Embed Size (px)

Citation preview

Accountingas a profession and Accounting

Information System

Pr. SAMLAL Zoubida , MBA, CFA & PHDcandidate for HBS program

ACCOUNTING INFORMATIONACCOUNTING INFORMATION

CHARACTERISTICS OF ACCOUNTINGINFORMATION

• Accounting information is composed principally of financialdata about business transactions, expressed in terms of money.

• The recorded data must be sorted and summarized beforesignificant reports and analyses can be prepared.

• The “basic raw materials” of accounting are composed ofbusiness transaction data.

• Its “primary end products” are composed of varioussummaries, analyses, and reports.

• Accounting information is composed principally of financialdata about business transactions, expressed in terms of money.

• The recorded data must be sorted and summarized beforesignificant reports and analyses can be prepared.

• The “basic raw materials” of accounting are composed ofbusiness transaction data.

• Its “primary end products” are composed of varioussummaries, analyses, and reports.

USERS OF ACCOUNTING INFORMATION

• Accounting provides the techniques for accumulating and thelanguage for communicating economic data to various categoriesof individuals and institutions:

• Investors in a business enterprise need information about itsfinancial status and its future prospects.

• The government agencies are concerned with the financialactivities of business organizations for purposes of taxation andregulation.

• The individuals most dependent upon and most involved with theend products of accounting are those charged with the responsibilityfor directing the operations of enterprises.

• Accounting provides the techniques for accumulating and thelanguage for communicating economic data to various categoriesof individuals and institutions:

• Investors in a business enterprise need information about itsfinancial status and its future prospects.

• The government agencies are concerned with the financialactivities of business organizations for purposes of taxation andregulation.

• The individuals most dependent upon and most involved with theend products of accounting are those charged with the responsibilityfor directing the operations of enterprises.

USERS OF ACCOUNTING INFORMATION

• For example, in the conduct of day-to-day operations,management relies upon accounting to provide the amountowed to each creditor and by each customer and the date eachpayment is due.

• The relevant information for one category of users may differmarkedly from that needed by other users.

• Once the user groups are identified, however, and the nature ofthe relevant data determined, the accountant is able toestablish an information network to assist each group informing judgments and making decisions regarding futureactions.

• For example, in the conduct of day-to-day operations,management relies upon accounting to provide the amountowed to each creditor and by each customer and the date eachpayment is due.

• The relevant information for one category of users may differmarkedly from that needed by other users.

• Once the user groups are identified, however, and the nature ofthe relevant data determined, the accountant is able toestablish an information network to assist each group informing judgments and making decisions regarding futureactions.

ACCOUNTING AS A PROFESSIONACCOUNTING AS A PROFESSION

RELATIONSHIP OF ACCOUNTING TOOTHER FIELDS

• Everyone engaged in business activities, from the youngestemployee to the manager and owner, comes into contact withaccounting.

• The higher the level of authority and responsibility, the greater isthe need for an understanding of accounting concepts andterminology.

• The importance of understanding accounting is not limited to thebusiness world.

• Many employees with specialized training in non-business areasalso make use of accounting data and should understand accountingprinciples and terminology.

• Everyone engaged in business activities, from the youngestemployee to the manager and owner, comes into contact withaccounting.

• The higher the level of authority and responsibility, the greater isthe need for an understanding of accounting concepts andterminology.

• The importance of understanding accounting is not limited to thebusiness world.

• Many employees with specialized training in non-business areasalso make use of accounting data and should understand accountingprinciples and terminology.

PROFESSION OF ACCOUNTANCY

• Accountancy is a profession with stature comparable to that ofengineering or law. The rapid development of accounting theory andtechnique during the current century has been accompanied by anexpansion of the career opportunities in accounting and anincreasing number of professionally trained accountants.

• Accountants who render accounting services on a fee basis, and staffaccountants employed by them, are said to be engaged in publicaccounting.

• Accountants employed by a particular business enterprise or not-for-profit organization, as chief accountant, controller, or financial vice-president, are said to be engaged in private accounting.

• Accountancy is a profession with stature comparable to that ofengineering or law. The rapid development of accounting theory andtechnique during the current century has been accompanied by anexpansion of the career opportunities in accounting and anincreasing number of professionally trained accountants.

• Accountants who render accounting services on a fee basis, and staffaccountants employed by them, are said to be engaged in publicaccounting.

• Accountants employed by a particular business enterprise or not-for-profit organization, as chief accountant, controller, or financial vice-president, are said to be engaged in private accounting.

PUBLIC ACCOUNTING

• The practice of public accounting is generally restricted tolicensed CPA’s.

• This act created the Board of Accountancy which was giventhe power among other, to issue the certificate of CertifiedPublic Accountant, abbreviated as CPA.

• The practice of public accounting is generally restricted tolicensed CPA’s.

• This act created the Board of Accountancy which was giventhe power among other, to issue the certificate of CertifiedPublic Accountant, abbreviated as CPA.

PRIVATE ACCOUNTING

• The scope of activities and duties of private accountants varies widely.Private accountants are frequently called management accountants.

• If they are employed by a manufacturing concern, they may be callindustrial or cost accountants. The chief accountant in a businessmay be call controller. Various governmental units and other not-for-profit organizations also employ accountants.

• Internal auditors are accountants who review the accounting andoperating procedures prescribed by their companies. Accountantswho specialize in internal auditing may be granted the CertifiedInternal Auditor (CIA) certificate.

• The scope of activities and duties of private accountants varies widely.Private accountants are frequently called management accountants.

• If they are employed by a manufacturing concern, they may be callindustrial or cost accountants. The chief accountant in a businessmay be call controller. Various governmental units and other not-for-profit organizations also employ accountants.

• Internal auditors are accountants who review the accounting andoperating procedures prescribed by their companies. Accountantswho specialize in internal auditing may be granted the CertifiedInternal Auditor (CIA) certificate.

RELATIONSHIP OF ACCOUNTING TOOTHER FIELDS

• For example, an engineer responsible for selecting the mostdesirable solution to a technical manufacturing problem mayconsider cost accounting data to be the decisive factor.

• Lawyers use accounting data in tax cases and in lawsuitsinvolving property ownership and damages from breach of contract.

• Governmental agencies rely on accounting data in evaluatingthe efficiency of government operations and for appraising thefeasibility of proposed taxation and spending programs.

• Accounting plays an important role in modern society and, broadlyspeaking, all citizens are affected by accounting in some way.

• For example, an engineer responsible for selecting the mostdesirable solution to a technical manufacturing problem mayconsider cost accounting data to be the decisive factor.

• Lawyers use accounting data in tax cases and in lawsuitsinvolving property ownership and damages from breach of contract.

• Governmental agencies rely on accounting data in evaluatingthe efficiency of government operations and for appraising thefeasibility of proposed taxation and spending programs.

• Accounting plays an important role in modern society and, broadlyspeaking, all citizens are affected by accounting in some way.

FIELDS OF ACCOUNTINGFIELDS OF ACCOUNTING

SPECIALIZED ACCOUNTING FIELDS

FINANCIAL ACCOUNTINGIt is concerned with the recording of transactions for a businessenterprise or other economic unit and the periodic preparation ofvarious reports from such records.

Corporate enterprise must employ such principles in preparing theirannual reports on profitability and financial status for theirstockholders and the investing public.

FINANCIAL ACCOUNTINGIt is concerned with the recording of transactions for a businessenterprise or other economic unit and the periodic preparation ofvarious reports from such records.

Corporate enterprise must employ such principles in preparing theirannual reports on profitability and financial status for theirstockholders and the investing public.

SPECIALIZED ACCOUNTING FIELDS

AUDITINGIt is a field of activity involving an independent review of the accountingrecords. In conducting an audit, public accountants examine the recordssupporting financial reports of an enterprise and express an opinionregarding their fairness and reliability.

COST ACCOUNTINGIt emphasizes the determination and control of costs. It is concernedprimarily with the costs of manufacturing processes and ofmanufactured products, but increasing attention is being given todistribution costs. In addition, one of the principal functions of costaccountants is to assemble and interpret cost data, both actual andprospective for the use of management in controlling current operations andin planning for the future.

AUDITINGIt is a field of activity involving an independent review of the accountingrecords. In conducting an audit, public accountants examine the recordssupporting financial reports of an enterprise and express an opinionregarding their fairness and reliability.

COST ACCOUNTINGIt emphasizes the determination and control of costs. It is concernedprimarily with the costs of manufacturing processes and ofmanufactured products, but increasing attention is being given todistribution costs. In addition, one of the principal functions of costaccountants is to assemble and interpret cost data, both actual andprospective for the use of management in controlling current operations andin planning for the future.

SPECIALIZED ACCOUNTING FIELD

MANAGEMENT ACCOUNTINGIt employs both historical and estimated data in assistingmanagement in daily operations and in planning futureoperations. It deals with the specific problems that confrontenterprise managers at various organizational levels. The managementaccountant is frequently concerned with identifying alternativecourses of action and in helping to select the best one.

TAX ACCOUNTINGIt encompasses the preparation of tax returns and the considerationof the tax consequences of proposed business transactions oradministrative courses of action. Accountants specializing in this field,particularly in the area of tax planning, must be familiar with taxstatutes affecting their employer or clients and also must keep up todate on administrative regulations and court decisions on tax cases.

MANAGEMENT ACCOUNTINGIt employs both historical and estimated data in assistingmanagement in daily operations and in planning futureoperations. It deals with the specific problems that confrontenterprise managers at various organizational levels. The managementaccountant is frequently concerned with identifying alternativecourses of action and in helping to select the best one.

TAX ACCOUNTINGIt encompasses the preparation of tax returns and the considerationof the tax consequences of proposed business transactions oradministrative courses of action. Accountants specializing in this field,particularly in the area of tax planning, must be familiar with taxstatutes affecting their employer or clients and also must keep up todate on administrative regulations and court decisions on tax cases.

SPECIALIZED ACCOUNTING FIELDS

ACCOUNTING SYSTEMIt is the special field concerned with the design and implementationof procedures for the accumulation and reporting of financial data.

The systems accountant must devise appropriate “checks andbalances” to safeguard business assets and provide for informationflow that will be efficient and helpful to management.

BUDGETARY ACCOUNTINGIt presents the plan of financial operations for a period and, throughrecords and summaries provides comparisons of actual operationswith the predetermined plans.

A combination of planning and controlling future operations, it issometimes concerned to be a part of management accounting.

ACCOUNTING SYSTEMIt is the special field concerned with the design and implementationof procedures for the accumulation and reporting of financial data.

The systems accountant must devise appropriate “checks andbalances” to safeguard business assets and provide for informationflow that will be efficient and helpful to management.

BUDGETARY ACCOUNTINGIt presents the plan of financial operations for a period and, throughrecords and summaries provides comparisons of actual operationswith the predetermined plans.

A combination of planning and controlling future operations, it issometimes concerned to be a part of management accounting.

SPECIALIZED ACCOUNTING FIELDS

INTERNATIONAL ACCOUNTINGIt is concerned with the special problems associated with the internationaltrade of multinational business organizations.

Accountants specialized in this area must be familiar with the influences ofcustoms law, and taxation of various countries bear on international operationsand accounting principles.

NOT-FOR-PROFIT ACCOUNTINGIt specializes in recording and reporting the transactions of variousgovernmental units and other not-for-profit organizations such as church,charities, and educational institutions.

An essential element in an accounting system that will insure strict adherenceon the part of management to restrictions and other requirements imposed bylaw, by other institutions, or by individual donors.

INTERNATIONAL ACCOUNTINGIt is concerned with the special problems associated with the internationaltrade of multinational business organizations.

Accountants specialized in this area must be familiar with the influences ofcustoms law, and taxation of various countries bear on international operationsand accounting principles.

NOT-FOR-PROFIT ACCOUNTINGIt specializes in recording and reporting the transactions of variousgovernmental units and other not-for-profit organizations such as church,charities, and educational institutions.

An essential element in an accounting system that will insure strict adherenceon the part of management to restrictions and other requirements imposed bylaw, by other institutions, or by individual donors.

SPECIALIZED ACCOUNTING FIELDS

SOCIAL ACCOUNTING

It is the newest field of accounting and is the most difficult to describeconcisely.

One of the engagement in this field involved measurement of trafficpatterns in a densely populated section of the nation as part of agovernment study to determine the most efficient use of transportationfunds, not only in terms of facilitating trade but also of assuring agood environment for the area’s residents.

SOCIAL ACCOUNTING

It is the newest field of accounting and is the most difficult to describeconcisely.

One of the engagement in this field involved measurement of trafficpatterns in a densely populated section of the nation as part of agovernment study to determine the most efficient use of transportationfunds, not only in terms of facilitating trade but also of assuring agood environment for the area’s residents.

BOOKKEEPING AND ACCOUNTING

BOOKKEEPING is the recording of business data in a prescribedmanner. A bookkeeper may be responsible for keeping all therecords of a business or only a minor segment, such portion ofcustomer accounts in department store. Much of the work of thebookkeeper is critical in nature and increasingly being accomplishedthrough the use of mechanical and electronic equipment.

ACCOUNTING is primarily concerned with the design of thesystem of records, the preparation of reports based on the recordeddata, and the interpretation of the reports. Accountants often directand review the work of bookkeeper. In event, the accountant mustpossess a much higher level of knowledge, conceptualunderstanding, and analytical skill than is required of thebookkeeper.

BOOKKEEPING is the recording of business data in a prescribedmanner. A bookkeeper may be responsible for keeping all therecords of a business or only a minor segment, such portion ofcustomer accounts in department store. Much of the work of thebookkeeper is critical in nature and increasingly being accomplishedthrough the use of mechanical and electronic equipment.

ACCOUNTING is primarily concerned with the design of thesystem of records, the preparation of reports based on the recordeddata, and the interpretation of the reports. Accountants often directand review the work of bookkeeper. In event, the accountant mustpossess a much higher level of knowledge, conceptualunderstanding, and analytical skill than is required of thebookkeeper.

The Study of AccountingInformation Systems

The Study of AccountingInformation Systems

WHAT IS A SYSTEM?

• A System is an entity consisting ofinteracting parts that are coordinated toachieve one or more common objectives.Systems must possess

• A System is an entity consisting ofinteracting parts that are coordinated toachieve one or more common objectives.Systems must possess

SYSTEM

INPUT OUTPUTPROCESSINPUT OUTPUTPROCESS

FEEDBACK

INFORMATION SYSTEM

INPUT OUTPUTPROCESS

DATA INFORMATION

INPUT OUTPUTPROCESS

FEEDBACK

• Data are raw facts and figures that are processed toproduce information

• Information is data that have been processed and aremeaningful and useful to users. The terms “meaningful”and “useful” are value-laden terms and usually subsumeother qualities such as timeliness, relevance, reliability,consistency, comparability, etc.

DATA VERSUS INFORMATION

• Data are raw facts and figures that are processed toproduce information

• Information is data that have been processed and aremeaningful and useful to users. The terms “meaningful”and “useful” are value-laden terms and usually subsumeother qualities such as timeliness, relevance, reliability,consistency, comparability, etc.

FUNCTIONAL STEPS IN TRANSFORMINGDATA INTO INFORMATION

• Data collection - capturing, recording, validating andediting data for completeness and accuracy

• Data Maintenance/Processing - classifying, sorting,calculating data

• Data Management - storing, maintaining and retrievingdata

• Data Control - safeguarding and securing data andensuring the accuracy and completeness of the same

• Information Generation - interpreting, reporting, andcommunicating information

• Data collection - capturing, recording, validating andediting data for completeness and accuracy

• Data Maintenance/Processing - classifying, sorting,calculating data

• Data Management - storing, maintaining and retrievingdata

• Data Control - safeguarding and securing data andensuring the accuracy and completeness of the same

• Information Generation - interpreting, reporting, andcommunicating information

THE UNIVERSAL DATA PROCESSINGMODEL

Processing

Storage

Processing

Consumers

Exchange EventsInternal EventsEnvironmental Events

}

FUNCTIONS OF AN INFORMATIONSYSTEM

INFORMATION SYSTEMINFORMATION SYSTEM

ENVIRONMENTENVIRONMENT

Customers SuppliersCustomers Suppliers

ORGANIZATIONORGANIZATION

INPUT OUTPUTPROCESS

FEEDBACK

INFORMATION SYSTEMINFORMATION SYSTEM

RegulatoryRegulatory Stockholders CompetitorsStockholders CompetitorsAgenciesAgencies

Sales/Marketing

ProductionInfo

AIS AS AN MIS SUBSYSTEM

AIS

Personnel Finance

RELATIONSHIP OF AIS & MIS

Sales/Marketing Production AIS Personnel

MIS

Finance

Order entry/Sales

Billing/A.Rec.Cash receipts

Production

General ledgerPayroll

InventoryPurchasing/A. Pay./Cash disb.

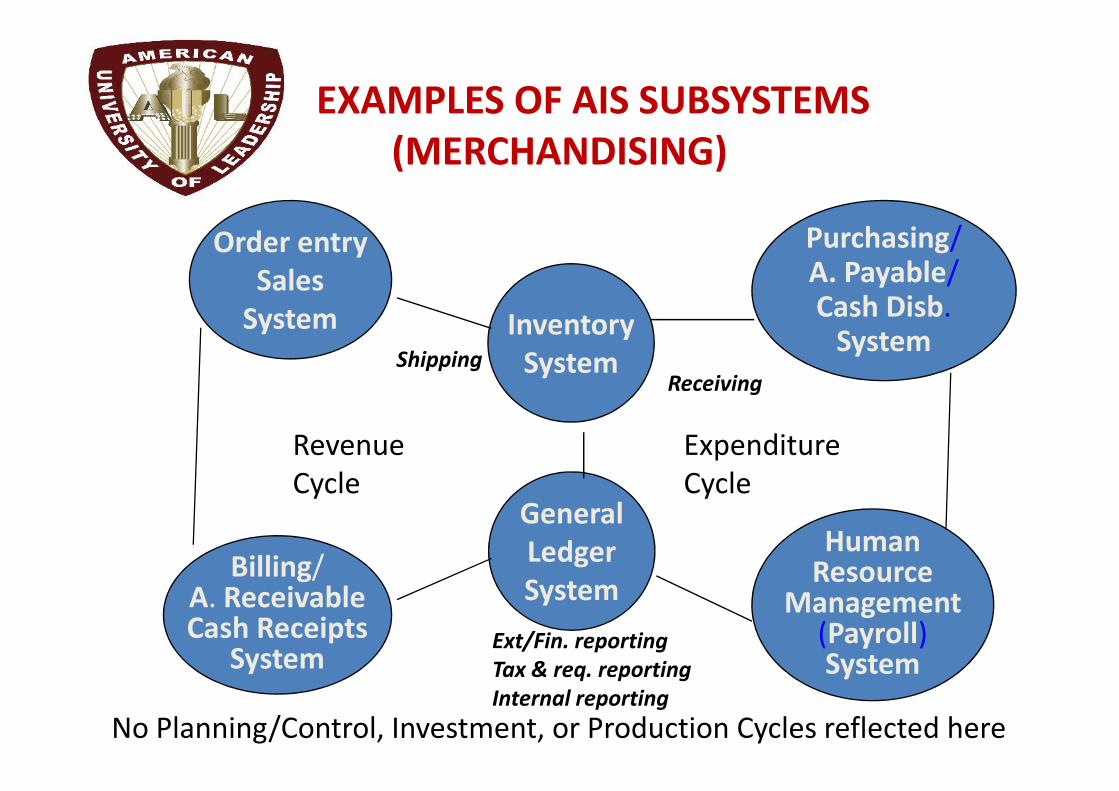

EXAMPLES OF AIS SUBSYSTEMS(MERCHANDISING)

InventorySystem

Order entrySales

System

Purchasing/A. Payable/Cash Disb.

SystemShipping

Receiving

No Planning/Control, Investment, or Production Cycles reflected here

GeneralLedgerSystem

Billing/A. ReceivableCash Receipts

System

HumanResource

Management(Payroll)System

RevenueCycle

ExpenditureCycle

Receiving

Ext/Fin. reportingTax & req. reportingInternal reporting

OBJECTIVES AND USERS OF AIS

• Support day-to-day operations– Transaction processing

• Support Internal Decision-Making– Trend Analyses

– Quantitative & Qualitative Data

– Non-transactional sources

• Help fulfill Stewardship Role

• Support day-to-day operations– Transaction processing

• Support Internal Decision-Making– Trend Analyses

– Quantitative & Qualitative Data

– Non-transactional sources

• Help fulfill Stewardship Role

RESOURCES REQUIRED FOR AN AIS

• Processor(s): Manual or Computerized

• Data Base(s): Data Repositories

• Procedures: Manual or Computerized• Input / Output Devices

• Miscellaneous Resources

• Processor(s): Manual or Computerized

• Data Base(s): Data Repositories

• Procedures: Manual or Computerized• Input / Output Devices

• Miscellaneous Resources

ROLES OF ACCOUNTANTS WITHRESPECT TO AN AIS

• Financial accountants prepare financial informationfor external decision-making in accordance with GAAP

• Managerial accountants prepare financial informationfor internal decision-making

• Financial accountants prepare financial informationfor external decision-making in accordance with GAAP

• Managerial accountants prepare financial informationfor internal decision-making

ROLES OF ACCOUNTANTS WITHRESPECT TO AN AIS

• Auditors - evaluate controls and attest to the fairness ofthe financial statements.

• Accounting managers - control all accountingactivities of a firm.

• Tax specialists - develop information that reflects taxobligations of the firm.

• Consultants - devise specifications for the AIS.

• Auditors - evaluate controls and attest to the fairness ofthe financial statements.

• Accounting managers - control all accountingactivities of a firm.

• Tax specialists - develop information that reflects taxobligations of the firm.

• Consultants - devise specifications for the AIS.

ETHICAL STANDARDS FOR CONSULTING

• Professional competence• Exercise due professional care• Plan and supervise all work• Obtain relevant data to support reasonable

recommendations• Maintain integrity and objectivity• Understand and respect the responsibilities of all

parties• Disclose any conflicts of interest

• Professional competence• Exercise due professional care• Plan and supervise all work• Obtain relevant data to support reasonable

recommendations• Maintain integrity and objectivity• Understand and respect the responsibilities of all

parties• Disclose any conflicts of interest

CASE STUDY- Price WaterhouseCoopers

CASE STUDY- Price WaterhouseCoopers