Embed Size (px)

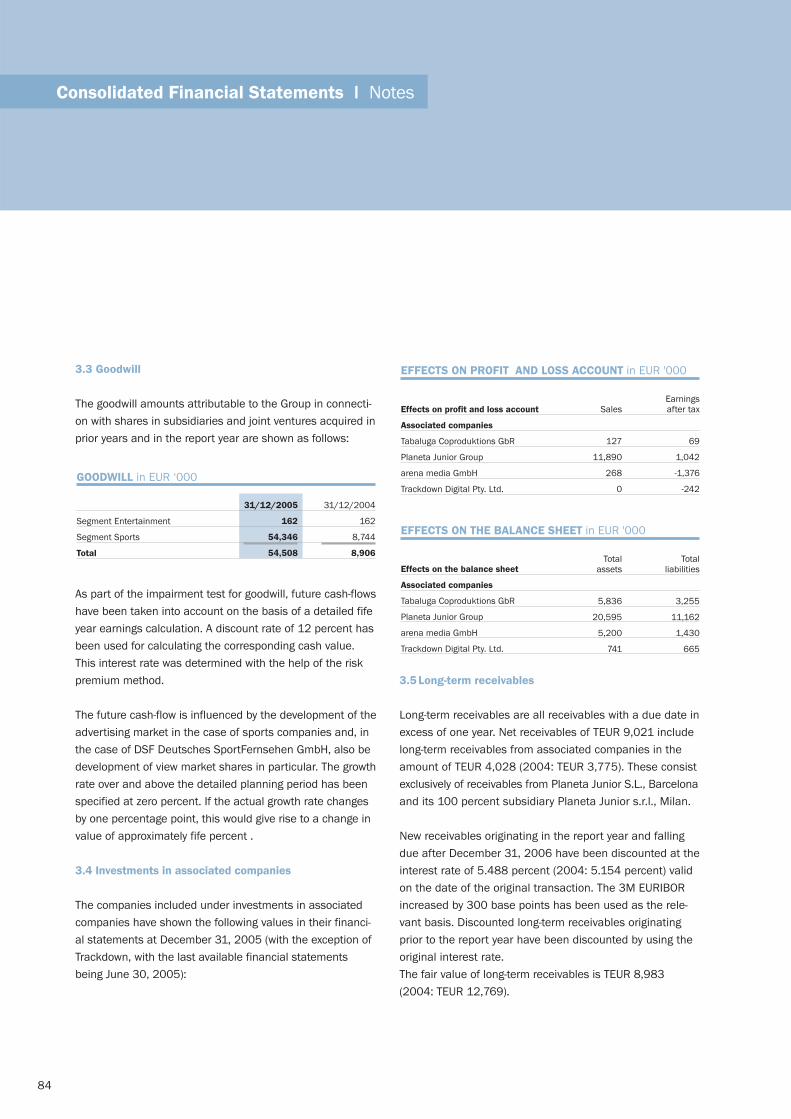

Citation preview

Annual Report 2005

The Year 2005

February 2005 EM.TV Beteiligungs GmbH & Co. KGcompletely repays the zero-coupon note to its holders,through the transfer of net proceeds from the sale ofits 45 percent stake in Tele München Gruppe (TMG).

EM.TV AG reaches an agreement with KarstadtQuelleNew Media AG and Swiss sports investor Dr. h. c.Hans-Dieter Cleven regarding the acquisition of theirstakes in sports TV station DSF and online sportsplatform Sport1. The EM.TV Group is now sole stake-holder of both sports companies.

With C&A and the Deichmann Group, EM.TV wins tworespected retail companies as new licensees for the2006 FIFA World Cup™. Their extensive national andinternational retail networks are a decisive contributi-on to the expansion of distribution channels.

March 2005 EM.TV subsidiary EM.EntertainmentGmbH reaches an agreement with ZDF on the exten-sion to their existing framework contract until 2012.The agreement relates to the period starting 2006and encompasses a total of around 625 half-hourprograms. Furthermore, the two companies agree tocontinue their joint co-production activities within thechildren’s and youth sector.

May 2005 DSF acquires an extensive rights packageto the UEFA Cup matches for the next three seasonsfrom sports rights marketing agency SPORTFIVE,beginning with the 2005/2006 season.

June 2005 EM.TV AG partially repays the 8% bondwith warrants attached of 2004/2009 with a nominalpayment of 10 million Euro on June 30, 2005.

September 2005 Following countless anniversaryinitiatives in celebration of the 30th TV birthday ofcartoon series Vicky the Viking, the three-part Vickypromotion run in 2004 by EM.Entertainment GmbHin co-operation with Autobahn Tank & Rast GmbH isvoted Promotion of the Year by licensing body LIMA.

December 2005 EM.Entertainment GmbH takes animportant step in the expansion of its home entertain-ment activities when it secures long-term program con-tracts with Munich-based Universum Film GmbH andHamburg-based Warner Bros. Entertainment GmbH.

In the course of the TV rights issue by DFL DeutscheFußball Liga GmbH in Frankfurt, DSF secures an exten-sive rights package to the Premier and Second GermanSoccer League for the next three seasons, starting withthe 2006/2007 season. The rights package encom-passes the exclusive first free-TV highlights to both theSunday matches played in the Premier Soccer League,as well as the exclusive free-TV highlights to the SecondSoccer League, including the live match on Mondays.

PLAZAMEDIA reaches an agreement with PREMIEREon the continuation of their long-term strategic partner-ship, as of January 1, 2007. Within the scope of thepartnership, PLAZAMEDIA will provide a wide rangeof services in studio production (contract term untilJune 30, 2011) and outside production (contract termuntil December 31, 2009).

In addition, PLAZAMEDIA takes over 100 percent ofthe stakes in PREMIERE subsidiary Creation Club (CC)GmbH. Creation Club and PREMIERE also agree onan extensive production framework contract with aterm of three years and an option to extend by a fur-ther two years.

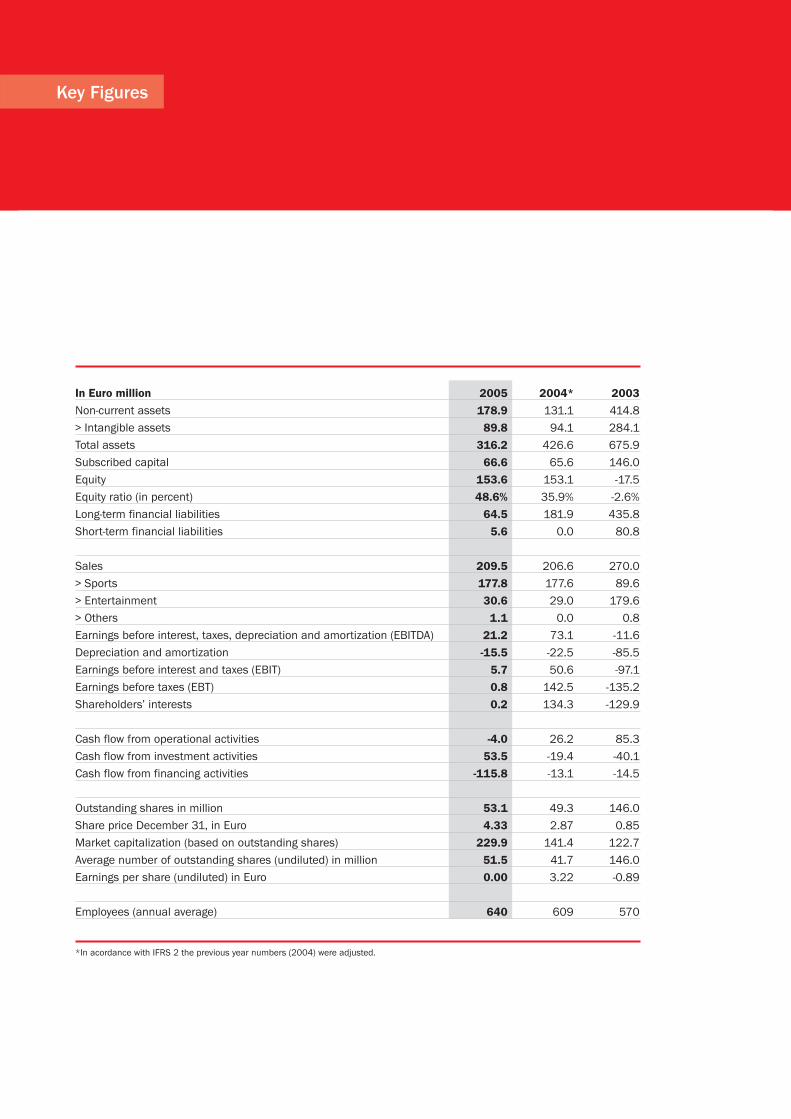

Key Figures

2003

414.8

284.1

675.9

146.0

-17.5

-2.6%

435.8

80.8

270.0

89.6

179.6

0.8

-11.6

-85.5

-97.1

-135.2

-129.9

85.3

-40.1

-14.5

146.0

0.85

122.7

146.0

-0.89

570

In Euro million

Non-current assets

> Intangible assets

Total assets

Subscribed capital

Equity

Equity ratio (in percent)

Long-term financial liabilities

Short-term financial liabilities

Sales

> Sports

> Entertainment

> Others

Earnings before interest, taxes, depreciation and amortization (EBITDA)

Depreciation and amortization

Earnings before interest and taxes (EBIT)

Earnings before taxes (EBT)

Shareholders’ interests

Cash flow from operational activities

Cash flow from investment activities

Cash flow from financing activities

Outstanding shares in million

Share price December 31, in Euro

Market capitalization (based on outstanding shares)

Average number of outstanding shares (undiluted) in million

Earnings per share (undiluted) in Euro

Employees (annual average)

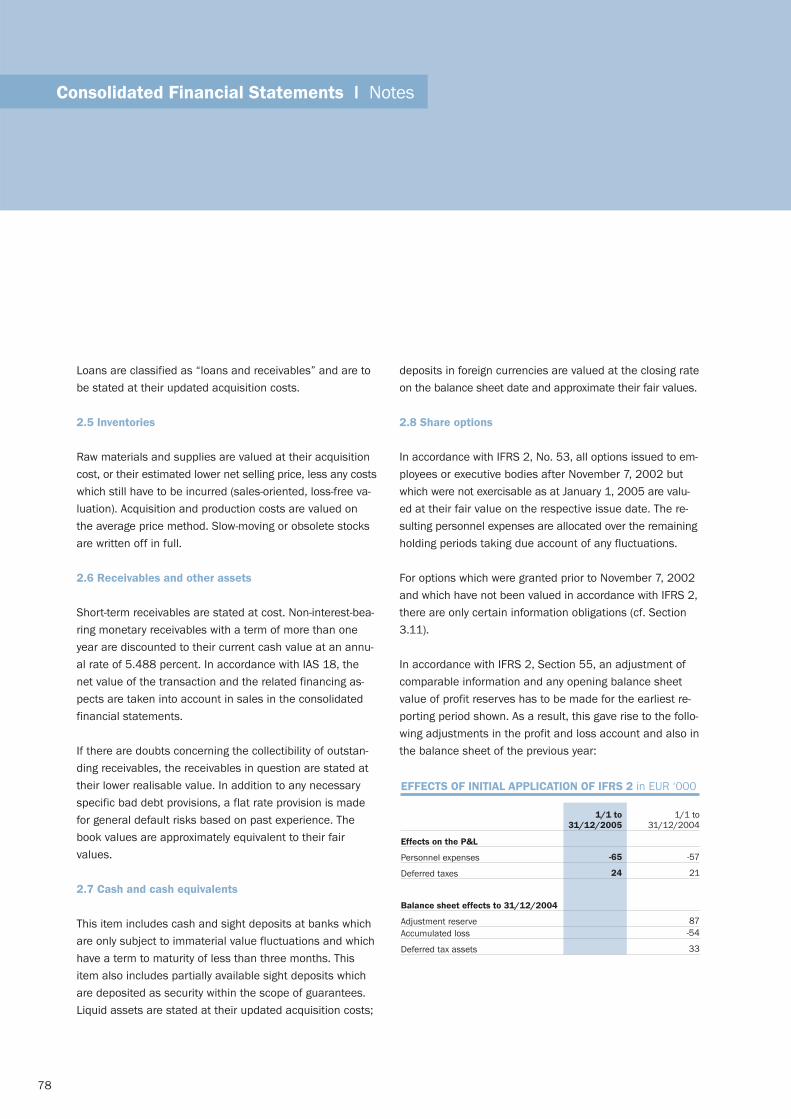

*In acordance with IFRS 2 the previous year numbers (2004) were adjusted.

2005

178.9

89.8

316.2

66.6

153.6

48.6%

64.5

5.6

209.5

177.8

30.6

1.1

21.2

-15.5

5.7

0.8

0.2

-4.0

53.5

-115.8

53.1

4.33

229.9

51.5

0.00

640

2004*

131.1

94.1

426.6

65.6

153.1

35.9%

181.9

0.0

206.6

177.6

29.0

0.0

73.1

-22.5

50.6

142.5

134.3

26.2

-19.4

-13.1

49.3

2.87

141.4

41.7

3.22

609

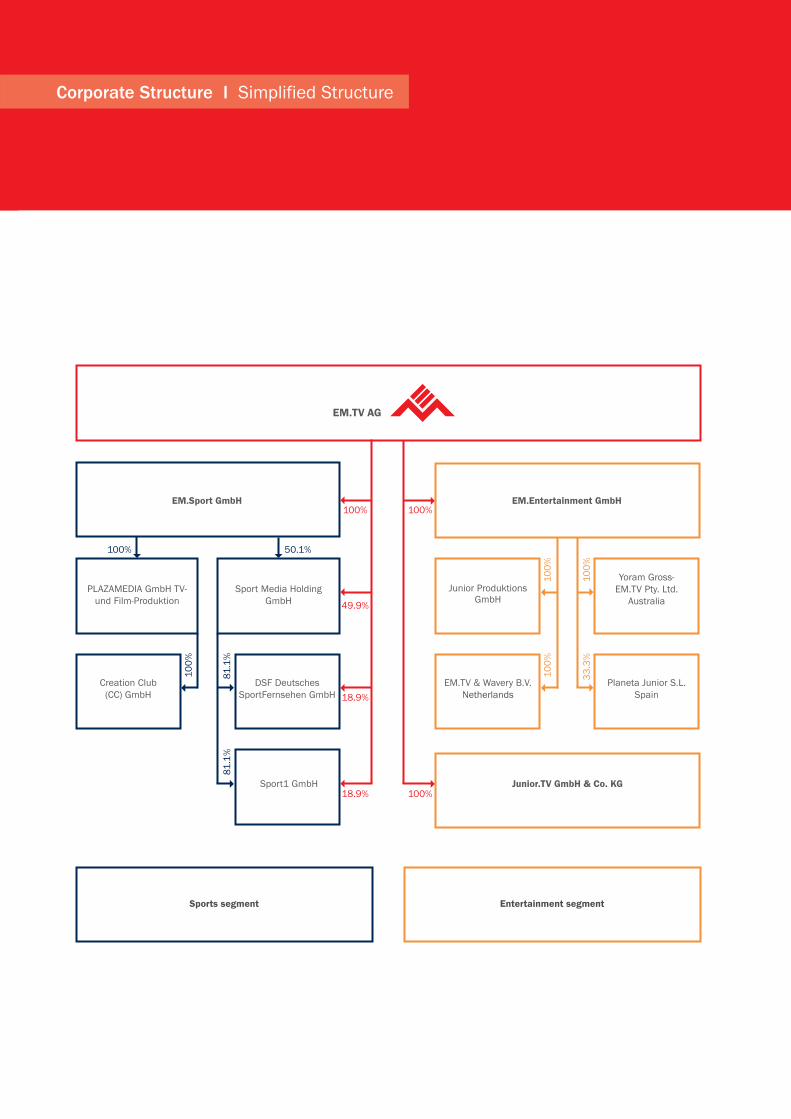

Corporate Structure I Simplified Structure

18.9% 100%Junior.TV GmbH & Co. KG

EM.Entertainment GmbHEM.Sport GmbH

Sport Media Holding GmbH

DSF DeutschesSportFernsehen GmbH

Sport1 GmbH

PLAZAMEDIA GmbH TV- und Film-Produktion

Creation Club (CC) GmbH

50.1%

100%

100%

100

%

81.1

%81

.1%

49.9%

18.9%

100%

Yoram Gross- EM.TV Pty. Ltd.

Australia

Planeta Junior S.L. Spain

Junior ProduktionsGmbH

EM.TV & Wavery B.V.Netherlands

100

%

33

.3%

100

%

100

%

Sports segment Entertainment segment

EM.TV – Our Profile

We are a medium-sized media company which operates in

the core sectors of Sports and Children and Youth

Entertainment. In sports business we are the leading

German TV production company and run the leading plat-

forms DSF and Sport1. In the entertainment business we

are internationally oriented, have one of the largest pro-

gram libraries in the children and youth sector and distin-

guish ourselves by many years of experience with the deve-

lopment and marketing of license themes and characters,

all of which are duly esteemed and appreciated in the mar-

ket. After a successful restructuring and reorientation from

2001 to 2004, we now have an attractive investment port-

folio, together with a sound financial basis for further

growth in the future.

EM.TV – Our Strengths

We are an independent group and on account of this inde-

pendent position an established partner for a large number

of companies. We encounter the challenges of our markets

with classical medium-sized virtues such as speed, flexibili-

ty, reliability and creativity.

EM.TV – Our Objectives

With our products and services, our aim is to satisfy the

emotional requirements of our ultimate customers. We will

only succeed in this respect if our products are marked by

a high level of creativity and quality.

As far as our shareholders are concerned, our aim is to

seize market opportunities with a due sense of proportion

by means of a growth strategy, to create added-value and

to ensure an attractive return on their investment.

EM.TV intends to comply with its social responsibilities with its productsand entrepreneurial actions.

Dr. Andreas Pres Werner E. Klatten Rainer Hüther

Forward-looking statementsThis annual report contains statements relating to future events that arebased on management’s assessments of future developments. A series offactors beyond the control of the company, such as changes in the generaleconomic and business environment and the incidence of individual risks oroccurrence of uncertain events, can result in the actual results differing sub-stantially from those forecast. EM.TV does not intend to continually updatethe forward-looking statements contained in the annual report.

Important noticeIn case of any differences the German version of the annual report prevails.

Content

2 Foreword by the Chairman of the Management Board

5 Boards6 Report of the Supervisory Board

10 Corporate Governance Report14 The EM.TV AG Share18 Company Strategy

22 Business Units Reports I Sports22 TV I DSF Deutsches SportFernsehen24 Online I Sport125 Production Services I PLAZAMEDIA27 Licensing I European Licensing Representative

2006 FIFA World Cup™

30 Business Units Reports I Entertainment30 Production31 TV-Sales33 Licensing I Merchandising34 Licensing I Home Entertainment35 TV I Junior Channel

38 Management Report on the Situation of the Group and the AG

38 Economic Conditions 42 Sales and Earnings45 Net Worth Position46 Financial Position48 Investments49 Personnel Report50 Innovation51 Risk and Opportunities Report57 Occurrences after the End of the Fiscal Year57 Forecast Report

63 Consolidated Financial Statements64 Consolidated Balance Sheet66 Consolidated Profit an Loss Account67 Consolidated Cash Flow Statement68 Changes in Consolidated Equity

69 Notes on the Consolidated Financial Statements69 General Explanation76 Accounting and Valuation Principles81 Explanations on Invidual Items in the Balance Sheet96 Explanations on Items in the Profit and Loss Account

102 Explanations on Items in the Cash Flow Statement103 Segment Reporting106 Contingent Liabilities and Other Financial

Commitments107 Occurrences after the End of the Fiscal Year108 Other Mandatory Disclosures108 Other Explanations and Disclosures111 Auditors’ Report

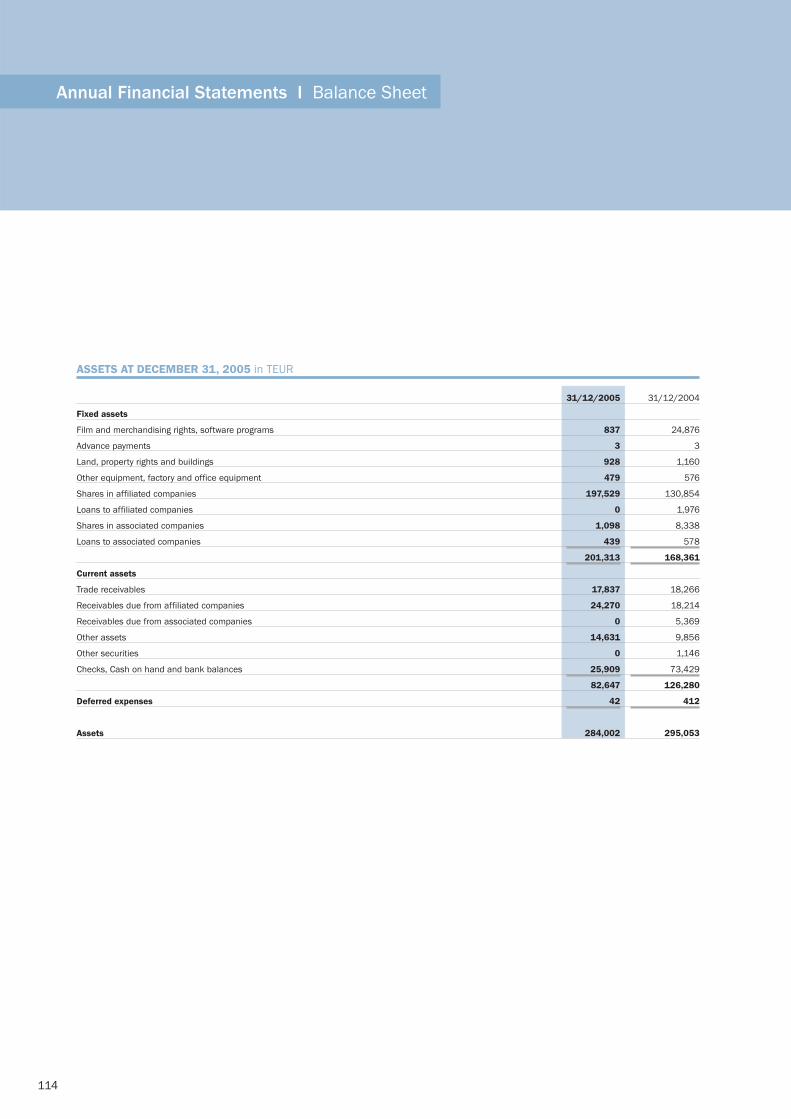

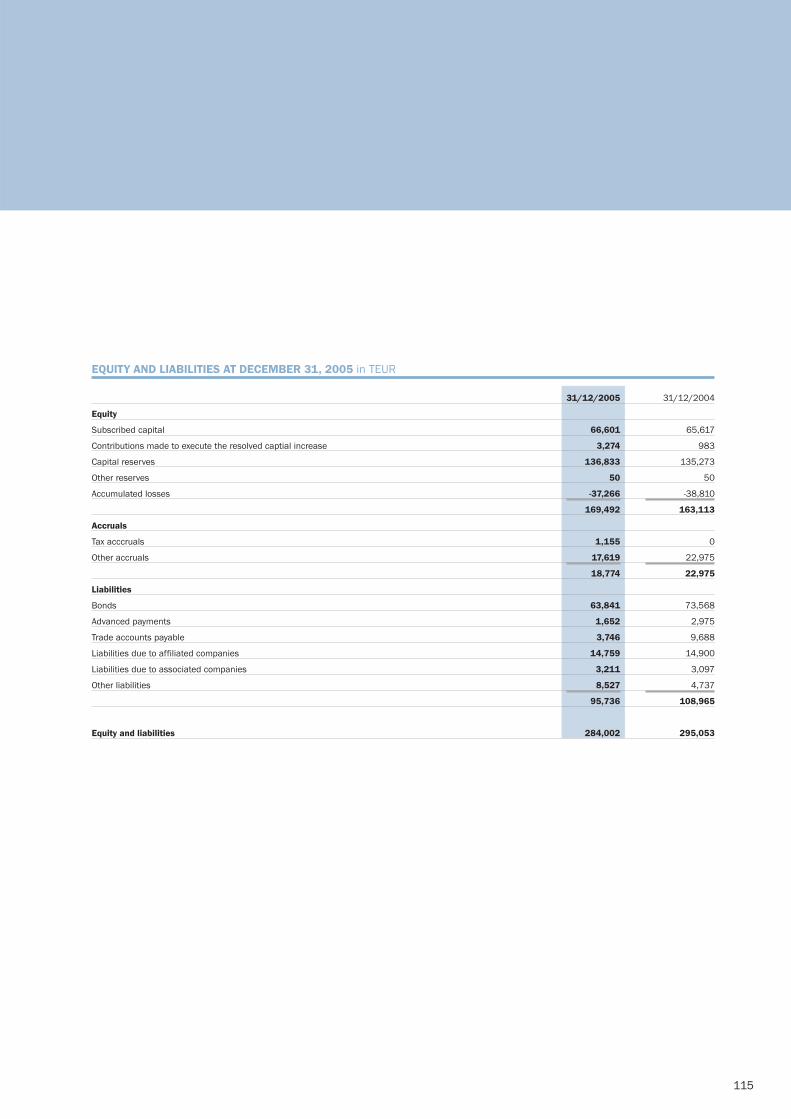

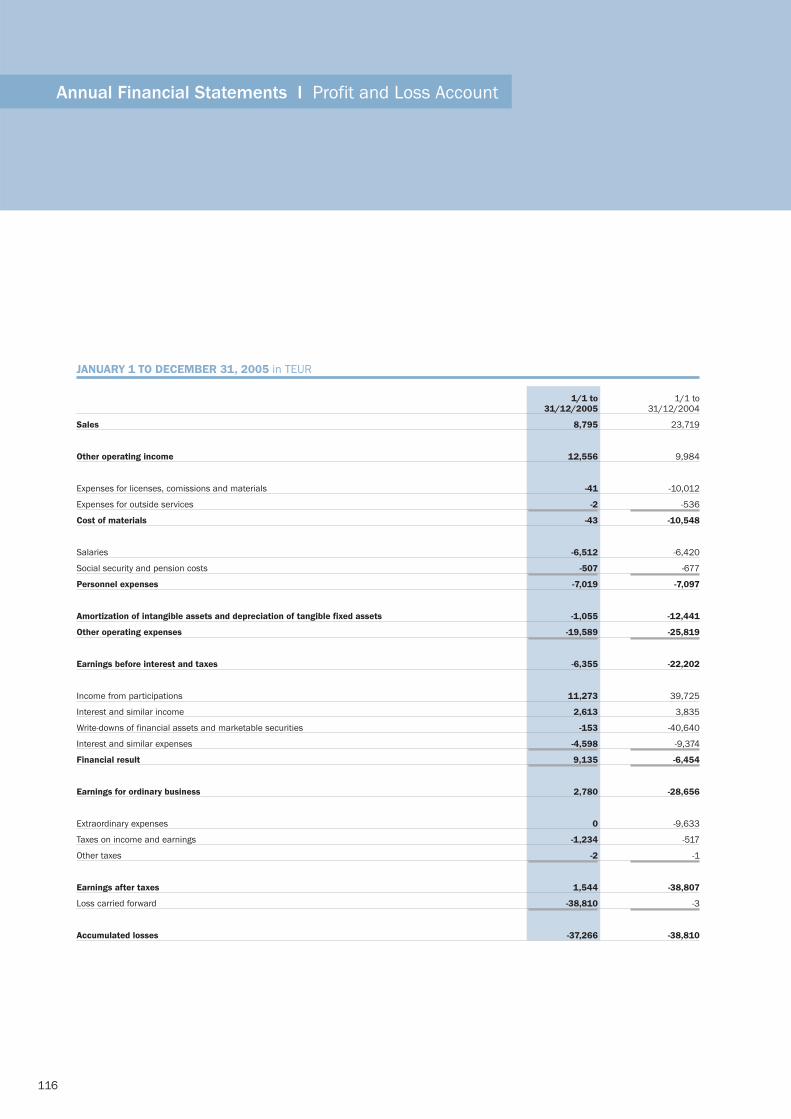

113 Annual Financial Statements of the AG114 Balance Sheet116 Profit an Loss Account

117 Finance Calendar117 Production Credits

1

2005 saw EM.TV AG continue on a path of positive deve-

lopment. For the first time since 1999, we have been able

to report a Group profit before tax and special or one-off

effects, as well as achieve a single figure percentage

growth in Group sales. This falls exactly within the forecast

that we issued at the beginning of the business year.

EM.TV has thus been true to its word. This is of great

importance to me, as the new EM.TV, which came into

being as a result of the restructuring of the former EM.TV &

Merchandising AG, must take its place on the capital mar-

ket as a reliable and predictable player.

The result that has been achieved pleases me all the more,

as we found ourselves facing numerous obstacles during

2005 that were either not apparent at the start of the year

or, at least, not as substantial:

> The development of the German economy in 2005 was

disappointing, and was unable to inject new life into

the advertising market. This had a subduing effect on

sales development at our free-TV station DSF.

> Due to the failure to pay on the part of two of its busi-

ness partners, DSF found itself obliged to make a sub-

stantial bad debt provisions.

> During the previous year, EM.TV made significant

investments in attractive programming and new busi -

ness activities. These included the acquisition of exten-

sive rights packages in sports, as well as expenditure

on the preparation for market entry into the “sports

betting” sector. While these investments had a nega-

tive short-term impact on performance, in the medium-

term they will significantly strengthen the operating

business and deliver a positive contribution to profitabi-

lity. In this respect, this money has been well invested.

The 2005 business year demonstrated that the EM.TV Group

is strategically well positioned with its two operating busi-

ness divisions Sports and Entertainment, and able to ope-

rate profitable. We have made progress in both segments

as well as securing and extending our market position.

Within the Sports segment, we took over the stakes of the

former co-owners of DSF and online portal Sport1 on attrac-

tive terms. This means that EM.TV now holds also, either

directly or indirectly, 100 percent of the stakes in these

companies.

> In the free-TV sector, the reporting year saw DSF stabi-

lize its market share within its core target group of

males aged 14 to 49 at 1.9 percent. With the acquisi-

tion of extensive rights packages to the UEFA Cup for

the 2005/2006 to 2007/2008 seasons, and to the

Premier and Second German Soccer League for the

2006/2007 to 2008/2009 seasons, DSF has secured

its ability to offer top soccer to its viewers. Therefore

DSF offers an attractive advertising environment for its

advertising customers. This is an important condition

for the station’s ongoing commercial success. These

rights acquisitions also demonstrate that, through the

establishment of a clear program profile, DSF has

achieved a position over the last three years as one of

the top players on the German TV market. The editorial

quality and the independence of the station is valued

and respected by not only the viewers, but also by the

sporting community.

> In terms of production services, our subsidiary PLAZA-

MEDIA enjoyed continued success with good levels of

capacity utilization across all its business units. The

company completed close to 90,000 program hours

2

Foreword by the Chairman of the Management Board

3

and handled around 1,500 national and international

productions. PLAZAMEDIA concentrates its service offe-

ring on state-of-the-art production technology, and thus

is increasingly able to offer its customers genuine added

value. One good example of this innovative spirit is the

company’s introduction of new television standard

HDTV (High Definition Television) throughout its entire

production chain, thus giving PLAZAMEDIA a unique

position within the market. At the end of 2005, we were

able to significantly strengthen the position as a provider

of creative production services through the acquisition

of Creation Club GmbH from PREMIERE. The Creation

Club is successfully positioned in promotion, on and

off-air design, advertising and TV formats, and thus

complements perfectly PLAZAMEDIA’s service portfolio.

> Within the online sector, sports portal Sport1 was yet

again successful in strengthening its position signifi-

cantly as the most popular German-language sports

website, with a 40 percent growth in ratings. Sport1

is also demonstrating increasing success in its media

sales activities, i.e. the sale of sports content for tele-

text and mobile platforms (SMS, MMS, and WAP) to

third parties.

> We have been delighted with the development during

the last year of our merchandising marketing activities

for the 2006 FIFA World Cup™. By the end of 2005 we

had secured contracts with a total of 53 license partners

– clear proof that the timely introduction of our marke-

ting strategy for this mega-event has been highly

successful. It is already evident that the commercial

success of the FIFA project will be significantly greater

than originally forecast.

Within the Entertainment segment – encompassing the pro-

duction and marketing of high quality program for children

and young people – 2005 saw us achieve the conditions

necessary in terms of structure and human resources in

order to put the business onto a path of sustainable growth.

These measures included the bundling of all production and

distribution activities into EM.Entertainment GmbH, with the

purpose of achieving clear and transparent divisional respon-

sibilities. This also included the strengthening of production

competence by means of a partial renewal of EM.Entertain-

ment’s management team. It remains our objective to en-

sure the continued attractiveness of our library with additio-

nal new, in-house program rights.

Although demand for children’s and youth program wit-

nessed a slight increase both nationally and internationally

during 2005, this trend has yet to impact pricing. EM.Enter-

tainment has, however, demonstrated that it remains possi-

ble to secure attractive business under these conditions,

with extensive and long-term agreements such as those se-

cured in the home entertainment sector during the fourth

quarter with Universum Film GmbH and Warner Bros. Enter-

tainment GmbH. Despite the difficult market conditions, the

entertainment division was nevertheless able to improve its

financial result – proof of the substance of our program

portfolio.

The global market for children’s and youth programming con-

tinues to find itself in a phase of consolidation. During the

reporting year, the Management Board considered various

options for the development of the Entertainment division

through M&A transactions. In the end, these intensive inve-

stigations did not produce any results that were commerci-

ally compelling. This notwithstanding, we will continue to

strive to play an active role in the consolidation of the sector.

The progress made in the operating business is also reflec-

ted in the development of the EM.TV share price. During

2005 it demonstrated a growth in value of 51 percent, thus

significantly exceeding the overall growth of the SDAX, which

increased by 35 percent. With a daily average of 500,000

shares, EM.TV was the most traded share of the SDAX. For

the sake of every one of our shareholders that stood by us

during the long process of restructuring, we are particularly

pleased by this positive share price development, which is

accompanied by an ever-increasing interest in our company

on the part of investors and analysts.

During the current business year, we want to develop our

market position within both of our key business sectors. One

significant step in this process is the agreement reached in

the Sports segment at the beginning of March between PLA-

ZAMEDIA and Arena Sport Rechte und Marketing GmbH,

making PLAZAMEDIA the exclusive production partner for

Arena’s pay-TV offer for the German Soccer League. In

order to improve our position in the market place, we will

also seek in future to make greater use of synergies between

our Sports segment stakeholdings in order to be able to

offer customers turnkey solutions.

The organizational and conceptual preparations for EM.TV’s

entry into the “sports betting” sector are well advanced.

The German market remains restricted, preventing our entry

for the time being. We continue to attribute substantial

sales and profit potential to this business, but are prepared

to take a decision to act only when the commercial concept

is fully cohesive and its legal basis beyond all possible

doubt.

Within the Entertainment segment, the focus of efforts du-

ring 2006 will be on the start of in-house productions. We

will also be pushing forward with the further internationali-

zation of our businesses, with particular emphasis on streng-

thening our presence within the Anglo-Saxon markets. In

this regard, added-value M&A activities are certainly con-

ceivable.

Dear shareholders,

in recent years, EM.TV has developed a market position

that presents many fascinating perspectives. Our ultimate

objective continues to be to guide the EM.TV Group into a

phase of sustainable growth, evidenced by an ongoing

improvement of profitability. In this spirit, EM.TV will enrich

the media market as an independent and flexible partici-

pant, operating on all the best principles of a medium-sized

enterprise.

Unterföhring, March, 2006

With best regards,

Werner. E. Klatten

Chairman of the Management Board

4

Foreword by the Chairman of the Management Board

5

Werner E. Klatten,

Chairman of the Management Board, CEO

Werner E. Klatten is Chairman of the Management Board

of the EM.TV AG. He is responsible for the the corporate

strategy, the Entertainment segment, central functions:

Legal Matters, Communication, Human Resources and

Administration, as well as for shareholdings.

Rainer Hüther,

Member of the Management Board, COO Sports

Rainer Hüther is resposible for the Sports segment. In addi-

tion to his Board Member activities at EM.TV, he is Chief

Executive of sports broadcaster DSF since June 2, 2003.

Dr. Andreas Pres,

Member of the Management Board, CFO

Dr. Andreas Pres is member of the Board and responsible

for Finance, Investor Relations, Accounting, Controlling, IT

and Process Management.

Management Board

Boards

Dr. Bernd Thiemann, Chairman

Dr. Hans-Holger Albrecht, Deputy Chairman

Arthur Bastings, Member

Supervisory Board

The Supervisory Board of EM.TV AG met a total of six times

during 2005, including one telephone conference. As in the

previous year, the board, which in accordance with legal

requirements consists of only three members, did not crea-

te any separate committees.

Under the terms of the German Stock Corporation Act, the

Supervisory Board is responsible for monitoring the activities

of the Management Board. During the reporting year, the

Supervisory Board of EM.TV regularly monitored the Manage-

ment Board and provided it with advice. By means of oral

and written reports from the Management Board, the Super-

visory Board was kept abreast with business operations at

EM.TV AG and the EM.TV Group, business planning, ongoing

business development, risk factors and significant business

events.

The Supervisory Board was represented in full at all mee-

tings held in 2005. Furthermore, all members of the Ma-

nagement Board also participated in those meetings in

order to report to the Supervisory Board and to answer its

questions. In keeping with previous years, the Supervisory

Board also called upon the advice of external experts, in

the form of lawyers and publicly certified accountants.

Furthermore, between meetings, there was ongoing contact

between the members of the Management and Supervisory

Boards, and between the Chairmen of the Management

and Supervisory Boards in particular. Where necessary in

the interests of timing, documentary information was circu-

lated between meetings in order to obtain decisions from

the Supervisory Board.

During 2005, the Supervisory Board of EM.TV AG dealt prin-

cipally with the following issues:

Business status and current business development

Throughout the entire business year, the Supervisory Board

dealt in detail with the current business status of EM.TV AG

and the EM.TV Group. This included principally the analysis

of business activities during the course of the year in both

the Sports and Entertainment divisions, with particular em-

phasis on positive and negative deviations from the budget.

Within this process, the Management Board gave clear and

detailed statements on the current status of the business

and on plans for the year ahead for the individual divisions

and for EM.TV AG as the holding company, as well as on the

risks to group business development.

Significant investments in the operating business

The Supervisory Board used the circulation procedure to ap-

prove the acquisition by DSF of extensive exploitation rights

to the UEFA Cup matches for the 2005/2006, 2006/2007

and 2007/2008 seasons. It likewise gave its approval to

the acquisition by DSF of exploitation rights to the Premier

and Second German Soccer League for the 2006/2007,

2007/2008 and 2008/2009 seasons. The Supervisory

Board is of the opinion that both rights acquisitions ensure

that DSF’s program portfolio is suitably stocked with attrac-

tive top-end sports on a long-term basis. This is a fundamen-

tal requirement for the further commercial success of the

station.

Portfolio initiatives

In 2005, EM.TV AG completed the reorganization of the

Entertainment division, as a result of which the company

takes on the role of holding company without direct business

operations. In the course of this process, the Supervisory

Board used the circulation procedure to approve the mea-

sures necessary in order to bundle all the production and

6

Report of the Supervisory Board

Dr. Bernd Thiemann I Chairman of the Supervisory Board

7

sales activities of the Entertainment division into EM.Enter-

tainment GmbH and its subsidiaries. EM.Entertainment is a

100 percent subsidiary of EM.TV AG.

The Supervisory Board also used the circulation procedure

to approve the acquisition of further shares in sports com-

panies DSF and Sport1 from the possession of their previous

co-owners KarstadtQuelle New Media AG and Dr. h. c. Hans-

Dieter Cleven. The acquisition means that EM.TV AG now

holds either directly or indirectly 100 percent of each sports

company. The Supervisory Board considers the transactions

as important to the strengthening of the Sports segment.

Using the circulation procedure, the Supervisory Board

granted its approval to the acquisition of all stakes in the

Creation Club (CC) GmbH from PREMIERE through EM.TV

subsidiary PLAZAMEDIA. This included an extension of the

current production services framework contract between

PLAZAMEDIA and PREMIERE, ending December 31, 2006,

for a period of three years (outside production) and 4.5

years (studio production). In acquiring the Creation Club, the

Supervisory Board is convinced that PLAZAMEDIA is now

able to broaden significantly the added value of its creative

activities, while at the same time having achieved a long-

term relationship with an important customer in the shape

of PREMIERE.

Legal issues

2005 also saw the Supervisory Board focus a great deal of

its advisory efforts on the investigation of corporate dama-

ges claims against former board members. The Supervisory

Board heard reports on a regular basis from the appointed

legal experts, as well as from the Management Board, on

the status of the investigations and the outcome of the claim

entered on October 13, 2004 at the Munich I Regional Court.

This claim is against former CEO Thomas Haffa, former

Deputy CEO Florian Haffa and former Supervisory Board

Chairman Dr. Nickolaus Becker, and cites negligent breach

of duty in respect of the acquisition of Formula 1 shares in

2000. The damages claims asserted run to almost 148 mil-

lion Euro, plus release from claims entered by the Morgan

Grenfell Group.

As a result of the oral hearing of March 31, 2005, the

Munich I Regional Court ruled on August 25, 2005 that the

evidence of expert witnesses be submitted for consideration

in respect of certain factual matters. It is estimated that

the report of the expert witnesses will be submitted in the

course of 2006.

The intensive examination of further factual circumstances

revealed possible breach of duty in respect of loans made

to TheatrO CentrO GmbH in 2000 and 2001, the acquisiti-

on of stakes in Tabaluga Film- und Fernsehproduktion GmbH,

a major charitable donation, and in respect of the closing

of several co-production and licensing contracts. Following

requisite statements made by the former board members,

neither the Management nor the Supervisory Board were

able to reach any alternative conclusion on these matters,

and thus the company entered claims with the Munich I

Regional Court in August and September 2005. The claims

for damages entered in respect of the combined TheatrO

CentrO/Tabaluga/donation issues amount to around 17 mil-

lion Euro, with those arising from the co-production and

licensing contracts totaling around 18 million Euro.

With the exception of the aforementioned issues, the highly

time intensive and complex investigations carried out into

the major business transactions of the former EM.TV & Mer-

chandising AG have not led to the establishment of any

enforceable damages claims resulting from the dealings of

former board members – despite repeated acts of negli-

gence. This is particularly the fact in respect of the acquisi-

tion of major holdings Junior.TV, Tele München Gruppe and

the Jim Henson Company. In spite of the necessary in-depth

investigation, insufficient grounds were found on which the

company could base a case for damages resulting from the

misconduct of the former company directors. The same

applies to around ten further, smaller company acquisitions;

to the majority of co-production, rights purchase and license

contracts agreed by the company; and to a series of other

business transactions.

Group strategic direction

During the reporting year, the Supervisory Board dealt inten-

sively with issues concerning the future strategic direction

of the EM.TV Group. This included, in particular, opportuni-

ties for strategic development in both the Sports and Enter-

tainment segments through acquisition or divestment ini-

tiatives, and on the development of new business sectors.

The Management Board called extensively upon advice in

the matter of its plans for entry into the “betting” sector. The

Supervisory Board considered detailed reports on the vario-

us strategic options associated with this potential venture.

Changes to the Boards of Directors

The Management Board saw no changes in the course of

the reporting year.

Supervisory Board Members Prof. Roland Berger and

Dr. Andreas Meissner stepped down from their positions

with effect from the Annual General Meeting (AGM) on July

5, 2005. Prof. Berger and Dr. Meissner were with the com-

pany throughout its restructuring and reorientation, and

brought their extensive knowledge and advice to bear

during a very difficult phase for EM.TV. The Chairman of

the Supervisory Board offers his sincere gratitude to both

Prof. Berger and Dr. Meissner for their commitment to the

good of the company.

At the AGM on July 5, 2005, Dr. Hans-Holger Albrecht and

Mr. Arthur Bastings were approved as new members of the

Supervisory Board. With these two individuals, EM.TV has

gained the services of two highly knowledgeable and hands-

on media managers, with huge international experience. In

its meeting of July 5, 2005, the Supervisory Board unani-

mously voted Dr. Albrecht to the position of Deputy Chairman

of the Board.

Having been tasked with auditing the company reports,

PricewaterhouseCoopers AG Wirtschaftsprüfungsgesell-

schaft, München audited the annual accounts of EM.TV AG,

the Group annual accounts and the combined company

and Group management reports of December 31, 2005,

and issued them with an unconditional audit certificate. The

company annual accounts, the Group annual accounts and

the combined Group and company management reports

were passed in a timely manner to all members of the Super-

visory Board along with the audit reports.

The auditors furnished the Supervisory Board with the

significant findings of their audit at the meeting of the

Supervisory Board on March 23, 2006. The Supervisory

Board examined in detail the annual accounts of the AG

and the Group, as well as the combined company and

Group management reports, and approved the findings of

the auditors. Following the completion of its examination,

the Supervisory Board raised no objections to either the

company annual accounts or the Group annual accounts

and thus approved the company and Group annual

accounts as presented by the Management Board on

March 27, 2006. The annual accounts are thus final.

8

Report of the Supervisory Board

9

In the aftermath of the far-reaching restructuring that took

place in 2004, the Supervisory Board is of the opinion that

the 2005 business year was a successful one. Despite initi-

ally unforeseen burdens such as those arising through im-

portant program investments and ongoing difficult market

conditions, the forecast of a positive Group financial result

before tax and special and one-off effects has been achie-

ved for the first time since 1999. In addition, the business

year saw the foundations laid for the continuation of this

positive business development through a series of success-

ful business agreements. The Supervisory Board thanks

the Management Board and all the employees of the EM.TV

Group for their enormous commitment.

March 2006

Supervisory Board of EM.TV AG

Dr. Bernd Thiemann

Chairman of the Supervisory Board

In accordance with Article 3.10 of the German Corporate

Governance Code, the Management Board and the Super-

visory Board hereby report on the corporate governance of

EM.TV AG.

The Management Board and the Supervisory Board work

together on a basis of mutual trust for the benefit of the

company, and are fundamentally committed to achieving

sustainable growth in the company’s corporate worth. It is

the objective of EM.TV AG to justify the trust put in it by its

shareholders, customers and employees, as well as to live

up to its corporate responsibilities. EM.TV AG thus stands

for transparent and timely communication.

Shareholders and Annual General Meeting

In its annual and quarterly reports, EM.TV AG regularly pub-

lishes information regarding the development of its business.

In so doing, shareholders are provided with regular opportu-

nities to follow analysts’ conferences on those reports live

in the internet. Further detailed information on EM.TV AG is

also available on our homepage www.em.tv.

EM.TV AG shareholders are able to exercise their rights, as

well as their voting rights at the Annual General Meeting

(AGM). Each and every shareholder is entitled to participate

in the AGM, to take the floor on any agenda item, to ask

questions and to submit requests. EM.TV AG simplifies the

process for its shareholders to exercise their rights perso-

nally, by providing proxy voting representation bound by the

instruction of the shareholder. The AGM for the 2004 busi-

ness year took place on July 5, 2005, at which around 1,150

shareholders were represented, with a total of some 9.8 mil-

lion votes. All agenda items were agreed with majorities of

over 99 percent.

Cooperation between the Management and Supervisory

Boards

As the Group’s holding company and a German incorporati-

on (Aktiengesellschaft), EM.TV AG has a two-tier manage-

ment and control system i.e. the Management and Super-

visory Boards operate on a strictly separate basis.

The Management Board of EM.TV AG comprises three mem-

bers. The Management Board is responsible for running

EM.TV AG’s operating business, and for representing the

company to third parties. The main tasks of the Management

Board include the establishment of strategic direction, ma-

nagement of the Group and monitoring of risk management.

The Supervisory Board of EM.TV AG comprises three mem-

bers. The Supervisory Board advises and monitors the

Management Board in its management of the company. Its

responsibilities include, but are not restricted to, the appoint-

ment of Management Board members and the determinati-

on of Management Board remuneration.

The Management Board works together with the Supervisory

Board. It provides the Supervisory Board in a regular and

timely manner with information on all planning issues rele-

vant to the company and the Group, as well as on business

development, risk exposure and risk management. In doing

so, the Management Board agrees the company’s strategic

direction with the Supervisory Board, and discusses strate-

gic implementation at regular intervals.

Documents requiring approval, in particular EM.TV AG’s an-

nual accounts, its consolidated financial statement and

audit report, are presented in front of a meeting of the

Supervisory Board members. Laid down in the internal regu-

lations governing the Management Board is the requirement

for the approval of the Supervisory Board in respect of busi-

ness decisions of fundamental importance to the company.

A total of six Supervisory Board meetings were held during

the 2005 business year.

10

Corporate Governance Report

Corporate Governance Report

11

Further information concerning the Management and Super-

visory Boards can be found in the section on corporate bo-

dies and within the Group appendix.

Management and Supervisory Board Remuneration

The Management Board contract with Mr. Werner E. Klatten

runs until December 31, 2007.

Following the acquisition in early 2005 of all stakes in DSF

GmbH and Sport1 GmbH from KarstatdtQuelle and Dr. h.c.

Hans-Dieter Cleven, both positions held by Mr. Rainer Hüther

– one with EM.TV AG and one with DSF GmbH – were trans-

ferred into a single contract effective as of June 1, 2005.

Mr. Hüther’s contract ends on February 28, 2009. The con-

tract of Chief Financial Officer Dr. Andreas Pres runs until

December 31, 2008.

In accordance with the German Code of Corporate Gover-

nance, the total remuneration of each Management Board

member comprises both fixed and variable elements. The

variable remuneration elements are made up of one-off com-

ponents granted by the Supervisory Board for extraordinary

performance, and from components based on the financial

performance of the Group and its subsidiaries. The values

of these variable components are set by the Supervisory

Board and have contractual limits.

As variable remuneration components with a long-term in-

centive, the members of the Management Board of the for-

mer EM.TV & Merchandising AG had, at an earlier juncture,

received stock option packages as part of the stock option

program 2000 (“Option Program 2000”).

As the result of a decision made by the AGM of the former

EM.TV & Merchandising AG on July 22, 1999 (“Option Pro-

gram 1999”), which was then changed by a decision made

by the AGM of the former EM.TV & Merchandising AG on

July 26, 2000 (“Option Program 2000”), the Management

Board of the former EM.TV & Merchandising AG was empo-

wered, with the approval of the Supervisory Board, to issue

a stock option program for employees and members of the

Management Board of the Group companies. These options

also retain their fundamental validity following the restruc-

turing that took place in 2004.

Within the scope of the restructuring process, the AGM of

EM.TV AG decided on March 19, 2004, to grant those entit-

led to stock options the right to take one 10/73 ordinary

share in EM.TV AG at the strike option price, in return for

the right to one ordinary share in EM.TV & Merchandising

AG at the strike option price. The original issue volume of

1,488,012 shares comes from the Conditional Capital III

set aside for this purpose. Of the total stock option volume,

30 percent was reserved for members of the Management

Board and Group directors, with 70 percent reserved for

group company employees. This notwithstanding, the opti-

on terms of the 1999 and 2000 Option Programs retain

their validity. In accordance with the option terms, this in-

cludes a reduction in strike price in respect of the issue of

share certificates to existing shareholders within the scope

of the merger (dilution protection).

The Option Program 2000 requires that 50 percent of the

stock options may be exercised at the earliest after no less

than 2 years (in subsequent tranche 1), with the remaining

50 percent to be exercised at the earliest after no less than

4 years (in subsequent tranche 2). The strike price is deter-

mined by averaging the opening and closing price of EM.TV

shares on the Frankfurt Stock Exchange on the day of the

decision to issue (reference price); the price being no less

than the pro-rata amount of the subscribed capital for one

share, plus an additional 10 percent for tranche 1 and 20

percent for tranche 2. The stock options are valid for ten

years. On exercising stock options, the holder receives

ordinary shares in EM.TV AG, whereby shares arising from

options are eligible for participation in profit sharing from

the start of the year in which the option was exercised.

As of December 31, 2005, members of the Management

Board were eligible for a total of 600,000 stock options from

the Option Program 2000, entitling them to a total of

82,190 shares in EM.TV AG. The stock options are appor-

tioned among the members of the Management Board as

follows:Notes:1 Original strike price per share in the former EM.TV & Merchandising AG

prior to increases in accordance with option terms and dilution protection2 Price payable per EM.TV AG share on exercising option following increase

in accordance with option terms. Adjustment in keeping with the merger ratio of 73:10 and dilution protection in respect of issued certificates

12

Corporate Governance Report

Stock options

Quantity

200,000

200,000

100,000

100,000

Name

Werner E. Klatten

Rainer Hüther

Dr. Andreas Pres

Issue Date

31/01/02

31/01/02

07/06/02

30/06/03

Original StrikePrice1

Euro/Share

2.28

2.28

1.29

1.60

Shares

Quantity

27,397

27,397

13,698

13,698

Price perShare2

Tranche 1Euro/Share

17.48

17.48

9.53

12.02

Price perShare2

Tranche 2Euro/Share

19.14

19.14

10.47

13.19

SharePrice

31/12/05Euro

4.33

4.33

4.33

4.33

Due to the share price performance of the former EM.TV &

Merchandising shares, as well as those of EM.TV AG, it has

thus far not been possible to exercise stock options held by

the Management Board. Therefore we currently attribute no

tangible value to the stock options.

Remuneration of Supervisory Board members is specified

in paragraph 12 of EM.TV AG’s articles of association.

Alongside the reimbursement of their expenses, Supervisory

Board members receive a fixed remuneration. The introduc-

tion of success-based remuneration for the Supervisory

Board has been deferred. The fixed remuneration of

Supervisory Board members in the 2005 business year

was as follows:

Name Function Period Fixed Remuneration

Dr. Bernd Thiemann Chairman / Supervisory Board 01/01/2005 to 31/12/2005 90,000.00 Euro

Dr. Hans Holger-Albrecht Deputy Chairman / Supervisory Board 05/07/2005 to 31/12/2005 22,068.49 Euro

Arthur Bastings Member / Supervisory Board 05/07/2005 to 31/12/2005 14,712.33 Euro

Prof. Dr. h.c. Roland Berger Deputy Chairman / Supervisory Board 01/01/2005 to 05/07/2005 22,931.51 Euro

Dr. Andreas Meissner Member / Supervisory Board 01/01/2005 to 05/07/2005 15,287.67 Euro

13

Neither the Management Board members nor the Supervi-

sory Board members conducted any acquisitions or dispo-

sals during the 2005 business year that were subject to

mandatory reporting requirements. The direct or indirect

ownership by any board member of any shares issued by

EM.TV AG was no greater than 1%. The position with regards

to shares and shares from stock options on the part of any

board member as of December 31, 2005 was as follows:

Further information regarding the remuneration of the

Management and Supervisory Boards can be found in the

group appendix and on our homepage.

Statement of Conformity with the German Code of

Corporate Governance

The Management and Supervisory Boards of EM.TV AG state

that the recommendations of the German Code of Corporate

Governance dated May 21, 2003 have been met, with the

exceptions detailed below, as will the recommendations of

the Code dated June 2, 2005 be met, with the same excep-

tions:

> Section 4.2.3 para. 2, final clause of the code

With regard to stock options, a cap will be agreed on new

option issues. In the case of existing share options, which

currently have no tangible value, it is not necessary to

amend finalized contracts in respect of a cap.

> Section 4.2.4 para. 2 of the code

The remuneration of Management Board members is not

individually reported as this is the personal information of

the Management Board members. The company will re-

port Management Board remuneration individually as of

the 2006 business year, as required by law.

> Sections 5.3.1 and 5.3.2 of the code

Separate committees were not formed, as the Supervisory

Board consists of only three members.

> Section 5.4.7 of the code

The introduction of success-based remuneration for the

Supervisory Board has been deferred, as there currently

remains a lack of clarity in respect of the reliability of

success-based remuneration.

> Section 7.1.2 of the code

The deadline for publication of quarterly reports (interim

reports) has not yet been reduced to 45 days after the end

of the reporting period. The Management Board is striving

to meet this recommendation as quickly as possible by

optimizing internal procedures.

The current version of the statement of conformity with the

German Code of Corporate Governance, as well as earlier

versions, can be found on our homepage.

Number of Shares fromShares Stock Options

Werner E. Klatten 0 27,397

Rainer Hüther 0 27,397

Dr. Andreas Pres 6,000 27,396

Supervisory Board Members 0 0

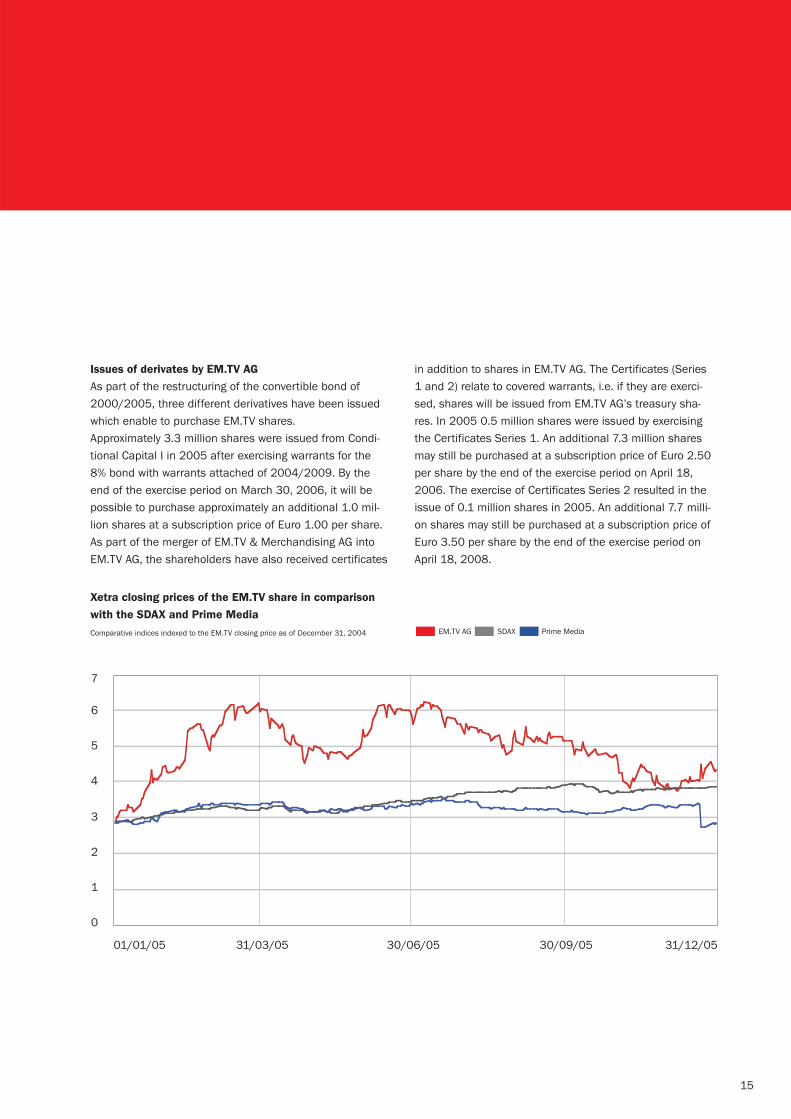

Development of the EM.TV share

The EM.TV Share developed with substantial price fluctu-

ations very positively in 2005 with a value increase of 51

percent. The percentage increase of the share price excee-

ded that of the SDAX therefore which advanced by 35 per-

cent and also the Prime Media which fell by 1 percent. The

share price rose from January to the middle of March and

reached its current 52-week high of Euro 6.37 during a pe-

riod of high trading volumes. A consolidation then set in un-

til the end of May, with the share price falling to Euro 4.76

in April. The share price then rose again until the middle of

July. Between July and the end of the year, the share price

declined and reached its current 52-week low of Euro 3.68.

The price of the EM.TV share closed the year at Euro 4.33.

This was equivalent to a price increase of Euro 1.46 and

51 percent respectively.

In 2005, the EM.TV share was the SDAX security with the

highest level of trading with a total volume of approximately

199 million shares (daily average of 0.5 million). Over the

12-month period, this was equivalent to a trading volume

of approximately four times the outstanding shares and re-

flected the high liquidity of the share.

Subscribed capital and shareholder structure

The subscribed capital of the EM.TV share amounted to

approximately Euro 69.9 million as of December 31, 2005,

including new shares from exercised warrants of the bond

with warrants attached, the entry of which in the Commercial

Register was still outstanding at the balance date.

EM.TV AG held 23.9 percent of the subscribed capital equi-

valent to 16.7 million non-voting shares. Approximately

15.0 million thereof were reserved for servicing the certifi-

cate series. After deducting the Company’s own, non-voting

shares, there were approximately 53.1 million outstanding

shares as of December 31, 2005.

On June 8, 2005, Centaurus Capital LP fell below the thres-

hold of 5 percent of the voting rights in EM.TV AG. As of

December 31, 2005, Constant Ventures B.V. held 6.9 per-

cent of the share capital, equivalent to 9.1 percent of the

voting rights. Scattered shareholders therefore held 69.2

percent of the share capital, equivalent to 90.9 percent of

the voting rights.

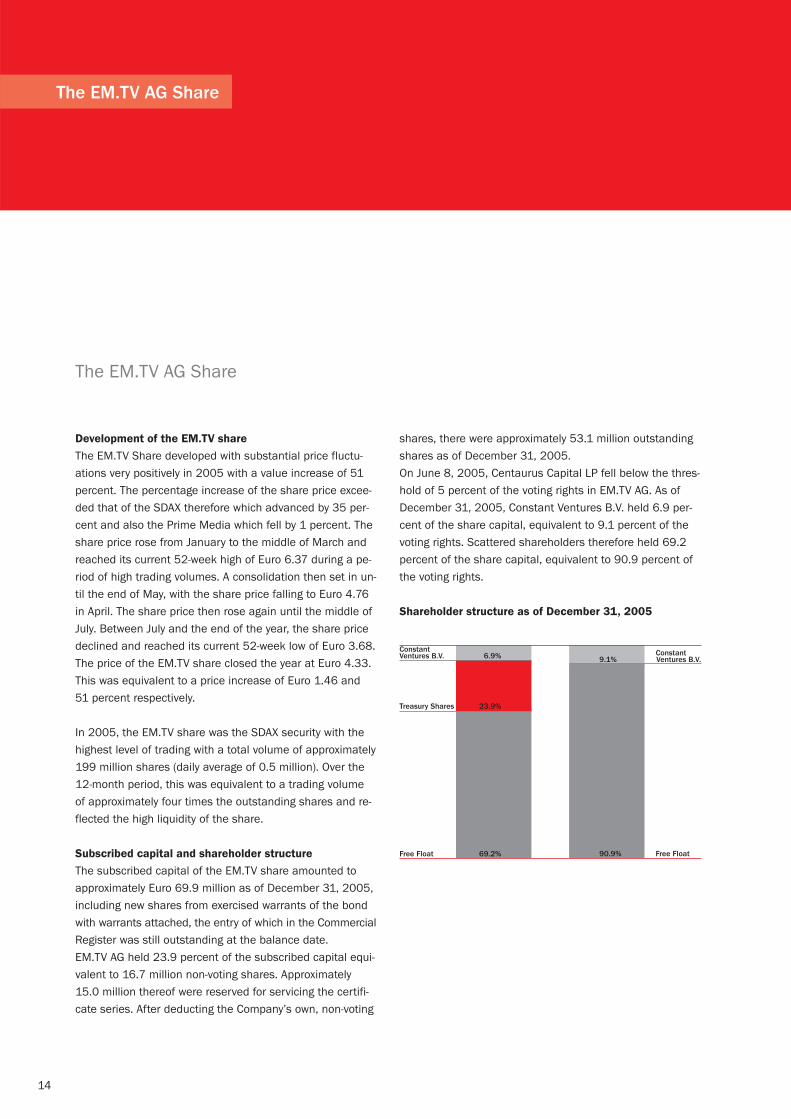

Shareholder structure as of December 31, 2005

14

The EM.TV AG Share

The EM.TV AG Share

Constant Ventures B.V. 6.9%

Treasury Shares 23.9%

Free Float 69.2%

Constant 9.1% Ventures B.V.

90.9% Free Float

15

Issues of derivates by EM.TV AG

As part of the restructuring of the convertible bond of

2000/2005, three different derivatives have been issued

which enable to purchase EM.TV shares.

Approximately 3.3 million shares were issued from Condi-

tional Capital I in 2005 after exercising warrants for the

8% bond with warrants attached of 2004/2009. By the

end of the exercise period on March 30, 2006, it will be

possible to purchase approximately an additional 1.0 mil-

lion shares at a subscription price of Euro 1.00 per share.

As part of the merger of EM.TV & Merchandising AG into

EM.TV AG, the shareholders have also received certificates

in addition to shares in EM.TV AG. The Certificates (Series

1 and 2) relate to covered warrants, i.e. if they are exerci-

sed, shares will be issued from EM.TV AG’s treasury sha-

res. In 2005 0.5 million shares were issued by exercising

the Certificates Series 1. An additional 7.3 million shares

may still be purchased at a subscription price of Euro 2.50

per share by the end of the exercise period on April 18,

2006. The exercise of Certificates Series 2 resulted in the

issue of 0.1 million shares in 2005. An additional 7.7 milli-

on shares may still be purchased at a subscription price of

Euro 3.50 per share by the end of the exercise period on

April 18, 2008.

0

1

2

3

4

5

6

7

01/01/05 31/03/05 30/06/05 30/09/05 31/12/05

EM.TV AG SDAX Prime Media

Xetra closing prices of the EM.TV share in comparison

with the SDAX and Prime Media

Comparative indices indexed to the EM.TV closing price as of December 31, 2004

7

6

5

4

3

2

1

0

16

The EM.TV AG Share

Investor Relations activities

EM.TV AG aims at justifying the trust of investors and the

public by timely and transparent publications of its finan-

cial data, business transactions, corporate strategy, oppor-

tunities and risks. Extensive information concerning EM.TV

AG is available on our homepage www.em.tv.

Investor Relations activities were intensified in 2005. All

quarterly figures were explained to analysts and investors

by telephone or in person. The results for the third quarter

were presented at the Deutsches Eigenkapitalforum 2005

(German Equity Capital Forum) in Frankfurt.

EM.TV AG participated in six capital market conferences

and a road-show in Frankfurt and London. It was also avai-

lable to institutional investors in a large number of additio-

nal one-on-one meetings. Various individual enquiries by

private investors were also handled by our Investor Rela-

tions team.

Investor Relations activities were particularly directed to a

systematic extension of analysts’ coverage. Three additio-

nal institutes initiated coverage during the course of 2005.

Regular contacts are currently being maintained with the

following institutes:

> CA Cheuvreux > Deutsche Bank

> DZ Bank > WestLB

The aim of Investor Relations activities in 2006 will be par-

ticularly directed to expanding the analyst coverage even

further and increasing the number of long-term oriented in-

stitutional investors.

17

ISIN

> Ordinary Share DE0009147207

> New Share* DE000A0AHSX7

Segment Prime Standard

Regulated Market

Indices SDAX, Prime Media Index

Bloomberg /Reuters EV4 GR/EV4G.DE

Share price Euro 4.33

52-week high/52-week low Euro 6.37/Euro 3.68

Subscribed capital (inkl. shares from exercised warrants of bond with warrants attached) Euro 69.9 million

Outstanding shares 53.1 million Shares

Potential shares from outstanding warrants

> Certificates Series 1 (Subscribed price Euro 2.50 until April 18, 2006) 7.3 million Shares

> Certificates Series 2 (Subscribed price Euro 3.50 until April 18, 2008) 7.7 million Shares

> Warrants of bond with warrants attached (Subscribed price Euro 1.00 until March 30, 2006) 1.0 million Shares

> Others (Employee participation programs and convertible bond) 0.4 million Shares

Market capitalization (based on outstanding shares) Euro 230.1 million

Market evaluation for own issues of outstsanding derivates Euro 29.2 million

Information on the EM.TV Share as of

December 31, 2005

*Since January 1, 2006, shares are issued by EM.TV AG from the conditional capital.These are being traded under a separate ISIN as “New Shares”. The background to thisis a deviating profit entitlement in comparison with ordinary shares. The “New Shares”will be transferred into ordinary shares after the resolution of the General Meeting on theappropriation of profits for the 2005 financial year.

The Company considers itself as a lean and flexible medium

sized media company which is able to manoeuvre indepen-

dently within the rapidly changing media industry, as it is

not part of one of the large media groups in Germany.

Therefore, the Company is able to cooperate with nearly all

other market participants from a neutral position.

The Company pursues a two segment strategy focusing on

sports and entertainment.

The Company is generally aiming to achieve organic growth

as well as growth by acquisitions in each segment. The

growth path will only be pursued provided that it does not

jeopardize the primary goal of the Company to achieve pro-

fitability for each segment and to generate a positive free

cash flow before extra ordinary investments.

However, due to currently consolidating markets, the Com-

pany may also decide to sell certain of its assets if the cir-

cumstances are favourable to the Company.

Strategy of Sports segment

The Sports segment comprises mainly of DSF, PLAZAMEDIA

and Sport1 with a range of seamlessly fitting services to

offer turnkey production solutions together with access to

distribution platforms in the TV and the internet and mobile

devices.

It is intended that DSF will further sharpen its profile as a

niche sports channel towards its target group of men aged

14 to 49 years by increasing the number of hours of natio-

nal and international premium sports as highlights or even

live formats. In addition, the channel will further seek to level

out the dependency on classical advertising with other add

on services such as T-Commerce i.e. revenue streams from

interactive formats. In the medium term, an expansion of

the existing broadcast activities by additional DSF channels,

particularly via digital distribution platforms could become

an attractive option.

PLAZAMEDIA shall further exploit its current market positi-

on as one of the leading sports production companies by

means of expanding its customer base. It shall seek to de-

velop itself further towards a general contractor for a varie-

ty of sport events. As such, its involvement in production

services during the upcoming 2006 FIFA World Cup™ may

qualify PLAZAMEDIA for additional sports production con-

tracts. Moreover, demand from foreign TV stations as well

as the changing environment for new broadcast technology

such as HDTV offer opportunities that PLAZAMEDIA intends

to take advantage of.

Sport1 shall further exploit its market position as the lead-

ing German sports internet platform in order to grow its ad-

vertising revenue and expand its strategic partnerships for

cross promotions. International expansion may also be con-

sidered. Given the strong development of online advertising

market in other countries, the Company believes that

Sport1 has potential to grow profits.

The market for sports betting has developed very positively

in the last few years in the German speaking area and offers

significant sales and earnings opportunities in the opinion

of the Company. In the event of liberalization, EM.TV would

be in a position to enter the market immediately as a result

of the extensive preparations carried out in 2005 and would

be able to participate with promising market perspectives.

With DSF and Sport1, the Group also has two extremely

18

Company Strategy

Company Strategy

19

appropriate advertising platforms for making appropriate

offers for sports betting.

Strategy of Entertainment segment

The Entertainment segment with its large library is aiming

at producing and acquiring youth and kids’ content and the

comprehensive exploitation of all its properties throughout

distribution channels and territories worldwide.

The Company, through its subsidiaries EM.Entertainment

GmbH and Junior Produktions GmbH, intends to increase

its production activities in order to heighten the value of the

library and its freshness. Further, it is intended to adjust its

rights library to older children and teenagers with an increa-

sed focus on distribution channels besides TV. Thus, the

aim is to grow the non-TV related revenue in order to lower

the dependency on TV license fees currently paid for kids’

and youth program.

The Company is also endeavouring to obtain increased

direct access to distribution platforms such as television

stations, audio and video distributors. Content exploitation

through mobile platforms and applications could become

an additional distribution tool.

In order to get access to territories, where the Company has

so far been weak distributing to such as UK, US and

Canada, the Company contemplates acquisitions, partner-

ships or distribution joint ventures and expand its entertain-

ment activities in a fragmented, but consolidating media

market.

20

21

With its products, EM.TV intends to satisfy the interests and emotionalrequirements of its customers and viewers. These products have to becreative, emotional, qualitatively equivalent to the „state of the art“ andupright from a contents point of view.

DSF has been an integral feature of the German media

landscape since the station was founded. With a clear

focus on the core advertising target group of males aged

14 to 49, DSF has achieved distinctive positioning. No

other German free-TV station provides such comprehensive

reporting on sporting events, with independence, neutrality

and critical distance being hallmarks of the station’s edito-

rial policy.

Long-term coverage secured

In keeping with the station’s motto “Mehr Sport, Mehr Live”

(more sport, more live), the top quality broadcast rights ac-

quired during the previous year were converted into attrac-

tive sports coverage. At the same time, the reporting period

saw comprehensive premium soccer rights secured for the

future. A further operational highlight was the successful

finalization of feeder contracts with cable companies, secu-

ring both analog and digital transmission on a long-term

basis. With these sports rights and new levels of transmis-

sion security, DSF has laid a firm foundation for the further

development of the station.

Financial result impacted by program investments and

special effects

Despite a difficult TV advertising market, in which DSF – in

contrast to 2004 – was no longer able to buck the general

trend in terms of advertising income, turnover remained on

the same level as the previous year.

DSF’s operating result was down against the 2004 business

year. This decrease was largely due to costs associated with

the acquisition of the UEFA Cup rights, and bad debt provi-

sions in respect of two service partners, which could not be

compensated for by other positive effects.

Co-operations with key customers expanded

In spite of difficult overall conditions, DSF was able to ex-

pand or extend co-operations with key customers, as well

as form new partnerships within the sponsoring and special

advertising sector. Top class customers such as Deutsche

Telekom, Hasseröder, Betandwin, DA Direkt, Nike, Erdinger

Weißbräu and BMW extended their partnerships, while other

customers have expanded their co-operations with DSF.

Thus, Krombacher (current title sponsor of DSF-Doppelpass)

is now also presenter of the UEFA Cup broadcasts. Suzuki

has now entered in soccer, in addition to its involvement in

motorsport projects. New customers in the sponsoring sec-

tor include König Pilsner, LG Electronics, Puma and DiBa.

DSF grows market share over previous year

Within the target group of viewers overall, DSF succeeded

in increasing its market share for the year from 1.1 to 1.2

percent against 2004. In the core target group of males

aged 14 to 49, DSF maintained its market share against

the previous year at 1.9 percent. The previous year’s level

was also reached in the fourth quarter 2005, with 1.1 per-

cent (viewers overall) and 1.9 percent (males aged 14 to

49) exactly matching the figures for the last quarter 2004.

Significant growth in market share was achieved by DSF-

teletext. For the full year 2005, DSF saw increases over

2004 among viewers overall (from 4.8 to 5.2 percent), as

well as among the target group of males aged 14 to 49

(from 6.3 to 7.6 percent).

Long-term rights secured: German Soccer League, UEFA

Cup, FA Cup and Davis Cup

DSF remains the soccer station in German free-TV. Following

the TV rights granted by the Deutsche Fußball Liga (German

Soccer League) (DFL), December 2005 saw DSF receive a

22

Business Units Reports I Sports

TV I DSF Deutsches SportFernsehen

23

renewal for the next three years of the exclusive first high-

lights in free-TV to the Premier Soccer League Sunday mat-

ches, as well as the exclusive first free-TV highlights to the

Second Soccer League, including the live match on Mon-

days. With this deal, DSF has secured its core rights for the

next three years. License expenditure for this is not due

until the start of each respective season.

Alongside the Soccer League, the 2005 business year saw

DSF invest in further long-term, top-class broadcasting rights.

The top event acquired by DSF next to the Soccer League

was the UEFA Cup. From the 2005/2006 season through

to the 2007/2008 season, DSF will be broadcasting at least

two UEFA cup matches live on every match day up to and

including the semi-finals. Furthermore, DSF has also secu-

red the exclusive live and highlights rights to the traditional

English FA Cup for a period of two years up to and including

the 2006/2007 season, as well as the live and exclusive

rights to the matches of the German Davis Cup team for

2005 and 2006.

DSF increases its share of live coverage against previous

year

DSF has stood by the motto it issued at the beginning of the

year “Mehr Sport, mehr Live” and presented a host of pro-

gram highlights during 2005. Alongside top soccer from the

Premier and Second Soccer League and the UEFA Cup, DSF

reported live from, among others, the Handball World Cham-

pionship (January), the Ice Hockey World Championship

(May), the Tour de Suisse (June) and the European Basket-

ball Championship and the Davis Cup (both in September).

Thus DSF demonstrated during 2005, an increase in live

reporting of a little over seven percent. In the fourth quar-

ter 2005 alone, DSF achieved an increase against the

same period the previous year of around 17 percent.

In addition, DSF also presented a program innovation in

2005. For the very first time, viewers were able to select

for themselves a live match from the Handball Bundesliga

over a period of six weeks. With this initiative, DSF presen-

ted something completely new in German sports free-TV.

On the road to success with Bundesliga formats and the

UEFA Cup

The soccer formats on DSF continue on the road to success.

All formats from the Premier and Second Soccer League

achieved significant increases in market share against the

previous year within the core target group of males aged 14

to 49. For example, during the reporting period, Bundesliga

– Der Sonntag recorded growth in market share against

2004 from 10.1 to 10.7 percent, while DSF-Doppelpass

witnessed an improvement from 7.9 to 9.3 percent.

With Bundesliga – Der Sonntag, DSF achieved a milestone

in its broadcast history on March 13, 2005. The highlights

of the Sunday matches Schalke 04 versus Bayern Munich,

and Borussia Dortmund versus VfB Stuttgart achieved ra-

tings of an average of 4.7 million, and a peak value of 5.5

million viewers. This saw DSF record its second best ratings

since the station was founded, and only narrowly missed its

absolute record from 1993 (an average of 4.8 million vie-

wers watched the UEFA Cup semi-final Dortmund versus

Auxerre). With 17.6 percent market share in the target group

of males aged 14 to 49, March 13 saw DSF achieve a new

best for Bundesliga – Der Sonntag since the acquisition of

the Bundesliga rights in 2003. Bundesliga – Der Sonntag

was also DSF’s highest-rating format for 2005 as a whole.

Alongside the Bundesliga, DSF also achieved very good

ratings with the UEFA Cup. An average of 1.8 million viewers

followed the broadcasts on DSF; with the station achieving

a market share of 11.7 percent among males aged 14 to

49. DSF achieved its top ratings for the UEFA Cup with FSV

Mainz 05 versus FC Sevilla. An average of 2.31 million vie-

wers overall followed the match live on DSF (market share

males 14 to 49 years – 13.3 percent). This was almost

equaled in the fourth quarter 2005, when the live transmis-

sion of HSV versus Viking Stavanger on November 3 brought

an average of 2.3 million viewers (market share males 14

to 49 – 11.9 percent).

Strong ratings with European Basketball Championship

and Handball World Championship

Other sporting disciplines also produced outstanding

ratings during 2005. With the final of the European Basket-

ball Championship in September between Germany and

Greece, DSF achieved strong ratings averaging 1.34 million

viewers, while the Handball World Championship at the end

of January was equally well received with up to 1.1 million

viewers.

24

Business Units Reports I Sports

Online I Sport1

Sport1.de continues to be the most popular German-lan-

guage sports website offering up-to-the-minute, well-re-

searched content from the exciting world of sports. In addi-

tion, as a multimedia sports platform, Sport1 provides

sports content for teletext and mobile platforms such as

SMS, MMS and WAP. Within this business sector, Sport1

includes private TV stations and leading telecommunica-

tions companies among its customers.

Focus on core business

Following the portfolio restructuring that took place in 2004,

efforts during the 2005 business year were focused entirely

on the core business activities of media sales and content

syndication. Due to the absence of major sporting events,

Sport1 took the opportunity to use 2005 as a preparation

year for the forthcoming major event – the 2006 FIFA

World Cup™ in Germany.

Sport1 further developed its successful strategy of mana-

ging operations outside of its core business with external

partners. The Auto&Motor unit saw a partnership agreed

with production service “onpact” during the first quarter, as

well as a co-operation with auto portal “mobile.de”. This

concept, which minimizes risk for Sport1, has also been

successfully implemented in a similar way within the

Games unit with partner “Gameduell”.

Successful business year for Sport1

Due to the ongoing focus on core business, Sport1 was able

to sustain the successful business development achieved

in the previous year, and to confirm its position as Germany’s

leading multimedia sports platform.

Massive growth in usage of more than 40 percent – mar-

ket leadership position expanded

With over 180 million visits and over 1.3 billion page im-

pressions during the 2005 business year, equating to an

increase in usage of well over 40 percent compared with

2004, Sport1 accomplished yet another significant expan-

sion in its market leadership. Sport1 achieved the highest

visit ratings in its six year history in September 2005 with

over 17.3 million visits.

Sport1 confirms position as teletext producer

In the second quarter 2005, the major contract with Seven

One Interactiv GmbH for the production and delivery of

25

editorial teletext content for the sports sector was extended

until December 31, 2008. Thus, Sport1 still produces and

delivers the entire editorial teletext sports content for TV

stations ProSieben, Sat.1, kabel eins, N24 and DSF.

Co-operations with Adidas and Suzuki

2005 saw a long-term strategic co-operation reached with

sporting goods manufacturer Adidas. This encompasses

exclusive advertising campaigns for the DAX group within

the soccer sector. Furthermore, “Suzuki” was also secured

as a strategic and long-term partner.

New marketing agency mediasquares GmbH

In recognition of the strong growth ongoing in the online ad-

vertising market, 2005 saw Sport1 further expand its sales

team. In another move, a contract was signed on March 1,

2005 with Hamburg-based online marketing agency medias-

quares GmbH for the marketing of classic advertising space

on www.sport1.de, as well as the associated ad manage-

ment. Mediasquares is one of Germany’s highest performers

in online marketing and is therefore an excellent strategic

partner for sport1.de, ideally complementing its in-house

marketing activities associated with sponsoring, co-opera-

tions and cross-media.

Sport1 with new sports database

In respect of future strategy at Sport1, the third quarter 2005

saw the implementation of an in-house sports database. This

technical project was realized in co-operation with Norwe-

gian sports data supplier “Betradar.com-Market Monitor AS”.

PLAZAMEDIA is a leading full-service company for TV and

new media, operating in outside production, studio produc-

tion, post production, new media, program management and

creative services. Within the reporting period, the company

created close to 90,000 hours of programming and mana-

ged around 1,500 national and international productions.

2005 business year sees positive development and posi-

tioning for further growth

The 2005 business year was marked by good capacity utili-

zation across all business activities. Despite the loss of the

contract to produce the base signal for the Premier and

Second Soccer League as of the 2004/2005 season,

PLAZAMEDIA’s business development in 2005 was in line

with expectations. Major contributors to the progress made

during the reporting period were increased profitability and

additional contracts. The opening up of new technologies

and business sectors was pushed forward, and will also con-

tinue to bring about sustainable business growth.

During the last year, PLAZAMEDIA was able to lay down the

foundations for forward-looking production technology.

Through the introduction of “HDTV” (High Definition Tele-

vision) throughout the entire production chain, the company

was able to secure its unique position in the marketplace.

This production capability has already won PLAZAMEDIA

significant contracts such as that for the production of the

2005 FIFA Confederation Cup from Host Broadcast Service

(HBS) based in Switzerland, which is also the official produc-

tion partner of the 2006 FIFA World Cup™. This tournament

functioned as a dress rehearsal for the imminent 2006

FIFA World Cup™ in Germany, which, for the first time ever,

will be produced entirely in the new HDTV technology.

Production Services I PLAZAMEDIA

The last business year also saw an agreement reached with

HBS to provide production services on the worldwide signal

for the 2006 FIFA World CupTM. HBS has contracted PLAZA-

MEDIA to generate the worldwide signal using two venue

production teams. The contract also covers the final of the

2006 FIFA World Cup™ in Berlin.

In addition to this, PLAZAMEDIA will also create, under con-

tract to HBS, the city profiles for all the host cities of the

2006 FIFA World Cup™. These profiles are the means by

which the individual host cities will be presented to the

event’s worldwide audience.

Numerous other contracts were also secured during the re-

porting period. These included the take over by PLAZAMEDIA

of playout for the PLANET documentary channel, the realiza-

tion of the PREMIERE SPORT PORTAL, as well as the first

live-capable program production in HDTV for PREMIERE HD

SPORT, plus production of the 2005 FIFA Confederation Cup

as well as the UEFA Champions League (2005/2006 sea-

son) for Premiere and the UEFA Cup for DSF. In addition,

the company also handled conception and production of

the Kabel Deutschland Info Channel under contract to Kabel

Deutschland GmbH.

Entry into international markets and capacity expansion

During 2005, Outside Production also realized numerous

national and international series productions, including pro-

duction of the Premier and Second Soccer League for DSF;

the Red Zac First League and T-Mobile Bundesliga for

PREMIERE Austria; Formula 1, the German BBL Basketball

League and the DEL German Ice Hockey League for Pre-

miere; plus the HBL German Handball League for DSF.

At the same time, the New Media business unit further

expanded its international activities. Under contract to US

internet company Bluelake Media, PLAZAMEDIA produced

the Premier and Second Soccer League, the 2005 IIHF Ice

Hockey World Championship, the 2005 European Basket-

ball Championship, the qualifying matches for the 2006

FIFA World Cup™ and the three-language highlights of all

16 of the 2005 FIFA Confederation Cup matches. Japanese

company Softbank and Brazilian telecommunications com-

pany Terra Networks received pre-prepared video clips of

the German Soccer League.

During the fourth quarter, PLAZAMEDIA reached an agree-

ment with PREMIERE for the continuation of their long-term

strategic partnership as of January 1, 2007, as well as ex-

tending the framework production contract covering exten-

sive studio and outside production services. In terms of

sports, the studio production services (period of agreement

extends until June 30, 2011) will in future also encompass

full program management of PREMIERE’s sports program

and HD portfolio, post production, studio production and

production of the conference channel for the Champions

League matches. In outside production, PLAZAMEDIA will