Embed Size (px)

Citation preview

President and CEO Mikael Mäkinen

15 June 2010

Paris road show

June 2010 2

Cargotec in briefg

Cargotec improves the efficiency of cargo flows on land and at sea –wherever cargo is on the move Cargotec’s daughter brands Hiabwherever cargo is on the move. Cargotec s daughter brands, Hiab, Kalmar and MacGregor are recognised leaders in cargo and load handling solutions around the world. Cargotec’s global network is

iti d l t t d ff t i i th tpositioned close to customers and offers extensive services that ensure the continuous, reliable and sustainable performance of

equipment. Cargotec’s sales totalled EUR 2.6 billion in 2009 and it employs approximately 9,500 people. Cargotec’s class B shares are

quoted on the NASDAQ OMX Helsinki.

June 2010 3

Cargotec is a global market leader

Sol tions for ports and Sol tions for marine cargoS l ti f i d t i l d Solutions for ports and container handlingCompetitors• Terex/Fantuzzi Group

Solutions for marine cargo handling and offshore load handlingCompetitors

Solutions for industrial and on-road load handlingCompetitors• Palfinger Terex/Fantuzzi Group

• ZPMC• Konecranes

Competitors• TTS

• Palfinger• Fassi• Hyva• Effer

June 2010 4

e

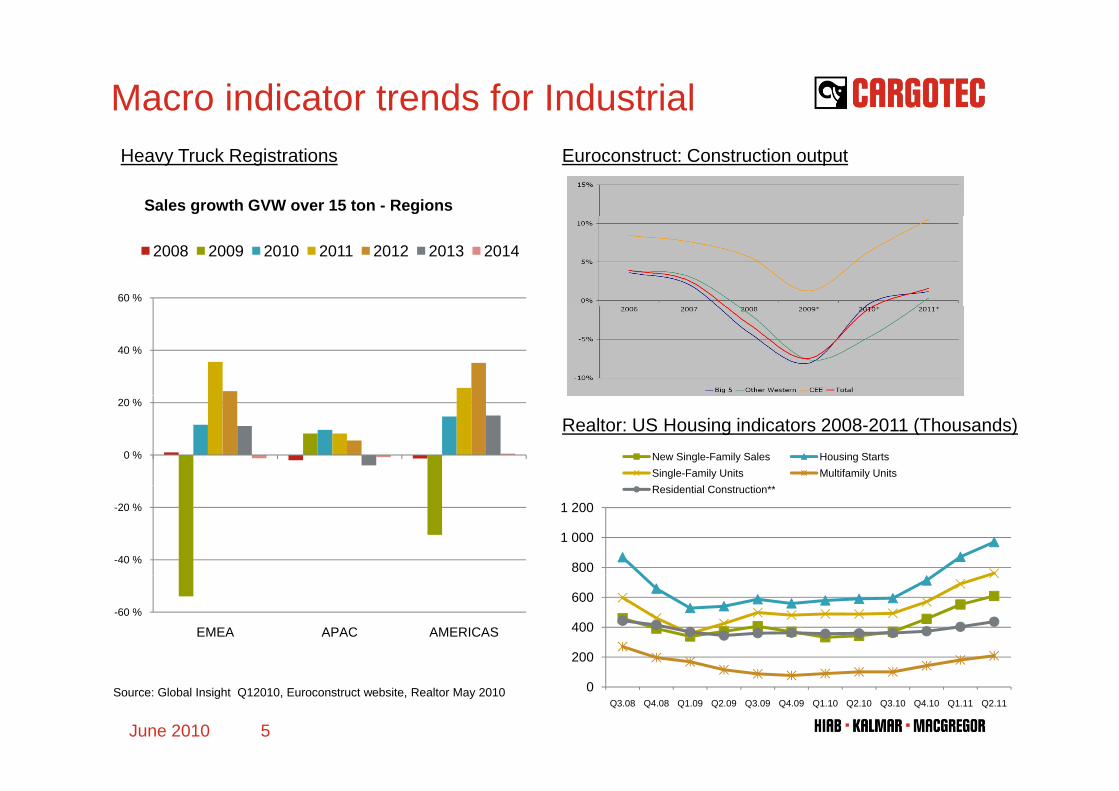

Macro indicator trends for IndustrialHeavy Truck Registrations Euroconstruct: Construction output

Sales growth GVW over 15 ton - Regions

60 %

2008 2009 2010 2011 2012 2013 2014

40 %

Realtor: US Housing indicators 2008-2011 (Thousands)New Single-Family Sales Housing StartsSingle-Family Units Multifamily Units

C **

0 %

20 %

800

1 000

1 200Residential Construction**

-40 %

-20 %

200

400

600-60 %

EMEA APAC AMERICAS

Source: Global Insight Q12010, Euroconstruct website, Realtor May 2010 0Q3.08 Q4.08 Q1.09 Q2.09 Q3.09 Q4.09 Q1.10 Q2.10 Q3.10 Q4.10 Q1.11 Q2.11

June 2010 5

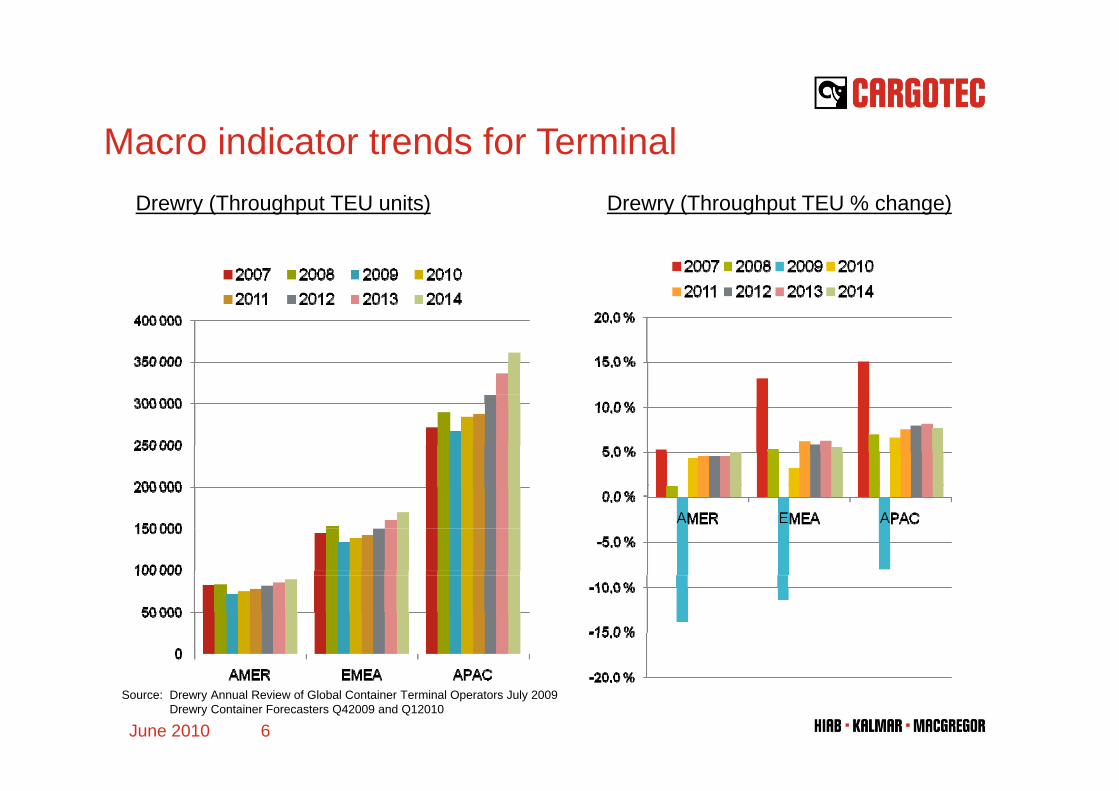

Macro indicator trends for TerminalDrewry (Throughput TEU % change)Drewry (Throughput TEU units)

Source: Drewry Annual Review of Global Container Terminal Operators July 2009Drewry Container Forecasters Q42009 and Q12010

June 2010 6

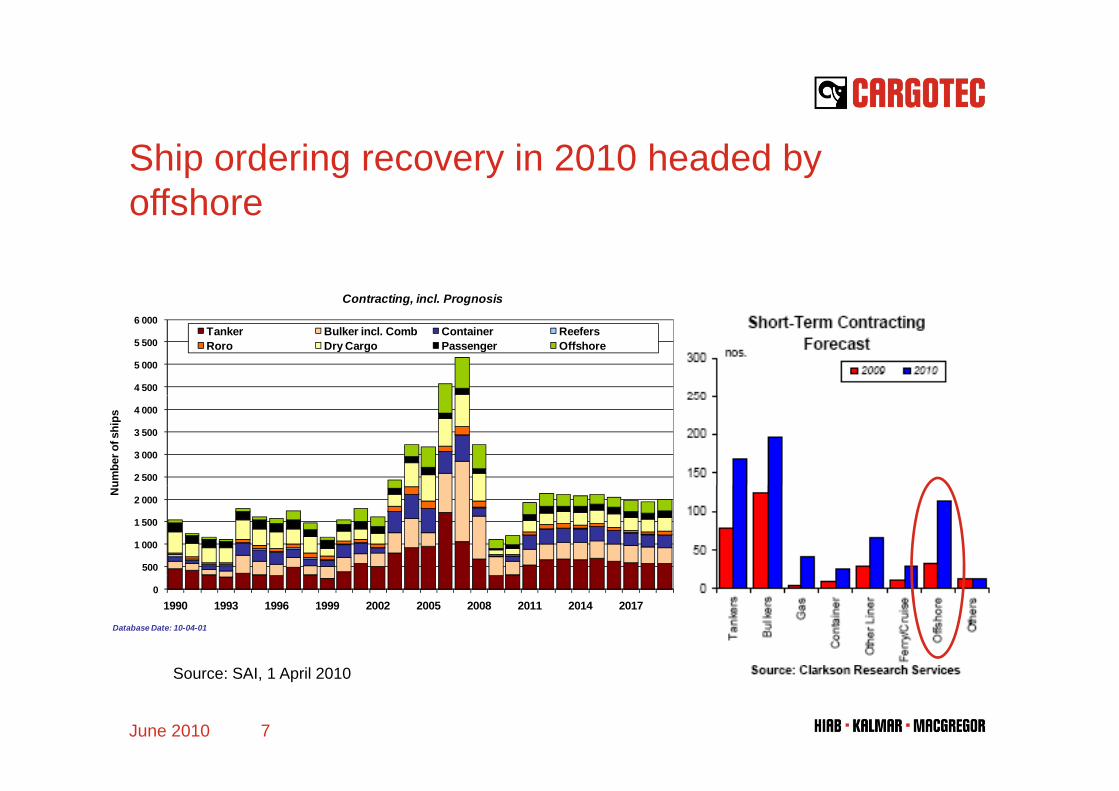

Ship ordering recovery in 2010 headed by offshore

Contracting, incl. Prognosis

4 500

5 000

5 500

6 000Tanker Bulker incl. Comb Container ReefersRoro Dry Cargo Passenger Offshore

2 500

3 000

3 500

4 000

umbe

r of s

hips

500

1 000

1 500

2 000

Nu

01990 1993 1996 1999 2002 2005 2008 2011 2014 2017

Database Date: 10-04-01

Source: SAI, 1 April 2010

7June 2010

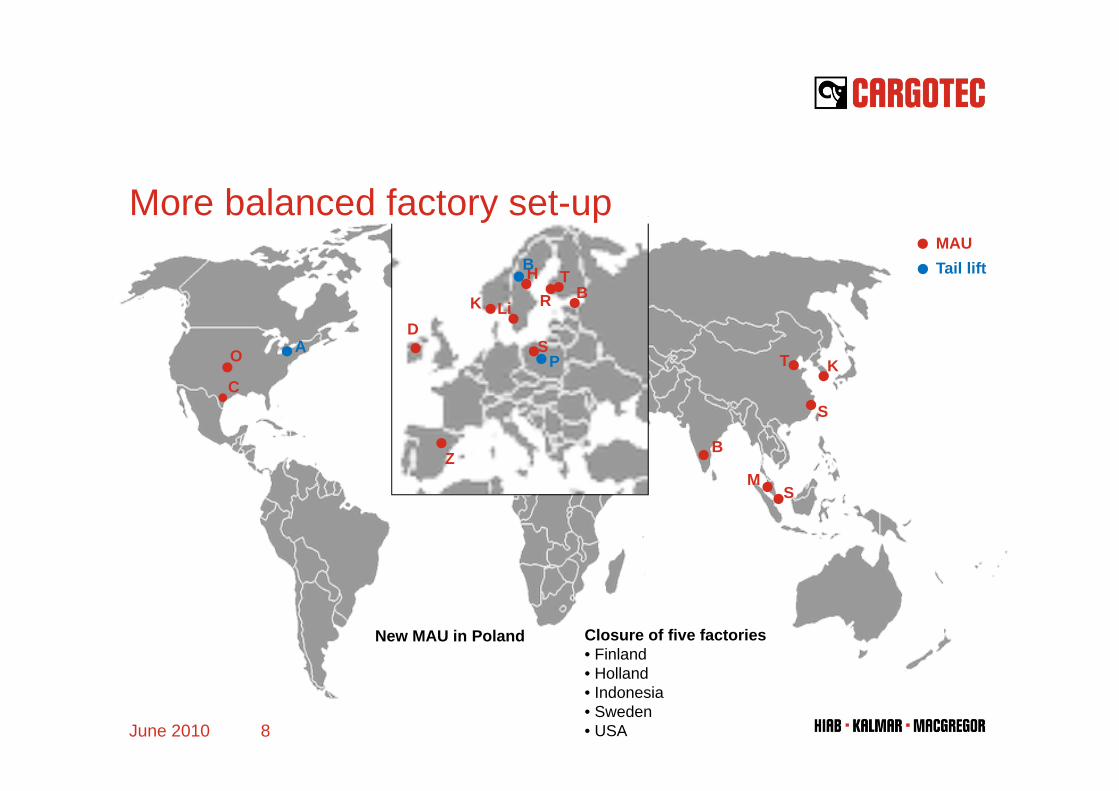

More balanced factory set-up

HR

T

Li

MAU

BK

Tail liftB

y p

RLiD

O KC

T

K

SP

A

Z

S

M

B

S

Closure of five factories• Finland

New MAU in Poland

• Holland• Indonesia• Sweden• USA8June 2010

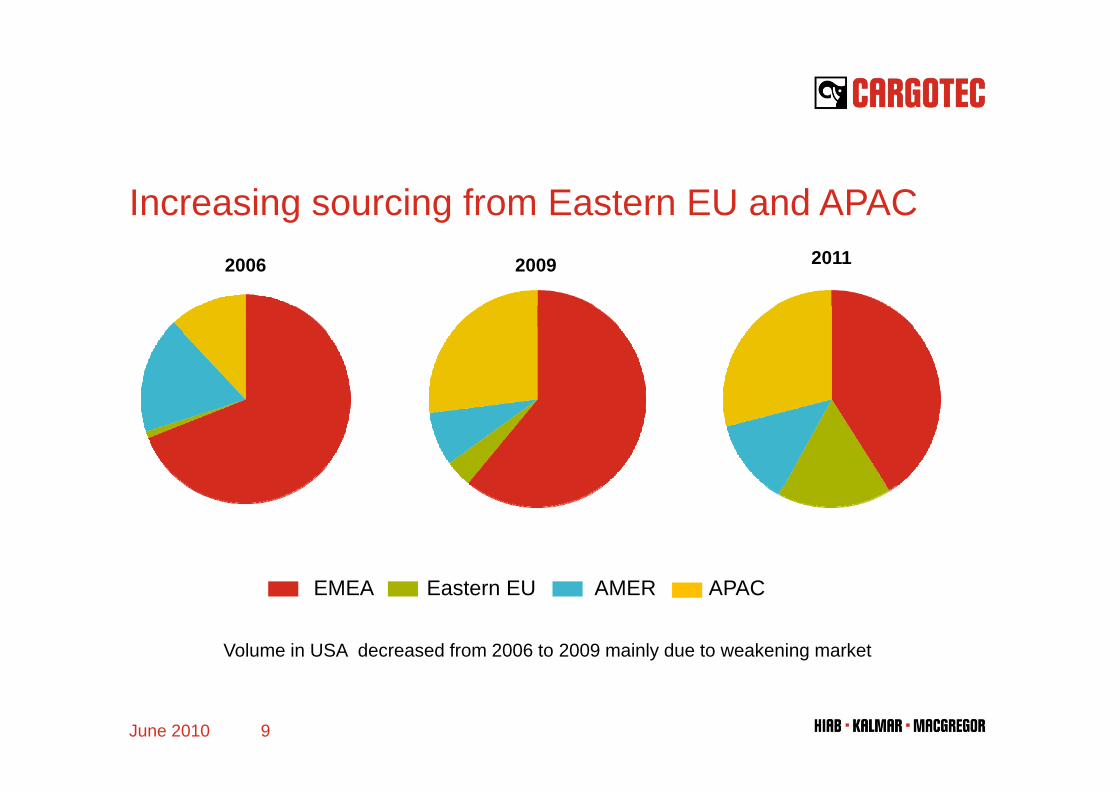

Increasing sourcing from Eastern EU and APAC2006 2009 2011

g g

EMEA Eastern EU AMER APAC

Volume in USA decreased from 2006 to 2009 mainly due to weakening market

9June 2010

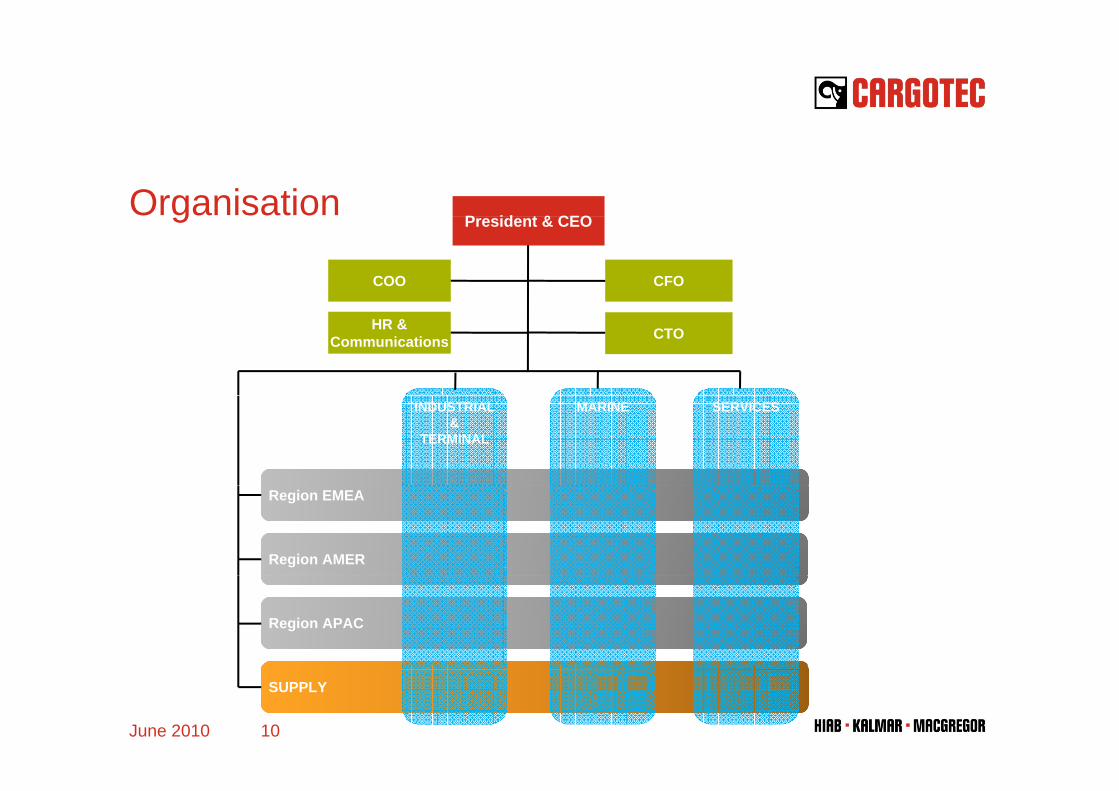

OrganisationP id t & CEO

gPresident & CEO

CFOCOO

CTOHR &Communications

INDUSTRIAL &

TERMINAL

MARINE SERVICES

Region EMEA

Region AMER

Region APAC

June 2010 10

SUPPLY

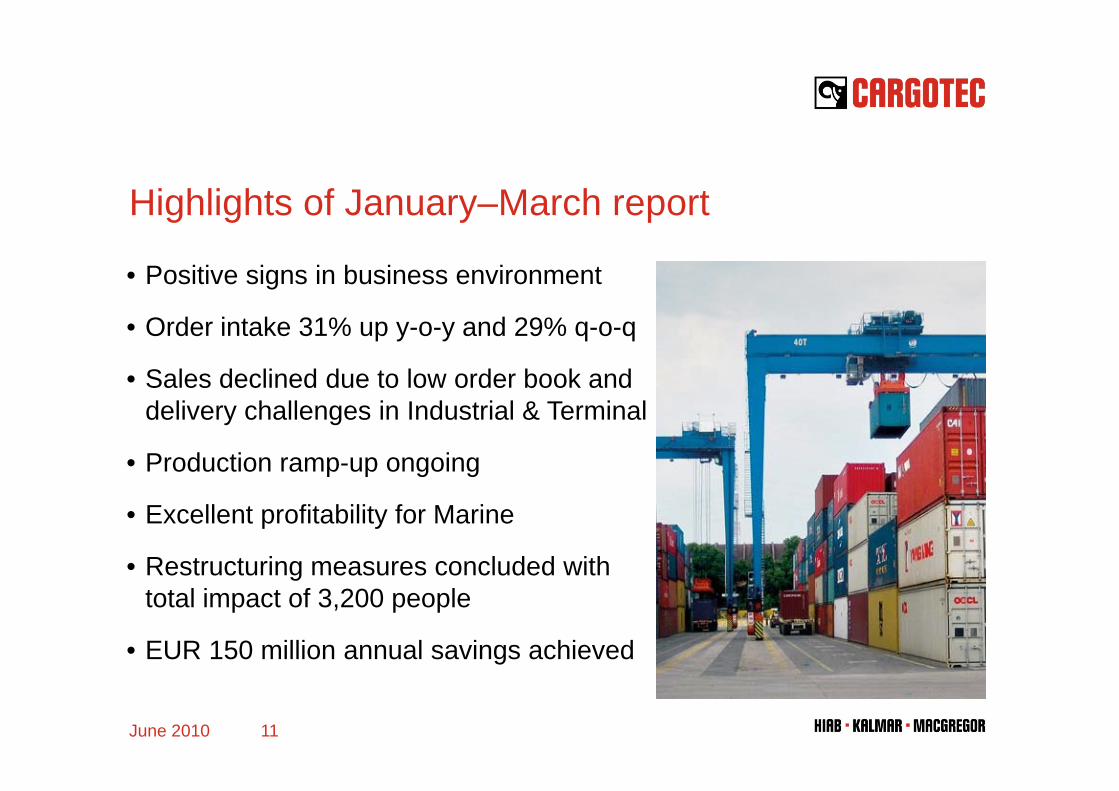

Highlights of January–March reportg g y p

• Positive signs in business environment

• Order intake 31% up y-o-y and 29% q-o-q

• Sales declined due to low order book and delivery challenges in Industrial & Terminal

• Production ramp-up ongoing

• Excellent profitability for Marine

• Restructuring measures concluded withRestructuring measures concluded with total impact of 3,200 people

• EUR 150 million annual savings achieved

June 2010 11

Market environment in January–March y

• Tentative recovery in demand for load handling equipment continued in both Europe and the USequipment continued in both Europe and the US

• Markets for container handling equipment in ports remained quiet to a large extent. The

b f t i h dl d h d i fnumber of containers handled showed signs of an upturn in the Asian ports.

• The market for marine cargo handling equipment g g q pshowed signs of picking up, especially in terms of equipment for offshore and bulk vessels.

• Services markets were fairly quiet at the• Services markets were fairly quiet at the beginning of the year, however, signs of recovery, especially in spare parts, glimpsed towards the end of the quarter.towards the end of the quarter.

June 2010 12

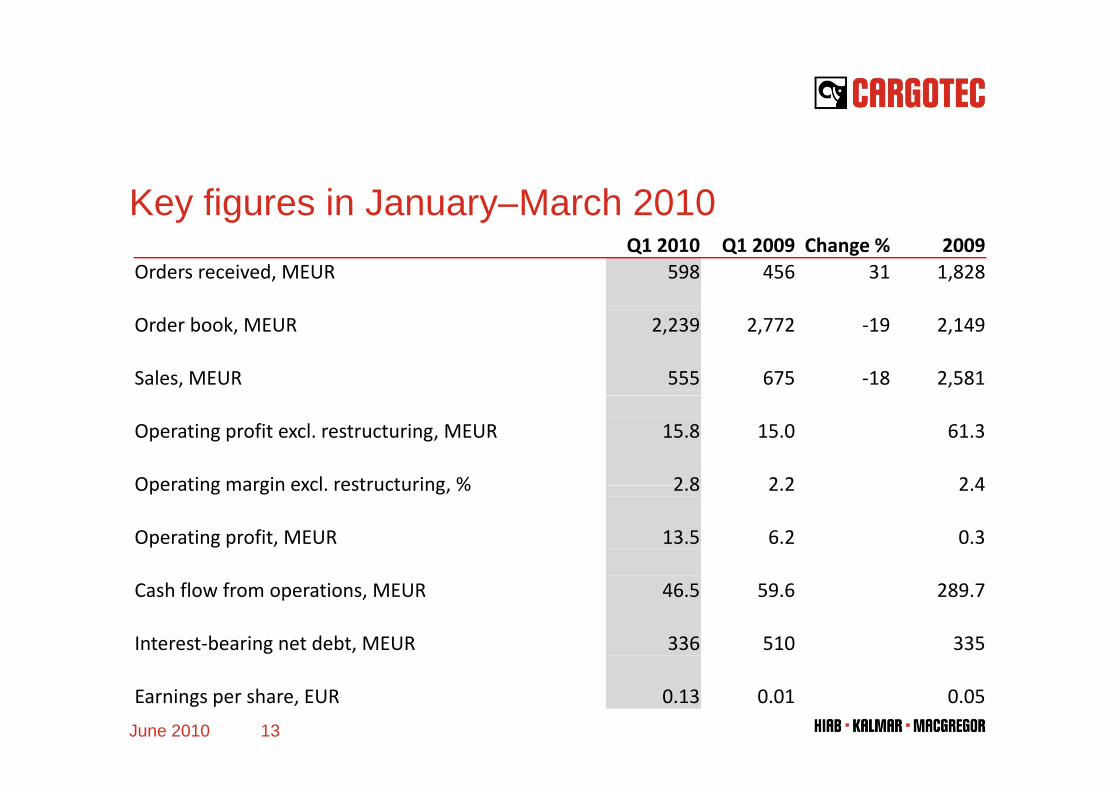

Key figures in January–March 2010y g yQ1 2010 Q1 2009 Change % 2009

Orders received, MEUR 598 456 31 1,828

Order book, MEUR 2,239 2,772 ‐19 2,149

Sales, MEUR 555 675 ‐18 2,581

Operating profit excl. restructuring, MEUR 15.8 15.0 61.3

Operating margin excl restructuring % 2 8 2 2 2 4Operating margin excl. restructuring, % 2.8 2.2 2.4

Operating profit, MEUR 13.5 6.2 0.3

Cash flow from operations, MEUR 46.5 59.6 289.7

Interest‐bearing net debt, MEUR 336 510 335

June 2010 13

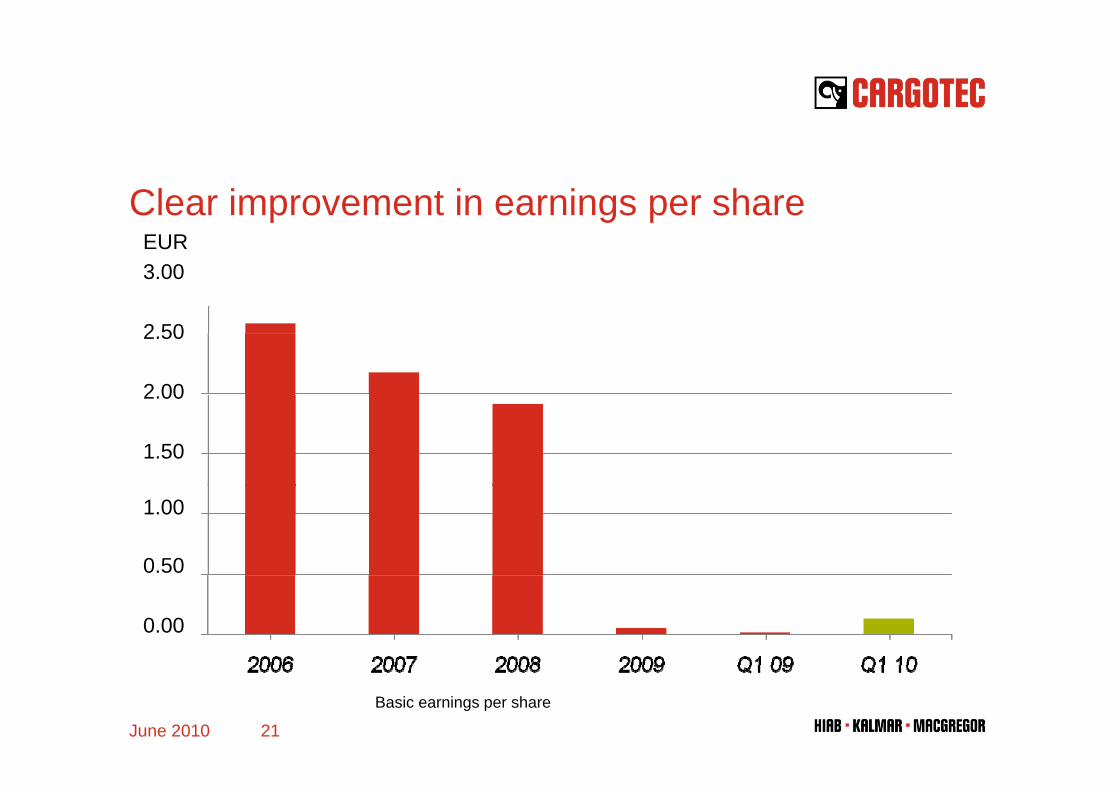

Earnings per share, EUR 0.13 0.01 0.05

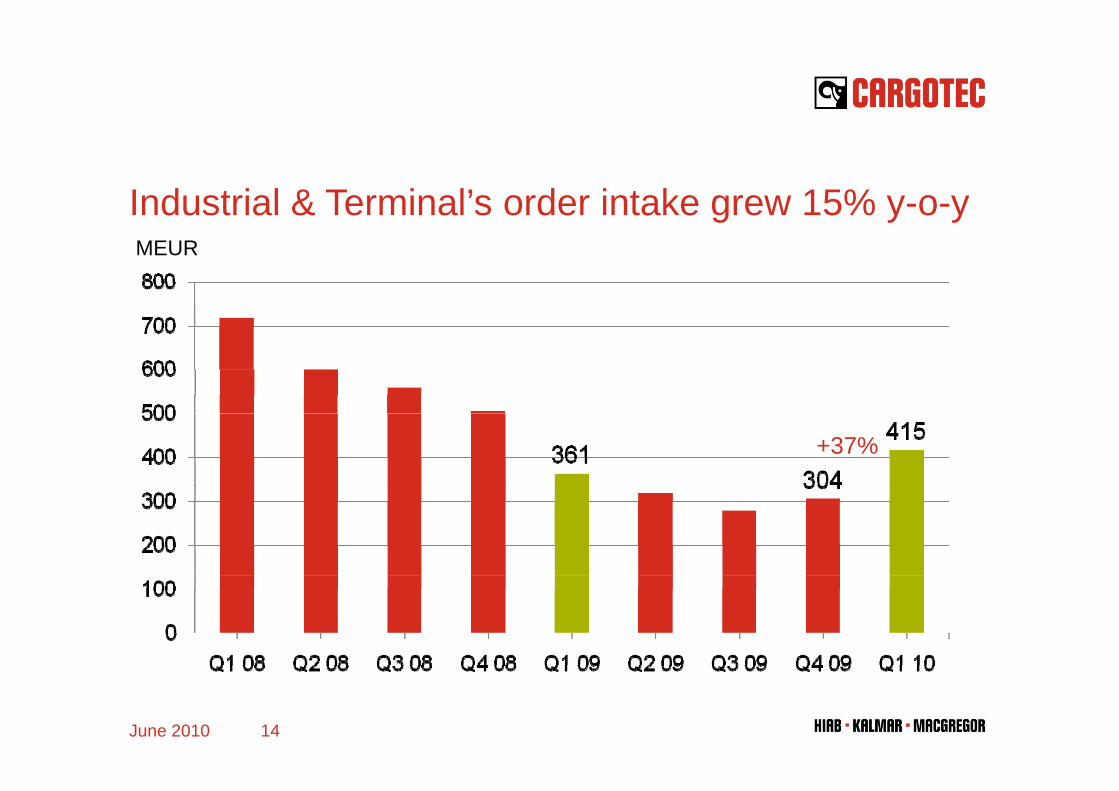

Industrial & Terminal’s order intake grew 15% y-o-yg % y yMEUR

+37%

June 2010 14

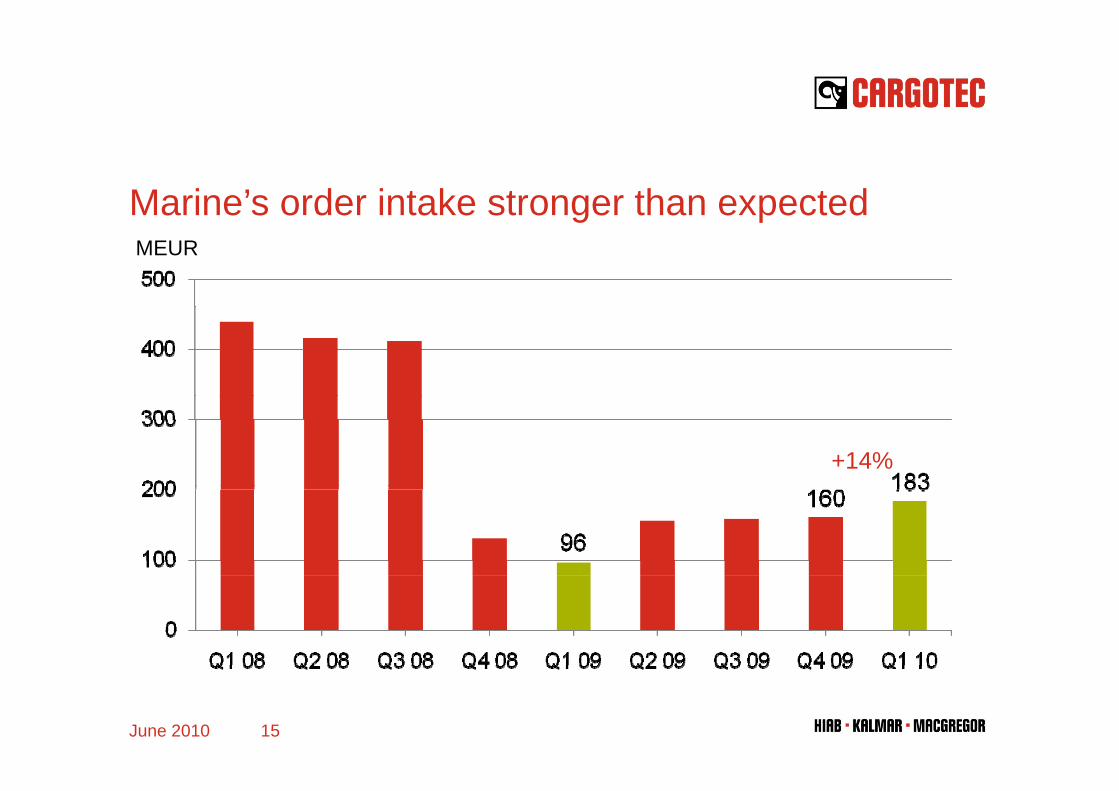

Marine’s order intake stronger than expectedg pMEUR

+14%

June 2010 15

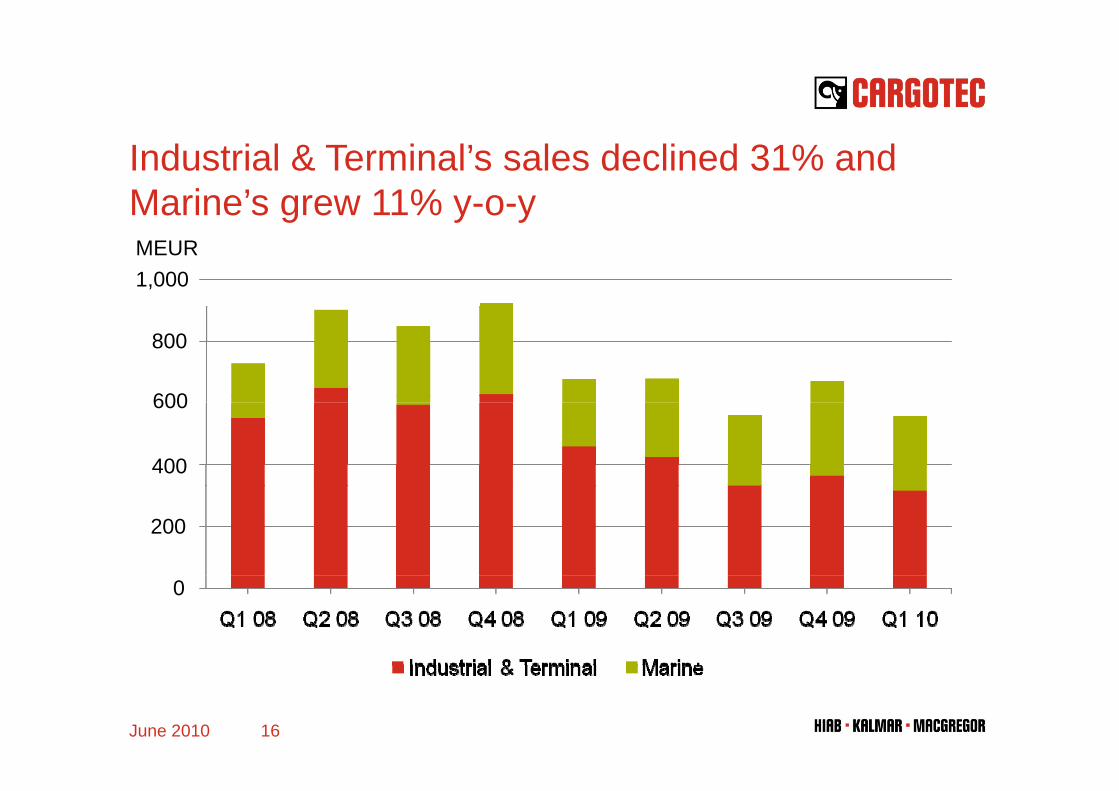

Industrial & Terminal’s sales declined 31% and Marine’s grew 11% y-o-yg % y yMEUR1,000

800

600600

400

200

0

June 2010 16

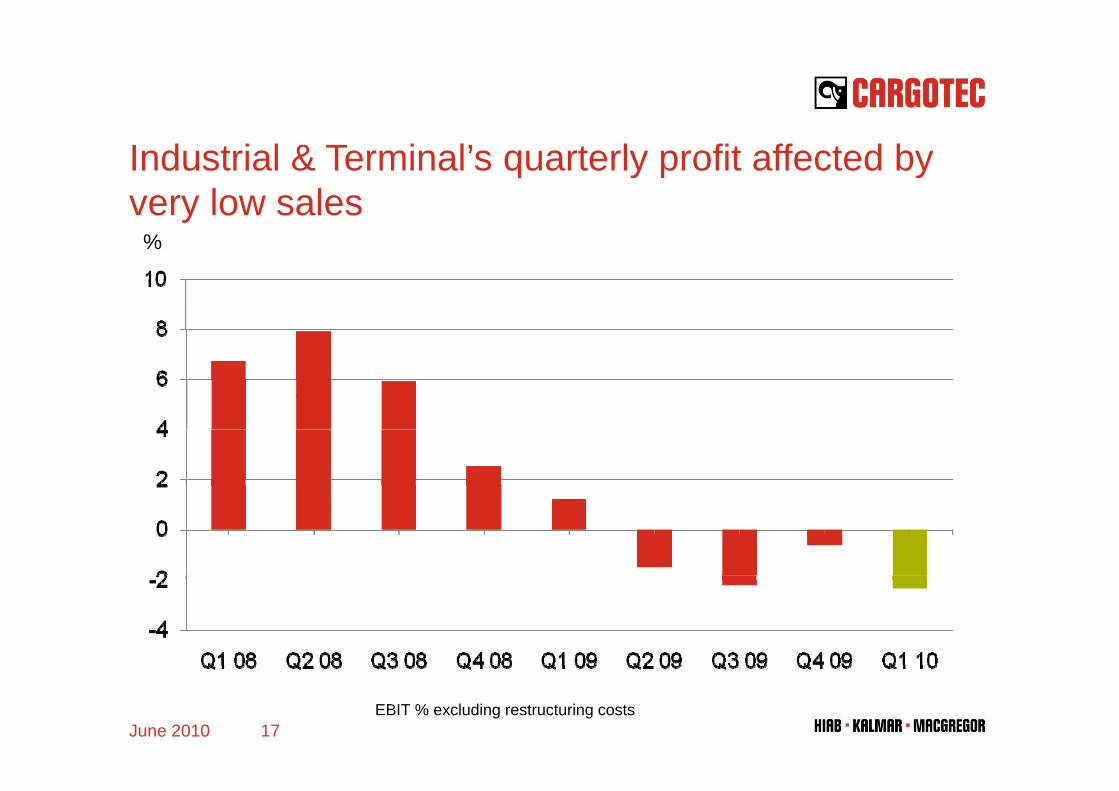

Industrial & Terminal’s quarterly profit affected by very low salesy

%

June 2010 17EBIT % excluding restructuring costs

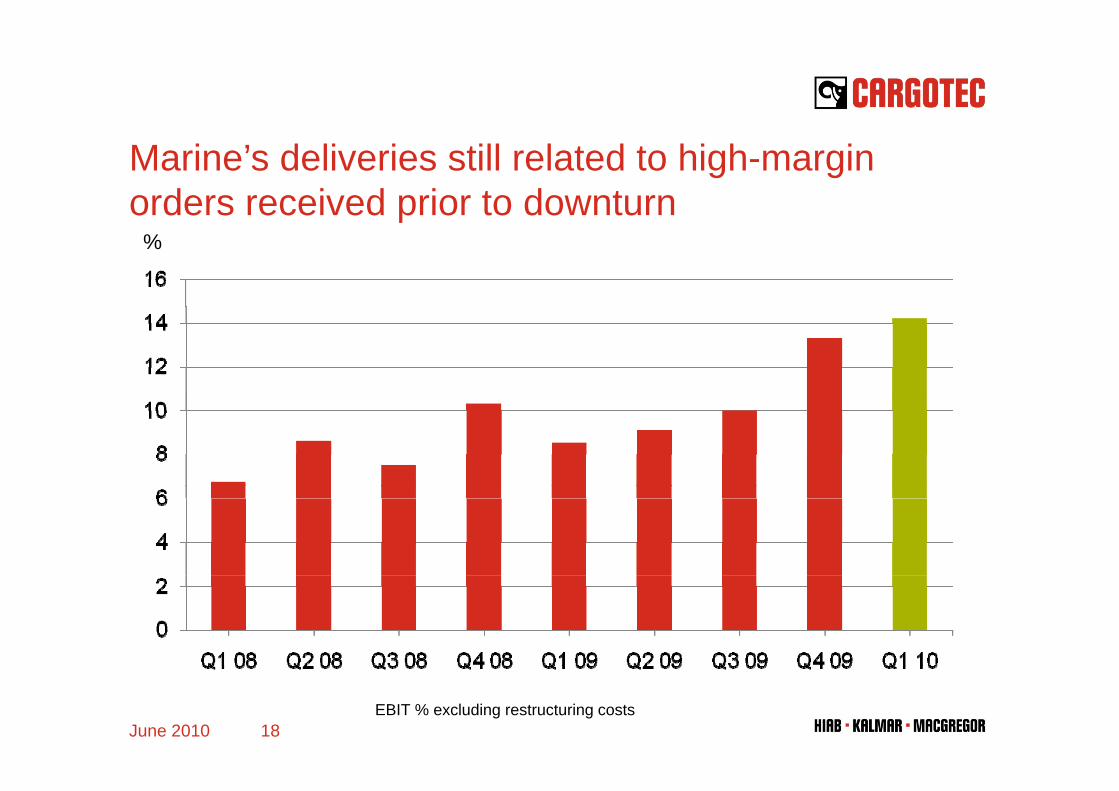

Marine’s deliveries still related to high-margin orders received prior to downturnp

%

June 2010 18EBIT % excluding restructuring costs

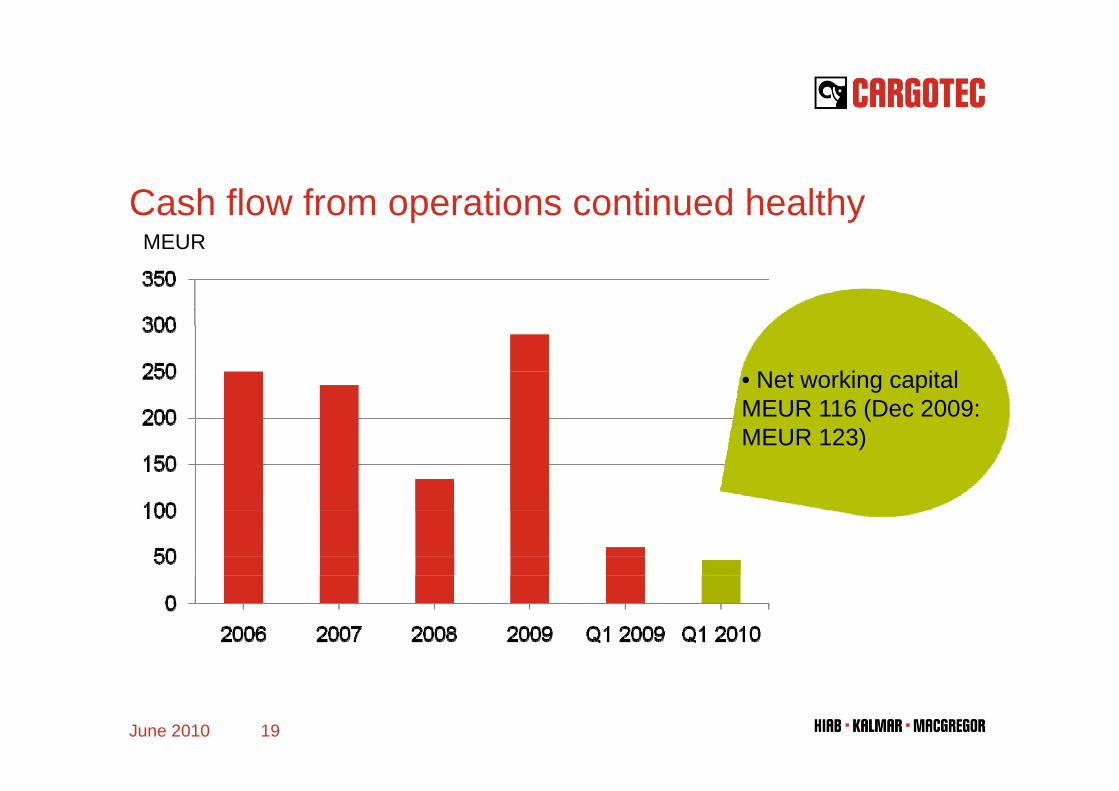

Cash flow from operations continued healthyp yMEUR

• Net working capital MEUR 116 (Dec 2009: MEUR 123)

June 2010 19

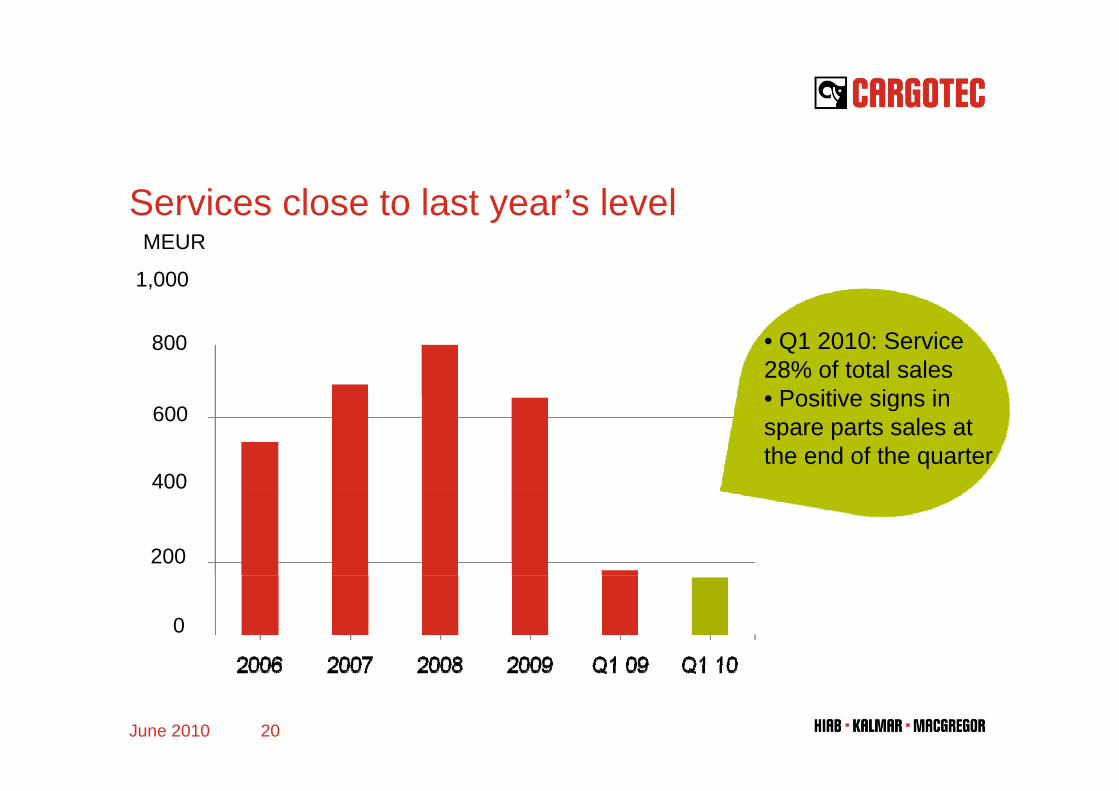

Services close to last year’s levelyMEUR

1,000

• Q1 2010: Service 28% of total sales• Positive signs in

800

• Positive signs in spare parts sales at the end of the quarter

600

400400

200

0

June 2010 20

Clear improvement in earnings per sharep g pEUR3.00

2.50

2 002.00

1.50

1.00

0.50

0.00

June 2010 21

Basic earnings per share

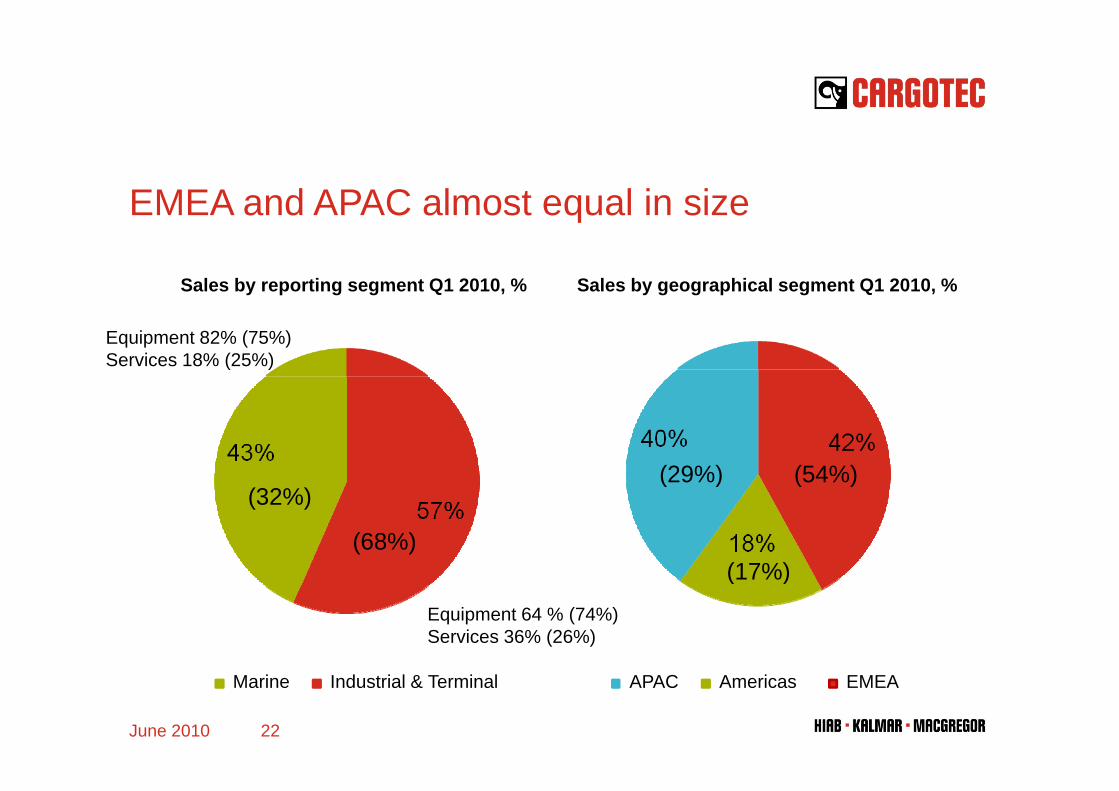

EMEA and APAC almost equal in sizeq

Sales by reporting segment Q1 2010, % Sales by geographical segment Q1 2010, %

Equipment 82% (75%)Services 18% (25%)

(54%)(29%)(32%)

(68%)

( )

(17%)

( )

Equipment 64 % (74%)Services 36% (26%)

(17%)

June 2010 22

Marine Industrial & Terminal APAC Americas EMEA

Investment in Poland proceeding according to planp

June 2010 23

Cargotec’s key priorities in 2010g y p• Preparing for growth strategy

F d h &• Focused research & development

• Service concept development• Service concept development

• Ensuring accomplishment of efficiency targetsefficiency targets

June 2010 24

Short-term outlook (29 April 2010)( p )

• There are tentative positive signs visible in the order intake for the Industrial business Uncertainty continues in the Terminal businessIndustrial business. Uncertainty continues in the Terminal business. Based on the strong order book, sales in the Marine business are expected to remain on a healthy level in 2010.

• Cargotec’s 2010 sales are estimated to be on 2009 level and operating profit to exceed EUR 100 million.

June 2010 25

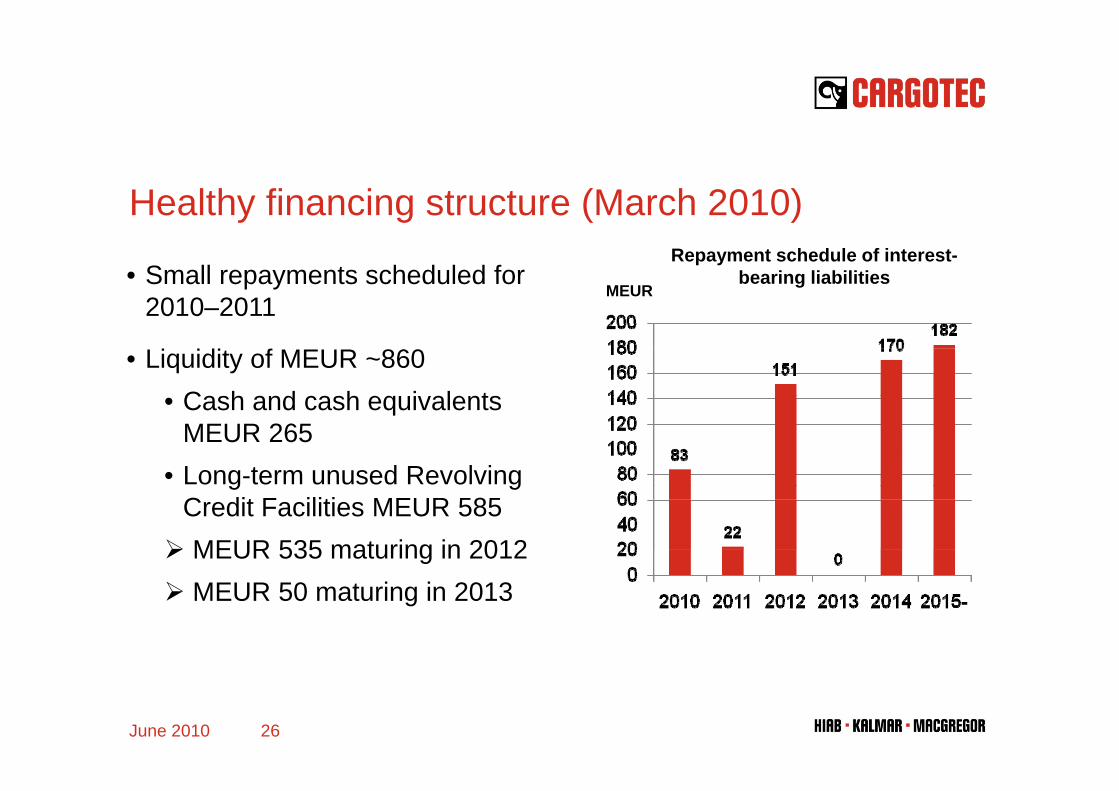

Healthy financing structure (March 2010)y g ( )

• Small repayments scheduled for 2010 2011

MEUR

Repayment schedule of interest-bearing liabilities

2010–2011

• Liquidity of MEUR ~860C h d h i l t• Cash and cash equivalents MEUR 265

• Long-term unused Revolving g gCredit Facilities MEUR 585MEUR 535 maturing in 2012MEUR 50 maturing in 2013

June 2010 26

Cargotec’s financial targets 2007–2011g g

Annual net sales growth exceeding 10% (incl acquisitions)Annual net sales growth exceeding 10% (incl. acquisitions)

R i i h i i i 10%Raising the operating income margin to 10%

G i b l 50%Gearing below 50%

Dividend 30–50% of earnings per share

June 2010 27

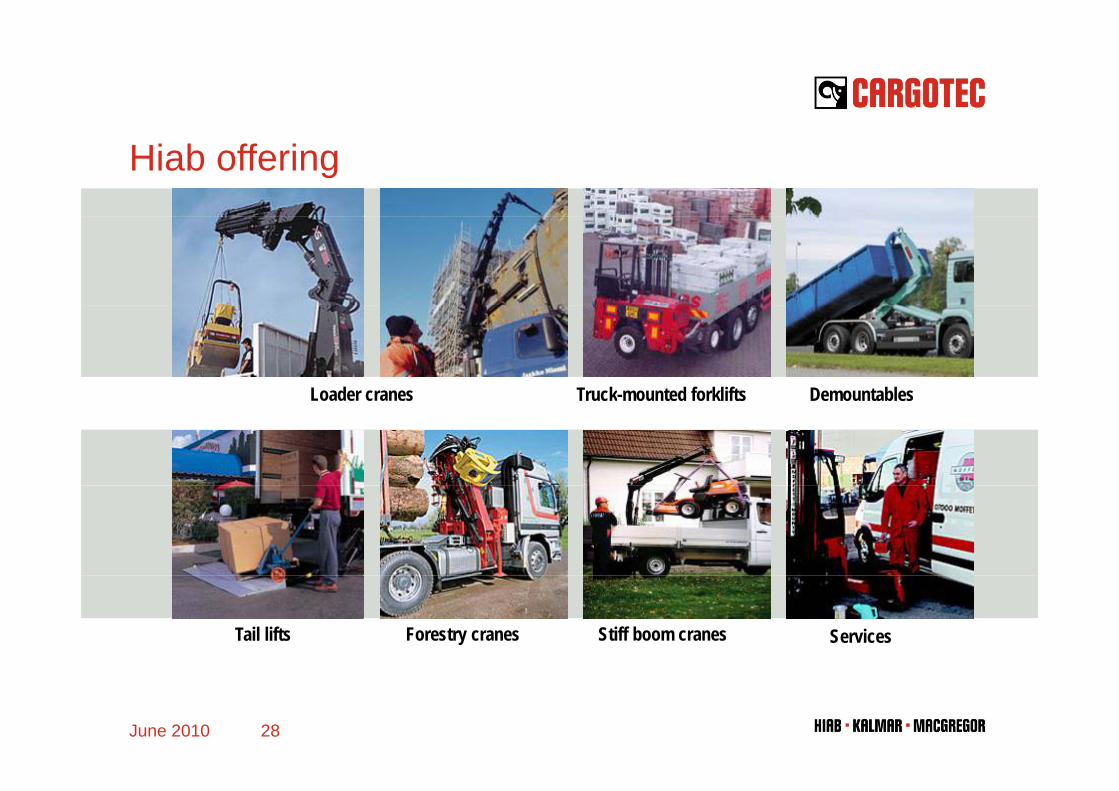

Hiab offering

Truck-mounted forklifts DemountablesLoader cranes Truck-mounted forklifts DemountablesLoader cranes

ServicesForestry cranes Tail lifts Stiff boom cranes

28June 2010

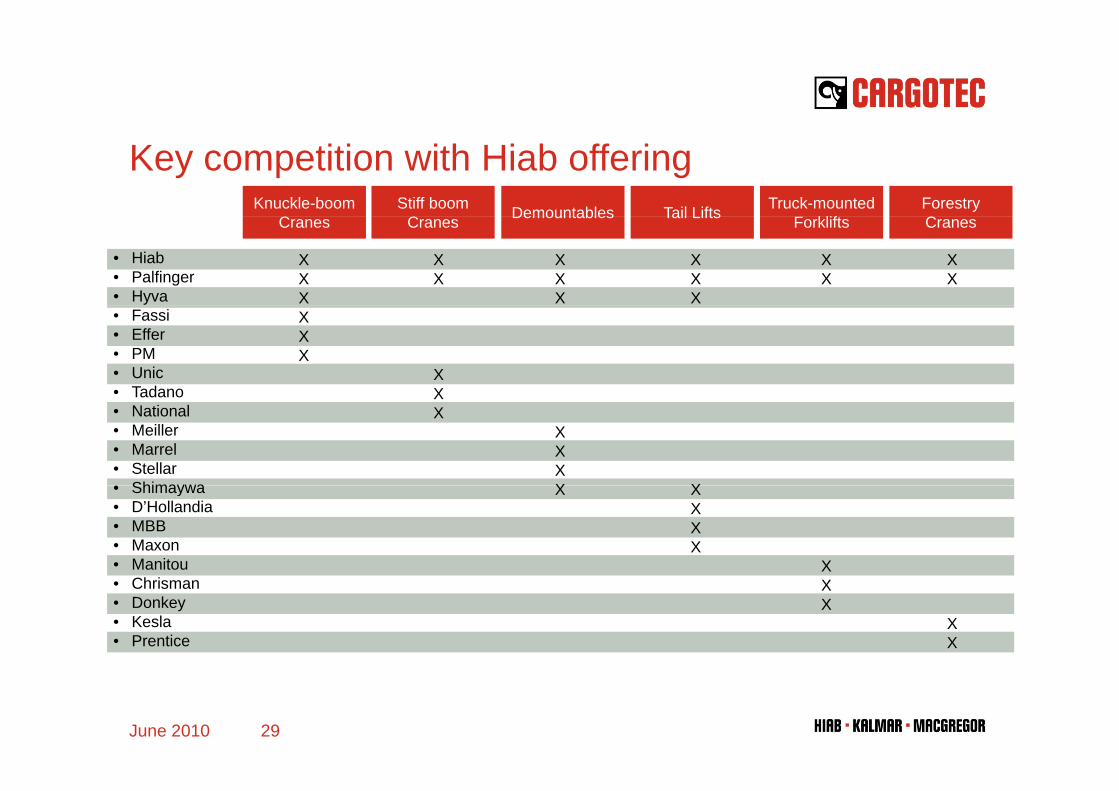

Key competition with Hiab offeringKnuckle-boom

C Demountables Truck-mountedf

ForestryCTail LiftsStiff boom

CCranes Demountables Forklifts CranesTail LiftsCranes

XXX

XXX

XXX

XX

XX

XX

• Hiab• Palfinger• Hyva

XXX

XX

• Fassi• Effer• PM• Unic• Tadano

XXXX X

XX

Tadano• National• Meiller• Marrel• Stellar

Shimaywa X X XXX

X

• Shimaywa• D’Hollandia• MBB• Maxon• Manitou

XX

XX

• Chrisman• Donkey• Kesla • Prentice

29June 2010

Kalmar offering

Terminal tractors Forklift trucksReachstackersStraddle carriers

Ship-to-Shore cranes RTGs, RMGs ServicesSpreaders

30June 2010

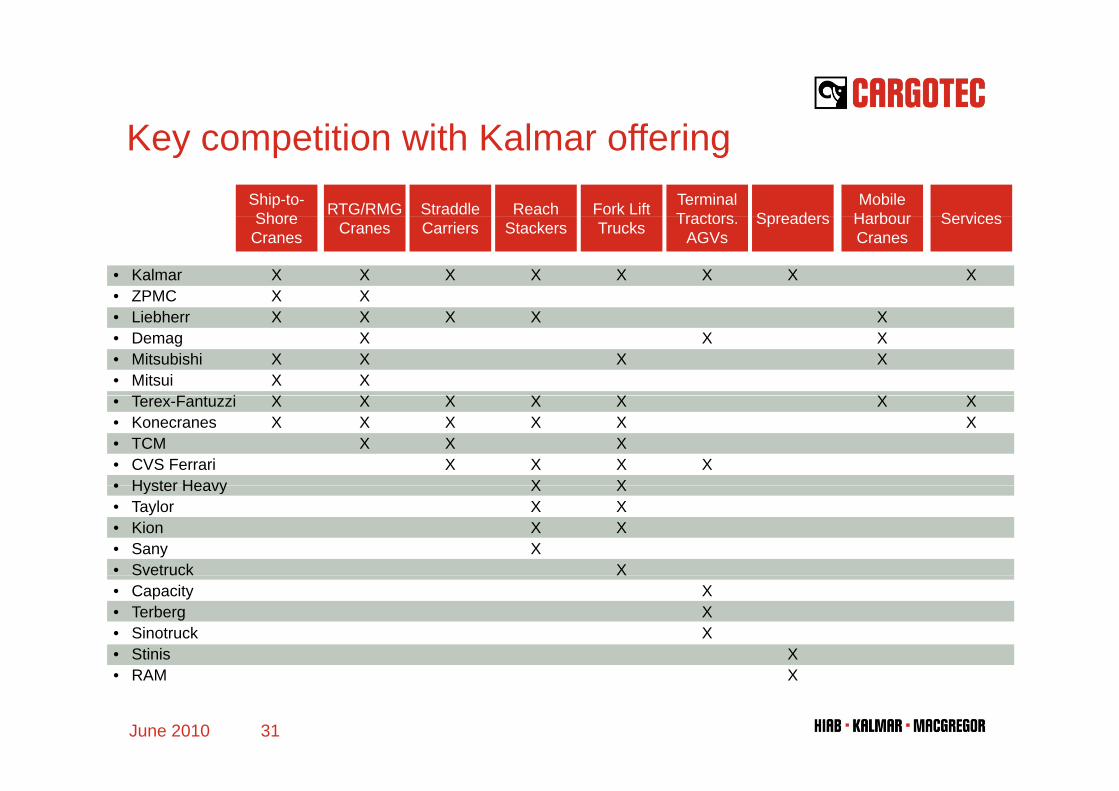

K titi ith K l ff iKey competition with Kalmar offeringShip-to-Shore

MobileHarbourRTG/RMG Straddle Reach Fork Lift Terminal

Tractors ServicesSpreadersShoreCranes

HarbourCranesCranes Carriers Stackers Trucks Tractors.

AGVsServicesSpreaders

XX

XXX

X X X X• Kalmar• ZPMC

X

X

XXX

XXX

X X

XXXXX

X

X

X

X

X

X

X• Liebherr• Demag• Mitsubishi• Mitsui

T F t i XX

X XX

XXX

XXXX

XX

XX

XXXXX

X

• Terex-Fantuzzi• Konecranes• TCM• CVS Ferrari• Hyster Heavy X

XXX

XXX

X

• Hyster Heavy• Taylor• Kion• Sany• Svetruck X

XXX

Svetruck• Capacity• Terberg• Sinotruck• Stinis X• RAM X

31June 2010

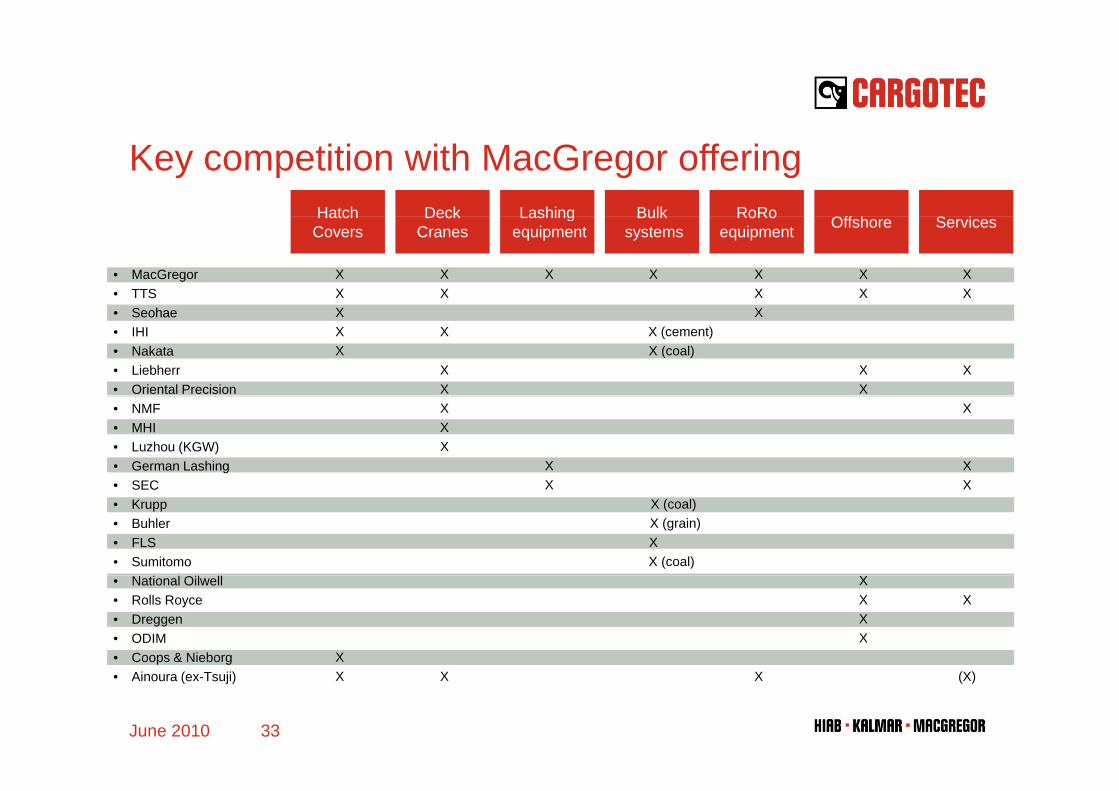

MacGregor offering

Ship cranes SecuringHatch covers Offshore deck equipmentp gq p

Link spansRoRo ServicesBulk loaders

32June 2010

Key competition with MacGregor offeringHatch Deck OffLashing SRoRoBulk

• MacGregor• TTS

HatchCovers

DeckCranes OffshoreLashing

equipment Services

XX

XX

X XX

XX

RoRoequipment

XX

Bulksystems

X

• Seohae• IHI• Nakata• Liebherr• Oriental Precision

XXX

X

XX

X (cement)X (coal)

XX

X

X

• NMF• MHI• Luzhou (KGW)• German Lashing• SEC

XXX

X

XX

XX• SEC

• Krupp• Buhler• FLS• Sumitomo

X (coal)X (grain)XX (coal)

XX

• National Oilwell• Rolls Royce• Dreggen• ODIM• Coops & Nieborg X

XXXX

X

• Ainoura (ex-Tsuji) X X (X)X

33June 2010