Embed Size (px)

Citation preview

1

Livestock, Liberalization and Trade Negotiations

in West Africa

PN. Dieye1, G. Duteurtre 2, JR Cuzon 3, D. Dia 4

Communication (Full Paper) to the 1st Inaugural Symposium of the African Association of Agricultural Economics(AAAE), Nairobi, 5-9 December, 2004

Abstract

West Africa is shifting towards an increasing liberalization of agricultural markets. This trends will continue in the context of current trade negotiations at WTO and between the European Union and ACP countries. The objective of this paper is to assess the impact of these negotiations on the livestock sector in the region. Livestock systems, in spite of their weak technical level, are strongly integrated to markets, especially by cattle, milk, poultry and pork marketing. The liberalization has an important impact on national livestock sub-sectors, especially in dairy and poultry sub-channels. Imports of poultry meat increased for example from 500 to 17000 tons between 1996 and 2002 in Senegal. Evolutions are similar in Ghana and Ivory Coast. The dairy sub-sector has been in competition with milk powder imports for years, but this competition seems limited by market segmentation, which explains good prospects for the local milk production. In addition, powder milk has been playing a significant role in the setting up of a local dairy industry. African countries should invest in trade negotiations more in depth in order to better use tariffs barriers (lists of products of reference, anti-dumping measures, etc.), and to better manage sanitary regulations. It is therefore necessary to increase national capacities i.e., power of negotiation of administration services and to encourage national and regional research networks working on domestic and regional markets analysis.

Key-Words : West Africa, World Trade, Livestock Agriculture, Markets.

1 Chercheur au Centre de Recherches Zootechniques (CRZ) de l’Institut Sénégalais de Recherches Agricoles (ISRA), BP 53, Kolda, Sénégal ([email protected])2 Chercheur au Cirad, actuellement détaché au Ministère des Affaires Etrangères (France), en poste au Bureau d’Analyses Macro-économiques de l’ISRA (ISRA-BAME), BP 3120, Dakar-Bel Air ([email protected])3 Expert à la Plateforme d’appui au Développement Rural en Afrique de l’Ouest et du Centre, S/C UNOPS, BP 15 702, Dakar-Fann ([email protected])4 Doctorant en géographie à l’Université Cheikh Anta Diop en poste au Bureau d’Analyses Macro-économiques de l’ISRA (ISRA-BAME), BP 3120, Dakar-Bel Air ([email protected])

2

Introduction

West Africa represents nowadays a market of 220 millions consumers. Demographic

projections show that this population is going to reach 350 millions in 2020 (FAO, 2004).

This increase of the population will be coupled with a very strong urbanization. The coastal

zones will constitute main demographic concentratio zones with an urban population of nearly

60 % in countries like Ivory Coast, Nigeria and Senegal. A mattering issue concerns the

satisfaction of the population needs and the supply of the urban areas which will continue to

be important poles of consumption. As regards to the markets of animal products, the

literature underline that these demographic changes will lead to fast and deep modifications of

the livestock systems and of marketing chains within the framework of the livestock

revolution (Delgado and al. 1999). Because of the high revenu elasticity of animal products,

the challenges of the livestock sector are very important for West Africa. Indeed, the gap

between demand and supply is important for various animal products, particularly for milk

and poultry meat. The levels of satisfaction of milk are from 60 to 70 % for Sahelian countries

and from 8 to 50 % for the coastal countries (Balami, 2004). Imports therefore contribute

strongly to the supply of domestic West African markets.

This paper analyzes current dynamics and issues in development of the livestock sector in

West Africa in the context of liberalization and international trade negotiations.

Material and methods

The analysis of the trade negotiations issues on the livestock sector in West Africa leans on

three sources of information. First, the use of the FOA-stat statistical databases and other

various information from FAO allow a general analysis of the importance of livestock in West

3

Africa, of the organization of the livestock sub-sector and of the intra zones and extra zone

exchanges. Second, statistical data from WAEMU, ECOWAS, and European Commission,

coupled with recent regional commissioned studies bring interesting elements on the expected

impact of current negotiations. Third, various secondary data but also published

bibliographical resources give key elements on livestock in West and Sub-Saharan Africa, on

the exchanges of the animal products, and on the implications of trade negotiations for West

Africa zone.

This statistical and bibliographical informations was completed by case studies led on the

impact of the imports surges on local production : case of the dairy production in Senegal and

case of the poultry sector in Senegal, Ghana and Ivory Coast.

Results and discussions

1. Livestock in West Africa : a sector strongly integrated into markets

West Africa is characterized by a wide variety of agro-ecological zones influencing very

strongly the various livestock systems and the organization of animal commodity chains. The

mobile pastoral systems in the Sahelian zones with important potentialities in term of cattle

trade contributes to the supply of the coastal areas where agro-pastoral sedentary and

intensive peri-urban systems take place. The livestock commodity chains benefit from agro-

pastoral complementarities between the agro-ecological zones. Sahelian Countries as Mali,

Burkina Faso and Niger contribute strongly to the supply in meat and cattle of coastal

countries as Nigeria and Ghana which, in return assure their supply in cereals.

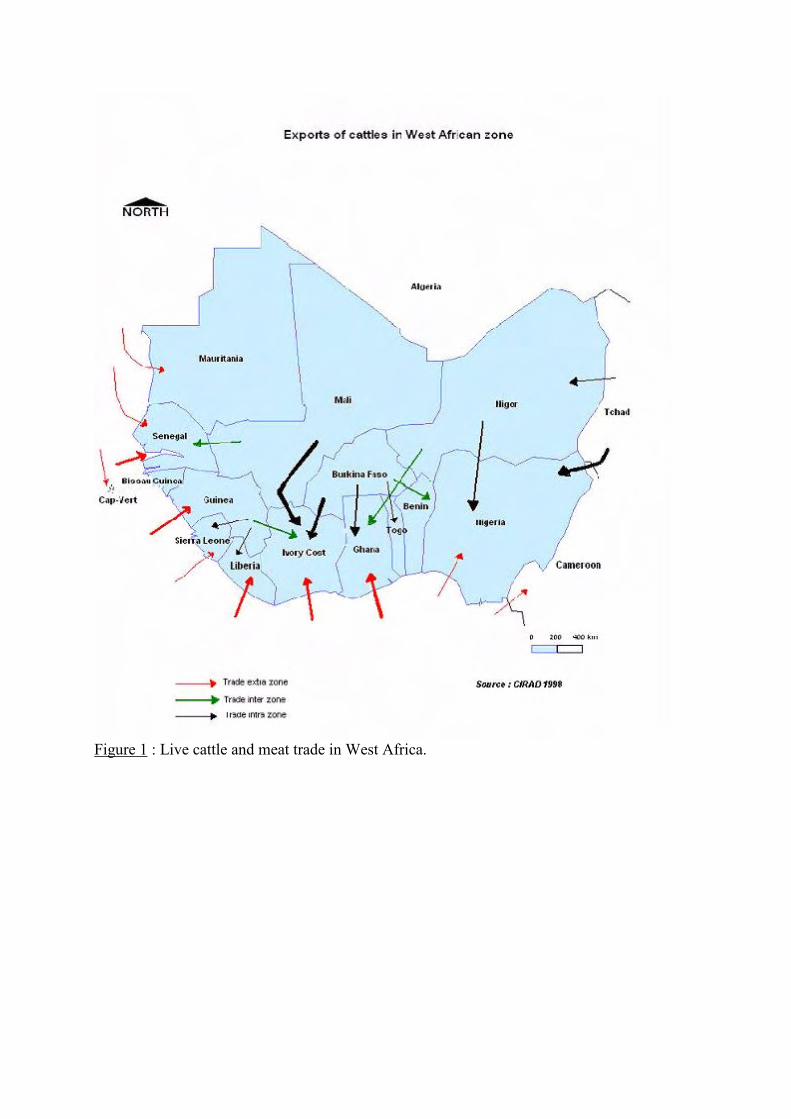

The exchanges of animal products essentially consist of live animals (cattle and small

ruminants), poultry and poultry meat, leather and skins. The organization of intra zone trade

4

show the importance of the flows of the Sahelian countries towards the coastal countries

(Figure 1).

Figure 1 : Live cattle trade in West Africa.

The intra zone trade of live cattle refers to three types of marketing channels (Akakpo and al.

1999). The " central corridor" zone : animals leave Mali and Burkina to supply Ivory Coast,

Ghana, Togo and in a lower extent Benin. The " Nigeria " zone : animals come from Chad,

Niger, Sudan, Centrafric Republic and additionally from Mali and Burkina to supply

Cameroon, Nigeria, Benin and Togo. The "west littoral" zone : animals leaving Mauritania

and Mali, to supply Senegal, Gambia and Guinea Bissau.

There is a very strong polarization of live animals trade towards the urban areas of the coastal

countries in relation of their demographic weight but also to the economic power of these

countries in the regional economy. Countries of the Guinea Gulf (Nigeria, Ivory Coast,

Ghana) represent 70 % of the regional GDP. Nigeria and Ivory Coast constitute two very

important trade poles in the region. More than 80 % of the whole cattle exported by Burkina

and Mali is intended for the Ivory Coast market (Perret, 2004).

The economic and social networks play a highly important role in the intra regional trade.

Indeed, various organizations refer to the same economic group shaped with the cross-border

networks where business and finance are strictly connected (Grégoire, 2004).

These networks involve also in the extra regional trade of animal products which is less

important. The most important exchanges concern the exports of camels from Niger towards

North Africa. The exports of skins of small ruminants towards the European Union in 2002

represented respectively 20.6 % and 31.4 % of the total of the agricultural exports of Burkina

5

Faso and Benin (Pricewhaterhousecoopers, 2004). But the extra regional trade is dominated

by imports of animal products from the European Union.

2. The current dynamics of animal products trade

2.1. The increasing opening of markets in imports

The liberalization of West African agricultural markets introduced in the 80s with the

Structural Adjustment Programs continues with the intensification of the regional integration

by the adoption of the Common External Tariff (CET) in West African Economic Monetary

Union (WAEMU) zone in January, 2000 and the current CET negotiation in Economic

Community of West African States (ECOWAS). The current trade negotiations concern the

Agricultural Agreement at World Trade Organization (WTO) as well as negotiations of free

trade agreements between European Union and ACP Countries (Economic Partnership

Agreements -EPAs). Most West African countries are members of WTO (except Cap Verde

and Liberia), signers of the Cotonou Agreement and eligible in the advantages offered by the

Africa Growth and Opportunity Act (AGOA) (except Burkina Faso, Liberia, and Togo). They

are for the greater part classified among least advanced countries with the exception of Ivory

Coast, Ghana and Nigeria. They enjoy also additional commercial preferences, notably

Initiative " All except weapons " of the European Union and the analogue preferential regime

set up by Canada.

Beyond the regional integration policies, the liberalization of West African markets is

strongly related to structural imbalance of livestock sector. With an increasing urbanization of

4.2 % per year in the coastal countries, the current level of livestock productivity does not

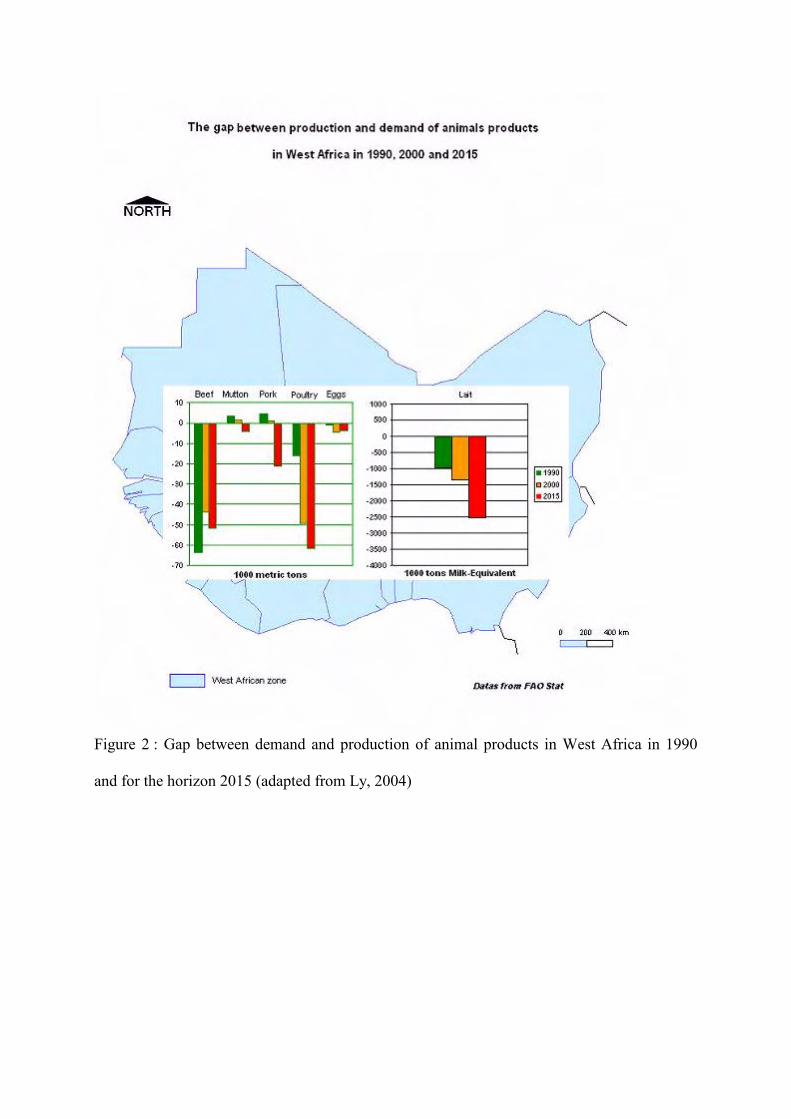

allow regional economies to cover the regional demand. The current imbalance between the

6

demand and the supply is very important notably for milk - 1,359 millions equivalent liter -

and the poultry meat - 49,400 metric tons. Projections on the horizon 2015 show that this gap

will be multiplied by 1.5 for poultry meat, 3 for sheep and 1.8 for milk (Figure 2).

Figure 2 : Gap between demand and production of animal products in West Africa in 1990

and for the horizon 2015

2.2. The imports surges and the disintegration of livestock sector

Current dynamics are shaped in most of West African countries by strong imports surges.

These trends are related to the evolution of consumption patterns in the urban areas of West

Africa brought by the availability of animal products, change of life style but also the rise of

purchasing power of the consumers (Boutonnet and al. 2000, Dia 1997, Duteurtre et al.,

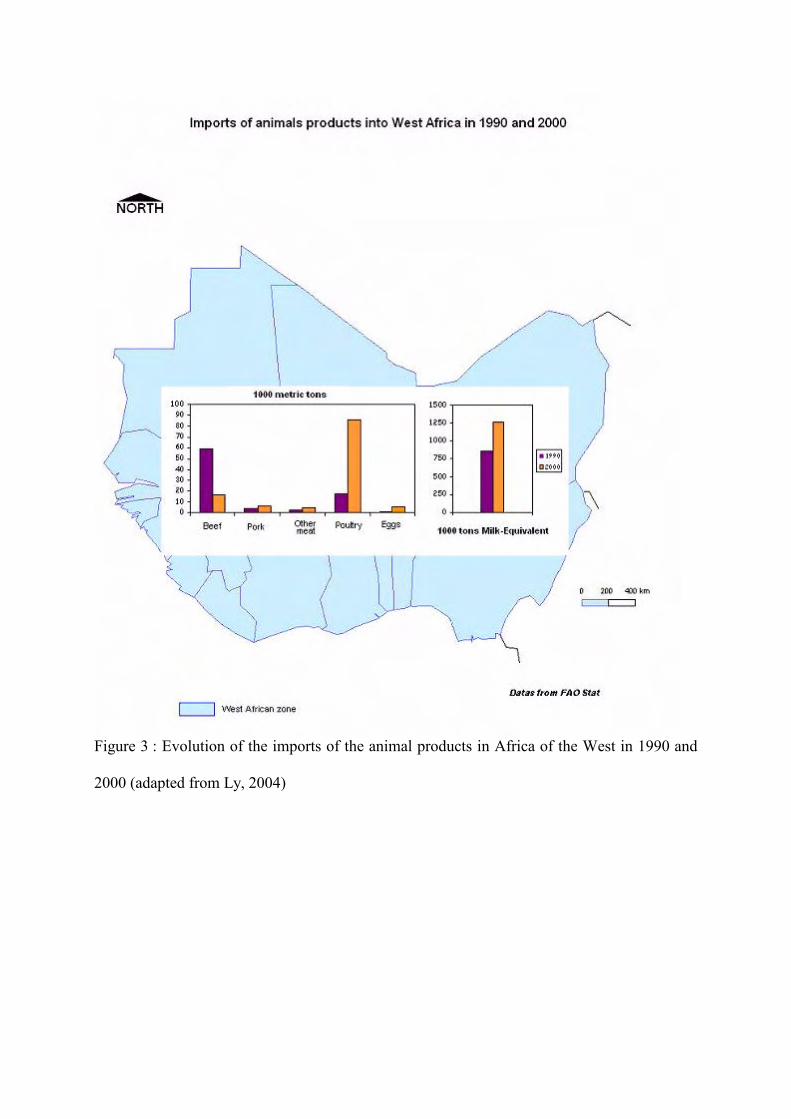

2004). During the decade 1990-2000, imports in West Africa were particularly massive for

poultry which was multiplied by 5, eggs by 7 and milk by 1.5 (Figure 3).

Figure 3 : Evolution of the imports of the animal products in Africa of the West in 1990 and

2000 (Source : FAOSTAT).

The impacts of imports are however more perceptible on the poultry sector and due to its level

of intensification and economical weight. In most West African countries except Guinea

Bissau, the poultry sector contributes to half of the livestock turnover : 49 % in Senegal and

7

Benin, and 56 % in Ivory Coast (UEMOA, 2002). For milk and dairy imports, the trends are

in the long-term and date for the most part of countries in the end of the 70s and the 80s. The

contribution of milk production on the livestock sector turnover is especially important in the

Sahelian countries where it is 40 % in Niger, 38 % in Mali and 32 % in Burkina Faso

(UEMOA, 2002). The market of milk and dairy products is also characterized by a very

strong segmentation due to the big variety of products and food utilization. From the point of

view of imports impact analysis on the local production, markets must be separated in relation

of the transport costs and the market organization different for the type of milk products(Von

Massow, 1989, Duteurtre, 2004)

The imports of poultry meat pieces were particularly massive on the coastal countries as Ivory

Coast, Ghana and Senegal. In Senegal, 86 % of the poultry imports are frozen pieces (legs and

wings) and the rest is whole chickens. The European Union contribute at 72 % of the poultry

imports and the rest comes from Brazil and United States (Duteurtre and al. 2004).

Poultry imports increased by 110 % in Ghana passing from 11,000 tons in 2001 to 23,100

tons in 2002. Situation is similar in Senegal with 7,900 tons in 2001 and 16,600 tons in 2002.

In Ivory Coast, the increase of imports was 44 % between 1998-1999. According ANOPACI

(2004), imports spent then from 2,840 tons in 2000 to 15,400 tons in 2003. This sudden

imports surges was also reported in the other countries of Africa notably in Cameroon where

they are crossed from 447 tons to 1996 to11,424 tons in 2002 (Takam and Nkamela, 2004).

Except the important demand and the low prices for poultry imports, the application of the

CET and the harmonization of the Value Added Tax (VAT) in the WAEMU zone constitute

favoring factors in Ivory Coast and Senegal.

Indeed, poultry legs and wings are industrial by-products in Europe, with low production

costs, due to the good valorisation of the breast but also due to the decrease of feed costs with

the reform of the cereal sector in Europe. The application of the CET lowered imports taxes

8

from 55 % before 1998 (Ly, 001) to 20 % in Senegal (Duteurtre et al., 2004). Negative effects

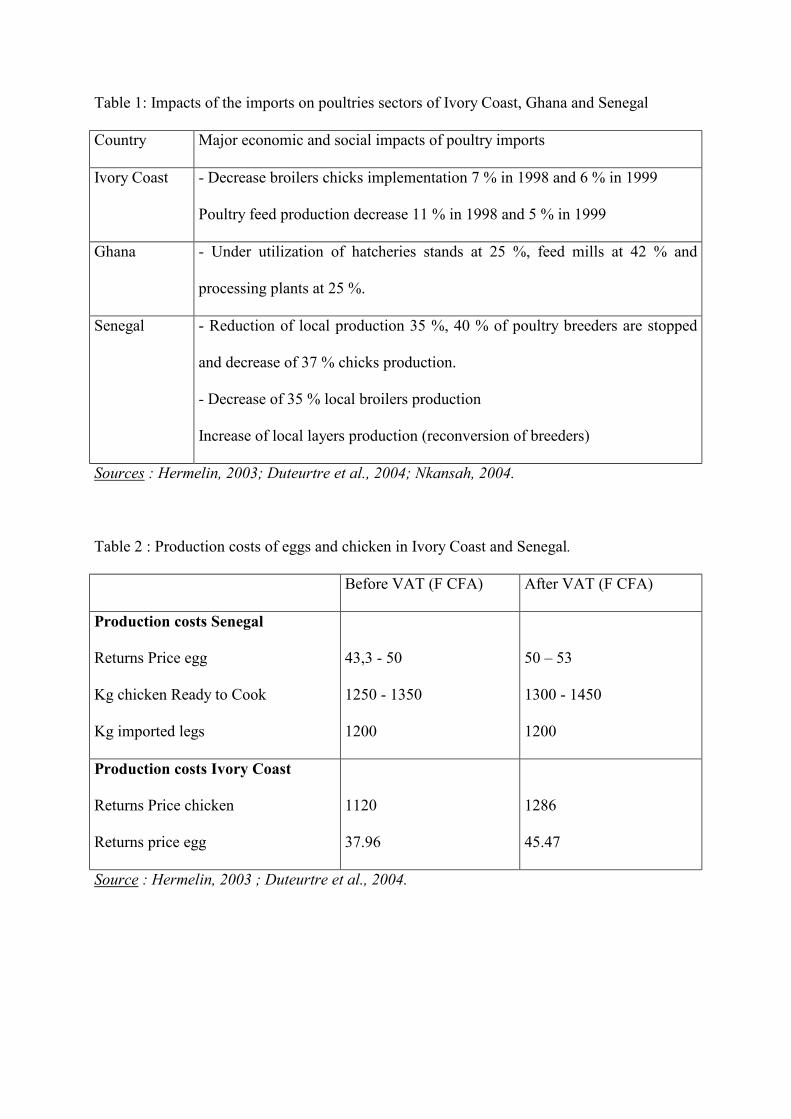

in local poultry are relative to economic and social costs (Table 1).

Table 1: Impacts of the imports on poultries sectors of Ivory Coast, Ghana and Senegal

In Ivory Coast, the implementation of the broilers chicks decreased from 7 % in 1998 to 6 %

in 1999 whereas the poultry feed production decreased respectively from 11 % to 5 % for the

same periods (Hermelin, 2003). In Ghana, poultry imports unfair competition had wasteful

under-utilization of poultry facilities in the country : utilization of hatcheries stands at 25 %,

feed mills at 42 % and processing plants at 25 % (Nkansah, 2004). In Senegal, the reduction

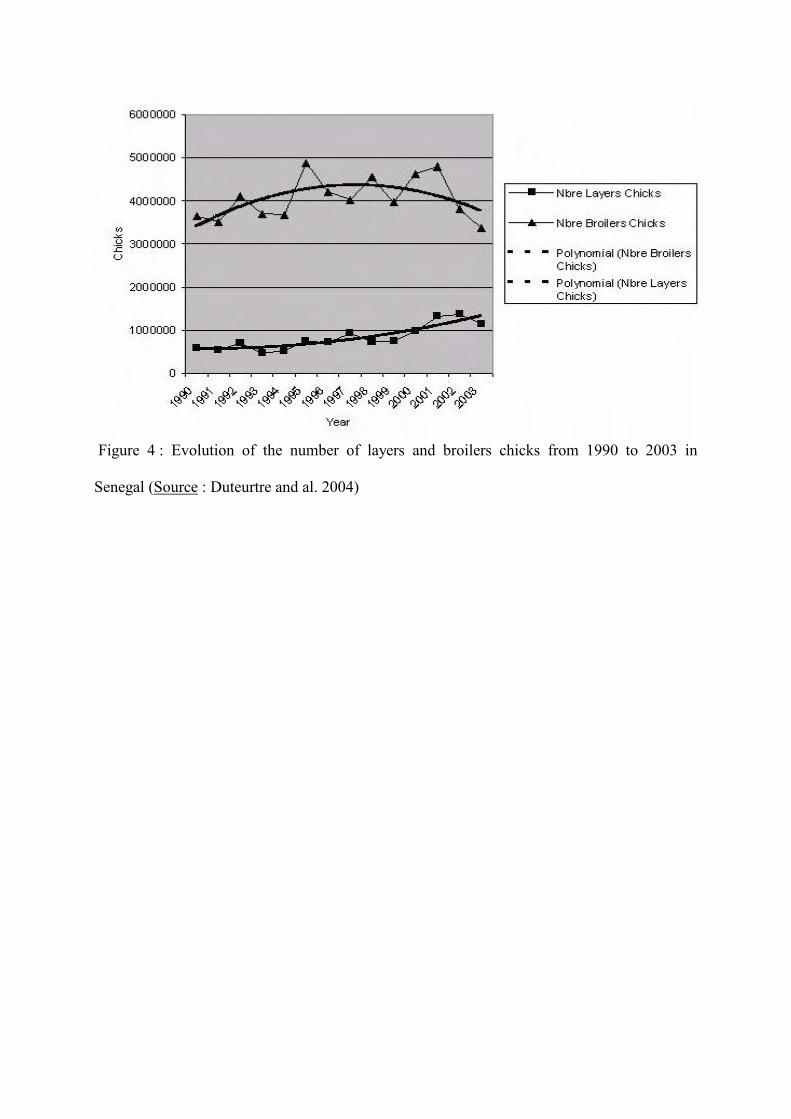

of the broilers production can be estimated to 30% in those 2 last years for the benefit of a

changeover in the layers production (Figure 4).

Figure 4 : Evolution of the number of layers and broilers chicks from 1990 to 2003 in Senegal

(Source : Duteurtre and al. 2004)

Impacts are also related to the increasing of market segmentation. The local broilers and local

farm chickens “poulet du pays” cost more than imported chickens. Price differential is due to

the relatively higher production cost of the local broiler meat notably the cost of feeds and

chicks. In Senegal and in Ivory Coast, the harmonization of the VAT with respective rates of

18 and 20 % created additional costs of inputs and the increase of poultry products returns

prices (Table 2). The application of the VAT in the poultry sector was so suspended in

9

Senegal in October 2002 and in Ivory Coast, the cattle feed was exempted from VAT since

October 2000.

Table 2 : Production costs of eggs and chicken in Ivory Coast and Senegal.

Those differences in costs of production lead to the necessity to differentiate local products

with specific quality signs in order for the local poultry sector not to be affected negatively. In

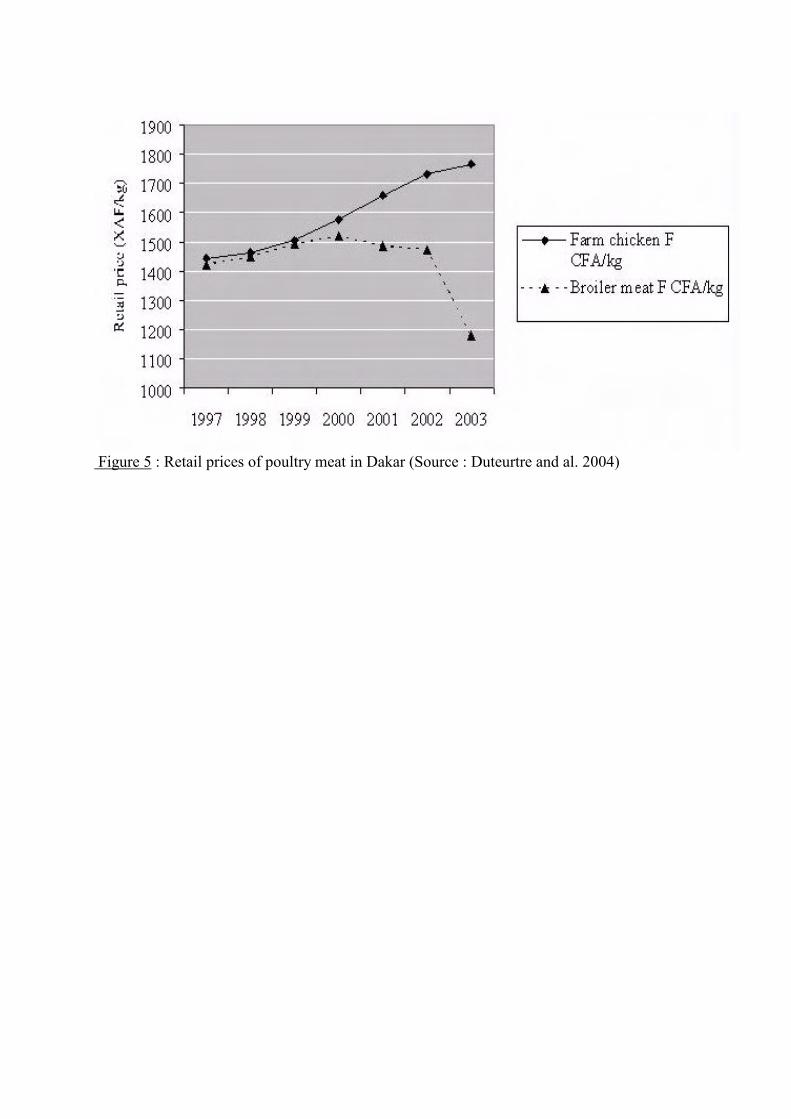

Senegal for exemple, in spite of the low price for the imported chickens due to the lower

imports and wholesale prices (542 F CFA on Gambian border and 1083 F CFA in Dakar), the

price for the local farm chicken (" Poulet du pays ") continues to grow (Figure 5).

Figure 5 : Retail prices of poultry meat in Dakar (Source : Duteurtre and al. 2004)

The market segmentation constitutes an important factor of valorization of the local

traditional domestic products and a mean for the improvement of its competitiveness.

Positive impacts of imports are related to public resources. The taxes generated by dairy

products and poultry imports in Senegal increased respectively by 77 % and 115 % spending

from 6.6 billions in 2000 to 11.7 billions in 2003 for dairy products and from 352 millions to

5 billions during the same period for poultry meat (Duteurtre and al. 2004). The positive

impacts also concern the concentration in the poultry sector allowing more professionalism

for a better organization and efficiency to cover the consumer’s demand.

The import surges in West Africa show the vulnerability of livestock local markets with the

liberalization. Indeed, the competition is often biased because of subsidized inputs European

10

and American markets,. In this context, producers organizations and NGOs often speak about

“dumping” as expressed by Mr Adjei Henaku, Executive Secretary of the Ghana Poultry

Farmers : " It is extremely difficult to figure how the dumping of cheap poultry parts-like,

legs, wings, necks that have no markets in the EU anyway, could be permitted in the name of

free trade that is supposed to promote competitiveness ".

Multilateral and bilateral commercial negotiations constitute a major issue for the small

farmers in West Africa for whom livestock activity is highly integrated to markets, but in the

same time plays an important role in the food security and welfare of the family.

According to Ndiogou Fall of the West Africa Network of the Farmers Organizations and

Producers ( ROPPA) " the farmers are there also to ask that subsidized exports do not come

to destabilize internal markets of the other countries " (Pigeaud, on 2003)

3. Trade perspectives in the livestock sector

3.1. International trade negotiations and construction of the regional economic

community in West Africa

Until 1986, agriculture (including livestock) was excluded from international trade

negotiations led within the framework of the General Agreement on Tariff and Trade

(GATT). Agriculture was considered as an sector of second importance, being even able to

benefit from a strong protection on borders and from an important political and financial

support. Agricultural policies in United States and in Europe have had an impact on the fast

and important development of their livestock sector, but have generated surplus which were

more and more difficult to sell on the international markets. For this reason, agriculture was

introduced into negotiations within the framework of the Uruguay Round, which ended in

11

1994 by the signature of the Marrakech Agreements in specifying the followings : reduction

of export subsidies, facilitation of market access by the transformation of the non tariff

barriers to customs duties and by the reduction of consolidated tariffs, introduction of

disciplines in internal supports for agriculture (with the classification of different national

support in 3 "boxes" ) and the reduction of supports creating most distortions and the clauses

on Sanitary and Phytosanitary (SPS) measures.

The Agreement on Agriculture (AOA) provides for the LDC a " Special Differentiate

Treatment " (weaker reduction and over long periods), and a specific mechanisms for sensible

agricultural products by temporarily increase of tariffs in case of strong decline of world

prices or high increase of imports.

The Agreement on Agriculture of WTO has not fundamentally changed the situation

concerning market access for West African countries, of preferential access for their main

export markets. On the contrary, we have been facing important zoosanitary crisis in recent

years (ESB and foot and mouth disease in Europe, Avian Influenza in Asia). Those crises led

to the growing importance of sanitary standards (Codex alimentarius, OIE). Since 1995, 875

announcements of sanitary and phytosanitary measures concerning meat and livestock

products were subjected by 59 countries to WTO and 60 % concern animal health (Kassum

and Morgan, 2004). For West African countries not unhurt to rinderpest and peripneumonia

bovine diseases, the small producers involved in the cattle trade can not reach these markets.

The regional integration, with the implementation of a common external tariff (CET) in

WAEMU zone in the beginning of 2000, has had a significant impact, by a reduction of tariffs

effectively applied to imports, leading to sudden imports surges (case of the frozen chicken in

the Countries of the Golf of Guinea). Regional integration however has had more positive

impacts on the development of exchanges within the sub-region, with in particular the

simplification of procedures (notably customs procedures) and the start of harmonization of

12

standards at a regional level (case of veterinarians products for example). With the

implementation of the CET, the weight of intra WAEMU exports increased from 11.97 % in

1996 to 14.97 % in 2001, while imports are spent from 8.27 % to 11.97 % during the same

period (Pricewhaterhousecoopers, 2004).

3.2. Trade policies, bilateral and multilateral negotiations.

There are numerous current negotiations in West Africa : WTO, EPAs, definition of the

Economic Community of West Africa Agricultural Policy (ECOWAAP), negotiation of the

CEDEAO CET, etc. The Cotonou Agreement signed in 2000 by 77 ACP countries and the 15

countries of the EU, in replacement of the Lome Agreement, is going to deeply modify trade

connections between the EU and the ACP countries, because it of the implementation in 2008

of "Economic Partnership Agreements " (EPAs), aiming at establishing free trade areas

between EU and ECOWAS, on one hand, and within regional ACP blocks on the other hand

(the ECOWAS and Mauritania for West Africa; the ECMAC and Sao Tome and Principe for

Central Africa). Indeed, the EPAs will certainly have a highly important impact on the

livestock sector because West African countries are going to negotiate an agreement of free

trade with their main commercial partner, the European Union.

The livestock sector must be prepared for a increased competition with European agricultural

imports (meat, powder of milk, etc.), which will enter eventually on the regional market

without customs duty from 2008 for those concerned with the APE. The current competition

of frozen chickens imports risks to strengthen if the products of the local poultry sector are

not retained in the regional list of sensitive products to be negotiated with the EU and which

will benefit a customs protection after 2008. It will also be a question of identifying

practicable earnings competitiveness within every livestock products sector and taking of

13

adequate capacities for an upgrade of their sector. The main issue in negotiations concerns the

definition of the products covered or not by the agreement of free exchange, and the possible

negotiation of the exclusion from the most sensitive livestock products (EPAU, 2004 ; IRAM,

2004).

The upgrade of the agriculture and livestock sector in the West Africa has also to be in the

heart of national and regional policies, notably the agricultural policy of ECOWAS (the

ECOWAAP) in current elaboration.

Priorities at regional level will be necessary and will imply that the national actors will

regroup themselves at a regional level to defend better their arguments with the authorities of

ECOWAS. They should also be more involved in the negotiation of the ECOWAS CET.

Studies should evaluate the level of tariffs likely to protect national and regional growing

industries from low cost imports. The empowerment of capacities of public and private actors

involved in the definition of livestock national and regional policies is urgent. This capacity

building is necessity to allow them to be better equipped for negotiations.

The role of the research is essential in this process : It should contribute to the development of

forward-looking tools and models likely to assist the decision making process including

producers organizations, various administrations and governments.

Conclusion

Beyond the aspects concerning trade negotiations, the current development of the poultry and

of the dairy production in peri urban zones shows that the livestock sector is very dynamic

West Africa. This evolution, results also in large part from strong population growth . The

increase of urban population shows that the livestock sector in West Africa is more and more

influenced by markets, notably urban markets. In this respect, the current development of

14

supermarkets in Africa is a process which takes more and more importance and which shows

a modification of the food marketing models to urban consumers. African livestock keepers

do not stayed apart this evolution and need resources and training to participate actively in the

domestic market rapidly changing. The main issue is notably to be able to supply these

domestic markets in a regular way and with qualitative products. The issue also concerns the

development of the regional market and the reduction of the supply deficit in animal products.

If livestock producers organizations and services are not able to face these new challenges, the

demand will supplied by imports.

Current negotiations led by ECOWAS for the adoption of a CET for all the countries of West

Africa is an opportunity to discuss the level of tariffs applied to animal products imports and

to think about the implementation of mechanisms allowing to encourage the development of

the regional agricultural sector. This negotiation of the ECOWAS CET must be led at the

same time with two other discussions: the one related to the elaboration of a common

agricultural policy (ECOWAAP); and the other related to the negotiation of Economic

Partnership Agreement with the European Union. The livestock sector must be entirely

associated to those current processes, with the risk of beeing marginalized during coming

decisions and strategic choices.

Livestock in West Africa conceals others trade development opportunities, including the

exports for honey, hides and skins, meat, etc.But those options are often insufficiently taken

into account in national policies.

Bibliographie

ANOPACI. 2004. Les importations de volaille en Côte d’Ivoire : contribution de l’IPRAVI. Abidjan : ANOPACI (Association Nationale des Organisations de Producteurs Avicoles de Côte d’Ivoire).

15

Akakpo, J. A. Ly, C. Bada-Alambedji, R. 1999. Le commerce du bétail et de la viande en Afrique de l’Ouest et du Centre, facteur d’intégration économique en Afrique tropicale. Revue Méd. Vét. 150, 5 : 453-462.

Balami, D. H. 2004. Le rôle de la filière élevage dans la compétitivité des pays ouest africains. OCDE/Club du Sahel et de l’Afrique de l’Ouest. Réunion du groupe d’orientation des politiques, Paris 29-31 Octobre 2003. 17 p.

Boutonnet, J. P. Griffon, M. Vallet, D. 2000. Compétitivité des productions animales en Afrique susaharienne et à Madagascar. Synthèse générale. MAE/DGCID, 100 p.

Delgado, C. Rosegrant, M. Steinfeld, H. Ehui, E. Courbois, C. 1999. Livestock Revolution to 2020. The next food revolution. IFFPRI/FAO/ILRI. Food, Agriculture,and the Environment Discussion Paper 28, 83 p.

DIA, P. I. 1997. Le consommateur urbain africain et les SADA. Communication présenté au séminaire sous régional FAO-ISRA : « Approvisionnement et distribution alimentaires des villes de l’Afrique Francophone ». Dakar, 14-17 avril 1997. 20 p.

Duteurtre G., 2004 : « Normes exogènes et tradition locale : la problématique de la qualité dans les filières laitières africaines », in Cahiers Agriculture, Numéro spécial « L’Alimentation des villes », 13 (1), pp. 91-98.

Duteurtre G., Corniaux C., Boutonnet J.P., 2003 : « Baisse de la consommation des produits laitiers en Afrique subsaharienne : mythe ou réalité ? », in Renc. Rech. Ruminants, 2003 (10), INRA, pp. 323-326

Duteurtre, G. Dieye, P. N. Dia, D. 2004. Assessment of the impact of poultry and dairy imports on local production in Senegal. Case-study : Import Surge Study. Bureau d’Analyses Macro-économique de l’ISRA, Unpublished Report, 44 p. + annexes.

EPAU, 2004 : « West Africa – European Union Pre-trade negotiations : Study on Agriculture”, Study conducted at the behest of the ECOWAS Executive Secretariat, Economic Policy Analysis Unit (EPAU), Cotonou, 114 p.,

FAO. 2003. Base de données statistiques FAOSTAT. Support CD ROM.

Grégoire, E. 2004. Réseaux et espaces économiques transétatiques. OCDE/Club du Sahel et de l’Afrique de l’Ouest. Réunion du groupe d’orientation des politiques, Paris 29-31 Octobre 2003. 18 p.

Hermelin, B. 2003. La politique agricole de l’UEMOA : aspects institutionnels et politiques. FAO/ Agricultural Policy Support Service/ TCAS working document n° 53. 57 p.

IRAM, 2004 : “Etude sur la compétitivité des grandes filières agricoles de l’espace UEMOA », Etude réalisée pour le compte de la Commission de l’UEMOA, IRAM, Paris, 246 p.

Kassum, J and Morgan, N. 2004. The SPS Agreement : Livestock and Meat Trade, unpublished working document, FAO Commodity and Trade Division, 16 p.

16

Ly, C. 2001. Les enjeux d’une politique avicole pour le Sénégal. Dakar : Communication pour le séminaire de lancement du projet Développement intégré de l’aviculture périurbaine. ISRA/EISMV/ENSA/FNRAA, 31 octobre 2001, 13 p.

Ly, C. 2004. De quelques statistiques sur l’élevage en Afrique de l’Ouest. Atelier sur les politiques de l’élevage : Modernisation de l’élevage et pratiques de recherche développement. Comment accompagner les politiques d’élevage en Afrique de l’Ouest. Dakar, Novembre 2004.

Nkansah, K. O. 2004. Ghana : a Case Study on Economic Partnership Agreements. In : Eurostep editor : New ACP-EU Trade Arrangements : New Barriers to Eradicating Poverty ? pp. 69-88.

Perret, C. 2004. L’état actuel de l’économie Ouest-Africaine. OCDE/Club du Sahel et de l’Afrique de l’Ouest. Réunion du groupe d’orientation des politiques, Paris 29-31 Octobre 2003. 25 p.

Pigeaud, F. 2003. Le poulet Sénégalais se débat devant l’OMC : Les importations subventionnées ruinent la filière. Paris : Journal Libération, 5th August 2003, 1 p.

Pricewhaterhousecoopers. 2004. Sustainability Impact Assessment (SIA) of the EU-ACP Economic Partnership Agreements. Regional SIA : West African ACP Countries. Institut de Prospective Africaine, 142 p.

Takan, M. Nkamela, G. P. 2004. Cameroon : a Case Study on Economic Partnership Agreements. In Eurostep editor : New ACP-EU Trade Arrangements : New Barriers to Eradicating Poverty ? pp. 53-68.

UEMOA. 2002. Les grandes orientations de la politique agricole de l’UEMOA. Rapport principal et annexes. Vol. 1 et 2. 296 p.

Von Massow, . Dairy Imports into Sub-Saharan Africa : Problems Policies and Prospects. ILCA Research Report, n° 17. 46 p.

Figure 1 : Live cattle and meat trade in West Africa.

Figure 2 : Gap between demand and production of animal products in West Africa in 1990

and for the horizon 2015 (adapted from Ly, 2004)

Figure 3 : Evolution of the imports of the animal products in Africa of the West in 1990 and

2000 (adapted from Ly, 2004)

Figure 4 : Evolution of the number of layers and broilers chicks from 1990 to 2003 in

Senegal (Source : Duteurtre and al. 2004)

Figure 5 : Retail prices of poultry meat in Dakar (Source : Duteurtre and al. 2004)

Table 1: Impacts of the imports on poultries sectors of Ivory Coast, Ghana and Senegal

Country Major economic and social impacts of poultry imports

Ivory Coast - Decrease broilers chicks implementation 7 % in 1998 and 6 % in 1999

Poultry feed production decrease 11 % in 1998 and 5 % in 1999

Ghana - Under utilization of hatcheries stands at 25 %, feed mills at 42 % and

processing plants at 25 %.

Senegal - Reduction of local production 35 %, 40 % of poultry breeders are stopped

and decrease of 37 % chicks production.

- Decrease of 35 % local broilers production

Increase of local layers production (reconversion of breeders)

Sources : Hermelin, 2003; Duteurtre et al., 2004; Nkansah, 2004.

Table 2 : Production costs of eggs and chicken in Ivory Coast and Senegal.

Before VAT (F CFA) After VAT (F CFA)

Production costs Senegal

Returns Price egg

Kg chicken Ready to Cook

Kg imported legs

43,3 - 50

1250 - 1350

1200

50 – 53

1300 - 1450

1200

Production costs Ivory Coast

Returns Price chicken

Returns price egg

1120

37.96

1286

45.47

Source : Hermelin, 2003 ; Duteurtre et al., 2004.