Embed Size (px)

Citation preview

Accounting

Chapter 8

Remember the Adjustment Column of the Work Sheet?Adjustments must be journalized and posted

WHY?Accounting Period CycleAdequate DisclosureMatching Expenses with Revenue

Adjusting Entries are journal entries recorded to update general ledger accounts at the end of a fiscal period

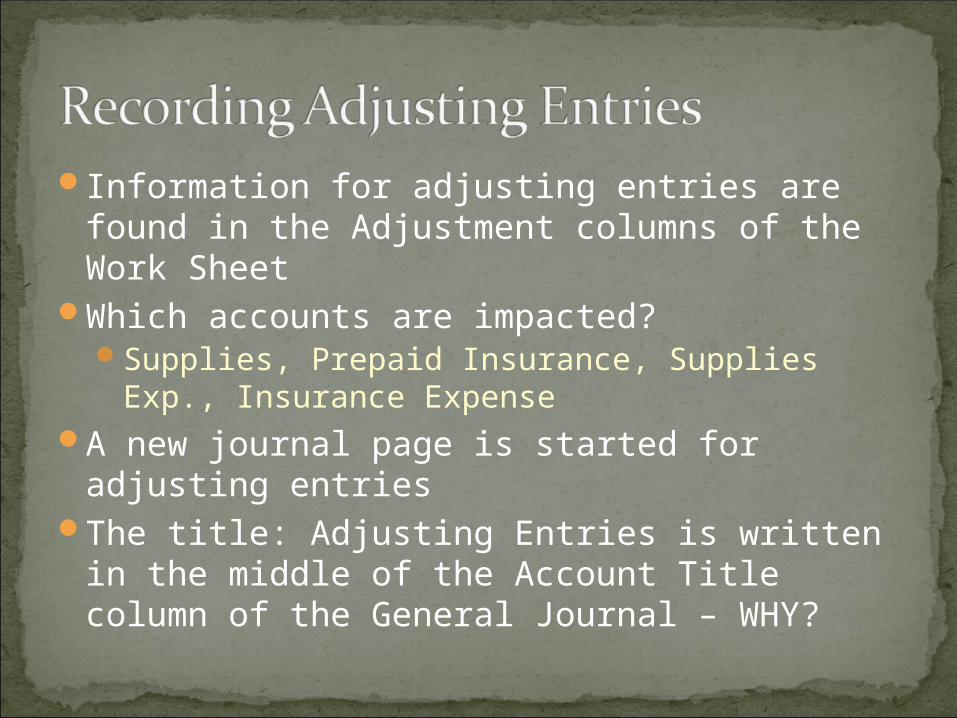

Information for adjusting entries are found in the Adjustment columns of the Work Sheet

Which accounts are impacted?Supplies, Prepaid Insurance, Supplies Exp.,

Insurance ExpenseA new journal page is started for adjusting

entriesThe title: Adjusting Entries is written in the

middle of the Account Title column of the General Journal – WHY?

Name of Company

General Journal

Page: n+1

Date Account TitleDoc No.

Post. Ref Debit Credit

Adjusting Entries

8 31 Supplies Expense 715

Supplies 715

All journal entries must be postedPosting to the General Ledger insures that

all account balances are up to date and match the information on the company’s financial statements

Remember the steps for posting?Don’t forget to record the account

number on the general journal entryWT 81-83.xls

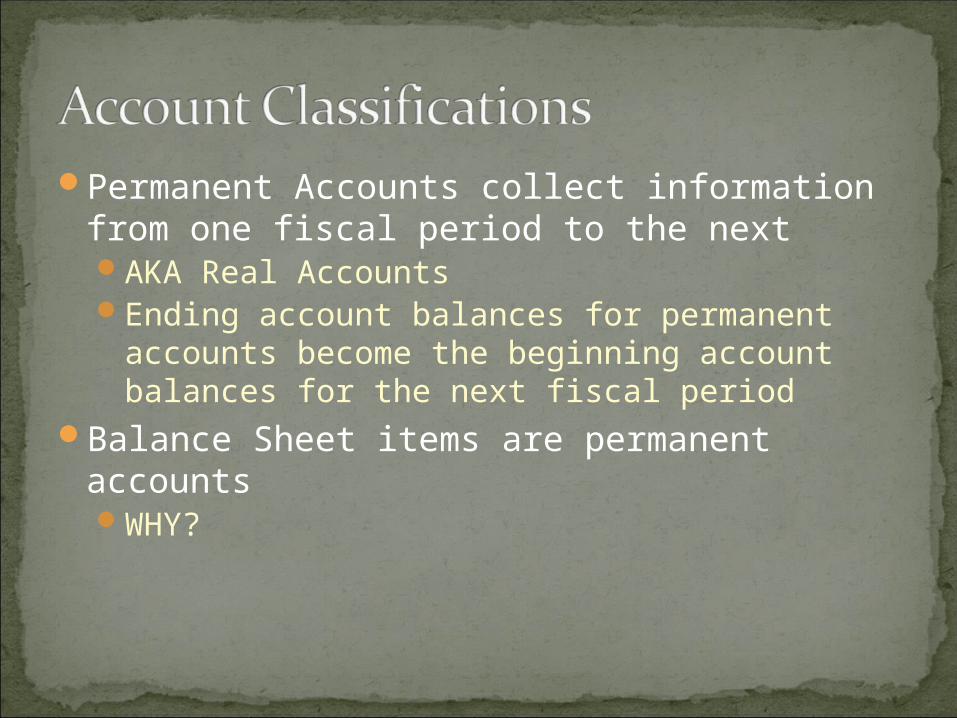

Permanent Accounts collect information from one fiscal period to the nextAKA Real AccountsEnding account balances for permanent

accounts become the beginning account balances for the next fiscal period

Balance Sheet items are permanent accountsWHY?

Temporary Accounts accumulate information that is transferred to the owner’s capital account at the end of the fiscal periodAKA Nominal Accounts

Income Statement items are temporary accountsWHY?

Temporary accounts begin a new fiscal period with a zero balance

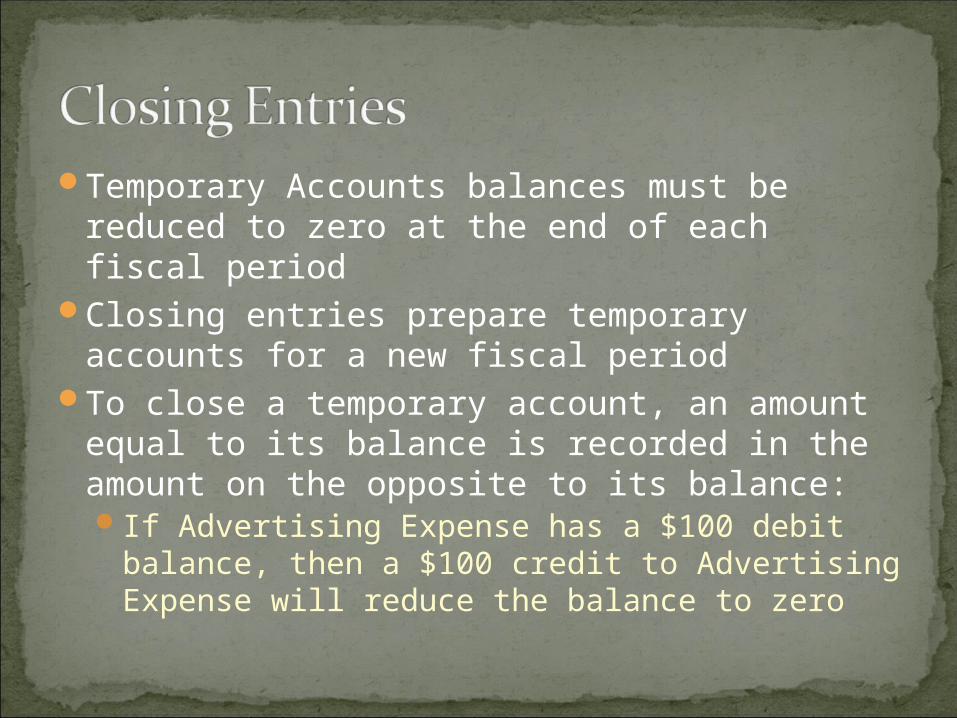

Temporary Accounts balances must be reduced to zero at the end of each fiscal period

Closing entries prepare temporary accounts for a new fiscal period

To close a temporary account, an amount equal to its balance is recorded in the amount on the opposite to its balance:If Advertising Expense has a $100 debit

balance, then a $100 credit to Advertising Expense will reduce the balance to zero

The Income Summary account is a temporary account that summarizes the closing entries associated with Revenues and Expenses

All expenses (debit normal balances) are debits to Income Summary

All revenues (credit normal balances) are credits to Income Summary

Income Summary is eventually closed to Capital

What is relationship between the Income Summary account and Net Income(Loss)?

The balance of the Income Summary account is determined by whether the business earns net income or suffers a net loss

There are four closing entries for a service business (sole proprietorship):An entry to close income statement accounts

with credit balancesAn entry to close income statement accounts

with debit balancesAn entry to record net income or loss and close

Income SummaryAn entry to close the owner’s drawing account

Which accounts are these?

Name of CompanyGeneral Journal

Page: n+1Date Account Title Doc No. Post. Ref Debit Credit

Closing Entries 31 Sales 3,565.00

Income Summary 3,565.00

Only one closing entry is required to close all expense accounts

Name of Company

General Journal

Page: n+1

Date Account Title

Doc No.

Post. Ref Debit Credit

Closing Entries

31 Sales 3,565.00

Income Summary 3,565.00

31 Income Summary 1,466.00 Advertising Expense 213.00 Insurance Expense 100.00 Miscellaneous Expense 28.00 Rent Expense 300.00 Supplies Expense 715.00 Utilities Expense 110.00

Income Summary is a temporary account that is closed to the Capital account – WHY?

If there is net income:

If there is net loss

Supplies Expense 715.00

Utilities Expense 110.00

31 Income Summary 2,099.00 Owner, Capital 2,099.00

Utilities Expense 110.00

31 Owner, Capital 2,099.00 Income Summary 2,099.00

Drawing is not a revenue or expense account and cannot be closed through the Income Summary account

WT 81-83.xls

Owner, Capital 2,099.00

31 Owner, Capital 625.00 Owner, Drawing 625.00

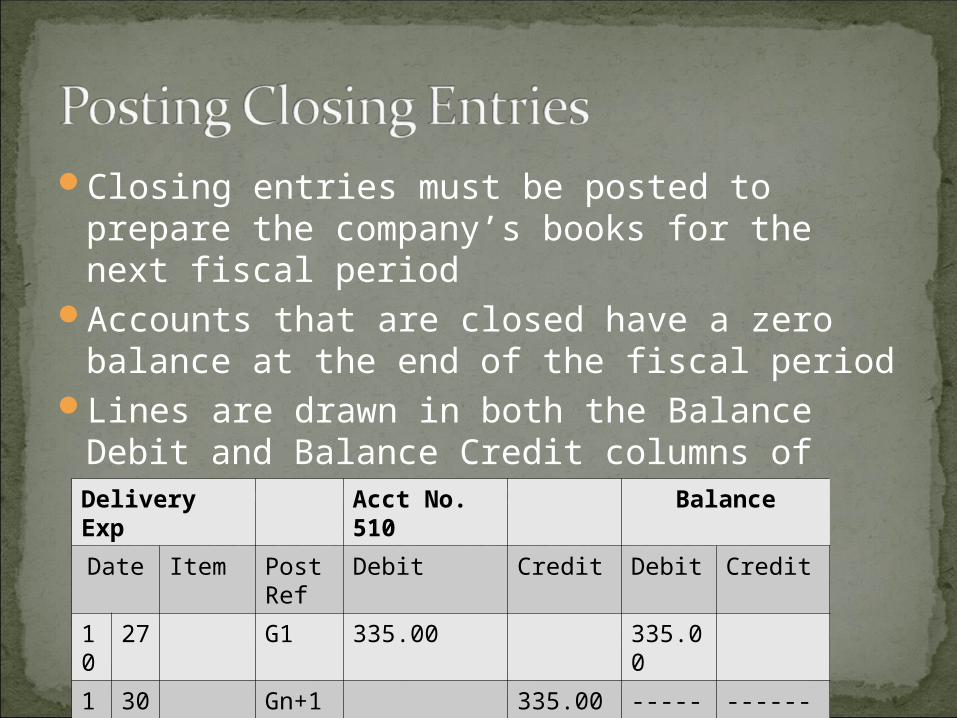

Closing entries must be posted to prepare the company’s books for the next fiscal period

Accounts that are closed have a zero balance at the end of the fiscal period

Lines are drawn in both the Balance Debit and Balance Credit columns of closed temporary accounts to verify that the account has been closedDelivery Exp

Acct No. 510

Balance

Date Item Post Ref

Debit Credit Debit Credit

10

27

G1 335.00 335.00

11

30

Gn+1

335.00 -------- ----------

A Post Closing Trial Balance is a trial balance prepared after the closing entries are postedVerifies that debits equal credits in the general

ledgerOnly general ledger accounts with balances

are included on a post-closing trial balanceOnly balance sheet items – WHY?

A Post-Closing Trial Balance is included on page 216It follows a similar format to the Trial Balance

prepared on the Work Sheet

The series of accounting activities included in recording financial information for a fiscal period

Since it is a cycle, step 1 begins again after step 8

Source documents are analyzedTransactions are recorded in the General JournalJournal Entries are posted to the General LedgerA Work Sheet is prepared from the General LedgerFinancial statements are prepared from the Work

SheetAdjusting and closing entries are journalized from

the Work SheetAdjusting an closing entries are posted to the

General LedgerA Post-Closing Trial Balance of the General Ledger

is preparedWT 81-83.xls