Embed Size (px)

Citation preview

Download our reports from Bloomberg: BOCM〈enter〉

08 June 2016

Financial Highlights Y/E 30 Jun 2014 2015 2016E 2017E 2018E

Revenue (HKD m) 365.2 429.5 498.7 561.8 703.6

YoY growth (%) 9.4% 17.6% 16.1% 12.7% 25.2%

*Adjusted net profit (HKD m) 38.7 41.1 42.0 52.5 61.0

*Adjusted EPS (HKD) - - 0.12 0.15 0.17

*Adjusted EPS growth (%) - - - 25.2% 16.2%

*Adjusted P/E (x) - - 22.5 18.0 15.5

P/B (x) - - 4.1 3.5 3.0

Dividend yield (%) - - 0.9% 1.7% 1.9%

*Excluding listing expenses Source: Company, BOCOM Int’l estimates

We initiate coverage on Human Health, a leading HK private healthcare service provider, with LT BUY and TP of HKD3.16. Despite its shares having rallied 89% since IPO in March, we see room for upside, led partly by the partnership with Ping An Health and Capital Healthcare Group that has set the stage for future cooperation with China’s public hospitals. At 18.0x adjusted FY2017E P/E, the stock is trading slightly below its HK-listed peers. In light of its clinics network in HK and growth potential, our DCF-derived TP is equivalent to 21.7x of adjusted FY2017E P/E.

The largest private healthcare service provider in Hong Kong with a wide range of services: According to the Euromonitor Report, Human Health was the largest private healthcare service provider in Hong Kong as of Aug 2015, in terms of the number of medical centres. The company has been engaged in hospital management for 19 years since the establishment of its first medical centre in 1997.

Rapid growth of the private healthcare service industry in HK: Due to aging demographics,

growing consumer spending and fast-growing demand for personalized and specialized services, the healthcare service industry in Hong Kong is expected to grow significantly in the following years. We believe such demand will spill over from public healthcare providers to the private ones

given the long waiting time and shortage of qualified healthcare service professionals. We are also of the view that private specialist medical centres will become one of the fastest growing subsectors in HK.

Positioned in a more developed and better regulated healthcare system compared with China: In Hong Kong, with the regulations of medical practitioners (including the Medical Registration Ordinance, Code of Professional Conduct, and Medical Clinics Ordinance) guiding the

general healthcare market, qualified practitioners successfully registered with the Medical Council can practise freely in the market. However, in China, doctors can only practise in their associated hospitals, which, together with the Social Security Fund issue, makes China’s hospital industry

closed to the market and private capital. We have compared the PRC healthcare market and Hong Kong healthcare market and believe the latter is more suitable for private hospitals to grow, in the aspects of more independent doctor practice, a developed medical insurance system, less

government intervention, and a more advanced private healthcare market. We believe these merits will help Human Health achieve robust growth in Hong Kong in future.

Cooperation with Ping An Health and Capital Healthcare Group to bring new catalysts: In light of the rapid growth of the healthcare industry in China, Human Health formed a joint venture with Ping An Health last year. In addition, Capital Healthcare Group stands as a cornerstone Investor, now holding around 7.25% of its shares. Human Health will have the

potential to build cooperation with China’s public hospitals via the partnership with the above two well-known healthcare platforms, in our view.

Initiate coverage at “LT Buy”: Considering its clinics network in HK and rapid growth in future,

we believe its intrinsic value is approximately HKD1141.7m, corresponding to 27.2x/21.7x FY16/17E adjusted P/E (excluding listing expense). We initiate its coverage with “LT Buy” rating and TP of HKD3.16, representing 21.1% upside potential.

Last Closing: HK$2.61 Upside: +21.1% Target Price: HK$3.16 Healthcare Sector

Human Health (1419.HK)

The largest private healthcare service provider in HK; Initiate with LT Buy & TP of HKD3.16 Initiation of coverage

Human Health is the largest

private healthcare service provider in Hong Kong.

Rapid growth of the private healthcare service industry in HK.

Positioned in a more developed and better regulated healthcare system compared with China.

Initiate with “ LT BUY” rating and TP of HKD3.16

Stock data

52w High (HKD) 3.51 8.57 8.57

52w Low (HKD) 1.38 5.81 5.81

Market cap ( HKD m) 943.52 40,719.30 42,196.77

Issued shares (m) 361.50 5,909.91 5,909.91

Avg daily vol (m) 12.10 9.98 9.96

1-mth change (%) -9.69 -1.85 2.15

YTD change (%) - 0.73 4.39

50d MA ( HKD ) - 6.94 6.93

200d MA ( HKD ) - 7.07 7.07

14-day RSI 54.4 51.7 59.6

Source: Company data, Bloomberg 1 Year Performance chart

Source: Company data, Bloomberg

David Li [email protected]

Tel: (852) 2977 9203

UP MP OPUP MP OP

SELL

NeutralLT

BUY

BUY

Stock

-5%

5%

15%

25%

35%

45%

55%

65%

75%

85%

95%

105%

115%

125%

135%

3/31/16

HSI 1419 HK Equity

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

2

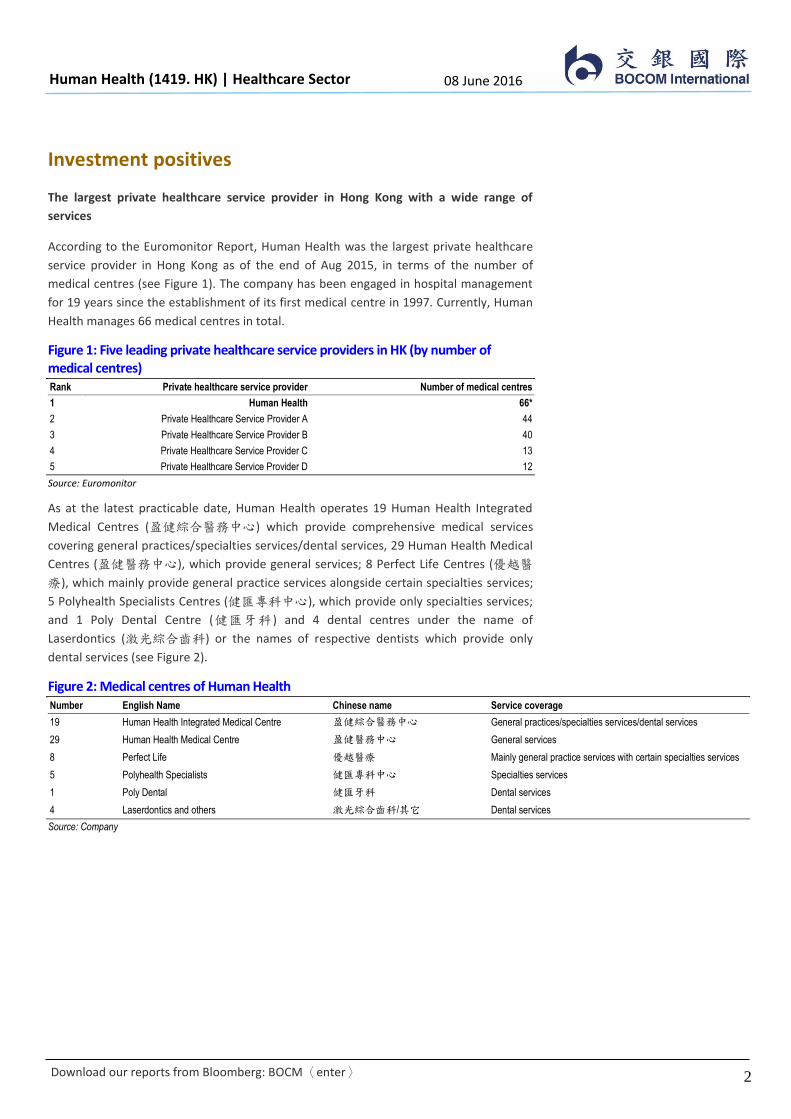

Investment positives

The largest private healthcare service provider in Hong Kong with a wide range of

services

According to the Euromonitor Report, Human Health was the largest private healthcare

service provider in Hong Kong as of the end of Aug 2015, in terms of the number of

medical centres (see Figure 1). The company has been engaged in hospital management

for 19 years since the establishment of its first medical centre in 1997. Currently, Human

Health manages 66 medical centres in total.

Figure 1: Five leading private healthcare service providers in HK (by number of medical centres) Rank Private healthcare service provider Number of medical centres

1 Human Health 66*

2 Private Healthcare Service Provider A 44

3 Private Healthcare Service Provider B 40

4 Private Healthcare Service Provider C 13

5 Private Healthcare Service Provider D 12

Source: Euromonitor

As at the latest practicable date, Human Health operates 19 Human Health Integrated

Medical Centres (盈健綜合醫務中心) which provide comprehensive medical services

covering general practices/specialties services/dental services, 29 Human Health Medical

Centres (盈健醫務中心), which provide general services; 8 Perfect Life Centres (優越醫

療), which mainly provide general practice services alongside certain specialties services;

5 Polyhealth Specialists Centres (健匯專科中心), which provide only specialties services;

and 1 Poly Dental Centre (健匯牙科 ) and 4 dental centres under the name of

Laserdontics (激光綜合齒科) or the names of respective dentists which provide only

dental services (see Figure 2).

Figure 2: Medical centres of Human Health Number English Name Chinese name Service coverage

19 Human Health Integrated Medical Centre 盈健綜合醫務中心 General practices/specialties services/dental services

29 Human Health Medical Centre 盈健醫務中心 General services

8 Perfect Life 優越醫療 Mainly general practice services with certain specialties services

5 Polyhealth Specialists 健匯專科中心 Specialties services

1 Poly Dental 健匯牙科 Dental services

4 Laserdontics and others 激光綜合齒科/其它 Dental services

Source: Company

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

3

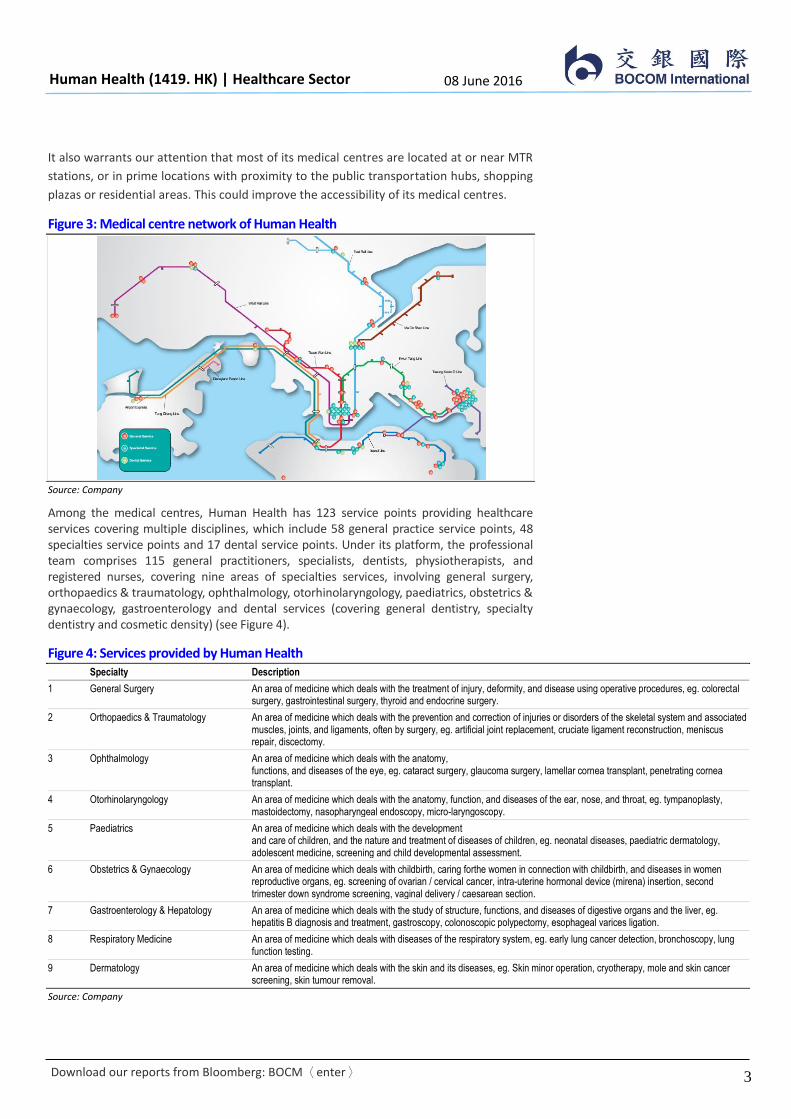

It also warrants our attention that most of its medical centres are located at or near MTR

stations, or in prime locations with proximity to the public transportation hubs, shopping

plazas or residential areas. This could improve the accessibility of its medical centres.

Figure 3: Medical centre network of Human Health

Source: Company

Among the medical centres, Human Health has 123 service points providing healthcare services covering multiple disciplines, which include 58 general practice service points, 48 specialties service points and 17 dental service points. Under its platform, the professional team comprises 115 general practitioners, specialists, dentists, physiotherapists, and registered nurses, covering nine areas of specialties services, involving general surgery, orthopaedics & traumatology, ophthalmology, otorhinolaryngology, paediatrics, obstetrics & gynaecology, gastroenterology and dental services (covering general dentistry, specialty dentistry and cosmetic density) (see Figure 4).

Figure 4: Services provided by Human Health Specialty Description

1 General Surgery An area of medicine which deals with the treatment of injury, deformity, and disease using operative procedures, eg. colorectal surgery, gastrointestinal surgery, thyroid and endocrine surgery.

2 Orthopaedics & Traumatology An area of medicine which deals with the prevention and correction of injuries or disorders of the skeletal system and associated muscles, joints, and ligaments, often by surgery, eg. artificial joint replacement, cruciate ligament reconstruction, meniscus repair, discectomy.

3 Ophthalmology An area of medicine which deals with the anatomy, functions, and diseases of the eye, eg. cataract surgery, glaucoma surgery, lamellar cornea transplant, penetrating cornea transplant.

4 Otorhinolaryngology An area of medicine which deals with the anatomy, function, and diseases of the ear, nose, and throat, eg. tympanoplasty, mastoidectomy, nasopharyngeal endoscopy, micro-laryngoscopy.

5 Paediatrics An area of medicine which deals with the development and care of children, and the nature and treatment of diseases of children, eg. neonatal diseases, paediatric dermatology, adolescent medicine, screening and child developmental assessment.

6 Obstetrics & Gynaecology An area of medicine which deals with childbirth, caring forthe women in connection with childbirth, and diseases in women reproductive organs, eg. screening of ovarian / cervical cancer, intra-uterine hormonal device (mirena) insertion, second trimester down syndrome screening, vaginal delivery / caesarean section.

7 Gastroenterology & Hepatology An area of medicine which deals with the study of structure, functions, and diseases of digestive organs and the liver, eg. hepatitis B diagnosis and treatment, gastroscopy, colonoscopic polypectomy, esophageal varices ligation.

8 Respiratory Medicine An area of medicine which deals with diseases of the respiratory system, eg. early lung cancer detection, bronchoscopy, lung function testing.

9 Dermatology An area of medicine which deals with the skin and its diseases, eg. Skin minor operation, cryotherapy, mole and skin cancer screening, skin tumour removal.

Source: Company

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

4

We believe that Human Health is able to leverage on the needs of patients to expand into

specialties services. In addition, its general practice team and specialties team can

achieve synergies. For example, its specialties team would receive patients internally

transferred from the general practice team, thus facilitating illness identification and

saving time.

Rapid growth of the private healthcare service industry in HK

Due to rapidly aging demographics, we expect the demand for healthcare services and

facilities to grow significantly in the following years. According to the Euromonitor Report,

the elderly residents require almost six times as much inpatient care as the rest of the

population; hence, the demand for healthcare services and facilities is expected to

expand at an exponential rate. We also expect such demand to spill over from public

healthcare providers to the private ones given the long waiting time and shortage of

qualified healthcare service professionals. It is estimated that private specialist medical

centres would become one of the fastest growing subsectors in HK in the following years.

Particularly, the demand for cataract surgery, cholecystectomy, percutaneous

transluminal coronary angioplasty, hip replacement, dementia, all of which are common

problems for the elderly, is expected to grow at a high speed.

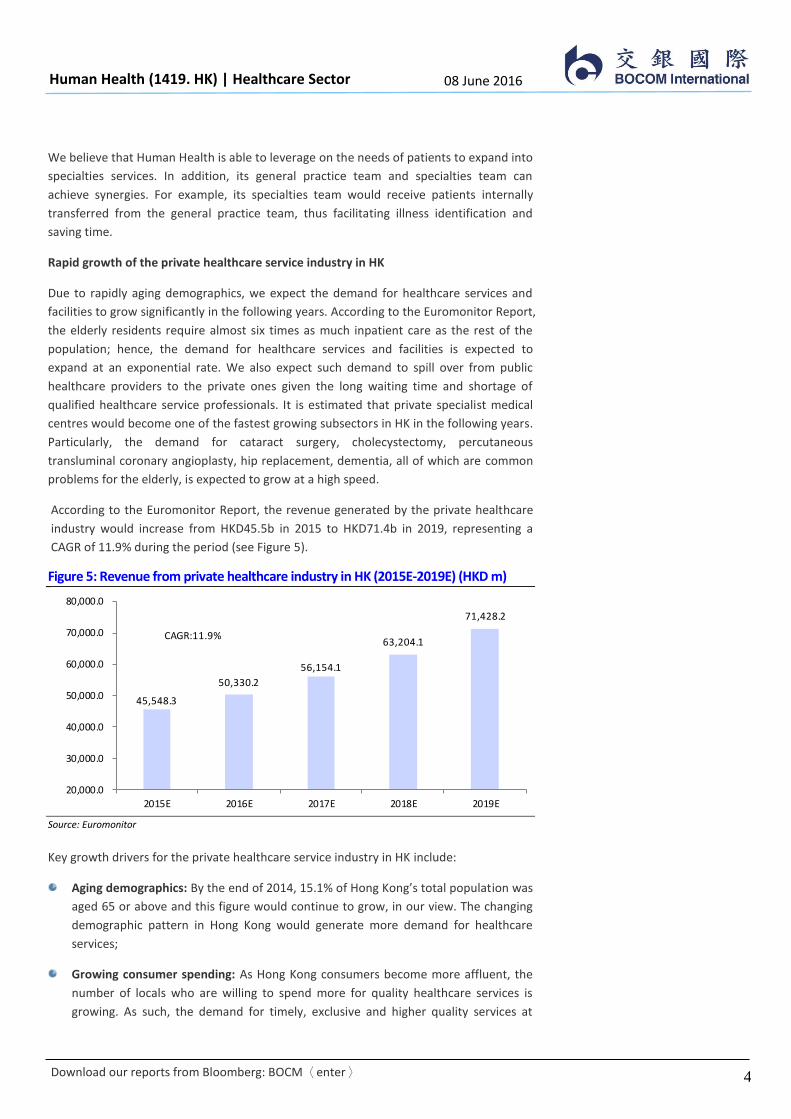

According to the Euromonitor Report, the revenue generated by the private healthcare

industry would increase from HKD45.5b in 2015 to HKD71.4b in 2019, representing a

CAGR of 11.9% during the period (see Figure 5).

Figure 5: Revenue from private healthcare industry in HK (2015E-2019E) (HKD m)

Source: Euromonitor

Key growth drivers for the private healthcare service industry in HK include:

Aging demographics: By the end of 2014, 15.1% of Hong Kong’s total population was

aged 65 or above and this figure would continue to grow, in our view. The changing

demographic pattern in Hong Kong would generate more demand for healthcare

services;

Growing consumer spending: As Hong Kong consumers become more affluent, the

number of locals who are willing to spend more for quality healthcare services is

growing. As such, the demand for timely, exclusive and higher quality services at

45,548.3

50,330.2

56,154.1

63,204.1

71,428.2

20,000.0

30,000.0

40,000.0

50,000.0

60,000.0

70,000.0

80,000.0

2015E 2016E 2017E 2018E 2019E

CAGR:11.9%

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

5

private facilities is far from peaking. This is a strong pull factor for the private

healthcare service sector in creating great potential for future growth;

Current public healthcare infrastructure squeeze: Hong Kong’s public healthcare

system is facing the problems of infrastructure squeeze, public hospitals operating

over capacity and long waiting time in some cases. All these issues would push

consumers to switch to non-subsidized private healthcare service providers. The

Hong Kong government’s recent focus on the supplemental healthcare financing

scheme in relation to the private sector will aim to facilitate greater use of private

healthcare services; and

More demand for personalized and specialized services: The healthcare market has

changed since the demand for specialized and personalized services, which cannot

be met by public healthcare service facilities, is growing. More consumers would turn

to private healthcare facilities to seek better healthcare service despite the relatively

higher costs.

Positioned in a more developed and better regulated healthcare system compared with

China

China is still at the early stage of healthcare system development, where government

authorities are trying to launch a new round of policies. The healthcare reform in China

aims to promote reasonable drug prices, the interaction between medicare and

healthcare, and the building of “Healthy China”. Developing processes like “promoting

the equal identity between public hospitals and private hospitals” and “prioritizing the

medical and healthcare institutions in China” were still on the agenda of The Fifth Plenary

Session of the 18th Central Committee. We believe China still needs time to achieve a

better developed healthcare system and modern hospital management system.

However, Hong Kong’s healthcare industry is more developed and better regulated

compared with the one in China, due to legacy from the British healthcare system. In

Hong Kong, with the regulations of medical practitioners (including the Medical

Registration Ordinance, Code of Professional Conduct, and Medical Clinics Ordinance)

guiding the general healthcare market, qualified practitioners successfully registered with

the Medical Council can practise freely in the market. However, in China, qualified

doctors can only practise in their affiliated hospitals, which make China’s hospital

industry closed to the market and private capital. In addition, the medicare system in

China, where only the public hospitals can get access to the Social Security Fund (SSF), is

also different from the rest of the world. Since the most qualified doctors are restricted

to public hospitals, where the SSF is available, demand outside public hospitals is

relatively small, leading to a weak relationship between commercial insurance and

medicare system.

We have compared the PRC healthcare market and Hong Kong healthcare market (see

Figure 6), and believe the latter is more suitable for private hospitals to grow, in the

aspects of more independent doctor practices, developed insurance medicare, less

government intervention, and a more advanced private healthcare market. We believe

these merits would help Human Health achieve robust growth in the future.

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

6

Figure 6: Comparison between HK healthcare market and PRC healthcare market

Hong Kong PRC

Independent practice of doctors ●●●●● ●

Developed insurance medicare ●●●●● ●●

Government intervention to healthcare industry ● ●●●●●

Price control in healthcare service ● ●●●●●

Supply chain business ● ●●●●●

Development of private healthcare market ●●●●● ●●

Source: BOCOM Int’l

Expansion to the PRC through partnership with Ping An Health

In light of the rapid growth of the healthcare industry in China, especially the significant

opportunities in the private hospital business, Yingjian Qiye (a wholly-owned company of

Human Health) formed a joint venture named Pingan Yingjian with Ping An Health (a

subsidiary of Ping An Financial Technology which is held as to 92.4% by Ping An Insurance)

in April 2015. Ping An Health is an established player in the private healthcare service

industry in the PRC and holds a large number of online customers. It also provides

consistent support for the outpatient services. Human Health plans to use its partner’s

marketing and well established online platform Ping An Hao Yi Sheng (平安好醫生),

which provides a new form of internet medical services with more than 10 million

existing users, as well as its experience and know-how in Shanghai, to expand the local

market.

Figure 7: Website of Ping An Hao Yi Sheng (平安好醫生)

Source: Website of Ping An Hao Yi Sheng (http://www.jk.cn/)

We believe Human Health also has the potential to build cooperation with China’s public

hospitals after establishing its reputation through the cooperation with Ping An. The

public hospital reform in China is still in its infancy. Hospitals with growth potential but

facing operating difficulties, low efficiency and capital shortage are keen to undertake

reform. In other words, demand for experienced hospital management in China’s public

hospitals is high. And cooperation with private capital is strongly supported by some local

governments. For example, the government of Beijing published in 2012 Certain Opinions

on Further Encouraging and Guiding Private Capital in Establishing Healthcare Institutions,

which encouraged and provided guidance for private companies to participate in the

public hospital reform in Beijing. In particular, the private sector partners with successful

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

7

track records will be given priority. In 2015, the Beijing government promulgated

Opinions on Encouraging Private Sector Participation in the Financing and Investment in

Key Fields of Innovation. We think the partnership with Ping An Health is the first step for

Human Health to enjoy the opportunities in hospital reform as a pioneer in the long run.

Additionally, Human Health plans to set up medical centres in Shanghai via the joint

venture company, Pingan Yingjian. It intends to leverage on its experience and knowledge

gained from Shanghai, and establish presence in other first-tier cities in the PRC. Either

setting up medical centres or making equity investment in local companies would be its

strategy. The company intends to set up four integrated medical centres in other first-tier

cities in the PRC in 2018 which provides general practice services, specialties services and

dental services to target customers.

Specialties services to drive significant revenue growth in the following years

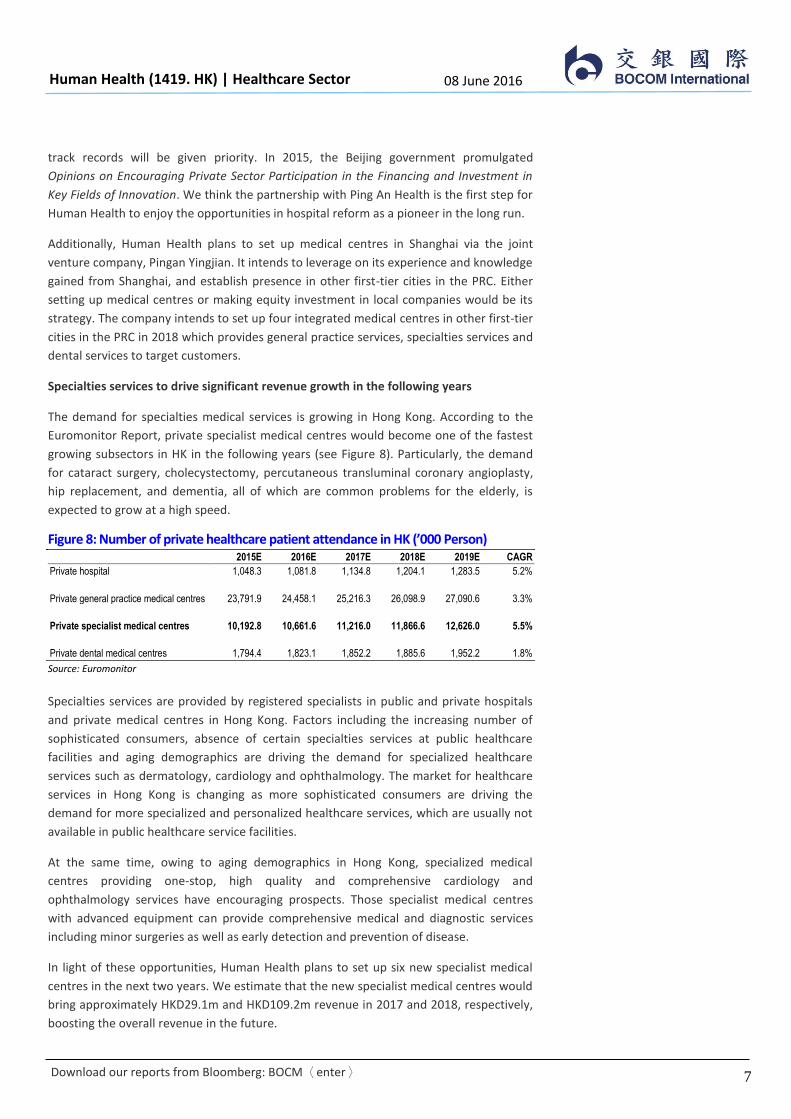

The demand for specialties medical services is growing in Hong Kong. According to the

Euromonitor Report, private specialist medical centres would become one of the fastest

growing subsectors in HK in the following years (see Figure 8). Particularly, the demand

for cataract surgery, cholecystectomy, percutaneous transluminal coronary angioplasty,

hip replacement, and dementia, all of which are common problems for the elderly, is

expected to grow at a high speed.

Figure 8: Number of private healthcare patient attendance in HK (’000 Person) 2015E 2016E 2017E 2018E 2019E CAGR

Private hospital 1,048.3 1,081.8 1,134.8 1,204.1 1,283.5 5.2%

Private general practice medical centres 23,791.9 24,458.1 25,216.3 26,098.9 27,090.6 3.3%

Private specialist medical centres 10,192.8 10,661.6 11,216.0 11,866.6 12,626.0 5.5%

Private dental medical centres 1,794.4 1,823.1 1,852.2 1,885.6 1,952.2 1.8%

Source: Euromonitor

Specialties services are provided by registered specialists in public and private hospitals

and private medical centres in Hong Kong. Factors including the increasing number of

sophisticated consumers, absence of certain specialties services at public healthcare

facilities and aging demographics are driving the demand for specialized healthcare

services such as dermatology, cardiology and ophthalmology. The market for healthcare

services in Hong Kong is changing as more sophisticated consumers are driving the

demand for more specialized and personalized healthcare services, which are usually not

available in public healthcare service facilities.

At the same time, owing to aging demographics in Hong Kong, specialized medical

centres providing one-stop, high quality and comprehensive cardiology and

ophthalmology services have encouraging prospects. Those specialist medical centres

with advanced equipment can provide comprehensive medical and diagnostic services

including minor surgeries as well as early detection and prevention of disease.

In light of these opportunities, Human Health plans to set up six new specialist medical

centres in the next two years. We estimate that the new specialist medical centres would

bring approximately HKD29.1m and HKD109.2m revenue in 2017 and 2018, respectively,

boosting the overall revenue in the future.

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

8

Great platform for retention of good talents

Human Health has attracted a lot of new members to join its professional team through

its reputation, competitive compensation and supportive working environment which is

conducive to professional growth. Its medical network provides a platform for the

professional team to develop their respective specialized fields given the following

advantages:

Established infrastructure. This could minimize administrative time and thereby

enhance productivity, enabling doctors to focus on providing quality healthcare

services to patients;

Ongoing support from the Doctor Advisory Board and network of general

practitioners, specialists and dentists. This could allow its professional team to

continuously develop their respective professional practices;

Portfolio of comprehensive healthcare services and patient-centric culture. This

could enable the professional team to access and retain a large pool of patients;

Wide range of services. This could help to achieve a large number of specialties

service referrals; and

Vast network. This could accommodate flexible working arrangements and flexible

working locations.

Due to the effective management of Human Health and the benefits brought by its brand,

the company has maintained long-term relationships with many of its professional team

members. Its professional team comprises 115 members, including general practitioners,

specialists, dentists, physiotherapists, pharmacists and registered nurses. A majority of its

professional team members have worked with Human Health for more than 3 years and

up to 18 years.

Figure 9: Number of its professional team members Team Number

1 General practitioners 67

2 Specialists 22

3 Dentists 15

4 Physiotherapists 3

5 Registered nurses 6

6 Pharmacist 1

7 Dental hygienist 1

Total 115

Source: Company

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

9

Experienced management team with a proven track record

Human Health is under the leadership of an experienced and dedicated management

team which comprises its founders, seasoned professionals and doctors who have

participated in the management for a number of years. Its founders, Mr. Chan Kin Ping

and Dr. Pang Lai Sheung, have been leading Human Health since they founded the

company 18 years ago. The senior management promotes a corporate culture and

standard operation procedures by working collaboratively with the professional team in

achieving a consistent client-focused approach to deliver quality healthcare services to

the patients.

Mr. Chan Kin Ping As the chairman of the board, chief executive officer and an executive

director of Human Health. Mr. Chan is also one of the co-founders of the company and

has been leading Human Health for over 18 years to serve in the private healthcare

industry. He is responsible for managing the overall operations and developments and

formulating the overall business plans.

In April 2015, Mr. Chan was appointed as the vice chairman cum director of Hong Kong

Kowloon City Industry and Commerce Association, the Vice Chairman of Kowloon West

Youth Care Committee for the Year of 2015 and a member of The Lok Sin Tong Benevolent

Society, Kowloon. Mr. Chan was also appointed as the principal adviser of the advisory

board to Auxiliary Medical Services Officers Club from June 2014 to May 2015. Moreover,

Mr. Chan has been a general committee member of The Hong Kong Shanxi Chamber of

Commerce and an ordinary member of the Hong Kong Professionals and Senior Executives

Association since May 2014 and November 2013, respectively. He has also been the Vice

President of the Hong Kong Real Property Federation since September 2013.

Dr. Pang Lai Sheung As the chief medical officer and an executive director of Human

Health, Dr. Pang is one of the co-founders of Human Health. Dr. Pang is mainly

responsible for overseeing and providing advice on the management of the professional

team and has contributed significantly to the developments of the company. Dr. Pang

obtained a Bachelor of Medicine and Bachelor of Surgery from The Chinese University of

Hong Kong in 1993. Dr. Pang has been a registered medical practitioner in Hong Kong

since 1993. Dr. Pang also completed a Diploma in Family Medicine and a Diploma

Programme in Advances in Medicine from the Chinese University of Hong Kong in August

2001 and March 2005, respectively. Dr. Pang was awarded a Master of Business

Administration issued jointly by Northwestern University and The Hong Kong University

of Science and Technology in December 2014. Moreover, she has been a Honorary

Clinical Assistant Professor in Faculty of Medicine of the Chinese University of Hong Kong

since June 2014.

Ms. Sat Chui Wan As the CFO and an executive director of Human Health, Ms. Sat is

mainly responsible for overseeing the financial, risk and human resources management

of Human Health. Ms. Sat obtained a Bachelor of Arts in Accountancy from the Hong

Kong Polytechnic University in October 1992. She subsequently obtained a Master of

Business Administration from the University of Lancaster in the United Kingdom in

November 2000 and completed the International Study Program (ISP) at the University of

St. Gallen in December 2000. She also completed the City University of Hong Kong

Advanced Management Programme at the University of California, Berkeley in August

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

10

2010. Ms. Sat is a member of the Hong Kong Institute of Certified Public Accountants

since September 1996. She was also admitted as an associate of the Chartered

Association of Certified Accountants since July 1996 and is a fellow of the Chartered

Association of Certified Accountants since July 2001. Ms. Sat has over 20 years of working

experience in accounting, finance, management and strategic planning in different

industries. Prior to joining Human Health, she was an assistant accountant of The Wing

On Department Stores (Hong Kong) Limited from September 1994 and was promoted to

accountant in January 1996 until April 1999. She joined Sun Fung Offset Binding Co. Ltd.

as the Financial Controller from October 2004 to June 2007 and was assigned the role of

Deputy Chief Executive Officer from October 2005 to June 2007.

Mr. Poon Chun Pong As the chief operating officer and an executive director of Human

Health, Mr. Poon obtained a Bachelor of Engineering with Honours and a Master of

Business Administration from The Chinese University of Hong Kong in December 2000

and December 2009, respectively. Mr. Poon has over 12 years of experience in

information technology in the medical field and over eight years of management

experience as he began his career as a senior technical analyst of Human Health

Associate in June 2003. He was later appointed as an assistant director of Actmax in April

2007 and is primarily responsible for overseeing the overall business operations of

Human Health.

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

11

Investment concerns/risks

Human Health may not be able to implement its business strategy on schedule

The growth of its business is heavily dependent on the implementation of its business

strategies, including setting up new general/specialist healthcare centres. The successful

implementation of its business strategies is subject to some uncertainties and

contingencies, including the continued growth of healthcare services in Hong Kong and

the PRC. We do not rule out the possibility that the integration of its resources and

management resulting from the expansion of new medical centres may take an extended

period of time, and the shortage of professionals in the future could also be another issue.

Thus, its profit growth might be negatively affected.

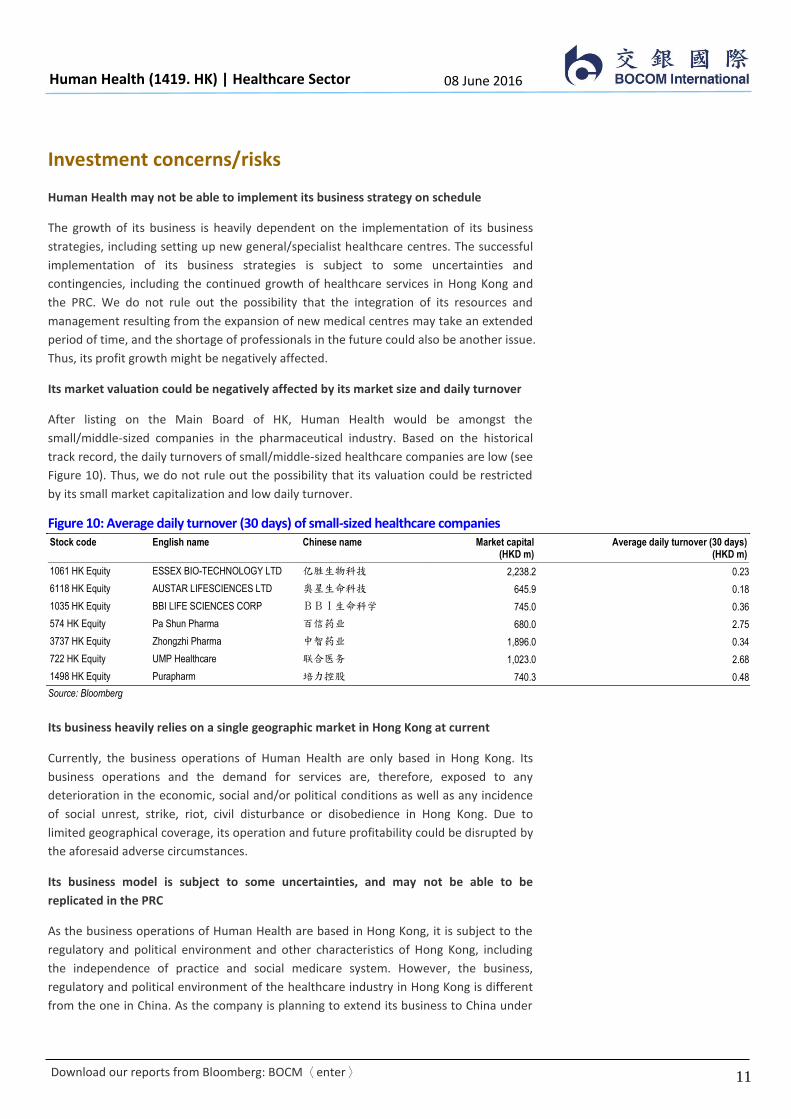

Its market valuation could be negatively affected by its market size and daily turnover

After listing on the Main Board of HK, Human Health would be amongst the

small/middle-sized companies in the pharmaceutical industry. Based on the historical

track record, the daily turnovers of small/middle-sized healthcare companies are low (see

Figure 10). Thus, we do not rule out the possibility that its valuation could be restricted

by its small market capitalization and low daily turnover.

Figure 10: Average daily turnover (30 days) of small-sized healthcare companies Stock code English name Chinese name Market capital

(HKD m) Average daily turnover (30 days)

(HKD m)

1061 HK Equity ESSEX BIO-TECHNOLOGY LTD 亿胜生物科技 2,238.2 0.23

6118 HK Equity AUSTAR LIFESCIENCES LTD 奥星生命科技 645.9 0.18

1035 HK Equity BBI LIFE SCIENCES CORP BBI生命科学 745.0 0.36

574 HK Equity Pa Shun Pharma 百信药业 680.0 2.75

3737 HK Equity Zhongzhi Pharma 中智药业 1,896.0 0.34

722 HK Equity UMP Healthcare 联合医务 1,023.0 2.68

1498 HK Equity Purapharm 培力控股 740.3 0.48

Source: Bloomberg

Its business heavily relies on a single geographic market in Hong Kong at current

Currently, the business operations of Human Health are only based in Hong Kong. Its

business operations and the demand for services are, therefore, exposed to any

deterioration in the economic, social and/or political conditions as well as any incidence

of social unrest, strike, riot, civil disturbance or disobedience in Hong Kong. Due to

limited geographical coverage, its operation and future profitability could be disrupted by

the aforesaid adverse circumstances.

Its business model is subject to some uncertainties, and may not be able to be

replicated in the PRC

As the business operations of Human Health are based in Hong Kong, it is subject to the

regulatory and political environment and other characteristics of Hong Kong, including

the independence of practice and social medicare system. However, the business,

regulatory and political environment of the healthcare industry in Hong Kong is different

from the one in China. As the company is planning to extend its business to China under

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

12

the partnership with Ping An, there is no assurance that its business model could be

replicated in the PRC.

Its businesses may be affected by intensified competition from the increasing number

of practitioners in the private sector

According to the Euromonitor Report, the number of private healthcare service facilities

grew by a CAGR of 4.9% from 2010 to 2014. We believe that the increasing number of

private healthcare service facilities will intensify the competition in the industry.

Competition from existing competitors and new entrants, both in terms of recruitment of

medical practitioners and market share, may intensify.

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

13

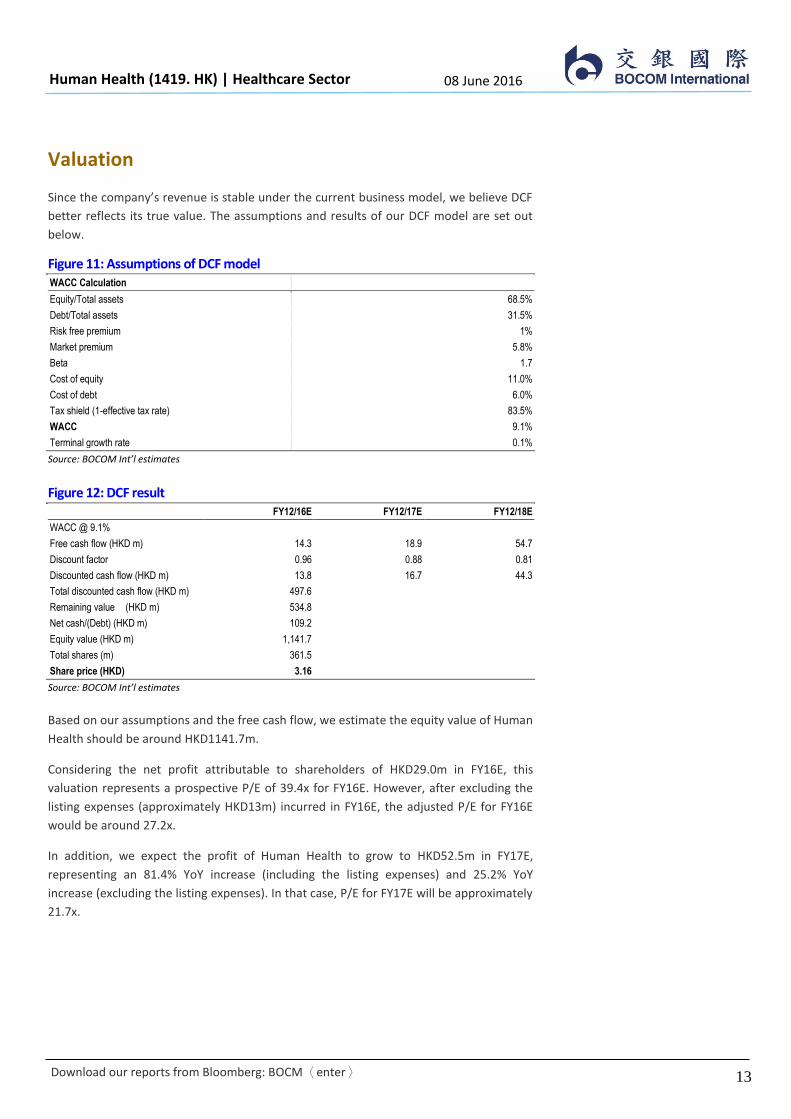

Valuation

Since the company’s revenue is stable under the current business model, we believe DCF

better reflects its true value. The assumptions and results of our DCF model are set out

below.

Figure 11: Assumptions of DCF model WACC Calculation

Equity/Total assets 68.5%

Debt/Total assets 31.5%

Risk free premium 1%

Market premium 5.8%

Beta 1.7

Cost of equity 11.0%

Cost of debt 6.0%

Tax shield (1-effective tax rate) 83.5%

WACC 9.1%

Terminal growth rate 0.1%

Source: BOCOM Int’l estimates

Figure 12: DCF result FY12/16E FY12/17E FY12/18E

WACC @ 9.1%

Free cash flow (HKD m) 14.3 18.9 54.7

Discount factor 0.96 0.88 0.81

Discounted cash flow (HKD m) 13.8 16.7 44.3

Total discounted cash flow (HKD m) 497.6

Remaining value (HKD m) 534.8

Net cash/(Debt) (HKD m) 109.2

Equity value (HKD m) 1,141.7 Total shares (m) 361.5 Share price (HKD) 3.16 Source: BOCOM Int’l estimates

Based on our assumptions and the free cash flow, we estimate the equity value of Human

Health should be around HKD1141.7m.

Considering the net profit attributable to shareholders of HKD29.0m in FY16E, this

valuation represents a prospective P/E of 39.4x for FY16E. However, after excluding the

listing expenses (approximately HKD13m) incurred in FY16E, the adjusted P/E for FY16E

would be around 27.2x.

In addition, we expect the profit of Human Health to grow to HKD52.5m in FY17E,

representing an 81.4% YoY increase (including the listing expenses) and 25.2% YoY

increase (excluding the listing expenses). In that case, P/E for FY17E will be approximately

21.7x.

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

14

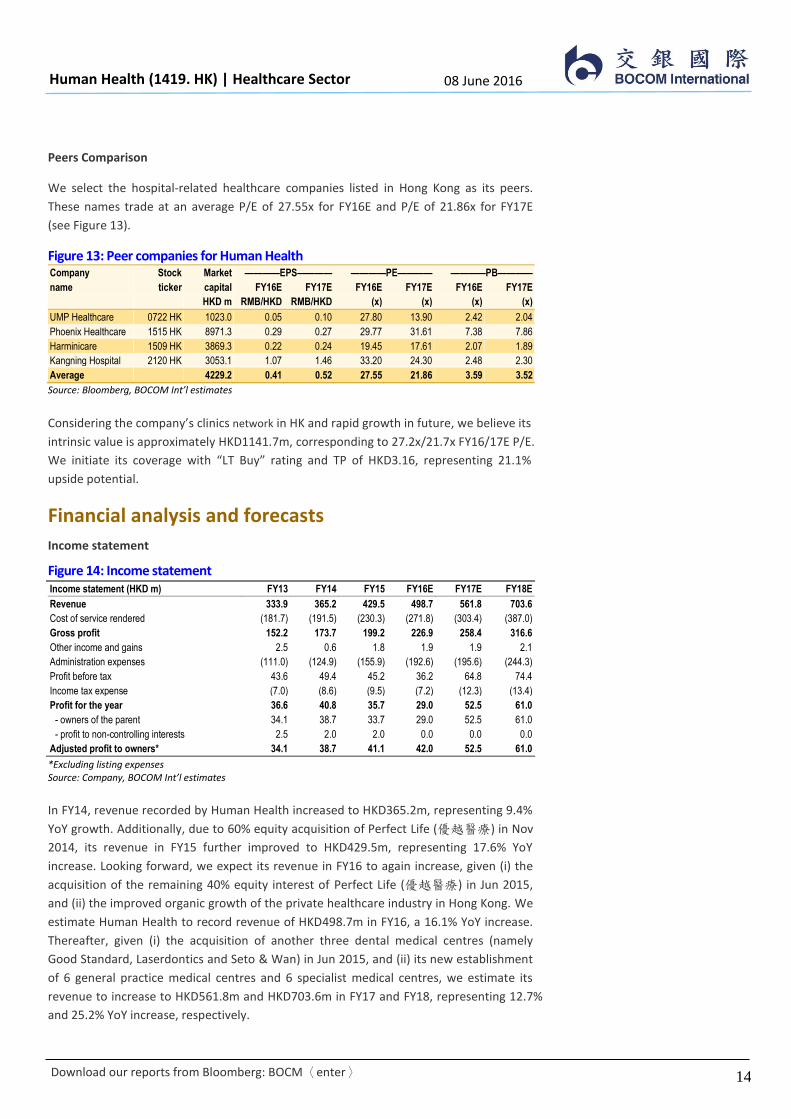

Peers Comparison

We select the hospital-related healthcare companies listed in Hong Kong as its peers.

These names trade at an average P/E of 27.55x for FY16E and P/E of 21.86x for FY17E

(see Figure 13).

Figure 13: Peer companies for Human Health Company Stock Market ————EPS———— ————PE———— ————PB————

name ticker capital FY16E FY17E FY16E FY17E FY16E FY17E

HKD m RMB/HKD RMB/HKD (x) (x) (x) (x)

UMP Healthcare 0722 HK 1023.0 0.05 0.10 27.80 13.90 2.42 2.04

Phoenix Healthcare 1515 HK 8971.3 0.29 0.27 29.77 31.61 7.38 7.86

Harminicare 1509 HK 3869.3 0.22 0.24 19.45 17.61 2.07 1.89

Kangning Hospital 2120 HK 3053.1 1.07 1.46 33.20 24.30 2.48 2.30

Average

4229.2 0.41 0.52 27.55 21.86 3.59 3.52

Source: Bloomberg, BOCOM Int’l estimates

Considering the company’s clinics network in HK and rapid growth in future, we believe its

intrinsic value is approximately HKD1141.7m, corresponding to 27.2x/21.7x FY16/17E P/E.

We initiate its coverage with “LT Buy” rating and TP of HKD3.16, representing 21.1%

upside potential.

Financial analysis and forecasts

Income statement

Figure 14: Income statement Income statement (HKD m) FY13 FY14 FY15 FY16E FY17E FY18E

Revenue 333.9 365.2 429.5 498.7 561.8 703.6

Cost of service rendered (181.7) (191.5) (230.3) (271.8) (303.4) (387.0)

Gross profit 152.2 173.7 199.2 226.9 258.4 316.6

Other income and gains 2.5 0.6 1.8 1.9 1.9 2.1

Administration expenses (111.0) (124.9) (155.9) (192.6) (195.6) (244.3)

Profit before tax 43.6 49.4 45.2 36.2 64.8 74.4

Income tax expense (7.0) (8.6) (9.5) (7.2) (12.3) (13.4)

Profit for the year 36.6 40.8 35.7 29.0 52.5 61.0

- owners of the parent 34.1 38.7 33.7 29.0 52.5 61.0

- profit to non-controlling interests 2.5 2.0 2.0 0.0 0.0 0.0

Adjusted profit to owners* 34.1 38.7 41.1 42.0 52.5 61.0

*Excluding listing expenses Source: Company, BOCOM Int’l estimates

In FY14, revenue recorded by Human Health increased to HKD365.2m, representing 9.4%

YoY growth. Additionally, due to 60% equity acquisition of Perfect Life (優越醫療) in Nov

2014, its revenue in FY15 further improved to HKD429.5m, representing 17.6% YoY

increase. Looking forward, we expect its revenue in FY16 to again increase, given (i) the

acquisition of the remaining 40% equity interest of Perfect Life (優越醫療) in Jun 2015,

and (ii) the improved organic growth of the private healthcare industry in Hong Kong. We

estimate Human Health to record revenue of HKD498.7m in FY16, a 16.1% YoY increase.

Thereafter, given (i) the acquisition of another three dental medical centres (namely

Good Standard, Laserdontics and Seto & Wan) in Jun 2015, and (ii) its new establishment

of 6 general practice medical centres and 6 specialist medical centres, we estimate its

revenue to increase to HKD561.8m and HKD703.6m in FY17 and FY18, representing 12.7%

and 25.2% YoY increase, respectively.

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

15

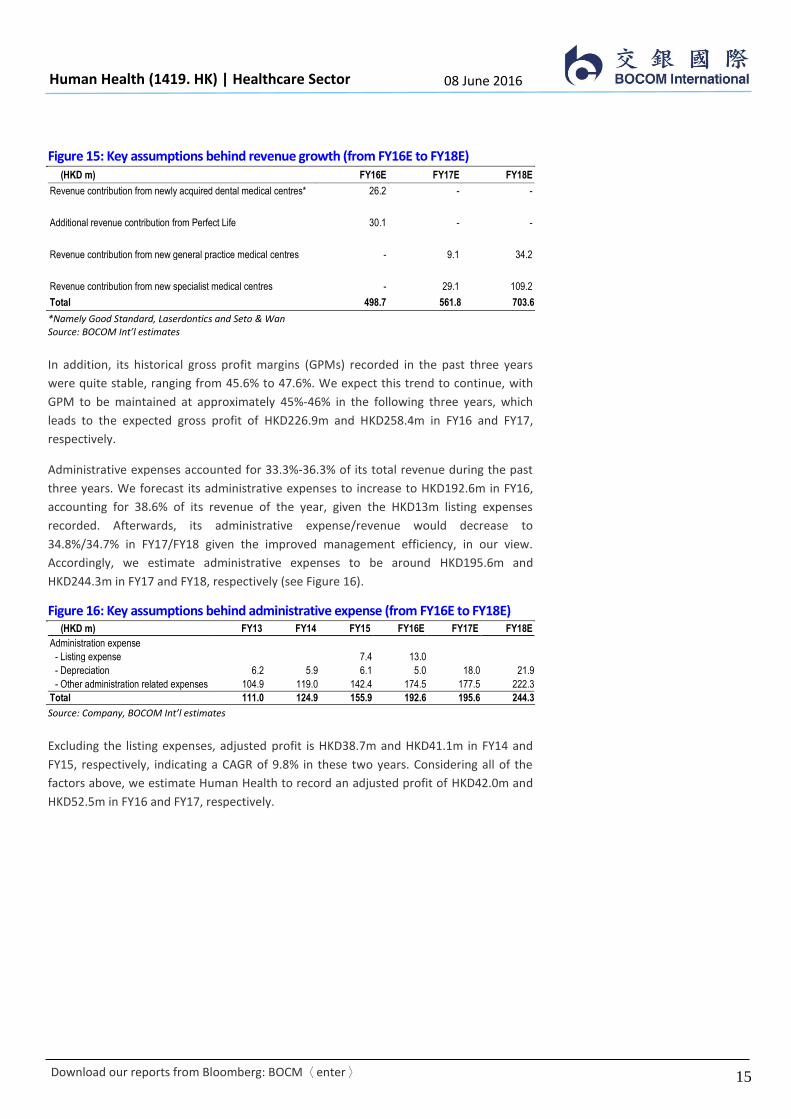

Figure 15: Key assumptions behind revenue growth (from FY16E to FY18E) (HKD m) FY16E FY17E FY18E

Revenue contribution from newly acquired dental medical centres* 26.2 - -

Additional revenue contribution from Perfect Life 30.1 - -

Revenue contribution from new general practice medical centres - 9.1 34.2

Revenue contribution from new specialist medical centres - 29.1 109.2

Total 498.7 561.8 703.6

*Namely Good Standard, Laserdontics and Seto & Wan Source: BOCOM Int’l estimates

In addition, its historical gross profit margins (GPMs) recorded in the past three years

were quite stable, ranging from 45.6% to 47.6%. We expect this trend to continue, with

GPM to be maintained at approximately 45%-46% in the following three years, which

leads to the expected gross profit of HKD226.9m and HKD258.4m in FY16 and FY17,

respectively.

Administrative expenses accounted for 33.3%-36.3% of its total revenue during the past

three years. We forecast its administrative expenses to increase to HKD192.6m in FY16,

accounting for 38.6% of its revenue of the year, given the HKD13m listing expenses

recorded. Afterwards, its administrative expense/revenue would decrease to

34.8%/34.7% in FY17/FY18 given the improved management efficiency, in our view.

Accordingly, we estimate administrative expenses to be around HKD195.6m and

HKD244.3m in FY17 and FY18, respectively (see Figure 16).

Figure 16: Key assumptions behind administrative expense (from FY16E to FY18E) (HKD m) FY13 FY14 FY15 FY16E FY17E FY18E

Administration expense

- Listing expense 7.4 13.0

- Depreciation 6.2 5.9 6.1 5.0 18.0 21.9

- Other administration related expenses 104.9 119.0 142.4 174.5 177.5 222.3

Total 111.0 124.9 155.9 192.6 195.6 244.3

Source: Company, BOCOM Int’l estimates

Excluding the listing expenses, adjusted profit is HKD38.7m and HKD41.1m in FY14 and

FY15, respectively, indicating a CAGR of 9.8% in these two years. Considering all of the

factors above, we estimate Human Health to record an adjusted profit of HKD42.0m and

HKD52.5m in FY16 and FY17, respectively.

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

16

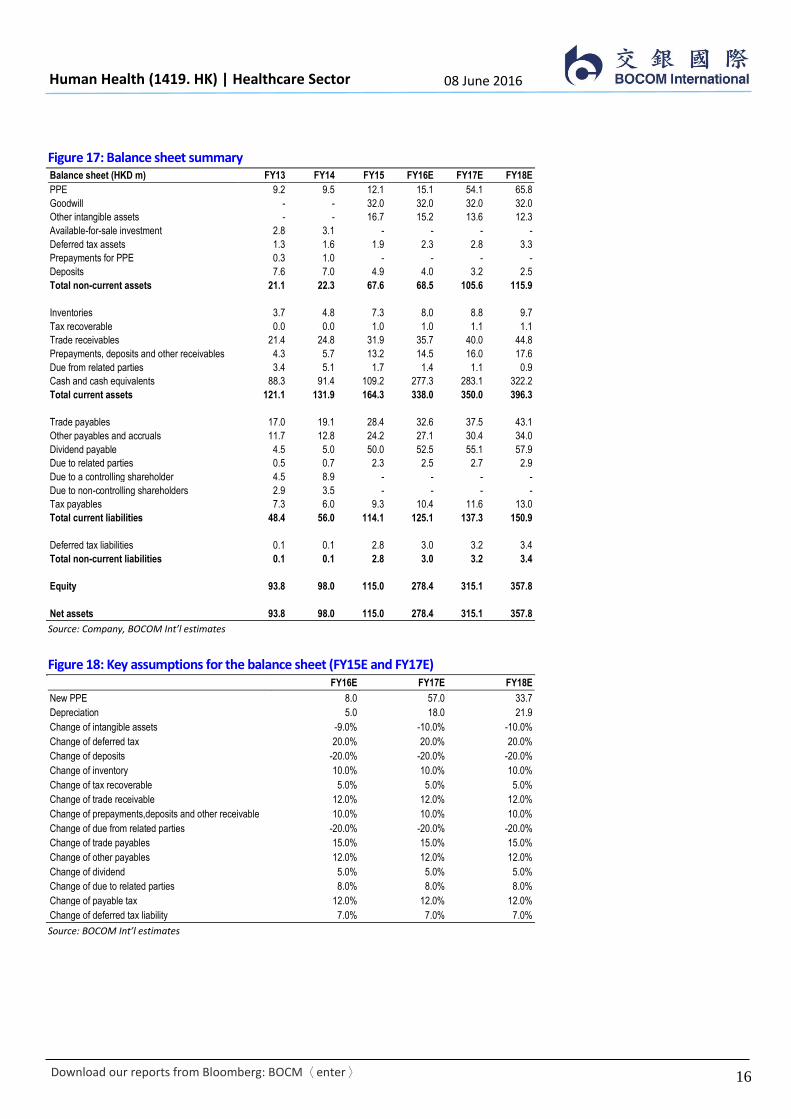

Figure 17: Balance sheet summary Balance sheet (HKD m) FY13 FY14 FY15 FY16E FY17E FY18E

PPE 9.2 9.5 12.1 15.1 54.1 65.8

Goodwill - - 32.0 32.0 32.0 32.0

Other intangible assets - - 16.7 15.2 13.6 12.3

Available-for-sale investment 2.8 3.1 - - - -

Deferred tax assets 1.3 1.6 1.9 2.3 2.8 3.3

Prepayments for PPE 0.3 1.0 - - - -

Deposits 7.6 7.0 4.9 4.0 3.2 2.5

Total non-current assets 21.1 22.3 67.6 68.5 105.6 115.9

Inventories 3.7 4.8 7.3 8.0 8.8 9.7

Tax recoverable 0.0 0.0 1.0 1.0 1.1 1.1

Trade receivables 21.4 24.8 31.9 35.7 40.0 44.8

Prepayments, deposits and other receivables 4.3 5.7 13.2 14.5 16.0 17.6

Due from related parties 3.4 5.1 1.7 1.4 1.1 0.9

Cash and cash equivalents 88.3 91.4 109.2 277.3 283.1 322.2

Total current assets 121.1 131.9 164.3 338.0 350.0 396.3

Trade payables 17.0 19.1 28.4 32.6 37.5 43.1

Other payables and accruals 11.7 12.8 24.2 27.1 30.4 34.0

Dividend payable 4.5 5.0 50.0 52.5 55.1 57.9

Due to related parties 0.5 0.7 2.3 2.5 2.7 2.9

Due to a controlling shareholder 4.5 8.9 - - - -

Due to non-controlling shareholders 2.9 3.5 - - - -

Tax payables 7.3 6.0 9.3 10.4 11.6 13.0

Total current liabilities 48.4 56.0 114.1 125.1 137.3 150.9

Deferred tax liabilities 0.1 0.1 2.8 3.0 3.2 3.4

Total non-current liabilities 0.1 0.1 2.8 3.0 3.2 3.4

Equity 93.8 98.0 115.0 278.4 315.1 357.8

Net assets 93.8 98.0 115.0 278.4 315.1 357.8

Source: Company, BOCOM Int’l estimates

Figure 18: Key assumptions for the balance sheet (FY15E and FY17E) FY16E FY17E FY18E

New PPE 8.0 57.0 33.7

Depreciation 5.0 18.0 21.9

Change of intangible assets -9.0% -10.0% -10.0%

Change of deferred tax 20.0% 20.0% 20.0%

Change of deposits -20.0% -20.0% -20.0%

Change of inventory 10.0% 10.0% 10.0%

Change of tax recoverable 5.0% 5.0% 5.0%

Change of trade receivable 12.0% 12.0% 12.0%

Change of prepayments,deposits and other receivable 10.0% 10.0% 10.0%

Change of due from related parties -20.0% -20.0% -20.0%

Change of trade payables 15.0% 15.0% 15.0%

Change of other payables 12.0% 12.0% 12.0%

Change of dividend 5.0% 5.0% 5.0%

Change of due to related parties 8.0% 8.0% 8.0%

Change of payable tax 12.0% 12.0% 12.0%

Change of deferred tax liability 7.0% 7.0% 7.0%

Source: BOCOM Int’l estimates

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

17

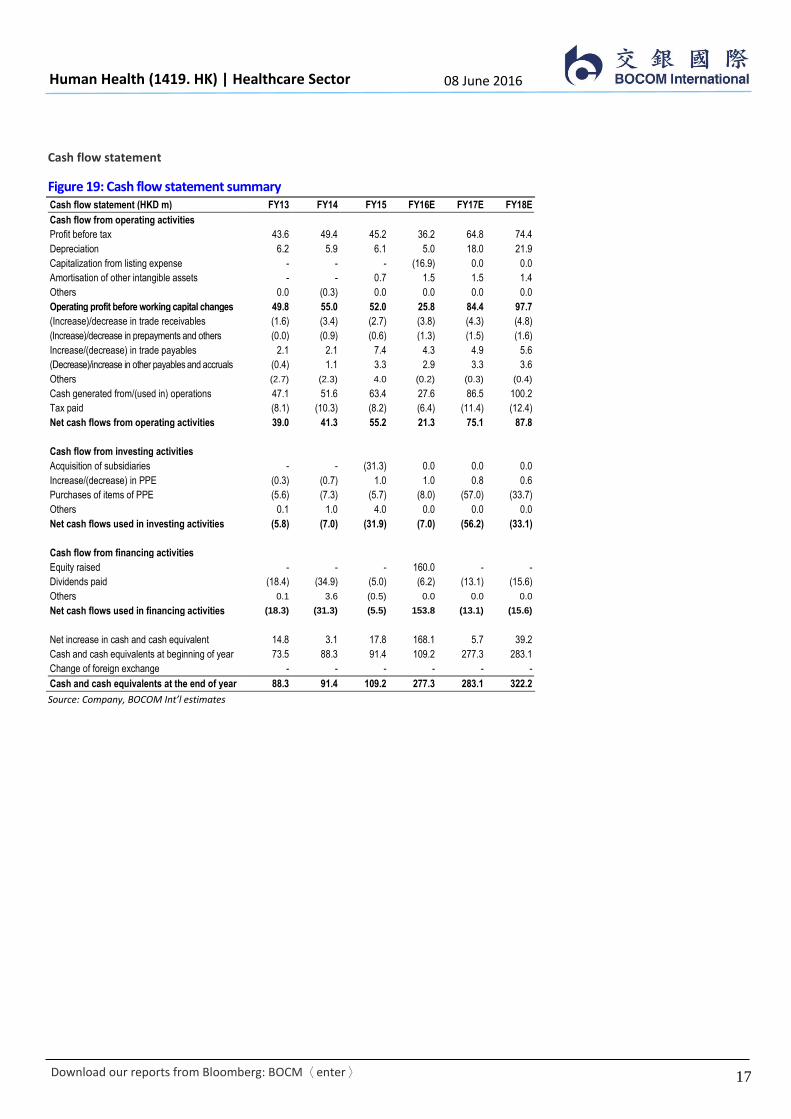

Cash flow statement

Figure 19: Cash flow statement summary Cash flow statement (HKD m) FY13 FY14 FY15 FY16E FY17E FY18E

Cash flow from operating activities

Profit before tax 43.6 49.4 45.2 36.2 64.8 74.4

Depreciation 6.2 5.9 6.1 5.0 18.0 21.9

Capitalization from listing expense - - - (16.9) 0.0 0.0

Amortisation of other intangible assets - - 0.7 1.5 1.5 1.4

Others 0.0 (0.3) 0.0 0.0 0.0 0.0

Operating profit before working capital changes 49.8 55.0 52.0 25.8 84.4 97.7

(Increase)/decrease in trade receivables (1.6) (3.4) (2.7) (3.8) (4.3) (4.8)

(Increase)/decrease in prepayments and others (0.0) (0.9) (0.6) (1.3) (1.5) (1.6)

Increase/(decrease) in trade payables 2.1 2.1 7.4 4.3 4.9 5.6

(Decrease)/increase in other payables and accruals (0.4) 1.1 3.3 2.9 3.3 3.6

Others (2.7) (2.3) 4.0 (0.2) (0.3) (0.4)

Cash generated from/(used in) operations 47.1 51.6 63.4 27.6 86.5 100.2

Tax paid (8.1) (10.3) (8.2) (6.4) (11.4) (12.4)

Net cash flows from operating activities 39.0 41.3 55.2 21.3 75.1 87.8

Cash flow from investing activities

Acquisition of subsidiaries - - (31.3) 0.0 0.0 0.0

Increase/(decrease) in PPE (0.3) (0.7) 1.0 1.0 0.8 0.6

Purchases of items of PPE (5.6) (7.3) (5.7) (8.0) (57.0) (33.7)

Others 0.1 1.0 4.0 0.0 0.0 0.0

Net cash flows used in investing activities (5.8) (7.0) (31.9) (7.0) (56.2) (33.1)

Cash flow from financing activities

Equity raised - - - 160.0 - -

Dividends paid (18.4) (34.9) (5.0) (6.2) (13.1) (15.6)

Others 0.1 3.6 (0.5) 0.0 0.0 0.0

Net cash flows used in financing activities (18.3) (31.3) (5.5) 153.8 (13.1) (15.6)

Net increase in cash and cash equivalent 14.8 3.1 17.8 168.1 5.7 39.2

Cash and cash equivalents at beginning of year 73.5 88.3 91.4 109.2 277.3 283.1

Change of foreign exchange - - - - - -

Cash and cash equivalents at the end of year 88.3 91.4 109.2 277.3 283.1 322.2

Source: Company, BOCOM Int’l estimates

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

18

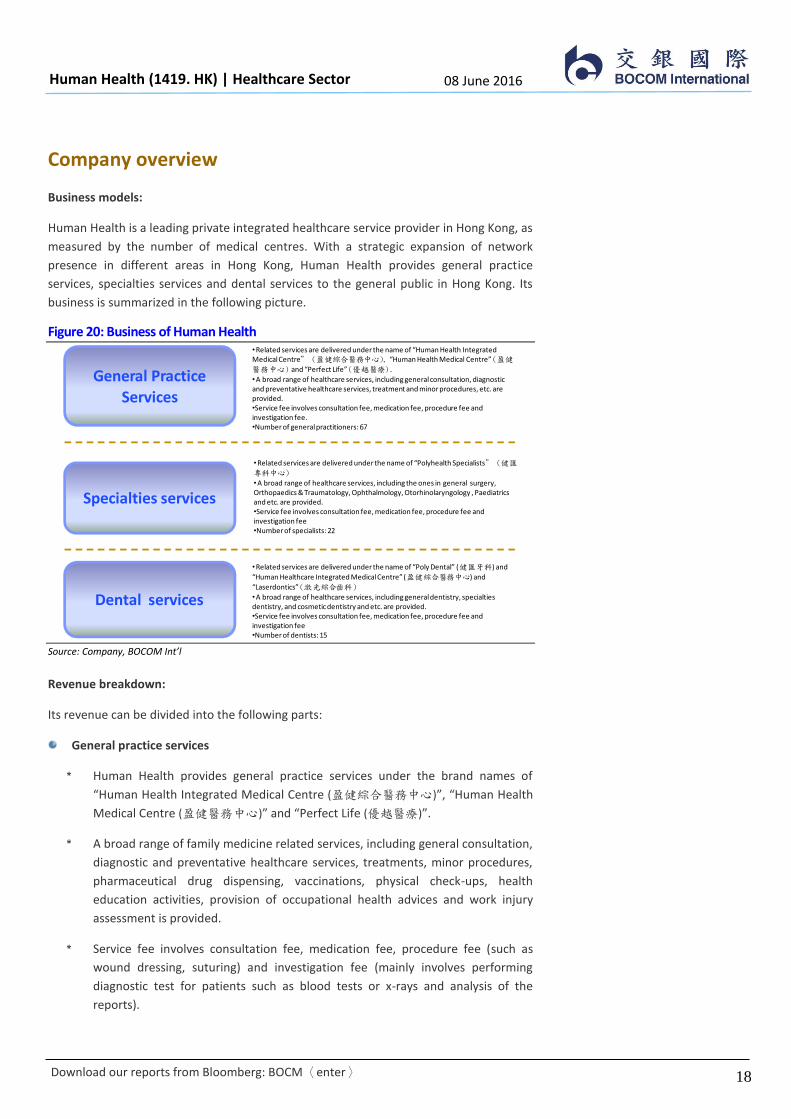

Company overview

Business models:

Human Health is a leading private integrated healthcare service provider in Hong Kong, as

measured by the number of medical centres. With a strategic expansion of network

presence in different areas in Hong Kong, Human Health provides general practice

services, specialties services and dental services to the general public in Hong Kong. Its

business is summarized in the following picture.

Figure 20: Business of Human Health

Source: Company, BOCOM Int’l

Revenue breakdown:

Its revenue can be divided into the following parts:

General practice services

* Human Health provides general practice services under the brand names of

“Human Health Integrated Medical Centre (盈健綜合醫務中心)”, “Human Health

Medical Centre (盈健醫務中心)” and “Perfect Life (優越醫療)”.

* A broad range of family medicine related services, including general consultation,

diagnostic and preventative healthcare services, treatments, minor procedures,

pharmaceutical drug dispensing, vaccinations, physical check-ups, health

education activities, provision of occupational health advices and work injury

assessment is provided.

* Service fee involves consultation fee, medication fee, procedure fee (such as

wound dressing, suturing) and investigation fee (mainly involves performing

diagnostic test for patients such as blood tests or x-rays and analysis of the

reports).

General Practice Services

Specialties services

Dental services

•Related services are delivered under the name of “Human Health Integrated Medical Centre” (盈健綜合醫務中心), “Human Health Medical Centre” (盈健

醫務中心) and “Perfect Life” (優越醫療) .

•A broad range of healthcare services, including general consultation, diagnostic and preventative healthcare services, treatment and minor procedures, etc. are provided. •Service fee involves consultation fee, medication fee, procedure fee and investigation fee. •Number of general practitioners: 67

•Related services are delivered under the name of “Polyhealth Specialists” (健匯

專科中心)

•A broad range of healthcare services, including the ones in general surgery, Orthopaedics & Traumatology, Ophthalmology, Otorhinolaryngology , Paediatrics and etc. are provided. •Service fee involves consultation fee, medication fee, procedure fee and investigation fee•Number of specialists: 22

•Related services are delivered under the name of “Poly Dental” (健匯牙科) and

“Human Healthcare Integrated Medical Centre” (盈健綜合醫務中心) and

“Laserdontics” (激光綜合齒科)

•A broad range of healthcare services, including general dentistry, specialties dentistry, and cosmetic dentistry and etc. are provided. •Service fee involves consultation fee, medication fee, procedure fee and investigation fee•Number of dentists: 15

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

19

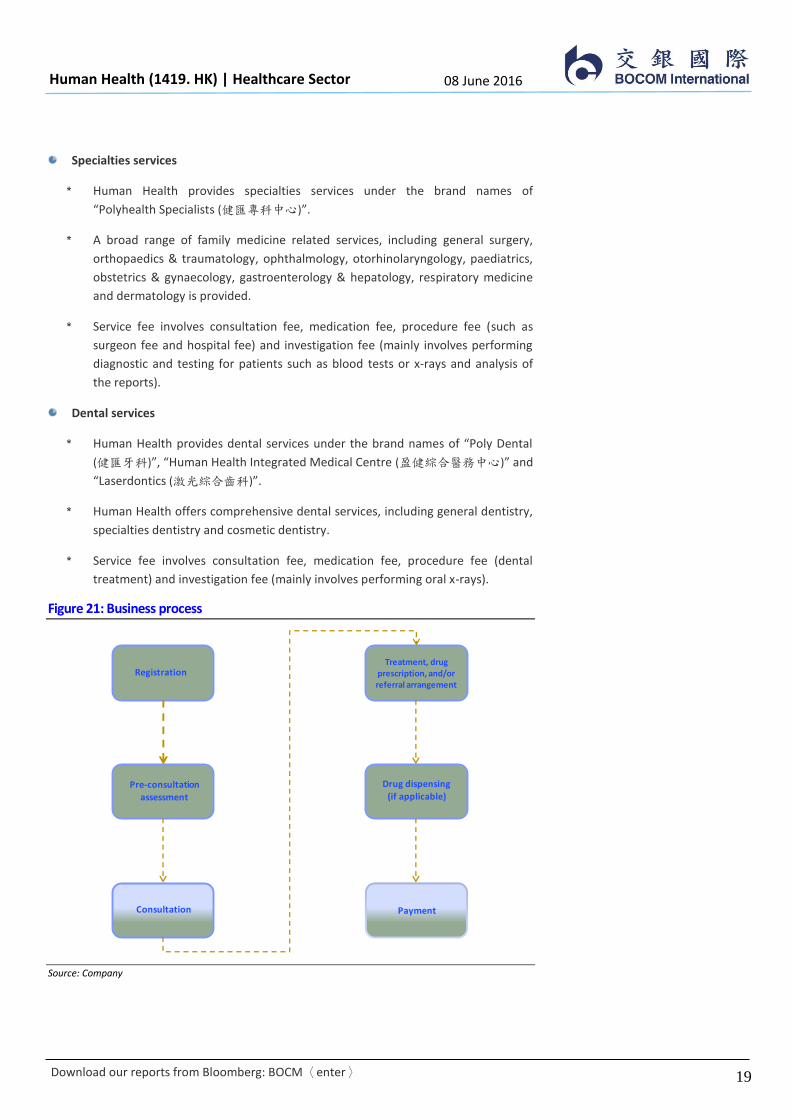

Specialties services

* Human Health provides specialties services under the brand names of

“Polyhealth Specialists (健匯專科中心)”.

* A broad range of family medicine related services, including general surgery,

orthopaedics & traumatology, ophthalmology, otorhinolaryngology, paediatrics,

obstetrics & gynaecology, gastroenterology & hepatology, respiratory medicine

and dermatology is provided.

* Service fee involves consultation fee, medication fee, procedure fee (such as

surgeon fee and hospital fee) and investigation fee (mainly involves performing

diagnostic and testing for patients such as blood tests or x-rays and analysis of

the reports).

Dental services

* Human Health provides dental services under the brand names of “Poly Dental

(健匯牙科)”, “Human Health Integrated Medical Centre (盈健綜合醫務中心)” and

“Laserdontics (激光綜合齒科)”.

* Human Health offers comprehensive dental services, including general dentistry,

specialties dentistry and cosmetic dentistry.

* Service fee involves consultation fee, medication fee, procedure fee (dental

treatment) and investigation fee (mainly involves performing oral x-rays).

Figure 21: Business process

Source: Company

Treatment, drug prescription, and/or referral arrangement

Registration

Drug dispensing(if applicable)

Pre-consultation assessment

Consultation Payment

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

20

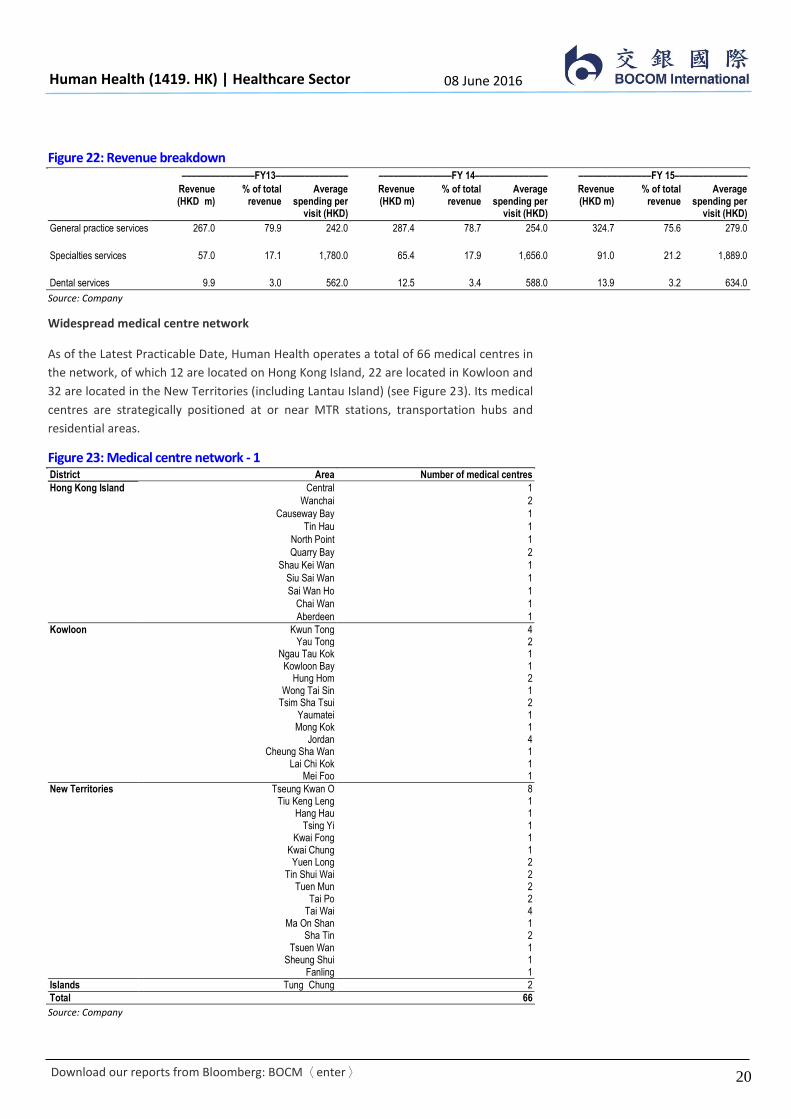

Figure 22: Revenue breakdown

–––––––––––––––FY13––––––––––––––– –––––––––––––––FY 14––––––––––––––– –––––––––––––––FY 15–––––––––––––––

Revenue (HKD m)

% of total revenue

Average spending per

visit (HKD)

Revenue (HKD m)

% of total revenue

Average spending per

visit (HKD)

Revenue (HKD m)

% of total revenue

Average spending per

visit (HKD)

General practice services 267.0 79.9 242.0 287.4 78.7 254.0 324.7 75.6 279.0

Specialties services 57.0 17.1 1,780.0 65.4 17.9 1,656.0 91.0 21.2 1,889.0

Dental services 9.9 3.0 562.0 12.5 3.4 588.0 13.9 3.2 634.0

Source: Company

Widespread medical centre network

As of the Latest Practicable Date, Human Health operates a total of 66 medical centres in

the network, of which 12 are located on Hong Kong Island, 22 are located in Kowloon and

32 are located in the New Territories (including Lantau Island) (see Figure 23). Its medical

centres are strategically positioned at or near MTR stations, transportation hubs and

residential areas.

Figure 23: Medical centre network - 1 District Area Number of medical centres

Hong Kong Island Central 1

Wanchai 2

Causeway Bay 1

Tin Hau 1

North Point 1

Quarry Bay 2

Shau Kei Wan 1

Siu Sai Wan 1

Sai Wan Ho 1

Chai Wan 1

Aberdeen 1

Kowloon

Kwun Tong 4 Yau Tong 2

Ngau Tau Kok 1 Kowloon Bay 1

Hung Hom 2 Wong Tai Sin 1

Tsim Sha Tsui 2 Yaumatei 1 Mong Kok 1

Jordan 4 Cheung Sha Wan 1

Lai Chi Kok 1 Mei Foo 1

New Territories Tseung Kwan O 8 Tiu Keng Leng 1 Hang Hau 1 Tsing Yi 1 Kwai Fong 1 Kwai Chung 1 Yuen Long 2 Tin Shui Wai 2 Tuen Mun 2 Tai Po 2 Tai Wai 4 Ma On Shan 1 Sha Tin 2 Tsuen Wan 1 Sheung Shui 1 Fanling 1

Islands Tung Chung 2

Total 66

Source: Company

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

21

Figure 24: Medical centre network - 2

Source: Company

Figure 25: Medical centre - 1

Source: BOCOM Int’l

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

22

Figure 26: Medical centre - 2

Source: BOCOM Int’l

Figure 27: Medical centre - 3

Source: BOCOM Int’l

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

23

Figure 28: Medical centre - 4

Source: BOCOM Int’l

Figure 29: Medical equipment

Source: BOCOM Int’l

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

24

Pricing of services

There is no pricing regulation in the Hong Kong healthcare service market. The prices

charged by each healthcare service provider are determined by the market. In order to

deliver quality healthcare services to the public and compete with other competitors,

Human Health positions its healthcare services at the mid-to-high end in terms of pricing

strategy. The company will review its pricing of service every year considering factors like

cost of operations, cost of premises leasing, market price charged by competitors and

inflation rates. More specifically, medication fee would be adjusted based on the

reference retail price of the pharmaceutical drugs, price charged by distributors of the

pharmaceutical drugs and relevant administration costs; and procedure fee would be

adjusted based on the risk and complexity in applying the treatment and the materials

and equipment used.

Types of clients

Its customers can be categorized into the following two parts, namely the Individual

Customers who settle their own medical payments by cash or cash equivalents, such as

government medical vouchers, credit cards or debit cards and Corporate Customers,

which entered into contractual arrangement with Human Healthcare, including i) medical

scheme management companies; ii) corporations; and iii) insurance companies.

Business milestones:

Figure 30: Business milestones Year Event

1997 Human Health established its first medical centre in Kowloon East in Hong Kong

2002 Established its first MTR medical centre at Tseung Kwan O MTR station. Since then, more than 10 are opened at MTR stations

2004 Noon and night medical services were offered at medical centres

2006 Commenced its specialties services in Tsim Sha Tsui

2008 Established its first dental centre in Centre

2009 Its one-stop specialist medical centre "Polyhealth Specialists" commenced operation in Jordan

2012 The second specialist medical centre "Polyhealth Specialists" commenced operation in Tseung Kwan O

2013 Poly Dental commenced operations in Jordan

2014 "Polyhealth Orthopaedic & Sports Medicine Centre" and "Polyhealth Physiotherapy & Rehabilitation Centre" commenced operation in Jordan

2014 Acquired a controlling interest in Perfect Life

2014 Network of medical centres covers all 18 districts in Hong Kong

2014 Extended its foothold in the PRC through the establishment of Yingjian Qiye

2015 Entered into JV with Ping An Health

2015 Completed the acquisitions of 3 dental companies

Source: Company

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

25

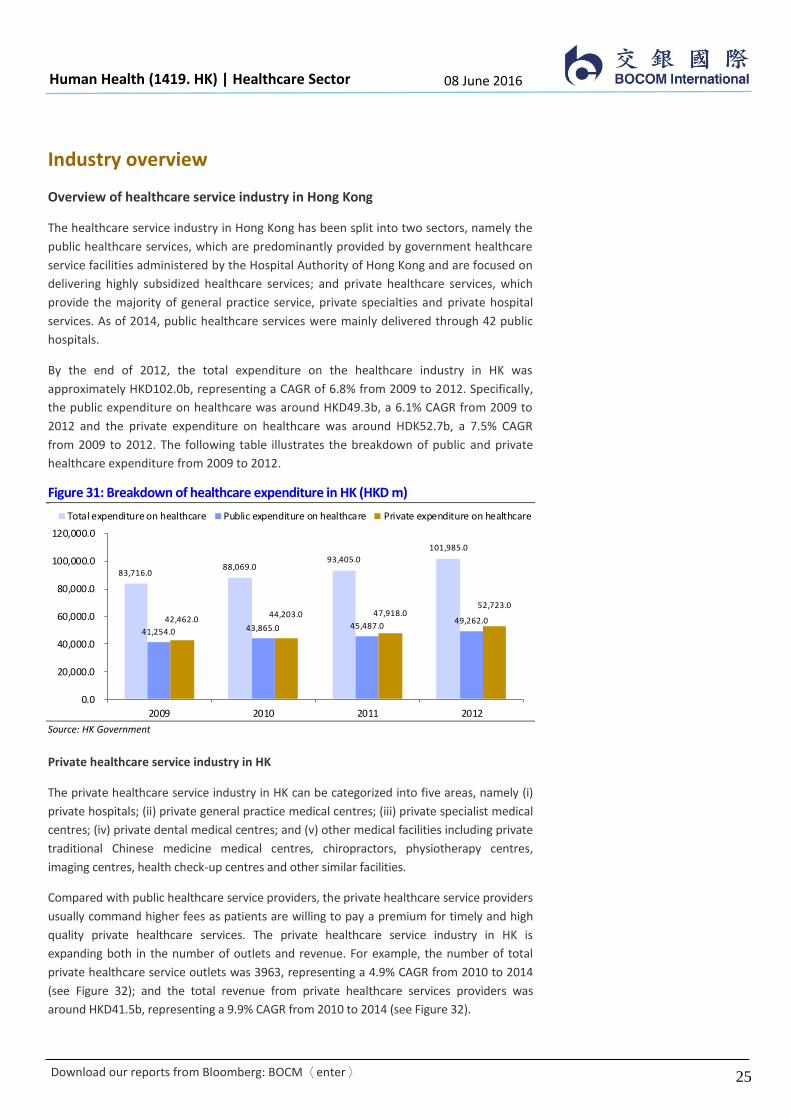

Industry overview

Overview of healthcare service industry in Hong Kong

The healthcare service industry in Hong Kong has been split into two sectors, namely the

public healthcare services, which are predominantly provided by government healthcare

service facilities administered by the Hospital Authority of Hong Kong and are focused on

delivering highly subsidized healthcare services; and private healthcare services, which

provide the majority of general practice service, private specialties and private hospital

services. As of 2014, public healthcare services were mainly delivered through 42 public

hospitals.

By the end of 2012, the total expenditure on the healthcare industry in HK was

approximately HKD102.0b, representing a CAGR of 6.8% from 2009 to 2012. Specifically,

the public expenditure on healthcare was around HKD49.3b, a 6.1% CAGR from 2009 to

2012 and the private expenditure on healthcare was around HDK52.7b, a 7.5% CAGR

from 2009 to 2012. The following table illustrates the breakdown of public and private

healthcare expenditure from 2009 to 2012.

Figure 31: Breakdown of healthcare expenditure in HK (HKD m)

Source: HK Government

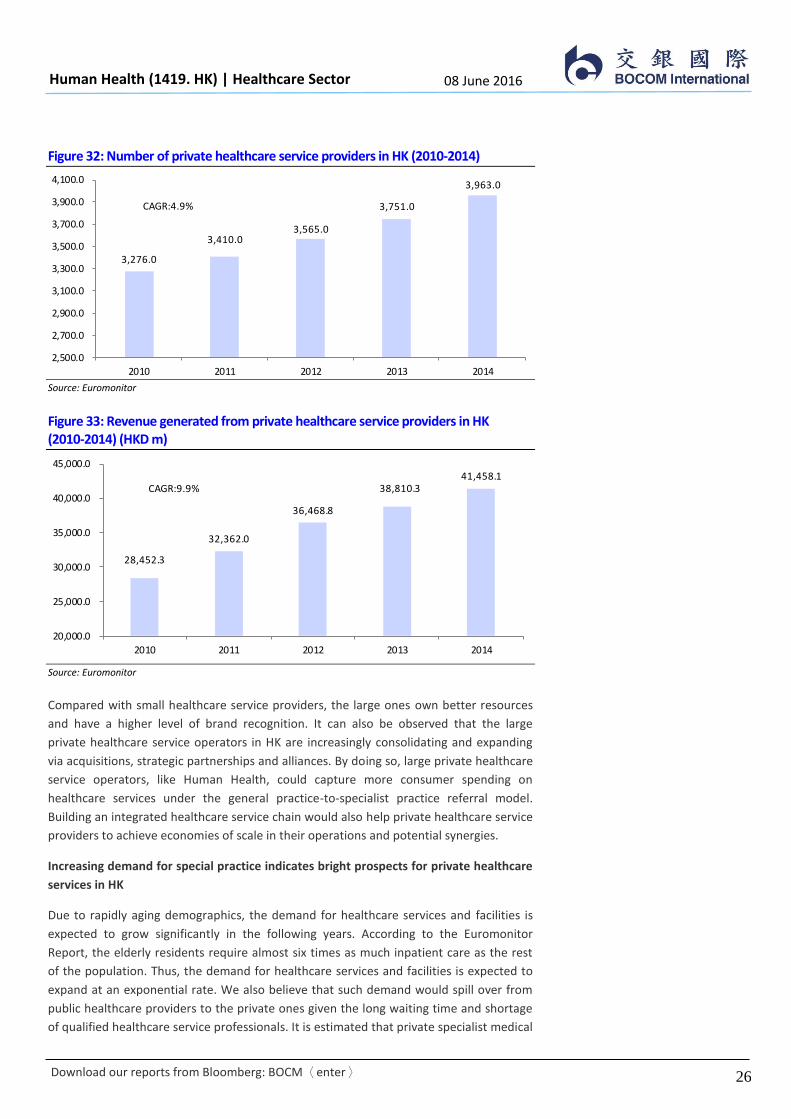

Private healthcare service industry in HK

The private healthcare service industry in HK can be categorized into five areas, namely (i)

private hospitals; (ii) private general practice medical centres; (iii) private specialist medical

centres; (iv) private dental medical centres; and (v) other medical facilities including private

traditional Chinese medicine medical centres, chiropractors, physiotherapy centres,

imaging centres, health check-up centres and other similar facilities.

Compared with public healthcare service providers, the private healthcare service providers

usually command higher fees as patients are willing to pay a premium for timely and high

quality private healthcare services. The private healthcare service industry in HK is

expanding both in the number of outlets and revenue. For example, the number of total

private healthcare service outlets was 3963, representing a 4.9% CAGR from 2010 to 2014

(see Figure 32); and the total revenue from private healthcare services providers was

around HKD41.5b, representing a 9.9% CAGR from 2010 to 2014 (see Figure 32).

83,716.0 88,069.0

93,405.0

101,985.0

41,254.0 43,865.0 45,487.0 49,262.0 42,462.0

44,203.0 47,918.0 52,723.0

0.0

20,000.0

40,000.0

60,000.0

80,000.0

100,000.0

120,000.0

2009 2010 2011 2012

Total expenditure on healthcare Public expenditure on healthcare Private expenditure on healthcare

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

26

Figure 32: Number of private healthcare service providers in HK (2010-2014)

Source: Euromonitor

Figure 33: Revenue generated from private healthcare service providers in HK (2010-2014) (HKD m)

Source: Euromonitor

Compared with small healthcare service providers, the large ones own better resources

and have a higher level of brand recognition. It can also be observed that the large

private healthcare service operators in HK are increasingly consolidating and expanding

via acquisitions, strategic partnerships and alliances. By doing so, large private healthcare

service operators, like Human Health, could capture more consumer spending on

healthcare services under the general practice-to-specialist practice referral model.

Building an integrated healthcare service chain would also help private healthcare service

providers to achieve economies of scale in their operations and potential synergies.

Increasing demand for special practice indicates bright prospects for private healthcare

services in HK

Due to rapidly aging demographics, the demand for healthcare services and facilities is

expected to grow significantly in the following years. According to the Euromonitor

Report, the elderly residents require almost six times as much inpatient care as the rest

of the population. Thus, the demand for healthcare services and facilities is expected to

expand at an exponential rate. We also believe that such demand would spill over from

public healthcare providers to the private ones given the long waiting time and shortage

of qualified healthcare service professionals. It is estimated that private specialist medical

3,276.0

3,410.0 3,565.0

3,751.0

3,963.0

2,500.0

2,700.0

2,900.0

3,100.0

3,300.0

3,500.0

3,700.0

3,900.0

4,100.0

2010 2011 2012 2013 2014

CAGR:4.9%

28,452.3

32,362.0

36,468.8

38,810.3 41,458.1

20,000.0

25,000.0

30,000.0

35,000.0

40,000.0

45,000.0

2010 2011 2012 2013 2014

CAGR:9.9%

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

27

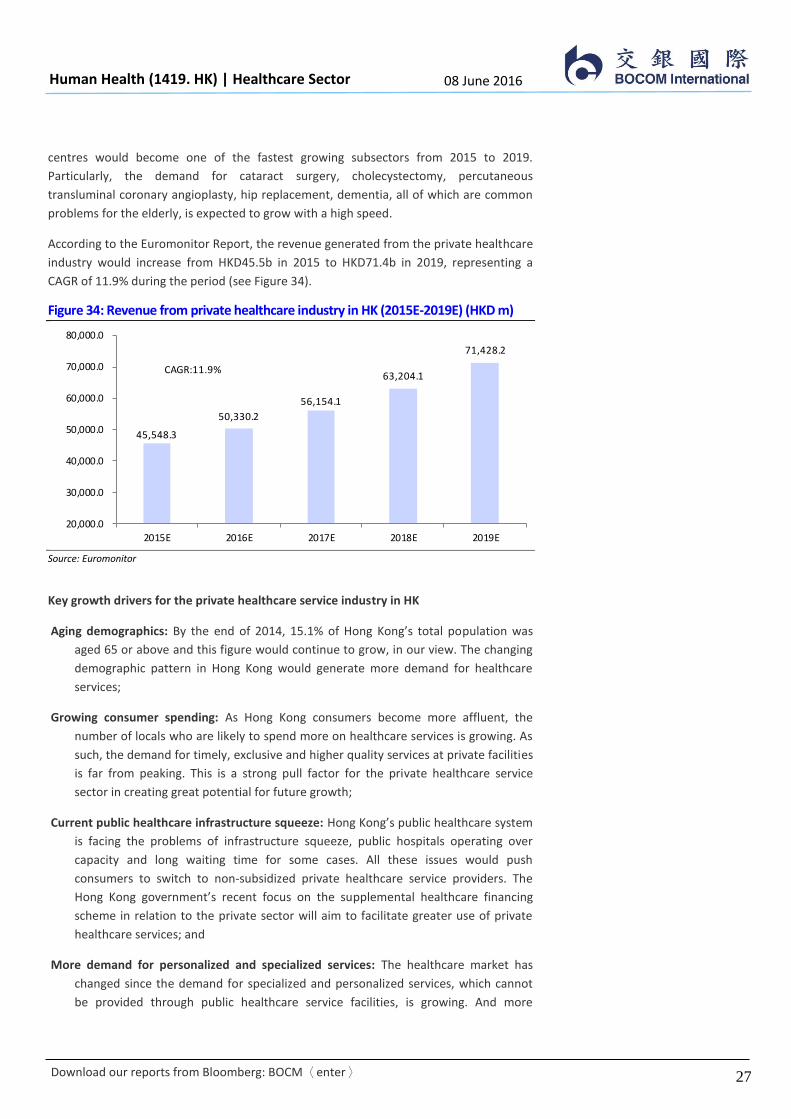

centres would become one of the fastest growing subsectors from 2015 to 2019.

Particularly, the demand for cataract surgery, cholecystectomy, percutaneous

transluminal coronary angioplasty, hip replacement, dementia, all of which are common

problems for the elderly, is expected to grow with a high speed.

According to the Euromonitor Report, the revenue generated from the private healthcare

industry would increase from HKD45.5b in 2015 to HKD71.4b in 2019, representing a

CAGR of 11.9% during the period (see Figure 34).

Figure 34: Revenue from private healthcare industry in HK (2015E-2019E) (HKD m)

Source: Euromonitor

Key growth drivers for the private healthcare service industry in HK

Aging demographics: By the end of 2014, 15.1% of Hong Kong’s total population was

aged 65 or above and this figure would continue to grow, in our view. The changing

demographic pattern in Hong Kong would generate more demand for healthcare

services;

Growing consumer spending: As Hong Kong consumers become more affluent, the

number of locals who are likely to spend more on healthcare services is growing. As

such, the demand for timely, exclusive and higher quality services at private facilities

is far from peaking. This is a strong pull factor for the private healthcare service

sector in creating great potential for future growth;

Current public healthcare infrastructure squeeze: Hong Kong’s public healthcare system

is facing the problems of infrastructure squeeze, public hospitals operating over

capacity and long waiting time for some cases. All these issues would push

consumers to switch to non-subsidized private healthcare service providers. The

Hong Kong government’s recent focus on the supplemental healthcare financing

scheme in relation to the private sector will aim to facilitate greater use of private

healthcare services; and

More demand for personalized and specialized services: The healthcare market has

changed since the demand for specialized and personalized services, which cannot

be provided through public healthcare service facilities, is growing. And more

45,548.3

50,330.2

56,154.1

63,204.1

71,428.2

20,000.0

30,000.0

40,000.0

50,000.0

60,000.0

70,000.0

80,000.0

2015E 2016E 2017E 2018E 2019E

CAGR:11.9%

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

28

consumers would turn to private healthcare facilities to seek better healthcare

services despite the relatively higher costs.

Entry barriers for the private healthcare industry in HK

We found several entry barriers, namely shortage of professionals, a lack of an

appropriate network of partners, difficulty in attracting patients, and a lack of reputation,

for potential new entrants into the market.

Figure 35: Entry barriers for the private healthcare industry in HK

Shortage of professional manpower:

Doctors are in short supply and medical facilities cannot be operated without

certified and registered medical professionals, and this would make it

difficult for new competitors to enter the market;

Lack of an appropriate network of partners:

Economies of scale in operation and synergies can be achieved with an

integrated healthcare service chain, network and partnerships. An

appropriate network of partners is critical to developing private healthcare

chains in HK. It is difficult for the new competitors to build a qualified

network and partnerships;

Difficulty in attracting patients:

New entrants may find it hard to attract patients as new industry players either

join a certain healthcare service network or a group of affiliated medical

centres, which has a large pool of potential customers;

Lack of reputation:

It is difficult for the new entrants to build a reliable reputation, which is crucial to

brand building.

Source: BOCOM Int’l

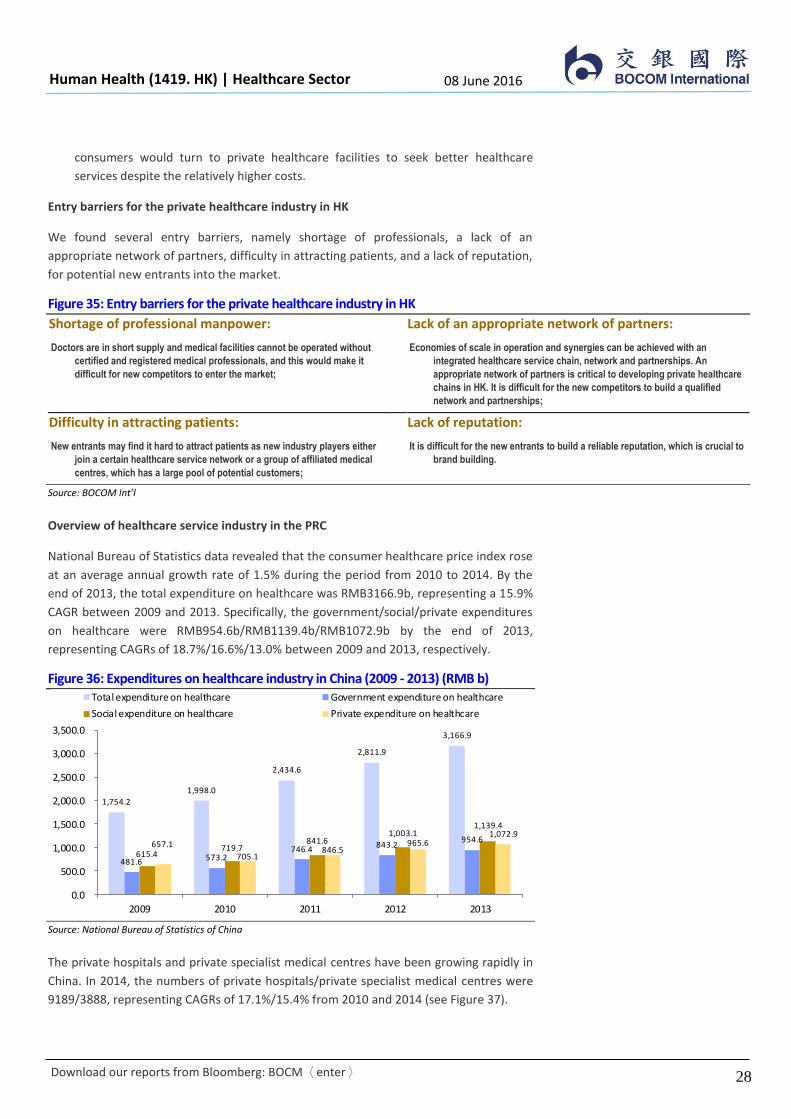

Overview of healthcare service industry in the PRC

National Bureau of Statistics data revealed that the consumer healthcare price index rose

at an average annual growth rate of 1.5% during the period from 2010 to 2014. By the

end of 2013, the total expenditure on healthcare was RMB3166.9b, representing a 15.9%

CAGR between 2009 and 2013. Specifically, the government/social/private expenditures

on healthcare were RMB954.6b/RMB1139.4b/RMB1072.9b by the end of 2013,

representing CAGRs of 18.7%/16.6%/13.0% between 2009 and 2013, respectively.

Figure 36: Expenditures on healthcare industry in China (2009 - 2013) (RMB b)

Source: National Bureau of Statistics of China

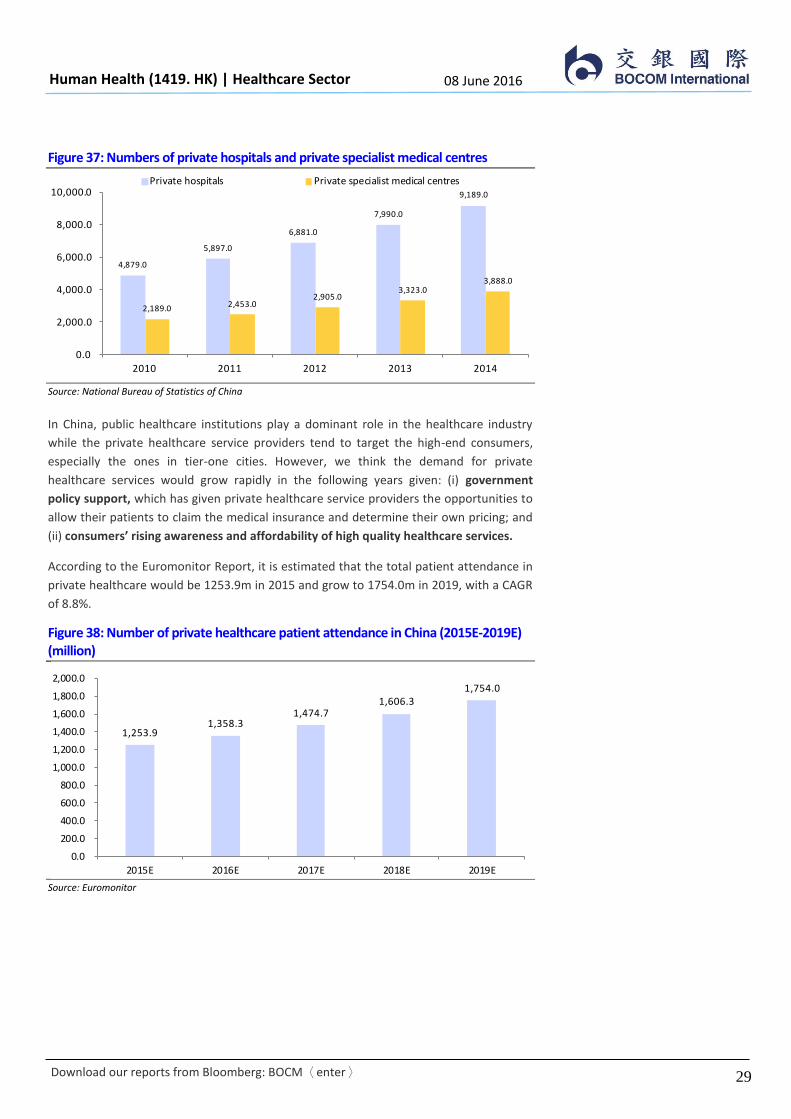

The private hospitals and private specialist medical centres have been growing rapidly in

China. In 2014, the numbers of private hospitals/private specialist medical centres were

9189/3888, representing CAGRs of 17.1%/15.4% from 2010 and 2014 (see Figure 37).

1,754.2

1,998.0

2,434.6

2,811.9

3,166.9

481.6 573.2 746.4

843.2 954.6

615.4 719.7

841.6 1,003.1

1,139.4

657.1

705.1 846.5

965.6 1,072.9

0.0

500.0

1,000.0

1,500.0

2,000.0

2,500.0

3,000.0

3,500.0

2009 2010 2011 2012 2013

Total expenditure on healthcare Government expenditure on healthcare

Social expenditure on healthcare Private expenditure on healthcare

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

29

Figure 37: Numbers of private hospitals and private specialist medical centres

Source: National Bureau of Statistics of China

In China, public healthcare institutions play a dominant role in the healthcare industry

while the private healthcare service providers tend to target the high-end consumers,

especially the ones in tier-one cities. However, we think the demand for private

healthcare services would grow rapidly in the following years given: (i) government

policy support, which has given private healthcare service providers the opportunities to

allow their patients to claim the medical insurance and determine their own pricing; and

(ii) consumers’ rising awareness and affordability of high quality healthcare services.

According to the Euromonitor Report, it is estimated that the total patient attendance in

private healthcare would be 1253.9m in 2015 and grow to 1754.0m in 2019, with a CAGR

of 8.8%.

Figure 38: Number of private healthcare patient attendance in China (2015E-2019E) (million)

Source: Euromonitor

4,879.0

5,897.0

6,881.0

7,990.0

9,189.0

2,189.0 2,453.0 2,905.0

3,323.0 3,888.0

0.0

2,000.0

4,000.0

6,000.0

8,000.0

10,000.0

2010 2011 2012 2013 2014

Private hospitals Private specialist medical centres

1,253.9 1,358.3

1,474.7 1,606.3

1,754.0

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

2,000.0

2015E 2016E 2017E 2018E 2019E

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

30

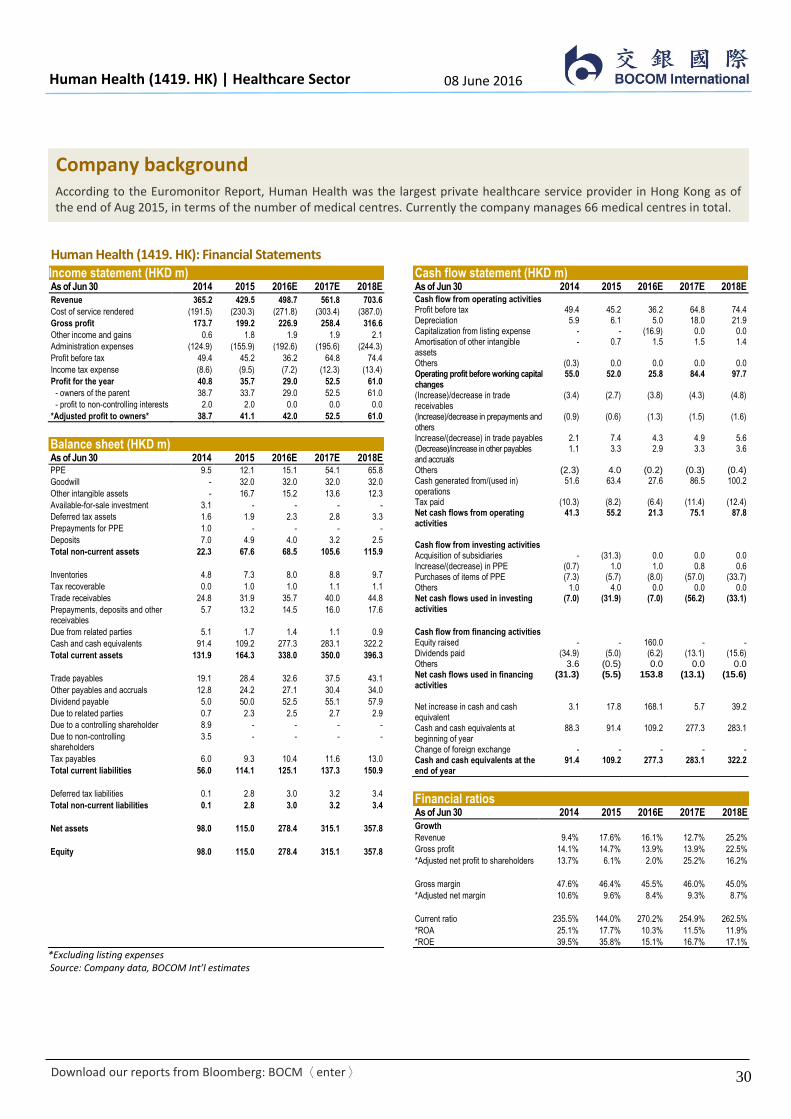

Company background According to the Euromonitor Report, Human Health was the largest private healthcare service provider in Hong Kong as of the end of Aug 2015, in terms of the number of medical centres. Currently the company manages 66 medical centres in total.

Human Health (1419. HK): Financial Statements Income statement (HKD m) As of Jun 30 2014 2015 2016E 2017E 2018E

Revenue 365.2 429.5 498.7 561.8 703.6

Cost of service rendered (191.5) (230.3) (271.8) (303.4) (387.0)

Gross profit 173.7 199.2 226.9 258.4 316.6

Other income and gains 0.6 1.8 1.9 1.9 2.1

Administration expenses (124.9) (155.9) (192.6) (195.6) (244.3)

Profit before tax 49.4 45.2 36.2 64.8 74.4

Income tax expense (8.6) (9.5) (7.2) (12.3) (13.4)

Profit for the year 40.8 35.7 29.0 52.5 61.0

- owners of the parent 38.7 33.7 29.0 52.5 61.0

- profit to non-controlling interests 2.0 2.0 0.0 0.0 0.0

*Adjusted profit to owners* 38.7 41.1 42.0 52.5 61.0

Balance sheet (HKD m) As of Jun 30 2014 2015 2016E 2017E 2018E PPE 9.5 12.1 15.1 54.1 65.8

Goodwill - 32.0 32.0 32.0 32.0

Other intangible assets - 16.7 15.2 13.6 12.3

Available-for-sale investment 3.1 - - - -

Deferred tax assets 1.6 1.9 2.3 2.8 3.3

Prepayments for PPE 1.0 - - - -

Deposits 7.0 4.9 4.0 3.2 2.5

Total non-current assets 22.3 67.6 68.5 105.6 115.9

Inventories 4.8 7.3 8.0 8.8 9.7

Tax recoverable 0.0 1.0 1.0 1.1 1.1

Trade receivables 24.8 31.9 35.7 40.0 44.8

Prepayments, deposits and other receivables

5.7 13.2 14.5 16.0 17.6

Due from related parties 5.1 1.7 1.4 1.1 0.9

Cash and cash equivalents 91.4 109.2 277.3 283.1 322.2

Total current assets 131.9 164.3 338.0 350.0 396.3

Trade payables 19.1 28.4 32.6 37.5 43.1

Other payables and accruals 12.8 24.2 27.1 30.4 34.0

Dividend payable 5.0 50.0 52.5 55.1 57.9

Due to related parties 0.7 2.3 2.5 2.7 2.9

Due to a controlling shareholder 8.9 - - - -

Due to non-controlling shareholders

3.5 - - - -

Tax payables 6.0 9.3 10.4 11.6 13.0

Total current liabilities 56.0 114.1 125.1 137.3 150.9

Deferred tax liabilities 0.1 2.8 3.0 3.2 3.4

Total non-current liabilities 0.1 2.8 3.0 3.2 3.4

Net assets 98.0 115.0 278.4 315.1 357.8

Equity 98.0 115.0 278.4 315.1 357.8

Cash flow statement (HKD m) As of Jun 30 2014 2015 2016E 2017E 2018E Cash flow from operating activities Profit before tax 49.4 45.2 36.2 64.8 74.4 Depreciation 5.9 6.1 5.0 18.0 21.9 Capitalization from listing expense - - (16.9) 0.0 0.0 Amortisation of other intangible assets

- 0.7 1.5 1.5 1.4

Others (0.3) 0.0 0.0 0.0 0.0 Operating profit before working capital changes

55.0 52.0 25.8 84.4 97.7

(Increase)/decrease in trade receivables

(3.4) (2.7) (3.8) (4.3) (4.8)

(Increase)/decrease in prepayments and others

(0.9) (0.6) (1.3) (1.5) (1.6)

Increase/(decrease) in trade payables 2.1 7.4 4.3 4.9 5.6 (Decrease)/increase in other payables and accruals

1.1 3.3 2.9 3.3 3.6

Others (2.3) 4.0 (0.2) (0.3) (0.4) Cash generated from/(used in) operations

51.6 63.4 27.6 86.5 100.2

Tax paid (10.3) (8.2) (6.4) (11.4) (12.4) Net cash flows from operating activities

41.3 55.2 21.3 75.1 87.8

Cash flow from investing activities Acquisition of subsidiaries - (31.3) 0.0 0.0 0.0 Increase/(decrease) in PPE (0.7) 1.0 1.0 0.8 0.6 Purchases of items of PPE (7.3) (5.7) (8.0) (57.0) (33.7) Others 1.0 4.0 0.0 0.0 0.0 Net cash flows used in investing activities

(7.0) (31.9) (7.0) (56.2) (33.1)

Cash flow from financing activities Equity raised - - 160.0 - - Dividends paid (34.9) (5.0) (6.2) (13.1) (15.6) Others 3.6 (0.5) 0.0 0.0 0.0 Net cash flows used in financing activities

(31.3) (5.5) 153.8 (13.1) (15.6)

Net increase in cash and cash equivalent

3.1 17.8 168.1 5.7 39.2

Cash and cash equivalents at beginning of year

88.3 91.4 109.2 277.3 283.1

Change of foreign exchange - - - - - Cash and cash equivalents at the end of year

91.4 109.2 277.3 283.1 322.2

Financial ratios As of Jun 30 2014 2015 2016E 2017E 2018E

Growth

Revenue 9.4% 17.6% 16.1% 12.7% 25.2%

Gross profit 14.1% 14.7% 13.9% 13.9% 22.5%

*Adjusted net profit to shareholders 13.7% 6.1% 2.0% 25.2% 16.2%

Gross margin 47.6% 46.4% 45.5% 46.0% 45.0%

*Adjusted net margin 10.6% 9.6% 8.4% 9.3% 8.7%

Current ratio 235.5% 144.0% 270.2% 254.9% 262.5%

*ROA 25.1% 17.7% 10.3% 11.5% 11.9%

*ROE 39.5% 35.8% 15.1% 16.7% 17.1%

*Excluding listing expenses Source: Company data, BOCOM Int’l estimates

Download our reports from Bloomberg: BOCM〈enter〉

08 June 2016 Human Health (1419. HK) | Healthcare Sector

31

BOCOM International

11/F, Man Yee Building, 68 Des Voeux Road, Central, Hong Kong

Main: + 852 3710 3328 Fax: + 852 3798 0133 www.bocomgroup.com

Rating System

Company Rating Sector Rating Buy: Expect more than 20% upside in 12 months Outperform (“OP”): Expect more than 10% upside in 12 months

LT Buy: Expect more than 20% upside but longer than 12 months Market perform (“MP”): Expect low volatility

Neutral: Expect low volatility Underperform (“UP”): Expect more than 10% downside in 12 months

Sell: Expect more than 20% downside in 12 months

Research Team

Head of Research @bocomgroup.com Head of Research/ Strategy @bocomgroup.com

Raymond CHENG, CFA, CPA, CA (852) 2977 9393 raymond.cheng Hao HONG, CFA (852) 2977 9384 hao.hong

Banks/Network Financials Mid-Cap Industrial & Building Materials/ Automobile

Shanshan LI, CFA (86) 10 8800 9788 - 8058 lishanshan Angus CHAN (852) 2977 9392 angus.chan

Li WAN, CFA (86) 10 8800 9788 - 8051 wanli

Hannah HAN (86) 10 8800 9788 - 8055 hannah.han

Consumer Oil & Gas/ Gas Utilities

Summer WANG, CFA (852) 2977 9221 summer.wang Tony LIU (852) 2977 9390 xutong.liu

Shawn WU (852) 2977 9386 shawn.wu

Environmental Services Property

Wallace CHENG (852) 2977 9387 wallace.cheng Alfred LAU, CFA, FRM (852) 2977 9235 alfred.lau

Philip TSE, CFA, FRM (852) 2977 9220 philip.tse

Luella GUO (852) 2977 9211 luella.guo

Gaming & Leisure Renewable Energy

Alfred LAU, CFA, FRM (852) 2977 9235 alfred.lau Louis SUN (86) 21 6065 3606 louis.sun

Healthcare Technology

David LI (852) 2977 9203 david.li Chris YIM (852) 2977 9243 christopher.yim

Insurance & Brokerage Telecom & Small/ Mid-Caps

Jupiter ZHENG (852) 2977 9389 jupiter.zheng Zhiwu LI (852) 2977 9209 lizhiwu

Jennifer ZHANG (852) 2977 9250 yufan.zhang

Internet Transportation & Industrial

Yuan MA, PhD (86) 10 8800 9788 - 8039 yuan.ma Geoffrey CHENG, CFA (852) 2977 9380 geoffrey.cheng

Connie GU, CPA (86) 10 8800 9788 - 8045 conniegu Fay ZHOU (852) 2977 9381 fay.zhou

Mengqi SUN (86) 10 8800 9788 - 8048 mengqi.sun

08 June 2016 Human Health (1419. HK) | Healthcare Sector

Download our reports from Bloomberg: BOCM〈enter〉

32

Analyst Certification The authors of this report, hereby declare that: (i) all of the views expressed in this report accurately reflect their personal views about any and all of the subject securities or issuers; and (ii) no part of any of their compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in this report; (iii) no insider information/ non-public price-sensitive information in relation to the subject securities or issuers which may influence the recommendations were being received by the authors.

The authors of this report further confirm that (i) neither they nor their respective associates (as defined in the Code of Conduct issued by the Hong Kong Securities and Futures Commission) have dealt in or traded in the stock(s) covered in this research report within 30 calendar days prior to the date of issue of the report; (ii)) neither they nor their respective associates serve as an officer of any of the Hong Kong listed companies covered in this report; and (iii) neither they nor their respective associates have any financial interests in the stock(s) covered in this report.