Embed Size (px)

DESCRIPTION

Игорь МАРИЧ Управляющий директор по Денежному рынку. ВАЛЮТНЫЙ РЫНОК И ДЕНЕЖНО-КРЕДИТНАЯ ПОЛИТИКА БАНКА РОССИИ. ОСНОВНЫЕ МАКРОФИНАНСОВЫЕ ИНДИКАТОРЫ РОССИИ. Рост реального ВВП, %. Суверенный долг в % к ВВП. Номинальный ВВП, $ трлн. Nominal GDP (2013E, USD trn ). - PowerPoint PPT Presentation

Citation preview

ВАЛЮТНЫЙ РЫНОК И ДЕНЕЖНО-КРЕДИТНАЯ ПОЛИТИКА БАНКА РОССИИ

Игорь МАРИЧУправляющий директор по Денежному рынку

2

CPI, RUB/USD, MosPrime3M

2006 2007 2008 2009 2010 2011 2012 2013

9.0%11.9% 13.3%

8.8% 8.8%6.1% 6.6% 6.2%

27.1 25.6 24.931.8 30.4 29.4 31.1 32.0

CPI RUB/USD (avr.)

5.1% 5.9% 9.8%13.7

%4.3% 5.0% 7.1% 7.0%

MosPrime3M (avr.)

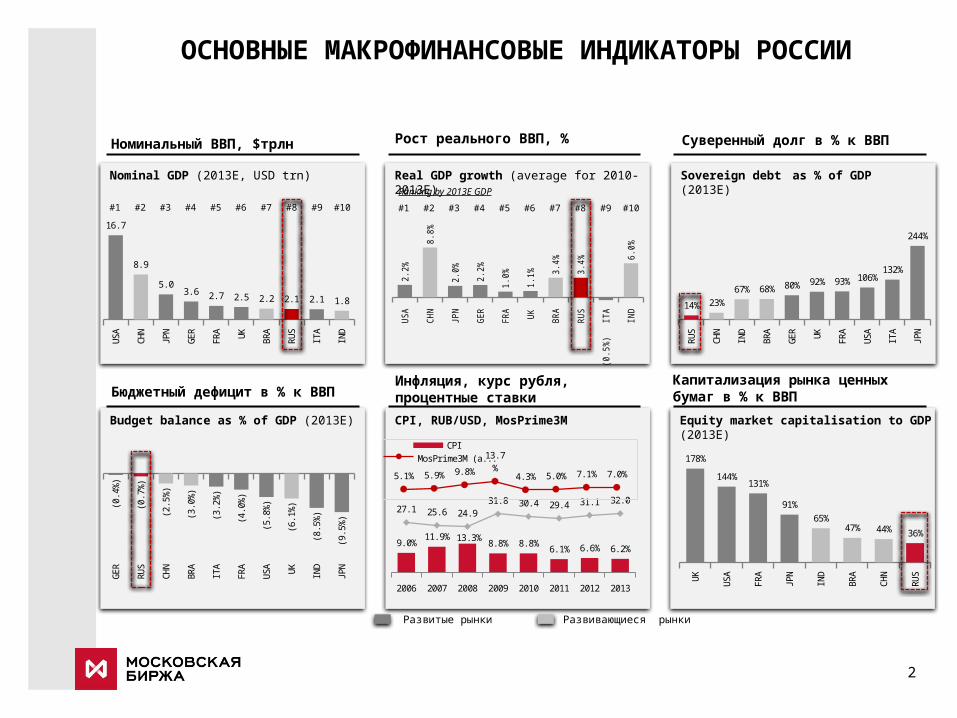

ОСНОВНЫЕ МАКРОФИНАНСОВЫЕ ИНДИКАТОРЫ РОССИИ

Nominal GDP (2013E, USD trn)

Номинальный ВВП, $трлн

Real GDP growth (average for 2010-2013E)

Рост реального ВВП, % Суверенный долг в % к ВВП

Sovereign debt as % of GDP (2013E)

Budget balance as % of GDP (2013E)

Бюджетный дефицит в % к ВВПИнфляция, курс рубля, процентные ставки

Капитализация рынка ценных бумаг в % к ВВП

Развитые рынки Развивающиеся рынки

US

A

CH

N

JPN

GE

R

FRA

UK

BR

A

RU

S

ITA

IND

16.7

8.9

5.03.6 2.7 2.5 2.2 2.1 2.1 1.8

US

A

CH

N

JP

N

GE

R

FR

A

UK

BR

A

RU

S

ITA

IND

2.2

%

8.8

%

2.0

%

2.2

%

1.0

%

1.1

% 3.4

%

3.4

%

(0.5

%)

6.0

%

RU

S

CH

N

IND

BR

A

GE

R

UK

FRA

US

A

ITA

JPN

14% 23%

67% 68% 80% 92% 93% 106%132%

244%

GE

R

RU

S

CH

N

BR

A

ITA

FRA

US

A

UK

IND

JPN

(0.4

%)

(0.7

%)

(2.5

%)

(3.0

%)

(3.2

%)

(4.0

%)

(5.8

%)

(6.1

%)

(8.5

%)

(9.5

%)

#1 #2 #3 #4 #5 #6 #7 #8 #9 #10 #1 #2 #3 #4 #5 #6 #7 #8 #9 #10

Equity market capitalisation to GDP (2013E)

UK

US

A

FRA

JPN

IND

BR

A

CH

N

RU

S

178%

144%131%

91%

65%47% 44% 36%

Ranking by 2013E GDP

ИЗМЕНЕНИЕ ДЕНЕЖНО-КРЕДИТНОЙ ПОЛИТИКИ

Переход к «инфляционному таргетированию»• Переход к плавающему курсу рубля• Примат цели по инфляции над всеми

иными целями ДКП• Основной инструмент ДКП –

процентные ставки• Повышение ликвидности и глубины

финансовых рынков, развитие инфраструктуры

• Эффективная передача сигнала (изменение процентных ставок ДКП) в реальную экономику

• Меры бюджетной политики, динамика курса рубля выступают как внешние по отношению к ДКП переменные

• Ориентир курсовой политики Банка России - рублевая стоимость бивалют ной корзины (0,55 доллара США и 0,45 ев ро)

• Управление валютным курсом путем валютных интервенций

• Сглаживание резких колебаний валютных курсов

• Регулирование ликвидности в банковской системе

Политика «управляемого плавания»

3

НОВАЦИИ В ПОЛИТИКЕ ВАЛЮТНОГО КУРСА

Банк России не препятствует формированию тенденций в динамике курса рубля Банк России не устанавливает фиксированные ограничения на уровень курса национальной

валюты или целевые значения его изменения Увеличе ние чувствительности границ операционно го интервала к объему совершенных Банком

России интервенций Банк России сглаживает резкие колебания валютного курса в целях обеспечения постепенной

адаптации экономических агентов к его изменению Постепенное повышение гибкости кур сообразования

01/12

03/12

05/12

07/12

09/12

11/12

01/13

03/13

05/13

07/13

09/13

11/13

01/14

28

30

32

34

36

38

38

40

42

44

46

48

USD/RUB

EUR/RUB

Курсы рубля к доллару и евро, руб.

4

2006 2007 2008 2009 2010 2011 2012 2013 2014*0%

2%

4%

6%

8%

10%

12%

14%

9.0%

11.9%

13.3%

8.8% 8.8%

6.1% 6.6% 6.2%5.5%

Инфляция, %

Источники: Росстат, *2014 - прогноз Минфина

МЕХАНИЗМ КУРСОВОЙ ПОЛИТИКИ В 2014 Режим управляемого плавающего валютного курса В качестве операционного ориентира используется рублевая стоимость бивалютной корзины (0,45 евро и

0,55 доллара США) Диапазон допустимых значений рублевой стоимости бивалютной корзины задан плавающим операционным

интервалом, границы которого корректируются в зависимости от объема совершенных валютных интервенций

Ширина данного интервала – 7 рублей При совершении Банком России продаж (покупок) иностранной валюты на сумму 350 млн долларов США

границы перемещаются на 5 копеек вверх (вниз) Механизм сглаживания колебаний курса рубля предполагает возможность осуществления покупок или

продаж иностранной валюты (доллара США и евро) при нахождении стоимости бивалютной корзины на границах плавающего операционного интервала и внутри его

В центральной части операционного интервала выделяется нейтральный диапазон, в котором не совершаются валютные интервенции

5

ДИНАМИКА КУРСА РУБЛЯ

Новации ДКП ведут к повышению гибкости курсообразования

Динамика курса рубля сопоставима с динамикой курсов валют большин ства стран с формирующимися рынками

Jan/1

2

Mar/12

May/1

2Jul/1

2

Sep/1

2

Nov/12

Jan/1

3

Mar/13

May/1

3Jul/1

3

Sep/1

3

Nov/13

Jan/1

40

1

2

3

4

5

6

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

Волатильность курса USDRUB Объем спот USD/RUB

6

Темп роста курсов, %Волатильность курса рубля (%) и объем торгов (трлн руб.)

7

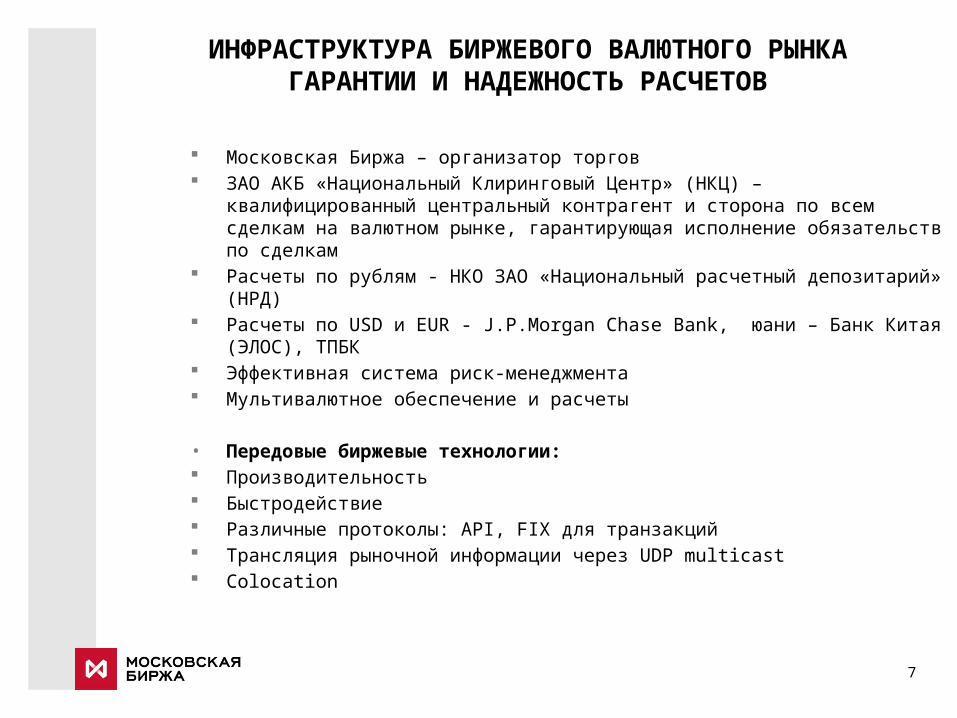

ИНФРАСТРУКТУРА БИРЖЕВОГО ВАЛЮТНОГО РЫНКАГАРАНТИИ И НАДЕЖНОСТЬ РАСЧЕТОВ

Московская Биржа – организатор торгов ЗАО АКБ «Национальный Клиринговый Центр» (НКЦ) –

квалифицированный центральный контрагент и сторона по всем сделкам на валютном рынке, гарантирующая исполнение обязательств по сделкам

Расчеты по рублям - НКО ЗАО «Национальный расчетный депозитарий» (НРД)

Расчеты по USD и EUR - J.P.Morgan Chase Bank, юани – Банк Китая (ЭЛОС), ТПБК

Эффективная система риск-менеджмента Мультивалютное обеспечение и расчеты

• Передовые биржевые технологии: Производительность Быстродействие Различные протоколы: API, FIX для транзакций Трансляция рыночной информации через UDP multicast Colocation

8

ДИНАМИКА, СТРУКТУРА, КОНКУРЕНТОСПОСОБНОСТЬБИРЖЕВОГО ВАЛЮТНОГО РЫНКА

2007 2008 2009 2010 2011 2012 20130

2

4

6

8

10

12

14

16

18

20

3.65.7 4.8 5.0 6.3 7.8 7,2

2.4

4.9 7.5 5.65.4

7.112,2

SPOT SWAP

Среднедневной объем торгов, $ млрд.

6,0

10,612,3

10,611,7

14,9

19,4

Объем торгов дек.2013

Дневной максимум – $35,6 млрд

Среднедневной – $24,3 млрд

569 Участников торгов (38 некредитных организаций)

По паре доллар/рубль на биржевой сегмент приходится 43,1%, евро/рубль — 66,4% российского межбанковского рынка

Соотношение валютного рынка Московской Биржи с мировыми FX

платформами, %

Структура рынка по парам валют, %

Q1.11Q2.11

Q3.11Q4.11

Q1.12Q2.12

Q3.12Q4.12

Q1.13Q2.13

Q3.13Q4.13

4

8

12

16

20

24

28

Биржа/ICAP Биржа/Reuters Биржа/FXall

9

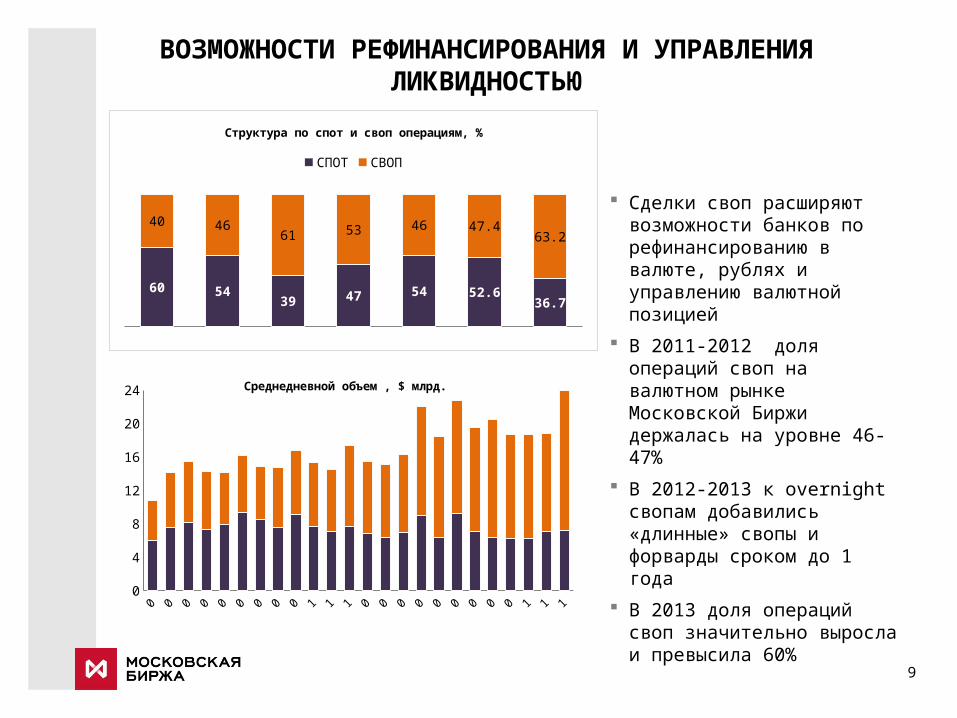

Сделки своп расширяют возможности банков по рефинансированию в валюте, рублях и управлению валютной позицией

В 2011-2012 доля операций своп на валютном рынке Московской Биржи держалась на уровне 46-47%

В 2012-2013 к overnight свопам добавились «длинные» свопы и форварды сроком до 1 года

В 2013 доля операций своп значительно выросла и превысила 60%

ВОЗМОЖНОСТИ РЕФИНАНСИРОВАНИЯ И УПРАВЛЕНИЯ ЛИКВИДНОСТЬЮ

2007 2008 2009 2010 2011 2012 2013

60 5439 47 54 52.6

36.7

40 4661 53 46 47.4

63.2

Структура по спот и своп операциям, %

СПОТ СВОП

01/12

03/12

05/12

07/12

09/12

11/12

01/13

03/13

05/13

07/13

09/13

11/13

0

4

8

12

16

20

24 Среднедневной объем , $ млрд.

10

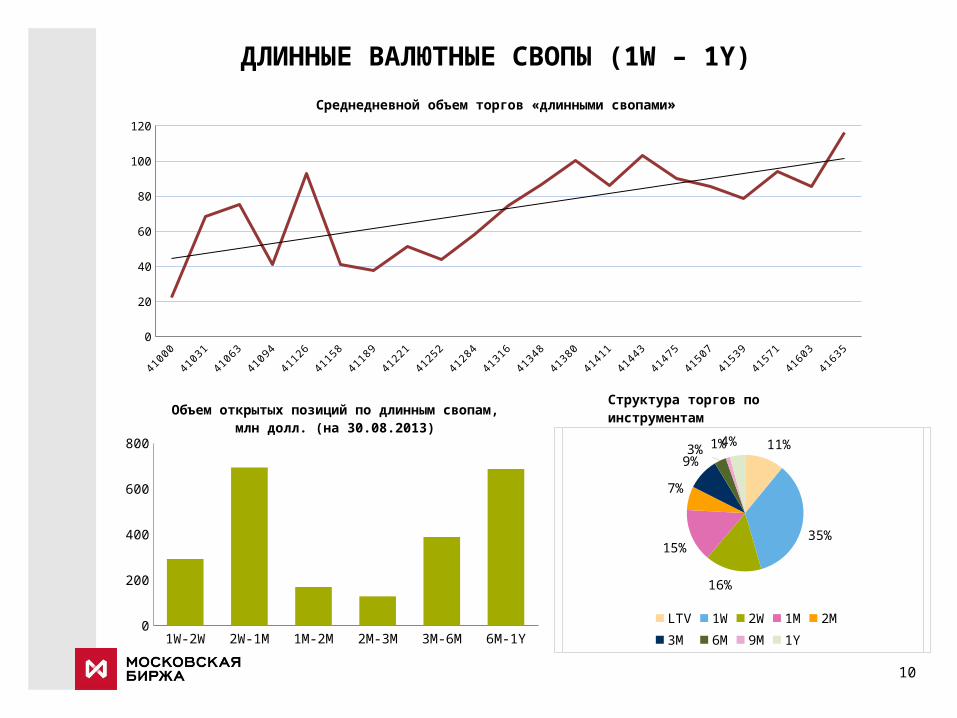

ДЛИННЫЕ ВАЛЮТНЫЕ СВОПЫ (1W – 1Y)

Структура торгов по инструментам

Среднедневной объем торгов «длинными свопами»

41000 41031 41063 41094 41126 41158 41189 41221 41252 41284 41316 41348 41380 41411 41443 41475 41507 41539 41571 41603 416350

20

40

60

80

100

120

1W-2W 2W-1M 1M-2M 2M-3M 3M-6M 6M-1Y0

200

400

600

800

Объем открытых позиций по длинным свопам, млн долл. (на 30.08.2013)

11%

35%

16%

15%

7%

9%3% 1%4%

LTV 1W 2W 1M 2M 3M 6M 9M 1Y

11

01/12

02/12

03/12

04/12

05/12

06/12

07/12

08/12

09/12

10/12

11/12

12/12

01/13

02/13

03/13

04/13

05/13

06/13

07/13

08/13

09/13

10/13

11/13

12/13

0

10

20

30

40

50

60

70

80

90

Новации 2013 года:

Новые инструменты - CNYRUB_TOM, CNYRUB_SPT, CNY_TODTOM, CNY_TOMSPT, свопы (1W - 6M)

Частичное депонирование и единая позиция (прием юаней в обеспечение)

Торги инструментами TOM, SPT (T+2), TOMSPT, свопы (1W - 6M) – до 23:50

Котировка n руб./1 юань

Унификация тарифов с тарифами по USD и EUR

Среднедневной объем торгов CNY/RUB на Московской Бирже, млн CNY

15.01.2014 на валютном рынке Московской Биржи объем торгов юанями достиг рекордного уровня – 350 млн юаней

РАЗВИТИЕ ТОРГОВ ЮАНЬ-РУБЛЬ

12

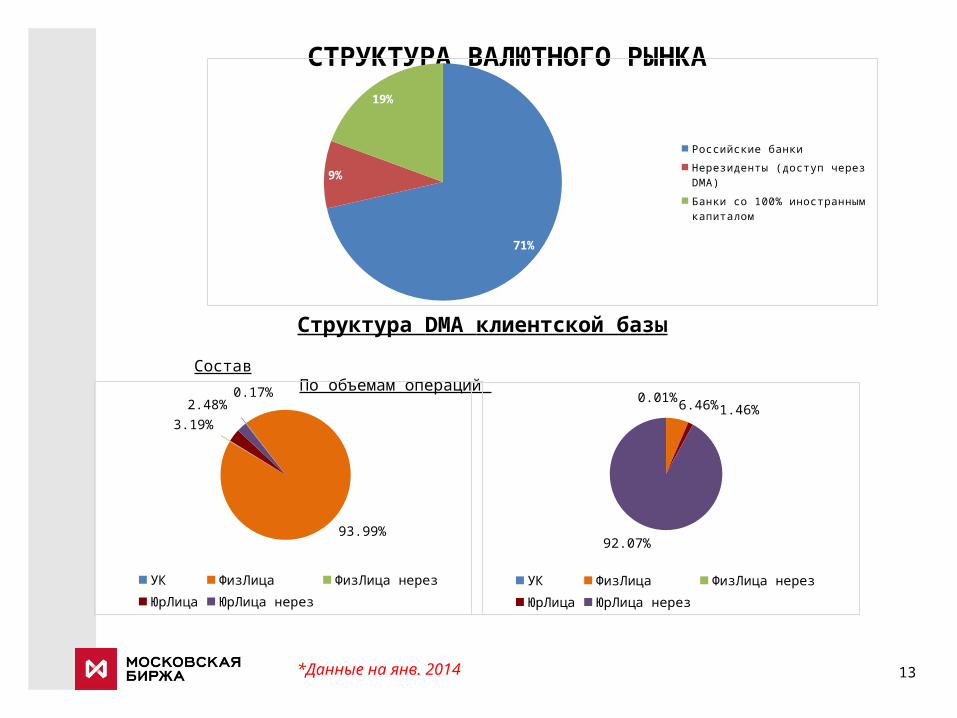

УЧАСТНИКИ ВАЛЮТНОГО РЫНКА

БАНКИ – 531

БРОКЕРЫ – 38

DMA КЛИЕНТЫ – НЕРЕЗИДЕНТЫ – >800

DMA КЛИЕНТЫ – РОССИЙСКИЕ КОРПОРАЦИИ -

>5000

DMA КЛИЕНТЫ – ФИЗИЧЕСКИЕ ЛИЦА - > 65 000*Данные на янв. 2014

13

СТРУКТУРА ВАЛЮТНОГО РЫНКА

*Данные на янв. 2014

Структура DMA клиентской базы

Состав По объемам операций

0.17%

93.99%

3.19%

2.48%

УК ФизЛица ФизЛица нерезЮрЛица ЮрЛица нерез

0.01%6.46% 1.46%

92.07%

УК ФизЛица ФизЛица нерезЮрЛица ЮрЛица нерез

71%

9%

19%

Российские банки

Нерезиденты (доступ через DMA)

Банки со 100% иностранным капиталом

14

НОВАЦИИ ВАЛЮТНОГО РЫНКА Развитие клиентского доступа

С февраля 2012 г. предоставлен полнофункциональный доступ на валютный

рынок всем категориям лиц через непосредственных участников (Sponsored

DMA)

Запуск длинных валютных свопов В апреле 2012 г. начались торги валютными свопами USD/RUB

(срок исполнения 2-й ноги от 1 недели до 1 года)

Доступ брокеров на валютный рынок С января 2013 г. брокеры, дилеры, ДУ могут стать прямыми участниками

торгов при условии соблюдения требований по достаточности собственных

средств (180 млн. руб.)

Продление времени торгов до 23:50 Синхронизация времени торгов разных рынков

Расширение географии участников торгов и валютных пар

››› 24h

Развитие торгов валютной парой юань/рубль С середины апреля 2013 г. расширена продуктовая линейка, продлено время

торгов, изменены тарифы, изменилась система риск-менеджмента

ДЕНЕЖНЫЙ РЫНОК: РЕПО, ДЕПОЗИТНО-КРЕДИТНЫЕ ОПЕРАЦИИ, РАЗМЕЩЕНИЕ

Цели Банка России: Предоставление ликвидности (прямое РЕПО, ломбардное кредитование, необеспеченные кредиты) Изъятие ликвидности (депозитные операции, размещение ОБР) Генеральный агент Минфина России (размещение ОФЗ)

Инструменты денежно-кредитной политики

Прямое РЕПО: на аукционной основе и на фиксированных условиях сроки РЕПО – 1 неделя сроки РЕПО от 1 до 6 дней (аукционы «тонкой настройки)

Аукционы по предоставлению кредитов, обеспеченных нерыночными активами сроки кредитов – 3 мес.

Депозитные операции / ломбардные кредиты: на аукционной основе и на фиксированных условиях сроки депозитов от 1 дня до 1 месяца сроки кредитов от 1 дня до 1 года

Размещение Облигаций Банка России (ОБР) и необеспеченные кредиты - в настоящее время не используются

Размещение Облигаций Федерального Займа (ОФЗ): Банк России действует по поручению Минфина России размещения проводятся регулярно

15

НОВАЦИИ В ДЕНЕЖНО-КРЕДИТНОЙ ПОЛИТИКЕ БАНКА РОССИИ

Ключевая ставка Банка России - ставка по операциям РЕПО на аукционной основе на срок 1 неделя

Банк России планирует приравнять к 1 января 2016 ставку рефинансирования к ставке по операциям РЕПО на срок 1 неделя

Операционная цель – поддержание однодневных ставок денежного рынка вблизи ключевой ставки

Межбанковское кредитование будет играть основную роль в перераспределении ликвидности между участниками рынка

Основа системы инструментов денежно-кредитной политики - коридор процентных ставок по операциям Банка России

16

ИЗМЕНЕНИЕ В СИСТЕМЕ ПРОЦЕНТНЫХ ИНСТРУМЕНТОВ ДКП

Основные инструменты регулирования банковской ликвидности - операции Банка России по рефинансированию кредитных организаций: аукционы РЕПО на срок 1 неделя

Операции «тонкой настройки» по предоставлению ликвидности будут проводится в форме аукционов РЕПО на сроки от 1 до 6 дней

При возникновения избытка ликвидности, основной инструмент - депозитные аукционы на срок 1 неделя

Ставки по операциям постоянного действия по абсорбированию и предоставлению ликвидности на срок 1 день образуют нижнюю (4,5%) и верхнюю (6,5%) границы процентного коридора. Ширина процентного коридора составляет 2 п.п.

Предоставление на аукционной основе кредитов, обе спеченных нерыночными активами, на срок 3 месяца по плавающей процентной став ке

17

ПРОЦЕНТНЫЕ СТАВКИ ПО ОСНОВНЫМ ОПЕРАЦИЯМ БАНКА РОССИИ (% ГОДОВЫХ)

Назначение Вид инструмента Инструмент Срок Ставка с 11.06.13 16.09.13

Предоставление ликвидности

Операции постоянного действия (по фиксированным процентным ставкам)

Кредиты «овернайт»

Сделки валютный «своп» (рублевая часть), ломбардные кредиты, РЕПО, кредиты, обеспеченные золотом Кредиты, обеспеченные нерыночными активами или поручительствами

Операции на аукционной основе (минимальные процентные ставки)

Аукционы по предоставлению кредитов, обеспеченных нерыночными активами

Аукционы РЕПО

Абсорбирование ликвидности

Операции на аукционной основе (максимальные процентные ставки)

Операции постоянного действия (по фиксированным процентным ставкам)

Депозитные аукционы

Депозитные операции

От 1 до 7 дней

1 день

1 день

1 день

3 месяца

1 неделя

1 день, до востребования

Справочно

Ставка рефинансирования

8,25

6,50

6,75

6,50

-

5,50

5,75

5,50я5,00

5,50

4,50 4,50

8,25 8,25

18

ПРОГРАММА РАЗМЕЩЕНИЯ ОФЗ

В I кв 2014 запланировано размещение облигаций федеральных займов (ОФЗ) на общую сумму 275 млрд руб. ($8,3 миллиарда)

Объем размещения трех- и пятилетних госбумаг составит в январе-марте 80 млрд руб.

Объем размещения семи- и 10-летних ОФЗ - 135 млрд руб.

Объем размещения 15-20-летних ОФЗ - 60 млрд руб.

19

41.2

48.7

82.9

130.0

165.7

ОПЕРАЦИИ РЕПО НА МОСКОВСКОЙ БИРЖЕ

РЕПО с акциями

Трлн. руб.

РЕПО с облигациями

Трлн. руб.

Объем торгов

Трлн.руб.

Среднедневной объем торгов РЕПО с ЦК

Млрд.руб.

CAGR: 40%

фев.13

мар.13

апр.13

май.13

июн.13

июл.13

авг.1

3

сен.13

окт.1

3

ноя.13

дек.13

(1 - 27

) янв

.14

0

10

20

30

40

50

60

0.8 2.5 1.9 1.06.1

11.116.7

25.1

31.9

38.3 40.6

49.9

4563

79 84 90104

122

146155

163176

187

Объем сделокКоличество участников

Операции РЕПО на Бирже(>90% оборота Российского рынка РЕПО)

20

РЕПО С ЦЕНТРАЛЬНЫМ КОНТРАГЕНТОМ

Междилерское РЕПО

РЕПО с ЦК

Сторона по сделкам – Центральный контрагент (ЗАО АКБ «Национальный Клиринговый Центр»)

Адресный режим Безадресный режим

Допущенные бумаги:

ОФЗ

Акции (топ-50 по ликвидности)

Корп. облигации (128 бумаг из ломбардного списка Банка России, рейтинг эмитента не хуже BBB-)

ОФЗ

Акции (23 бумаги, отвечающие критериям: допущены к клирингу с частичным обеспечением, мин. уровни ставки 1-го уровня не превышают 30%)

Корп. облигации (128 бумаг из ломбардного списка Банка России, рейтинг эмитента не хуже BBB-)

Код расчетов:

Y0/Y1 (поставка актива в 17:00)

Т0/Y1 (моментальная поставка актива по 1-ой части сделки РЕПО)

Т0/Y2 (моментальная поставка актива по 1-ой части сделки РЕПО)

Y1/Y2 (поставка актива на следующий день в 17:00)

Y0/Y2 (поставка актива в 17:00)

Y0/Y1 (поставка актива в 17:00)

Время торгов: с 10:00 до 16:00 (код расчетов: Y0/Y1, Y0/Y2)

с 10:00 до 19:00 (код расчетов: T0/Y1, T0/Y2, Y1/Y2)

Прекращение обязательств по сделкам с частичным обеспечением: 17:00.

Расчеты: 19:00

5 февраля 2013г. - Московская Биржа запустила РЕПО с Центральным Контрагентом

21

Депозитные операции

Ломбардные кредиты Банка России

Необеспеченные кредиты

Депозитные операции Внешэкономбанка

Депозитные операции Федерального Казначейства

Депозитные операции Пенсионного Фонда РФ

ДЕПОЗИТНО-КРЕДИТНЫЕ ОПЕРАЦИИ

Источник: информация Биржи

Депозитно-кредитные операции, трлн. руб.

2009 2010 2011 2012 2013

5.7 4.9

9.0 8.5 8.00.1

0.1 0.9

5.0

5.75.0

9.1 9.4

13.0

Остальные (ВЭБ, ФК, ПФР)Операции Банка России

22

Центральный Банк

Участники

Банки

Участники

Рынок РЕПО Депозитный рынок

Участники, размещающие

деньгиБанки

БанкиЦентральный Контрагент

Проф. Участники

Банки

Корпорации

РЕПО

РЕПОРЕПО

Проф. Участники

Пул обеспечения

Депозиты

Кредиторы

Заемщики

Центральный Банк

Другие организации

УПРАВЛЕНИЕ ЛИКВИДНОСТЬЮ

23

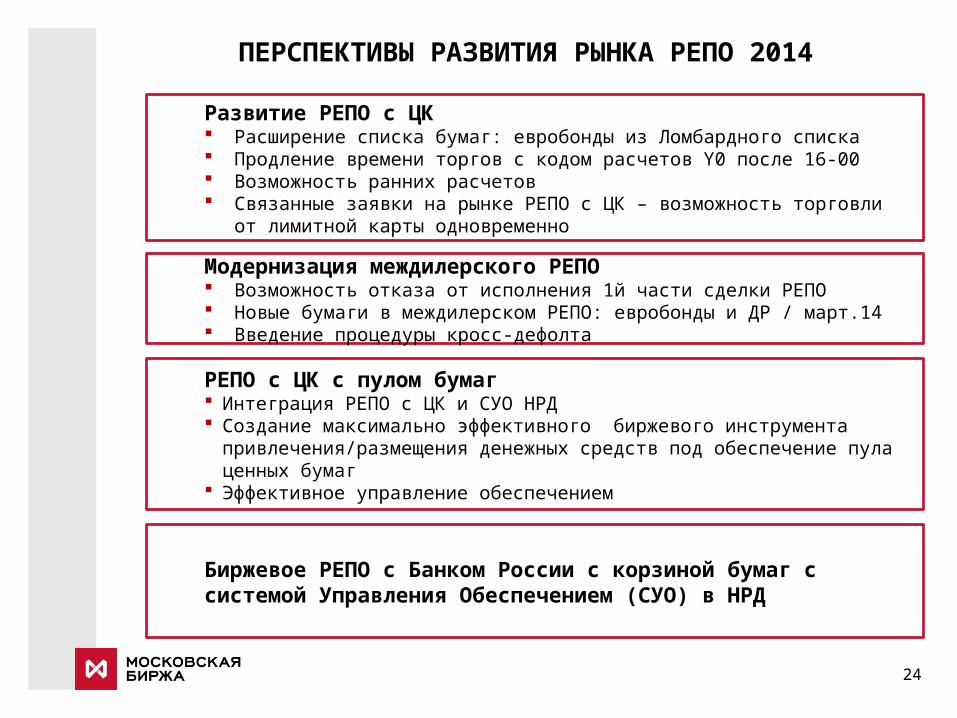

ПЕРСПЕКТИВЫ РАЗВИТИЯ РЫНКА РЕПО 2014

Биржевое РЕПО с Банком России с корзиной бумаг с системой Управления Обеспечением (СУО) в НРД

РЕПО с ЦК с пулом бумаг Интеграция РЕПО с ЦК и СУО НРД Создание максимально эффективного биржевого инструмента

привлечения/размещения денежных средств под обеспечение пула ценных бумаг

Эффективное управление обеспечением

Развитие РЕПО с ЦК Расширение списка бумаг: евробонды из Ломбардного списка Продление времени торгов с кодом расчетов Y0 после 16-00 Возможность ранних расчетов Связанные заявки на рынке РЕПО с ЦК – возможность торговли от

лимитной карты одновременно по всем стаканам РЕПО

Модернизация междилерского РЕПО Возможность отказа от исполнения 1й части сделки РЕПО Новые бумаги в междилерском РЕПО: евробонды и ДР / март.14 Введение процедуры кросс-дефолта

24

СПАСИБОЗА ВНИМАНИЕ

26

РАСКРЫТИЕ ИНФОРМАЦИИ

Настоящая презентация была подготовлена и выпущена Открытым акционерным обществом «Московская Биржа ММВБ-РТС» (далее – «Компания»). Если нет какой-либо оговорки об ином, то Компания считается источником всей информации, изложенной в настоящем документе. Данная информация предоставляется по состоянию на дату настоящего документа и может быть изменена без какого-либо уведомления. Данный документ не является, не формирует и не должен рассматриваться в качестве предложения или же приглашения для продажи или участия в подписке, или же, как побуждение к приобретению или же к подписке на какие-либо ценные бумаги, а также этот документ или его часть или же факт его распространения не являются основанием и на них нельзя полагаться в связи с каким-либо предложением, договором, обязательством или же инвестиционным решением, связанными с ним, равно как и он не является рекомендацией относительно ценных бумаг компании. Изложенная в данном документе информация не являлась предметом независимой проверки. В нем также не содержится каких-либо заверений или гарантий, сформулированных или подразумеваемых и никто не должен полагаться на достоверность, точность и полноту информации или мнения, изложенного здесь. Никто из Компании или каких-либо ее дочерних обществ или аффилированных лиц или их директоров, сотрудников или работников, консультантов или их представителей не принимает какой-либо ответственности (независимо от того, возникла ли она в результате халатности или чего-то другого), прямо или косвенно связанной с использованием этого документа или иным образом возникшей из него. Данная презентация содержит прогнозные заявления. Все включенные в настоящую презентацию заявления, за исключением заявлений об исторических фактах, включая, но, не ограничиваясь, заявлениями, относящимися к нашему финансовому положению, бизнес-стратегии, планам менеджмента и целям по будущим операциям являются прогнозными заявлениями. Эти прогнозные заявления включают в себя известные и неизвестные риски, факторы неопределенности и иные факторы, которые могут стать причиной того, что наши нынешние показатели, достижения, свершения или же производственные показатели, будут существенно отличаться от тех, которые сформулированы или подразумеваются под этими прогнозными заявлениями. Данные прогнозные заявления основаны на многочисленных презумпциях относительно нашей нынешней и будущей бизнес-стратегии и среды, в которой мы ожидаем осуществлять свою деятельность в будущем. Важнейшими факторами, которые могут повлиять на наши нынешние показатели, достижения, свершения или же производственные показатели, которые могут существенно отличаться от тех, которые сформулированы или подразумеваются этими прогнозными заявлениями являются, помимо иных факторов, следующие: восприятие рыночных услуг, предоставляемых Компанией и ее дочерними обществами; волатильность (а) Российской экономики и рынка ценных бумаг и (b) секторов с высоким уровнем конкуренции, в которых Компания и ее дочерние общества осуществляют свою

деятельность; изменения в (a) отечественном и международном законодательстве и налоговом регулировании и (b) государственных программах, относящихся к финансовым рынкам и рынкам

ценных бумаг; ростом уровня конкуренции со стороны новых игроков на рынке России; способность успевать за быстрыми изменениями в научно-технической среде, включая способность использовать расширенные функциональные возможности, которые популярны

среди клиентов Компании и ее дочерних обществ; способность сохранять преемственность процесса внедрения новых конкурентных продуктов и услуг, равно как и поддержка конкурентоспособности; способность привлекать новых клиентов на отечественный рынок и в зарубежных юрисдикциях; способность увеличивать предложение продукции в зарубежных юрисдикциях.Прогнозные заявления делаются только на дату настоящей презентации, и мы точно отрицаем наличие любых обязательств по обновлению или пересмотру прогнозных заявлений в настоящей презентации в связи с изменениями наших ожиданий, или перемен в условиях или обстоятельствах, на которых основаны эти прогнозные заявления.