Embed Size (px)

Citation preview

Electronic copy available at: http://ssrn.com/abstract=1924364

Effects of financial liberalization and competition

F. Balmaceda

U. de Chile

R. Fischer F. Ramirez

U. de Chile 1

June 1, 2011

1Very preliminary. Center for Applied Economics (CEA), Department of Industrial Engineering, Uni-versity of Chile, Av. República 701, Santiago, Chile. Tel. +56-2-978-4072. Fax: +56-2-689-7895. Theauthors acknowledge the support of Fondecyt Project # 1110052 and the support of the Instituto Mileniode Sistemas Complejos en Ingenier’ia.

Electronic copy available at: http://ssrn.com/abstract=1924364

Abstract

This paper presents a simple model that shows the effects of financial liberalization on the

credit market of a small, relatively capital poor economy. The empirical evidence regarding the

effect of foreign bank entry is mixed. Some studies show that financial liberalization leads to

an increase in credit to businesses (Micco, Panizza and Ya’nez, 2004), while others show that

some businesses loose access to credit (Gormley 2008).

In our model entrepreneurs are heterogenous in their wealth and are subject to moral haz-

ard, which leads to some potential entrepreneurs being credit constrained. We show that the

effects of financial liberalization depend on the competitive structure of domestic banks prior

to liberalization. In the case of ex ante banking competition, liberalization lowers domestic

interest rates and credit penetration increases. In the case of a monopolist bank ex ante, the

effects of liberalization can be reversed, increasing the number of entrepreneurs that do not

receive credit. We also show that the benefits of liberalization under competition are larger in

economies with better loan recovery rates, but that this might not be the case when ex ante the

market is not competitive.

Electronic copy available at: http://ssrn.com/abstract=1924364

1 Introduction

In the last two decades, financial markets that had been closed, specially in developing countries

began to liberalize their access permitting international banks access to the domestic markets

or the free flow of international capital. The expectation was that the increased competition

and the lower rates (because of access to international financial markets) would increase access

to credit and lower financial costs. In some countries this was observed (Claessens , Demigurc-

Kunt and Huizinga (2001), Micco et al (2004)), while in others, while the access and conditions

facing larger firms improved, the effects on smaller firms have been mixed or negative, with

reduced access to the market. This is the case of the study of Gormley (2009) for India. What

could explain this wide divergence in the results of financial liberalization? We provide an

answer given by the ex ante degree of competition in the market. In markets where there is ex

ante competition, financial liberalization leads to the expected results, while in markets where

initially the financial sector is non-competitive, liberalization can lead to an increase to the

exclusion from the credit market of some for smaller (or weaker) businesses, while the stronger

companies are served by international banks.

An alternative to our answer is provided by Detriagache et al (2008) who proposes that in the

closed market, firms find it convenient (in order to reduce monitoring costs) to pool creditors,

and therefore to implicitly to provide a subsidy to smaller borrowers. When the international

firms arrive, with improved ability to screen hard numerical data, they compete in advantageous

conditions for the larger firms. This leaves the domestic banks to concentrate on the local firms

and now, under certain conditions on the monitoring cost, there is market separation. This is

too expensive for some borrowers, who drop out of the market. The end result is that loans to

the private market decrease and the portfolio of foreign banks is less risky than the domestic

portfolio. The authors provide empirical support for these results. Apparently, however, the

model is empirically verified.

However, for this argument to hold, it requires that banks do not differentiate among poorer

creditors, but pool them with stronger businesses. However, there is a lot of evidence that infor-

mal financial markets do differentiate among borrowers (Conning and Udry 2007, Bannerjhee,

2003, etc). While there is less evidence of discrimination among formal banks Boucher and

Guirkinger (2005) show that formal banks in developing countries discriminate by the use of

collateral. Hence, the basic premise of the pooling model appears to be fail. The object of this

paper is to provide an alternative explanation for the effect of financial market liberalization on

the domestic credit market that is a better fit for the empirical facts.

In this paper, it is the initial degree of competition that drives the results. Consider an

economy which is underdeveloped, so that with a competitive internal financial market, the

internal interest rate is higher than the world rate. Moreover, the spread between deposit rates

and loan rates is at the margin (for the best borrowers and the largest deposits). Hence, when

the financial markets are liberalized, the foreign banks with access to lower rates come in and

in general, rates fall. As expected, the effect is to increase access to credit and lower rates.

However, when the initial market situation is one of imperfect financial markets, the re-

sults are different. The reason is that a financial market where there is imperfect competition

and there are no international financial flows is one in which not only the lending rate is non-

competitive, but the deposit market is also uncompetitive. This means that the cost of funds

to banks can be lower than the competitive rate, because of lack of competition. In that case

it is possible that agents that would be excluded from credit in a competitive market for loan-

able funds have access to it. When the economy liberalizes, the cost of funds for domestic

banks goes up and some agents are now excluded from the market. Assuming, as we do, that

international banks do not have the detailed knowledge of clients that domestic banks have,

they will specialize in lending to the more solid firms (and are better off because we assume

that international banks are more efficient in their internal operations), while other firms are

served at a higher cost by domestic banks, and finally, there is as set of firms that is excluded

from the market. Hence, we have explained the fact the conflicting evidence on the effects of

liberalization on access to credit.

1.1 Empirical support in the literature

In this section we examine the evidence for our model. While there is no direct evidence for

our results, i.e., a study that relates ex ante competitive conditions in the domestic financial

market to the effects of financial market liberalization on different types of borrowers, we have

evidence for each intermediate step of our reasoning.

First, we note that, as we mentioned before, domestic lenders have a lot of knowledge of

borrowers and tailor their loan conditions to the lender. Second, we show that there is evidence

that after outside entry into concentrated financial markets, the interest rate on deposit rises

and there are better conditions for large business loans, while there are fewer consumer loans

(and we show evidence that consumer loans are often used for small businesses). Third, we

show that foreign firms have an informational disadvantage when lending in other markets.

Adding all of this together, we have all of the conditions of our results.

Differentiated credit conditions In both developed and developing countries, financial inter-

mediaries have developed techniques to discriminate among borrowers, both in terms of mea-

suring their ability to repay loans, and thus increase the return on loans once adjusted by risk.

In general, the use of collateral measures has been shown to be the principal determinant of

credit rationing (Binswanger, McIntire, and Udry 1989).

In developing countries, both formal lenders and informal moneylenders coexist, notwith-

standing the large differences in the rates they charge on loans. Formal lenders (usually com-

mercial banks) have fairly limited amounts of local information, so they demand collateral in

order to separate good from bad debtors. Informal moneylenders, on the other hand, have bet-

2

ter local information so they monitor and screen as a substitute for collateral and therefore can

offer loans to those who are rationed in the formal market (Boucher and Guirkinger (2005)).

Careful studies of rural areas in emerging countries describe the ability of moneylenders to

solve the problems on asymmetric information with their clients. The studies show that the

markets are “fragmented” in the sense that different sets of borrowers are treated differently

and are financed on the basis of their characteristics, the characteristics of their borrowers and

other local conditions. Businesses will use financial instruments that can vary substantially

in terms of interest rates, type and quantity or required collateral, monitoring cost, among

other variables (Conning and Udry (2007)). Bannerjee (2003) describes the extreme variability in

interest rates charged to superficially similar businesses and farmers in rural India. We conclude

that there is little pooling in developing markets, and therefore not much subsidization across

borrowers.1

Effect of entry into concentrated markets In highly concentrated financial markets, new en-

trants can lead to drastic changes in the market. These changes affect not only potential bor-

rowers, but also savers. In a study of the rural areas in the US, Mccall and Peterson (1997)

study the effects of entry in financial markets with less than three participant banks. They find

large decreases in the profits of established banks (as expected), but also alterations in the rate

paid on deposits, and therefore on the cost of funds of the incumbent banks. One year after

entry they observed a large raise in the interest rate paid on time deposits and a change in

lending policies, with a larger fraction of assets directed at commercial loans and a reduction

on consumer loans. It is well known that consumer loans are often used by small businesses

as a source of credit.2 Therefore, it appears that entry into a concentrated financial market

–consistent with our model– reduces credit penetration for entrepreneurs with fewer assets.

Notice also that the cost of funds following entry increases also consistent with our model.

Informational disadvantage of foreign banks There is ample evidence showing that foreign

banks are handicapped in providing services that require a close association with domestic

firms. Mian (2006) suggests that when a foreign bank opens a branch in another country, it faces

relatively higher costs in providing loans that require close knowledge of domestic borrowers.

More precisely, the evidence shows that foreign banks face difficulties in lending to small and

medium enterprizes given the opacity of their financial conditions. Berger, Klapper, and Udell

(2001) argue that the distance between the CEO of the foreign bank and the domestic firms,

the different local commercial cultures or institutional barriers constrain the contacts between

foreign banks and the domestic firms. Among others, Detragiache, Tressel, and Gupta (2008),

1Other papers that describe this variability in credit conditions are: Aleem (1990), Timberg and Aiyar (1984),Dasgupta (1989), Ghate (1992) y Udry (1991).

2Kneiding and Kritikos (2007) show that households with no dependent workers use consumer loans to financebusinesses, while Trumbull (2010)estimates that 30% of consumer loans are used to finance entrepreneurial projects.

3

and Gormley (2011) assume that domestic banks have better knowledge of local conditions and

therefore can forge closer associations with domestic firms.

Thus, the empirical evidence shows that there is ample circunstancial evidence for our

model. Moreover, contrary to the alternative explanation for the observation of different ef-

fects of financial liberalization in developing countries, domestic financial markets in devel-

oping countries do not pool borrowers. On the contrary, lenders use sophisticated means for

discriminating among them, and this is reflected in different lending rates or in the exclusion

from loans. In addition, for the case of rural markets in the US, the evidence above shows that

our mechanism fits the facts directly.

Methodology of the paper The way we proceed is by considering successively four cases. First

we look at the equilibrium in the closed economy with competition and under monopoly. Next,

we open the economy by allowing the entry of foreign banks while simultaneously allowing

depositors to lend abroad. In the case of competition, the effects of opening the economy are,

as expected, increased credit penetration and lower domestic rates. Opening the economy does

not deprive the domestic monopoly of all its monopoly power because of the informational

disadvantage of foreign banks means that there is a range of (weak) entrepreneurs who are

not given credit by foreign banks and thus can only be served by the single domestic bank.

The problem for the bank is that increased competition for deposits raises its cost of funds,

and this means that some creditors that had access to the banking system before financial

liberalization are now excluded. The effect is to reduce the credit penetration in the economy

following opening. Hence the model explains the phenomena observed by Detriagache et al

(2008), without the assumption of pooling, which is not observed in the real world.

2 The closed economy model

We begin by considering a small closed economy, with two types of risk neutral agents: en-

trepreneurs and bankers. There is a continuum of entrepreneurs indexed by z ∈ [0,1], who

are protected by limited liability. We divide the single period into four stages (see figure 1).

Agents are born in the first stage endowed with one unit of inalienable specific capital (an idea,

a project or an ability) and different amounts of wealth, Kz. The wealth distribution of en-

trepreneurs is given by G(·), which has a continuous density g and bounded support given by

[0,1]. Bankers intermediate between agents as owners of wealth and agents as entrepreneurs

who require funds to carry put their projects, and are therefore the sole source of financing in

this economy. In order to carry out a project, the entrepreneur must invest I > 1 ≥ Kz, ∀z.

Thus she needs to obtain a loan Lz = I −Kz.In order to grant a loan, the banker checks –at no cost– whether the entrepreneur really

is the owner of the declared wealth of the entrepreneur. On the other hand, bankers find it

4

Agents bornowning Kz .

Agents apply forloan I −Kz .

Agents that receive loantake (or not) action forprivate benefit.

If project succeeds, loanis paid back. Otherwise,bankruptcy.

Figure 1: Time line of the model

difficult to determine whether an entrepreneur is wealthier than she declares. In other words,

entrepreneurs can hide some of their wealth Kz from bankers, but bankers can always determine

whether particular assets declared by an entrepreneur effectively belong to him. The origination

cost of a loan is co, a constant independent of the size of the loan.

If an entrepreneur receives financing, he invests in his risky project which can be successful,

with probability p or fail with probability 1−p. If successful, it returns observable R, otherwise

it returns 0 (it has no residual value).3 We assume that the expected net social value of the

projects is positive, i.e.,

Assumption 1

pR − (1+ ρ)I > co

where ρ is the cost of funds for the banks. The problem, as in ? or ?, is that there is moral

hazard in the sense that entrepreneurs can abscond with the loan. In that case, only a fraction

1−φ of the loan is recovered, with φ < 1. Note that if there is total recovery of absconded debt

(φ = 0) Assumption 1 implies that all projects should be financed if there is sufficient capital.

Apart from their role as intermediaries, domestic banks fulfill two additional roles. First,

optionally, borrowers can contract for the bank to monitor the project at a cost cm per loan. By

monitoring they reduce the benefit of absconding to βφLz , with β < 1. Second, in the process

of monitoring, the banks provide an advising role which increases the probability of success of

the project from p to p + ε (see ?). We assume that the cost of monitoring is sufficiently small

that the expected value of projects always increases, so that entrepreneurs which get loans from

domestic banks always choose to pay for monitoring:

Assumption 2

(p + ε)R − cm > pRa εR > cm

This means that we can conflate the cost of origination and the cost of monitoring into a

single domestic bank cost: c ≡ co + cm. The possibility of monitoring establishes a difference

between domestic and foreign banks. We assume foreign banks are unable to provide monitor-

ing services at a reasonable cost, due to distance, different legal and institutional cultures or

other factors.

3For an analysis of the effect of a residual value, see ?.

5

3 The closed economy model

Initially the economy is closed, so there is no access to international capital. The only possible

source of financing for entrepreneurs is the domestic banking system. Consider first the system

under competition.

3.1 Competition

By our assumption 2, all entrepreneurs under competition choose to get a loan with the moni-

toring services included. The problem facing entrepreneur z is:

Maxrz ,Lz≥0

Πz = (p + ε)[R − (1+ rz)Lz] (P1)

s.t. (p + ε)[R − (1+ rz)Lz] ≥ βφLz (ICb)

(p + ε)(1+ rz)Lz − c − (1+ ρ)Lz = 0 (IRl)

(p + ε)(1+ rz)Lz − cm ≥ p(1+ rz)Lz (ICl)

I ≤ Kz + Lz (MP)

The first restriction is the no absconding condition, while the second restriction is the zero profit

condition for banks. The third condition is the incentive compatibility condition on banks for

them to perform the monitoring role. From the (??) condition we obtain the interest rate charged

to agent z if the project is successful.

1+ rz =1+ ρp + ε +

c + Co(p + ε)Lz

(1)

In turn, we use (1) in the no absconding condition (??) to obtain the minimum level of capital

that an entrepreneur needs to have to receive a loan:

K(ρ) ≡ I − (p + ε)R − c − Co1+ ρ + βφ (2)

Agents with higher amounts of capital receive loans. In addition, if the monitoring activity

of banks is non-verifiable, in the case of agents which require small loans, (??) might not hold.

We avoid this complication by assuming that the required investment is sufficiently large:

Assumption 3

I > 1+cmpε − co1+ ρ

Finally, to ensure that the problem is interesting, we assume that even when the cost of funds

ρ − 0, there are credit-rationed agents, i.e., K(0) = 0. Now, consider the equilibrium in the of

this economy by equating the supply of loanable funds from agents to the demand for funds.

6

The supply of loanable finds is independent of the interest rate and given by:4

KS =∫ 10KzdG (3)

Demand for loans is the sum of the investments made by all entrepreneurs that receive loans:

KcbD = I [1−G(K(ρ))] (eq:DemandK1)

Since∂KcbD∂ρ = −Ig(K(ρ)) ∂K(ρ)∂ρ < 0, the demand curve for capital is downwards sloping. We

assume that at the minimum interest rate of zero, there is excess demand for capital, and

therefore there is a competitive interest rate ρcb that equates supply and demand. Hence,

Proposition 1 In a closed, competitive economy, only entrepreneurs with wealth Kz < K(ρcb)receive loans.

Note that E ≡ 1−G(K(ρ)) is a natural measure of the efficiency of the economy. However, with

a fixed supply of capital, the measure is not interesting.

3.2 The case of monopoly

First, note that the banking monopoly will only offer contracts with monitoring, as it gets to

extract more rents from entrepreneurs. Second, since the bank is also a monopoly on the

depositors side, it sets the cost of funds at zero, the lowest rate at which lenders will hand over

their wealth to the bank in this static model.5

There are two cases we must examine. First, the case in which the capital of the entrepreneur

is perfectly observable by the bank. In that case, the bank will extract all rents from en-

trepreneurs (so long as the no absconding condition is met). This means the interest rate

charged rises with wealth, and this does not seem reasonable. For this reason, we assume next

that the bank can verify if an entrepreneur has a declared amount of capital, but cannot find

out if she has more than that level of wealth.

4It is slightly more complex to have the supply of loanable funds be an increasing function of the interest rate.However, for the purposes of this paper, nothing is gained by this complication.

5The assumption that in an uncompetitive market the cost of funds is low is reasonable, as the example of XXXXin Mexico xhows.

7

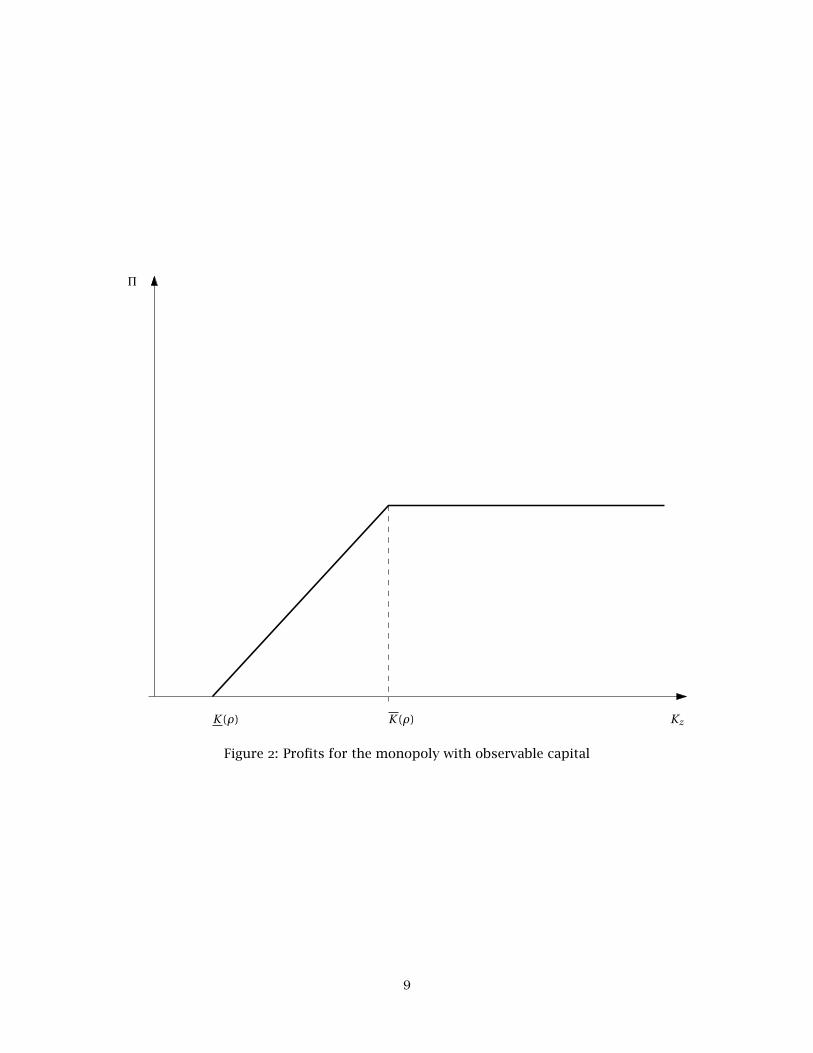

3.2.1 Capital is observable

When the bank can observe the wealth of entrepreneurs, it will extract all the rents that are

compatible with the no-absconding condition. The problem for the monopoly bank is:

Maxrz ,Lz≥0

Πz = (p + ε)(1+ rz)Lz − c − (1+ ρ)Lz (P2)

(p + ε)[R − (1+ rz)Lz] ≥ βφLz (ICb)

(p + ε)[R − (1+ rz)Lz] ≥ (1+ ρ)Kz (IRb)

(p + ε)(1+ rz)Lz − cm ≥ p(1+ rz)Lz (ICl)

I ≤ Kz + Lz (MP)

Note that the participation constraint for entrepreneurs considers the alternative that she

does not invest and puts all her capital at interest. We divide the analysis of the problem into

two cases. In the first, the Individual rationality constraint for borrowers (??) is binding and the

bank extracts all rents from those entrepreneurs. The interest charged these entrepreneurs is:

1+ rz =1+ ρp + ε +

(p + ε)R − (1+ ρ)I(p + ε)Lz

(9)

The monopoly bank receives the same amount of rent out of each entrepreneur in this category.

This requires that the interest rate be inversely proportional to the size of the loan. The least

wealthy entrepreneur that satisfies the constraint with equality, and hence loses all rents, is:

K(ρ) ≡ βφI1+ ρ + βφ (11)

For agents with less wealth, i.e., K(ρ) <≤ Kz ≤ K(ρ) the bank is unable to extract all rents,

because otherwise the no-absconding condition is not met. Hence, the bank sets the no-

absconding condition (??) to be active and solves the resulting problem to maximize profits.

The interest rate charged an entrepreneur in this wealth range is :

1+ rz =RLz− βφp + ε (12)

Replacing this interest rate in the objective function, the profits the bank obtains from en-

trepreneur z are:

(p + ε)R − c − (1+ ρ + βφ)(I −Kz) (13)

Observe that the lowest z that obtains credit is the same as in the case of competition. The

reason is that the monopoly bank will serve all agents for which the no-absconding condition

is met. As a perfectly discriminating monopoly, the equilibrium is efficient in that the same

number of firms is served as under competition. the equilibrium is described in Figure 2.

8

K (ρ)K (ρ) Kz

Π

Figure 2: Profits for the monopoly with observable capital

9

3.3 The bank does not observe Kz

Recall that in this case the bank can verify that an entrepreneur has the declared amount of

wealth, but has no means of determining if that is all his wealth. The entrepreneur knows that if

she declares all her wealth, the bank will extract all rents, so she prefers to hide part of it (unless

she has the lowest level of capital that receives a loan). Therefore entrepreneurs ask for larger

loans than strictly needed and get interest on the unneeded capital. There are two options here.

First, the bank may choose to bunch entrepreneurs, by fixing a single lowest value of capital

that it will lend to and serving all higher ranked entrepreneurs at a fixed rate.Alternatively,

the monopoly bank must provide incentives for the firms to reveal their true values of Kz.6

Contrary to the previous case, the monopolist cannot maximize profits at the individual level.

The problem for the monopolist is:

maxρ,K,r(Kz)

∫ 1K(p + ε)(1+ r(Kz))(I −Kz)− c − (1+ ρ)(I −Kz)dGz (P3)

(p + ε)(R − (1+ r(Kz))(I −Kz)) ≥ βφ(I −Kz) ∀Kz ∈ [K,1] (ICb)

s.t r ′(Kz) =(p + ε)(1+ r(Kz))− (1+ ρ)

(p + ε)(I −Kz)∀Kz ∈ [K,1] (IC2b)

(p + ε)(1+ rz)Lz − cm ≥ p(1+ rz)Lz (ICl)

KS ≥ I(1−G(K)) (CA)

Defining ϕ ≡ K(ρcb)− 1−G(K(ρcb)g(K(ρcb)) , and assuming:

Assumption 4 g′(K)(K −K(ρ))+ 2g(K) > 0 ∀K ∈ [0,1] ∀ρ ∈ [0, ρmax]

the truth-revealing equilibrium is characterized by:

Proposition 2 The monopoly bank sets the cost of funds at ρM = 0. Only entrepreneurs with

wealth Kz ≥ KM are given loans, where KM is determined from:

• If ϕ ≥ K(0) then the monopolist is efficient in the sense that KM = K(ρcb).

• If ϕ < K(0), then the monopolist is inefficient in the sense that KM ∈ (K(ρcb),1] and is

determined from

KM −K(0) =[1−G(KM)]g(KM)

.

Proof See Ramirez (2011).

Note that in the second case, the monopolist is inefficient in the sense that it provides less

credit than a competitive banking system. Solving the differential equation (IC2b) we obtain:

r(Kz) =(1+ r0)−

(1+ρp+ε

)Kz

I −Kz6RF: Can we can show that bunching is worse than separating for the monopoly?

10

which is increasing. Observe that the interest rate is increasing in Kz, which seems unreason-

able, but recall that in the symmetric information case, the monopoly can extract all the rent. To

do this it increases the interest rate at a faster rate than in the truth revealing case, where firms

are rewarded by revealing the truth about Kz with an interest rate that increases at a slower

pace.7

4 The Open Economy

We now go onto the open economy case. Again here we consider the case of initial competition

and initial monopoly. In the case of financial liberalization, we assume that domestic agents

have access to unlimited amounts of capital at a rate ρ∗. This is also true for agents as providers

of funds, and in particular, it means that the cost of funds for the monopoly could go up.

Foreign banks set up local subsidiaries (alternatively they buy local banks in an attempt at

obtaining local talent and knowledge). The foreign banks are risk neutral and competitive.

The main disadvantage of large banks is that they cannot provide monitoring services, because

of the distance they have to use arm’s length relationships.8 Hence they can operate in the

local market only if they are more efficient providers of credit. We assume that their cost of

originating a loan is c∗o < co.Foreign banks are excluded from the local market if: (p + ε)R − c − (1+ ρ∗)I > pR − c∗o −

(1 + ρ∗)I a εR − cm > co − c∗o , where the right hand side of the second equation represents

the difference in originating efficiency between local and foreign banks, and the left hand side

represents the net social benefit from monitoring due to the increased probability of success of

the project.

The case in which the inequality is reversed is one in which local banks have sufficiently high

originating costs compared to foreign banks that the net effect of the increased probability of

success is not sufficient to eliminate foreign banks. Hence, monitoring is an expensive proposi-

tion and only provides benefits to those firs that require it to receive loans. Entrepreneurs with

sufficient capital will operate with foreign banks, while those with less backing will continue to

pay for monitoring services with the domestic firms. the limit capital stock is given by:

K∗ ≡ I − pR − co1+ ρ +φ

7The fact that the interest rate is increasing with the wealth of the agent is an artifact of the fact that we haveassumed that investment size is fixed. If investment sizes are variable, the monopoly can reward the wealthierentrepreneur with a larger loan, without having to raise the interest rate, because the rate per unit is higher.

8Alternatively they are less efficient at providing monitoring and advisory services because of distance and fewerpossibilities of controlling local account executives.

11

4.1 Ex-ante competition

In this case, financial liberalization does not change the competitive situation. Hence we have

that:

Proposition 3 Assume K∗ > K(ρ∗). so that there is a range of agents for which only domestice

banks can loan. Then, with ex ante financial competition, financial liberalization means that en-

trepreneurs with wealth Kz > K∗(ρ∗) operate with foreign banks. Entrepreneurs with wealth in

the range K∗ > Kz > K(ρ∗) must operate with domestic banks that provide monitoring services.

Note that, unless we assume that ρcb < ρ∗, the number of entrepreneurs that have access

to loans must increase. The opposite case would mean that the closed economy is relatively

abundant in capital, which is unlikely for a developing economy. Assuming that the cost of

funds for banks falls (ρ < ρ∗), under competition both ex ante and ex post, we have the expected

result that:

Proposition 4 If there is ex ante competition , financial liberalization produces an inflow of cap-

ital, leading to an increase in the number of entrepreneurs that receive financing.

This is the result expected by those who promoted financial liberalization for poor countries.

4.2 Ex ante Monopoly

This is the interesting case, in the sense that it leads to the counterintuitive result that has been

observed: financial liberalization leads to a decrease in credit market penetration, as agents

with less wealth are excluded from credit.

Before financial liberalization, the single bank operates as a monopoly in the funds market

and therefore sets a low rate on funds. After liberalization, the cost of finds for the bank rises

to the international level ρ∗. Financial liberalization means not only the end of the monopoly,

but a rise in the cost of funds for the bank because its monopsony power disappears.

Consider now the effects on borrowers. Wealthy agents, as in the previous subsection, will

switch to foreign banks and will not ask for monitoring services. Hence, the domestic bank

loses all the customers that do not require monitoring services, i.e., with Kz > K∗. However,

the domestic firms has an advantage over entrepreneurs with less capital, since these require

monitoring in order to receive loans. These are the entrepreneurs in the range K∗ < Kz <K(ρ∗). The behavior of the domestic bank is described by the solution to the following problem,

recalling that the domestic bank continue to operate as a monopoly over agents that do not have

access to loans from the foreign banks:

12

MaxK

∫ K∗Kp(1+ r(Kz))(I −Kz)− c − (1+ ρ∗)(I −Kz)dG (P7)

(p + ε)(R − (1+ r(Kz))(I −Kz)) ≥ βφ(I −Kz) ∀Kz ∈[K,K∗

](4)

r ′(Kz) =(p + ε)(1+ r(Kz))− (1+ ρ∗)

(p + ε)(I −Kz)∀Kz ∈

[K,K∗

](5)

s.t. K∗ ≥ K ≥ K(ρ∗) (32)

the following result describes the equilibrium:

Proposition 5 After liberalization the domestic bank finances and provides monitoring services

to entrepreneurs with wealth in the range Kz ∈ [K∗M , K∗), where K∗M > K(ρ∗). The limit capital

K∗M is determined from

K∗M −K(ρ∗) =[G(K∗)−G(K∗M)

]g(K∗M)

Proof In Ramirez (2011).

Note that there is a difference between the effects of liberalization depending on the com-

petitive conditions in the ex ante market: if the market was competitive, the number of en-

trepreneurs that receive financing after liberalization is larger than if the market was a monopoly:

K∗M > K∗(ρcb). Now, it can be shown that

Proposition 6 K∗M is strictly increasing in ρ ∈ [0, ρcb].

Proof In Ramirez (2011).

It is possible that entrepreneurs that received financing ex ante under monopoly conditions

are now excluded form the credit market. This happens if

K∗M(ρ∗) > K(ρcb) (6)

Hence, under condition (6) there is a group of entrepreneurs who are worse off by financial

liberalization. The reason is that the no absconding conditions for the entrepreneur are not

satisfied given the increased cost of funds for the monopoly bank.

4.2.1 A simplified version

In this section we verify that the reason for the exclusion of firms is the increased cost of funds

for the monopoly bank due to liberalization, and not the entry of foreign banks. To see this,

consider a simplified model in which financial liberalization does not include the possibility

of foreign banks lending directly to domestic entrepreneurs. Liberalization only implies that

the domestic banks have access to international funds and that domestic savers can invest

13

overseas. To simplify the expressions, we will assume that there is no monitoring activity, since

it is unnecessary for our results. Hence there is no increase in the probability of success due to

monitoring.

Clearly, in the case of ex ante competition in the domestic market, there is no difference with

the results obtained before: if the external rate of return on funds is lower than the domestic

rate, the number of entrepreneurs with access to credit increases and by the same amount as if

international banks were allowed to operate domestically.

Consider now the case of an ex ante monopoly. The effect of financial liberalization is to

raise its cost of funds from zero to a positive value, since it now must compete for deposits.

The problem facing the monopolist is

MaxK

∫ 1Kp(1+ r(Kz))(I −Kz)− c − (1+ ρ∗)(I −Kz)dG (7)

p(R − (1+ r(Kz))(I −Kz) ≥ φ(I −Kz) ∀Kz ∈[K,K∗

]r ′(Kz) =

p(1+ r(Kz))− (1+ ρ∗)p(I −Kz)

∀Kz ∈[K,K∗

]s.t. 1 > K ≥ K(ρ∗)

As in the proof of proposition 2, we can rewrite the problem as:

MaxK

[1−G(K)[[K −K(ρ∗)]

s.t. 1 ≥ K ≥ K(ρ∗)

From which we reproduce the fact that there is restricted lending if

K∗M(ρ∗)−K(ρcb) =

1−G(K∗M)g(K∗M)

(8)

5 Conclusions

The object of this paper is to explain the apparently inconsistent results that are observed

after financial liberalization in a developing country. While the expectation is that this will lead

to increased credit penetration, in some countries the opposite is observed: domestic banks

cease lending to some (weaker) businesses and therefore credit penetration falls. Moreover,

foreign banks, which are at an informational disadvantage, lend only to the stronger firms.

These inconsistent results are explained by Detriagache et al (2008) in the context of a model in

which the domestic banks pool the loans of strong and weak firms thus providing and implicit

subsidy to the weaker firms. Once foreign firms enter, they cream-skim the stronger domestic

firms because the informational problems are smaller for them, and the domestic banks start

14

to separate their lending.

While Detriagache’s model explains the facts, there is no evidence of pooling in lending in

developing markets. The evidence seems to go towards extreme separation in credit conditions

in developing countries. Our model is closer to the empirical evidence and while we do not have

the direct confirmation that in ex ante less competitive markets financial liberalization leads

to reduced credit penetration similar effects in isolated markets have been observed in the US.

The reason in our model for the decrease in the access to the market after liberalization is not

foreign entry per se on the loan market, but rather the effects of increased competition on the

cost of funds of the domestic monopoly bank.

15

6 References

Berger, Allen N., Leora F. Klapper, and Gregory F. Udell “The Ability of Banks to Lend to Infor-

mationally Opaque Small Businesses.” Journal of Banking and Finance 2001.

Todd A. Gormley, "The impact of foreign bank entry in emerging markets: Evidence from

India" J. Finan. Intermediation 2009

Enrica Detragiache, Thierry Tressel, and Poonam Gupta, “Foreign Banks in Poor Countries:

Theory and Evidence”, The Journal of Finance 2008.

Atif Mian, “Distance Constraints: The Limits of Foreign Lending in Poor Economies”, The

Journal of Finance 2006

Alan S. Mccall and Manferd 0. Peterson, “The Impact Of De Novo Commercial Bank Entry”,

The journal of finance 1977.

Beck, Thorsten, Berrak Büyükkarabacak, Felix Rioja and Neven Valev, “Who Gets the Credit?

And Does it Matter? Enterprise vs. Household Credit across Countries.” CentER Discussion

Paper.2009-41, Tilburg University, 2008

DeYoung, R., and Nolle, D., “Foreign-owned banks in the United States: Earning market share

or buying it?”, Journal of Money, Credit, and Banking 1996.

Christoph Kneiding and Alexander Kritikos, “Funding Self-Employment - The Role of Con-

sumer Credit”, GfA Discussion Paper No. 06, 2007

Steve Boucher, Michael Carter and Catherine Guirkinger, SRisk Rationing and Wealth Ed’ects

in Credit Markets: Implications for Agricultural De- velopment,T American Journal of Agricul-

tural Economics, forthcoming.

Gunnar Trumbull, “Regulating for Legitimacy: Consumer Credit Access in France and Amer-

ica”, Harvard Business School BGIE Unit Working Paper No. 11-. 047, 2010.a

Micco, Alejandro, Ugo Panizza, and Mónica Yanez, 2004, Bank ownership and performance:

Are public banks different? Working paper, Inter-American Development Bank.

Petersen and Rajan, “The effect of credit market competition on lending relationships.”

Quarterly Journal of Economics 1995

Marquez, “Competition, adverse selection, and information dispersion in the banking indus-

try”, Review of financial studies, 2002

Rebecca Zarutskie, “Evidence on the effects of bank competition on firm borrowing and

investment”, Journal of Financial Economics 2005

Emilia Bonaccorsi di Patti and Giovanni Dell’Ariccia, “Bank Competition and Firm Creation”,

Journal of Money, Credit and Banking, 2004.

16

Kwangwoo Park and George Pennacchi, “Harming Depositors and Helping Borrowers: The

Disparate Impact of Bank Consolidation”, The Review of Financial Studies, 2009

Jith Jayaratne and Philip E. Strahan, “Entry Restrictions, Industry Evolution, and Dynamic

Efficiency: Evidence from Commercial Banking”, Journal of Law and Economics, 1998

Ben R. Craig and Valeriya Dinger, “Bank mergers and the dynamics of deposit interest rates”,

"Discussion Paper Series 2: Banking and Financial Studies

Robert N. Collender a, Sherrill Shaffer “"Local bank office ownership, deposit control, market

structure, and economic growth”, Journal of Banking and Finance.

Ramirez, Felipe, “Liberalización Financiera, Competencia Bancaria y el Mercado Del Crédito”,

Tesis Magister de Economía Aplicada, 2011.

17