Embed Size (px)

DESCRIPTION

公 司 理 財 研 討. MA0A0204 王詩婷 MA0A0205 許睿烜 497A0009 陳欣妤. 2.4 How Analysts Value Firms : An Illustrative Example Analyst Mary Meeker. 2.4 如何分析企業價值:舉例說明 分析師 Mary Meeker. - PowerPoint PPT Presentation

Citation preview

公 司 理 財 研 討

MA0A0204 王詩婷MA0A0205 許睿烜 497A0009 陳欣妤

2.4 How Analysts Value Firms : An Illustrative

Example

Analyst Mary Meeker

2.4 如何分析企業價值:舉例說明 分析師 Mary Meeker

In the Spring of 2003, 24 analysts followed eBay. Among these, the most well known was Mary Meeker from the firm Morgan Stanley. Mary Meeker’s analysis of eBay used a series of valuation techniques, each of which gave a different target price for eBay.

在 2003 年的春天, 24 名分析師跟隨 eBay 。其中,最知名的是從 Morgan Stanley 公司來的Mary Meeker 。 Mary Meeker 分析 eBay 是採用一系列的估價技術,對 eBay 的每一項都給予不同的目標價格。

Her April 2003 report offers a rich set of insights into how analysts apply these various techniques.

在 2003 年 4 月她的報告中,對分析師如何應用各種技術提供了一套豐富的見解。

Behavioral Pitfalls Wall-Marting of the Web

行為陷阱網路 Wall-Marting 化

During the late 1990s Mary Meeker was a security analyst at Morgan Stanley and was one of the highest-paid analysts on Wall Street, having earned approximately $15 million in 1999 and $23 million in 2000. At the time, she placed very high valuations on some internet firms, and as a result came to be called Queen of the internet.

在 20 世紀 90 年代後期, Mary Meeker 在 Morgan Stanley 是位安全分析師並且在華爾街是薪酬最高的分析師之一,在 1999 年賺得約 1500 萬在 2000 年是 2300 萬。當時,她放置在一些互聯網公司的估價非常高,因此後來被稱為網際網路。

In 1998, Time Magazine interviewed Mary Meeker, asking her to justify the high valuations of internet companies that prevailed at the time. She began by stating that the development of the commercial internet was “the biggest new technology cycle ever.”

在 1998 年,時代雜誌採訪了 Mary Meeker ,問她理由,當時盛行的互聯網公司的高估價。她開始指出商業互聯網的發展是“最大的新技術循環不斷”

Continuing, she pointed out that just as the traditional retailer Wal-Mart came to dominate the retail sector, Web-based counterparts would emerge and dominate internet commerce. Mary Meeker described the phenomenon as the “Wal-Marting of the Web.”

繼續,她指出正如傳統的零售商 Wal-Mart 來主導零售業,基於網站的同行也將會出現支配互聯網電子商務。 Mary Meeker 將這種現象稱為“網站上的 Wal-Marting”

Wal –Mart had built its business by beating its competition in regard to convenience, product selection, and low prices. She argued that the internet provided the opportunity for other firms to follow Wal-Mart, but on the Web.

Wal –Mart 已經建立的業務,產品的選擇,價格低廉,擊敗了在購物方便方面的競爭。她認為,互聯網所提供的機會,對於其他公司效仿 Wal –Mart ,但是是在網站上。

In 2000, after period of excessive optimism, if not irrational exuberance, the prices of many internet stocks fell dramatically. This event has been described as the bursting of the dot-com bubble. In May 2002 Fortune magazine placed Mary Meeker’s picture on their cover and asked if investors could ever trust Wall Street again.在 2000 年,過度樂觀的時期之後,如果不是非理性繁榮,很多互聯網股票價格大幅下跌。這個事件已經被描述為網路泡沫的破滅。 2002 年 5 月財富雜誌在他們封面上放入 Mary Meeker 的圖片,並詢問如果投資者能夠重新再信任華爾街。

In the wake of the collapse in stock prices, regulators from New York State’s attorney general’s office and the U.S. Securities and Exchange Commission launched a major investigation. Among those investigated was Mary Meeker. In 2003, the attorney general’s office and the SEC criticized her valuations as excessive, but they did not bring charges against her.在股價大跌之後,從紐約州的總檢察長辦公室到美國證券和交易委員會 (SEC) 的監管機構都發起了一項重大調查。在那些人之中被調查的是 Mary Meeker 。在 2003 年,總檢察長辦公室和 SEC 過度批評她的估價,但是他們並沒有對她提出起訴。

On February 23, 2004, The Wall Street Journal ran a feature titled “Ah, the 1990s” updating the fates of key Wall Street personalities from the 1990s stock market bubble. Regarding Mary Meeker, the article notes that she was recently named Morgan Stanley’s coleader of tech-sector research.

2004 年 2 月 23 日,華爾街日報發表了標題“啊, 20 世紀 90 年代” 修訂從 20 世紀 90 年代股市泡沫的關鍵是華爾街人士的命運。關於 Mary Meeker ,本文指出她最近被任命為 Morgan Stanley 高科技部門研究合作的領導人。

Mary Meeker’s

Target Prices for eBay

EBay Mary Meeker目標價格

At the time Mary Meeker released her April 2003 report, eBay’s price was $89.22. She used all three valuation heuristics described earlier, as well as a discounted cash flow (DCF) computation.

當時, Mary Meeker 在 2003 年 4 月發布了她的報告, eBay 的價格是 89.22 美元。她使用三個計價捷思如前所述,以及現金流量折現法 DCF計算

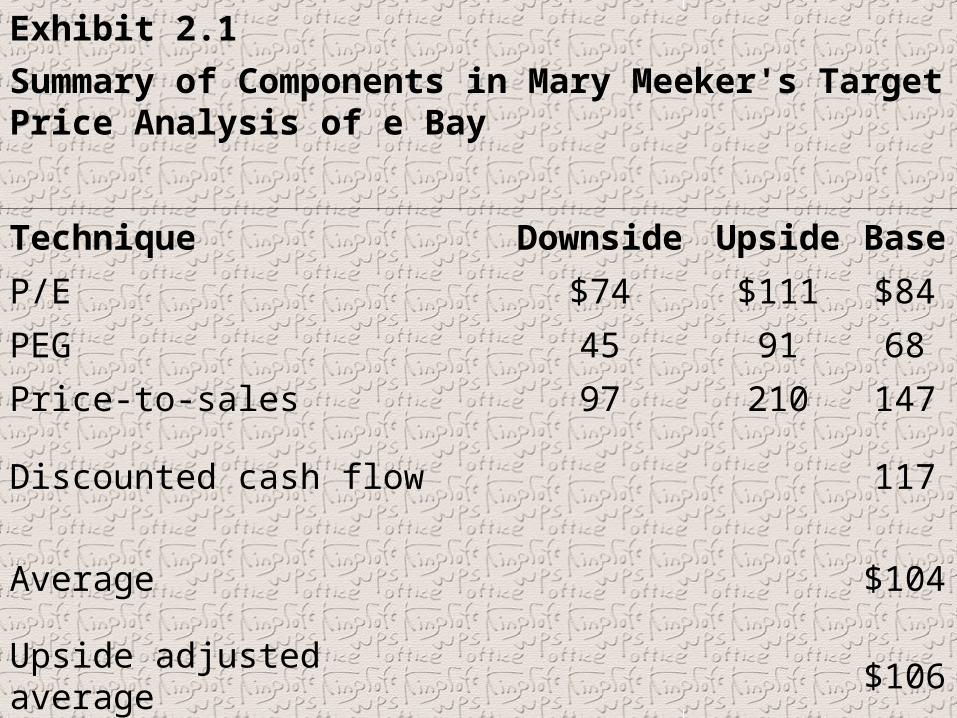

Exhibit 2.1 provides a summary of the components of Mary Meeker’s target price analysis. For each of the first three heuristics, Meeker computed a low, high, and intermediate guess. She then averaged these together with her DCF valuation to arrive at a target price of $106 per share.

圖表 2.1Mary Meeker 的目標價格分析提供了一個總結。對於前三個捷思, Meeker計算低,高、 中級推測。她平均這些計價,到達了每股 106 美元的目標價格。

Exhibit 2.1

Summary of Components in Mary Meeker's Target Price Analysis of e Bay

Technique DownsideUpsid

eBase

P/E $74 $111 $84

PEG 45 91 68

Price-to-sales 97 210 147

Discounted cash flow 117

Average$10

4

Upside adjusted average $106

Exhibit 2.2

Valuation Methodologies in Mary Meeker's Target Price Analysis of eBay

Year

2002 2003E 2004E 2005E

EPS at 32% growth

$0.86 $1.14 $1.50 $1.98

EPS at 38% growth

$0.86 $1.19 $1.64 $2.26

GMS/share at 38% grown

$39.53 $54.55 $75.27 $103.88

P/E 103 63 47 33

Price-to-

GMS Target Target

P/E PEG SalesSales per

Price Price

Method Ratio Ratio Ratio EPSGrowt

hShare Dec-04

(Discounted)

P/E 40 $2.26 $90 $84

PEG 1.5 1.5 32 72 68

Price-to-sales

1.5 2.26 $103.88 156 147

In Exhibit 2.2, an E after a year (for example, 2004E) designates that the numbers are estimates, not actual values. In all cases target prices were computed for year-end 2004 and then discounted back to mid-2004.

在表 2.2 中,經過一年的 E (下例如, 2004E)指定的數字是估計,而不是實際值。在所有情況下的目標價格計算,截至 2004 年底,然後貼現至 2004 年年中。

To arrive at her target price for December 2004,Meeker used a P/E value of 40 for 2005, the midpoint of 47 and 33 shown in the table. For sales, she used the gross global sales activity on all eBay Web sites, called gross merchandise sales (GMS).

2004 年 12 月得出她的目標價, Meeker 用於2005 年的 33 和 2004 年的 47 目標價中間點,顯示P / E 值 40 。對於銷售,她用 eBay 的網站上的總全球銷售,被稱為商品銷售總額( GMS)。

As can be seen in Exhibit 2.1, Mary Meeker used a DCF approach, applied to eBay’s free cash flows. This computation comes closest to traditional textbook technique and is the only one of the four that purports to derive the target price in terms of intrinsic or fundamental value.

表 2.1 中可以看到, Mary Meeker使用的 DCF 方法,適用於 eBay 的自由現金流量。這種計算最接近傳統教科書,四個計價中唯一最基本能得出目標價格。

A firm generates positive free cash flows when its after-tax cash flows from operations are positive and it does not spend all those after-tax flows acquiring working capital and fixed assets.

一家公司產生正的自由現金流量時,當稅後營業活動的現金流量 (OCF) 是正的,這些稅後營業活動的現金流量 (OCF) 沒有花費在營運資本和固定資產。

The difference between after-tax cash flow from operations and investment in working capital and fixed assets is paid out to the firm’s owners.

營業活動的現金流量( OCF)與營運資本和固定資產投資的區別是在付給該公司的股東。

Free cash flows are akin to dividends, but are paid to all investors, meaning debtholders and stockholders. Just as the present value of the future expected dividend stream comprises the value of the firm’s equity, the present value of the firm’s expected free cash flows comprise the value of the entire firm.

自由現金流量類似於股息,但支付給所有投資者,是債權人和股東。正如對未來的預期股息的現值,包括該公司的股權價值,公司的預期自由現金流量的現值占整個公司的價值。

Exhibit 2.3

Free Cash Flow Computation in Mary Meeker's Target Price Analysis of eBay

2000

2001

2002

2003E

2004E

2005E

2006E

2007E

2008E

2009E

2010E

2011E on

EBITDA84,

072

229,43

8

444,61

4

723,735

1,005,27

6

1,401,68

2

1,853,23

0

2,426,29

7

3,110,99

0

3,985,08

5

4,982,03

2

Taxes - - - - -140,168

370,646

849,204

1,088,84

6

1,394,78

0

1,743,71

1

Cange in

(47582

)

(41091

)

39232

(26792)

6849

(58695)

9709 (520

96)7375

(53278)

4105

working

capital

Capital49,

75357,

420

138,67

0

188,908

190,000

190,000

190,000

190,000

190,000

190,000

190,000

expenditures

Free cash flow

-13,

263

130,92

7

345,17

6

508,035

822,125

1,012,81

9

1,302,29

2

1,334,99

7

1,839,51

9

2,347,02

7

3,052,42

6

65,321,907

Target Price-Dec 31, 2003

Present value eBay free cash flows

$36,478,759

Less debt $79,592

Plus cash $2,280,857

eBay's full value $38,680,023

Shares outstanding('000)

330,259

Discount rate 12%

Future growth rate 7%

DCF per share value

$117

In her April 2003 report, Mary Meeker forecast free cash flows through the end of 2010. She used a terminal value to capture the free cash flows that would occur after 2010 and discounted these at a rate of 12 percent.

Mary Meeker 在她 2003 年 4 月的報告,預計2010 年底通過自由現金流量。她用一個終值抓取自由的現金流量將出現 2010 年後,這些折現率是 12%。

In Exhibit 2.3, she obtained her $65.3 billion terminal value in 2011 by assuming that free cash flows would grow at the rate of 7 percent from 2011 on, and then valued the future expected free cash flow stream beginning in 2011 using the constant-growth-rate perpetuity formula.

圖表 2.3 中, 2011 年她獲得了 65.3億美元的終值,假設,從 2011 年,自由現金流量將 7 %的固定成長率,然後預計未來自由現金流量值在 2011 年開始增長採用永續年金現值公式。

Specifically, she forecast that free cash flows in 2011 would be $3,266,096=1.07*$3,052,426. She then applied the perpetuity formula:

具體來說,她預計在 2011 年的自由現金流量將$3,266,096=1.07*$3,052,426 。然後,她採用了永續年金現值的公式:

PV= =$65,321,90707.012.0096,266,3$

As shown in Exhibit 2.3, that sum came to $36.5 billion. Then she added eBay’s $2.3 billion cash holdings to arrive at the value of the firm as a whole and subtracted the value of eBay’s $79 million in debt to arrive at the value of eBay’s equity. The net result was $38 billion, which Meeker called eBay’s “full value.”

正如表 2.3 所示,該款項來到 365億美元。然後她補充說: eBay 的 23億美元的現金持有到達公司作為一個整體的價值和 eBay 的 7900 萬美元債務的價值相減到達 eBay 的股票價值。最終的結果是 380億美元,其中 Meeker 稱 eBay 的“完整的價值。”

Dividing full value by eBay’s shares outstanding (330 million) lead to a target value of about $117 per share at year-end 2003. In using this amount, she did not take the future value of the $117 to mid-2004.

完整的價值除以 eBay 流通在外股數( 33億元),導致 2003 年底的目標價值每股 117 美元。 2004 年中沒有到這 117 美元金額。

2.5 BIASES 偏見

Biases and Heuristics

偏見與捷思

At the end of June 2004 , eBay’s stock price reached $180 (on a presplit basis ), well above Meekers’ target price of $106.

在 2004 年 6 月底, eBay 的股價達到 $180 ( 分割前為基礎 ),高於 Meeker 的目標價格 $106 。

At year-end 2004 its stock price closed 2004 ( pre-split ) at $232, and its forward P/E for eBay was 70, well above Meeker’s forecast of 47. Those facts alone in no way indicate that Meeker’s analysis was biased.

在 2004 年年底股價收盤 ( 分割前 ) 為 $232 ,和eBay 的 P/E為 70 ,高於 Meeker預測的 47 。這些事實沒辦法指出 Meeker 分析是有偏見的。

The rate of return associated with a target price of $106 lies above Meeker’s discount rate of 12 percent.

實際價格 $106 以折現率 12%推估目標價格

In this respect , $106 would be upwardly biased , if in April 2003 Meeker judged eBay’s stock to have been fairly priced. Of course, in April 2003 Meeker might have judged eBay’s stock to be undervalued.

在 這 方 面 , 如 果 在 2003 年 4 月 Meeker 認 為eBay 股價是公平的價格 $106 美元將會往上漲。當然,在 2003 年 4 月 Meerker 認為 eBay 股價是被低估的。

The P/E heuristic is the approach most favored by analysts.

以P/E 捷思是接近分析師贊成的方法。

Meeker’s range for the P/E target price was $74 to $111. Her base case estimate of $84 lies below the April 2003 price of $89.22 and therefore gives rise to a negative return.

Meeker 目標價格範圍為 $74 到 $111 。她的基本估計是 $84 在 2003 年 4 月價格 $89.22 之下,因此是上漲的負報酬。

The PEG heuristic produces a value range that is more negative and is therefore even worse.

以 PEG捷思產生的價格範圍是負數因此更差的。

Unless Meeker judged eBay stock to have been overvalued at the time, it is safe to conclude that the P/E heuristic or the PEG heuristic, or both, produced downward biased estimates of future value.

除非 Meeker 認為 eBay 股票被高估,它是安全的結論是以P/E 捷思或 PEG捷思,或兩者皆是,產生向下偏誤估計的未來價格。

Moreover, the assumptions that underlie the two techniques are not consistent. The P/E heuristic target price computation is premised on a growth rate of 38 percent, whereas the PEG heuristic target price computation is premised on a growth rate of 32percent.

此外,這兩種技術基礎假設是不一致。 P/E 捷 思目標價格計算成長比率為 38% ,反之, PEG 捷思目標價格計算成長比率為 32% 。

Moreover, for her PEG calculation, Meeker appears to have used an EPS number of $1.50 for 2004 rather than 2005. Actually, she used $1.42 for EPS, which corresponds to $1.50 discounted back to mid-2004, but which she listed as expected cash earnings for the year 2003.

此外,她的 PEG計算, Meeker使用 2004 年的EPS$1.50而不是 2005 年。實際上,她使用 EPS為 $1.42 ,如她預期 2003 年的現金收益推算至2004 年中期 $1.50 。

The target price range of $97 to $210 based on the price-to-sales ratio might well be biased upward. The average of this range produces a return of 63 percent, far above the required return (discount rate) of 12 percent.

目標價格範圍在 $97 到 $210 基於價格銷售比率將會向上偏。在此範圍內的平均產生 63%的回報,遠遠高於要求回報率 12%(貼現率)。