Embed Size (px)

Citation preview

Roskill | Approachable. Independent. Expert

54, Russell Road, London SW19 1QL, UK Tel: +44 20 8417 0087 Fax: +44 20 8417 1308

Online: www.roskill.com Email: [email protected]

Lithium: Market Outlook to 2017

Twelfth Edition, 2013

Copyright © Roskill Information Services Ltd. ISBN 978 0 86214 589 7

This report is copyright It is illegal to copy it without obtaining a licence

The customer number of the organisation receiving this report has been encrypted

throughout the report so that any copies made can be tracked back to the original source

Copyright © April 2013 Roskill Information Services Ltd

The contents of this report may not be reproduced, stored or transmitted in any form

or by any means, without prior permission in writing.

We want you to get the best value from your investment in this report. If you wish to

photocopy a few pages of the report for use within your own organisation, you can

obtain the necessary licence and make copies at a cost of £4/$8 per page from the

Copyright Licensing Agency, 90 Tottenham Court Road, London, W1P 9HE, from the

Copyright Clearance Center in the USA, and from similar organisations in other

countries.

Please do not allow this report to be photocopied without a licence. Illegal

photocopying harms us because cannot afford to update reports as often as we would

like, and it may harm you too when you next want an up-to-date report from us. Your

co-operation is much appreciated.

Table of Contents

Page

1. Summary 1

2. Lithium Mineralogy, Occurrences and Reserves 10

2.1 Occurrence of lithium 10

2.1.1 Lithium minerals 10

2.1.2 Lithium clays 12

2.1.3 Lithium brines 12

2.2 Lithium reserves 14

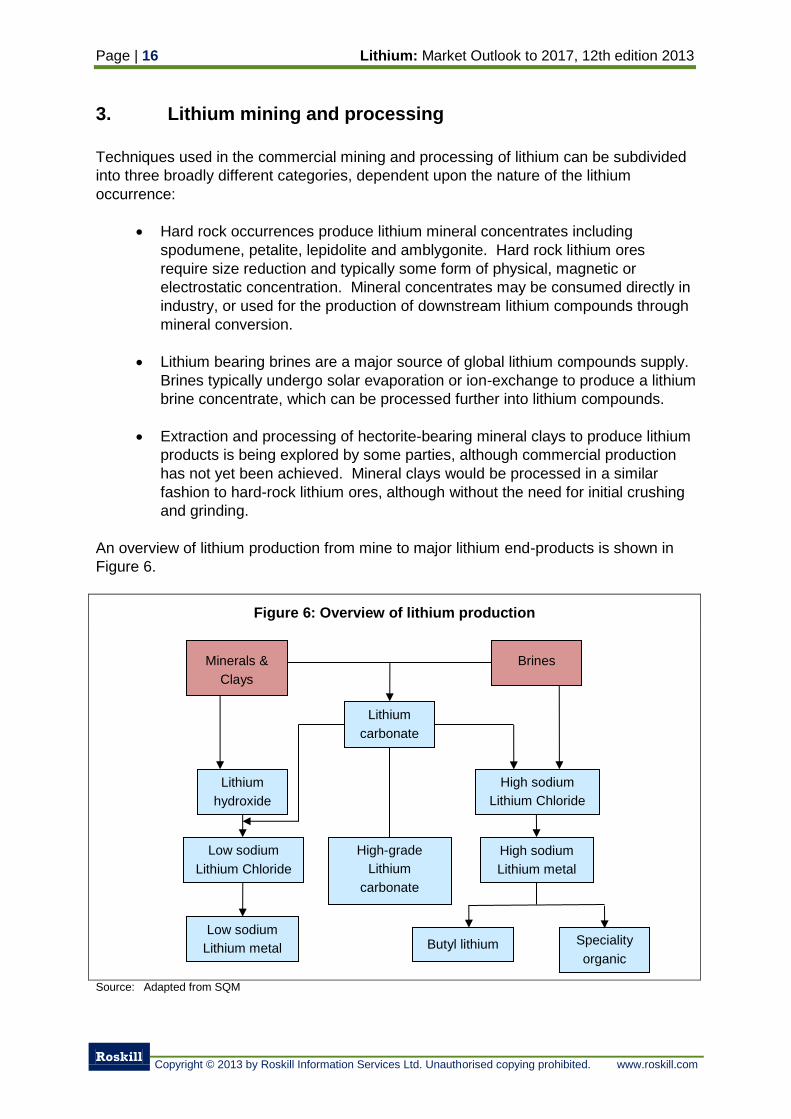

3. Lithium mining and processing 16

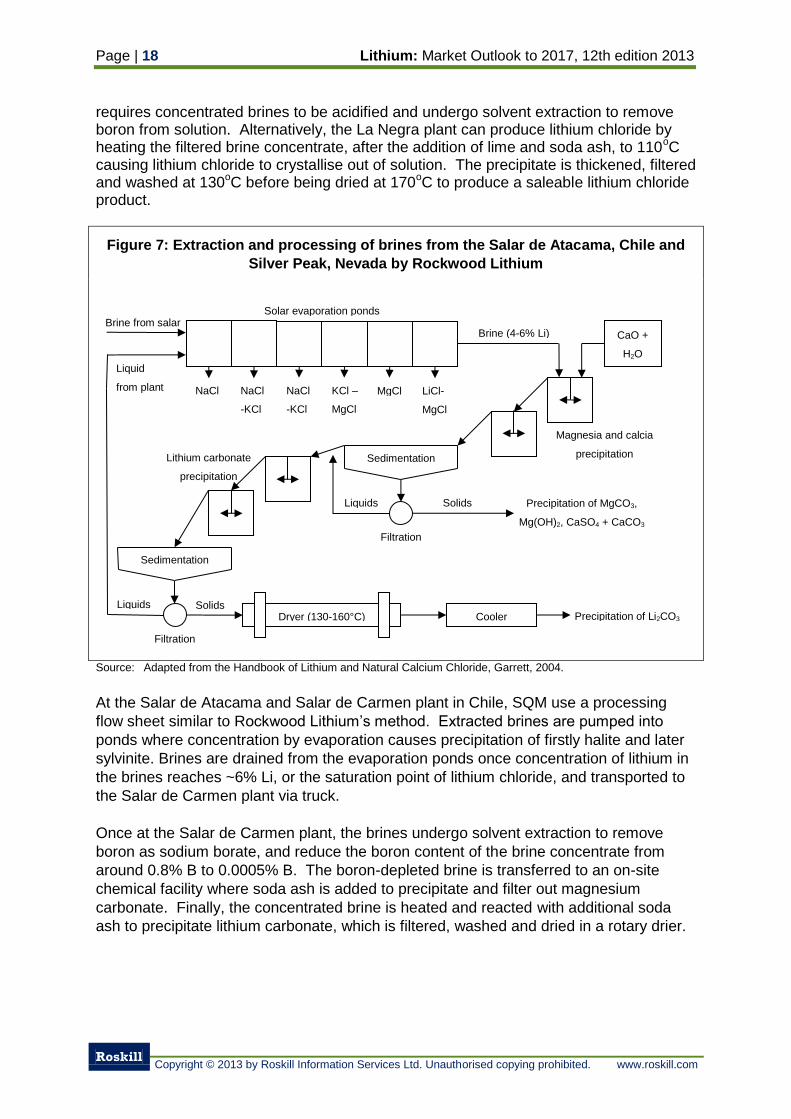

3.1 Extraction and processing of lithium brines 17

3.1.1 Other methods of brine extraction 20

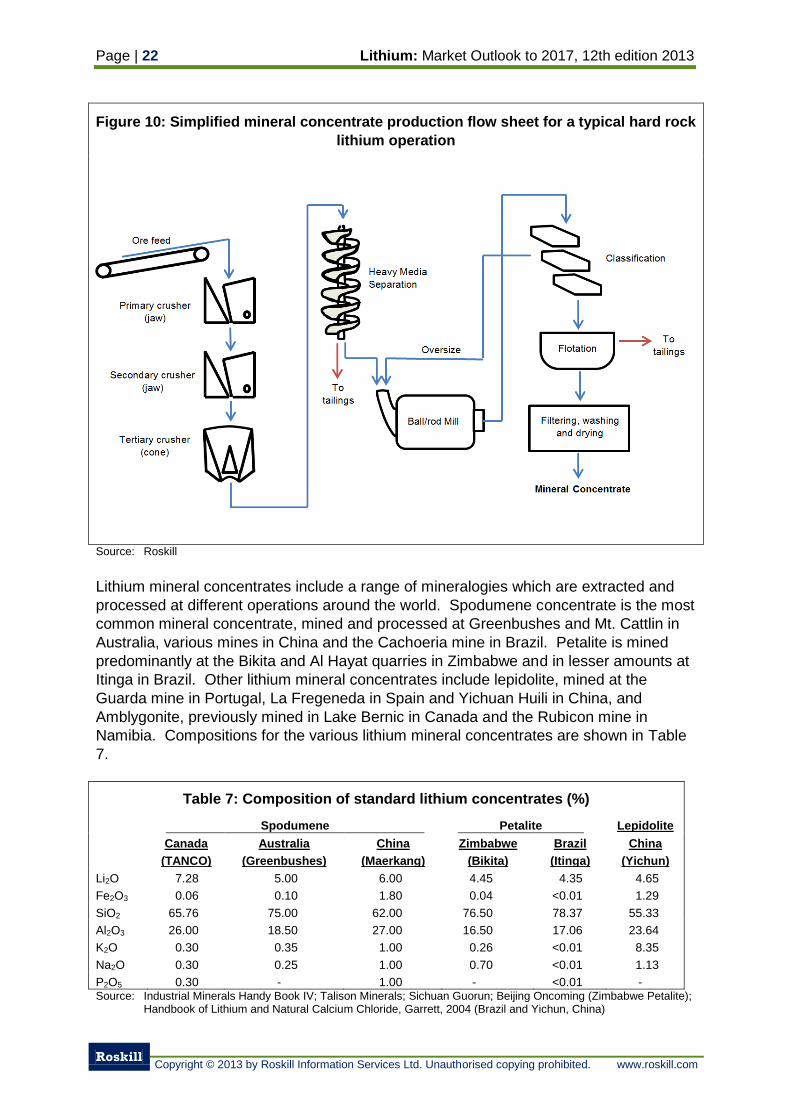

3.2 Mining and processing of lithium minerals 21

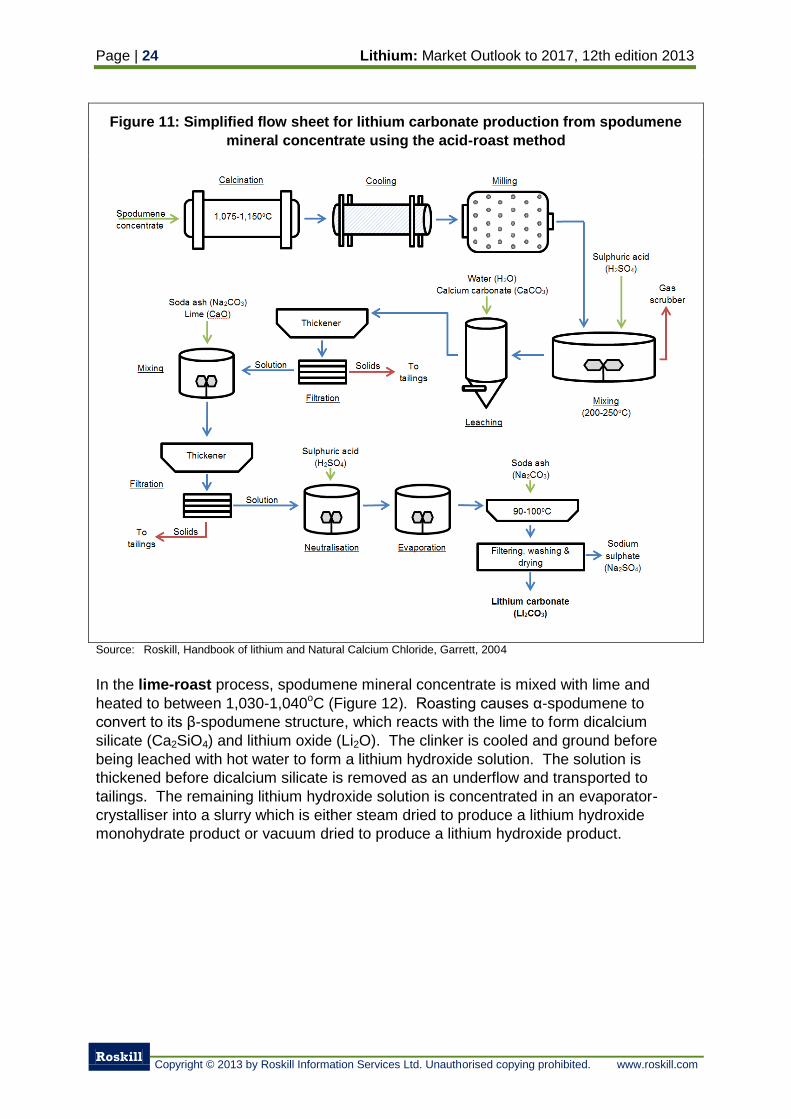

3.3 Processing lithium mineral concentrates to lithium compounds 23

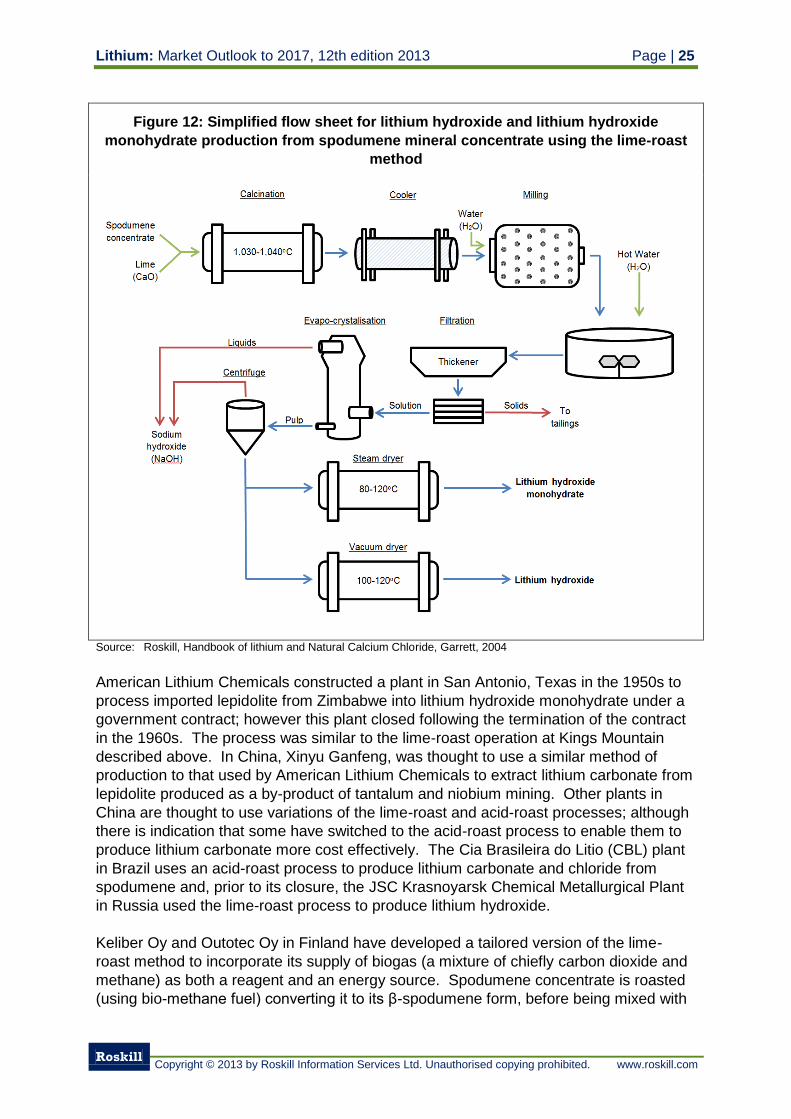

3.4 Processing lithium bearing clays into lithium compounds 26

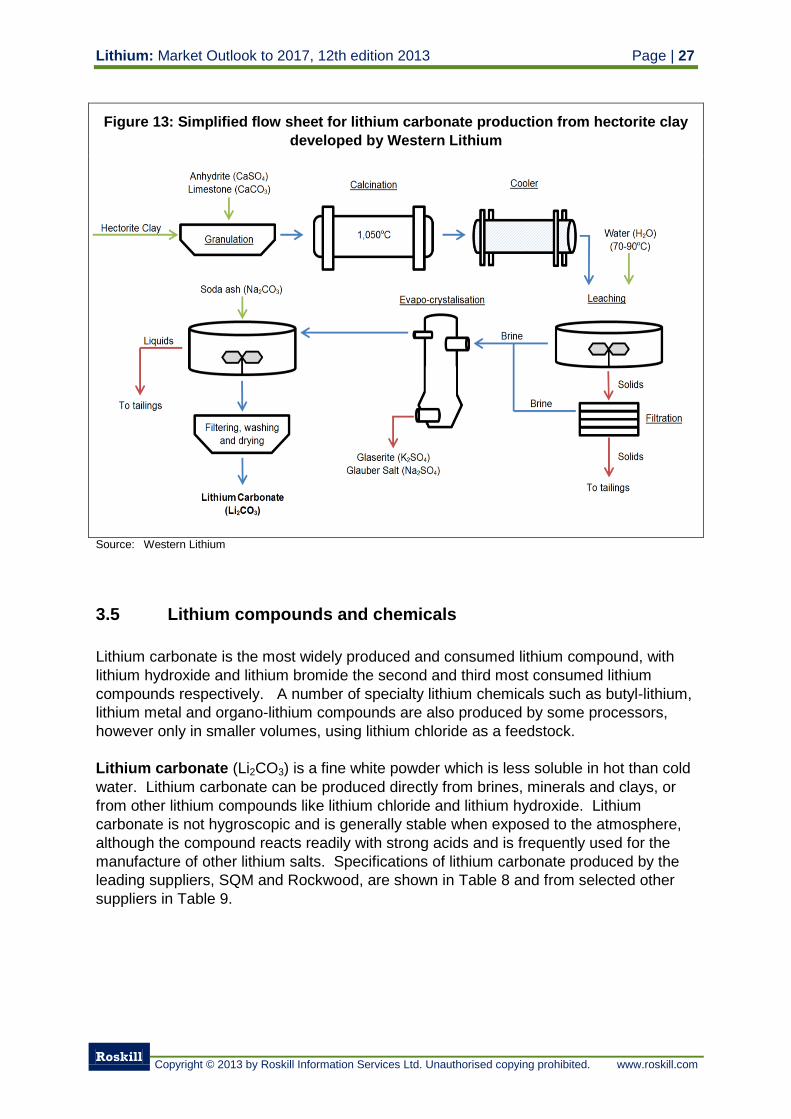

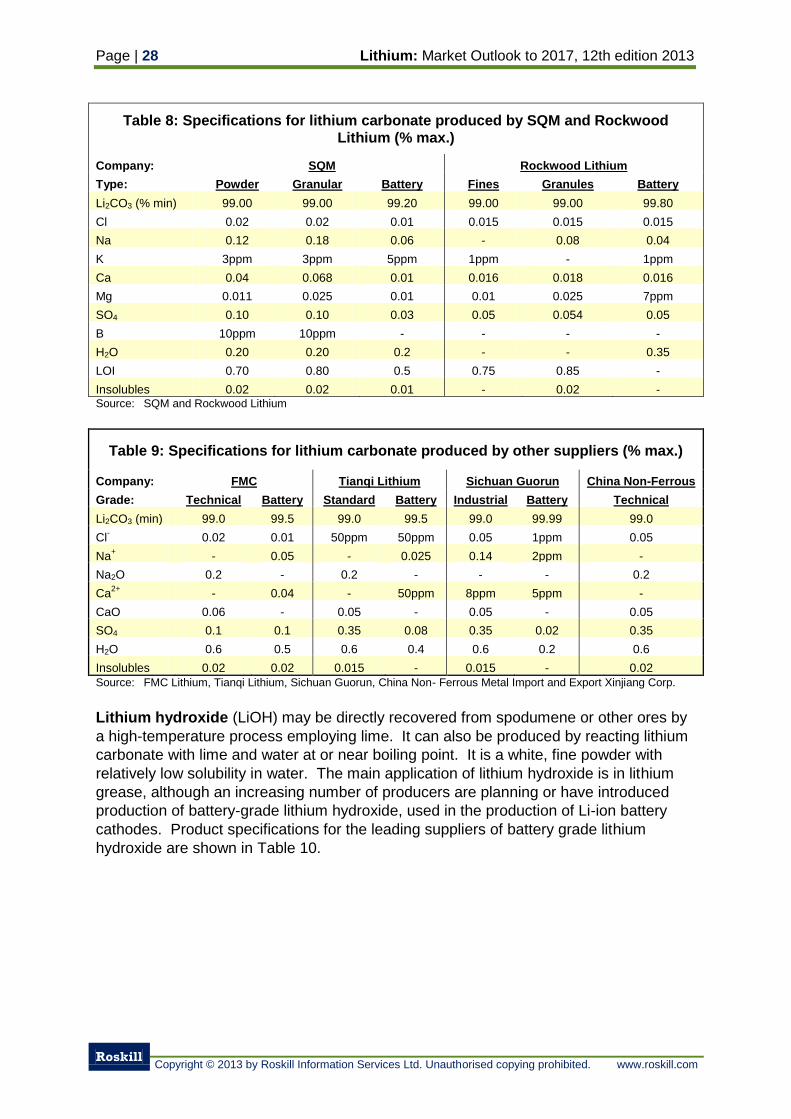

3.5 Lithium compounds and chemicals 27

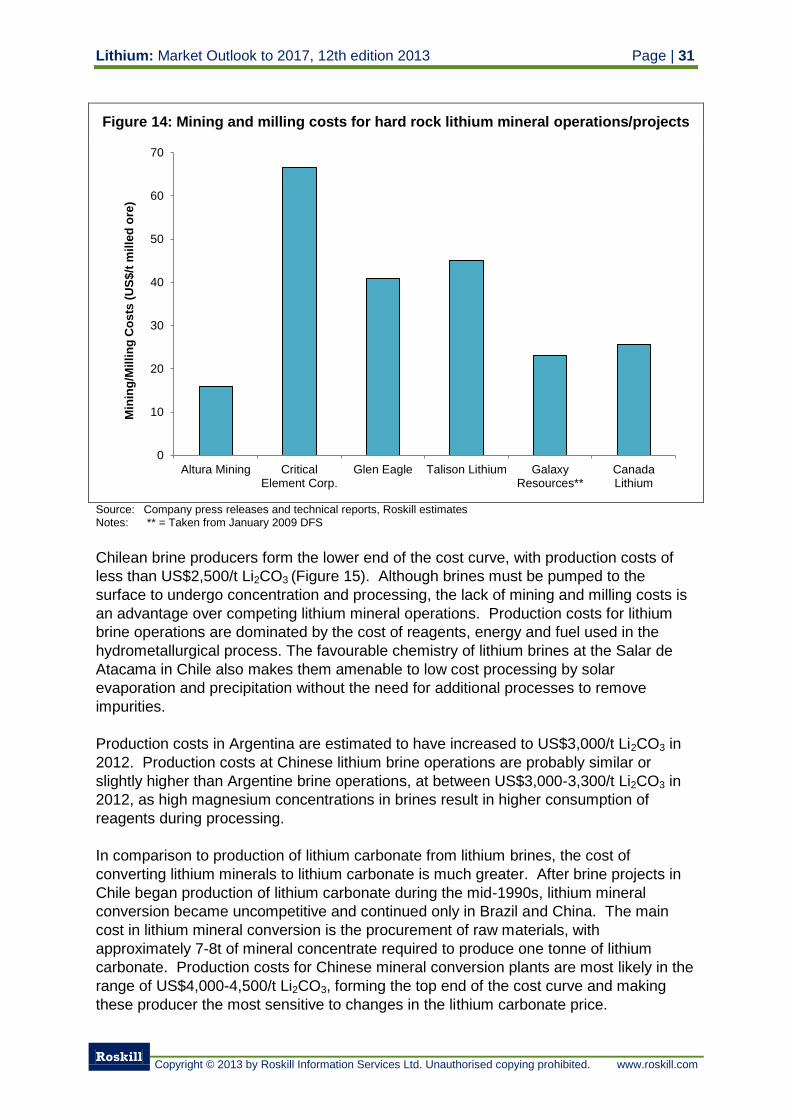

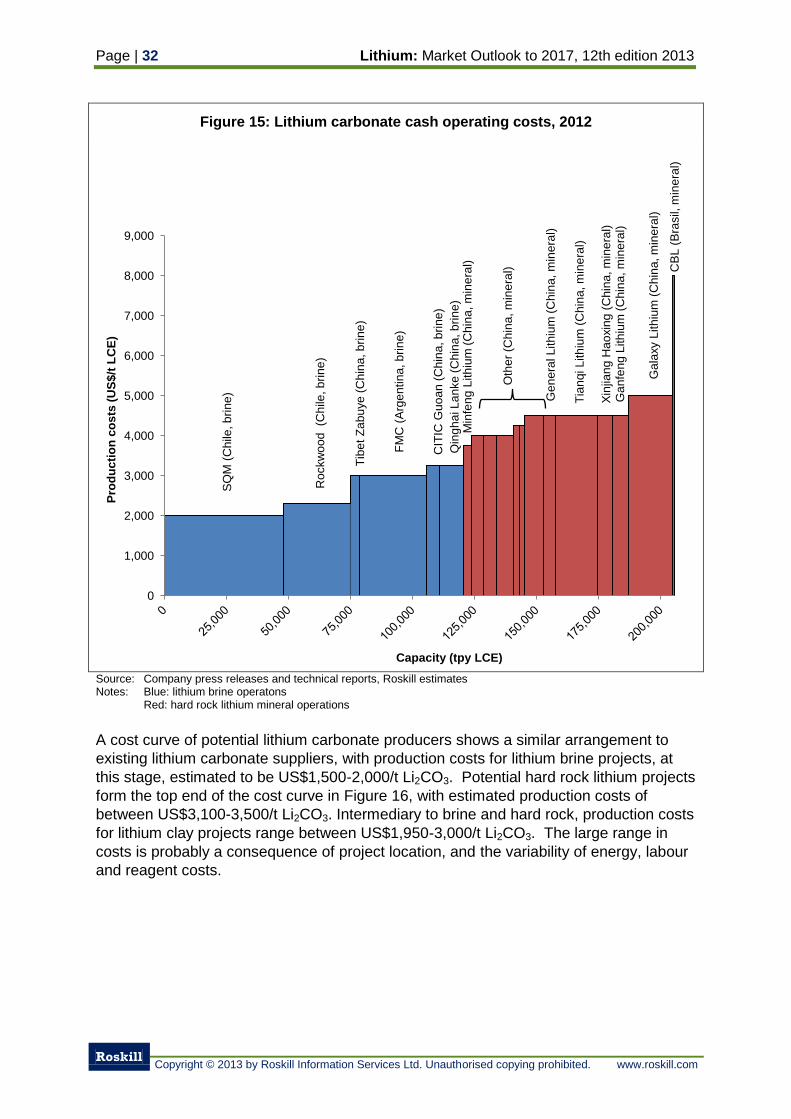

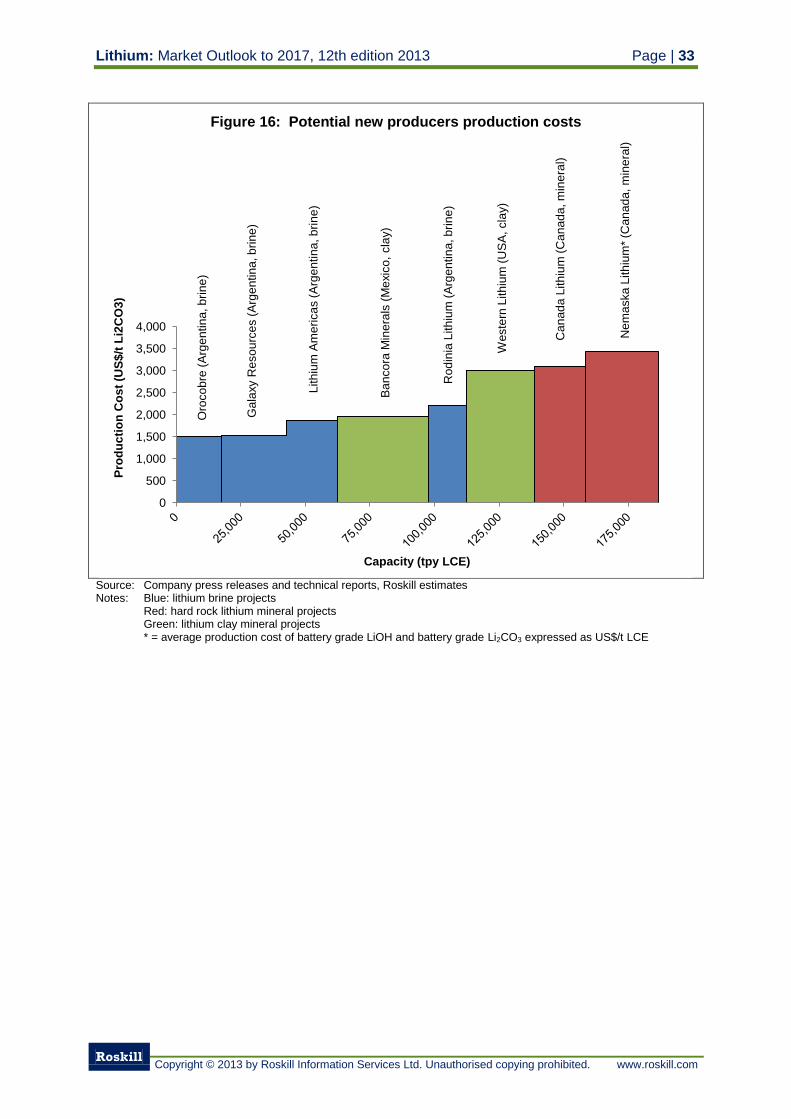

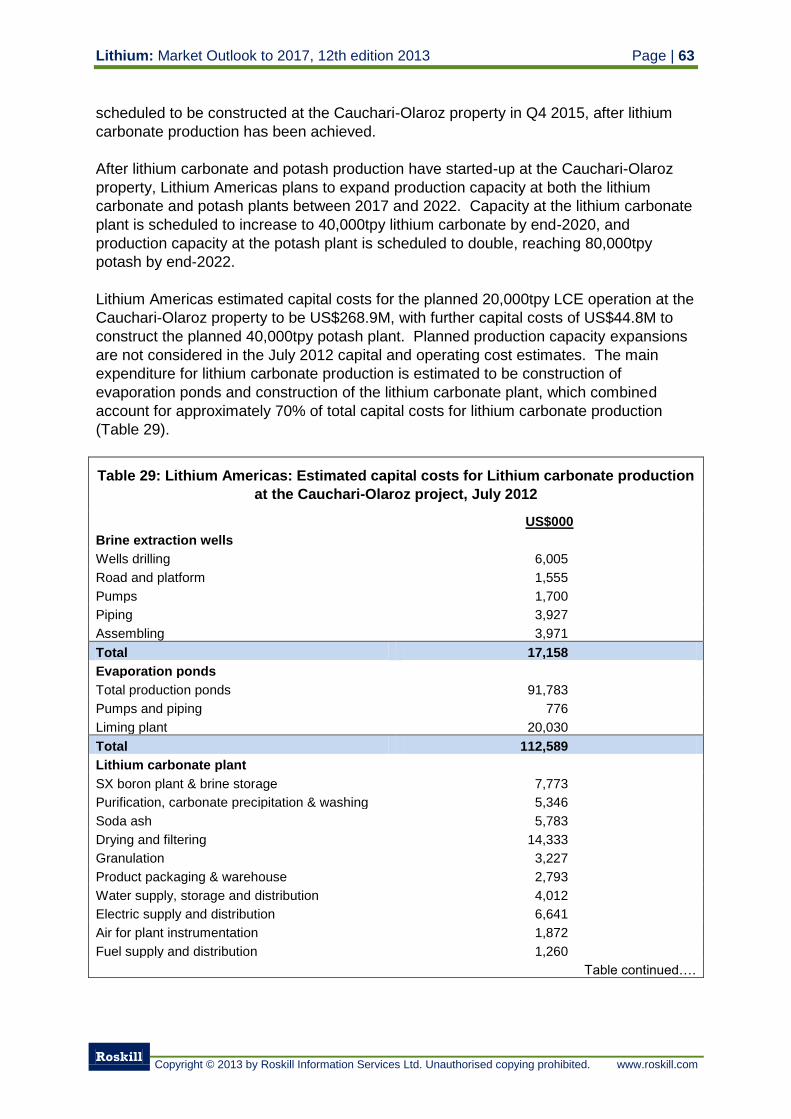

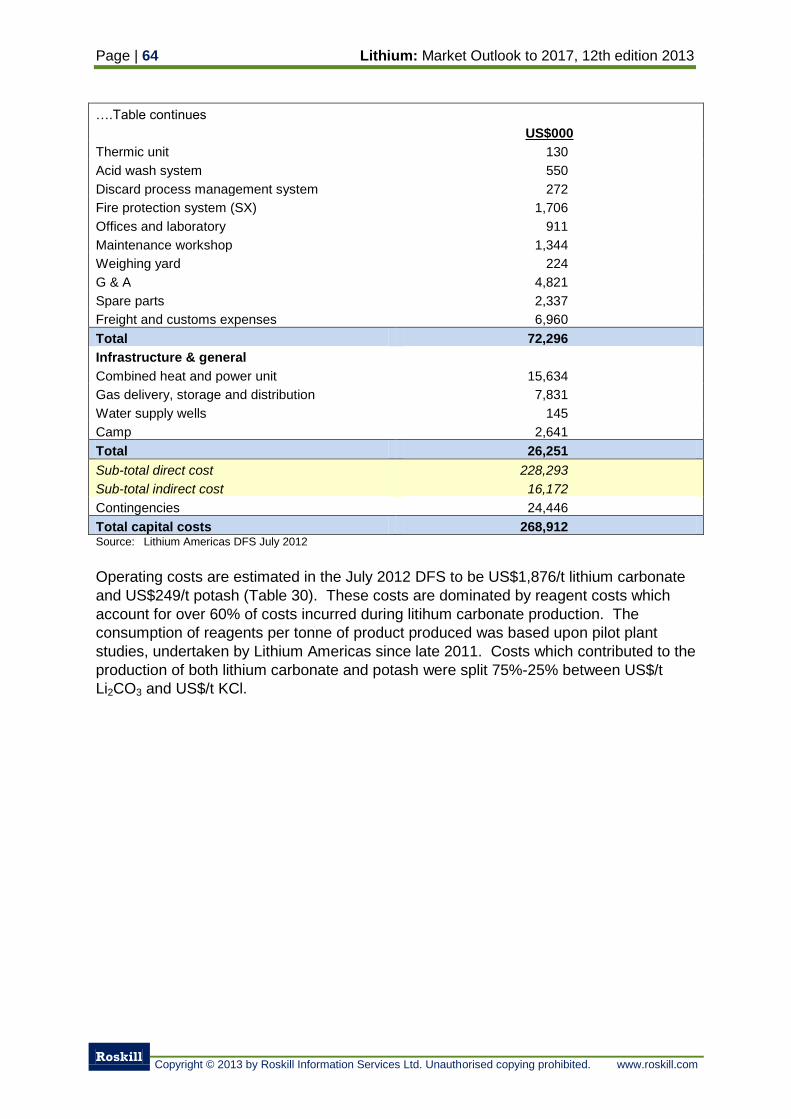

3.6 Production costs 30

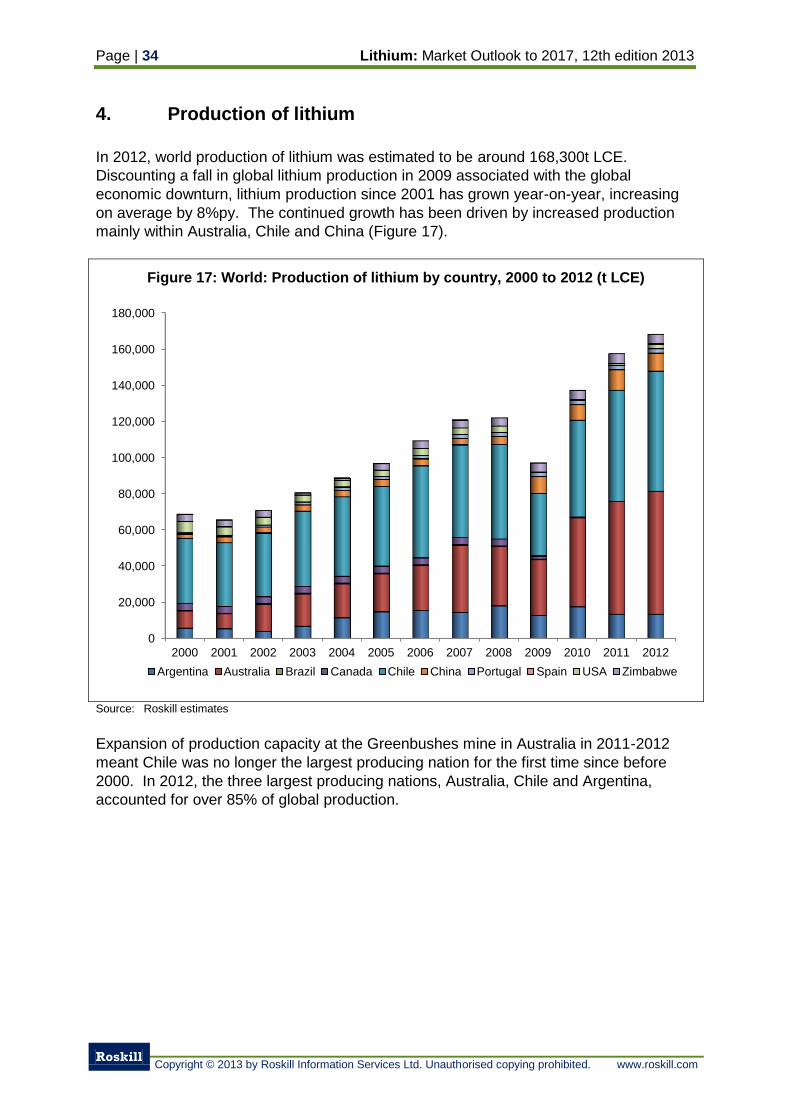

4. Production of lithium 34

4.1 Lithium production by source 35

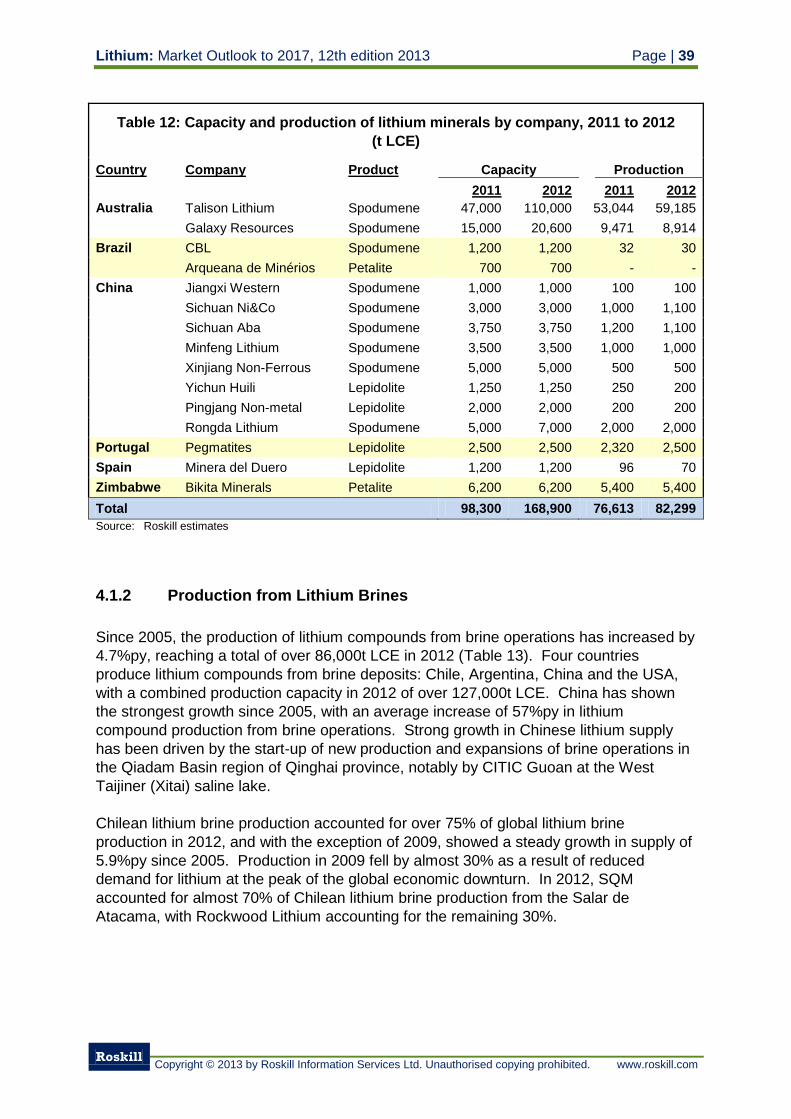

4.1.1 Production of Lithium Minerals 37

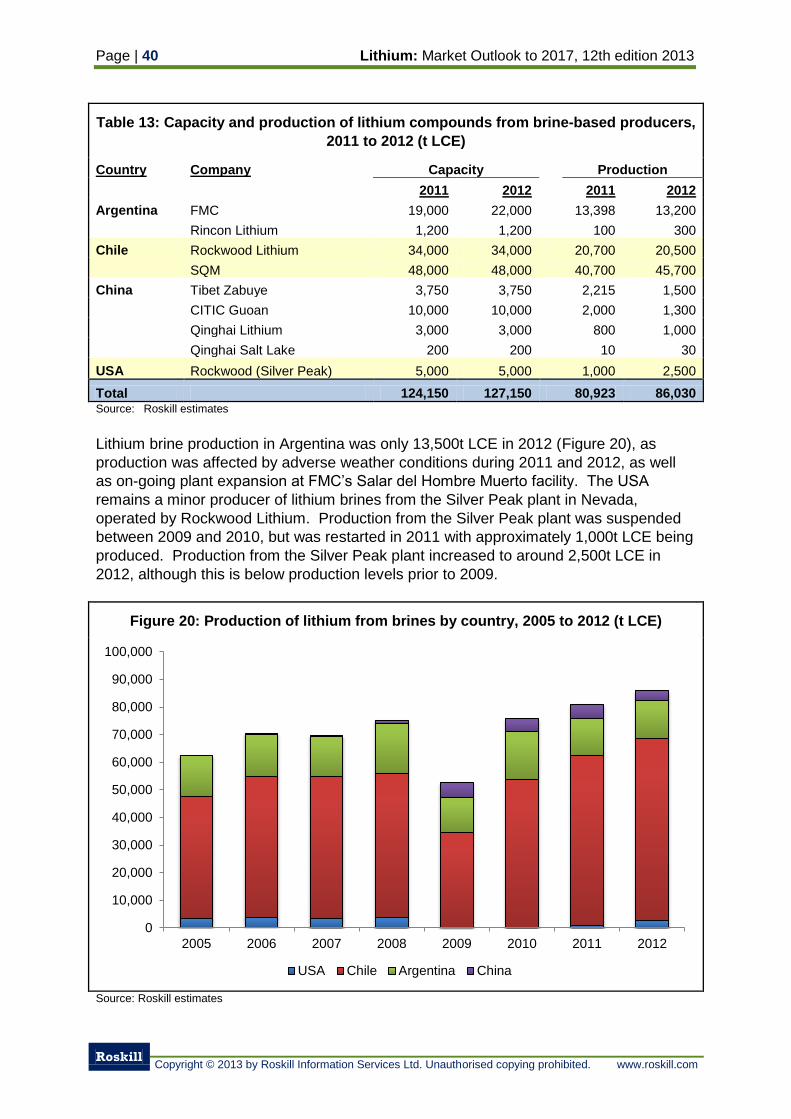

4.1.2 Production from Lithium Brines 39

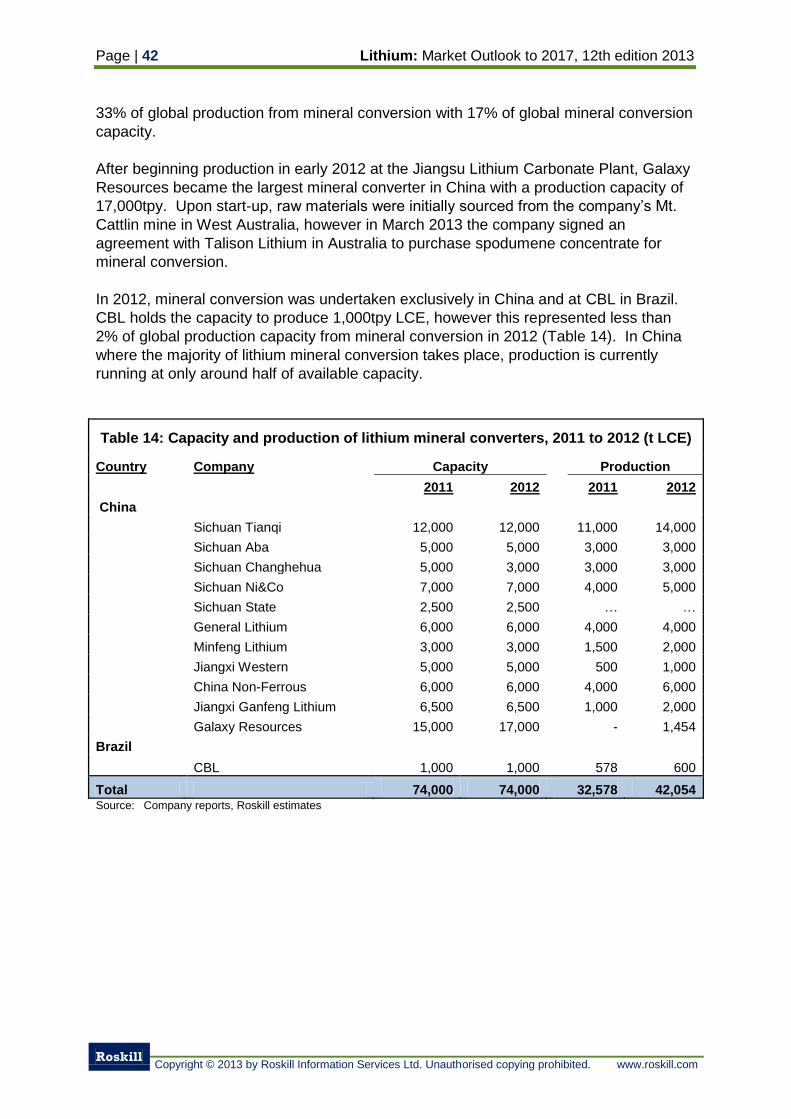

4.1.3 Production of lithium compounds from mineral conversion 41

4.1.4 Production of downstream lithium chemicals 43

4.2 Outlook for production capacity of lithium to 2017 44

4.2.1 Outlook for production capacity of lithium minerals 45

4.2.2 Outlook for lithium production capacity from brines 48

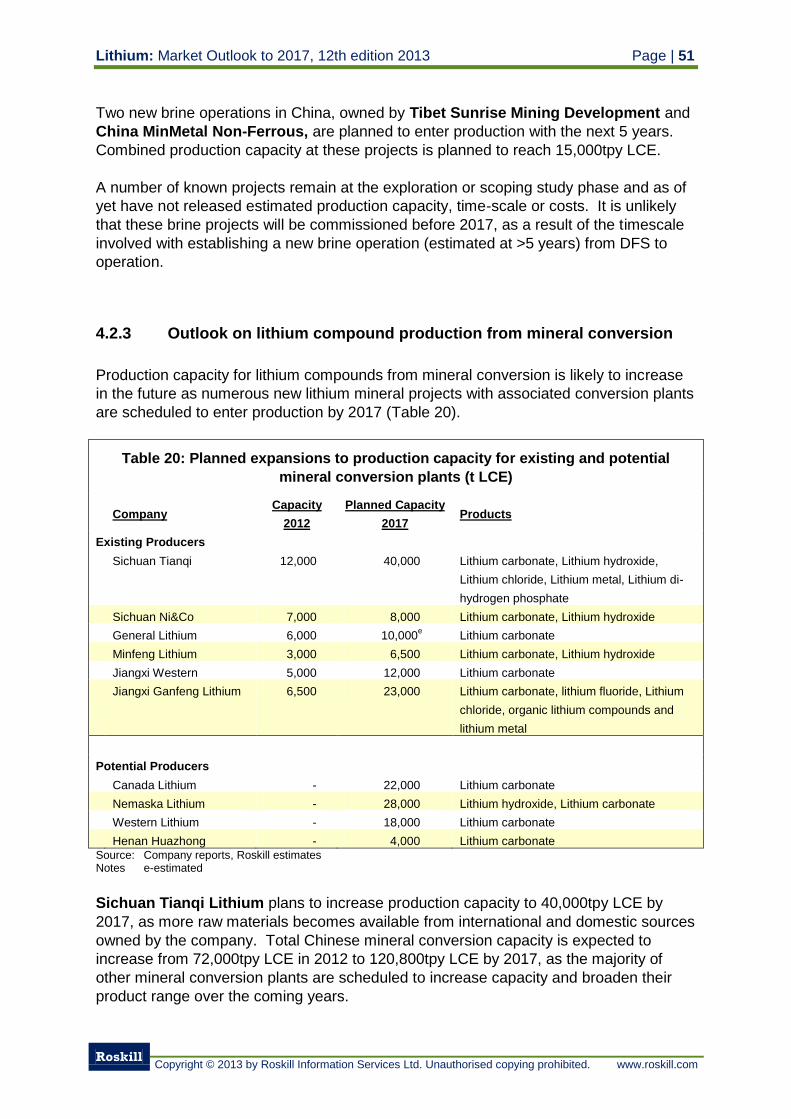

4.2.3 Outlook on lithium compound production from mineral conversion 51

4.3 Forecast production of lithium to 2017 52

5. Review of lithium producing countries 55

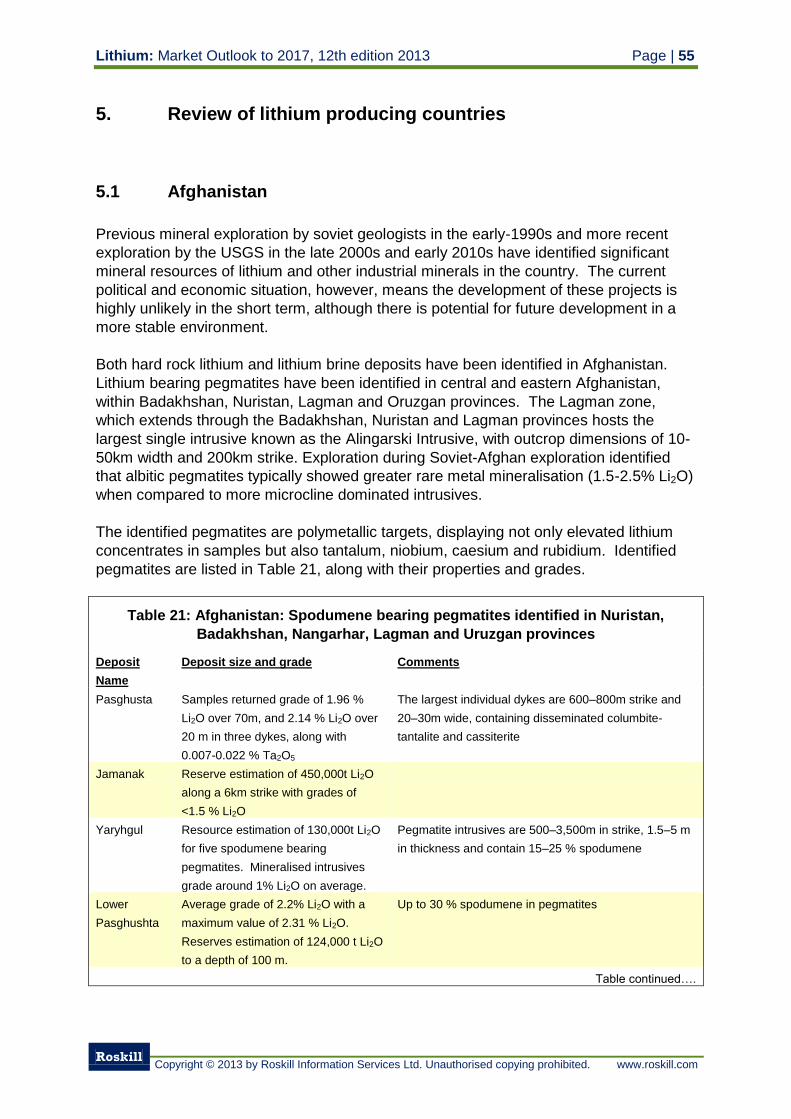

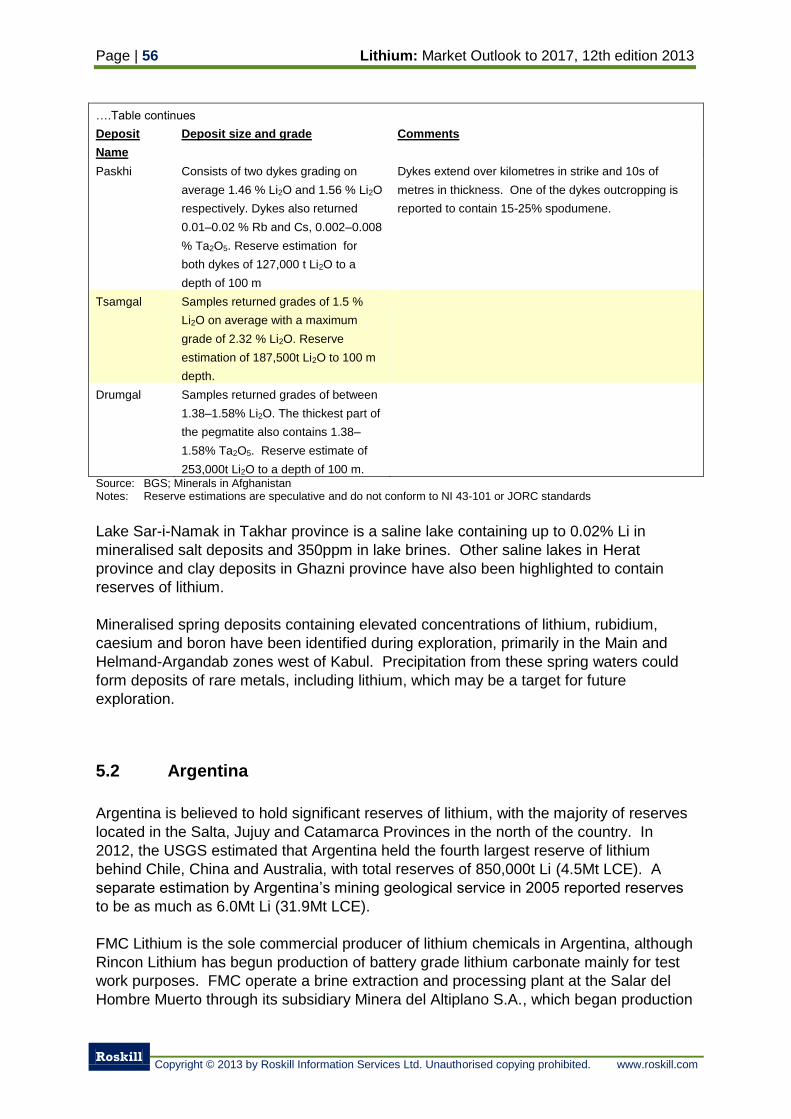

5.1 Afghanistan 55

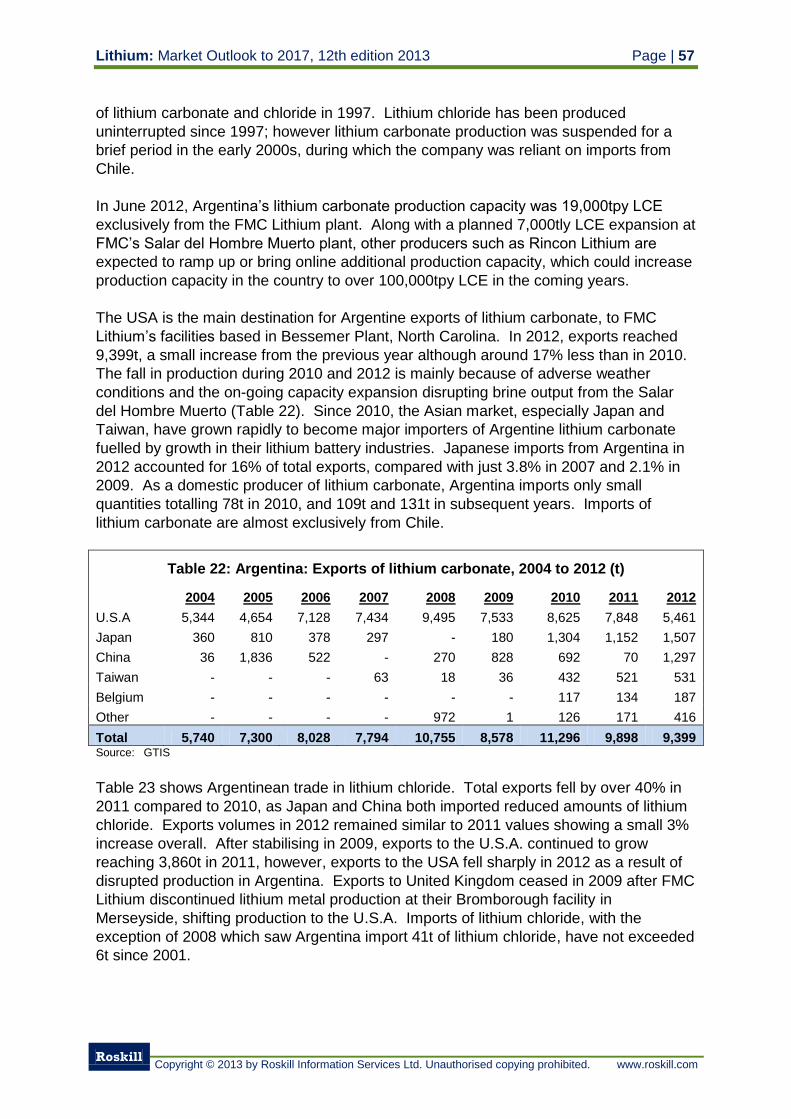

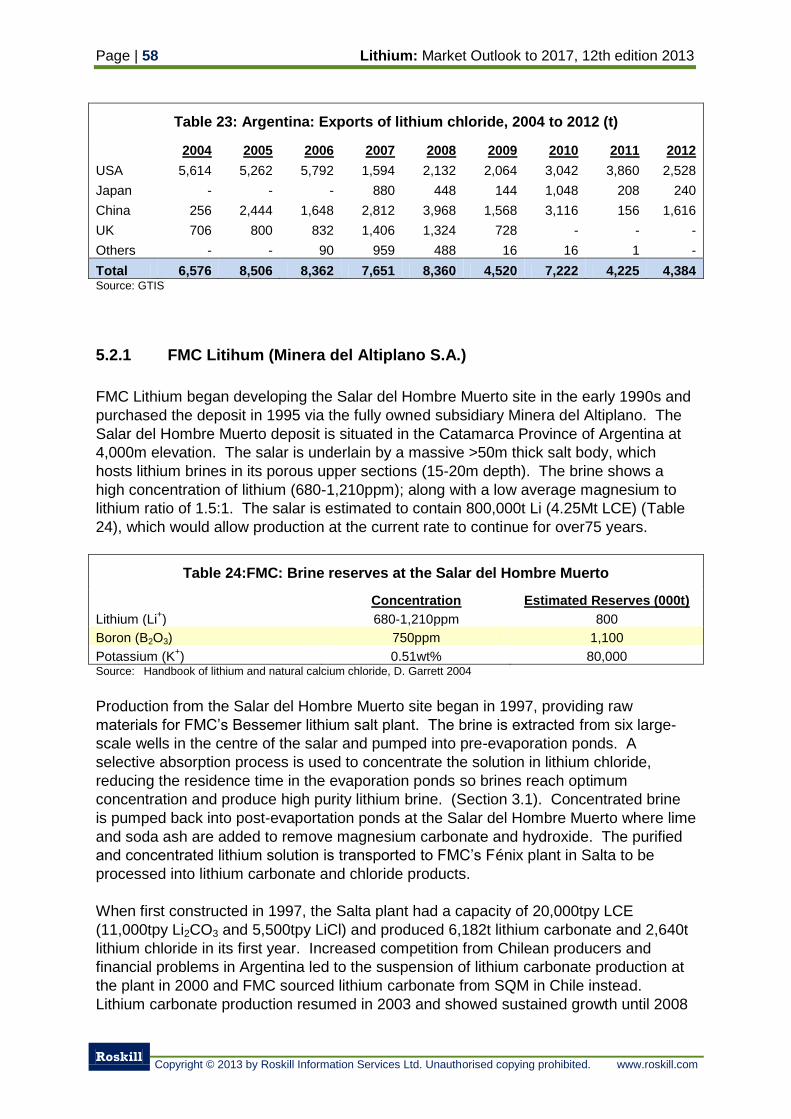

5.2 Argentina 56

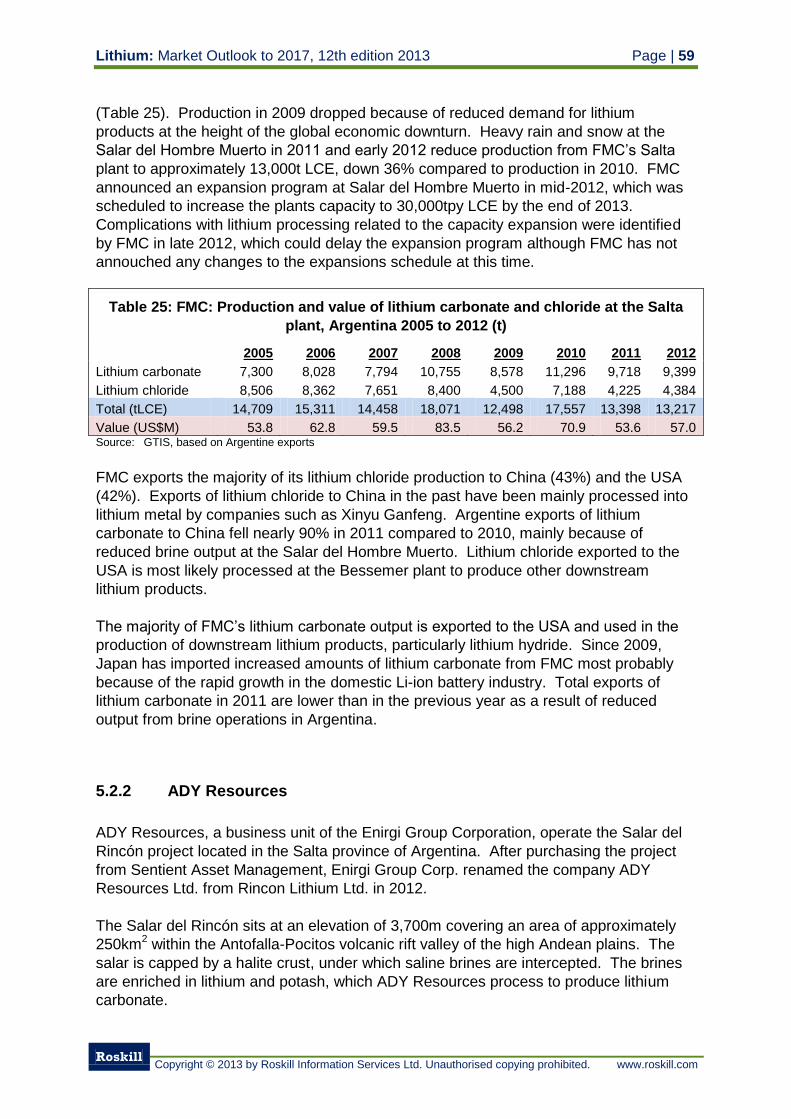

5.2.1 FMC Litihum (Minera del Altiplano S.A.) 58

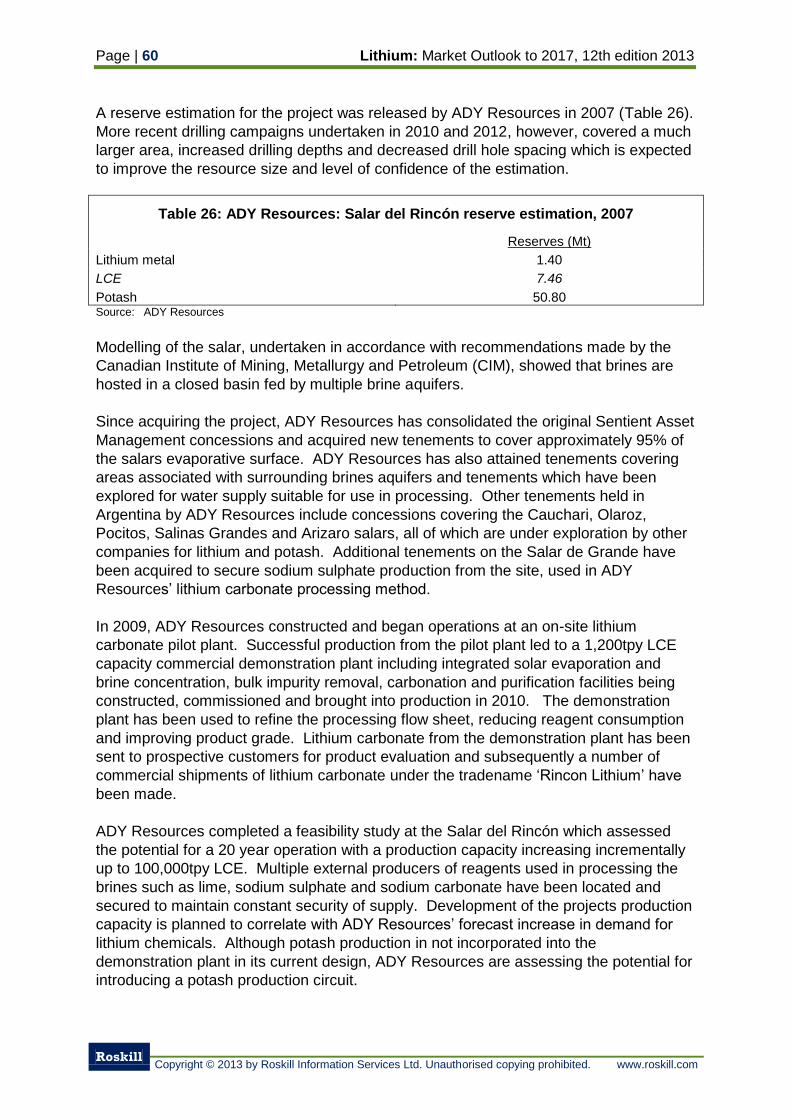

5.2.2 ADY Resources 59

5.2.3 Lithium Americas 61

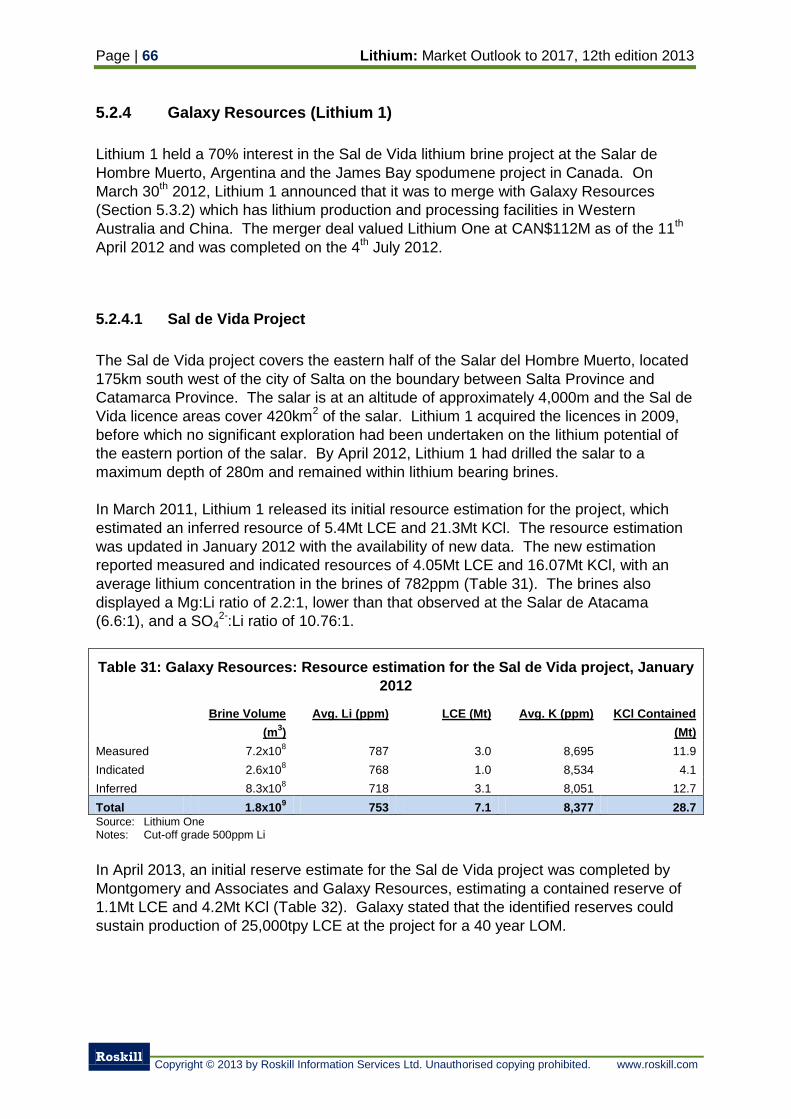

5.2.4 Galaxy Resources (Lithium 1) 66

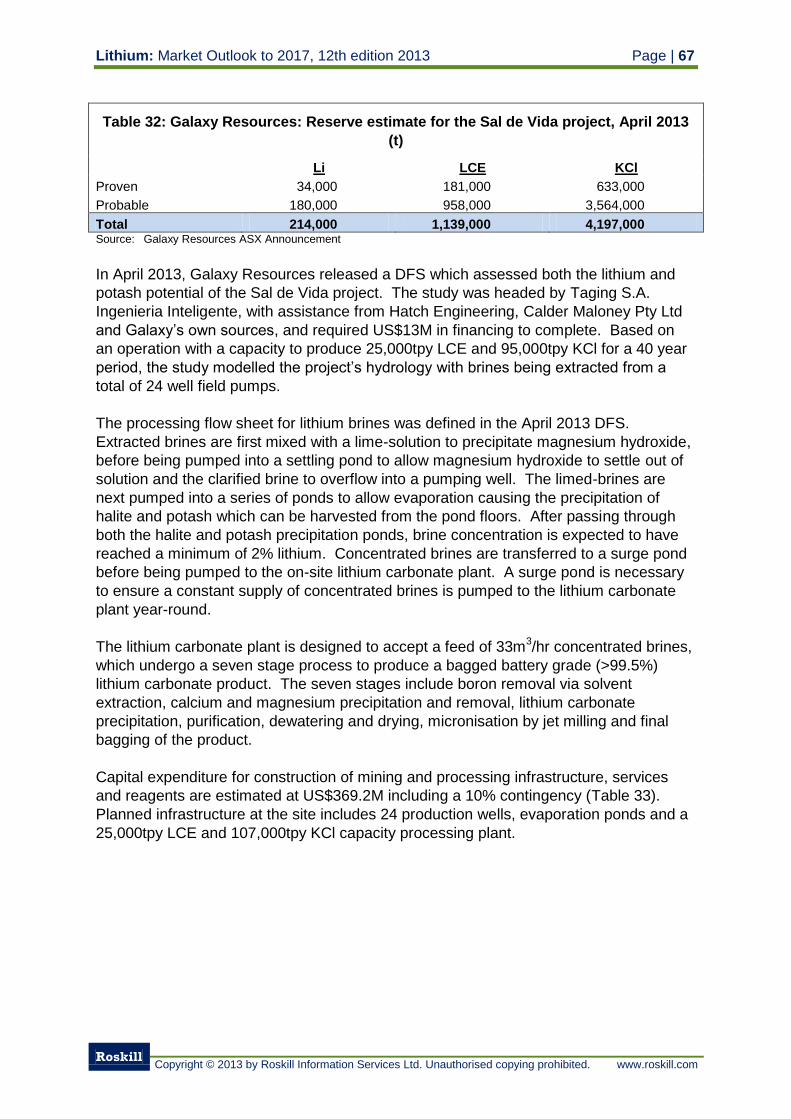

5.2.4.1 Sal de Vida Project 66

5.2.4.2 James Bay Hard-rock Lithium Project 68

5.2.5 Orocobre Ltd. 69

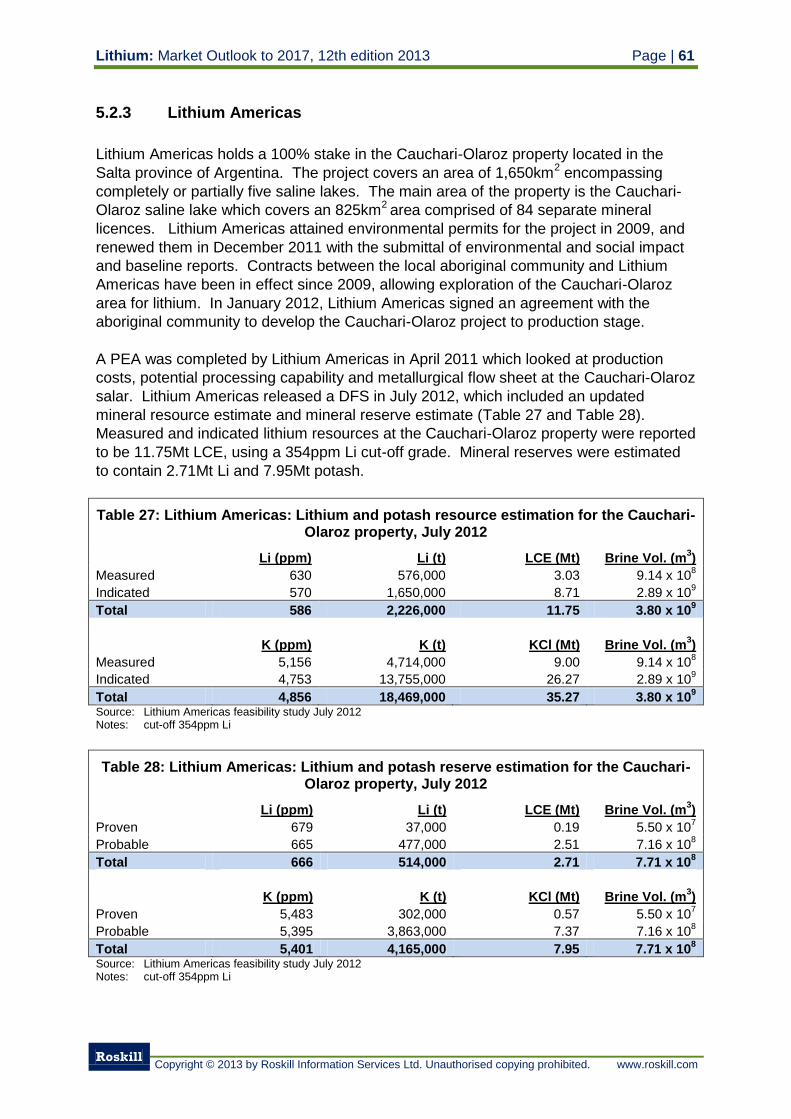

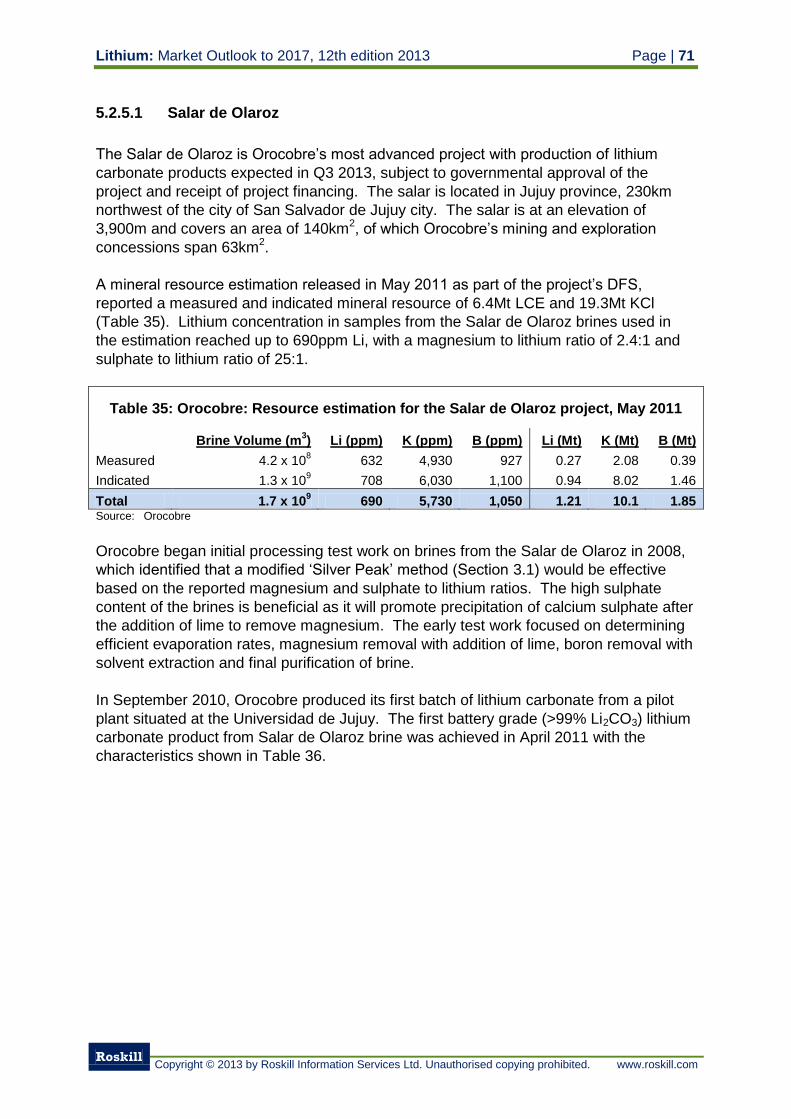

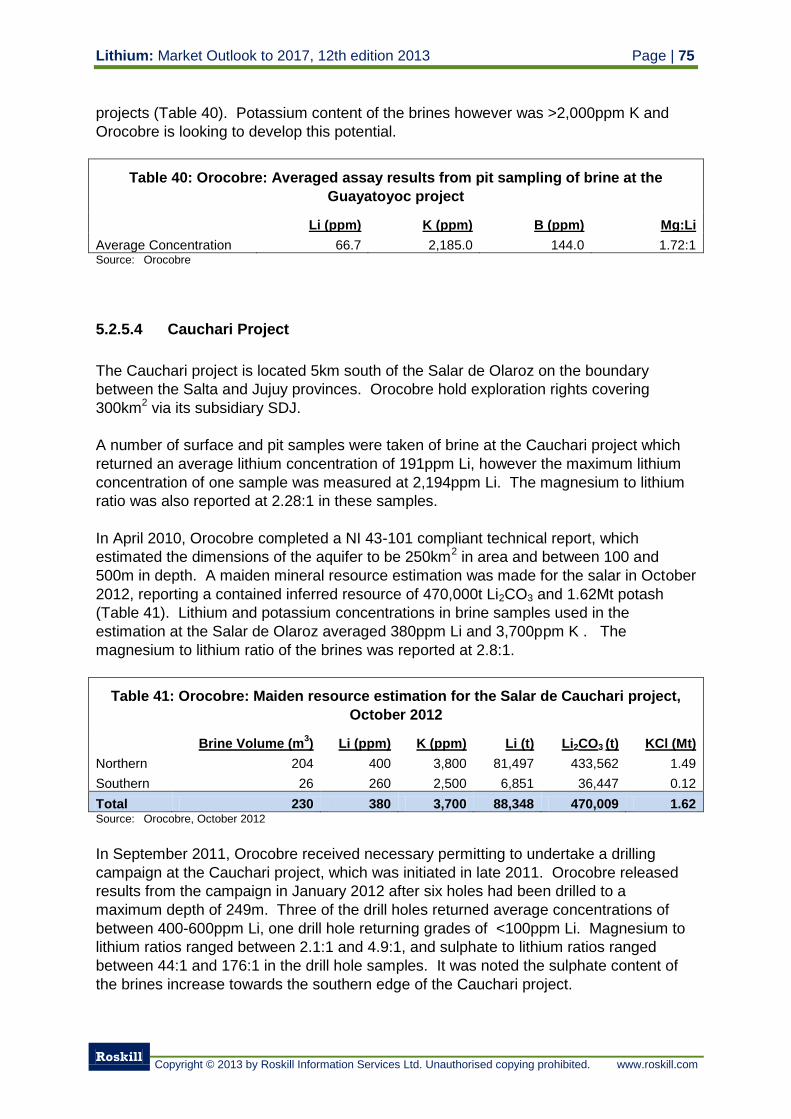

5.2.5.1 Salar de Olaroz 71

5.2.5.2 Salinas Grandes (Cangrejillo) 74

5.2.5.3 Guayatoyoc Project 74

5.2.5.4 Cauchari Project 75

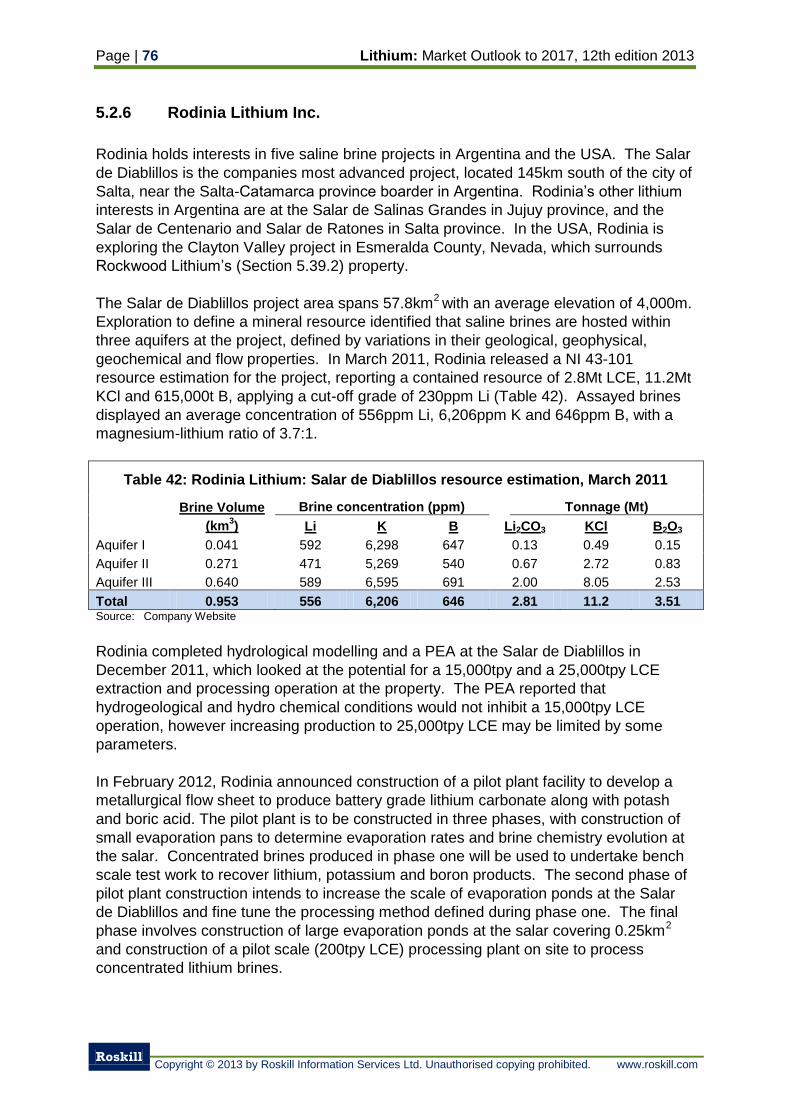

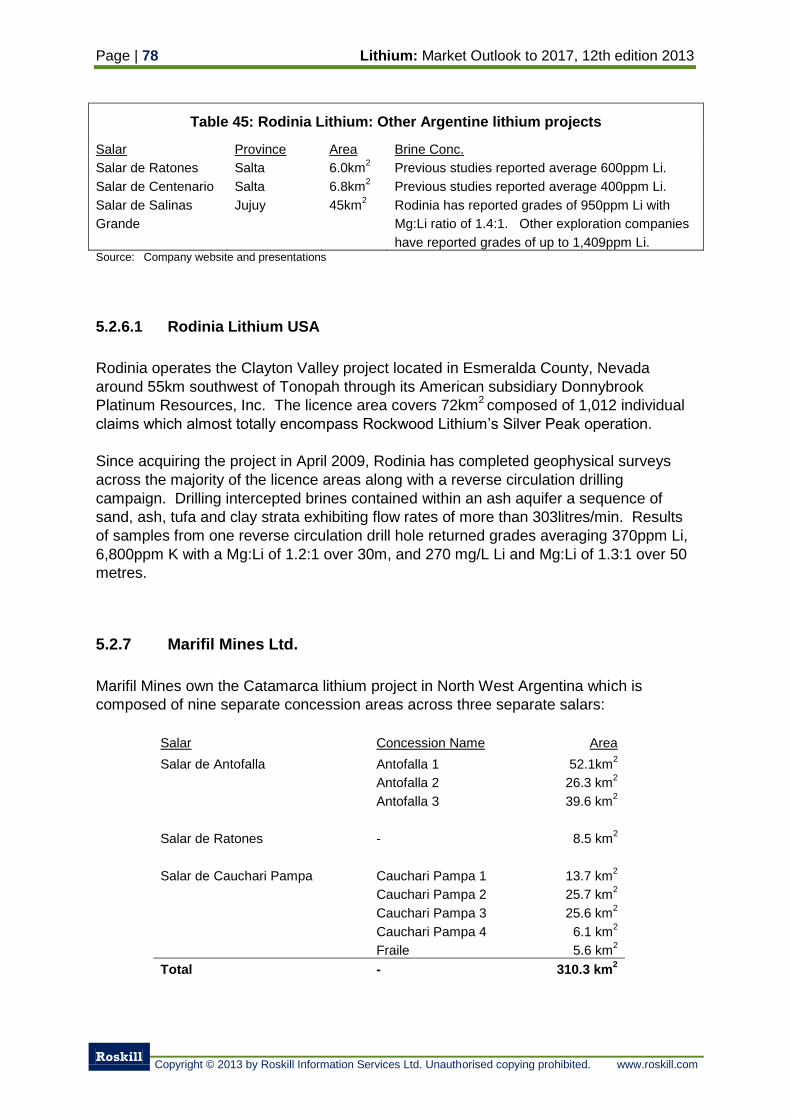

5.2.6 Rodinia Lithium Inc. 76

5.2.6.1 Rodinia Lithium USA 78

5.2.7 Marifil Mines Ltd. 78

5.2.8 International Lithium Corporation 79

5.2.9 Other prospects for Lithium Production 79

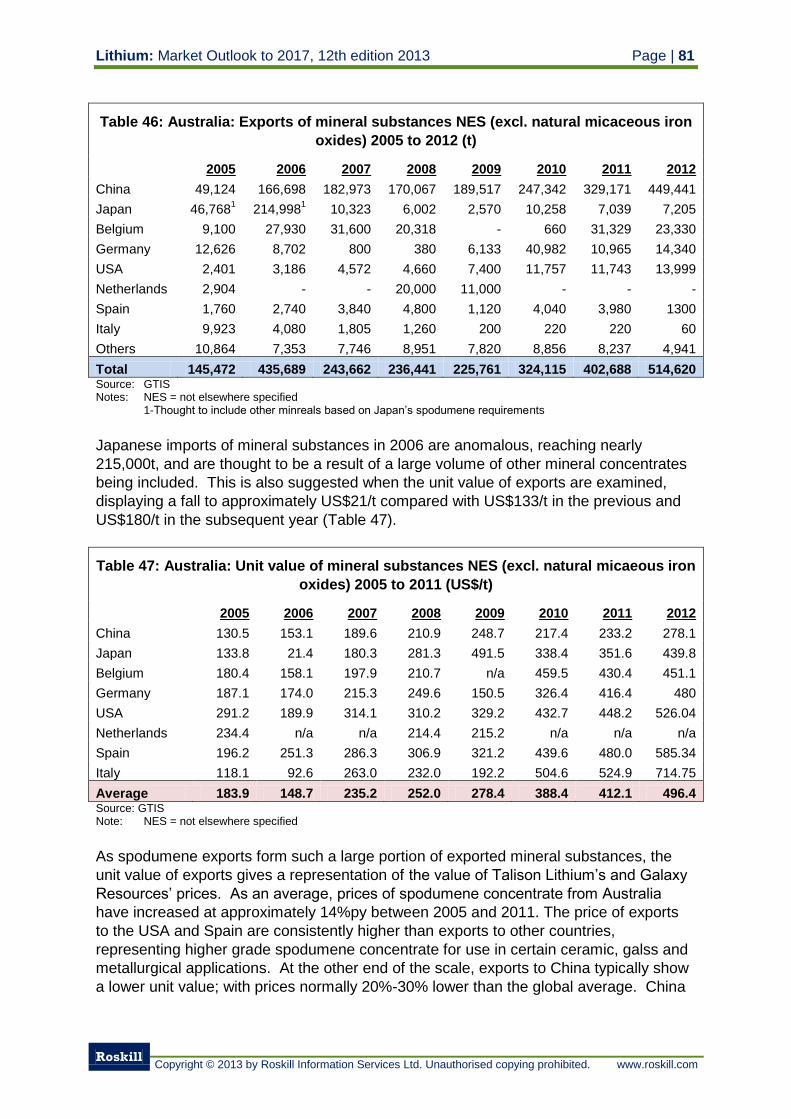

5.3 Australia 80

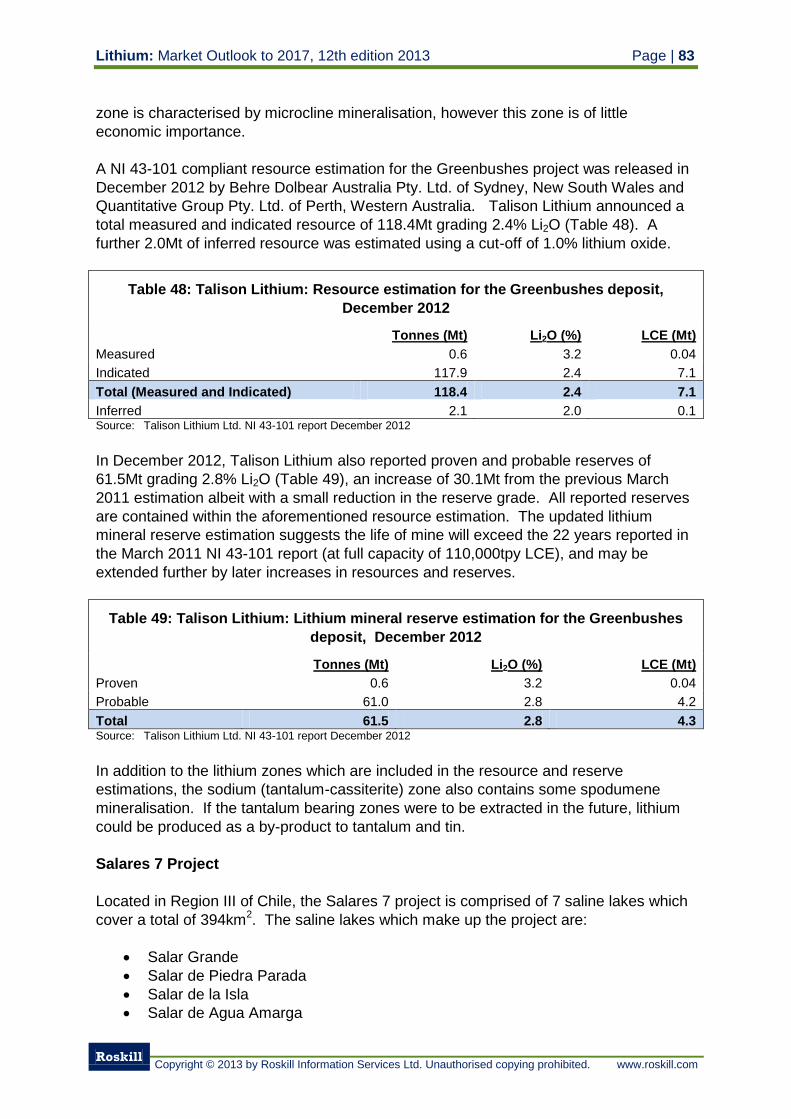

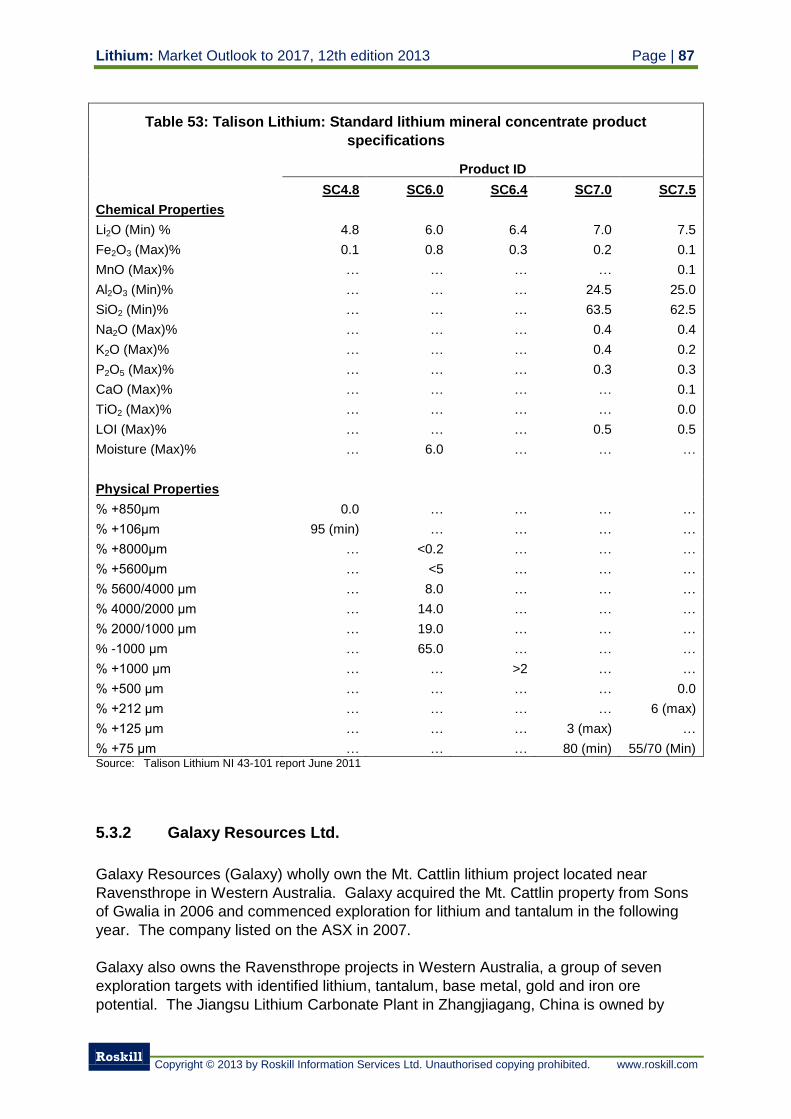

5.3.1 Talison Lithium 82

5.3.1.1 Resources and Reserves 82

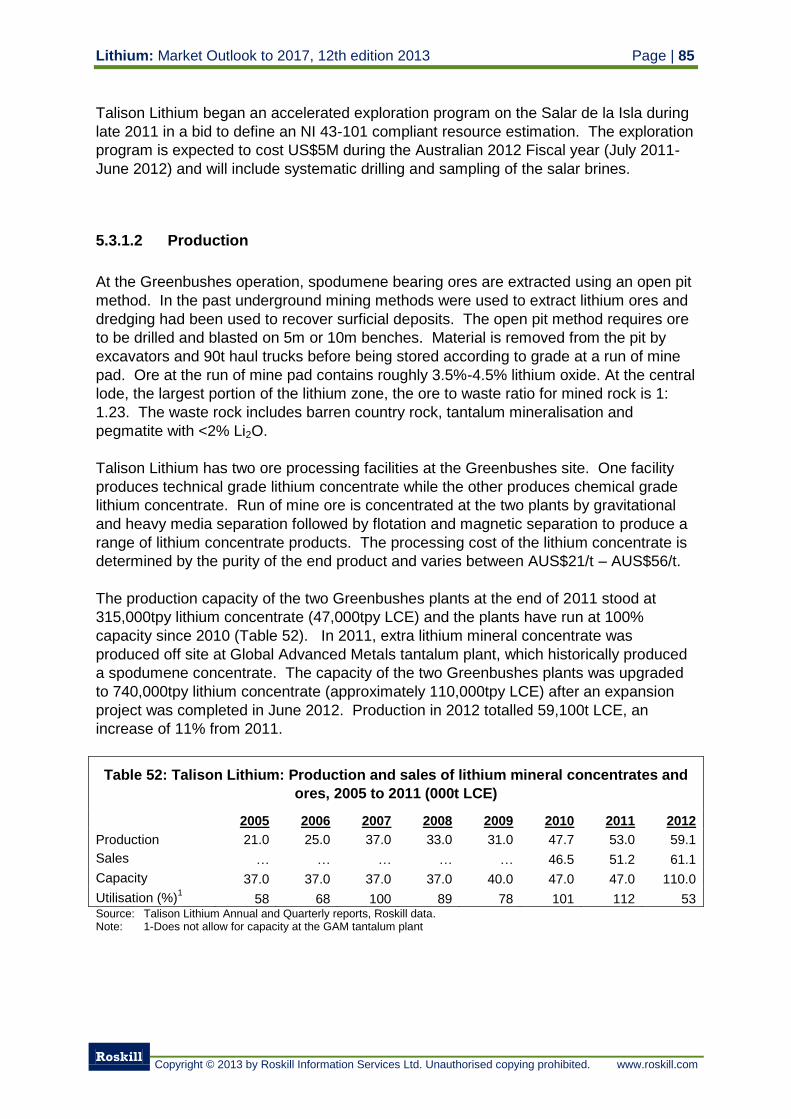

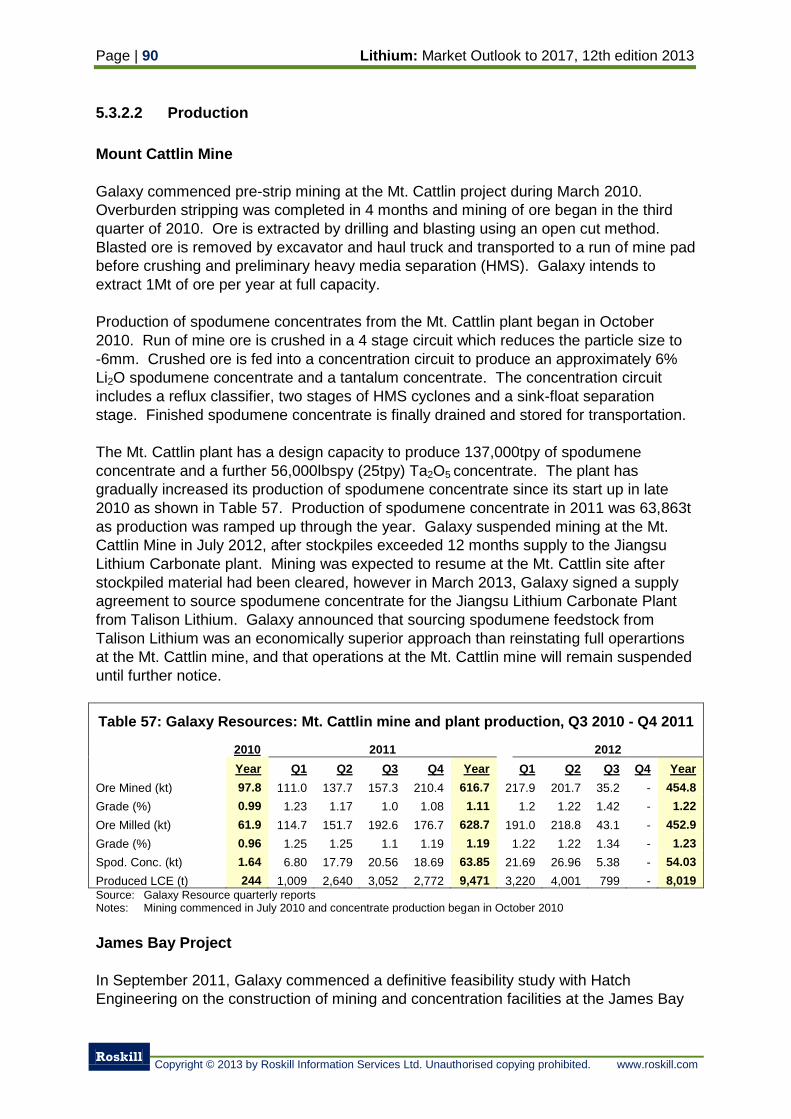

5.3.1.2 Production 85

5.3.1.3 Products 86

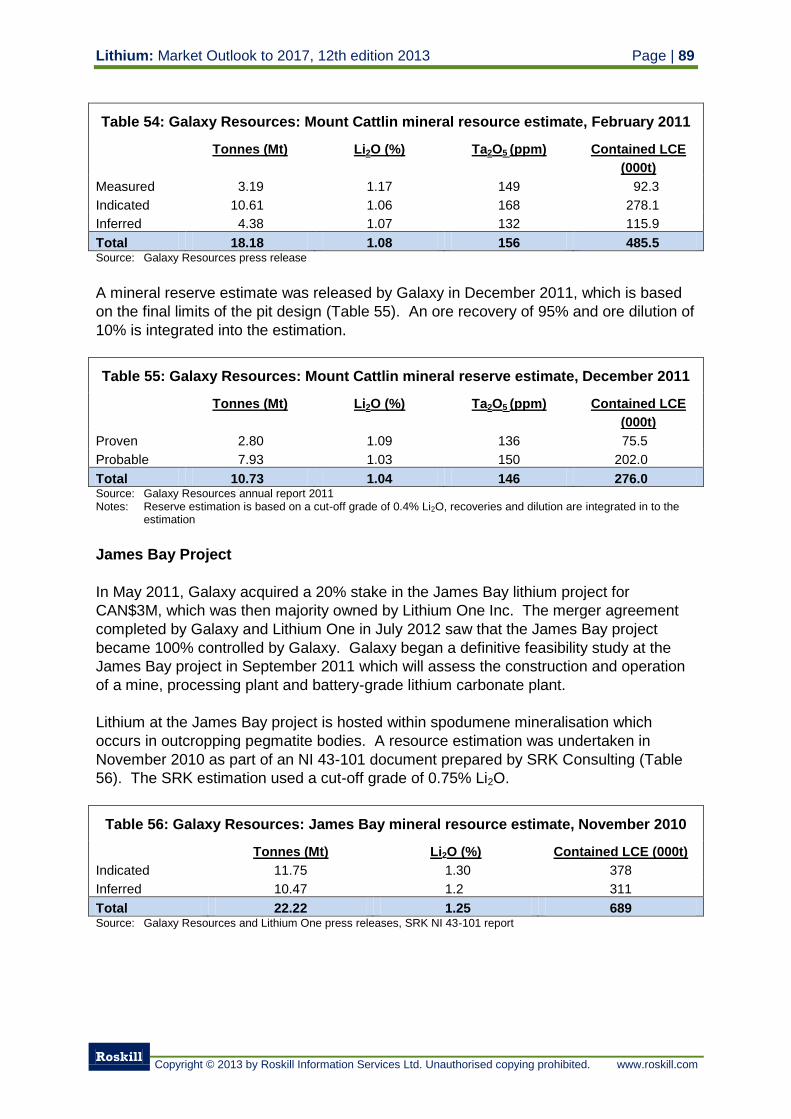

5.3.2 Galaxy Resources Ltd. 87

5.3.2.1 Reserves and Resources 88

5.3.2.2 Production 90

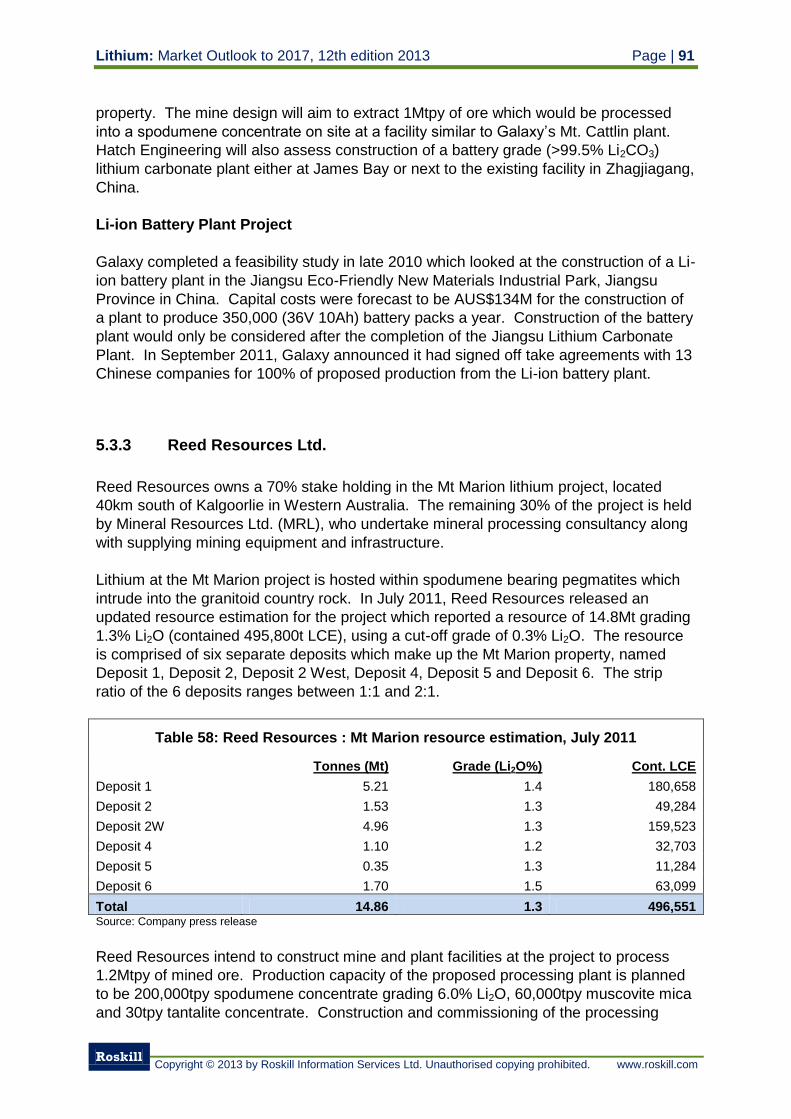

5.3.3 Reed Resources Ltd. 91

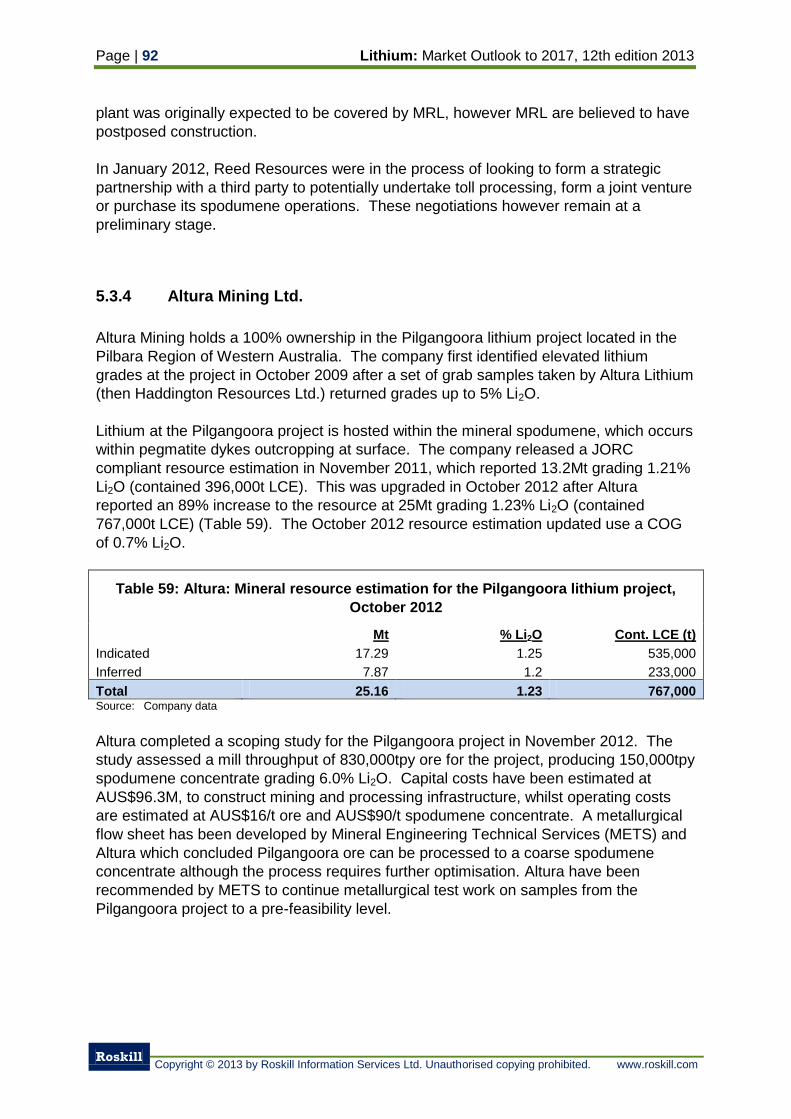

5.3.4 Altura Mining Ltd. 92

5.3.5 Artemis Resources 93

5.3.6 Amerilithium 93

5.3.7 Reward Minerals 93

5.4 Austria 93

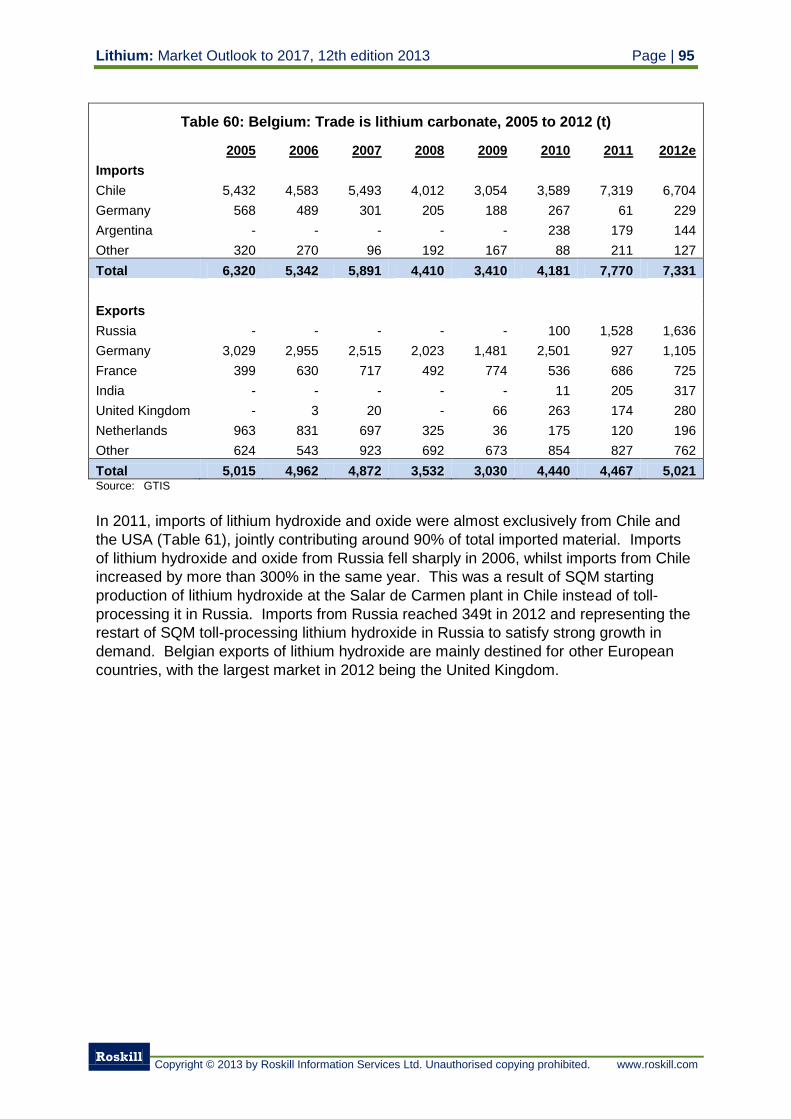

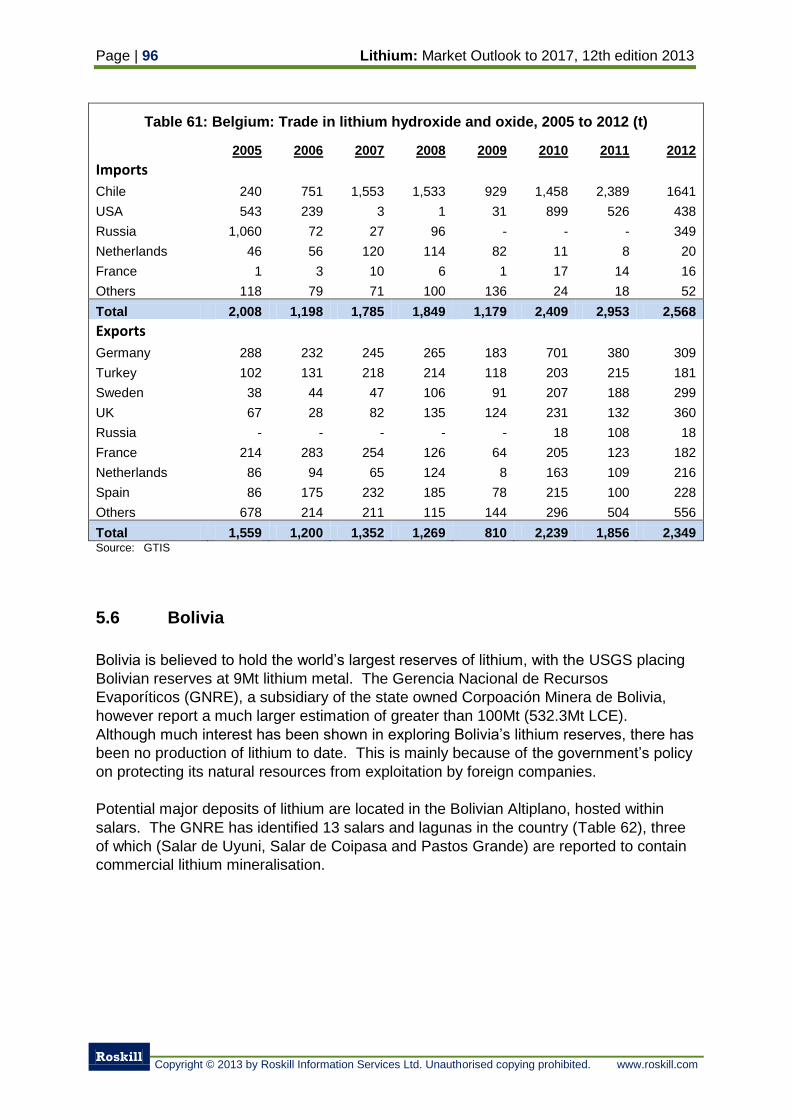

5.5 Belgium 94

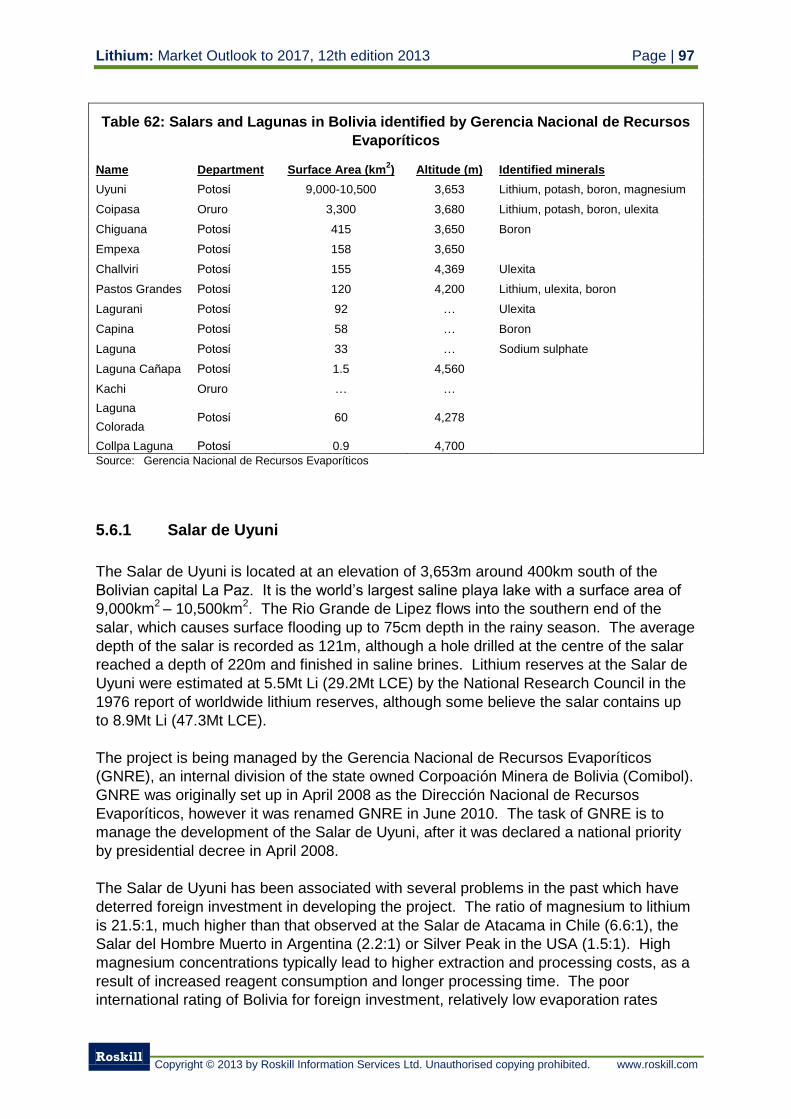

5.6 Bolivia 96

5.6.1 Salar de Uyuni 97

5.6.2 Salar de Coipasa 99

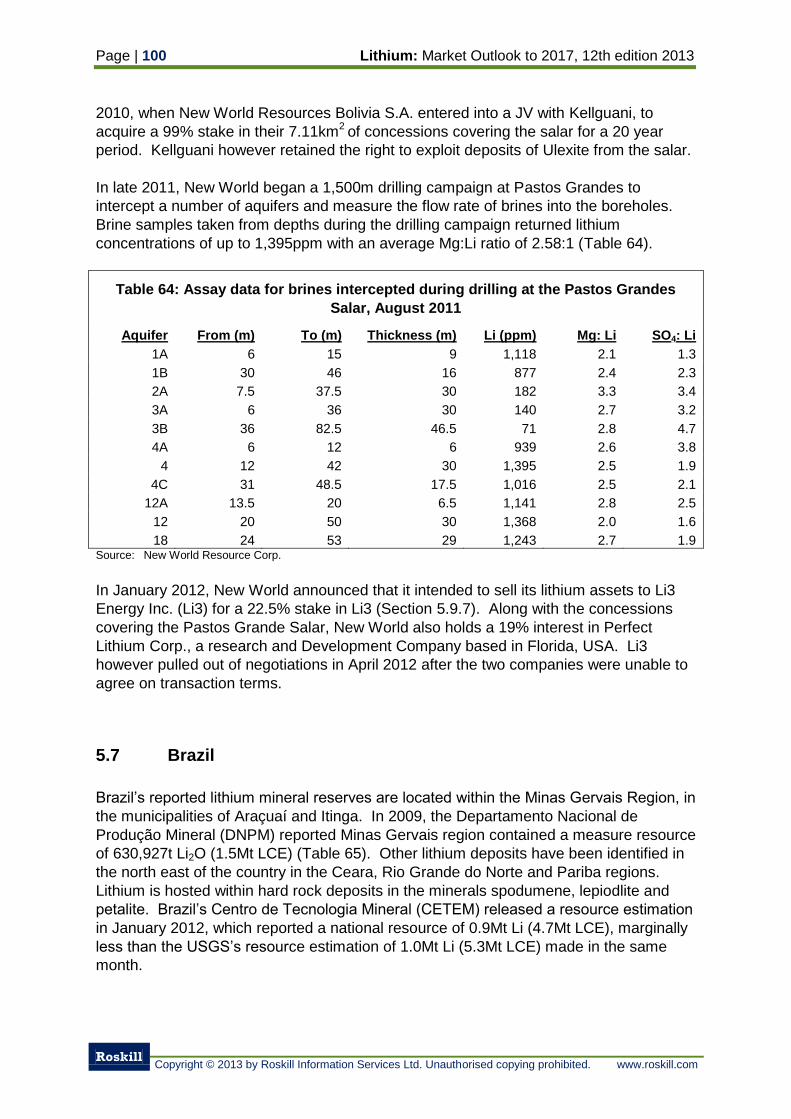

5.6.3 New World Resource Corp. 99

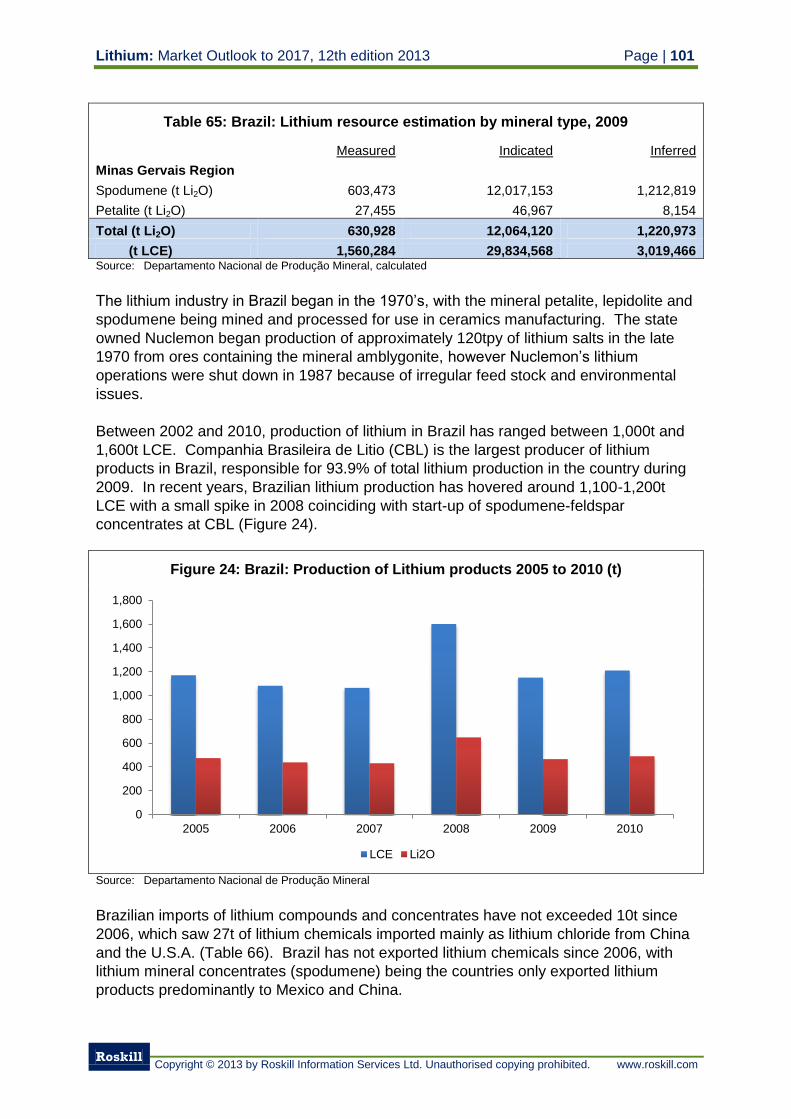

5.7 Brazil 100

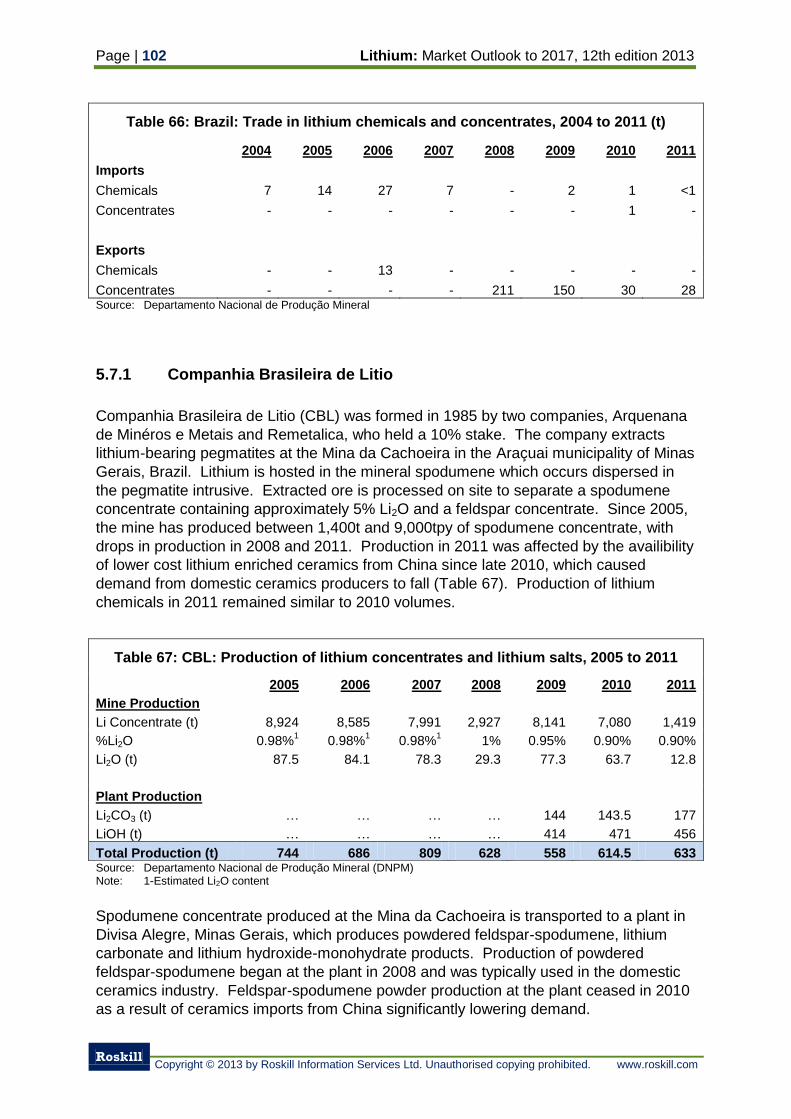

5.7.1 Companhia Brasileira de Litio 102

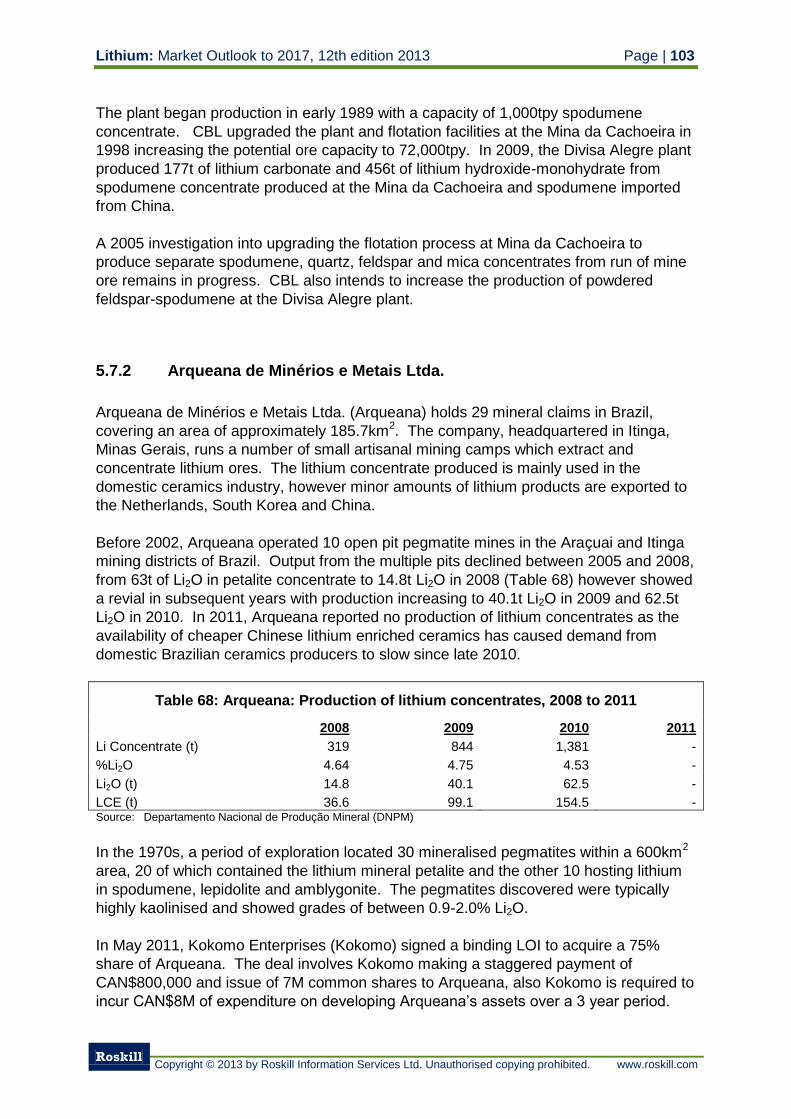

5.7.2 Arqueana de Minérios e Metais Ltda. 103

5.7.3 Advance Metallurgical Group (AMG) 104

5.8 Canada 104

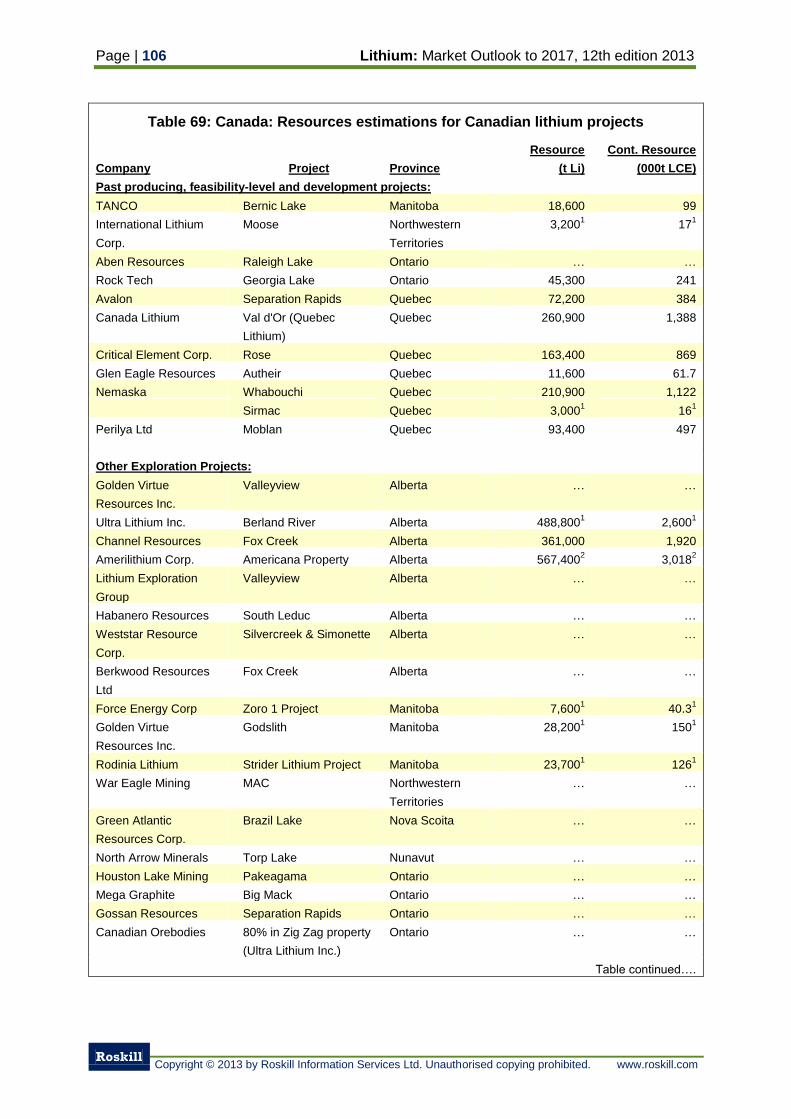

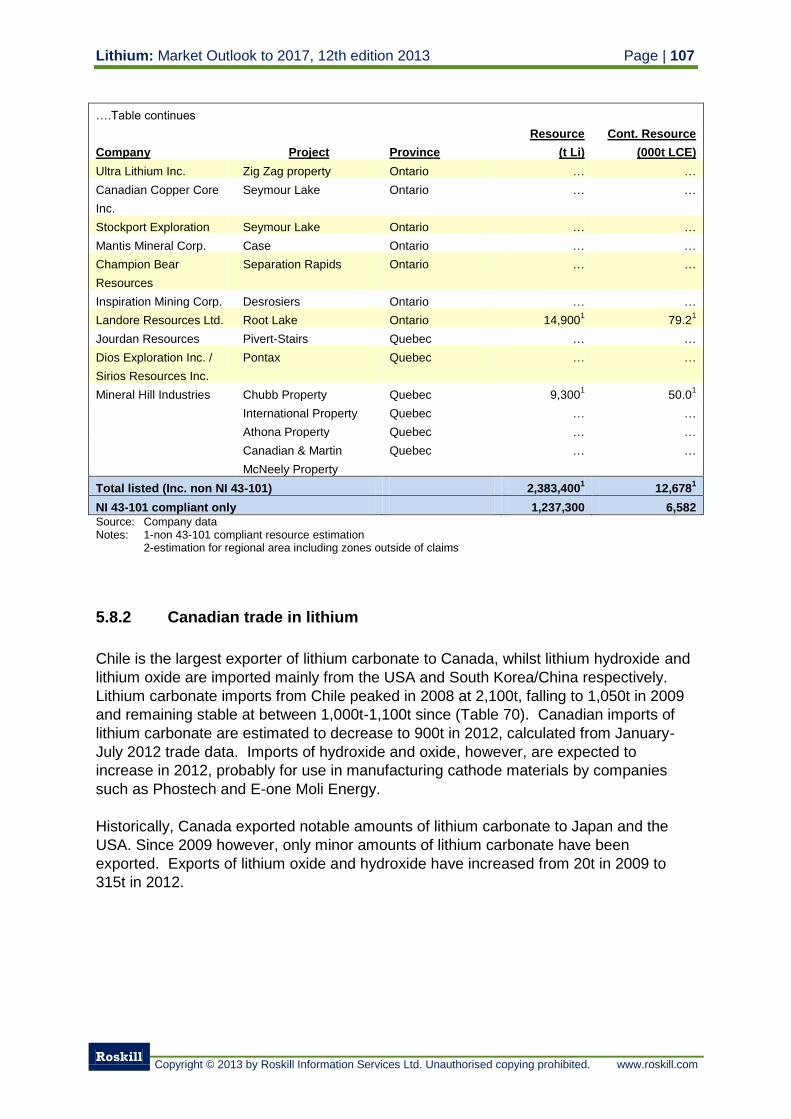

5.8.1 Lithium resources in Canada 105

5.8.2 Canadian trade in lithium 107

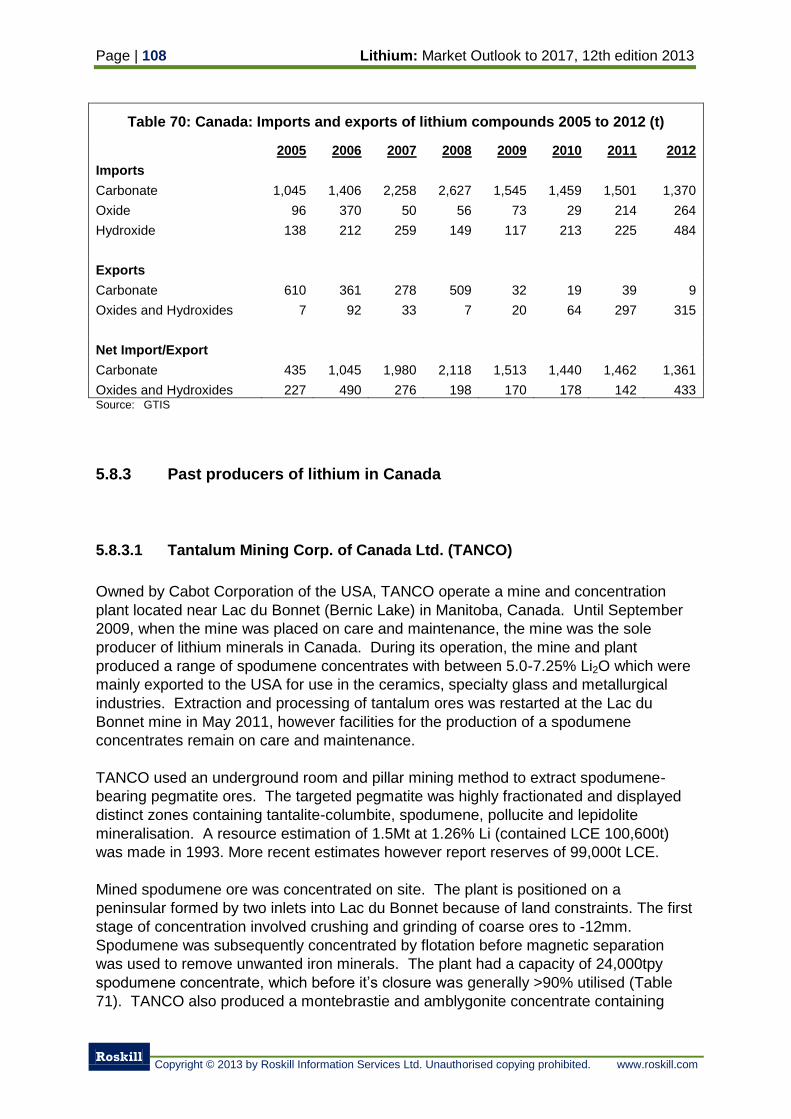

5.8.3 Past producers of lithium in Canada 108

5.8.3.1 Tantalum Mining Corp. of Canada Ltd. (TANCO) 108

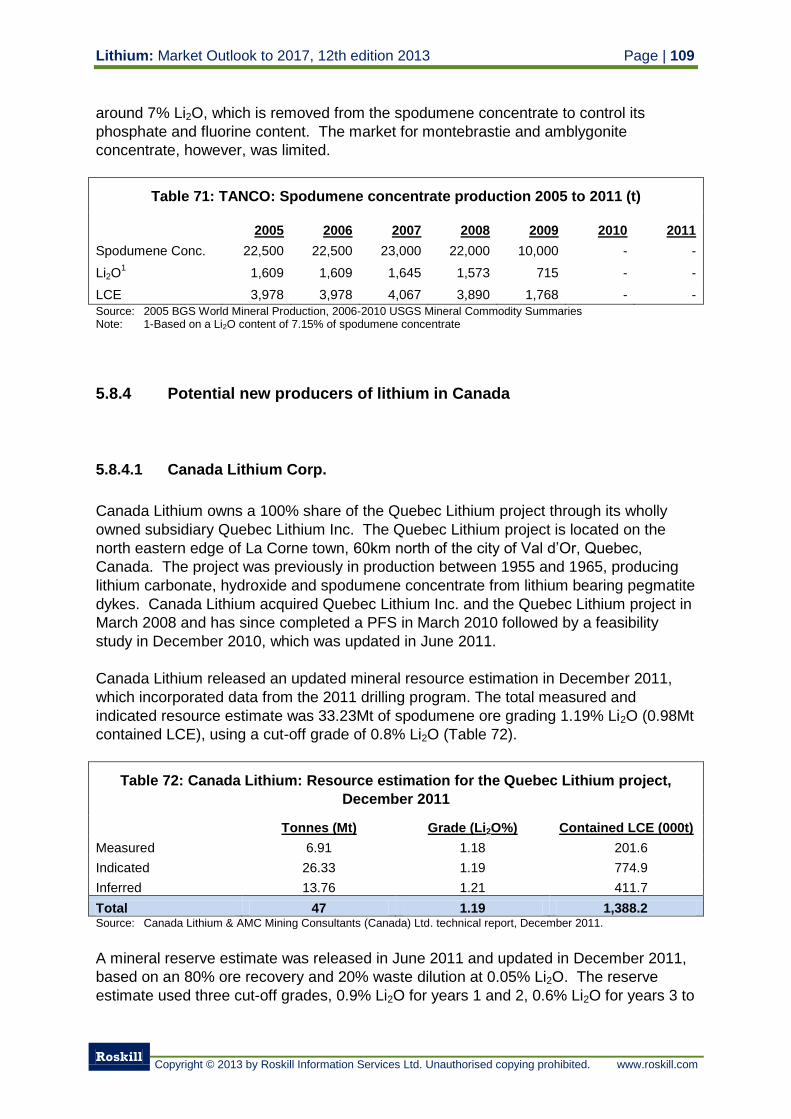

5.8.4 Potential new producers of lithium in Canada 109

5.8.4.1 Canada Lithium Corp. 109

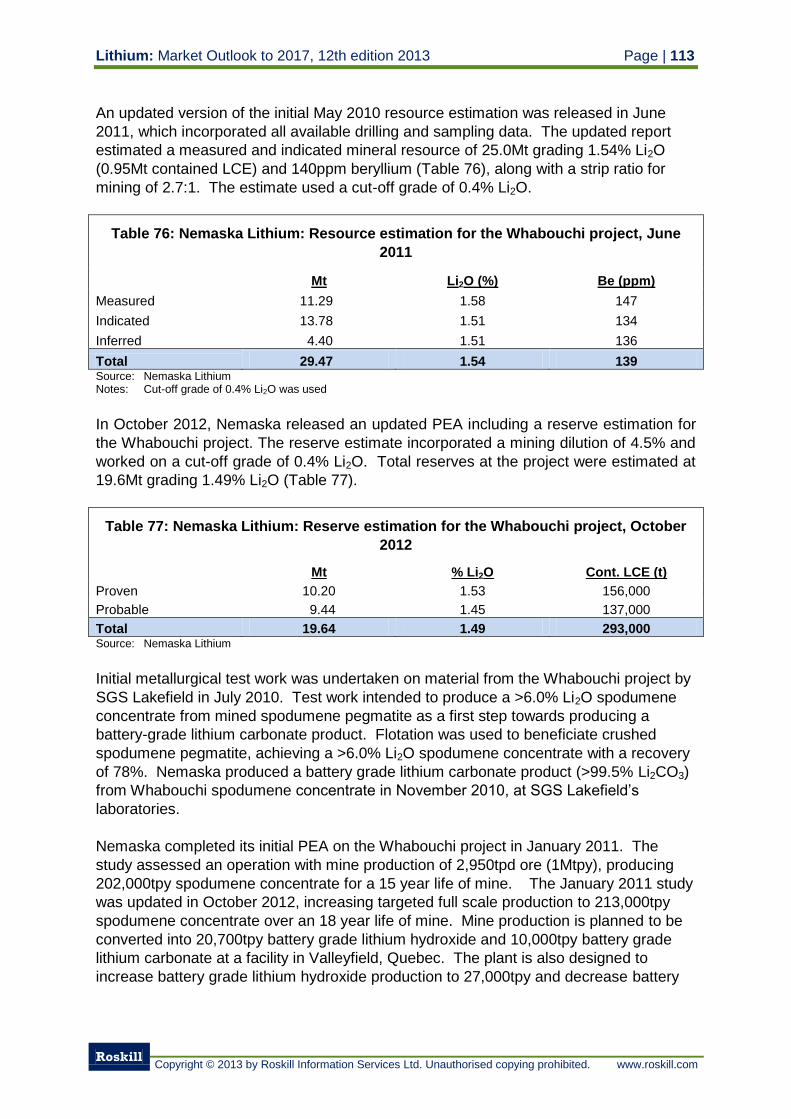

5.8.4.2 Nemaska Lithium 112

5.8.4.3 Avalon Rare Metals Inc. 115

5.8.4.4 Perilya Limited 116

5.8.4.5 Rock Tech Lithium Inc. 117

5.8.4.6 Critical Elements Corporation 120

5.8.4.7 Glen Eagle Resources Inc. 120

5.8.4.8 Aben Resources Ltd. 121

5.8.4.9 Toxco Inc. Canada 122

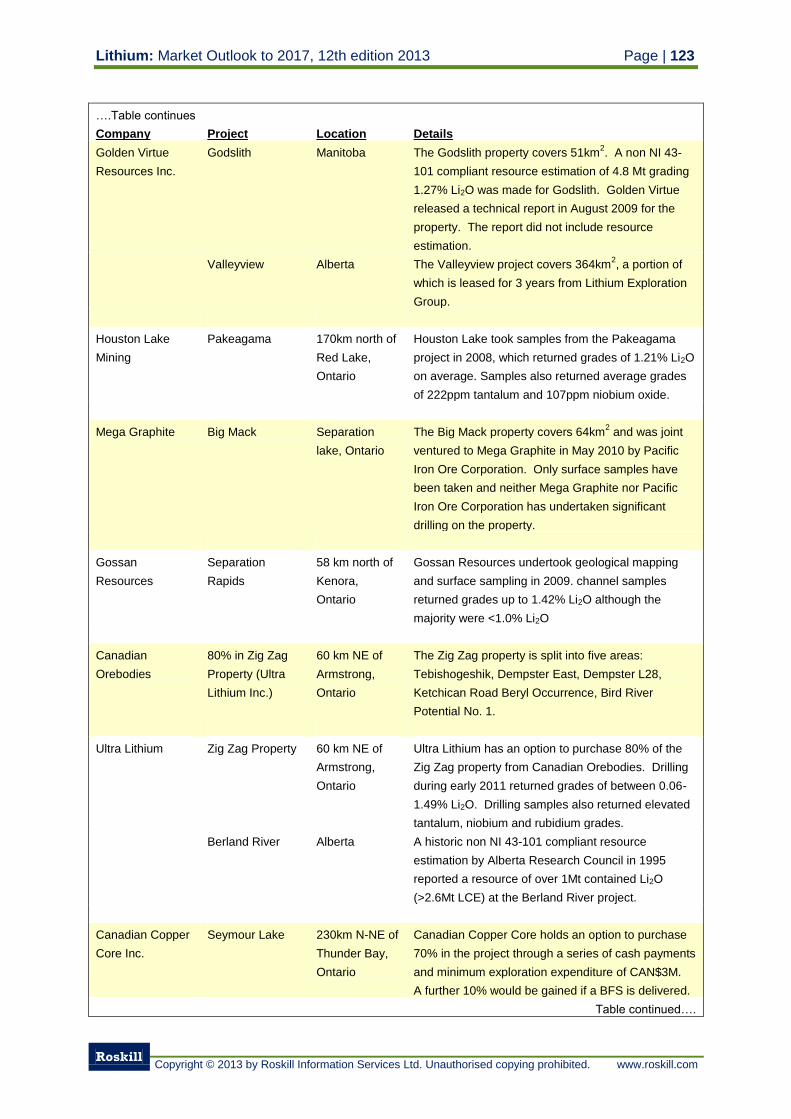

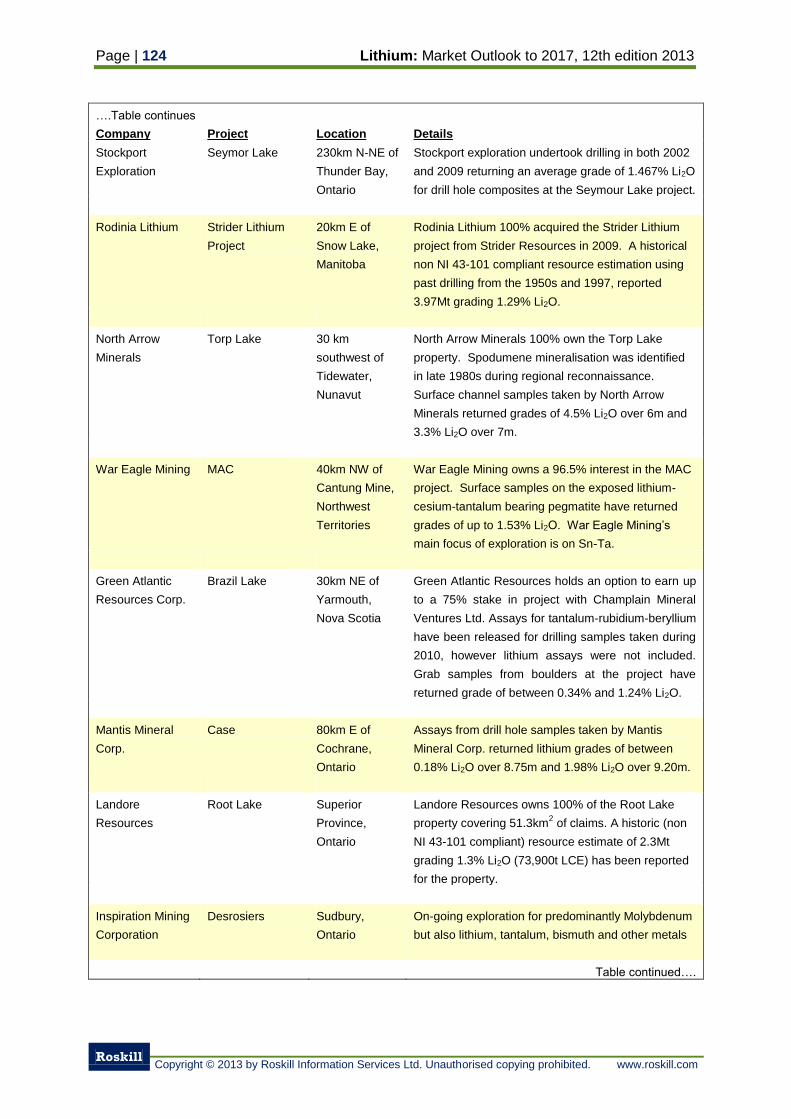

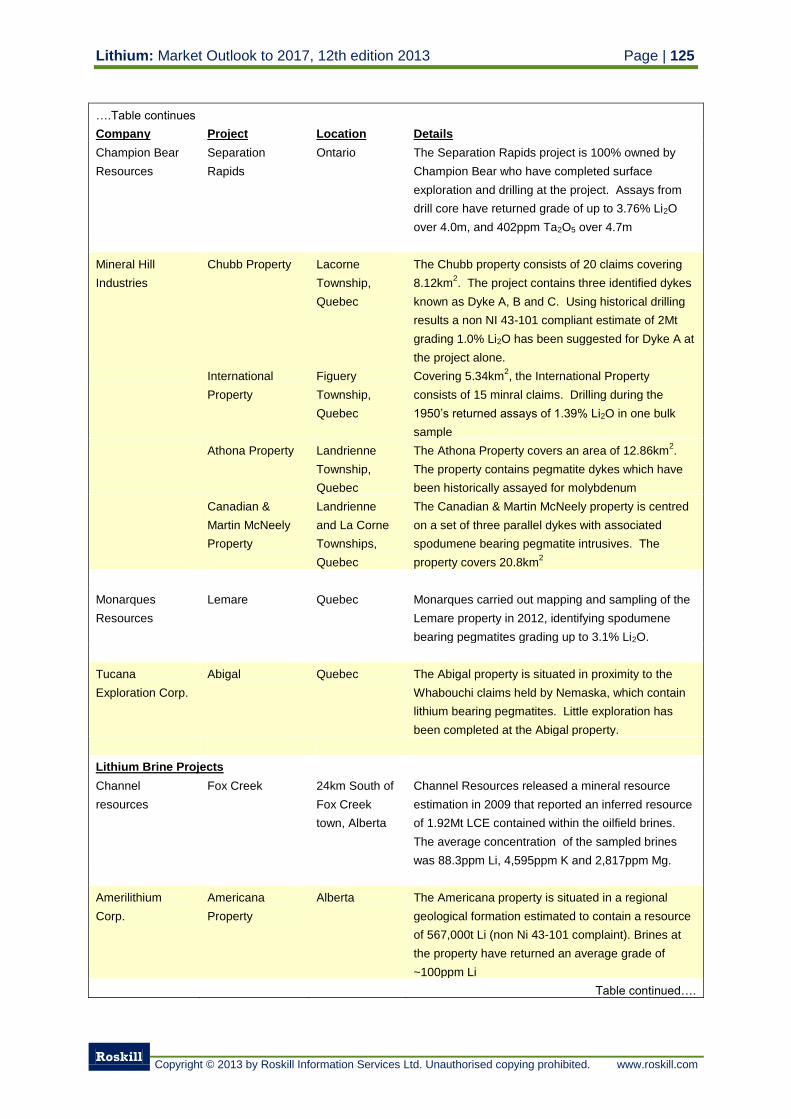

5.8.4.10 Other Canadian Lithium Projects 122

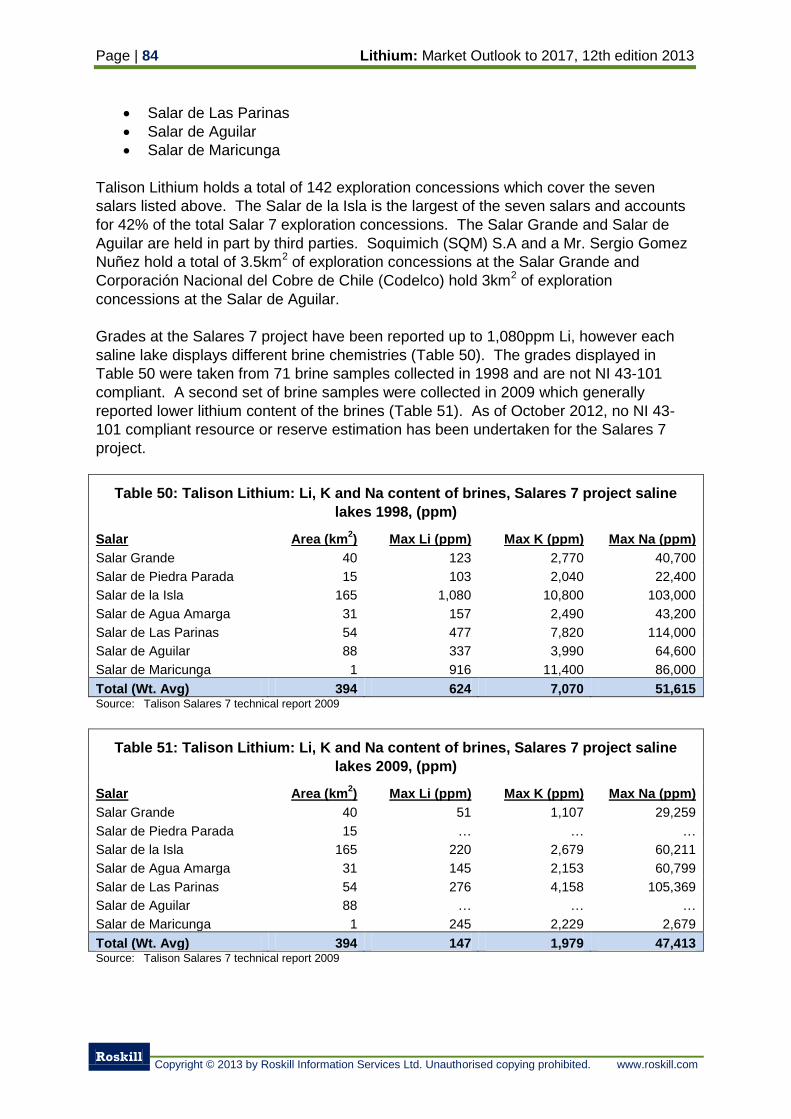

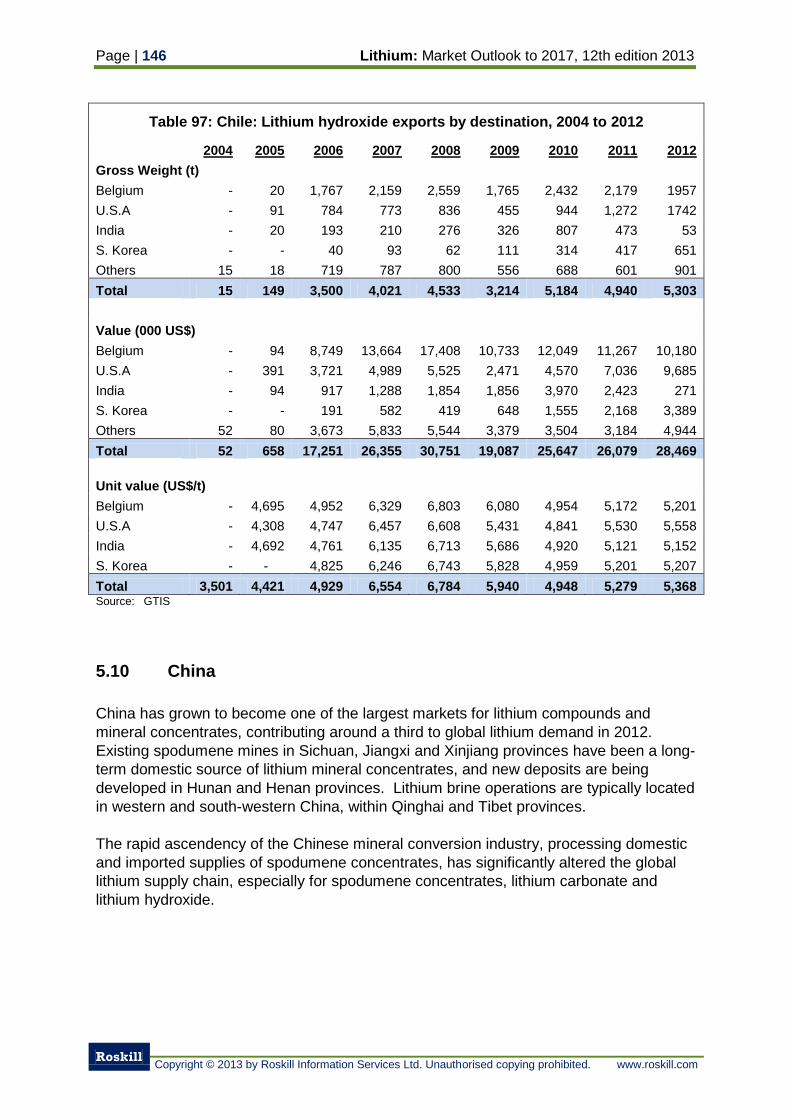

5.9 Chile 126

5.9.1 Chilean lithium reserves 127

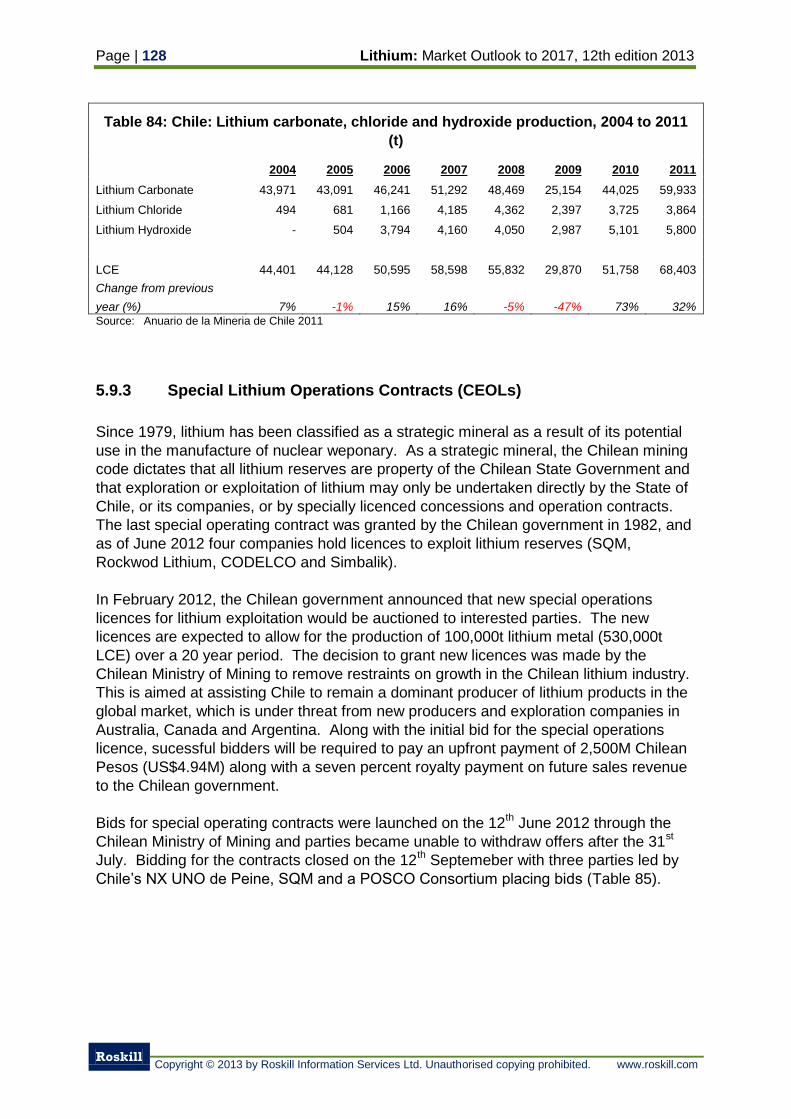

5.9.2 Chilean lithium production 127

5.9.3 Special Lithium Operations Contracts (CEOLs) 128

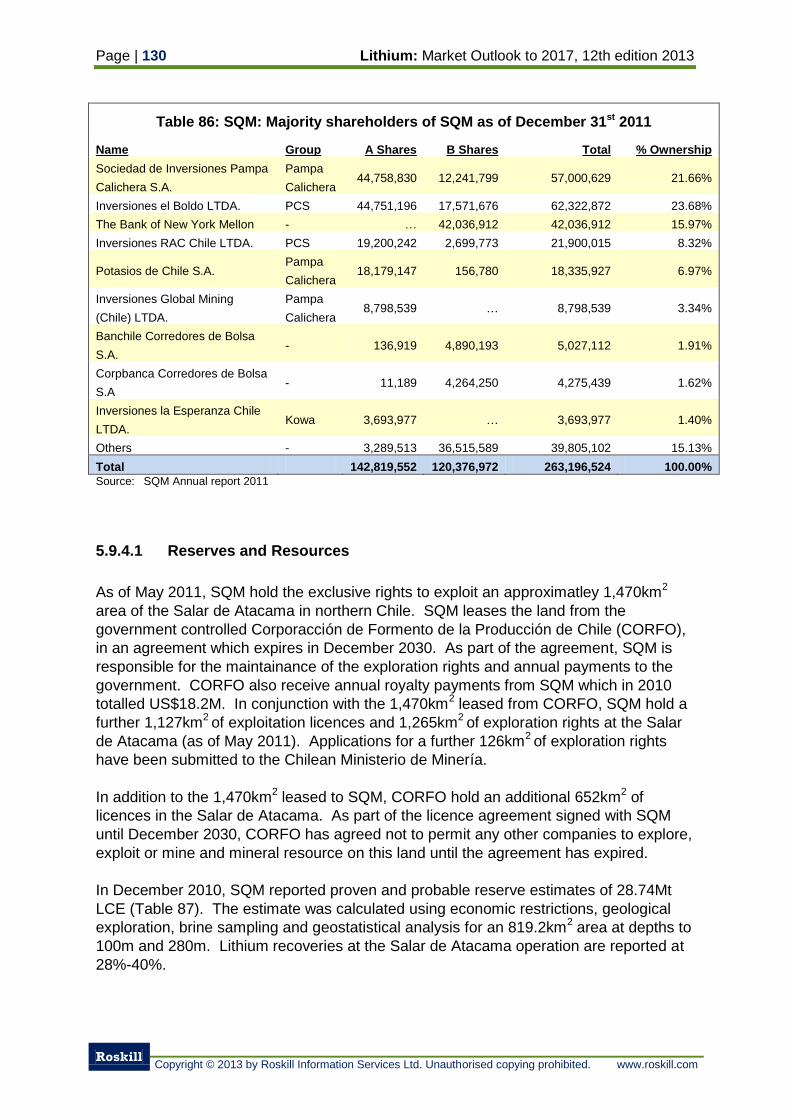

5.9.4 Sociedad Química y Minera 129

5.9.4.1 Reserves and Resources 130

5.9.4.2 Production 131

5.9.4.3 Products 132

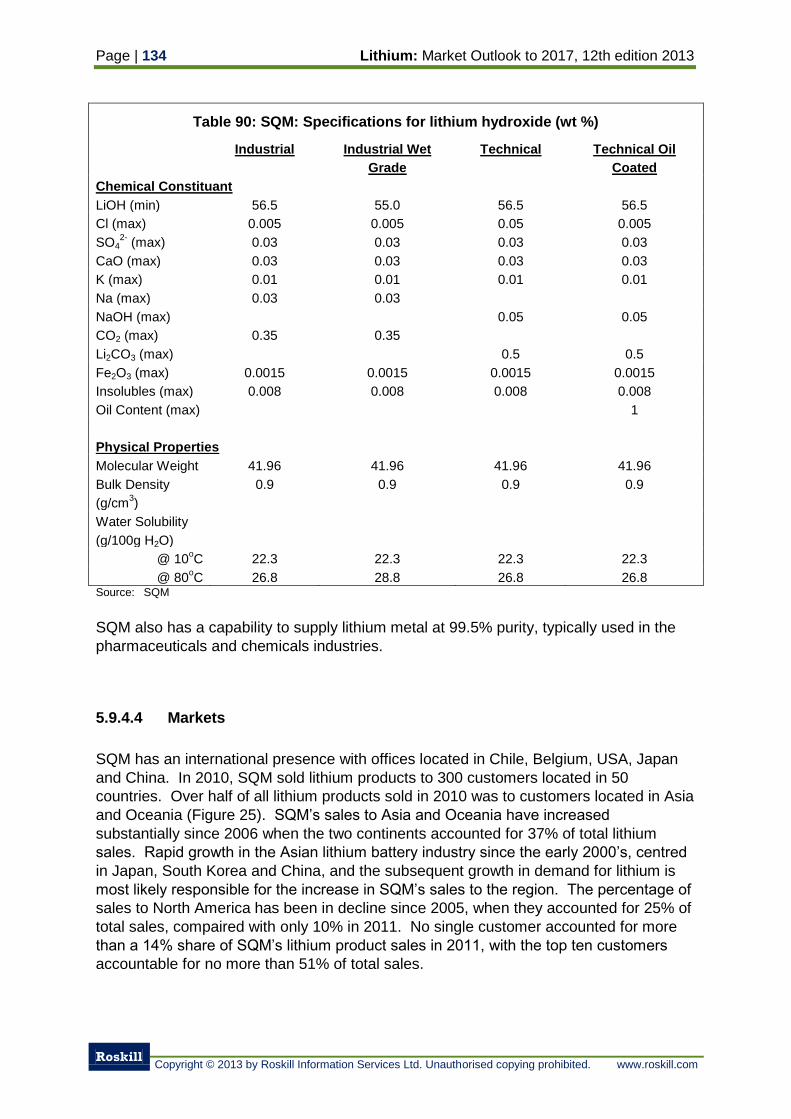

5.9.4.4 Markets 134

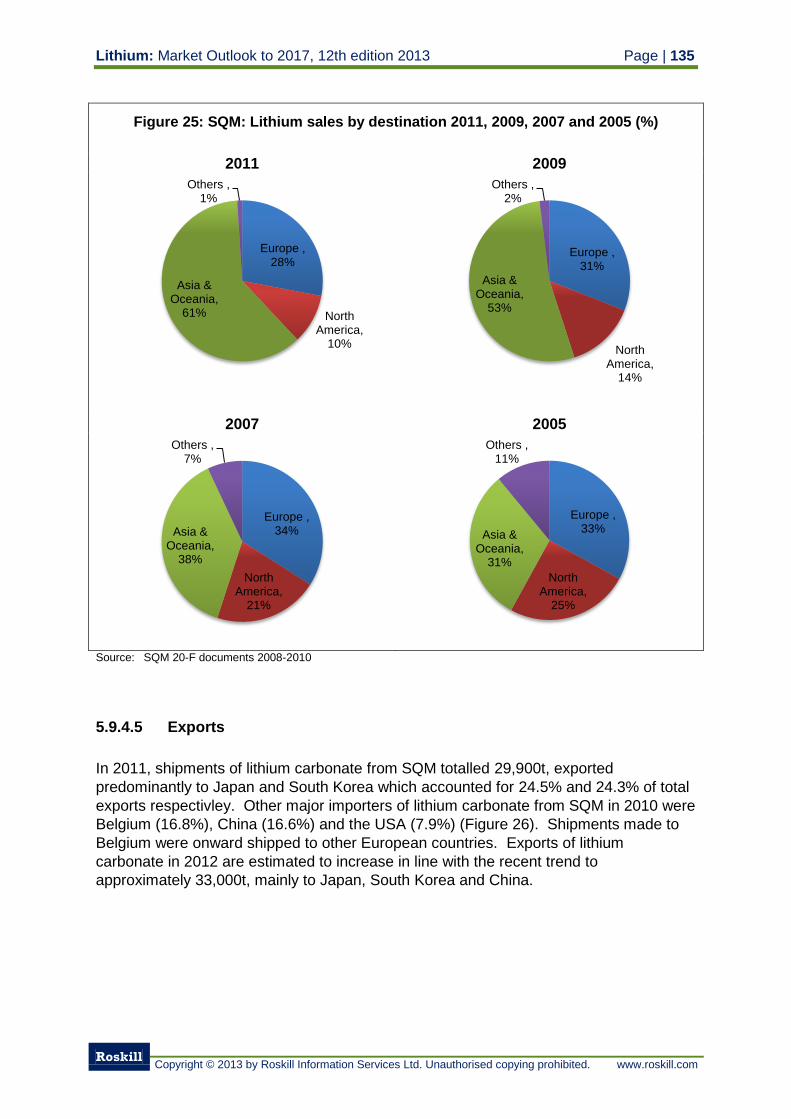

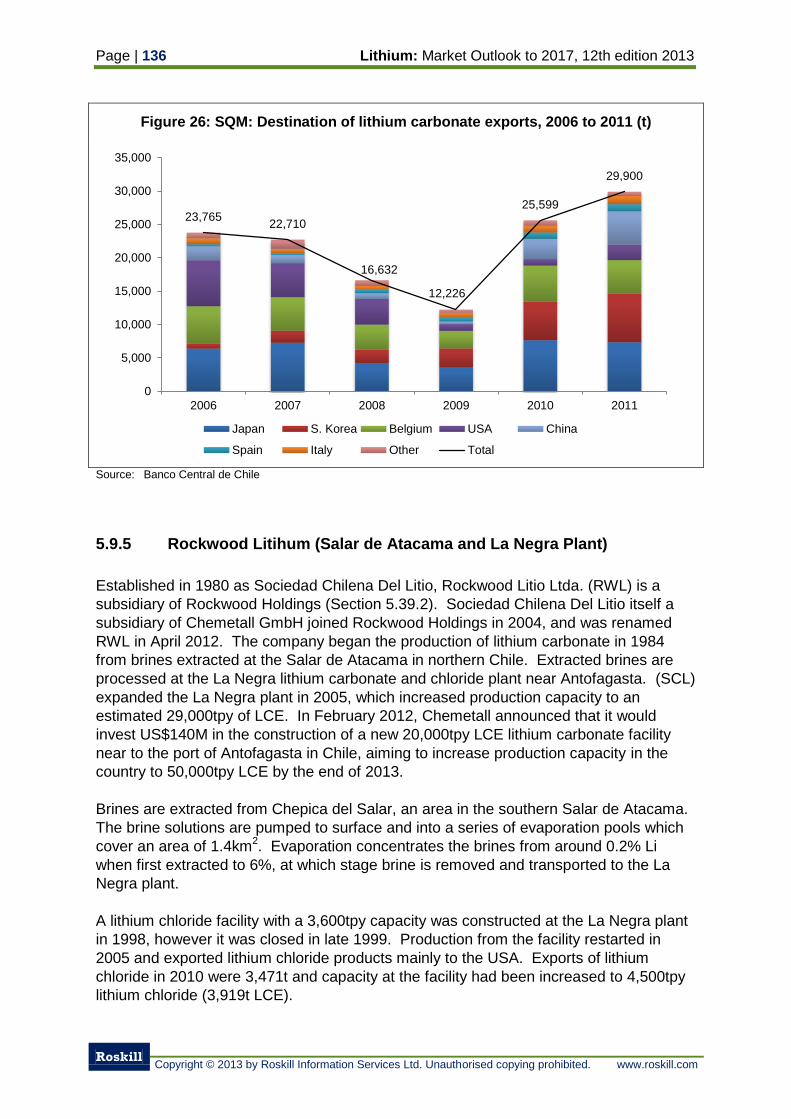

5.9.4.5 Exports 135

5.9.5 Rockwood Litihum (Salar de Atacama and La Negra Plant) 136

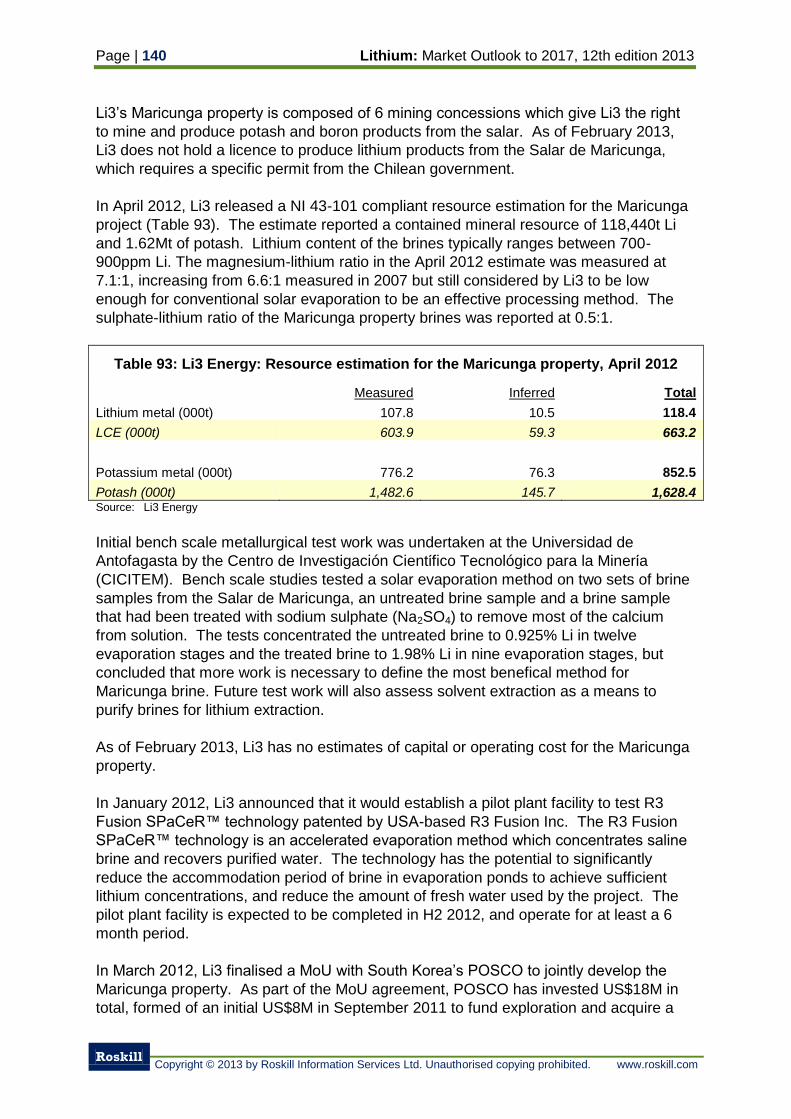

5.9.6 Simbalik Group 138

5.9.7 Li3 Energy Inc. 139

5.9.7.1 Maricunga Property 139

5.9.7.2 Li3 Energy Peruvian Projects 141

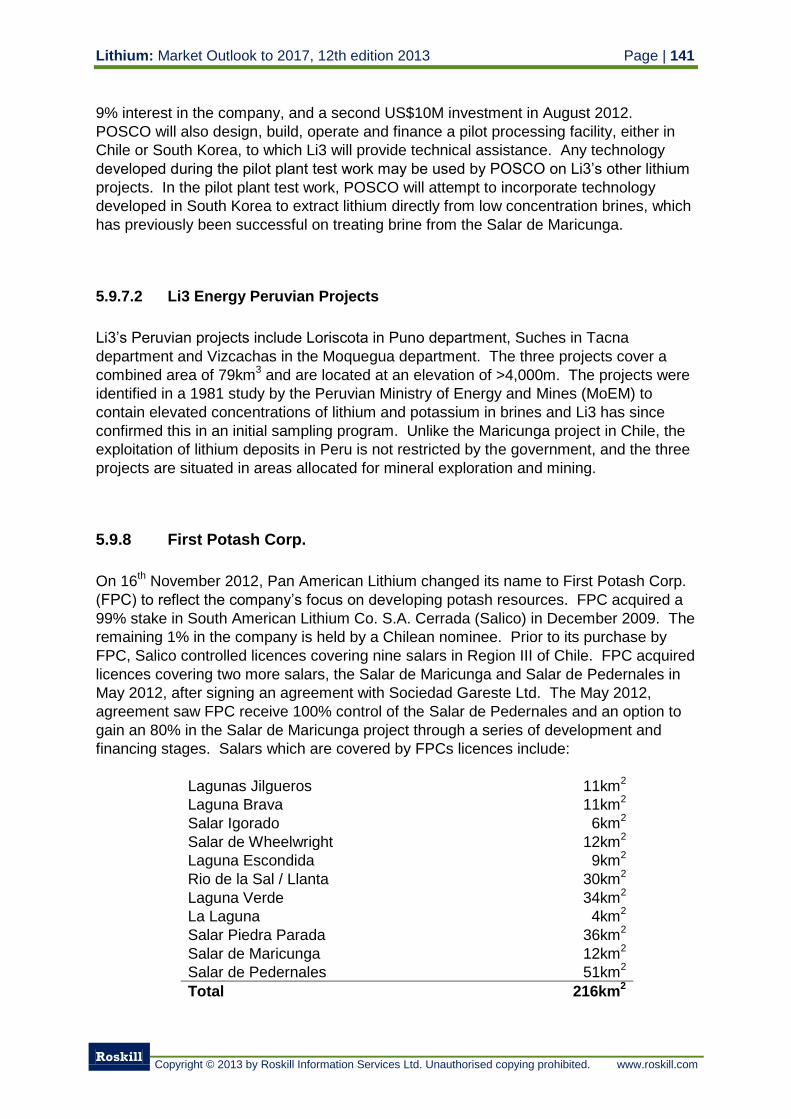

5.9.8 First Potash Corp. 141

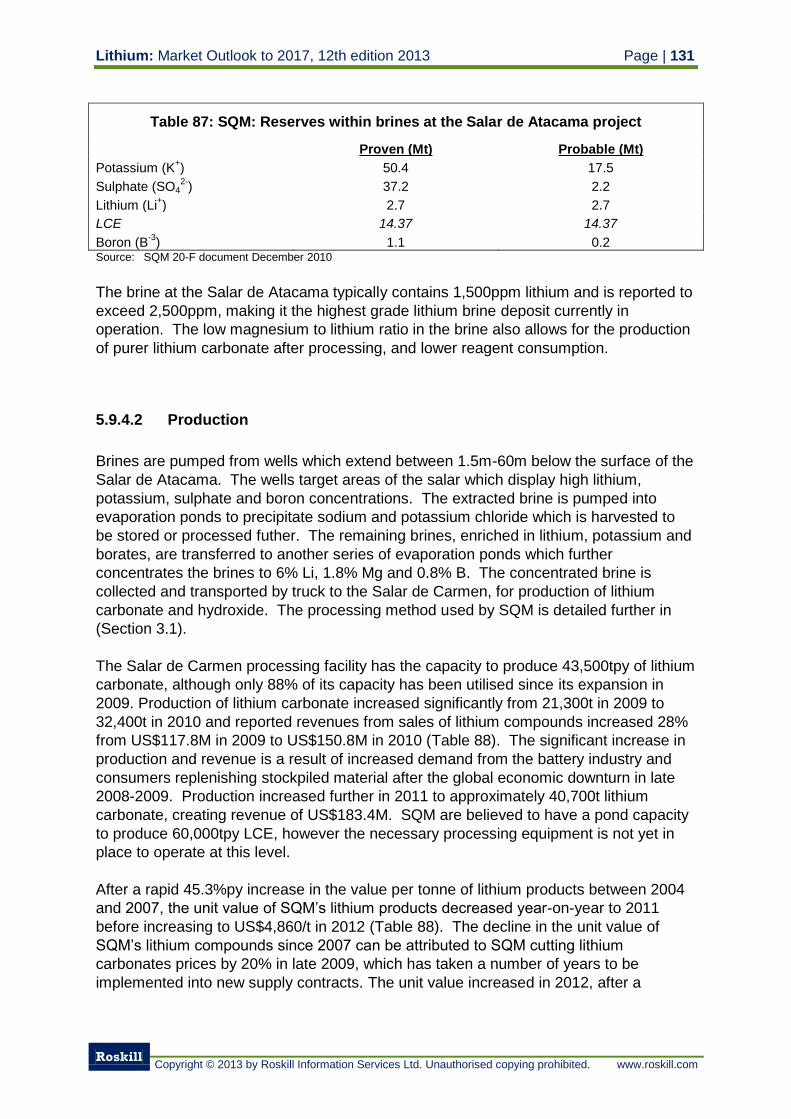

5.9.9 CODELCO 142

5.9.10 Mammoth Energy Group Inc. 142

5.9.11 Lomiko Metals Inc. 143

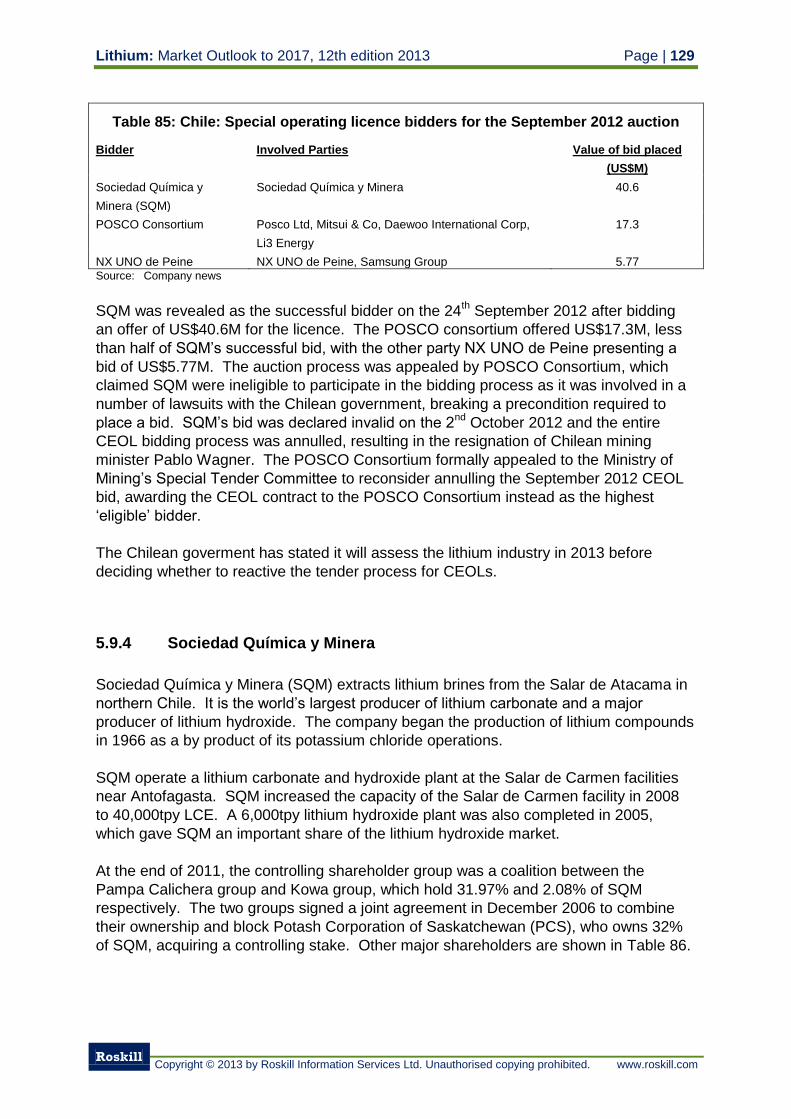

5.9.12 Errázuriz Lithium 143

5.9.13 Exports of litihum from Chile 143

5.10 China 146

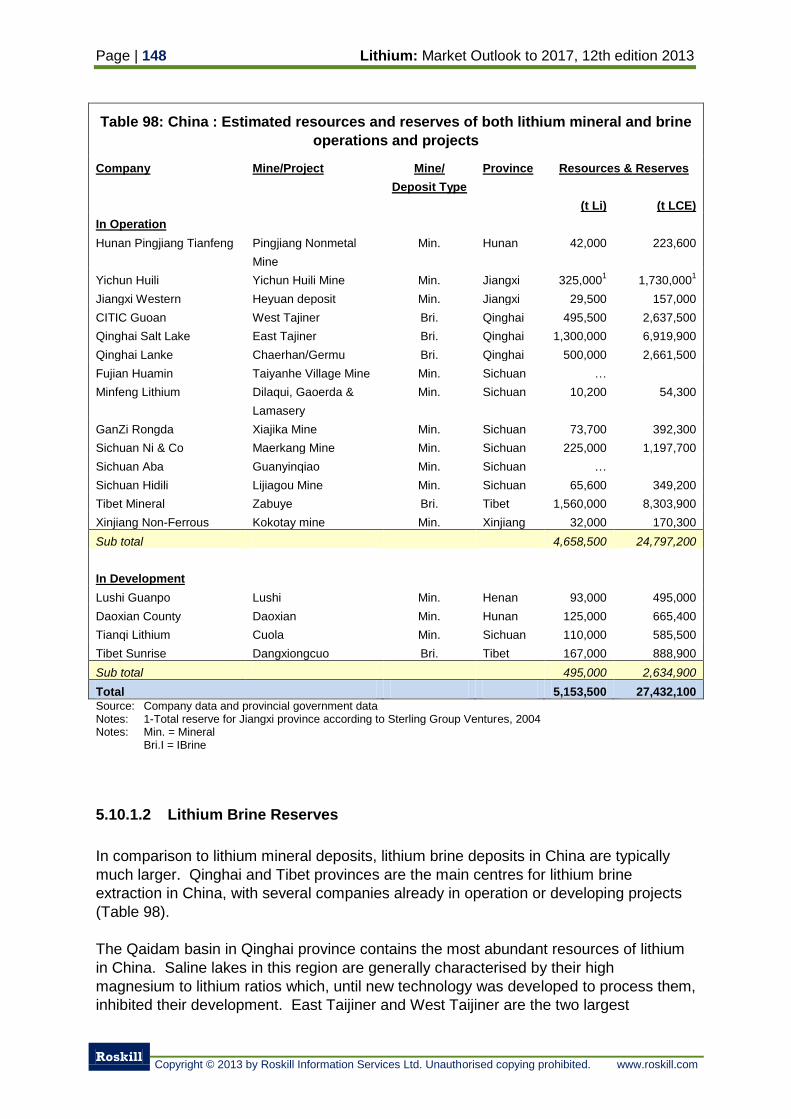

5.10.1 Chinese reserves of lithium 147

5.10.1.1 Lithium Mineral Reserves 147

5.10.1.2 Lithium Brine Reserves 148

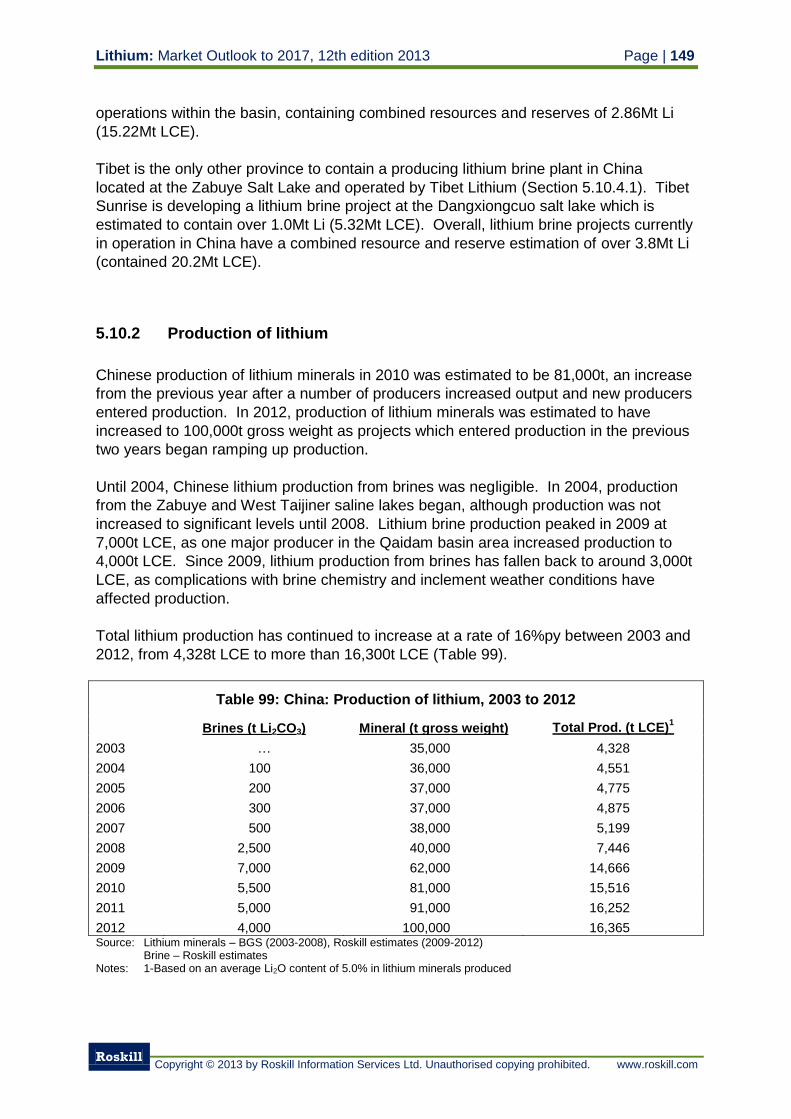

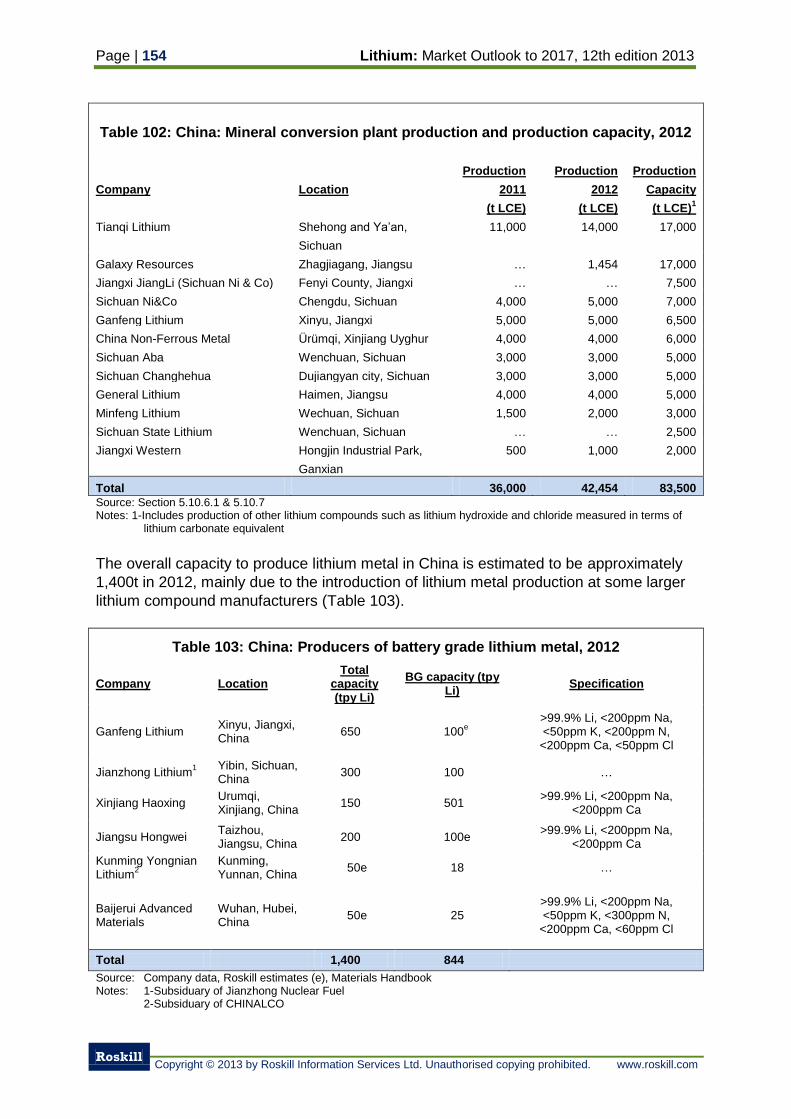

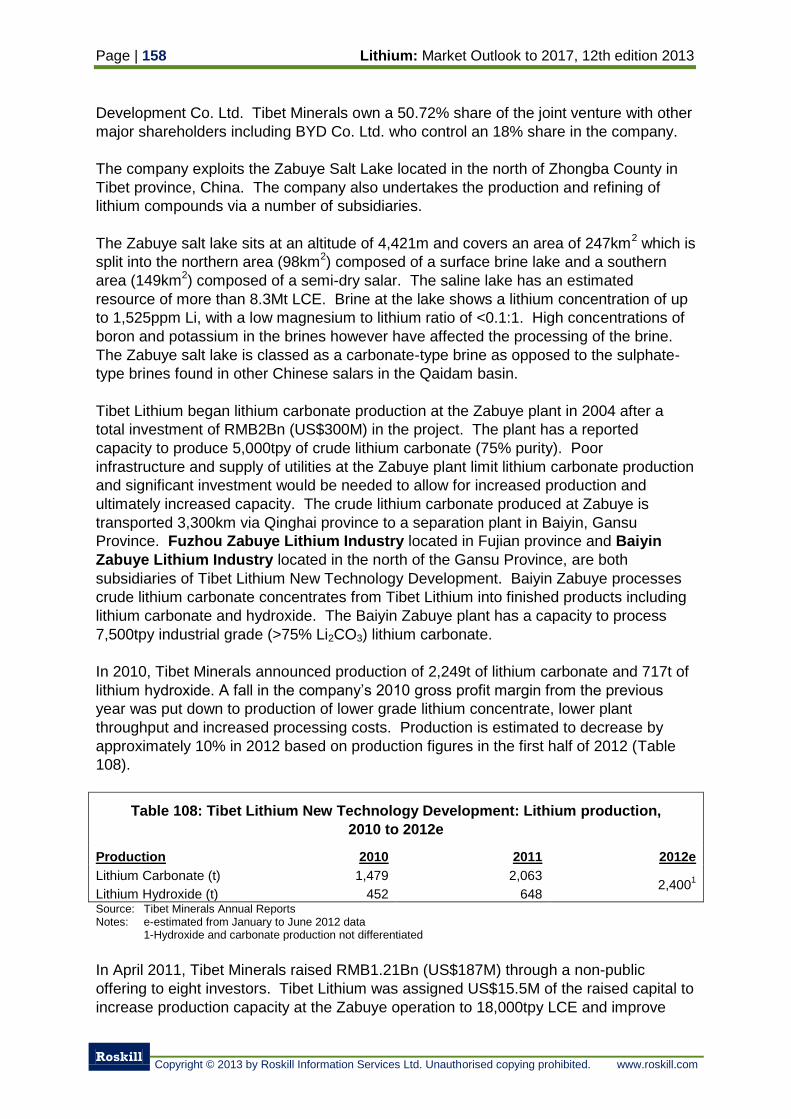

5.10.2 Production of lithium 149

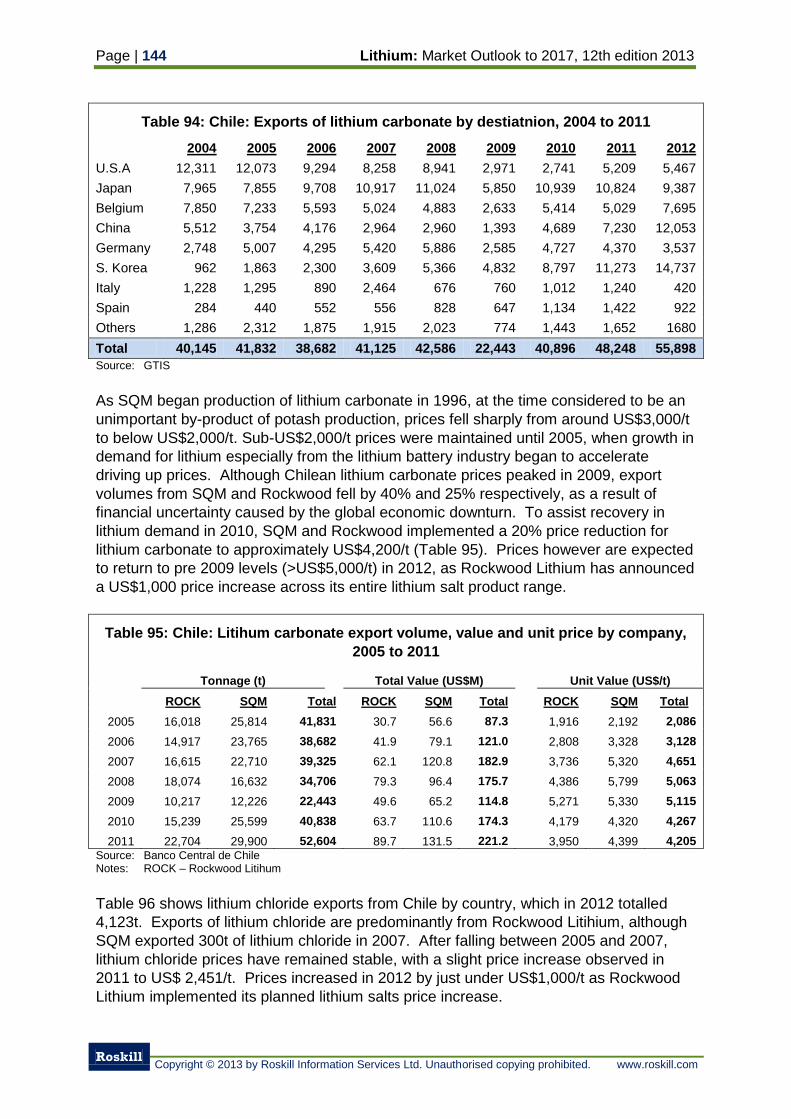

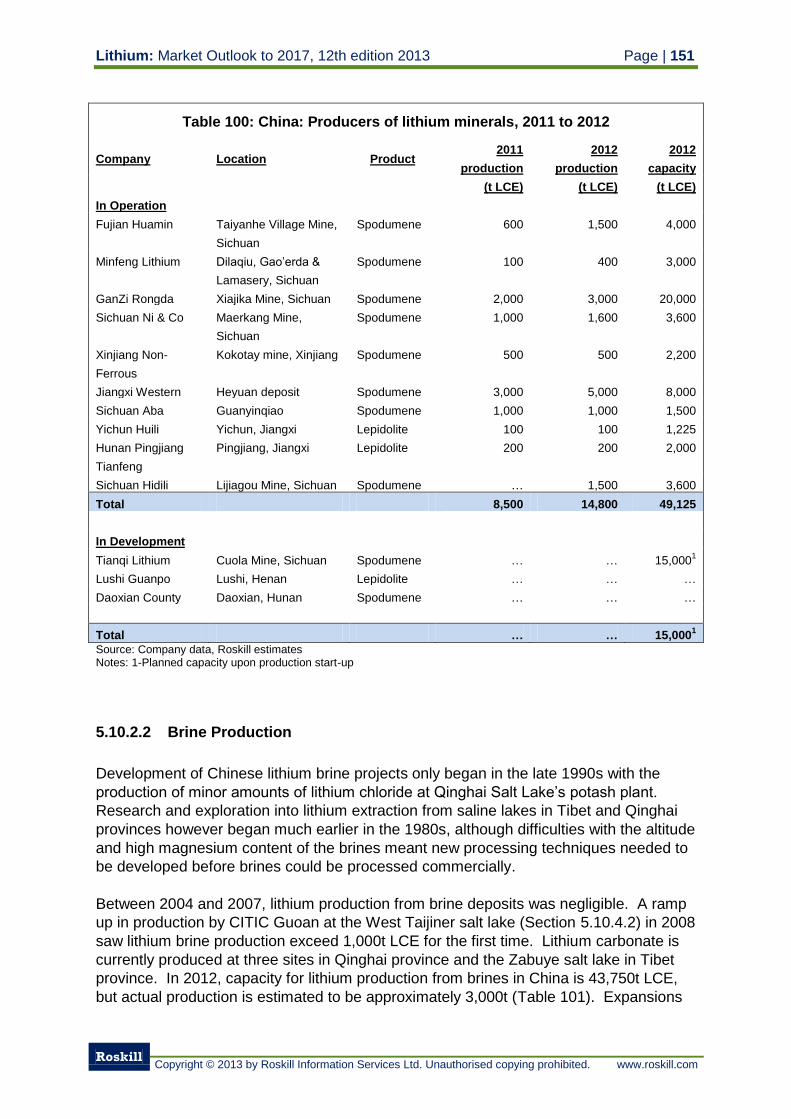

5.10.2.1 Mineral Production 150

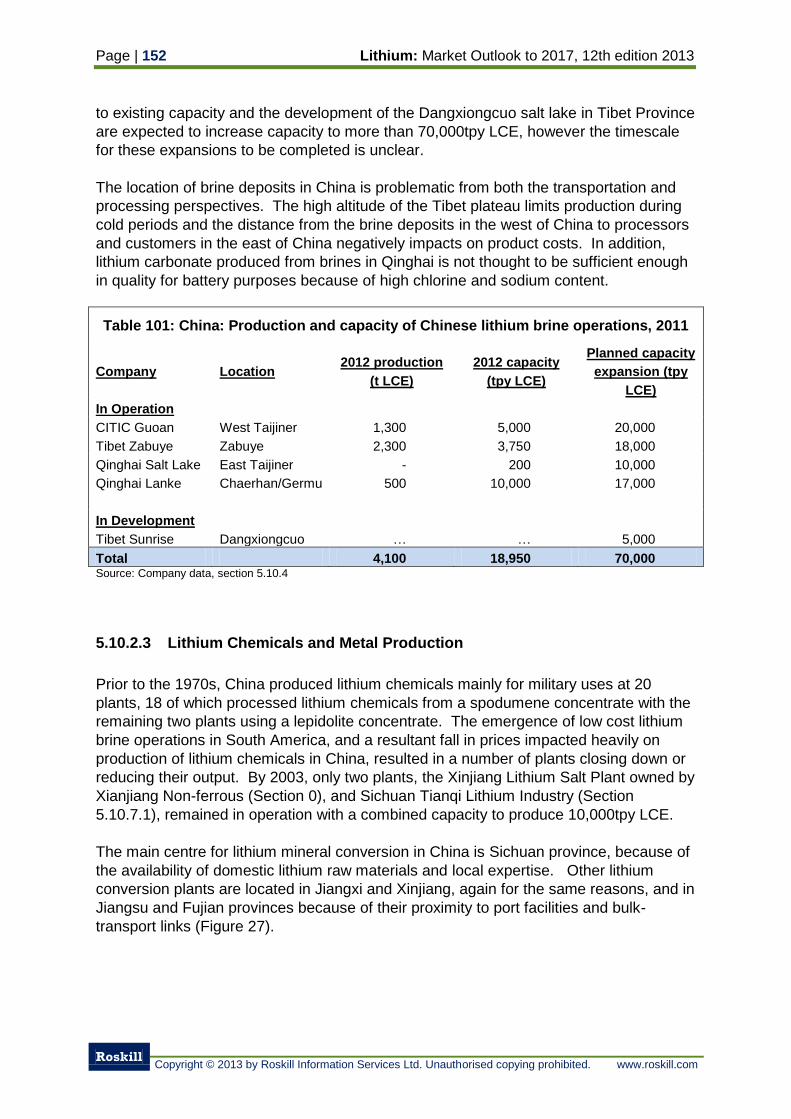

5.10.2.2 Brine Production 151

5.10.2.3 Lithium Chemicals and Metal Production 152

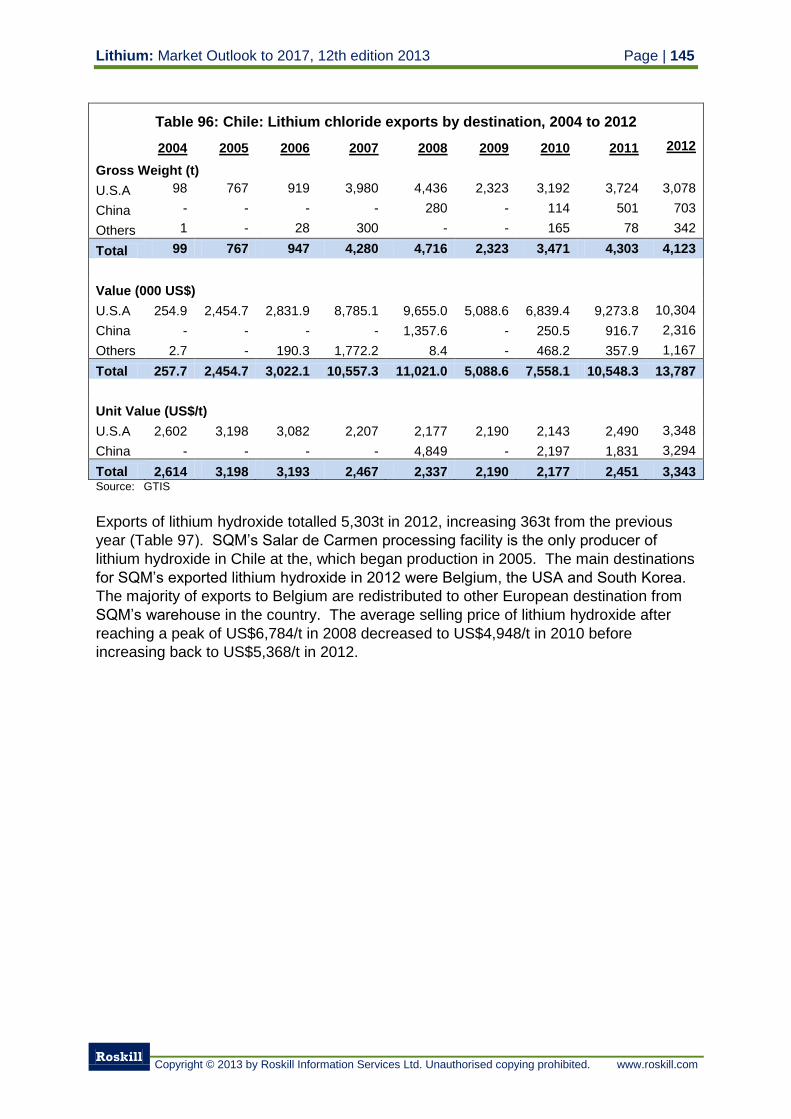

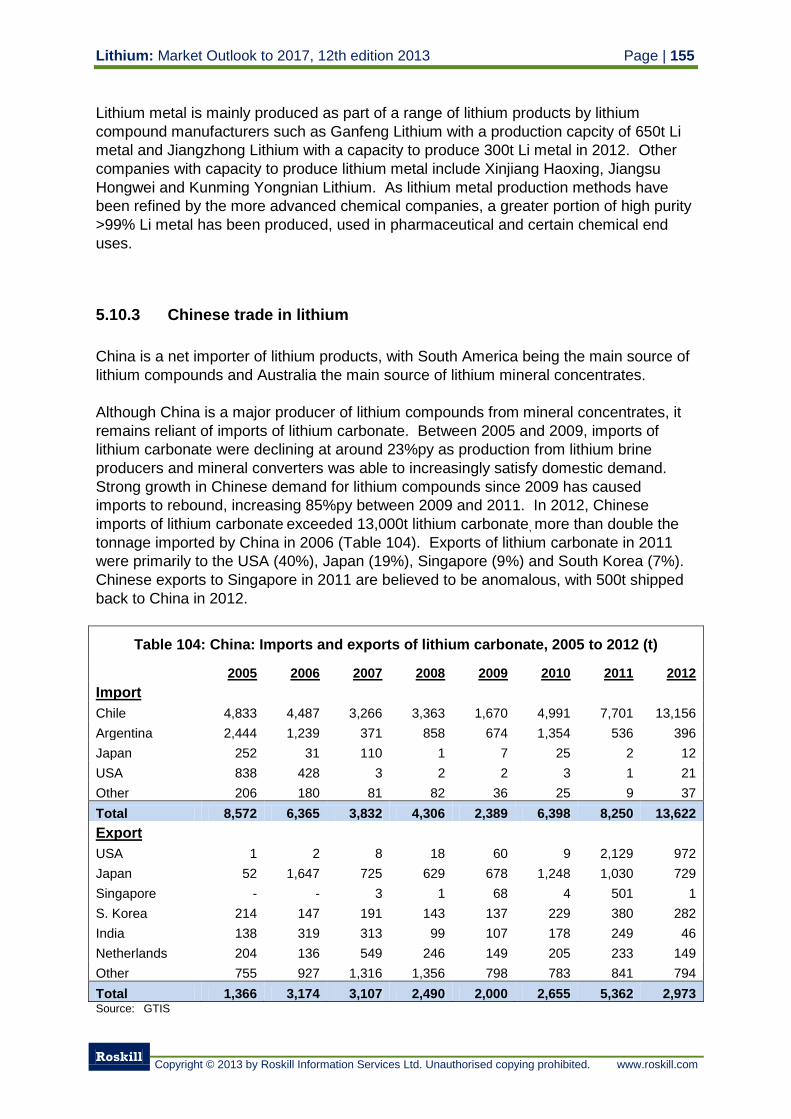

5.10.3 Chinese trade in lithium 155

5.10.4 Chinese lithium brine producers 157

5.10.4.1 Tibet Lithium New Technology Development Co. Ltd. 157

5.10.4.2 Qinghai CITIC Guoan Technology Development Co. Ltd. 159

5.10.4.3 Qinghai Salt Lake Industry Co. Ltd. 160

5.10.4.4 Qinghai Lanke Lithium Industry Co. Ltd. 161

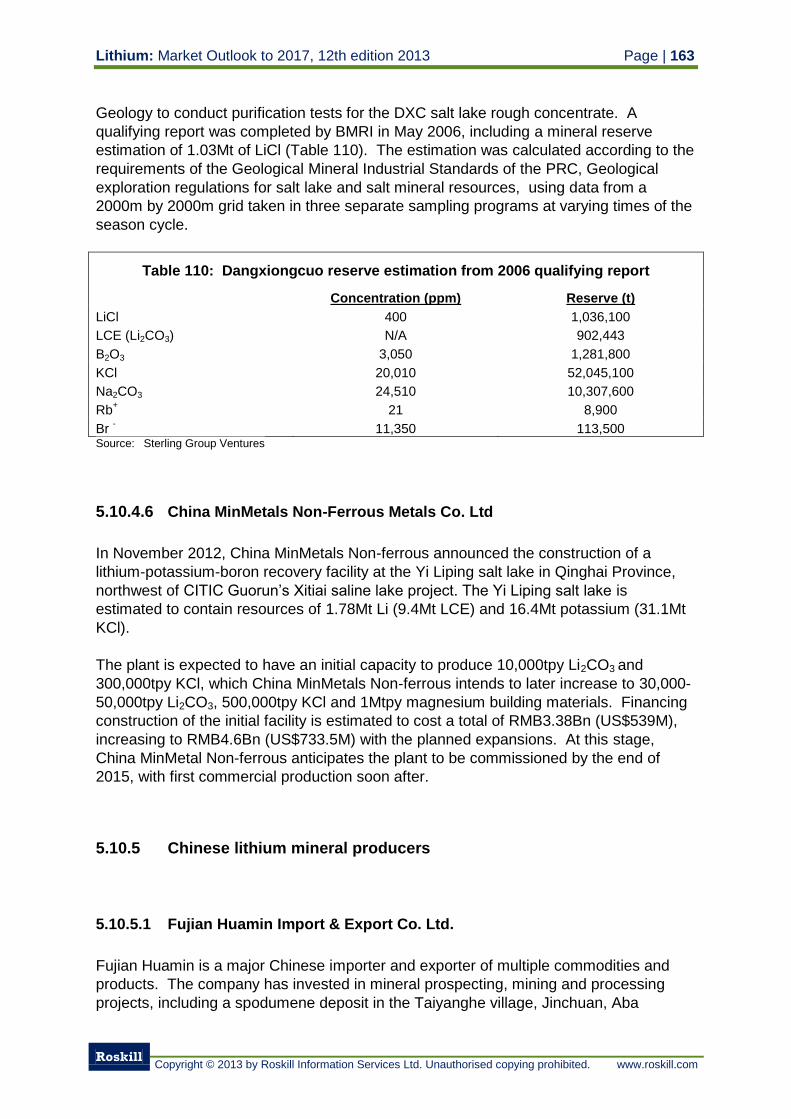

5.10.4.5 Tibet Sunrise Mining Development Ltd. 162

5.10.4.6 China MinMetals Non-Ferrous Metals Co. Ltd 163

5.10.5 Chinese lithium mineral producers 163

5.10.5.1 Fujian Huamin Import & Export Co. Ltd. 163

5.10.5.2 Yichun Huili Industrial Co. Ltd. 164

5.10.5.3 GanZi Rongda Lithium Co., Ltd. 164

5.10.5.4 Sichuan Hidili Dexin Mineral Industry 165

5.10.5.5 Xinjiang Non-Ferrous Metals (Group) Ltd. 166

5.10.6 Chinese lithium mineral producers with mineral conversion capacity 166

5.10.6.1 Jiangxi Western Resources Lithium Industry 166

5.10.6.2 Sichuan Aba Guangsheng Lithium Co. Ltd. 167

5.10.6.3 Minfeng Lithium Co. Ltd. 167

5.10.6.4 Sichuan Ni&Co Guorun New Materials Co. Ltd. 168

5.10.7 Chinese mineral conversion plants 169

5.10.7.1 Sichuan Tianqi Lithium Shareholding Co. Ltd. 169

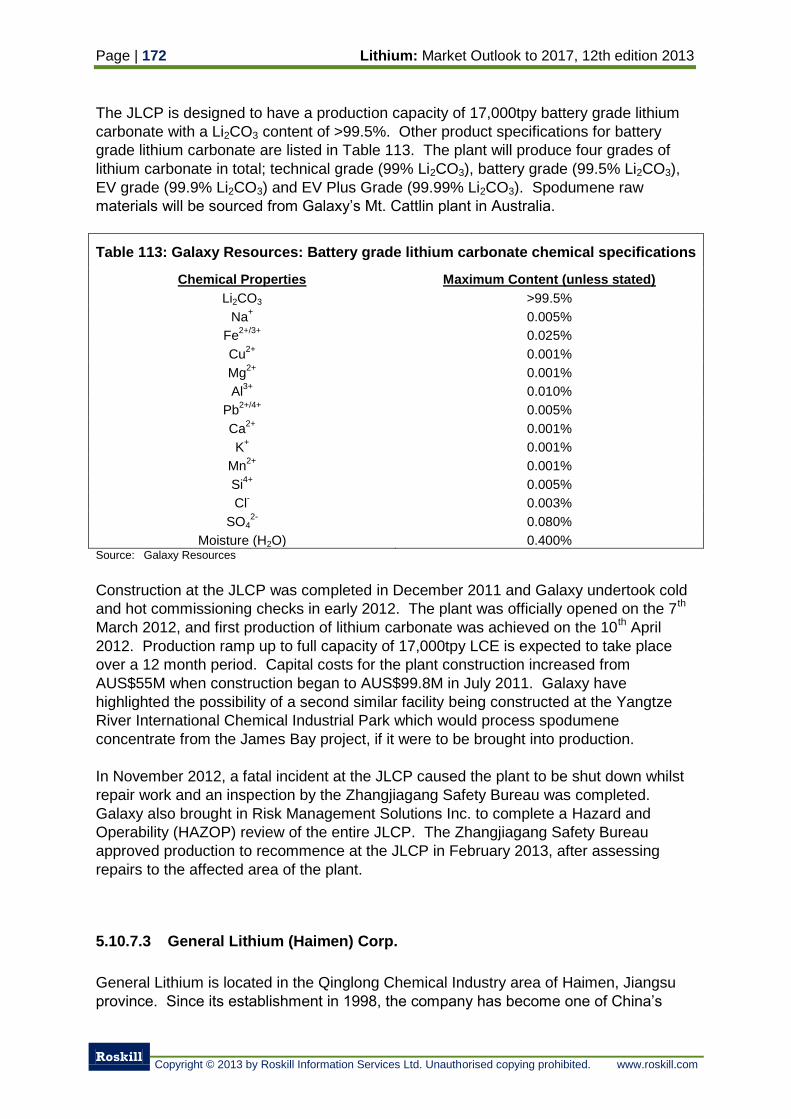

5.10.7.2 Galaxy Resources (Jiangsu Lithium Carbonate Plant) 171

5.10.7.3 General Lithium (Haimen) Corp. 172

5.10.7.4 China Non-Ferrous Metal Import & Export Xinjiang Corp. 173

5.10.7.5 Sichuan State Lithium Materials Co. Ltd. 174

5.10.7.6 Jiangxi Ganfeng Lithium Co. Ltd. 174

5.10.7.7 Sichuan Chenghehua Lithium Technology Co. Ltd. 176

5.10.8 Chinese lithium chemical producers 176

5.10.9 Specialist lithium bromide producers 177

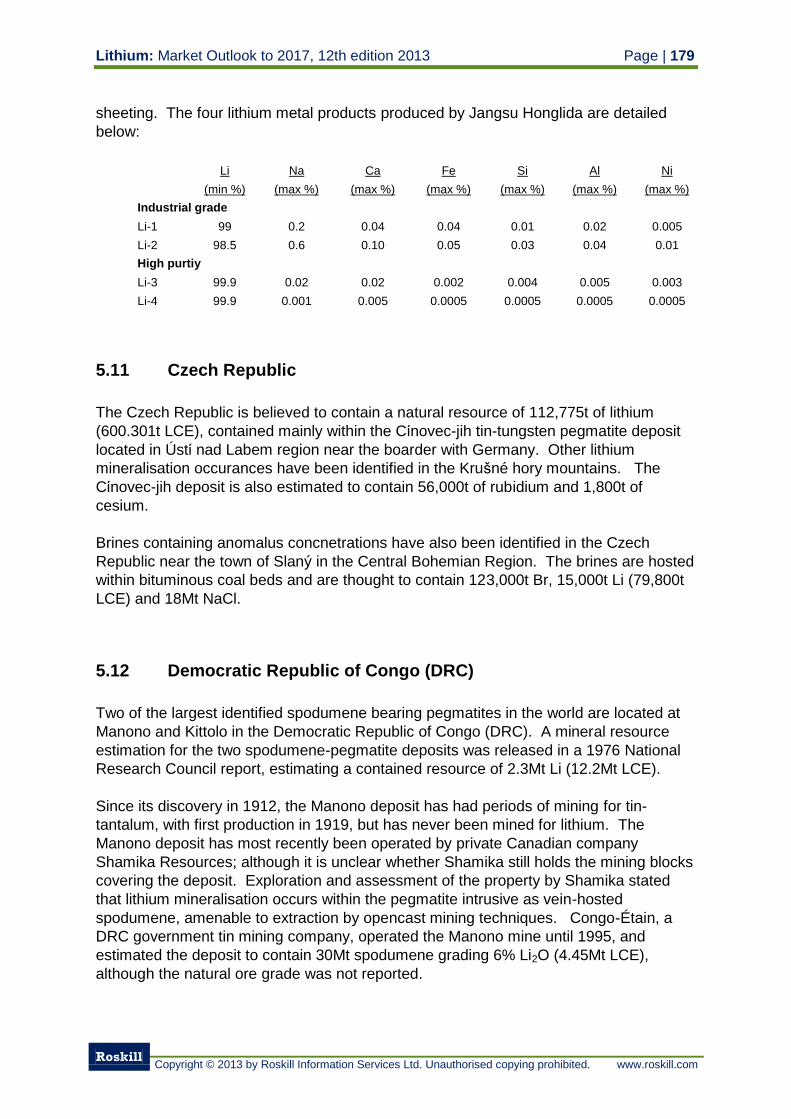

5.10.10 Specialist lithium metal producers 178

5.11 Czech Republic 179

5.12 Democratic Republic of Congo (DRC) 179

5.13 Finland 180

5.13.1 Keliber Oy 180

5.13.2 Nortec Minerals Corp. 181

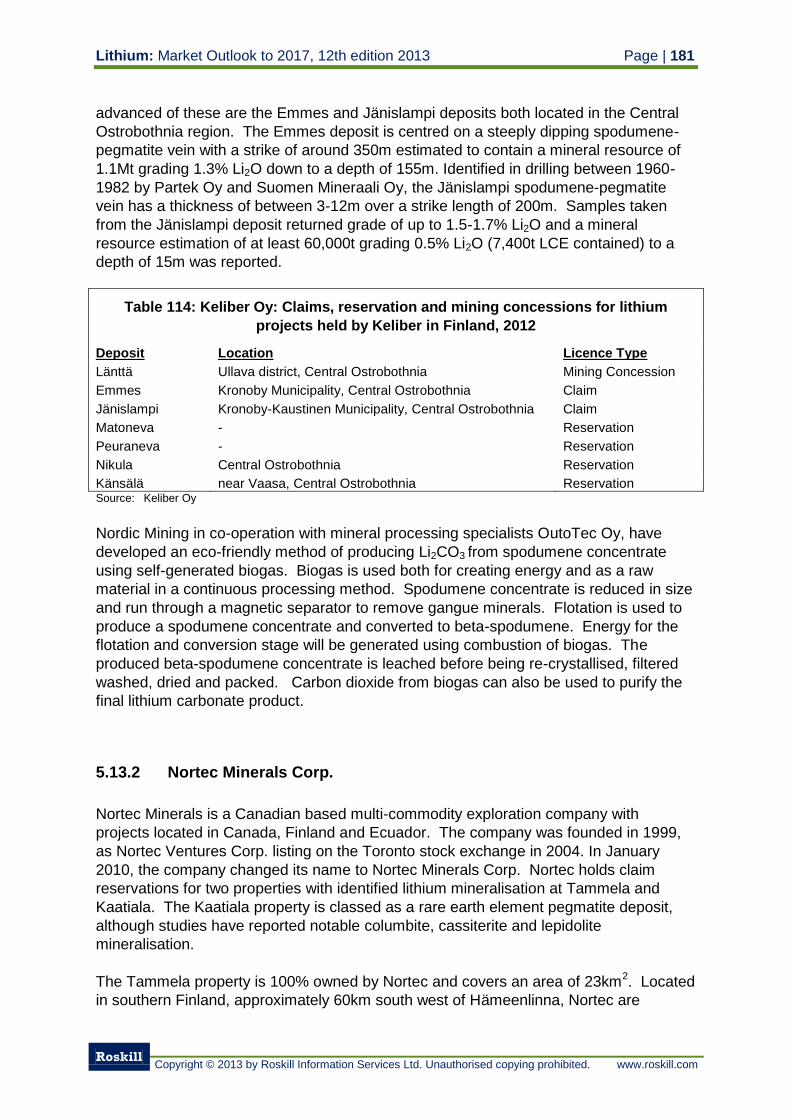

5.13.3 Leviäkangas Deposit 182

5.13.4 Syväjärvi Deposit 182

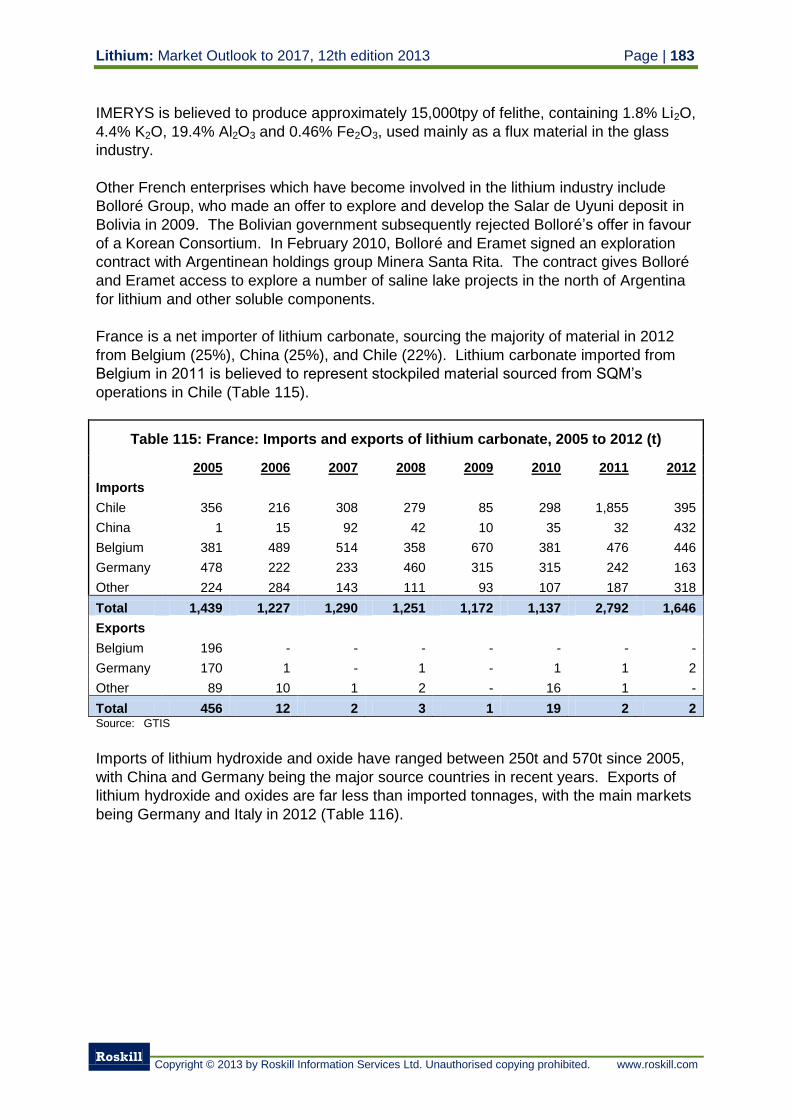

5.14 France 182

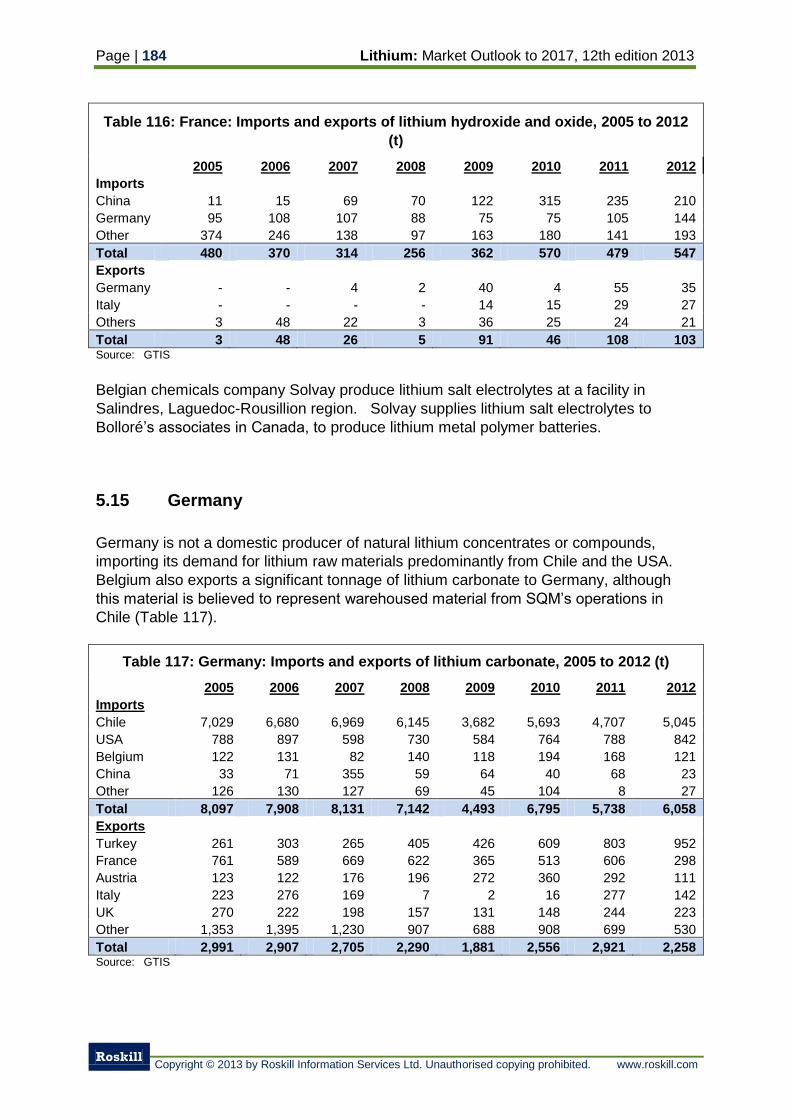

5.15 Germany 184

5.15.1 Rockwood Lithium (Langelsheim Plant) 185

5.15.2 Helm AG 185

5.15.3 Lithium exploration in Germany 185

5.16 Greece 186

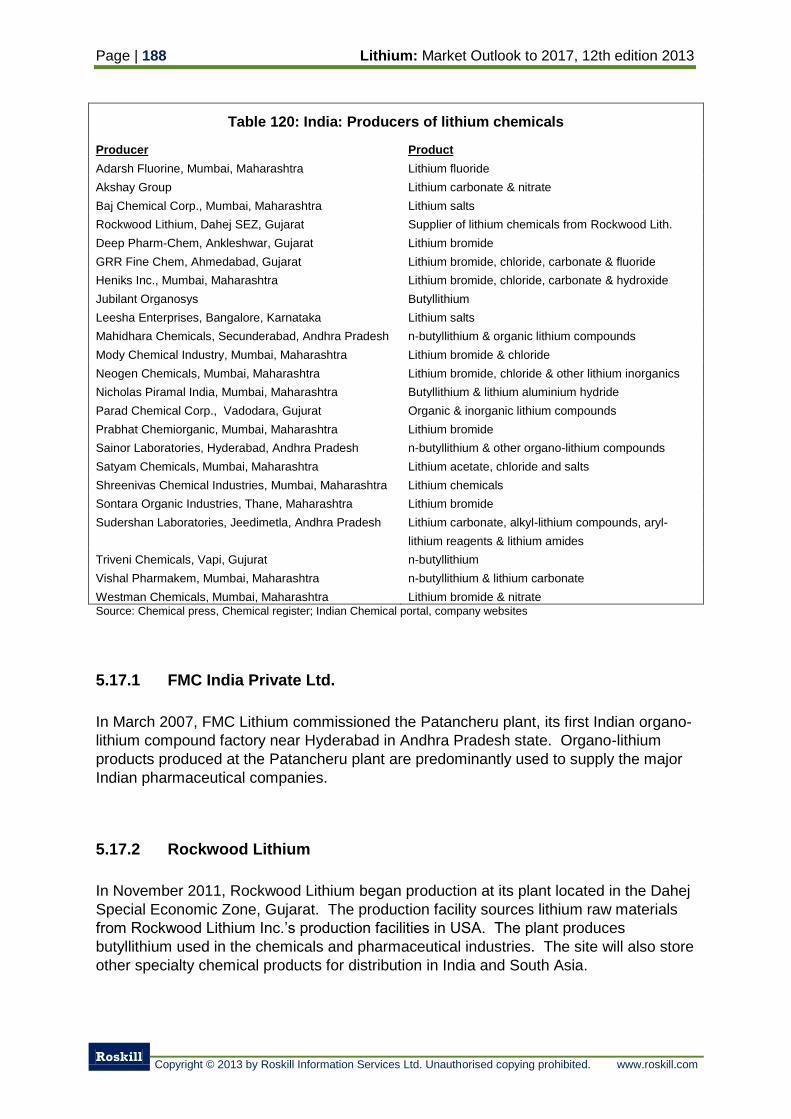

5.17 India 186

5.17.1 FMC India Private Ltd. 188

5.17.2 Rockwood Lithium 188

5.18 Ireland 189

5.19 Israel 189

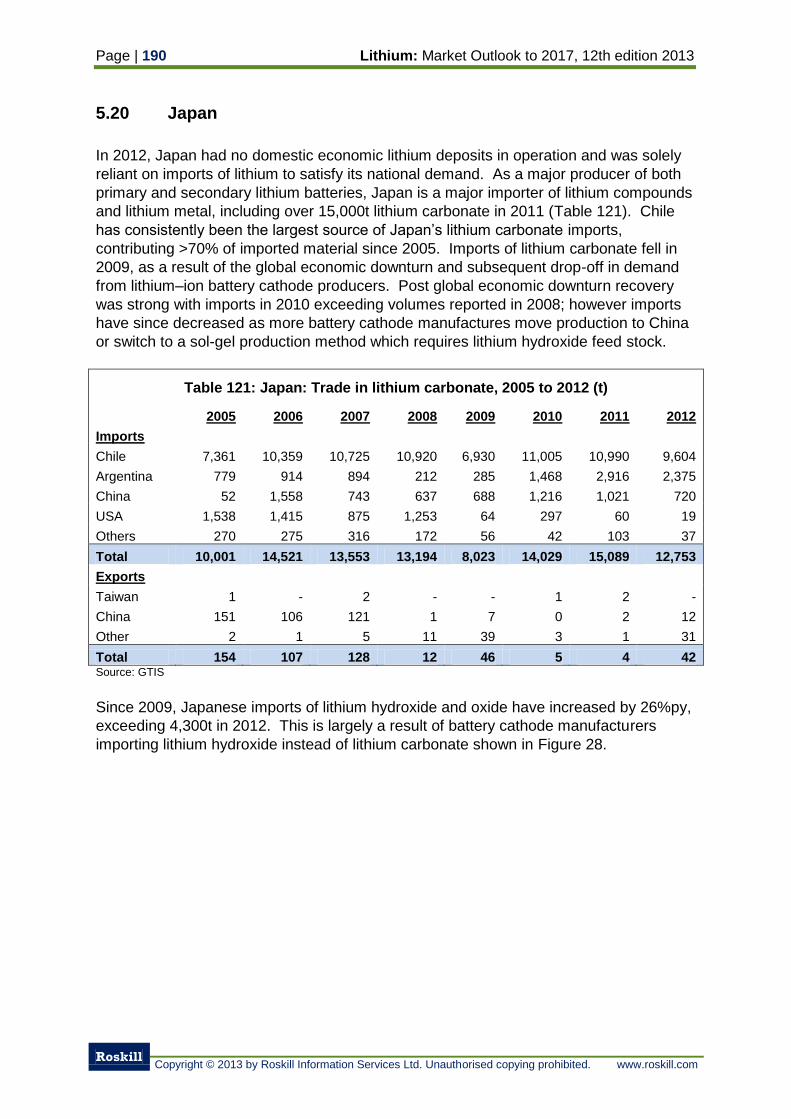

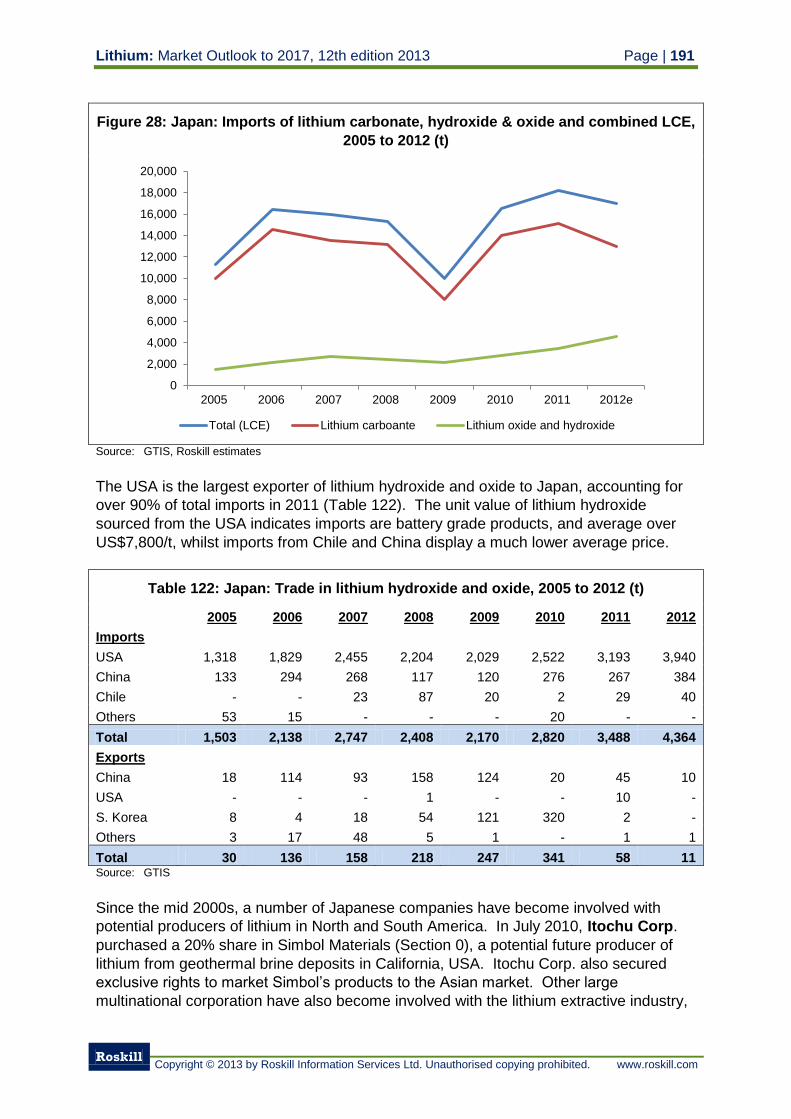

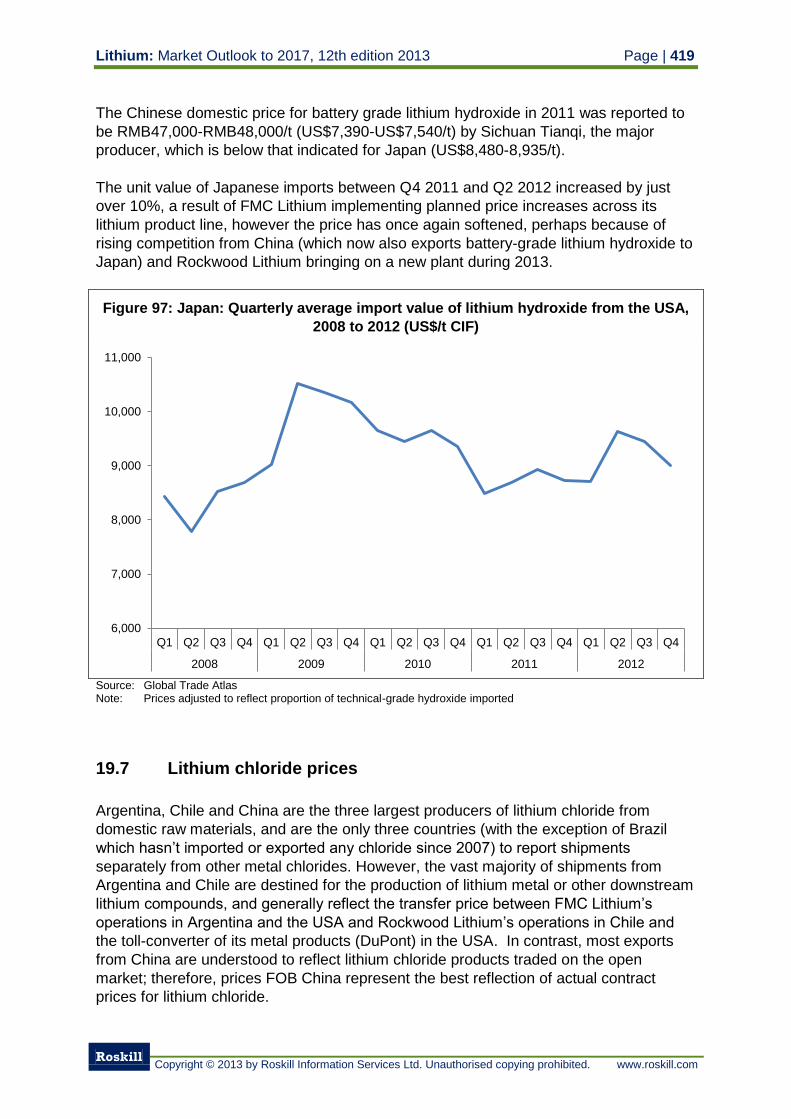

5.20 Japan 190

5.21 Kazakhstan 192

5.22 Mali 193

5.23 Mexico 193

5.23.1 Litio Mex S.A. de C.V. (Piero Sutti S.A. de C.V.) 193

5.23.2 First Potash Corp. (Mexico) 195

5.23.3 Bacanora Minerals Ltd. 195

5.24 Mongolia 196

5.25 Mozambique 196

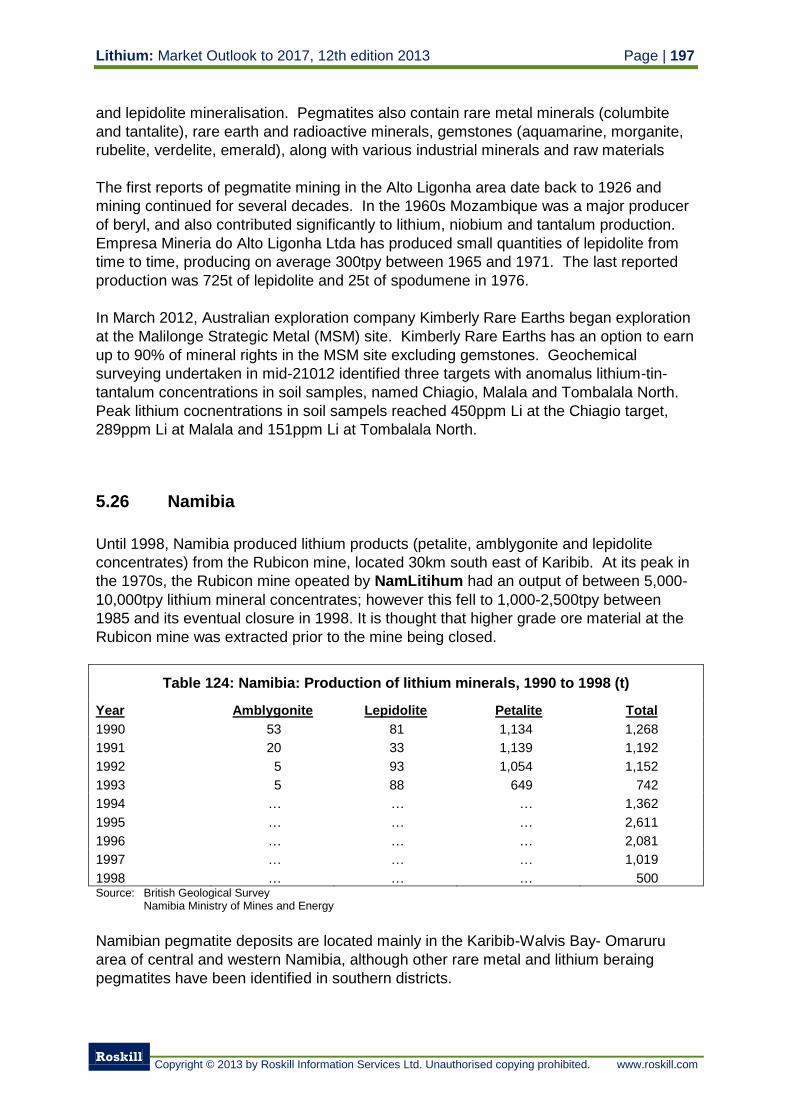

5.26 Namibia 197

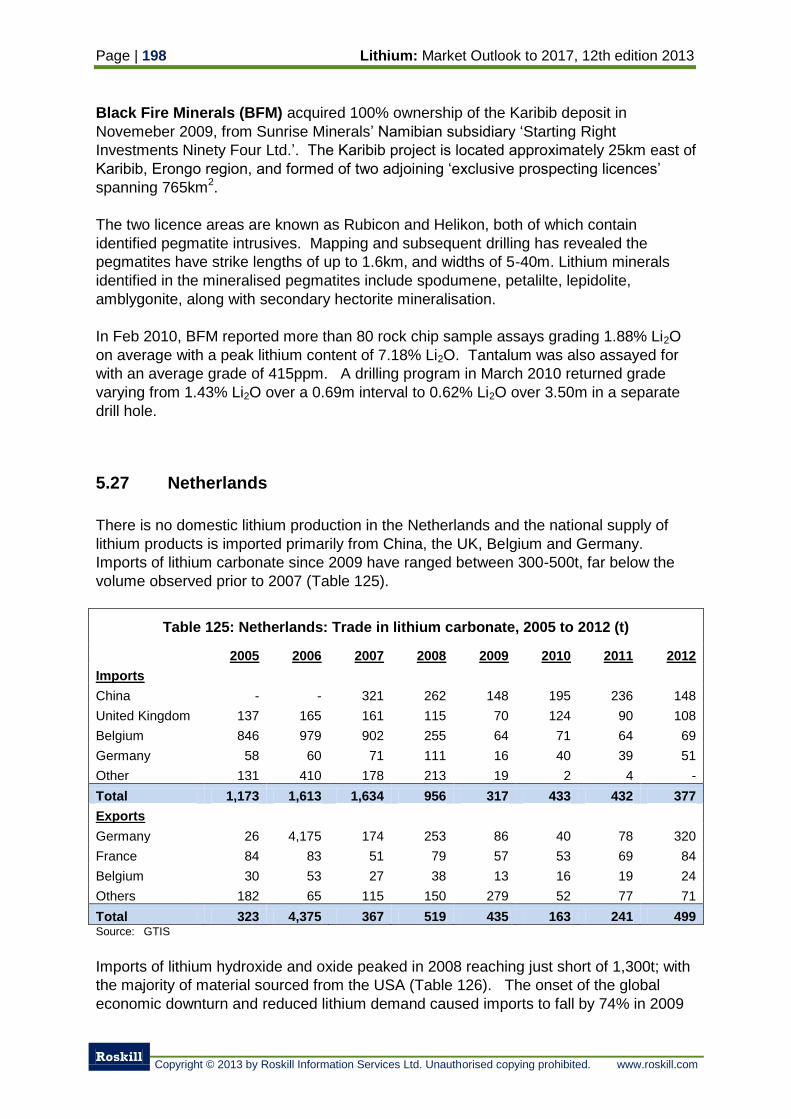

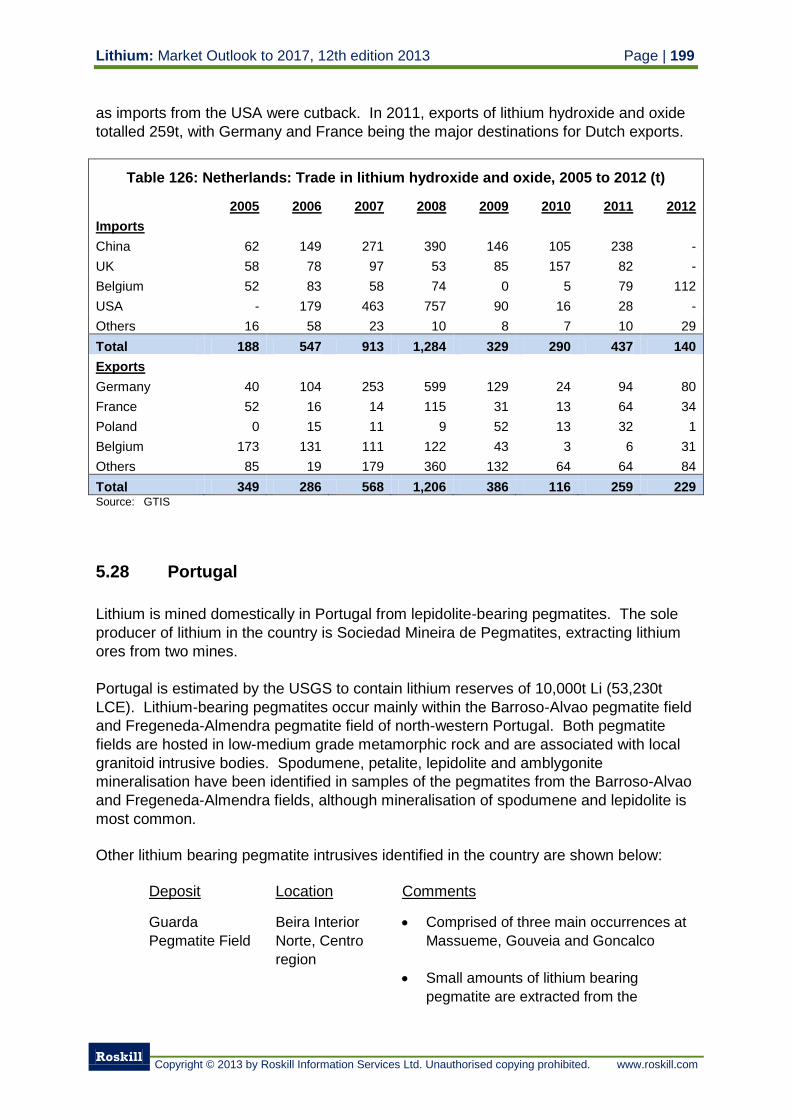

5.27 Netherlands 198

5.28 Portugal 199

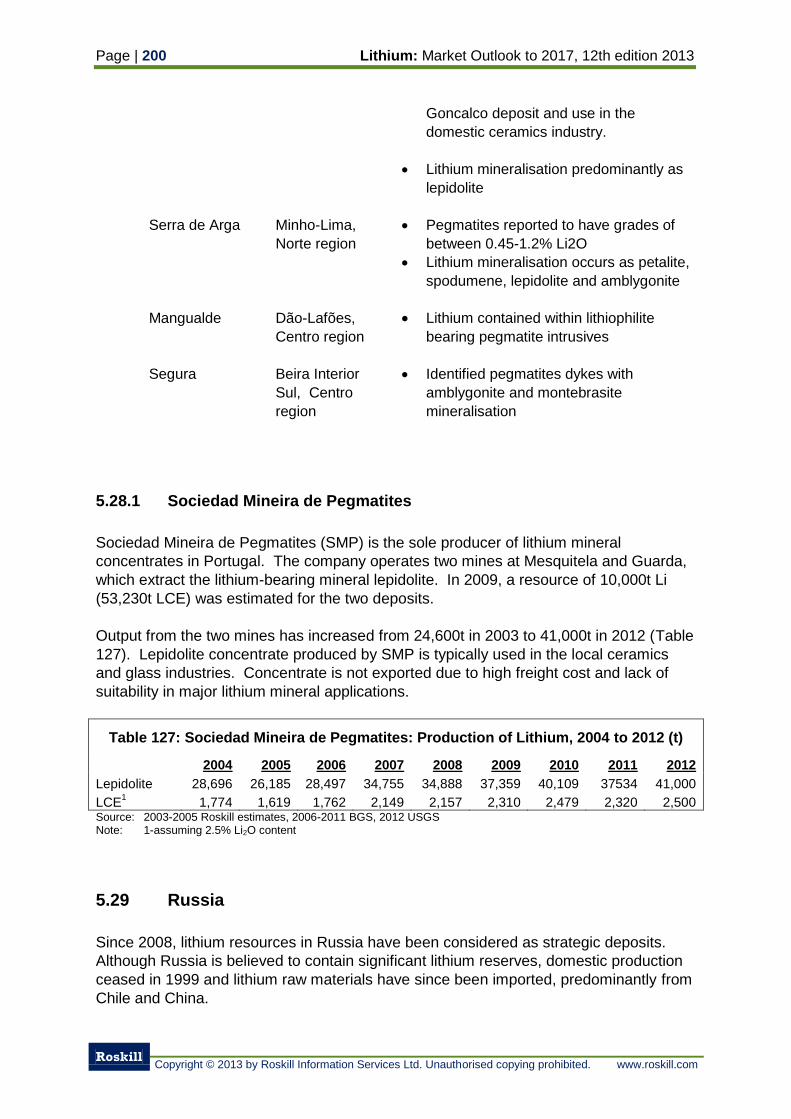

5.28.1 Sociedad Mineira de Pegmatites 200

5.29 Russia 200

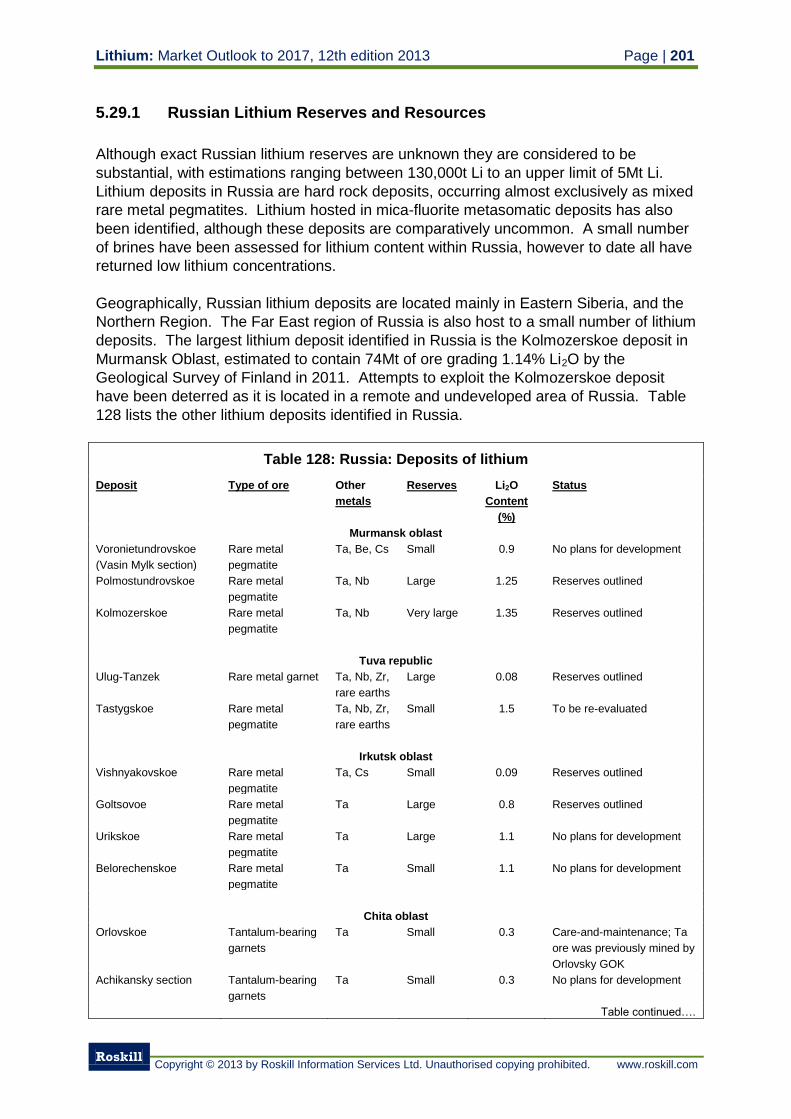

5.29.1 Russian Lithium Reserves and Resources 201

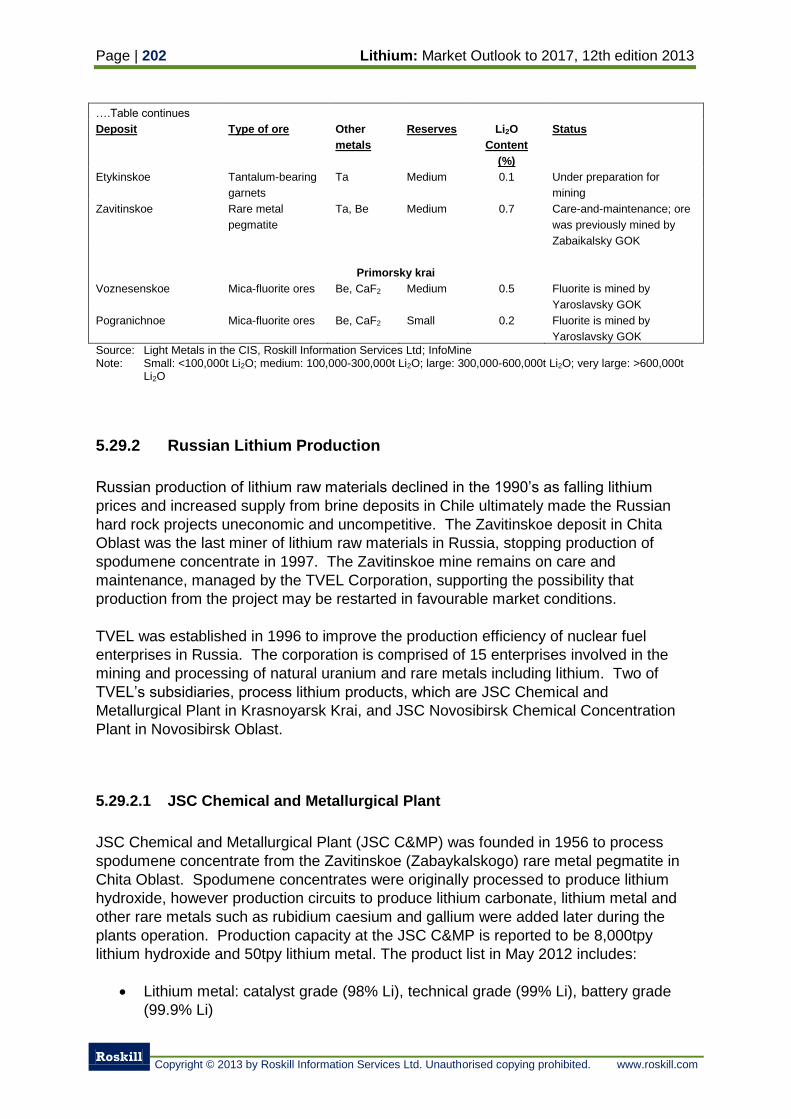

5.29.2 Russian Lithium Production 202

5.29.2.1 JSC Chemical and Metallurgical Plant 202

5.29.2.2 JSC Novosibirsk Chemical Concentration Plant 203

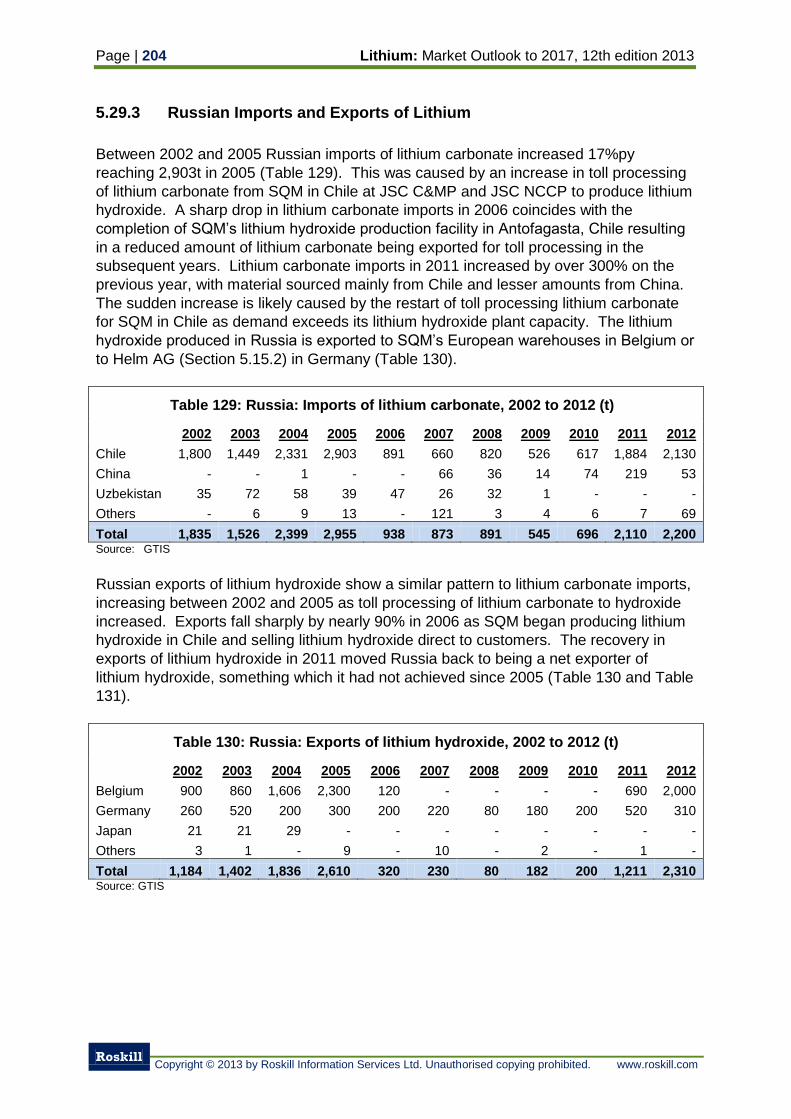

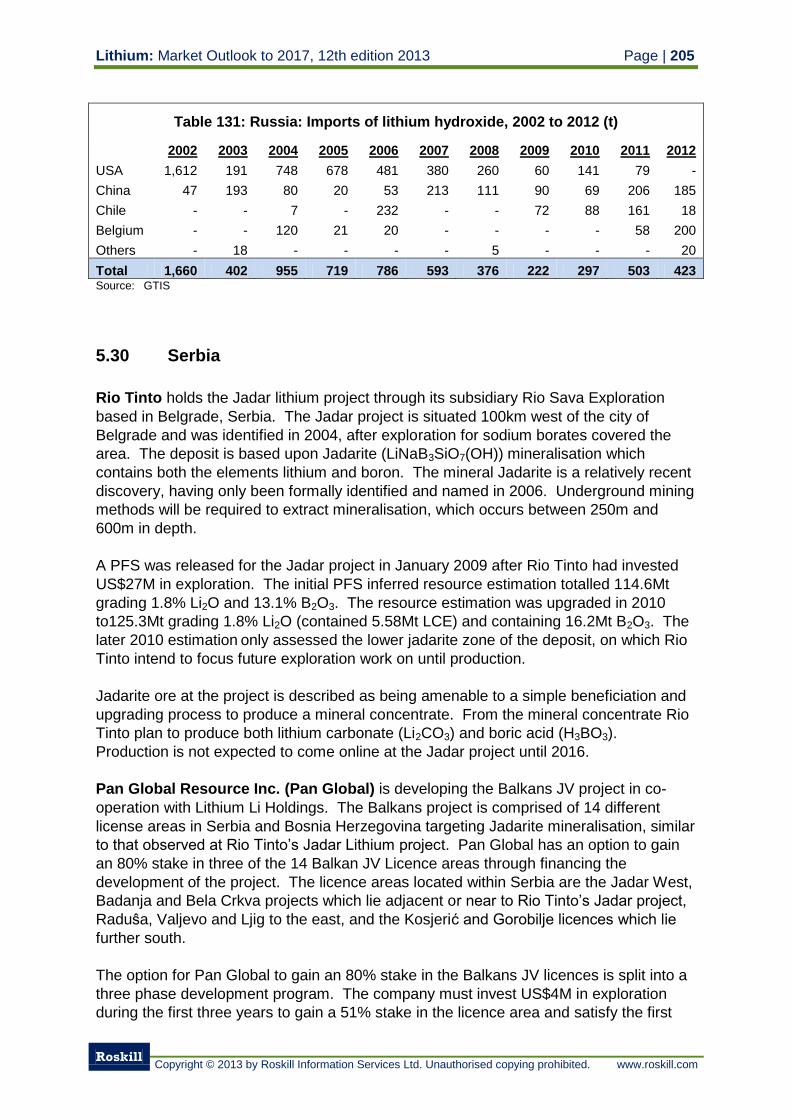

5.29.3 Russian Imports and Exports of Lithium 204

5.30 Serbia 205

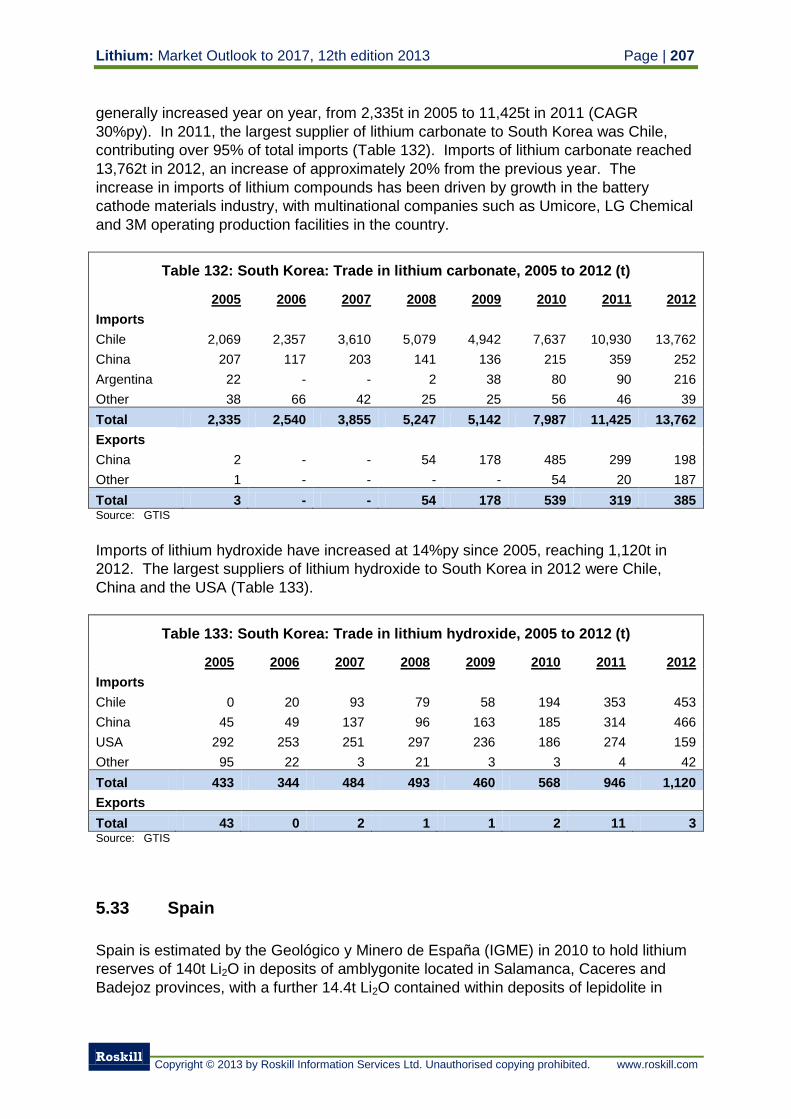

5.31 South Africa 206

5.32 South Korea 206

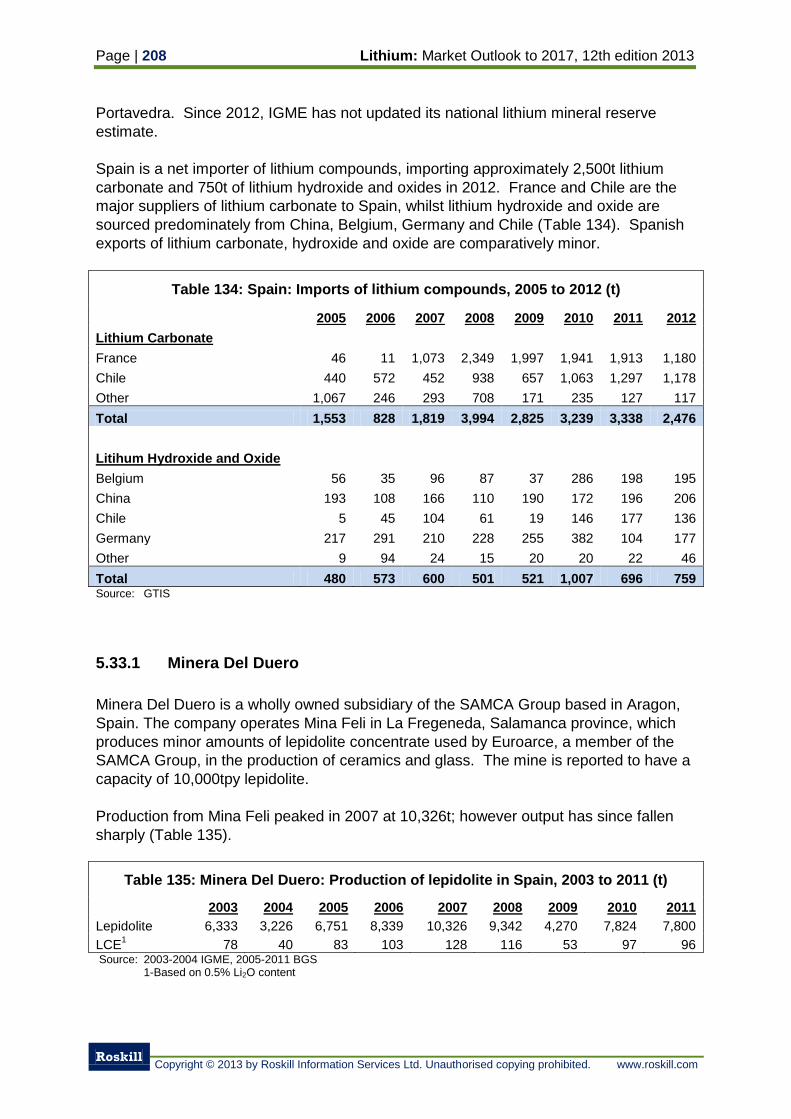

5.33 Spain 207

5.33.1 Minera Del Duero 208

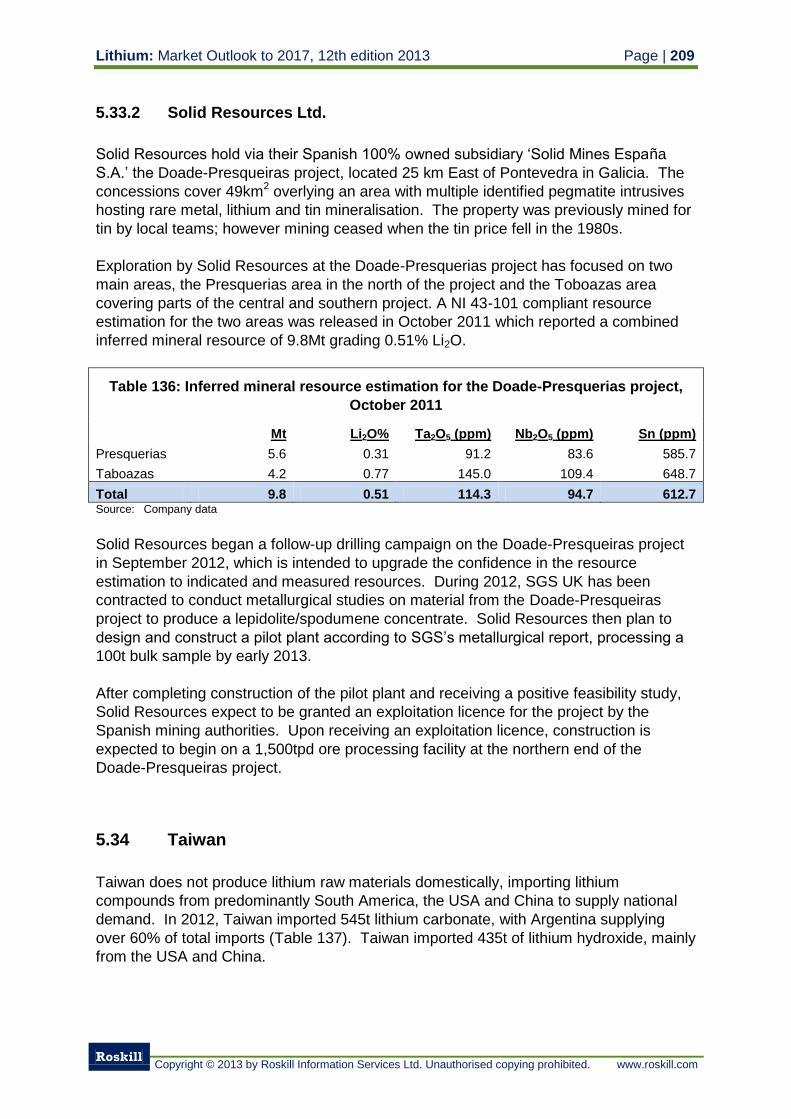

5.33.2 Solid Resources Ltd. 209

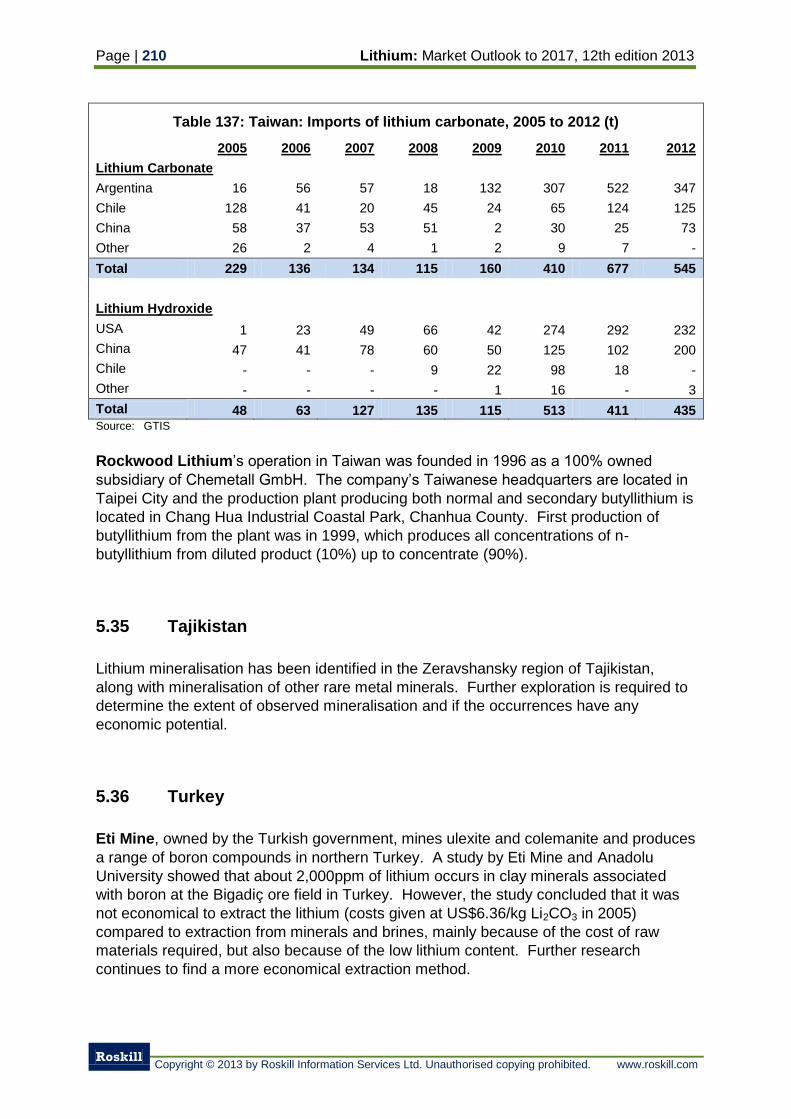

5.34 Taiwan 209

5.35 Tajikistan 210

5.36 Turkey 210

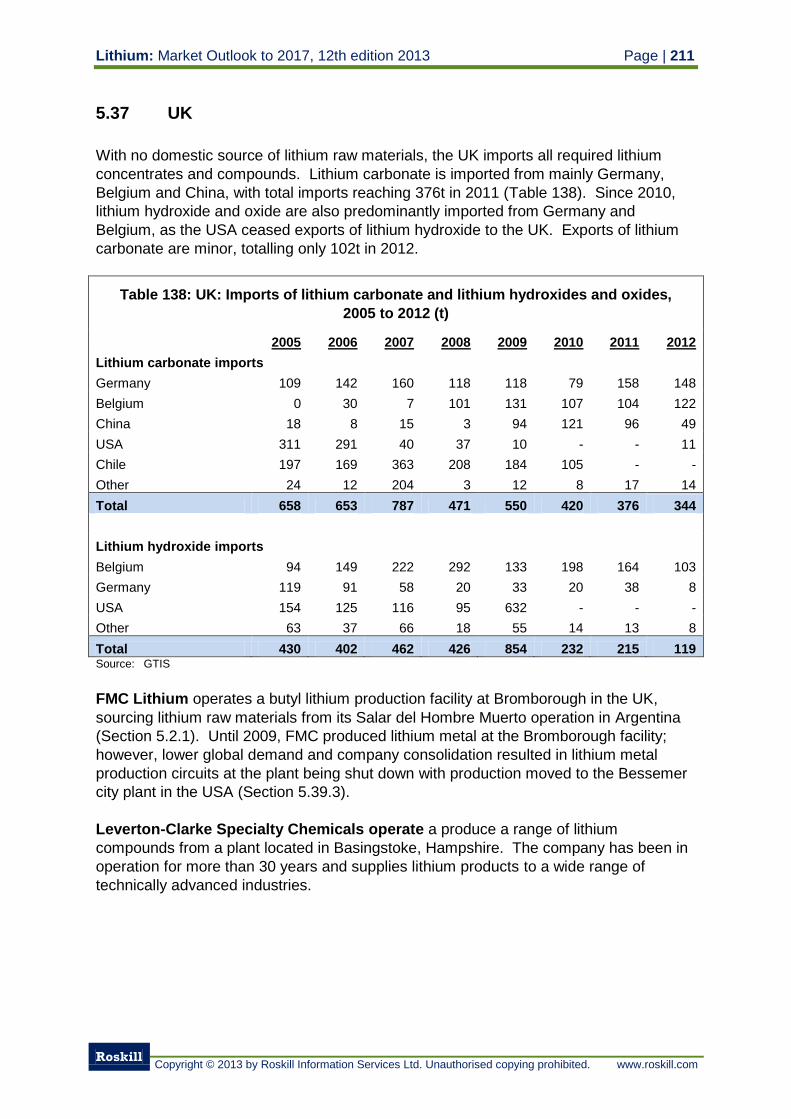

5.37 UK 211

5.38 Ukraine 212

5.39 USA 212

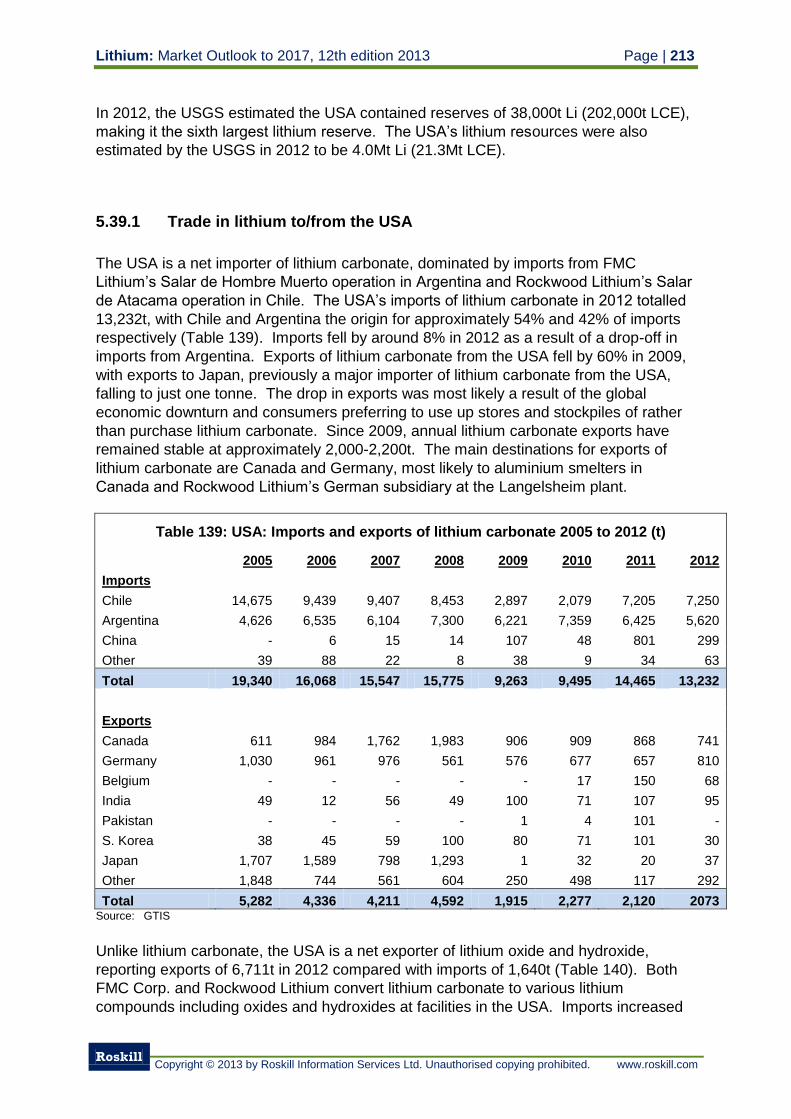

5.39.1 Trade in lithium to/from the USA 213

5.39.2 Rockwood Lithium (Chemetall Group) 214

5.39.2.1 Silver Peak, Kings Mountain and New Johnsonville operations

(USA) 215

5.39.3 FMC Corporation 216

5.39.3.1 FMC Lithium 217

5.39.3.2 Other FMC Corporation facilities 218

5.39.4 Western Lithium Corporation 219

5.39.5 Simbol Materials Corp. 222

5.39.6 Albemarle Corporation 223

5.39.7 Toxco Inc. 223

5.39.8 AusAmerican Mining Corp. Ltd. 223

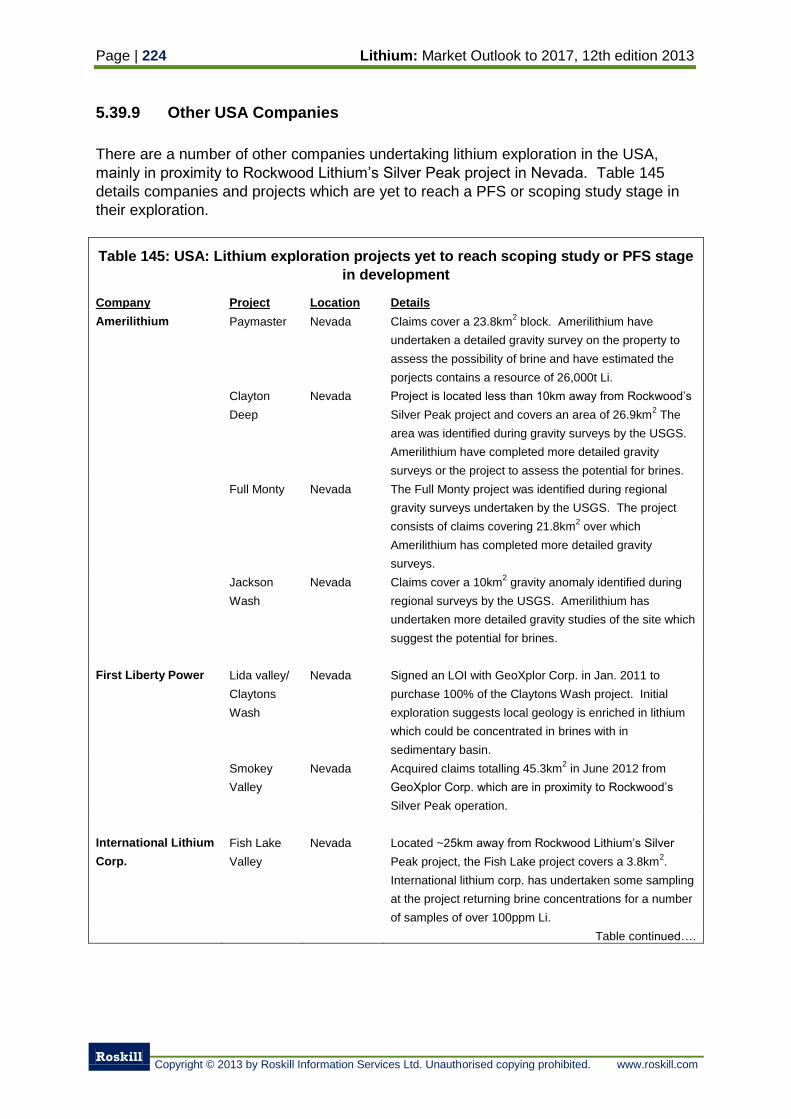

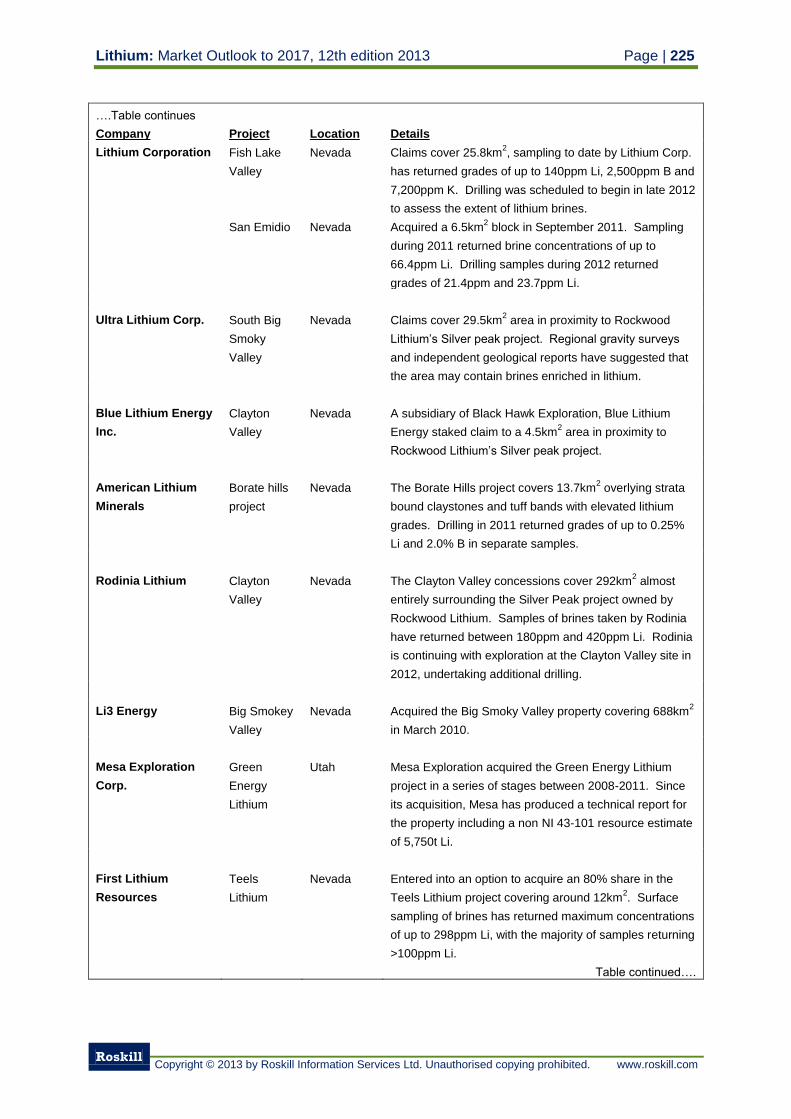

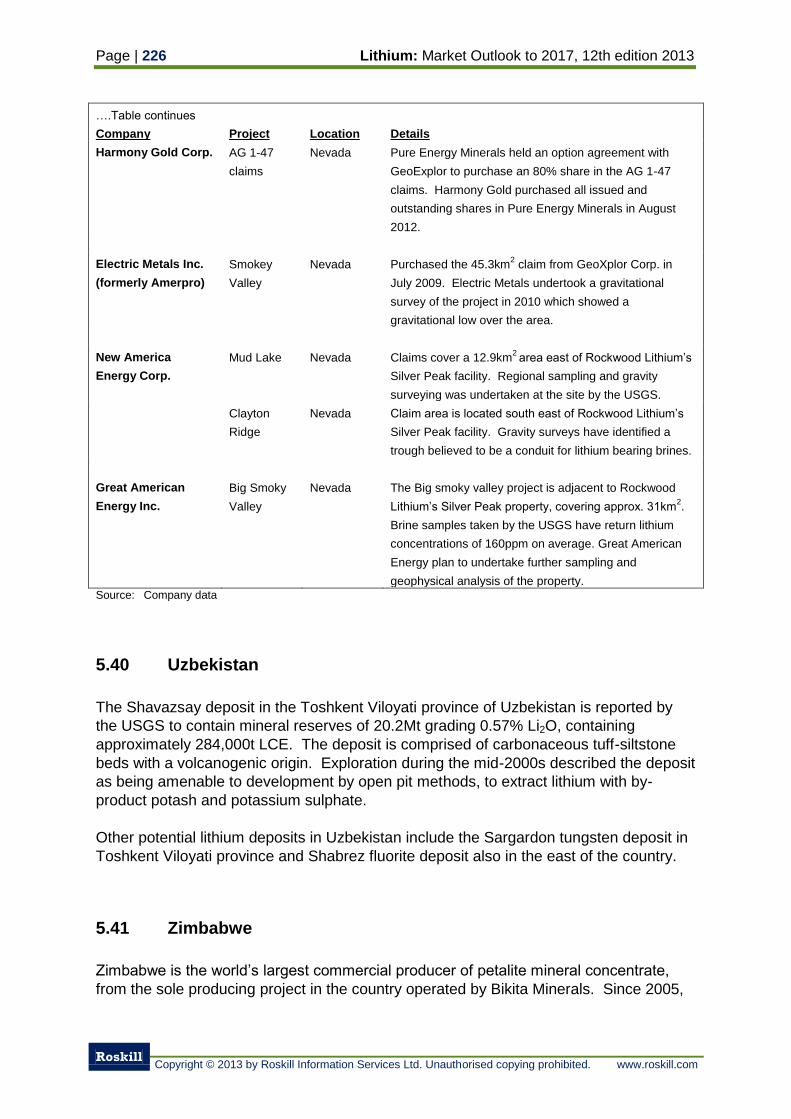

5.39.9 Other USA Companies 224

5.40 Uzbekistan 226

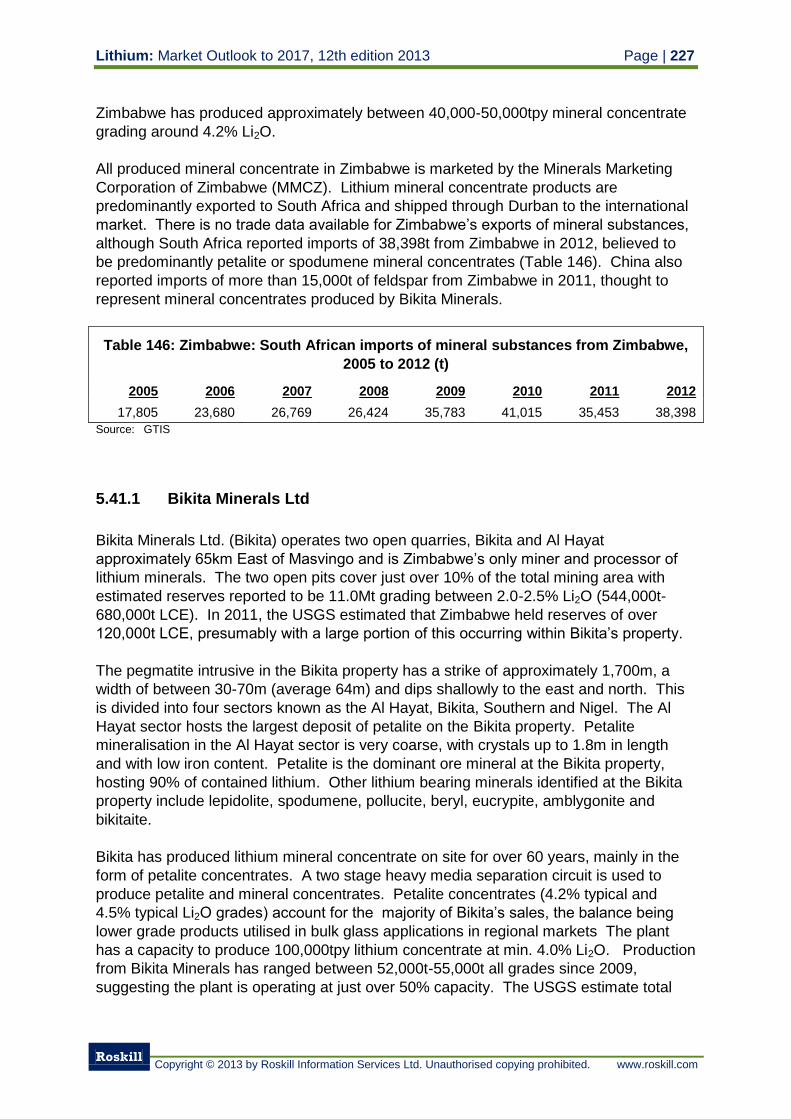

5.41 Zimbabwe 226

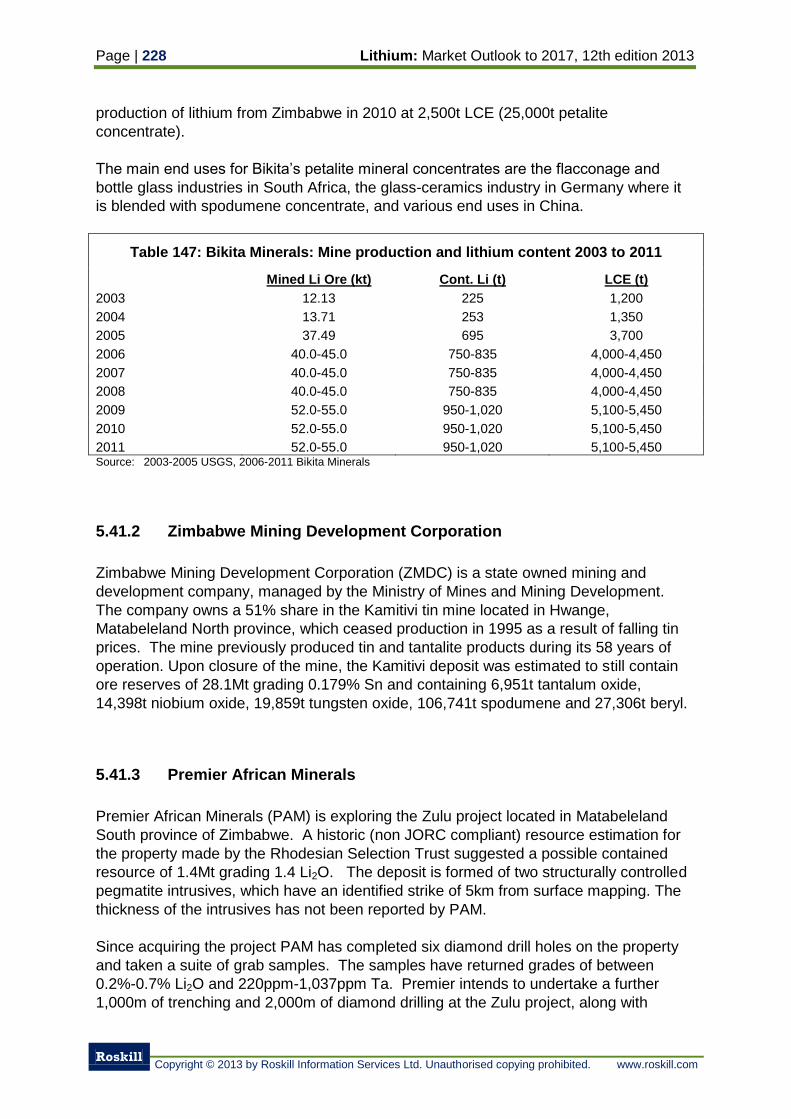

5.41.1 Bikita Minerals Ltd 227

5.41.2 Zimbabwe Mining Development Corporation 228

5.41.3 Premier African Minerals 228

5.41.4 Cape Range Ltd. 229

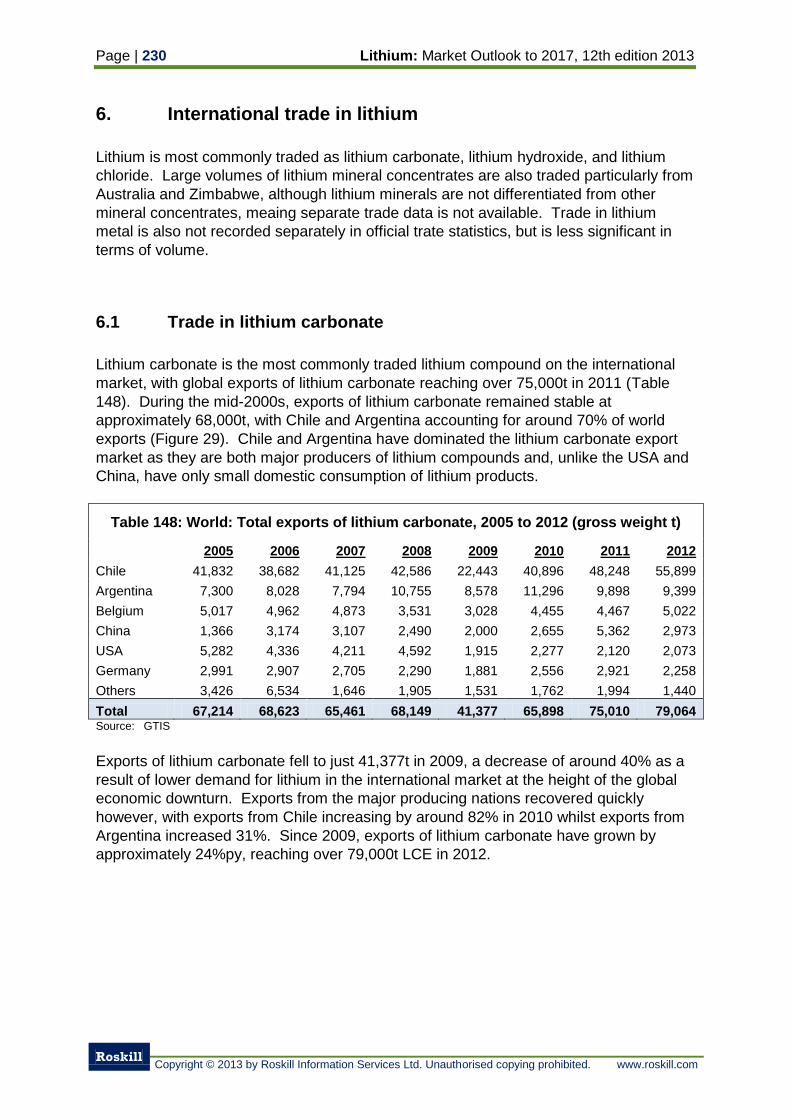

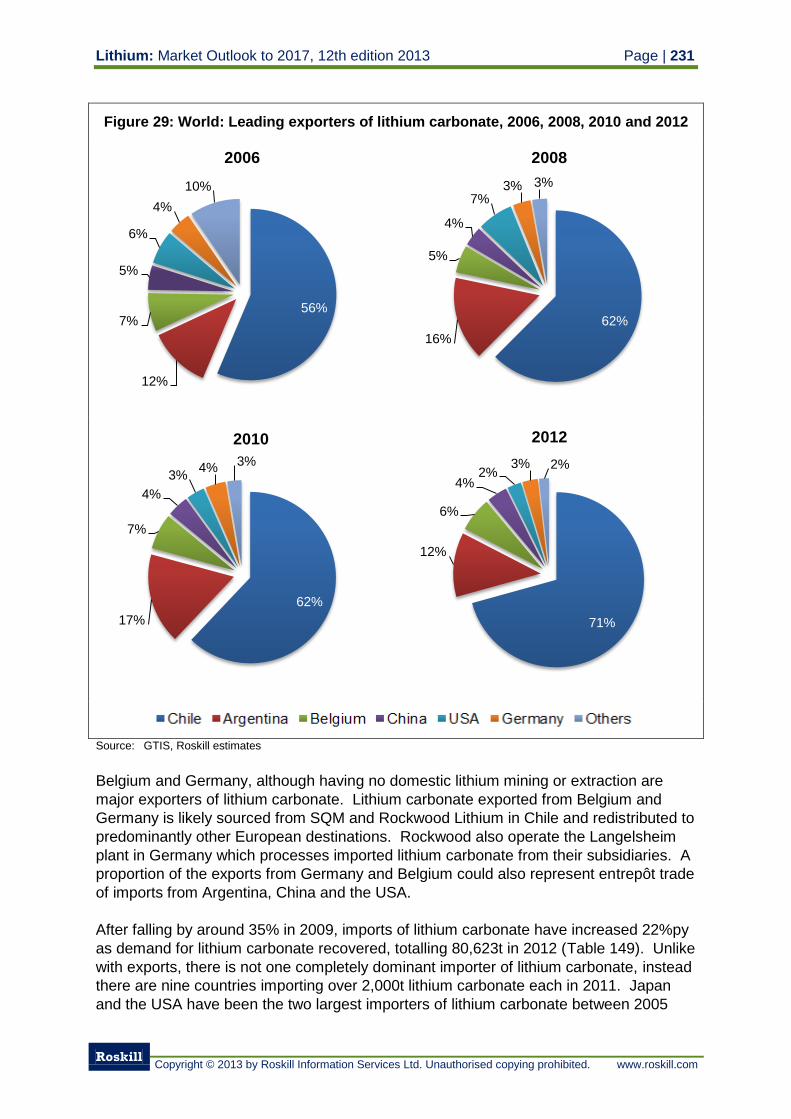

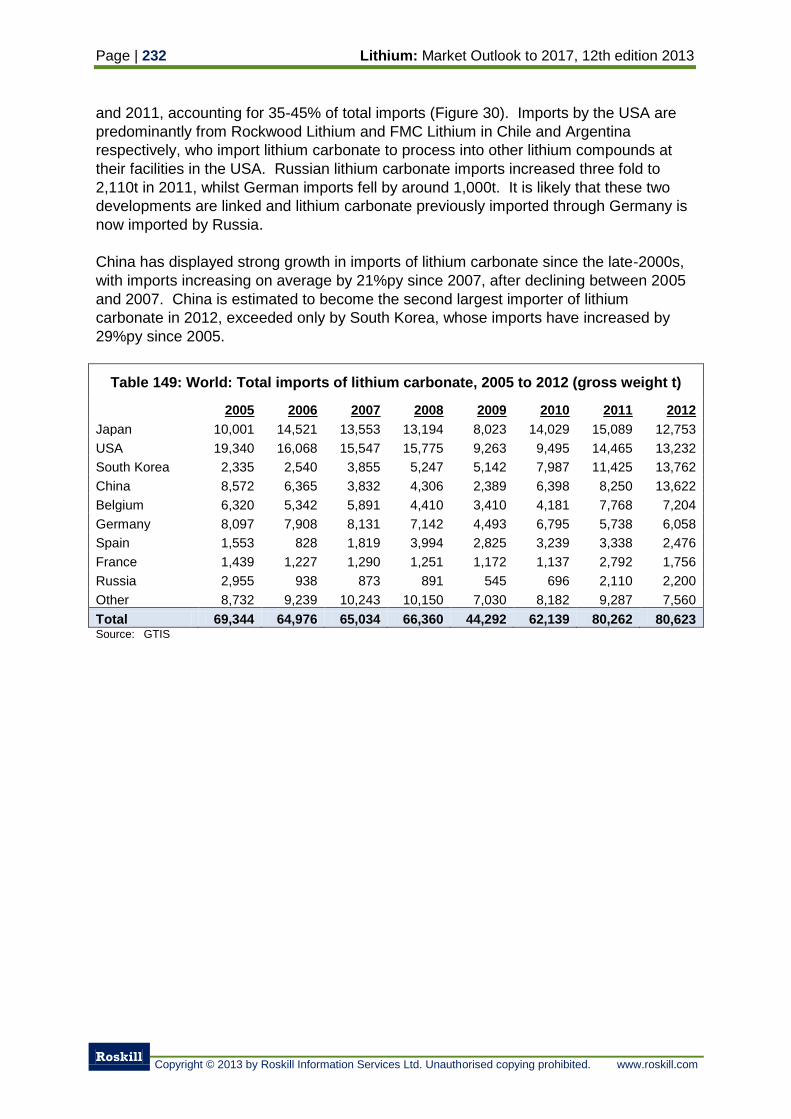

6. International trade in lithium 230

6.1 Trade in lithium carbonate 230

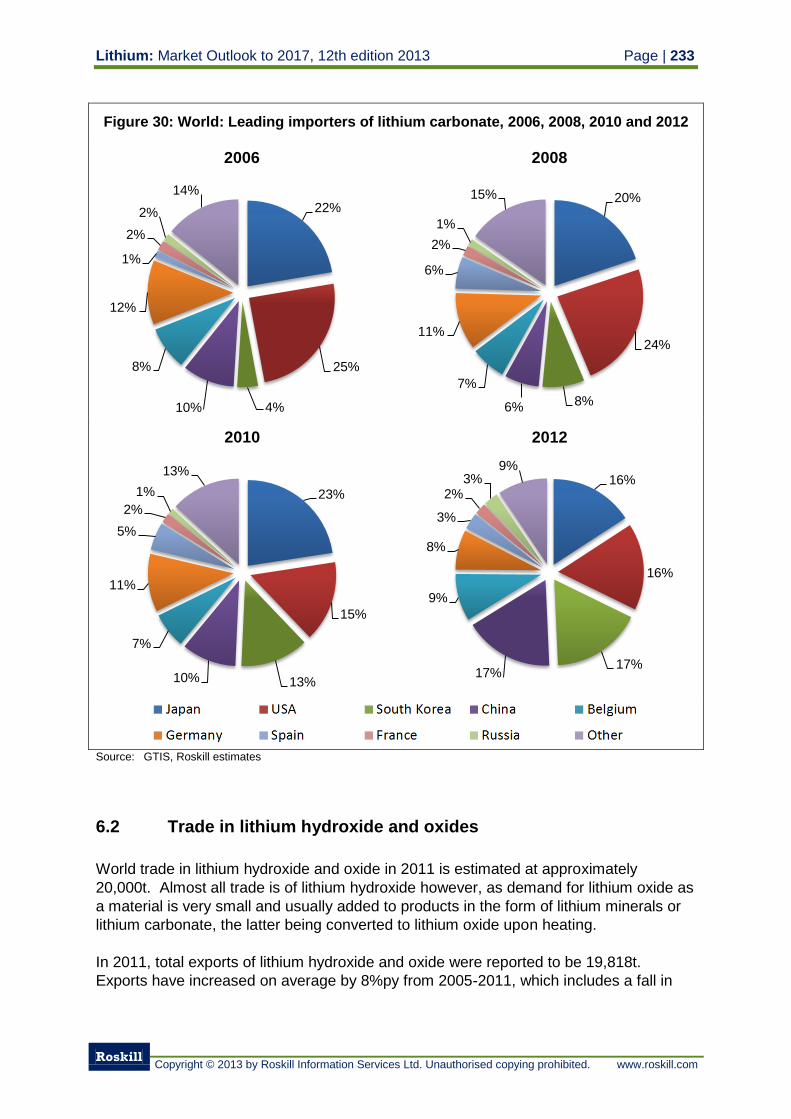

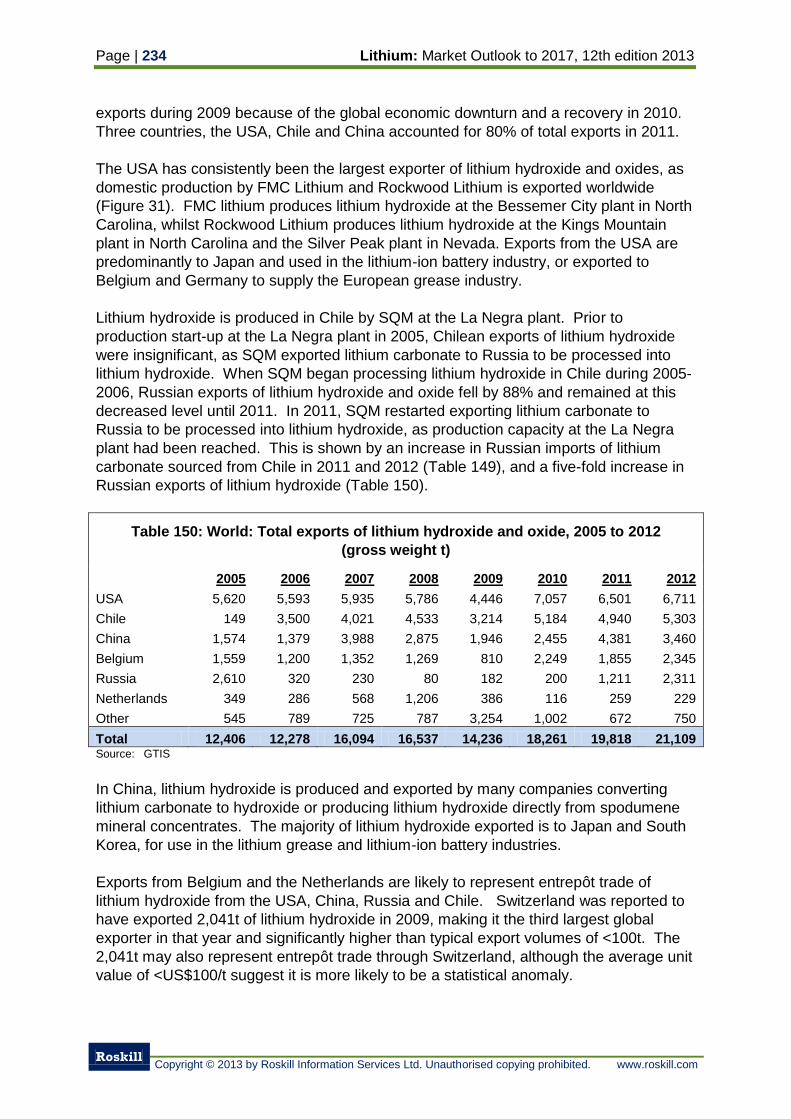

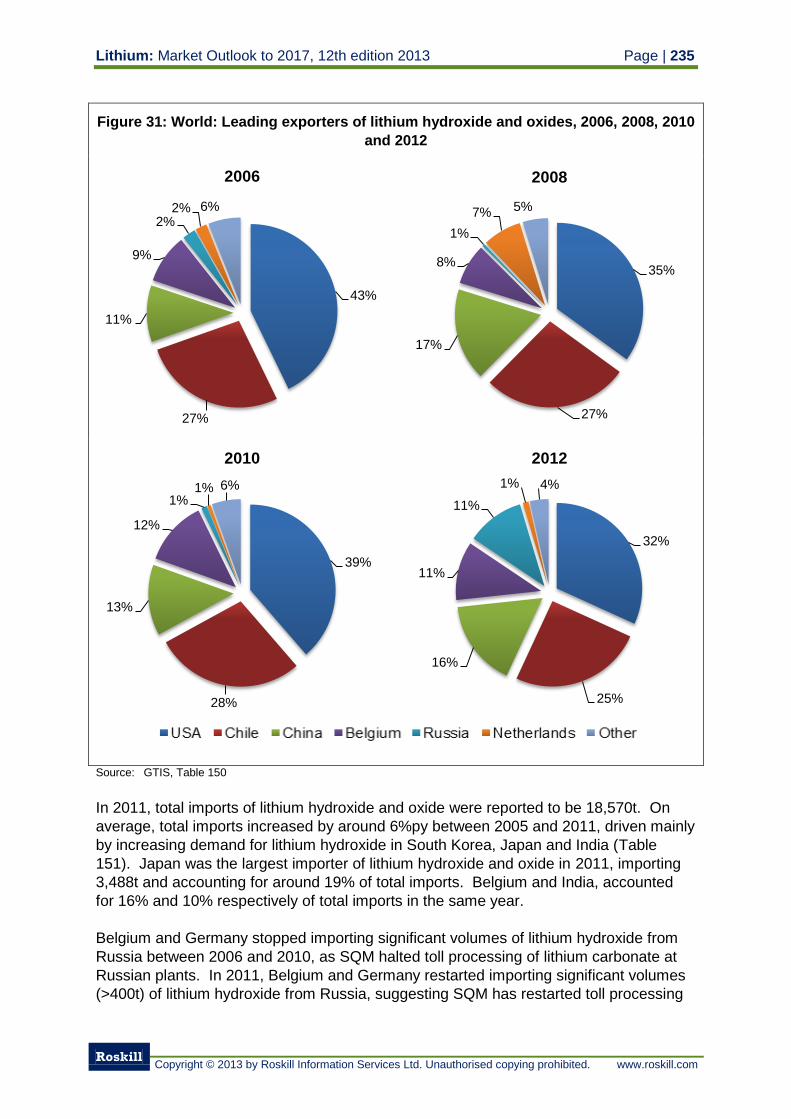

6.2 Trade in lithium hydroxide and oxides 233

6.3 Trade in lithium chloride 236

6.4 Trade in mineral concentrates 237

6.5 Trade in lithium brines 238

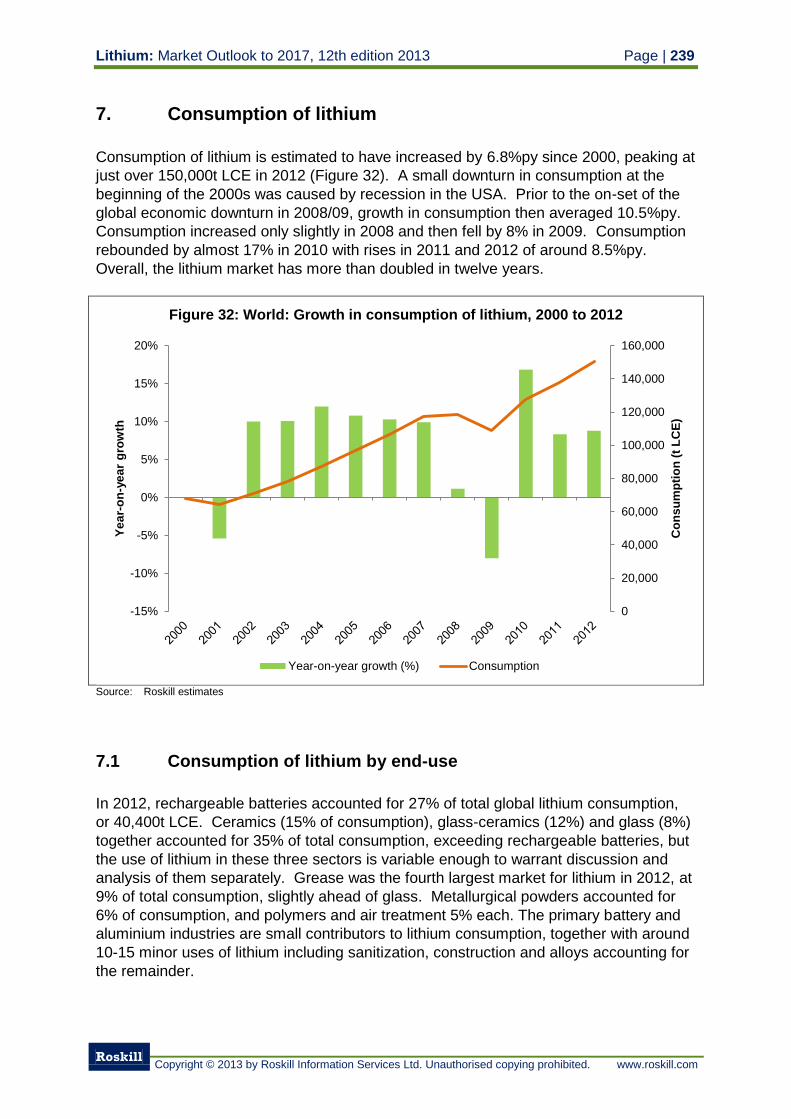

7. Consumption of lithium 239

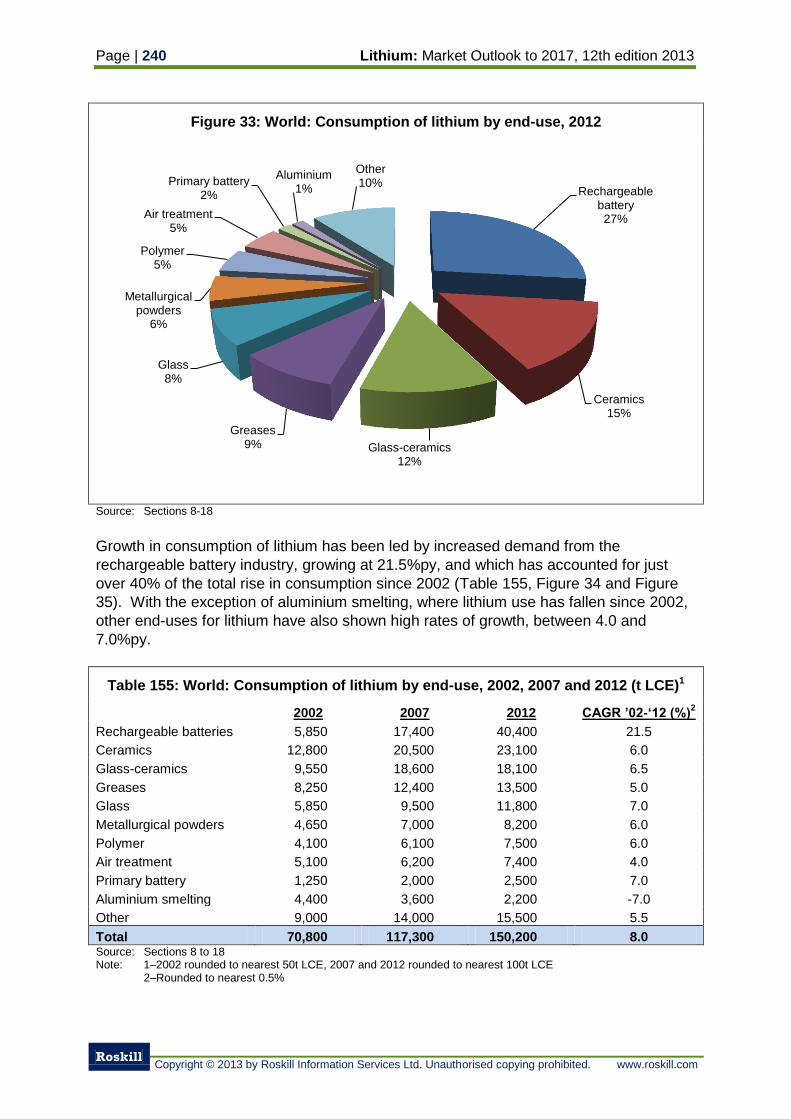

7.1 Consumption of lithium by end-use 239

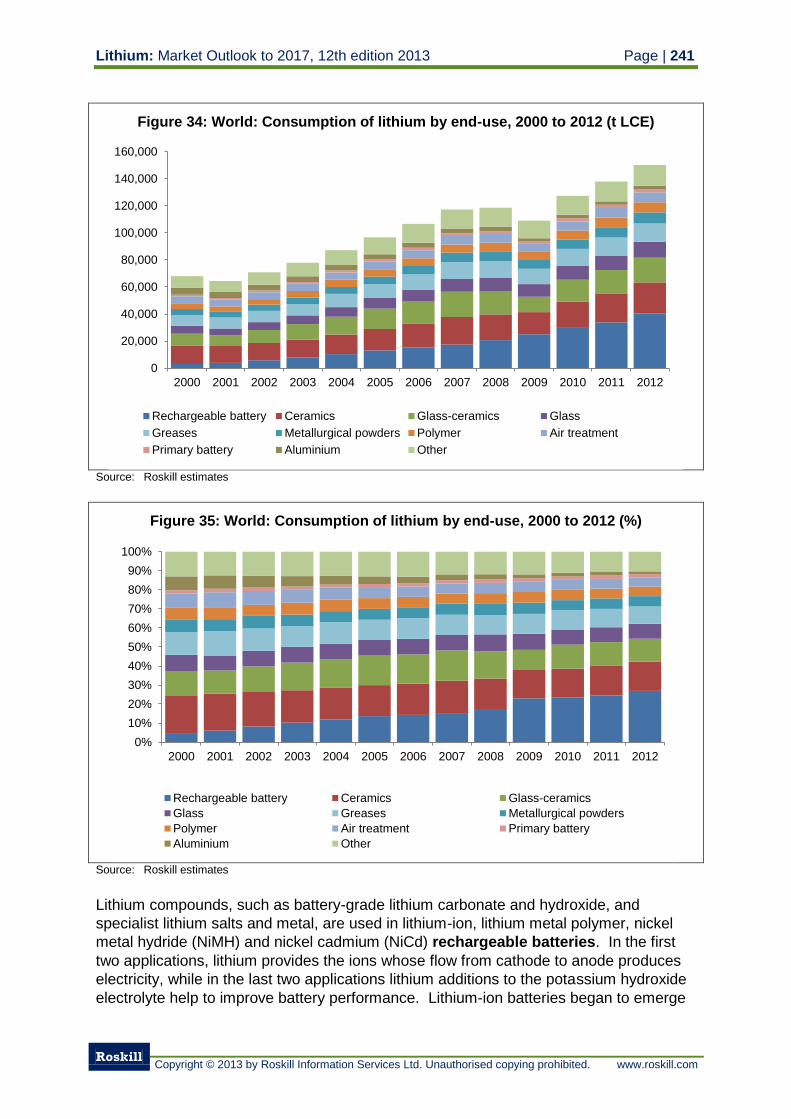

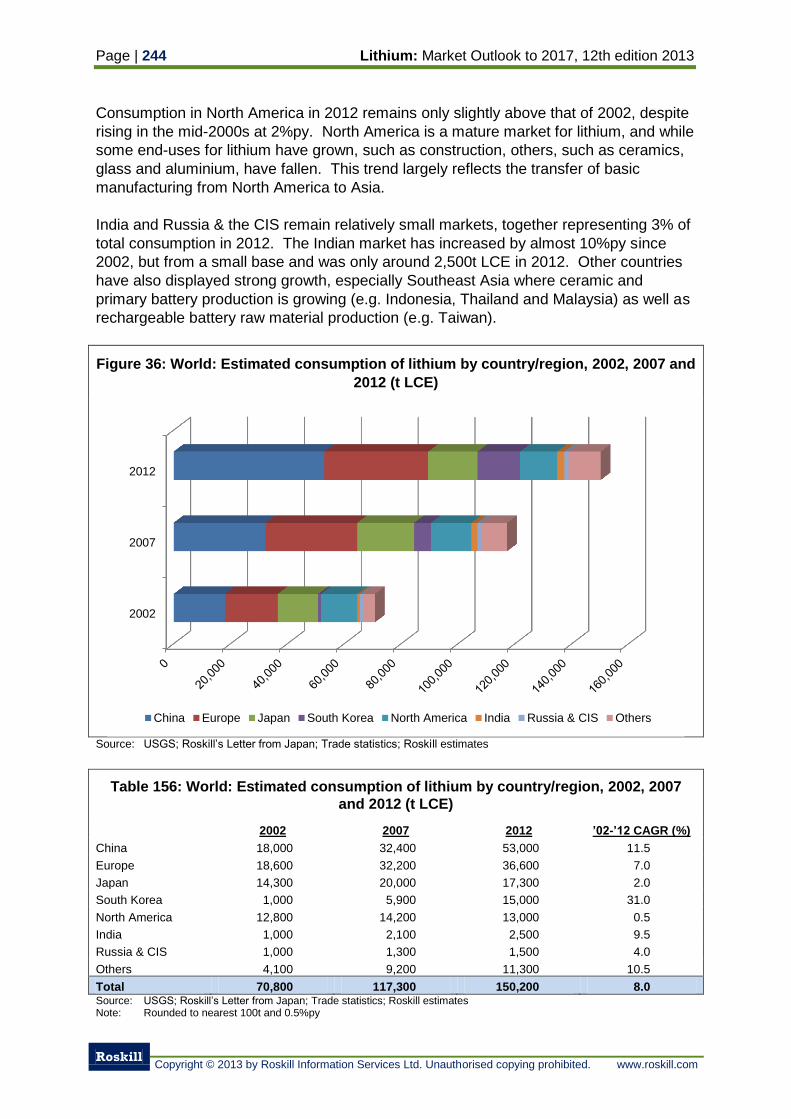

7.2 Consumption of lithium by country/region 243

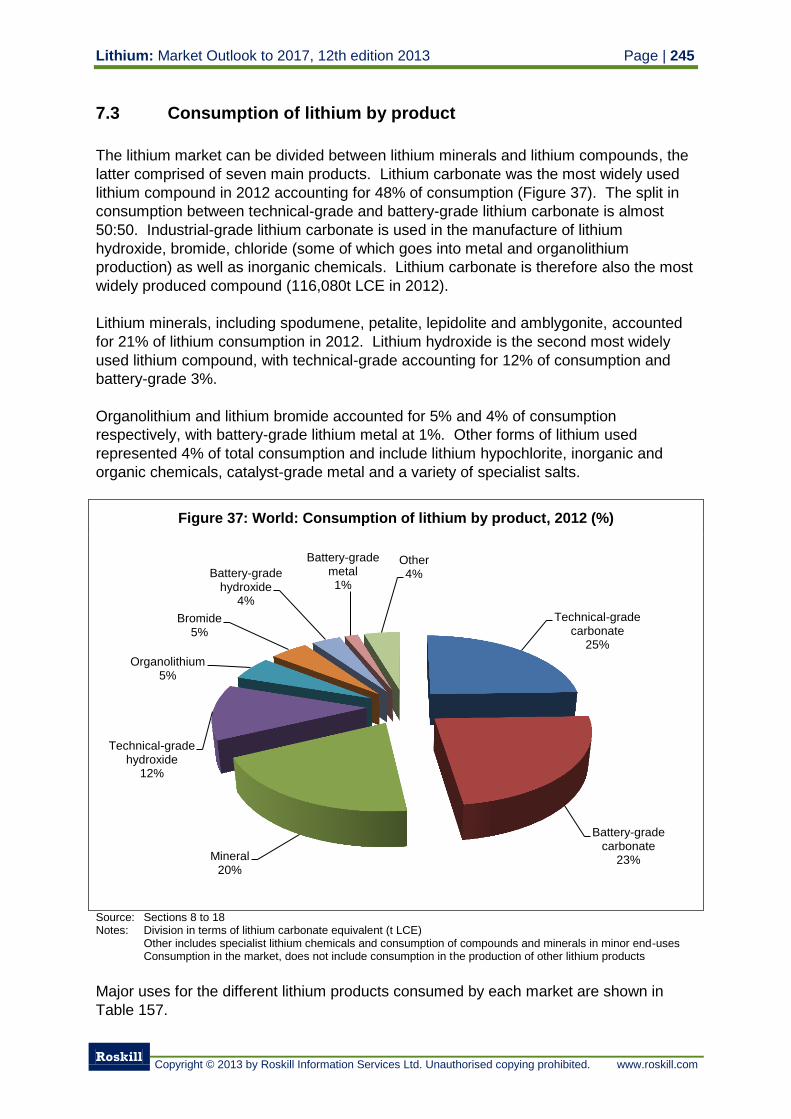

7.3 Consumption of lithium by product 245

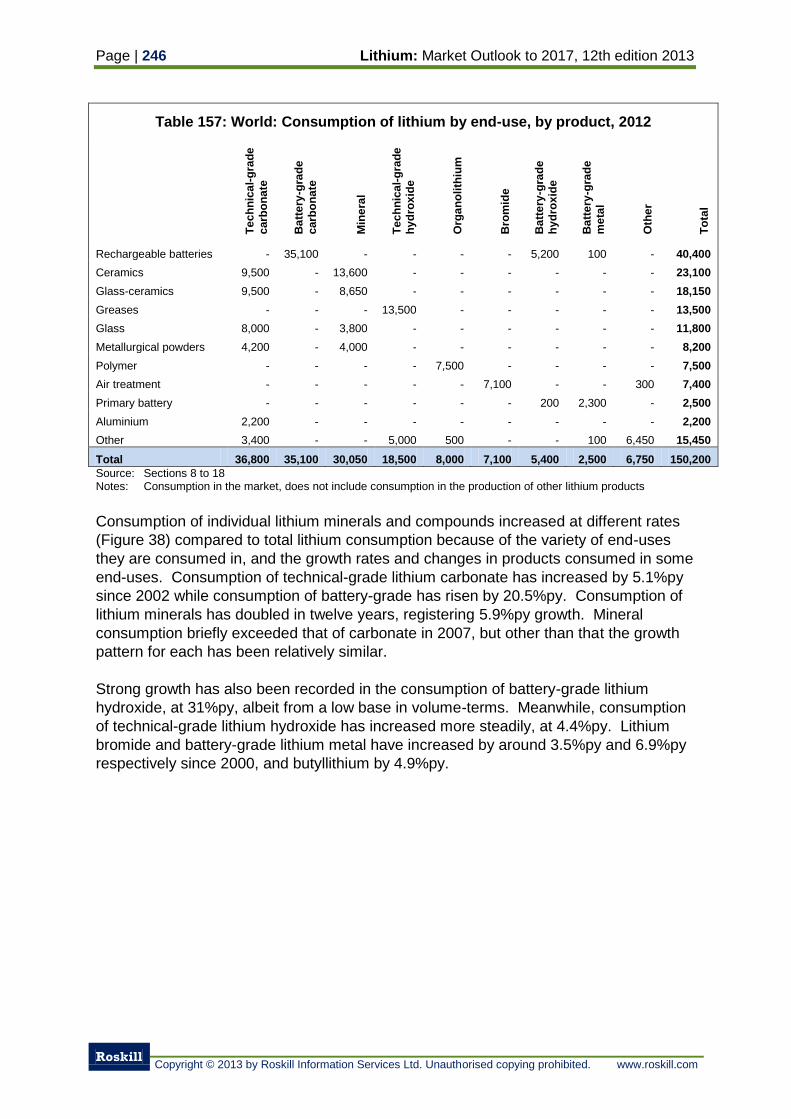

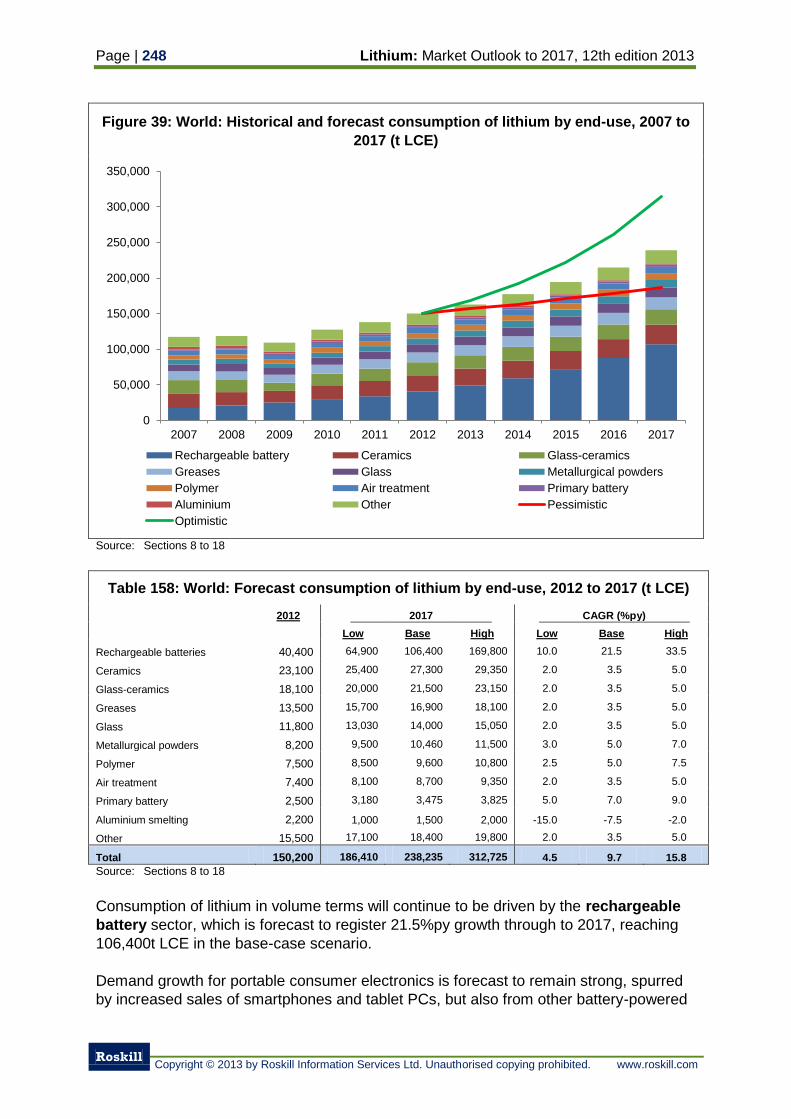

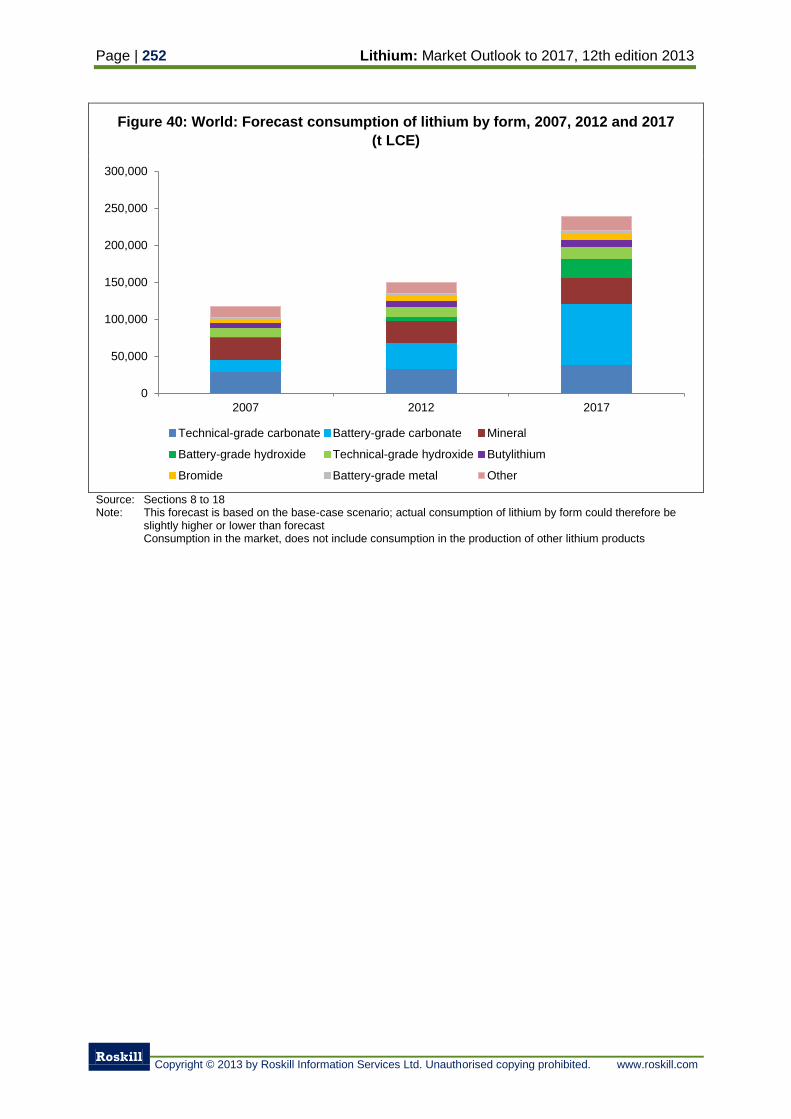

7.4 Outlook for consumption of lithium by end-use 247

7.5 Outlook for lithium consumption by product 251

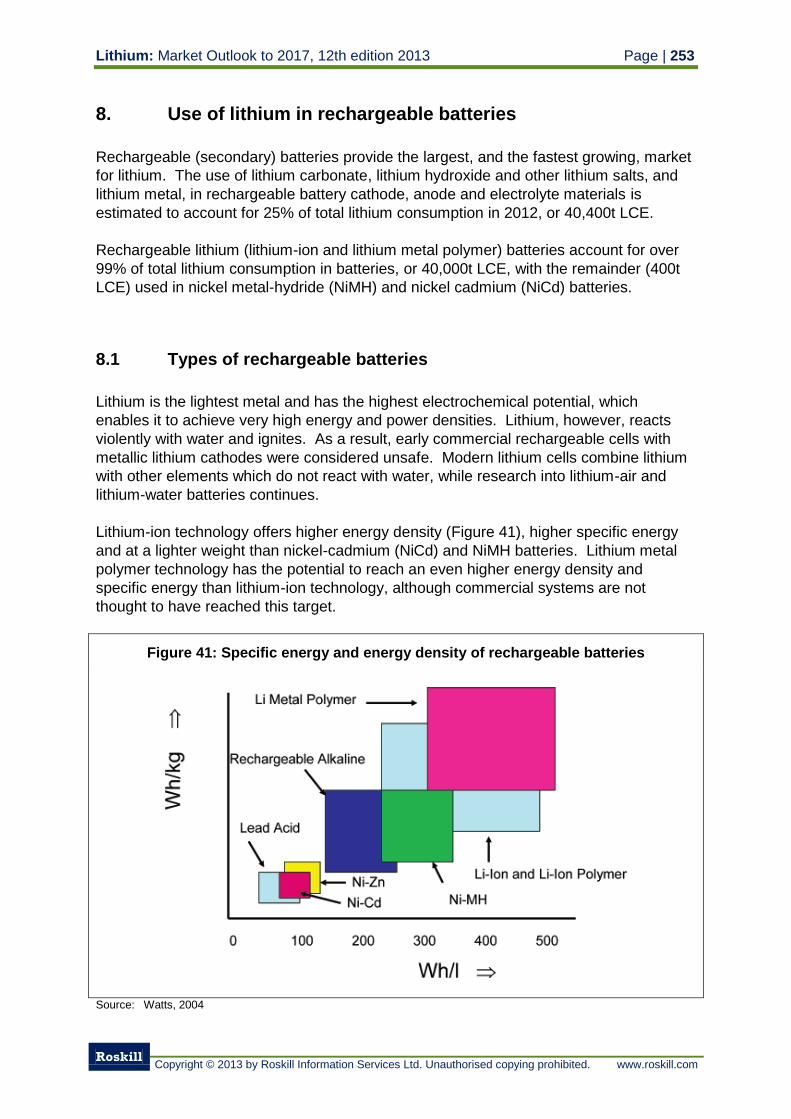

8. Use of lithium in rechargeable batteries 253

8.1 Types of rechargeable batteries 253

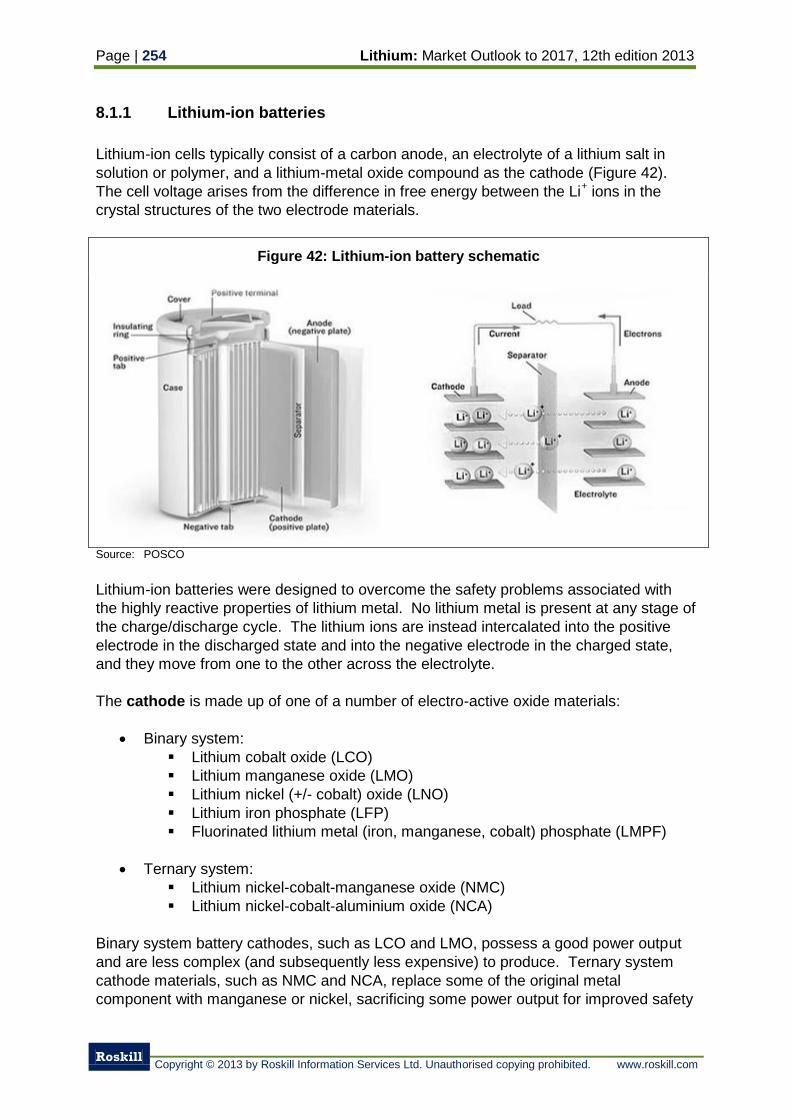

8.1.1 Lithium-ion batteries 254

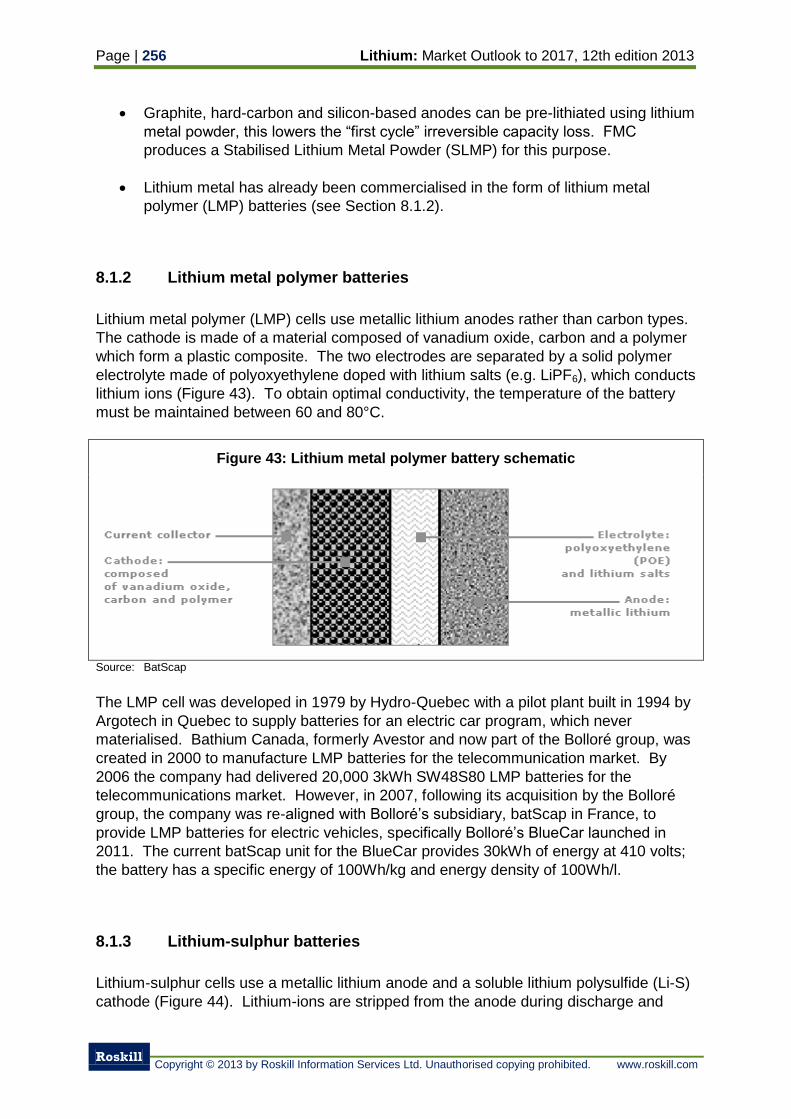

8.1.2 Lithium metal polymer batteries 256

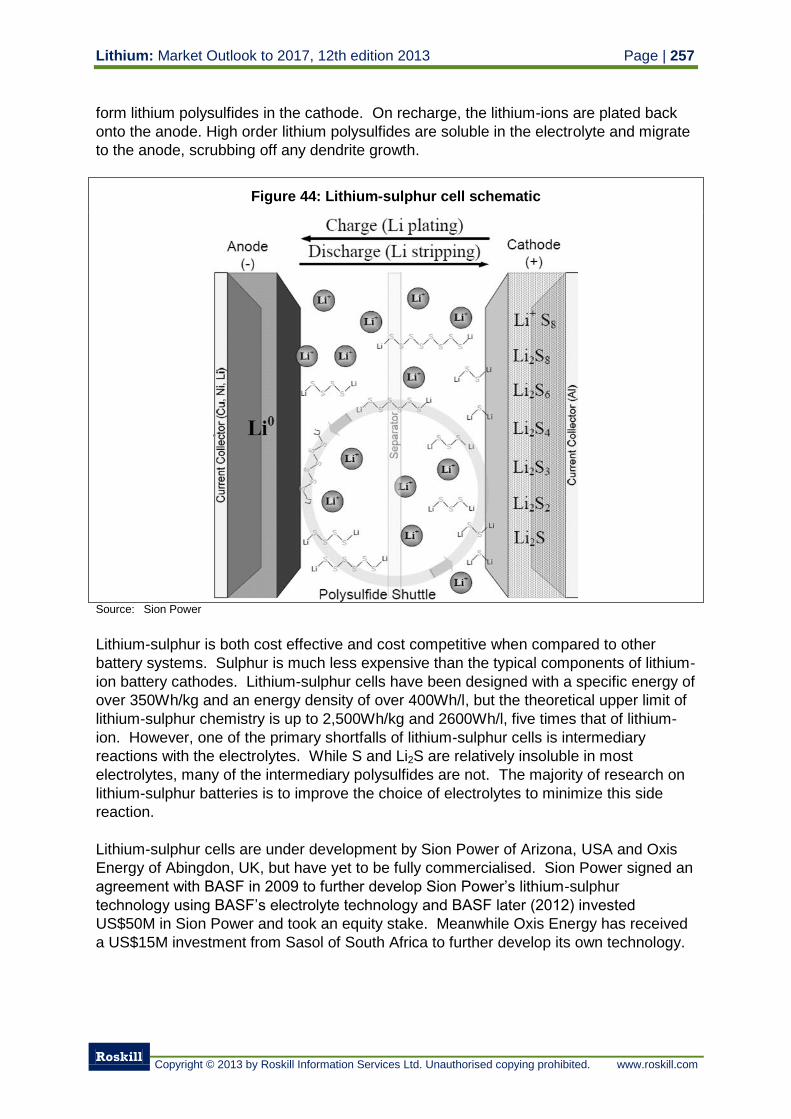

8.1.3 Lithium-sulphur batteries 256

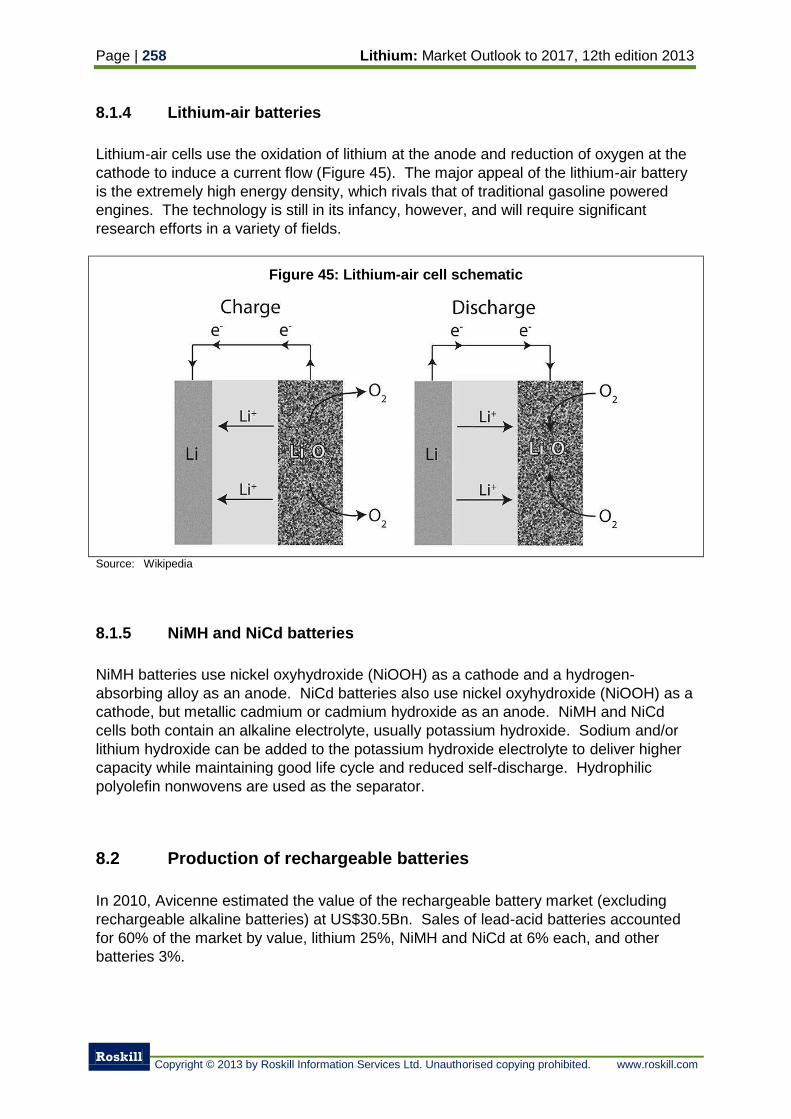

8.1.4 Lithium-air batteries 258

8.1.5 NiMH and NiCd batteries 258

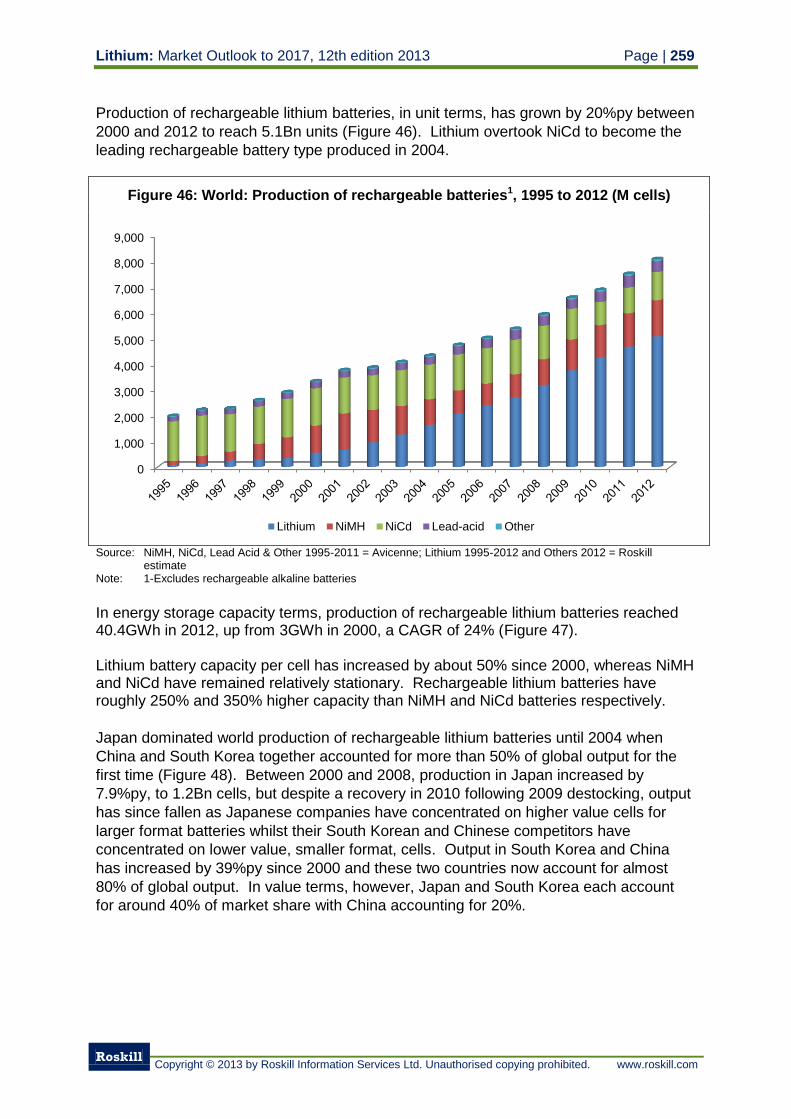

8.2 Production of rechargeable batteries 258

8.2.1 Producers of rechargeable lithium batteries 261

8.2.2 Producers of nickel metal hydride batteries 262

8.3 Production of rechargeable lithium battery materials 262

8.3.1 Producers of rechargeable lithium battery materials 264

8.3.1.1 Cathode materials 264

8.3.1.2 Electrolyte salts 267

8.3.1.3 Anode materials 268

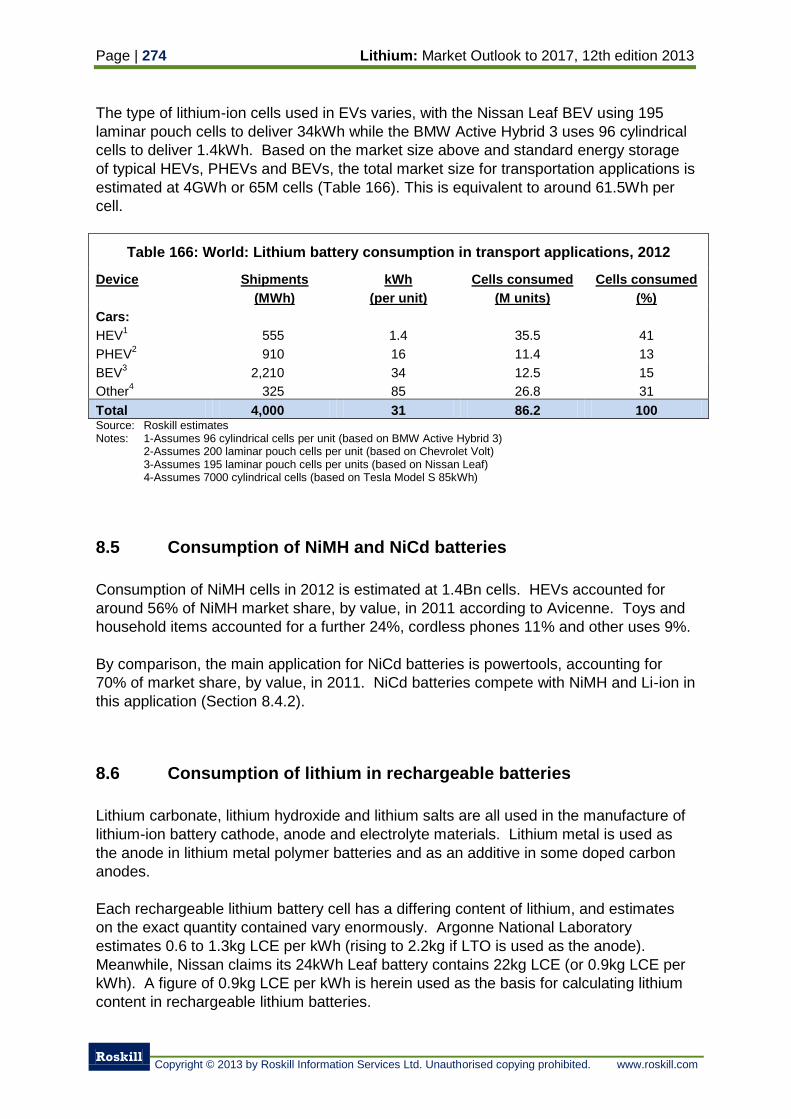

8.4 Consumption of rechargeable lithium batteries 268

8.4.1 Computing, communication and consumer (3C) market 269

8.4.2 Power devices and motive power 270

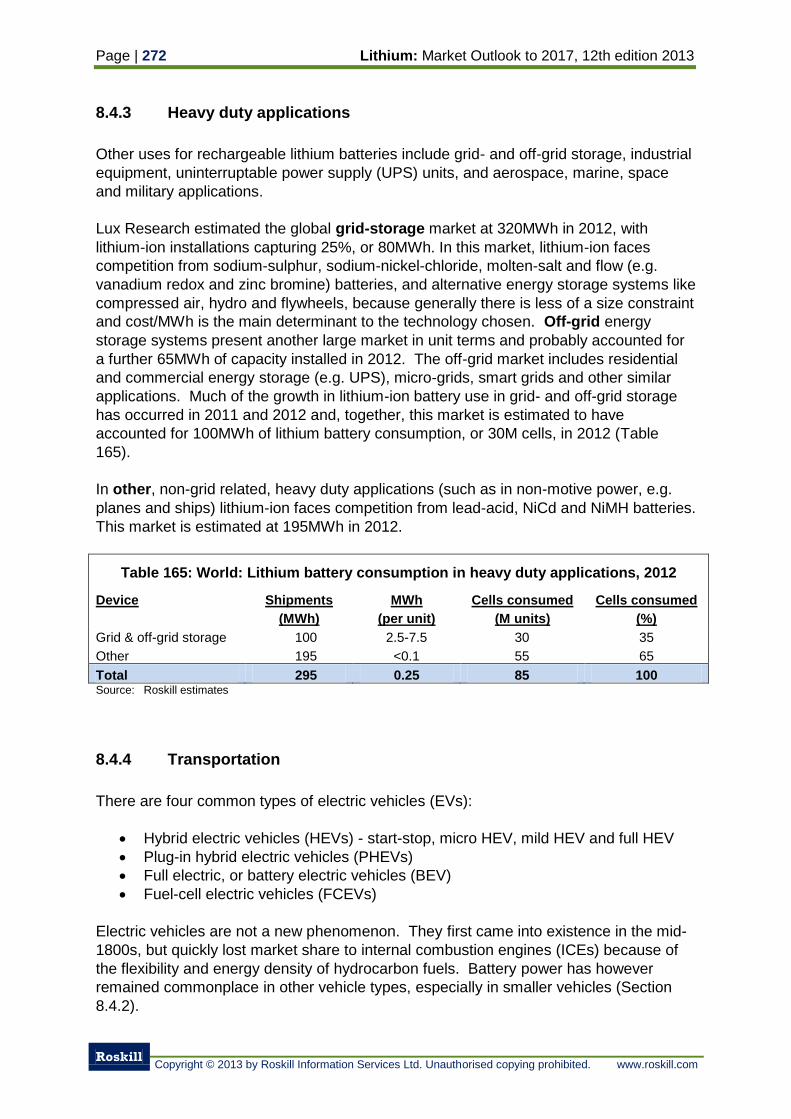

8.4.3 Heavy duty applications 272

8.4.4 Transportation 272

8.5 Consumption of NiMH and NiCd batteries 274

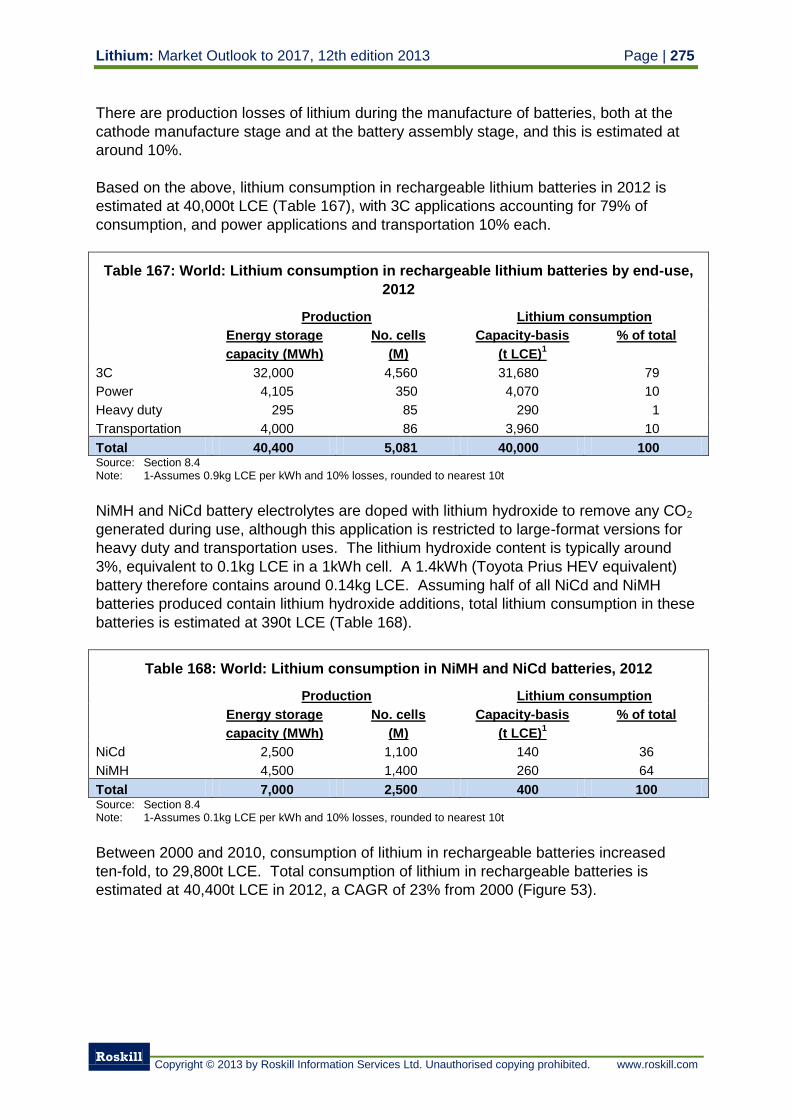

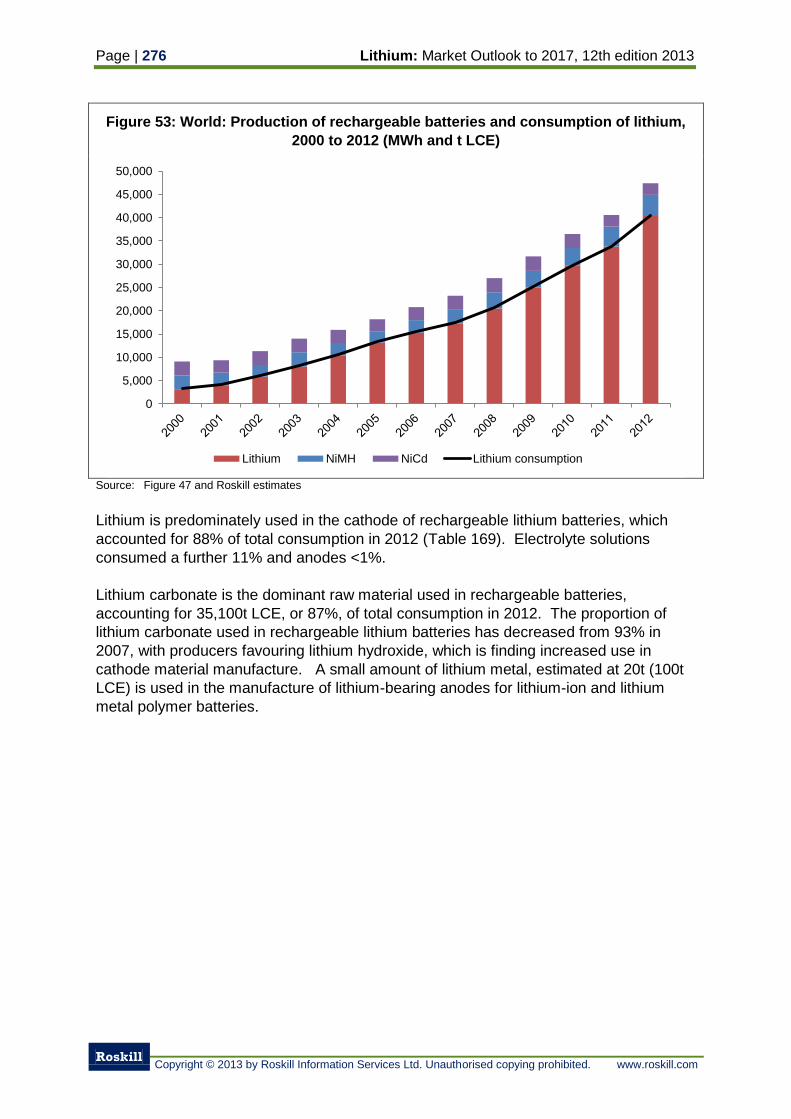

8.6 Consumption of lithium in rechargeable batteries 274

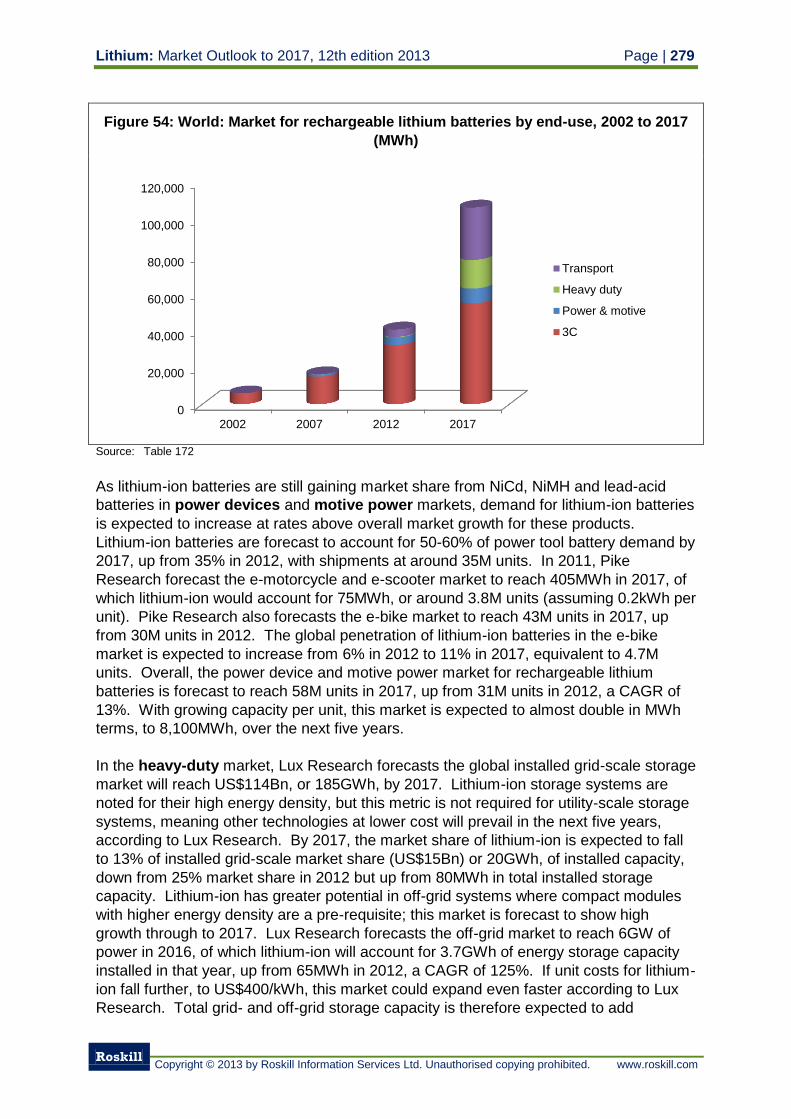

8.7 Outlook for demand for rechargeable batteries 278

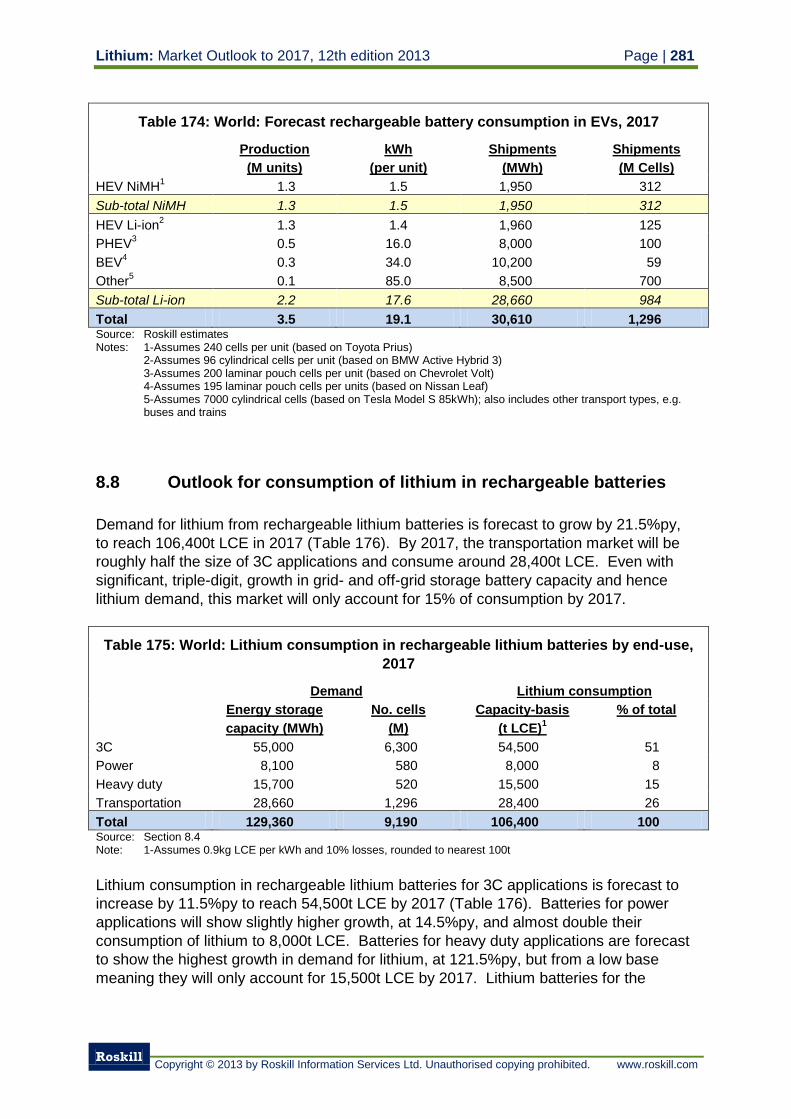

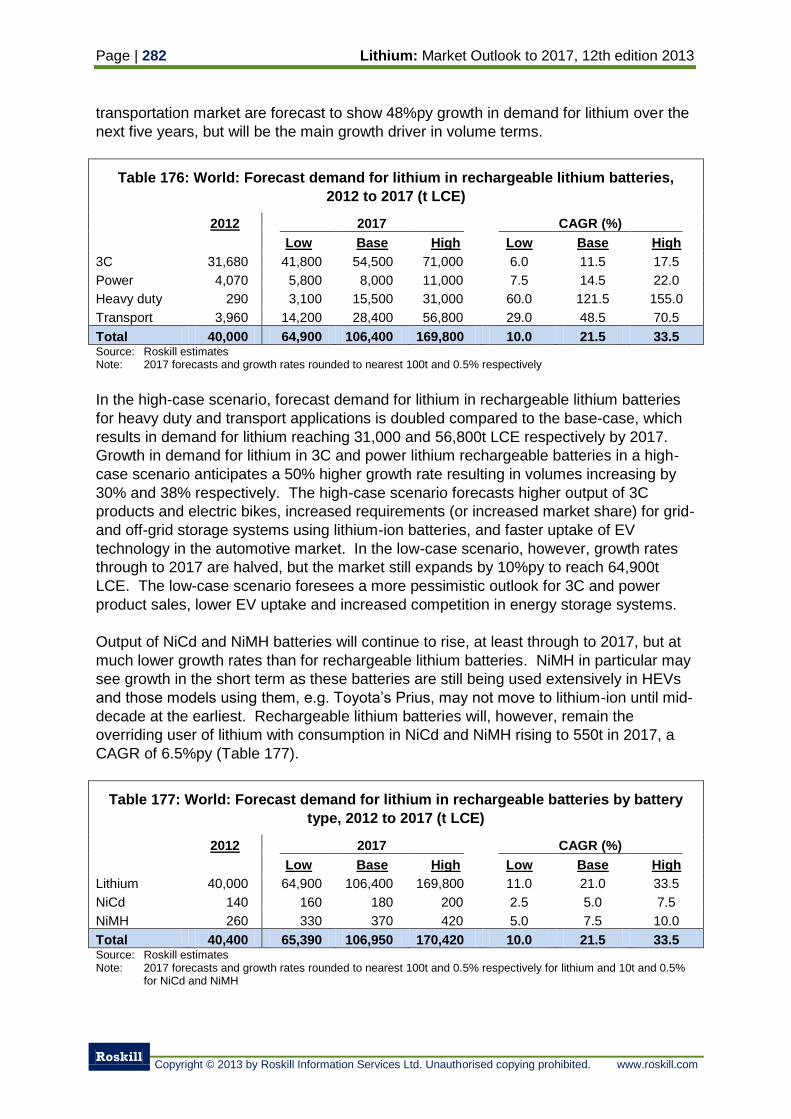

8.8 Outlook for consumption of lithium in rechargeable batteries 281

9. Use of lithium in ceramics 284

9.1 Use of lithium in ceramics 284

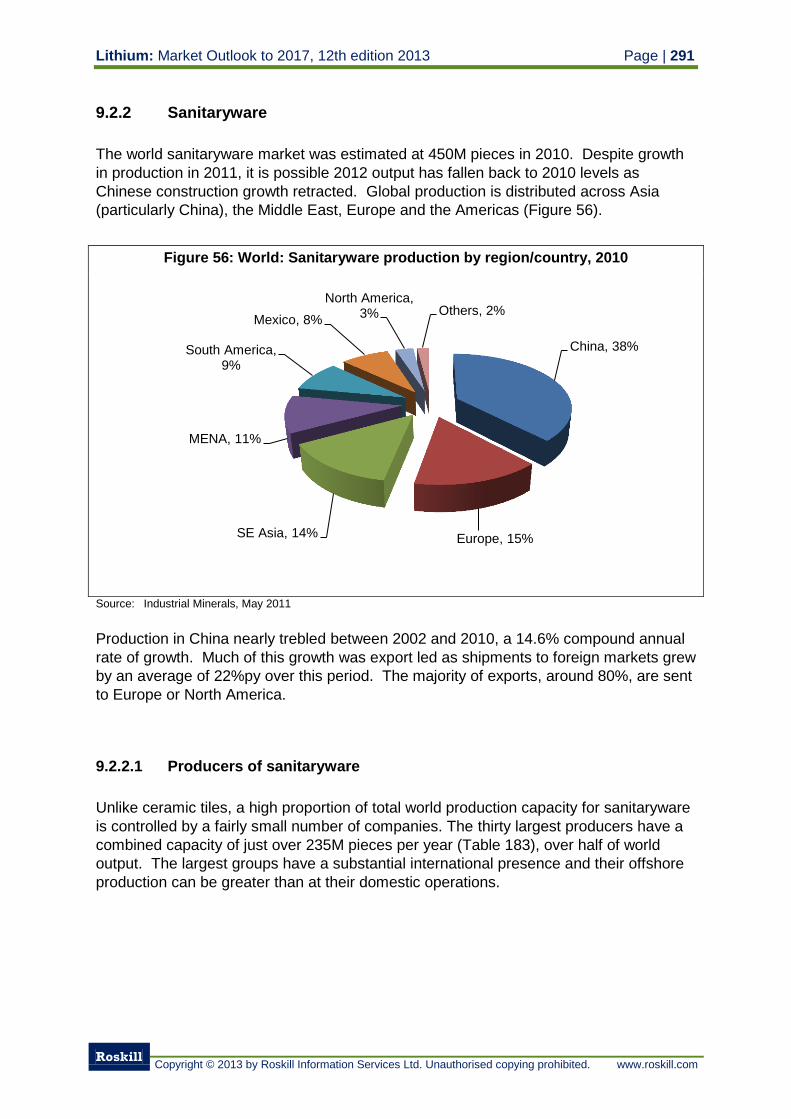

9.2 Production and consumption of ceramics 286

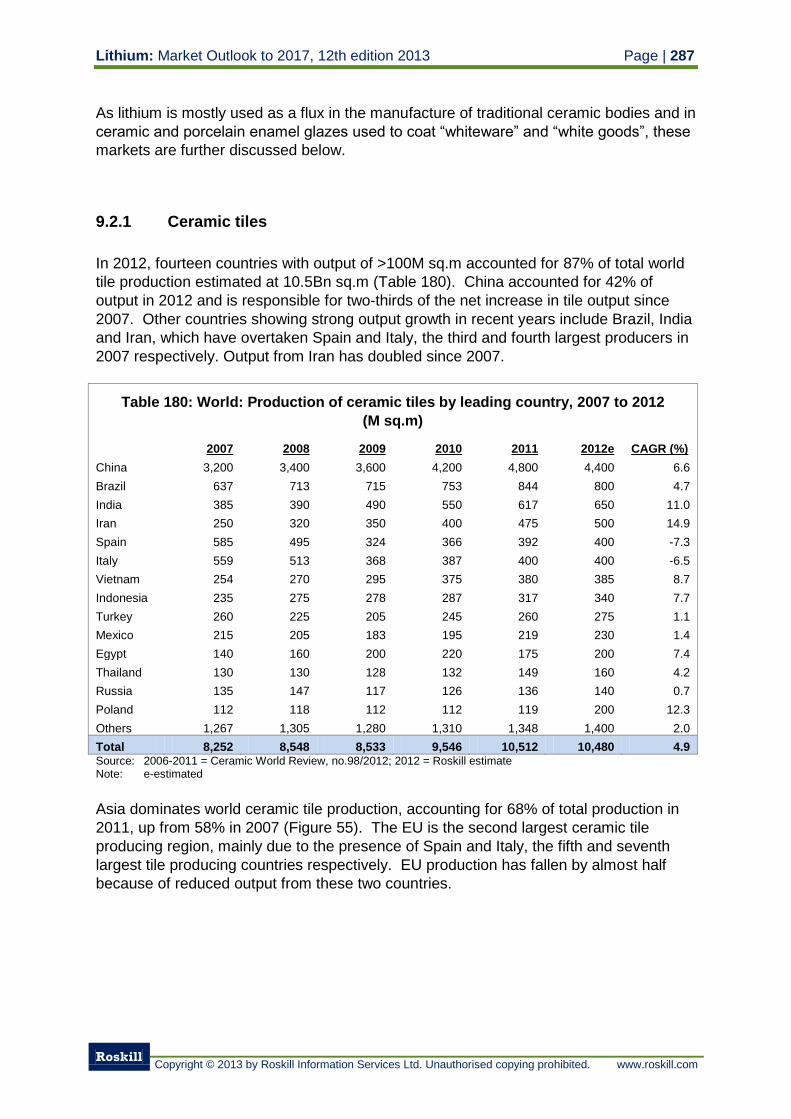

9.2.1 Ceramic tiles 287

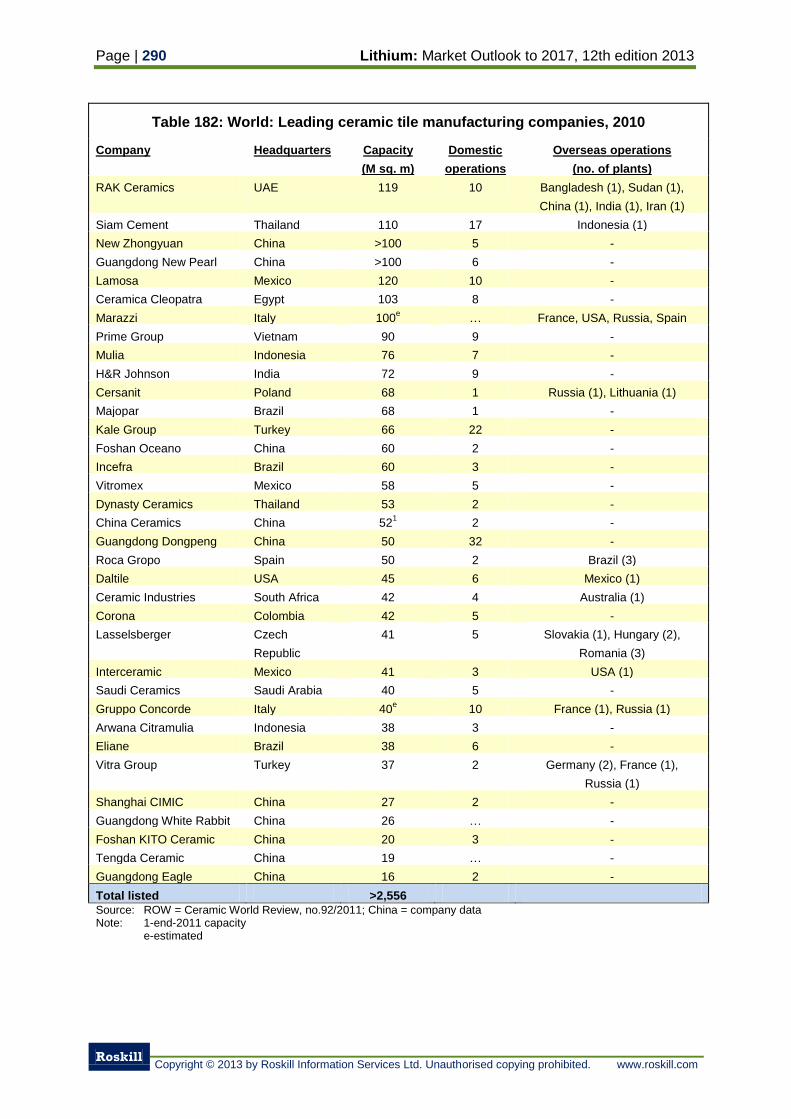

9.2.1.1 Producers of ceramic tiles 289

9.2.2 Sanitaryware 291

9.2.2.1 Producers of sanitaryware 291

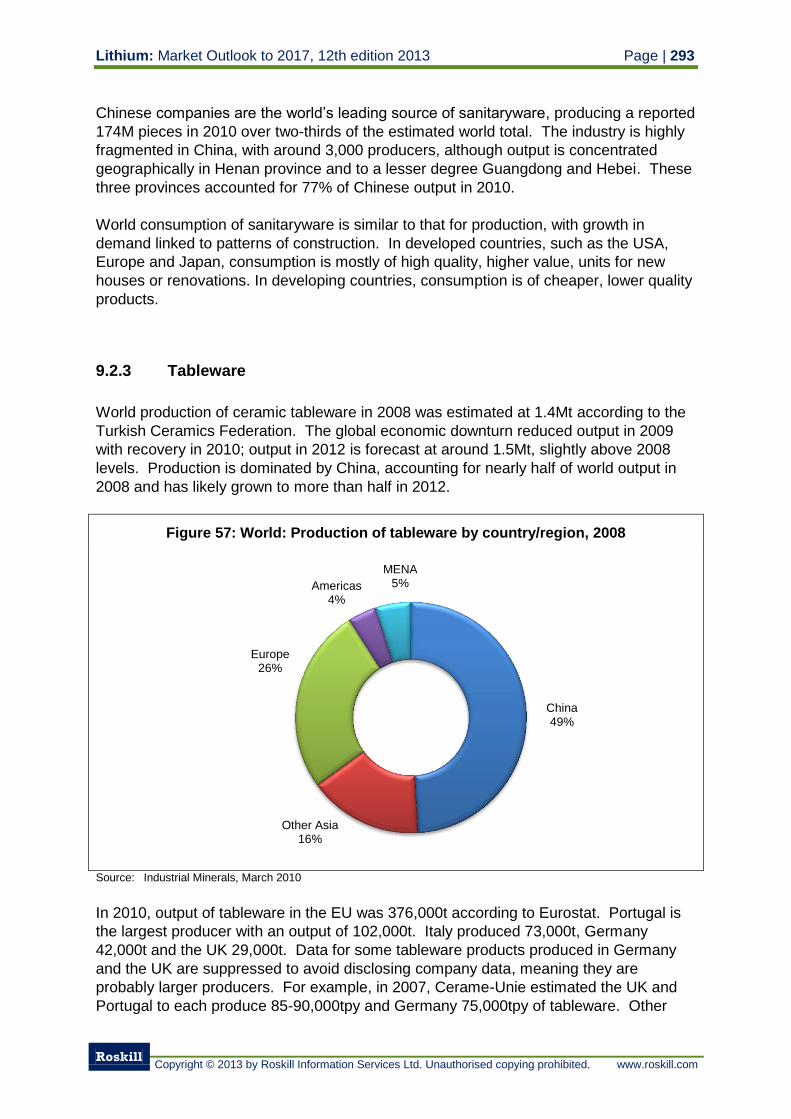

9.2.3 Tableware 293

9.2.3.1 Producers of tableware 294

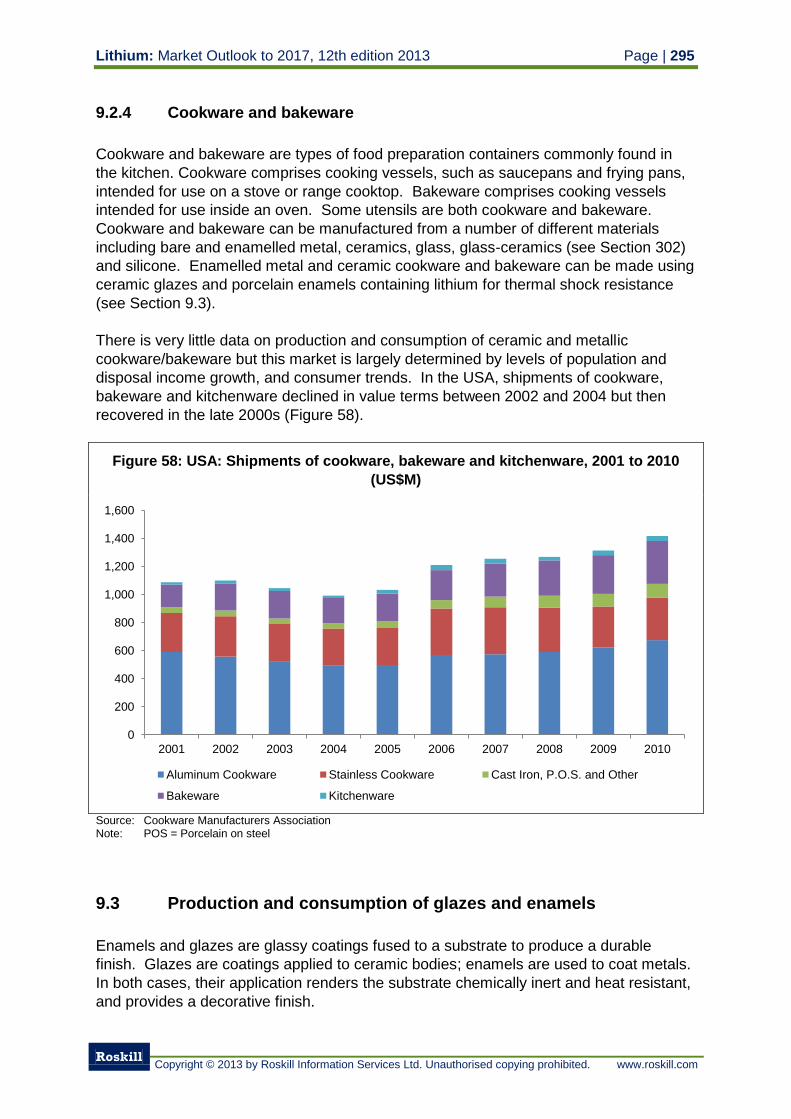

9.2.4 Cookware and bakeware 295

9.3 Production and consumption of glazes and enamels 295

9.3.1 Producers of glazes and enamels 297

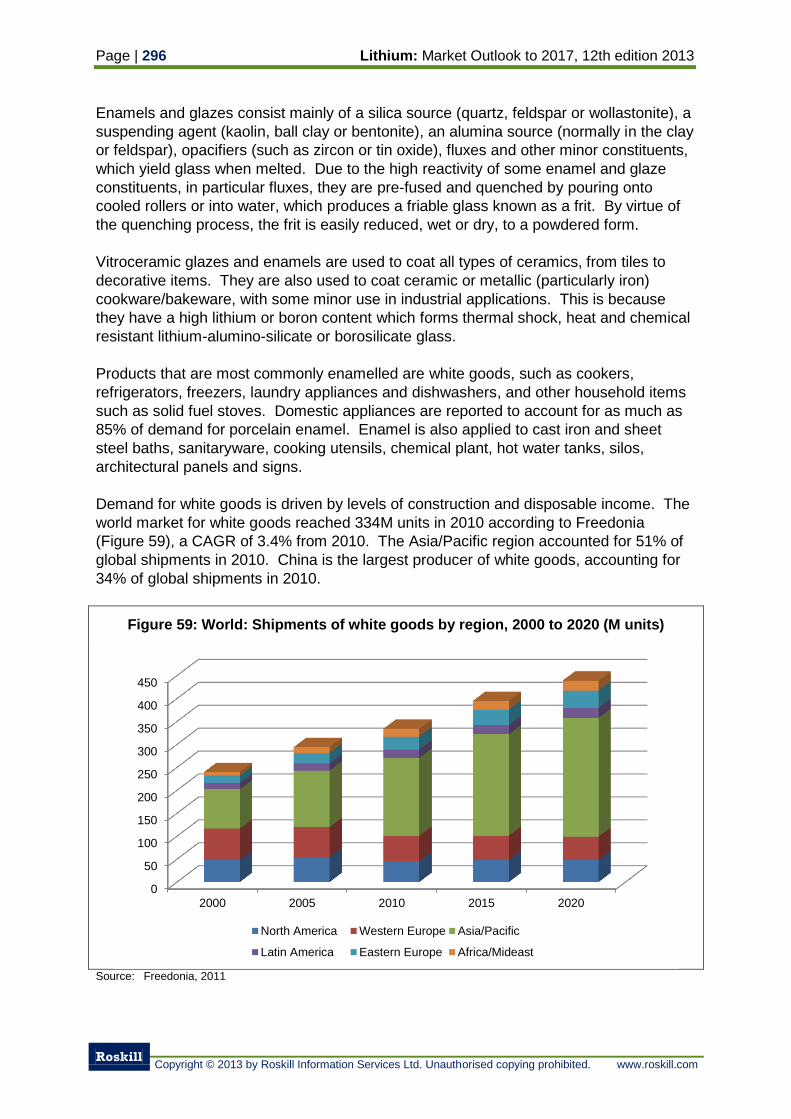

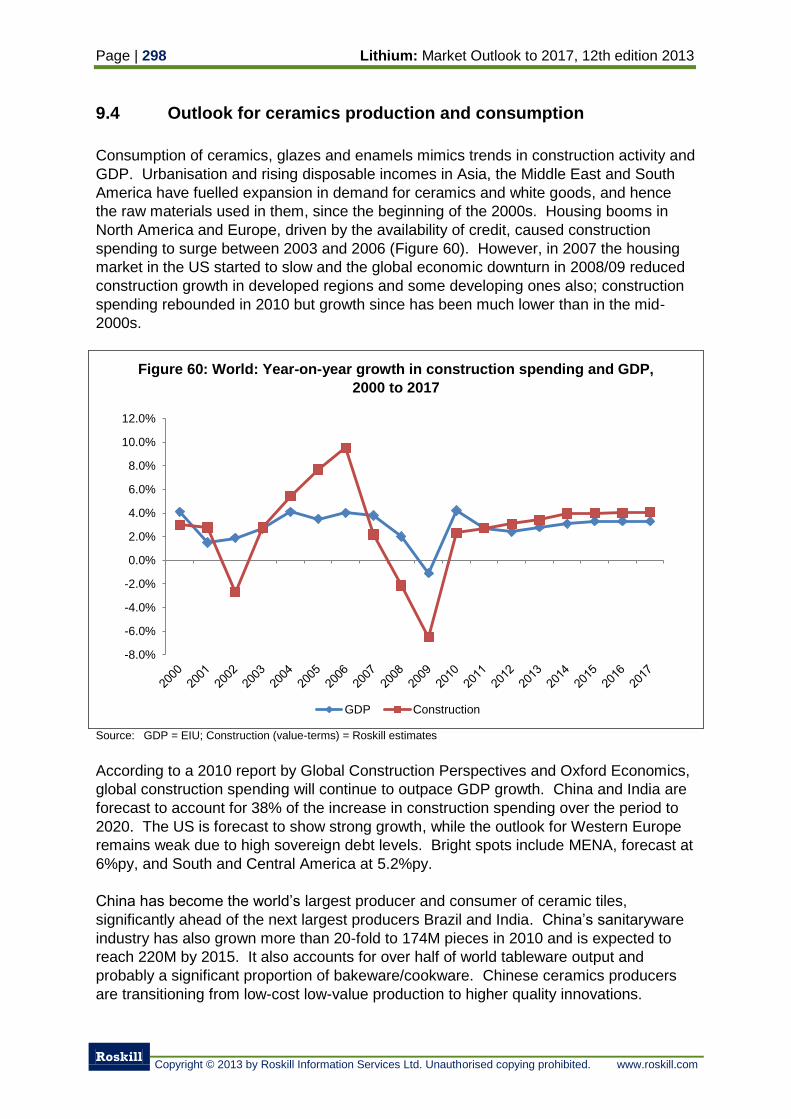

9.4 Outlook for ceramics production and consumption 298

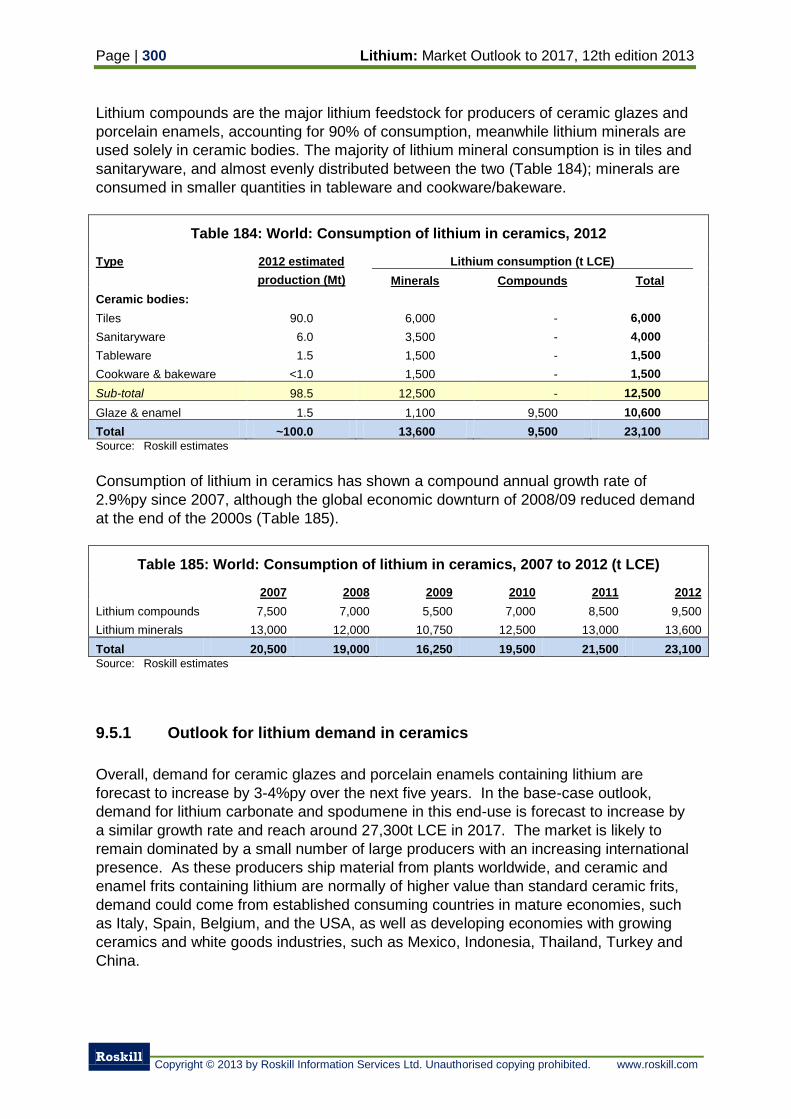

9.5 Consumption of lithium in ceramics 299

9.5.1 Outlook for lithium demand in ceramics 300

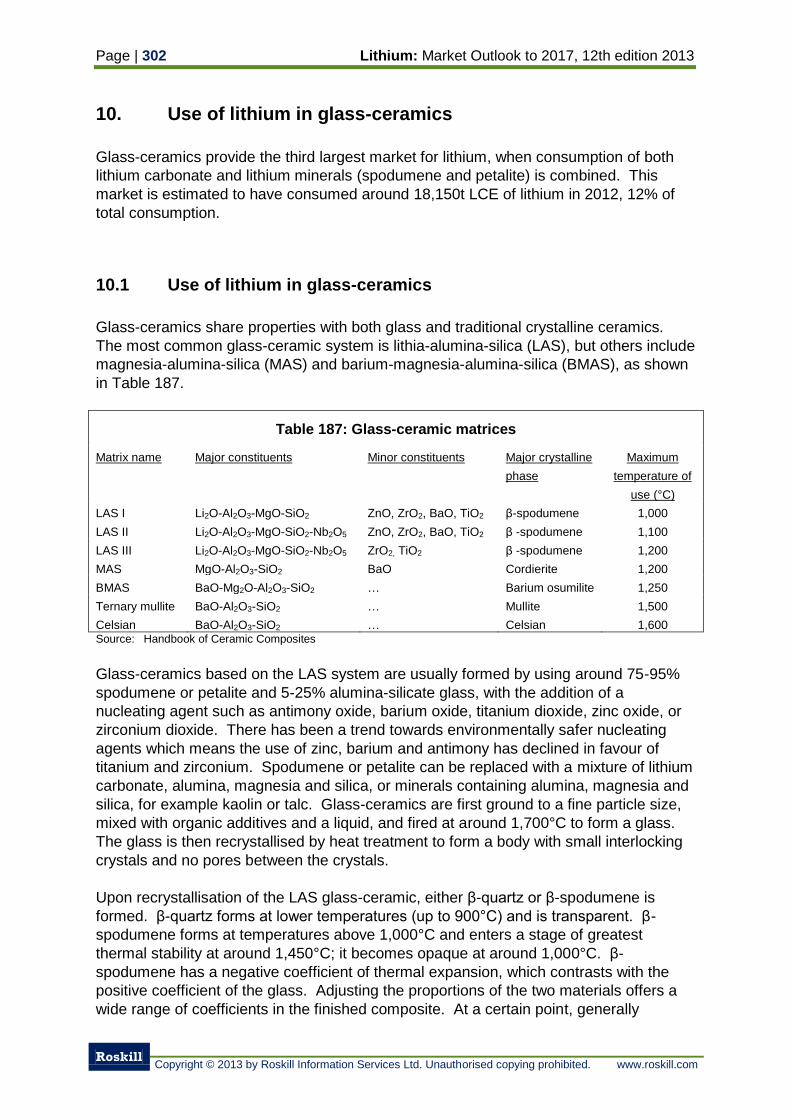

10. Use of lithium in glass-ceramics 302

10.1 Use of lithium in glass-ceramics 302

10.2 Production and consumption of glass-ceramics 304

10.2.1 Producers of glass-ceramics 305

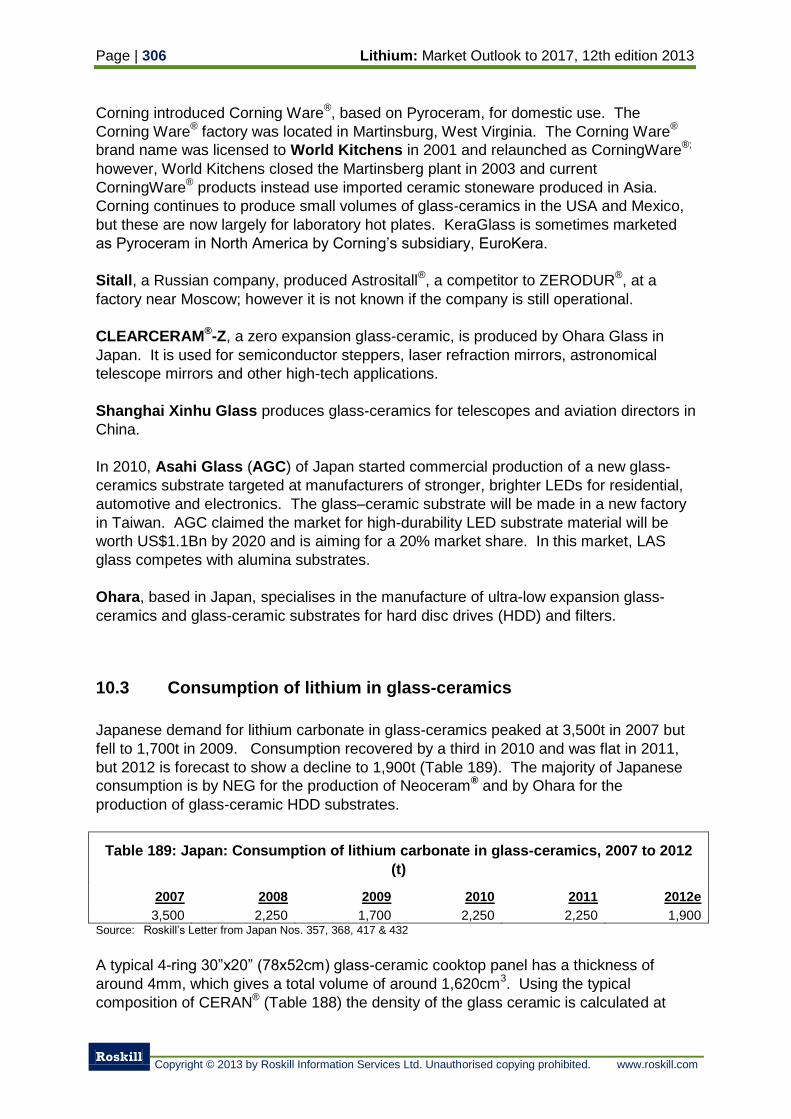

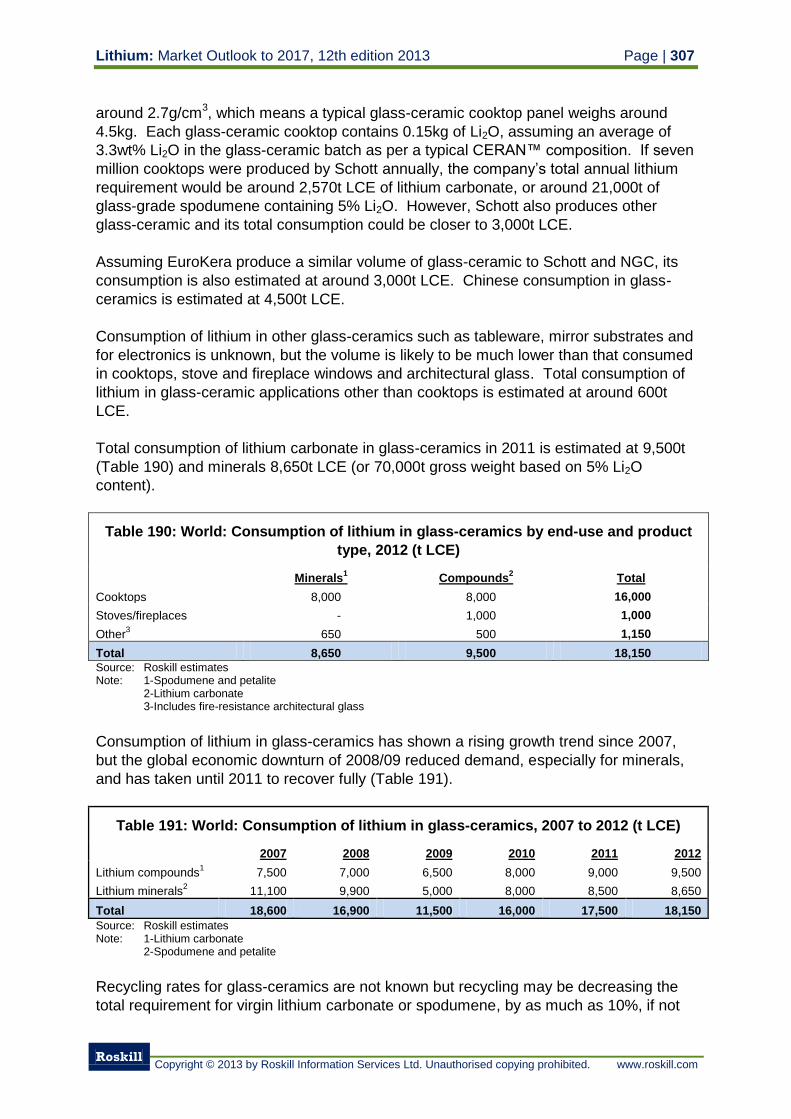

10.3 Consumption of lithium in glass-ceramics 306

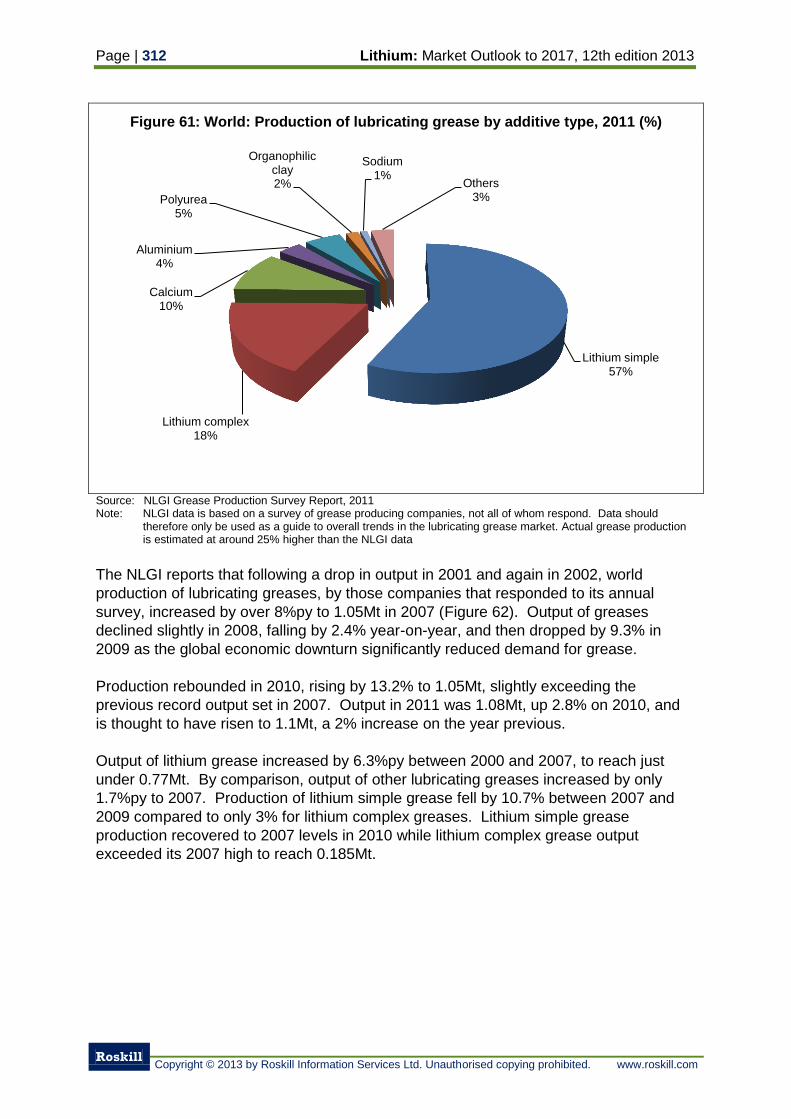

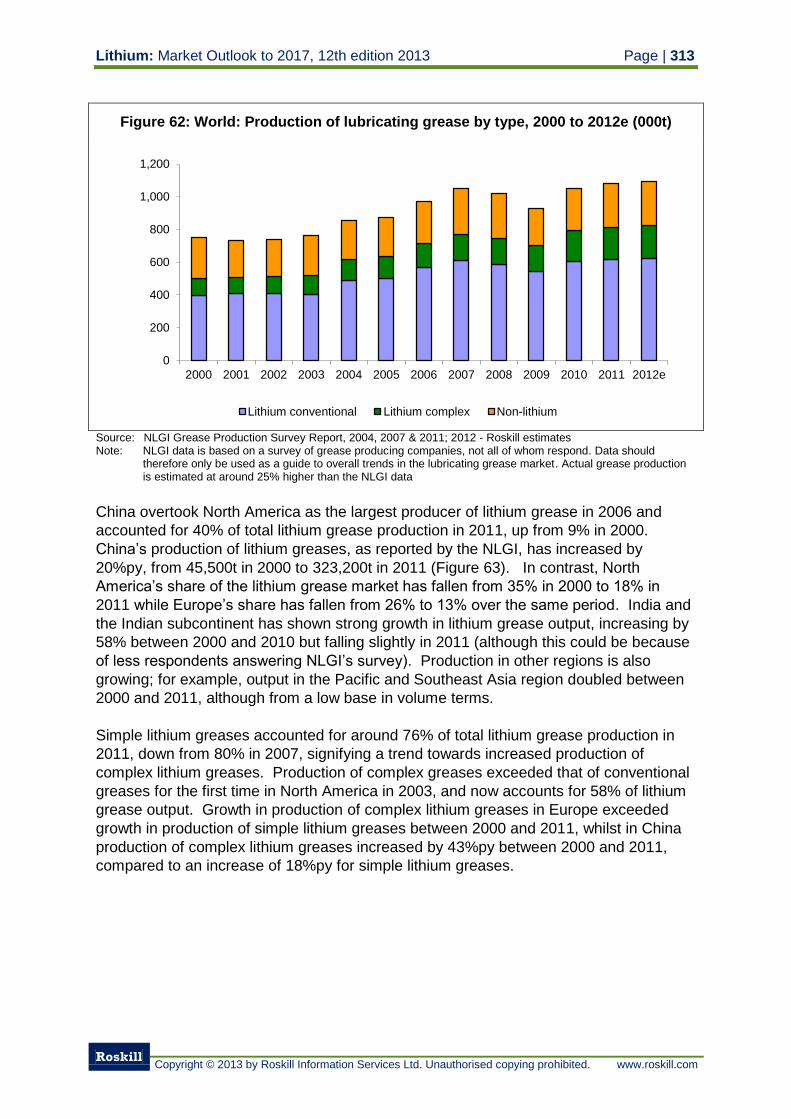

11. Use of lithium in lubricating grease 309

11.1 Types of lubricating grease 309

11.2 Production of grease 311

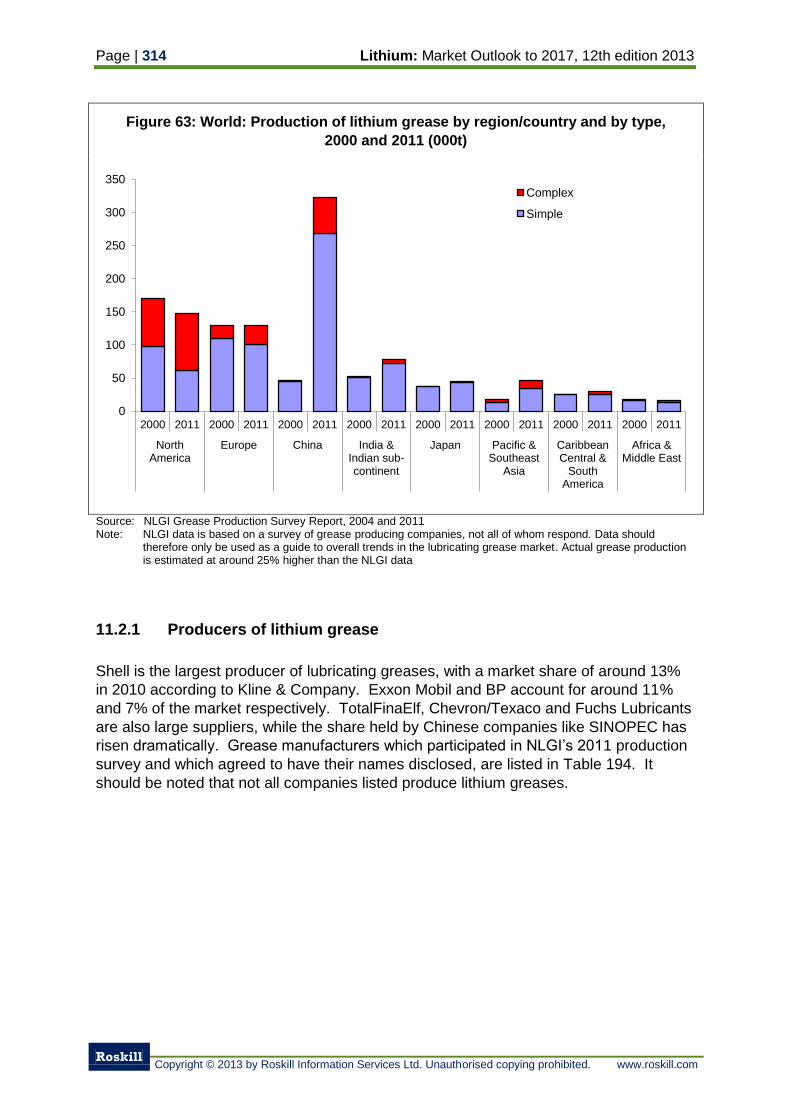

11.2.1 Producers of lithium grease 314

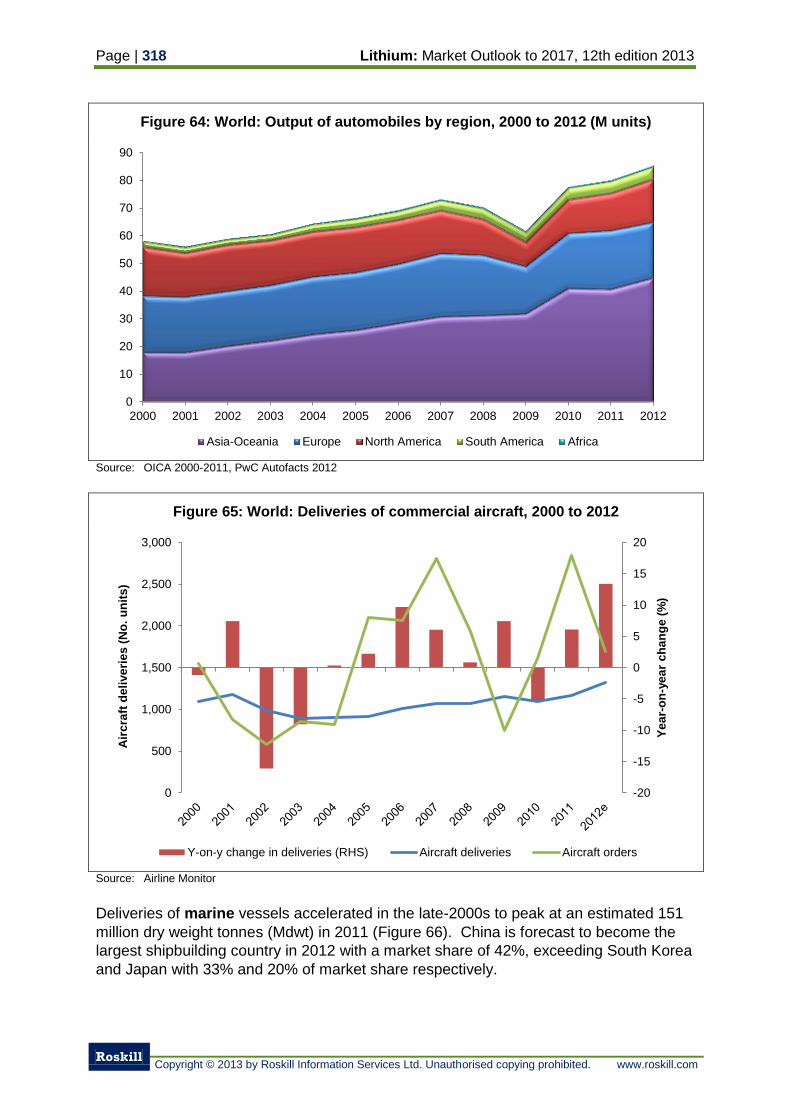

11.3 Consumption of lithium greases 317

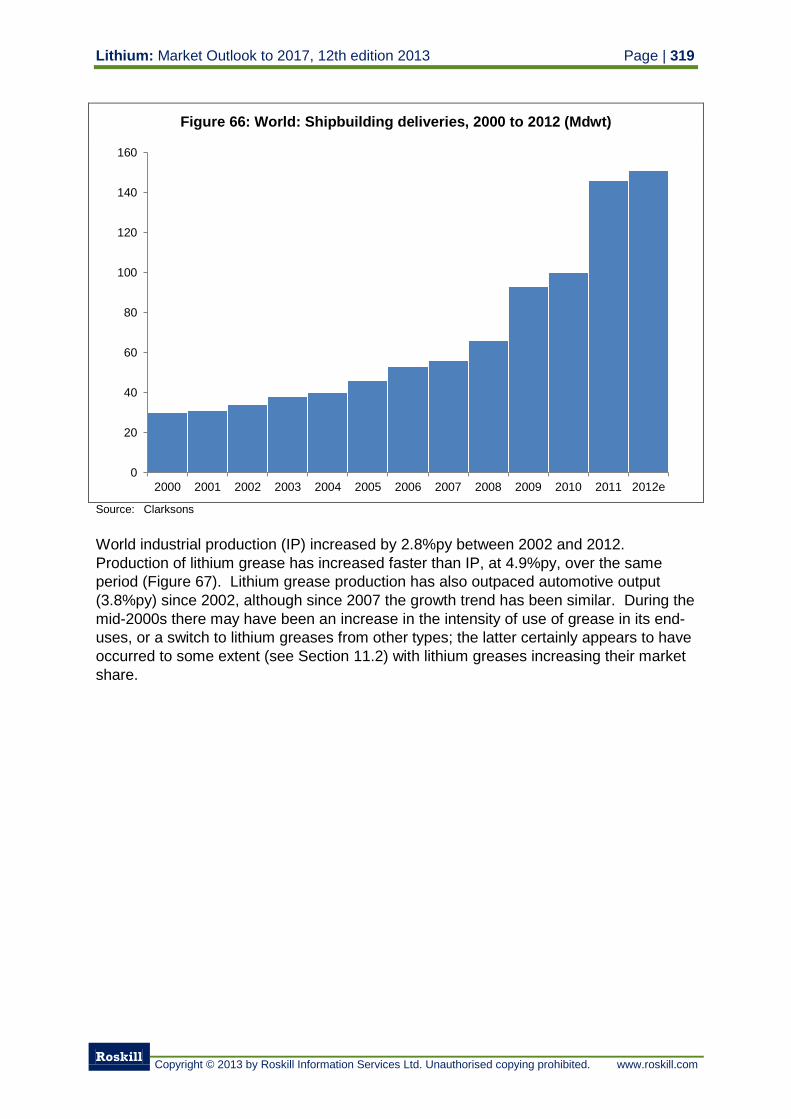

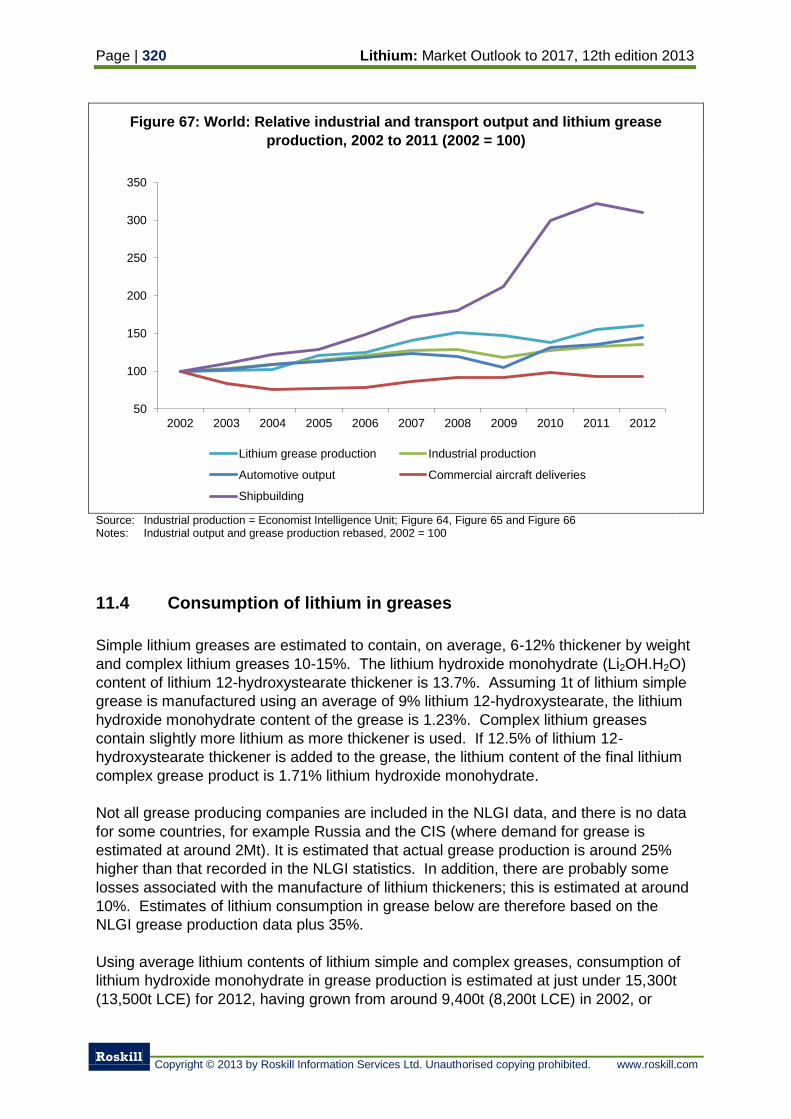

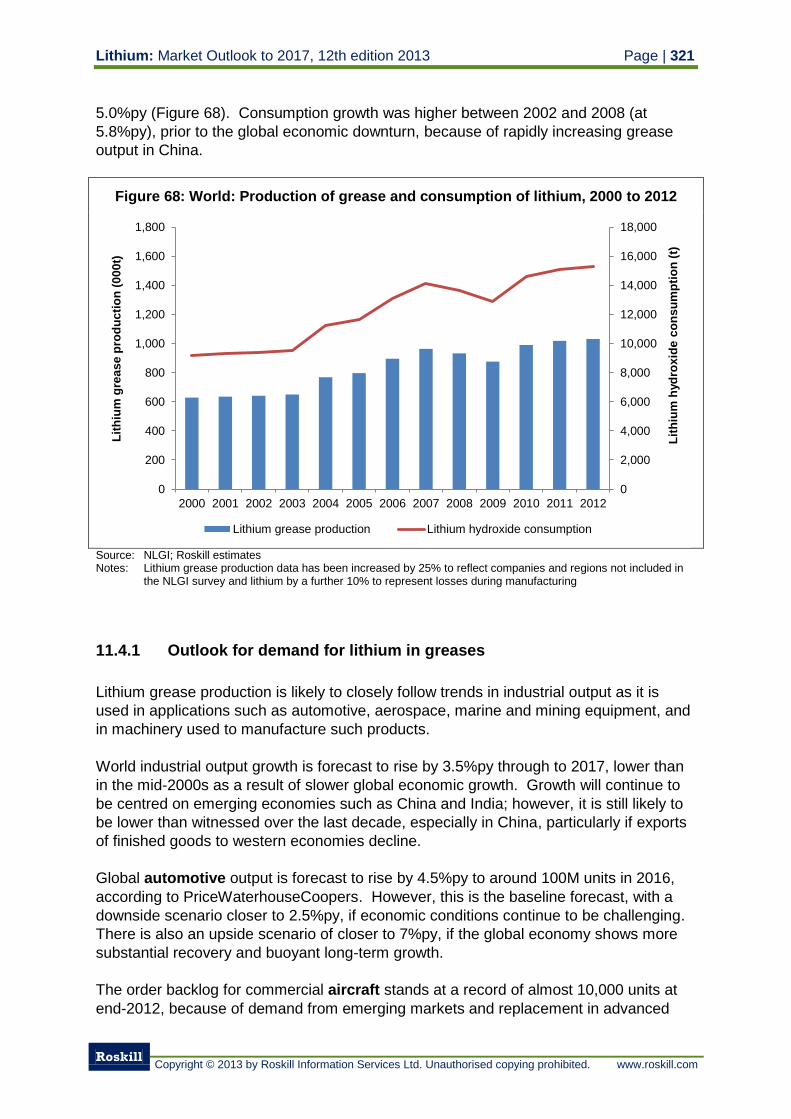

11.4 Consumption of lithium in greases 320

11.4.1 Outlook for demand for lithium in greases 321

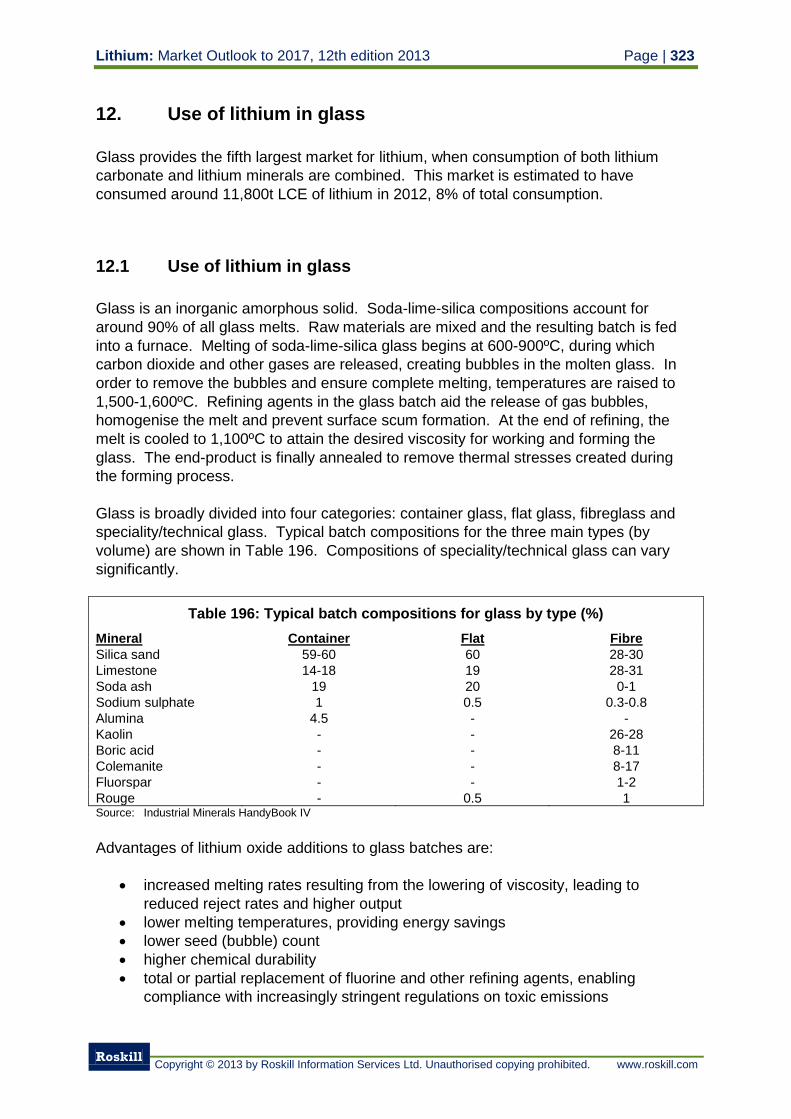

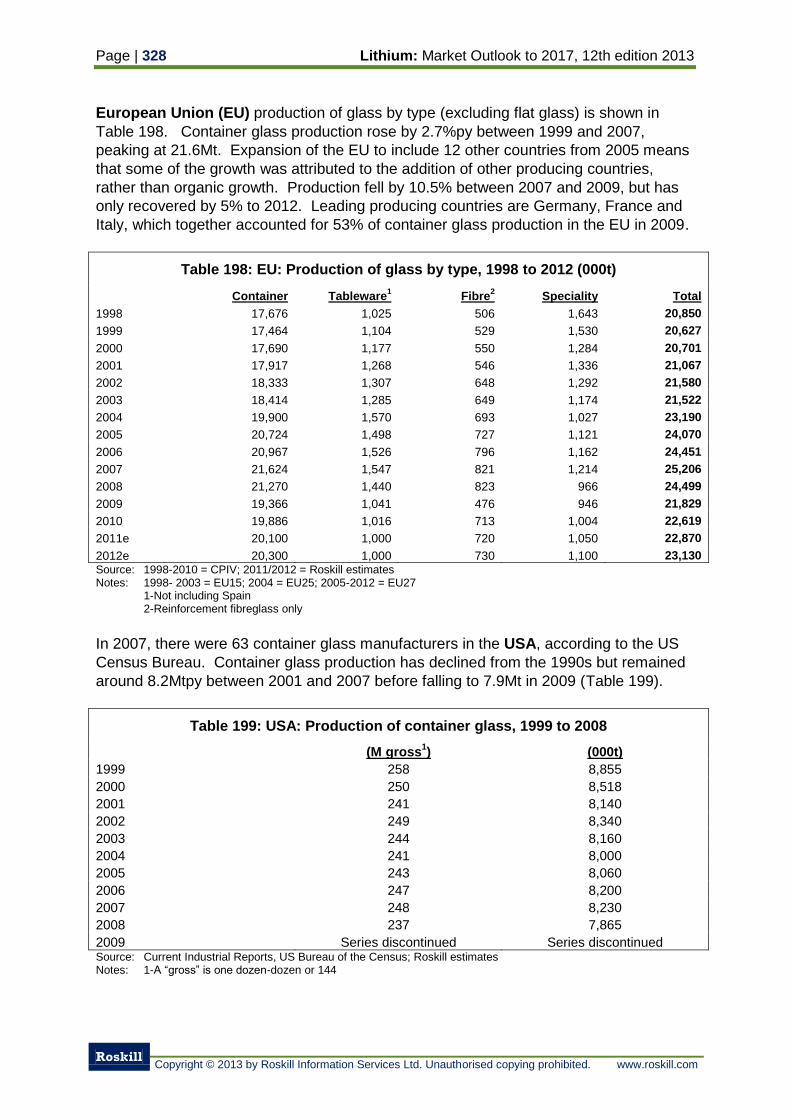

12. Use of lithium in glass 323

12.1 Use of lithium in glass 323

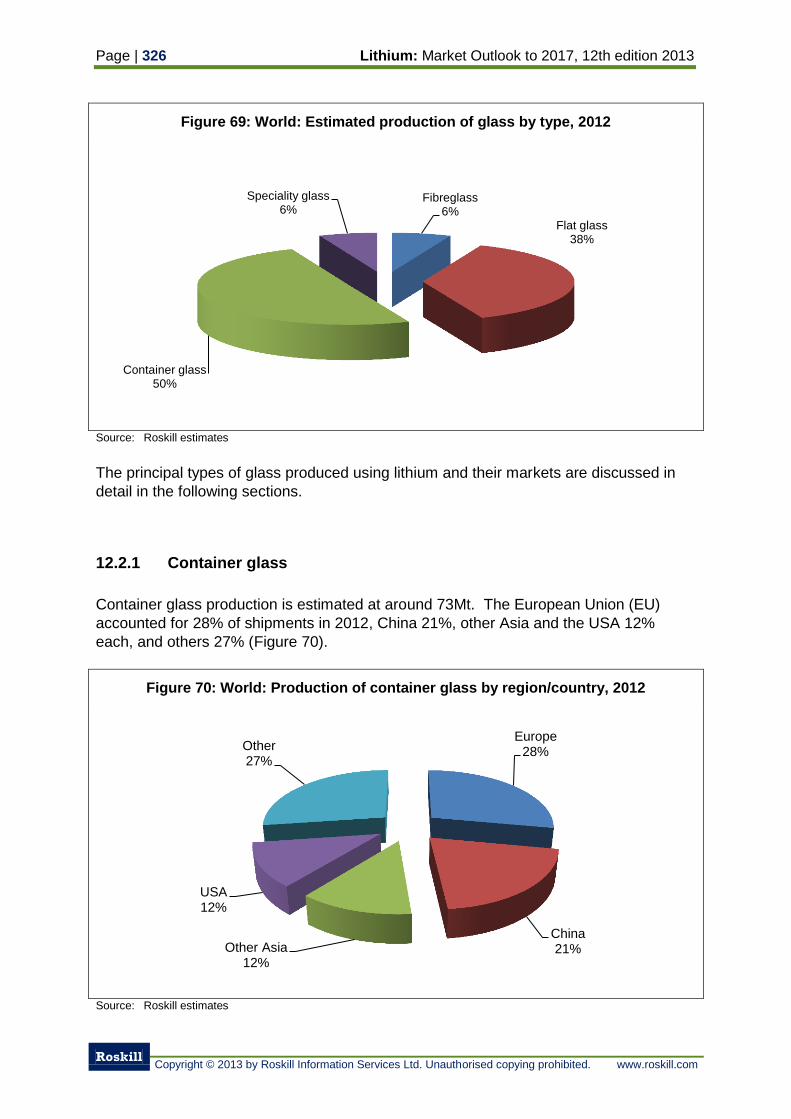

12.2 Production and consumption of glass 325

12.2.1 Container glass 326

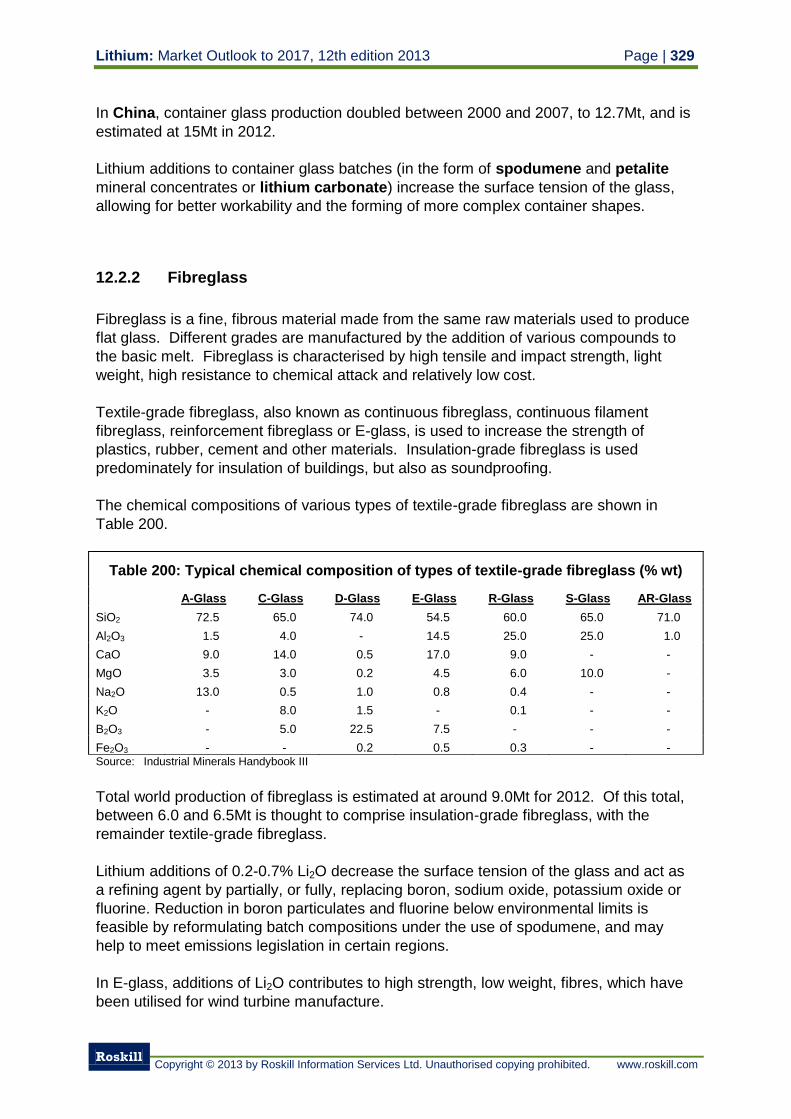

12.2.2 Fibreglass 329

12.2.3 Speciality glass 330

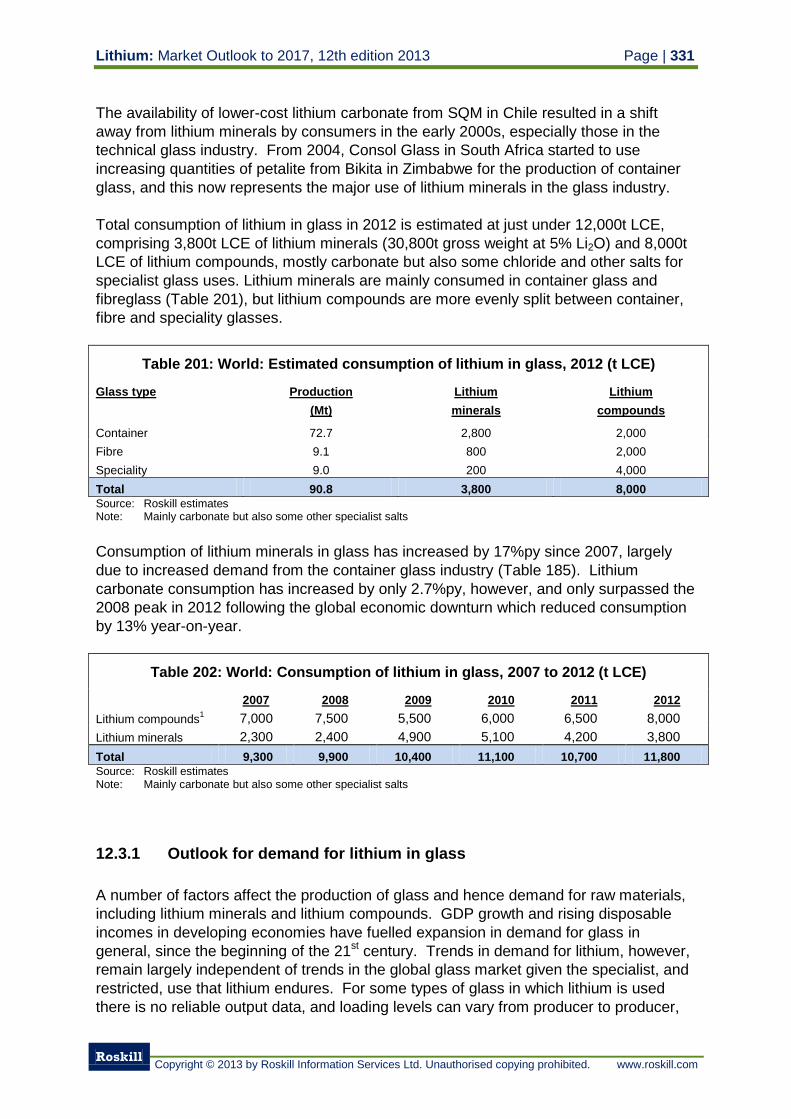

12.3 Consumption of lithium in glass 330

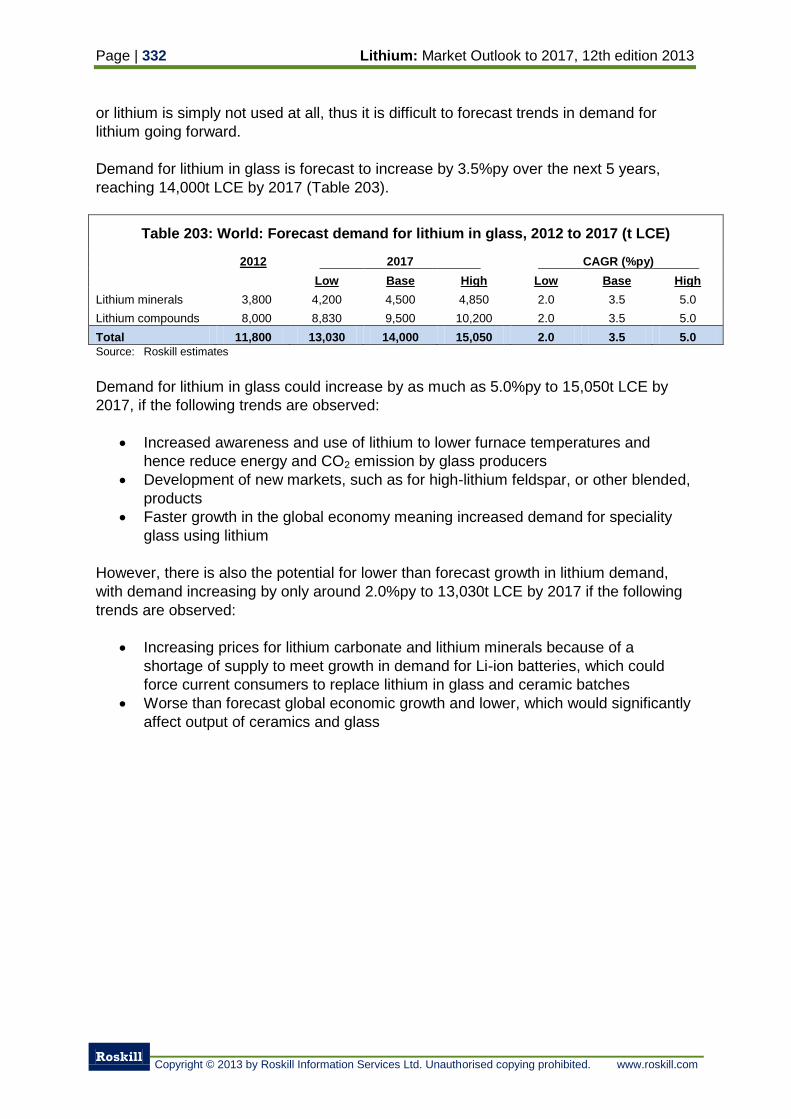

12.3.1 Outlook for demand for lithium in glass 331

13. Use of lithium in metallurgical powders 333

13.1 Continuous casting 333

13.1.1 Producers of continuous casting mould powders 334

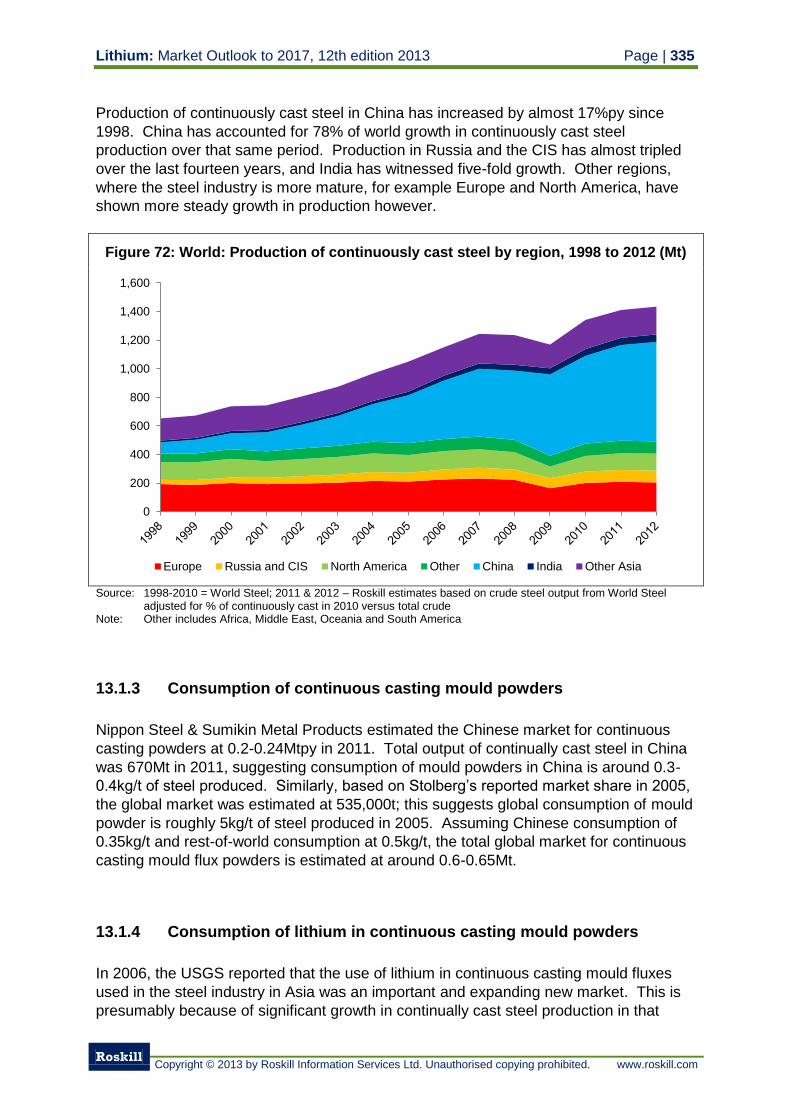

13.1.2 Continually cast steel production 334

13.1.3 Consumption of continuous casting mould powders 335

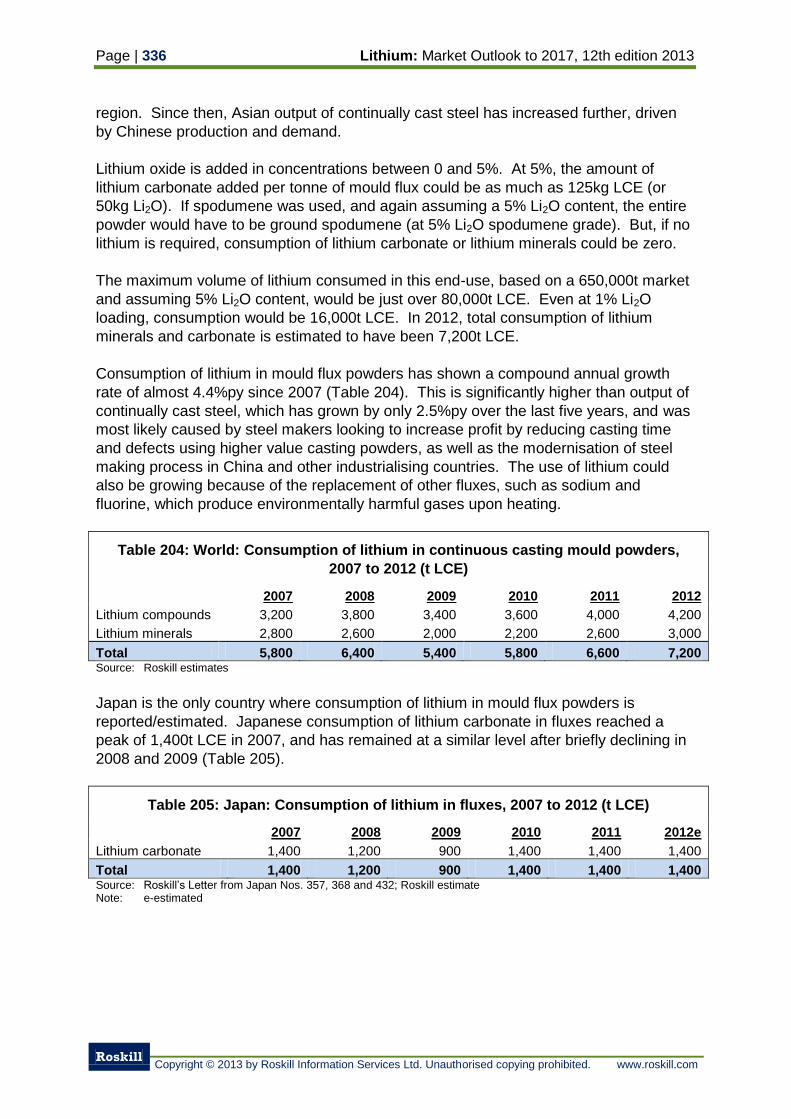

13.1.4 Consumption of lithium in continuous casting mould powders 335

13.2 Traditional metal casting 337

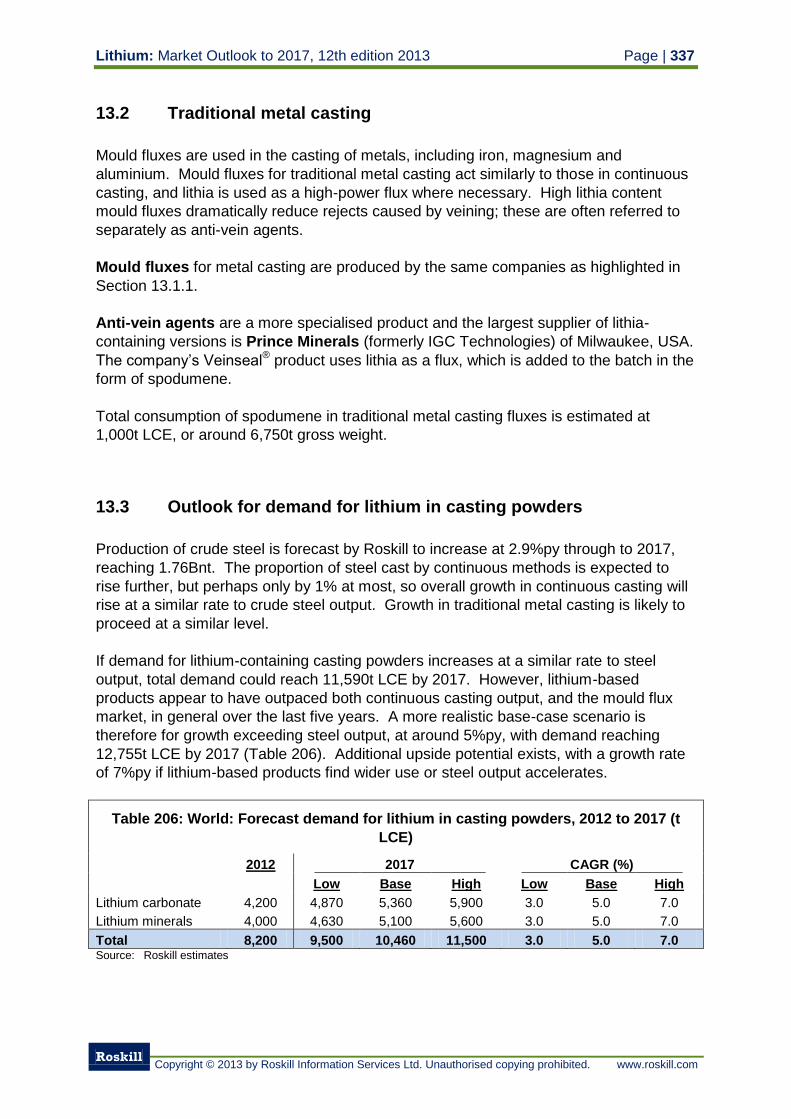

13.3 Outlook for demand for lithium in casting powders 337

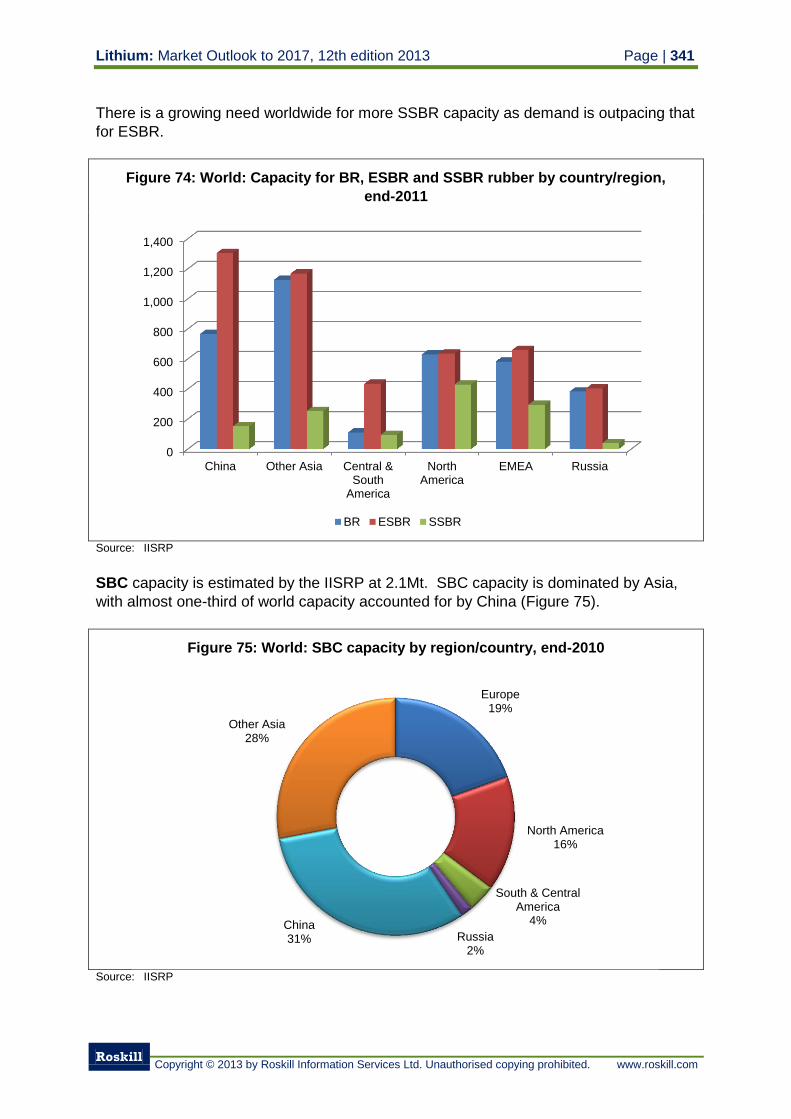

14. Use of lithium in polymers 338

14.1 Types of polymers 338

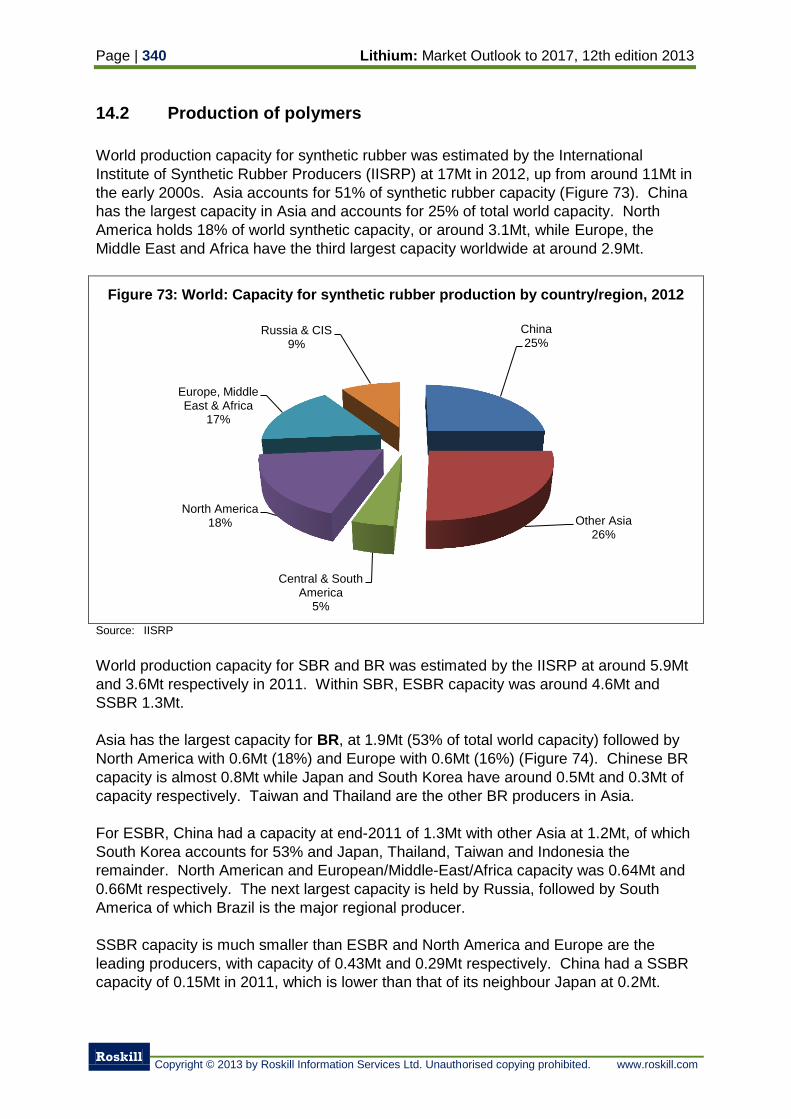

14.2 Production of polymers 340

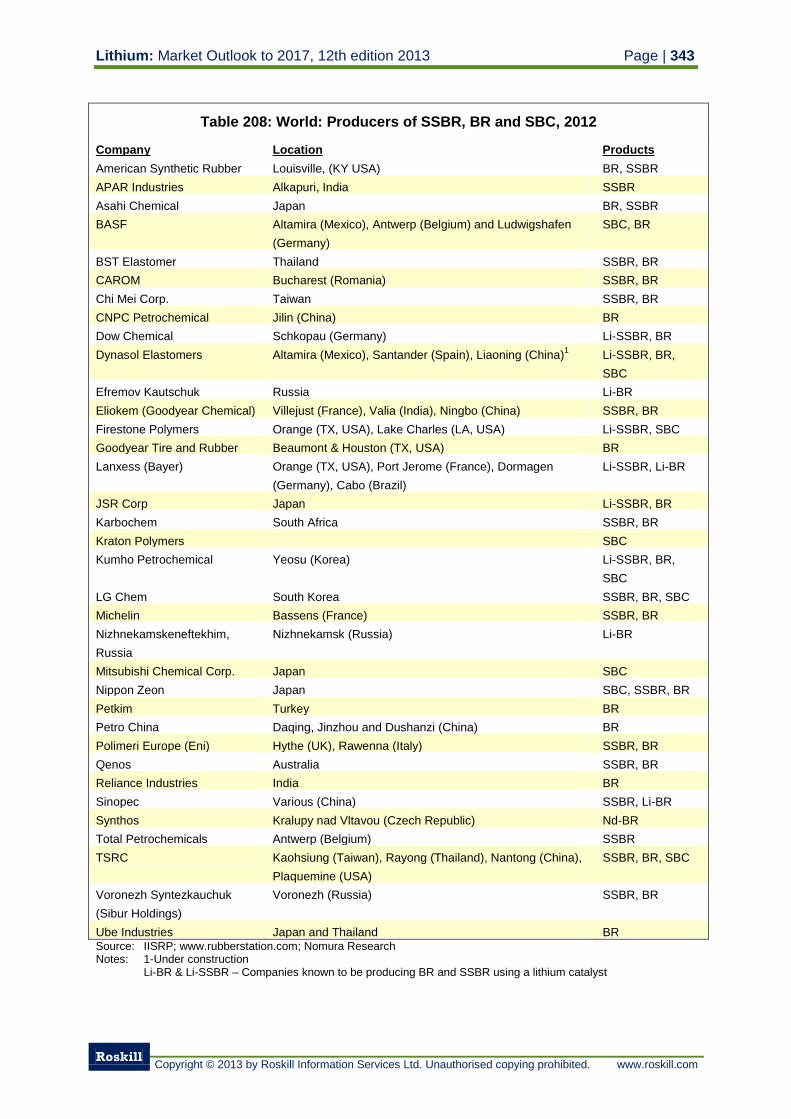

14.2.1 Producers of polymers 342

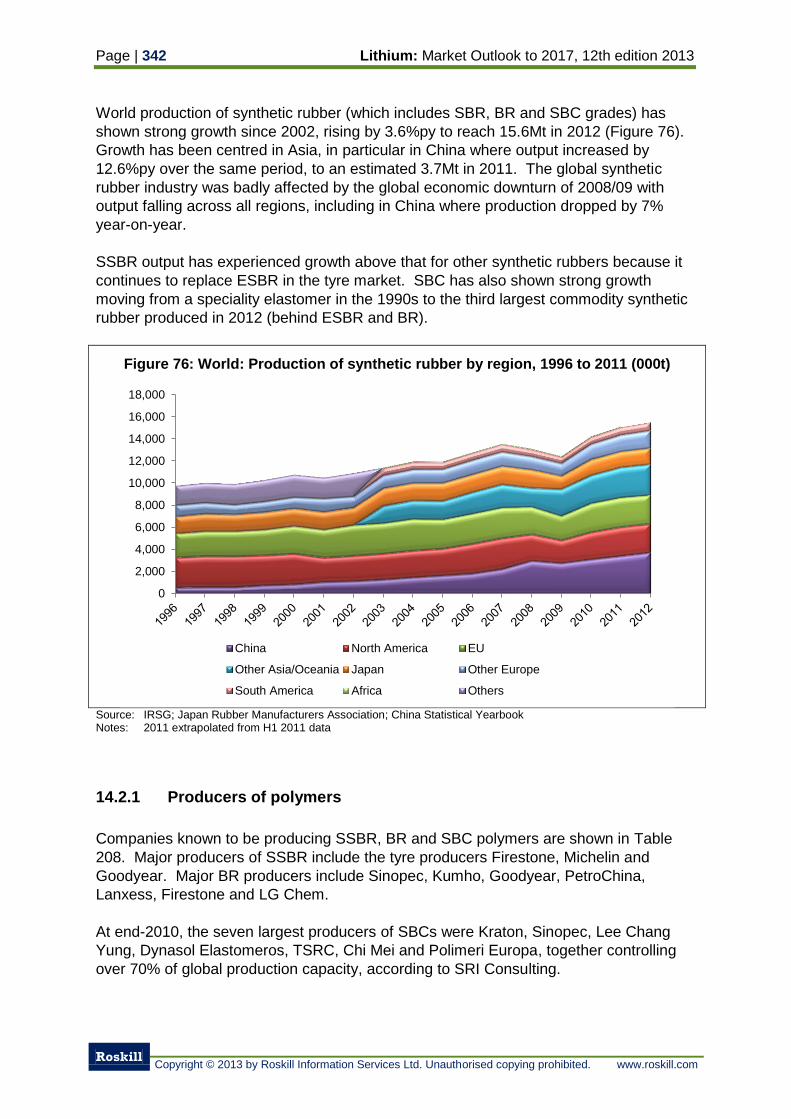

14.3 Consumption of polymers 344

14.4 Consumption of lithium in polymers 348

14.4.1 Outlook for lithium demand in polymers 348

15. Use of lithium in air treatment 350

15.1 Absorption chillers 350

15.1.1 Production of absorption chillers 351

15.1.2 Producers of adsorption chillers 352

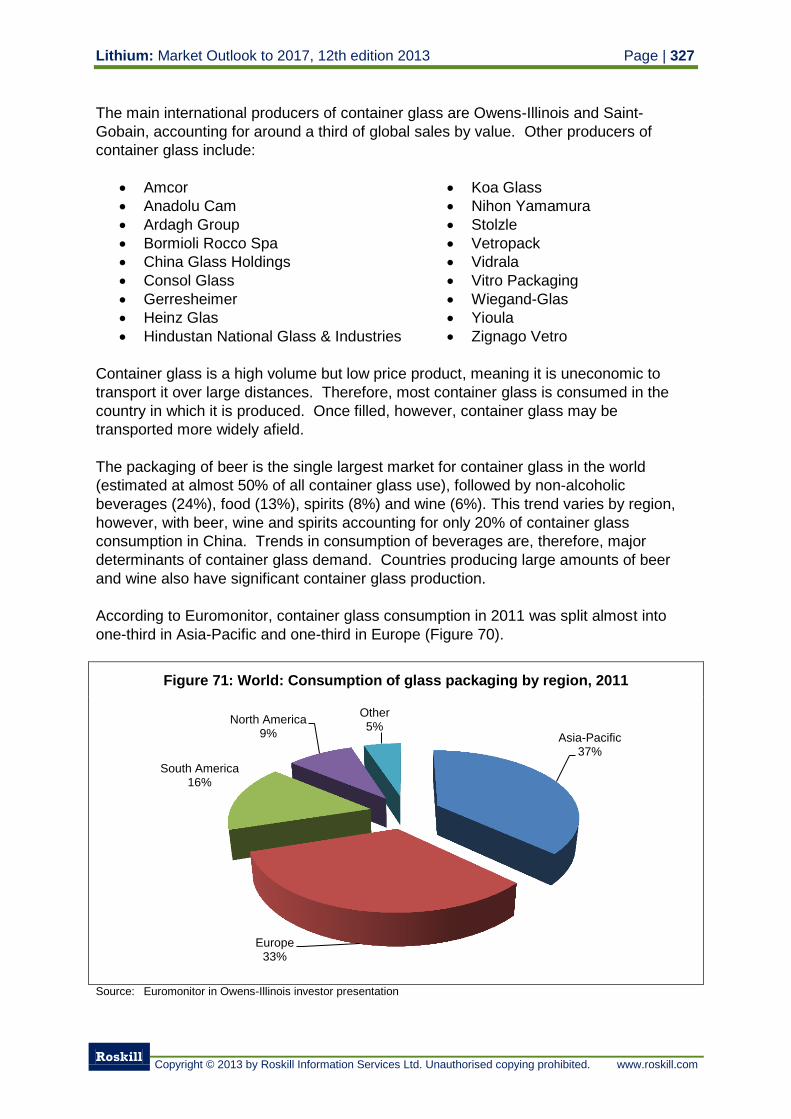

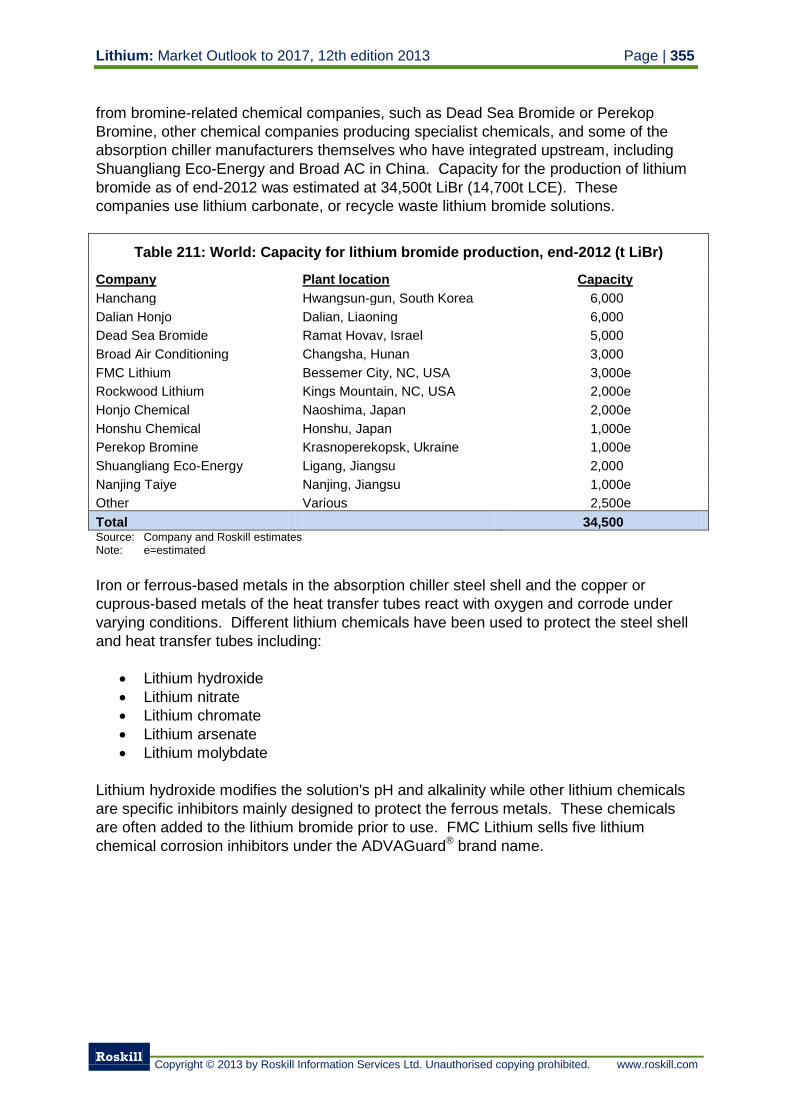

15.1.3 Producers of lithium bromide for absorption chillers 354

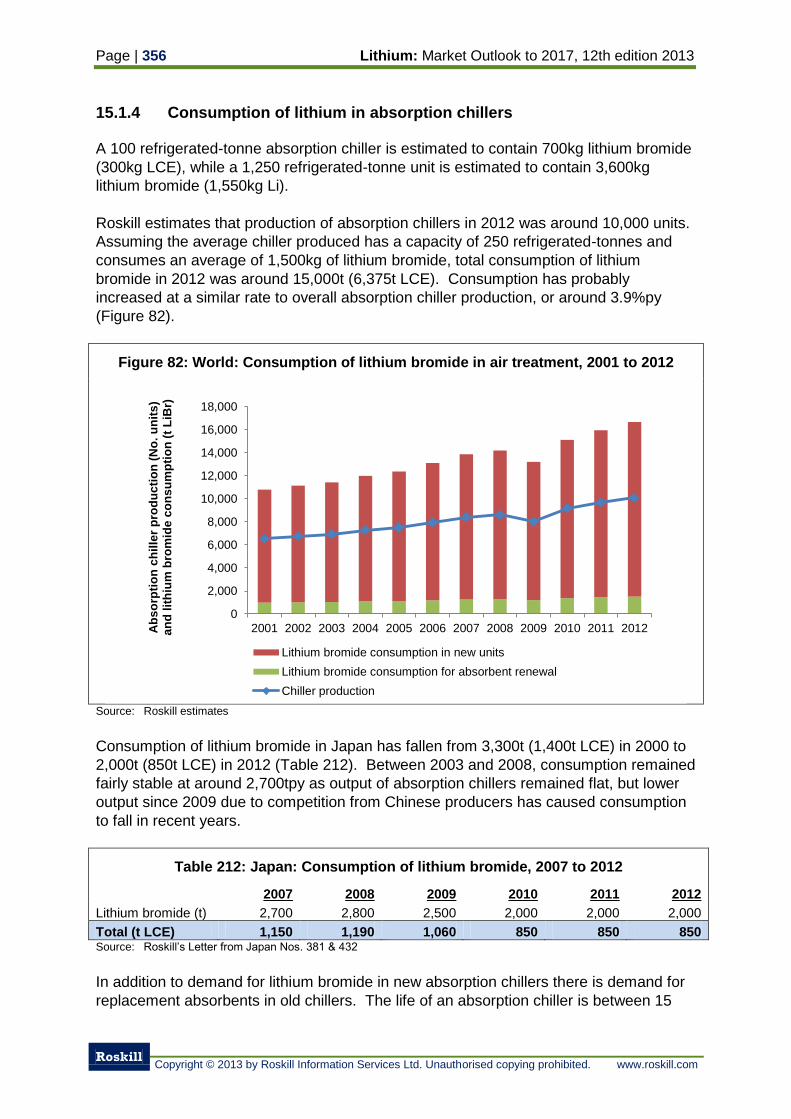

15.1.4 Consumption of lithium in absorption chillers 356

15.2 Dehumidification 357

15.2.1 Production of desiccant dehumidification systems 358

15.2.2 Producers of desiccant dehumidification systems 358

15.2.3 Consumption of lithium in desiccant dehumidifiers 359

15.3 Air purification 359

15.5 Outlook for demand for lithium in air treatment 360

16. Use of lithium in primary batteries 362

16.1 Types of primary batteries 362

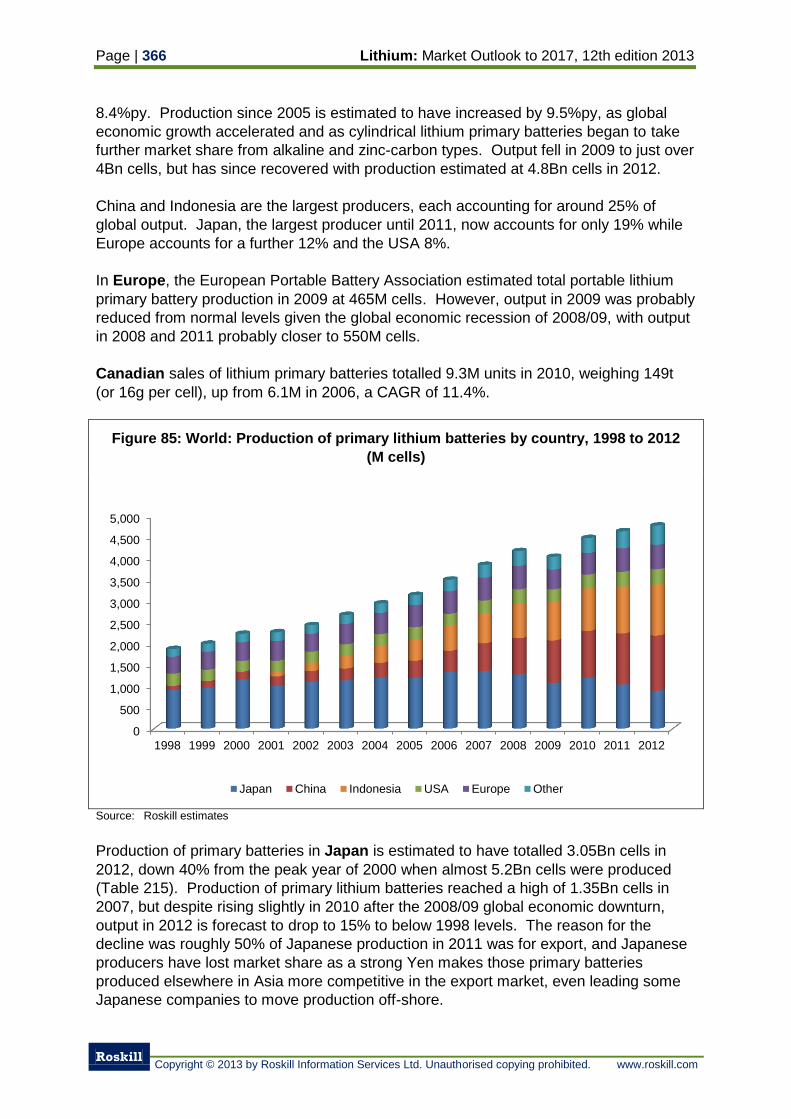

16.2 Production of lithium primary batteries 365

16.2.1 Producers of lithium primary batteries 367

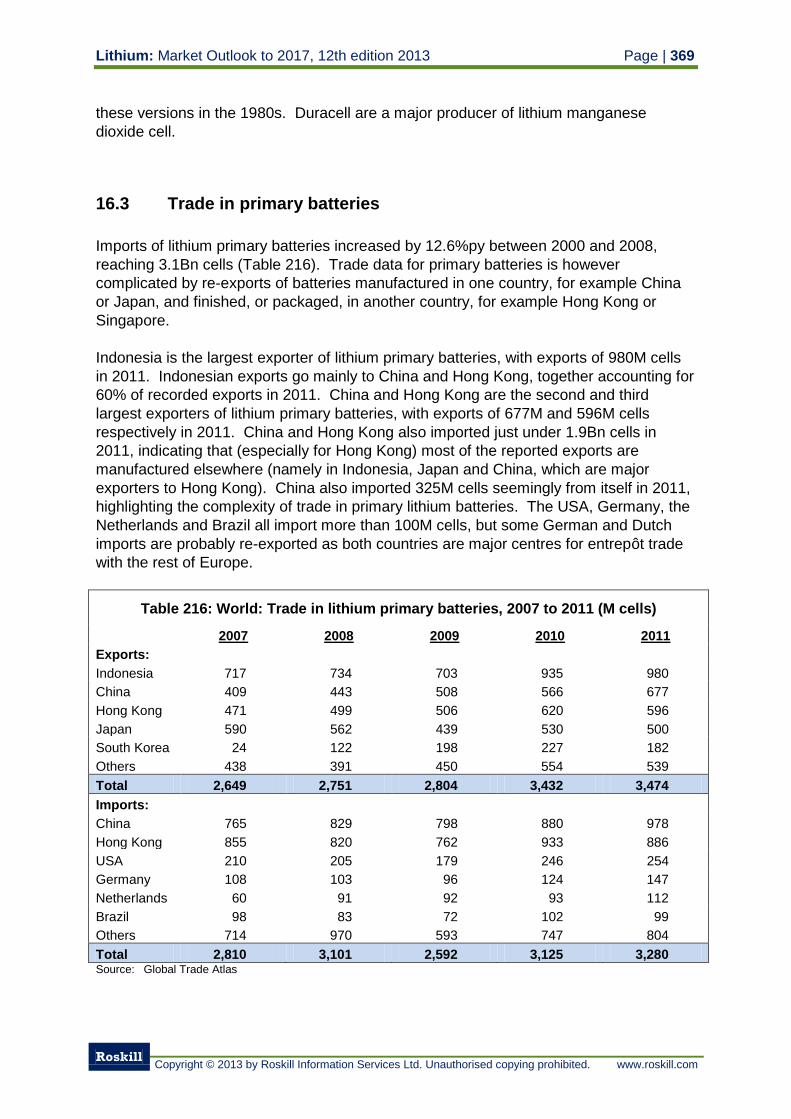

16.3 Trade in primary batteries 369

16.4 Production of primary lithium battery materials 370

16.4.1 Producers of lithium primary battery anodes 371

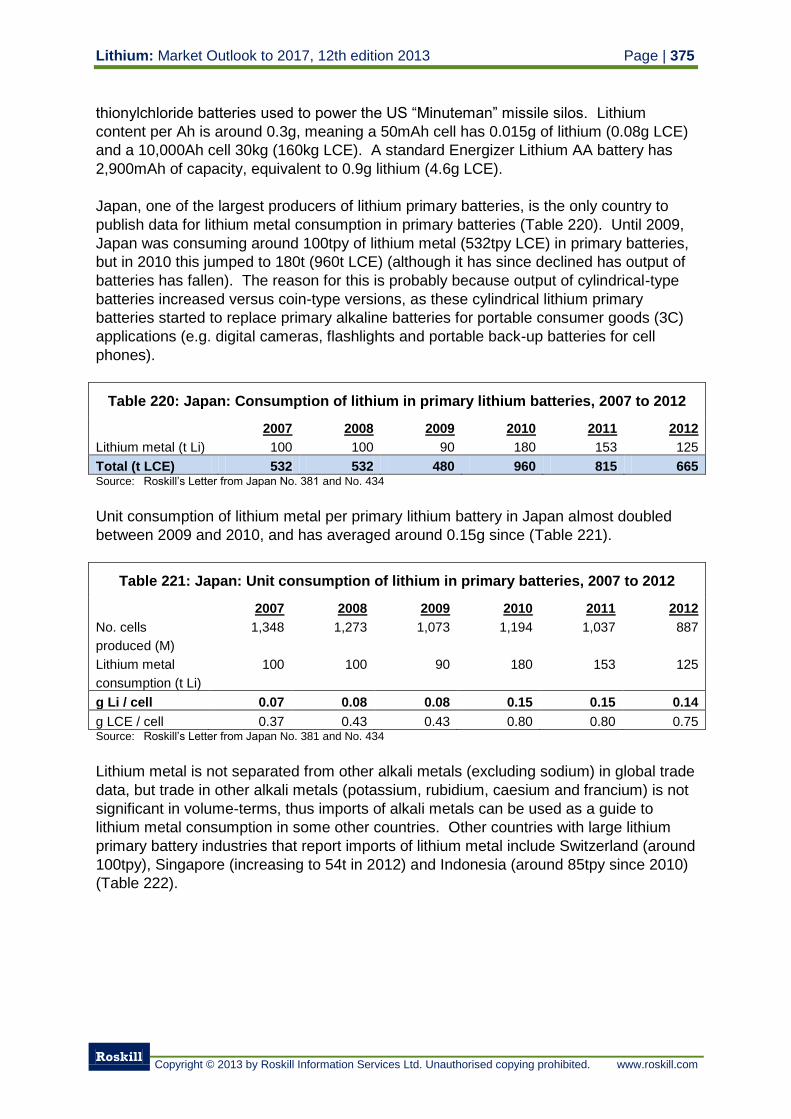

16.5 Consumption of lithium primary batteries 373

16.5.1 Outlook for primary lithium battery consumption 374

16.6 Consumption of lithium in primary batteries 374

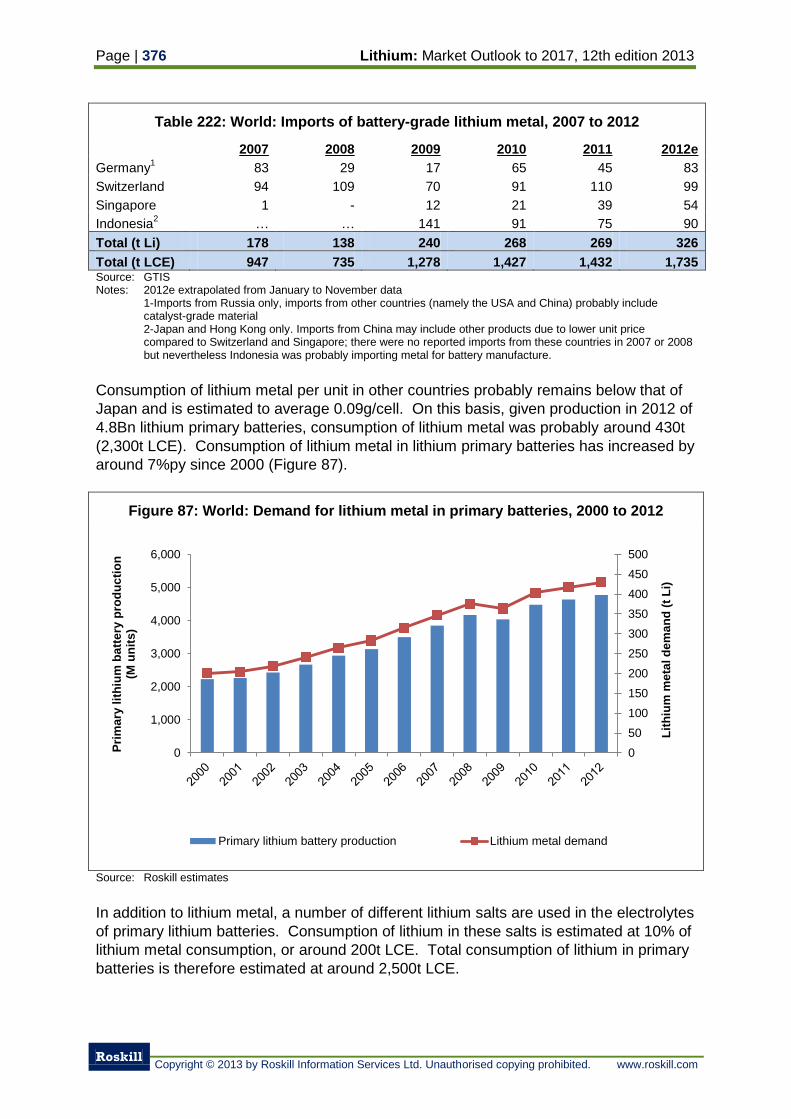

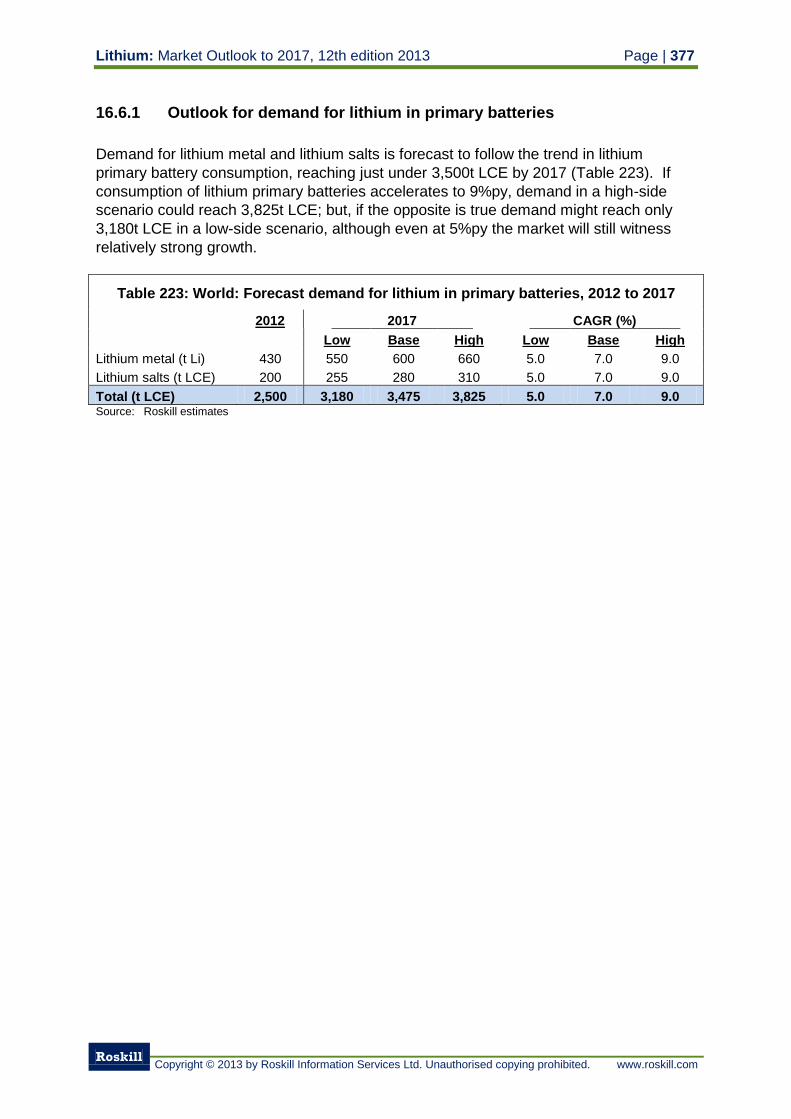

16.6.1 Outlook for demand for lithium in primary batteries 377

17. Use of lithium in aluminium smelting 378

17.1 Process of aluminium smelting 378

17.2 Consumers of lithium in aluminium smelting 380

17.3 Consumption of lithium in aluminium smelting 382

17.3.1 Outlook for lithium demand in aluminium smelting 383

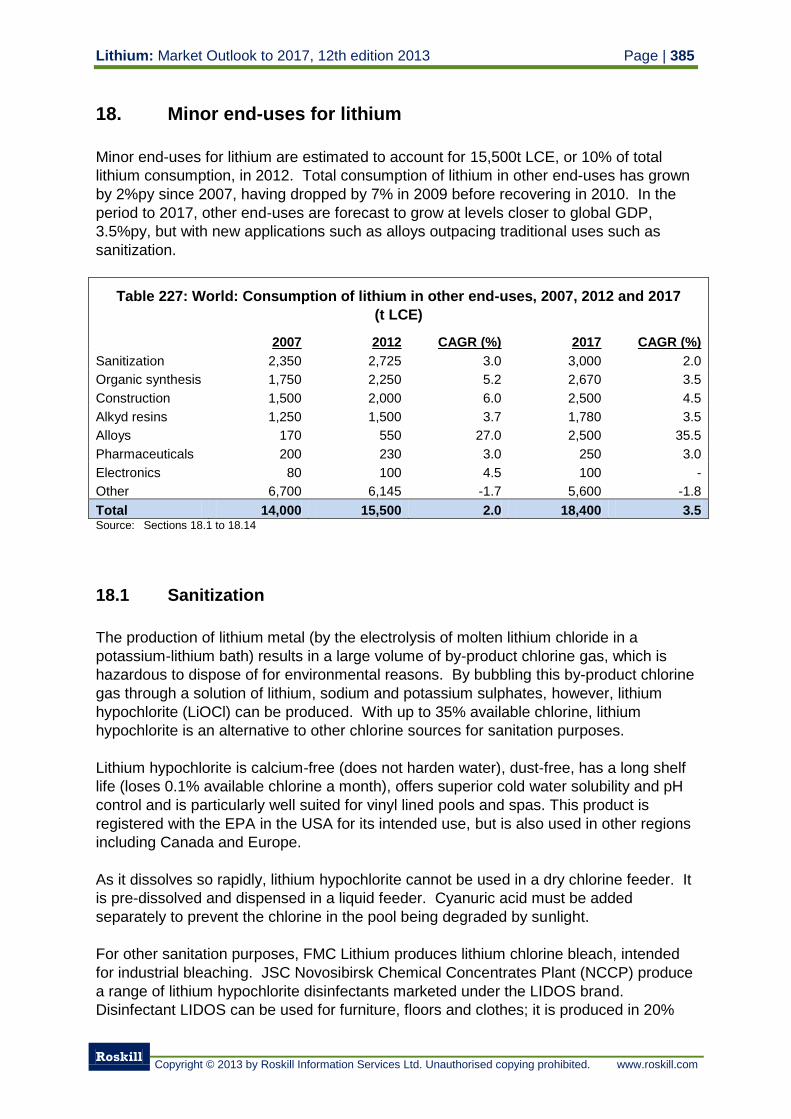

18. Minor end-uses for lithium 385

18.1 Sanitization 385

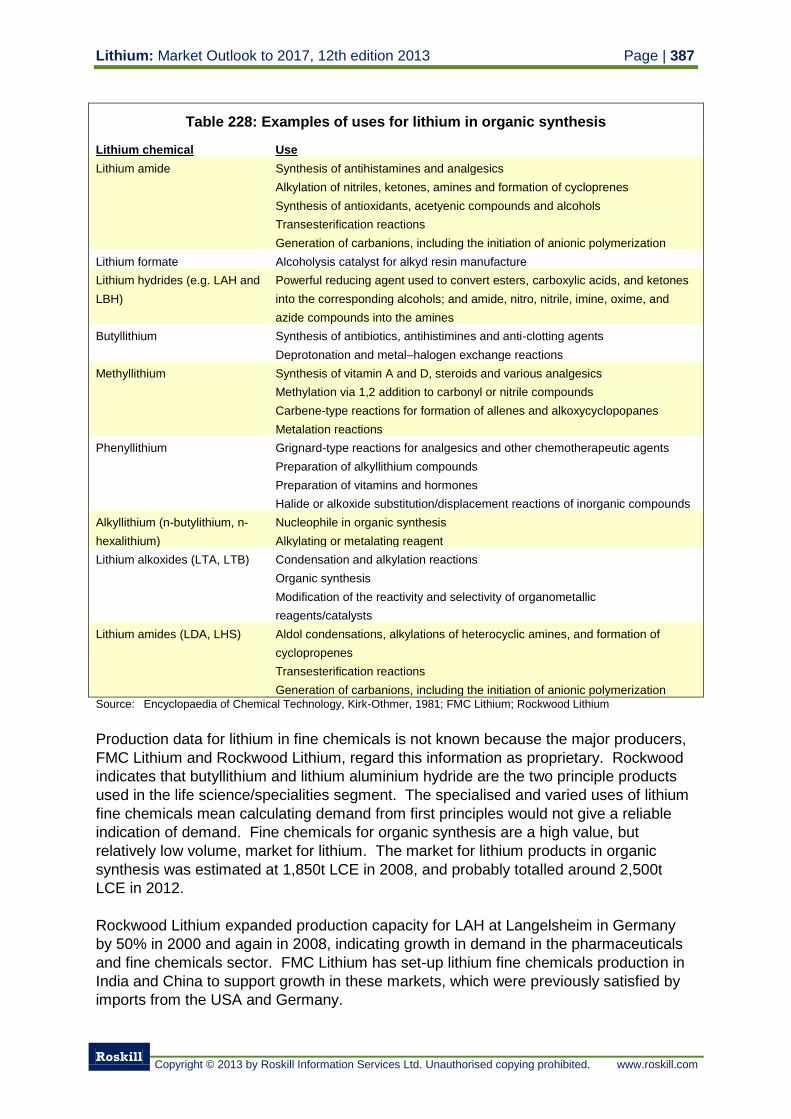

18.2 Organic synthesis 386

18.3 Construction 388

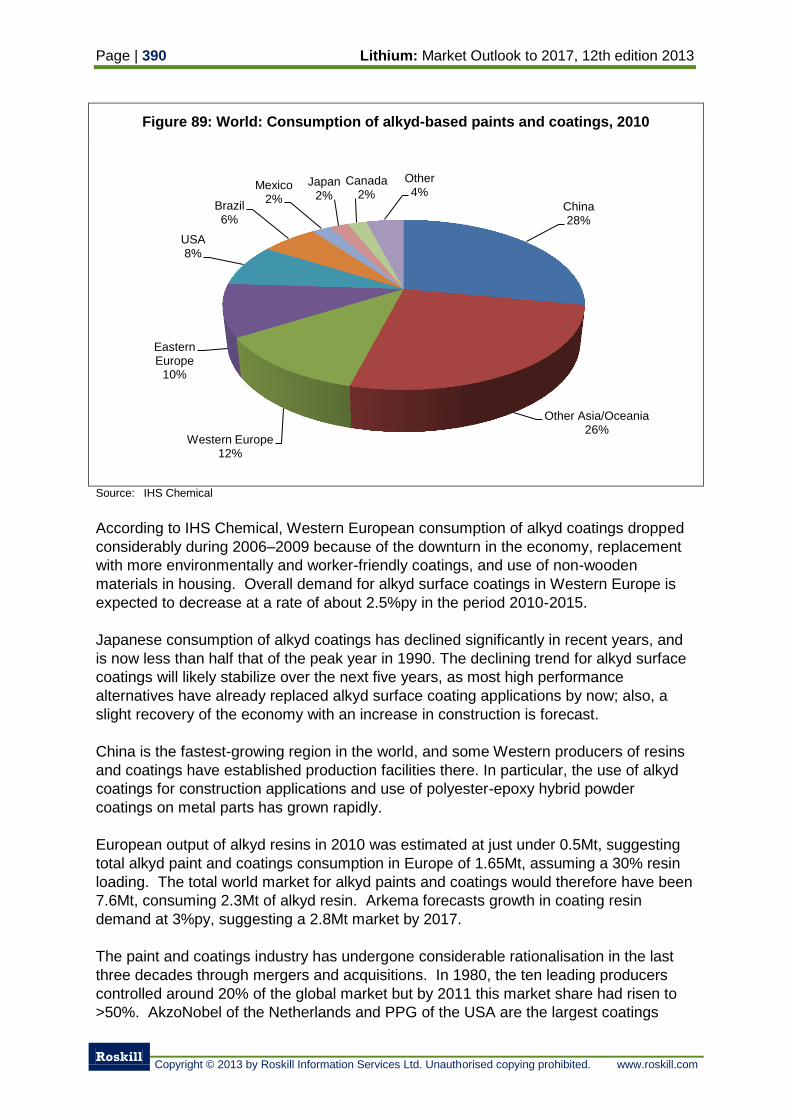

18.4 Alkyd resins 388

18.5 Alloys 391

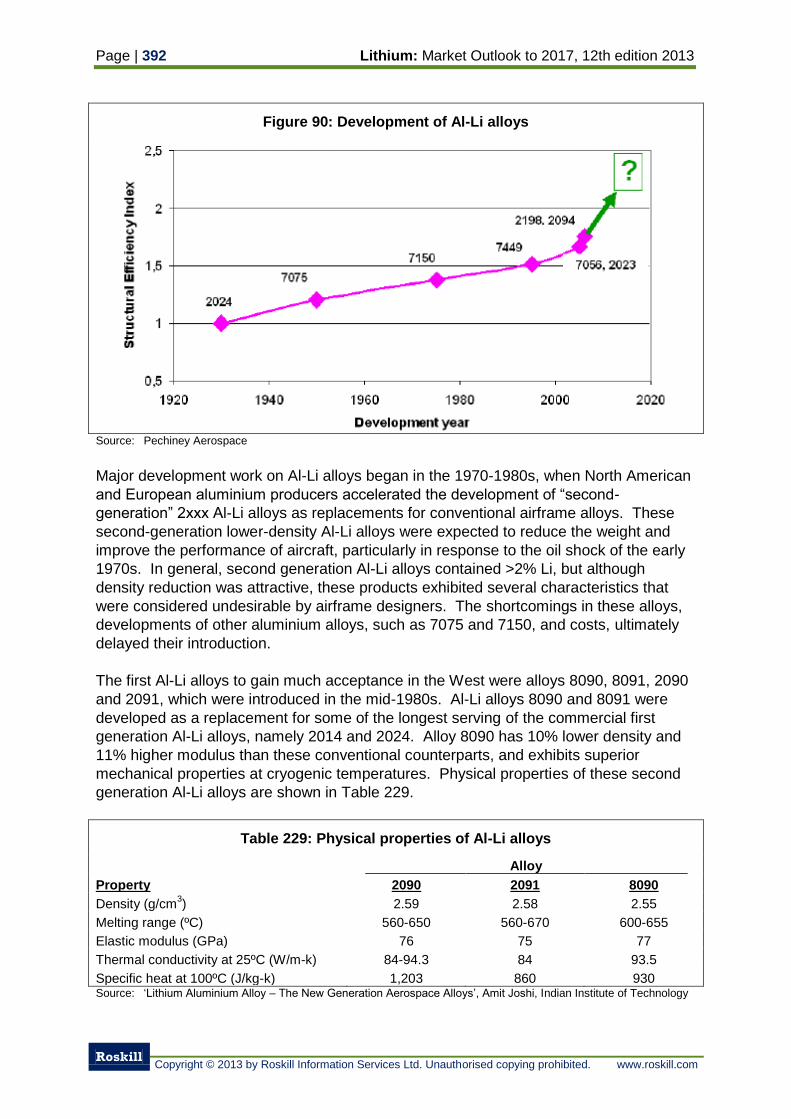

18.5.1 Aluminium-lithium alloy 391

18.5.1.1 Producers of aluminium-lithium alloys 394

18.5.1.2 Applications for aluminium-lithium alloys 395

18.5.1.3 Consumption of lithium in aluminium-lithium alloys 398

18.5.1.4 Outlook for demand for lithium in aluminium-lithium alloys 398

18.5.2 Magnesium-lithium alloy 400

18.6 Electronics 400

18.7 Analytical agents 402

18.8 Dyestuffs 402

18.9 Metallurgy 402

18.10 Photographic industry 402

18.11 Welding fluxes 402

18.12 Electrochromic glass 403

18.13 Pharmaceuticals 403

18.13.1 Producers of lithium-based pharmaceuticals 404

18.13.2 Production and consumption of lithium-based pharmaceuticals 404

18.13.3 Consumption of lithium in pharmaceuticals 405

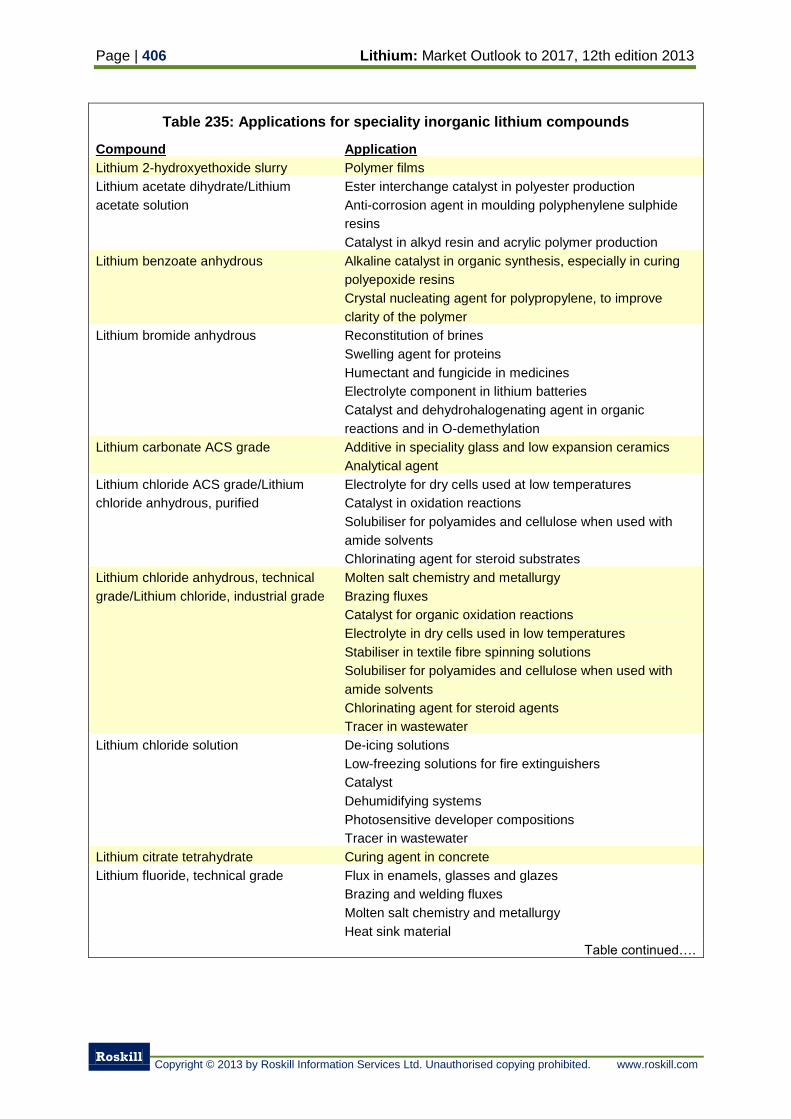

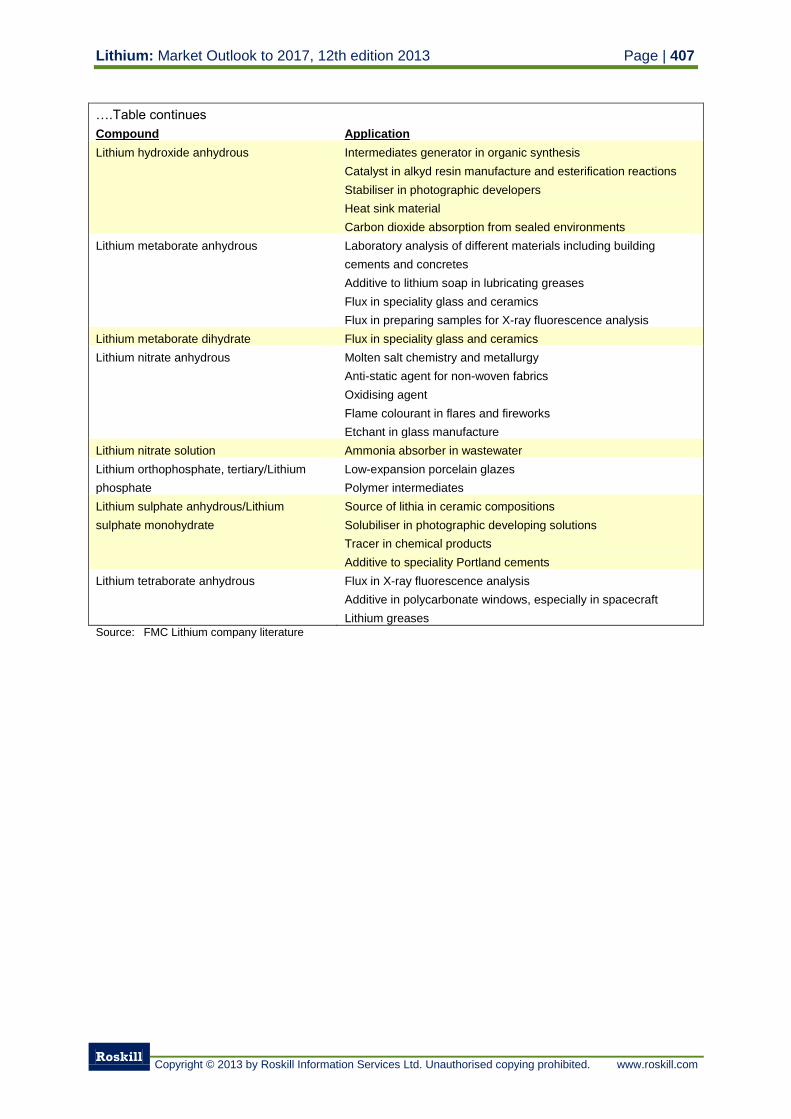

18.14 Speciality lithium inorganics 405

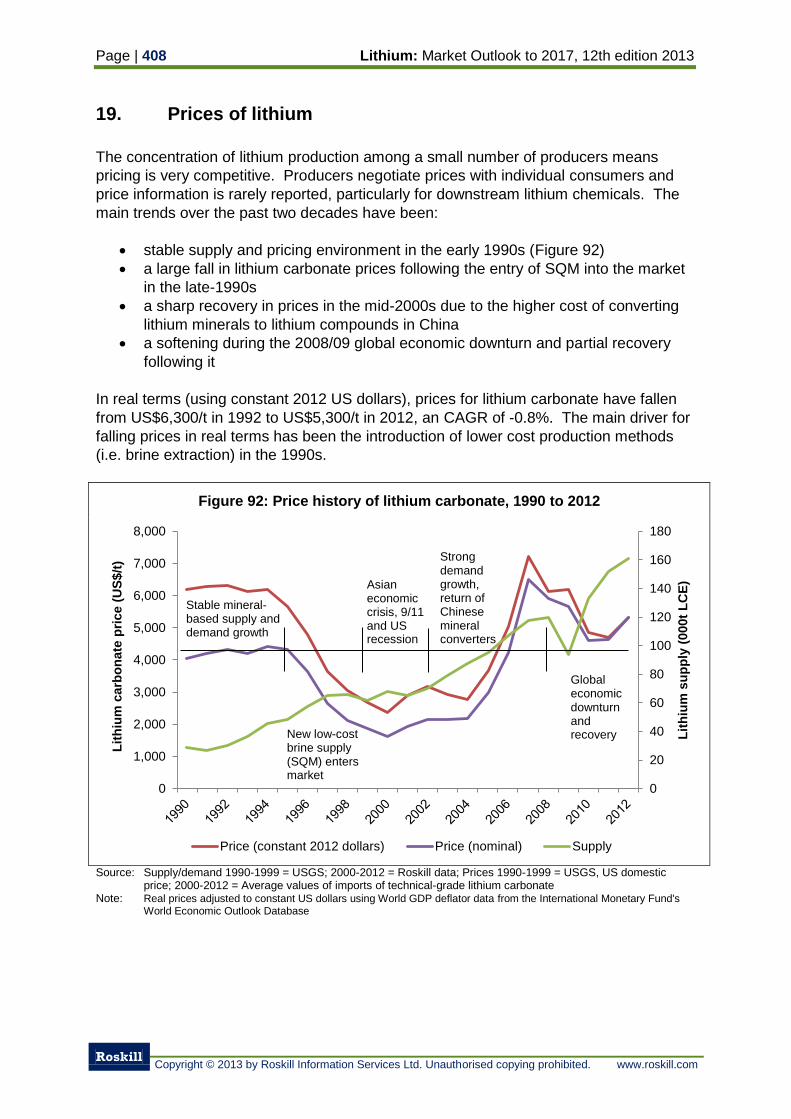

19. Prices of lithium 408

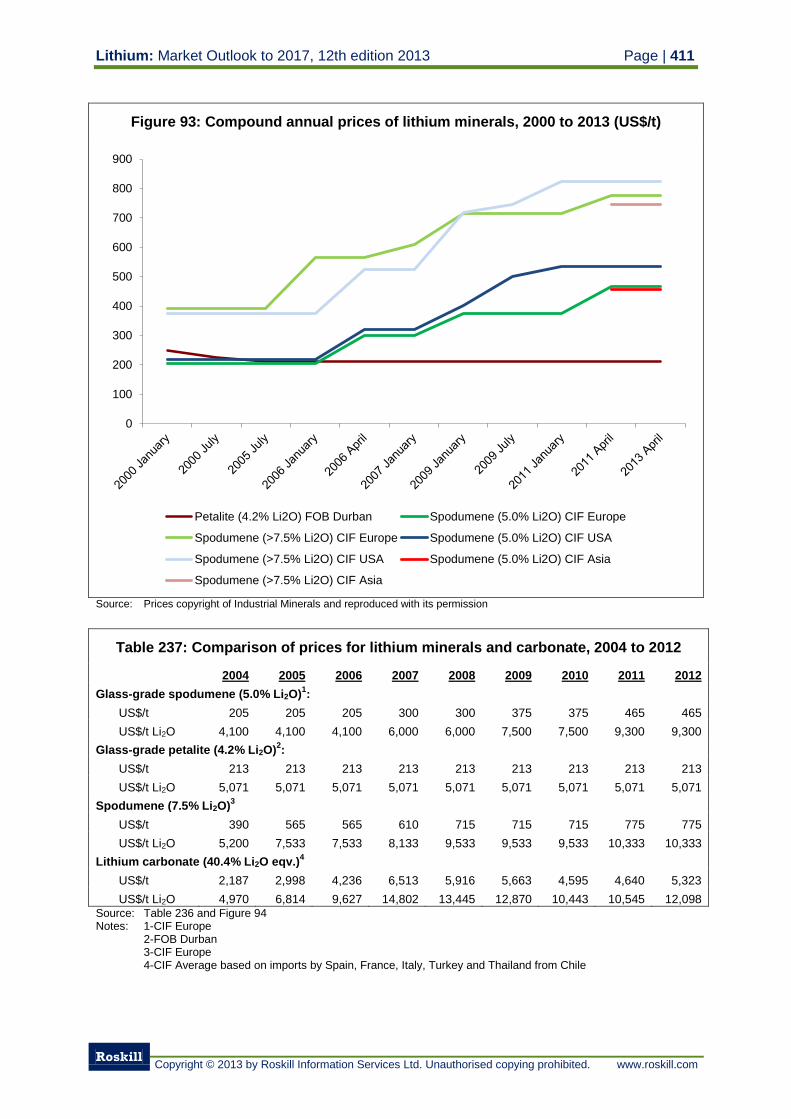

19.1 Technical-grade lithium mineral prices 409

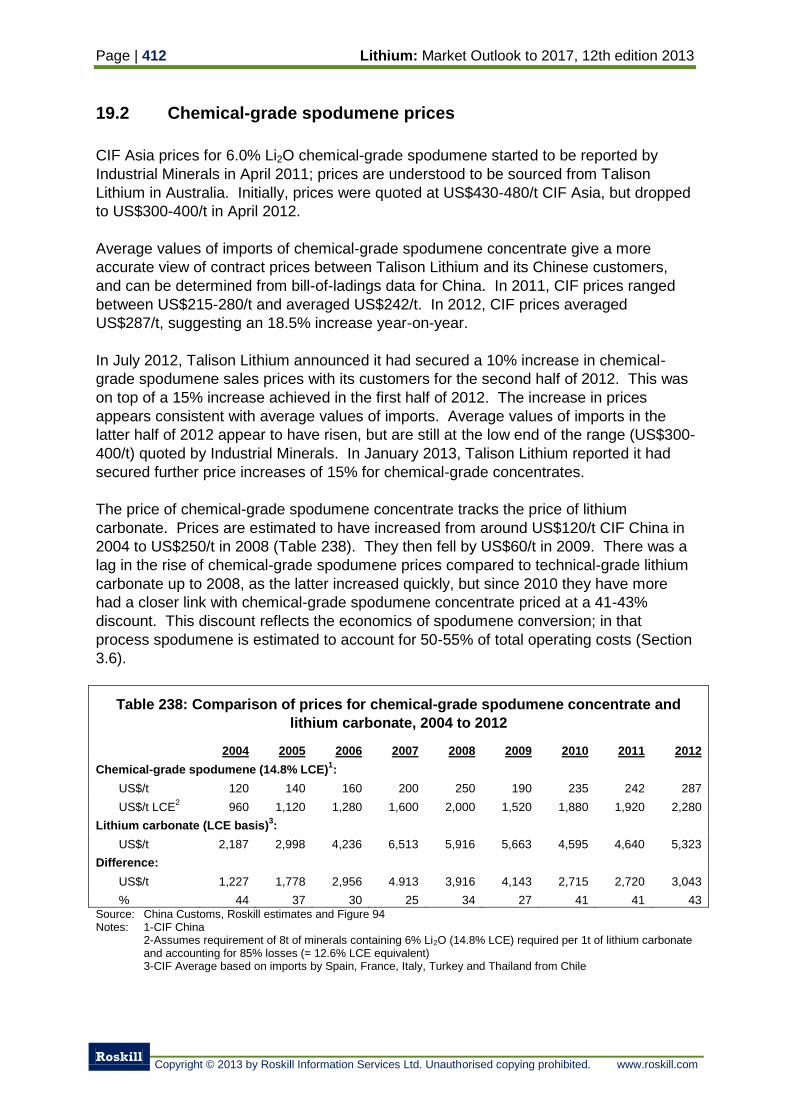

19.2 Chemical-grade spodumene prices 412

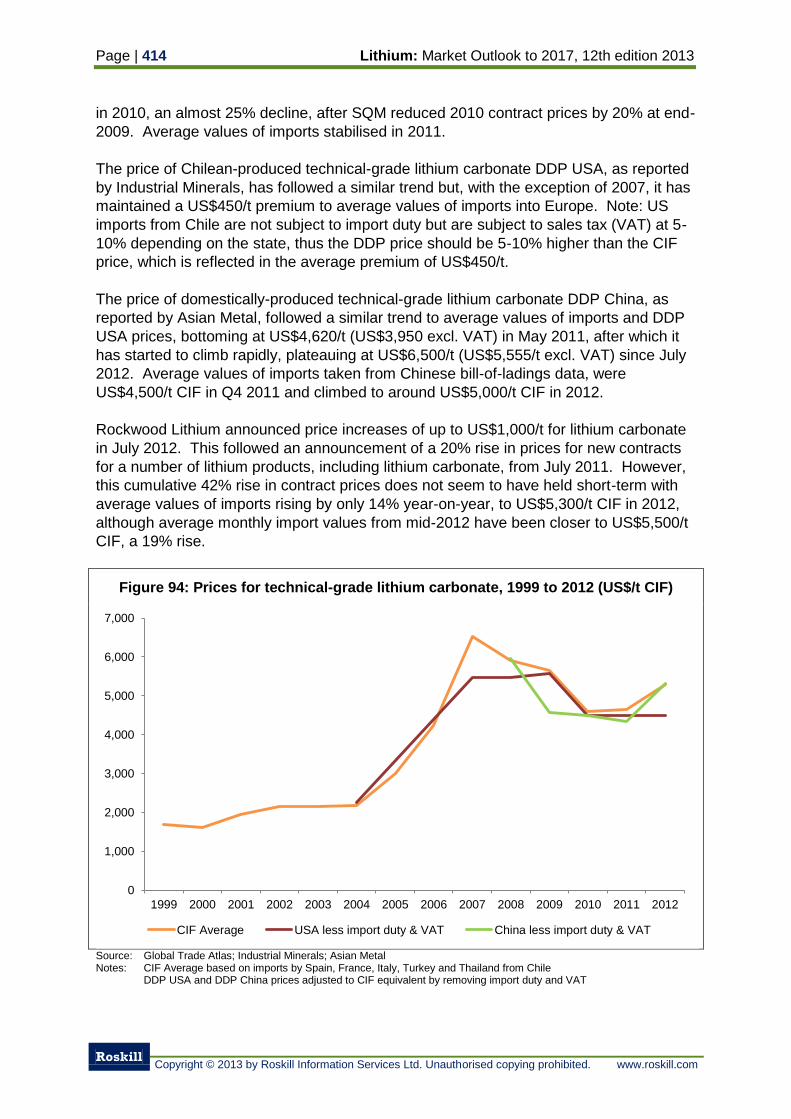

19.3 Technical-grade lithium carbonate prices 413

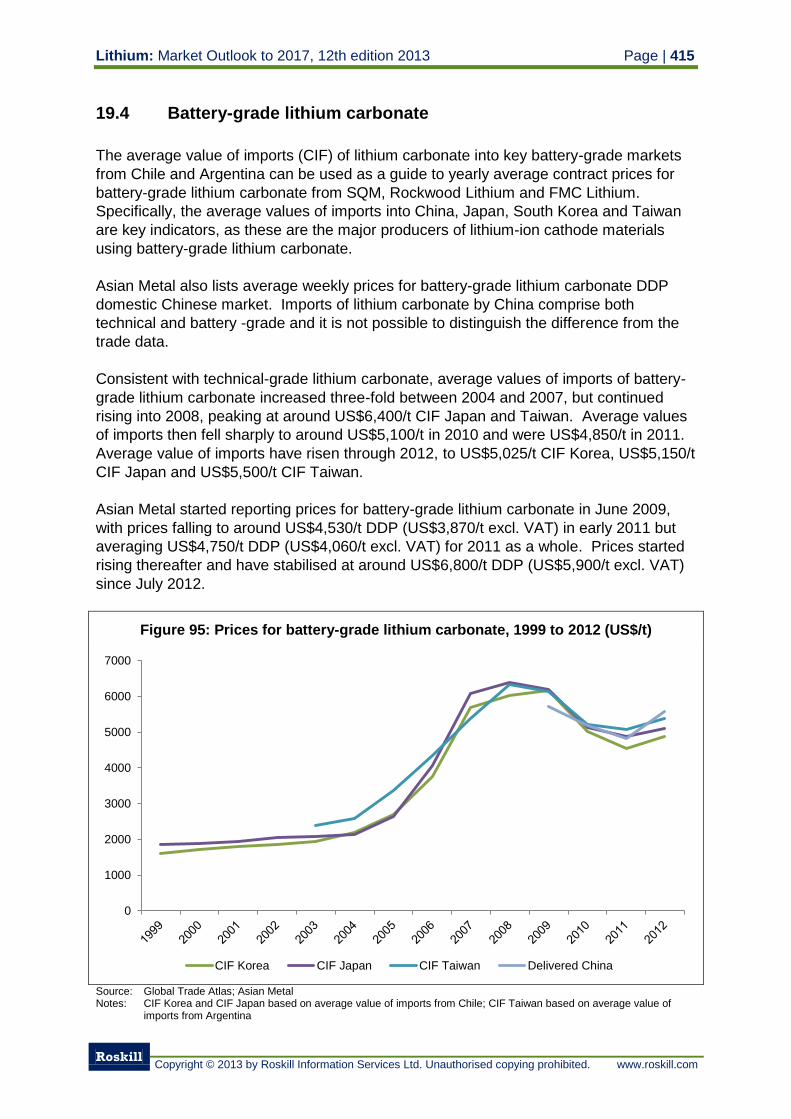

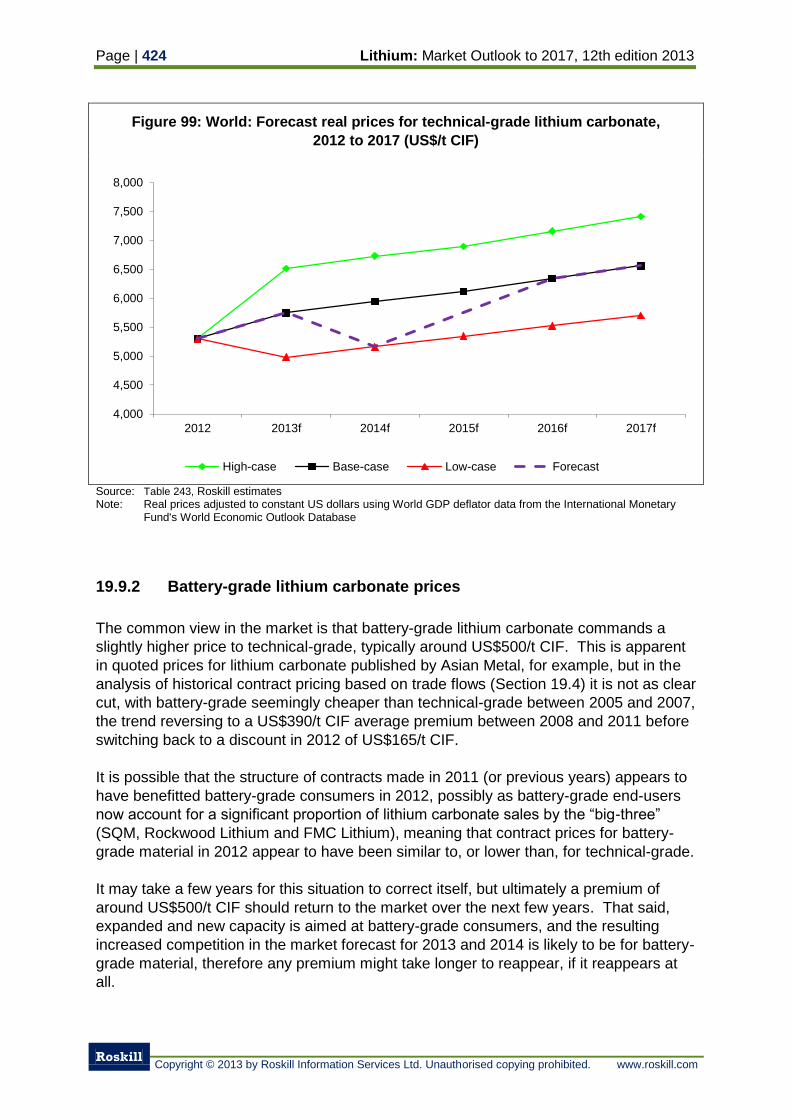

19.4 Battery-grade lithium carbonate 415

19.5 Technical-grade lithium hydroxide prices 416

19.6 Battery-grade lithium hydroxide prices 418

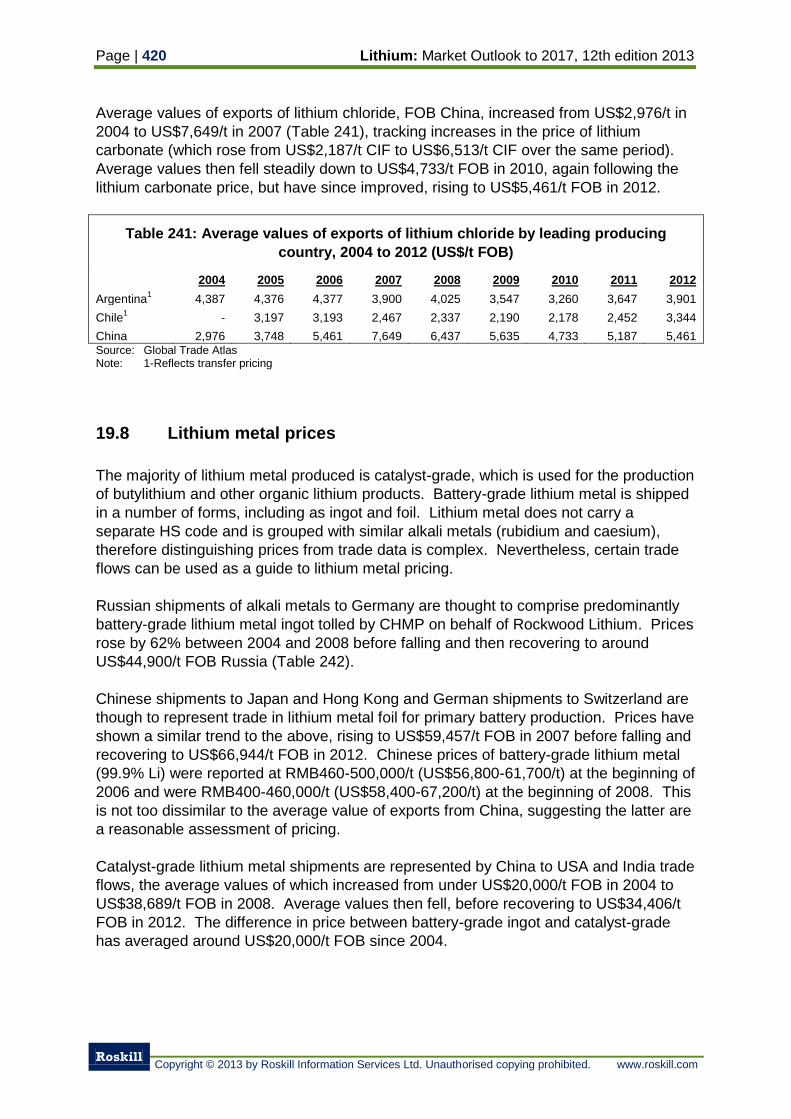

19.7 Lithium chloride prices 419

19.8 Lithium metal prices 420

19.9 Outlook for lithium prices 421

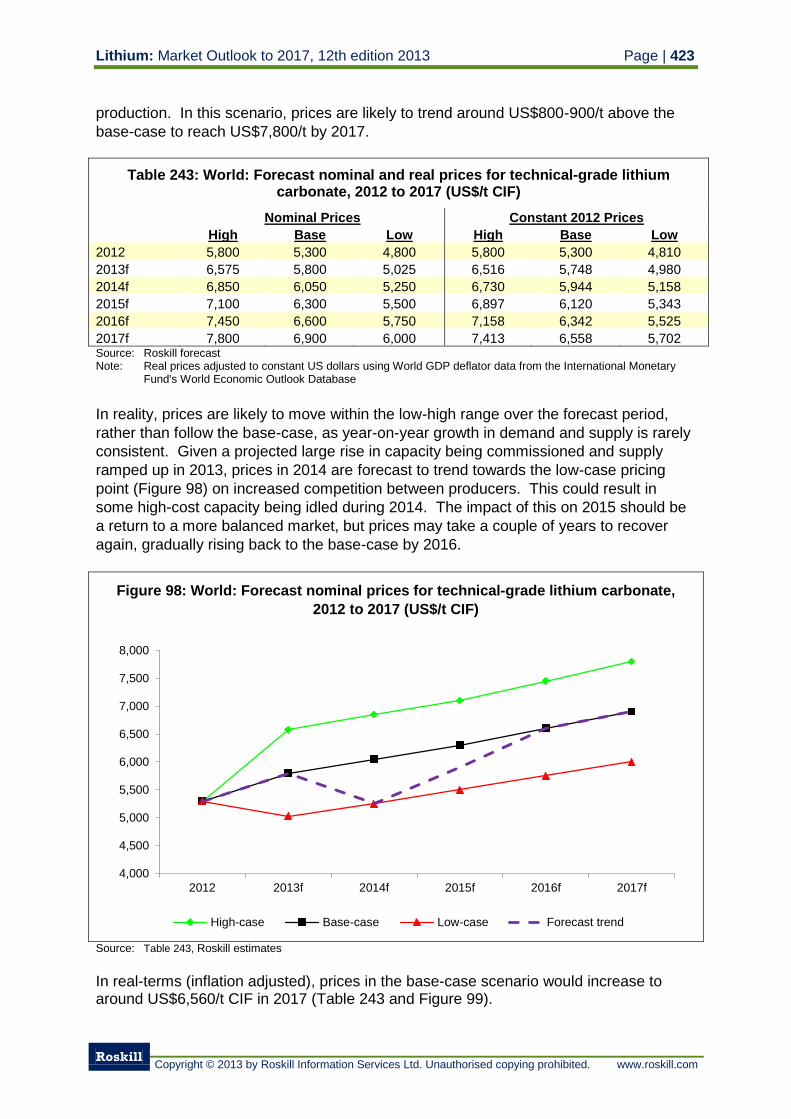

19.9.1 Technical-grade lithium carbonate prices 421

19.9.2 Battery-grade lithium carbonate prices 424

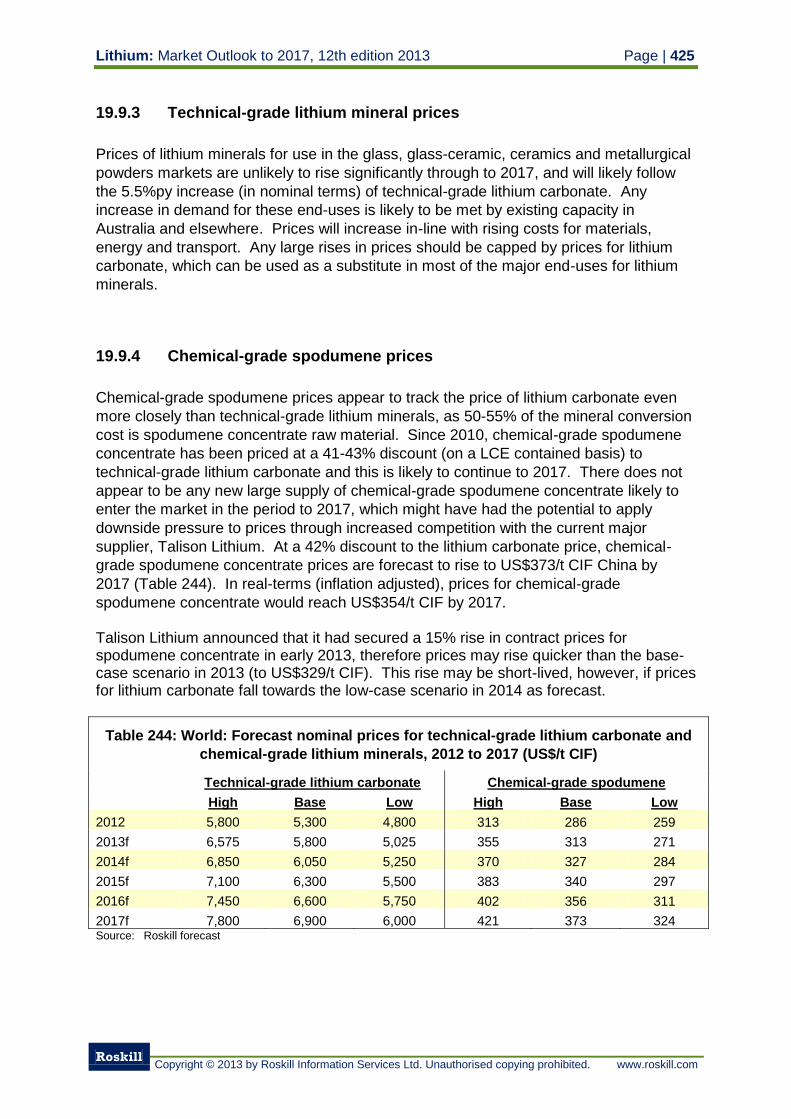

19.9.3 Technical-grade lithium mineral prices 425

19.9.4 Chemical-grade spodumene prices 425

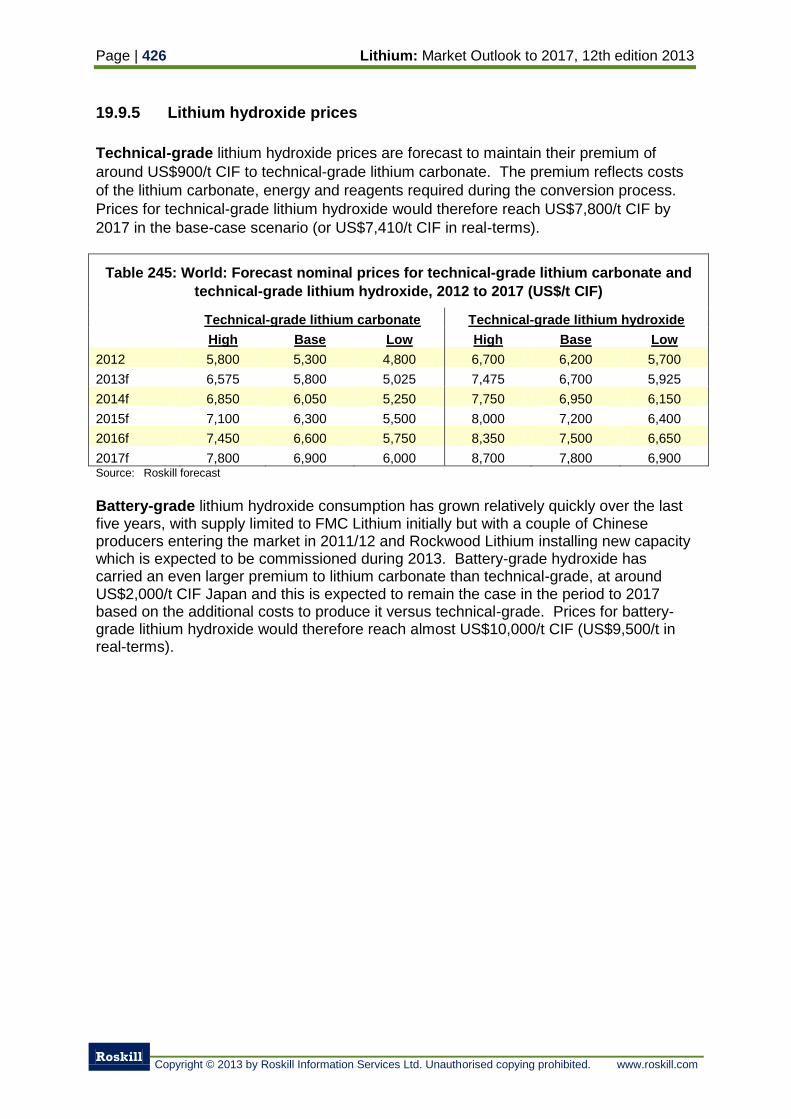

19.9.5 Lithium hydroxide prices 426

List of Tables

Page

Table 1: World: Forecast nominal and real prices for technical-grade lithium

carbonate, 2012 to 2017 8

Table 2: Properties of lithium 10

Table 3: Significant lithium minerals 11

Table 4: Major lithium bearing smectite group members 12

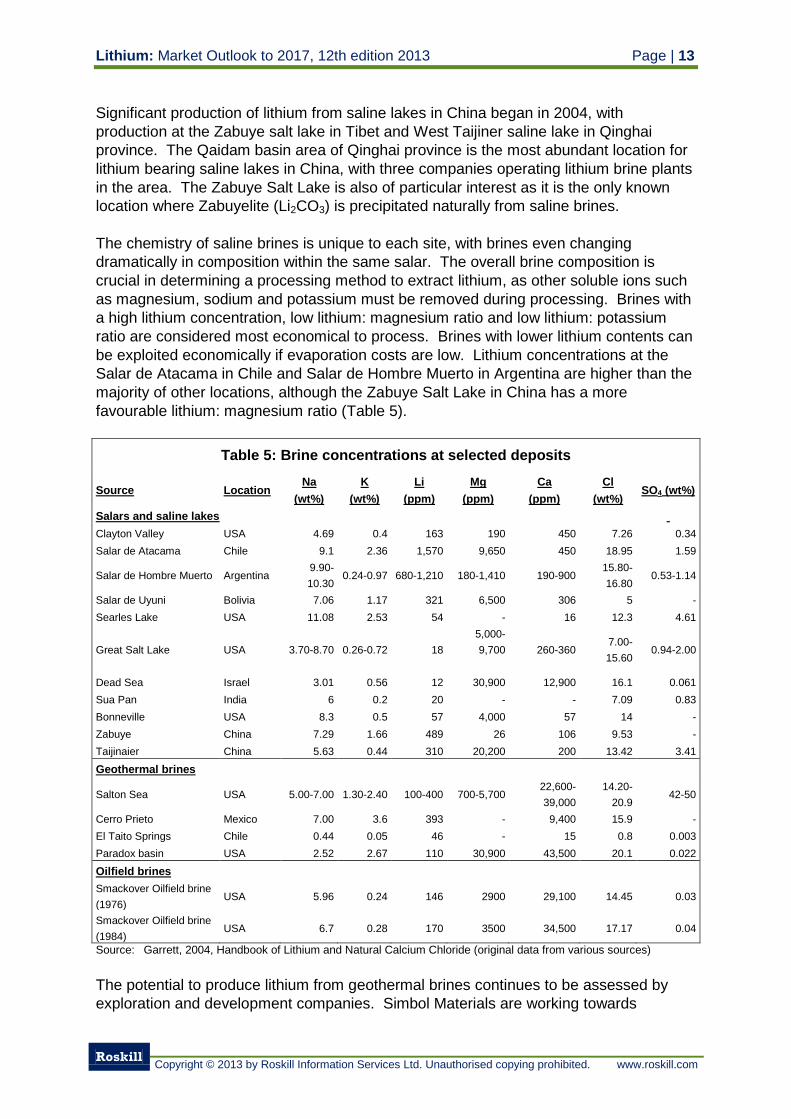

Table 5: Brine concentrations at selected deposits 13

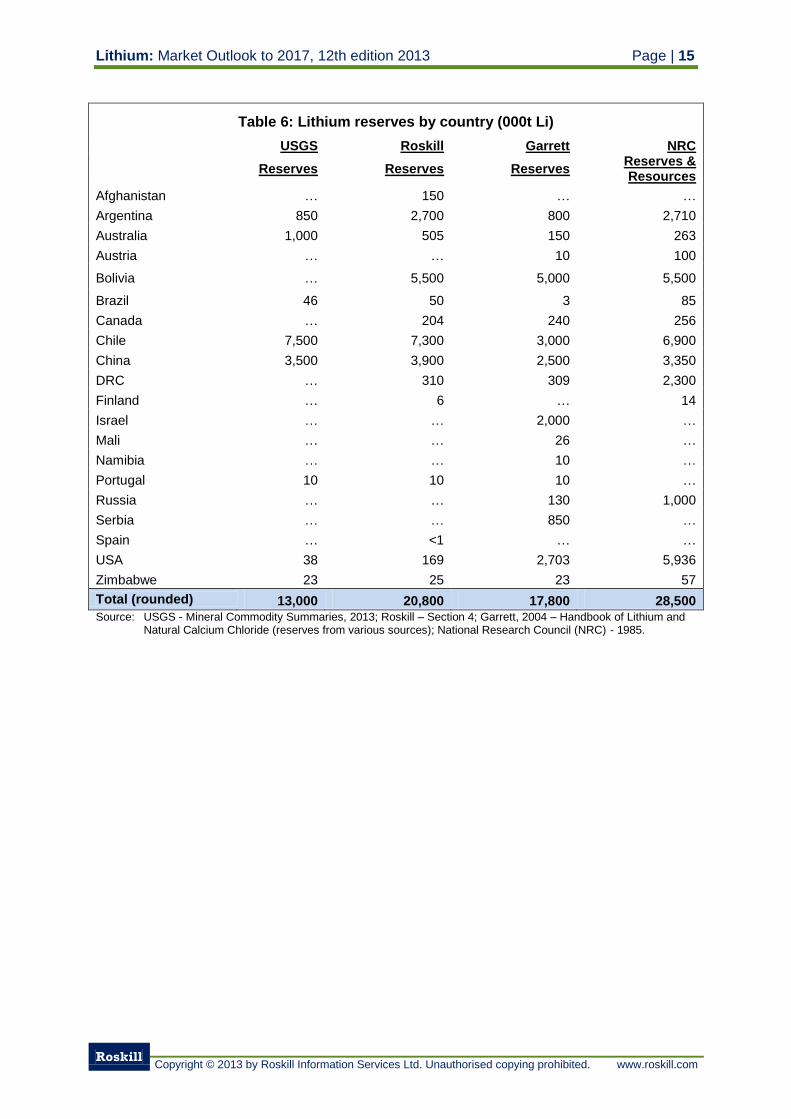

Table 6: Lithium reserves by country 15

Table 7: Composition of standard lithium concentrates 22

Table 8: Specifications for lithium carbonate produced by SQM and Rockwood

Lithium 28

Table 9: Specifications for lithium carbonate produced by other suppliers 28

Table 10: Battery grade lithium hydroxide product specifications of major producers 29

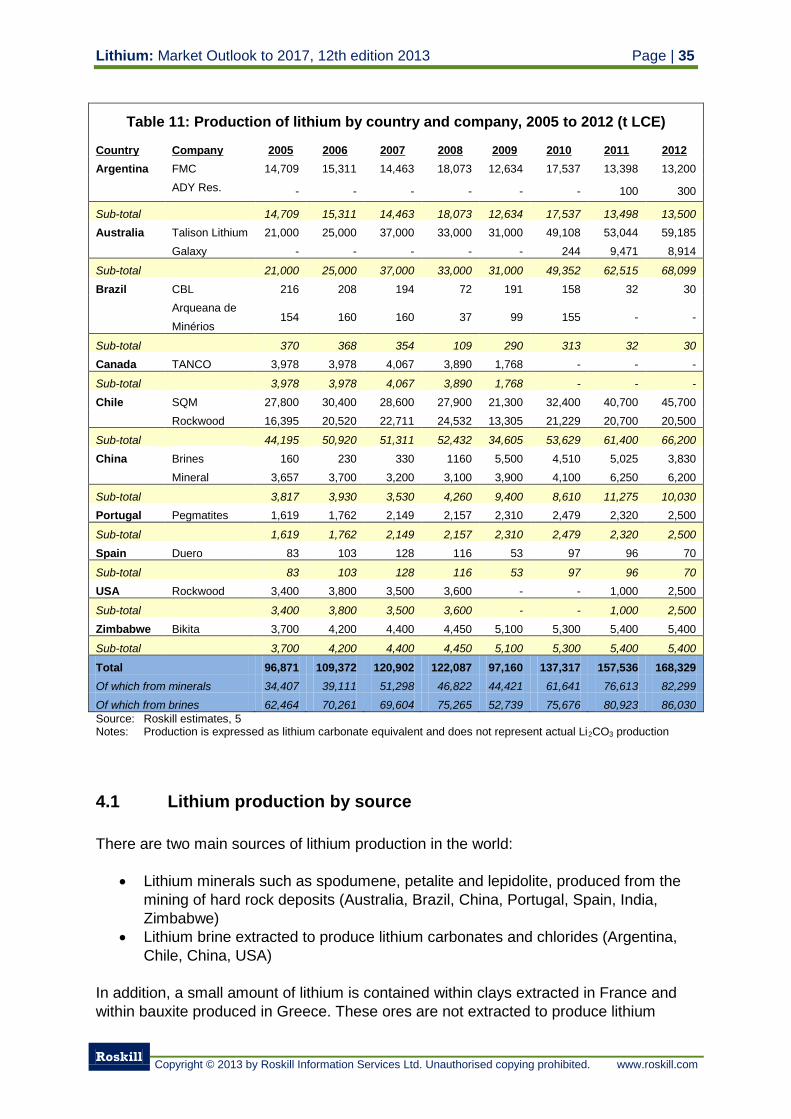

Table 11: Production of lithium by country and company, 2005 to 2012 35

Table 12: Capacity and production of lithium minerals by company, 2011 to 2012 39

Table 13: Capacity and production of lithium compounds from brine-based

producers, 2011 to 2012 40

Table 14: Capacity and production of lithium mineral converters, 2011 to 2012 42

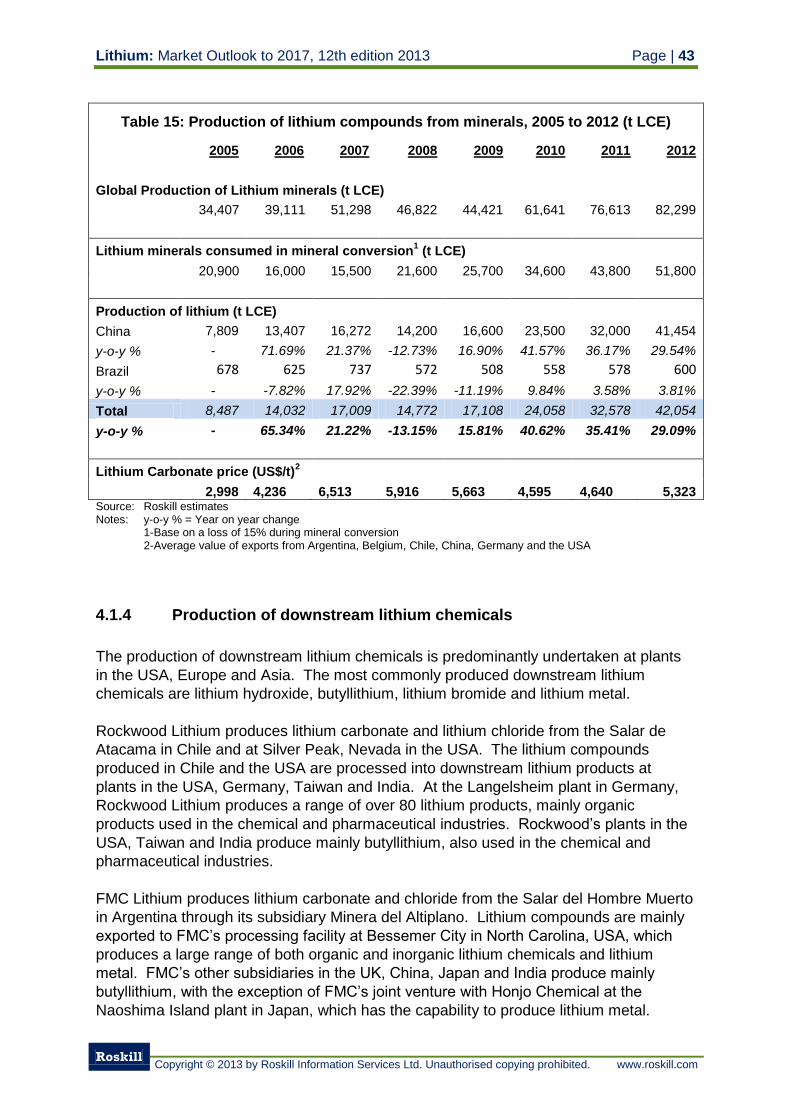

Table 15: Production of lithium compounds from minerals, 2005 to 2012 43

Table 16: Planned expansions as reported by existing lithium mineral producers

to 2017 46

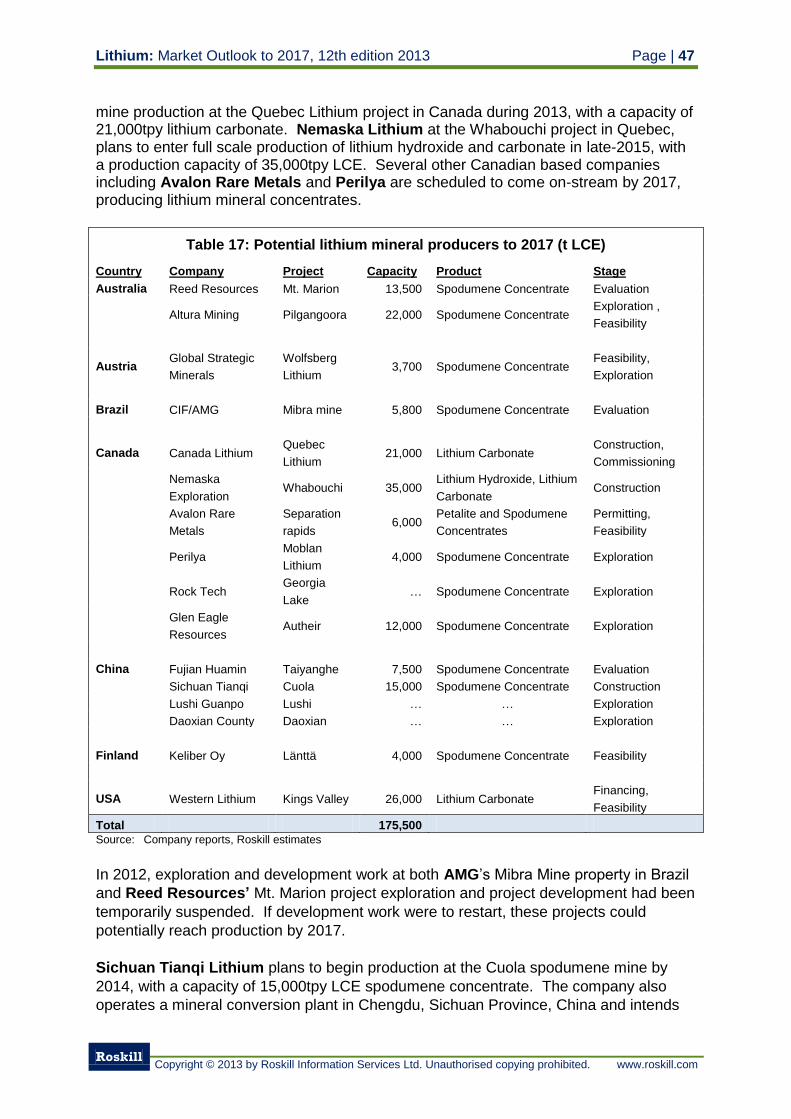

Table 17: Potential lithium mineral producers to 2017 47

Table 18: Planned expansions by existing lithium brine producers to 2017 49

Table 19: Potential new lithium brine projects to 2017 50

Table 20: Planned expansions to production capacity for existing and potential

mineral conversion plants 51

Table 21: Afghanistan: Spodumene bearing pegmatites identified in Nuristan,

Badakhshan, Nangarhar, Lagman and Uruzgan provinces 55

Table 22: Argentina: Exports of lithium carbonate, 2004 to 2012 57

Table 23: Argentina: Exports of lithium chloride, 2004 to 2012 58

Table 24:FMC: Brine reserves at the Salar del Hombre Muerto 58

Table 25: FMC: Production and value of lithium carbonate and chloride at the Salta

plant, Argentina 2005 to 2012 59

Table 26: ADY Resources: Salar del Rincón reserve estimation, 2007 60

Table 27: Lithium Americas: Lithium and potash resource estimation for the

Cauchari-Olaroz property, July 2012 61

Table 28: Lithium Americas: Lithium and potash reserve estimation for the Cauchari-

Olaroz property, July 2012 61

Table 29: Lithium Americas: Estimated capital costs for Lithium carbonate

production at the Cauchari-Olaroz project, July 2012 63

Table 30: Lithium Americas: Estimated operating costs for Cauchari-Olaroz project,

July 2012 65

Table 31: Galaxy Resources: Resource estimation for the Sal de Vida project,

January 2012 66

Table 32: Galaxy Resources: Reserve estimate for the Sal de Vida project,

April 2013 67

Table 33: Galaxy Resources: Estimated capital costs for Sal de Vida project ,

October 2011 68

Table 34: Orocobre: Agreements between Borax Argentina and other lithium

companies 70

Table 35: Orocobre: Resource estimation for the Salar de Olaroz project, May 2011 71

Table 36: Orocobre: Assay results of first battery grade lithium carbonate product

from the Orocobre pilot plant 72

Table 37: Orocobre: Capital costs for 16,400tpy LCE operation at the Salar de

Olaroz, May 2011 73

Table 38: Orocobre: Operating costs for battery grade lithium carbonate

for the Salar de Olaroz, May 2011 73

Table 39: Orocobre: Resource estimation for the Salinas Grande project, April 2012 74

Table 40: Orocobre: Averaged assay results from pit sampling of brine at the

Guayatoyoc project 75

Table 41: Orocobre: Maiden resource estimation for the Salar de Cauchari project,

October 2012 75

Table 42: Rodinia Lithium: Salar de Diablillos resource estimation, March 2011 76

Table 43: Rodinia Lithium: Estimated capital costs for the Salar de Diablillos project 77

Table 44: Rodinia Lithium: Estimated operating costs for the Salar de Diablillos

project 77

Table 45: Rodinia Lithium: Other Argentine lithium projects 78

Table 46: Australia: Exports of mineral substances NES (excl. natural micaceous

iron oxides) 2005 to 2012 81

Table 47: Australia: Unit value of mineral substances NES (excl. natural micaeous

iron oxides) 2005 to 2011 81

Table 48: Talison Lithium: Resource estimation for the Greenbushes deposit,

December 2012 83

Table 49: Talison Lithium: Lithium mineral reserve estimation for the Greenbushes

deposit, December 2012 83

Table 50: Talison Lithium: Li, K and Na content of brines, Salares 7 project saline

lakes 1998, (ppm) 84

Table 51: Talison Lithium: Li, K and Na content of brines, Salares 7 project saline

lakes 2009, (ppm) 84

Table 52: Talison Lithium: Production and sales of lithium mineral concentrates and

ores, 2005 to 2011 85

Table 53: Talison Lithium: Standard lithium mineral concentrate product

specifications 87

Table 54: Galaxy Resources: Mount Cattlin mineral resource estimate, February

2011 89

Table 55: Galaxy Resources: Mount Cattlin mineral reserve estimate, December

2011 89

Table 56: Galaxy Resources: James Bay mineral resource estimate, November

2010 89

Table 57: Galaxy Resources: Mt. Cattlin mine and plant production, Q3 2010 –

Q4 2011 90

Table 58: Reed Resources : Mt Marion resource estimation, July 2011 91

Table 59: Altura: Mineral resource estimation for the Pilgangoora lithium project,

October 2012 92

Table 60: Belgium: Trade is lithium carbonate, 2005 to 2012 95

Table 61: Belgium: Trade in lithium hydroxide and oxide, 2005 to 2012 96

Table 62: Salars and Lagunas in Bolivia identified by Gerencia Nacional de

Recursos Evaporíticos 97

Table 63: Results of sampling campaign by Université de Liegé and Universidad

Tecnica de Oruro at the Salar de Coipasa, 2002 99

Table 64: Assay data for brines intercepted during drilling at the Pastos Grandes

Salar, August 2011 100

Table 65: Brazil: Lithium resource estimation by mineral type, 2009 101

Table 66: Brazil: Trade in lithium chemicals and concentrates, 2004 to 2011 102

Table 67: CBL: Production of lithium concentrates and lithium salts, 2005 to 2011 102

Table 68: Arqueana: Production of lithium concentrates, 2008 to 2011 103

Table 69: Canada: Resources estimations for Canadian lithium projects 106

Table 70: Canada: Imports and exports of lithium compounds 2005 to 2012 108

Table 71: TANCO: Spodumene concentrate production 2005 to 2011 109

Table 72: Canada Lithium: Resource estimation for the Quebec Lithium project,

December 2011 109

Table 73: Canada Lithium: Reserve estimation for the Quebec Lithium project,

December 2011 110

Table 74: Canada Lithium: Estimated capital expenditure for Quebec Lithium

project (inc. LiOH and Na2SO4 plant costs), October 2012 111

Table 75 :Canada Lithium: Estimated operating expenditure for Quebec Lithium

project, October 2012 111

Table 76: Nemaska Lithium: Resource estimation for the Whabouchi project,

June 2011 113

Table 77: Nemaska Lithium: Reserve estimation for the Whabouchi project,

October 2012 113

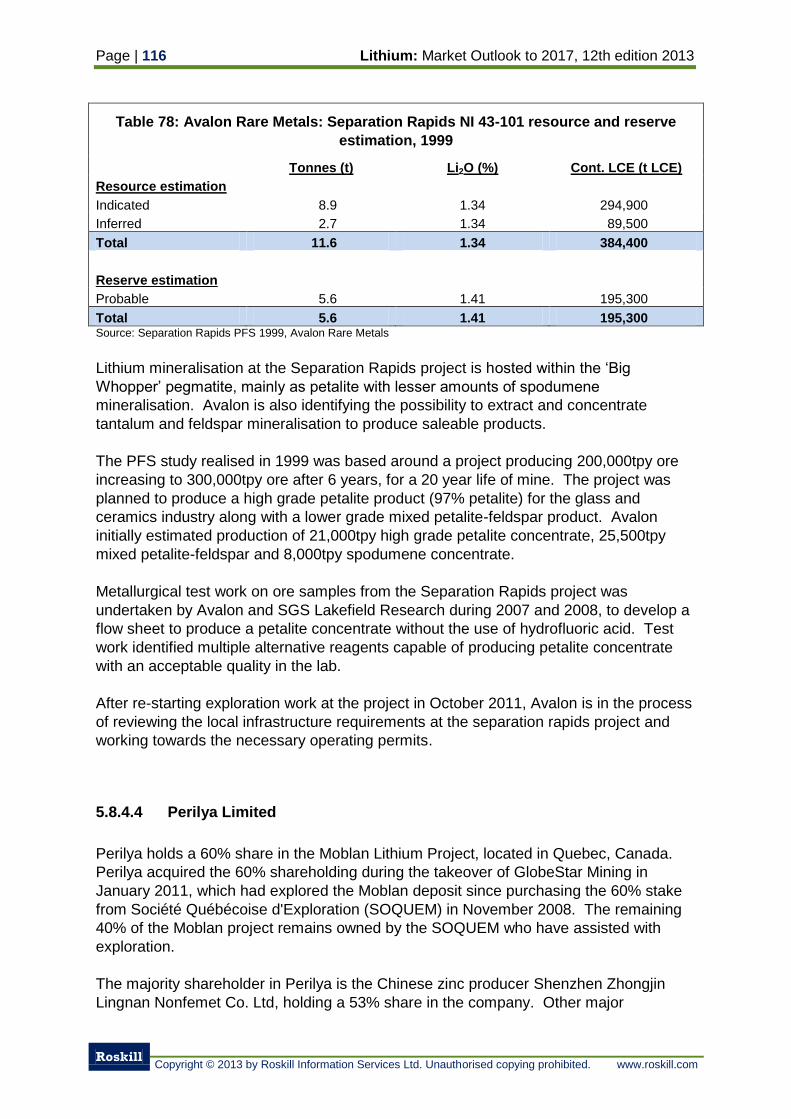

Table 78: Avalon Rare Metals: Separation Rapids NI 43-101 resource and reserve

estimation, 1999 116

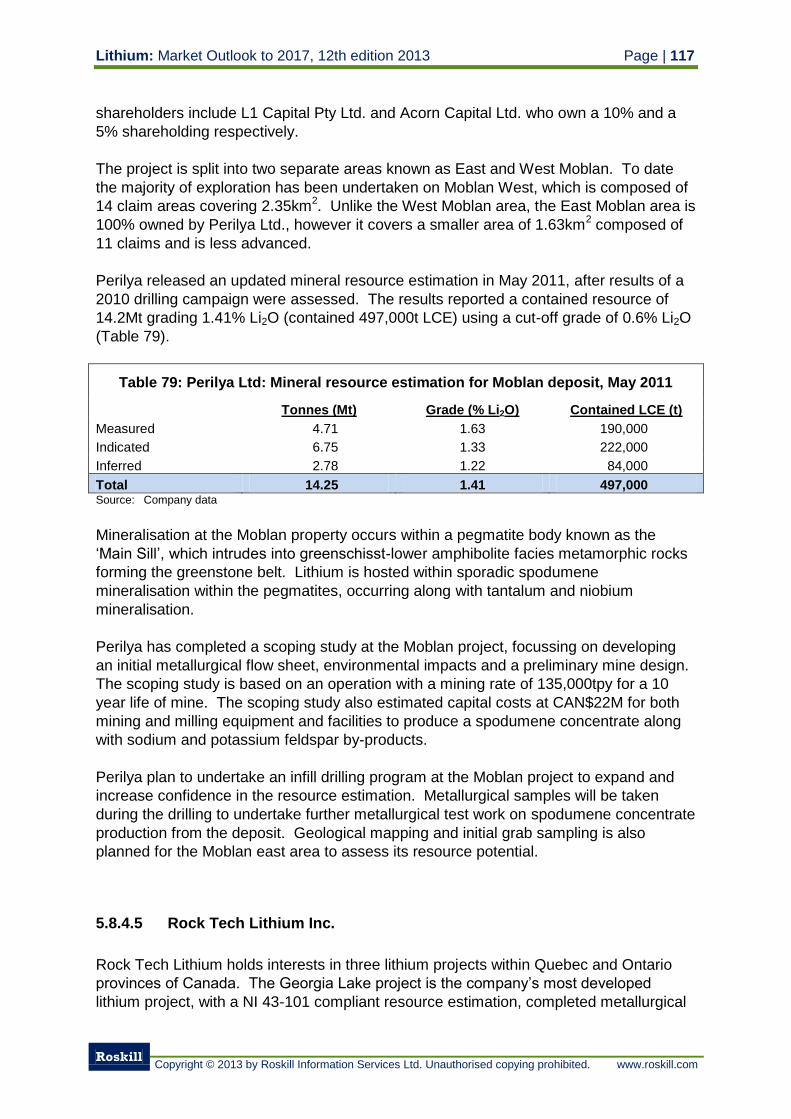

Table 79: Perilya Ltd: Mineral resource estimation for Moblan deposit, May 2011 117

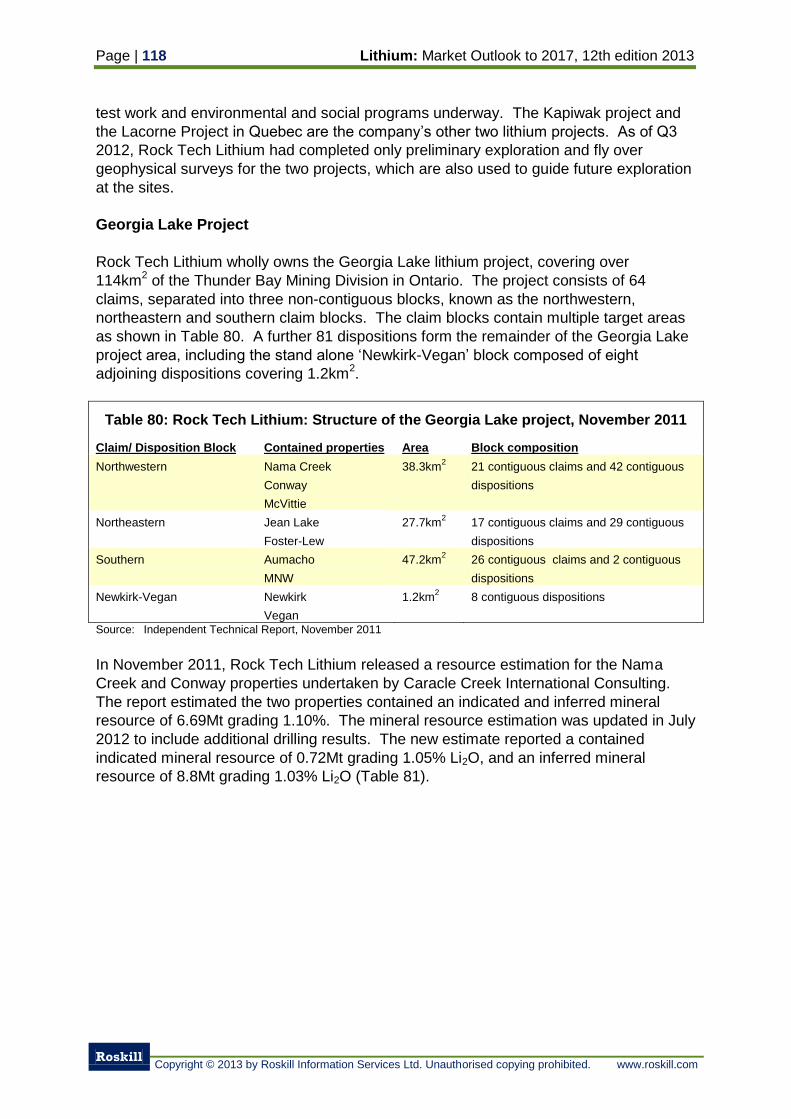

Table 80: Rock Tech Lithium: Structure of the Georgia Lake project, November

2011 118

Table 81: Rock Tech Lithium: Updated mineral resource estimation for Georgia

Lake project, July 2012 119

Table 82: Glen Eagle: Resource estimation for Authier lithium property, January

2012 121

Table 83: Canada: Lithium exploration projects in Canada with uncompleted

scoping studies or PFS in October 2012 122

Table 84: Chile: Lithium carbonate, chloride and hydroxide production, 2004 to 2011 128

Table 85: Chile: Special operating licence bidders for the September 2012 auction 129

Table 86: SQM: Majority shareholders of SQM as of December 31st 2011 130

Table 87: SQM: Reserves within brines at the Salar de Atacama project 131

Table 88: SQM: Production, revenue and value per tonne of lithium compounds,

2003 to 2012 132

Table 89: SQM: Specifications for lithium carbonate 133

Table 90: SQM: Specifications for lithium hydroxide 134

Table 91: RWL: Gross tonnage, value and unit value of lithium carbonate exports,

2006 to 2012 137

Table 92: RWL: Gross tonnage, value and unit value of lithium chloride exports,

2006 to 2012 138

Table 93: Li3 Energy: Resource estimation for the Maricunga property, April 2012 140

Table 94: Chile: Exports of lithium carbonate by destiatnion, 2004 to 2011 144

Table 95: Chile: Litihum carbonate export volume, value and unit price by company,

2005 to 2011 144

Table 96: Chile: Lithium chloride exports by destination, 2004 to 2012 145

Table 97: Chile: Lithium hydroxide exports by destination, 2004 to 2012 146

Table 98: China : Estimated resources and reserves of both lithium mineral and

brine operations and projects 148

Table 99: China: Production of lithium, 2003 to 2012 149

Table 100: China: Producers of lithium minerals, 2011 to 2012 151

Table 101: China: Production and capacity of Chinese lithium brine operations,

2011 152

Table 102: China: Mineral conversion plant production and production capacity,

2012 154

Table 103: China: Producers of battery grade lithium metal, 2012 154

Table 104: China: Imports and exports of lithium carbonate, 2005 to 2012 155

Table 105: China: Imports and exports of lithium chloride, 2005 to 2012 156

Table 106: China: Imports and exports of lithium hydroxide, 2005 to 2012 157

Table 107: China: Imports and exports of lithium oxide, 2005 to 2012 157

Table 108: Tibet Lithium New Technology Development: Lithium production,

2010 to 2012 158

Table 109: Qinghai CITIC: Lithium carbonate production, 2008 to 2012 160

Table 110: Dangxiongcuo reserve estimation from 2006 qualifying report 163

Table 111: Jiangxi Western Resources: Lithium Production, 2010 167

Table 112: Sichuan Tianqi: Production and sales of lithium products, 2010 to 2011 169

Table 113: Galaxy Resources: Battery grade lithium carbonate chemical

specifications 172

Table 114: Keliber Oy: Claims, reservation and mining concessions for lithium

projects held by Keliber in Finland, 2012 181

Table 115: France: Imports and exports of lithium carbonate, 2005 to 2012 183

Table 116: France: Imports and exports of lithium hydroxide and oxide, 2005

to 2012 184

Table 117: Germany: Imports and exports of lithium carbonate, 2005 to 2012 184

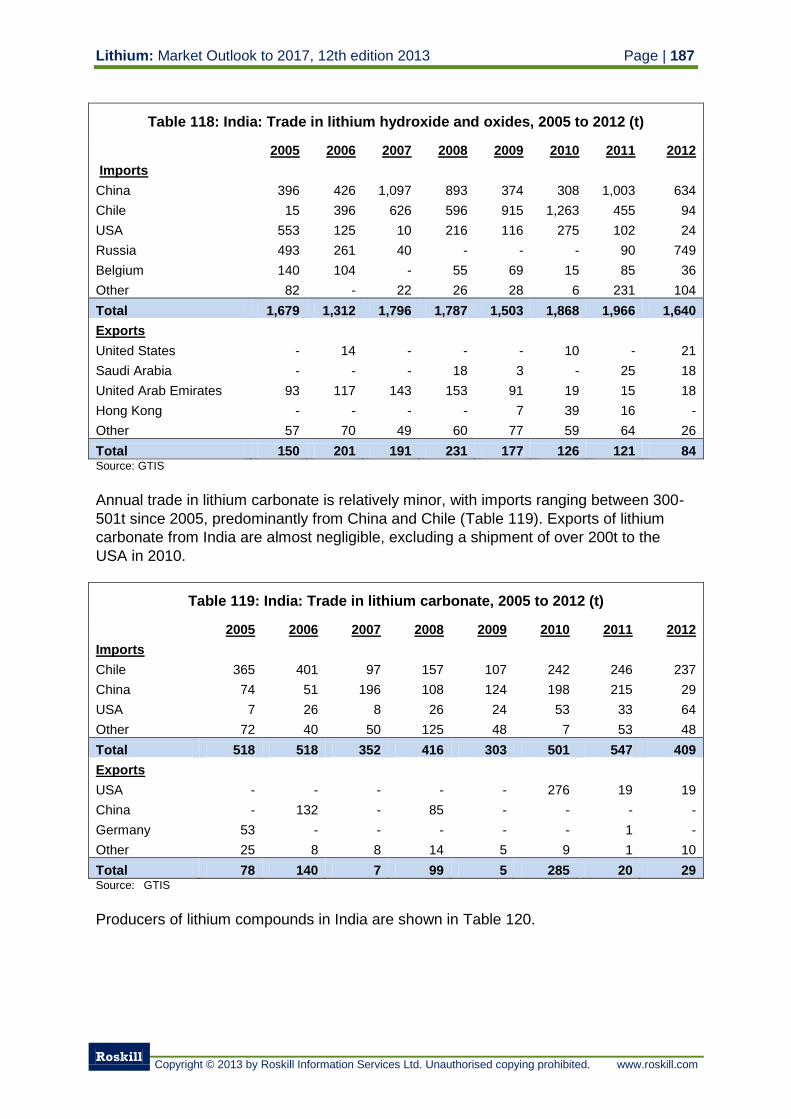

Table 118: India: Trade in lithium hydroxide and oxides, 2005 to 2012 187

Table 119: India: Trade in lithium carbonate, 2005 to 2012 187

Table 120: India: Producers of lithium chemicals 188

Table 121: Japan: Trade in lithium carbonate, 2005 to 2012 190

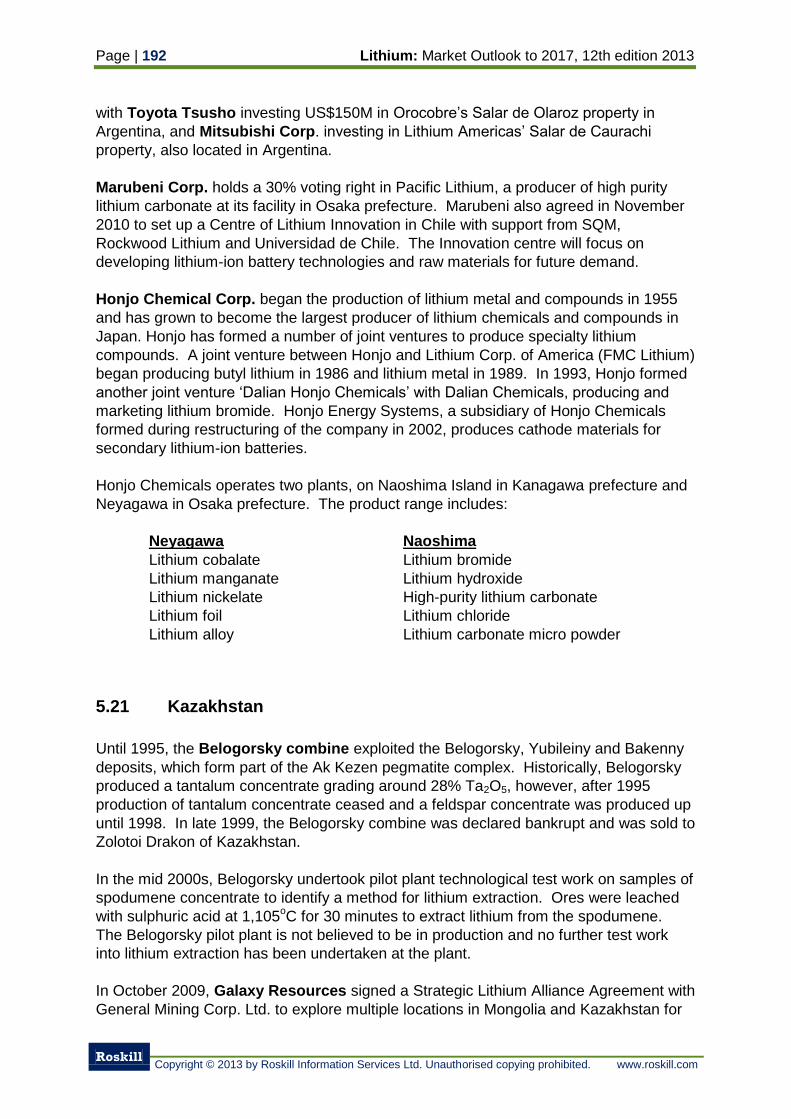

Table 122: Japan: Trade in lithium hydroxide and oxide, 2005 to 2012 191

Table 123: Mexico: Litio Mex S.A. concessions and resource estimations 194

Table 124: Namibia: Production of lithium minerals, 1990 to 1998 197

Table 125: Netherlands: Trade in lithium carbonate, 2005 to 2012 198

Table 126: Netherlands: Trade in lithium hydroxide and oxide, 2005 to 2012 199

Table 127: Sociedad Mineira de Pegmatites: Production of Lithium, 2004 to 2012 200

Table 128: Russia: Deposits of lithium 201

Table 129: Russia: Imports of lithium carbonate, 2002 to 2012 204

Table 130: Russia: Exports of lithium hydroxide, 2002 to 2012 204

Table 131: Russia: Imports of lithium hydroxide, 2002 to 2012 205

Table 132: South Korea: Trade in lithium carbonate, 2005 to 2012 207

Table 133: South Korea: Trade in lithium hydroxide, 2005 to 2012 207

Table 134: Spain: Imports of lithium compounds, 2005 to 2012 208

Table 135: Minera Del Duero: Production of lepidolite in Spain, 2003 to 2011 208

Table 136: Inferred mineral resource estimation for the Doade-Presquerias project,

October 2011 209

Table 137: Taiwan: Imports of lithium carbonate, 2005 to 2012 210

Table 138: UK: Imports of lithium carbonate and lithium hydroxides and oxides

2005 to 2012 211

Table 139: USA: Imports and exports of lithium carbonate 2005 to 2012 213

Table 140: USA: Imports and exports of lithium oxide and hydroxide 2005 to 2012 214

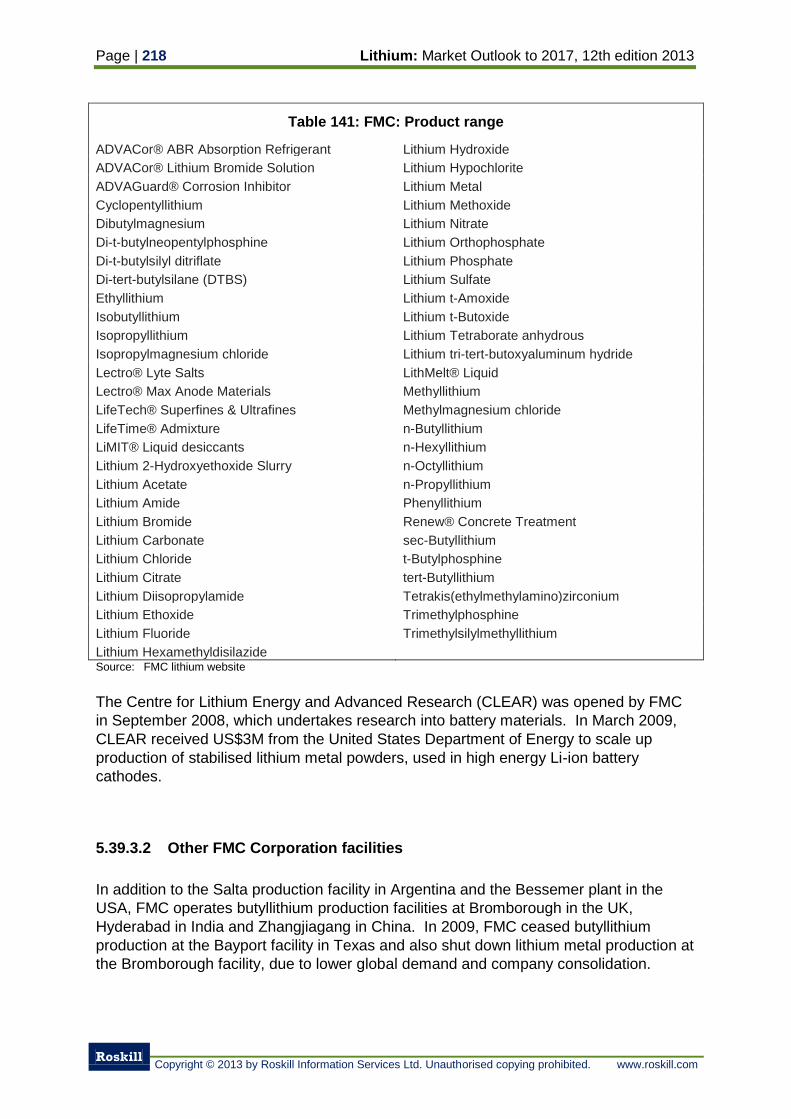

Table 141: FMC: Product range 218

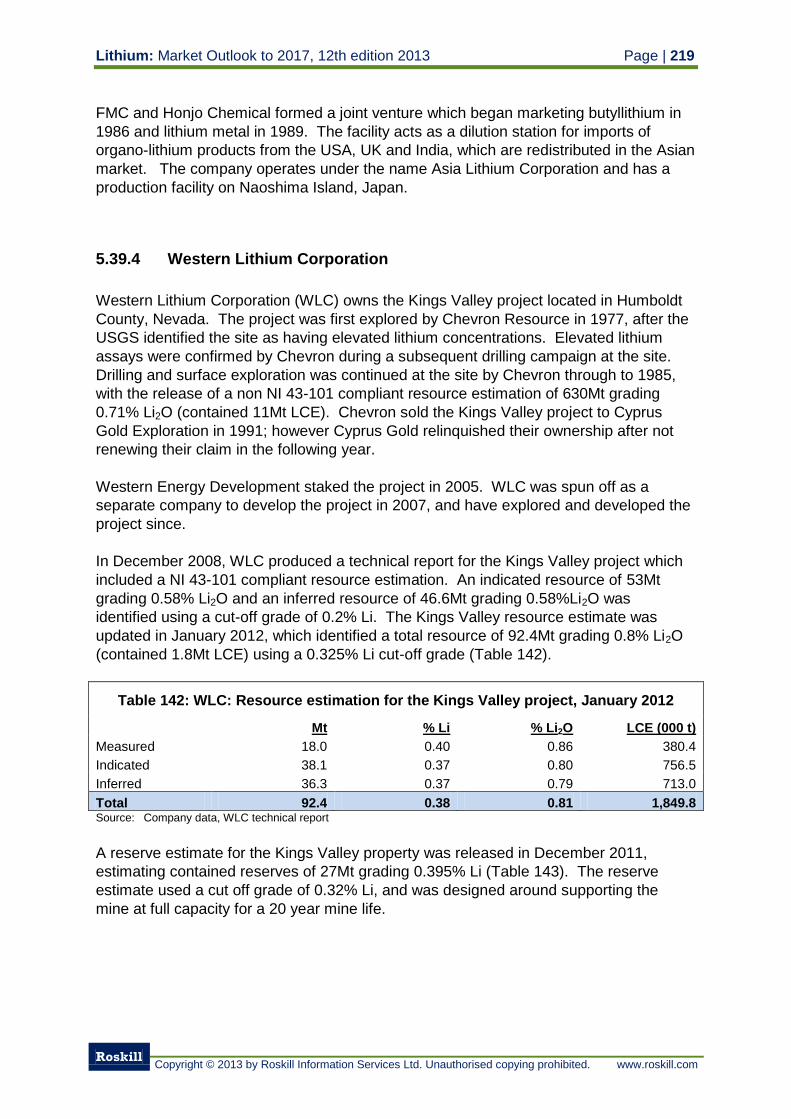

Table 142: WLC: Resource estimation for the Kings Valley project, January 2012 219

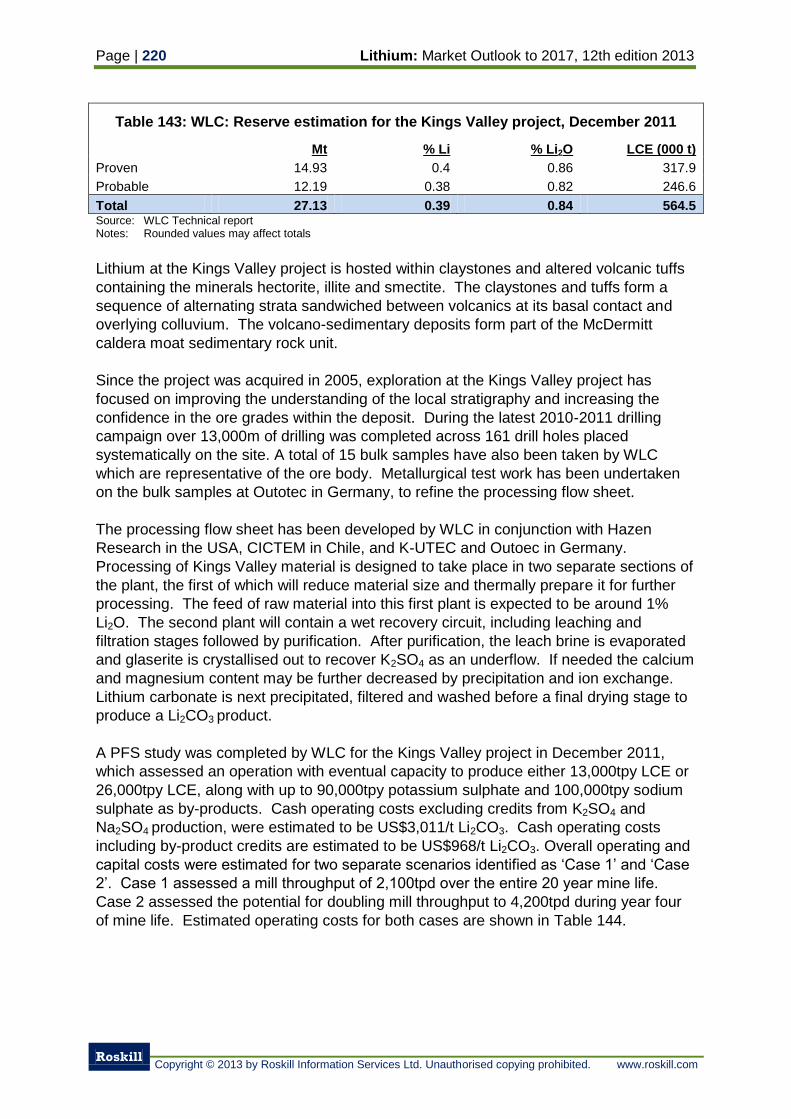

Table 143: WLC: Reserve estimation for the Kings Valley project, December 2011 220

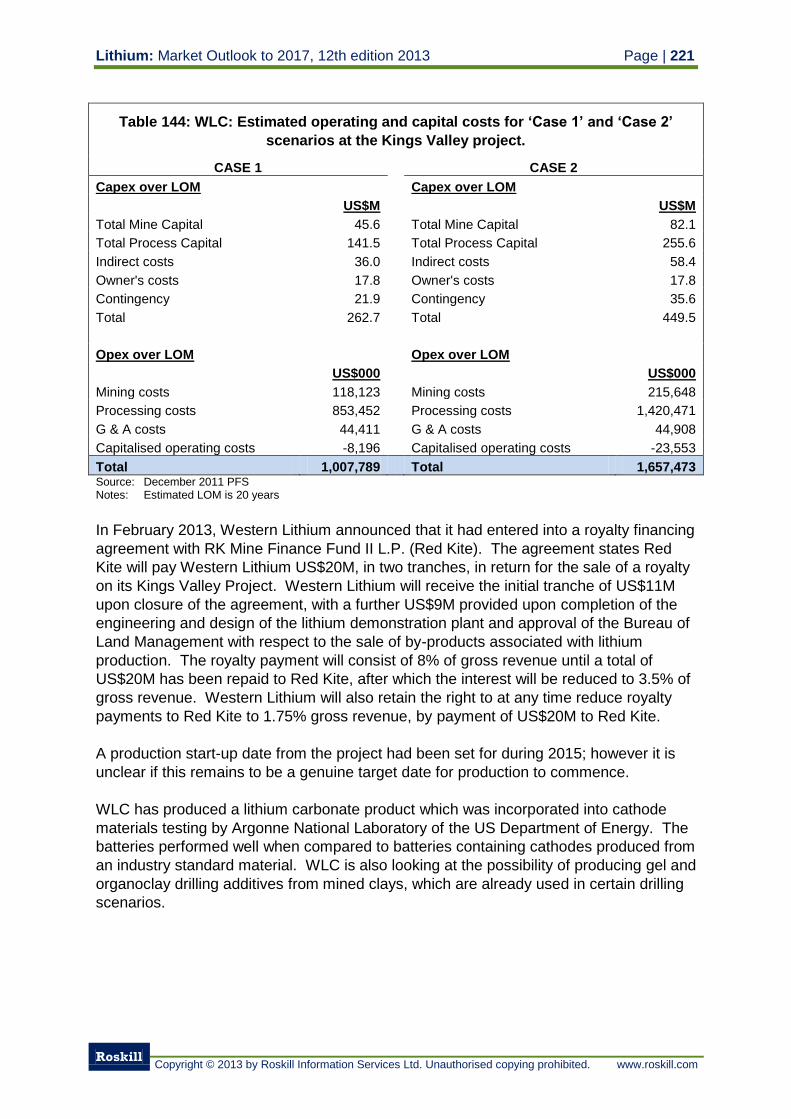

Table 144: WLC: Estimated operating and capital costs for ‘Case 1’ and ‘Case 2’

scenarios at the Kings Valley project. 221

Table 145: USA: Lithium exploration projects yet to reach scoping study or PFS

stage in development 224

Table 146: Zimbabwe: South African imports of mineral substances from

Zimbabwe, 2005 to 2012 227

Table 147: Bikita Minerals: Mine production and lithium content 2003 to 2011 228

Table 148: World: Total exports of lithium carbonate, 2005 to 2012 230

Table 149: World: Total imports of lithium carbonate, 2005 to 2012 232

Table 150: World: Total exports of lithium hydroxide and oxide, 2005 to 2012 234

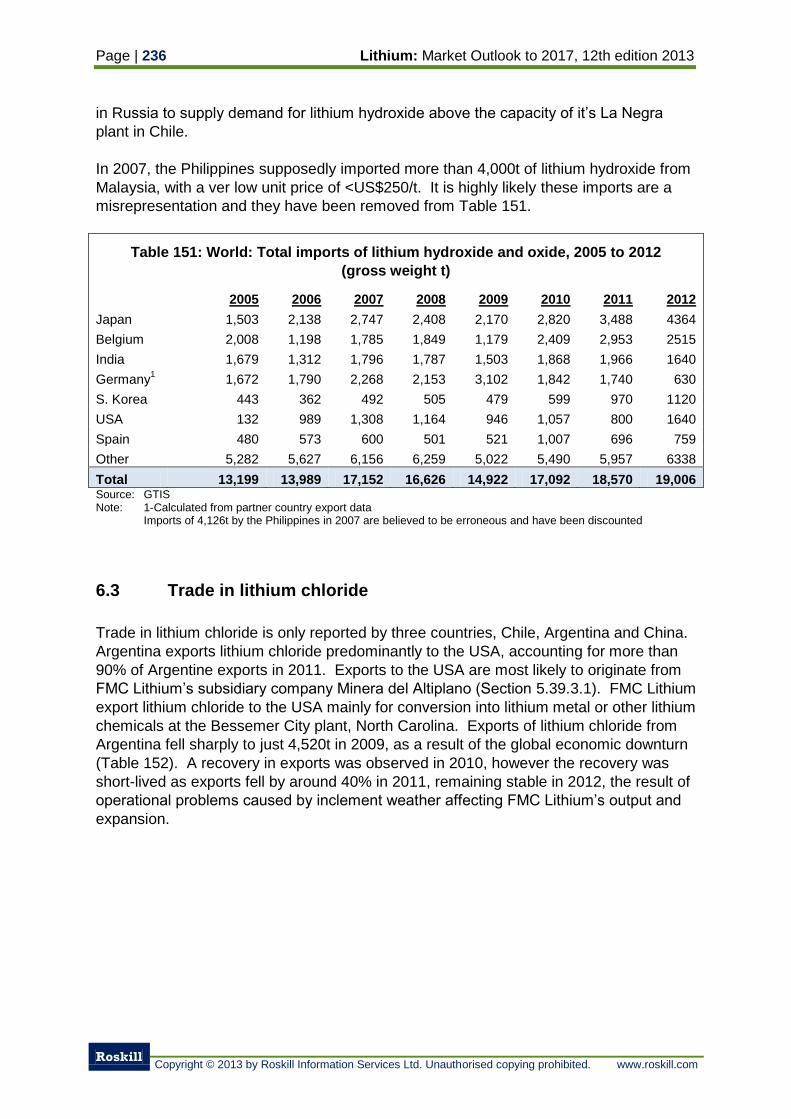

Table 151: World: Total imports of lithium hydroxide and oxide, 2005 to 2012 236

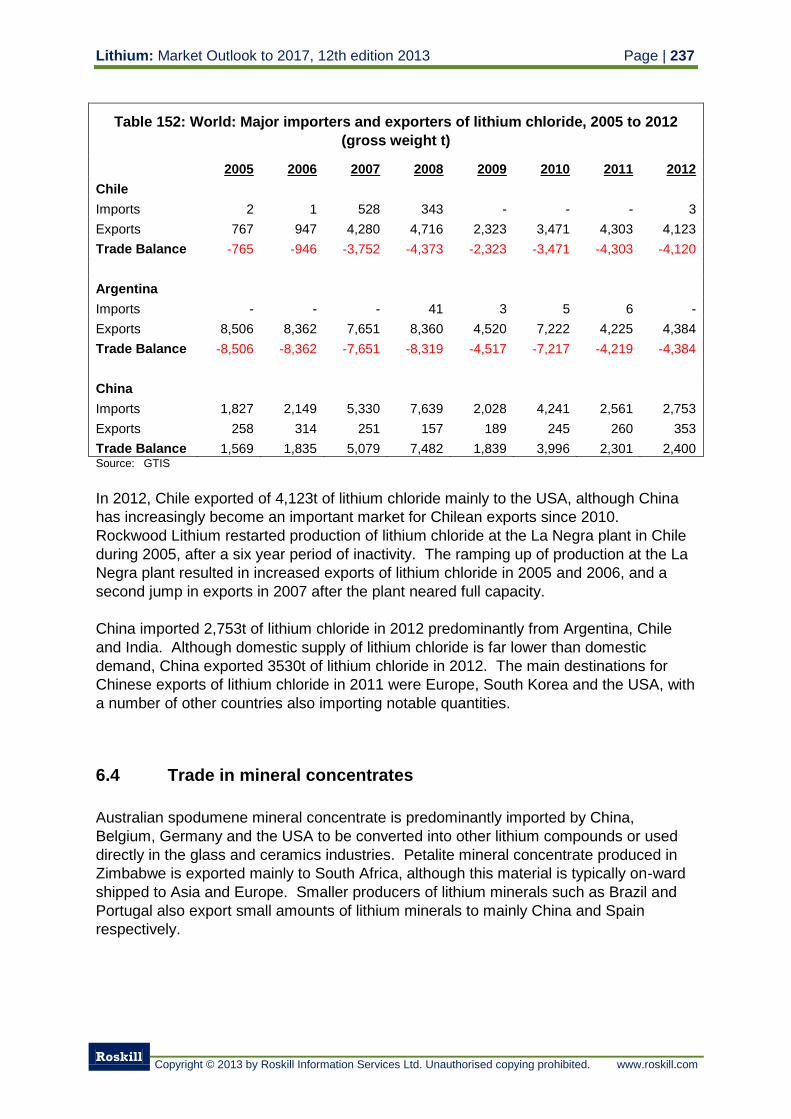

Table 152: World: Major importers and exporters of lithium chloride, 2005 to 2012 237

Table 153: World: Exports of lithium minerals by major lithium mineral producing

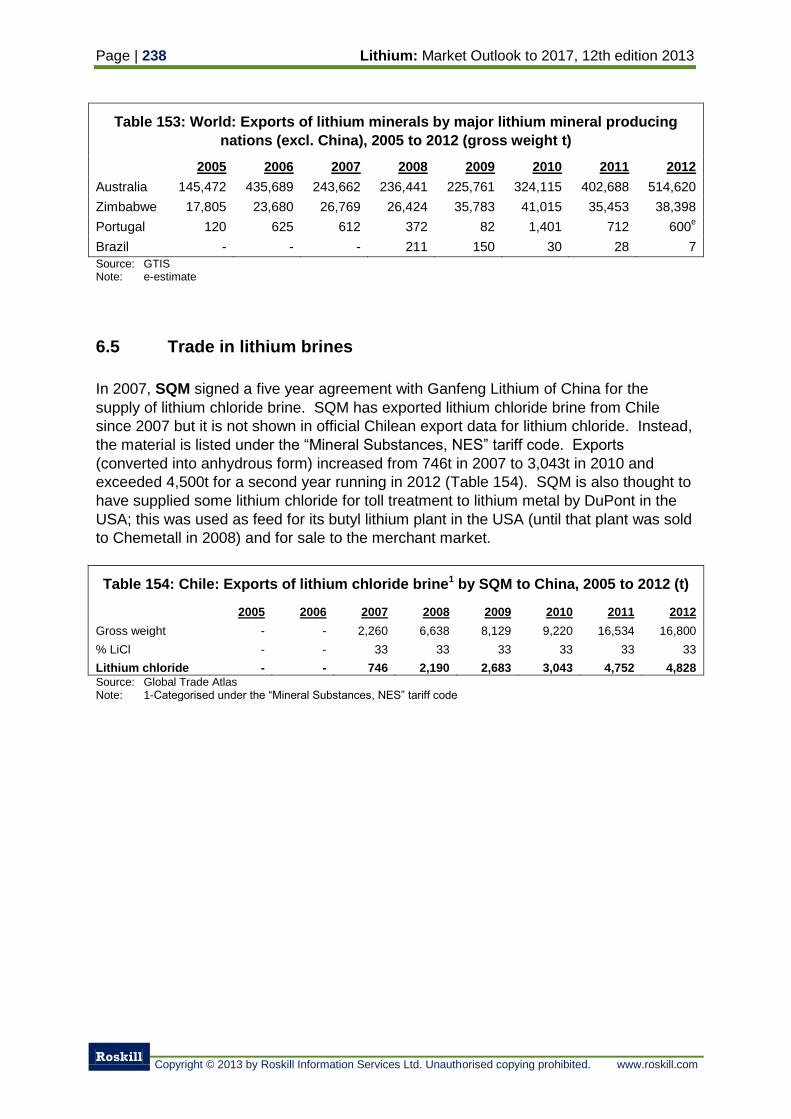

nations (excl. China), 2005 to 2012 238

Table 154: Chile: Exports of lithium chloride brine1 by SQM to China, 2005 to 2012 238

Table 155: World: Consumption of lithium by end-use, 2002, 2007 and 2012 240

Table 156: World: Estimated consumption of lithium by country/region, 2002, 2007

and 2012 244

Table 157: World: Consumption of lithium by end-use, by product, 2012 246

Table 158: World: Forecast consumption of lithium by end-use, 2012 to 2017 248

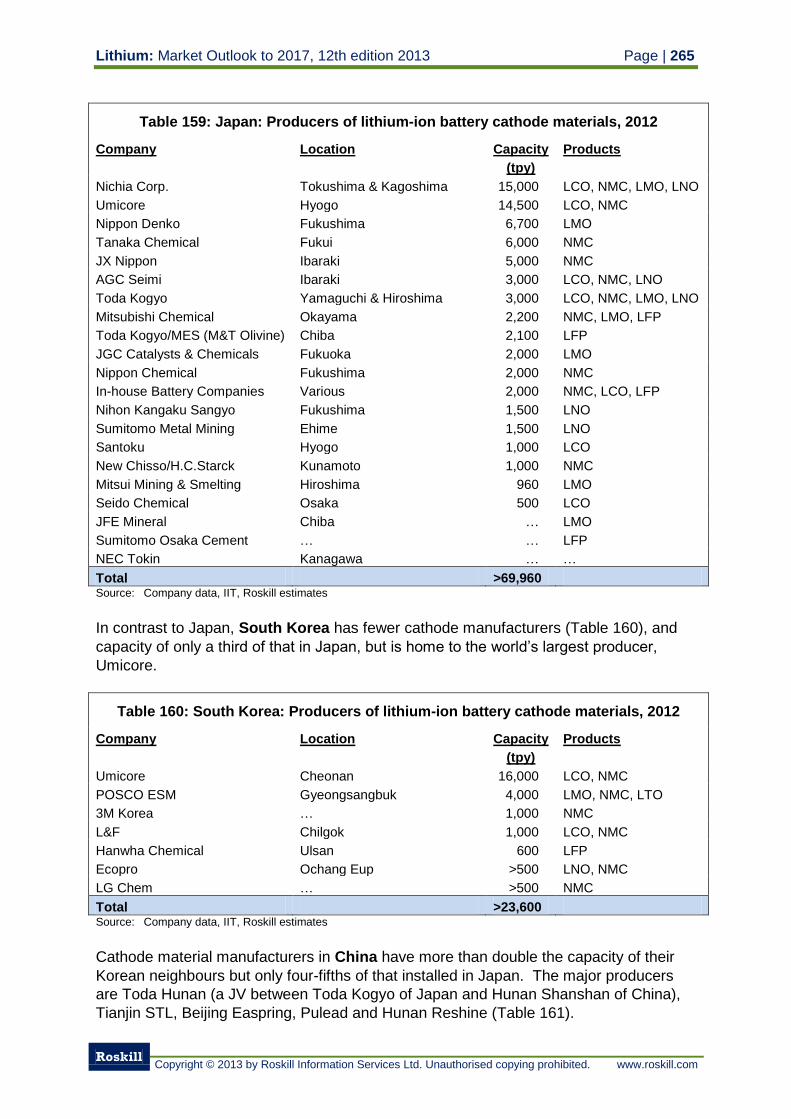

Table 159: Japan: Producers of lithium-ion battery cathode materials, 2012 265

Table 160: South Korea: Producers of lithium-ion battery cathode materials, 2012 265

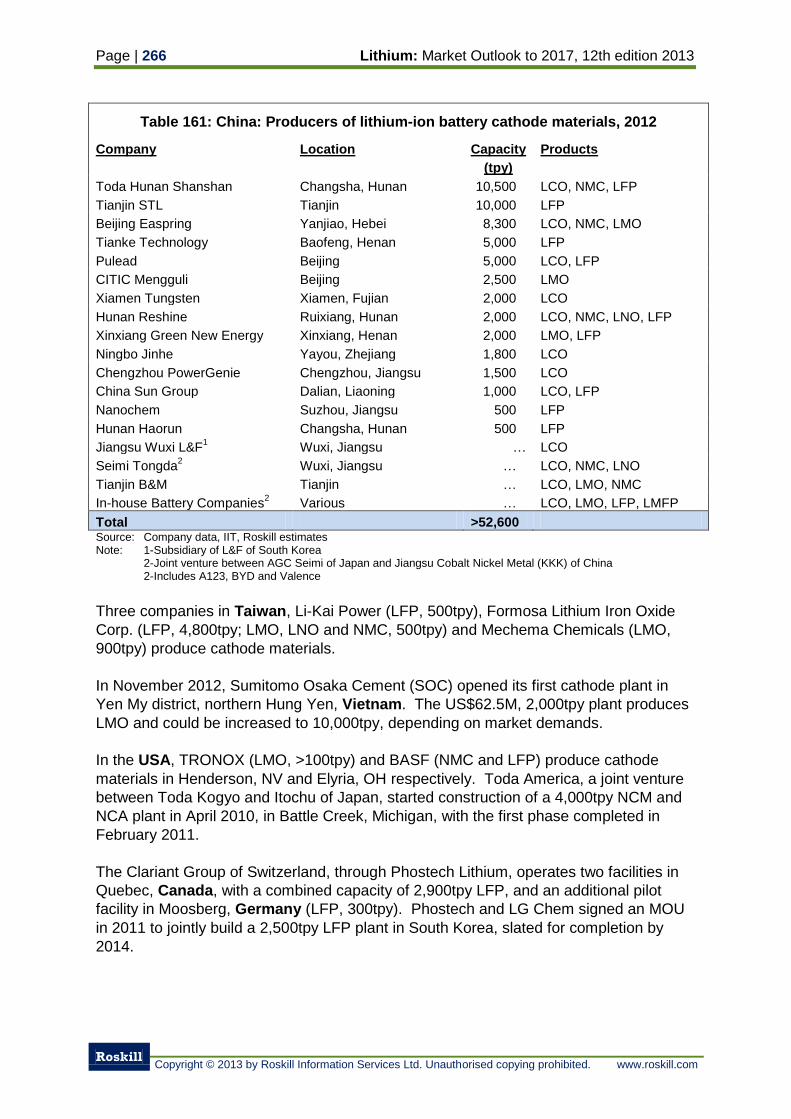

Table 161: China: Producers of lithium-ion battery cathode materials, 2012 266

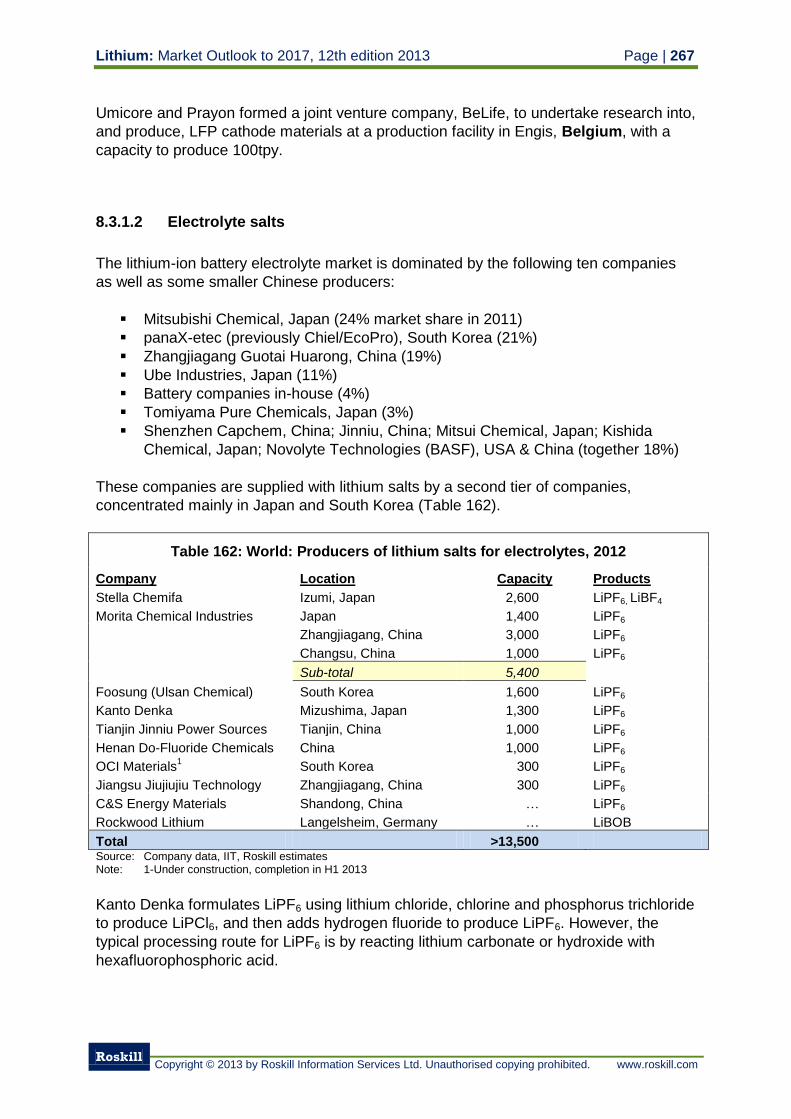

Table 162: World: Producers of lithium salts for electrolytes, 2012 267

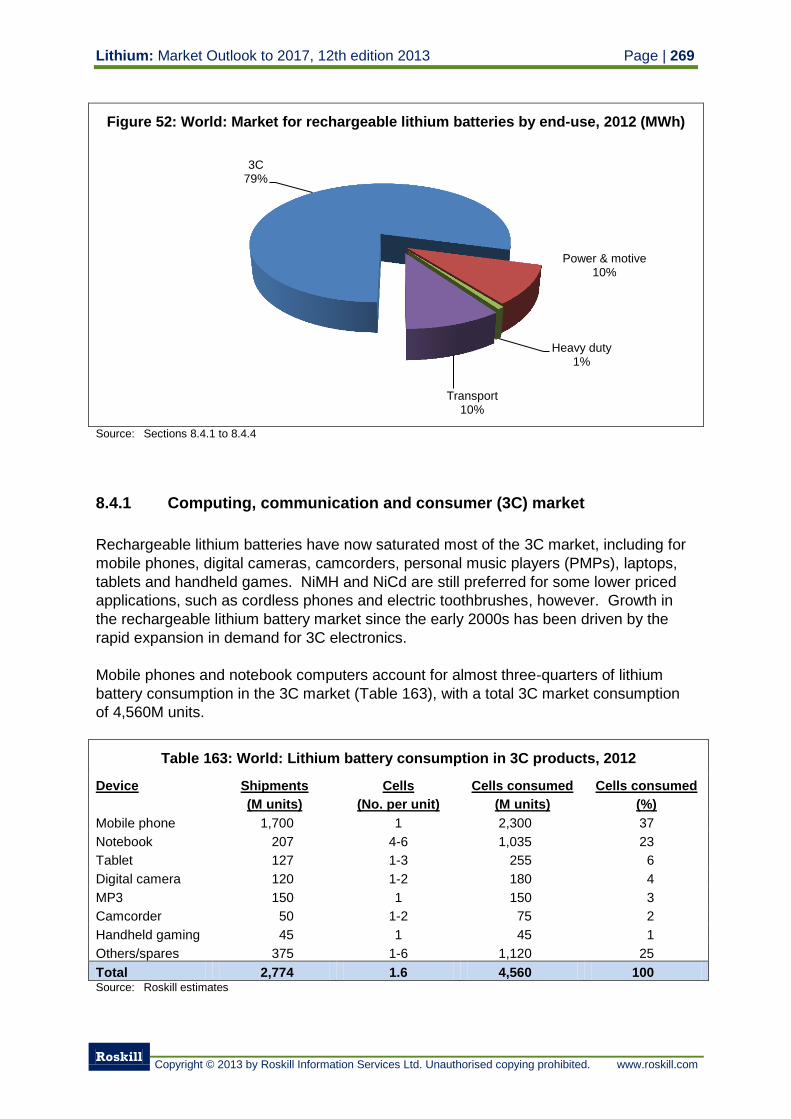

Table 163: World: Lithium battery consumption in 3C products, 2012 269

Table 164: World: Lithium battery consumption in power devices and motive

power, 2012 271

Table 165: World: Lithium battery consumption in heavy duty applications, 2012 272

Table 166: World: Lithium battery consumption in transport applications, 2012 274

Table 167: World: Lithium consumption in rechargeable lithium batteries

end-use, 2012 275

Table 168: World: Lithium consumption in NiMH and NiCd batteries, 2012 275

Table 169: World: Consumption of lithium in rechargeable batteries by type, 2007

to 2012 277

Table 170: Japan: Consumption of lithium in rechargeable batteries, 2007 to 2012 277

Table 171: World: Consumption of lithium in rechargeable batteries by country,

2007 to 2012 278

Table 172: World: Rechargeable lithium battery demand by market, 2012 and 2017 278

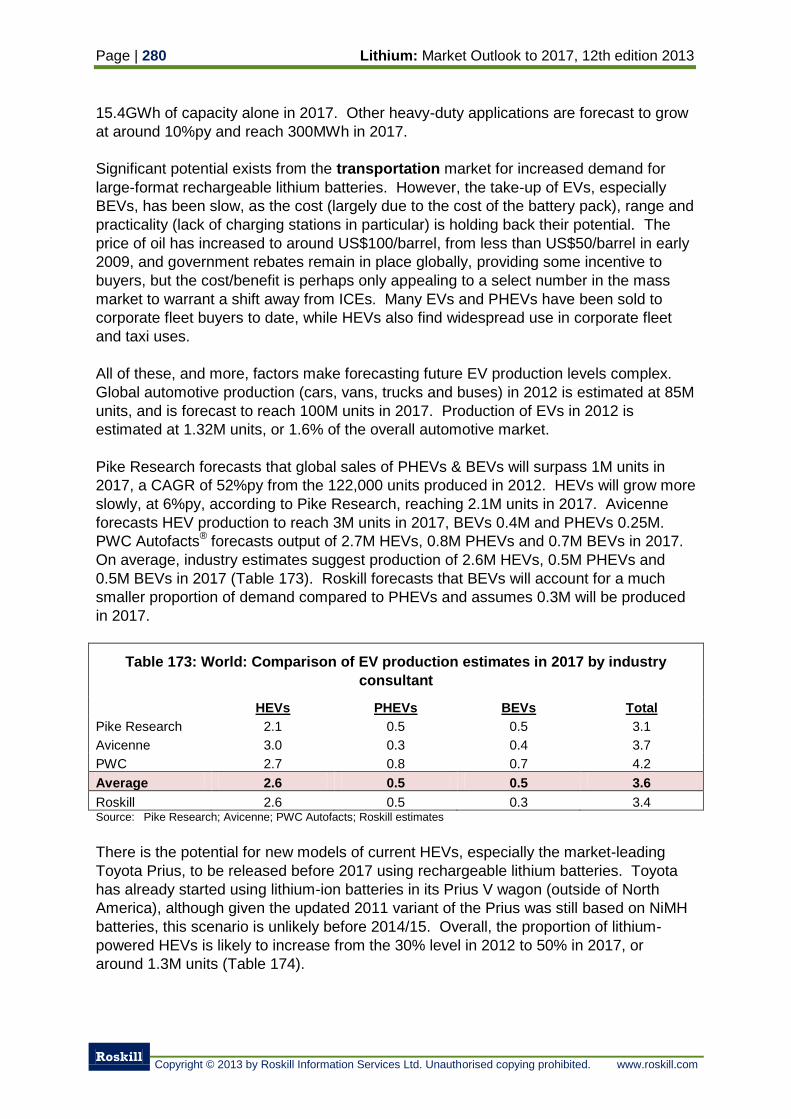

Table 173: World: Comparison of EV production estimates in 2017 by industry

consultant 280

Table 174: World: Forecast rechargeable battery consumption in EVs, 2017 281

Table 175: World: Lithium consumption in rechargeable lithium batteries by

end-use, 2017 281

Table 176: World: Forecast demand for lithium in rechargeable lithium batteries,

2012 to 2017 282

Table 177: World: Forecast demand for lithium in rechargeable batteries by battery

type, 2012 to 2017 282

Table 178: World: Forecast demand for lithium in rechargeable batteries by

product type, 2007 to 2012 283

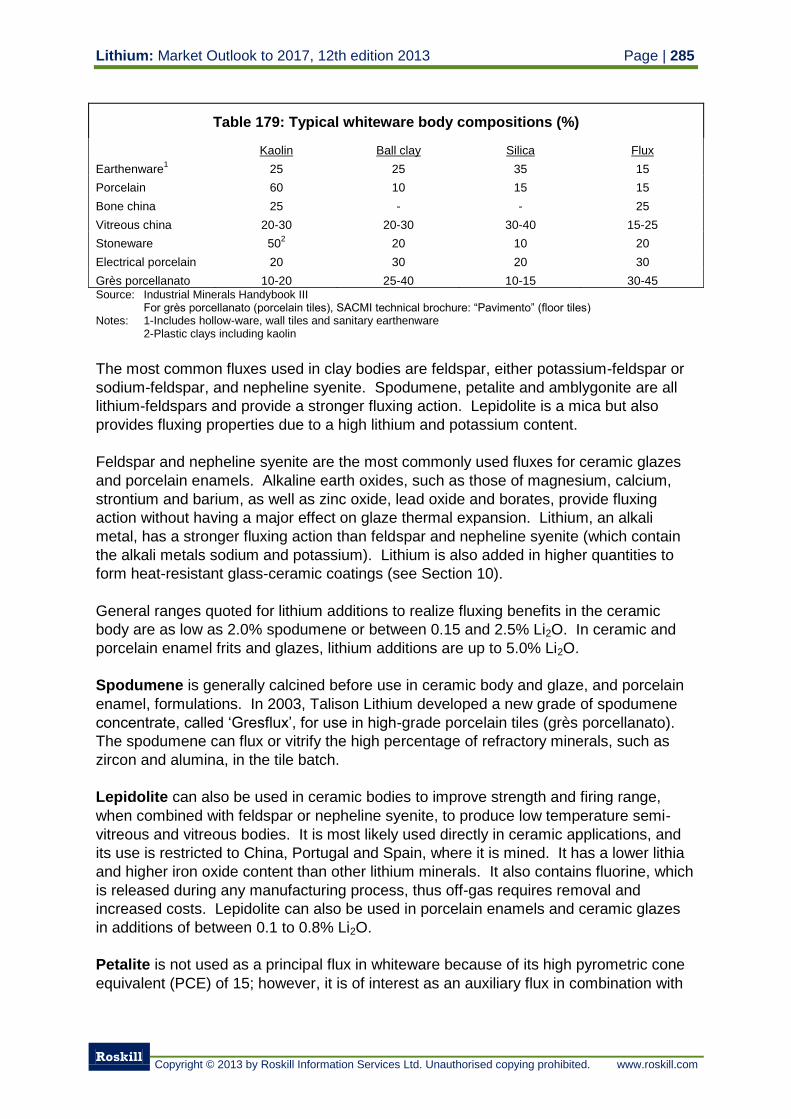

Table 179: Typical whiteware body compositions 285

Table 180: World: Production of ceramic tiles by leading country, 2007 to 2012 287

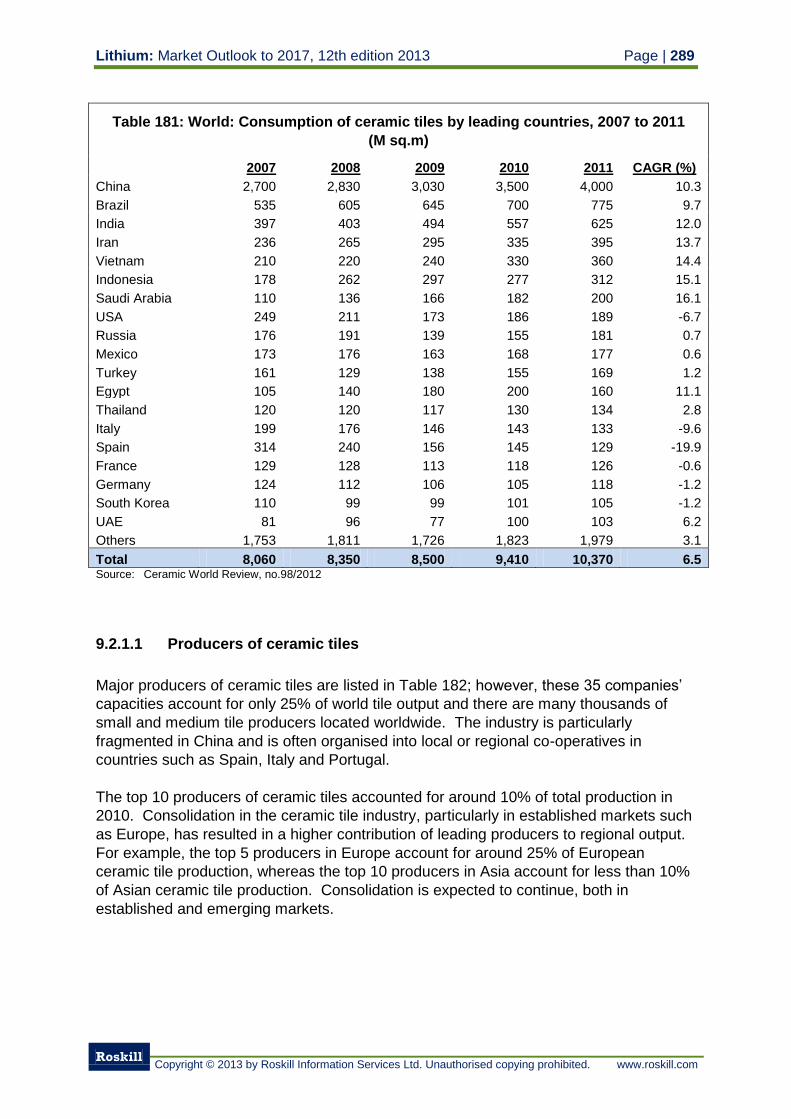

Table 181: World: Consumption of ceramic tiles by leading countries, 2007 to 2011 289

Table 182: World: Leading ceramic tile manufacturing companies, 2010 290

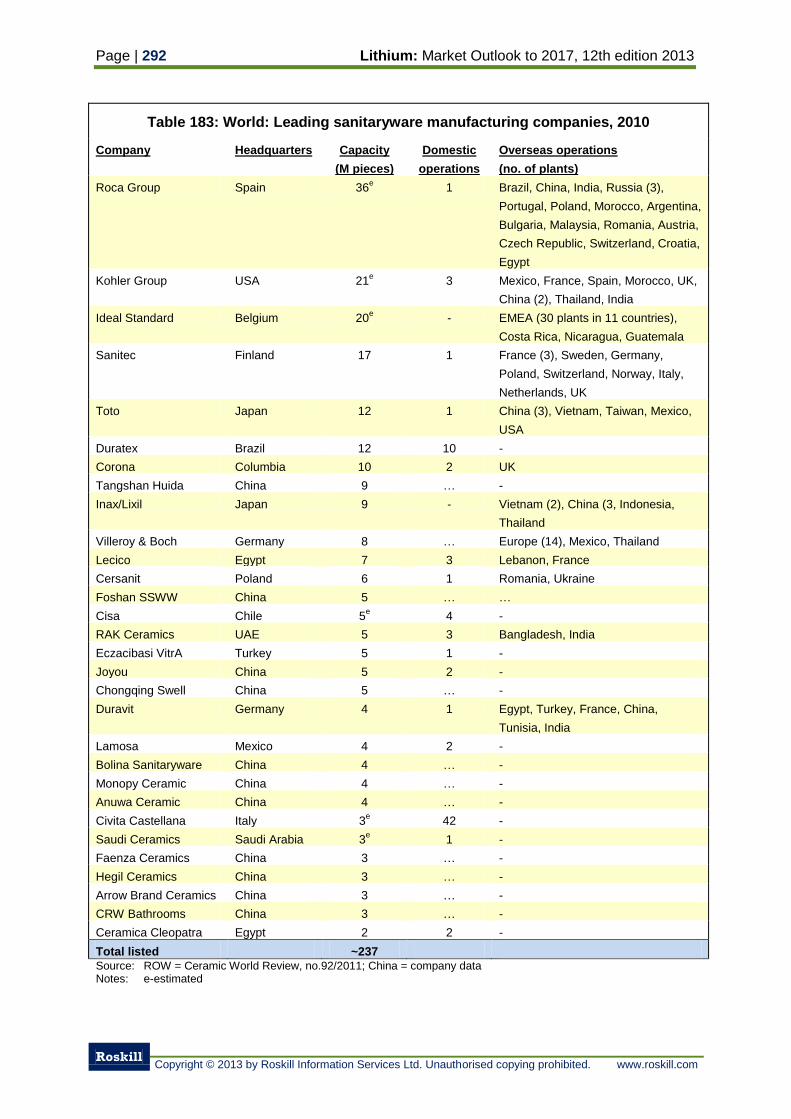

Table 183: World: Leading sanitaryware manufacturing companies, 2010 292

Table 184: World: Consumption of lithium in ceramics, 2012 300

Table 185: World: Consumption of lithium in ceramics, 2007 to 2012 300

Table 186: World: Forecast demand for lithium in ceramics, 2012 to 2017 301

Table 187: Glass-ceramic matrices 302

Table 188: Compositions of commercial glass-ceramics 303

Table 189: Japan: Consumption of lithium carbonate in glass-ceramics, 2007

to 2012 306

Table 190: World: Consumption of lithium in glass-ceramics by end-use and

product type, 2012 307

Table 191: World: Consumption of lithium in glass-ceramics, 2007 to 2012 307

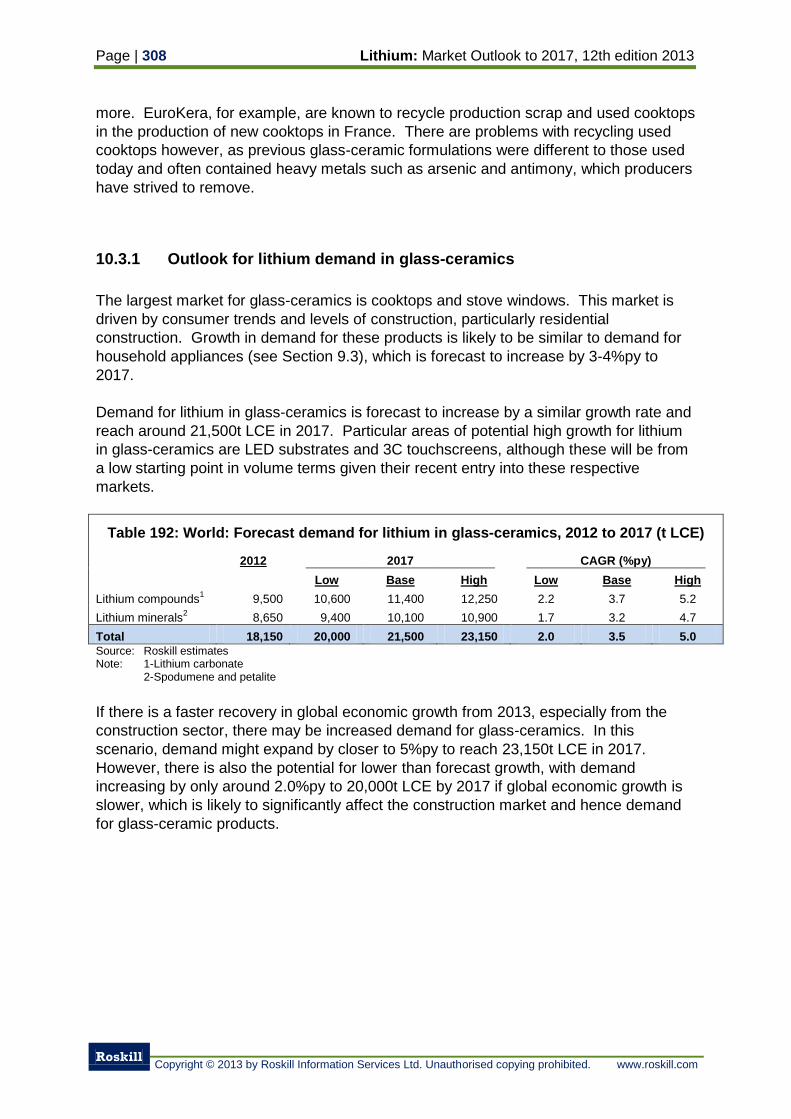

Table 192: World: Forecast demand for lithium in glass-ceramics, 2012 to 2017 308

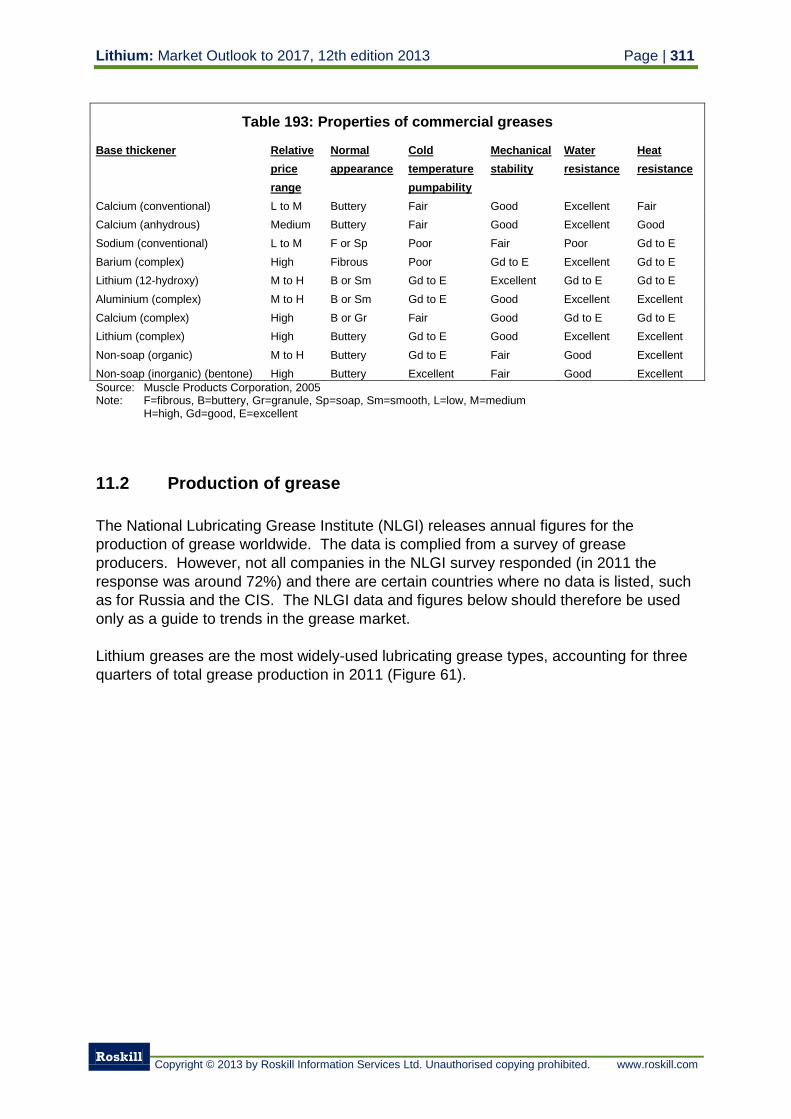

Table 193: Properties of commercial greases 311

Table 194: World: Producers of lubricating grease 315

Table 195: World: Forecast demand for lithium in greases, 2012 to 2017 322

Table 196: Typical batch compositions for glass by type 323

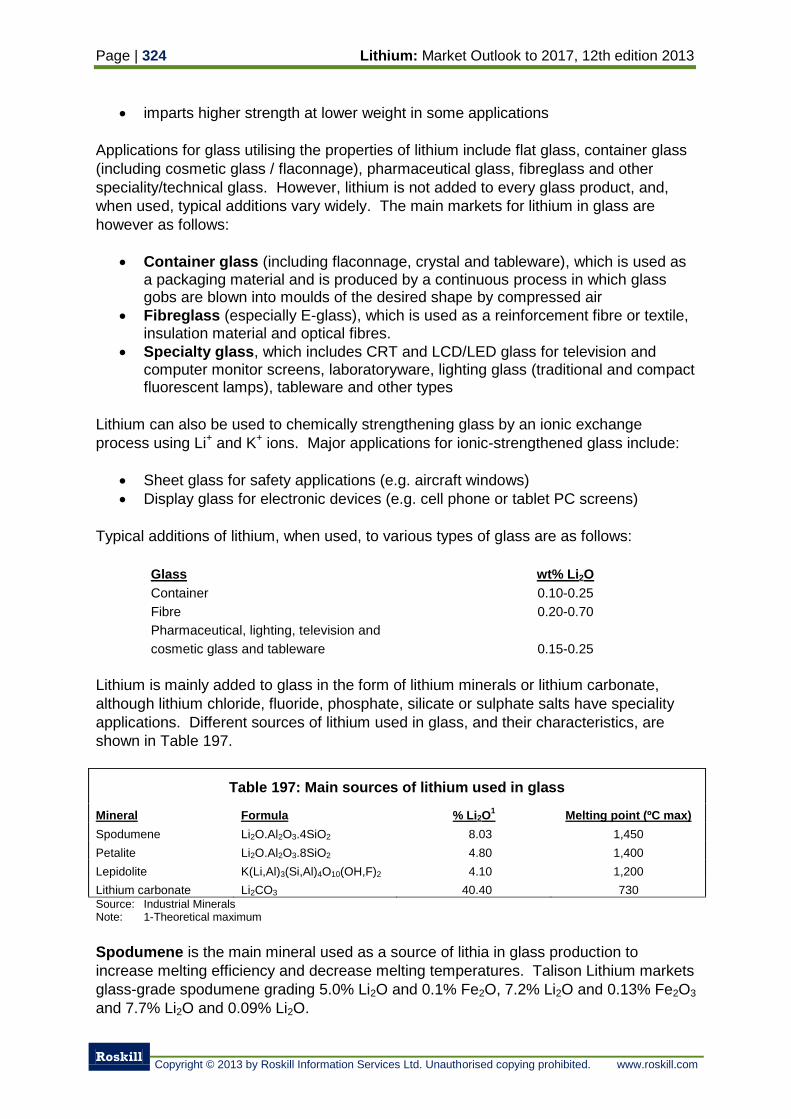

Table 197: Main sources of lithium used in glass 324

Table 198: EU: Production of glass by type, 1998 to 2012 328

Table 199: USA: Production of container glass, 1999 to 2008 328

Table 200: Typical chemical composition of types of textile-grade fibreglass 329

Table 201: World: Estimated consumption of lithium in glass, 2012 331

Table 202: World: Consumption of lithium in glass, 2007 to 2012 331

Table 203: World: Forecast demand for lithium in glass, 2012 to 2017 332

Table 204: World: Consumption of lithium in continuous casting mould powders,

2007 to 2012 336

Table 205: Japan: Consumption of lithium in fluxes, 2007 to 2012 336

Table 206: World: Forecast demand for lithium in casting powders, 2012 to 2017 337

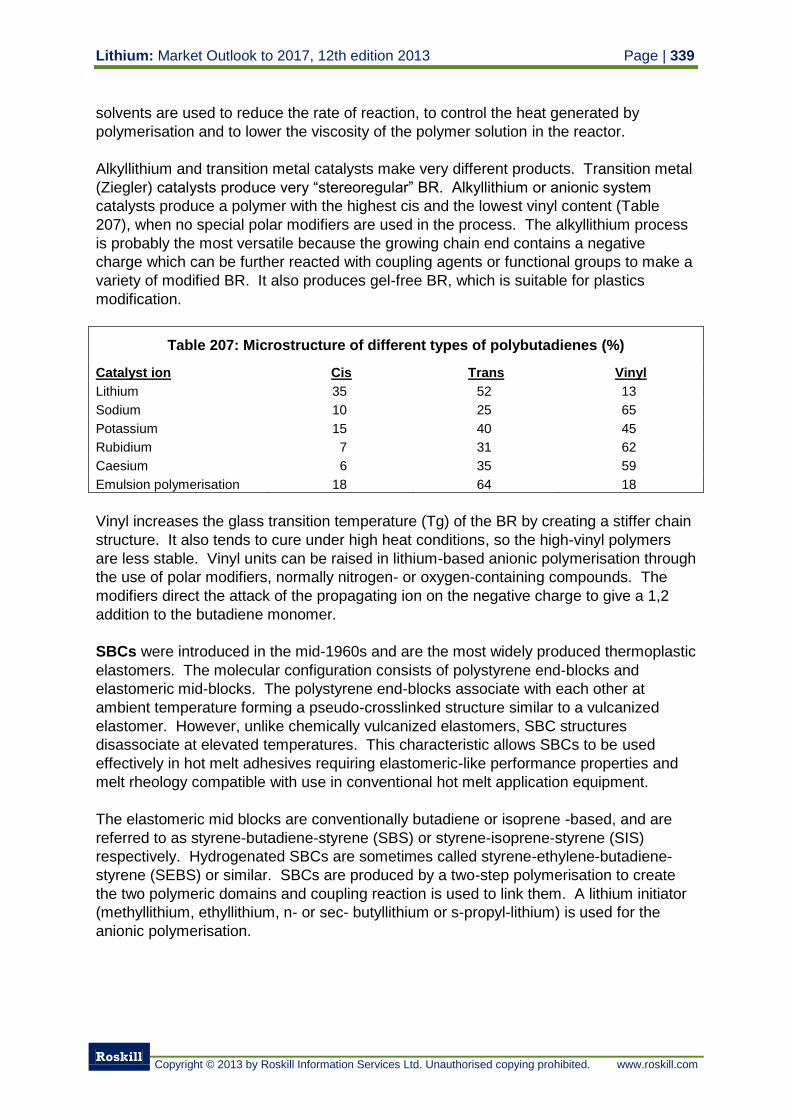

Table 207: Microstructure of different types of polybutadienes 339

Table 208: World: Producers of SSBR, BR and SBC, 2012 343

Table 209: World: Planned new/expanded SBR, BR and SBC plants 344

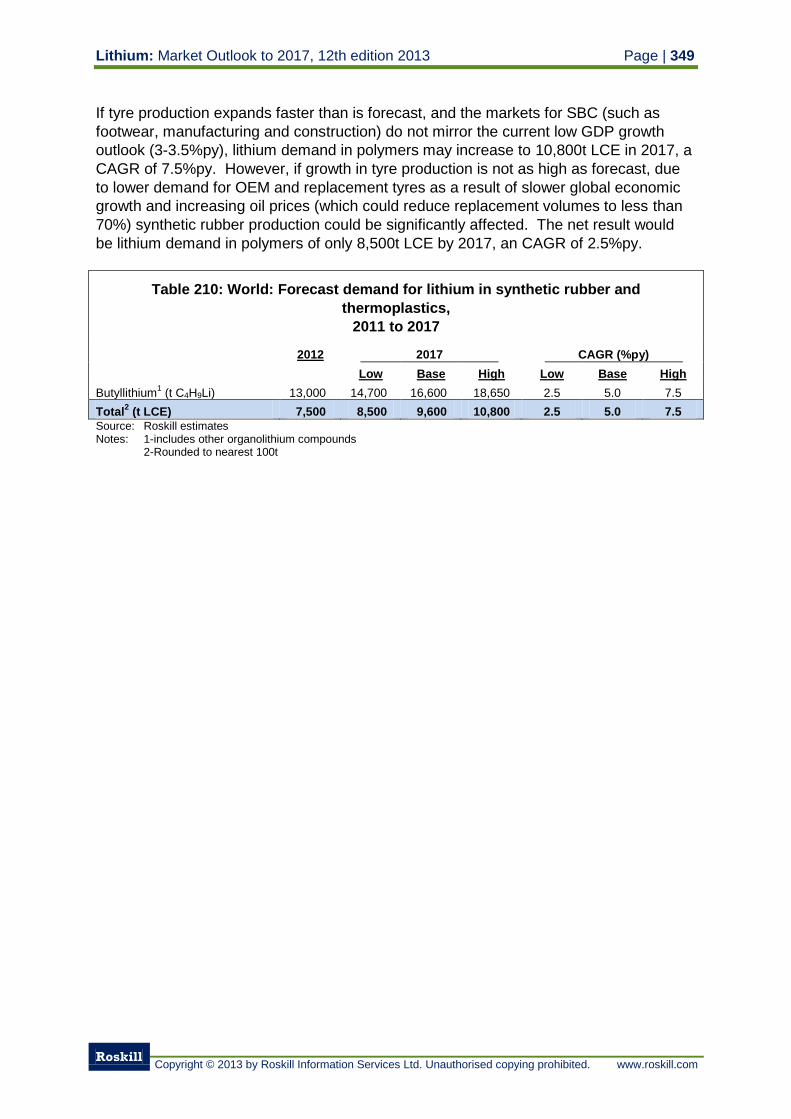

Table 210: World: Forecast demand for lithium in synthetic rubber and

thermoplastics, 2011 to 2017 349

Table 211: World: Capacity for lithium bromide production, end-2012 355

Table 212: Japan: Consumption of lithium bromide, 2007 to 2012 356

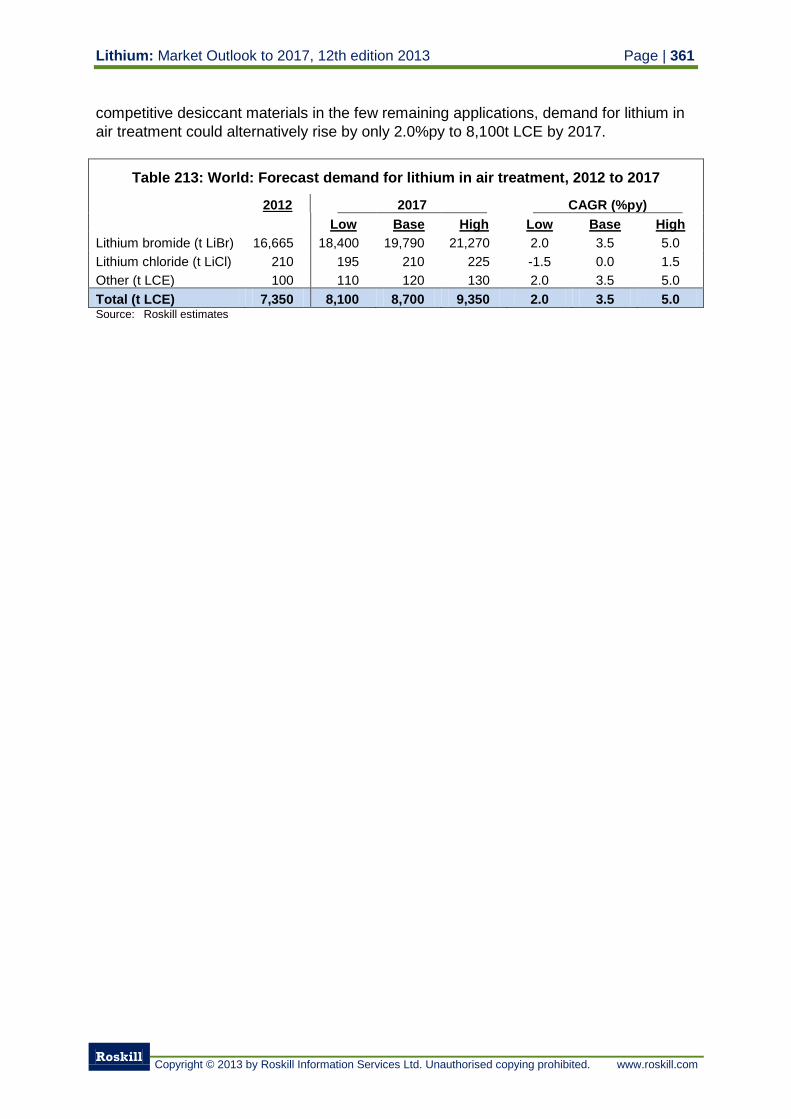

Table 213: World: Forecast demand for lithium in air treatment, 2012 to 2017 361

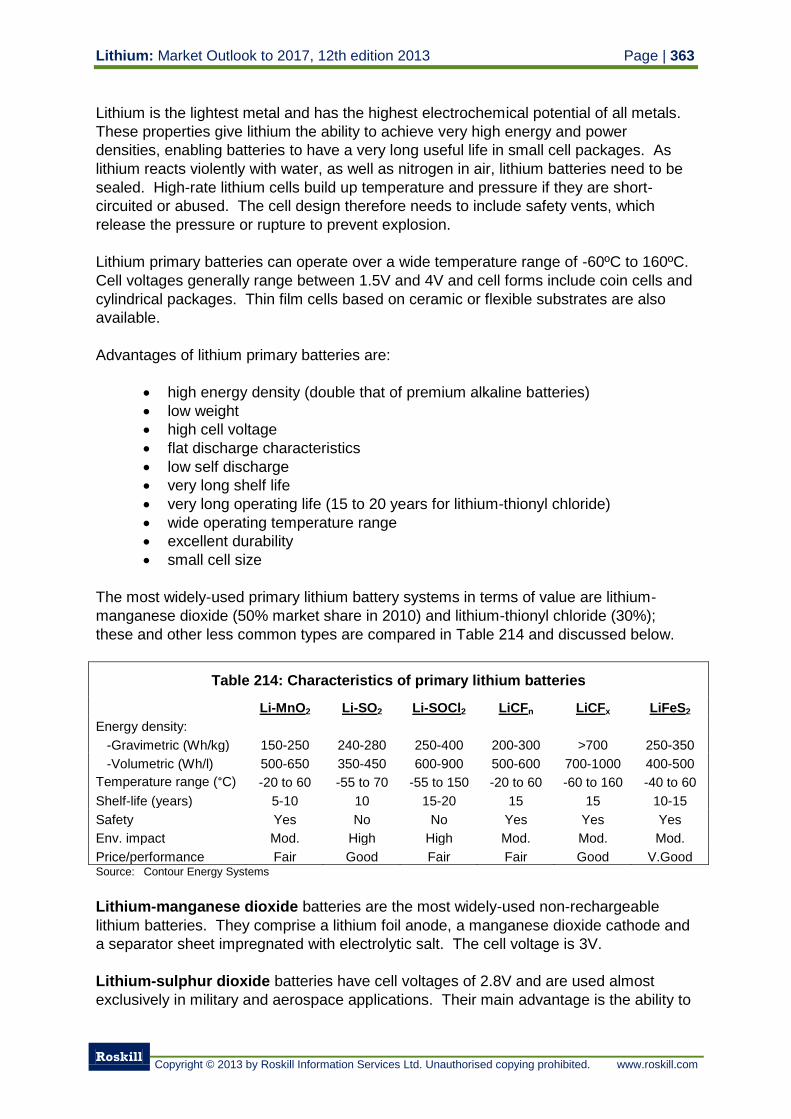

Table 214: Characteristics of primary lithium batteries 363

Table 215: Japan: Production of primary batteries by type, 1998 to 2012 367

Table 216: World: Trade in lithium primary batteries, 2007 to 2011 369

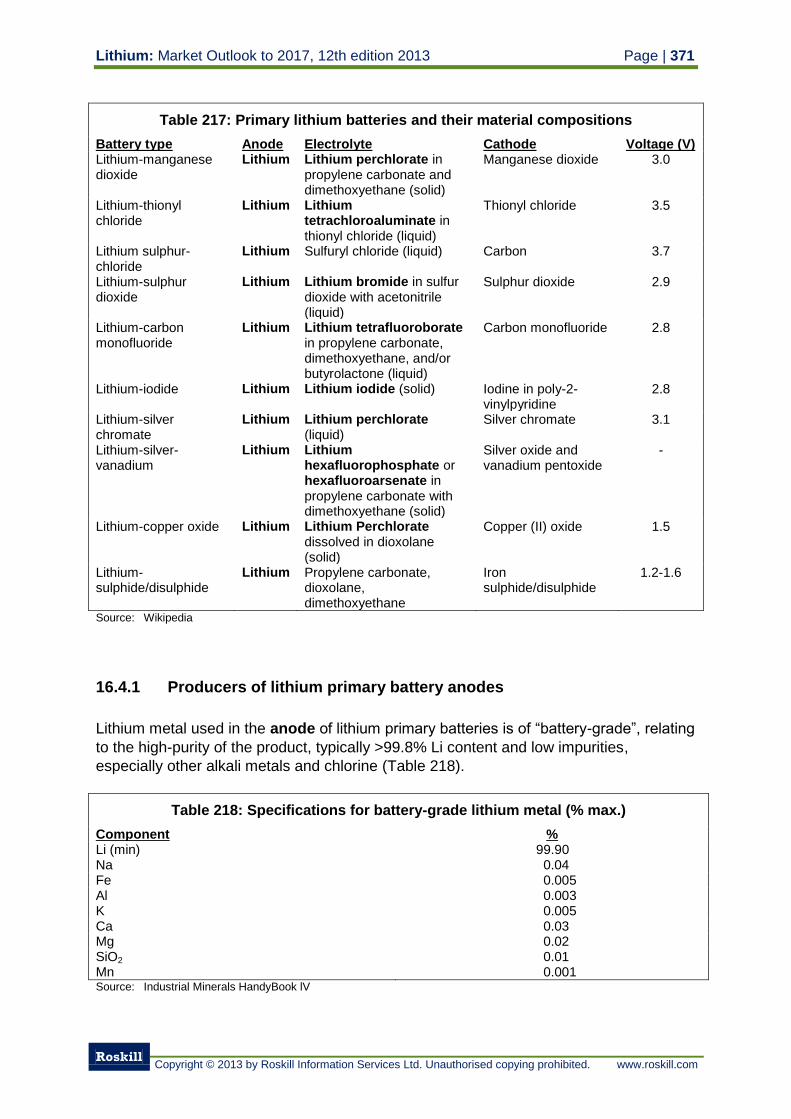

Table 217: Primary lithium batteries and their material compositions 371

Table 218: Specifications for battery-grade lithium metal 371

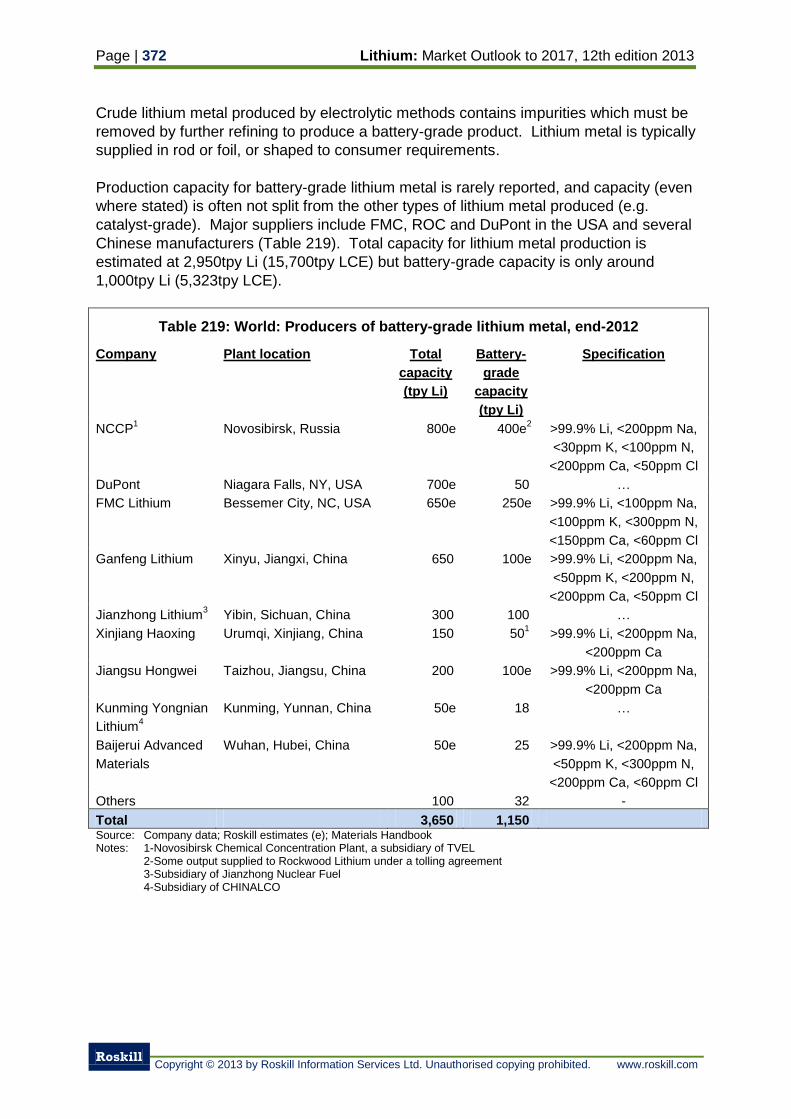

Table 219: World: Producers of battery-grade lithium metal, end-2012 372

Table 220: Japan: Consumption of lithium in primary lithium batteries, 2007 to 2012 375

Table 221: Japan: Unit consumption of lithium in primary batteries, 2007 to 2012 375

Table 222: World: Imports of battery-grade lithium metal, 2007 to 2012 376

Table 223: World: Forecast demand for lithium in primary batteries, 2012 to 2017 377

Table 224: Effects of additives and temperatures on properties of molten cryolite 379

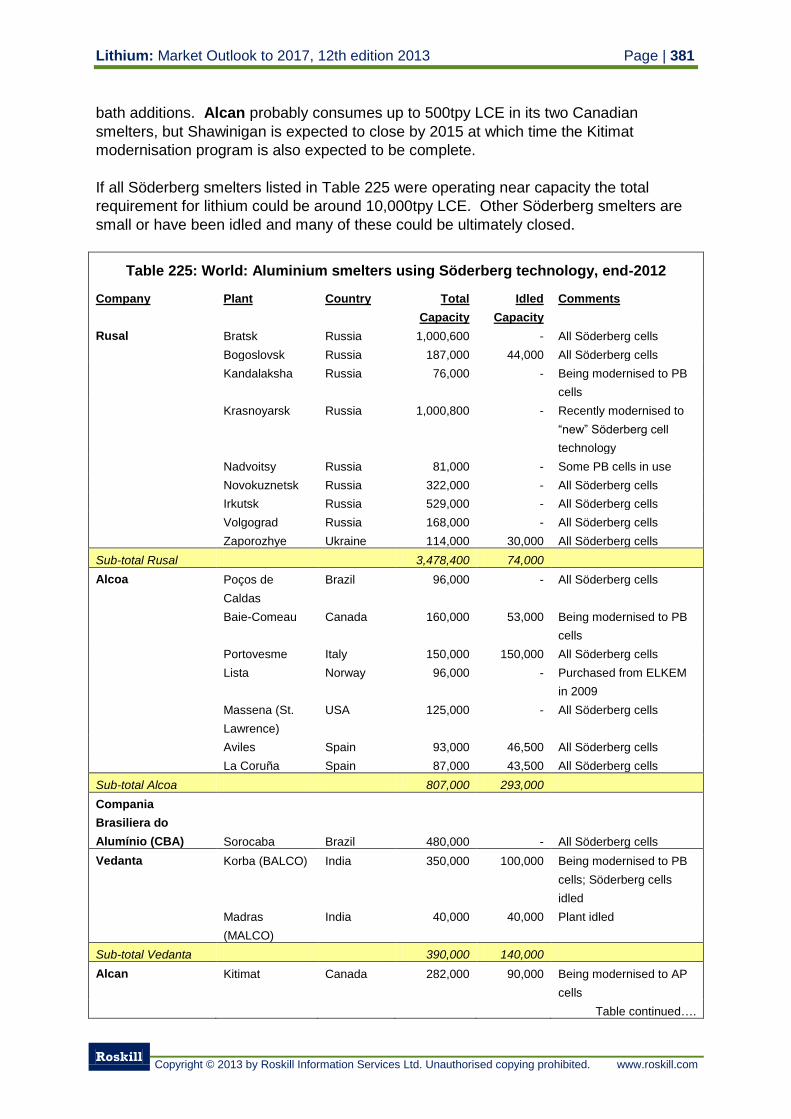

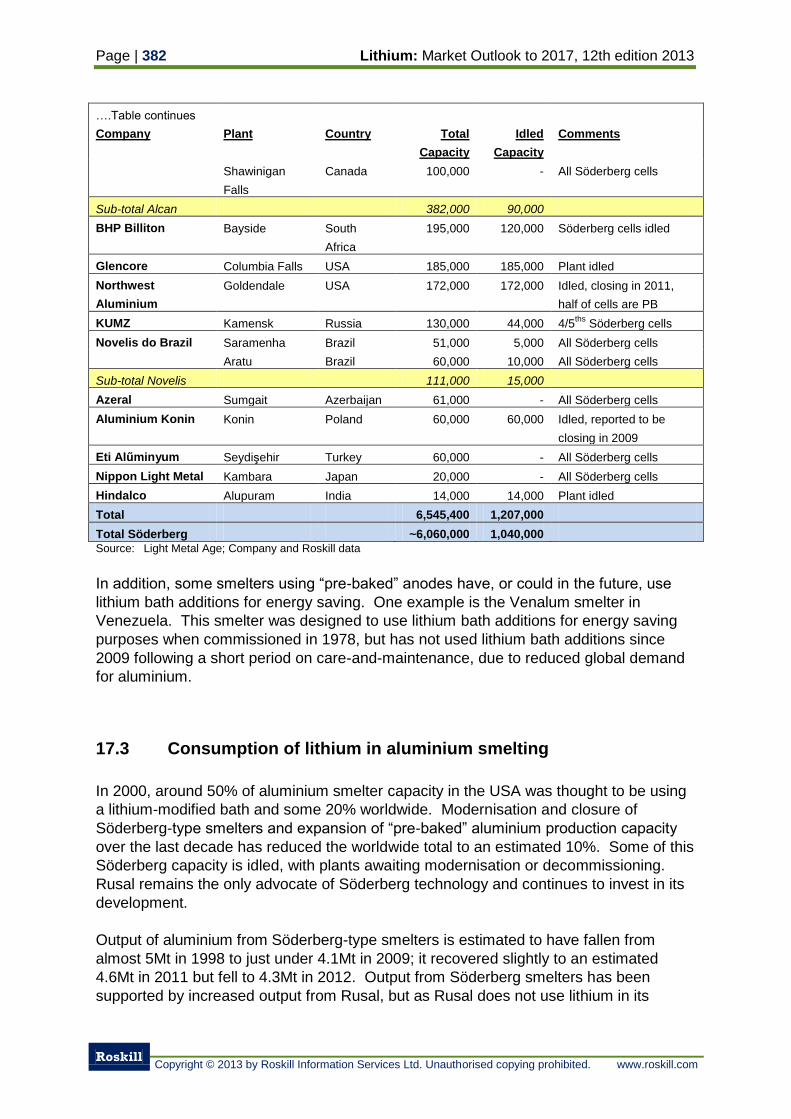

Table 225: World: Aluminium smelters using Söderberg technology, end-2012 381

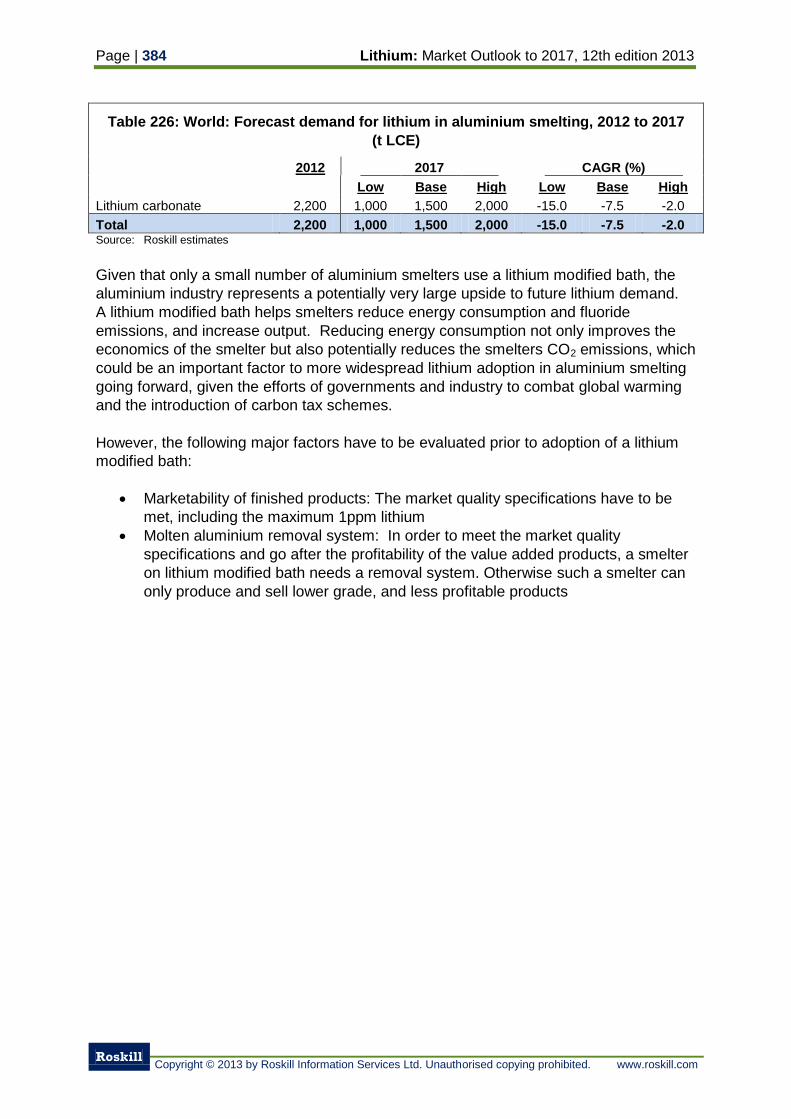

Table 226: World: Forecast demand for lithium in aluminium smelting, 2012 to 2017 384

Table 227: World: Consumption of lithium in other end-uses, 2007, 2012 and 2017 385

Table 228: Examples of uses for lithium in organic synthesis 387

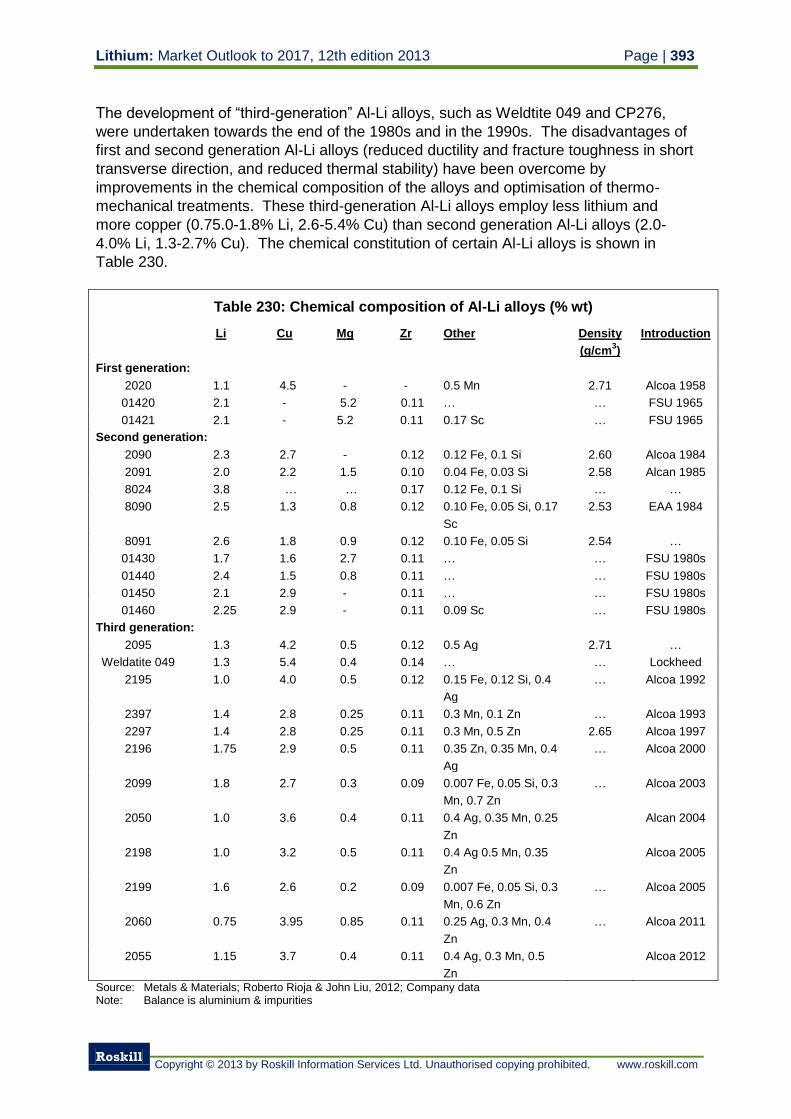

Table 229: Physical properties of Al-Li alloys 392

Table 230: Chemical composition of Al-Li alloys 393

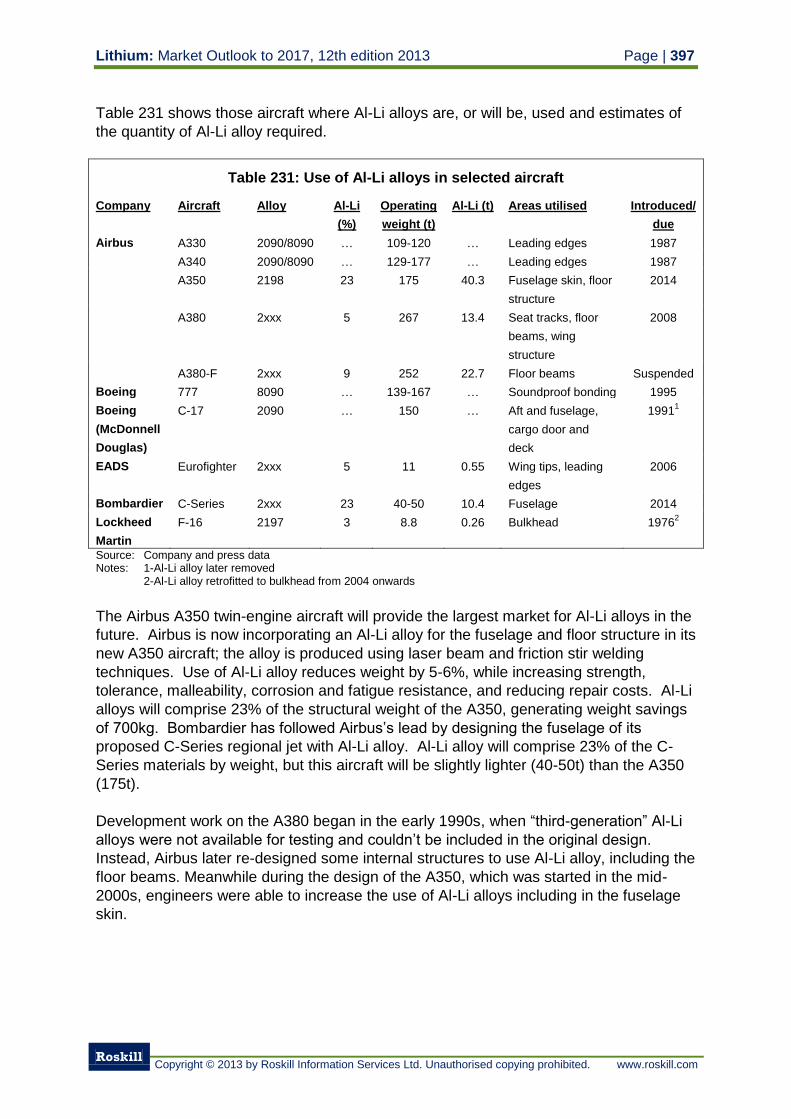

Table 231: Use of Al-Li alloys in selected aircraft 397

Table 232: World: Forecast demand for lithium in aluminium-lithium alloys, 2012

to 2017 399

Table 233: Properties of lithium niobate and lithium tantalite 401

Table 234: Applications for SAW components 401

Table 235: Applications for speciality inorganic lithium compounds 406

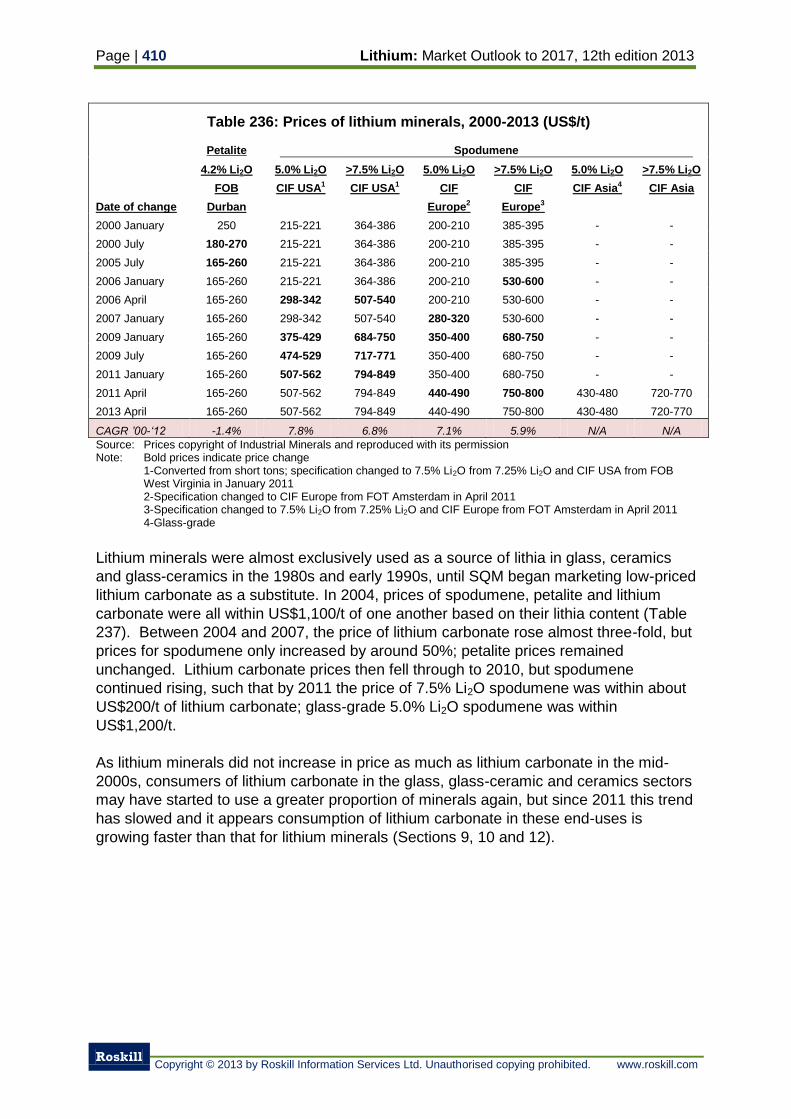

Table 236: Prices of lithium minerals, 2000-2013 410

Table 237: Comparison of prices for lithium minerals and carbonate, 2004 to 2012 411

Table 238: Comparison of prices for chemical-grade spodumene concentrate and

lithium carbonate, 2004 to 2012 412

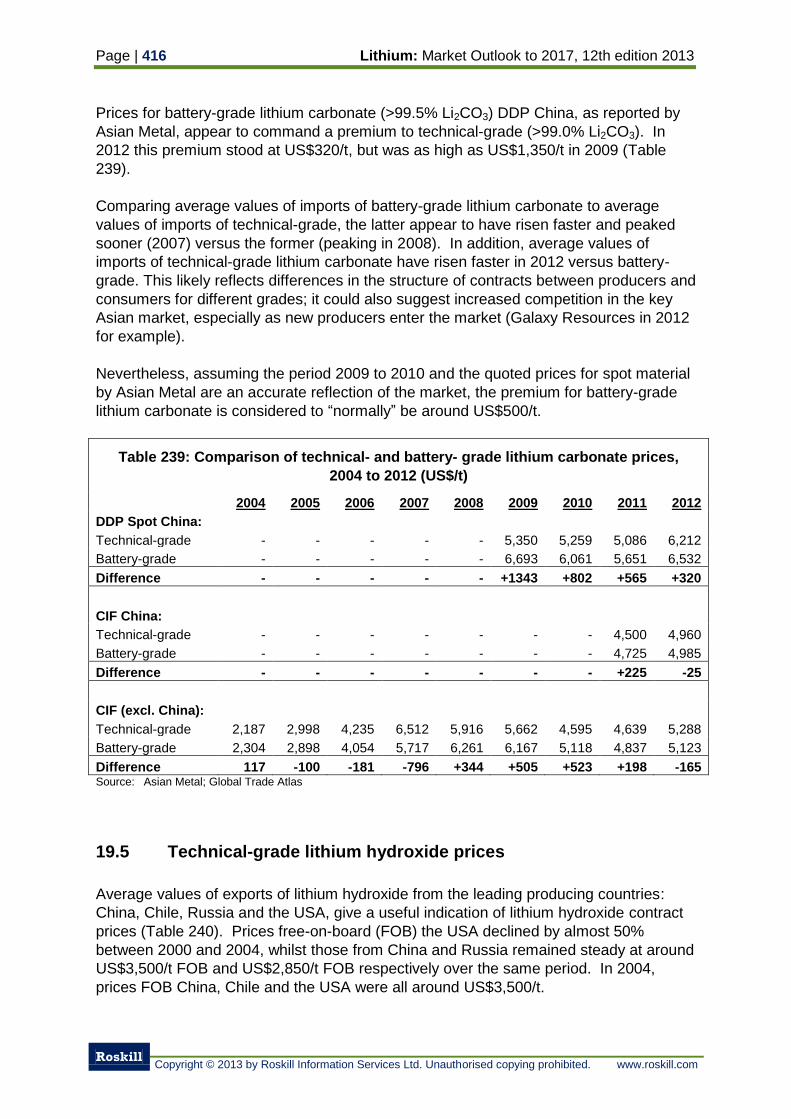

Table 239: Comparison of technical- and battery- grade lithium carbonate prices,

2004 to 2012 416

Table 240: Average values of exports/imports of lithium oxides and hydroxides by

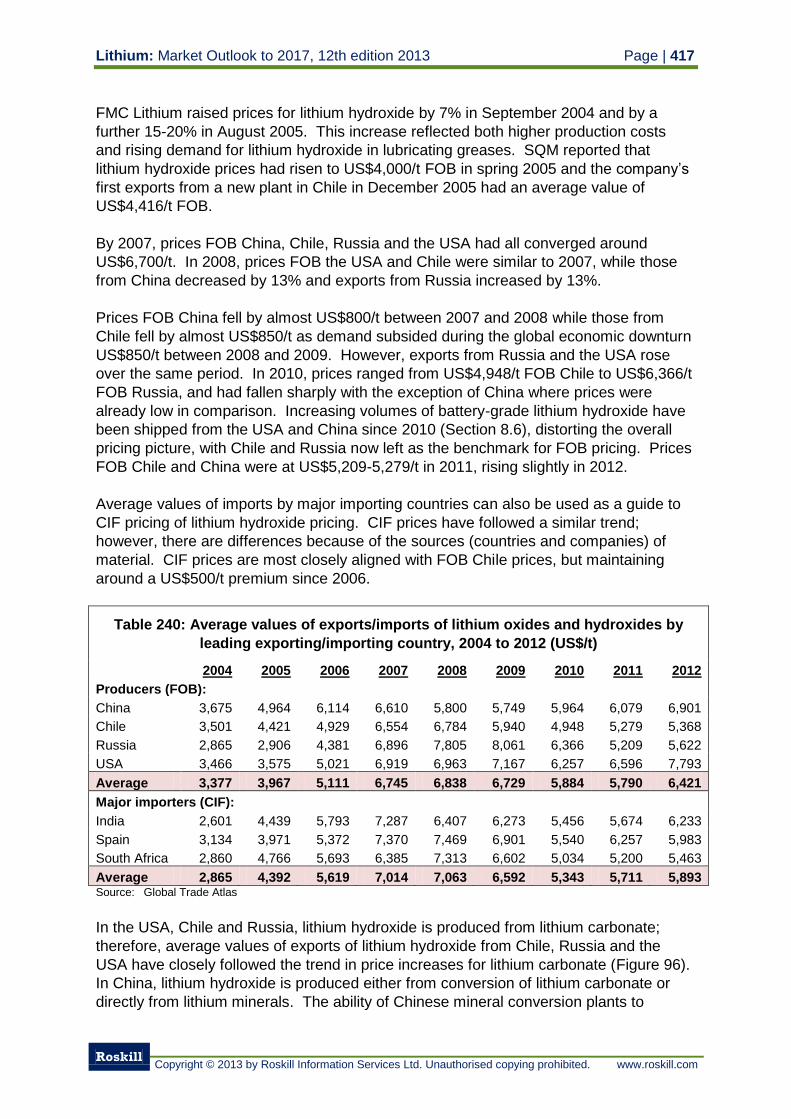

leading exporting/importing country, 2004 to 2012 417

Table 241: Average values of exports of lithium chloride by leading producing

country, 2004 to 2012 420

Table 242: Average values of exports of lithium metal by leading producing

country, 2004 to 2012 421

Table 243: World: Forecast nominal and real prices for technical-grade lithium

carbonate, 2012 to 2017 423

Table 244: World: Forecast nominal prices for technical-grade lithium carbonate

and chemical-grade lithium minerals, 2012 to 2017 425

Table 245: World: Forecast nominal prices for technical-grade lithium carbonate

and technical-grade lithium hydroxide, 2012 to 2017 426

List of Figures

Figure 1: Lithium product flow chart and main end-uses, 2012 1

Figure 2: Consumption of lithium by end-use, 2000 to 2012 2

Figure 3: Production of lithium by country, 2000 to 2012 4

Figure 4: Price history of lithium carbonate, 1990 to 2012 6

Figure 5: World: Forecast real prices for technical-grade lithium carbonate, 2012

to 2017 9

Figure 6: Overview of lithium production 16

Figure 7: Extraction and processing of brines from the Salar de Atacama, Chile and

Silver Peak, Nevada by Rockwood Lithium 18

Figure 8: Flow sheet showing the processing of brines at Salar de Carmen by SQM 19

Figure 9: Simplified flow sheet of the Li SX™ method patented by Bateman Lithium

Projects 21

Figure 10: Simplified mineral concentrate production flow sheet for a typical hard

rock lithium operation 22

Figure 11: Simplified flow sheet for lithium carbonate production from spodumene

mineral concentrate using the acid-roast method 24

Figure 12: Simplified flow sheet for lithium hydroxide and lithium hydroxide

monohydrate production from spodumene mineral concentrate using the

lime-roast method 25

Figure 13: Simplified flow sheet for lithium carbonate production from hectorite clay

developed by Western Lithium 27

Figure 14: Mining and milling costs for hard rock lithium mineral operations/projects 31

Figure 15: Lithium carbonate cash operating costs, 2012 32

Figure 16: Potential new producers production costs 33

Figure 17: World: Production of lithium by country, 2000 to 2012 34

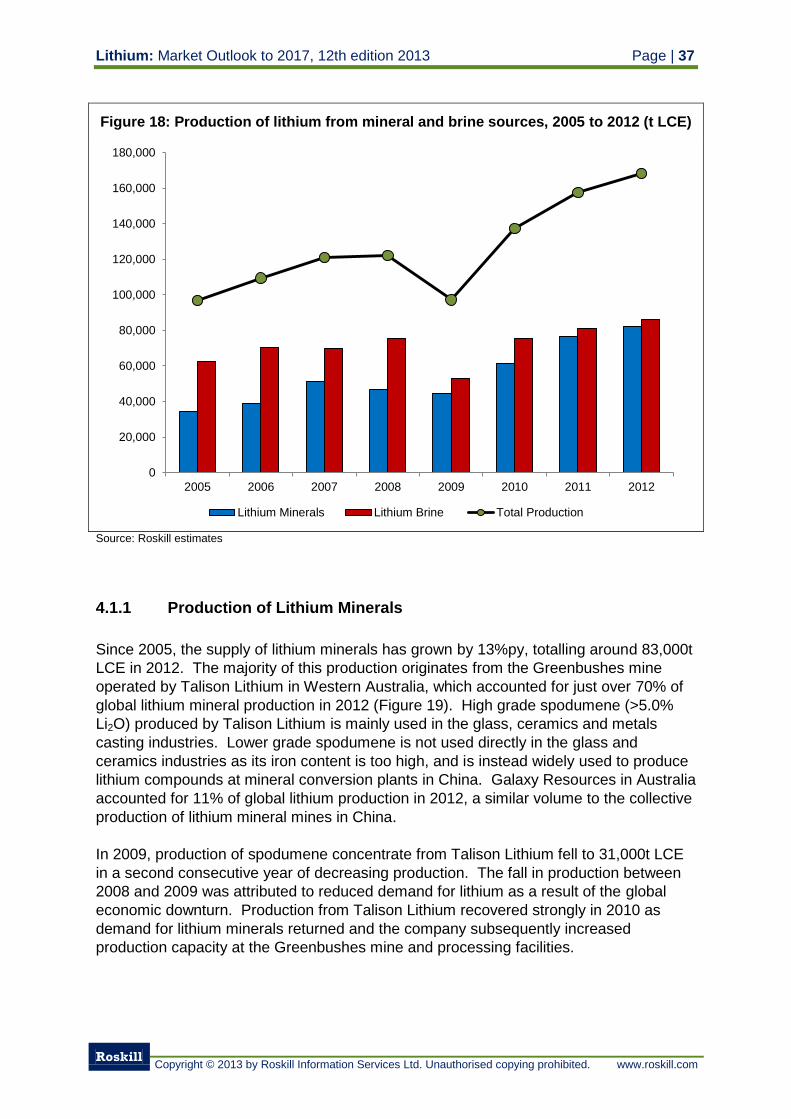

Figure 18: Production of lithium from mineral and brine sources, 2005 to 2012 37

Figure 19: Production of lithium minerals by company, 2012 38

Figure 20: Production of lithium from brines by country, 2005 to 2012 40

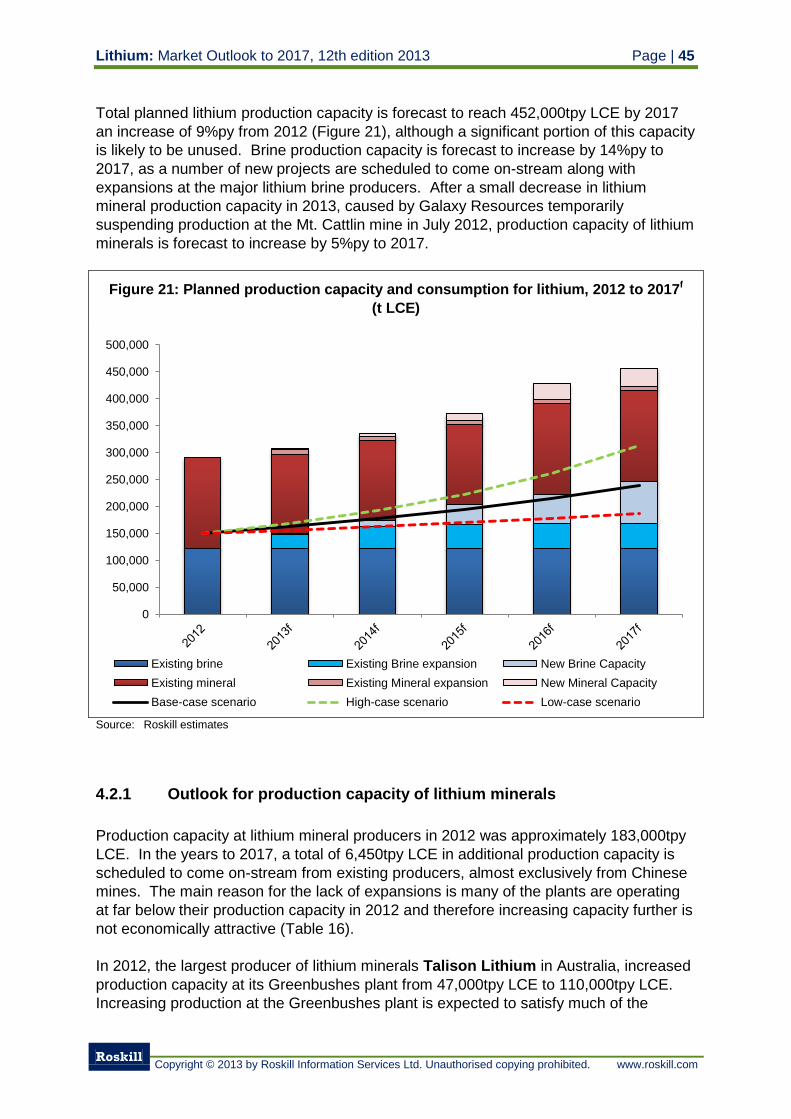

Figure 21: Planned production capacity and consumption for lithium, 2012 to 2017 45

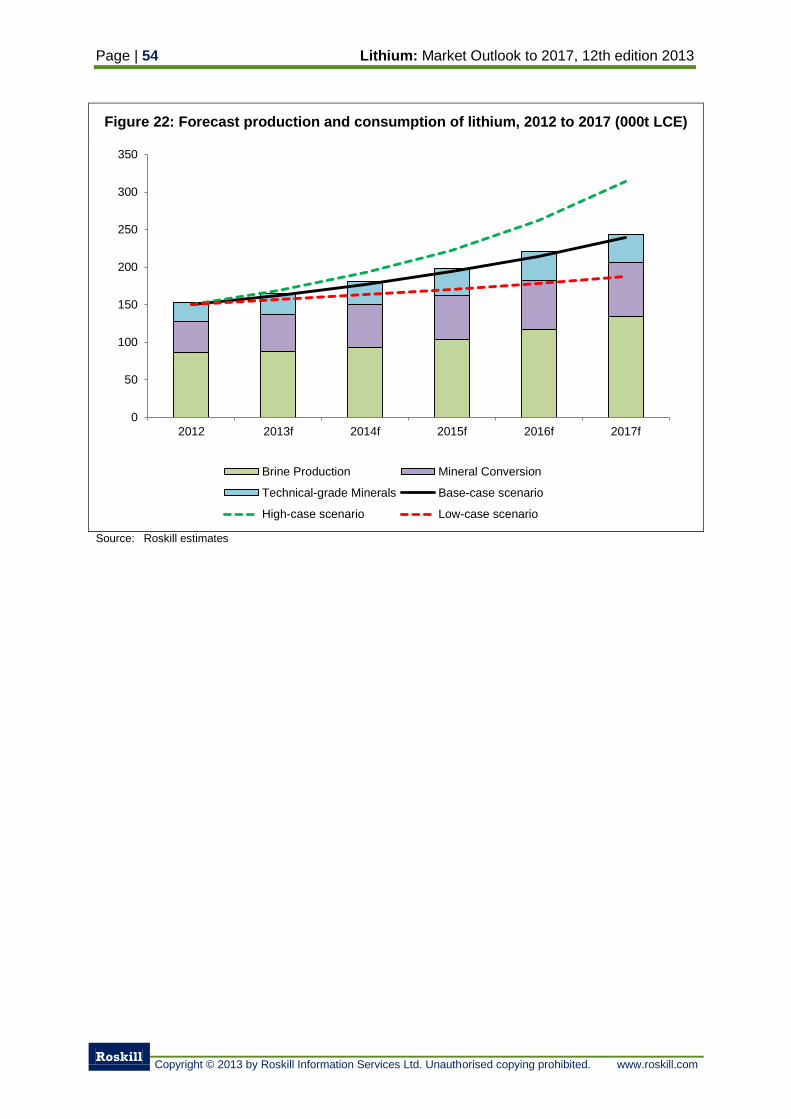

Figure 22: Forecast production and consumption of lithium, 2012 to 2017 54

Figure 23: Pilot plant flow sheet developed for Lithium Americas at SGS Mineral

Services 62

Figure 24: Brazil: Production of Lithium products 2005 to 2010 101

Figure 25: SQM: Lithium sales by destination 2011, 2009, 2007 and 2005 135

Figure 26: SQM: Destination of lithium carbonate exports, 2006 to 2011 136

Figure 27: China: Location of mineral conversion and lithium chemical/metal plants

in China, 2012 153

Figure 28: Japan: Imports of lithium carbonate, hydroxide & oxide and combined

LCE, 2005 to 2012 191

Figure 29: World: Leading exporters of lithium carbonate, 2006, 2008, 2010

and 2012 231

Figure 30: World: Leading importers of lithium carbonate, 2006, 2008, 2010

and 2012 233

Figure 31: World: Leading exporters of lithium hydroxide and oxides, 2006, 2008,

2010 and 2012 235

Figure 32: World: Growth in consumption of lithium, 2000 to 2012 239

Figure 33: World: Consumption of lithium by end-use, 2012 240

Figure 34: World: Consumption of lithium by end-use, 2000 to 2012 241

Figure 35: World: Consumption of lithium by end-use, 2000 to 2012 241

Figure 36: World: Estimated consumption of lithium by country/region, 2002, 2007

and 2012 244

Figure 37: World: Consumption of lithium by product, 2012 245

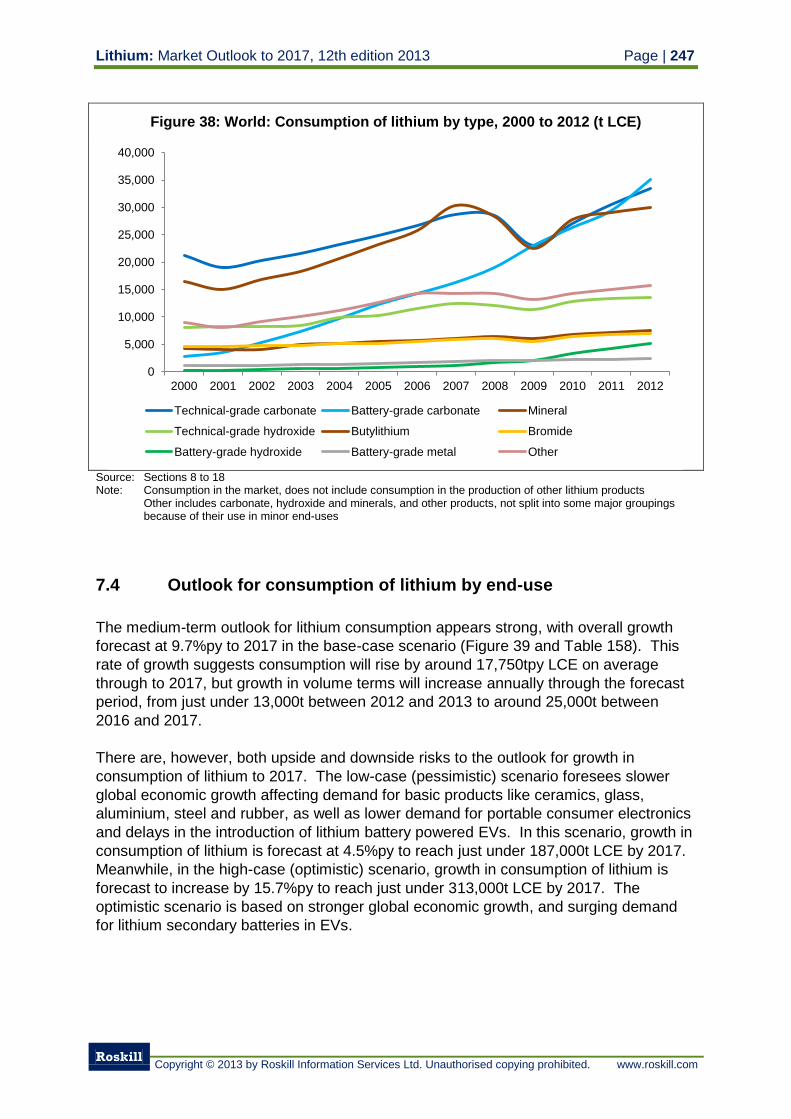

Figure 38: World: Consumption of lithium by type, 2000 to 2012 247

Figure 39: World: Historical and forecast consumption of lithium by end-use, 2007

to 2017 248

Figure 40: World: Forecast consumption of lithium by form, 2007, 2012 and 2017 252

Figure 41: Specific energy and energy density of rechargeable batteries 253

Figure 42: Lithium-ion battery schematic 254

Figure 43: Lithium metal polymer battery schematic 256

Figure 44: Lithium-sulphur cell schematic 257

Figure 45: Lithium-air cell schematic 258

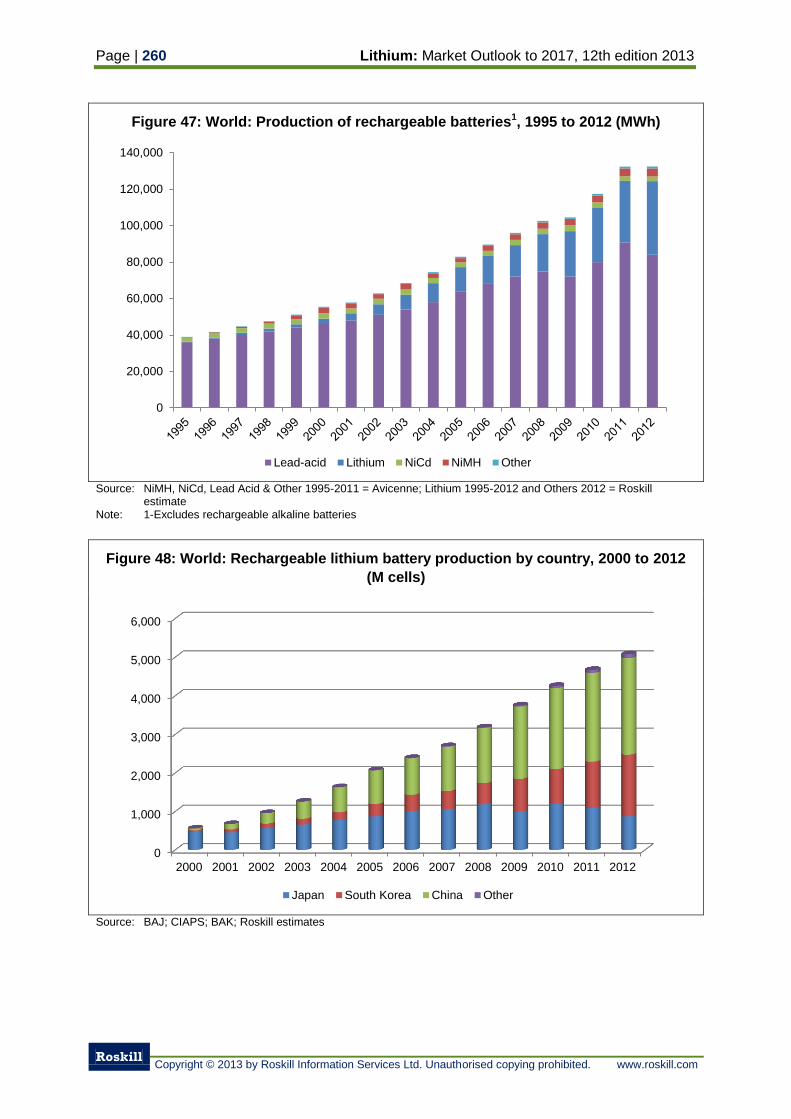

Figure 46: World: Production of rechargeable batteries1, 1995 to 2012 259

Figure 47: World: Production of rechargeable batteries1, 1995 to 2012 260

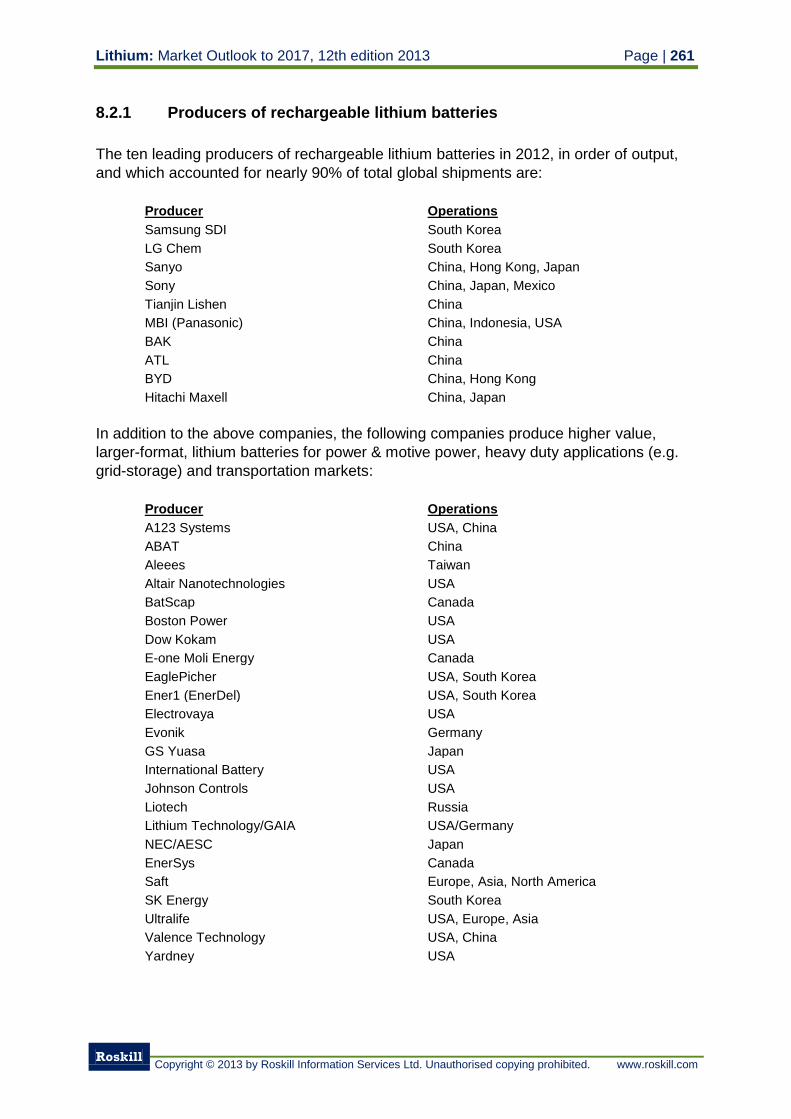

Figure 48: World: Rechargeable lithium battery production by country, 2000 to 2012 260

Figure 49: Lithium-ion battery materials value chain 263

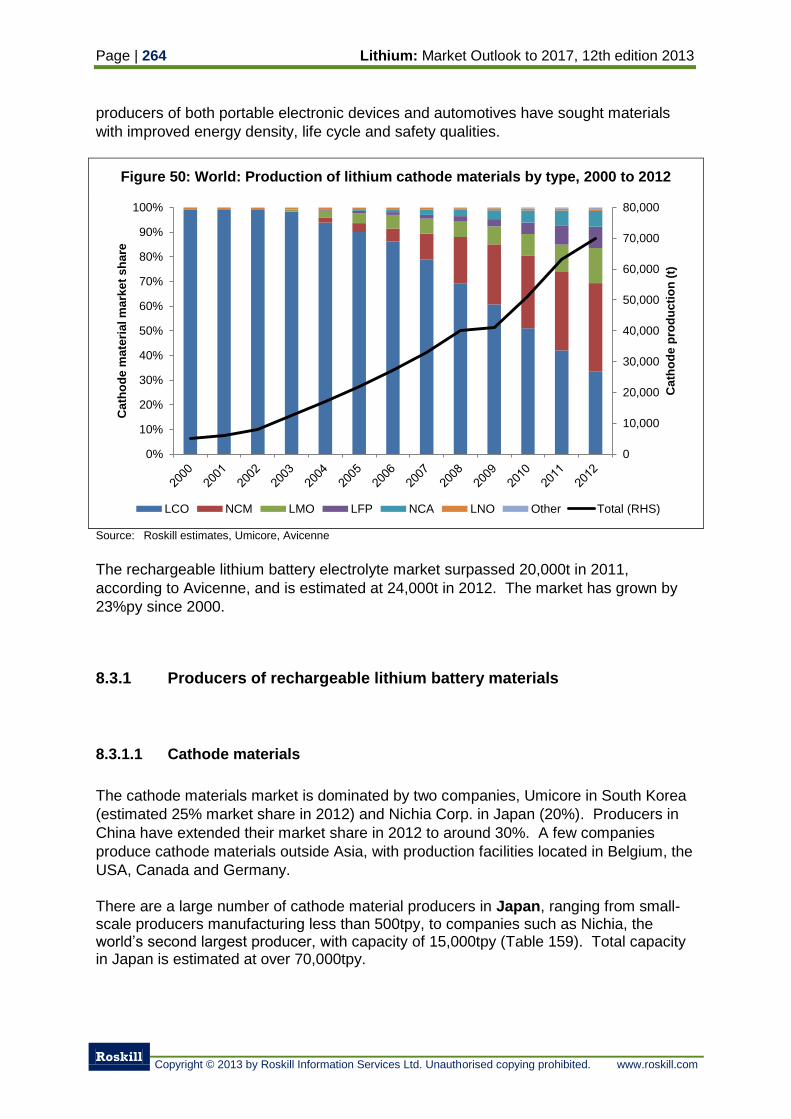

Figure 50: World: Production of lithium cathode materials by type, 2000 to 2012 264

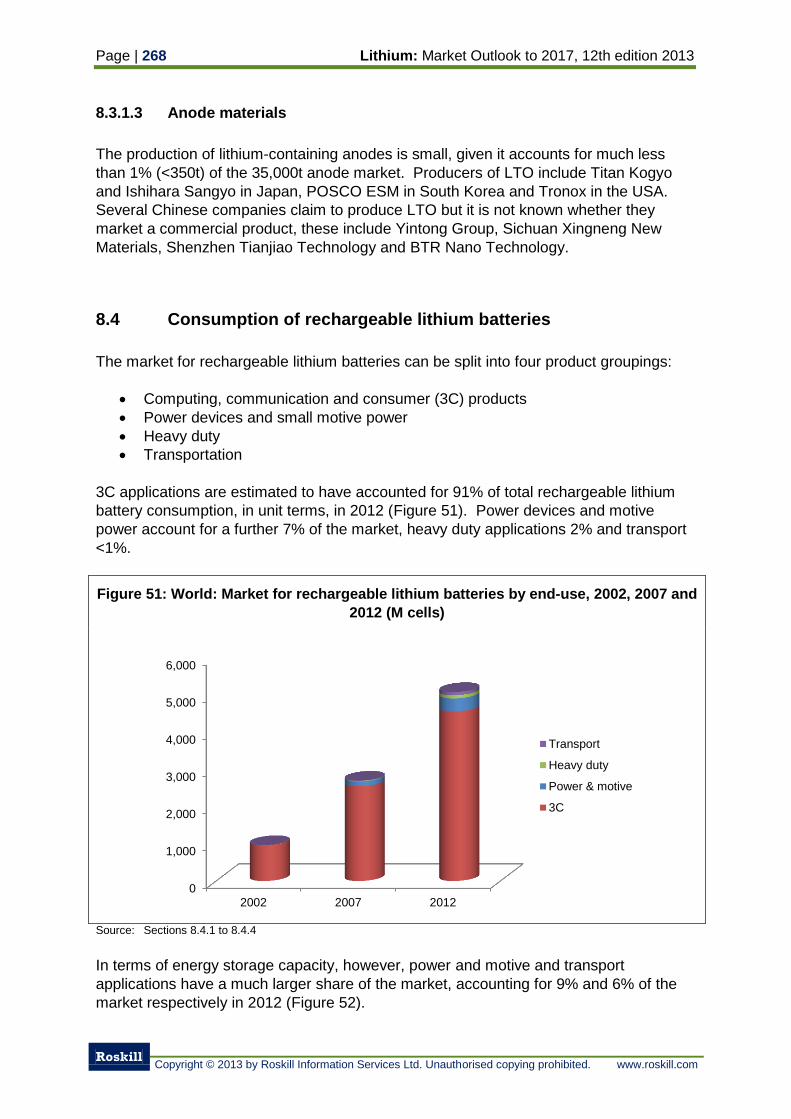

Figure 51: World: Market for rechargeable lithium batteries by end-use, 2002, 2007

and 2012 268

Figure 52: World: Market for rechargeable lithium batteries by end-use, 2012 269

Figure 53: World: Production of rechargeable batteries and consumption of lithium,

2000 to 2012 276

Figure 54: World: Market for rechargeable lithium batteries by end-use, 2002

to 2017 279

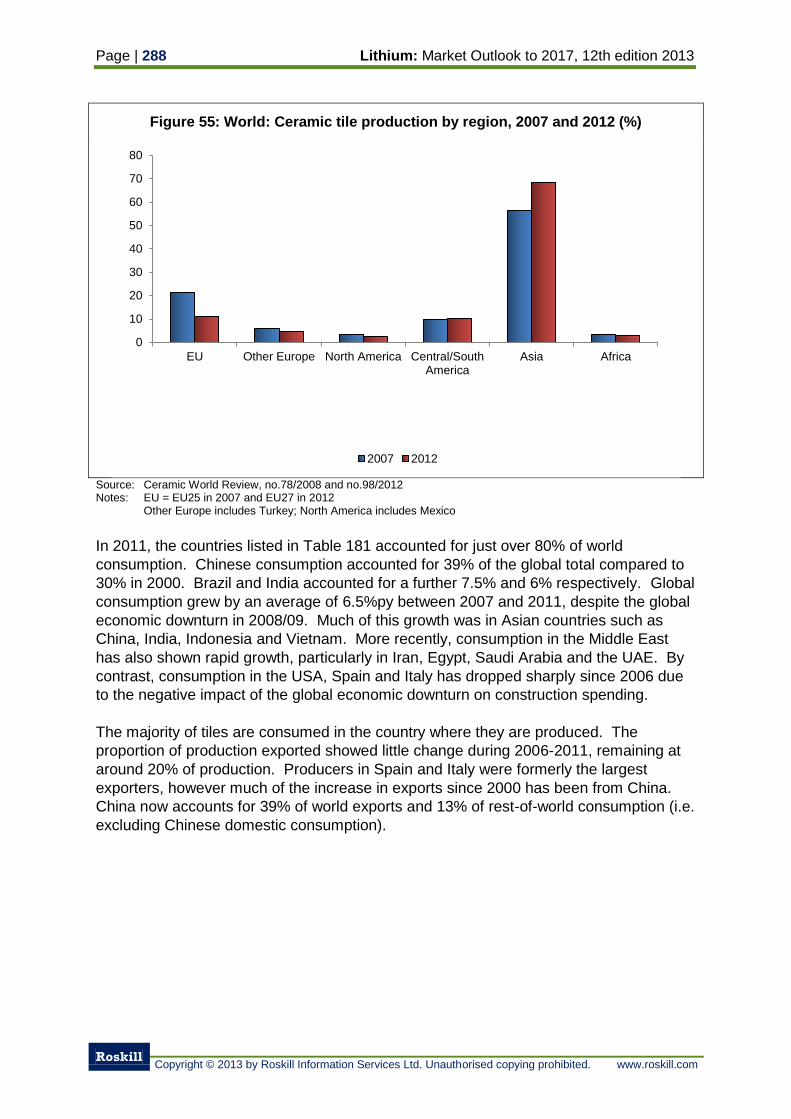

Figure 55: World: Ceramic tile production by region, 2007 and 2012 288

Figure 56: World: Sanitaryware production by region/country, 2010 291

Figure 57: World: Production of tableware by country/region, 2008 293

Figure 58: USA: Shipments of cookware, bakeware and kitchenware, 2001 to 2010 295

Figure 59: World: Shipments of white goods by region, 2000 to 2020 296

Figure 60: World: Year-on-year growth in construction spending and GDP, 2000

to 2017 298

Figure 61: World: Production of lubricating grease by additive type, 2011 312

Figure 62: World: Production of lubricating grease by type, 2000 to 2012 313

Figure 63: World: Production of lithium grease by region/country and by type, 2000

and 2011 314

Figure 64: World: Output of automobiles by region, 2000 to 2012 318

Figure 65: World: Deliveries of commercial aircraft, 2000 to 2012 318

Figure 66: World: Shipbuilding deliveries, 2000 to 2012 319

Figure 67: World: Relative industrial and transport output and lithium grease

production, 2002 to 2011 320

Figure 68: World: Production of grease and consumption of lithium, 2000 to 2012 321

Figure 69: World: Estimated production of glass by type, 2012 326

Figure 70: World: Production of container glass by region/country, 2012 326

Figure 71: World: Consumption of glass packaging by region, 2011 327

Figure 72: World: Production of continuously cast steel by region, 1998 to 2012 335

Figure 73: World: Capacity for synthetic rubber production by country/region, 2012 340

Figure 74: World: Capacity for BR, ESBR and SSBR rubber by country/region,

end-2011 341

Figure 75: World: SBC capacity by region/country, end-2010 341

Figure 76: World: Production of synthetic rubber by region, 1996 to 2011 342

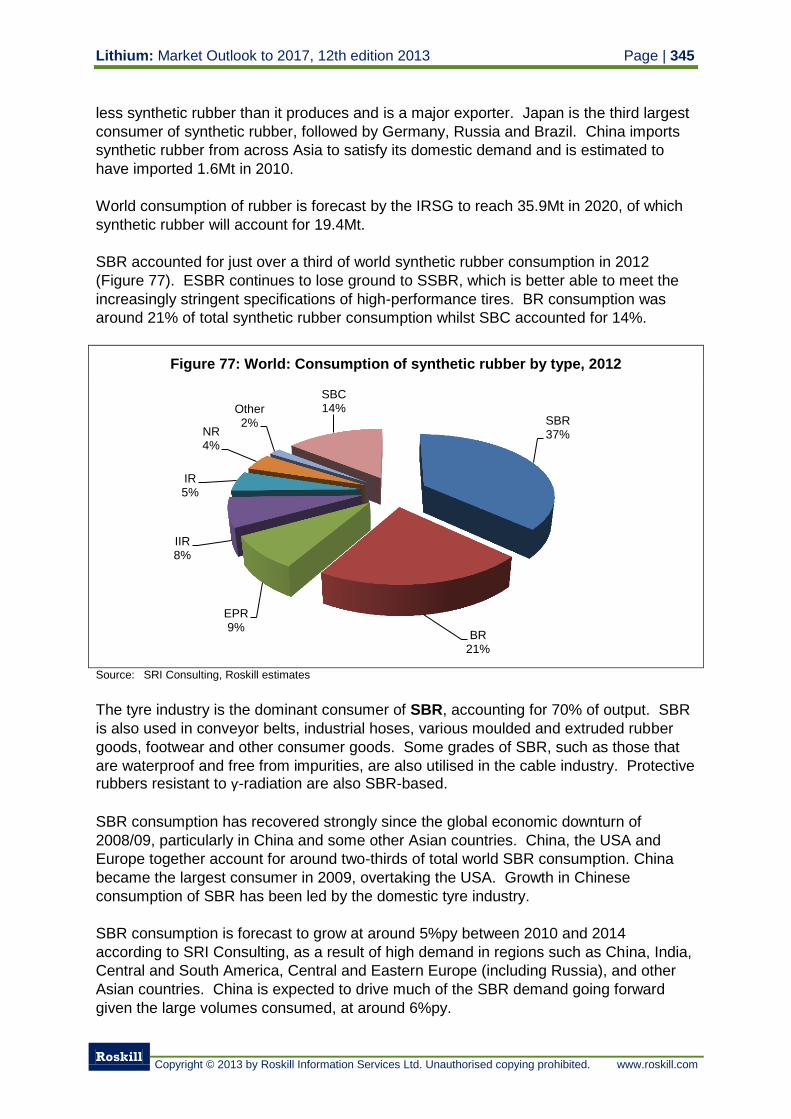

Figure 77: World: Consumption of synthetic rubber by type, 2012 345

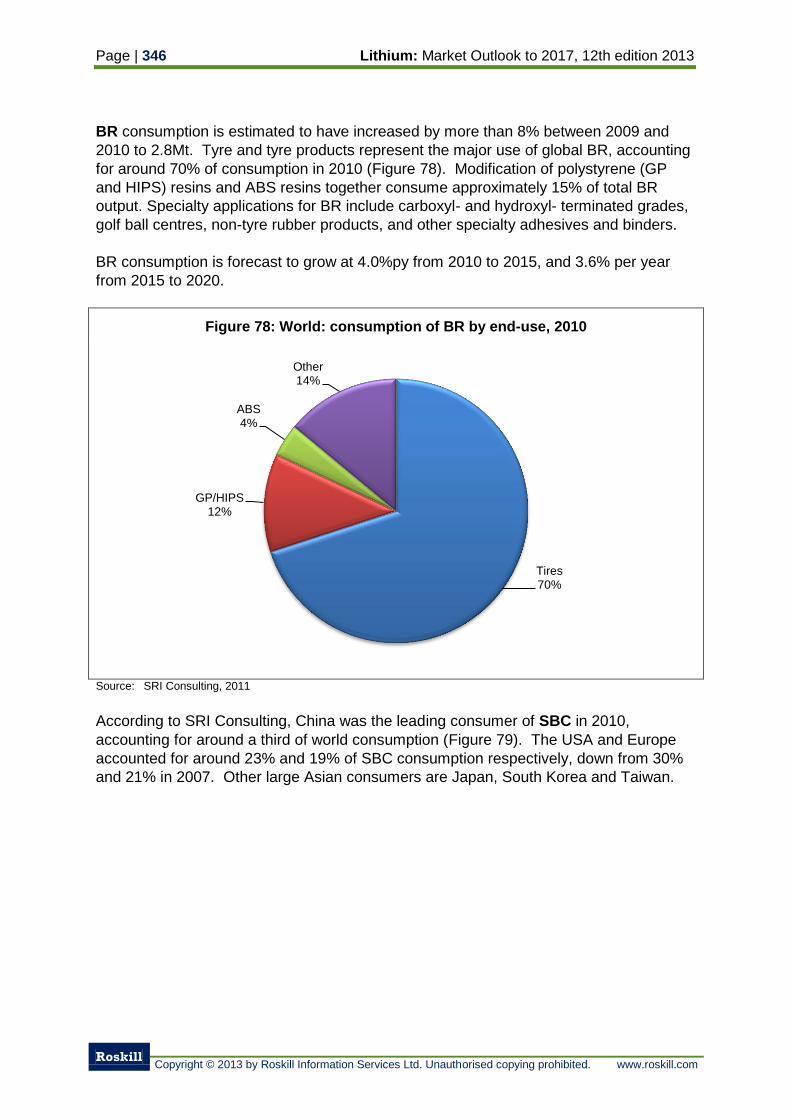

Figure 78: World: consumption of BR by end-use, 2010 346

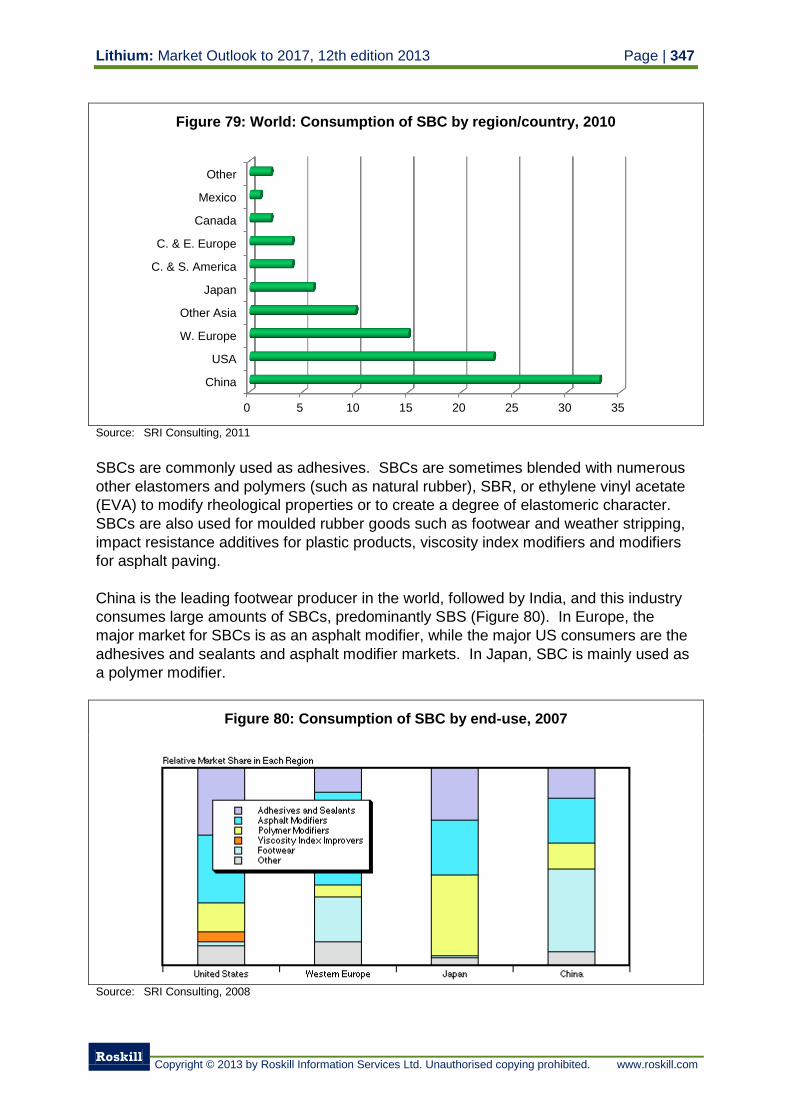

Figure 79: World: Consumption of SBC by region/country, 2010 347

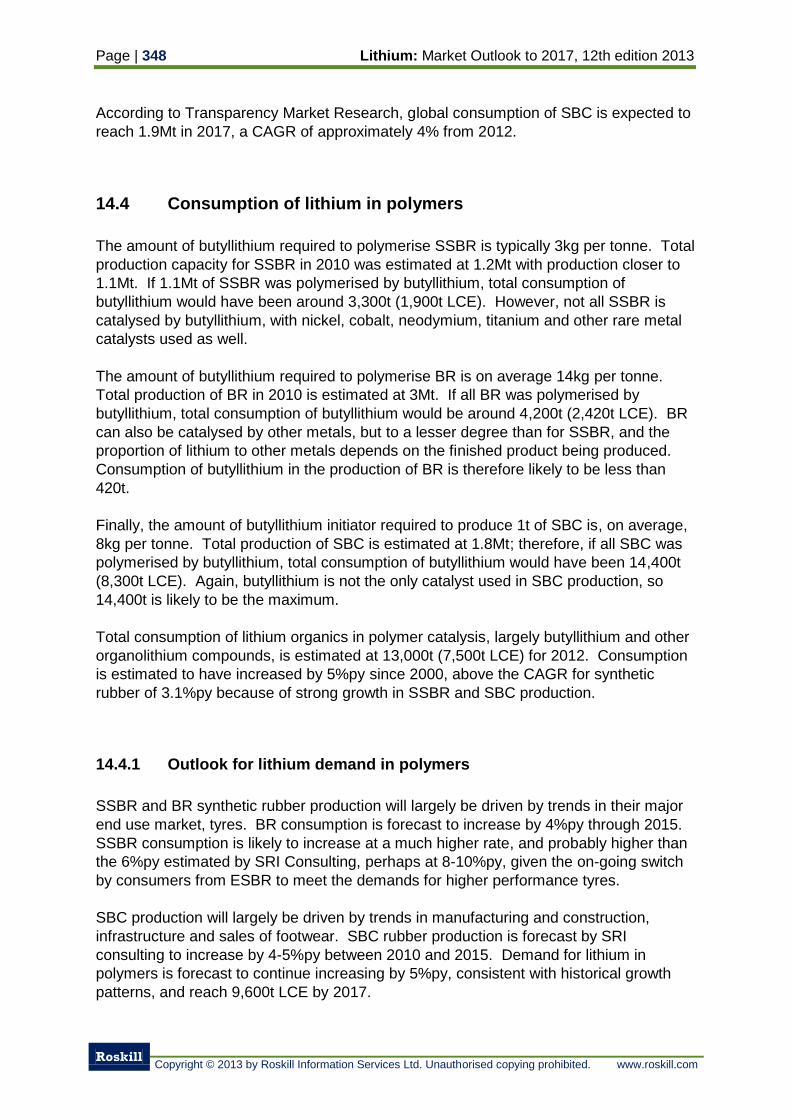

Figure 80: Consumption of SBC by end-use, 2007 347

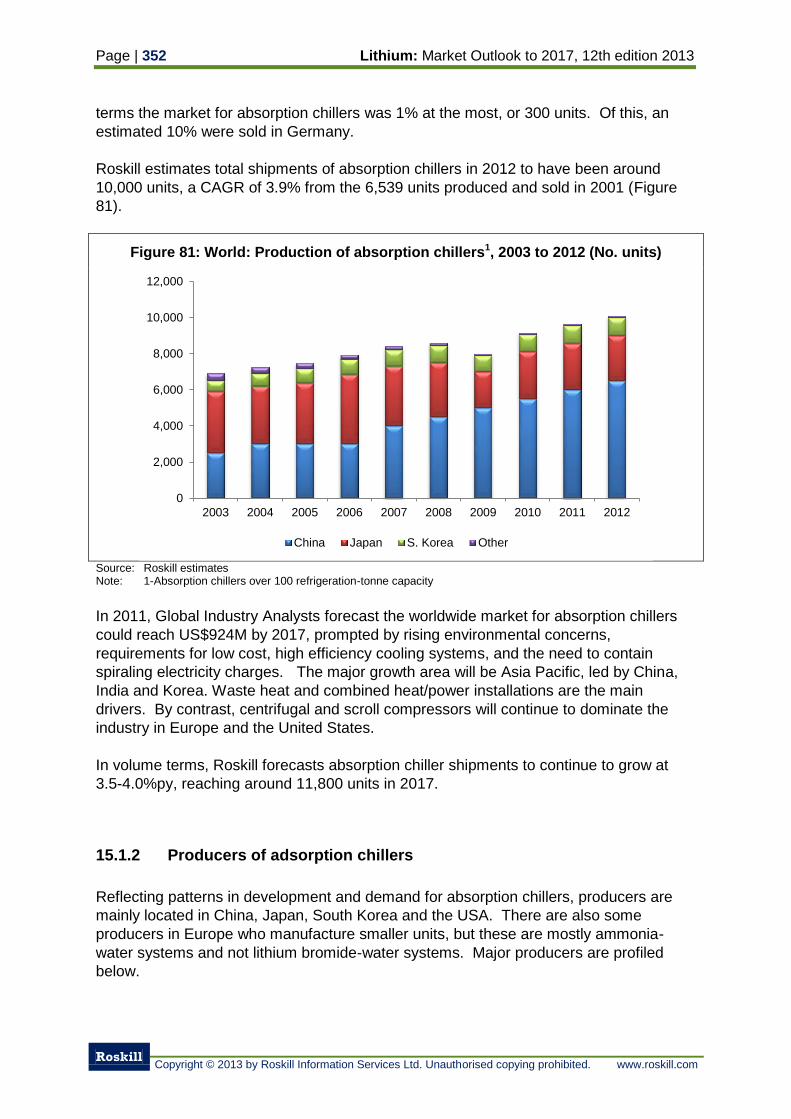

Figure 81: World: Production of absorption chillers, 2003 to 2012 352

Figure 82: World: Consumption of lithium bromide in air treatment, 2001 to 2012 356

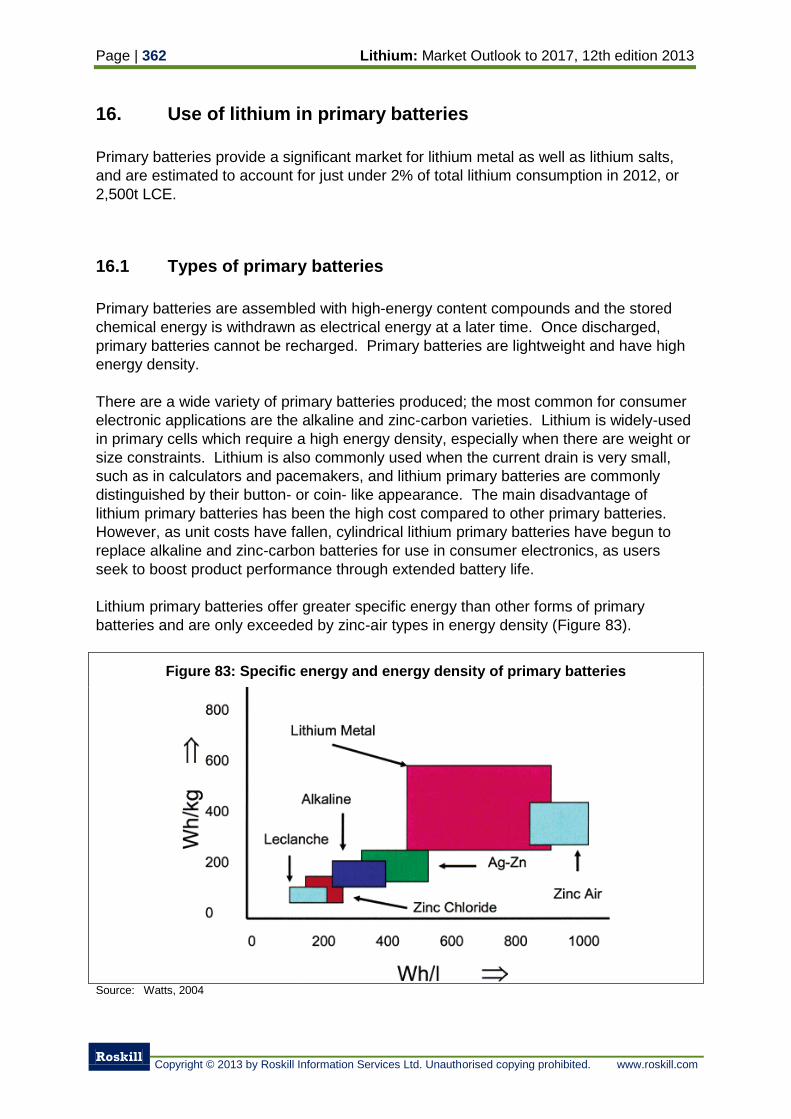

Figure 83: Specific energy and energy density of primary batteries 362

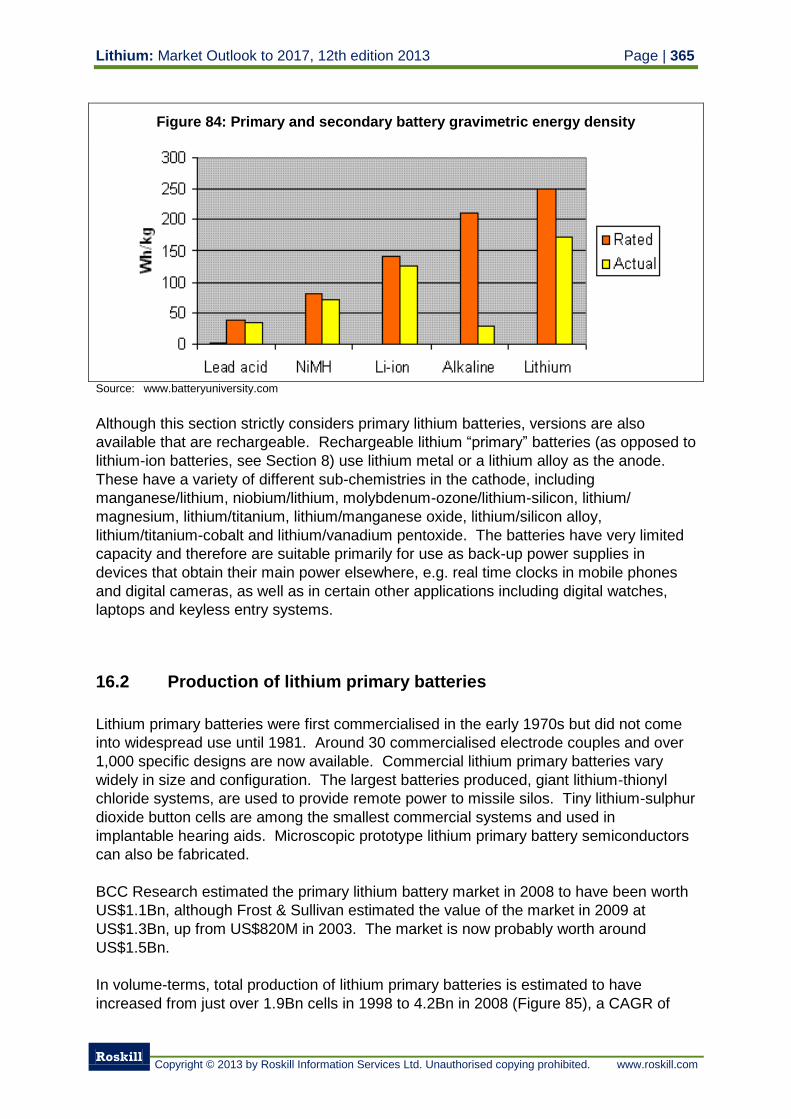

Figure 84: Primary and secondary battery gravimetric energy density 365

Figure 85: World: Production of primary lithium batteries by country, 1998 to 2012 366

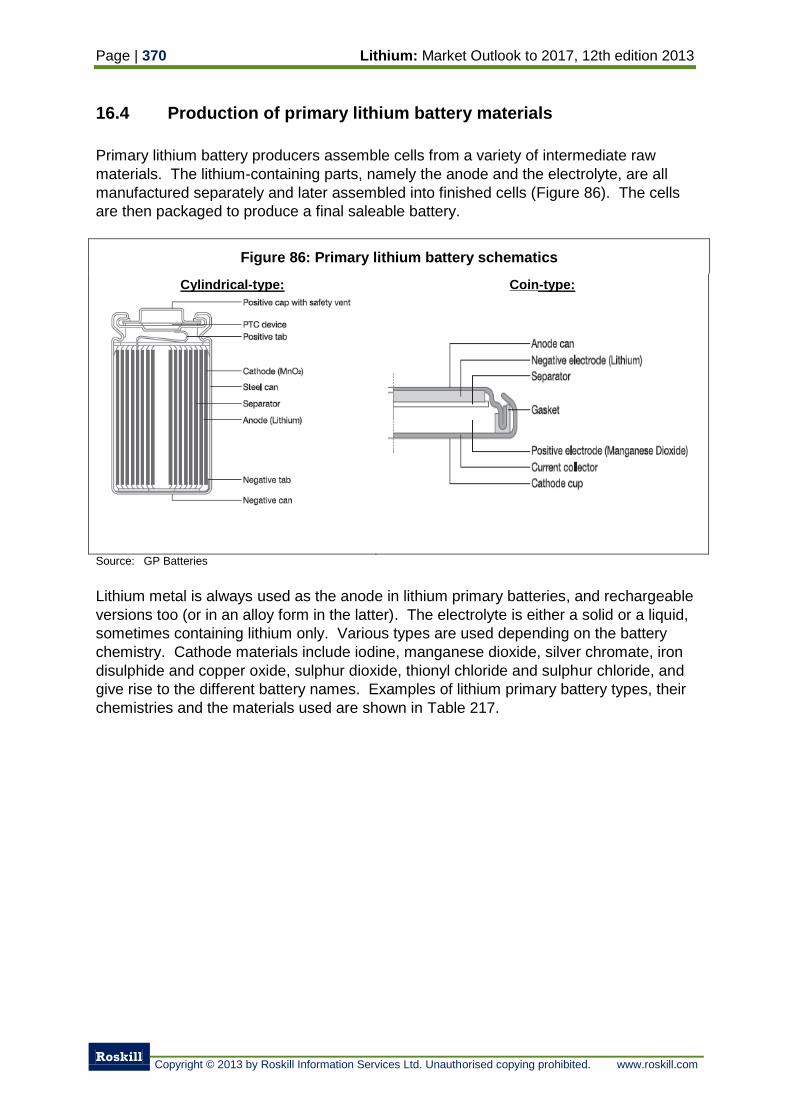

Figure 86: Primary lithium battery schematics 370

Figure 87: World: Demand for lithium metal in primary batteries, 2000 to 2012 376

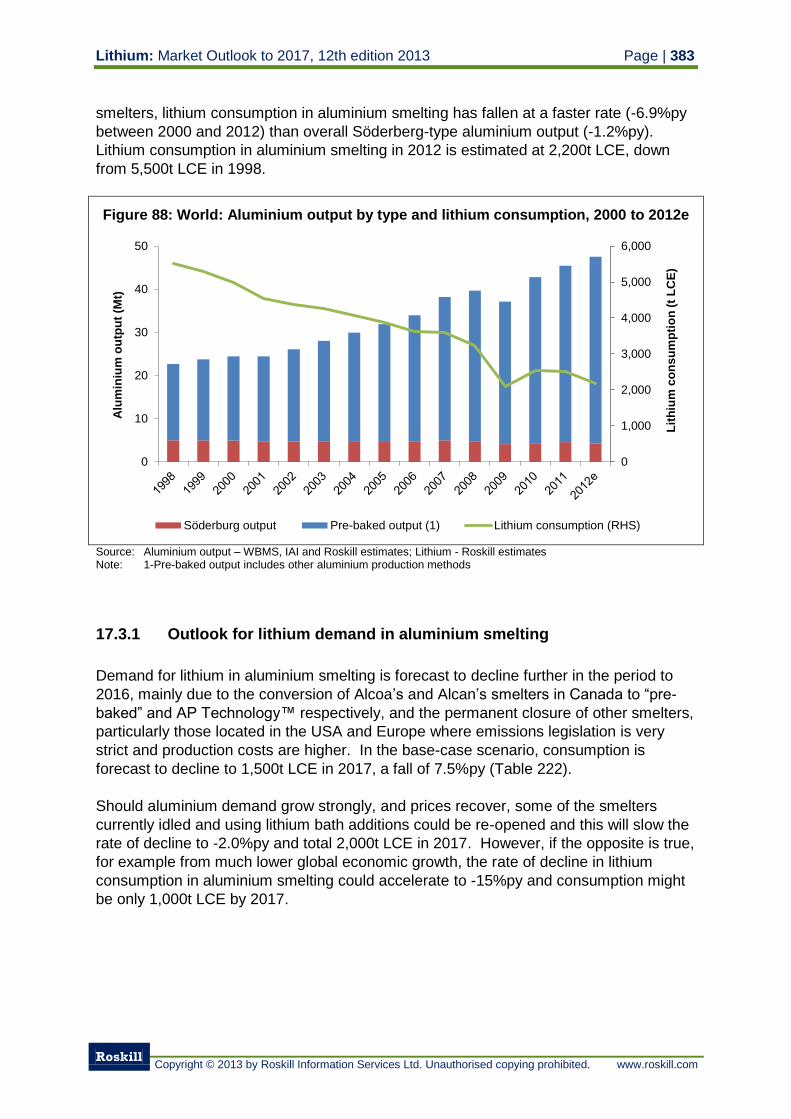

Figure 88: World: Aluminium output by type and lithium consumption, 2000 to 2012 383

Figure 89: World: Consumption of alkyd-based paints and coatings, 2010 390

Figure 90: Development of Al-Li alloys 392

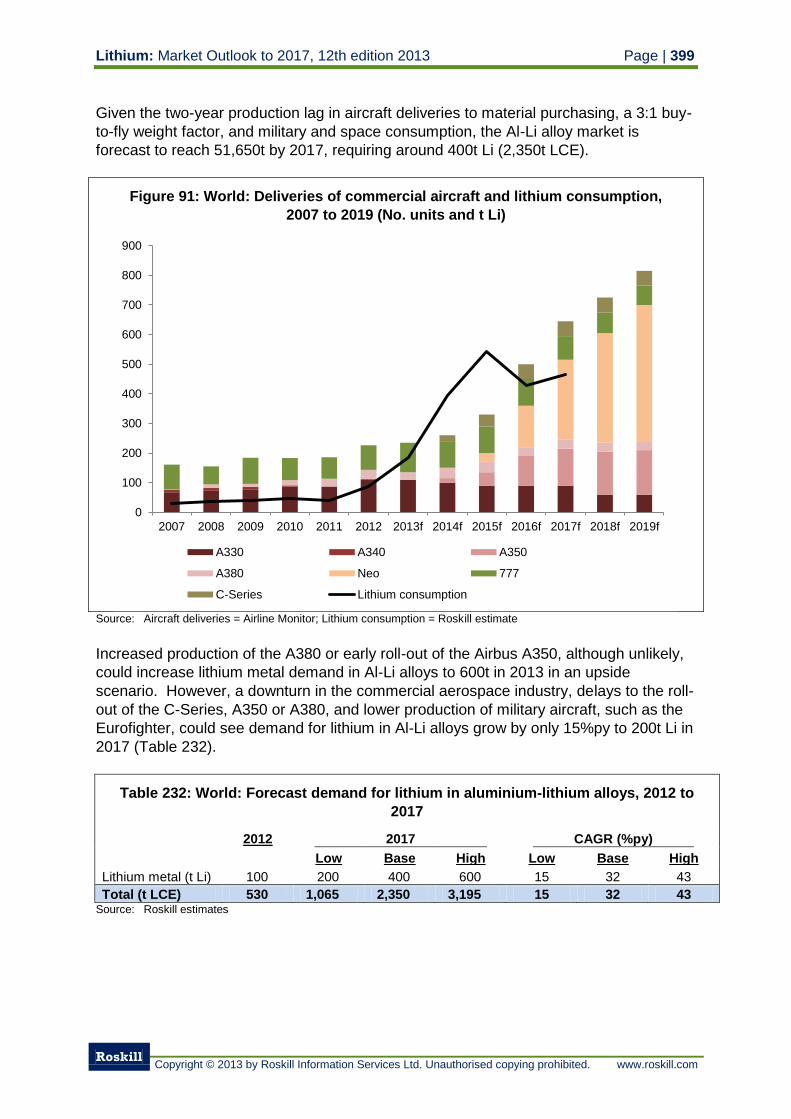

Figure 91: World: Deliveries of commercial aircraft and lithium consumption, 2007

to 2019 399

Figure 92: Price history of lithium carbonate, 1990 to 2012 408

Figure 93: Compound annual prices of lithium minerals, 2000 to 2013 411

Figure 94: Prices for technical-grade lithium carbonate, 1999 to 2012 414

Figure 95: Prices for battery-grade lithium carbonate, 1999 to 2012 415

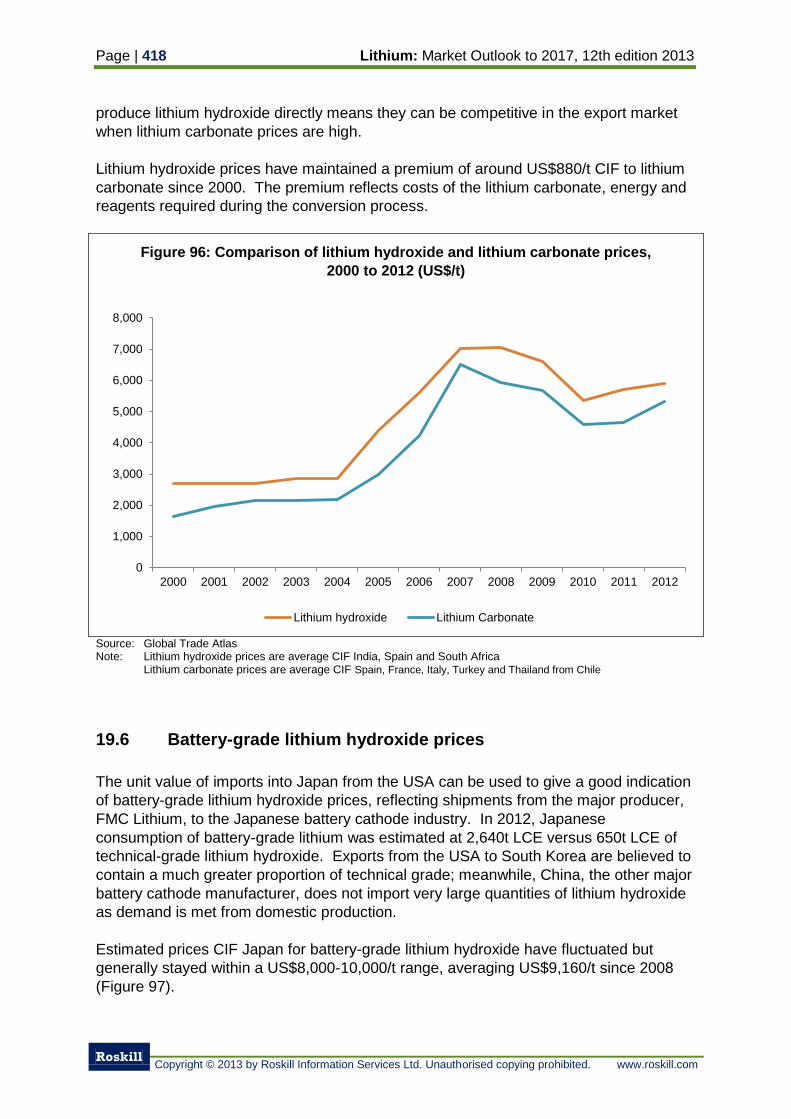

Figure 96: Comparison of lithium hydroxide and lithium carbonate prices, 2000

to 2012 418

Figure 97: Japan: Quarterly average import value of lithium hydroxide from the

USA, 2008 to 2012 419

Figure 98: World: Forecast nominal prices for technical-grade lithium carbonate,

2012 to 2017 423

Figure 99: World: Forecast real prices for technical-grade lithium carbonate,

2012 to 2017 424

List of Appendices (See attached CD)

Appendix A: International trade statistics

List of Symbols and Abbreviations

Symbols

p Preliminary ø Under half of one unit

e Estimated … Not available

r Revised - Nil

Abbreviations

M Million

Bn Billion

t Tonne

Mt Million tonnes

tpd Metric tonne per day

tpm Metric tonne per month

tpy Metric tonne per year

g Gramme

kg Kilogramme

mg Milligramme

lb Pound

l Litre

μm Micrometre

m Metre

m3 Cubic metre

km Kilometre

km2

Square kilometre

wt % Weight percent

ppm Parts per million

V Volt

Ah Ampere-hour

kWh KiloWatt hour

Wh/kg Watt hours/kg oC Degrees Celsius

K Kelvins

Pa Pascal

dwt Deadweight tonnage

3C Computing, communication & consumers

HLF High lithium feldspar

BR Polybutadiene rubber

SBR Styrene butadiene rubber

SBC Styrenic block polymers

SBS Styrene-butadiene-styrene

SSBR Solution based styrene butadiene rubber

BQM Bank Cubic Metre

LCE Lithium Carbonate Equivalent

LCO Lithium cobalt oxide

LMO Lithium manganese oxide

LNO Lithium nickel (+/- cobalt) oxide

LFP Fluorinated lithium iron phosphate

LMPF Fluorinated lithium metal phosphate

NCM Lithium nickel-cobalt-manganese oxide

NCA Lithium nickel-cobalt-aluminium oxide

PEA Preliminary Economic Assessment

PFS Preliminary Feasibility Study

DFS Definative Feasibility Study

BFS Bankable Feasibility Study

USGS US Geological Survey

BGS British Geological Survey

DNPM Departamento Nacional de Produção Mineral

IGME Instituto Geológico y Minero de España

CIS Commonwealth of Independent States

Equivalent values kg lb kg 1 2.204662 t 1,000 2,204.62

Conversion Table

The lithium content of minerals and compounds is referred to in three units depending

on the source quoted and the end-use referred to:

lithium (Li) content

lithium oxide (lithia, Li2O) content

lithium carbonate (Li2CO3) content or lithium carbonate equivalent (LCE)

Lithium oxide content is widely-used in the glass and ceramics industry, while lithium

carbonate content is mainly used for processed lithium compounds. The conversion

factors for the main commercial lithium compounds are shown in the table below.

Conversion factors for lithium compounds

To convert from: to Li to Li2O to Li2CO3

Lithium: x x x

Li (100% Li) 1.000 2.153 5.323

Lithium oxide (lithia):

Li2O (46.4% Li) 0.464 1.000 2.473

Lithium bromide:

LiBr (8.0% Li) 0.080 0.172 0.425

Lithium carbonate:

Li2CO3 (18.8% Li) 0.188 0.404 1.000

Lithium hydroxide monohydrate:

LiOH.H2O (16.5% Li) 0.165 0.356 0.880

Lithium chloride:

LiCl (16.3% Li) 0.163 0.362 0.871

Lithium fluoride:

LiF (26.8% Li) 0.268 0.576 1.420

Lithium hypochlorite:

LiOCl (11.89% Li) 0.119 0.256 0.633

Butyllithium:

C4H9Li (10.83% Li) 0.108 0.233 0.576

Lithium: Market Outlook to 2017, 12th edition 2013 Page | 1

Roskill

Copyright © 2013 by Roskill Information Services Ltd. Unauthorised copying prohibited. www.roskill.com

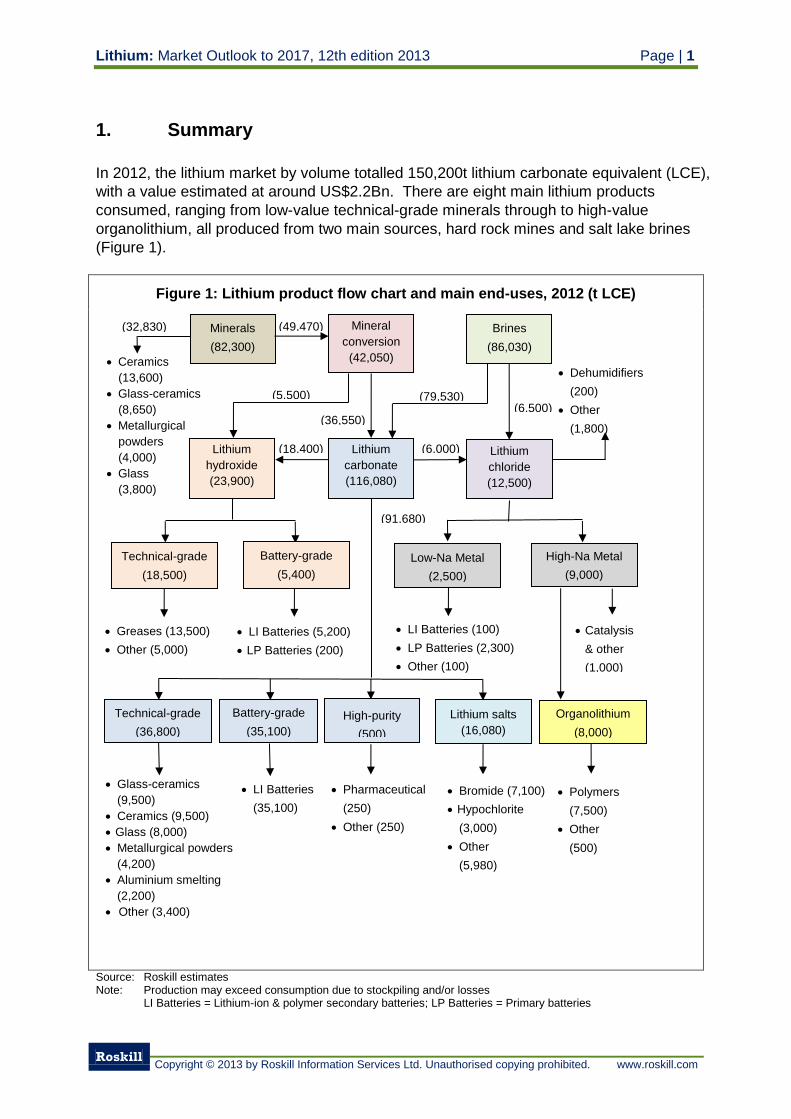

1. Summary

In 2012, the lithium market by volume totalled 150,200t lithium carbonate equivalent (LCE),

with a value estimated at around US$2.2Bn. There are eight main lithium products

consumed, ranging from low-value technical-grade minerals through to high-value

organolithium, all produced from two main sources, hard rock mines and salt lake brines

(Figure 1).

Figure 1: Lithium product flow chart and main end-uses, 2012 (t LCE)

Source: Roskill estimates Note: Production may exceed consumption due to stockpiling and/or losses LI Batteries = Lithium-ion & polymer secondary batteries; LP Batteries = Primary batteries

Minerals

(82,300)

Brines

(86,030)

Lithium

carbonate

(116,080)

Lithium

hydroxide

(23,900)

Lithium

chloride

(12,500)

Glass-ceramics

(9,500)

Ceramics (9,500)

Glass (8,000)

Metallurgical powders

(4,200)

Aluminium smelting

(2,200)

Other (3,400)

Low-Na Metal

(2,500)

Pharmaceutical

(250)

Other (250)

LI Batteries

(35,100)

Technical-grade

(36,800)

Mineral

conversion

(42,050)

Battery-grade

(35,100)

Technical-grade

(18,500)

Battery-grade

(5,400)

Greases (13,500)

Other (5,000)

LI Batteries (5,200)

LP Batteries (200)

Lithium salts

(16,080)

High-purity

(500)

Bromide (7,100)

Hypochlorite

(3,000)

Other

(5,980)

LI Batteries (100)

LP Batteries (2,300)

Other (100)

(49,470)

(6,500)

(6,000)

(79,530)

(36,550)

(5,500)

(18,400)

Organolithium

(8,000)

(91,680)

Polymers

(7,500)

Other

(500)

(32,830)

High-Na Metal

(9,000)

Catalysis

& other

(1,000)

Ceramics

(13,600)

Glass-ceramics

(8,650)

Metallurgical

powders

(4,000)

Glass

(3,800)

Dehumidifiers

(200)

Other

(1,800)

Page | 2 Lithium: Market Outlook to 2017, 12th edition 2013

Roskill

Copyright © 2013 by Roskill Information Services Ltd. Unauthorised copying prohibited. www.roskill.com

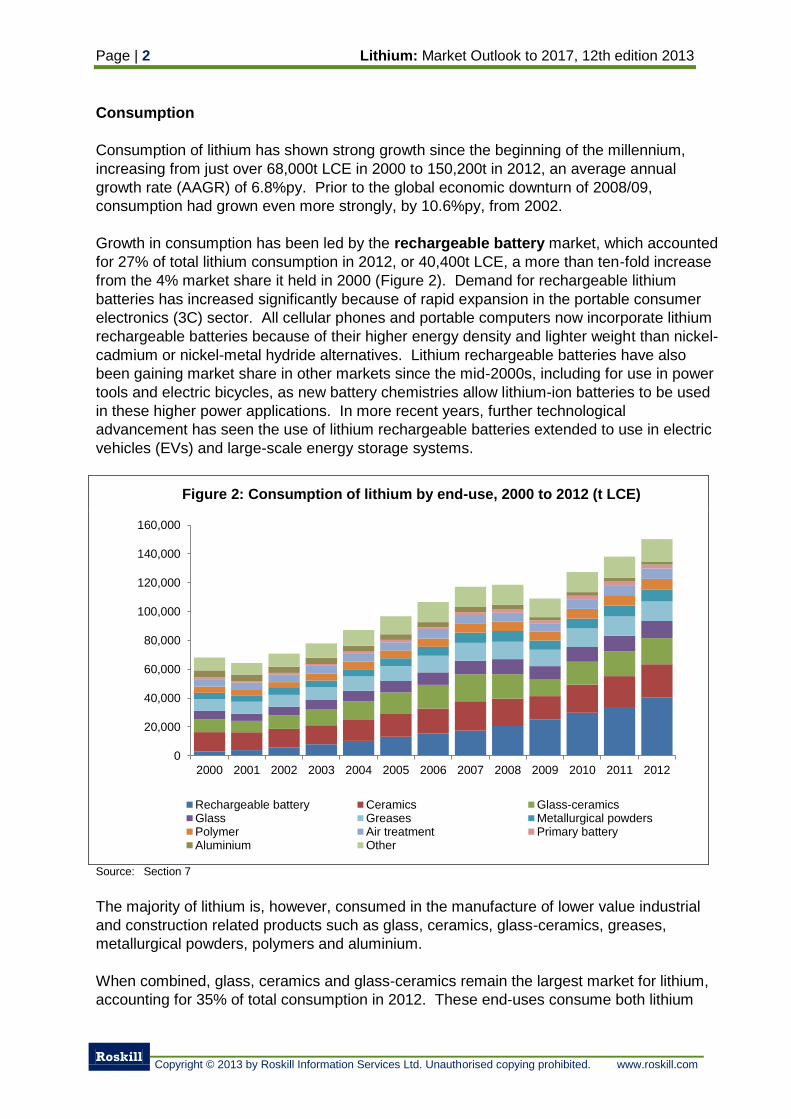

Consumption

Consumption of lithium has shown strong growth since the beginning of the millennium,

increasing from just over 68,000t LCE in 2000 to 150,200t in 2012, an average annual

growth rate (AAGR) of 6.8%py. Prior to the global economic downturn of 2008/09,

consumption had grown even more strongly, by 10.6%py, from 2002.

Growth in consumption has been led by the rechargeable battery market, which accounted

for 27% of total lithium consumption in 2012, or 40,400t LCE, a more than ten-fold increase

from the 4% market share it held in 2000 (Figure 2). Demand for rechargeable lithium

batteries has increased significantly because of rapid expansion in the portable consumer

electronics (3C) sector. All cellular phones and portable computers now incorporate lithium

rechargeable batteries because of their higher energy density and lighter weight than nickel-

cadmium or nickel-metal hydride alternatives. Lithium rechargeable batteries have also

been gaining market share in other markets since the mid-2000s, including for use in power

tools and electric bicycles, as new battery chemistries allow lithium-ion batteries to be used

in these higher power applications. In more recent years, further technological

advancement has seen the use of lithium rechargeable batteries extended to use in electric

vehicles (EVs) and large-scale energy storage systems.

Figure 2: Consumption of lithium by end-use, 2000 to 2012 (t LCE)

Source: Section 7

The majority of lithium is, however, consumed in the manufacture of lower value industrial

and construction related products such as glass, ceramics, glass-ceramics, greases,

metallurgical powders, polymers and aluminium.

When combined, glass, ceramics and glass-ceramics remain the largest market for lithium,

accounting for 35% of total consumption in 2012. These end-uses consume both lithium

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Rechargeable battery Ceramics Glass-ceramicsGlass Greases Metallurgical powdersPolymer Air treatment Primary batteryAluminium Other

Lithium: Market Outlook to 2017, 12th edition 2013 Page | 3

Roskill

Copyright © 2013 by Roskill Information Services Ltd. Unauthorised copying prohibited. www.roskill.com

compounds and lithium minerals, with an almost 50:50 share of demand between the two

products. Growth in consumption of lithium in ceramics and glass-ceramics has averaged

6.0 and 6.5%py, to 23,100t and 18,100t LCE, respectively since 2002, driven by a boom in

construction in emerging and developed economies, especially before 2008/09, and hence

increased use of construction materials and kitchen equipment. In glass, lithium lowers the

viscosity of the melt and can partially replace fluorine and other refining agents, and is

especially valued in the manufacture of flaconnage and container glass. The glass market

for lithium grew by 7.0%py between 2002 and 2012, to 11,800t LCE.

Rapid growth in construction and manufacturing output in emerging economies, particularly

China, has also led to increased lithium consumption in metallurgical powders used in the

continuous casting of steel, and in the production of lithium-based greases. Lithium

consumption in greases increased by 5.0%py between 2002 and 2012, to 13,500t LCE,

while the metallurgical powders market expanded by 6.0%py over the same period to 8,200t

LCE. The use of organolithium products for catalysing certain synthetic rubbers and

thermoplastics has also provided strong growth, of around 6.0%py, in consumption of lithium

in polymers since 2002 as demand for tyres, tubes and consumer goods increased in

emerging economies.

Lithium is added during aluminium smelting using Söderberg pot lines to reduce fluorine

emissions, as well as occasional use to decrease the melting point of alumina and raise

electrical conductivity of the bath in newer smelters using pre-baked anode pot lines. In

absorption chillers, lithium bromide is used as the absorption medium to produce chilled air

from waste heat in large commercial and industrial complexes. The air treatment market

for lithium also includes desiccant dehumidifiers and air purification systems. While

consumption of lithium in aluminium has declined by 7.0%py to 2,200t LCE since 2002, as outdated Söderberg smelters are decommissioned or replaced, the air treatment market has

grown by 4.0%py to 7,400t LCE, again largely due to emerging economy industrialisation.

The primary battery industry has witnessed growth, albeit on a much smaller scale than for

rechargeable batteries (7.0%py compared to 21.5%py) since 2002 to total 2,500t LCE.

Primary batteries are used for memory back-up in 3C electronics and remote monitoring

systems through to industrial equipment.

China is the world’s largest consumer of lithium, accounting for 35% of consumption in 2012,

with domestic demand having grown three-fold since 2002, to 53,000t LCE. Europe

represented a further 24% of consumption followed by Japan and South Korea. South

Korea and China are the dominant rechargeable battery and battery material producers,

hence their consumption has increased rapidly during the mid-2000s on increased

rechargeable battery output. Japan is also a major battery material producer, but has faced

growing competition from its Asian neighbours. China, Europe and North America consume

lithium in the manufacture of industrial and construction –related products, such as

ceramics, glass-ceramics, greases, polymers and aluminium.

The surge in consumption of lithium in rechargeable batteries in the 2000s has led to a

sharp rise in battery-grade lithium carbonate, and battery-grade lithium hydroxide,

consumption, the latter growing particularly strongly since 2008. Together, these two

products account for a similar volume (40,300t LCE) of consumption to technical-grade

lithium carbonate (40,000t LCE). Lithium mineral use is also significant, at over 30,000t

Page | 4 Lithium: Market Outlook to 2017, 12th edition 2013

Roskill

Copyright © 2013 by Roskill Information Services Ltd. Unauthorised copying prohibited. www.roskill.com

LCE, followed by technical-grade lithium hydroxide at 18,500t LCE. Other lithium products

such as butylithium, lithium bromide and lithium metal together account for the remaining

20% of lithium consumption by product.

Production

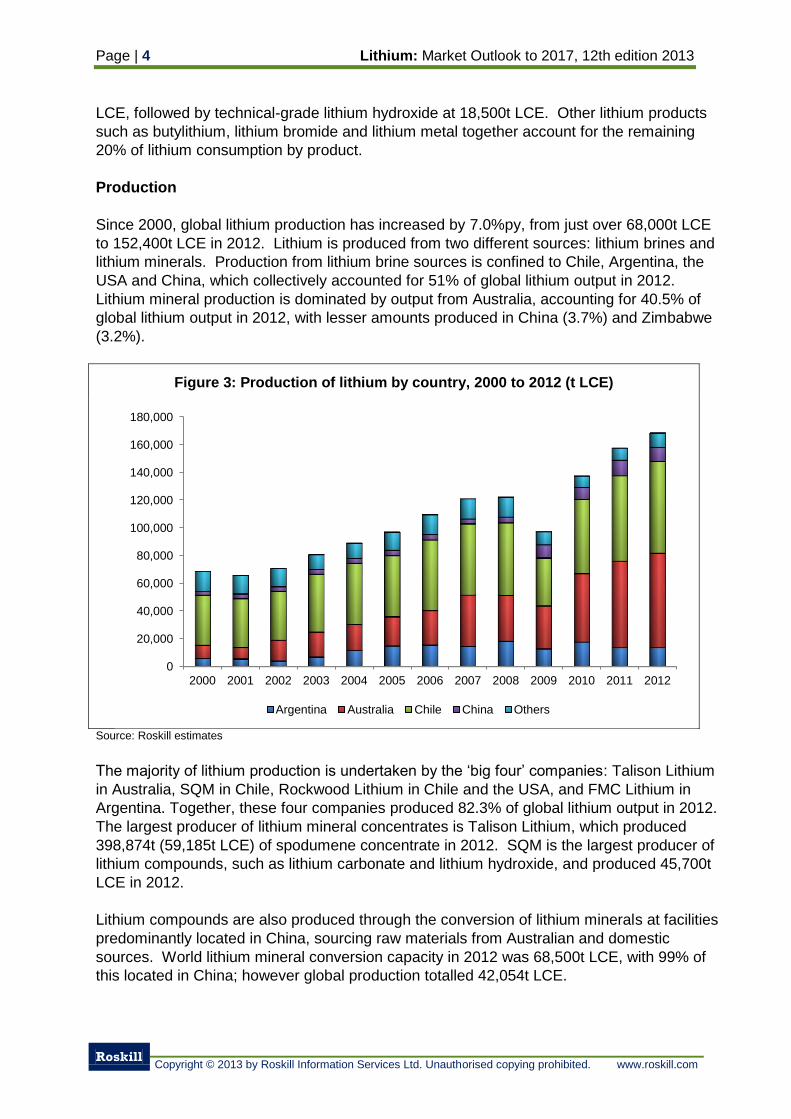

Since 2000, global lithium production has increased by 7.0%py, from just over 68,000t LCE

to 152,400t LCE in 2012. Lithium is produced from two different sources: lithium brines and

lithium minerals. Production from lithium brine sources is confined to Chile, Argentina, the

USA and China, which collectively accounted for 51% of global lithium output in 2012.

Lithium mineral production is dominated by output from Australia, accounting for 40.5% of

global lithium output in 2012, with lesser amounts produced in China (3.7%) and Zimbabwe

(3.2%).

Figure 3: Production of lithium by country, 2000 to 2012 (t LCE)

Source: Roskill estimates

The majority of lithium production is undertaken by the ‘big four’ companies: Talison Lithium

in Australia, SQM in Chile, Rockwood Lithium in Chile and the USA, and FMC Lithium in

Argentina. Together, these four companies produced 82.3% of global lithium output in 2012.

The largest producer of lithium mineral concentrates is Talison Lithium, which produced

398,874t (59,185t LCE) of spodumene concentrate in 2012. SQM is the largest producer of

lithium compounds, such as lithium carbonate and lithium hydroxide, and produced 45,700t

LCE in 2012.

Lithium compounds are also produced through the conversion of lithium minerals at facilities

predominantly located in China, sourcing raw materials from Australian and domestic

sources. World lithium mineral conversion capacity in 2012 was 68,500t LCE, with 99% of

this located in China; however global production totalled 42,054t LCE.

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Argentina Australia Chile China Others

Lithium: Market Outlook to 2017, 12th edition 2013 Page | 5

Roskill

Copyright © 2013 by Roskill Information Services Ltd. Unauthorised copying prohibited. www.roskill.com

The production of downstream lithium chemicals and lithium metal is undertaken by a

number of companies in China. Outside of China, Rockwood Lithium and FMC Lithium are

the largest producers of lithium chemicals and metal, from facilities in Germany, the USA,

Taiwan, India, the UK and Japan.

Trade

As the main centres of lithium production are in countries that have little domestic

consumption (with the exception of China), trade in lithium is significant, with world exports

reaching 79,064t (gross weight) of lithium carbonate, 21,109t (gross weight) of lithium

hydroxide and 8,860t (gross weight) lithium chloride in 2012. The largest exporter of lithium

compounds in 2012 was Chile, which exported 55,899t (gross weight) of lithium carbonate,

6,711t (gross weight) of lithium hydroxide and 4,123t (gross weight) of lithium chloride in

2012, mainly to Asia, the USA and Europe. Lithium minerals are predominantly exported by

Australia and Zimbabwe, to markets in China, Japan, Europe and the USA.

Prices

The concentration of lithium production among a small number of producers means pricing

is very competitive. Producers negotiate prices with individual consumers and price

information is rarely reported, particularly for downstream lithium chemicals.

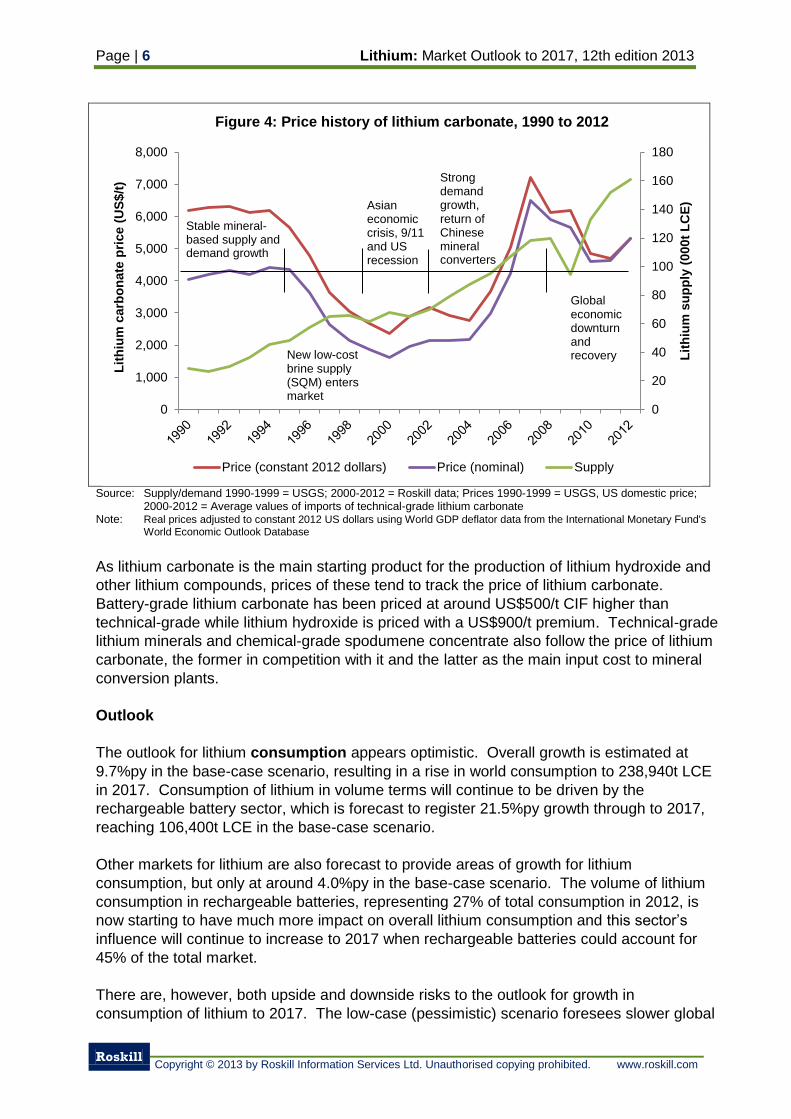

The entry of SQM into the lithium market in 1996 resulted in a fundamental restructuring of

the industry. Between 1995 and 1999, average technical-grade lithium carbonate prices

plunged from US$4,400/t CIF (US$6,175/t in constant 2012 dollars) to US$1,625/t CIF

(US$2,350 in constant 2012 dollars), causing the closure of mineral-based operations in

China, Russia and the USA.

In the mid-2000s, the combination of accelerating consumption and a lag in the response

time of brine producers to increase output (due to the time taken to concentrate brine by

natural evaporation) led to rising prices as higher-cost (>US$4,000/t LCE compared to

<US$3,000/t for brine operations) lithium mineral conversion plants re-started to fulfil market

requirements.

Prices peaked in 2007 at just over US$6,500/t CIF (US$7,230/t in constant 2012 dollars) but

then gradually fell as the global economic downturn of 2008/09 reversed the tightness in

supply leading up to the peak.

Page | 6 Lithium: Market Outlook to 2017, 12th edition 2013

Roskill

Copyright © 2013 by Roskill Information Services Ltd. Unauthorised copying prohibited. www.roskill.com

Figure 4: Price history of lithium carbonate, 1990 to 2012

Source: Supply/demand 1990-1999 = USGS; 2000-2012 = Roskill data; Prices 1990-1999 = USGS, US domestic price;

2000-2012 = Average values of imports of technical-grade lithium carbonate Note: Real prices adjusted to constant 2012 US dollars using World GDP deflator data from the International Monetary Fund's

World Economic Outlook Database

As lithium carbonate is the main starting product for the production of lithium hydroxide and

other lithium compounds, prices of these tend to track the price of lithium carbonate.

Battery-grade lithium carbonate has been priced at around US$500/t CIF higher than

technical-grade while lithium hydroxide is priced with a US$900/t premium. Technical-grade

lithium minerals and chemical-grade spodumene concentrate also follow the price of lithium

carbonate, the former in competition with it and the latter as the main input cost to mineral

conversion plants.

Outlook

The outlook for lithium consumption appears optimistic. Overall growth is estimated at

9.7%py in the base-case scenario, resulting in a rise in world consumption to 238,940t LCE

in 2017. Consumption of lithium in volume terms will continue to be driven by the

rechargeable battery sector, which is forecast to register 21.5%py growth through to 2017,

reaching 106,400t LCE in the base-case scenario.

Other markets for lithium are also forecast to provide areas of growth for lithium

consumption, but only at around 4.0%py in the base-case scenario. The volume of lithium

consumption in rechargeable batteries, representing 27% of total consumption in 2012, is

now starting to have much more impact on overall lithium consumption and this sector’s

influence will continue to increase to 2017 when rechargeable batteries could account for

45% of the total market.

There are, however, both upside and downside risks to the outlook for growth in

consumption of lithium to 2017. The low-case (pessimistic) scenario foresees slower global

0

20

40

60

80

100

120

140

160

180

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Lit

hiu

m s

up

ply

(000t

LC

E)

Lit

hiu

m c

arb

on

ate

pri

ce (

US

$/t

)

Price (constant 2012 dollars) Price (nominal) Supply

Stable mineral-based supply and demand growth

New low-cost brine supply (SQM) enters market

Asian economic crisis, 9/11 and US recession

Strong demand growth, return of Chinese mineral converters

Global economic downturn and recovery

Lithium: Market Outlook to 2017, 12th edition 2013 Page | 7

Roskill

Copyright © 2013 by Roskill Information Services Ltd. Unauthorised copying prohibited. www.roskill.com

economic growth affecting demand for basic products like ceramics, glass, aluminium, steel

and rubber, as well as lower demand for portable consumer electronics and delays in the

introduction of lithium battery powered EVs. In this scenario, growth in consumption of

lithium is forecast at 4.5%py to reach just under 187,000t LCE by 2017. Meanwhile, in the

high-case (optimistic) scenario, growth in consumption of lithium is forecast to increase by

15.7%py to reach just under 313,000t LCE by 2017. The optimistic scenario is based on

stronger global economic growth, and surging demand for lithium secondary batteries in

EVs.

Installed capacity for lithium production at end-2012 (279,000t LCE) is sufficient to meet

forecast demand to 2017 in the base-case demand scenario (238,940t LCE). Installed

capacity for lithium compound production, however, is only 190,650t LCE (comprising

122,150t LCE of brine and 68,500t LCE of mineral conversion capacity), versus projected

consumption of compounds at around 200,000t LCE. New or expanded capacity is

therefore required to satisfy future demand for lithium compounds (around 200,000t LCE) in

the base-case demand scenario.

Two new projects (Canada Lithium, 19,000tpy LCE and Orocobre, 17,000tpy LCE) are

expected to be commissioned in 2013 and 2014 meaning that capacity should be more than

sufficient to meet market requirements to 2017. In addition to these new projects, however,

FMC Lithium in Argentina is ramping up its 7,000tpy LCE expansion in mid-2013 and

Rockwood Lithium is expanding its operations in Chile by 20,000tpy LCE by late-2013.

SQM has also stated its intention to increase capacity to 60,000tpy LCE. Chinese mineral

converters have also recently expanded their plants (Sichuan Tianqi by 5,000tpy LCE and

Ganfeng Lithium by 10,000tpy LCE), utilising increased availability of spodumene from

Talison Lithium’s newly (2012) expanded chemical-grade spodumene capacity in Australia.

From a situation of relative market balance in 2011/12, following re-stocking in 2010 after

the global economic downturn, 2013 and 2014 are likely to witness supply-side pressure on

pricing. Nevertheless, there is insufficient low-cost capacity entering the market to displace

all of the high-cost mineral conversion capacity. The lithium market will therefore continue to

be reliant on supplies of lithium compounds from higher-cost producers in China through to

2017, and this effectively puts a floor under pricing. Retaining some higher-cost production

in the supply chain is also advantageous for lower-cost producers, because despite

potentially losing some market share its means low-cost producers can operate at very

healthy margins on commodity lithium products (carbonate and hydroxide in particular).

Lithium carbonate prices appear to have reached a floor of US$4,600/t CIF for technical-

grade and US$4,830/t CIF for battery-grade in 2011. Cost inflation for both brine-based and

mineral-based producers is forecast at 4.5%py and will be the main underlying driver for

increased prices in the long-term. Assuming a 4.5%py rise in operating costs, the floor price

in 2017 would be US$6,000/t CIF (US$5,702/t in constant 2012 dollars) (Table 241). This

forms the basis for the low-case scenario for pricing.

A US$250-500/t CIF (~10%) increase is considered likely in the base-case scenario for

2013, given the 20% increase already pushed through for 2012 contracts and increased

supply entering the market during 2013. Under the base-case scenario, average prices for

technical-grade lithium carbonate are expected to rise by 4.5%py to around US$6,900/t CIF

(US$6,558/t in constant 2012 dollars) in 2017.

Page | 8 Lithium: Market Outlook to 2017, 12th edition 2013

Roskill

Copyright © 2013 by Roskill Information Services Ltd. Unauthorised copying prohibited. www.roskill.com

With current and forecast capacity more than sufficient to meet demand, it is unlikely prices

will test 2007 highs of US$6,500/t CIF, but if demand was to accelerate as per the optimistic

growth forecast (15.8%py, to 312,725t LCE by 2017) then prices would likely rise on

tightening capacity. In this scenario, prices are likely to trend around US$800-900/t above

the base-case to reach US$7,800/t by 2017.

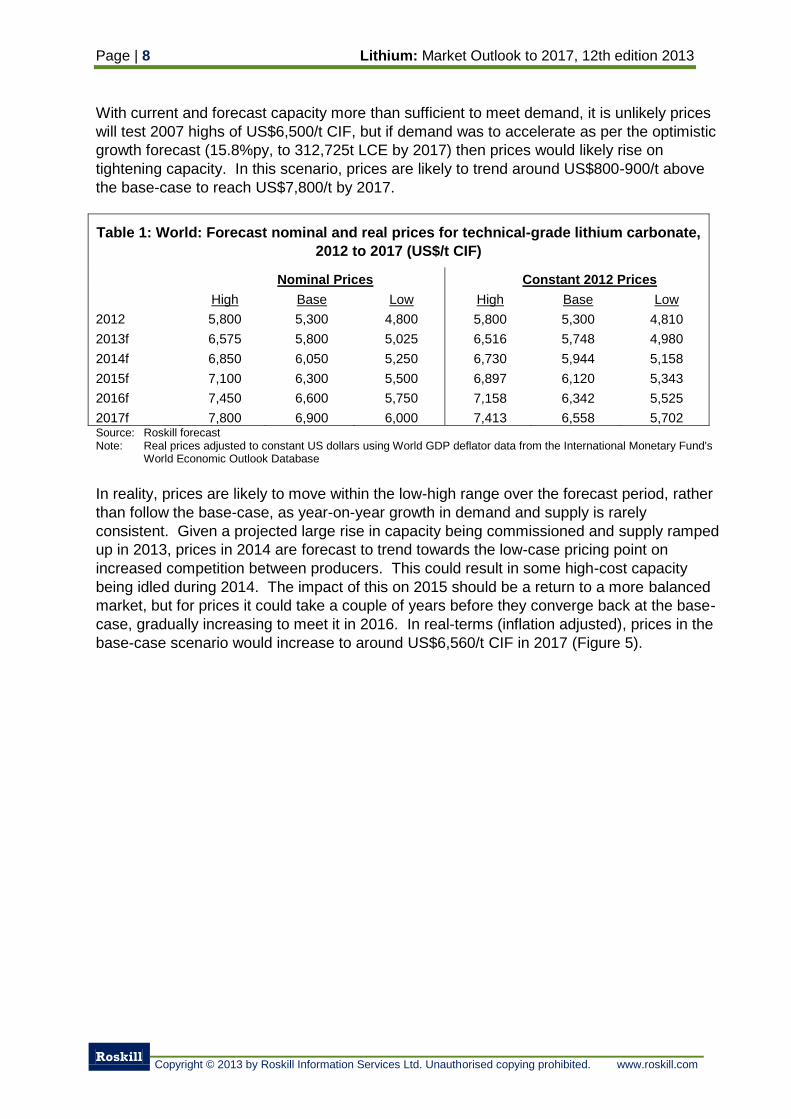

Table 1: World: Forecast nominal and real prices for technical-grade lithium carbonate,

2012 to 2017 (US$/t CIF)

Nominal Prices Constant 2012 Prices

High Base Low High Base Low

2012 5,800 5,300 4,800 5,800 5,300 4,810

2013f 6,575 5,800 5,025 6,516 5,748 4,980

2014f 6,850 6,050 5,250 6,730 5,944 5,158

2015f 7,100 6,300 5,500 6,897 6,120 5,343

2016f 7,450 6,600 5,750 7,158 6,342 5,525

2017f 7,800 6,900 6,000 7,413 6,558 5,702 Source: Roskill forecast Note: Real prices adjusted to constant US dollars using World GDP deflator data from the International Monetary Fund's

World Economic Outlook Database

In reality, prices are likely to move within the low-high range over the forecast period, rather

than follow the base-case, as year-on-year growth in demand and supply is rarely

consistent. Given a projected large rise in capacity being commissioned and supply ramped

up in 2013, prices in 2014 are forecast to trend towards the low-case pricing point on

increased competition between producers. This could result in some high-cost capacity

being idled during 2014. The impact of this on 2015 should be a return to a more balanced

market, but for prices it could take a couple of years before they converge back at the base-

case, gradually increasing to meet it in 2016. In real-terms (inflation adjusted), prices in the

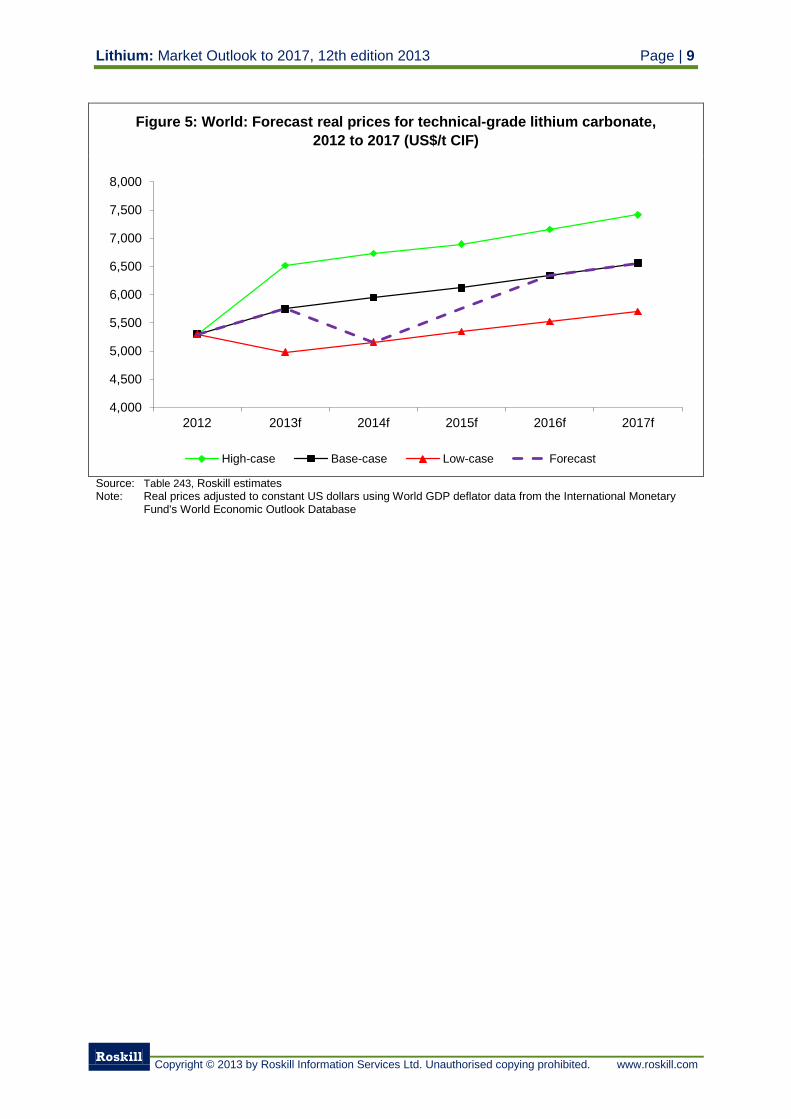

base-case scenario would increase to around US$6,560/t CIF in 2017 (Figure 5).

Lithium: Market Outlook to 2017, 12th edition 2013 Page | 9

Roskill

Copyright © 2013 by Roskill Information Services Ltd. Unauthorised copying prohibited. www.roskill.com

Figure 5: World: Forecast real prices for technical-grade lithium carbonate,

2012 to 2017 (US$/t CIF)

Source: Table 243, Roskill estimates Note: Real prices adjusted to constant US dollars using World GDP deflator data from the International Monetary

Fund's World Economic Outlook Database

4,000

4,500

5,000

5,500

6,000

6,500

7,000

7,500

8,000

2012 2013f 2014f 2015f 2016f 2017f

High-case Base-case Low-case Forecast

Page | 10 Lithium: Market Outlook to 2017, 12th edition 2013

Roskill

Copyright © 2013 by Roskill Information Services Ltd. Unauthorised copying prohibited. www.roskill.com

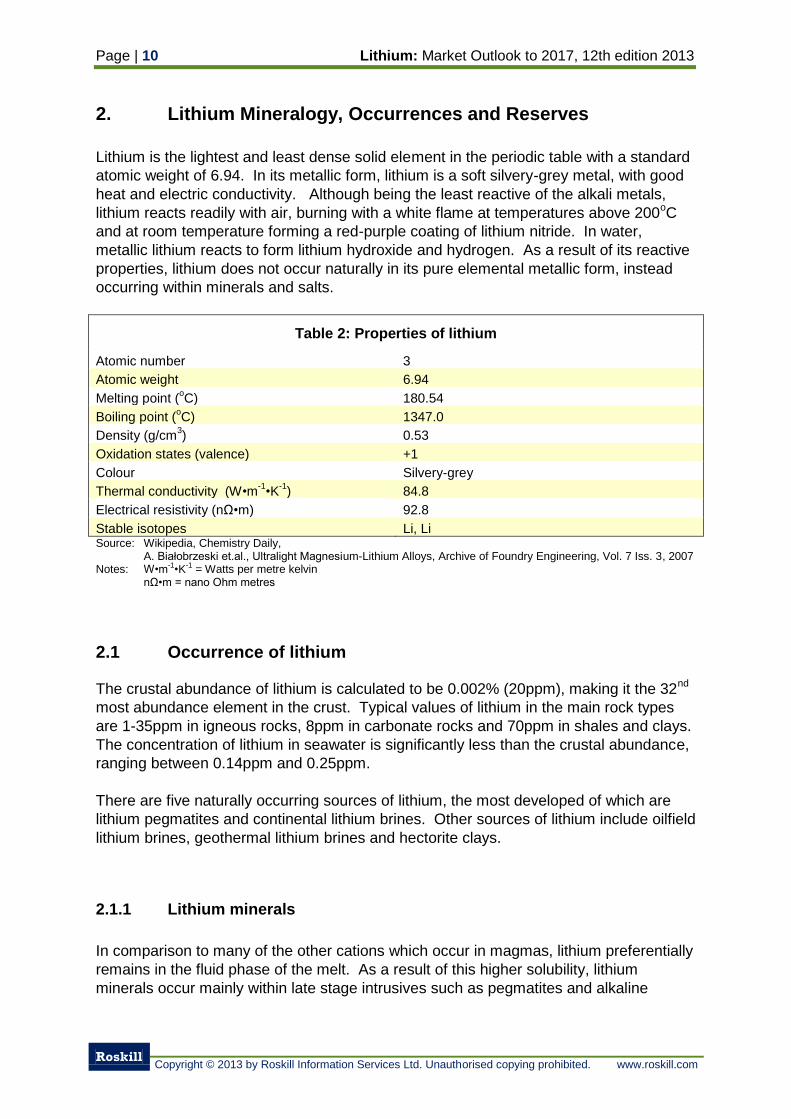

2. Lithium Mineralogy, Occurrences and Reserves

Lithium is the lightest and least dense solid element in the periodic table with a standard

atomic weight of 6.94. In its metallic form, lithium is a soft silvery-grey metal, with good

heat and electric conductivity. Although being the least reactive of the alkali metals,

lithium reacts readily with air, burning with a white flame at temperatures above 200oC

and at room temperature forming a red-purple coating of lithium nitride. In water,

metallic lithium reacts to form lithium hydroxide and hydrogen. As a result of its reactive

properties, lithium does not occur naturally in its pure elemental metallic form, instead

occurring within minerals and salts.

Table 2: Properties of lithium

Atomic number 3

Atomic weight 6.94

Melting point (oC) 180.54

Boiling point (oC) 1347.0

Density (g/cm3) 0.53

Oxidation states (valence) +1

Colour Silvery-grey

Thermal conductivity (W•m-1

•K-1

) 84.8

Electrical resistivity (nΩ•m) 92.8

Stable isotopes Li, Li Source: Wikipedia, Chemistry Daily,

A. Białobrzeski et.al., Ultralight Magnesium-Lithium Alloys, Archive of Foundry Engineering, Vol. 7 Iss. 3, 2007 Notes: W•m-1•K-1 = Watts per metre kelvin nΩ•m = nano Ohm metres

2.1 Occurrence of lithium

The crustal abundance of lithium is calculated to be 0.002% (20ppm), making it the 32nd

most abundance element in the crust. Typical values of lithium in the main rock types

are 1-35ppm in igneous rocks, 8ppm in carbonate rocks and 70ppm in shales and clays.

The concentration of lithium in seawater is significantly less than the crustal abundance,

ranging between 0.14ppm and 0.25ppm.

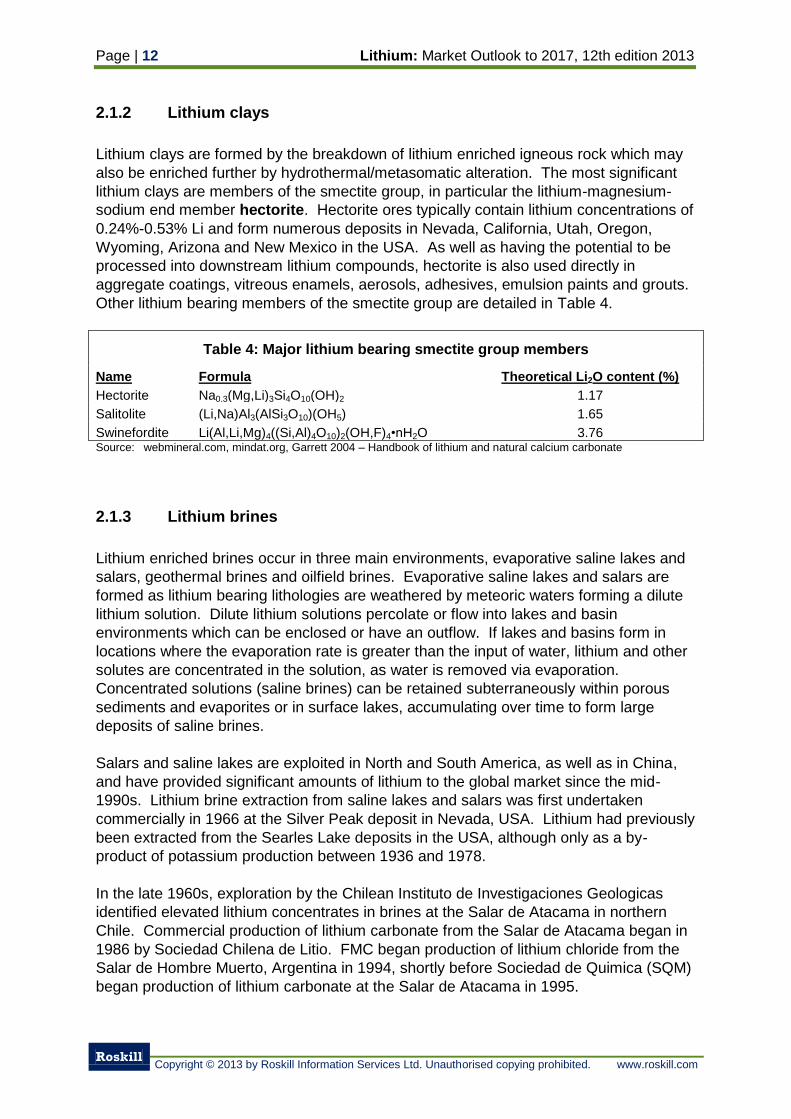

There are five naturally occurring sources of lithium, the most developed of which are

lithium pegmatites and continental lithium brines. Other sources of lithium include oilfield

lithium brines, geothermal lithium brines and hectorite clays.

2.1.1 Lithium minerals

In comparison to many of the other cations which occur in magmas, lithium preferentially

remains in the fluid phase of the melt. As a result of this higher solubility, lithium

minerals occur mainly within late stage intrusives such as pegmatites and alkaline

Lithium: Market Outlook to 2017, 12th edition 2013 Page | 11

Roskill

Copyright © 2013 by Roskill Information Services Ltd. Unauthorised copying prohibited. www.roskill.com

intrusives. Lithium minerals also occur within hydrothermal deposits which have been

derived from magmatic fluids.

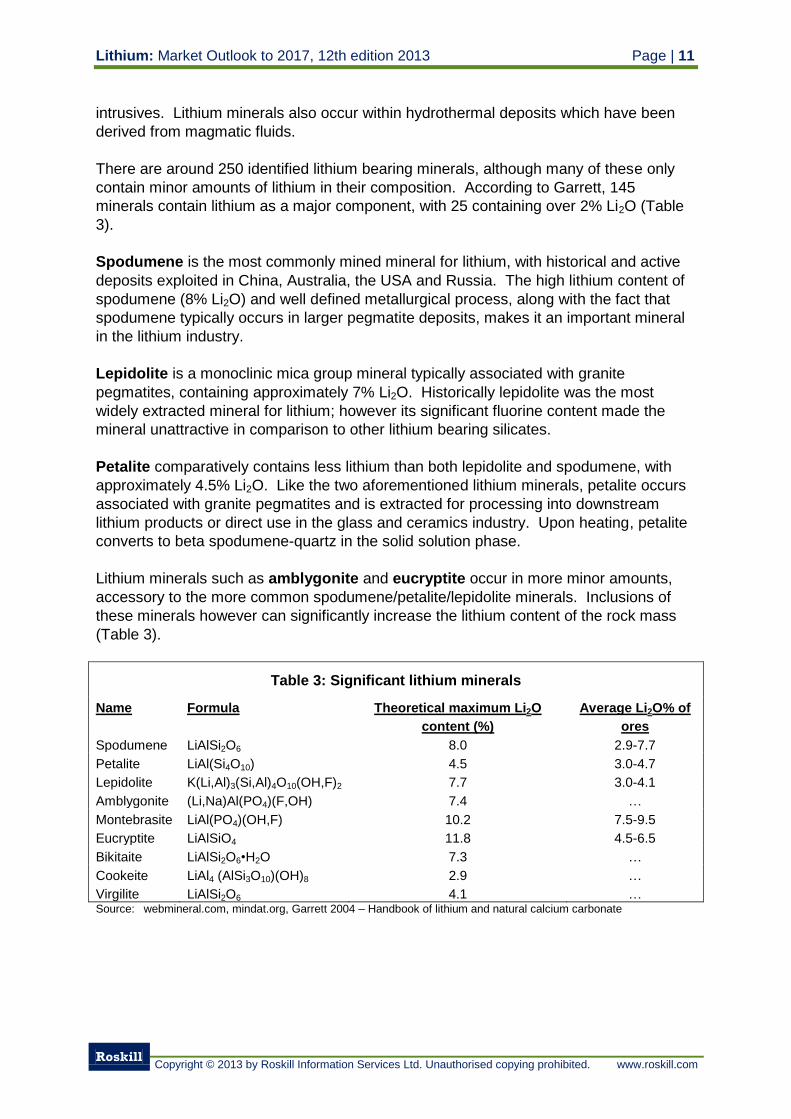

There are around 250 identified lithium bearing minerals, although many of these only

contain minor amounts of lithium in their composition. According to Garrett, 145

minerals contain lithium as a major component, with 25 containing over 2% Li2O (Table

3).

Spodumene is the most commonly mined mineral for lithium, with historical and active

deposits exploited in China, Australia, the USA and Russia. The high lithium content of

spodumene (8% Li2O) and well defined metallurgical process, along with the fact that

spodumene typically occurs in larger pegmatite deposits, makes it an important mineral

in the lithium industry.

Lepidolite is a monoclinic mica group mineral typically associated with granite

pegmatites, containing approximately 7% Li2O. Historically lepidolite was the most

widely extracted mineral for lithium; however its significant fluorine content made the

mineral unattractive in comparison to other lithium bearing silicates.

Petalite comparatively contains less lithium than both lepidolite and spodumene, with

approximately 4.5% Li2O. Like the two aforementioned lithium minerals, petalite occurs

associated with granite pegmatites and is extracted for processing into downstream