Embed Size (px)

Citation preview

PROJECT REPORT

on

A STUDY ON CAPITAL BUDGETING AT SUNNESS

CAPITAL INDIA PVT LTD

BY

JEEVITHA

USN: 1NZ18MBA33

Submitted to

DEPARTMENT OF MANAGEMENT STUDIES

NEW HORIZON COLLEGE OF ENGINEERING,

OUTER RING ROAD, MARATHALLI,

BENGALURU

In partial fulfilment of the requirements for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

Under the guidance of

Guide Name: Mr. SANTOSH KUMAR S

Asst. Professor

2018-2020

CERTIFICATE

This is to certify that Jeevitha bearing USN 1NZ18MBA33, is a

bonafide student of Master of Business Administration course of the

Institute 2018-2020, autonomous program, affiliated to Visvesvaraya

Technological University, Belgaum. Project report on “A Study on

Capital Budgeting at Sunness Capital India Pvt Ltd” is prepared by her

under the guidance of Mr. Santosh Kumar S, in partial fulfillment of

requirements for the award of the degree of Master of Business

Administration of Visvesvaraya Technological University, Belgaum

Karnataka.

Signature of Internal Guide Signature of HOD Principal

Name of the Examiners with affiliation Signature with date

1. External Examiner

2. Internal Examiner

DECLARATION

I, Jeevitha, hereby declare that the project report on “A Study on Capital Budgeting at

Sunness Capital India Pvt Ltd” with reference to” Sunness Capital India Pvt Ltd” prepared

by me under the guidance of Mr. Santosh Kumar S, faculty of M.B.A Department, New

Horizon College of Engineering.

I also declare that this project report is towards the partial fulfilment of the university

regulations for the award of the degree of Master of Business Administration by

Visvesvaraya Technological University, Belgaum.

I have undergone an industry project for a period of Eight weeks. I further declare that this

report is based on the original study undertaken by me and has not been submitted for the

award of a degree/diploma from any other University / Institution.

Signature of Student

Place:

Date:

ACKNOWLEDGEMENT

The successful completion of the project would not have been possible without

the guidance and support of many people. I express my sincere gratitude to (Mr.

Ananth P, Manager, Sunness Capital India Pvt Ltd, Bengaluru, for allowing to

do my project at Sunness Capital India Pvt Ltd.

I thank the staff of Sunness Capital India Pvt Ltd, Bengaluru for their support

and guidance and helping me in completion of the report.

I am thankful to my internal guide Mr. Santosh Kumar S, for his constant

support and inspiration throughout the project and invaluable suggestions,

guidance and also for providing valuable information.

Finally, I express my gratitude towards my parents and family for their

continuous support during the study.

STUDENT NAME: JEEVITHA

USN NO.: 1NZ18MBA33

TABLE OF CONTENTS

SL. NUMBER CONTENTS PAGE NUMBERS

1 Executive Summary 2

2 Theoretical Background of The Study 3-5

3 Industry Profile &Company Profile 6-13

4 Application of Theoretical Framework 14-18

5 Analysis and Interpretation of Financial

Statements and Reports 19-48

6 Learning Experience- Findings,

Suggestions and Conclusion 49-54

7 Bibliography 55

2

EXECUTIVE SUMMARY

I got an opportunity to do project work in a stock broking company called SUNNESS

INDIA CAPITAL PVT LTD who deals with buying and selling of shares on behalf of

their investors, as well they are into commodity trading, currency trading, promoting

various companies health plans and insurance to its clients, they also provide consultancy

service to its investors before investing.

I was basically working as an clients acquisition where in I had to meet new customers

explain them some basics about the stock market and make them to invest on shares, well

it was an challenging job and personally had a good hands on experience and learnt a

loads of things regarding the stock market.

The internship duration was nearly eight weeks and i did a project on “A STUDY ON

CAPITAL BUDGETING AT SUNNESS CAPITAL INDIA PVT LTD” which deals with

currency trading and also provide services to the traders which were newly introduced by

the company.

For this study the data were collected from both through questionnaire and through

internet sources. Since currency exchange services was newly introduced the number of

clients were limited the sample size were limited to only twenty.

This study was conducted just to know what are the risks faced by the clients, what are

techniques or strategies used by them to reduce the risk involved in the foreign exchange,

and also what kind of services clients are expecting from other brokers other than the

regular services.

The main motto of this project is to know the gap created by the SUNNESS PVT LTD

with its clients and try to bridge them and makes satisfy its clients, therefore this in turn

would increase the growth of the number of clients.

3

INTRODUCTION

CAPITAL BUDGETING:

An efficient allocation of capital is the most important finance function in modern times. It

involves decisions to commit firm’s funds to long-term assets. Such decisions are tend to

determine the value of company/firm by influencing its growth, profitability & risk.

Investment decisions are generally known as capital budgeting or capital expenditure

decisions. It is clever decisions to invest current in long term assets expecting long-term

benefits firm’s investment decisions would generally include expansion, acquisition,

modernization and replacement of long-term assets.

Such decisions can be investment decisions, financing decisions or operating decisions.

Investment decisions deal with investment of organization’s resources in Long tern (fixed)

Assets and / or Short term (Current) Assets. Decisions pertaining to investment in Short term

Assets fall under “Working Capital Management”. Decisions pertaining to investment in

Long term Assets are classified as “Capital Budgeting” decisions.

Capital budgeting decisions are related to allocation of investible funds to different long-term

assets. They have long-term implications and affect the future growth and profitability of the

firm.

In evaluating such investment proposals, it is important to carefully consider the expected

benefits of investment against the expenses associated with it.

Organizations are frequently faced with Capital Budgeting decisions. Any decision that

requires the use of resources is a capital budgeting decisions. Capital budgeting is more or

less a continuous process in any growing concern.

4

NEED FOR THE STUDY

The Project study is undertaken to analyze and understand the Capital

Budgeting process in cement manufacturing sector, which gives mean

exposure to practical implication of theory knowledge.

To know about the company’s operation of using various Capital Budgeting

techniques.

To know how the company gets funds from various resources.

OBJECTIVES OF THE STUDY

To study the relevance of capital budgeting in evaluating the project for project

finance.

To study the technique of capital budgeting for decision- making.

To measure the present value of rupee invested.

To understand an item wise study of the company financial performance of the

company.

To make suggestion if any for improving the financial position if the company.

To understand the practical usage of capital budgeting techniques

To understand the nature of risk and uncertainty

METHODOLOGY

To achieve aforesaid objective the following methodology has been adopted. The

information for this report has been collected through the primary and secondary sources.

PRIMARY SOURCES

It is also called as first handed information; the data is collected through the

observation in the organization and interview with officials. By asking question with

the accounts and other persons in the financial department. A part from these some

information is collected through the seminars, which were held by Sunness.

5

SECONDARY SOURCES

The secondary data have been collected through the various books, magazines, brouchers &

websites

LIMITATION OF THE STUDY:

Lack of time is another limiting factor, ie., the schedule period of 8 weeks are not

sufficient to make the study independently regarding Capital Budgeting in Sunness.

The busy schedule of the officials in the Sunness is another limiting factor. Due to

the busy schedule officials restricted me to collect the complete information about

organization.

Non-availability of confidential financial data.

The study is conducted in a short period, which was not detailed in all aspects.

All the techniques of capital budgeting are not used in Sunness. Therefore it was

possible to explain only few methods of capital budgeting.

6

INDUSTRY AND COMPANY PROFILE

1. INDUSTRY PROFILE

Evolution:

Stock broking industry came from the history of say two hundred years ago east India

institutions and companies were the most popular and dominant when compared to any other

Indian companies in those days, during the eighteenth centuries east India companies used to

provide loans for the and invest on other companies. During the time say in 1830s business

on corporate stocks and shares in bank and cotton presses took place in Bombay. during 1839

many people started investing on shares, equities which in turn saw a huge list getting

broader day by day and also even merchant banks and financial banks list got broader in

investing during 1840s- 1850s.

During 1840s we could see only half a dozen entering into stock broking industry and that is

how at the early years of 1850s many men started being an stock broker started pooling of

public money and invested on equities this is the period India witnessed a greater revolution

in the stock broking industry many of the brokers started attracting many investors and made

them understand the importance of investing on companies shares, commodities, and

currencies this lead to even more increase in the number of stock brokers. However with in

few years due to American civil war there was a disastrous began.

After a great American civil war by the time they could stabilize stock brokers found a place

in a street which is at presently called as Dhala Street. This place made each and every stock

broker to meet and transact business very easily, this is how brokers formally established in

Bombay which is known as “the stock exchange” similarly a premise was built for the stock

exchange in the same street and had got inaugurated in 1899.

Important leading cities in operating stock market: if you see in cotton textile industry

Mumbai was gained a major importance followed to it Ahmadabad also gained an importance

in this industry.

At the early years of 1881s mills which were originated in Ahmadabad had rapidly forged.

Once this forged mills where removed and new mills were created then expected for the

existence of a stock exchange in Ahmadabad. And by 1849 all the brokers together formed an

association called “The Ahmadabad share and stock brokers association

7

With the help of swadeshi movement the industry was expecting to have an tremendous

industrial revolution coming on its way to India with the help of inauguration of the TATA

iron and steel company in 1907 and because of the first world war all the companies who

deals with the commodities like cotton, steel, sugar, textiles, paper, and flour mills said to

have an tremendous prosperity. All these things were happening during the beginning of

twentieth century.

During the time of 1920s in the city of Madras had a wonderful thrill in trading the stock

exchange in the name of “The Madras Stock Exchange” with a number of hundred members,

gradually when we could see boom getting faded the members started getting reduced from

hundred to three which is a single digit and that is how it lost its existence.

In 1935, the stock market activity improved, especially in South India where there was a

rapid increase in the number of textile mills and many plantation companies were floated. In

1937, a stock exchange was once again organized in Madras - Madras Stock Exchange

Association (Pvt) Limited. (In 1957 the name was changed to Madras Stock Exchange

Limited). Lahore Stock Exchange was formed in 1934 and it had a brief life. It was merged

with the Punjab Stock Exchange Limited, which was incorporated in 1936.

Indian Stock Exchanges - An Umbrella Growth:

The Second World War broke out in 1939. It gave a sharp boom which was followed by a

slump. But, in 1943, the situation changed radically, when India was fully mobilized as a

supply base.

Exchange Limited (1989), Bhubaneswar Stock Exchange Association Limited (1989),

Saurashtra Kutch Stock Exchange Limited (at Rajkot, 1989), Vadodara Stock Exchange

Limited (at Baroda, 1990) and recently established exchanges - Coimbatore and Meerut.

Thus, at present, there are totally 23 recognized stock exchanges in India.

• This has made the system to be more effective and efficient enough to work and reduce

the time barrier.

• The system is been created in such a way that it is clear crystal and are transparent to the

investors.

• Since the trading happens online investors need not approach any of the brokers to buy or

sell the shares, the share prices are being displayed on the screen hence before buying or

selling the investor will come to know the value of the share.

8

• During the process each and every steps are been updated to the investors by sending mail

therefore the investor need not worry about the process involved in the transaction.

Similar to that of BSE we have NSE that is National Stock Exchange in which 50

companies are listed under this are operating in all over the world due to globalization

and liberalization companies have been performing really effective and efficiently in

entering into globally, for any company the goal will be getting globally and operating all

over the world this is because of many rival companies entering globally and to survive

many companies are going globally. NSE plays an important role for such companies the

companies listed under this can pool in money more and are safe too.

NSE has several advantages over the traditional trading exchanges. They are as follows:

It helps in pooling the many investors all over the nation and are made to invest

Investors need not to worry regarding the transactions since the steps are been updated to

the investor therefore transactions happens very faster and there is no chance of getting

delayed in the process.

NSE works very effective and efficiently to make sure that investors interest are safe

guard and make sure that process involved in this transactions are transparent and not

only in this the companies listed under this are transparent.

NATURE OF BUSINESS CARRIED

The company were acting as an agent/ broker or rather we could call them as stock

brokers who acts as a middle men on behalf of its investors and make their investors to

invest on shares, bonds, foreign currencies.

Equities:

SUNNESS CAPTIAL offers a wide spectrum of services that includes Equity Broking in

Cash and Derivatives, Internet based trading, Demat services & Research services. When

people deal with SUNNESS CAPTIAL people are dealing with a professional broker who

has centralized risk management system in place at Bangalore. SUNNESS CAPTIAL

follows a hub and spoke model of Branch management where in all the branches &

9

franchise interact with the hub/regional office & in turn the regional/hub office talks to

Head office. This company a great level of flexibility in managing the risk level of the

clients, which in turn benefit the client. SUNNESS CAPTIAL is the first brokerage house

to offer Direct Market Access (DMA) to Institutional Clients on FT Platform. They offer

research based broking services on the equity as well as derivative segments to their

institutional clients.

Fixed Income Securities:

Keeping the middle class people or public in the mind SUNNESS CAPTIAL can

understand the importance of money market and debt market, therefore deals with so

many companies who are into health plans, mutual funds, primary dealers, insurance

companies so as to provide as per the requirements of its customers.

SUNNESS CAPTIAL is one of the leading merchant bankers who helps in issue

management for the new companies entering BSE or NSE, and also provides

consultancy services, and also provides t-bills, bonds, debentures, floating rates etc.

Retail Distribution: The company caters services in retail such as in 1) Primary Market

Division 2) Mutual Funds & Insurance Advisory

Commodities: A sister concern of the renowned and trusted SUNNESS CAPTIAL,

Alpha Commodities offers a complete bouquet of client- friendly services in the

burgeoning Commodity Futures market. Alpha Commodities provides a host of facilities

to their clients, ranging from dealing, investing or hedging in Commodity Futures which

includes Bullions, Metals, Energy and Agro Commodities.

Currency: currency derivatives are newly services by joining with SEBI and RBI so as

to give currency exchange services for commodities trading where in any of the two

parties enter into a future contract for a certain quantity of goods, for certain exchange

rate on a certain date therefore for this the company helps in supplying the particular

currency for trading.

DIRECTORS:

1. SASITOTA PRABHAKARA SHREESHA

2. PADMAHYOTHI SREESHA

10

VISION, MISSION AND QUALITY POLICY

Vision:

Vision: “To become a globally renowned organization that provides state of the art

trading solutions and infrastructure and to grow with latest technology and services, by

delivering the best solutions by best-in-class people.”

Mission: “To achieve our objectives in an environment of fairness, honesty, and courtesy

towards our clients, employees, vendors and society at large.”

Quality Policy: “To achieve and retain leadership, Sunness shall aim for complete

customer satisfaction, by combining its human and technological resources, to provide

superior quality financial services. In the process, Sunness will strive to exceed

Customer's expectations.”

Quality Objectives: As per the Quality Policy, SUNNESS CAPITAL will:

The company believes in building up the trust in the investors mind therefore it is been

trying to be more transparent to its clients and avoid ambiguity.

The company’s main motto is to build up a good relationship with its investors and its

vendors so as to keep up the words in finishing the obligations and be committed to its

clients

The employees are being treated well and are given training so that employees can

acquire skills and deal the customer’s requirements.

SUNNESS CAPITAL has a very strong feeling to maintain the business standards and

being honesty is one of the motive therefore the company tries to be unbiased and

uphold the ethics of the business.

PRODUCTS/SERVICE PROFILE:

SUNNESS CAPITAL is a renowned well established, dynamic broking house in India. It

is known for its state-of-the-art systems and innovative processes, Sunness has been

offering a single window advantage to its investors, clients for all capital and money

market related requirements. Sunness is a one store like shop which will cater all your

financial requirements & caters a wide spectrum of services that includes

Equity Broking in Cash and Derivatives

11

Internet based trading

The company provides services for dematerialization

The company has a wonderful research providing services

Company deals with money market and debt market broking

Company helps in serving merchant banking

Currency exchange services

Caters and provides loans for investing shares and for funding of margin Also helps

in any merging and acquiring of companies.

SUNNESS CAPITAL provides trading of commodities.

AMFI registered all India Mutual Fund Distributors

IPO (New Issue) distribution

Life Insurance distribution Value Added Services

Research and Advisory Services

Technology that guarantees seamless connectivity for trading

Flexibility of a local broking house and sophistication of corporate brokerage

A dedicated Relationship Manager to help in sales and other business related queries

Online Back-office systems for the Partner as well as all their customers. SUNNESS

CAPITAL views its clients or investors has its king, since years the company has been

respecting the feedbacks and the expectations of its clients, SUNNESS CAPITAL has

been bridging the gap created by its competitors and have been catering the services

which is expected and a requirement for its clients, the company’s main motto is to

bridge the gap and satisfy all the investors needs. In order to be prompt in providing

good consultancy service it has formed a most sophisticated research department where

in advanced techniques are used to predict and assume the future rates and its trends

which shall have an accurate results. Therefore, SUNNESS CAPITAL has a good

competitive edge.

AREAS OF OPERATION:

12

The company operates in the financial areas such as like insurance for both life and

general and also insurance policies for travel related, it helps in the IPOs, provide

consultancy services, has a wide range of health plans for its customers, also provide

finance for leasing and hire purchasing of machineries and also exchange of currency

derivatives, etc. It has presence in 147 cities through its network of longstanding

franchisees and sub brokers.

INFRASTRUCTURE FACILITY:

• Has a very good holding over to tackle the huge transactions and have a good risk

management taking which happens in a very sophisticated and are carried in a well

processed way.

• The company owns its branches in places like Bangalore, Chennai, Mumbai, Kolkata, and

Pune and also almost spread and present over many cities in INDIA.

• The company holds a very good research department in which advanced methods, tools or

techniques are been used in predicting the market, which are highly accurate and are

expected by the clients and investors this is one of the most important infrastructure

should be used in by almost all the stock brokers.

• The company owns a broad-based team of more than 300 personnel

COMPETITORS INFORMATION

1. VLS FINANCE LTD:

When compared to any other stock broking company VLS FINANCE LTD holds a good

position of market capitalization of up to rupees 177.07 cores which is really huge and

great when compared to others, the company has been successful in making a sales worth

rupees 896.82 cores which is again a big value compared to its competitors, VLS holds a

huge place and are reputed in the market, it has also been providing a wide classic

products like any other stock brokers, and not only that though it has a very good sales

worth the net profit is comparatively less that is it has made a net profit of worth rupees

1.76 cores when compared to BNK, and many other stock broking companies.

2. BNK SECURITIES PRIVATE LTD:

13

BNL SECURITIES PVT LTD is one of the best stock broking and a competitor

for the LKP, by holding the market capitalization of rupees 48.85 cores and has made

sales worth rupees 0.74 cores. The company has a wide range of services just like any

other stock broker who provides insurance, health plans, provides consultancy services

for its clients and also help many new firms for the issue management, the company has

hold the membership in BSE and NSE exchanges, the company has a capacity to earn a

net profit of rupees 2.71 cores. Therefore, it is one of the tough competitors for all the

stock brokers.

3.GEOJIT BNP PARIBAS:

GEOJIT BNP PARIBAS is one of the competitors and has the market capitalization of

rupees 869.44 cores. The company deals and caters with a line of products like mutual

funds, life and general insurance and also deals with the commodity, derivatives and

online trading services to its clients. The company has earned a profit of rupees 17.65

cores in last year end quarter in 2014, the company is been one of the best stock broker

acquiring the clients and has increased its volume of number of customers by making a

presence in all over 130 cities in INDIA.

4. R K GLOBAL SHARES & SECURITIES LTD:

R.K GLOBAL SHARES AND SECURITIES LTD is one of the INDIAN based stock

broking who caters products like commodities, currencies, derivatives, shares, mutual

funds, and also provides services for the new firms for issuing IPOs. the company is been

presented almost all over 150 cities in INDIA, the company was established during 2004

and from then started growing enormously, the company is been successfully running.

5. ZERODHA:

ZERODHA is one of the competitor, zerodha caters a wide range of services like stock

broking, currency derivatives, trading in commodity markets and also provide online

trading services, the company charges only 0.01% on the trades happening or usually the

company charge rupees 20 per transaction irrespective to number of shares bought by the

investors, more over the company has been successful in increasing the volume of

number of customers and its growth.

14

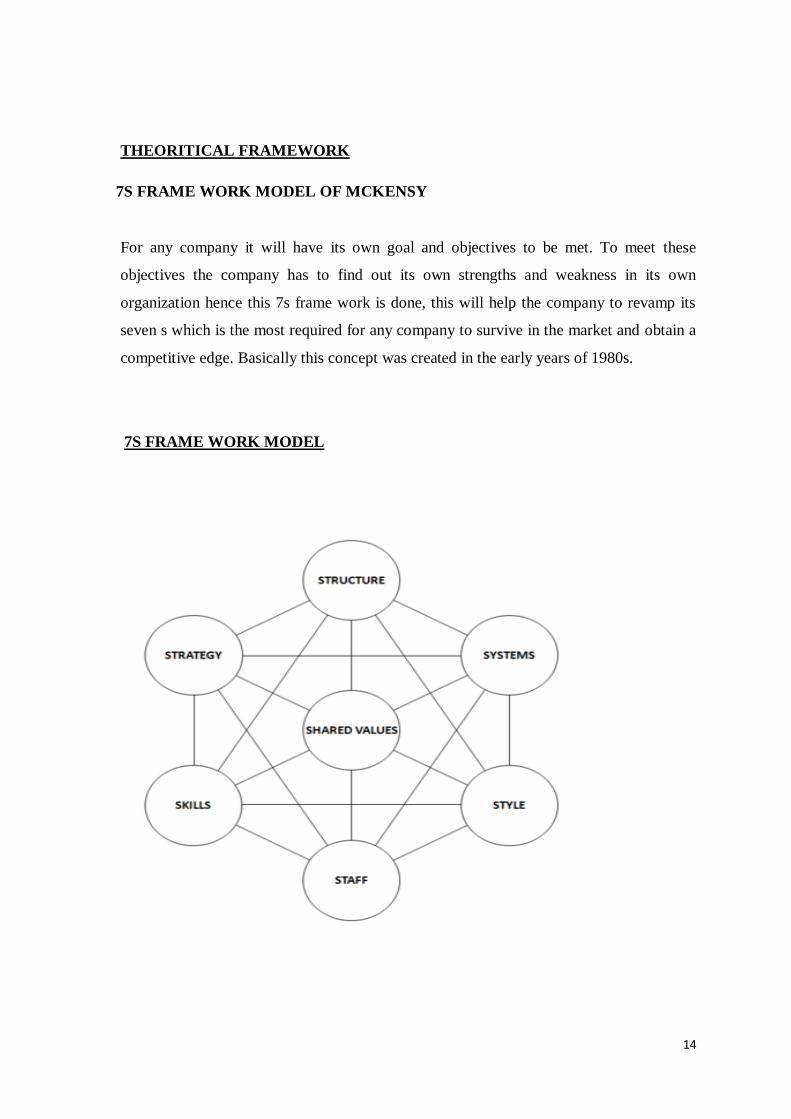

THEORITICAL FRAMEWORK

7S FRAME WORK MODEL OF MCKENSY

For any company it will have its own goal and objectives to be met. To meet these

objectives the company has to find out its own strengths and weakness in its own

organization hence this 7s frame work is done, this will help the company to revamp its

seven s which is the most required for any company to survive in the market and obtain a

competitive edge. Basically this concept was created in the early years of 1980s.

7S FRAME WORK MODEL

15

SYSTEM OF SUNNESS CAPITAL:

SUNNESS CAPITAL has a team leadership style that is each and every message or

information’s or the plan which is to executed has to flow vertically from the top level

management to the bottom level of the management so everything happens in a process to

avoid the ambiguity, and not only that the employee will receive only commands from his

head therefore we can see a clear cut efficiency in the process.

STRUCTURE OF SUNNESS CAPITAL:

SCIP has a clear cut organization structure which prevents from ambiguity and avoids the

miscommunication from the top level management to the bottom level management. Here

in SCIP we can see a formal relationship between the employees, the structure of the

organization is developed in such a way that each and every department as a link, and has

a good support between the departments this will improvise the effectiveness of the work

carried on.

STYLE OF SUNNESS CAPITAL:

Here style refers to how the SCIP work effectively and are carried on by the top level

management people, actually the important decisions related to the organization is

decided only by the top level executives, lower level executives are not consulted while

take important decisions of the organization, similarly any disputes or any decisions

related to between the departments are solved and decided only by the department heads

that kind of freedom is given to the department heads in order to maintain a good

relationship, therefore the style adopted by the SCIP is viable.

STAFF IN SUNNESS CAPITAL:

For any companies staffs are the most important and complex asset to be handled in that

case staffs in SCIP are very friendly and supportive in nature, more over staffs are

expected to obtain a self responsibility in growing the firm which in turn the employees

will be well treated and rewarded with reasonable rewards and bonus SCIP views its

staffs as an big strength and an valuable asset to the company simultaneously staffs are

recognized with the work done by them.

16

SKILLS EXPECTED IN SUNNESS CAPITAL:

Skills of employees are supposed to be the greater strengths for any organization that

might obtain an competitive edge, here company expects for a good analytical, logical,

and should have a good communicational skills this things can alone sell the products of

the organization and that is what SCIP believes in. At the same time they are soft enough

in teaching you these kinds of skills if any of the employees lack in any of the skills.

STRATEGIES ADOPTED BY THE SUNNESS CAPITAL:

For any organization strategies plays an important role in attracting the clients and make a

positive relationship with the clients, here SCIP does a wonderful job in that case, for

these people investors are the kings, the company tries to bridge the gap which was

created by its competitors, the company initially fixes an appointment and then explain

the basics of the stock market which is not done by any other company. Not only that

SCIP provides frequent updates expected by the clients this is what the strategy adopted

by the company in increasing the number of clients.

SHARED VALUES:

Here shared values refers to the feed backs given by the clients to the company, company

usually give values to the feedbacks which will improvise the company. More over

company takes feedbacks as their objectives and take it as an challenge in solving the gap

created by them this in turn will make the clients to retain from switching over to the

other brokers, similarly the company respects its employees feedbacks and make sure that

it is solved and both the employees and clients are satisfied with the service provided by

SCIP.

17

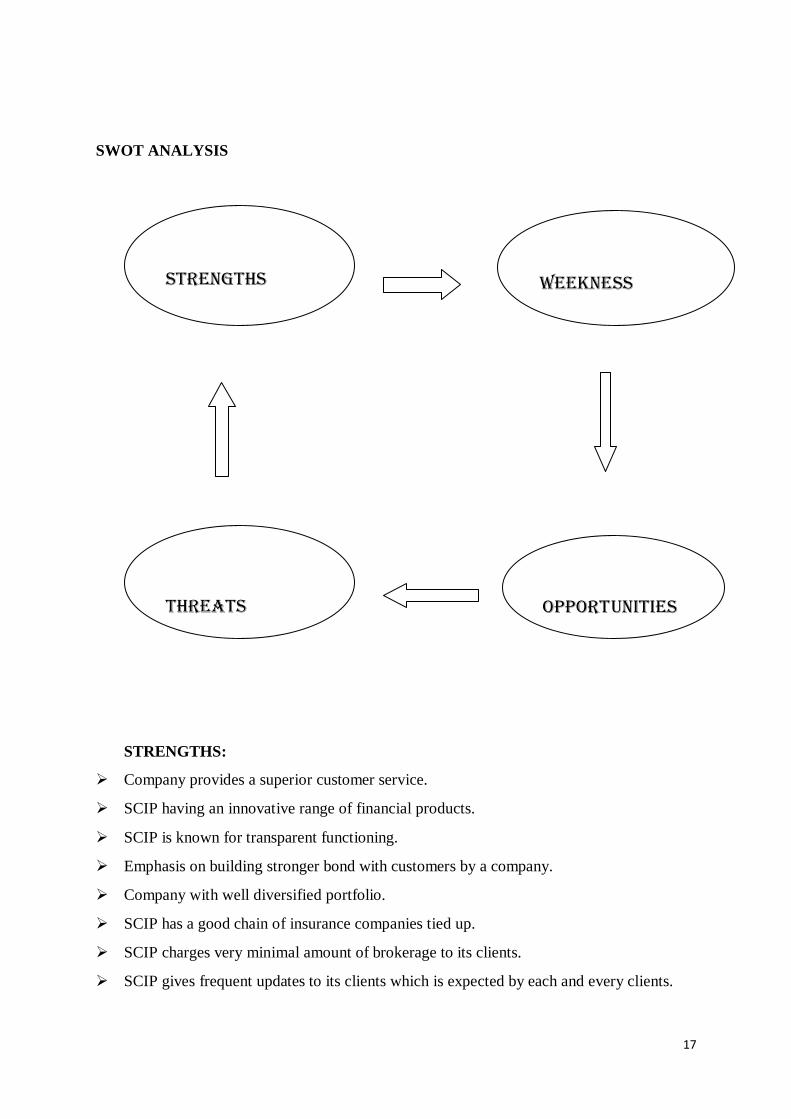

SWOT ANALYSIS

STRENGTHS:

Company provides a superior customer service.

SCIP having an innovative range of financial products.

SCIP is known for transparent functioning.

Emphasis on building stronger bond with customers by a company.

Company with well diversified portfolio.

SCIP has a good chain of insurance companies tied up.

SCIP charges very minimal amount of brokerage to its clients.

SCIP gives frequent updates to its clients which is expected by each and every clients.

STRENGTHS

WEEKNESS

OPPORT UNITIES

THREATS

18

WEAKNESS:

SCIP having limited sales executives.

Low advertisements from the company.

SCIP does not have any segments, or target customers.

SCIP does not give any seminar to investors prior to investing.

OPPORTUNITY:

Growing consumer awareness about equity related product

Positive outlook of people towards financial products

Growing rural market is the best opportunity for the company

THREATS:

Uncertainty of the market volatility and fluctuations in the stock prices

Threat from new entrants into the field of stock broking

Stringent economic measures by Government and RBI

Banks entering to stock broking industry

19

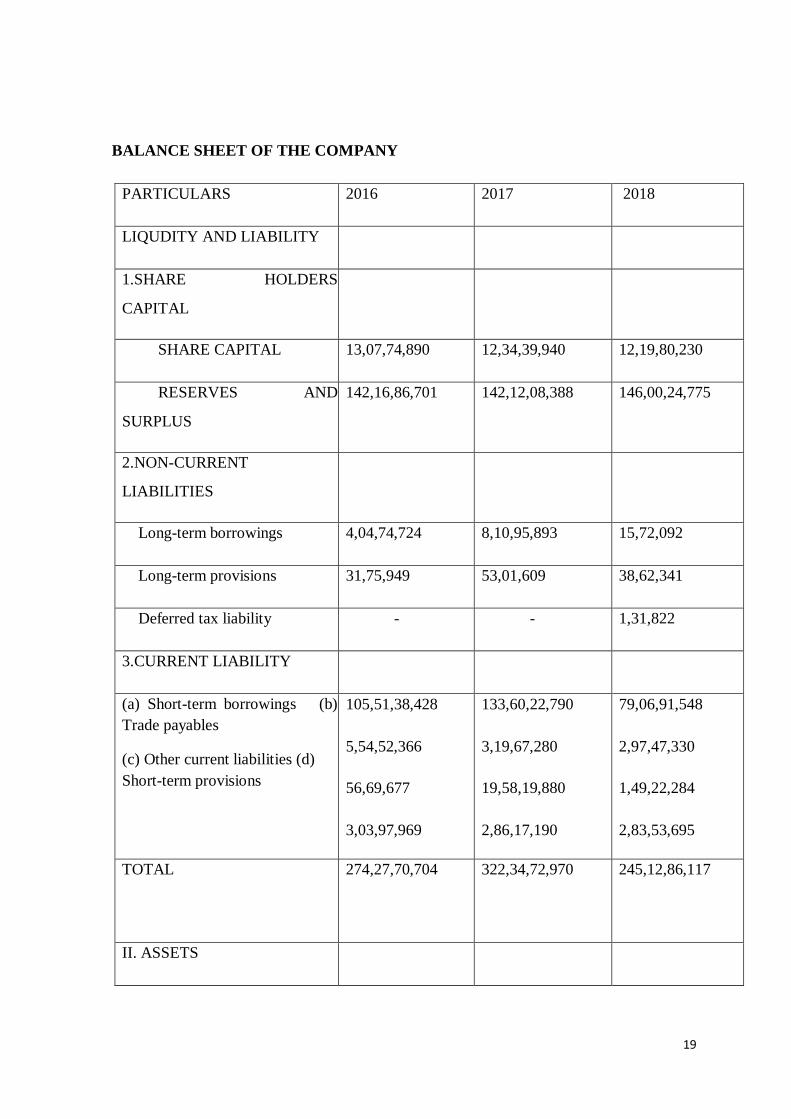

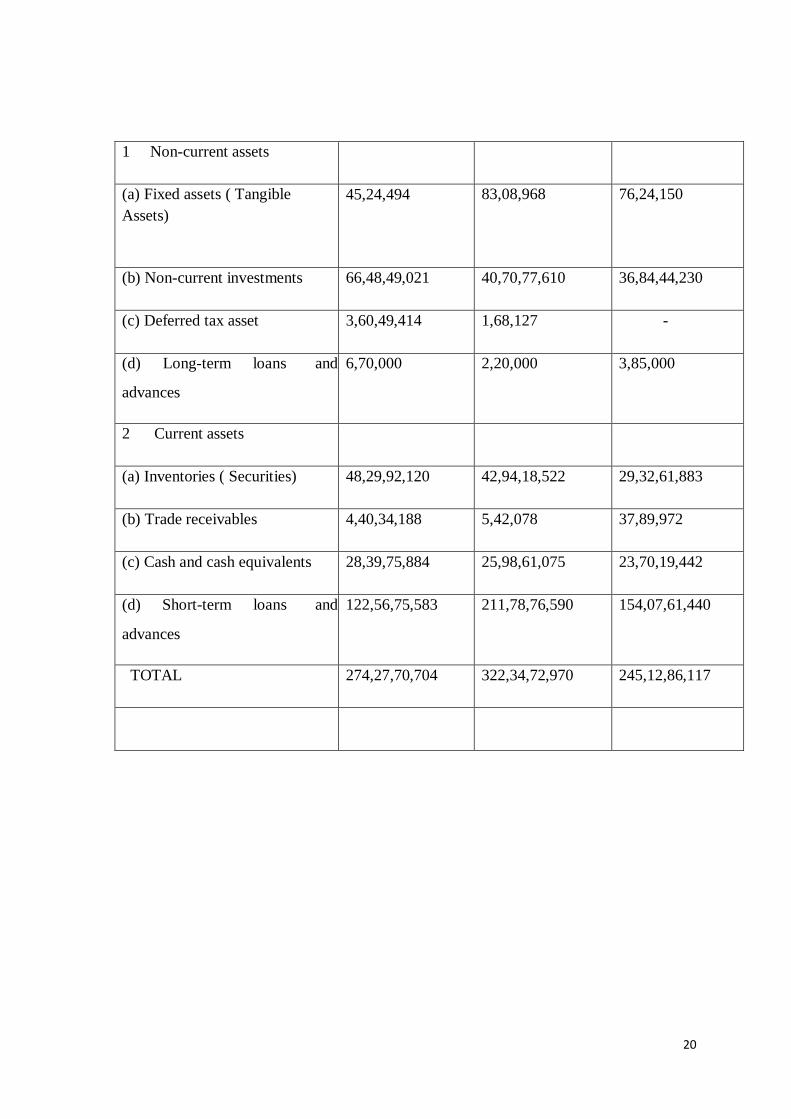

BALANCE SHEET OF THE COMPANY

PARTICULARS 2016 2017 2018

LIQUDITY AND LIABILITY

1.SHARE HOLDERS

CAPITAL

SHARE CAPITAL 13,07,74,890 12,34,39,940 12,19,80,230

RESERVES AND

SURPLUS

142,16,86,701 142,12,08,388 146,00,24,775

2.NON-CURRENT

LIABILITIES

Long-term borrowings 4,04,74,724 8,10,95,893 15,72,092

Long-term provisions 31,75,949 53,01,609 38,62,341

Deferred tax liability - - 1,31,822

3.CURRENT LIABILITY

(a) Short-term borrowings (b)

Trade payables

(c) Other current liabilities (d)

Short-term provisions

105,51,38,428

5,54,52,366

56,69,677

3,03,97,969

133,60,22,790

3,19,67,280

19,58,19,880

2,86,17,190

79,06,91,548

2,97,47,330

1,49,22,284

2,83,53,695

TOTAL 274,27,70,704 322,34,72,970 245,12,86,117

II. ASSETS

20

1 Non-current assets

(a) Fixed assets ( Tangible

Assets)

45,24,494

83,08,968 76,24,150

(b) Non-current investments 66,48,49,021 40,70,77,610 36,84,44,230

(c) Deferred tax asset 3,60,49,414 1,68,127 -

(d) Long-term loans and

advances

6,70,000 2,20,000 3,85,000

2 Current assets

(a) Inventories ( Securities) 48,29,92,120 42,94,18,522 29,32,61,883

(b) Trade receivables 4,40,34,188 5,42,078 37,89,972

(c) Cash and cash equivalents 28,39,75,884 25,98,61,075 23,70,19,442

(d) Short-term loans and

advances

122,56,75,583 211,78,76,590 154,07,61,440

TOTAL 274,27,70,704 322,34,72,970 245,12,86,117

21

CAPITAL BUDGEING:

An efficient allocation of capital is the most important finance function in modern times. It

involves decisions to commit firm’s funds to long-term assets. Such decisions are tend to

determine the value of company/firm by influencing its growth, profitability & risk.

Investment decisions are generally known as capital budgeting or capital expenditure

decisions. It is clever decisions to invest current in long term assets expecting long-term

benefits firm’s investment decisions would generally include expansion, acquisition,

modernization and replacement of long-term assets.

Such decisions can be investment decisions, financing decisions or operating decisions.

Investment decisions deal with investment of organization’s resources in Long tern (fixed)

Assets and / or Short term (Current) Assets. Decisions pertaining to investment in Short term

Assets fall under “Working Capital Management”. Decisions pertaining to investment in

Long term Assets are classified as “Capital Budgeting” decisions.

Capital budgeting decisions are related to allocation of investible funds to different long-term

assets. They have long-term implications and affect the future growth and profitability of the

firm.

In evaluating such investment proposals, it is important to carefully consider the expected

benefits of investment against the expenses associated with it. Organizations are frequently

faced with Capital Budgeting decisions. Any decision that requires the use of resources is a

capital budgeting decisions. Capital budgeting is more or less a continuous process in any

growing concern.

For Example: Purchase of Land is an example of Capital Budgeting decision. Similarly

replacement of outdated equipment with modern machines, purchase of a brand or business,

computerization and networking the organization, investment in research and development

of a product launch of a major promotional campaign etc are all example of Capital

Budgeting decisions.

However, in all cases, the decisions have a long-term impact on the performance of the

organization. Even a single wrong decision may in danger the existence of the firm as a

profitable entity.

22

IMPORTANCE OF CAPITAL BUDGETING:

There are several factors that make capital budgeting decisions among the critical decisions

to be taken by the management. The importance of capital budgeting can be understood from

the following aspects of capital budgeting decisions.

1. Long Term Implications: Capital Budgeting decisions have long term effects on the

risk and return composition of the firm. These decisions affect the future position of

the firm to a considerable extent. The finance manger is also committing to the future

needs for funds of that project.

2. Substantial Commitments: The capital budgeting decisions generally involve large

commitment of funds. As a result, substantial portion of capital funds is blocked.

3. Irreversible Decisions: Most of the capital budgeting decisions are irreversible

decisions. Once taken the firm may not be in a position to revert back unless it is

ready to absorb heavy losses which may result due to abandoning a project midway.

4. After the Capacity and Strength to Compete: Capital budgeting decisions affect

the capacity and strength of a firm to face competition. A firm may lose

competitiveness if the decision to modernize is delayed.

PROBLEMS & DIFFICULTIES IN CAPITAL BUDGETING:

Future uncertainty:

Capital Budgeting decisions involve long-term commitments. There is lot of

uncertainty in the long term. The uncertainty may be with reference to cost of the

project, future expected returns, future competition, legal provisions, political

situation etc.

Time Element:

The implications of a Capital Budgeting decision are scattered over a long period. The

cost and benefits of a decision may occur at different point of time. The cost of a

project is incurred immediately. However, the investment is recovered over a number

of years. The future benefits have to be adjusted to make them comparable with the

cost. Longer the time period involved, greater would be the uncertainty.

23

Difficulty in Quantification of Impact:

The finance manager may face difficulties in measuring the cost and benefits of

projects in quantitative terms.

Example: The new product proposed to be launched by a firm may result in increase

or decrease in sales of other products already being sold by the same firm. It is very

difficult to ascertain the extent of impact as the sales of other products may also be

influenced by factors other than the launch of the new product.

ASSUMPTIONS IN CAPITAL BUDGETING:

The Capital Budgeting decision process is a multi-faceted and analytical process. A number

of assumptions are required to be made.

1. Certainty with respect to cost & Benefits:

It is very difficult to estimate the cost and benefits of a proposal beyond 2-3 years in

future.

2. Profit Motive:

Another assumption is that the capital budgeting decisions are taken with a primary

motive of increasing the profit of the firm.

The activities can be listed as follows:

Dis-investments i.e., sale of division or business.

Change in methods of sales distribution.

Undertakings an advertisement campaign.

Research & Development programs.

Launching new projects.

Diversification.

Cost reduction.

FEATURES OF INVESTMENT DECISIONS:

The exchange of current funds for future benefits.

24

The funds are invested in long-term assets.

The future benefits will occur to the firm over a series of years.

IMPORTANT OF INVESTMENT DECISIONS:

They influence the firm’s growth in long run.

They effect the risk of the firm.

They involve commitment of large amount of funds.

They are irreversible, or reversible at substantial loss.

They are among the most difficult decisions to make.

TYPE OF INVESTMENT DECISIONS:

Expansion of existing business.

Expansion of new business.

Replacement & Modernization.

INVESTMENT EVALUATION CRITERIA:

Estimation of cash flows.

Estimation of the required rate of return.

Application of a decision rule for making the choice.

Consideration of cash flows is to determine true profitability of the project and it is an

unambiguous way of identifying good projects from the pool. Ranking is possible it should

recognize the fact that bigger cash flows are preferable to smaller ones & early cash flows

are referable to later ones I should help to choose among mutually exclusive projects that

which maximizes the shareholders wealth. It should be a criterion which is applicable to

any considerable investment project independent of other. There are number of techniques

that are in use in practice. The chart of techniques can be outlined as follows:

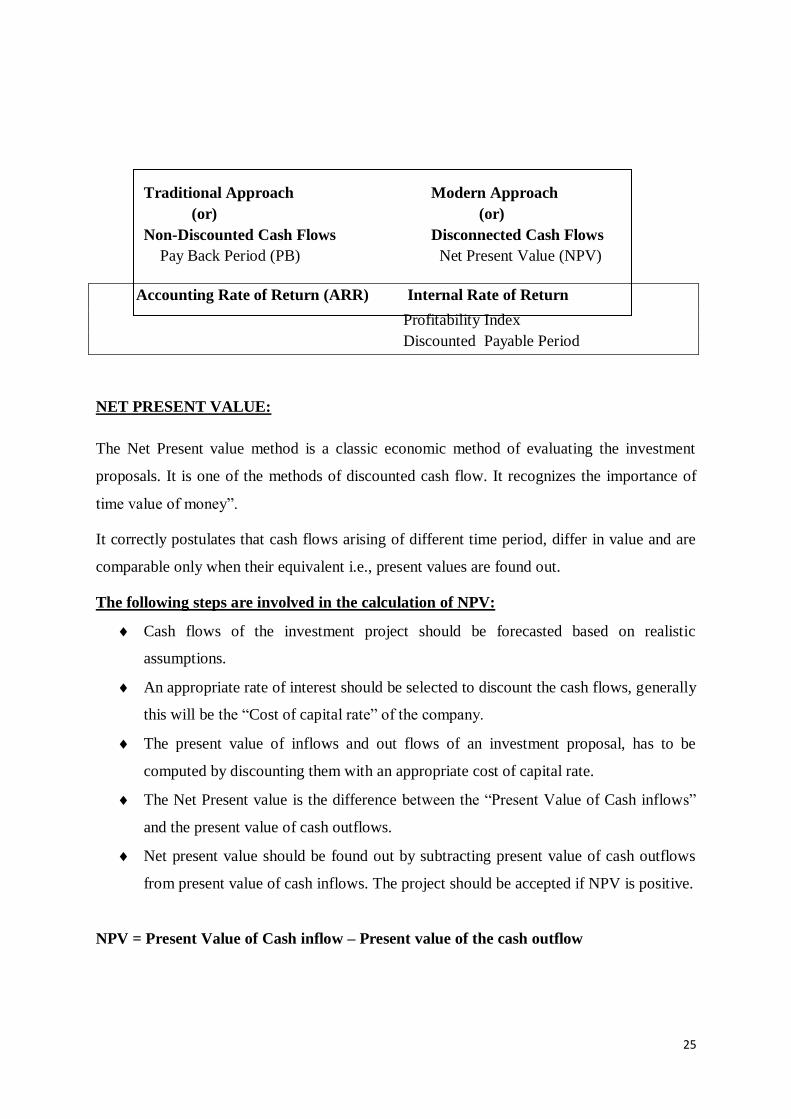

Capital Budgeting Techniques:

25

Traditional Approach Modern Approach

(or) (or)

Non-Discounted Cash Flows Disconnected Cash Flows

Pay Back Period (PB) Net Present Value (NPV)

Accounting Rate of Return (ARR) Internal Rate of Return

Profitability Index

Discounted Payable Period

NET PRESENT VALUE:

The Net Present value method is a classic economic method of evaluating the investment

proposals. It is one of the methods of discounted cash flow. It recognizes the importance of

time value of money”.

It correctly postulates that cash flows arising of different time period, differ in value and are

comparable only when their equivalent i.e., present values are found out.

The following steps are involved in the calculation of NPV:

Cash flows of the investment project should be forecasted based on realistic

assumptions.

An appropriate rate of interest should be selected to discount the cash flows, generally

this will be the “Cost of capital rate” of the company.

The present value of inflows and out flows of an investment proposal, has to be

computed by discounting them with an appropriate cost of capital rate.

The Net Present value is the difference between the “Present Value of Cash inflows”

and the present value of cash outflows.

Net present value should be found out by subtracting present value of cash outflows

from present value of cash inflows. The project should be accepted if NPV is positive.

NPV = Present Value of Cash inflow – Present value of the cash outflow

26

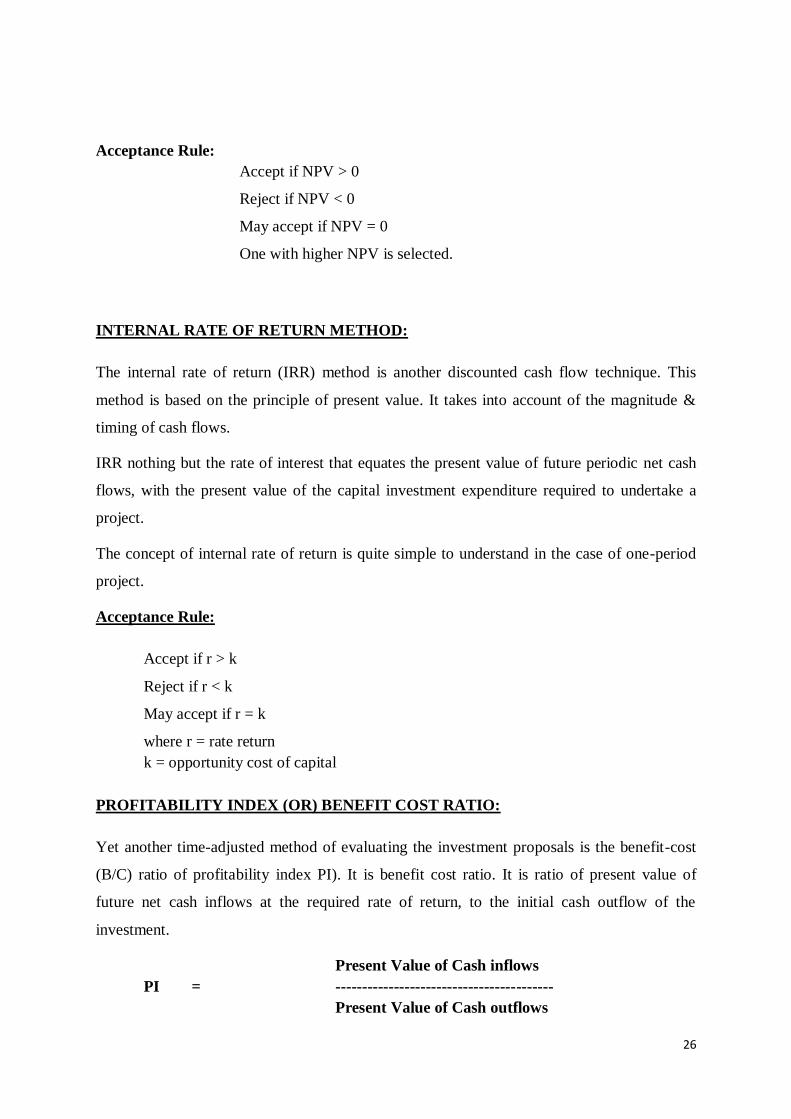

Acceptance Rule:

Accept if NPV > 0

Reject if NPV < 0

May accept if NPV = 0

One with higher NPV is selected.

INTERNAL RATE OF RETURN METHOD:

The internal rate of return (IRR) method is another discounted cash flow technique. This

method is based on the principle of present value. It takes into account of the magnitude &

timing of cash flows.

IRR nothing but the rate of interest that equates the present value of future periodic net cash

flows, with the present value of the capital investment expenditure required to undertake a

project.

The concept of internal rate of return is quite simple to understand in the case of one-period

project.

Acceptance Rule:

Accept if r > k

Reject if r < k

May accept if r = k

where r = rate return

k = opportunity cost of capital

PROFITABILITY INDEX (OR) BENEFIT COST RATIO:

Yet another time-adjusted method of evaluating the investment proposals is the benefit-cost

(B/C) ratio of profitability index PI). It is benefit cost ratio. It is ratio of present value of

future net cash inflows at the required rate of return, to the initial cash outflow of the

investment.

Present Value of Cash inflows

PI = -----------------------------------------

Present Value of Cash outflows

27

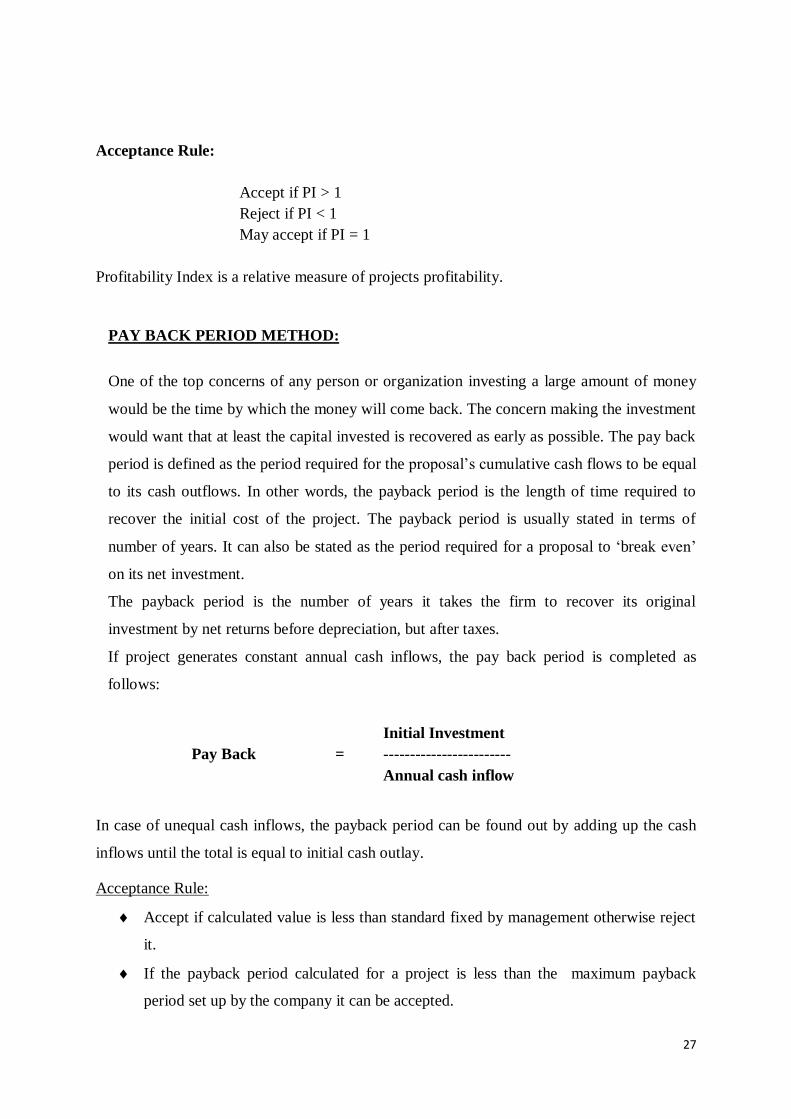

Acceptance Rule:

Accept if PI > 1

Reject if PI < 1

May accept if PI = 1

Profitability Index is a relative measure of projects profitability.

PAY BACK PERIOD METHOD:

One of the top concerns of any person or organization investing a large amount of money

would be the time by which the money will come back. The concern making the investment

would want that at least the capital invested is recovered as early as possible. The pay back

period is defined as the period required for the proposal’s cumulative cash flows to be equal

to its cash outflows. In other words, the payback period is the length of time required to

recover the initial cost of the project. The payback period is usually stated in terms of

number of years. It can also be stated as the period required for a proposal to ‘break even’

on its net investment.

The payback period is the number of years it takes the firm to recover its original

investment by net returns before depreciation, but after taxes.

If project generates constant annual cash inflows, the pay back period is completed as

follows:

Initial Investment

Pay Back = ------------------------

Annual cash inflow

In case of unequal cash inflows, the payback period can be found out by adding up the cash

inflows until the total is equal to initial cash outlay.

Acceptance Rule:

Accept if calculated value is less than standard fixed by management otherwise reject

it.

If the payback period calculated for a project is less than the maximum payback

period set up by the company it can be accepted.

28

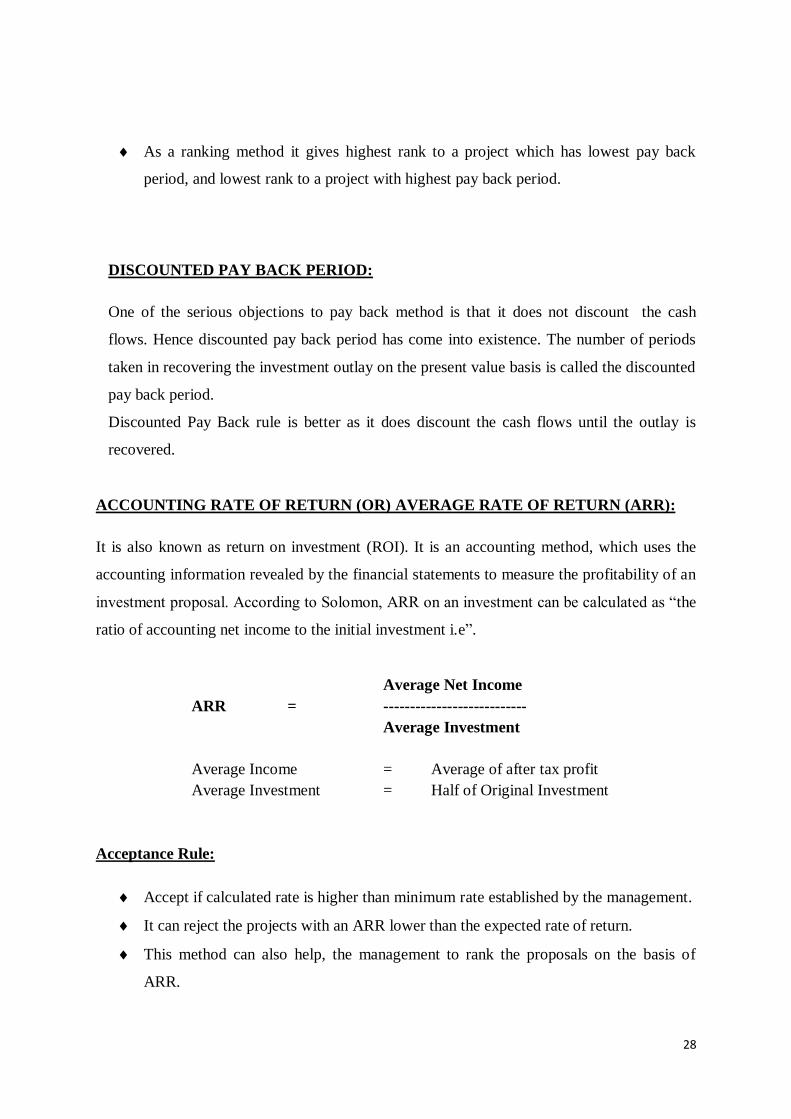

As a ranking method it gives highest rank to a project which has lowest pay back

period, and lowest rank to a project with highest pay back period.

DISCOUNTED PAY BACK PERIOD:

One of the serious objections to pay back method is that it does not discount the cash

flows. Hence discounted pay back period has come into existence. The number of periods

taken in recovering the investment outlay on the present value basis is called the discounted

pay back period.

Discounted Pay Back rule is better as it does discount the cash flows until the outlay is

recovered.

ACCOUNTING RATE OF RETURN (OR) AVERAGE RATE OF RETURN (ARR):

It is also known as return on investment (ROI). It is an accounting method, which uses the

accounting information revealed by the financial statements to measure the profitability of an

investment proposal. According to Solomon, ARR on an investment can be calculated as “the

ratio of accounting net income to the initial investment i.e”.

Average Net Income

ARR = ---------------------------

Average Investment

Average Income = Average of after tax profit

Average Investment = Half of Original Investment

Acceptance Rule:

Accept if calculated rate is higher than minimum rate established by the management.

It can reject the projects with an ARR lower than the expected rate of return.

This method can also help, the management to rank the proposals on the basis of

ARR.

29

A highest rank will be given to a project with highest ARR, whereas a lowest rank to

a project with lowest ARR.

CAPITAL BUDGETING METHODS IN PRACTICE:

In a study of the capital budgeting practices of fourteen medium to large size

companies in India, it was found tat almost all companies used by back.

With pay back and/or other techniques, about 2/3rd of companies used IRR and about

2/5th NPV. IRR s found to be second most popular method.

Pay back gained significance because of is simplicity to use & understand, its

emphasis on the early recovery of investment & focus on risk.

It was found that 1/3rd of companies always insisted on computation of pay back for

all projects, 1/3rd for majority of projects & remaining for some of the projects.

Reasons for secondary of DCF techniques in India included difficulty in

understanding & using threes techniques, lack of qualified professionals &

unwillingness of top management to use DCF techniques.

One large manufacturing and marketing organization mentioned that conditions of its

business were such that DCF techniques were not needed.

Yet another company stated that replacement projects were very frequent in the

company, and it was not considered necessary to use DCF techniques for evaluating

such projects. techniques in India included difficulty in understanding & using threes

techniques, lack of qualified professionals & unwillingness of top management to use

DCF techniques.

PROCESS

CAPITAL BUDGETING PROCESS:

Atleast five phases of capital expenditure planning & control can be identified:

Identification (or Organization) of investment opportunities.

30

Development of forecasts of benefits and costs.

Evaluation of the net benefits.

Authorization for progressing and spending capital expenditure.

Control of capital projects.

INVESTMENT IDEAS:

Investment opportunities have to be identified or created investment proposals arise at

different levels within a firm.

Nature of Idea Level

Cost reduction ------

Replacement Plant Level

Process/Product Development (50% in India cover this level)

Expansion Top management

Diversification in India, it is insignificant

Replacing an old

Machine (or)

Improving the Factory Level.

Production techniques.

Investment proposals should be generated to employ the firm’s funds fully well & efficiently.

FORECASTING :

Cash flow estimates should be development by operating managers with the help of finance

executives. Risk associated should be properly handled. Estimation of cash flows requires

collection and analysis of all qualitative and quantitative data, both financial and non-

financial in nature. MIS provide such data.

Correct treatment should be given to:

Additional working capital

Sale proceeds of existing assets.

Depreciation

Financial flows (to be distinguished from operation flows)

EVALUATION:

31

Group of experts who have no ake to grind should be taken in selecting the methods of

evaluation as NPV, IRR, PI, Pay Back, ARR & Discounted Pay Back.

Pay Back period is used as “Primary” method & IRR/NPV as “Secondary” method in India.

The following are to be given due importance.

For evaluation, minimum rate of return or cut-off is necessary.

Usually if is computed by means of weighted Average cost of Capital (WACC)

Opportunity cost of capital should be based on risky ness of cash flow of

investment proposals.

Assessment of risk is an important aspect. Sensitivity Analysis & Conservative

for costs are two important methods used in India.

AUTHORIZATION:

Screening and selecting may differ from one company to another. When large sums are

involved usually final approval rests with top management. Delegation of approval authority

may be effected subject to the amount of outlay. Budgetary control should be rigidly

exercised.

CONTROL AND MONITORY:

A Capital projects reporting system is required to review and monitor the performance of

investment projects after completion and during their life. Follow up comparison of the actual

performance with original estimates to ensure better forecasting besides sharpening the

techniques for improving future forecasts. As a result company may re-praise its projects and

take necessary action.

Indian Companies use regular project reports for controlling capital expenditure reports may

be quarterly, half-yearly, monthly, bi-monthly continuous reporting.

Expenditure to date

Stage and physical completion

Approved total cost

Revised total cost

32

DECISION MAKING LEVEL:

For planning and control purpose three levels of Decision making have been identified:

Operating

Administrative

Strategic

OPERATING CAPITAL BUDGETING:

Includes routine minor expenditure, as office equipment handled by lower level management.

ADMINISTRATIVE CAPITAL BUDGETING:

Falls in between these two levels involves medium size investments such as business handled

by middle level management.

STRATEGIC CAPITAL BUDGETING:

Involves large investment as acquisition of new business or expansion in a new time of

business, handled by top management unique nature.

Long Term Capital Budgeting In Sunness:

PRE – INVESTMNET STAGE:

In a planned economy, as in India, the identification of public sector projects needs to be

done within the overall framework of national the sectoral planning. All projects of every

sector need to be identified scientifically at the time of plan formulation. In actual

practice,however, it is observed that ‘identification’ stage is the most neglected stage of the

project planning.

The five year plans indicate the broad strategy of planning economic growth rate and other

basic objectives to be achieved during the plan period. The macro level planning exercise

undertaken at the beginning of every five year plan indicates broadly the role of each sector’s

physical targets to be achieved and financial outlays, which could be made available for the

development of the sector during the plan period.

33

The identification of a project in the Five Year Plan is not the sanction of the project for

implementation. It provides only the ‘green signal’ for the preparation of feasibility report

(FR0 for appraisal and investment decision. A preliminary scrutiny of the FR of the project

is done in the Ministry and thereafter copies of the feasibility report are submitted to the

appraising agencies, viz., Planning Commission, Bureau of Public Enterprises and the Plan

Finance Division of the Ministry of Finance. Thus the organizational responsibility for

identifying these projects rests with the concerned administrative ministry, in consultation

with its public enterprises.

The essential steps for project identification and preparation relates to studying (i) imports (ii)

substitutes(iii) available and raw material (iv) available technology and skills (v) inter-

industry relationship (vi) existing industry (vii) development plans (viii) old projects etc.

It may be mentioned that in actual practice, these steps are hardly scientifically studied and

followed by the administrative ministry public sector undertaking at the time of project

identification. The public sector projects many a time come spontaneously on the basis of

ideas and possibilities of demand or availability of some raw materials and not an outcome of

scientific investigation and systematic search for feasible projects.

PROJECT FORMULATION:

The second stage of “Project Cycle” viz. Project Formulation, is a pre-investment exercise to

determine whether to invest, where to invest, when to invest and how much to invest. The

project/feasibility reports are meant to provide required information for assessing technical,

financial, commercial, organization and economic viability of the project planning in India,

mainly because of relatively late realization of its importance. As a result, the investment

decisions for large projects in the past were taken on half-baked and ill-conceived projects

and time-over runs and cost-over runs of public sector projects have become a regular feature

rather than exception.

In early seventies along with the setting up of the Public Investment Board (PIB) the

Government created a new project Appraisal Division in the Planning Commission. This

Division prepared and circulated “Guidelines for preparing Feasibility Reports of Industrial

Projects” in 1974.

34

This guidelines, unlike earlier manual, indicates all the information and data required to be

presented and analysed in the feasibility report, so as to enable the appraisal agency to carry

out (i) technical analysis – to determine whether the specification of technical parameters are

realistic, (ii) financial anaylsis – to determine whether the proposal is financially viable, (iii)

commercial analysis – to determine soundness of the product specifications, marketing plans

and organization structure and (iv) economic analysis, to determine whether a project is

worthwhile from the point of view of nation and economy as a whole.

The guidelines describes in details, the information required to be given and analysed on the

following issues : (a) general information of the sector, (b) objective of the proposal, (c)

alternative ways, if any of attaining the objectives and better suitability of the proposed

project, (d) project description – gestation period, costs, technology proposed, anticipated

life of the project etc., (e) demand analysis, total demand / requirements of the country,

including anticipated imports and exports and share of the proposed project, (f) capital costs

and norms assumed, activity wise and year wise, (g) operating costs and norms, (h) revenue

and benefits estimation etc.

PROJECT APPRAISAL :

The appraisal of the project follows the formulation stage. The objective of the appraisal

process is not only to decide whether to accept or reject the investment proposal, but also to

recommend the ways in which the project can be redesigned or reformulated so as to ensure

better technical, financial, commercial and economic viabilities.

The project appraised which is an essential tool for judicious investment decisions and

project selection is a multi-disciplinary task. But many a times this is considered doubt, have

played an important role in contributing systematic methods for forecasting the future and

evolving appraisal methods to quantify socials costs and benefits, but they alone can not carry

out complete appraisal of an investment proposal.

The need for project appraisal and investment decisions based on social profitability arises

mainly because of the basic characteristics of developing countries limited resources for

development and multiple needs – objective of planning being ‘Economic Growth with

Social Justice’. The project appraisal is a convenient and comprehensive fashion to achieve,

35

the laid down objectives of the economic development plan. The appraisal work presupposes

availability of a certain minimum among of reliable and up to date data in the country, as well

as the availability of trained persons to carry out the appraisal analysis.

As stated earlier the investment decision of public sector projects are required to be taken

within the approved plan frame work. The Project Appraisal Division (PAD) that prepares

the comprehensive appraisal note of projects of Central Plans was therefore set up in

Planning Commission. The Finance Ministry issues expenditure sanction for all investment

proposals within the frame work of annual budget. The plan Finance Division and the

Bureau of Public Enterprises of the Finance Ministry are also required to examine and give

comments on the investment proposals of public.

36

DATA ANALYSIS

All finance activity commences with an investment proposal, which calls for a financial

appraisal of a project. Here, capital Budgeting has its role. Each one of the projects is

appraised on following basis”

Cost Estimates.

Cost Generations.

Cost Estimates:-

Feasibility Report of the project is prepared based on the cost of similar units prevailing at the

time of preparation of projects report of the latest costs are not available, the same should be

escalated. Collection of data with regard to the cost of the various equipment should from

part of a continuous planning so tat a realistic cost estimate is made for the project Reports

for civil works are generally based on Sunness schedule of rates with reasonable premium

there on.

Cost of Generation:-

The financing of public sector company is generally based on Debt Equity of 3:1 the general rate of

interest chargeable by the central Government on loan components is 10.5% (Now enhanced to 11%)

The plant life as provided under the Electricity Supply Act, 1948 is 25 years and depreciation based

on this period has to be calculated on straight line method, on 90% of the cost fixed assets. The

operation & maintenance expenses are generally of the order 2.5% of the capital cost based on the

above assumptions, the cost of generation could be worked out discounted cash flow basis taking 12%

IRR (Internal Rate of Return). This rate has been generally accepted by various appraising agencies

of the power projects.

Feasibility Report based on above methodology and indicating site selection, coal linkage,

power distribution examined by Central Electricity Authority in all cases where investment is

Rs.1 Crore and above. Since Sunness is public sector undertaking, all the investment

decisions have to be formally sanctioned by Government after PIB’s (Public Investment

Board’s) clearance.

37

SHARE CAPITAL:

The entire share capital is owned by Government of India. During the Year no addition has

been made. However the authorized capital has been increased from Rs. 80,000 million to

Rs.1,00,000 million and the face value or share has been split to Rs.10/- each from Rs.1000/-

each.

ROLE OF FINANCE MANAGEMENT IN INVESTMENT DECISIONS IN

SUNNESS:

Finance Manager is the number of a project team. He plays an important role in investigation

stage of the project, when various alternatives are analysed & the most optimum solution is

decided upon. The soundness upon the accuracy of the data & as a finance manager has to

questing and satisfy himself on the validity of the data.

The power projects are extremely capital intensive and before large resources are committed

to a scheme a detailed feasibility study need to be prepared covering-

The need of the project

The demand projections

The alternatives of the site locations

The broad parameters of the plant and equipment

The cost estimates

The viability of the scheme.

Cost Estimates:

Cost estimates and financial justification and returns of the projects are the areas where

financial management has to play its role. Cost estimates should be prepared by the cost

engineers and vetted by the finance manager. Cost engineering is a specialized filed & need

to be developed in the contest of power projects because of insufficient cost data on the

components of the projects.

This raises an important question of the present methodology of preparing the cost estimates

without any provision for price contingencies. Because of time lag between preparation of

38

cost estimates and investment decisions, After its scrutiny by the appraising agencies, these

estimates are already out of data and hence would need updating.

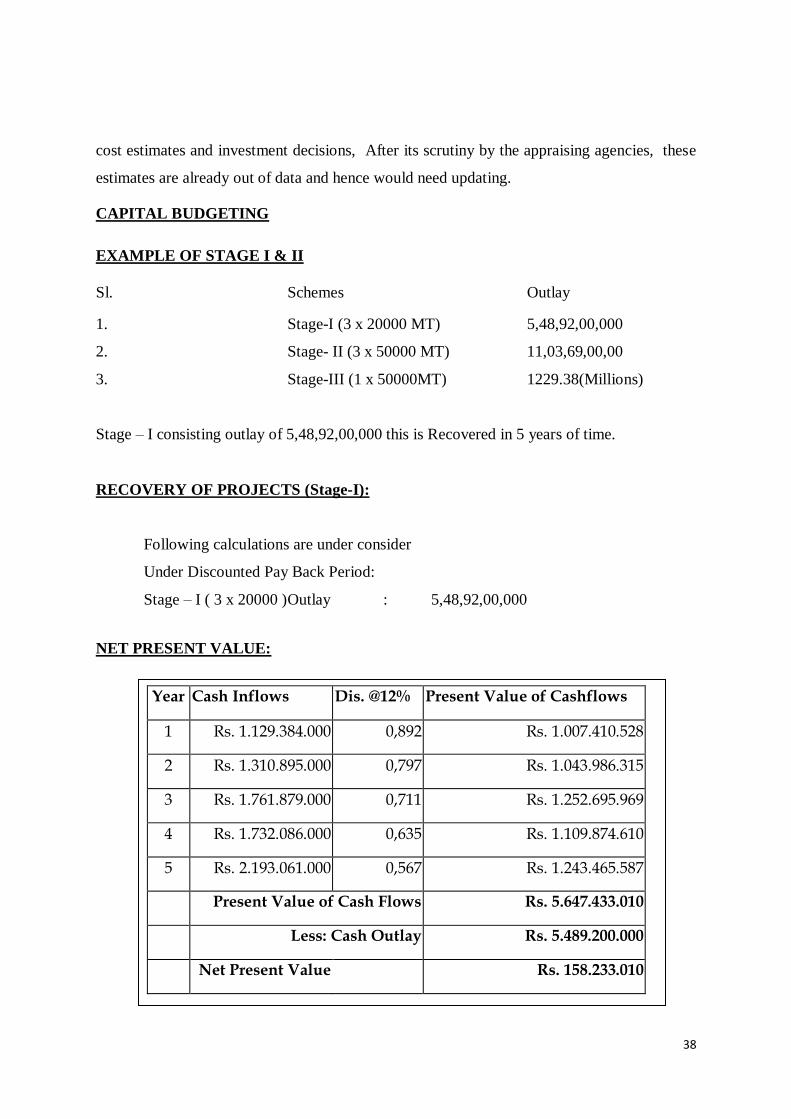

CAPITAL BUDGETING

EXAMPLE OF STAGE I & II

Sl. Schemes Outlay

1. Stage-I (3 x 20000 MT) 5,48,92,00,000

2. Stage- II (3 x 50000 MT) 11,03,69,00,00

3. Stage-III (1 x 50000MT) 1229.38(Millions)

Stage – I consisting outlay of 5,48,92,00,000 this is Recovered in 5 years of time.

RECOVERY OF PROJECTS (Stage-I):

Following calculations are under consider

Under Discounted Pay Back Period:

Stage – I ( 3 x 20000 ) Outlay : 5,48,92,00,000

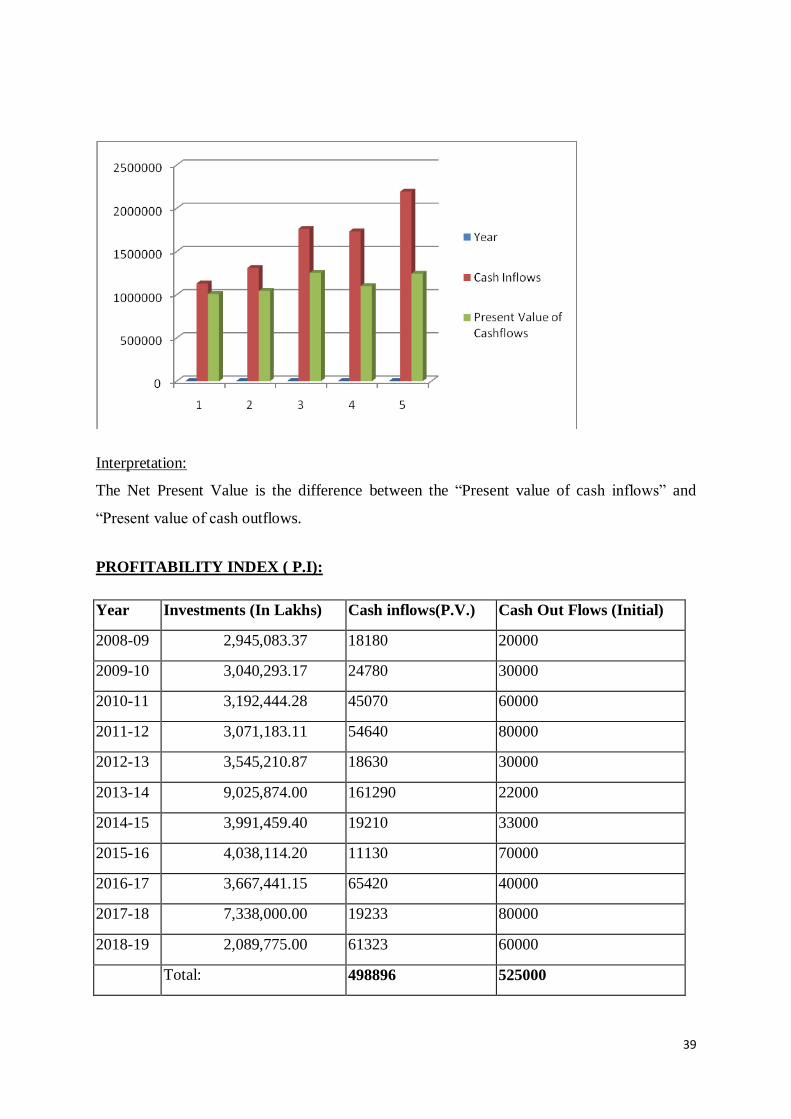

NET PRESENT VALUE:

Year Cash Inflows Dis. @12% Present Value of Cashflows

1 Rs. 1.129.384.000 0,892 Rs. 1.007.410.528

2 Rs. 1.310.895.000 0,797 Rs. 1.043.986.315

3 Rs. 1.761.879.000 0,711 Rs. 1.252.695.969

4 Rs. 1.732.086.000 0,635 Rs. 1.109.874.610

5 Rs. 2.193.061.000 0,567 Rs. 1.243.465.587

Present Value of Cash Flows Rs. 5.647.433.010

Less: Cash Outlay Rs. 5.489.200.000

Net Present Value Rs. 158.233.010

39

Interpretation:

The Net Present Value is the difference between the “Present value of cash inflows” and

“Present value of cash outflows.

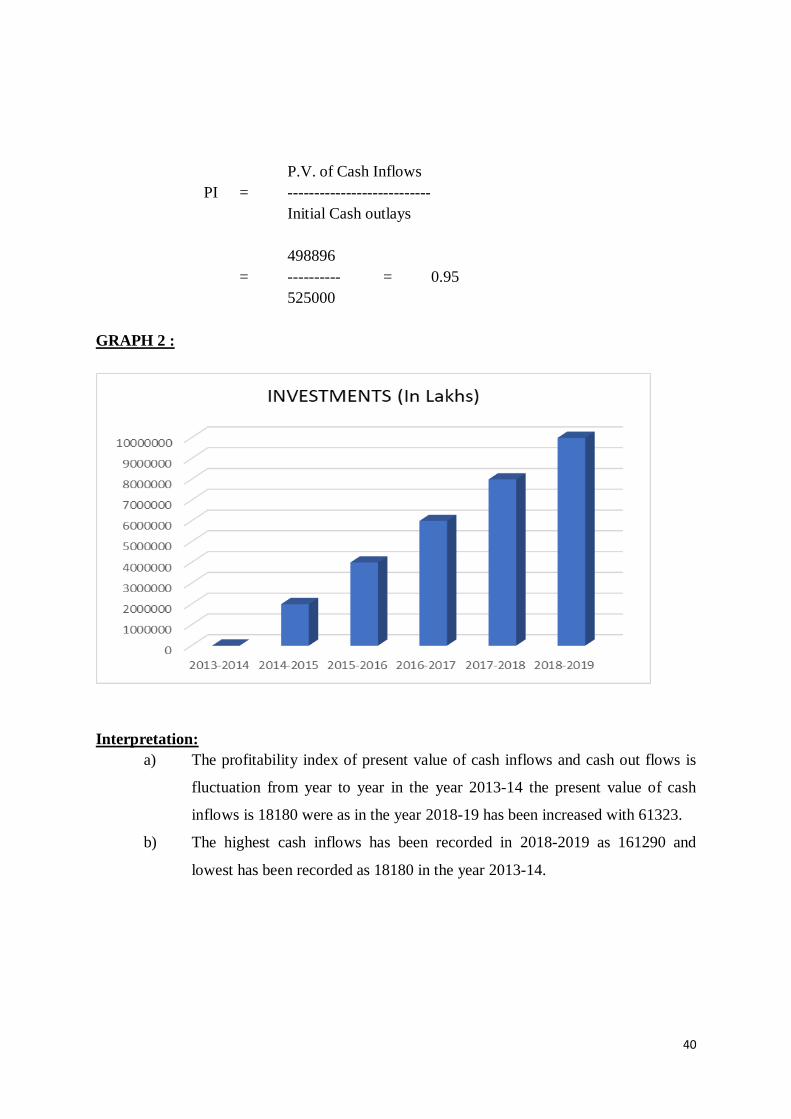

PROFITABILITY INDEX ( P.I):

Year Investments (In Lakhs) Cash inflows(P.V.) Cash Out Flows (Initial)

2008-09 2,945,083.37 18180 20000

2009-10 3,040,293.17 24780 30000

2010-11 3,192,444.28 45070 60000

2011-12 3,071,183.11 54640 80000

2012-13 3,545,210.87 18630 30000

2013-14 9,025,874.00 161290 22000

2014-15 3,991,459.40 19210 33000

2015-16 4,038,114.20 11130 70000

2016-17 3,667,441.15 65420 40000

2017-18 7,338,000.00 19233 80000

2018-19 2,089,775.00 61323 60000

Total: 498896 525000

40

P.V. of Cash Inflows

PI = ---------------------------

Initial Cash outlays

498896

= ---------- = 0.95

525000

GRAPH 2 :

Interpretation:

a) The profitability index of present value of cash inflows and cash out flows is

fluctuation from year to year in the year 2013-14 the present value of cash

inflows is 18180 were as in the year 2018-19 has been increased with 61323.

b) The highest cash inflows has been recorded in 2018-2019 as 161290 and

lowest has been recorded as 18180 in the year 2013-14.

41

PAY BACK PERIOD:

Year Investments (In Lakhs) Cash inflows(P.V.) Cash Out Flows (Initial)

2008-09 40,000.00 8000 20000

2009-10 60,000.00 1600 30000

2010-11 70,000.00 2200 60000

2011-12 20,000.00 4500 80000

2012-13 10,000.00 4000 30000

2013-14 66,000.00 3000 22000

2014-15 25,000.00 2900 33000

2015-16 12,000.00 1100 70000

2016-17 90,000.00 1600 40000

2017-18 30,000.00 1200 80000

2018-19 50,000.00 1800 60000

Total: 473,000.00 31900 525000

Initial Investments

Pay Back Period = ---------------------------

Annual Cash inflows

40,000

= --------- 5 Years

8000

GRAPH 3:

42

Interpretation:

a) In the Pay Back method the Investment and the case inflows are fluctuating

from year to year where as in the year 2013-14 it is 40000 and in the year

2018-19 is 50000.

b) Cash inflows are in the order of increasing to decreasing from 2013-14 and

2018-19.

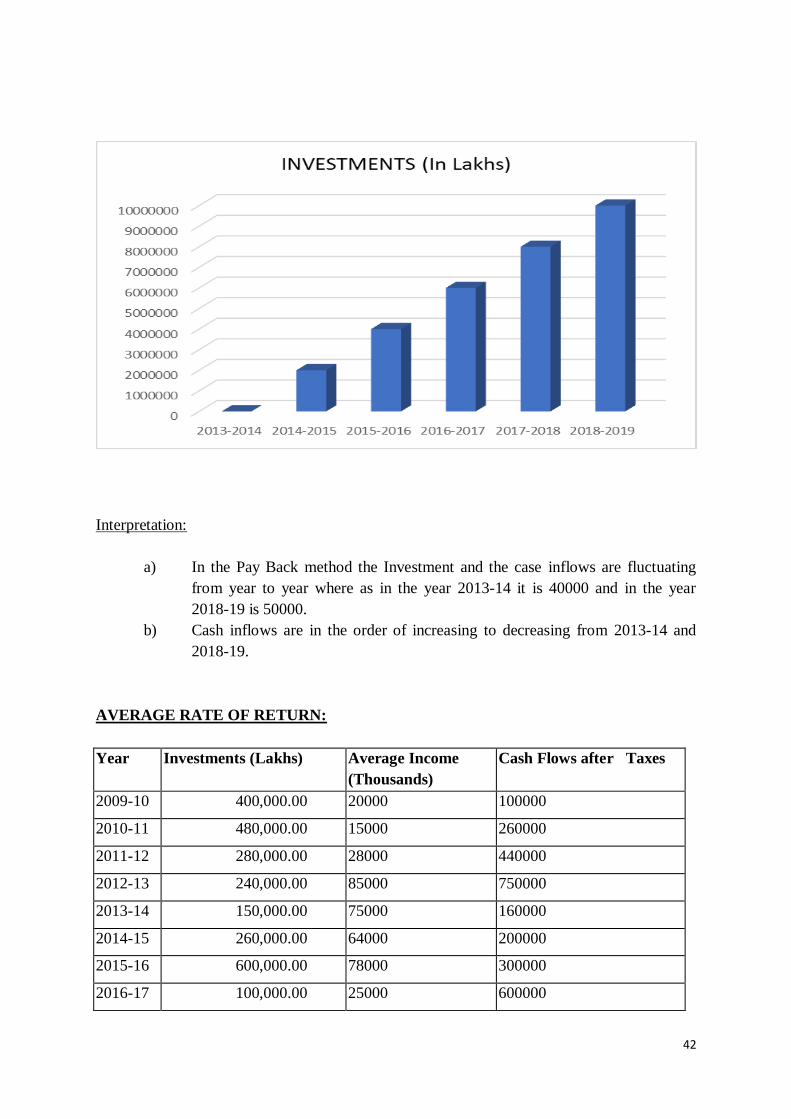

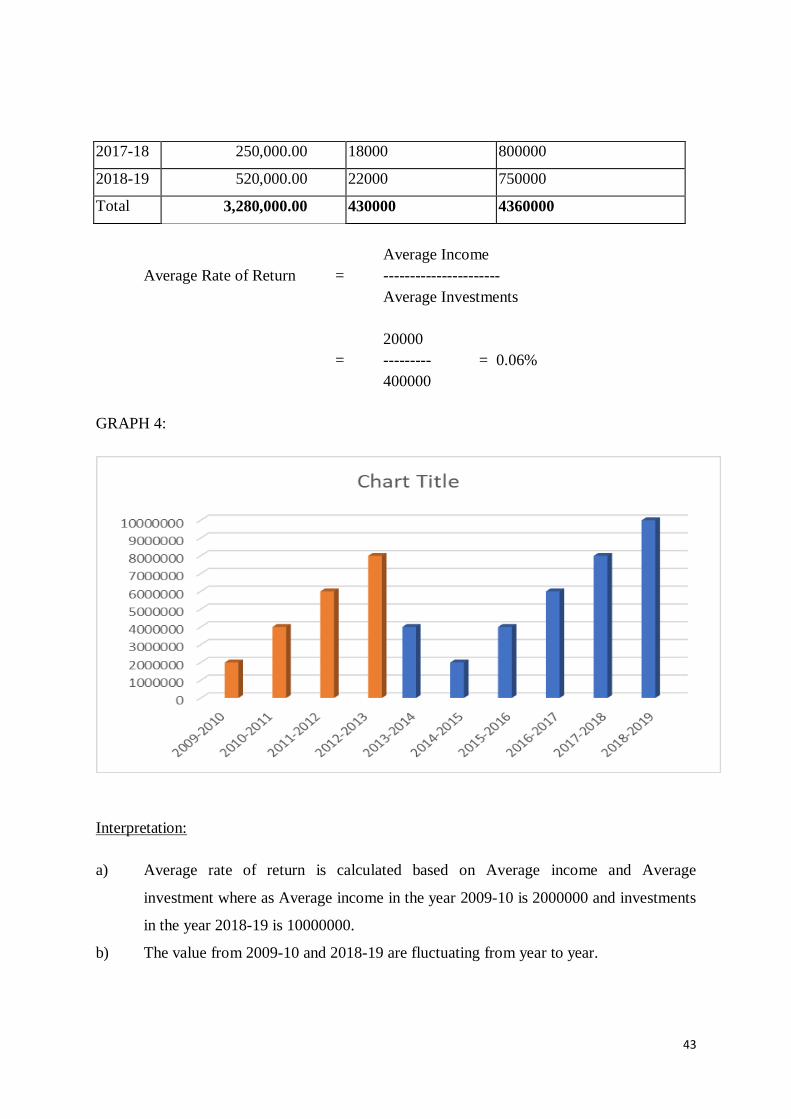

AVERAGE RATE OF RETURN:

Year Investments (Lakhs) Average Income

(Thousands)

Cash Flows after Taxes

2009-10 400,000.00 20000 100000

2010-11 480,000.00 15000 260000

2011-12 280,000.00 28000 440000

2012-13 240,000.00 85000 750000

2013-14 150,000.00 75000 160000

2014-15 260,000.00 64000 200000

2015-16 600,000.00 78000 300000

2016-17 100,000.00 25000 600000

43

2017-18 250,000.00 18000 800000

2018-19 520,000.00 22000 750000

Total 3,280,000.00 430000 4360000

Average Income

Average Rate of Return = ----------------------

Average Investments

20000

= --------- = 0.06%

400000

GRAPH 4:

Interpretation:

a) Average rate of return is calculated based on Average income and Average

investment where as Average income in the year 2009-10 is 2000000 and investments

in the year 2018-19 is 10000000.

b) The value from 2009-10 and 2018-19 are fluctuating from year to year.

44

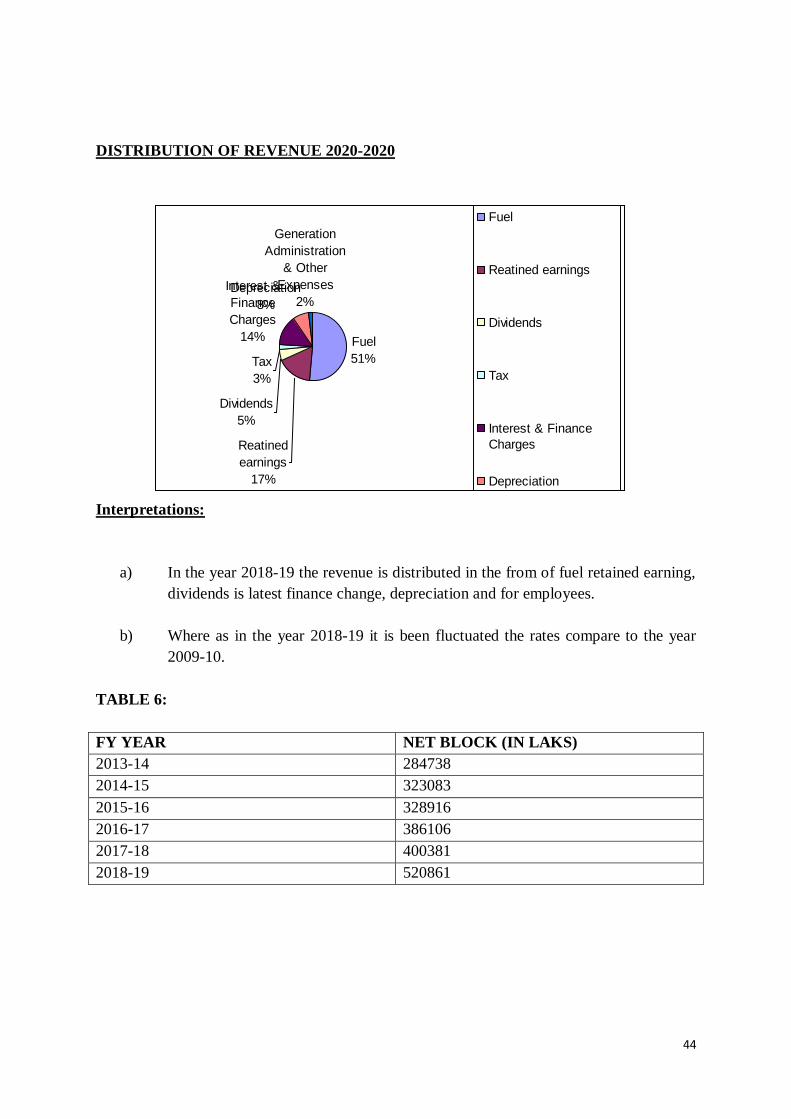

DISTRIBUTION OF REVENUE 2020-2020

Interpretations:

a) In the year 2018-19 the revenue is distributed in the from of fuel retained earning,

dividends is latest finance change, depreciation and for employees.

b) Where as in the year 2018-19 it is been fluctuated the rates compare to the year

2009-10.

TABLE 6:

FY YEAR NET BLOCK (IN LAKS)

2013-14 284738

2014-15 323083

2015-16 328916

2016-17 386106

2017-18 400381

2018-19 520861

Fuel

51%

Reatined

earnings

17%

Dividends

5%

Tax

3%

Interest &

Finance

Charges

14%

Depreciation

8%

Generation

Administration

& Other

Expenses

2%

Fuel

Reatined earnings

Dividends

Tax

Interest & Finance

Charges

Depreciation

Generation

Administration & Other

Expenses

45

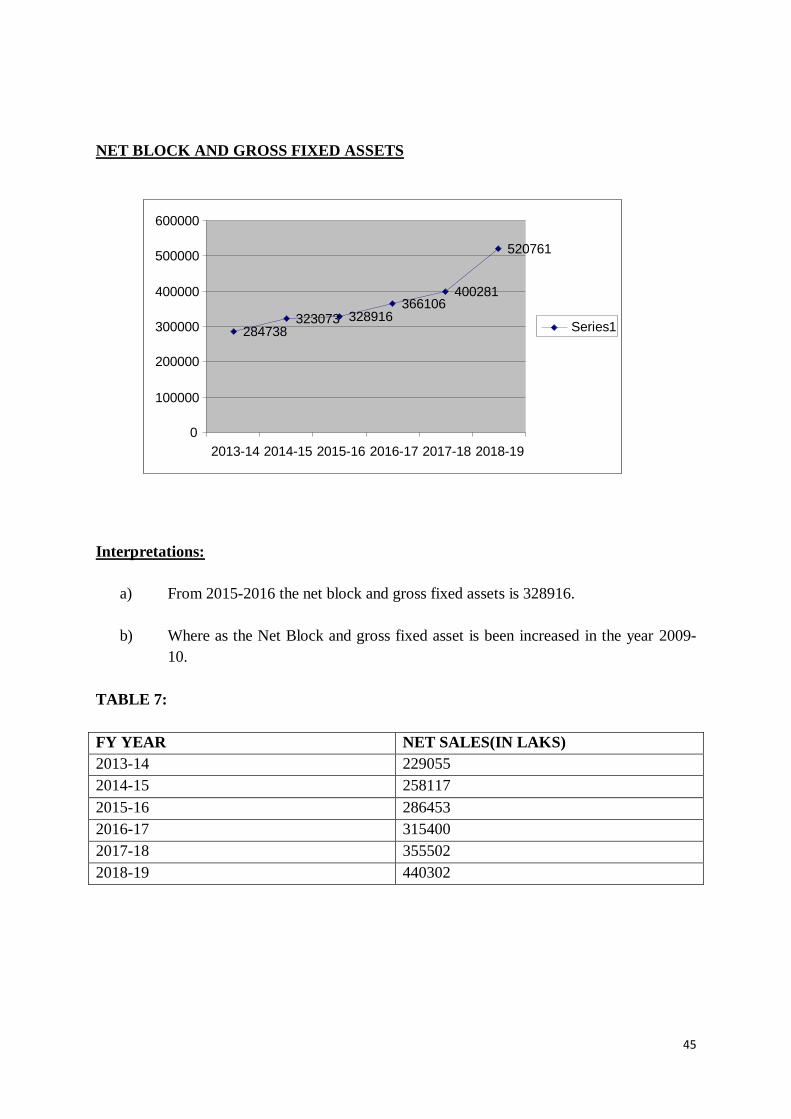

NET BLOCK AND GROSS FIXED ASSETS

Interpretations:

a) From 2015-2016 the net block and gross fixed assets is 328916.

b) Where as the Net Block and gross fixed asset is been increased in the year 2009-

10.

TABLE 7:

FY YEAR NET SALES(IN LAKS)

2013-14 229055

2014-15 258117

2015-16 286453

2016-17 315400

2017-18 355502

2018-19 440302

284738 323073 328916

366106 400281

520761

0

100000

200000

300000

400000

500000

600000

2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

Series1

46

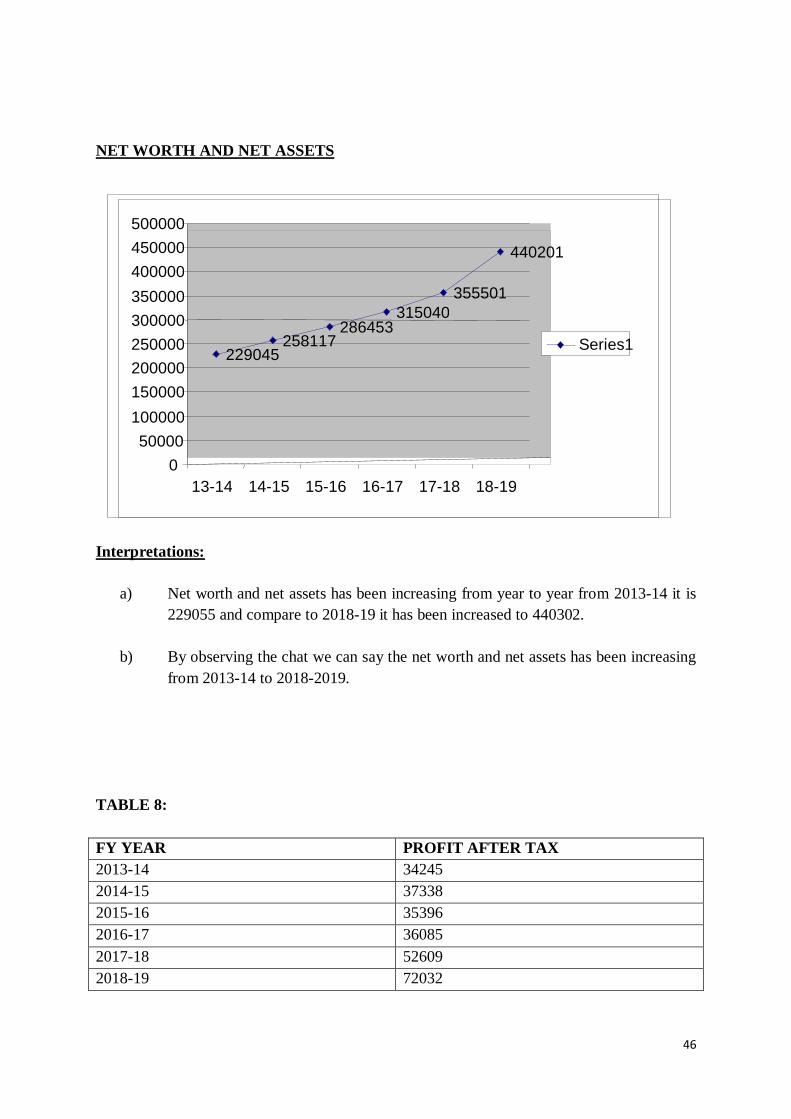

NET WORTH AND NET ASSETS

Interpretations:

a) Net worth and net assets has been increasing from year to year from 2013-14 it is

229055 and compare to 2018-19 it has been increased to 440302.

b) By observing the chat we can say the net worth and net assets has been increasing

from 2013-14 to 2018-2019.

TABLE 8:

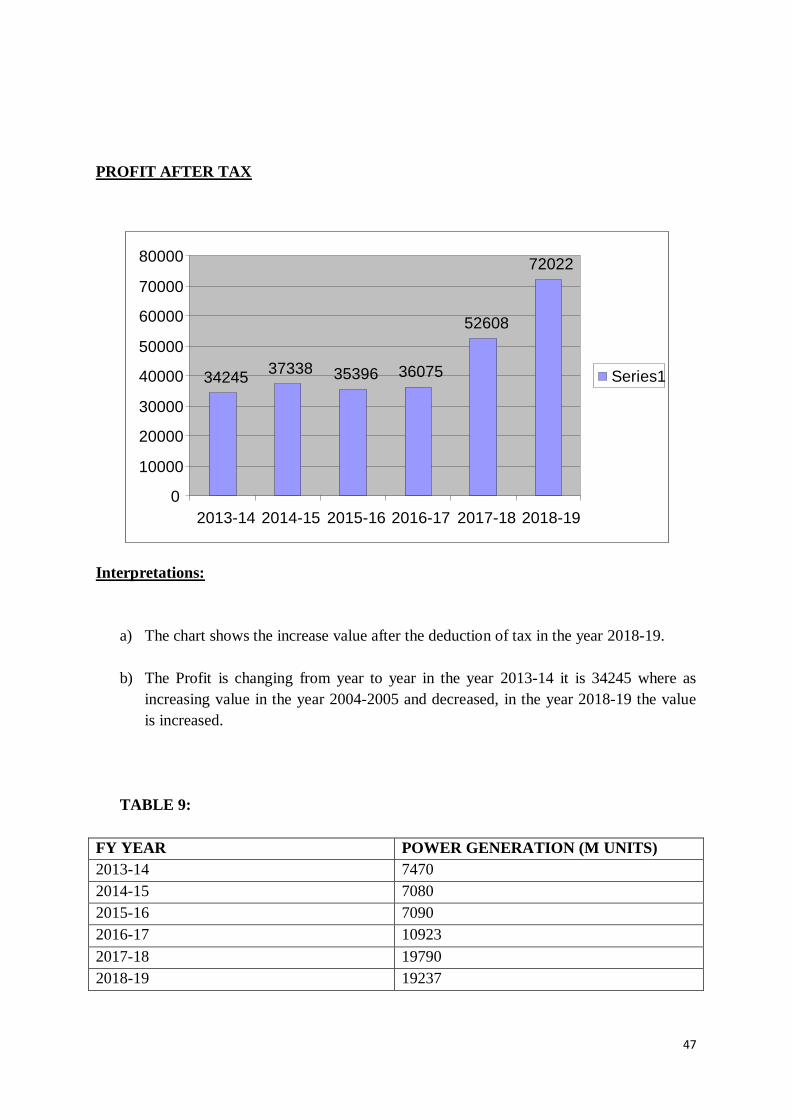

FY YEAR PROFIT AFTER TAX

2013-14 34245

2014-15 37338

2015-16 35396

2016-17 36085

2017-18 52609

2018-19 72032

229045 258117

286453 315040

355501

440201

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

13-14 14-15 15-16 16-17 17-18 18-19

Series1

47

PROFIT AFTER TAX

Interpretations:

a) The chart shows the increase value after the deduction of tax in the year 2018-19.

b) The Profit is changing from year to year in the year 2013-14 it is 34245 where as

increasing value in the year 2004-2005 and decreased, in the year 2018-19 the value

is increased.

TABLE 9:

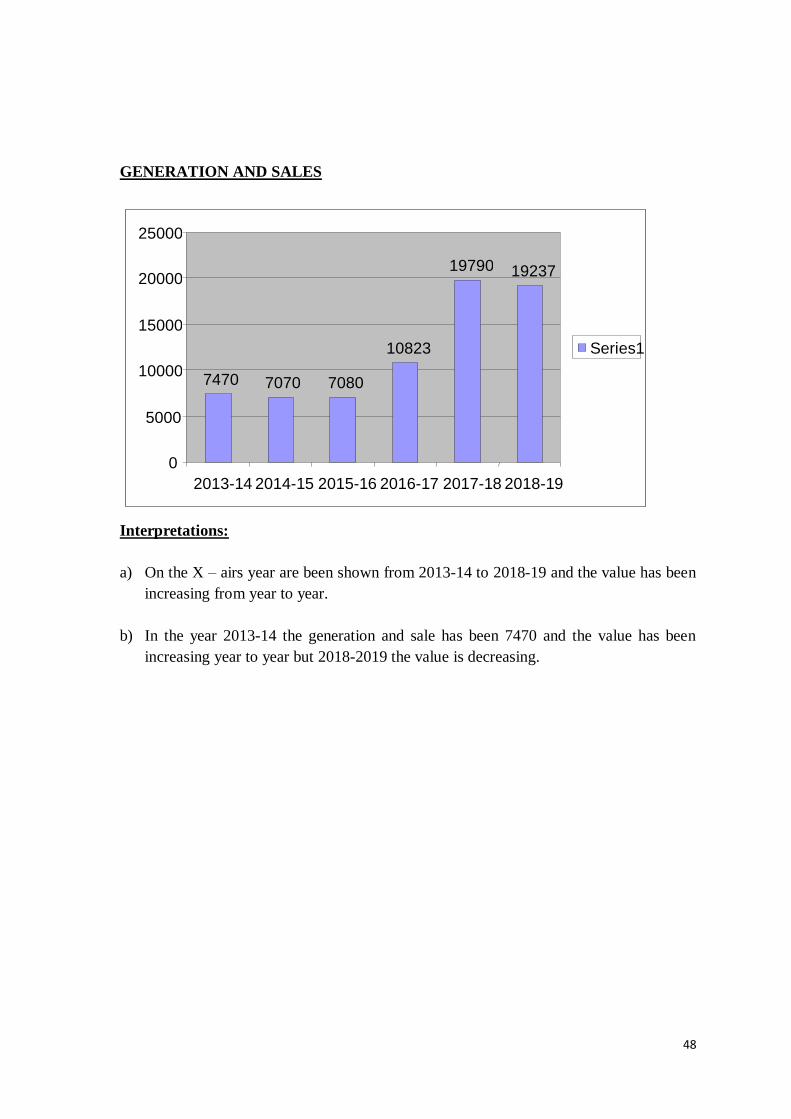

FY YEAR POWER GENERATION (M UNITS)

2013-14 7470

2014-15 7080

2015-16 7090

2016-17 10923

2017-18 19790

2018-19 19237

34245 37338 35396 36075

52608

72022

0

10000

20000

30000

40000

50000

60000

70000

80000

2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

Series1

48

GENERATION AND SALES

Interpretations:

a) On the X – airs year are been shown from 2013-14 to 2018-19 and the value has been

increasing from year to year.

b) In the year 2013-14 the generation and sale has been 7470 and the value has been

increasing year to year but 2018-2019 the value is decreasing.

7470 7070 7080

10823

19790 19237

0

5000

10000

15000

20000

25000

2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

Series1

49

LEARNING EXPERIENCE- FINDINDS, SUGGESTION AND CONCLUSION

An empirical study of the practices of the Capital Budgeting for evaluation of investment

proposals in the corporate sector in India has been made in the preceding chapters.

Comparison, wherever possible, has been made with the practices and procedures in the

foreign countries. It has to be noted that conclusions based upon a study of this type have to

be taken as indicative of broad trends only. However, the results of this study do indicate that

majority of large scale companies in India are aware of the need for a well formulated capital

budgeting decisions. It is proposed to review the important findings of this study and venture

to outline some suggestions and recommendations for the benefit of academicians, industry

as well as for post doctoral research.

An in-depth analysis has been carried out to observe the trend and insight into factors that

influence capital budgeting decisions. The results of the survey and its analysis have been

provided in chapter 5.

The companies in India do have specific amount of average size of annual capital budget and

all project size requires formal quantitative analysis. However, such analysis and use of

capital budgeting method differ on the basis of nature and size of a particular project under

consideration. Surprisingly, the companies under study in India seem to be planning one year

in advance only but here also the period of planning is different for different projects. This

may be due to volatile business environment. The authority to take final capital budgeting

decision rests with the chief finance officer and top management officials of all the

organizations under study.

One of the objectives of this study is to determine the types of capital investments

undertaken and the methods of appraisal used. The responding firms ranked pay back period

as the most important technique followed by internal rate return and net present value. Thus,

pay back period method (59.3%) still continues to be the most favoured technique though it

ignores time value of money and also the cash flow beyond pay back period followed by

IRR. But almost all the company’s are using now multiple techniques for evaluating their

capital budgeting proposals. In this research study, the company’s prefer IRR and NPV with

the PBP method. The investment in the new projects being strategic decisions in nature IRR,

50

PBP and NPV are the most preferred techniques while for expansion, replacement,

modernization, etc. PBP is favoured by the respondents.

Another objective of this study is to analyze the problems faced to estimate the cash flows

associated with each capital investment accurately. The cash flow estimation is considered as

the most difficult task in capital budgeting decisions. This can be understood from the

responses of the respondents of the present study. Many respondents have replied that items

like expenses incurred on R&D, market survey, test marketing, interest on borrowings,

depreciation, income taxes etc. have been included in the cash flows which requires to be

excluded actually. In fact, many of them might have been intending to convey that they

include it in the project cost. Even the firms are using different inflation adjustment methods

for their investment appraisal.

One of the objectives of this research is to analyze how ‘Risk’ and ‘Uncertainty’ in the future

estimates in investment projects is being taken care of. Sensitivity analysis is considered as

the most important technique while scenario analysis is considered as the second important

technique for assessing risk. The other more sophisticated techniques like Decision tree,

Monte Carlo simulation, Certainty equivalent, Probability analysis, Beta analysis has got

very low ratings that means these techniques are rarely used in practice by firms in India.

The researcher wanted to assess suitability of Discounted Cash Flow (DCF) Techniques in

India and the preferences between Net Present Value (NPV) and Internal Rate of Return

(IRR) methods. All the companies responded to my study are using DCF techniques either

IRR or NPV or both which indicates that now these techniques are very well accepted and

used by finance officials of the organizations. With reference to this Porwal (1976) in his

study has mentioned, “As long term planning under the present conditions is not quite

possible in India, the use of DCF methods do not seem to be efficacious. However, it needs

to be mentioned that as conditions improve, it would be desirable for Indian companies to

apply ‘theoretically correct’ techniques in a larger measure.” Prasanna Chandra (1975) in his

study conducted on 20 companies made the following observations. “The most commonly

used method for evaluating the investments of small size is payback period method….For

investments of large size, the average rate of return is commonly used as the principle

criterion and the payback period is used as a supplementary criterion. DCF techniques,

51

though not commonly used, are gaining importance, particularly in the evaluation of large

investments.” It appears that now though the government restrictions are minimized on

business but firms are always working under highly volatile environment. Still no

respondents in my study is using only pay back period method at the same time no

organizations are using single technique for evaluating capital budgeting proposals. Though

Pay back period is still a popular technique, it is always used with some other DCF

techniques which are in most of the cases IRR or NPV. The suitability of DCF techniques

even depends on how professional the organization is. But all the respondents in my study

appreciate and use the suitability of these techniques. In capital budgeting literature, two

widely discussed methods for appraisal of capital investments are the NPV and IRR methods.

There is good amount of controversy exist regarding the superiority of one method over the

other. Many authors argue that the NPV method leads to correct decision (Bierman and

Smidt S, 1980). On the other hand Merret A J and Sykes A (1966) prefer the yield method.

In some situations the NPV and yield methods give contradictory results. Babu C P (1984)