Embed Size (px)

Citation preview

STRATEGIC ROLE OF MARKETING AS A COMPETITIVE TOOL FOR GROWTH ANDSURVIVAL IN NIGERIA BANKING INDUSTRY

Shittu Oladipupo Ibrahim [email protected], [email protected]

08032495760, 08077223399

And

Dr. Samaila Idi Ningi [email protected]

08024138052, 08031125430

Accounting and Finance Technology Department, Faculty ofManagement Technology

Abubakar Tafawa Balewa University, Bauchi

ABSTRACTPrior to bank consolidation in Nigeria, some banks are referred to as bestperforming banks, with the hope that they are highly liquid and efficient. Butafter the consolidation exercise in 2005, it is paramount to understand thatbanking industry became more intensely competitive which calls for asignificant tool to survive in the competitive market. This research thenexamines the role of marketing as a competitive tool for growth and survivalin Nigerian banking industry. 5 banks were selected from which 50 staff of theselected banks (ten from each) and total of 446 customers were used as thesample with the use of questionnaire. Tables and percentages were used to makeanalyses. The hypothesis was tested using chi-square statistical method. Itwas concluded that marketing plays a vital role for growth and survival in TheNigerian banking industry, the problem of distinctive characteristics ofservice marketing have effects on banks and that customers’ service functionshould be considered in rendering efficient banking services. It wasrecommended that Nigerian banks should be more customer-focused in order toidentify customers’ needs and satisfy them; Nigerian banks should adopteffective marketing strategies to differentiate their product from that of thecompetitors; use brand names among others.

Keywords: customers’ service, marketing mix, marketing strategy,service marketing.

Introduction 1

Banking is of strategic importance to the economy, this is

because the performance of other industry depends on the

soundness of the banking sector. In Nigeria, the industry has

witness many phases as described by Bamidele and Kama (2003), and

most especially the 2005 consolidation exercise. Prior to the

consolidation, some banks are referred to as best performing

banks, with the hope that they are highly liquid and efficient.

But after the consolidation exercise in 2005, it is paramount to

understand that the Nigerian banking industry became more

intensely competitive, which calls for a significant tool to

survive in the competitive market.

There are basically four principal areas of operations within all

firms, namely: Accounting, Finance, Management and Marketing.

Adebisi and Abdulazeez(2000) defined Accounting as the process of

collecting, classifying, recording, summarizing and interpreting

the financial events of a business for the purpose of making

decision on the financial state and progress of the business. Van

Horne (2002) described the main functions of finance to include

investment in assets and new products, determining the best mix

of financing and dividends in relation to company’s overall

valuation. Management is defined by Oyekunle and Adeniyi (2001)

2

as a mental activity, which is concerned with the work of

planning, organizing, staffing, directing or leading and

controlling for the accomplishment of the stated objectives of an

organization. While marketing is described in ATS Distance

Learning Pack: Management (2001) as the process of determining

consumer wants for a product or service, motivating its sale and

distributing it to ultimate consumption at a profit. So,

marketing is majorly responsible for generation of revenue,

through the exchange process and customer’s satisfaction, which

makes the unit to be indispensable in every organization. Dwivedi

(2007) explained that finance functions are important, but not as

important as the marketing functions. Thus, every firm that

produces products either tangible or intangible, to existing or

potential customers need marketing personnel and strategy for its

growth, survival and profit maximization. Some people thought

that marketing is just about advertising or sales, but it goes

beyond that, it also involve everything a company does to

acquire customers and maintain good relationship with them,

creation of demand for company’s products, its distribution and

other services for customers who purchase the product and/or

service.

3

Kotler (2003) described industrial marketing as the marketing

activities across borders. Bolaji (2006) defined service as an

act or performance, offered by one party to another, but which is

essentially intangible and does not result in ownership of

anything. He as well described it (service) as an economic

activity that create value and provide benefits for customers’

want as a result of bringing about a desired change on behalf of

the recipient of service.

Ikpefan (2013) explains that the need for marketing of services

and products in the banking system to satisfy customers and to

improve profit levels cannot be over emphasized since the

sustainability of any economic system is predicated on the

viability of the financial system of that country.

Banking institution as a major sector in the service industry

occupies a central position in the financial system in any

economy as described by Bamidele and Kama (2003). Marketing scope

in banking sector is considered under the service marketing

framework. Bank marketing does not only include service selling

but also the function which gets personality and image for bank

on its customers’ mind in order to solve the problem of

intangibility among others. As described by Nokandeh, Poorhabib,

4

Seyedi and Niknafs (2013) banks marketing involve creating a

comprehensive marketing plan for assessment and finding hidden

and visible need of customer and finding most useful markets. In

today's competitive environment, the survival of bank depends on

their ability to deal with environmental challenges which also

lies on marketing. Marketing of banking service is so important

because of banks’ aim to increase its profit. Banks need to

increase their profit in order to create new markets, to protect

and develop their market shares and to survive on basis of

intense competition through customers’ retention and strategic

marketing. Many Banks in recent time failed and went out of

business probably, because the insignificant tool (marketing) for

organization’s success was not properly utilized. So, marketing

consideration should be an integral part of every organization

because the success of every firm is the result of satisfying the

wants, needs and demands of its customers.

The need of maintaining customers in terms of waiting hours, bank

lending, unpleasant attitude of some bank staff and lack of

awareness of certain products and services offered by banks call

for the research work. It also arises from the problem of

competition which has become intense since the bank consolidation

5

(re-capitalisation) exercise in 2005 as most banks that survive

the exercise were believed to be strong in terms of capital base

and management which as well increased competition which

moreover, calls for a tool that could aid banks for growth and

survival in the industry.

The objectives of the study is to access the role of marketing as

a competitive tool for growth and survival in banking industry as

well as to access an efficient customer service as an essential

tool in rendering efficient service to customers.

LITERATURE REVIEW

Frank and Bernanke (2007) defined commercial banks as privately

owned firms that accept deposits from individual and businesses

and use those deposits to make loans. It explained further that,

the determination of money supply in a modern economy depends in

part, on the behavior of commercial banks and their depositors,

which makes the industry, and their customers deposit to be very

essential. So, to improve those deposits, marketing is very

essential.

As described by Perreault & McCarthy (2002), people think that

marketing is about selling and advertisement only but, it also

extended to identifying customer’s needs, as well as making those

6

needs so well that the product almost sells itself. This is

applicable to whether the product is a physical good or services

or even an idea. So, if the whole marketing has been done well,

the customers might not need much persuasion but customers will

always be ready to buy. Kotler and Keller (2006) pronounce that

marketing is everywhere, formally or informally.

Every organizations/ business firm intends to remain in business

profitably as Dwivedi (2002) revealed and that the major

objectives of all business firm is not only profit maximization

but as well include the following: maximizing sales revenue/

deposit, maximizing firms growth rate, maximizing utility

function, making satisfactory rate of profit, long run survival

of the firm, entry prevention and risk avoidance among others, so

it was to be noted that all these could be possibly achieved

through marketing strategies.

Zikmund and Michael (2006) explained that financial success often

depends on marketing ability, finance, operations, accounting and

other business functions but the success will not be actually

realized if there is no sufficient demand for product and service

offering of the firm which makes marketing function to be so

important.

7

Bamidele and Kama (2003) described the increase in the use of

marketing in banking industry as a result of four accruing

factors, which are:

Increase competition to customers

Increase sophistication of those customers

Increase technology, and

Increase cost of meeting customers need profitably

Therefore, marketing is important tool to be considered in

banking industry.

Marketing of Banking Services

There are several services offered by commercial banks, which

needs to be marketed with the deployment of various marketing

strategies and mixes. Banking industry falls under the service

industry, so its’ meaning and nature to be understood.

Meaning and nature of service

There are varieties of organizations that are referred to as

‘service industry’ which include health care sector, legal firm,

Education, Real estate, Hotel and Tourism, Communication sector,

Insurance, Baking among others.

Kotler (1999) defined service as any act or performance that one

party can offer to another that is essentially intangible and

8

does not result in the ownership of anything. It also defined

service as the production of an essentially intangible benefit

either in its own right or as a significant element of a tangible

product, which through some form of exchange, satisfying and

identifying need. Service Providers/ Service firms offer

varieties of service to their customers and tend to satisfy them

profitably which requires distinctive marketing strategies of

service marketing.

Services are intangible unlike a tangible product. It cannot be

touched, felt or held to determine its quality, which pose threat

to service marketers but with better understanding and use of

service marketing mixes and strategies the problems could be

overcome.

Some Marketing Strategies Employed by Banks

Traditionally, there are four P’s of marketing but, there are

three additional P’s which makes service marketing to be seven (7

P’s), as described by Mas’ud and Yamzid (2009), which are

Product, Price, Place, Promotion, People, Process and Physical

Evidence. The appropriate mix of these are good ingredient for

bank sound performance. Marketing Strategy is a major tool used

9

by marketers to penetrate the market with programs that will

convince potential customers and retain the existing ones

THE ROLE OF MARKETING AS A COMPETITIVE TOOL IN BANKING INDUSTRY

Marketing has been a good competitive tool for growth and

survival in banking industry through series of role it performed

in the industry. Some of these roles are:

1. Marketing Research

2. Product and Business Development

3. Market Plan Formulation and Strategy

4. Marketing of Banking Services

5. Strengthening Customer Relationship

Marketing Research

Alvin and Ronald (2001) defined marketing research as the

systematic and objective search for an analysis of information to

guide managers in marketing planning and problem solving.

Marketing research assists marketers to identify customers’ need

and want and how to satisfy them. It helps marketers to get

customers information in terms of income level, socio-cultural

factors that could affect sales volume and any barrier that could

affect demand.

10

Product and Business Development

It is the role of the marketing unit of the bank to develop new

products and look for ways of developing businesses for the bank

within the society. They make sure that they produce an evenly

challenging and competitive product to withstand the competitive

market in to retain and gain more customers as well as surviving

in the industry.

Market Plan Formulation and Strategy

This is a function of the marketer, which play a significant role

as a tool for survival and growth in the competitive market. It

helps banks to plan about how to carry out their activities and

programs and as well formulate differentiated strategies that

could be used to offer products that are better than that of the

competitors. As concluded by Uppal (2010) only those banks who face

the competition with the effective ways of marketing will survive.

Marketing of Banking Services

This is the most common role of marketers understood by the

majority. They (bank marketers) ensure that the products and

services offered by the banks are demanded for by the customers,

they try as much as possible to create personal awareness to

customers and convince them of the benefit they could derive.

11

Many constraints are faced by bank marketers as a result of the

distinctive characteristics of bank service, which requires

special skills.

Strengthening Customer Relationship

It is the role of the marketer to ensure smooth bank-customer

relationship. They make sure that customers always get what they

want at the right time as they are the closest staff to the

customers. To achieve this, every bank customers is attached to

every staff called ‘Account Officer’, whom must know everything

(mostly financial) about his customer.

Methodology

The descriptive survey is adopted in carrying out this research

and its success was based on the administration of questionnaire.

The population covers all commercial banks in Bauchi State out of

which five (5) banks (GTBank, Skye bank, Keystone bank, Zenith

Bank and Sterling Bank) were selected as the sample size. A total

number of fifty (50) questionnaires were distributed to the

marketing and customer care unit of the five banks, ten (10)

questionnaires to each of the banks from the total marketing and

customer care staff population of 12 (GTBank), 11 (Skye Bank),

10(keystone), 13(Zenith Bank), and 10 (Sterling Bank). And total

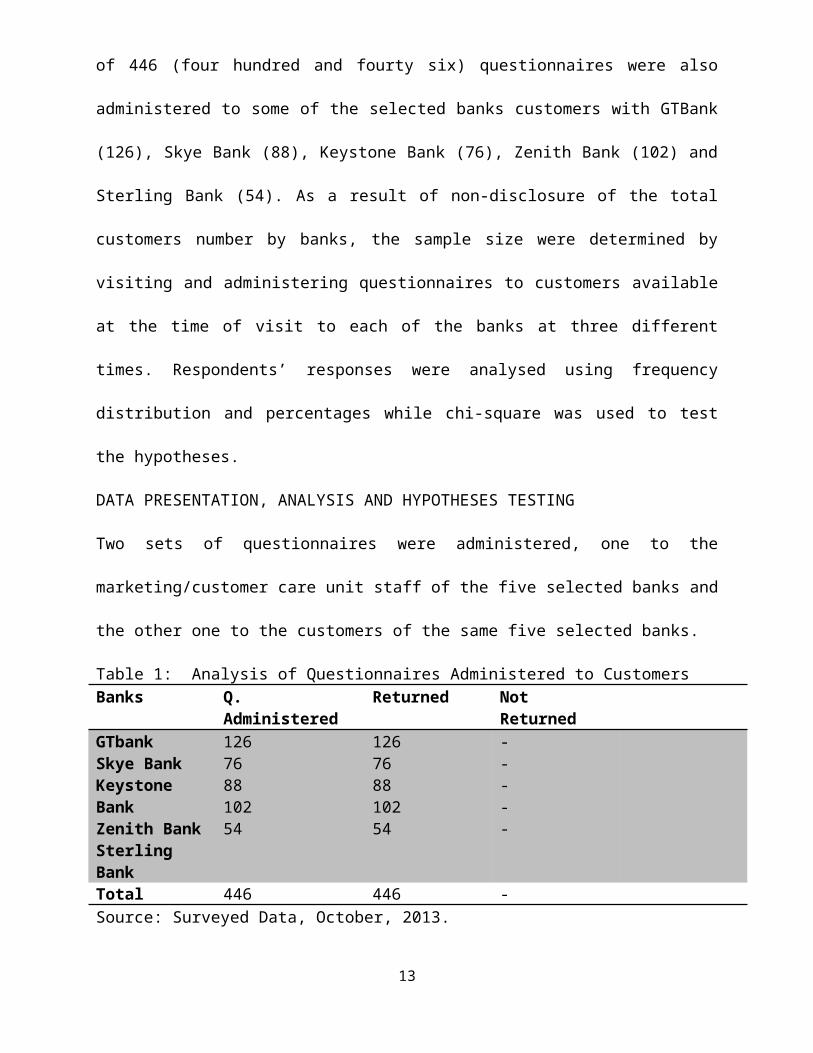

12

of 446 (four hundred and fourty six) questionnaires were also

administered to some of the selected banks customers with GTBank

(126), Skye Bank (88), Keystone Bank (76), Zenith Bank (102) and

Sterling Bank (54). As a result of non-disclosure of the total

customers number by banks, the sample size were determined by

visiting and administering questionnaires to customers available

at the time of visit to each of the banks at three different

times. Respondents’ responses were analysed using frequency

distribution and percentages while chi-square was used to test

the hypotheses.

DATA PRESENTATION, ANALYSIS AND HYPOTHESES TESTING

Two sets of questionnaires were administered, one to the

marketing/customer care unit staff of the five selected banks and

the other one to the customers of the same five selected banks.

Table 1: Analysis of Questionnaires Administered to Customers Banks Q.

AdministeredReturned Not

ReturnedGTbankSkye BankKeystoneBankZenith BankSterlingBank

126768810254

126768810254

-----

Total 446 446 -Source: Surveyed Data, October, 2013.

13

Table 1 displayed the numbers of questionnaires that were

administered to each of the five banks customers in which all the

distributed questionnaires were returned.

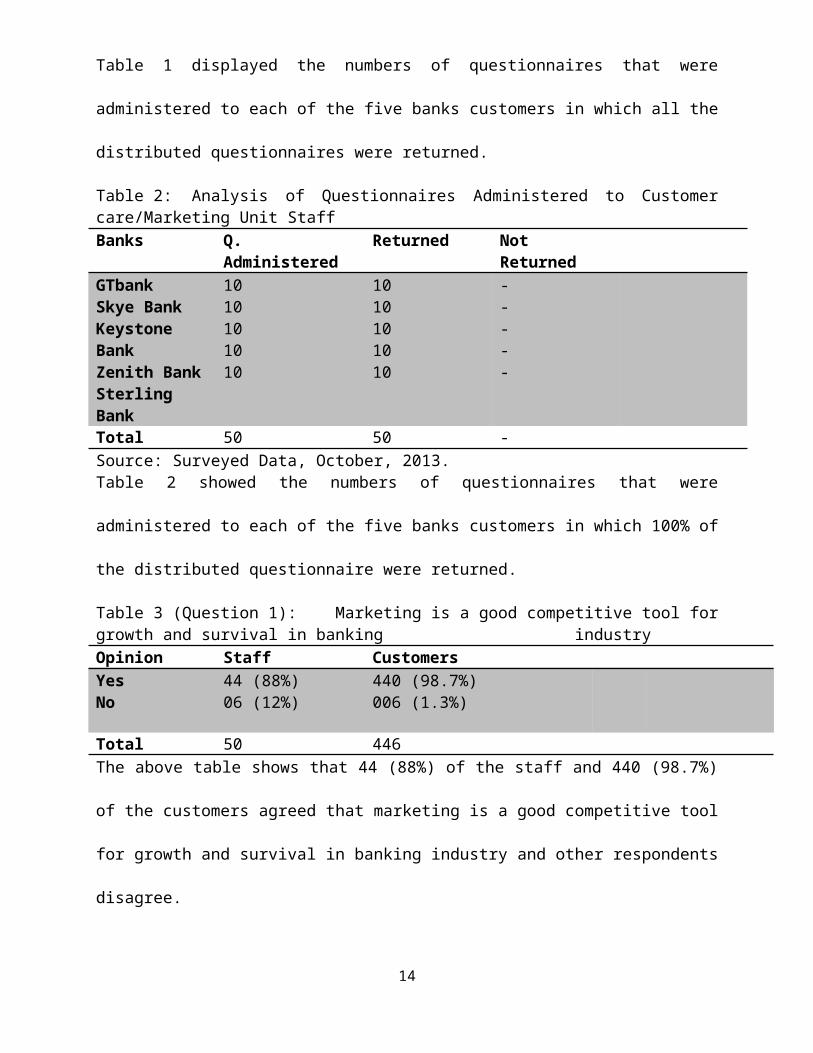

Table 2: Analysis of Questionnaires Administered to Customercare/Marketing Unit Staff Banks Q.

AdministeredReturned Not

ReturnedGTbankSkye BankKeystoneBankZenith BankSterlingBank

1010101010

1010101010

-----

Total 50 50 -Source: Surveyed Data, October, 2013.Table 2 showed the numbers of questionnaires that were

administered to each of the five banks customers in which 100% of

the distributed questionnaire were returned.

Table 3 (Question 1): Marketing is a good competitive tool forgrowth and survival in banking industryOpinion Staff CustomersYesNo

44 (88%)06 (12%)

440 (98.7%)006 (1.3%)

Total 50 446The above table shows that 44 (88%) of the staff and 440 (98.7%)

of the customers agreed that marketing is a good competitive tool

for growth and survival in banking industry and other respondents

disagree.

14

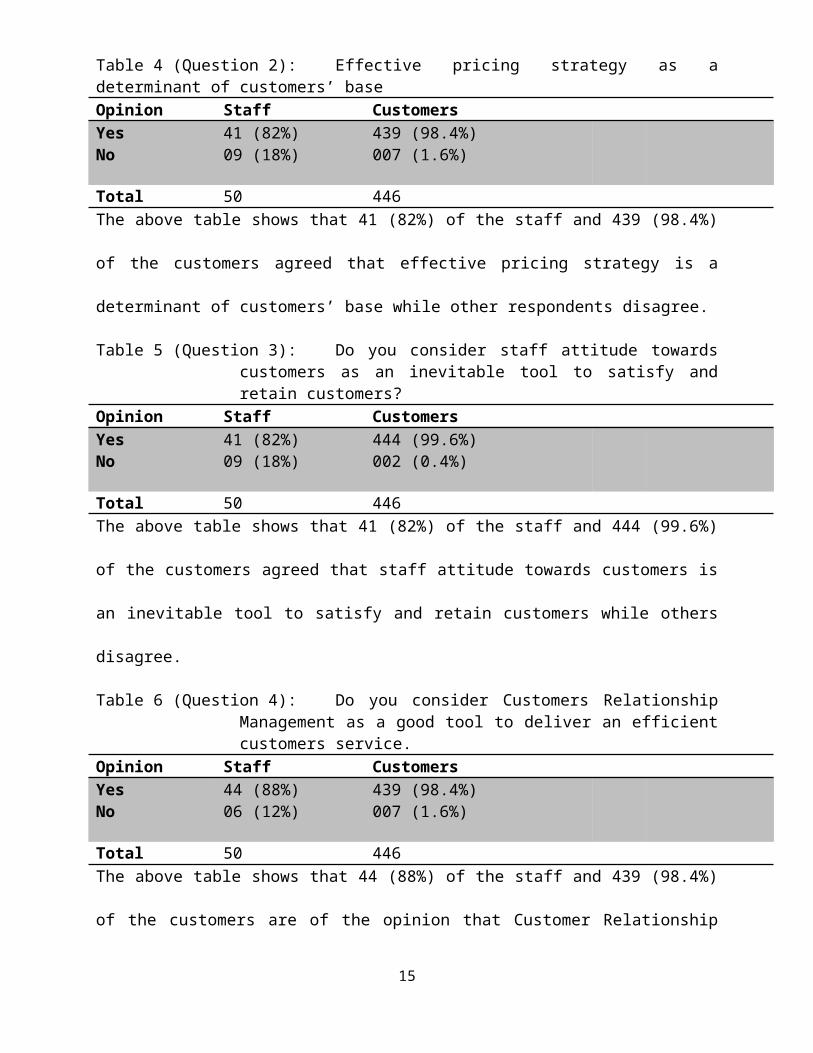

Table 4 (Question 2): Effective pricing strategy as adeterminant of customers’ baseOpinion Staff CustomersYesNo

41 (82%)09 (18%)

439 (98.4%)007 (1.6%)

Total 50 446The above table shows that 41 (82%) of the staff and 439 (98.4%)

of the customers agreed that effective pricing strategy is a

determinant of customers’ base while other respondents disagree.

Table 5 (Question 3): Do you consider staff attitude towardscustomers as an inevitable tool to satisfy andretain customers?

Opinion Staff CustomersYesNo

41 (82%)09 (18%)

444 (99.6%)002 (0.4%)

Total 50 446The above table shows that 41 (82%) of the staff and 444 (99.6%)

of the customers agreed that staff attitude towards customers is

an inevitable tool to satisfy and retain customers while others

disagree.

Table 6 (Question 4): Do you consider Customers RelationshipManagement as a good tool to deliver an efficientcustomers service.

Opinion Staff CustomersYesNo

44 (88%)06 (12%)

439 (98.4%)007 (1.6%)

Total 50 446The above table shows that 44 (88%) of the staff and 439 (98.4%)

of the customers are of the opinion that Customer Relationship

15

Management (CRM) is a good tool to deliver an efficient customer

service while other respondents disagree.

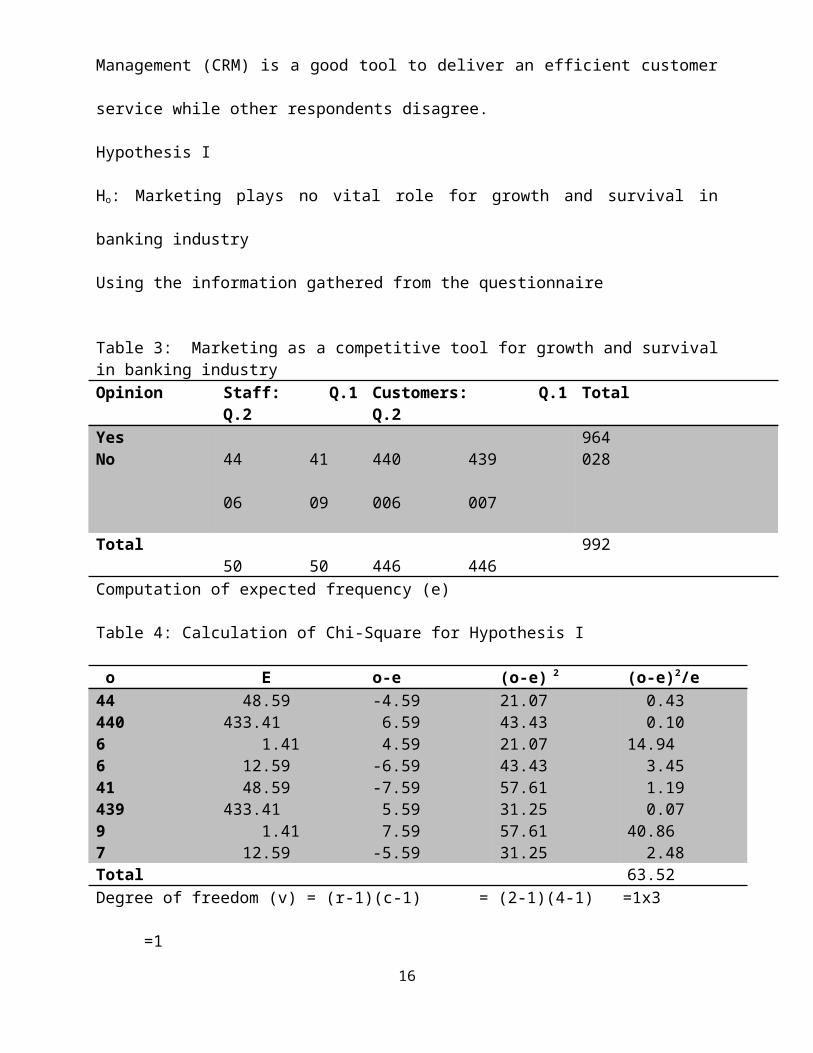

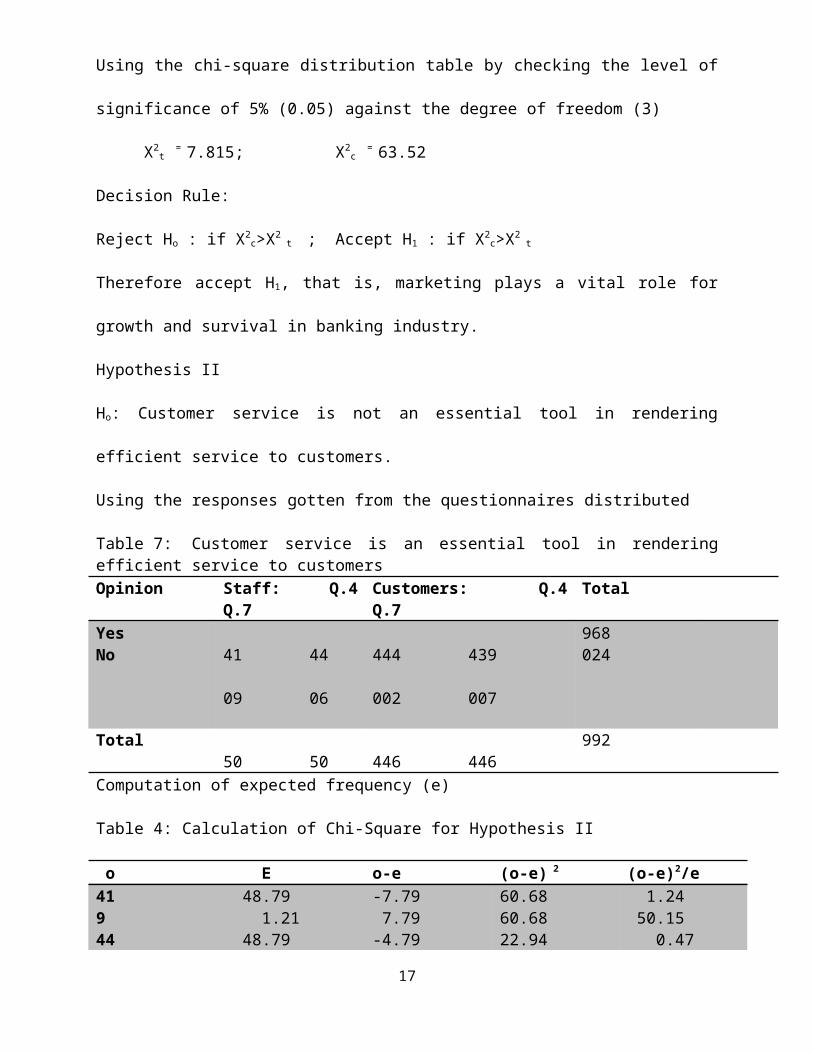

Hypothesis I

Ho: Marketing plays no vital role for growth and survival in

banking industry

Using the information gathered from the questionnaire

Table 3: Marketing as a competitive tool for growth and survivalin banking industryOpinion Staff: Q.1

Q.2Customers: Q.1Q.2

Total

YesNo

44 41 06 09

440 439 006 007

964028

Total 50 50

446 446

992

Computation of expected frequency (e)

Table 4: Calculation of Chi-Square for Hypothesis I

o E o-e (o-e) 2 (o-e)2/e44440664143997

48.59433.41 1.41 12.59 48.59433.41 1.41 12.59

-4.59 6.59 4.59-6.59-7.59 5.59 7.59-5.59

21.0743.4321.0743.4357.6131.2557.6131.25

0.43 0.1014.94 3.45 1.19 0.0740.86 2.48

Total 63.52Degree of freedom (v) = (r-1)(c-1) = (2-1)(4-1) =1x3

=1

16

Using the chi-square distribution table by checking the level of

significance of 5% (0.05) against the degree of freedom (3)

X2t = 7.815; X2

c = 63.52

Decision Rule:

Reject Ho : if X2c>X2

t ; Accept H1 : if X2

c>X2 t

Therefore accept H1, that is, marketing plays a vital role for

growth and survival in banking industry.

Hypothesis II

Ho: Customer service is not an essential tool in rendering

efficient service to customers.

Using the responses gotten from the questionnaires distributed

Table 7: Customer service is an essential tool in renderingefficient service to customers Opinion Staff: Q.4

Q.7Customers: Q.4Q.7

Total

YesNo

41 44 09 06

444 439 002 007

968024

Total 50 50

446 446

992

Computation of expected frequency (e)

Table 4: Calculation of Chi-Square for Hypothesis II

o E o-e (o-e) 2 (o-e)2/e41944

48.79 1.21 48.79

-7.79 7.79-4.79

60.6860.6822.94

1.24 50.15 0.47

17

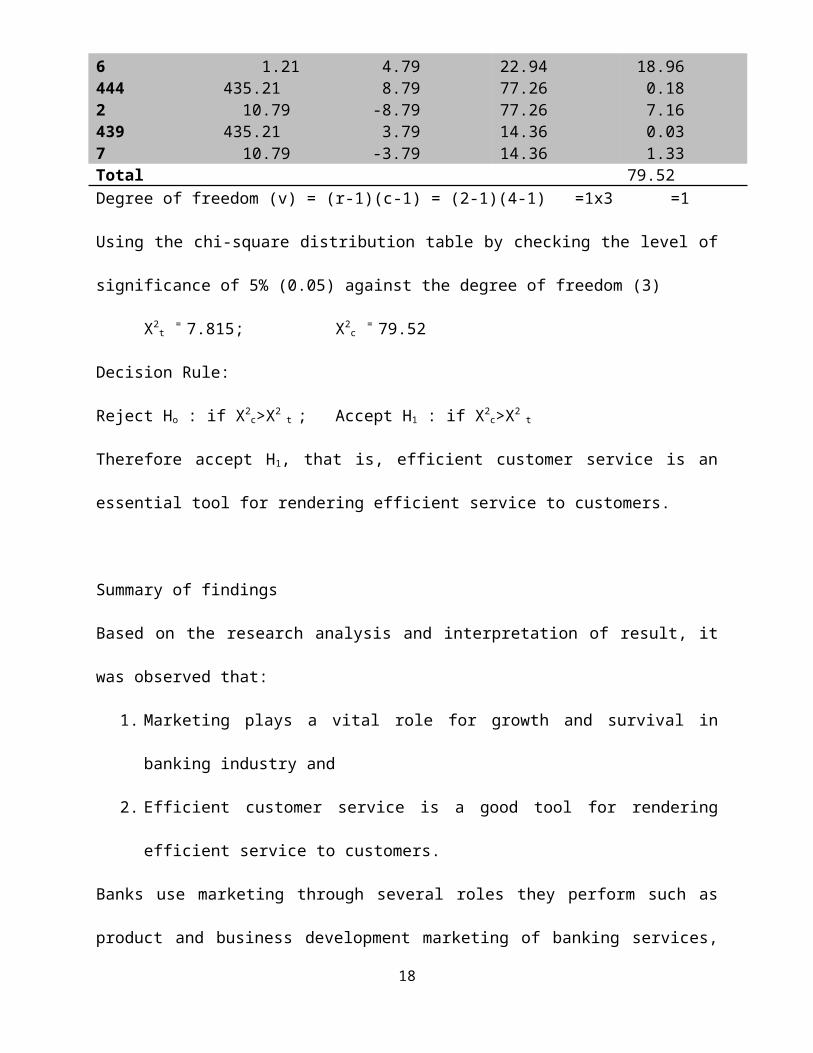

644424397

1.21435.21 10.79435.21 10.79

4.79 8.79-8.79 3.79-3.79

22.9477.2677.2614.3614.36

18.96 0.18 7.16 0.03 1.33

Total 79.52Degree of freedom (v) = (r-1)(c-1) = (2-1)(4-1) =1x3 =1

Using the chi-square distribution table by checking the level of

significance of 5% (0.05) against the degree of freedom (3)

X2t = 7.815; X2

c = 79.52

Decision Rule:

Reject Ho : if X2c>X2

t ; Accept H1 : if X2

c>X2 t

Therefore accept H1, that is, efficient customer service is an

essential tool for rendering efficient service to customers.

Summary of findings

Based on the research analysis and interpretation of result, it

was observed that:

1. Marketing plays a vital role for growth and survival in

banking industry and

2. Efficient customer service is a good tool for rendering

efficient service to customers.

Banks use marketing through several roles they perform such as

product and business development marketing of banking services,

18

strengthening customer relationship, marketing planning strategy

formulation, marketing research among others. Since service is

different from product with some features referred to as

distinctive characteristics of service which are intangibility,

variability, perishability, inseparability of ownership these

then posed threat to marketing of banking service as customers

wish to see what they intend to purchase, verify its reliability

before consumption, to get service without visiting the bank and

even want best service of same degree every time.

Efficient customer service was discovered to be a significant

tool for rendering efficient service to customers as they want

staff to treat them with care, pay special attention to them and

talk to them in an appropriate manner.

Summary

Marketing is an indispensable tool for the realization of

organization’s objective as they (organization) need it

(marketing) for growth, survival and profit maximization. Many

people earlier believed that marketing is just about advertising

or sales but others believed that marketing is just about

advertising or sales but others believed that it goes beyond

that, as it involves everything a company does to acquire

19

customers and maintain good relationship with them, creation of a

demand for a company’s products/services, distribution and other

service for customer who purchase the product. This research then

study the situation especially the banking industry to determine

whether marketing truly plays a significant role for growth and

survival in banking industry among other objectives with the aid

of survey design and questionnaire which is being validated by

the use of chi-square statistical method of testing.

Authors’ views related to marketing were reviewed with emphasis

on marketing in banks, various marketing definitions, major banks

division marketing concepts, banking services and its marketing,

marketing planning and strategies and importantly the role of

marketing in banking industry.

The study as well focuses on all the 21 banks in Bauchi state

while 5 selected banks in Bauchi were used as sample size in

which both staff of marketing/customer care unit as well as

customers were used as respondents with the use of table and

percentages, and also interpreted to give a clear understanding

before the hypotheses were tested for acceptance or rejection

using chi-square statistical method.

20

It was concluded that marketing plays a vital role for growth and

survival in banking industry,. Marketers should always focus on

benefits to be derived from their differentiated product and

service to minimize the problems of intangibility, Banks should

be more customer-focused and more innovative in order to identify

customer’s needs and satisfy them timely and Marketers should

always follow the know your customer (KYC) and Customers Address

Verification (CAV) procedures and conduct proper credit

assessment before giving out loan to customers.

Conclusion

After several study, assessment analyses and proper

interpretation of the data obtained from the respondents it was

concluded that marketing is an important tool used by banks for

growth and survival in the industry. It was as well realized that

marketing also play a vital role, in terms of customer service

function, to render efficient service to customers while there by

increase customers loyalty and retention.

Banks use advertisement, promotion, branding and corporate social

responsibility as a service marketing strategy to create

awareness of their products/services in order for customers to

know much about the products/services offered by the banks. They

21

also adopt management of credit facilities extension, pricing

strategy, customer relationship management and electronic banking

products/services as an aid for customers’ retention and

acquisition.

It was observed that male are the majority of banks customers

as they cover 80% of the respondents, while female covers only

20%, which was concluded that they (female) don’t really deposit

and transact with banks.

Recommendations

The following recommendations were suggested which if properly

implemented will further enhance marketing of banking service and

solve the problem posed by the distinctive characteristics of

service.

1. Banks should be more customer-focused and more innovative in

order to identify customer’s needs and satisfy them timely.

2. Marketers should always follow the Know Your Customer (KYC)

and Customers Address Verification (CAV) procedures and

conduct proper credit assessment before giving out loan to

customers.

3. Benchmarking should be deployed by banks in order to compare

organization’s performance with that of their competitors.

22

4. The banks should continue to improve their corporate social,

responsibility function and branding so as to create more

awareness of the banks to both existing and potential

customers.

5. Banks should adopt effective marketing planning and

strategy to differentiate their product/service from that of

the competitors.

6. Banks should encourage adequate training and re-training to

their marketing and customer care staff in order to boost

their efficiency and equip them with adequate practical

marketing knowledge, idea and tactics.

7. Banks should focus more on the additional 3p’s of marketing

mix (people, process and physical evidence), so that

customers will be best satisfied.

8. Ensure that standards are always monitored to overcome the

problems of variability.

References

Adebisi, I. & Abdulazeez, A. (2000). Principles and Practice of FinancialAccounting. Ilorin: Rajah Dynamic Printers.

Alvin, C. & Ronald, F. (2001). Marketing Research (Second Edition). NewJersey: Prentice Hall Inc.

23

ATS (2001). ATS Distance Learning Pack: Management Study, Questions & Answers.Lagos: Accountancy Training Publications.

Bamidele, A. & Kama, U. (2003). A Case Study of Distress Banks inNigeria. Journal of Research & Statistics Department of Central Bank ofNigeria. 26(3): 28-37.

Bolaji, B. (2006). Service Marketing and Management. New Delhi: SChand and Company Ltd.

Dwivedi, D. (2002). Managerial Economics (Sixth Revised Edition). India:Vikas Publishing House PVT Ltd.

Dwivedi, R. (2007), “Managing Marketing-Finance Interface”, Journal of Commerce and Trade. 2(2): 32

Frank, R. & Bernanke, B. (2007). Principles of Economics (Third Edition).New York: McGraw Hill Publishing Company.

Ikpefan, O. (2013). The Impact of marketing of Financial Servicesin the Nigerian banking industry. Journal of Business Administration andManagement Sciences Research 2(6): 148-162. Retrieved November 18,2013 from

www.eprints.covenantuniversity.edu.ng/1329/1/ikpefan.pdf

Kotler, P. (2003). Marketing Management (Eleventh Edition). India:Pearson Education Ltd.

Kotler, P. & Keller, K. (2006). Marketing Management (12th Edition).Singapore: Pearson Education Ltd.

Mas’ud, R. & Yamzid, A. (2009). Problems and Strategies inService Marketing: Bangladesh Perspectives. Journal of ServiceMarketing. Retrieved June 18, 2012 from

www.ssrn/abstract=1349449.

Nokandeh, B. Poorhabib, A. Seyedi, S. & Niknafs, M. (2013). Marketing Research Services of Banks and their Impact on Perception of Service Users. Interdisciplinary Journalof

Comtemporary Research in Business. Retrieved November 21, 2013 from www.journal –archives31.webs.com/472-477.

24

Oyekunle, O. & Adeniyi, W. (2000). Integrated Management. Oshogbo:Adekola Commercial Press.

Perreault, D. & McCarthy, E. (2002). Basic Marketing. A GlobalManagerial Approach. London: McGraw-Hill Irwin.

Uppal, R. (2010). Marketing of Bank Product-Emerging Challenges &New Strategies. JM International Journal of Management Research. Retrieved November 24, 2013 from

www.jmijitm.com/papers/130082034035_45.pdf.

Van Horne, C. (2004). Financial Management and Policy (12th Edition). India:Pearson Education (Singapore) Pte. Ltd.

Zikmund, D. & Michael, W. (2006). Marketing (5th Edition). Minneapolis:West Publishing Company Minneapolis/St. Paul.

25