Embed Size (px)

Citation preview

NEWSLETTER

SE

CT

IO

N

OF

T

AX

AT

IO

NS U M M E R 2 0 0 2Vo l u m e 2 1 N u m b e r 4

LOSANGELESFALL MEETING, OCTOBER 17-19, 2002

ABA LA

NEW NY C

LE RULES –

see p. 3

26945_ABA_Newletter_Summer 8/2/02 11:13 AM Page 1

SE

CT

IO

N

OF

T

AX

AT

IO

N 2

CONTENTSIMPORTANT SECTION DATES AND SERVICES . . . . .3

FROM THE EDITOR . . . . . . . . . . . . . . . . . . . . . . . . . . .4

FROM THE CHAIR . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

FROM THE CHAIR-ELECT . . . . . . . . . . . . . . . . . . . . . .7

COUNCIL ACTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

POINTS TO REMEMBER . . . . . . . . . . . . . . . . . . . . . . .10

SPECIAL REPORT . . . . . . . . . . . . . . . . . . . . . . . . . . .15

INTERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19

SPOTLIGHT ON COMMITTEES . . . . . . . . . . . . . . . . . .23

PRO BONO AWARD RECIPIENTS . . . . . . . . . . . . . . .24

NEWS BRIEFS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26

2002 FALL MEETING . . . . . . . . . . . . . . . . . . . . . . . . . .27

General Information . . . . . . . . . . . . . . . . . . . . . . . . .27

Preliminary Program Topics . . . . . . . . . . . . . . . . . . .29

Hotel Reservation Form . . . . . . . . . . . . . . . . . . . . . .30

Registration and Ticket Purchase Form . . . . . . . . . 32

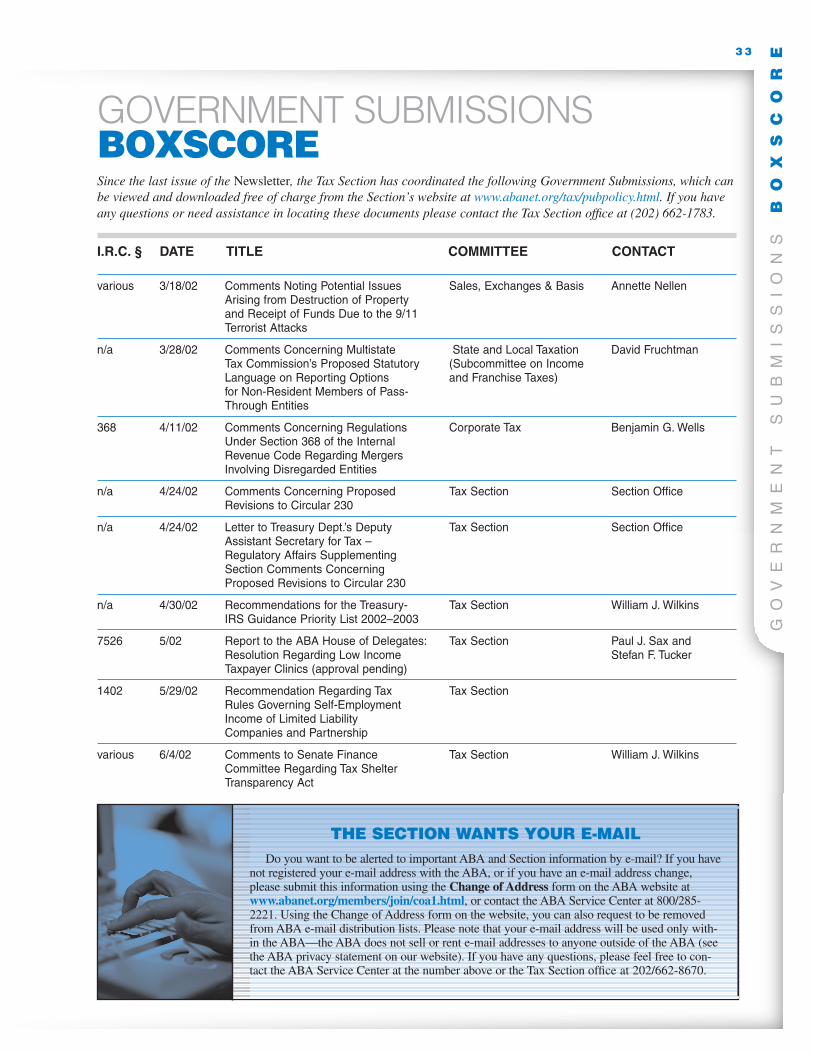

GOVERNMENT SUBMISSIONS BOXSCORE . . . . . .33

PUBLICATIONS ORDER FORM . . . . . . . . . . . . . . . . .34

MATERIALS ORDER FORM . . . . . . . . . . . . . . . . . . . .35

NEWSLETTERABA SECTION OF TAXATIONSUMMER 2002 VOLUME 21 NUMBER 4

ISSN 0277-2361

EDITORIAL BOARDCOUNCIL DIRECTORPatricia Ann Metzer

SUPERVISING EDITORAlice G. Abreu

INTERVIEW EDITORSJasper L. Cummings, Jr.Alan J.J. Swirski

SPECIAL FEATURES EDITORChristopher S. Rizek

PRODUCTION EDITORAnne B. Dunn

ASSOCIATE EDITORSNancy M. BecknerDianne BennettDavid A. BrennenAlexander DrapatskyEdward KesselBernice J. KoplinAnnette NellenDavid L. SilvermanKathleen A. Stephenson

EDITORIAL POLICYThe ABA Section of Taxation Newsletter is

published quarterly to provide information ondevelopments pertaining to taxation, Section ofTaxation news, and other information of profes-sional interest to Section of Taxation membersand other readers.

The Newsletter cannot be responsible forunsolicited manuscripts and reserves the right toaccept or reject any manuscript and the right tocondition acceptance upon revision of materialto conform to its criteria.

Articles and reports reflect the view of theindividuals or committees that prepared themand do not necessarily represent the position ofthe American Bar Association, the Section ofTaxation, or the editors of the Newsletter.

Manuscripts and letters should be mailed to:ABA Section of Taxation, 740 15th Street, NW,10th Floor, Washington, DC 20005.

Nonmembers of the Tax Section may subscribe to the Newsletter for $15.00 per yearor may obtain back issues for $4.00 per copy. To order, contact the ABA Service Center,750 N. Lake Shore Drive, Chicago, IL 60611,tel. 800/285-2221.

26945_ABA_Newletter_Summer 8/2/02 11:13 AM Page 2

3

IM

PO

RT

AN

T

SE

CT

IO

N

DA

TE

S

AN

D

SE

RV

IC

ES

FUTURE SECTION MEETINGS

2002 FALL MEETING—OCTOBER 17-19, CENTURY PLAZA AND ST. REGIS HOTEL, LOS ANGELES, CA

2003 MIDYEAR MEETING—JANUARY 23-26, MARRIOTT RIVERCENTER AND RIVERWALK, SAN ANTONIO, TX

2003 MAY MEETING—MAY 8-10, GRAND HYATT, WASHINGTON, DC

2003 FALL MEETING—SEPTEMBER 11-13, SHERATON CHICAGO, CHICAGO, IL

2004 MIDYEAR MEETING—JANUARY 29-31, GAYLORD PALMS, KISSIMEE, FL

IMPORTANT SECTION DATES AND SERVICES

ABA SERVICE [email protected]

The ABA Service Center is your one-stop shop forinquiries and orders related to ABA publications,ABA/CLE-sponsored programs, membership status anddues information, change of address requests, and theABA Member Advantage Program. You can reach theService Center by phone toll-free at 800/285-2221.

ABANETWORK—FOR MEMBERS ONLYAs a member of the ABA Tax Section, you are entitled

to browse exclusive “Members Only” content throughoutthe ABANetwork. On the Tax Section website, SectionMembers can download articles from the Newsletter andThe Tax Lawyer, research materials on Comm-Online,join committees, and view career opportunities for taxprofessionals.To access this privileged content, membersmust log in.

To log in, your username on the ABANetwork is yourABA Membership ID number, and your password is yourlast name. If you do not know your password, or if you

encounter problems when you attempt to log in, pleasecontact the ABA Service Center at [email protected],or by phone at 312/988-5522, or toll-free at 800/285-2221. Please have your Membership ID number readywhen you call.

COMM-ONLINE—WHAT ARE YOUWAITING FOR?

Cosponsored by the Tax Section and its primary cor-porate sponsor, LexisNexis™, Comm-Online providesinstant access to meeting materials, including valuablelegislative analysis, discussions of new regulations,important developments, and more, collected from TaxSection programs from May 1999 to the present. Accessis free to Tax Section members. Click on Comm-Onlinefrom the lefthand menu on the Tax Section’s homepage.

E-MAIL v. SNAIL MAILHave you registered your e-mail address with the

ABA? The Tax Section is communicating with 70% of itsmembership by e-mail. Why wait for snail mail, whenyou can receive regular notification of teleconferencesand other CLE opportunities, Section meetings, Sectiondeadline reminders, and other important announcementsfrom the Tax Section delivered right to your desktop.

We know it is not perfect—managing your e-mailboxis quite a task—but these days, e-mail is faster, cheaper,and more effective than snail mail.We don’t spam, and wecommunicate with you only when we have information toconvey. Sign up today at www.abanet.org/members/join/coa1.html.

CONTACT USABA Section of Taxation, 740 15th Street, NW,

Washington, DC 20005, tel. 202/662-8670,fax 202/662-8682, e-mail [email protected].

URGENT NOTICE FOR NY-LICENSED ATTORNEYSThe NYSBA recently notified the ABA that it mustdistribute NY Certificate of Attendance forms to allNY-licensed attorneys who wish to receive CLEcredit for attending any of the 2001-2002 TaxSection Meetings. The Section is in the process ofsending the forms to everyone who registered forany 2001-2002 meeting using a New York mailingaddress. If you are a NY-licensed attorney whodoes not have a New York mailing address, ANDyou wish to receive credit for attending any 2001-2002 Tax Section meeting, please contact theSection Office at 202/662-8670 or by e-mail [email protected] with your name and address toreceive a form.

26945_ABA_Newletter_Summer 8/2/02 11:13 AM Page 3

FR

OM

T

HE

E

DI

TO

R 4

“Summertime, an’ the livin’ iseasy . . .” The languid sensu-

ality of the world evoked by themusic and lyrics of GeorgeGershwin’s Porgy and Bess wereaspirational even within the contextof that opera, but they seem evenmore so as the summer of 2002 nearsits end. Summer marks the end of acycle even for the Section and offersan opportunity to reflect on chal-lenges met and new spheres left toconquer. This issue, a child of itstime, does likewise.

The issue itself marks the end ofan era, as it is the last issue that willcarry the name Newsletter. At itsMay meeting, Council approvedchanging the name of this publicationfrom the Tax Section Newsletter tothe Tax Section NewsQuarterly. Thechange in name reflects the changesin the content of the publication overthe last several years, in particularthose changes made by my predeces-sor, Ellen Aprill, to whom I continueto be grateful. While we still carrySection news, the publication is nowso much more. Points to Rememberprovide substantive practice pointers,Point/Counterpoint articles offerstimulating debates on important top-ics, Special Reports offer in-depthanalyses, and the Interviews give us aglimpse into the life and views ofpeople important to the developmentof the tax system or the work of theSection. The NewsQuarterly will beeven more informative, as it will havean expanded board of AssociateEditors who will be able to contributePoints to Remember and other fea-tures over a broader range of practiceareas. I’ll tell you more about them inthe Fall. In the meantime, if you havesuggestions for items you’d like tosee in the NewsQuarterly, or if youwould like to become involved withits work, please contact me [email protected].

This issue is not only the last ofthe Newsletter, but it is also the last

issue for which Dick Lipton has hadto write a Chair’s column. Dick’sleadership of the Section has beenexemplary despite the many chal-lenges events have posed; I haveespecially appreciated the dedicationthat has led him to submit hiscolumns before they are due. In thisissue Dick provides a thoughtfulassessment of the Section’s initiativesand its accomplishments during histenure at its helm. He discusses theSection’s efforts on various fronts,including tax system simplification,increasing member value, the impor-tance of pro bono service, the dedi-cated work of the 9/11 task force, aswell as numerous comments filed onproposed tax shelter legislation andrevisions to Circular 230. Reading hiscolumn should make you proud to bea member of the Section.

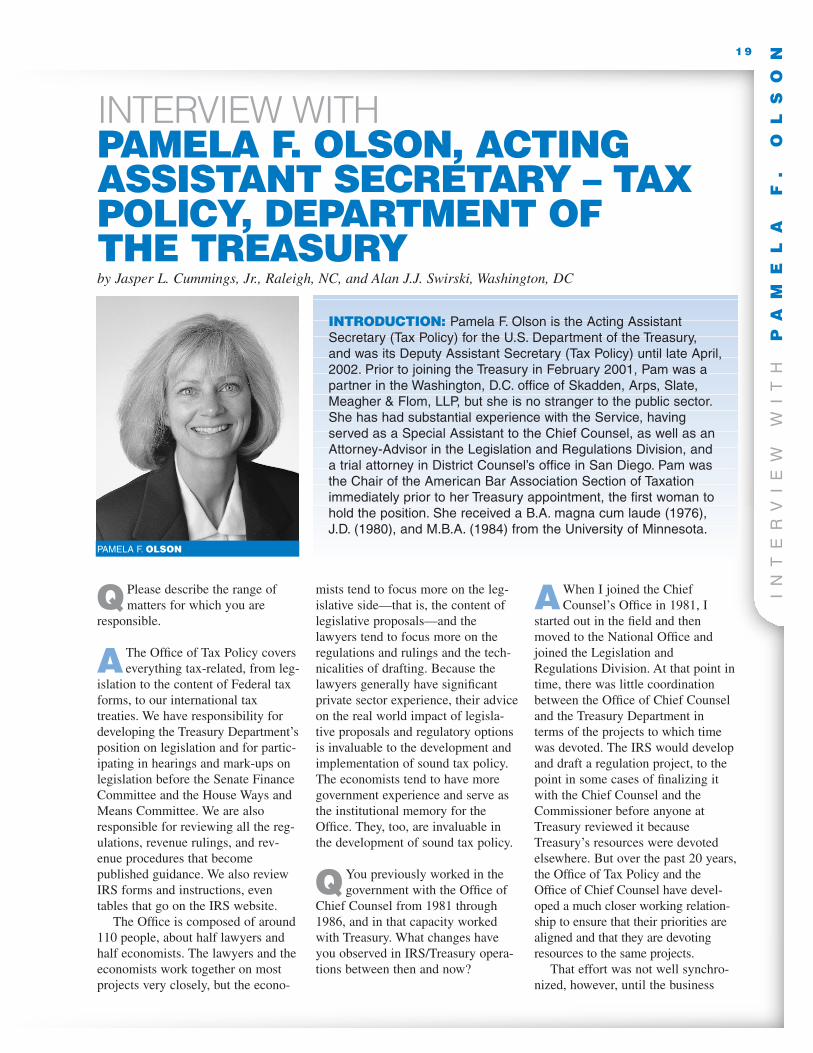

Of course, Dick’s tenure has beenunusually long, since he agreed toassume the leadership of the Sectionwhen his predecessor, Pam Olson,left private practice to enter govern-ment service. It is therefore fittingthat Pam, now in her role as theTreasury’s Acting Assistant Secretaryfor Tax Policy, is the subject of thisissue’s interview. As always, JackCummings and Alan Swirski haveposed a set of questions that begin byeliciting a detailed description of thework of the Office of Tax Policy andmove through Pam’s reflections onchanges in the relationship betweenthe Service and Treasury from thetime of her first government servicein 1981 to the present, as well as thechallenges of tax administration andthe prospects for a significant efforton tax simplification during the sec-ond half of the current administra-tion.

In the Tax Section, as often in life,the end of one era marks the begin-ning of another, so it is fitting thatthis issue also contains a column byHerb Beller, the incoming Chair.Herb not only describes the genesis

of his longstanding involvement withthe Section but also shares his aspira-tions for his term as Chair. We learn,for example, that Herb will continueto build on the successful initiativesof his predecessors and, will, in addition, strengthen the Section’srelationship with the Service’s operating divisions.

This issue marks another begin-ning, for it features the recipients of anew award, the Pro Bono ServiceAward, which was presented at theMay meeting. The first recipients ofthis award, Victoria Bjorklund andElizabeth Atkinson, are individualswhose accomplishments will inspireus and who have set a standard forpublic and professional service thatshould make us proud to claim themas members of the Section.

In light of the commitment to pub-lic and pro bono service which hasbeen one hallmark of Dick Lipton’stenure as Chair, and which is exem-plified by the inauguration of the ProBono award, it is fitting that thisissue’s Spotlight be on the LowIncome Taxpayers Committee. TheSpotlight reveals the breadth of issuesto which the Committee devotes itsattention, including many that shouldbe of interest to tax practitioners generally, regardless of whether they represent low income taxpayers.Reading it may even prompt you towant to get up in time to attend theCommittee meetings, typically heldat 7 a.m. on Saturday mornings during Section meetings.

On the substantive side, this issuecontains a Special Report and twoPoints to Remember, both of whichgive their subjects a more in-depthtreatment than is usual for this fea-ture. In the Special Report, BerniceKoplin discusses a recent but veryimportant Supreme Court case whichheld that property owned by a tax-payer as a tenant by the entirety

FROM THE EDITORby Alice G. Abreu, Philadelphia, PA

SEE EDITOR, PAGE 18

26945_ABA_Newletter_Summer 8/2/02 11:13 AM Page 4

5

FR

OM

T

HE

C

HA

IR

In the Tax Section, as in life, allgood things must come to an end.

My term as Chair of the Section isnow ending. In this, my final Fromthe Chair column, I will highlight themost important activities of theSection during the past 18 months.

In my first column I set forth thethree primary goals for my term: pro-moting simplification of the tax laws,increasing the value of membershipfor our members, and encouragingpro bono activities. The unfoldingevents over the past 18 months haveadded a number of other importantgoals and actions, but these threegoals remained paramount through-out that time.

SIMPLIFICATIONAs David Richmond, who chaired

the Section in the early 1960s, recent-ly reminded me, simplification of thetax laws has been an (unachieved)goal of the Tax Section virtually fromthe time of its formation. Althougheveryone is in favor of tax law sim-plification (just like everyone favorsmotherhood and apple pie), no grouphas come forward to volunteer thattheir tax liability be increased inorder to make the tax laws simplerfor everyone else.

The Tax Section has joined overthe past several years with the othermajor national groups of tax practi-tioners—the American Institute ofCertified Public Accountants and theTax Executives Institute—in order toincrease the public focus on the needfor tax simplification. My predeces-sor, Pam Olson, placed considerableimportance on tax law simplificationbefore she assumed her current posi-tion in the Administration. During myterm, I was fortunate to have a groupof committed members, led by DavidGlickman of Dallas and HelenHubbard of Washington, DC, whodevoted substantial time and energyto the cause of tax simplification. We

were aided greatly in this endeavorby the significant work of the JointCommittee on Taxation (JCT) which,in response to the mandate fromCongress in the 1997 Tax Act, pub-lished a detailed analysis of the prob-lems caused by tax complexity andvarious alternatives for simplifyingthe Code.

Although simplification of the taxlaws will remain an uphill struggle,slow progress is being made. When Itestified before Congress in 2001, Iemphasized three primary simplifica-tion goals of the Section—repeal ofthe alternative minimum tax, repealof rules commonly referred to as PEP(personal exemption phase-out) andPease (limitation on itemized deduc-tions), and enactment of a uniformdefinition of a child. We can reportsome success in this regard. Congressapproved in the 2001 bill the repealof PEP and Pease (albeit with adelayed effective date), and theAdministration proposed a uniformdefinition of a child for tax law pur-poses in its “white paper” issued onApril 15, 2002. Moreover, leadingmembers of both political partiesappear to recognize the need torepeal the individual AMT, althoughthe high budgetary cost of this actionhas been an impediment.

Perhaps more importantly, simpli-fication is now part of the discussionin every tax bill that is proposed. TheJCT recently began to include a “sim-plification analysis” in its discussionof proposed legislation, and theAdministration has publicly calledfor simplification of the Code. Thecontinuing focus on tax simplificationwill, hopefully, eventually result inreal simplification of the tax laws.

MEMBER VALUEThe Tax Section is, first and fore-

most, a membership organization.The leadership of the Section mustnever forget that their primary obliga-tion is to our members, whose duessupport the Section and whose partic-ipation gives the Section its vitality.My “member value initiative” wasintended to focus on providingincreased value to members for theirmembership in the Section.

I asked Dick Shaw of San Diego,who will succeed Herb Beller asChair of the Section, to lead thiseffort. Dick prepared a lengthy reportwhich highlighted many ways for theSection to provide value to our mem-bers. But most importantly, the reportemphasized a fundamental fact—before we try to deliver value to ourmembers, we need to know what ourmembers want. In response, theSection has authorized a detailed sur-vey of our members in order to deter-mine what YOU want from the TaxSection. This survey should be dis-tributed soon, and I hope that, if youare selected randomly to receive asurvey, you will take the time torespond so that the Tax Section canstrive to deliver the benefits that youbelieve are important.

PRO BONOThe third of my goals was to

increase the pro bono activities of theSection and its members. To provideus guidance, I asked Terri Hyde of

FROM THE CHAIRby Richard M. Lipton, Chicago, IL

RICHARD M. LIPTON

26945_ABA_Newletter_Summer 8/2/02 11:13 AM Page 5

FR

OM

T

HE

C

HA

IR 6

Washington, DC, to head a pro bonotask force, which reported to Councilin November. Terri’s efforts wereincredible, and Council unanimouslyadopted her proposals, which includ-ed the formation of a standing com-mittee on pro bono activities, theestablishment of a Pro Bono Awardto honor Section members involvedin pro bono activities, and an “out-reach” program through which theSection would assist low-income tax-payers through increased awarenessof their rights and responsibilities aswell as legal assistance.

We have begun to take steps inthis direction. At the Plenary Sessionof the May 2002 Meeting inWashington, I had the pleasure ofpresenting the first Tax Section ProBono Awards to Elizabeth Atkinsonof Norfolk, Virginia, and VictoriaBjorklund of New York, New York.These two members of the Sectionhave, through their long-standingcommitment to pro bono activities,set an example for all of us. ThePlenary Session also included a paneldiscussion of pro bono opportunitiesthat featured comments from B. JohnWilliams, the Chief Counsel of theIRS, Nina Olson, the NationalTaxpayer Advocate, Judge PeterPanuthos of the US Tax Court, andElizabeth Atkinson.

In addition to focusing internally, Iimplemented an outreach program forthe Section through the media. Weprepared video and audio newsreleases on the topics of charitablegiving and tax return preparation,which were aired on hundreds of tel-evision and radio stations in virtuallyevery major market. These releaseswere highly successful; more than 40million Americans heard or saw oneof these media releases. In addition,we launched a new platform on ourwebsite, Tax Tips 4 U.org, which fea-tures helpful hints for consumersconcerning their tax rights andresponsibilities.

There is still much to be accom-plished. I am very pleased that mysuccessor, Herb Beller, and Councilappear to be committed to increasingthe pro bono activities of the Section

and its members. Like tax law simpli-fication, this will not be an easy task,but unlike simplification, this is agoal that is within the control of ourmembers. I hope that all of you willjoin me in making pro bono activitiesa regular part of your legal career.

9/11 TASK FORCEIn addition to the planned activi-

ties during my term, there were threeadditional matters that arose andbecame a significant focus of theSection. The first was one that nonewould have wished to occur—theresponse to the events of September11, 2001. The tragedy on that daybrought forth, however, some of the best from many members of the Section.

Immediately after the terroristattacks, I appointed a special taskforce, which was headed by MichaelHirschfeld of New York. The taskforce served as an important resourcefor Congress, the Administration andthe media in addressing the tax con-sequences of the attacks. Most impor-tantly, the 9/11 Task Force was ableto focus on problems in the tax lawthat made it difficult for Americans tomake charitable contributions to ben-efit the individuals and businessesthat were most directly affected. Inresponse, Congress enacted legisla-tion and the IRS issued guidancespecifically addressing the concernsraised by our task force. The con-structive role of the task force, inresponse to the destructive attacksmade against our country, is some-thing that the Section can be veryproud of.

CIRCULAR 230 AND TAXSHELTERS

Another major development dur-ing my term as Chair was created bythe tax-shelter phenomenon of thelate 1990s. In response to inappropri-ate behavior by both taxpayers andpractitioners, Congress and theAdministration proposed legislationand regulations, respectively, intend-ed to clamp down on tax shelters.These proposals included a substan-

tial revision to Circular 230, whichsets forth the rules for practice beforethe IRS.

Although Congress’ and the IRS’goals were appropriate, their propos-als were not always on the mark. Anumber of members of the Sectiondevoted an unbelievable amount oftime and energy towards preparingcomments on the various legislativeand regulatory proposals. Four indi-viduals—Rick Ballard, Greg Jenner,Bill Wilkins and Herb Beller—spear-headed the preparation of three setsof comments concerning the pro-posed revisions to Circular 230 aswell as several responses to legisla-tive proposals from the Hill.

As I write this column, we areembarking on the preparation of yetanother set of comments, this time inresponse to the legislative proposalsintroduced in the Senate in May 2002and the regulatory proposals issuedby the Administration the precedingMarch, which are specifically focusedon tax shelters and tax shelter pro-moters. The Tax Section has longargued that the best way to addresstax shelters is to focus sunshine onthem, and the latest proposals appearto take this approach through theimposition of various disclosurerequirements. I anticipate that ourcomments will applaud these effortsaimed at increasing the disclosure ofpotentially-abusive transactions whilepointing out problems and issuesraised by the proposals.

ANNUAL MEETINGIn the last issue of the Newsletter,

I addressed the decision of Councilthat the Section would cease to holdcommittee meetings at the AnnualMeeting of the ABA. Although thisdecision was not an easy one, it hadbeen long in coming—the question ofthe Section’s role at the AnnualMeeting had been on the agendawhen I joined Council in 1990, and12 years later the issue has finallybeen resolved. When the ABAannounced last fall that the format forthe Annual Meeting was changing in

SEE CHAIR, PAGE 8

26945_ABA_Newletter_Summer 8/2/02 11:13 AM Page 6

7

FR

OM

T

HE

C

HA

IR

-E

LE

CT

FROM THE CHAIR-ELECTby Herbert N. Beller, Washington, DC

Early in my career I had the goodfortune to work closely with Ed

Kahn, an outstanding Washington taxlawyer who was very active in theSection. One day Ed enlisted my helpin putting together the Section’s com-ments on the recently enacted TaxReform Act of 1969. The manySection committees that were affect-ed by this important new legislationhad been asked to prepare drafts ofseparate comments regarding priorityareas for administrative guidance onthe multitude of issues that werebeginning to surface. My task was toreview, edit, and coordinate thesedrafts into a single, well-organizedsubmission. For the next few days(and evenings too), client work wentby the wayside as I immersed myselfin the intricacies of some fairly hefty,and seemingly incomprehensible,changes to the Internal RevenueCode—the maximum tax on earnedincome, private foundation excisetaxes, revamped stock dividend rules,section 83 and the minimum tax onpreferences, to name but a few. Theresulting “cut and paste” job waspromptly reviewed and surelyimproved by Ed and others, and offit went to Treasury and the Service.For me, the experience was challeng-ing, educational, and ultimately very

useful in my practice. It also markedthe beginning of more than threedecades of involvement with anorganization that has helped me growboth professionally and personally incountless ways.

I remember well my early years inthe Section, including spring meet-ings at the Shoreham Hotel inWashington. All of the committeesmet at the same time in the ballroom,each at its own table. There usuallywere about 10 or 12 of us at theCorporate-Shareholder table, includ-ing Jim Holden, Jere McGaffey, andothers who would go on to becomeleaders of the Section. Saturdayswere devoted primarily to an endlessstream of committee reports present-ed to the entire group, a practice thattended to induce considerable drowsi-ness. Not infrequently, however, thesesessions became quite lively as aresult of heated floor debates on leg-islative recommendations or otherburning issues of the day.

Over the years the Section hasbecome a much larger organization,with a much broader plate of activi-ties. We provide to our almost 20,000members unparalleled CLE program-ming, valuable networking opportuni-ties, and more than 50 activecommittees and task forces throughwhich they can work to hone theirareas of specialization and to improveour nation’s tax system. My prede-cessor, Dick Lipton, has done a greatjob enhancing even further theSection’s premier reputation as atrusted and well-respected voice onthe national tax scene. When PamOlson answered the call to publicservice early last year, Dick steppedin without missing a beat. He hasgone full steam ever since and leavesbig shoes to fill. (My own size 13D’shopefully will give me a leg up onthe matter!)

The overriding theme for myupcoming term as Chair is quite sim-ple: to make a difference for our

members and for the tax system. Lastyear a special task force headed byDick Shaw produced a comprehen-sive report containing many goodsuggestions for increasing the valueof Section membership. Dick willcontinue to focus on this area duringhis upcoming term as Chair-Elect ofthe Section. In addition, I am delight-ed that Susan Serota, a formerSection Vice-Chair for ProfessionalServices, will chair our Membershipand Marketing Committee, and thatMelinda Merk, outgoing Chair of ourYoung Lawyers Forum, will serve asher Vice-Chair.

Perhaps the most important of ourmember-oriented goals is the need tocontinue recent successful efforts toattract as new members youngerlawyers and lawyers from diversebackgrounds. Our Young LawyersForum and Diversity Committee haveboth been very productive, and theircontinuing vitality is critical to theSection’s future. I also would like tosee us do more in the way of“between meetings” CLE and com-mittee activity, taking full advantageof our excellent online and otherremote communication capabilities.And finally, we need to make surethat Section activities and initiativesare compatible with the needs anddesires of our membership. We soonwill be sending a comprehensive sur-vey to a broad cross-section of ourmembership. This is a good way forSection management to learn abouthow we can better serve you. I urgeall who receive the survey to com-plete and return it as promptly as possible.

Among our priorities relating toimprovement of the tax system, Iview the following as especiallyimportant:• Government interface.

Strengthening Section relation-ships with all of the IRS operatingdivisions; encouraging and facili-tating opportunities for direct

HERBERT N. BELLER

26945_ABA_Newletter_Summer 8/2/02 11:14 AM Page 7

8

interaction between more of ourcommittees and their governmentcounterparts; improving responsetime and increasing follow-upactivity on regulation commentsand other government submis-sions; and seeking opportunitiesfor earlier and more intensiveSection involvement in the devel-opment of published guidance.

• Simplification. Continuing to beatthe drum on the desperate need formajor simplification of the taxlaws. Tax simplification is one ofABA’s top legislative priorities,and the Section’s joint efforts withthe AICPA and Tax ExecutivesInstitute have been instrumental infocusing national attention on theissue. No matter how difficult theroad to achieving significant

progress may be, we cannot affordto relax our commitment to thisimportant cause.

• Pro bono. Building on the signifi-cant steps that were taken duringDick Lipton’s term to enhance theSection’s profile and participationin the pro bono arena. The excel-lent report of the special task forcechaired by Terri Hyde outlines sev-eral ways in which Section mem-bers might contribute their talentsand time to low-income taxpayerand other pro bono initiatives. Dickwill chair our newly formed ProBono Committee, and will nodoubt bring considerable energyand devotion to the job of imple-menting these recommendations.

• Tax shelters. Continuing our sub-stantial and longstanding support

for the development of workable,fair and effective mechanisms forshining the spotlight on (andappropriately sanctioning) notonly the taxpayers who engage inabusive tax shelters, but also thepromoters and advisers who prodand assist them. It is imperativethat the Section stand on the high-est ground possible in evaluatingand providing input on administra-tive and legislative proposals thatare designed to eradicate this seri-ous blight on the integrity of ourtax system.

As always, there is much to do. Ilook forward to the privilege of lead-ing the Section and am confident that,working together, we will continue to make a difference in many important ways. �F

RO

M

TH

E

CH

AI

R-

EL

EC

T

a manner that would make it moredifficult for the Tax Section to con-duct “business as usual,” the time hadfinally come to sever our links withthe Annual Meeting.

As I noted in my prior column, Iview this action not as a step awayfrom the ABA, but, rather, as a nec-essary response to the needs anddesires of our members. At the sametime, the Tax Section has begun toplay a larger role in the ABA throughthe Section Officers Conference, thepromotion of ABA goals in Congressand with the Administration, andthrough our efforts to increase theprofile of the ABA. I look forward toour stand-alone meetings in LosAngeles in October 2002 and inChicago in September of 2003, inwhich the Tax Section can focus onour members without the distractionsand difficulties caused by being partof the larger Annual Meeting.

CONCLUSIONA chair for the Tax Section is only asgood as the people who support him.I was fortunate to be supported by anable Council and a wonderful groupof officers, including Nick Freud,Karen Hawkins, George Howell, DonKorb, Pat Metzer, Bill Wilkins, SusanStone and Helen Hubbard. Each ofthem spent large amounts of time andenergy making the Section functionsmoothly. Space does not permit meto laud each of their efforts, but theyall contributed greatly to the successof the Section.

I will be succeeded by HerbBeller as Chair of the Section. Herbhas provided superb support andinput to me during my term, and I amconfident that he is fully prepared toassume leadership of the Section. Ilook forward to watching the Sectioncontinue to grow in importance underHerb’s leadership.

Last, but by no means least, Iwant to thank the entire staff of the

Section and particularly our Director,Christine Brunswick. Most membersare unaware of the incredible amountof staff effort that goes into every-thing the Section does, from publica-tion of the Newsletter to mediaoutreach to successful meetings.Christine and her staff make it alllook effortless, but that is onlybecause they are so good at whatthey do. Our staff is one of the finestin the ABA, and we are very proudof them. The Tax Section could not function without their efforts and support.

In summary, it has been an honorand a privilege to serve as the Chairof the Tax Section for the past 18months. I am confident that theSection is in a leadership position inthe tax arena, and I look forward towatching as the Section continues itsrole as the voice of the legal profes-sion in tax matters. �

CHAIRFROM PAGE 5

FR

OM

T

HE

C

HA

IR

26945_ABA_Newletter_Summer 8/2/02 11:14 AM Page 8

9

CO

UN

CI

L

AC

TI

ON

S

COUNCIL ACTIONSBy N. Susan Stone, Secretary, Houston, Texas

The Council of the ABA Sectionof Taxation met on May 9, 2002,

at the Spring Meeting of the Sectionin Washington, DC. The Councilheard reports and took action on thefollowing topics.

MJP COMMISSIONRULE 5.5

Stef Tucker, one of the Section’sDelegates to the ABA House ofDelegates and former Chair of theSection, led Council in a review ofproposed Rule 5.5 and associatedcomments recently released by theABA Commission on Multijurisdic-tional Practice (“MJP Commission”).Proposed Rule 5.5, which addressesthe unauthorized practice of law in amultijurisdictional practice context,contains at least two provisions thatwould typically allow a tax lawyer topractice in a state other than thestate where he or she is licensedwithout being deemed to beengaged in the unauthorized prac-tice of law. Among other excep-tions to unauthorized practice,proposed Rule 5.5 provides that

a lawyer admitted in onestate may provide legal

services on a tempo-rary basis in another

state if those tempo-rary services rea-

sonably relate tothe lawyer’s

practice in thejurisdiction in

which thelawyer is

admitted. Furthermore, a lawyeradmitted in one state may providelegal services in another state,whether or not on a temporary basis,if the services are those that thelawyer is authorized by federal orother law to provide in another state.After discussion, Council unanimous-ly agreed to join other sections of theABA in supporting proposed Rule5.5. Proposed Rule 5.5 will be debat-ed by the ABA House of Delegatesduring the ABA Annual Meeting inWashington, DC, in August 2002.

DIVERSITYCOMMITTEE REPORT

Jessica Hough and WayneHamilton, both Co-Chairs of theCommittee on Diversity, delivered areport to Council on the goals andaccomplishments of the Committee.The Committee’s twin goals are: (1)to recruit minority attorneys to theSection, and (2) to encourage andenable minority attorneys to takeleadership positions within theSection. Recent Committee accom-plishments include completion of theCommittee’s web page, the cospon-sorship with tax practitioners of vari-ous career panels for minoritystudents at New York, Chicago andBoston universities, and participationof minority attorneys on panels spon-sored by Section substantive commit-tees. Council commended theCommittee for its hard work and con-tinued progress.

LAW STUDENTINVOLVEMENT

Council considered steps toencourage and increase the

involvement of law studentsin the activities of the Tax

Section. Dick Lipton,Section Chair, report-

ed that the ABA actively encourageslaw student memberships and that theABA dues for law students are low.Mr. Lipton further reported that mostsections provide free section mem-berships for law students. Councilconsidered the fact that younglawyers are more likely to join theTax Section if they become familiarwith the benefits of Section member-ship during their law school years.After discussion, Council unanimous-ly agreed to provide free Sectionmembership for law students.Council also agreed that the ViceChair-Administration has discretionto approve reimbursement for a lawstudent’s travel expenses if the stu-dent has worked on a project that willbe presented at a Section meeting.Council further agreed that a requestfor reimbursement must be submittedto and approved by the Vice-ChairAdministration before any commit-ment is made to a student regardingreimbursement.

SECOND READING OFSTANDARDS OF TAXPRACTICE STATEMENT2001-1

Charles Pulaski, Vice Chair-LawImprovement of the Committee onStandards of Tax Practice, led thesecond reading of proposedStandards of Tax Practice Statement2001-1 (the “Statement”). Mr.Pulaski reported that the proposedStatement articulates standards ofacceptable practice in the preparationand distribution of written tax opin-ions. After significant discussion byCouncil regarding the application ofthe proposed Statement’s definitionof a “tax opinion,” Council did notapprove a motion to return the pro-posed Statement to the Committeefor publication. �

26945_ABA_Newletter_Summer 8/2/02 11:14 AM Page 9

PO

IN

TS

T

O

RE

ME

MB

ER 1 0

JUST THE FACTS,PLEASE: SUBSTANCECAN PREVAIL OVER FORM

by Edward Kessel and Kathleen A.Stephenson, Philadelphia, PA

In his “Practice Strategies”column, which appeared in the

March 2002 ABA Journal, ProfessorJames W. McElhaney’s alter ego,Angus, states that there are fourthings required of any brief—thelegal setting, the issues, the statementof facts, and the legal argument. Hethen persuasively argues that of thefour, the most important element isthe statement of facts. Those of uswho live in the arcane, esoteric worldof the tax code can be in danger ofgetting hung up on the legal argu-ment and giving short shrift to thefacts. Here are just a few examples ofthe dangers inherent in doing so.

In the days before charitableremainders were required to be in theform of a unitrust or annuity trust,Mary Cotton Wood established a tes-tamentary trust to pay the income toher brother-in-law for life and, uponhis death, to distribute one-sixth ofthe corpus to each of two charities.The trustee was also authorized topay to the brother-in-law so much ofthe principal as the trustee deemednecessary to provide for his “support,

maintenance, welfare and comfort.”The Service denied a charitablededuction, maintaining that the termsof the trustee’s powers of invasionwere subjective in character and wereso broad as to be incapable of beingconfined within any ascertainablestandard. In other words, the standardsfor invasion of principal were so looseas to be virtually nonexistent, or, atleast were incapable of being translat-ed in terms of money. The Tax Court ruled otherwise. Wood v.Commissioner, 39 T.C. 919 (1963).

Just three and a half years later, atax attorney, relying on the Woodcase, again asked the Tax Court todecide whether a trustee’s power toinvade principal for the “welfare andcomfort” of the income beneficiariesof a charitable remainder trust madethe value of the charitable remainderunascertainable. Judge Raum stoodwith his interpretation of the law, asset forth in the Wood decision, but,this time, ruled in favor of theService and denied the charitablededuction, reasoning that: “[T]hemere fact that the will fixes measura-ble limits to the power of invasion isnot sufficient to justify the claimeddeduction. It must appear further thatthe possibility of invasion, with itsconsequent diversion of corpus fromthe charitable donee, is so remote asto be negligible. . . . And it is at thispoint that petitioner has failed tocarry its burden of proof. . . .Thequestion is purely one of fact andmust be examined in the light of therecord made by the parties.”Buckwalter v. Commissioner, 46 T.C.805 (1966) (emphasis added).

The same legal concept of “ascer-tainable standard” arises in the con-text of treating gifts by one spouse ashaving been made one-half by eachspouse under section 2513 of theInternal Revenue Code. In this areathe case law again demonstrates thateven though the language of the doc-ument may meet the legal standard, itis still necessary to apply that stan-

dard to the facts of the case. InRobertson v. Commissioner, 26 T.C.246 (1956), Mr. Robertson created atrust to pay the income to his wife,along with so much of the principalas deemed necessary for her mainte-nance and support, “giving dueregard to her other sources of funds.”The remainder in the trust was givento third parties. Mrs. Robertson con-sented to treating the gift of theremainder as a split gift. This time itwas the Service that rested on a legalargument that the trustee’s power todistribute principal to the wife madethe gift to the remainder beneficiariesunascertainable and, therefore, thedonor was not permitted to split thegift. However, the Tax Court held thatthe trustee’s power to invade princi-pal was restricted by an ascertainablestandard and that the taxpayer’s evi-dence proved that, in applying thatstandard, there was no likelihood thatprincipal would be invaded. Thecourt therefore allowed the taxpayersto treat the transfer as having beenmade one half by each spouse.

Falk v. Commissioner, T.C. Memo1965-22, refined the result inRobertson. In Falk, the trustee’spower to distribute income and prin-cipal to the donor’s spouse were bothheld to be governed by ascertainablestandards. After examining the cou-ple’s finances, however, the TaxCourt found that in the event of thedonor husband’s death there wouldbe a possibility that the trustee wouldbe required to distribute income tothe wife, but that there would be noreason, under the standard, to distrib-ute principal. Since the facts, asdeveloped, showed that it was notpossible to quantify how much of theincome might be used for the benefitof the spouse, and how much wouldnecessarily benefit parties other thanthe spouse, the Court did not allowthe value of the income interest to betreated as having been made one-halfby each spouse. Nevertheless, sincethe facts showed that there would be

POINTS TO REMEMBEREditor’s Note: POINTS TOREMEMBER are individual sub-missions to the Newsletter fromAssociate Editors and Section ofTaxation members with insights toshare. Although these items aresubject to selection and editing, theSection conducts no systematicreview of them. Accordingly, eachitem states the view of the individ-ual contributor and does not neces-sarily represent the views of theABA or of the Section of Taxation.We welcome new submissions aswell as responses to previously pub-lished material found in this sec-tion.

26945_ABA_Newletter_Summer 8/2/02 11:14 AM Page 10

1 1

PO

IN

TS

T

O

RE

ME

MB

ER

no invasion of principal, gift splittingwas allowed as to the remainder.

Buckwalter, Robertson and Falk alldemonstrate the importance of build-ing a strong factual record to supportour legal arguments. In each case, theresult did not turn on the legal issueof whether there was an ascertainablestandard but, rather, on whether thefacts established a likelihood thatincome or principal would be invadedunder that ascertainable standard.

This brings us to several morerecent cases dealing with family lim-ited partnerships. The Tax Court hasindicated quite clearly, in Strangi v.Commissioner, 115 T.C. 478 (2000),and in Knight v. Commissioner, 115T.C. 506 (2000), that family limitedpartnerships will be respected forestate and gift tax purposes, and thatto the extent that the partnershipagreements create impediments forpartners who wish to gain access tothe assets of the partnership, thevalue of the partnership units willreflect discounts to account for those impediments.

Given this legal analysis, considerthe following. Within a year of herdeath, Dorothy Schauerhamer createdthree limited partnerships, one witheach of her three children. In eachpartnership Dorothy held a 1% inter-est as general partner and a 95%interest as limited partner. Her chil-dren each paid for and held a 4%general partnership interest in thepartnerships. Dorothy then funded thepartnerships with substantial assetsand followed that with transfers toher children of some of her limitedpartnership units in the three partner-ships. Each transfer was not subjectto gift tax by virtue of annual exclu-sions. After her death, the Servicerevalued the partnership interestsremaining in the estate as if the threepartnerships did not exist and includ-ed in her gross estate all the assetsshe had used to fund the partnerships,as transfers with a retained life estateunder section 2036(a)(1).

Had the Tax Court simply appliedthe logic it later espoused in Strangiand Knight, the Schauerhamer part-nerships should have been valued at a

discount. However, the court lookedbehind the partnership agreementsthemselves. Dorothy, in contraventionof the partnership agreements, haddeposited the income earned by thepartnerships into her own personalchecking account, where it was com-mingled with income from othersources. Furthermore, Dorothy’s chil-dren testified that they knew Dorothywas depositing the funds into her per-sonal account and they also acknowl-edged that the assets and incomewere to be managed exactly as theyhad been before they were transferredto the partnership. The Tax Courtruled for the government, holdingthat the facts did not support the exis-tence of a partnership. Dorothy’sactions ignored the partnership andso did the court, finding an impliedagreement that Dorothy retained pos-session and enjoyment of the eco-nomic benefits of the underlyingassets. Schauerhamer v.Commissioner, T.C. Memo 1997-242.

Likewise, in Reichardt v.Commissioner, 114 T.C. 144 (2000),the decedent transferred, during hislifetime, virtually all of his propertyto a family limited partnership.However, after the transfer he contin-ued to control all of the notes receiv-able, investment accounts, and cashin the same manner as he had beforethe transfer. He commingled partner-ship assets with his own and contin-ued to live in the house that he hadalso transferred to the partnership.Although the estate argued that thedecedent’s fiduciary duties as a gen-eral partner (and as trustee of a trustwhich served as one of the limitedpartners) affected his ability to retainthe enjoyment of the transferredassets, the Tax Court saw otherwise.The fact that the other partners didnot limit his actions was taken asproof that there was an impliedagreement to allow the decedent tocontinue to enjoy the partnershipproperty. Again, the partnership formfailed to deliver the expected dis-count to taxable value.

Family limited partnerships havebecome a favored estate planningtool. If the partnership, in addition to

providing benefits such as simplifiedmanagement within a fractionalizedownership, is also to provide thebenefit of a discount to taxable valuefor estate and gift tax purposes, it iscritical that the partners respect thepartnership form and follow, to theletter, the terms of the partnershipagreement.

These cases are a telling reminderof the importance tax planners mustplace on building a firm factual base.We must not only provide an efficienttax structure but must also impressupon our clients the importance ofbehaving in a manner that is consis-tent with that structure. Actions willoften speak as loud, if not louder,than words. Arguments that preferform over substance are destined tobe rejected, and our clients’ actions,which will become the facts of anycase that subsequently arises, mustcreate that substance. These casesoffer a cautionary tale—one whichmany of us would be wise to pass onto our clients.

ALIMONY AND CHILDSUPPORT: PLANNINGOPPORTUNITIES

by David L. Silverman,Great Neck, NY

GENERAL PRINCIPLES

Tax planning in the context ofdivorce requires familiarity with

sections 71 and 1041, the first ofwhich governs the taxation of alimo-ny (support) payments and latter ofwhich sets forth the general rule ofnonrecognition with respect to prop-erty transfers incident to divorce. As Iwill discuss in this Point, some famil-iar tax principles cease to apply whensection 1041 is applicable. For exam-ple, a recent ruling, Rev. Rul. 2002-22, 2002-19 I.R.B. 849, examines theincome tax consequences of transfersof nonstatutory stock options orrights to deferred compensationbetween divorcing spouses and holdsthat the assignment of income doc-trine does not apply. In addition,

26945_ABA_Newletter_Summer 8/2/02 11:14 AM Page 11

PO

IN

TS

T

O

RE

ME

MB

ER 1 2

certain rules operate to discourage“alimony” payments that tend to dis-appear upon the emancipation of achild. To a considerable extent, thisproblem can be diminished by carefultax planning. The structuring of alimo-ny payments presents an opportunityto utilize careful tax planning toachieve a fair and tax-favored resultfor both parties.

FLEXIBILITY IN TAX PLANNINGFOR ALIMONY PAYMENTS

A payment will be deductible asalimony under section 215 only if itfits the definition of alimony or sepa-rate maintenance payment providedby section 71(b). Section 71(b)defines alimony or separate mainte-nance payments as payments made toor on behalf of a spouse pursuant to awritten divorce or separation agree-ment. Among other requirements,such payments must terminate at the death of the payee spouse. I.R.C.§ 71(b)(1)(D). The Tax Reform Actof 1984 eliminated the requirementthat alimony payments be “periodic”and be made in discharge of a legalobligation of support. See Temp.Treas. Reg. § 1.71-1T(a), Q & A 3.

Parties may therefore structureagreements so that alimony paymentscontinue following what would other-wise have been a terminating event,such as the remarriage of the payeespouse (which would have terminatedthe support obligation). A provisionrequiring alimony payments evenafter the recipient spouse remarriesmight appeal to the payor spouse,since it would provide an incentivefor the recipient spouse to remarry.

The elimination of the supportrequirement also facilitates the struc-turing of an overall settlement whereilliquidity exists. To illustrate:Assume that spouse X’s business isworth $1 million and comprises thepredominant asset in the maritalestate. However, no portion of thatasset can be allocated to spouse Y ina settlement because the asset is indi-visible, as is, for example, a profes-sional license. Assume further thatthe parties agree that a court would

award spouse Y $15,000 per year forten years in spousal support, butspouse X lacks the cash with which topay such an award. One solution tothe illiquidity problem would be forspouse X to make payments supple-menting the assumed spousal supportaward as a proxy for an even alloca-tion of the illiquid net marital estate.These payments, being a substitute forproperty division, could be designedto survive otherwise terminatingevents, such as remarriage or death ofspouse Y. (Recall that payments con-tinuing after the death of the recipientspouse do not constitute alimony fortax purposes, and consequently are notdeductible by the payor spouse.Payments continuing after the remar-riage of the recipient spouse could,however, qualify as deductible alimo-ny payments.)

A frequent objective in structuringalimony payments is to time adiminution in payments with theemancipation of a child. The problemis that section 71(c) provides thatamounts paid for child support willnot qualify as alimony and the regu-lations make it clear that amountswill be treated as child support if theyare either reduced “(a) on the hap-pening of a contingency relating to achild or (b) at a time which can clear-ly be associated with such a contin-gency.” Temp. Reg. § 1.71-1T(c) A16. Nevertheless, the regulations cre-ate a presumption which has theeffect of creating a safe harbor. Thus,Temp. Treas. Reg. section 1.71-1T(c),Q & A 18, provides that a reductionwill be presumed to be “clearly asso-ciated” with a contingency relating tothe child if (i) the payments arereduced within 6 months before orafter the date when the child reachesthe age of 18, 21, or the local age ofmajority; or (ii) the payments arereduced on two occasions within oneyear, before or after another child ofthe payor attains the age of 18through 24. If the payments arereduced under either of these circum-stances an amount equal to the reduc-tion will not constitute alimony butwill instead be treated as non-

deductible child support unless thepresumption is rebutted.

Nevertheless, since the regulationsstate that if the terms of the presump-tion are not met, “reductions in pay-ments will not be treated as clearlyassociated with the happening of acontingency relating to a child of thepayor,” Temp. Reg. section 1.71-1T(c) A18, the presumption has theeffect of creating a safe harbor:reductions outside the presumptionwill not turn otherwise qualifyingalimony payments into non-deductible child support. Therefore, atermination seven months before achild reaches the age of 21 will notresult in recharacterization, but a ter-mination five months prior to theattainment of the same age will resultin recharacterization. Although multi-ple reductions will trigger recharac-terization under the second part oftest, circumstances may necessitatemultiple reductions. When multiplereductions would, but for tax conse-quences, be considered, the partiesmay be able to achieve a better over-all economic result by (i) schedulingonly a single reduction; (ii) foregoingthe second reduction; (iii) calculatingthe present after-tax value of the sec-ond foregone reduction; and (iv)reducing the payee’s share of the netmarital estate by the amount deter-mined under (iii). For example, if theparties would, but for tax considera-tions, schedule a second reduction of$5,000 effective for years six throughten, the reduction could be foregone,and the present after-tax value of$25,000 could instead be subtractedfrom the payee’s portion of the marital estate.

MAXIMIZING BENEFIT OF TAX-FREE TRANSFERS INCIDENTTO DIVORCE

Tax planning opportunities alsoarise in connection with the transferof property to a spouse incident todivorce. Under section 1041, no gainor loss is recognized on the transferof property from an individual to aspouse or former spouse incident todivorce, whether or not the transferor

26945_ABA_Newletter_Summer 8/2/02 11:14 AM Page 12

1 3

PO

IN

TS

T

O

RE

ME

MB

ER

spouse receives consideration for thetransfer. Since no gain or loss is rec-ognized in such transfers, the trans-feree spouse takes a carryover basisin the property. If marital assets con-sist of properties with varyingdegrees of appreciation, equity wouldsuggest that each party receive a mixof property with the same relativedegree of built-in gain. If this is notpossible (e.g., one spouse retains thepersonal residence with a higherbasis), the parties may wish to com-pensate the spouse who takes thelower basis property since that spousewill be required to pay tax on all ofthe gain when the property is sold.

SALES OF PERSONALRESIDENCES

An important planning opportunityinvolving the sale of a residenceshould also not be overlooked: The$250,000 exclusion provided for bysection 121 is increased to $500,000for married couples filing a jointreturn. To preserve the full $500,000exclusion, the couple would berequired to file a joint return. There-fore, it may be prudent for the sale tooccur in a taxable year in which par-ties can still file a joint return.

REV. RUL. 2002-22 AND NOTICE2002-31 CLARIFY THE TAXTREATMENT OF TRANSFERSOF STOCK OPTIONS ANDDEFERRED COMPENSATIONRIGHTS INCIDENT TO DIVORCE

Under the laws of many states, stockoptions and deferred compensationrights earned by a spouse during mar-riage are subject to equitable distribu-tion. The question arises whethersection 1041 will operate to prevent arecognition event when stock optionsor deferred compensation rights aretransferred incident to divorce, andwhether the assignment of incomedoctrine will operate to provide thatthe transferor is taxed on the incomerecognized upon exercise of theoptions or receipt of the deferred com-pensation. In Rev. Rul. 2002-22, theService examined these issues.

In the factual situation presentedin Rev. Rul. 2002-22, Spouse A,employed by Corporation Y, received(i) nonstatutory stock options as partof A’s compensation, and (ii) rights tofuture income from two unfunded,nonqualified deferred compensationplans. With respect to the stockoptions, no amount had been includ-ed in A’s gross income because theoptions did not have a reasonablyascertainable fair market value upongrant within the meaning of Treas.Reg. section 1.83-7(b).

Rev. Rul. 2002-22 first stressedthe breadth of section 1041 and con-cluded that the transfer of the optionsand rights to retirement paymentswere not taxable events. The Servicereached this conclusion despite thefact that normally, under section 83,the exercise or arm’s length disposi-tion of a nonstatutory stock optionresults in income inclusion to theextent the fair market value of thestock subject to the option exceedsthe price paid. While recognizing thatthe transfer of stock options pursuantto divorce might well be consideredan “arm’s length disposition,” the rul-ing declined to hold that the transferof such options resulted in income tothe transferor.

That conclusion did not resolvethe question of who would be taxedupon exercise of the options orreceipt of the retirement payments.Although the assignment of incomedoctrine ordinarily imposes tax onthe person who earned the income,“the courts and the Service have longrecognized that [the doctrine] doesnot apply to every transfer of futureincome rights.” Applying the assign-ment of income doctrine in the con-text of divorce, the Serviceconcluded, would be “inappropriate”because it would be inconsistent withthe policy behind section 1041.Therefore, the Service concluded thatthe non-employee spouse would rec-ognize income at the time the optionswere exercised. The Service alsofound that the ownership rightsacquired by the non-employee spousewould yield income to the transferee

non-employee spouse under section83(a) of the same character and to thesame extent as if that non-employeespouse had been the person who pro-vided the services. Similarly, thetransferee spouse would be requiredto include in income amounts real-ized from deferred compensationrights in the taxable year in whichpayments were made (or made avail-able) to the transferee spouse.

Notice 2002-31, 2002-19 I.R.B.908, a companion announcement toRev. Rul. 2002-22, contains a propos-ed revenue ruling that discusses theFederal Insurance Act (FICA) andFederal Unemployment Tax Act(FUTA) consequences of the transfersdescribed in Rev. Rul. 2002-22.

First, the proposed ruling con-cludes that the transfer of nonstatutorystock options and nonqualifieddeferred compensation from anemployee to a non-employee spouseincident to divorce does not result in apayment of wages for FICA andFUTA tax purposes. This is the corol-lary of the result reached in Rev. Rul.2002-22, discussed above.

Second, the proposed ruling con-cludes that, for FICA purposes, whenthe non-employee spouse exercisesnonstatutory stock options, FICA tax will be imposed on that non-employee spouse to the extent thatthe fair market value of the stockreceived exceeds the exercise price ofthe option. According to the Service,this result is required because “noth-ing in section 1041 excludes pay-ments to a person other than anemployee from wages for purposes of FICA.” Moreover, the proposedruling holds that because the com-pensatory interests transferred undersection1041 to the non-employeespouse remain taxable for employ-ment tax purposes, the income recog-nized by the non-employee spouse isremuneration for employment andwages for purposes of income taxwithholding under 3402. The pro-posed ruling states that FUTA taxa-tion issues will be treated in amanner similar to that provided forFICA issues.

26945_ABA_Newletter_Summer 8/2/02 11:14 AM Page 13

PO

IN

TS

T

O

RE

ME

MB

ER 1 4

Rev. Rul. 2002-22 is prospective.Until November 9, 2002, an impor-tant planning opportunity exists withrespect to both existing and newcourt orders and agreements. Withinthis narrow window of time, itappears that divorcing spouses mayelect whether the transferor or thetransferee will report income uponthe actual or constructive receipt ofdeferred compensation or the exerciseof nonstatutory stock options. Theruling effectively creates this electionby providing that the Service willapply assignment of income princi-ples to treat income attributable to aninterest in nonstatutory stock optionsand unfunded deferred compensationrights (or similar intangible rights) asgross income of the transferor pro-vided: (i) the options or rights weretransferred pursuant to a divorce; (ii)the transfer was required by a provi-sion of an agreement or court order;(iii) the agreement or court orderrequires that the transferor reportsuch income and that such income isshown to be reported; and (iv) theprovision or order precedes the dateof November 9, 2002.

To illustrate: Assume that divorc-ing spouses are structuring a divorceagreement to be executed prior toNovember 9, 2002. As part of theagreement, spouse X is to transfernonstatutory stock options to spouseY on December 31, 2002. The trans-fer of these options is not a taxableevent under prevailing law; nor doesRev. Rul. 2002-22 alter that result.However, Rev. Rul. 2002-22 affordsparties the opportunity to designate inthe agreement (or the court may des-ignate in its order) whether spouse Xor spouse Y shall be responsible forreporting income attributable to theexercise of the stock options. Recallthat as a result of companion Notice2002-31, the person responsible forreporting income will also berequired to pay applicable FICA and FUTA taxes as well.

Note that the application of theassignment of income doctrinerequires several affirmative steps: ifan existing or new agreement (or

court order) omits even one require-ment, e.g., that the provision be con-tained in the agreement or court orderbefore November 9, 2002, the resultwill be that the transferee will betaxed when the options are exercisedor the compensation is received.(Query what result would obtain ifthe agreement made all appropriatereferences to the required transfer,and to the transferor reporting theincome, but the document was notexecuted (or the Judge failed to signthe order) before November 9, 2002.In this case, although the transferormight be contractually required toreport income upon exercise of theoptions (or receipt of the income), thetransferee would be required to reportthe income as a federal tax matteraccording to the ruling.)

Note also that parties to an exist-ing agreement (or court order) mayalso be able to avail themselves ofthe “election” provided by Rev. Rul.2002-22 until November 9, 2002. Forexample, assume parties to an agree-ment (or court order) dated January1, 1990 provided for the transfer ofnonstatutory stock options onDecember 31, 1999. Although notcrystal clear, the ruling appears toprovide that parties even to thisagreement may amend the agreementto comply with requirements whichwould result in operation of theassignment of income doctrine uponexercise (or receipt) and the attendanttax liability to the transferor.

CONCLUSION

Careful tax planning between divorc-ing spouses can result in a loweroverall tax burden if a significant taxrate bracket differential exists.Section 71, which governs alimonypayments, now gives divorcingspouses considerable flexibility instructuring support obligations. Bystructuring agreements to continuebeyond a contingency which wouldnormally terminate support obliga-tions, divorcing spouses may resolvedifficulties associated with illiquidmarital estates. If parties contemplatethat payments should diminish as

children mature, the regulations pro-vide a safe harbor preventing theapplication of section 71(c), whichwould otherwise operate to precludethose amounts from being treated as alimony for federal income tax purposes.

The tax rule that no gain or loss isrecognized when property is trans-ferred between spouses incident todivorce also requires a careful plan-ning eye. For example, a party trans-ferring low-basis property might berequired to compensate the otherspouse for the built-in gain.

Finally, recently issued Rev. Rul.2002-22 and Notice 2002-31 providea blueprint for tax planning wheredivorcing spouses contemplate thetransfer of nonstatutory stock optionsor rights to nonqualified deferredcompensation. Henceforth, the recipi-ent spouse will be taxed when theoptions are exercised or the deferredcompensation is received. However,until November 9, 2002, parties to anew or an existing agreement mayelect to tax the transferor—evenmany years later—if certain technicalrequirements are met. This tax treat-ment is accomplished by virtue of the application of assignment ofincome principles.

After November 9, 2002, whenassignment of income principles willno longer apply, the transfer of non-statutory stock options and deferredcompensation will result in income tothe transferee when the options areexercised or the income is received.Moreover, but the transferee will alsobe treated as the employee for FICAand FUTA employment tax purposes.This result also illustrates the reachof section 1041, which provides fornonrecognition with respect to trans-fers between divorcing spouses.Since the transferee spouse may nothave expected to pay income oremployment taxes upon the exerciseof stock options or receipt of deferredcompensation, the tax implications ofthe transfer could affect the terms ofthe overall agreement. �

26945_ABA_Newletter_Summer 8/2/02 11:15 AM Page 14

1 5

SP

EC

IA

L

RE

PO

RT

FEDERAL TAXCOLLECTION TRUMPSRIGHTS ACCORDEDBY STATE PROPERTYLAWS: FEDERAL TAXLIEN ATTACHES TOENTIRETIES PROPERTY

by Bernice J. Koplin,Philadelphia, PA

In United States v. Craft, 122 S. Ct.1414 (April 17, 2002), the

Supreme Court held that eachspouse’s interest in property held astenants by the entirety constitutes“property” or “rights to property” towhich a federal tax lien may attach.Craft thus stands for the propositionthat a federal tax lien for onespouse’s tax liability attaches toentireties property, and furthers atrend to subjugate state law fictions tofederal tax law in connection with thecollection of federal taxes. Althoughthe case left open the question of val-uation of such interests, Craft is sig-nificant both within and outsidefederal tax law.

First, Craft not only shows thatentireties property is not imperviousto attachment in satisfaction of thedebts of one of the owners, but alsocements a trend in this regard.Second, Craft suggests that partner-ships may be more desirable vehiclesfor holding property if asset protec-tion is a goal. In addition, theSupreme Court’s opinion in Craftraises significant issues which arebeyond the scope of this SpecialReport. Those include includewhether the principles enunciated bythe Court in Craft apply equally to allforms of property, real and personal,in states that have adopted some formof a multiple party account act;whether the Court’s shift away fromthe traditional protection of the fami-ly home for the stay-at-home spouse(Dissent, Scalia, Slip Opinion at 1)may have been addressed sufficiently

by the recent provisions in favor ofthe “innocent spouse,” and whetherthere is any potential impact on thedisclaimer of interests in entiretiesproperty as part of a married couple’sestate planning.

Craft is procedurally complicatedbecause it resulted from an appeal ofa case that went to the Court ofAppeals for the Sixth Circuit twicebefore reaching the Supreme Court,and because both Sixth Circuit deci-sions were divided. By contrast, thefacts of the case are simple. After aNotice of Lien was filed and in con-nection with their divorce, Don andSandra Craft jointly executed a quit-claim deed whereby Don purportedto transfer to Sandra his interest in apiece of Michigan real property thatthe two of them had owned as tenantsby the entirety. It was Don’s interestin that property that was at issuebecause Don failed to pay federalincome tax liabilities assessed againsthim and a federal tax lien attached tohis “rights to property” under section6321. Section 6321 is the general ruleof attachment, and provides that theunpaid amount of tax (after theService issues a notice and demandand the taxpayer fails to pay), includ-ing interest, penalties, and costs“shall be a lien in favor of the UnitedStates upon all property and rights toproperty, whether real or personal.”

Tenancy by the entirety is a formof ownership available only to mar-ried individuals, and pursuant to itownership is considered to be vestedin the marital unit “as if they were asingle personality.” See, e.g., Raffaelev. Granger, 196 F.2d 620, 622 (3rdCir. 1952). Accordingly, such proper-ty is not considered to be ownedexclusively by either spouse. In themajority of states that recognizeentireties ownership, neither spousehas a separate or severable interestthat can be reached by creditors, andbefore the Supreme Court’s decisionin Craft, it was the accepted wisdomthat federal tax liens could not gener-

ally attach in such states until theentireties form of ownership was bro-ken. See, e.g. Internal RevenueService v. Gaster, 42 F. 3d 787, 791(3d Cir. 1994)(despite propriety oflevy, Delaware law prohibited theService from using funds from anaccount held as tenants by the entire-ty to satisfy tax liability of onespouse); Raffaele, supra, (accountheld as tenants by the entirety underPennsylvania law renders ineffectivethe Service’s attempt to deal sepa-rately with or dispose of the interestof one spouse in derogation of theother spouse’s ownership of the entireproperty). Even under the minorityrule, the lien would attach, but theService had to wait to collect on thelien until the death of one of thespouses. See, e.g., United States v.Avila, 88 F.3d 229 (3d. Cir. 1996)(federal tax lien attaches to taxpayer-spouse’s life estate and right of sur-vivorship in the subject entiretiesproperty and if taxpayer-spouse predeceases nontaxpayer spouse,lien is extinguished), citing Freda v. Commercial Trust Co., 118 N.J. 36 (1990).

When Sandra wanted to sell theproperty the Service agreed to releasethe lien and allow her to sell theproperty, but required that half thenet proceeds be held in escrow pend-ing determination of the Govern-ment’s interest in the property. Dondied during the pendency of thesevarious proceedings, and Sandrabrought an action to quiet title to theescrowed proceeds. The DistrictCourt granted summary judgment for the government, holding that thefederal tax lien attached to Don’sinterest in the tenancy by the entiretyat the moment of transfer to Sandra,and that the transfer to the buyerswas invalid as a fraud on creditors.Craft v. United States, 94-2 U.S. TaxCas. (CCH) P50493 (W.D.Mich.1994). The parties cross-appealed, Sandra challenging the lienand the Service challenging the

SPECIAL REPORT

26945_ABA_Newletter_Summer 8/2/02 11:15 AM Page 15

SP

EC

IA

L

RE

PO

RT 1 6

amount of the invalid transfer. Amajority of the Sixth Circuit panelreversed on the issue involving thefederal tax lien, holding that no lienattached because Don had no sepa-rate interest, or any severable futureinterest, in the entireties propertyunder Michigan law, and remandedthe case to the District Court on theissue of the fraudulent transfer. Craftv. United States, 140 F.3d 638, 644(6th Cir. 1998)(hereinafter “Craft I”).

On the fraudulent transfer issue,the court held that Don Craft’s actionof paying the mortgage while insol-vent had effectuated a type of fraudu-lent conveyance under Michigan lawbecause the payments had placednon-exempt funds beyond the reachof a creditor (the Service), thusenhancing the value of the entiretiesproperty by the amount of the pay-ments. 233 F.3d at 371-372.Nevertheless, both the District Courton remand, 65 F. Supp. 2d 651, 657-659 (W.D. Mich. 1999), and theSixth Circuit, 233 F.3d 358, 370 (6th

Cir. 2000)(hereinafter “Craft II”),later concluded that since the federaltax lien could not attach to the prop-erty under Michigan law, then payingthe mortgage on it could not consti-tute a fraudulent conveyance. Thisresult was described by the SupremeCourt as “somewhat anomalous” inlight of its holding, which empha-sized that in future cases this ques-tion would undoubtedly be answereddifferently. Slip Opinion at 14-15.

Although Michigan considersentireties property to be a form ofsingle ownership and characterizesits tenancy by the entirety as creatingno separate or severable individualrights except survivorship, theSupreme Court, validating theDistrict Court and the concurrencesin both Sixth Circuit decisions, deter-mined that each spouse had manyother kinds of rights under Michiganlaw in addition to survivorship. Ineffect, the Court found that the tenan-cy gave each spouse a bundle ofsticks, not just one stick. While theCraft court did not address directlythe question whether rights heldunder a state’s law which gives the

spouse only the right of survivorshipwould also qualify as “property” or“rights to property” under section6321, it would be consistent with theSupreme Court’s holding that if aspouse has at least one property“stick,” such spouse has “rights inproperty” within the meaning of sec-tion 6321, and that the bigger thebundle of “sticks,” the more valuablethe bundle of rights should be. Theemphasis by the Craft Court on aspouse’s “rights in property” utilizedand thus validated the analysis of theDistrict Court, which had initiallydetermined that the lien did not attachto the property per se, but insteadattached to the spouse’s “rights inproperty,” 65 F. Supp. 2d at 651.

The dissent in Craft I had correct-ly pointed out that the majority ofthat panel had erred by accepting atface value Michigan’s description ofthe property interests held by a tenantby the entirety, rather than looking atthe substance of those interests. Theconcurring judge in Craft I had chal-lenged the majority’s reversal of theDistrict Court by agreeing with theDistrict Court that the legal land-scape in Michigan had changed since1971 and that the case of Cole v.Cardoza, 441 F.2d 1337, 1343 (6thCir. 1971)(federal tax lien againstindividual taxpayer cannot attach toproperty held by that individual as atenant by the entirety), upon whichthe majority relied, was antiquatedbecause it did not assure the collec-tion of federal taxes. 140 F. 3d at645. In describing this change inlegal landscape, the District Courtand the concurring judge in Craft Irelied upon United States v. NationalBank of Commerce, 472 U.S. 713,105 S. Ct. 2919, 2924, 86 L.Ed.2d565 (1985)(Service can levy on thejoint accounts of a delinquent taxpay-er even though state law did notallow ordinary creditors to do so),and emphasized that this changedlegal landscape was intended to facil-itate the collection of federal taxesdespite state laws that might frustrateother types of creditors. When thecase returned to the Sixth Circuit onthe issue of the lien attachment, the

Government argued that the SupremeCourt’s intervening decision in Dryev. United States, 528 U.S. 49, 120 S.Ct. 474 (1999) should cause thepanel to reconsider the result in Craft I. See also, Brett A. Bluestein,Disclaimers and Federal Tax Liens’Effect on Inheritances, 36 REAL

PROPERTY, PROBATE AND TRUST

JOURNAL 391 (2001), ClaudioOrsorio, Disclaimer of Intestate’sEstate Under Arkansas Law CannotPrevent Attachment of Federal TaxLien: Drye v. United States, 53 TAX

LAWYER 951 (2000).Nevertheless, the determination

that no federal tax lien attached to theentireties property was, according tothe majority in Craft II, the law of thecase which it could not reverse.Because the majority of the SixthCircuit in Craft II believed that it wasboth constrained by the law of thecase and the law of the Circuit, andthat the government was wrong, it dis-missed the Government’s claim and,in Craft II affirmed its decision inCraft I. The concurring judge in CraftII correctly pointed out that Craft Ihad reached the wrong result becausethat result was inconsistent withSupreme Court precedent, includingDrye, and that the Sixth Circuitshould have reversed Craft I. The con-curring judge emphasized his positionby paraphrasing language from Dryeand stating that he “believed that themajority in Craft I was ‘struck blind’by Michigan’s ‘legal fictions.” 233F.3d at 376. The Supreme Court’sreversal of the Sixth Circuit’s decisionin Craft II shows that the SupremeCourt refused to be “struck blind” inconnection with federal tax liens. Asthe Court itself explained, by decidingas it did it eliminated a perceivedabuse detrimental to the collection offederal taxes.

The Supreme Court’s analysis inCraft was consistent with the two-step analysis it had described inDrye. That analysis requires an initialdetermination of the state-definedrights the taxpayer has in the proper-ty the government seeks to attach,followed by an application of federallaw to determine whether such state-

26945_ABA_Newletter_Summer 8/2/02 11:15 AM Page 16

1 7

SP

EC

IA

L

RE

PO

RT

defined rights qualify as “property orrights to property” under section6321. (See 120 S. Ct. at 481, 528U.S. at 58). Accordingly, in Craft theCourt first looked to Michigan lawand found that Michigan law gives anindividual spouse, among otherrights, the right to use the entiretiesproperty, the right to exclude othersfrom it, the right of survivorship, theright to become a tenant in commonwith equal shares upon divorce, theright to sell the property with theother spouse’s consent and to receivehalf the proceeds from such a sale,the right to encumber the propertywith the consent of the other spouse,and the right to block the otherspouse from selling or encumberingthe property unilaterally. The Courtthen determined that the rights grant-ed to a spouse under Michigan lawqualify as “property” or “rights toproperty” under section 6321, SlipOpinion at 8, because the broad statu-tory language authorizing the tax lien“reveals on its face that Congressmeant to reach every interest in prop-erty that a taxpayer might have,” cit-ing United States v. National Bank ofCommerce, 472 U.S. at 719-720, thepurpose of which was to assure thecollection of taxes, id. at 8, citingGlass City Bank v. United States, 326U.S. 265, 267 (1945). The Court rea-soned that a Michigan spouse’s sub-stantial degree of control over theproperty was sufficient to justifyattaching a federal tax lien to it, citingDrye v. United States, 528 U.S. 49(1999), and that a spouse’s ability uni-laterally to alienate the property wasnot required for the attachment of afederal tax lien, citing United States v.Rodgers, 461 U.S. 677 (1983).