Embed Size (px)

Citation preview

THE MALAYSIAN REIT DEVELOPMENT ANDTHEIR ROLE IN A PORTFOLIO

By

ATASYA OSMADI

A thesis submitted in fulfilment of the requirements for the Degree ofDoctor of Philosophy at the University of Western Sydney

March 2010

ii

UNIVERSITY OF WESTERN SYDNEY

This thesis has been produced by a student of this University to satisfy learning

requirements of a postgraduate course.

While University staff may have offered supervision and advice to the author, the

University is unable to accept responsibility for any advice, recommendations,

suggestions or conclusions contained in this piece of work.

The University gratefully acknowledges the co-operation given to the student author

since studies such as these permit students to examine real world issues in a context

which provides an opportunity for meaningful research to be conducted and reported.

iii

DECLARATION

This thesis has been prepared by me to meet the requirements of a Doctor of

Philosophy degree at the University of Western Sydney.

I declare that this thesis represents my own work, except where due acknowledgement

is made, and that it has not been previously included in a thesis, dissertation or report

submitted to this University or to any other institution for a degree, diploma or other

qualification.

All possible care has been taken in the preparation of the information in this thesis;

however, I expressly disclaim any liability for the accuracy and sufficiency of the

information and under no circumstances shall either be liable in negligence or

otherwise in and arising out of the preparation or supply of the information in this

thesis.

Signed

Atasya Osmadi

iv

ACKNOWLEDGMENTS

This thesis was made possible with the assistance of the following people. Professor

Graeme Newell, my principal supervisor, has been very supportive and constructive

throughout my candidature. I would like to take this opportunity to express my

utmost gratitude for his guidance, encouragement and continuous support throughout

my research. Numerous property scholars and practitioners have also provided

constructive input to this thesis and I sincerely thank them. I would also like to

express my gratitude to my sponsors from the Public Service Department of Malaysia,

Ministry of Higher Education (Malaysia) and University Sains Malaysia for giving

me the privilege to do my PhD with Professor Graeme Newell in University of

Western Sydney.

I also gratefully acknowledge anonymous professionals and respondents to my

surveys who have been of assistance and supplied me with information important to

this thesis which have helped me to accomplish my PhD. Last, but not least, I

sincerely thank my family and friends especially my parents for their continuous

support throughout this period.

v

Table of Contents

Declaration iii

Acknowledgments iv

Table of Contents v

List of Tables x

List of Figures xvi

List of Abbreviations xvii

Executive Summary xix

Chapter 1: Introduction

1.1 Overall Context 1

1.1.1 Significance of Direct Property 8

1.1.2 Significance of Indirect Property 9

1.2 General Significance of the Malaysian Economy and Commercial Property

Markets 11

1.2.1 Significance of REITs in Malaysia 15

1.3 Objectives of the Study 17

1.4 Literature Review 19

1.4.1 Property in a Portfolio 19

1.4.2 REITs 22

1.4.2.1 REITs in US 22

1.4.2.2 A-REITs in Australia 23

1.4.3 REITs in Asia 24

1.4.4 M-REITs in Malaysia 25

1.5 Organisation of the Thesis 33

Chapter 2: Global Real Estate Investment Trusts and

Property Trust Vehicles

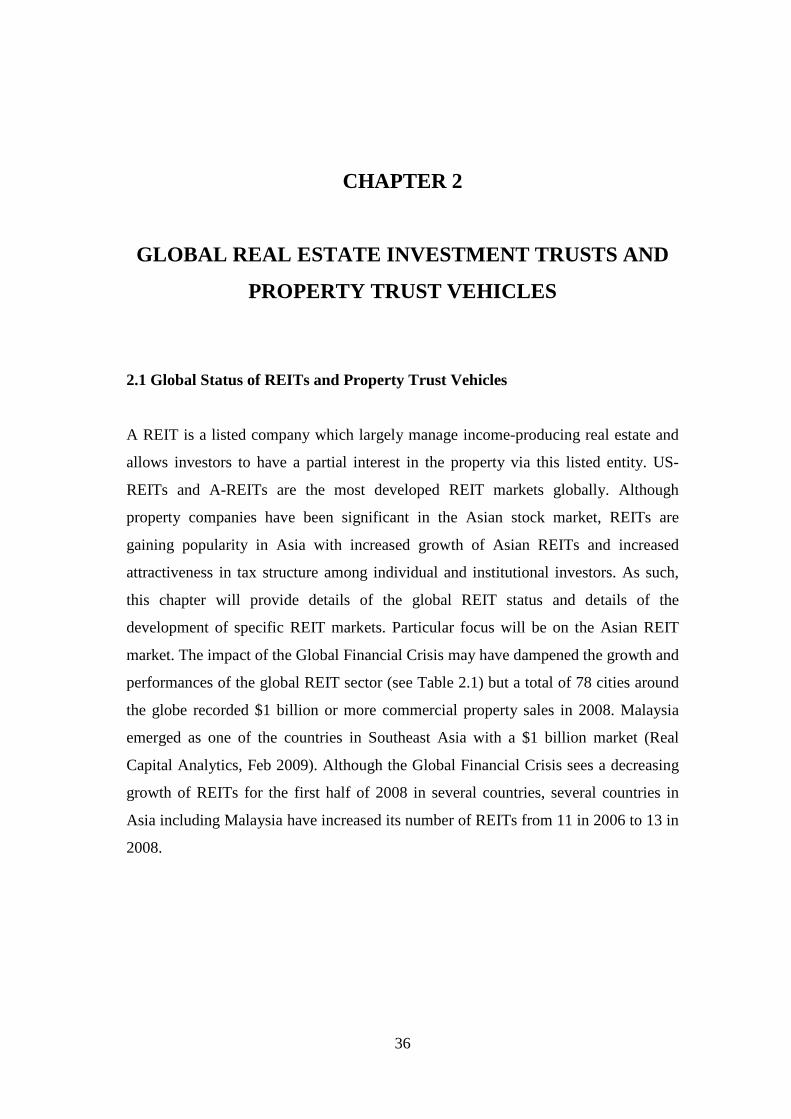

2.1 Global Status of REITs and Property Trust Vehicles 36

2.2 Malaysia REITs 52

vi

2.3 Global Property Securities Funds 55

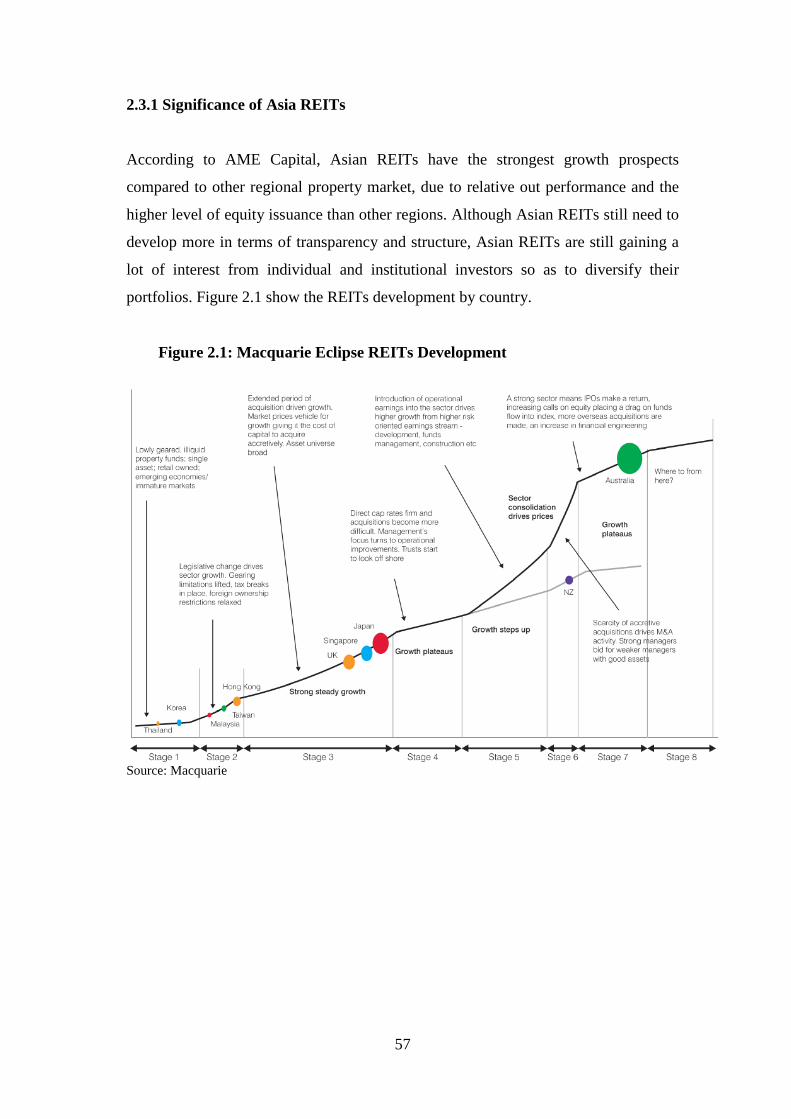

2.3.1 Significance of Asia REITs 57

Chapter 3: Significance of Malaysian Commercial Property Markets

3.1 Significance of Malaysia: Social, Economic Activity and Demographics 58

3.2 Commercial Property Market Universe 60

3.2.1 Global Property Investor Interest 64

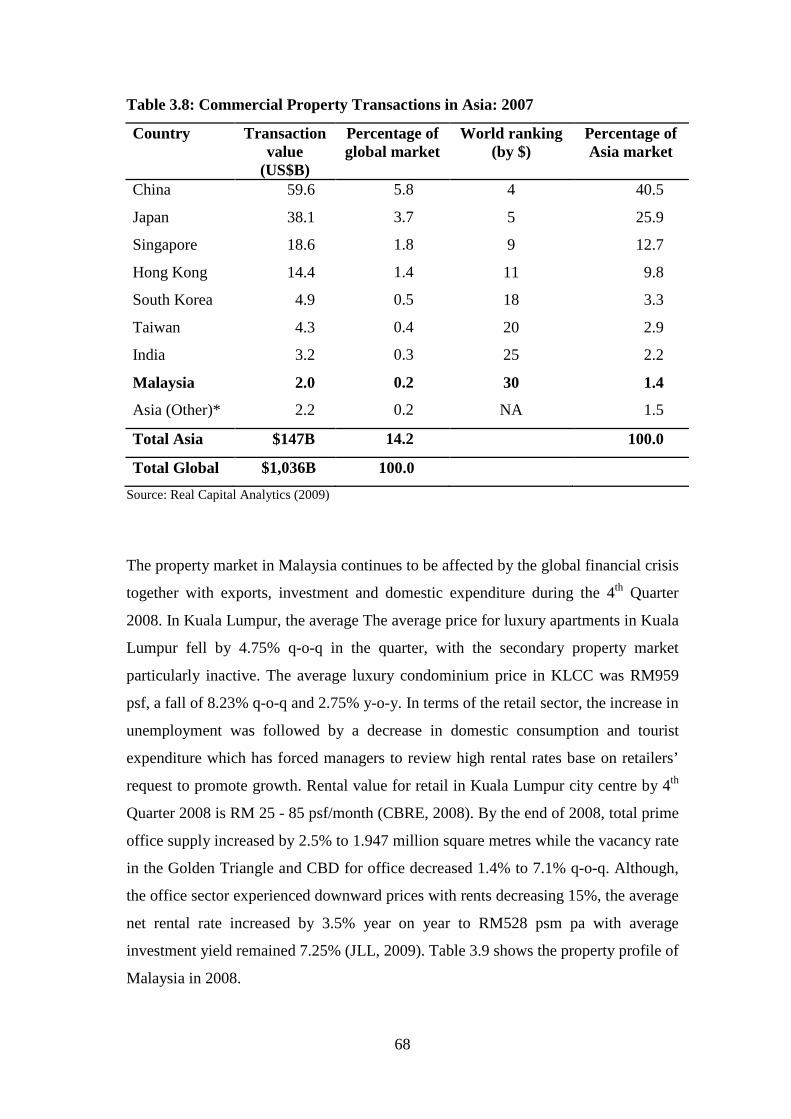

3.3 Malaysian Commercial Property: Asia Context 67

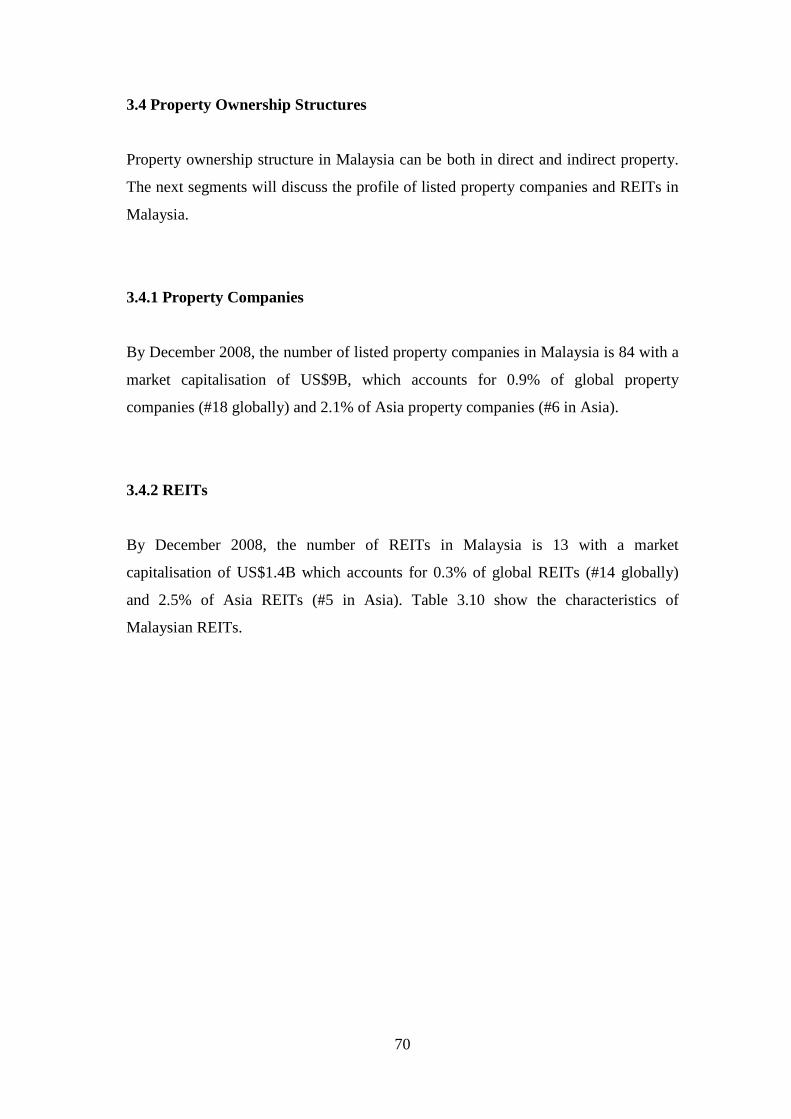

3.4 Property Ownership Structures 70

3.4.1 Property Companies 70

3.4.2 REITs 70

3.4.3 PTFs 72

3.4.4 REITs 74

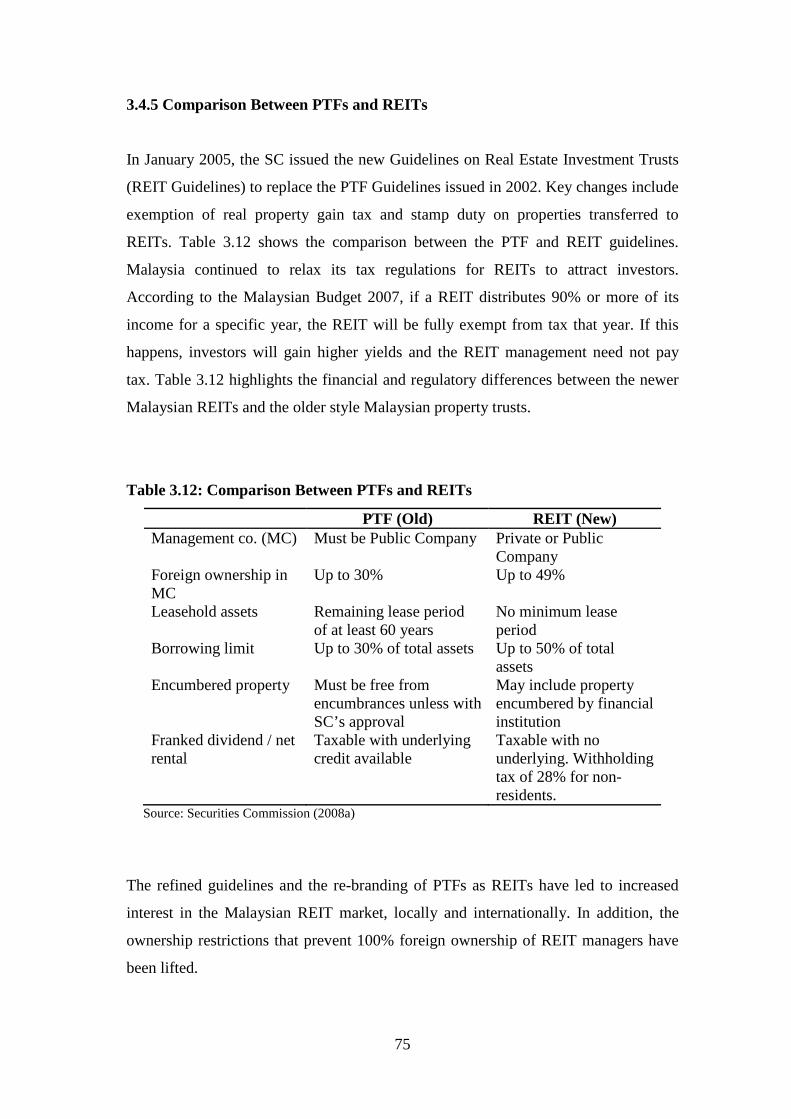

3.4.5 Comparison Between PTFs and REITs 75

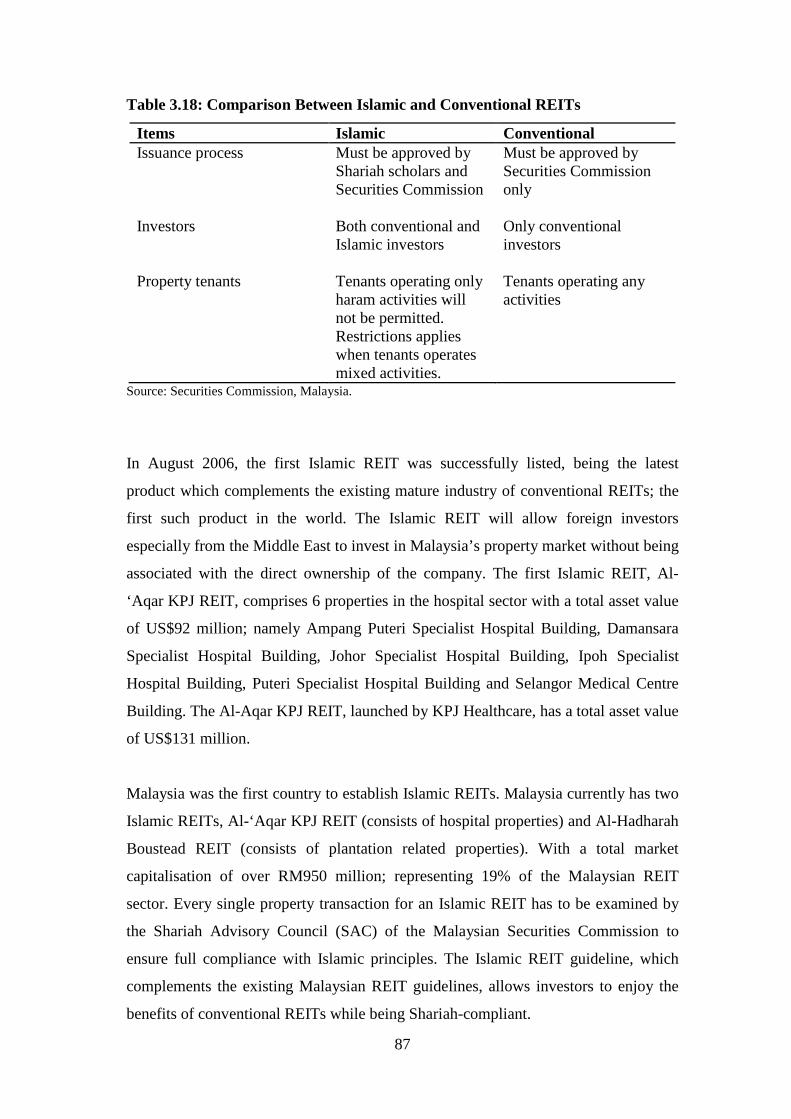

3.4.6 Comparison Between Conventional REITs and Islamic REITs 76

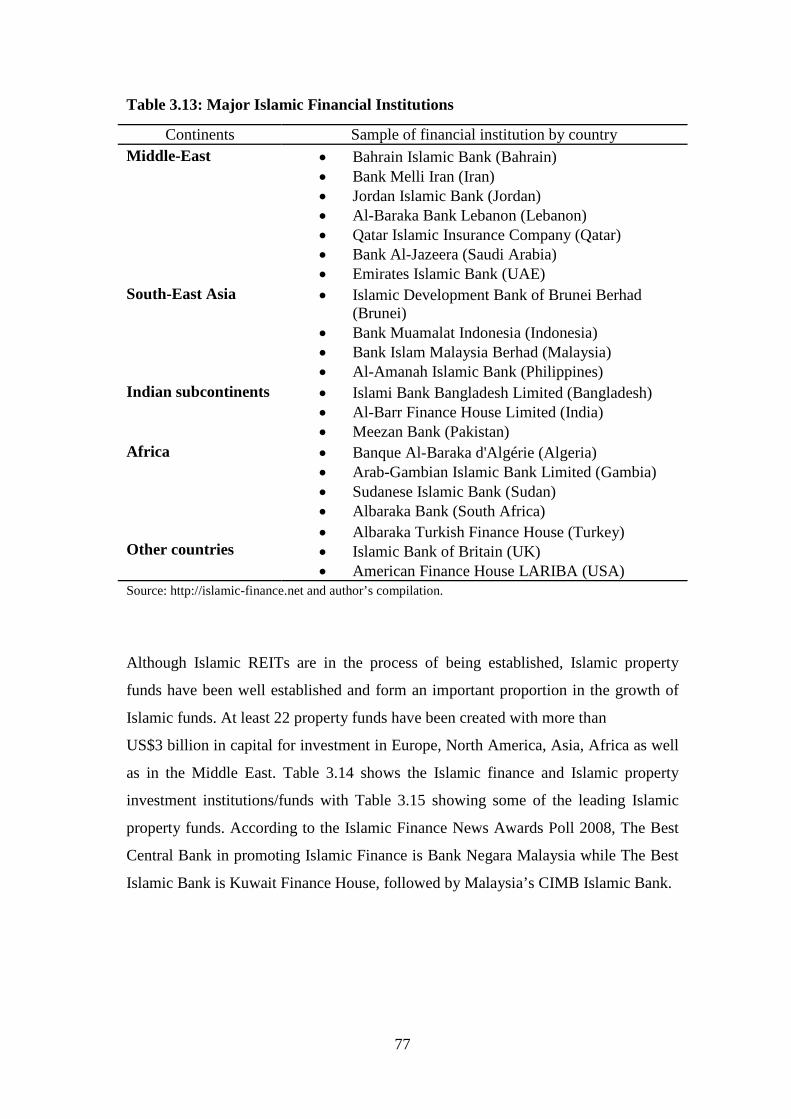

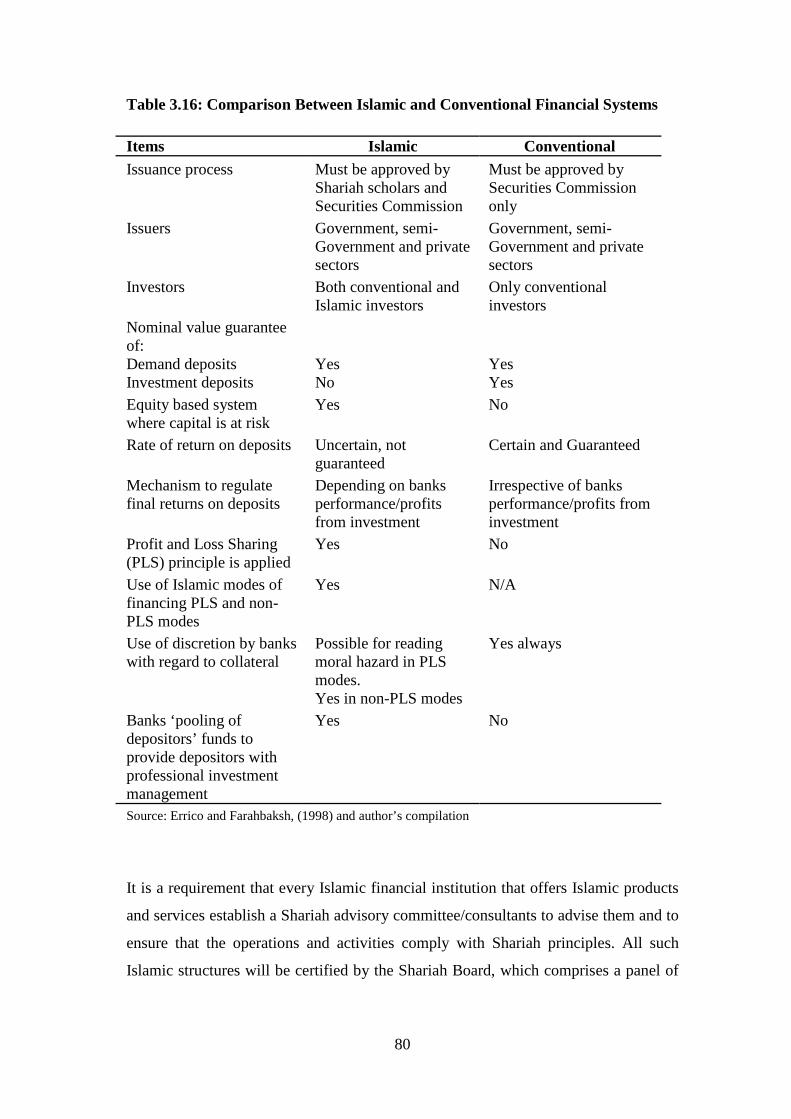

3.4.6.1 Characteristics of Islamic Finance 76

3.4.6.2 Characteristics of Islamic REITs 84

3.5 Market Size – Liquidity Issues 88

3.6 Future Opportunities 89

Chapter 4: Methodology

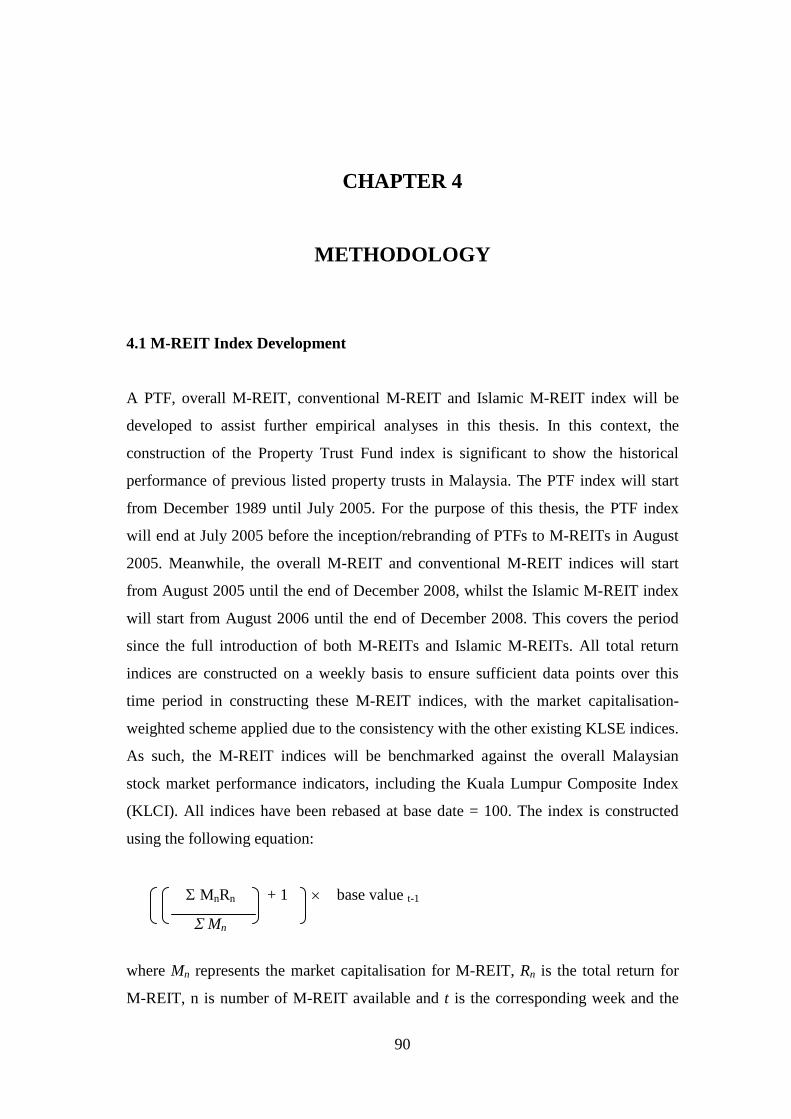

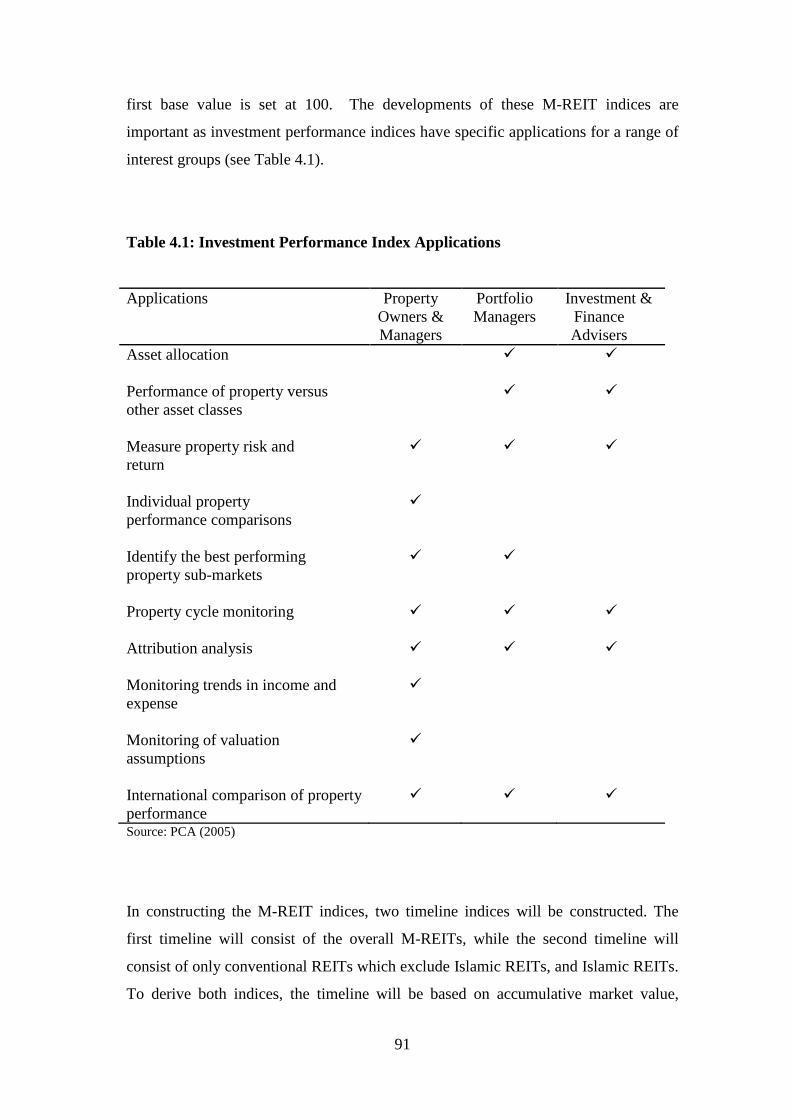

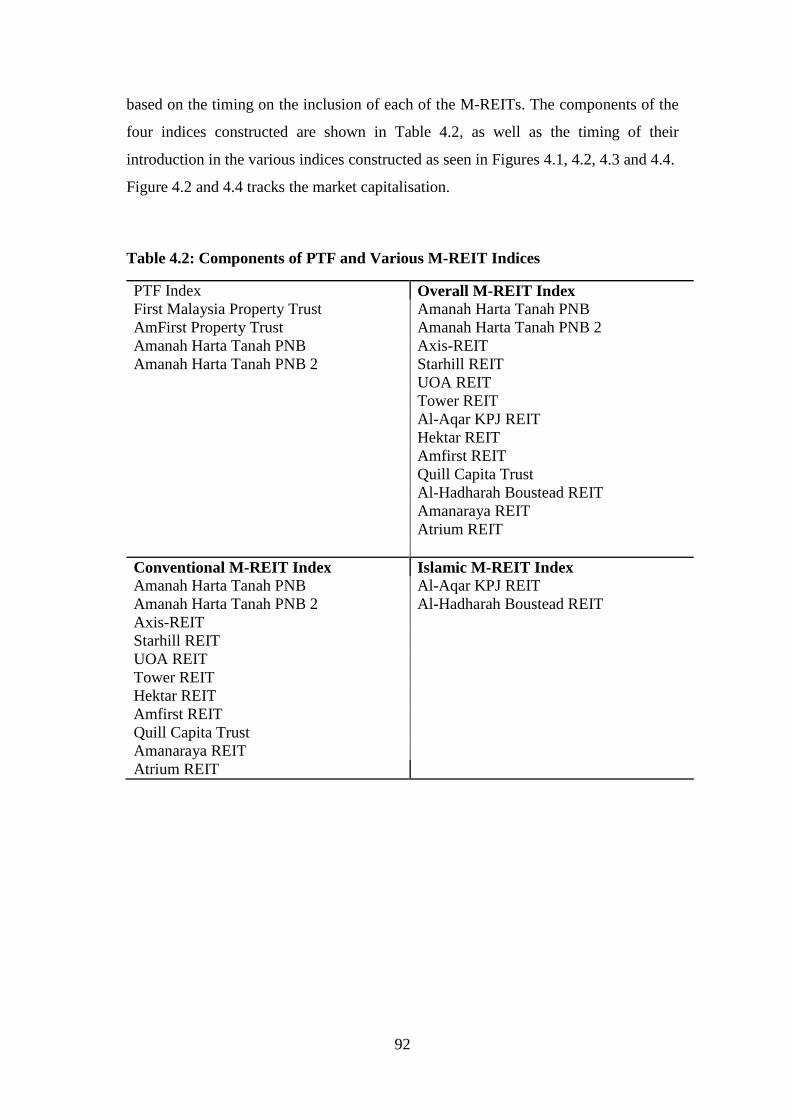

4.1 M-REIT Index Development 90

4.2 M-REIT Performance Analysis and Other Asset Classes 95

4.3 M-REIT Surveys 98

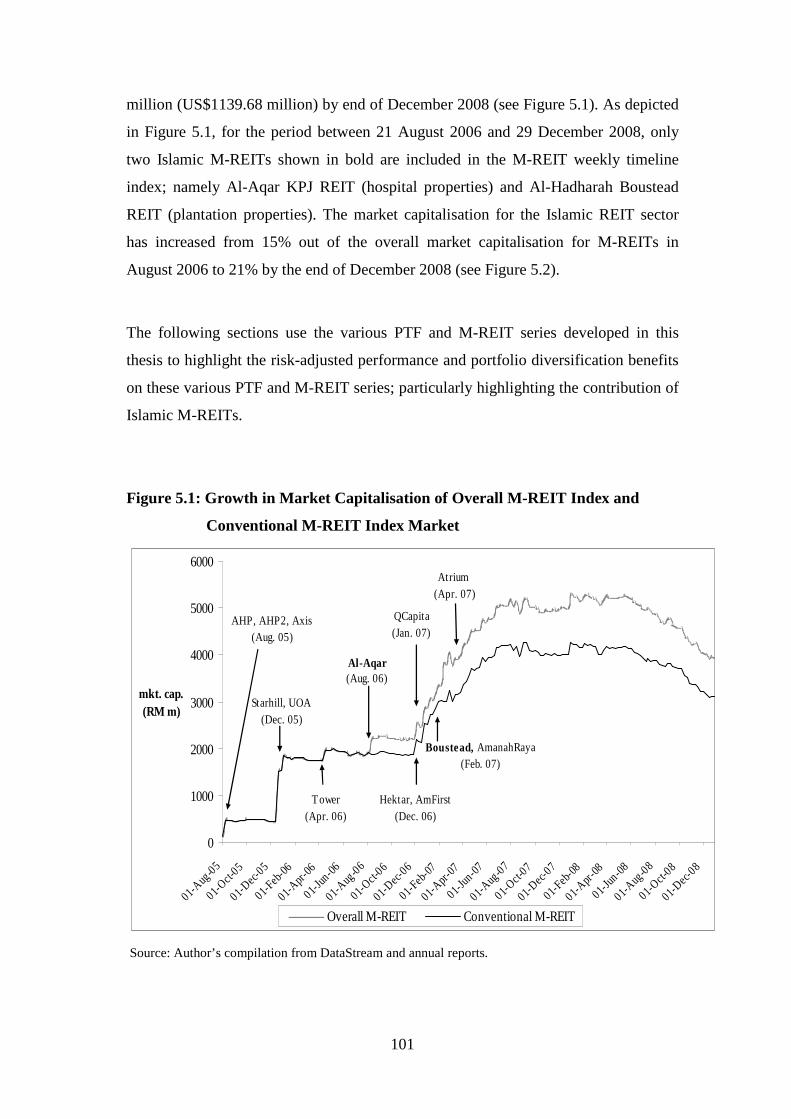

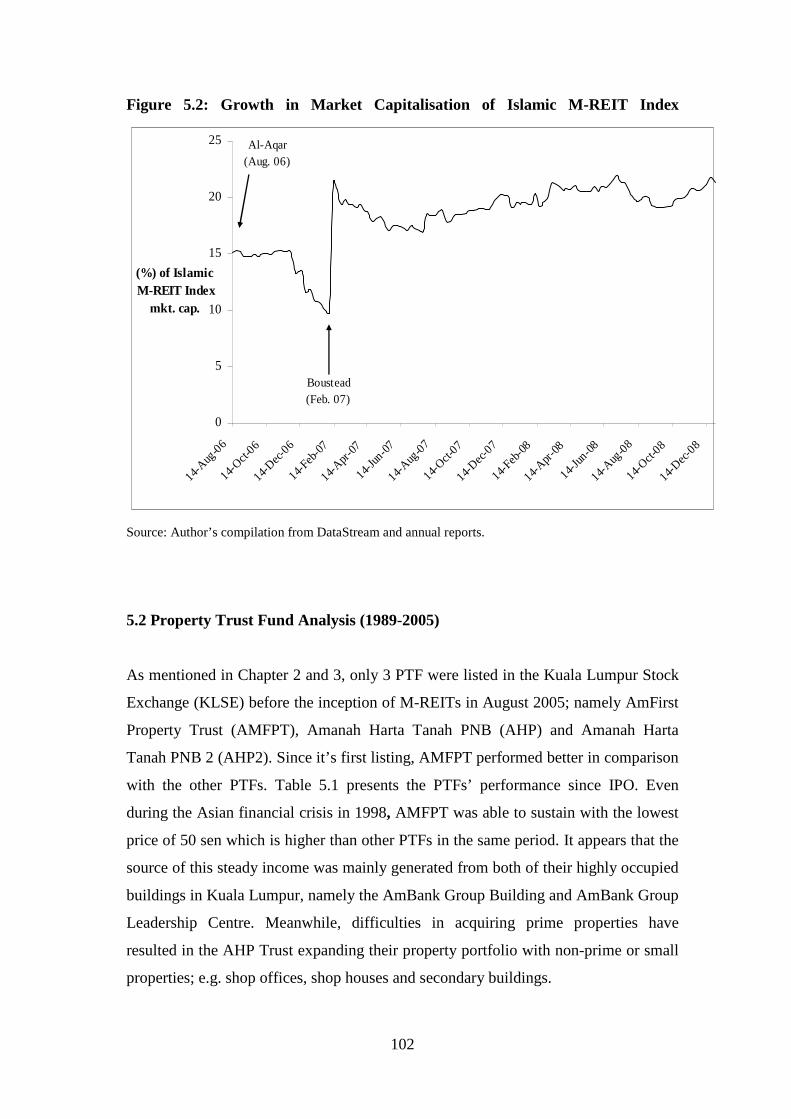

Chapter 5: Malaysian REIT Performance Analysis

5.1 Introduction 100

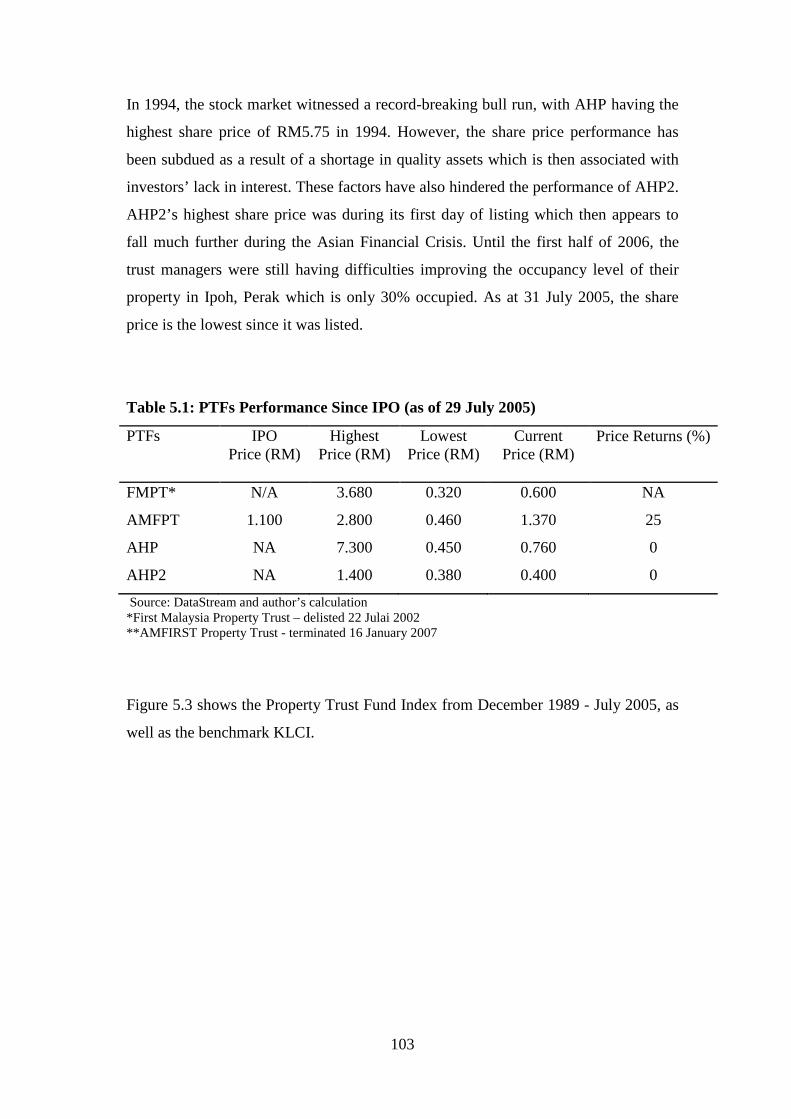

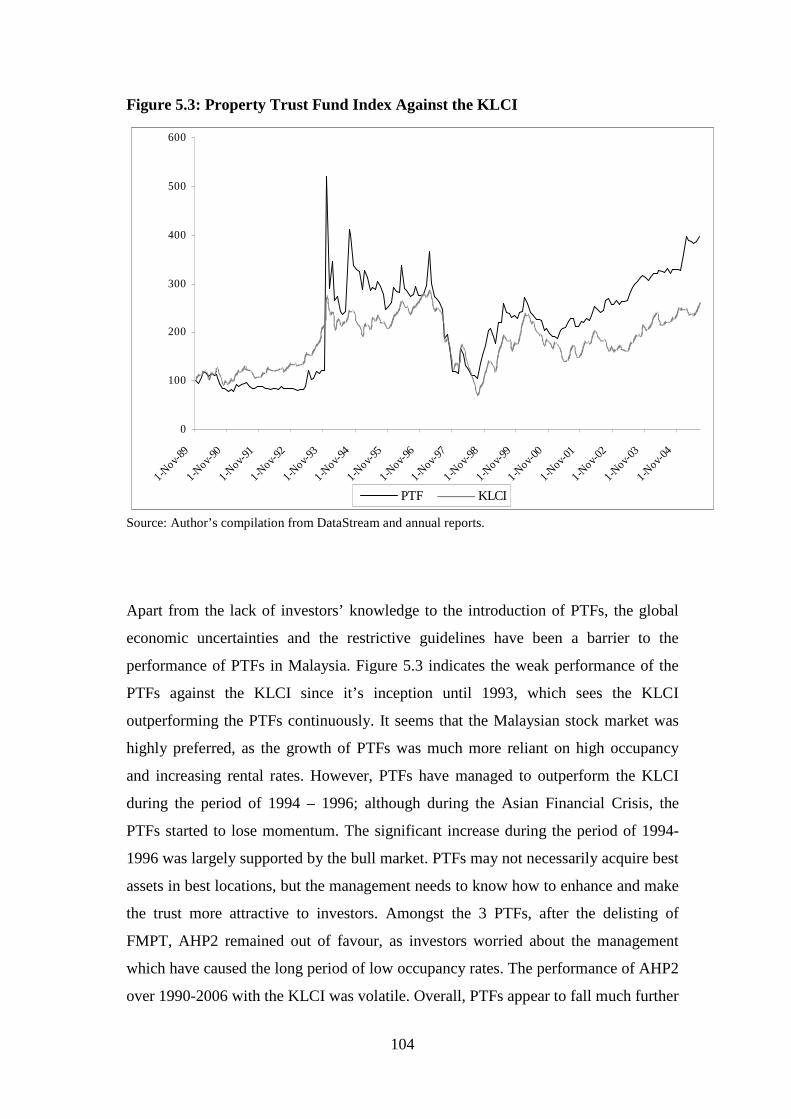

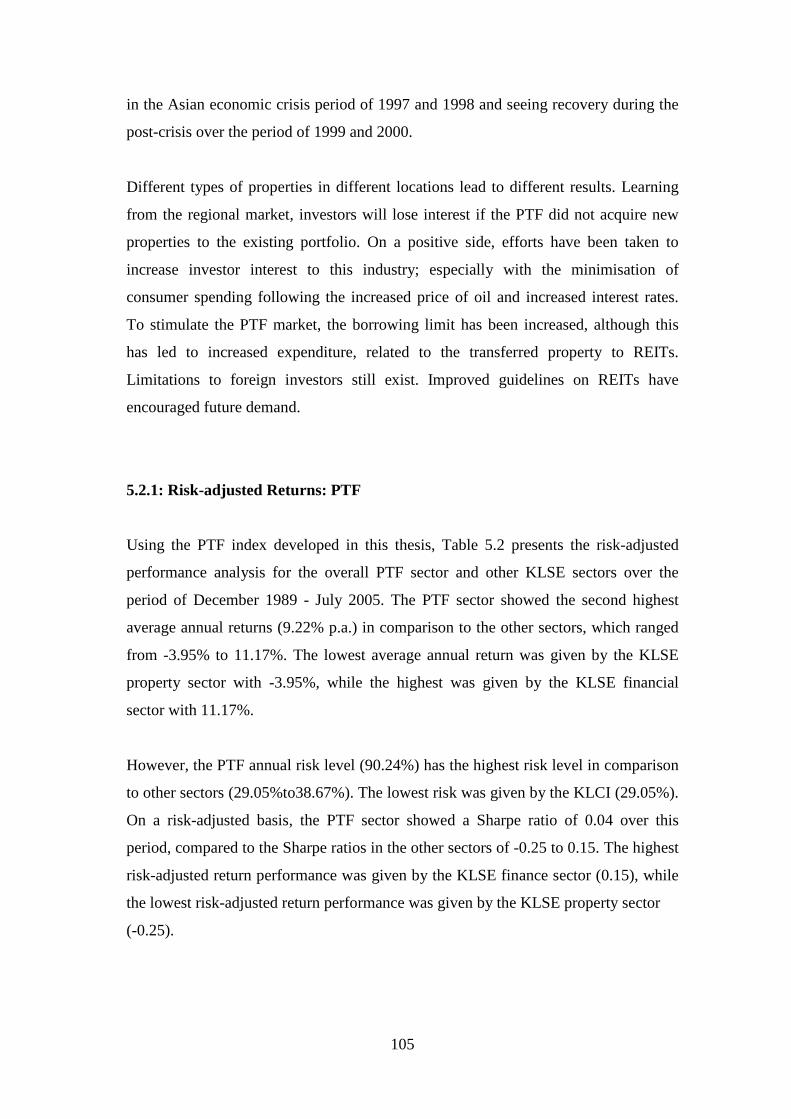

5.2 Property Trust Fund Analysis (1989-2005) 102

5.2.1: Risk-adjusted Returns: PTF 105

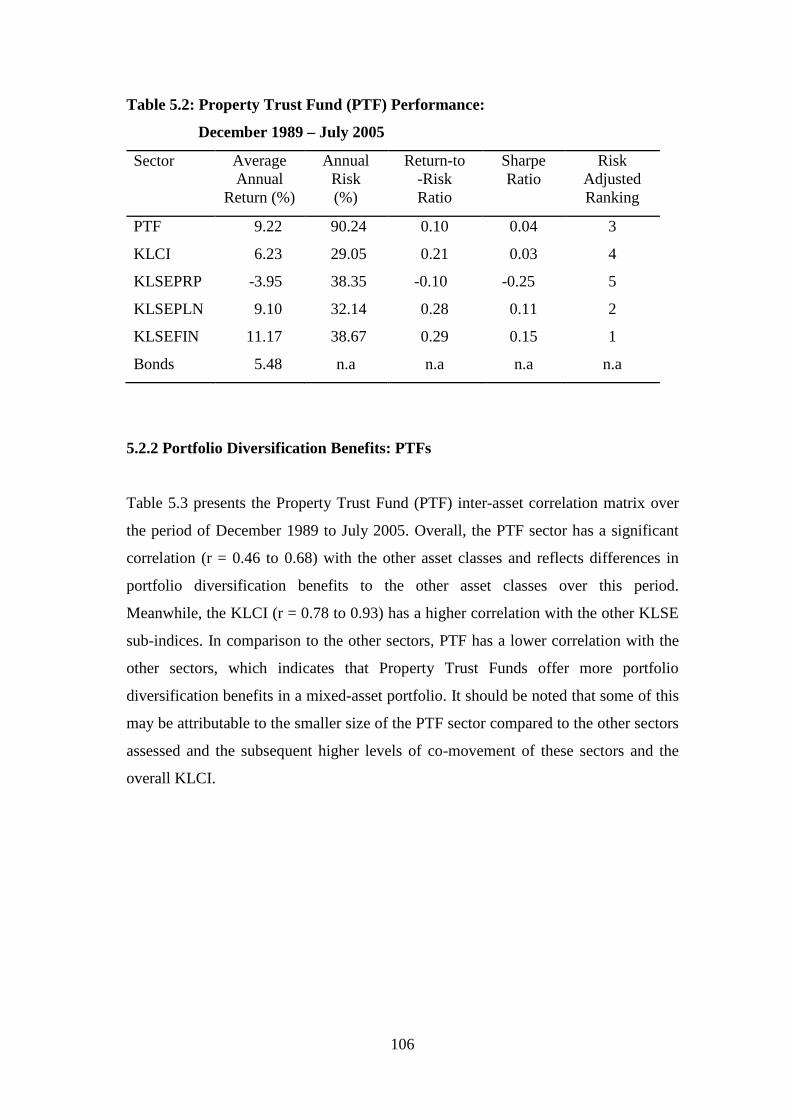

5.2.2 Portfolio diversification benefits: PTFs 106

5.3 Overall M-REIT Analysis (2005-2008) 107

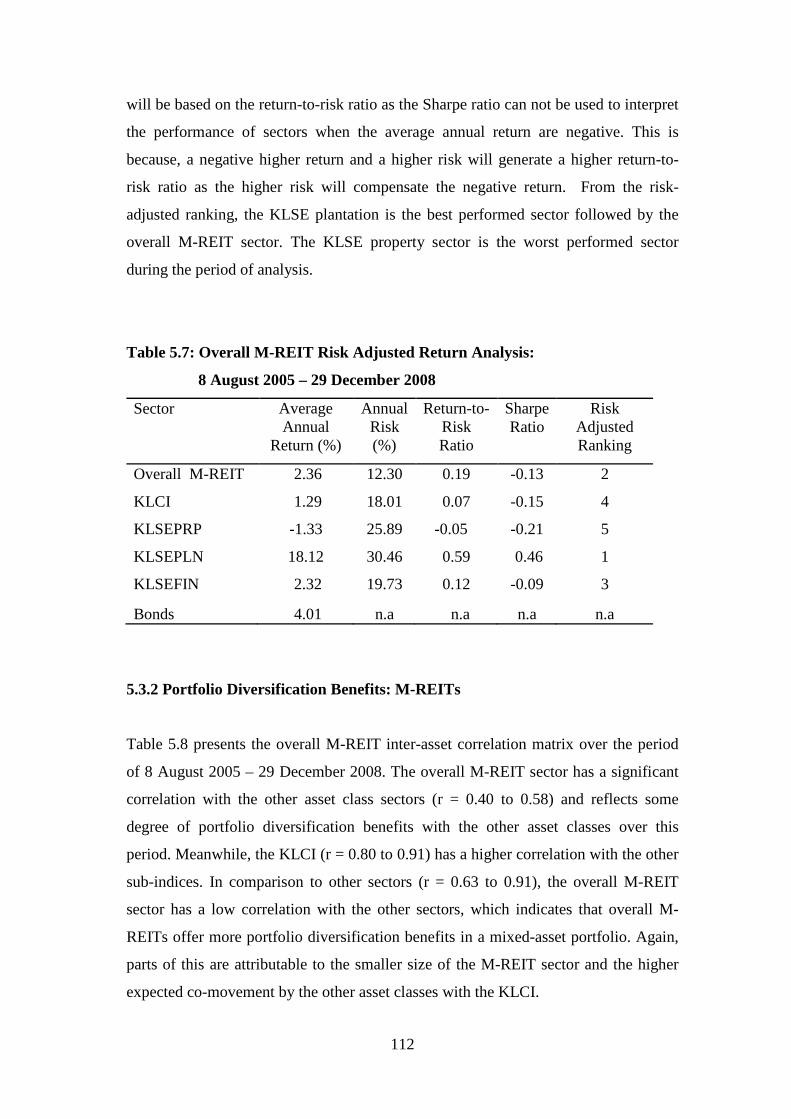

5.3.1 Risk-adjusted Returns: M-REITs 111

5.3.2 Portfolio Diversification Benefits: M-REITs 112

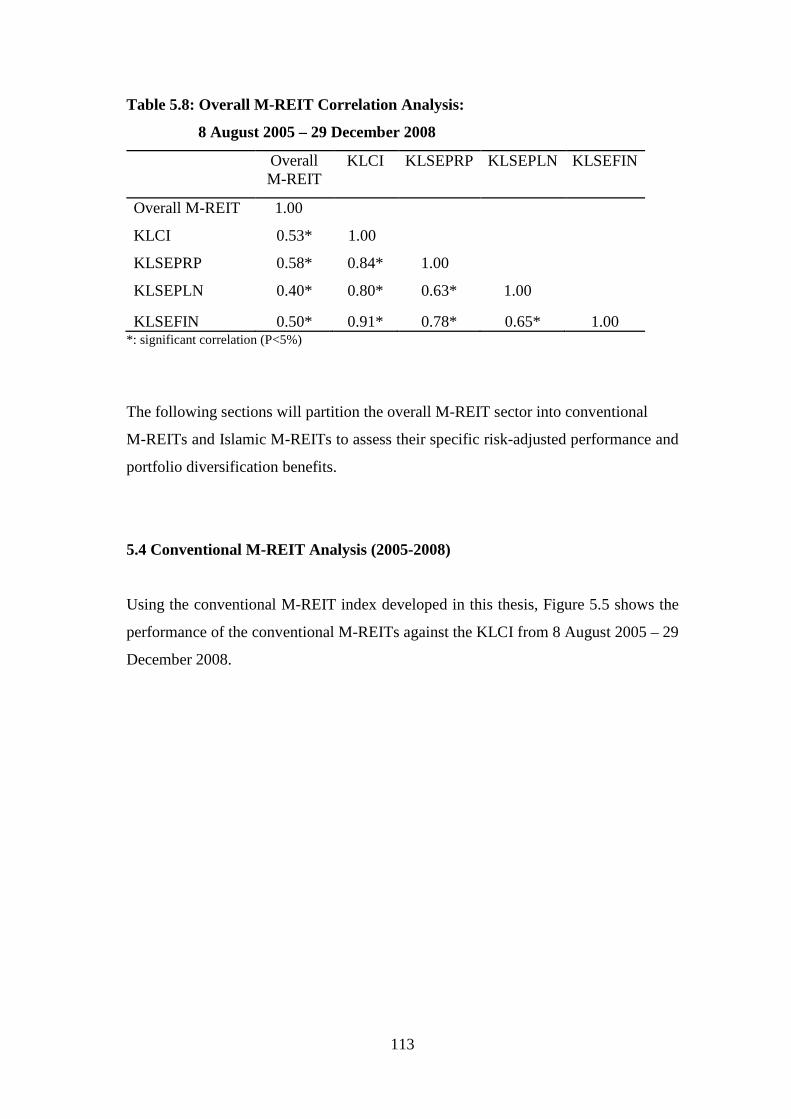

vii

5.4 Conventional M-REIT Analysis (2005-2008) 113

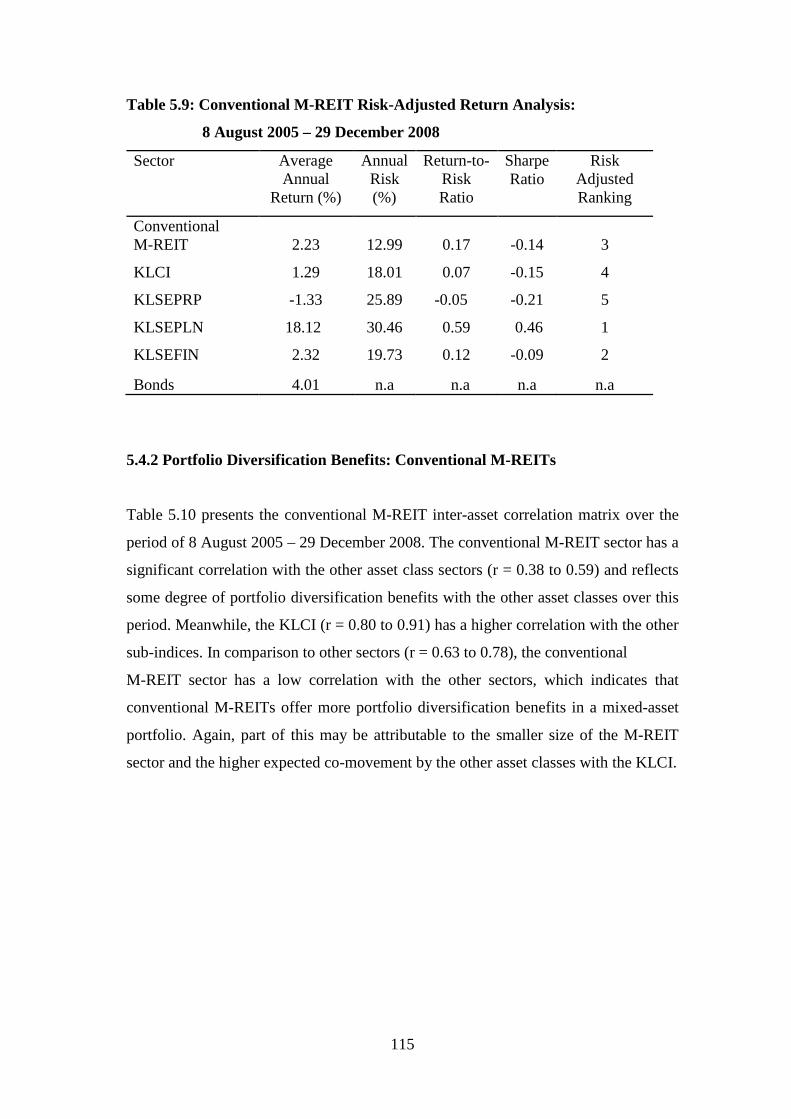

5.4.1 Risk-adjusted Returns: M-REITs 114

5.4.2 Portfolio Diversification Benefits: Conventional M-REITs 115

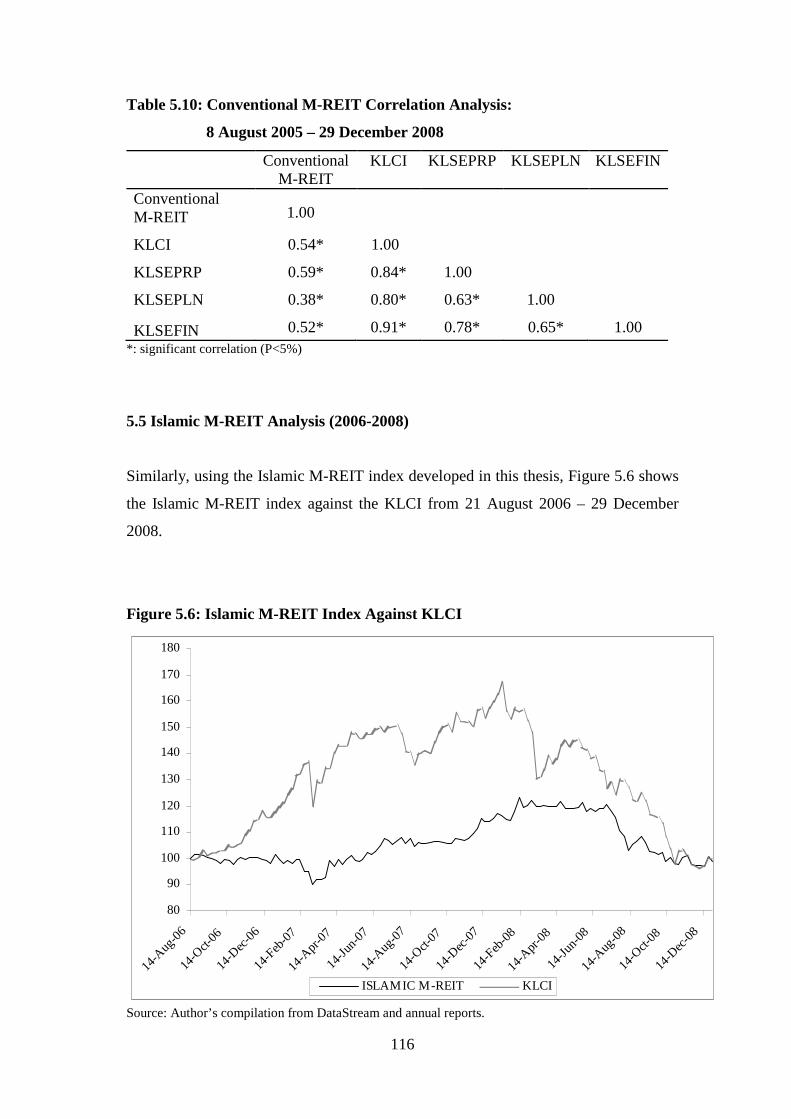

5.5 Islamic M-REIT Analysis (2006-2008) 116

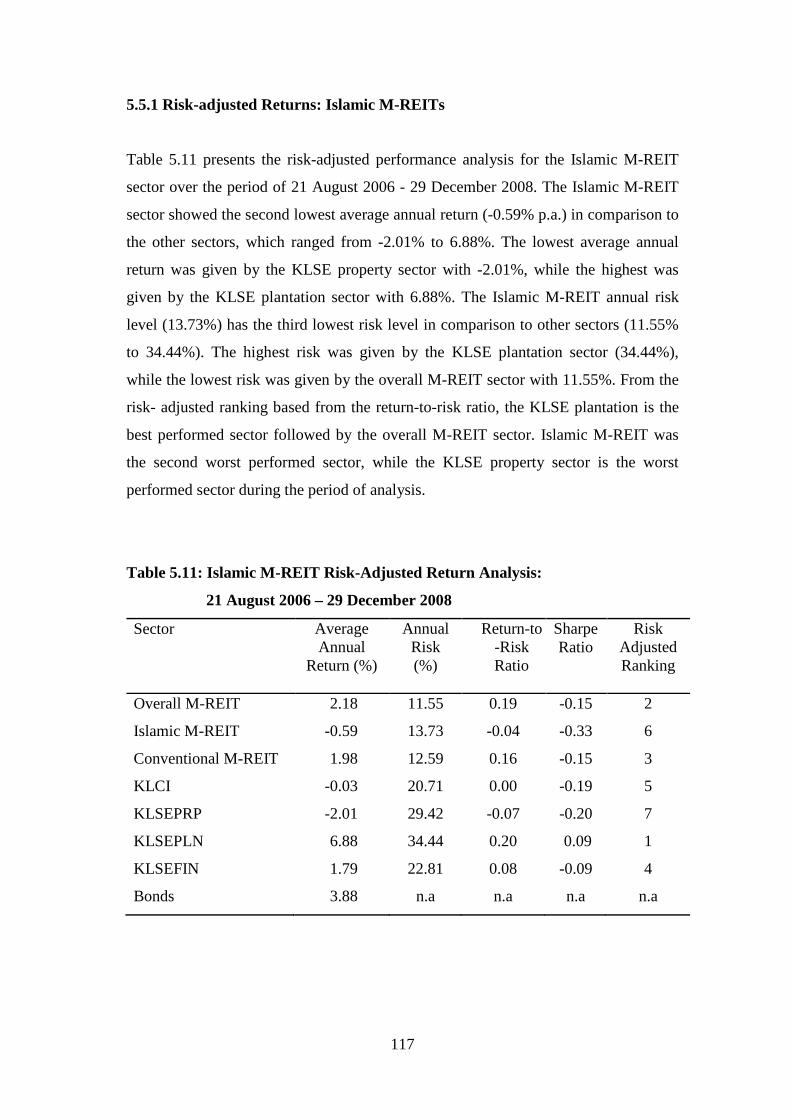

5.5.1 Risk-adjusted Returns: Islamic M-REITs 117

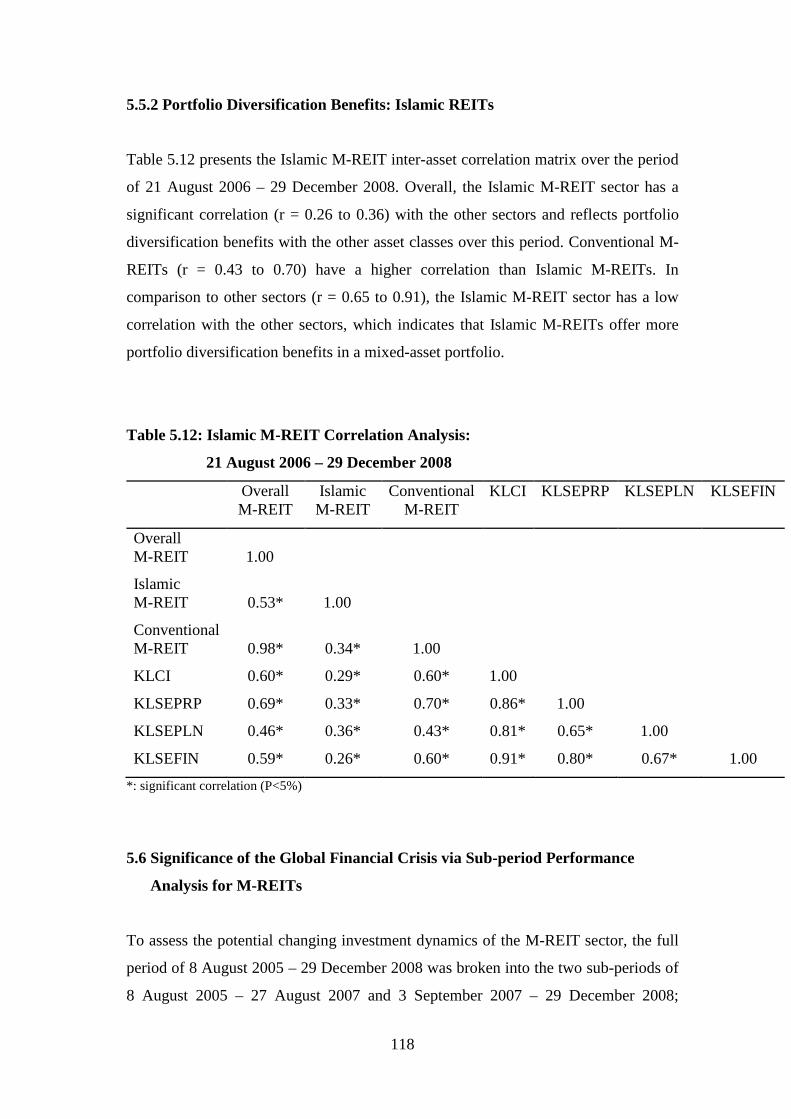

5.5.2 Portfolio Diversification Benefits: Islamic REITs 118

5.6 Significance of the Global Financial Crisis Via Sub-period

Performance Analysis for M-REITs 118

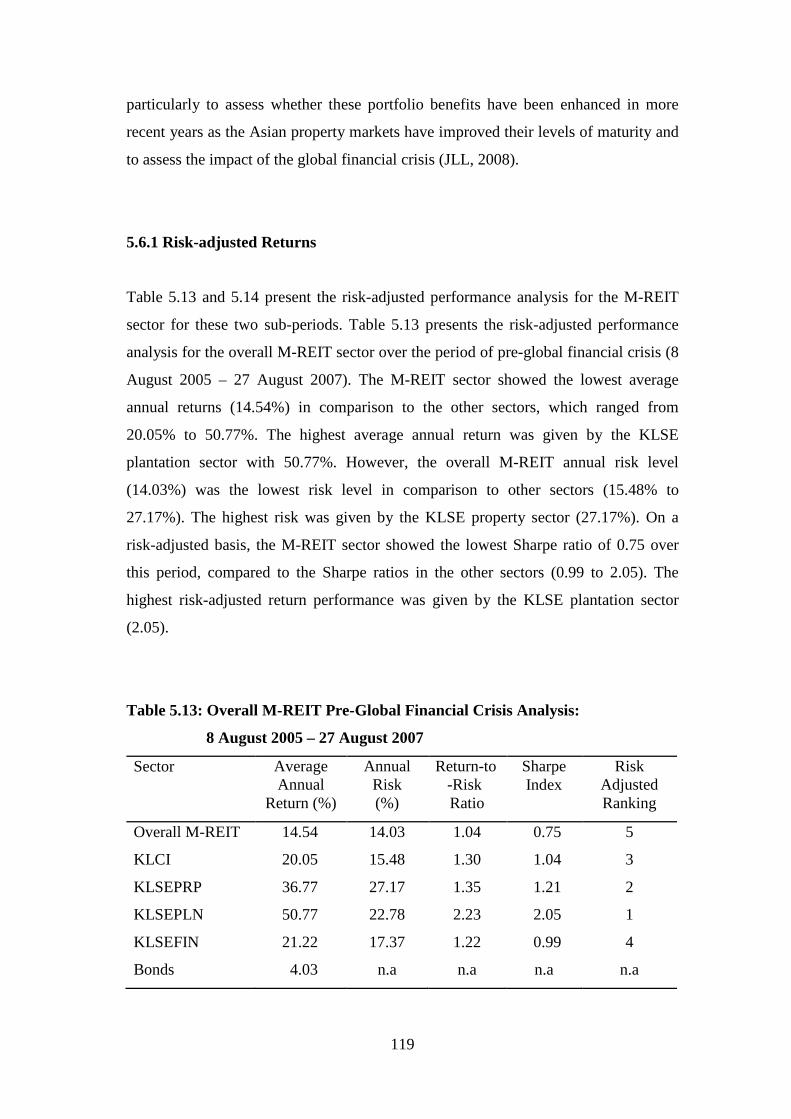

5.6.1 Risk-adjusted Returns 119

5.6.2 Portfolio Diversification Benefits 121

5.7 Significance of Global Financial Crisis Via Sub-period

Performance Analysis for Islamic M-REITs 122

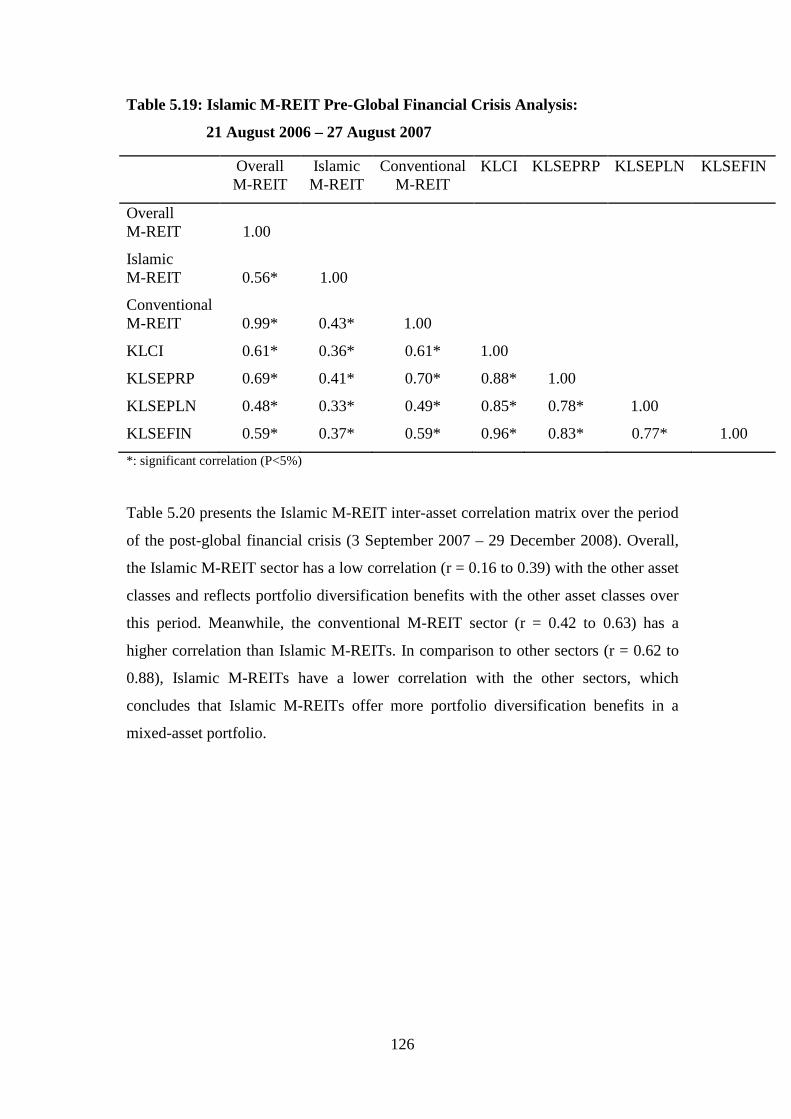

5.7.1 Risk-adjusted Returns 122

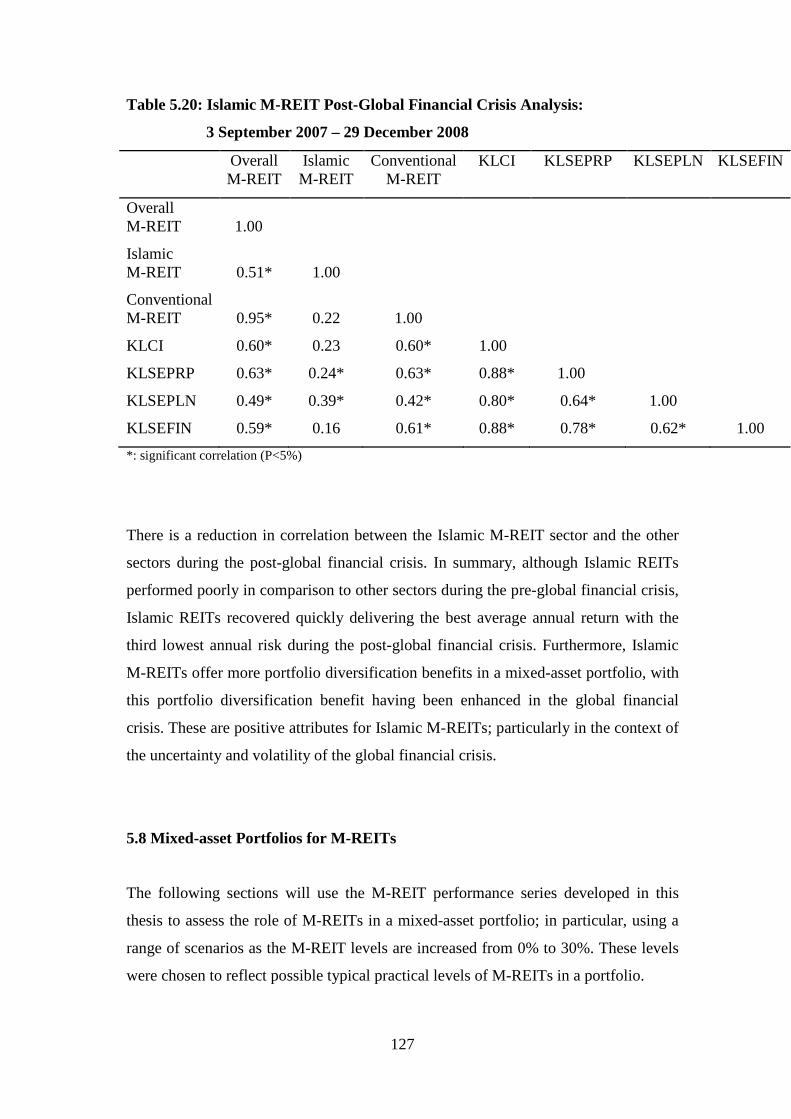

5.7.2 Portfolio Diversification Benefits 125

5.8 Mixed-asset Portfolios for M-REITs 127

5.8.1 Mixed-asset Portfolios for Overall M-REITs 128

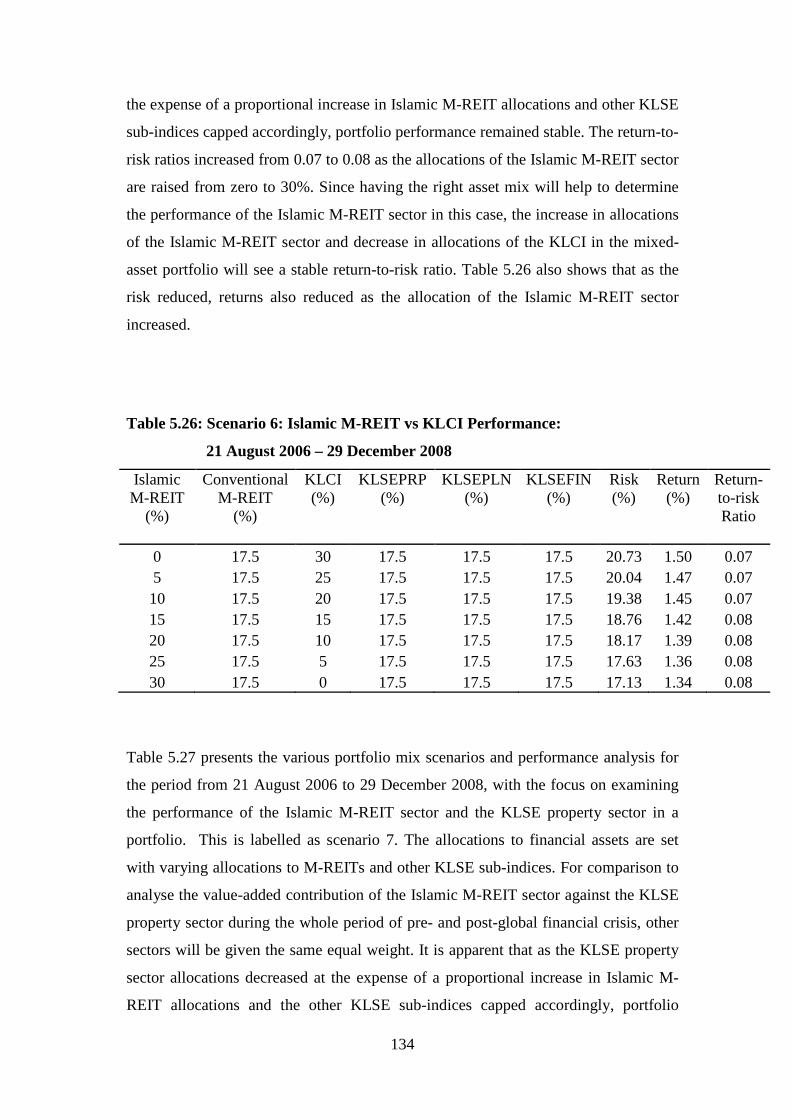

5.8.2 Mixed-asset Portfolios for Islamic M-REITs 132

5.8.3 Importance of Global Financial Crisis on Overall M-REITs and

Islamic M-REITs 138

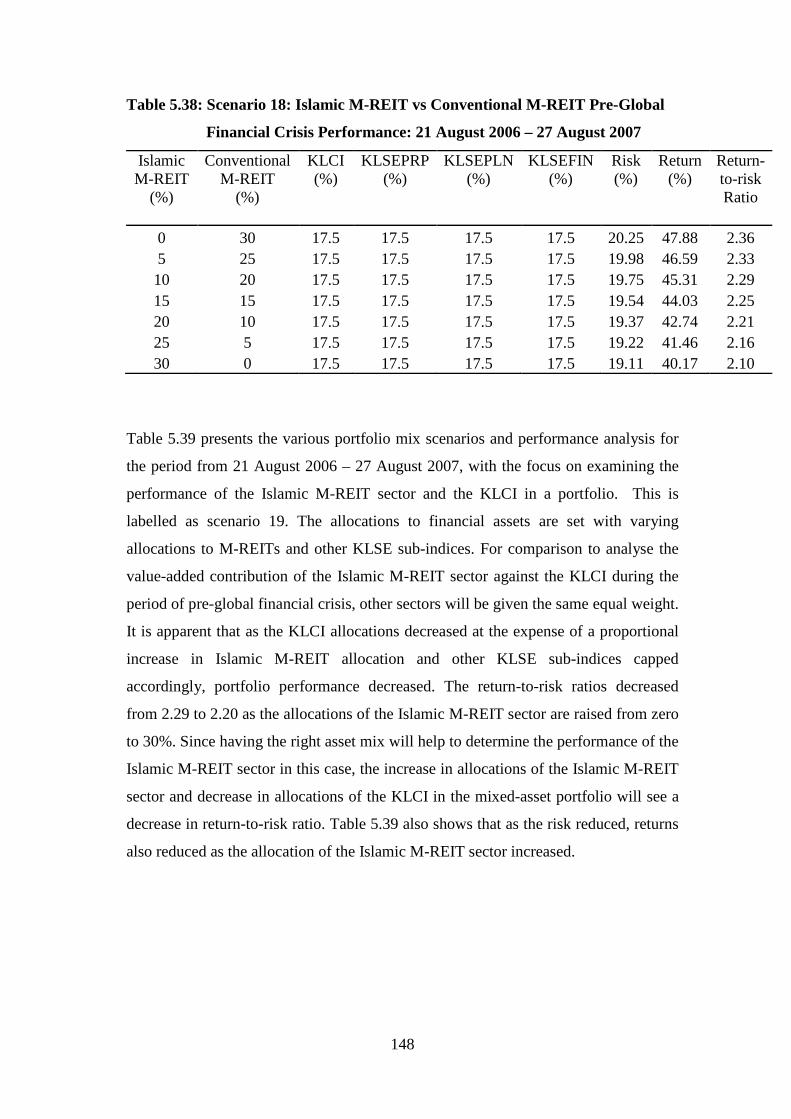

5.8.3.1 Overall M-REITs 138

5.8.3.2 Islamic M-REITs 147

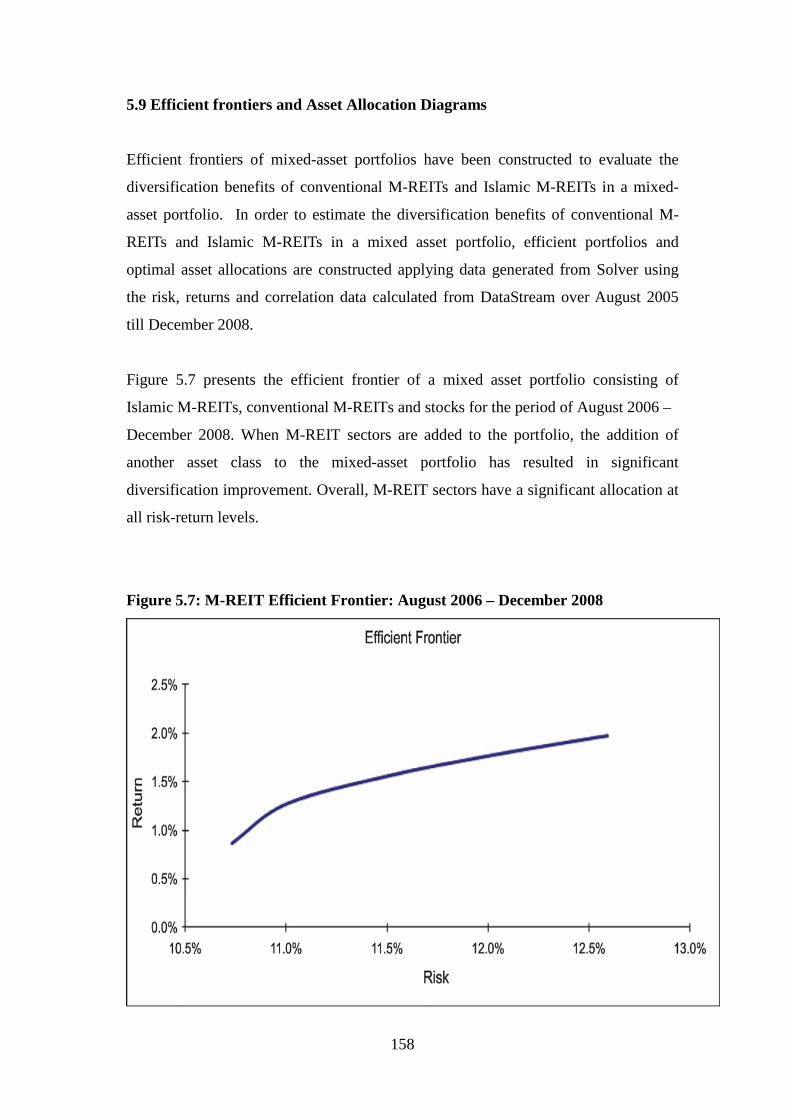

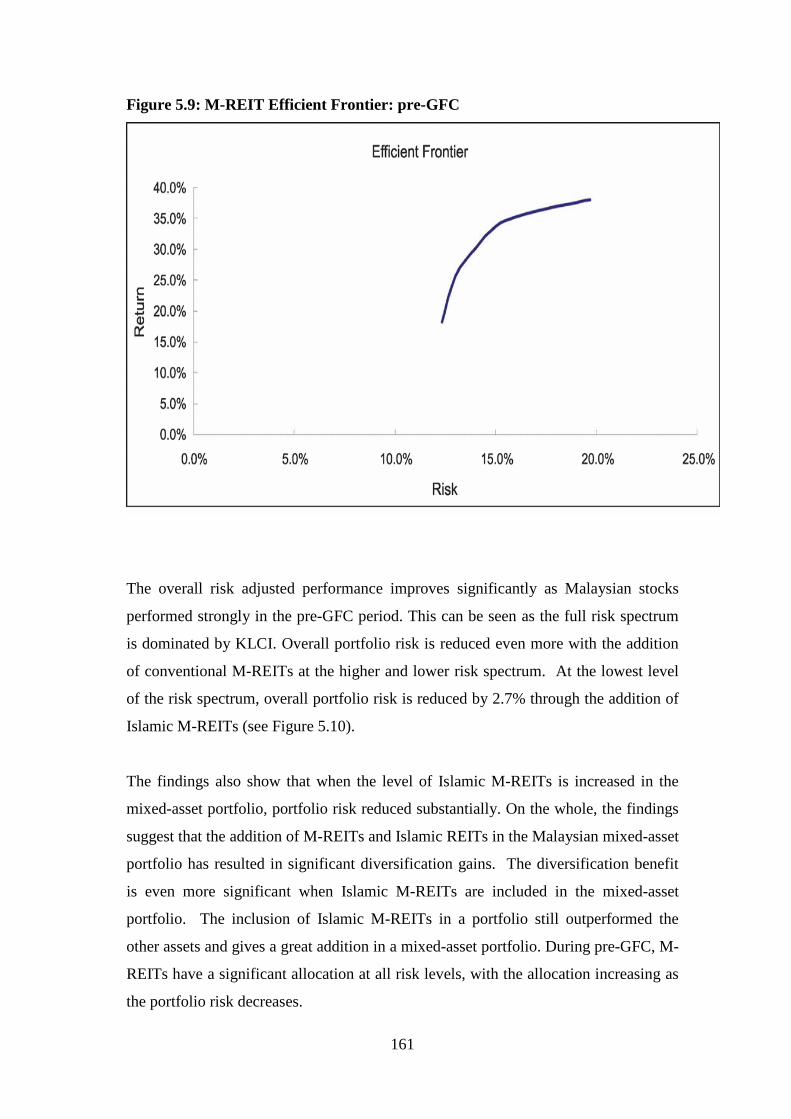

5.9 Efficient Frontier and Diagrams 158

5.9.1 Impact of Global Financial Crisis 160

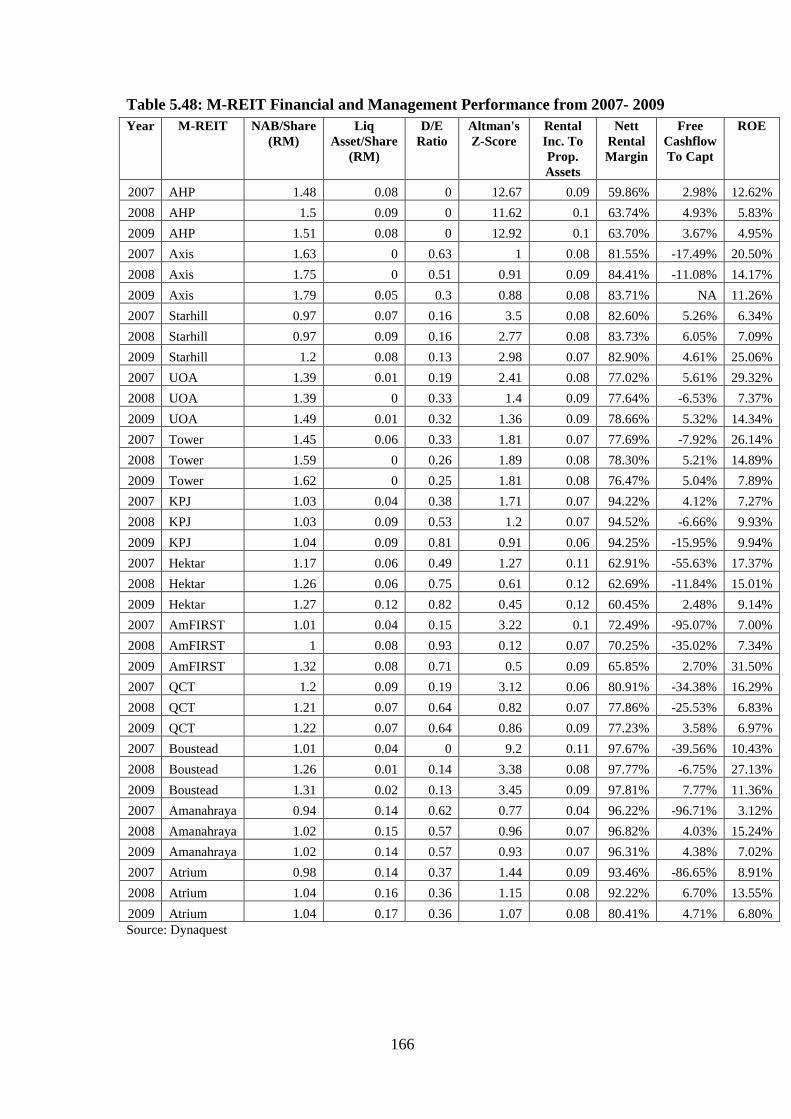

5.10 M-REITs Panel Regression 165

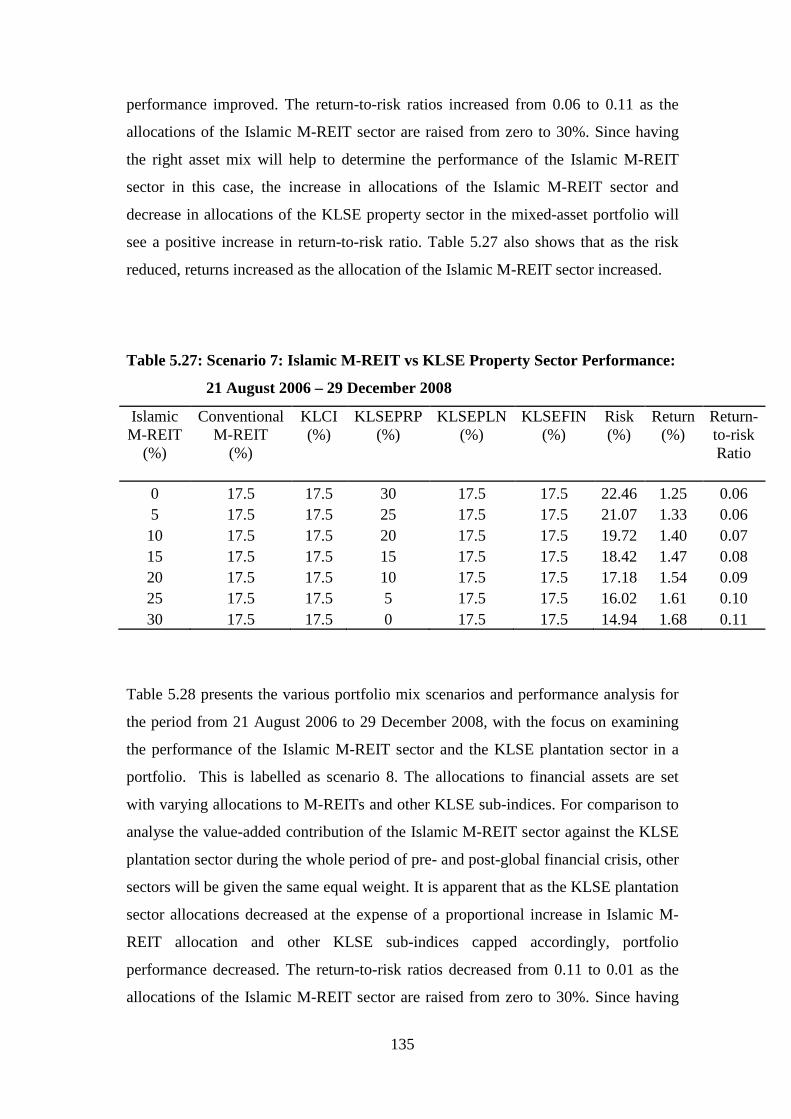

5.11 Conclusion 168

Chapter 6: M-REIT Surveys

6.1 Introduction 180

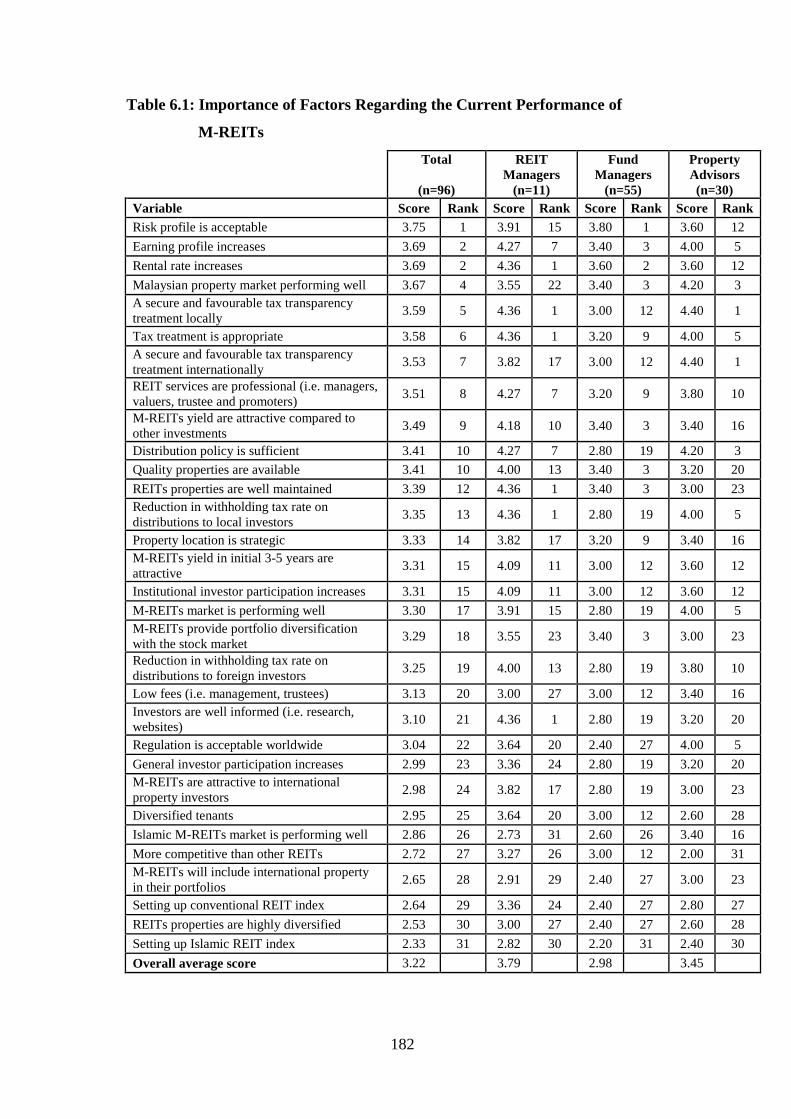

6.2 Importance of Factors Regarding the Current Performance of M-REITs 181

6.2.1 Overall 181

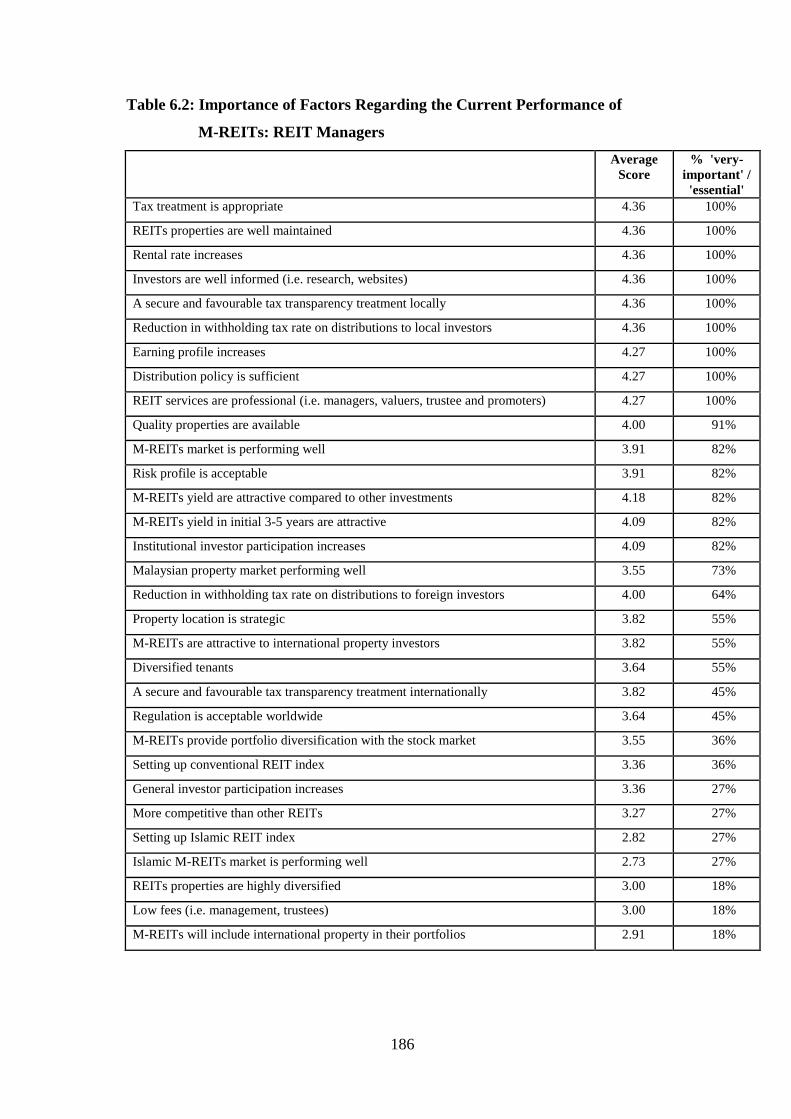

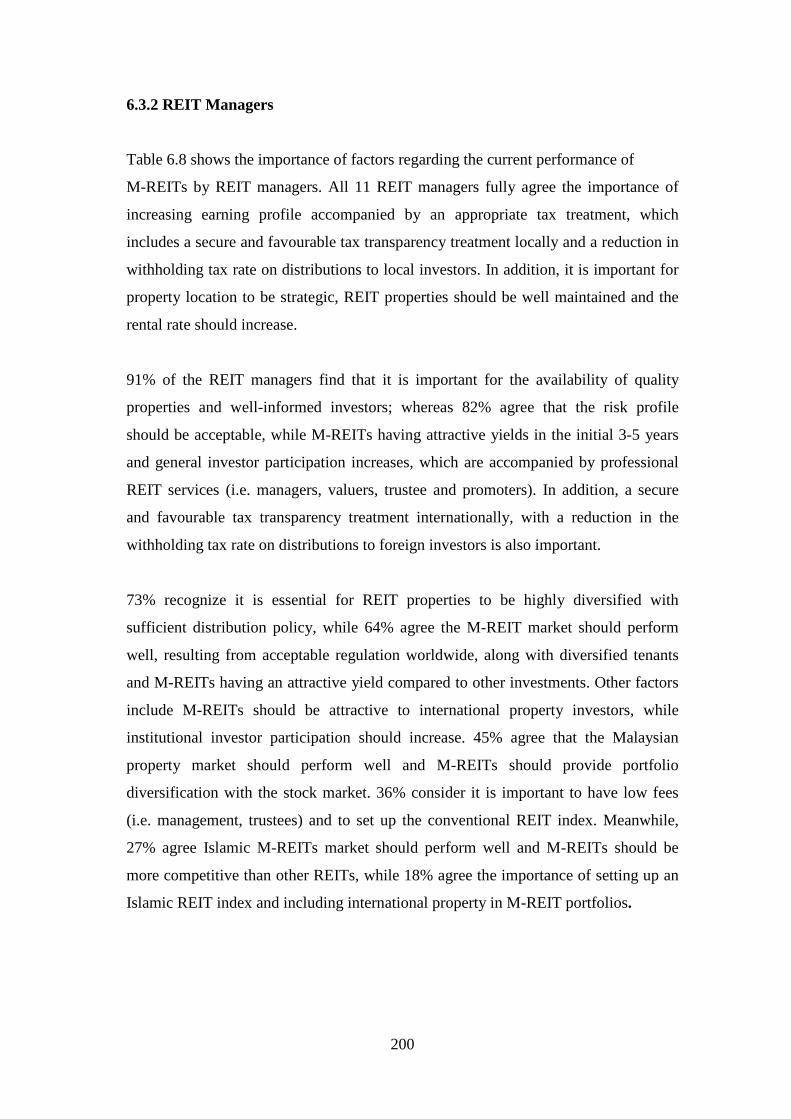

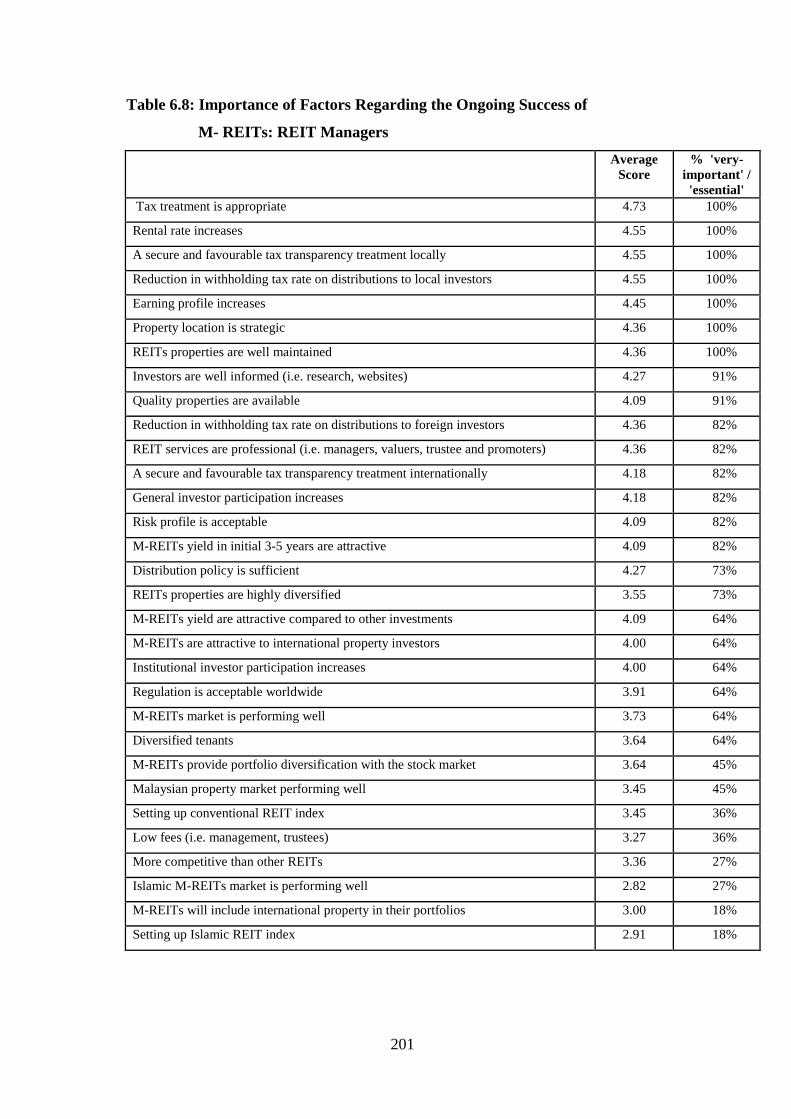

6.2.2 REIT Managers 184

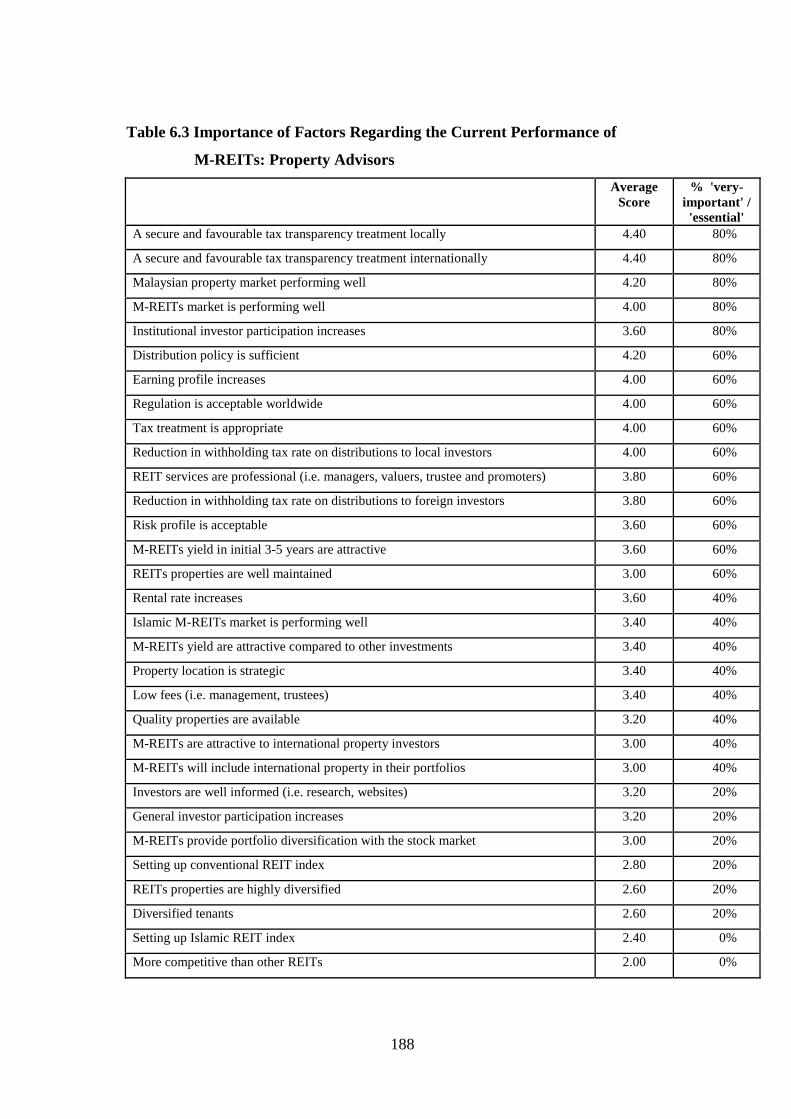

6.2.3 Property Advisors 187

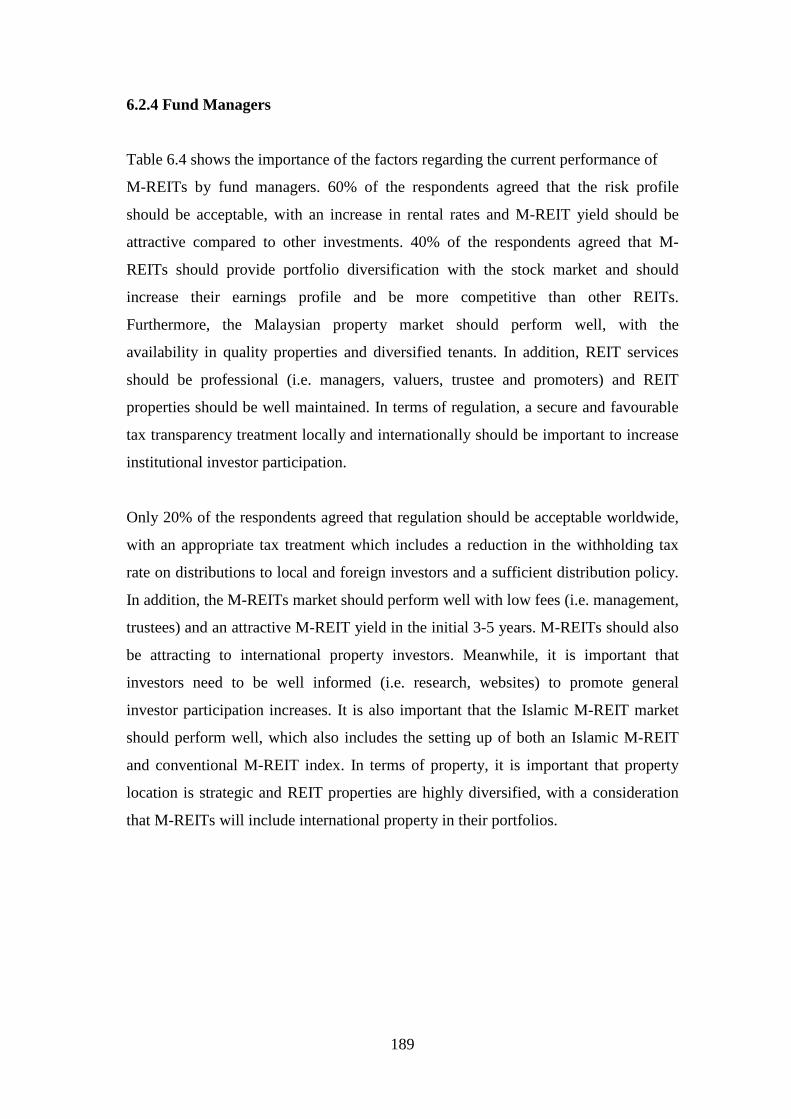

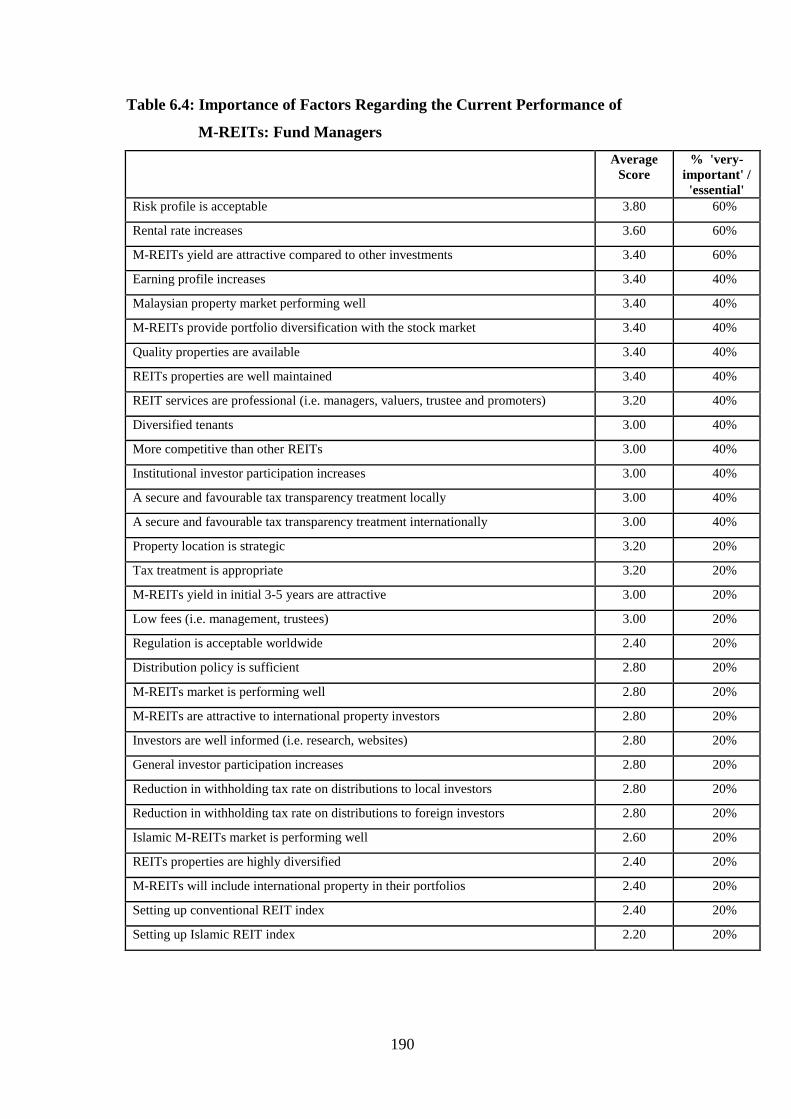

6.2.4 Fund Managers 189

viii

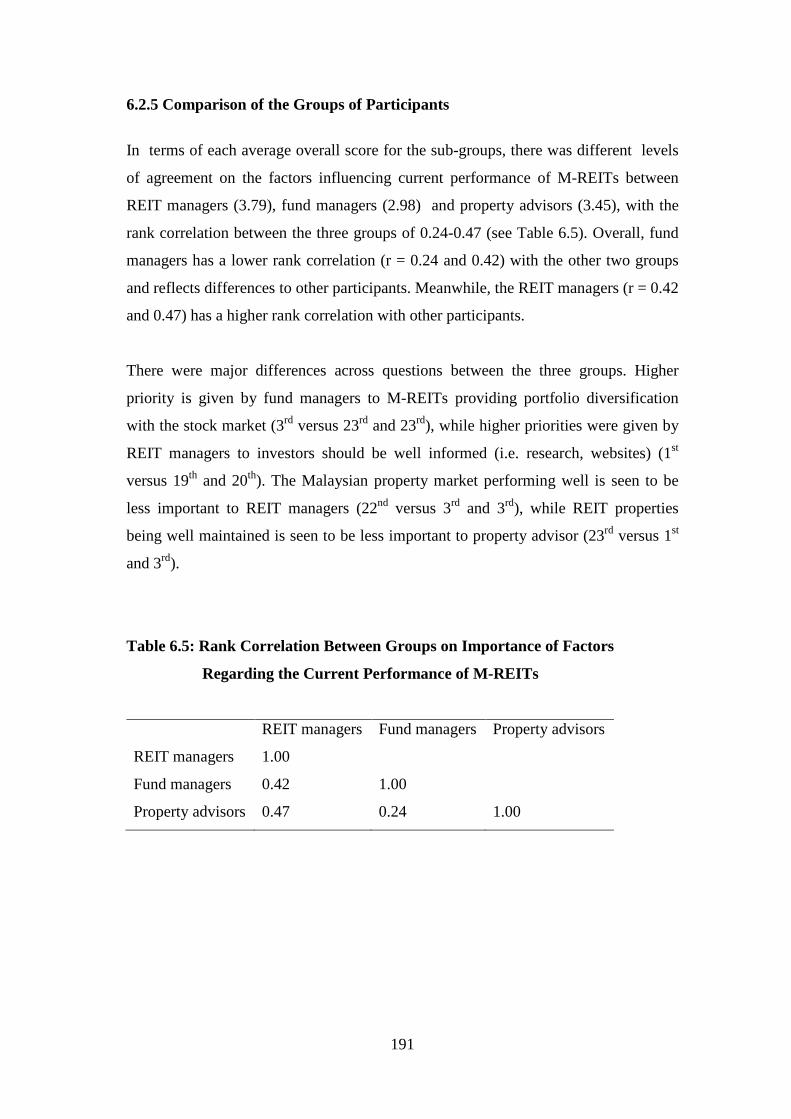

6.2.5 Comparison of the Groups of Participants 191

6.2.6 Factor Analysis Regarding Current Performance Factors 195

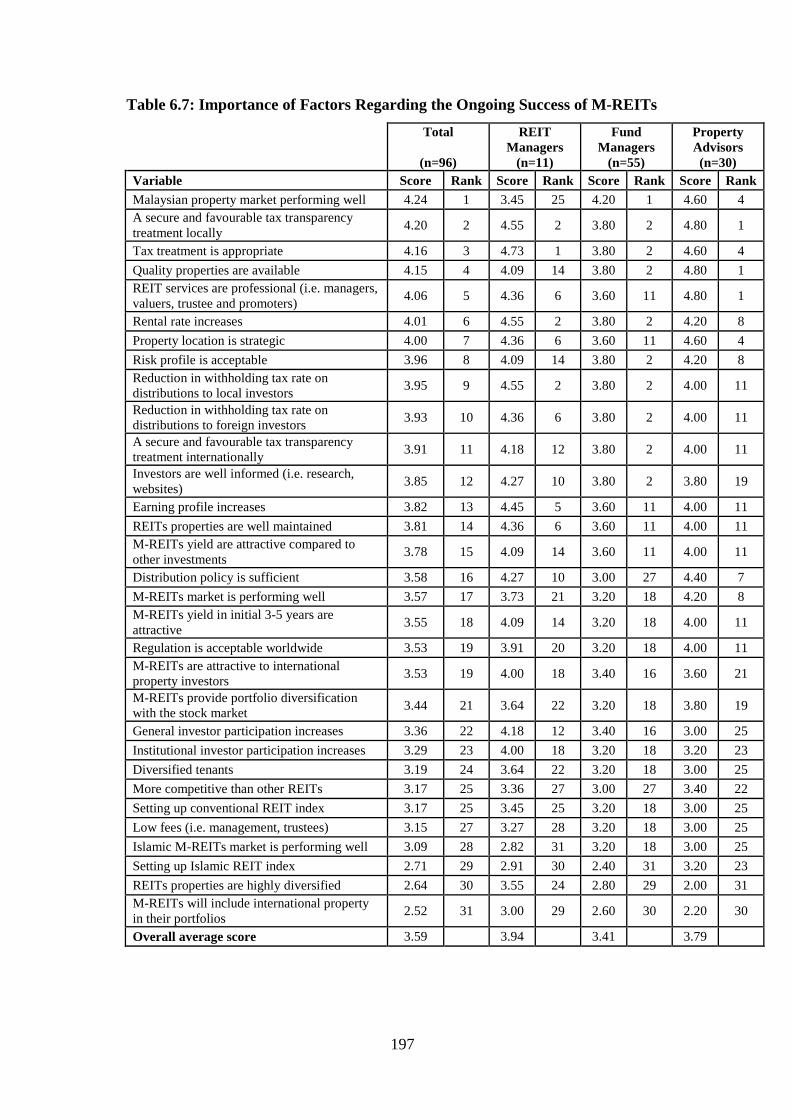

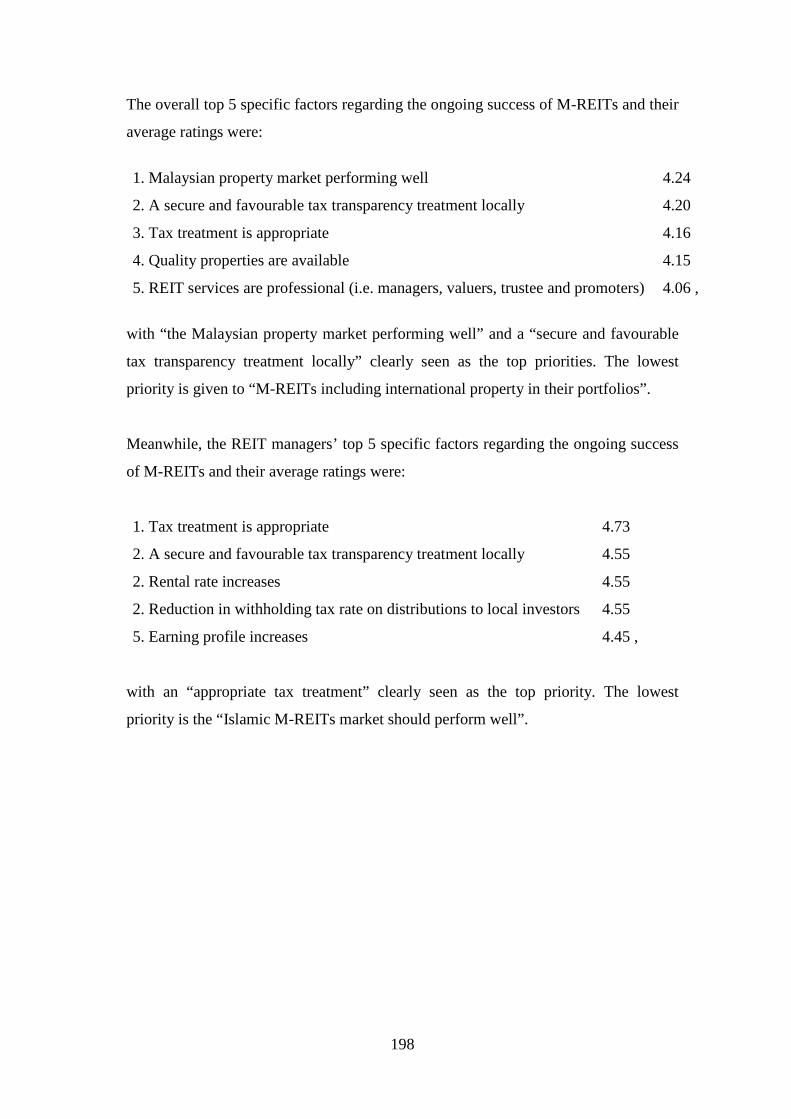

6.3 Importance of Factors Regarding the Ongoing Success of M-REITs 196

6.3.1 Overall 196

6.3.2 REIT Managers 200

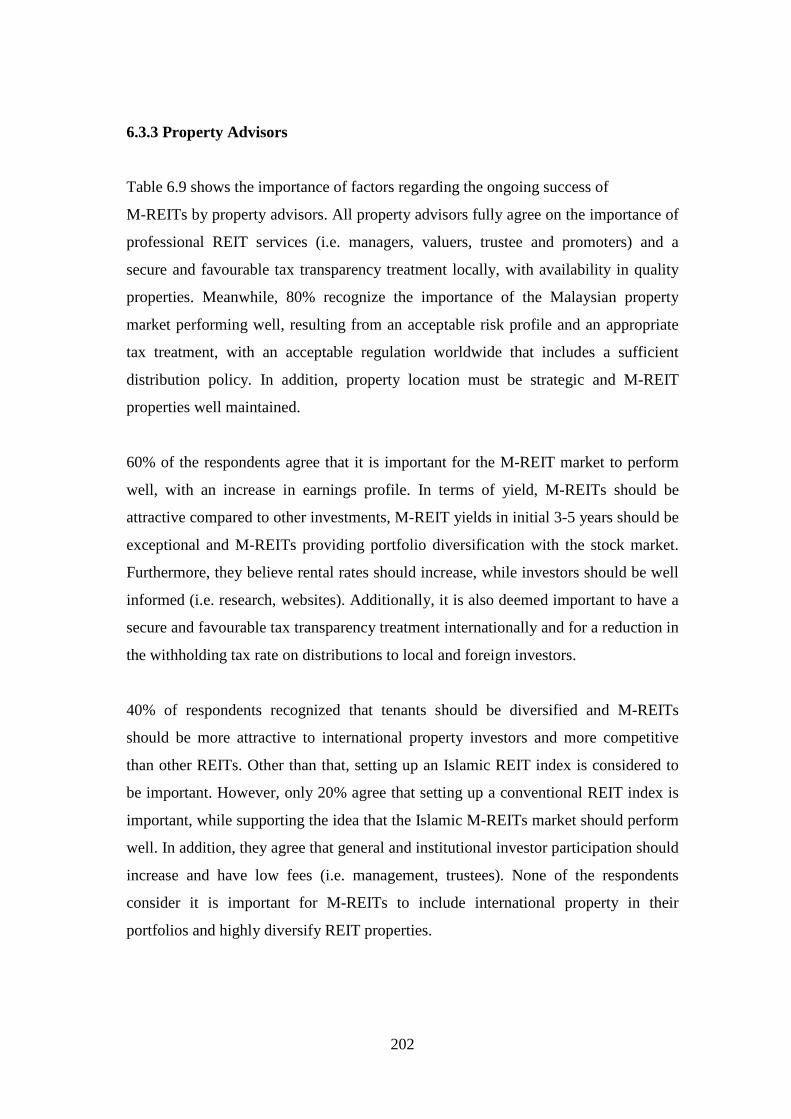

6.3.3 Property Advisors 202

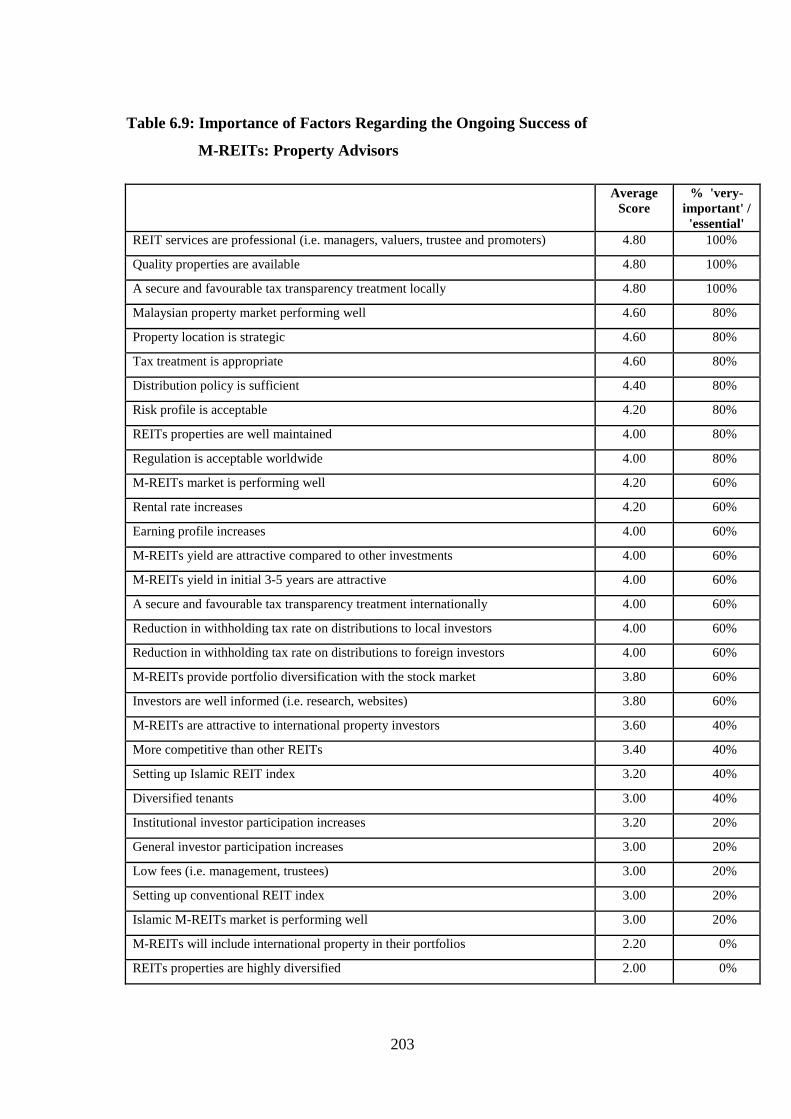

6.3.4 Fund Managers 204

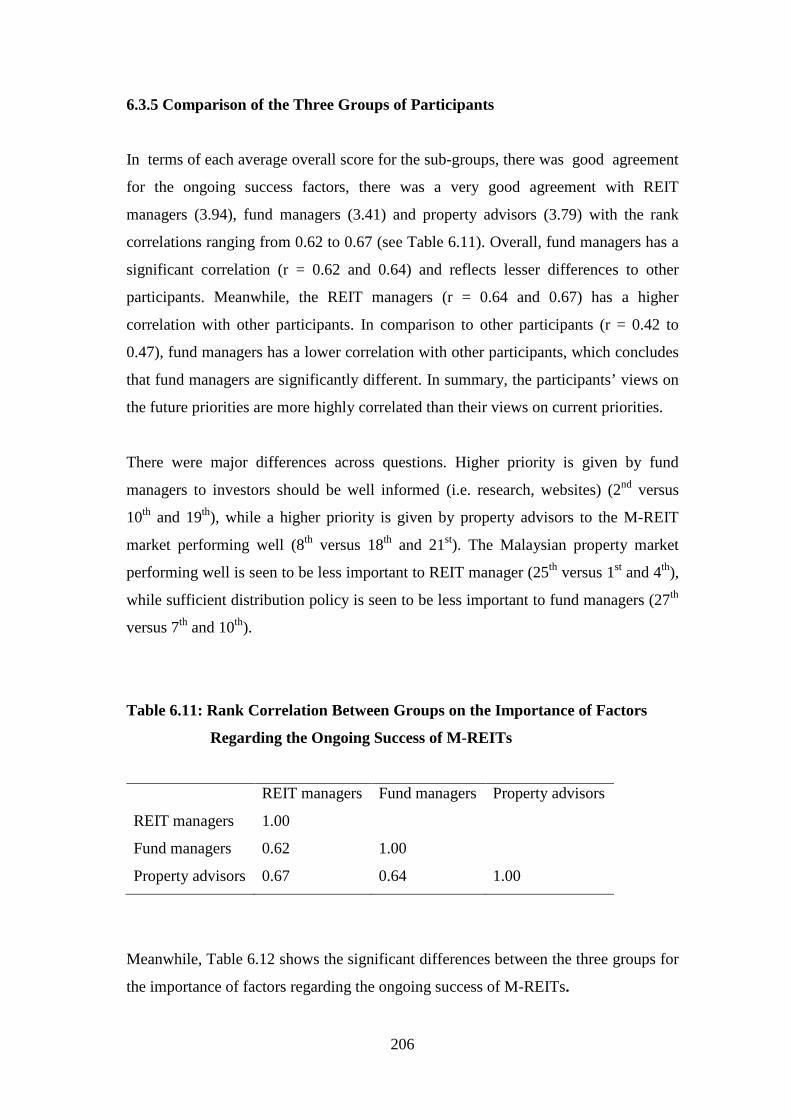

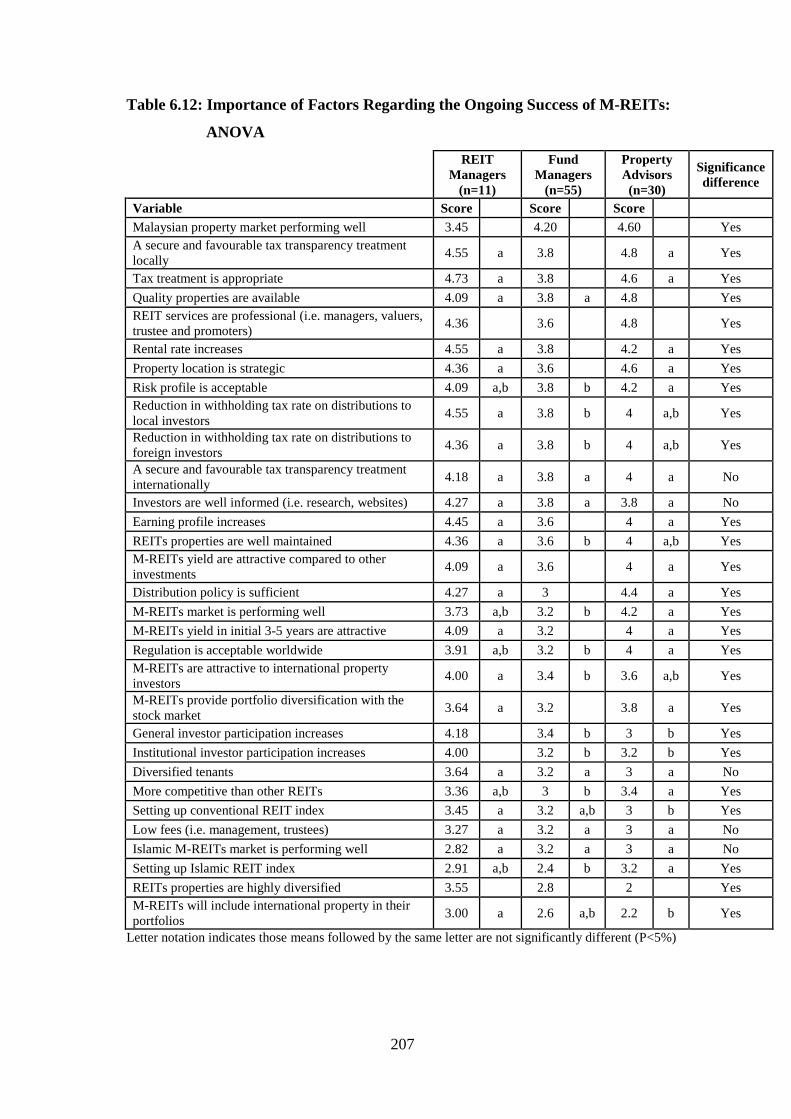

6.3.5 Comparison of the Three Groups of Participants 206

6.3.6 Factor Analysis Regarding Ongoing Success Factors for M-REITs 209

6.4 Comments From Respondents 210

6.4.1 M-REIT Fund Managers 211

6.4.2 Property Advisors 213

6.4.3 Fund Managers 214

6.5 Conclusion 216

Chapter 7: Summary

7.1 Summary of Contributions of the Research 217

7.2 Summary of Limitations 217

7.3 Suggestions 218

7.4 Summary of Future Research 220

References 224

Appendices 237

Appendix I The Survey Questionnaire for REIT Managers 238

Appendix II The Survey Questionnaire for Property Managers 239

Appendix III The Survey Questionnaire for Fund Managers 240

Appendix IV Global REITs 241

Appendix V M-REIT Case Studies 242

Appendix VI Paper Published for Journal of Property Research 243

Appendix VII Paper Published for PRPRJ 244

ix

List of Tables

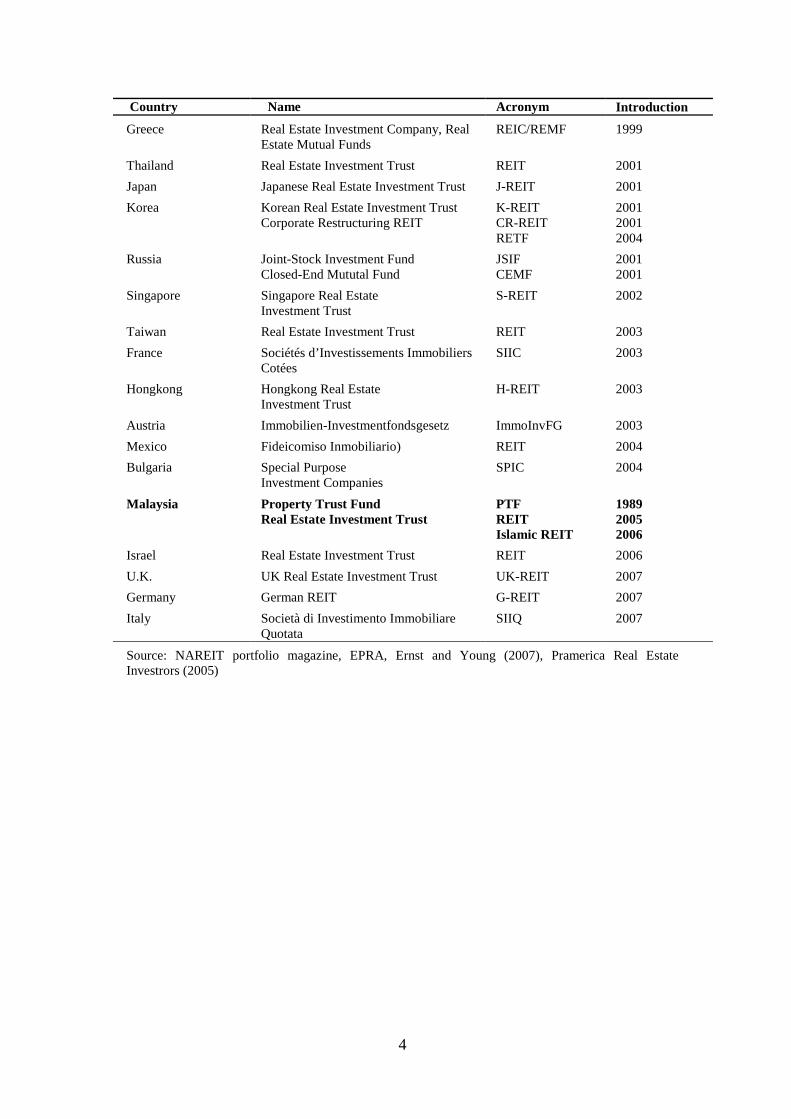

Table 1.1: Countries with Existing and Considering REIT-like Structures 3

Table 1.2: Global REIT Comparison 5

Table 1.3: List of Advantages and Disadvantages of Direct Property 8

Table 1.4: Advantages and Disadvantages of Indirect Property 10

Table 1.5: Private/Unlisted Property 10

Table 1.6: Listed Securities in a REIT Structure 11

Table 1.7: Economic and Financial Profile of Malaysia: 2008 12

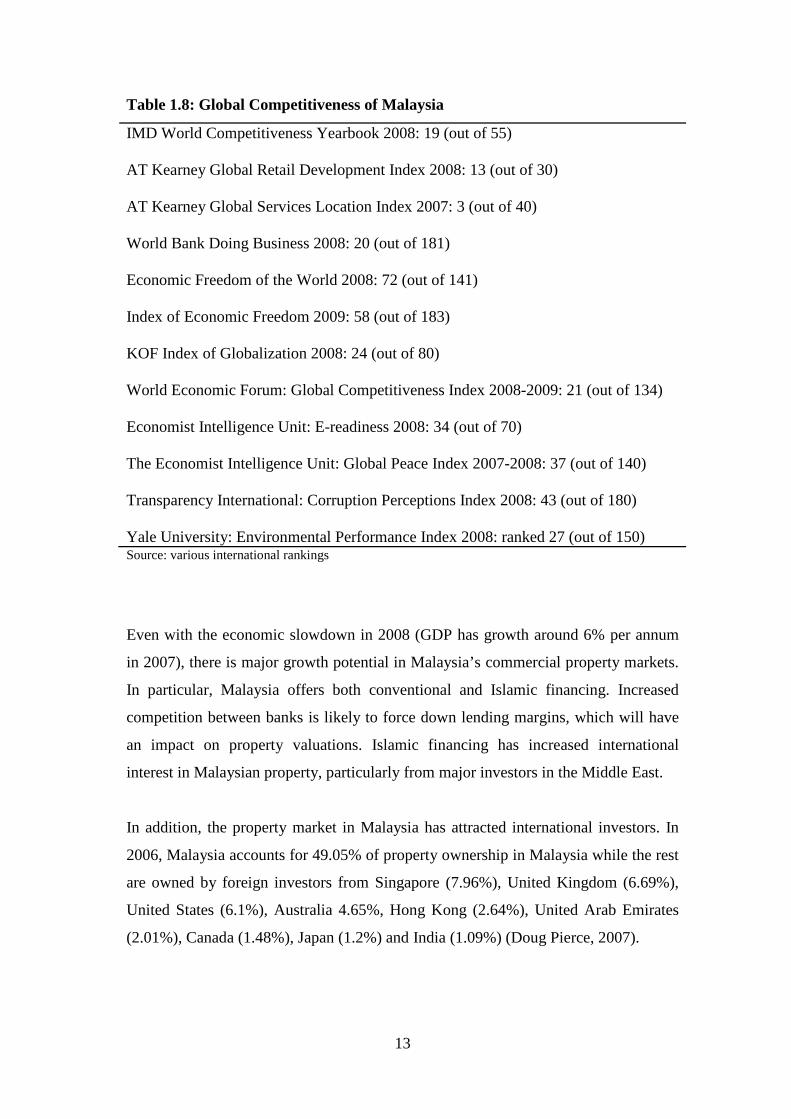

Table 1.8: Global Competitiveness of Malaysia 13

Table 1.9: Commercial Property Transactions in Asia: 2008 14

Table 1.10: Breakdown of Malaysia’s Commercial Property Sales by Market:

2008

14

Table 1.11: Asia Office Market Performance: 2008 16

Table 1.12: Asia Retail Market Performance: 2008 16

Table 1.13: Asia Industrial Market Performance: 2008 16

Table 2.1: Growth of REITs 37

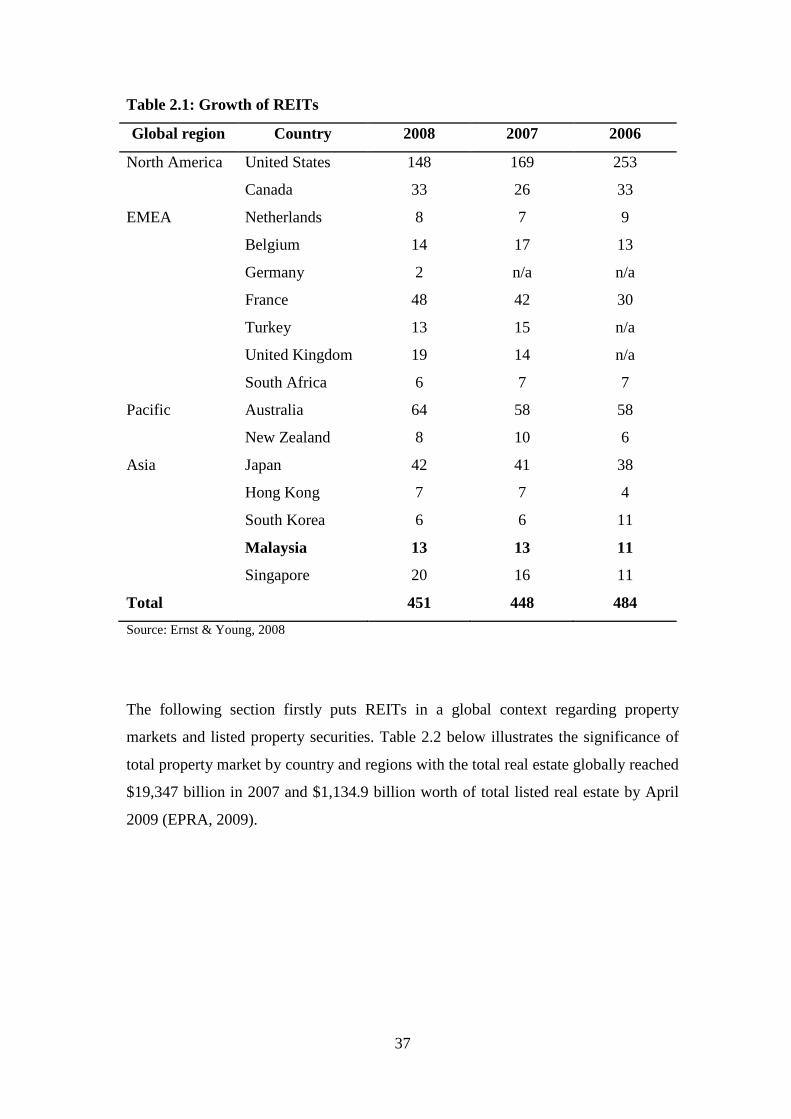

Table 2.2 Global Real Estate Universe: 2009 38

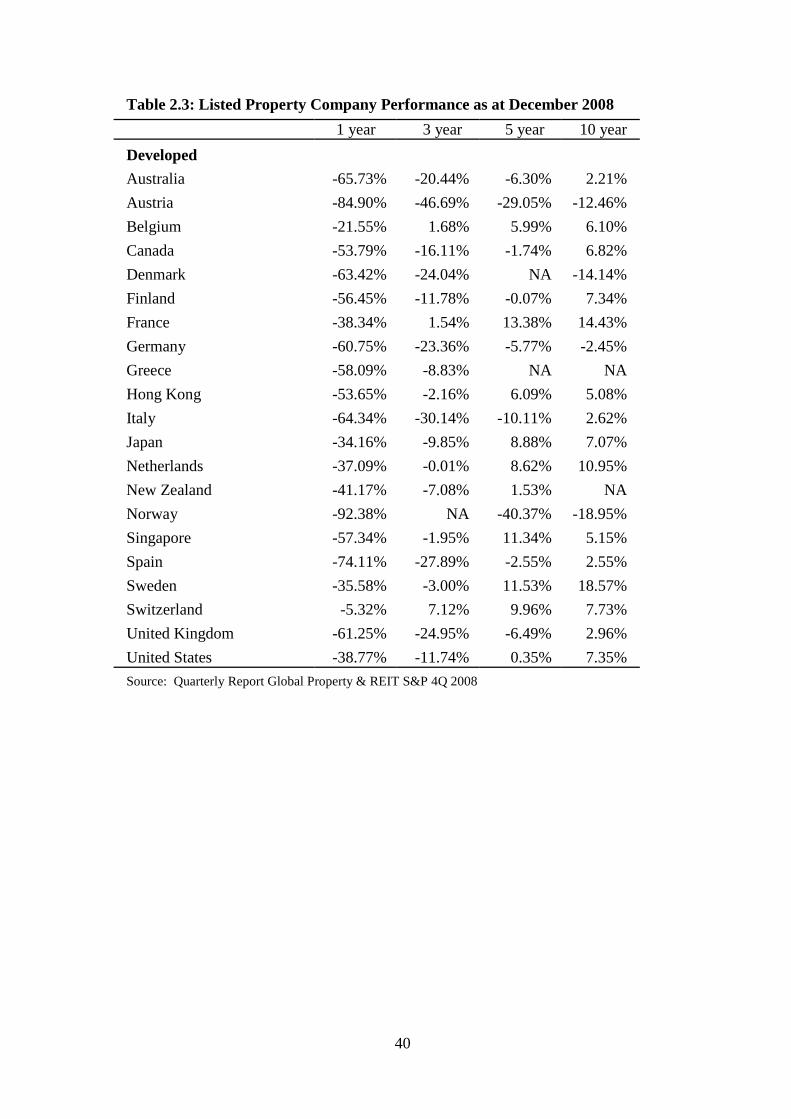

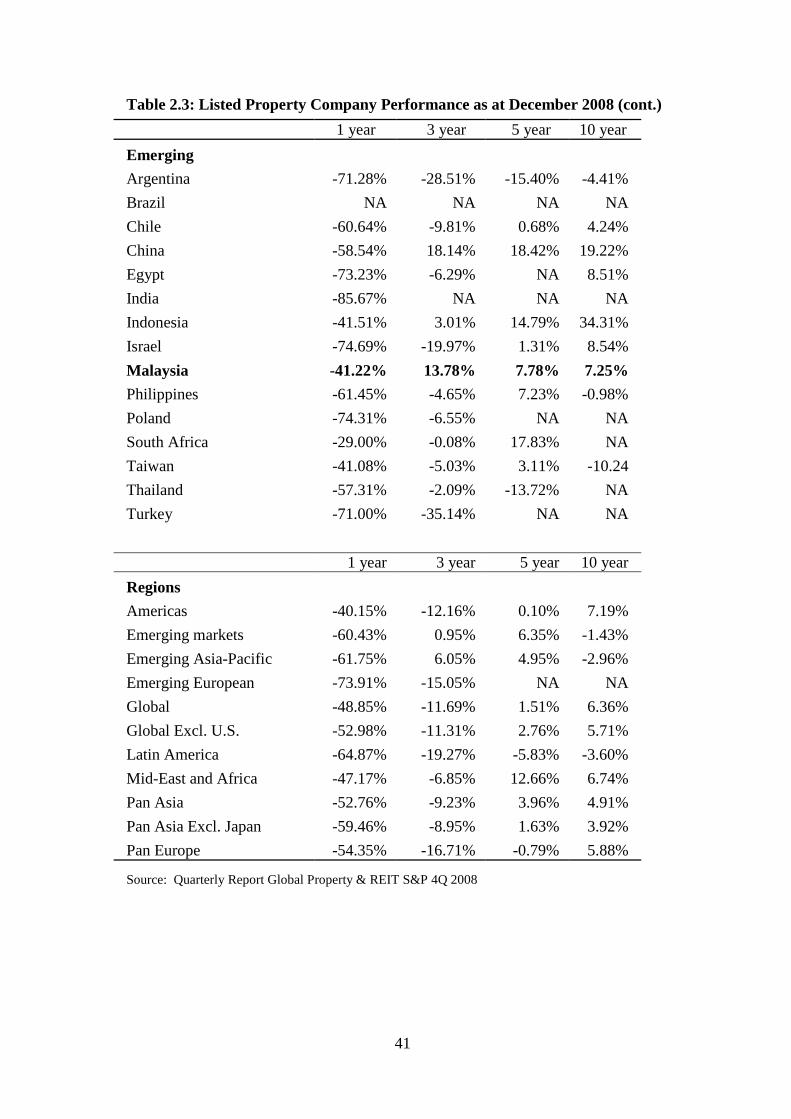

Table 2.3: Property Performance as at December 2008 40

Table 2.3: Property Performance as at December 2008 (cont.) 41

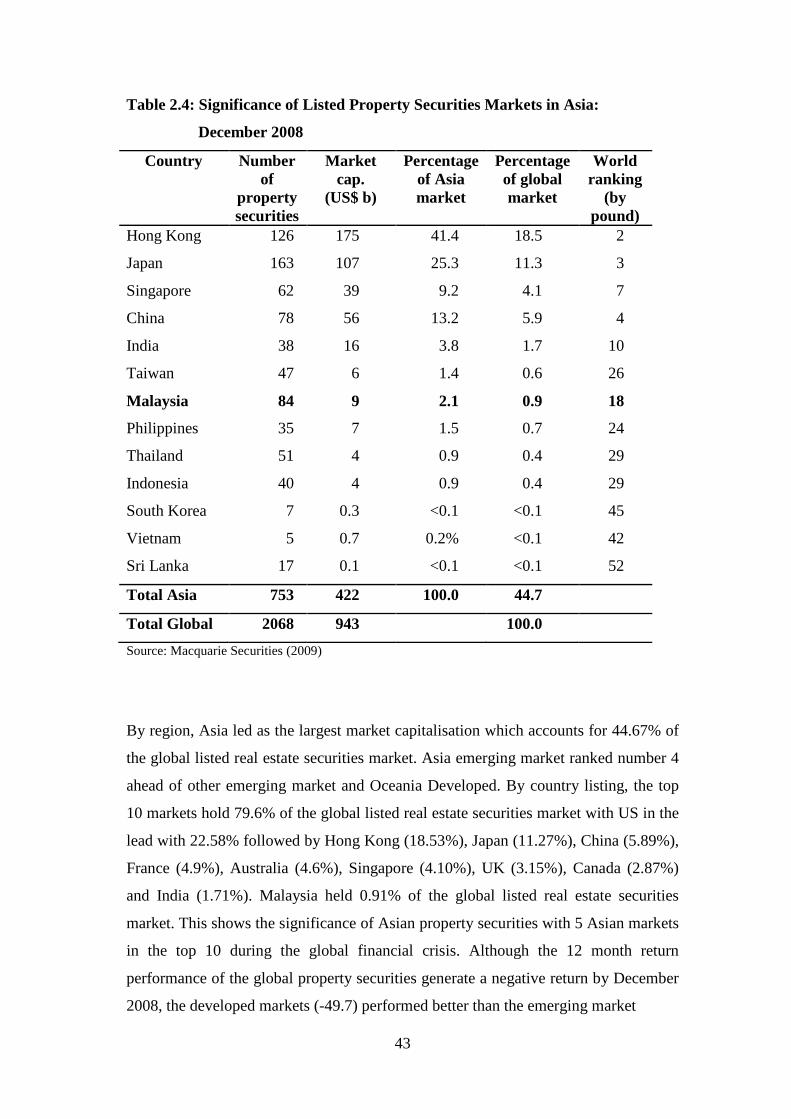

Table 2.4: Significance of Listed Property Securities Markets in Asia:Dec.2008 43

Table 2.5: Global REIT Market: December 2008 45

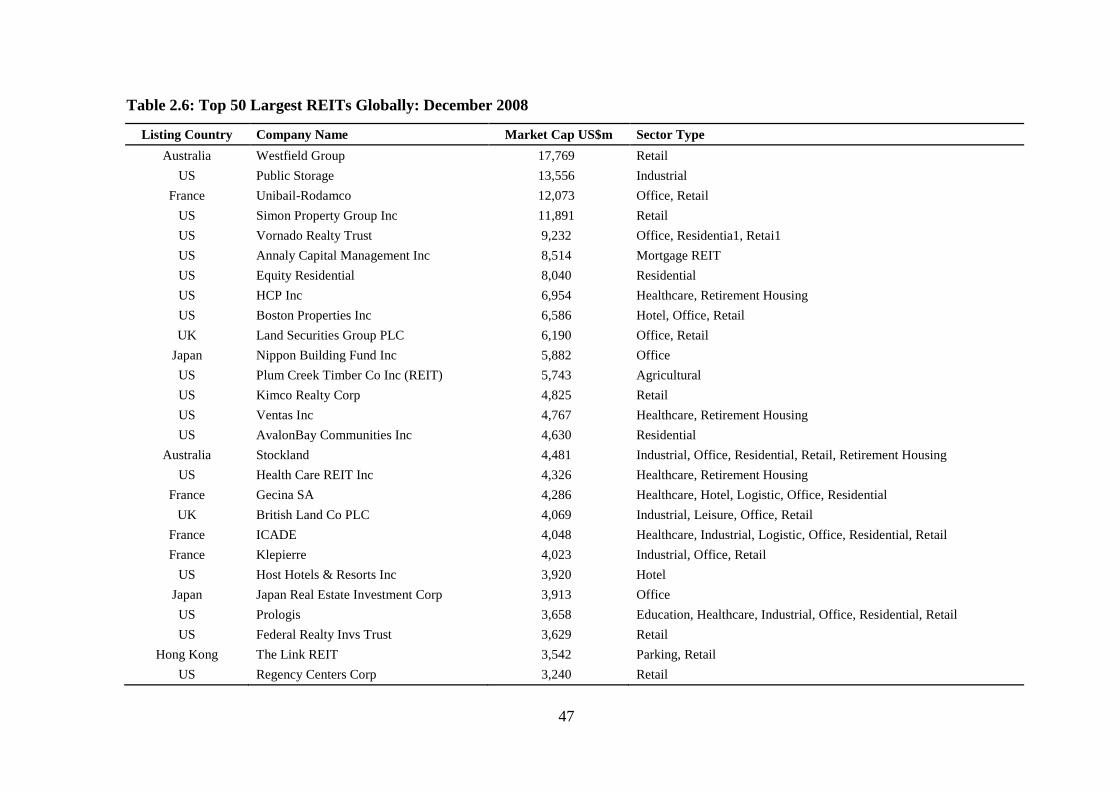

Table 2.6: Top 50 Largest REITs Globally: December 2008 47

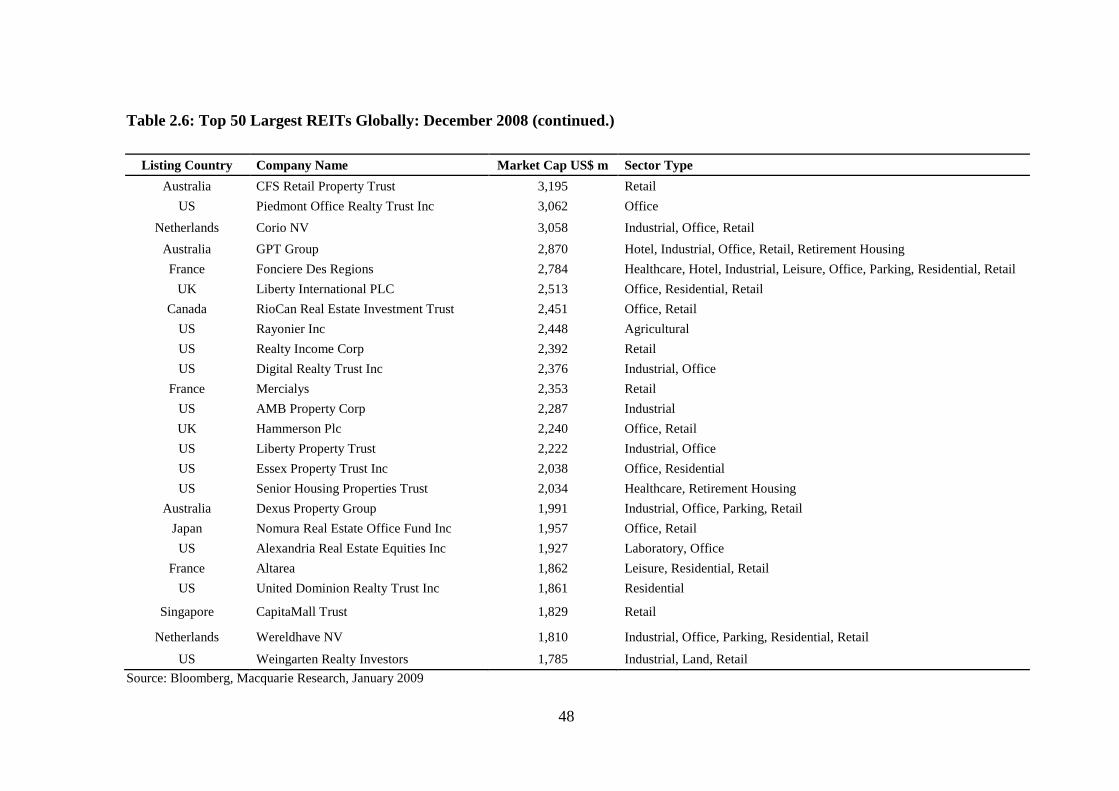

Table 2.6: Top 50 Largest REITs Globally: December 2008 (cont.) 48

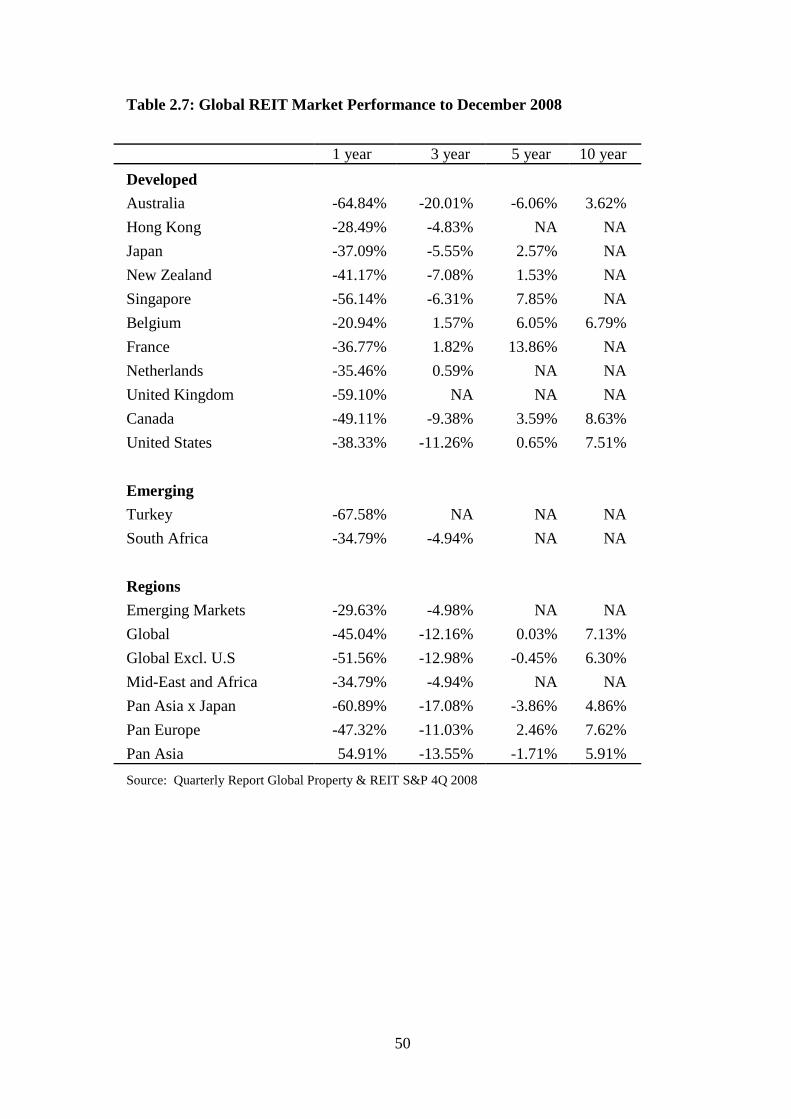

Table 2.7: Global REIT Market Performance to December 2008 50

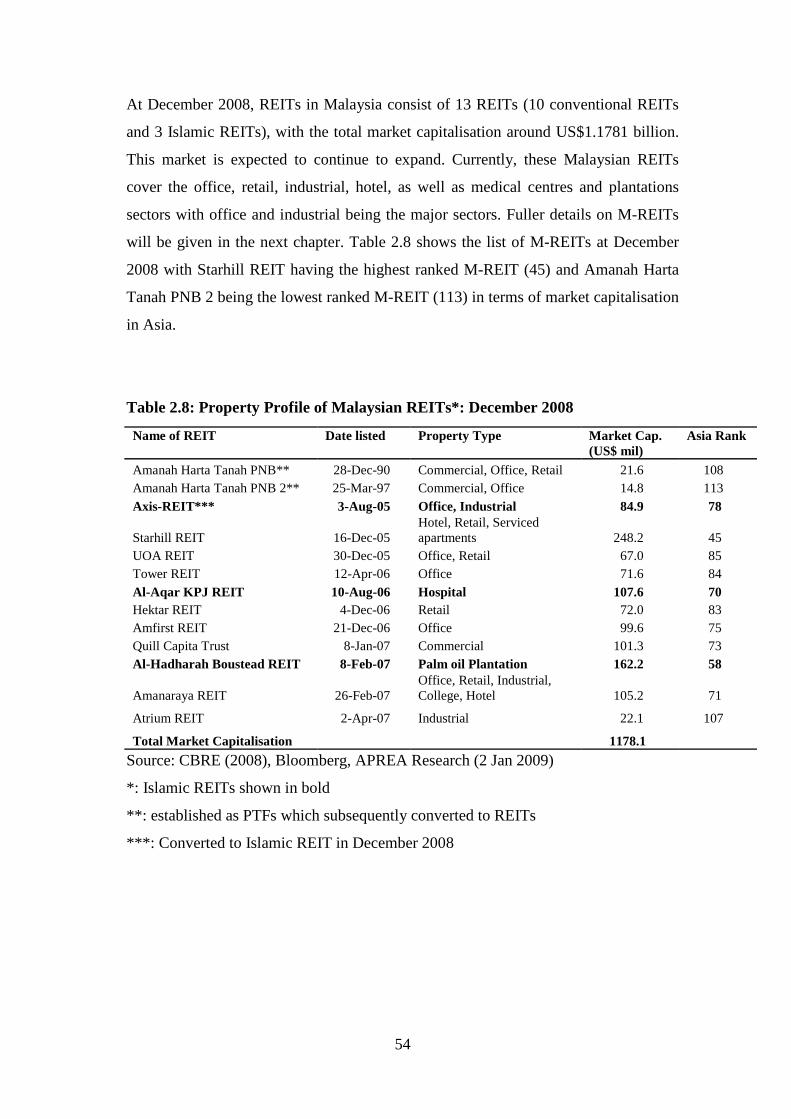

Table 2.8: Property Profile of Malaysian REITs*: December 2008 54

Table 2.9: Global Properties Securities Funds in 2007 56

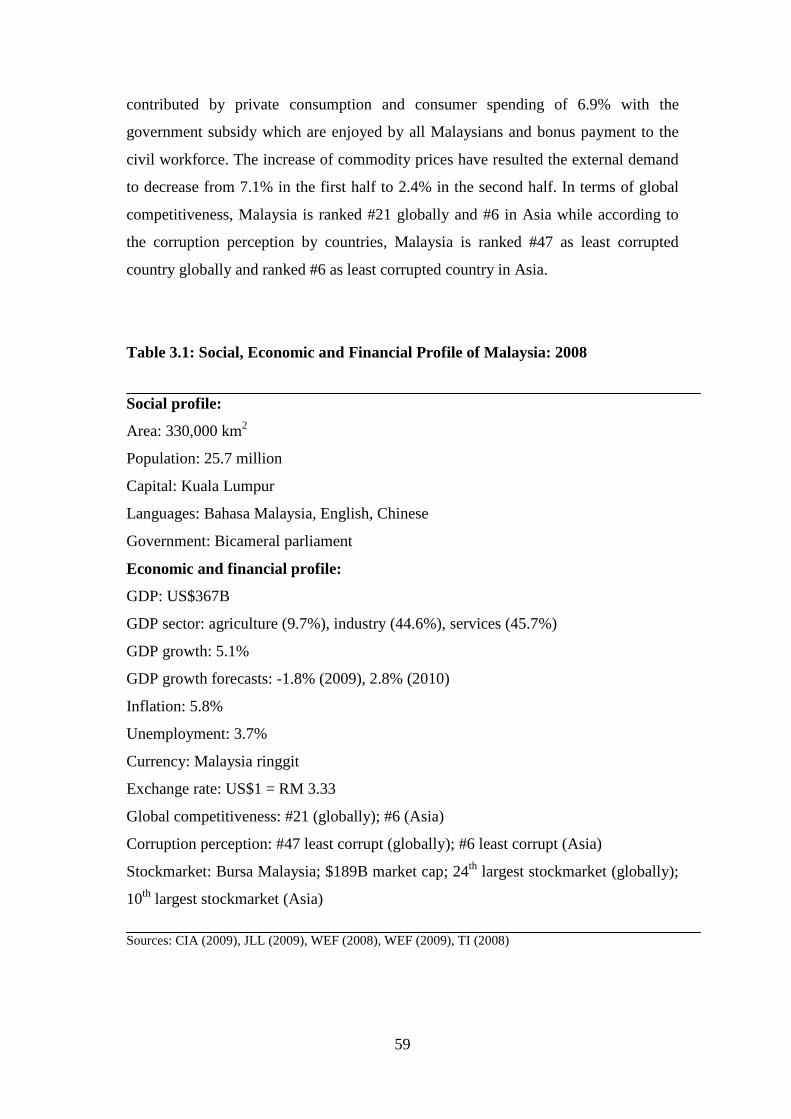

Table 3.1: Social, Economic and Financial Profile of Malaysia: 2008 59

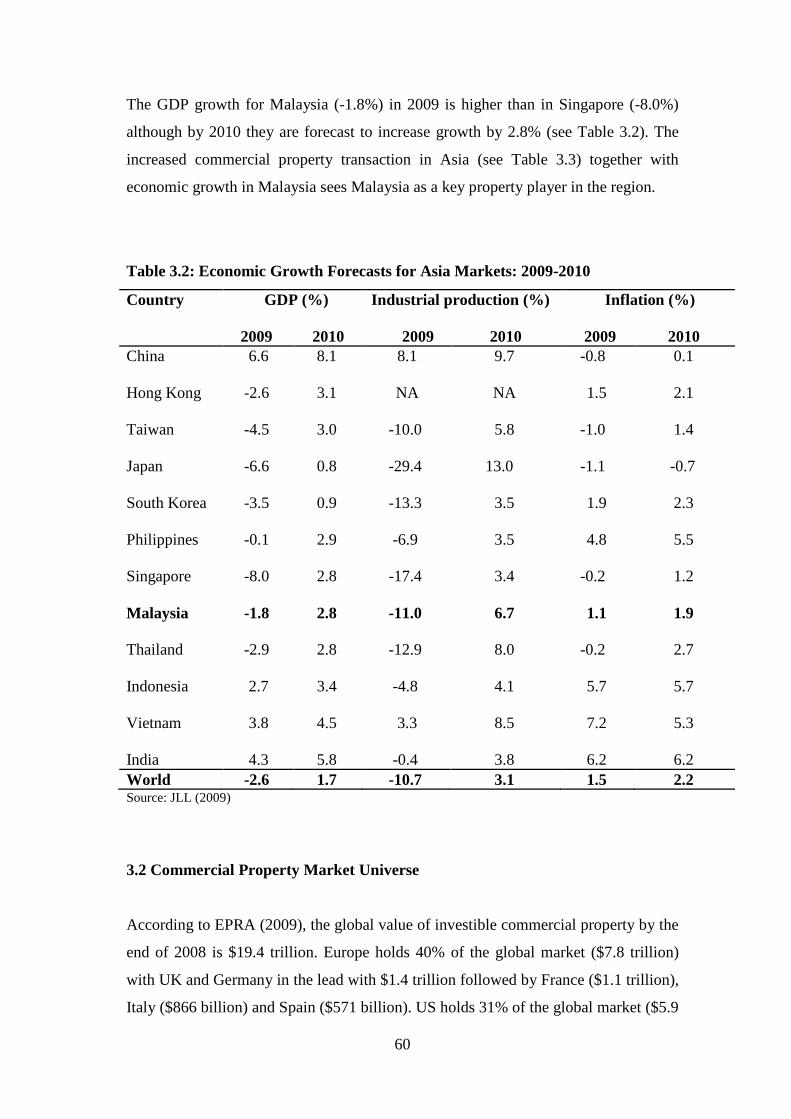

Table 3.2: Economic Growth Forecasts for Asia markets: 2009-2010 60

x

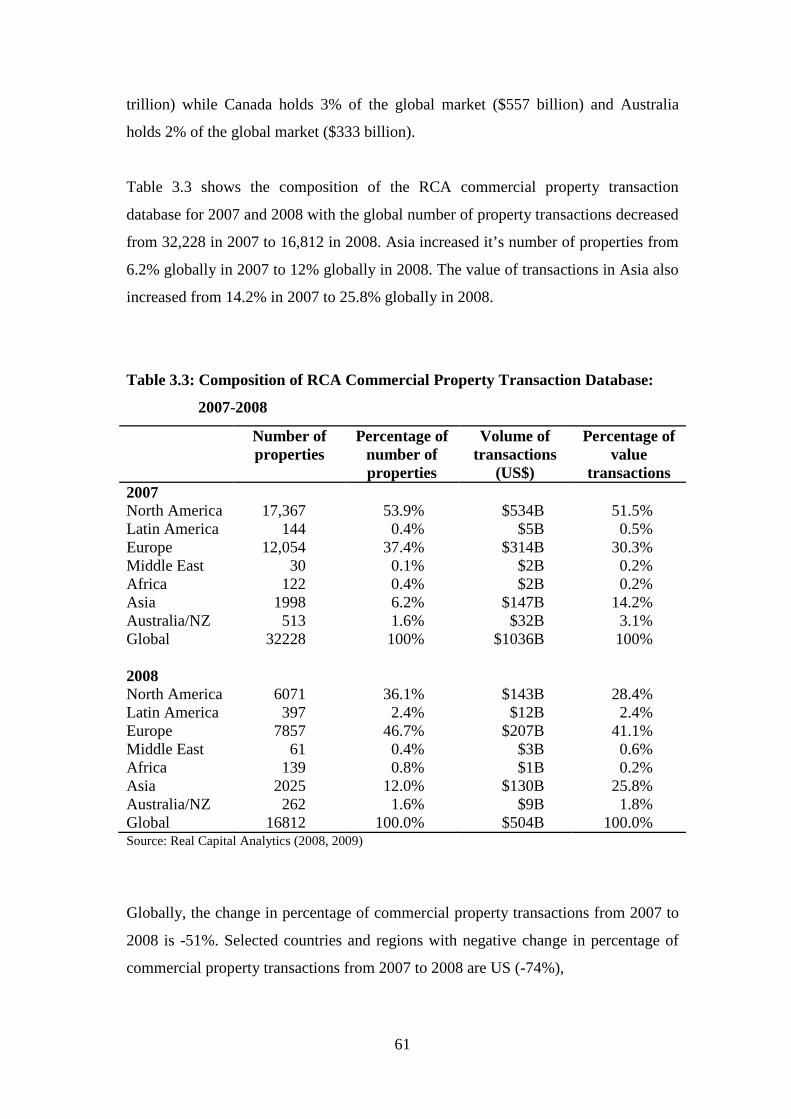

Table 3.3: Composition of RCA Commercial Property Transaction Database:

2007-2008 61

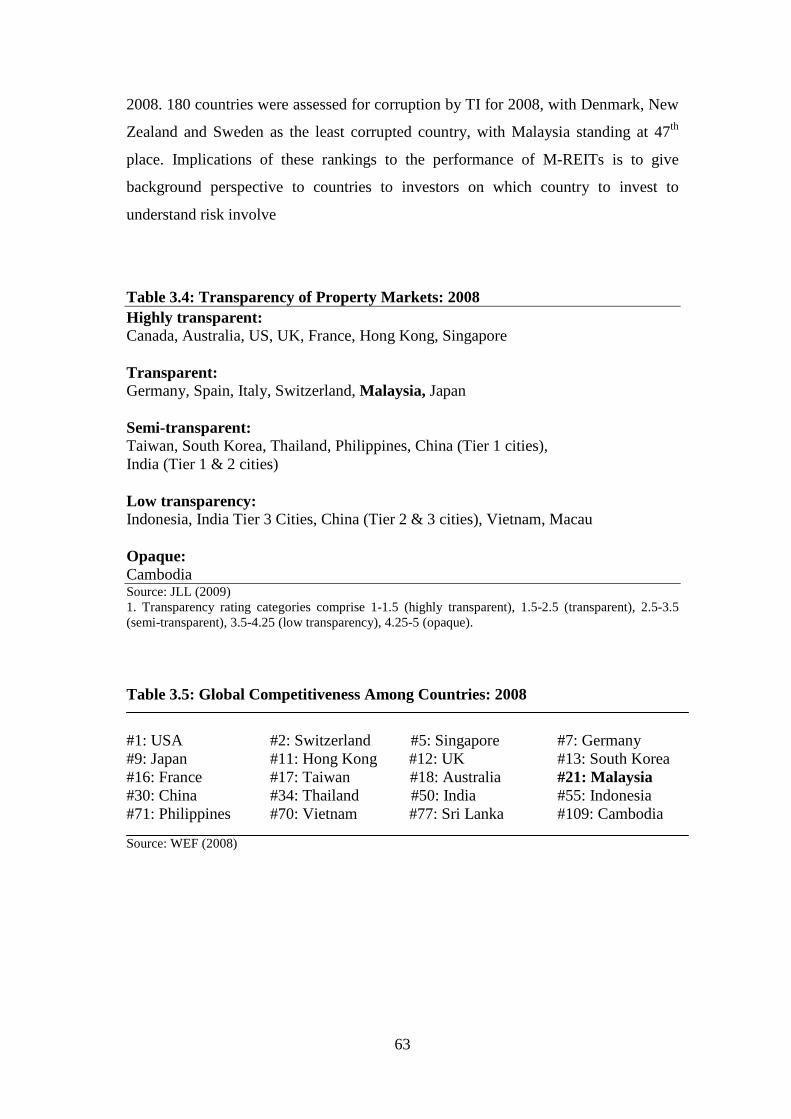

Table 3.4: Transparency of Property Markets: 2008 63

Table 3.5: Global Competitiveness Among Countries: 2008 63

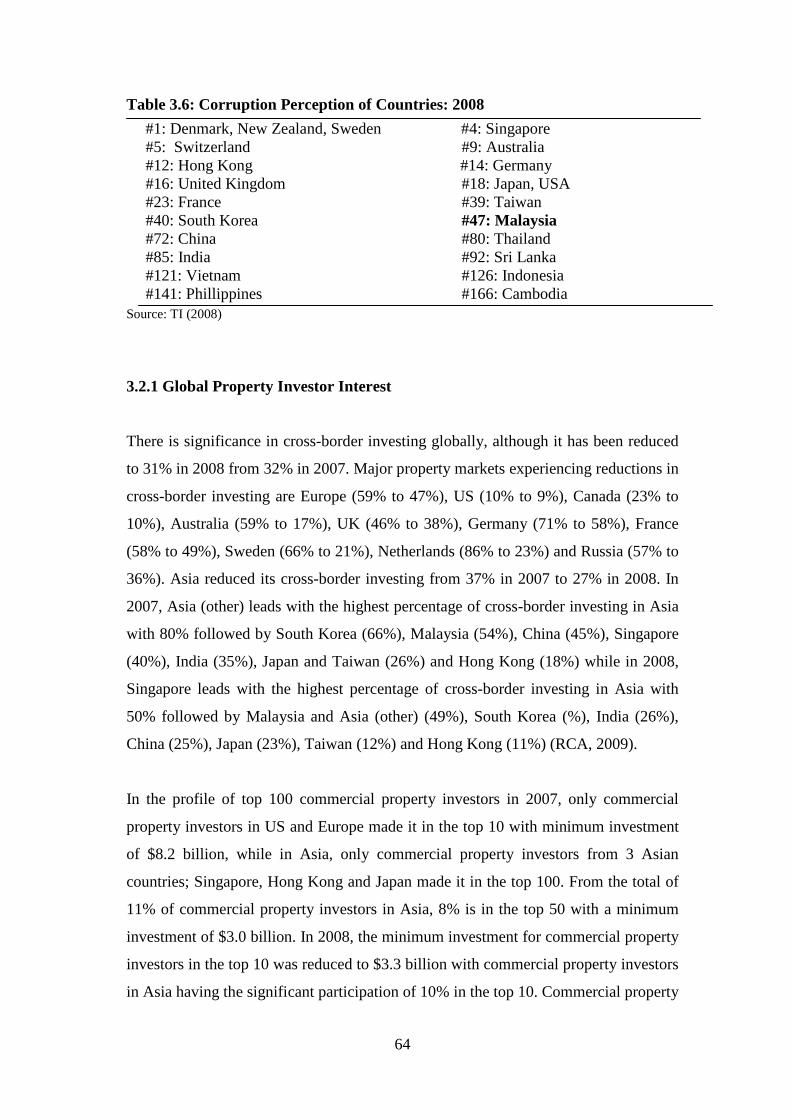

Table 3.6: Corruption Perception of Countries: 2008 64

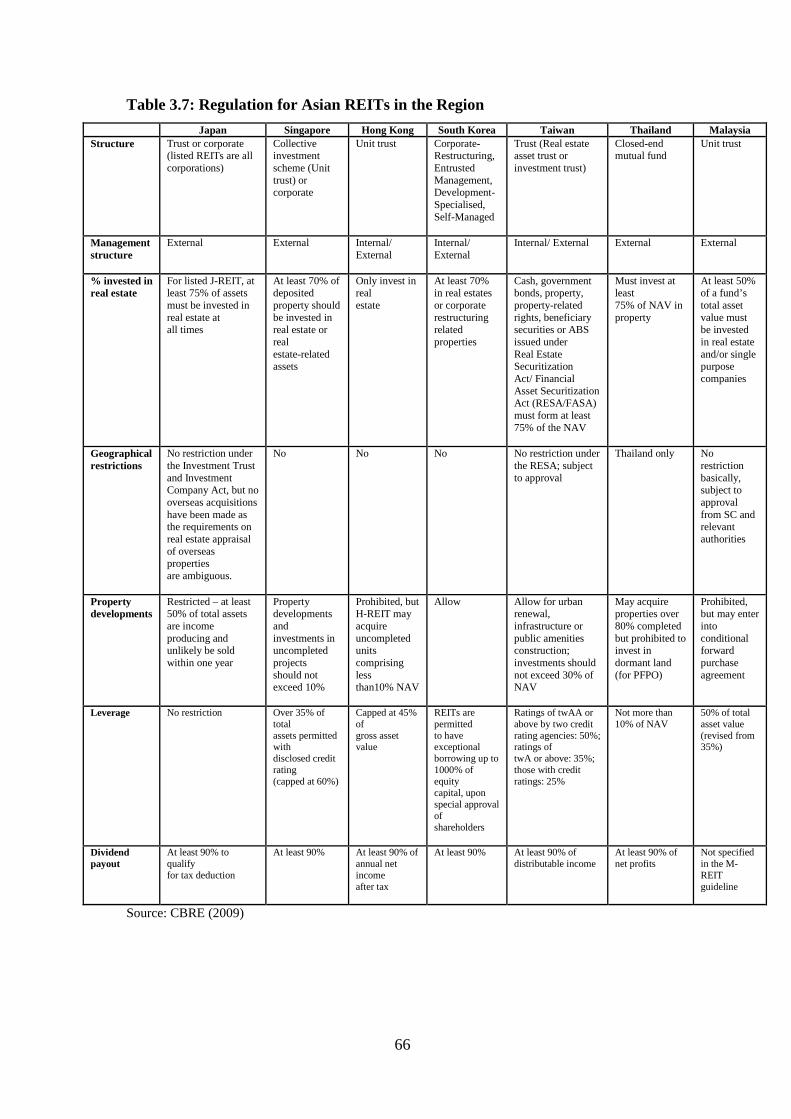

Table 3.7: Regulation for Asian REITs in the Region 66

Table 3.8: Commercial Property Transactions in Asia: 2007 68

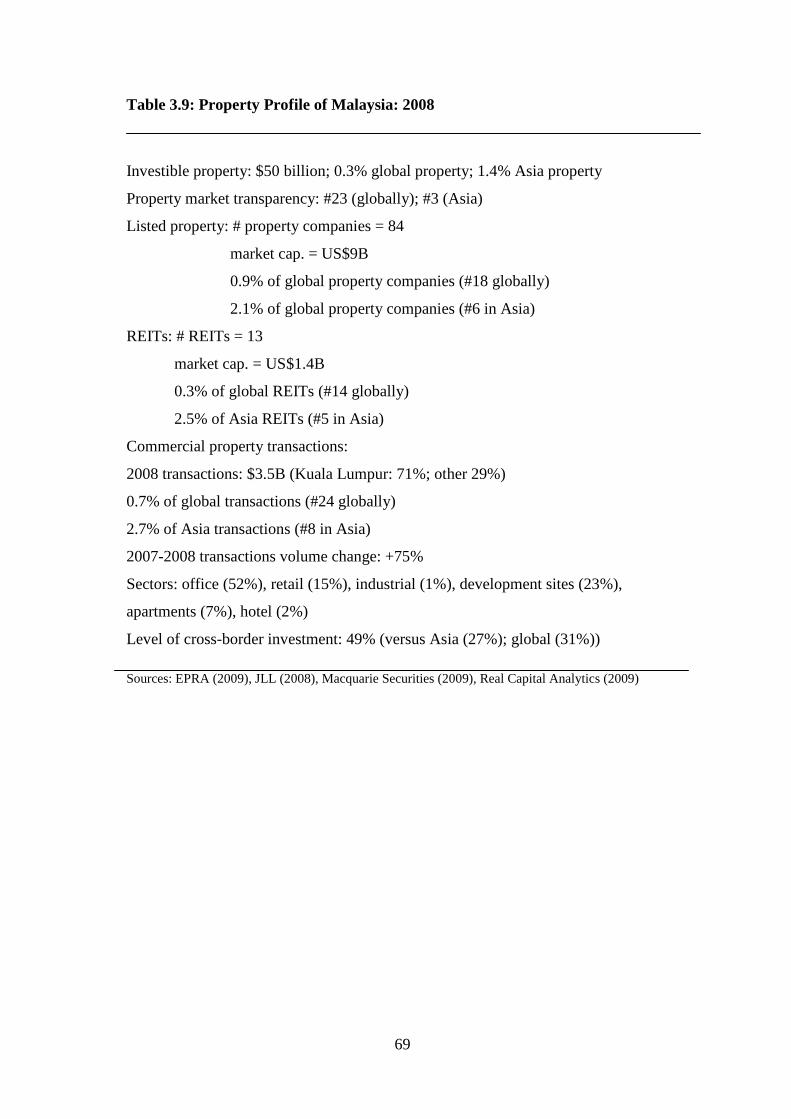

Table 3.9: Property Profile of Malaysia: 2008 69

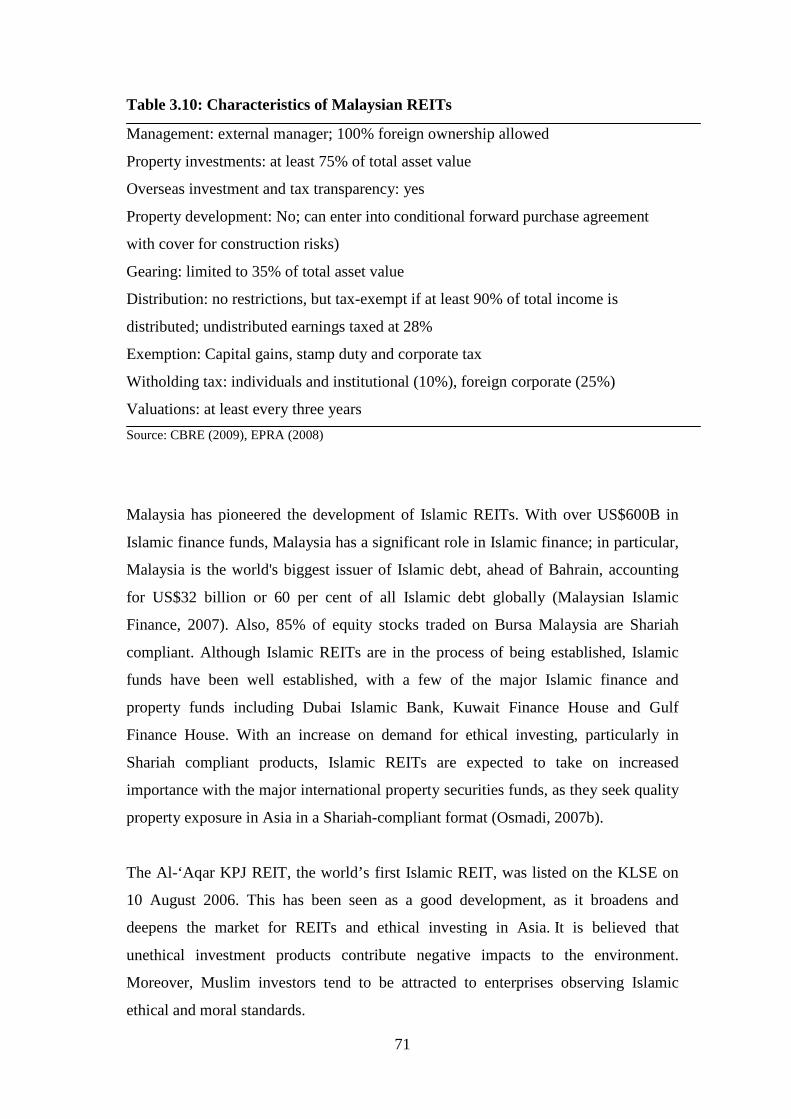

Table 3.10: Characteristics of Malaysian REITs 71

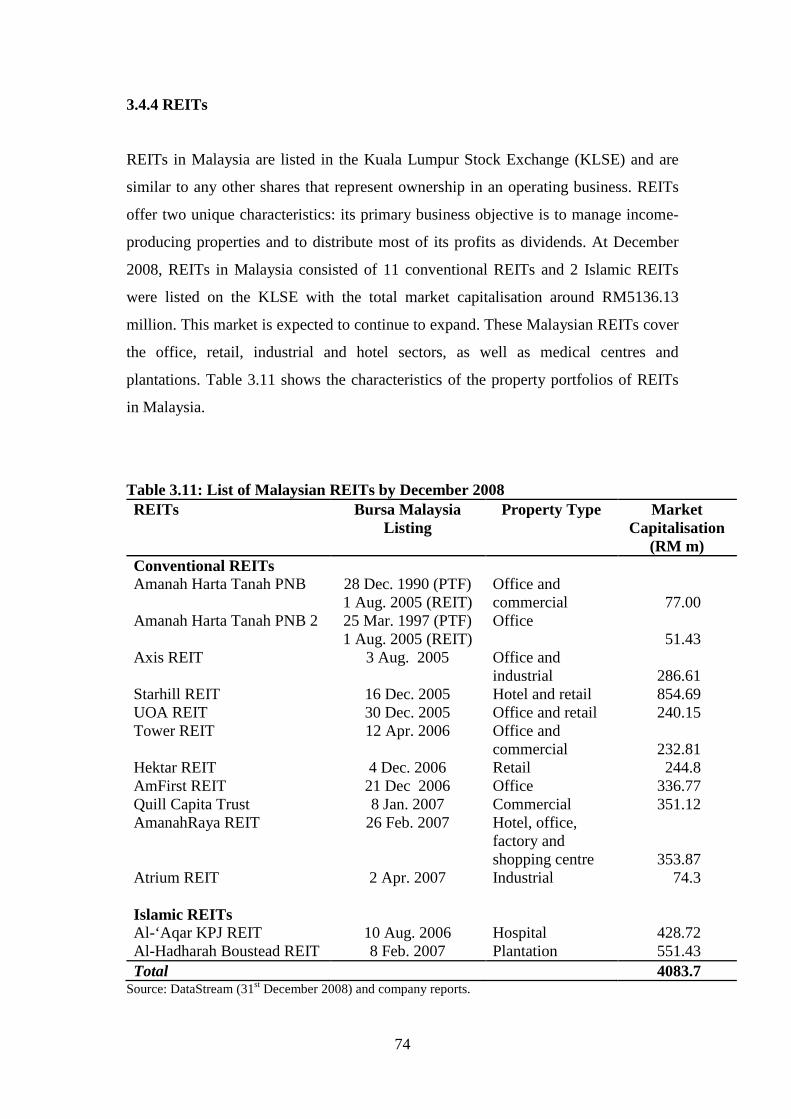

Table 3.11: List of Malaysian REITs by December 2008 74

Table 3.12: Comparison Between PTFs and REITs 75

Table 3.13: Major Islamic Financial Institutions 77

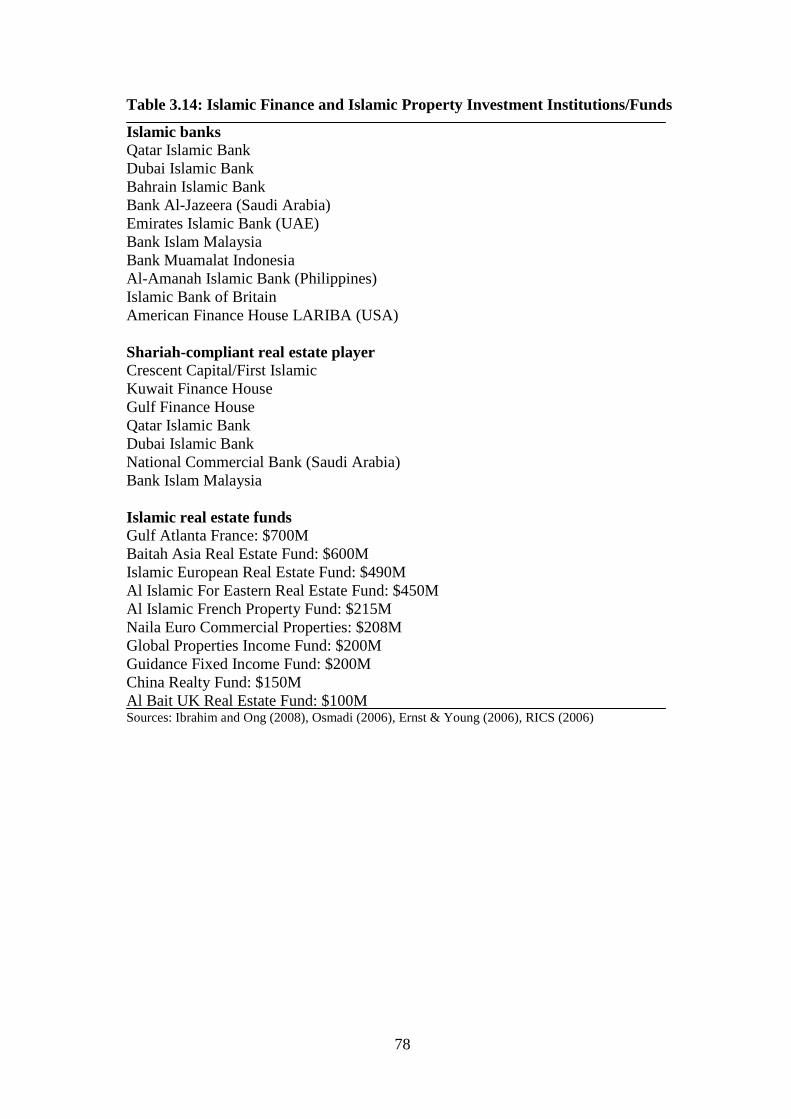

Table 3.14: Islamic Finance and Islamic Property Investment Institutions/Funds 78

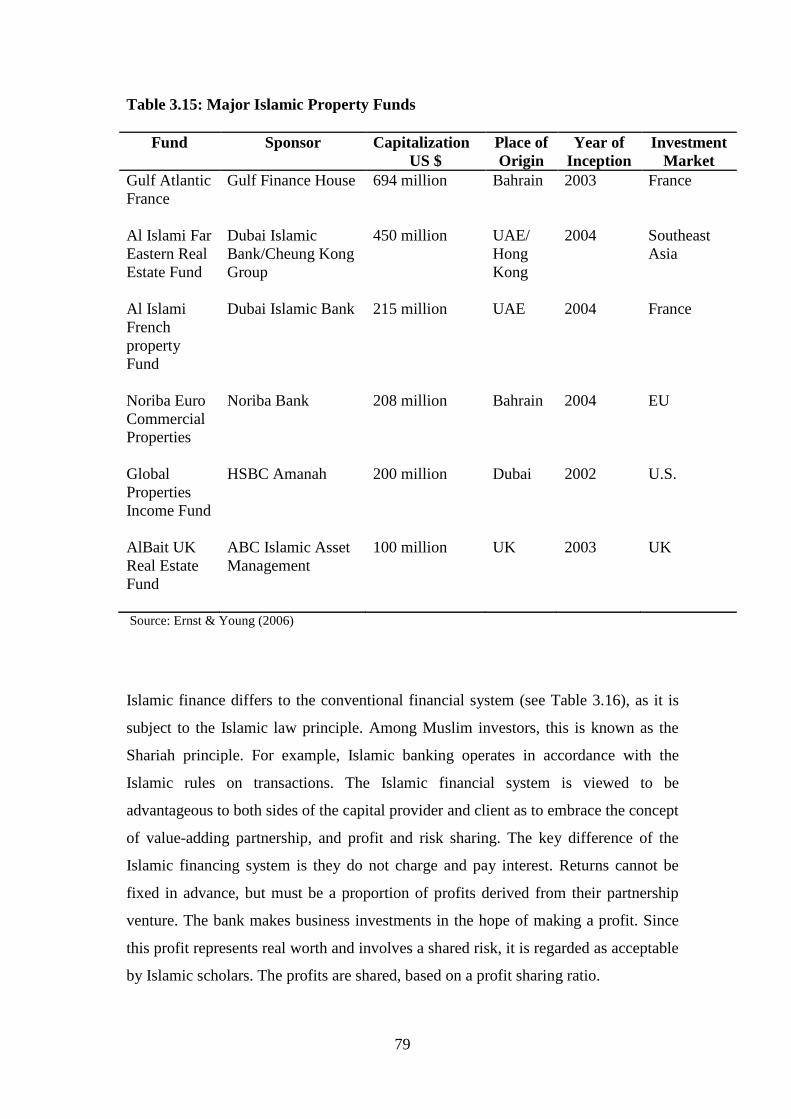

Table 3.15: Major Islamic Property Funds 79

Table 3.16: Comparison Between Islamic and Conventional Financial Systems 80

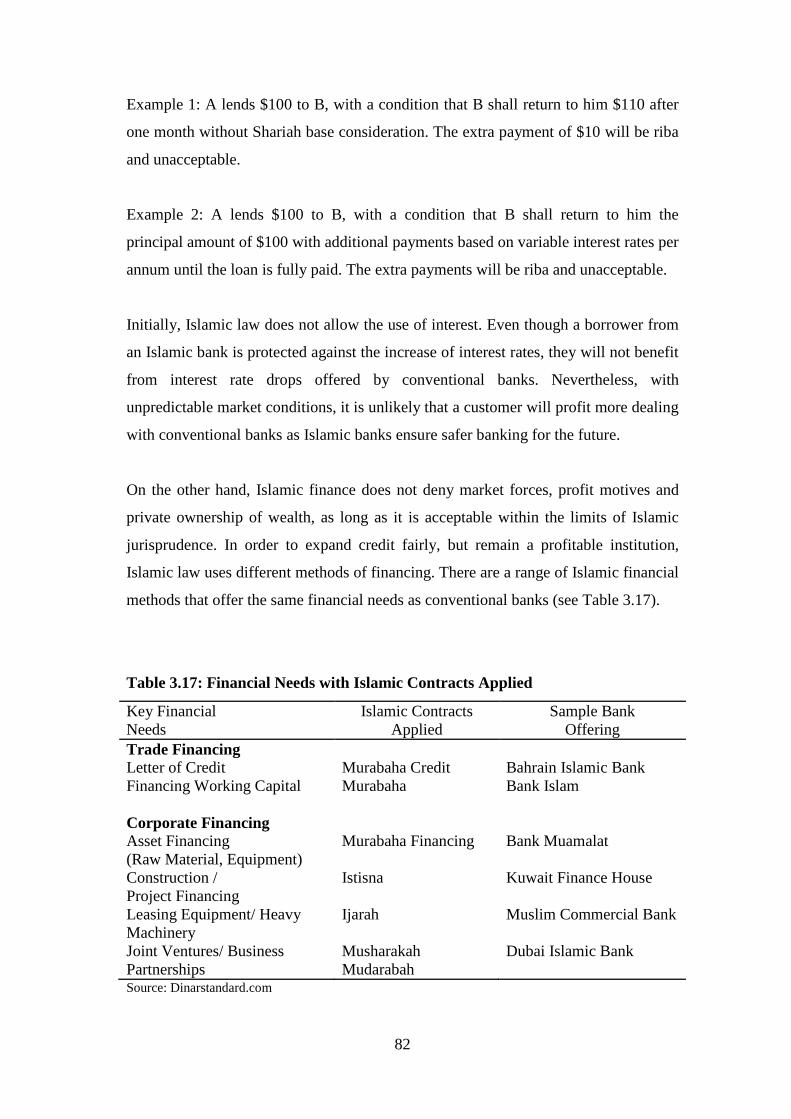

Table 3.17: Financial Needs with Islamic Contracts Applied 82

Table 3.18: Comparison Between Islamic and Conventional REITs 87

Table 4.1: Investment Performance Index Applications 91

Table 4.2: Components of PTF and Various M-REIT Indices 92

Table 5.1: PTFs Performance Since IPO (as of 29 July 2005) 103

Table 5.2: Property Trust Fund (PTF) Performance: Dec. 1989 – July 2005 106

Table 5.3: Property Trust Fund (PTF) Correlation: Dec. 1989 – July 2005 107

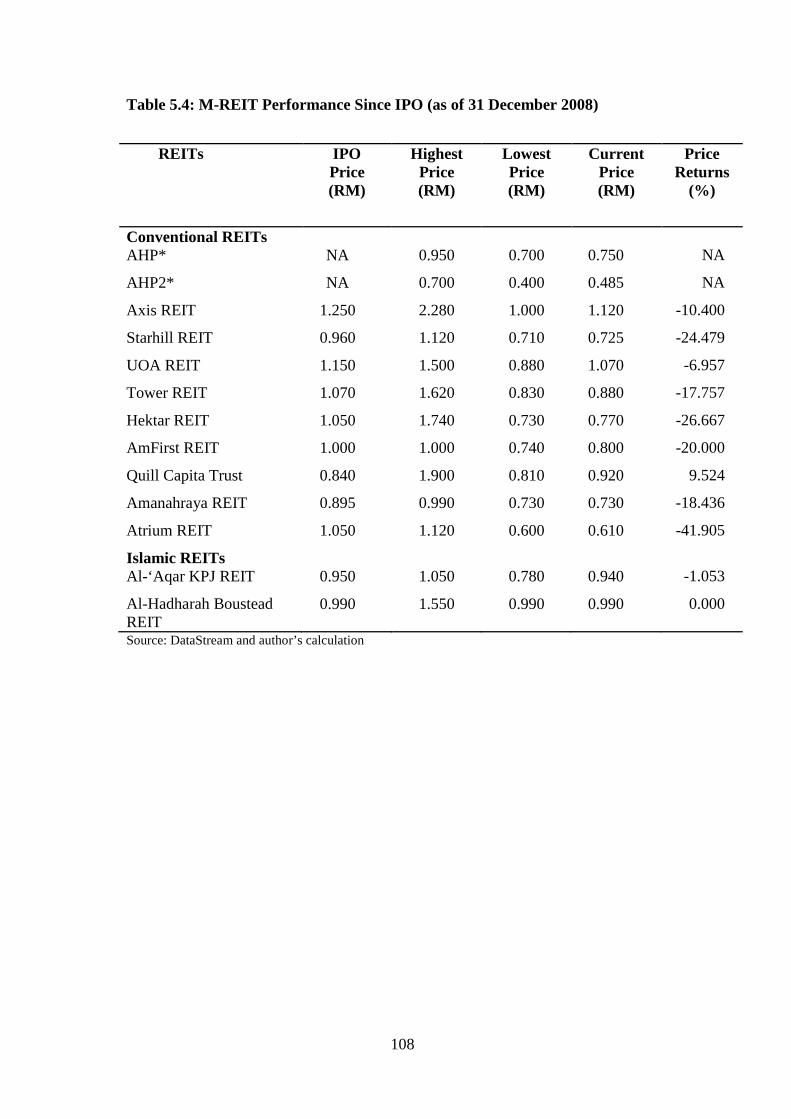

Table 5.4: M-REIT Performance Since IPO (as of 31 December 2008) 108

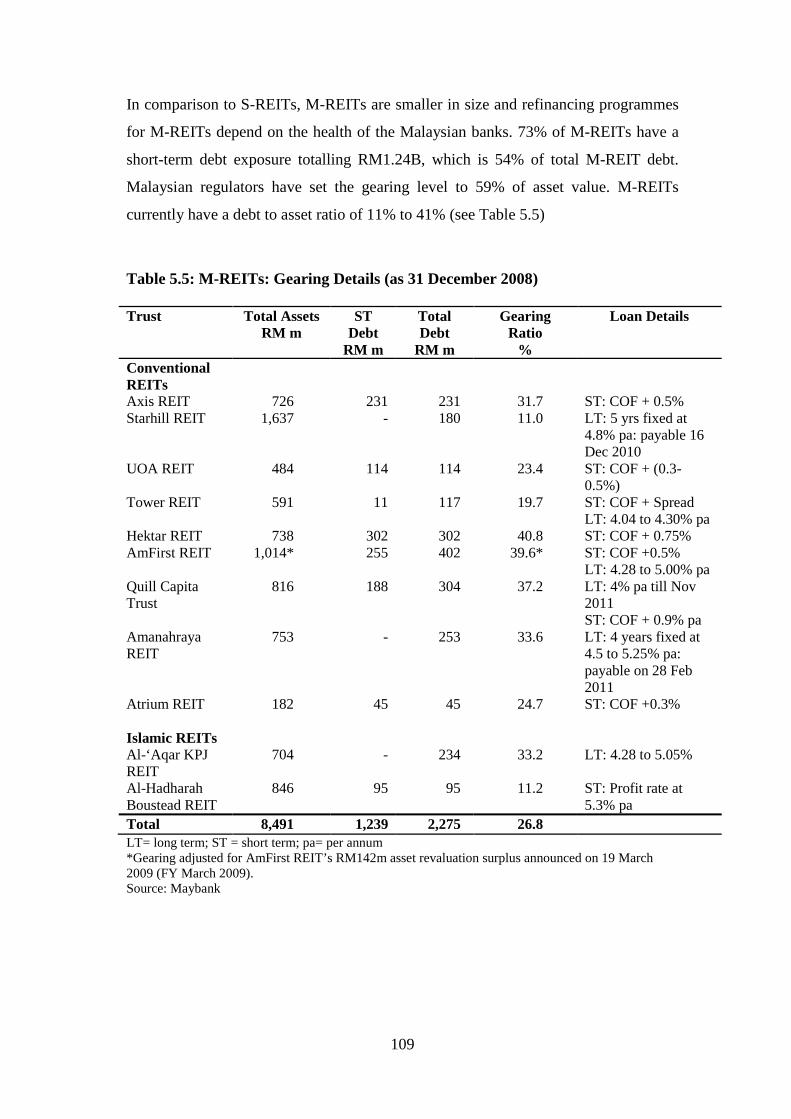

Table 5.5: M-REITs: Gearing Details (as 31 December 2008) 109

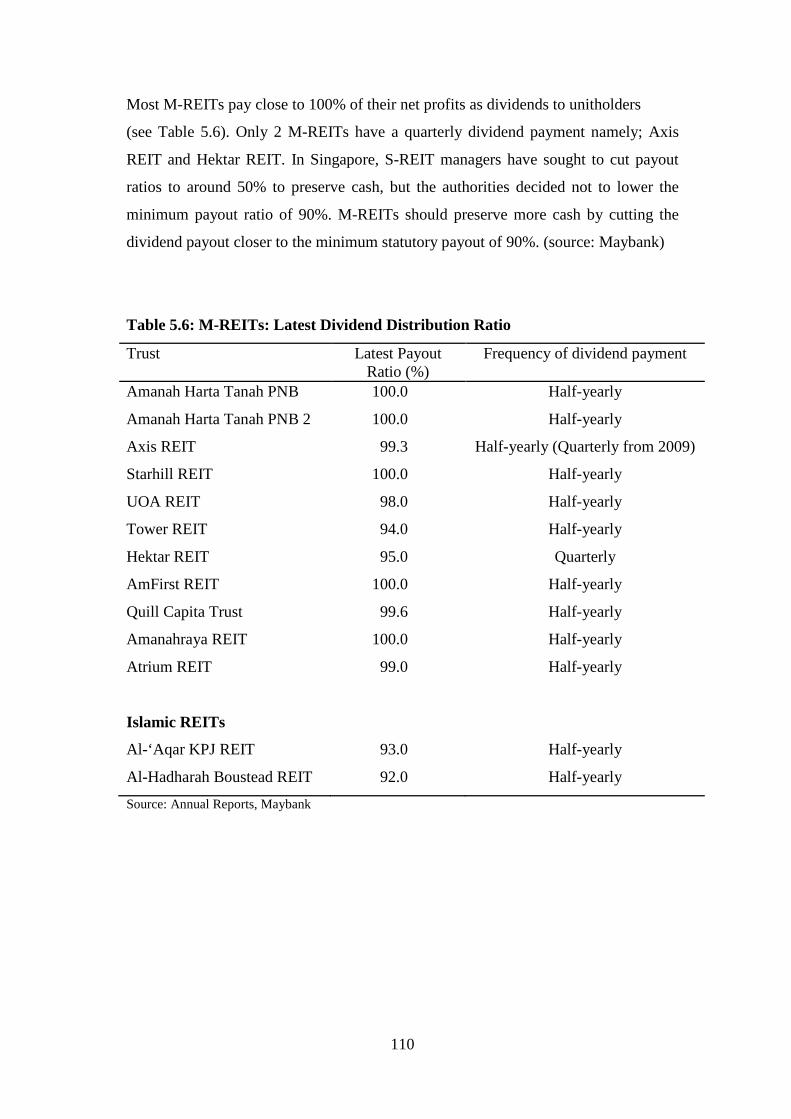

Table 5.6: M-REITs: Latest Dividend Distribution Ratio 110

Table 5.7: Overall M-REIT Risk Adjusted Return Analysis:

8 August 2005 – 29 December 2008 112

Table 5.8: Overall M-REIT Correlation Analysis:

8 August 2005 – 29 December 2008 113

Table 5.9: Conventional M-REIT Risk-Adjusted Return Analysis:

8 August 2005 – 29 December 2008 115

xi

Table 5.10: Conventional M-REIT Correlation Analysis:

8 August 2005 – 29 December 2008 116

Table 5.11: Islamic M-REIT Risk-Adjusted Return Analysis:

21 August 2006 – 29 December 2008 117

Table 5.12: Islamic M-REIT Correlation Analysis:

21 August 2006 – 29 December 2008 118

Table 5.13: Overall M-REIT Pre-Global Financial Crisis Analysis:

8 August 2005 – 27 August 2007 119

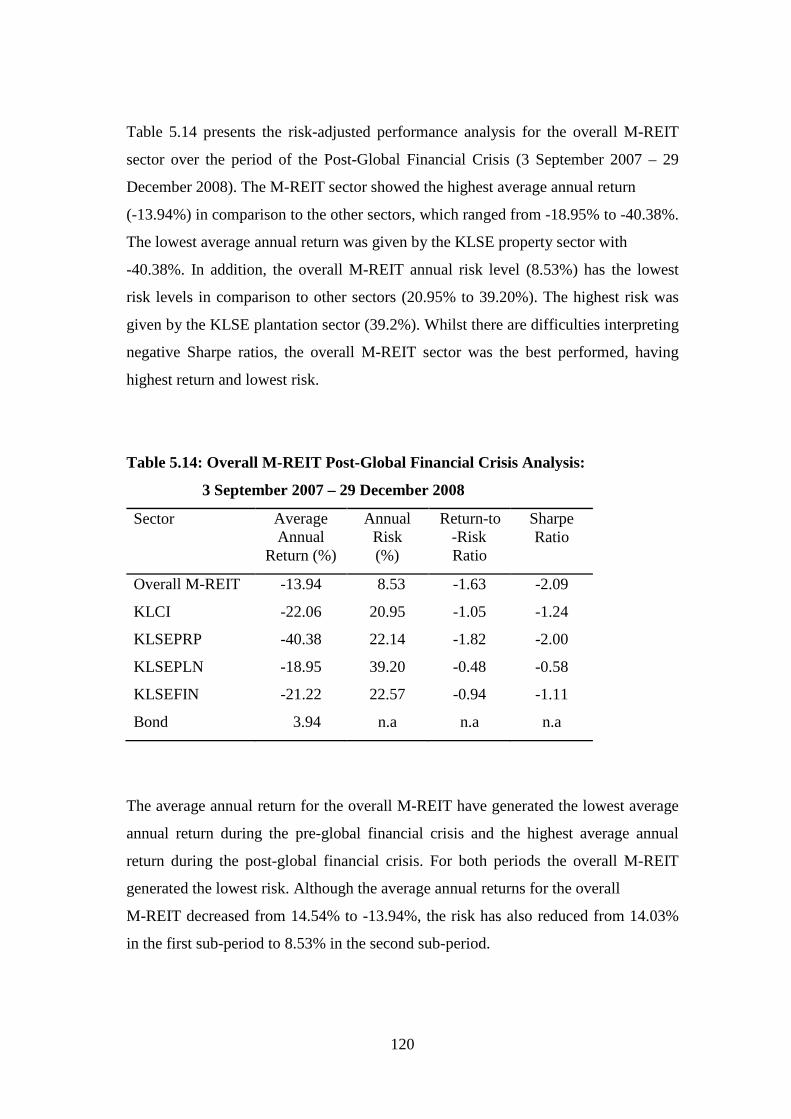

Table 5.14: Overall M-REIT Post-Global Financial Crisis Analysis:

3 September 2007 – 29 December 2008 120

Table 5.15: Overall M-REIT Pre-Global Financial Crisis Analysis:

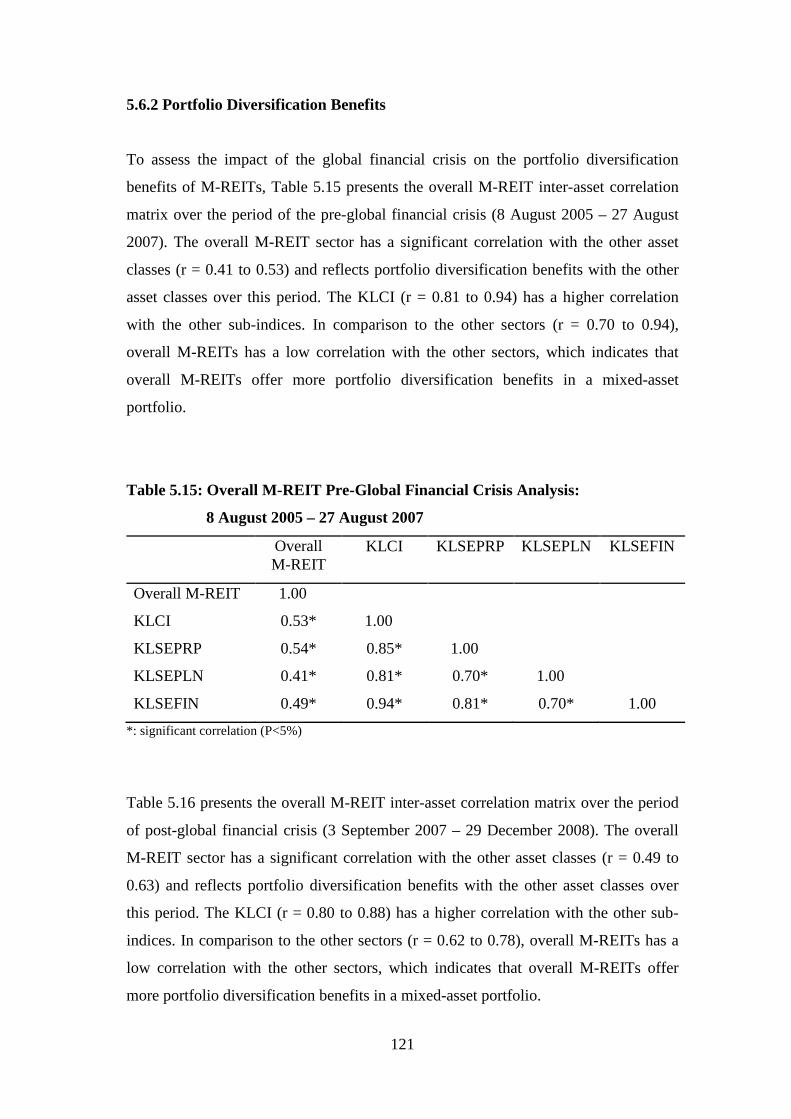

8 August 2005 – 27 August 2007 121

Table 5.16: Overall M-REIT Post-Global Financial Crisis Analysis:

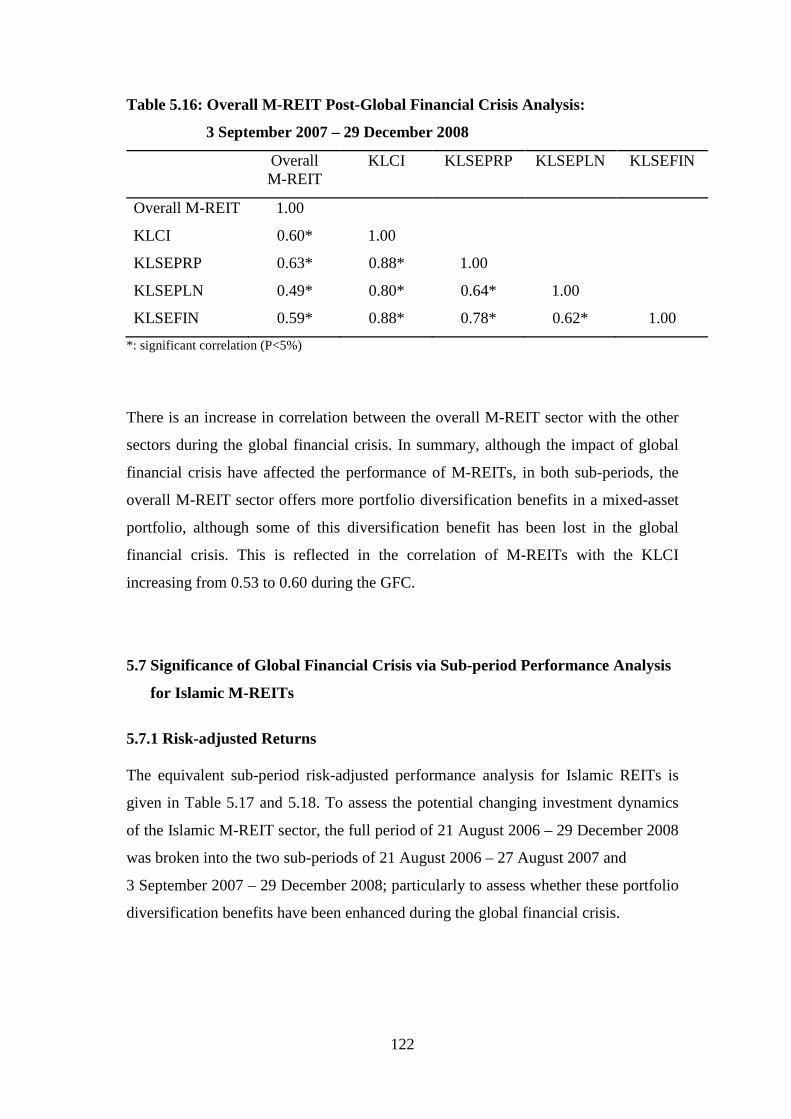

3 September 2007 – 29 December 2008 122

Table 5.17: Islamic M-REIT Pre-Global Financial Crisis Analysis:

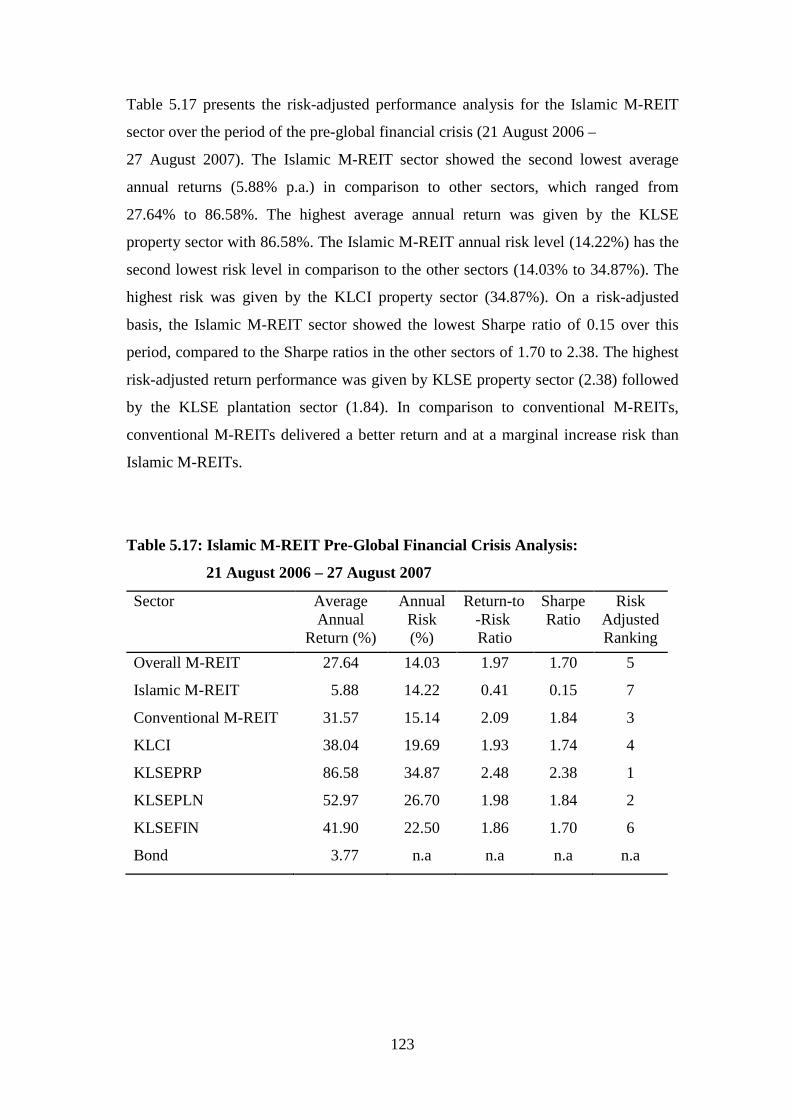

21 August 2006 – 27 August 2007 123

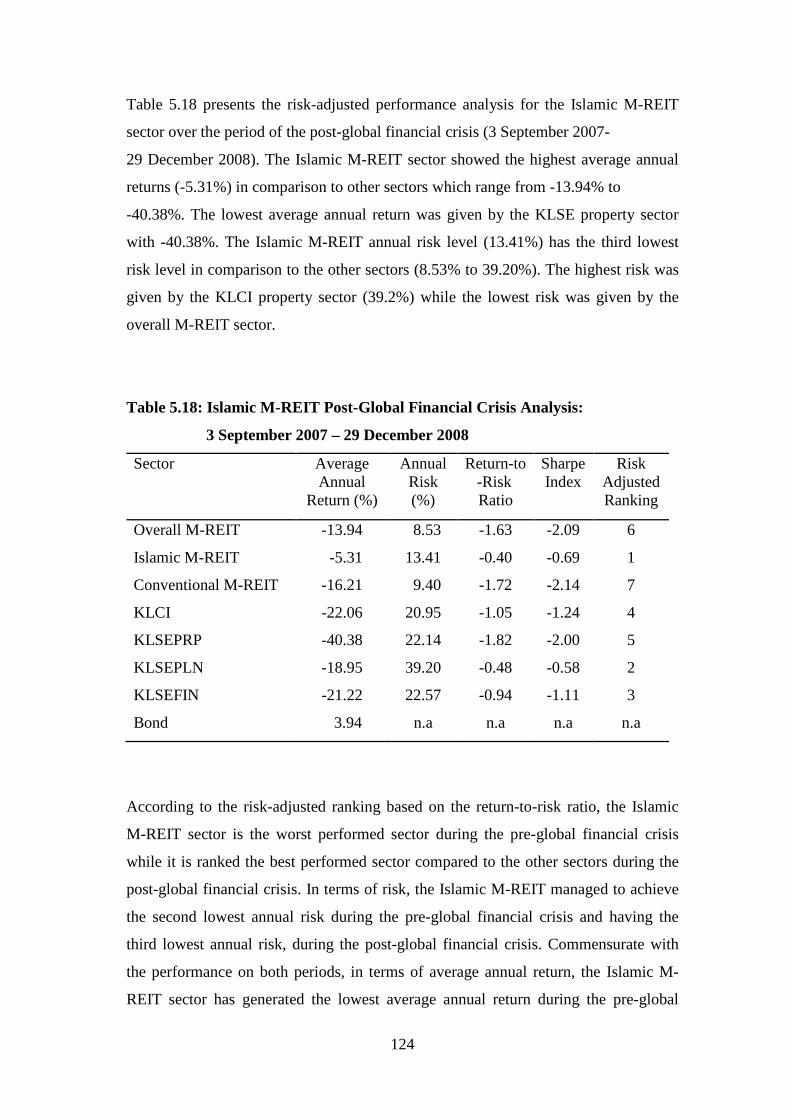

Table 5.18: Islamic M-REIT Post-Global Financial Crisis Analysis:

3 September 2007 – 29 December 2008 124

Table 5.19: Islamic M-REIT Pre-Global Financial Crisis Analysis:

21 August 2006 – 27 August 2007 126

Table 5.20: Islamic M-REIT Post-Global Financial Crisis Analysis: 3 September

2007 – 29 December 2008 127

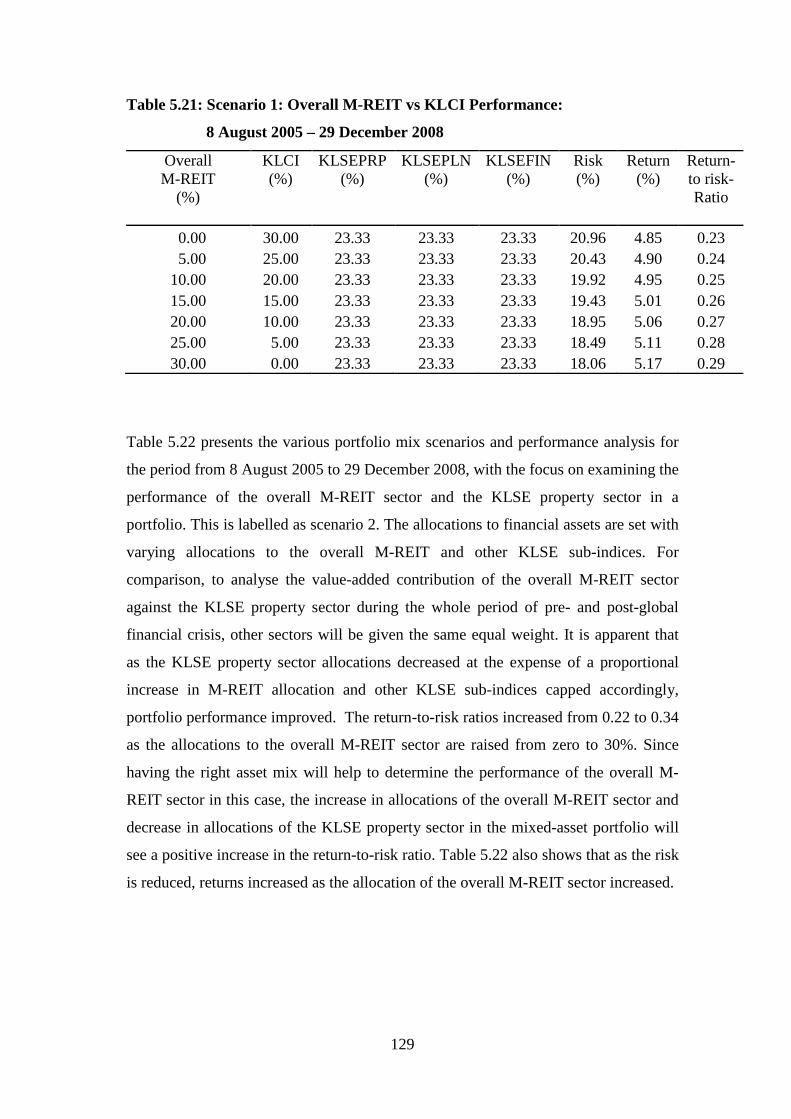

Table 5.21: Scenario 1: Overall M-REIT vs KLCI Performance:

8 August 2005 – 29 December 2008 129

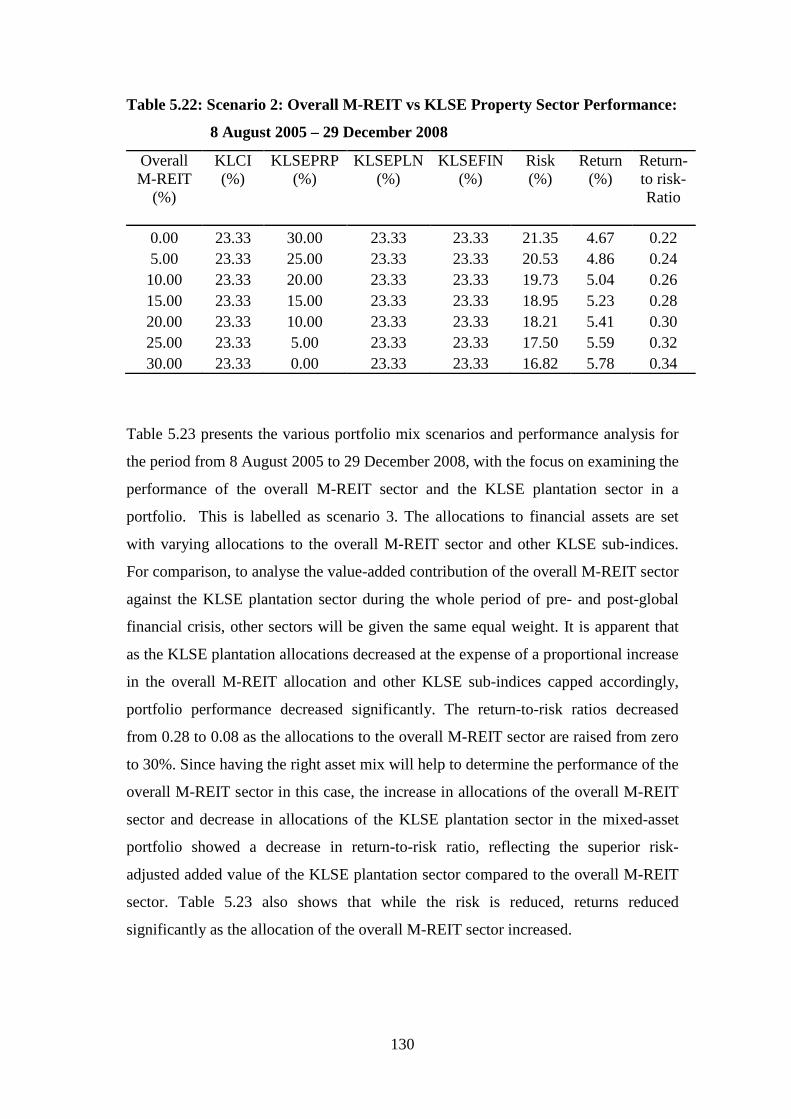

Table 5.22: Scenario 2: Overall M-REIT vs KLSE Property Sector Performance:

8 August 2005 – 29 December 2008 130

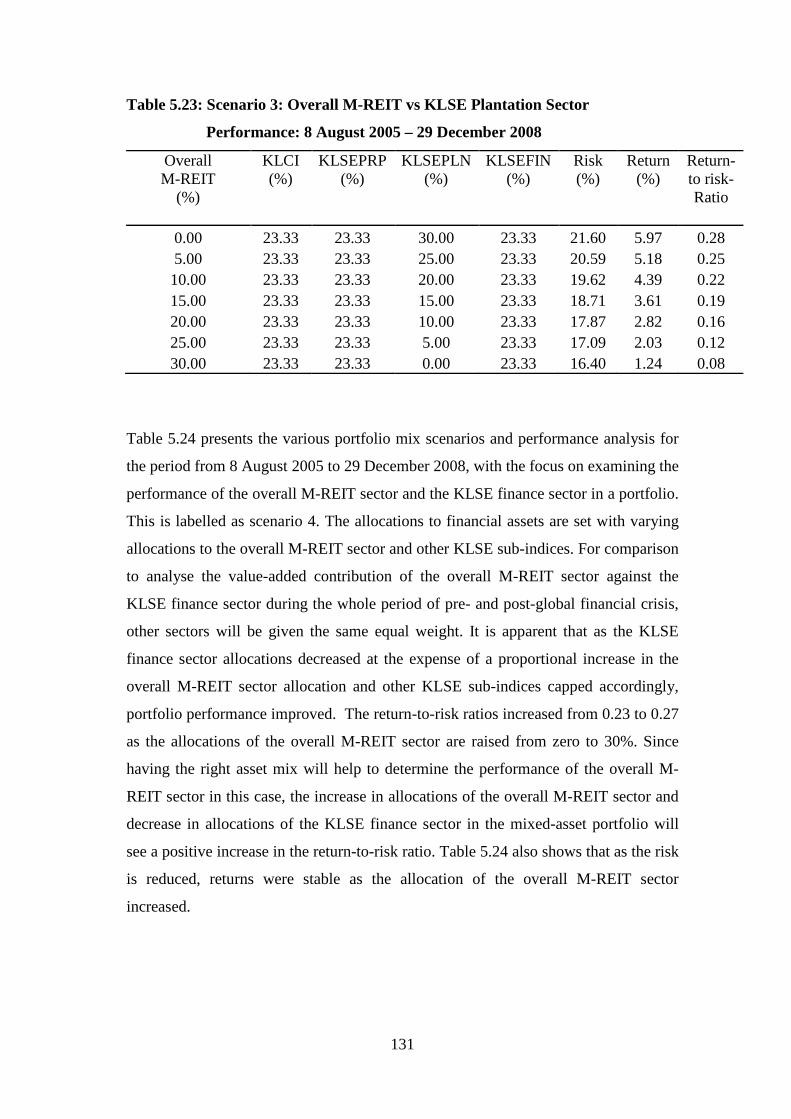

Table 5.23: Scenario 3: Overall M-REIT vs KLSE Plantation Sector

Performance: 8 August 2005 – 29 December 2008 131

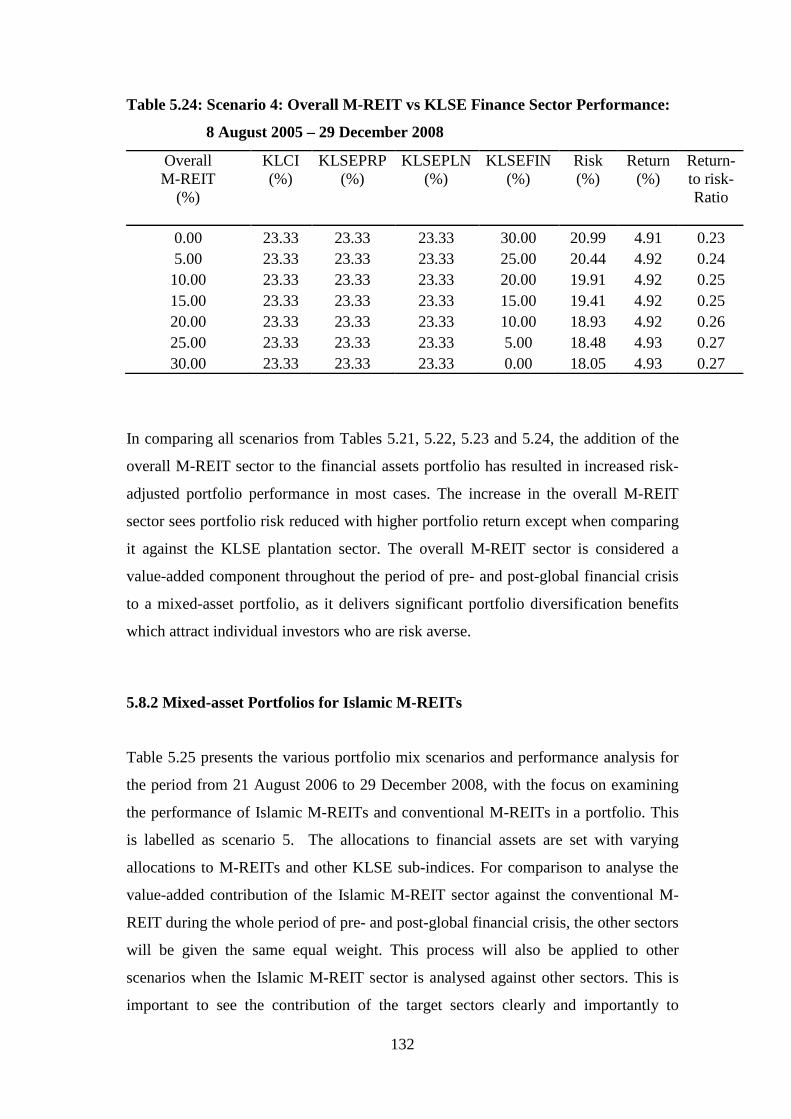

Table 5.24: Scenario 4: Overall M-REIT vs KLSE Finance Sector Performance:

8 August 2005 – 29 December 2008 132

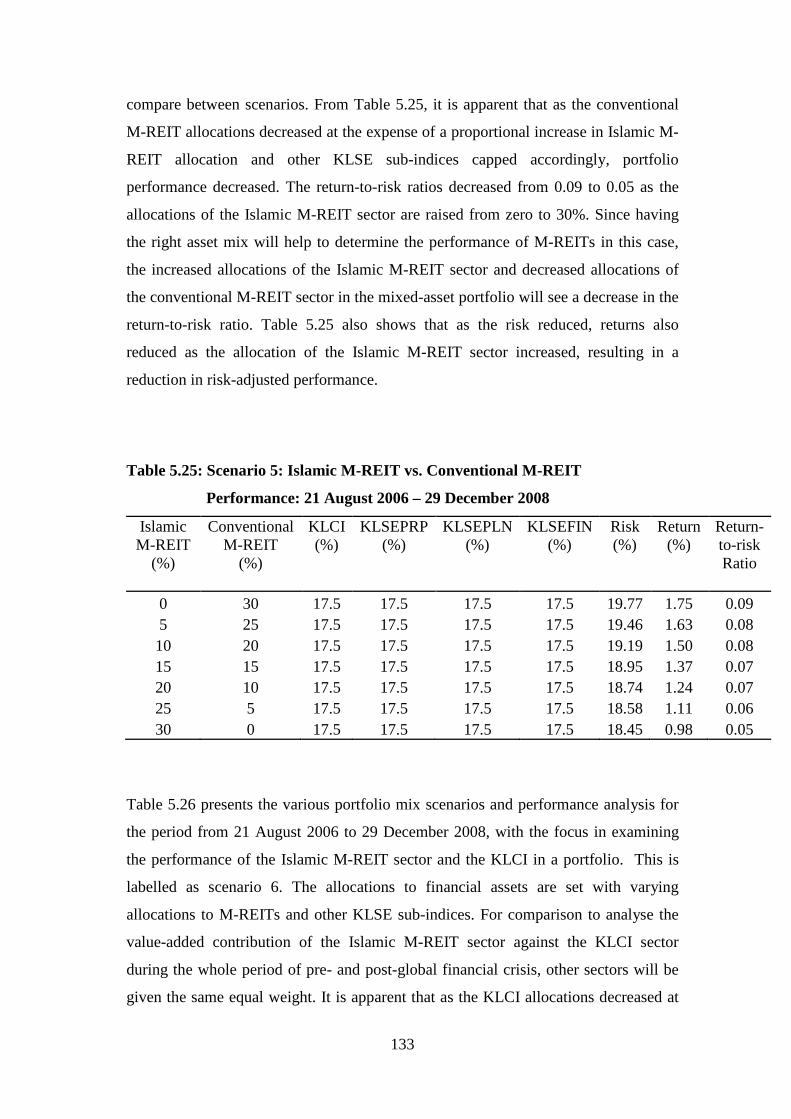

Table 5.25: Scenario 5: Islamic M-REIT vs. Conventional M-REIT

Performance: 21 August 2006 – 29 December 2008 133

xii

Table 5.26: Scenario 6: Islamic M-REIT vs KLCI Performance:

21 August 2006 – 29 December 2008 134

Table 5.27: Scenario 7: Islamic M-REIT vs KLSE Property Sector Performance:

21 August 2006 – 29 December 2008 135

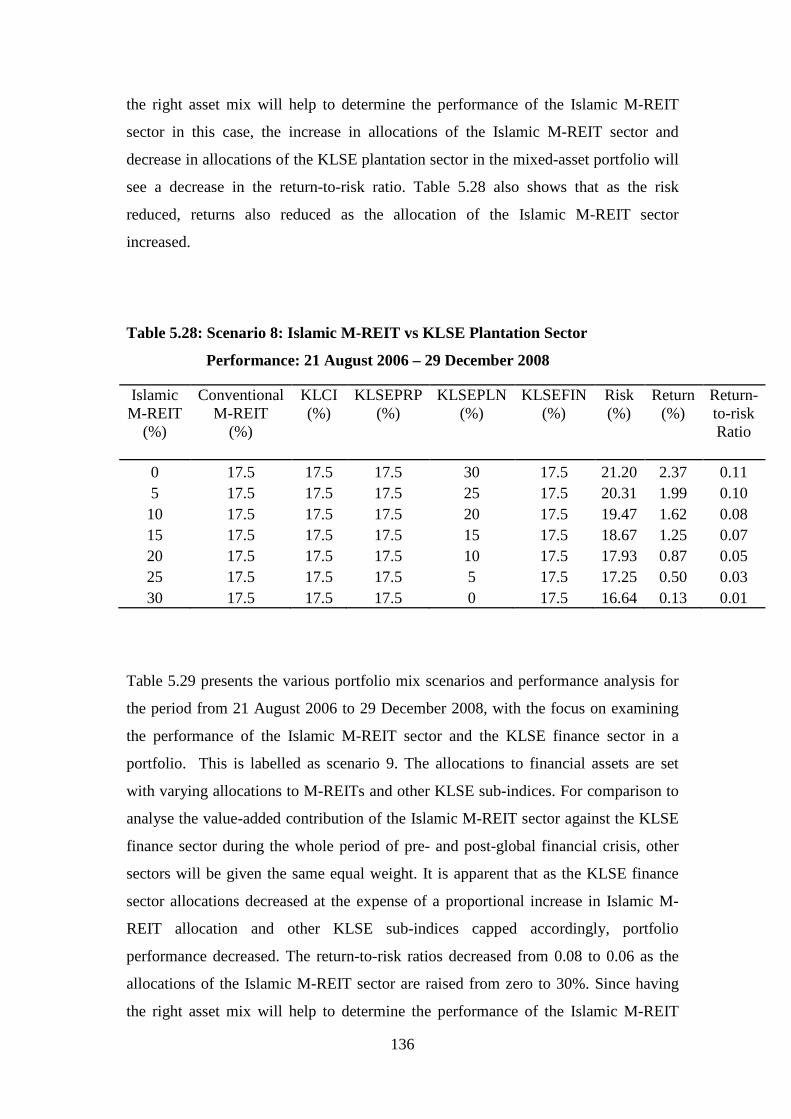

Table 5.28: Scenario 8: Islamic M-REIT vs KLSE Plantation Sector

Performance: 21 August 2006 – 29 December 2008 136

Table 5.29: Scenario 9: Islamic M-REIT vs KLSE Finance Sector Performance:

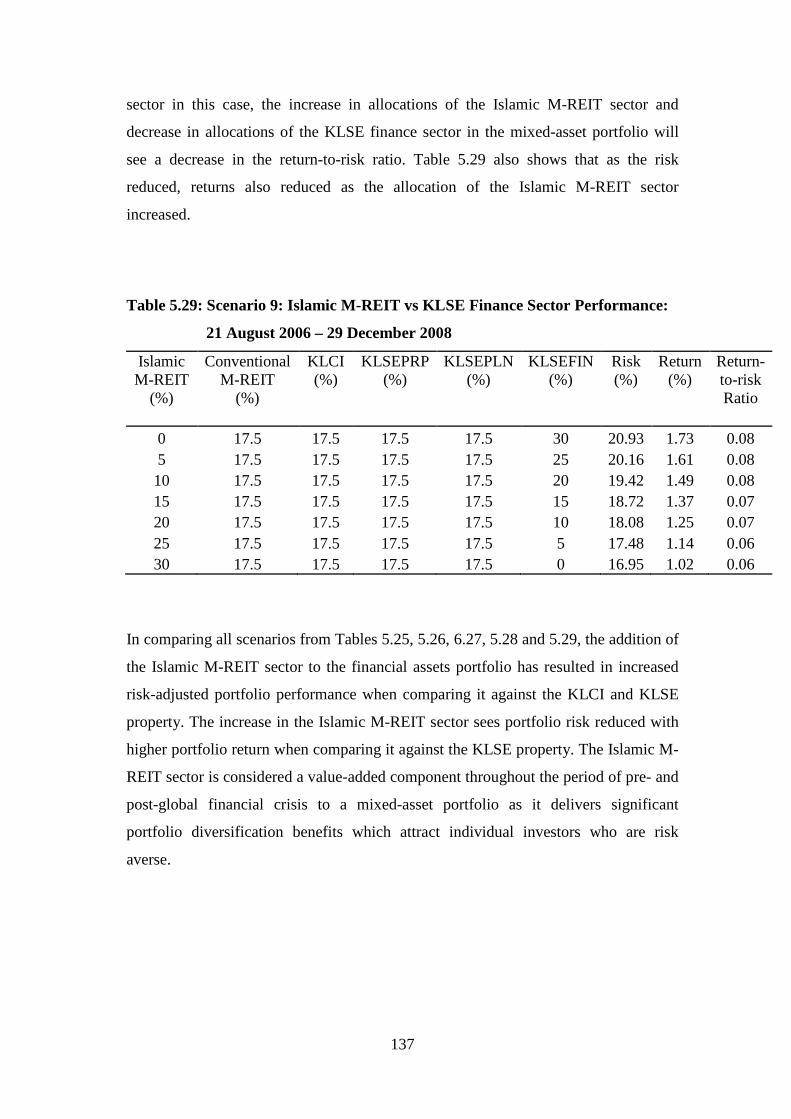

21 August 2006 – 29 December 2008 137

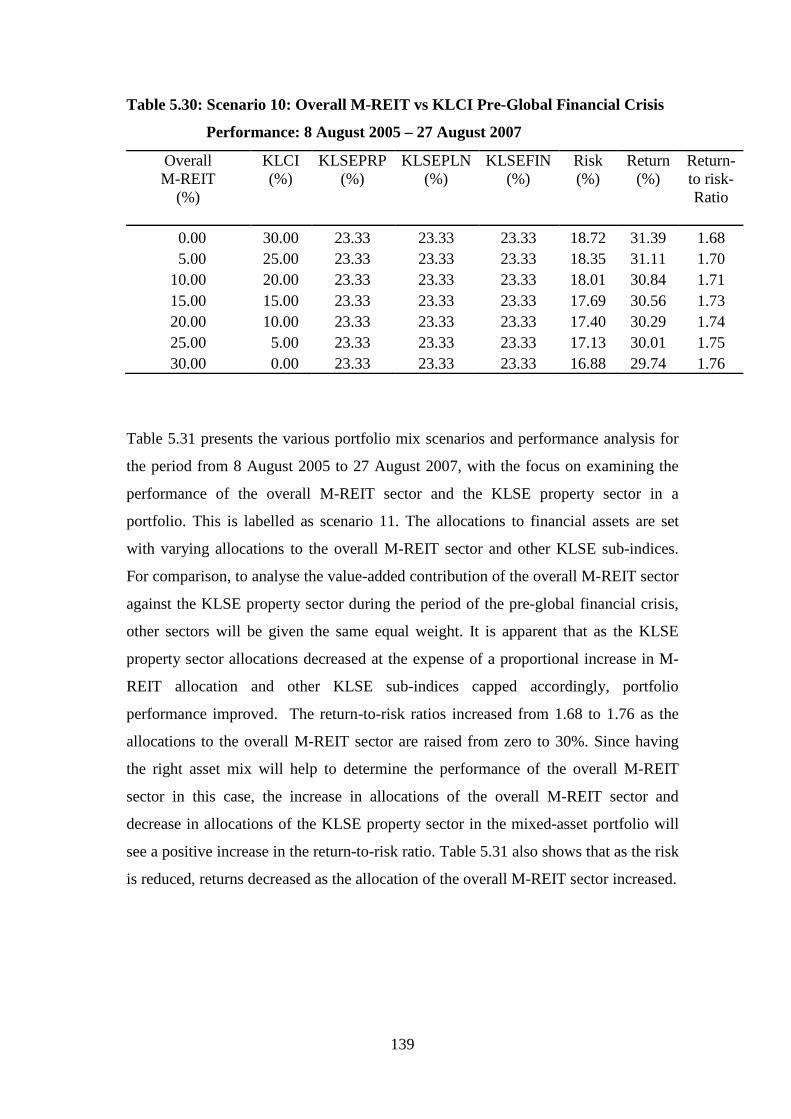

Table 5.30: Scenario 10: Overall M-REIT vs KLCI Pre-Global Financial Crisis

Performance: 8 August 2005 – 27 August 2007 139

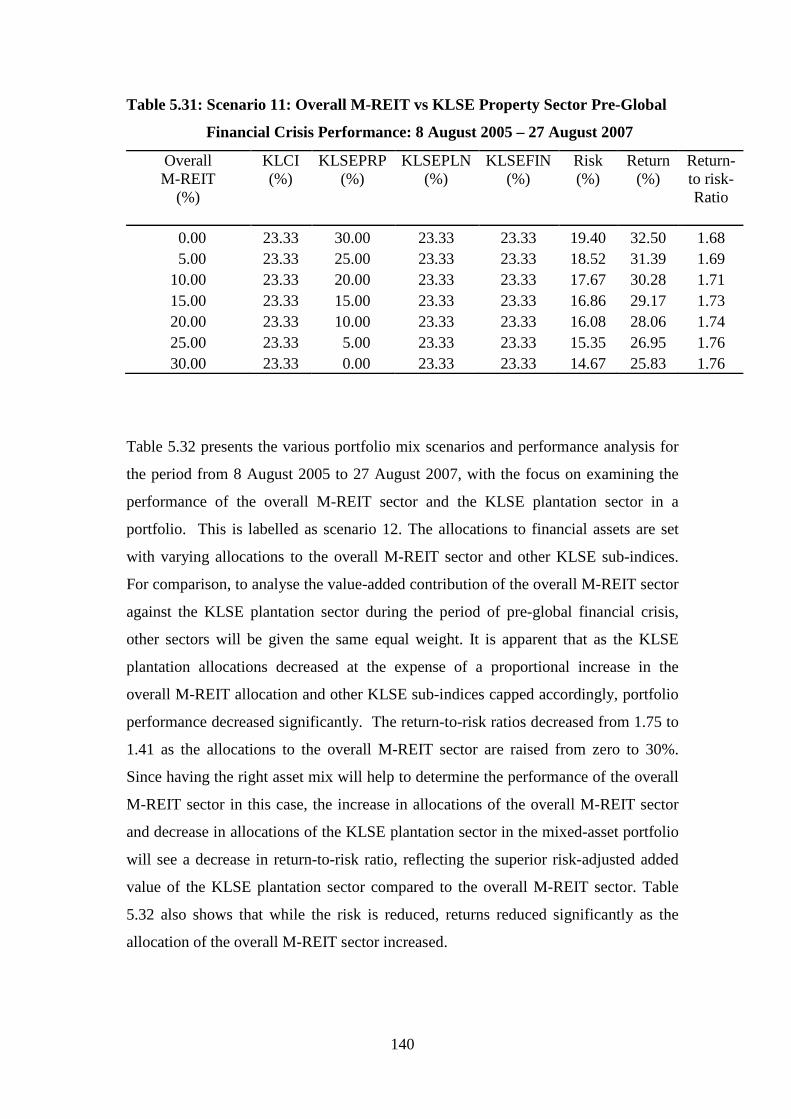

Table 5.31: Scenario 11: Overall M-REIT vs KLSE Property Sector Pre-Global

Financial Crisis Performance: 8 August 2005 – 27 August 2007 140

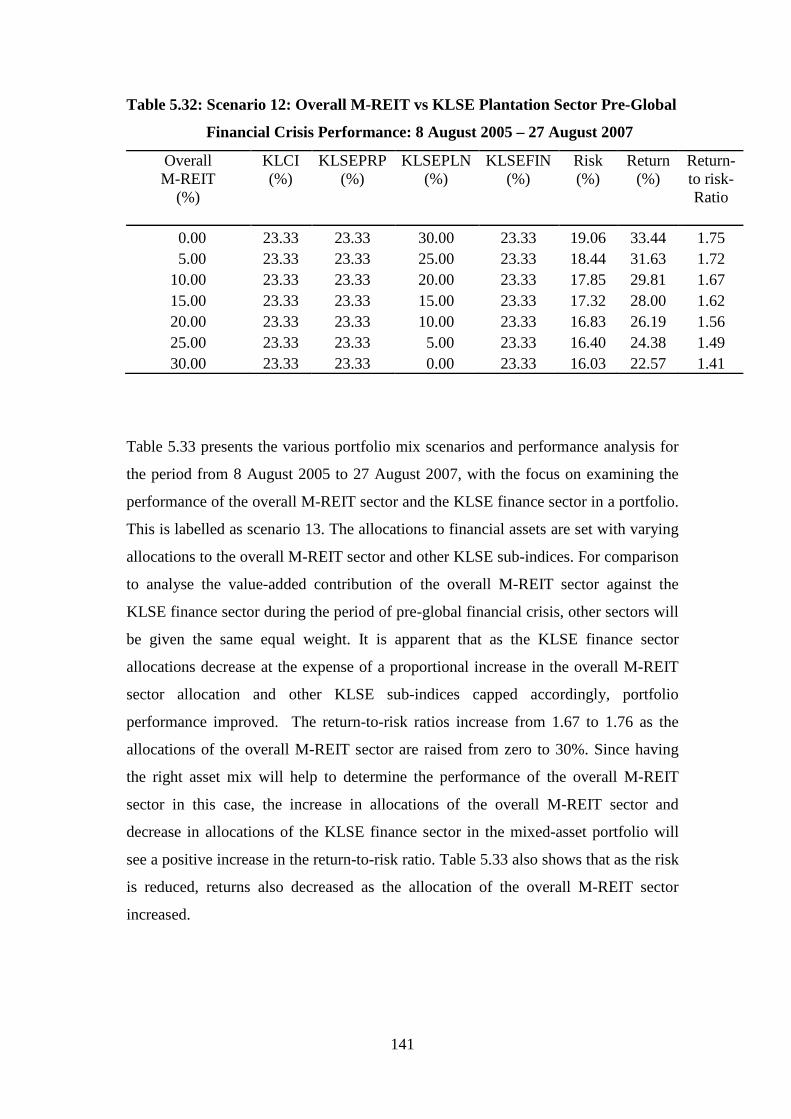

Table 5.32: Scenario 12: Overall M-REIT vs KLSE Plantation Sector Pre-

Global Financial Crisis Performance: 8 August 2005 –

27 August 2007 141

Table 5.33: Scenario 13: Overall M-REIT vs KLSE Finance Sector Pre-Global

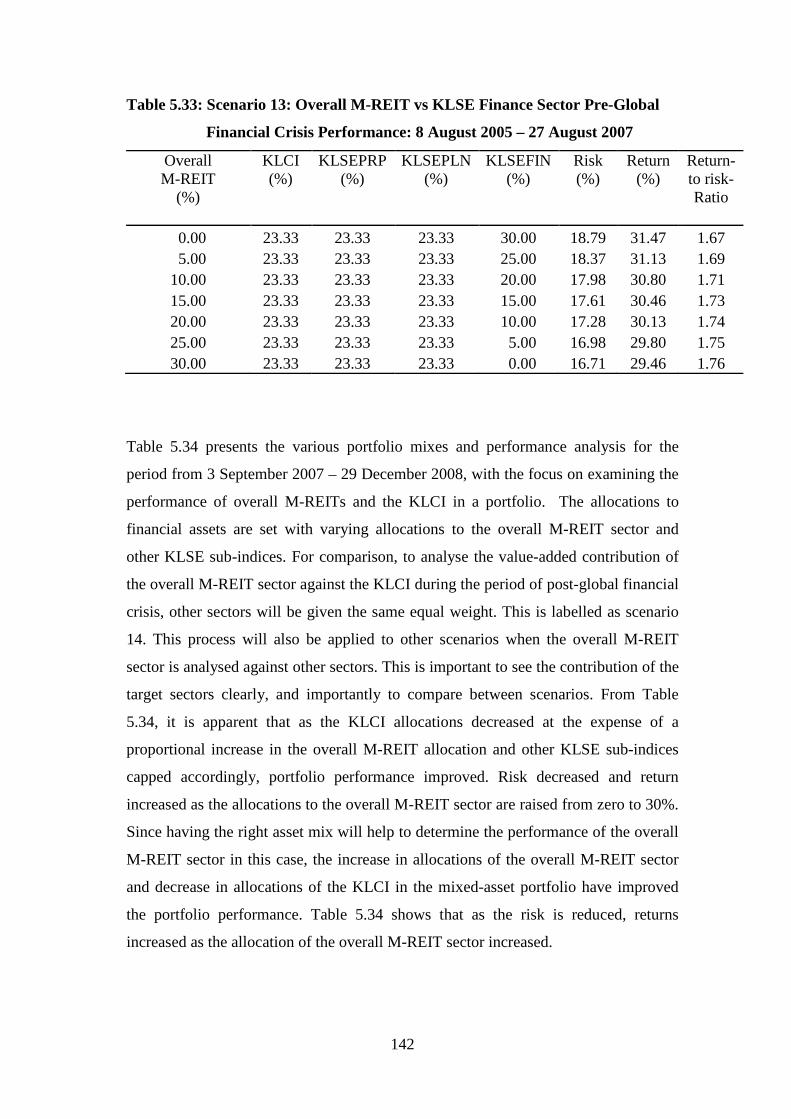

Financial Crisis Performance: 8 August 2005 – 27 August 2007 142

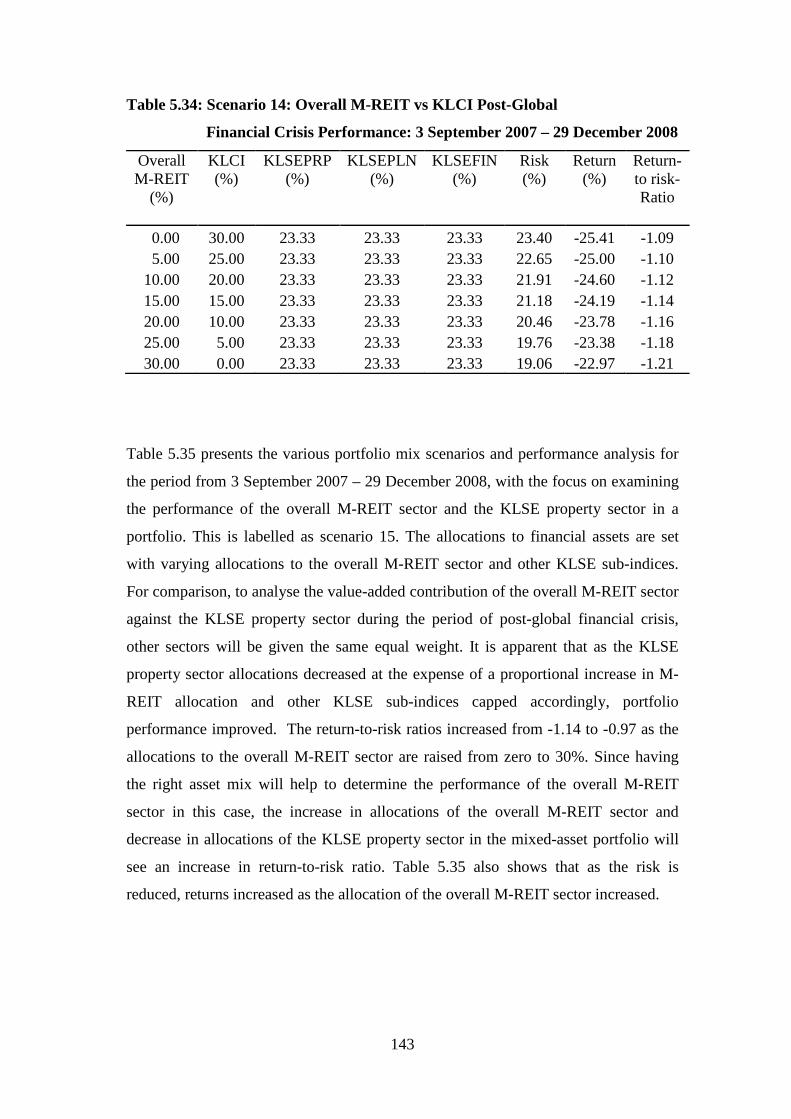

Table 5.34: Scenario 14: Overall M-REIT vs KLCI Post-Global

Financial Crisis Performance: 3 September 2007 – 29 Dec. 2008 143

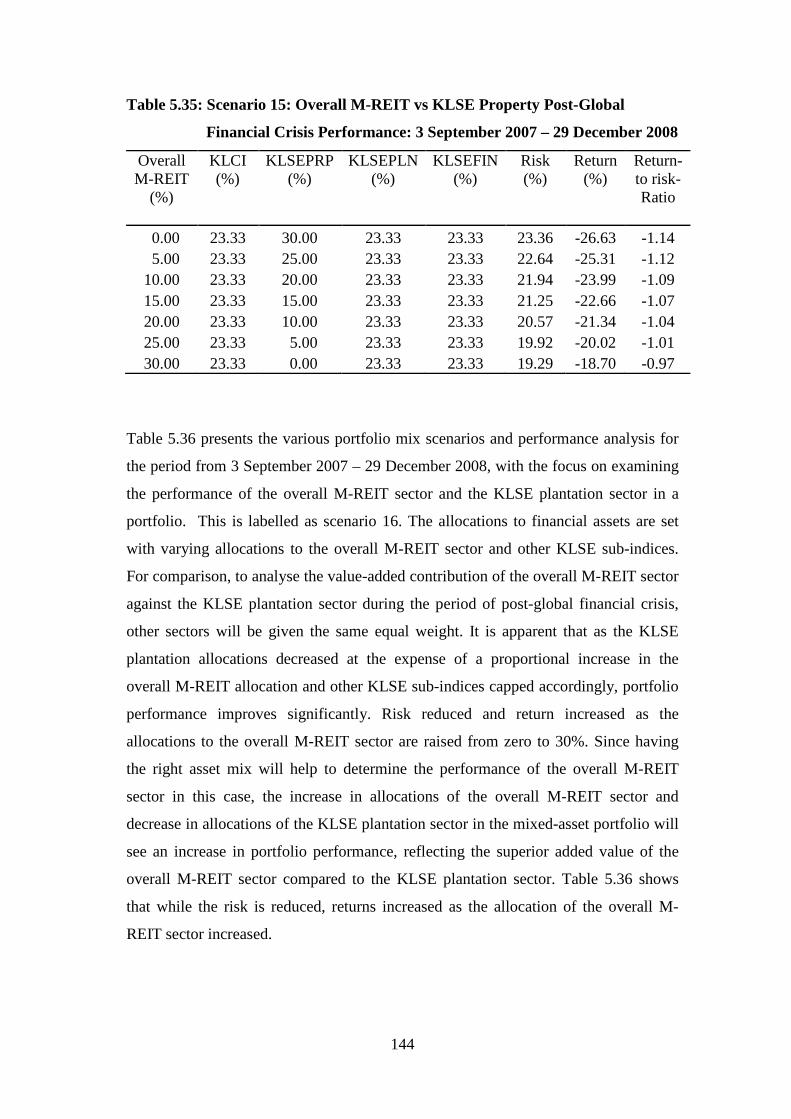

Table 5.35: Scenario 15: Overall M-REIT vs KLSE Property Post-Global

Financial Crisis Performance: 3 September 2007 – 29 Dec. 2008 144

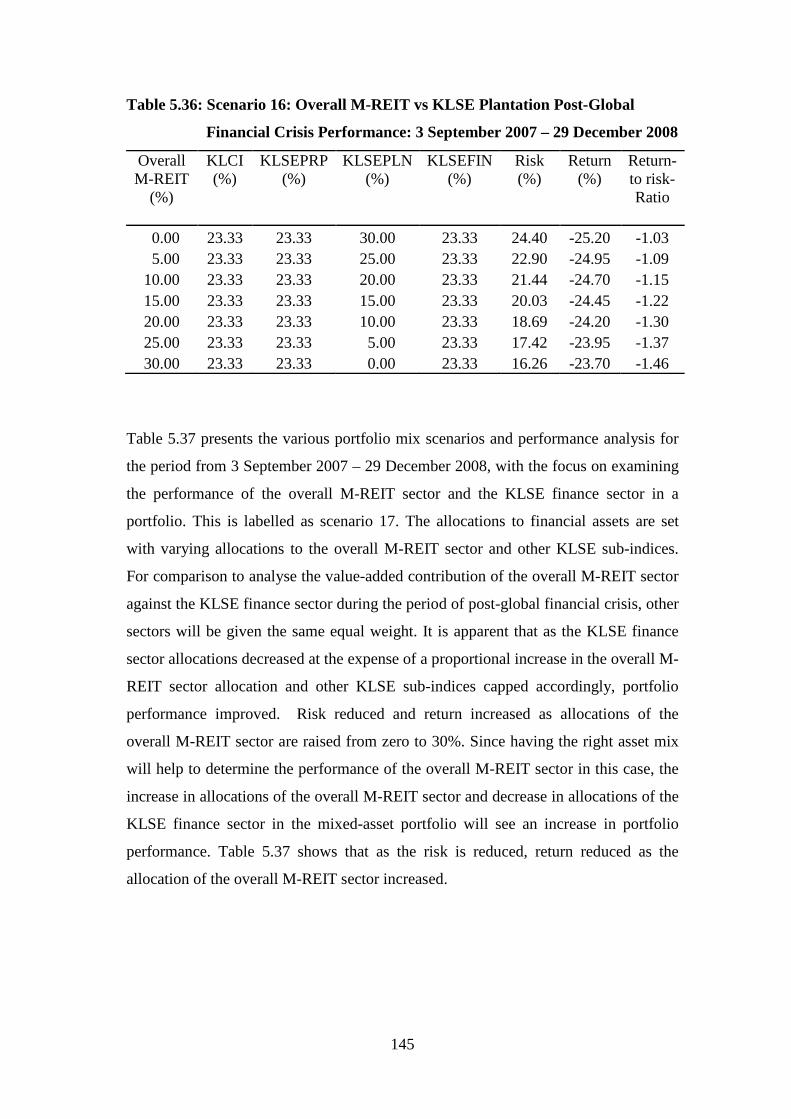

Table 5.36: Scenario 16: Overall M-REIT vs KLSE Plantation Post-Global

Financial Crisis Performance: 3 September 2007 – 29 Dec. 2008 145

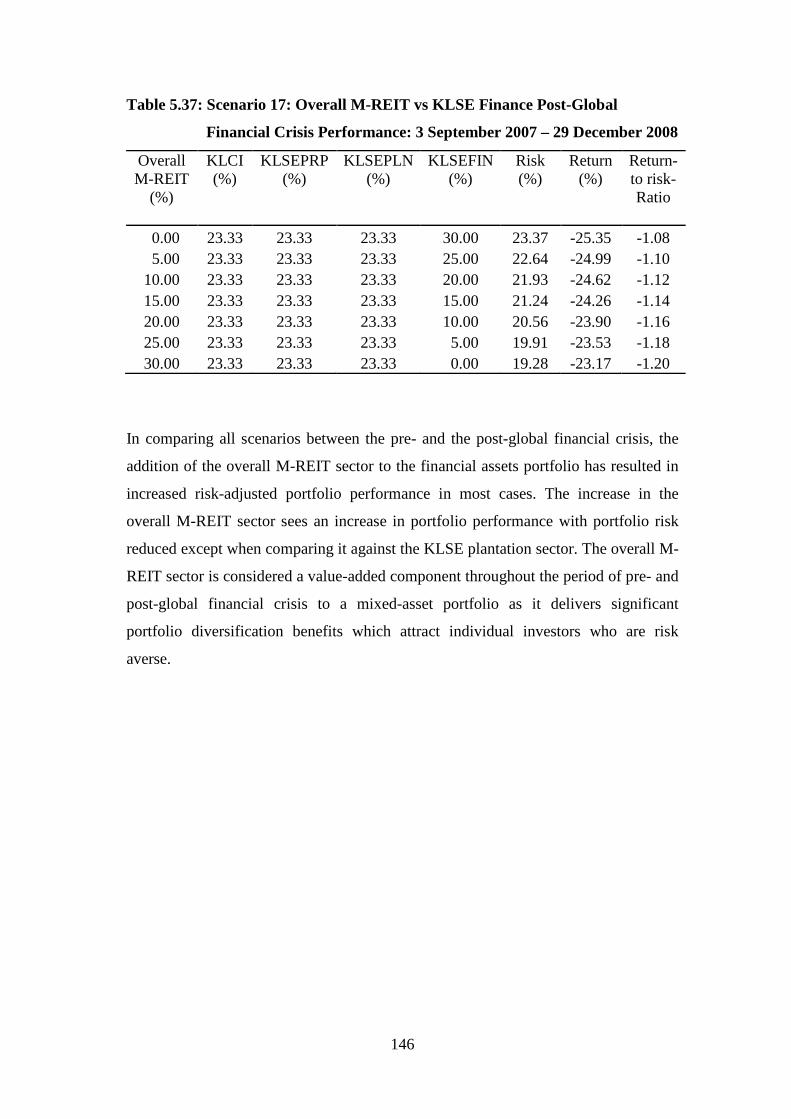

Table 5.37: Scenario 17: Overall M-REIT vs KLSE Finance Post-Global

Financial Crisis Performance: 3 September 2007 – 29 Dec. 2008 146

Table 5.38: Scenario 18: Islamic M-REIT vs Conventional M-REIT Pre-Global

Financial Crisis Performance: 21 August 2006 – 27 August 2007 148

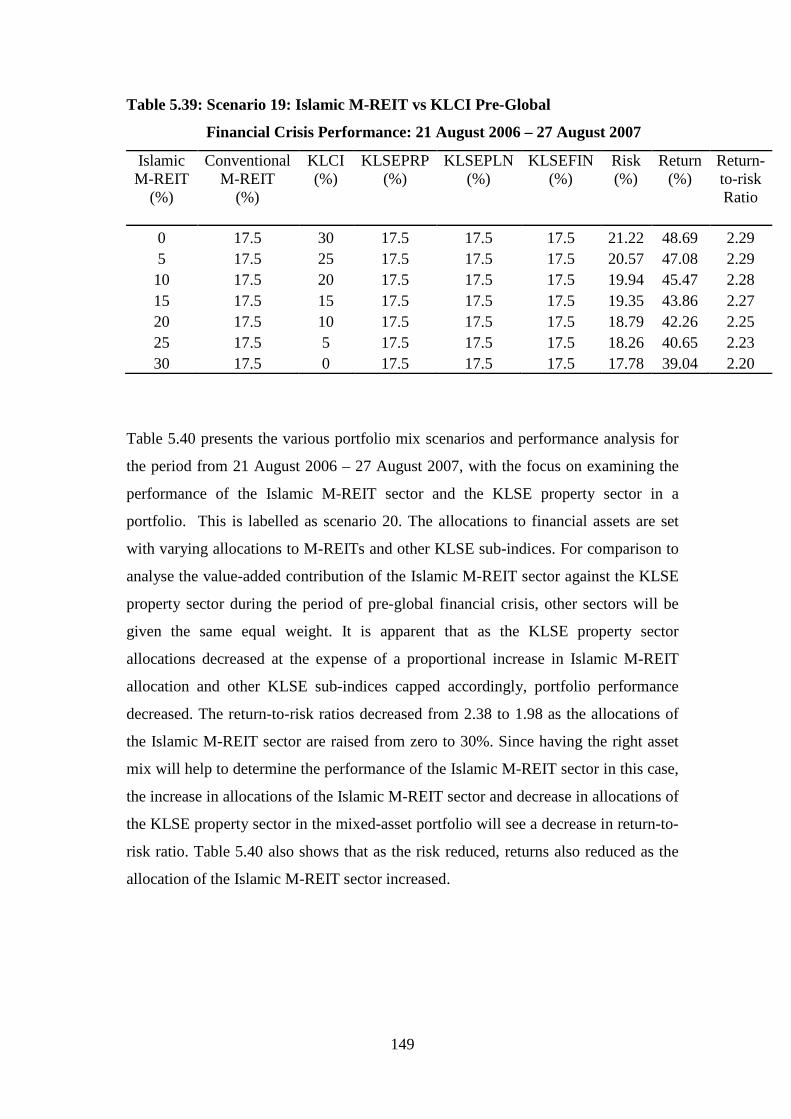

Table 5.39: Scenario 19: Islamic M-REIT vs KLCI Pre-Global

Financial Crisis Performance: 21 August 2006 – 27 August 2007 149

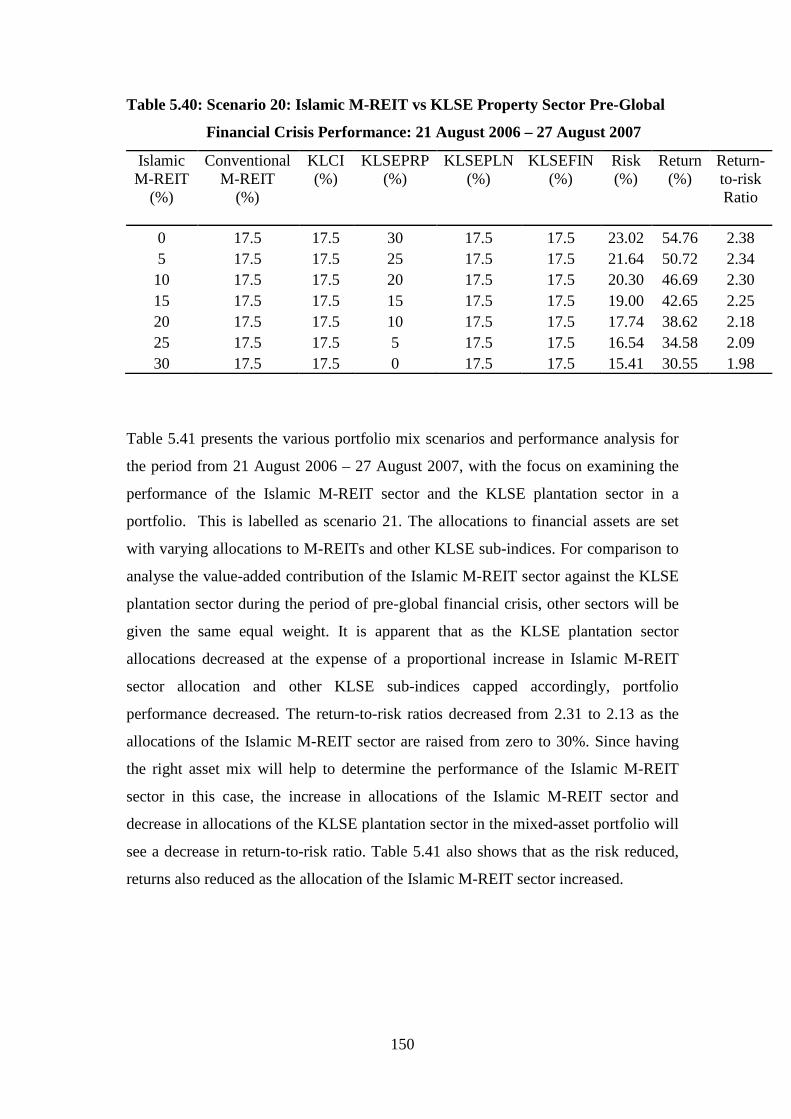

Table 5.40: Scenario 20: Islamic M-REIT vs KLSE Property Sector Pre-Global

Financial Crisis Performance: 21 August 2006 – 27 August 2007 150

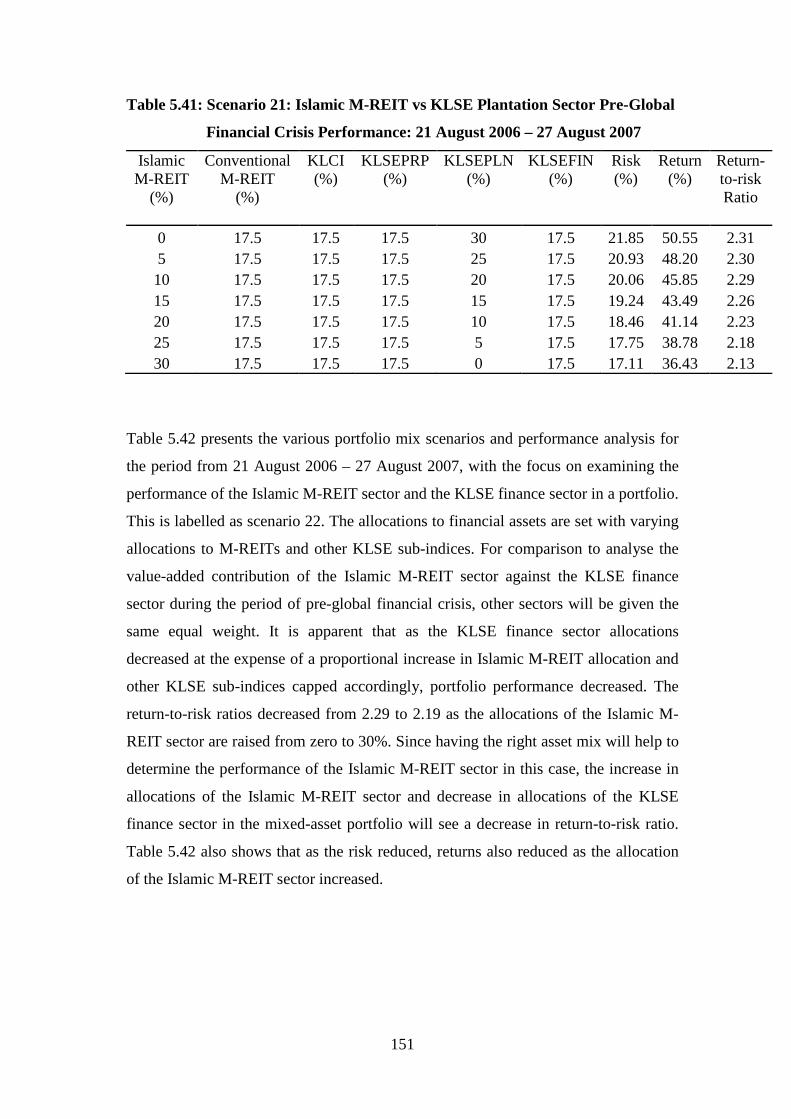

Table 5.41: Scenario 21: Islamic M-REIT vs KLSE Plantation Sector Pre-Global

Financial Crisis Performance: 21 August 2006 – 27 August 2007 151

xiii

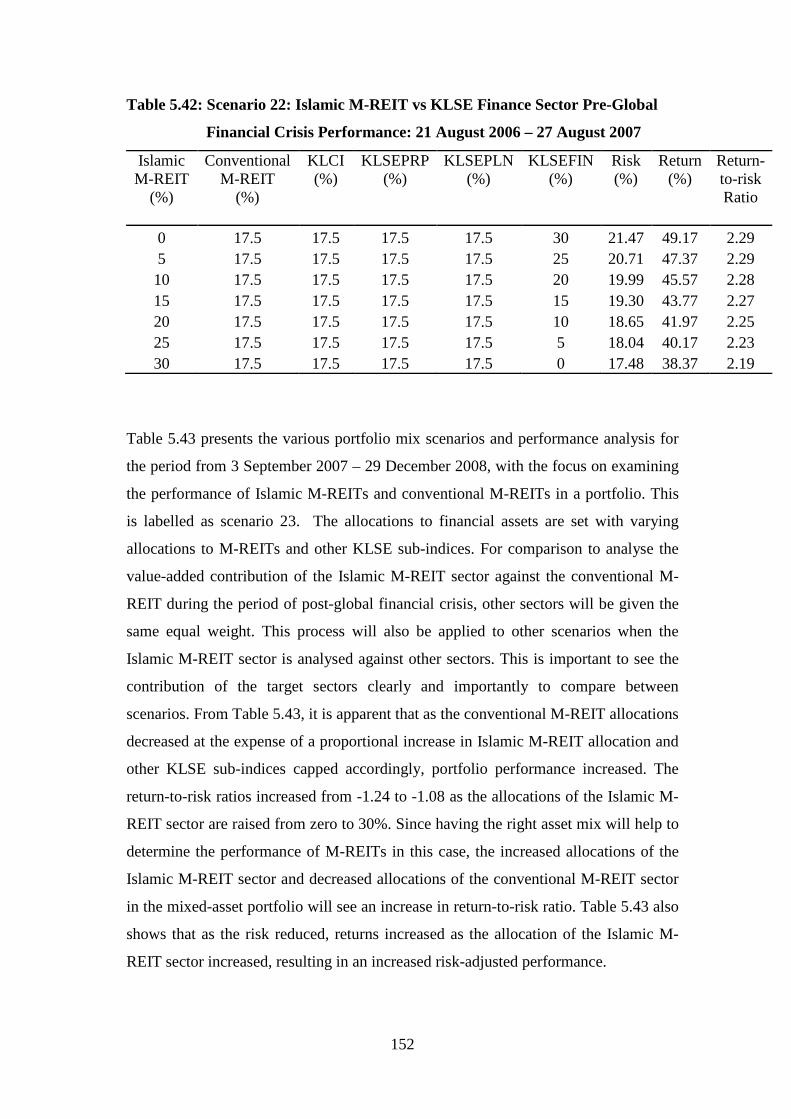

Table 5.42: Scenario 22: Islamic M-REIT vs KLSE Finance Sector Pre-Global

Financial Crisis Performance: 21 August 2006 – 27 August 2007 152

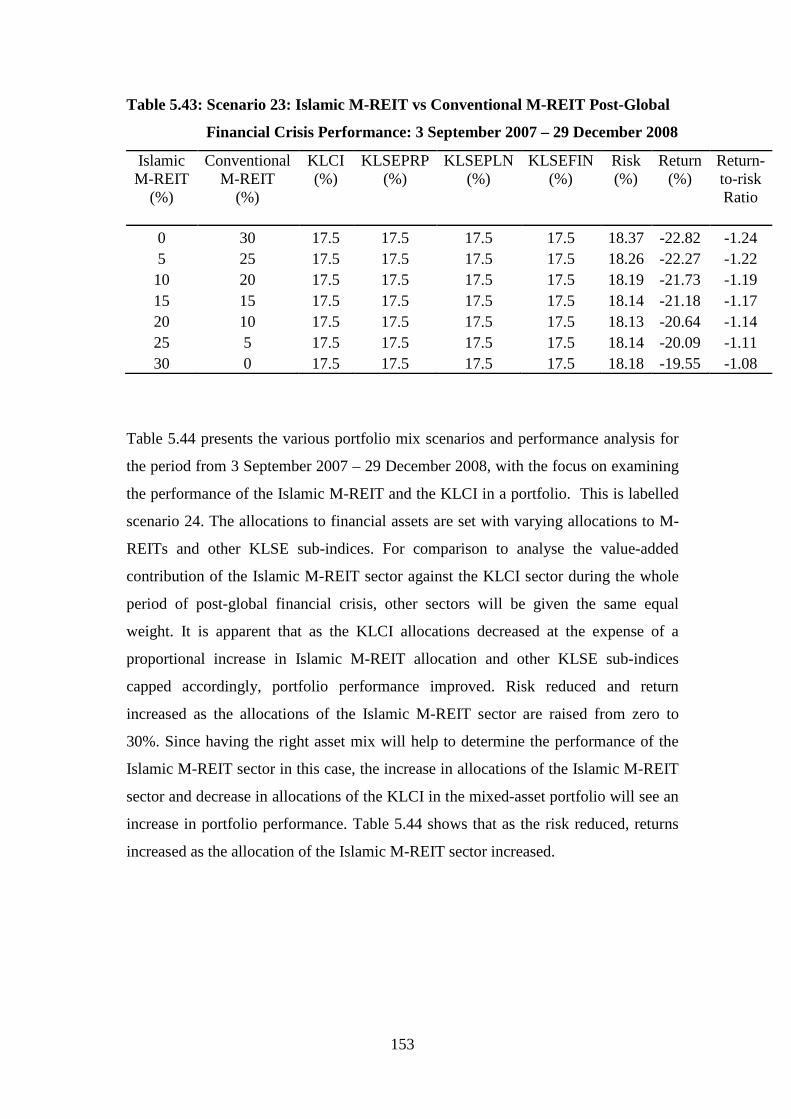

Table 5.43: Scenario 23: Islamic M-REIT vs Conventional M-REIT Post-Global

Financial Crisis Performance: 3 September 2007 – 29 Dec. 2008 153

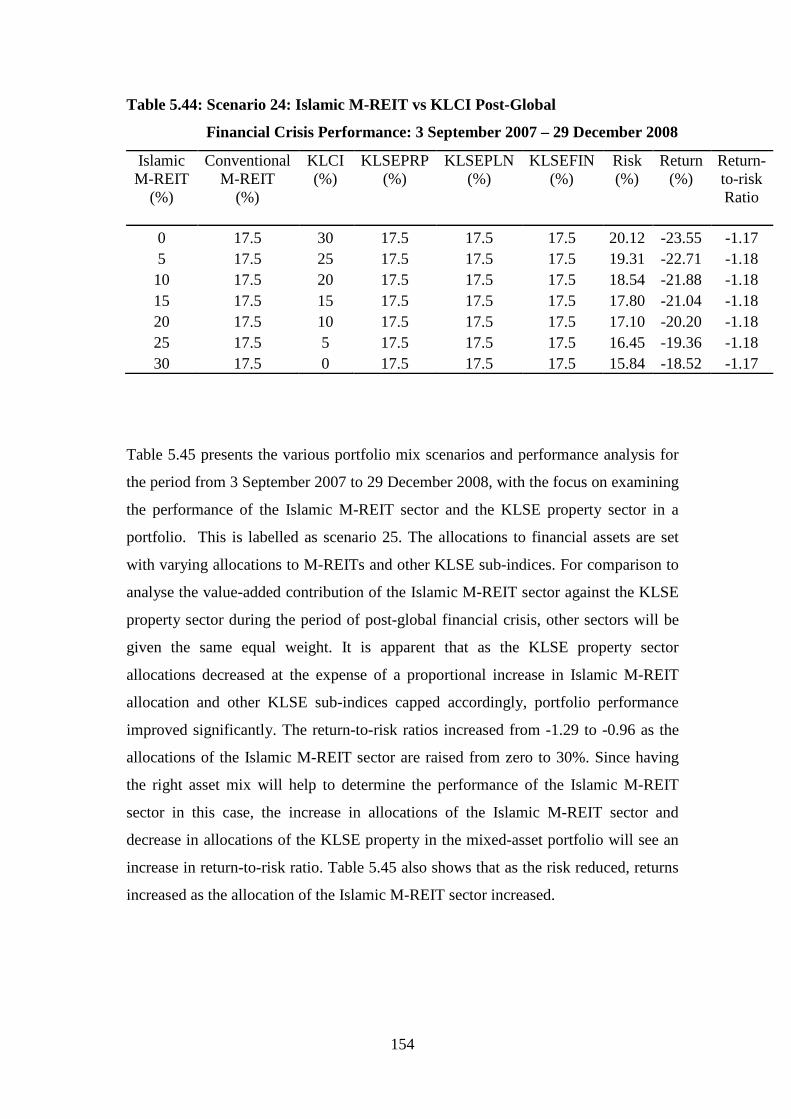

Table 5.44: Scenario 24: Islamic M-REIT vs KLCI Post-Global

Financial Crisis Performance: 3 September 2007 – 29 Dec. 2008 154

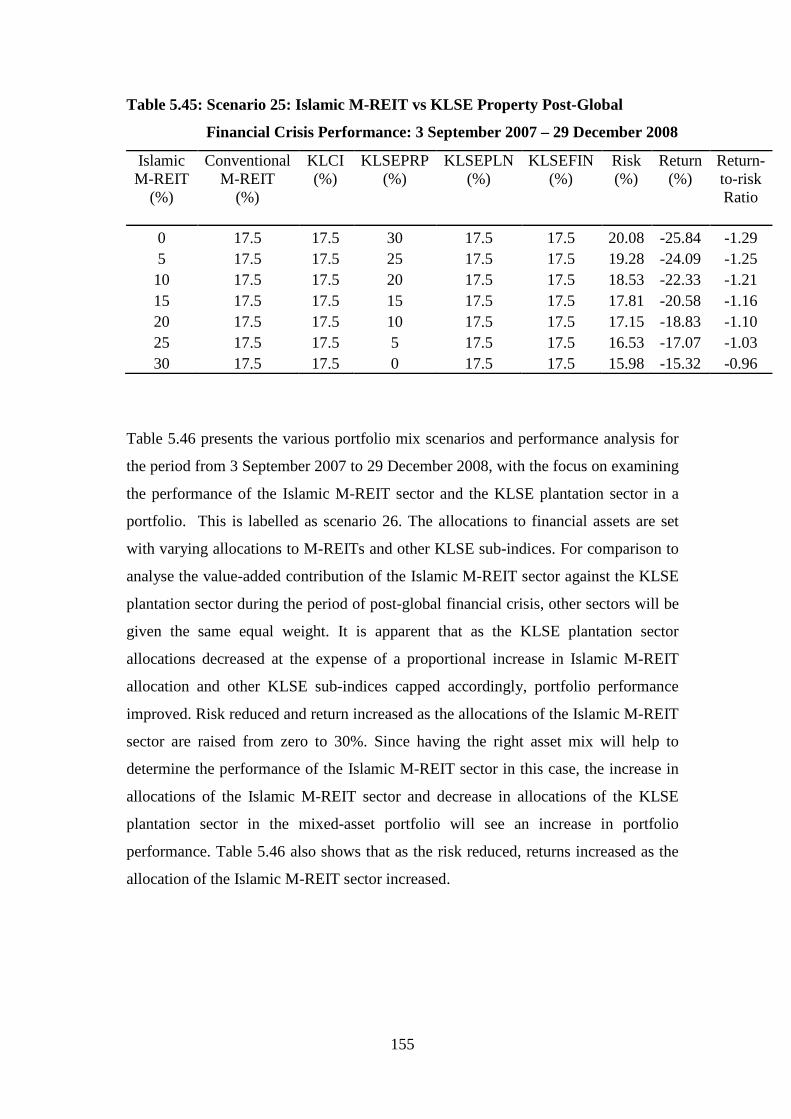

Table 5.45: Scenario 25: Islamic M-REIT vs KLSE Property Post-Global

Financial Crisis Performance: 3 September 2007 – 29 Dec. 2008 155

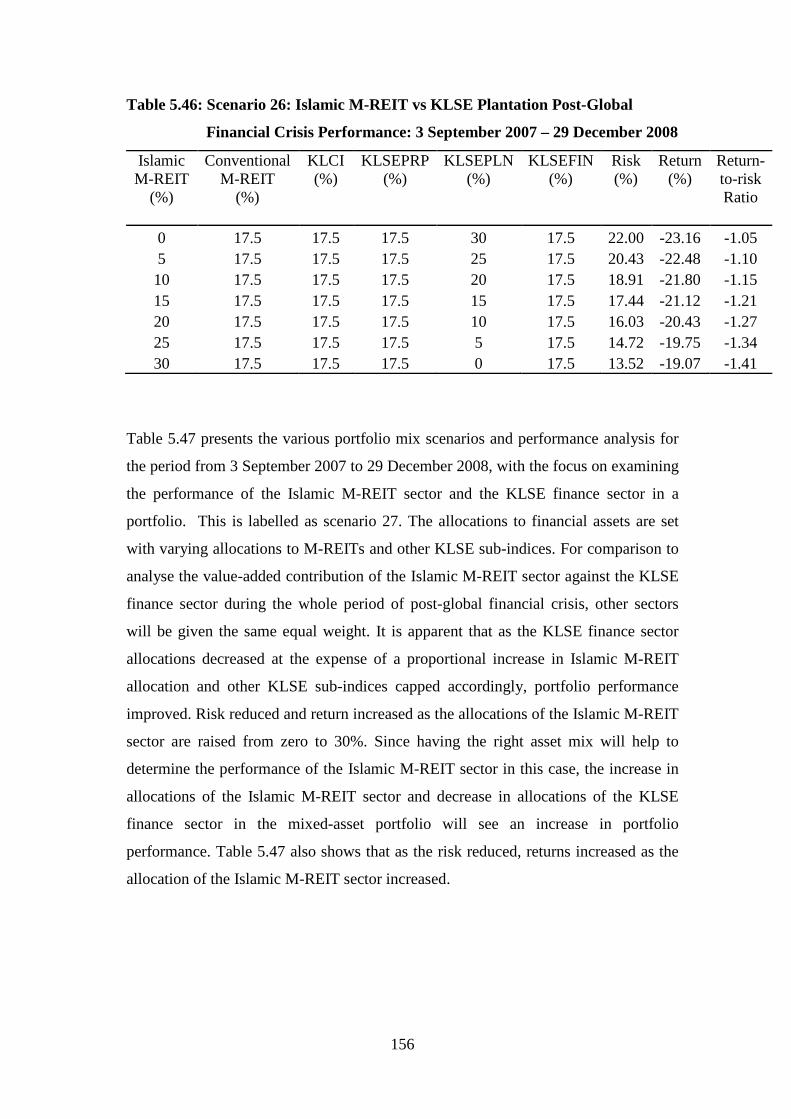

Table 5.46: Scenario 26: Islamic M-REIT vs KLSE Plantation Post-Global

Financial Crisis Performance: 3 September 2007 – 29 Dec. 2008 156

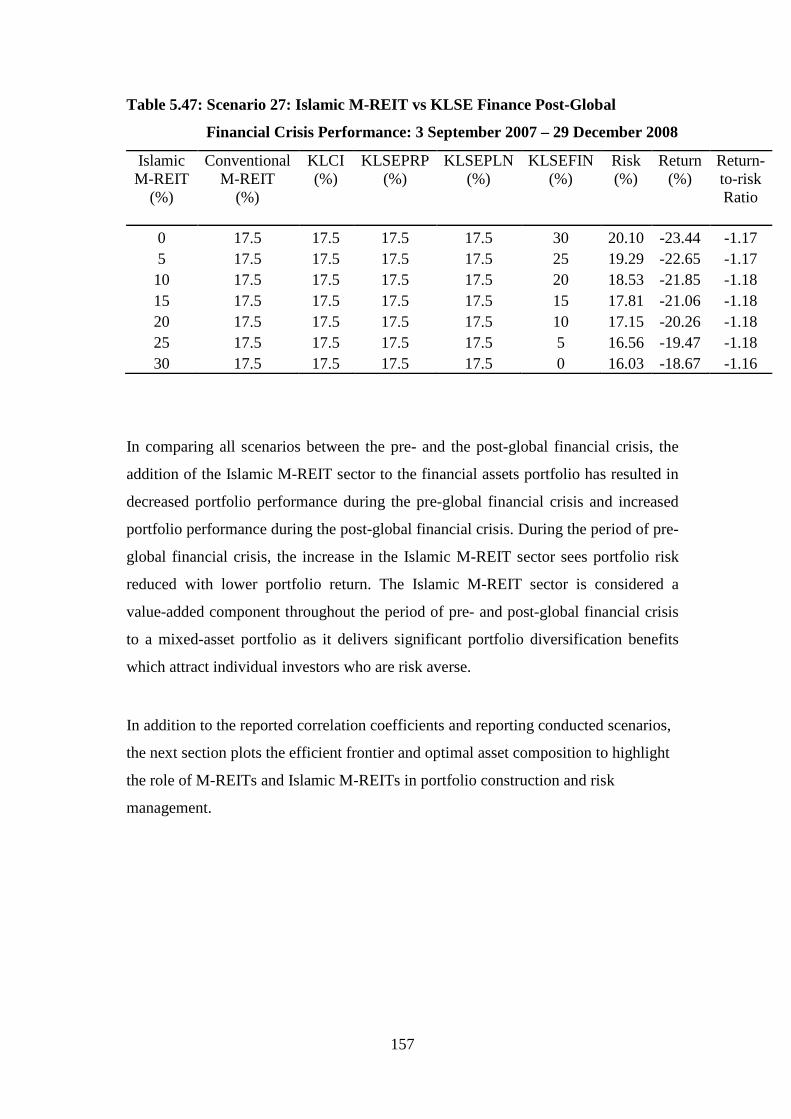

Table 5.47: Scenario 27: Islamic M-REIT vs KLSE Finance Post-Global

Financial Crisis Performance: 3 September 2007 – 29 Dec. 2008 157

Table 5.48: M-REIT Financial and Management Performance From 2007- 2009 166

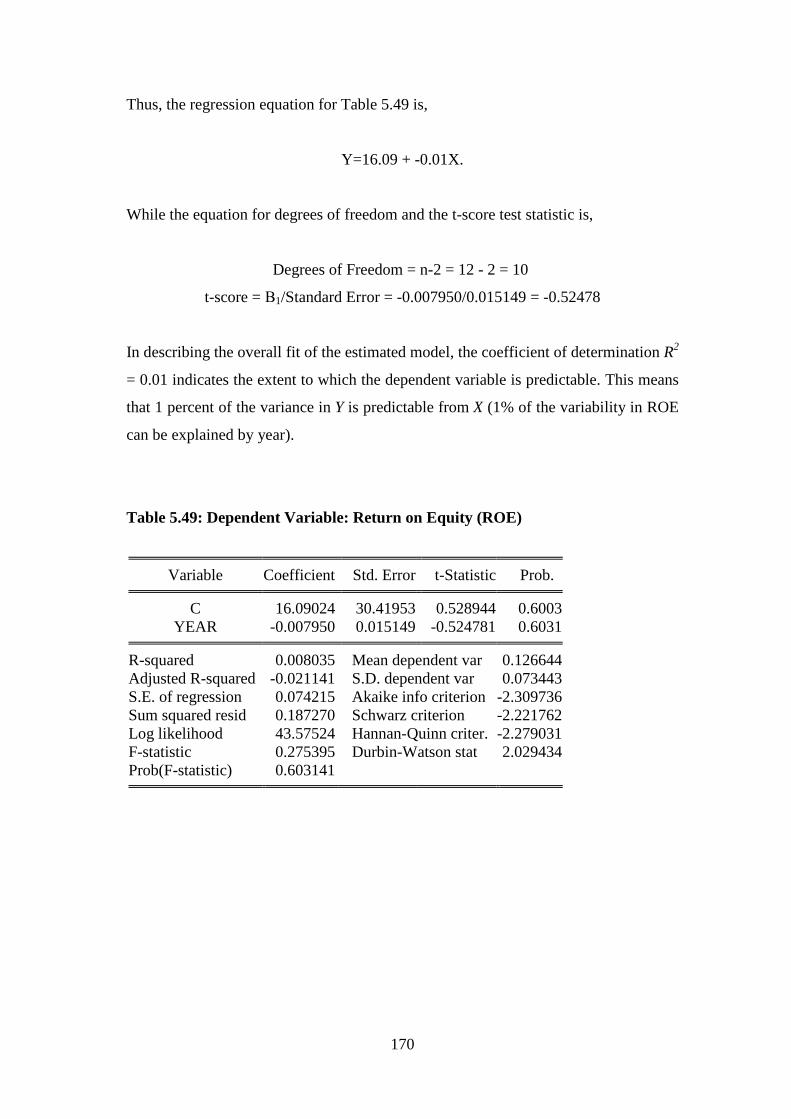

Table 5.49: Dependent Variable: Return on Equity (ROE) 170

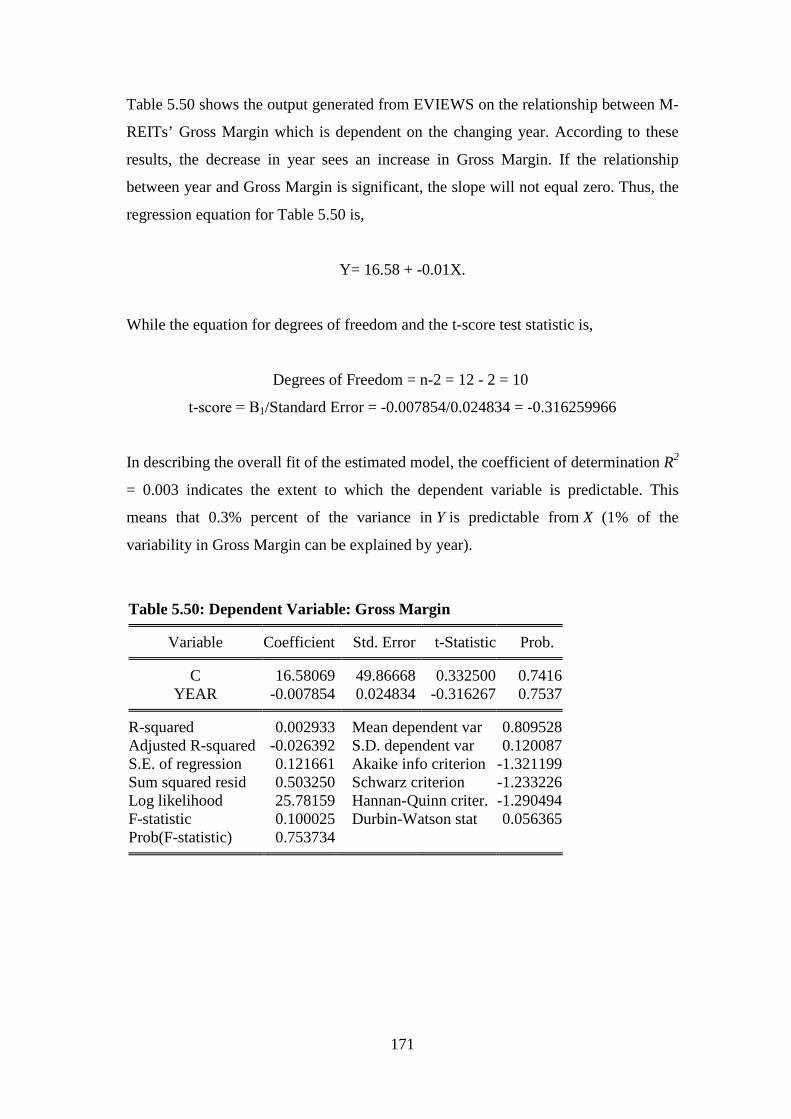

Table 5.50: Dependent Variable: Gross Margin 171

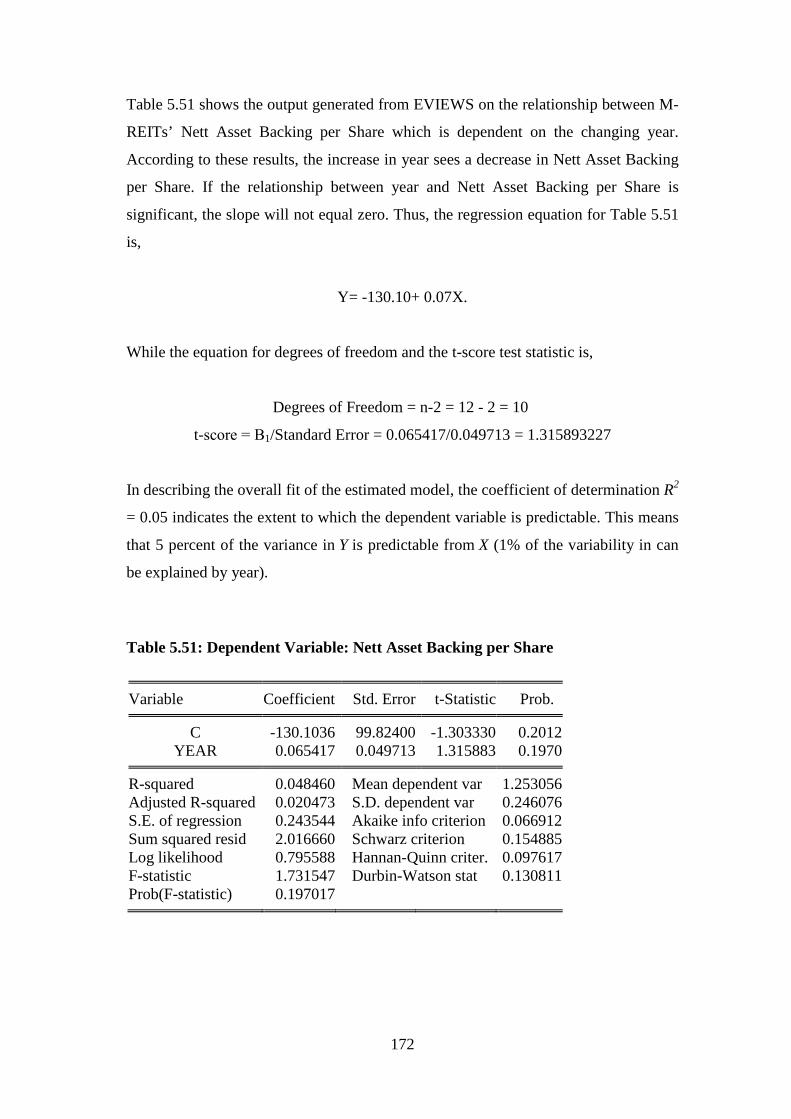

Table 5.51: Dependent Variable: Nett Asset Backing per Share 172

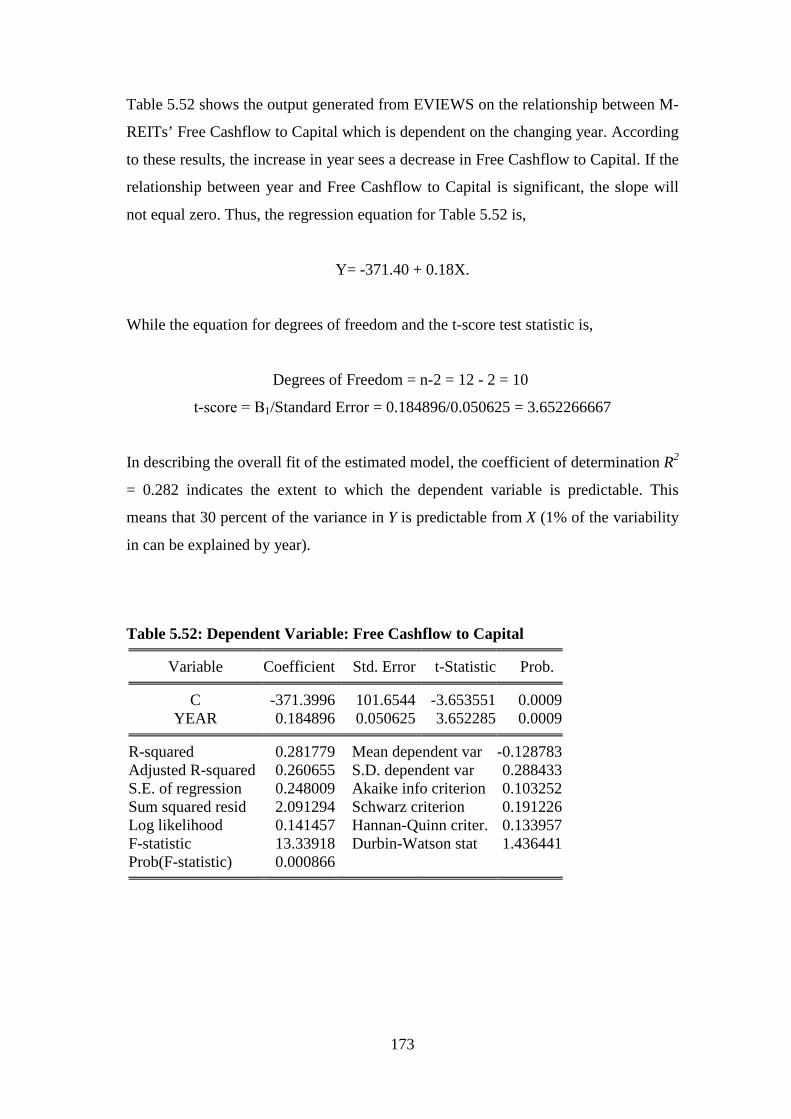

Table 5.52: Dependent Variable: Free Cashflow to Capital 173

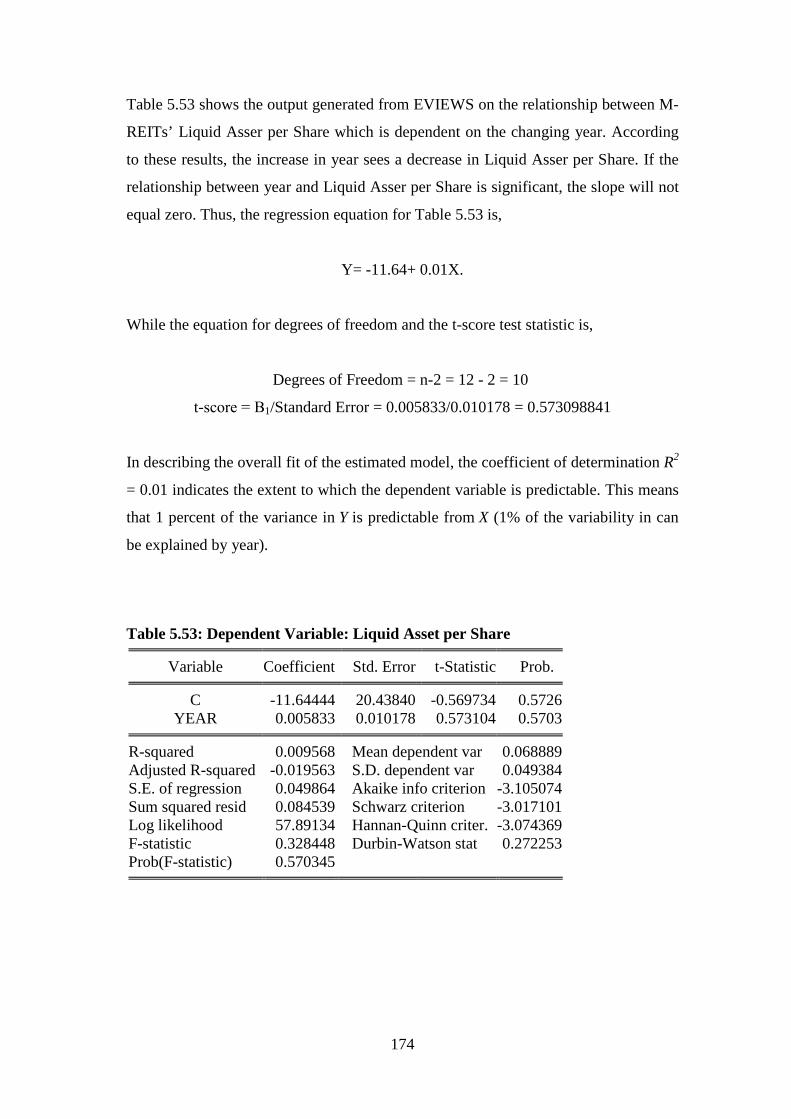

Table 5.53: Dependent Variable: Liquid Asset per Share 174

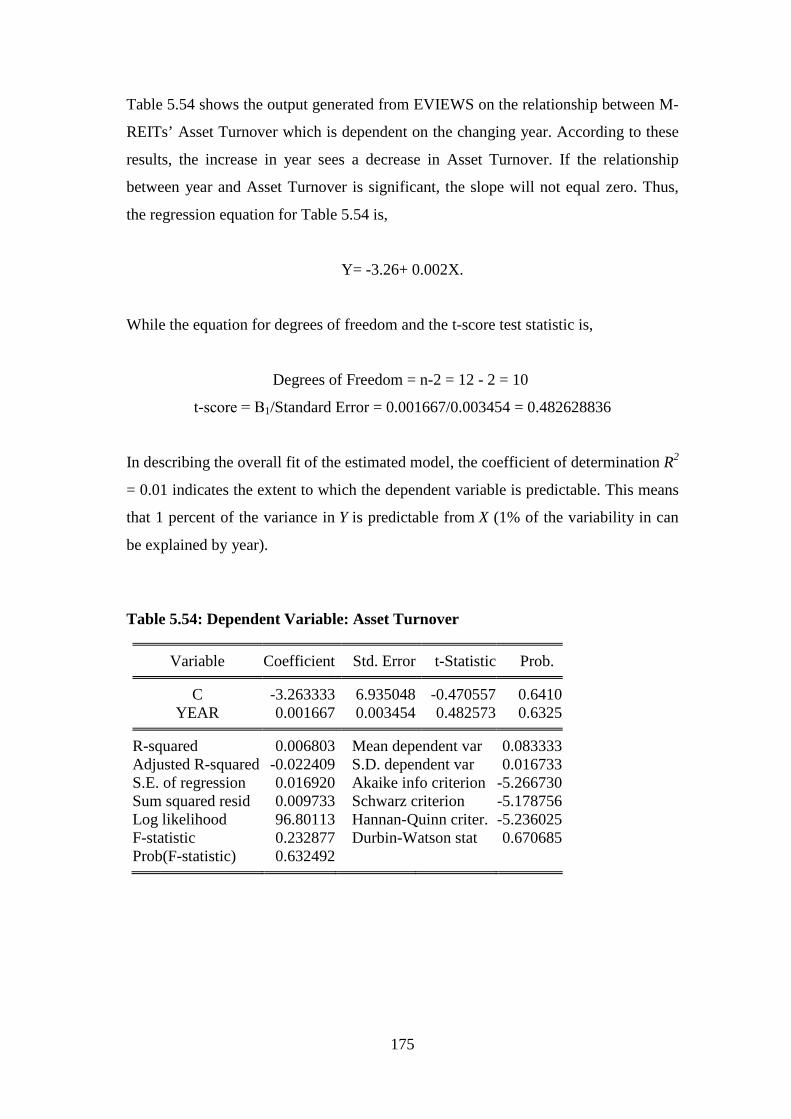

Table 5.54: Dependent Variable: Asset Turnover 175

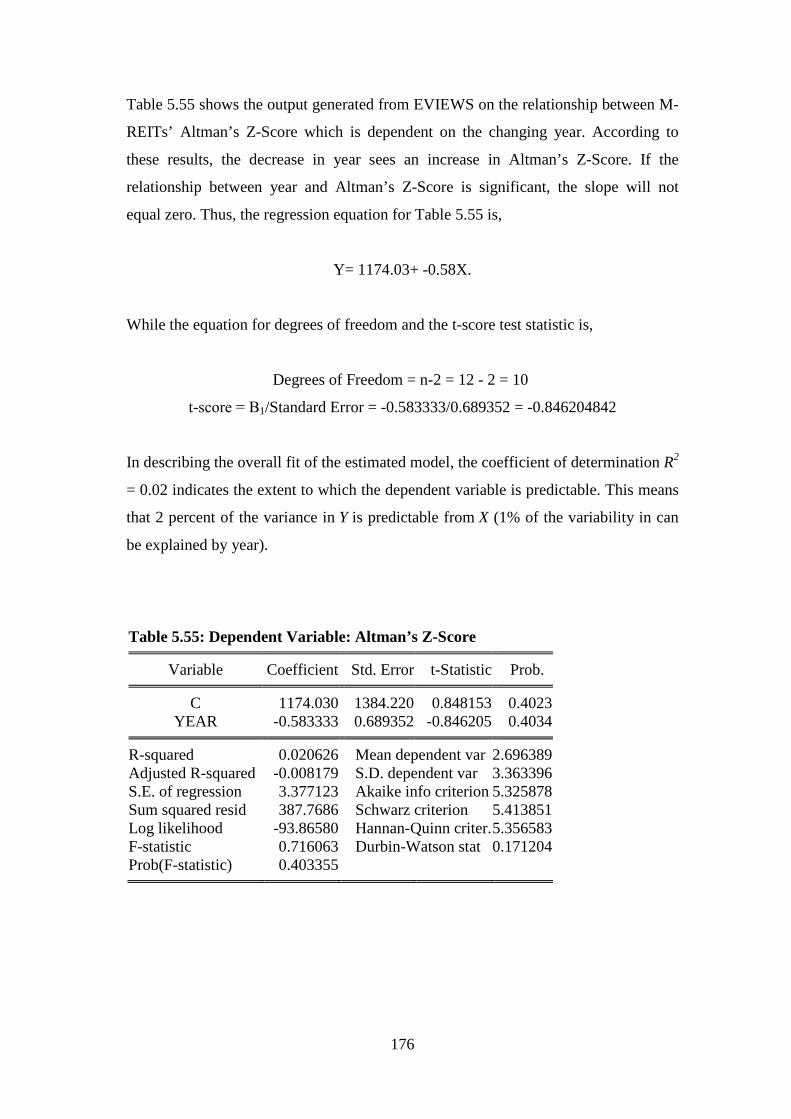

Table 5.55: Dependent Variable: Altman’s Z-Score 176

Table 5.56: Dependent Variable: Debt per Equity Ratio 177

Table 5.57: Overall M-REIT and Performance Report Card:

8 August 2005 – 28 December 2008 179

Table 5.58: Islamic M-REIT Performance Report Card:

21 August 2006 – 28 December 2008 179

Table 6.1: Importance of Factors Regarding the Current Performance of

M-REITs 182

Table 6.2: Importance of Factors Regarding the Current Performance of

M- REITs: REIT Managers 186

Table 6.3: Importance of Factors Regarding the Current Performance of

M-REITs: Property Advisors 188

Table 6.4: Importance of Factors Regarding the Current Performance of

M-REITs: Fund Managers 190

xiv

Table 6.5: Rank Correlation Between Groups on Importance of Factors

Regarding the Current Performance of M-REITs 191

Table 6.6: Importance of Factors Regarding the Current Performance of

M-REITs: ANOVA 193

Table 6.7: Importance of Factors Regarding the Ongoing Success of M-REITs 197

Table 6.8: Importance of Factors Regarding the Ongoing success of M-REITs:

REIT Managers 201

Table 6.9: Importance of Factors Regarding the Ongoing Success of M-REITs:

Property Advisors 203

Table 6.10: Importance of Factors Regarding the Ongoing Success of M-REITs:

Fund Managers 205

Table 6.11: Rank Correlation Between Groups on the Importance of Factors

Regarding the Ongoing Success of M-REITs 206

Table 6.12: Importance of Factors Regarding the Ongoing Success of M-REITs:

ANOVA 207

xv

List of Figures

Figure 1.1: Risk-return Spectrum of Commercial Property Investment

Opportunities 6

Figure 1.2: Profile of Commercial Property Investment Opportunities 7

Figure 2.1: Macquarie Eclipse REITs Development 57

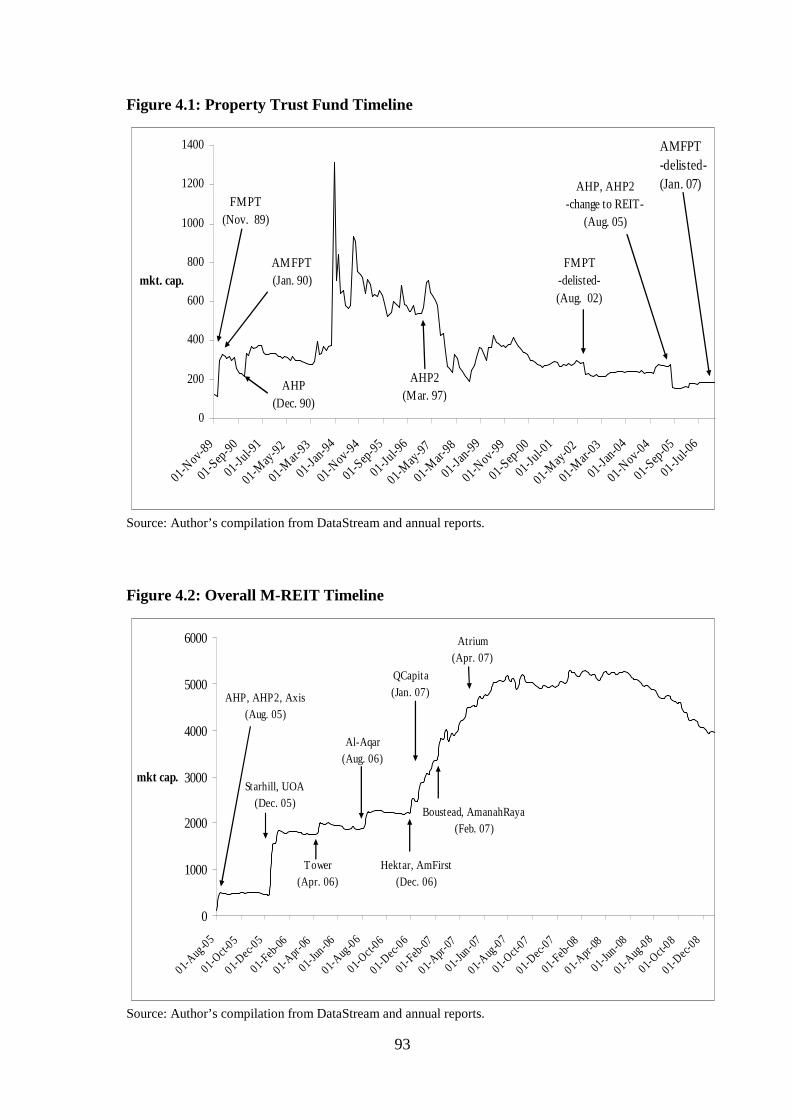

Figure 4.1: Property Trust Fund Timeline 93

Figure 4.2: Overall M-REIT Timeline 93

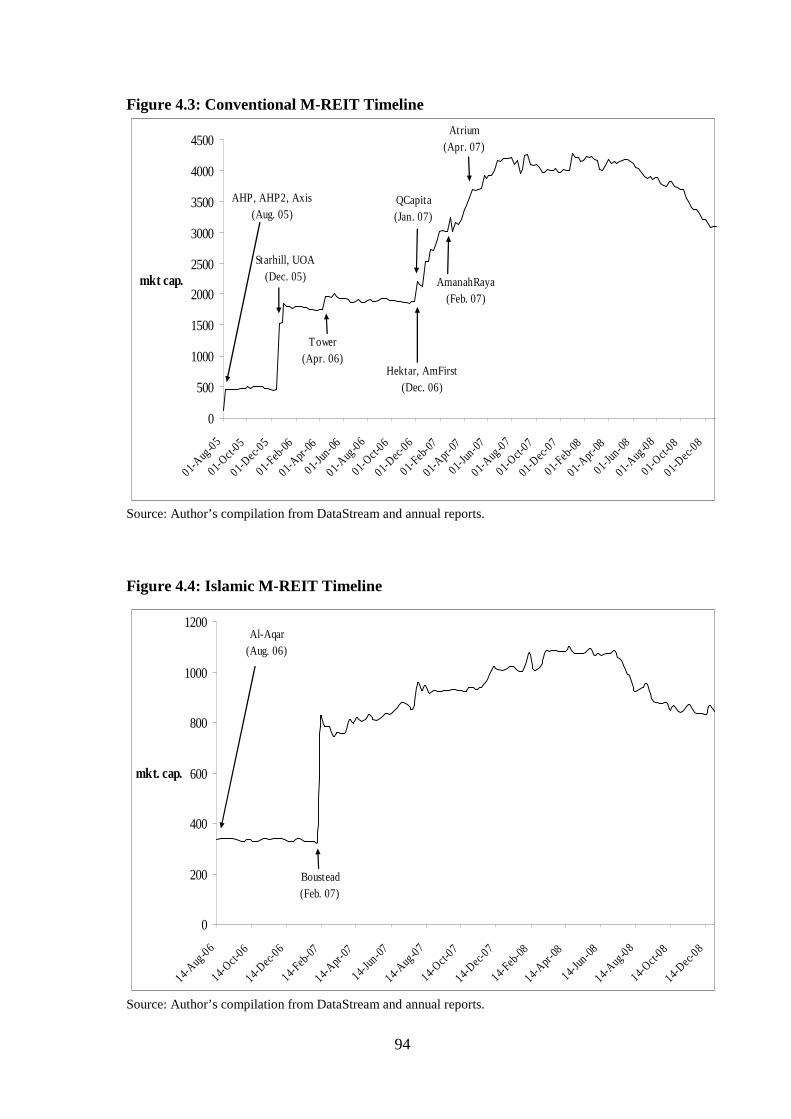

Figure 4.3: Conventional M-REIT Timeline 94

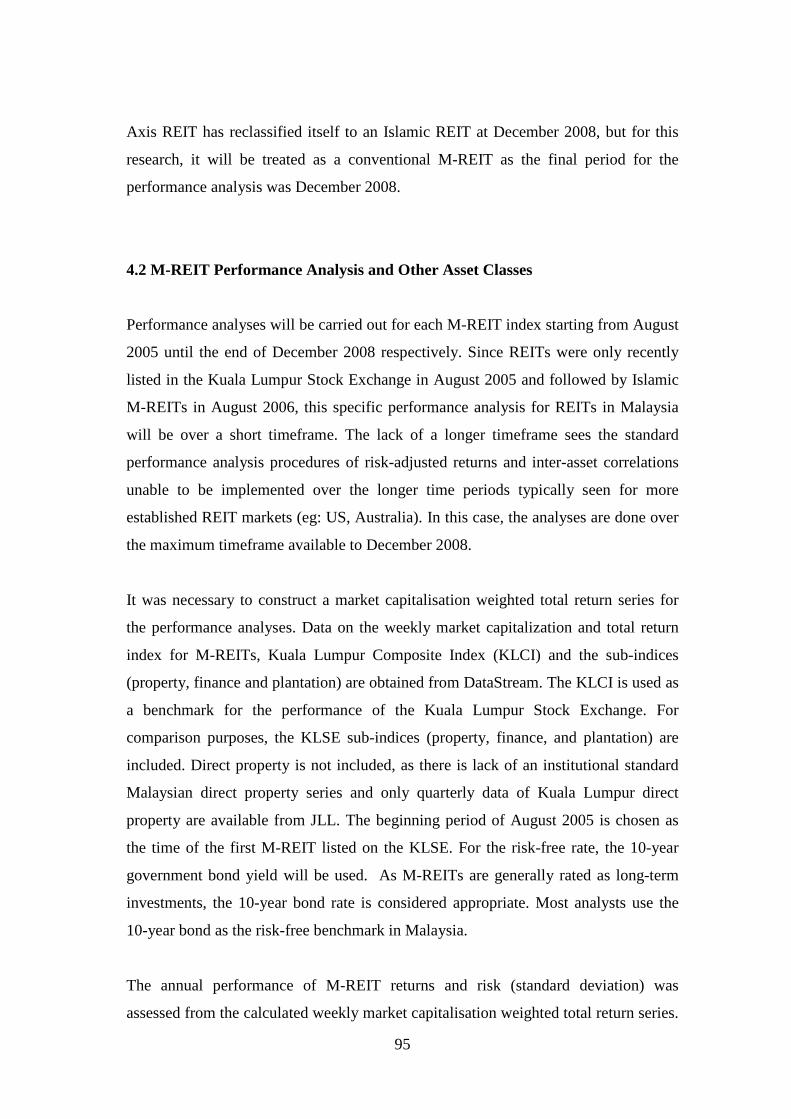

Figure 4.4: Islamic M-REIT Timeline 94

Figure 5.1: Growth in Market Capitalisation of Overall M-REIT Index and

Conventional M-REIT Index Market 101

Figure 5.2: Growth in Market Capitalisation of Islamic M-REIT Index 102

Figure 5.3: Property Trust Fund Index Against the KLCI 104

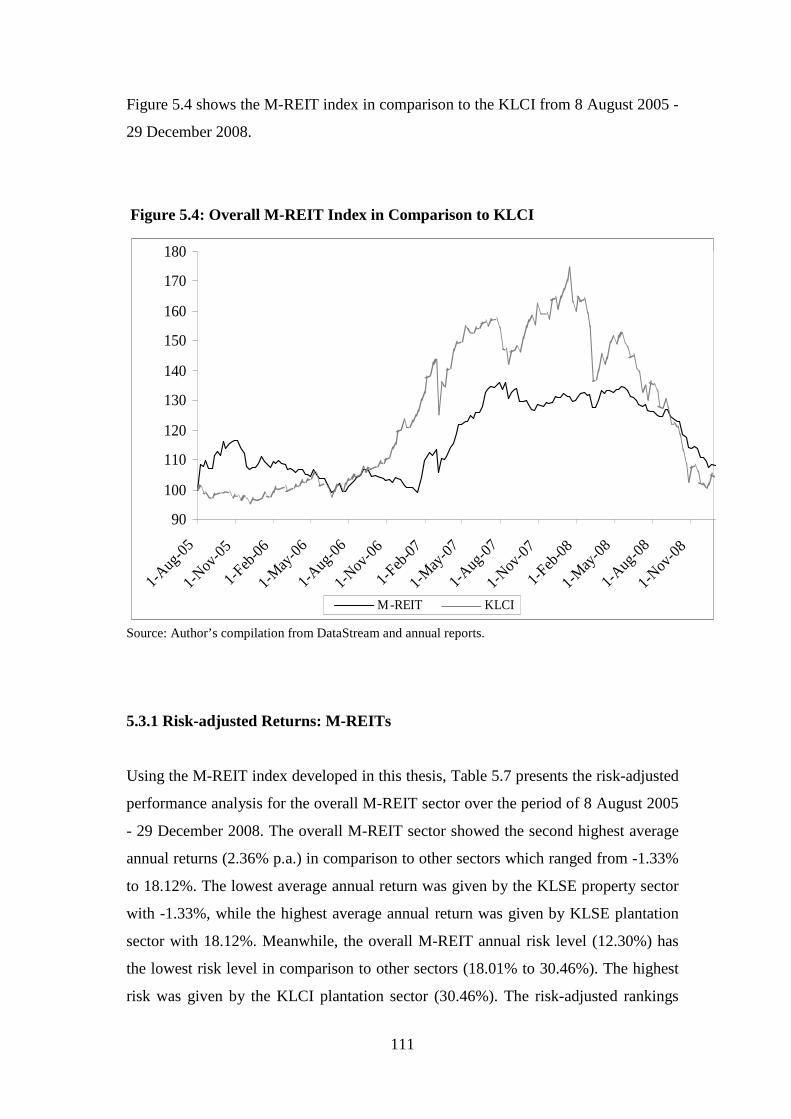

Figure 5.4: Overall M-REIT Index in Comparison to KLCI 111

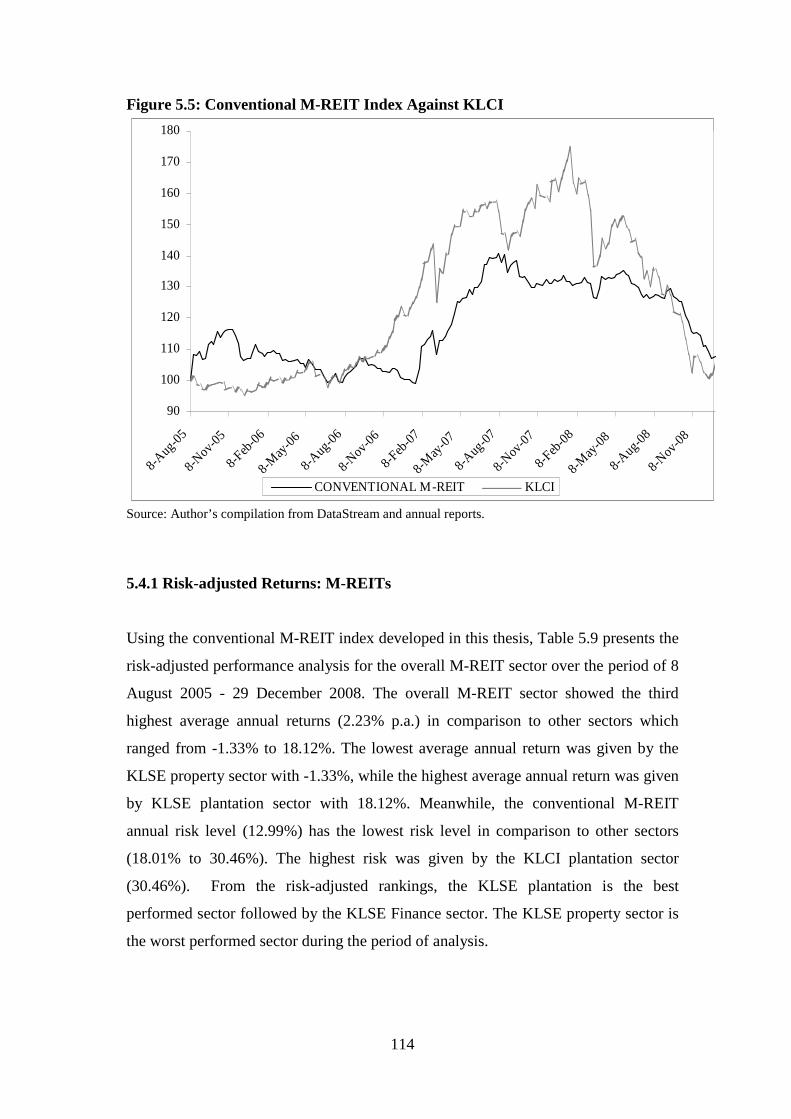

Figure 5.5: Conventional M-REIT Index Against KLCI 114

Figure 5.6: Islamic M-REIT Index Against KLCI 116

Figure 5.7: M-REIT Efficient Frontier: August 2006 – December 2008 158

Figure 5.8: M-REIT Asset Allocation Diagram: August 2006 – December 2008 160

Figure 5.9: M-REIT Efficient Frontier: pre-GFC 161

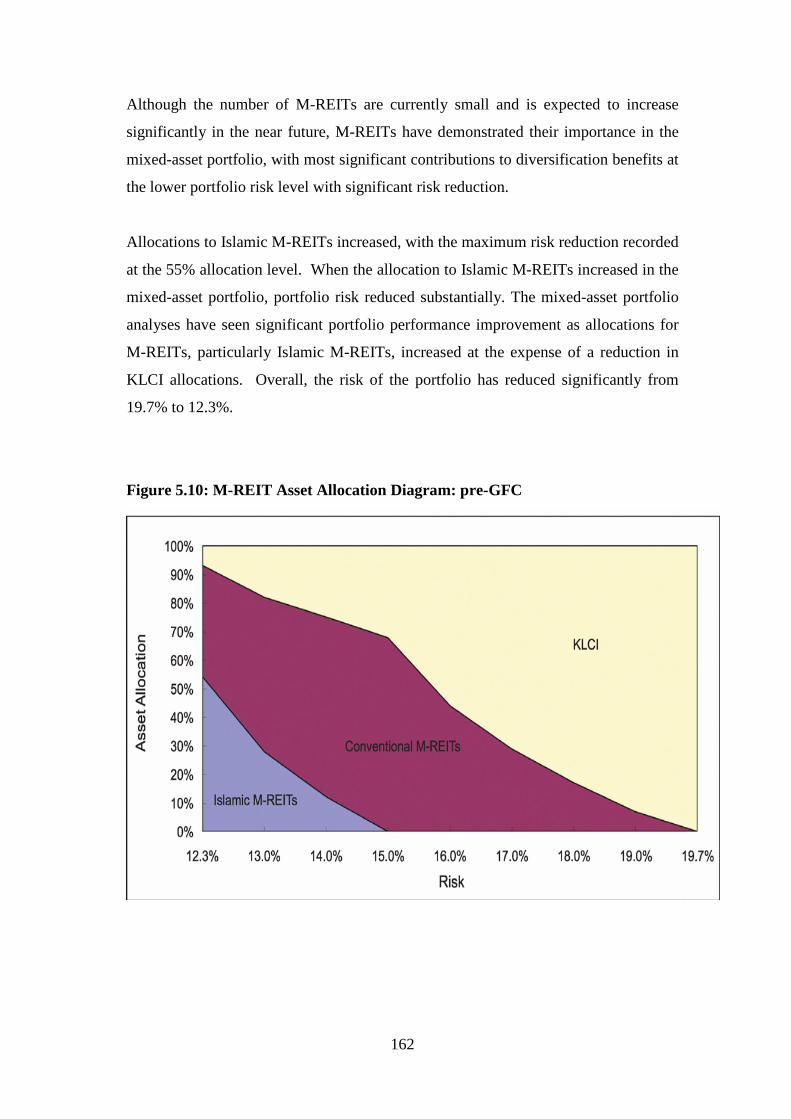

Figure 5.10: M-REIT Asset Allocation Diagram: pre-GFC 162

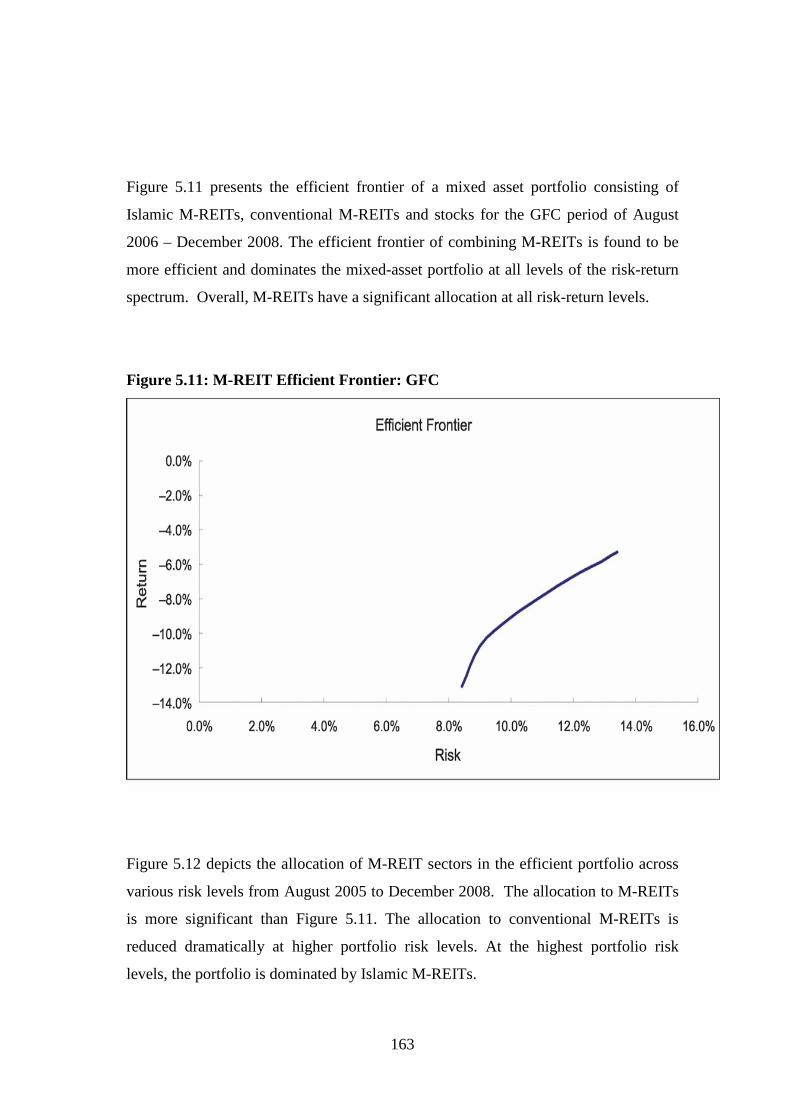

Figure 5.11: M-REIT Efficient Frontier: GFC 163

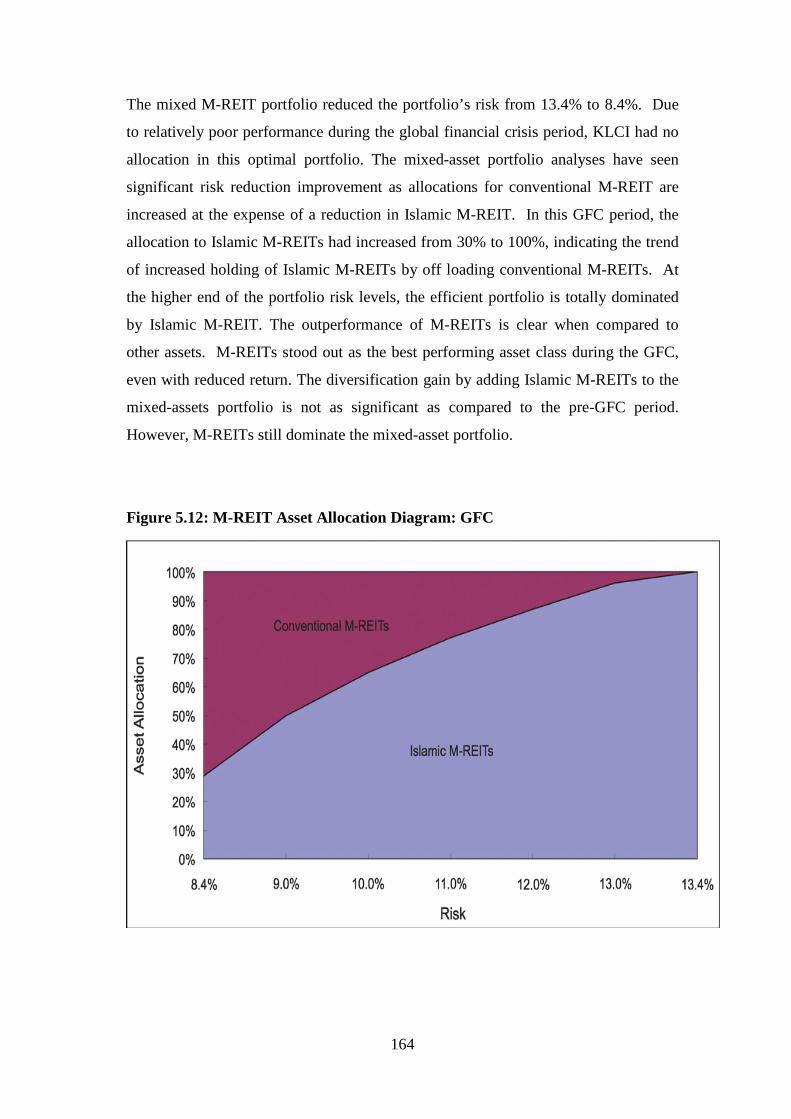

Figure 5.12: M-REIT Asset Allocation Diagram: GFC 164

Figure 5.13: Calculation Using EVIEWS 169

xvi

List of Abbreviations

Abbreviation Full Name/Term

A-REIT Australian REIT

ASX Australian Stock Exchange

CBRE CB Richard Ellis

CPO Crude Palm Oil

CR-REIT Corporate Restructuring Real Estate Investment Trust

Dec. December

EMEA Europe, the Middle East and Africa

EPRA European Public Real Estate Association

EREIT Equity Real Estate Investment Trusts

Excl. Excluding

GBP Pound Sterling

HK-REIT Hong Kong Real Estate Investment Trust

IPG Investa Property Group

J-REIT Japanese Real Estate Investment Trust

JLL Jones Lang LaSalle

K-REIT Korean Real Estate Investment Trust

KLCI Kuala Lumpur Composite Index

KLSE Kuala Lumpur Stock Exchange

KLSEFIN Kuala Lumpur Stock Exchange Finance

KLSEPLN Kuala Lumpur Stock Exchange Plantation

KLSEPRP Kuala Lumpur Stock Exchange Property

KSE Korea Stock Exchange

LPT Listed Property Trust

M-REIT Malaysia REIT

MER Management Expense Ratio

Mkt. cap. Market Capitalisation

xvii

Abbreviation Full Name/Term

NAREIT National Association for Real Estate Investment Trusts

NCREIF National Council of Real Estate Investment Fiduciaries

PIR Property Investment Research

PRRES Pacific Rim Real Estate Society

PTF Property Trust Fund

PSF Property Securities Fund

South Africa Property Unit Trust

REIT Real Estate Investment Trust

RM Ringgit Malaysia

S$ Singapore Dollar

SFC Hong Kong Securities and Futures Commission

SGX Stock Exchange of Singapore

SICAFI Sociétés d'investissement a capital fixe en immobiliere

SIIC Sociétés d'investissements immobiliers cotees

S-REIT Singaporean Real Estate Investment Trust

T-REIT Taiwanese Real Estate Investment Trust

TSE Tokyo Stock Exchange

UK United Kingdom

US United States of America

US$ US Dollar

xviii

Executive Summary

This PhD research will examine the development, performance and impact of

Malaysian REITs in the local, Asian and global REIT investment market; particularly

focusing on Islamic REITs in Malaysia. This issue is important as REITs have

emerged as a topic of considerable interest to the academic community, international

investors, policy makers and the public at large; particularly with the recent

significant development of REITs in Asia in recent years.

The objectives for this research are:

1. To compare the structure and regulation of Malaysian REITs with other

countries; both in Asia and internationally and differentiate the structure

between Malaysian conventional M-REITs and Islamic M-REITs

2. To develop an Malaysian REIT performance index and a sub-sector Islamic

M-REIT performance index and identify the impact of the Global Financial

Crisis on Malaysian REIT performance by analysing the risk-adjusted returns

performance for Malaysian REITs and Islamic M-REITs and analysing the

portfolio diversification benefits of Malaysian REITs and Islamic M-REITs in

a mixed-asset portfolio

3. To conduct an investment industry survey to identify the problems, challenges

and the possible solutions relating to a successful Malaysian REIT market

4. To identify Malaysian REIT prospects by determining the strategy for its

further strategic development and investor acceptance.

In terms of portfolio diversification for the whole period of 8 August 2005 till

December 2008, the overall M-REIT and Islamic M-REIT sector delivered strong

portfolio diversification benefit. However, one should be cautious before concluding

that Islamic M-REITs and conventional M-REITs have a smaller role in the mixed-

asset portfolio. Factors such as small sample bias as well as short study period (2½

years) should be taken into consideration.

xix

The survey results have revealed the key elements on the importance of the factors

regarding the current performance and the ongoing success of M-REITs. For all three

groups (property managers, fund managers and property advisors), the key points in

which they have equal agreement on the importance of factors regarding the current

performance of M-REITs are dividend growth and acquisition of new assets, while

the significant risk factors regarding M-REITs is the level of borrowings. In terms of

factors for the ongoing success, growth strategy is considered to be a significant

factor, which includes professional management, acquisition of new assets, dividend

growth and transparency in every aspect; especially in terms of regulation and

finance.

Overall, further research is clearly needed to further expand the understanding of

REITs in Malaysia, their investment dynamics and investor appeal. With the expected

future growth of M-REITs after the global financial crisis, this research will provide

increased understanding of M-REITs in an investment portfolio. In particular, this

understanding will also be relevant to the development of Islamic REITs, with the

expected future growth in Islamic property investment products and opportunities

globally.

1

CHAPTER 1

INTRODUCTION

1.1 Overall Context

Real estate investment trusts (REITs) are a form of property securitisation which has

proven to be a successful property investment vehicle in Australia, as well as in the

US. REITs provide investors with exposure to quality commercial property portfolios

via being listed on the stock market; serving as a hybrid investment vehicle. Recent

years have seen an increase of interest in real estate investment trusts (REITs) at a

global level; particularly amongst global property securities funds and international

investors. However, with this growing REIT awareness from international property

investors, there is a need for the further development of more innovative performance

analysis, products and opportunities to identify enhanced property portfolio

diversification benefits.

REITs have developed rapidly in recent years, with the number of REITs growing

significantly. This has seen REITs established (or legislated) in over 21 countries.

There has been substantial growth particularly in Asia (Japan, Singapore, Hong Kong,

Malaysia, Korea) and Europe (France, UK). Table 1.1 shows the status of global

REITs and the size of REIT markets in the various countries. However, the global

REIT market has been severely affected by the global financial market crisis in 2008,

with the total market capitalisation of listed REITs having declined significantly (eg:

November 2008: US$325bn, October: US$363.6bn, September: US$467.6bn, August:

US$484.9bn).

2

By December 2008, the number of REITs had grown to 509, with a market

capitalisation of US$375.6 billion. In Asia, there were 101 REITs with US$47.1

billion in market capitalisation, representing 12.5% of the global REIT market, with

REITs only being established in Asia in 2001, with the launching of the first Japanese

REIT (Whiting, 2007). Malaysia has 13 REITs and represents 0.3% of the global

REIT market. Within Asia, Malaysia accounts for 2.5% of the Asian REIT market.

One unique development in this REIT area has been the establishment of the world’s

first Islamic REIT in Malaysia in 2006, which include the principles of Shariah - the

body of Islamic law. Importantly, this development is significant, as it is another form

of ethical investment and will increase liquidity and transparency to the international

REIT market; particularly via increased acceptance from Islamic investors globally.

By the end of 2008, there were only three Islamic REITs in the world, with all three in

Malaysia; namely Al-‘Aqar KPJ REIT (hospital properties), Al-Hadharah Boustead

REIT (plantation properties) and Axis REIT (office/industrial properties). Axis REIT,

which was the first Malaysian REIT, has reclassified itself to being an Islamic REIT

in December 2008. By end of December 2008, the total market capitalisation of these

Islamic REITs was US$354.7 million (RM1228.9 million), representing 30% of

Malaysian REIT market capitalisation (APREA, 2009).

The US has the largest percentage of the global REIT market with 52%, followed by

Europe (21%), Asia (13%) and Australia (11%). The top 10 global REIT markets are:

#1: US #2: France #3: Australia #4: Japan #5: UK

#6: Canada #7: Singapore #8: Netherlands #9: Hong Kong

#10: Belgium

Japan dominates the Asian REIT market with US$29.5 billion in market

capitalisation, accounting for 7.8 % of the global REIT market and 62.6% of the

Asian REIT market.

3

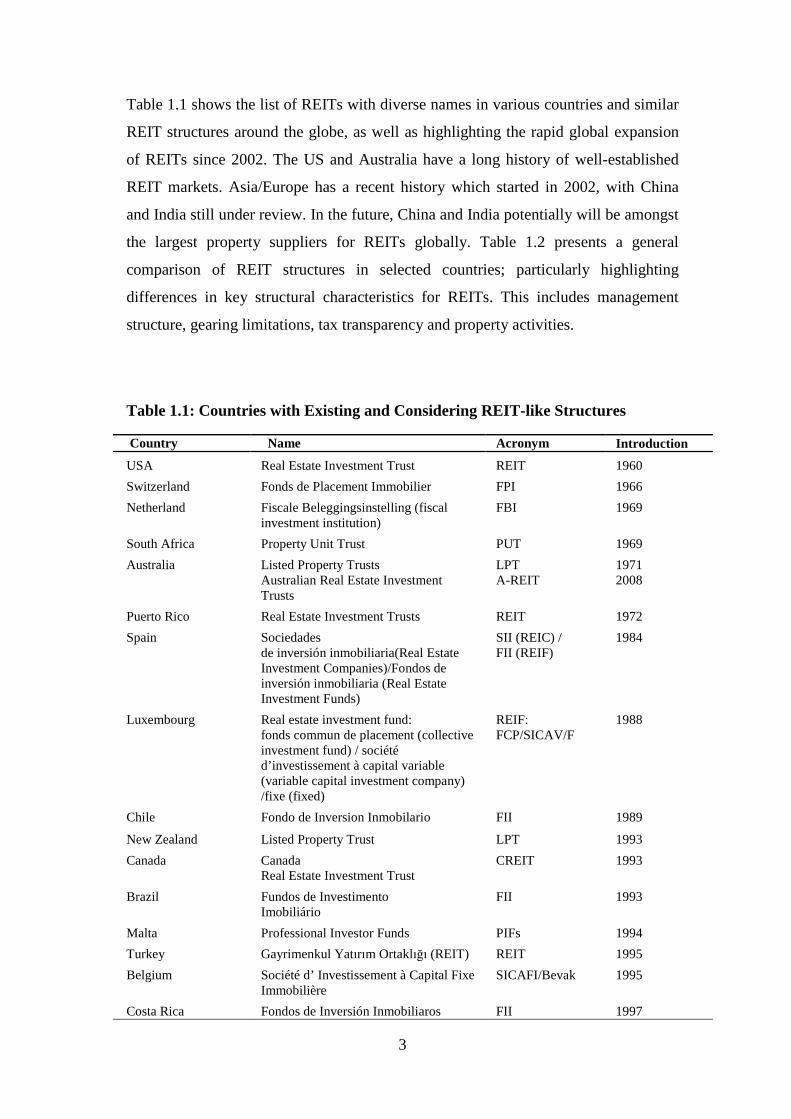

Table 1.1 shows the list of REITs with diverse names in various countries and similar

REIT structures around the globe, as well as highlighting the rapid global expansion

of REITs since 2002. The US and Australia have a long history of well-established

REIT markets. Asia/Europe has a recent history which started in 2002, with China

and India still under review. In the future, China and India potentially will be amongst

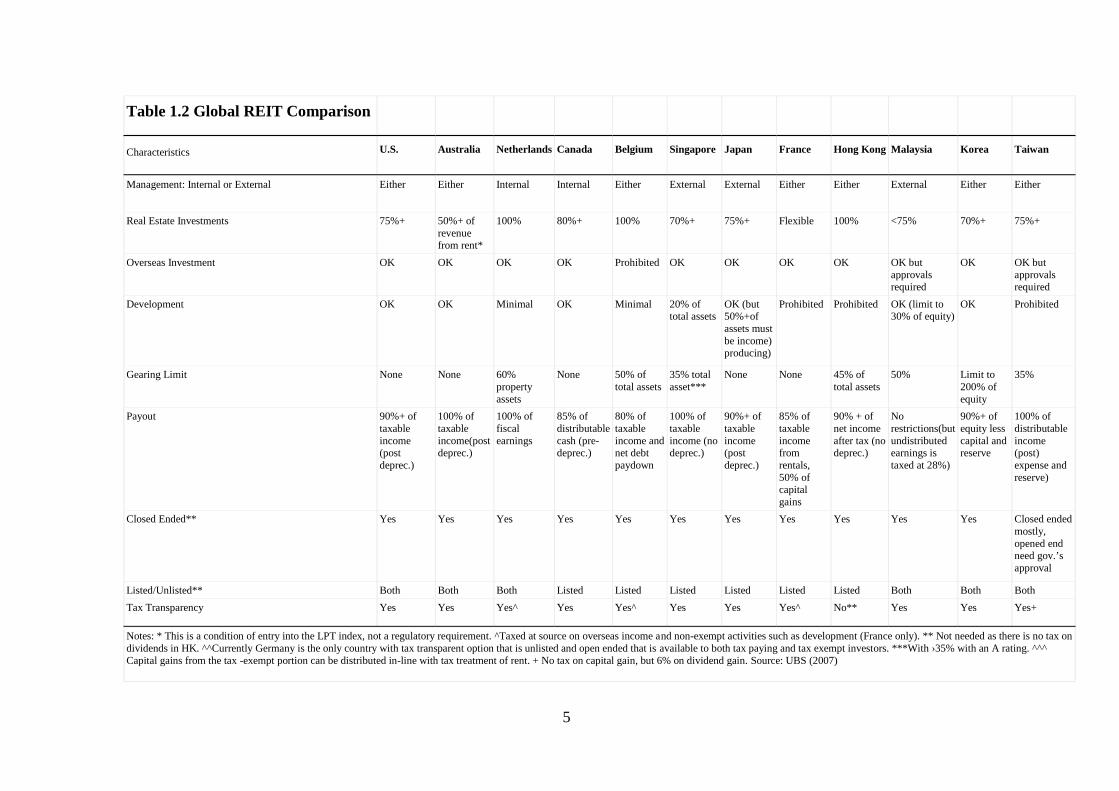

the largest property suppliers for REITs globally. Table 1.2 presents a general

comparison of REIT structures in selected countries; particularly highlighting

differences in key structural characteristics for REITs. This includes management

structure, gearing limitations, tax transparency and property activities.

Table 1.1: Countries with Existing and Considering REIT-like Structures

Country Name Acronym Introduction

USA Real Estate Investment Trust REIT 1960

Switzerland Fonds de Placement Immobilier FPI 1966

Netherland Fiscale Beleggingsinstelling (fiscalinvestment institution)

FBI 1969

South Africa Property Unit Trust PUT 1969

Australia Listed Property TrustsAustralian Real Estate InvestmentTrusts

LPTA-REIT

19712008

Puerto Rico Real Estate Investment Trusts REIT 1972

Spain Sociedadesde inversión inmobiliaria(Real EstateInvestment Companies)/Fondos deinversión inmobiliaria (Real EstateInvestment Funds)

SII (REIC) /FII (REIF)

1984

Luxembourg Real estate investment fund:fonds commun de placement (collectiveinvestment fund) / sociétéd’investissement à capital variable(variable capital investment company)/fixe (fixed)

REIF:FCP/SICAV/F

1988

Chile Fondo de Inversion Inmobilario FII 1989

New Zealand Listed Property Trust LPT 1993

Canada CanadaReal Estate Investment Trust

CREIT 1993

Brazil Fundos de InvestimentoImobiliário

FII 1993

Malta Professional Investor Funds PIFs 1994

Turkey Gayrimenkul Yatırım Ortaklığı (REIT) REIT 1995

Belgium Société d’ Investissement à Capital FixeImmobilière

SICAFI/Bevak 1995

Costa Rica Fondos de Inversión Inmobiliaros FII 1997

4

Country Name Acronym Introduction

Greece Real Estate Investment Company, RealEstate Mutual Funds

REIC/REMF 1999

Thailand Real Estate Investment Trust REIT 2001

Japan Japanese Real Estate Investment Trust J-REIT 2001

Korea Korean Real Estate Investment TrustCorporate Restructuring REIT

K-REITCR-REITRETF

200120012004

Russia Joint-Stock Investment FundClosed-End Mututal Fund

JSIFCEMF

20012001

Singapore Singapore Real EstateInvestment Trust

S-REIT 2002

Taiwan Real Estate Investment Trust REIT 2003

France Sociétés d’Investissements ImmobiliersCotées

SIIC 2003

Hongkong Hongkong Real EstateInvestment Trust

H-REIT 2003

Austria Immobilien-Investmentfondsgesetz ImmoInvFG 2003

Mexico Fideicomiso Inmobiliario) REIT 2004

Bulgaria Special PurposeInvestment Companies

SPIC 2004

Malaysia Property Trust FundReal Estate Investment Trust

PTFREITIslamic REIT

198920052006

Israel Real Estate Investment Trust REIT 2006

U.K. UK Real Estate Investment Trust UK-REIT 2007

Germany German REIT G-REIT 2007

Italy Società di Investimento ImmobiliareQuotata

SIIQ 2007

Source: NAREIT portfolio magazine, EPRA, Ernst and Young (2007), Pramerica Real EstateInvestrors (2005)

5

Table 1.2 Global REIT Comparison

Characteristics U.S. Australia Netherlands Canada Belgium Singapore Japan France Hong Kong Malaysia Korea Taiwan

Management: Internal or External Either Either Internal Internal Either External External Either Either External Either Either

Real Estate Investments 75%+ 50%+ ofrevenuefrom rent*

100% 80%+ 100% 70%+ 75%+ Flexible 100% <75% 70%+ 75%+

Overseas Investment OK OK OK OK Prohibited OK OK OK OK OK butapprovalsrequired

OK OK butapprovalsrequired

Development OK OK Minimal OK Minimal 20% oftotal assets

OK (but50%+ofassets mustbe income)producing)

Prohibited Prohibited OK (limit to30% of equity)

OK Prohibited

Gearing Limit None None 60%propertyassets

None 50% oftotal assets

35% totalasset***

None None 45% oftotal assets

50% Limit to200% ofequity

35%

Payout 90%+ oftaxableincome(postdeprec.)

100% oftaxableincome(postdeprec.)

100% offiscalearnings

85% ofdistributablecash (pre-deprec.)

80% oftaxableincome andnet debtpaydown

100% oftaxableincome (nodeprec.)

90%+ oftaxableincome(postdeprec.)

85% oftaxableincomefromrentals,50% ofcapitalgains

90% + ofnet incomeafter tax (nodeprec.)

Norestrictions(butundistributedearnings istaxed at 28%)

90%+ ofequity lesscapital andreserve

100% ofdistributableincome(post)expense andreserve)

Closed Ended** Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Closed endedmostly,opened endneed gov.’sapproval

Listed/Unlisted** Both Both Both Listed Listed Listed Listed Listed Listed Both Both Both

Tax Transparency Yes Yes Yes^ Yes Yes^ Yes Yes Yes^ No** Yes Yes Yes+

Notes: * This is a condition of entry into the LPT index, not a regulatory requirement. ^Taxed at source on overseas income and non-exempt activities such as development (France only). ** Not needed as there is no tax ondividends in HK. ^^Currently Germany is the only country with tax transparent option that is unlisted and open ended that is available to both tax paying and tax exempt investors. ***With ›35% with an A rating. ^^^Capital gains from the tax -exempt portion can be distributed in-line with tax treatment of rent. + No tax on capital gain, but 6% on dividend gain. Source: UBS (2007)

6

Given the increasing significance of REITs in Asia and specifically in Malaysia, this

thesis focuses on the significance and performance of REITs in Malaysia from August

2005 to December 2008; particularly focusing on the development, risk-adjusted

performance and portfolio diversification benefits of Islamic REITs in Malaysia, as

well as their investor acceptance.

To further establish this property context, the next segment will discuss property

investment, as property is considered to be a significance asset class, with a unique

role in a diversified portfolio. Property investment can be divided into two

fundamental approaches; direct property (unsecuritised physical asset/ private

property) and indirect property (securitized investment backed by property/ public

property). Different concepts, rules and regulations for investing in property may

apply for every country. Figure 1.1 shows the typical risk-return spectrum for

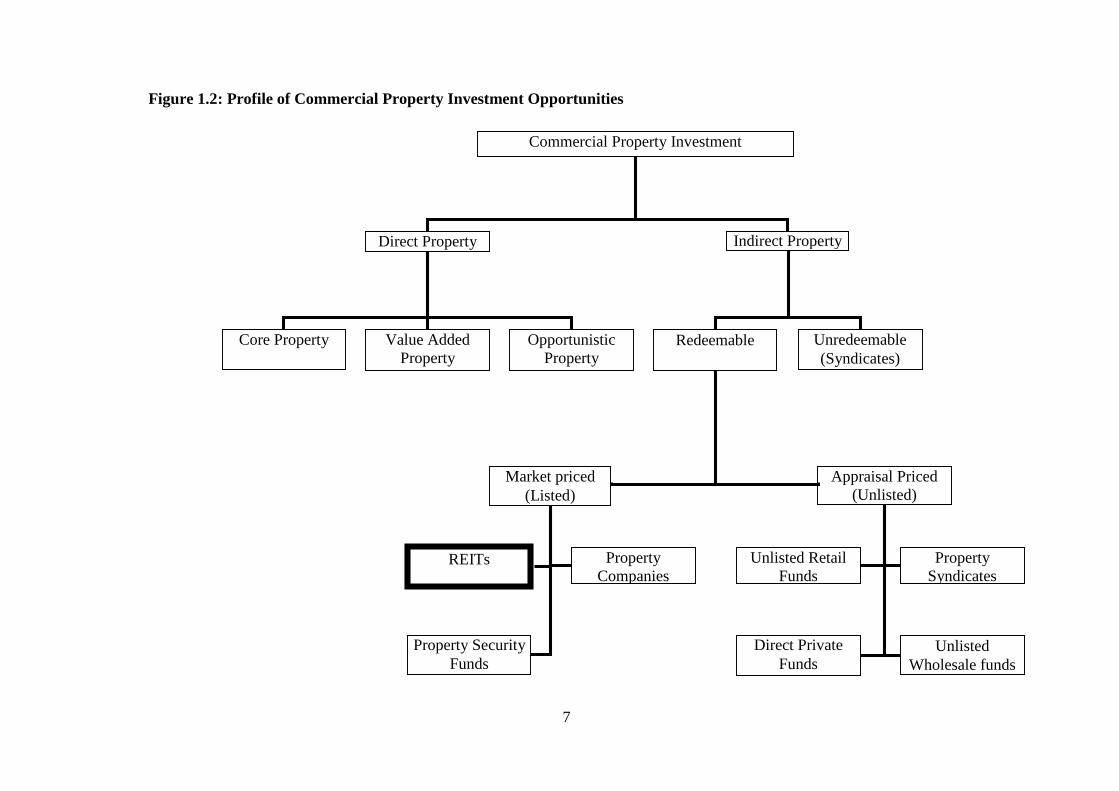

different types of property investment, while Figure 1.2 shows the profile of

commercial property investment opportunities; with this thesis focusing on REITs in

Malaysia.

Figure 1.1: Risk-return Spectrum of Commercial Property Investment

Opportunities

7

Figure 1.2: Profile of Commercial Property Investment Opportunities

Commercial Property Investment

Direct Property

Core Property

Indirect Property

Redeemable Unredeemable(Syndicates)

Market priced(Listed)

Appraisal Priced(Unlisted)

OpportunisticProperty

Value AddedProperty

REITs PropertyCompanies

Property SecurityFunds

Unlisted RetailFunds

PropertySyndicates

Direct PrivateFunds

UnlistedWholesale funds

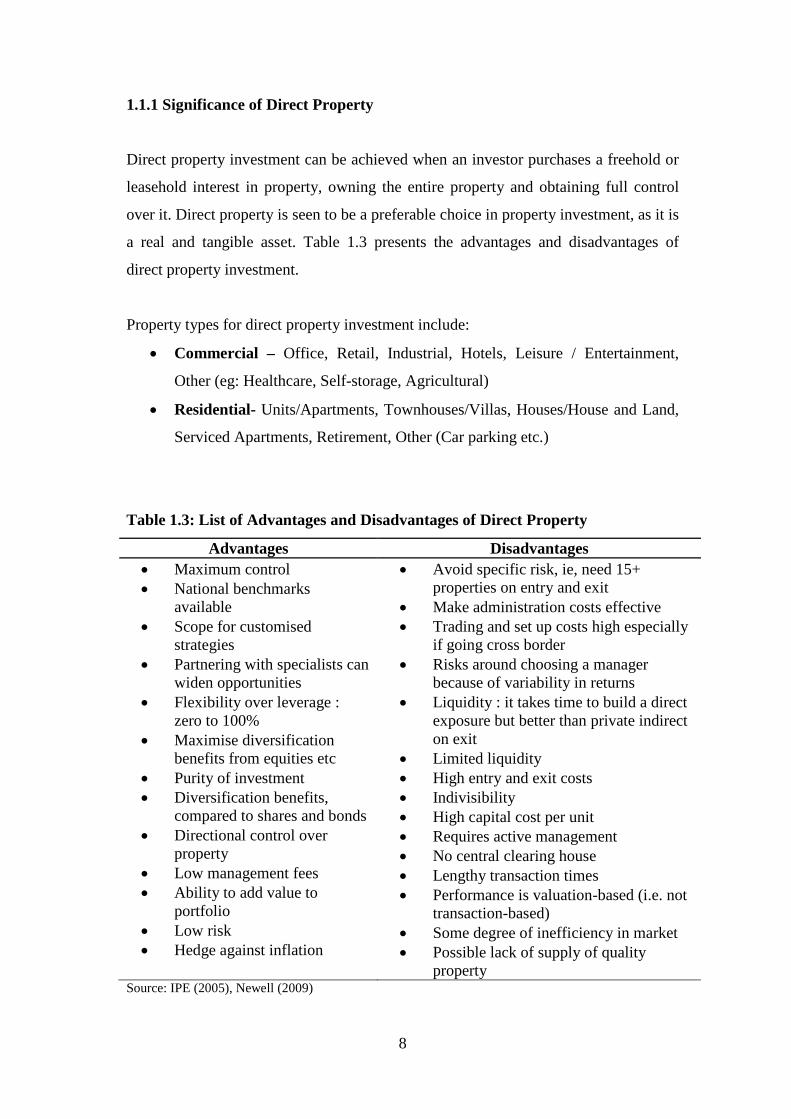

8

1.1.1 Significance of Direct Property

Direct property investment can be achieved when an investor purchases a freehold or

leasehold interest in property, owning the entire property and obtaining full control

over it. Direct property is seen to be a preferable choice in property investment, as it is

a real and tangible asset. Table 1.3 presents the advantages and disadvantages of

direct property investment.

Property types for direct property investment include:

Commercial – Office, Retail, Industrial, Hotels, Leisure / Entertainment,

Other (eg: Healthcare, Self-storage, Agricultural)

Residential- Units/Apartments, Townhouses/Villas, Houses/House and Land,

Serviced Apartments, Retirement, Other (Car parking etc.)

Table 1.3: List of Advantages and Disadvantages of Direct Property

Advantages Disadvantages

Maximum control National benchmarks

available Scope for customised

strategies Partnering with specialists can

widen opportunities Flexibility over leverage :

zero to 100% Maximise diversification

benefits from equities etc Purity of investment Diversification benefits,

compared to shares and bonds Directional control over

property Low management fees Ability to add value to

portfolio Low risk Hedge against inflation

Avoid specific risk, ie, need 15+properties on entry and exit

Make administration costs effective Trading and set up costs high especially

if going cross border Risks around choosing a manager

because of variability in returns Liquidity : it takes time to build a direct

exposure but better than private indirecton exit

Limited liquidity High entry and exit costs Indivisibility High capital cost per unit Requires active management No central clearing house Lengthy transaction times Performance is valuation-based (i.e. not

transaction-based) Some degree of inefficiency in market Possible lack of supply of quality

propertySource: IPE (2005), Newell (2009)

9

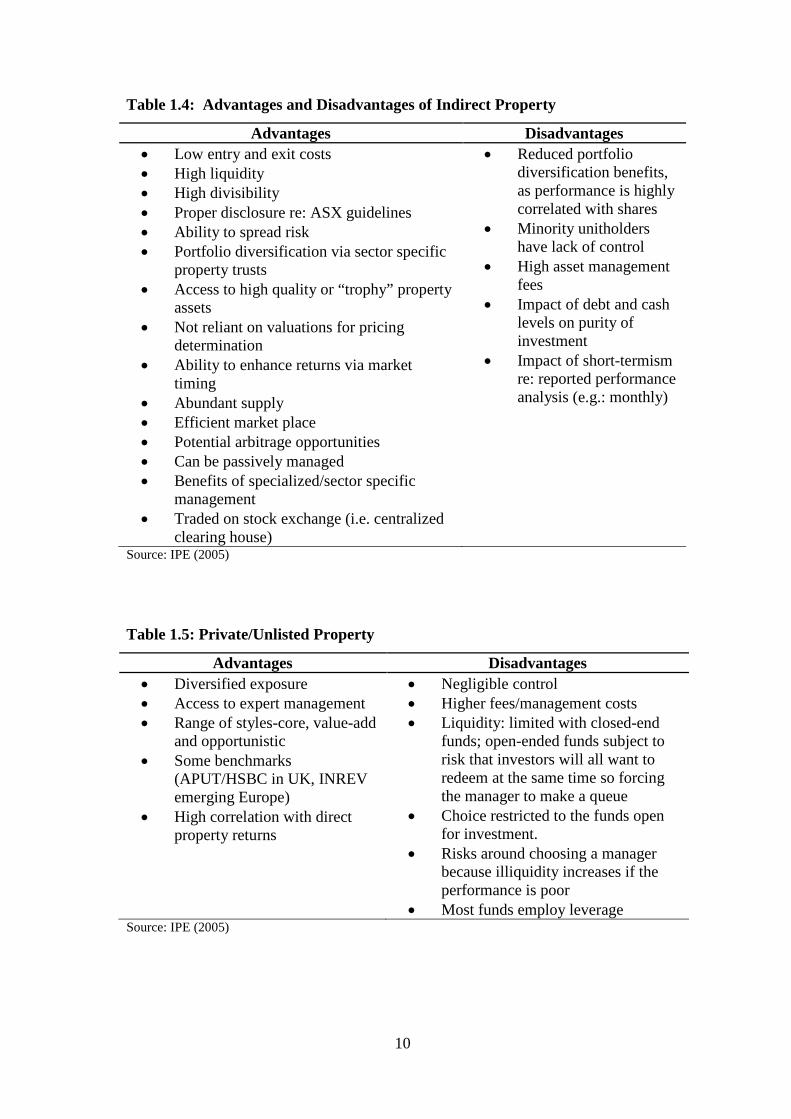

1.1.2 Significance of Indirect Property

Indirect property is generally considered to be a financial asset. Indirect property

investment can be achieved when an investor purchases units in a pooled investment;

thus gaining partial ownership of the property (i.e. shares in property company, REIT,

property trust or any company specialising in property dealings). Investors do not

have full control over this ownership, although they will obtain liquidity aspects of a

property asset. Investors will receive financial returns without having to use

substantial capital on purchasing. Tables 1.4, 1.5 and 1.6 show the advantages and

disadvantages of indirect property investment for these various property investment

vehicles.

Types of indirect property investment include:

Real Estate Investment Trust/Property Securities Funds – Real Estate

Investment Trust or Company (REIT)

Unlisted Property Trusts - Unlisted Wholesale Fund, Unlisted Retail Fund

Other Unlisted Entities- eg: Direct Private Fund

Mortgage Securities/Mezzanine Funds & Debentures -Mortgage Scheme

Debentures, Mortgage Fund Pooled, Mortgage Scheme Select

Property Investment Schemes Syndicates-Property Investment Schemes,

Strata Title Scheme, Direct Property Syndicates

10

Table 1.4: Advantages and Disadvantages of Indirect Property

Advantages Disadvantages

Low entry and exit costs High liquidity High divisibility Proper disclosure re: ASX guidelines Ability to spread risk Portfolio diversification via sector specific

property trusts Access to high quality or “trophy” property

assets Not reliant on valuations for pricing

determination Ability to enhance returns via market

timing Abundant supply Efficient market place Potential arbitrage opportunities Can be passively managed Benefits of specialized/sector specific

management Traded on stock exchange (i.e. centralized

clearing house)

Reduced portfoliodiversification benefits,as performance is highlycorrelated with shares

Minority unitholdershave lack of control

High asset managementfees

Impact of debt and cashlevels on purity ofinvestment

Impact of short-termismre: reported performanceanalysis (e.g.: monthly)

Source: IPE (2005)

Table 1.5: Private/Unlisted Property

Advantages Disadvantages

Diversified exposure Access to expert management Range of styles-core, value-add

and opportunistic Some benchmarks

(APUT/HSBC in UK, INREVemerging Europe)

High correlation with directproperty returns

Negligible control Higher fees/management costs Liquidity: limited with closed-end

funds; open-ended funds subject torisk that investors will all want toredeem at the same time so forcingthe manager to make a queue

Choice restricted to the funds openfor investment.

Risks around choosing a managerbecause illiquidity increases if theperformance is poor

Most funds employ leverageSource: IPE (2005)

11

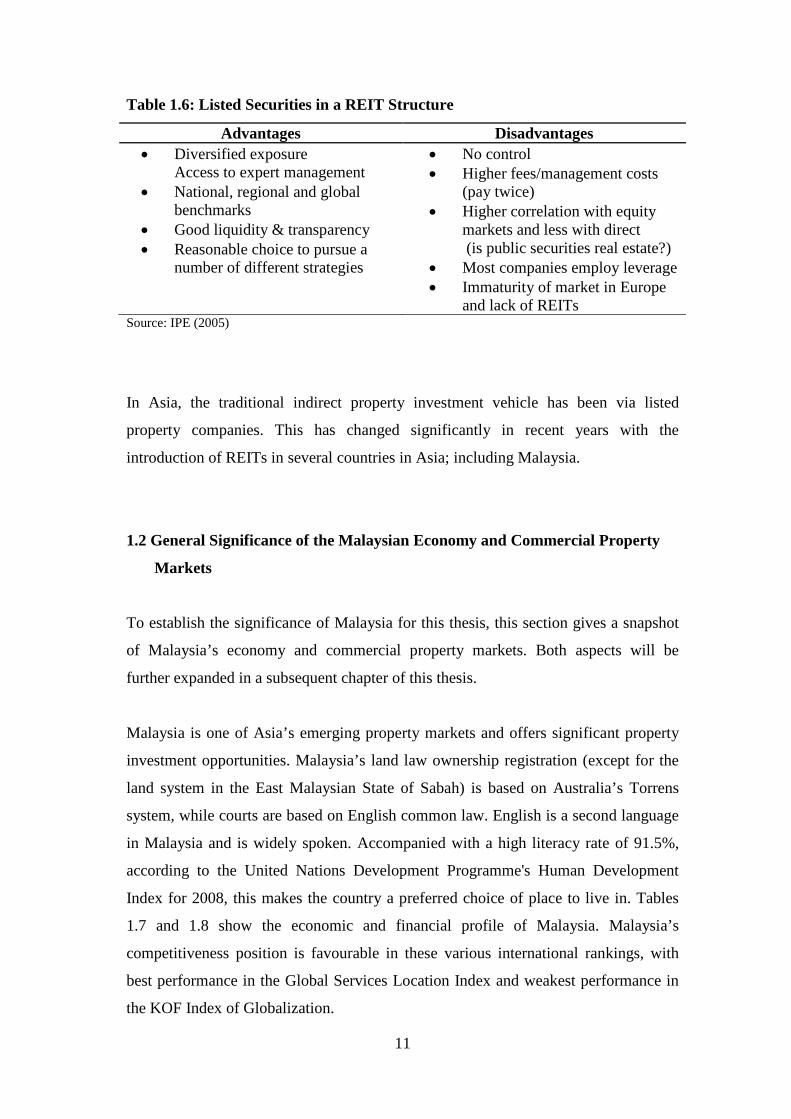

Table 1.6: Listed Securities in a REIT Structure

Advantages Disadvantages

Diversified exposureAccess to expert management

National, regional and globalbenchmarks

Good liquidity & transparency Reasonable choice to pursue a

number of different strategies

No control Higher fees/management costs

(pay twice) Higher correlation with equity

markets and less with direct(is public securities real estate?)

Most companies employ leverage Immaturity of market in Europe

and lack of REITsSource: IPE (2005)

In Asia, the traditional indirect property investment vehicle has been via listed

property companies. This has changed significantly in recent years with the

introduction of REITs in several countries in Asia; including Malaysia.

1.2 General Significance of the Malaysian Economy and Commercial Property

Markets

To establish the significance of Malaysia for this thesis, this section gives a snapshot

of Malaysia’s economy and commercial property markets. Both aspects will be

further expanded in a subsequent chapter of this thesis.

Malaysia is one of Asia’s emerging property markets and offers significant property

investment opportunities. Malaysia’s land law ownership registration (except for the

land system in the East Malaysian State of Sabah) is based on Australia’s Torrens

system, while courts are based on English common law. English is a second language

in Malaysia and is widely spoken. Accompanied with a high literacy rate of 91.5%,

according to the United Nations Development Programme's Human Development

Index for 2008, this makes the country a preferred choice of place to live in. Tables

1.7 and 1.8 show the economic and financial profile of Malaysia. Malaysia’s

competitiveness position is favourable in these various international rankings, with

best performance in the Global Services Location Index and weakest performance in

the KOF Index of Globalization.

12

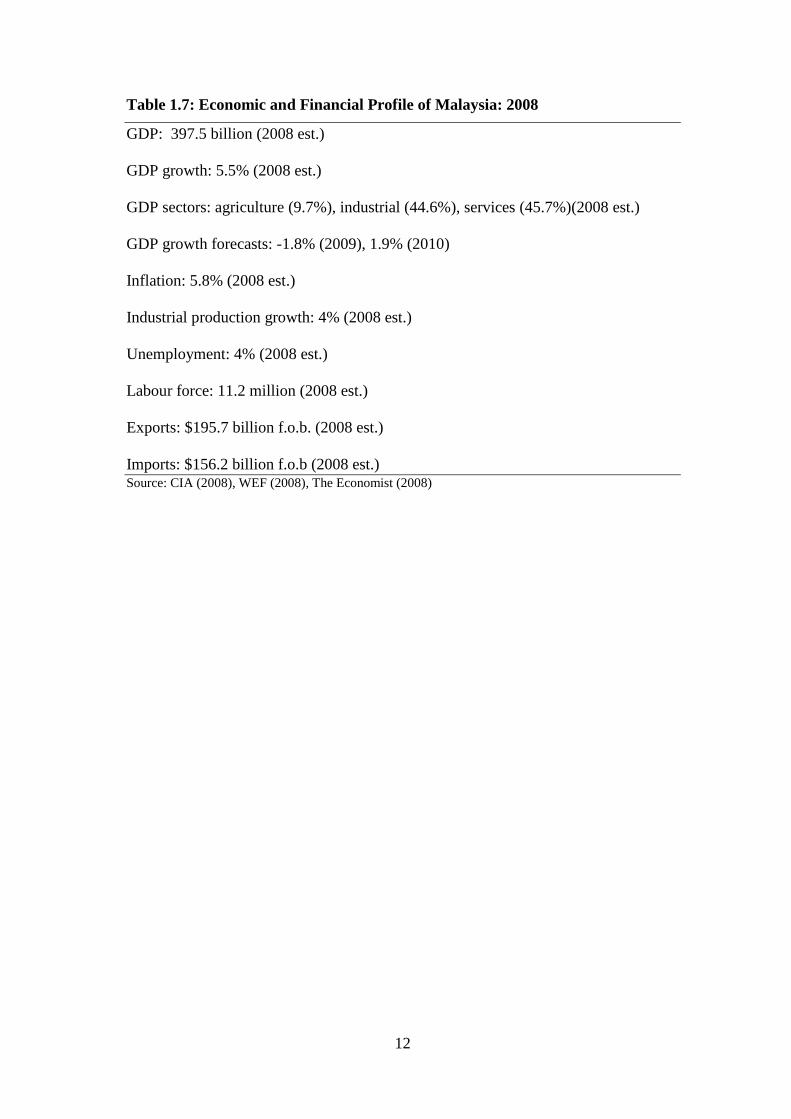

Table 1.7: Economic and Financial Profile of Malaysia: 2008

GDP: 397.5 billion (2008 est.)

GDP growth: 5.5% (2008 est.)

GDP sectors: agriculture (9.7%), industrial (44.6%), services (45.7%)(2008 est.)

GDP growth forecasts: -1.8% (2009), 1.9% (2010)

Inflation: 5.8% (2008 est.)

Industrial production growth: 4% (2008 est.)

Unemployment: 4% (2008 est.)

Labour force: 11.2 million (2008 est.)

Exports: $195.7 billion f.o.b. (2008 est.)

Imports: $156.2 billion f.o.b (2008 est.)Source: CIA (2008), WEF (2008), The Economist (2008)

13

Table 1.8: Global Competitiveness of Malaysia

IMD World Competitiveness Yearbook 2008: 19 (out of 55)

AT Kearney Global Retail Development Index 2008: 13 (out of 30)

AT Kearney Global Services Location Index 2007: 3 (out of 40)

World Bank Doing Business 2008: 20 (out of 181)

Economic Freedom of the World 2008: 72 (out of 141)

Index of Economic Freedom 2009: 58 (out of 183)

KOF Index of Globalization 2008: 24 (out of 80)

World Economic Forum: Global Competitiveness Index 2008-2009: 21 (out of 134)

Economist Intelligence Unit: E-readiness 2008: 34 (out of 70)

The Economist Intelligence Unit: Global Peace Index 2007-2008: 37 (out of 140)

Transparency International: Corruption Perceptions Index 2008: 43 (out of 180)

Yale University: Environmental Performance Index 2008: ranked 27 (out of 150)Source: various international rankings

Even with the economic slowdown in 2008 (GDP has growth around 6% per annum

in 2007), there is major growth potential in Malaysia’s commercial property markets.

In particular, Malaysia offers both conventional and Islamic financing. Increased

competition between banks is likely to force down lending margins, which will have

an impact on property valuations. Islamic financing has increased international

interest in Malaysian property, particularly from major investors in the Middle East.

In addition, the property market in Malaysia has attracted international investors. In

2006, Malaysia accounts for 49.05% of property ownership in Malaysia while the rest

are owned by foreign investors from Singapore (7.96%), United Kingdom (6.69%),

United States (6.1%), Australia 4.65%, Hong Kong (2.64%), United Arab Emirates

(2.01%), Canada (1.48%), Japan (1.2%) and India (1.09%) (Doug Pierce, 2007).

14

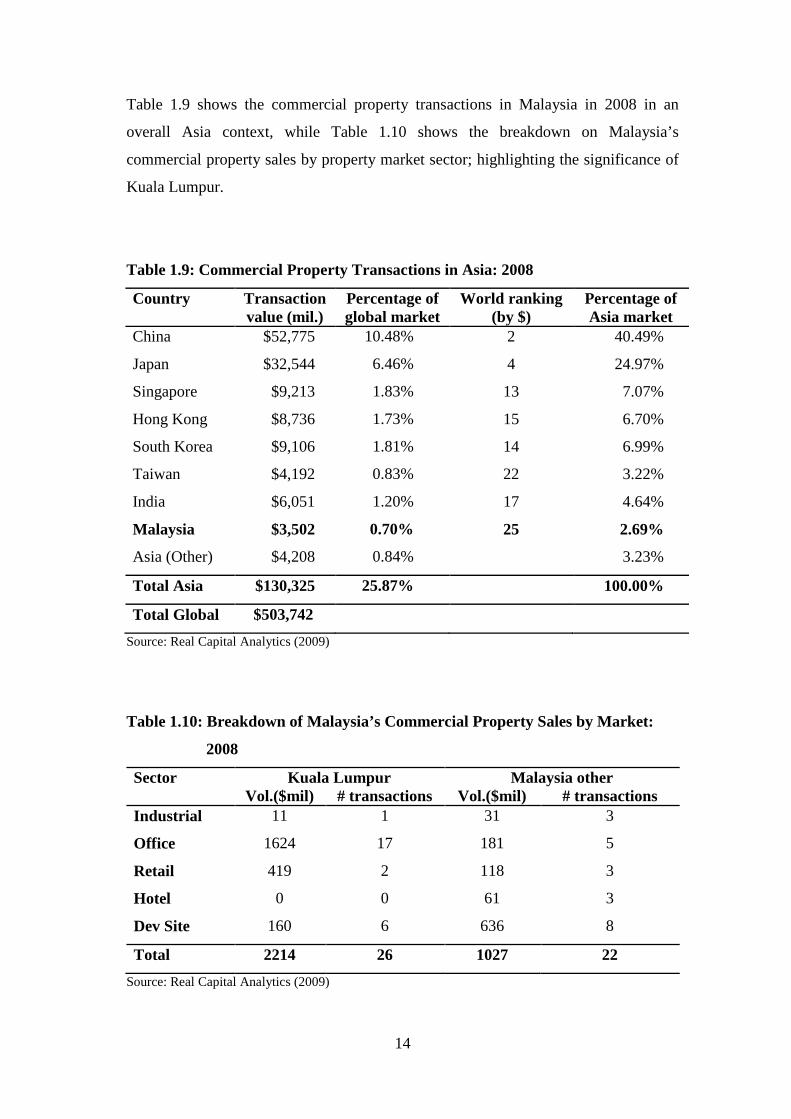

Table 1.9 shows the commercial property transactions in Malaysia in 2008 in an

overall Asia context, while Table 1.10 shows the breakdown on Malaysia’s

commercial property sales by property market sector; highlighting the significance of

Kuala Lumpur.

Table 1.9: Commercial Property Transactions in Asia: 2008

Country Transactionvalue (mil.)

Percentage ofglobal market

World ranking(by $)

Percentage ofAsia market

China $52,775 10.48% 2 40.49%

Japan $32,544 6.46% 4 24.97%

Singapore $9,213 1.83% 13 7.07%

Hong Kong $8,736 1.73% 15 6.70%

South Korea $9,106 1.81% 14 6.99%

Taiwan $4,192 0.83% 22 3.22%

India $6,051 1.20% 17 4.64%

Malaysia $3,502 0.70% 25 2.69%

Asia (Other) $4,208 0.84% 3.23%

Total Asia $130,325 25.87% 100.00%

Total Global $503,742

Source: Real Capital Analytics (2009)

Table 1.10: Breakdown of Malaysia’s Commercial Property Sales by Market:

2008

Sector Kuala Lumpur Malaysia otherVol.($mil) # transactions Vol.($mil) # transactions

Industrial 11 1 31 3

Office 1624 17 181 5

Retail 419 2 118 3

Hotel 0 0 61 3

Dev Site 160 6 636 8

Total 2214 26 1027 22

Source: Real Capital Analytics (2009)

15

1.2.1 Significance of REITs in Malaysia

Since the new issuance of REIT guidelines in 2005 and coupled with tax incentives,

REITs in Malaysia are seen to have a positive outlook following their wider

acceptance and increasing attention from institutional investors. Revised guidelines

have allowed more flexibility in terms of management, acquisition and borrowing

limits, while the inclusion of Islamic REITs in 2006 has encouraged participation of

international investors.

To further strengthen the M-REIT context, this is under-pinned by a strong local

commercial property market in Malaysia. Despite the global financial crisis, office

and retail markets managed to attain a post-stage (low but increasing vacancy rates)

position in 2008, with an increase in rent momentum. Meanwhile, the industrial

market is at growth stage (low and declining vacancy rates stage) with a stable rent

momentum (RREEF Research, 2009).

The office sector in Malaysia still has the capability to attain lower vacancy rates,

which decreased from 8.5% to 7.1% in 4Q:2008 in the Golden Triangle and CBD,

Kuala Lumpur (JLL, 2009) accompanied with an average rising rental rate of RM

7.10 psf. (US$2.05 psf.) per month, an increase of 9.2% (q-o-q) and 19.3% (y-o-y)

(CBRE, 2008). Although, Grade A vacancy rate fell by 80 bps to 6.9%, net absorption

was a positive 919,000 sf. for the fourth quarter of 2008. Unfortunately, retail rent

dropped, as the Consumer Sentiment Index fell from 88.9 points to 71.4 points in the

fourth quarter of 2008. It is also projected for the office and retail sectors to be under

contraction with a decrease in rent momentum until 2010. However, the industrial

sector will be in post-growth condition, with a stable rent momentum until 2010. This

indicates that industrial REITs could still generate a good return for investment.

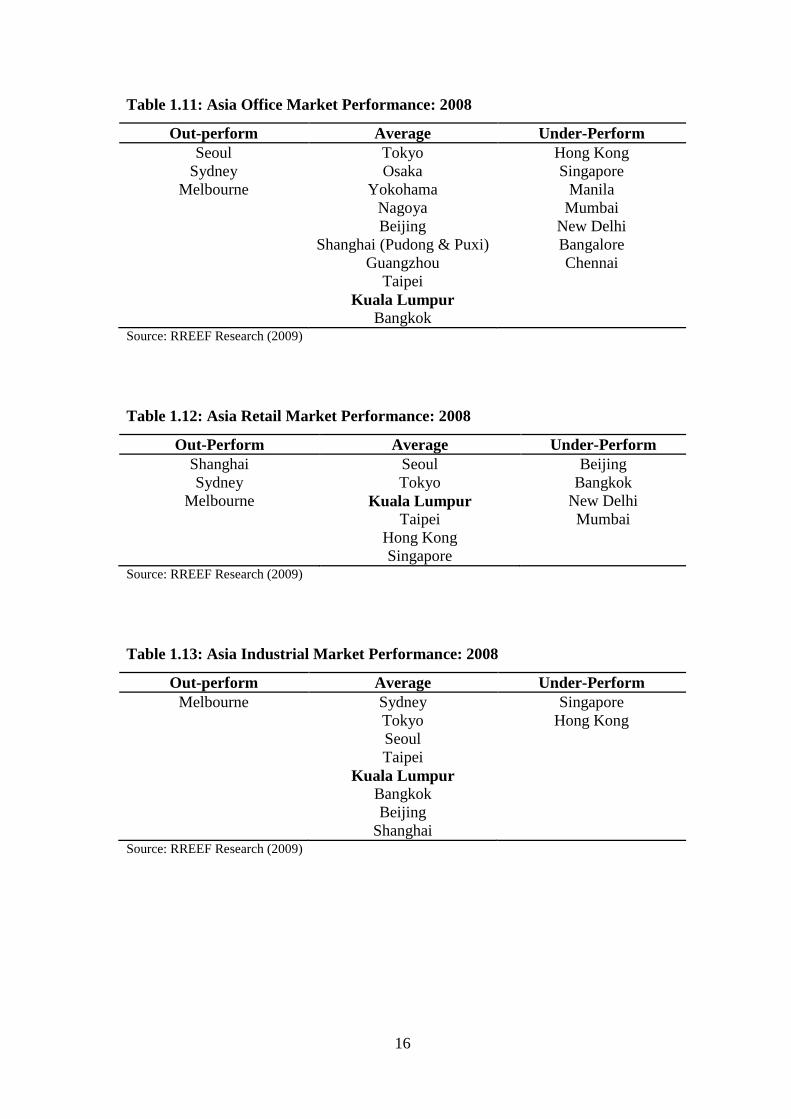

Tables 1.11, 1.12 and 1.13 shows the strong performance of the office, retail and

industrial property markets in Malaysia in an Asia context.

16

Table 1.11: Asia Office Market Performance: 2008

Out-perform Average Under-PerformSeoul

SydneyMelbourne

TokyoOsaka

YokohamaNagoyaBeijing

Shanghai (Pudong & Puxi)Guangzhou

TaipeiKuala Lumpur

Bangkok

Hong KongSingapore

ManilaMumbai

New DelhiBangaloreChennai

Source: RREEF Research (2009)

Table 1.12: Asia Retail Market Performance: 2008

Out-Perform Average Under-PerformShanghaiSydney

Melbourne

SeoulTokyo

Kuala LumpurTaipei

Hong KongSingapore

BeijingBangkok

New DelhiMumbai

Source: RREEF Research (2009)

Table 1.13: Asia Industrial Market Performance: 2008

Out-perform Average Under-PerformMelbourne Sydney

TokyoSeoulTaipei

Kuala LumpurBangkokBeijing

Shanghai

SingaporeHong Kong

Source: RREEF Research (2009)

17

1.3 Objectives of Study

This PhD research will examine the development, performance and impact of

Malaysian REITs in the local, Asian and global REIT investment market; particularly

focusing on Islamic REITs in Malaysia. This issue is important as REITs have

emerged as a topic of considerable interest to the academic community, international

investors, policy makers and the public at large; particularly with the recent

significant development of REITs in Asia in recent years. The main feature of this

thesis is the introduction and role of Islamic REITs as conventional REITs have been

studied vastly.

The objectives for this research are:

1. To compare the structure and regulation of Malaysian REITs with other

countries; both in Asia and internationally and differentiate the structure

between Malaysian conventional M-REITs and Islamic M-REITs

2. To develop an Malaysian REIT performance index and a sub-sector Islamic

M-REIT performance index and identify the impact of the Global Financial

Crisis on Malaysian REIT performance by analysing the risk-adjusted returns

performance for Malaysian REITs and Islamic M-REITs and analysing the

portfolio diversification benefits of Malaysian REITs and Islamic M-REITs in

a mixed-asset portfolio

3. To conduct an investment industry survey to identify the problems, challenges

and the possible solutions relating to a successful Malaysian REIT market.

4. To identify Malaysian REITs prospects by determining the strategy for its

further strategic development and investor acceptance.

This thesis aims to contribute to the development of a Malaysian REIT index, since a

Malaysian REIT performance series is currently not available. This will provide

investors and fund managers with more information about the returns on Malaysian

REITs. Furthermore, the development of the first Islamic M-REIT index in this thesis

will open greater opportunity and attract more Islamic investors in the future.

18

There are limitations in this research due to the short time series of Malaysian REIT

data. Even though Malaysian Property Trust Funds (PTF) data has existed since 1989,

REITs in Malaysia were only listed in August 2005, while an Islamic REIT in

Malaysia was only listed in August 2006. This research acknowledges that there is not

the equivalent extensive time series of performance data for Malaysian REITs that

typically can be used for empirical analyses for the traditional REIT markets of

Australia and US. This shorter time series is clearly evident for all research involving

REITs in Asia, given they have only been established since 2002. Whilst the

performance data may not cover a full investment or property cycle, this limitation is

recognized, and should not be considered to be an impediment to a rigorous and

insightful PhD research study seeking to enhance our understanding on the strategic

contribution of M-REITs in a global REIT context.

The key issue in this thesis is to develop Malaysian REIT performance indicators and

to do the analyses over August 2005- December 2008 for Malaysian REITs to provide

the basis for future research regarding the risk-adjusted performance, portfolio

diversification benefits and strategic development of Malaysian REITs as a successful

REIT product in Asia. The associated investors’ survey will see a much richer and

informed analysis than that just provided by the empirical performance analysis. This

research aims to contribute to and expand on the existing research on REITs;

particularly concerning the significance of Malaysian REITs and Islamic REITs.

Appropriate research questions and methodology used for analysis will be discussed

further in the next section on literature review. Literature review is the critical

component to see the understanding of relevant literature. The next section will

summarize the body of knowledge in this field including the major research questions,

techniques employed as well as their limitations. This will motivate the proposed

study by how it hopes to contribute to this body of knowledge.

19

1.4 Literature Review

1.4.1 Property in a Portfolio

This chapter will discuss the literature on international property research and REITs.

The major focus will be on the Asia property research; specifically Malaysian REITs.

Direct and indirect commercial property have been a major component of the global

investment universe (PREI, 2005) and property is seen to be an alternative asset due

to its inherent characteristics and relative immaturity in some developing markets

(RREEF, 2007). Direct property has consistently been found to be an effective hedge

against inflation in the US (Fama and Schwert, 1977; Hartzell et al, 1987; Gyourko

and Linneman, 1988; Rubens et al, 1989; Wurtzebach et al, 1991; Liu et al, 1997),

U.K. (Limmack and Ward, 1988; Matysiak et al, 1996; Liu et al, 1997), Australia

(Newell, 1996), New Zealand (Newell and Boyd, 1995), Canada (Newell, 1995),

Hong Kong (Ganesan and Chiang, 1998) and Singapore (Sing and Low, 2000). An

empirical study of the inflation-hedging characteristics of the four Chinese major

cities found the contrary, where direct property in these cities was not an effective

hedge against inflation (Chu and Sing, 2004). The widely accepted finding of

Wurtzebach et al (1991) concludes that direct property is a good hedge against

inflation when the vacancy rate is low, and failed as an inflation hedge when the

vacancy rate is high.

The role of direct property in mixed-asset portfolios is well documented. In one of the

earliest studies on direct property as a separate asset class in a mixed-asset portfolio,

Webb et al (1988) found that not only should property be included in a mixed-asset

portfolio, but also approximately two-thirds of the investment wealth should be

allocated to property. Subsequent studies by Ennis and Burik (1991), Hamelink and

Hoesli (1996), Ziobrowski and Ziobrowski (1997), Byrne and Lee (1997) also

confirmed mixed-asset portfolios containing direct property and financial assets

always dominated the financial assets portfolio and the allocation of property in a

mixed-asset portfolio is 15% to 30%. However, when the property data were

desmoothed to factor in appraisal bias, the portfolio diversification gain was reduced.

Despite the favourable findings of numerous studies, the actual allocation for property

in institutional investors’ portfolios is substantially lower than the suggested level

20

(Geltner and Miller, 2001). When the market imperfections of direct property such as

indivisibility and no short sales are taken into consideration (Kallberg et al, 1996) and

the allocation to property is evaluated in the framework of asset-liability (Craft,

2001), the lower allocation of property in institutional investors’ portfolios is justified.

Meanwhile, indirect property have been found to be a poor hedge against inflation in

the US (Gyourko and Linneman, 1988; Liu and Mei, 1992; Liu et al, 1997), U.K.

(Hoesli et al, 1997; Liu et al, 1997), Australia (Newell, 1996), Hong Kong (Ganesan

and Chiang, 1998) and Singapore (Sing and Low, 2000).

The indirect property market was found to lead the direct property market, indicating

indirect (securitised) property reflects information on prices quicker than direct

property appraisal values (Barkham and Geltner, 1995, 1996). As such, Stevenson

(2001) suggested that property trust vehicles might be used as a short-term market-

timing device. This is perhaps the greatest potential benefit for a property fund

manager considering REITs and other property trust vehicles as portfolio assets. The

higher volatility found in the REIT sector is always going to mean that risk-adjusted

asset allocation results are going to be biased towards direct property; however, such

tests will not accurately pick up the short-term market timing benefits that investors

could obtain. In such a case, a portfolio manager could use individual funds both to

switch the property exposure of the portfolio and to use REIT vehicles to gain access

to markets where there are limited property investment opportunities

Liang and McIntosh (1998) and Newell and Tan (2003) have provided evidence for

the diversification benefits of including REITs/LPTs in a mixed-asset portfolio. By

investigating the style and exposure of REITs, Liang and McIntosh (1998) concluded

that REITs have become more “unique” and consequently REITs should be included

in a mixed-asset portfolio to achieve a better risk-return trade-off, despite the styles of

REITs changing over time. However, Glascock et al (2000) found REITs were

cointegrated with direct property and argue that there was no role for REITs in

portfolio risk reduction. Despite the contrary evidence of Glascock et al (2000), it is

widely accepted that both REITs/LPTs (indirect property) and direct property warrant

an allocation in mixed-asset portfolios.

21

Studies reveal the improvements of portfolio diversification benefits by including

international property in a mixed-asset portfolio (eg: Bardhan et al, 2008; Hoesli et al,

2004; Bond et al, 2003; Ling and Naranjo, 2002; Conover et al, 2002; Steinert and

Crowe, 2001; Wilson and Okunev, 1996; Wilson and Zurbruegg, 2003; Worzala and

Sirmans, 2003), while Asian property markets have been proven to be more effective

than European property markets in international diversification (Bond et al, 2003).

Studies have shown international diversification benefits by investing into the Asian

property markets (eg: Bond et al, 2003; Garvey et al, 2001; Liow and Adair, 2009),

with property companies in Asia showing long-term diversification benefits (Garvey

et al, 2001). Property performance has also been specifically examined in selected

Asian countries; namely Singapore (eg: Liow, 2000, 2001a, 2001b; Ong, 1994, 1995;

Sing and Low, 2000), Hong Kong (eg: Newell and Chau, 1996; Schwann and Chau,

2005), India (eg: Newell and Kamineni, 2007). Major factors also contributing to this

increased international property exposure have included the need for portfolio

diversification, potential for higher returns, lower cost of capital and favourable

exchange rates (Worzala and Newell, 1997).

Recent research have examined various aspects of property performance in Asia (eg:

Bond et al, 2003; Jin et al, 2007; Liow, 2007, 2008; Liow and Adair, 2009; Liow and

Sim, 2006; Ooi and Liow, 2004; Wilson et al, 2007; Wilson and Zurbruegg, 2004)

Numerous papers have assessed the significance of Asian property companies,

including Liow (2000, 2001, 2008), Liow and Adair (2008), Liow and Sim (2006),

Newell and Chau (1996).

In terms of financial performance, Liang and McIntosh (1998) concludes direct

property should be classified as a different asset class with indirect property. Other

studies (Gyourko and Linneman, 1988; Liu et al, 1990) indicates that direct property

is uncorrelated with indirect property, while other studies found that they are linked to

one another by common property factors (Giliberto, 1990; Liu and Mei, 1992;

Gyourko and Keim, 1992).

22

1.4.2 REITs

1.4.2.1 REITs in US

Previous research on REITs has been extensive. The significant research in US REITs

has been reviewed (Corgel, Mcintosh and Ott, 1995; Zietz, Sirmans and Friday 2003).

It has been divided into 4 distinct categories and several subcategories; 1) REITs as

real estate and common stocks, 2) REIT asset acquisitions and dispositions, 3)

restructuring of REITs and 4) asset market information and REIT prices.

Research have shown that US REITs are viewed as hybrid securities (eg: Liu and

Mei, 1992), and REITs are integrated with the stock market (Li and Wang, 1995; Ling

and Naranjo, 1999). After 1992, Clayton and Mackinnon (2003) found equity REITs

behave more like real estate, although Lee, Lee and Chiang (2005) do not support this

finding. In terms of inflation hedging characteristics, Gyourko and Linneman (1988),

Park, Mullineux and Chew (1990), Chan, Hendershott and Sanders (1990), Liu and

Mei (1992) and Liu, Hartzell and Hoesli (1997) perceived REITs as having poor

ability against inflation. There is an indication of inflation-hedging capabilities in

other countries (Liu, Hartzell and Hoesli, 1997) and in the long-term (Goebel and

Kim, 1989). REITs are also seen as ideal for reducing portfolio risk (Goldstein and

Nelling, 1999).

Researchers such as Smith and Shulman (1976), Titman and Warga (1986), and

Goebel and Kim (1989) also suggested that the performance of REITs was worse

than, or comparable to, the market portfolio. Others such as Burns and Epley (1982),

Kuhle (1987), and Sagalyn (1990) found that REITs outperformed the stock market

portfolio. According to Smith and Shulman (1976), 16 REITs in the period of 1963-

1973 and 102 REITs in the period of 1977-1984 (Kuhle and Walther, 1986)

outperformed the S&P index although in 1974, both research conducted suggested

REITs underperformed the S&P index during the recession period. Mixed results

were also reported by Chan, Hendershott and Sanders (1990), and Howe and Shilling

(1990), while Liu, Hartzell, Grissom and Wylie (1990) investigated the sensitivity of

performance measures to the choice of market portfolios. Subsequently, Han and

Liang (1995) in assessment of the long-term performance of US-REITs from 1970 to

23

1993 found that the performance of survivors-only samples may not be a good

representation of the performance of the overall REIT industry.

Newell and Fife (1995) report that based on the REITs analysed for the period of

1980 to 1995, the success of US REITs was contributed to by the improved

management structures and benefits of the Tax Reform Act 1986 which allows REIT

owners to own and manage properties. In corporate restructuring, mergers provide

significant wealth increases for the acquiring REIT shareholders especially with

similar portfolio of assets (Allen and Sirmans, 1987). In term of dividends, REITs pay

out high dividends than mortgage REITs (Chan, Erickson and Wang, 2003) and other

regular REITs and firms with fluctuating dividends will be penalised (Kallberg, Liu

and Srinivasan, 2003).

1.4.2.2 A-REITs in Australia

LPTs was the previous name for REITs in Australia, which were rebadged as A-

REITs in 2008. Research has shown that LPTs have been a successful indirect

vehicle; largely because of its tax transparency and investor acceptance. LPTs account

for 40% of institutional property exposure compared to 20% in mid to late 1980s.

Newell (2005) observed and documented these past studies and used a variance

decomposition procedure to assess the proportion of LPT volatility that is attributable

to stock, bond and property factors over 1985-2004. The dynamics of this LPT

performance is also assessed. Property is seen to only make a small contribution to

LPT variability, with the contribution of property only marginally increasing in recent

years with the increased maturity of the LPT sector. The importance of stocks in LPT

performance has decreased significantly, with bonds being the most dominant

component in LPT performance in recent years.

The success of A-REITs has also been examined in specific research on performance

analysis issues (Lee et al, 2007, 2008; Newell, 2006; Newell and Peng, 2006; Newell

and Tan, 2003, 2004; Peng, 2004; Tan, 2004a, 2004b; Ratcliffe and Dimovski, 2007),

as well as IPO or financing issues (Chikolwa, 2007, 2008; Dimovski and Brooks,

2006a, 2006b, 2007) and investor acceptance (Newell, 2007a, 2007b, 2008). In terms

24

of fund manager decision making (Newell and McIntosh, 2007; Newell and Peng,

2008; Tan, 2004c, 2004d). According to Ratcliffe and Dimovski (2007), there is an

increase in the market risk profile of LPTs, suggesting an erosion of the defensive

benefits of LPTs against stockmarket volatilities. The study also finds that the degree

of financial leverage has a positive and significant impact on the level of market and

interest rate risk for LPTs. There is also some evidence that the level of diversification

across different property types reduces market risk.

1.4.3 REITs in Asia

Recent years have seen improvement in maturity and transparency in many

international commercial property markets in Asia (Chin and Dent , 2006; Chin et al,

2006; JLL, 2008) which have led to the introduction of Asian REITs in recent years

(Chin et al, 2006; JLL, 2008; Ooi et al, 2006; Lin, 2007). Although research on Asian

property companies has been extensive, research on Asia REITs is limited. Given the

recent establishment of REITs in Asia, only limited research has been conducted in

this increasingly important area; this includes Chiang et al (2008), Kutsuna et al.

(2008), Lin (2007), Ooi et al. (2006), and Quek and Ong (2008); largely concentrating

on developmental and IPO aspects of REITs in the larger REIT markets in Asia;

namely Japan, Singapore and Hong Kong. Ooi and Newell (2005) examined the

different background of Asian REIT markets, while Kutsuna, Dimovski and Brooks

(2008) have assessed the success of the J-REIT IPO market, which have influenced

the legislation and listing of other Asian REIT markets. From 2001 to 2006, the J-

REIT market reported a 0.5% average underpricing, which was not a statistically

different to zero underpricing. Chua and Kitamura (2004) showed that the

development of Japan REITs was supported by the improved transparency of the

property market and the development of non-recourse loans and a low interest rate

which is close to zero. Meanwhile, in Singapore and Korea, higher entrance

thresholds and restrictions on borrowing have constrained their REIT development.

Carr, Dimovski, Newell, Ooi and Yap (2009) assessed the REIT IPO underpricing in

3 Asian countries; Singapore, Hong Kong and Malaysia. The study reveals the mean

25

underpricing for 34 REIT IPOs from 2000-2007 is 5.77%, which is the highest

amongst the published Singapore and Malaysia REIT literature to date.

1.4.4 M-REITs in Malaysia

Earlier research on Malaysian property markets was on property companies, largely

concerning the role of Malaysian property companies in a pan-Asia context (Liow,

2008; Liow & Adair, 2009; Liow & Sim, 2006; Newell, Liow, Ooi & Haihong, 2005),

board composition issues (Shakir, 2008a, 2008b, 2009), capital structure (Ameer,

2007; Mahmood & Zakaria, 2007), sustainability issues (Newell & Manaf, 2008) and

corporate real estate (Ting, Nassir, Newell and Hassan, 2006). Published evidence on

the performance of listed property trusts in Malaysia is very limited. REITs/LPTs

were established in Malaysia in 1990 as property trust funds (PTFs), but were not

successful due to restrictive LPT market conditions and the restrictive Guidelines on

Property Trust Funds (Ting, 2002; Foong, 2005). Kok and Khoo (1995) examined the

performance and the systematic risk of three PTFs, namely Arab Malaysian First

Property Trust, First Malaysia Property Trust and Amanah Harta Tanah PNB, over the

January 1991-April 1995 period. The PTFs did not give consistent performance over

time. The systematic risks of the listed property trusts were low before the period of

over-speculation. However, after the period of over-speculation, the systematic risks

were higher than those of the market. They also discovered that the systematic risk

rankings of the listed property trusts were not consistent over time.

Newell, Ting and Acheampong (2002) analysed the performance of four Malaysian

property trusts, over the 1991-2000 period. Based on a coefficient of variation

measure, they concluded that PTFs in Malaysia underperformed other competing

investment vehicles such as shares. Other factors contributing to this lesser

performance include a low level of institutional investors’ participation (Ting, 2000),

thin volume of trading, too small market capitalisation of LPTs in Malaysia, slow

capital appreciation, poor historical returns of LPTs, low dividend yield compared to

other investment options, low fluctuation in returns, lack of portfolio management

expertise in LPTs and non-performing of the property sector (Lee, Hishamuddin and

Lee, 2005). This has seen the Malaysian government revive their REIT regulations in

26

2005 to stimulate the REIT market in Malaysia, resulting in a surge in the

establishment of REITs since 2005.

An online survey was conducted by Latham Consulting between 20th November 2007

and 16th December 2007. Their survey was distributed to senior, very experienced

and well respected property professionals, ranging from Fund Managers (31%),

Property Professionals (28%), Lawyers/Tax/Accounting professionals (22%) and

Merchant Bankers/Property owners (18%) from 49 companies in 6 key countries. The

sample quality of respondents are exceptional, with 98% having spent their time

residing or working in Asia, while 60% worked with international companies.

According to the report prepared by Trust, the objectives of the survey were to

understand the perceptions and attitudes of key stakeholders in the region of the

relevant REIT markets. They have presented the results from all respondent for their

survey by converting the five-point ratings scale to an index where 100 equals the

average score. From 11 countries, Malaysia has improved its rank from 8 to 7 (5%

increase in index) for ‘Overall Potential’ and from 6 to 5 for ‘Regulatory Support’

(+7%), while maintaining the same rank for ‘Property Market Growth’ (+1%) and

‘REIT Opportunity’ (+7%).

Several factors may have affected the performance and development of REITs in

Malaysia such as market size, advisor type, tax rate, interest rate, inflation rate and

institutional investor participation. In Malaysia, M-REITs have a low level of

institutional investor participation. In particular, the average annual unit holdings of

institutional possession for the sample period of 1989 to 1997 were 3.43% (Ting,

2000). A study conducted by Lee, Hishamuddin and Lee (2005) inspected the lack of

interests from institutional investors to REITs. The study surveyed 21 of 57 senior

fund managers which 10% are from insurance companies, 24% from asset

management and 66% from unit trusts. Results from the study suggest that

institutional investors have poor perception of LPTs in Malaysia. In Malaysia, trading

volume was found as the most important factor for lack of interest in M-REITs

followed by small market size of LPTs, slow capital appreciation, poor historical

returns of LPTs, low dividend yield compared to other investment types, low

fluctuation in returns, lack of management expertise and property sector not

performing well. Yaakop Yahaya Al-Haj and Hashim (2007) support the findings by

27

Lee, Hishamuddin and Lee (2005) which found that trading volume is the most

important factor that attracts institutional investors to invest in REITs.

On the other hand, an analysis by Ting (2000) of the annual stock turnover ratio

demonstrated that the transactional activities of REITs are low. The mean annual

stock turnover ratio of 0.33 for the 1990 to 1997 period contrasts poorly against the

ratio of other sectors of Bursa Malaysia. This shows poor demand and interest from

Malaysian investors on REIT stock. The unstable dividends declared by LPTs may

also have an affect on investor’s lack of interest on LPTs (Ting, 2007). This research

aims to examine the Malaysian REIT market and investors participation which will be

discuss in detail in the next chapters.

The only research specifically on M-REITs assessed the development of Islamic M-

REITs (Osmadi, 2006), and the risk-adjusted performance and portfolio

diversification benefits of Islamic M-REITs in a portfolio over 2006-2008;

particularly contrasting the performance of Islamic M-REITs and conventional M-

REITs over this period and during the global financial crisis (Newell and Osmadi,

2009). Overall, Islamic M-REITs were seen to be a differentiating property

investment product from conventional M-REITs, as well as displaying the defensive

characteristics of low risk levels and portfolio diversification benefits. The robustness

of these characteristics were further enhanced during the GFC (Newell and Osmadi,

2009). Ibrahim and Ong (2008) have assessed Islamic REITs by establishing synthetic

Shariah-compliant US REIT portfolios to assess their risk-adjusted performance

against the broader US REIT sectors and the 'cost' of Shariah-compliance. An

assessment by establishing synthetic Shariah-compliant A-REIT portfolios to assess

their risk-adjusted performance against the broader A-REIT sectors and the 'cost' of

Shariah-compliance is yet to be discovered. In order to understand how well the M-

REIT company performs, an analysis which provide the financial and management

strength statistics and ratios will be conducted as financial strength is one of the most

critical measures of the worth of an investment (the other two are stability and

growth) and buying companies with high management quality (Dynaquest). Greater

detail on these statistics will be analysed further in the following chapters.

28

A survey to assess the importance of factors influencing the future development of M-

REITs was conducted over October – December 2007. The survey addressed a range

of factors influencing the future development of M-REITs. These factors were

identified by a literature review of the development of REITs in Asia (eg: Ooi et al.,

2006) and an assessment of previous REIT surveys conducted by one of the authors.

These factors comprehensively covered the areas of M-REIT structure, tax, regulatory

environment, industry structure, investor acceptance, property market environment,

property performance and individual property-specific issues.

Previous empirical research has generally found no significant differences between

the risk-adjusted performances of Islamic stocks versus non-Islamic stocks. This has

included studies concerning the US (e.g. Girard & Hassan, 2008; Hakim & Rashidian,

2002; Hussein, 2004; Hussein & Omran, 2005), UK (Kok, Giorgioni & Lewis, 2009)

and Malaysia (e.g. Abdullah, Hassan & Mohamad, 2007; Ahmad & Ibrahim, 2002;

Albaity & Ahmad, 2008; Sadeghi, 2008; Yusof & Majid, 2006, 2007). The results of

these Islamic stock studies are consistent with similar studies involving the more

general aspects of the performance of ethical portfolios (e.g. Sauer, 1997) and socially

responsible investing (e.g. Guerard, 1997; Kreander, Gray, Power & Sinclair, 2005).

There was also some evidence of Islamic stocks out-performing conventional stocks