Embed Size (px)

Citation preview

Presented by,Mrinalini singhAnurag samaddar

Total income

First head: House property. Second head: Business and

Profession. Third head: Capital gain. Forth head: Other sources. Set off and carry forward of

loses. Total income

Contents First head: House property. Second head: Business and

Profession. Third head: Capital gain. Forth head: Other sources. Set off and carry forward of

loses. Total income

Total income

Houseproperty

Business And

profession

Capital gains

Other sources

Total income comprise

with 4 heads

First headHouse property

Three ways to use house property:

1.Self occupied.2.Business.3.Rented.

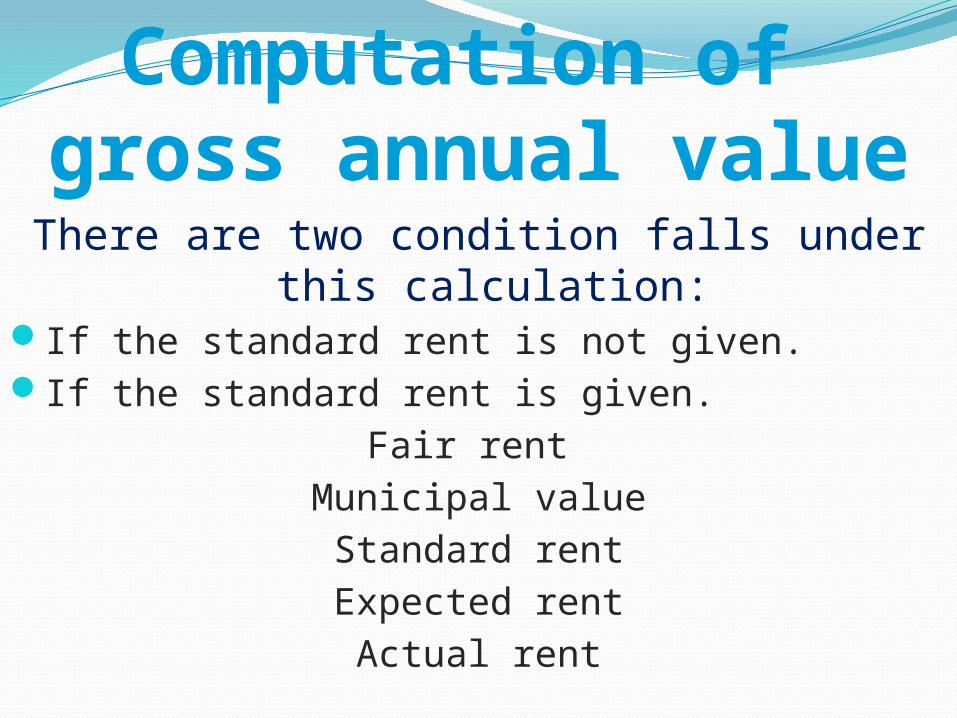

There are two condition falls under this calculation:

If the standard rent is not given.If the standard rent is given.

Fair rent Municipal valueStandard rentExpected rentActual rent

Computation of gross annual value

particulars

amount

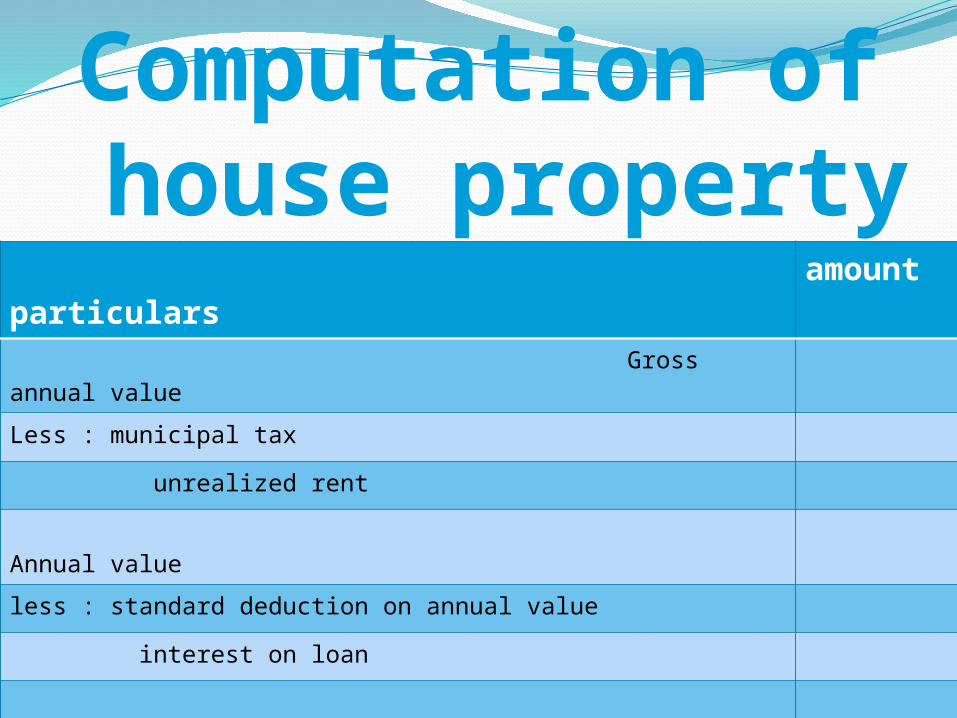

Gross annual valueLess : municipal tax unrealized rent Annual valueless : standard deduction on annual value interest on loan

Taxable income

Computation of house property

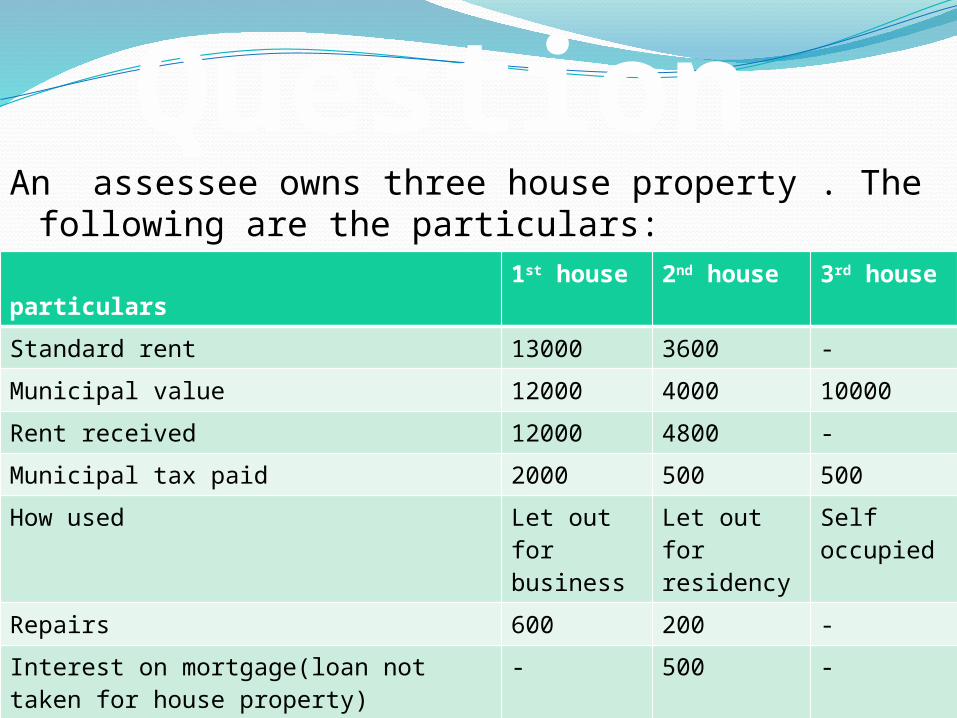

An assessee owns three house property . The following are the particulars:

particulars

1st house 2nd house 3rd house

Standard rent 13000 3600 -Municipal value 12000 4000 10000Rent received 12000 4800 -Municipal tax paid 2000 500 500How used Let out

for business

Let out for residency

Self occupied

Repairs 600 200 -Interest on mortgage(loan not taken for house property)

- 500 -

Ground rent 50 30 -Fire insurance premium 70 - -

Question

particulars

Amount

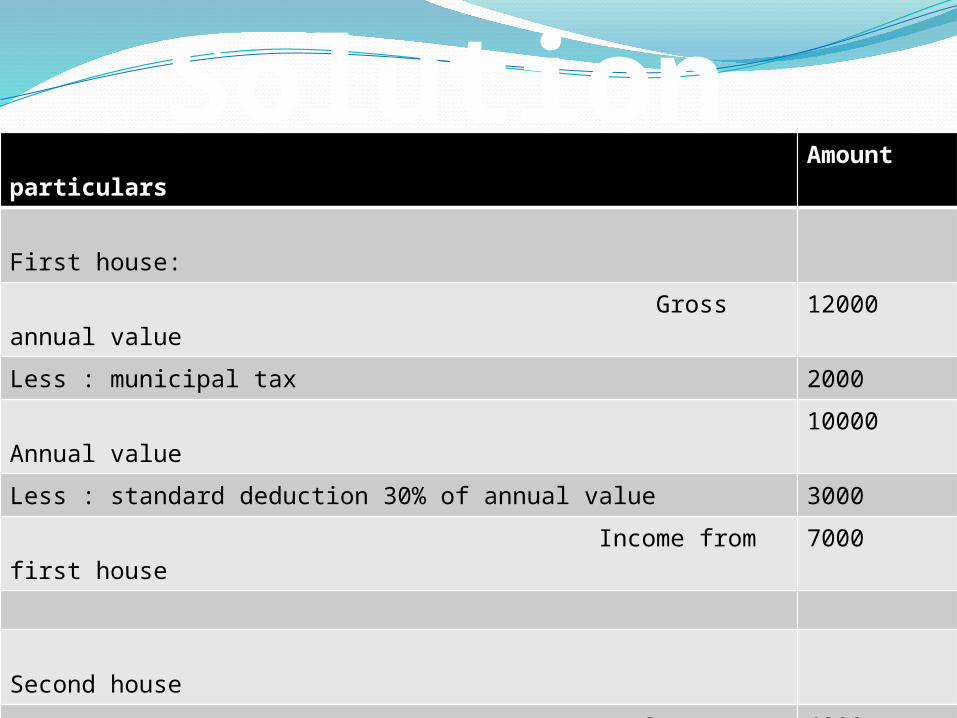

First house: Gross annual value

12000

Less : municipal tax 2000 Annual value

10000

Less : standard deduction 30% of annual value 3000 Income from first house

7000

Second house Gross annual value

4800

Less : municipal tax 500 Annual value

4300

Less : standard deduction 30% of annual value 1290 Interest of loan Nil Income from second house

3010

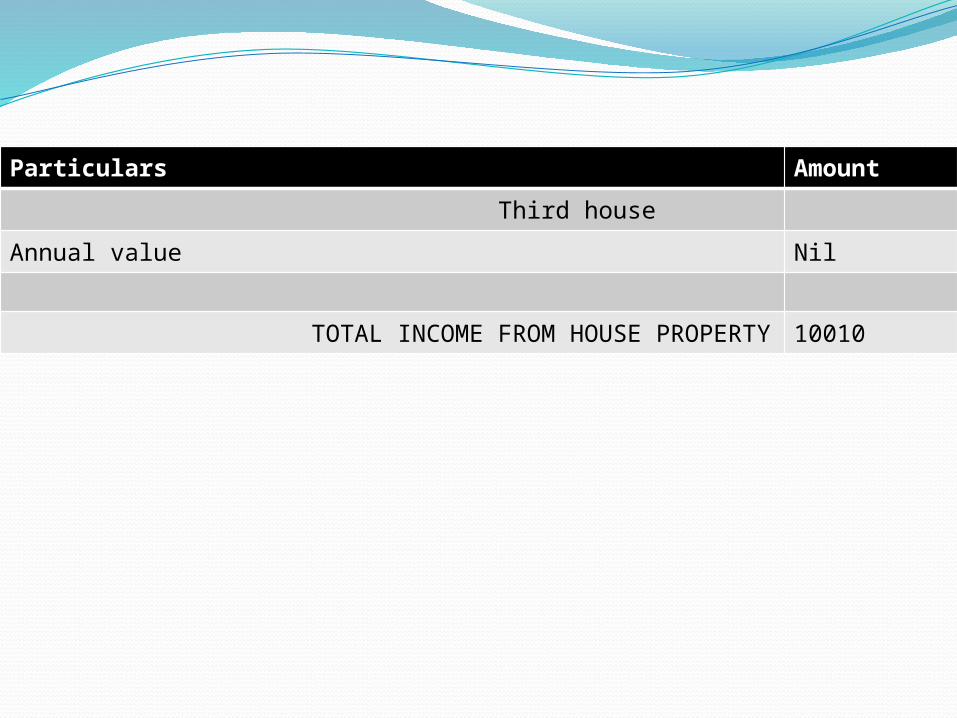

Solution

Particulars Amount Third houseAnnual value Nil

TOTAL INCOME FROM HOUSE PROPERTY 10010

Second head

Business and

profession

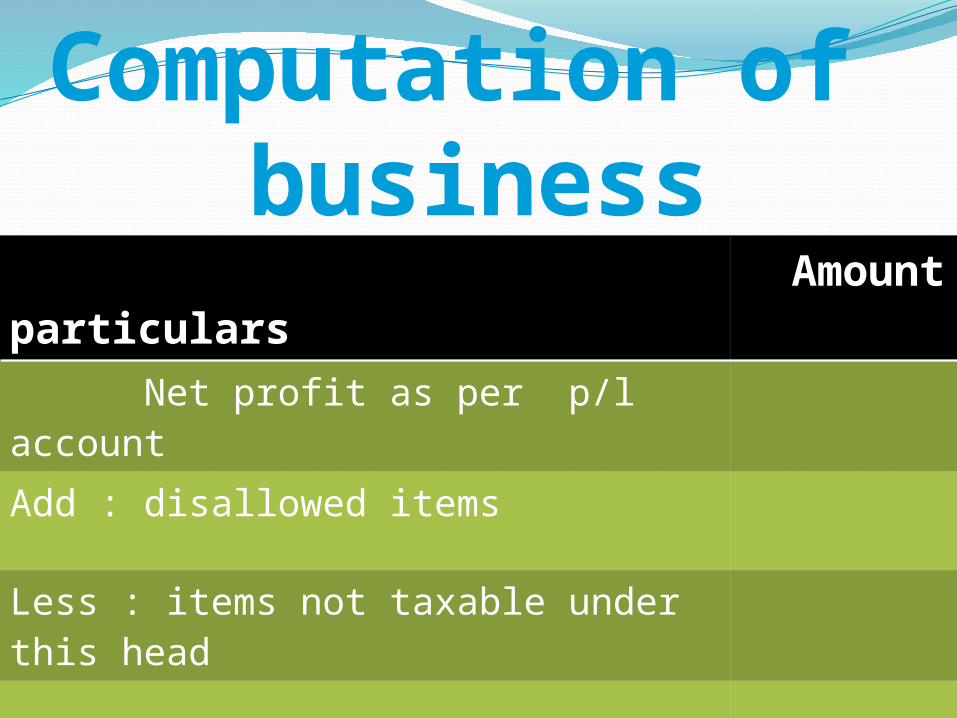

particulars

Amount

Net profit as per p/l account Add : disallowed items

Less : items not taxable under this head Income from business

Computation of business

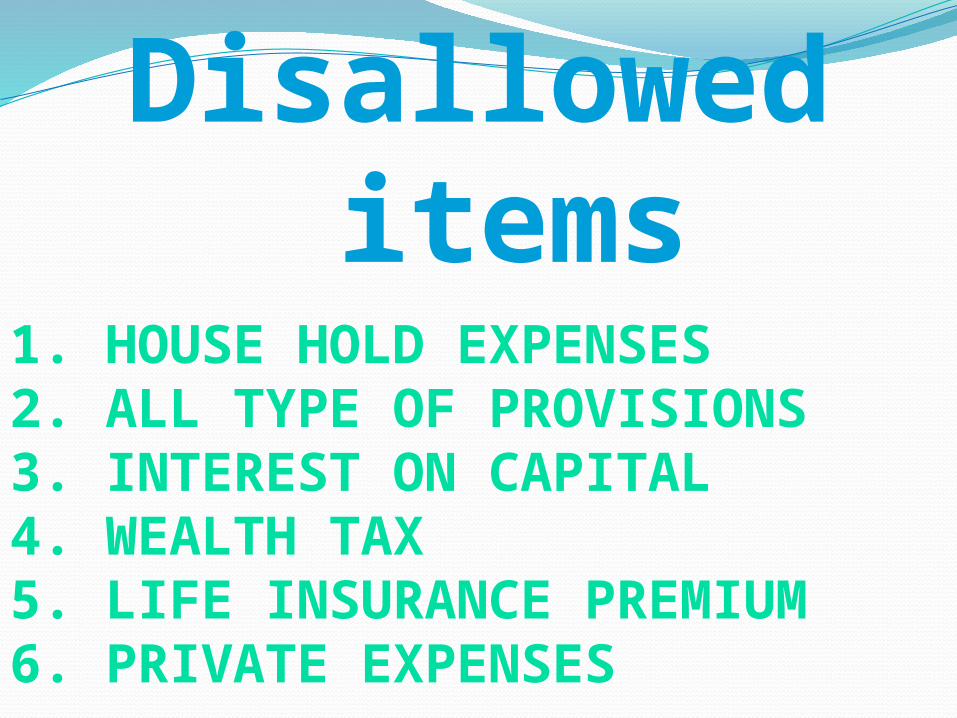

1. HOUSE HOLD EXPENSES2. ALL TYPE OF PROVISIONS3. INTEREST ON CAPITAL4. WEALTH TAX5. LIFE INSURANCE PREMIUM6. PRIVATE EXPENSES

Disallowed items

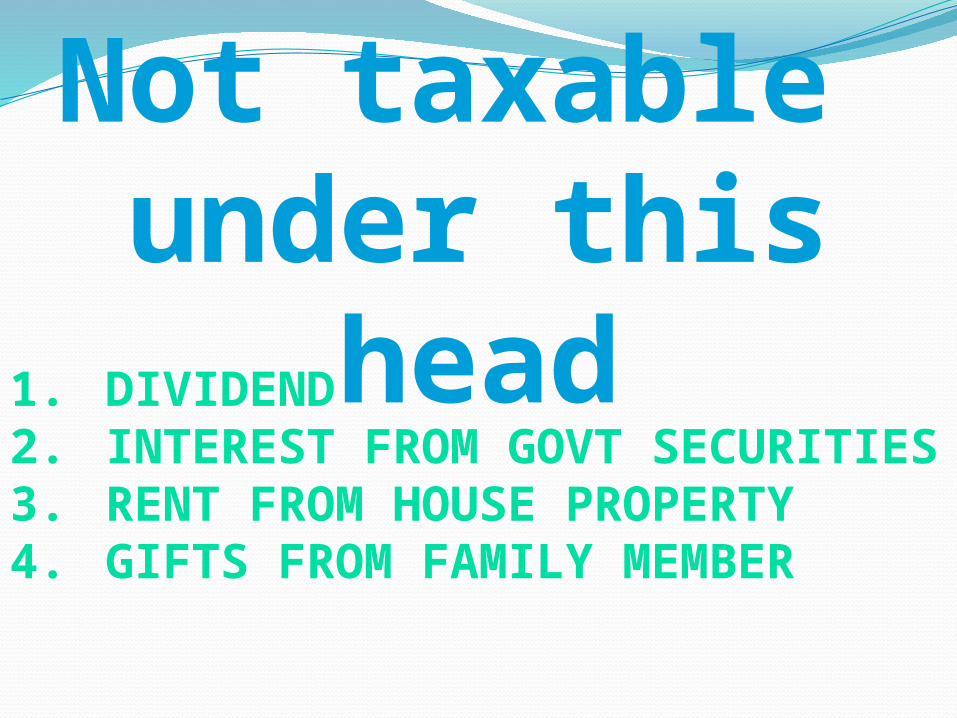

1. DIVIDEND2. INTEREST FROM GOVT SECURITIES3. RENT FROM HOUSE PROPERTY4. GIFTS FROM FAMILY MEMBER

Not taxable under this

head

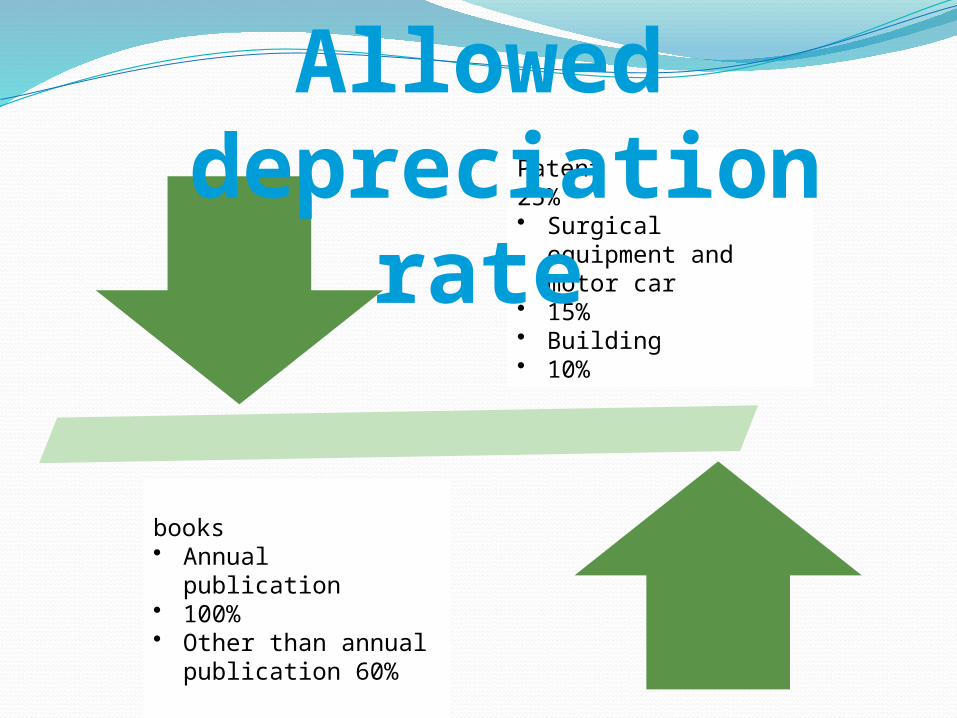

Patent25%• Surgical

equipment and motor car

• 15%• Building• 10%

books• Annual

publication• 100%• Other than annual

publication 60%

Allowed depreciation

rate

particular

amount

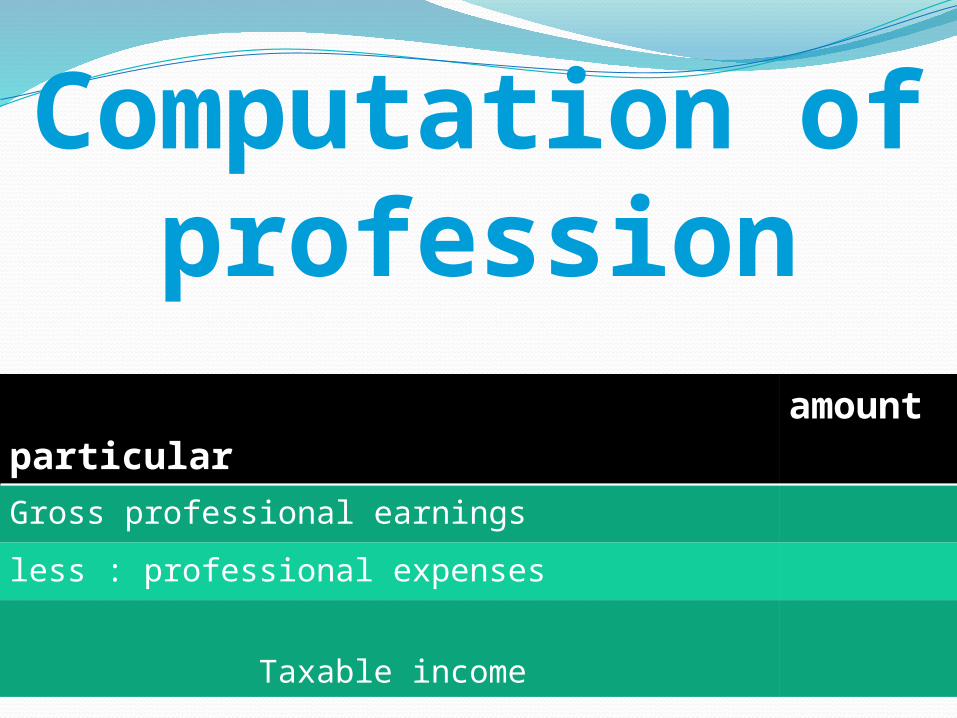

Gross professional earningsless : professional expenses Taxable income

Computation of profession

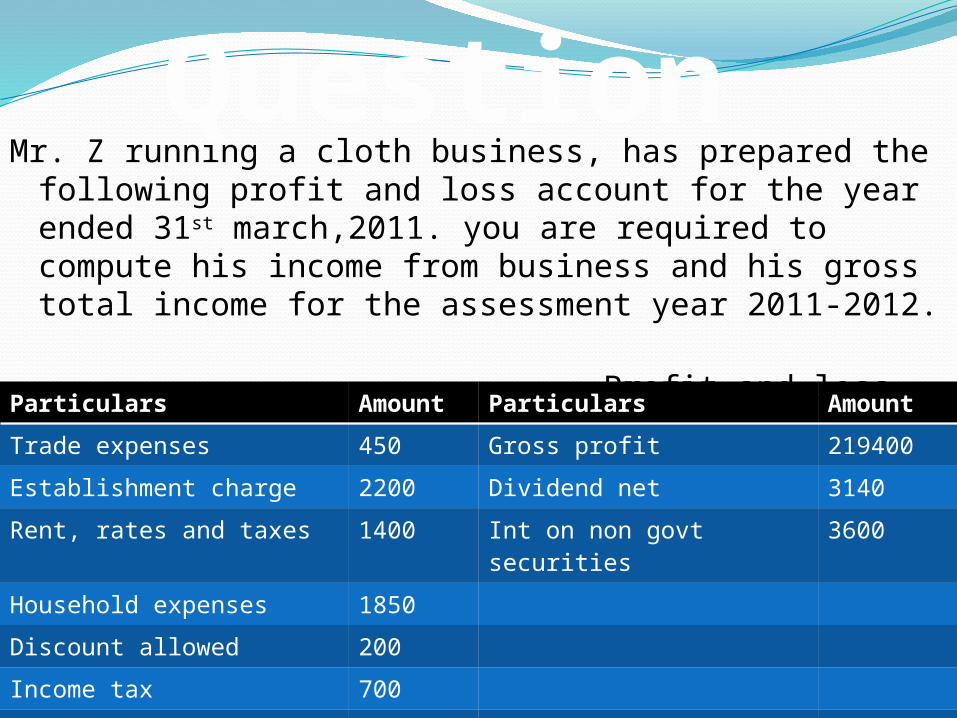

Mr. Z running a cloth business, has prepared the following profit and loss account for the year ended 31st march,2011. you are required to compute his income from business and his gross total income for the assessment year 2011-2012.

Profit and loss account

Particulars Amount Particulars Amount Trade expenses 450 Gross profit 219400Establishment charge 2200 Dividend net 3140Rent, rates and taxes 1400 Int on non govt

securities3600

Household expenses 1850Discount allowed 200Income tax 700Advertisement 450

Question

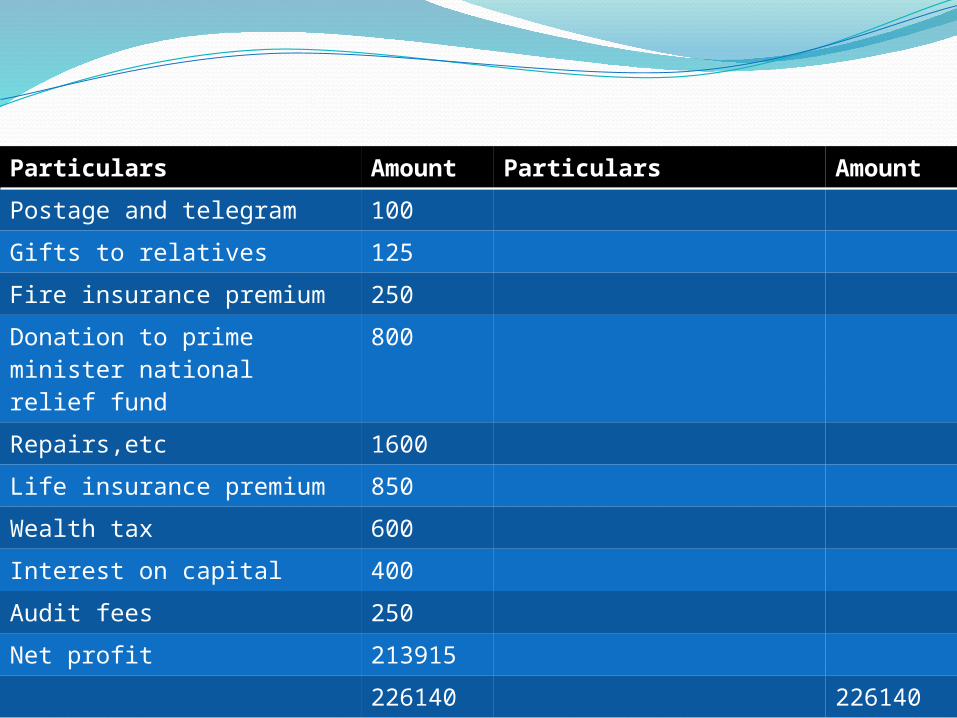

Particulars Amount Particulars Amount Postage and telegram 100Gifts to relatives 125Fire insurance premium 250Donation to prime minister national relief fund

800

Repairs,etc 1600Life insurance premium 850Wealth tax 600Interest on capital 400Audit fees 250Net profit 213915

226140 226140

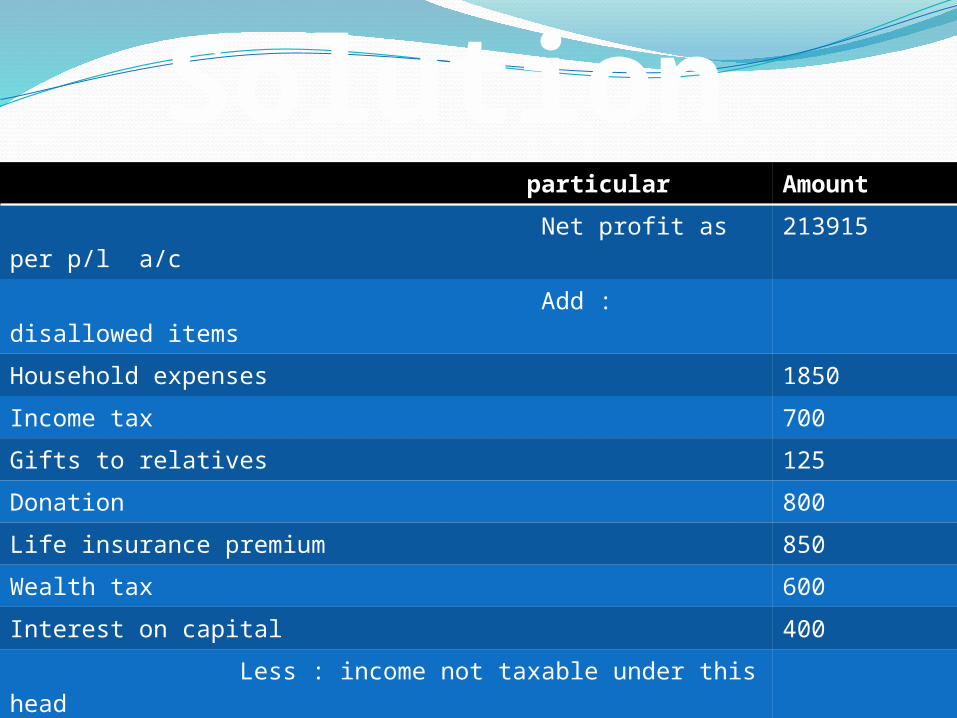

particular Amount Net profit as per p/l a/c

213915

Add : disallowed items Household expenses 1850Income tax 700Gifts to relatives 125Donation 800Life insurance premium 850Wealth tax 600Interest on capital 400 Less : income not taxable under this headDividend 3140Interest on non government securities 3600 Income from business

212500

Solution

CAPITAL GAIN

THIRD HEAD

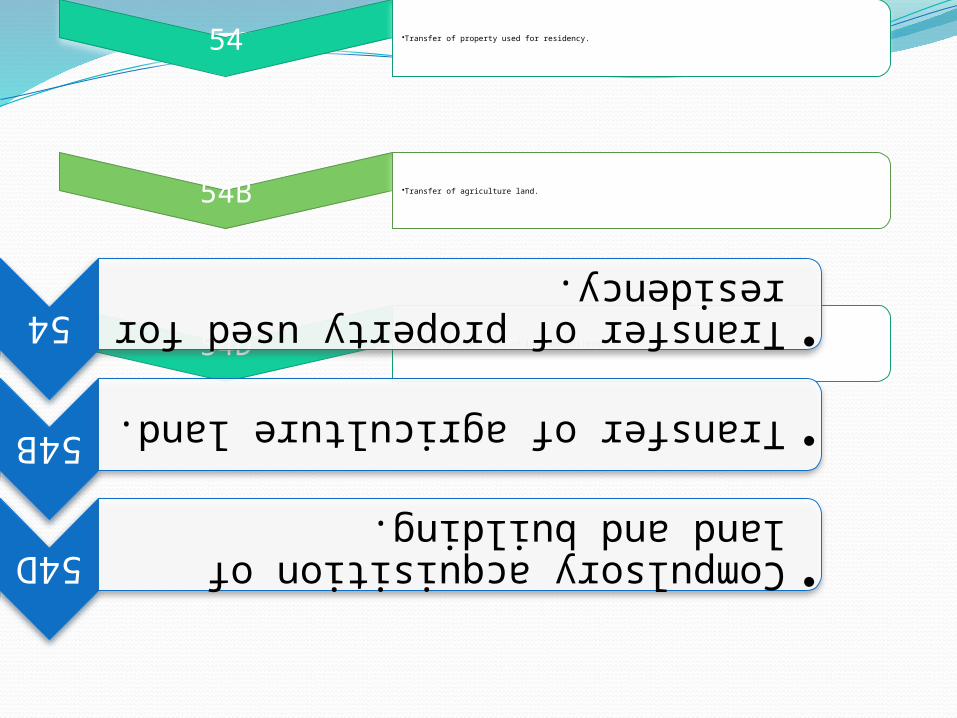

54 •Transfer of property used for residency.

54B •Transfer of agriculture land.

54D •Compulsory acquisition of land and building.

54 •Transfer of property used for residency.

54B •Transfer of agriculture land.

54D •Compulsory acquisition of land and building.

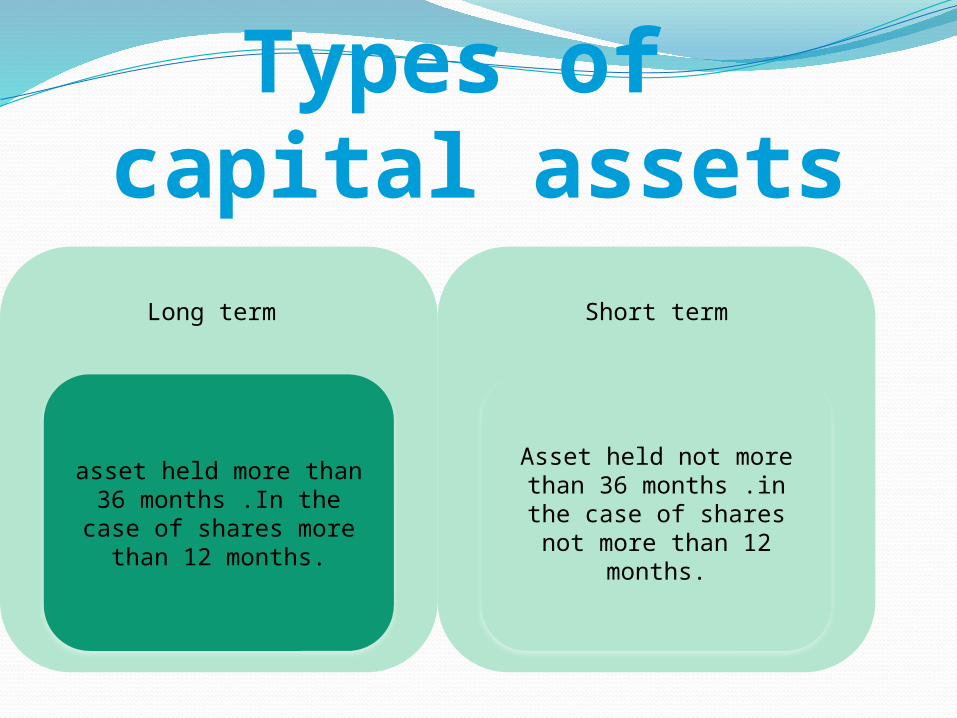

Long term

asset held more than 36 months .In the case of shares more

than 12 months.

Short term

Asset held not more than 36 months .in the case of shares not more than 12

months.

Types of capital assets

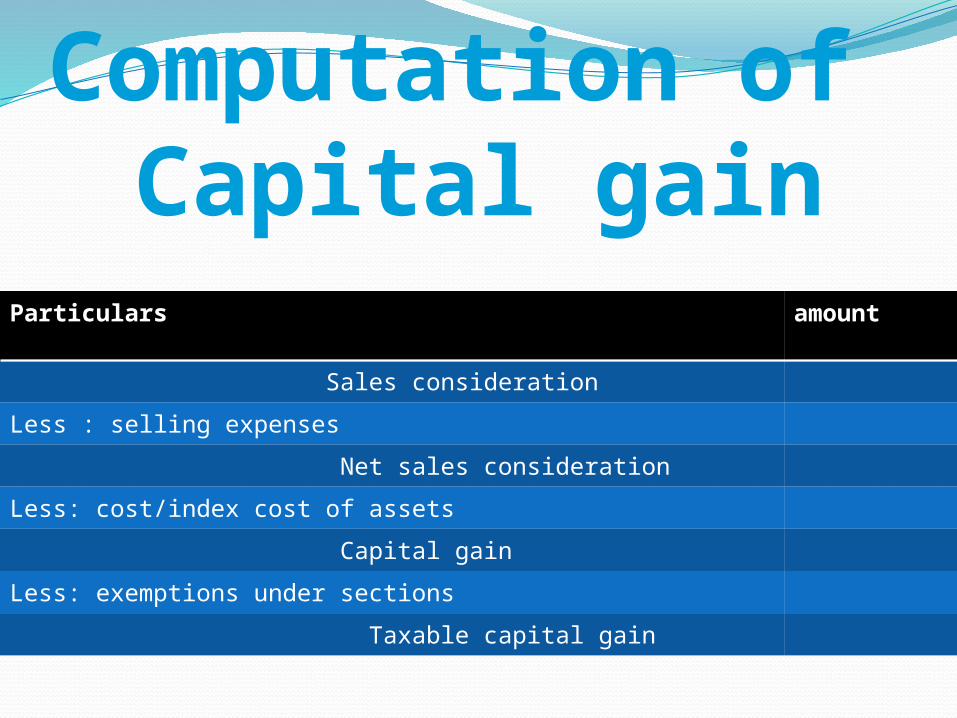

Particulars amount

Sales consideration Less : selling expenses Net sales considerationLess: cost/index cost of assets Capital gain Less: exemptions under sections Taxable capital gain

Computation of Capital gain

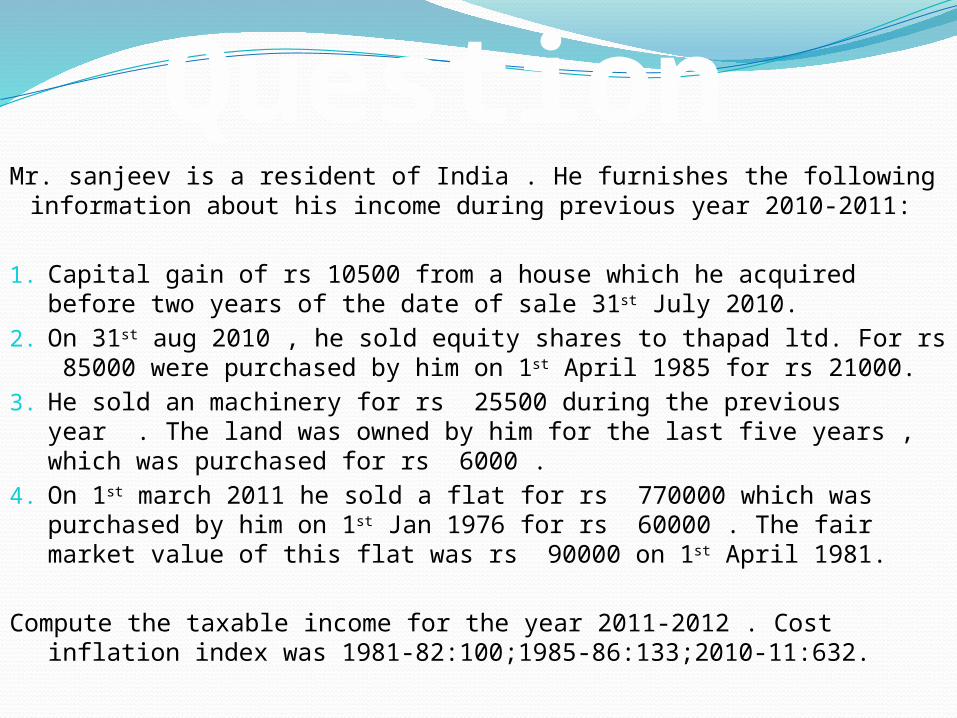

Mr. sanjeev is a resident of India . He furnishes the following information about his income during previous year 2010-2011:

1. Capital gain of rs 10500 from a house which he acquired before two years of the date of sale 31st July 2010.

2. On 31st aug 2010 , he sold equity shares to thapad ltd. For rs 85000 were purchased by him on 1st April 1985 for rs 21000.

3. He sold an machinery for rs 25500 during the previous year . The land was owned by him for the last five years , which was purchased for rs 6000 .

4. On 1st march 2011 he sold a flat for rs 770000 which was purchased by him on 1st Jan 1976 for rs 60000 . The fair market value of this flat was rs 90000 on 1st April 1981.

Compute the taxable income for the year 2011-2012 . Cost

inflation index was 1981-82:100;1985-86:133;2010-11:632.

Question

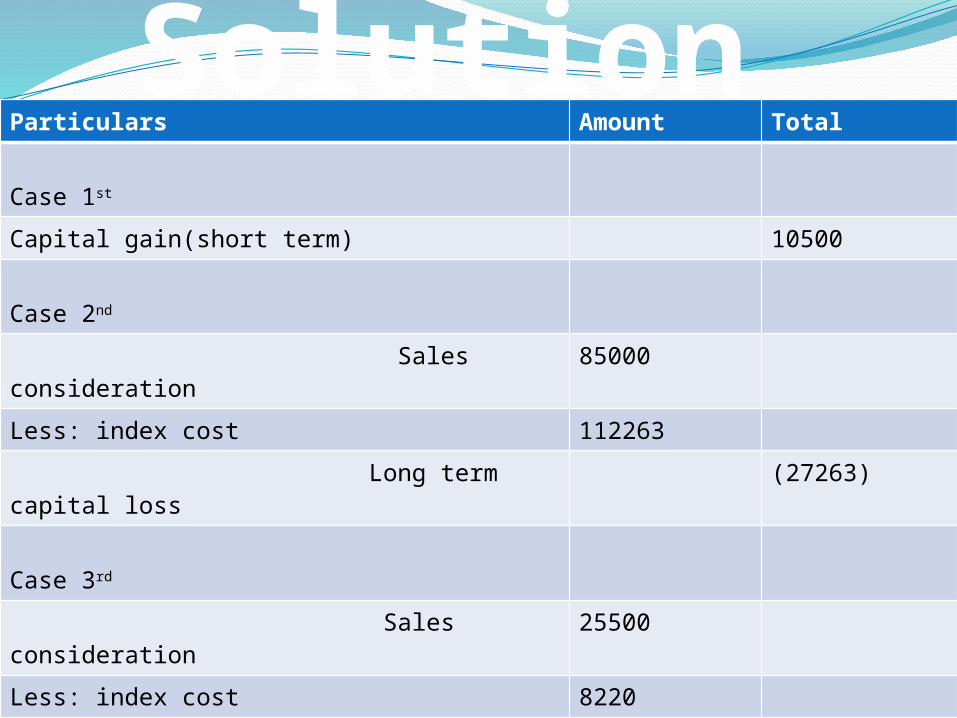

Particulars Amount Total Case 1st

Capital gain(short term) 10500 Case 2nd

Sales consideration

85000

Less: index cost 112263 Long term capital loss

(27263)

Case 3rd

Sales consideration

25500

Less: index cost 8220 Long term capital gain

17280

Case 4th

Sales consideration

770000

Less: index cost 639900 Long term capital gain

130100

TOTAL INCOME FROM CAPITAL GAIN 130617

Solution

Forth head

Othersources

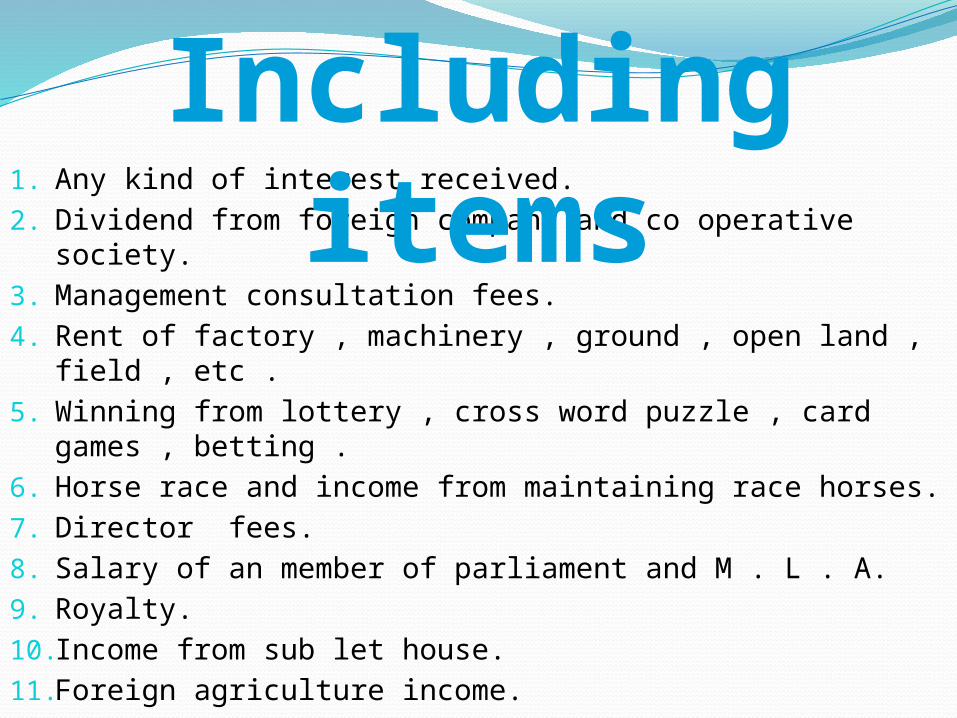

1. Any kind of interest received.2. Dividend from foreign company and co operative

society.3. Management consultation fees. 4. Rent of factory , machinery , ground , open land ,

field , etc .5. Winning from lottery , cross word puzzle , card

games , betting .6. Horse race and income from maintaining race horses.7. Director fees.8. Salary of an member of parliament and M . L . A.9. Royalty.10.Income from sub let house.11.Foreign agriculture income.

Including items

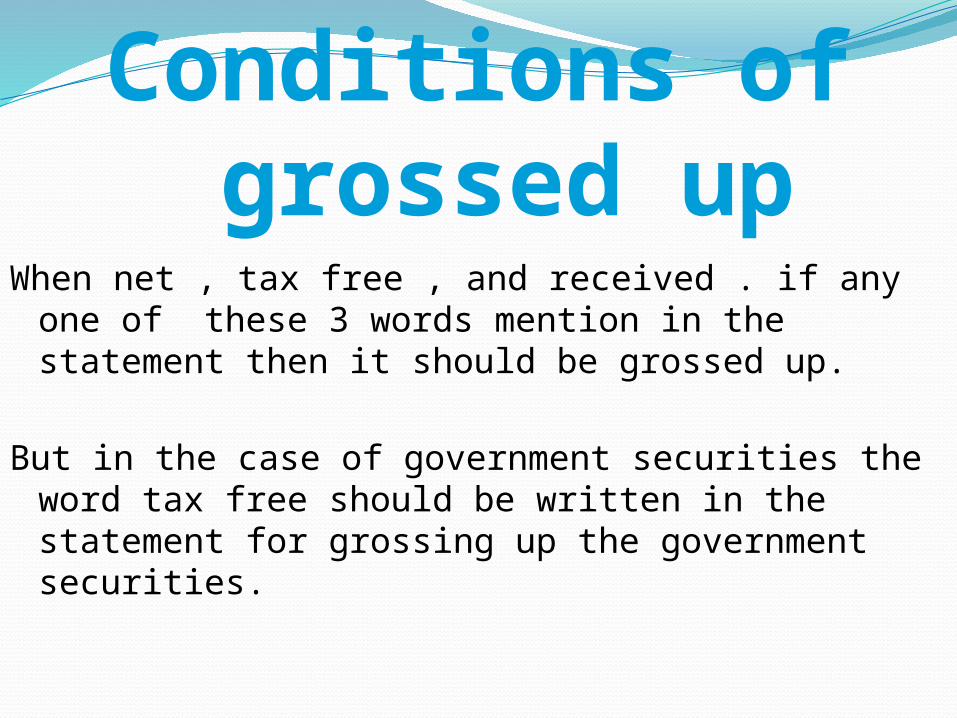

When net , tax free , and received . if any one of these 3 words mention in the statement then it should be grossed up.

But in the case of government securities the word tax free should be written in the statement for grossing up the government securities.

Conditions of grossed up

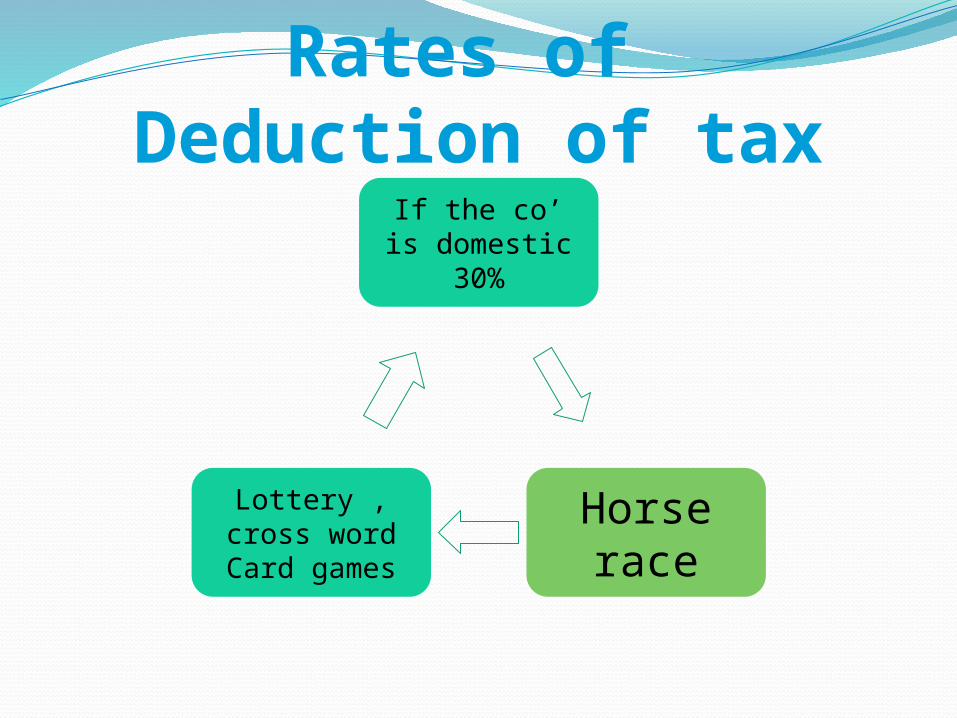

If the co’ is domestic

30%

Horse race

Lottery , cross wordCard games

Rates of Deduction of tax

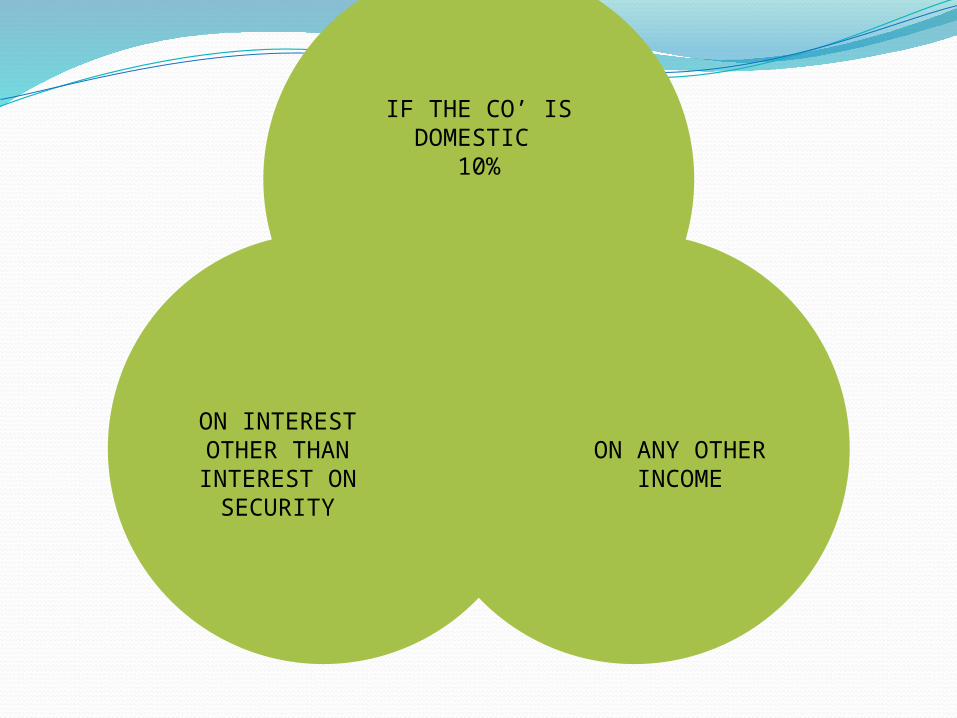

IF THE CO’ IS DOMESTIC

10%

ON ANY OTHER INCOME

ON INTEREST OTHER THAN INTEREST ON SECURITY

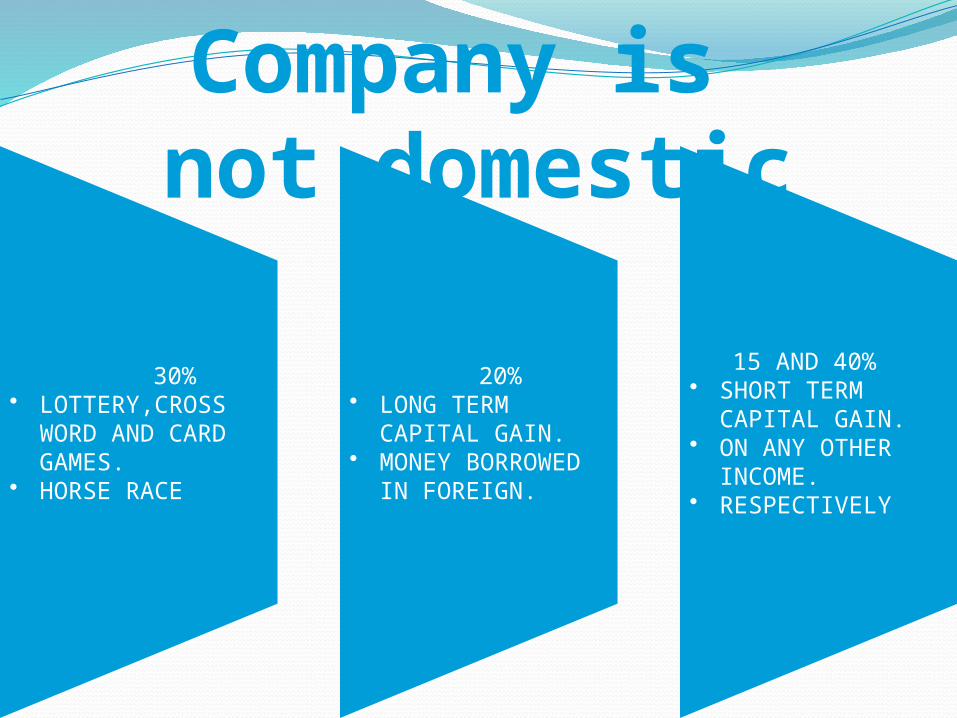

30%• LOTTERY,CROSS

WORD AND CARD GAMES.

• HORSE RACE

20%• LONG TERM

CAPITAL GAIN.• MONEY BORROWED

IN FOREIGN.

15 AND 40%• SHORT TERM

CAPITAL GAIN.• ON ANY OTHER

INCOME.• RESPECTIVELY

Company is not domestic

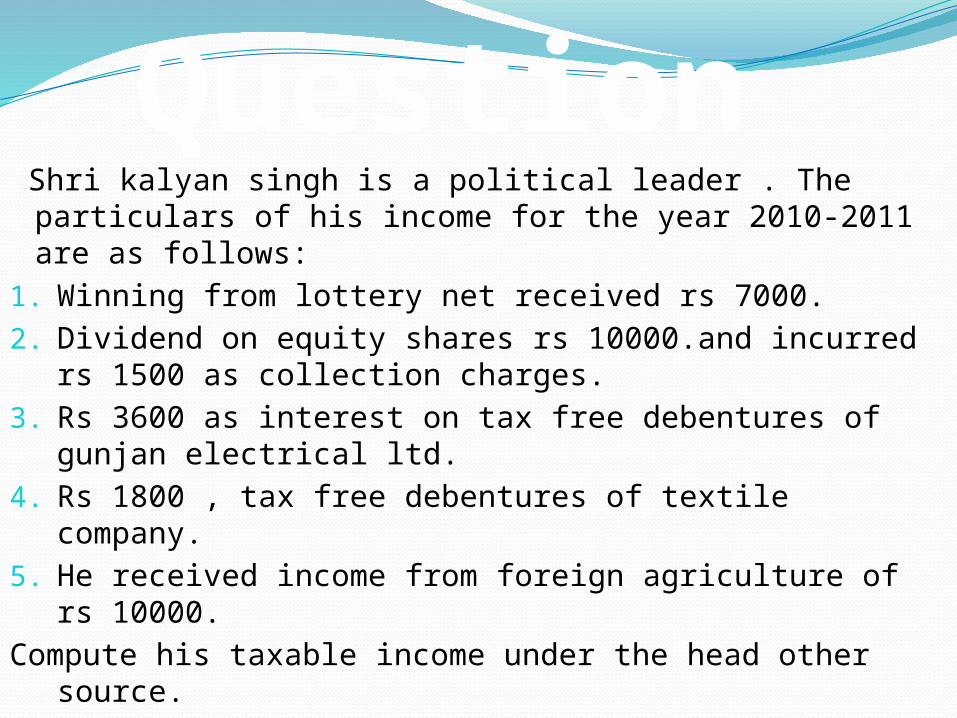

Shri kalyan singh is a political leader . The particulars of his income for the year 2010-2011 are as follows:

1. Winning from lottery net received rs 7000.2. Dividend on equity shares rs 10000.and incurred

rs 1500 as collection charges.3. Rs 3600 as interest on tax free debentures of

gunjan electrical ltd.4. Rs 1800 , tax free debentures of textile

company.5. He received income from foreign agriculture of

rs 10000.Compute his taxable income under the head other

source.

Question

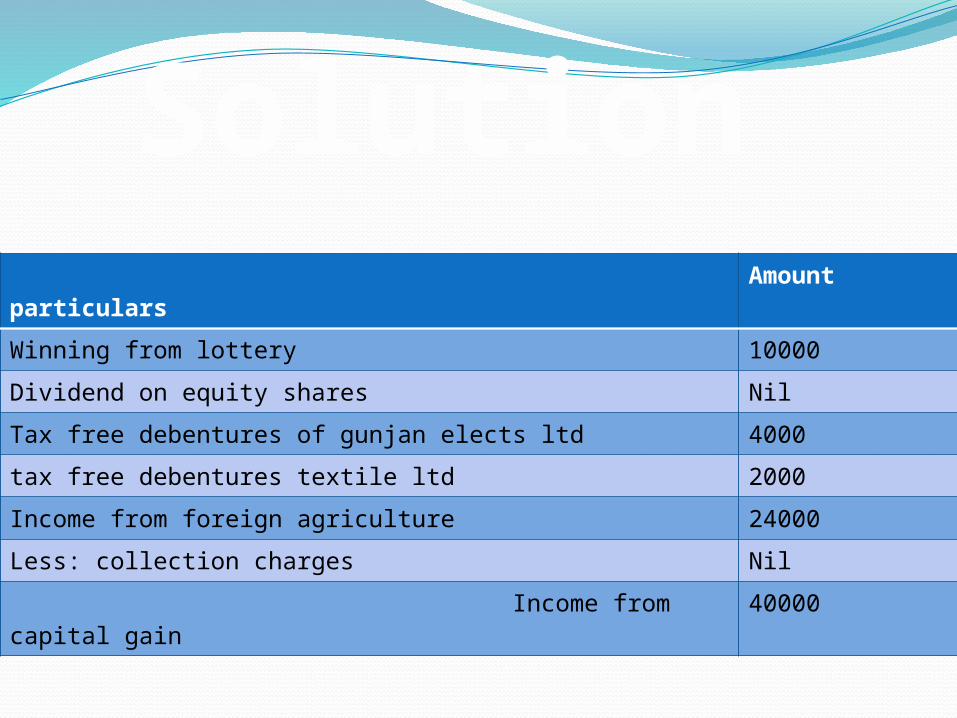

particulars

Amount

Winning from lottery 10000Dividend on equity shares NilTax free debentures of gunjan elects ltd 4000tax free debentures textile ltd 2000Income from foreign agriculture 24000Less: collection charges Nil Income from capital gain

40000

Solution

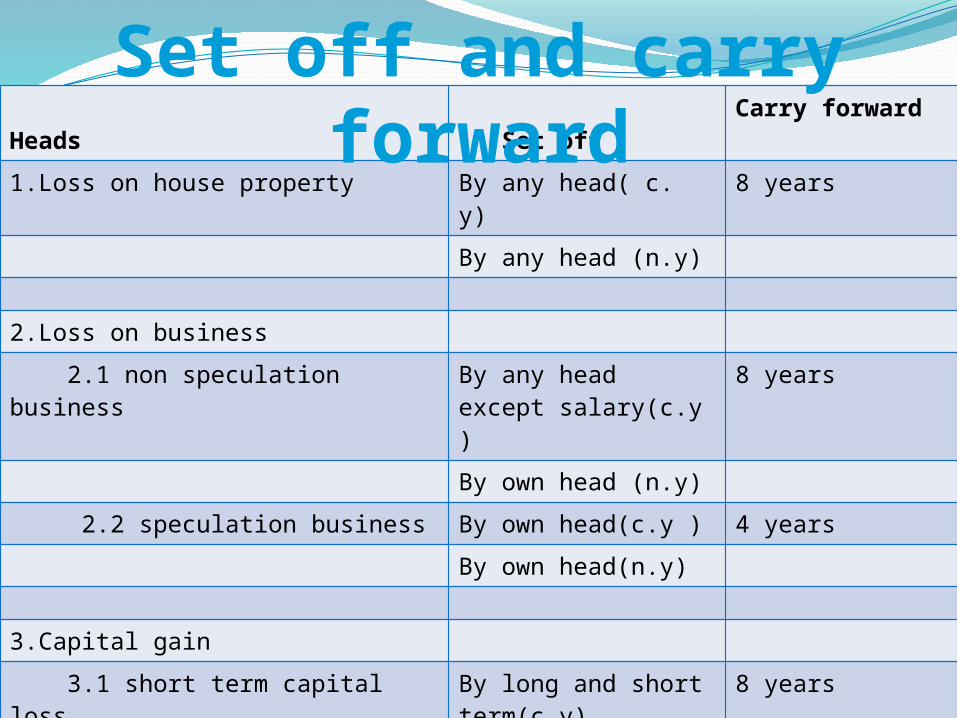

Heads

Set off

Carry forward

1.Loss on house property By any head( c. y)

8 years

By any head (n.y)

2.Loss on business 2.1 non speculation business

By any head except salary(c.y )

8 years

By own head (n.y) 2.2 speculation business By own head(c.y ) 4 years

By own head(n.y)

3.Capital gain 3.1 short term capital loss

By long and short term(c.y)

8 years

By short term 3.2 long term capital loss

By own head 8 years

By own head

Set off and carry forward

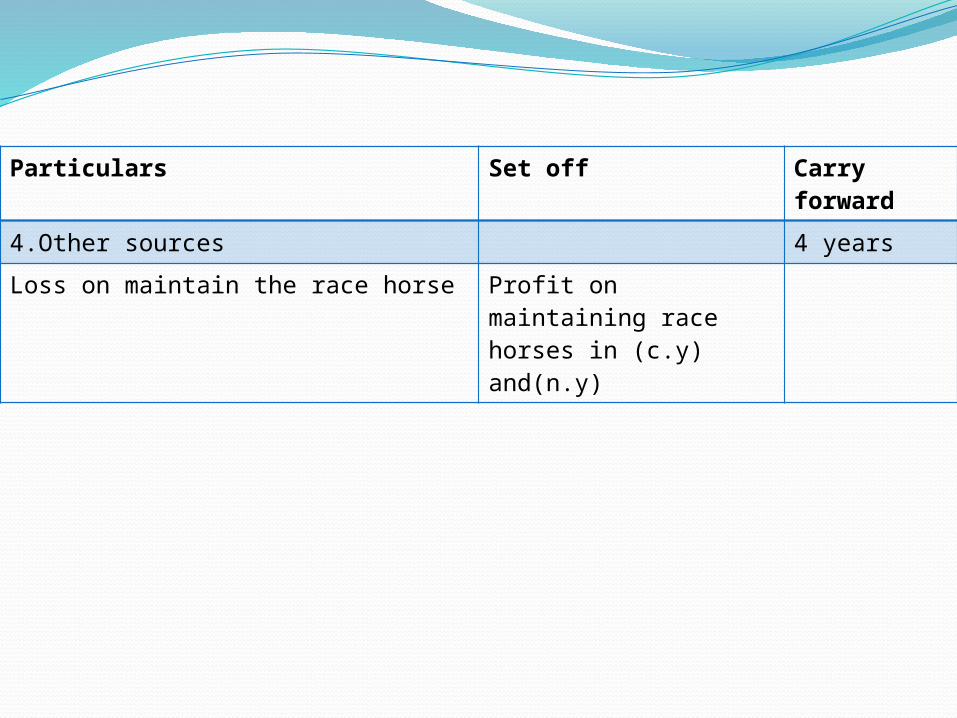

Particulars Set off Carry forward

4.Other sources 4 yearsLoss on maintain the race horse Profit on

maintaining race horses in (c.y) and(n.y)

Totalincome

80G- Deductions in respect of donations TO APPROVED FUNDS OR INTITUTIONS.

80GGA- Payment to scientific research or to a university and college etc. for scientific, social and statistical research.

80GGB- Deduction in respect of contribution given by companies to political parties.

80IA- Deduction in respect of infrastructural facilities.

80IAB- Regarding development of special economic zone.80IB- Deduction in respect of profits OF NEW INDUSTRIAL

UNDERTAKINGS OR HOTEL BUSINESS.

Exemptions

80IC- Special provision in respect of certain undertakings or enterprises in certain special category states.

80ID- Provides for a five year tax holiday to new hotel of two, three ,four, star category and conventions centers.

80IE- An undertakings engaged in the business of hotel(not below two star category)located in north eastern states.(states are A.P , ASSAM , MANIPUR , MEGHALAYA , MIZORAM , NAGALAND , SIKKIM , AND TRIPURA.

80JJA- Deduction in respect of profit and gain from business of collecting and processing of bio-degradable waste.

80JJAA- Deduction in respect of employment of new workmen.

80LA- Deduction in respect of certain incomes of offshore banking units and international financial service centers.

From the following particulars of income of Mr. Ashok Kumar for the year ended on 31st march 2011, calculate his total income for the assessment year 2011-12:

Rent receive from house property let out to state bank of India Rs. 200000.

Business profit Rs. 352000. setting off Rs. 20000 paid as donation to the chief

minister relief fund Long term capital gain Rs. 180000 and having a short

term capital loss of Rs. 1300. he received interest of Rs. 10000. He paid Rs. 50000 in respect of scientific research. He contribute Rs.20000 in respect of political

parties.

Question

Provide money for development for special economic zone Rs. 15500.

Income from 3 star hotel situated in Manipur Rs. 12000.

Having a business which relates to bio degradable processing and receive a profit of Rs. 6100.

His winning from lottery Rs. 100000. he had purchased a lottery ticket of Rs. 500.