Embed Size (px)

DESCRIPTION

Coach Inc (NYSE:COH) reported a higher-than-expected quarterly profit and its shares hit a three-year high as the upscale leather goods maker had strong sales both at home and abroad and said it expects robust holiday results. Sales rose 19.7 percent to $911.7 million, boosted by an increase in business at U.S. department stores, particularly for handbags, and sales in Western Europe and China, where Coach is relatively new to the market. Even in the mature North American market, stores open at least a year rose by a better-than-expected 8.5 percent during the first quarter, as customer traffic picked up, reversing the slowdown last quarter that alarmed investors.

Citation preview

COACH INCNYSE:COH

Chutinush Taksinapinunt

About the Company

Coach was founded in 1941 as a family-run workshop. In a Manhattan loft, six artisans handcrafted a collection of leather goods using skills handed down from generation to generation. Discerning consumers soon began to seek out the quality and unique nature of Coach craftsmanship.

Now greatly expanded, Coach continues to maintain the highest standards for materials and workmanship. Coach’s exceptional work force remains committed to carefully upholding the principles of quality and integrity that define the company. We attribute the prominence of the Coach brand to the unique combination of our original American attitude and design, our heritage of fine leather goods and custom fabrics, our superior product quality and durability and our commitment to customer service.

During the last decade, Coach has emerged as America's preeminent designer, producer, and marketer of fine accessories and gifts for women and men including handbags, business cases, luggage and travel accessories, wallets, outerwear, eyewear, gloves, scarves, fragrance and fine jewelry. Continued development of new categories has further established the signature style and distinctive identity of the Coach brand. Together with our licensing partners, we also offer watches, footwear, and office furniture bearing the Coach brand name.

Coach’s distribution strategy is multi-channel. There are currently over 400 Coach stores in the United States and Canada, with more expected to open this calendar year. In addition, Coach has built a strong presence in the U.S. through Coach boutiques located within select department stores and specialty retailer locations. The catalogue is an important advertising and sales vehicle for Coach, both domestically and abroad. In 1999, Coach launched its on-line store at www.coach.com.

While Coach continues to be one of the best recognized accessories brands in the United States, its long-term strategic plan is to increase international distribution and target international consumers, with an emphasis on the Japanese consumer. Through Coach Japan, Inc., now wholly owned by Coach, the company is leveraging a significant growth opportunity in this important market. Intent on maintaining a consistent brand strategy domestically and abroad, this ownership structure provides Coach with complete control of its distribution in Japan. With a global vision in place, Coach is available at over 900

department store locations in the US, 182 international department stores, retail store and duty free shop locations in over 20 countries, 161 department store shop-in-shops and retail and factory store locations operated by Coach Japan, Inc.

Coach’s corporate headquarters remain in mid-town Manhattan on 34th Street, in the location of our former factory lofts. Coach is a publicly traded company listed on the New York Stock Exchange, traded under the symbol COH.

www.coach.com

Latest NewsCORRECTED-Luxury brands wrest back China market, eye smaller cities

(Corrects attribution for figures on China's luxury goods market in bullet and 7th paragraph to World Luxury Association, instead of Bain. Corrects market size to $9.4 billion, not $9.6 billion. Removes reference in same paragraph to 12 pct sales growth rate)

* Luxury brands taking control of China sales networks

* China seen as world's top luxury market in 5 yrs - WLA

* Brands eyeing smaller, inland cities for growth

Top global luxury brands like Burberry (BRBY) and Coach (NYSE:COH) are pouring funds into China's multi-billion dollar luxury market, wresting control of their brands from Chinese partners as they swoop back into a market set to become world No.1.

Many piled into China over the last decade, pairing with re-sellers and joint venture partners, but with so much at stake, they are severing these ties and bringing their own considerable financial and marketing muscle as well as expertise to China.

"This is definitely a trend for luxury brands to operate in China themself," said Marie Jiang, retail analyst from Pacific Epoch, a China focused advisory firm.

"Its a booming market and is in a period of high growth at least in the next 3 to 5 years," she said, adding she expects to see about 30 percent sales growth in luxury brands each year in the coming few years.

China is now the world's No.2 luxury goods market, with sales in 2009 of $9.4 billion, accounting for 27.5 percent of the global market, according to the World Luxury Association.

The figure is expected to grow further to $14.6 billion in the next five years, making it the world's top luxury market.

"Many of them gained experience after more than a decade of operation in the mainland, and are ready to roll over to the next phase of development of operating on their own, so they can reduce the distribution cost and raise the operating

margin," said William Lo, an analyst at Ample Finance.

Coach profit beats on handbags, overseas sales

Coach Inc (NYSE:COH) reported a higher-than-expected quarterly profit and its shares hit a three-year high as the upscale leather goods maker had strong sales both at home and abroad and said it expects robust holiday results.

Sales rose 19.7 percent to $911.7 million, boosted by an increase in business at U.S. department stores, particularly for handbags, and sales in Western Europe and China, where Coach is relatively new to the market.

Even in the mature North American market, stores open at least a year rose by a better-than-expected 8.5 percent during the first quarter, as customer traffic picked up, reversing the slowdown last quarter that alarmed investors.

"People were valuing Coach based a lot on their U.S. sales -- the luxury market has already turned up this year, and it just wasn't reflected in the stock price," said Morningstar analyst Paul Swinand, noting that Coach shares had been weighed down by more modest U.S. growth in earlier quarters.

Coach shares were up $5.46, or 12.2 percent, at $49.89 in afternoon trading, a level they last reached in September 2007.

Despite the surge in the stock, analysts still think there is value in Coach shares. Wall Street Strategies analyst Brian Sozzi said the stock still had at least 15 percent upside potential in the next 12 to 18 months.

Buoyed by its quarterly results, the company slightly raised its outlook for North American same-store sales for the holidays and the rest of its fiscal year and said on a call with Wall Street analysts it now expects an increase in the mid-single percentage range from low-to-mid single digits.

Coach reported net income of $188.9 million, or 63 cents per share, for the fiscal first quarter ended October 2, up 34 percent from $140.8 million, or 44 cents per share, a year earlier.

"NEW NORMAL"

Coach has positioned itself in the "affordable luxury" segment in the past two years as shoppers have cut back on discretionary spending, lowering average prices on its handbags by about 10 percent and expanding its outlet stores.

For example, many handbags in its "Poppy" collection retail for $298 and less, reflecting what Chief Executive Lew Frankfort told Reuters was the "new normal" in high end consumption. That compares with other handbags that can run to about $900 and the thousands that Louis Vuitton bags can cost.

Sales of handbags and accessories at Coach's North American stores rose 20 percent and the company is planning to introduce other moderately priced handbag lines in the coming months.

Fundamentals

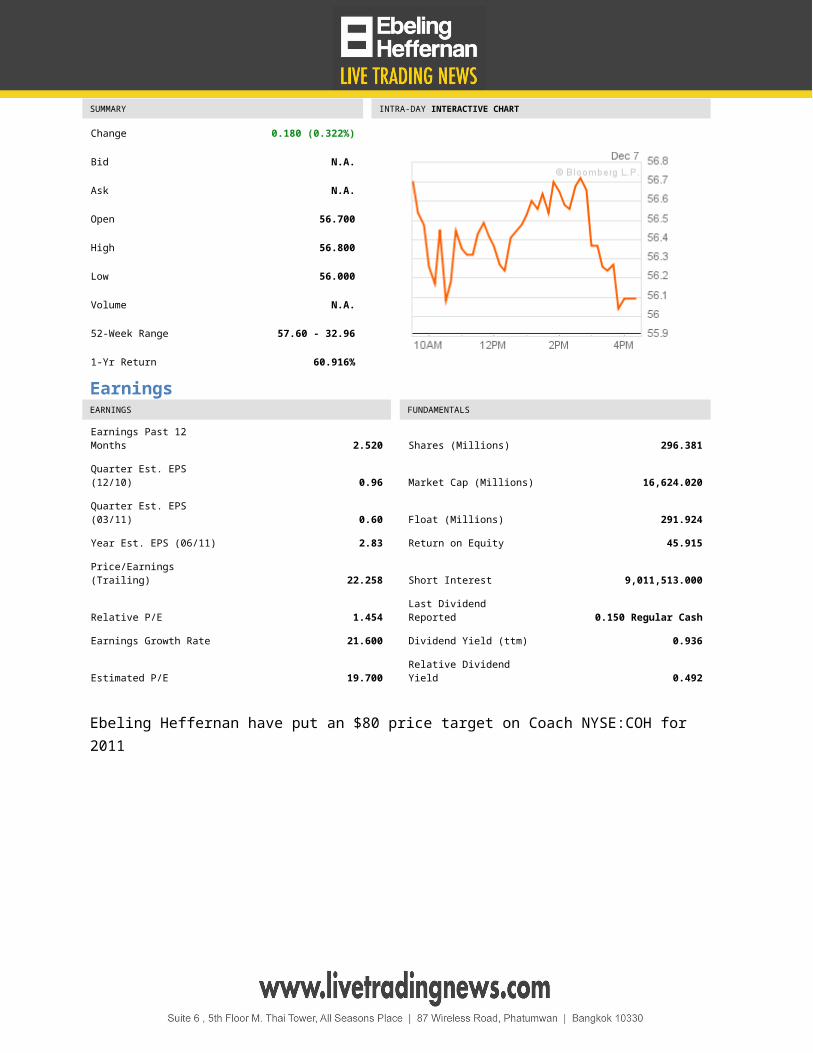

Current Price 56.09

SUMMARY INTRA-DAY INTERACTIVE CHART

Change 0.180 (0.322%)

Bid N.A.

Ask N.A.

Open 56.700

High 56.800

Low 56.000

Volume N.A.

52-Week Range 57.60 - 32.96

1-Yr Return 60.916%

EarningsEARNINGS FUNDAMENTALS

Earnings Past 12 Months 2.520 Shares (Millions) 296.381

Quarter Est. EPS (12/10) 0.96 Market Cap (Millions) 16,624.020

Quarter Est. EPS (03/11) 0.60 Float (Millions) 291.924

Year Est. EPS (06/11) 2.83 Return on Equity 45.915

Price/Earnings (Trailing) 22.258 Short Interest 9,011,513.000

Relative P/E 1.454 Last Dividend Reported 0.150 Regular Cash

Earnings Growth Rate 21.600 Dividend Yield (ttm) 0.936

Estimated P/E 19.700 Relative Dividend Yield 0.492

Ebeling Heffernan have put an $80 price target on Coach NYSE:COH for 2011

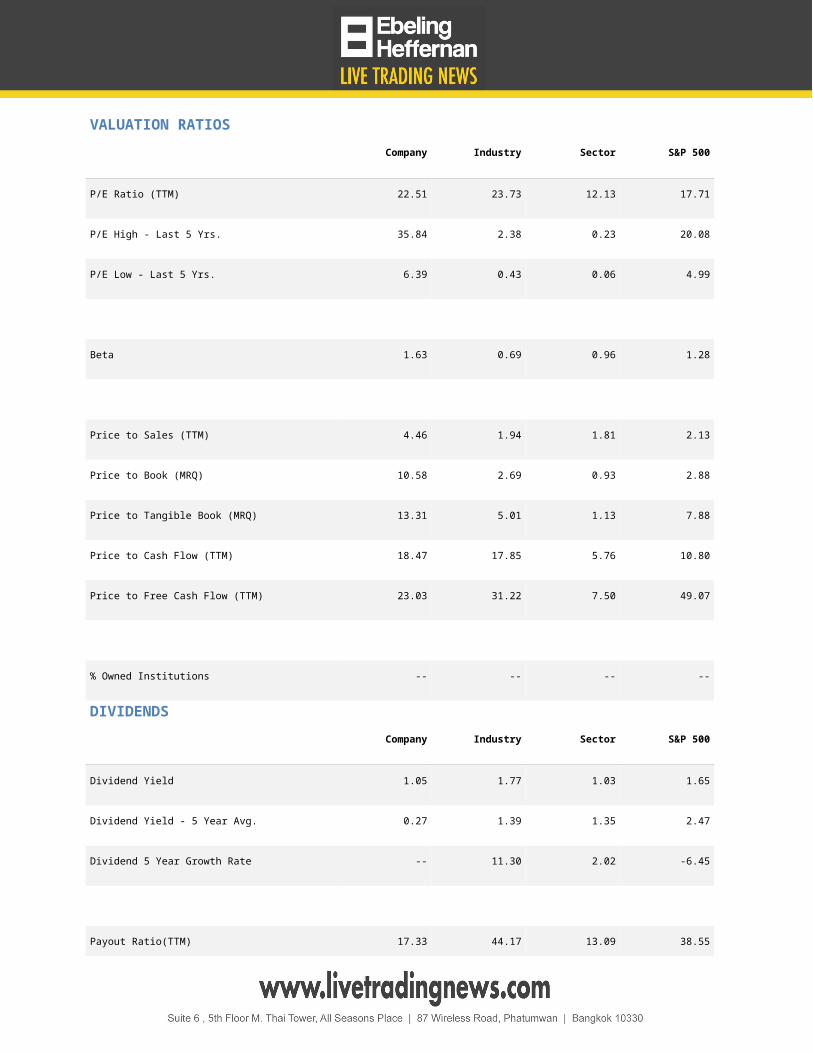

VALUATION RATIOS

Company Industry Sector S&P 500

P/E Ratio (TTM) 22.51 23.73 12.13 17.71

P/E High - Last 5 Yrs. 35.84 2.38 0.23 20.08

P/E Low - Last 5 Yrs. 6.39 0.43 0.06 4.99

Beta 1.63 0.69 0.96 1.28

Price to Sales (TTM) 4.46 1.94 1.81 2.13

Price to Book (MRQ) 10.58 2.69 0.93 2.88

Price to Tangible Book (MRQ) 13.31 5.01 1.13 7.88

Price to Cash Flow (TTM) 18.47 17.85 5.76 10.80

Price to Free Cash Flow (TTM) 23.03 31.22 7.50 49.07

% Owned Institutions -- -- -- --

DIVIDENDS

Company Industry Sector S&P 500

Dividend Yield 1.05 1.77 1.03 1.65

Dividend Yield - 5 Year Avg. 0.27 1.39 1.35 2.47

Dividend 5 Year Growth Rate -- 11.30 2.02 -6.45

Payout Ratio(TTM) 17.33 44.17 13.09 38.55

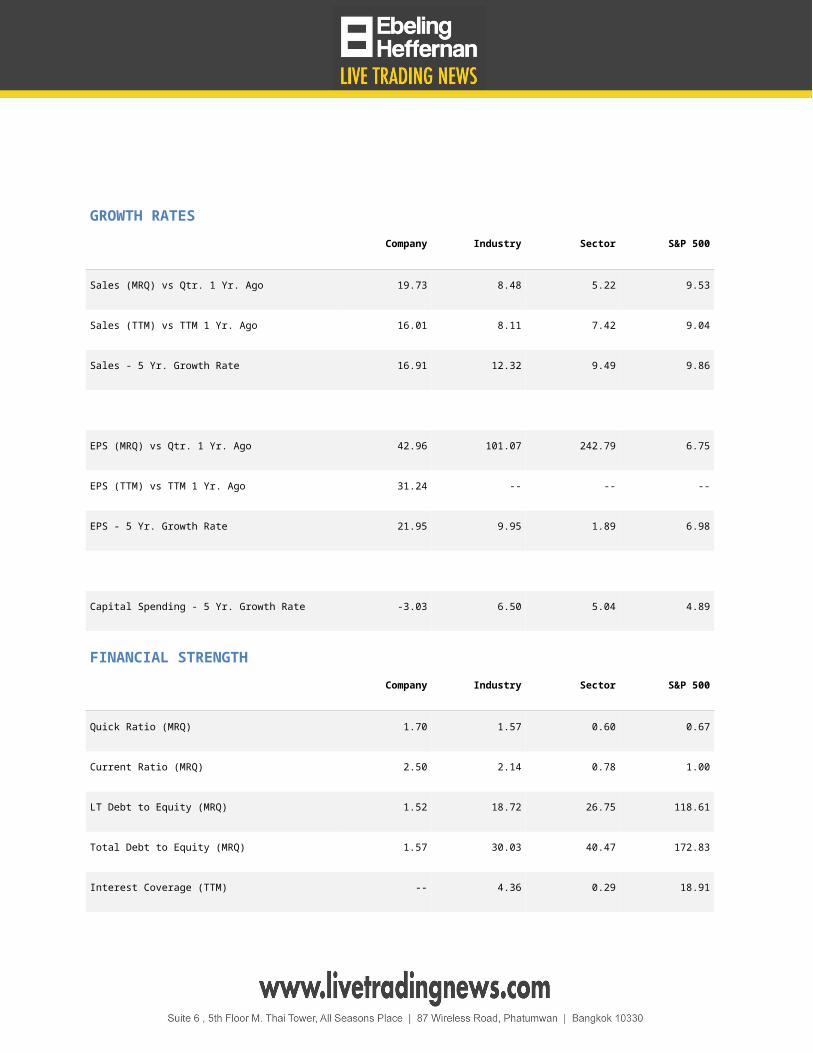

GROWTH RATES

Company Industry Sector S&P 500

Sales (MRQ) vs Qtr. 1 Yr. Ago 19.73 8.48 5.22 9.53

Sales (TTM) vs TTM 1 Yr. Ago 16.01 8.11 7.42 9.04

Sales - 5 Yr. Growth Rate 16.91 12.32 9.49 9.86

EPS (MRQ) vs Qtr. 1 Yr. Ago 42.96 101.07 242.79 6.75

EPS (TTM) vs TTM 1 Yr. Ago 31.24 -- -- --

EPS - 5 Yr. Growth Rate 21.95 9.95 1.89 6.98

Capital Spending - 5 Yr. Growth Rate -3.03 6.50 5.04 4.89

FINANCIAL STRENGTH

Company Industry Sector S&P 500

Quick Ratio (MRQ) 1.70 1.57 0.60 0.67

Current Ratio (MRQ) 2.50 2.14 0.78 1.00

LT Debt to Equity (MRQ) 1.52 18.72 26.75 118.61

Total Debt to Equity (MRQ) 1.57 30.03 40.47 172.83

Interest Coverage (TTM) -- 4.36 0.29 18.91

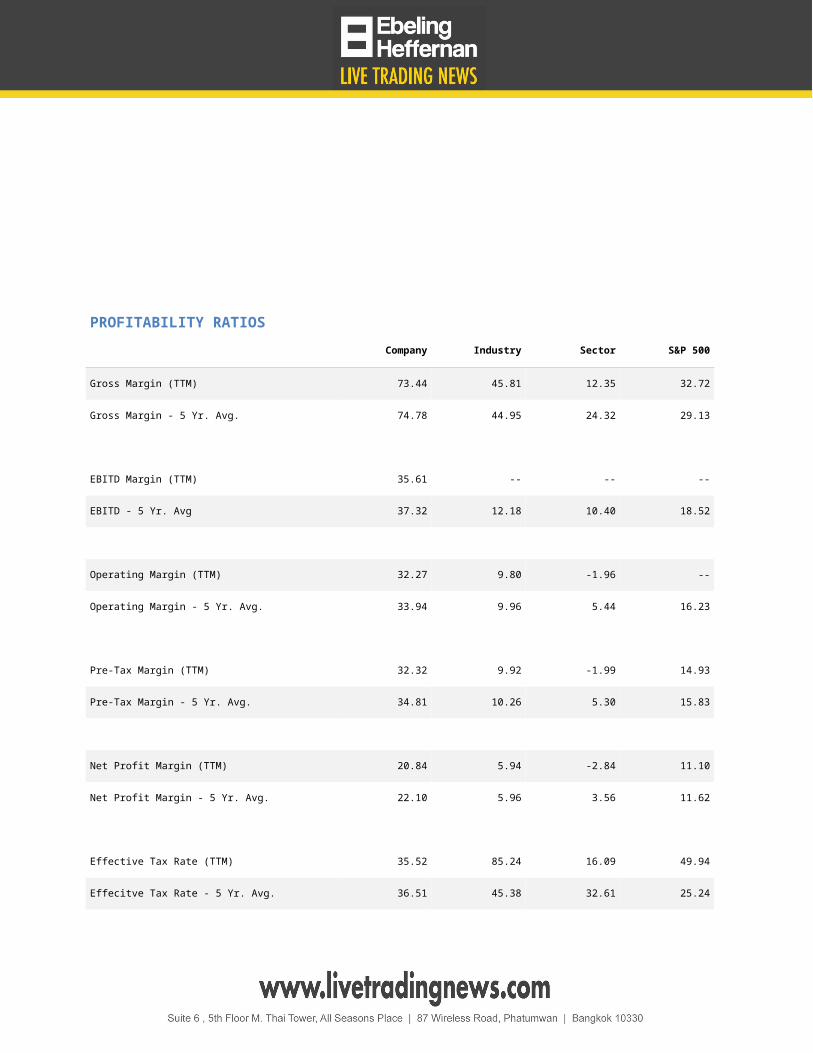

PROFITABILITY RATIOS

Company Industry Sector S&P 500

Gross Margin (TTM) 73.44 45.81 12.35 32.72

Gross Margin - 5 Yr. Avg. 74.78 44.95 24.32 29.13

EBITD Margin (TTM) 35.61 -- -- --

EBITD - 5 Yr. Avg 37.32 12.18 10.40 18.52

Operating Margin (TTM) 32.27 9.80 -1.96 --

Operating Margin - 5 Yr. Avg. 33.94 9.96 5.44 16.23

Pre-Tax Margin (TTM) 32.32 9.92 -1.99 14.93

Pre-Tax Margin - 5 Yr. Avg. 34.81 10.26 5.30 15.83

Net Profit Margin (TTM) 20.84 5.94 -2.84 11.10

Net Profit Margin - 5 Yr. Avg. 22.10 5.96 3.56 11.62

Effective Tax Rate (TTM) 35.52 85.24 16.09 49.94

Effecitve Tax Rate - 5 Yr. Avg. 36.51 45.38 32.61 25.24

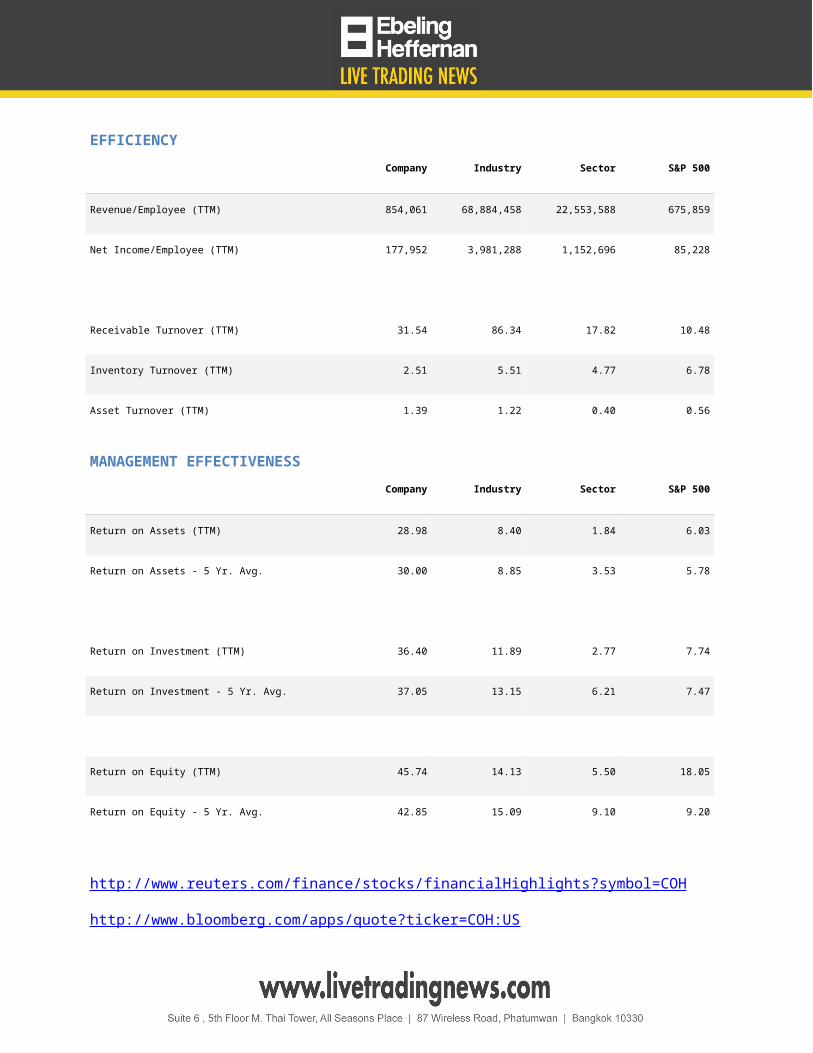

EFFICIENCY

Company Industry Sector S&P 500

Revenue/Employee (TTM) 854,061 68,884,458 22,553,588 675,859

Net Income/Employee (TTM) 177,952 3,981,288 1,152,696 85,228

Receivable Turnover (TTM) 31.54 86.34 17.82 10.48

Inventory Turnover (TTM) 2.51 5.51 4.77 6.78

Asset Turnover (TTM) 1.39 1.22 0.40 0.56

MANAGEMENT EFFECTIVENESS

Company Industry Sector S&P 500

Return on Assets (TTM) 28.98 8.40 1.84 6.03

Return on Assets - 5 Yr. Avg. 30.00 8.85 3.53 5.78

Return on Investment (TTM) 36.40 11.89 2.77 7.74

Return on Investment - 5 Yr. Avg. 37.05 13.15 6.21 7.47

Return on Equity (TTM) 45.74 14.13 5.50 18.05

Return on Equity - 5 Yr. Avg. 42.85 15.09 9.10 9.20

http://www.reuters.com/finance/stocks/financialHighlights?symbol=COH

http://www.bloomberg.com/apps/quote?ticker=COH:US

Contact Detail:

Chutinush Taksinapinunt

Corporate Account Executive

Heffernan Capital Management

Email: [email protected]

Chutinush Taksinapinunt holds a Bachelor of Business Administrators degree Majoring in Finance and Banking. Chutinush Taksinapinunt is an experienced market maker and Portfolio Manager, having worked with some of Thailand’s largest Securities Company and Financial Institutions.

Price Estimate by Shayne Heffernan PhD

Shayne Heffernan of Ebeling Heffernan holds a PhD in Economics serves as CEO of Heffernan Holdings Inc and Co Founder of Ebeling Heffernan www.ebeling-heffernan.com

BangkokSuite 53 Athenee Tower 63 Wireless Road, Lumpini, Pathumwan, Bangkok 10330 THAILANDTel: +66 2 126 8000 Fax: +66 2 126 8080New York347 5th Avenue, Suite 1402-508 Ny, NY 10016

Tel: +1 646-403-9881 Fax: +1 646-403-8014 Singapore3 Raffles Place #07-01 Bharat Building Singapore 048617 Tel: +65 6329 6408Fax: +65 6329 9699

Disclaimer

Ebeling Heffernan (EH) distributes research and other information purchased and compiled from outside sources and analysts. This report/release/advertisement is a commercial advertisement and is for general information purposes only. Do not base any investment decision on information in this report/release/advertisement. EH is not a registered Investment Advisor or a member of any association for other research providers. Under no circumstances is this report/release/advertisement to be used or considered as an offer to sell or a solicitation of any offer to buy any security or other debt instruments, or any options, futures or other derivatives related to such securities herein. All information herein is not intended to be used for investment advice. Price Targets are academic theory and should not be relied upon. The majority of these profiled companies are highly risky OTC Bulletin Board or Pink Sheet companies. All readers of this information indemnify EH from any liability for all accessed information. EH will not be responsible for updating any of its information in its report/release/advertisements. EH advises recipients of all such data to be validated from the issuing company including all statistical information derived from SEC filings, from data sources or financial information and data from the issuing company contained herein. The reader should seek professional financial advice, verify all claims and do his/her own research and due diligence before investing in any securities mentioned. EH will not be liable to any person or entity for the quality, accuracy, completeness, reliability or timeliness of information in this report/release/advertisement, or for any direct, indirect, consequential, incidental, special or punitive damages that may arise out of the use of information, products or services from any person or entity including but not limited to lost profits, loss of opportunities, trading losses, and damages that may result from any incompleteness or inaccuracy in any of EH’s profiled companies. When paid in stock, EH its affiliates, directors, officers, outside sources, investor awareness groups and employees may liquidate shares at any time or hold for investment purposes. Readers are advised to review SEC periodic reports: Forms 10-Q, 10K, Form 8-K, insider reports, Forms 3, 4, 5 Schedule 13D, www.sec.gov .nasd.com , www.pinksheets.com, www.sec.gov and www.finra.com. SPC is compliant with the Can Spam Act of 2003. Investing in micro cap and small cap securities is speculative and carries a high degree of risk. Investors can lose their entire investment. The Private Securities Litigation Reform Act of 1995 provides investors a 'safe harbor' in regard to forward-looking statements. EH cautions all investors that such forward-looking statements in this report/release/advertisement are not guarantees of future performance. Investors should understand that statements regarding future prospects may not be realized. This report/release/advertisement does not have regard to the specific investment objective, financial situation, suitability, and the particular need of any specific person who may receive this report/release/advertisement. Investors should note that income from such securities, if any, may fluctuate and that each security's price or value may rise or fall substantially. Accordingly, investors may receive back less than originally invested, or lose their entire investment. Past performance is not indicative of future performance. The Company has not paid compensation for this commercial advertisement. HCM. has written this commercial advertisement for EH.