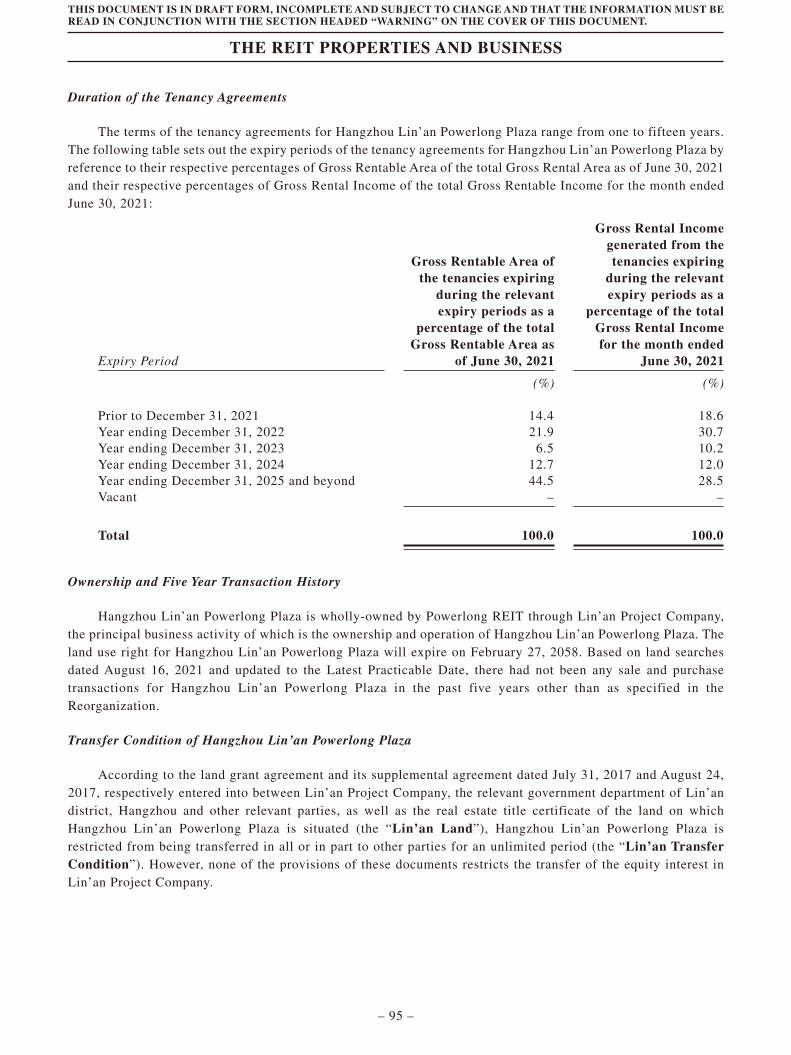

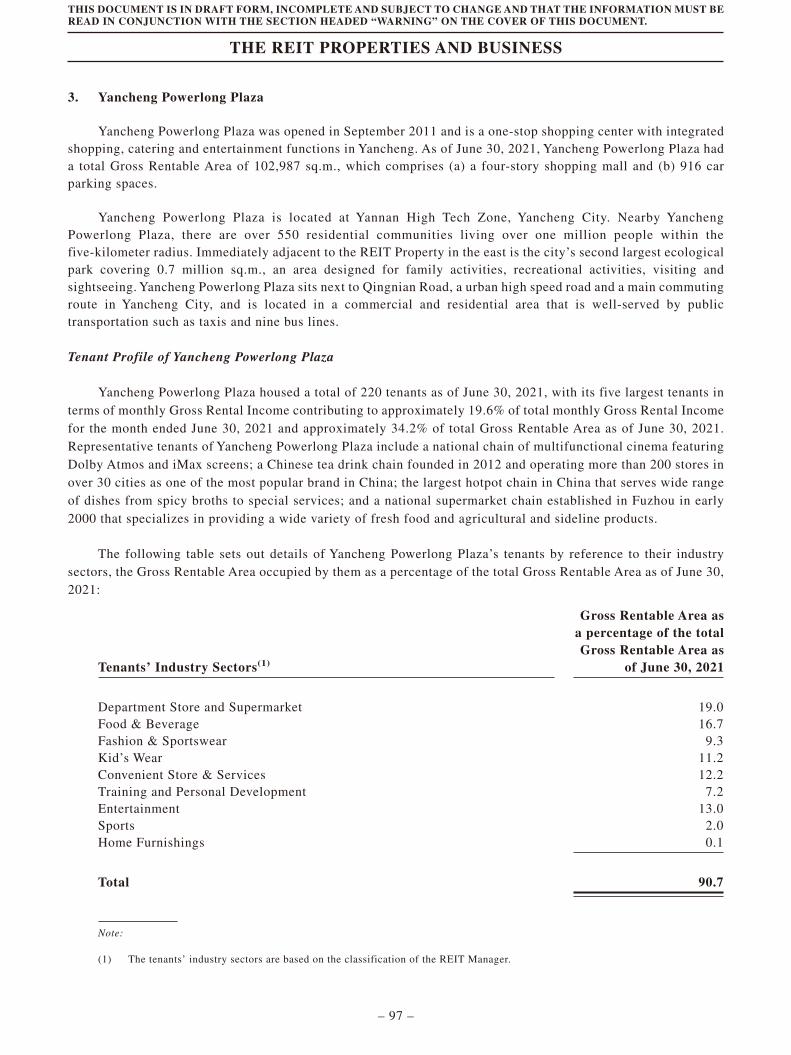

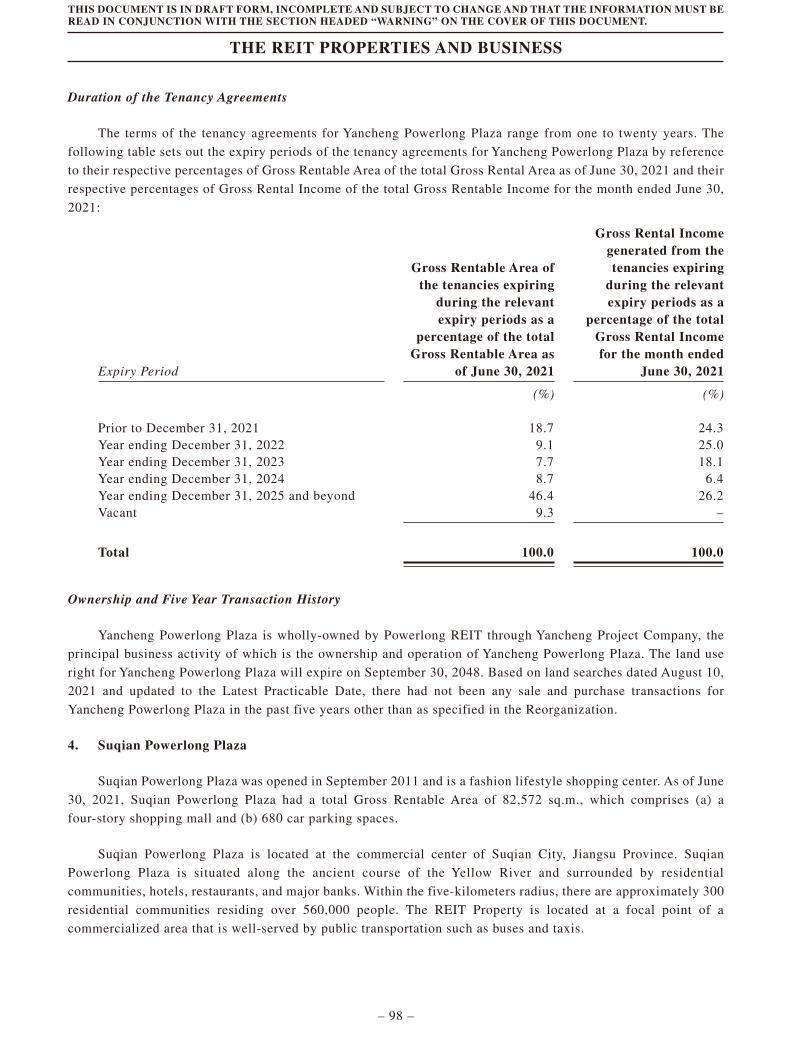

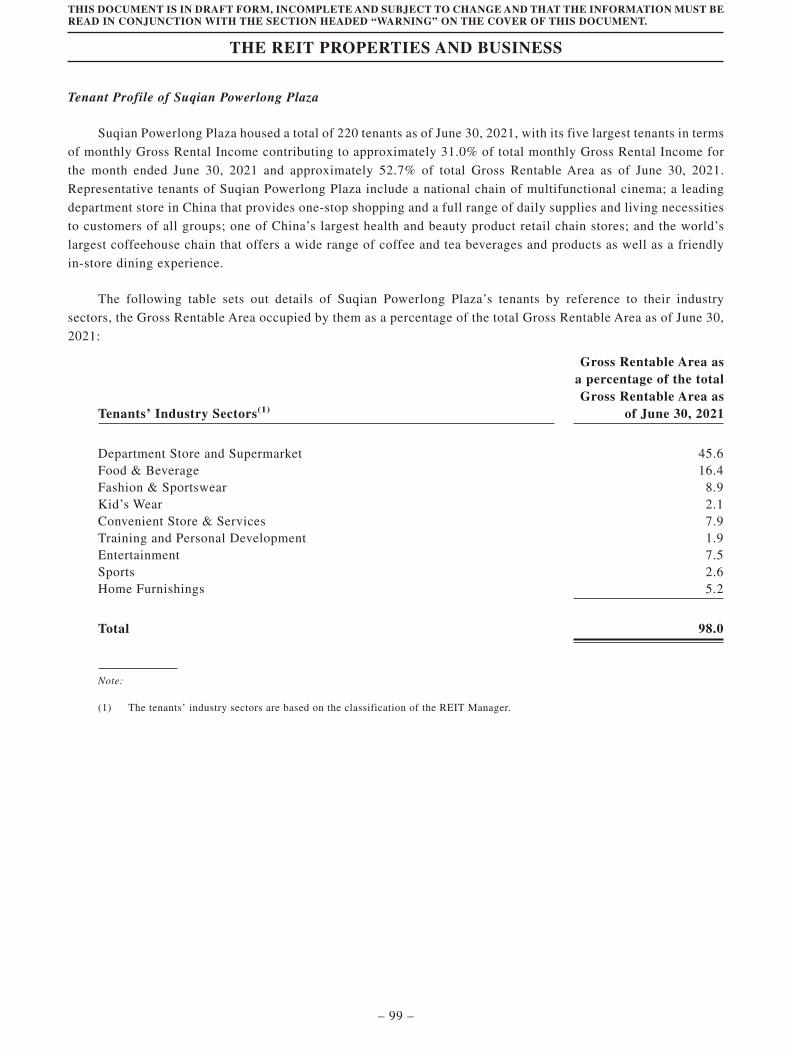

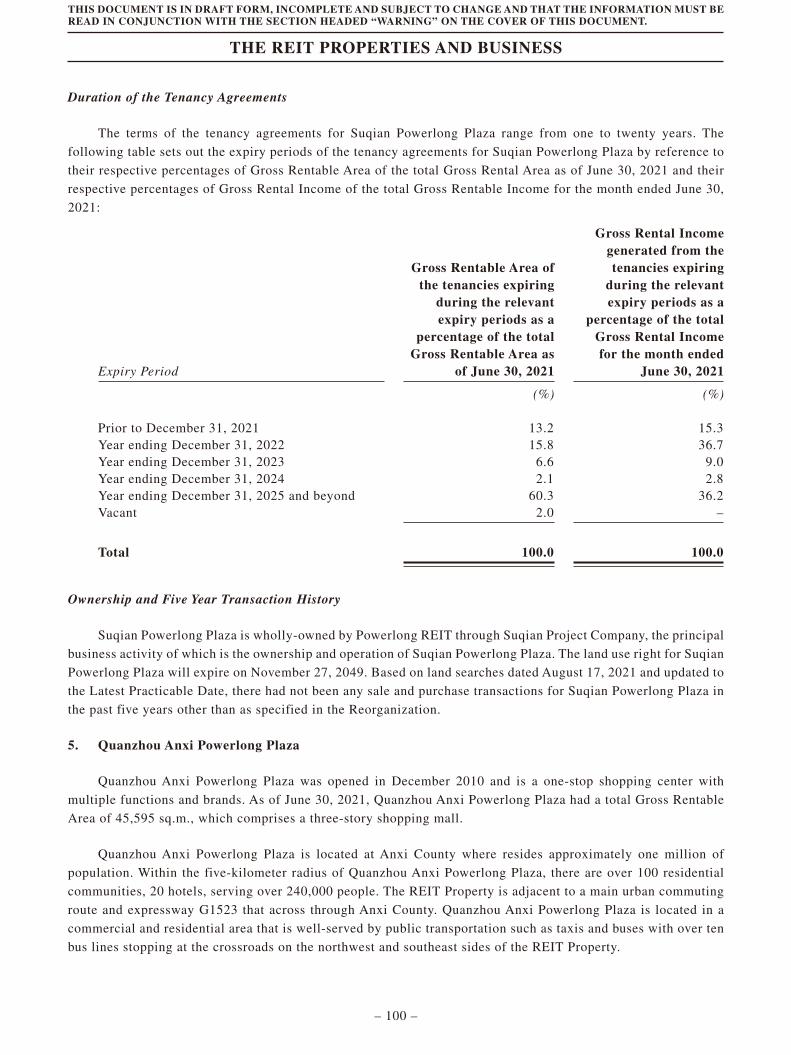

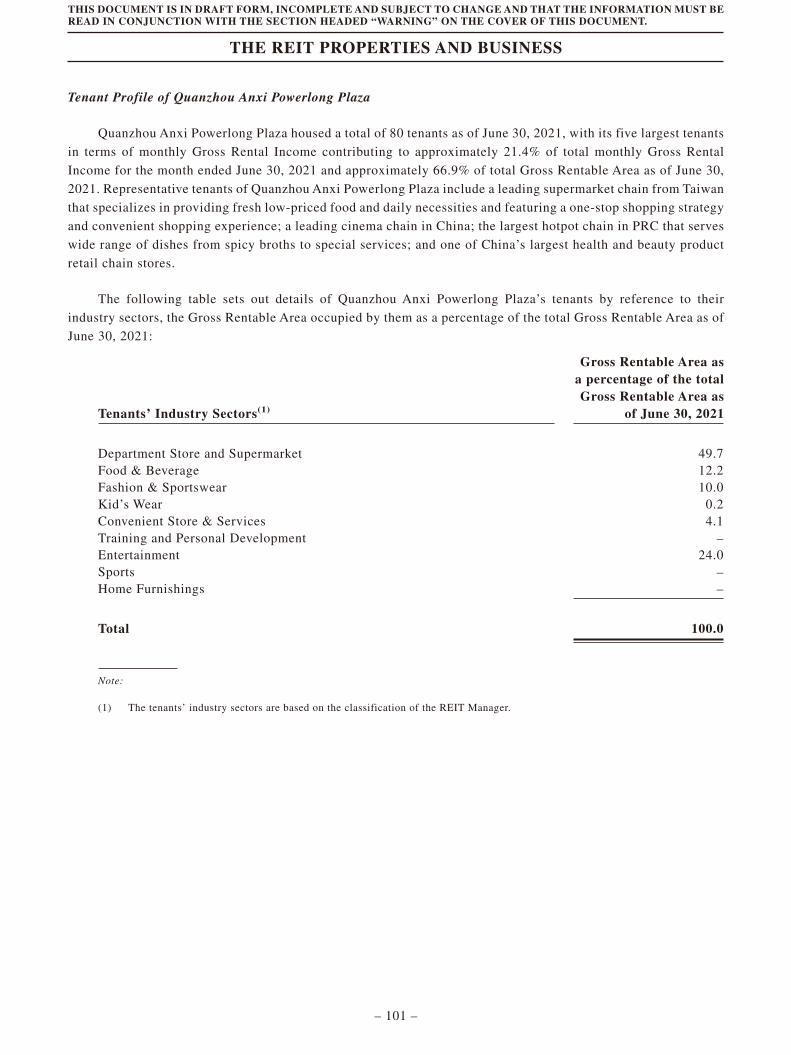

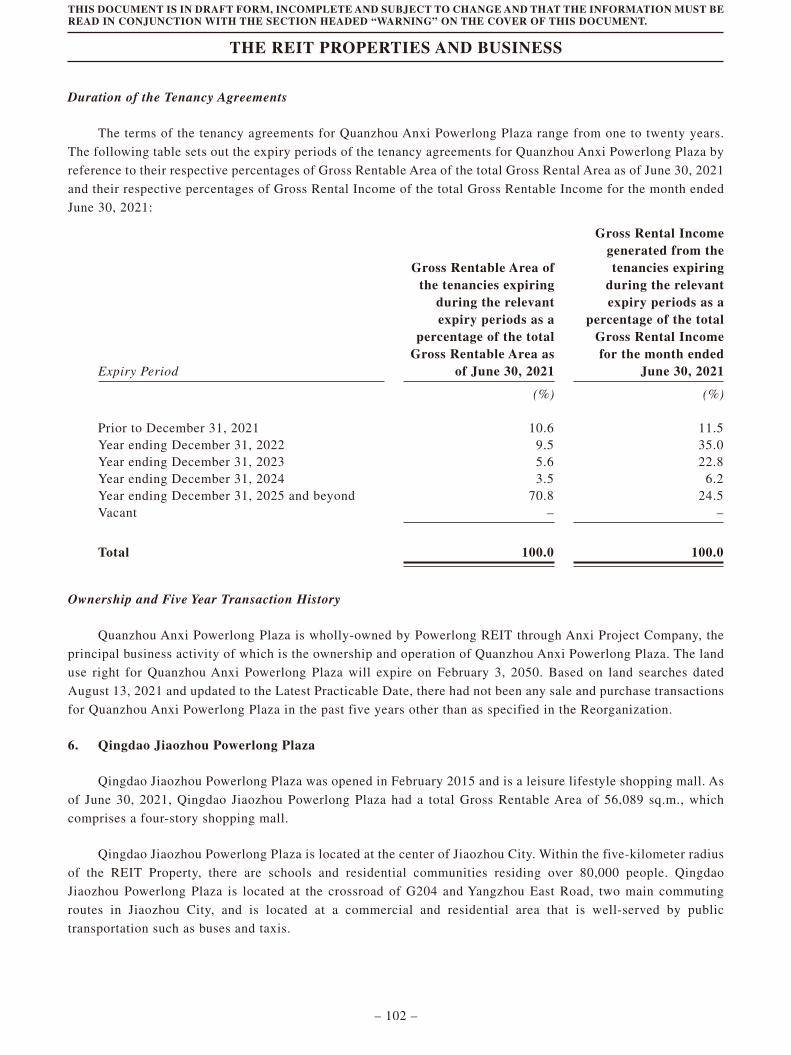

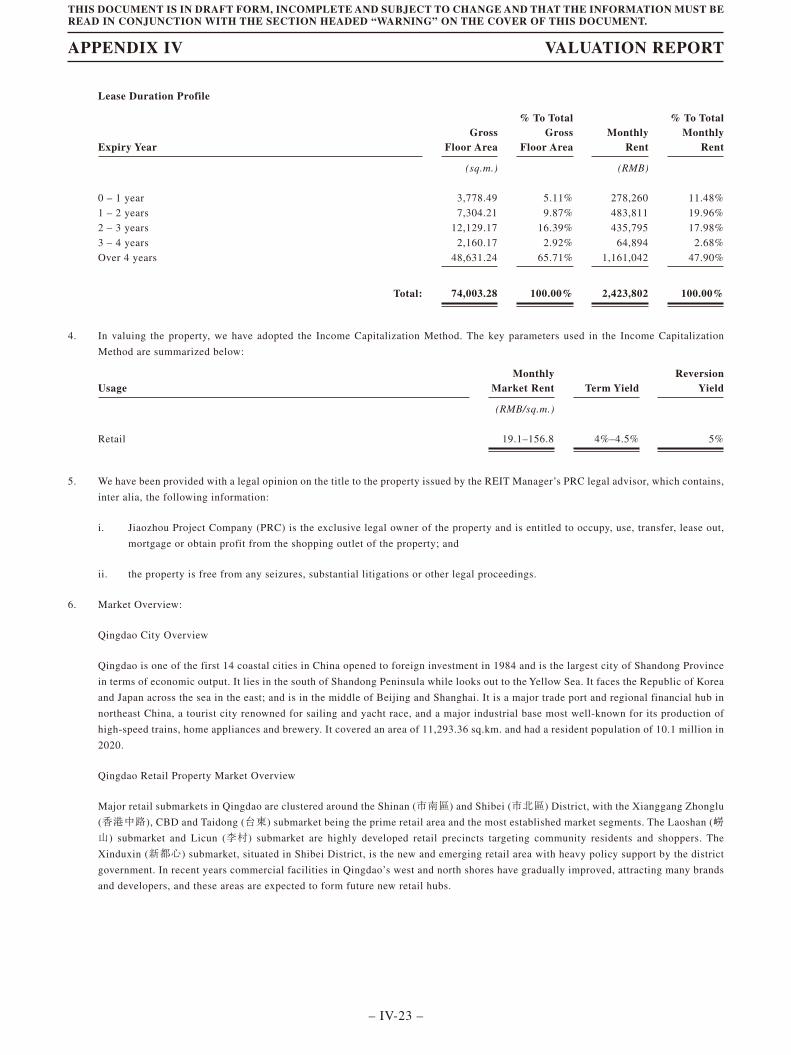

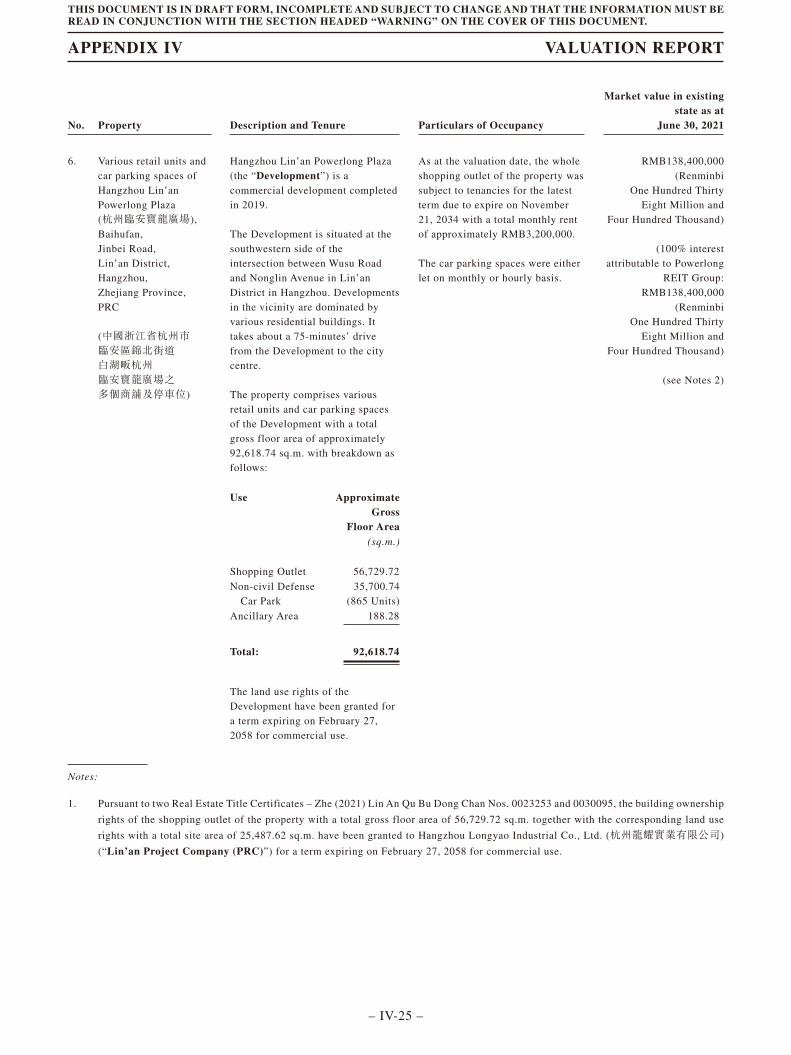

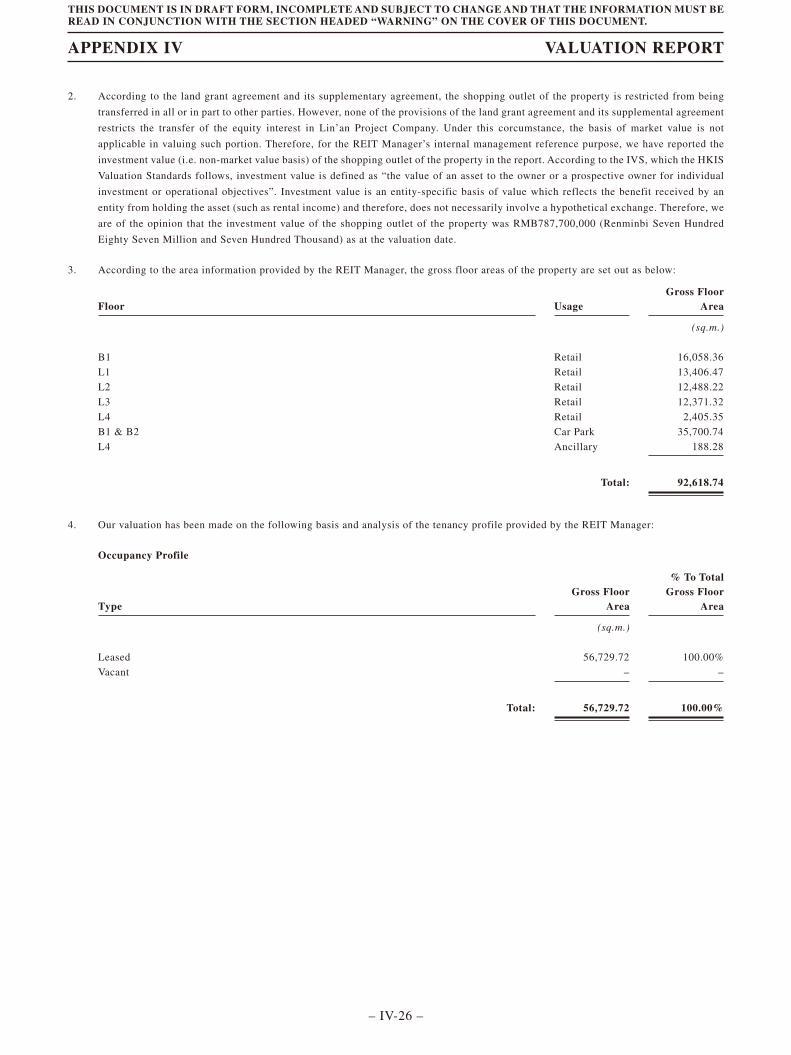

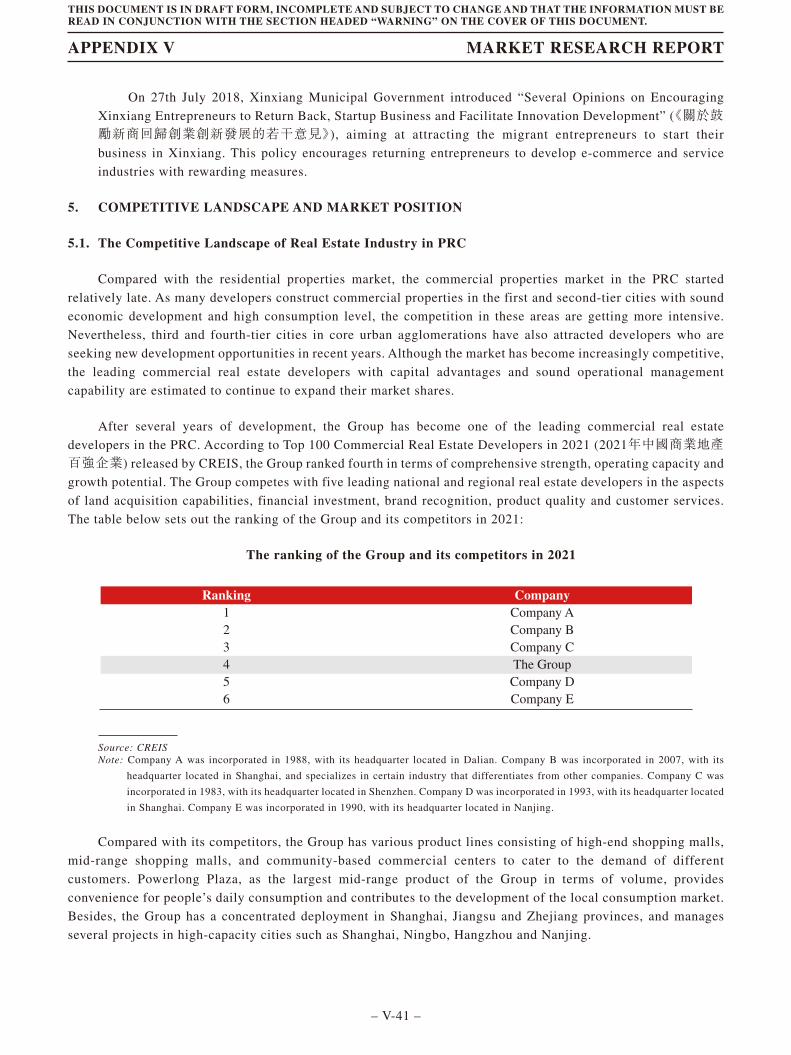

Embed Size (px)

Citation preview

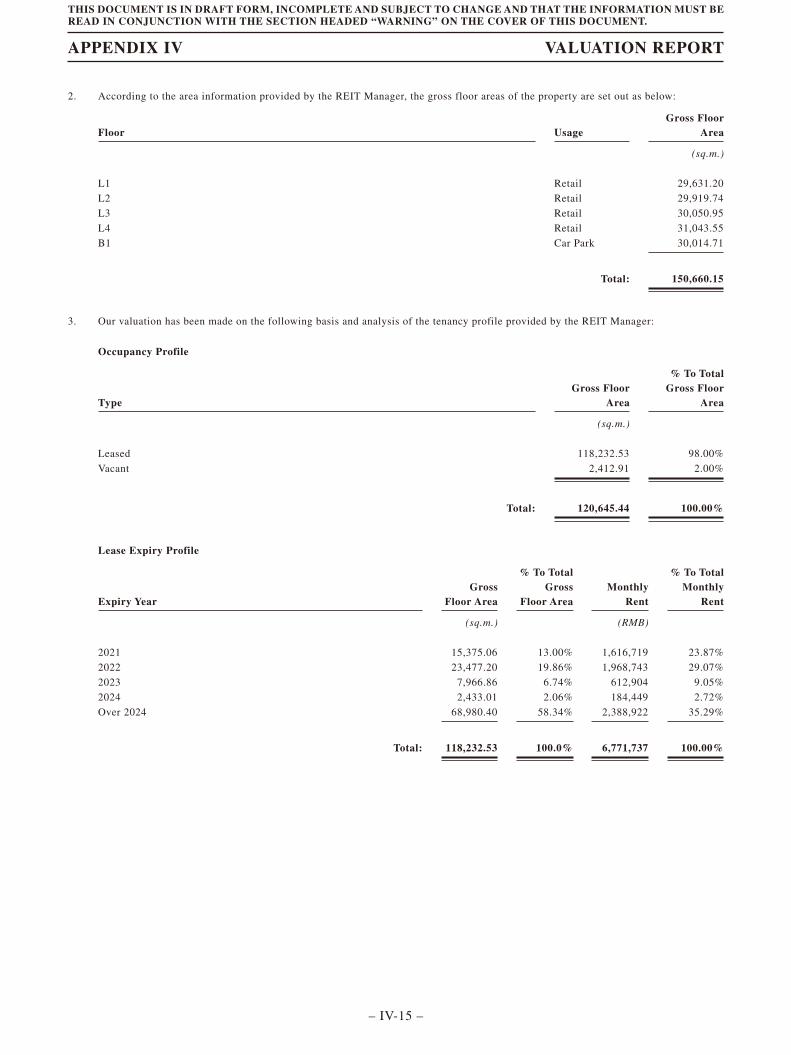

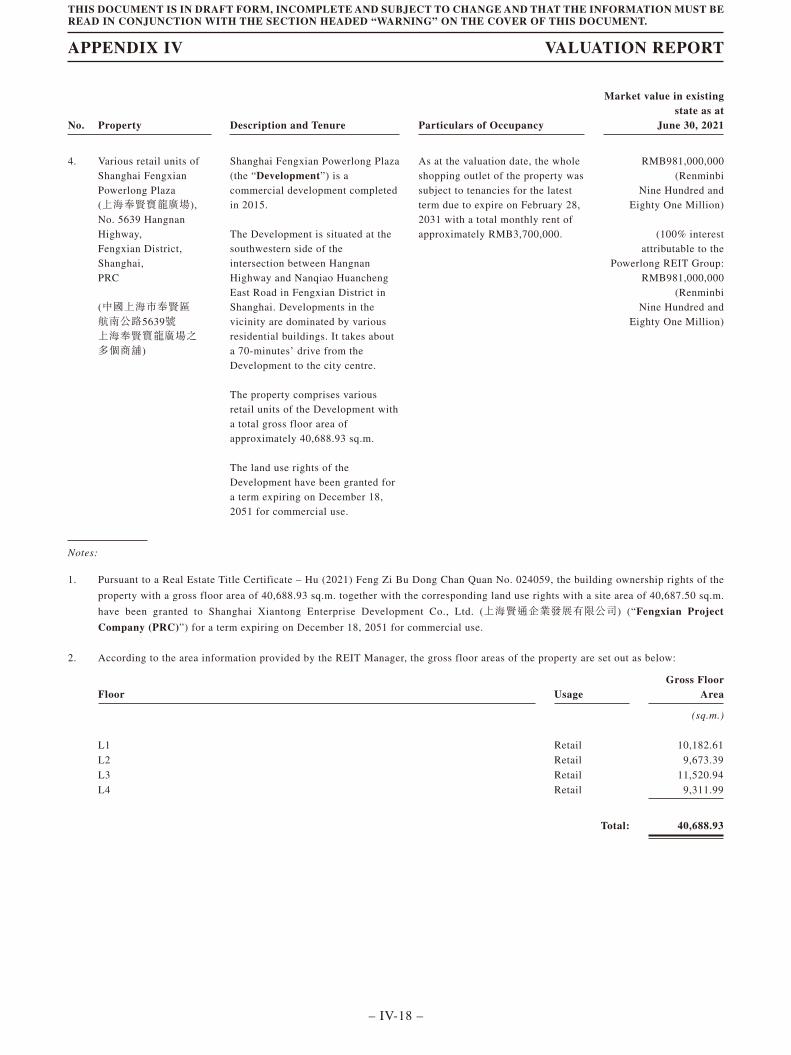

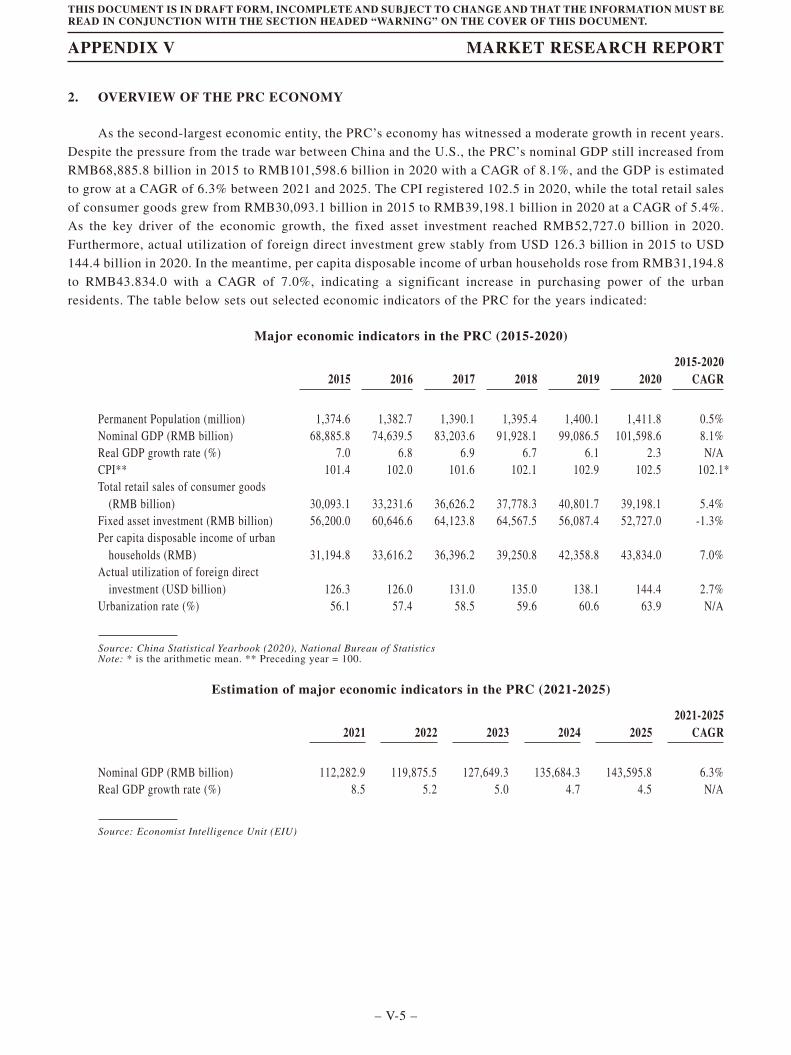

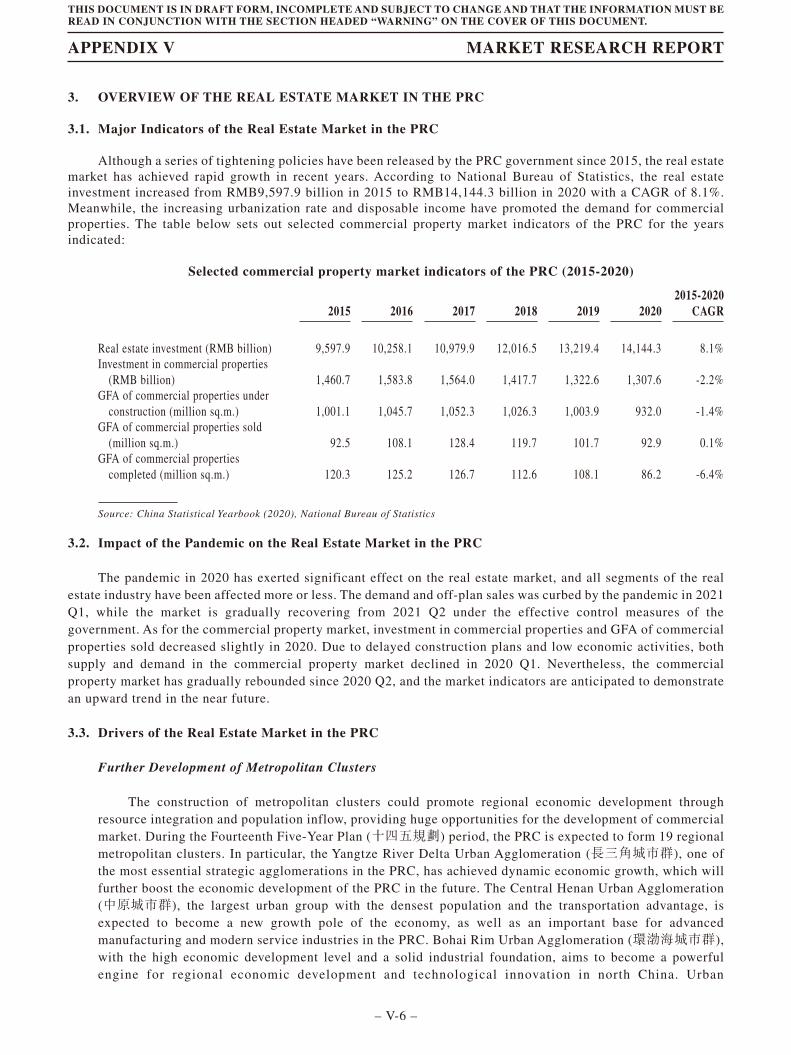

The Stock Exchange of Hong Kong Limited and the Securities and Futures Commission take no responsibility for the contents of thisApplication Proof, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever forany loss howsoever arising from or in reliance upon the whole or any part of the contents of this Application Proof.

Powerlong Commercial Real Estate Investment Trust寶龍商業房地產投資信託基金

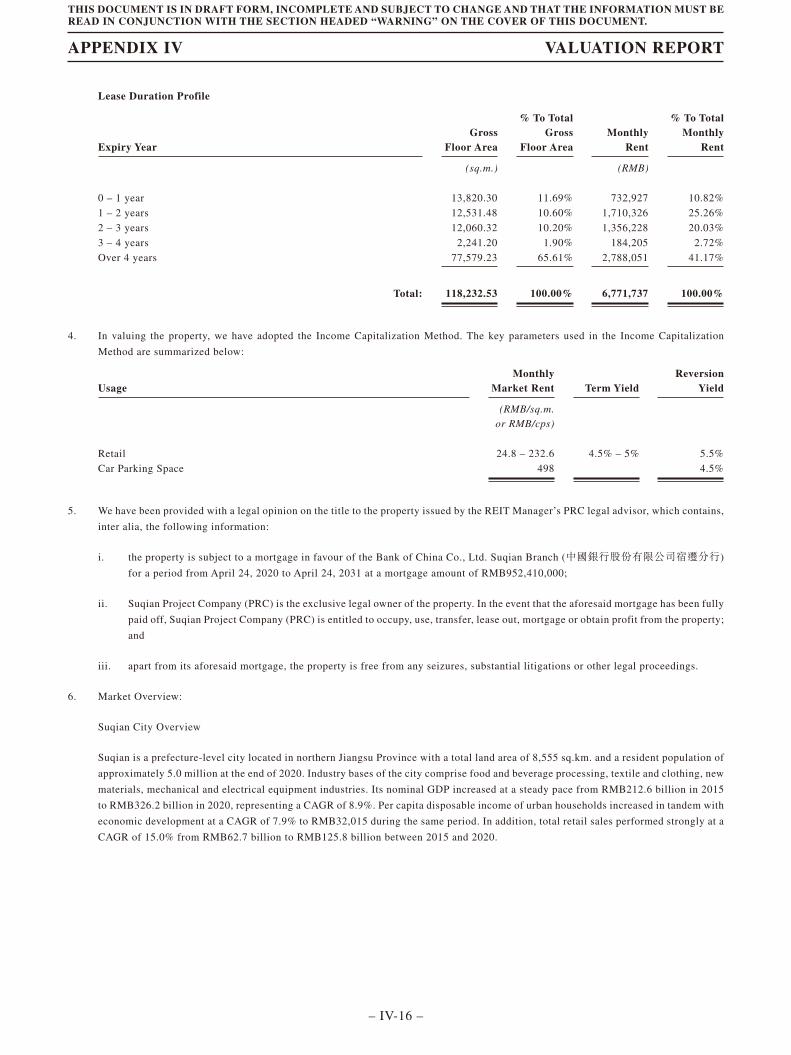

(a Hong Kong collective investment scheme authorized under section 104 of the Securities and Futures Ordinance(Chapter 571 of the Laws of Hong Kong))

WARNINGThe publication of this Application Proof is required by The Stock Exchange of Hong Kong Limited (the “Stock Exchange”) andthe Securities and Futures Commission (the “Commission”) solely for the purpose of providing information to the public in HongKong.

This Application Proof is in draft form. The information contained in it is incomplete and is subject to change which can bematerial. By viewing this document, you acknowledge, accept and agree with Powerlong Commercial Real Estate Investment Trust(the “Scheme”), Powerlong REIT Management Limited (in its capacity as manager of the Scheme) (the “REIT Manager”), DBTrustees (Hong Kong) Limited (in its capacity as trustee of the Scheme) (the “Trustee”), the Scheme’s joint listing agents, advisersand members of the underwriting syndicate that:

(a) this document is only for the purpose of providing information about the Scheme to the public in Hong Kong and not for anyother purposes. No investment decision should be based on the information contained in this document;

(b) the publication of this document or any supplemental, revised or replacement pages on the Stock Exchange’s website doesnot give rise to any obligation of the Scheme, the REIT Manager, the Trustee, the Scheme’s joint listing agents, advisers ormembers of the underwriting syndicate to proceed with an offering in Hong Kong or any other jurisdiction. There is noassurance that the Scheme will proceed with any offering;

(c) the contents of this document or supplemental, revised or replacement pages may or may not be replicated in full or in part inthe actual final listing document;

(d) this document is not the final listing document and may be updated or revised by the Scheme from time to time in accordancewith the Rules Governing the Listing of Securities on the Stock Exchange and the Securities and Futures Ordinance (Chapter571 of the Laws of Hong Kong);

(e) this document does not constitute a prospectus, offering circular, notice, circular, brochure or advertisement offering to sellany securities to the public in any jurisdiction, nor is it an invitation to the public to make offers to subscribe for or purchaseany securities, nor is it calculated to invite offers by the public to subscribe for or purchase any securities;

(f) this document must not be regarded as an inducement to subscribe for or purchase any securities, and no such inducement isintended;

(g) neither the Scheme nor any of its affiliates, the REIT Manager, the Trustee, the Scheme’s joint listing agents, advisers ormembers of its underwriting syndicate is offering, or is soliciting offers to buy, any securities in any jurisdiction through thepublication of this document;

(h) no application for the securities mentioned in this document should be made by any person nor would such application beaccepted;

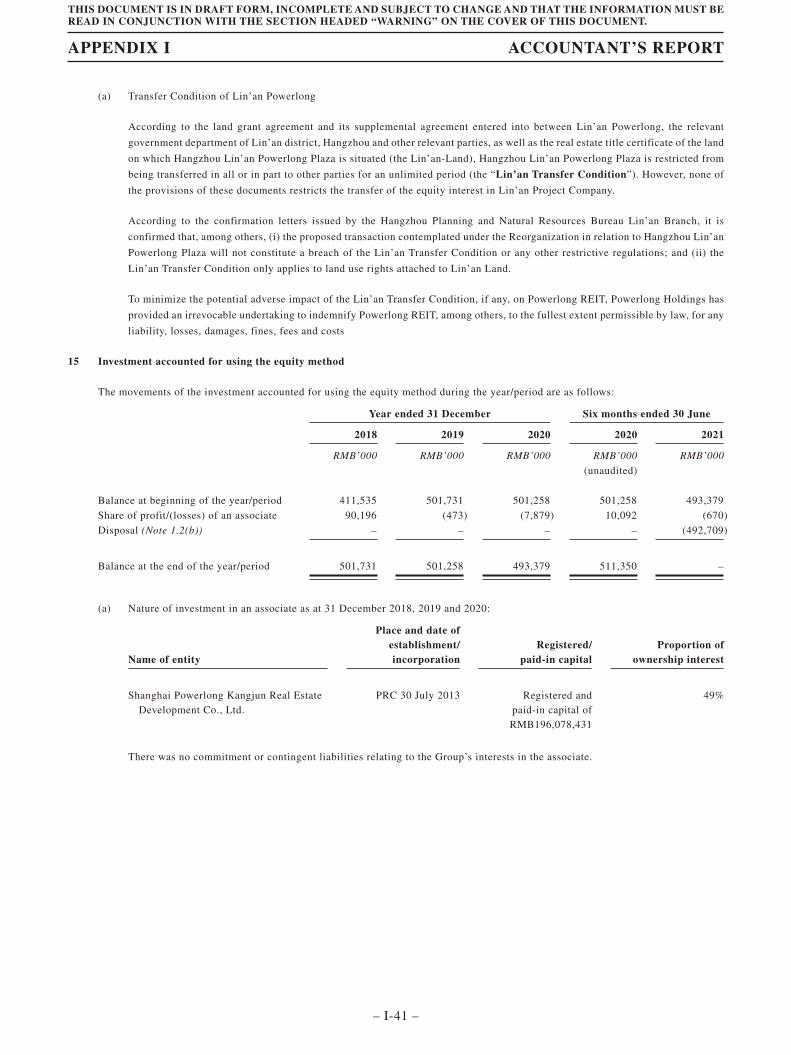

(i) the Scheme has not and will not register the securities referred to in this document under the U.S. Securities Act of 1933, asamended, or any state securities laws of the United States;

(j) as there may be legal restrictions on the distribution of this document or dissemination of any information contained in thisdocument, you agree to inform yourself about and observe any such restrictions applicable to you; and

(k) the application to which this document relates has not been approved or authorised for listing and the Stock Exchange and theCommission may accept, return or reject the application for the subject public offering and/or listing.

THIS APPLICATION PROOF IS NOT FOR PUBLICATION OR DISTRIBUTION TO PERSONS IN THE UNITEDSTATES. ANY SECURITIES REFERRED TO HEREIN HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDERTHE U.S. SECURITIES ACT OF 1933, AND MAY NOT BE OFFERED OR SOLD IN THE UNITED STATES WITHOUTREGISTRATION THEREUNDER OR PURSUANT TO AN AVAILABLE EXEMPTION THEREFROM. NO PUBLICOFFERING OF THE SECURITIES WILL BE MADE IN THE UNITED STATES.

NEITHER THIS APPLICATION PROOF NOR ANY INFORMATION CONTAINED HEREIN CONSTITUTES AN OFFERTO SELL OR THE SOLICITATION OF AN OFFER TO BUY ANY SECURITIES IN THE UNITED STATES OR IN ANYOTHER JURISDICTIONS WHERE SUCH AN OFFER OR SALE IS NOT PERMITTED. THIS APPLICATION PROOF ISNOT BEING MADE AND MAY NOT BE DISTRIBUTED OR SENT INTO ANY JURISDICTION WHERE SUCHDISTRIBUTION OR DELIVERY IS NOT PERMITTED.

If an offer or an invitation is made to the public in Hong Kong in due course, prospective investors are reminded to make theirinvestment decisions solely based on the final listing document issued by the Scheme, copies of which will be distributed to thepublic during the offer period.

IMPORTANT: If you are in any doubt about the contents of this Document, you should seek independent professional financial advice.

Powerlong Commercial Real Estate Investment Trust寶龍商業房地產投資信託基金

(a Hong Kong collective investment scheme authorized under section 104 of the Securities and Futures Ordinance(Chapter 571 of the Laws of Hong Kong))

Managed by

Powerlong REIT Management Limited

[REDACTED]

Number of [REDACTED] underthe [REDACTED]

: [REDACTED] (subject to the [REDACTED])

Number of [REDACTED] underthe [REDACTED]

: [REDACTED] (subject to reallocation)

Number of [REDACTED] underthe [REDACTED]

: [REDACTED] (including [REDACTED] [REDACTED]under the [REDACTED]) (subject to reallocation andthe [REDACTED])

[REDACTED] : HK$[REDACTED] per [REDACTED], plus brokerageof 1.0%, Stock Exchange trading fee of 0.005% andSFC transaction levy of 0.0027% (payable in full onapplication in Hong Kong dollars and subject torefund)

[REDACTED] : [●]

Joint Listing Agents

[REDACTED], [REDACTED] and [REDACTED]

The Securities and Futures Commission of Hong Kong, Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong KongSecurities Clearing Company Limited take no responsibility for the contents of this Document, make no representation as to its accuracy or completeness andexpressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this Document.

The [REDACTED] is expected to be determined by agreement between the [REDACTED] (for themselves and on behalf of the [REDACTED]) and the REITManager on the [REDACTED]. The [REDACTED] is expected to be on or about [REDACTED], and in any event, not later than [REDACTED]. The[REDACTED] will be no more than HK$[REDACTED] and is currently expected to be no less than HK$[REDACTED].

The [REDACTED] (for themselves and on behalf of the [REDACTED]), with the consent of the REIT Manager, may reduce the number of Units being[REDACTED] under the [REDACTED] and/or the indicative [REDACTED] below that stated in this Document (which is HK$[REDACTED] toHK$[REDACTED] per [REDACTED]) at any time on or prior to the morning of the last day for lodging applications under the [REDACTED]. In such a case, anannouncement will be published and on the websites of the Stock Exchange at www.hkexnews.hk and Powerlong REIT at www.powerlongreit.com not later thanthe morning of the last day for lodging applications under the [REDACTED]. Before submitting applications for the [REDACTED], applicants under the[REDACTED] should note that applications cannot be withdrawn once submitted. However, if the number of Units being [REDACTED] under the [REDACTED]and/or the [REDACTED] range is reduced, applicants under the [REDACTED] will be entitled to withdraw their applications unless positive confirmations fromthe applicants to proceed with their applications are received. Further details are set forth in the sections headed “Structure of the [REDACTED]” and “How toApply for [REDACTED]” in this Document.

The [REDACTED] have not been and will not be registered under the U.S. Securities Act or any state securities law in the United States. The [REDACTED] arebeing offered and sold only outside the United States in offshore transactions in accordance with Regulation S under the U.S. Securities Act.

Prior to making an investment decision, prospective investors should consider carefully all of the information set out in this Document, including the risk factorsset out in the section headed “Risk Factors” in this Document. The obligations of the [REDACTED] under the [REDACTED] to subscribe for, and to procureapplications for the subscription of, the [REDACTED], are subject to termination by the [REDACTED] (for themselves and on behalf of the [REDACTED]) ifcertain grounds arise prior to 8: 00 a.m. on the [REDACTED]. Such grounds are set out in the section headed “[REDACTED]” in this Document. It is importantthat you refer to that section for further details.

[REDACTED]

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

IMPORTANT

[REDACTED]

[REDACTED]

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

IMPORTANT

[REDACTED]

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

IMPORTANT

[REDACTED]

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

IMPORTANT

[REDACTED]

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

EXPECTED TIMETABLE

– i –

[REDACTED]

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

EXPECTED TIMETABLE

– ii –

[REDACTED]

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

EXPECTED TIMETABLE

– iii –

This Document is issued by Powerlong Commercial Real Estate Investment Trust solely in connectionwith the [REDACTED] and the [REDACTED] and does not constitute an offer to sell or a solicitation of anoffer to buy any securities other than the [REDACTED] and the [REDACTED] offered by this Documentpursuant to the [REDACTED] and the [REDACTED]. This Document may not be used for the purpose of, anddoes not constitute, an offer or invitation in any other jurisdiction or in any other circumstances. No actionhas been taken to permit a [REDACTED] of the [REDACTED] or the distribution of this Document in anyjurisdiction other than Hong Kong (save for the [REDACTED] made to the Qualifying PowerlongShareholders). The distribution of this Document and the [REDACTED] of the [REDACTED] in otherjurisdictions are subject to restrictions and may not be made except as permitted under the applicablesecurities laws of such jurisdictions pursuant to registration with or authorization by the relevant securitiesregulatory authorities or an exemption therefrom. You should rely only on the information contained in thisDocument and the [REDACTED] to make your investment decision. Powerlong REIT has not authorizedanyone to provide you with information that is different from what is contained in this Document. Anyinformation or representation not made in this Document must not be relied on as having been authorized byPowerlong REIT, the Joint Listing Agents, [REDACTED], [REDACTED], [REDACTED], [REDACTED],any of their respective directors, officers, representatives, employees, agents or professional advisors or anyother person or party involved in the [REDACTED] and the [REDACTED].

Page

EXPECTED TIMETABLE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i

CONTENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iv

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

DEFINITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

TECHNICAL TERMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

THE [REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

INFORMATION ABOUT THIS DOCUMENT AND THE [REDACTED] . . . . . . . . . . . . . . . . . . . . . 40

PARTIES INVOLVED IN THE [REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

USE OF [REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

OWNERSHIP OF AND INTEREST IN UNITS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

DISTRIBUTION POLICY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

KEY INVESTMENT HIGHLIGHTS OF POWERLONG REIT . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

STRATEGY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

THE REIT PROPERTIES AND BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

SELECTED FINANCIAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

CONTENTS

– iv –

Page

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUTURE OPERATIONS . . . . . . . . . . . . . . 136

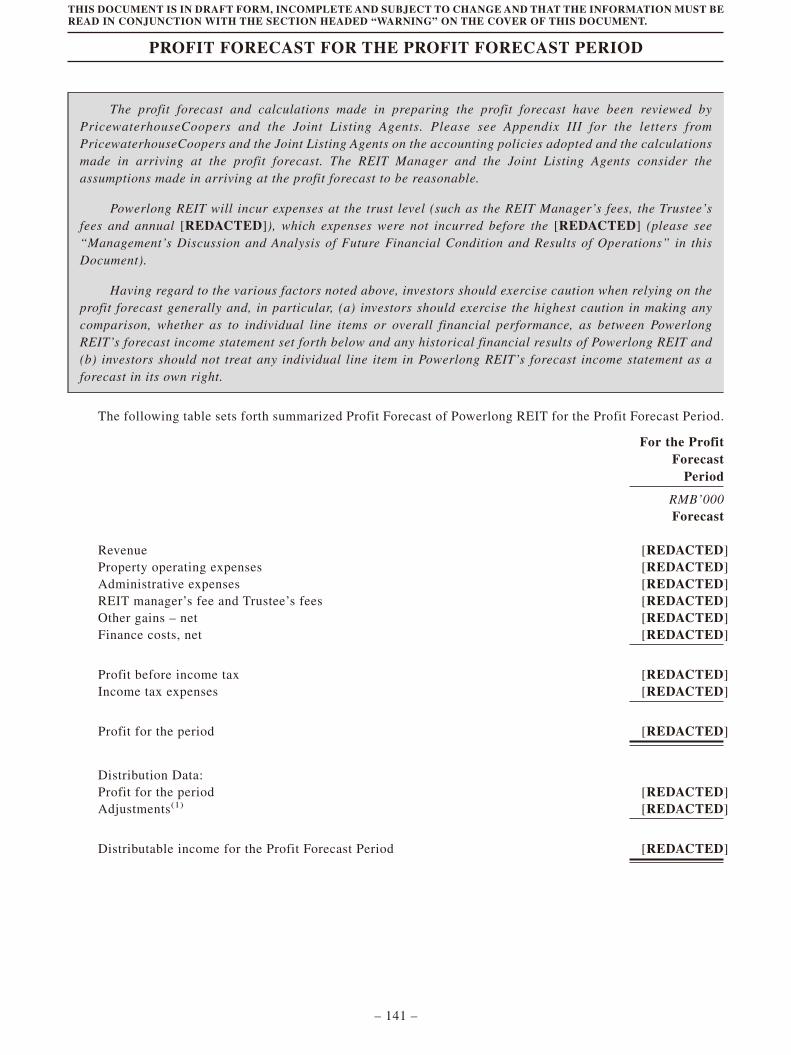

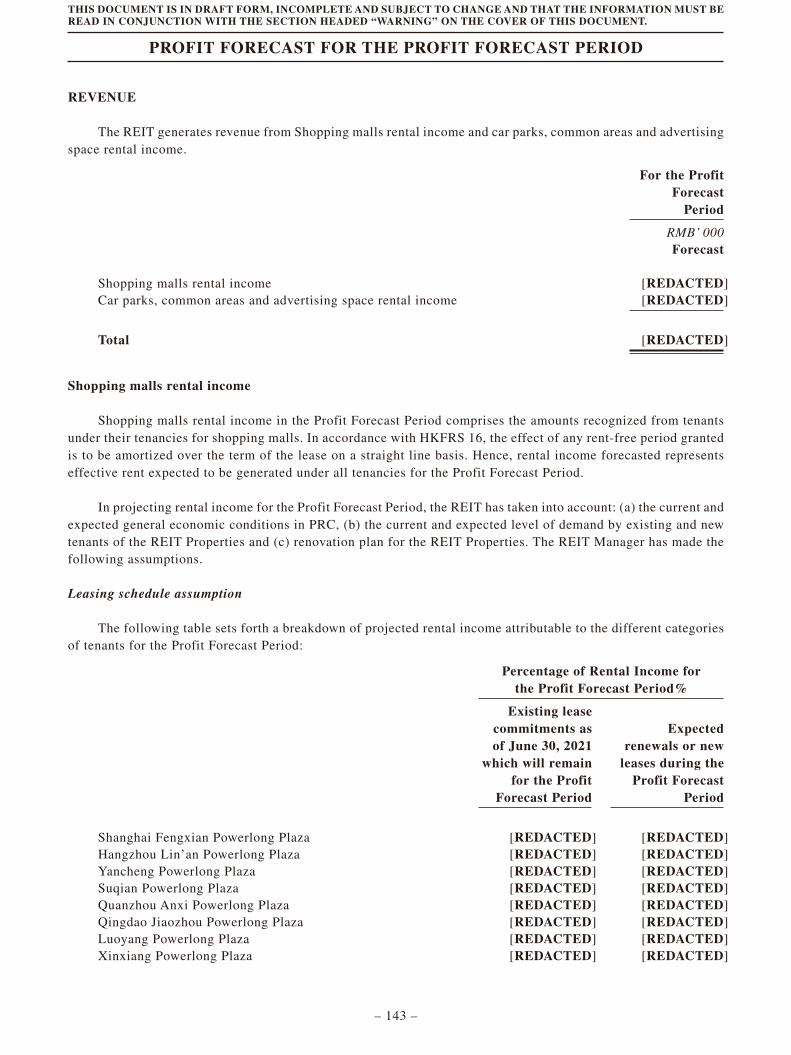

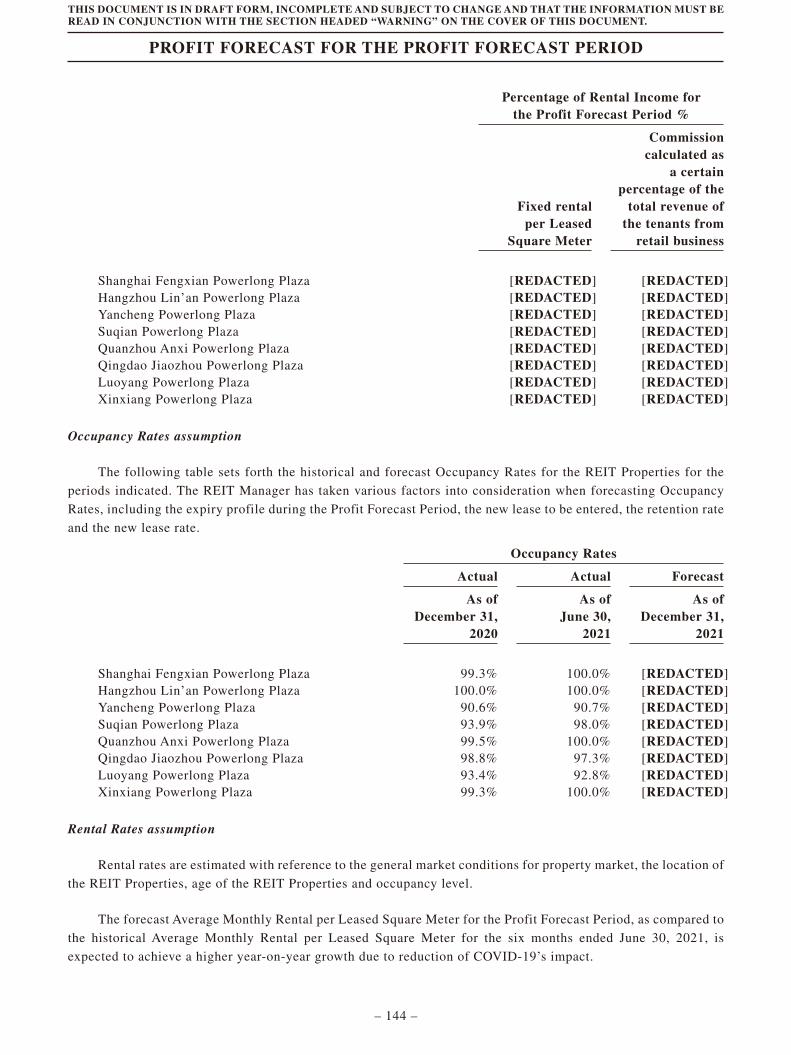

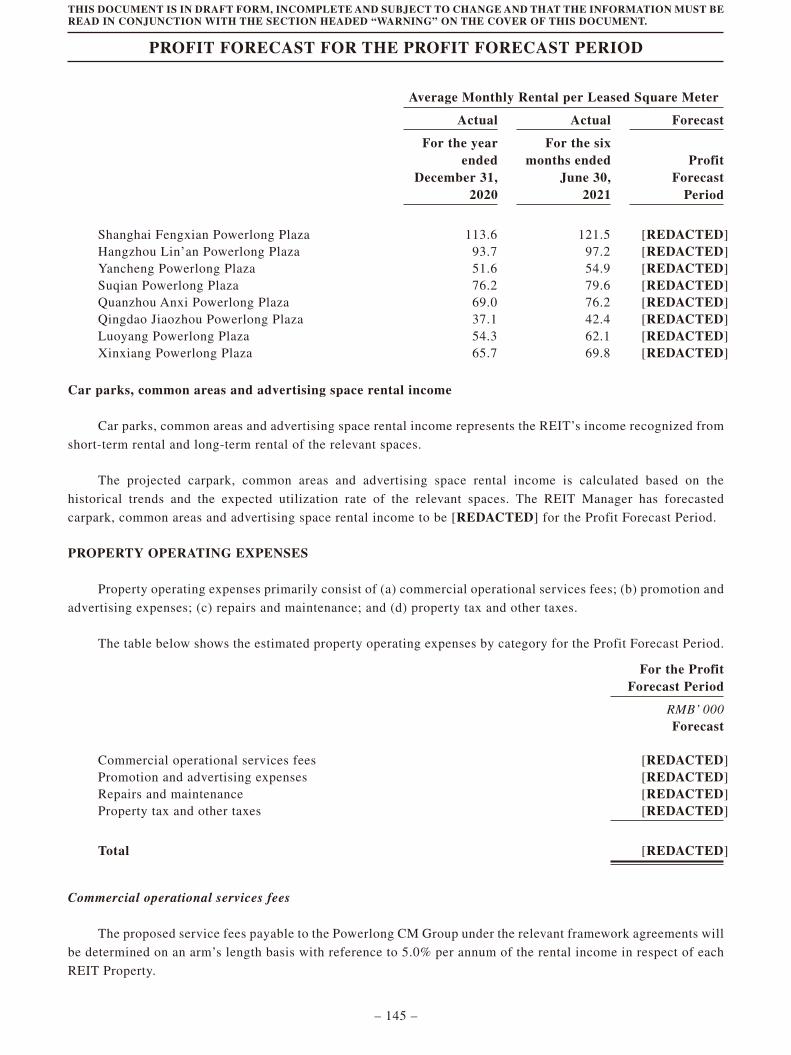

PROFIT FORECAST FOR THE PROFIT FORECAST PERIOD . . . . . . . . . . . . . . . . . . . . . . . . . . 140

STATEMENT OF DISTRIBUTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 150

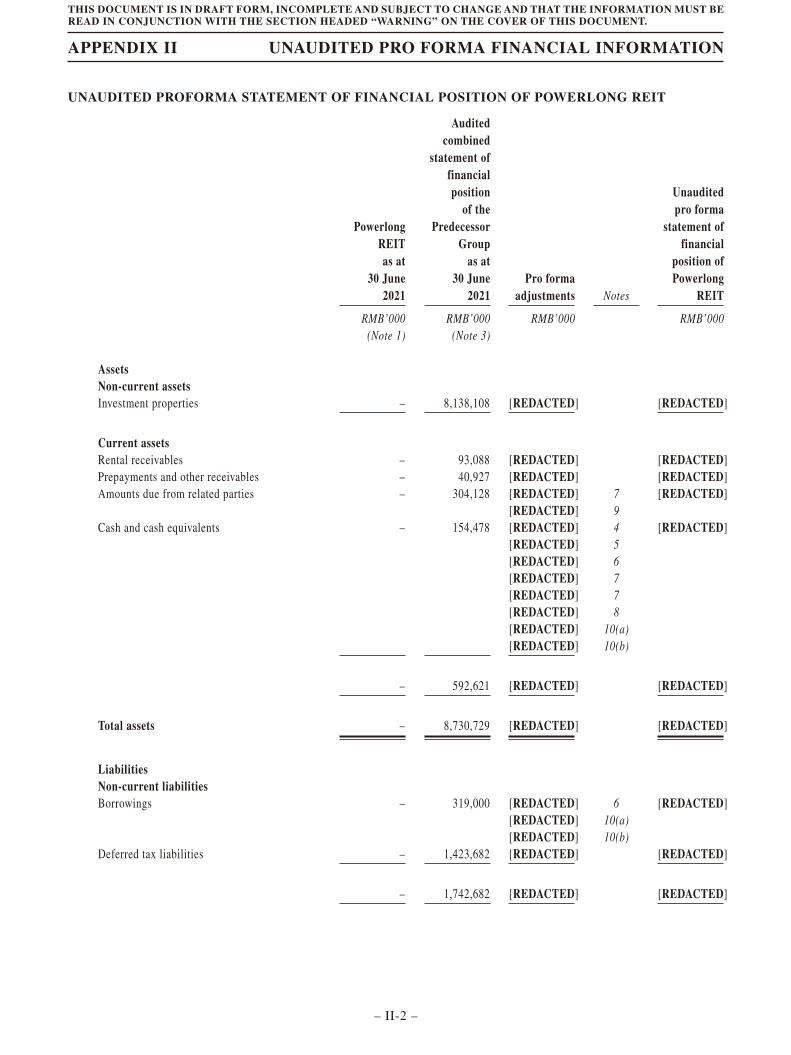

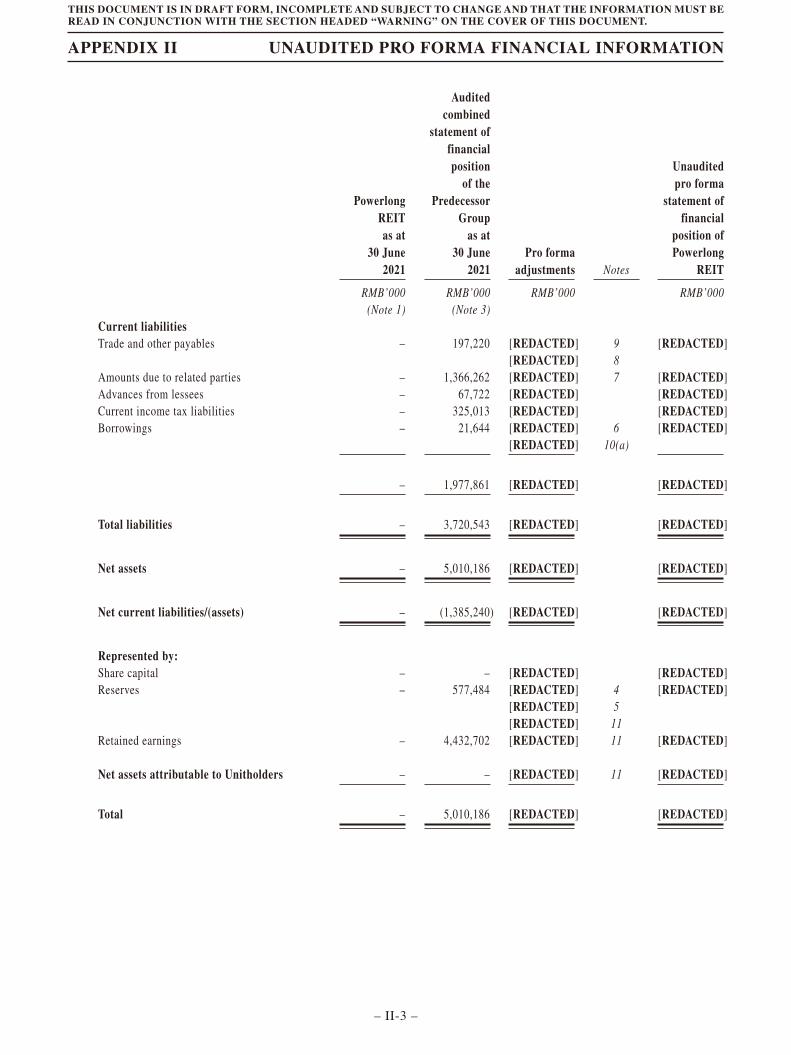

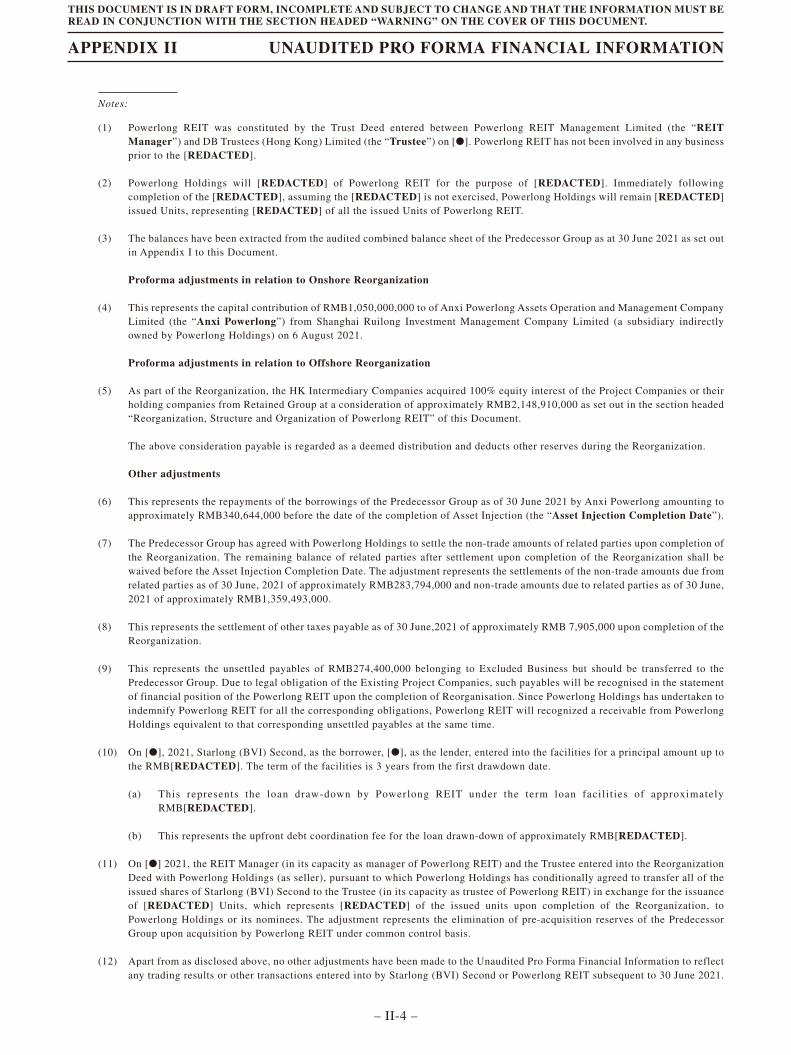

UNAUDITED PRO FORMA STATEMENTS OF FINANCIAL POSITION . . . . . . . . . . . . . . . . . . . 151

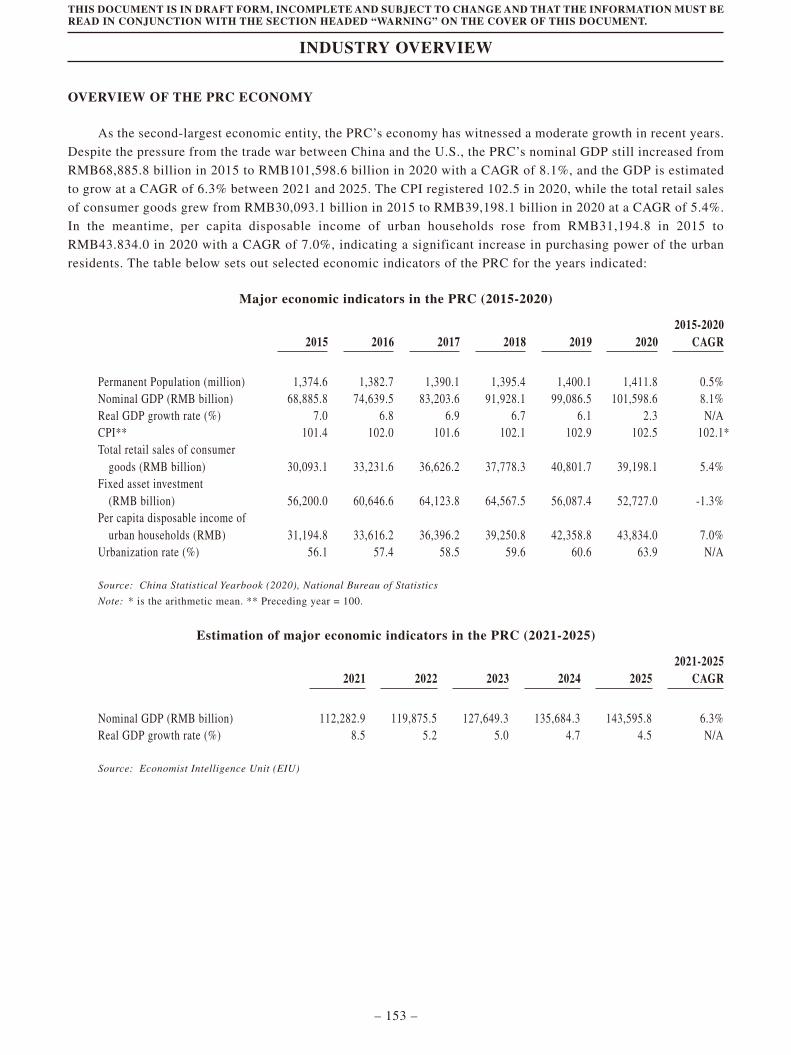

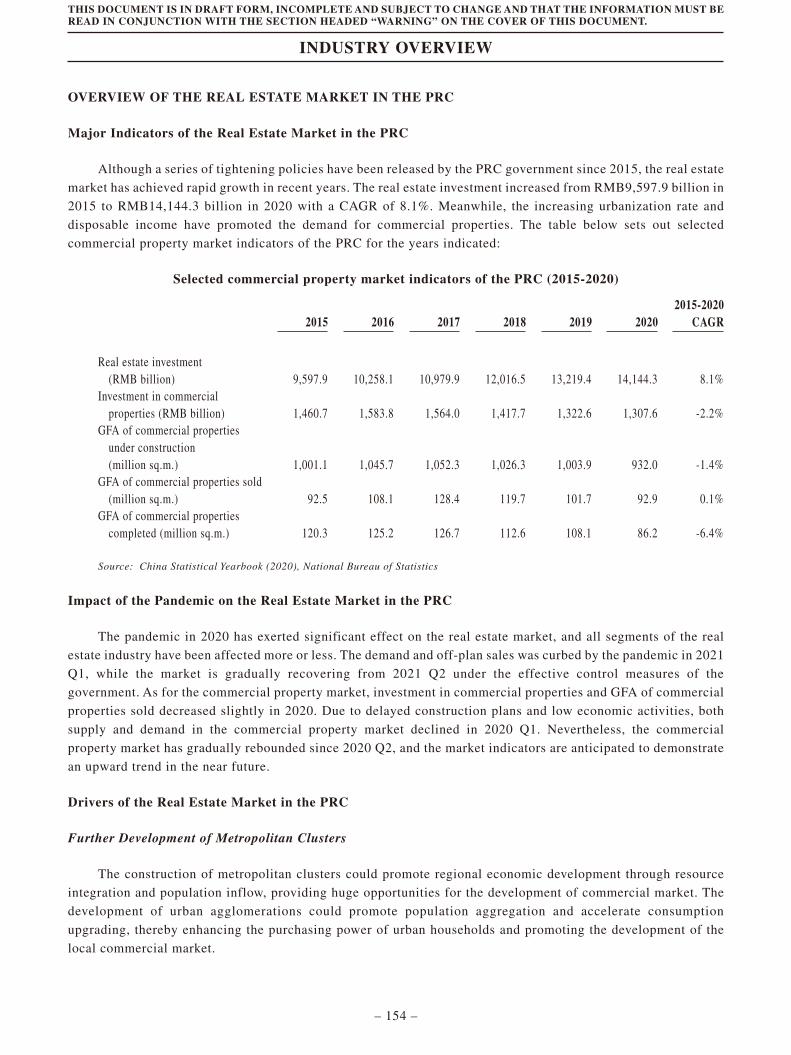

INDUSTRY OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152

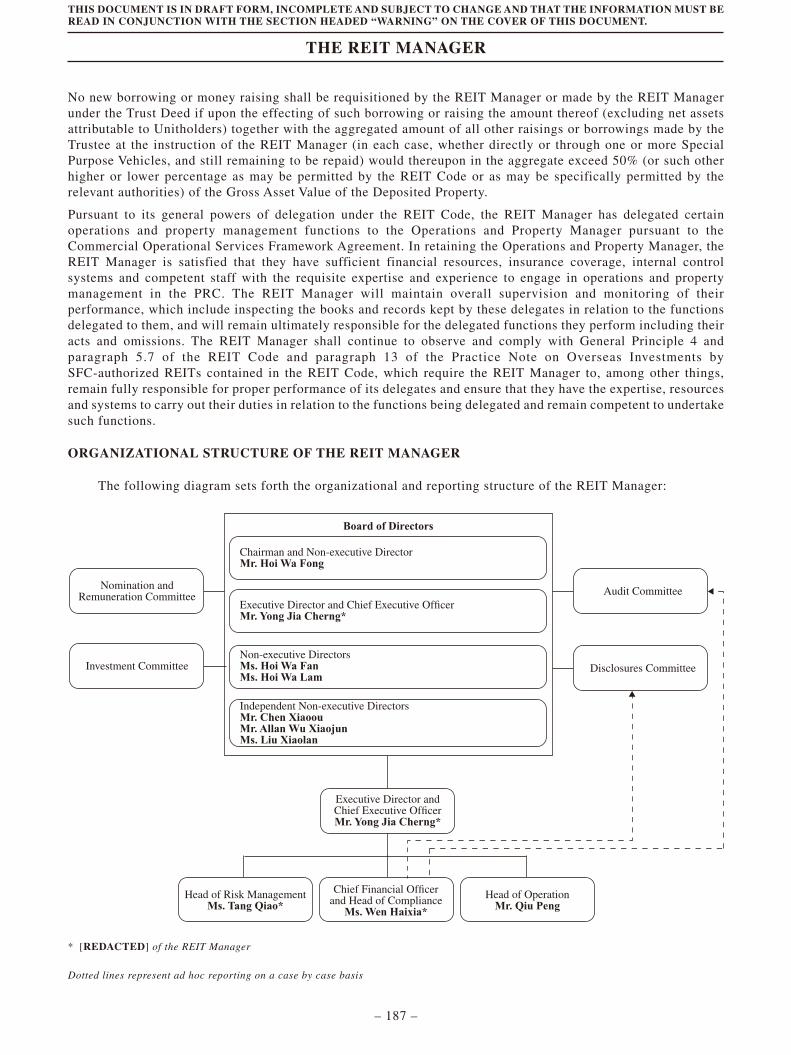

REORGANIZATION, STRUCTURE AND ORGANIZATION OF POWERLONG REIT . . . . . . . . . 170

THE REIT MANAGER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 185

THE OPERATIONS AND PROPERTY MANAGER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 202

INFORMATION ABOUT AND RELATIONSHIP WITH POWERLONG HOLDINGS . . . . . . . . . . 207

CORPORATE GOVERNANCE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 212

THE TRUST DEED . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 221

MATERIAL AGREEMENTS AND OTHER DOCUMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 240

CONNECTED PARTY TRANSACTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 246

MODIFICATIONS, WAIVERS AND LICENSING CONDITIONS . . . . . . . . . . . . . . . . . . . . . . . . . 257

TAXATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 260

[REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 268

STRUCTURE OF THE [REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 277

HOW TO APPLY FOR [REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 289

EXPERTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 314

APPENDIX I – ACCOUNTANT’S REPORT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . I-1

APPENDIX II – UNAUDITED PRO FORMA FINANCIAL INFORMATION . . . . . . . . . . . II-1

APPENDIX III – LETTERS IN RELATION TO THE PROFIT FORECAST . . . . . . . . . . . . III-1

APPENDIX IV – VALUATION REPORT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . IV-1

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

CONTENTS

– v –

Page

APPENDIX V – MARKET RESEARCH REPORT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . V-1

APPENDIX VI – LETTER FROM THE BUILDING SURVEYOR IN RELATION TO ITSBUILDING SURVEY REPORT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . VI-1

APPENDIX VII – OVERVIEW OF THE RELEVANT LAWS AND REGULATIONS INTHE PRC AND OF COMPARISON CERTAIN ASPECTS OF ITSPROPERTY LAWS AND THE LAWS OF HONG KONG . . . . . . . . . . . . VII-1

APPENDIX VIII – GENERAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . VIII-1

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

CONTENTS

– vi –

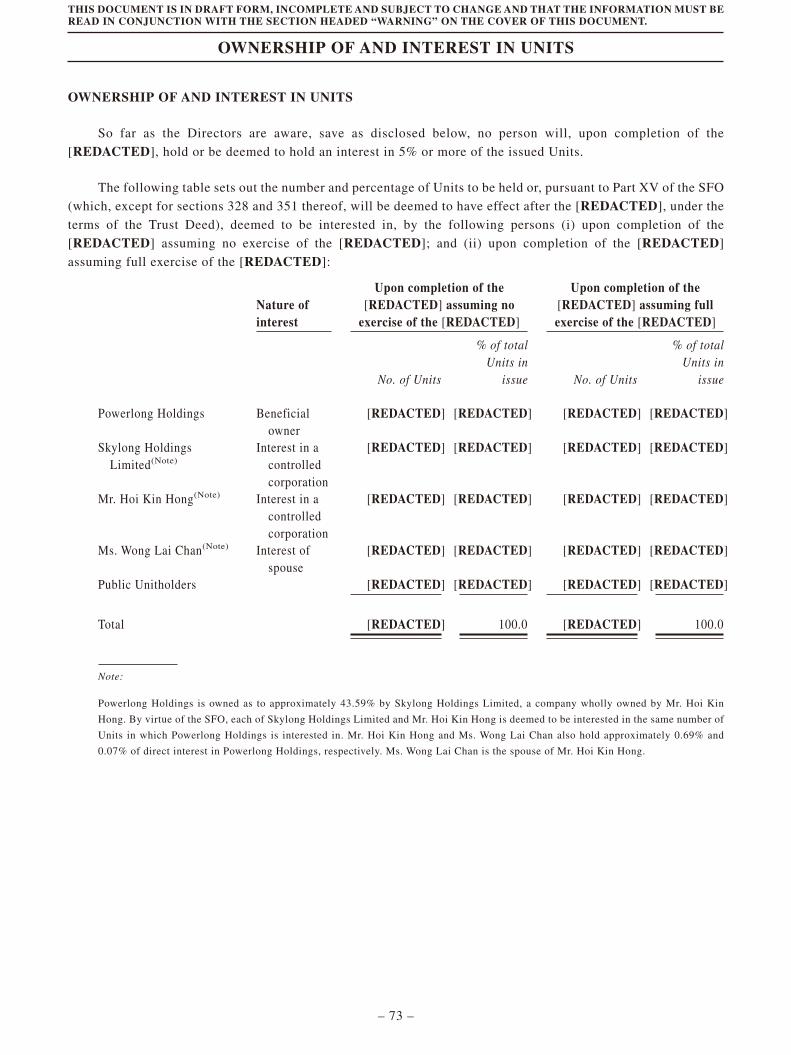

The following summary aims to provide you with an overview of the information contained in thisDocument and should be read in conjunction with the full text of this Document. As it is a summary only, itdoes not contain all the information that may be important to you. You should read the whole Documentcarefully before deciding to invest in the Units. There are risks involved in any investment. Some of theparticular risks involved in investing in the Units are set out in “Risk Factors” in this Document, which youshould read carefully before you decide to invest in the Units.

In making your investment decision, you should rely on the information contained in this Document.Neither Powerlong REIT, Powerlong Holdings, the REIT Manager, the Trustee, the [REDACTED], the JointListing Agents nor any of their respective directors, agents, employees or advisers or any other personsinvolved in the [REDACTED] has authorized anyone to provide you with information or make anyrepresentation that is different from that contained in this Document.

Statements contained in this summary that are not historical facts may be forward-looking statements,based on certain reasonable assumptions, expectations and beliefs of the REIT Manager. You are cautionedthat there are certain risks and uncertainties associated with Powerlong REIT and the actual results may differmaterially from those projected by such forward-looking statements.

A REIT AS AN INVESTMENT VEHICLE

A REIT is a collective investment scheme constituted as a unit trust that invests primarily in

income-generating properties and uses the income to provide stable returns to its unitholders. Holding units in a

REIT allows investors to share the benefits and risks of owning the properties held by the REIT. An investment in

the units of a REIT in Hong Kong is governed primarily by the REIT Code and also the trust deed constituting the

REIT and offers the following benefits: (i) certainty as to business focus of the REIT, as a REIT does not have

complete discretion to diversify outside of the real estate sector or to own significant non-real estate assets; (ii) a

distribution which is required by the REIT Code to be at least 90% of the REIT’s audited net income after tax for

each financial year, subject to certain adjustments; (iii) significantly enhanced liquidity in comparison to direct

investments in real estate; (iv) a REIT manager licensed and regulated on an ongoing basis by the SFC; and (v) a

corporate governance framework, compliance with which is overseen by an independent trustee.

OVERVIEW OF POWERLONG REIT

Powerlong REIT is a Hong Kong collective investment scheme constituted as a unit trust and authorized

under section 104 of the SFO. Powerlong REIT is a REIT formed to primarily own and invest in quality

income-generating commercial properties in the PRC. Powerlong REIT is managed by the REIT Manager whose

key investment objectives are to provide Unitholders with stable distributions, sustainable and long-term

distribution growth, and enhancement in the value of Powerlong REIT’s properties.

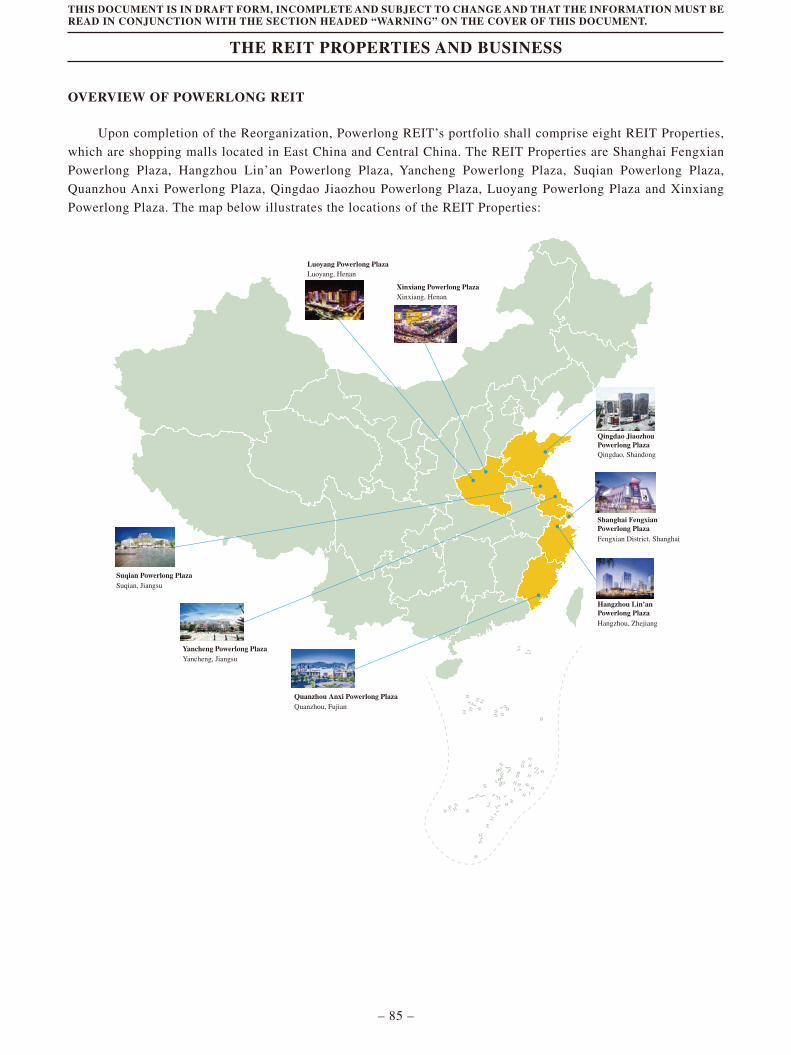

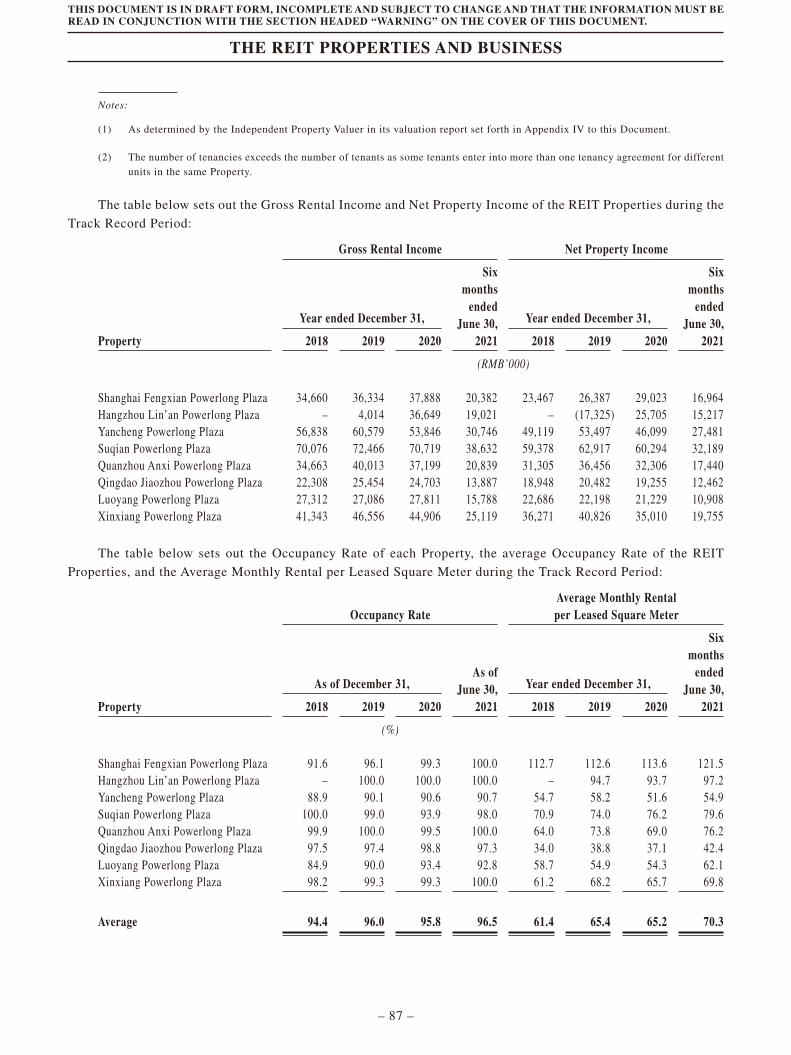

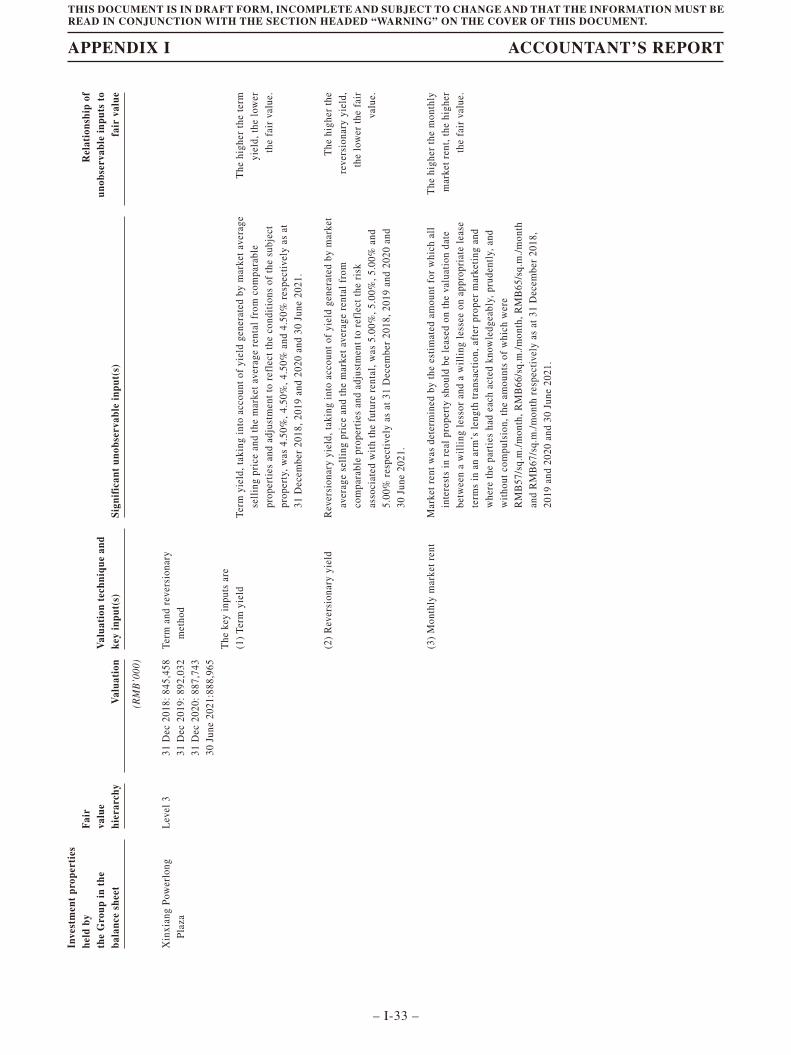

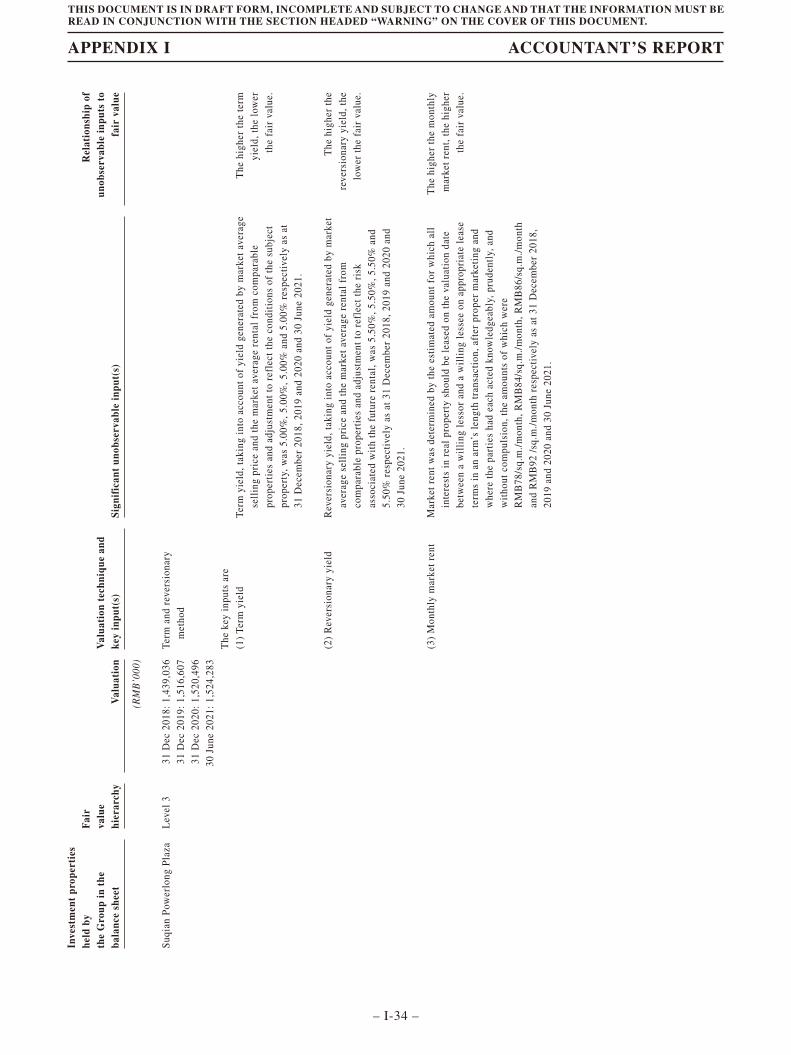

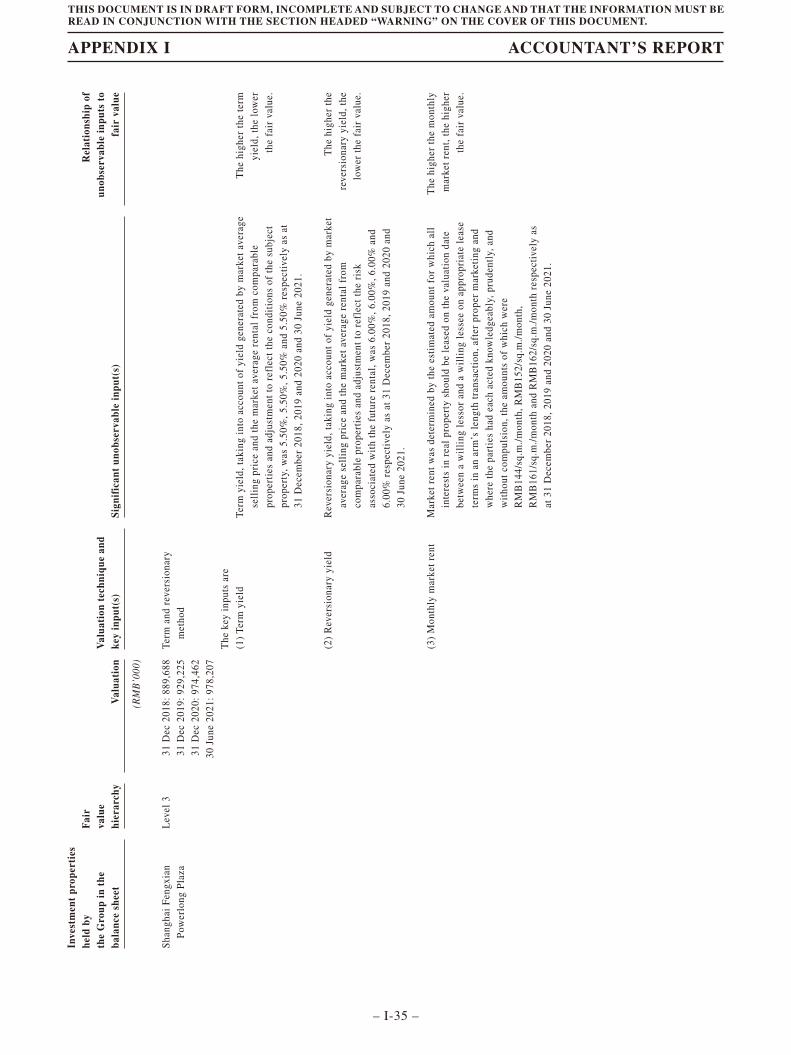

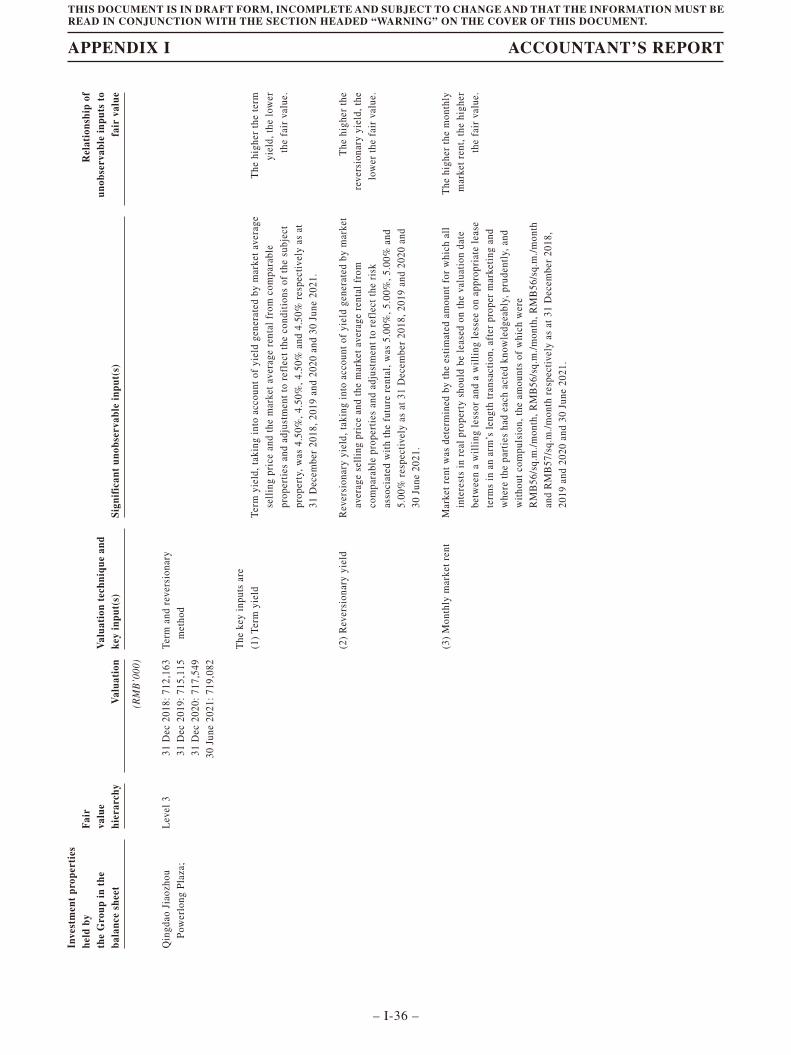

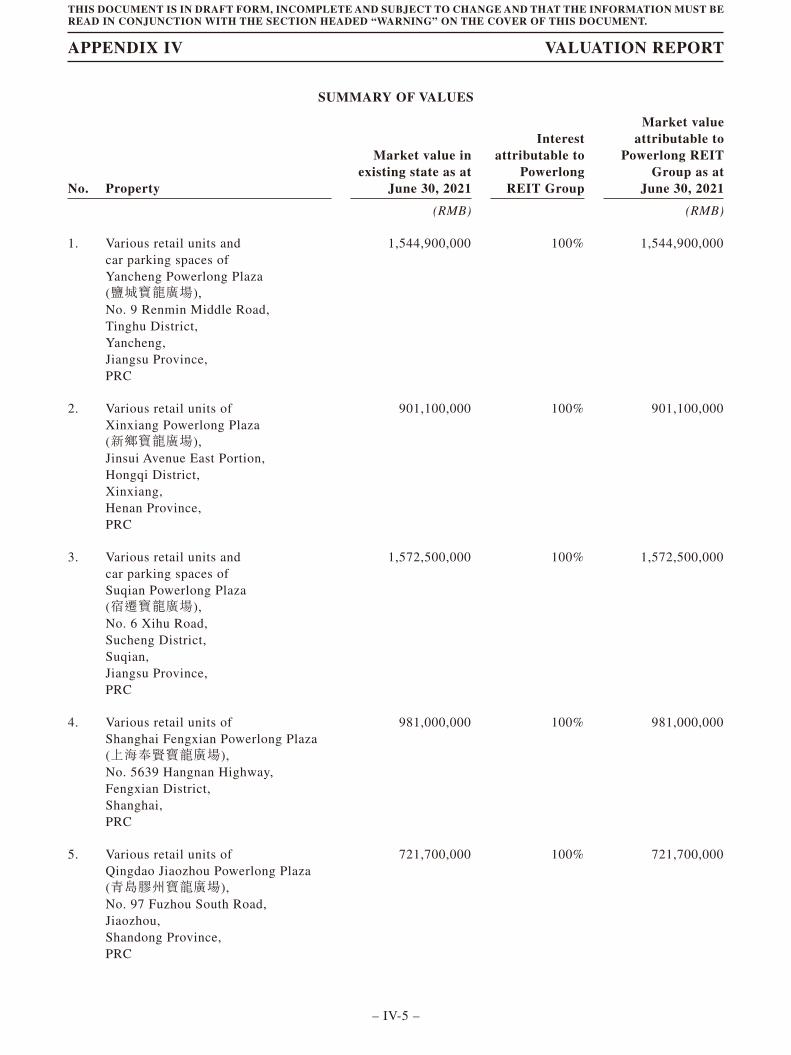

Powerlong REIT shall initially comprise the following eight REIT Properties in the PRC, all of which are

shopping malls located in East China and Central China: Shanghai Fengxian Powerlong Plaza, Hangzhou Lin’an

Powerlong Plaza, Yancheng Powerlong Plaza, Suqian Powerlong Plaza, Quanzhou Anxi Powerlong Plaza, Qingdao

Jiaozhou Powerlong Plaza, Luoyang Powerlong Plaza, and Xinxiang Powerlong Plaza.

As of June 30, 2021, the REIT Properties had an aggregate Gross Rentable Area of approximately 453,475

sq.m. with an Appraised Value of RMB8,231.3 million and an average Occupancy Rate of approximately 96.5%.

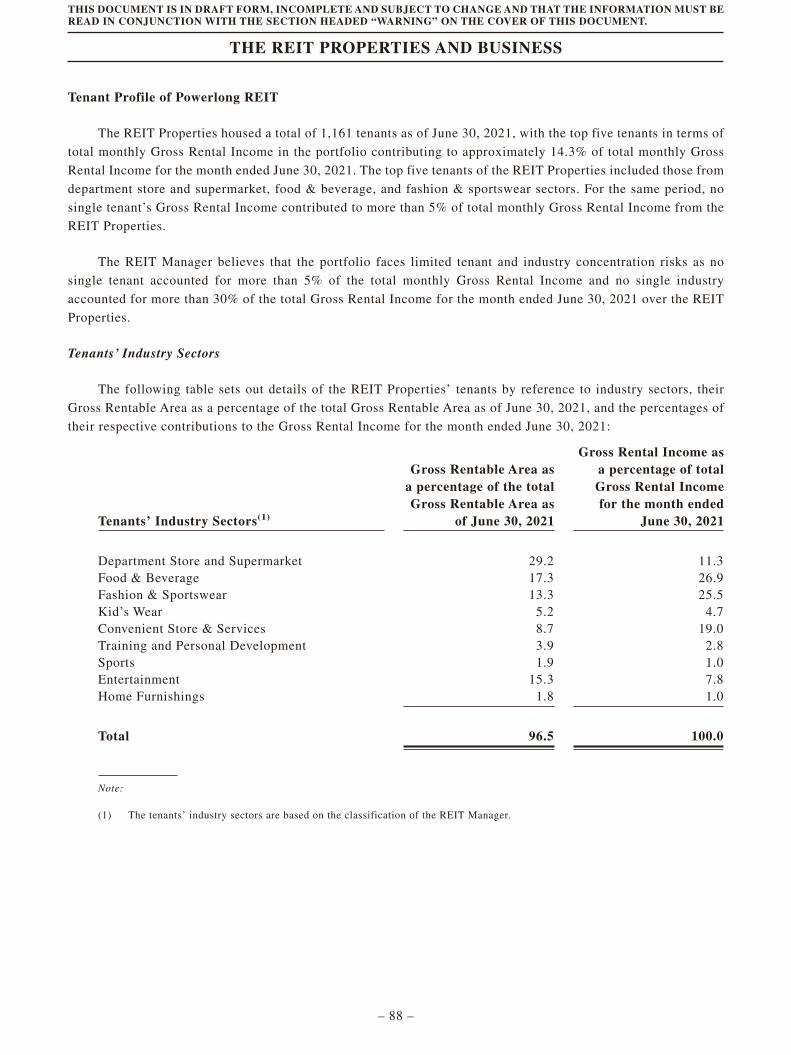

As of June 30, 2021, the REIT Properties housed a total of 1,161 tenants, with the top five tenants in terms of total

monthly Gross Rental Income contributing to approximately 14.3% of the total monthly Gross Rental Income for

the month ended June 30, 2021.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

SUMMARY

– 1 –

KEY INVESTMENT HIGHLIGHTS OF POWERLONG REIT

The REIT Manager believes that the REIT Properties have the following competitive strengths: (i) firstPRC-based commercial property REIT in Hong Kong with a focus on shopping malls strategically located tobenefit from the high growth in local economies; (ii) quality and diverse tenants with high Occupancy Ratemanaged by Powerlong CM, the first PRC commercial operation services provider listed on the Stock Exchange;(iii) strong organic growth and future acquisitions supported by reputable sponsor; and (iv) highly experienced andcommitted management team with a proven track record. For further details, please see “Key InvestmentHighlights of Powerlong REIT” in this Document.

OBJECTIVES AND INVESTMENT STRATEGIES OF POWERLONG REIT

The REIT Manager’s key objectives for Powerlong REIT are to provide Unitholders with stable distributions,sustainable and long-term distribution growth, and enhancement in the value of Powerlong REIT’s properties. TheREIT Manager intends to achieve this through holding and investing in quality income-generating commercialproperties located in the PRC. The REIT Manager’s strategy can be broadly categorized as follows: (i) assetmanagement strategy: proactively managing Powerlong REIT’s property portfolio to maintain optimaloccupancy level and operational efficiency; seeking asset enhancement opportunities through property upgradeand/or renovation to promote rental income growth; (ii) investments and acquisition strategy: investing in andacquiring quality properties in the PRC from Powerlong Group or third parties that satisfy the REIT Manager’sinvestment strategy; and (iii) capital and risk management strategy: optimizing returns on Powerlong REIT’sportfolio and distributions to Unitholders, while maintaining an appropriate level of financial prudence. Forfurther details, please see “Strategy” in this Document.

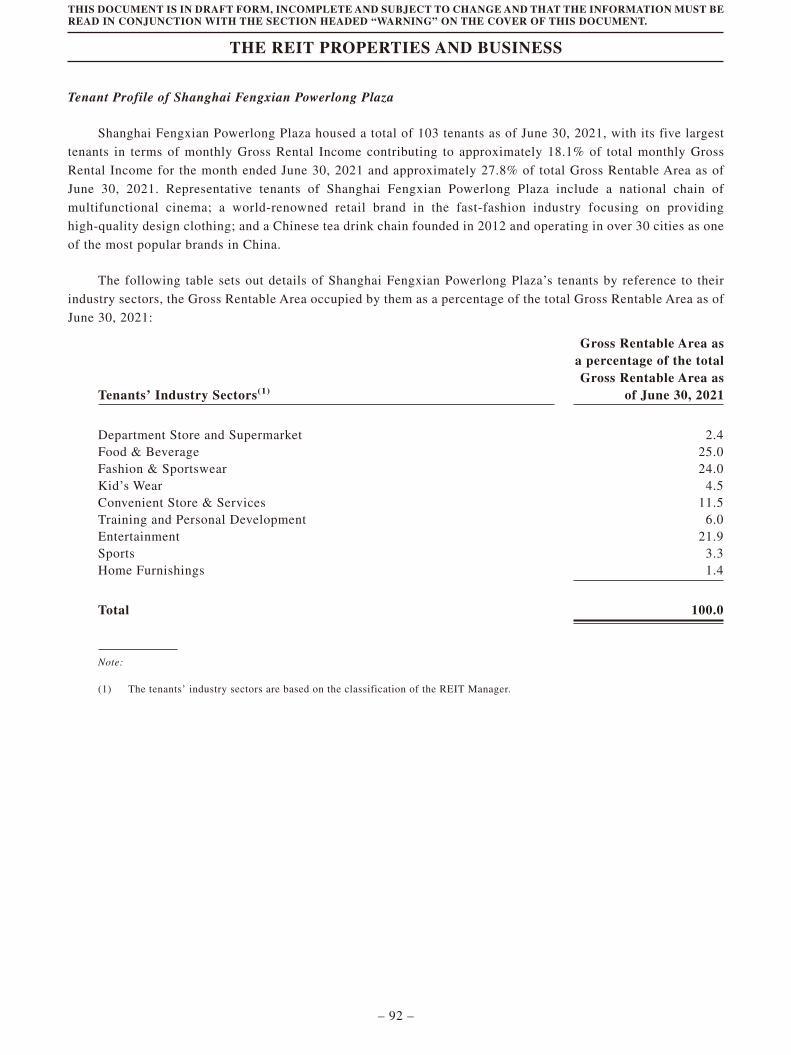

SUMMARY INFORMATION OF THE REIT PROPERTIES AS OF JUNE 30, 2021

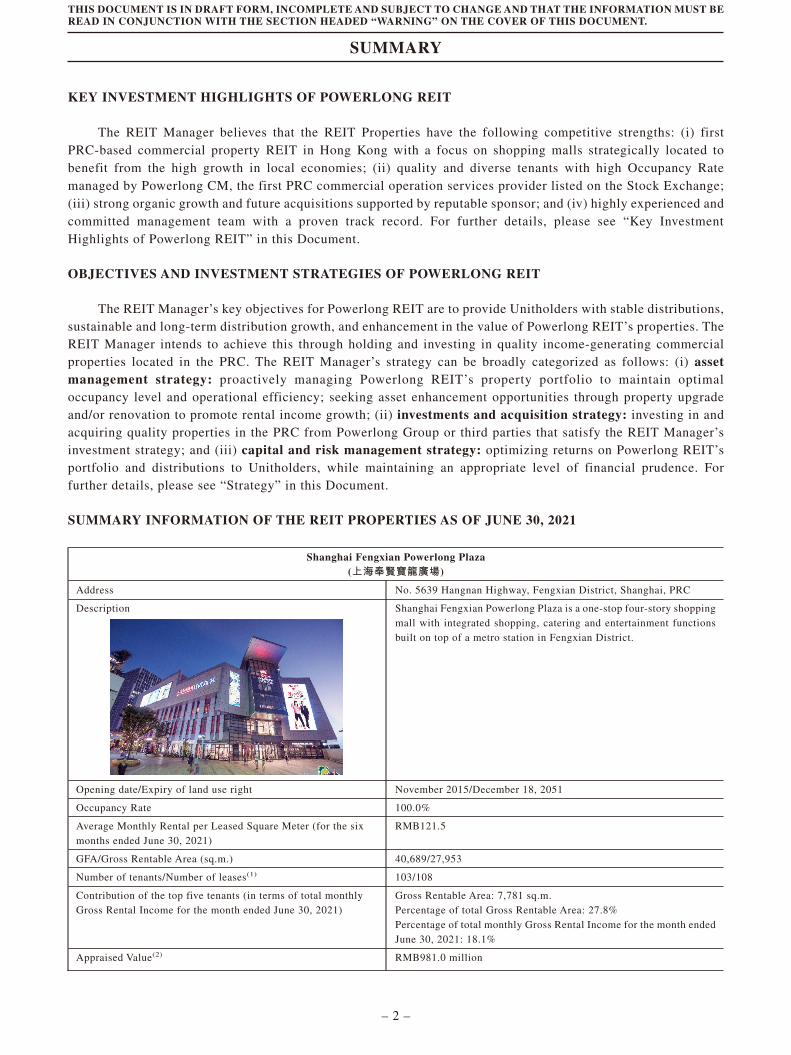

Shanghai Fengxian Powerlong Plaza(上海奉賢寶龍廣場)

Address No. 5639 Hangnan Highway, Fengxian District, Shanghai, PRC

Description Shanghai Fengxian Powerlong Plaza is a one-stop four-story shoppingmall with integrated shopping, catering and entertainment functionsbuilt on top of a metro station in Fengxian District.

Opening date/Expiry of land use right November 2015/December 18, 2051

Occupancy Rate 100.0%

Average Monthly Rental per Leased Square Meter (for the sixmonths ended June 30, 2021)

RMB121.5

GFA/Gross Rentable Area (sq.m.) 40,689/27,953

Number of tenants/Number of leases(1) 103/108

Contribution of the top five tenants (in terms of total monthlyGross Rental Income for the month ended June 30, 2021)

Gross Rentable Area: 7,781 sq.m.Percentage of total Gross Rentable Area: 27.8%Percentage of total monthly Gross Rental Income for the month endedJune 30, 2021: 18.1%

Appraised Value(2) RMB981.0 million

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

SUMMARY

– 2 –

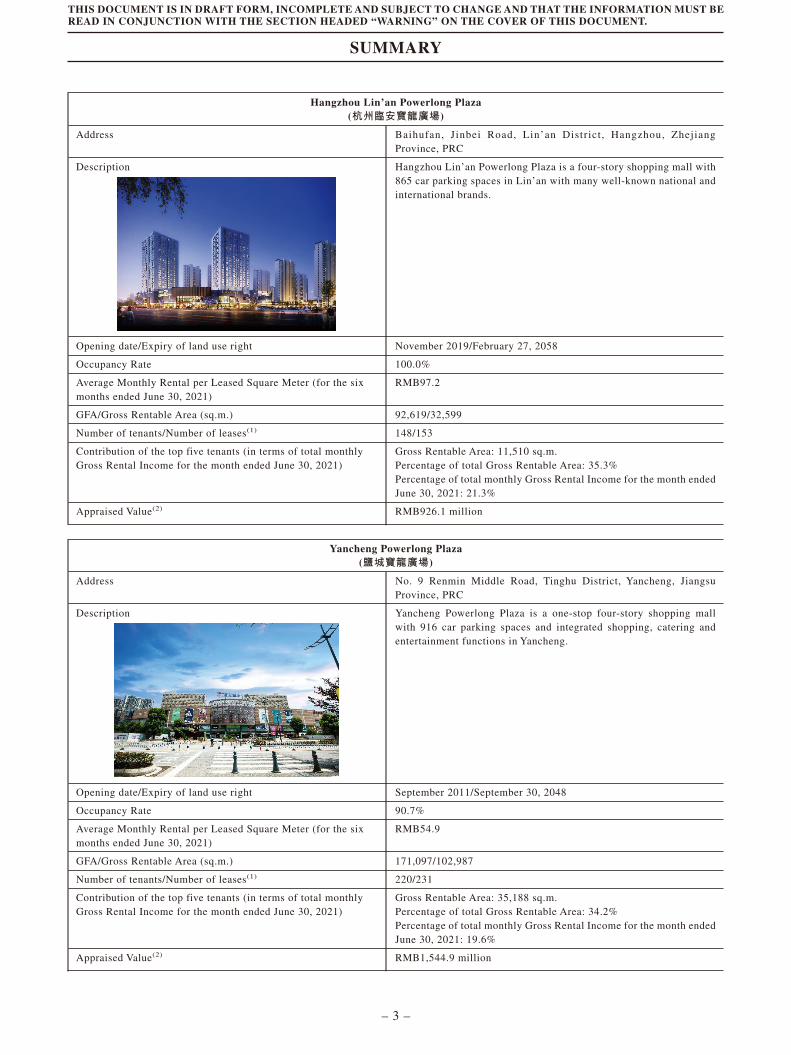

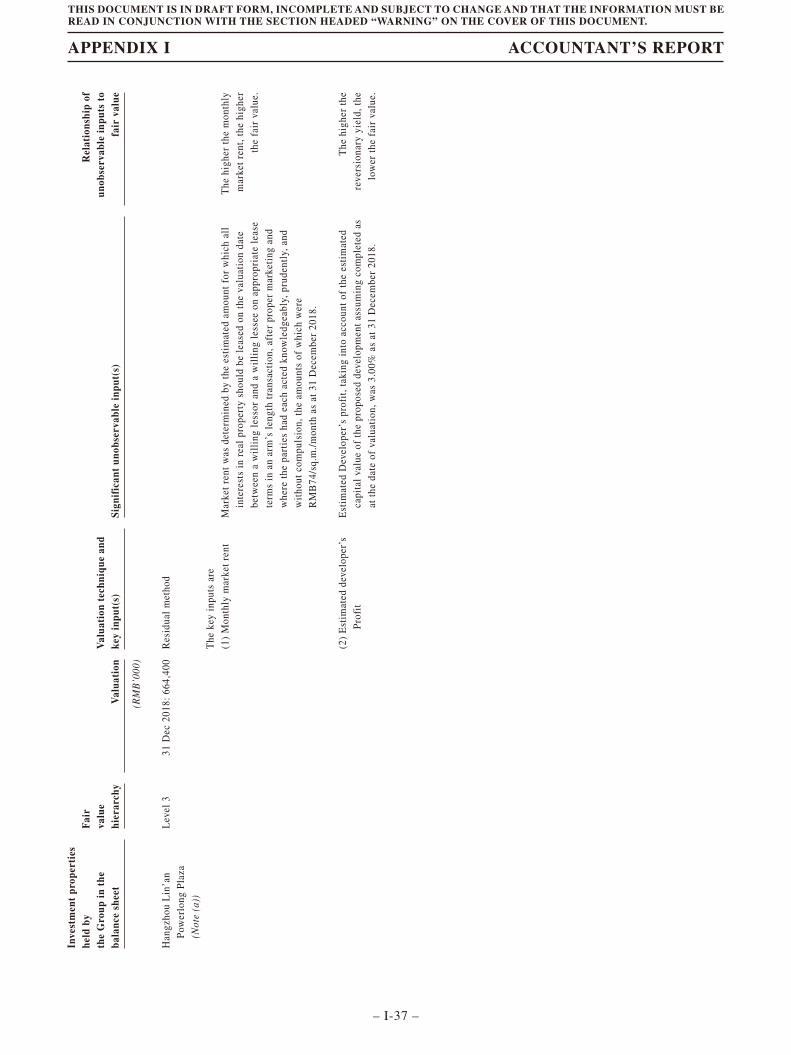

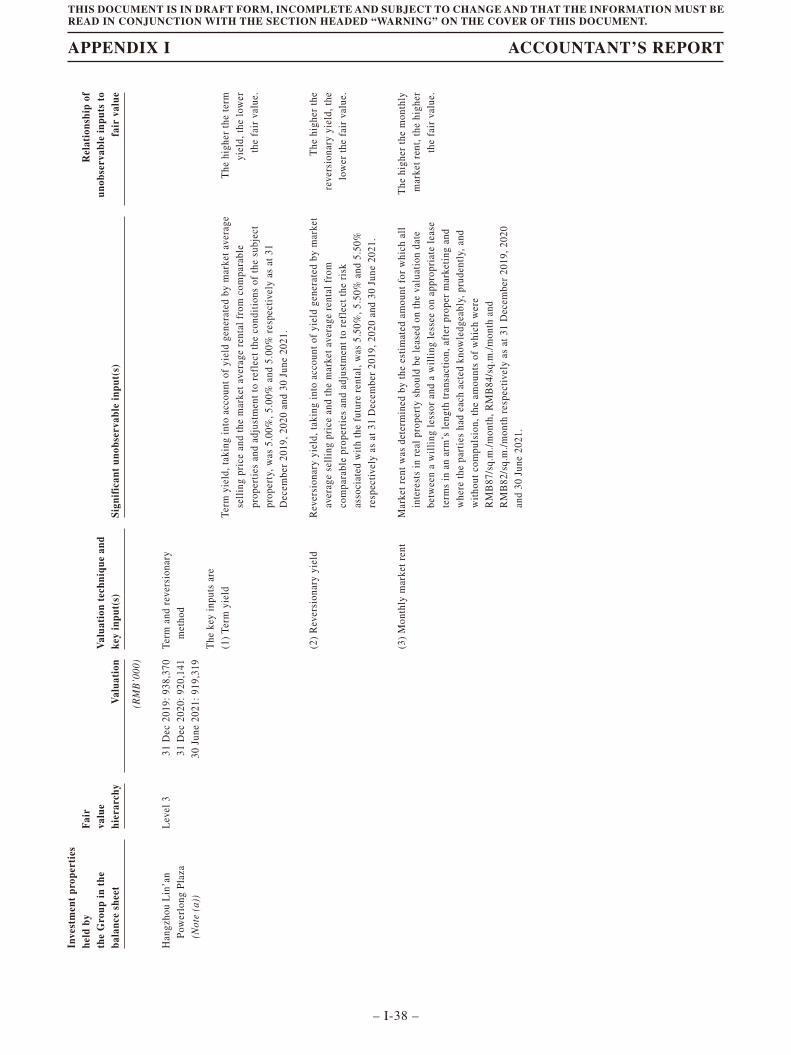

Hangzhou Lin’an Powerlong Plaza(杭州臨安寶龍廣場)

Address Baihufan, Jinbei Road, Lin’an District, Hangzhou, ZhejiangProvince, PRC

Description Hangzhou Lin’an Powerlong Plaza is a four-story shopping mall with865 car parking spaces in Lin’an with many well-known national andinternational brands.

Opening date/Expiry of land use right November 2019/February 27, 2058

Occupancy Rate 100.0%

Average Monthly Rental per Leased Square Meter (for the sixmonths ended June 30, 2021)

RMB97.2

GFA/Gross Rentable Area (sq.m.) 92,619/32,599

Number of tenants/Number of leases(1) 148/153

Contribution of the top five tenants (in terms of total monthlyGross Rental Income for the month ended June 30, 2021)

Gross Rentable Area: 11,510 sq.m.Percentage of total Gross Rentable Area: 35.3%Percentage of total monthly Gross Rental Income for the month endedJune 30, 2021: 21.3%

Appraised Value(2) RMB926.1 million

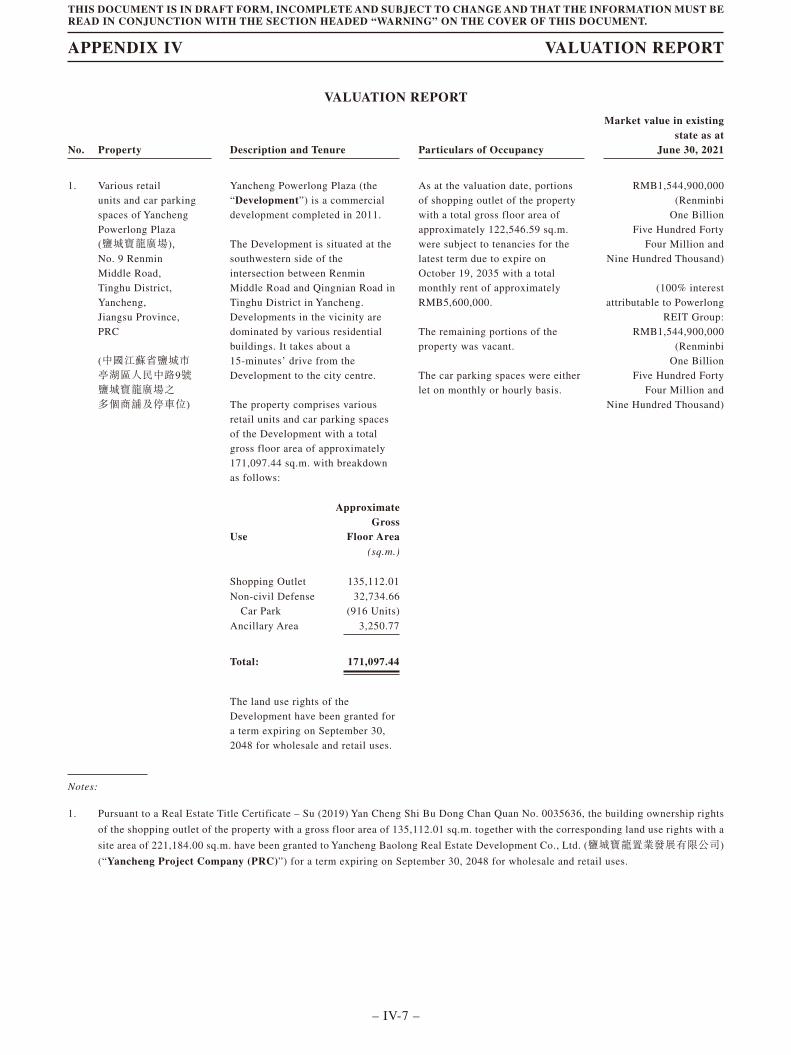

Yancheng Powerlong Plaza(鹽城寶龍廣場)

Address No. 9 Renmin Middle Road, Tinghu District, Yancheng, JiangsuProvince, PRC

Description Yancheng Powerlong Plaza is a one-stop four-story shopping mallwith 916 car parking spaces and integrated shopping, catering andentertainment functions in Yancheng.

Opening date/Expiry of land use right September 2011/September 30, 2048

Occupancy Rate 90.7%

Average Monthly Rental per Leased Square Meter (for the sixmonths ended June 30, 2021)

RMB54.9

GFA/Gross Rentable Area (sq.m.) 171,097/102,987

Number of tenants/Number of leases(1) 220/231

Contribution of the top five tenants (in terms of total monthlyGross Rental Income for the month ended June 30, 2021)

Gross Rentable Area: 35,188 sq.m.Percentage of total Gross Rentable Area: 34.2%Percentage of total monthly Gross Rental Income for the month endedJune 30, 2021: 19.6%

Appraised Value(2) RMB1,544.9 million

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

SUMMARY

– 3 –

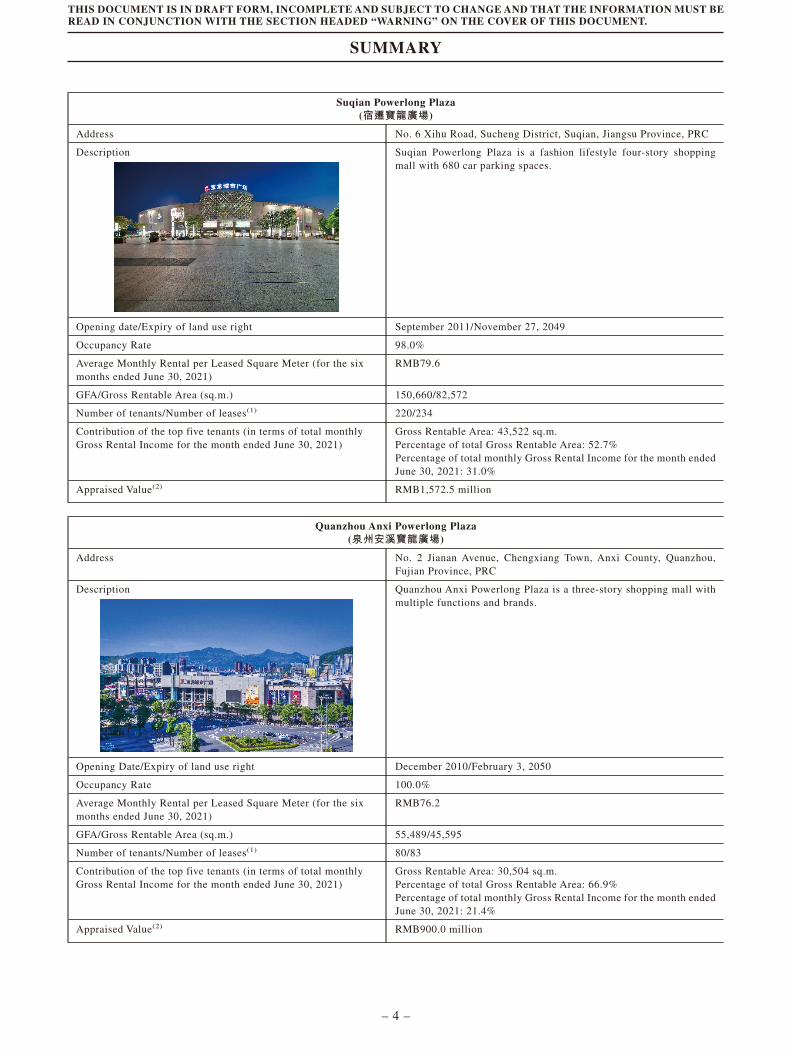

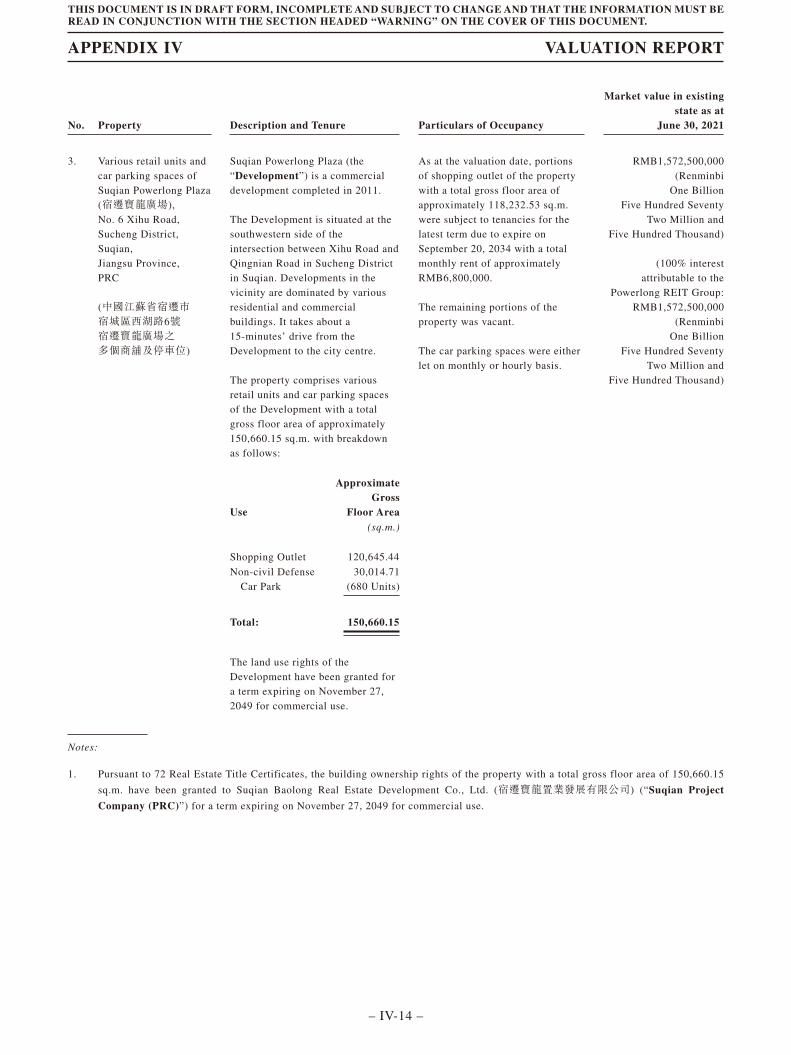

Suqian Powerlong Plaza(宿遷寶龍廣場)

Address No. 6 Xihu Road, Sucheng District, Suqian, Jiangsu Province, PRC

Description Suqian Powerlong Plaza is a fashion lifestyle four-story shoppingmall with 680 car parking spaces.

Opening date/Expiry of land use right September 2011/November 27, 2049

Occupancy Rate 98.0%

Average Monthly Rental per Leased Square Meter (for the sixmonths ended June 30, 2021)

RMB79.6

GFA/Gross Rentable Area (sq.m.) 150,660/82,572

Number of tenants/Number of leases(1) 220/234

Contribution of the top five tenants (in terms of total monthlyGross Rental Income for the month ended June 30, 2021)

Gross Rentable Area: 43,522 sq.m.Percentage of total Gross Rentable Area: 52.7%Percentage of total monthly Gross Rental Income for the month endedJune 30, 2021: 31.0%

Appraised Value(2) RMB1,572.5 million

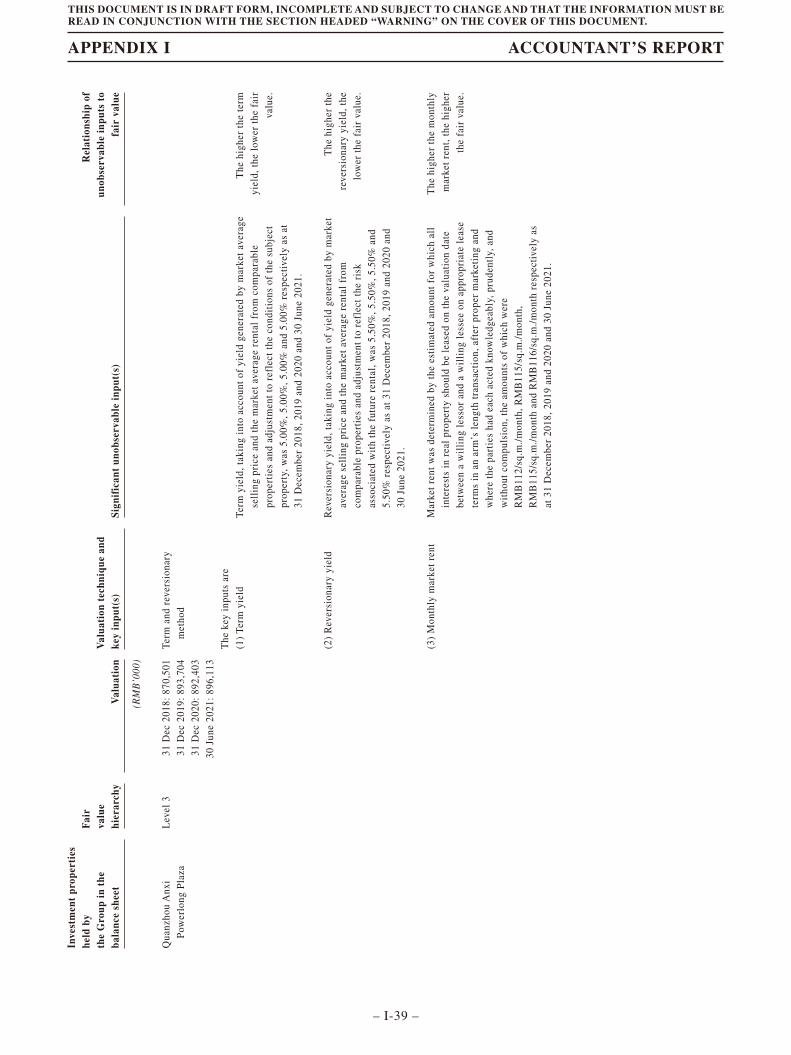

Quanzhou Anxi Powerlong Plaza(泉州安溪寶龍廣場)

Address No. 2 Jianan Avenue, Chengxiang Town, Anxi County, Quanzhou,Fujian Province, PRC

Description Quanzhou Anxi Powerlong Plaza is a three-story shopping mall withmultiple functions and brands.

Opening Date/Expiry of land use right December 2010/February 3, 2050

Occupancy Rate 100.0%

Average Monthly Rental per Leased Square Meter (for the sixmonths ended June 30, 2021)

RMB76.2

GFA/Gross Rentable Area (sq.m.) 55,489/45,595

Number of tenants/Number of leases(1) 80/83

Contribution of the top five tenants (in terms of total monthlyGross Rental Income for the month ended June 30, 2021)

Gross Rentable Area: 30,504 sq.m.Percentage of total Gross Rentable Area: 66.9%Percentage of total monthly Gross Rental Income for the month endedJune 30, 2021: 21.4%

Appraised Value(2) RMB900.0 million

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

SUMMARY

– 4 –

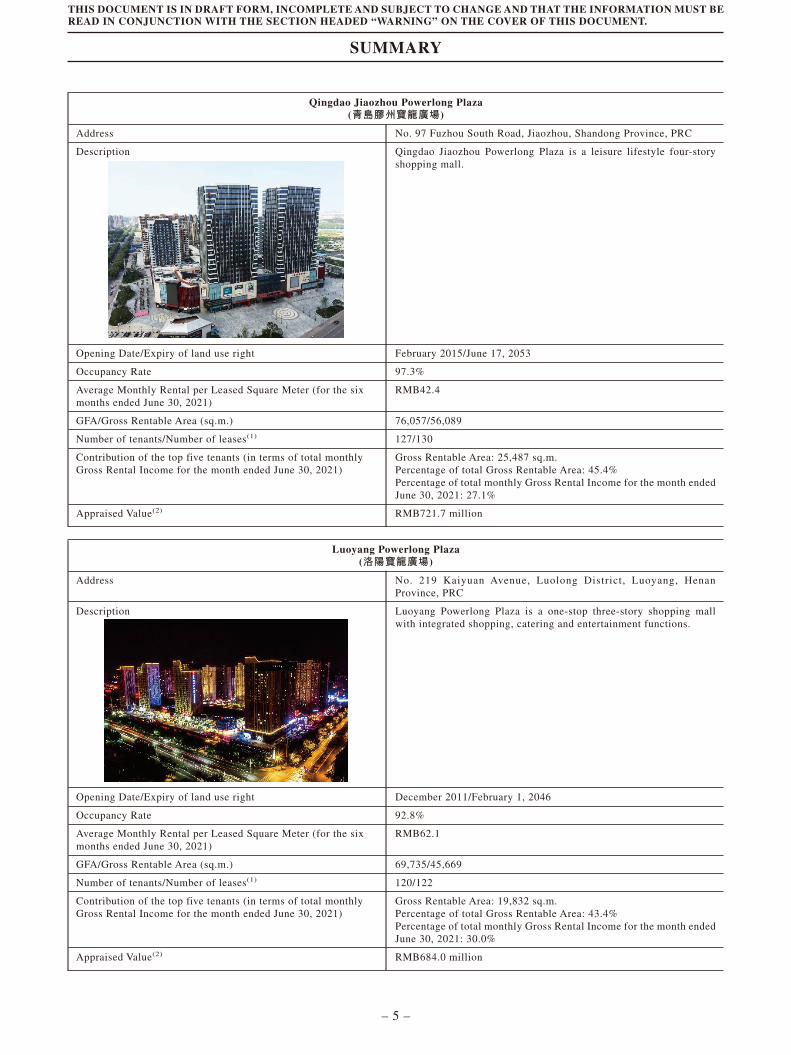

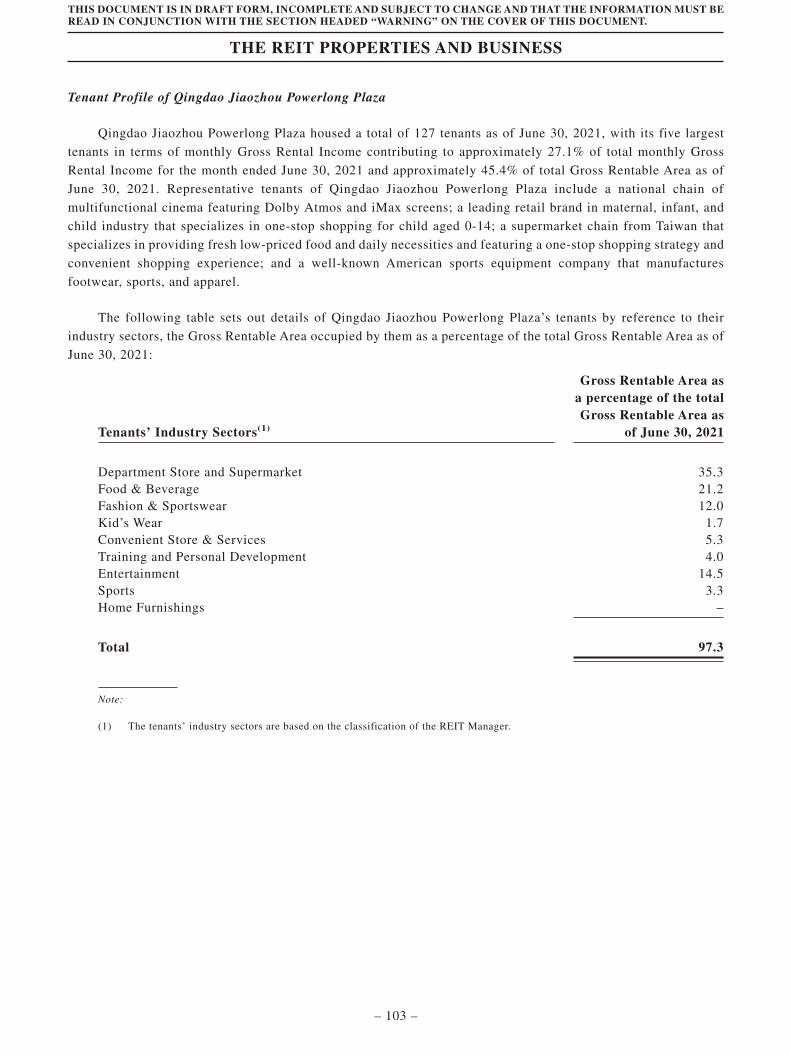

Qingdao Jiaozhou Powerlong Plaza(青島膠州寶龍廣場)

Address No. 97 Fuzhou South Road, Jiaozhou, Shandong Province, PRC

Description Qingdao Jiaozhou Powerlong Plaza is a leisure lifestyle four-storyshopping mall.

Opening Date/Expiry of land use right February 2015/June 17, 2053

Occupancy Rate 97.3%

Average Monthly Rental per Leased Square Meter (for the sixmonths ended June 30, 2021)

RMB42.4

GFA/Gross Rentable Area (sq.m.) 76,057/56,089

Number of tenants/Number of leases(1) 127/130

Contribution of the top five tenants (in terms of total monthlyGross Rental Income for the month ended June 30, 2021)

Gross Rentable Area: 25,487 sq.m.Percentage of total Gross Rentable Area: 45.4%Percentage of total monthly Gross Rental Income for the month endedJune 30, 2021: 27.1%

Appraised Value(2) RMB721.7 million

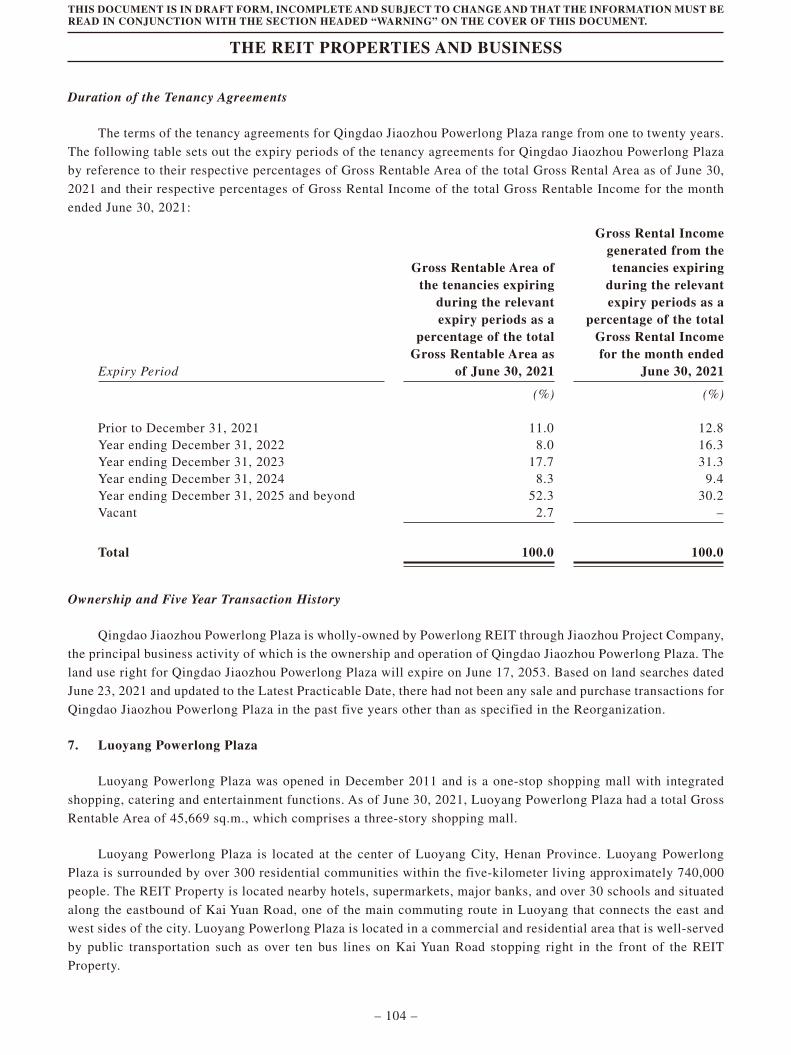

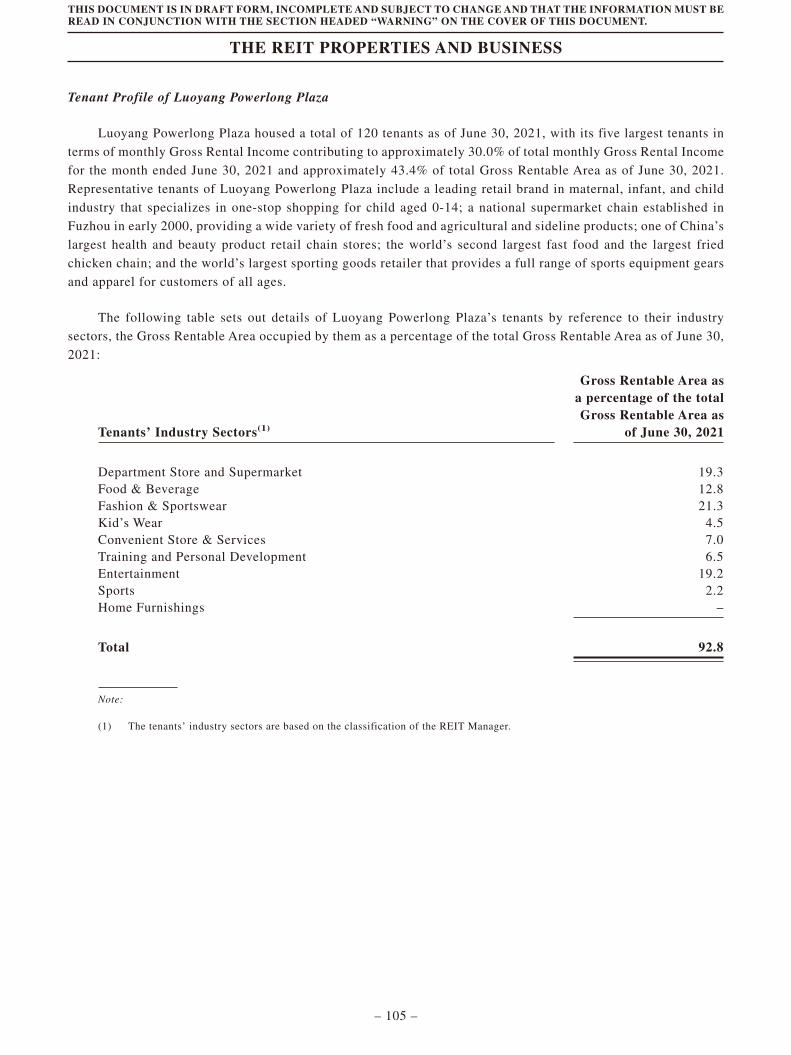

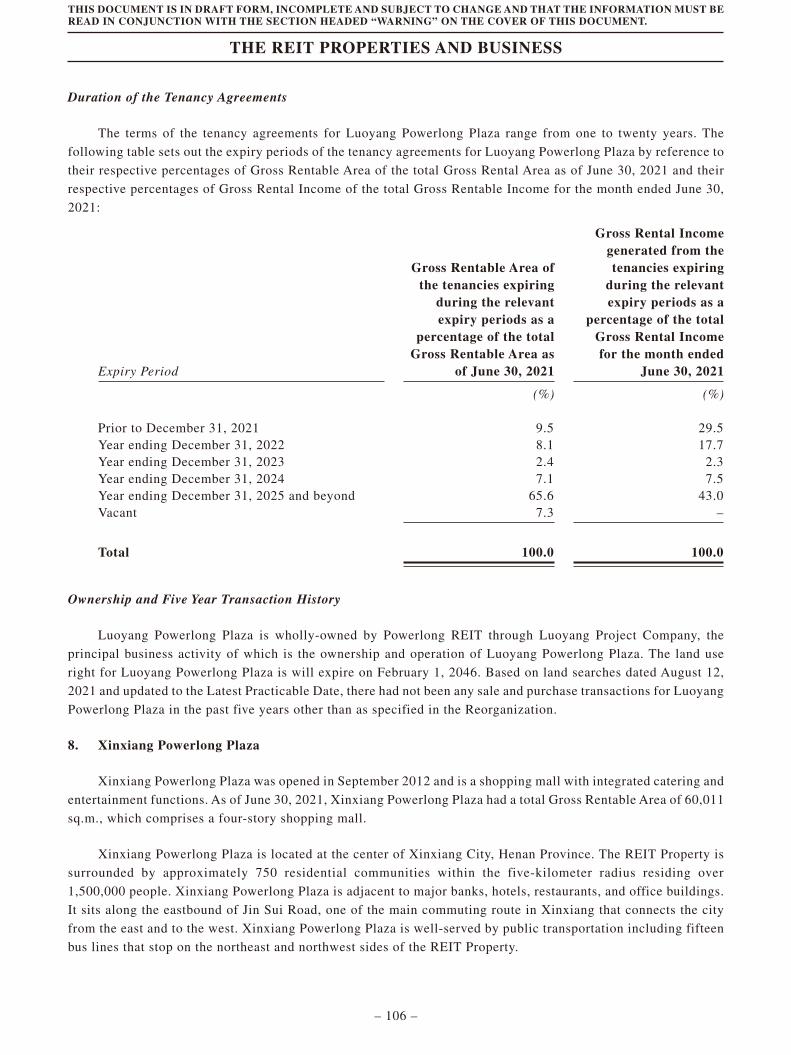

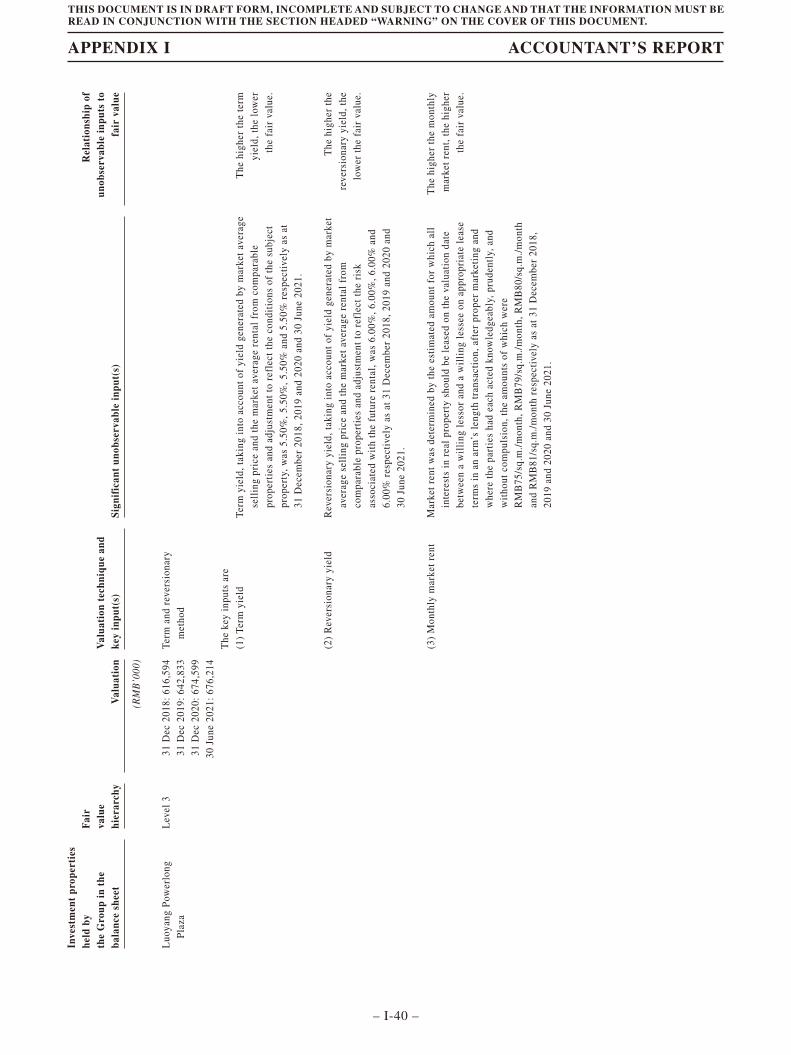

Luoyang Powerlong Plaza(洛陽寶龍廣場)

Address No. 219 Kaiyuan Avenue, Luolong District, Luoyang, HenanProvince, PRC

Description Luoyang Powerlong Plaza is a one-stop three-story shopping mallwith integrated shopping, catering and entertainment functions.

Opening Date/Expiry of land use right December 2011/February 1, 2046

Occupancy Rate 92.8%

Average Monthly Rental per Leased Square Meter (for the sixmonths ended June 30, 2021)

RMB62.1

GFA/Gross Rentable Area (sq.m.) 69,735/45,669

Number of tenants/Number of leases(1) 120/122

Contribution of the top five tenants (in terms of total monthlyGross Rental Income for the month ended June 30, 2021)

Gross Rentable Area: 19,832 sq.m.Percentage of total Gross Rentable Area: 43.4%Percentage of total monthly Gross Rental Income for the month endedJune 30, 2021: 30.0%

Appraised Value(2) RMB684.0 million

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

SUMMARY

– 5 –

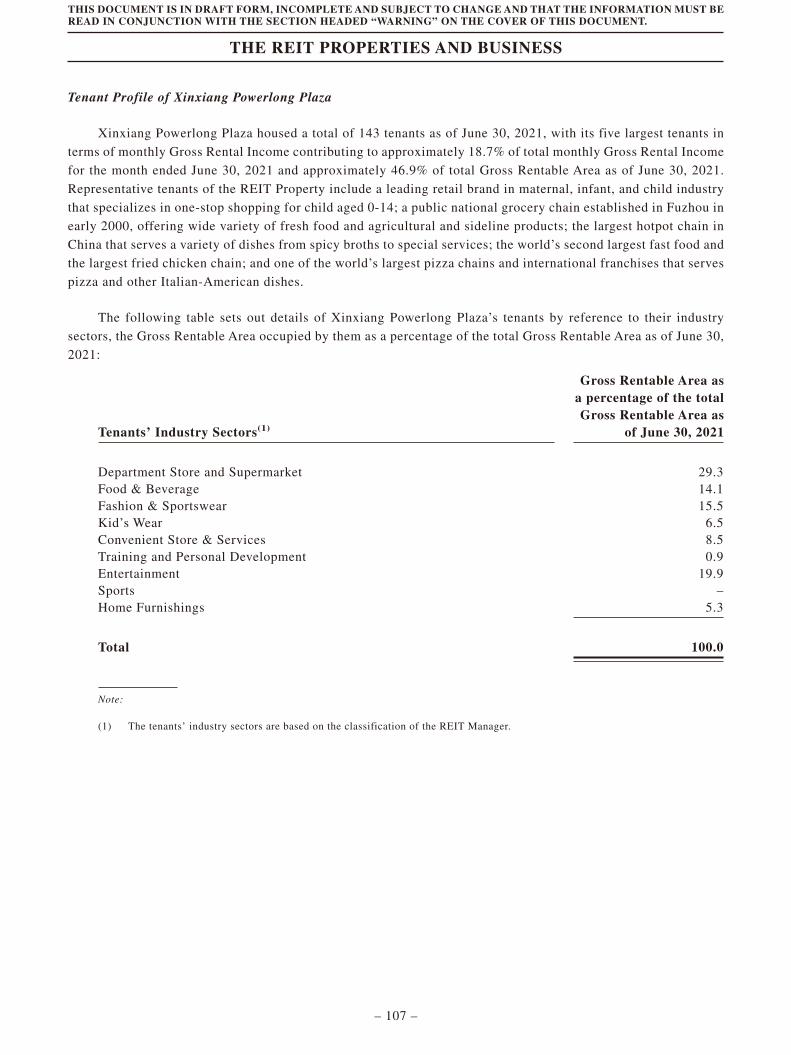

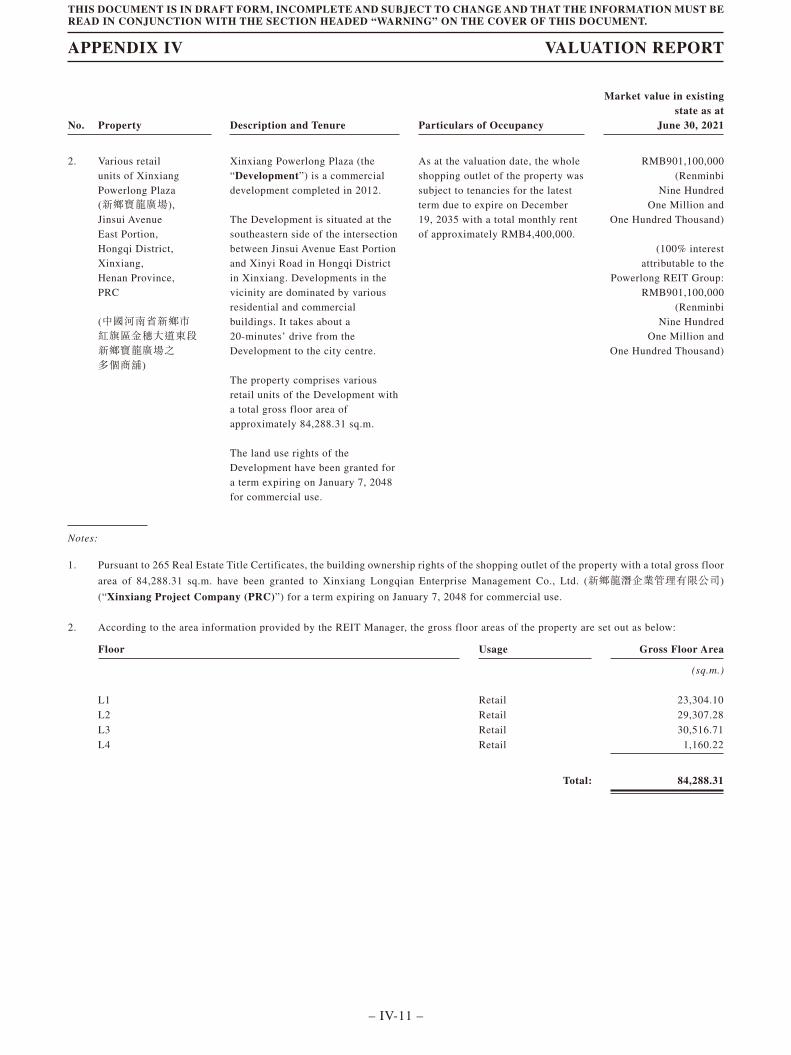

Xinxiang Powerlong Plaza(新鄉寶龍廣場)

Address Jinsui Avenue East Portion, Hongqi District, Xinxiang, HenanProvince, PRC

Description Xinxiang Powerlong Plaza is a four-story shopping mall withintegrated catering and entertainment functions.

Opening Date/Expiry of land use right September 2012/January 7, 2048

Occupancy Rate 100.0%

Average Monthly Rental per Leased Square Meter (for the sixmonths ended June 30, 2021)

RMB69.8

GFA/Gross Rentable Area (sq.m.) 84,288/60,011

Number of tenants/Number of leases(1) 143/154

Contribution of the top five tenants (in terms of total monthlyGross Rental Income for the month ended June 30, 2021)

Gross Rentable Area: 28,158 sq.m.Percentage of total Gross Rentable Area: 46.9%Percentage of total monthly Gross Rental Income for the month endedJune 30, 2021: 18.7%

Appraised Value(2) RMB901.1 million

Notes:

(1) The number of leases exceeds the number of tenants as some tenants enter into more than one lease for different units in the REIT

Properties.

(2) As determined by the Independent Property Valuer in its valuation report set forth in Appendix IV to this Document.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

SUMMARY

– 6 –

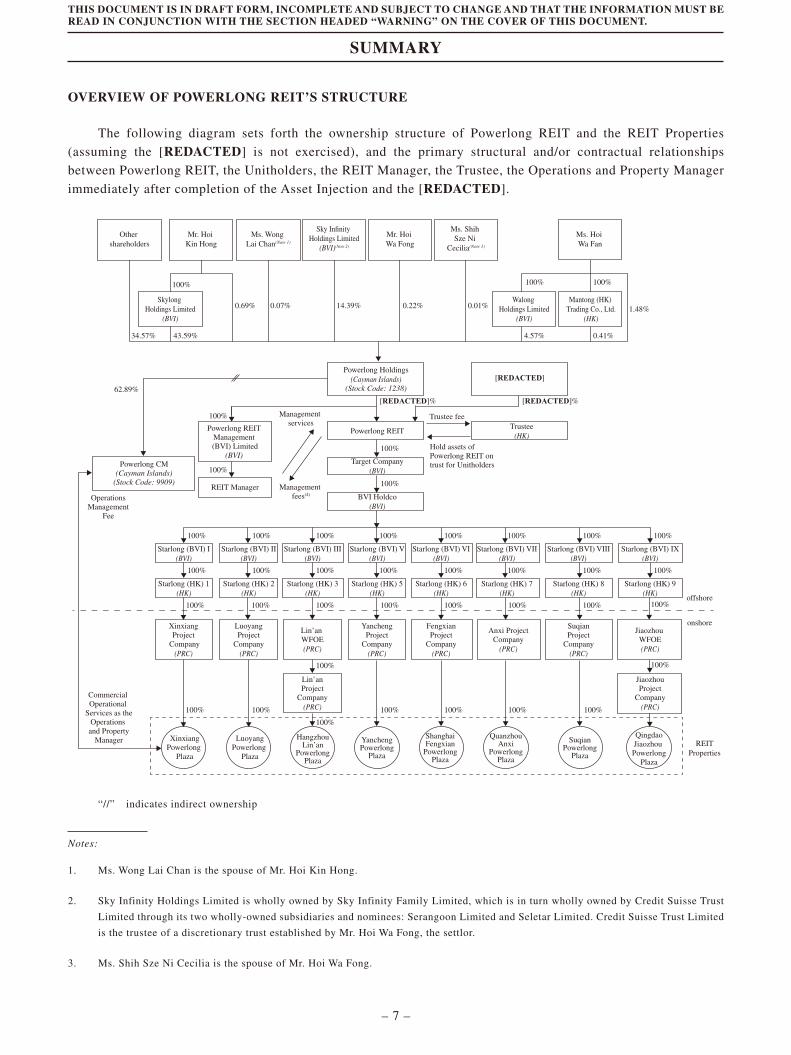

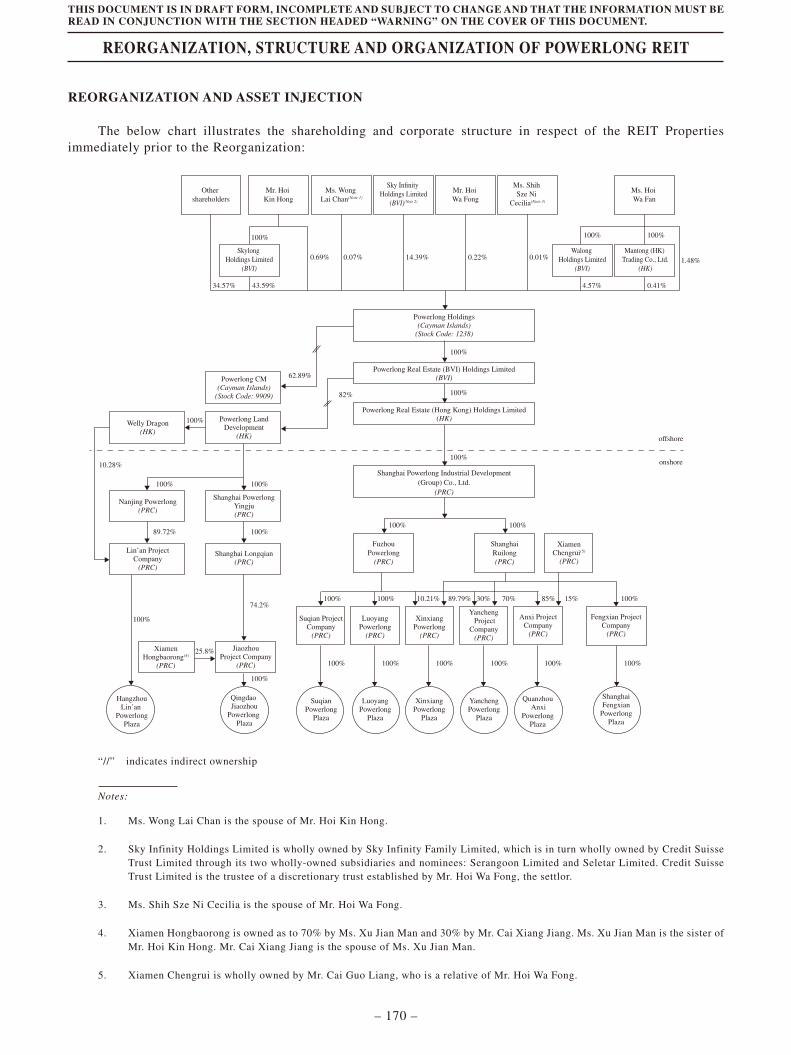

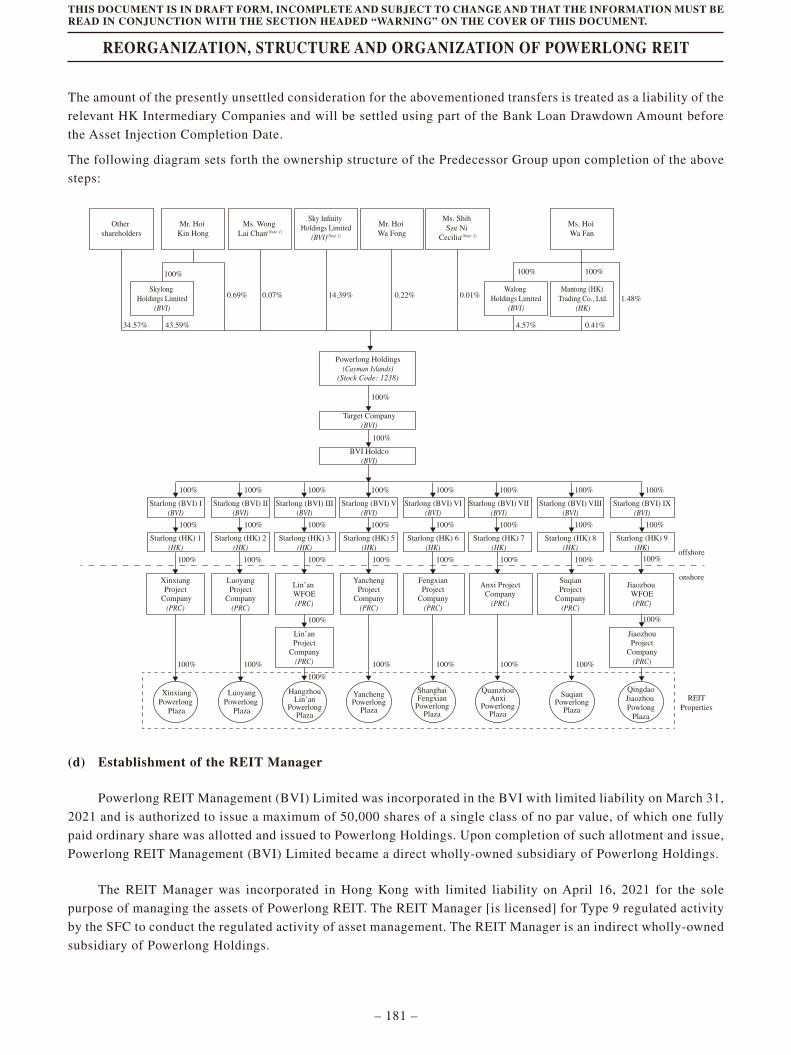

OVERVIEW OF POWERLONG REIT’S STRUCTURE

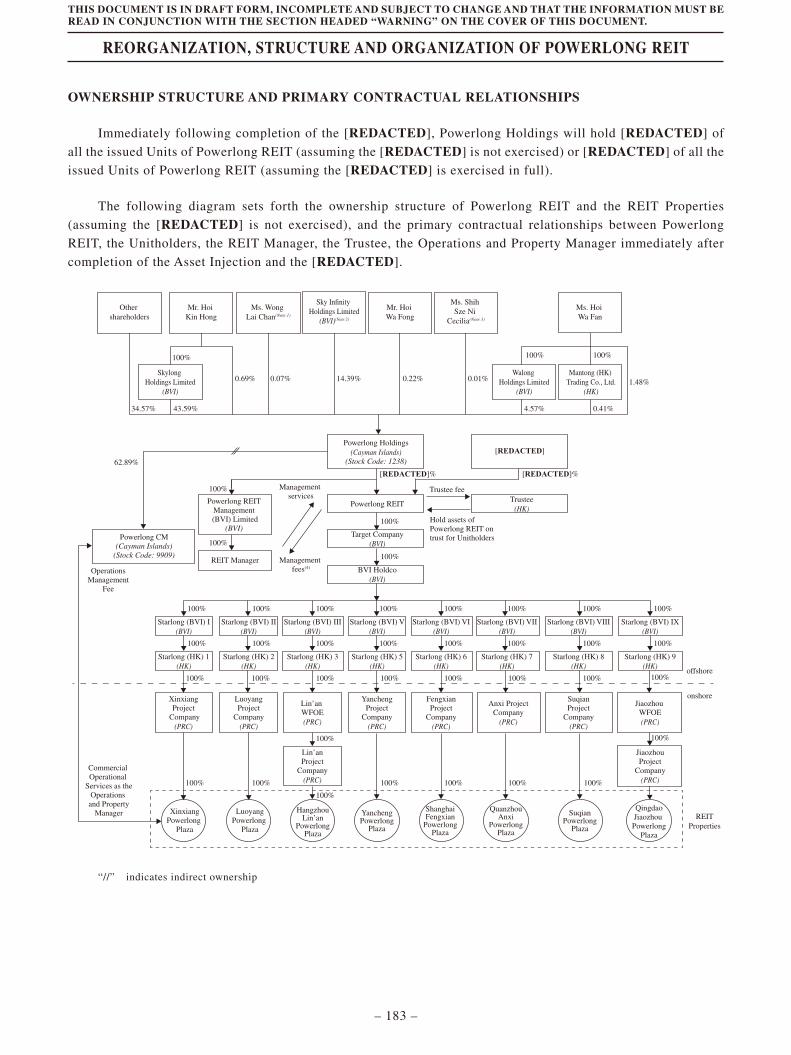

The following diagram sets forth the ownership structure of Powerlong REIT and the REIT Properties

(assuming the [REDACTED] is not exercised), and the primary structural and/or contractual relationships

between Powerlong REIT, the Unitholders, the REIT Manager, the Trustee, the Operations and Property Manager

immediately after completion of the Asset Injection and the [REDACTED].

[REDACTED]%

100%

100%

100%

100%

62.89%

Powerlong CM(Cayman Islands)

(Stock Code: 9909)

Powerlong Holdings(Cayman Islands)

(Stock Code: 1238)

Powerlong REIT

Management services

Trustee fee

Hold assets ofPowerlong REIT ontrust for Unitholders

Management fees(4)

Target Company(BVI)

OperationsManagement

Fee

Commercial Operational

Services as theOperations

and PropertyManager

BVI Holdco(BVI)

Powerlong REIT Management (BVI) Limited

(BVI)

REIT Manager

Trustee(HK)

100%

Starlong (BVI) I(BVI)

100%

Starlong (HK) 1(HK)

100%

Starlong (BVI) II(BVI)

100%

Starlong (HK) 2(HK)

100%

100%100%

100%

HangzhouLin’an

PowerlongPlaza

Starlong (BVI) III(BVI)

100%

Starlong (HK) 3(HK)

100%100%

Lin’an WFOE(PRC)

100%

100%

Lin’anProject

Company(PRC) 100%

100%

SuqianPowerlong

Plaza

Starlong (BVI) VIII(BVI)

100%

Starlong (HK) 8(HK)

100%

SuqianProject

Company(PRC)

100%

100%

100%

100%

YanchengPowerlong

Plaza

Starlong (BVI) V(BVI)

Starlong (HK) 5(HK)

YanchengProject

Company(PRC)

100%

100%

QuanzhouAnxi

PowerlongPlaza

Starlong (BVI) VII(BVI)

100%

Starlong (HK) 7(HK)

100%

Anxi ProjectCompany

(PRC)

100%

100%

ShanghaiFengxian

PowerlongPlaza

Starlong (BVI) VI(BVI)

100%

Starlong (HK) 6(HK)

100%

FengxianProject

Company(PRC)

Ms. Hoi Wa Fan

Other shareholders

Mr. Hoi Kin Hong

Skylong Holdings Limited

(BVI)

Ms. Wong Lai Chan(Note 1)

Ms. Shih Sze Ni

Cecilia(Note 3)

Walong Holdings Limited

(BVI)

Mantong (HK) Trading Co., Ltd.

(HK)

Sky Infinity Holdings Limited

(BVI)(Note 2)

Mr. Hoi Wa Fong

1.48%

100%100%

0.01%0.22%14.39%0.07%0.69%

100%

43.59%34.57% 0.41%4.57%

XinxiangProject

Company(PRC)

LuoyangProject

Company(PRC)

XinxiangPowerlong

Plaza

LuoyangPowerlong

Plaza

100%

Starlong (BVI) IX(BVI)

100%

Starlong (HK) 9(HK)

100%

100%

Jiaozhou WFOE(PRC)

JiaozhouProject

Company(PRC)

QingdaoJiaozhou

PowerlongPlaza

offshore

onshore

REITProperties

[REDACTED]%

[REDACTED]

“//” indicates indirect ownership

Notes:

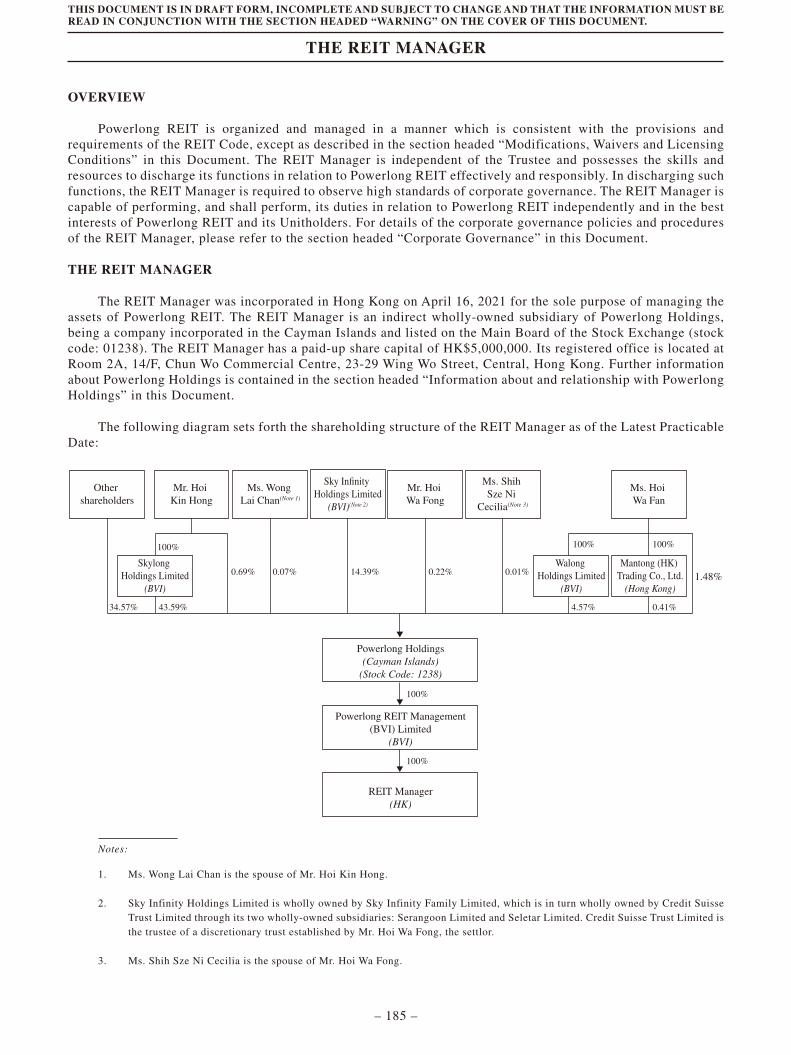

1. Ms. Wong Lai Chan is the spouse of Mr. Hoi Kin Hong.

2. Sky Infinity Holdings Limited is wholly owned by Sky Infinity Family Limited, which is in turn wholly owned by Credit Suisse Trust

Limited through its two wholly-owned subsidiaries and nominees: Serangoon Limited and Seletar Limited. Credit Suisse Trust Limited

is the trustee of a discretionary trust established by Mr. Hoi Wa Fong, the settlor.

3. Ms. Shih Sze Ni Cecilia is the spouse of Mr. Hoi Wa Fong.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

SUMMARY

– 7 –

4. Pursuant to the Trust Deed, the REIT Manager will manage Powerlong REIT and will receive management fees from Powerlong REIT.

Please refer to the section headed “The REIT Manager—Further Details Regarding the REIT Manager—Fees, Costs and Expenses of the

REIT Manager” in this Document for further details.

5. Pursuant to the Commercial Operational Services Framework Agreement, the Powerlong CM Group will provide Commercial

Operational Services in respect of the REIT Properties including, among other things, leasing services, marketing services and property

management services, and will receive Operations Management Fee from the Powerlong REIT Group. Please refer to “The Operations

and Property Managers—The Commercial Operational Services Framework Agreement” and “Connected Party

Transactions—Continuing Connected Party Transactions—Non-Exempt Continuing Connected Party Transactions with Connected

Persons—The Commercial Operational Services Framework Agreement” in this Document for further details.

THE REIT MANAGER

The REIT Manager was incorporated in Hong Kong on April 16, 2021 for the sole purpose of managing theassets of Powerlong REIT. The REIT Manager is an indirect wholly-owned subsidiary of Powerlong Holdings,being a company incorporated in the Cayman Islands and listed on the Main Board of the Stock Exchange (stockcode: 1238).

The REIT Manager is licensed by the SFC to conduct the regulated activity of asset management. The REITManager is responsible for the overall management of Powerlong REIT and ensuring compliance with theapplicable provisions of the REIT Code, the SFO, the Listing Rules, the Trust Deed, all relevant contracts and allother relevant laws, rules and regulations.

For further details on the REIT Manager, see “The REIT Manager” in this Document.

THE TRUSTEE

The trustee of Powerlong REIT is DB Trustees (Hong Kong) Limited. The Trustee is a company incorporatedin Hong Kong and registered as a trust company under section 77 of the Trustee Ordinance. The Trustee is qualifiedto act as a trustee for collective investment schemes authorized under the SFO pursuant to the REIT Code.

The Trustee has the fiduciary duty to hold assets of Powerlong REIT in trust for the benefits of theUnitholders, and to oversee the activities of the REIT Manager for compliance with the relevant constitutivedocuments of, and relevant regulatory requirements applicable to, Powerlong REIT. This includes ensuring that allinvestment activities carried out by the REIT Manager are in line with the investment objective and policy ofPowerlong REIT and the constitutive documents of Powerlong REIT, and are in the interest of the Unitholders.

For details of the Trustee’s obligations under the Trust Deed and the REIT Code, see “The Trust Deed” in thisDocument.

THE OPERATIONS AND PROPERTY MANAGER

The Operations and Property Manager, Powerlong CM, is an indirect non-wholly owned subsidiary ofPowerlong Holdings which is a Substantial Unitholder, and therefore it is a connected person of Powerlong REIT.The Operations and Property Manager is a commercial operational service provider in the PRC and a companylisted on the Main Board of the Stock Exchange (stock code: 9909).

Pursuant to the Commercial Operational Services Framework Agreement, the Powerlong CM Group [hasagreed] to provide, among other things, the Commercial Operational Services including leasing services,marketing services and property management services, and is entitled to receive the Operations Management Feefrom the Powerlong REIT Group.

For details, see “The Operations and Property Manager” in this Document.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

SUMMARY

– 8 –

CORPORATE GOVERNANCE

With the objectives of establishing and maintaining high standards of corporate governance, certain policiesand procedures have been put in place to promote the operation of Powerlong REIT in a transparent manner andwith built-in checks and balances. The Trustee and the REIT Manager are independent of each other, with theirrespective roles in relation to Powerlong REIT set out in the REIT Code and the Trust Deed. The REIT Manager isrequired under the REIT Code to act in the best interests of Unitholders, to whom the Trustee also owes fiduciaryduties. The Board comprises seven members, three of whom are independent non-executive Directors. Policies andprocedures have been established for, amongst other things, monitoring and supervising dealings in Units by theDirectors and the REIT Manager. For further details, see “Corporate Governance” in this Document.

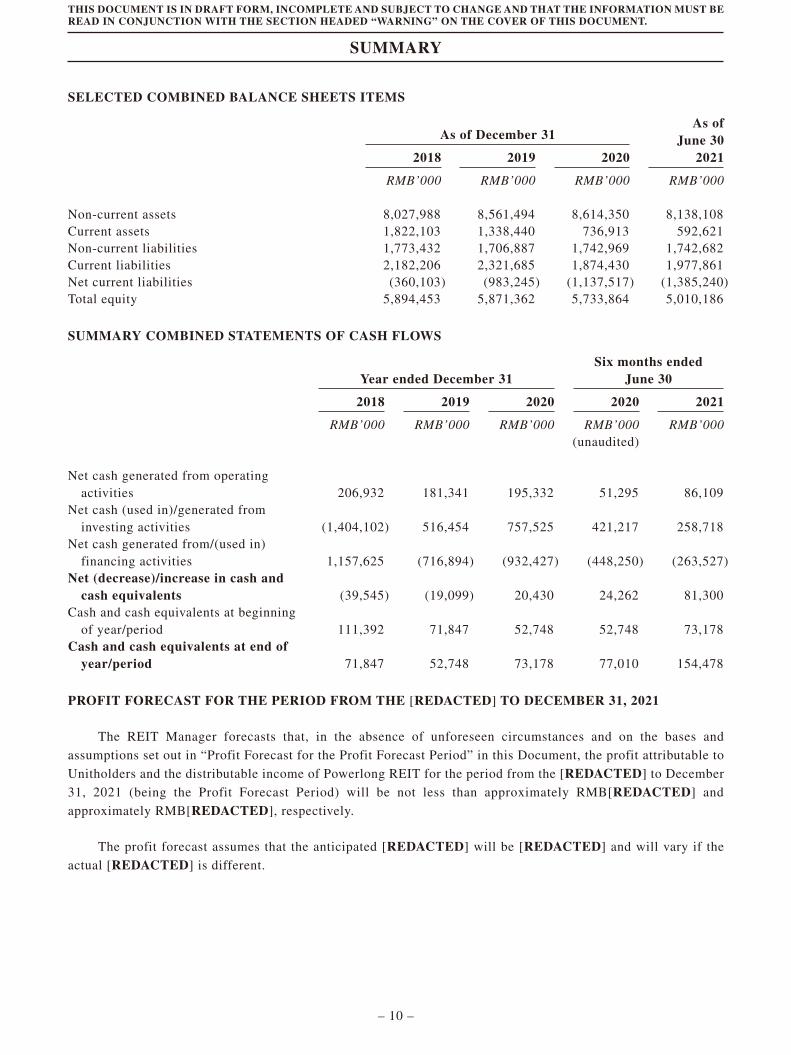

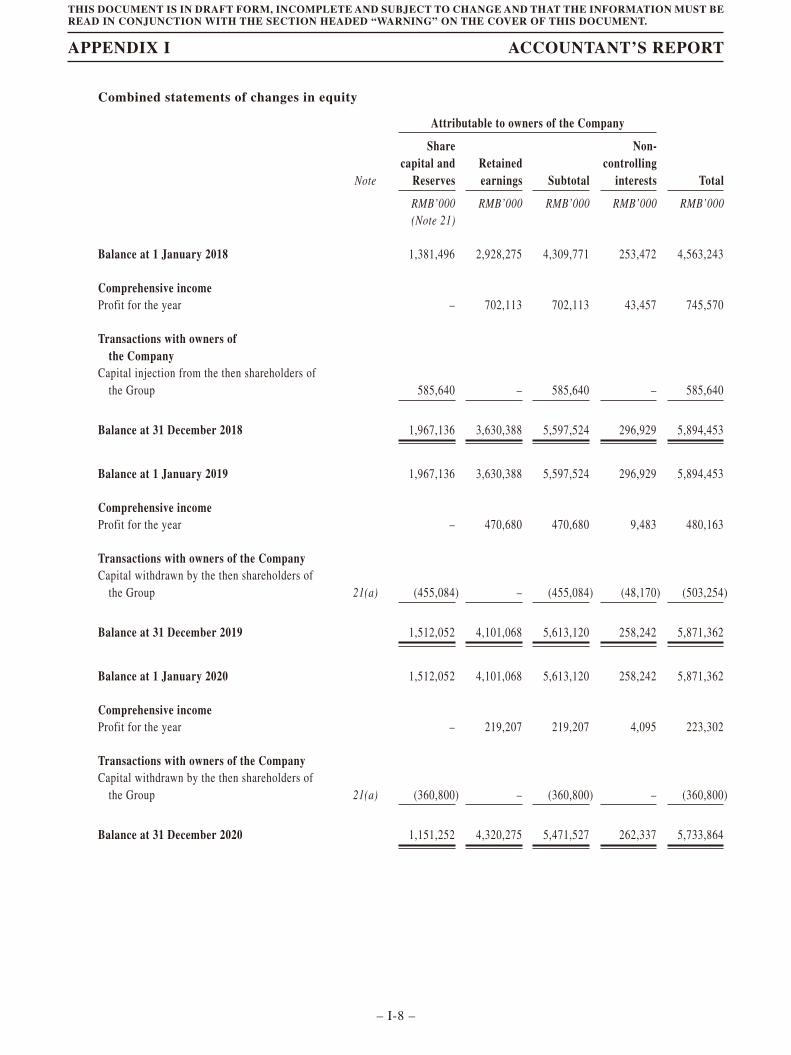

SUMMARY FINANCIAL INFORMATION

The following tables set forth summary financial information on a historical basis for the Predecessor Group.

The combined balance sheets as of December 31, 2018, 2019 and 2020 and June 30, 2021 and the combinedstatements of comprehensive income, the combined statements of changes in equity and the combined statementsof cash flows for each of the years ended December 31, 2018, 2019 and 2020 and the six months ended June 30,2021 have been derived from the Predecessor Group’s financial information and related notes thereto, which havebeen included in Appendix I to this Document. Such financial information and related notes have been prepared inaccordance with HKFRS and have been audited by PricewaterhouseCoopers, the reporting accountant of thePredecessor Group. The combined statements of comprehensive income and the combined statements of cashflows for the six months ended June 30, 2020 have been derived from the Predecessor Group’s unaudited financialinformation and related notes thereto, which have been included in Appendix I to this Document.

The selected historical financial included below and set forth in Appendix I to this Document is not indicativeof Powerlong REIT’s future performance. You should read the following summary of financial informationtogether with “The REIT Properties and Business,” “Management’s Discussion and Analysis of FinancialCondition and Results of Operations” and “Unaudited Pro Forma Statement of Financial Position” in thisDocument and the historical financial information of the Predecessor Group and related notes thereto set forth inAppendix I to this Document. For a discussion of Powerlong REIT’s future financial condition and results ofoperations, please see “Management’s Discussion and Analysis of Future Operations” in this Document.

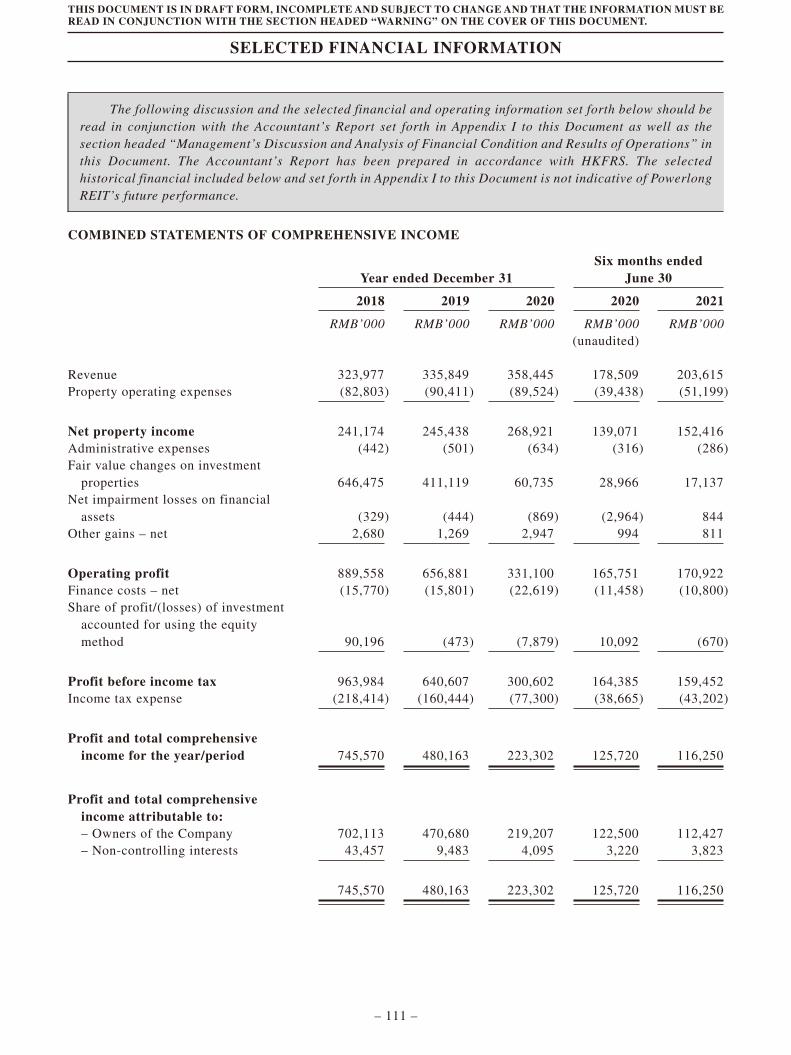

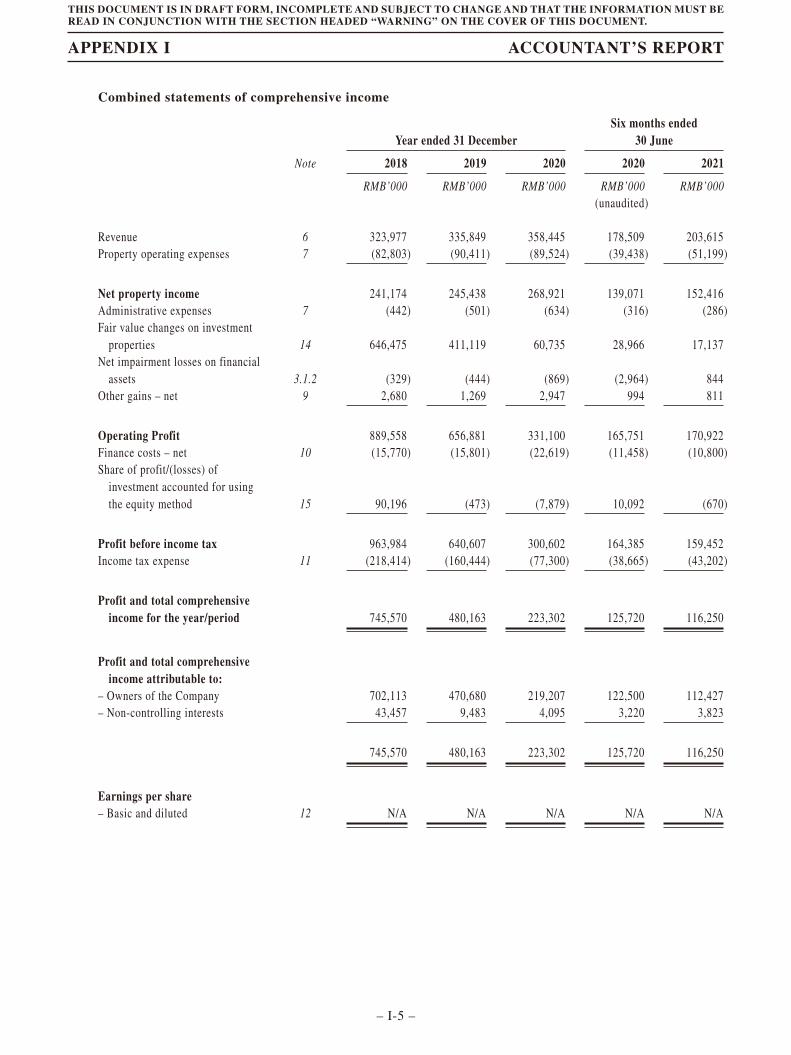

SELECTED COMBINED STATEMENTS OF COMPREHENSIVE INCOME ITEMS

Year ended December 31Six months ended

June 30

2018 2019 2020 2020 2021

RMB’000 RMB’000 RMB’000 RMB’000 RMB’000(unaudited)

Revenue 323,977 335,849 358,445 178,509 203,615Property operating expenses (82,803) (90,411) (89,524) (39,438) (51,199)

Net property income 241,174 245,438 268,921 139,071 152,416

Operating profit 889,558 656,881 331,100 165,751 170,922

Profit before income tax 963,984 640,607 300,602 164,385 159,452Income tax expense (218,414) (160,444) (77,300) (38,665) (43,202)

Profit for the year/period and totalcomprehensive income 745,570 480,163 223,302 125,720 116,250

Profit and total comprehensive incomeattributable to:– Owners of the Company 702,113 470,680 219,207 122,500 112,427– Non-controlling interests 43,457 9,483 4,095 3,220 3,823

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

SUMMARY

– 9 –

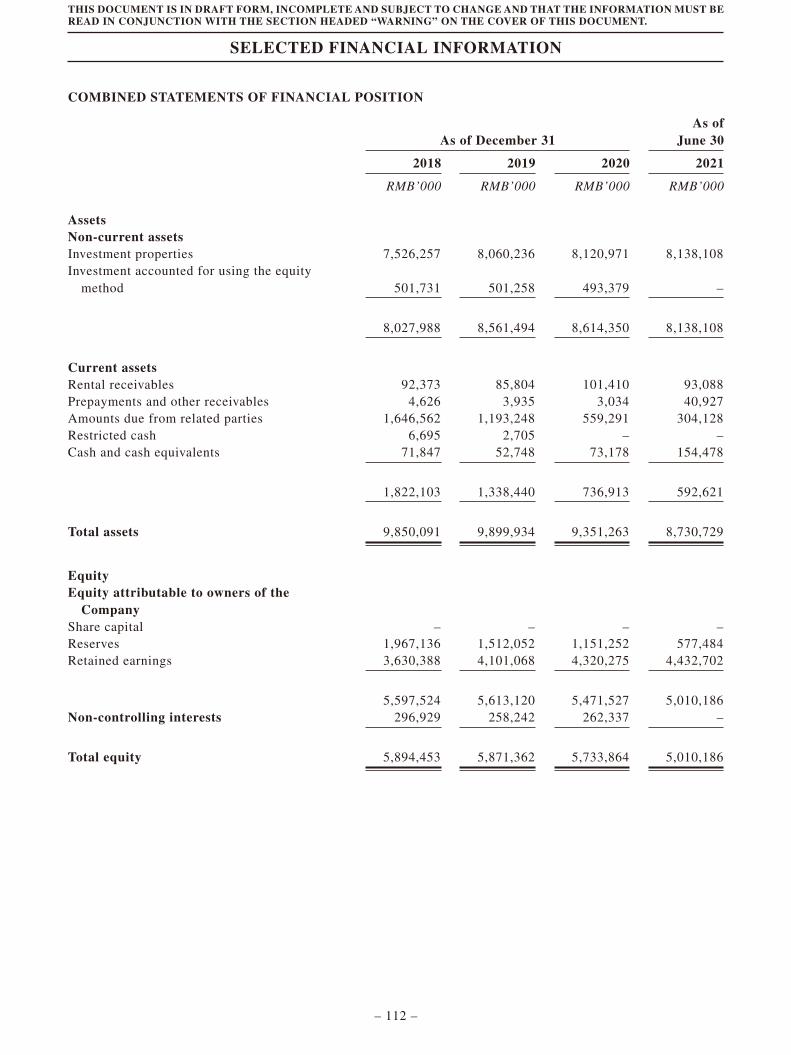

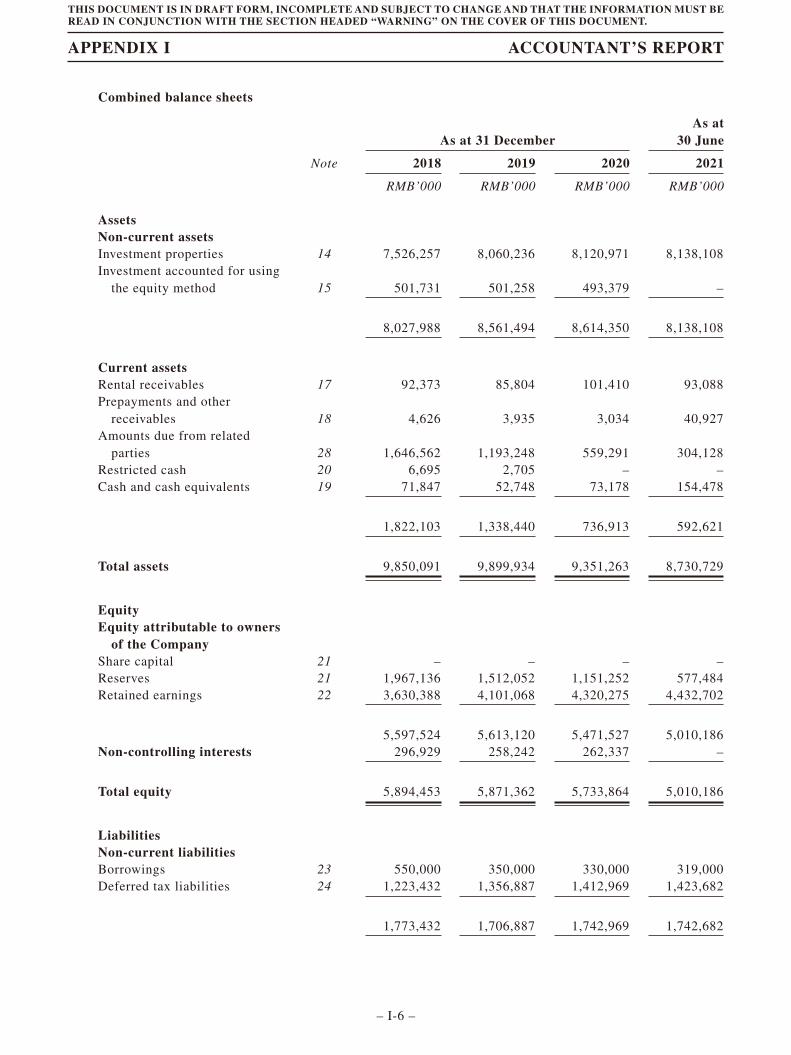

SELECTED COMBINED BALANCE SHEETS ITEMS

As of December 31As of

June 3020212018 2019 2020

RMB’000 RMB’000 RMB’000 RMB’000

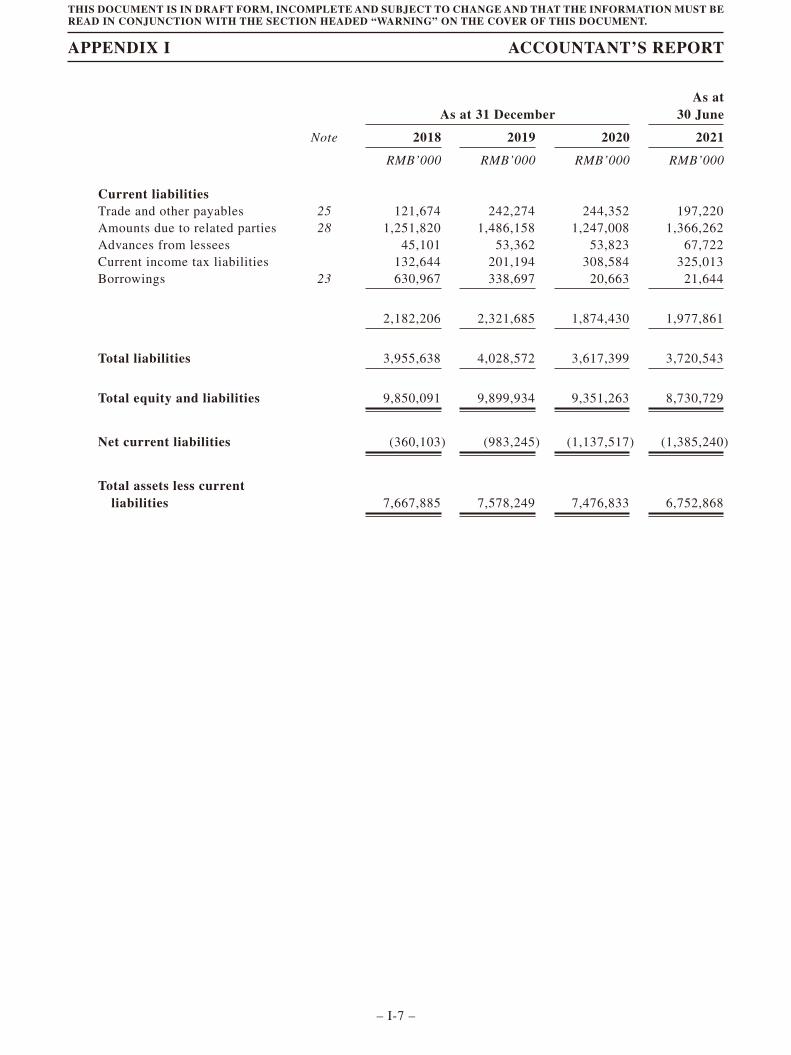

Non-current assets 8,027,988 8,561,494 8,614,350 8,138,108Current assets 1,822,103 1,338,440 736,913 592,621Non-current liabilities 1,773,432 1,706,887 1,742,969 1,742,682Current liabilities 2,182,206 2,321,685 1,874,430 1,977,861Net current liabilities (360,103) (983,245) (1,137,517) (1,385,240)Total equity 5,894,453 5,871,362 5,733,864 5,010,186

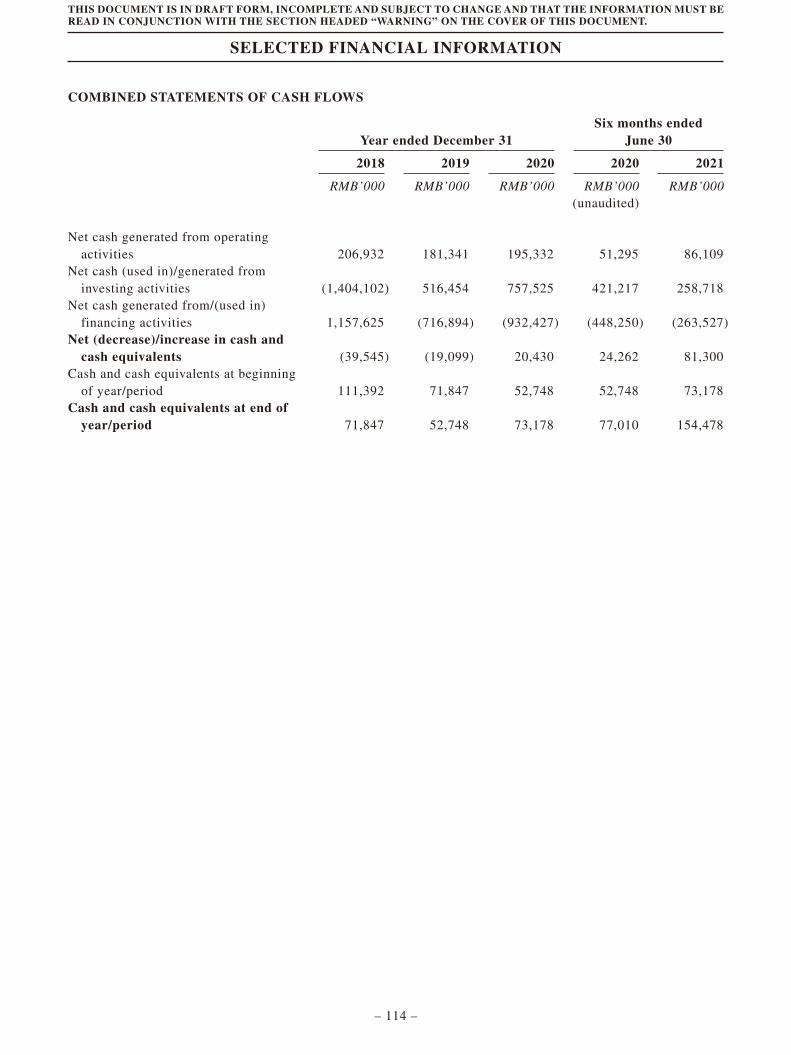

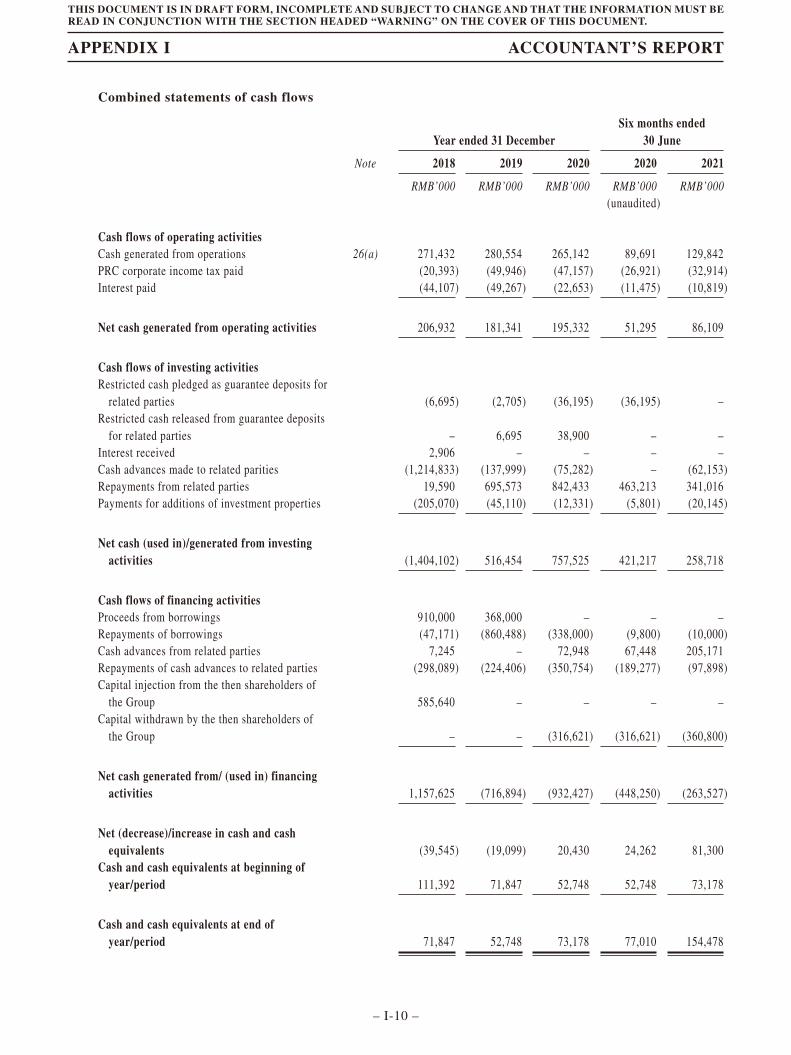

SUMMARY COMBINED STATEMENTS OF CASH FLOWS

Year ended December 31Six months ended

June 30

2018 2019 2020 2020 2021

RMB’000 RMB’000 RMB’000 RMB’000 RMB’000(unaudited)

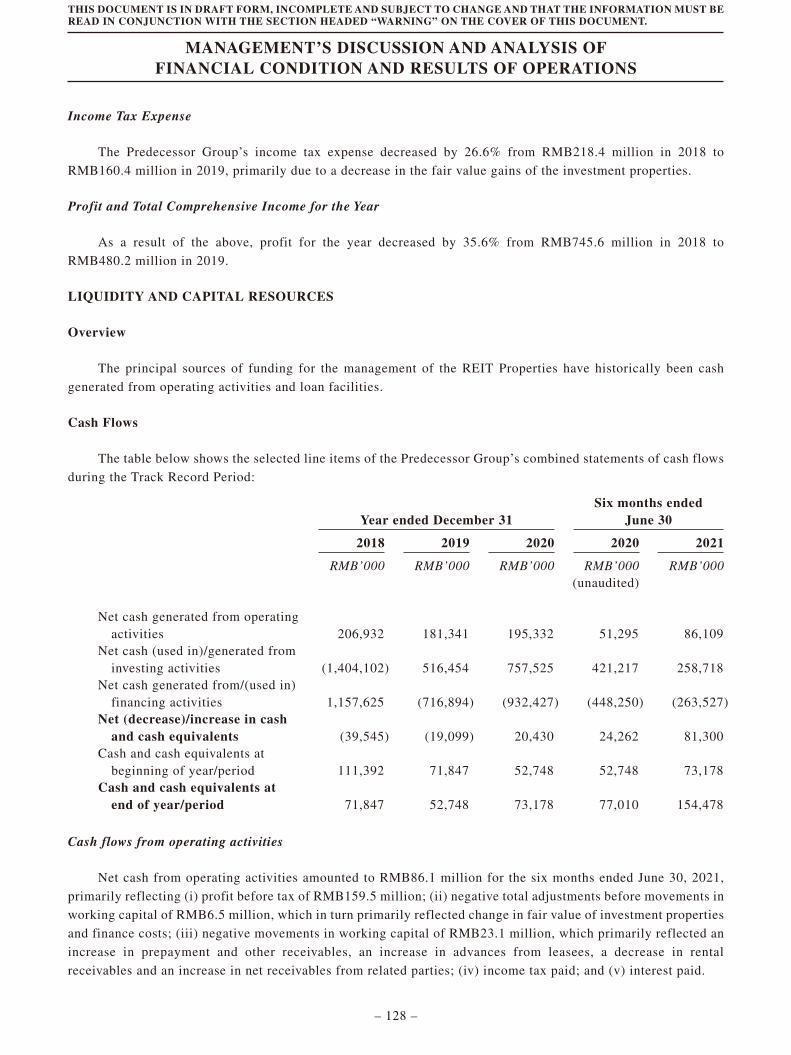

Net cash generated from operatingactivities 206,932 181,341 195,332 51,295 86,109

Net cash (used in)/generated frominvesting activities (1,404,102) 516,454 757,525 421,217 258,718

Net cash generated from/(used in)financing activities 1,157,625 (716,894) (932,427) (448,250) (263,527)

Net (decrease)/increase in cash andcash equivalents (39,545) (19,099) 20,430 24,262 81,300

Cash and cash equivalents at beginningof year/period 111,392 71,847 52,748 52,748 73,178

Cash and cash equivalents at end ofyear/period 71,847 52,748 73,178 77,010 154,478

PROFIT FORECAST FOR THE PERIOD FROM THE [REDACTED] TO DECEMBER 31, 2021

The REIT Manager forecasts that, in the absence of unforeseen circumstances and on the bases and

assumptions set out in “Profit Forecast for the Profit Forecast Period” in this Document, the profit attributable to

Unitholders and the distributable income of Powerlong REIT for the period from the [REDACTED] to December

31, 2021 (being the Profit Forecast Period) will be not less than approximately RMB[REDACTED] and

approximately RMB[REDACTED], respectively.

The profit forecast assumes that the anticipated [REDACTED] will be [REDACTED] and will vary if the

actual [REDACTED] is different.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

SUMMARY

– 10 –

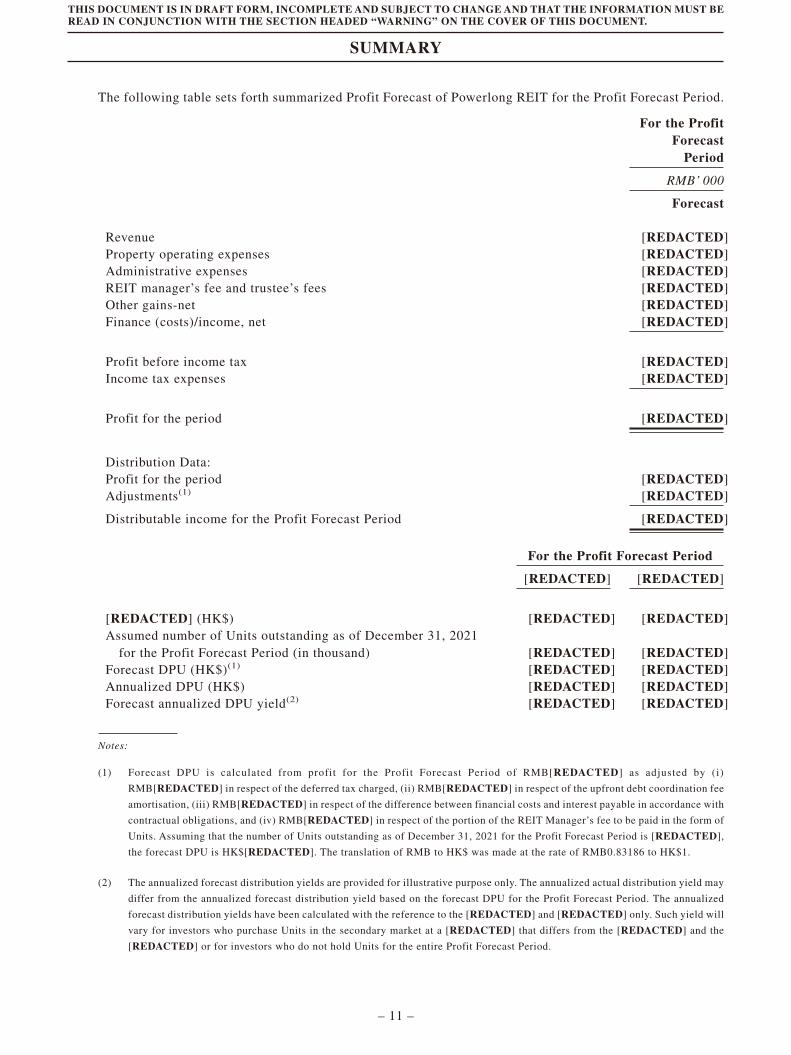

The following table sets forth summarized Profit Forecast of Powerlong REIT for the Profit Forecast Period.

For the ProfitForecast

Period

RMB’ 000

Forecast

Revenue [REDACTED]Property operating expenses [REDACTED]Administrative expenses [REDACTED]REIT manager’s fee and trustee’s fees [REDACTED]Other gains-net [REDACTED]Finance (costs)/income, net [REDACTED]

Profit before income tax [REDACTED]Income tax expenses [REDACTED]

Profit for the period [REDACTED]

Distribution Data:Profit for the period [REDACTED]Adjustments(1) [REDACTED]

Distributable income for the Profit Forecast Period [REDACTED]

For the Profit Forecast Period

[REDACTED] [REDACTED]

[REDACTED] (HK$) [REDACTED] [REDACTED]Assumed number of Units outstanding as of December 31, 2021

for the Profit Forecast Period (in thousand) [REDACTED] [REDACTED]Forecast DPU (HK$)(1) [REDACTED] [REDACTED]Annualized DPU (HK$) [REDACTED] [REDACTED]Forecast annualized DPU yield(2) [REDACTED] [REDACTED]

Notes:

(1) Forecast DPU is calculated from profit for the Profit Forecast Period of RMB[REDACTED] as adjusted by (i)

RMB[REDACTED] in respect of the deferred tax charged, (ii) RMB[REDACTED] in respect of the upfront debt coordination fee

amortisation, (iii) RMB[REDACTED] in respect of the difference between financial costs and interest payable in accordance with

contractual obligations, and (iv) RMB[REDACTED] in respect of the portion of the REIT Manager’s fee to be paid in the form of

Units. Assuming that the number of Units outstanding as of December 31, 2021 for the Profit Forecast Period is [REDACTED],

the forecast DPU is HK$[REDACTED]. The translation of RMB to HK$ was made at the rate of RMB0.83186 to HK$1.

(2) The annualized forecast distribution yields are provided for illustrative purpose only. The annualized actual distribution yield may

differ from the annualized forecast distribution yield based on the forecast DPU for the Profit Forecast Period. The annualized

forecast distribution yields have been calculated with the reference to the [REDACTED] and [REDACTED] only. Such yield will

vary for investors who purchase Units in the secondary market at a [REDACTED] that differs from the [REDACTED] and the

[REDACTED] or for investors who do not hold Units for the entire Profit Forecast Period.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

SUMMARY

– 11 –

REORGANIZATION DEED

The REIT Manager (in its capacity as manager of Powerlong REIT) and the Trustee entered into the

Reorganization Deed with Powerlong Holdings (as seller), pursuant to which Powerlong Holdings has

conditionally agreed to transfer all of the issued shares of the Target Company to the Trustee (in its capacity as

trustee of Powerlong REIT) in exchange for the issue of [REDACTED] Units (which represents [REDACTED]%

of the issued Units upon completion of the Reorganization) to Powerlong Holdings or its nominees.

CERTAIN FEES AND CHARGES

The following is a summary of certain fees and charges payable by Powerlong REIT in connection with the

establishment and ongoing management of Powerlong REIT:

Payable by Powerlong REIT Amount Payable

(a) REIT Manager’s fees Base Fee

On a semi-annual basis, a Base Fee not exceeding 0.25%per annum (and being 0.25% as of the [REDACTED]) ofthe Value of the Deposited Properties.

Variable Fee

On an annual basis, a Variable Fee of 3.0% per annum ofthe Net Property Income (in respect of each REITProperty, provided that the NAV per Unit exceeds theNAV Unit on which the Variable Fee was last calculatedand paid)

Acquisition Fee

An Acquisition Fee not exceeding 1.0% (and being 1.0%as of the [REDACTED]) of the acquisition price of eachreal estate asset in the form of land acquired, directly orindirectly, by Powerlong REIT (pro-rated if applicable tothe proportion of Powerlong REIT’s interest in the realestate acquired)

Divestment Fee

A Divestment Fee not exceeding 0.5% (and being 0.5% asof the [REDACTED]) of the sale price of each real estateasset in the form of land sold or divested, directly orindirectly, by Powerlong REIT (pro-rated if applicable tothe proportion of Powerlong REIT’s interest in the realestate sold).

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

SUMMARY

– 12 –

Payable by Powerlong REIT Amount Payable

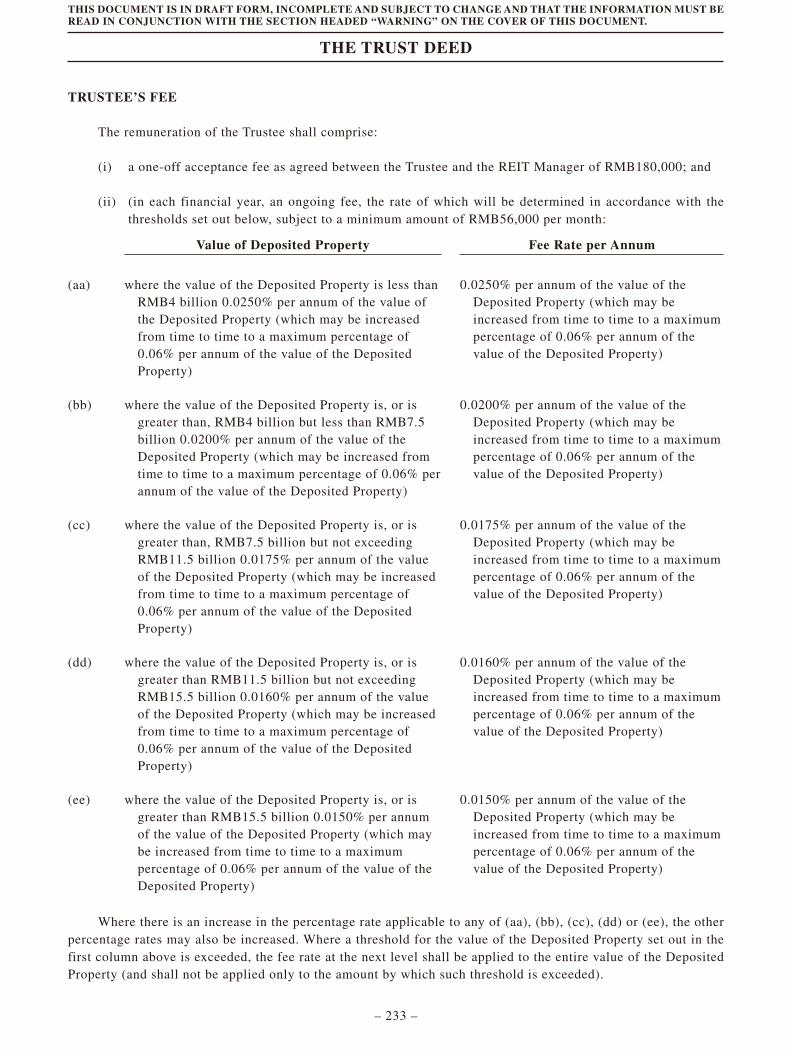

(b) Trustee’s fees Currently 0.0150% to 0.0250% per annum of the value ofthe Deposited Property payable semi-annually in arrears,which may be adjusted from time to time but subject to aminimum of RMB56,000 per month and a maximum capof 0.06% per annum of the value of the DepositedProperty. Powerlong REIT will also pay to the Trustee aone-off acceptance fee of RMB180,000 upon[REDACTED].

The Trustee may also charge Powerlong REIT additionalfees on a time-cost basis at a rate to be agreed with theREIT Manager from time to time if the Trustee were toundertake duties that are of an exceptional nature orotherwise outside the scope of its normal duties in theordinary course of normal day-to-day business operationof Powerlong REIT, such as acquisition or divestment ofinvestments by Powerlong REIT after [REDACTED].

(c) Operations Management Fee An amount equivalent to 5% per annum of the rentalincome in respect of each REIT Property.

USE OF [REDACTED]

The REIT Manager estimates that the total [REDACTED] from the [REDACTED], which consist entirely of

[REDACTED] to the [REDACTED] from the [REDACTED] of the [REDACTED], will be approximately

HK$[REDACTED] (based on the [REDACTED]), and approximately HK$[REDACTED] (based on the

[REDACTED]), assuming the [REDACTED] is not exercised.

[REDACTED]

The total expenses for the [REDACTED] are estimated to be approximately RMB[REDACTED] assuming

an [REDACTED] of HK$[REDACTED] per [REDACTED] (which is the [REDACTED] of the [REDACTED]

range), which includes [REDACTED] and other legal and professional fees directly related to the [REDACTED],

assuming the [REDACTED] is not exercised. All [REDACTED] will be borne by the [REDACTED].

RISK FACTORS

There are risks associated with any investment. These risks include without limitation: (i) the REIT

Properties are all located in the PRC, which exposes Powerlong REIT to economic and property market conditions

in the PRC; (ii) Powerlong REIT’s results of operations may be adversely affected if the Operations and Property

Manager fails to operate or manage the REIT Properties in an effective and efficient manner or the REIT Manager

decides to terminate the Commercial Operational Services Framework Agreement before expiration or decides not

to renew such agreement upon expiration; (iii) the REIT Manager may not be able to achieve its key objectives for

Powerlong REIT and its stated strategies for accomplishing such objectives may change; (iv) Powerlong REIT’s

portfolio growth depends on its ability to obtain external sources of capital; (v) Powerlong REIT’s investments or

acquisitions in the future may not be successful, which may adversely affect the results of operations of Powerlong

REIT.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

SUMMARY

– 13 –

For further information, please see “Risk Factors” in this Document. Investors should read that entire section

carefully before they decide to invest in the Units.

NO MATERIAL ADVERSE CHANGE

The Directors have confirmed that, since June 30, 2021 and up to the date of this Document, there had been

no material adverse change in Powerlong REIT’s financial or trading position or prospects and no event had

occurred that would materially and adversely affect the financial information in the Accountant’s Report included

as Appendix I to this Document.

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

SUMMARY

– 14 –

In this Document, unless the context otherwise requires, the following terms shall have the meanings setout below. Certain terms are explained in ”Technical Terms” in this Document,

“Accountant's Report” the accountant's report prepared by PricewaterhouseCoopers, asset out in Appendix I to this Document

“Acquisition Fee” as used in the Trust Deed, the acquisition fee not exceeding 1%(and being 1% as of the date of the Trust Deed) of the acquisitionprice of any real estate acquired directly or indirectly byPowerlong REIT (pro-rated if applicable to the proportion ofPowerlong REIT’s interest in the real estate acquired) payable tothe REIT Manager pursuant to the Trust Deed

“Adjustments” has the meaning set out in “Distribution Policy” in this Document

“Affected Units” has the meaning set out in “The Trust Deed—Deemed Applicationof Part XV of the SFO” in this Document

“Annual Distributable Income” has the meaning set out in “Distribution Policy” in this Document

“Anxi Project Company” Anxi Powerlong Asset Management Co., Ltd.* (安溪寶龍資產經營管理有限公司), a company established in the PRC with limitedliability on August 29, 2012, an indirect wholly-owned subsidiaryof Powerlong REIT and the direct owner of Quanzhou AnxiPowerlong Plaza

“Applicable Rules” the SFO, the REIT Code, the Listing Rules and all other law, rulesand regulations applicable to Powerlong REIT

[REDACTED]

“Appraised Value” the value of the REIT Properties as of June 30, 2021, as appraisedby the Independent Property Valuer and set out in Appendix IV tothis Document

“Asset Injection” the transactions contemplated under the Reorganization Deed

“Asset Injection Completion” completion of the Asset Injection

“Asset Injection Completion Date” the date of Asset Injection Completion

“associate(s)” has the meaning ascribed to it under Chapter 14A of the ListingRules (modified as appropriate pursuant to the REIT Code),unless the context otherwise defines

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

DEFINITIONS

– 15 –

“Assured Entitlement” the entitlement of Qualifying Powerlong Shareholders to applyfor [REDACTED] on an assured basis under the [REDACTED]to be determined on the basis of their respective shareholdings inPowerlong Holdings at 4:30 p.m. on the Assured EntitlementRecord Date

“Assured Entitlement Record Date” [●], 2021, being the record date for ascertaining the AssuredEntitlement

“Audit Committee” the audit committee of the REIT Manager

[REDACTED]

“Bank Loan Drawdown Amount” the gross amount borrowed by the Target Company under theFacilities

“Banking Ordinance” the Banking Ordinance (Chapter 155 of the Laws of Hong Kong),as amended, supplemented or otherwise modified from time totime

“Base Fee” the base fee payable to the REIT Manager on a semi-annual basisunder the Trust Deed, being 0.25% per annum of the aggregatedvaluation value of the Deposited Property

“Beneficial Powerlong Shareholder(s)” any beneficial owner of Powerlong Shares whose PowerlongShares are registered, as shown in the register of members ofPowerlong Holdings, in the name of a registered PowerlongShareholder at 4:30 p.m. on the Assured Entitlement Record Date

[REDACTED]

“Board” the board of Directors

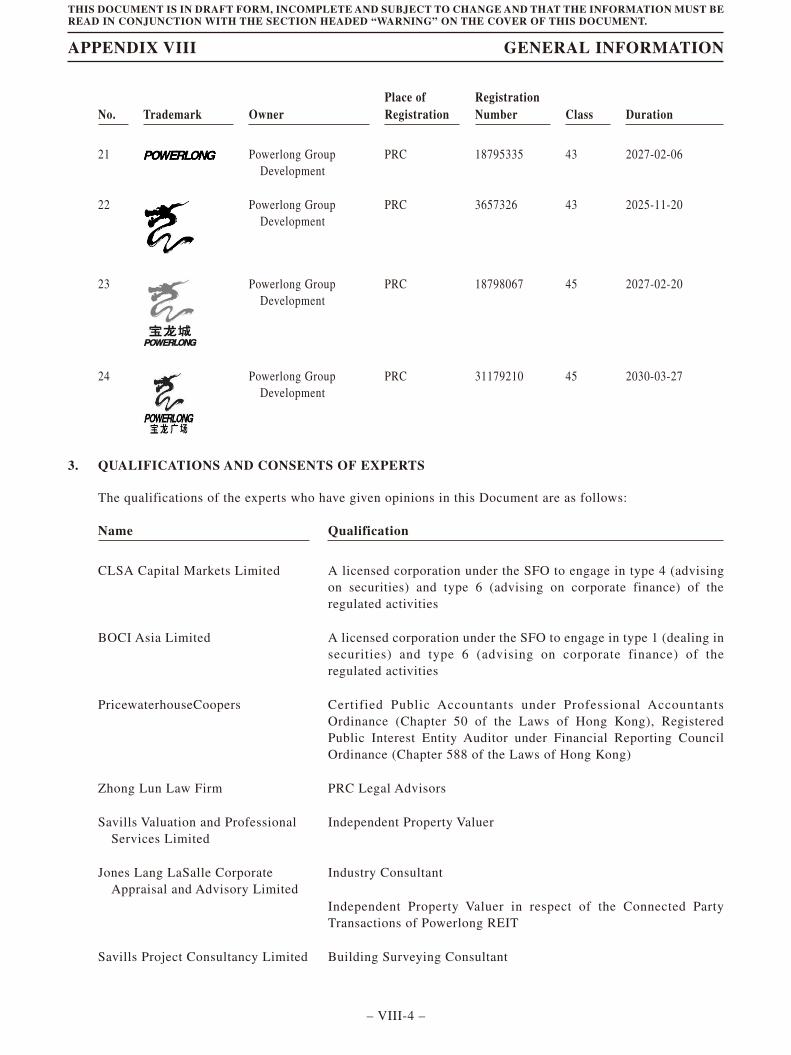

“Building Surveyor” Savills Project Consultancy Limited

“Bulletin 7” has the meaning set out in “Taxation” in this Document

“Bulletin 9” the Bulletin on Certain Issues relating to “Beneficial Owners” inTax Treaties, State Taxation Administration Bulletin 2018 No.9,issued by the SAT

“Business Day” any day (excluding Saturdays, Sundays, public holidays and anyday on which a tropical cyclone warning number 8 or above or a“black” rainstorm warning signal is hoisted in Hong Kong at anytime between the hours of 9:00 a.m. and 5:00 p.m.) on whichlicensed banks are open for general business in Hong Kong

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

DEFINITIONS

– 16 –

“BVI” the British Virgin Islands

“BVI Holdco” Starlong (BVI) Third Limited, a company incorporated in the BVIwith limited liability on March 31, 2021 and an indirectwholly-owned subsidiary of Powerlong REIT

“BVI Intermediary Companies” has the meaning set out in “Reorganization, Structure andOrganization of Powerlong REIT—Reorganization and AssetInjection” in this Document

“CAGR” compound annual growth rate

[REDACTED]

“Central China” a geographical region in China that covers the provinces ofHenan, Hubei, and Hunan

“Chairman” the chairman of the Board

“Chief Executive Officer” the chief executive officer of the REIT Manager

“Chief Financial Officer” the chief financial officer of the REIT Manager

“Chief Investment and AssetManagement Officer”

the chief investment and asset management officer of the REITManager

“Circular 82” the Circular on the Determination of Chinese-ControlledOffshore-Incorporated Enterprises as China Tax ResidentEnterprises on the Basis of Place of Effective Management, GuoShui Fa 2009 No. 82, issued by the SAT

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

DEFINITIONS

– 17 –

“Commercial Operational Services” has the meaning set out in “The Operations and PropertyManager—Commercial Operat ional Services FrameworkAgreement” in this Document

“Commercial Operational ServicesFramework Agreement”

the commercial operational services framework agreemententered into between the Operations and Property Manager andthe REIT Manager (for itself and on behalf of the PowerlongREIT Group) relating to the provision of Commercial OperationalServices in respect of the REIT Properties

“Companies Ordinance” the Companies Ordinance (Chapter 622 of the Laws of HongKong), as amended, supplemented or otherwise modified fromtime to time

“connected party rules” has the meaning set out in “Connected Party Transactions—Introduction” in this Document

“connected person(s)” has the meaning ascribed to it in the REIT Code

“Convertible Instruments” any securities convertible or exchangeable into Units, or anyoptions or warrants or similar rights for the subscription or issueof Units (or securities convertible or exchangeable into Units),issued by the REIT Manager on behalf of Powerlong REIT or anySpecial Purpose Vehicle; and references to an issue of Units“pursuant to” any Convertible Instruments means an issue ofUnits pursuant to exercise of any conversion, exchange,subscription or similar rights (as the case may be) under the termsand conditions of such Convertible Instruments

“COVID-19” a coronavirus disease caused by severe acute respiratorysyndrome coronavirus 2

“Deposited Property” as used in the Trust Deed, all of the assets of Powerlong REIT,including all its authorized investments for the time being held ordeemed to be held upon the trusts of the Trust Deed and anyinterest arising on subscription monies from the issuance of Units

“Directors” the directors of the REIT Manager

“Disclosures Committee” the disclosures committee of the REIT Manager

“Distribution Entitlement Record Date” the date or dates in respect of each distribution period determinedby the REIT Manager for the purpose of determining thedistribution entitlement to the distribution amount of theUnitholders

“distribution yield” DPU, on an annualized basis, divided by the [REDACTED] of aUnit

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

DEFINITIONS

– 18 –

“Divestment Fee” the divestment fee not exceeding 0.5% (and being 0.5% as of the[REDACTED]) of the sale price of each real estate asset sold ordivested directly or indirectly by Powerlong REIT (pro-rated ifapplicable to the proportion of Powerlong REIT’s interest in thereal estate sold) payable to the REIT Manager pursuant to theTrust Deed

“DPU” distribution(s) per Unit

“East China” a geographical region that covers the eastern coastal area ofChina, including provinces of Shandong, Jiangsu, Zhejiang, andFujian and the municipality of Shanghai

“EIT” the PRC enterprise income tax

“EIT Law” the PRC Enterprises Income Tax Law

“Existing Project Companies” has the meaning set out in “Reorganization, Structure andOrganization of Powerlong REIT—Reorganization and AssetInjection” in this Document

“Extreme Conditions” extreme conditions caused by a super typhoon as announced bythe government of Hong Kong, or any extreme conditions orevents, the occurrence of which causes serious interruption to theordinary course business operations in Hong Kong

“Facilities” the Onshore Facilities and the Offshore Facilities

“Fengxian Project Company” Shanghai Xiantong Enterprise Development Co., Ltd.* (上海賢通企業發展有限公司), a company established in PRC with limitedliability on March 12, 2021, an indirect wholly-owned subsidiaryof Powerlong REIT and the direct owner of Shanghai FengxianPowerlong Plaza

“Fuzhou Powerlong” Fuzhou Powerlong Trading Co., Ltd.* (福州寶龍貿易有限公司),a company established the PRC with limited liability on October21, 2003 and an indirect wholly-owned subsidiary of PowerlongHoldings

“GDP” gross domestic product

[REDACTED]

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

DEFINITIONS

– 19 –

“Guangdong-Hong Kong-MacauGreater Bay Area”

the geographical region that consists of Hong Kong, Macao andnine cities in Guangdong (namely Guangzhou, Shenzhen, Zhuhai,Foshan, Huizhou, Dongguan, Zhongshan, Jiangmen andZhaoqing) with a total land area of 56,000 square kilometers

“Head of Operation” the head of operation of the REIT Manager

“HK$,” “HKD” or “Hong Kong dollars” Hong Kong dollars, the lawful currency of Hong Kong

[REDACTED]

“Hong Kong” or “HK” the Hong Kong Special Administrative Region of the PRC

“Hong Kong Government” the Government of the Hong Kong

“HK Intermediary Companies” has the meaning set out in “Reorganization, Structure andOrganization of Powerlong REIT—Reorganization and AssetInjection” in this Document

[REDACTED]

“HKFRS” Hong Kong Financial Reporting Standards

“Independent Property Valuer” Savills Valuation and Professional Services Limited

“Independent Unitholders” Unitholders other than those who have a material interest in therelevant transactions within the meaning of the REIT Code

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

DEFINITIONS

– 20 –

“Interim Distributable Income” for any distribution period, the amount calculated by the REITManager (based on the interim unaudited financial statements ofPowerlong REIT for that distribution period) as representing theconsolidated audited net profit of Powerlong REIT for thatdistribution period, after provision for tax, and taking intoaccount the Adjustments and, for the avoidance of doubt,excludes any additional discretionary distributions out of capital

[REDACTED]

“Investment Committee” the investment committee of the REIT Manager

“Jiaozhou Project Company” Qingdao Powerlong Yingju Land Development Co., Ltd.*(青島寶龍英聚置地發展有限公司), a company established in thePRC with limited liabili ty on June 5, 2013, an indirectwholly-owned subsidiary of Powerlong REIT and the directowner of Qingdao Jiaozhou Powerlong Plaza

[REDACTED]

“Joint Listing Agents” CLSA Capital Markets Limited and BOCI Asia Limited

“Joint Venture Entity” an entity, partnership or other arrangement in which or throughwhich Powerlong REIT invests in any jointly owned property aspermitted under the REIT Code

“Land Use Grant Rules” the Rules Regarding the Grant of State-owned Land Use Rightsby Way of Tender, Auction and Listing-for-sale of the PRC whichare effective from November 1, 2007

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

DEFINITIONS

– 21 –

“Lapse Event” has the meaning set out in “Material Agreements and OtherDocuments—Deed of Right of First Refusal—Failure to Exercisethe Right of First Refusal” in this Document

“LAT” Land Appreciation Tax

“Latest Practicable Date” August 20, 2021, being the latest practicable date for the purposesof ascertaining certain information contained in this Document

“Lin'an Project Company” Hangzhou Longyao Industrial Co., Ltd.* (杭州龍耀實業有限公司), a company established in the PRC with limited liability onAugust 3, 2017, an indirect wholly-owned subsidiary ofPowerlong REIT and the direct owner of Hangzhou Lin’anPowerlong Plaza

[REDACTED]

“Listing Rules” the Rules Governing the Listing of Securities on the StockExchange

“Luoyang Powerlong” Luoyang Powerlong Property Development Co., Ltd.* (洛陽寶龍置業發展有限公司), a company established in the PRC withlimited liability on March 3, 2006 and an indirect wholly-ownedsubsidiary of Powerlong Holdings

“Luoyang Project Company” Luoyang Longqian Commercial Management Co., Ltd.*(洛陽龍潛商業管理有限公司), a company established in the PRCwith limited liabil i ty on March 23, 2021, an indirectwholly-owned subsidiary of Powerlong REIT and the directowner of Luoyang Powerlong Plaza

“Macao” Macao Special Administrative Region of the PRC

“Main Board” the stock exchange (excluding the option market) operated by theStock Exchange which is independent from and operated inparallel with GEM

“Management Person(s)” has the meaning set out in “Corporate Governance—Interests of,and Dealings in Units by, Directors, the REIT Manager or theSubstantial Unitholders” in this Document

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

DEFINITIONS

– 22 –

“Market Consultant” Jones Lang LaSalle Corporate Appraisal and Advisory Limited

“Market Research Report” a market research report prepared by the Market Consultant inconnection with the [REDACTED], as set out in Appendix V tothis Document

[REDACTED]

“MOFCOM” the Ministry of Commerce of the PRC

“Nanjing Powerlong” Nanjing Powerlong Kangjun Property Development Co., Ltd.*(南京寶龍康浚置業發展有限公司), a company established thePRC with limited liability on November 7, 2017 and an indirectnon-wholly owned subsidiary of Powerlong Holdings

“NAV” net asset value, which is calculated as total assets minus totalliabilities

“New Project Companies” has the meaning set out in “Reorganization, Structure andOrganization of Powerlong REIT—Reorganization and AssetInjection” in this Document

“Nomination and RemunerationCommittee”

the nomination and remuneration committee of the REITManager

“Non-qualifying PowerlongShareholder”

registered holders of Powerlong Shares whose addresses on theregister of members of Powerlong Holdings is, at 4:30 p.m. on theAssured Entitlement Record Date, in a place outside Hong Kongand who the directors of Powerlong Holdings, after makingenquiries regarding the legal restrictions under the laws of therelevant place or the requirements of the relevant regulatory bodyor stock exchange in that place, consider his/her/its exclusionfrom the definition of “Qualifying Powerlong Shareholder” isnecessary or expedient

“Non-REIT Properties” has the meaning set out in “Reorganization, Structure andOrganization of Powerlong REIT—Reorganization and AssetInjection” in this Document

“Notice on Land Supply” the Notice on Problems Regarding Strengthening the Supply andRegulation of Land Used for Real Estates Supply promulgated bythe Ministry of Land and Resources on March 8, 2010

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

DEFINITIONS

– 23 –

[REDACTED]

“Offshore Investors” has the meaning set out in “Taxation—PRC Taxation ofPowerlong REIT—China Indirect Transfer Tax” in this Document

“Offshore Facilities” has the meaning set out in “Material Agreements and OtherDocuments—Facilities Agreements” in this Document

“Offshore Property Holding Companies” collectively, BVI Holdco, the BVI Intermediary Companies andHK Intermediary Companies

“Onshore Facilities” has the meaning set out in “Material Agreements and OtherDocuments—Facilities Agreements” in this Document

“Operations Management Fee” has the meaning set out in “The Operations and PropertyManager—Commercial Operat ional Services FrameworkAgreement” in this Document

“Operations and Property Manager” Powerlong CM

“Ordinary Resolution” a resolution of Unitholders proposed and passed by a simplemajority of the votes of those present and entitled to vote inperson or by proxy where the votes shall be taken by way of poll,but with a quorum of two or more Unitholders registered asholding together not less than 10.0% of Units for the time being inissue

[REDACTED]

“PBOC” The People’s Bank of China

“Percentage Threshold” has the meaning set out in “The Trust Deed—Issue of Units and/or Convertible Instruments and Issue Price” in this Document

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

DEFINITIONS

– 24 –

“Powerlong CM” Powerlong Commercial Management Holdings Limited (寶龍商業管理控股有限公司) (stock code: 9909), an exempted companyincorporated in the Cayman Islands with limited liability onMarch 25, 2019 and the shares of which are listed on the MainBoard of the Stock Exchange

“Powerlong CM Group” Powerlong CM and its subsidiaries

“Powerlong Group” Powerlong Holdings and its subsidiaries

“Powerlong Group Development” Powerlong Group Development Co., Ltd.* (寶龍集團發展有限公司), a company established in the PRC with limited liability onJuly 11, 1992, which is indirectly owned as to 88.9% and 1% byMr. Hoi Kin Hong and Ms. Hoi Wa Lam, respectively

“Powerlong Holdings” Powerlong Real Estate Holdings Limited (寶龍地產控股有限公司) (stock code: 1238), an exempted company incorporated in theCayman Islands with limited liability on July 18, 2007 and theshares of which are listed on the Main Board of the StockExchange

“Powerlong Shareholders” holders of the Powerlong Shares

“Powerlong Shares” ordinary shares of HK$0.01 each in the share capital ofPowerlong Holdings

“Powerlong Land Development” Powerlong Land Development Limited, a company incorporatedin Hong Kong with limited liability on October 3, 2008 and anindirect non-wholly owned subsidiary of Powerlong Holdings

“Powerlong REIT” Powerlong Commercial Real Estate Investment Trust, a collectiveinvestment scheme constituted as a unit trust and authorizedunder section 104 of the SFO

“Powerlong REIT Group” Powerlong REIT and its subsidiaries

“PRC” The People’s Republic of China excluding, for the purposes ofthis Document only (unless otherwise expressly specified), HongKong, Macao and Taiwan

“PRC GAAP” the Generally Accepted Accounting Principles of the PRC

“PRC Government” the Government of the PRC

“PRC Legal Advisors” Zhong Lun Law Firm, the legal advisors to the REIT Manager asto PRC laws

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

DEFINITIONS

– 25 –

[REDACTED]

“Project Companies” the respective direct owners of the REIT Properties, being (i)Xinxiang Project Company; (ii) Luoyang Project Company; (iii)Lin’an Project Company; (iv) Yancheng Project Company; (v)Fengxian Project Company; (vi) Anxi Project Company; (vii)Suqian Project Company; (viii) Jiaozhou Project Company, and“Project Company” means any one of them

“Predecessor Group” Target Company and its subsidiaries, whose results of operationsare set out in the combined financial statements in Appendix I tothis Document

[REDACTED]

“Promotional Expenses” has the meaning set out in “Modifications, Waivers and LicensingConditions—Payment of Promotional Expenses from theProperties of Powerlong REIT—Paragraph 9.13(b) of the REITCode” in this Document

“Property Development and RelatedActivities”

the acquisition of incomplete units in a building by a REIT andproperty developments (including both new development projectsand re-development of existing properties) undertaken inaccordance with Chapter 7 of the REIT Code

[REDACTED]

“Qualifying Powerlong Shareholder” the holders of Powerlong Shares, whose names appeared on theregister of members of Powerlong Holdings as holding PowerlongShares at the close of business on the Assured Entitlement RecordDate, other than Non-qualifying Powerlong Shareholders

“Registration Regulations” the Land Registration Regulations promulgated by the State LandAdministration Bureau on December 28, 1995 and implementedon February 1, 1996

“Regulation S” Regulation S under the U.S. Securities Act

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT THE INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

DEFINITIONS

– 26 –

“REIT” real estate investment trust

“REIT Code” the Code on Real Estate Investment Trusts published by the SFC(as amended, supplemented or otherwise modified for the timebeing) or, for the purpose of the Trust Deed, from time to time,including but not limited to by published practice statements or inany particular case, by specific written guidance issued orexemptions or waivers granted by the SFC

“REIT Manager” Powerlong REIT Management Limited, the manager ofPowerlong REIT, a company incorporated in Hong Kong withlimited liability on April 16, 2021 and an indirect wholly-ownedsubsidiary of Powerlong Holdings

“REIT Manager’s Remuneration” has the meaning set out in “Modifications, Waivers and LicensingConditions—Payment of REIT Manager’s Fee by way ofUnits—Chapter 12 of the REIT Code” in this Document