Embed Size (px)

Citation preview

i

UNDERVALUING INCUMBENCY:

REGULATORY FAILURE OR REGULATORY CAPTURE

By Christo Grozev January 2013

ii

Contents

1. INTRODUCTION .......................................................................................................................... 1

2. ECONOMIC COSTS OF ORDER OF MARKET ENTRY: EMPIRICAL

EVIDENCE AND CONCEPTUAL THEORY ................ ERROR! BOOKMARK NOT DEFINED.

3. CASE STUDY: VALUATION OF DUTCH BROADCASTING SPECTRUM ......18

3.1 Background: 2003 tender ................................................................................................................. 18

3.2 New tender versus extension: policy decision 2011 ........................................................................... 20

3.3 SEO valuation model ............................................................................................................................. 22

3.4 A7 Valuation ........................................................................................................................................... 27

3.5 Empirical outcome of regulatory decisions ........................................................................................ 29

4. ECONOMIC AND LEGAL ANALYSIS OF EXTENSION OF LICENSES TO

INCUMBENTS ...............................................................................................................................................30

4.1 Abstract .................................................................................................................................................... 30

4.2 Economic analysis .................................................................................................................................. 31

4.3 Legal analysis .......................................................................................................................................... 40

4.4 Legitimate alternative approach to extension valuation .................................................................. 52

1

1. INTRODUCTION

The economic disadvantage of late market entry is significant; its structural

existence, sustainability across time, and susceptibility to quantification have been

confirmed time and again in hundreds of empirical studies spanning geographical

regions, market sectors and product taxonomies. At the same time, this source of

business “cost” traditionally has been viewed with distrust, or lack of understanding,

by adjudicators in tort disputes over economic losses--especially in Europe, where

courts and arbitrators are traditionally more conservative, lest their judgment

overspills into that characteristically American judicial instrument, the punitive

damage. This author’s review of available court records in the Netherlands, Germany,

Austria and France has uncovered not one verdict which honored a plaintiff’s

arguments for quantifiable damage caused by the delayed market entry. In fact,

econometric forensic analysis – effectively the only route to quantifying delayed-entry

damages – is rarely applied, or accepted as evidence, in European tort litigation. As

observed by Martinez-Granado and Siotis in their seminal 2006 study of damages

suffered by a telecoms operator prevented from entering the Spanish market1,

“In Europe, the use of rigorous forensic economic analysis in competition cases

is both new and rare […] To the best of our knowledge, only the EU Commission

1 “Sabotaging entry: an estimation of damages in the directory enquiry service market,” Maite Martinez-

Granado‡and Georges Sioti; 2006

2

and a few Member States (the UK among them) have accepted (or requested)

econometric analyses in competition cases.”

The European Commission itself recognizes the difficulty in substantiating

economic losses caused by exclusionary market or regulatory behavior. In its White

paper on damages actions for breach of the EC antitrust rules {SEC (2008), the

Commission notes that:

“This calculation [of the quantum of damages from exclusionary market

behavior], implying a comparison with the economic situation of the victim in

the hypothetical scenario of a competitive market, is often a very cumbersome

exercise. It can become excessively difficult or even practically impossible, if

the idea that the exact amount of the harm suffered must always be precisely

calculated is strictly applied.”

To facilitate the calculation of damages the Commission points to the need “to draw

up a framework with pragmatic, non-binding guidance for quantification of

damages in antitrust cases, e.g. by means of approximate methods of calculation or

simplified rules on estimating the loss”

The implications of the cost of delayed market entry, in the broadest sense of this

term, are most apparent in the area of determination of damages in antitrust cases, as

well as state liability and other tort cases where a party suffers economic losses due to

the exclusionary or unlawful regulatory behavior of another party. Clearly, in these

cases, the omission or incomplete determination of this cost component would lead to

3

underassessment of the total damage suffered, and in return create conditions for

recidivism and perpetuation of the unlawful market or regulator’s conduct.

The implications of the lack of conceptual understanding on this topic go much

farther than the potential for under-compensation in damage award arbitration.

Failure to understand the systemic nature of “cost of late entry,” and conversely, of the

“premium of early entry” has also far-reaching policy implications in another context

– in valuations of scarce resources, which governments allocate to parties through

tenders, comparative competitive procedures or via direct negotiation. Failure to

understand and capture, in valuation, this cost – respectively, premium--may result in

significant underpricing of resources – when (re-)allocating a resource to an

incumbent, for instance; and conversely – in significant overpricing; when empirical

data from incumbents’ economic performance is applied to resource valuations

imposed on new entrants. Such valuation failures tend to lead to allocation decisions

that distort market competition by creating entry barriers to new market entrants, or

by granting effective “state aid” to incumbents. In both cases, failures of this type lead

to inefficient use of scarce resources; a consequence that is both economically

undesirable and, in certain cases (such as in allocation of telecommunications

spectrum), contrary to special legal imperatives2.

2 The Framework Directive, as well as the other directives of the Telecommunications Package of the

European Parliament, impose an obligation on national governments to ensure efficient usage of telecommunications spectrum.

4

Given the vast empirical data substantiating the relationship between timing and

sequence of market entry, on one hand, and long-term economic performance, on the

other, it is surprising that courts, arbitrators3 and market regulators in Europe have

failed to acknowledge this factor in dispute resolutions and in scarce-resource

valuations. A likely cause to this failure is the abstract nature of the empirical findings,

which are based on aggregated empirical data from different geographies, from

(potentially) different market segments, and subject to (seemingly) other market forces

and relationships. As an example, in arguing against the inclusion of “delayed-entry”

costs in the computation of economic damage to a market participant in 2008, the

Dutch Ministry of Economic Affairs asserted that “the empirical research and

corresponding regression analysis put forward [by the claimant], which purports to

prove and quantify the impact of delayed entry, is based on data from foreign

markets and other industries and therefore cannot be used in the case at hand4.” Along

the same lines, Dutch courts have discarded claims for damages based on the abstract

computation of cost of delay as “speculative5.”

Clearly therefore, arbitrators and regulators are not easily convinced by the

overwhelming consensus among researchers of the systemic, predictable, market-

agnostic, yet quantifiable economic effects of delayed market entry. Absent a

normative rule-book for computation of damages in competitive foreclosure cases,

3 Arbitrators are used herein in the sense not only of extrajudicial arbitration tribunals, but also of dispute

resolution agencies, such as competition boards, anti-trust regulators and the like. 4 Position paper of the Dutch Ministry of Economic Affairs in negotiations over damage award for delayed

licensing award to RadioCorp BV; 2008 5 Verdict in case BJ5924, Zutphen regional court, 2007

5

such as the one the European Commission is currently pondering, it is likely that

claimants will need to resort to case-specific, in-context substantiation and

quantification of any claimed components of economic losses or gains caused by time

of entry. The fact that the burden of proof and quantification lies with the claimant

makes this task all the more formidable.

The impact of late entry would appear to be less prone to misunderstanding in cases

of regulator-side resource pricing, simply because regulators tend to resort to expert

advice by third-party professionals with sufficient knowledge in economics and

econometrics. However, failure of government regulators to grasp, on a conceptual

level, the market dynamics and specifically, the economics of order-of-entry and time-

of-entry into a market, inevitably results in perfunctory or incorrect application of such

third-party expertise. This trend may be compounded by regulator’s desire to maximize

revenues from resource allocation, especially where this may lead to political or career

gains. From a more pessimistic perspective, such failures may be non-apparent

instances of regulatory capture. One version thereof may be by regulators being

induced to consciously meander around the issue the value of incumbency in resource-

pricing to large, incumbent firms, or to overprice scarce resources for new entrants to

an extent where the regulator substitutes the proverbial monopolist in market-

exclusionary pricing practices. Another version may be regulators committing the same

market crimes unconsciously, by being motivated to not spend time and effort

understanding the value of incumbency and the cost of late entry.

6

Thus, as in the case with damage litigation, the burden of proof of erroneous

valuation rests with the disadvantaged party – be that a disadvantaged incumbent or

precluded entrant.

The remainder of this paper reviews a specific case in which the failure of a regulator

to understand (or recognize) the economics of order of entry in the radio broadcasting

market led to an improper application of an otherwise sophisticated econometric

model for resource valuation. This in turn resulted in a king-maker intervention by the

regulator, which, through value redistribution among market players, changed the

dynamics of a market in a way that, this author believes, is not permissible under EU

or national legislation. It also resulted in an excessively high reserve price for additional

spectrum offered in a tender procedure, which in turn led to failure to allocate it

altogether and, inevitably, to failure in government policy in relation to efficient usage

of scarce resources. Again, from a more pessimistic stance, these failures may be a

symptom of regulatory capture, given that the net benefit of these regulatory decisions

has been in favor of the largest incumbent firms with most extensive lobbying practices.

The case is based on the Dutch government’s decision to extend all radio

broadcasting licenses, which were set to expire in 2011, for a period of six additional

years. While the extension was desirable for political and social goals and generally

permissible under European and local legislation, extending the licenses could be

interpreted as (forbidden) state aid to the incumbents unless they were charged an

appropriate amount to offset the “aid” they were receiving. Therefore the Dutch

government commissioned a third party to produce a valuation of the fees that were to

7

be imposed on the incumbents, who accepted the extension in return for payments of

such fees. The government proceeded to use the same license valuation model also as

a basis for setting a reserve price for auctioning the only remaining unoccupied

frequency, without consideration for the mature market of incumbents in which the

newcomer was expected to enter. As a result, no applicants were willing to bid on top

of this reserved price, and the government refused to allocate the frequency to the only

candidate who was willing to pay a price lower than the set reserve price. In

consequence, the government has failed to allocate this national frequency for more

than a year.

The rest of this paper is structured as follows. The next chapter presents the

conceptual framework and empirical data substantiating the correlation between order

of market entry in and market share.

The following chapter presents the key facts of the Dutch case, including the (two)

regulatory tasks facing the regulator, and the relevant regulatory and legislative

framework. The second part of this chapter presents, directionally, the general

implications of the theory and empirical data on order of entry and market share, on

the current case.

The subsequent chapter presents the approach undertaken by the Dutch

government to address the regulatory tasks.

8

The following chapter addresses the methodological errors, committed by the Dutch

government in addressing the regulatory task, which resulted in inefficient use of

scarce resources.

The last chapter presents a correct, feasible method of valuation of the scarce

resource, and compares the outcomes of the incorrect and correct application of

empirical market data. This chapter also addresses the plausible market impact of the

regulatory failure.

9

2. ECONOMIC COSTS OF ORDER OF MARKET ENTRY: EMPIRICAL

EVIDENCE AND CONCEPTUAL THEORY

The systemic reduced capability of a late-comer to build market share (both short-

term and long-term), relative to an early entrant, is a market phenomenon which has

been widely acknowledged in economics and marketing literature and confirmed by

extensive empirical research, which has proven definitively and quantifiably the

advantages, ceteris paribus, of pioneers and early movers in a given market over late

entrants. Researchers into the relationship between market share and order of entry

have converged onto three generalizations, summarized by Kalanaryam, Robinson and

Urban in 1995.

The first generalization is that there is a negative relationship between order of

entry and long-term market share, both in the markets for consumer and industrial

products (Robinson and Fornell 19856; Robinson 19887; Parry and Bass 19908; Kerin

et al. 19929; Urban et al. 198610; Kalynaram and Urban 199211; Golder and Tellis 199312;

6 William T. Robinson; Claes Fornell, “Sources of Market Pioneer Advantages in Consumer Goods

Industries”, Journal of Marketing Research, Vol. 22, No. 3. (Aug., 1985), pp. 305-317 7 William T. Robinson, “Sources of Market Pioneer Advantages: The Case of Industrial Goods Industries”,

Journal of Marketing Research, Vol. 25, No. 1. (Feb., 1988), pp. 87-94 8 Parry, M. and F. M. Bass. "When to Lead or Follow? It Depends," Marketing Letters. 1 (November 1990), pp.

187-198. 9 Kerin. R. A., P. R. Varadarajan and R. A. Peterson, "First-Mover Advantage: A Synthesis. Conceptual

Framework and Research Propositions." Journal yf .llarkering. 56 (October 1992), pp 33-52. 10 Urban. G. L., T. Carter, S. Gaskin, and Z. Mucha, "Market Share Rewards to Pioneering Brands: An

Empirical Analysis and Strategic Implications", Marketing Science, 32 (June 1986), pp 645-659. 11 Kalyanaram, G. and G. L. Urban, "Dynamic Effects of the Order of Entry on Market Share. Trial Penetration, and Repeat Purchases for Frequently Purchased Consumer Goods," Marketing Science. I I (Summer 1992). 235-250 12 Colder. P. N. and G. J. Tellis , "Pioneer Advantage: Marketing Logic or Marketing Legend?', Journal of Marketing Research, 30 (May 1993). 158- 170

10

Kalyanaram and Wittink 199413; Berndt et al. 199414; Brown and Lattin 199415; Huff

and Robinson 199416; Glazer 198517; Lieberman 198918; Sullivan 199219; Mitchell 1991).

Later empirical studies have confirmed this generalization, both for consumer and

industrial goods (VanderWerf and Mahon 1997 20 ; Lieberman and Montgomery,

199821), and for services (Tufano 198922; Makadok 199823; Lopez and Roberts, 200224,

Fernandez and Belen Usero 200625).

The theoretical support for this empirical generalization is multi-faceted, intuitive

and plausible. Marketing science predicts that sustainable pioneer advantages arise at

nearly every level of a company’s operation, and are both endogenous and exogenous.

At the consumer level, theory assumes that pioneer’s products tend to shape

consumer tastes and preferences in their favor, a phenomenon termed protypicality by

13 Kalyanaram and D. R. Wittink, "Heterogeneity in Entry Effects Between Nondurable Consumer Product

Categories," International Journal ofResearch in Marketing, 1994 14 Berndt. E.. L. T. Bui, D. H. Reiley, and G. L. Urban, "The Roles of Marketing. Product Quality. and Price Competition in the Growth and Composition of the U.S Anti-Ulcer Drug Industry," Working Paper # 19-94 (May 1994), Sloan School, MIT 15 Brown. C. L. and J. M. Lattin. "Investigating the Relationship Between Time in the Market and Pioneering Advantage,"Management Science 40 (October 1994). I36 1- 1369 16 Huff. L. C. and W. T. Robinson , "The Impact of Leadtime and Years of Competitive Rivalry on PioneerMarket Share Advantages." Management Science. 40 (October 1994). 1370-1377 17 Glazer. A., "The Advantages of Being First," American Economic Review 75 (June 1985). 473-480. 18 Lieberman. M. B., "The Learning Curve. Technology Barriers to Entry. and Competitive Survival in the Chemical Processing Industries," Strategic Management Journal, 10 (September-October 1989), 431-447 19 Sullivan. M. W., "Brand Extensions: When to Use Them." Management Science 38 (June 1992). 793-806 20 VanderWerf, Pieter A. and John F. Mahon “Meta-Analysis of the Impact of Research Methods on Findings of

First Mover Advantage,” Management Science, 43 (Nov 1997), 1510-9. 21 Lieberman, Marvin B. and David B. Montgomery, "First Mover (Dis)Advantages: Retrospective and Link with the Resource Based View,” Strategic Management Journal, 19 (December 1998), 1111-25. 22 Tufano, P., “Financial innovation and first mover advantages”, Journal of Financial Economics 25 (1989):213-

240. 23 Makadok, Richard, “Can First-Mover and Early-Mover Advantages Be Sustained in an Industry with Low

Barriers to Entry/Imitation?”, Strategic Management Journal, 19 (7, 1998): 683-696 24 López LE, Roberts EB. “First-mover advantages in regimes of weal appropriability: the case of financial services innovations”,. J Bus Res 2002;55:997-1005. 25 Fernández Z, Usero B. “The erosion of pioneer advantage in the European mobile telecommunications industry.” Serv Bus 2007;1:195–210.

11

Carpenter and Nakamoto (1989)26. In addition, consumer risk aversion is assumed to

entrench the early entrant’s products with the consumers (Schmalensee, 1982 27 ),

similarly to the effects of consumer learning (Kardes and Kalyanaram, 1992 28 ).

Furthermore, it can be logically expected that the expected incremental benefit from a

new brand or service declines as the number of brands increases (Hauser and

Wernerfelt, 199029), and that the opportunity to serve unmet consumer needs declines

as the number of brands increases (Prescott and Visscher 197730).

The two mechanisms through which these theoretical predictions are transformed

into higher market share are (a) through higher initial trial rate and (b) through a

higher rate of repeat purchase/usage.

(a) Trial rate is higher for pioneers: Schmalensee (1982) argues that even for identical

products, the risk of an unfavorable experience motivates rational consumers to

continue buying the pioneering brand. Along similar lines, Hauser and Wernerfelt

(1990) state that, "if two brands enter the market with the same distribution of

perceived utility, the brand that enters earlier will be considered more often. If it

is considered more often, it should have a higher market share.” Kardes et al.

(1993) also find that pioneers are included more often in the consideration set by

26 Carpenter, Gregory S., and Kent Nakamoto, “Consumer Preference Formation and Pioneering Advantage,”

Journal of Marketing Research, 26, 3 (August 1989), 285-298 27 Schmalensee. R. "Product Differentiation Advantages of Pioneering Brands," Amerlcan Economic

Review 72 (June 1982). 349-365. 28 Kardes. F. R. and G. Kalyanaram (1992). "Order-of-Entry Effects on Consumer Memon and Judgment: An Information Integration Perspective," Journal of Marketing Research, 29 (August 1992). 343-357. 29 Hauser. J. R. and B. Wernerfelt, "An Evaluation Cost Model of Consideration Sets," Journal of Consumer

Research. 16 (March 1990). 393-408 30 Prescott. E. C. and M. Visscher . "Sequential Location Among Firms with Foresight," Bell Jolrrnal of Economlcs, 8, 1977, 378-393.

12

consumers. All of these forces should lead to greater consumer trial for pioneering

brands.

(b) Repeat purchase/usage is also higher for pioneering brands. One reason is that

consumers learn more about pioneering brands because of their longer time on the

market. Kardes and Kalyanaram (1992) conclude, "The learning advantage

conferred to the pioneering brand translates into more extreme and confidently

held judgments of the pioneer. Judgments held with conviction are persistent over

time and resistant to competitors' activities. Together, these judgmental processes

lead to long-run pioneering advantage" (p. 356)”

In distribution channels, pioneers are also likely to establish long-term advantages

through intensive distribution (Porter, 197431) and to dominate scarce retail shelf space

(White, 1983)32. Distribution channels in this context must be interpreted broadly as

any instruments of leverage over exposure to the end consumer; be those the traditional

physical distribution mechanisms (retail shelf space), media of distribution of

information goods (mobile spectrum, broadcasting frequencies, broadband spectrum),

or other gate-keeper capacity (such as agreements with media-buying agencies, in the

case of advertising businesses that do not sell their space directly to end consumers).

At the firm level, economies of scale and experience advantages are assumed for market

pioneers (Schere and Ross, 1990 33 ). Furthermore, Prescott and Visscher (1977) 34

31 Porter, M. E., "Consumer Behavior, Retailer Power. and Market Performance in Consumer Goods Industries." Review of Economics and Statistics, 56, 1074. 419-436 32 White. A. P., “The Dominant Firm – A Study of Market Power”, Ann Arbor.,1983. MI: UMI Research Press 33 Scherer. F. M and D. Ross , “Industrial Markets Structure and Econonlic Performance, (third Ed.. 1990),

Boston:Houghton Mifflin. 34 Prescott. E. C. and M. Visscher, "Sequential Location Among Firms with Foresight," Bell Jolrrnal of Economlcs, 8, 1977, 378-393.

13

theorize that early entrants have the option to develop a broad product line, whereas

later entrants are frequently forced to enter a market niche with a narrow product line.

Furthermore, it can be theorized that in markets which require specialized and thus

scarce human resources (specialized management skills, knowledge, talent, etc), early

entrants may be able to preempt later entrants from access to the necessary skill- or

talent-set.

The secondly generalization is that there exists a quantifiable relationship

between a market entrant’s market share and the pioneer’s market share. According to

regression results on cross-sectional empirical data, the entrant’s forecasted market

share divided by the first entrant’s market share broadly equals one divided by the

square root of the order of market entry, or expressed differently, MSi = MS1/��√� ,

where MSi is the market share of the ith entrant and MS1 is the market share of the first

entrant in that specific market. This relationship was originally derived through

regression analysis of data for markets of packaged consumer goods; but has since been

replicated, broadly to the same regression results, in many different single-sided

markets, including services markets and industrial-goods markets.35

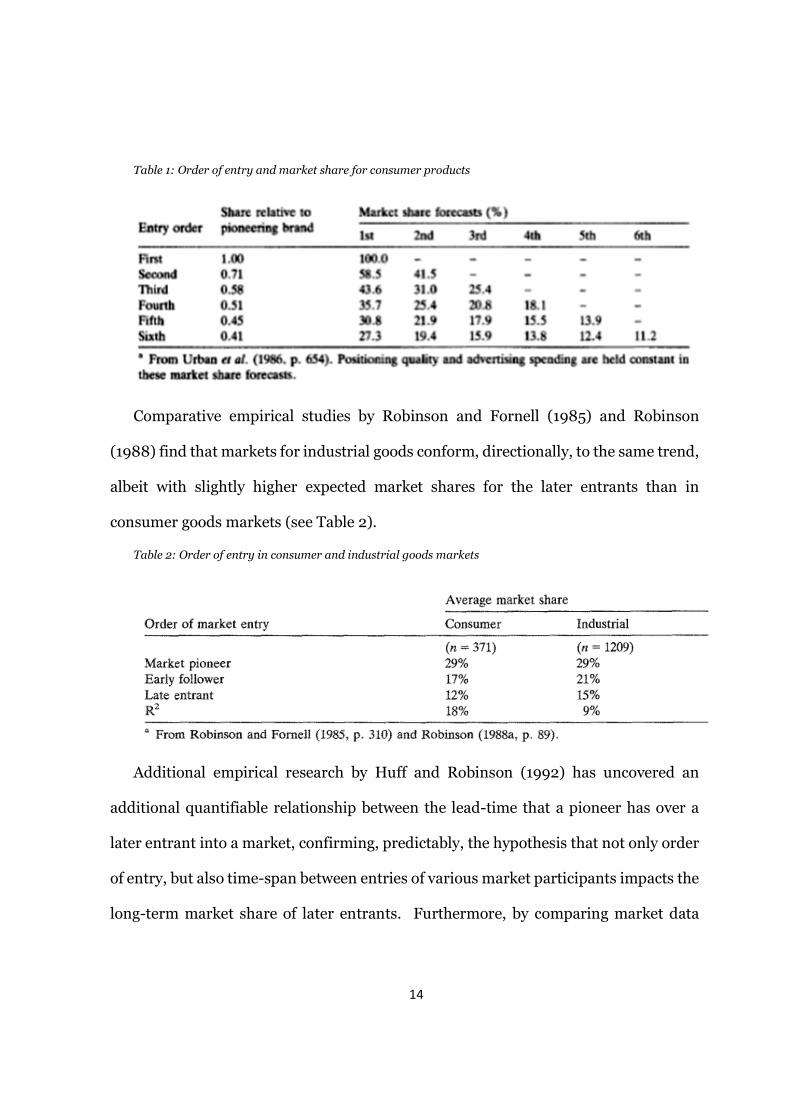

The following table, from Urban et al’s 1986’s cross-sectional meta-study involving

136 firms in 34 market sectors, exemplifies the long-term market-share expectations

for markets for consumer goods with sequential entry of up to six competitors.

35 Single-sided markets denote markets in which there is a single relationship between business and

consumer; different from two-sided markets, such as advertising based businesses that leverage one market (share) into another.

14

Table 1: Order of entry and market share for consumer products

Comparative empirical studies by Robinson and Fornell (1985) and Robinson

(1988) find that markets for industrial goods conform, directionally, to the same trend,

albeit with slightly higher expected market shares for the later entrants than in

consumer goods markets (see Table 2).

Table 2: Order of entry in consumer and industrial goods markets

Additional empirical research by Huff and Robinson (1992) has uncovered an

additional quantifiable relationship between the lead-time that a pioneer has over a

later entrant into a market, confirming, predictably, the hypothesis that not only order

of entry, but also time-span between entries of various market participants impacts the

long-term market share of later entrants. Furthermore, by comparing market data

15

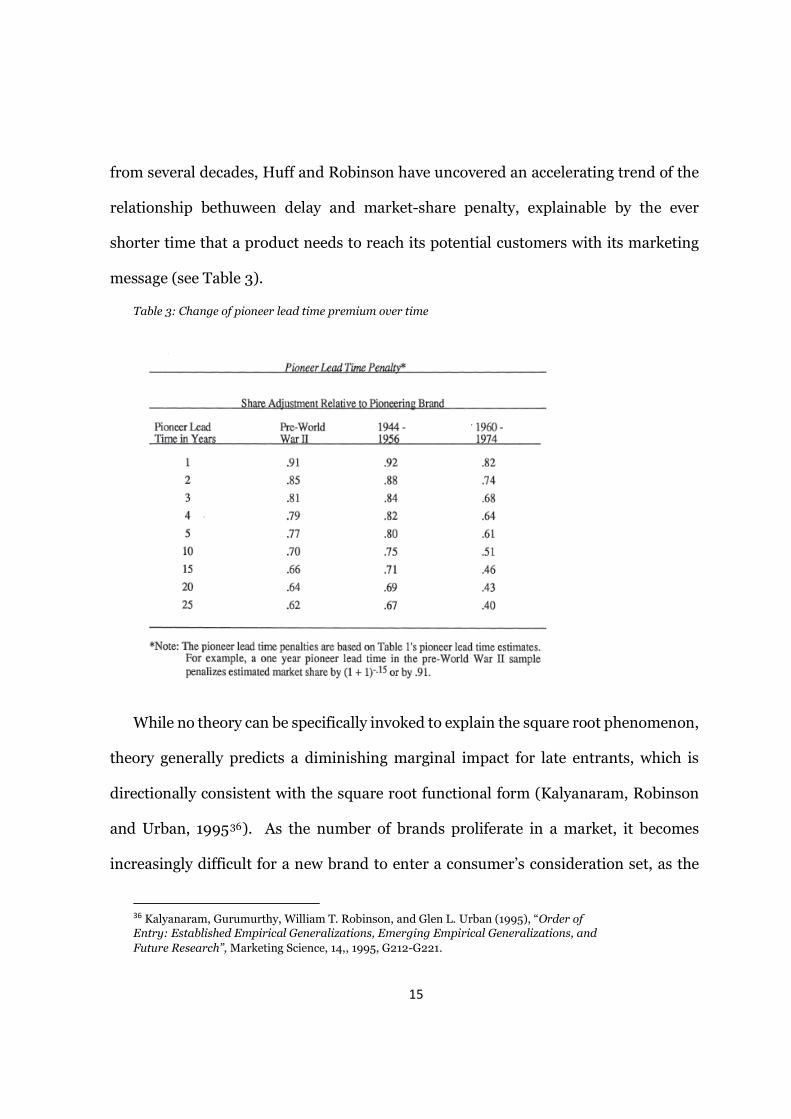

from several decades, Huff and Robinson have uncovered an accelerating trend of the

relationship bethuween delay and market-share penalty, explainable by the ever

shorter time that a product needs to reach its potential customers with its marketing

message (see Table 3).

Table 3: Change of pioneer lead time premium over time

While no theory can be specifically invoked to explain the square root phenomenon,

theory generally predicts a diminishing marginal impact for late entrants, which is

directionally consistent with the square root functional form (Kalyanaram, Robinson

and Urban, 199536). As the number of brands proliferate in a market, it becomes

increasingly difficult for a new brand to enter a consumer’s consideration set, as the

36 Kalyanaram, Gurumurthy, William T. Robinson, and Glen L. Urban (1995), “Order of

Entry: Established Empirical Generalizations, Emerging Empirical Generalizations, and

Future Research”, Marketing Science, 14,, 1995, G212-G221.

16

expected incremental benefits decline (Hauser and Wernerfelt, 1990). Further to the

decline in subjective “expectation of benefits” from new brands, the objective

opportunity to serve an unmet consumer need also declines as the number of brands

increases (Prescott and Visscher, 1977). Even with a broad product line usurped by the

pioneer, the second and third entrant often succeed in capturing the obvious niches,

while the subsequent entrants have to seek niches amongst the niches, thus leading to

ever diminishing returns in market share.

The third generalization is that in mature markets, pioneer market share

advantages decline slowly over time. Empirical evidence suggests that early market

share advantages are sustainable in the long term and “span decades” (Kalyanaram,

1994); however, these advantages decline slowly over time. This empirical result is

observed in consumer-goods markets at a significant statistical level by Brown and

Lattin (1994), Huff and Robinson (1994) and Robinson and Fornell (1985), as well as

for industrial goods (Robinson 1988). By way of example, Brown and Lattin (1994)

predict that in a three-player consumer-good market of 25 years, the pioneer would

have a 43% market share, the second entrant a 32% share, and the third entrant a 25%

share. As the market approaches infinity, these shares would converge somewhat, but

not fully, to 36%, 33% and 31% respectively. Similar findings, directionally, are

produced by a study of European mobile telephone operators in the 1995-2005 period

(Fernandez and Usero, 2006).

The theoretical substantiation of this observation can be derived, on one hand, from

theories relating to dominant and/or “old” firms. Scherer and Ross (1990) theorize

17

that after a given market share has been accumulated, it becomes more profitable for a

firm to slowly “sell off” a portion of its market share than to expend resources on

keeping every individual customer it has had. Per Geroski (1989), “dominant firms

decline when they become sleepy and thus vulerable” to innovative, sudden or simply

reckless competitive behavior of challengers. On the other hand, it can be theorized

that as later entrants reach profitable operation and potentially high profit margins,

they are more incentivized than early entrants to spend aggressively on marketing

namely in order to offset their structural late-entry disadvantage. With the passage of

time consistent marketing overspending is likely to minimize the impact of the package

of pioneering advantages.

In addition to the three generalizations, other researchers have observed

higher survival rate for pioneers than for early followers (Robinson and Min, 2002)37

and a negative relationship between the stages of entry by product life cycle and

survival rate (Agarwal and Gort, 1996, 1997)38. In addition, a meta-study by Mallik and

Sudharshtan (2002) 39 finds that market shares follow a stable Zipf-law form

distribution as a function of rank of entry into the market. This finding however does

not contradict materially the second generalization, but rather makes a further

generalization of that very generalization.

37 Robinson, William T and Sungwook Min, “Is the first to market the first to fail? Empirical evidence for

industrial goods businesses,” 2002, Journal of Marketing 38 Agarwal, R., and M. Gort, “The evolution of markets and entry, exit and survival of firms”, The Review of

Economics and Statistics, 78 (3), 1996, 489-498. 39 Riemer H Mallik S and Sudharshan D .2002. “Market Shares follow a Zipf Distribution”

http://www.business.illinois.edu/research/020125paper.pdf

18

Substantially, and certainly directionally, therefore, there appears to be consensus

among researchers in relation to a statistically significant and quantifiable relationship

between order and timing of entry into a market, and market share. The dissenting

scientific opinions have typically drawn attention to possible exaggeration of the effects

observed in the empirical data due to potential survival bias; however there does not

seem to be any body of research literature that purports to prove the null hypothesis on

this issue.

3. CASE STUDY: VALUATION OF DUTCH BROADCASTING

SPECTRUM

3.1 Background: 2003 tender

On July 1st 2003, the Dutch government re-distributed the radio broadcasting

spectrum across the Netherlands in what was termed officially “the zero-base radio

project.” It involved a completely new national plan of frequencies allocated to

commercial broadcasters, coupled with revocation of all existing radio licenses (which

had since expired and had been extended for temporary periods until the zero-base

redistribution). As a result of this major reshuffle, nine new national radio stations

were licensed for a license period of eight years, with no provision for automatic

renewal upon the expiration of such term.

Four of the national licenses were earmarked for “restriction-free” programming,

allowing their recipients to broadcast any possible mix of programming, subject to

general media and advertising laws only. These four licenses were allocated through a

closed, single-round auction. Applicants were invited to bid for the respective license,

19

having the knowledge of an additional, fixed, one-time fee that they would have to pay

upon receipt of the license.

The remaining five licenses were earmarked for specific content, including news,

serious music, Dutch-language music, alternative music, and old music. The procedure

through which these five licenses were allocated included both a financial auction of

the type described above, and a “beauty” contest based on content commitments. The

latter criterion had priority; i.e. applications which excelled in their programming offer

would be awarded the respective licenses, and only in the case of neck-to-neck

competition in content commitments would the financial bid be used as a tie-breaker.

The one-time financial fee, which de facto served as a reserve price in the auction,

was computed as a percentage (7.5%) of the cumulative net revenues that each license

was expected to generate over the license term, discounted to the date of the award. In

absolute numbers, the one-time fee ranged from €1,7 m to €5,5 m, depending on the

each license’s perceived earning potential.

The winning financial bids for each frequency exceeded significantly the one-time

fee (reserve price), with the bid range for the unrestricted licenses being between €30

m and €80 m. On average, the one-time fee represented approximately 10% of the

actual cumulative financial instrument, paid for each license.

The zero-base re-allocation project was accompanied by high publicity, both due to

the self-referential interest of the media in the issue, and as a result of high-profile

(unsuccessful) litigation by several incumbents trying to retain their licenses.

20

Additionally, the Dutch government funded a national direct-mail campaign

announcing the new radio landscape in the country to each and every Dutch resident.

On July 1st 2003, nine new radio stations (of which three had been incumbents

began broadcasting on the newly allocated frequency positions.

3.2 New tender versus extension: policy decision 2011

As the original license terms neared their expiration date in September 2011, the

Dutch government found itself under intensive lobbying by incumbent operators to

offer extensions to the existing license-holders, as opposed to hold new tenders open

to any party. Privately, this request was rationalized by the fact that in 2003, all parties

had overbid and, in retrospect, no incumbent had been able to recoup their investment

over the eight-year term. The 2008 financial crisis was put forward as a key exculpating

factor for the incumbents overbidding. Publicly, the argument for extension was

supported with public opinion surveys, evidencing that (predictably) audiences loved

their existing radio offerings and preferred to continue to listen to stations they knew

and liked. The Dutch government had internal pressures from bureaucrats in the

Ministry of Economy and technocrats in the Telecoms Agency to go for a new tender,

which would ensure (plausibly) higher revenues than an extension would and, from a

legal perspective, would be a bullet-proof regulatory decision. These proponents

argued that an extension was not provided for in the original licenses, and that

potential newcomers would object – and possibly litigate – in the event of extensions

that would lock up the market for incumbents only. On the other hand, the more

politically minded officials saw a new tender as a messy project, at that one that would

21

likely pitch the existing media operators against the government and induce them to

possibly transfer their lobbying efforts to over-the-air campaigning, as some stations

had done prior to the 2003 zero-base reallocation. Ultimately, the Minister of the

Economy (in charge of spectrum allocation policy) decided to outsource the decision to

a consortium of legal and economic experts, who were tasked with determining (a)

whether license term extensions were compatible with national and EU legislation and

(b) if so, under what financial terms such extensions must be offered to prevent possible

implications in unlawful state aid being offered to incumbents.

The consortium, including University of Amsterdam law professors and

econometrists from the economic consultancy SEO, produced a report that concluded

that a license extension was legally permissible, both under EU and national law, under

certain conditions. Key among them was the “avoidance of state aid” condition, which

meant that the incumbents would have to pay, as a license fee, essentially the full value

of the license; thus offsetting any aid that might be construed to have been granted. A

critical further question was, predictably, whether the “value of the license” should be

determined from the perspective of the incumbent or from that of a new operator –

clearly, these values would be significantly different. The consulting consortium

concluded that the valuation must be conducted from the perspective of an anonymous

newcomer. The logic was that the State would be granting to the incumbents a resource

of a certain value (which must be recouped via a license fee) which was equivalent to

quantum of the highest bid that an average efficient newcomer would be expected to

submit in a hypothetical auction. A different conceptual approach to valuation which

22

would lead to the same outcome was to establish the highest value, at which the

incumbents were likely to be able to sell their existing license to a newcomer. In other

words, this would represent the opportunity cost for an incumbent to dispose of the

license. The consortium also provided a full-fledged econometric model which

ascertained the corresponding values for each license.

A second key condition contained in the legal assessment by the consulting

consortium was that the market should not be fully locked up for new entry. Clearly,

licenses are tradable, and as such newcomers could enter the market through

acquisition. Conveniently, however, two of the nine national licenses – one unrestricted

and one restricted--had ended up being vacant, their operator having gone bankrupt in

2009. This lent the Government the opportunity to extend the seven active licenses to

their incumbents for an additional six year term, while addressing the “market lock-

up” issue through an allocation of the remaining two licenses through an auction, for

the same term.

The Dutch government opted to follow the advice of the consulting consortium and

published the consortium’s report (including both the legal conclusions and valuation

models) for public consultations in early 2011.

3.3 SEO valuation model

SEO, the Dutch economics and research consulting firm, produced the valuation

model for the one-time financial instruments to be paid by each of the incumbents. The

model was built around a macroeconomic projection of the radio advertising market

for a six-year period, econometrically derived market-share forecasts for each of the

23

license operators – under the explicit assumption that they would be operated by a

party other than the incumbent (i.e., a hypothetical new-comer), and econometrically

derived operating cost estimates for each license. The projected market share, as a

function of the forecasted market for each year, would result in the revenue projections

per year; and the projected revenue less the projected (cash-based) expenditures would

result in the expected pre-tax cash flows per year. Those would be then discounted for

taxation and for the time value of money, and the resulting net amounts would

constitute the (maximum) value of the licenses from the perspective of efficient

newcomers.

For the econometric computation of both market share (and thus revenues), and

operating costs, SEO had approached each incumbent in the radio market and had

gathered confidential data on revenues and costs by category for the years 2006,2007

and 2008. Based on these inputs and other publicly available data, SEO had produced

a series of highly-explanatory regression models, which identified a number of

independent variables for market share and for the key cost categories.

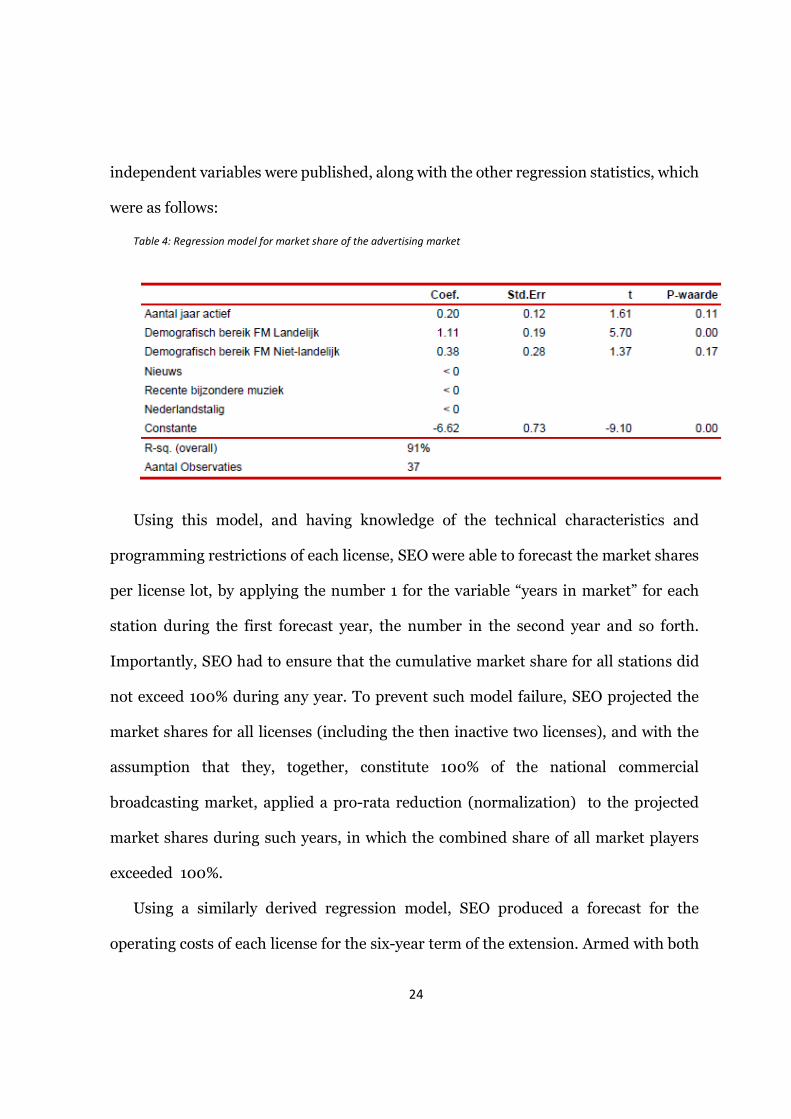

The regression modeling of market share had established that the key independent

variables, explaining 91% of variability in market share, were the following: (a)

technical reach as a percentage of the population covered by the license signal, (b)

number of years that a station has been active in the Dutch radio market, and (c)

whether or not the station has a programming restriction. Each of the program

restrictions had a different, negative impact on market share; however SEO did not

publish the corresponding coefficients due to confidentiality concerns. The remaining

24

independent variables were published, along with the other regression statistics, which

were as follows:

Table 4: Regression model for market share of the advertising market

Using this model, and having knowledge of the technical characteristics and

programming restrictions of each license, SEO were able to forecast the market shares

per license lot, by applying the number 1 for the variable “years in market” for each

station during the first forecast year, the number in the second year and so forth.

Importantly, SEO had to ensure that the cumulative market share for all stations did

not exceed 100% during any year. To prevent such model failure, SEO projected the

market shares for all licenses (including the then inactive two licenses), and with the

assumption that they, together, constitute 100% of the national commercial

broadcasting market, applied a pro-rata reduction (normalization) to the projected

market shares during such years, in which the combined share of all market players

exceeded 100%.

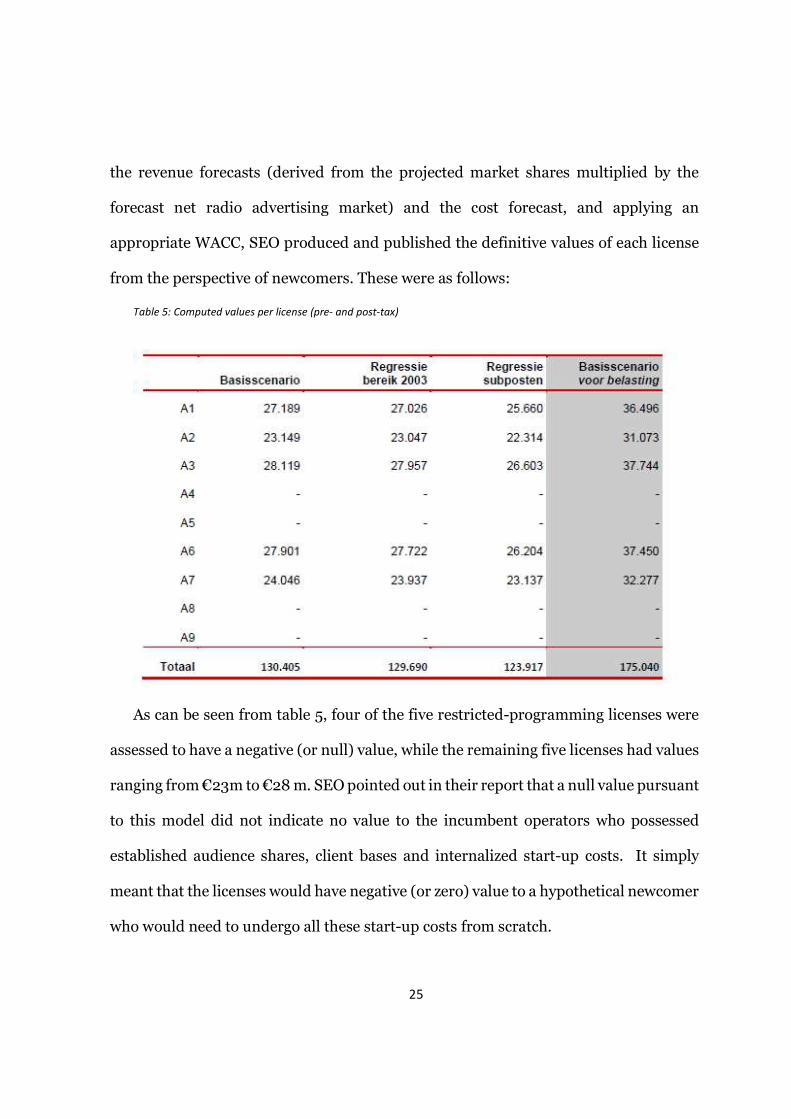

Using a similarly derived regression model, SEO produced a forecast for the

operating costs of each license for the six-year term of the extension. Armed with both

25

the revenue forecasts (derived from the projected market shares multiplied by the

forecast net radio advertising market) and the cost forecast, and applying an

appropriate WACC, SEO produced and published the definitive values of each license

from the perspective of newcomers. These were as follows:

Table 5: Computed values per license (pre- and post-tax)

As can be seen from table 5, four of the five restricted-programming licenses were

assessed to have a negative (or null) value, while the remaining five licenses had values

ranging from €23m to €28 m. SEO pointed out in their report that a null value pursuant

to this model did not indicate no value to the incumbent operators who possessed

established audience shares, client bases and internalized start-up costs. It simply

meant that the licenses would have negative (or zero) value to a hypothetical newcomer

who would need to undergo all these start-up costs from scratch.

26

Similarly, SEO stated, the value of the remaining (positive-value) licenses would be

higher to the actual incumbents to which they were to be awarded through the

envisaged extensions, than to a newcomer. However, SEO maintained, the only

economically justified method of determining the intrinsic value of the scarce resource,

net of the value created by (and at the expense of) the incumbent, was to assess the

value from the perspective of a newcomer.

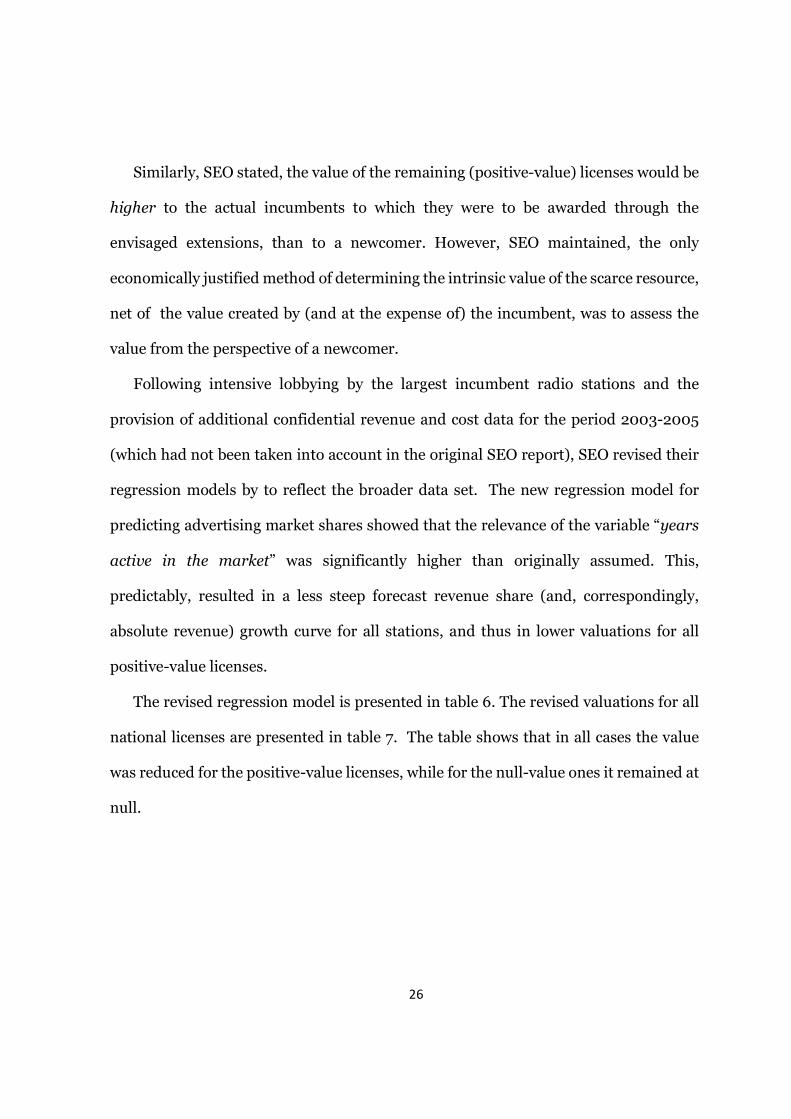

Following intensive lobbying by the largest incumbent radio stations and the

provision of additional confidential revenue and cost data for the period 2003-2005

(which had not been taken into account in the original SEO report), SEO revised their

regression models by to reflect the broader data set. The new regression model for

predicting advertising market shares showed that the relevance of the variable “years

active in the market” was significantly higher than originally assumed. This,

predictably, resulted in a less steep forecast revenue share (and, correspondingly,

absolute revenue) growth curve for all stations, and thus in lower valuations for all

positive-value licenses.

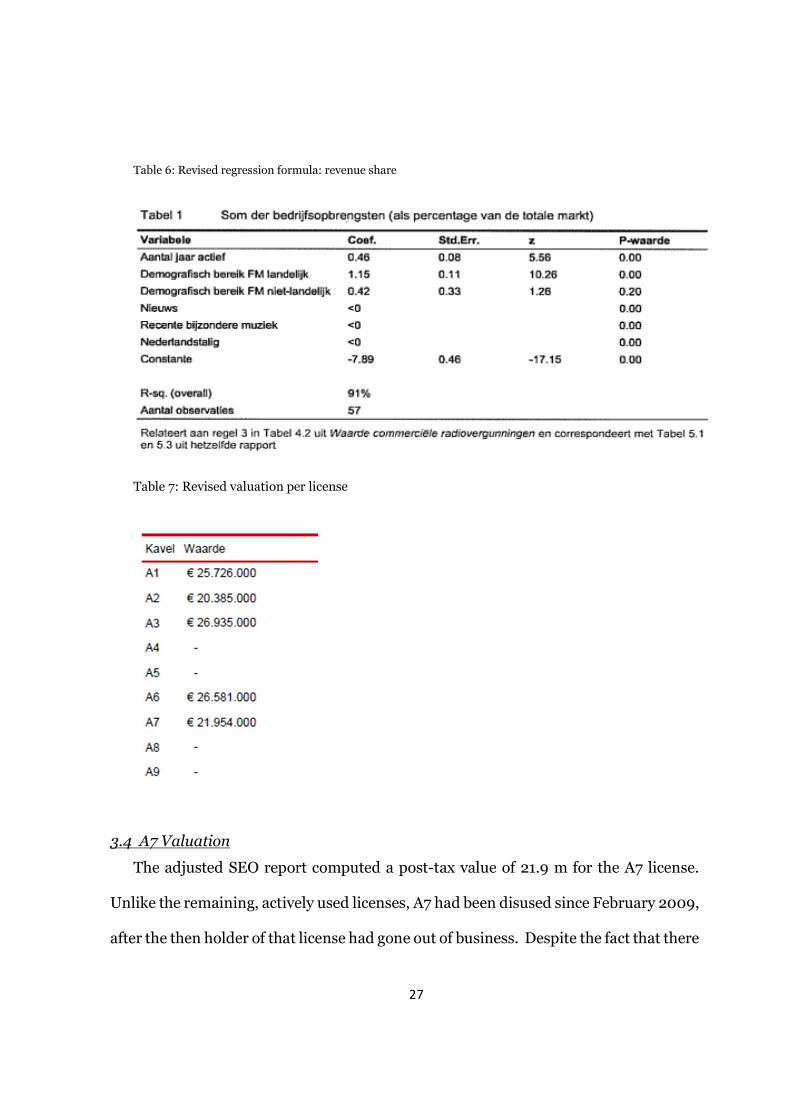

The revised regression model is presented in table 6. The revised valuations for all

national licenses are presented in table 7. The table shows that in all cases the value

was reduced for the positive-value licenses, while for the null-value ones it remained at

null.

27

Table 6: Revised regression formula: revenue share

Table 7: Revised valuation per license

3.4 A7 Valuation

The adjusted SEO report computed a post-tax value of 21.9 m for the A7 license.

Unlike the remaining, actively used licenses, A7 had been disused since February 2009,

after the then holder of that license had gone out of business. Despite the fact that there

28

could be no extension of A7 to an incumbent, the inclusion of that license in SEO’s

valuation model was necessary, as otherwise the forecast for the extended licenses

would have been based on an incomplete market – 7 versus 9 national competitors40.

The latter assumption was consistent with the expectation that as of 2011, both A7 and

A8 would be issued in new tender procedures, and thus active as of September 2011.

Failure to include A7 and A8 in the model would have resulted in inflated market share

forecasts for each of the remaining licenses, and thus possibly overcharging for the

incumbents. Furthermore, the empirical data from which the regression analysis had

been built had come from the period 2003-2008 when all nine national licenses had

been active; and thus the regression model derived from such data might not have been

robust for different market conditions with fewer players.

The Dutch government proceeded to use the valuation for A7, computed in the SEO

model, as a basis for determining the financial instrument to be paid by the successful

bidder for that license in the new tender procedure for that lot in September 2011. The

financial instrument was to be comprised of two parts – the one-time fee (set by the

Government and payable upon receipt of the license), and the financial bid, to be

offered by the applicants on top of the one-time fee. The one-time fee was to be set at

80% of the full value computed by SEO: i.e. at €17 m. The stated rationale behind this

discount was that “sufficient bidding space should be allowed on top of the one-time

fee,” in other words, the discounted one-time fee was perceived as the reserve price in

the auction, and the reserve price and the incremental bid together would represent

40 A8 was also disused since 2009, but it was a restricted (classical/jazz music) license with a negligible

audience potential with zero value, and thus is left out of the current analysis

29

the actual bid, which was expected to range anywhere between the reserve price and

the full value of €21,9 m41.

The Dutch government announced an auction for A7 in September 2011, setting

forth a requirement for a one-time license fee of €17 m and requiring a financial bid on

top of it. Furthermore, a pre-tender vetting requirement was that the applicant submits

a realistic business plan and financial forecast, evidencing their capability to exploit the

license efficiently and with a positive return during its six-year term (the latter was an

ex-lege requirement). A separate requirement set forth by the government was that

simultaneously with the application, candidates should provide a bank guarantee in the

amount of ¼ of the one-time license fee.

3.5 Empirical outcome of regulatory decisions

The decision to extend the seven active licenses at costs ranging from €0 (for three

restricted licenses) to €26 m was accepted by the incumbents, somewhat reluctantly so

by the un-restricted license-holders which were all forced to pay in excess of €20 m,

while having lobbied for even lower fees. One restricted-format incumbent, a station

with a relatively loose prescription to play “music older than 5 years,” whose license

was evaluated at €20 m, accepted the extension under protest and subsequently

litigated to have its fee reduced, a case currently in judicial proceedings.

In August 2011 the Dutch government held a tender for the A7 license with the

above-described terms. Two applicants took part, of which one was disqualified due to

41 theoretically, a higher price might also be offered; this however would mean that the applicant is more

than average efficient – for instance, has pre-existing market presence that could be leveraged into the

business case for this license

30

failure to comply with the formal pre-qualification requirements. The second applicant

made a financial bid but in its application explicitly disavowed he applicability of the

€17 m license fee, arguing that it was incorrectly computed, was based on false

economic logic, and was thus non-binding (null). In further support of this argument,

the applicant claimed that it was impossible to submit a business plan that

incorporated such license fee and at the same time complied with the requirement that

the financial result of operating the license over 6 years be positive.

The government rejected the application based on the absence of the bank

guarantee and the non-inclusion of the one-time fee into the business plan, without

considering on the merit the bidder’s arguments for the nullity of the fee regulation.

The rejected bidder appealed the rejection. The first-instance decision of the Court of

Rotterdam is pending at press-time.

In August 2012 the Government announced plans to re-auction the A7 license in

quarter four of 2012 – this time without a one-time fee, citing changed market

conditions and a shorter remaining license period. As of December 2012, no tender has

been initiated and the frequency network remains vacant.

4. Economic and legal analysis of extension of licenses to incumbents

4.1 Abstract

A key feature of the SEO model is that it determines the license extension fee on the

basis of a license (scarce resource) valuation that is agnostic of the identity of the

current license operator; of its current license fee level and programming restrictions.

31

In taking this approach, SEO achieves the stated goal of avoiding penalization of

incumbents for their empirical, firm-specific success; and thus assumes away the

subjective value of the resource. However, in so doing, the regulatory application of the

SEO model may lead to forward-looking distortion of competition, by introducing

disproportionate changes in similar circumstances, and by offering effective risk

mitigation to some operators while none (or less) is offered to others. In particular, this

valuation approach leads to increased business risk being imposed on holders of

restricted licenses, at the expense of holders of free-form ones.

Furthermore, a forward-looking DCF approach is likely to lead to actual changes of

license conditions which are larger than the objectively justified change, which may

result in a legal hypothesis of effective issuance of new licenses without the legally

required due process; as opposed to extension of existing ones.

In addition, , the “opportunity cost” approach adopted by the regulator would lead

to distortion of competition due to the fact that it would artificially assign equal

“newcomer” status to all market parties in 2011; whereas they in fact have starkly

different time-in-market backgrounds.

All of these market-interventionist effects of the terms of extension are likely to be

unlawful under EU and national legislation requiring non-discriminatory,

proportionate and non-interventionist spectrum regulation, as well as under broad

competition legal principles. More broadly, they may represent a form of regulatory

capture.

4.2 Economic analysis

32

The operator-agnostic DCF valuation model “resets” the values of all licenses as of

September 2011, reflecting their value in a hypothetical reality in which all operators

are newcomers. The theoretical framework relating to the cost of order-of-entry on

market-share predicts that such resetting would lead to structural, unavoidable cost

transfers– and thus, value--transfers between the actual market players. Market

players that have entered the market earlier will have their correspondingly lower costs

assumed away. More recent entrants will also have some of their costs assumed away,

assuming none of them will be a true newcomer in 2011; however the quantum of such

cost elimination – respectively, value subsidy – will be a function of the time in market.

Stated simply, earlier market entrants will get a higher value subsidy than more recent

entrants.

The empirical models described in the first chapter allow us to quantify, broadly,

the size of such value, or subsidy, misbalance. However, we do not need to depend on

market-agnostic empirical data to compute such misbalance. Given a large enough

time-series of market shares of radio stations in the Dutch market, we would be in a

position to regress the market-specific cost of order-of-entry onto market share, and

thus on value. In order to distill specifically the delay of entry as an explanatory

variable, we would need to identify those variables that have an exogenous impact on

market share (unrelated to time-in-market), in order to isolate their interference. To

simplify the regression model, however, a generous assumption will have to be made

that firm-quality and marketing expenditures are held constant for all periods and all

players, and thus have no (explanatory) impact on market share.

33

We had access to reliable audience-share data from public sources for 7 national

radio stations in the market for 4.5 years. In order to capture the faster dynamics of

early market share development, we chose to use semi-annual averaged market shares

as the dependent variables. Therefore the dataset amounted to 63 observations –

sufficient to produce a formula that is at the very least directionally predictive.

The next step was to identify the independent variables that were knowable for each

observation. Clearly one of the variables was the one we needed to test for significance:

rank of entry. We decided to add a second variable, which, while potentially correlated

with rank of entry, might turn out to improve the explanatory power of the regression

formula.

Other plausibly important independent variables were (a) geographical coverage of

each radio station during each time-period, expressed as a percentage of the

population, and (b) product restriction – relevant for those 5 national stations, which

could not deviate from a certain program prescription and were therefore limited to a

certain product and niche.

By conducting a regression analysis on these independent variables, we were able

to produce a regression model with a high explanatory power, having the following

regression statistics:

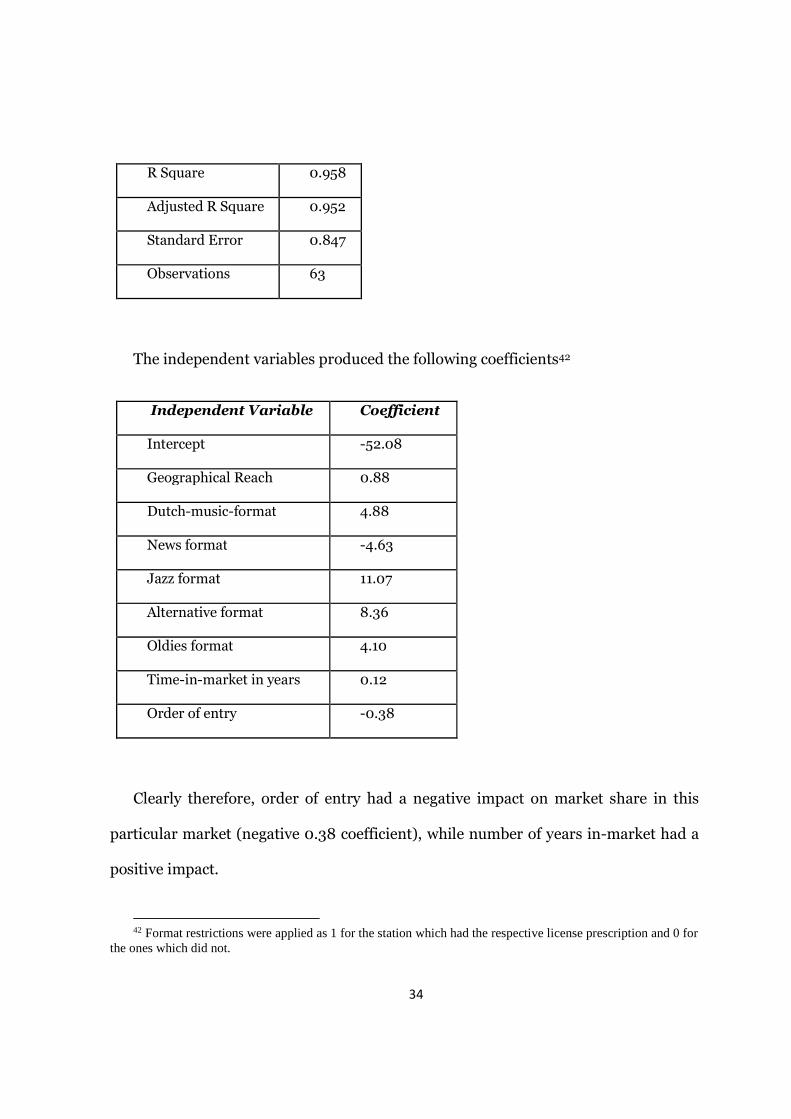

Multiple R 0.979

34

R Square 0.958

Adjusted R Square 0.952

Standard Error 0.847

Observations 63

The independent variables produced the following coefficients42

Independent Variable Coefficient

Intercept -52.08

Geographical Reach 0.88

Dutch-music-format 4.88

News format -4.63

Jazz format 11.07

Alternative format 8.36

Oldies format 4.10

Time-in-market in years 0.12

Order of entry -0.38

Clearly therefore, order of entry had a negative impact on market share in this

particular market (negative 0.38 coefficient), while number of years in-market had a

positive impact.

42 Format restrictions were applied as 1 for the station which had the respective license prescription and 0 for

the ones which did not.

35

The empirical findings in SEO’s report confirmed the same predictions for cost of

order-of-entry as the market-agnostic research studies cited in Chapter 1 and our own

regression analysis. Indeed, SEO did not isolate “order of entry” as a specific

explanatory variable, but instead captured a compound variable – number of years in

market; which combined both variables “order of entry” and “delay, in years, between

entries.” This was the result of the use of empirical data from 2003 to 2008 which

comprised both variables, expressed by the compound variable “number of years in

market.”

By applying the regression model from SEO and using two different scenarios for a

launch-year – the hypothetical and the actual one, for each market operator, we are

able to quantify, broadly43 and using a strict mutatis mutandis comparison, the value

misbalance in the two scenarios.

43 As SEO did not identify certain license-specific variables, such as the exact coefficient by which the

different license restrictions affect market shares, the model can be only be approximately reverse-engineered

by using the final values per license as published in SEO’s report. This is only possible for the “positive-value”

licenses, with a degree of +- 5%; and not feasible for the negative-value licenses.

36

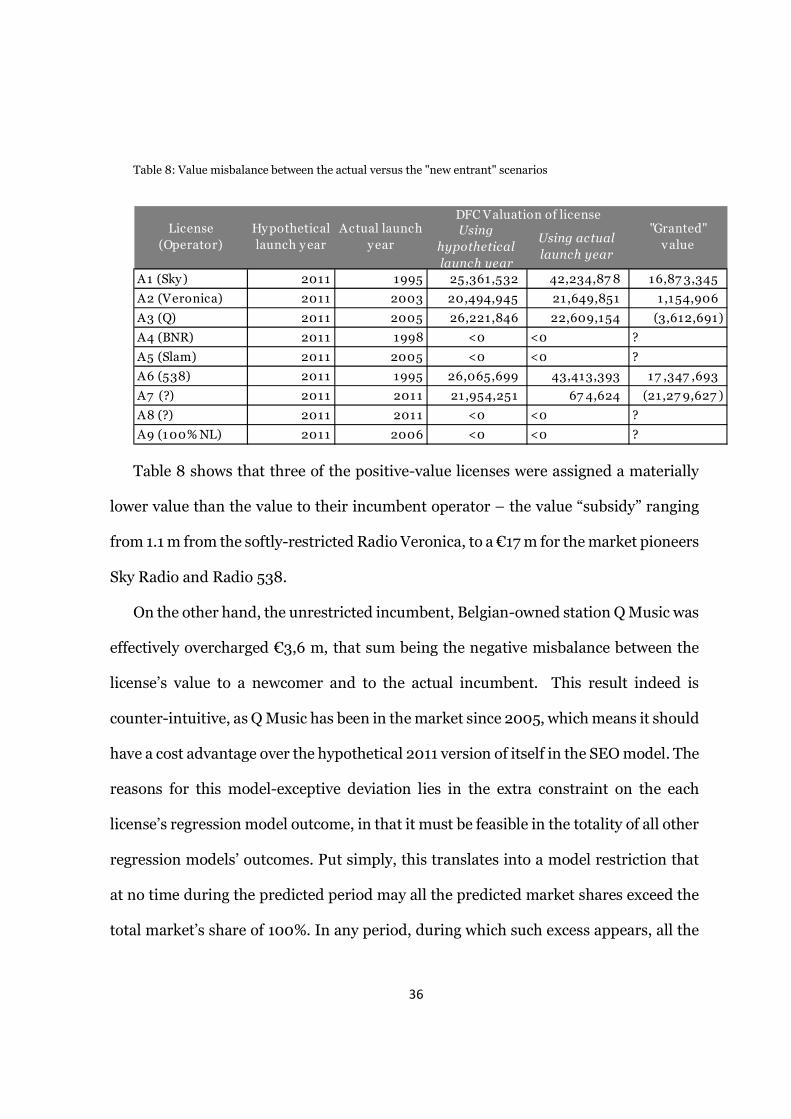

Table 8: Value misbalance between the actual versus the "new entrant" scenarios

Table 8 shows that three of the positive-value licenses were assigned a materially

lower value than the value to their incumbent operator – the value “subsidy” ranging

from 1.1 m from the softly-restricted Radio Veronica, to a €17 m for the market pioneers

Sky Radio and Radio 538.

On the other hand, the unrestricted incumbent, Belgian-owned station Q Music was

effectively overcharged €3,6 m, that sum being the negative misbalance between the

license’s value to a newcomer and to the actual incumbent. This result indeed is

counter-intuitive, as Q Music has been in the market since 2005, which means it should

have a cost advantage over the hypothetical 2011 version of itself in the SEO model. The

reasons for this model-exceptive deviation lies in the extra constraint on the each

license’s regression model outcome, in that it must be feasible in the totality of all other

regression models’ outcomes. Put simply, this translates into a model restriction that

at no time during the predicted period may all the predicted market shares exceed the

total market’s share of 100%. In any period, during which such excess appears, all the

Using

hypothetical

launch year

Using actual

launch year

A1 (Sky) 2011 1995 25,361,532 42,234,87 8 16,87 3,345

A2 (Veronica) 2011 2003 20,494,945 21 ,649,851 1 ,154,906

A3 (Q) 2011 2005 26,221,846 22,609,154 (3,612,691)

A4 (BNR) 2011 1998 <0 <0 ?

A5 (Slam) 2011 2005 <0 <0 ?

A6 (538) 2011 1995 26,065,699 43,413,393 17 ,347 ,693

A7 (?) 2011 2011 21 ,954,251 67 4,624 (21 ,27 9,627 )

A8 (?) 2011 2011 <0 <0 ?

A9 (100% NL) 2011 2006 <0 <0 ?

DFC Valuation of licenseLicense

(Operator)

Hypothetical

launch y ear

Actual launch

year

"Granted"

v alue

37

market share outcomes must be prorated down by such percentage as to comply with

the market totality of 100%. This normalization method is not only logically

indispensable, but was also explicitly identified as a necessary model step in the SEO

report.

In the case of Q Music, this constraint translated in the “dipping” of market shares

in the actual scenario, where other stations – such as Sky Radio, Radio 538 and

Veronica--had a seniority advantage over it and cornered it out of a part of its

hypothetical terminal market share, which it would have achieved in an all-newcomer

market in which no seniority advantages would have existed.

The value misbalance in the cases of the restricted, negative value licenses cannot

be precisely computed using the available coefficients from SEO’s model, but

directionally, and using Q Music as proxy, we would expect that more recent entrants

100% NL and Slam FM have a significantly lower value in the actual scenario than in

the hypothetical one.

A7 and A8 are licenses that are not operated by incumbents and thus no comparison

is possible; however A7, predictably, shows the largest divergence in values between

the “hypothetical” and “actual” scenarios, despite the fact that in both scenarios the

license would be used as of 2011. The implications of this divergence are discussed in

detail in the next sections.

This valuation comparison quantifies the very significant economic value

redistribution between market players that was the consequence of the application of

SEO’s model by the Dutch government for determining the license extension one-time

38

fees. It shows that by focusing on the (legitimate) goal to solve one economic and legal

problem – to isolate the subjective from the objective value of the license, respectively

to preclude penalization of incumbents for their prior strategy – the regulator

committed a serious market intervention, and granted effective subsidies to some

players at the expense of lesser ones – or in some cases, of taking value – from others.

In the null hypothesis for existence of regulatory capture, this market-distorting

regulatory policy may be explained by a lack of understanding of the economics behind

the cost/value implications of order-of-entry, as well as poor conceptual understanding

of the necessity to value a resource in the totality of a market, as opposed to in abstract,

market-agnostic isolation such as the one proposed in SEO’s report.

However, given the direction of the effective value transfers – away from smaller,

more recent and foreign-owned market-participants, and in favor of larger, older and

local players, there seems to be empirical evidence to suggest at least a plausible case

of regulatory capture.

Table 9 lists the value-redistribution for the positive-value licenses, along with

time-in market, profitability and ownership data for the period immediately preceding

the license extensions.

39

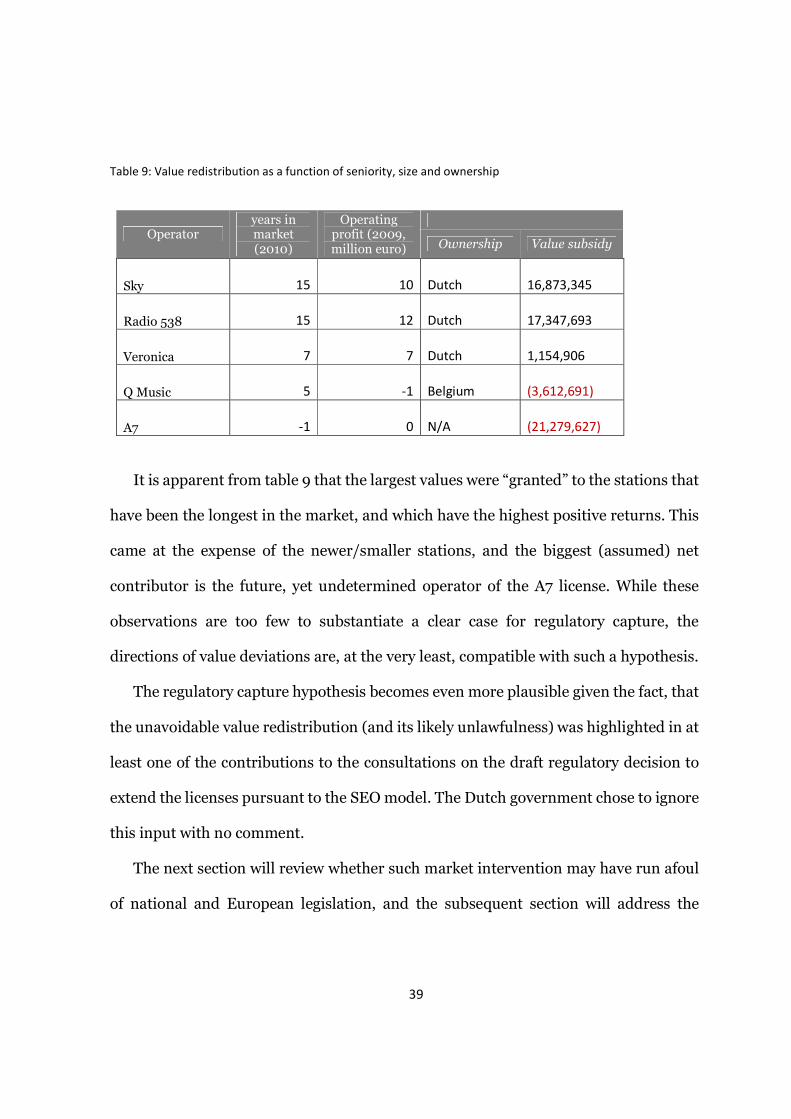

Table 9: Value redistribution as a function of seniority, size and ownership

Operator years in market (2010)

Operating profit (2009, million euro)

Ownership Value subsidy

Sky 15 10 Dutch

16,873,345

Radio 538 15 12 Dutch

17,347,693

Veronica 7 7 Dutch

1,154,906

Q Music 5 -1 Belgium

(3,612,691)

A7 -1 0 N/A

(21,279,627)

It is apparent from table 9 that the largest values were “granted” to the stations that

have been the longest in the market, and which have the highest positive returns. This

came at the expense of the newer/smaller stations, and the biggest (assumed) net

contributor is the future, yet undetermined operator of the A7 license. While these

observations are too few to substantiate a clear case for regulatory capture, the

directions of value deviations are, at the very least, compatible with such a hypothesis.

The regulatory capture hypothesis becomes even more plausible given the fact, that

the unavoidable value redistribution (and its likely unlawfulness) was highlighted in at

least one of the contributions to the consultations on the draft regulatory decision to

extend the licenses pursuant to the SEO model. The Dutch government chose to ignore

this input with no comment.

The next section will review whether such market intervention may have run afoul

of national and European legislation, and the subsequent section will address the

40

question of what alternative valuation scenarios could have produced better results for

the extension-valuation regulatory task.

4.3 Legal analysis

4.3.1 Legal framework in relation to granting of licenses

1. The award of radio-broadcasting licenses must be made in accordance to art. 3.3

(4) of the Dutch Telecommunications law (Tw):

“The awarding of licenses in other than the foreseen in the second article cases

may occur:

(a) on a first–come, first-serve basis based in order of application

(b) by means of a comparative test, with or without the use of a financial bid;

(c) by means of an auction

2. Extension of licenses is permitted in accordance with art 3.3 (11) Tw:

“The license must be awarded for a specific term, to be set in the license. The license

may be extended by a term to be determined by Our Minister”

On the fees payable for the use of licenses

3. Article 3.3a of the Tw establishes the possibility for the State to charge a one-

time or periodic amount for the use of frequency space for commercial broadcasting,

exclusively “…with a goal to warrant optimal use of frequency space”

Alinea 2 of Art. 3.3a defines the possible methods of establishing such charge: either

through a DCF model based on the expected turnover or projected cash-flows,

estimated ex-ante during the year of the license award (or extension), or through the

periodic charge of a percentage of the cash-flows (or turnover) during the period of

41

exploitation of the license. In any event, the fee must be related to the expected benefits

(voordelen) of exploitation of the license.

Alinea 3 of art. 3.3a allows the State to set additional rules relating to the

determination of the benefits expected from the exploitation of licenses.

4. The clarification to the Ministerial Regulation TK 2000-2001, 27 607, nr. 3,

which set the one-time amounts used in the 2003 tenders (Regeling VEB),

explained the rationale for the introduction of a one-time fixed charge; i.e. it was

to serve as a minimum financial threshold for market-entry, which would allow

only market participants who plan to use the resources with at least minimal

efficiency to be considered in the test. Furthermore, the combination of the

financial instrument and the financial bid would, together, be a measure of the

efficiency with which applicants intend to use the resources:

“De voorgestelde wijziging brengt hier verandering in door te bepalen dat van

de vergelijkende toets ook deel uit kan maken een toets op de bereidheid van de

aanvrager een bindend financieel bod uit te brengen. Langs deze weg kan, zoals

gezegd, ook bij de vergelijkende toets het financiële instrument worden ingezet

om het optimaal gebruik van de toe te kennen frequentieruimte te waarborgen.

(...)

Voor de volledigheid zij voorts opgemerkt dat ook een combinatie van een

eenmalig of periodiek bedrag met een (vrijwillig) bod bij de vergelijkende toets

op grond van het wetsontwerp mogelijk is. (...) "

42

(...) Het inzetten van een financieel instrument kan er toe leiden dat bepaalde

potentiële aanvragers afzien van het aanvragen van een vergunning. Hierdoor

komen er wellicht andere partijen op de markt dan wanneer van de inzet van het

financiële instrument zou zijn afgezien. (...)

Rationeel handelende partijen baseren hun biedingen op hun eigen waarde-

bepalingen van de te verdelen frequenties. Op een veiling komen die

waarderingen tot uiting in het bied-gedrag van de deelnemers. Indien er een

financieel instrument wordt gehanteerd naast de veiling, zal vooraf bekend zijn

wat bij een eenmalig bedrag de hoogte van dat bedrag is (...). Deze wetenschap

zal door de aanvragers worden verdisconteerd in hun bied-gedrag.

(...)

5. In the court case LJN: BA216944, the court further clarified and confirmed the

interpretation of the one-time license fee as a threshold (drempel) having the purpose

to preclude from participation parties who are likely to make sub-optimal use of the

frequencies, and (b) that the one-time license fee and the self-imposed financial bid

collectively represent such payment which ensures optimal use of the frequency.

“9.3.3 Het College ziet evenmin aanleiding om de keuze voor een financieel

bod in strijd met een doelmatig gebruik van de frequentieruimte te oordelen.

In een situatie waarin de overige relevante omstandigheden gelijk zijn, is het

doelmatig om een vergunning voor het gebruik van frequentieruimte toe te

kennen aan degene die hiertoe het hoogste financiële bod heeft uitgebracht. In

44 College van Beroep voor het bedrijfsleven , AWB 05/811 en 06/17,

43

dit verband acht het College het aannemelijk, zoals ook door de commerciële

radio-omroepen ter zitting is onderschreven, dat in het geval van commerciële

radio-omroep het de marktpartijen zijn, die beschikken over de meeste kennis

en informatie om de economische waarde van de verschillende kavels te

kunnen inschatten. Op grond van dit gegeven, dat de bepaling van de

marktwaarde aan de marktpartijen dient te worden overgelaten omdat zij

degenen zijn die een inschatting kunnen maken van de

exploitatiemogelijkheden van een kavel, heeft het toenmalige kabinet dan ook

gekozen voor een verdelingssystematiek voor de commerciële radio-omroep

waarbij, in het belang van een doelmatige verdeling van frequentieruimte, bij

gelijk gewaardeerde aanvragen de vergunning wordt vergeven aan de

aanvrager met het hoogste financieel bod.

(...)

9.4. (…). Met name niet nu, zoals hierboven is overwogen, uit de gekozen

verdelingssystematiek volgt, dat de aanvragers worden geacht zelf de

bovengrens te kunnen bepalen van hetgeen zij bereid zijn te betalen door

vooraf de waarde van het kavel vast te stellen, inclusief de verplichting bij

verkrijging van de vergunning het eenmalig bedrag te voldoen.

9.6.2 Anders dan de commerciële radio-omroepen, is het College van

oordeel dat het eenmalig bedrag noch het financieel bod een (para-)fiscale

heffing is. Beide bedragen zijn daarentegen (financiële) instrumenten om de

44

allocatie van schaarse vergunningen efficiënt te laten verlopen. Er kan

derhalve geen sprake zijn van een verboden dubbele heffing”

6. The provisions of the Tw and the Regeling VEB must be interpreted in the

context of the relevant art. 13 of Directive 2002/20/EC (the “Authorization Directive”):

“Member States may allow the relevant authority to impose fees for the

rights of use for radio frequencies or numbers or rights to install facilities on,

over or under public or private property which reflect the need to ensure the

optimal use of these resources. Member States shall ensure that such fees shall

be objectively justified, transparent, non-discriminatory and proportionate in

relation to their intended purpose and shall take into account the objectives in

Article 8 of Directive 2002/21/EC (Framework Directive).”

7. The invocation of art. 8 of the Framework Directive imposed a competition-

promoting obligation to the imposition of license fees:

“2. The national regulatory authorities shall promote competition in the

provision of electronic communications networks, electronic communications

services and associated facilities and services by inter alia:

[…]

(b) ensuring that there is no distortion or restriction of competition in the

electronic communications sector;

[….]

3. The national regulatory authorities shall contribute to the development

of the internal market by inter alia:

45

[…]

(c) ensuring that, in similar circumstances, there is no discrimination in the

treatment of undertakings providing electronic communications networks and

services…”

Interim Conclusion 1:

The financial instrument (one-time fee) introduced by Regeling VEB represents a

minimum threshold for the value of the license. It does not represent the optimal use

of the frequency space. Only the payment of the sum of the financial instrument and

the financial bid, (along with the programming offer in the case of restricted licenses),

ensures optimal use of the frequency space.

Interim Conclusion 2:

Only the market parties themselves are able to determine the actual value of each

license. This value has been expressed, in the 2003 tender, in the form of their financial

bids (which already took into account the amount of the one-time fee), together with

their programming offers, where relevant. This license value is therefore captured in

the current license terms of the incumbents, which include the obligation to pay the

financial instrument, the financial bid and to conform to the programming offer (where

relevant).

In relation to extension and amendment of licenses

8. Art.3.3 al. 9 of the Tw states:

46

“By means of general administrative measures, and taking into account

Directive 2002/20/EC, rules shall be set in the area of granting, amending and

extending of licenses”

9. Article 14 of the Directive 2002/20/EG (Authorization Directive) states:

“1. Member States shall ensure that the rights, conditions and procedures

concerning general authorisations and rights of use or rights to install facilities

may only be amended in objectively justified cases and in a proportionate

manner.”

Interim conclusion 3:

License fees for the existing commercial radio licenses (whether during their

current term or during their extended term) may be amended only (i) in objectively

justified cases and only (ii) in a proportionate manner. Furthermore, in setting the new

license terms, (iii) distortion of competition and (iv) discriminatory treatment of

certain market parties must be precluded.

It follows that a forward-looking, player-agnostic DCF-based valuation approach to

revising the license fees would run contrary to the Authorization Directive because it

would lead to disproportionate change of conditions among market players. A DCF

approach would, as evidenced by the comparison in the previous section, result in

different levels of amelioration or deterioration of financial terms for different market

participants, relative to the current terms. This would lead to an unwarranted

distortion of competition relative to the current market.

47

The specific application of the DCF method in an “opportunity cost” approach

appears unlawful, as it distorts competition and represents discrimination of the type

“similar treatment in dissimilar circumstances”

The valuation of the licenses from a “newcomer’s perspective” as of 2011 would

effectively assign new-entrant status to all licenses. This determination, however,

would be untrue, as it concerns existing license holders. Each license would have had a

different time-in-market, and therefore a different income-earning capability in 2011

and onward. Some of the licenses would have been operated by the current holder as

of the 80’s, while others only 5 or fewer years before the extension date.

On the contrary, the time-in-market was well captured in the (self) setting of the

original license fees in 2003.

Interim conclusion 4:

To value all licenses from the point of view of a new entrant would mean to

artificially lower the license fee costs for the long-time incumbents (pioneers), thus

effectively discriminating against recent entrants.

Interim conclusion 5

The change of the license conditions must be limited only to such change which is