All Other

Toy Stores

Toys & Games

Soft Drinks

Chain Restaurants

Food

31% 35%26%

8%22%

£28m £31m £32m £57m £147m

©Ofcom 25

Source: Nielsen, 2003Sum of impacts on commercial terrestrial channels + non-terrestrial channels Children’s Airtime = Children’s airtime on terrestrial channels + Dedicated children’s channels

Impacts in Children's Airtime(Children), 2003

28% 27% 24%9%

21%

5%4% 4%

1%5%

3%

59%35%

43% 42% 36%26%

36%

5%6%

20% 30%22%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1 2003 Q2 2003 Q3 2003 Q4 2003 2003

Prop

ortio

n of

Impa

cts

in C

hild

ren'

s A

irtim

e, %

All Other

Toy Stores

Toys & Games

Soft Drinks

Chain Restaurants

Food

35% 38% 34%

14%29%

TV advertising impacts for Toys in children’s airtime shows the most seasonal variation