Embed Size (px)

Citation preview

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

NYSE: SNA | Price Target: $198 | Upside: 17.3% | 10 Shares

Snap-On Inc. Sector Head: Vienna BuscherJunior Analyst: Christopher SucheckiNovember 5, 2019

BINGHAMTONINVESTMENT FUND

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

Agenda2

SNA Company Overview

Industry Overview

Valuation

Risks & Mitigations

SNA Market Position

Investment Thesis & Catalysts

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

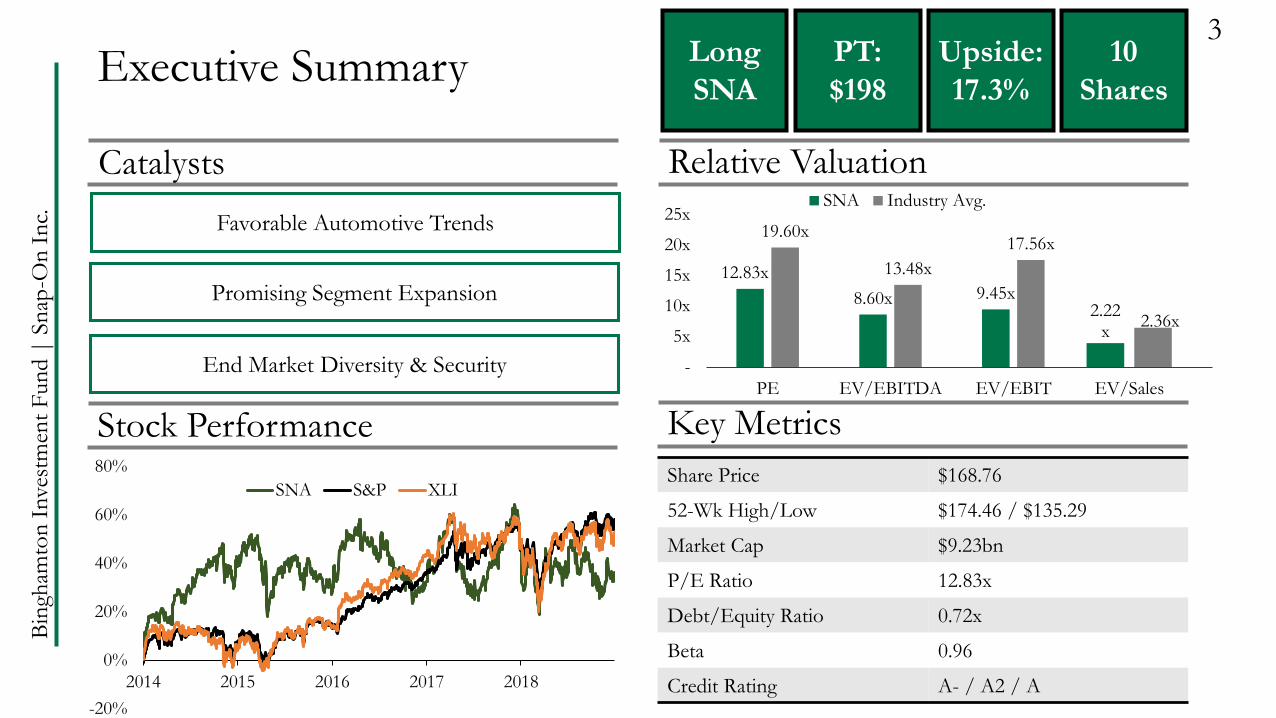

Executive Summary3

Catalysts Relative Valuation

Stock Performance Key Metrics

Favorable Automotive Trends

End Market Diversity & Security

Promising Segment Expansion12.83x

8.60x 9.45x

19.60x

13.48x

17.56x

-

5x

10x

15x

20x

25x

PE EV/EBITDA EV/EBIT

SNA Industry Avg.

2.22x

2.36x

EV/Sales

Long

SNA

PT:

$198

Upside:

17.3%

Share Price $168.76

52-Wk High/Low $174.46 / $135.29

Market Cap $9.23bn

P/E Ratio 12.83x

Debt/Equity Ratio 0.72x

Beta 0.96

Credit Rating A- / A2 / A-20%

0%

20%

40%

60%

80%

2014 2015 2016 2017 2018

SNA S&P XLI

10

Shares

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

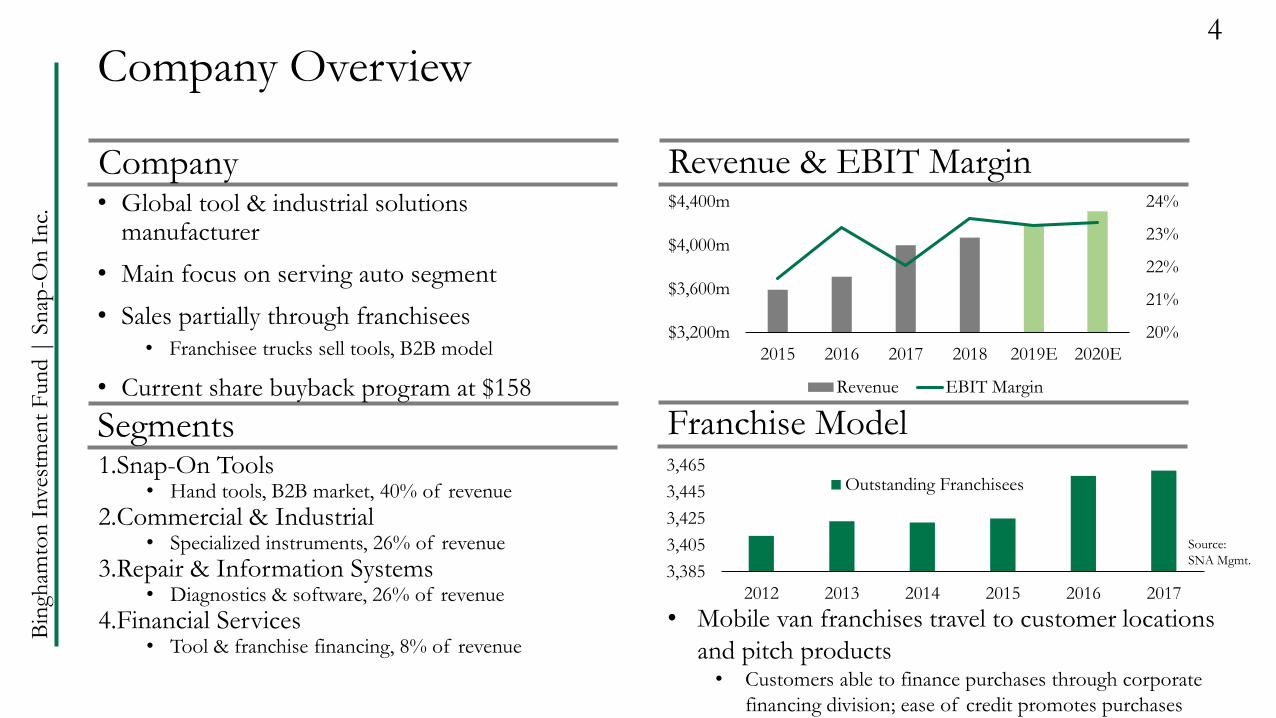

• Global tool & industrial solutions manufacturer

• Main focus on serving auto segment

• Sales partially through franchisees

• Franchisee trucks sell tools, B2B model

• Current share buyback program at $158

1.Snap-On Tools• Hand tools, B2B market, 40% of revenue

2.Commercial & Industrial• Specialized instruments, 26% of revenue

3.Repair & Information Systems• Diagnostics & software, 26% of revenue

4.Financial Services • Tool & franchise financing, 8% of revenue

Company Overview4

Company Revenue & EBIT Margin

Segments Franchise Model

20%

21%

22%

23%

24%

$3,200m

$3,600m

$4,000m

$4,400m

2015 2016 2017 2018 2019E 2020E

Revenue EBIT Margin

3,385

3,405

3,425

3,445

3,465

2012 2013 2014 2015 2016 2017

Outstanding Franchisees

• Mobile van franchises travel to customer locations

and pitch products• Customers able to finance purchases through corporate

financing division; ease of credit promotes purchases

Source:

SNA Mgmt.

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

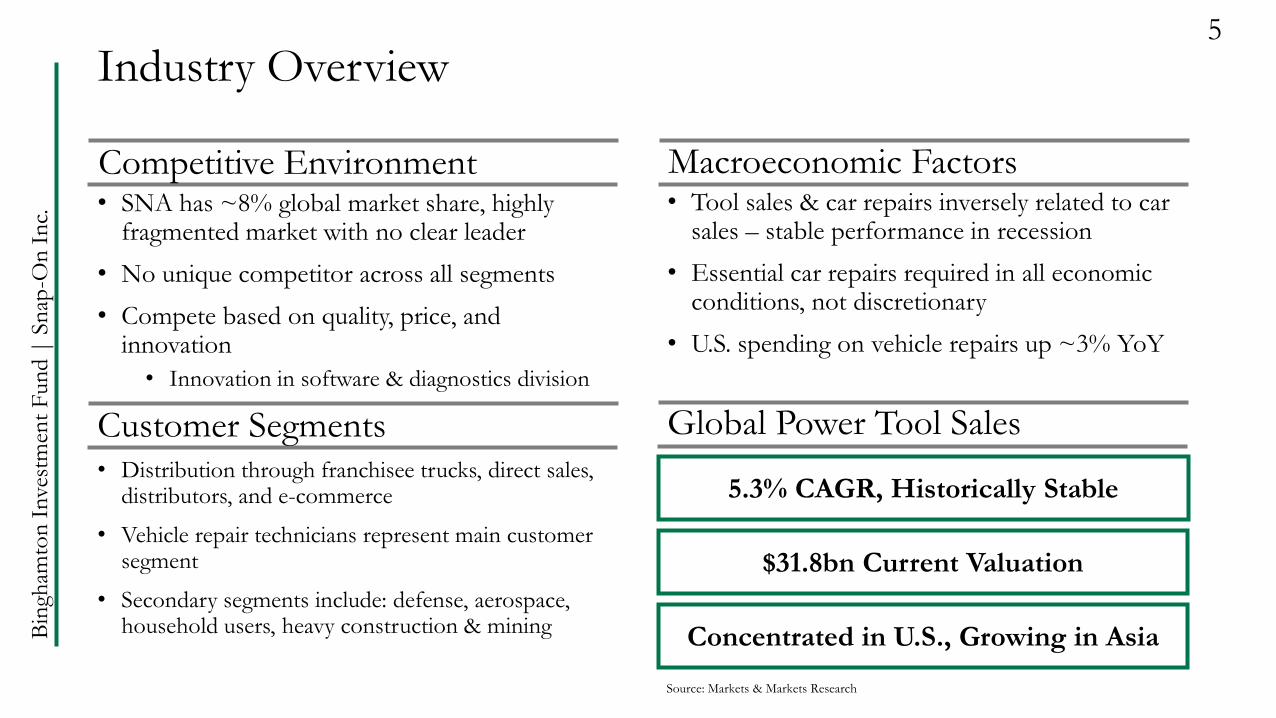

• SNA has ~8% global market share, highly fragmented market with no clear leader

• No unique competitor across all segments

• Compete based on quality, price, and innovation

• Innovation in software & diagnostics division

• Distribution through franchisee trucks, direct sales, distributors, and e-commerce

• Vehicle repair technicians represent main customer segment

• Secondary segments include: defense, aerospace, household users, heavy construction & mining

• Tool sales & car repairs inversely related to car sales – stable performance in recession

• Essential car repairs required in all economic conditions, not discretionary

• U.S. spending on vehicle repairs up ~3% YoY

Industry Overview5

Competitive Environment Macroeconomic Factors

Customer Segments Global Power Tool Sales

5.3% CAGR, Historically Stable

$31.8bn Current Valuation

Concentrated in U.S., Growing in Asia

Source: Markets & Markets Research

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

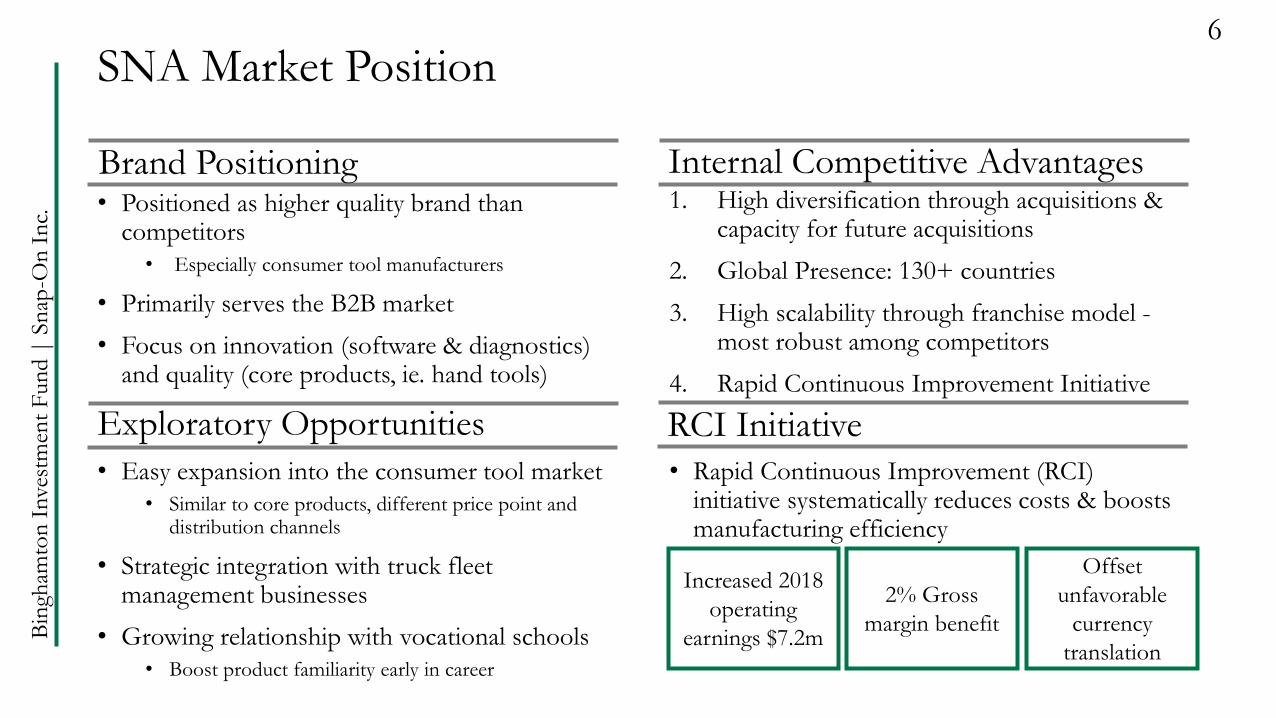

• Positioned as higher quality brand than competitors

• Especially consumer tool manufacturers

• Primarily serves the B2B market

• Focus on innovation (software & diagnostics) and quality (core products, ie. hand tools)

1. High diversification through acquisitions & capacity for future acquisitions

2. Global Presence: 130+ countries

3. High scalability through franchise model -most robust among competitors

4. Rapid Continuous Improvement Initiative

• Rapid Continuous Improvement (RCI) initiative systematically reduces costs & boosts manufacturing efficiency

SNA Market Position6

Brand Positioning Internal Competitive Advantages

Exploratory Opportunities RCI Initiative

Increased 2018

operating

earnings $7.2m

2% Gross

margin benefit

Offset

unfavorable

currency

translation

• Easy expansion into the consumer tool market

• Similar to core products, different price point and distribution channels

• Strategic integration with truck fleet management businesses

• Growing relationship with vocational schools

• Boost product familiarity early in career

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

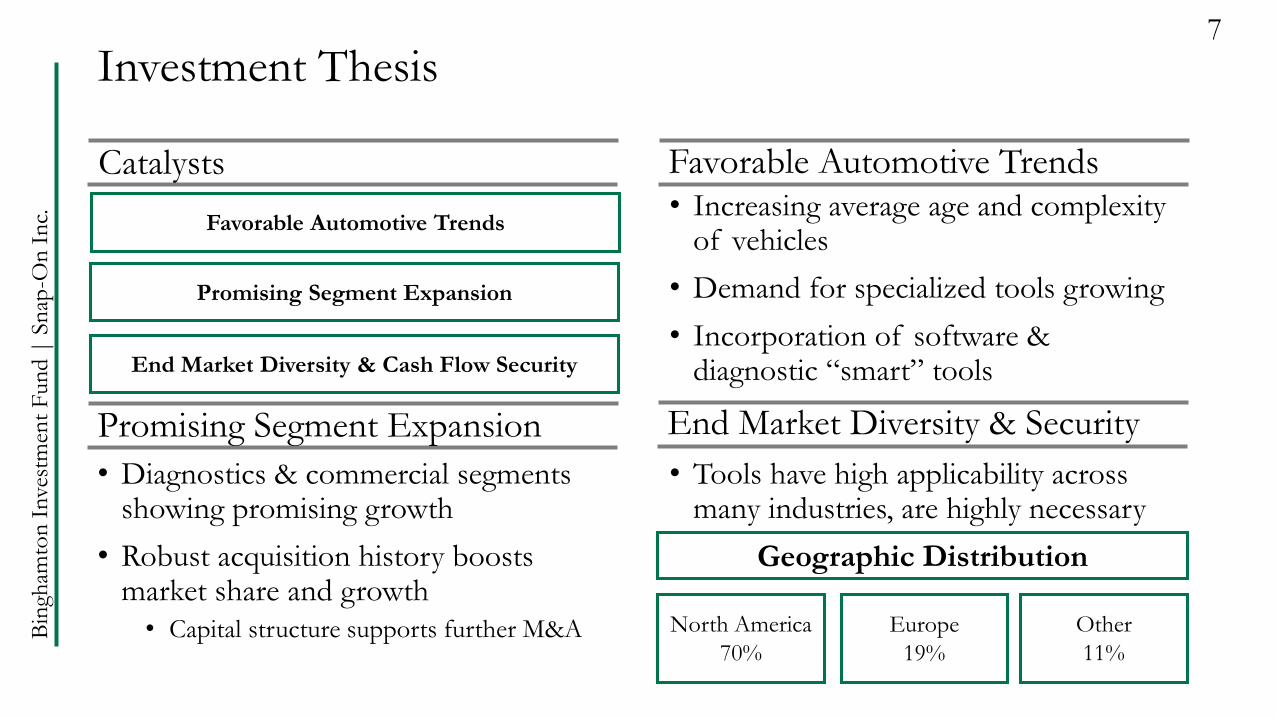

• Increasing average age and complexity of vehicles

• Demand for specialized tools growing

• Incorporation of software & diagnostic “smart” tools

• Diagnostics & commercial segments showing promising growth

• Robust acquisition history boosts market share and growth

• Capital structure supports further M&A

• Tools have high applicability across many industries, are highly necessary

Investment Thesis7

Catalysts Favorable Automotive Trends

Promising Segment Expansion End Market Diversity & Security

Favorable Automotive Trends

End Market Diversity & Cash Flow Security

Promising Segment Expansion

Geographic Distribution

North America

70%

Europe

19%

Other

11%

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

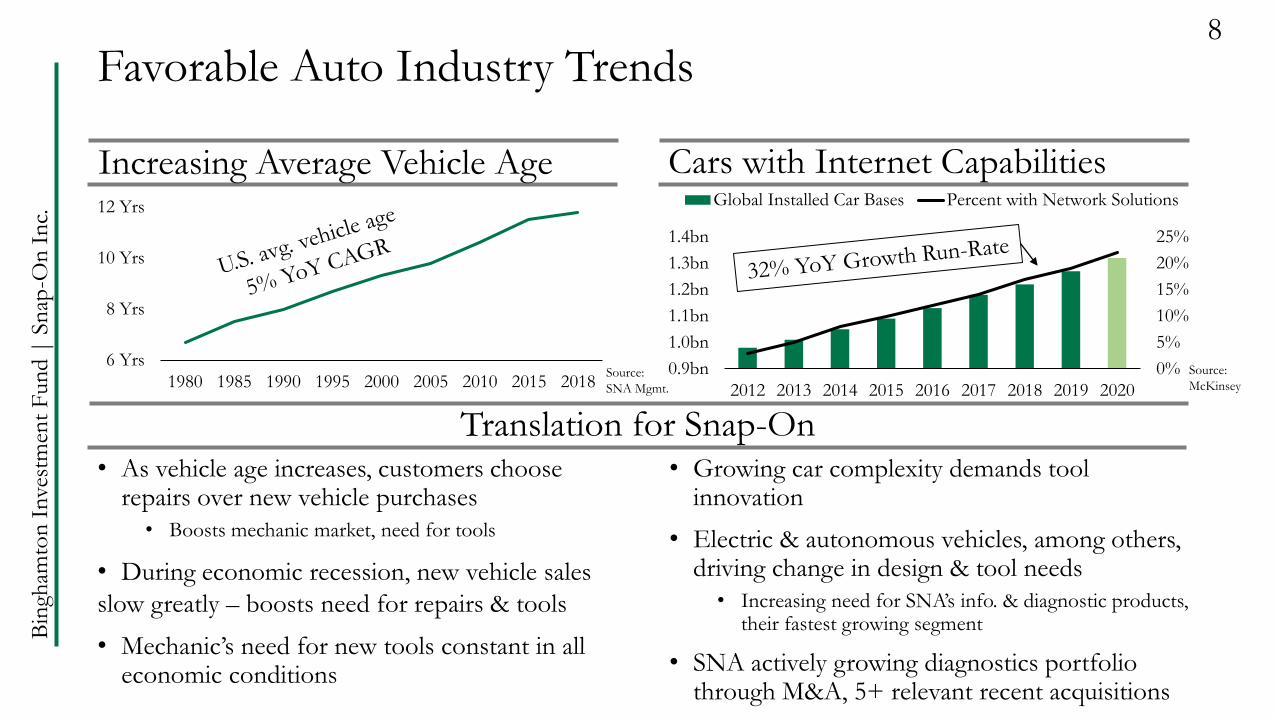

Translation for Snap-On• As vehicle age increases, customers choose

repairs over new vehicle purchases

• Boosts mechanic market, need for tools

• During economic recession, new vehicle sales

slow greatly – boosts need for repairs & tools

• Mechanic’s need for new tools constant in all economic conditions

• Growing car complexity demands tool innovation

• Electric & autonomous vehicles, among others, driving change in design & tool needs

• Increasing need for SNA’s info. & diagnostic products, their fastest growing segment

• SNA actively growing diagnostics portfolio through M&A, 5+ relevant recent acquisitions

Favorable Auto Industry Trends8

Increasing Average Vehicle Age Cars with Internet Capabilities

6 Yrs

8 Yrs

10 Yrs

12 Yrs

1980 1985 1990 1995 2000 2005 2010 2015 2018Source:

McKinseySource:

SNA Mgmt.

0%

5%

10%

15%

20%

25%

0.9bn

1.0bn

1.1bn

1.2bn

1.3bn

1.4bn

2012 2013 2014 2015 2016 2017 2018 2019 2020

Global Installed Car Bases Percent with Network Solutions

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

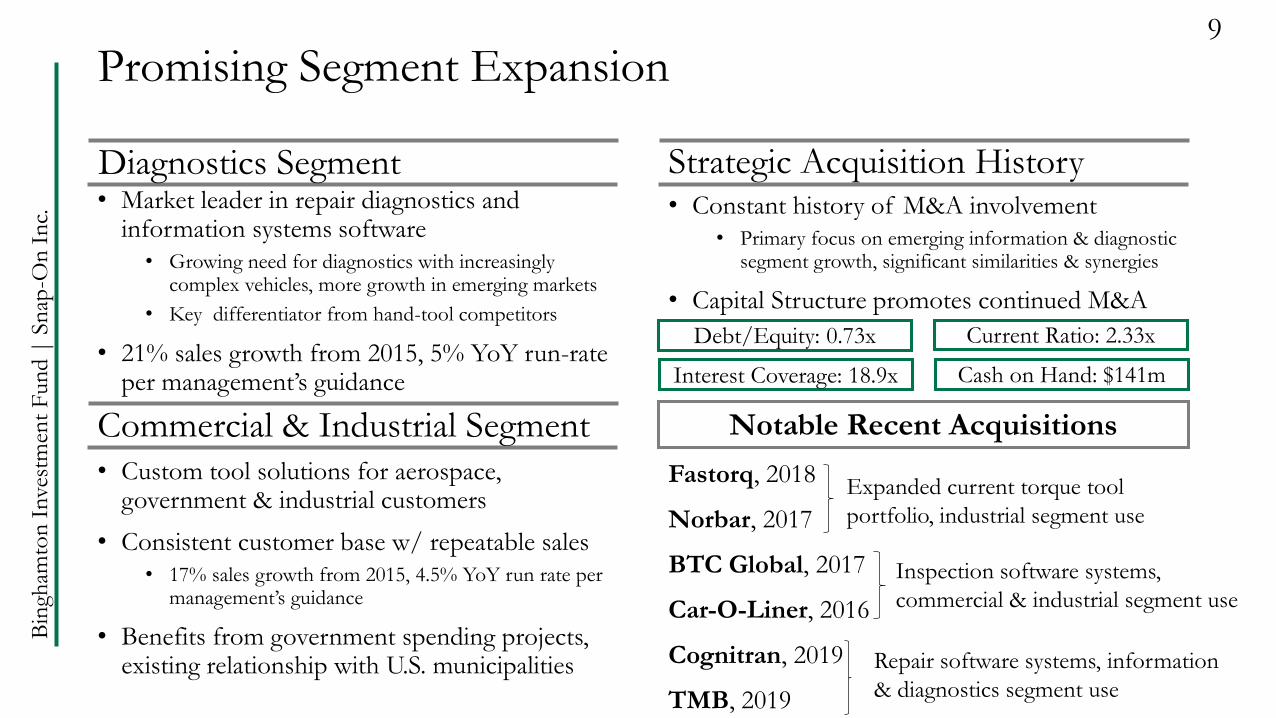

• Custom tool solutions for aerospace, government & industrial customers

• Consistent customer base w/ repeatable sales

• 17% sales growth from 2015, 4.5% YoY run rate per management’s guidance

• Benefits from government spending projects, existing relationship with U.S. municipalities

Promising Segment Expansion9

Diagnostics Segment Strategic Acquisition History

Commercial & Industrial Segment Notable Recent Acquisitions

Fastorq, 2018

Norbar, 2017

BTC Global, 2017

Car-O-Liner, 2016

Cognitran, 2019

TMB, 2019

Expanded current torque tool

portfolio, industrial segment use

Inspection software systems,

commercial & industrial segment use

Repair software systems, information

& diagnostics segment use

• Market leader in repair diagnostics and information systems software

• Growing need for diagnostics with increasingly complex vehicles, more growth in emerging markets

• Key differentiator from hand-tool competitors

• 21% sales growth from 2015, 5% YoY run-rate per management’s guidance

• Constant history of M&A involvement

• Primary focus on emerging information & diagnostic segment growth, significant similarities & synergies

• Capital Structure promotes continued M&A

Debt/Equity: 0.73x

Interest Coverage: 18.9x

Current Ratio: 2.33x

Cash on Hand: $141m

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

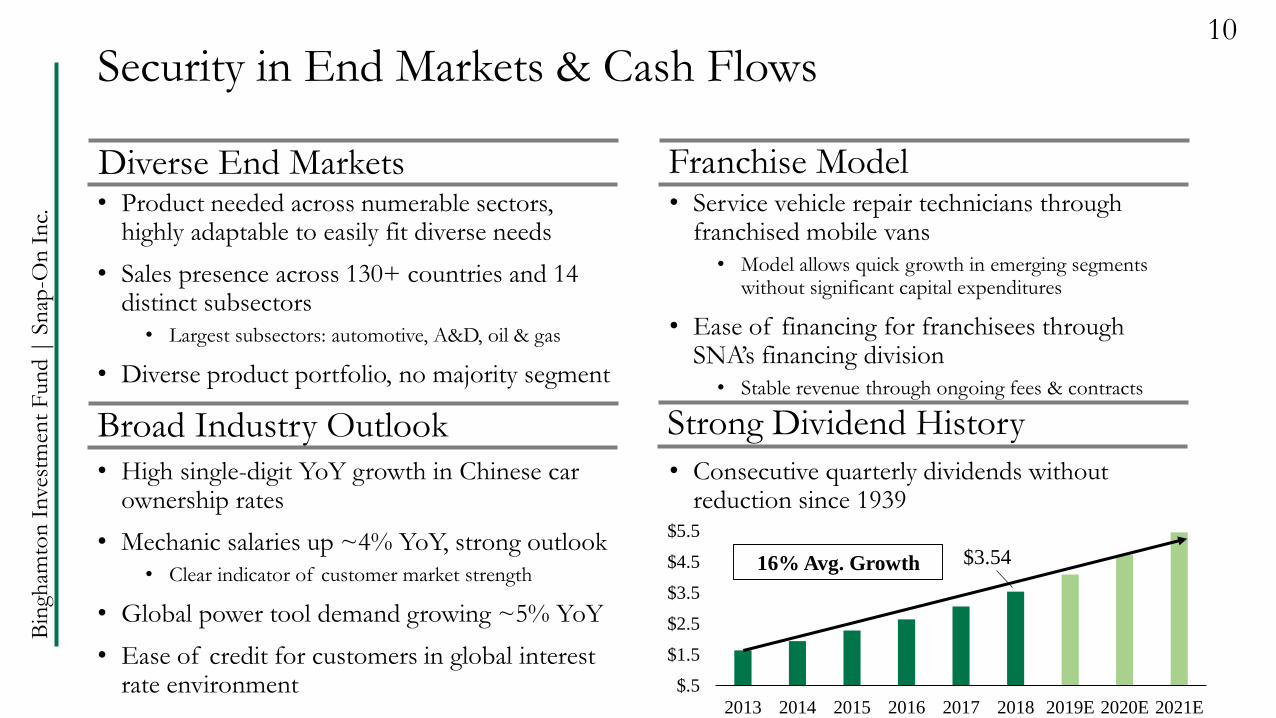

• Product needed across numerable sectors, highly adaptable to easily fit diverse needs

• Sales presence across 130+ countries and 14 distinct subsectors

• Largest subsectors: automotive, A&D, oil & gas

• Diverse product portfolio, no majority segment

• Service vehicle repair technicians through franchised mobile vans

• Model allows quick growth in emerging segments without significant capital expenditures

• Ease of financing for franchisees through SNA’s financing division

• Stable revenue through ongoing fees & contracts

• High single-digit YoY growth in Chinese car ownership rates

• Mechanic salaries up ~4% YoY, strong outlook

• Clear indicator of customer market strength

• Global power tool demand growing ~5% YoY

• Ease of credit for customers in global interest rate environment

• Consecutive quarterly dividends without reduction since 1939

Security in End Markets & Cash Flows10

Diverse End Markets Franchise Model

Broad Industry Outlook Strong Dividend History

$.5

$1.5

$2.5

$3.5

$4.5

$5.5

2013 2014 2015 2016 2017 2018 2019E 2020E 2021E

$3.5416% Avg. Growth

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

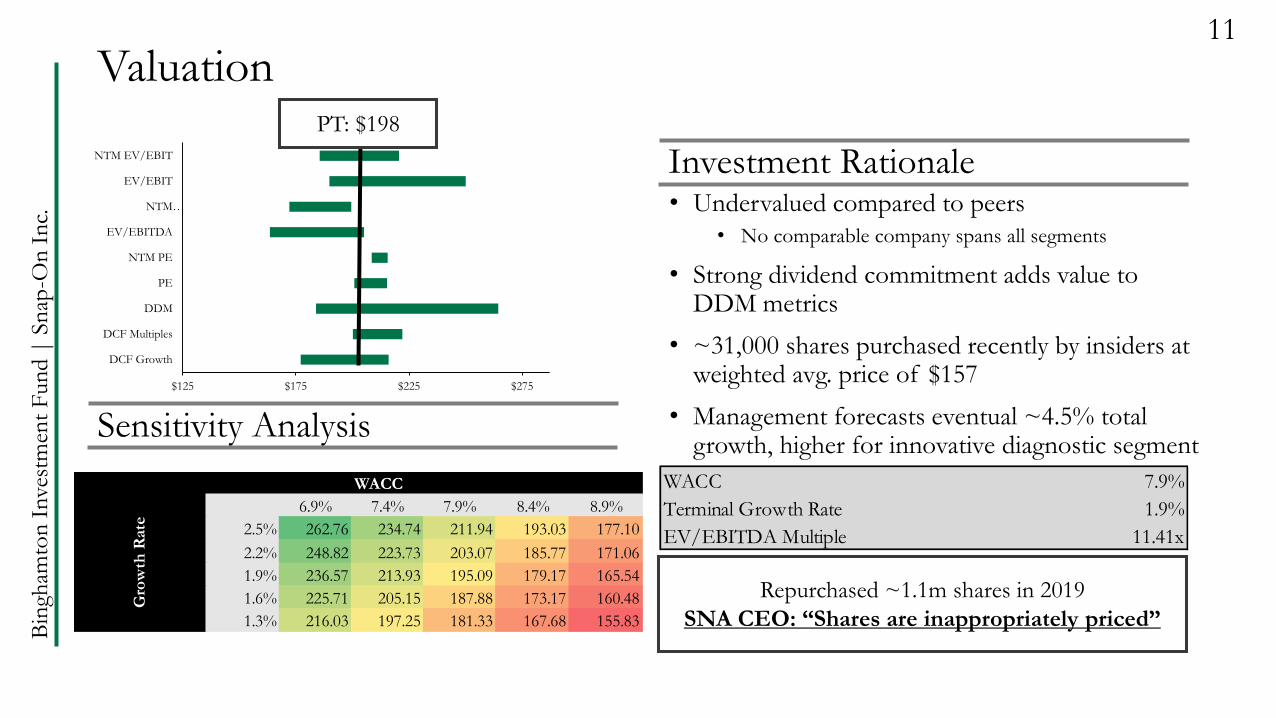

$125 $175 $225 $275 $325

DCF Growth

DCF Multiples

DDM

PE

NTM PE

EV/EBITDA

NTM…

EV/EBIT

NTM EV/EBIT

• Undervalued compared to peers

• No comparable company spans all segments

• Strong dividend commitment adds value to DDM metrics

• ~31,000 shares purchased recently by insiders at weighted avg. price of $157

• Management forecasts eventual ~4.5% total growth, higher for innovative diagnostic segment

Valuation11

Investment Rationale

Sensitivity Analysis

Repurchased ~1.1m shares in 2019

SNA CEO: “Shares are inappropriately priced”

PT: $198

WACC

194.82$ 6.9% 7.4% 7.9% 8.4% 8.9%

2.5% 262.76 234.74 211.94 193.03 177.10

2.2% 248.82 223.73 203.07 185.77 171.06

1.9% 236.57 213.93 195.09 179.17 165.54

1.6% 225.71 205.15 187.88 173.17 160.48

1.3% 216.03 197.25 181.33 167.68 155.83

Gro

wth

Rate

WACC 7.9%

Terminal Growth Rate 1.9%

EV/EBITDA Multiple 11.41x

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

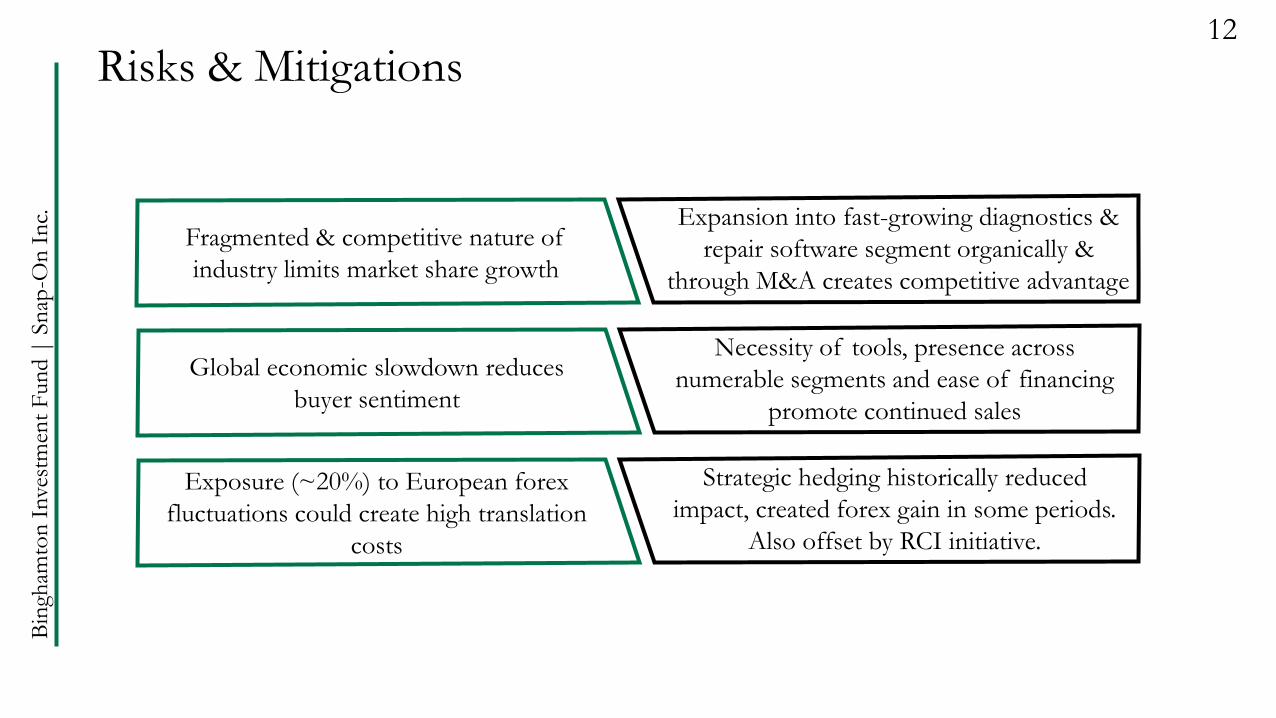

Risks & Mitigations12

Fragmented & competitive nature of

industry limits market share growth

Expansion into fast-growing diagnostics &

repair software segment organically &

through M&A creates competitive advantage

Exposure (~20%) to European forex

fluctuations could create high translation

costs

Strategic hedging historically reduced

impact, created forex gain in some periods.

Also offset by RCI initiative.

Global economic slowdown reduces

buyer sentiment

Necessity of tools, presence across

numerable segments and ease of financing

promote continued sales

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

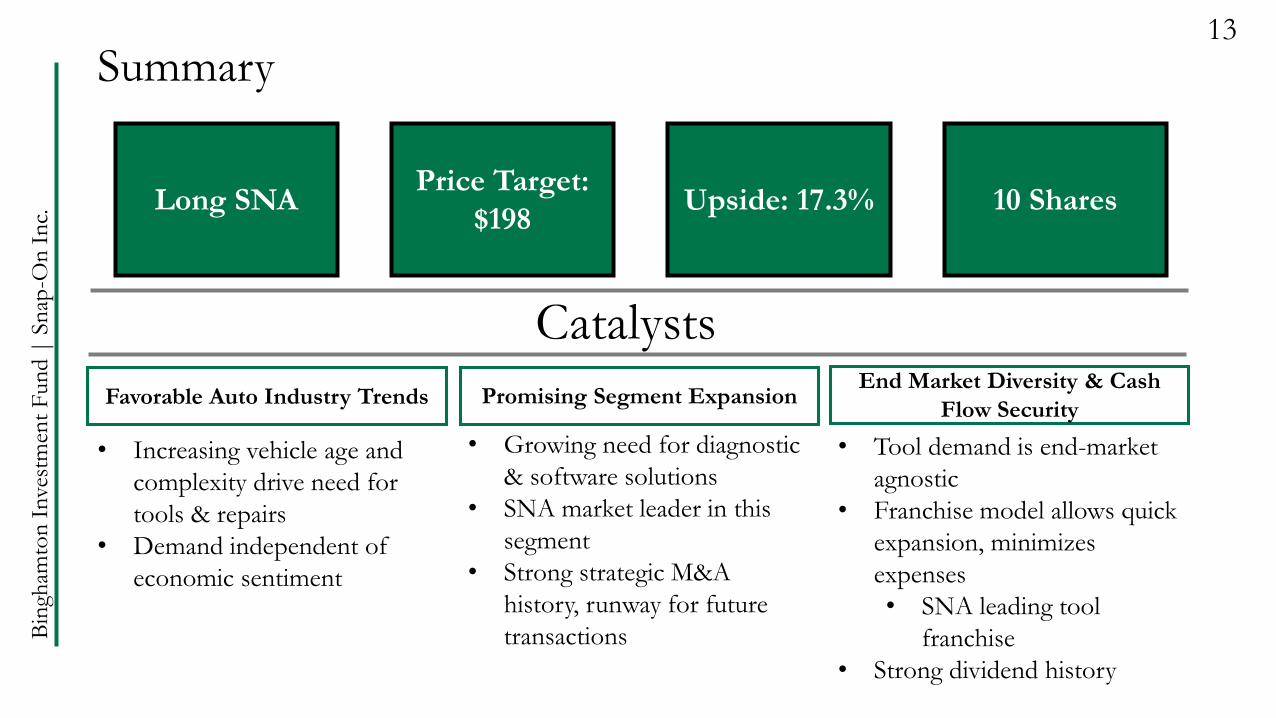

Summary13

Catalysts

Long SNAPrice Target:

$198Upside: 17.3%

End Market Diversity & Cash

Flow SecurityFavorable Auto Industry Trends Promising Segment Expansion

• Increasing vehicle age and

complexity drive need for

tools & repairs

• Demand independent of

economic sentiment

• Growing need for diagnostic

& software solutions

• SNA market leader in this

segment

• Strong strategic M&A

history, runway for future

transactions

• Tool demand is end-market

agnostic

• Franchise model allows quick

expansion, minimizes

expenses

• SNA leading tool

franchise

• Strong dividend history

10 Shares

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

14

Thank You

Questions?

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

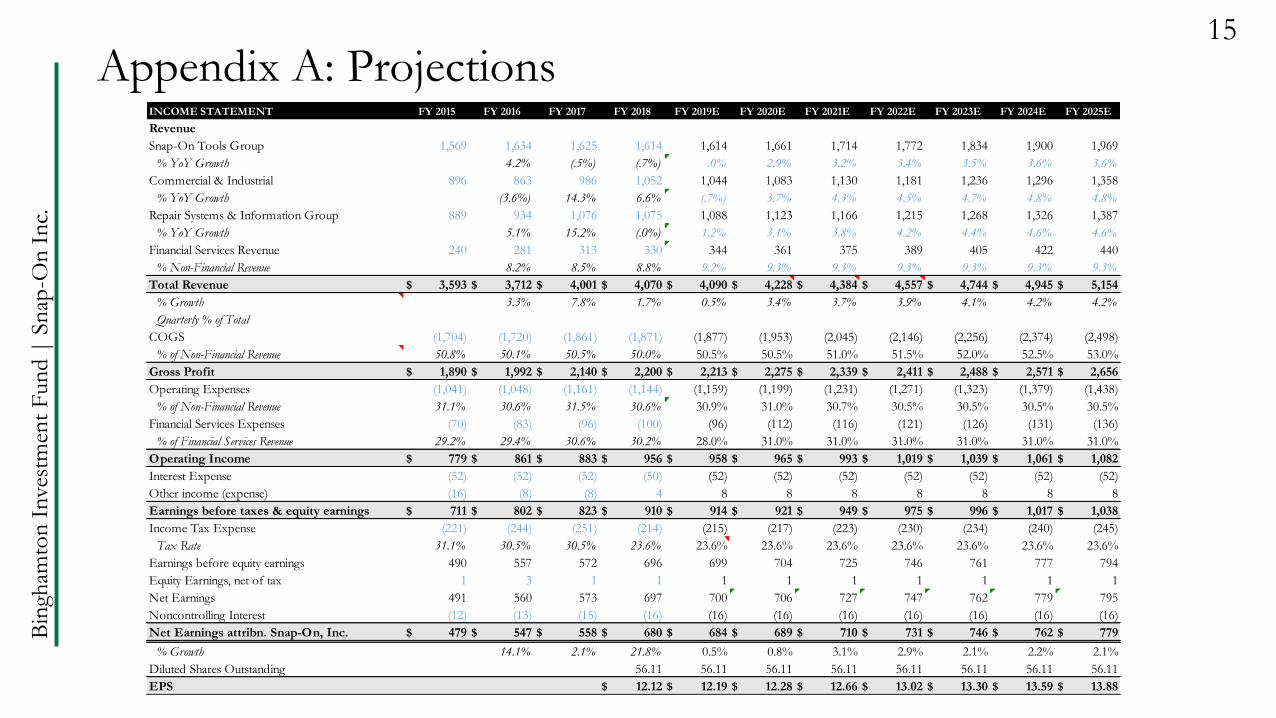

INCOME STATEMENT FY 2015 FY 2016 FY 2017 FY 2018 FY 2019E FY 2020E FY 2021E FY 2022E FY 2023E FY 2024E FY 2025E

Revenue

Snap-On Tools Group 1,569 1,634 1,625 1,614 1,614 1,661 1,714 1,772 1,834 1,900 1,969

% YoY Growth 4.2% (.5%) (.7%) .0% 2.9% 3.2% 3.4% 3.5% 3.6% 3.6%

Commercial & Industrial 896 863 986 1,052 1,044 1,083 1,130 1,181 1,236 1,296 1,358

% YoY Growth (3.6%) 14.3% 6.6% (.7%) 3.7% 4.3% 4.5% 4.7% 4.8% 4.8%

Repair Systems & Information Group 889 934 1,076 1,075 1,088 1,123 1,166 1,215 1,268 1,326 1,387

% YoY Growth 5.1% 15.2% (.0%) 1.2% 3.1% 3.8% 4.2% 4.4% 4.6% 4.6%

Financial Services Revenue 240 281 313 330 344 361 375 389 405 422 440

% Non-Financial Revenue 8.2% 8.5% 8.8% 9.2% 9.3% 9.3% 9.3% 9.3% 9.3% 9.3%

Total Revenue 3,593$ 3,712$ 4,001$ 4,070$ 4,090$ 4,228$ 4,384$ 4,557$ 4,744$ 4,945$ 5,154$

% Growth 3.3% 7.8% 1.7% 0.5% 3.4% 3.7% 3.9% 4.1% 4.2% 4.2%

Quarterly % of Total

COGS (1,704) (1,720) (1,861) (1,871) (1,877) (1,953) (2,045) (2,146) (2,256) (2,374) (2,498)

% of Non-Financial Revenue 50.8% 50.1% 50.5% 50.0% 50.5% 50.5% 51.0% 51.5% 52.0% 52.5% 53.0%

Gross Profit 1,890$ 1,992$ 2,140$ 2,200$ 2,213$ 2,275$ 2,339$ 2,411$ 2,488$ 2,571$ 2,656$

Operating Expenses (1,041) (1,048) (1,161) (1,144) (1,159) (1,199) (1,231) (1,271) (1,323) (1,379) (1,438)

% of Non-Financial Revenue 31.1% 30.6% 31.5% 30.6% 30.9% 31.0% 30.7% 30.5% 30.5% 30.5% 30.5%

Financial Services Expenses (70) (83) (96) (100) (96) (112) (116) (121) (126) (131) (136)

% of Financial Services Revenue 29.2% 29.4% 30.6% 30.2% 28.0% 31.0% 31.0% 31.0% 31.0% 31.0% 31.0%

Operating Income 779$ 861$ 883$ 956$ 958$ 965$ 993$ 1,019$ 1,039$ 1,061$ 1,082$

Interest Expense (52) (52) (52) (50) (52) (52) (52) (52) (52) (52) (52)

Other income (expense) (16) (8) (8) 4 8 8 8 8 8 8 8

Earnings before taxes & equity earnings 711$ 802$ 823$ 910$ 914$ 921$ 949$ 975$ 996$ 1,017$ 1,038$

Income Tax Expense (221) (244) (251) (214) (215) (217) (223) (230) (234) (240) (245)

Tax Rate 31.1% 30.5% 30.5% 23.6% 23.6% 23.6% 23.6% 23.6% 23.6% 23.6% 23.6%

Earnings before equity earnings 490 557 572 696 699 704 725 746 761 777 794

Equity Earnings, net of tax 1 3 1 1 1 1 1 1 1 1 1

Net Earnings 491 560 573 697 700 706 727 747 762 779 795

Noncontrolling Interest (12) (13) (15) (16) (16) (16) (16) (16) (16) (16) (16)

Net Earnings attribn. Snap-On, Inc. 479$ 547$ 558$ 680$ 684$ 689$ 710$ 731$ 746$ 762$ 779$

% Growth 14.1% 2.1% 21.8% 0.5% 0.8% 3.1% 2.9% 2.1% 2.2% 2.1%

Diluted Shares Outstanding 56.11 56.11 56.11 56.11 56.11 56.11 56.11 56.11

EPS 12.12$ 12.19$ 12.28$ 12.66$ 13.02$ 13.30$ 13.59$ 13.88$

Appendix A: Projections15

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

Appendix A: Projections16

INCOME STATEMENT FY 2015 FY 2016 FY 2017 FY 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019E FY 2019E FY 2020E FY 2021E FY 2022E FY 2023E FY 2024E FY 2025E

Revenue

Snap-On Tools Group 1,569 1,634 1,625 1,614 410 406 385 413 1,614 1,661 1,714 1,772 1,834 1,900 1,969

% YoY Growth 4.2% (.5%) (.7%) 1.4% (1.5%) (1.2%) 1.3% .0% 2.9% 3.2% 3.4% 3.5% 3.6% 3.6%

Commercial & Industrial 896 863 986 1,052 250 263 257 274 1,044 1,083 1,130 1,181 1,236 1,296 1,358

% YoY Growth (3.6%) 14.3% 6.6% (3.6%) (1.5%) .5% 1.6% (.7%) 3.7% 4.3% 4.5% 4.7% 4.8% 4.8%

Repair Systems & Information Group 889 934 1,076 1,075 262 283 260 284 1,088 1,123 1,166 1,215 1,268 1,326 1,387

% YoY Growth 5.1% 15.2% (.0%) (3.7%) 2.5% 2.8% 3.3% 1.2% 3.1% 3.8% 4.2% 4.4% 4.6% 4.6%

Financial Services Revenue 240 281 313 330 86 84 84 90 344 361 375 389 405 422 440

% Non-Financial Revenue 8.2% 8.5% 8.8% 9.3% 8.8% 9.3% 9.2% 9.2% 9.3% 9.3% 9.3% 9.3% 9.3% 9.3%

Total Revenue 3,593$ 3,712$ 4,001$ 4,070$ 1,007 1,035 986 1,061 4,090$ 4,228$ 4,384$ 4,557$ 4,744$ 4,945$ 5,154$

% Growth 3.3% 7.8% 1.7% (1.1%) (.1%) .6% 2.5% 0.5% 3.4% 3.7% 3.9% 4.1% 4.2% 4.2%

Quarterly % of Total 24.6% 25.3% 24.1% 26.0%

COGS (1,704) (1,720) (1,861) (1,871) (450) (478) (454) (496) (1,877) (1,953) (2,045) (2,146) (2,256) (2,374) (2,498)

% of Non-Financial Revenue 50.8% 50.1% 50.5% 50.0% 48.8% 50.2% 50.3% 51.0% 50.5% 50.5% 51.0% 51.5% 52.0% 52.5% 53.0%

Gross Profit 1,890$ 1,992$ 2,140$ 2,200$ 557 558 532 566 2,213$ 2,275$ 2,339$ 2,411$ 2,488$ 2,571$ 2,656$

Operating Expenses (1,041) (1,048) (1,161) (1,144) (284) (284) (280) (311) (1,159) (1,199) (1,231) (1,271) (1,323) (1,379) (1,438)

% of Non-Financial Revenue 31.1% 30.6% 31.5% 30.6% 30.8% 29.8% 31.1% 32.0% 30.9% 31.0% 30.7% 30.5% 30.5% 30.5% 30.5%

Financial Services Expenses (70) (83) (96) (100) (24) (24) (23) (26) (96) (112) (116) (121) (126) (131) (136)

% of Financial Services Revenue 29.2% 29.4% 30.6% 30.2% 27.5% 27.9% 27.5% 29.0% 28.0% 31.0% 31.0% 31.0% 31.0% 31.0% 31.0%

Operating Income 779$ 861$ 883$ 956$ 250 251 229 230 958$ 965$ 993$ 1,019$ 1,039$ 1,061$ 1,082$

Interest Expense (52) (52) (52) (50) (13) (12) (12) (15) (52) (52) (52) (52) (52) (52) (52)

Other income (expense) (16) (8) (8) 4 2 2 3 2 8 8 8 8 8 8 8

Earnings before taxes & equity earnings 711$ 802$ 823$ 910$ 239 240 220 216 914$ 921$ 949$ 975$ 996$ 1,017$ 1,038$

Income Tax Expense (221) (244) (251) (214) (57) (56) (50) (52) (215) (217) (223) (230) (234) (240) (245)

Tax Rate 31.1% 30.5% 30.5% 23.6% 23.8% 23.1% 22.9% 24.2% 23.6% 23.6% 23.6% 23.6% 23.6% 23.6% 23.6%

Earnings before equity earnings 490 557 572 696 182 185 170 164 699 704 725 746 761 777 794

Equity Earnings, net of tax 1 3 1 1 1 1 1 1 1 1 1 1

Net Earnings 491 560 573 697 182 185 170 164 700 706 727 747 762 779 795

Noncontrolling Interest (12) (13) (15) (16) (4) (5) (5) (3) (16) (16) (16) (16) (16) (16) (16)

Net Earnings attribn. Snap-On, Inc. 479$ 547$ 558$ 680$ 178 181 165 161 684$ 689$ 710$ 731$ 746$ 762$ 779$

% Growth 14.1% 2.1% 21.8% 8.9% .9% 1.0% (8.1%) 0.5% 0.8% 3.1% 2.9% 2.1% 2.2% 2.1%

Diluted Shares Outstanding 56.11 56.11 56.11 56.11 56.11 56.11 56.11 56.11 56.11 56.11 56.11 56.11

EPS 12.12$ 3.17$ 3.22$ 2.94$ 2.87$ 12.19$ 12.28$ 12.66$ 13.02$ 13.30$ 13.59$ 13.88$

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

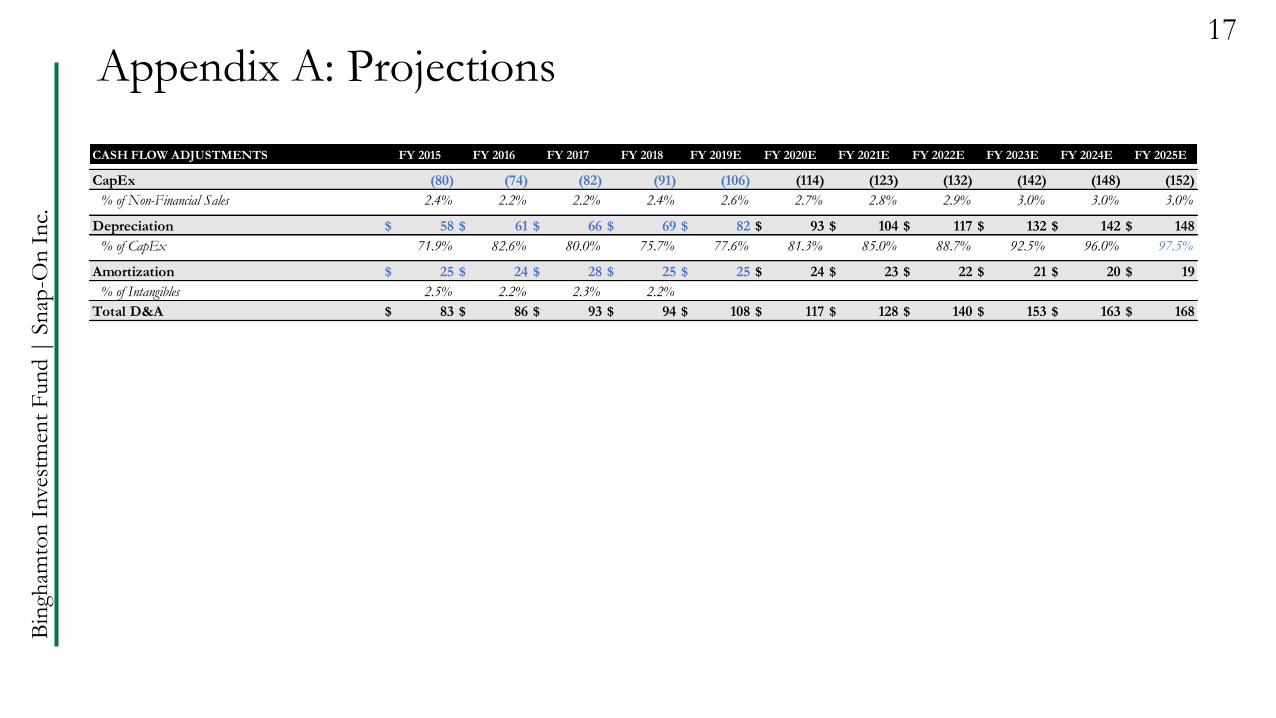

CASH FLOW ADJUSTMENTS FY 2015 FY 2016 FY 2017 FY 2018 FY 2019E FY 2020E FY 2021E FY 2022E FY 2023E FY 2024E FY 2025E

CapEx (80) (74) (82) (91) (106) (114) (123) (132) (142) (148) (152)

% of Non-Financial Sales 2.4% 2.2% 2.2% 2.4% 2.6% 2.7% 2.8% 2.9% 3.0% 3.0% 3.0%

Depreciation 58$ 61$ 66$ 69$ 82$ 93$ 104$ 117$ 132$ 142$ 148$

% of CapEx 71.9% 82.6% 80.0% 75.7% 77.6% 81.3% 85.0% 88.7% 92.5% 96.0% 97.5%

Amortization 25$ 24$ 28$ 25$ 25$ 24$ 23$ 22$ 21$ 20$ 19$

% of Intangibles 2.5% 2.2% 2.3% 2.2%

Total D&A 83$ 86$ 93$ 94$ 108$ 117$ 128$ 140$ 153$ 163$ 168$

Appendix A: Projections17

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

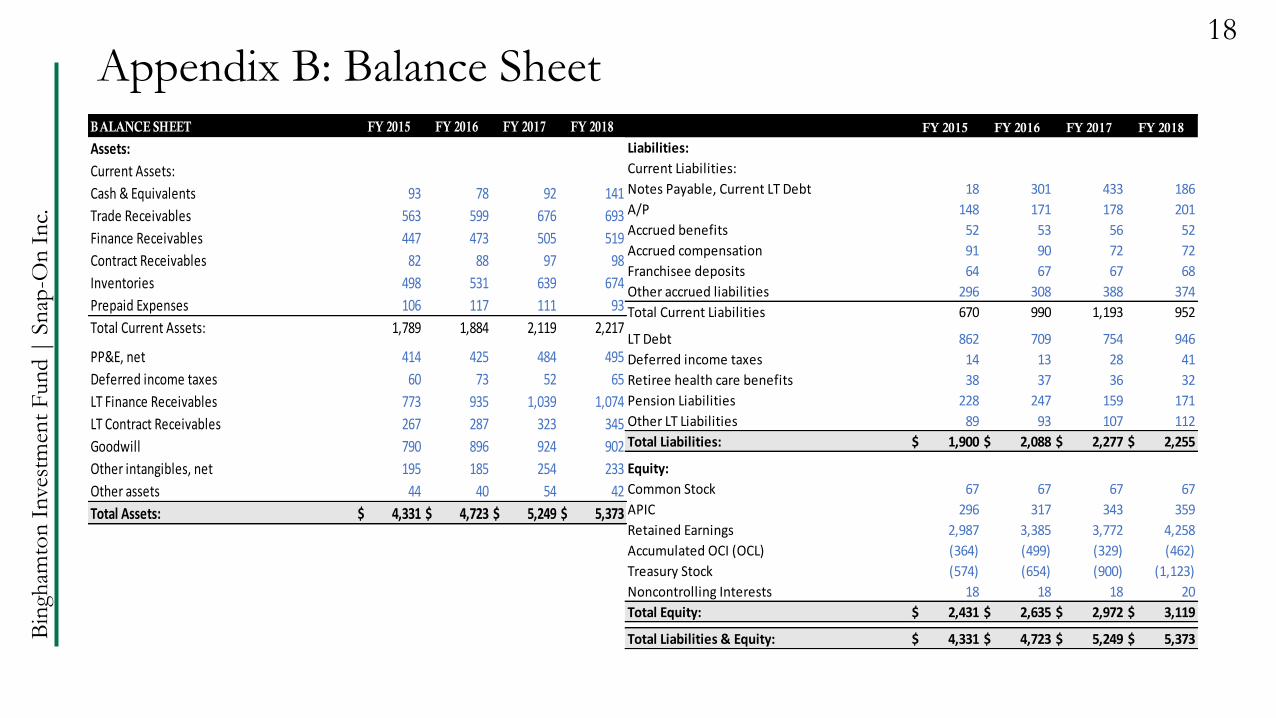

Appendix B: Balance Sheet18

BALANCE SHEET FY 2015 FY 2016 FY 2017 FY 2018

Assets:

Current Assets:

Cash & Equivalents 93 78 92 141

Trade Receivables 563 599 676 693

Finance Receivables 447 473 505 519

Contract Receivables 82 88 97 98

Inventories 498 531 639 674

Prepaid Expenses 106 117 111 93

Total Current Assets: 1,789 1,884 2,119 2,217

PP&E, net 414 425 484 495

Deferred income taxes 60 73 52 65

LT Finance Receivables 773 935 1,039 1,074

LT Contract Receivables 267 287 323 345

Goodwill 790 896 924 902

Other intangibles, net 195 185 254 233

Other assets 44 40 54 42

Total Assets: 4,331$ 4,723$ 5,249$ 5,373$

FY 2015 FY 2016 FY 2017 FY 2018

Liabilities:

Current Liabilities:

Notes Payable, Current LT Debt 18 301 433 186

A/P 148 171 178 201

Accrued benefits 52 53 56 52

Accrued compensation 91 90 72 72

Franchisee deposits 64 67 67 68

Other accrued liabilities 296 308 388 374

Total Current Liabilities 670 990 1,193 952

LT Debt 862 709 754 946

Deferred income taxes 14 13 28 41

Retiree health care benefits 38 37 36 32

Pension Liabilities 228 247 159 171

Other LT Liabilities 89 93 107 112

Total Liabilities: 1,900$ 2,088$ 2,277$ 2,255$

Equity:

Common Stock 67 67 67 67

APIC 296 317 343 359

Retained Earnings 2,987 3,385 3,772 4,258

Accumulated OCI (OCL) (364) (499) (329) (462)

Treasury Stock (574) (654) (900) (1,123)

Noncontrolling Interests 18 18 18 20

Total Equity: 2,431$ 2,635$ 2,972$ 3,119$

Total Liabilities & Equity: 4,331$ 4,723$ 5,249$ 5,373$

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

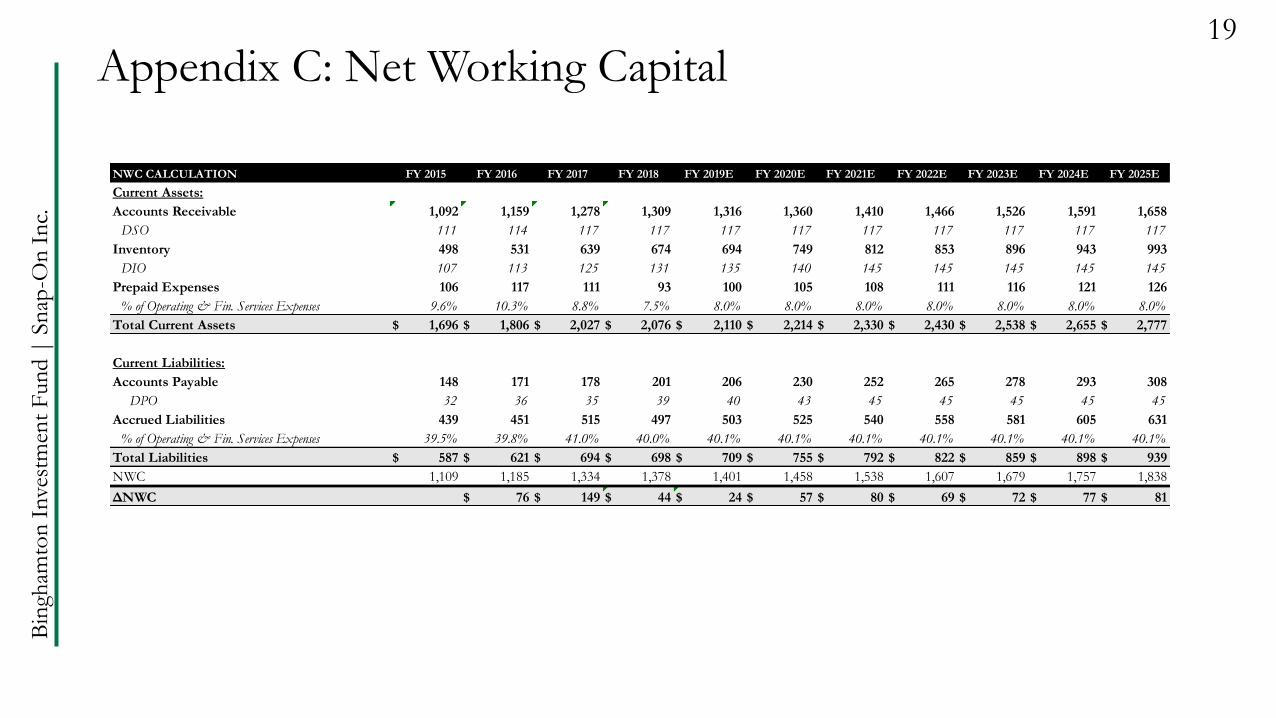

Appendix C: Net Working Capital 19

NWC CALCULATION FY 2015 FY 2016 FY 2017 FY 2018 FY 2019E FY 2020E FY 2021E FY 2022E FY 2023E FY 2024E FY 2025E

Current Assets:

Accounts Receivable 1,092 1,159 1,278 1,309 1,316 1,360 1,410 1,466 1,526 1,591 1,658

DSO 111 114 117 117 117 117 117 117 117 117 117

Inventory 498 531 639 674 694 749 812 853 896 943 993

DIO 107 113 125 131 135 140 145 145 145 145 145

Prepaid Expenses 106 117 111 93 100 105 108 111 116 121 126

% of Operating & Fin. Services Expenses 9.6% 10.3% 8.8% 7.5% 8.0% 8.0% 8.0% 8.0% 8.0% 8.0% 8.0%

Total Current Assets 1,696$ 1,806$ 2,027$ 2,076$ 2,110$ 2,214$ 2,330$ 2,430$ 2,538$ 2,655$ 2,777$

Current Liabilities:

Accounts Payable 148 171 178 201 206 230 252 265 278 293 308

DPO 32 36 35 39 40 43 45 45 45 45 45

Accrued Liabilities 439 451 515 497 503 525 540 558 581 605 631

% of Operating & Fin. Services Expenses 39.5% 39.8% 41.0% 40.0% 40.1% 40.1% 40.1% 40.1% 40.1% 40.1% 40.1%

Total Liabilities 587$ 621$ 694$ 698$ 709$ 755$ 792$ 822$ 859$ 898$ 939$

NWC 1,109 1,185 1,334 1,378 1,401 1,458 1,538 1,607 1,679 1,757 1,838

ΔNWC 76$ 149$ 44$ 24$ 57$ 80$ 69$ 72$ 77$ 81$

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

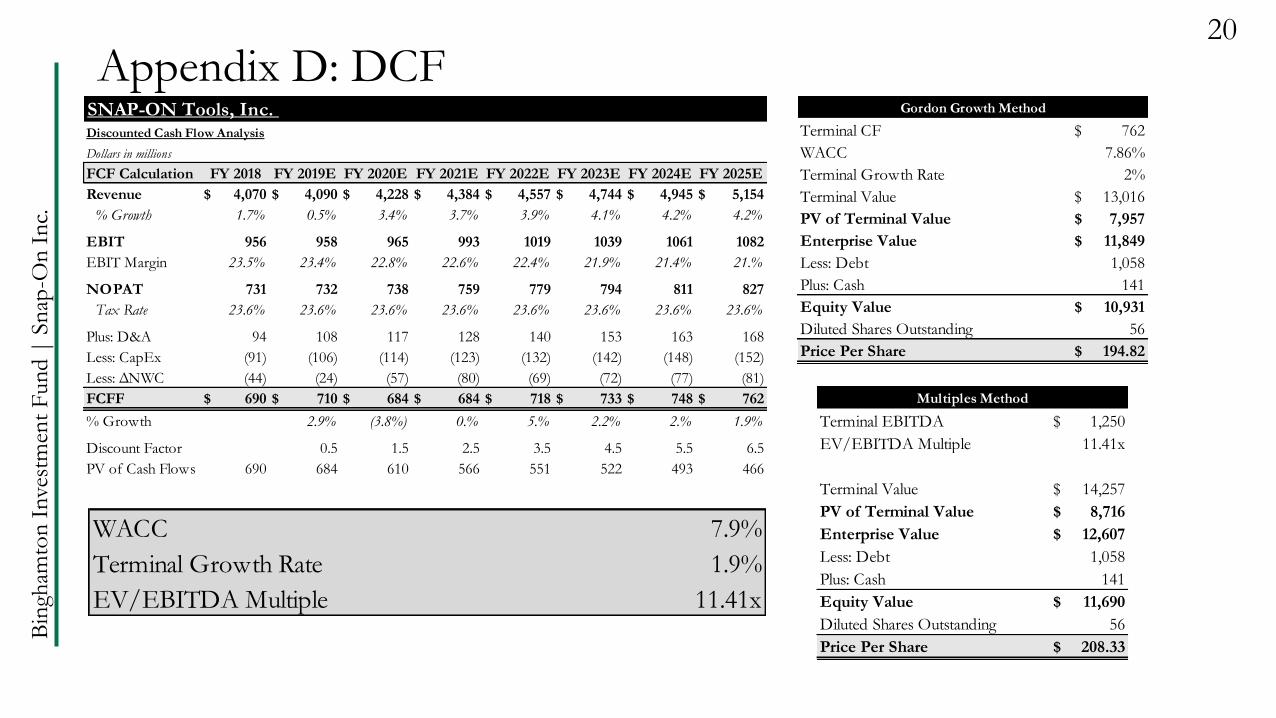

Appendix D: DCF20

SNAP-ON Tools, Inc. Discounted Cash Flow Analysis

Dollars in millions

FCF Calculation FY 2018 FY 2019E FY 2020E FY 2021E FY 2022E FY 2023E FY 2024E FY 2025E

Revenue 4,070$ 4,090$ 4,228$ 4,384$ 4,557$ 4,744$ 4,945$ 5,154$

% Growth 1.7% 0.5% 3.4% 3.7% 3.9% 4.1% 4.2% 4.2%

EBIT 956 958 965 993 1019 1039 1061 1082

EBIT Margin 23.5% 23.4% 22.8% 22.6% 22.4% 21.9% 21.4% 21.%

NOPAT 731 732 738 759 779 794 811 827

Tax Rate 23.6% 23.6% 23.6% 23.6% 23.6% 23.6% 23.6% 23.6%

Plus: D&A 94 108 117 128 140 153 163 168

Less: CapEx (91) (106) (114) (123) (132) (142) (148) (152)

Less: ΔNWC (44) (24) (57) (80) (69) (72) (77) (81)

FCFF 690$ 710$ 684$ 684$ 718$ 733$ 748$ 762$

% Growth 2.9% (3.8%) 0.% 5.% 2.2% 2.% 1.9%

Discount Factor 0.5 1.5 2.5 3.5 4.5 5.5 6.5

PV of Cash Flows 690 684 610 566 551 522 493 466

Gordon Growth Method Multiples Method

Terminal CF 762$

WACC 7.86%

Terminal Growth Rate 2%

Terminal Value 13,016$

PV of Terminal Value 7,957$

Enterprise Value 11,849$

Less: Debt 1,058

Plus: Cash 141

Equity Value 10,931$

Diluted Shares Outstanding 56

Price Per Share 194.82$

Multiples Method

Terminal EBITDA 1,250$

EV/EBITDA Multiple 11.41x

Terminal Value 14,257$

PV of Terminal Value 8,716$

Enterprise Value 12,607$

Less: Debt 1,058

Plus: Cash 141

Equity Value 11,690$

Diluted Shares Outstanding 56

Price Per Share 208.33$

WACC 7.9%

Terminal Growth Rate 1.9%

EV/EBITDA Multiple 11.41x

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

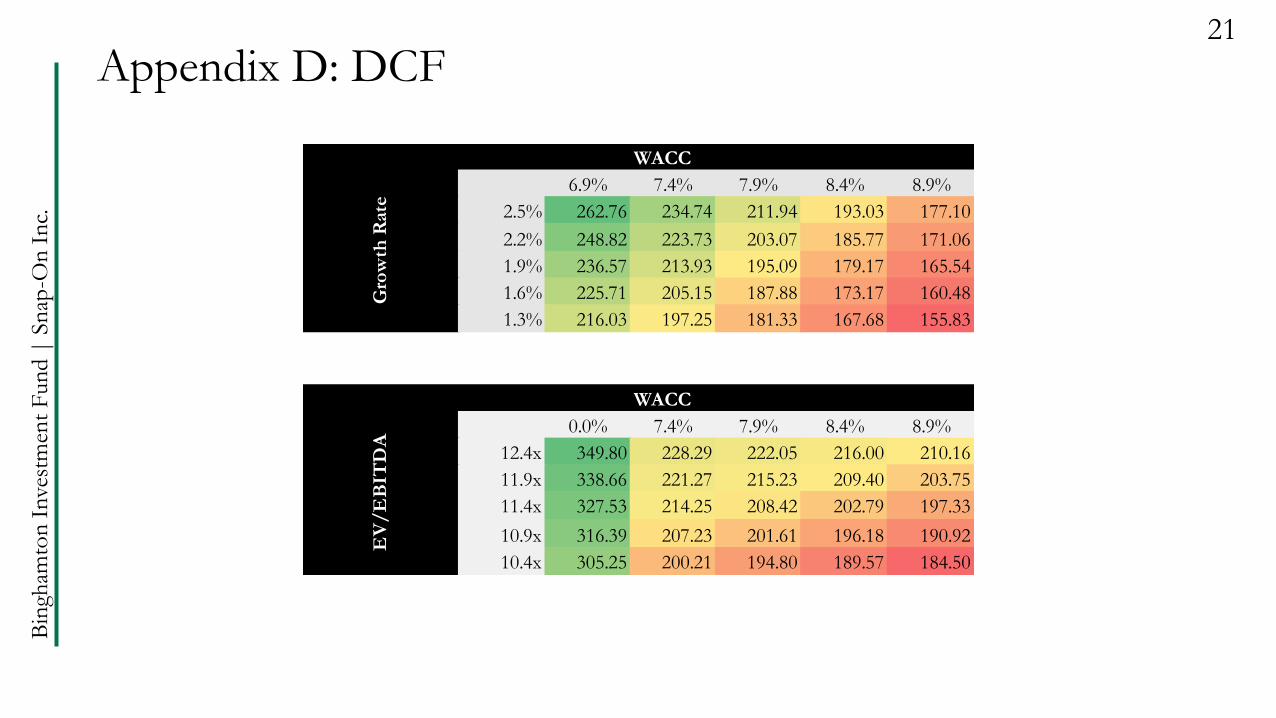

Appendix D: DCF21

WACC

194.82$ 6.9% 7.4% 7.9% 8.4% 8.9%

2.5% 262.76 234.74 211.94 193.03 177.10

2.2% 248.82 223.73 203.07 185.77 171.06

1.9% 236.57 213.93 195.09 179.17 165.54

1.6% 225.71 205.15 187.88 173.17 160.48

1.3% 216.03 197.25 181.33 167.68 155.83

WACC

208.33$ 0.0% 7.4% 7.9% 8.4% 8.9%

12.4x 349.80 228.29 222.05 216.00 210.16

11.9x 338.66 221.27 215.23 209.40 203.75

11.4x 327.53 214.25 208.42 202.79 197.33

10.9x 316.39 207.23 201.61 196.18 190.92

10.4x 305.25 200.21 194.80 189.57 184.50

Gro

wth

Rate

EV

/E

BIT

DA

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

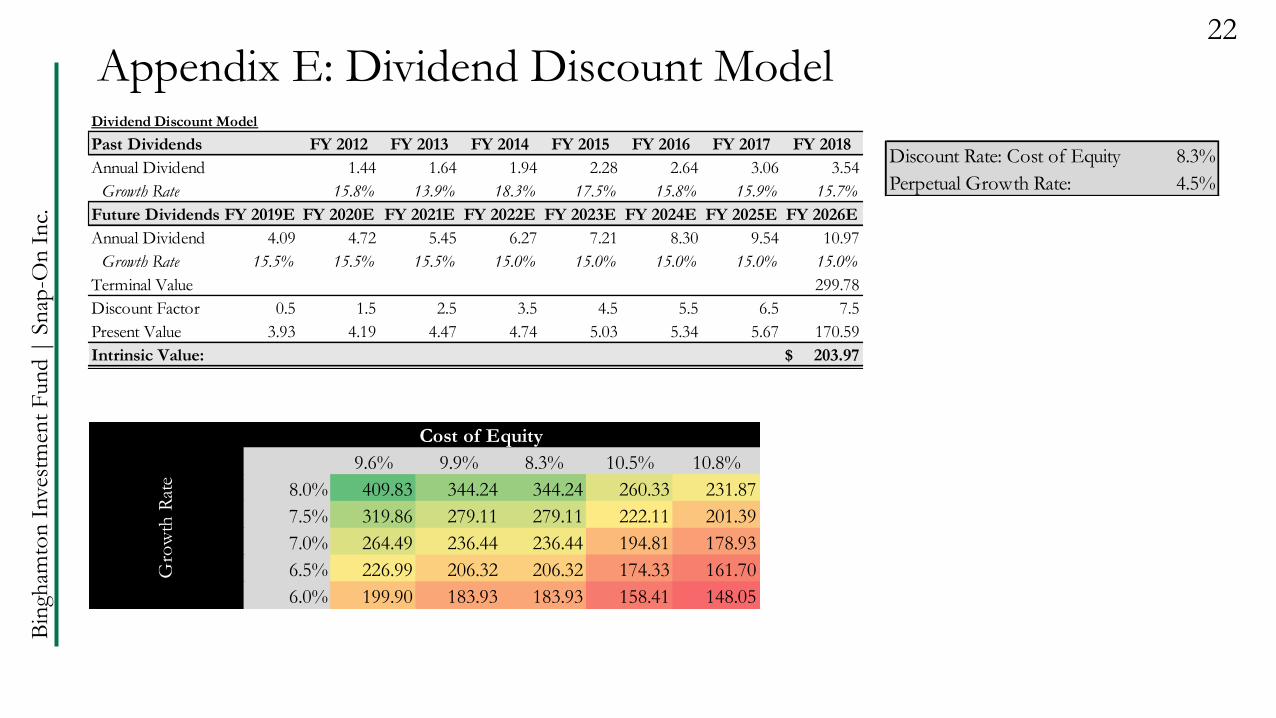

Appendix E: Dividend Discount Model22

Dividend Discount Model

Past Dividends FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

Annual Dividend 1.44 1.64 1.94 2.28 2.64 3.06 3.54

Growth Rate 15.8% 13.9% 18.3% 17.5% 15.8% 15.9% 15.7%

Future Dividends FY 2019E FY 2020E FY 2021E FY 2022E FY 2023E FY 2024E FY 2025E FY 2026E

Annual Dividend 4.09 4.72 5.45 6.27 7.21 8.30 9.54 10.97

Growth Rate 15.5% 15.5% 15.5% 15.0% 15.0% 15.0% 15.0% 15.0%

Terminal Value 299.78

Discount Factor 0.5 1.5 2.5 3.5 4.5 5.5 6.5 7.5

Present Value 3.93 4.19 4.47 4.74 5.03 5.34 5.67 170.59

Intrinsic Value: 203.97$

Discount Rate: Cost of Equity 8.3%

Perpetual Growth Rate: 4.5%

Cost of Equity

203.97$ 9.6% 9.9% 8.3% 10.5% 10.8%

8.0% 409.83 344.24 344.24 260.33 231.87

7.5% 319.86 279.11 279.11 222.11 201.39

7.0% 264.49 236.44 236.44 194.81 178.93

6.5% 226.99 206.32 206.32 174.33 161.70

6.0% 199.90 183.93 183.93 158.41 148.05

Gro

wth

Rat

e

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

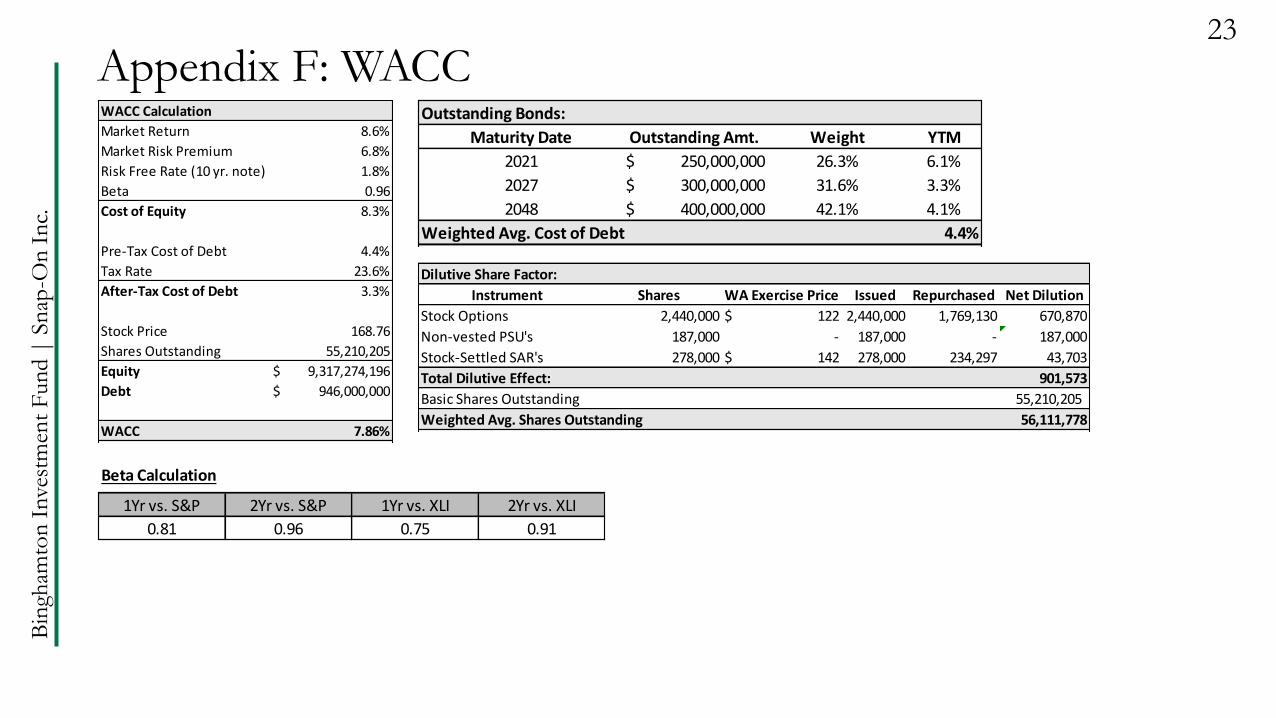

Appendix F: WACC23

Beta Calculation

1Yr vs. S&P 2Yr vs. S&P 1Yr vs. XLI 2Yr vs. XLI

0.81 0.96 0.75 0.91

WACC Calculation

Market Return 8.6%

Market Risk Premium 6.8%

Risk Free Rate (10 yr. note) 1.8%

Beta 0.96

Cost of Equity 8.3%

Pre-Tax Cost of Debt 4.4%

Tax Rate 23.6%

After-Tax Cost of Debt 3.3%

Stock Price 168.76

Shares Outstanding 55,210,205

Equity 9,317,274,196$

Debt 946,000,000$

WACC 7.86%

Outstanding Bonds:

Maturity Date Outstanding Amt. Weight YTM

2021 250,000,000$ 26.3% 6.1%

2027 300,000,000$ 31.6% 3.3%

2048 400,000,000$ 42.1% 4.1%

Weighted Avg. Cost of Debt 4.4%

Dilutive Share Factor:

Instrument Shares WA Exercise Price Issued Repurchased Net Dilution

Stock Options 2,440,000 122$ 2,440,000 1,769,130 670,870

Non-vested PSU's 187,000 - 187,000 - 187,000

Stock-Settled SAR's 278,000 142$ 278,000 234,297 43,703

Total Dilutive Effect: 901,573

Basic Shares Outstanding 55,210,205

Weighted Avg. Shares Outstanding 56,111,778

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

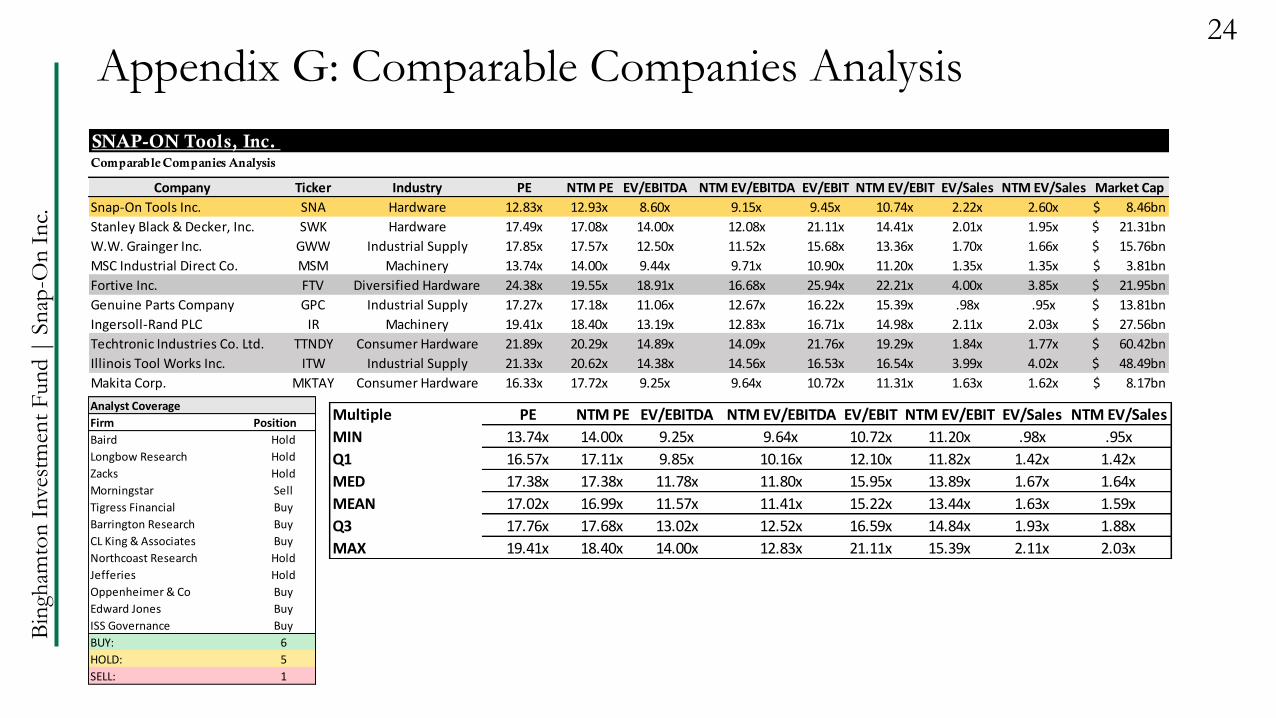

SNAP-ON Tools, Inc. Comparable Companies Analysis

Company Ticker Industry PE NTM PE EV/EBITDA NTM EV/EBITDA EV/EBIT NTM EV/EBIT EV/Sales NTM EV/Sales Market Cap

Snap-On Tools Inc. SNA Hardware 12.83x 12.93x 8.60x 9.15x 9.45x 10.74x 2.22x 2.60x 8.46bn$

Stanley Black & Decker, Inc. SWK Hardware 17.49x 17.08x 14.00x 12.08x 21.11x 14.41x 2.01x 1.95x 21.31bn$

W.W. Grainger Inc. GWW Industrial Supply 17.85x 17.57x 12.50x 11.52x 15.68x 13.36x 1.70x 1.66x 15.76bn$

MSC Industrial Direct Co. MSM Machinery 13.74x 14.00x 9.44x 9.71x 10.90x 11.20x 1.35x 1.35x 3.81bn$

Fortive Inc. FTV Diversified Hardware 24.38x 19.55x 18.91x 16.68x 25.94x 22.21x 4.00x 3.85x 21.95bn$

Genuine Parts Company GPC Industrial Supply 17.27x 17.18x 11.06x 12.67x 16.22x 15.39x .98x .95x 13.81bn$

Ingersoll-Rand PLC IR Machinery 19.41x 18.40x 13.19x 12.83x 16.71x 14.98x 2.11x 2.03x 27.56bn$

Techtronic Industries Co. Ltd. TTNDY Consumer Hardware 21.89x 20.29x 14.89x 14.09x 21.76x 19.29x 1.84x 1.77x 60.42bn$

Illinois Tool Works Inc. ITW Industrial Supply 21.33x 20.62x 14.38x 14.56x 16.53x 16.54x 3.99x 4.02x 48.49bn$

Makita Corp. MKTAY Consumer Hardware 16.33x 17.72x 9.25x 9.64x 10.72x 11.31x 1.63x 1.62x 8.17bn$

Appendix G: Comparable Companies Analysis24

Analyst Coverage

Firm Position

Baird Hold

Longbow Research Hold

Zacks Hold

Morningstar Sell

Tigress Financial Buy

Barrington Research Buy

CL King & Associates Buy

Northcoast Research Hold

Jefferies Hold

Oppenheimer & Co Buy

Edward Jones Buy

ISS Governance Buy

BUY: 6

HOLD: 5

SELL: 1

Multiple PE NTM PE EV/EBITDA NTM EV/EBITDA EV/EBIT NTM EV/EBIT EV/Sales NTM EV/Sales

MIN 13.74x 14.00x 9.25x 9.64x 10.72x 11.20x .98x .95x

Q1 16.57x 17.11x 9.85x 10.16x 12.10x 11.82x 1.42x 1.42x

MED 17.38x 17.38x 11.78x 11.80x 15.95x 13.89x 1.67x 1.64x

MEAN 17.02x 16.99x 11.57x 11.41x 15.22x 13.44x 1.63x 1.59x

Q3 17.76x 17.68x 13.02x 12.52x 16.59x 14.84x 1.93x 1.88x

MAX 19.41x 18.40x 14.00x 12.83x 21.11x 15.39x 2.11x 2.03x

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

Appendix H: Product Examples25

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

Appendix I: Product Divisions26

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

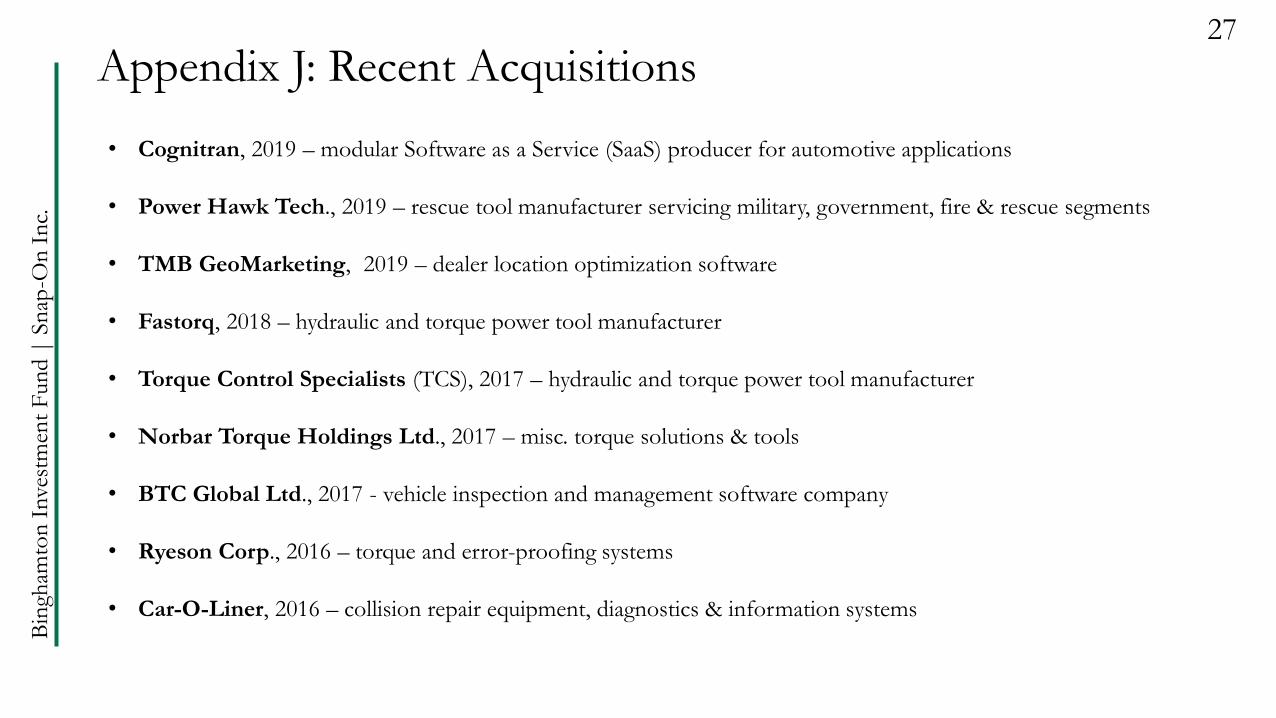

Appendix J: Recent Acquisitions27

• Cognitran, 2019 – modular Software as a Service (SaaS) producer for automotive applications

• Power Hawk Tech., 2019 – rescue tool manufacturer servicing military, government, fire & rescue segments

• TMB GeoMarketing, 2019 – dealer location optimization software

• Fastorq, 2018 – hydraulic and torque power tool manufacturer

• Torque Control Specialists (TCS), 2017 – hydraulic and torque power tool manufacturer

• Norbar Torque Holdings Ltd., 2017 – misc. torque solutions & tools

• BTC Global Ltd., 2017 - vehicle inspection and management software company

• Ryeson Corp., 2016 – torque and error-proofing systems

• Car-O-Liner, 2016 – collision repair equipment, diagnostics & information systems

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

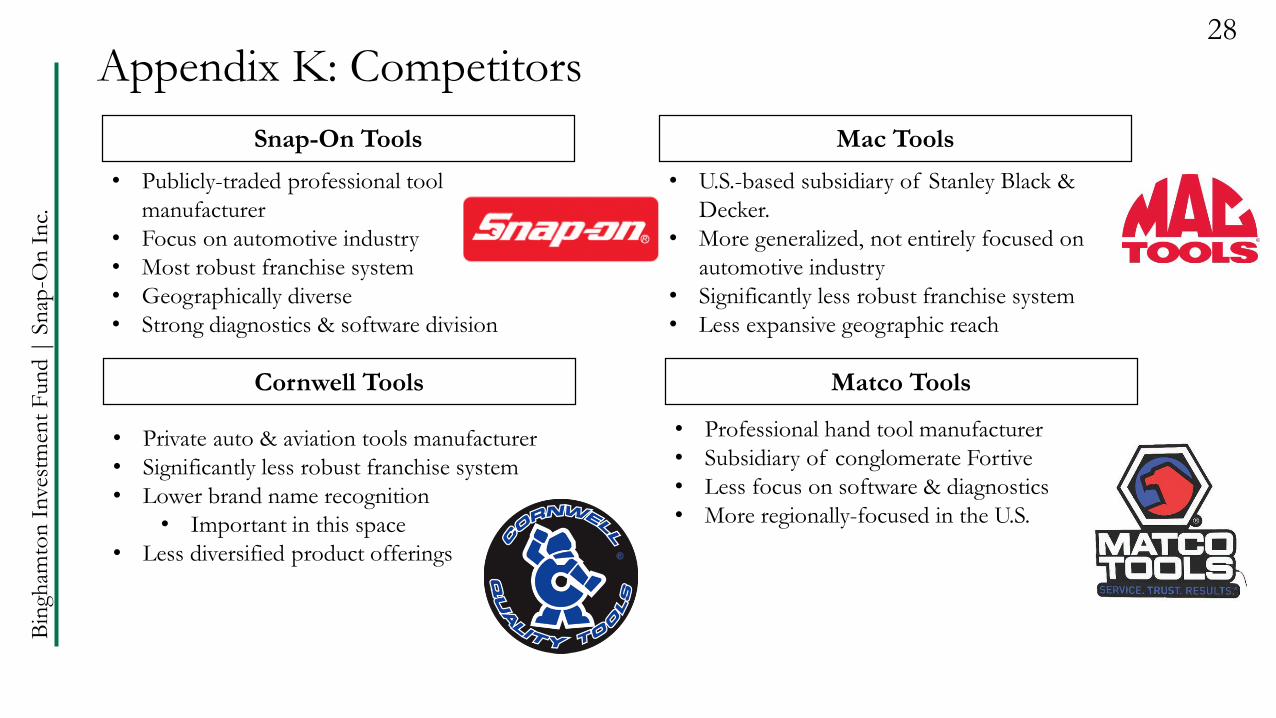

Appendix K: Competitors28

Snap-On Tools Mac Tools

• Publicly-traded professional tool

manufacturer

• Focus on automotive industry

• Most robust franchise system

• Geographically diverse

• Strong diagnostics & software division

• U.S.-based subsidiary of Stanley Black &

Decker.

• More generalized, not entirely focused on

automotive industry

• Significantly less robust franchise system

• Less expansive geographic reach

• Private auto & aviation tools manufacturer

• Significantly less robust franchise system

• Lower brand name recognition

• Important in this space

• Less diversified product offerings

• Professional hand tool manufacturer

• Subsidiary of conglomerate Fortive

• Less focus on software & diagnostics

• More regionally-focused in the U.S.

Cornwell Tools Matco Tools

Bin

gham

ton

Inve

stm

ent

Fun

d |

Sn

ap-O

n I

nc.

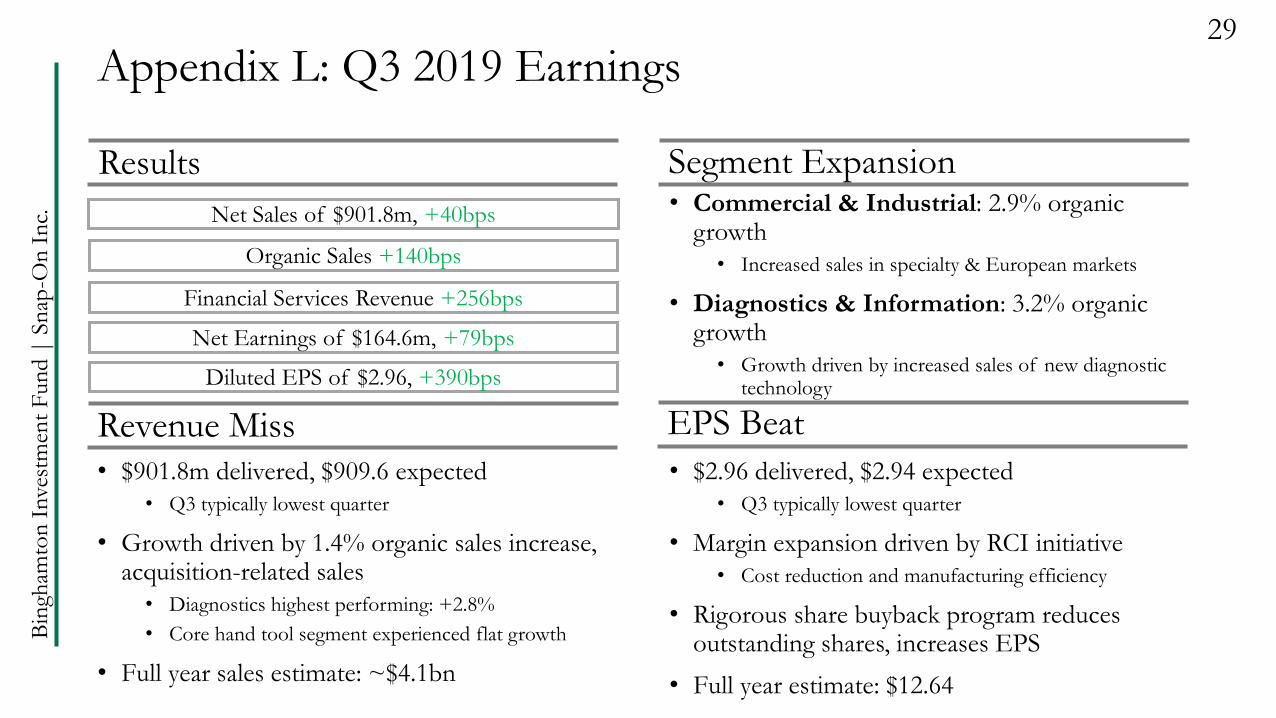

• Commercial & Industrial: 2.9% organic growth

• Increased sales in specialty & European markets

• Diagnostics & Information: 3.2% organic growth

• Growth driven by increased sales of new diagnostic technology

• $901.8m delivered, $909.6 expected

• Q3 typically lowest quarter

• Growth driven by 1.4% organic sales increase, acquisition-related sales

• Diagnostics highest performing: +2.8%

• Core hand tool segment experienced flat growth

• Full year sales estimate: ~$4.1bn

• $2.96 delivered, $2.94 expected

• Q3 typically lowest quarter

• Margin expansion driven by RCI initiative

• Cost reduction and manufacturing efficiency

• Rigorous share buyback program reduces outstanding shares, increases EPS

• Full year estimate: $12.64

Appendix L: Q3 2019 Earnings29

Results Segment Expansion

Revenue Miss EPS Beat

Net Sales of $901.8m, +40bps

Organic Sales +140bps

Financial Services Revenue +256bps

Net Earnings of $164.6m, +79bps

Diluted EPS of $2.96, +390bps