Embed Size (px)

Citation preview

© Pearson Education New Zealand 2007

Contents1. The Statement of Accounting Policies

2. Balance Day adjustments (review)

3. Income Statement – Service business

4. Income Statement – Trading business

5. Balance Sheet

6. Statement of Changes in Cash Position

End

© Pearson Education New Zealand 2007

1 The Statement of Accounting Policies

NOTES

QUESTIONS

Back to Contents

© Pearson Education New Zealand 2007

Statement of Accounting Policies

PurposeThe Statement of Accounting Policies shows the assumptions that have been followed in preparing all of the financial statements for a sole proprietor and how the financial elements have been measured.

© Pearson Education New Zealand 2007

Return to 1 Statement of Accounting Policies

Layout

The layout for the Statement of Accounting Policies is as follows:

(Business Name)

Statement of Accounting Policies

Name and nature

Financial statements have been prepared for – list the name of the business and the nature of the entity (e.g. a sole proprietor retail business).

Measurement basis

The measurement base adopted is Historical cost.

Property, plant and equipment

Property, plant and equipment are recorded at their original purchase price, less any accumulated depreciation.

Depreciation policy

Property, plant and equipment are depreciated over their estimated useful lives.

© Pearson Education New Zealand 2007

Question:The Statement of Accounting Policies

Complete a Statement of Accounting Policies for

Graham’s Café.

© Pearson Education New Zealand 2007

Answer

Graham’s Café

Statement of Accounting Policies for the period ended…

Name and nature

These statements have been prepared for Graham’s Café, a sole proprietor café business.

Measurement basis

The measurement base adopted is historical cost.

Property, plant and equipment

Property, Plant and Equipment are recorded at their original purchase price, less any accumulated depreciation.

Depreciation policy

Depreciation is charged on a straight line basis so as to allocate the cost (less the salvage value) of the Property, Plant and Equipment over its estimated useful life.

Return to 1 Statement of

Accounting Policies

© Pearson Education New Zealand 2007

3 Income Statement – Service business

NOTES

QUESTIONS

Back to Contents

© Pearson Education New Zealand 2007

Income Statement – Service business

PurposeThe purpose of the Income Statement is to show the net profit of the business.

A service business is one who offers services to their customers such as:plumbing, legal services, hairdressing, etc.

© Pearson Education New Zealand 2007

Return to

3 Income Statement – Service business

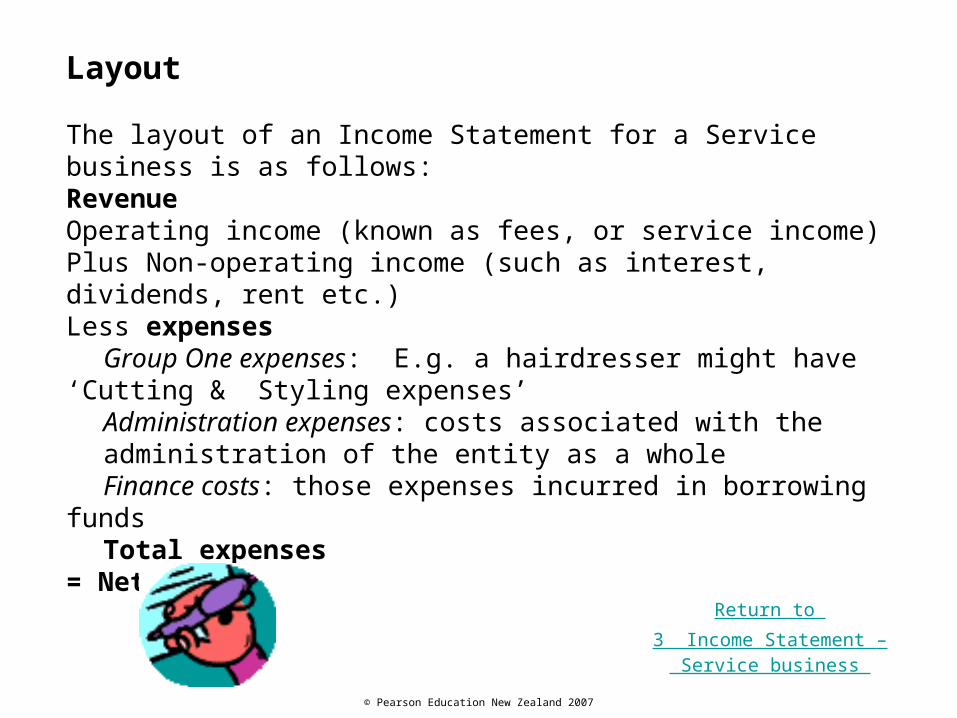

Layout

The layout of an Income Statement for a Service business is as follows:RevenueOperating income (known as fees, or service income)Plus Non-operating income (such as interest, dividends, rent etc.) Less expenses

Group One expenses: E.g. a hairdresser might have ‘Cutting & Styling expenses’Administration expenses: costs associated with the

administration of the entity as a wholeFinance costs: those expenses incurred in borrowing funds Total expenses

= Net profit

© Pearson Education New Zealand 2007

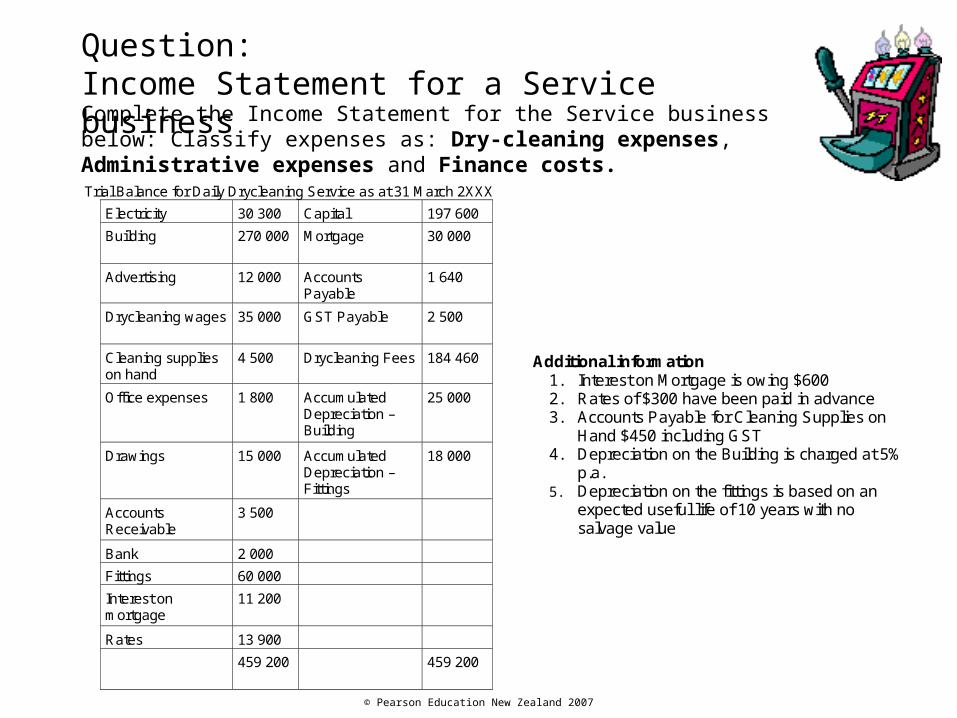

Trial Balance for Daily Drycleaning Service as at 31 March 2XXX

Electricity 30 300 Capital 197 600

Building 270 000 Mortgage 30 000

Advertising 12 000 Accounts Payable

1 640

Drycleaning wages 35 000 GST Payable 2 500

Cleaning supplies on hand

4 500 Drycleaning Fees 184 460

Office expenses 1 800 Accumulated Depreciation – Building

25 000

Drawings 15 000 Accumulated Depreciation –Fittings

18 000

Accounts Receivable

3 500

Bank 2 000

Fittings 60 000

Interest on mortgage

11 200

Rates 13 900

459 200 459 200

Additional information 1. Interest on Mortgage is owing $600 2. Rates of $300 have been paid in advance 3. Accounts Payable for Cleaning Supplies on Hand $450 including GST 4. Depreciation on the Building is charged at 5%

p.a. 5. Depreciation on the fittings is based on an

expected useful life of 10 years with no salvage value

Complete the Income Statement for the Service business below: Classify expenses as: Dry-cleaning expenses, Administrative expenses and Finance costs.

Question: Income Statement for a Service business

© Pearson Education New Zealand 2007

AnswerDaily Drycleaning Service

Income Statement for the year ended 31 March 2XXX

Revenue

Drycleaning fees 184 460

Less Expenses

Drycleaning expenses

Advertising 12 000

Drycleaning wages 35 000

Depreciation on fittings 6 000 53 000

Administrative expenses

Electricity 30 300

Office expenses 1 800

Rates 13 600

Depreciation on building 13 500 59 200

Financial costs

Interest on mortgage 11 800

Total expenses 124 000

Net Profit 60 460

Return to

3 Income Statement – Service business

© Pearson Education New Zealand 2007

4 Income Statement – Trading business

NOTES

QUESTIONS

Back to Contents

© Pearson Education New Zealand 2007

Income Statement – Trading business

PurposeThe purpose of the Income Statement is to show the net profit of the business.

A trading business buys goods from a supplier and on-sells them at a higher price to customers.

© Pearson Education New Zealand 2007

Return to 4 Income Statement – Trading business

Layout

The layout of an Income Statement for a Service business is as follows:RevenueOperating income (Sales)Less Sales ReturnsLess Cost of Goods SoldOpening inventory+ Purchases– Purchase returns+ Costs (Freight inwards, packaging, customs duty etc.)– Closing inventory= Cost of Sales= Gross ProfitPlus Non-operating income (such as interest, dividends, rent etc.) Less ExpensesDistribution expenses: (costs incurred in transferring the finished goods to the customer)Administration expenses: (costs associated with the administration of the entity as a whole)Finance costs: (those expenses incurred in borrowing funds) Total Expenses= Net Profit

© Pearson Education New Zealand 2007

Questions:Income Statement – Trading business

Trial Balance (extract) of The Curtain and Fabric Store as at 31March 2XX2

I nventory 1/ 4/ X1

17,000 Sales 180,000

Purchases 50,000 Purchase Returns

2,800

Freight I nwards

870

Advertising 4,900

I nventory on hand at 31 March 2XX2 $22,000

1) Using the trial balance extract below, complete the Trading section of the Income Statement (Sales to Gross Profit).

© Pearson Education New Zealand 2007

Answer

The Curtain and Fabric Store

I ncome Statement f or the year ended 31 March 2XX2

Revenue

Sales 180 000

Less Cost of Goods Sold

Opening I nventory 17 000

+ Purchases 50 000

- Purchase Returns 2 800 47 200

64 200

+ Freight I nwards 870

65 070

- Closing I nventory 22 000

Cost of Sales 43 070

Gross Profi t 136 930

1)

© Pearson Education New Zealand 2007

Trial Balance of The Plant Shop as at 31 March 2XX2

Delivery Van (cost)

30 000 Sales 260,000

Advertising 10 500 Loan 20,000

Freight Inwards 5 000 Capital 70000

Inventory 1/4/X1 65 000 GST Payable 1,500

Shop Equipment 60 000 Bank 2,700

Accountancy Fee

1 800 Accumulated Depreciation – Shop Equipment

5,000

Delivery Van Expenses

7 500 Accumulated Depreciation –- Delivery Van

2,950

Interest on Loan 1 750

Rent 40 000

Purchases 45 000

General Expenses

15 000

Drawings 20 000

Shop Wages 34 000

Insurance 15 000

Goodwill 8 000

Freight Outwards 3 600

362,150 362,150

Inventory on hand at 31 March 2XX2 $40,000

Additional information:

1. Invoices on hand for sales $9 000 including GST.

2. Advertising paid in advance $500.

3. Shop Wages owing $2 000.

4. Depreciation on Shop Equipment $4 000 p.a.

5. Depreciation on Delivery Van 20% per annum on cost.

2) Complete the Income Statement for the Trading Business below. Classify expenses as: Distribution expenses, Administrative expenses and Finance costs.

© Pearson Education New Zealand 2007

AnswerThe Plant Shop

Income Statement for the year ended 31 March 2XX2

Revenue

Sales 268 000

Less Cost of Goods Sold

Opening Inventory 65 000

+ Purchases 45 000

110 000

+ Freight Inwards 5 000

115 000

– Closing Inventory 40 000

Cost of Sales 75 000

Gross Profit 193 000

Less Expenses

Distribution Expenses

Advertising 10 000

Delivery Van Expense 7 500

Shop Wages 36 000

Freight Outwards 3 600

Depreciation on Shop Equipment 4 000

Depreciation on Delivery Van 6 000 67 100

Administration Expenses

Accountancy Fee 1 800

Rent 40 000

General Expenses 15 000

Insurance 15 000 71 800

Finance Costs

Interest on Loan 1 750

Total Expenses 140 650

Net Profit 52 350

Return to 4 Income Statement

– Trading business

2)

© Pearson Education New Zealand 2007

5 Balance Sheet

NOTES

QUESTIONS

Back to Contents

© Pearson Education New Zealand 2007

Balance Sheet

PurposeThis statement reports the value of the business’s assets, liabilities and equity at a particular point in time.

This statement is made up of two parts:

1. Assets minus liabilities

2. Equity – this shows the value of the owner’s share in the

business.

© Pearson Education New Zealand 2007

Layout

The layout of a Balance Sheet is as follows:Current Assets+ Non Current AssetsInvestment AssetsProperty, Plant and EquipmentIntangible AssetsTotal AssetsLess LiabilitiesCurrent AssetsNon Current LiabilitiesTotal Liabilities= Net Assets * Note: Net Assets Equity and Closing Capital Opening Capital totals must equal. + Net Profit– Drawings= Closing Capital *

© Pearson Education New Zealand 2007

Return to 5 Balance Sheet

Property, Plant and Equipment Note:

The layout is as follows:

Property, Plant and Equipment

Historical Cost of Asset less Accumulated depreciation

= Carrying amount of asset

The total carrying amount of the assets is transferredto the Balance Sheet.

© Pearson Education New Zealand 2007

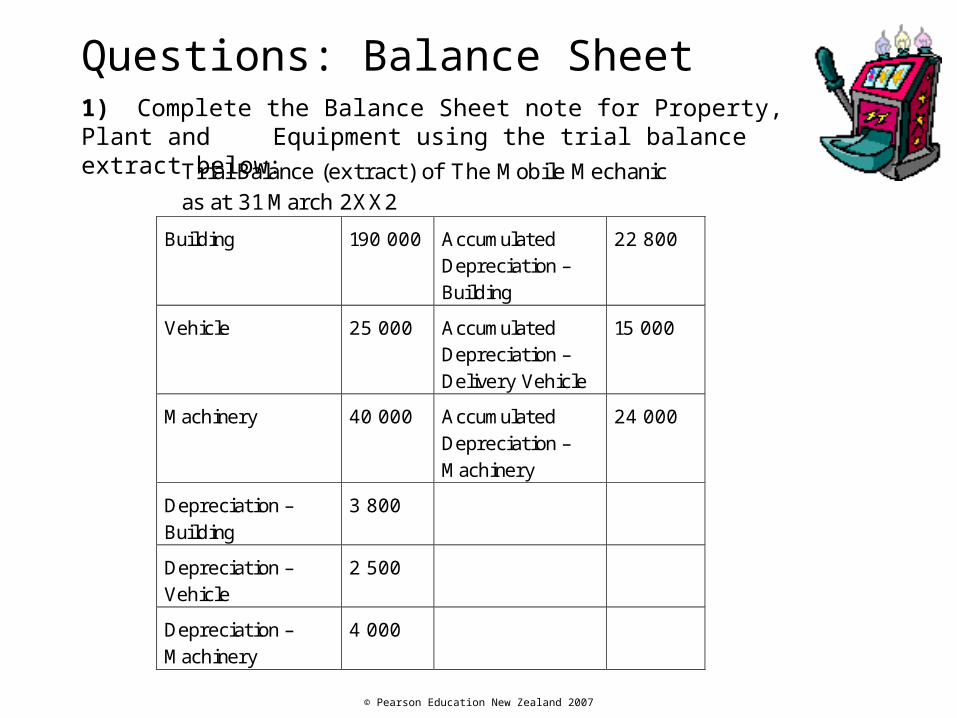

Questions: Balance Sheet

Trial Balance (extract) of The Mobile Mechanic as at 31 March 2XX2

Building 190 000 Accumulated Depreciation – Building

22 800

Vehicle 25 000 Accumulated Depreciation – Delivery Vehicle

15 000

Machinery 40 000 Accumulated Depreciation – Machinery

24 000

Depreciation – Building

3 800

Depreciation –Vehicle

2 500

Depreciation – Machinery

4 000

1) Complete the Balance Sheet note for Property, Plant and Equipment using the trial balance extract below:

© Pearson Education New Zealand 2007

Answers

Note to the Balance Sheet –

Property, Plant and Equipment

Building Vehicle Machinery Total $

$ $ $

Cost 190 000 25 000 40 000 255 000

Accumulated Depreciation

26 600 17 500 28 000 72 100

Carrying Amount 163 400 7 500 12 000 182 900

1)

© Pearson Education New Zealand 2007

Trial Balance for Daily Drycleaning Service as at 31 March 2XXX

Electricity 30 300 Capital 197 600

Building 270 000 Mortgage 30 000

Advertising 12 000 Accounts Payable 2 090

Drycleaning Wages 35 000 GST Payable 2 450

Cleaning Supplies on hand

4 900 Drycleaning Fees 184 460

Offi ce expenses 1 800 Accumulated Depreciation – Building

33 500

Drawings 15 000 Accumulated Depreciation –Fittings

24 000

Accounts Receivable 3 500 Accrued Expense 600

Bank 2 000

Fittings 60 000

I nterest on mortgage 11 800

Rates 13 600

Prepayments 300

Depreciation – Building 8 500

Depreciation – Fittings 6 000

474 700 474 700

2) Complete a) the Balance Sheet and b) the Property, Plant & Equipment note using the adjusted trial balance below:

© Pearson Education New Zealand 2007

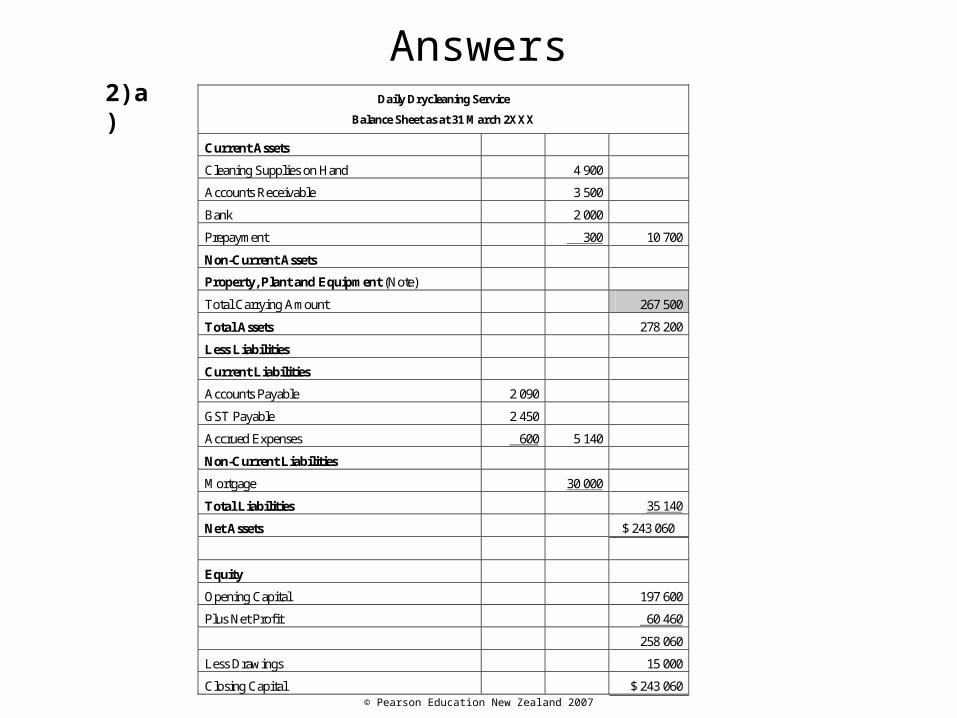

Answers

Daily Drycleaning Service

Balance Sheet as at 31 March 2XXX

Current Assets

Cleaning Supplies on Hand 4 900

Accounts Receivable 3 500

Bank 2 000

Prepayment 300 10 700

Non-Current Assets

Property, Plant and Equipment (Note)

Total Carrying Amount 267 500

Total Assets 278 200

Less Liabilities

Current Liabilities

Accounts Payable 2 090

GST Payable 2 450

Accrued Expenses 600 5 140

Non-Current Liabilities

Mortgage 30 000

Total Liabilities 35 140

Net Assets $ 243 060

Equity

Opening Capital 197 600

Plus Net Profit 60 460

258 060

Less Drawings 15 000

Closing Capital $ 243 060

2)a)

© Pearson Education New Zealand 2007

Note to the Balance Sheet –

Property, Plant and Equipment

Building Fittings Total $

$ $

Cost 270 000 60 000 330 000

Accumulated Depreciation

38 500 24 000 57 500

Carrying Amount 231 500 36 000 267 500

b)

© Pearson Education New Zealand 2007

Trial Balance of The Plant Shop as at 31 March 2XX2

Delivery Van (cost) 30 000 Sales 268,000

Advertising 10 000 Loan 20,000

Freight I nwards 5 000 Capital 70000

I nventory 1/ 4/ X1 65 000 GST Payable 2,500

Shop Equipment 60 000 Bank 2,700

Accountancy Fee 1 800 Accumulated Depreciation – Shop Equipment

9,000

Delivery Van Expenses

7 500 Accumulated Depreciation - Delivery Van

8,950

I nterest on Loan 1 750 Accrued Expenses 2 000

Rent 40 000

Purchases 45 000

General Expenses 15 000

Drawings 20 000

Shop Wages 36 000

I nsurance 15 000

Goodwill 8 000

Freight Outwards 3 600

Accounts Receivable 9 000

Prepayments 500

Depreciation – Shop Equipment

4 000

Depreciation - Van 6 000

383,150 383,150

3) Complete a) the Balance Sheet and b) the Property, Plant & Equipment note using the adjusted trial balance below :

© Pearson Education New Zealand 2007

The Plant Shop

Balance Sheet as at 31 March 2XX2

Current Assets

Accounts Receivable 9 000

Prepayment 500

I nventory 40 000 49 500

Non- Current Assets

Property, Plant and Equipment (Note)

Total Carrying Amount 172 050

I ntangible Asset

Goodwill 8 000

Total Assets 129 550

Less Liabilities

Current Liabilities

GST Payable 2 500

Bank 2 700

Accrued Expenses 2 000 7 200

Non- Current Liabilities

Loan 20 000

Total Liabilities 27 200

Net Assets $ 102 350

Equity

Opening Capital 70 000

Plus Net Profi t 52 350

122 350

Less Drawings 20 000

Closing Capital $ 102 350

3) a)Answers

© Pearson Education New Zealand 2007

Return to

5 Balance Sheet

Note to the Balance Sheet –

Property, Plant and Equipment

Delivery Van Shop Equipment

Total $

$ $

Cost 30 000 60 000 90 000

Accumulated Depreciation

8 950 9 000 17 950

Carrying Amount 21 050 51 000

72 050

b)

© Pearson Education New Zealand 2007

2 Balance Day adjustments (Review)

Accrued income

Prepayments

Accrued expenses

Income received in advance

Depreciation

Accounts receivable

Accounts payable

Purchasing assets on creditBack to Contents

© Pearson Education New Zealand 2007

Balance Day adjustments

Accrued income

Dividends Owing $180

The effect of this Balance Day adjustment on the trial balance is to create a new current asset, Accrued Income for $180, on the debit side of the trial balance and to increase the dividends by $180 on the credit side of the trial balance.

31/3 Accrued Income 180

Dividends 180

Return to

2 Balance Day adjustments

© Pearson Education New Zealand 2007

Prepayments

Insurance paid in advance $300

The effect of this Balance Day adjustment on the trial balance is to create a new current asset, Prepayments for $300, on the debit side of the trial balance and to decrease (credit) the Insurance paid by $300.

31/3 Prepayments 300

Insurance 300

Return to

2 Balance Day adjustments

© Pearson Education New Zealand 2007

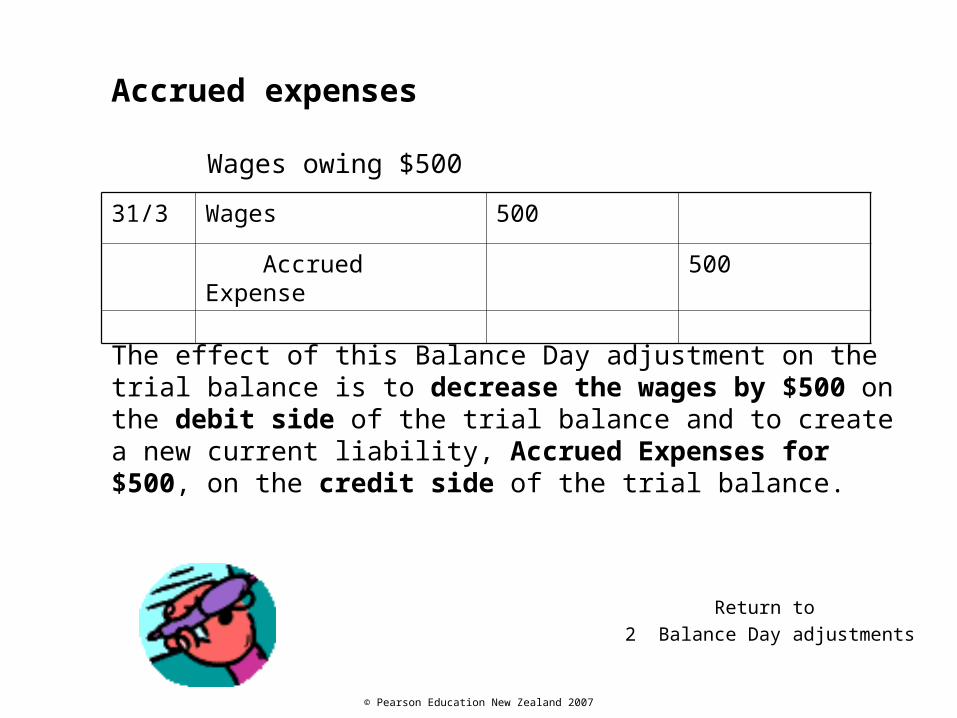

Accrued expenses

Wages owing $500

The effect of this Balance Day adjustment on the trial balance is to decrease the wages by $500 on the debit side of the trial balance and to create a new current liability, Accrued Expenses for $500, on the credit side of the trial balance.

31/3 Wages 500

Accrued Expense 500

Return to

2 Balance Day adjustments

© Pearson Education New Zealand 2007

Income received in advance

Fees received in advance $400

The effect of this Balance Day adjustment on the trial balance is to create a new current liability, Income received in advance for $400, on the credit side of the trial balance and to decrease (debit) the Fees by $400.

31/3 Fees 400

Income received in advance

400

Return to

2 Balance Day adjustments

© Pearson Education New Zealand 2007

Return to

2 Balance Day adjustments

31/3 Depreciation - Vehicle 4 500

Accumulated Depreciation -

Vehicle

4 500

The effect of this Balance Day adjustment on the trial balance is to create a new expense, Depreciation - Vehicle for $4 500, on the debit side of the trial balance and to increase (credit) the Accumulated Depreciation - Vehicle by $4 500.

Depreciation example

© Pearson Education New Zealand 2007

Accounts receivable

Credit sales of $540 were made

The effect of this Balance Day adjustment on the trial balance is to create a new / increase the existing current asset, Accounts Receivable for / by $540 on the debit side of the trial balance and to increase the Sales on the credit side by $480 and increase (credit) the GST by $60.

31/3 Accounts Receivable 540

Sales 480

GST 60

Return to

2 Balance Day adjustments

© Pearson Education New Zealand 2007

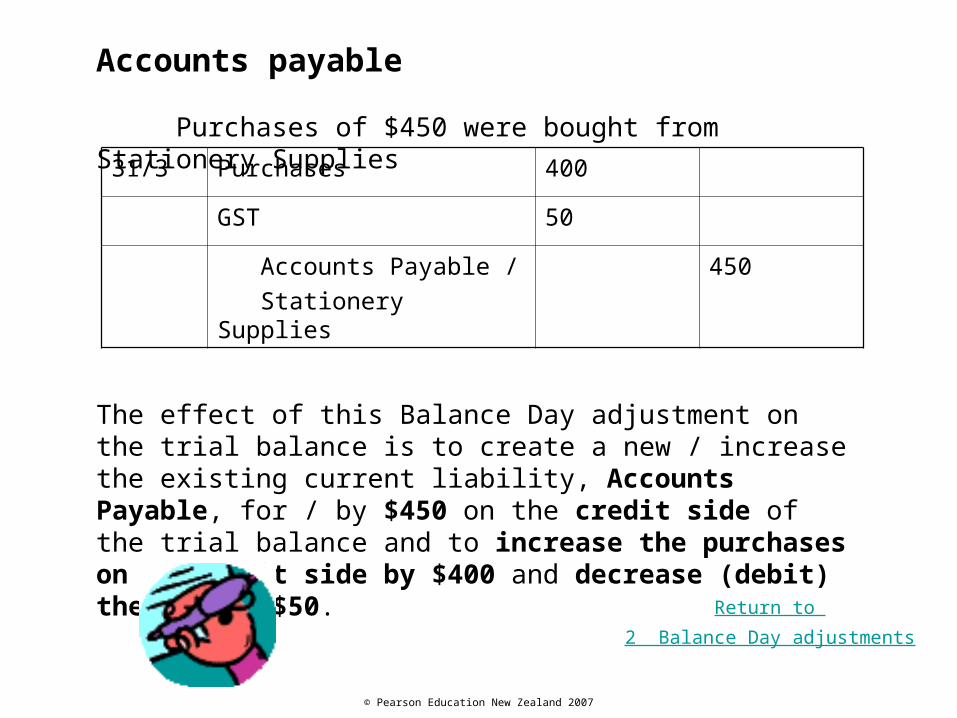

Accounts payable

Purchases of $450 were bought from Stationery Supplies

The effect of this Balance Day adjustment on the trial balance is to create a new / increase the existing current liability, Accounts Payable, for / by $450 on the credit side of the trial balance and to increase the purchases on the debit side by $400 and decrease (debit) the GST by $50.

31/3 Purchases 400

GST 50

Accounts Payable / Stationery Supplies

450

Return to

2 Balance Day adjustments

© Pearson Education New Zealand 2007

Return to

2 Balance Day adjustments

Purchasing Property, Planning, and Equipment on credit

Purchased a new office chair $270 from Executive Furnishings

The effect of this Balance Day adjustment on the trial balance is to create a new / increase the existing current liability, Accounts Payable, for / by $270 on the credit side of the trial balance and to increase the office equipment on the debit side by $240 and decrease (debit) the GST by $30.

31/3 Office chair 240

GST 30

Accounts Payable / Executive Furnishings

270

© Pearson Education New Zealand 2007

6 Statement of Changes in Cash Position

NOTES

QUESTIONS

Back to Contents

© Pearson Education New Zealand 2007

Statement of Changes in Cash Position

PurposeThe Statement of Changes in Cash Position (aka Cash Flow Statement) records the sources and uses of cash during the financial period.

A cash flow statement only records cash transactions. Therefore, we need to be able to classify transaction as being cash or credit items.

© Pearson Education New Zealand 2007

Return to 6 Statement of Changes in Cash Position

Layout

The layout of this statement is as follows:

Cash was received from:Total cash received

Cash was applied to:Total cash paid

Net increase / decrease in cash held+ Opening bank balance= Closing Bank balance

© Pearson Education New Zealand 2007

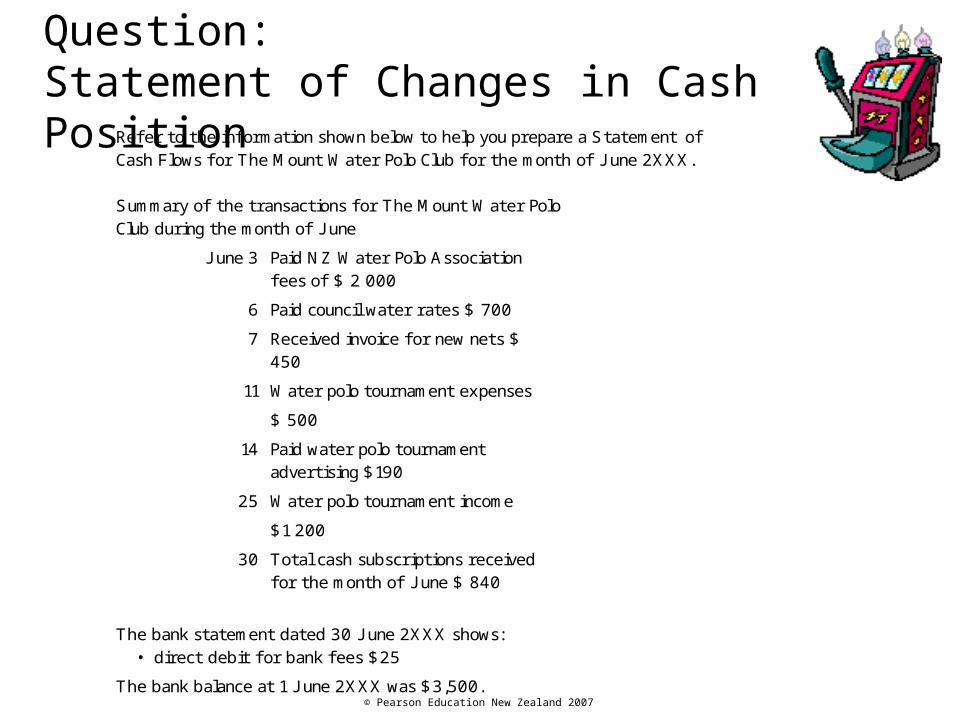

Question:Statement of Changes in Cash Position

Ref er to the information shown below to help you prepare a Statement of Cash Flows f or The Mount Water Polo Club f or the month of J une 2XXX. Summary of the transactions f or The Mount Water Polo Club during the month of J une

J une 3 Paid NZ Water Polo Association f ees of $ 2 000

6 Paid council water rates $ 700

7 Received invoice f or new nets $ 450

11 Water polo tournament expenses

$ 500

14 Paid water polo tournament advertising $190

25 Water polo tournament income

$1 200

30 Total cash subscriptions received f or the month of J une $ 840

The bank statement dated 30 J une 2XXX shows:

• direct debit f or bank f ees $25

The bank balance at 1 J une 2XXX was $3,500.

© Pearson Education New Zealand 2007

Answer

Return to 6

Statement of Changes

in Cash Position

The Mount Water Polo Club

Statement of Changes in Cash Position for the month ended

30 J une 2XXX

Cash was received f rom:

Water Polo Tournament I ncome 1 200

J une Subscriptions 840

Total cash received 2 040

Cash was applied to:

Water Polo Fees 2 000

Council Water Rates 700

Water Polo Tournament Advertising 190

Bank Fees 25

Total cash paid 2 915

Net decrease in cash held 875

Add: Cash at 1 J une 2XXX 3 500

Balance at 30 J une 2XXX $2 625