Embed Size (px)

Citation preview

1

Economic Diversification for Sustainable and Inclusive Growth

Vandana Chandra (PRMED)Inclusive Growth Course

March 24, 2009

2

Rationale

• By the mid-1990s, most developing countries had implemented the macroeconomic reforms that are a necessary condition for economic growth. Various other reforms also followed. BUT

• Economic diversification that was expected to follow ex post reform and is essential for sustained prosperity and inclusive growth did not ensue in many of the Bank’s client countries.

• Absence of economic diversification – has become the source of social and political pressures.

• Impatient to diversify, some client governments have announced industrial policies targeted at industries they believe can deliver faster and more inclusive growth.

• Government’s choice of industries is often ad hoc and uninformed, and targets non-traditional industries in which the country has no comparative advantage. Most choices are also driven by pro-poor or inclusive growth considerations.

• This recent shift in public policy from an industry-neutral to an industry-specific approach in our client countries has created among their development partners a demand for analytical tools to study the economic growth implications of active development policies.

3

Course Objective

• Introduce questions and concepts that can be useful in exploring the nexus between economic diversification and income-enhancing, sustainable, and inclusive growth.

• Provide a measure of the income potential of a country’s total exports based on Hausmann, Hwang and Rodrik (2007).

• Offer an EXCEL-based toolkit (A) to study these approaches and measures.

• The country economist (CE) may not be able to dissuade an impatient client (government) from implementing its industrial policy but may find the concepts useful in informing policy decisions.

4

Warning

• Industrial policy discussions warrant industry-level analysis. BUT• The toolkits are not intended to produce a menu of industries that

should be recommended to clients as candidates that deserve government’s special attention.

• Wanting a hi Tech industry does not imply that the country will be able to develop an efficient and competitive hi Tech industry .

• The application of the toolkit is a desk exercise that uses disaggregated product-level statistical evidence from the trading patterns of all countries, developed and developing over a long time series.

• Strength: Statistically robust. Objective. Transparent.• Weakness: Cannot substitute for in-depth country-knowledge. • Needs to be complemented with a proper field assessment of the

state of existing industries, what works and why.

Why does economic diversification matter for sustainable growth in developing countries? -Outline

1. How can we measure economic diversification? 2. What is the relationship between economic diversification and sustained

growth ?3. Openness, diversification and growth – some stylized facts 4. Are some patterns of diversification more income-enhancing than

others? Examine the traditional approaches to diversification.5. Explain PRODY - a concept that measures a product or industry’s export

sophistication by linking it with a notional level of income. 6. Explain EXPY - a concept that measures the sophistication of a country’s

export basket by linking it with a notional level of per capita income. 7. The framework we use is useful for cross-country and country-specific

analysis over a long period. Example: an application to Burkina Faso.

5

6

Two simple measures of economic diversification

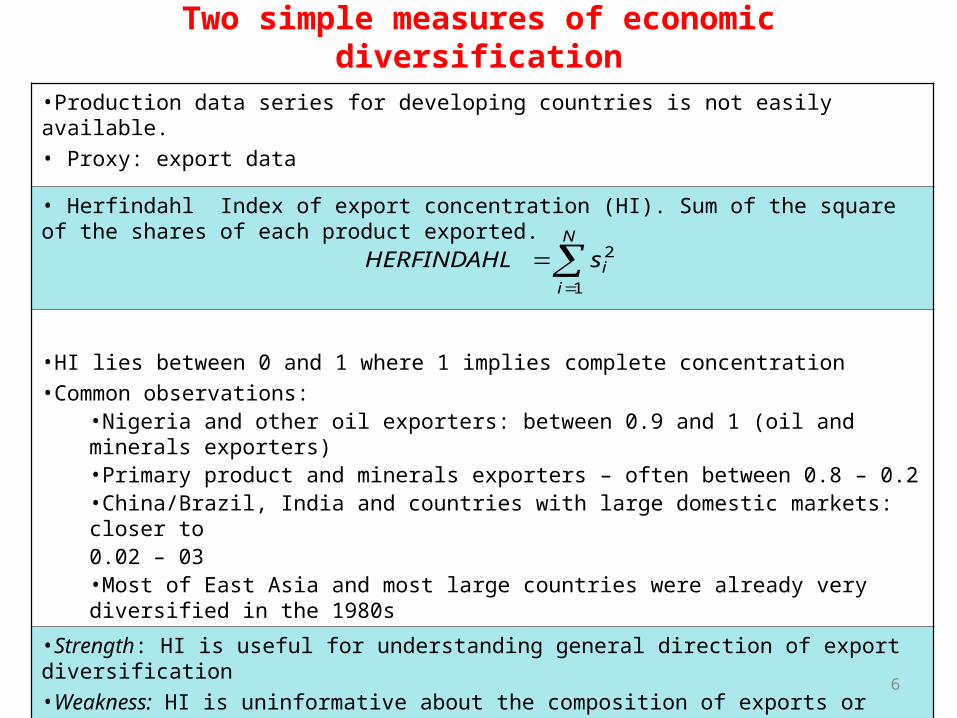

•Production data series for developing countries is not easily available. • Proxy: export data

• Herfindahl Index of export concentration (HI). Sum of the square of the shares of each product exported.

•HI lies between 0 and 1 where 1 implies complete concentration•Common observations:

•Nigeria and other oil exporters: between 0.9 and 1 (oil and minerals exporters)•Primary product and minerals exporters – often between 0.8 – 0.2•China/Brazil, India and countries with large domestic markets: closer to 0.02 – 03 •Most of East Asia and most large countries were already very diversified in the 1980s

•Strength: HI is useful for understanding general direction of export diversification •Weakness: HI is uninformative about the composition of exports or their income potential

6

N

iisHERFINDAHL

1

2

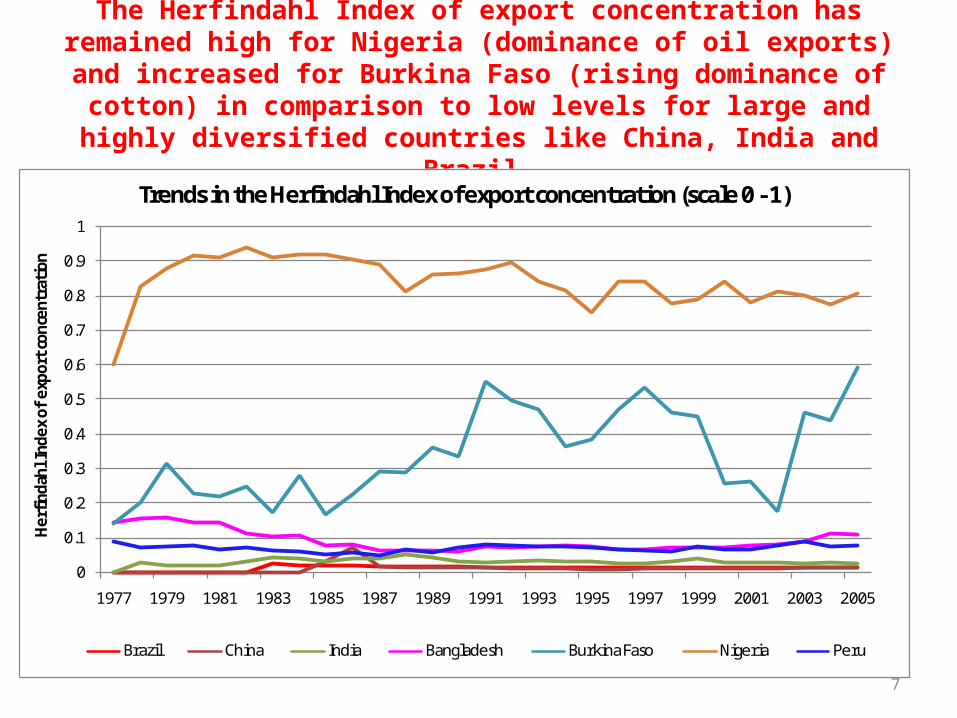

The Herfindahl Index of export concentration has remained high for Nigeria (dominance of oil exports) and increased for Burkina Faso (rising

dominance of cotton) in comparison to low levels for large and highly diversified countries like China, India and Brazil.

7

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

Her

finda

hl I

ndex

of

expo

rt co

ncen

trati

on

Trends in the Herfindahl Index of export concentration (scale 0 - 1)

Brazil China India Bangladesh Burkina Faso Nigeria Peru

Another measure of diversification: trends in the export share of the top 5, 10 or 20 products is consistent with the Herfindahl Index

8

0

10

20

30

40

50

60

1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

Shar

e of

tot

al e

xpor

ts (%

)

Share of the top 5 products in total exports in large economies

Brazil China South Africa India

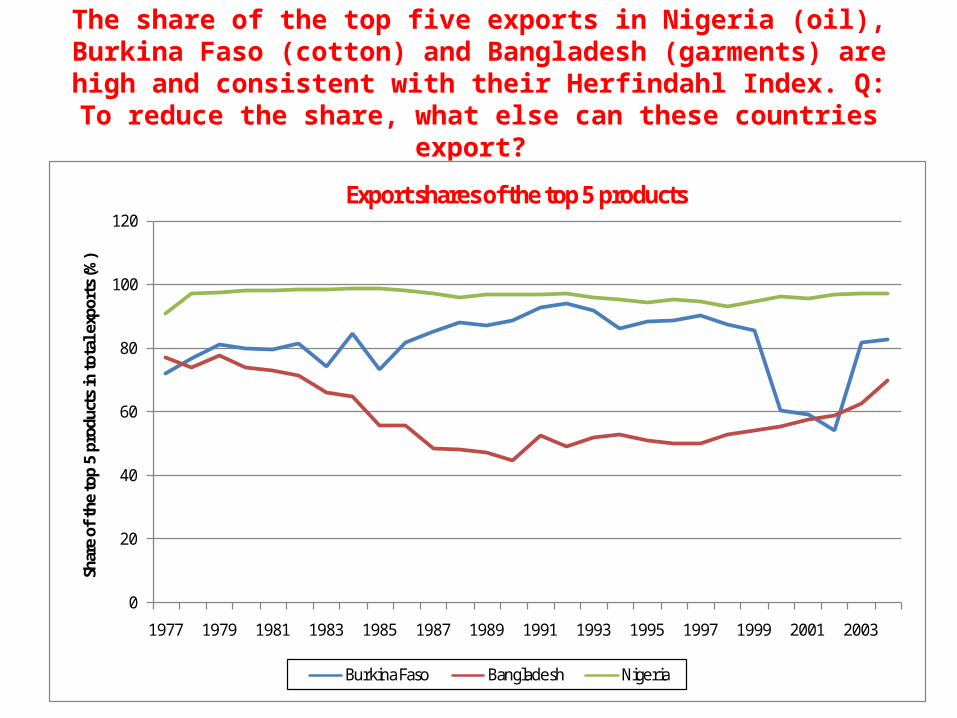

The share of the top five exports in Nigeria (oil), Burkina Faso (cotton) and Bangladesh (garments) are high and consistent with their Herfindahl Index.

Q: To reduce the share, what else can these countries export?

9

0

20

40

60

80

100

120

1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003

Shar

e of

the

top

5 pr

oduc

ts in

tota

l exp

orts

(%)

Export shares of the top 5 products

Burkina Faso Bangladesh Nigeria

10

The relationship between sustained growth and openness/exports

Conventional theory - as economies diversify, their income grows (positive relationship). Hesse (2009) confirms that diversification and per capita income are positively correlated.

Imbs and Wacziarg (2003) – empirical evidence indicates that there is a U-shaped relationship between sectoral diversification and income. Initially, negative, i.e., as diversification increases, per capita income increases. After reaching $10,000 (2000 constant USD), sectoral diversification decreases and the relationship becomes positive (based on employment and production data for developed and developing countries).

In natural resource-based economies, diversification helps to dissipate the negative effects of terms of trade shocks. In more developed ones, agglomeration effects reinforce economic concentration.

We find that for most of the Bank’s client countries, the relationship is L-shaped. Along the vertical axis are low income countries in Sub-Saharan Africa, South Asia and even China. The range of the HI is very large. Close to 0.9 for Nigeria and 0.02 for India!

Hesse (2009) confirms that diversification and per capita income are positively correlated.

We need a better measure of diversification that links exports to a country’s per capita GDP. Q: What type of products should China export to catch up with Brazil? Cannot answer with the HI.

10

11

In low income countries, the relationship between HI and income is L-shaped. The HI for China and Korea is similar but it does not tell us what China must

export to catch up with Korea.

ETH

KEN

BDI

NGA

TZA

BFA

ZWE

UGA

ZAF

AGO

BWA

TGO

GAB

SYC

RWA

COG

ZAR

LBRMOZ

MLI

ZMB

GHA

TCD

GNQ

ZAR

ETH

TZA

BDI

GHA

LBR

ZMB

ZAF

MLI

SYC

MOZ

RWA

GNQ

GAB

COG

ZWE

AGO

UGA

NGA

BWA

BFA

TGO

TCD

KEN

ZMB

ZAR

MLI

AGO

GNQ

MOZ

TGO

BFA

LBRSYC

COG

BDI

BWA

NGA

GHA

TZA

RWA

ZAF

ZWE

GAB

ETH

UGA

KEN

TCD

KEN

MLI

TGO

TCD

AGO

ETH

COG

RWA

ZAF

ZAR

LBR

UGA

BWA

BDI

BFA

GNQ

GHA

NGA

GAB

ZWE

SYC

TZA

MOZ

ZMB

NGA

ZAF

TCD

RWA

GNQ

ETH

BDI

UGA

LBR

TZA

ZAR

ZWE

ZMB

GHA

GABBWA

AGO

MOZ

KEN

MLI

BFA

COG

SYC

TGO

VENVENVENVENVEN

MEX

CHL

ARGIDN HKGCHN BRATHACHNMEX HKGTHAIDN

CHL

ARGBRA MEXTHAIDN

CHNARG

BRA HKG

CHL

HKGTHA

CHL

BRAIDNCHN

ARGMEXIDN THA MEX HKGBRAARG

CHL

CHN

SGP

BHR

HKG

BRB MAC

MLT

KOR

MLT

MAC

HKG

BRB

BHR

SGP

KORKORMACBRB

MLTBHR

SGP

HKGHKG

MLT

MACKOR

BHR

SGPBRB MAC

BHR

SGP

HKG

MLT

KOR

BRB

0.2

.4.6

.8H

erf

inda

hl In

dex o

f E

xp

ort

s

0 5000 10000 15000 20000 25000GDP per capita constant US$(2000)

Author's calculations

Data Source: UN Comtrade (SITC Rev. 2 - 4 digit) and the World Bank (World Development Indicators)

GDP per capita and Export Diversification, 2000-2004

11

China

Korea

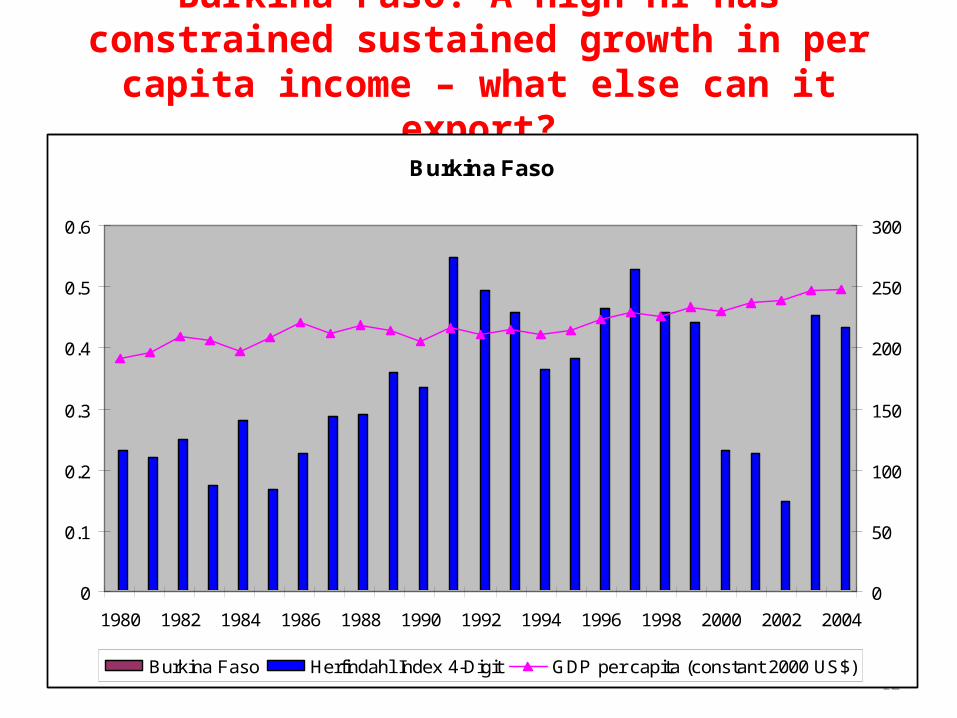

Burkina Faso: A high HI has constrained sustained growth in per capita income – what else can it export?

12

Burkina Faso

0

0.1

0.2

0.3

0.4

0.5

0.6

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

0

50

100

150

200

250

300

Burkina Faso Herfindahl Index 4-Digit GDP per capita (constant 2000 US$)

A drop in HI drove growth in per capita GDP but the level of the HI is still very high and of income too low. What else can

Bangladesh export?

13

Bangladesh

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

0

50

100

150

200

250

300

350

400

450

Bangladesh Herfindahl Index 4-Digit GDP per capita (constant 2000 US$)

A low HI has helped but what China exports explains why it has grown so fast

14

China

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

0

200

400

600

800

1000

1200

1400

China Herfindahl Index 4-Digit GDP per capita (constant 2000 US$)

Openness fosters diversification and sustained growth

• Export led-growth played an important role in fostering fast and sustained growth.

• In small or poor countries, the purchasing power of the domestic market is low and exports are often the only source of growth.

• Between 1980 – 2007: in most low and middle income countries, the export/GDP ratio was small – less than 20 percent. In these economies, per capita GDP (constant USD) increased little.

• Examples: Brazil, India, Burkina Faso, Ghana. • In fast growing countries, growth was export-led and compensated

for small domestic markets. A high share of exports in GDP was matched by a faster increase in per capita income. Many countries graduated from a low to a middle income status. Examples: South Korea, Malaysia. More recently, China.

15

Openness and its nexus with per capita income. Note, SSA is more open than even China. What explains the differences in income within a region,

and between regions?

• Macro Stability?

• Openness?

Or

• Is it the Export Mix?

0.2.4.6.8Total exports/GDP, (%)

First_EA

Second_EA

SSAnoZAF

CHN

LAC

SA

Data: WDI and COMTRADE

Regional average Total exports/GDP

1990-95 2000-04

17

Sustained growth was led by exports in East Asia

Growth was export-led in fast growing East Asia

-10

10

30

50

70

90

110

130

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

Exp

orts

of g

oods

& s

ervi

ces

/GD

P (%

)

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

GD

P p

er c

apita

(200

0 co

nsta

nt U

SD

)

China Exports of goods and services (% of GDP) Malaysia Exports of goods and services (% of GDP)

Thailand Exports of goods and services (% of GDP) China GDP per capita (constant 2000 US$)

Malaysia GDP per capita (constant 2000 US$) Thailand GDP per capita (constant 2000 US$)17

18

Herfindahl Index of export concentration (0 – 1) and share of exports in GDP (%) – no clear relationship!

China - HI (0-1) and exports as a share of GDP (%)

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

0

5

10

15

20

25

30

35

40

China Herfindahl Index 4-Digit Exports of goods and services (% of GDP)

Burkina Faso - HI (0-1) and exports as a share of GDP (%)

0

0.1

0.2

0.3

0.4

0.5

0.6

1 3 5 7 9 11 13 15 17 19 21 23 25

0

2

4

6

8

10

12

14

Burkina Faso Herfindahl Index 4-Digit Exports of goods and services (% of GDP)

Bangladesh - HI (0-1) and exports as a share of GDP (%)

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

1 3 5 7 9 11 13 15 17 19 21 23 25

0

2

4

6

8

10

12

14

16

18

Bangladesh Herfindahl Index 4-Digit Exports of goods and services (% of GDP)

Ghana - HI (0-1) and exports as a share of GDP (%)

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

1 3 5 7 9 11 13 15 17 19 21 23 25

0

10

20

30

40

50

60

Ghana Herfindahl Index 4-Digit Exports of goods and services (% of GDP)

18

When can diversification be income-enhancing and inclusive?

1. Is there empirical evidence to suggest that certain patterns of diversification can be more income-enhancing than others?

2. East Asia relied on export diversification in manufactured products to achieve faster and sustained growth. Is the East Asian diversification pattern optimal and feasible for all developing countries that are eager to catch up?

3. Are natural resources a curse for a low income country?” 4. Country-specific level examination:

1. Can Burkina Faso’s (BF) current exports transform it into a MIC even in the next several decades?

2. Do the trends in BF’s exports reflect the level of its technological capabilities and indicate how it compares with comparators, ie., other landlocked, cotton or primary product exporters over the longer term?

19

20

Some hypotheses about the export mix and the growth path

• Technology classification (Lall, 2005)– Links a product to its technology content. – Cereals and fish are primary (PP), minerals are resource-based (RB) and

manufactured products are low, medium or hi tech (LT, MT,HT)

• Is there a natural resource curse? Prebisch and Singer in 50s and 60s and Sachs and Warner ’90s). “Natural Resources are Neither Curse nor Destiny” – Lederman and Maloney, 2006.

• Is Sub-Saharan Africa special? Transactions costs, and risks of manufactured exports (Collier, 1998, 1999), Primary Commodity Dependence and Africa’s Future, Paul Collier (2002), low skills, land abundance (Mayer and Woods, 2001) and low Net TFP (Eifert, Gelb and Ramachandran, 2005); infrastructure (Habiyaremya and Ziesemer,2006).

• Deterministic – These hypotheses suggest that in poor countries, manufactured exports are the PATH to growth

Why natural resources and primary products appear to be a curse?

Ex: the relationship between the export share of cotton and per capita income is negative. Burkina Faso, Benin and Mali did not diversify away

from it.

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

5 5.5 6 6.5 7 7.5

Log of GDP pc (constant US$)

Co

tton

(%

To

tal E

xpo

rts)

TCD

MLI

BFA BEN

SDNTGO

TZACAF KGZ PAK

NICAZE

EGY

TKM

PRY

21

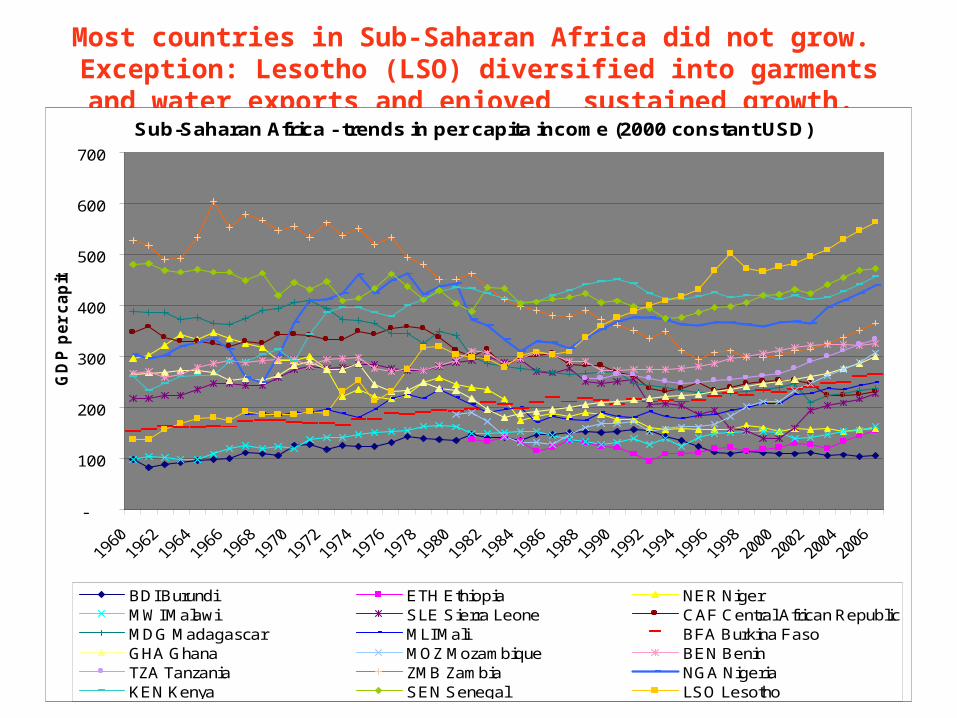

Most countries in Sub-Saharan Africa did not grow. Exception: Lesotho (LSO) diversified into garments and water exports and

enjoyed sustained growth. Sub-Saharan Africa - trends in per capita income (2000 constant USD)

-

100

200

300

400

500

600

700

GD

P p

er

ca

pit

a

BDI Burundi ETH Ethiopia NER NigerMWI Malawi SLE Sierra Leone CAF Central African RepublicMDG Madagascar MLI Mali BFA Burkina FasoGHA Ghana MOZ Mozambique BEN BeninTZA Tanzania ZMB Zambia NGA NigeriaKEN Kenya SEN Senegal LSO Lesotho

Technology hypothesis: High and sustained growth has occurred in countries that export mostly LT, MT and HT products

Cereals and fish are primary (PP), minerals are resource-based (RB) and manufactured products are low, medium or hi tech (LT, MT,HT)

• Problem: Too deterministic and ad hoc. Implies manufactured exports are the only path to growth. Can PP and RB exporters leapfrog into LT, MT and HT exports?

0.2

.4.6

.81

SA LAC SSAnoZAF OECD First_EA

First EA: HKG, TWN, KOR and SGP

1990-95

HT MT

LT RB

HV PP

0.2

.4.6

.81

SA SSAnoZAF LAC OECD First_EA

First EA: HKG, TWN, KOR and SGP

2000-04

HT MT

LT RB

HV PP

Regional export composition, Tech categories

Must all countries export manufactured products to grow?

Trade patterns have changed and are indeterminate in this era of globalization. Production networks are fragmented globally. For example:

1. East Asia – exports mostly Hi-tech products now. China is replicating the East Asian model. Imports parts and exports hi Tech products. They have acquired a competitive advantage in these products.

2. Some other countries have successfully reversed export patterns and discovered new products. Chile has diversified from copper to fish and wine; Columbia from coffee to cut flowers ; Kenya and Uganda from coffee, tea and cotton to fish and flowers. India has reversed the historical flow of services exports. Where the share of new exports is large, income growth has been fast and sustained.

These approaches to diversification do not offer a metric that objectively indicates whether the new products are good or bad for a sustained increase in per capita income.

25

Metric: PRODY denotes a product’s sophistication which suggests a notional level of per capita income

• Designed by Hausmann, Hwang, and Rodrik (2007).• PRODY and EXPY are indexes that measure export

sophistication or which suggest a notional level of income for a product and country’s exports respectively.

• The core idea is that (ceteris paribus) “An economy is better off producing goods that richer countries export.”

• “Countries that export goods associated with higher productivity levels grow more rapidly”

• Sources: Hausmann, Ricardo, Jason Hwang, and Dani Rodrik. 2007. What you export matters. Journal of Economic Growth (U.S.) 12, No. 1:1-25.

• Rodrik, D. (2006). “What’s So Special About China’s Exports,” NBER Working Paper Series, No. 11947.

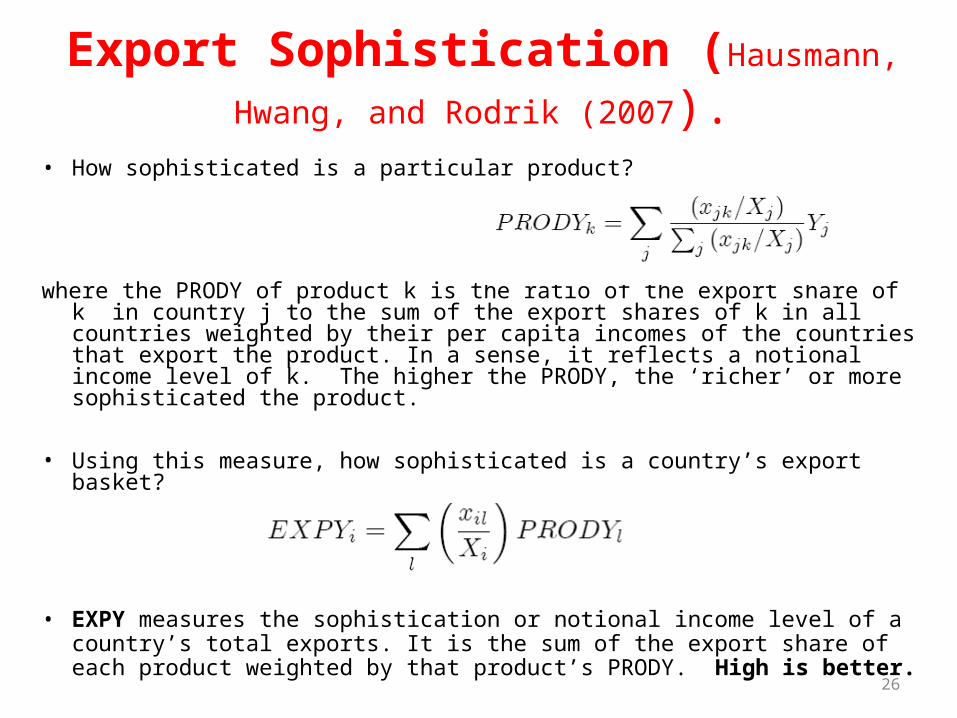

Export Sophistication (Hausmann, Hwang, and Rodrik

(2007).• How sophisticated is a particular product?

where the PRODY of product k is the ratio of the export share of k in country j to the sum of the export shares of k in all countries weighted by their per capita incomes of the countries that export the product. In a sense, it reflects a notional income level of k. The higher the PRODY, the ‘richer’ or more sophisticated the product.

• Using this measure, how sophisticated is a country’s export basket?

• EXPY measures the sophistication or notional income level of a country’s total exports. It is the sum of the export share of each product weighted by that product’s PRODY. High is better. 26

27

PRODY for Selected Products – natural resources are neither curse nor destiny – it all depends on what you do with them

0

5

10

15

20

25E

lect

ron

icm

icro

circ

uits

Inte

rna

lco

mb

ust

ion

Wo

od

an

dre

sin

ba

sed

Te

levi

sio

nre

ceiv

ers

,A

rtic

les

of

lea

the

rK

nitt

ed

/cro

ch.

Fa

bri

cF

ish

, pre

pa

red

or

pre

serv

ed

Pri

ntin

g a

nd

wri

ttin

g p

ap

er

Ba

con

, ha

m &

oth

er

dri

ed

Po

tato

es,

fre

sho

r ch

ille

dC

offe

e, w

he

the

ro

r n

ot r

oa

ste

d

Co

coa

, be

an

s

Fru

it, fr

esh

or

dri

ed

Milk

an

d c

rea

m

Oliv

e O

il

Pa

lm O

il

Ma

ize

(co

rn),

un

mill

ed

PR

OD

Y (

'00

0)

High and Medium TechLow Tech

Resource Based

Primary Products

Source: Authors’ calculations using UN Comtrade Database

28

Certain products have been good for Catch-up in East Asia, (see Rodrik (2006))

• Leapfrogging does not require all exported products to be transformed immediately into high PRODY ones.

• China’s catch up with Hong Kong and Korea occurred when it started exporting some High Prody products.

Country Product Description Prody share (%) Product Description Prody share (%)

Petrol.oils & crude oils from bitum. Minerals 5127 8 Peripheral units,incl.control & ada 13315 4

Cotton(other than linters) not carded 1531 3Parts of and accessories suitable for Office mach and elect. Appliances 13526 4

Other parts & accessories of motor vehicles 13511 3 Footwear 14349 3Fabrics woven of silk or noil or other 8685 3 Children's toys, indoor games, etc 13962 3Cotton yarn 4183 2 Parts of apparatus of radios, TVs, etc. 12278 3

Children's toys, indoor games, etc 13962 8 Electronic microcircuits 15002 9

Watches, watch movements and cases 21281 6Parts of and accessories suitable for Office mach and elect. Appliances 13526 5

Other outer garment of textile fabrics 5155 5 Electronic appliances 13924 5Jersey, pullovers, twinsets, cradigans. 4591 5 Jersey, pullovers, twinsets, cradigans. 4591 4Trousers, breeches, etc of textile fabric. 5022 3 Other outer garment of textile fabrics 5155 3

Footwear 14349 7 Electronic microcircuits 15002 12Fabrics woven of continuous synth. 10361 3 Passenger motos cars, for transport 18851 8Electronic microcircuits 15002 3 Radiotelegraphic and radiotelephonic 18331 8Art. of apparel & colthing accessories 6379 3 Peripheral units,incl.control & ada 13315 4

Jersey, pullovers, twinsets, cradigans. 4591 3Parts of and accessories suitable for Office mach and elect. Appliances 13526 4

1980

-84

2000

-04

Five main exports (2000-04) Five main exports (1980-84)

China

Hong Kong, China

Korea Rep.

29

Manufactured Exports are not the only path to faster and sustainable growthOther developing countries’ success stories are natural resource-based

CountryMain exports, 1980 Shares Prody Country

Main exports, 2004 Shares Prody

Copper alloys 37.4% 6825 Copper alloys 31.2% 6825Flours & meals,of meat/fish 8.1% 10625 Copper ores 16.7% 1825Grapes 4.7% 5492 Fish,frozen 2.5% 5932

Coffee,whether or 60.7% 638 Petrol.oils & crude 19.3% 5261

Sugars,beet and cane 4.2% 1515

Other coal,whether/not pulverized 11.4% 7534

Cotton (other than linters),not car 2.1% 530

Coffee,whether or not roasted 6.2% 638

Cut flowers and foliage 2.5% 2286

Cut flowers and foliage 4.5% 2286

Coffee,whether or not roasted 40.0% 638

Cut flowers and foliage 17.5% 2286

Tea 17.7% 517 Tea 16.2% 517Coffee,whether or not roasted or fr 5.8% 638

Coffee,whether or not roasted 33.0% 638Fish fillets,fresh or chilled 21.0% 6034Cut flowers 6.4% 2286U

gand

a

Keny

aCo

lom

bia

Chile

Uga

nda

Coffee,whether or not roasted 95.3% 638

Chile

Colo

mbi

aKe

nya

USA and Canada: Fish fillet and Frozen Fish

Netherlands: Cut flowers

30

EXPY is a good measure of the export sophistication of a country’s exports. EXPY & GDP per capita are highly correlated

Source: Hausmann, Hwang and Rodrik (2005)

Summing up (1)

1. Openness and diversification matter for sustainable growth. But not any type of diversification. The L-shaped curve for the Herfindahl Index and per capita income in low income countries shows this.

2. There are alternative growth paths for primary and natural resource-based product exporters. They are not cursed.

• To leapfrog and grow faster – a country needs to diversify into and scale up at least some sophisticated (higher PRODY) products.

2. Country and product/industry specificity are key.

• The diversity of country experiences indicates that there is more than one way to do it.

3. Comparative advantage can be created/developed. Technological capabilities can be acquired and can change what you export. There is no need to rely only on your natural endowments to guide export patterns.

4. As usual, there are trade-offs.

Summing up (2)Should we make policy recommendations based on these new

concepts that link a product to its sophistication level – NO.1. EXPY indicates that higher PRODY products can lead to a higher level of per

capita income. BUT it does not tell us which high PRODY products.

2. A higher PRODY suggests that one product is more sophisticated than another.

BUT it does not indicate whether the country has a comparative advantage in

exporting that product.

3. Judging whether a high PRODY product is optimal for a country depends on

whether the country has the technological capabilities and other

complementary inputs required to produce that product profitably.

4. This requires a lot more homework, analysis and in-depth knowledge of what

constrains the emergence and scaling up of high PRODY products that seems

suitable for a country.

An analysis of diversification and growth in Burkina Faso

Brief background: In 1977, BF had a per capita income of US$ 186 (constant 200 dollars). In 2004, after 27 years, it had increased to only $248. Annual growth rate was only 1.1%. Central question: If Burkina Faso wants to become a middle income country,

can it continue to pursue the same growth path that it has tread in the past 30 or more years?

Outline: International comparisons are useful Sources of growth Why exports matter Why diversification matters Into what can it diversify? Whatever it is, it must be income-enhancing diversification. For more details, refer to the diversification and growth chapter in CEM 2009

(draft)

Table 2.1: Trends in per capita Gross National Income in Burkina Faso and Comparators (current PPP US $)

Burkina Faso 86 148 270 269 250 340 400 420 430 Landlocked (LL), cotton

Nepal 65 99 165 205 232.5 270 300 320 340 LL, leather, beans

Lao PDR 378 302 320 420 450 500 580 LL, coffee, wood

Kyrgyz Republic 388 298 400 450 500 590 LL, cotton, gold, tobacco

Uzbekistan 605 515 460 530 610 730 Landlocked

Turkmenistan 850 686 650 LL, nuts, tobacco, cotton

Mongolia 1474 579 475 690 810 1000 1290 LL, wool, wood,minerals

Bolivia 490 851 867 953 960 1020 1110 1260 LL, petroleum, tin

Paraguay 1569 1185 1080 1230 1410 1670 LL,cotton, soya beans, wood

Cambodia 286 305 380 440 490 540 Sya beans, wood, rubber

Senegal 250 366 548 591 485 640 740 760 820 Groundnuts, seafood,min.

Nicaragua 224 484 670 467 738 820 890 930 980 Coffee, cotton, bananas

Sri Lanka 154 234 371 664 875 1070 1200 1350 1540 Tea, rubber

Guatemala 294 611 1101 1328 1700 1930 2080 2250 2440 Cotton, coffee, sugar

Burkina Faso 86 148 270 269 250 340 400 420 430 Landlocked, cotton

Burundi 63 109 231 165 100 90 90 100 110 Landlocked, coffee

Malawi 58 116 168 186 155 220 220 230 250 Landlocked, tobacco

Rwanda 44 112 284 274 218 210 250 280 320 Landlocked, coffee

Uganda 283 243 240 250 270 300 340 Landlocked, cotton, coffee

Mali 70 144 241 293 270 390 450 460 500 Cotton

Benin 114 193 319 328 340 450 510 530 570 Cotton

Zambia 270 483 443 356 323 410 500 640 800 Landlocked, copper Source: WDI

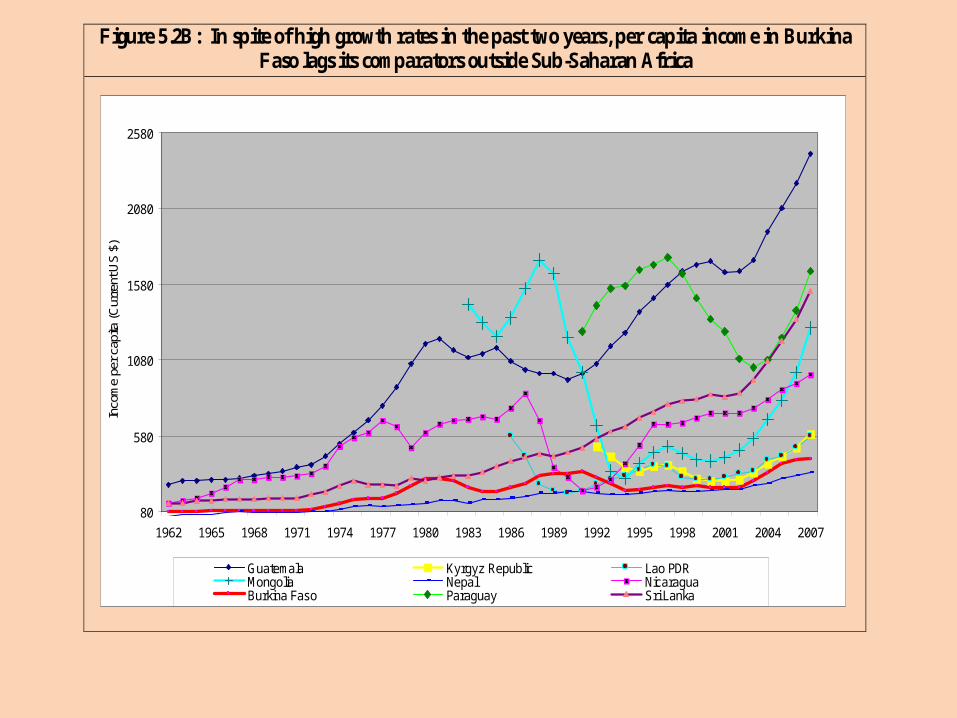

Figure 5.2B: In spite of high growth rates in the past two years, per capita income in Burkina Faso lags its comparators outside Sub-Saharan Africa

80

580

1080

1580

2080

2580

1962 1965 1968 1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007

Inco

me

per

capi

ta (

Cur

rent

US

$)

Guatemala Kyrgyz Republic Lao PDRMongolia Nepal NicaraguaBurkina Faso Paraguay Sri Lanka

Figure 5.2: Income Potential (EXPY) of Burkina Faso’s exports (EXPY) has remained low relative to landlocked and cotton exporters outside Sub-Saharan Africa

EXPY (cosntant 2000 $)

500

1000

1500

2000

2500

3000

3500

4000

4500

5000E

XP

Y

Benin Burkina Faso Bangladesh Guatemala

Lao PDR Paraguay Nicaragua Mali

Our framework: A classification of Burkina Faso’s exports by Revealed Comparative Advantage (table 1)

CLASSICS – prodcuts in which BF’s RCA in the earlier period was high and in recent period continues to remain high. Implication – its strong, maintain it

1980-84: RCA = 1 2001-05: RCA = 1

DISAPPEARANCES – prodcuts in which BF’s RCA in the earlier period was high but in recent period is low. Implication – declining competitiveness, leave them alone.

1980-84: RCA = 1 2001-05: RCA = 0

MARGINALS – products in which BF did not and does not have a RCA Implication – observe and let them grow

1980-84: RCA = 0 2001-05: RCA = 0

EMERGING CHAMPIONS – products in which BF’s RCA was low in the earlier period but high in recent period. Implication – build on these new discoveries and nascent products.

1980-84: RCA = 0 2001-05: RCA = 1

RCA 80-84 = 1 SHARE SHARE RCA 80-84 = 1 SHARE SHARE

RCA 00-04 = 1 80-84 00-06 RCA 00-04 = 0 80-84 00-06

Cotton uncarded 32.1 62.3 1,500 Gold 2.3 1.2 5,716

Sesame seeds 4.0 3.9 1,179 Oil cake & residues 2.6 0.3 5,718

Leather 0.9 1.5 2,159 Sheep and lamb skins 2.1 - 4,956

Other Vegetables 4.0 1.3 5,477 Basketwork, wickerwork 0.2 - 7,789

RCA 80-84 = 0 SHARE SHARE PRODY RCA 80-84 = 0 SHARE SHARE PRODY

RCA 00-04 = 1 80-84 00-06 RCA 00-04 = 0 80-84 00-06

Sugar - 3.4 4,516 Cotton seeds - 0.9 2,473

Cigarretes - 3.2 12,204 Cotton yarn - 0.8 4,262

Sheep/lamb skin leather 0.1 1.7 2,526 Bovine animals 3.4 0.1 4,391

Cotton seed oil - 0.8 3,173 Work of Art 0.2 0.2 8,542

(a) The Classics (b) Disappearances

(c) Emerging Champions (d) Marginals

PRODY PRODY

A classification of Burkina Faso’s exports by Revealed Comparative Advantage and PRODY (table 2)

A classification of Burkina Faso’s exports – thinking at the industry or more aggregated level (table 3 )

• Classics: These are Burkina Faso’s traditional exports and the group is formed by 6 product categories. It includes some

• fresh or chilled vegetables; • fresh fruits, • sesame seeds, • oil seeds and oleaginous fruits; • not carded cotton; and • leather of other hides or skins. They tend to have low PRODYs but the highest densities for

Burkina Faso.

• Disappearances: It includes 4 categories of bovine, goat, sheep, and lamb skins; basketwork; and notably gold. Hides and skins exports to Europe have declined systematically. Gold was one major product exported by Burkina Faso whose production decline. Now gold mining has a promising recovery.

• Emerging champions, High PRODY products but small in number (only 15) and export values. Some reversals in exports during 2005-06 suggest the existence of constraints in the economic environment that prevents them from scaling up. Cotton seed oil, soap, horticultural products, some low tech manufactures, and two leather and skin products.

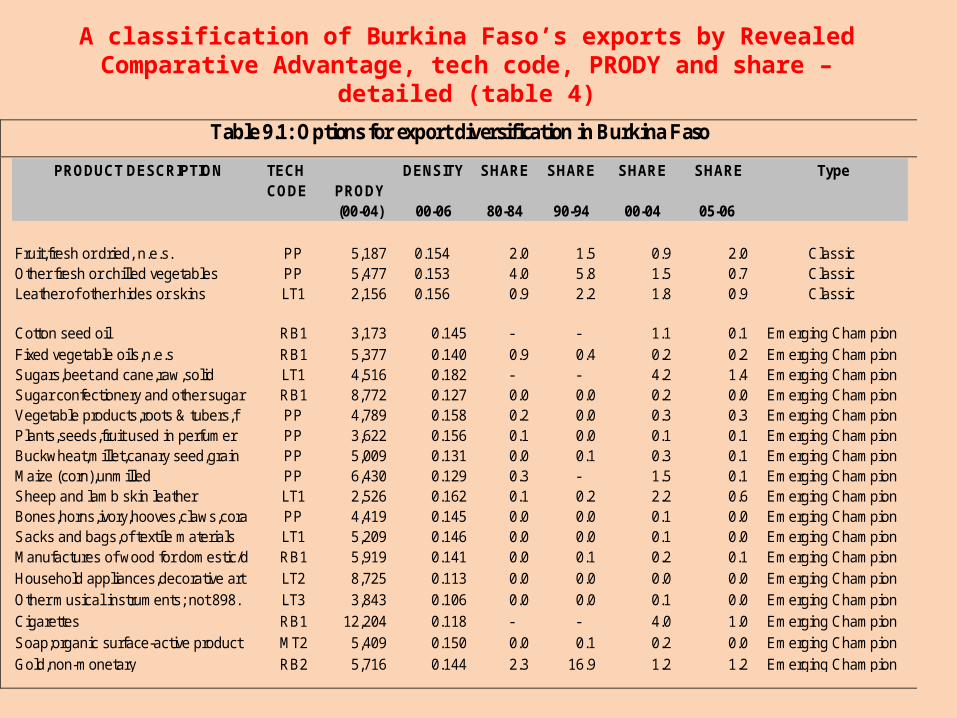

Table 9.1: Options for export diversification in Burkina Faso

PRODUCT DESCRIPTION TECH CODE PRODY

DENSITY SHARE SHARE SHARE SHARE Type

(00-04) 00-06 80-84 90-94 00-04 05-06

Fruit,fresh or dried, n.e.s. PP 5,187 0.154 2.0 1.5 0.9 2.0 ClassicOther fresh or chilled vegetables PP 5,477 0.153 4.0 5.8 1.5 0.7 ClassicLeather of other hides or skins LT1 2,156 0.156 0.9 2.2 1.8 0.9 Classic

Cotton seed oil RB1 3,173 0.145 - - 1.1 0.1 Emerging Champion

Fixed vegetable oils,n.e.s RB1 5,377 0.140 0.9 0.4 0.2 0.2 Emerging ChampionSugars,beet and cane,raw,solid LT1 4,516 0.182 - - 4.2 1.4 Emerging ChampionSugar confectionery and other sugar RB1 8,772 0.127 0.0 0.0 0.2 0.0 Emerging ChampionVegetable products,roots & tubers,f PP 4,789 0.158 0.2 0.0 0.3 0.3 Emerging ChampionPlants,seeds,fruit used in perfumer PP 3,622 0.156 0.1 0.0 0.1 0.1 Emerging ChampionBuckwheat,millet,canary seed,grain PP 5,009 0.131 0.0 0.1 0.3 0.1 Emerging ChampionMaize (corn),unmilled PP 6,430 0.129 0.3 - 1.5 0.1 Emerging ChampionSheep and lamb skin leather LT1 2,526 0.162 0.1 0.2 2.2 0.6 Emerging ChampionBones,horns,ivory,hooves,claws,cora PP 4,419 0.145 0.0 0.0 0.1 0.0 Emerging ChampionSacks and bags,of textile materials LT1 5,209 0.146 0.0 0.0 0.1 0.0 Emerging ChampionManufactures of wood for domestic/d RB1 5,919 0.141 0.0 0.1 0.2 0.1 Emerging Champion

Household appliances,decorative art LT2 8,725 0.113 0.0 0.0 0.0 0.0 Emerging Champion

Other musical instruments; not 898. LT3 3,843 0.106 0.0 0.0 0.1 0.0 Emerging Champion

Cigarettes RB1 12,204 0.118 - - 4.0 1.0 Emerging Champion

Soap;organic surface-active product MT2 5,409 0.150 0.0 0.1 0.2 0.0 Emerging Champion

Gold,non-monetary RB2 5,716 0.144 2.3 16.9 1.2 1.2 Emerging Champion

A classification of Burkina Faso’s exports by Revealed Comparative Advantage, tech code, PRODY and share – detailed (table 4)

Policy Implications - What can this framework tell us of income-enhancing export possibilities in Burkina Faso? Part 1

1. GOOD NEWS: there are alternative growth paths for Burkina Faso which is a primary commodity exporter.

2. What our framework shows:– That Burkina Faso’s traditional or “Classic” export products are mostly

low PRODY.– That there are some “Disappearing” exports. Some are high PRODY.

We don’t know why they are disappearing but we need to get more information.

– There is a long list of “Marginal “ products. We should be reluctant to suggest they might be good products. We need more information.

– There is a set of high PRODY “Emerging Champions” which seems attractive. We don’t know why they have not scaled up and what is holding them back. We need more information.

– MOST importantly, we do not know whether Burkina Faso has the technological capabilities and inputs to produce the “Emerging Champions.” We need more information.

Are we ready to comment on Burkina Faso’s industrial policy yet? NO

We should feel comfortable sharing information and comment on the sophistication of the Classics, Disappearances, Marginals and Emerging Champions as identified by our framework.

BUT

We are not ready to endorse any product or industrial policy. We need to do more homework. How much more?

Some answers can be found in a companion course.How do we prepare a report that helps us how to replicate the

concepts in this course for other countries or products? We recommend that you play with our toolkit, and cut and paste charts and tables into your reports.

42