Embed Size (px)

Citation preview

Chennai-Kanyakumari Industrial Corridor: Power Sector Investment Project (RRP IND 51308-001)

Project Number: 51308-001 Loan and/or Grant Number: {LXXXX; GXXXX} October 2019

India: Chennai–Kanyakumari Industrial Corridor:

Power Sector Investment Project

Project Administration Manual

ABBREVIATIONS

ADB – Asian Development Bank

ADF – Asian Development Fund

AFS – audited financial statements

APFS – audited project financial statements

ARR – aggregate revenue requirement

CAAA – controller of aid accounts and audit

CAG – Comptroller and Auditor General of India

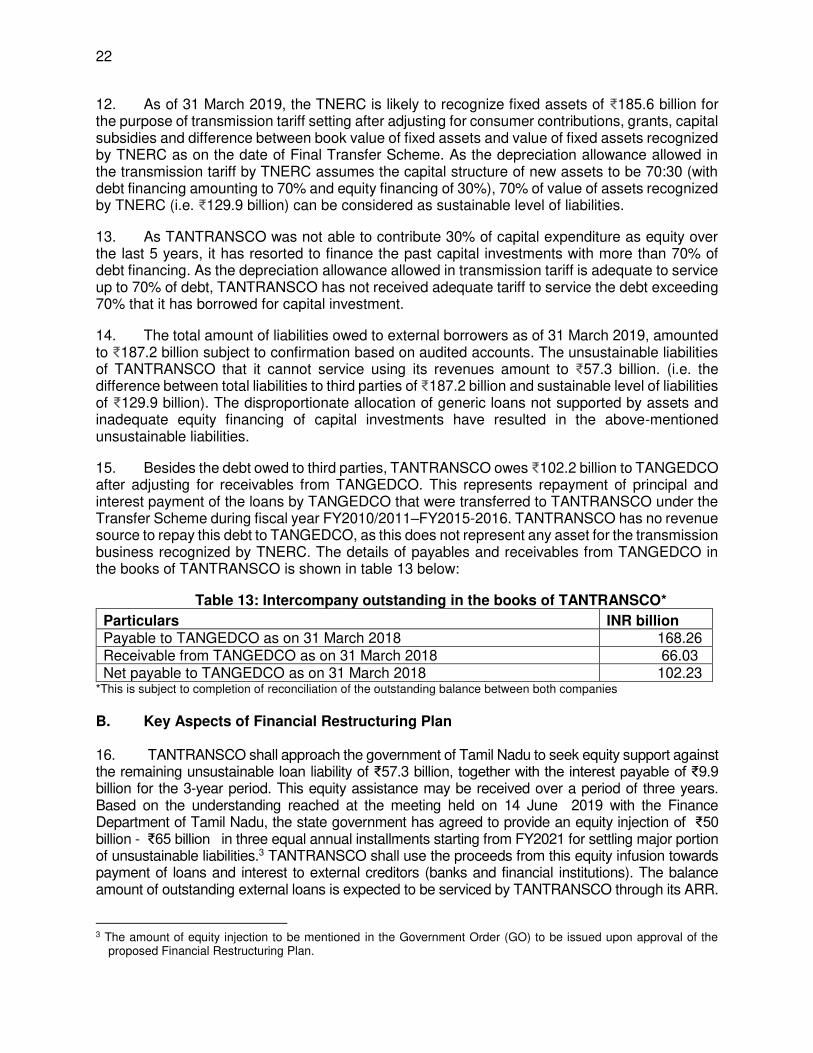

CERC – Central Electricity Regulatory Commission

CPS – country partnership strategy

CWIP DEA

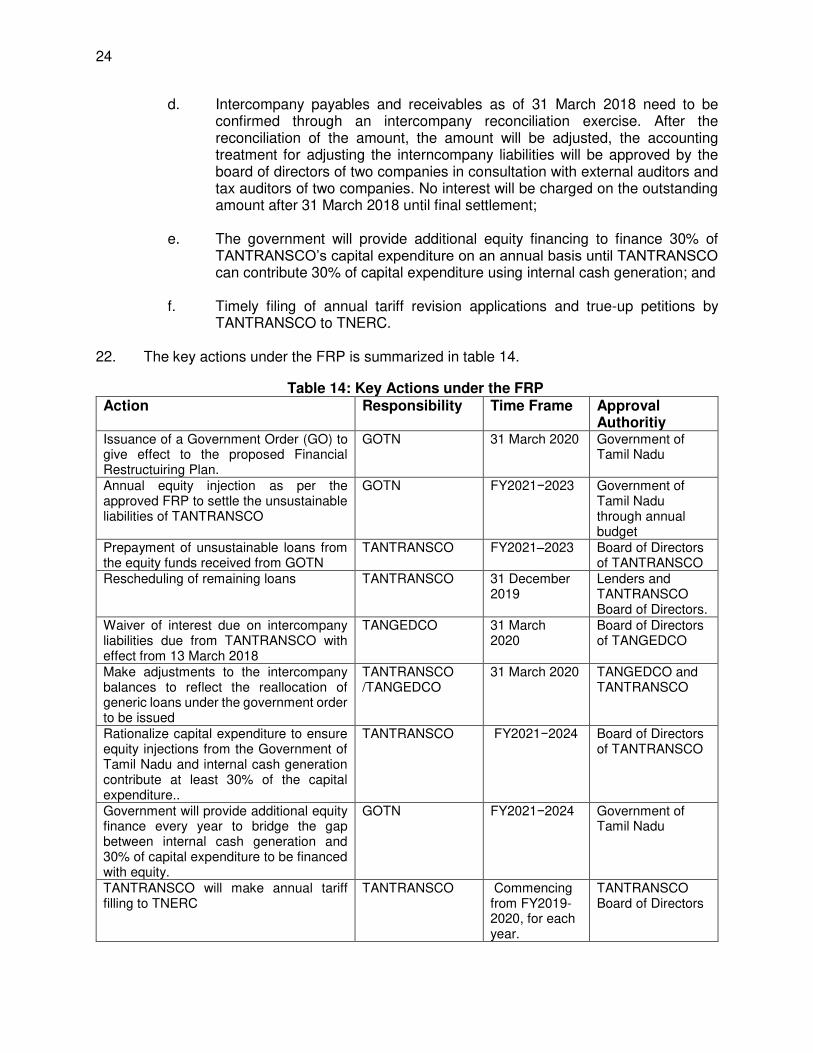

– –

capital works in progress Department of Economic Affairs

EMP EPC

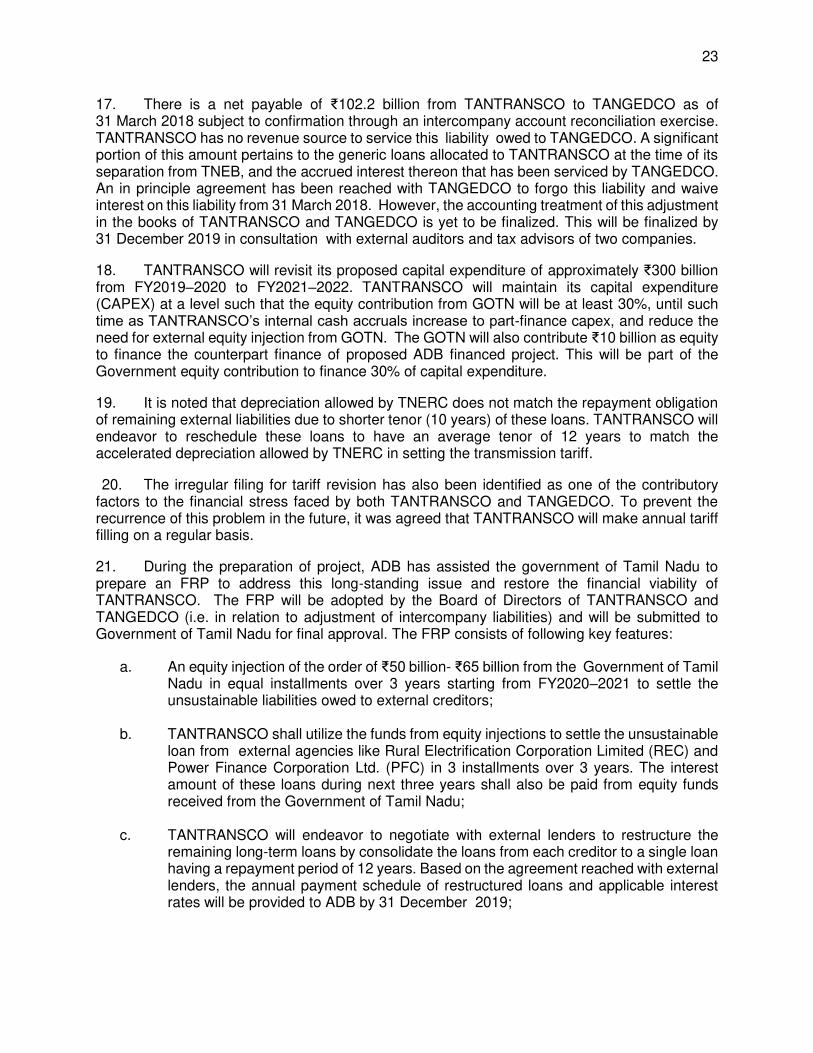

– –

environment management plan engineering procurement and construction contractors

ESMR – environment and social monitoring report

FIRR – financial internal rate of return

FMA FMAP

– –

financial management assessment financial management action plan

FMAQ FRP

– –

financial management assessment questionnaire financial restructuring plan

GCC – general construction circle

GIS – gas insulated switchgear

GST – goods and services tax

H&S – health and safety

IEE – initial environment examination

Ind-AS km kV

– – –

Indian accounting standards kilometer kilovolt

LIBOR LOA MVA PAM

– – – –

London interbank offered rate letter of award megavolt ampere project administration manual

PF-I – Plan Finance Division of the Department of Expenditure

PFM – public financial management

PIU – project implementation unit

RBI – Reserve Bank of India

RRP – report and recommendation of the President to the Board

SOE – statement of expenditure

STU – state transmission utility

TA – technical assistance

TANGEDCO – Tamil Nadu Generation and Distribution Corporation Ltd

TANTRANSCO – Tamil Nadu Transmission Corporation Ltd.

TNEB – Tamil Nadu Electricity Board

TNERC – Tamil Nadu Electricity Regulatory Commission

TOR – terms of reference

Chennai-Kanyakumari Industrial Corridor: Power Sector Investment Project (RRP IND 51308-001)

CONTENTS

I. PROJECT DESCRIPTION 1

II. IMPLEMENTATION PLANS 2

A. Project Readiness Activities 2

B. Overall Project Implementation Plan 3

III. PROJECT MANAGEMENT ARRANGEMENTS 5

A. Project Implementation Organizations: Roles and Responsibilities 5

B. Key Persons Involved in Implementation 9

C. Project Organization Structure 11

IV. COSTS AND FINANCING 12

A. Cost Estimates Preparation and Revisions 12

B. Key Assumptions 13

C. Detailed Cost Estimates by Expenditure Category 14

D. Allocation and withdrawal of Loan Proceeds 15

E. Detailed Cost Estimates by Financier 16

F. Detailed Cost Estimates by Outputs and/or Components 17

G. Detailed Cost Estimates by Year 18

H. Contract and Disbursement S-Curve 19

I. Fund Flow Diagram 20

V. FINANCIAL MANAGEMENT 21

A. Financial Restructuring Plan 21

C. Financial Management Assessment 25

D. Disbursement 30

E. Accounting 31

F. Auditing and Public Disclosure 32

VI. PROCUREMENT AND CONSULTING SERVICES 33

A. Advance Contracting and Retroactive Financing 33

B. Procurement of Goods, Works, and Consulting Services 33

C. Procurement Plan 34

D. Consultant’s Terms of Reference 35

VII. SAFEGUARDS 36

VIII. GENDER AND SOCIAL DIMENSIONS 37

IX. PERFORMANCE MONITORING, EVALUATION, REPORTING, AND COMMUNICATION 39

A. Project Design and Monitoring Framework 39

B. Monitoring 42

C. Evaluation 42

D. Reporting 43

E. Stakeholder Communication Strategy 43

X. ANTICORRUPTION POLICY 43

XI. ACCOUNTABILITY MECHANISM 43

XII. RECORD OF CHANGES TO THE PROJECT ADMINISTRATION MANUAL 44

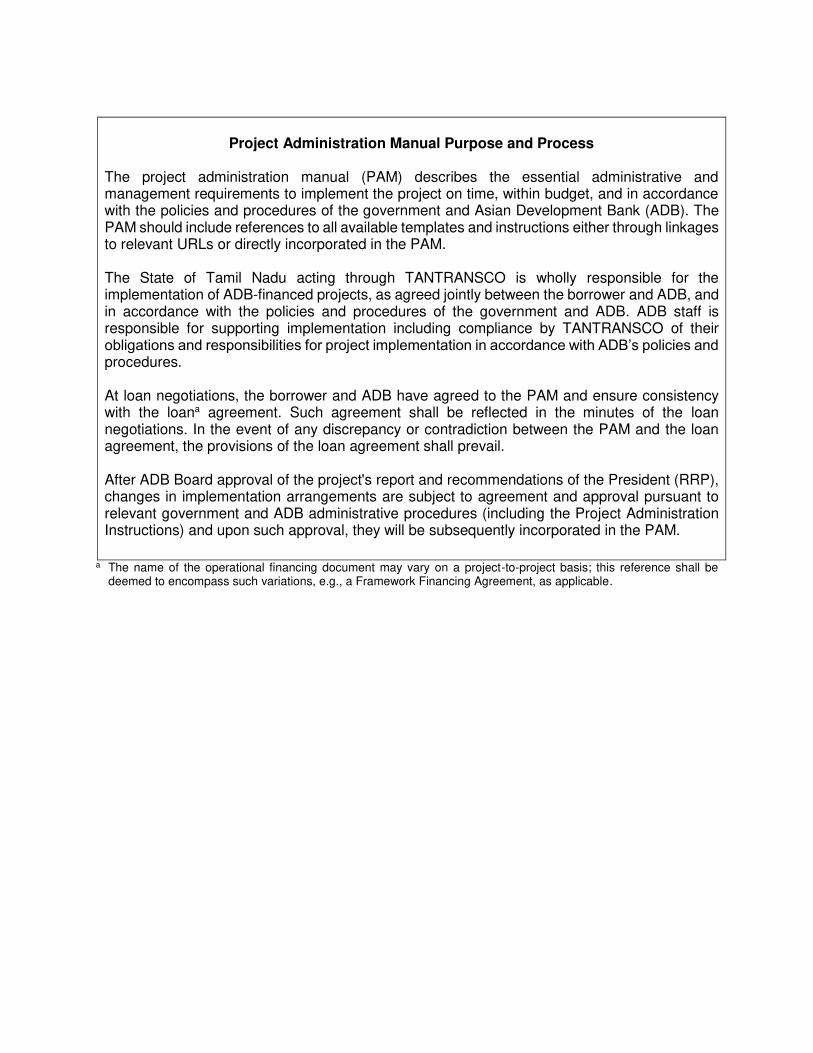

Project Administration Manual Purpose and Process

1. The project administration manual (PAM) describes the essential administrative and management requirements to implement the project on time, within budget, and in accordance with the policies and procedures of the government and Asian Development Bank (ADB). The PAM should include references to all available templates and instructions either through linkages to relevant URLs or directly incorporated in the PAM.

2. The State of Tamil Nadu acting through TANTRANSCO is wholly responsible for the implementation of ADB-financed projects, as agreed jointly between the borrower and ADB, and in accordance with the policies and procedures of the government and ADB. ADB staff is responsible for supporting implementation including compliance by TANTRANSCO of their obligations and responsibilities for project implementation in accordance with ADB’s policies and procedures.

3. At loan negotiations, the borrower and ADB have agreed to the PAM and ensure consistency with the loana agreement. Such agreement shall be reflected in the minutes of the loan negotiations. In the event of any discrepancy or contradiction between the PAM and the loan agreement, the provisions of the loan agreement shall prevail.

4. After ADB Board approval of the project's report and recommendations of the President (RRP),

changes in implementation arrangements are subject to agreement and approval pursuant to relevant government and ADB administrative procedures (including the Project Administration Instructions) and upon such approval, they will be subsequently incorporated in the PAM.

a The name of the operational financing document may vary on a project-to-project basis; this reference shall be

deemed to encompass such variations, e.g., a Framework Financing Agreement, as applicable.

I. PROJECT DESCRIPTION

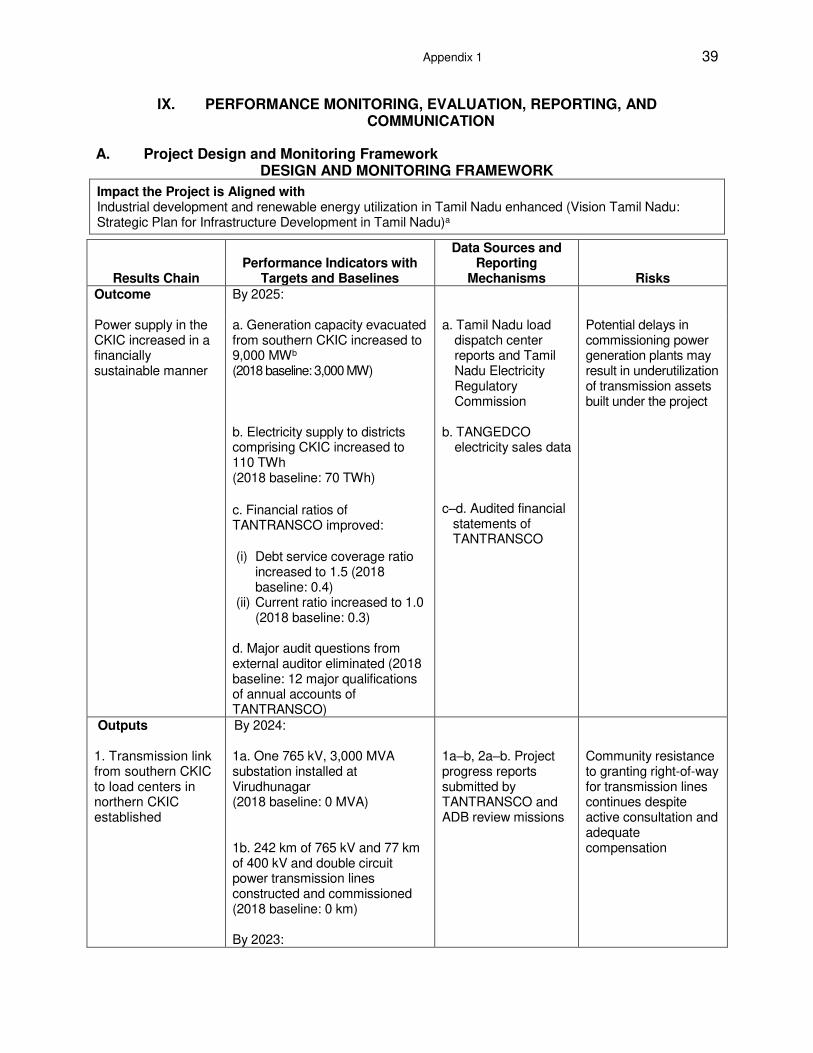

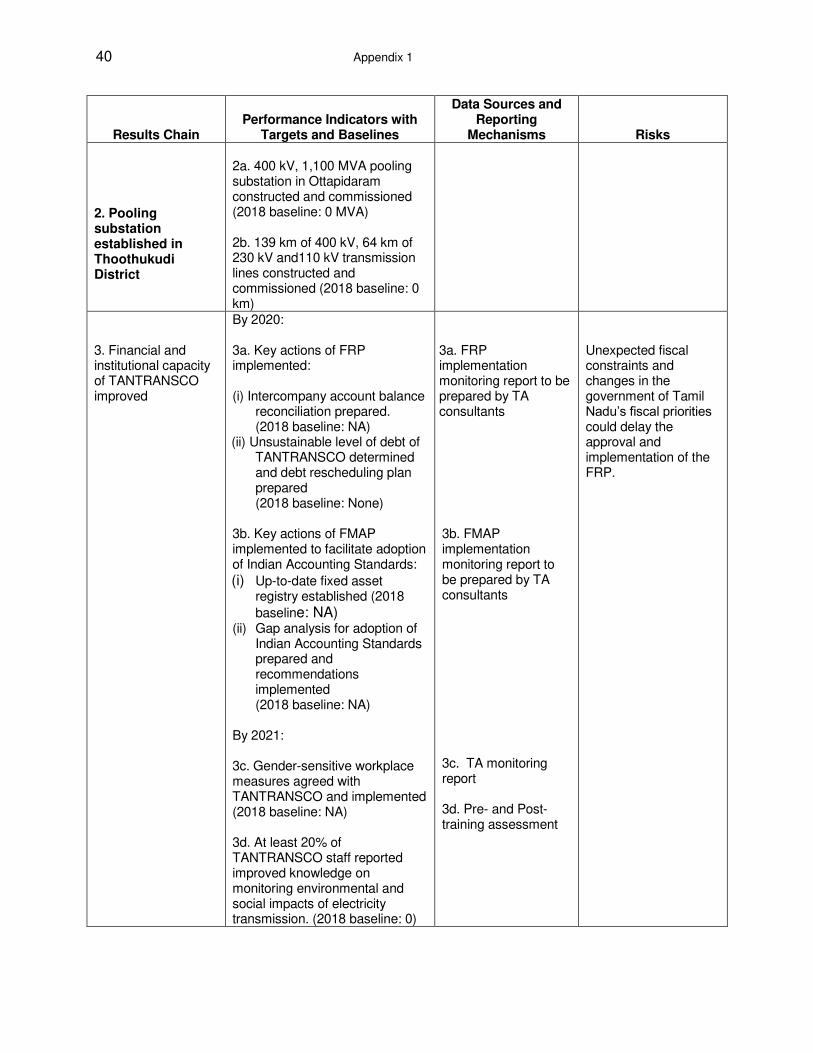

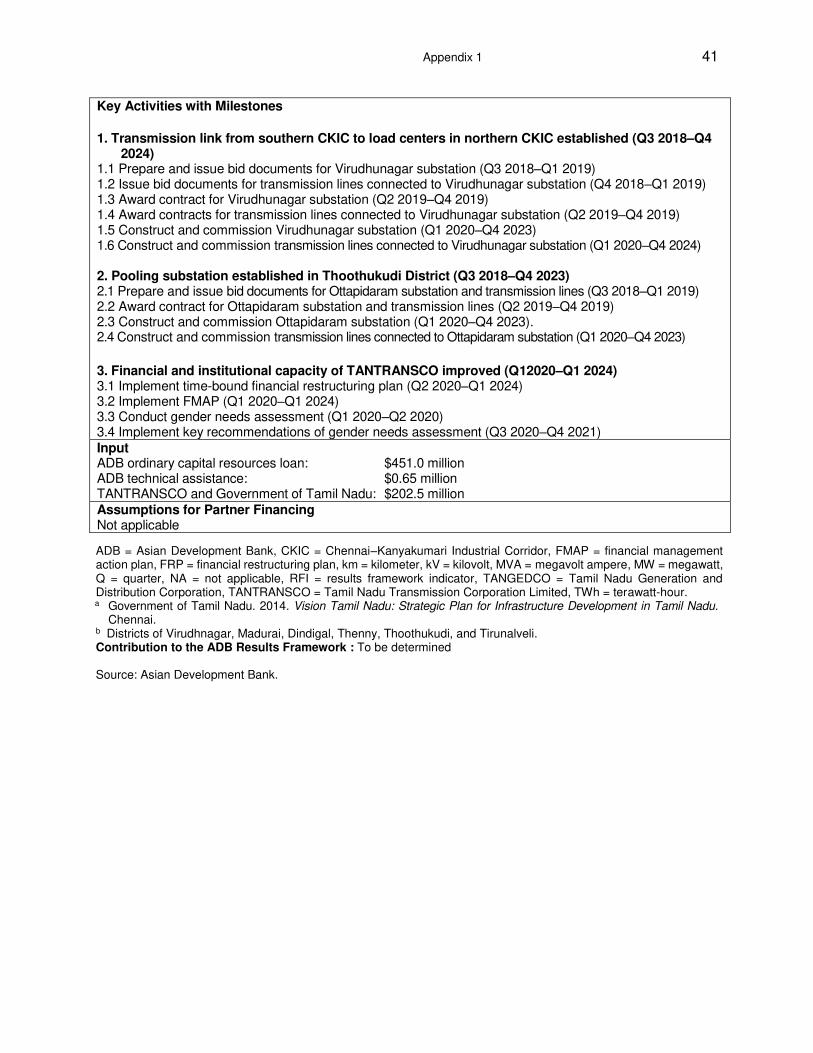

1. The proposed project will strengthen power transmission connectivity between the southern part of the Chennai–Kanyakumari Industrial Corridor (CKIC) and the northern part of the CKIC by augmenting the 765 kilovolt (kV) and 400 kV networks. This will allow more power including renewable energy to be evacuated from new generation facilities in the south CKIC to the energy hungry north CKIC. The project will also enhance the institutional capacity of TANTRANSCO by (i) supporting the implementation of a financial restructuring plan (FRP) to restore the financial sustainability of TANTRANSCO; (ii) facilitating the introduction of gender sensitive workplace practices; and (iii) building TANTRANSCO’s capacity to monitor the environmental and social impacts of power transmission projects.

2. The project is aligned with the following impact: industrial development and renewable energy utilization in Tamil Nadu enhanced. The project will have the following outcome: power supply in CKIC increased in a financially sustainable manner.

3. The proposed project will have the following outputs:

Output 1: Transmission link from southern Chennai–Kanyakumari Industrial Corridor to load centers in northern Chennai–Kanyakumari Industrial Corridor established. This output will establish a 765 kV substation and 765 kV power transmission link between the power generation hub in the Madurai–Thoothukudi area (southern part of the CKIC ) and load centers in the northern parts of the CKIC.

Output 2: Pooling substation established in Thoothukudi District. This output will establish a 400 kV pooling substation to receive electricity generated from power plants in the Thoothukudi district with associate transmission lines.

Output 3: Financial and institutional capacity of Tamil Nadu Transmission Corporation Limited improved. This output will (i) assist TANTRANSCO in implementing the FRP to restore its financial sustainability; (ii) support the financial management action plan (FMAP) to improve the financial management capacity and corporate governance of TANTRANSCO; (iii) facilitate the introduction of gender-sensitive workplace practices; and (iv) enhance the capacity of TANTRANSCO to monitor the environmental and social impacts of transmission projects. The attached TA will support these activities.

2

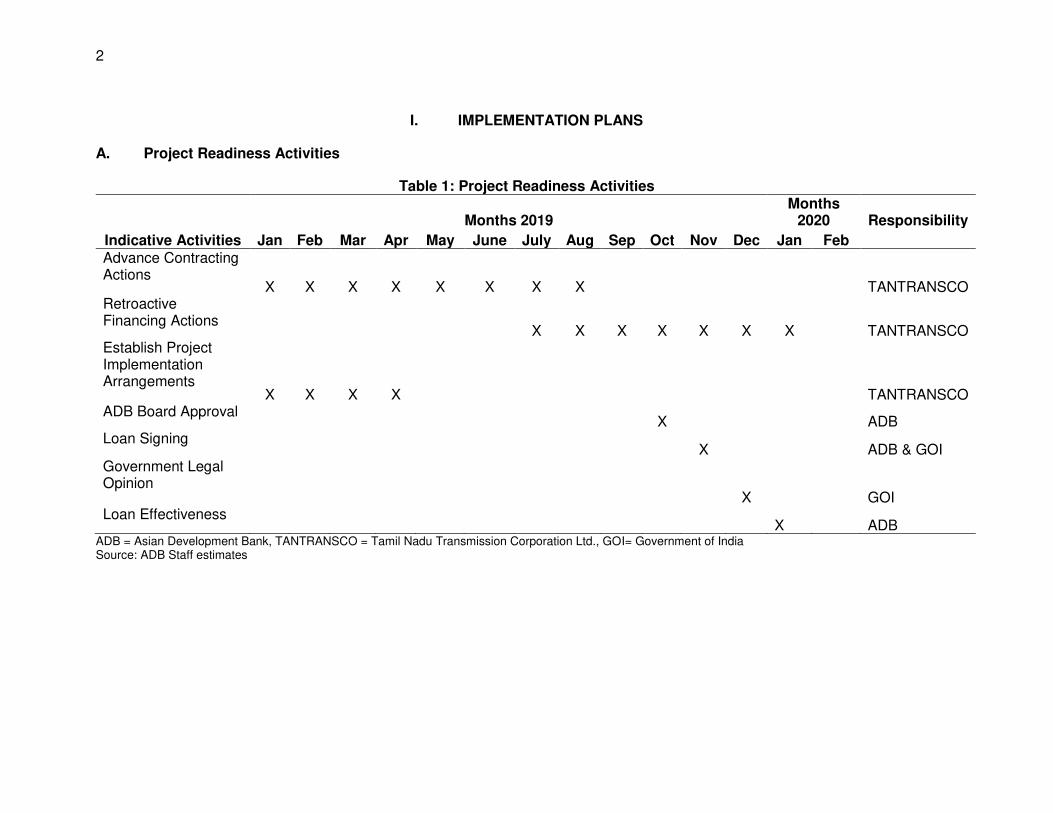

I. IMPLEMENTATION PLANS

A. Project Readiness Activities

Table 1: Project Readiness Activities

Months 2019 Months

2020 Responsibility

Indicative Activities Jan Feb Mar Apr May June July Aug Sep Oct Nov Dec Jan Feb Advance Contracting Actions

X X X X X X X X TANTRANSCO Retroactive Financing Actions

X X X X X X X TANTRANSCO Establish Project Implementation Arrangements

X X X X TANTRANSCO ADB Board Approval

X ADB Loan Signing

X ADB & GOI Government Legal Opinion

X GOI Loan Effectiveness

X ADB ADB = Asian Development Bank, TANTRANSCO = Tamil Nadu Transmission Corporation Ltd., GOI= Government of India Source: ADB Staff estimates

3

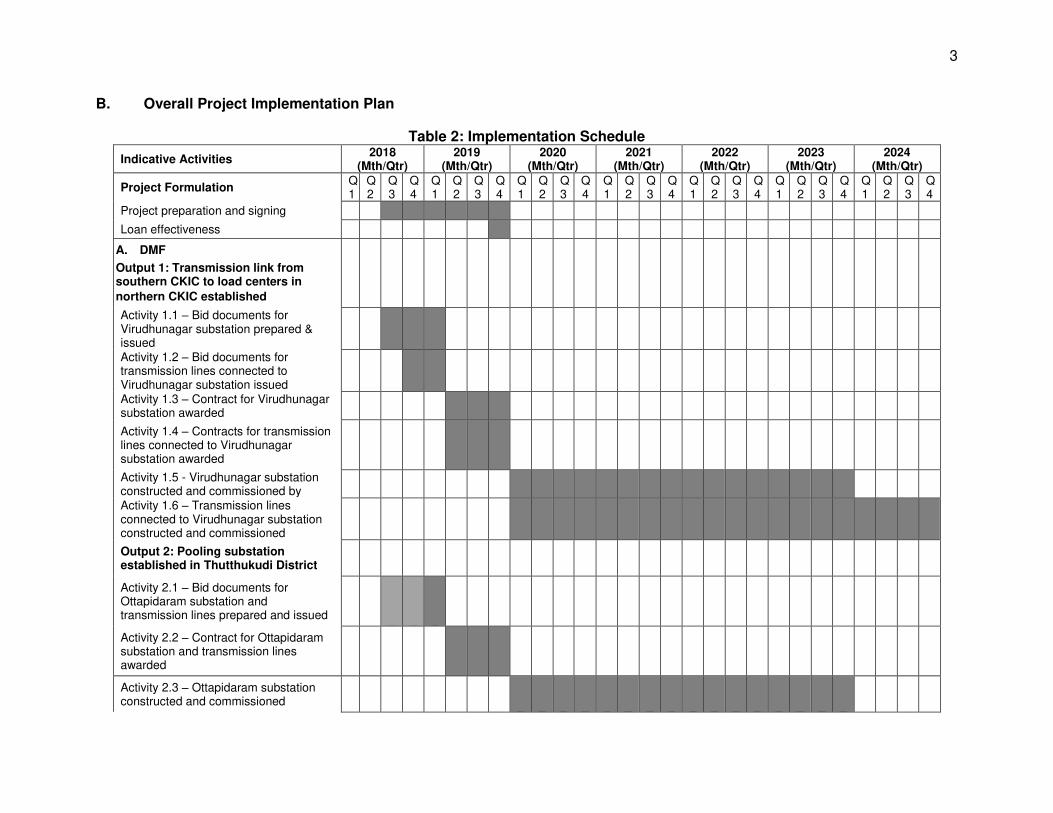

B. Overall Project Implementation Plan

Table 2: Implementation Schedule

Indicative Activities 2018

(Mth/Qtr) 2019

(Mth/Qtr) 2020

(Mth/Qtr) 2021

(Mth/Qtr) 2022

(Mth/Qtr) 2023

(Mth/Qtr) 2024

(Mth/Qtr)

Project Formulation Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Project preparation and signing

Loan effectiveness

A. DMF

Output 1: Transmission link from southern CKIC to load centers in

northern CKIC established

Activity 1.1 – Bid documents for Virudhunagar substation prepared & issued

Activity 1.2 – Bid documents for transmission lines connected to Virudhunagar substation issued

Activity 1.3 – Contract for Virudhunagar substation awarded

Activity 1.4 – Contracts for transmission lines connected to Virudhunagar substation awarded

Activity 1.5 - Virudhunagar substation constructed and commissioned by

Activity 1.6 – Transmission lines connected to Virudhunagar substation constructed and commissioned

Output 2: Pooling substation established in Thutthukudi District

Activity 2.1 – Bid documents for Ottapidaram substation and transmission lines prepared and issued

Activity 2.2 – Contract for Ottapidaram substation and transmission lines awarded

Activity 2.3 – Ottapidaram substation constructed and commissioned

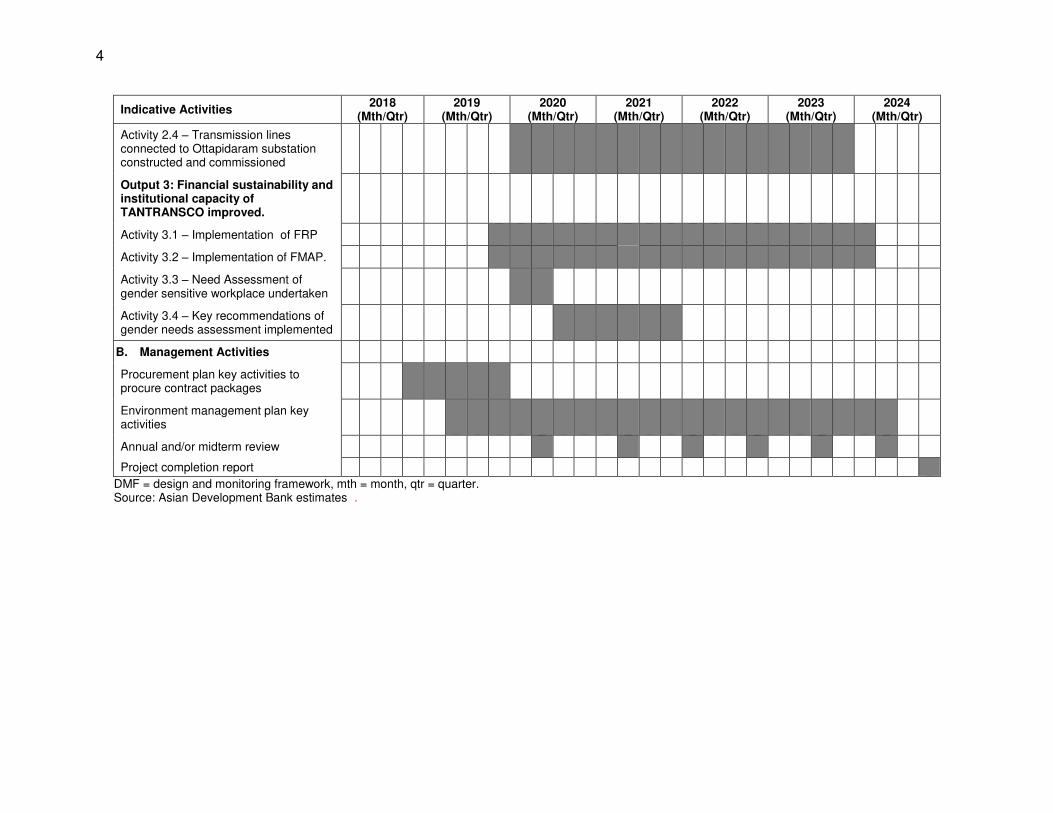

4

Indicative Activities 2018

(Mth/Qtr) 2019

(Mth/Qtr) 2020

(Mth/Qtr) 2021

(Mth/Qtr) 2022

(Mth/Qtr) 2023

(Mth/Qtr) 2024

(Mth/Qtr)

Activity 2.4 – Transmission lines connected to Ottapidaram substation constructed and commissioned

Output 3: Financial sustainability and institutional capacity of TANTRANSCO improved.

Activity 3.1 – Implementation of FRP

Activity 3.2 – Implementation of FMAP.

Activity 3.3 – Need Assessment of gender sensitive workplace undertaken

Activity 3.4 – Key recommendations of gender needs assessment implemented

B. Management Activities

Procurement plan key activities to procure contract packages

Environment management plan key activities

Annual and/or midterm review

Project completion report DMF = design and monitoring framework, mth = month, qtr = quarter. Source: Asian Development Bank estimates .

5

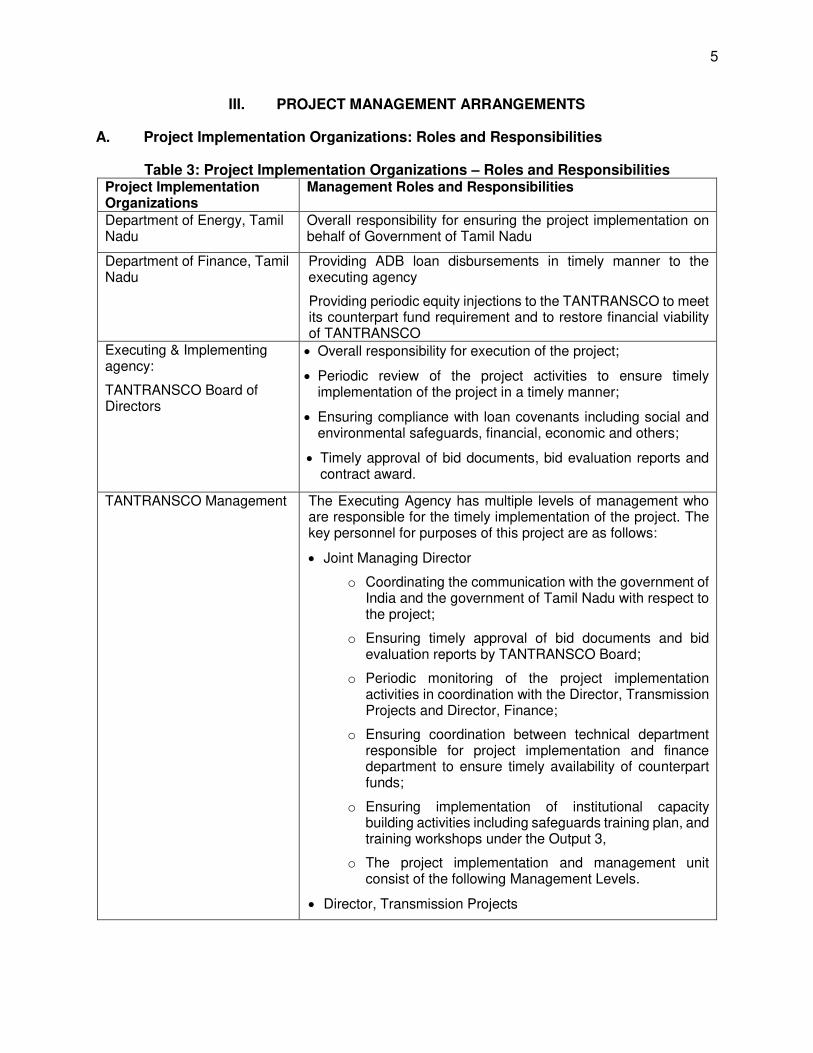

III. PROJECT MANAGEMENT ARRANGEMENTS

A. Project Implementation Organizations: Roles and Responsibilities

Table 3: Project Implementation Organizations – Roles and Responsibilities Project Implementation Organizations

Management Roles and Responsibilities

Department of Energy, Tamil Nadu

Overall responsibility for ensuring the project implementation on behalf of Government of Tamil Nadu

Department of Finance, Tamil Nadu

Providing ADB loan disbursements in timely manner to the executing agency

Providing periodic equity injections to the TANTRANSCO to meet its counterpart fund requirement and to restore financial viability of TANTRANSCO

Executing & Implementing agency:

TANTRANSCO Board of Directors

• Overall responsibility for execution of the project;

• Periodic review of the project activities to ensure timely implementation of the project in a timely manner;

• Ensuring compliance with loan covenants including social and environmental safeguards, financial, economic and others;

• Timely approval of bid documents, bid evaluation reports and contract award.

TANTRANSCO Management The Executing Agency has multiple levels of management who are responsible for the timely implementation of the project. The key personnel for purposes of this project are as follows:

• Joint Managing Director

o Coordinating the communication with the government of India and the government of Tamil Nadu with respect to the project;

o Ensuring timely approval of bid documents and bid evaluation reports by TANTRANSCO Board;

o Periodic monitoring of the project implementation activities in coordination with the Director, Transmission Projects and Director, Finance;

o Ensuring coordination between technical department responsible for project implementation and finance department to ensure timely availability of counterpart funds;

o Ensuring implementation of institutional capacity building activities including safeguards training plan, and training workshops under the Output 3,

o The project implementation and management unit consist of the following Management Levels.

• Director, Transmission Projects

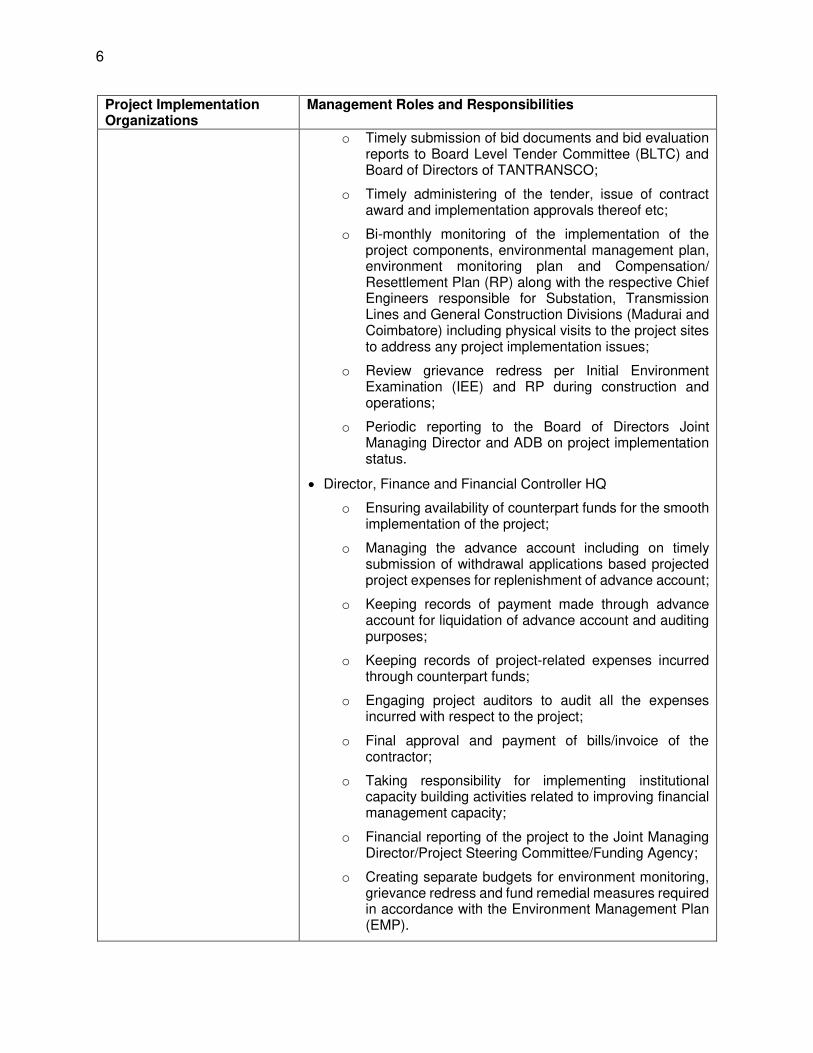

6

Project Implementation Organizations

Management Roles and Responsibilities

o Timely submission of bid documents and bid evaluation reports to Board Level Tender Committee (BLTC) and Board of Directors of TANTRANSCO;

o Timely administering of the tender, issue of contract award and implementation approvals thereof etc;

o Bi-monthly monitoring of the implementation of the project components, environmental management plan, environment monitoring plan and Compensation/ Resettlement Plan (RP) along with the respective Chief Engineers responsible for Substation, Transmission Lines and General Construction Divisions (Madurai and Coimbatore) including physical visits to the project sites to address any project implementation issues;

o Review grievance redress per Initial Environment Examination (IEE) and RP during construction and operations;

o Periodic reporting to the Board of Directors Joint Managing Director and ADB on project implementation status.

• Director, Finance and Financial Controller HQ

o Ensuring availability of counterpart funds for the smooth implementation of the project;

o Managing the advance account including on timely submission of withdrawal applications based projected project expenses for replenishment of advance account;

o Keeping records of payment made through advance account for liquidation of advance account and auditing purposes;

o Keeping records of project-related expenses incurred through counterpart funds;

o Engaging project auditors to audit all the expenses incurred with respect to the project;

o Final approval and payment of bills/invoice of the contractor;

o Taking responsibility for implementing institutional capacity building activities related to improving financial management capacity;

o Financial reporting of the project to the Joint Managing Director/Project Steering Committee/Funding Agency;

o Creating separate budgets for environment monitoring, grievance redress and fund remedial measures required in accordance with the Environment Management Plan (EMP).

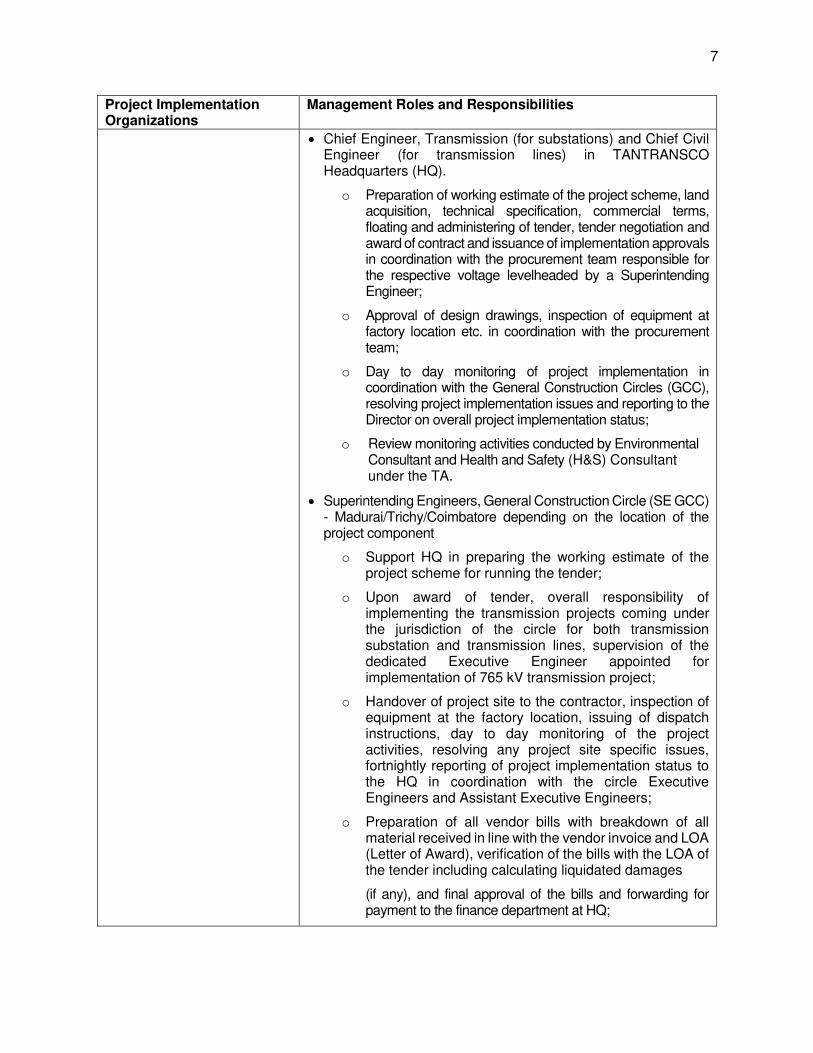

7

Project Implementation Organizations

Management Roles and Responsibilities

• Chief Engineer, Transmission (for substations) and Chief Civil Engineer (for transmission lines) in TANTRANSCO Headquarters (HQ).

o Preparation of working estimate of the project scheme, land acquisition, technical specification, commercial terms, floating and administering of tender, tender negotiation and award of contract and issuance of implementation approvals in coordination with the procurement team responsible for the respective voltage levelheaded by a Superintending Engineer;

o Approval of design drawings, inspection of equipment at factory location etc. in coordination with the procurement team;

o Day to day monitoring of project implementation in coordination with the General Construction Circles (GCC), resolving project implementation issues and reporting to the Director on overall project implementation status;

o Review monitoring activities conducted by Environmental Consultant and Health and Safety (H&S) Consultant under the TA.

• Superintending Engineers, General Construction Circle (SE GCC) - Madurai/Trichy/Coimbatore depending on the location of the project component

o Support HQ in preparing the working estimate of the project scheme for running the tender;

o Upon award of tender, overall responsibility of implementing the transmission projects coming under the jurisdiction of the circle for both transmission substation and transmission lines, supervision of the dedicated Executive Engineer appointed for implementation of 765 kV transmission project;

o Handover of project site to the contractor, inspection of equipment at the factory location, issuing of dispatch instructions, day to day monitoring of the project activities, resolving any project site specific issues, fortnightly reporting of project implementation status to the HQ in coordination with the circle Executive Engineers and Assistant Executive Engineers;

o Preparation of all vendor bills with breakdown of all material received in line with the vendor invoice and LOA (Letter of Award), verification of the bills with the LOA of the tender including calculating liquidated damages

(if any), and final approval of the bills and forwarding for payment to the finance department at HQ;

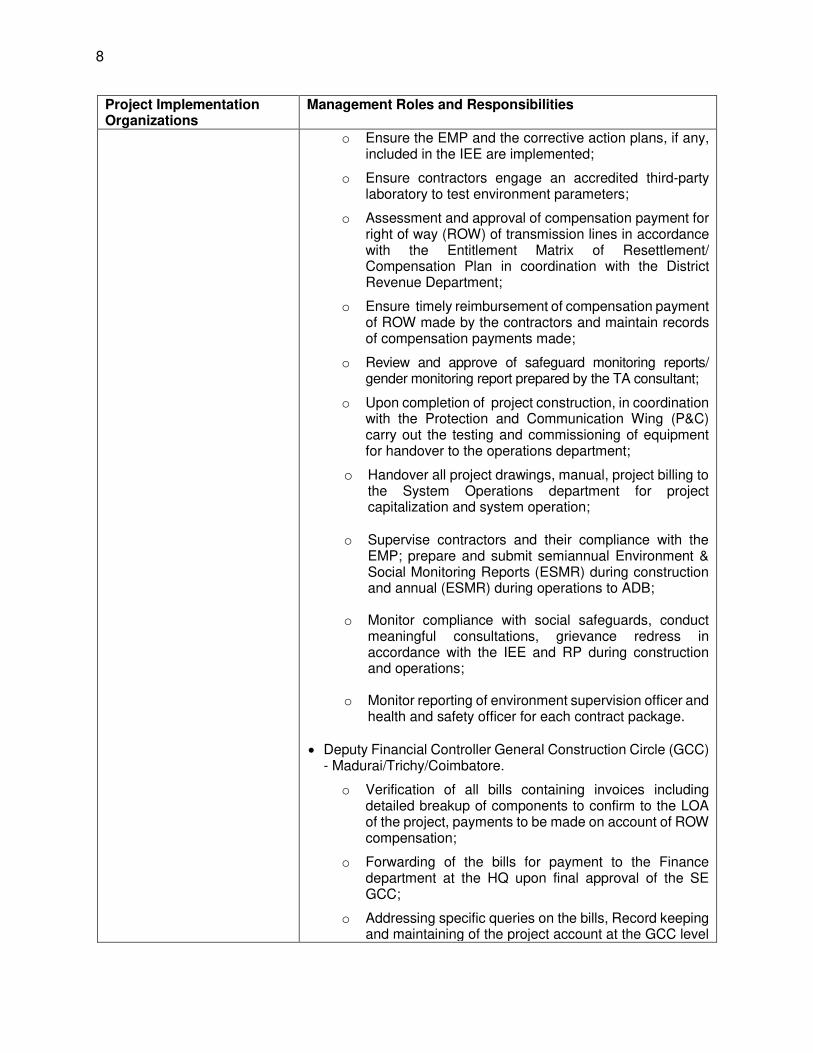

8

Project Implementation Organizations

Management Roles and Responsibilities

o Ensure the EMP and the corrective action plans, if any, included in the IEE are implemented;

o Ensure contractors engage an accredited third-party laboratory to test environment parameters;

o Assessment and approval of compensation payment for right of way (ROW) of transmission lines in accordance with the Entitlement Matrix of Resettlement/ Compensation Plan in coordination with the District Revenue Department;

o Ensure timely reimbursement of compensation payment of ROW made by the contractors and maintain records of compensation payments made;

o Review and approve of safeguard monitoring reports/ gender monitoring report prepared by the TA consultant;

o Upon completion of project construction, in coordination with the Protection and Communication Wing (P&C) carry out the testing and commissioning of equipment for handover to the operations department;

o Handover all project drawings, manual, project billing to the System Operations department for project capitalization and system operation;

o Supervise contractors and their compliance with the EMP; prepare and submit semiannual Environment & Social Monitoring Reports (ESMR) during construction and annual (ESMR) during operations to ADB;

o Monitor compliance with social safeguards, conduct meaningful consultations, grievance redress in accordance with the IEE and RP during construction and operations;

o Monitor reporting of environment supervision officer and

health and safety officer for each contract package.

• Deputy Financial Controller General Construction Circle (GCC) - Madurai/Trichy/Coimbatore.

o Verification of all bills containing invoices including detailed breakup of components to confirm to the LOA of the project, payments to be made on account of ROW compensation;

o Forwarding of the bills for payment to the Finance department at the HQ upon final approval of the SE GCC;

o Addressing specific queries on the bills, Record keeping and maintaining of the project account at the GCC level

9

Project Implementation Organizations

Management Roles and Responsibilities

including reporting on the financial progress of the project;

o Supervising budgets for EMP and environment monitoring, compensation payment, meaningful consultation, grievance redress and fund remedial measures required in accordance with IEE and RP.

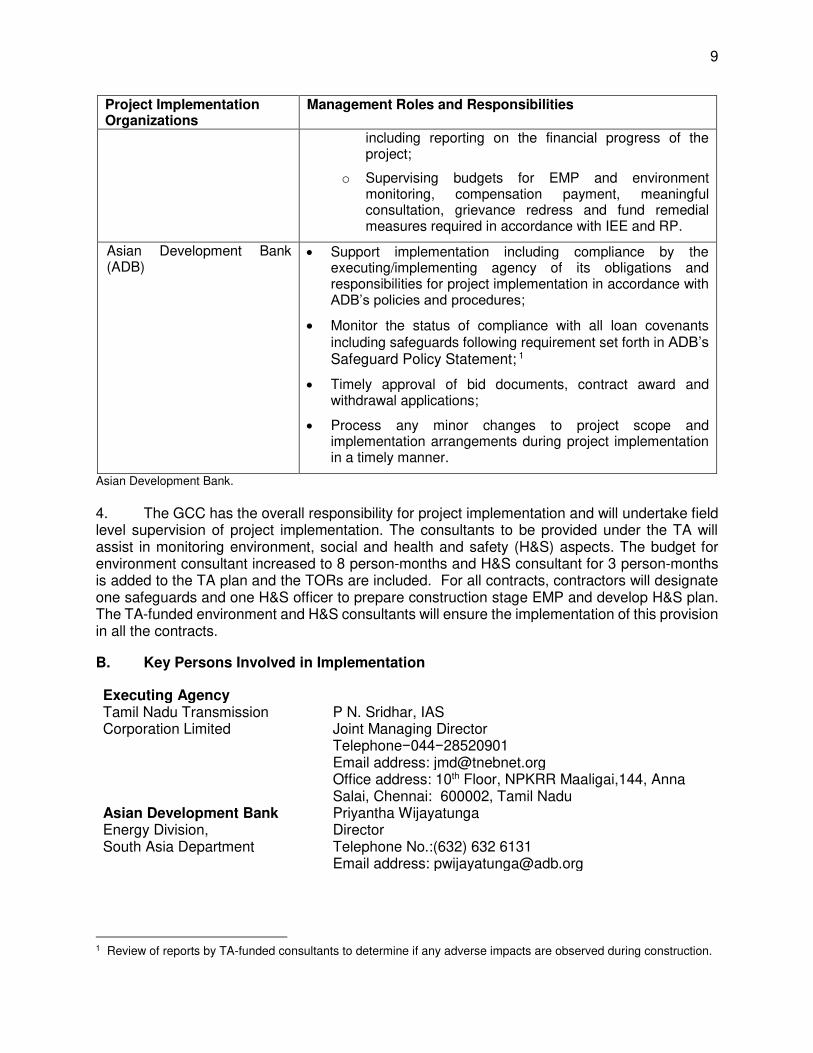

Asian Development Bank (ADB)

• Support implementation including compliance by the executing/implementing agency of its obligations and responsibilities for project implementation in accordance with ADB’s policies and procedures;

• Monitor the status of compliance with all loan covenants including safeguards following requirement set forth in ADB’s Safeguard Policy Statement; 1

• Timely approval of bid documents, contract award and withdrawal applications;

• Process any minor changes to project scope and implementation arrangements during project implementation in a timely manner.

Asian Development Bank.

4. The GCC has the overall responsibility for project implementation and will undertake field level supervision of project implementation. The consultants to be provided under the TA will assist in monitoring environment, social and health and safety (H&S) aspects. The budget for environment consultant increased to 8 person-months and H&S consultant for 3 person-months is added to the TA plan and the TORs are included. For all contracts, contractors will designate one safeguards and one H&S officer to prepare construction stage EMP and develop H&S plan. The TA-funded environment and H&S consultants will ensure the implementation of this provision in all the contracts.

B. Key Persons Involved in Implementation

Executing Agency Tamil Nadu Transmission Corporation Limited

P N. Sridhar, IAS Joint Managing Director Telephone−044−28520901 Email address: [email protected]

Office address: 10th Floor, NPKRR Maaligai,144, Anna Salai, Chennai: 600002, Tamil Nadu

Asian Development Bank Energy Division, South Asia Department

Priyantha Wijayatunga Director Telephone No.:(632) 632 6131 Email address: [email protected]

1 Review of reports by TA-funded consultants to determine if any adverse impacts are observed during construction.

10

Mission Leader

Pradeep Perera Principal Energy Specialist Telephone No.: +91 11 2419 4246 Email address: [email protected]

11

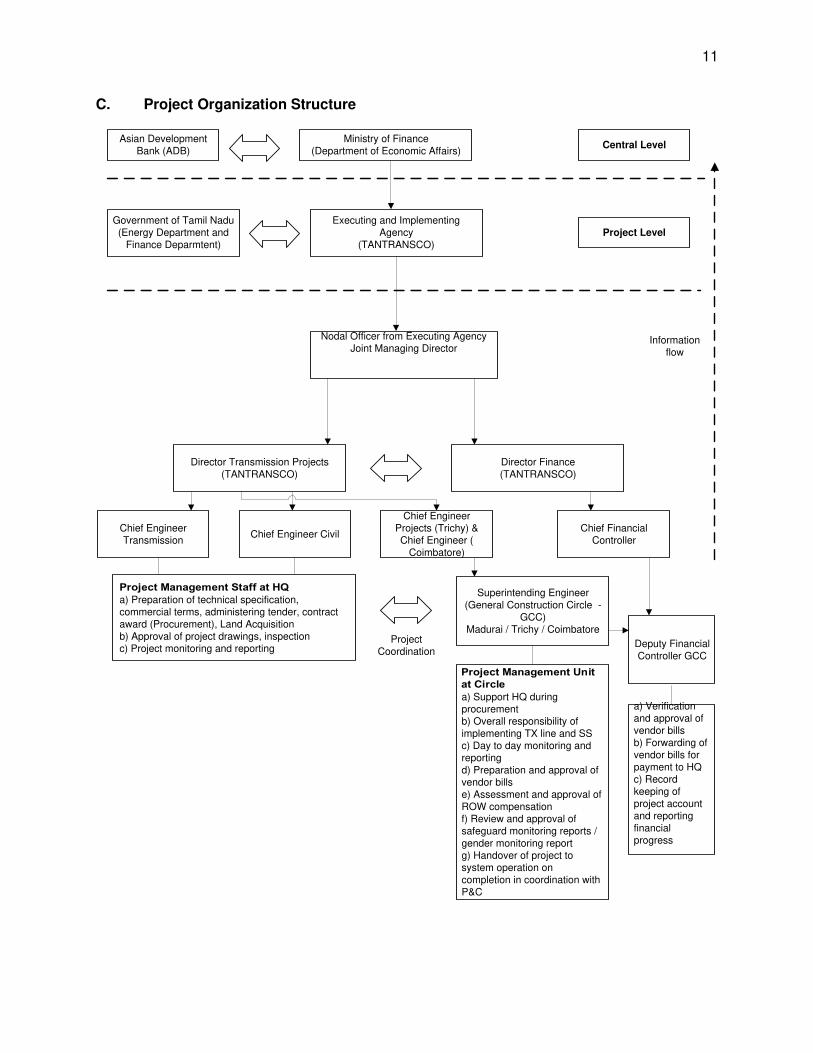

C. Project Organization Structure

a) Preparation of technical specification, commercial terms, administering tender, contract award (Procurement), Land Acquisitionb) Approval of project drawings, inspectionc) Project monitoring and reporting

Ministry of Finance(Department of Economic Affairs)

Asian Development Bank (ADB)

Executing and Implementing Agency

(TANTRANSCO)

Nodal Officer from Executing AgencyJoint Managing Director

Director Transmission Projects (TANTRANSCO)

Central Level

Project Level

Director Finance(TANTRANSCO)

Chief Engineer Transmission

Chief Engineer Civil

Chief Engineer Projects (Trichy) & Chief Engineer (

Coimbatore)

Superintending Engineer (General Construction Circle -

GCC)Madurai / Trichy / Coimbatore

Project Coordination

Chief Financial Controller

a) Support HQ during procurementb) Overall responsibility of implementing TX line and SSc) Day to day monitoring and reportingd) Preparation and approval of vendor billse) Assessment and approval of ROW compensationf) Review and approval of safeguard monitoring reports / gender monitoring report g) Handover of project to system operation on completion in coordination with P&C

Deputy Financial Controller GCC

a) Verification and approval of vendor billsb) Forwarding of vendor bills for payment to HQc) Record keeping of project account and reporting financial progress

Information flow

Government of Tamil Nadu(Energy Department and

Finance Deparmtent)

12

IV. COSTS AND FINANCING

A. Cost Estimates Preparation and Revisions

5. The project is estimated to cost $653.5 million (Table 4). The major cost categories are for the procurement of engineering procurement and construction contractors (EPC) including goods and service tax (GST) for implementing the proposed substations and transmission lines. The capacity building activities to be undertaken under Output 3 will be financed by the proposed attached TA. In addition, the cost of land acquisition and payment of compensation for right of way for transmission lines and financial charges during implementation to be financed using counterpart funding is included in the cost estimates. The project investment plan is summarized in Table 4.

Table 4: Summary Cost Estimates ($ million)

Item Amounta

A. Base Costb

1. Transmission link from southern CKIC to northern CKIC 438.3

2. Pooling substation in Thutthukudi District 120.2

Subtotal (A) 558.5

B. Contingenciesc 60.3

C. Financing Charges During Implementationd 34.7

Total (A+B+C) 653.5 CKIC = Chennai–Kanyakumari Industrial Corridor a Includes taxes of $68.8 million. such amount does not represent an excessive share of the project cost. ADB will

finance taxes and duties of $68.8 million. The environment management cost of $2.69 million to be incurred by the contractors. Excludes output 3 because it will be funded by the Technical Assistance Special Fund of the Asian Development Bank (ADB) under the attached technical assistance.

b In January 2019 prices. c Physical and price contingencies, and a provision for exchange rate fluctuations are included. . d Includes interest and commitment charges. Interest during the construction for the ordinary capital resources loan

has been computed at the 5-year United States dollar fixed swap rate plus an effective contractual spread of 0.5%. Commitment charges are 0.15% per year to be charged on the undisbursed loan amount.

Source: Tamil Nadu Transmission Corporation and Asian Development Bank estimates.

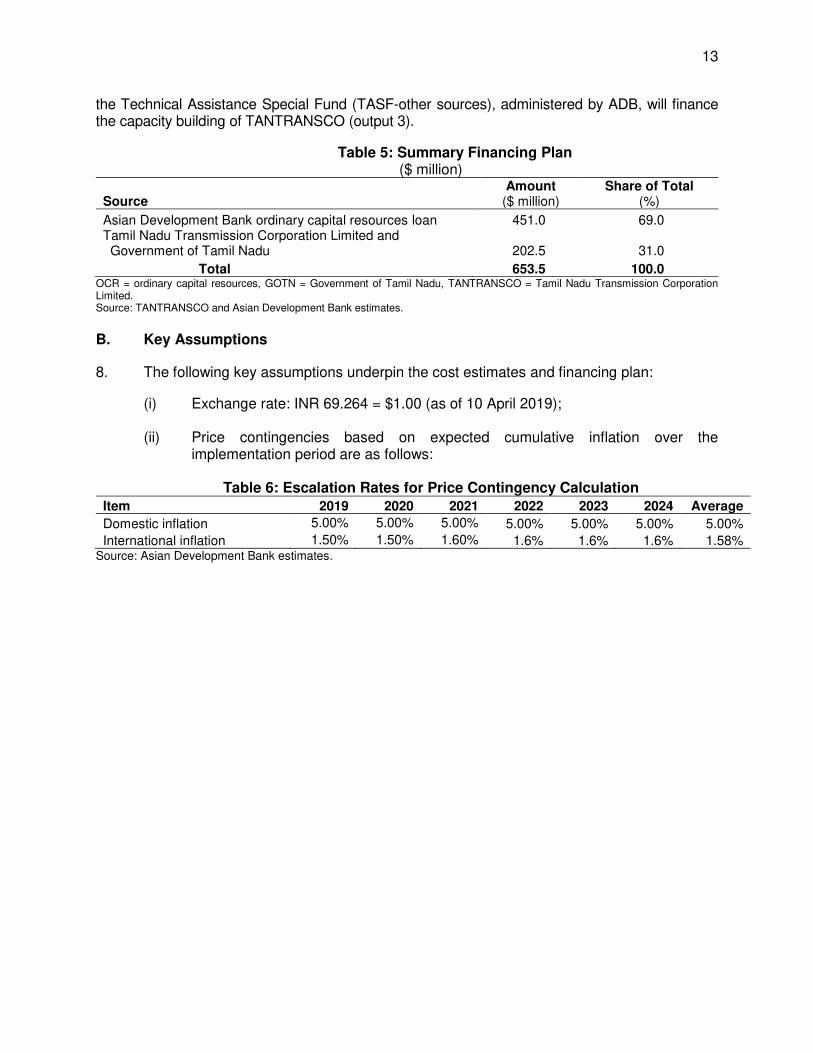

6. The government has requested a regular loan of $451 million from ADB’s ordinary capital resources to help finance the project. The loan will have a 20-year term, including a grace period of 5 years; an annual interest rate determined in accordance with ADB’s London interbank offered rate (LIBOR)-based lending facility; a commitment charge of 0.15% per year; and such other terms and conditions set forth in the draft loan and project agreements. Based on the customized amortization schedule of semiannual repayment, the average maturity is 13 years, and there is no maturity premium payable to ADB.2 The government will provide the proceeds of the ADB loan on a back-to-back basis to TANTRANSCO.

7. The summary financing plan is in Table 2. ADB will finance eligible expenditures in relation to supply and installation of substations and transmission lines on a turnkey basis, including goods and services tax. The counterpart funds to be provided by the government of Tamil Nadu through TANTRANSCO will be utilized for payment of compensation for right-of-way for transmission lines, land acquisition for substations, financial charges during implementation, project management expenses, and price and physical contingencies. The attached TA grant funded by

2 The customized amortization schedule is based on government’s choice of repayment option.

13

the Technical Assistance Special Fund (TASF-other sources), administered by ADB, will finance the capacity building of TANTRANSCO (output 3).

Table 5: Summary Financing Plan ($ million)

Source Amount ($ million)

Share of Total (%)

Asian Development Bank ordinary capital resources loan 451.0 69.0 Tamil Nadu Transmission Corporation Limited and Government of Tamil Nadu 202.5 31.0

Total 653.5 100.0 OCR = ordinary capital resources, GOTN = Government of Tamil Nadu, TANTRANSCO = Tamil Nadu Transmission Corporation Limited. Source: TANTRANSCO and Asian Development Bank estimates.

B. Key Assumptions

8. The following key assumptions underpin the cost estimates and financing plan:

(i) Exchange rate: INR 69.264 = $1.00 (as of 10 April 2019);

(ii) Price contingencies based on expected cumulative inflation over the implementation period are as follows:

Table 6: Escalation Rates for Price Contingency Calculation

Item 2019 2020 2021 2022 2023 2024 Average

Domestic inflation 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00%

International inflation 1.50% 1.50% 1.60% 1.6% 1.6% 1.6% 1.58% Source: Asian Development Bank estimates.

14

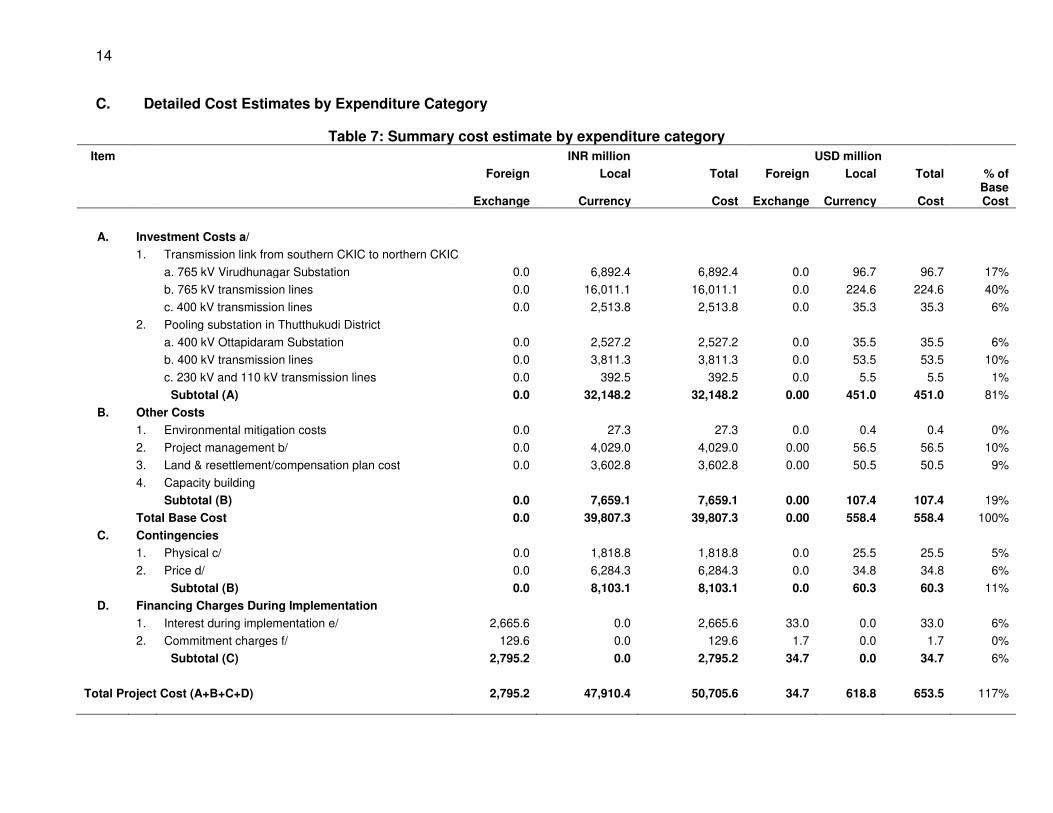

C. Detailed Cost Estimates by Expenditure Category

Table 7: Summary cost estimate by expenditure category

Item INR million USD million

Foreign Local Total Foreign Local Total % of

Exchange Currency Cost Exchange Currency Cost Base Cost

A. Investment Costs a/

1. Transmission link from southern CKIC to northern CKIC

a. 765 kV Virudhunagar Substation 0.0 6,892.4 6,892.4 0.0 96.7 96.7 17%

b. 765 kV transmission lines 0.0 16,011.1 16,011.1 0.0 224.6 224.6 40%

c. 400 kV transmission lines 0.0 2,513.8 2,513.8 0.0 35.3 35.3 6%

2. Pooling substation in Thutthukudi District

a. 400 kV Ottapidaram Substation 0.0 2,527.2 2,527.2 0.0 35.5 35.5 6%

b. 400 kV transmission lines 0.0 3,811.3 3,811.3 0.0 53.5 53.5 10%

c. 230 kV and 110 kV transmission lines 0.0 392.5 392.5 0.0 5.5 5.5 1%

Subtotal (A) 0.0 32,148.2 32,148.2 0.00 451.0 451.0 81%

B. Other Costs

1. Environmental mitigation costs 0.0 27.3 27.3 0.0 0.4 0.4 0%

2. Project management b/ 0.0 4,029.0 4,029.0 0.00 56.5 56.5 10%

3. Land & resettlement/compensation plan cost 0.0 3,602.8 3,602.8 0.00 50.5 50.5 9%

4. Capacity building

Subtotal (B) 0.0 7,659.1 7,659.1 0.00 107.4 107.4 19%

Total Base Cost 0.0 39,807.3 39,807.3 0.00 558.4 558.4 100%

C. Contingencies

1. Physical c/ 0.0 1,818.8 1,818.8 0.0 25.5 25.5 5%

2. Price d/ 0.0 6,284.3 6,284.3 0.0 34.8 34.8 6%

Subtotal (B) 0.0 8,103.1 8,103.1 0.0 60.3 60.3 11%

D. Financing Charges During Implementation

1. Interest during implementation e/ 2,665.6 0.0 2,665.6 33.0 0.0 33.0 6%

2. Commitment charges f/ 129.6 0.0 129.6 1.7 0.0 1.7 0%

Subtotal (C) 2,795.2 0.0 2,795.2 34.7 0.0 34.7 6%

Total Project Cost (A+B+C+D) 2,795.2 47,910.4 50,705.6 34.7 618.8 653.5 117%

15

a/In January 2019 prices. Includes taxes of $68.8 million. Includes the Environment Management cost of $2.69 million to be incurred by the contractors. b/Includes all project management and supervision costs, including staff. c/Physical contingency computed at 5% of base costs (excluding right-of-way compensation included in land & resettlement/compensation plan cost). d/Price contingency computed using ADB's forecasts of international and domestic inflation and includes provision for potential exchange rate fluctuation under the

assumption of a purchasing power parity exchange rate. e/Interest during the implementation period has been computed at 3.15%. f/Commitment charge has been computed at 0.15% of undisbursed loan amounts for ADB loan. Numbers may not sum precisely because of rounding. Source: Executing Agency and Asian Development Bank estimates.

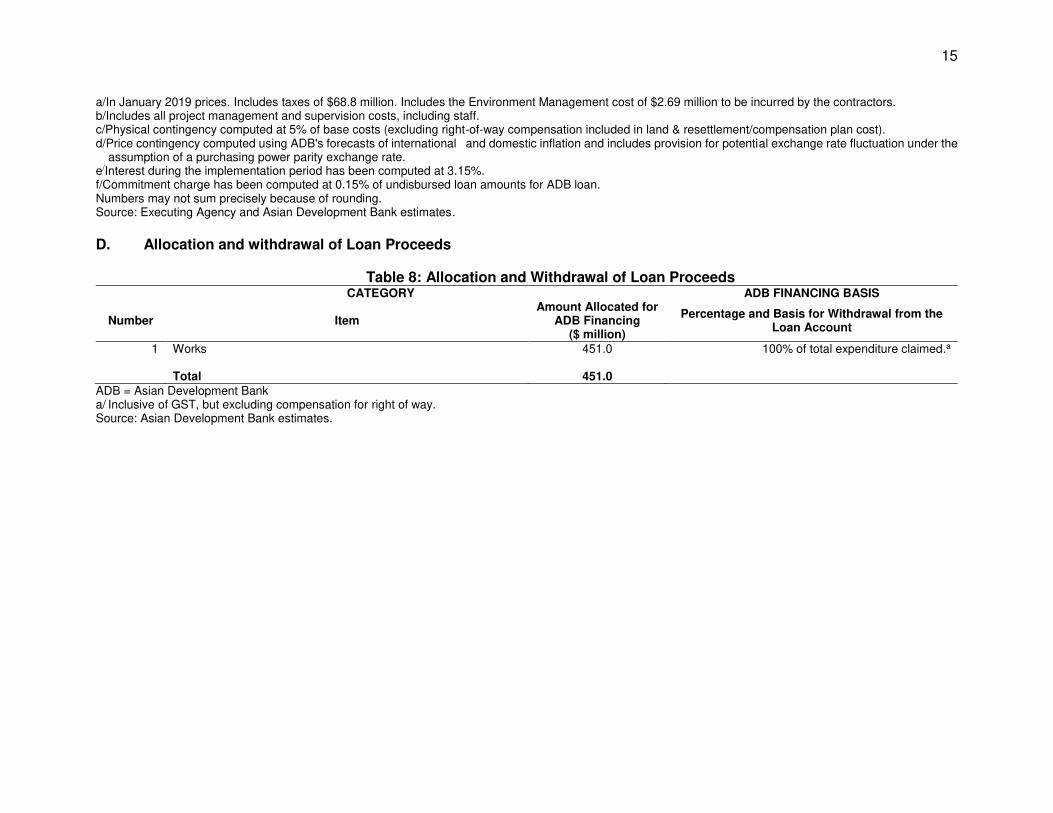

D. Allocation and withdrawal of Loan Proceeds

Table 8: Allocation and Withdrawal of Loan Proceeds CATEGORY ADB FINANCING BASIS

Number Item Amount Allocated for

ADB Financing ($ million)

Percentage and Basis for Withdrawal from the Loan Account

1 Works 451.0 100% of total expenditure claimed.a

Total 451.0 ADB = Asian Development Bank a/ Inclusive of GST, but excluding compensation for right of way. Source: Asian Development Bank estimates.

16

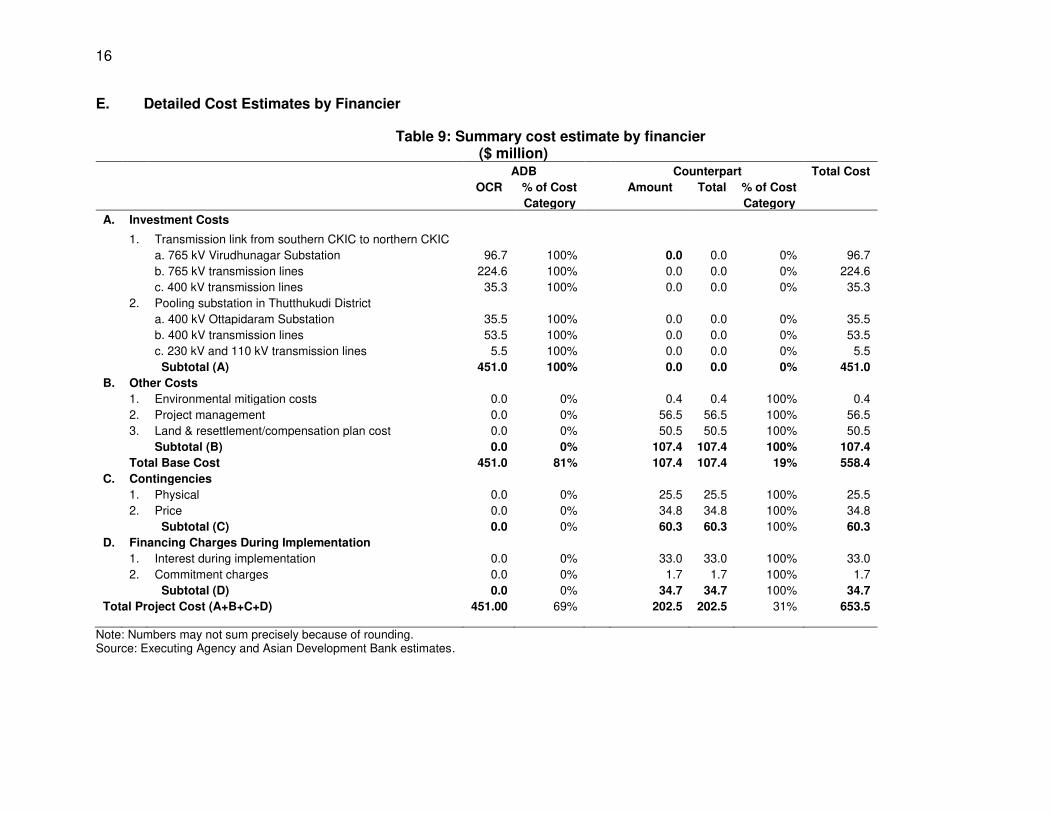

E. Detailed Cost Estimates by Financier

Table 9: Summary cost estimate by financier ($ million)

ADB Counterpart Total Cost

OCR % of Cost Amount Total % of Cost

Category Category

A. Investment Costs

1. Transmission link from southern CKIC to northern CKIC a. 765 kV Virudhunagar Substation 96.7 100% 0.0 0.0 0% 96.7

b. 765 kV transmission lines 224.6 100% 0.0 0.0 0% 224.6

c. 400 kV transmission lines 35.3 100% 0.0 0.0 0% 35.3

2. Pooling substation in Thutthukudi District a. 400 kV Ottapidaram Substation 35.5 100% 0.0 0.0 0% 35.5

b. 400 kV transmission lines 53.5 100% 0.0 0.0 0% 53.5

c. 230 kV and 110 kV transmission lines 5.5 100% 0.0 0.0 0% 5.5

Subtotal (A) 451.0 100% 0.0 0.0 0% 451.0

B. Other Costs

1. Environmental mitigation costs 0.0 0% 0.4 0.4 100% 0.4

2. Project management 0.0 0% 56.5 56.5 100% 56.5

3. Land & resettlement/compensation plan cost 0.0 0% 50.5 50.5 100% 50.5

Subtotal (B) 0.0 0% 107.4 107.4 100% 107.4

Total Base Cost 451.0 81% 107.4 107.4 19% 558.4

C. Contingencies

1. Physical 0.0 0% 25.5 25.5 100% 25.5

2. Price 0.0 0% 34.8 34.8 100% 34.8

Subtotal (C) 0.0 0% 60.3 60.3 100% 60.3

D. Financing Charges During Implementation

1. Interest during implementation 0.0 0% 33.0 33.0 100% 33.0

2. Commitment charges 0.0 0% 1.7 1.7 100% 1.7

Subtotal (D) 0.0 0% 34.7 34.7 100% 34.7

Total Project Cost (A+B+C+D) 451.00 69% 202.5 202.5 31% 653.5

Note: Numbers may not sum precisely because of rounding. Source: Executing Agency and Asian Development Bank estimates.

17

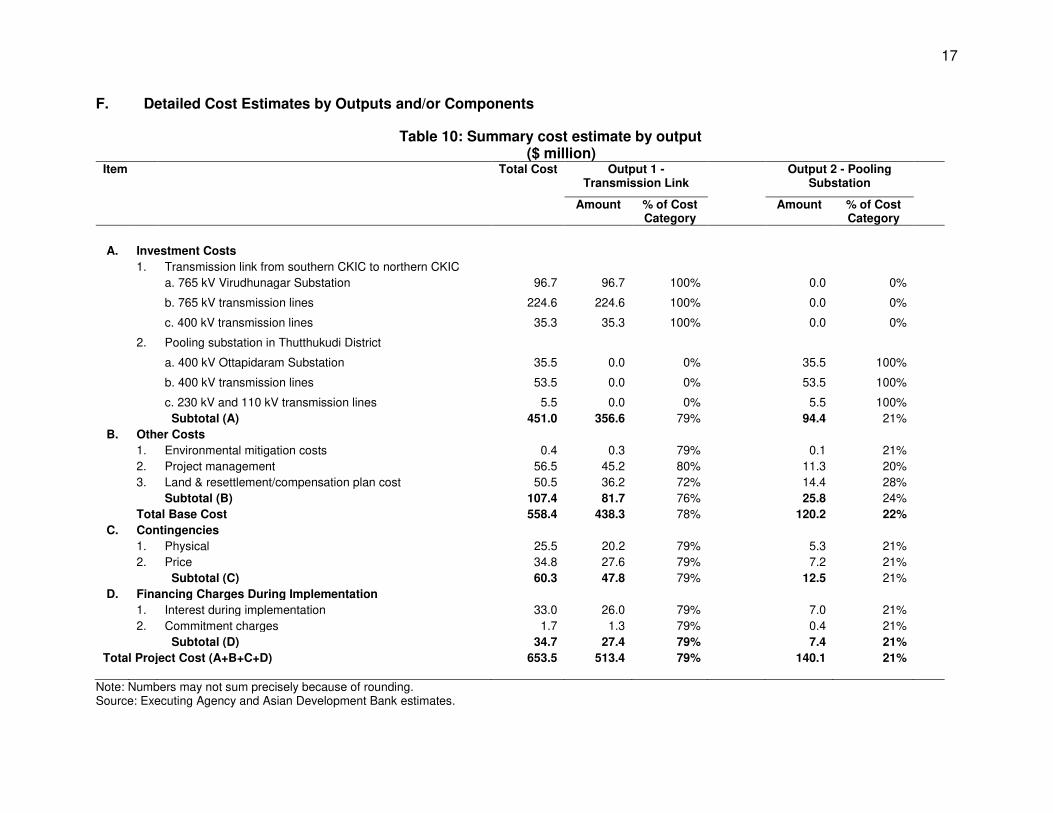

F. Detailed Cost Estimates by Outputs and/or Components

Table 10: Summary cost estimate by output ($ million)

Item Total Cost Output 1 - Transmission Link

Output 2 - Pooling Substation

Amount % of Cost Category

Amount % of Cost Category

A. Investment Costs

1. Transmission link from southern CKIC to northern CKIC

a. 765 kV Virudhunagar Substation 96.7 96.7 100% 0.0 0%

b. 765 kV transmission lines 224.6 224.6 100% 0.0 0%

c. 400 kV transmission lines 35.3 35.3 100% 0.0 0%

2. Pooling substation in Thutthukudi District

a. 400 kV Ottapidaram Substation 35.5 0.0 0% 35.5 100%

b. 400 kV transmission lines 53.5 0.0 0% 53.5 100%

c. 230 kV and 110 kV transmission lines 5.5 0.0 0% 5.5 100%

Subtotal (A) 451.0 356.6 79% 94.4 21%

B. Other Costs

1. Environmental mitigation costs 0.4 0.3 79% 0.1 21%

2. Project management 56.5 45.2 80% 11.3 20%

3. Land & resettlement/compensation plan cost 50.5 36.2 72% 14.4 28%

Subtotal (B) 107.4 81.7 76% 25.8 24%

Total Base Cost 558.4 438.3 78% 120.2 22%

C. Contingencies

1. Physical 25.5 20.2 79% 5.3 21%

2. Price 34.8 27.6 79% 7.2 21%

Subtotal (C) 60.3 47.8 79% 12.5 21%

D. Financing Charges During Implementation

1. Interest during implementation 33.0 26.0 79% 7.0 21%

2. Commitment charges 1.7 1.3 79% 0.4 21%

Subtotal (D) 34.7 27.4 79% 7.4 21%

Total Project Cost (A+B+C+D) 653.5 513.4 79% 140.1 21%

Note: Numbers may not sum precisely because of rounding. Source: Executing Agency and Asian Development Bank estimates.

18

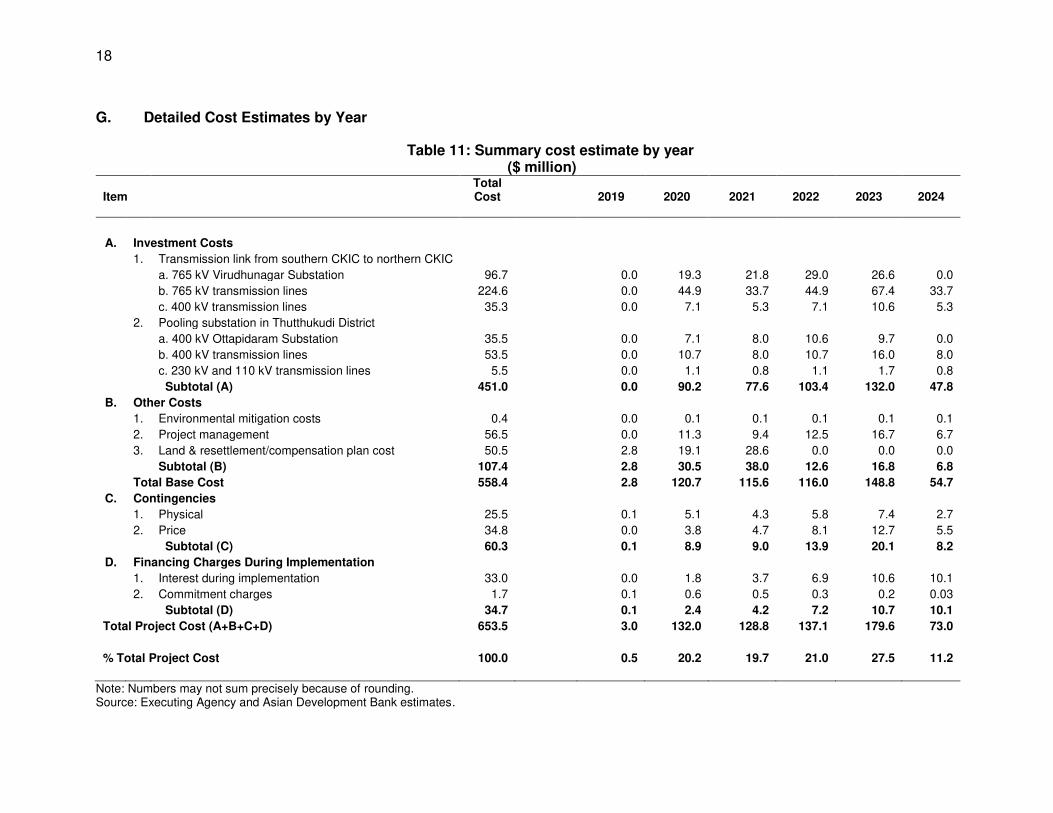

G. Detailed Cost Estimates by Year

Table 11: Summary cost estimate by year ($ million)

Item Total Cost 2019 2020 2021 2022 2023 2024

A. Investment Costs

1. Transmission link from southern CKIC to northern CKIC

a. 765 kV Virudhunagar Substation 96.7 0.0 19.3 21.8 29.0 26.6 0.0

b. 765 kV transmission lines 224.6 0.0 44.9 33.7 44.9 67.4 33.7

c. 400 kV transmission lines 35.3 0.0 7.1 5.3 7.1 10.6 5.3

2. Pooling substation in Thutthukudi District

a. 400 kV Ottapidaram Substation 35.5 0.0 7.1 8.0 10.6 9.7 0.0

b. 400 kV transmission lines 53.5 0.0 10.7 8.0 10.7 16.0 8.0

c. 230 kV and 110 kV transmission lines 5.5 0.0 1.1 0.8 1.1 1.7 0.8

Subtotal (A) 451.0 0.0 90.2 77.6 103.4 132.0 47.8

B. Other Costs

1. Environmental mitigation costs 0.4 0.0 0.1 0.1 0.1 0.1 0.1

2. Project management 56.5 0.0 11.3 9.4 12.5 16.7 6.7

3. Land & resettlement/compensation plan cost 50.5 2.8 19.1 28.6 0.0 0.0 0.0

Subtotal (B) 107.4 2.8 30.5 38.0 12.6 16.8 6.8

Total Base Cost 558.4 2.8 120.7 115.6 116.0 148.8 54.7

C. Contingencies

1. Physical 25.5 0.1 5.1 4.3 5.8 7.4 2.7

2. Price 34.8 0.0 3.8 4.7 8.1 12.7 5.5

Subtotal (C) 60.3 0.1 8.9 9.0 13.9 20.1 8.2

D. Financing Charges During Implementation

1. Interest during implementation 33.0 0.0 1.8 3.7 6.9 10.6 10.1

2. Commitment charges 1.7 0.1 0.6 0.5 0.3 0.2 0.03

Subtotal (D) 34.7 0.1 2.4 4.2 7.2 10.7 10.1

Total Project Cost (A+B+C+D) 653.5 3.0 132.0 128.8 137.1 179.6 73.0

% Total Project Cost 100.0 0.5 20.2 19.7 21.0 27.5 11.2

Note: Numbers may not sum precisely because of rounding. Source: Executing Agency and Asian Development Bank estimates.

19

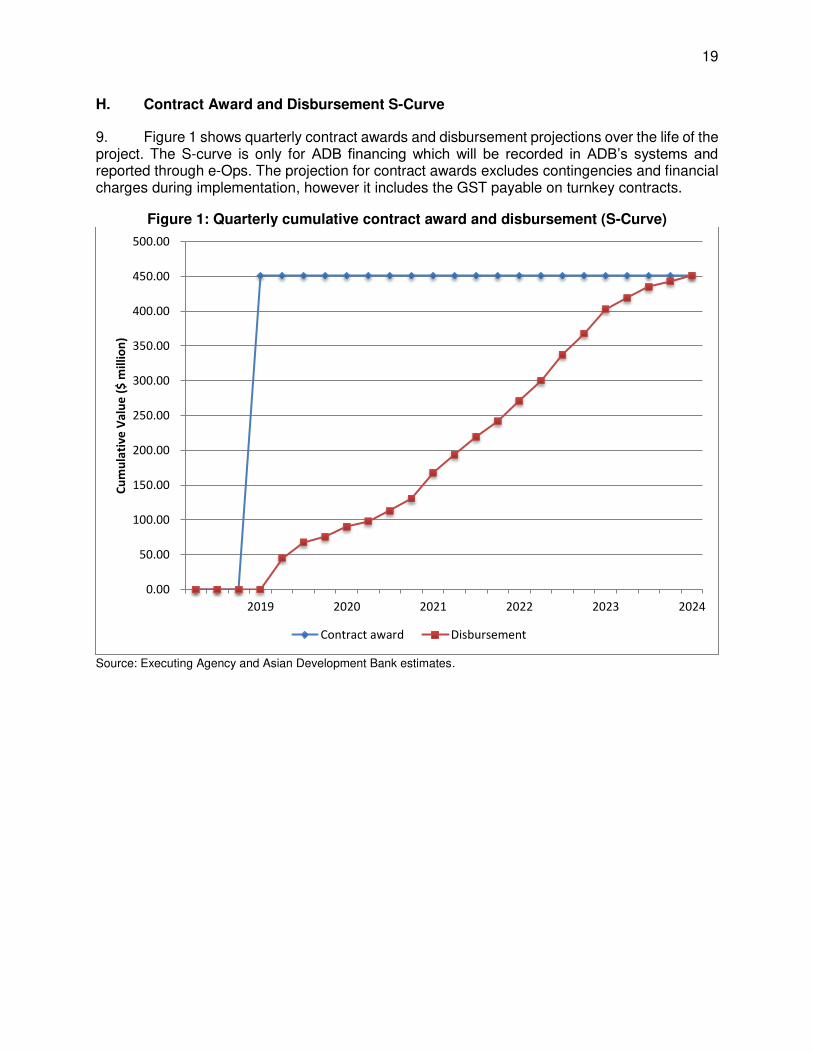

H. Contract Award and Disbursement S-Curve

9. Figure 1 shows quarterly contract awards and disbursement projections over the life of the project. The S-curve is only for ADB financing which will be recorded in ADB’s systems and reported through e-Ops. The projection for contract awards excludes contingencies and financial charges during implementation, however it includes the GST payable on turnkey contracts.

Figure 1: Quarterly cumulative contract award and disbursement (S-Curve)

Source: Executing Agency and Asian Development Bank estimates.

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

400.00

450.00

500.00

2019 2020 2021 2022 2023 2024

Cu

mu

lati

ve

Va

lue

($

mil

lio

n)

Contract award Disbursement

20

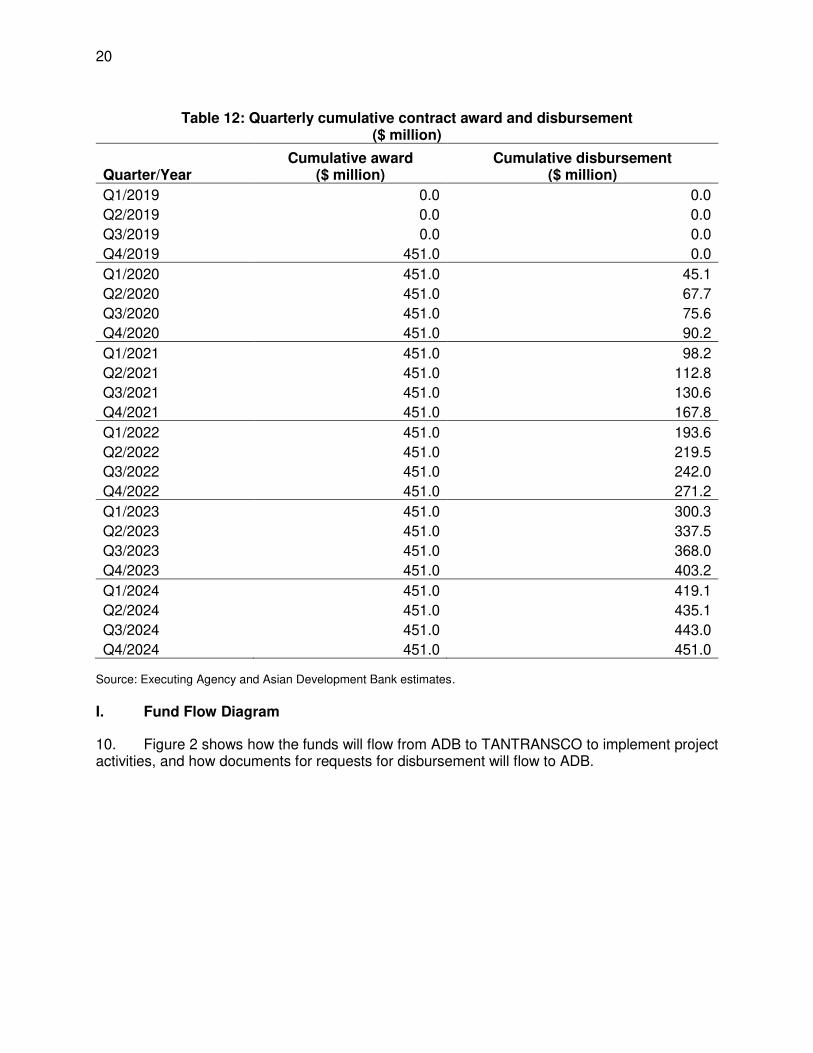

Table 12: Quarterly cumulative contract award and disbursement ($ million)

Quarter/Year Cumulative award

($ million) Cumulative disbursement

($ million)

Q1/2019 0.0 0.0

Q2/2019 0.0 0.0

Q3/2019 0.0 0.0

Q4/2019 451.0 0.0

Q1/2020 451.0 45.1

Q2/2020 451.0 67.7

Q3/2020 451.0 75.6

Q4/2020 451.0 90.2

Q1/2021 451.0 98.2

Q2/2021 451.0 112.8

Q3/2021 451.0 130.6

Q4/2021 451.0 167.8

Q1/2022 451.0 193.6

Q2/2022 451.0 219.5

Q3/2022 451.0 242.0

Q4/2022 451.0 271.2

Q1/2023 451.0 300.3

Q2/2023 451.0 337.5

Q3/2023 451.0 368.0

Q4/2023 451.0 403.2

Q1/2024 451.0 419.1

Q2/2024 451.0 435.1

Q3/2024 451.0 443.0

Q4/2024 451.0 451.0 Source: Executing Agency and Asian Development Bank estimates.

I. Fund Flow Diagram

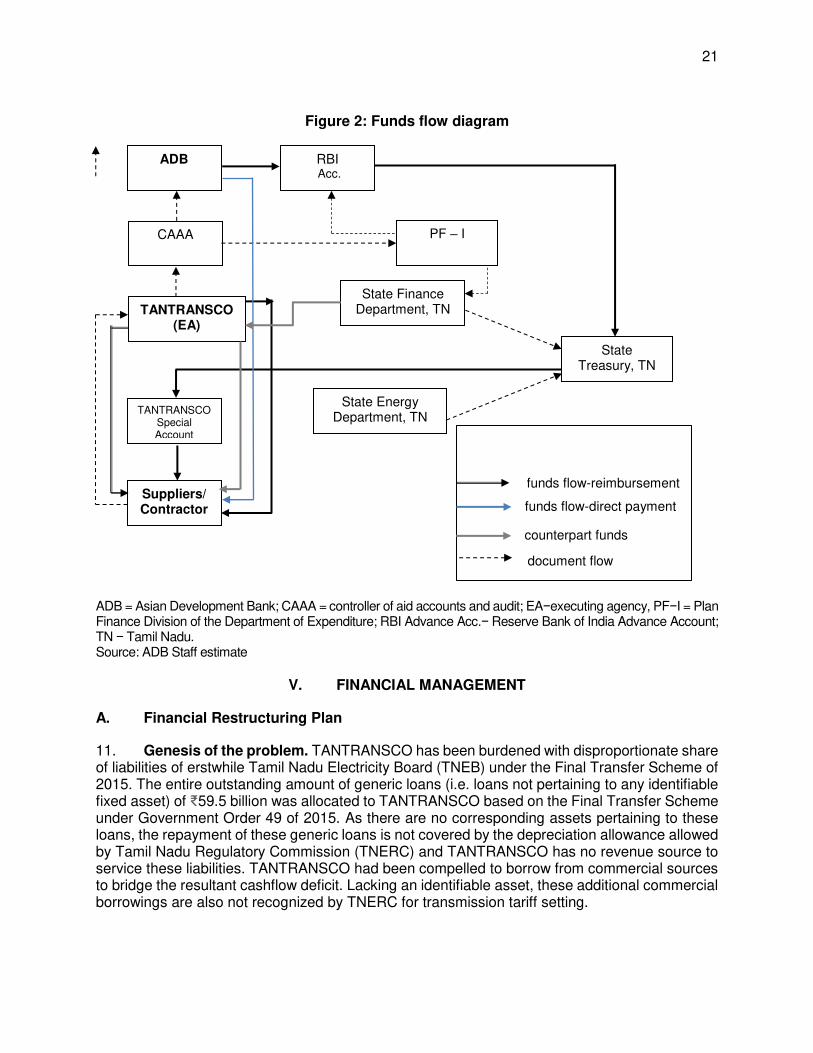

10. Figure 2 shows how the funds will flow from ADB to TANTRANSCO to implement project activities, and how documents for requests for disbursement will flow to ADB.

21

Figure 2: Funds flow diagram

ADB = Asian Development Bank; CAAA = controller of aid accounts and audit; EA−executing agency, PF−I = Plan Finance Division of the Department of Expenditure; RBI Advance Acc.− Reserve Bank of India Advance Account; TN − Tamil Nadu. Source: ADB Staff estimate

V. FINANCIAL MANAGEMENT

A. Financial Restructuring Plan

11. Genesis of the problem. TANTRANSCO has been burdened with disproportionate share of liabilities of erstwhile Tamil Nadu Electricity Board (TNEB) under the Final Transfer Scheme of 2015. The entire outstanding amount of generic loans (i.e. loans not pertaining to any identifiable fixed asset) of ₹59.5 billion was allocated to TANTRANSCO based on the Final Transfer Scheme under Government Order 49 of 2015. As there are no corresponding assets pertaining to these loans, the repayment of these generic loans is not covered by the depreciation allowance allowed by Tamil Nadu Regulatory Commission (TNERC) and TANTRANSCO has no revenue source to service these liabilities. TANTRANSCO had been compelled to borrow from commercial sources to bridge the resultant cashflow deficit. Lacking an identifiable asset, these additional commercial borrowings are also not recognized by TNERC for transmission tariff setting.

TANTRANSCO (EA)

CAAA

ADB RBI Acc.

TANTRANSCO Special Account

Suppliers/ Contractor

s

State Energy Department, TN

PF – I

State Treasury, TN

State Finance Department, TN

document flow

funds flow-reimbursement

funds flow-direct payment

counterpart funds

22

12. As of 31 March 2019, the TNERC is likely to recognize fixed assets of ₹185.6 billion for the purpose of transmission tariff setting after adjusting for consumer contributions, grants, capital subsidies and difference between book value of fixed assets and value of fixed assets recognized by TNERC as on the date of Final Transfer Scheme. As the depreciation allowance allowed in the transmission tariff by TNERC assumes the capital structure of new assets to be 70:30 (with debt financing amounting to 70% and equity financing of 30%), 70% of value of assets recognized by TNERC (i.e. ₹129.9 billion) can be considered as sustainable level of liabilities.

13. As TANTRANSCO was not able to contribute 30% of capital expenditure as equity over the last 5 years, it has resorted to finance the past capital investments with more than 70% of debt financing. As the depreciation allowance allowed in transmission tariff is adequate to service up to 70% of debt, TANTRANSCO has not received adequate tariff to service the debt exceeding 70% that it has borrowed for capital investment.

14. The total amount of liabilities owed to external borrowers as of 31 March 2019, amounted to ₹187.2 billion subject to confirmation based on audited accounts. The unsustainable liabilities of TANTRANSCO that it cannot service using its revenues amount to ₹57.3 billion. (i.e. the difference between total liabilities to third parties of ₹187.2 billion and sustainable level of liabilities of ₹129.9 billion). The disproportionate allocation of generic loans not supported by assets and inadequate equity financing of capital investments have resulted in the above-mentioned unsustainable liabilities.

15. Besides the debt owed to third parties, TANTRANSCO owes ₹102.2 billion to TANGEDCO after adjusting for receivables from TANGEDCO. This represents repayment of principal and interest payment of the loans by TANGEDCO that were transferred to TANTRANSCO under the Transfer Scheme during fiscal year FY2010/2011–FY2015-2016. TANTRANSCO has no revenue source to repay this debt to TANGEDCO, as this does not represent any asset for the transmission business recognized by TNERC. The details of payables and receivables from TANGEDCO in the books of TANTRANSCO is shown in table 13 below:

Table 13: Intercompany outstanding in the books of TANTRANSCO*

Particulars INR billion Payable to TANGEDCO as on 31 March 2018 168.26 Receivable from TANGEDCO as on 31 March 2018 66.03 Net payable to TANGEDCO as on 31 March 2018 102.23

*This is subject to completion of reconciliation of the outstanding balance between both companies

B. Key Aspects of Financial Restructuring Plan 16. TANTRANSCO shall approach the government of Tamil Nadu to seek equity support against the remaining unsustainable loan liability of ₹57.3 billion, together with the interest payable of ₹9.9 billion for the 3-year period. This equity assistance may be received over a period of three years. Based on the understanding reached at the meeting held on 14 June 2019 with the Finance Department of Tamil Nadu, the state government has agreed to provide an equity injection of ₹50 billion - ₹65 billion in three equal annual installments starting from FY2021 for settling major portion of unsustainable liabilities.3 TANTRANSCO shall use the proceeds from this equity infusion towards payment of loans and interest to external creditors (banks and financial institutions). The balance amount of outstanding external loans is expected to be serviced by TANTRANSCO through its ARR.

3 The amount of equity injection to be mentioned in the Government Order (GO) to be issued upon approval of the

proposed Financial Restructuring Plan.

23

17. There is a net payable of ₹102.2 billion from TANTRANSCO to TANGEDCO as of 31 March 2018 subject to confirmation through an intercompany account reconciliation exercise. TANTRANSCO has no revenue source to service this liability owed to TANGEDCO. A significant portion of this amount pertains to the generic loans allocated to TANTRANSCO at the time of its separation from TNEB, and the accrued interest thereon that has been serviced by TANGEDCO. An in principle agreement has been reached with TANGEDCO to forgo this liability and waive interest on this liability from 31 March 2018. However, the accounting treatment of this adjustment in the books of TANTRANSCO and TANGEDCO is yet to be finalized. This will be finalized by 31 December 2019 in consultation with external auditors and tax advisors of two companies.

18. TANTRANSCO will revisit its proposed capital expenditure of approximately ₹300 billion from FY2019–2020 to FY2021–2022. TANTRANSCO will maintain its capital expenditure (CAPEX) at a level such that the equity contribution from GOTN will be at least 30%, until such time as TANTRANSCO’s internal cash accruals increase to part-finance capex, and reduce the need for external equity injection from GOTN. The GOTN will also contribute ₹10 billion as equity to finance the counterpart finance of proposed ADB financed project. This will be part of the Government equity contribution to finance 30% of capital expenditure.

19. It is noted that depreciation allowed by TNERC does not match the repayment obligation of remaining external liabilities due to shorter tenor (10 years) of these loans. TANTRANSCO will endeavor to reschedule these loans to have an average tenor of 12 years to match the accelerated depreciation allowed by TNERC in setting the transmission tariff.

20. The irregular filing for tariff revision has also been identified as one of the contributory factors to the financial stress faced by both TANTRANSCO and TANGEDCO. To prevent the recurrence of this problem in the future, it was agreed that TANTRANSCO will make annual tariff filling on a regular basis.

21. During the preparation of project, ADB has assisted the government of Tamil Nadu to prepare an FRP to address this long-standing issue and restore the financial viability of TANTRANSCO. The FRP will be adopted by the Board of Directors of TANTRANSCO and TANGEDCO (i.e. in relation to adjustment of intercompany liabilities) and will be submitted to Government of Tamil Nadu for final approval. The FRP consists of following key features:

a. An equity injection of the order of ₹50 billion- ₹65 billion from the Government of Tamil Nadu in equal installments over 3 years starting from FY2020–2021 to settle the unsustainable liabilities owed to external creditors;

b. TANTRANSCO shall utilize the funds from equity injections to settle the unsustainable loan from external agencies like Rural Electrification Corporation Limited (REC) and Power Finance Corporation Ltd. (PFC) in 3 installments over 3 years. The interest amount of these loans during next three years shall also be paid from equity funds received from the Government of Tamil Nadu;

c. TANTRANSCO will endeavor to negotiate with external lenders to restructure the remaining long-term loans by consolidate the loans from each creditor to a single loan having a repayment period of 12 years. Based on the agreement reached with external lenders, the annual payment schedule of restructured loans and applicable interest rates will be provided to ADB by 31 December 2019;

24

d. Intercompany payables and receivables as of 31 March 2018 need to be confirmed through an intercompany reconciliation exercise. After the reconciliation of the amount, the amount will be adjusted, the accounting treatment for adjusting the interncompany liabilities will be approved by the board of directors of two companies in consultation with external auditors and tax auditors of two companies. No interest will be charged on the outstanding amount after 31 March 2018 until final settlement;

e. The government will provide additional equity financing to finance 30% of

TANTRANSCO’s capital expenditure on an annual basis until TANTRANSCO can contribute 30% of capital expenditure using internal cash generation; and

f. Timely filing of annual tariff revision applications and true-up petitions by

TANTRANSCO to TNERC. 22. The key actions under the FRP is summarized in table 14.

Table 14: Key Actions under the FRP Action Responsibility Time Frame Approval

Authoritiy Issuance of a Government Order (GO) to give effect to the proposed Financial Restructuiring Plan.

GOTN 31 March 2020 Government of Tamil Nadu

Annual equity injection as per the approved FRP to settle the unsustainable liabilities of TANTRANSCO

GOTN FY2021−2023 Government of Tamil Nadu through annual budget

Prepayment of unsustainable loans from the equity funds received from GOTN

TANTRANSCO FY2021–2023 Board of Directors of TANTRANSCO

Rescheduling of remaining loans TANTRANSCO 31 December 2019

Lenders and TANTRANSCO Board of Directors.

Waiver of interest due on intercompany liabilities due from TANTRANSCO with effect from 13 March 2018

TANGEDCO 31 March 2020

Board of Directors of TANGEDCO

Make adjustments to the intercompany balances to reflect the reallocation of generic loans under the government order to be issued

TANTRANSCO /TANGEDCO

31 March 2020 TANGEDCO and TANTRANSCO

Rationalize capital expenditure to ensure equity injections from the Government of Tamil Nadu and internal cash generation contribute at least 30% of the capital expenditure..

TANTRANSCO FY2021−2024 Board of Directors of TANTRANSCO

Government will provide additional equity finance every year to bridge the gap between internal cash generation and 30% of capital expenditure to be financed with equity.

GOTN FY2021−2024 Government of Tamil Nadu

TANTRANSCO will make annual tariff filling to TNERC

TANTRANSCO Commencing from FY2019-2020, for each year.

TANTRANSCO Board of Directors

25

C. Financial Management Assessment

23. The financial management assessment (FMA) was conducted over the period January-March 2019 in accordance with ADB’s Guidelines for the Financial Management and Analysis of Projects 2005, Financial Due Diligence: A Methodology Note (2009) and Financial Management Technical Guidance Note (2015) of the ADB.

24. The FMA considered the capacity of TANTRANSCO, including funds-flow arrangements, staffing, accounting and financial reporting systems, financial information systems, and internal and external auditing arrangements. TANTRANSCO’s relative strengths in the area of financial management, identified during the FMA, include governance by a robust legislative framework periodic audit by Comptroller and Auditor General of India (CAG), its operations and tariffs regulated by state and central electricity regulatory commissions, and experience with disbursement and procurement processes and procedures of international development agencies such as JICA and KFW. The key weaknesses include a substantial dependency by TANTRANSCO on TANGEDCO as all its staff are on deputation from TANGEDCO, financial accounts with numerous unresolved audit observations, high levels of intra-company and inter-company unreconciled balances, lack of a completed fixed asset register, and low levels of computerization and automation. The overall pre-mitigation financial management risk of TANTRANSCO is assessed as substantial.

25. TANTRANSCO has agreed to implement an action plan as key measures to address the deficiencies. The financial management action plan is provided in Table 16.

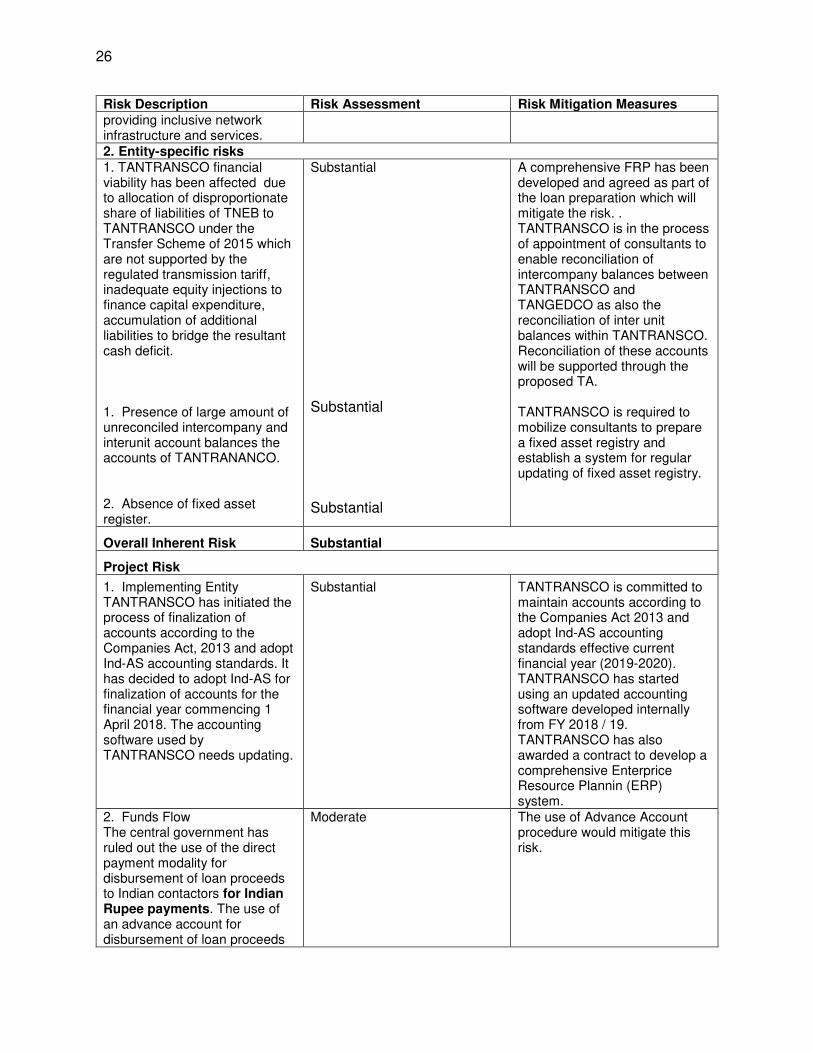

Table 15: Financial Management Internal Control and Risk Assessment (FMICRA) Risk Description Risk Assessment Risk Mitigation Measures Inherent Risk 1. Country specific risks 1. Country Specific Strong public financial management (PFM) is one of the key elements of the Government of India’s strategy for strengthening governance, optimizing outputs from public resources and ensuring inclusive and broad-based development. The 2010 Public Financial Management Performance Assessment Report for India identified that the PFM system is well structured but unevenly implemented.

ADB’s 2018-2022 Country Partnership Strategy for India notes that public financial management at the state level needs to be improved to facilitate the strategic pillar of

Moderate No particular mitigation measures are proposed.

26

Risk Description Risk Assessment Risk Mitigation Measures providing inclusive network infrastructure and services. 2. Entity-specific risks 1. TANTRANSCO financial viability has been affected due to allocation of disproportionate share of liabilities of TNEB to TANTRANSCO under the Transfer Scheme of 2015 which are not supported by the regulated transmission tariff, inadequate equity injections to finance capital expenditure, accumulation of additional liabilities to bridge the resultant cash deficit. 1. Presence of large amount of unreconciled intercompany and interunit account balances the accounts of TANTRANANCO. 2. Absence of fixed asset register.

Substantial

Substantial Substantial

A comprehensive FRP has been developed and agreed as part of the loan preparation which will mitigate the risk. . TANTRANSCO is in the process of appointment of consultants to enable reconciliation of intercompany balances between TANTRANSCO and TANGEDCO as also the reconciliation of inter unit balances within TANTRANSCO. Reconciliation of these accounts will be supported through the proposed TA. TANTRANSCO is required to mobilize consultants to prepare a fixed asset registry and establish a system for regular updating of fixed asset registry.

Overall Inherent Risk Substantial

Project Risk

1. Implementing Entity TANTRANSCO has initiated the process of finalization of accounts according to the Companies Act, 2013 and adopt Ind-AS accounting standards. It has decided to adopt Ind-AS for finalization of accounts for the financial year commencing 1 April 2018. The accounting software used by TANTRANSCO needs updating.

Substantial TANTRANSCO is committed to maintain accounts according to the Companies Act 2013 and adopt Ind-AS accounting standards effective current financial year (2019-2020). TANTRANSCO has started using an updated accounting software developed internally from FY 2018 / 19. TANTRANSCO has also awarded a contract to develop a comprehensive Enterprice Resource Plannin (ERP) system.

2. Funds Flow The central government has ruled out the use of the direct payment modality for disbursement of loan proceeds to Indian contactors for Indian Rupee payments. The use of an advance account for disbursement of loan proceeds

Moderate The use of Advance Account procedure would mitigate this risk.

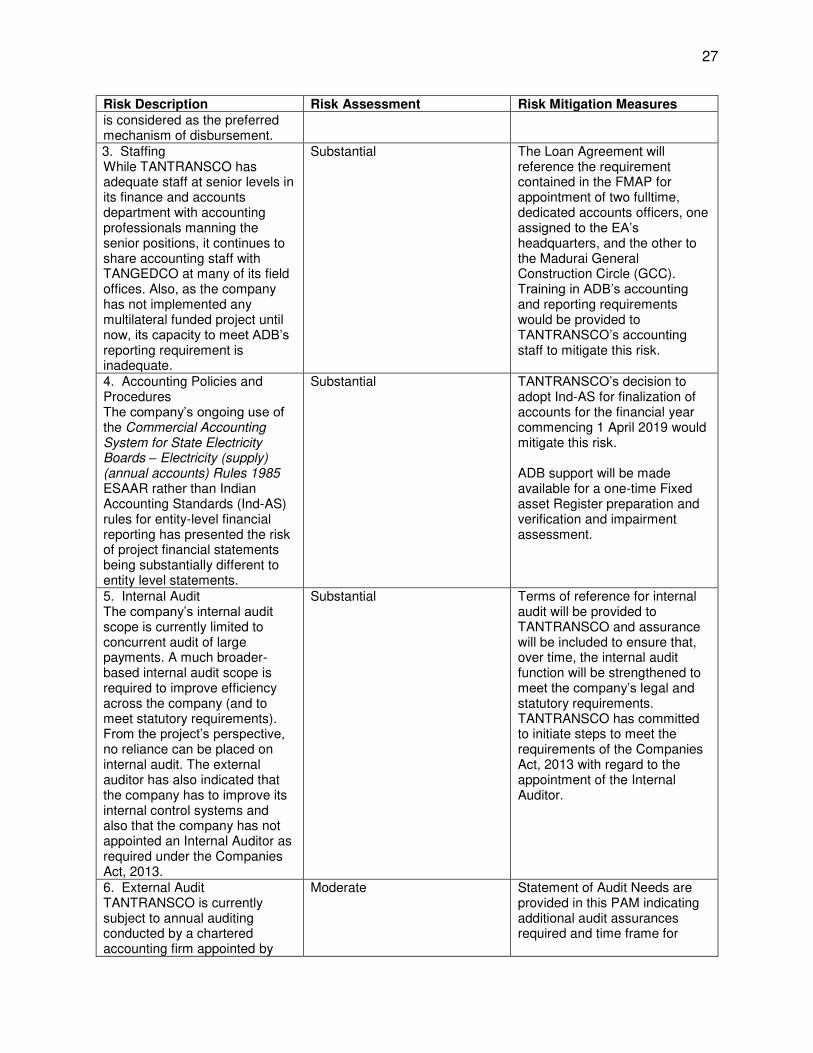

27

Risk Description Risk Assessment Risk Mitigation Measures is considered as the preferred mechanism of disbursement. 3. Staffing While TANTRANSCO has adequate staff at senior levels in its finance and accounts department with accounting professionals manning the senior positions, it continues to share accounting staff with TANGEDCO at many of its field offices. Also, as the company has not implemented any multilateral funded project until now, its capacity to meet ADB’s reporting requirement is inadequate.

Substantial The Loan Agreement will reference the requirement contained in the FMAP for appointment of two fulltime, dedicated accounts officers, one assigned to the EA’s headquarters, and the other to the Madurai General Construction Circle (GCC). Training in ADB’s accounting and reporting requirements would be provided to TANTRANSCO’s accounting staff to mitigate this risk.

4. Accounting Policies and Procedures The company’s ongoing use of the Commercial Accounting System for State Electricity Boards – Electricity (supply) (annual accounts) Rules 1985 ESAAR rather than Indian Accounting Standards (Ind-AS) rules for entity-level financial reporting has presented the risk of project financial statements being substantially different to entity level statements.

Substantial TANTRANSCO’s decision to adopt Ind-AS for finalization of accounts for the financial year commencing 1 April 2019 would mitigate this risk. ADB support will be made available for a one-time Fixed asset Register preparation and verification and impairment assessment.

5. Internal Audit The company’s internal audit scope is currently limited to concurrent audit of large payments. A much broader-based internal audit scope is required to improve efficiency across the company (and to meet statutory requirements). From the project’s perspective, no reliance can be placed on internal audit. The external auditor has also indicated that the company has to improve its internal control systems and also that the company has not appointed an Internal Auditor as required under the Companies Act, 2013.

Substantial Terms of reference for internal audit will be provided to TANTRANSCO and assurance will be included to ensure that, over time, the internal audit function will be strengthened to meet the company’s legal and statutory requirements. TANTRANSCO has committed to initiate steps to meet the requirements of the Companies Act, 2013 with regard to the appointment of the Internal Auditor.

6. External Audit TANTRANSCO is currently subject to annual auditing conducted by a chartered accounting firm appointed by

Moderate Statement of Audit Needs are provided in this PAM indicating additional audit assurances required and time frame for

28

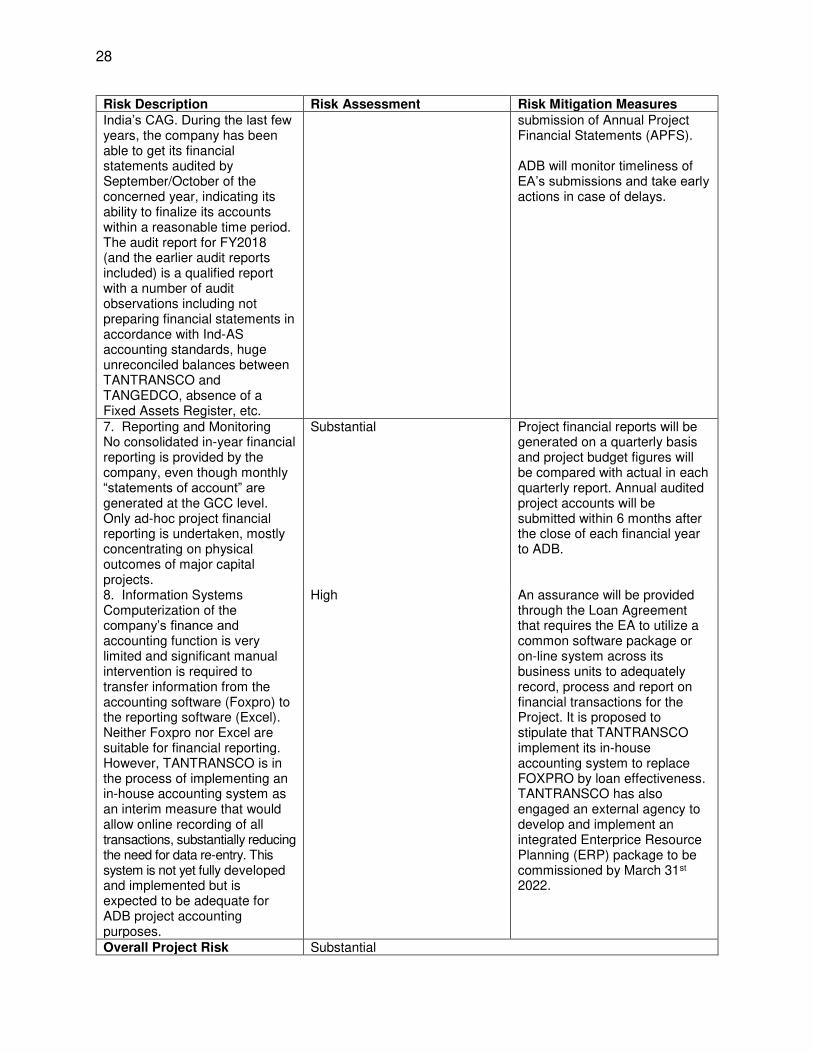

Risk Description Risk Assessment Risk Mitigation Measures India’s CAG. During the last few years, the company has been able to get its financial statements audited by September/October of the concerned year, indicating its ability to finalize its accounts within a reasonable time period. The audit report for FY2018 (and the earlier audit reports included) is a qualified report with a number of audit observations including not preparing financial statements in accordance with Ind-AS accounting standards, huge unreconciled balances between TANTRANSCO and TANGEDCO, absence of a Fixed Assets Register, etc.

submission of Annual Project Financial Statements (APFS). ADB will monitor timeliness of EA’s submissions and take early actions in case of delays.

7. Reporting and Monitoring No consolidated in-year financial reporting is provided by the company, even though monthly “statements of account” are generated at the GCC level. Only ad-hoc project financial reporting is undertaken, mostly concentrating on physical outcomes of major capital projects.

Substantial Project financial reports will be generated on a quarterly basis and project budget figures will be compared with actual in each quarterly report. Annual audited project accounts will be submitted within 6 months after the close of each financial year to ADB.

8. Information Systems Computerization of the company’s finance and accounting function is very limited and significant manual intervention is required to transfer information from the accounting software (Foxpro) to the reporting software (Excel). Neither Foxpro nor Excel are suitable for financial reporting. However, TANTRANSCO is in the process of implementing an in-house accounting system as an interim measure that would allow online recording of all transactions, substantially reducing the need for data re-entry. This system is not yet fully developed and implemented but is expected to be adequate for ADB project accounting purposes.

High An assurance will be provided through the Loan Agreement that requires the EA to utilize a common software package or on-line system across its business units to adequately record, process and report on financial transactions for the Project. It is proposed to stipulate that TANTRANSCO implement its in-house accounting system to replace FOXPRO by loan effectiveness. TANTRANSCO has also engaged an external agency to develop and implement an integrated Enterprice Resource Planning (ERP) package to be commissioned by March 31st 2022.

Overall Project Risk Substantial

29

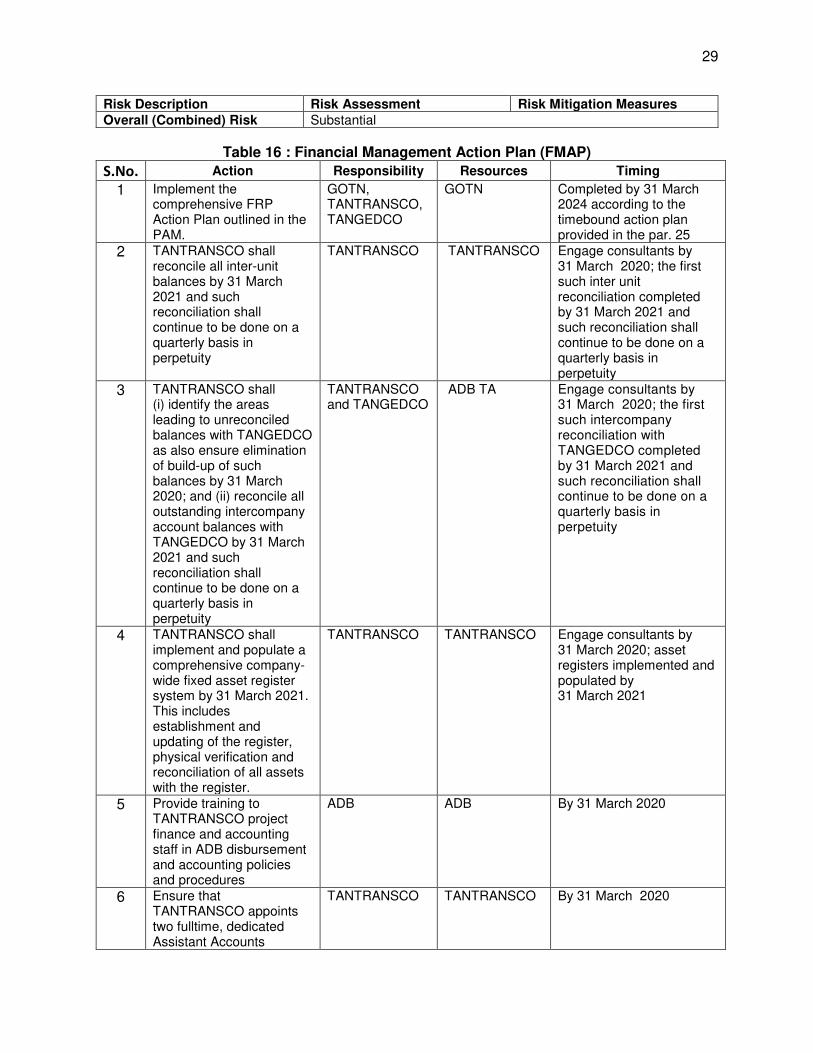

Risk Description Risk Assessment Risk Mitigation Measures Overall (Combined) Risk Substantial

Table 16 : Financial Management Action Plan (FMAP)

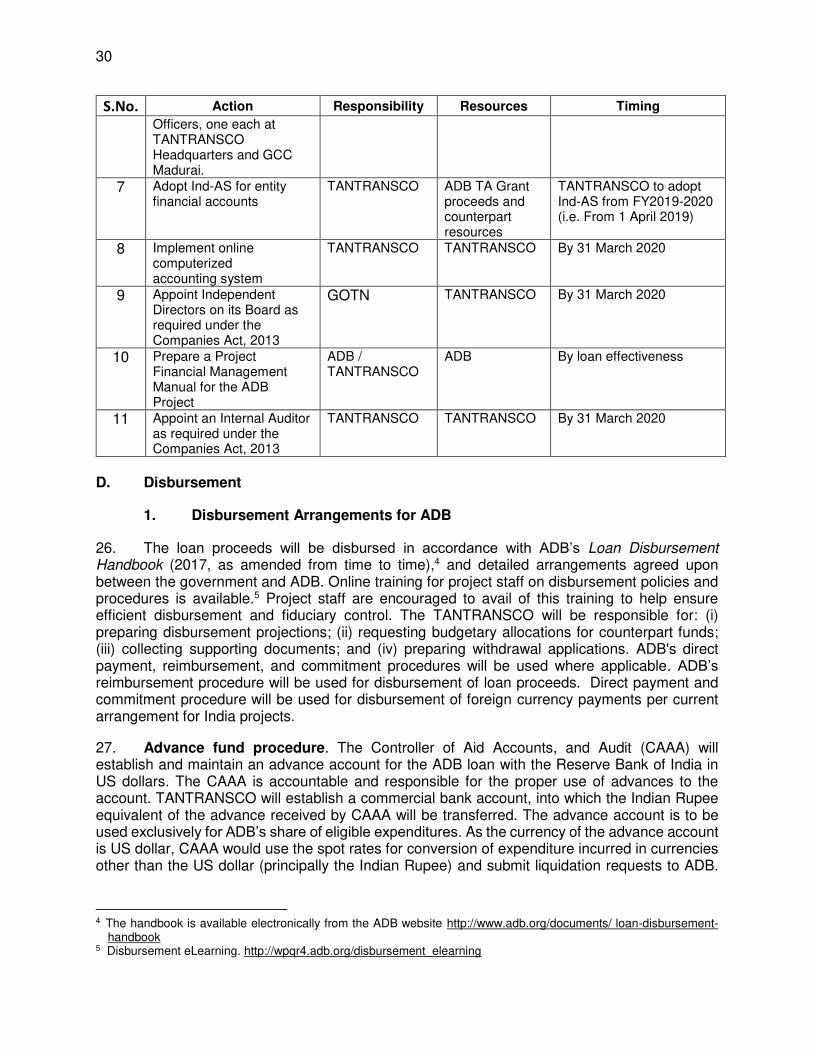

S.No. Action Responsibility Resources Timing

1 Implement the comprehensive FRP Action Plan outlined in the PAM.

GOTN, TANTRANSCO, TANGEDCO

GOTN Completed by 31 March 2024 according to the timebound action plan provided in the par. 25

2 TANTRANSCO shall reconcile all inter-unit balances by 31 March 2021 and such reconciliation shall continue to be done on a quarterly basis in perpetuity

TANTRANSCO TANTRANSCO Engage consultants by 31 March 2020; the first such inter unit reconciliation completed by 31 March 2021 and such reconciliation shall continue to be done on a quarterly basis in perpetuity

3 TANTRANSCO shall (i) identify the areas leading to unreconciled balances with TANGEDCO as also ensure elimination of build-up of such balances by 31 March 2020; and (ii) reconcile all outstanding intercompany account balances with TANGEDCO by 31 March 2021 and such reconciliation shall continue to be done on a quarterly basis in perpetuity

TANTRANSCO and TANGEDCO

ADB TA Engage consultants by 31 March 2020; the first such intercompany reconciliation with TANGEDCO completed by 31 March 2021 and such reconciliation shall continue to be done on a quarterly basis in perpetuity

4 TANTRANSCO shall implement and populate a comprehensive company-wide fixed asset register system by 31 March 2021. This includes establishment and updating of the register, physical verification and reconciliation of all assets with the register.

TANTRANSCO TANTRANSCO Engage consultants by 31 March 2020; asset registers implemented and populated by 31 March 2021

5 Provide training to TANTRANSCO project finance and accounting staff in ADB disbursement and accounting policies and procedures

ADB ADB By 31 March 2020

6 Ensure that TANTRANSCO appoints two fulltime, dedicated Assistant Accounts

TANTRANSCO TANTRANSCO By 31 March 2020

30

S.No. Action Responsibility Resources Timing Officers, one each at TANTRANSCO Headquarters and GCC Madurai.

7 Adopt Ind-AS for entity financial accounts

TANTRANSCO ADB TA Grant proceeds and counterpart resources

TANTRANSCO to adopt Ind-AS from FY2019-2020 (i.e. From 1 April 2019)

8 Implement online computerized accounting system

TANTRANSCO TANTRANSCO By 31 March 2020

9 Appoint Independent Directors on its Board as required under the Companies Act, 2013

GOTN TANTRANSCO By 31 March 2020

10 Prepare a Project Financial Management Manual for the ADB Project

ADB / TANTRANSCO

ADB By loan effectiveness

11 Appoint an Internal Auditor as required under the Companies Act, 2013

TANTRANSCO TANTRANSCO By 31 March 2020

D. Disbursement

1. Disbursement Arrangements for ADB

26. The loan proceeds will be disbursed in accordance with ADB’s Loan Disbursement Handbook (2017, as amended from time to time),4 and detailed arrangements agreed upon between the government and ADB. Online training for project staff on disbursement policies and procedures is available.5 Project staff are encouraged to avail of this training to help ensure efficient disbursement and fiduciary control. The TANTRANSCO will be responsible for: (i) preparing disbursement projections; (ii) requesting budgetary allocations for counterpart funds; (iii) collecting supporting documents; and (iv) preparing withdrawal applications. ADB's direct payment, reimbursement, and commitment procedures will be used where applicable. ADB’s reimbursement procedure will be used for disbursement of loan proceeds. Direct payment and commitment procedure will be used for disbursement of foreign currency payments per current arrangement for India projects.

27. Advance fund procedure. The Controller of Aid Accounts, and Audit (CAAA) will establish and maintain an advance account for the ADB loan with the Reserve Bank of India in US dollars. The CAAA is accountable and responsible for the proper use of advances to the account. TANTRANSCO will establish a commercial bank account, into which the Indian Rupee equivalent of the advance received by CAAA will be transferred. The advance account is to be used exclusively for ADB’s share of eligible expenditures. As the currency of the advance account is US dollar, CAAA would use the spot rates for conversion of expenditure incurred in currencies other than the US dollar (principally the Indian Rupee) and submit liquidation requests to ADB.

4 The handbook is available electronically from the ADB website http://www.adb.org/documents/ loan-disbursement-

handbook 5 Disbursement eLearning. http://wpqr4.adb.org/disbursement_elearning

31

TANTRANSCO would bear the risks arising from any adverse exchange rate movements during liquidation of the advance account.

28. The total outstanding advance to the advance account should not exceed the estimate of ADB’s share of expenditures to be paid through the advance account for the forthcoming 3 months. TANTRANSCO may request for initial and additional advances to the advance account based on an Estimate of Expenditure Sheet6 setting out the estimated expenditures to be financed through the account{s} for the forthcoming 6 months. Supporting documents should be submitted to ADB or retained by TANTRANSCO in accordance with ADB’s Loan Disbursement Handbook (2017, as amended from time to time) when liquidating or replenishing the advance account.

29. Statement of expenditure procedure.7 The statement of expenditure (SOE) procedure may be used for reimbursement of eligible expenditures or liquidation of advances to the advance account(s). There will be an SOE ceiling of $100,000 per claim. Supporting documents and records for the expenditures claimed under the SOE should be maintained and made readily available for review by ADB's disbursement and review missions, upon ADB's request for submission of supporting documents on a sampling basis, and for independent audit.

30. Before the submission of the first withdrawal application (WA), the borrower should submit to ADB sufficient evidence of the authority of the person(s) who will sign the withdrawal applications on behalf of the government, together with the authenticated specimen signatures of each authorized person. The minimum value per WA is $200,000 equivalent unless otherwise accepted by ADB. Individual payments below such amount should be paid (i) by TANTRANSCO and subsequently claimed to ADB through reimbursement; or (ii) through the advance fund procedure, unless otherwise accepted by ADB. The borrower should ensure sufficient category and contract balances before requesting disbursements. "Use of ADB’s Client Portal for Disbursements (CPD)8 system is mandatory for submission of withdrawal applications to ADB."

2. Disbursement Arrangements for Counterpart Funds

31. Disbursement for counterpart funds will be carried out in accordance with guidelines and practices of the state government. The quantity and timing of counterpart funding will be determined and advised by the EA, who will then initiate defined processes to ensure that counterpart funding is reflected in the approved state government budget and the annual capital expenditure budget of the EA. This will be undertaken on an annual basis.

E. Accounting 32. TANTRANSCO will maintain, or cause to be maintained, separate books and records by funding source for all expenditures incurred on the project accrual-based accounting following the equivalent national accounting standards. In case of Project Management expenditure, apart from direct expenditure incurred by TANTRANSCO for this project, it would also include general overhead expenditure incurred by TANTRANSCO on a company wide basis which would then be allocated to each of the projects being implemented by TANTRANSCO (including this project) based on principles acceptable to ADB. TANTRANSCO will prepare project financial statements

6 Estimate of Expenditure sheet is available in Appendix 8A of ADB’s Loan Disbursement Handbook (2017, as

amended from time to time), 7 SOE forms are available in Appendix 7B and 7D of ADB’s Loan Disbursement Handbook (2017, as amended from

time to time). 8 The CPD facilitates online submission of WA to ADB, resulting in faster disbursement. The forms to be completed

by the Borrower are available online at https://www.adb.org/documents/client-portal-disbursements-guide.

32

in accordance with the government's accounting laws and regulations which are consistent with international accounting principles and practices.

F. Auditing and Public Disclosure 33. TANTRANSCO will cause the detailed project financial statements to be audited following the Standards on Auditing (SA) as formulated by the Institute of Chartered Accountants of India (ICAI) by an independent auditor acceptable to ADB. The audited project financial statements together with the auditor’s opinion will be presented in the English language to ADB within 6 months from the end of the fiscal year by TANTRANSCO.

34. The audited entity financial statements, together with the auditor’s report, will be submitted in the English language to ADB within 1 month after their approval by the relevant authority.

35. TANTRANSCO shall prepare the computations demonstrating compliance with the financial ratios as defined in the legal agreements every year, as part of its entity financial reporting. The STATUTORY auditors will provide an ADDITIONAL opinion on achievement of the financial ratios under ISAE 3000 (as applicable in India).

36. The audit report for the project financial statements will include a management letter and auditor’s opinions, which cover (i) whether the project financial statements present an accurate and fair view or are presented fairly, in all material respects, in accordance with the applicable financial reporting standards; and (ii) whether the proceeds of the loan were used only for the purpose(s) of the project.

37. Compliance with financial reporting and auditing requirements will be monitored by review missions and during normal program supervision, and followed up regularly with all concerned, including the external auditor.

38. The government and TANTRANSCO have been made aware of ADB’s approach to delayed submission, and the requirements for satisfactory and acceptable quality of the audited project financial statements.9 ADB reserves the right to require a change in the auditor (in a manner consistent with the constitution of the borrower), or for additional support to be provided to the auditor, if the audits required are not conducted in a manner satisfactory to ADB, or if the audits are substantially delayed. ADB reserves the right to verify the project's financial accounts to confirm that the share of ADB’s financing is used in accordance with ADB’s policies and procedures.

9 ADB’s approach and procedures regarding delayed submission of audited project financial statements:

(i) When audited project financial statements are not received by the due date, ADB will write to the executing agency advising that (a) the audit documents are overdue; and (b) if they are not received within the next 6 months, requests for new contract awards and disbursement such as new replenishment of advance accounts, processing of new reimbursement, and issuance of new commitment letters will not be processed.

(ii) When audited project financial statements are not received within 6 months after the due date, ADB will withhold processing of requests for new contract awards and disbursement such as new replenishment of advance accounts, processing of new reimbursement, and issuance of new commitment letters. ADB will (a) inform the executing agency of ADB’s actions; and (b) advise that the loan may be suspended if the audit documents are not received within the next 6 months.

(iii) When audited project financial statements are not received within 12 months after the due date, ADB may suspend the loan.

33

39. Public disclosure of the audited project financial statements, including the auditor’s opinion on the project financial statements, will be guided by ADB’s Access to Information Policy 2018.10 After the review, ADB will disclose the audited project financial statements and the opinion of the auditors on the project financial statements no later than 14 days of ADB’s confirmation of their acceptability by posting them on ADB’s website. The management letter, additional auditor’s opinions, and audited entity financial statements will not be disclosed.11

VI. PROCUREMENT AND CONSULTING SERVICES

A. Advance Contracting and Retroactive Financing

40. All advance contracting and retroactive financing will be undertaken in conformity with ADB’s Procurement Policy (2017, as amended from time to time) and ADB’s Procurement Regulations (2017, as amended from time to time). The issuance of invitations to bid under advance contracting and retroactive financing will be subject to ADB approval. TANTRANSCO have been advised that approval of advance contracting and retroactive financing does not commit ADB to finance the project.

41. Advance contracting. ADB has approved the advanced contracting including preparation of tender documents, bid evaluation of turnkey contract packages for transmission lines and substations and contract award.

42. Retroactive financing. Except as otherwise agreed with ADB, the eligible expenses incurred for works will be eligible for retroactive financing, provided that these are incurred before the effectiveness of the related loan agreement, but not earlier than 12 months preceding the signing of the related loan agreement, and as long as they do not exceed an amount of 20% of the loan.

B. Procurement of Goods, Works, and Consulting Services

43. All procurement of goods and works will be undertaken in accordance with ADB’s Procurement Policy (2017, as amended from time to time) and Procurement Regulations (2017, as amended from time to time). All turnkey contract packages will be procured through open competitive bidding with prior review by ADB. An 18-month procurement plan indicating threshold and review procedures of contract packages to be procured under the loan is provided. There are no consulting service contract packages to be procured using the Loan.

44. Achievement of Value for Money (VFM) through Strategic Procurement Planning. VFM in procurement will be achieved through the use of ADB Standard Bidding Document Plant: Design, Supply, and Installation with Single Envelope Two Stage procedure.

10 Access to Information Policy: https://www.adb.org/documents/access-information-policy 11 This type of information would generally fall under public communications policy exceptions to disclosure. ADB. 2011.

Access to Information Policy. Paragraph 97(iv) and/or 97(v).

Appendix 1 34

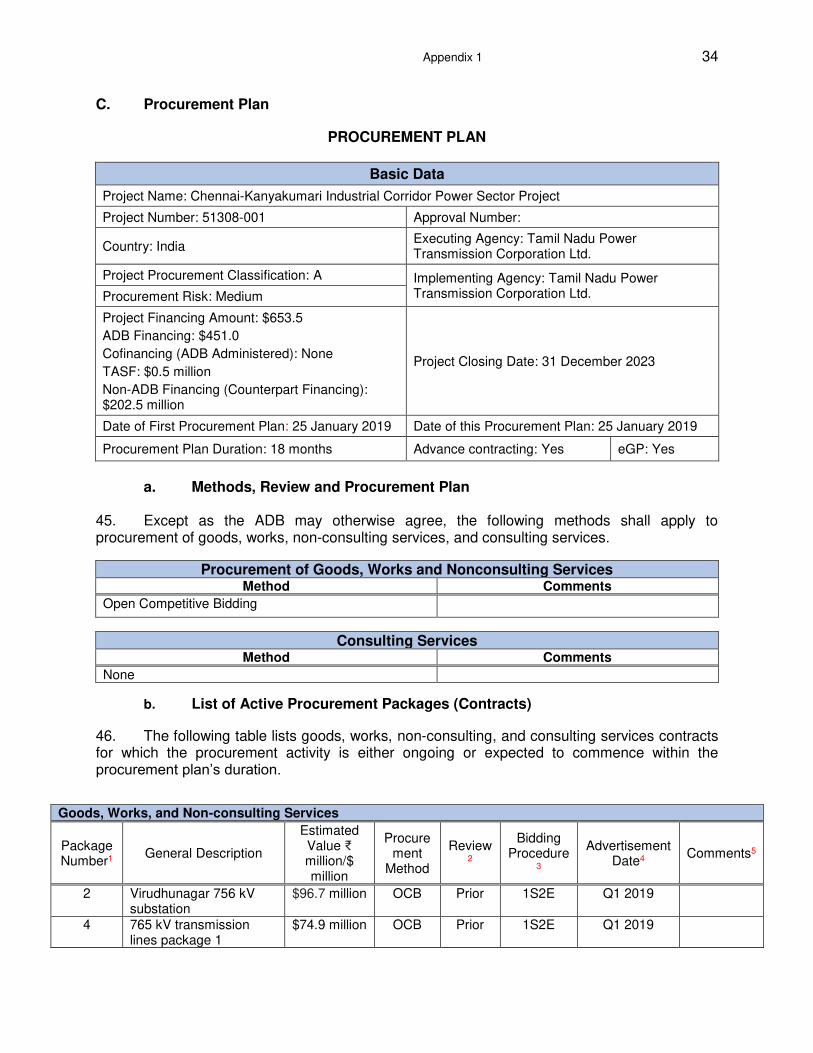

C. Procurement Plan

PROCUREMENT PLAN

Basic Data

Project Name: Chennai-Kanyakumari Industrial Corridor Power Sector Project

Project Number: 51308-001 Approval Number:

Country: India Executing Agency: Tamil Nadu Power Transmission Corporation Ltd.

Project Procurement Classification: A Implementing Agency: Tamil Nadu Power Transmission Corporation Ltd. Procurement Risk: Medium

Project Financing Amount: $653.5

ADB Financing: $451.0

Cofinancing (ADB Administered): None

TASF: $0.5 million

Non-ADB Financing (Counterpart Financing): $202.5 million

Project Closing Date: 31 December 2023

Date of First Procurement Plan: 25 January 2019 Date of this Procurement Plan: 25 January 2019

Procurement Plan Duration: 18 months Advance contracting: Yes eGP: Yes

a. Methods, Review and Procurement Plan

45. Except as the ADB may otherwise agree, the following methods shall apply to procurement of goods, works, non-consulting services, and consulting services.

Procurement of Goods, Works and Nonconsulting Services Method Comments

Open Competitive Bidding

Consulting Services Method Comments

None

b. List of Active Procurement Packages (Contracts)

46. The following table lists goods, works, non-consulting, and consulting services contracts for which the procurement activity is either ongoing or expected to commence within the procurement plan’s duration.

Goods, Works, and Non-consulting Services

Package Number1

General Description

Estimated Value ₹ million/$ million

Procurement

Method

Review2

Bidding Procedure

3

Advertisement Date4

Comments5

2 Virudhunagar 756 kV substation

$96.7 million OCB Prior 1S2E Q1 2019

4 765 kV transmission lines package 1

$74.9 million OCB Prior 1S2E Q1 2019

Appendix 1 35

Goods, Works, and Non-consulting Services

associated with Virudhunugar substation

5 765 kV transmission lines package 2 associated with Virudhunagar substation

$74.9 million OCB Prior 1S2E Q1 2019

10 765kV transmission lines package 3 associated with Virudhunagar substation

$74.9 million OCB Prior 1S2E Q12019

6 400kV transmission lines associated with Virudhunagar substation

$35.3 million OCB Prior 1S2E Q1 2019

7 Ottapidaram 400 kV substation & 400 kV transmission lines associated with Ottapidaram substation

$88.2 million OCB Prior 1S2E Q1 2019

9 230 kV and 110 kV Transmission lines associated with Ottapidaram substation

$5.5 million OCB Prior 1S2E Q3 2019

c. List of Indicative Packages (Contracts) Required under the Project

47. The following table lists goods, works, non-consulting, and consulting services contracts for which the procurement activity is expected to commence beyond the procurement plan duration and over the life of the project (i.e. those expected beyond the current procurement plan’s duration).

48. None.

d. List of Awarded and Completed Contracts

49. The following table lists the awarded contracts and completed contracts for goods, works, non-consulting, and consulting services.

50. None.

e. Non-ADB Financing